WELCOME WISH YOU HAPPY NEW YEAR 2018 - C-PEC

40

WELCOME WISH YOU HAPPY NEW YEAR 2018

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of WELCOME WISH YOU HAPPY NEW YEAR 2018 - C-PEC

WELCOME

WISH YOU

HAPPY NEW

YEAR

2018

Presentation on

By

Dr. Rajendra N. Sarkale

CEO,

The Satara DCC Bank Ltd.,Satara

Satara, district is located

in the western part of

Maharashtra State

Bank Slogan is in Sanskrit Language

m/njsnkReukRekue%Means

Get empowered by making others empowered

A)Historical Background of the Satara District

Satara is a historical place blessed by theShrimant Chha. Shivaji Maharaj, a GreatMaratha King & warrior.

Satara was the capital of Maratha Kingdom.

Several great warriors, kings, saints, and greatpersonalities of our district had left theirfootprints in the history of our country.

The district had been very active in the freedommovement; number of individuals hadsacrificed their lives for getting freedom for ourcountry.

B) General information of The Satara District

1) Satara, district is located in the western part of Maharashtra State.

2) Total Geographical area: 10,480 (sq.km.)

(i.e. 3.40% of Maharashtra area of 3,07,710 sq.km.)

3) Total : 11 Blocks/ Tehsils and 1,788 Villages

4) Population: 30 Lacs out of which 80 % is Rural Population

5) High Literacy rate is 82.34%.

(Male : 88.38%, Female: 75.87%)

6) Satara district is situated in the river basin of the

Krishna and Koyana.

7) There are 3 major irrigation projects : Koyana,

Dhom and Kanher Dams. Most of the electricity

of Maharashtra is being generated through

Koyana power grid.

8) Min. Temp is 11.6 o Celsius and Max. Temp 37.5 o

Celsius

9) Average annual rainfall is 1426 mm

10) Irrigation percentage of District : 36%

(Maharashtra:16%) (India: 35%)

C) Rainfall and Geographical condition of the district Considering the Geographical Situation of district it is divided in three

zones.

1. Eastern Zone: Block /Tehsils - Phaltan, Man and Khatav

a) Soil type : Poor to Medium.

b) Average annual rainfall ranging from 250-300mm.

c) Major Crops: Food Grains - Jawar & Bajara,

Horticulture – Pomegranate, Grapes.

d)Fruit Vegetables-Potato and Onion.

2.Western Zone:Block/Tehsils-Mahabaleshwar, Jaoli, Patan and Wai.

a) The land is Hilly and Forests. Undulated land, generally of low fertility.

b) Average Annual rainfall more than 3000 mm. Highest rainfall atMahabaleshwar 5000 – 6000 mm.

c) Main crops are Paddy, Nagali & Strawberry.

3.Central Zone:Block/Tehsils– Khandala, Koregaon, Satara & Karad.

a) Most of the land plane & fertile.

b) Average Annual rainfall ranging from 500 to 600 mm.

c) Main crops are Sugarcane, Ginger, Turmeric, Vegetables, Groundnut& Food Grains.

History of the Bank

•The Satara District Central Cooperative Bank Ltd., Satara, is a leading

cooperative bank in India. Bank has emerged as the economic power house of

the Satara district. The Bank leads the Co-operative Credit Banking.

•Ex-Deputy Prime Minister of India Late Hon. Yashwantrao Chavan and Great

Freedom Fighters Late Balasaheb Desai, Late R. D. Patil & Late Kisan Veer

established the bank on 15th August 1949 with great vision of development in

mind.

•Bank has Lion’s share in the economic development of Cooperatives in the

district.

Bank Network

•The Bank has wide network of 272 Branches and 46 extension counters.

•80% branches are located in rural area to flow the banking services to grass

root level.

•Bank is the Apex Institute operating in the District.

•The most working of the bank is based on three tier system. The loans to

Most of Agriculture and allied activities are provided by the Bank to ultimate

borrower through affiliated Primary Agricultural Co-operative Societies (PACS).

It helps to provide fast and direct service to farmer members to cater their

financial needs.

Name of the Bank : The Satara District Central Co-operative Bank Ltd., Satara.

Address : New Administrative Building, ‘Kisan Bhavan’, C.T.S.No. 523 A/1, Plot No. 5 & 6, Sadarbazar, Camp, P.O. Box No.6, Satara - 415 001

Website : www.sataradccb.com

E-mail Address : [email protected]

Phone Nos. : (02162) 227636 to 227643

Fax No. : (02162) 227645

Registration No : 13179/1961 Dated 15th August 1949

License No. : RPCD Bombay 53 C Dated 06th September 1994License renewed on 20th December 2011.

Audit Class : “A” (Since inception)

Total Branches : 272 Branches and 46 Extension counters

Total Members* : 2738 (2639 - Coop. Societies and 102 - Individuals)

Total Deposits* : 5900.00 Crore

Total Loans* : 3862.98 Crore

Mixed Business* : 9762.98 Crore (* as on 31.03.2017)

General Information of the Bank

Business Performance of the Bank(Rs. in Crores)

Sr. No.

Particulars As on 31-3-2015

As on 31-3-2016

As on 31-3-2017

1 Share Capital 123.43 145.25 159.58

2 Total reserves 284.23 283.22 302.27

3 Free reserves 230.10 248.63 270.52

4 Capital Fund (1 + 3) 353.53 393.88 430.10

5 Deposits 4494.74 5246.82 5900.15

6 Investment 1814.07 2267.74 2904.70

7 Loans & advances 3505.38 4024.24 3862.98

8 % of recovery (June ) 99.50 % 98.13 % 92.00 %

9 Working Capital 5746.77 6763.24 7347.01

10 Gross Profit 66.93 71.58 65.13

11 Net Profit 25.00 33.00 40.00

12 Per Branches Business 25.65 30.27 32.88

Sr. No.

Particulars As on

31-3-2015

As on

31-3-2016

As on

31-3-2017

13 Per Employee Business 4.89 6.086.93

14 Net worth 392.12 406.89441.31

15 Total Branches 272 272272

16 Total employees 1425 13531291

17 CD Ratio ( % ) NABARD 77.98 % 76.69 %65.47%

18 Gross NPA 0.29 % 0.37 %0.37%

19 Net NPA 0 % 0 %0%

20 C.R.A.R. 10.83 10.5511.82

21 Average CRR 4.30 4.204.15

22 Audit Class "A" "A""A"

A) 1) Gross profit before tax 85.36

2) Income Tax paid 20.24

3) Profit after Tax 65.12

4) Net Profit 40.00

B) Net Profit is Distributed as per the Norms

C) Gross Profit Distribution

1) Interest Subvention to Society Borrowers (ST (SAO) @ 2%) 2.00

2) Interest Subvention to Society Borrowers (MTLT @ 2%) 1.62

3) ) Recovery Incentive to PACS having 100 % recovery at Bank level 2.75

4) Recovery Incentive to PACS having 100 % recovery at PACS level 0.15

5) Interest Incentive to PACS Godown / Building Loan 0.11

6) Interest Incentive for Education Loan 1.06

7) Interest Incentive for Drip Irrigation Loan 1.08

8) Secretary Reward Pay (12 % & 15 %) 1.25

9) Reward to Staff ( 2 Salary) 6.41

10) Ex-Grecia to Staff (21 %) 8.07

11) Gratuity Premium 14) Rural Artizen Society Interest Subvention 0.63

Total 25.12

Net Profit 40.00

Gross Profit 65.12

Financial Year 2016-17 – Gross & Net profit ( Rs in Crores)

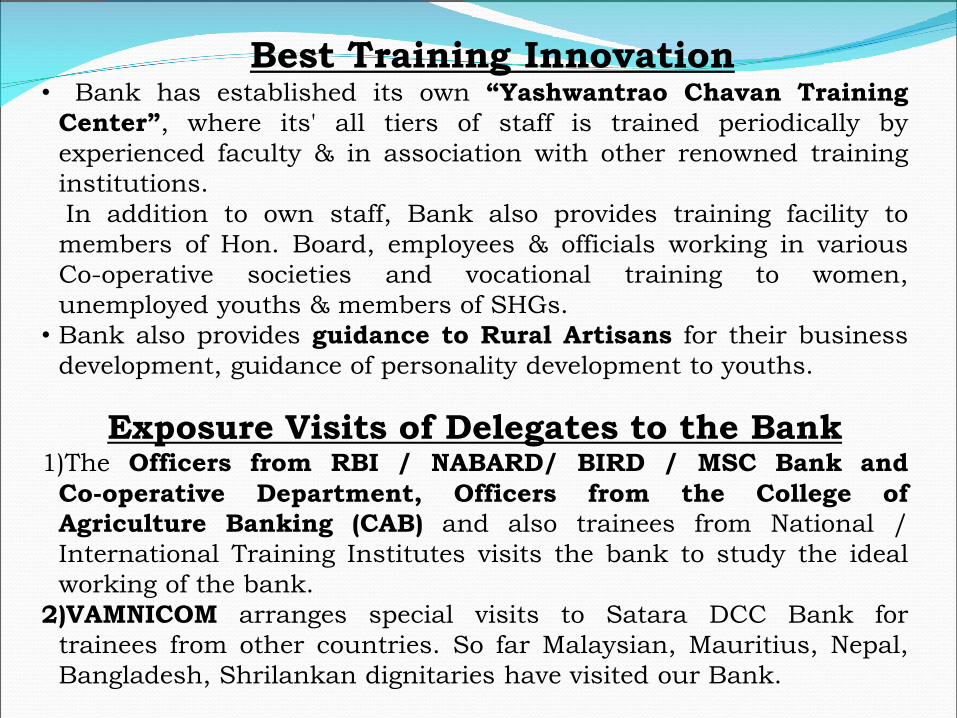

Best Training Innovation• Bank has established its own “Yashwantrao Chavan Training

Center”, where its' all tiers of staff is trained periodically by

experienced faculty & in association with other renowned training

institutions.

In addition to own staff, Bank also provides training facility to

members of Hon. Board, employees & officials working in various

Co-operative societies and vocational training to women,

unemployed youths & members of SHGs.

• Bank also provides guidance to Rural Artisans for their business

development, guidance of personality development to youths.

Exposure Visits of Delegates to the Bank1)The Officers from RBI / NABARD/ BIRD / MSC Bank and

Co-operative Department, Officers from the College of

Agriculture Banking (CAB) and also trainees from National /

International Training Institutes visits the bank to study the ideal

working of the bank.

2)VAMNICOM arranges special visits to Satara DCC Bank for

trainees from other countries. So far Malaysian, Mauritius, Nepal,

Bangladesh, Shrilankan dignitaries have visited our Bank.

Sr. No

Particular

FY 2014-15 FY 2015-16 FY 2016-17

Target Achiev. % Target Achiev. % Target Achiev. %

1CommercialBanks

2950.49 2312.27 78.00 3273.53 2787.18 85 % 3928.96 2813.73 93 %

2The SataraDCC Bank

1693.88 2773.46 163.73 1876.47 3115.08166%

2021.73 3251.57 161%

Total 4644.37 5085.73 109% 5150.00 5902.26 115% 5950.69 6065.30 102%

1) Role in District Credit Plan

* Bank is playing vital role in respect of Annual Credit Plan of

the district.

* Share of our Bank in District Credit Plan is more than 50 %.

* Relative performance for last three years is as under:

(Rs in Crores)

2) Loan Facilities

Customer oriented Loan Policies

Considering the need of agricultural development of the district,

the Bank has introduced more than 75 agri-oriented loan

policies and implemented it successfully.

a) Short Term Loan for Crop: ST (SAO)

•The Short Term Credit is mainly required to the poor farmers for

purchase of various inputs viz. Seeds, Fertilizers, Insecticides etc.

•Taking in to consideration these basic needs, Bank makes

available Crop Loan facility to the farmers as per their need from

Rs. 1 lac to Rs. 3 lacs @ 0%.

•953 Primary Agriculture Cooperative Societies affiliated to our

Bank. Out of which 734 are in profit as on 31.03.2017.

•There are 9.41 lacs revenue account holders, out of which 6.5

Lacs are Society member and 3.50 Lacs are Borrowers.

b) Medium & Long Term Loan for Agri allied activities

•Taking into consideration farmer’s shelter need and easy monitoring and

management of farm, bank has launched the “Shetkari Niwas Scheme”.

Bank introduced Hi- Technology to the farmers for changing traditional

farming to technosavy farming as per the need of time. Bank provides Loans

for Horticulture and Floriculture, Nursery, Green House Project etc

•After harvesting, if the produce is graded, sorted and packed in proper

manner; it gets higher rates in National and International Market. Also due

to lack of proper storage facility, farmers incur heavy losses because of

fluctuating trends in the market. To avoid this, our bank has launched loan

Schemes for Pack House, Onion Storage Sheds, “Rural Godowns”, “Cold

Storage and Pre-cooling Unit etc.

•To make available the additional income source to the farmers, Bank

motivates the farmers for agri-allied business parallel to agriculture for self

development. Accordingly, bank provides the loan for Dairy, Poultry

Farming, Sericulture, Agro-Clinics, Agro truism House.

•Lion’s share in development of Water Resources: Bank has taken

initiatives for development of water resources & bringing more waste &

barren land under irrigation in the district. Bank is also financing for lift

irrigation, Drip / Sprinkler irrigation, renovation of well, farm pond and

water supply by tanker to fruit orchards during drought conditions etc. For

Drip irrigation system Rs. 5000/ per Acre Assistant is provided by the Bank.

c) Direct Finance to Individual

District Central Cooperative Banks mainly provides advances for

Agriculture and Agriculture related activities. The income of the farming families

are improving due to use of advanced technology & industrialization which has

raised their standard of living resulting into changing needs & preference.

Considering this trend and changing requirements of customer, our bank

has established individual direct loan section. This section caters to the

individual needs of customers. Bank has introduced more than 30 schemes

under Individual Direct Finance. Few of them are narrated as below:

1) Loan against Gold Ornaments,

2) Hire Purchase loan for purchase of consumer goods like TV, Refrigerator,

Computer

3) Loan Facility for purchase of four wheeler vehicle

4) Cash Credit Hypothecation facility to traders

5) Housing Loan facility

6) Education Loan Scheme

7) Loan Scheme to purchase Sugarcane Harvesting Machine:

8)Loan facility for purchase of JCB Machine, Bulldozer, Pock lain Machine,

Dozer etc.

9)Composite No. 3 : Loan facility to Rural Artisans, Small entrepreneurs

10)Overdraft against Deposits and against Saving Bank Account for salary

earners

11)Loan against Deposits, Ware-house Receipts, NSC/KVP & Purchase

receipt of Cocoons

d) Non Agriculture Loan Schemes

1) Loan Policy for the Marketing, Processing, Industrial and Consumer

Societies.

a) Cash Credit Clean,

b) Hypothecation,

c) Cash Credit Pledge

2) Fixed Loan policy for the Urban Cooperative Credit Society

(Patasansta)

3) Cash Credit Clean & Fixed Loan policy for the Salary Earners Society

& Bank (where Salary Earners Society is converted in to bank).

4) Medium Term and Long Term Loan facility for Building Construction

to Educational Society.

5) Loan facility for Land Purchase & Building Construction to PACS for

Office Building.

6) Loan facility for Warehouse and Construction to Non Agriculture

Cooperative Societies and Sugar Industries.

7) Medium Term Loan facility to PACS for Computer Software &

Hardware

8) Composite Loan No 2 facility for Village Artisan.

9) Loan Facility for the Sugar Factories

3) CBS Implementation

The bank has fully computerised its' branches in 2009 and

implemented CBS since 2013, the details of which are as under:

1) MIS is being generated through CBS application.

2) The bank is taking utmost precaution for security ot its' data.

3) Bank is providing range of Delivery channels like RTGS, NEFT,

CTS clearing, SMS facility, Mobile Banking and IMPS etc.

Accordingly, Bank is direct member of RBI

4) Bank had already linked Aadhar to accounts for various

benefits distribution. More than 5 lacs accounts are already

seeded with Aadhar.

5) Bank had procured own ATM switch for all types of card based

transactions.

6) Bank has successfully deployed 29 ATMs so far. ATM network is

connected to NFS since inception

7) The Bank is also planning to have network of 650 Micro ATMs

to cater the enrolment of accounts and card based/AEPS

transactions.

8) Out of the 953 PACS in the district, about 878 PACS are already

computerized. The rest are in the process of computerisation

9) Rupay KCC: Under guidance of GOI., RBI and NABARD Rupay

KCC are provided which are in operation on all ATMs and POS

in NPCI network. Bank has distributed 299500 Rupay KCC

and 70000 Rupay debit cards.

DATA CENTRE SETUP

• Data center : Bank has established well equipped data center

(IBM Blade Servers, Storage, CISCO ASR Routers, Firewall,

Security equipments like FM200 Fire protection, VESDA

system, CCTV, Water leakage, Rodent repellent, etc ) at

Satara. Redundancy is maintained at each level.

• Disaster Recovery (DR) site : Well equipped with

redundancy at Nasik.

• Connectivity : Primary connectivity (BSNL LL + RF)

Secondary connectivity (MPLS+ RF)

Insurance Cover to the customers

Bank has implemented Government sponsored Insurance

Schemes like -

•Prime Minister “Jivan Jyoti Bima Yojana” (PMJJBY)

•Prime Minister “Suraksha Bima Yojana”(PMSBY)

•Prime Minister Jan Dhan Yojana (PMJDY)

•Crop Insurance/ Pradhan Mantri Fasal Bima Yojana (PMFBY)

•Horticulture Insurance

And All Government Schemes are effectively Implemented.

Number of Farmers are benefited.

Financial Inclusion Scheme

• Bank has adopted and implemented this policy since 2007

• Financial inclusion improves economic and social development of the

country.

• "Reach to Un reach" is the motto of this programme.

• Bank has achieved excellent success to provide banking services under

Financial Inclusion Scheme to people who are away from the banking

system in the Satara district.

• Bank has 53% S.B. A/C holders from total district population.

Best Financial Literacy

• Taking in to consideration NABARD has sanctioned permission to open

11 FLCs one for each block. Accordingly, bank has started its first

Financial Literacy Centre at Satara on 12/3/2013. i.e. ''Yashwantrao

Chavan Financial Literacy Center''

• The needy people are being benefited by this Financial Literacy Centers.

• Bank has its wide network of 318 branches, through which bank

organizes the seminars to give information regarding the banking

services to the people.

Active participation in Development of Women and Farmers.

Self Help Groups

• Bank has actively implemented the policy of formation of Self Help

Groups for empowering women since 1999.

• More than 23000 Self Help Groups of women are formed by the bank.

• Bank provides loan to SHGs at only 4 % interest rate through PACS.

•SHGs are working under the guidance of bank and most of them got

awards from NABARD.

•Under SHG programme 32 Crores loan is sanctioned and 16000 SHGs

are credit linked.

Farmers Clubs•Bank has established 636 Farmers Clubs under “Vikas Voluntary

Vahini” scheme of NABARD introduced in 1982.

•Bank has been arranging seminars to provide guidance to the farmers in

relation to advanced technique and scientific methods to be used in

their agriculture field to increase quality and quantity of agriculture

production by the successful farmers and by the experts.

•Most of the Farmers Club have received awards from NABARD.

Total Number of Farmers Club 636

NABARD Sanctioned 446

Granted by NABARD 356

Total Grant received 41.28 Lakh

1) The NPA and recovery position of the bank

during the last 10 years

2) Excellence in Recovery

3) Linking Recovery

4) Direct Recovery

5) Review and follow-up

6) Special Schemes of the bank for prompt paying

Borrower

7) Introduction of Mirror accounting system in

PACS:

The NPA and recovery position of the bank

Sr. No. Financial Year Total Loans &

Advances Total NPA

% to Total

Loans &

Advances

% of Recovery

Agri loan

% of Total Recovery Agri+

Non Agri loans

1 2007-2008 97819.54 1132.05 1.16 99.0 98.90

2 2008-2009 97658.93 1329.76 1.36 100.0 99.60

3 2009-2010 109333.32 1347.34 1.23 100.0 98.30

4 2010-2011 157231.86 1536.67 0.97 100.0 99.03

5 2011-2012 193530.22 1535.12 0.79 100.0 99.18

6 2012-2013 264909.65 1490.78 0.56 100.0 98.56

7 2013-2014 293802.15 1604.87 0.54 99.52 98.60

8 2014-2015 350538.39 1020.32 0.29 99.50 98.31

9 2015-2016 402423.96 1470.71 0.36 98.13 97.96

10 2016-2017 386298.18 1430.17 0.37 92.00 95.12

Through figures you would have observed that Loan Recovery of

our bank is very excellent.

Bank has achieved 100 % recovery of loan consecutively for 5 years.

(i.e. from 30th June - 2009 to 2013) and from 2013-14 Bank has

succeeded to recover almost 100 %., even in the scenario of declaration

of Debt Waiver scheme.

Excellence in Recovery

Factors of Effective recover

Proper Assessment of Borrower

Proper Scrutiny and Appraisal of Loan Proposal

Monitoring of Schemes and utilisation of Loans

Technical guidance during implementation of schemes.

Continuous Rapport with Borrower.

Involvement of all segments of the Bank i.e. from Chairman to

Sub staff for recovery. Chairman, Directors, Bank Officers, Co-

operative Department Officers and Society Managing Committee

is actively involved in the recovery process.

For effective recovery, bank has formed separate Recovery Section

at H.O. which is headed by Dy. Manager. There are 11 Blocks /

Tahasils in the district. In every tahasil bank has appointed 1 or 2

Recovery Officers taking into consideration loan portion and area of

operation. Presently there are 13 Recovery Officers. Every officer has

provided separate vehicle for Recovery purpose. Recovery is effected

through linking and through direct approach.

Linking Recovery

Sugarcane is the major crop in the district.

Out of total loan disbursed for short duration purpose, the

quantum of sugarcane loans is around 80% i.e. 800 Crores.

After harvest most of the Sugarcane Growers send their

sugarcane to the Sugar Factories for crushing.

The list of Borrowers with their outstanding including

overdue amount and interest is prepared and submitted to

sugar factories for recovery . As per list of Borrowers

members, Sugar factory used to send bill credit amount

directly to the farmer's bank branch account.

The branch deducts loan portion amount and remaining

amount is being transferred

to farmer's saving account. This is continuous and effective

process.

By this way linking recovery is around 50 %. All the sugar

factories extends best co-operation for making recovery

Direct Recovery :The role of Recovery Officers is to pursue chronic, willful, prestigious willful and

powerful defaulters at first instance. Thereafter, defaulters having amount

outstanding over Rs. 50,000/- is put to necessary action. Personal visits to

defaulter and persuasion are the main tools in recovery process. Sometimes the

measures of possession of movable assets and publishing of Auction notice of

land in local news papers is one of the effective tool of recovery. In very rare

cases land needs to be auctioned. Lastly Legal measures are also adopted for

recovery.

The recovery work of overdue amount is very hard. However DDR has delegated

powers to our sale officers to recover the default amount by way of Legal

measures like attachment of property. It is suggested to make visit on door to

door of every defaulter to give simple intimation and make awareness to pay due

amount in stipulated period of time.

Review and follow-up :Every month review of recovery work done by Recovery Officers is

taken at H.O. level and recovery position is assessed. If any Block /

tahshil is comparatively lagging behind in recovery, then special squad

from HO is deputed, meanwhile HO recovery section is daily in touch

with Block /taluka officers.

After every 3 months overall performance i.e. Loan Target, Deposit

and Recovery is assessed by Chairman, Directors and Senior Officers of

the Bank. These meetings are arranged at Divisional Offices. All

officers, involved in Development and Recovery Process, are called and

branch wise and individual review is taken.

Special Incentive Schemes of the bank for prompt repayment

The bank had introduced many borrower benefit schemes, as under:

Zero percent interest on ST (SAO) loan upto Rs. 3.00 lakh on prompt

repayment (the bank bears the 2% subvention for loans between Rs.1.00 lakh

and Rs.3.00 lakh, which remains after GoI and State Govt, subvention). Bank

has made provision of Rs.200.00 Lacs for the year 2016-17 from its own

profit.

Interest rebate for MT/LT loans: Bank has introduced Interest rebate to

the farmers on the interest for the current year instalment since last 7 years .

Bank has made provision of Rs.162.00 Lacs for the year 2016-17 from its

own profit.

Zero percent interest is offered on Education Loans, Society Godown,

Building Construction Loan and Drip Irrigation for prompt repaying

borrowers. Bank has made provision of Rs.225.00 Lacs for the year 2016-17

from it's profit.

The bank has a “Farmers Group Mediclaim Insurance Scheme” for 2.5 lakh

borrowers, which offers Mediclaim to the couple (borrower & spouse) as an

additional benefit for prompt repayment.

Incentive to PACs and its Secretary is also granted for 100% recovery of

Loans.

Support from the Board:

The bank had also created Planning, Development & Follow up

Sub Committee of the Board. The meetings of the Committee are

organized twice in a year at block level. Chairman, Vice Chairman

and other Sub Committee Members including the block level Asst.

Registrar, Board Members of PACS and their Secretaries, attend

these meeting, which discusses issues including recovery and

sanction of loans.

Board members take keen interest in recovery matters and

assist the PACS / bank officers in solving issues pertaining to

recovery.

The Board of director is very transparent. They never interfere

in appraisal, monitoring or recovery but contribute to the

efforts of the banks staff wherever required.

Hon. Board of Directors has given freedom therefore management

can work effectively without favour and fear.

Imbalance Reduction Scheme

The Bank had adopted the policy in 1997, to Bring imbalanced societies into balanced

The bank had appointed a committee in order to help, guide, and supervise the imbalanced

societies and do the exercise as follows :

Made Ten installments of accumulated interest i.e. given relief to interest

Stopped charging of Interest on principle

Started finance to such societies :

Total period for repayment was given 10 years hence all societies came in Balance

within 5 years.

We are proud to say that, from 1997 - 2004 our bank has got success to maintain all

affiliated societies in balanced state. Now, there is no single PACS in Imbalance. This is

truly success of “Satara Imbalance Reduction Scheme”.

Introduction of Mirror Accounting System in PACSTo ensure that no further Imbalance is created at the PACS level and to minimise the

occurrence of Frauds, the bank introduced a concept called Mirror accounting system.

First each PACS was linked to nearby specified bank branch. This could be done as the

bank had its own branch within 50 – 500 mt of every PACS.

Secondly every cash transaction of the PACS member was linked to the specified branch.

This was done through a mechanism of triplicate challan one for the customer, second

one for the society and third for the Bank.

Every borrower member when he repays the loan amount would pay it through the branch

only and not at PACS. Ultimately this leads to check fraudulent transactions and

giving control over PACs working.

Bank’s Role in Development of affiliated PACs

Support to increase the Share Capital of the PACS

To strengthening the PACS bank gives Special incentives to PACS for its good performance

for 100% recovery from last 9 years. i.e. from 2008-09.

Total Amount of Rs. 22.22 Crore has been made available by the bank as recovery

incentive through its own profit and contributed to each PACs which is converted in to

share Capital during the respective years.

Bank has provided 13 % dividend on their Share Holding to the PACS from last 5

years upto 2015-16 and 12% for the year 2016-17.

PACS as Multi Activities Centers (MACs)

The PACS implemented the “Business Development Plan” to increase the loans and

arrange the programme to introduce the different types of business like Petrol Pumps,

Wedding Hall, commercial buildings, Xerox center, etc.

NABARD has sanctioned the PACS Development Cell (PDC) to the Bank.

More than 3 Lacs KCC Rupay cards SB accounts are opened.

Bank to submit claim to NABARD for release of grant assistance under the project for 22

PACS as MSCs already sanctioned.

NABARD has Sanctioned refinance of Rs. 165.59 lakh for 22 PACS.

Major Achievements of the Bank

Bank has secured 65 awards from different renowned agencies /

institutions in the country and the details are as under.

1)State Government of Maharashtra has awarded the bank by “Sahakar

Bhushan Puraskar 2014” and “Sahakar Nishta Puraskar 2013”.

2) We are the first District Central Cooperative Bank from India, recorded as

“Co-operative Banking Topper” In “Limca Book of Records 2014”

3) Bank has obtained the International Standard Certification i.e. ISO

9001:2008 Certificate by British Standard Institution. Now going to

upgrade on ISO 9001:2015 Certificate.

4) Bank has been awarded by National Bank for Agriculture & Rural

Development (NABARD) by "Best Performance Award" from 1997 to 2004

for 6 times consecutively.

5) Bank has been awarded by National Level “Best Overall Performance

Award” by National Federation of State Co-operative Bank Ltd., (NAFSCOB)

for the year 2013 and 2015.

6) Maharashtra State Co-op. Bank Ltd, Mumbai has been awarded the bank

by “Late Yashwantrao Chavan Award 2012” for Best Performance.

7) Maharashtra State Co-operative Banks Association Ltd., Mumbai (MSCBA)

has awarded the bank by “Best District Central Co-op. Bank Award” from

1998 to 2017 for 16 times consecutively.

Also our 6 officials have been awarded by the association by “Late

Bapusaheb Deshmukh Best Coop. Bank Employee”.

8) Bank has been honoured by 19 Awards in different Categories by Banking

Frontiers, Mumbai from the year 2011 to 2016.

9) TIME RESEARCH, New Delhi has selected the Bank for "Business

Leadership Award 2013”.

10) Avies Publication, Kolhapur has been awarded the bank by “Banco

Award” in 2013, 2014 and 2016.

11) “Lokmat” has been awarded the bank by “BFSI Award 2013”

12) NABARD has been awarded for 5 times from 2007 to 2010 for

“Development of Best Farmers Clubs”

13) NABARD has been awarded 4 times from 2010 to 2012 for “Best Self Help

Group Linkage”

Uniqueness of the Bank

1)Highest Award Winner Bank:

2)as “Co-operative Banking Topper” In “Limca Book of Records 2014”

2) Audit Classification:

3) Profit Making Bank:

4) Consistency in 100 % Recovery of Loan at Bank Level:

5) 0 % Net NPA:

6) Dividend more than 10 % to the Share Holders:

.

7) Free mediclaim for the Borrowers :

8) 0 % interest on Crop Loan:

9) Interest rebate to the farmers for Medium Term (MT) and Long

Term (LT) Loan :

Website : www.sataradccb.com