Bahasa

Halaman

Hukum

1

..........................

IS LABOUR THE FALL GUY OF A FINANCIAL-LED GLOBALISATION?

A CROSS-COUNTRY INQUIRY ON GLOBALISATION, FINANCIALISATION AND EMPLOYMENT AT THE INDUSTRY LEVEL

Cédric Durand

CEPN - Paris13/CNRS, 99 av. Jean-Baptiste Clément, 93430 Villetaneuse

Sébastien Miroudot*

OECD1, 2 rue André-Pascal, 75775 Paris Cedex 16

Abstract: This paper looks at the relationship between globalisation, employment and financialisation at the industry level by providing an analytical framework describing three modes of insertion into global production (fragmentation of production, global competition and domestic positioning) and four industry dynamics (decline, predation, rent-seeking and expansion). This analytical framework is then tested econometrically in a panel of 38 countries and 30 industries over the period 1995-2009. While regressions pooling all industries appear inconclusive, there is some evidence of contrasted outcomes across industries when they are grouped into the categories proposed in the theoretical framework. In some sectors, the productivity gains from offshoring seem to have benefited employment and the expansion of production through investment while in others they have led to rents and a higher share of the gross operating surplus going to shareholders and financial institutions (i.e. financialisation). The debate on offshoring and trade would benefit from a better understanding of the mechanisms that explain these differences among industries.

Keywords: globalisation, offshoring, financialisation, employment, industry-level.

* The authors are writing in a personal capacity. The views expressed are theirs only, and do not reflect in any way those of the OECD Secretariat or the member countries of the OECD.

JEL codes: F16, F66

.

Is labour the fall guy of financial-led globalisation? A cross-country inquiry on globalisation, financialisation and employment at the industry level"

N° 2014-1

2

1. Introduction

How does globalisation affect employment? There has been a huge amount of research and

controversies dedicated to the relationship between offshoring and jobs. Some authors (Amiti and

Wei 2005; Cohen 2006; Mankiw and Swagel 2006) have argued that the direct effects on

employment are rather limited and that they are more than compensated by the productivity

enhancing effects of trade liberalisation. At the firm (or plant) level, numerous studies have shown

that an intensification of import competition in manufacturing industries leads to the exit of the least

productive firms, while increasing the productivity of remaining firms (Pavcnik 2002; Amiti and

Konings 2007; Fernandes 2007; De Loecker 2011; Hayakawa et al. 2012). Some evidence has also

been collected at the industry level (Ferreira and Rossi 2003; Hijzen and Swaim 2007; Foster-

McGregor et al. 2013).

However, the overall impact of the globalisation of production on the economy is still debated. In a

famous paper, Samuelson (2004) has shown that when a large developed economy trades with a

large developing country, the Ricardian theory does not guarantee in each region that the net gains

of the winners will be greater than the net losses of the losers. It has also been argued that

globalisation may foster at the same time higher manufacturing productivity and de-industrialisation

in developed countries because labour-intensive manufacturing activities have been offshored and

there is a higher demand for services (Kollmeyer 2009). Moreover, McMillan and Rodrik (2011)

suggest that in some developing economies the productivity-enhancing effects of trade liberalisation

may have produced growth-reducing structural change, displacing workers in even lower-

productivity activities.

Despite this huge amount of research, the role of financialisation in explaining the impact of

globalisation on employment has been less studied. Financialisation can be defined as an increase in

the share of profit (at the firm or industry level) dedicated to financial payments at the expense of

investment and employment. To our knowledge, only the work conducted by Deborah Winckler and

Will Milberg has pointed out financialisation as a possible leak between the gains from offshoring

and employment in high-income countries (Milberg 2008; Milberg and Winckler 2010; Milberg et

Winkler 2013). Following their original insights, we propose in this study to broaden the argument

empirically and analytically. More specifically, we develop an analytical framework to jointly

explore the co-determinants of financialisation and employment at the industry level, according to

their exposure to international trade and offshoring. We then test this framework with data for 30

manufacturing and services industries over the period 1995-2009 in a panel of 38 developed and

emerging economies representing about 87% of world GDP.

3

The aim of the paper is to bring new insights on differences across industries to introduce new

elements in the policy debate surrounding globalisation and employment. Most of the literature has

not been able to capture the roots of public concerns related to the destructive socio-economic

effects of globalisation in high-income countries. What our contribution suggests is that it is not

globalisation per se that produces negative welfare outcomes, but its association in some industries

with the financialisation of non-financial firms.

The paper is organised as follows. Section 2 explains our analytical framework with four industry

dynamics (decline, predation, rent-seeking and expansion) and three modes of insertion into global

production (fragmentation of production, global competition and domestic positioning). Section 3

describes the data and the econometric methodology to test the hypothesis made in Section 2.

Section 4 presents the main econometric results with regressions on labour demand, the investment

to profit ratio (IPR) and the categories of our analytical framework. Section 5 discusses these results

in the context of the analytical framework and its underlying assumptions. Section 6 concludes.

2. Analytical framework

In order to investigate the globalisation-employment-financialisation nexus, we propose an

analytical framework that will allow us to identify the diversity in industry dynamics and the variety

of outcomes across countries. Due to data limitations and the complexity of the relationships

involved, we limit our analysis to the impact of globalisation on employment and do not consider

important related issues such as wages and inequalities.

Following the literature (Boyer 2000; Lazonick and O’Sullivan 2000; Stockhammer 2004; Krippner

2005; Aglietta and Berrebi 2007; Orhangazi 2008), financialisation can be described as a divorce

between profits and accumulation. Financialisation has been defined as a shift in the use of profits

with an increase in the acquisition of financial assets and/or a higher share of profits distributed to

shareholders and lending institutions at the expense of fixed capital formation. The ratio of

reinvested earnings can thus be used as a proxy for financialisation and measured by the ratio of

fixed investment (I) to profit (P), both being taken as a share of value added.

Financialisation, i.e. a reduction in the fixed investment share to profit share ratio, is occurring (F+)

between and when

. It may result from an increase in profits and/or a diminution in

fixed investment relatively to value added. There is no financialisation (F-) when

.

4

The share of profit not dedicated to investment is used for the remuneration of capital, including

several types of assets that can be regarded as immaterial investment, such as technology payments.

This can be an issue in our analysis, especially since measuring this knowledge-based capital is very

difficult (Plihon and Mouhoub 2009; OECD 2013). However, it should be pointed out that most of

knowledge-related expenditures are captured in national accounts data either as services

intermediate inputs (for example R&D services, especially when R&D is outsourced) or as are part

of the definition of fixed investment (I). Softwares, for example, should be included in fixed

investment according to the 2008 System of National Accounts. Therefore, the bias should be

limited and in our empirical analysis we include skill and technology variables to take it into

account.

We define employment simply as the number of hours worked. In a context of global under-

employment, such measure better reflects the dynamic of the labour market because, contrary to the

number of employee, it is not affected by the changing importance of part-time jobs. (E+) means an

increase in the number of hours worked; (E-) a reduction.

2.1 Typologies

The starting point in our analysis is the definition of four types of industry dynamics based on the

change in employment and financialisation (i.e. the investment to profit ratio). These four categories

are described in Table 1.

The combination of growing employment and financialisation is associated with Rent-seeking. It

concerns expanding industries in terms of employment where firms manage to maintain their

competitive position while giving priority to the retribution of shareholders and/or financial

operations rather than to investments.

The combination of employment improvement and no financialisation corresponds to a dynamic of

Expansion. Firms expand their activity and dedicate the gains to higher investment and/or to wage

increase.

Predation results from a combination of diminishing employment and financialisation: facing a

lower demand for their products or strong productivity gains, firms choose not to invest but rather

to maintain or expand their payments to shareholders and/or to sustain their profitability thanks to

financial operations.

Finally, Decline is associated with diminishing employment and no financialisation. While the

industry faces adverse market conditions, profits are squeezed by the diminution of productivity and

the rigidity of wages and employment.

5

F + F -

Employment + Rent-seeking Expansion

Employment - Predation Decline

Table 1: Industry dynamics according to the evolution of employment and financialisation

To assess the involvement of industries in global production networks, we also create a typology

with three globalisation dynamics. Fragmentation corresponds to a significant increase in

offshoring. We define offshoring here as the increase in the use of foreign inputs in domestic

industries, following Feenstra and Hanson (1999). Fragmentation can also be regarded as part of

vertical trade where countries specialise in a stage of production and further process a good (or

service) imported as an input and shipped to another destination, either to be further processed or to

be consumed (Hummels et al. 2001). This vertical segmentation is the basis for the recent literature

on global value chains (Bair 2009).

Global competition is characterised by the prevalence of imports of final products in the industry,

pointing to an intense international competition on this market segment. We measure it through a

significant increase in foreign value added in domestic final demand which is not explained by the

offshoring of inputs but rather by imports of final goods and services. This captures traditional trade

in final products but also another form of offshoring, which is the offshoring of the assembly of

goods. When goods are assembled off-shore, traditional measures of offshoring looking only at the

use of foreign inputs do not increase but this can also lead to increased foreign value added in

domestic consumption.

Finally, Domestic positioning is the situation in which industries experience neither a significant

increase in the offshoring of inputs, nor an increase in the foreign goods and services sold in the

domestic market (imports of value added). While there can be some overlap between the

fragmentation of production and global competition (when foreign value added in domestic

consumption increases both through imports of inputs and final products), domestic positioning is a

distinct category. Industries which are relatively isolated from the global economy vertically (trade

in inputs) as well as horizontally (global competition) are mostly domestically positioned.

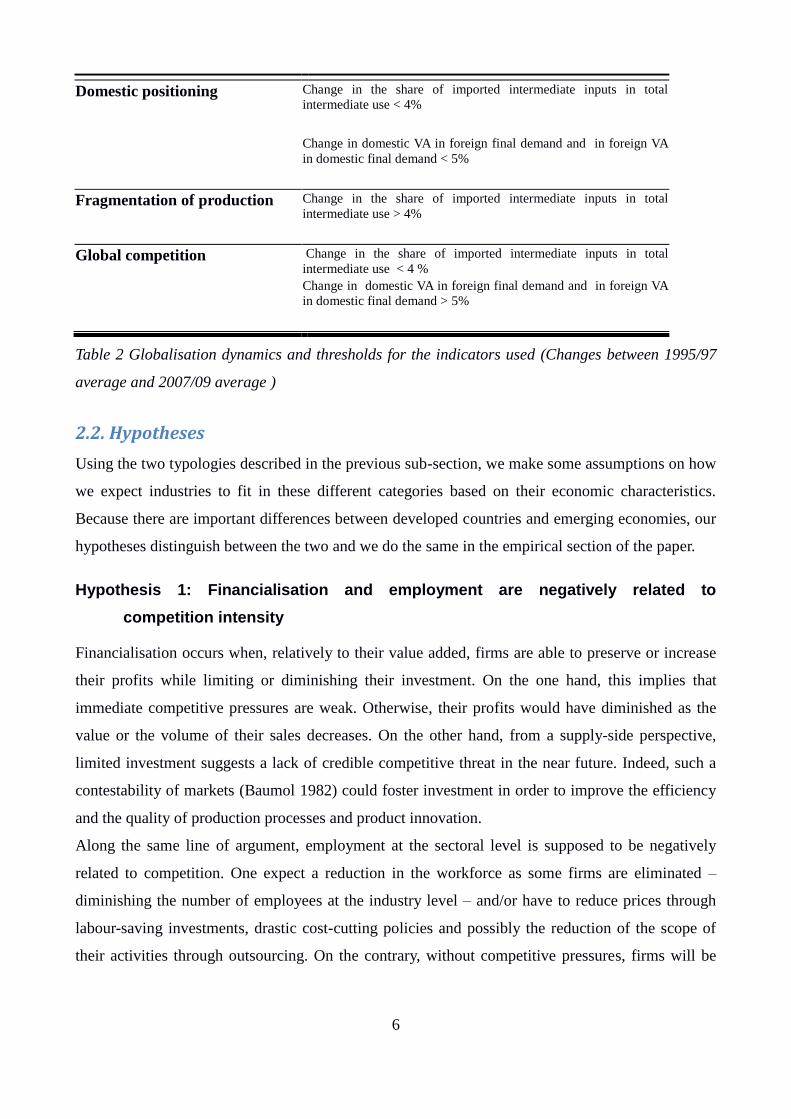

Table 2 summarizes the typology and indicates the threshold we use to distinguish between

domestic positioning, fragmentation and global competition dynamics for the period of our study.

Data and indicators are presented in detail in the section 3.

6

Domestic positioning Change in the share of imported intermediate inputs in total

intermediate use < 4%

Change in domestic VA in foreign final demand and in foreign VA

in domestic final demand < 5%

Fragmentation of production Change in the share of imported intermediate inputs in total

intermediate use > 4%

Global competition Change in the share of imported intermediate inputs in total

intermediate use < 4 %

Change in domestic VA in foreign final demand and in foreign VA

in domestic final demand > 5%

Table 2 Globalisation dynamics and thresholds for the indicators used (Changes between 1995/97

average and 2007/09 average )

2.2. Hypotheses

Using the two typologies described in the previous sub-section, we make some assumptions on how

we expect industries to fit in these different categories based on their economic characteristics.

Because there are important differences between developed countries and emerging economies, our

hypotheses distinguish between the two and we do the same in the empirical section of the paper.

Hypothesis 1: Financialisation and employment are negatively related to

competition intensity

Financialisation occurs when, relatively to their value added, firms are able to preserve or increase

their profits while limiting or diminishing their investment. On the one hand, this implies that

immediate competitive pressures are weak. Otherwise, their profits would have diminished as the

value or the volume of their sales decreases. On the other hand, from a supply-side perspective,

limited investment suggests a lack of credible competitive threat in the near future. Indeed, such a

contestability of markets (Baumol 1982) could foster investment in order to improve the efficiency

and the quality of production processes and product innovation.

Along the same line of argument, employment at the sectoral level is supposed to be negatively

related to competition. One expect a reduction in the workforce as some firms are eliminated –

diminishing the number of employees at the industry level – and/or have to reduce prices through

labour-saving investments, drastic cost-cutting policies and possibly the reduction of the scope of

their activities through outsourcing. On the contrary, without competitive pressures, firms will be

7

less keen to reduce employment and will consider an increase in employment as long as they are

able to maintain or improve their margins.

Competition intensity results from (i) the tradability of products and (ii) the level of barriers to

entry. Traditionally, such barriers result from sunk costs and the presence of scales economies.

However, there is mounting evidence of increasing competition in capital intensive core industries

as catching-up by developing countries has added excess producing capacities. This suggests that

knowledge intensity could be a better proxy for protection against competitive pressure.

As pointed out in Figure 1, one would thus expect both financialisation and employment to expand

primarily in activities characterised by low tradability and/or sectors which are knowledge

intensive.

Hypothesis 2: Global competition is the dominant form in activities where

technologies and know-how are widely diffused, while fragmentation is

relatively more important for knowledge intensive industries. Both of them

decrease in relevance when tradability of the products lowers

Tradability of goods and services is a key determinant of global competition and fragmentation;

non-tradable products are supposed to be mostly produced domestically, although some inputs

could be imported. Global competition plays a dominant role in sectors where barriers to entry are

low and, especially, where technologies and know-how are widely diffused. This does not preclude

possibilities of offshoring. However, fragmentation is supposed to be a more distinctive feature of

sectors where firms benefit from barriers to entry and could increase their mark-up thanks to lower

input prices.

Figure 1 summarizes hypotheses 1 and 2.

Figure 1: Financialisation, employment and globalization in the light of the determinants of

competition

8

Hypotheses 1 and 2 can explain two dynamics in our analytical framework: “rent seeking” (E+ ;

F+) where competition is weak due to low tradability and knowledge intensity and “decline” (E- ;

F-) where competition is strong due to high tradability and commonality of technology. As we will

further see in the discussion of our empirical results, knowledge intensity and technology

commonality are two different notions and should not be used interchangeably. Knowledge is not

only involved in technology but also in other intangible assets for which skills are important.

What is not explained on Figure 1 are the other socio-economic dynamics, “expansion” (E+ ; F-)

and “predation” (E- ; F+), as well as the importance of uneven development across countries. We

need complementary hypotheses to deal with this.

KNOWLEDGE INTENSITY

HIG

H T

RA

DA

BIL

ITY

COMMONALITY OF TECHNOLOGY

LO

W T

RA

DA

BIL

ITY

E+ F+

E- F-

do

me

sti

c c

en

teri

ng

fragmentation

global competition

9

Hypothesis 3: Late comers in global production are less prone to financialisation

than core countries

For similar industries, investment opportunities are higher in emerging countries for two reasons.

First, more than in high-income economies, there are some cheap and unexploited resources, in

particular labour. Second, these economies can benefit from late-comer advantages: they have the

possibility to rapidly catch-up with industries in more advanced economies by leap-frogging to the

most efficient techniques of production and are not constrained by the disadvantages of the front-

runners - what Thornstein Veblen (1915) called “systemic obsolescence” - in terms of old-fashioned

social and technical standards and material infrastructures.

This is almost a tautology to say that catching-up necessitates important investments and all

development policies throughout history have insisted on investment (Gerschenkron 1962;

Hirschman 1988; Amsden 1989; Wade 2004; Huang 2010). Consequently, industries in catching-up

countries are more prone to “expansion” (E+; F-) than to any other category, for any level of

knowledge intensity or tradability and for all globalisation dynamics.

Hypothesis 4: The combination of fragmentation and financialisation in high-income

economies is adverse to employment

Taking into account the case of tradable “knowledge intensive” products, the relationship between

financialisation and employment is ambivalent in high-income economies. Indeed, financialisation

and growing or stable employment could occur as long as feeble competition intensity allows firms

to preserve their profits while they are neither constrained to invest, nor to diminish the workforce.

Fragmentation could also be compatible with employment stability or growth of offshoring if (i) it

allows firms to improve their competitiveness and (ii) these gains from lower input prices translate

into expanding market shares and/or in higher profits and higher capacity investment.

However, as suggested my Milberg and Winkler (2013), the combination of offshoring and

financialisation in oligopolistic markets of high-income economies should be adverse to

employment, as mark-up gains from cheaper inputs neither translate into lower prices and higher

sales, nor into investment-led expansion, but rather into higher payments to financial markets. As a

consequence, we assume that offshoring by industries in high-income economies will favour

“predation” (E- ; F+) rather than “expansion” (E+; F-).

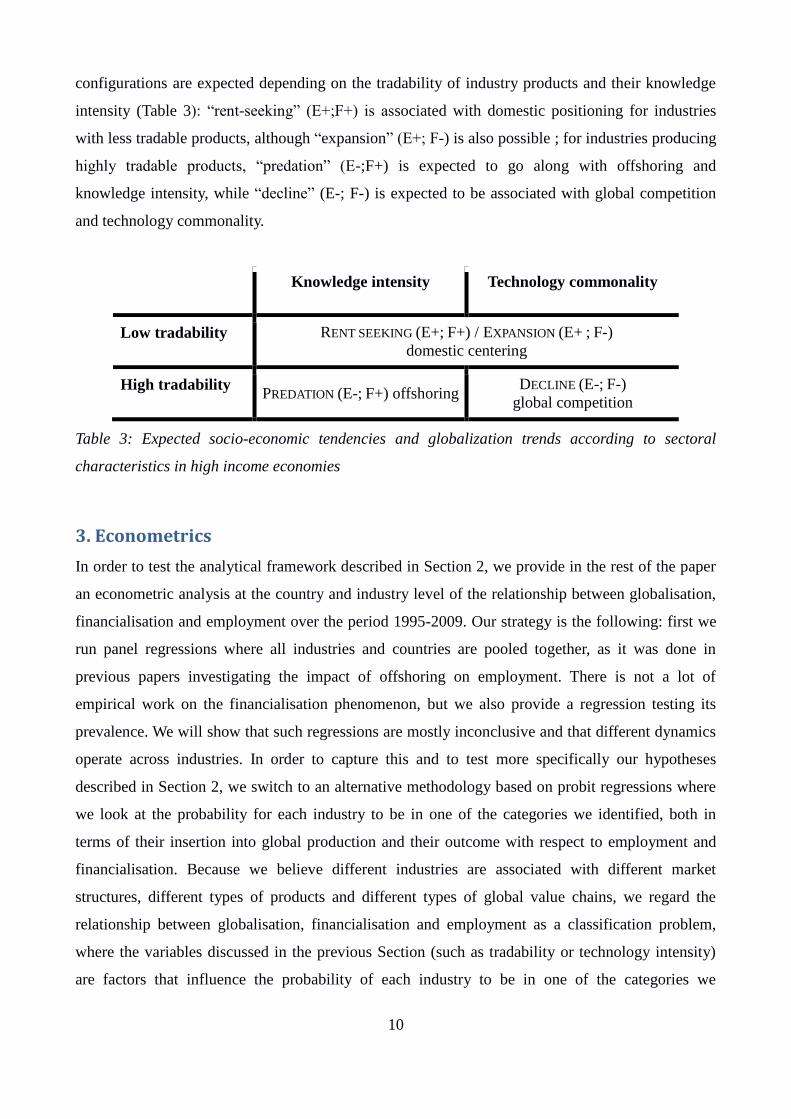

To put it in a nutshell, our hypotheses suggest that the main socio-economic dynamic for industries

in emerging countries is “expansion” (E+; F-). For high-income economies, three dominant

10

configurations are expected depending on the tradability of industry products and their knowledge

intensity (Table 3): “rent-seeking” (E+;F+) is associated with domestic positioning for industries

with less tradable products, although “expansion” (E+; F-) is also possible ; for industries producing

highly tradable products, “predation” (E-;F+) is expected to go along with offshoring and

knowledge intensity, while “decline” (E-; F-) is expected to be associated with global competition

and technology commonality.

Knowledge intensity Technology commonality

Low tradability RENT SEEKING (E+; F+) / EXPANSION (E+ ; F-)

domestic centering

High tradability PREDATION (E-; F+) offshoring

DECLINE (E-; F-)

global competition

Table 3: Expected socio-economic tendencies and globalization trends according to sectoral

characteristics in high income economies

3. Econometrics

In order to test the analytical framework described in Section 2, we provide in the rest of the paper

an econometric analysis at the country and industry level of the relationship between globalisation,

financialisation and employment over the period 1995-2009. Our strategy is the following: first we

run panel regressions where all industries and countries are pooled together, as it was done in

previous papers investigating the impact of offshoring on employment. There is not a lot of

empirical work on the financialisation phenomenon, but we also provide a regression testing its

prevalence. We will show that such regressions are mostly inconclusive and that different dynamics

operate across industries. In order to capture this and to test more specifically our hypotheses

described in Section 2, we switch to an alternative methodology based on probit regressions where

we look at the probability for each industry to be in one of the categories we identified, both in

terms of their insertion into global production and their outcome with respect to employment and

financialisation. Because we believe different industries are associated with different market

structures, different types of products and different types of global value chains, we regard the

relationship between globalisation, financialisation and employment as a classification problem,

where the variables discussed in the previous Section (such as tradability or technology intensity)

are factors that influence the probability of each industry to be in one of the categories we

11

described. At the micro level, firm strategies are the determinants of employment, financialisation

and offshoring. This is why we can regard these categories as the aggregation of choices made by

firms on the basis of their socio-economic environment.

3.1 Data

The empirical analysis relies on the World Input Output Database described in Timmer et al. (2012),

which is a set of world input-output tables (WIOTs) covering 40 countries and 35 industries over

the years 1995-2011. This dataset is particularly relevant for a comparison across countries and

industries as it is based on harmonised national accounts. In addition, WIOTs cover all inter-country

inter-industry transactions and are the ideal tool to understand global production, with indicators

going beyond the traditional measures of offshoring.

Moreover, the WIOD database includes tables in previous year prices for 1995-2009, allowing the

comparison of output and value added over time in real terms and the calculation of chain price

indexes for gross output and the cost of inputs. There are also socio-economic accounts with data on

labour, capital and investment for 1995-2009. To take advantage of these data, we limit our dataset

to this period. We keep all countries, except two very small European Union economies (Cyprus

and Malta). The dataset thus covers 38 countries, which are mostly high income countries

(Australia, Austria, Canada, Belgium, Bulgaria, the Czech Republic, Denmark, Estonia, Finland,

France, Germany, Greece, Hungary, Japan, Korea, Ireland, Italy, Latvia, Lithuania, Luxembourg,

the Netherlands, Poland, Portugal, Romania, the Slovak Republic, Slovenia, Spain, Sweden, the

United Kingdom and the United States) but also includes 8 emerging economies (Brazil, China,

Mexico, India, Indonesia, Russia, Chinese Taipei and Turkey).

From the world input-output tables (WIOTs), we collect information at the industry level on output,

value added and the use of intermediate inputs. We calculate offshoring indexes following Feenstra

and Jensen (2012) as the share of foreign intermediate inputs in total intermediate use (for a given

industry). Building on the work of the OECD and WTO on trade in value added1, we also calculate

the foreign content in domestic final demand (imports of value added) and the domestic content in

foreign final demand (exports of value added). These flows are obtained by multiplying a vector of

value added by industry and country by the Leontief inverse of the WIOTs and then by a vector of

final demand. For each country, we obtain a matrix that describes the origin of the value added in

final demand and summing the foreign and domestic elements, we can decompose final demand

into domestic and foreign value added.

1 See //oe.cd/tiva for documents describing the concepts we refer to in this section and more details on the methodology.

12

From the WIOD socio-economic accounts, we have directly for each country and industry: the

number of hours worked (our employment variable), the labour compensation, the gross operating

surplus (calculated as value added minus labour compensation), investment (gross fixed capital

formation) and a real capital stock.

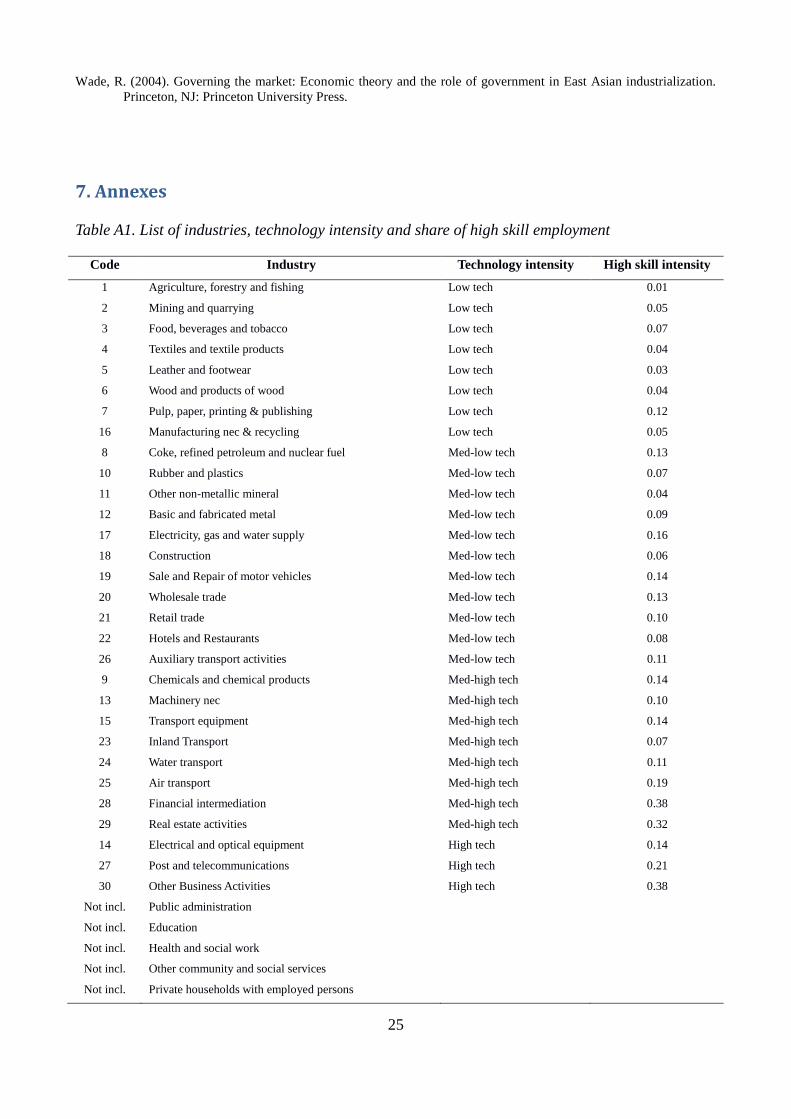

The WIOD industry classification is based on NACE Rev. 1 and we use Eurostat definitions for the

technology and knowledge intensity of these sectors. We associate each industry with a technology

level from 1 (low tech industries) to 4 (high tech industries) with 2 corresponding to mid-low tech

industries and 3 to mid-high tech industries. Knowledge intensive services sectors are either mid-

low tech (2), mid-high tech (3) or high tech (4). We drop from the dataset 5 sectors that are mostly

non-market services: ‘public administration and defence’, ‘education’, ‘health and social work’,

‘other community, social and personal services’ and ‘private households with employed persons’.

These activities are not part of global production networks and less relevant for our analysis. Inputs

coming from these industries are however included in all our calculations. The list of industries and

their technology level can be found in Table A1 in the Annex. We have also included the average

share of high skill employment in this Table to highlight that the technology level of industries and

their share of high skill jobs are not strongly correlated.

3.2 Regressions on employment and the investment profit ratio

We first run the traditional labour demand regressions found in the offshoring literature,

distinguishing between an unconditional labour demand and a conditional labour demand (Hijzen

and Swaim, 2007). Using the same WIOD dataset, Foster-McGregor et al. (2013) have shown that

offshoring has an overall neutral or slightly positive effect on employment. The variable in their

results is not always significant and our own analysis will confirm its lack of robustness

We estimate two functions at the industry level, pooling observations for all years and countries.

First the unconditional (or capital-constrained) labour demand:

(1)

where is the demand for labour in country i, industry j at year t, is the price of variable

inputs (the ratio of the hourly wage to the price of intermediate inputs), is the capital stock,

the price of output (relative to the price of intermediate inputs), and is a set of demand

shifters that includes an offshoring index but also value-added trade flows, industry mark-ups –the

price-cost margin, which is a proxy for the degree of competition- and the share of high skill labour

in employment. Rather than adding fixed effects to control for unobserved time invariant factors

influencing labour demand, we estimate the function in difference. We use a 5-year difference to

13

allow a sufficient number of years for labour to adjust.2 This type of estimation is also better to

capture the dynamic (the evolution over time) of employment and how it is affected by the change

in the independent variables. We add year fixed effects for unobserved time-varying heterogeneity.

Equation (1) measures the overall impact of the fragmentation of production on employment.

However, this total impact is the result of two opposing effects. On the one hand, offshoring is

expected to decrease employment because less labour is required in the industry to produce the

same output (the technology effect). On the other hand, as companies are more productive through

offshoring, the output of the industry can be higher with more jobs created (the scale effect). The

impact of offshoring on industry employment is therefore ambiguous, depending on the effect that

dominates. In order to assess the respective importance of the scale and technology effects, a second

labour demand function is estimated where gross output ( ) is added as an independent variable

(instead of the price of output relative to the price of intermediate inputs), so that all other

coefficients are estimated for a given level of output. This conditional labour demand measures the

technology effect of offshoring:

(2)

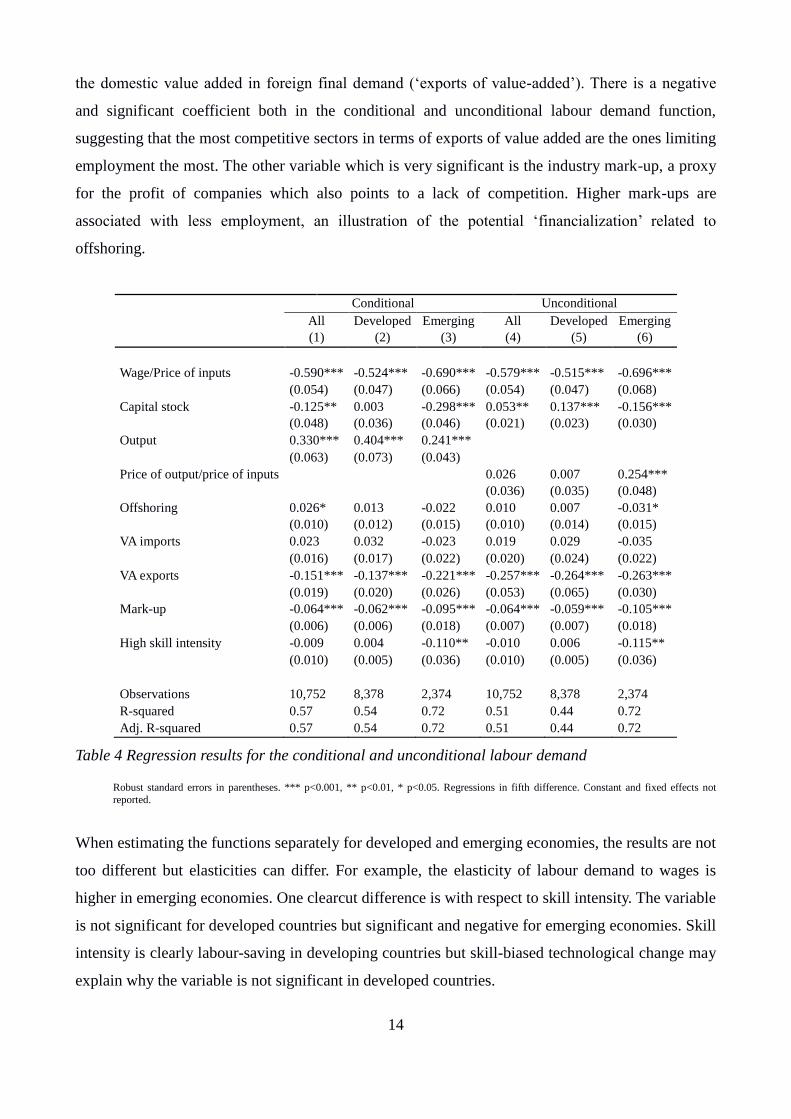

Results of the estimation of the unconditional and conditional labour demand are presented in Table

1. We run the regressions for all countries and then separately for developed countries and emerging

economies. For the whole dataset, the main variables are significant and have the expected sign.

Higher wages (relative to the price of inputs) are associated with lower employment both in the

conditional and unconditional labour demand. An increase in the capital stock also decreases

employment for a given level of output (substitution effect) but in the unconditional labour demand,

a higher capital stock is associated with more output and more employment (positive coefficient).

Output is very significant and positively correlated with employment in the conditional demand, as

one can expect. The ratio of the price of output to the price of intermediate inputs is also significant

and positive in the unconditional labour demand.

When looking at the demand shifters, the offshoring index is positive and weakly significant in the

conditional labour demand and not significant in the unconditional function. We would expect the

opposite sign for the conditional labour demand, as the theory predicts that for the same level of

output there should be less employment when part of the production is offshored. But our result is

in line with other papers that find no clear relationship between the offshoring of inputs and

employment. The foreign value added in domestic final demand is also not significant in the

regression. Interestingly, the most significant demand shifter is on the export side, when looking at

2 Hijzen and Swaim (2007) also use 5-year differences, while Foster-McGregor et al. (2013) have first differences. It

partly explains why our results are different despite using the same dataset.

14

the domestic value added in foreign final demand (‘exports of value-added’). There is a negative

and significant coefficient both in the conditional and unconditional labour demand function,

suggesting that the most competitive sectors in terms of exports of value added are the ones limiting

employment the most. The other variable which is very significant is the industry mark-up, a proxy

for the profit of companies which also points to a lack of competition. Higher mark-ups are

associated with less employment, an illustration of the potential ‘financialization’ related to

offshoring.

Conditional Unconditional

All Developed Emerging All Developed Emerging

(1) (2) (3) (4) (5) (6)

Wage/Price of inputs -0.590*** -0.524*** -0.690*** -0.579*** -0.515*** -0.696***

(0.054) (0.047) (0.066) (0.054) (0.047) (0.068)

Capital stock -0.125** 0.003 -0.298*** 0.053** 0.137*** -0.156***

(0.048) (0.036) (0.046) (0.021) (0.023) (0.030)

Output 0.330*** 0.404*** 0.241***

(0.063) (0.073) (0.043)

Price of output/price of inputs 0.026 0.007 0.254***

(0.036) (0.035) (0.048)

Offshoring 0.026* 0.013 -0.022 0.010 0.007 -0.031*

(0.010) (0.012) (0.015) (0.010) (0.014) (0.015)

VA imports 0.023 0.032 -0.023 0.019 0.029 -0.035

(0.016) (0.017) (0.022) (0.020) (0.024) (0.022)

VA exports -0.151*** -0.137*** -0.221*** -0.257*** -0.264*** -0.263***

(0.019) (0.020) (0.026) (0.053) (0.065) (0.030)

Mark-up -0.064*** -0.062*** -0.095*** -0.064*** -0.059*** -0.105***

(0.006) (0.006) (0.018) (0.007) (0.007) (0.018)

High skill intensity -0.009 0.004 -0.110** -0.010 0.006 -0.115**

(0.010) (0.005) (0.036) (0.010) (0.005) (0.036)

Observations 10,752 8,378 2,374 10,752 8,378 2,374

R-squared 0.57 0.54 0.72 0.51 0.44 0.72

Adj. R-squared 0.57 0.54 0.72 0.51 0.44 0.72

Table 4 Regression results for the conditional and unconditional labour demand

Robust standard errors in parentheses. *** p<0.001, ** p<0.01, * p<0.05. Regressions in fifth difference. Constant and fixed effects not

reported.

When estimating the functions separately for developed and emerging economies, the results are not

too different but elasticities can differ. For example, the elasticity of labour demand to wages is

higher in emerging economies. One clearcut difference is with respect to skill intensity. The variable

is not significant for developed countries but significant and negative for emerging economies. Skill

intensity is clearly labour-saving in developing countries but skill-biased technological change may

explain why the variable is not significant in developed countries.

15

When pooling all industries, there is not much we can learn from the econometric analysis. The

average effect of offshoring is not robust and the scale versus technology effect does not seem to be

supported by the data. This is why we have developed an alternative theoretical framework, looking

at how the above variables are likely to lead to different outcomes in different industries.

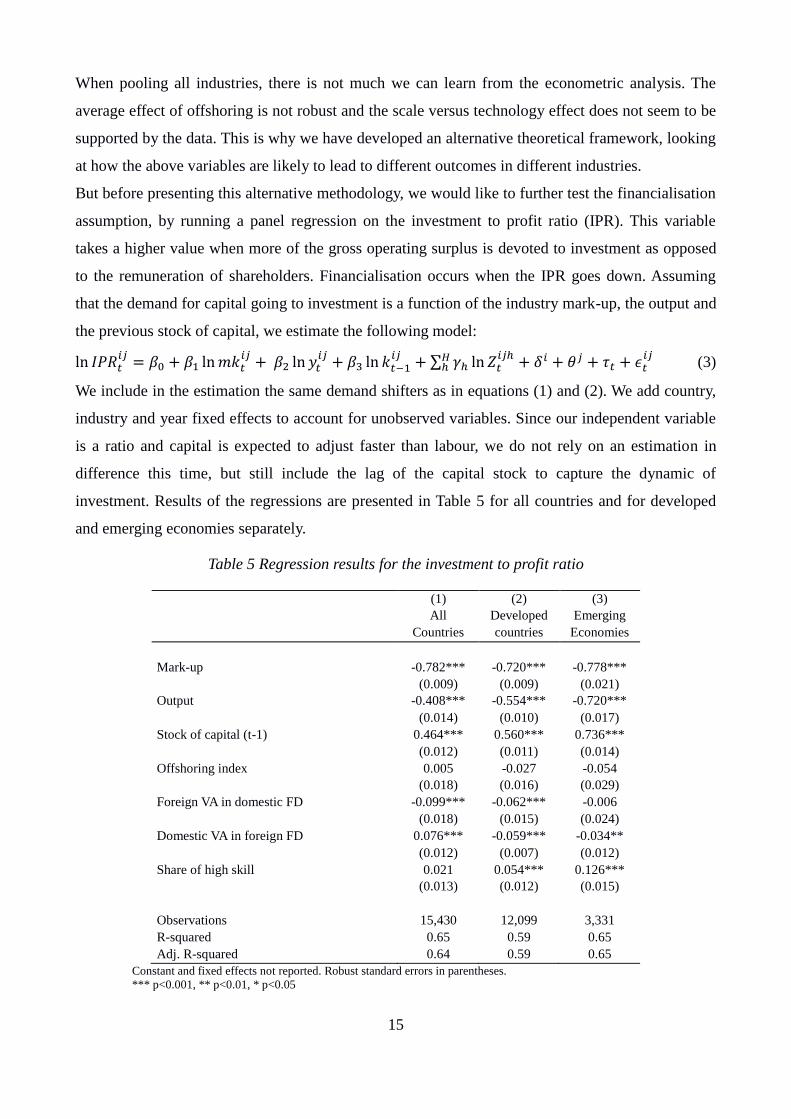

But before presenting this alternative methodology, we would like to further test the financialisation

assumption, by running a panel regression on the investment to profit ratio (IPR). This variable

takes a higher value when more of the gross operating surplus is devoted to investment as opposed

to the remuneration of shareholders. Financialisation occurs when the IPR goes down. Assuming

that the demand for capital going to investment is a function of the industry mark-up, the output and

the previous stock of capital, we estimate the following model:

(3)

We include in the estimation the same demand shifters as in equations (1) and (2). We add country,

industry and year fixed effects to account for unobserved variables. Since our independent variable

is a ratio and capital is expected to adjust faster than labour, we do not rely on an estimation in

difference this time, but still include the lag of the capital stock to capture the dynamic of

investment. Results of the regressions are presented in Table 5 for all countries and for developed

and emerging economies separately.

Table 5 Regression results for the investment to profit ratio

(1) (2) (3)

All Developed Emerging

Countries countries Economies

Mark-up -0.782*** -0.720*** -0.778***

(0.009) (0.009) (0.021)

Output -0.408*** -0.554*** -0.720***

(0.014) (0.010) (0.017)

Stock of capital (t-1) 0.464*** 0.560*** 0.736***

(0.012) (0.011) (0.014)

Offshoring index 0.005 -0.027 -0.054

(0.018) (0.016) (0.029)

Foreign VA in domestic FD -0.099*** -0.062*** -0.006

(0.018) (0.015) (0.024)

Domestic VA in foreign FD 0.076*** -0.059*** -0.034**

(0.012) (0.007) (0.012)

Share of high skill 0.021 0.054*** 0.126***

(0.013) (0.012) (0.015)

Observations 15,430 12,099 3,331

R-squared 0.65 0.59 0.65

Adj. R-squared 0.64 0.59 0.65

Constant and fixed effects not reported. Robust standard errors in parentheses.

*** p<0.001, ** p<0.01, * p<0.05

16

Because we have fixed effects in all the dimensions of the panel, the R-squared is reasonably high

but the main variables of the model explain more than 40% of the variation in the data. The industry

mark-up is strongly correlated with lower levels of IPR, indicating that industries with high profits

are less likely to have higher levels of investment. Output is also negatively correlated with the IPR,

as more productive capacity in an industry leads (in the short term) to lower investment. The lag of

the stock of capital is positively correlated with the IPR, suggesting that past investment is

associated with more investment as a share of gross operating surplus (we have a similar result if

we introduce in equation (3) the lag of investment).

As we observed with the labour demand function, there is no significant relationship between the

IPR and the offshoring index, even when limiting the data sample to developed economies. But

interestingly, another variable measuring the insertion in globalisation is significant, the foreign

value added in domestic final demand. The more an industry is ‘globalised’, importing value added

either through the use of foreign inputs (offshoring of inputs) or imports of final goods and services

(the other side of offshoring), the lower the IPR and thus the higher the ‘financialisation’. This

regression is another starting point for looking further at the relationship between employment,

financialisation and globalisation, but still does not capture what makes the outcome different

across industries.

3.3 Understanding industry dynamics using probit regressions

To test the theoretical framework described in Section 2 with an alternative methodology, we run a

series of probit regressions on the 3 different types of insertion into the global economy previously

identified: fragmentation of production (offshoring of inputs), global competition (higher foreign

value added in domestic final demand explained by imports of final goods and services) and

domestic positioning (for industries where no fragmentation or global competition occurs).

The probit models are the following (omitting subscripts for the country, industry and year):

(4)

(5)

(6)

where is the variation of the number of hours worked (over the last year), IPR is the

investment to profit ratio previously described, Mk is the industry mark-up, Skill is the skill

17

intensity (share of high skill employment) and technology is a factor variable representing the

technology level of the industry (from 1 =low tech to 4=high tech).

We pool all industries, countries and year and estimate simple probit regressions. Since our

dependent variable does not reflect a choice, we don’t run a multinomial probit.

We use a similar methodology to test the role of globalisation variables in explaining the evolution

of employment and financialisation. The typology described in Section 2 is used to look at the

probability for each industry/country to be in one of the four categories: decline, predation, rent-

seeking or expansion.

The probit models are:

=14 + (7)

=14 + (8)

=14 + (9)

=14 + (10)

Table A2 in the Annex shows the distribution of industries for developed and emerging countries

across all the categories. Results for the globalisation dynamics are presented in Table 6 below

where we report only the marginal effect of each variable in the different models. We run

independently regressions for developed and emerging economies.

Table 6 indicates a negative relation to employment in sectors where fragmentation plays a key role

in both developed and emerging economies, suggesting that foreign labour is substituted for

domestic labour through offshoring. On the contrary, a relative insulation from fragmentation and

global competition is associated with a positive correlation for domestically positioned sectors.

Interestingly, in sectors characterised by an intensification of global competition, we observe

different signs in the relation to employment: while in developed economies the impact on

employment is negative, there is no significant relationship for emerging economies.

Financialisation is associated with fragmentation in developed economies (diminishing IPR), which

points to the possibility that gains from cheaper imported inputs may be transferred to financial

markets in a context where their mark-up tend to diminish. This is in contrast with industries under

pressure of global competition where a negative mark-up trend is not associated with

financialisation, firms of developed and emerging economies not being able to increase the share of

their profits allocated to financial markets. Among developing economies, financialisation occurs

18

only in domestically positioned sectors where mark-us are on the rise, a correlation which is not

confirmed for developed countries.

Global competition is associated with low-tech industries among developed economies but not in

emerging countries, related to the difference in the level of development of these two groups.

Interestingly, among developed economies, fragmentation is associated with lower skills but also

with more mid-high technology, pointing to the possibility for some industries to retain a wide

range of employment in some segments relatively insulated from competition on final products.

Higher skills and technology are typically associated with domestic positioning, which reflects the

rapid expansion of business services and telecoms industries.

(1) (2) (3) (4) (5) (6)

Fragmentation competition domestic fragmentation competition domestic

VARIABLES Developed developed developed Emerging emerging Emerging

Employment -0.012*** -0.025*** 0.037*** -0.022*** -0.004 0.028***

(0.002) (0.002) (0.002) (0.004) (0.004) (0.004)

IPR -0.003** 0.002* 0.001 0.001 0.012* -0.041***

(0.001) (0.001) (0.001) (0.005) (0.006) (0.010)

Mark-up -0.039*** -0.131*** 0.105*** -0.036*** -0.430*** 0.186***

(0.008) (0.012) (0.006) (0.009) (0.030) (0.013)

Skill intensity -0.578*** 0.061 0.474*** 0.155* -0.256*** 0.189**

(0.040) (0.038) (0.033) (0.067) (0.077) (0.073)

2.tech -0.036*** -0.147*** 0.193*** -0.061*** -0.056** 0.137***

(0.011) (0.010) (0.009) (0.018) (0.019) (0.020)

3.tech 0.039** -0.082*** 0.045*** 0.034 0.108*** -0.137***

(0.012) (0.011) (0.010) (0.022) (0.022) (0.021)

4.tech -0.078*** -0.036* 0.115*** -0.040 -0.028 0.101**

(0.016) (0.016) (0.014) (0.027) (0.030) (0.031)

Observations 13,458 13,458 13,458 3,570 3,570 3,570

Table 6 Probit estimations – Globalisation dynamic - Average marginal effects

Standard errors in parentheses *** p<0.001, ** p<0.01, * p<0.05

dy/dx for technology levels is the discrete change from the base level (low tech industries = 1)

Tables 7 and 8 present the results for the socio-economic dynamic, respectively for developed countries and

emerging economies. Because the offshoring index and the foreign value added in domestic final demand

can be collinear, these variables are in separate regressions.

Only expansion –i.e. an increase in both the IPR ratio and employment - is associated with higher mark-ups.

As expected, decline and predation are both associated with offshoring and foreign VA. One can also note the

19

strong weight of foreign VA in the case of decline and the fact that the relationship between offshoring and

decline is more robust than in the case of predation. Offshoring thus appears to be associated to an increase

in competitive pressures which sometimes can allow firms to increase their financialisation. Interestingly,

offshoring is also associated with rent-seeking – i.e. an expansion of both employment and financialisation.

In this case, as in predation, offshoring could be considered to be at the origin of the possibility for firms to

increase their payments to financial markets and institutions.

As expected, low skills intensity and low tech levels are associated with decline, whereas rent-seeking is

associated with higher skills and higher technology. Decline occurs where technology is common. On the

contrary, firms manage to increase both employment and financialisation when their knowledge intensive

production is protected from competition.

Regarding predation and expansion, there are interesting opposite signs with respect to skill intensity and

technology. One way to interpret them would be to think about industries such as business services, telecoms

services or electrical and optical equipment. As they expand, they increase their workforce to take care of

more standardised activities which require fewer skills. In the case of predation, the logic could be one of

specialisation in the higher-end segments of mature industries.

(1) (2) (3) (4) (5) (6) (7) (8)

decline decline predation Predation Rentseeking rentseeking expansion expansion

VARIABLES developed developed developed Developed Developed developed developed developed

Mark-up -0.112*** -0.078*** -0.076*** -0.060*** -0.038*** -0.052*** 0.147*** 0.123***

(0.013) (0.013) (0.009) (0.009) (0.008) (0.008) (0.008) (0.008)

Offshoring 0.098*** 0.066** 0.056** -0.187***

(0.022) (0.023) (0.020) (0.022)

Foreign VA 0.166*** 0.107*** -0.060*** -0.186***

(0.015) (0.015) (0.013) (0.015)

Exported VA -0.002 -0.009** -0.001 -0.003 -0.000 -0.000 0.001 0.002

(0.002) (0.003) (0.001) (0.002) (0.000) (0.000) (0.001) (0.001)

Skill intensity -0.221*** -0.200*** 0.100** 0.121*** 0.202*** 0.166*** -0.105** -0.137***

(0.037) (0.037) (0.036) (0.036) (0.031) (0.032) (0.035) (0.035)

2.tech -0.173*** -0.146*** -0.258*** -0.241*** 0.169*** 0.160*** 0.273*** 0.240***

(0.010) (0.010) (0.010) (0.010) (0.008) (0.008) (0.009) (0.009)

3.tech -0.105*** -0.107*** -0.187*** -0.187*** 0.141*** 0.147*** 0.154*** 0.160***

(0.011) (0.011) (0.011) (0.011) (0.009) (0.009) (0.009) (0.010)

4.tech -0.295*** -0.285*** -0.119*** -0.110*** 0.230*** 0.230*** 0.183*** 0.174***

(0.011) (0.010) (0.015) (0.015) (0.014) (0.014) (0.014) (0.014)

Observations 13,468 13,468 13,468 13,468 13,468 13,468 13,468 13,468

Table 7 Probit estimations for developed countries – Socio-economic dynamic - Average marginal

effects

Standard errors in parentheses *** p<0.001, ** p<0.01, * p<0.05

dy/dx for technology levels is the discrete change from the base level (low tech industries = 1)

For emerging economies, the coefficients tend to be similar to the ones observed for high-income

countries. There are, however, two interesting differences to report. First, rent-seeking tends to be

negatively correlated with offshoring, which could be explained by the fact that there is not much

20

room for gains from cheaper inputs from lower wage countries in the case of emerging economies.

The second difference concerns the role of exports of domestic value-added. While the variable is

mostly not significant for developed economies, we observe on the contrary some weak but still

significant coefficients in the group of emerging countries. While rent-seeking is associated with a

lower specialisation in exports, there is a positive link between the expansion of industries and

export activities.

(1) (2) (3) (4) (5) (6) (7) (8)

decline decline predation Predation Rentseeking rentseeking expansion expansion

VARIABLES emerging emerging emerging Emerging Emerging emerging emerging emerging

Mark-up -0.094*** -0.073*** -0.041*** -0.038*** -0.020** -0.023** 0.080*** 0.070***

(0.022) (0.021) (0.011) (0.011) (0.007) (0.008) (0.013) (0.012)

Offshoring 0.217*** 0.279*** -0.181** -0.405***

(0.051) (0.039) (0.062) (0.073)

Foreign VA 0.256*** 0.114*** -0.113** -0.282***

(0.030) (0.026) (0.038) (0.044)

Exported VA 0.048*** -0.005 -0.022 -0.033* -0.062** -0.046* 0.017 0.064**

(0.013) (0.015) (0.012) (0.014) (0.019) (0.021) (0.020) (0.023)

Skill intensity -0.816*** -0.855*** 0.415*** 0.437*** 0.189** 0.173** -0.328*** -0.352***

(0.087) (0.087) (0.042) (0.042) (0.057) (0.058) (0.079) (0.079)

2.tech -0.176*** -0.163*** 0.031* 0.047*** 0.066*** 0.061*** 0.127*** 0.110***

(0.017) (0.017) (0.014) (0.014) (0.015) (0.015) (0.022) (0.022)

3.tech -0.133*** -0.130*** 0.016 0.017 0.173*** 0.174*** -0.013 -0.015

(0.019) (0.019) (0.015) (0.014) (0.019) (0.019) (0.024) (0.024)

4.tech -0.258*** -0.256*** -0.048** -0.040** 0.421*** 0.416*** -0.067* -0.080*

(0.019) (0.018) (0.015) (0.015) (0.030) (0.030) (0.032) (0.032)

Observations 3,570 3,570 3,570 3,570 3,570 3,570 3,570 3,570

Table 8 Probit estimations for emerging economies – Socio-economic dynamic - Average marginal

effects

Standard errors in parentheses *** p<0.001, ** p<0.01, * p<0.05

dy/dx for technology levels is the discrete change from the base level (low tech industries = 1)

4. Discussion

In this section we discuss our initial hypotheses in light of the econometric results and descriptive

statistics presented in the Annex.

When looking at how industries are distributed across the categories introduced in the analytical

framework (Table A2), there is already some evidence supporting our third hypothesis, which is

about marked differences between developing and developed economies. Expansion is the dominant

socioeconomic dynamics among developing economies (47,9%) and financialisation is a limited

phenomenon concerning about 33% of the industries. In developed economies, 48% of the

industries are under financialisation and employment is declining for 51% of them, against 30,2% in

21

emerging economies. Expansion (28.1%) ranks first, as in emerging economies, but not very far

from predation (27,1%), followed by decline (23, 9%) and rent-seeking (20,9%).

With respect to the relevance of the employment-globalisation-financialisation nexus, finding a

negative relationship between mark-ups and employment in the labour demand estimation seems to

contradict our first hypothesis that protection from competition is favourable to employment.

However, a positive link between mark-ups and financialisation (diminishing IPR), is in line with

the other part of this first hypothesis, which suggests a trade-off between financialisation and

employment. We can see here some support for our general argument that a consistent assessment

of the impact of globalisation on labour requires to take into account the financialisation

phenomenon.

The results of the econometric analysis also support the other argument we made about the lack of

robustness of regressions trying to establish a generic relationship between offshoring and

employment. This may be partly related to the definition and measurement of offshoring, as

suggested by the different results we have for an offshoring index based on the use of foreign inputs

versus more sophisticated value-added measures of the offshoring of production. But the main

result of the analysis is that it is important to look at the specificities of industries, in particular

along the dimensions of tradability, competition and skill or technology intensity.

Our empirical results tend to support the idea that global competition –only for developed

economies- and fragmentation are adverse to employment at the industry level, contrary to domestic

positioning. However, one needs to distinguish between fragmentation which is associated with

financialisation and globalisation where there is no financialisation. This result is in line with our

fourth hypothesis and is relevant for both developing and developed economies. It is supported by

the probit analysis of socio-economic dynamics that shows a positive relationship between

predation and offshoring, which means that gains offshoring could be used to maintain payments to

financial markets and institutions at the expense of employment. Interestingly, in developed

countries, rent-seeking is also associated with offshoring which also suggests a positive relationship

between offshoring and financialisation but in a context where limited competition allows firms to

expand employment.

As expected, the dynamic of expansion, i.e. an increase in both employment and the IPR ratio, is at

the opposite of predation: it occurs (in developed countries) only when the mark-up is increasing

and in the context of diminishing offshoring and diminishing imports of foreign VA.

Finally, decline is associated with both offshoring and increased foreign VA, as firms facing an

intensification of competition (diminishing mark-up) are not able to increase the share of their

22

profits dedicated to financial markets but have to squeeze employment and try to diminish their

input costs thanks to offshoring.

Skills and technology indicators also show a good fit to the analytical framework as shown on

Figure 2 below. Decline is associated with technological commonality and low skills. At the

opposite side of the Figure, rent-seeking is associated with higher skills and higher technology.

However, there seems to be a more subtle relationship for the predation dynamic, where there is a

positive relationship with skills and negative relationship with technology. This suggests that in

some mature industries, firms focus on the high quality end of the spectrum of products thanks to

highly qualified workers. The case of expansion is less surprising: new medium to high-tech

expanding industries enlarge their workforce and in doing so recruit less skilled workers than

before.

Figure 2. An empirical test of Figure 1 (all industries and countries)

Note: Tradability is the average of the offshoring index and the foreign value in domestic final demand (to capture both

the tradability of inputs and final products). The technology intensity is as defined in Table A.1. Values for each

category are the unweighted average across all industries and countries.

5. Conclusion

From the above analysis, there are two important implications regarding the relationship between

globalisation and employment. First, it is important to take into account differences across

industries and the fact that in a non-competitive environment or in markets where technology

matters, the gains from offshoring do not automatically lead to higher levels of employment and

23

investment. This is also expected as offshoring is about specialisation and specialisation implies that

some industries are declining while others expand their output. In the context of global value

chains, however, we could expect specialisation to be more within industries than across industries.

Therefore, there are other mechanisms to take into account, such as financialisation. The first

conclusion is that industries matter and that future research on offshoring and employment should

focus on differences across industries. We refer to industries because this is the statistical unit used

in national accounts but we should rather refer to global value chains in the context of the

international fragmentation of production.

The second conclusion of the paper is, however, that using such industry-level data, we cannot find

strong econometric relationships between globalisation, employment and financialisation, and this

is why we used as our main methodology probit regressions that highlight some differences in the

probability for each industry of going into one direction or the other. More analysis at the firm level

(or the global value chain level) would be needed to bring more robust evidence. The aggregate

analysis presented in this paper should be regarded as a starting point.

Nevertheless, we believe such analysis can bring more concrete policy implications in the debate on

the globalisation of production by focusing on how policies can encourage firms to use the gains

from offshoring to increase employment and investment.

6. References

Aglietta, M., & Berrebi, L. (2007). Désordres dans le capitalisme mondial. Paris: Odile Jacob.

Amiti, M. & Konings, J. (2007). Trade Liberalization. Intermediate Inputs, and Productivity: Evidence from Indonesia .

The American Economic Review, 97(5), 1611-1638.

Amiti, M. & Wei, S.J., (2005). Fear of service outsourcing: is it justified?, Economic Policy, 20 (42), 308-347.

Amsden, A. (1989). Asia's next giant: South Korea and late industrialization. New-York: Oxford University Press.

Bair, Jennifer (2009). Frontiers of commodity chain research. Stanford, Calif: Stanford University Press.

Baumol, W. J. (1982). Contestable markets: an uprising in the theory of industry structure. American economic review,

72(1), 1-15.

Boyer, R. (2000). Is a Finance-led growth regime a viable alternative to Fordism? A preliminary analysis . Economy and

Society 29 (1) (janvier 1), 111-145.

Cohen, D. (2006), Les effets du commerce international sur l'emploi dans les pays riches. In P. Auer, G. Besse & Meda,

D. (2006), Délocalisation, normes de travail et politique de l'emploi: vers une mondialisation plus juste. Paris :

La Découverte.

De Loecker, J. (2011). Product differentiation, multiproduct firms, and estimating the impact of trade liberalization on

productivity . Econometrica, 79 (5), 1407-1451.

Feenstra, R. C. & Jensen, J. B. (2012). Evaluating Estimates of Material Offshoring from US Manufacturing.

Economics Letters, 117(1), 170-173.

24

Feenstra, R.C. and Hanson, G.H. (1999). The Impact of Outsourcing and High-Technology Capital on Wages: Estimates

for the United States, 1979-1990. Quarterly Journal of Economics, 114(3), 907-940.

Fernandes, A. (2007). Trade policy, trade volumes and plant-level productivity in Colombian manufacturing industries.

Journal of International Economics, 71(1), 52-71.

Ferreira, P. & Rossi, J..(2003). New Evidence from Brazil on Trade Liberalization and Productivity Growth.

International Economic Review, 44 (4), 1383-1405.

Foster-McGregor, N., Stehrer, R. & de Vries, G. J. (2013). Offshoring and the Skill Structure of Labour Demand.

Review of World Economics, 149(4), 631-662.

Gerschenkron, A., (1962). Economic backwardness in historical perspective. Cambridge, MA: Harvard University

Press.

Hayakawa, K., Machikita, T. & Kimura, F. (2012), Globalization and Productivity: A Survey of Firm-Level Analysis.

Journal of Economic Surveys. 26 (2), 332-350.

Hijzen, A. & Swaim, P. (2007). Does Offshoring Reduce Industry Employment? National Institute Economic Review,

201(1), 86-96.

Hirschman, A.(1988). The strategy of economic development. Boulder: Westview Press.

Huang, H. (2010). Capitalism with Chinese Characteristics, Cambridge University Press.

Hummels, D., Ishii, J. and Yi, K.-M. (2001). The Nature and Growth of Vertical Specialization in World Trade. Journal

of International Economics, 54(1), 75-96.

Kollmeyer, C. (2009). Explaining Deindustrialization: How Affluence, Productivity Growth, and Globalization

Diminish Manufacturing Employment. American Journal of Sociology, 114(6), 1644-1674.

Krippner, G. (2005). The financialisation of the American economy . Socio-Economic Review 3 (2),173-208.

Lazonick, W. & O’Sullivan, M. (2000). Maximizing shareholder value: a new ideology for corporate governance .

Economy and Society 29 (1), 13-35.

Mankiw, G. and P. Swagel (2006), The Politics and Economics of Offshore Outsourcing”, Journal of Monetary

Economics, 53(5), 1027-1056.

McMillan, M. & Rodrik, D. (2011). Globalization, structural change and productivity growth. NBER Working Paper,

171-143.

Milberg, W, & Winkler, D. 2010. Financialisation and the dynamics of offshoring in the USA. Cambridge Journal of

Economics, 34 (2), 275 293.

Milberg, W. & Winckler, D. (2013). Outsourcing Economics: Global Value Chains in Capitalist Development.

Cambridge; New York: Cambridge University Press.

Milberg, W. (2008). Shifting sources and uses of profits: sustaining US financialisation with global value chains.

Economy and Society, 37(3), 420-451.

OECD (2013). Supporting Investment in Knowledge Capital, Growth and Innovation. Paris: OECD Publishing.

Orhangazi, Ö. (2008). Financialisation and capital accumulation in the non-financial corporate sector: A theoretical and

empirical investigation on the US economy: 1973–2003 . Cambridge Journal of Economics, 32(6), 863-886.

Pavcnik, N. (2002). Trade liberalization, exit, and productivity improvements: Evidence from Chilean plants. The

Review of Economic Studies, 69(1), 245-276.

Plihon, D. & Mouhoub, E.M. (2009). Le savoir et la finance. Paris : La Découverte.

Samuelson, P. (2004). Where Ricardo and Mill Rebut and Confirm Arguments of Mainstream Economists Supporting

Globalization. The Journal of Economic Perspectives, 18(3), 135-146.

Stockhammer, E. 2004. Financialisation and the slowdown of accumulation . Cambridge Journal of Economics, 28 (5).

719-741.

Timmer, M. P. (ed) (2013). The World Input-Output Database (WIOD): Contents, Sources and Methods”. WIOD

Working Paper Number 10, downloadable at http://www.wiod.org/publications/papers/wiod10.pdf

Veblen T. [1915] (1994). Imperial Germany and the Industrial Revolution. In The Collected Work of Thorstein Veblen.

vol. 4. London: Routledge.

25

Wade, R. (2004). Governing the market: Economic theory and the role of government in East Asian industrialization.

Princeton, NJ: Princeton University Press.

7. Annexes

Table A1. List of industries, technology intensity and share of high skill employment

Code Industry Technology intensity High skill intensity

1 Agriculture, forestry and fishing Low tech 0.01

2 Mining and quarrying Low tech 0.05

3 Food, beverages and tobacco Low tech 0.07

4 Textiles and textile products Low tech 0.04

5 Leather and footwear Low tech 0.03

6 Wood and products of wood Low tech 0.04

7 Pulp, paper, printing & publishing Low tech 0.12

16 Manufacturing nec & recycling Low tech 0.05

8 Coke, refined petroleum and nuclear fuel Med-low tech 0.13

10 Rubber and plastics Med-low tech 0.07

11 Other non-metallic mineral Med-low tech 0.04

12 Basic and fabricated metal Med-low tech 0.09

17 Electricity, gas and water supply Med-low tech 0.16

18 Construction Med-low tech 0.06

19 Sale and Repair of motor vehicles Med-low tech 0.14

20 Wholesale trade Med-low tech 0.13

21 Retail trade Med-low tech 0.10

22 Hotels and Restaurants Med-low tech 0.08

26 Auxiliary transport activities Med-low tech 0.11

9 Chemicals and chemical products Med-high tech 0.14

13 Machinery nec Med-high tech 0.10

15 Transport equipment Med-high tech 0.14

23 Inland Transport Med-high tech 0.07

24 Water transport Med-high tech 0.11

25 Air transport Med-high tech 0.19

28 Financial intermediation Med-high tech 0.38

29 Real estate activities Med-high tech 0.32

14 Electrical and optical equipment High tech 0.14

27 Post and telecommunications High tech 0.21

30 Other Business Activities High tech 0.38

Not incl. Public administration

Not incl. Education

Not incl. Health and social work

Not incl. Other community and social services

Not incl. Private households with employed persons

26

Table A2. Number of observations in each category

Developed countries

Decline Predation Rent-seeking Expansion Total

Fragmentation 102 117 60 91 370

Competition 78 84 48 68 278

Domestic 35 42 80 93 250

Total 215 243 188 252 898

% 23,9 27,1 20,9 28,1 100

Emerging economies

Decline Predation Rent-seeking Expansion Total

Fragmentation 12 9 12 28 61

Competition 19 10 18 39 86

Domestic 15 7 22 47 91

Total 46 26 52 114 238

% 19,3 10,9 21,8 47,9 100

Top Related

Copyright © 2022 FDOKUMEN