Bahasa

Halaman

Hukum

Going Global: Predicting the Next Tight Oil Revolution

IHS CERA

Going Global: Predicting the Next

Tight Oil Revolution A comprehensive screening of tight oil opportunities beyond North America

Going Global: Predicting the Next Tight Oil Revolution

What is it?

The Going Global: Predicting the Next Tight Oil Revolution is a

Multiclient Study that will screen 148 potential tight oil plays

around the world, providing a consistent framework of data and

analysis that can be used to prioritize areas of possible investment

and opportunity

The Study will leverage the full breadth of IHS resources globally

including IHS databases and subsurface experts

Study opportunity to interact with IHS experts in workshops and

conference calls

Completed by May 2013

2

Going Global: Predicting the Next Tight Oil Revolution

Global Screening builds on IHS Experience

2010 2011 2012 2013 Q1

• First authoritative

study at play level of

unconventional gas

potential in North

America

• Integrated study

(from geological

screening to market

impact) of shale and

CBM potential in key

markets

• Europe

• East Europe

• South America

• Australia

• India

• China

Cream of the Crop

Unconventional Frontier: The Potential for

Gas Shale and CBM

Prospects North

American Tight

Oil

• First authoritative

study at play level of

Tight oil potential in

North America

• Covering 11

maturing plays and

17 emerging plays in

USA and Canada

Going Global:

Predicting the Next

Tight Oil Revolution

• Screening study of

potential tight oil

opportunities beyond

North America

Going Global: Predicting the Next Tight Oil Revolution

IHS Credentials and Sources

A team of regionally based basin/geological researchers will work

with several resources to create the analytical background for

international screening of tight oil plays

• IHS Upstream Researchers

• IHS International Exploration and Production Database — IRIS21.

This is the most comprehensive and reliable data set of E&P industry

professionals available, featuring a fully integrated data area with over

13,000 E&P data attributes

• IHS Global Exploration and Production Services (GEPS). This ongoing

service provides a worldwide picture of E&P activity

• IHS Petroleum Economics and Policy Solutions (PEPS). This ongoing

resource for the oil and gas industry reports on political, contractual,

environmental, and legal policies around the globe

• IHS Background Sources. Include several reports on worldwide basins

made as Multiclient Studies (i.e. Petroconsultants, IEDS, IHS)

4

• Databases and

services leverage 50

years of information

gathering and

analysis

• Locally based experts

keep databases

updated

• Publicly available

information

• Academic

publications

• Scientific reports

• All these resources

are leveraged by the

global tight oil team

Going Global: Predicting the Next Tight Oil Revolution

A Global Revolution Starts?

• The application of horizontal drilling technology

and hydraulic fracturing to tight oil formations

has led to an oil supply renaissance in North

America, reversing a two-decade production

decline

• Using production and well data, IHS CERA has

recently concluded an authoritative assessment

of tight oil prospects in North America for 27

plays*. IHS CERA estimates that tight oil will

add over 40 billion barrels to recoverable

Supply- and the global prospects could be

almost 500 billion barrels- but where, and

when?

• Going Global: Predicting the Next Tight Oil

Revolution will help companies screen and

indentify opportunities in regions outside North

America.

* Source: IHS CERA North America Tight Oil Multiclient Study

North America Tight Oil Play Areas

5

Going Global: Predicting the Next Tight Oil Revolution

North American Supply

North America’s Tight Oil Revolution will go global—Why?

– Tight Oil Supply Outlook confirms 40 billion barrels of recoverable oil by 2035

– U.S. and Canada will ramp up to and sustain an increase of 4.5 million barrels of

oil/condensate per day between 2018 and 2033

– Recoverable dry gas associated with Tight Oil plays is about 270 TCF

– Recoverable NGLs will increase to 4 million barrels per day by 2021 and exceed 5

million by 2035—a recoverable total of 36 billion barrels

– Total hydrocarbons production could be 9 million barrels per day by the end of the

decade

Implications:

– U.S Oil demand is about 18 million barrels per day with current imports at 8.8 million

per day—i.e. 48 percent of demand. Tight Oil almost cuts the imports in half!

– Add Canadian oil sands production to current U.S. imports from Canada and North

America becomes energy self sufficient

– Global rebalance of supply, investment and economies.

– Inspires tight oil exploitation worldwide—BUT where is the best potential?

Going Global: Predicting the Next Tight Oil Revolution

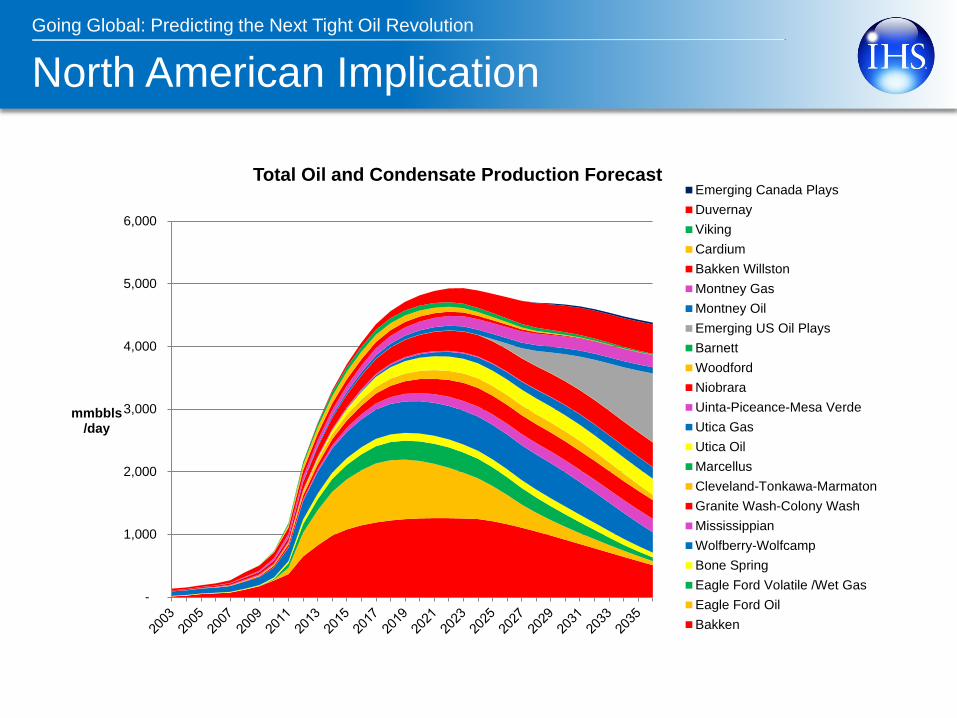

North American Implication

-

1,000

2,000

3,000

4,000

5,000

6,000

mmbbls /day

Total Oil and Condensate Production Forecast Emerging Canada Plays

Duvernay

Viking

Cardium

Bakken Willston

Montney Gas

Montney Oil

Emerging US Oil Plays

Barnett

Woodford

Niobrara

Uinta-Piceance-Mesa Verde

Utica Gas

Utica Oil

Marcellus

Cleveland-Tonkawa-Marmaton

Granite Wash-Colony Wash

Mississippian

Wolfberry-Wolfcamp

Bone Spring

Eagle Ford Volatile /Wet Gas

Eagle Ford Oil

Bakken

Going Global: Predicting the Next Tight Oil Revolution

Going Global: Predicting the Next

Tight Oil Revolution

A screening study

Going Global: Predicting the Next Tight Oil Revolution

Study Scope

The Study will provide members with a toolkit to

screen and prioritize possible Tight Oil plays. The

Study will also provide a more detailed analysis of

a smaller set of high ranking opportunities.

Study members will be able to:

– Identify potential tight oil areas and

analyze key parameters

– Understand main geological risks

for key areas

– View general information about above-

ground issues related to tight oil

– Assessment of commercial

characteristics of top opportunities

9

PHASE 3: OPPORTUNITY ANALYSIS

For top ranking opportunities

General play information

Distribution maps

Commercial characteristics and key above ground

parameters and risks

PHASE 2: OPPORTUNITY RISKING AND RANKING

Rank opportunities based parameters established in

conjunction with members

PHASE 1: GLOBAL SCREENING

Identify major potential tight oil plays outside

North America

Collection of key data per tight oil opportunity

Going Global: Predicting the Next Tight Oil Revolution

Geographic Scope

10

South America

14 play areas

Africa

15 play areas

Europe

27 play areas

CIS

13 play areas

South Asia

20 play areas

North Asia

26 play areas

Australasia

17 play areas

Going Global: Predicting the Next Tight Oil Revolution

General Statistics

• Total of 95 shale oil and 53 tight reservoirs plays analyzed

11

Number of Tight Reservoir Plays by Lithology

Carbonate

Mudstone

Sand/siltstone

Conglomerate

Granite

Going Global: Predicting the Next Tight Oil Revolution

Depositional Environments

Alluvial-fluvial

Lacustrine

Lacustrine-fluvial

Fluvial Delta Plain

Transition Zone

Restricted Marine

Shallow Marine

Open Marine

Deep Marine

Going Global: Predicting the Next Tight Oil Revolution

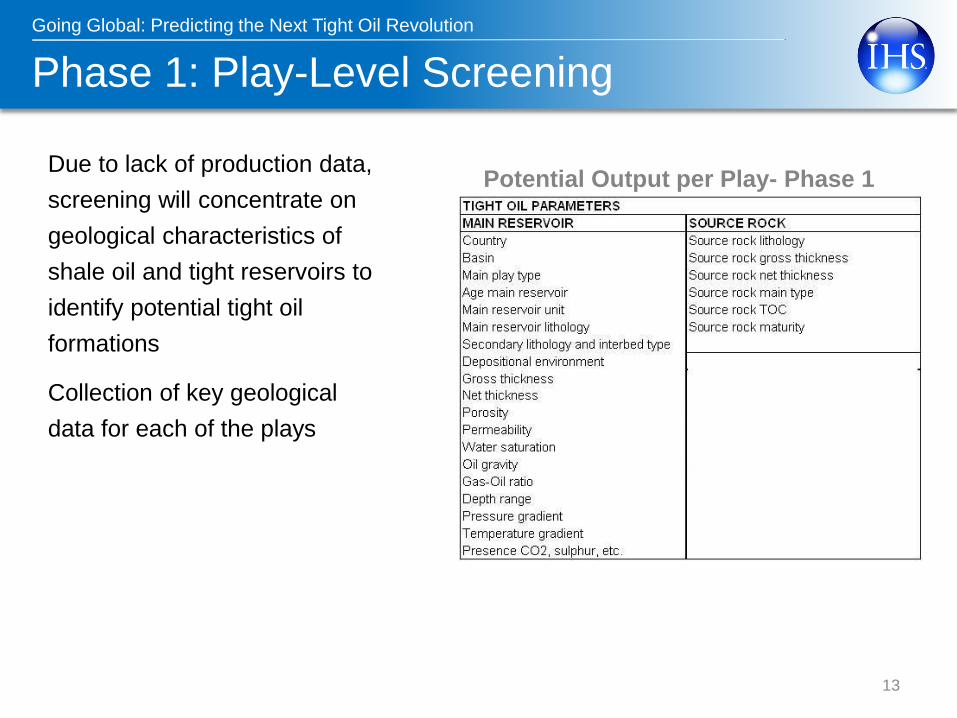

Phase 1: Play-Level Screening

Due to lack of production data,

screening will concentrate on

geological characteristics of

shale oil and tight reservoirs to

identify potential tight oil

formations

Collection of key geological

data for each of the plays

13

Potential Output per Play- Phase 1

Going Global: Predicting the Next Tight Oil Revolution

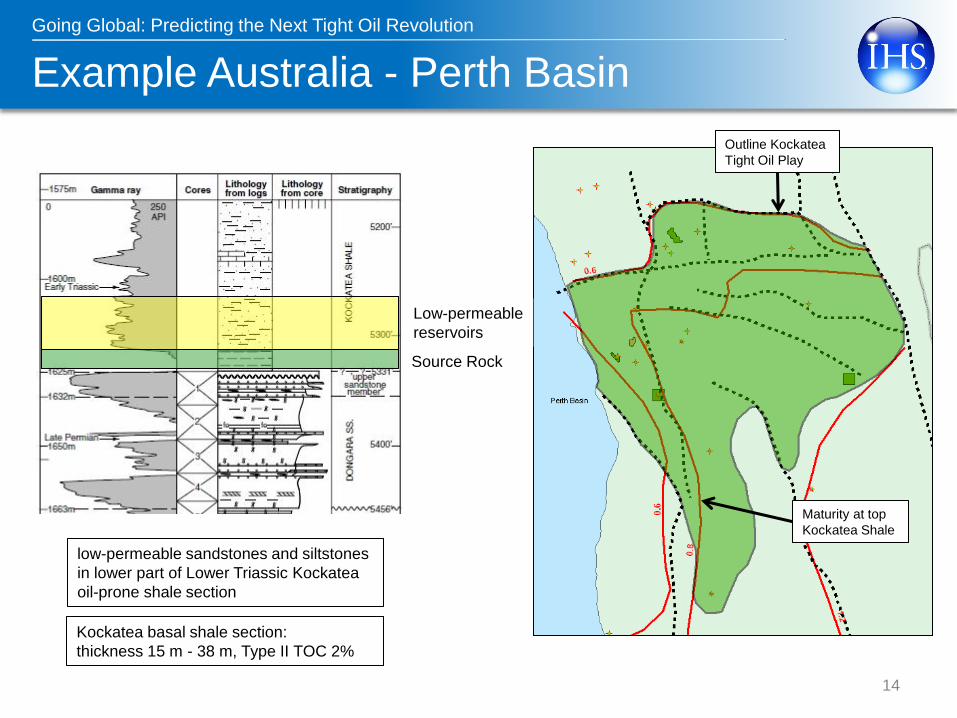

Example Australia - Perth Basin

14

Maturity at top

Kockatea Shale

Outline Kockatea

Tight Oil Play

low-permeable sandstones and siltstones

in lower part of Lower Triassic Kockatea

oil-prone shale section

Kockatea basal shale section:

thickness 15 m - 38 m, Type II TOC 2%

Source Rock

Low-permeable

reservoirs

Going Global: Predicting the Next Tight Oil Revolution

Phase 2 and 3

Phase 2: Tight Oil Play Risk and Ranking

– IHS will risk potential tight oil plays according to a basic set

of criteria collected in Phase 1

– Final output of this phase will be a catalogue of plays and a

ranking of potential tight oil plays with the possibility for

Study members to re-arrange the risking and ranking

Phase 3: Opportunity analysis

– For a limited number (20-30) of the most attractive tight oil

play areas additional information will be provided: • A short geological description characterizing the play and indication of

resource size

• Summary of infrastructure, license and fiscal terms, business environment

• A summary of above ground issues in the form of a matrix highlighting areas with opportunity and/or with potential above ground challenges

15

Going Global: Predicting the Next Tight Oil Revolution

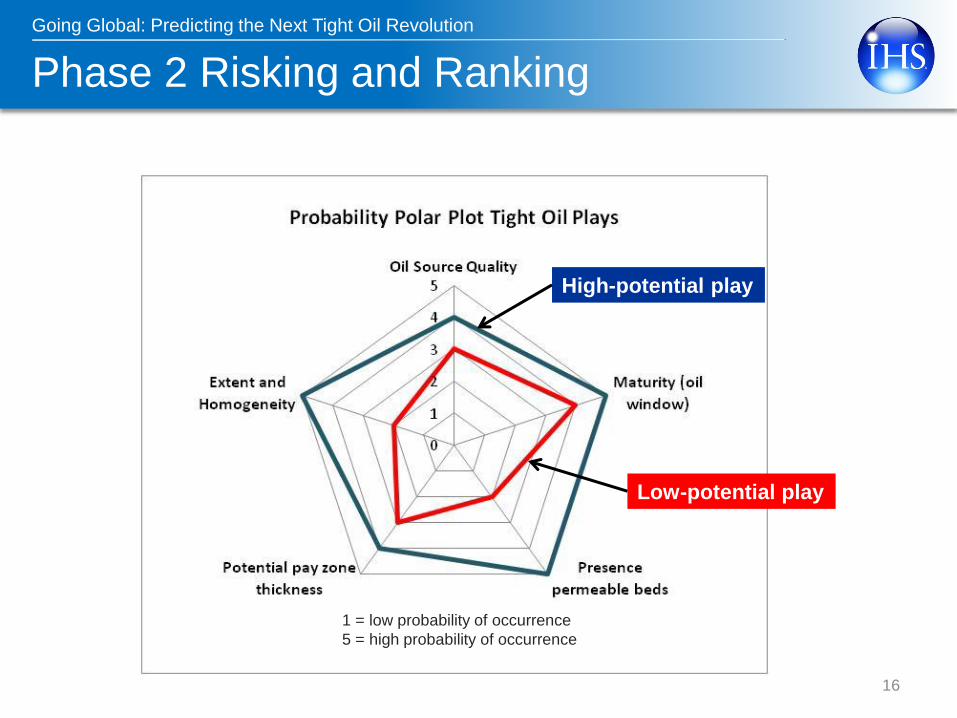

Phase 2 Risking and Ranking

16

1 = low probability of occurrence

5 = high probability of occurrence

Low-potential play

High-potential play

Going Global: Predicting the Next Tight Oil Revolution

Phase 2 Score Card

17

Weight 1.2 1.2 0.8 0.8 1.1 1.1 0.8 1.0 1.3 1.4 0.7 0.4 1.2

Information

quality

Geology

Information

quality

Geochem

Source/

Reservoir

Thickness

Source/

Reservoir

Extent

Presence

low perm

beds

Natural

fractures Brittleness

Over-

pressure

Sealing

capacity

Source

Rock

Type

Source

Rock

TOC

Source

Rock

Maturity

Oil

gravity

Contami

nation

HC

content

1 1 2 1 1 3 3 1 1 1 2 1 3 2 1

1 1 1 1 1 3 2 2 2 1 3 1 2 2 1

2 2 2 2 1 1 2 1 2 1 1 1 3 2 1

1 1 1 2 4 3 3 1 2 2 2 1 1 2 1

2 2 1 2 2 2 2 1 2 1 2 1 2 2 1

1 1 1 1 3 3 2 1 1 1 1 3 2 2 3

Geological Parameters Geochemical ParametersInformation Quality

provide score 1 to 5

for each parameter

(1 is best)

provide score

for information

quality

Weight

importance of

each parameter

Average Weight 1.00 1.00

Play Name Play_ID Main play type

Average

weighted risk

Average

Geological

risk

Average

Geochemical

risk

Proterozoic Shale Oil GTO_02 Shale Oil 1.67 1.8 1.5

Cretaceous Shale Oil GTO_05 Shale Oil 1.69 1.8 1.6

West Siberia Upper Jurassic Bazhenov Shale Oil GTO_01 Shale Oil 1.70 1.7 1.3

Permian Shale Oil GTO_09 Shale Oil 1.70 2.0 1.5

Cambrian Tight Oil GTO_03 Tight Oil 1.72 1.6 1.4

Silurian Shale Oil GTO_10 Shale Oil 1.75 1.5 2.1

Risk Results

Average weighted risk

for geological and

geochemical risk

(1 is best)

Going Global: Predicting the Next Tight Oil Revolution

Detailed description: example Ordos, China

18

Play description:

• lithological variation, fractures, brittleness

• source potential, oil quality, GOR

• pressure regime

Going Global: Predicting the Next Tight Oil Revolution

Policy/ Public

opinion Land Access

Business

Terms Supply Chain

Downstream

Infrastructure

Water

Availability

and

Management

Other

Regulatory

Play 1

Play 2

Play 3

Play 4

Play 5

Play 6

Play 7

Play 8

Phase 3 Evaluation of Opportunities

Example of a scorecard to characterize, assess and rank unconventional gas

exploration regions. This will be adapted to score a set of criteria specific to

international tight oil opportunities.

19

Going Global: Predicting the Next Tight Oil Revolution

Study Timeline

PLAY-LEVEL SCREENING RISKING

AND RANKING OPPORTUNITY ANALYSIS

20

October November December January February March April May

2012 2013

Kick-off webinar Mid-project webinar Final workshop Final report

• Overview methodology

• Overview of key map

areas

• Present key data

parameters

• Short report describing the

first results of analysis and

risk analysis

• List of potential 20-30 tight oil

play areas to be analyzed in

more detailed in Phase 3

• Short description of the top

tight oil plays (20-30):

• General play

information

• Distribution maps

• Geological risk analysis

• Commercial

characteristics

• Overview of above ground

issues for selected key areas

Going Global: Predicting the Next Tight Oil Revolution

For more information about this presentation or IHS CERA in general,

please contact Roberto Futuro +33 1 7676 0092

Beijing San Francisco

Washington, DC

Cambridge, MA

Calgary

Mexico City

Rio de Janeiro

Paris

Oslo Moscow

Dubai

Singapore

Bangkok

Tokyo

Houston

Denver

London

Geneva

21

For technical questions, please contact [email protected] or [email protected]

Top Related

Copyright © 2022 FDOKUMEN