To provide for settlement of old arrears and disputes arising ...

11

Jharkhand Ordinance no .... .12021 THE JHARKHAND KARADHAN ADmNIYAMON KI BAKAYA RASm KA SAMADHAN ADmYADESHlADmNIYAM 2021 Preamble- To provide for settlement of old arrears and disputes arising from proceedings under Part I of the Bihar Finance Act 1981 (Bihar Act 5 of 1981) and the Bihar Finance Act, 1981 as adopted in the state of Jharkhand and arrears arising from and dispute under the Jharkhand Value Added Tax Act 2005 (Act 5 of 2006), the Central Sales Tax Act, 1956 (Act 74 of 1956), the adopted Bihar Electricity duty Act, 1948 (Bihar Act 36 of 1948), the Jharkhand Hotel and Luxury Tax Act (Jharkhand Act 21 of 2011), the Jharkhand Advertisement Act, 2012 (Jharkhand Act, 14 of 2012) Jharkhand Tax on Professions, Trades, Calling and Employment Act, 2011, the Jharkhand Entertainment Tax Act, 2012 (Jharkhand Act 13 of 2012),and Jharkhand Entry Tax on Consumption or Use of Goods Act, 2011. An Act to promulgate "The Jharkhand Karadhan Adhiniyamo ki Bakaya Rashi ka Samadhan Adhyadesh 2021" to take immediate action to generate revenue for the State and to grant relief to arrear holder, Be it enacted by Legislature of Jharkhand in the seventy second year of the Republic of India as follows :-

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of To provide for settlement of old arrears and disputes arising ...

Jharkhand Ordinance no .... .12021

THE JHARKHAND KARADHAN ADmNIYAMON KI

BAKAYA RASm KA SAMADHAN

ADmYADESHlADmNIYAM 2021

Preamble- To provide for settlement of old arrears and disputes arising from

proceedings under Part I of the Bihar Finance Act 1981 (Bihar Act 5 of

1981) and the Bihar Finance Act, 1981 as adopted in the state of Jharkhand

and arrears arising from and dispute under the Jharkhand Value Added Tax

Act 2005 (Act 5 of 2006), the Central Sales Tax Act, 1956 (Act 74 of 1956),

the adopted Bihar Electricity duty Act, 1948 (Bihar Act 36 of 1948), the

Jharkhand Hotel and Luxury Tax Act (Jharkhand Act 21 of 2011), the

Jharkhand Advertisement Act, 2012 (Jharkhand Act, 14 of 2012) Jharkhand

Tax on Professions, Trades, Calling and Employment Act, 2011, the

Jharkhand Entertainment Tax Act, 2012 (Jharkhand Act 13 of 2012),and

Jharkhand Entry Tax on Consumption or Use of Goods Act, 2011.

An Act to promulgate "The Jharkhand Karadhan Adhiniyamo ki Bakaya

Rashi ka Samadhan Adhyadesh 2021" to take immediate action to generate

revenue for the State and to grant relief to arrear holder,

Be it enacted by Legislature of Jharkhand in the seventy second year of the

Republic of India as follows :-

9.

CHAPTERl

Preliminary

1. Short title, Extent and commencement-

(1) This Ordinance may be called the Jharkhand Karadhan Adhiniyamon ki

Bakaya Rashi ka Samadhan Adhydesh/ Adhiniyam, 2021 (in short Kar

Samadhan Y ojna)

(2) It shall extend to whole of the State of Jharkhand,

(3) It shall come into force on the date of publication in the official Gazette

and effective up to six months from the date of its notification.

Provided that the State Government may, by notification published in

official Gazette in this behalf, extend the said period of six months by such

further period, not exceeding six months, as may be specified in the said

notification.

2. Definitions-

(1) In this Ordinance unless the context otherwise requires:-

(i) "Admitted tax"- means the amount of tax, interest and penalty

admitted as being payable by the person under relevant Act;

(ii) "Assessed tax"- means tax, interest and penalty determined as being

payable under an order of assessment or reassessment under the relevant

Act' , (iii) "Applicant"-means a person, who is liable to pay old arrears under the

relevant Acts and also includes a person willing to settle the amount of old

arrears of any other person, who desires to avail benefit of settlement by

complying with the condition under this Ordinance;

(iv) "Appeal"- means an appeal under the relevant Act, pending before the

Appellate Authority under respective Act;

(v) " Arrear of tax, penalty, interest or fine" - means tax, interest, penalty or fine by whatever name called, payable by an assesses pursuant to an order of assessment, re-assessment or scrutiny or any other order made or passed under the relevant Acts relating to any period ending on or before 31 "March, 2018 which is due for payment as on the date of filing application under this Ordinance; Provided that old arrears shall not include any arrears related to deferment of tax schemes, issued by the State Government under the relevant Acts, from time to time;

Provided further that arrear does not include where penalty has been

levied in lieu of prosecution.

(vi) "Commissioner"- means the Commissioner of Commercial

Taxes or Additional Commissioner of Commercial/State Tax appointed by

the Government

(vii) "Dispute" means an appeal, revision, review, reference, Writ Petition,

or Special Leave Petition, arising out of any order passed under the relevant

Act and pending before, as the case may be, the following.-

(i) The Joint Commissioner of Commercial Taxes (Appeal)

(ii) The Joint Commissioner of Commercial Taxes (Administration)

(iii) The Commissioner of Commercial Taxes

(iv) The Commercial Taxes Tribunal

(v) The High Court (vi) The Supreme Court of India

Explanation:- For the purposes of this clause a dispute includes:

(i) Any levy of tax, interest, and penalty by an authority prescribed and/or

authorized under the relevant Acts, which has not been paid into Government

Treasury, or

(UJ A proceeding for recovery of any tax, interest, fine or penalty,

initiated by or pending before any authority appointed or prescribed or

authorized under the relevant Act or under the Bihar and Orissa Public

Demand Recovery Act, 1914;

(viii) "Disputed Amount" , in relation to a dispute, means any tax or

interest or fine or penalty which has been determined as being payable

by the person pursuant to an order of assessment, re-assessment,

scrutiny or any other order made or passed under the Relevant Acts

and which is not admitted and for such demand a litigation has been

filed before any Appellate Authority or Forum but shall not include

any demand in pursuant to an order of assessment, re-assessment,

scrutiny or any other order made or passed under the Relevant Acts

where the Government has filed any case against such demand before

any Appellate Authority or higher Courts

(ix) "Relevant Act" means :-

1. The Bihar Finance Act, 1981(Bihar Act 5 of 1981) and The Bihar

Finance Act, 1981 as adopted in the State of Jharkhand.

2. The Central Sales Tax Act 1956 (Act74 Of 1956)

3. Jharkhand Value Added Tax Act, 2005 (Act 05 0f2006)

4. Adopted and amended the Bihar Electricity Duty Act, 1948

(Bihar Act 36 of 1948) and amended Act 10 of 2011 by

Jharkhand

5. Jharkhand Taxation on Luxuries in Hotels Act, 2011 (Jharkhand

Act 21 of 20 11)/ Act administered before this

6. Jharkhand Advertisement Act 2012 (Jharkhand Act 14 of

2012)/ Act administered before this

7. Jharkhand Tax on Professions, Trades, Calling and Employment Act, 2011.

8. Jharkhand Entertainment Tax Act, 2012(Jharkhand Act 13 of

2012)/ Act administered before this

9. Jharkhand Entry Tax on Consumption or Use of Goods Act, 2011.

(x) . ''Person'' means any authorized signatory/representative/dealer/

legal heir who is a party to a dispute/holder of old arrears and wants to

settle the dispute/old arrears under the Relevant Act and who files an

application under this Ordinance for settlement

(xi) "Prescribed" means as prescribed in the Rules made under this

Ordinance; (xii) ''prescribed authority", for the purposes of this Ordinance,

means authorities referred to section 4 of Jharkhand Value added Tax

Act, 2005;

(xiii) "Revision" means a petition for revision under the relevant Act

pending before the Commissioner of Commercial Taxes Department or

before the Jharkhand Commercial Tax Tribunal Jharkhand;

(xiv) "Settled", in relation to a dispute, means disposal and conclusion

of the proceeding in relation to such dispute;

(xv) "Settlement Amount" means the amount to be paid by 'the

applicant after determination by the authority, the amount to be paid

finally;

(xvi) "Statutory Certijicates/DeclarationsIForms" for the purpose of

the Ordinance means declarations and certificates mentioned under

Rule 12 of the Central Sales Tax (Registration & Turnover) Rules

1957 and includes any Form of declaration prescribed under any other

rule framed under the Relevant Act;

(xvii) "Tribunal" means the Commercial Taxes Tribunal constituted

under section 8 of Part I of the Bihar Finance Act, 1981 or section 3 of

the lharkhand Value Added Tax Act, 2005 or any relevant Act.

The words or expressions not defmed herein shall have the meanmgs

respectively assigned to them under the relevant Act or under the rules

framed there under.

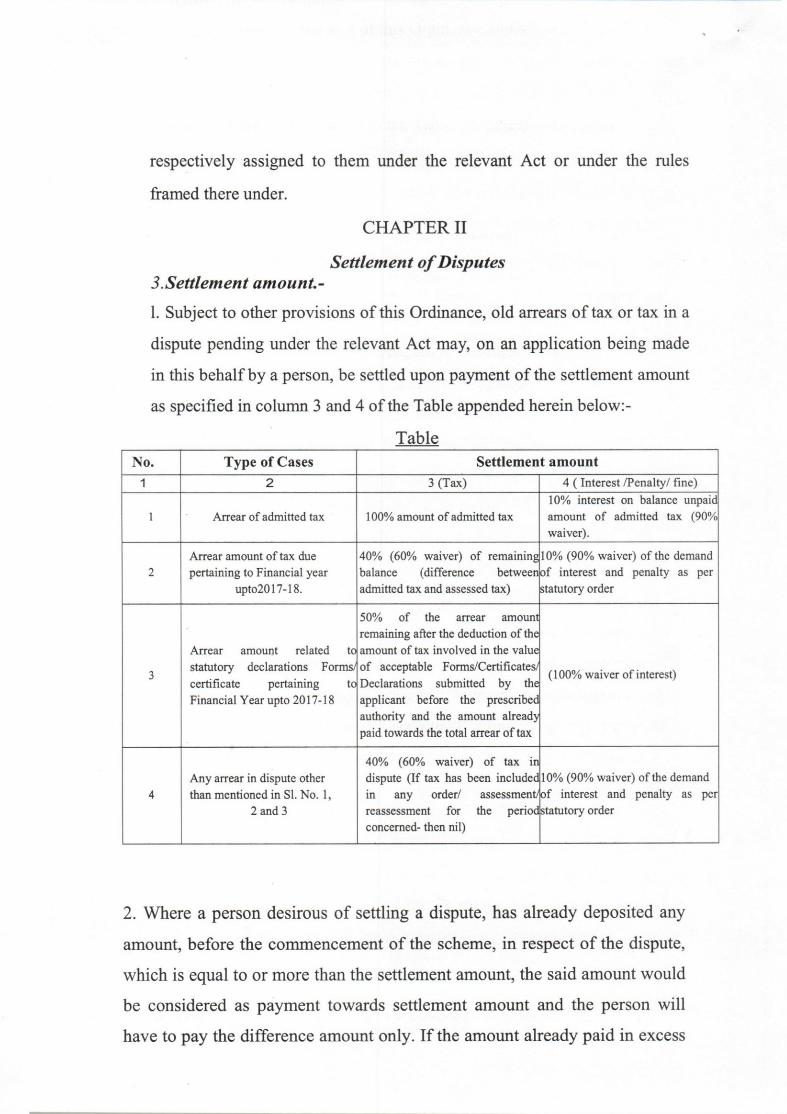

CHAPTER II

Settlement of Disputes 3.Settlement amount.- 1. Subject to other provisions of this Ordinance, old arrears of tax or tax in a

dispute pending under the relevant Act may, on an application being made

in this behalf by a person, be settled upon payment of the settlement amount

as specified in column 3 and 4 of the Table appended herein below:-

Table No. Type of Cases Settlement amount

1 2 3 (Tax) 4 ( Interest /Penalty/ fine) 10% interest on balance unpaid

1 Arrear of admitted tax 100% amount of admitted tax amount of admitted tax (90% waiver).

Arrear amount of tax due 40% (60% waiver) of remaining 10% (90% waiver) of the demand 2 pertaining to Financial year balance (difference between k>f interest and penalty as per

upto2017-18. admitted tax and assessed tax) statutory order

50% of the arrear amoun remaining after the deduction of the

Arrear amount related tc amount of tax involved in the value

3 statutory declarations Forms of acceptable Forms/Certificates

(100% waiver of interest) certificate .. tc Declarations submitted by th( pertauung Financial Year upto 2017-18 applicant before the prescribec

authority and the amount already paid towards the total arrear of tax

40% (60% waiver) of tax ir Any arrear in dispute other dispute (If tax has been includee 10% (90% waiver) of the demand

4 than mentioned in Sl. No. I, m any order/ assessment k>f interest and penalty as per 2 and 3 reassessment for the perioe statutory order

concemed- then nil)

2. Where a person desirous of settling a dispute, has already deposited any

amount, before the commencement of the scheme, in respect of the dispute,

which is equal to or more than the settlement amount, the said amount would

be considered as payment towards settlement amount and the person will

have to pay the difference amount only. If the amount already paid in excess

of settlement amount, will not be refunded.

3. No application for settlement shall be entertained by the authority, III

which the State Government! Department has moved to higher court.

Explanation-I For the purposes of this sub-section, the expression

"settlement amount" shall not include any payment towards any arrear of

admitted tax, interest, penalty and the person shall deposit the total amount

of such admitted tax, interest and penalty;

Explanation-II Where settlement application IS made for an independent

interest and penalty order, it shall be considered only when the relevant tax

in demand has been paid;

Explanation-III for the purpose of resolution of dispute, each proceeding

initiated by the department! authority shall be construed as one dispute and

person has to apply separately for settlement for each such dispute.

CHAPTER III

Manner of Settlement of Disputes

4. Application for settlement- (1) Any person desiring settlement of

arrears, shall apply to the prescribed authority, separate applications

for each statutory order under each relevant Act, in such form and

manner as prescribed within 90 days from the date of this Ordinance coming

into force along with proof of payment of admitted tax as per

sub-section (l) of section 3 of this Ordinance and other documents as

may be prescribed.

Provided that the Commissioner may, by a notification published in

the Official Gazette in this behalf, extend the said period for filing the

application by such further period, not exceeding two months, as may

be specified in the said notification.

(2) The applicant shall make disclosure about any pending appeal, revision or

any petition before any Authority or Forum with respect to such arrear in

dispute under relevant Acts and in case any appeal, revision or any petition is

pending before any Authority or Forum, an undertaking shall be furnished by

him stating that in case of availing the benefit of settlement under this

Ordinance, he shall withdraw such case against the statutory order pending

before any Authority or Forum. When the settlement order is passed by the

Prescribed Authority, the applicant shall forthwith produce such application

regarding withdrawal of such pending relevant appeal, revision or any petition

and shall produce appropriate evidence of doing so before the prescribed

Authority within 90-days of receiving the settlement order, failing which the

order of settlement shall liable to be revoked by the Prescribed Authority after

giving the applicant a reasonable opportunity of being heard.

(3). The prescribed Authority as specified in Clause (xii) of Sub-Section 2 shall

have the fmancial Jurisdiction as per the following limits of old arrears with

respect to an application-

(i) Commercial Taxes/ State Tax Officer for the amount not exceeding 5 lakh;

(ii) Assistant Commissioner of Commercial Taxes/ State Tax not exceeding

151akh;

(iii) Deputy Commissioner of Commercial Taxes / State Tax for any amount;

Provided that the Commissioner may authorize/transfer any or all

applications from one prescribed authority to another.

5. Disposal of application.-

(l) The prescribed authority will scrutinize the application filed and

if he finds correct and complete, will process for disposal in manner

prescribed, and if it is found incomplete or incorrect in any manner, a

notice will be issued to the applicant within 15 days, intimating deficiency to

rectify the same within 15 days from the date of service of such notice;

Provided that where the applicant fails to comply the notice or fails to

submit the required documents within 15 days of service of such notice,

the prescribed authority may, after giving reasonable opportunity and for the

reasons to be recorded in writing, process or reject the application.

(2) Every application furnished under section 4 shall be processed III

such manner and within such time as may be prescribed.

(3) The prescribed authority shall, on being satisfied about the fulfillment

and correctness, pass the order of settlement, within 30 days, for each

application separately, specifying therein the amount of settlement to be paid

and intimate the applicant in the manner prescribed.

Provided that where an application is remanded under sub section 2 of

section 9 to the prescribed authority for reconsideration, the order of

settlement or the order of rejection of the application as per provision

of sub section 1 and 3, as the case may be, shall be passed within 30

days of passing of the order by the appellate authority,

6. Rectification of mistakes- The prescribed authority may

(a) on his own motion or on direction of the Commissioner; or

(b) on an application submitted by an applicant within 30 days of receipt of the

order of settlement;

Pass an order; within 60 days of passing of order or receipt of the application

whichever is earlier, rectify the order of settlement for correcting apparent

mistakes on the record.

Provided that if it has the effect of enhancing the tax/interest/penalty, the

prescribed authority concerned shall give the applicant, a reasonable

opportunity of being heard.

--------

7. Revocation of order of settlement-Notwithstanding anything contained in

the Ordinance, where it appears to the prescribed authority on his own motion

or any information or direction from the Commissioner, that the applicant has

obtained the benefit of settlement by suppressing any material fact or particulars

or by furnishing false or incorrect information or has concealed any fact, the

prescribed authority may, for the reasons to be recorded in writing and after

giving the applicant a reasonable opportunity of being heard, revoke the order

of settlement passed by him under the Ordinance, within a period of one year of

passing the order of settlement;

Provided the period of one year may be extended to five years with the

approval of the Commissioner.

The amount of settlement deposited by the applicant pursuant to a settlement

order, shall be adjusted against the outstanding dues of the year concerned.

8. Power of the Commissioner under the Ordinance

(i) The Commissioner may, from time to time, issue instructions and

directions as he may deem fit for carrying out the purpose of the Ordinance,

(ii) The Commissioner may prescribe any Form/annexure/worksheet required

for the purpose of the Ordinance

(iii) The Commissioner may authorize/ transfer any or all application from one

prescribed authority to another

(iv) The Commissioner may, on his own motion or on application or

information, direct the authority to re verify the Order of Settlement. He may,

reasons to believe, that applicant has suppressed any material

facts/particulars/information or has given false information/concealed any

particulars, may revoke the Order of Settlement passed by any prescribed

authority and direct to pass a fresh order after giving the applicant a reasonable

opportunity of being heard.

r

9. Appeal- An appeal against the order of settlement passed by the Prescribed

Authority, shall be filed before the Additional/Joint commissioner (Appeal) of

the Division, having jurisdiction as specified in sub- section (2) of Section 4 of

the Jharkhand Value Added Tax Act, 2005 within 30 days from the date of

service of such order

(2) Appellate authority shall pass an order, after giving opportunity of

hearing, within 60 days of filing of such application of appeal.

(3) No appeal shall lie against the order passed under proVISO of

sub-Section (2) of Section 3.

(4) In disposing of the appeal, the appellate authority may,-

(i) set aside the order of rejection of the application and remand the

application to the prescribed authority for consideration;

(ii) reject the appeal.

(5) Order passed by appellate authority shall be final

(6) The Commissioner may, on his own motion or on application, transfer any

or all appeals from one appellate authority to another

10. Power to make rules.-

(1) The Government may by notification, make rules for carrying out the

provisions of this Ordinance.

(2) Without prejudice to the generality of the provisions of sub-section (1), the

Government may make rules for all or any of the matters which by this

Ordinance are required to be, or may be prescribed or in respect of which

provisions are to be or may be made by rules.