Tsogo Sun Heritage

80

-

Upload

khangminh22 -

Category

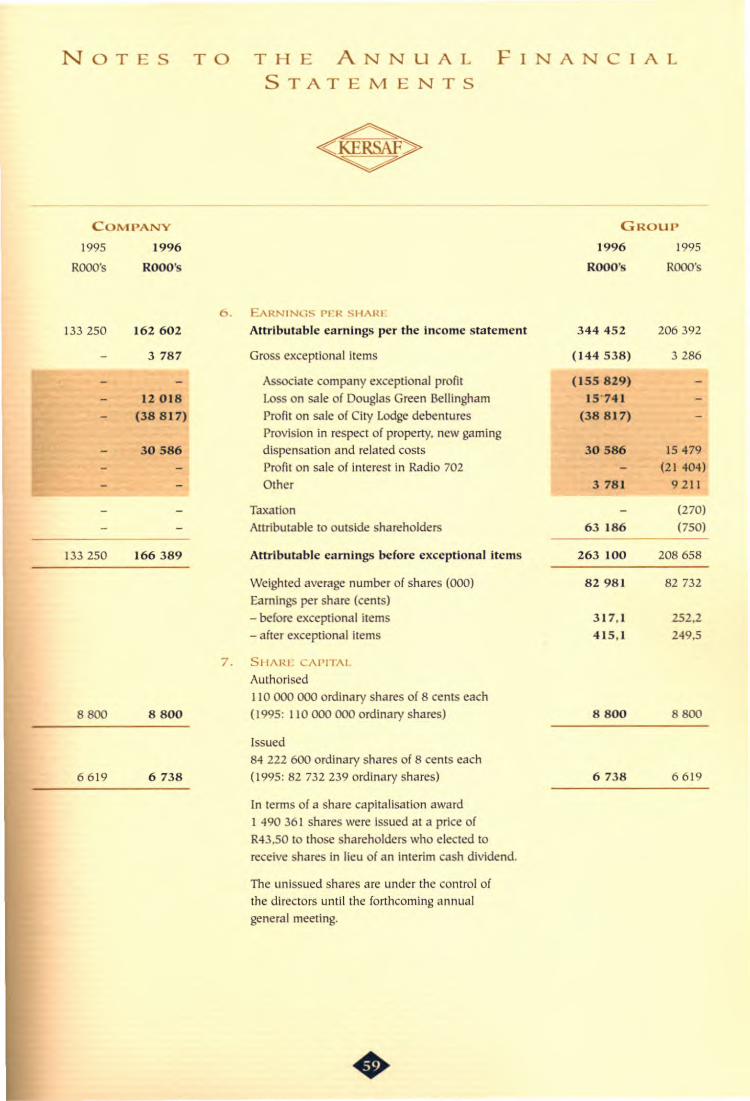

Documents

-

view

0 -

download

0

Transcript of Tsogo Sun Heritage

lE.'TS L I KERSAF INVEST IT ED

CORPORATE PROFILE

KERSAF INVESTMENTS LIMITED IS INVESTED IN AND PROVIDES THE RELEVANT

MANAGEMENT SERVICES FOR BUSINESSES IN THE LEISURE INDUSTRY

IN SOUTHERN AFRICA AND OVERSEAS.

THE GROUP FOCUSES ON GAMING, CASINO RESORTS, HOTELS AND

THE CINEMA BUSINESS.

CORPORATE VISION

KERSAF INVESTMENTS LIMITED PROVIDES SHAREHOLDERS WITH THE OPPORTUNITY

TO INVEST IN A RANGE OF LEISURE RELATED ACTIVITIES WITHIN A FOCUSED VISION.

By SPREADING ITS INTERESTS BOTH GEOGRAPHICALLY AND OPERATIONALLY, THE GROUP

IS ABLE TO MINIMISE RISK AND BY FOCUSING SECTORALLY TI-IE GROUP CAN

MAXIMISE SYNERGIES.

\.VITHIN ITS MARKETS THE GROUP ENJOYS STRONG TO DOMINANT POSITIONS DUE

TO ITS ABILITY TO TAKE ADVANTAGE OF MARKET OPPORTUNITIES AND

ITS INNOVATIVE APPROACH TO NEW IDEAS AND CONCEPTS.

BOTH IN SOUTHERN AFRICA AND INTERNATIONALLY, THE GROUP VIGOROUSLY

PURSUES INVESTMENT OPPORTUNITIES WHICH IT BELIEVES WILL

CONTRIBUTE SIGNIFICANTLY TO FUTURE GROWTH.

CONTENTS

FINANCIAL HIGHLIGI-ITS 1 CORPQRAT.': CODE OF ETI-IICS 2 VALUE ADDED STATEMENT 3

GROLIP STRUCTURE 4 DIRECTORATE AND ADMINISTRATION 6 CIIAIRMAN'S REVIE'-'V B

I~EVIEW OF OPERATIONS - SUN INTI:RNATIONAL 18 REVlE\N OF OPI:RATIONS - Cj-r-v LODGE 30

REVIE\I\I OF OPERATIONS - INTERLE,SURE 34 FINANCIAL COMMENTARY 38

O\tVNERSI-IlP OF SI-IARI: CAPITAl. 43 SEVEN YEAR FINANCIAL I:tEVIEW 44

CORPORATE GOVERNANCE STATCM[:NT 48 ApPROVAL OF ANNUAL FINANCIAL. STATEMENTS 49

REPORT OF THE INDEPENDENT AUDITORS 50 REPORT OF TI-IE DIRl:CTORS 51

ANNUAL FINANCIAL STATI:MI:NTS 52

FORM OJ.' PROXY 75

NOTICE OF ANNUAL GJ:NI:I~L MEI:TING 74

SHAREI-IOLDERS' DIARY IBC

FINANCIAL HIGHLIGHTS

----_._- -----

1996 1995 Change

Rm Rn1 %

TJ:ading (excluding exceptional items)

Ia-enue 2649,8 2428,3 9

Operating profit 766,3 661,5 16

t after taxation 549, I 500,9 10

.\mibutable earnings 263,1 208,7 26

Ordinary share performance Earnings (before exceptional items) 317c 252c 26

Oi\;dends 183c 162c 13

"'et worth R16,88 R15,53 9

Fmancial ratios ~ to equity shareholders 18% 17%

rest bearing debt to total shareholders' funds 3% 170/0

t cover (times) II 12

loIarket share price at 30 June R44,40 R32,SO

Employees at 30 June 15 815 16410

REVENUE (R million)

3000---------------------------------

2 SOD - - - • ~ - -- - - , I

- ,- - - - -

- -

2000

1500

1000

500

o 95 96 90 91 92 93 94

EARNINGS AND DIVIDENDS PER SHARE (cents)

350-----------------------------------

90 91 96 92 93 94 95

... Earnings .... Dividends

•

CORPORATE CODE OF ETHICS

THE GROLIP RECOGNISES THE VESTED INTERESTS OF ALL STAKEHOLDERS IN THE MANNER

IN WHICH ITS VARIOUS BUSINESSES ARE CONDUCTED. THIS CODE OF ETHICS WILL ASSIST

IN FLILFILLING OLIR RESPONSI131LITY TO THESE STAI<EHOLDER$.

THE GROUP VVILL ACT IN A WAY THAT WILL EARN IT AND ITS $LIBSIDIARIES AND

ASSOCIATES THROUGHOUT THE WORLD THE REPUTATION OF BEING:

.:. OPEN AND HONEST IN ALL DEALINGS

.:. CONSISTENT IN FLILFILLING ITS MORAL AND LEGAL OBLIGATIONS

.:. SOCIALLY RESPONSIBLE

.:. ENVIRONMENTALLY RESPONSIBLE

.:. NON-SECTIONAL

.:. NON-POLITICAL

-e- SUPPORTIVE OF LOYALTY AND LONG STANDING RELATIONSHIPS

.:. PROTECTIVE OF THE QUALIT'i OF ITS SERVICES AND PRODUCTS

As REGARDS ITS PEOPLE RESOURCES, THE GROUP IS COMMITTED TO ENLIGHTENED

EMPLOYMENT POLICIES AND PRACTICES WHEREBY:

.:. DISCRIMINATION IS ELIMINATED

.:. TRAINING AND SKILLS DEVELOPMENT IS EMPHASISED

.:. EMPLOYEES HAVE AN LINCONTESTED RIGHT TO ORGANISE AND NEGOTIATE Tl-IEIR

CONDITIONS OF EMPLOYMENT

•

ADDED STATEMENT

2649,8 2428,3

(rom investments 291,6 71,8

generated 2 941,4 2500,1 18

- to suppliers for materials and services (1010,6) (784,2)

value added 1 930,8 I 715,9 13

tion to stakeholders

613,6 576,9 6

ents 581,5 444,6 31 ers and lenders

idmds to shareholders 208,0 340,1 (39)

costs 70,7 55,8 27

1 473,8 I 417,4 4

in business

capitalisation awards 139,8

retentions 317,2 298,5

e to fund the replacement of assets and facilitate further growth 457,0 298.5 53

FOR THE YE,\R ENDED 30 JUNE 1996

1996

Rm 1995

Rnl Change

%

lI'I[]JDO"- VALUE ADDED (R million)

1996

DISTRIBUTION TO STAKEHOLDERS (%)

1995

... Employees 42%

.... Gove ... nrnents 39%

... Shareholders 14% • -~--+--_'--+---'--~--I'

... Lenders 5% 90 91 92 93 94 95 96

• .... Employees 4 I %

... Governments 3 1%

... Shareholders 24%

... Lenders 4%

GROUP STRUCTURE

-7 ACTIVITIES ~

<@P 80%

SUN INTERNATIONAL INC CASINO RESORTS, HOTELS AND CASINOS

41% SUN INTERNATIONAL

SOUTH AFRICA+

• 100% NORTH WEST PROVINCE SUN CITY' The Palace of the Lost City (350 rooms) Cascades (245 rooms) Sun City Hotel and Enrertainmenr Centre (340 rooms) Cabanas (380 rooms)

MMABATHO Mmabatho Sun" (150 rooms) Molopo Sun" (220 rooms)

MABOPANE Morula Sun" (74 rooms)

BABELEGI The Carousel Casino and Entertainment World* (60 rooms)

TLHABANE Tlhabane Sun" (30 rooms)

TAUNG Taung Sun= (40 rooms)

• 100% EASTERN CAPE PROVINCE BISHO Amatola Sun" (85 rooms)

PEDDIE Mpekwenl Sun Marine Resort (100 rooms) Fish River Sun* (120 rooms)

MDANTSANE Mdantsane Hotel and Entertainment Centre" (8 rooms)

MZAMBA Wild Coast Sun" (400 rooms)

UMTATA Ttansgamesf

BUTTERWORTH Transgames*

• 100% NORTHERN PROVINCE THOHOYANDOU Venda Sun* (82 rooms)

• 100% FREE STATE PROVINCE THABA 'NCHU Thaba 'Nchu Sun" (120 rooms) Nalcdl Sun" (30 rooms)

OTHER SOUTHERN

AFRICA

• 80% BOTSWANA Gaborone Sun" (203 rooms)

• 47% LESOTHO Maseru Sun Cabanas" (J 12 rooms)

• 49% LESOTHO Lesotho Sun" (236 rooms)

• 51 % NAMIBIA Kalahari Sands" (J 87 rooms)

• 51 % SWAZILAND Royal Swazi Sun" (145 rooms) Ezulwini Sun (120 rooms) Lugogo Sun (202 rooms) Nhlangano Sun" (47 rooms)

• 100% RIVIERA The Riviera International (100 rooms)

•

73°.16 ROYALE RESORTS

HOLDINGS LIMITED

• 100% SI MANAGEMENT LIMITED Southern African management contracts

• 19% SUN INTERNATIONAL HOTELS LIMITED·

23% SUN RESORTS LIMITED+ MAURITIUS Le Saint Geran (175 rooms) La Pirogue (248 rooms) Le Touessrok (200 rooms) Le Coco Beach (333 rooms)

COMORES Lc Galawa Beach Hotel" (182 rooms)

100% PARADISE ISLAND Atlantis Resort and Casino" (1147 rooms) Paradise Paradise Beach Resort (/00 rooms) Ocean Club Golf and Tennis Resort (59 rooms)

25% FRANCE Ruhl'" Cassls'" Carry-le-Rouet" Chamontx"

50% TRADING COVE ASSOCIATES Mohegan Sun casino management contract

Casino licence " 1Wo casino licences • Listed on the Johannesburg Stock Exchange • Listed on New York Stock Exchange to Listed on Mauritius Stock Exchange

GROUP STRUCTURE

~ ACTIVITIES ~

43%

LODGE HOTELS LIMITED'" AFFORDABLE HIGH QUALITY HOTELS

• CITY LODGE BwEMFONTEIN \\lortrekker Street (152 rooms)

CAPE TOWN ),Iowbray Golf Park (134 rooms) :"ittoria and Alfred ~aterfront (164 rooms)

DuRBAN - khill Road (I6 J rooms)

joHANNESBURG labannesburg International Mpon (J6/ rooms) &mdburg (123 r00111s) Sandran Katherine Street (J 59 rooms) Saldton Morningside (161 r00111s)

PORT ELIZABETH Scac:h Road (I48 rooms)

• TOWN LODGE eWE TOWN

rille (106 rooms)

esburg International (135 r00111s)

nd (118 rooms)

NELSPRUIT General Dan Pienaar Street (106 rooms)

• ROAD LODGE JOHANNESBURG Johannesburg International Airport (92 rooms)

• THE COURTYARD INN CAPE TOWN Mowbray (70 rooms)

JOHANNESBURG Bruma Lake (69 rooms) Rosebank (83 rooms) Sandron (69 rooms)

PRETORIA Arcadia (69 rooms)

•

37%

INTERLEISURE'" LIMITED

CINEMA AND FILM RELATED ENTERTAINMENT

• fILM EXHIBITION AND DISTRIBUTION

100% STER-KINEKOR 283 cinema screens at 48 locations countrywide and t3 drive-ins Distribution rights in South Africa for Columbta-Tri Star, Twentieth Century Fox and Disney

50% STER-MoRIBO 24 cinema screens at 6 locations 60% of Maxi-Movies Franchising (Pry) Limited which franchises cinemas in rural and disadvantaged areas

85% STER-KINEKOR HOME ENTERTAINMENT

• FILM AND TELEVISION PRODUCTION

100% TORON INTERNATIONAL

50% THE VIDEO LAB GROUP

• ANCILLARY SERVICES 100% COMPUTICKET

100% CINEMARK

DIRECTORATE AND AD.1I.ISTRATION

~ BOARD OF DIRECTORS ~

EXECUTIVE DIRECTORS D A HAWTON (59) F.c.I.S.

Chairman Appointed to the board in 1987

Chairman and chief executive, Safrnartne and Rennies Holdings Limited

P D BACON (50) M.H.C.I.M.A. (BRITISII) Reappointed to the board in 1994

Originally appointed in 1985 Managing director, Sun International

DC CouTTs-TROTTER (34) B.Bus.SCI., B.Acc .. C.A.(S.A.) Appointed to the board in 1996

Group financial director

M P EGAN (41) B.Co,1., C.A.(S.A.) Appointed to the board in 1992

Managing director, Interleisure Limited

H R ENDERLE (53) Appointed to the board in 1994

Executive chairman, City Lodge Hotels Limited

F W J KILBOURN (34) B.CoM.LLB, B.A. (HONS), H.DIP.TAX Appointed to the board in 1996

Corporate development director, Safmarine and Rennies Holdings Llmited

NON-EXECUTIVE DIRECTORS t*W F DE LA H BECK (73) B.COM., C.A.(S.A.)

Appointed to the board in 1985 Director of companies

t*G A MACMILLAN (75) C.A.(S.A.) Appointed to the board in 1984

Director of companies

*1 N MATTHEWS (50) M.A. (OXON), M.B.A. Appointed to the board in 1996

Director of companies

'" Member of the audit committee t Menlber of the remuneration committee

ADMINISTRATION

KERSAF Il\rvESTi\1ENTS LIMITED

Incorporated in the Republic of South Africa Registration number 67/07528/06

GROLIP SECI~[TAnY S A Bailes EC.I.S .. EC.I.B.M.

ATTORNEYS Edward Nathan & Friedland Inc

TRANSfER OFFICE Fraser Street Registrars (Pty) Limited Ground Floor, Sage Centre 10 Fraser Street Johannesburg, 2001 Gauteng

REGISTERED OFFICE

3 Sandown Valley Crescent Sandown Sandton, 2031 Gauteng Republic of South Africa Telephone (+2711) 780-7444 Telefax (+2711) 783-7446

AUDITORS

Price Waterhouse

BANKERS

Nedcor Bank Limited The Standard Bank of South Africa Limited

•

Hails Enderle. David Contts-Trouer; A4il.'e Egan, I.'ralll., Kilbourn, Seated: Elldtl), Hasaou alit I Peter Bacon

I N Matthews

•

W Fdeta H Bed

G A Macmilloll

CHAIRMAN'S REVIEVV

~ KERSAF INVESTMENTS LIMITED ~

Buddy Hawton EXECUTIVE CHA1Rl,lAN

his year's results are particularly pleasing as they clearly reflect the strength inherent in the broad spread of Ke r safs investments within the leisure sector as well as the benefits of their geographic diversity. The

material impact on the earnings of Sun International in South Africa by the activities of

the illegal casinos and by the higher taxation was mitigated by the excellent progress achieved in the offshore operations, the strong performance from City Lodge and the sustained improvement in Interleisure's profitability.

Sun International South Africa faced difficult market conditions in gaming, particularly due to increased competition from illegal casino operators although the hotel operations generally performed well and pre-tax profit showed a healthy increase. City Lodge had another

excellent year with increased margins reflecting the improved efficiencies achieved during the year and the benefits of the Courtyard a cqu i sition. Interleisure benefited from focusing on its core cinema businesses and has progressed in its planned move to expand internationally.

Trading conditions prevailing during the year were generally satisfactory although consumer and business confidence was somewhat dampened during the second half and in particular the last quarter of the year by the sharp depreciation in the rand and increases in interest rates. The rate of growth in personal consumption expenditure declined from 5% in the six months to December 1995 to 2% in the six month period to June 1996.

RESULTS

Revenues for the year at R2,7 billion were 9% higher than in 1995 and 10% higher if the disposed Douglas Green Bellingham business is excluded. Improved margins and foreign exchange gains raised profit from operations by 11% to R677,3 million. Strong cash flows and capitalisation share awards in lieu of intcr im dividends, resulted in net interest inC0111e of R 18.3 million versus a net expense of

. R2,6 million in the prior year and consequently a 14% improve me nr in profit before tax to R684,3 million notwithstanding the R8,0 million increase in exceptional costs. The '4,1 percentage point increase in the effective tax rate, due mainly to the full applicability of the South African legislation to the earnings of Sun International South Africa, reduced the increase in profit after tax to 8%.

Normal associate company profits were up 156% to R46,8.million as a result of the excellent results achieved by City Lodge and Sun

•

CHAIRMAN'S REVIEW

•

CHAIRMAN'S REVIEW

International's offshore operations conducted CHANG ES IN TH E G RO U P through Sun International Hotels Limited. An STRUCTU RE exceptional associate C0l11pany profit arose

during the year, representing the increase in

the value of the group's interest in the net assets of Sun International Hotels, following

the successful public offering which raised $285 million.

Earnings attributable to ordinary shareholders increased 67% to R344,5 million although on

exclusion of the exceptional items the improve ment reduced to 26%. Earnings per share before

exceptional items for the year were 26% higher. It is notable that dollar based earnings in 1996

contributed 16% of total attributable earnings before exceptional items, up substantially on the

II%ofI995.

The aggregate of the capitalisation share award

and the final cash dividend totalling 183 cents

per share is 13% higher than the total dividends for the previous year. In accordance with the

indication given last year, the percentage payout has reduced Irorn the previous year's 640/0 to 580/0. It is likely that the payout ratio will be further

reduced in the year ahead so as to achieve the

targeted two times dividend cover.

The group's balance sheet remains strong with

gearing reducing from 17% in the previous year to 3% at the year end. Furthermore, the group has

significant cash resources at its disposal which is pleasing as it is the intention of the group to

actively pursue new investment opportunities within the hotel, ganling and leisure industries both in southern Africa and internationally. The

return on net assets for the year of 24% repre sents an increase of 3 percentage points over the previous year and continues the positive trend re established last year.

During the year Sun International's South African

gaming and hotel interests were successfully restructured under one listed cOI1'pany, the former Sun International (Bophuthatswana) Limited. which was renamed Sun International (South Africa) Limited ("SISA"). This restructure

will facilitate any future rationalisation of SISA's

operations in compliance with the new gaming dispensation in South Africa and enhances the ability of SISA to finance potential new gaming developments.

The group divested its 50% interest in the Douglas Green Bellingham partnership ("DGB") to its joint venture partner, Kangra Holdings (Proprietary) Limited, with effect from 26 April 1996. DGB did not form part of the group's core activities being gaming, hotels and leisure. The

disposal consideration was not materia l and nor was the i mpac t on current or future earnings.

SOCIO-POLITICAL AND ECONOMIC CONSIDERATIONS

South Africa's remarkable political transforma

tion and re-acceptance into the world community are now substantially complete. The recent announcement of the Government's Gr owth , Employment and Redistribution strategy is encouraging as it appears to contain many of the

elements required for South Africa to achieve Government's target of sustained economic growth in excess of 6% by the year 2000. The Government's c o mrn i trne n t s to monetary and fiscal discipline, the accelerated reduction of the

fiscal deficit. the relaxation of exchange controls, the privatisation of state assets, an increase in labour market Ilexibf htv and productivity, and a reduction in real interest rates are to be welcomed. The success of this strategic plan and

CHAIRMAN'S REVIEVV

CHAIRMAN'S

its acceptance by local and international investors and markets requires specific action plans and tangible evidence of this corurnitrnc nt. In particular there should be further relaxation of exchange controls and more rapid progress to privatise state assets, so as to improve their efficiency and reduce the level of state borrowing.

The achievement of an investor friendly environ ment is essential if South Africa is to attract the levels of long-term international investment required to achieve significant development, empowerment and economic growth. A serious threat to the achievement of such an environment is the current level of crime and violence that pervades our society. This situation discourages direct investment, inhibits the growth of tourism and is eroding the country's skills base through emigration. It is particularly noteworthy that the rate of growth in foreign tourism to South Africa has declined over the last two quarters. The full cornmttrnenr of Government, business and com munities is essential if law and order are to prevail and the human rights and dignity of every citizen are to be protected.

Whilst the sharp decline in the value of the rand has had a positive impact on the group's earnings from its international investments, it has also, over the past few months, placed upward pres sures on real interest rates and inflation. The resultant slowdown in the economy and in particular consumer discretionary expenditure is of concern although it still appears possible that gross domestic product growth of 3% can again be achieved over the next twelve months.

GAMING IN SOUTH AFRICA

The National Gambling Bill, which is intended to provide a national fr a mewo rk within which the gaming industry will operate, was passed by Parliament during June this year. This Bill contains certain specific issues that are

REVIEW

of particular relevance to the group, i.e ,

.:. a maximum of 40 licences are to be granted nationally, with specified maxima per province;

.:. a limitation per investor or operator to 16 licences nationally and 2 per province with the exception of the Eastern Cape and the North West provinces where, in recognition of its existing investments and the related employment, Sun International will be allowed to operate 3 licences in each province; and

.:. the prohibition of the State or any of its bodies from having a financial interest in companies holding, managing or operating casino licences.

Sun International has until 10 May 1999 to com ply with these provisions of the national gambling legislation.

Sun International has committed significant resources so as to continue its success in a regulated gaming industry in South Africa. Applications for new casino licences are well advanced and strong alliances have been forged with a number of national and provincial partners recognising the principles of black economic ernpowermcnr and the participation of histori cally disadvantaged persons and communities. Strategies for the rationalisation and sale of certain existing licences have been developed but their implementation is not d ee med practicable until such time as clarity on the location of new casino licences and the rcquirc m e n t s of provincial gaming legislation and the respective provincial gaming boards are clarified.

The group has assumed a prudent view and made full provision against the costs incurred in progressing plans for new casino projects, inter alia acquiring options over properties, engaging consultants and relevant experts and preparing licence applications.

CHAIRMAN'S REVIEW

ment is at its greatest. The group promotes

improvements through the lnvesrrnenr of finan cial resources as well as skills, advice, leadership and capacity building. The communities, how

ever, lead the way in identifying [heir real nee and the cornerstone of the process is the involve rne nt of staff and community reprc sentatives ] the analysis, planning and implementation of the various projects.

CHAIRMAN'S REVIEW

CORPORATE RESPONSIBILITY in rural areas where the need for social invest-

The Kersaf group believes that the new democracy in South Africa must be supported by creating a just and equitable society where all stakeholders take responsibility for and make a

positive contribution to their economic develop ment and well-being.

To this end the group is committed to both the principle and spirit of economic empowerment and devotes time, effort and resources to ensure that previously disadvantaged individuals and communities are brought into the mainsrream of the economy, have access to employment opportunities and have access to facilities and training to ensure the transference of skills and knowledge.

Our employees, which number over 15500 at year end, participated in 42% of the value added that was distributed to stakeholders in the period under review. The principle of affirmative action is fully supported by the group and is aimed at developing and promoting the skills and abilities of those disadvantaged by past discrimination. The ultimate objective is to establish a workforce that at all levels reflects the demographics of the economically active population in southern Africa. Sun International, which employs over three quarters of the total staff complement of the group, has already made Significant progress in this regard with over 50% of management and supervisory positions being occupied by black, coloured and Asian staff.

It is recognised that the community is a stakeholder in the group and that a social respcnsibi lity exists to assist with the upliftment and development of those communities where the group operates. This is especially important given that nlany of the group's operations arc situated

•

Projects undertaken and sponsored in rural areas include the upgrading of the Greenville Hospital and Vulindlela Technical School ncar the Wild Coast Sun, upgrading of the Sekampaneng Primary School near the Carousel, establishment of the Saulspoort Sewing Centre and partic ipatton in the building of the Sandfontien Clinic near Sun City. Other donations include those made to the Nelson Mandela Children's Fund, Keep South Africa Beautiful project, Rustenburg Street Children's project, Lambani water relief scheme and the construction of the Mdantsane indoor sports complex.

On a broader front various corporate sponsorship initiatives have been undertaken. These include being a founding trustee to The Sports Trust and the Arts and Culture Trust as well as being an official sponsor to the national team which successfully participated in the 1996 Atlanta Olympic Games.

In pursuing its cornrnirrnenr to the principle of black economic empowerment the group has forged strong alliances with a number of national and provincial partners in applying for new casino licences in terms of the new gaming dispensation. City Lodge launched an employees share trust scheme during the year in which approximately 4% of its share capital has been

CHAIRMAN'S REVIEW

CHAIRMAN'S

issued to the IrUSl, which will enable all employees to participate in the wealth they help to create. Interleisure has continued to develop Ster-Moribo, a joint venture with Thebe Investment Corporation, with t he opening of Dobsonville and Davey ton cinema complexes and the establishment of Maxi-Movies Franchis ing. wh ich franchises cinemas to rural and disadvantaged areas.

PROSPECTS

The year ahead will be a very important one for the Kersaf group. There are many challenges to

face, particularly with regard to the group's gaming interests in South Africa. However, the year also holds a number of significant develop ments and opportunities including:

+:+ the finalisation of the structure of South Africa's casino gaming industry, with applica tions for new casino licences and, in the case of certain provinces, the award of these licences;

+:+ further rapid growth of the group's offshore earnings with commencement of operations at the Mohegan Sun, which was recently awarded a permanent licence, as well as expansion of Sun International Hotels' existing facilities and the planned major expansion and refurbishment of the recently acquired Atlantic City casino resort;

.:. lnterleisure's venture into international cinema markets and, potentially, domestic television; and

+:+ City Lodge's further expansion through the development of new locations.

The slowdown in the growth in the economy and particularly in personal consumption expenditure will place pressure on Sun International's local operations. We nevertheless expect that with

REVIEW

the imminent closure of the illegal casinos, which has C0l11111cnced in certain provinces, and given the group's strong positioning in the market place, revenues should show growth in real terms in the year ahead. This growth, coupled with the strong performances anticipated from Sun International's offshore operations and the increased earnings expected from Interleisure and City Lodge, indicate that the group should achieve real earnings growth for the year.

ApPRECIATION

I would like to thank the management and staff of all the group's many enterprises for their significant contribution to the group's success over the past year, particularly in the face of the uncertainty created by the unresolved future of casino ganling in South Africa. The commitment. profe ssionalism and loyalty shown by all has been extremely encouraging and augurs well as we e nte r into an even more competitive environment and as South Africa establishes itself in the global market place.

I wish particularly to thank Alan van Biljon, who resigned during the year, for his very valuable contribution to the group over the past len years. Alan's integrity, energy and dedication will be missed and we wish him every success in the future. Finally, it is my pleasure to welcome Frank Kilbourn, David Coutts-Trotter and Nigel Matthews onto the board and I believe that they will make a Significant contribution in the years to come.

D A Hawton Executive Chairman

CHAIRMAN'S REVIEW

•

REVIEW OF OPERATIONS

~ SUN INTERNATIONAL ~

SUN INTERNATIONAL WAS FORMED IN OCTOBER 1983 TO ACQUIRE CONTROL

OF THE CASINO RESORTS OF SOUTIIERN SUN HOTEL HOLDINGS LIMITED AND

RENNIES CONSOLIDATED HOLDINGS LIMITED IN SOUTHERN AFRICA AND MAURITIUS.

THE GROLlI' IS 80% OWNED BY KERSAF.

- ... r---

I! un International's philosophy is to acquire a

substantial equity interest in the casino resorts

and hotels under its banner as well as to

provide the necessary management services.

The focus of the group is the development and

management of casino resorts with a range of gaming,

entertainment and sporting facilities available to guests

and visitors. The group's portfolio currently includes

35 hotels with over 6 000 rooms in southern Africa, the

Indian Ocean Islands of Mauritius and Cornores, and in

the Bahamas. In addition to its hotel and resort facilities,

Sun International has casino operations in France. The

group's interest in the Marrakech casino was sold during

the year.

Sun International Inc's overall results for the year were

satisfactory, with revenues up 10% and profit before tax up

12% due to containment of costs and higher net interest

income. Attributable income before exceptional items was

19% higher due mainly to the increase in the offshore

associate company profits.

SOUTHERN AFRICA

The South African hotel industry enjoyed an increase in

occupancy levels over the year as the number of business

and holiday visitors again increased over the prior

year, albeit at a slower rate. The hotel room capacity in

the more important business and tourist regions is I

increasing rapidly and if current high occupancies are to

continue, more rapid economic growth and a significant

reduction in the current levels of crime and violence are

required.

The status and future of a regulated ganling industry in

South Africa, which is of great importance to the group,

has been dealt with by the Chairman in his review. It

is hoped that over the next year the Significant outstand

ing issues will be addressed by central and provincial

governments and that the process of awarding licences will

be well advanced. The group will then be in a position to

plan any rationalisation that may be required and there

after to proceed with the expansion of existing facilities

and in the event of obtaining new licences, the develop

ment of new casino based projects.

Sun International's resorts in southern Africa continued to

enjoy strong demand for accommodation, with an average

occupancy attained of 63% being I percentage point up on

last year at an average room rate! 4% higher. This demand

unfortunately did not extend to gaming, particularly slots

revenues, which continue to be impacted by the activities

of the illegal casinos, most notably in KwaZulu Natal and

Gauteng. Casino revenues have also to an extent been

impacted by the n1any other entertainment activities

on offer and the downward pressure on consumer

discretionary spending, which was particularly evident

during the last quarter.

Sun International (South Africa) Limited ("SISA"),

was constituted following the acquisition by Sun Inter

national (Bophuthatswana) Limited, renamed SISA, of the

entire issued share capitals of Transkei Sun International

Limited, Sun International (Ciskei) Limited and Venda

Sun Limited. The acquisition was funded by an issue

of shares or at the election of the shareholders, cash. This

restructuring resulted in the rationalisation of Sun

REVIEW OF OPERATIONS

•

REVIEVV OF OPERATIONS

~ SUN INTERNATIONAL ~ (continued)

International's existing South African gaming and resort

interests under one listed company. All shareholders will

now be afforded the opportunity to participate in the

benefits of new investment opportunities in South Africa

and the group's ability to fund future expansion is

enhanced. Kersaf's effective interest in the reconstituted

S[SA group is 33%.

SUN INTERNATIONAL (SOUTH AFRICA) LIMITED

% Rm [996 change 1995

Revenue 2 160,7 10 1 957,9

Profit from operations 519,9 11 469,2

Atrributable earnings 386,3 6 364,1

Earnings per share (cents) 49,8 6 47,2

Total assets 2624,0 - 2626,9

Operating margin (%) 24 24

Rooms available 2767 2763

Average occupancy (%) 70 68

Slot machines 6867 6595

Employees 11 912 11 941

SISA's results for the year were satisfactory bearing in mind

that revenue growth was restricted to 10% prtmartly as a

result of the increased level of activity of the illegal

casinos. Hospitality revenues showed good growth as a

result of improved occupancy, 2 percentage points higher

than last year at 70%, and strong rate growth of 15%

due largely to the strong foreign demand which was

particularly evident at Sun City. Management continues

to place emphasis on overhead cost containment, which,

together with the significantly reduced net interest cost

boosted the growth in profit before taxation to 14%. The

growth in attributable earnings was reduced to 6% by the

taxation charge that was 52% higher than last year and at

an effective rate of 22%, up 5 percentage points. This

•

increase was due to the full applicability of South African

tax legislation to the earnings of the SISA group

companies, including the imposition of STC on the final

cash dividend. The relatively 10v,1 effective tax rate is as a

result of the utilisation of the tax equalisation reserve

which it is anticipated will be utilised over the next two to

three years. The results for the second half of the year

reflected the slowdown in consumer spending and the

slower rate of growth of tourism with revenues and

attributable earnings growth of S% and 4% versus 13% and

10% during the first half.

The Sun City resort continued to benefit from strong

international demand with occupancy for the year of

79%, up 4 percentage points on last year. Table revenues

benefited from the increase in the number of hotel

guests although slots revenues continued to decline in

the face of illegal competition and hence reduced day

visitor numbers. Overall the resort increased revenues by

15% while, increasing margins and containment of costs

resulted in the attributable loss at the resort being

materially reduced. The refurbishment of the Main Hotel

was completed during the year and enhancements were

made to the Entertainment Centre so as to improve the

day visitor experience at Sun City. The total cost of

these refurbishments was RII7,S million and the resort

is now in a position where all the facilities are in an

excellent condition having been recently refurbished.

In response to the demand for more affordable

accommodation at Sun City, the Sun City Vacation Club

was launched. This innovative concept will allow club

members access to the refurbished staff flats on a

reservation basis. To date the response from the public has

been excellent. The development is anticipated to be

completed by mid 1997 at a total cost, including

construction of the new improved staff facilities, of approxi

marely R97 million. Sun City continued to host numerous

major events and the Miss World pageant was held at the

resort for the fourth consecutive year creating considerable

international exposure for Sun City and the region.

REVIEW OF OPERATIONS

REVIEW OF OPERATIONS

~ SUN INTERNATIONAL ~ (con tin LIed)

The Million Dollar Golf Challenge was again held in

December and continued to generate substantial local and

foreign support and ranks amongst the top invitational golf

tournaments.

The Carousel and Morula Sun, SISA's two major day

visitor gaming facilities both of which are dependent on

the Gauteng marker. experienced mixed fortunes. The

Ca.rousel traded very well while the Morula Sun was

somewhat disappointing, with the combined revenues

of these operations 100/0 higher at R870,S million and

operating profit showing a similar Improvement. The

~loruJa Sun was impacted by the refurbishment which was

completed during the first half year, the poor condition of

the major access road and the ongoing security threat

posed to customers by local criminal elements and taxi

violence. The Implementation of an on-line player tracking

system through the Most Valued Guest program has been

successful in reducing the impact of illegal competition

and has been very well received by punters. In addition

to this, the market for substantial linked progressive

jackpots continues to grow and has resulted in the

successful addition of two new products, Dream Machine

and Poker Magic.

The Wild Coast Sun achieved an occupancy of 76%,

3 percentage points up, which assisted in raising r00l11

revenues 17% v v hile casino revenues were 10% higher.

This performance is commendable given the level of illegal

competition in and around Durban where it is estimated

that there are currently at least 3 500 unlicensed slot

machines. The resort improved margins despite these

competitive pressures resulting in an increase in operating

profit of 13%.

The Arnatola Sun and the Fish River Sun resort both

showed improved occupancies while casino revenues,

particularly slots revenues, were noticeably impacted by

the illegal casinos that opened in both Port Elizabeth and

East London during the second half of the year. The region

•

achieved revenue growth of 12% and with improved

margins increased profit from operations by 14%.

The smaller operations located in Mmabatho, Tlhabane,

Taung, Thaba 'Nchu. Naledi, Umtata, Butterworth,

Mdantsane and Thohoyandou did not trade as well with

revenue growth generally disappointing and negative in

real terms. This was due to a movement of business away

from the old TBVC centres as well as the impact of the

illegal casinos that opened in and around these centres.

Except for the Sun City staff flats and Vacation Club

development, no major capital expenditure on new projects

has been planned for the 1997 financial year. SISA will

continue with the regular replacement of operating assets,

and in particular slot machines, to ensure that customers

are offered the highest quality of entertainment and

comfort. Capital expenditure for 1997 is budgeted at

R151,9 million.

SISA has formed strong consortia comprising SISA,

AfriSun Leisure Investments, a consortium of significant

black controlled companies with a wide spread of

shareholders including Real Africa Holdings and Thebe

Investment Corporation, and regiona!ly based empower ment partners. It is intended that these consortia will make

application for the casino licences to be granted in terms of

the new ganling dispensation in South Africa. Significant

progress has been made in progressing the project design,

shareholder and management structure, financial feasi

bility and structuring, as well as the economic, social,

environmental and other impact studies on five major

projects in each of Mpurnalanga. Western Cape, Eastern

Cape, KwaZuJu Natal and Gauteng. Several smaller

projects are also being investigated and it is likely that at

least one other bid for a major casino project will be

tendered for in Gauteng. SISA and Sun International

Management Limited have the necessary expertise and

resources, which should enable the Sun International

consortia to produce winning and yet deliverable

REVIEVV OF OPERATIO S

REVIEW OF OPERATIONS

-7 SUN INTERNATIONAL ~ (contil1ued)

and viable casino projects which will contribute to

employment, empowerment and tourism in South Africa.

Mpumalanga is the province most advanced in the casino

licencing process and the Sun International consortium's

preliminary bid is due to be submitted to that province's

ganling board on 2 September 1996. The four licences in

Mpumalanga are expected to be awarded late in March

1997. The licencing process in the other eight provinces is

likely to commence shortly and should be concluded by

late 1997. The group therefore does not anticipate any

capital expenditure on new casino projects during the

1997 financial year.

Other southern African operations, include the casino, resort and hotel facilities in Swaziland, Lesotho, Botswana

and Namibia, and the Riviera International.

OTHER SOUTHERN AFRICAN OPERATIONS

% Rm 1996 change 1995

Revenue 146,1 6 138.3

Profit (rom operations 17,4 (4) 18,2

Atrributable earnings 13,5 22 11.1

Total assets 91,0 8 84,6

Operating margin (0/0) 12 t3

R00l11S available 1 327 1 338

Average occupancy (%) 48 49

Slot machines 507 483

Employees 2059 2006

These units produced mixed results wlth overall revenues

only 6% higher than last year and profit from operations

declining by 40/0 although strong associate company profits

from the Lesotho operations Improved attributable

earnings by 229{:' over last year. The Swaziland and

Lesotho units traded well lifting revenues by 11 % and 23%

respectively. Occupancy in Swaziland remained at 53%,

with Lesotho improving 3 percentage points to 34%. The

casinos in both regions performed well. The trading at both

the Gaborone Sun and the Kalahari Sands was adversely

impacted by increased cornpetitlon and at Gaborone by

the major refurbishment currently underway. Occupancy

at the Kalahari Sands was down 13 percentage points at

41 % with average room rate achieved up only 2% while

casino revenues in Gaborone remained unchanged on

last year. Operating profit at these two units declined

310/0. The Kalahari Sands vilas recently awarded a casino

licence and a new casino is currently under construction

together with a refurbishrnent of the hotel facilities at

a total cost of R25,8 million. This casino is expected

to open early in November 1996. The Gaborone Sun is

likewise undergoing a major refurbishment of the hotel

and casino at a cost of R 18,6 million and is expected to

resume normal operations during September 1996. In

addition a small casino facility is being constructed at

Selebe Pikwe at a cost of R3,5 million. The profitability of

the Botswanan and Namibian operations is expected to

lmprove during 1997.

REVIEW OF OPERATIONS

REVIEW OF OPERATIONS

~ SUN INTERNATIONAL ~ (continued)

OFFSHORE

Sun International's offshore interests include the opera

tions of Royale Resorts Holdings, in which Kersaf holds an

effective 59% interest, and cash available for investment

which is held on short tern, deposit and amounted to $54 million at 30 June 1996. The Royale interests include

an indirect equity investment in the New York Stock

Exchange listed Sun International Hotels Limited ("SIHL"),

Sun International Management Limited's contracts to

manage the casino and hotel operations in southern

Africa, and the portfolio funds and cash.

Royale Resorts Holdings Limited's earnings before exceptional items for the year were 28% up on those of

1995 in Rand terms. This improvement was due to

the substantial increase in the income from the portfolio

funds, with dollar income up by 32%, and the equity

earnings attributable to 51 HL that increased from

$1,4 rnilllon to $7,2 million. Earnings attributable to

the management activities were only 2% higher despite

the 100/0 minority equity interest acquired effective I July

1995. The portfolio funds and cash held by Royale, which

are available for the pursuit of future investment

opportunities, totalled $93 million at 30 June 1996. The

improved returns on the portfolio funds were as a result

of the strong performance of dollar denominated bond

markets during the year, and particularly during the first six

months of the year.

Sun International Management Limited's management

activities in southern Africa generated fee income 90/0

higher than in the previous year. Costs however rose

39% as a result of the additional resources and

expenditure relating to potential new casino developments

in South Africa, the effects of the Rand devaluation

on offshore costs and the higher rate of taxation

payable. This increase in costs resulted in Sun Inter

national Management's earnings declining by 8% on the

prior year.

Sun International Hotels Limited currently comprises

the Paradise Island operations, equity interests in Sun

Resorts Limited (Mauritius and Comores) of 23%, and the

casino facilities in France of 25%, and the management

activities relating to all of these operations. During March

1996 Royale Resorts' effective equity interest in SIHL

reduced from 26% to 190/0 as a result of the public offering

in SIHL. The public offering was extremely well received

by the investment C0l11111unity allowing the company to

raise $285 million on an historic earnings multiple of over

40. These funds were used to redeem debt of approxi

mately $135 million, with the balance to be applied to

funding SIHL's commitments to the Mohegan Sun as well

as the planned expansion of the Paradise Island facilities.

SUN INTERNATIONAL HOTELS LIMITED

% $111 1996 change 1995

Revenue 242,1 52 159,8

Profit from operations 26,4 (0,9)

Attributable earnings 28,3 (1,0)

Earnings per share ($) 1,04 (0,08)

Total assets 517,5 40 370,4

Operating margin (%) II

Rooms available 2444 2 165

SIHL's results for the year to [une 1996 were excellent with

attributable earnings of $28,3 million and earnings per

share of $1,04 versus an operating loss of RO,9 million and

a loss per share of $0,08 for the previous year. This

performance is due mainly to the Paradise Island resort

which has traded exceptionally well since re-opening in

December 1994. The three hotels achieved an average

occupancy for the year of 87%, and for the six months

to June 1996 of 9 I %, 5 percentage points up 011 the

comparable period last year. The average room rate

REVIEW OF OPERATIONS

REVIEW OF OPERATIONS

~ SUN INTERNATIONAL ~ (conltnuecl)

achieved for the six months to June was $167, almost

30% higher than last year. Growth in casino revenues

has been relatively less spectacular while margins have

shown continual lmprovernent. The Mauritian, Comorian

and French operations all experienced improved trading

although their earnings are equity accounted by SIHL and

represent a relatively small contribution to SIHL earnings.

The hotels in Mauritius and Comores achieved occupan

cies ahead of last year at 75% and 61 % respectively,

although rate growth was marginal.

SIHL recently acquired the 562-f00111 Holiday Inn which is

located adjacent to Atlantis on Paradise Island and will be

completely renovated and integrated into the overall

Atlantis Resort. In addition to the Holiday Inn acquisition,

SIHL will shortly be commencing a $380 million expan

sion progran1 to Atlantis, which will include a new 1 200-

room hotel, a new casino, convention facilities and various

themed attractions around the wonders of the ocean and

the spectacular Bahamian beaches. Following the

completion of the Atlantis expansion and the Holiday Inn

acquisition and renovation, the Paradise Island complex

will comprise over 3 000 rooms in five hotels, each appeal

ing to a different market segment, and will become one of

the most unique resort destinations in the world.

SIHL and the required executive personnel recently

received permanent gaming licences from the State of

Connecticut for the Mohegan Sun Casino that is expected

to open during October this year. SIHL has a 50% interest

in Trading Cove Associates, the company that holds a

seven year contract to manage the Mohegan Sun.

The 333-ro0111 Le Coco Beach resort was opened in

Mauritius during April 1996 and has immediately found

acceptance in the value conscious family marker, achiev

ing occupancy of 70% in the period to June. A fifth hotel in

Mauritius, the 240-r00111 Sugar Beach is scheduled to open

during October 1996.

SIHL announced recently that it had reached agreement to

acquire AMEX-listed Griffin Gaming & Entertainment Inc.

in a share for share merger with a total equity value of

approximately $210 million. It is intended that Griffin's

existing resort in Atlantic City will be extensively

refurbished and revitalised following which a major new

project will be developed on an adjacent property which is

owned by Griffin. A further major project in Atlantic City is

also under consideration. The merger reams Sun

International's proven expertise in casino and hotel

development and management with Griffin's excellently

located existing facility and property in Atlantic City. SIHL

has applied to the New Jersey Casino Commission for a

licence to operate in Atlantic City.

REVIEW OF OPERATIONS

REVIEW OF OPERATIONS

~ CITY LODGE ~

CITY LODGE WAS ESTABLISHED WHEN THE FIRST LODGE OPENED IN

AUGUST 1985 AND THE GROUP WAS SUCCESSFULLY LISTED ON THE

JOHANNESBURG STOCK EXCHANGE IN NOVEMBER 1992. KERSAF ACQU IRED ITS

INTERESTS IN THE GROUP IN JANUARY 1995 AT WHICH TIME THE GROUP HAD A MARKET

CAPITALISATION OF R391 MILLION. THE GROUP CURRENTLY OPERATES

20 HOTELS AND HAS A MARKET CAPITAUSATION OF Rl 328 MILLION.

his year the City Lodge group consolidated iIS

position as South Africa's premier selected services hotel chain and laid the foundations for further sound growth in its four brands;

Courryard Suite Hotels, City Lodge, Town

Lodge and Road Lodge.

The group produced another impressive financial perfor mance with the maintenance of high occupancy levels and

an improvement in operating margins contributing to the

excellent results. Revenues grew by 17% to R I 08,7 million, pre-tax profit increased by 31 % to R4S,O million and

attributable earnings before exceptional items were up

CITY LODGE HOTELS LIMITED

% Rm 1996 change 1995

Revenue 108,7 17 92,S

Profit from operations 55, I 22 45,2

Attributable earnings* 33,S 40 23,9

Earnings per share (cents)* 128,7 35 95,3

Total assets 289,7 33 218,2

Operating margin (0,.6) 51 49

Rooms available 2278 2 162

Average occupancy (%) 81 80

Employees 796 787

* Excludes the Impact of exceptional items

40% to R33,S million. Average room occupancy levels at

City Lodge, Town Lodge and Road Lodge increased by I percentage point to 82% and with the inclusion of the

five Courtyard Suite Hotels, overall occupancy was 810/0

compared with 80% in the previous year. Although the

expected high growth in international guests did not

materialise, the group experienced strong demand for accommodation from corporate travellers.

The group continued its ongoing refurbishment pro

gramme in order to maintain the high standards guests

have come to expect in addition to which 26 new suites

were added to the Courtyard hotel in Pretoria. The imple mentation of the 'Room 2000' conversion commenced

during the current year. This progranlme focuses 011

meeting the changing needs of guests and includes

reducing noise pollution; using information technology to

maxirnlse business inforrnation and entertainment for

guests; implementing card-based access and security measures: improved bathroom layouts: and enhanced

overall comfort and appeal. The first of these conversions

was successfully completed at City Lodge Randburg and

similar conversions will take place at two further City

Lodges during the 1997 financial year.

The group continued to expand capacity and began

construction on t\VO new lodges during the year, a 142-

room Town Lodge in Sandton and a 92-ro0111 Road Lodge

in the Cape Peninsula. Prospects for both Lodges are

good as they meet the growing demand for affordable accommodation in two of the country's major economic

REVIEW OF OPERATIONS

REVIEW OF OPERATIONS

-7 CITY LODGE ~ (continued)

growth areas. The Road Lodge will open its doors to the

public on 25 August 1996 and the Town Lodge is due to open in November 1996.

Significant progress has been made in gaining further sites

in Gauteng, Durban and other parts of South Africa, which will enable the group to increase its accommodation

offering in 1997, Foreign exchange approval from the Zimbabwe authorities is still awaited on the joint venture

agreement signed with Cresta Hospitality, a division of

Zimbabwe's TA Holdings group, which will enable City Lodge to expand into Zimbabwe and Botswana. City

Lodge's total capital expenditure for the past year was R23,O million and given the further expansion planned,

it is expected to increase to at least R59,O million in the year ahead.

The continued success of the group lies in its ability to attract, retain and develop a highly motivated and dedi cated staff committed to providing guests with excellent

service. With this in mind, the directors, with the

approval of the shareholders, introduced the City Lodge

lOth Anniversary Employees Share Trust as a mechanism whereby all employees share in the group's wealth

creation. Employees, who in November each year have been in the full time employ of the City Lodge group for one year or longer, will be eligible to participate in the

distribution of dividends and in the allocation of shares.

The board believes this to be a true empowerment scheme

that will enable all employees to become shareholders and thus share in the wealth that they help to create.

Marketing efforts are to be increased during the forth

coming year, in order to increase weekend occupancies

and the 'Team Scheme' and 'Spouse 011 the House' week

end specials are proving popular with guests around the country.

With four distinctive brands covering the one to four star

selected services hotel market, the group is ideally posi

tioned to take advantage of any futur.e expansion in the economy and the growth of local and foreign business and leisure travel. The resounding success of the first Road

Lodge has stimulated the intention to rapidly expand this

brand within the next few years. Courtyard too, in its first

full year in the group, made a significant contribution and is "veil placed to strengthen its position at the upper end of the quality, selected services hotel market.

REVIEVV OF OPERATIONS

REVIEW OF OPERATIONS

~ INTERLEISURE ~

THE INTERI.EISURE GROUP, \VHICH HAS l'J.:COMr: THE LEADING FORCE IN THE

SOL1TH AFI~ICAN FILM /\ND CINEMA lNDL1Sl-RY, WAS FORMI:L) (_jN 1 fL1LY 1987 AND

LISTED ON TIlE IOHANNI:Sl1URG STOCK EXCHANGE ON 24 ALI(_~L1ST OF TIIAT YEAR.

KERSAF HAS AN EFFECTIVE 37% SHAREHOLDING IN THE GROLlP, AND ITS

RESL1LTS IIAVE BEEN INCLL1DED ON TI-IE PROP(_)RTIONATE C()NSOLIDAT[ON METI-{OD

IN ReCOGNrTION OF TIlE IOINT CONTR<.)L SITLIATION TIIAT I":XISTS "VITI I

SI:RVGRO INTCRNATIONAl LIMI1-1_:[).

he Interleisure group grew earnings before

exceptional items by 18% for the year and has

shown a good three-year profit trend since the

decision to focus on its core cinema and film interests.

Group revenues increased by 14% reflecting real growth,

despite Ster-Kinekor's continued policy of low price

increases. The increase in Ster-Klnekor's average admis

sion price was contained to only 4% for the year due

primarily to the half-price Tuesday promotion which ran

from October 1995 to year end. This promotion signifi

cantly gre\v market share, with attendances increasing by

INTERLEISURE LIMITED %

Rm 1996 change 1995

Revenue 462,5 14 407,4

Profit from operations 78,3 15 68,0

Attributable earnings* 51,7 18 43,7

Earnings per share (cents)* 27,2 18 23,1

Total assets 293,6 12 262,7

Operating margin (%) 17 17

Employees 2080 1990

Cinema attendances (millions) 19,9 17,9

.. Excludes the impact of exceptional items

10% for the year. The concomitant boost to catering was

evident as these revenues rose by 23% with price increases

accounting for only I 00/0 of this increment. Drive-in

attendances and revenues were dampened by the heavy

seasonal rains over the summer months. Ster-Kinekor

invested in additional people and infrastructure in

advance of its planned entry into the European cinema

market in the forthcoming year. This higher overhead

served to dilute the 18°;6 operating profit growth achieved

at the cinema level.

The other business units in the group had mixed results.

Ster-Moribo, lnterleisure's joint venture with the Thebe

group, grew revenues by 24%, helped by the opening of

the Davey ton complex during the year. This venture

produced a positive cash flow, but high depreciation on

its predominantly new assets gave rise to a break-even

at operating profit level, Srer-Ktnekor Home Entertainment

experienced a resurgence in market share growing

revenues by 35% and more than doubling its operating

profit during the year. Cinemark provided revenue growth

of 23% despite the uncertainty surrounding Cigarette

advertising, and achieved similar growth in operating

profit. Toran increased revenues by 12% despite no feature

film production with a strong demand for its television

production and editing facilities. Computicket's innovative

telephone booking system was well supported by South

African consumers and helped boost its revenues and

operating profit by 19% for the year,

•

REVIEW OF OPERATIONS

~ ,:-~

}. ;"~~I

REVIEW OF OPERATIONS

~ INTERLEISURE ~ (continued)

The group's overall operating margin was maintained at last year's level of 17% despite the additional overhead

incurred to investigate and develop expansion opportu

nities, Interleisure continues to be a strong cash generator

with borrowings all but eliminated at year end. This

resulted in net interest paid of only RO,7 million against last year's R2,3 million and a healthy interest cover of over 100 times. The effective tax rate approximated that of last

year, resulting in earnings per share before exceptional

items of 27,2 cents, an 18% increase on last year, and after

exceptional items of 26,4 cents, some 25% higher.

The plan to rapidly develop the Ster-Kinekor chain in the late eighties and early nineties has been achieved although

there was little expansion over the past year. lnterleisure's

total capital expenditure was consequently reduced from

last year's R44,6 million to R24,9 million in the year under review. Ster-Kinekor accounted for Rl I ,3 million

of this through the opening of two new complexes - the six-screen Kolonade in Pretoria and three screens in

Windhoek - and the refurbishment of two existing

complexes. Srer-Moribo opened a three-screen complex in

Davey ton, Benoni. The Video Lab spent R12,O million on

editing, graphics origination and post-production equipment, half of which cost is attributable to the Inter

leisure group. Computicker accounted for R3,O rnllllon,

with this expenditure incurred on the telephone booking

system and automatic dispensing technology.

Interleisure plans to spend a further R24,7 million on

capital items in the year ahead. Ster-Kinekor will open the

new eight-screen Bayside complex in Tableview, Cape Town and will extend its Stellenbosch complex from four

to six screens. Major refurbishments will be undertaken at five existing complexes. Srer-Moribo plans to open a five

screen complex in Mabopane near Pretoria. The Video Lab

and Computicket will incur further capital expenditure in continuing to advance their respective technologies.

Interleisure has formed a development company together

with Kerry Packer's Nine Network Australia and the Thebe

group to investigate the viability of launching a free-to-air terrestrial television station in South Africa. Business plans

are well advanced and the development company is awaltlng guidelines for the issue of television licences from

the Independent Broadcasting Authority.

Ster-Kinekor is well advanced in its plans to extend its

cinema operations into Europe, with the first partnership agreement finalised in Greece, where the group plans to open several cinema complexes over the next three years.

REVIEW OF OPERATIONS

FINANCIAL

NCOME STATEMENT

Overall, trading for the year "vas pleasing wlrh the strength arising front the group's geo

graphic diversity becoming evident in the earnings as illustrated in the segmental

information on page 40.

Revenues for the year of R2 649,8 million were 9%

higher than the prior year, impacted by the disposal of Douglas Green Bellingham during April 1996 and the

pedestrian growth in gaming revenues due to the activities of the illegal casinos, the quantum of alternative enter tainrnent on offer and, particularly during the final quarter,

the decline in consumer discretionary spending. In

contrast rooms revenues grew by 17% as occupancies and rates improved on the strength of foreign tourist and

business travellers.

Operating profit for the year of R755,O million was 15%

higher (160/0 on excluding exceptional items). with the

operating margin 0,5 percentage points up as a result of overhead savings. Interest income, which is included in

operating profit, was substantially higher than the previous year due mainly to the increase in the rates of interest at which the group's cash resources were deployed.

The interest expense for the year of R70,7 million was 27% higher than in 1995, with this increase mainly related to higher rates on borrowings whose average level was similar to that of 1995. The group's interest cover at II times, although marginally down on last year's

12 times, remains satisfactory despite being below the group's longer term average.

Profit after taxation of R537,8 million was 8% higher, with the effective rate of taxation for the year of 21 %

compared with the 170/0 of the previous year. The 40%

increase in the tax charge was due to the full applicability

of (he South African legislation to the earnings of Sun International South Africa, although the part utilisation of the tax equalisation reserve provided some relief. It is

COMMENTARY

anticipated that the effective rate of taxation will increase further in 1997.

Attributable earnings for the year increased 67% to

R344,5 million although on exclusion of exceptional items the

Improvement was 26%, with earnings per share before exceptional items up similarly to 317 cents. The group's share of normal associate companies' profits of R46,8 million was

considerably higher than the R18,3 million of the previous

year due to the continued excellent growth in earnings from

City Lodge and the profitability achieved by the New York

Stock Exchange listed Sun International Hotels Limited.

The total dividend for the year of 183 cents per share

is 13°Al higher than last year's 162 cents. The dividend

payout percentage of 58% is lower than the previous year's

payout of 64% and it is expected that this percentage will be further reduced in the coming year, closer to a target

of 50%. This payout percentage is in line with the dividend policies of certain of the subsidiary companies

and is necessary in recognition of the fact that the major

associates have to date not paid cash dividends and are

unlikely to do so in their current growth phases.

BALANCE SHEET

The balance sheet at the year end reflects a strong financial position, with the group well able to finance

substantial expansion in the years ahead both in South

Africa and offshore. Significant movements in important balance sheet components over the year were as follows:

Shareholders' funds of R3 358,6 million were R528,9 mil

lion higher with this increase mainly due to the profit

retentions at both equity and outside shareholder levels, the capitalisation share awards in lieu of interim dividends, the R155,8 million associate cornpany exceptional profit,

and the gains arising on the translation of the balance sheets of offshore subsidiaries,

Interest bearing borrowings of RI09,3 million were

R379,2 million lower, with the percentage of interest

FINANCIAL COMMENTARY

bearing borrowings to total shareholders' funds at 3% declines were caused by the large scale capital projects compared with the previous year's 170/0 and the group's completed over this period, in addition to which earnings

self-imposed constraint of 60% of shareholders' funds. declined in real terms as a result of the cconomlc down-

This substantial reduction results mainly from the turn and the erosion of gaming revenues caused by the relatively ]O\V level of capital expenditure and the activities of the illegal casinos.

capitalisation share awards which were made in lieu of interim dividends. In the presentation of the balance sheet.

cash resources of R733,8 million have not been set off against the interest bearing borrowings although the

availability of such should be taken into account when

assessing the resources, gearing and associated risk profile

of the group.

RETURN TO EQUITY SI-tAREHOLDERS (%)

35

5

• • ~, • - f-

" - 1-11.- I _,1,,· I

- - - -

- - - ~ - - ~ f-

~

30

25

20

15

Operating assets were R42,2 million higher with this

increase being the net movement of capital expenditures,

depreciation and disposals. Capital expenditures which

totalled R 188,8 million were again lower than the group's

historic average with the amounts comprislng mainly the expansion of existing facilities and the replacement of equipment, The offshore capital expenditures over the

year are not included in the group's operating assets due to

the equity basis of accounting adopted for these investments.

10

o 90 91 92 93 94 95 96

RETUR.N ON SHAREHOLDERS' FUNDS (%)

40----------------------------------

Investments and loans were R237,9 million higher due

mainly to the equity accounted earnings of the group's

associates which include the R155,8 million exceptional

profit, and the translation gains arising on the devaluation of the SA rand.

15

- I

- ~ • - ~

- .. - -

- - - - , . , •• 1'1 ~, ~ f-' ~

- ~ - - - ---

35

30

25

20

10

5

o 90 91 92 93 94 95 96

Current assets and interest free liabilities were

RI06,9 million and R237,3 million higher respectively.

The increases in accounts receivable and payable relate

primarily to the higher trading levels while the significantly

higher taxation provision is a function of the higher normal and STC taxation charges.

RETURN ON NET ASSETS ('",)

50--------------------------------

RETURNS

30-

20-

The returns for the year, as graphed alongside, were

satisfactory and continued the improvement of the prior year after the declines of the previous four years. These

I 0 -11---- __ ---111---'

o--·f---~----'~---r---'-----~ ~- 90 91 92 93 94 95 96

FINANCIAL

SEGMENTAL INFORMATION

The group's main divisions comprising

Sun International Inc with:

Sun International South Africa ("SISA"), currently

the only legal casino operator in South Africa with

investments in major casino resorts, day visitor casino

entertainment complexes and hotels. Other southern African operations, with casinos and

hotels in Swaziland. Lesotho, Botswana and Namibia,

and the Riviera International.

Management activities, being the services provided

by SUIl International Management Limited to the casino and hotel operations throughout southern Africa.

Other international activities, including New York Stock Exchange listed Sun International Hotels Limited

with its operations in Mauritius, C0I110reS, France and

the Bahamas, and cash resources held offshore.

Intcrleisure, focused on (ibn and cinema related leisure activities.

City Lodge, which occupies a leading position in the

limited services sector of the South African hotel market,

and

COMMENTARY

Kcrsaf central office and other comprising cash resources, certain local activities undertaken all behalf

of the offshore management c0l11pany and Douglas Green

Bellingham from which the group divested during

April 1996.

Accounting conventions make segmental analysis complex

as associate companies do not contribute to revenue

and operating profit. The information presented below

does however take into account these accounting

conventions and excludes exceptional items so as to

enable comparability and yet reflect the information

as ill the income statements and balance sheets contained

in the annual financial statements. SISA continues to

provide the majority of the group's revenues with casino

gaming the group's dominant activity. The contribution

of the group's interests in SIHL and offshore funds

increased fro 111 R22,4 million to R43,4 million in 1996

and 110\V comprises 16% of total attributable earnings.

The pie charts presented opposite provide additional

information on the composition of Kersaf's revenue,

attributable earnings and net assets.

SEGMENTAL ANALYSIS Revenue Profit front Kersaf share Net assets

operations # of earnings # Rm 1996 1995 1996 1995 1996 1995 1996 t995

Sun International Inc 2 312,2 2 101,4 627,2 577,3 216,6 182,6 3 087,9 2590,5

Sun International (South Nrica) Limited 2 160,7 I 957,9 519,9 469.2 127,9 t21,2 1 955,2 I 754,4 Other southern African activities 146,0 138,t 17,4 18,2 10,8 8,8 102,1 95,3 Management activities 5,5 5,4 122,1 106,2 65,7 60,5 - - Other international activities - - - - 43,4 22,4 1 096,9 759,4 Central office costs and other - - (32,2) (16,3) (31,2) (30,3) (66,3) (18,6)

Interleisure 231,1 203,7 39,1 32,9 19,4 t6,2 80,0 70.8 City Lodge (shares and debentures) - - - - 16,8 13,7 164,0 175.2 Central office and other" 106,5 123,2 11,0 (1,9) 10,3 (3,8) 26,7 (6,8)

2649,8 2428,3 677,3 608,3 263,1 208,7 3358,6 2829,7

.. Includes Douglas Green Bellingham. # Excludes the impact of exceptional items (normal and associate).

FINANCIAL

SEGMENTAL INFORMATION (continued)

REVENUE (Activity analysis)

... Casino gaming 61 % (61 t){,)

... Hospitality 26% (26%)

... Fllnl and cf ne rrm 9"X, (S'X.)

... Other 4% (5%)

SOURCE OF KERSAF EARNINGS

(Currency analysis)

... SA rands 80% (85%)

... US dollars 16% (11%)

... Other 4% (4%)

NET ASSETS (Currency analysis)

... US dollo:lrs 33% (27%)

... Other 3% (4%)

( ) - 1995

COMMENTARY

INFLATION

In the absence of any generally applied and accepted

practice regarding accounting for the effects of inflation, and

recognising that the taxation system in South Africa does not

provide for relief in this area, the group has decided not to

prepare and publish inflation adjusted financial statements.

As in past years. however, in order to provide an indication

of the quality of earnings and dividends per share, these

have been restated below in 1990 base year terms:

DEFLATED EARNINGS

7 year

compound

1996 % 1995 annual

cents change cents growth (%)

Earnings per share

Reported 317 26 252

Deflated 174 18 147

Dividends per share

Reported 183 13 162

Deflated 101 6 95

Consumer price index (1990: 100) 182 171

II

10

As per the above, the growth in reported earnings per share of 26°;6 reduces to 18% on the restatement of the earnings in both years in 1990 base year terms. The increase in real terms of both earnings a~d dividends reverses the trend of

declining real earnings and dividends experienced during

the early to mid 19905 .

FINANCIAL

CAPITAL EXPENDITURE

Details of the group's capital expenditure for the year under review and that proposed for the year ahead are contained

in the individual operational reviews preceding this review and in the cash flow statement and notes 12 and 20

in the annual financial statements.

The 320-room Table Bay Hotel at the Victoria and Alfred

Waterfront in Cape Town is due to be completed by April

1997. The Transnet Pension Fund is funding the building at a total cost of R 190 million with the furniture and fittings

of R60 million to be funded by a subsidiary currently wholly owned by Kersaf.

As a general policy, the holding company does not guarantee the borrowing obligations of subsidiary

companies and, accordingly, approved capital expenditures must be appropriately financed at subsidiary company

level with due regard to the group's overall gearing and

interest cover limitations. The planned capital expenditures

COMMENTARY

for the 1997 year will be financed from internal resources

and existing borrowing facilities. These planned

expenditures do not include any amounts in respect of new

casino resort opportunities in South Africa as it is not

anticipated that any such developments will commence

during the 1997 financial year.

CAPITAL EXPENDITURE (R nlillion)

900 ------------------

800 ----- ... ~-----------

700 -----.' .. -----------

600 -----1.' .f------------

100 - -'1--1 o - --,_--'--I~-'---I--"

90 91 92 93 94 95 96 97

.... Actual ..... Buctgctcct

OVVNERSHIP OF SHARE CAPITAL

AT 30 JUNE 1996

Number of Category Number of 0/0 of total

shareholders shares owned issued shares

Size of shareholding

571 1- 500 shares 92493 0,11

105 501 - I 000 shares 71 572 0.08 116 1001 - 5 000 shares 224928 0,27

19 5 001- 10 000 shares 128692 0,15

29 10 001 - 50 000 shares 569275 0,68

8 50 00 I - 100 000 shares 478782 0,57

16 100 00 I + shares 82656858 98,14

864 84222600 100,00

Type of shareholder

706 Individuals 338973 0,40

27 Investment and trust companies 778690 0,92

6 Insurance and assurance companies 2552 768 3,03

62 Banks and nominee companies 18215402 21,63

32 Pension and provident funds 638827 0,76

30 Other corporate bodies 109837 0,13

Holding company 61 588 103 73,13

864 84222600 100,00

Ten largest shareholders at 30 June 1996

Safrnartne and Rennies Holdings Limited 61588 103 73,13

Standard Bank Nominees (Transvaal) (Pty) Limited 8 091501 9,61

First National Nominees (Pty) Limited 3186371 3,78

CMB Nominees (Pty) Limited 2771568 3,29

South African Mutual Life Assurance Society 2510 569 2,98

Eighty-One Main Street Nominees Limited 2 082 415 2,47

5MBL Nominees (Pty) Limited 528 163 0,63

Sun International Executive Investments Limited 388760 0,46

Indo-China Nominees (Pry) Limited 344492 0,41

edbank Nominees Limited 270 834 0,32

81762776 97.08

•

SEVEN YEAR FINANCIAL REVIEW

GROUP Rm 1996 1995 1994 1993 1992 1991 1990

Consolidated income statements

Revenue 2649,8 2428,3 2217,2 2 05], 7 1861,5 1599,7 1367,2

Profit from operations 677,3 608,3 571,4 534,0 515,4 468,5 412,9 Interest income 89,0 53,2 25,2 27,8 43,3 70,2 68,3

Operating profit 766,3 661,5 596,6 561,8 558,7 538,7 481,2

Interest expense (70,7) (55,8) (54,9) (48,8) (24,S) ( 17,5) (23,7)

Profit before taxation 695,6 605,7 541,7 513,0 534,2 521,2 457,5

Taxation (146,5) (104,8) (98,3) (85,4) (102,8) ( 130,4) ( 122,3)

Profit after taxation 549,1 500,9 443,4 427,6 431,4 390,8 335,2

Share of associate companies' profits 46,8 18,3 6,0 4,0 8,7 6,5 4,5

Outside shareholders (332,8) (310,5) (270,7) (267,3) (258,8) (233,7) (200,4)

Attributable earnings 263,1 208,7 178,7 164,3 181,3 163,6 139,3 Dividends ( 152,9) ( 134,0) (121,0) (I 15,1) ( 111,6) (101,4) (87,0)

110,2 74,7 57,7 49,2 69,7 62,2 52,3

Note: - All exceptional items have been excluded to provkie a more meaningful comparison of historical operating performance. - The above figures have been restated where necessary 10 provide a nlcaningfu[ comparison of perfonnance of the seven years.

A.TTRIBUTABLE EARNINGS (R million) OPERATING MARGIN ('X.)

300 ---------------------------------- 30

5

• • • - - • • - - ,-- -- -- _ _ _

-

- ,_ - - ~ ,_ _ _ - - - ,_ ~ --

50

-

'. - . • ,_ ,_ "r - , __ I ,_ _ ~ - _

-

25 250

200 20

ISO IS

100 10

o o 90 91 92 93 94 95 96 90 91 92 93 94 95 96

•

SEVEN YEAR FINANCIAL REVIEW

<@P :;; ~

--_---- ---- ----

GROUP Rm 1996 1995 1994 1993 1992 1991 1990

Consolidated balance sheets Ordinary shareholders' equiry 1421,9 1284,6 1 205,7 924,4 770,8 575,2 429,5 Outside shareholders' interests I 936,7 1 545,1 1 432,3 1283,7 1 159,3 749,6 578,0

Total shareholders' funds 3358,6 2829,7 2638,0 2208,1 1930,1 1 324,8 1007,5 Interest bearing debt 109,3 488,5 530,1 537,4 368.2 176,5 196,0