Value-based management and corporate governance: A study of Serbian corporations

20

93 ECONOMIC ANNALS, Volume LVII, No. 193 / April – June 2012 UDC: 3.33 ISSN: 0013-3264 * Department of Accounting, Auditing and Business Finance, Faculty of Economics, University of Kragujevac, Serbia, [email protected] ** Department of Accounting and Business Finance, Faculty of Economics, University of Belgrade, Serbia, [email protected] *** Department of Accounting, Auditing and Business Finance, Faculty of Economics, University of Kragujevac, Serbia, [email protected] JEL CLASSIFICATION: L21, L25, G34, G32 ABSTRACT: e aim of this paper is to determine the place and role of corporate governance and performance measures in the efforts of managers to maximize shareholder value, and the attitude of Serbian corporations toward these issues. e paper first analyses the importance of corporate governance and performance measures in the context of value-based management. en, through the multiple case study, we investigate the attitude of seven Serbian corporations toward defining the general corporate objective, corporate governance, and performance measurement. Finally, we point out the factors and preconditions that determine corporate culture, objective definition, and performance measures used by Serbian corporations. KEY WORDS: shareholder value, corporate governance, performance measures DOI:10.2298/EKA1293093S Predrag Stančić* Miroslav Todorović** Milan Čupić*** VALUE-BASED MANAGEMENT AND CORPORATE GOVERNANCE: A STUDY OF SERBIAN CORPORATIONS

Transcript of Value-based management and corporate governance: A study of Serbian corporations

93

ECONOMIC ANNALS, Volume LVII, No. 193 / April – June 2012UDC: 3.33 ISSN: 0013-3264

* Department of Accounting, Auditing and Business Finance, Faculty of Economics, University of Kragujevac, Serbia, [email protected]

** Department of Accounting and Business Finance, Faculty of Economics, University of Belgrade, Serbia, [email protected]

*** Department of Accounting, Auditing and Business Finance, Faculty of Economics, University of Kragujevac, Serbia, [email protected]

JEL CLASSIFICATION: L21, L25, G34, G32

ABSTRACT: The aim of this paper is to determine the place and role of corporate governance and performance measures in the efforts of managers to maximize shareholder value, and the attitude of Serbian corporations toward these issues. The paper first analyses the importance of corporate governance and performance measures in the context of value-based management. Then, through the multiple case study, we investigate the attitude

of seven Serbian corporations toward defining the general corporate objective, corporate governance, and performance measurement. Finally, we point out the factors and preconditions that determine corporate culture, objective definition, and performance measures used by Serbian corporations.

KEY WORDS: shareholder value, corporate governance, performance measures

DOI:10.2298/EKA1293093S

Predrag Stančić*Miroslav Todorović**Milan Čupić***

VALUE-BASED MANAGEMENT AND CORPORATE GOVERNANCE: A STUDY OF SERBIAN CORPORATIONS

94

Economic Annals, Volume LVII, No. 193 / April – June 2012

1. INTRODUCTION

Companies face the different and often conflicting demands of a number of stakeholders. This problem is particularly evident when defining the primary objective of a company’s business. Although companies often define their general business objectives as profit maximization, growth and development, and market share increase, none of these is sufficiently comprehensive to ensure that the requirements of all stakeholders are met. Some authors (Rappaport, 2006; Lazonick and O’Sullivan, 2000) suggest that the majority of modern companies, as a general objective (mission) of their businesses, identify shareholder value maximization, usually defined as the present value of future free cash flows. Shareholder value maximization is considered to be a sufficiently comprehensive objective to ensure the satisfaction of the requirements of most stakeholders (Stančić, 2006; Jensen, 2001), and is a cornerstone of the value-based management (VBM) approach.

At the base of all value creation models are several key value drivers that determine the amount and the present value of expected cash flows. These key value drivers are return on invested capital (ROIC), weighted average cost of capital (WACC), expected company growth rate, and competitive advantage period (the period during which the company expects to generate a difference between the return on invested capital and the weighted average cost of capital). The value is created when a company succeeds in achieving a positive performance spread, i.e., when ROIC exceeds WACC. Negative performance spread is a reliable sign that current business activity is destroying the value of a company. The amount of value created or destroyed is the product of invested capital and performance spread.

Moskalev and Park (2010) suggest that the corporation must be built on the core concept of value, and that the firm’s organization, strategy, processes, communication, everything the firm does, must be consistently aligned with the key value drivers. They further suggest that if VBM is successfully implemented, then corporate culture will support and encourage corporate governance mechanisms consistent with value creation at all levels within the organization. The link between corporate governance and corporate valuation has been investigated in several studies (Dahya et al., 2008; Durnev and Kim, 2005). These studies show that strong governance can protect the interests of minority shareholders and improve company performance, even more in countries with weak than in countries with strong legal protection of investors.

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

95

This paper aims to investigate characteristics of internal governance mechanisms in the context of value-based management and the specific economic and cultural conditions within which corporations in Serbia operate. We conduct the analysis using a multiple case method on a sample of seven corporations in Serbia. We build our analysis on several previous papers that use the multiple case method to investigate similar corporate problems. We expect that our research will provide an insight into the corporate culture, corporate objectives, and performance measures used in the large publicly traded companies from different industry sectors in Serbia. This insight is the basis for understanding the factors influencing the corporate culture and governance of Serbian companies, and for the future theoretical and empirical investigation of this problem.

2. THEORETICAL BACKGROUND

Value-based management (VBM) can be defined as a framework for targeting those business decisions that consistently add economic value to a company (Morin and Jarrell, 2001). It is also a managerial approach in which company objectives, systems, strategies, processes, performance measurements, and culture have as their guiding objective shareholder value maximization. The simple concepts behind VBM are value and value creation. The value of a company is determined by its discounted future cash flows, and value is created when a company invests capital at returns that exceed the cost of that capital. Copeland et al. (1994) point out that VBM extends these concepts by focusing on how companies use them to make strategic and operating decisions.

Copeland et al. (1994) also suggest that VBM focuses on better decision making at all levels in an organization, and calls on managers to use value-based performance measures for making better decisions. Similarly, todorović (2010) points out that value-based performance measures are particularly useful because they show managers how they can create value, while Kaličanin (2005) points out that these measures provide the motivation for managers in the selection and implementation of those options that maximize value. However, managers still often use measures based on accounting data (according to Fitzgerald, 2007). Although this approach is obviously simpler, it results in only partially accurate indications and suboptimal decisions, since accounting data weakly correspond with factors determining shareholder value (Čupić, 2011; Rappaport, 2006; Stewart 2003). This is confirmed in many empirical studies showing that value measures are more significantly related to shareholder returns than accounting measures (e.g., Wet and toit, 2007; Wortington and West, 2004; O’Byrne, 1996).

96

Economic Annals, Volume LVII, No. 193 / April – June 2012

Although the original idea behind VBM was to align the measurement system with value creation in a way that accounting measurement systems did not, some authors suggest that too much focus on performance measurement caused serious problems in VBM implementation. For example, Koller et al. (2005) argue that many VBM programmes failed because companies developed objective and comprehensive value-based measurement systems, but neglected management processes and corporate governance. Morin and Jarrell (2001) argue that investing in relationships with shareholders and other stakeholders can add value, while Rappaport (2005) believes that a company can better realize its potential for value creation by aligning the interests of shareholders and managers, and providing investors with value-relevant information.

Some authors empirically investigate the importance of corporate governance for improving company performance. Dahya et al. (2008) and Durnev and Kim (2005) find that strong governance (primarily a strong board) can protect the interests of minority shareholders and improve company performance, and even more so in countries with weak than in countries with strong legal protection of investors. Coombes and Watson (2000) show that investors in the US and UK are willing to pay up to 18% more for shares of companies with good governance than for the shares of companies with similar performance but poor practice of corporate governance. Barton and Wong (2006) show that investors in developing countries are ready to pay from 20%-40% more for shares with good governance. Mitton (2002) finds that firms with higher disclosure quality, greater transparency, and higher outside ownership concentration experience better stock price performance during periods of crisis.

The general model of corporate governance, aimed at resolving the agency problem that arises between the agent (manager) and the principal (shareholders), which is typical in economic systems with strong legal protection of investors where the roles of managers and owners are clearly divided (Jensen and Meckling, 1976), cannot be used as a starting point for investigating the relationship between corporate governance and company performance in developing economies. An insufficiently developed institutional context in developing economies makes the enforcement of agency contracts and protection of investors more costly and problematic (Wright et al., 2005). This results in the prevalence of concentrated firm ownership, which acts as the major governance mechanism in developing countries. Concentrated ownership, combined with an absence of effective protection of minority investors, results in more frequent conflicts between dominant (ultimate, controlling) shareholder and minority shareholders (Young et al., 2008; Shleifer and Vishny, 1997), with negative consequences for firm performance.

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

97

In developing countries with weak legal protection of investors, corporate governance is the means by which minority shareholders are protected from expropriation of their rights by managers and the dominant shareholder. Institutions that are important external governance mechanisms in developed countries, such as the stock exchange, securities regulators, institutional investors, and the judiciary, are weak in developing economies. A high quality of disclosure and strong boards of directors are, therefore, besides ownership concentration, the most important internal governance mechanisms in developing economies. Many authors stress the importance of internal governance mechanisms regardless of economy development. Morin and Jarrell (2001) pointed out that the three main areas of corporate governance are performance measurement, the compensation system, and investor communication, while Mitton (2002) put special emphasis on disclosure quality, ownership structure, and corporate diversification. La Porta et al. (1998) argue that accounting standards play a critical role in corporate governance by informing investors and by making contracts more verifiable.

3. EMPIRICAL RESEARCH

3.1. Context of the analysis

Serbia has a civil law legal system, and belongs to the group of emerging and developing countries. In many studies (e.g., Johnson et al., 2000; La Porta et al., 2000) civil law countries have been linked with strong regulation but weak effective (institutional) protection of investors, particularly minority shareholders. In the case of Serbia this is confirmed in The World Bank global report Doing Business 2011, which shows that Serbia ranks better in legal (measured by strength of investor protection index) than in effective judicial (measured by enforcing contracts index) protection of investors. Among 183 economies Serbia is ranked 74th in protecting investors, and 94th in enforcing contracts. Kaličanin (2005) argues that Serbian corporations are not motivated to be transparent in business and do not feel pressure from shareholders to deliver the required returns or to create value for them. The shareholders are subjects of attention only if they are dominant (which is often); but then the problem of protecting minority shareholders arises.

The process of transition, which caused changes in the institutional and economic system and in the ways companies operate and in which managers and staff behave, has motivated some Serbian companies to introduce technology and management

98

Economic Annals, Volume LVII, No. 193 / April – June 2012

systems recognized and used by the successful companies operating in developed market economies (Bogićević Milikić et al., 2008). For example, Bogićević Milikić and Janićijević (2009) show that performance evaluation systems (PES) have become an institutionally accepted way of operating in Serbian companies such as tarket, telekom Srbija, etc. Medicinal products manufacturer Hemofarm was one of the pioneers among Serbian corporations in using VBM methodologies. In the annual report for 2003 Hemofarm reports: “In the course of 2003 Hemofarm Group introduced innovative instruments of monitoring financial performance in cooperation with the structurally major shareholder Aktiva. The “Economic Value Added” concept became the key instrument for performance evaluation at the Strategic Business Unit levels”.

3.2. Research methodology

The attitude of companies in Serbia toward value-based management, corporate governance, and performance measurement is relatively unknown. That is why we use the multiple case method, which is suited to researching unknown subjects (Bogićević Milikić and Janićijević, 2009), i.e., for getting in-depth and first-hand understanding of a particular situation (Yin, 2004). Yin (2004) defines the case study research method as an empirical inquiry that investigates a contemporary phenomenon within its real-life context, when the boundaries between the phenomenon and the context are not clearly evident, and in which multiple sources of evidence are used. Unlike single case studies, multiple case studies permit replication and extension between individual cases, which helps researchers to understand patterns more easily, to eliminate chance associations, and to form better theoretical structure (Eisenhardt, 1991).

The multiple case method has been used in several studies on corporate governance and performance measurement systems (Bogićević Milikić and Janićijević, 2009; Chen and Guliang, 2009; Kennerly and Neely, 2002). While there is no ideal number of cases, a number between four and ten usually works (Eisenhardt, 1989), so we design a seven-case study. We analyse seven large (according to Serbian Accounting and Audit Law, RS Official Gazette, Nos. 46/2006 and 111/2009) publicly traded companies. As in Chen and Guliang (2009) and Kennerly and Neely (2002), companies from different industry sectors and with a wide variety of competitive and organizational characteristics were intentionally chosen to introduce diversity into the sample, and to enable the identification of factors affecting the evolution of measurement in a variety of different circumstances. We also chose companies from different Belgrade Stock Exchange (BSE) markets (regulated and unregulated) because we wanted to

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

99

investigate if listing requirements had influenced the way companies behaved. General characteristics of the companies involved in the research are shown in table 1.

The research took place during 2008, and the data was collected by referring to publicly available data (annual reports, Business Registers Agency, and company web sites), and through questionnaires and phone interviews with top managers and employees designated by the top manager. The questionnaire and interview were designed to get the answers to the following four questions:

a) How does the company communicate with its shareholders?b) How does the company define its general and additional objectives? c) Is the company aware of the existence of the value-based management concept?

Does the company use this concept, or try to implement it?d) What performance measures does the company use?

This research is intended to provide an insight into the corporate culture, corporate objectives, and performance measures used in the large publicly traded companies from different industry sectors. This insight is the basis for understanding the factors influencing corporate culture and governance of Serbian companies, and for the future theoretical and empirical investigation of this issue.

Table 1. Basic information on business cases

Company IndustryTotal sales

in 2008 (000 €)

Total assets in 2008 (000 €)

Belgrade stock exchange market

1 Production of non-electrical household appliances 35,515 40,537 Regulated

market

2 Production of rusks, biscuits, preserved pastry goods and cakes 64,547 72,125 Unregulated

market

3 Production of soft drinks, mineral waters and other bottled waters 71,880 78,674 Unregulated

market

4 Production of enamel, stainless steel and non-stick cookware 6,300 39,317 Regulated

market

5 Production of furniture 62,591 190,214 Unregulated market

6 Production of footwear, technical rubber goods and chemical products 2,845 45,909 Regulated

market

7 Wholesaler of medications and medical products 129,913 298,761 Unregulated

marketSource: Belgrade Stock Exchange, Business Registers Agency and company web sites

100

Economic Annals, Volume LVII, No. 193 / April – June 2012

3.3. Research findings

We first analyse the ownership and board structure of the companies in our study. table 2 shows that all the companies in our study have a controlling shareholder. Controlling shareholder is defined as a single owner of voting rights in a company, providing that it controls at least 10% of the company’s votes (Dahya et al., 2008; La Porta, 1998). The mean of equity holdings of the three largest shareholders is 56%, which is considerably more than in emerging (51%) and developed economies (41%), as reported by Young et al. (2008).

The mean of board size is 8.43 directors, which is consistent with the 7-12 directors reported in several studies on boards of non-financial firms from developed and developing countries (Dahya et al., 2008; Andres et al., 2005). On average, independent directors account for 30.08% of directors on the board, which is considerably less than the average proportion of independent directors (around 80%) reported for banks (Adams and Mehran, 2008; Andres and Vallelado, 2008), and the average proportion of independent directors (at least 38%) reported for non-financial firms (Dahya et al., 2008; Andres et al., 2005).

The implication of these results is that the dominant shareholders of companies in Serbia tend to appoint weak boards, which can lead to serious conflicts between dominant and minority shareholders in the absence of developed external governance mechanisms. In addition, companies that are traded on the regulated markets of the BSE (1, 4 and 6) have a lower ownership concentration ratio, which could be due to the requirement for these companies to have at least 25% of shares in free float. These companies also tend to have smaller boards of directors and a lower proportion of independent directors on the board.

Table 2. Ownership and board structure in the business cases

CompanyEquity holding of the largest

owner

Equity holdings of the largest three owners

Board size

% of non-executives on

the board

% of independent directors on the

board1 24.77% 41.65% 7 57.14% 14.29%2 63.72% 69.61% 7 100.00% 28.57%3 58.07% 99.29% 7 100.00% 28.57%4 11.07% 24.69% 7 71.43% 71.43%5 44.26% 44.81% 11 63.63% 27.27%6 33.70% 47.02% 9 55.55% 22.22%7 23.02% 64.91% 11 63.63% 18.18%

Mean 36.94% 56.00% 8.43 73.05% 30.08%Source: Authors’ survey data

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

101

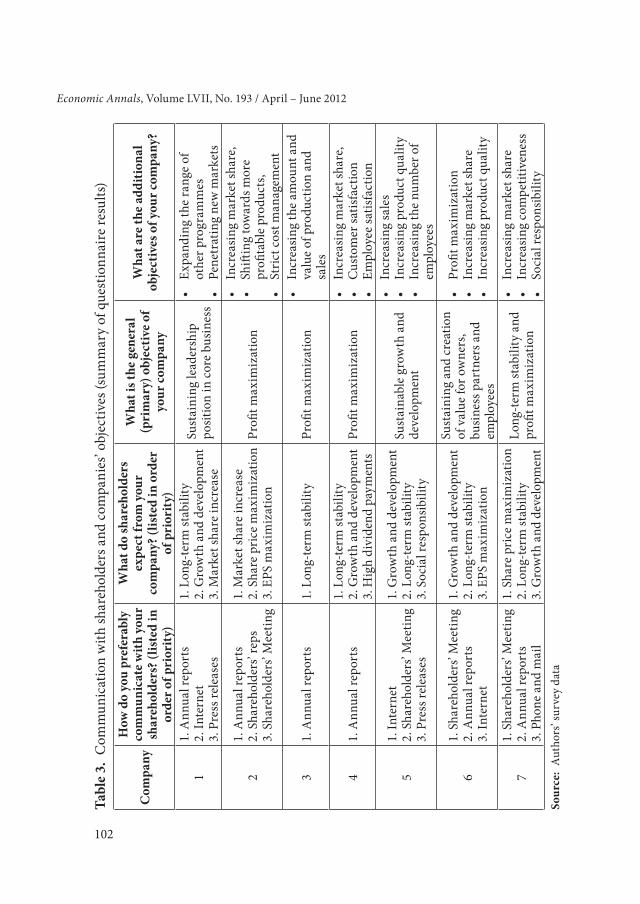

We further analyse the way companies communicate with their shareholders. table 3 shows that all the companies, except for company 5, use annual reports as the most important or second most important means of communication with shareholders, which is consistent with some recommendations for enhancing shareholder value (Morin and Jarrell, 2001). Companies also tend to communicate with shareholders at Shareholders’ Meetings, described by Strenger (2006) as the premier governance instrument for shareholders to directly articulate their concerns. Companies rarely use phone, mail, Internet, or dividend payments; methods of communication and signals that have become preferred in developed economies over the past ten years (Romanek and Lee, 2006).

Companies traded on the regulated BSE markets offer more publicly available information and pay dividends to shareholders on an annual basis. Information on companies traded on the unregulated market is often hard to find, and these companies do not pay dividends on a regular basis. This is more often the case if a company has higher ownership concentration ratio and a lower proportion of independent directors on the board. This could be due to stricter criteria for listing on the regulated market, and the fact that controlling shareholders with larger equity holdings are less interested in shareholder expectations and dividend signalling. The implication of this finding is that the corporations in Serbia are interested in communication with shareholders only to the degree that is required by law or other regulations. This is consistent with studies showing that countries with civil law legal systems have strong regulation but weak protection of investors, particularly minority shareholders (La Porta et al., 2000).

We continue our multiple case study by investigating the way companies include shareholder expectations in general and additional objective definitions. table 3 shows that all the companies, except for company 2, believe that shareholders expect long-term stability from them, as opposed to four companies (2,3, 4 and 7), which list short-term profit maximization as their primary objective. Furthermore, two (2 and 7) out of four “profit maximization companies” list share price increase as the primary shareholder expectation. Share price increase is one of the elements of total shareholder return and in line with shareholder value maximization. Hence the controversy: this implies that the fact that a company recognizes shareholder expectations does not have to mean that the company is shareholder value-oriented.

102

Economic Annals, Volume LVII, No. 193 / April – June 2012Ta

ble

3. C

omm

unic

atio

n w

ith sh

areh

olde

rs a

nd c

ompa

nies

’ obj

ectiv

es (s

umm

ary

of q

uest

ionn

aire

resu

lts)

Com

pany

How

do

you

pref

erab

ly

com

mun

icat

e w

ith y

our

shar

ehol

ders

? (lis

ted

in

orde

r of p

rior

ity)

Wha

t do

shar

ehol

ders

ex

pect

from

you

r co

mpa

ny? (

liste

d in

ord

er

of p

rior

ity)

Wha

t is t

he g

ener

al

(pri

mar

y) o

bjec

tive

of

your

com

pany

Wha

t are

the

addi

tiona

l ob

ject

ives

of y

our c

ompa

ny?

11.

Ann

ual r

epor

ts2.

Inte

rnet

3. P

ress

rele

ases

1. L

ong-

term

stab

ility

2. G

row

th a

nd d

evel

opm

ent

3. M

arke

t sha

re in

crea

se

Sust

aini

ng le

ader

ship

po

sitio

n in

cor

e bu

sine

ss

•Ex

pand

ingtherang

eof

othe

r pro

gram

mes

•

Penetratingnewm

arkets

21.

Ann

ual r

epor

ts2.

Sha

reho

lder

s’ re

ps3.

Sha

reho

lder

s’ M

eetin

g

1. M

arke

t sha

re in

crea

se2.

Sha

re p

rice

max

imiz

atio

n3.

EPS

max

imiz

atio

nPr

ofit m

axim

izat

ion

•Increasing

marketsha

re,

•Sh

iftingtowardsm

ore

profi

tabl

e pr

oduc

ts,

•Strictcostm

anagem

ent

31.

Ann

ual r

epor

ts1.

Lon

g-te

rm st

abili

ty

Profi

t max

imiz

atio

n•

Increasing

theam

ountand

va

lue

of p

rodu

ctio

n an

d sa

les

41.

Ann

ual r

epor

ts1.

Lon

g-te

rm st

abili

ty2.

Gro

wth

and

dev

elop

men

t3.

Hig

h di

vide

nd p

aym

ents

Profi

t max

imiz

atio

n•

Increasing

marketsha

re,

•Customersa

tisfaction

•Em

ployeesa

tisfaction

51.

Inte

rnet

2. S

hare

hold

ers’

Mee

ting

3. P

ress

rele

ases

1. G

row

th a

nd d

evel

opm

ent

2. L

ong-

term

stab

ility

3. S

ocia

l res

pons

ibili

ty

Sust

aina

ble

grow

th a

nd

deve

lopm

ent

•Increasing

sales

•Increasing

produ

ctqua

lity

•Increasing

thenu

mbero

fem

ploy

ees

61.

Sha

reho

lder

s’ M

eetin

g2.

Ann

ual r

epor

ts3.

Inte

rnet

1. G

row

th a

nd d

evel

opm

ent

2. L

ong-

term

stab

ility

3. E

PS m

axim

izat

ion

Sust

aini

ng a

nd c

reat

ion

of v

alue

for o

wne

rs,

busi

ness

par

tner

s and

em

ploy

ees

•Profi

tmaxim

ization

•Increasing

marketsha

re•

Increasing

produ

ctqua

lity

71.

Sha

reho

lder

s’ M

eetin

g2.

Ann

ual r

epor

ts3.

Pho

ne a

nd m

ail

1. S

hare

pri

ce m

axim

izat

ion

2. L

ong-

term

stab

ility

3. G

row

th a

nd d

evel

opm

ent

Long

-ter

m st

abili

ty a

nd

profi

t max

imiz

atio

n

•Increasing

marketsha

re•

Increasing

com

petitiveness

•So

cialre

spon

sibility

Sour

ce:

Aut

hors

’ sur

vey

data

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

103

The ability of companies 1, 5 and 6 to recognize long-term stability and sustainable growth and development and not to highlight profit maximization as the primary corporate objective implies that they take care of shareholders’ interests. Furthermore, managers in company 1 state that they “make decisions consistent with the aim of exceeding the minimal required rate of return of 10%”, while managers in company 6 are focused on “obtaining and exceeding the rate of return expected by owners.” However, only companies 5 and 6 directly build shareholders’ expectations into their primary objective. Company 5 is completely dedicated to fulfilling shareholders’ expectations, since it defines its primary objective precisely as recognizing shareholders’ expectations – sustainable growth and development. Company 6 is the only company in our study that defines its primary objective as “sustaining and creating value for owners, business partners and employees,” i.e., as creating value for shareholders and other stakeholders. Besides company 6, traces of orientation to other stakeholders can be found in the objective definitions of companies 5 and 7, while other companies do not mention other stakeholders even in secondary objectives. Interestingly, companies 1 and 6, which are the only companies in our study that pay dividends on an annual basis, do not believe that shareholders expect high dividend payments.

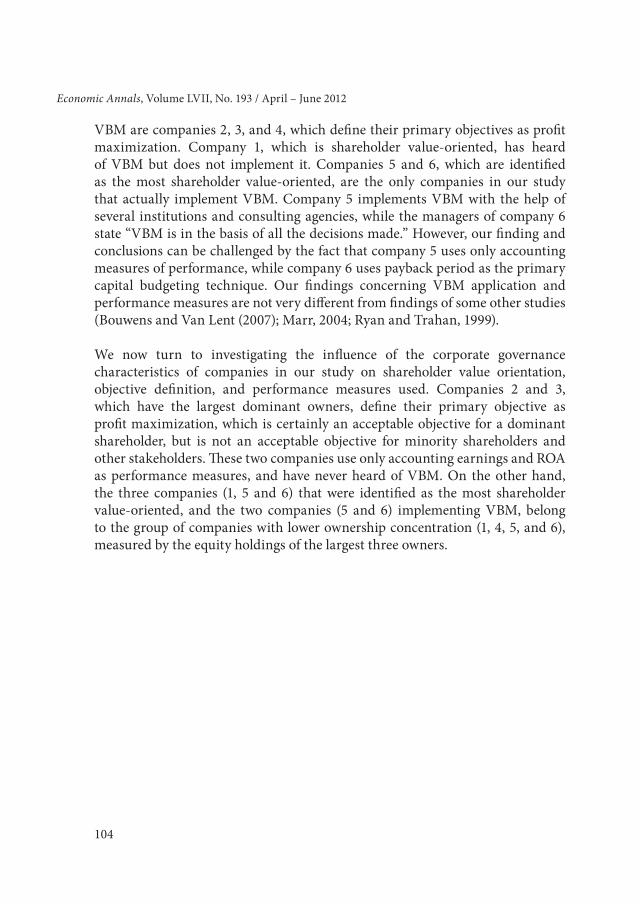

table 4 shows that all the companies in our study use traditional accounting and market measures of performance. Company 6 uses the largest set of measures, and it is the only company in our study where other measures besides traditional accounting (net profit and earnings before interest and taxes) or market (dividend per share) measures are used. This company uses total shareholder return (tSR) and cash flow return on investment (CFROI). None of the companies use economic value added (EVA), market value added (MVA), or total business return (tBR). Companies tend to rely on traditional capital budgeting techniques (payback period and accounting rate of return), but all the companies use at least one discounted cash flow investment appraisal technique (net present value, internal rate of return, or benefit/cost ratio). In four companies managers use payback period as a primary capital budgeting technique, which means that managers in these corporations are more interested in capital turnover rate (project liquidity) than in profitability. This fact can be explained by the lack of shareholder value orientation among companies in our study, as well as by the liquidity problems of Serbian corporations and the limited number of funding mechanisms. The majority of companies use internal rate of return, which again shows that Serbian corporations are concerned with the way each unit of capital is used.

table 4 shows that the managers of four companies have heard of VBM, while two companies implement VBM. Among companies that have never heard of

104

Economic Annals, Volume LVII, No. 193 / April – June 2012

VBM are companies 2, 3, and 4, which define their primary objectives as profit maximization. Company 1, which is shareholder value-oriented, has heard of VBM but does not implement it. Companies 5 and 6, which are identified as the most shareholder value-oriented, are the only companies in our study that actually implement VBM. Company 5 implements VBM with the help of several institutions and consulting agencies, while the managers of company 6 state “VBM is in the basis of all the decisions made.” However, our finding and conclusions can be challenged by the fact that company 5 uses only accounting measures of performance, while company 6 uses payback period as the primary capital budgeting technique. Our findings concerning VBM application and performance measures are not very different from findings of some other studies (Bouwens and Van Lent (2007); Marr, 2004; Ryan and trahan, 1999).

We now turn to investigating the influence of the corporate governance characteristics of companies in our study on shareholder value orientation, objective definition, and performance measures used. Companies 2 and 3, which have the largest dominant owners, define their primary objective as profit maximization, which is certainly an acceptable objective for a dominant shareholder, but is not an acceptable objective for minority shareholders and other stakeholders. These two companies use only accounting earnings and ROA as performance measures, and have never heard of VBM. On the other hand, the three companies (1, 5 and 6) that were identified as the most shareholder value-oriented, and the two companies (5 and 6) implementing VBM, belong to the group of companies with lower ownership concentration (1, 4, 5, and 6), measured by the equity holdings of the largest three owners.

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

105

Tabl

e 4.

Val

ue-b

ased

man

agem

ent a

nd p

erfo

rman

ce m

easu

res (

sum

mar

y of

que

stio

nnai

re re

sults

)

Com

pany

Wha

t per

form

ance

mea

sure

s do

you

use?

Wha

t cap

ital b

udge

ting

te

chni

ques

do

you

use?

(lis

ted

in o

rder

of p

rior

ity)

Hav

e yo

u ev

er h

eard

of

VBM

?

Are

you

im

plem

enti

ng

VBM

?

1•

Accou

ntingearnings

•Re

turnonassets(R

OA)

•Dividendpersha

re(D

PS)

1. P

ayba

ck p

erio

d2.

Ben

efit/c

ost r

atio

3. A

ccou

ntin

g ra

te o

f ret

urn

Yes

No

2•

Accou

ntingearnings

•Re

turnonassets(R

OA)

1. N

et p

rese

nt v

alue

2. In

tern

al ra

te o

f ret

urn

3. P

ayba

ck p

erio

dN

oN

o

3•

Accou

ntingearnings

•Re

turnonassets(R

OA)

1. P

ayba

ck p

erio

d2.

Acc

ount

ing

rate

of r

etur

n3.

Net

pre

sent

val

ueN

oN

o

4•

Accou

ntingearnings

•Re

turnonassets(R

OA)

•Dividendpersha

re(D

PS)

1. P

ayba

ck p

erio

d2.

Inte

rnal

rate

of r

etur

nN

oN

o

5•

Accou

ntingearnings

•Re

turnonassets(R

OA)

1. B

enefi

t/cos

t rat

io2.

Rec

ipro

cal o

f pay

back

per

iod

3. In

tern

al ra

te o

f ret

urn

Yes

Yes

6

•Accou

ntingearnings

•Re

turnonassets(R

OA)

•Price-earningsra

tio(P

/E)

•Dividendpersha

re(D

PS)

•To

talsha

reho

lderre

turn(T

SR)

•Cashflo

wre

turnoninvestment(CFR

OI)

1. P

ayba

ck p

erio

d2.

Inte

rnal

rate

of r

etur

n3.

Acc

ount

ing

rate

of r

etur

nYe

sYe

s

7•

Accou

ntingearnings

•Re

turnonassets(R

OA)

•Price-earningsra

tio(P

/E)

1. N

et p

rese

nt v

alue

2. In

tern

al ra

te o

f ret

urn

Yes

No

Sour

ce:

Aut

hors

’ Sur

vey

data

106

Economic Annals, Volume LVII, No. 193 / April – June 2012

In regard to the influence of the board structure as a second important variable of corporate governance, it seems that the percentage of non-executive and independent directors does not play a role in corporate shareholder value orientation, implementation of VBM, performance measurement, and capital budgeting techniques choice. Company 2 with 100% of non-executive directors is the only one that does not list long-term stability as the shareholders’ expectation, has never heard of VBM, and quotes profit maximization as its primary objective. Similarly, company 3, whose board also consists entirely of non-executive directors, uses only accounting earnings and return on assets (ROA) as performance measures and payback period as its primary capital budgeting technique, states profit maximization as its primary objective, and has never heard of VBM. Company 4 is in the same situation, which is the company with the highest proportion of independent directors on the board. In contrast, companies that are value oriented (1 and 6) have the lowest percentages of non-executive and independent directors. The implications of our findings concerning corporate governance are that ownership concentration is the major governance mechanism of Serbian corporations, and that the structure of the boards of directors is a weak governance variable (mechanism) in Serbian corporations.

Based on research findings, we identify several factors influencing corporate culture, corporate objectives, and choice of performance measures of large publicly traded companies in Serbia. These are:

1) Civil law legal system - Serbia is a civil law country with weak de jure and de facto shareholder protection. Consequently, companies have a high degree of ownership concentration and tend to take shareholder interests and requirements into consideration only to the degree that is required by law and other regulations.

2) Belgrade stock exchange (BSE) rules - Companies traded on the regulated (Prime and Standard) BSE markets communicate better with their shareholders. The reason is stricter rules for listing the shares on regulated than on unregulated markets.

3) Funding mechanisms - Along with characteristics of the legal system, BSE does not provide incentives for using IPO as a funding mechanism for corporations. Therefore, corporations do not feel pressure from the capital market and shareholders to create high shareholder returns, pay dividends, and regularly inform shareholders.

4) Uninformed managers – Managers of three of the surveyed corporations have never heard of value-based management, while managers of another three corporations heard about this concept thanks to Serbian scientific sources.

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

107

That is, scientific and professional papers are available in the Serbian language, and several institutions (or agencies) provide consulting services in the area of value based management, but still many managers have not heard anything about value-based methodologies and value measures of performance.

Bearing in mind key factors determining the relations between corporations and shareholders in Serbia, we identify two important preconditions for improving these relations. The first precondition is improvement of the legal framework. The New Law on the Capital Market (Official Gazette RS, No. 31/2011) relies on a new market development strategy advocating an upgrade of the stature of the BSE by removing from admission to trading those companies in which there is no significant trading interest. It provides better protection of shareholders’ rights and provides for the establishment of an Investor Protection Fund. The law also regulates public offerings, which could motivate corporations in Serbia to use this funding mechanism. Also, the new Law on Companies (RS Official Gazette, No. 36/2011), although not substantially different from its previous version, provides more detailed and precise provisions and allows corporations to choose between a one-tier and a two-tier board, which is in accordance with EU regulations. These two laws should provide a better legal framework for the operation of Serbian corporations, better protection of investors, and better communication between corporations and their shareholders.

The second precondition is development of the BSE and strengthening of the Securities Commission by providing adequate supervision and enforcement. Along with a better legal framework that clearly defines the supervisory role of the Securities Commission by directing its focus on those regulatory activities that are the most important in achieving investor protection and fair and orderly trading of securities, this precondition should provide efficient functioning of the market and attract more individuals and foreign investors to the BSE. We believe that these two preconditions, as well as institutional investors and foreign direct investment, are going to significantly determine the direction and degree of the development of corporate governance and performance measures in Serbian corporations.

4. CONCLUSIONS

Value-based management places the need for an integrated approach to company management at the forefront, which includes the definition, implementation, and evaluation of strategic and operational decisions with respect to the objective

108

Economic Annals, Volume LVII, No. 193 / April – June 2012

of shareholder value maximization. The performance measures developed in the context of value-based management are an important factor of value-based management implementation and business improvements. However, too much focus on performance measurement can cause serious problems in VBM implementation, as reported in several studies. Companies must also rely on governance mechanisms and comprehensive management processes in order to meet different information requirements and improve business performance.

The ownership concentration in Serbian corporations is very high, while the proportion of independent directors on the board is small if compared to statistics reported from samples of non-financial firms in developed countries. In other words, dominant shareholders tend to appoint weak boards, which can lead to serious conflicts between dominant and minority shareholders. In the absence of strong boards, policy makers in Serbia should develop better legal and institutional mechanisms for protecting minority shareholders. Companies traded on the regulated markets of the Belgrade Stock Exchange have a lower ownership concentration ratio, tend to have smaller boards of directors and a lower proportion of independent directors on the board, and are more likely to take expected rate of return into consideration.

Corporations in Serbia are interested in communicating with shareholders only to the degree that is required by law or other regulations. Companies that are not traded on the regulated markets of the Belgrade Stock Exchange have a higher ownership concentration ratio and a lower proportion of independent directors on the board, offer less publicly available information, and do not pay dividends on a regular basis.

Corporations usually believe that shareholders expect long-term stability, growth, and development, as well as market share increase, but only three of them are really shareholder value-oriented. This means that, although a company can recognize shareholder expectations, it is not consequently oriented towards shareholder value maximization.

All the surveyed companies use traditional accounting and market measures of performance, while none of the companies use EVA, MVA, or tBR. Only one company in our study uses total shareholder return (tSR) and cash flow return on investment (CFROI). Companies tend to rely on traditional capital budgeting techniques, but all the companies use at least one discounted cash flow investment appraisal technique. As for value-based management, we find that the three most shareholder value-oriented companies have heard of VBM,

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

109

and two of them are actually implementing VBM. The implications of our findings concerning the relation between corporate governance and VBM are that ownership concentration is the major governance mechanism of Serbian corporations, and that boards of directors are the weak governance mechanism in Serbian corporations.

Based on research findings, we identify four factors influencing corporate governance, corporate objectives, and choice of performance measures of large publicly traded companies in Serbia. These are the civil law legal system, the Belgrade Stock Exchange market on which company’s shares are traded, limited funding mechanisms, and uninformed managers. Bearing in mind these factors, we identify two important preconditions for improving relations between corporations and shareholders and the ability of corporations to create shareholder value: 1) improving the legal framework, and 2) the development of the Belgrade Stock Exchange and strengthening of the Securities Commission. We emphasize external factors and preconditions for improving relations between corporations and shareholders because the characteristics of Serbian culture (see Janićijević, 2003) and the legal system foreground external incentives to managers’ and investors’ actions, and not internal or individual initiatives.

Our research has several limitations, one of which is the small number of corporations that are investigated. However, we believe that it gives a useful insight into the corporate culture, corporate governance, and performance measures used in large publicly traded companies from different industry sectors in Serbia. This insight provides a basis for understanding the factors influencing the corporate governance and performance measurement systems of Serbian corporations, and for the future theoretical and empirical investigation of this problem. Future research should focus on investigating the particular business areas in which VBM is used and factors that limit or motivate the use of specific governance mechanisms or performance measures.

REFERENCES

Adams, R.B. & Mehran, H. (2008). Corporate Performance, Board Structure, and their Determinants in the Banking Industry. Federal Reserve Bank of New York Staff Report No. 330. June 2008.

Andres, P. de & Vallelado, E. (2008). Corporate Governance in Banking: The Role of the Board of Directors. Journal of Banking and Finance, 32 (12), pp. 2570-2580.

110

Economic Annals, Volume LVII, No. 193 / April – June 2012

Andres, P., Azofra, V., & Lopez, F.J. (2005). Corporate Boards in OECD Countries: Size, Composition, Compensation, Functioning and Effectiveness. Corporate Governance: an International Review, 13 (2), pp. 197–210.

Barton, D. & Wong, S.C.Y. (2006). Improving board performance in emerging markets. The McKinsey Quarterly, 1, pp. 35-43.

Bogićević Milikić, B., Janićijević, N. & Petković, M. (2008). HRM in transition Economies: The Case of Serbia. South East European Journal of Economics and Business, 3 (2), pp. 75-88.

Bogićević Milikić, B. & Janićijević, N. (2009). Cultural Divergence and Performance Evaluation Systems: A Comparative Analysis Study of Three Serbian Companies. Economic Annals, 54 (180), pp. 40-55.

Bouwens, J. & Van Lent, L. (2007). Assessing the Performance of Business Unit Managers. Journal of Accounting Research, 45 (4), pp. 667-697.

Chen, G. & Guliang, t. (2009). Subjective Performance Measurement: Multi-Case Study Based on Chinese Corporations. (Paper presented at PMA Conference 2009). Retrieved from http://www.pma.otago.ac.nz/pma-cd/papers/1093.pdf.

Coombes, P. & Watson, M. (2000). Three surveys on corporate governance. The McKinsey Quarterly, 4, pp. 74-77.

Copeland, t., Koller, t., Murrin, J. (1994). Valuation: Measuring and Managing the Value of Companies. Hoboken, NJ: John Wiley and Sons.

Čupić, M. (2011). Usaglašenost računovodstvenih merila sa ciljem maksimiziranja vrednosti za akcionare. Ekonomske teme, 49 (1), pp. 123-136.

Dahya, J., Dimitrov, O. & McConnell, J. (2008). Dominant Shareholder, Corporate Boards, and Corporate Value: A Cross-Country Analysis. Journal of Financial Economics, 87 (1), pp. 73-100.

Durnev, A. & Kim, E.H. (2005). to Steal or Not to Steal: Firm Attributes, Legal Environment, and Valuation. Journal of Finance, 60 (3), pp. 1461-1493.

Eisenhardt, K. (1989). Building Theories from Case Study Research. Academy of Management Review, 14 (4), pp. 532-550.

Eisenhardt, K. (1991). Better Stories and Better Constructs: The Case for Rigor and Comparative Logic. Academy of Management Review, 16 (3), pp. 620-627.

Fitzgerald, L. (2007). Performance Measurement. In t. Hopper, D. Horthcott and R. Scapens (eds.), Issues in Management Accounting (pp. 223-241). Harlow, UK: Pearson Education Limited.

Hemofarm Group. (2003). Annual Report 2003. Retrieved from http://www.vibilia.rs/srpski/izvestaj/0401/hemofarm_160804.pdf.

Јаnićijević, N. (2003). Uticaj nacionalne kulture na organizacionu strukturu preduzeća u Srbiji. Economic Annals, 48 (156), pp. 45-66.

VALUE-BASED MANAGEMENt IN SERBIAN CORPORAtIONS

111

Jensen, M. (2001). Value Maximization, Shareholder Theory, and the Corporate Objective Function. Journal of Applied Corporate Finance, 14 (3), pp. 8-21.

Jensen, M., & Meckling, W. (1976). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3 (4), pp. 305-360.

Johnson, S., La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2000). tunneling. American Economic Review Papers and Proceedings, 90 (2), pp. 22-27.

Kaličanin, Đ. (2005). Menadžment zasnovan na vrednosti: teorijska osnova, akcionarski zahtev i koncept. Economic Annals, 50 (165), pp. 165-184.

Kennerly, M. & Neely, A. (2002). A Framework of the Factors Affecting the Evolution of Performance Measurement Systems. International Journal of Operations and Production Management, 22 (11), pp. 1222-1245.

Koller, t., Goedhart, M. & Wessels, D. (2005). Valuation: Measuring and Managing the Value of Companies. New Jersey: John Wiley & Sons.

La Porta, R., Lopez‐de‐Silanes, F., Shleifer, A., & Vishny, R.W. (1998).

Law and Finance. Journal of Political Economy, 106 (6), pp. 1113-1155. La Porta, R., Lopez‐de‐Silanes, F., Shleifer, A., & Vishny, R. (2000).

Investor Protection and Corporate Governance. Journal of Financial Economics, 58 (1-2), pp. 3-27.

Lazonick, W. & O’Sullivan, M. (2000). Maximizing Shareholder Value: A New Ideology for Corporate Governance. Economy and Society, 29 (1), pp. 13-35.

Marr, B. (2004). Business Performance Management: Current State of the Art. Cranfield School of Management and Hyperion Solutions.

Mitton, t. (2002). A Cross-Firm Analysis of the Impact of Corporate Governance on the East Asian Financial Crisis. Journal of Financial Economics 64 (2), pp. 215-241.

Morin, R. & Jarrell, S. (2001). Driving Shareholder Value: Value-Building Techniques for Creating Shareholder Wealth. New York, NY: McGraw-Hill.

Moskalev, S. & Park, S.C. (2010). South Korean Chaebols and Value-Based Management. Journal of Business Ethics, 92 (1), pp. 49-62.

O’Byrne, S. (1996). EVA and Market Value. Journal of Applied Corporate Finance, 9 (1), pp.116-125.

Rappaport, A. (2005). The Economics of Short-term Performance Obsession. Financial Analysts Journal, 61 (3), pp. 65-79.

Rappaport, A. (2006). ten Ways to Create Shareholder Value. Harvard Business Review, 84 (9), pp. 66-77.

112

Economic Annals, Volume LVII, No. 193 / April – June 2012

Romanek, B. & Lee, D. (2006). E-Communication to Shareholders outside the Offering Process. University of Toledo Law Review, 37 (2), pp. 387-402.

Ryan, H. & trahan, E. (1999). The Utilization of Value-Based Management: An Empirical Analysis. Financial Practice and Education, 9 (1), pp. 46-58.

Shleifer, A., & Vishny, R. (1997). A Survey of Corporate Governance. Journal of Finance, 52 (2), pp. 737-789.

Stančić, P. (2006). Savremeno upravljanje finansijama preduzeća. Kragujevac: Ekonomski fakultet Univerziteta u Kragujevcu.

Stewart, B. (2003). How to Fix Accounting – Measure and Report Economic Profit. Journal of Applied Corporate Finance, 15 (3), pp. 63-82.

Strenger, C. (2006). Best Practice for Dealing with Non-Controlling Shareholders – An Institutional Investor’s Perspective. OECD Policy dialogue 2006 – Corporate Governance in India. Retrieved from http://www.capital-governance-advisory.com/060223StrengerOECDIndia.pdf.pdf.

The World Bank. Doing Business 2011. Retrieved from http://www.doingbusiness.org/reports/global-reports/doing-business-2011/.

todorović, M. (2010). Poslovno i finansijsko restrukturiranje preduzeća. Beograd: Centar za izdavačku delatnost Ekonomskog fakulteta u Beogradu.

Wet, J. & toit, E. (2007). Return on Equity: A Popular, But Flawed Measure of Corporate Financial Performance. South African Journal of Business Management, 38 (1), pp. 59-69.

Worthington, A. & West, t. (2004). Australian Evidence Concerning the Information Content of Economic Value-Added. Australian Journal of Management, 29 (2), pp. 201-224.

Wright, M., Filatotchev, I., Hoskinsson, R., & Peng, M. (2005). Strategy Research in Emerging Economies: Challenging the Conventional Wisdom. Journal of Management Studies, 42 (1), pp. 1-33.

Yin, R. (2004). Case Study Research: Design and Methods. Thousand Oaks, CA: Sage Publications.

Young, M., Peng, M., Ahlstrom, D., Bruton, G., & Jiang, Y. (2008). Corporate Governance in Emerging Economies: A Review of the Principal–Principal Perspective. Journal of Management Studies, 45 (1), pp. 196-220.

Accounting and Audit Law, RS Official Gazette, Nos. 46/2006 and 111/2009.

Law on Companies, RS Official Gazette, No. 36/2011.

Law on the Capital Market, RS Official Gazette, No. 31/2011.

Received: October 24, 2011Accepted: November 07, 2011