Bahasa

Halaman

Hukum

Available online at www.sciencedirect.com

Research in Social and

Administrative Pharmacy j (2010) jej

Original Research

Evaluating pharmacists’ views, knowledge,and perception regarding generic medicines

in New ZealandZaheer-Ud-Din Babara,*, Piyush Grovera, Joanna Stewartb,Michele Hogga, Leanne Shorta, Hee Gyung Seoa, Anne Rewa

aSchool of Pharmacy, Faculty of Medical and Health Sciences, University of Auckland, Private Mail Bag 92019, Auckland,

New ZealandbSchool of Population Health, Faculty of Medical and Health Sciences, University of Auckland, Private Mail Bag 92019,

Auckland, New Zealand

Abstract

Background: Generic medicines are commonly used in New Zealand; however, Pharmaceutical

Management Agency of New Zealand (PHARMAC) has indicated a need for better information to thepublic. Studies on consumers’ perceptions suggest that pharmacists play an important role in consumers’choice; hence, “quality use of generic medicines” can be promoted with a better understanding of pharma-

cists’ views, knowledge, and perception.Objectives: (1)To evaluate pharmacists’ perceptions, views, and knowledge of and willingness to recom-mend generic medicines. (2) To explore pharmacists perceptions of the safety, quality, and efficacy of ge-

neric medicines. (3) To assess pharmacists’ views on current policy with respect to substitution of genericmedicines.Methods: A cross-sectional survey using a postal questionnaire was conducted, and questionnaires were

sent to 625 randomly selected pharmacists from a list of 1594 pharmacists who had agreed to release theirdetails for research purposes.Results: Three-hundred and sixty pharmacists responded to the questionnaire (a response rate of 58%).Seventy percent of pharmacists stated there is no difference in safety between original brand and generic

medicines. However, 65% stated that original brand medicines were of higher quality than their genericcounterparts, and half stated that generic medicines and original brand medicines are equally effective. Alarge number of pharmacists reported concerns regarding brand substitution and offered suggestions, such

as the need for advertising campaigns, patient pamphlets, updating prescribers’ software, and distinctpackaging for generic medicines. It was found that pharmacists’ perceptions of generic medicines are pri-marily driven by PHARMACs policies and their experiences with consumers.

Conclusions: About one-third of pharmacists correctly defined the term “generic medicines,” suggestingdiscrepancies in pharmacists’ knowledge and perceptions of generic medicines. Concerns were raisedregarding: quality, safety, and effectiveness; however, most of the pharmacists acknowledged the

economic benefits to the health care system.� 2010 Elsevier Inc. All rights reserved.

* Corresponding author. Telephone: þ64 9 373 7599 ext 88436; fax: þ64 9 367 7192.

E-mail address: [email protected], [email protected] (Z-U-D. Babar).

1551-7411/$ - see front matter � 2010 Elsevier Inc. All rights reserved.

doi:10.1016/j.sapharm.2010.06.004

2 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

Keywords: Generic medicines; Pharmacists; Perceptions; Knowledge; New Zealand

Introduction and background

New Zealand’s health care system

Medicines play a critical role in the health ofNew Zealanders, with 7 out of 10 New Zealandersusing medicines.1 New Zealand has a publicly

funded health care system, with government fund-ing accounting for 78% of health care cost.2 ThePharmaceutical Management Agency of NewZealand (PHARMAC) is responsible formanaging

the pharmaceutical subsidy expenditure, particu-larly for pharmaceuticals accessed in primarycare.2-4 New Zealand has been successful in con-

taining medicine costs because from 1993 to 2006pharmaceutical expenditures in New Zealand in-creased by 11% compared with a 212% increase

in Australia.5 Although New Zealand spends lesson medicines per capita, arguably it achieves bettervalue for money largely as a result of effective

purchasing by the PHARMAC.6,7 AlthoughPHARMAC has played an important role in con-taining the pharmaceutical budget inNewZealand,in 2009 medicines expenditure was recorded as 694

million a year.8,9 Health care expenditures are agrowing concern for many countries includingNew Zealand, and the widespread use of generic

medicines can lead to significant savings.10,11

Generic medicines around the globe

Although most generic medicines provide the

same quality, safety, and efficacy as the originalbrand name product, they are typically 20-90%less expensive than the brand name original.12 The

use of generic medicines saves European patientsand health care systems an estimated V25 billioneach year.12 Generic substitution has reached be-

tween 50% and 60% of the total pharmaceuticalconsumption in the United States, Denmark,United Kingdom, and Germany.13The prescribingof generic medicines in Britain is higher than in

many other European countries, as more than55% of all prescriptions for National Health Ser-vice patients in England are now written generi-

cally.14 In United Kingdom, in some generalpractitioner (GP) surgeries, generic prescribing ismore than 90%.14 In Australia, it is estimated

that approximately 30% of Pharmaceutical Bene-fits Scheme (PBS) scripts, representing around15% of PBS sales by value, are now filled with

generics.15 According to IMS Health Canada, ge-

neric drugs were dispensed to fill 54% of all pre-scriptions in Canada and in 2009, the use ofgeneric prescription drugs saved Canada’s health

care system more than $4 billion. In the UnitedStates, IMS Health reports that 75% of all pre-scriptions are dispensed with generic medicines.16

New Zealand and generic medicines

In New Zealand, Medsafe is the regulatoryauthority for approving new pharmaceuticals and

generic medicines.17 The bioequivalence betweenthe original brand and the generic version of amedicine is the fundamental basis of generic substi-

tution.18 Medsafe compares pharmacokinetic vari-ables of a generic with the innovator medicine, andthe 2 products are considered bioequivalent if the

90% confidence intervals for their mean Cmax,

Tmax, and area under curve (AUC) are within�20%.17 Once these criteria are met, Medsafe

grants bioequivalence status and then the productcan be considered by PHARMAC for subsidy.17

PHARMAC manages the subsidies to medi-cines through The Pharmaceutical Schedule,

which lists the subsidized medicines and thecriteria for eligibility. The schedule has approxi-mately 2000 funded medicines (either brand or

generic), and everyone eligible for subsidy paysa $3 copayment.19 Most of the drugs listed byPHARMAC for subsidy are generics; however,

branded medicines are also listed in the Schedule.In New Zealand, GPs generally prescribe subsi-dized medicines, which in many cases20 is a genericmedicine. (In theory, pharmacists dispense in ac-

cordance with a GPs instructions, as a specialagreement with the prescriber is required beforesubstitution is permitted.) There is currently no

generic policy or generic substitution guidelinesavailable for pharmacists in New Zealand.

Rationale of the study

In certain instances, patients in New Zealandmay have a choice of whether to accept a subsidized

medicine (usually a generic), or choose to pay foranother brand which in many cases is an InnovatorBrand (IB) or another generic which may not be

subsidized. However, patient loyalty to a brand cancome into play and theymay choose20 to pay for aninnovator brand. Also, the perceptions regarding

3Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

generics as “lower quality” are widespread.22,23

This was confirmed in a recent study conductedin Auckland, where it was observed that many con-sumers hadmisconceptions regarding generic med-

icines.24 This should not be the case, as in NewZealand where Medsafe ensures bioequivalencybetween an IB and the generic medicine before it

is released onto the market indicating that mostof the genericmedicines should be safe.25 It was dis-cussed during a PHARMACmeeting that the term

“generic” is well understood by PHARMAC, yetthe public may simply regard them as “cheap”and there is an opportunity to educate consumers

regarding generics.22

An information leaflet produced byPHARMAC targeting stakeholders and distrib-uted to consumers through pharmacies and GPs

states “though a generic medicine is cheaper how-ever they are equally effective.”26 A previous studyon consumer perceptions of generic medicines un-

dertaken in Auckland24 along with evidence fromthe literature suggests that pharmacists play a keyrole in providing information to consumers, in

turn enabling them tomake informed choices aboutgenerics.27

Another factor that could affect consumers’

confidence in generic drugs is that a therapeutic re-sponse of somemedicines may differ in a small pro-portion of the population.28 Some of thesemedicines are drugs with a narrow therapeutic in-

dex and modified release formulations. In July2007, GlaxoSmithKline (United Kingdom) intro-duced a new formulation of levothryoxine

(Eltroxin�) containing different excipients fromthe originator product, which resulted in weightgain, lethargy, and visual disturbances. By Septem-

ber 2008, the Center for Adverse Reactions Moni-toring (CARM) in New Zealand had received 746adverse reaction reports on Eltroxin�.28 Such dif-ferent therapeutic responses can cause the generic

medicine to be perceived as substandard and inef-fective by prescribers, pharmacists, and con-sumers.29 Also, confusion among consumers with

differences in the appearance, taste, and color couldlead to reduced adherence.30-32 In New Zealand,feedback fromaproposal indicated that prescribers

opposed the idea of generic substitutionwhile phar-macy organizations and two-thirds of the con-sumers supported the idea.33

Switching patients to different brands of med-icines has been highlighted as a key medicine useissue in New Zealand, with some of the therapeuticclasses affected most being statins and angiotensin

converting enzyme (ACE) inhibitors.34,35 This

necessitates additional support from the healthcare professionals, and pharmacists could playa key role in generating support for improved usageof generic medicines.36 In promoting quality use of

generic medicines37 and in directing consumers’choice, pharmacists and prescribers play a crucialrole35,38,39; however, no research has been pub-

lished in this area and very little has been discussedinMedicines NZ. Although PHARMAC has com-missioned some research on the topic,40 the results

are not available in the public domain.

Study objectives

1. To evaluate pharmacists’ perceptions, views, andknowledge of and willingness to recommend ge-neric medicines.

2. To explore pharmacists perceptions of the safety,quality, and efficacy of generic medicines.

3. To assess pharmacists’ views on current policywith respect to substitution of generic medicines.

The term “knowledge” applies to the pharma-cists’ knowledge regarding the definition of ge-

neric medicine, regulatory understanding of theterm generic, knowledge about possible substitu-tion, and sources of information regarding ge-

nerics. The term “views” has been used in thisresearch as something believed or accepted astrue by a person, or as an opinion.41

Methods

Study design

A cross-sectional survey using a postal ques-tionnaire was conducted across New Zealandbetween 22nd June 2009 and 20th July 2009. Surveyresearch techniques have been widely used in the

past to identify the views, beliefs, and attitudes ofpharmacists on pharmacy-related issues. The ad-vantages of quantitative research on a random

sample of the population of interest are that itallows hypothesis testing that the generalizationscan be made to the total population.41

Questionnaire development

Electronic databases Embase, Medline, ScienceDirect, and Springer Link were used to conduct

a literature review regarding generic medicinesissues in New Zealand (approximately 60 articles).This developed insights into the issues surrounding

the use of generics and provided information abouttheir safety, quality, and efficacy. A particularfocus was placed on similar studies that examined

4 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

pharmacists’ knowledge and perceptions regardinggeneric medicines. In addition to the literature re-view, an informal group discussion was conducted

with 4 New Zealand-registered community phar-macists to gain understanding on the issues sur-rounding generics medicines.

Once the questionnaire was constructed, it was

examined for face validity by 16 fourth-yearstudents from the School of Pharmacy.The selectedstudents were asked to provide feedback on their

understanding of questions, layout, and sequenceof questions and themes. The students interpretedmost of the questions as anticipated, and there was

uniformity in their understanding. Questions thatpilot testing revealed were ambiguous or partici-pants had difficulty deciphering were changedaccordingly.

Following these initial modifications, the ques-tionnaire was piloted on 5 New Zealand-registeredpharmacists and further modifications made. The

piloting investigated the understanding of ques-tions and that all important aspects regarding useof generic medicines were explored adequately. In

addition to this, the pharmacists also were ques-tioned regarding the relevance of the question-naire as a tool to investigate the aims of this

study so as to evidence content validity. Contentvalidity of the questionnaire was also assessedfrom a pool of questions derived from the GroupDiscussion with pharmacists.

The first part of the questionnaire covered thedemographic data; age, gender, and years ofexperience in pharmacy. The second part explored

the pharmacists’ knowledge of generic medicines,relevant policies, profitability, brand substitution,safety, and effectiveness. Knowledge was assessed

by asking “ what is a generic medicine?” with op-tions: the medicine is (1) bioequivalent to the brandmedicine, (2) a less expensive version of the brandmedicines, (3) of equivalent quality and efficacy as

of the brand medicines, and (4) less costly than thebrand medicines. A score of 0-4 was given depend-ing on the number of options correctly answered

with a score of 4 required for correct knowledge.There was a mixture of questions on pharmacists’views and perceptions. Most of the questions were

close ended; however, respondents were given theopportunity to provide qualitative comments.Close-ended questions solicited pharmacists; views

of support and conditions they would recommendgeneric substitution. Their views also were solicitedabout profitability and dispensing generic medi-cines, how to make brand substitution safer, and

the consequences of using generic medicines.

Sampling and data collection

A list of 1594 pharmacists, who had agreed torelease their details for research purposes whenapplying for their Annual Practicing Certificate

with The Pharmacy Council of New Zealand, wasobtained. The total number of pharmacists regis-tered with The Pharmacy Council of New Zealandwas 3050, so the details of approximately 50%of all

registered pharmacists were available. Six hundredand twenty-five pharmacists were randomly se-lected using Microsoft Excel randomization soft-

ware and were sent the questionnaire, a ParticipantInformation Sheet, a return self-addressed postage-paid envelope, and a letter of recommendation

issued by The Pharmacy Guild of New Zealand.42

A news article on this study was also published inthe July edition of Pharmacy Today to increasethe response rate.43 A random sample of 300 would

result ina95%confidence intervalaroundapercent-age of a maximum of �6%, which was consideredsufficient precision. A sample twice this size was

taken to allow for a response rate as low as 50%.A period of 2 weeks was allowed for a return of

questionnaires from the first mail drop. After 2

weeks, a second mail drop was undertaken to thesame 625 pharmacists. Pharmacists were againgiven 2 weeks to complete the questionnaire. After

4 weeks, any further returns were not included inthe study.

Statistical analysis

All data entry and the basic summary of thedata were conducted using SPSS version 16 withstatistical analysis conducted in SAS 9.1 Data were

summarized using frequencies and percentages.The association of years of experience (! or �5years) with knowledge of generics (a score from0 to 4) was investigated using a Mann-Whitney U

test. To investigate factors associated with supportfor generics (yes or no), a logistic regression anal-ysis was run with knowledge of generics (100%

correct or not) and years of experience (! or �5years) included as the 2 explanatory variables.

Results

Out of 625 pharmacists, 360 pharmacists

responded to the questionnaire, a response rateof 58%.

Demographics of the respondents

More than 60% of respondents were female;most of the respondents were in the age range of

5Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

30-40 years and were community pharmacists(Table 1). Respondent demographics are similarto those from other studies from the PharmacyCouncil of New Zealand.44,45

Pharmacists’ knowledge of generic medicines

Most of the respondents (91.9%) defined a ge-neric medicine as a medicine with the same activeingredient as an original brand medicine butwithout the same excipients. Approximately 70%

of the respondents believed that a generic medicineis bioequivalent to the original brand medicine andis less expensive than original brand medicine.

Close to 70%of respondents reported no differencein safety between generics and originator brands,whereas 28% mentioned that original brands were

safer than generics. Although 65% respondentssuggested the originator brands are of higherquality, half of the respondents believed that theoriginator brands are more effective. Only 30% of

respondents had fully correct knowledge of a ge-neric medicine (by correctly identifying all 4 op-tions of safety, effectiveness, quality, and cost).

Factors affecting pharmacists’ perceptions

The major factors that affected pharmacists’

perceptions of generic medicines were consumers’experiences and the pharmacists’ own judgment.Generic substitution was supported by 89.4% of

respondents. Among those, most support genericsubstitution most of the time, whereas approxi-mately 8% believe that generic substitution is ap-

propriate all of the time. Approximately 60% of

Table 1

Demographic characteristics of pharmacists

Characteristics Frequency (%)

Gender (n¼ 359)

Male 142 (39.6)

Female 217 (60.4)

Age (n¼ 359) (yr)

!30 72 (20.1)

30-50 170 (47.4)

O50 117 (32.6)

Number of years of practice (n¼ 359)

!5 68 (18.9)

5-10 41 (11.4)

11-20 85 (23.7)

O20 165 (46.0)

Pharmacist respondents (by categories) (n¼ 352)

Community 307 (87.2)

Hospital 45 (12.8)

respondents routinely recommended generics asthey believed they had no other choice, whereas5.6% of respondents never recommended genericmedicines. The main reasons to support generic

substitution were cost, consumer preference or de-mand, appearance, and the availability (Table 2).

Association of pharmacists’ work experience with

knowledge of generics

There was a statistically significant differencein pharmacists’ knowledge of generic medicines de-pending on the length of time in practice (P¼ .03).

Pharmacists with less than 5 years in practice hada better understanding of generic medicines thanthose with greater than or equal to 5 years in

practice.

Factors associated with support for genericsubstitution

Examination of odds ratios revealed no asso-

ciation between pharmacists’ years of practice andtheir support or knowledge of generic medicines.

Pharmacists, generic medicines, and monetarybenefits

Of the 287 community pharmacists who re-

sponded, 80% stated that generic medicines affectthe profitability of community pharmacy. Of thosewho believed profitability was affected, 11% men-

tioned that generic medicines increased profit,whereas 89% felt profits were decreased. Most(84.0%) of the respondents believed that profits

were reduced because of greater time required toexplain frequent medication changes to patients.Approximately 68% stated that the profit (dollar

value) of generic medicines was less; therefore, itwas necessary to increase sales volume to maintainprofitability (Table 3).

Information sources for generics and concerns

about generic medicines

Nearly half of the respondents (49.7%) be-lieved pharmacists were primarily responsible forinforming consumers about issues relating to

generic medicines. Approximately 30% viewedPHARMAC, 13% doctors, and 7% Medsafe tobe the responsible informants of consumers about

generic medicines.Approximately 50% of respondents choose to

voice their concerns about generic medicines to

PHARMAC directly, whereas 47% of respondentsnotified Medsafe of any issues they may have. ThePharmaceutical Society of New Zealand, the

Table 2

Pharmacists and generic medicines

Reasons why pharmacists

recommend generic medicines

Frequency (%)

of pharmacists’

response (n¼ 359)

Factors that affect pharmacists’

perception

of generic medicines

Frequency (%)

of pharmacists’

response (n¼ 359)

Cost to the customer 297 (82.5) Reputation of manufacturer

(recall record)

161 (44.7)

Having no other choice 228 (63.3) Consumers’ experiences 273 (75.8)

Consumer preference/demand 226 (62.8) Professional judgment 260 (72.2)

Availability of stock 164 (45.6) Information from Medsafe 246 (68.3)

Do not recommend generic

medicines

20 (5.6) Problem reports in media/

journals

148 (41.1)

Customer’s appearance 11 (3.1) Information available on brand

substitution

5 (1.4)

Cost-effectiveness of generic

medicines

5 (1.4) Practice based on PHARMAC

funding and information

5 (1.4)

Proven bioequivalence to

original brand medicines

5 (1.4) Personal experience 5 (1.4)

Personal faith in the product 2 (0.6) Appearance of product and

packaging

2 (0.6)

Substitution agreement with

prescriber

1 (0.3)

6 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

Pharmacy Guild, and the Pharmacy Council ofNew Zealand were the preferred organizations forreferring generic issues by 16.7%, 13.6%, and 8.1%of the respondents, respectively. Approximately

20% of respondents chose not to voice theirconcerns anywhere.

Generic medicinesdpharmacists’ perceptions ofconsumer compliance and therapeutic response

More than half of the respondents (56.1%)

believed that generic medicines had no impact onmedication compliance. Of those respondents thatthought generics could affect compliance, 43.6%

of them believed that compliance was reduced bygeneric medicine use. Most of the respondents(67%) estimated 10% of patients would

Table 3

Community pharmacists’ perception of the impact of generic

Methods by which generic medicines impact on the profitabili

Greater time spent explaining the change to customers

Stock level planning is required

The profit (dollar value) of generic medicines is less; therefore,

to increase sales volume to maintain profit

Less money spent purchasing inventory medicines

Impact on relationship with patient when generic medicine do

Lower margin and mark-up

Better purchase deals from wholesaler

Having to stock for customer’s choice

Time consuming to explain the change in generic medicines to

experience a change in therapeutic responsewhen brand substitution took place.

Ninety-three percent of respondents estimatedthat 20% or less of consumers specifically re-

quested an original brand with 70% estimating10% or less.

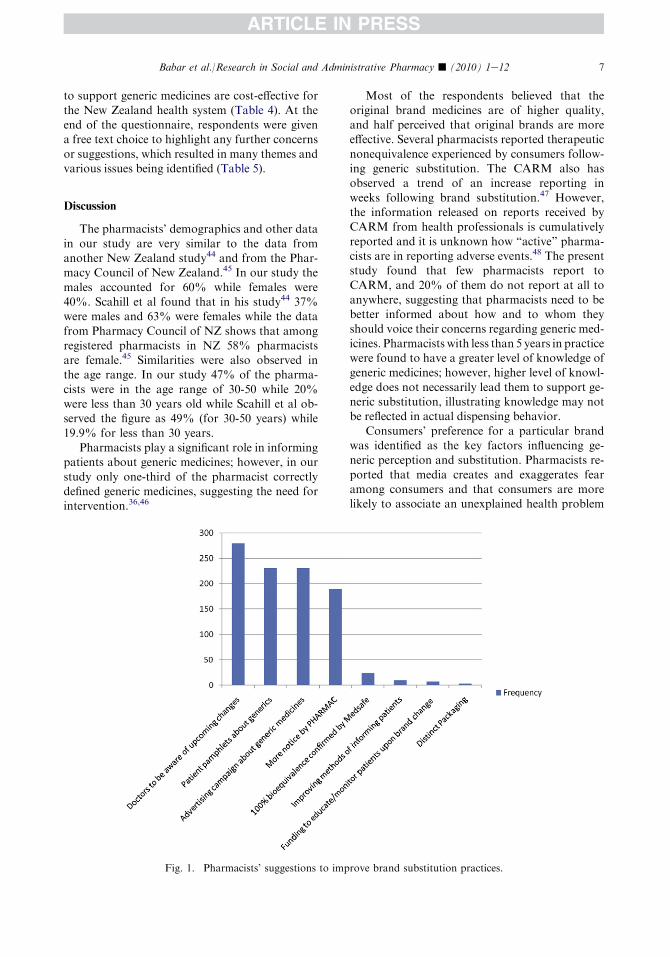

Suggestions to improve generic substitution

Seventy-seven percent of the respondents be-lieved that prescribers needed to be aware of

upcoming brand changes. Other suggestions in-cluded the need for advertising campaigns, patientpamphlets, updating doctors’ software, prescribing

generically, funding for monitoring patients, anddistinct packaging for generic medicines (Fig. 1).Pharmacists also mentioned that current policies

medicines on the profitability of their pharmacies

ty Frequency (%) of pharmacists’

response (n¼ 306)

257 (84.0)

186 (60.8)

it is necessary 207 (67.6)

5 (1.6)

es not work 4 (1.3)

3 (1.0)

3 (1.0)

3 (1.0)

patients 2 (0.7)

7Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

to support generic medicines are cost-effective forthe New Zealand health system (Table 4). At theend of the questionnaire, respondents were givena free text choice to highlight any further concerns

or suggestions, which resulted in many themes andvarious issues being identified (Table 5).

Discussion

The pharmacists’ demographics and other data

in our study are very similar to the data fromanother New Zealand study44 and from the Phar-macy Council of New Zealand.45 In our study the

males accounted for 60% while females were40%. Scahill et al found that in his study44 37%were males and 63% were females while the data

from Pharmacy Council of NZ shows that amongregistered pharmacists in NZ 58% pharmacistsare female.45 Similarities were also observed inthe age range. In our study 47% of the pharma-

cists were in the age range of 30-50 while 20%were less than 30 years old while Scahill et al ob-served the figure as 49% (for 30-50 years) while

19.9% for less than 30 years.Pharmacists play a significant role in informing

patients about generic medicines; however, in our

study only one-third of the pharmacist correctlydefined generic medicines, suggesting the need forintervention.36,46

Fig. 1. Pharmacists’ suggestions to imp

Most of the respondents believed that theoriginal brand medicines are of higher quality,and half perceived that original brands are moreeffective. Several pharmacists reported therapeutic

nonequivalence experienced by consumers follow-ing generic substitution. The CARM also hasobserved a trend of an increase reporting in

weeks following brand substitution.47 However,the information released on reports received byCARM from health professionals is cumulatively

reported and it is unknown how “active” pharma-cists are in reporting adverse events.48 The presentstudy found that few pharmacists report to

CARM, and 20% of them do not report at all toanywhere, suggesting that pharmacists need to bebetter informed about how and to whom theyshould voice their concerns regarding generic med-

icines. Pharmacists with less than 5 years in practicewere found to have a greater level of knowledge ofgeneric medicines; however, higher level of knowl-

edge does not necessarily lead them to support ge-neric substitution, illustrating knowledge may notbe reflected in actual dispensing behavior.

Consumers’ preference for a particular brandwas identified as the key factors influencing ge-neric perception and substitution. Pharmacists re-

ported that media creates and exaggerates fearamong consumers and that consumers are morelikely to associate an unexplained health problem

rove brand substitution practices.

Table 4

Frequency (%) of pharmacists’ agreement response to item statements

Statement Frequency (%) of pharmacists’ response

Strongly

agree/agree

Neutral Strongly

disagree/disagree

PHARMAC allows sufficient time for pharmacists to prepare for

a change in brand (n¼ 358)

144 (40.2) 89 (24.9) 125 (34.9)

Generic medicines enable PHARMAC to fund more medicines

(n¼ 359)

291 (81.1) 40 (11.1) 28 (7.8)

The wider use of generic medicines means that less money will be

available for research to develop new medicines (n¼ 360)

207 (57.5) 85 (23.6) 68 (18.9)

Generic medicines are responsible for many therapeutic failures

(n¼ 360)

85 (23.6) 108 (30.0) 167 (46.4)

Generic medicines are cost-effective for the health system (n¼ 360) 272 (75.6) 48 (13.3) 40 (11.1)

Overall current policies to support generic medicines are effective

(n¼ 359)

135 (37.6) 126 (35.1) 98 (27.3)

8 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

with generic medicines. Direct-to-consumer ad-vertising and poor understanding of issues sur-

rounding generic medicines are other factorsaffecting pharmacists’ perception and their will-ingness to recommend generics.

Although most of the respondents were gener-ally supportive of generics, only a few believe thatgeneric substitution is appropriate all the time.

Another major factor influencing generic substi-tution is stock availability. As a result of subsidyarrangements made by PHARMAC, pharmacies

stock the subsidized branddoften a generic. Nev-ertheless, some consumers who experience thera-peutic nonequivalence may request an originalbrand. This could be problematic as it is usually

difficult to obtain stock of the originator brand.Sole supply agreements between PHARMAC andthe pharmaceutical industry significantly reduce

the likelihood of obtaining the originator brand ina small country such as New Zealand.

A large proportion of pharmacists reported that

generic medicines might reduce compliance. It isrecognized that consumers are more accepting ofgeneric medicines if substitution is explainedclearly.49For this reason,PHARMAChasdeveloped

several information leaflets such as “My medicationlooks different” and “The truth about generic medi-cines.” Most of the pharmacists believed that generic

medicines are not responsible for significant changesin therapeutic response.Thesefindingsare in linewiththose found in the literature.50,51Most of the respon-

dents reported that approximately10%of consumersexperience a change in therapeutic response withbrand substitution. The main classes of medication

that require caution are those with a narrow thera-peutic index such as anticonvulsants, psychotropicagents, and cardiovascular medicines.47,52,53

Also, there should be stringent substitutionguidelines for critical patients (elderly) and

for critical diseases such as arrhythmias.49

PHARMAC and Medsafe could potentiallydevelop some guidelines, which could result in

pharmacists gaining greater confidence when deal-ing with generic substitution. There was in exis-tence an Interchangeable Multi-source Medicines

list published by Medsafe that stated which med-icines could be generically substituted; however, itwas discontinued in July 2006.54

Most of the respondents believed that genericmedicines are cost-effective. It has been reportedthat switching from original brand to generic couldlead to an 11% reduction in annual overall medi-

cine costs.55 Although it is less expensive to use ge-neric medicines, reactions to an excipient orineffectiveness in controlling a condition are likely

to result in hidden costs. This could be a big prob-lem, as has been seen with the adverse events of sta-tins and ventolin substitution in New Zealand.

Likewise, respondents reported cases where 3 timesthe generic medicine dose was required to maintaintherapeutic levels for their patients.56 Others alsoreported that substitution of narrow therapeutic in-

dexmedicines resulted in additional blood tests andmore visits to their GP, resulting in greater costs topatients and the health care system as a whole.55

The respondents believed that PHARMAC istoo concerned about the price and not the qualityof medicine. They also believed that the money

saved by PHARMAC is not being used to maxi-mum benefit for New Zealanders. For example,PHARMAC made significant savings last year on

Lipex� [Merck Sharp & Dohme (MSD)] andLosec� (Astra Zeneca, UnitedKingdom), yet listedvery few medicines in return.

Table 5

Pharmacists’ comments on generic medicines’ issues

Theme Sub themes/issues Number of

respondents

Pharmacists and generic substitution Impact of brand substitution on community

pharmacies and patients’ health outcomes

often underestimated.

5

Pharmacists to be reimbursed for the time spent

with brand substitution and explaining the

change to patients.

21

Frequent brand substitution increases the

likelihood of dispensing the unintended brand.

4

Problems faced by consumers with generic

substitution

Frequent brand substitution causes confusion

and frustration among patients and affects

their acceptance to generic medicines.

15

Therapeutic nonequivalence or failure

encountered by patients from substitution to

generic medicines.

20

Patients have a lack of information or biased

information on generics.

15

Erratic stock supply of some generic medicines is

a problem especially when there is sole supply

agreement.

4

Suggestions to improve generic substitution PHARMAC should allow greater time

notification for a brand substitution.

3

In some cases, more than one brand of a medicine

needs to be subsidized or made available.

20

Prescribers to update their software regularly 2

Prescribers need to prescribe more generics and/

or use generic names

13

Improvements in information dissemination

of generic medicines

PHARMAC to invest more on advertising

generics to consumers and explaining their

rational.

8

Pharmacists’ perception of generic medicines Appearance of generic medicines influences their

acceptance from patients.

4

Generic medicines reduce the pharmaceutical

expenditure in the health care system.

12

Quality of generic medicines is dubious especially

with those manufactured in third world

countries.

16

At least in New Zealand patients get the same

generic throughout.

2

PHARMAC and generic substitution Money saved from funding generic medicines not

going back into purchasing more medicines.

7

PHARMAC is more concerned about money and

takes little notice for health outcomes for

patients. Unseen costs involved are neglected.

7

There is monopoly in funding of medicines by

PHARMAC. There is no choice but to accept

their decisions.

11

Pharmaceutical companies are withdrawing from

New Zealand as a result of sole supply and

generics.

6

9Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

Many countries use financial incentivesto encourage generic substitution.2,32 In NewZealand, many pharmacists mentioned thatgeneric medicines could affect the profitability of

their pharmacies. In New Zealand, patients paya $3 copayment for any funded drug. The fundeddrug could be a generic or nonoriginal brand. Phar-macists in New Zealand are permitted to claim

10 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

government subsidies for dispensing subsidizedmedicines. For these transactions, the pharmacistcan claim the manufacturer’s price of the medicine

plus a mark-up, which is a percentage of the price.In addition, on each occasion that medicine is dis-pensed, thepharmacist is entitled toclaimadispens-ing fee for each individual medicine for each

patient. The dispensing fee is currently calculatedat $5.80 per item of medicine dispensed.57 The dis-pensing fee does not change if generic or branded

however as the mark-up is a percentage of themedicine cost, if generics are cheaper the amountreceived as mark-up will be less, meaning the phar-

macy would need to increase volume to maintainprofit.

Approximately half of the respondents identi-fied pharmacists as being primarily responsible for

informing consumers; however, pharmacists arenot currently reimbursed for the time spentexplaining the change to patients. Many respon-

dents suggested that some of the savings madefrom brand substitution need to be passed ontopharmacists as they are doing a significant

amount of work. Germany, the United States ofAmerica, and the United Kingdom have all21 suc-cessfully used financial incentives for pharmacists

to dispense generics. In New Zealand, a similarapproach could be considered; allowing commu-nity pharmacies to maintain their profit marginswhile facilitating generic substitution.

Most of the respondents believed that if pre-scribers were aware of upcoming changes andnotified patients, this would reduce the problems

of brand substitution. In this scenario, the patientwould get the information from 2 health pro-fessionals. Patient pamphlets about generic medi-

cines are already used and many pharmacists inour study agreed that this made substitutionsafer. Other suggestions to make substitutiontransition better were advertising campaigns, fund-

ing for pharmacists, educating and monitoringpatients, and also for Medsafe to ensure stringentbioequivalence.

Study limitations

The sample consisted of only those pharmacistswho had agreed to release their details for research,

which is approximately 50% of New Zealand’sregistered pharmacists. The method of samplingpharmacists (instead of pharmacies) was used to

avoid cluster bias. The pharmacists who releasetheir details for research may differ from thosewho choose not to be involved in research;

however, this difference does not seem to be largeas the demographic data from our study is similarwith the data from other sources.44,45 Although

there was evidence to support face and content val-idity of the items composing the questionnaire,there was no means by which to assess constructvalidity or reliability in those same items.

Impact of the current research and suggestions forfuture research

Generic medicines are a vital component of

New Zealand’s medicine cost management poli-cies; however, the full impact of use of genericmedicines is not known. Exploring pharmacists’

perceptions is 1 step in this direction and has en-abled us to understand use of generics and theirlikely impact on patient compliance. The knowl-edge gained can be used to develop strategies to

better inform patients about generic medicines,with pharmacists being the main health profes-sionals likely to positively affect patient knowl-

edge and views. The data provides a foundationto develop, implement, and evaluate primarycare interventions designed to provide accurate in-

formation to the public about generic medicines.This knowledge is indeed very helpful to current

consultative processes involved in developing phar-

maceutical policy in New Zealand. Some of thefuture research questions could be how to furtherimprovegeneric penetrationandbrand substitutionpractices. One important research question could

be to explore the savings made by generics and thelikely impact of this change on health outcomes.

Conclusion

Many pharmacists were in favor of a greater

number of subsidized brands being made avail-able for consumer choice, and consumer’s prefer-ence and stock availability were identified as key

factors influencing generic substitution. Pharma-cist’s perceptions toward generics are being pri-marily driven by PHARMACs’ policies andconsumer experiences, and by the current laws re-

garding brand substitution. Community pharma-cists believed brand substitution reduces theirpharmacies profitability, highlighting the need

for financial incentives for pharmacists. Approxi-mately one-fifth of the pharmacists in this studydo not report their concerns regarding generic

medicines to anyone, indicating the need for inter-vention. Most of the respondents believed thatprescribers needed to be aware of upcoming brand

11Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

changes. The results of this study should help toinform policy and future research on generic med-ication use in New Zealand and elsewhere.

Acknowledgments

We would like to say thank you to Ms. Charon

Lessing and Mr. Shane Scahill for reviewing themanuscript and for their helpful comments. Wewould also like to say thankyou toMs.Yanwei Pan.

References

1. Associate Minister of Health, Minister of Health.

Medicines New Zealand: Contributing to GoodHealth

Outcomes for All NewZealanders.Wellington:Minis-

try of Health [Internet Site]. [cited 2009 Aug 25].

Available at: http://www.moh.govt.nz/moh.nsf/pages

mh/7236/$File/medicines-nz.pdf; 2007.

2. Glover J, Hetzel D, Tennant S. Australia and New

Zealand, Health Systems of International Encyclope-

dia of Public Health. Oxford: Academic Press; 2008.

255e267.3. Pharmaceutical Management Agency. Information

SheetsdIntroduction to PHARMAC. Wellington:

PHARMAC [Internet Site]. [cited 2009 Aug 25].

Available at: http://pharmac.govt.nz/2008/12/16/01

_PHARM_Infsheet_INTRO.pdf; 2009 Jul 27.

4. Williams G, Poynton M. PHARMAC Lectured

Professional Pharmacy Studies [Pharmacy 409].

Auckland,NewZealand: TheUniversity ofAuckland;

May 5, 2009.

5. Morgan S, Boothe K. Prescription drug subsidies in

Australia and New Zealand. Aust Prescr 2010;33:

2e4.

6. Morgan S, Henley G, McMahon M, Barer M. Influ-

encing drug prices through formulary-based policies:

lessons from New Zealand. Healthc Policy 2007;3:

1e20.

7. McCormackP,Quigley J, HansenP.Review ofAccess

to High-Cost, Highly-Specialised Medicines in New

Zealand. Report Presented to Minister of Health.

Available at: http://www.beehive.govt.nz/sites/all/

files/Review%20of%20Access%20to%20High%20

Cost%20Highly%20Specialised%20Medicines%2031

%20April%202010.pdf; 2007. Accessed 28.05.10.

8. Ryall T. Health Minister confirms new medi-

cines spending, 30th July 2009. Available at:

http://www.beehive.govt.nz/release/healthþministerþconfirmsþnewþmedicinesþspending; 2007. Accessed

13.06.10.

9. PHARMAC. Pharmaceutical Management Agency

Annual Review, New Zealand Government. Avail-

able at: http://www.pharmac.govt.nz/2007/11/21/

ARev071.pdf; 2007. Accessed 15.09.09.

10. Kanavos P. Do generics offer significant savings to

the UK National Health Service? Curr Med Res

Opin 2007;23:105e116.

11. KingDR,Kanavos P. Encouraging the use of generic

medicines: implications for transition economies.

Croat Med J 2002;43:462e469.

12. Generic medicines, basic notions: European Generic

Medicines Association. Available at: http://www.ega

generics.com/gen-basics.htm; 2002. Accessed 15.06.10.

13. IMS. IMS health data 2003. Available at: http://

www.imshealth.com; 2003.

14. Generic Prescribing. Association of British Pharma-

ceutical Industry. BSC/5/99/3k. Available at: http://

www.kidney.org.uk/main/switch_meds/generic.pdf;

2003. Accessed 16.06.10.

15. Lofgran H. Generic medicines in Australia: busi-

ness dynamics and recent policy reform. South

Med Rev:24e28. Available at: http://apps.who.int/

medicinedocs/documents/s16383e/s16383e.pdf, 2009;

2. Accessed 17.05.10.

16. MatchingUSGenericDrugUseWould Save Canada

$1.6-Billion, Toronto, April 6, 2010. Available at:

http://www.canadiangenerics.ca/en/news/apr_06_10.

asp; 2009. Accessed 18.05.10.

17. Medsafe. 6.3 ed.. In: New Zealand Regulatory Guide-

lines for Medicines, Vol. 1. Wellington: Medsafe.

[cited 2009 Jul 8]. Available at: http://medsafe.

govt.nz/regulatory/Guideline/Full%20-%20NZ%20

Regulatory%20Guidelines%20for%20Medicines.

pdf; 2009. Accessed 24.06.10.

18. Borgheini G. The bioequivalence and therapeutic ef-

ficacy of generic versus brand-name psychoactive

drugs. Clin Ther 2003;25:1578e1592.

19. Cumming J, Mayes N, Daube J. How New Zealand

has contained expenditures on drugs. BMJ 2010;

340:1224e1227.

20. Upfront: Brand Change. Changing to a generic drug.

BPac NZ [cited 1 May 2008]. Available at: http://

www.bpac.org.nz/magazine/2007/june/upfront.asp;

2007. Accessed 15.05.10.

21. Kalisch L, Roughead E, Gilbert A. Pharmaceutical

brand substitution in Australiadare there multiple

switches per prescription? Aust N Z J Public Health

2007;31:348e352.

22. Minutes of the PHARMAC Consumer Advisory

Committee (CAC) Meeting, Friday 13 July 2007.

Available at: http://www.pharmac.govt.nz/pdf/0210

07a.pdf; 2007. Accessed 13.02.10.

23. Generic medicines: dealing with multiple brands. Na-

tional Prescribing ServiceNewsletter. Australia. Avail-

able at: http://www.nps.org.au/health_professionals/

publications/nps_news/current/generic_medicines_

dealing_with_multiple_brands; 2007. Accessed

16.06.10.

24. Babar ZU, Stewart J, Reddy S, et al. An evaluation of

consumers’ knowledge, perceptions and attitudes re-

garding generic medicines in Auckland [Online first].

Available at: http://www.springerlink.com/content/

2n22020r2x366782/?p¼ed9bd33d6e5347b49bc417ad

89486317&pi¼1; 2007. Accessed 28/6/2010.

25. Why you should prescribe generically. Best Pract

Gen:24e27. Available at: http://www.bpac.org.nz/

12 Babar et al./Research in Social and Administrative Pharmacy j (2010) 1e12

magazine/2008/june/generic.asp, 2008;14. Accessed

26.06.10.

26. Pharmaceutical Management Agency. Information

SheetsdThe Truth About Generic Medicines [Inter-

net Site]. [cited 2009 August 25]. Available at: http://

pharmac.govt.nz/2008/12/16/07_PHARM_Infosheets

_GENERIC_MEDS.pdf; 2008. Accessed 27.07.09.

27. Mott D, Cline R. Exploring generic drug use behav-

ior: the role of prescribers and pharmacists in the op-

portunity for generic drug use and generic

substitution. Med Care 2002;40(8):662e674.

28. Medsafe, Minister of Health. EltroxindMedsafe Sum-

mary Review of Eltroxin (Media Conference Informa-

tion). Wellington: Medsafe [Internet Site]. [cited 2009

May 23]. Available at: http://www.medsafe.govt.nz/

hot/MediaContents.asp; 2008Sep11.Accessed25.06.10.

29. Ford N, t’Hoen E. Generic medicines are not sub-

standard medicines. Lancet 2002;359:1351e1352.

30. Kjoenniksen I, Lindbaek M, Granas A. Patients’ at-

titudes towards and experiences of generic drug

substitution in Norway. Pharm World Sci 2006;28:

284e289.

31. Mason J, Bearden W. Generic drugs: consumer,

pharmacist and physician perceptions of the issues.

J Consum Aff 1980;14:193e206.

32. Bearden W, Mason J. Physician and pharmacist per-

ceptions of generic drugs. Ind Market Manag 1979;8

(1):63e68.

33. Medsafe. Regulatory IssuesdNo Immediate

Changes to Generics [Internet Site]. [cited 2009

May 23]. Available at: http://medsafe.govt.nz/profs

/RIss/gensubleg.asp; 1979. Accessed 15.05.10.

34. Maling T. Finding a better balance between pharma-

ceutical supply and demandda medicinal issue. N Z

Fam Phys 2002;29:3.

35. Perkins E,Dovey S, TilyardM,BoyleK,&PenroseA.

A 30 change management strategy to modify ACE-

inhibitor prescribing. RNZCGPResearch Unit; 1999.

36. Babar Z, Awaisu A. Evaluating community pharma-

cists’ perceptions and practices on generic medicines:

a pilot study from Peninsular Malaysia. J Generic

Med 2008;5:315e330.37. Hassali A, Stewart K. Quality use of generic medi-

cines. Aust Prescr:80e81. Available at: http://www.

australianprescriber.com/upload/pdf/articles/488.

pdf, 2004;27. Accessed 26.06.10.

38. SSRI antidepressants and brand changing. Best

Pract J. Special edition. Available at: http://www.

bpac.org.nz/magazine/2007/march/changing.asp#

ssri, March 2007;27. Accessed 20.06.10.

39. Al-Gedadi NA, Hassali MA, Shafie AA. A pilot

survey on perceptions and knowledge of generic med-

icines among consumers in Penang,Malaysia.Pharm

Pract 2008;6:93e97.

40. Request for proposal (RFP) supply of market ser-

vices research (medication brand changes). Pharm

Manag Agency N Z Jan 2008;25th.

41. Smith FJ. Research Methods in Pharmacy Practice.

Pharmaceutical Press; 2002. 1e286.

42. PharmacyGuildofNewZealand.About thePharmacy

GuilddFacts at a Glance. Wellington: Pharmacy

Guild of New Zealand [Internet Site]. Available at:

http://www.pgnz.org.nz/about-us/; 2006. Accessed

26.06.10.

43. Sinclair N, ed. Generics Survey. Pharmacy Today.

Auckland: CMPMedica (NZ) Ltd; 2009, Jul 5.

44. Scahill S, Harrison J, Sheridan J. The ABC of New

Zealand’s Ten Year Vision for pharmacists: aware-

ness, barriers and consultation. Int J Pharm Pract

2009;17:135e142.

45. Pharmacy Council of New Zealand. Workforce De-

mographics as at 30th June 2009. Available at: http://

www.pharmacycouncil.org.nz/cms_show_download.

php?id¼125; 2009. Accessed 20.06.10.

46. Allenet B, Barry H. Opinion and behaviour of phar-

macists towards the substitution of branded drugs by

generic drugs: survey of 1,000 French community

pharmacists. Pharm World Sci 2003;25:197e202.

47. TatleyM.Monitoringof genericmedicines andbrand

changes. BPJ Spec Ed Generics:18e20. Available at:

http://www.bpac.org.nz/magazine/2009/generics/

generics.asp?article¼6; 2009. Accessed 26.05.10.

48. New Zealand Pharmacovigilance CentredCARM.

CARM Background Information. Dunedin: CARM

[Internet Site]. [cited 2009 Sep 15]. Available at:

http://carm.otago.ac.nz/index.asp?link¼carm; 2009

Sep. Accessed 19.06.10.

49. Lamy PP. Generic equivalents: issues and concerns.

J Clin Pharmacol 1986;26:309e316.

50. Al-Gedadi N, Azmi Hassali M. Pharmacists’ views

on generic medicines: a review of the literature. J Ge-

neric Med 2008;5:209e218.

51. Barrett LL, AARP Knowledge Management. Phar-

macists’ Attitudes and Practices Regarding Generic

Drugs. Washington: AARP [Serial on the Internet].

[cited 2009 Aug 18]. Available at: http://www.aarp.

org/research; 2005 Sep. Accessed 27.06.10.

52. KirkingDM,GaitherCA,AscioneFJ,WelageLS.Phy-

sicians individual and organizational views on generic

medications. J Am Pharm Assoc 2001;41:718e722.

53. Meredith PA. Generic drugsdtherapeutic equiva-

lence. Drug Saf 1996;15:233e242.

54. Medsafe. Interchangeable Status (IMM) [Internet

Site]. [cited 2009 Sep 23]. Available at: http://medsafe.

govt.nz/profs/imm.asp; 1996. Accessed 07.07.06.

55. Purvis L, AARP Public Policy Institute. Strategies to

Increase Generic Drug Utilization and Associated Sav-

ings. Washington: AARP [Serial on the Internet].

[cited 2009 Aug 18]. Available at: http://assets.aarp.

org/rgcenter/health/i16_generics.pdf; 2008 Dec.

Accessed 15.06.10.

56. Banahan BF III, Kolaassa EM. Generic Substitution

and Narrow Therapeutic Index DrugsdA National

Survey of Retail and Hospital Pharmacies. Oxford,

Mississippi: University of Mississippi; 1994.

57. Pharmacist claiming, Media Release. Available at:

http://www.moh.govt.nz/moh.nsf/pagesmh/5284?

Open; 1994. Accessed 22.06.10.

Top Related

Copyright © 2022 FDOKUMEN