Vodafone vs Mannesmann - Ho Keng Mun Mervin

29

Vodafone vs Mannesmann Case Study of a Hostile Takeover Group 40 Huizhu Zhang Ho Keng Mun Mervin Wenye Hao Yixin Ye Yuhan Liu Zhou Yu 2378343 2378411 2377326 2378795 2377803 2378298

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Vodafone vs Mannesmann - Ho Keng Mun Mervin

Vodafone vs

MannesmannCase Study of a Hostile Takeover

Group 40Huizhu Zhang Ho Keng Mun MervinWenye Hao Yixin Ye Yuhan Liu Zhou Yu

23783432378411 2377326237879523778032378298

What is a Takeover?1

Case Study Introduction2

Takeover Process3

Post-merger Analysis4

CONTENTS

What is a Takeover?01

Takeover

Proxy Contest

Management Buyout

Acquisition

Merger

Leverage Buyout

Definition of Takeover

Tender Offer

A takeover refers to the transfer of control of a firm from one group of shareholders to another.

Easier to succeed

With the support of

stockholders

Lower cost

输入文本

Friendly Takeover vs Hostile Takeover

Against the wishes of

stockholders

Higher cost

Harder to succeed

Case Study Introduction02

Two mergers

transformed its

regional influence

and industry status

Initially expanded

into the market

through licensing

2012 – One of the

largest and most

successful

companies in UK

1983 – A

subsidiary of

British electronics

company Racal

UK-based

Telecommunications company

Introduction of Vodafone

Vodafone

Düsseldorf-

based company

Introduction of Mannesmann

Disappeared,

automotive and

telecommunications

after Vodafone merger

1995 - Controlled

D2 company

1990 - Successful

entry into

telecommunications

field

German-basedIndustrial conglomerate

Mannesmann AG

Motivation of Vodafone’s Takeover

Orange

Vodafone Mannesmann

Mannesmann’s Expansion Plan

A.

B.

Influence interest of domestic businesses in UK

Compete with Vodafone's position in European market

Takeover Process03

An estimated amount of

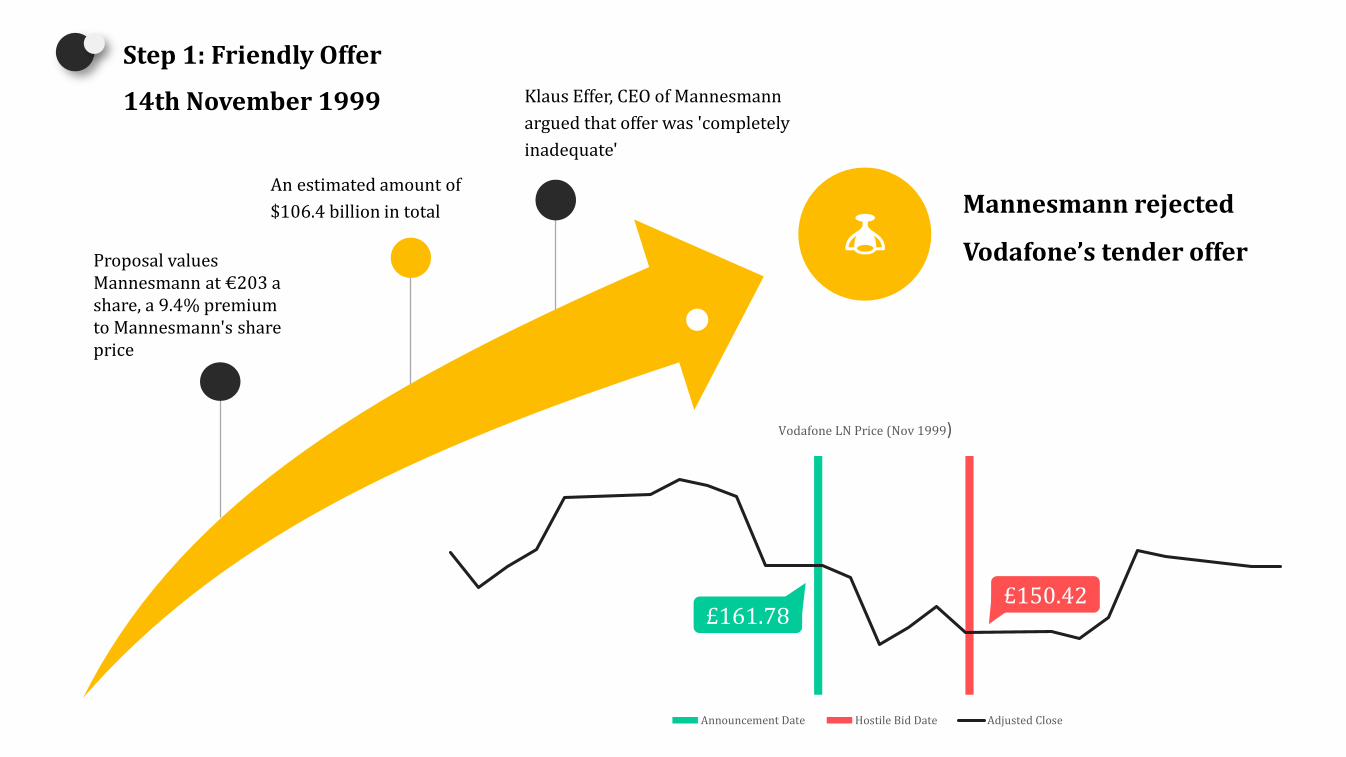

$106.4 billion in total Mannesmann rejected

Vodafone’s tender offer

Step 1: Friendly Offer

14th November 1999

Proposal values Mannesmann at €203 a share, a 9.4% premium to Mannesmann's share price

Klaus Effer, CEO of Mannesmann

argued that offer was 'completely

inadequate'

Vodafone LN Price (Nov 1999)

Announcement Date Hostile Bid Date Adjusted Close

£161.78£150.42

Vodafone rose offer

to almost €125

billion in total

Mannesmann still rejected,

justifying that it will see an

outstanding growth rate of

D2/Orange in the future

Due to Mannesmann's

nationalistic position in

Germany, there was a very

intense reaction throughout

the country in response to

Vodafone's hostile takeover'

Step 2: Hostile Bid: Higher Price Offered

19th November 1999

Mannesmann share price was €185 on 12th Nov 1999 (Friday), share price has been rising from the month before due to speculation.

Step 2: Hostile Bid: Higher Price Offered

19th November 1999

140

150

160

170

180

190

200

210

220

Mannesmann AG Price (Nov 1999)

Announcement Date Hostile Bid Date Last Price

€203

€191.40

“We seek ‘mutual agreement’ and shareholders should take this offer for their profits.”

“We do not wish to lose potential growth, It’s ‘simple mathematics’ to decide.”

Step 2: Hostile Bid: Higher Price Offered

Vodafone directly approached Mannesmann's board

Step 3: White Knight Strategy

18th January 2000

Mannesmann found Vivendi SA, a French leading media conglomerate, as a ‘white knight’. Vivendi

finds itself in talks with both Mannesmann and Vodafone.

Stock Price changes of Vodafone and Mannesmann during the negotiation

Vodafone LN Price (Jan 2000)

White Knight Start Date White Knight End Date Adjusted Close

£185.09 £182.73

Mannesmann AG Price (Jan 2000)

White Knight Start Date White Knight End Date Last Price

€261 €266.5

Vodafone AirTouch and Mannesmann reached agreement

with combine in a $185 billion takeover deal

Please replace text, click add

relevant headline, modify the text

content, also can copy your

content to this directly.

Step 4: Agreement of Merger

4th February 2000

Stock Price changes after Merger

150

160

170

180

190

200

210

220

Vodafone LN Price (Feb-Apr 2000)

Agreement Date Completion Date Adjusted Close

£189.75

£170.96

260

280

300

320

340

360

380

400

Mannesmann AG Price (Feb-Apr 2000)

Agreement Date Completion Date Last Price

€321.5

€305

Post-merger Analysis04

♦Mannesmann was disintegrated.

In addition to the telecommunications business, the industrial

sector is divided and sold according to different sub-sectors. Vodafone suffered huge deficit of £7.71 million due to debt repayment after acquisition

Orange is sold to France Telecom

After the Merger

Brand advertising investment

Integration of cultures

Broaden market presence in Japan

and Hong Kong

♦Continue merging ♦ Establishing an image

♦Vodafone

After the Merger

To maintain Vodafone's position in the market in the light of the debt:

Acquired BT's shares in Airtel and

Japan Telecom

Acquired additional shares in other

company (Swisscom, Iusacell, Eircell)

ROA and ROE was high before merger, but profitability dropped drastically from 2000 onwards. Possible reason is the burst of the dotcom bubble in the early 2000s.

Financial Ratio Analysis

-30

-10

10

30

50

70

90

110

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Vodafone LN (1999-2010)

ROA ROE

EPS dropped from 2000-2001, again possibly due to dotcom bubble. It increased from 2003 onwards, with the exception of 2006. In 2006, Vodafone recorded the biggest loss in the UK thus far, due to write-downs of the values of acquisitions in Italy and Germany, amongst which included Mannesmann.

Financial Ratio Analysis

-1.3

-1.1

-0.9

-0.7

-0.5

-0.3

-0.1

0.1

0.3

0.5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Vodafone LN (1999-2010)

EPS

Vodafone's Situation Today

Vodafone ranked 4th in the number

of mobile customers

Ranked 158th in Fortune 500

companies

In 2018

Investments in 27 countries around

the world

Jointly operated with local mobile

operators in 14 countries

Vodafone's Situation Today

0.00

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

9,000.00

0

50

100

150

200

250

01

/06

/19

99

01

/10

/19

99

01

/02

/20

00

01

/06

/20

00

01

/10

/20

00

01

/02

/20

01

01

/06

/20

01

01

/10

/20

01

01

/02

/20

02

01

/06

/20

02

01

/10

/20

02

01

/02

/20

03

01

/06

/20

03

01

/10

/20

03

01

/02

/20

04

01

/06

/20

04

01

/10

/20

04

01

/02

/20

05

01

/06

/20

05

01

/10

/20

05

01

/02

/20

06

01

/06

/20

06

01

/10

/20

06

01

/02

/20

07

01

/06

/20

07

01

/10

/20

07

01

/02

/20

08

01

/06

/20

08

01

/10

/20

08

01

/02

/20

09

01

/06

/20

09

01

/10

/20

09

01

/02

/20

10

01

/06

/20

10

01

/10

/20

10

01

/02

/20

11

01

/06

/20

11

01

/10

/20

11

01

/02

/20

12

01

/06

/20

12

01

/10

/20

12

01

/02

/20

13

01

/06

/20

13

01

/10

/20

13

01

/02

/20

14

01

/06

/20

14

01

/10

/20

14

01

/02

/20

15

01

/06

/20

15

01

/10

/20

15

01

/02

/20

16

01

/06

/20

16

01

/10

/20

16

01

/02

/20

17

01

/06

/20

17

01

/10

/20

17

01

/02

/20

18

01

/06

/20

18

01

/10

/20

18

Vodafone vs FTSE100 (1999-2019)

Vodafone FTSE100

Vodafone's Situation Today:

Was the takeover good or bad?

For Vodafone

Expansion into new German market

Absolute leadership in Europe

Increased in adveristing and investor awareness

Increased financial performance

A

B

C

D

For Mannesmann

Acquired into Vodafone and dissolution of departments

Mass retrenchment occured except for telecommunications

division

Huge impact on German industry

Loss of culture as Mannesmann had more than 100 years history

A

B

C

D

Vodafone's Situation Today:

Are takeovers are always a good strategy in business competition?

In December 2008, Bank of America bought Merrill Lynch for $50 billion and at the time executives knew

that the deal would sour BofA's earnings for years.

The losses were ultimately so huge that the bank required a second bailout worht $20 billion.

In 2000, Time Warner merged with AOL in a deal valued at $240.07 billion. The two companies lost

billions of dollars as both failed to capitalize on each other's strengths.

Time Warner CEO remarked that the merger was “the biggest mistake in the history of the company”.

(n.d.). Retrieved from https://academic-eb-com.ezproxy.lib.gla.ac.uk/levels/collegiate/article/Vodafone/50582

Bloomberg, Yahoo Finance (2019).

Deutsche Welle. (n.d.). Mannesmann: The mother of all takeovers | DW | 03.02.2010. Retrieved from https://www.dw.com/en/mannesmann-the-mother-of-all-takeovers/a-5206028

Higson, C. (2009). Value Creation at Vodafone. Online: http://faculty.london.edu/chigson/casestudies/pdfs/Vodafone.pdf [Accessed 29/1/2019]

Managing Tax by Organizational Means: The Case of Vodafone, 34(2014), 5th ser., 371-378. (2014). Retrieved February 2, 2019, from https://www-tandfonline-com.ezproxy.lib.gla.ac.uk/doi/full/10.1080/09540962.2014.945809?scroll=top&needAccess=true.

Ross, A. S., Westerfield, W. R., Jaffe, J. & Jordan, D. B. (2013) Corporate Finance. New York: McGraw-Hill Education, 880-922.

Thorsten, S. (1999) Vodafone's hostile takeover bid for Mannesmann highlights debate on the German capitalist model. Online: https://www.eurofound.europa.eu/publications/article/1999/vodafones-hostile-takeover-bid-for-mannesmann-highlights-debate-on-the-german-capitalist-model [Accessed 29/1/2019]

Ulrich, K. (2010) Mannesmann: The mother of all takeovers. Online: https://www.dw.com/en/mannesmann-the-mother-of-all-takeovers/a-5206028 [Accessed 29/1/2019]

Wang, D. and Zhang, Q. (2004). Corporate Mergers and Acquisitions. Beijing: Tsinghua University Press.

References

Thank youfor your

attention!