Bahasa

Halaman

Hukum

EMPOWERING MINDS

A Study On The Financial Performance Of Big Bazaar

Organization StudyAt

BIG BAZAAR MALLESWARAM BANGALORE

Submitted in Partial Fulfilment of the Requirements ofBangalore University for the Award of the Degree of

MASTER OF BUSINESS ADMINISTRATION

By

BIPROJIT DEYREG No: 13SKCMA161

Under the Guidance of

Prof. VENKATRAMAN SUBRAMANIAN

AIMS(ACHARYA INSTITUTE OF MANAGEMENT AND SCIENCES)

Peenya, Bangalore

2013 - 2015

DECLARATION

I, BIPROJIT DEY, hereby declare that thisOrganisation Study Report titled A Study On The FinancialPerformance Of Big Bazaar is based on the original studyconducted by me under the guidance of Prof. VenkatramanSubramanian.

This report has not been submitted earlier for the award of

any other degree / diploma by Bangalore University or any

other University.

Place : Bangalore

Date :

BIPROJIT DEY

CERTIFICATE

Certified that this organization StudyReport titled “A STUDY ON THE FINANCIAL PERFORMANCE OF BIGBAZAAR ” based on an original study conducted by BIPROJIT DEYof IIIrd Semester MBA under the guidance of Prof.VENKATRAMAN SUBRAMANIAN Professor MBA department.

This report is based on the original study undergone and has

not formed the basis for the award of any other degree/diploma

by Bangalore University or any other University.

Prof. Venkatraman Subramanian Dr. Kerron G Reddy

Professor MBA department

CEO and Principal

Place: Bangalore Place:

Bangalore

Date: Date:

Acknowledgement

An undertaking of work life - this is never an outcome of asingle person; rather it bears the imprints of a number ofpeople who directly or indirectly helped me in completing thepresent study. I would be failing in my duties if I don't saya word of thanks to all those who made my training periodeducative and pleasurable one. I am thankful to Big Bazaar,Malleshwaram for giving me an opportunity to do the internshipin the company.

First of all, I am extremely grateful to Mr. Tarun Saha (StoreKarta) for his guidance, encouragement and tutelage during thecourse of the internship despite his extremely busy schedule.My very special thanks to him for giving me the opportunity todo this project and for his support throughout as a mentor.

I must also thank my faculty guide Prof. VenkatramanSubramanian (Faculty, Acharya Institute of Management &Sciences) for his continuous support, mellow criticism andable directional guidance during the project.

I would also like to thank all the respondents for giving

their precious time and relevant information and experience, I

required, without which the Project would have been

incomplete.

Finally I would like to thank all lecturers, friends and my

family for their kind support and to all who have directly or

indirectly helped me in preparing this project report. And at

last I am thankful to all divine light and my parents, who

kept my motivation and zest for knowledge always high through

the tides of time.

Biprojit Dey

Date:

Contents :

CHAPTER CONTENTS Page No.

CHAPTER 1

1.1 Introduction

1.2 Industry Profile

1.3 Company profile

1.4 Products Profile

1.5 Competitors Profile

1

8

21

33

34

CHAPTER 2 Organization Structure 36

CHAPTER 3

Functional Departments

3.1 Human Resource Dpmt

3.2 Customer Service Desk

3.3 Administration

3.4 Logistics

3.5 Marketing Department

3.6 Sales Department

39

40

40

41

42

43

43

CHATPER 4 Ethical / Best Policies / Policies in the organisation

45

CHAPTER 5 SWOT Analysis 48

CHAPTER 6 McKinsay 7 Model Discussion 51

CHAPTER 7 Research Problem Study 57

CHAPTER 8 Findings, Suggestions & Conclusion

70

CHAPTER 9 Bibliography & Annexure 74

LIST OF FIGURES/CHARTS

SERIAL NO. FIGURES/ CHARTS NAMEFig. 1 Various Retail formats across value & lifestyle Segments

Fig. 2 Future Group

Fig. 3 3B Model of Management

Fig. 4 Formats of Retailing

Fig. 5 Strategy used in Big Bazaar

Fig. 6 Product Mix

Fig. 7 Organization Structure

i ) Zonal

ii) Big Bazaar

Fig. 8 Functional Departments

Fig. 9 Administrative Department

Fig. 10 Core Values

Fig. 11 Quality Policy

Fig. 12 SWOT Analysis

Fig.13 McKinsay Elements

Fig.14 McKinsay 7s Model

Fig.15 Organization Structure

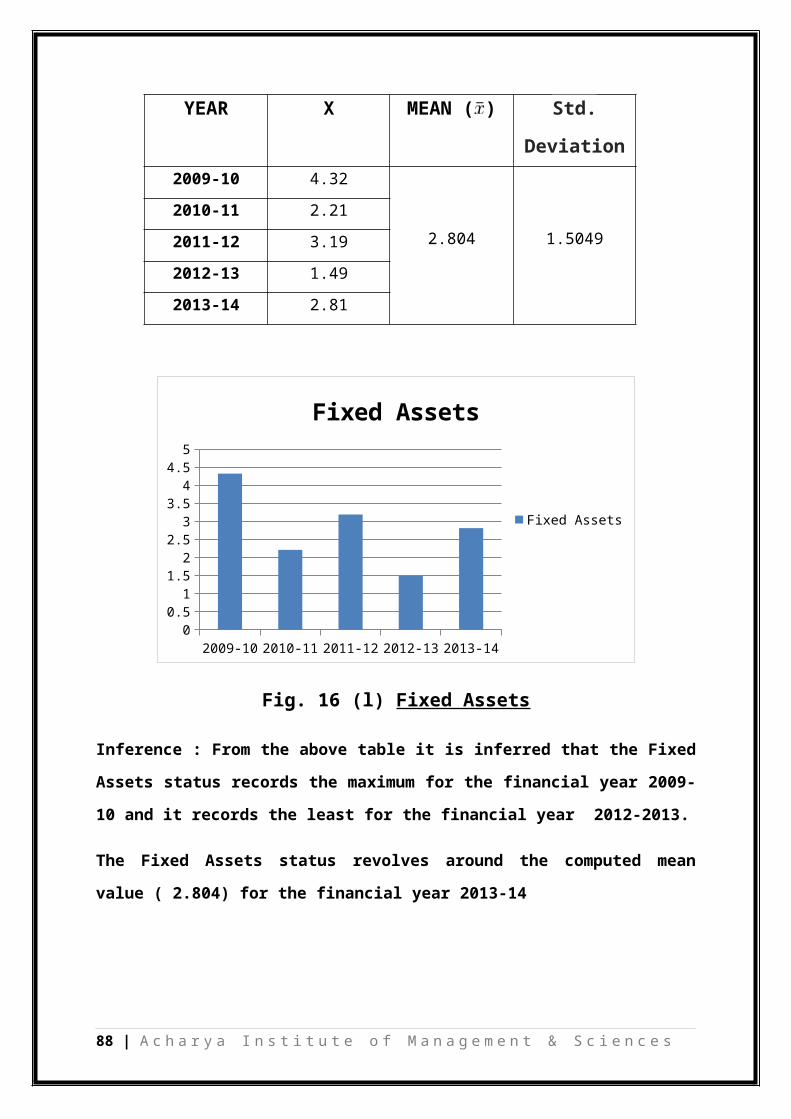

Fig. 16 Current Ratio, Liquid Ratio, Gross Profit Ratio, Net profit

Ratio, Proprietors Fund, Earnings Per Share, Stock

Velocity Ratio, Inventory Turnover Ratio, Interest

Coverage Ratio, Degree of Operating Leverage, Fixed

Asset

LIST OF TABLES

SERIAL NO. TABLE NAMETab. 1 Future Group In Brief

Tab. 2 Founder Board

Tab. 3 Company Profile of Big Bazaar

Chapter 1

1.1 INTRODUCTION

Future Group understands the soul of Indian consumers. As one

of India’s retail pioneers with multiple retail formats,

Future Group connects a diverse and passionate community of

Indian buyers, sellers and businesses. The collective impact

on business is staggering. Around 300 million customers walk

into the stores each year and choose products and services

supplied by Future Group's 30,000 small, medium and large

entrepreneurs and manufacturers from across India. And this

number is set to grow.

Future Group employs 30,000 people directly from every section

of our society. They source their supplies from enterprises

across the country, creating fresh employment, impacting

livelihoods, empowering local communities and fostering mutual

growth.

Future Group believe in the ‘Indian dream’ and have aligned

our business practices to their larger objective of being a

premier catalyst in India’s consumption-led growth story.

Working towards this end, Future Group are ushering positive

socio-economic changes in communities to help the Indian dream

fly high and the ‘Sone Ki Chidiya’ soar once again. This

approach remains embedded in Future Group's ethos even as they

rapidly expand their footprints deeper into India.

Future Group makes every effort to delight its

customers, tailoring store formats to changing Indian

1 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

lifestyles and adapting products and services to their

desires. Future Group operate some of India’s most

popular retail formats. Across value and lifestyle

segments, Future Group's multi-format retail strategy

caters to the complete consumption needs of a wide cross-

section of Indian consumers.

As modern retail drives fresh demand and consumption

in new categories, Future Group's strategy is based on a

deep understanding of Indian consumers, the products they

want, and making these products available in every city,

in every store format.

2 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

LIFESTYLE

Style for Every Occasion

DIGITAL

Connecting the Youth ofIndia

FIG. 1: Various Retail Formats

3 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

VALUE

Helping India Save

HOME

Building Dreams in a New India

Future Group offers innovative offerings at affordable prices

tailored to the needs of every Indian household.

Pioneers in the India’s retail space, Future Group's

formats are household names in more than 93 cities and 60

rural locations across the country

Future Group's stores cover around 17 million square feet

of retail space and attract around 300 million customers

each year

Pantaloon Retail (India) Limited focuses on the lifestyle

retail segment led by the Pantaloons and Central formats

Future Value Retail focuses on the value retail segment

through the Big Bazaar, Food Bazaar and KB’s Fair

price formats.

BRANDS KNOWLEDGE SERVICES RETAIL

SHOPPING MALLS

E-TAILING

LEISURE

CAPITAL

4 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

FUTURE GROUP

&

ENTERTAINMENT

CONSUMER FINANCE INSURANCE

LEARNING

&

DEVELOPMENT MEDIA VENTURES

LOGISTICS

Type Private

Industry Retail

Founder(s) Mr. Kishore Biyani (MD & CEO)

Headquarte

rs

Mumbai, Maharashtra, India

Products Discount, grocery and convenience

stores, cash and carry, hypermarkets,

financial services

Employees 35,000

Divisions Pantaloon Retail, Future Value Retail 5 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Limited

Websites www.futuregroup.in

www.futurebazaar.com

Tab. 1 : Future Group in Brief

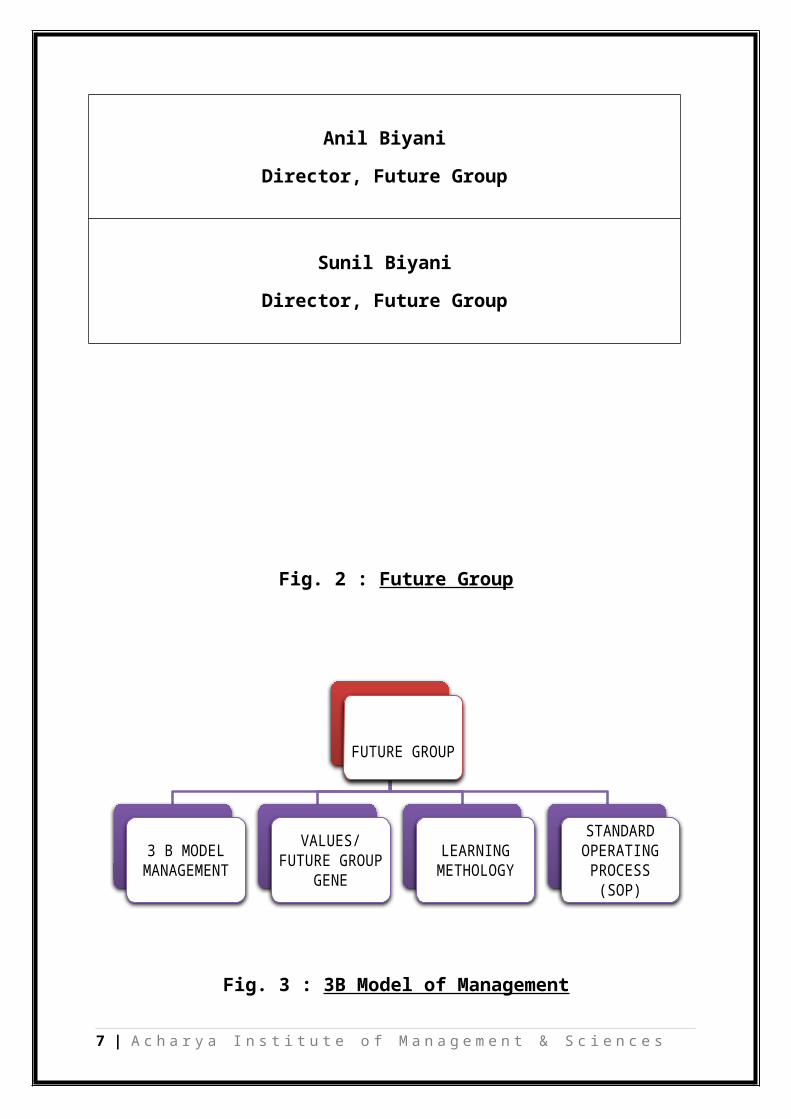

Tab. 2 : Founder Board

Kishore Biyani

Group CEO, Future Group

Rakesh Biyani

Director, Future Group

Vijay Biyani

Director, Future Group

6 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Anil Biyani

Director, Future Group

Sunil Biyani

Director, Future Group

Fig. 2 : Future Group

Fig. 3 : 3B Model of Management

7 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

FUTURE GROUP

3 B MODEL MANAGEMENT

VALUES/FUTURE GROUP

GENELEARNING METHOLOGY

STANDARD OPERATING PROCESS (SOP)

1.1.2 VISION

“Future Group shall deliver everything, everywhere & every

time for every customer in the most profitable manner”

1.1.3 MISSION

We share the vision & believe that our customers &

stakeholders shall be served only by creating &

executing the future scenarios in the consumption space

leading to economic development.

We will be the trendsetters in evolving:

8 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

VISHWASBELIEF VYAVHARBEHAVIOR VYAPARBUSINESS

OUR BELIEF

OUR BEHAVIO

ROUR

CULTURE

delivery formats

Creating retail reality.

Making consumption affordable for all customer

segments –for classes & for masses.

We shall infuse Indian brands with confidence & renewed

ambition.

We shall be:

Efficient

Cost conscious

Committed to quality in whatever we do.

We shall ensure that our positive attitude, sincerity,

humility & united determination shall be the driving

force to make us successful.

1.2 INDUSTRY PROFILE

The contracting global economy, advances in technology, a

proliferationin the number of shopping channels, and an

increasingly well-informed and mobile consumer base are

altering the means, modes, and manner in which consumers shop.

9 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

1.2.1 HISTORIES AND EVOLUTION OF RETAIL INDUSTRY:India retail industry is the largest industry in India, with

an employment of around 8% and contributing to over 10% of the

country's GDP. Retail industry in India is expected to rise

25% yearly being driven by strong income growth, changing

lifestyles, and favourable demographic patterns.

It is expected that by 2016 modern retail industry in India

will be worth US$ 175- 200 billion. India retail industry is

one of the fastest growing industries with revenue expected in

2007 to amount US$ 320 billion and is increasing at a rate of

5% yearly. A further increase of 7-8% is expected in the

industry of retail in India by growth in consumerism in urban

areas, rising incomes, and a steep rise in rural consumption.

It has further been predicted that the retailing industry in

India will amount to US$ 22.5 billion by 2015 from the current

size of US$ 18.5 billion. Shopping in India has witnessed a

revolution with the change in the consumer buying behaviour

and the whole format of shopping also altering. Industry of

retail in India which has become modern can be seen from the

fact that there are multi- stored malls, huge shopping

centres, and sprawling complexes which offer food, shopping,

and entertainment all under the same roof.

India retail industry is expanding itself most aggressively;

as a result a great demand for real estate is being created.

Indian retailers preferred means of expansion is to expand to

other regions and to increase the number of their outlets in a

city. It is expected that by 2015, India may have 600 new

shopping centres.

10 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

In the Indian retailing industry, food is the most dominating

sector and is growing at a rate of 9% annually. The branded

food industry is trying to enter the India retail industry and

convert Indian consumers to branded food. Since at present 60%

of the Indian grocery basket consists of non- branded items.

India retail industry is progressing well and for this to

continue retailers as well as the Indian government will have

to make a combined effort.

1.2.2 RETAIL IN INDIA: HISTORICAL PERSPECTIVERetailing provides a crucial link between producers and

consumers in a modern market economy. The performance of this

sector has a strong influence on consumer welfare. Retailers

not only provide consumers with a wide variety of products,

but also a wide range of complementary services (such as

assurance of product delivery), which can lead to more

informed choice and greater convenience in shopping. They also

provide producers with much needed information on consumers

demand pattern. Productivity and efficiency in retail

operations lowers price level and reduce distortions in the

price structure. Through backward and forward linkage,

performance of retailing services affects the performance of

interlinked sectors such as tourism, recreational and cultural

services, manufacturing of consumers goods agro-good producing

industries etc.

The present paper is an attempt to explore retailing in India

in Historical perspective. Retailing is the largest private

industry in India and second largest employer after

11 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

agriculture. The sector contributes to around 10 per cent of

GDP and 6-7 per cent of employment. With over 15 million

retail outlets, India has the highest retail outlet density in

the world. This sector witnessed significant development in

the past 15 years – from small-unorganized family-owned retail

formats to organized retailing. Liberalization of the economy,

rise in per capita income and growing consumerism has

encourage larger business houses and manufactures to set up

retail formats; real estate companies and venture capitalist

are investing in retail infrastructure. Many foreign retailers

have also entered the market through different routes such as

wholesale cash-and-carry, local manufacturing, franchising,

test marketing, etc. With the growth in organized retailing,

unorganized retailers are fast changing their business models

and implementing new technologies and modern accounting

practices to face competition. The retailing sector in India

has undergone significant transformation in the past 10 years.

Traditionally, Indian retail sector has been characterized by

the presence of a large number of small-unorganized retailers.

However, in the past decade there has been development of

organized retailing, which has encouraged large private sector

player to invest in this sector. Many foreign players have

also entered India through different routes such as test

marketing, franchising, and wholesale cash-and-carry

operation. With high GDP growth, increased consumerism and

liberalization of the manufacturing sector, India is being

portrayed as an attractive destination for foreign direct

investment (FDI) in retailing. At present this is one of the

12 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

few sectors, which has 51% FDI in multi-brand retail sector &

100% FDI in single brand. On one hand farmers will benefit

from it but on the other hand small traders feel they will not

be able to withstand the competition. In India, the retail

sector is the 2nd

largest employers after agriculture. In fact

due to wide network of retailing in India it is known as

nation of shopkeepers. There are about 12 millions retail

outlet spread across India and the country has the highest

density of shops in the world i.e. one shop for every 20 to 25

families or 11 retail shop for every 1000 persons. While, it

is only four shops per 1000 in USA. Retailing in India

provides employment to about 7% of total work force in the

country and contributes about 14% to GDP of India. However the

retailing sector in India is highly fragmented and consists

predominantly of small, independent and owner managed shop.

The Global Retail Development Index developed by A.T Kearney

has ranked India first among the top 30 emerging markets in

the world. A look at the landscape of most of the cities in

India shows the rapid phase of change. This changes in

reflection of the changes in the Indian consumers his

lifestyle and his habits. Goldman Sachs has estimated that the

Indian economic growth could actually exceed that of China by

year 2015. It is believed that the country has the potential

to deliver the fast growth over the next 50 years. It took 10

years for the first 2500 organized retail stores to emerge in

India; the next 2500 could easily get added in the next 5

years. Formats new to the India market place have emerged

rapidly over the past ten years. There is little doubt that

13 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

retail in India is revelling up for an exciting phase ahead.

1.2.3 EVOLUTION OF RETAIL IN INDIA: The origins of retail are old as trade itself. Barter was the

oldest form of trade. For centuries, most merchandise was sold

in market place or by peddlers. Medieval markets were

dependent on local sources for supplies of perishable food

because Journey was far too slow to allow for long distance

transportation. However, customer did travel considerable

distance for specialty items. The peddler, who provided people

with the basic goods and necessities that they could not be

self sufficient in, followed one of the earliest forms of

retail trade. Even in prehistoric time, the peddler travelled

long distances to bring products to locations, which were in

short supply. They could be termed as early entrepreneurs who

saw the opportunity in serving the needs of the consumers at a

profit. Later retailers opened small shops, stocking them with

such produce. As towns and cities grew, these retail stores

began stocking a mix of convenience merchandise, enabling the

formation of high-street bazaars that become the hub retail

activity in every city.

1.2.4 TRADITIONAL RETAIL FORMAT IN INDIA:It is important that for centuries now, India has been

operating within her unique concept of retailing. Retailing in

its initial period was witnessed at the weekly Haats or

Gathering in a market place where vendors put on displays

their produce. Off course this practice is still prevalent in

many towns and cities in India: then the market saw the

emergence of the Local banias and his neighbourhood Kirana

14 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

shop. In fact these were the common local mummy-daddy or

multipurpose departmental store located in the residential

areas such shops stocked goods and multipurpose utility and

were with the vision of providing convenience at the doorstep

of the consumer.

While barter would be considered to be the oldest form of

retail trade, since Independence, retail in India has evolved

to support the unique needs of our country, given its size and

complexity. Haats, mandis and melas have been a part of India

landscape. They will continue to be present in most part of

the country and form an essential part of life and trade in

various areas.

1.2.5 EMERGENCE OF ORGANISED RETAIL IN INDIA:The emergence of first phase of organized retailing in India

can be traced back when a shopping centre into existence in

the year 1869 with Mumbai Crawford Market. After that, in the

year 1874 Hogg market, popularly and better known as new

market came into existence in Kolkata. This shopping centre

was designed by an East Indian Railways Co. Architect R.R.

Banya and was named after the then municipal commissioner of

Kolkata, Sir Stuart Hogg. Earlier the Hogg market even had a

garden with a beautiful fountain adding to its ambience and

benches too for tired shoppers.

Today, the New Market continues to be a premier shopping area

in Kolkata despite a part of it being incinerated in late

1985. Its redbrick Gothic clock tower today bears testimony to

the past Grandeur of this first shopping centre in India.

Today from linen to cakes and fruits to fishes everything is

15 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

available at the New Market Atta reasonable price and this has

made the New Market sustain its popularity among the metro

customers of Kolkata. The tenant mix of this first shopping

centre is unique as it has a large number of 2000 stalls,

which are organized in an order of merchandize. There are rows

of stalls dealing with one particular line of Goods.

A retail researcher by name Christine Furedy in 70s has

observed in her article in the capital on 24th

Dec. 1979

tracing the emergence of the New Market, thus “The most

complex retail business of late nineteenth century Kolkata,

establishment which were to dominate the modern retail sector,

were the departmental stores. Although everyone has closed its

doors, many Calcuttians still remember the name or recognize

their converted, subdivided building: Francis, Harrison and

Hathaway; Hall and Anderson; the Army and Navy stores; white a

way; laid low and Co. In their scope and outreach these shops

rivalled those to be found in cities of the same size in

Britain, Europe or the United States”.

The second phase of development of organized retailing can be

traced back to the year 1931 when Bata shoe Co. took lead in

opening its chain stores at various cities & towns. DCM and

Raymond’s followed it extensively.

The earliest seed of the so-called specialty malls can be

traced to shopkeepers who stocked goods of the same product

category in a particular locality. If one were to go back to

the early 80s, it can be said that organized retail, to a

great extent was visible in the functioning of stores such as

Akbar Ally in Mumbai and Nilgiris and Spencer’s in Chennai.

16 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

These stores later evolved into multi-chain outlet and were

the first to bring on the ‘onset of organized retail’ in

India.

The evolution of PDS (Public Distribution System) of Grains in

India having its origin in the rationing system introduced by

the British during World War II was example of single largest

retail chain in the country the canteen stores Department and

the Post Offices in India are also among the largest network

of outlets in the country, reaching populations across state

boundaries. The Khadi and Village Industries (KVIC) was set

during post Independence and today it has more than 7000

stores across the country.

While Independence retail stores like Akbar Ally's, Vivek’s

and Nallis have existed in India for a long time, Reliance,

Garden Silk Mills, Madhura Garments, Arvind Mills etc. have

set up show rooms for retail sale of their branded products.

At present India is rapidly evolving in to an existing and

Competitive market place with potential target consumers in

both the rich and middle class segments. Manufacturer owned

and retail chain stores are springing up in urban area to

market consumer goods in a style similar to that of mall in

more affluent countries. Even though big retail chains like

Crossroad, Saga and Shopper’s stop are concentrating on the

upper segment and selling products at higher prices, some like

A.V Birla Retails More, RPG’s Spencer’s, Food World and Big17 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Bazaars are tapping the huge middle class population. During

the past two years, there has been tremendous amount of

Interest in the Indian retail trade from global majors as well

as over the years, International brands like McDonalds,

Swarovski, Lacoste, Domino’s, Pepsi, Benetton among a host of

others have come in and thrived in India.

1.2.6 RETAIL FORMATS IN INDIA:In India, at present, retailing activities are being carried

through wide varieties of formats ranging from ‘pheri wala’ in

streets to Modernized Malls in Metro cities. However from

study point of view these formats can easily classified into

following three Groups.

Fig. 4 : Formats of Retailing

18 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

EMERGING

MORDERN KIOSKSCONVINIENCE STORESDEPARTMENTAL STORESCHAIN STORESFRANCHISESPECIALITY STORESSHOPPING MALL/PLAZA

ESTABLISHED

KIOSKKIRANA SHOPSINDEPENDENT STORESCO-OPERATIVE

TRADITIONAL

ITENEREANT SALESMAN HATS

A) TRADITIONAL FORMATS :

1. ITINERANT SALESMAN : It is a type of direct selling,which stated centuries ago. It is an example of door-to-door

office-to-office delivery or marketing. Morning milk man and

sabji wala are the most famous examples of this category.

This type of format has been very popular throughout India

in coping with daily needs. In rural areas this sales man

use cycles, for carrying their stock for display of Goods.

2. HAATS : Haats are the unique examples of traditionalmalls in India. Just like Malls, different sellers sells

different types of items along with the sale of vegetables,

fruits, sweets, chart etc. Some entertainment arrangements

are also made in available in these haats. There was

tendency in rural as well as semi-urban area in India for

visiting these haats with family members as a part of picnic

cum purchasing programs. In fact Haats are periodic markets

(generally organized once in week or fortnight at a

particular place & time) that form a major part of the rural

market system in India. In other words the term Haats refers

to locations, which witness a public gathering of buyers and

sellers at fixed time, and fixed locations. On account of

organization of these haats these are called with the name

of a particular day also such as Mangal Bazaar, Budh Bazaar

etc. According to one estimate about 42,000 haats are

organized in our country.

3. MELAS : Melas are fairs & they can range from

commodities fairs to religious fairs. Virtually every state

19 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

in India has meals for which it is known. It is estimated

that more than 2500 melas are held annually in the country.

It is also estimated that the average outlets in every Mela

would be more than 800 & the average sale per mela would be

Rs. 143 lakhs. Nauchandi is an example of important annual

mela in Meerut, at many places such as Gwalior, Aligarh,

Bulendshahr annual exhibitions are organized. At government

level, a number of fairs such as book fair, trade fair and

specific commodity fair are organized by Trade Fair

Authority of India.

4. MANDIS : Mandis are markets set up & regulated bystate government for the sale of agricultural produce

directly from farmers. At present the number of such markets

stand at 7521. These mandis are playing significant role in

providing better prices to farmers.

B) ESTABLISHED FORMATS :

1. KIOSKS : A kiosk is a small freestanding pavilion or

stall often open on one or more sides and used for

information sales and promotion. Generally a kiosks is

placed in a shopping centre, a bus stand or near by the

prospective customers.

2. KIRANA SHOP & INDEPENDENT STORES : This is one of theimportant & popular established formats of retailing in India.

These shops are usually shops with a very small area, stocking

a limited range of products, varying from region to region

according to the need of the clientele or the whims of the

owners.

These are low cost structures mostly owner operated, have

20 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

reliable real estate & labours cost. Consumer familiarity that

runs from generation to generation is one big advantage

enjoyed by such Kirana Shops.

It is worth mentioning that India retail sector has

traditionally been structured around 3 small retail entities –

the grocer, the general store and the chemist. The grocer

stocks non-packaged, unbranded/Generic commodities such as

rice, floor, pulses, spices, salt etc. for sale. The Grocery

Stores or Kirana shops located in neighbour-hood centres also

sale branded & packaged fast moving consumer goods.

The General store stocks only branded & packaged FMCGs. These

are generally located prominently in the neighbourhood centre

& residential areas. Chemists are a part of dispensing

pharmaceutical. Products, sales branded FMCGs such as personal

Carrier Products & health food. Alongside the three retail

outfit, exist a large segment of smaller, unorganized players

- paan, beedi stores which stock products in sachets,

batteries, confectionary & soaps, bakery & confectioners,

fruit juice/tea salts, ice-cream parlour, electrical,

furniture & hardware stores.

Kirana shops & independent small stores provide a wide variety

of facilities to their customers, such as telephone order

credit facilities, home delivery, customization on account of

offerings & packaging & specific products produced on order in

case of stock out. More importantly they’re available next

door to offer personalized service. In this way their able to

develop a strong relationship with their customer, who over a

period of time, become extremely loyal.

21 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

3. SUPER MARKETS/HYPER MARKETS : These are large (90,000square feet plus) self-service stores selling a variety of

products at discounted price. The best practice chains in this

format are Carrefour (France) Wal-Mart (US). Supermarkets tend

to be located in key residential markets and malls and offer

competitive prices due to economics of scale in logistics and

purchasing. The format is new to India and some important

players in this field are Food World, Big Bazaar. Indian Super

Market are smaller than others countries.

4. DEPARTMENTAL STORES : These large stores primarily sellnon-food items such as apparel, footwear household products.

They stock multiple brands across product categories, though

some of them focus as their own store labels. Departmental

stores are found on high streets and as anchor shops of

shopping malls. Some department stores chains are opened in

India e.g. Shopper’s stop, Westside and Ebony.

5. SPECIALTY CHAINS : These outlets focus on a particularbrand as product category, usually non-food items and are

located on high streets and in shopping malls. The most famous

specialty chains include Gap, Levi’s and Benetton.

6. DISCOUNT STORE : It is a general merchandise retailerthat offers a wide variety of merchandises limited service and

low prices. Subhiksha and Margin free markets are operating in

this format in India.

7. WHOLESALE CASH AND CARRY : The wholesale cash and carryoperation is defined as any trading outlets where goods are

sold at the wholesale rate for retailers and business to buy.

The transactions are only for the business purpose and not for

22 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

personal consumption. Metro, cash and carry, Gmbh of Germany

entered the India in this format.

8. CONVENIENCE STORE : It is a retail business of lessthan 5,000 square feet with primary emphasis on providing the

public a convenient location to quickly purchase an assortment

of food, gasoline and other consumable products. They are

usually open seven days a week for extended hours

C) CO-OPERATIVE SHOPS/GOVT. ORGANISATION :Cooperative stores in India are the result of the cooperative

movement that can be traced to the Pre-independence period.

They emerged as a reaction to the feudal system & attempted to

place the fruit of labour in the hands of the producer himself

to make him relevant. The Cooperative movement was

strengthened after independent in Western India?

A consumer cooperative is a retail institution owned by member

customers. A consumer cooperative is generally formed either

because of dissatisfied consumers who's needs are not

fulfilled by the existing retailers or on account of

initiative by enlightened consumer.

D) MOTHER DAIRY, DELHI & FRUIT & VEGETABLE

PROJECT, DELHI :Mother Dairy, Delhi & the fruit & vegetable project Delhi, set

up by the National Dairy Development Board in 1974, 1986,

respectively, were merged to form Mother Dairy Fruit &

Vegetable Limited in April 2000.

23 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

The new Company, a wholly owned subsidiary of NDDB, is

involved in marketing & distribution of milk, milk products &

horticulture produce. The companies’ dairy plant handles more

than 1.3 million litres of milk daily & undertakes its

marketing operations through 636 own milk shops & more than

6500 retail outlets in and around Delhi. Ice-creams market

The company market horticulture produce in fresh, frozen &

processed from under the brand named 'SAFAL' through a chain

of 263 own fruit & vegetable shops & more than 20000 retail

outlets in various parts of the country. Fresh produce from

the producers is handled at the Companies modern processing

facility in Delhi with an annual capacity of 120000 MT.

A state of the art fruit processing plant, a 100% EOU, set up

in 1996 at Mumbai, supplies quality products in the

international market. The Companies unique distribution

network of bulk vending booths, retail outlets & mobile units

gives it a significant competitive advantage.

It is worth mentioning that the consumer cooperative structure

in the country has 4 tiers, with the National Cooperative

Consumer Federation of India Ltd. (NCCF) at the national

level. Thirty State Cooperative Consumers Organization are

affiliated to the NCCF, the central/wholesale level there are

800 consumer cooperative stores. At the primary level, there

are 21,903 primary stores. In the rural area there are about

44,418 village level Primary Agricultural Credit Societies &

Marketing Societies undertaking the distribution of consumer

goods along with their normal business. In the urban & semi-

urban areas, the consumer cooperative societies are operating

24 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

about 37,226 retail outlets to meet the requirement of the

consumers.

Established formats of retailing in India also include certain

retail organizations initiated & promoted by Govt. They

include Canteen stores, department, CCIE, KVIC and various

cottage & Handicraft Emporium. The canteen store department

has opened Canteen for Army persons & Govt. employees

providing consumer goods at constitutional prices. It has

about 3400 outlets throughout the country.

E) PDS/FAIR PRICE SHOP :The PDS or Public Distribution System would easily emerge as

the single largest retail chain existing in the country. The

evolution of PDS of Grains in India has its origin in the

rationing system introduce by the British during World War II.

The system was started in 1939 in Bombay & Subsequently

extended to other cities and towns. By the year 1946, as many

as 771 cities/towns were covered. The system was abolished

post war, however, on at attaining Independence India was

forced to reintroduce it in 1950 in the face of renewed

inflationary pressures in the economy.

The system, however, continued to remain an essentially urban

oriented activity. In fact, towards the end of the First 5-

year plan (1956) the system was closing its relevance due to

comfortable food grains availability. At this point in time,

PDS was reintroduced and other essential commodities like

sugar, cooking coal & kerosene oil were added to the commodity

basket of PDS. There was also a rapid increase in the Ration

shop and their number went up from 18000 in 1957 to 51000 in

25 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

1961. Thus, by the end of the second 5 year Plan, PDS had

changed from the typical rationing system to a social safety

system, making available food grains at a 'fair-price' so that

access of household to food grain could be improved & such

distribution could keep a check on the speculative tendencies

in the market. The PDS has been functioning for more than 4

decades now and its greatest achievement lies in preventing

famines in India.

F) CONVENIENCE SHOPS :These shops are relatively small shops that are located near

residential areas, are open for long house & 7 days a week and

offer a limited line of convenience products like beverages,

ready to eat snack (Pastry, Sandwiches) bread, eggs, milk,

confectionary etc. These shops have been quite common

throughout the country.

G) SPECIALTY SHOPS :A Specialty shop is a retail shop displaying merchandise,

which has narrow product line, specializing in a particular

type of merchandise & offering, specialized service to

customers. Generally these shops concentrate on a specific

item such as Appeal, Jewellery, Fabric, Sporting Goods, and

Furniture etc. Specialty shop can be sub classified by the

degree of narrowness in their product line. E.g. a clothing

stock would be a single line shop, a men’s clothing shop would

be limited time shop & a men’s shirt store would be a super

specialty shop. Such shop have always played significant role

in relating of consumer durables throughout the country but

particularly in urban & sub-urban areas.

26 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

1.2.7 RURAL MALLS HAVE MADE A BEGINNING:Rural retailing is an important segment of the retail industry

and it is only lately that companies are making investments in

this area. ITC launched Chaupal Sagar, the first rural mall,

with a variety of products and offering farmer’s tools to

adapt to new technologies and methods of farming and selling

their produce. The DCM Sriram Group has opened a Hariyali

Bazaar, offering farm-related services and plans to increase

their product line to a full-fledged grocery store. Godrej

Group has opened Adhaar, a one-stop shop for farmers, focusing

on farm related products. Escorts and Tata Chemicals are also

in the process of setting up agri-stores targeting the rural

market

1.2.8 HYPERMARKETS:In commerce, a hypermarket is a superstore combining a

supermarket and a department store. The result is an expansive

retail facility carrying a wide range of products under one

roof, including full groceries lines and general merchandise.

In theory, hypermarkets allow customers to satisfy all their

routine shopping needs in one trip.

It is often a very large establishment; hypermarkets offer a

large variety of products such as appliances, clothing and

groceries.The hypermarket appeared first in France at the beginning of

the sixties as a synthesis of the main features of modern

retailing. But in France, the decline of this retail format

seems to have begun and Spain could follow quickly. In the

same time, the German hard-discounters continue their

27 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

invasion. According to the retail life cycle theory, this

paper displays curves to demonstrate the evolution of this

retail concept in France, Spain and Italy and tries to evoke

some managerial and strategic issues. The retail wheel seems

to go on turning!

1.2.9 HISTORY OF HYPERMARKET:At the end of the 1950's and at the beginning of the 1960's,

many French retailers came to United States to listen to

Bernardo Trujillo, director of the International Management

Systems Seminars. One of his arguments during his seminars on

modern retailing was: “No parking, no business”. Most of these

French retailers came back to France very enthusiastic. A new

concept then was launched in the French market: the

hypermarket.

The hypermarket was defined as a retail concept with a floor

space over 2,500 m2. Every kind of products was supposed to be

sold through self-service techniques even though there are

today exceptions. Despite several bank support refusals, the

families Fournier, Badin, and Defforey, native from

Switzerland, decided to open the first hypermarket. It was in

the Southern Paris in 1963 under the name Carrefour. Its size

was exactly 2,500 m2. This first hypermarket was immediately a

big success.

Ten years after, there were more than 250 hypermarkets in

France. Today, there are more than 1,300 hypermarkets in this

country. And the group Carrefour, composed of several chains,

is now the second world largest retailer after Wal-Mart. This

public company has more than 10,000 stores in the world today

28 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

located in more than 30 countries. Carrefour began its

internationalization process very early in the 1970's. The

group is present of course in Europe but also in South and

Central America, and in North Africa. In Asia, Carrefour is

very successful in China and Thailand but not in Japan where

they located only four hypermarkets at this time.

BIG BAZAAR

Type Public

Industry Retailing

Founded 2001

Headquarters Mumbai, Maharashtra, India

Products Hypermarket

Revenue 11500 crores (US$1.8 billion) crores (in 2014) (Big Bazaar and Food Bazaar combined)

Employees 36000 people

Parent Future Group

Divisions 214

Website http://www.pantaloonretail.in/businesses/big-bazaar.html

1.3 COMPANY PROFILE

29 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Tab. 3 : Company Profile of Big Bazaar

Big Bazaar is the largest hypermarket chain in India. As of

June 2, 2014 there are 214 stores across 90 cities and towns

in India covering around 16 million m2 of retail space. Big

Bazaar is designed as an agglomeration of bazaars or Indian

markets with clusters offering a wide range of merchandise

including fashion and apparels, food products, general

merchandise, furniture, electronics, books, fast food and

leisure and entertainment sections.

Big Bazaar stores are aimed at providing a local marketplace

feel to the shoppers. They offer a wide variety of household

items including retail apparels, food products, general

merchandise, furniture, electronics, books, fast food, etc.

Several stores also have leisure and entertainment sections.

The hypermarket chain crossed the 100 store mark in 2008.

Future Bazaar is an online business venture of Future Group,

which sells an assortment of products such as fashion, which

includes merchandise for men and women, mobile accessories,

mobile handsets and electronics like home theatres, video

cameras, digital camera, LCD TVs, kitchen appliances and many

more.

Discounts: “Hafte ka sabse sasta din was introduced by

the Big Bazaar, wherein extra and special discounts were

30 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

offered on Wednesday every week, to attract the potential

buyers into their store.

Security check: At each exit of Big Bazaar, they use

alarm systems or Electronic Article Surveillance system,

which detects the products that has attached tags or not.

FUTURE GROUP ALSO OWNS

Central Hypermarket

Brand Factory

Pantaloons

e - ZONE

31 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Hometown

futurebazaar.com

KB's Fair Price

.

1.3.1 HISTORY

2001 to 2010

Big Bazaar was introduced by the Future Group in September

2001 with the opening of its first four stores in Kolkata,

Indore, Bangalore and Hyderabad within a period of 22 days.

Started by Kishore Biyani, Big Bazaar was launched mainly as a

fashion format selling apparel, cosmetics, accessories and

general merchandise. Over the years, the retail chain has

included in its portfolio a wide range of products and

services, ranging from grocery to electronics.

The current retail formats of the Future Group include Big

Bazaar, Food Bazaar, Electronic Bazaar and Furniture Bazaar.

32 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

According to Kishore Biyani, the inspiration behind this

entire retail format was from Saravana Stores, a local store

in T. Nagar, Chennai. Big Bazaar is popularly known as the

‘Indian Wal-Mart’ today.

In the second year of operations, Big Bazaar tied up with

Indian banking giant ICICI Bank and launched the Big Bazaar

ICICI Bank Card. In the same year, the first Food Bazaar store

was also launched at High Street Phoenix mall in Mumbai,

marking the retailer’s entry into dedicated food retail.

In 2003, Big Bazaar made its foray into small towns and

cities. The first store in this category was launched that

year in Nagpur. The franchise also welcomed its 10 millionth

customer at its new store in Gurgaon in the same year.

Over the next two years, Big Bazaar consolidated its position

in the Indian retail landscape. This phase of growth included

the setting up of the Mumbai store in Lower Parel, which

registered a record Rs 10 million turnover in a single day on

Diwali-eve in 2004. In 2005, the first Big Bazaar Exchange

Offer was launched, which has quickly gained popularity among

customers.

In 2006, further changes in loyalty marketing took place with

the launch of the housewife-centric credit card, Shakti.

Jewellery store ‘Navaras’ was also launched that year within

Big Bazaar stores which became the first store-in-store

concept to be launched by the brand. Another dedicated retail

format launched in 2006 is Furniture Bazaar.

33 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

In 2007, Big Bazaar partnered with a shopping portal

Futurebazaar.com and expanded its retail footprint to 50

stores.

The following year, 2008, witnessed by far the fastest growth

in terms of retail expansion for Big Bazaar, with the launch

of the 101st store. Joining the league of India’s Super brands

and voted among the top ten service brands in the country by

the Pitch-IMRB international survey, Big Bazaar became much

more than a household name.

The year also saw the launch of the Monthly Bachat Bazaar

(Monthly Budget Market) campaign, which provided significantly

low prices and gave discounts on bulk purchases in the first

week of the month.

Over the next two years, Big Bazaar carved its own niche in

modern retail and became the largest brand in the hypermarket

format. Capturing one-third of the food and grocery market in

modern retail, celebrity endorsements and tie-ups with other

brands allowed it to enhance its retail footprint. In 2009,

Big Bazaar won the CNBC Awaaz Consumer Awards for the third

consecutive year. It was adjudged the Most Preferred Multi

Brand Food & Beverage Chain, Most Preferred Multi Brand Retail

Outlet and Most Preferred Multi Brand One Stop Shop.

2010 to present

On successful completion of 10 years in the Indian retail

industry, in 2011, Big Bazaar came up a new logo with a new

tag line: "Naye India Ka Bazaar.

In 2012, Big Bazaar signed a multi-million dollar deal with

Cognizant Technology Solutions for the development of an IT

34 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

infrastructure, encompassing Future Group’s entire network of

stores, warehousing and data centers.

Recently, Big Bazaar announced its plans to add more retail

services to its portfolio such as grinding, de-seeding and

cutting of fruits and vegetables.

1.3.2 OPERATIONS

Various formats and store concept

Most Big Bazaar outlets are multi-leveled stores and are

located in stand-alone buildings in city centers as well as

within shopping malls. These stores have more than 2,00,000

Stock Keeping Units (SKU) in a wide range of categories, led

primarily by fashion and food products. The retail space of

these stores in the metros range between 50,000 and 1,60,000

sq. ft. Since its launch in 2001 in metro cities like Kolkata,

Bangalore and Hyderabad, Big Bazaar is the largest Hypermarket

chain with presence in 90 cities and towns across the country

1.3.3 CSR ACTIVITIES

As a part of Future Group, Big Bazaar is involved in various

social activities that include green initiatives for the35 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

community, blood donation camps, Diwali celebrations with

orphanages, visits to orphanages and other NGOs helping

underprivileged children. These activities usually involve all

members of the management as well as staff of Big Bazaar.

• In September 2011, Future Group signed a strategic

partnership with the Himachal Pradesh Government to directly

source, market and promote the state’s products and services

through its Big Bazaar stores under the brand ‘Himachal’. The

aim of this partnership is to aid the development of various

‘source-to-market’ initiatives to enhance livelihoods for more

than 25,000 families in the state.

• Big Bazaar created a platform called Yatra to provide women

of self-help groups across various towns and regions of

Maharashtra and Gujarat the opportunity to market their wide

assortment of indigenous food and non-food products. As part

of the programme, women from over 30 regional self-help groups

were invited, encouraged and helped to set up stalls to

exhibit their products at Big Bazaar stores.

• Big Bazaar Mysore started offering a free wholesome meal to

all its customers, who in return contribute ‘Shraddha Anussar’

for a community cause. In other words, the customers donate

any amount for the meal which would be used for a local,

regional or topical cause.

1.3.4 SCHEMES & INNOVATIONS

The introduction of ‘Sabse Sasta Din’ (Cheapest Day) in the

year 2005 was a turning point for the Big Bazaar franchise. As

part of this effort, the Republic Day holiday was used to

36 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

ensure that consumers visited Big Bazaar outlets across the

country in large numbers to get required household items at

cheaper rates.

Taking cue from this highly successful concept, another

initiative was introduced, named the ‘Purana do aur naya lo’

(give old and get new) scheme. In this scheme, consumers were

asked to bring and sell old clothes, utensils and other

household items in exchange of discount coupons.

The concept proved to be a success yet again as people from

across the country responded spontaneously, in spite of the

different preconditions associated with it.

The franchise further inaugurated the concept of ‘Hafte ka

sabse sasta din’ (Cheapest Day of the Week), wherein Wednesday

was designated to be the day when special discounts were

offered to consumers during a week.

Wednesday Bazaar

The concept of Wednesday Bazaar was promoted as ‘Hafte Ka

Sabse Sasta Din’ (Cheapest Day of the Week). Initiated in

January 2007, the idea behind this scheme was to draw

customers to stores on Wednesdays, the day when consumer

37 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

presence is usually less. According to the chain, the aim of

the concept was ‘to give homemakers the power to save the

most’.

Sabse Sasta Din

Big Bazaar introduced ‘Sabse Sasta Din’ (Cheapest Day) with

the intention of attaining a sales figure of Rs 26 crores in a

single day. The concept became such a hit that the time period

for the offer had to be increased from one day to three days

in 2009 (January 24 to 26) and to five days in 2011 (January

22 to 26).

Maha Bachat

38 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

The concept of ‘Maha Bachat’ (Mega Saving) was introduced in

the year 2006 as a single day campaign with attractive

promotional offers across the company outlets. Over the years,

the concept has grown to become a six-day biannual campaign.

During this campaign, attractive offers are given in all the

value formats including Big Bazaar, Food Bazaar, Electronic

Bazaar and Furniture Bazaar.

The Great Exchange Offer

Introduced on February 12, 2009, ‘The Great Exchange Offer’

allows customers to exchange their old goods for Big Bazaar

coupons. The coupons can be redeemed later for buying brand

new goods from Big Bazaar outlets across the nation.

1.3.5 ADVERTISING CAMPAIGNS & MARKETING INITIATIVES

In view of the increasing competition in the retail market,

Big Bazaar has introduced certain steps to keep itself updated

and continue promoting the band.

39 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Advertising initiatives

Big Bazaar has recently launched a 360-degree promotion drive

covering the three prime media, television, print and social

media, to mark the launch of the new logo. The entire media

campaign was developed by Mudra Communications as Big Bazaar

celebrating April Utsav on 2013. They Offering Rs. 50 off on

Rs. 500 or Rs. 100 off on Rs. 500 or Rs. 200 off on Rs. 500

coupon through missed call.

1.3.6 STRATEGY USED IN BIG BAZAAR

3-C Theory

According to Kishore Biyani's 3-C theory, Change and

Confidence among the entire population is leading to rise in

Consumption, through better employment and income which in

turn is creating value to the agricultural products across the

country.

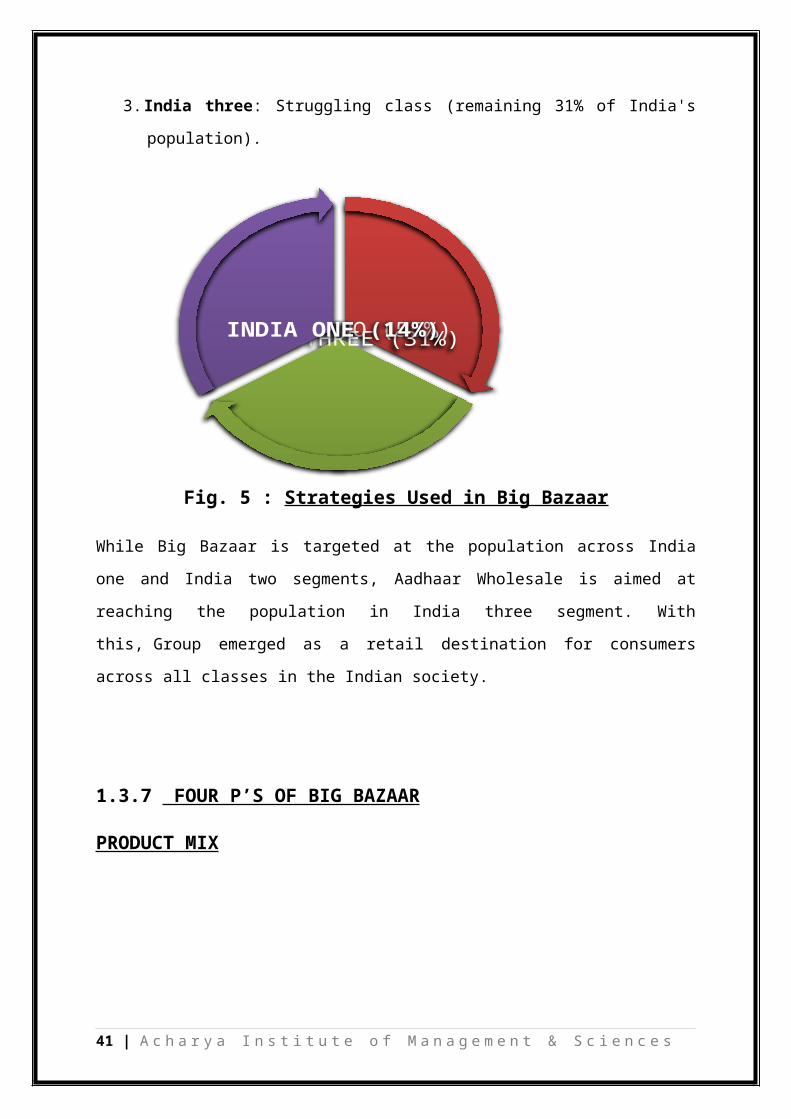

Big Bazaar has divided India into three segments:

1.India one: Consuming class which includes upper middle

and lower middle class (14% of India's population).

2.India two: Serving class which includes people like

drivers, household helps, office peons, liftmen, washer

men, etc. (55% of India's population) and

40 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

3.India three: Struggling class (remaining 31% of India's

population).

Fig. 5 : Strategies Used in Big Bazaar

While Big Bazaar is targeted at the population across India

one and India two segments, Aadhaar Wholesale is aimed at

reaching the population in India three segment. With

this, Group emerged as a retail destination for consumers

across all classes in the Indian society.

1.3.7 FOUR P’S OF BIG BAZAAR

PRODUCT MIX

41 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

INDIA TWO (55%)INDIA THREE (31%)INDIA ONE (14%)

Fig. 6 : Product Mix

PRICE MIX

Value Pricing (EDLP) Promotional Pricing Low Interest Financing Psychological Discounting Special Event Pricing Differentiated Pricing Time Pricing Bundling

PLACE MIX

Initially Identifies Future/Potential development areas. Acquire such areas at an early phase before the real

estate value booms. Located at high traffic areas. Design to look crowded.

42 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

APPARELS

Denims & ShirtsFabricsFormal WearCasual Wear

HOME CARE

ShampoosDetergents Soaps Liquid Wash

CHILL STATION

Soft DrinkPackaged Juices Milk Items Frozen Foods

FARM PRODUCE

FruitsImported FruitsVegetablesDairy Products

PROMOTION MIX

“Saal Ke Sabse Sasta 3 Din” Future Card(3%Discount) Advertising(Print ads, TV Ads, Radio) Brand Endorsement by M.S Dhoni Exchange Offer Weekend Discount Point of Purchase Promotion

1.4 PR ODUCTS PROFILE

The product profile of Big Bazaar is as follows. They are

dealing with various types of products and so they had divided

them into various departments for the customer’s convenience.

The departments are:

43 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

FOOD BAZAAR

HOME CARE PRODUCTS

HEAD TO TOE

FIT & HEALTHY

BOOKS & STATIONARIES

APPARELS & GARMENTS

MEN & WOMEN ACCESSORIES

KIDS ACCESSORIES

CROCKERY & PLASTIC ITEMS

UTENSILS

HOME DECORS

HOME LINEN

GIFTS

BAGS & TRALLIES

FURNITURES

ELECTRONIC GOODS

FOOT WEARS

1.5 COMPETITORS PROFILE

44 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Big Bazaar faces competition from other retailers of similar

products & services. These include stand alone stores in the

organised & unauthorised sector, as well as other chain of

stores including Department stores.

It is because of this and the service and ambience that Big

Bazaar believes have been able to create a differentiation in

the mind of the customer vis-a-vis our competitors where

similar products and Brands are available.

COMPETITORS OF BIG BAZAAR

More

Easy Day

Lifestyle International

Reliance Trend

Wal-Mart

Reliance

Shoppers stop

Vishal Mega Mart

Local retailers

Spencer's

Reliance Fresh

45 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

CHAPTER 2

46 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

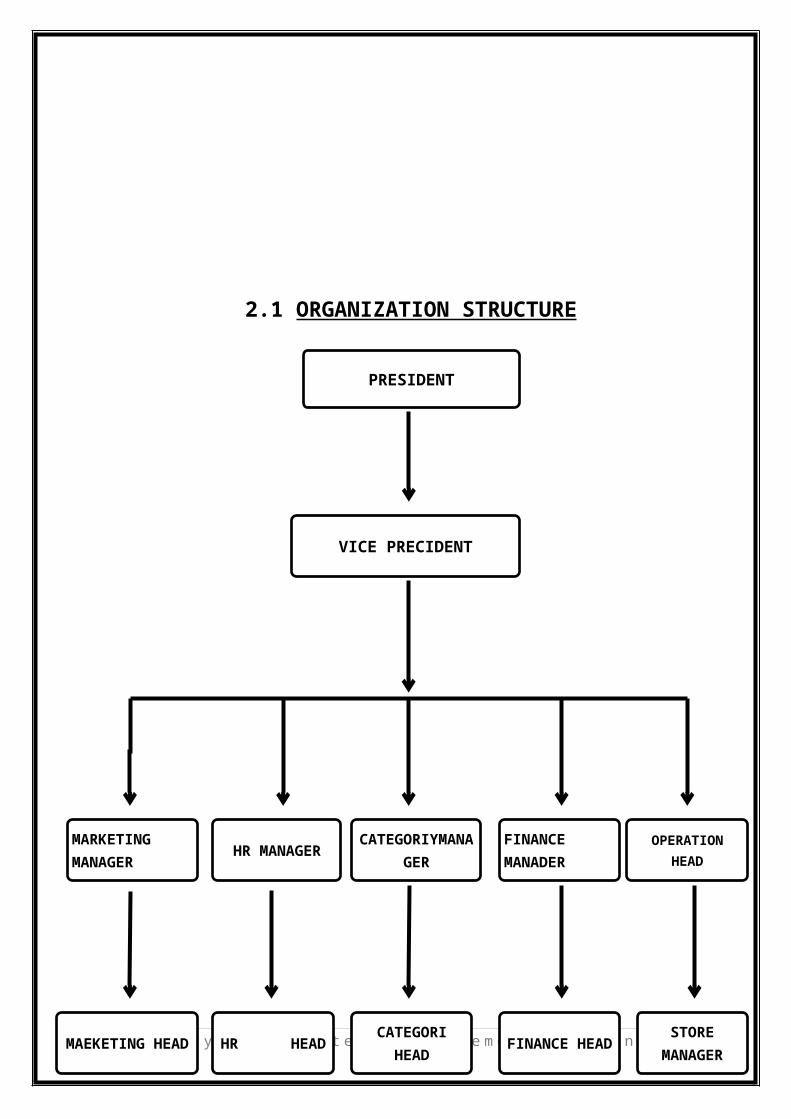

2.1 ORGANIZATION STRUCTURE

47 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

PRESIDENT

VICE PRECIDENT

MARKETING MANAGER HR MANAGER FINANCE

MANADERCATEGORIYMANA

GEROPERATION

HEAD

MAEKETING HEAD HR HEAD CATEGORIHEAD FINANCE HEAD STORE

MANAGER

Fig. 7 (i) : Zonal Organization Structure

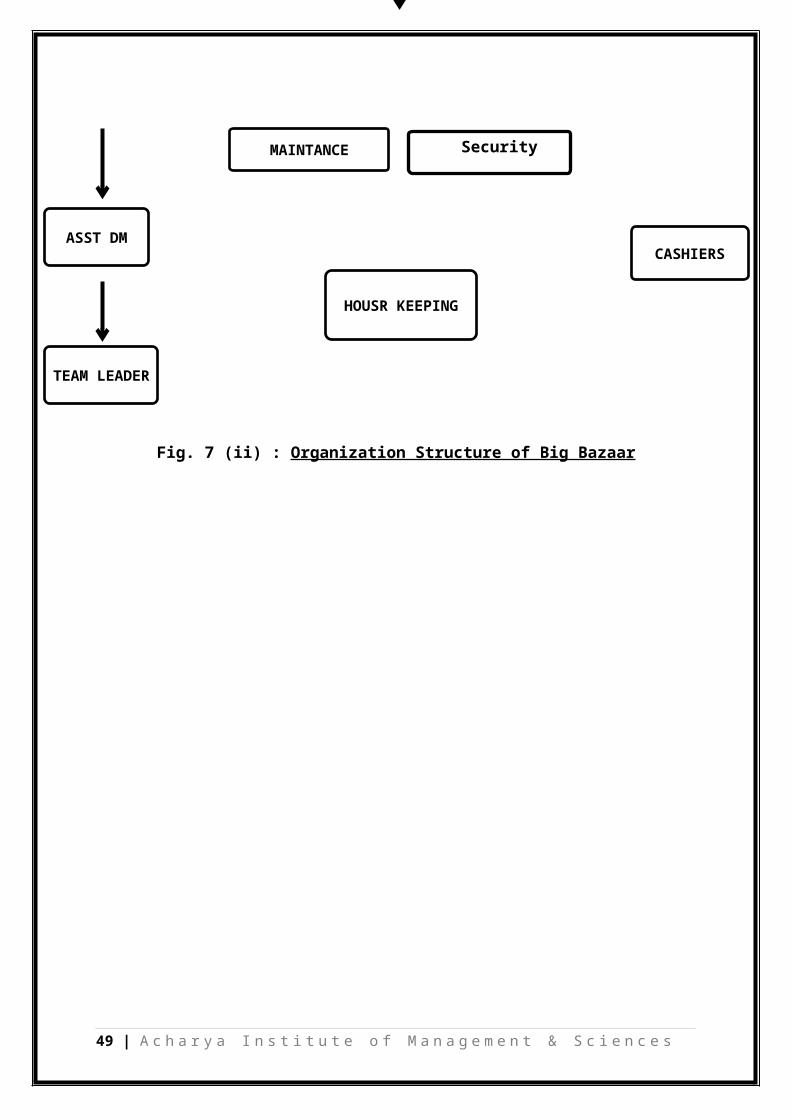

48 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

CSD

HRMANAGER

ADMINISTRATION

LOGISTICS

MARKETING

SALESMANAGER

ASST STORE MANAGER

STORE MANAGER

DEPT MANAGER

TEAM MEMBERS

Fig. 7 (ii) : Organization Structure of Big Bazaar

49 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

MAINTANCE

HOUSR KEEPING

CASHIERS

TEAM LEADER

Security

ASST DM

Chapter 3

FunctionalDepartments

50 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Fig. 8 : Functional Department

3.1 Human Resource Department

51 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

FUNCTIONALDEPARTMENTS

SUPPORT SYSTEM

DEPARTMENT

ADMINISTRATION

DEPARTMENT

CUSTOMER SERVICE DESK

MAINTENANCE DEPARTMENT

LOGISTICS DEPARTMENT

FINANCE DEPARTMENT

HUMAN RESOURCE

DEPARTMENT

MARKETING DEPARTMENT

SALES DEPARTMENT

The HR department of Big Bazaar is very dynamic. Employees are

the biggest Strength and asset of any organization and the HR

dept. realises this very well. This is very evident from the

way the HR department handles all its employees. They take

utmost care to select, train, motivate and retain all tile

employees. They have continuous developmental programmes for

all the employees.

Currently Big Bazaar Malleshwaram is employing 220 full time

and 60 part time employees. There are two shifts for the

employees. The first shift employees arrive at 9am in the

morning and leave at 7.30 in the evening, while the second

shift employees report at 1:30 and leave at the time of store

closing which is 10pm.

3.2 Customer Service Desk (CSD)

Every service industry today has a desk where customers can

express their problems and get them resolved. Similarly in

retail stores, the customer services desk acts as the face

of the organization and listens to customers' problems and

builds their trust on the organization. Thus it is important

for all stores to have a customer service desk. Customers may

approach the customer service desk (CSD) with various types

of queries which may range from asking 'where the wash rooms

are' to 'what is the telephone number of the CEO of the

52 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

organisation: All such queries should be answered by the CSD

with a smile on their face and an acceptable body language.

3.3 Administration

Safety is always a concern for any business specially safety

of the customers and staff. Also, it is very essential that a

store is well maintained, clean and tidy. The administration

department is in charge of the security, housekeeping, packers

and loaders. They handle the police interaction whenever

required.

53 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Fig. 9 : Administration Department

The housekeeping staffs have to maintain cleanliness of the

stores and the departments. They must make sure that cleaning

of the floors is done from time to time during a day. The

security manages the entry and exit of the customers,

protection against theft at the stores, etc. Strict checking

is done before a customer or employee enters the store and at

the time they are leaving.

Every product has a security tag that will prevent the

customers from smuggling the product out of the stores without

paying for it. There are 3 kinds of tags: hard tag, soft tag

and string tag. These tags help to keep a track of the product

and prevent theft.

54 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Admin Head

Admin Assistant(2 people)

Houskeeping Security Maintance

3.4 Logistics

Logistics is considered to be the complete process involving

planning, managing and controlling the flow of goods and

services, information, real-time data and human resources from

the point of origin to the point of destination. There is

hardly any manufacturing or marketing activity that can be

achieved without the support of an effective logistical

department.

The logistics process consists of the process of integration

of several aspects such as material handling, warehousing,

information, transportation, packaging and inventory. The

primary duty of an effective logistics system is to ensure

geographical repositioning of unfinished goods, and it is also

concerned with the finished inventories of the organization

being at the required place at the lowest possible cost.

The various tasks performed by the department may be

summarized as follows:

Ensuring all the requirements of the customers are met on

time in an efficient and safe manner.

To coordinate with third party logistics (3PLs).

To ensure that there is a safe and timely dispatch of

goods.

To draft plans, policies and procedures for successful

implementation of logistics system.

55 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

To ensure that the business goals of the organization are

in synchronization with logistics system.

To create and maintain customer support.

To maintain coordination with vendors, service providers

and transport carriers.

To ensure that no fraud is committed.

To ensure timely supply and reduce inventories.

3.5 Marketing Department

Marketing concept is a customer orientation backed by

integrated marketing aimed at generating customer

satisfaction as the key to satisfying organizational goals.

For a firm in order to implement the marketing concept it

has to focus its attention on the consumer, ascertain

his/her needs, discuss and wants before

Every Brand appeals to individual customers in different

ways. Good customer service is the life blood of any

business. Good customer service is all about attending to

existing and potential customers. This maintaining good

relationship with the customers is the key to business

success and hence the concept relationship marketing.

56 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Traditionally, marketers have located their target market

segments, presented their offer, and made the sales. It's

always been a single step process. Relationship marketing

looks at customers and clients over a longer term

3.6 Sales Department

This department is responsible for the collection of sales

amount i.e., cash sales. There are in all 25 cash counters

in the Store. There is a Head Cashier to whom all the

cahiers report and submit the total sales amount collected

throughout the by the cashiers. In addition to cash all

leading credit and debit cards are accepted at no extra

charge. Also Big Bazaar vouchers and Sodexho coupons are

also accepted.

57 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Chapter 4

ETHICAL/BEST PRACTICES/POLICIES IN THE ORGANIZATION58 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Fig. 10 : Core Values

1. INDIANNESS: Confidence in ourselves.

2. LEADERSHIP: To be leader both in business & thought.

3. RESPECT & HUMILITY: To respect every individual & behumble in our conduct.

4. INTROSPECTIVE: Leading to purposeful thinking.

5. OPENNESS: To be open to receptive to new ideas, knowledge& information.

6. VALUING & NATURING RELATIONSHIP: To build long termrelationship.

7. SIMPLICITY & POSITIVITY: Simplicity & positivity in ourthought, business & action.

59 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

INDIANNESS LEADERSHIP RESPECT & HUMILITY

INTROSPECTIVE OPENNESS

VALUING & NATURING

RELATIONSHIP

SIMPLICITY &

POSITIVITYADAPTABILIT

Y FLOW

8. ADAPTABILITY: To be flexible & adaptable to meetchallenges.

9. FLOW: To respect & understand the universal laws ofnature.

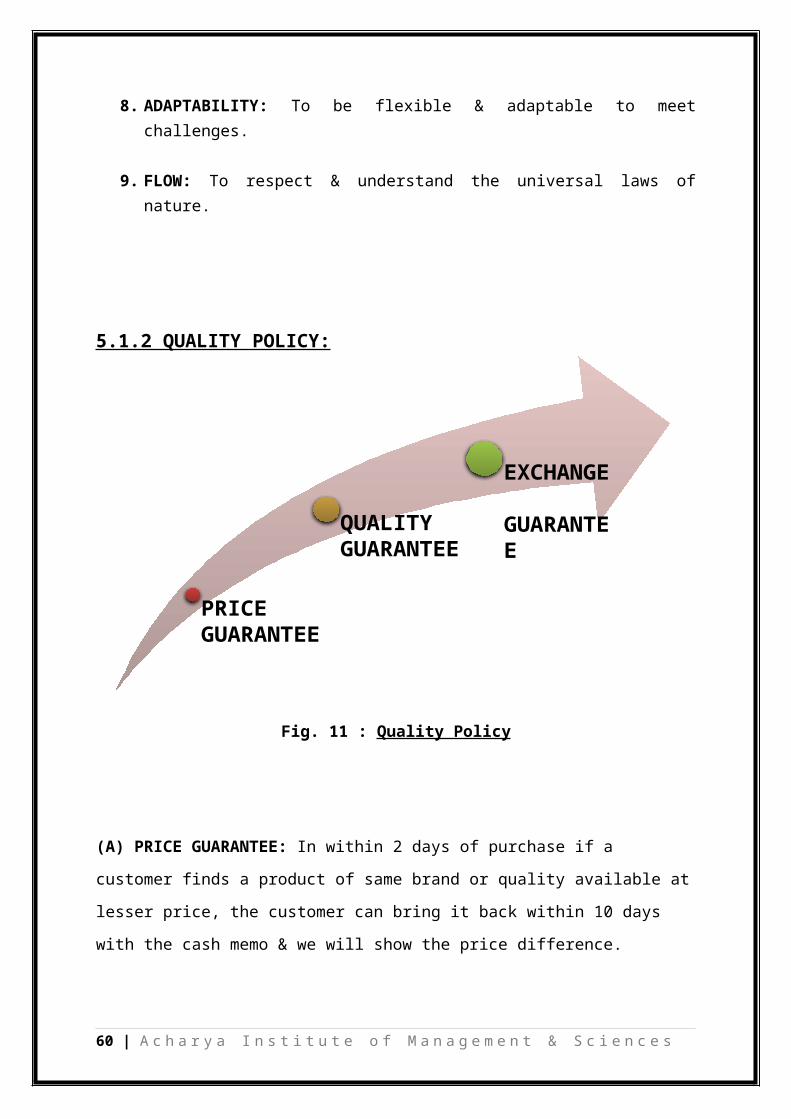

5.1.2 QUALITY POLICY:

Fig. 11 : Quality Policy

(A) PRICE GUARANTEE: In within 2 days of purchase if a

customer finds a product of same brand or quality available at

lesser price, the customer can bring it back within 10 days

with the cash memo & we will show the price difference.

60 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

PRICE GUARANTEE

QUALITY GUARANTEE

EXCHANGE GUARANTEE

(B) QUALITY GUARANTEE: All products sold at Big Bazaar are

guaranteed to be at a good price & of good quality.

(C) EXCHANGE GUARANTEE: The exchange of any product that

have been bought from Big Bazaar & are not satisfied by the

customer can be return back with the cash memo within 15 days

from purchase.

Chapter 461 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

SWOT ANALYSIS

62 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Fig. 12 : SWOT Analysis

STRENGTHS:

High brand equity.

Better understanding of customers helping the company to

serve them better.

Vast range of products under one roof helping in aerating

customer & their family.

Diversified business operating all over India in various

retail formats.

Ability to get products from customers at the rate of

discounted price due to the scale of business.

Professional management.

Good employee & employer relationship.

Strong cultural ethics & values are followed.

63 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

STRENGTHS

WEAKNESSES

OPPORTUNITIES

THREATS

Provides loans for purchase of furniture & electronic

products.

Provides home delivery facilities to customers

WEAKNESSES:

High cost of operation due to large fixed cost.

Specific items are not consistently available.

Poor supply chain management & weak support

infrastructure

Unable to meet store opening targets.

Unavailability of popular brand items with regard to

clothing.

Weak in technology.

OPPORTUNITIES:

Population of the country is growing where the scope of

the market is kept on increasing for the retail sector.

Can enter into the production of various products due to

its in depth understanding of customer’s taste &

preference.

Growth in the income of the customers.

Expand their business at global level.

Provide quality services to the customers.

THREATS:64 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Lot of competitors coming up to tap the market potential.

Shrinkage

High business risk involved.

Advancement of technology day by day.

CHAPTER 665 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

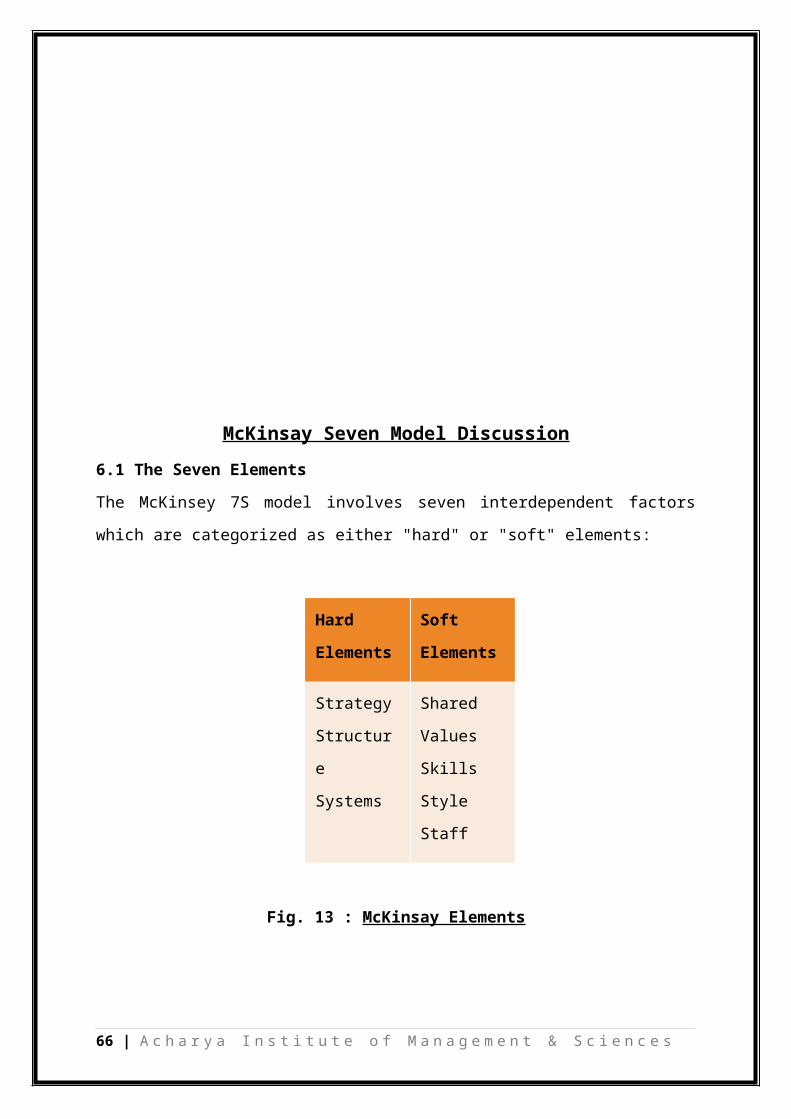

McKinsay Seven Model Discussion6.1 The Seven Elements

The McKinsey 7S model involves seven interdependent factors

which are categorized as either "hard" or "soft" elements:

Hard

Elements

Soft

Elements

Strategy

Structur

e

Systems

Shared

Values

Skills

Style

Staff

Fig. 13 : McKinsay Elements

66 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

"Hard" elements are easier to define or identify and

management can directly influence them: These are strategy

statements; organization charts and reporting lines; and

formal processes and IT systems.

"Soft" elements, on the other hand, can be more difficult to

describe, and are less tangible and more influenced by

culture. However, these soft elements are as important as the

hard elements if the organization is going to be successful.

The way the model is presented in Figure 6.2.6 below depicts

the interdependency of the elements and indicates how a change

in one affects all the others.

Fig. 14 : McKinsay 7s Model

6.2 MC KINESEY’S 7 S MODEL

The 7 S Framework of Mc Kinsey is a model that describes 7

factors to organize a company in a holistic and effective way.

67 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

Together these factors determine the way in which a retail

store operates. Store Manager should take into account all

seven factors, to be sure of successful implementation of

strategy. Richard Pascal and Anthony Athos first mentioned the

7-S Framework in “The Art of Japanese Management ’’ in 1981.

6.3 McKinsey’s 7s frame work with reference to organization.

STRATEGY

The business strategy of Big Bazaar Retail has been to capture

the entire consumption space of the Indian consumers. The

company has moved from one retail business to another, keeping

in pace with the changing needs and aspirations of the Indian

consumer. The company which primarily started as a garment

retailing company has moved into multiple businesses on the

backdrop of the endless opportunities being provided by the

growing Indian economy.

The company has adopted a strategy of catalyzing consumption

and not just capturing it. The company follows a strategy of

discovering new customers, new markets, new geographies and

new business possibilities.

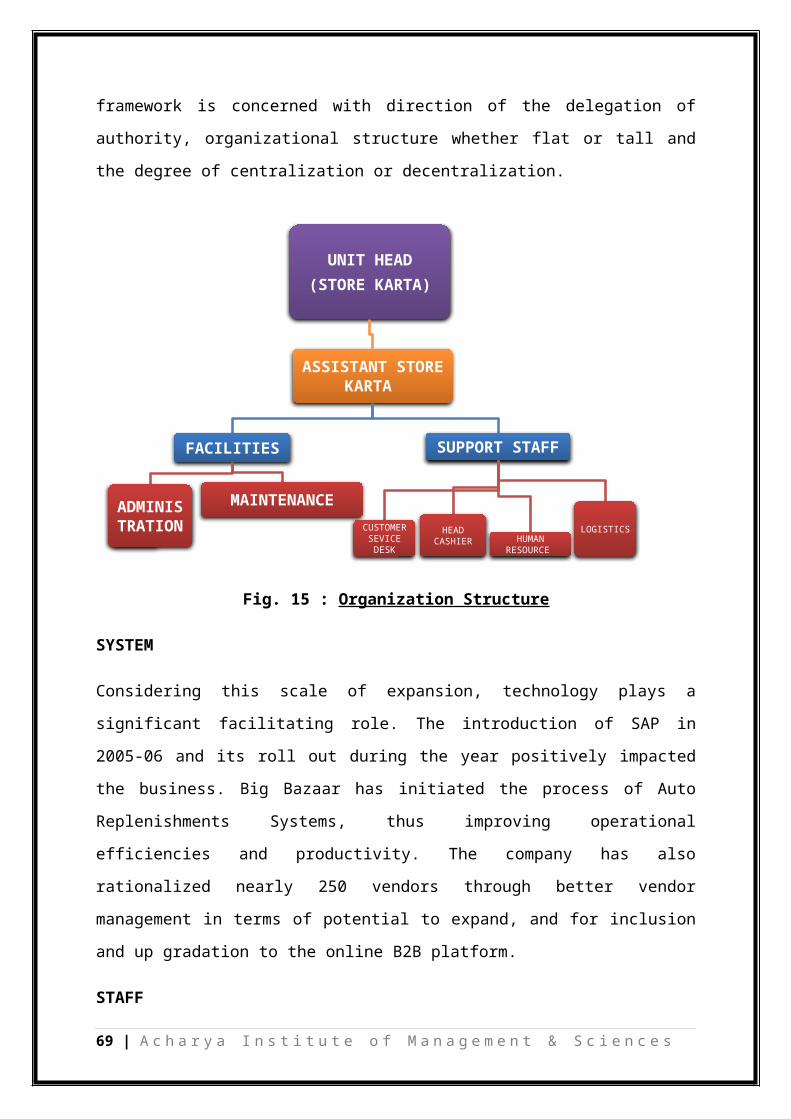

STRUCTURE

“Structure” is the organizational structure or the hierarchy

of the organization that comprises of the authority,

responsibility and relationships in the firm. This function of

68 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

framework is concerned with direction of the delegation of

authority, organizational structure whether flat or tall and

the degree of centralization or decentralization.

Fig. 15 : Organization Structure

SYSTEM

Considering this scale of expansion, technology plays a

significant facilitating role. The introduction of SAP in

2005-06 and its roll out during the year positively impacted

the business. Big Bazaar has initiated the process of Auto

Replenishments Systems, thus improving operational

efficiencies and productivity. The company has also

rationalized nearly 250 vendors through better vendor

management in terms of potential to expand, and for inclusion

and up gradation to the online B2B platform.

STAFF

69 | A c h a r y a I n s t i t u t e o f M a n a g e m e n t & S c i e n c e s

UNIT HEAD(STORE KARTA)

ASSISTANT STORE KARTA

FACILITIES

ADMINISTRATION

MAINTENANCE

SUPPORT STAFF

CUSTOMER SEVICE DESK

HEAD CASHIER HUMAN

RESOURCE

LOGISTICS

Big Bazaar has been successful in keeping its workforce of

25000 highly satisfied and motivated. The company has an

attrition rate of 8.12%, much below industry levels.

Big Bazaar would not have been able to expand and have the

same level of success without hiring and taking care of

quality employees. Some of Pantaloon human resource activities

include employee advancement, employee recruitment on college

universities, and employee training and development.

Additionally, while most firms in retail facing talent crunch.

Big Bazaar has tied up with various college and institutes to

ensure it has fresh supply of talent at its disposal. Close to

46% of the employees in the organization are women and the

average age within the organization is 27 years.

The company has a adopted a policy of collaborating on joint

degree programs with 15 management schools, design institutes

and institutes of higher learning in areas like food business,

supply chain management, design experience management etc.

This ‘Seekho’ programme for the external and internal

candidates ensures a steady stream of mid-level, well trained

retail professionals every year. The company’s ‘Gurukool’

programme provides the front-end employees an opportunity to

imbibe the company’s values and a sense of ownership to the

company.

SKILLS

Pantaloon by tying with various management institutes in India