Bahasa

Halaman

Hukum

Auditing Complex Fair Value

Measurements: The Battle of Interpretations

Emil Otterskog

Ted Wanning

Stockholm Business School

Bachelor’s Degree Thesis 15 HE Credits

Subject: Business Administration

Spring semester 2020

Supervisor: Gunilla Eklöv Alander

Acknowledgements

We want to say our thanks to everyone who helped us with this thesis. Our supervisor Gunilla

Eklöv Alander who was of tremendous help, our interviewees and everyone who helped us

find possible interviewees. Their efforts were much appreciated in these difficult times with

the Covid-19 pandemic. We would also like to thank our fellow students for contributing

useful feedback, as well as, everyone who helped us proofread the thesis.

Stockholm, June 2020

Emil Otterskog and Ted Wanning

Abstract

Level: Bachelor Thesis in Accounting, 15 HE credits

Date: 2020-06-04 (June 4th, 2020)

Title: Auditing Complex Fair Value Measurements: The Battle of Interpretations

Authors: Ted Wanning, [email protected]

Emil Otterskog, [email protected]

Supervisor: Gunilla Eklöv Alander

Fair Value Accounting is becoming increasingly more prominent, and auditing such

measurements is at times difficult as a great deal of estimates and judgments are involved. This

makes auditors jobs more challenging. Research has found that there is a need for

understanding how auditing standards affect the audit process. Furthermore, some studies have

shown that there is a gap between auditors and inspectors view of what constitutes sufficient

and appropriate audit evidence regarding fair value measurements, the “FVM gap”. The aim

of this study is to provide new insight on how auditing standards and inspectors affect the

judgment of auditors in regards to fair value measurements. This study contributes to audit

standard setters by illuminating how current auditing standards affect auditor judgment when

auditing fair value measurements. It also contributes knowledge on how inspections affect

judgment in the auditing process. Finally, it provides insight to practitioners on how box-

checking and similar tools affect auditor judgment. We performed semi-structured interviews

with respondents who have considerable experience of fair value measurements. The empirical

data was thematically analysed and related to theories on judgment and decision-making as

well as structure versus judgment research. A number of interesting findings were made;

auditing standards seem to be well adjusted to auditors’ needs, documentation is one of the

major issues when dealing with fair value measurements and the toughness of inspections

between countries seem to differ. Some potential topics for future research were identified:

whether or not a gap of interpretations exists between auditors and the lawyers of inspecting

entities, and what effects such a gap could have; if the documentation of both audit clients and

auditors needs to be improved upon. More potential areas for future research can be found in

the Conclusion.

Keywords

Fair Value; Fair Value Measurements; Auditing; Auditing Standards; Audit Inspections;

Judgment; Decision-Making; Structure; FVM Gap

Abbreviations FV - Fair Value

FVMs - Fair Value Measurements

FVA - Fair Value Accounting

FVOEs - Fair Value and Other Estimates

Big 4 - Deloitte, EY, KPMG, PwC

RI - Revisorsinspektionen (The Swedish Audit Inspection)

JDM - Judgment Decision-Making

ISA - International Standards on Auditing

IFRS - International Financial Reporting Standards

US GAAP - US Generally Accepted Accounting Principles

PCAOB - Public Company Accounting Oversight Board

IAASB - International Auditing and Assurance Standards Board

MBS - Mortgage-Backed Securities

Table of Contents

1. Introduction ................................................................................................................................................................. 1

1.1 Background ............................................................................................................................................................. 1

1.2 Previous Research ................................................................................................................................................ 2

1.3 Problematization and Research Question .................................................................................................. 3

1.4 Aim and Contribution ......................................................................................................................................... 4

2. Theory ............................................................................................................................................................................. 5

2.1 Literature Review ................................................................................................................................................. 5

2.1.1 IFRS 13 – Fair Value Measurement ...................................................................................................... 5

2.1.2 ISA 540 – Auditing Accounting Estimates and Related Disclosures ....................................... 6

2.1.3 The Challenges of Auditing FVMs and its Impact on the Audit Process ................................ 7

2.1.4 Regulatory and Legal Influences in regard to Auditing FVMs ................................................... 9

2.1.5 Summary of Previous Research on Auditing FVMs ..................................................................... 10

2.2 Theoretical Framework ................................................................................................................................... 11

2.2.1 Judgment and Decision-Making Expertise ...................................................................................... 12

2.2.2 Structure versus Judgment .................................................................................................................... 13

2.2.3 Theoretical Framework .......................................................................................................................... 15

3. Method ......................................................................................................................................................................... 17

3.1 Ontological and Epistemological Assumptions ...................................................................................... 17

3.2 Research Design .................................................................................................................................................. 17

3.2.1 Data Collection Technique ..................................................................................................................... 17

3.2.2 Sample ............................................................................................................................................................ 18

3.2.3 Operationalization..................................................................................................................................... 19

3.3 Data Analysis ........................................................................................................................................................ 20

3.4 Ethical Reflections .............................................................................................................................................. 21

3.5 Quality Criteria .................................................................................................................................................... 21

3.6 Limitations and Weaknesses ......................................................................................................................... 22

4. Empirical Findings and Analysis ................................................................................................................... 24

4.1 The Complexity of FVMs .................................................................................................................................. 24

4.1.1 An Increased Work Burden ................................................................................................................... 24

4.1.2 What the Focus is Put on When Auditing FVMs ............................................................................ 25

4.1.3 How FVMs Are Handled .......................................................................................................................... 27

4.2 Auditing Standards ............................................................................................................................................ 28

4.2.1 Audit Standard Rigidness and Box-Checking ................................................................................. 29

4.2.2 Differences Between ISA and US GAAS ............................................................................................. 30

4.3 Inspector Influence ............................................................................................................................................ 32

4.3.1 The Role of Inspectors and Revisorsinspektionen ...................................................................... 32

4.3.2 Documentation and Checklists ............................................................................................................. 33

4.3.3 The FVM Gap ................................................................................................................................................ 34

4.3.4 Differences in Inspections Internationally ...................................................................................... 35

4.4 Interplay Between the Complexity of FVMs, Auditing Standards, Inspector Influence, and

its Application on the Framework ...................................................................................................................... 36

5. Discussion .................................................................................................................................................................. 38

5.1 Discussion of Findings ...................................................................................................................................... 38

5.2 Contribution ......................................................................................................................................................... 41

6. Conclusion ................................................................................................................................................................. 43

7. References ................................................................................................................................................................. 45

8. Appendix ..................................................................................................................................................................... 50

1

1. Introduction

In this section we present a short background of the field of research and concisely present

what previous studies have found. With this we introduce the problem that we have identified

and present the research question. We then establish the aim and contribution of this thesis as

well as how we intend to conduct the research.

1.1 Background

“Bailout Plan Rejected, Markets Plunge, Forcing New Scramble to Solve Crisis”

(Lueck et al., 2008)

The 2008 financial crisis saw large parts of the world fall into a deep recession that greatly

affected companies and individuals alike. Mortgage-backed securities (MBS) played a pivotal

role in the continuation of the crisis as loan-takers could not repay what they owed, essentially

making the MBS worthless leading to some banks going belly up (Gilreath, 2018). A largely

debated, contributing factor to the MBS issues was fair values (Pozen, 2009). Fair value1 is a

way of valuing assets held by corporations based on their estimated values as opposed to

observed prices and is as such open to interpretation and debate, which makes the assets value

subject to considerable uncertainty. This uncertainty has proven troublesome in several areas

beyond the financial crisis, especially in the field of auditing (Bell & Griffin, 2012).

Since the inception of fair values, the field of accounting has developed at a rapid pace to see

fair value accounting (FVA) take on an increasingly prominent role. In many ways FVA can

be said to be a “game-changer” in modern financial accounting (Bell & Griffin, 2012). Experts

and decision makers in the field of auditing are forced to revise and review practices, standards

and regulations regarding how to handle FVA in order to stay on par with the changes in the

accounting field (Power, 2010). This has proven to be a great challenge for firms and auditors

alike when dealing with the changing demands of assurance that these complex, fair value

based financial systems impose (Bell & Griffin, 2012).

1 Level 2 and Level 3 inputs which have no/limited active markets to compare with. More on this in the theory

section.

2

1.2 Previous Research

What is it then that makes FVA and FVMs complex? According to Martin et al. (2006) FVMs

often incorporate estimates of future events and are therefore subject to uncertainty and “(...)

an element of judgment is always involved” (p. 289). When dealing with estimates it is often

difficult to get a high level of assurance and even small adjustments to estimated values can

have significant impact on financial statements (Christensen et al., 2012). Bratten et al. (2013)

found that since fair value estimations are carried out according to models and specifications

set by the management of organizations, there is a risk that the assumptions made and models

used are adjusted to suit their personal agendas and incentives.

How does this affect auditors and the auditing process? Martin et al. (2006) and Singh (2015)

established that auditors need to acquire specialised knowledge on FVMs in order to properly

evaluate them in the auditing process. It is reasonable to assume that this is not a trivial task as

Bratten et al. (2013) state that many auditors lack essential knowledge of the FVA methods

employed by their clientele. FVMs also seem to increase the difficulty to make proper risk

assessments amongst auditors. Cannon and Bedard (2017) conducted a study based on

experiences of audit team personnel, in which they examined how the complex nature of FVMs

caused estimation uncertainty to exceed materiality in over 70 percent of the cases studied.

They also found that despite this, in over 30 percent of the cases where estimation uncertainty

exceeded materiality, the auditors only assessed the inherent risk as low to moderate. Bratten

et al. (2013) suggest that a contributing factor to this may be that estimation uncertainty

significantly increases the task difficulty of an FVA audit. One of the measures auditors use to

try to tackle this is seeking expert help from specialists (Martin et al., 2006; Griffith et al.,

2015).

Another issue is that standard setters and practicing auditors seem to not always be on the same

page regarding new standards introduced to address FVMs (Power, 2010; Christensen et al.,

2012). Furthermore, Power (2010) found that when it comes to FVA, auditing standards seem

to have been left behind forcing them to be reactive to changes of accounting standards rather

than proactive. Glover et al. (2019) found a gap between what inspectors and auditors feel is

sufficient evidence for assurance when auditing FVMs and Christensen et al. (2012) add that

new, complicated standards2 hinder auditors’ ability to perform an adequate audit.

2 Christensen et al. (2012) investigated both PCAOB and ISA standards.

3

1.3 Problematization and Research Question

Overall there seems to exist a fair amount of research on the topic of FVMs in auditing (e.g.

Martin et al., 2006; Christensen et al., 2012; Bratten et al., 2013; Cannon & Bedard, 2017).

However, one area that is in need of development, as recognised by Glover et al. (2019), is

whether the way current auditing standards3 are formulated is too ambiguous or rigid, which

may cause issues in the auditing process. Bratten et al. (2013) bring up the fact that auditors in

general seem somewhat adverse to the standards in effect and Christensen et al. (2012) suggest

that further studies on auditors’ views and opinions on how the standards affect audits are of

importance. Furthermore, Glover et al. (2019) state that there is a phenomenon known as the

FVM gap, in which auditors and inspectors have such differing views of what qualifies as

sufficient, appropriate audit evidence when auditing FVMs, that the behaviour of auditors may

change and the quality of audits suffers as a result. For example, they mention that 70 percent

of participants in their study believed that inspectors expected more audit evidence than the

relevant standard required. Glover et al. (2019) note that, since their study was conducted in

America, their findings are tied to the American system and therefore may not be as applicable

internationally. This is another point of inquiry for this thesis; to investigate whether there are

indications of the FVM gap on the Swedish market and what effects inspections may have on

auditors’ judgment, or if different regulatory systems have different implications for the

interpretations made by auditors and inspectors.

This thesis looks into the issue of the FVM gap and the configuration of current audit standards

by hearing from auditors, a valuation specialist, and an inspector in what ways they find current

fair value audit standards affect the auditing of FVMs. Furthermore, how their interactions and

interpretations during inspections affect the audit process and auditor judgment. We attempt to

address these issues and lessen the gap in the understanding of FVM auditing by answering the

question:

What effects do auditing standards and inspectors have on auditor judgment regarding

the audit of FVMs?

3 In our case, we are focusing on ISA 540. More on this in the Theory section.

4

1.4 Aim and Contribution

The overarching aim of this thesis is to shed light on how the potential ambiguities and

deficiencies in current fair value auditing standards affect auditor judgment when auditing

FVMs. Furthermore, to explore the possible gap between auditors’ and inspectors’ ideas of

what qualifies as sufficient audit evidence in a FV auditing context, as described by Glover et

al (2019), and its potential effects on auditor judgment. This is a vital area to explore further in

order to improve the quality of audits including uncertain estimates which are continuously

increasing in frequency in modern accounting (Power, 2010; Bell & Griffin, 2012). This study

may inform standard setters about improvement possibilities in order to increase the

effectiveness, accuracy and level of assurance of audits when FVMs are a major influence.

Other researchers may use this study’s findings to guide them in further studies on topics such

as the FVM gap, and also other areas of potential future research which are suggested in the

Conclusion.

To answer the research question we sought out auditors, an inspector from an inspecting entity4

and a valuation specialist who had experience of working with FVMs. We conducted an

interview study where we asked about FVMs, auditing standards, and inspector influence

which gave us the necessary empirical data needed to address the research question. More on

this in the method section of the thesis.

4 Revisorsinspektionen (RI), the Swedish equivalent to PCAOB.

5

2. Theory

This section has two parts: the literature review and the theoretical framework. In the literature

review we first present the relevant accounting and auditing standards. We then present the

challenges, and the regulatory and legal influences when auditing FVMs. The theoretical

framework is explained, and a figure is added as a visual aid for comprehension.

2.1 Literature review

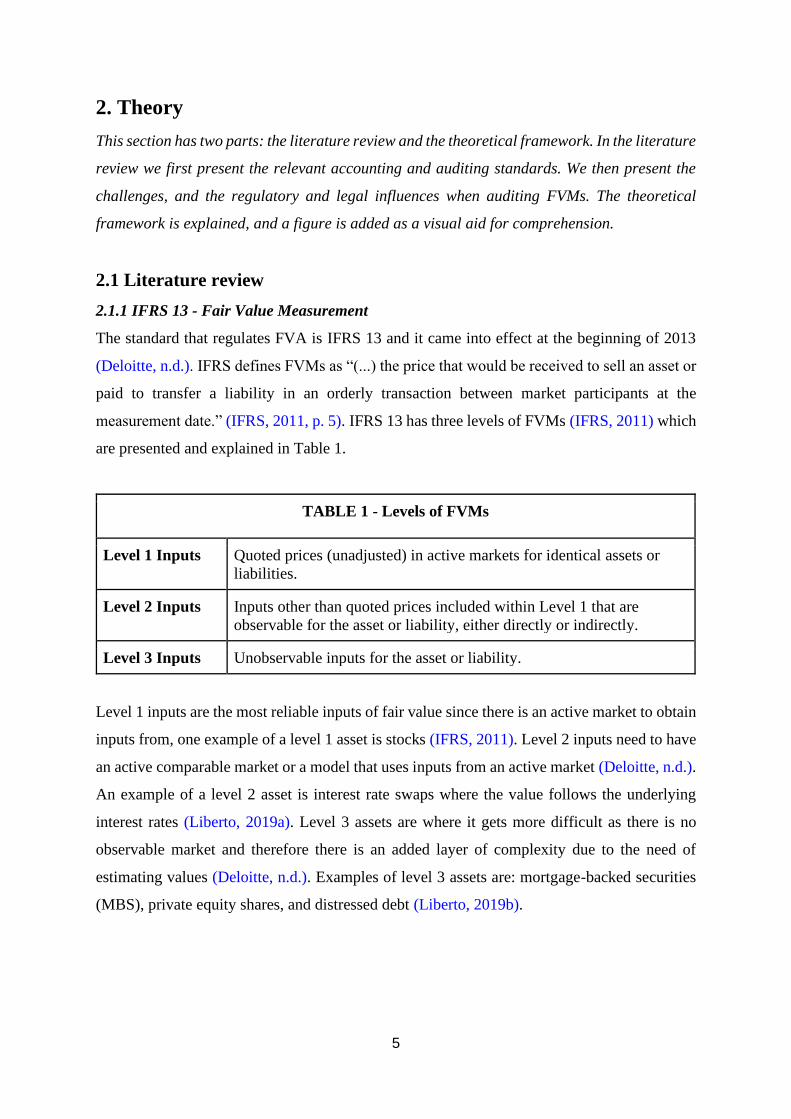

2.1.1 IFRS 13 - Fair Value Measurement

The standard that regulates FVA is IFRS 13 and it came into effect at the beginning of 2013

(Deloitte, n.d.). IFRS defines FVMs as “(...) the price that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants at the

measurement date.” (IFRS, 2011, p. 5). IFRS 13 has three levels of FVMs (IFRS, 2011) which

are presented and explained in Table 1.

TABLE 1 - Levels of FVMs

Level 1 Inputs Quoted prices (unadjusted) in active markets for identical assets or

liabilities.

Level 2 Inputs Inputs other than quoted prices included within Level 1 that are

observable for the asset or liability, either directly or indirectly.

Level 3 Inputs Unobservable inputs for the asset or liability.

Level 1 inputs are the most reliable inputs of fair value since there is an active market to obtain

inputs from, one example of a level 1 asset is stocks (IFRS, 2011). Level 2 inputs need to have

an active comparable market or a model that uses inputs from an active market (Deloitte, n.d.).

An example of a level 2 asset is interest rate swaps where the value follows the underlying

interest rates (Liberto, 2019a). Level 3 assets are where it gets more difficult as there is no

observable market and therefore there is an added layer of complexity due to the need of

estimating values (Deloitte, n.d.). Examples of level 3 assets are: mortgage-backed securities

(MBS), private equity shares, and distressed debt (Liberto, 2019b).

6

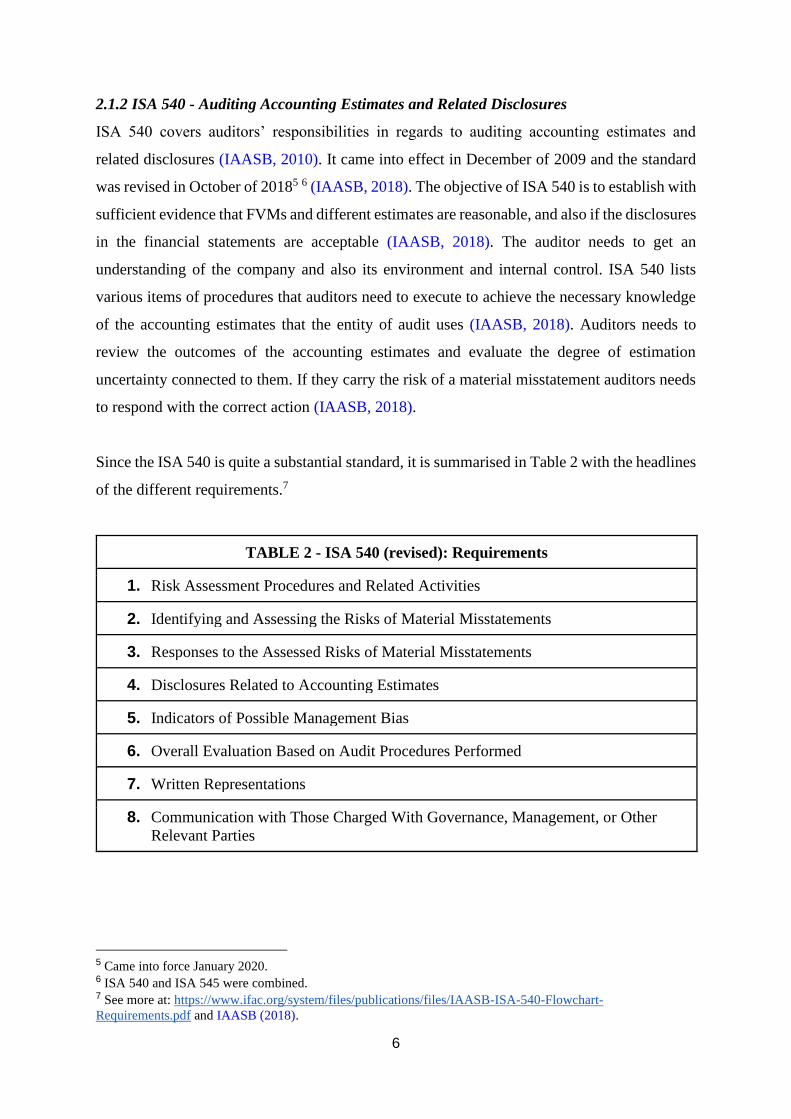

2.1.2 ISA 540 - Auditing Accounting Estimates and Related Disclosures

ISA 540 covers auditors’ responsibilities in regards to auditing accounting estimates and

related disclosures (IAASB, 2010). It came into effect in December of 2009 and the standard

was revised in October of 20185 6 (IAASB, 2018). The objective of ISA 540 is to establish with

sufficient evidence that FVMs and different estimates are reasonable, and also if the disclosures

in the financial statements are acceptable (IAASB, 2018). The auditor needs to get an

understanding of the company and also its environment and internal control. ISA 540 lists

various items of procedures that auditors need to execute to achieve the necessary knowledge

of the accounting estimates that the entity of audit uses (IAASB, 2018). Auditors needs to

review the outcomes of the accounting estimates and evaluate the degree of estimation

uncertainty connected to them. If they carry the risk of a material misstatement auditors needs

to respond with the correct action (IAASB, 2018).

Since the ISA 540 is quite a substantial standard, it is summarised in Table 2 with the headlines

of the different requirements.7

TABLE 2 - ISA 540 (revised): Requirements

1. Risk Assessment Procedures and Related Activities

2. Identifying and Assessing the Risks of Material Misstatements

3. Responses to the Assessed Risks of Material Misstatements

4. Disclosures Related to Accounting Estimates

5. Indicators of Possible Management Bias

6. Overall Evaluation Based on Audit Procedures Performed

7. Written Representations

8. Communication with Those Charged With Governance, Management, or Other

Relevant Parties

5 Came into force January 2020. 6 ISA 540 and ISA 545 were combined. 7 See more at: https://www.ifac.org/system/files/publications/files/IAASB-ISA-540-Flowchart-

Requirements.pdf and IAASB (2018).

7

2.1.3 The Challenges of Auditing FVMs and the Impact on the Audit Process

FVAs prominence in new standards has been continuously increasing and as such the need for

auditing FVMs has subsequently increased (Martin et al., 2006; Bell & Griffin, 2012). As

previously mentioned, there is an element of judgment involved with FVMs8 and hence, a great

deal of uncertainty (Martin et al., 2006). Christensen et al. (2012) found that in selected public

companies, small changes could impact the FVMs in quantities larger than materiality due to

the high estimation uncertainty. Cannon and Bedard (2017) displayed how high estimation

uncertainty is a difficult problem for auditors; they concluded that in more than 70 percent of

the cases of estimation uncertainty, the uncertainty was larger than materiality. Bratten et al.

(2013) divide the phenomenon estimation uncertainty into two categories, measurement

uncertainty, and macroeconomic risks. When referring to measurement uncertainty, Bratten et

al. (2013) point out the ambiguity of the valuation of an item. There is not a great deal of

measurement uncertainty for Level 1 assets, where there are observable prices, but when

climbing up to Level 2 and Level 3 where models are used to produce the FVMs, measurement

uncertainty increases because of the assumptions made in the models. Folpmers and de Rijke

(2009) demonstrated that the difference in using a Level 2 and Level 3 model on a MBS was

so large that the expected value failed to capture the true risk of the asset. Furthermore, the

macroeconomic risks are a big part of estimation uncertainty since many models of the

complicated FVOEs incorporate estimates of macroeconomic factors. Bratten et al. (2013)

found that in macroeconomic crises, even observed prices may not be considered fair. During

the 2008 crisis the IAASB (2008) told auditors that changing valuation models from price to a

model that would produce a more appropriate value, could be acceptable. Further proof of the

macroeconomic risks with FVMs was found by Vyas (2011), showing that financial institutions

delayed write-downs of securitized assets during the 2008 crisis.

After establishing the fact that there is a great deal of estimation uncertainty in FVMs, it is

important to bring to light what research has found to be the impact on the audit process.

Christensen et al. (2012) found that the complexity and estimation uncertainty of FVMs

resulted in the auditors feeling that they could not give satisfactory levels of assurance.

Similarly, Cannon and Bedard (2017) found that even though a suitable approach was used in

most cases, auditors still felt that they could not give satisfactory assurance. Cannon and Bedard

(2017) found that in over 30 percent of the cases where the estimation uncertainty was larger

8 Level 2 & Level 3.

8

than materiality, the auditors classified the inherent risk as low to moderate. This highlights a

large problem due to the magnitude of the risk and how, in these cases, the inherent risk is rated

far too incautiously by the auditors.

By establishing that fair value and other estimates are complex it is important to know how this

affects auditor judgment and the auditing process. Bratten et al. (2013) list task difficulty as one

factor affecting the audit of FVOEs. Task difficulty is an important aspect to consider because

of how it affects the audit and the auditor. Psychological studies have found that the more

difficult a task is, the greater the negative impact on an individual’s decision-making (Payne et

al., 1997). This is relevant because of the uncertain nature of FVMs, and auditors whose

decision-making is impaired due to the difficulty of the auditing task makes for a lesser quality

audit. The models that are used to generate the FVMs are complex and a more advanced

knowledge of finance may be needed (Bratten et al., 2013), which is why auditors often opt to

use valuation specialists, either internal or external (Bratten et al., 2013; Martin et al., 2006;

Kumarasiri & Fisher, 2011). Bratten et al. (2013) also recognised the difficulties when the

management uses multiple models and how that requires the auditor to also determine whether

the models are weighted appropriately. To accomplish that, the auditor needs to have a great

deal of understanding how the models work, and how or if, they are applicable (IAASB, 2008).

Research has found that auditors often lack the necessary knowledge to tackle the difficulties

of FVMs by themselves (Martin et al., 2006; Kumarasiri & Fisher, 2011) and Griffith et al.

(2015) found this to be partly due to the aftermath of audit firms often dividing knowledge

between auditors and in-house specialists. Consequently, auditors in charge of the audit may

lack the necessary specialised knowledge. This, however, does not necessarily need to be a

major problem since using an in-house specialist is still the same firm doing the work. High

estimation uncertainty was found by Cannon and Bedard (2017) to potentially lead to

disagreements between specialists, and furthermore, Cannon and Bedard (2017) found that

there is a correlation between the use of specialists and the level of inherent and control risk,

but not estimation uncertainty. Further making the point how important it is for auditors to

classify the inherent risk appropriately, which Cannon and Bedard (2017) found to not always

be the case.

9

2.1.4 Regulatory and Legal Influences in regards to Auditing FVMs

When auditing FVMs there is an aspect of regulatory and legal influence. Christensen et al.

(2012) highlight this by showing that the expectations of standard setters seem to have

increased and the limitations have been narrowed. Power (2010) found that whereas FVA keeps

evolving, auditing standards seem to get left behind and are forced to be reactive to new

accounting standards. Bratten et al. (2013) make the argument that a greater regulatory scrutiny

should improve audit quality, but this may not always be the case. During the 2008 crisis

auditors claimed that they followed the rules carefully fearing lawsuits of “Enron-size” and

facing the same destiny as Arthur Andersen (Hughes & Tett, 2008), however, Dickey et al.

(2008) recognised that the core issue of most legal cases was the integrity of the financial

statements and their fair value methodologies. This suggests that greater regulatory discipline

not necessarily always improves audit quality.

In a similar sense, Dowling et al. (2018) found that auditing has shifted further into a “box-

checking”-style of auditing to increase the visibility of compliance to regulatory bodies and

thus avoid scrutiny from inspectors. Power (2009) found that “box-checking” gives both

auditors and inspectors a sense of comfort and Dowling et al. (2018) argue that this could lead

to auditors relying on checklists and failing to contemplate alternative factors. Power (2009)

further argues that the increasing use of checklists leads to standardisation and according to

Dowling et al. (2018) increases the commoditization of auditing. Thus, holding down the

development of knowledge amongst auditors, putting pressure on audit fees and profits while

constricting innovation and development. This may lead to a multitude of negative effects on

the auditor profession, for example graduates avoiding the profession and an increasing

departure of auditors from audit firms (Dowling et al., 2018). Dowling et al. (2018) also found

that audit firms will work proactively to establish mechanisms and routines that minimise the

risk of getting inspected which, as discussed, does not increase audit quality.

Several previous studies (Bratten et al., 2013; Cannon & Bedard, 2017; Glover et al., 2017;

Griffith et al., 2015) take the standpoint that all deficiencies identified by regulators represent

actual deficient auditor performance. However, Glover et al. (2019) find that this view is

incomplete and that it overlooks other perspectives. Peecher et al. (2013) support this

standpoint by finding that regulators and inspectors tend to see a lack of consensus between

auditors and inspectors as evidence of deficient auditor performance. Glover et al. (2019)

present this as the FVM gap, where auditors’ and inspectors’ view of what is sufficient and

10

appropriate evidence when auditing FVMs differ. Glover et al. (2019) find that auditors do

perceive that there is a gap and feel that inspectors often expect more evidence than the audit

standards require, which challenges the authority of auditing standards.

According to Glover et al. (2019) there are four factors that contribute to the disagreement

between inspectors and auditors: (1) high subjectivity and uncertainty rooted in auditing FVMs

with high EU; (2) lack of inspector expertise and judgment bias; (3) differing roles or

affiliations, and incentives between auditors and inspectors; and lastly (4) lack of clear

guidance regarding what constitutes sufficient and appropriate audit evidence. They argue that

the presence of an FVM gap can have unintended negative consequences on audit quality due

to a change in auditor behaviour emerging from the current inspection process.

Glover et al. (2019) recognise that a potentially rewarding area for future research is one that

will shed light on potential needs for revisions to auditing standards, in regards to auditing

complex FVMs. We believe that this study will be able to cover this to a degree. By looking at

how auditors reason about current auditing standards we will help both auditors and regulators

understand what some deficiencies and ambiguities are in current auditing standards of FVMs.

The newly revised ISA 540 is also a hot topic for us and we believe that we can also clarify if,

and how, this impacts the current practices when auditing FVMs.

2.1.5 Summary of Previous Research on Auditing FVMs

Previous research on FVM auditing has found that the prominence of FVA has increased and

thus the need for auditing complex FVMs has increased (Martin et al., 2006; Power, 2010; Bell

& Griffin, 2012; Christensen et al., 2012). Complex FVMs often incorporate judgments and

estimates, thus there is uncertainty involved (Martin et al., 2006; Christensen et al., 2012;

Cannon & Bedard, 2017). Auditors seemingly struggle with these FVMs and were found to

feel that they could not give satisfactory assurance (Christensen et al., 2012; Cannon & Bedard,

2017), sometimes classifying inherent risk as fairly low even though there is considerable

estimation uncertainty (Cannon & Bedard, 2017). The task of auditing FVMs is consequently

complex and auditors sometimes lack the necessary specialised knowledge to tackle the task.

Auditors thus frequently rely on valuation specialists (Bratten et al., 2013; Martin et al., 2006;

Kumarasiri & Fisher, 2011; Cannon & Bedard, 2017; Griffith et al., 2015).

11

When auditing FVMs there are regulatory and legal aspects to consider and Power (2010)

showed how despite FVA evolving, auditors seemingly feel left behind in auditing standards

and are forced to be reactive to changes in accounting standards. Bratten et al. (2013) argue

that a greater regulatory scrutiny should improve the quality of the audit but during the 2008

crisis auditors claimed that they followed the rules (Hughes & Tett, 2008) yet most of the legal

cases revolved around the financial statements and FVMs (Dickey et al., 2008). Dowling et al.

(2018) found that there has been a shift towards more of a box-checking approach in auditing

due to fears of scrutiny from inspectors (Dowling et al., 2018) and box-checking seemingly

gives a sense of comfort (Power, 2009). Box-checking is argued to lead auditors to rely too

much on the lists, failing to contemplate outside aspects (Power, 2009; Dowling et al., 2018).

Glover et al. (2019) found a gap between auditors and inspectors views of what constitutes

sufficient and relevant audit evidence when auditing FVMs. Glover et al. (2019) also

recognised that a potential area for future research is showing and discussing how auditing

standards may need to be revised.

2.2 Theoretical Framework

For this study there was a need for a theoretical base for analysing the empirical data, and one

fundamental aspect of FVMs is judgment. We found two theoretical bases in judgment and

decision-making (JDM) expertise research and structure versus judgment research. The JDM

expertise research exists in both psychology (e.g. Einhorn, 1974; Mumpower & Stewart, 1996;

Weiss et al., 2006) and auditing (e.g. Solomon & Shields, 1995; Peecher et al., 2013) whereas

structure versus judgment mainly covers auditing (e.g. Cushing & Loebbecke, 1986; Bamber

et al., 1989; Francis, 1994; McDaniel, 1990).

The reason we chose JDM expertise research is because of the complexity of FVMs. When

auditing FVMs there is a need for an expert and a need to implement professional judgment to

evaluate the estimations made by the management. The reason we chose structure versus

judgment is because this study also covers the auditing standards part of auditing FVMs. Since

standards structure the way a person carries out a task, it is highly relevant to know how

structure affects the auditing process and its interplay with judgments which is a big part of

FVMs.

12

2.2.1 Judgment and Decision-Making Expertise

Judgment and decision-making (JDM) expertise research has been conducted on both auditing

and other fields such as psychology. The literature emerges from experts having differing

opinions and judgments, especially when faced with complex problems and tasks. We believe

that this can help us tackle and analyse the intricacy of auditing FVMs by showing that experts

do differ in judgments and the JDM expertise literature helps us understand why. Mumpower

and Stewart (1996) argued that the knowing and understanding of why experts have differing

opinions is important to help reduce the gap.

Mumpower and Stewart (1996) found that complex tasks with subjective assessments lead to

differences in experts’ opinions and judgments. Glover et al. (2019) found this to be resonating

with the complexity of FVMs, thus recognising the usefulness of using JDM expertise research

for studies of FVM auditing. Einhorn (1974) studied the psychology behind judgments made

by experts. He wanted to find out whether the experts acted in the same way according to three

criteria: (1) they should show a tendency to cluster variables in the same way, (2) their

judgment should be reliable, and (3) they should weight and combine information in similar

ways. Einhorn (1974) showed that for the first two criteria the experts acted alike but he saw

differences in how they weighted and used information. However, Weiss et al. (2006) discredit

Einhorn (1974) by claiming that the approach of using consistency in judgments is not an

optimal way of measuring expertise. They support this by claiming that a person can be

consistent in how they make judgments but that does not necessarily mean the judgments are

correct. Furthermore, Weiss et al. (2006) claim that the consensus aspect of Einhorn (1974) is

also flawed due to groupthink (Janis, 1972, as cited in Weiss et al., 2006, p. 444), i.e. when the

pressure to conform to a consensus hinders dissenting views and opinions. A consensus does

not mean that the experts are correct and therefore, Weiss et al. (2006) claim that expert

consensus is a flawed approach for evaluating expertise.

Weiss et al. (2006) argue that expertise is hard to measure, and that experience is not a reliable

measure. They assert that experts often have considerable experience, but at the same time,

experience is not a guarantee of expertise. An example is Goldberg (1968, as cited in Weiss et

al., 2006, p. 443) which found that when asking psychologists with varying amounts of

experience, there was no clear association between the experience of the psychologist and their

diagnosis accuracy. Mumpower and Stewart (1996) however, argue that disagreements based

on judgments emanate from either systematic or non-systematic differences in the process in

13

which the judgment was made. Mumpower and Stewart (1996) see four reasons why systematic

differences exist in the judgment process of experts: (1) missing or poor quality feedback, (2)

missing or poor quality information, (3) difficulty in evaluating the quality of one’s own

judgment, and finally (4) causal texture of the environment. Non-systematic differences, on the

other hand, are seen as more of a random occurrence and a product of a concept found by

Hammond and Summers (1972, as cited in Mumpower & Stewart, 1996, p. 197); called

cognitive control, which accounts for judgments not being made with cues in an ideal order or

fashion. The systematic differences are, however, of great interest because of a clear impact on

judgment.

One aspect of Mumpower and Stewart (1996) is that an individual’s self-interest may shape

the way a person judges certain things. For example, an auditor’s or inspector’s self-interest

could affect the way they make judgments during audits or inspections. This can also be

expanded to the interest of one’s organization shapes the way judgments are made. There is

evidence of such occurrences in other fields, such as politics (Mumpower and Stewart, 1996;

Peecher et al., 2013).

2.2.2 Structure versus Judgment

The structure versus judgment debate is the debate of audit methodology and how the audit

process should involve more judgments or a more structured approach. Cushing and Loebbecke

(1989, p. 32), define a structured audit methodology as:

“a systematic approach to auditing characterized by a prescribed, logical sequence of

procedures, decisions, and documentation steps, and by a comprehensive and integrated

set of audit policies and tools to assist the auditor in conducting the audit”. (as cited in

Bamber et al., 1989, p. 286)

Bamber et al. (1989) claimed that audit firms, to improve audit quality and efficiency,

embraced a more structured audit process. They used Cushing and Loebbecke (1986) as the

foundation for their study to ascertain the association between the degree of structure in the

auditing approach, and auditor’s role conflict and ambiguity experienced (Bamber et al., 1989).

While Cushing and Loebbecke (1986, as cited in Bamber et al., 1989, p. 290) used a

institutional approach with interviews, Bamber et al. (1989) used a questionnaire to compare

structured and unstructured audit firms. They found that auditors from structured firms tended

14

to perceive their task as more analysable than auditors from unstructured firms. They also found

that auditors from structured firms perceived that there was a great degree of formalization of

standard practices, policies, and responsibilities. They also showed lower levels of role conflict

than auditors from unstructured firms (Bamber et al., 1989).

McDaniel (1990) also recognised how structure helped auditors. With a quantitative study

McDaniel (1990) researched the implications of time constraints and structure to audit

programs, and the results indicate that there are possible benefits of structure when it comes to

consistency, for example in “making global judgments about sample sizes” (p. 283). At a more

relaxed time constraint level the structure audit program test group had significant increases in

audit effectiveness, efficiency, and consistency. However, just how much consistency that can

be derived from such structures seems to depend on the nature of the current task at hand for

an auditor. McDaniel (1990) also discusses that structured audit programs may not always lead

to the sought-after effects. More specifically9, McDaniel (1990) points out that since the

experiment is based on testing details-tasks it may be less applicable on more complex,

unstructured tasks that include multiple components and require more judgment. Pentland

(1993) expanded on the judgment part by showing that previous studies on judgment always

viewed it as a cognitive process, leaving no room for gut-feel which Pentland (1993) found to

be critical throughout the audit process. Pentland (1993) puts this as the relationship between

the “micro-level behaviour of the engagement team and macro-level context in which they

work” (p. 605). Auditors not only have to form a cognitive connection to their work but also

an emotional one and the way an audit team seems to achieve this is through a sense of comfort

which is obtained by following a ritualistic process. Pentland (1993) further discussed how

trying to, in a purely rational sense, describe auditor's judgment via a rule-abiding system is

insufficient because for any given rule there needs to be a contemplation of when and how to

apply it which in turn requires more rules.

Francis (1994) contributes to the structure versus judgment debate, claiming that “merely

following rules10 is not inherently virtuous because it does not involve reflection on and choice

over one's actions” (p. 263). Francis (1994) is concerned that the rational, technocratic

approach11 compromises the ability of the moral good to develop in auditors as it increasingly

9 And most relevant to this thesis. 10 Such as structured audits. 11 I.e. introducing more rigid standards in auditing.

15

colonises their mindspace. According to Francis (1994); in order for an auditor to do good work

he needs to execute a “self-consciously hermeneutical or interpretative practice” (p. 235) with

a good amount of self-reflection on the work that one does and the goodness that it comprises.

2.2.3 Theoretical Framework

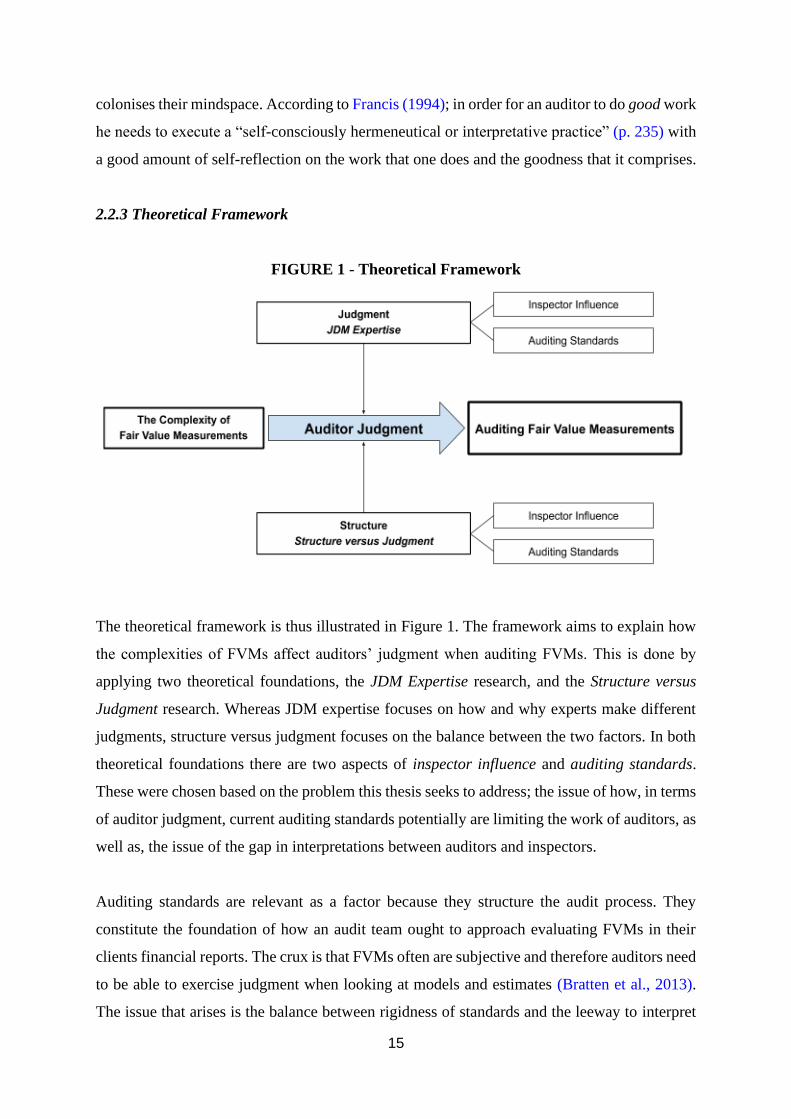

FIGURE 1 - Theoretical Framework

The theoretical framework is thus illustrated in Figure 1. The framework aims to explain how

the complexities of FVMs affect auditors’ judgment when auditing FVMs. This is done by

applying two theoretical foundations, the JDM Expertise research, and the Structure versus

Judgment research. Whereas JDM expertise focuses on how and why experts make different

judgments, structure versus judgment focuses on the balance between the two factors. In both

theoretical foundations there are two aspects of inspector influence and auditing standards.

These were chosen based on the problem this thesis seeks to address; the issue of how, in terms

of auditor judgment, current auditing standards potentially are limiting the work of auditors, as

well as, the issue of the gap in interpretations between auditors and inspectors.

Auditing standards are relevant as a factor because they structure the audit process. They

constitute the foundation of how an audit team ought to approach evaluating FVMs in their

clients financial reports. The crux is that FVMs often are subjective and therefore auditors need

to be able to exercise judgment when looking at models and estimates (Bratten et al., 2013).

The issue that arises is the balance between rigidness of standards and the leeway to interpret

16

made available to auditors. We analyse this by taking previous research on the interplay

between structure and judgment and making it one of the two theoretical viewpoints of the

framework.

Inspector influence is another aspect that we argue is relevant as inspections impact the audit

process, especially when working under the assumption that auditors and inspectors potentially

do not share a consensus regarding how to interpret and apply auditing standards (Glover et al.,

2019). Expert opinions may differ for several reasons and we will analyse the supposed FVM

gap. By interviewing both auditors and an inspector this study aims to uncover some hidden

causes for differing opinions with the help of JDM expertise research and judgment versus

structure research.

17

3. Method

In this section we present the research method used to conduct this study. We give a summary

of the arguments for the choices made as well as an account of sampling and techniques used.

We start off by discussing the methodological stances taken, followed by the research design,

data analysis and reflections on the ethical and procedural limitations of the thesis, as well as,

the quality assurances.

3.1 Ontological and Epistemological Assumptions

Ontology is the nature of social science, asking if social entities are objective entities or social

constructions (Bryman & Bell, 2011). For this study we have opted to use a constructionist

viewpoint. Because we are dealing with people and differing opinions, a constructionist

approach is most relevant (Bryman & Bell, 2011).

Epistemology on the other hand is the study of knowledge and how it is understood.

Epistemology deals with what should or should not be considered legitimate knowledge about

specific areas of study (Bryman & Bell, 2011). We have chosen an interpretivist approach

because it coincides with our reasoning behind the choice of branch of ontology in the sense

that we are talking to people and focusing on how individuals understand and interpret their

surroundings based on context (Bryman & Bell, 2011).

3.2 Research Design

This study’s aim is to answer the research question “What effects do auditing standards and

inspectors have on auditor judgment regarding the audit of FVMs?“ and thus, as discussed

above, a qualitative mindset is used. The research design is therefore based on the notion that

the best way to yield answers to the research question is to speak to people and try to dig deep

into their views, opinions and beliefs on the subject matter. This will yield the best possible

data for the analysis (Klopper, 2008).

3.2.1 Data collection technique

The empirical data for this thesis was originally intended to be collected by conducting semi-

structured, face-to-face interviews. However, due to the global Covid-19 pandemic of 2020 we

were instead forced to resort to carrying out the interviews digitally with Zoom and Microsoft

18

Teams12. Semi-structured interviews are a useful tool when you want the interview to follow a

certain scheme but at the same time give the interviewees some leeway in what their answers

are or main focus is (Bryman & Bell, 2011; Qu & Dumay, 2011). We believe that semi-

structured interviews were the most appropriate to use for this thesis because we have a specific

topic in FVMs that we wanted to pervade the conversations. Furthermore, we wanted to avoid

the rigidness of structured interviews and argue that this would not have brought answers of

any substance for the analysis. The interviews followed the structure of the interview guide

found in Appendix 1, but at times we needed to ask follow-up questions not included in the

guide and go with the flow of the interview as is the nature of the semi-structured approach.

3.2.2 Sample

For the sample we needed to have auditors and inspectors with experience of auditing FVMs,

in particular using ISA 540. We argue that this was the most relevant and efficient way to get

the empirical data needed to answer the research question. We were quite open to what the

interviewees exact role within their organizations was since we found that by having an open

mind to who, in the audit-spectrum, you interview you may yield richer data with a wider range

of perspectives and points-of-view. We performed a lesser amount of interviews than initially

intended due to limitations discussed later on. 5 interviews were performed and since this is a

qualitative study this should not necessarily have a significant negative impact (Slevitch, 2011;

Farquhar, 2012), one of the reasons being that the interviewees have all been carefully selected

based on their extensive experience in the area of FVMs.

Because this study was specific to FVMs, the knowledge required for the sample group was

also specific and we needed interviewees with a specialised knowledge of FVMs and of

auditing FVMs. The selected interviewees held high competence and experience in the field,

which allowed us to gather the necessary knowledge of FVMs from the sample. By having

well-informed and extensively experienced interviewees we prevented speculative and

uninformed answers to our questions. We focused the search on auditors from Big 4 firms13.

The reason being them having the majority of the complex FVMs cases, and thus, their auditors

would have the greatest experience of FVM auditing. To reach out to our desired sample group

we used secondary contacts by either emailing or calling and when the opportunity arose we

12 Which software was used had no notable effect on this study. 13 The Big 4 consists of Deloitte, EY, KPMG & PwC.

19

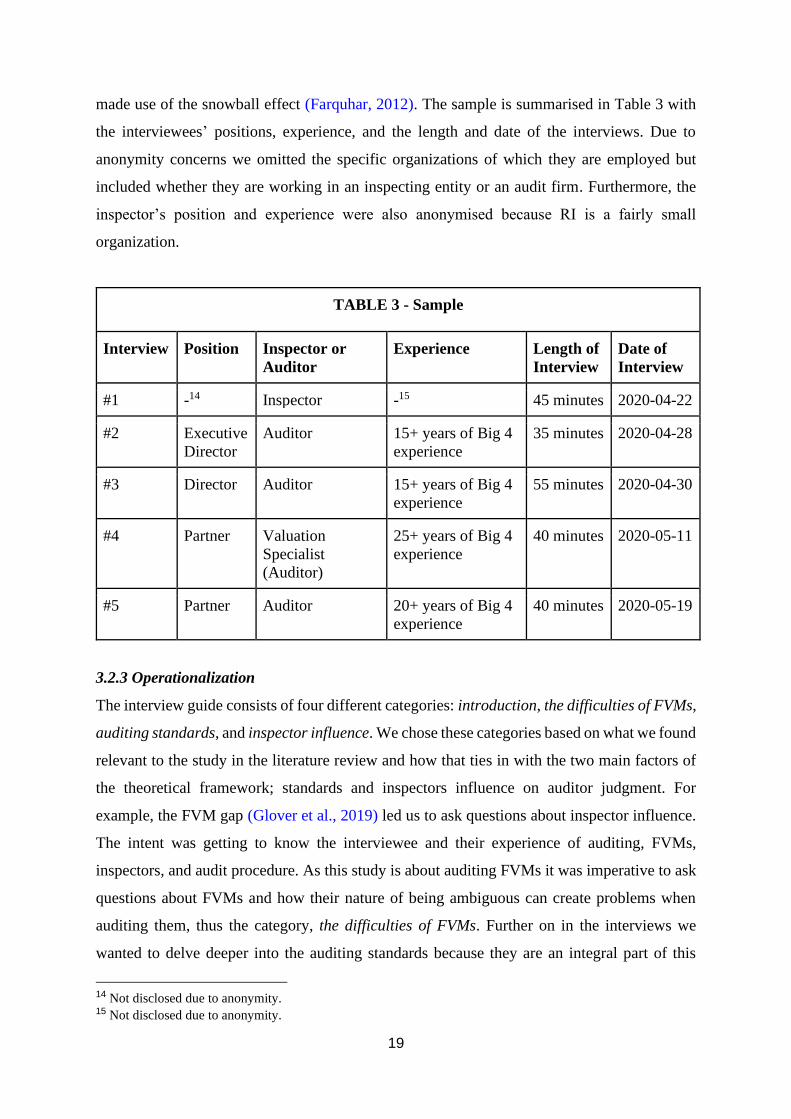

made use of the snowball effect (Farquhar, 2012). The sample is summarised in Table 3 with

the interviewees’ positions, experience, and the length and date of the interviews. Due to

anonymity concerns we omitted the specific organizations of which they are employed but

included whether they are working in an inspecting entity or an audit firm. Furthermore, the

inspector’s position and experience were also anonymised because RI is a fairly small

organization.

TABLE 3 - Sample

Interview Position Inspector or

Auditor

Experience Length of

Interview

Date of

Interview

#1 -14 Inspector -15 45 minutes 2020-04-22

#2 Executive

Director

Auditor 15+ years of Big 4

experience

35 minutes 2020-04-28

#3 Director Auditor 15+ years of Big 4

experience

55 minutes 2020-04-30

#4 Partner Valuation

Specialist

(Auditor)

25+ years of Big 4

experience

40 minutes 2020-05-11

#5 Partner Auditor 20+ years of Big 4

experience

40 minutes 2020-05-19

3.2.3 Operationalization

The interview guide consists of four different categories: introduction, the difficulties of FVMs,

auditing standards, and inspector influence. We chose these categories based on what we found

relevant to the study in the literature review and how that ties in with the two main factors of

the theoretical framework; standards and inspectors influence on auditor judgment. For

example, the FVM gap (Glover et al., 2019) led us to ask questions about inspector influence.

The intent was getting to know the interviewee and their experience of auditing, FVMs,

inspectors, and audit procedure. As this study is about auditing FVMs it was imperative to ask

questions about FVMs and how their nature of being ambiguous can create problems when

auditing them, thus the category, the difficulties of FVMs. Further on in the interviews we

wanted to delve deeper into the auditing standards because they are an integral part of this

14 Not disclosed due to anonymity. 15 Not disclosed due to anonymity.

20

study. We asked questions about ISA 540, but also how auditing standards in general affect the

audit process in different ways. Lastly in the inspector part of the interview our intentions were

to get an understanding of how inspectors influence the audit process and what the opinions,

of both auditors and inspectors, are on what the role of an overseeing organization such as RI16

is. The interview guide can be found in Appendix 1.

3.3 Data Analysis

For data analysis, a thematic analysis method to identify themes from the interview transcripts

was used. A thematic analysis was chosen due to it being one of the most commonly used

techniques in qualitative interview studies (Bryman & Bell, 2011). The procedure of the

analysis was constructed in accordance to Burnard’s (1991) method where we began by taking

notes right after the interviews were finished and then transcribing them in their entirety. The

transcription process included both authors listening back to the recorded interviews at least

two times and carefully writing them down word for word, leading to 55 pages of empirical

data. The next step was reading the transcripts thoroughly, identifying different themes and

patterns in the answers given. We used the thematic method to identify important codes that

could support different perspectives in the analysis section. These codes were based on the

operationalization, which had us divide the problem into the main themes of the difficulties of

FVMs, auditing standards, and inspector influence. We defined subheadings to those three

main themes that we believe capture the essence of the two main factors of the theoretical

framework; the influence on auditor judgment imposed by auditing standards and inspectors.

We went on to scour the interview transcripts for responses that could help spotlight those

discussion points. Some examples of the subheadings are: rigidness of standards and

differences in inspections internationally. We chose to exclude some parts of Burnard’s (1991)

process, for example we chose not to ask an outsider to identify themes to compare to our own.

Data that was deemed irrelevant to the research was omitted (Smagorinsky, 2008) to keep the

study focused on the main subjects of the complexities of FVMs, audit standards, and inspector

influence.

After organizing and categorising the data and isolating the parts deemed most vital and

insightful we started to construct the empirical findings and analysis chapter of the thesis. We

began by structuring the chapter according to key questions asked during the interviews that

16 The Swedish equivalent to PCAOB.

21

tie neatly into the themes described above. We then went on to make connections between

responses given by the interviewees and key points made by previous research presented in the

theory chapter. Lastly, we applied the theoretical framework to the empirical findings and

analysed them accordingly. In the Empirical Findings and Analysis section follows a summary

of the most interesting and important findings from this process.

3.4 Ethical Reflections

Diener and Crandall (1978, as cited in Bryman & Bell, 2011, p. 128) broke down ethical

principles in business research into four categories. However, for this study we only really need

to address one of the four17; whether there is a lack of informed consent or not. We believe that

we have taken this into consideration. It was made clear from first contact that the interviews

would be anonymous and that the interviewees had the option to opt out of the process at any

time. We also informed the respondents ahead of the interview what we were going to discuss

and they were given some example questions to use for preparation. The interviews were

recorded in audio format and consent was given by all participants.

3.5 Quality Criteria

For the study’s quality criteria, we have chosen to evaluate it with trustworthiness and

authenticity. According to Bryman and Bell (2011) and Lincoln and Guba (1985), there are

four different criteria when evaluating a study’s trustworthiness: credibility, transferability,

dependability, and confirmability. We will now explain and evaluate each criterion to the thesis

and how we can achieve trustworthiness.

Credibility can be achieved by detailing how the study was carried out with good practice

(Bryman & Bell, 2011). We have in this section described how the study was done and taken

research ethics into account thus achieving credibility. Transferability can be achieved in a

similar way, by thoroughly detailing how we made this study, assumptions, theoretical

framework, or procedure of interviewing. Transferability is achieved when a study can be

transferred to another social context or study (Bryman & Bell, 2011), and we argue that we

achieve transferability by presenting a detailed methodology section which could be adapted

in further studies. Dependability is according to Lincoln and Guba (1985) similar to an “audit-

approach” in the way that you can achieve dependability by saving for example interview

17 Due to a lack of relevance for the study on the other 3 categories.

22

transcripts and other records that are not found to its entirety in the study itself (Bryman &

Bell, 2011). Finally, to achieve confirmability in a study the authors need to show how they

acted in good faith (Bryman & Bell, 2011). We argue that by showing every step of the process

and how we did act in good faith, by showing that we have been as objective as we realistically

can be, we achieve confirmability.

Those four criteria were comprised in the larger quality criterion of trustworthiness,

followingly, the second criterion is authenticity (Lincoln & Guba, 1985; Bryman & Bell, 2011).

According to Lincoln and Guba (1985) there are five different criteria within authenticity. One

example of those is educative authenticity, which argues whether a study helps people to

understand other perspectives better (Bryman & Bell, 2011). For this study we find ontological

authenticity the most relevant to the study. We believe that by highlighting how judgments can

differ when auditing FVMs, we contribute to the understanding of social contexts which is

highly relevant to this thesis’ research question.

3.6 Limitations and Weaknesses

Because of the Covid-19 pandemic, the study suffered in several ways. Due to social distancing

regulations we could not perform the interviews face-to-face. Instead we opted for digital

interviews. Furthermore, our target sample group were seemingly more hesitant to agree to

interviews during the pandemic and the snowball-sampling method was not as effective as

planned. According to some of the people we contacted, this was due to them working remotely

from home and the workload had increased with this change. We struggled therefore to get the

desired amount of interviewees; however, in the end we managed to get an adequate,

knowledgeable sample.

All interviews of this study were held in Swedish because it is the native tongue of all the

interviewees and the researchers. This means that the translated quotes may lack certain

nuances that are hard to capture in a translation. We have done our utmost to ensure that the

translations are accurate and true to the original statements, but it is important to keep in mind

that translations may have a possible negative effect.

23

Since this is a bachelor’s thesis, there is a limited amount of time one has to plan and conduct

their study. But we believe that during this timeframe we managed to create a study that is of

interest to the field of auditing FVMs.

24

4. Empirical Findings and Analysis

In this section we begin by giving a short description of the object of study in this thesis.

Followed by an organized description of the empirical data gathered with a selection of quotes

from the interviews. We also draw parallels between patterns in the empirical data and the

literature study. Lastly, we present the application of the theoretical framework on the

empirical findings.

4.1 The Complexity of FVMs

FVMs have become increasingly more prominent in accounting (Bell & Griffin, 2012; Power

2010) and this has led to an increased burden on auditors. Level 2 and Level 3 inputs require

estimates and assumptions since there is no active market to gather prices from (Deloitte, n.d.).

The models used and the assumptions related to them play a big part when producing these

complex FVMs (Bratten et al., 2013). We interviewed auditors, a valuation expert18 and an

inspector19 from the Swedish equivalent to the American PCAOB, Revisorsinspektionen (RI).

We wanted to get an understanding of their view on complex FVMs as well as auditing

standards in general, of ISA 540 and of the inspector influence. In this first section we will

present quotes from the interviews about the complexity of FVMs and discuss their potential

implications.

4.1.1 An Increased Work Burden

We asked the interviewees if they think that complex FVMs increase the burden on auditors.

Every respondent agreed that the increasing prominence of FVMs in accounting and auditing

brings with it a new level of complexity for the people who work in the field. Consequently,

the amount and difficulty of the work has increased.

“Definitely, especially now that there is a new standard, well not new but revised ISA

540, where the demands on us auditors are extended.” (Interview #5)

18 The valuation expert is referred to as Interviewee #4 henceforth. 19 The inspector is referred to as Interviewee #1 henceforth.

25

Interviewee #1 said:

“That is the way it is and it is a part of being an auditor, partly understanding when you

should not take on a job and when you should. The answer is really that it gets more

complex and it most likely has to, it is not possible to go around it (...) the job has to be

done and an increased burden has to be accepted otherwise maybe you should not be

an auditor.” (Interview #1)

Interviewee #1 was adamant that the increased burden is something natural and has to be

accepted and Interviewee #5 mentioned that FVA is increasingly more prominent and an

important part of financial reports. This largely coincides with what previous research has

found, that the complexity of FVMs increases the work burden for auditors (Martin et al., 2006;

Bratten et al., 2013; Cannon & Bedard, 2017).

4.1.2 What the Focus is Put on When Auditing FVMs

To understand why FVMs increase the work burden we need to understand what the focus is

when auditing FVMs, and why it is difficult. We asked the interviewees which they thought

were the most important parts, and what the focus is when auditing FVMs. Interviewee #2

responded:

“I would say that we put the most time on estimations and the data for the models. Not

so much time on the models themselves as they are often standardised.” (Interview #2)

The judgments and estimation of FVMs was one of the focal points found by the interviewees.

Interviewee #3 mentioned three areas that are important when talking about estimations and

judgments; that it is important to have good methods, good assumptions, and good input data.

“(...) it is primarily in these important estimations and judgments where, if you go

wrong, it can really go wrong. That is why we have an important role in challenging

and looking, Do they have enough precision in these?” (Interview #3)

“(...) if you have bad data and do your estimates on it, then it all falls apart.” (Interview

#3)

26

Interviewee #3 claimed that the problems with auditing FVMs often emanate from the

documentation provided by the client and how it is often too thin and inadequate, especially in

smaller companies. The challenge is that in order to make an adequate audit of the judgments

and estimates made by the management, there needs to be quite robust supporting

documentation. If the documentation is poor, it does not matter what the auditing standards

says since it is difficult to perform an adequate audit when the material is thin. This viewpoint

was supported by Interviewee #2 and Interviewee #4 elaborated by claiming that if the material

submitted to the valuation specialist team is of low quality, the time it takes them to do their

work is often increased as a result of them needing to make their own models and calculations.

Interviewee #5 claimed that what could be improved upon from the client’s side is the

reasoning behind different estimations and judgments made about the future and also how the

demands on the clients, from auditors, will likely increase with the newly revised ISA 540.

Interviewee #5 mentioned that there are two aspects of assumptions: technical20 and business

assumptions. The business assumptions were recognised as the most challenging part of

auditing FVMs which Interviewee #3 also supported by mentioning how important it is that

you as an auditor challenge the business assumptions made by the client when evaluating their

assets.

“We have to make sure it is not fantasy with these forecasts (...) These forecasts assume

a large revenue and profit increase, what support do you have for this?” (Interview #3)

Overall it seems auditors most heavily emphasize the subjective aspects of FVMs with

judgments and estimates. They have to make sure that the clients have used a thorough and

reliable methodology but most importantly that the assumptions made hold water based on the

financial reality they operate within. If the assumptions and inputs are not solid the valuations

lose their reliability and credibility. This coincides with what previous research has found; that

judgments and estimates are the main culprit of the complexity when auditing FVMs

(Christensen et al., 2012; Bratten et al., 2013; Cannon & Bedard, 2017).

20 E.g. the WACC in a discounted cash flow-model.

27

“The problem is that they are judgments. There is nothing that is entirely right or wrong

so you can have one opinion and the client can have another, and it can sometimes be

hard to completely rebuff it” (Interview #5)

Ultimately, when subjectivity is involved, there is always going to exist a level of uncertainty.

How FVMs are handled will be uncovered in the upcoming section.

4.1.3 How FVMs Are Handled

We asked the interviewees if they find that audit firms and auditors in general deal with FVMs

appropriately. Interviewee #1 said:

“(...) generally for the big firms, since it is those who above all work with complex fair

value measurements, it does work well. They have specialists and so on, I would say

that the quality is good.” (Interview #1)

Interviewee #1 expressed that with the help of specialists an auditor can get sufficient assurance

of the validity of the FVMs. Similarly, when looking at RI’s latest quality controls on the Big

4 firms, no specific mention of problems regarding FVMs was presented (RI, 2017; RI, 2018;

RI, 2019a; RI, 2019b). It was repeated many times by Interviewee #1, that the use of a specialist

is a very useful tool and that without them, Interviewee #1 claimed that they would not feel

comfortable signing off on an audit21. Interviewee #2 supported this:

“Relatively well, I would say. In these companies where there are large items and large

sums that are valuated with fair value, then you often call in specialists to help.”

(Interview #2)

Previous research has found that the use of specialists is customary when auditing FVMs (e.g.

Martin et al., 2006; Cannon & Bedard, 2017) and seemingly RI does not necessarily see this as

problematic, at least from Interviewee #1’s viewpoint. The valuation specialist in Interview #4

shared:

21 Referring to their own experiences as an auditor.

28

“(...) we (valuation specialists) often come in to the audit when there is Level 2 and

above all Level 3 in IFRS 13, where there is a need for more qualified judgments. Partly

because the choice of method is not always evident but rather you need to judge what

is a suitable method in the context, and also you need to judge what is reasonable data

in these valuation methods. And I suppose it is often there we contribute the most.”

(Interview #4)

When asked about what can be improved upon in the audit of FVMs Interviewee #1 found that

there is always room for improvement and how the documentation part of the audit can always

be better. Interviewee #1 also recognised the importance of keeping a professional skepticism

toward the client. Interviewee #3 responded to this by shifting the blame, to some extent, on

the clients:

“I think we share that viewpoint22, in how important it is. Then it can vary from mission

to mission in how well it is documented. But often it emanates from that we have not

been clear enough with our demands on the clients.” (Interview #3)

The findings from these interviews suggest that perhaps the difficulty of auditing FVMs does

not lie in actually carrying out the appropriate auditing measures and techniques when faced

with fair value but rather in the aspect of communication. Documentation was brought up as a

main concern both on the auditor and client side as well as auditors not always approaching

their tasks with sufficient professional skepticism. The interviewees did recognise that auditing

FVMs is complex, but they did not paint a picture as dreary as previous research suggests

(Christensen et al., 2012; Bratten et al., 2013; Cannon & Bedard, 2017; Glover et al., 2019).

4.2 Auditing Standards

As FVA has evolved to become one of the most important parts of modern day accounting

various standards in accounting and auditing alike have changed accordingly (Bell & Griffin,

2012; Power, 2010). However, some researchers have found that the change of the standards

may have brought with it issues. Christensen et al. (2012) claim that the standards are complex

and therefore impact the auditor’s ability to perform audits to an adequate level of assurance.

Are the standards in need of change or improvement or are there other factors that are more

22 That documentation could be better.

29

vital to address? During the interviews we inquired about current auditing and accounting

standards23 to find possible explanations.

4.2.1 Audit Standard Rigidness and Box-Checking

We asked regarding the strictness of auditing standards, whether the interviewees find the

current standards too rigid or perhaps problematic in some other fashion. The general consensus

amongst every interviewee was that the standards are well adjusted to the demands of

contemporary fair value auditing. Interviewee #2 said:

“In some parts I do not find ISA very strict (...) overall, I prefer looser rules because

they allow for more interpretations of your own, based on what you find reasonable in

the current context you find yourself in. Anything else can get very square.” (Interview

#2)

Interviewee #3 agrees that the standards fulfill their purpose adequately and suggests that

issues in the audit process occur due to reasons other than the standards:

“The standards and tools and such are good, but the problem is that the customer, the

companies, that create these financial reports according to IFRS or whatever they use,

they are the ones responsible for valuing assets (...) and the documentation that lays

the foundation of what we as auditors examine and take a stand on is often too thin.”

(Interview #3)

This connects to the next point of inquiry which was checklists. The interviewees were asked

whether they find checklists useful, in what ways they might assist during an audit and if they

potentially cause issues as well. The respondents were unified in that checklists can become

problematic if auditors rely heavily upon them, compromising their professional skepticism

approach as a result. Interviewee #3 highlighted the importance of professional skepticism and

judgment:

23 Specifically, IFRS 13 and ISA 540.

30

“When you ask the critical questions and judge, that is where you usually find if

something is amiss, rather than when filling out a checklist. I believe that it is important

that there are sufficiently experienced individuals who can judge and critically question

information; is this really reasonable?” (Interview #3)

Interviewee #1 also made clear the importance of thinking critically:

“I do agree that it can lead to auditors relying too much on checklists. Checklists are

good in many respects, they do ensure that you have done the task that you are expected

to (...) but there is a risk of it becoming more focused on checking boxes than thinking

about what you actually have done. Checklists are a useful tool for getting an oversight

if you have done certain tasks but there is a risk of not reflecting enough.” (Interview

#1)