The impact of internal audit on public service organisation

63

1 The impact of internal audit on public service organization. By: Richard Nsiah [email protected] CHAPTER ONE INTRODUCTION It has come to realisation all over the world that the activities of internal audit have significant impact on the progress of every organisation. The potential auditors possess have tuned into a challenge and task and performed their duties to enable the organisation to achieve its goal and objectives. Background of the Study Ancient history of accounting and auditing started in 8500 BC. The history did not prove any record until 1397 when a double entry form of record at Medici family of Florence, Italy. As early as 2500 years ago Zenon Papyli really recorded the application of audit in Egyptian Estate of the Greek ruler Ptolemy Philadelpus. Greek and Roman writers such as Aristophanes Ceasar and Cicero made mention of accountants auditors and auditing accounts and audit rooms. Internal auditing existed among the minor houses of England in year 1700 where the Lord serves as managers of the audit function. The earliest external audit was independently by public accountant Charles Snells as a result of the South Sea Bubble scandal in England .The total market value of the company exceeded the value of all money in England. After the investigation fictitious entries were discovered in the books and because of this incident major auditing events

Transcript of The impact of internal audit on public service organisation

1

The impact of internal audit on public service organization.

By: Richard Nsiah

CHAPTER ONE

INTRODUCTION

It has come to realisation all over the world that the activities of internal audit

have significant impact on the progress of every organisation. The potential

auditors possess have tuned into a challenge and task and performed their duties to

enable the organisation to achieve its goal and objectives.

Background of the Study

Ancient history of accounting and auditing started in 8500 BC. The history did not prove any

record until 1397 when a double entry form of record at Medici family of Florence, Italy. As

early as 2500 years ago Zenon Papyli really recorded the application of audit in Egyptian Estate

of the Greek ruler Ptolemy Philadelpus. Greek and Roman writers such as Aristophanes Ceasar

and Cicero made mention of accountants auditors and auditing accounts and audit rooms.

Internal auditing existed among the minor houses of England in year 1700 where the Lord

serves as managers of the audit function. The earliest external audit was independently by public

accountant Charles Snells as a result of the South Sea Bubble scandal in England .The total

market value of the company exceeded the value of all money in England. After the investigation

fictitious entries were discovered in the books and because of this incident major auditing events

2

that focus on improvement of standards tends to focused on public exposure of scandals and

fraud.

Later industrial revolution resulted in family systems that were finance by stakeholders. It

became necessary for both internal and external auditors to protect the public organisations

which brought about the establishment of British Company Act1844 provided for mandatory

audit.

In 1853 organisation of chartered accountants were formed in Scotland. In 1880 five

organisations of chartered accountants formed a unified Institute of Charted Accountants. In

1917 an American Institute of Certified Public Accountant (AICPA) began the preparation of the

uniform examination by all the states which was passed as laws. Sixteen Amendments on income

tax was pass in 1913.One of the provision of the law was that, all companies must maintain

adequate record that will enable large and small firms to obtain proper record for planning and

controlling.

The American auditors of the 1800 were devoted to the accuracy of bookkeeping details,

vouchers examination and payment verifications. In 1918 the approve method of preparation of

Balance sheet statements was issued ,this document declared the generally accepted principles

and audit programme , instruction for auditing specific account and standardise audit report.

The 1936 document placed emphasis on internal controls balance sheets and income statements.

This document became the reliable source of document more than two decades. Internal audit

practice has come a long way since the establishment of the Institute of Internal Auditors in

1941. Ours is now a full fledge profession with a standards ,a code of ethics and a certification

programme , prestige and enjoys much better compensation and a working conditions than in

earlier times. The Institute itself is much larger offers a great variety of services and has ventured

far beyond its original birth place in North America.

3

The interest to our analysis is a determination of what has not change in the Internal Auditing

concept. Internal auditing practice continues to be an internal appraisal activities serving interest

to the organisation and functioning over broad area, including accounting and other operations.

What has also not changed is an overview of” independence” bore upon the honesty, diligence,

and objectivity of the auditors, as well as the support of the management.

It can be concluded that the authoritative view of internal auditing remains pretty much like what

it has always been. Many pronouncements have been issued but this has done little more than

flesh out of the basic vision that was established in 1941.

Although internal auditing does not appear to have change very much of the conceptual level, it

does not follow the same kind of internal audit practice. Internal auditing has, in fact changed in

the field.

Ghana audit service was created in London as Colonial audit department. It later became known

as Auditor General Department.In1969 constitution of Ghana extended financial and

administrative autonomy to the agency and in 1972 Audit service Decree established it as Ghana

audit service which strengthened its independence by a seven -member audit service board as it’s

governing body. The board consist of chairman, four representatives appointed by the president

acting in consultation with the council of state, auditor general and the head of civil service.

The audit service Act 2000(Act584) which derives most of its provision from the 1992

constitution further enhanced the mandate of Ghana Audit Service. Ghana audit service exists for

good governance, transparency, accountability and probity in public financial management

system of Ghana resources in accordance with the recognized international auditing standards

reporting to parliaments.

The internal audit agency Acts, 2003 [Act 658] was established by parliament as apex body to

facilitate, coordinate and provide quality assurance for the internal audit activities within the

4

republic of Ghana. The success of internal auditor depends on how well he has contributed to

development of organizations. The internal auditor should make his /herself very important by

providing the relevant information and advice that enable management take decisions that

enhance the welfare of the organizations. The knowledge and experience of internal auditor has

acquired and his ability to provide timely advice to management helps the organization to reach

it goals and objectives.

However research has proved that the activities of internal auditors has been restrictive in terms

of scope and ability to take right decision that will bring inefficiencies of management to bear

and expose financial malfeasance of management. There is therefore the need to address these

issues to ensure internal auditors can work effectively and efficiently to achieve the mission of

Ghana Education service in Kumasi and safeguard its finances.

Statement of the Problem

The internal audit function in Ghanaian public service faces a lot of challenges, difficulties, and

perceptions and to some extent a credibility problems which hamper their activities. Sometimes

auditors are seen by management as threat to the organization and therefore the necessary

corporation and support are not given them to carry out their mandate. The money voted for

them to carry out their duty at the financial year is woefully inadequate and logistics they need

from the state are very difficult to get them. Internal auditors are not seen as partners in

developmental agenda of government but rather fault funders and this perception does not

motivate internal auditor to execute their work effectively. Our concern is to assess the impact of

this unfortunate development on work of Ghana Education service in Kumasi.

In addition to these problems public service are measured by three key factors which are

effectiveness, efficiencies and economy it chops at any given time. However most of public

service organizations are not able to achieve these objectives upon all the resources at their

disposal. The auditor’s report of government exposes financial embezzlements,

misappropriations and misapplication of public money every year. The quality of service

provided by some public service to citizens leave much to be desired. Most people see public

service as government property and needed attention is not given. These unfortunate situations

5

forced the public to ask whether internal auditors are actually in this organization and if they are

what measures are they putting in place to prevent such menace. Concerned are also raised as to

action the parliament is taking to ensure those who commit this act are brought to book to face

the full rigor of the law and if possible all the property they have use the nation resources to

acquire for themselves are sold to state. There is no doubt that integrity of internal auditor and

cordial relationship and support of management and shareholders can promote image of the

organization and eliminate wasteful use of nation resources so as to get value for money.

Purpose of the Study

Internal audit functions bring a systematic disciplined approach to evaluate the risk and add

value to internal control. It also makes recommendation to increase the effectiveness of risk

management effort by improving the internal control structure and promote good corporate

governance

Below are the purposes of the study:

To find out whether the auditors have the right qualification and experience.

To examine how effective internal audit unit in Ghana education service in Kumasi are

putting the proper measures in place to ensure that the service complied with the proper

procedure, rules, regulation, standards etc.

To lay more emphasis on the need for the government and management to speed up

implementation of recommendations made by Internal Auditors.

Examine the independence of internal auditor in helping to promote good governance in

the education service.

6

To identify reasons why most public service organizations are not able to leave up to

expectation looking at all resources they have and the ways to curb these problems.

Research Questions

Do the auditors have the required qualification, expertise and resources that facilitate

their work?

Do the recommendation and advisory service provided by internal auditors are accepted

and implemented by management and government?

Are the internal auditors independent in public service organisation?

Are the public service organisation workers able to comply with the internal control

measure, are they able to safeguard assets and reduce fraud in public service?

To what extent does the operation of Ghana Education Service conform to financial and

accounting regulations and internal control measures?

What account for low performance of some public service organizations upon the all the

appropriate measures internal auditors are putting in place and how can these problems

be solved?

To what extent can effective internal audit better the performance of the public service

organisation?

Significance of the Study

At the end of the study, the following should be ascertained by the public:

7

The study would help bring up issues of how an internal audit practice has changed the

thinking of interest groups like staff, shareholders, suppliers, creditors among many

others who contribute to the public service organisation.

The study would help to identify weaknesses, risk and potential areas of fraud which will

serve as a guide to management to fashion out policies and strategies that will mitigate

the perceived and inherent dangers in public service organisation.

Assist government to know the type of skills public officer need to acquire before any

high position is handed to him and properly address factors which affect managers for not

achieving the best result.

Increase the general public holasiosm whether the internal auditors are doing enough to

assist manager of organization to achieve the objectives of public service organizations.

Help the general public to identify factors affecting the internal auditors that serve as a

hindrance for them to perform satisfactory to improve the fortune of public service.

Limitations of the Study

Recognized research limitation is necessary to assist users assess the percentage of reliability of

research outcome. The challenge of this research work is finances which prevents us to cover

wider area of institution in Kumasi that will help to ascertain more information about the

activities of Ghana Education Service. In addition to this, some of the respondents were not

given much attention for the filling of questionnaires and granting audience for the interview.

Time factor cannot be ignored, as combining the work and academics is very tedious task but

upon all this challenges we did our best to examine the reasons why our most public service

organizations like Ghana Education service are not leaving up to expectations upon all vast

resources they possess.

Scope of the Study

8

The study covers the following aspect of the research topic: the independence of the conduct of

internal audit unit , the effectiveness of the audit structure to ensure the prescribe procedure and

principle for the conduct of the organisation’s business are followed , the attitude of the segment

of the organisation to the notices of lapses discovered by internal audit unit, the attention and

support accorded the internal audit unit by the management and the board and the impact of work

of the internal audit unit on attainment of the overall goal of the organisation.

Organisation of the Study

The study consists of five chapters. Chapter one describes the background of the study, the

problem statement, the research objective, research questions, the limitation of the study.

Review of related literature in relation to public works and research topics and problem

statement is given in chapter two.

Methodology is given in chapter three and this consist of Research design , Population, Sample

and Sampling Procedure for collecting data, Research Instruments, Data Collection Procedures

and Analysis of data collected.

The chapter4 shows the analysis of key findings arising from the study. Chapter 5 ends the study

and provide the necessary recommendations.

9

CHAPTER TWO

LITERATURE REVIEW

Internal audit agency (IAA) was established by the Internal Audit Agency Act 2003 (Act658)

with a mandate to co-ordinate, facilitate, monitor, supervise and provide adequate assurance for

the Internal audit Unit in MDA’S or MMDA’s. The key requirement of Act are the provision of

internal auditing Assurance service and consulting services that will lead to the enhancement of

efficiency accountability and transparency in the management of resources in the public sector.

The creation of the Internal Audit Agency was predicated on the need for the government to put

in place a structure that could support the eventual transfer of budgetary authority and

expenditure.

The initiative is part of government effort under the public financial management reform

programmes (PUFMARN). The achieved presidential assent on 31 December 2003,

Administration was allowed up to 31 August for the effective implementation stated in 2005.

The internal auditing has gained considerable interest in modern organization since it drives

every organization toward achieving it visions and missions. The agency set standard and

procedures for conduct of internal audit activities in the organisations. They ensure national

resources are adequately safeguarded; financial activities of public service organization are in

line with laws, policies, plans, standard and procedures. Without limiting their powers, they see

to it that managerial, financial and operating information’s are reported internally is accurate,

reliable and timely. The agency facilitates the prevention and detection of fraud and undertakes

inspections and evaluates the internal auditing of the organizations. One could easily say the

agency strengthen the performance of internal auditing, it helps to promote economy, efficiency

and effectiveness in the administration of public service organizations.

10

According to Anderson and Bragg (1996), the existence of qualified internal audit department or

unit, certainly is the medium to a large organisation is an important element of the system of

internal control. They emphasize that the internal audit is the eyes and ears of management for

ascertaining that status of internal control system, especially the accounting or financial control

and thus internal auditor must ensure that adequate control measures exist and that the system are

effective for the intended purposes and therefore any deficiency should be brought to the

attention of the management for the necessary action to be taken “.

Internal Auditing

The Wikipedia encyclopaedia (n.d) defined internal auditing as “an independents, objective,

assurance and consulting activities design to add value and improve an organisation’s

operations”. Internal auditing is a catalyst for improving an organizations effectiveness and

efficiency by improving insight and recommendation based on analysis and assessment of data

and business process. It helps an organisation to accomplish its objective by bringing a

systematic disciplined approach to evaluate and improve the effectiveness of risk management

control and governance processes.

Independence is established by the organisational and reporting structure .objectivity is achieved

by an appropriate mind-set .The internal audit activity evaluates risk exposures relating to the

organisations governance operation and information system in relating to the:

Effectiveness and efficiency of operation.

Reliability and integrity of financial and operating information.

Safeguarding of assets.

Compliance with law, regulations and contract.

11

Based on the result of the risk assessment, the internal auditors evaluate the adequacy and

effectiveness of how risks are identified and manage in the above areas. They also assess other

aspect such as ethics and value the organisation in order to facilitate the governance process

Institute of Internal Audit Research Foundation (IIARF) define an internal audit as “an ongoing

appraisal of financial health of a company operation by its own employees”. Employees who

carry this function are called internal auditors will evaluate and monitor the company risk

management, reporting and control practices and make suggestions for improvement.

It covers not an organisational finance function but all operations and system of the firms.

Internal auditing is performed by professionals with in-depth understanding of the business

culture, systems and processes in effective and efficient manner to ensure organisational goals

and objectives are met. While internal auditors are typically accountants, theses activities can

also be carried out by professionals who are well versed with a company function and the

relevant regulatory requirements. Auditing therefore can be defined as the independent

examination of, an expression of opinion on the financial statement of an enterprise by an

appointed auditor in pursuance of that appointment and in compliance any relevant stationery

obligation. Auditing Practice Committee.

The internal auditors are expected to provide recommendations for improvement in the areas

where opportunities or deficiencies are identified while management is responsible for internal

control, the internal audit activities provide assurance to management and audit committee that

internal controls are effective and working as intended. The internal audits are led by Chief Audit

Executive (CAE). The audit executive delineates the scope of activities, authority and

independent for internal auditing in a written charter that is approved by audit committee.

An effective internal audit activity is a valuable resource for the management and the board or

its equivalent and audit committee due to its understanding of the organisation and its culture,

operation and risk profile. The objectivity skills and knowledge of a competent internal auditors

12

can significantly add value to an organisational internal control, risk management and

governance processes.

Similarly, an effective audit activity can provide assurance to other stakeholders such as

regulators, employees, providers of finance and shareholders.

Objective of Audit

The objective of an audit is to enable the auditor to express opinion whether the financial

statements are prepared in all material respect in accordance with an identified financial

recording frameworks.

The phrase used to express the opinion is to ‘give true and fair view” or present fairly in all the

material respect. Auditors opinion enhance the credibility of the financial statements, the users

cannot assumes that the opinion is an assurance to the future viability of the entity or

effectiveness or efficiency with which the auditor has conducted the affairs of the entity.

Other objective is to prevent errors, fraud and to improve client internal and accounting control

systems. It must emphasize that audit work is not design to identify fraud, errors and significant

weakness in the client system but audit work should be carried out in such a manner as to be

unearth errors, fraud and weakness if they exist.

Ethical Principles Govern Professional Auditors

A professional internal auditor should need to demonstrate some quality like objectivity and

independence, professional competence and due care, confidentiality, integrity and professional

behaviour as established by IFAC to enable him exercise his duty diligently.

Independence

Auditor’s independence refers to the independent of the internal auditors from various parties

that may have a financial interest in the business being audited .It requires integrity and

13

objectivity approach to the audit process. The concept requires the auditor to carry out his work

freely and in an objective manner. Independence of the internal auditor means independence

from parties whose might be harmed by the result of an audit. The United States Panel on Audit

effectiveness (2000) stressed that the independence of the auditor was fundamental to the

reliability of auditor’s report. Specific internal management are inadequate, risk management,

internal controls and poor governance. The charter and the reporting committee provide

independence from management, the code of ethics of the company (and of the internal audit

profession) helps give guidance on independence from suppliers, client and the third parties

(Sarbanes-Oxley Act2002).

Programming independence is a type which essentially protects the auditor’s ability to select the

most appropriate strategy when conducting an audit.

Investigative independence protect the auditors ability to implement the strategies in whatever

manner they considered necessary .Auditor must have unlimited access to all the company

information. Queries must be answered and the collection of audit evidence is an essential

process and cannot be restricted in any way by the client.

Reporting independence protects the auditor ability to choose to reveal to the public any

information they believe should be disclosed, if the company’s directive have been misleading.

Shareholders by falsifying accounting information, they will strive to prevent the auditors from

reporting this. It is a situation like this when auditor’s independence is mostly likely to be

compromised.

Perceived independence suggests that the auditor must not act independently, but must be seen to

be independent too. The auditor’s independence must be beyond doubt but how can this be

guaranteed and measured.

Professional Competence

Professional competence requires auditors apply reasonable skill in whatever they do and adopt

proper techniques in all their dealings. It is the duty of every auditor to ensure care; diligence and

expedition are taken in consideration in executing their duties. It must be noted that the

14

professional knowledge and skills of an auditor is not absolute as sometime advice could lead to

unexpected result

Scope of Audit

The term scope of the audit refers to the audit procedure deemed necessary in the circumstances

to achieve the objective of the audit. The procedures required to conduct the audit in accordance

with ISA’s should be determined by the auditor having regard for the requirement of ISA

relevant professional bodies, legislation, regulations and where appropriate, the term of the audit

engagement and the reporting requirement.

Assurance Audit

Audit is designed to provide reasonable assurance that financial statement is taken as a whole are

free from material misstatements. The concept relating to the accumulation evidence necessary

for the auditor to conclude that there is no material misstatements in the financial statement taken

as a whole. The auditor cannot obtain an absolute assurance because there is an inherent

misstatement that result from this factor. The use of testing the inherent limitation of internal

control and persuasive audit evidence gathered rather than the conclusive audit evidence relating

to timing, nature and the extent of the audit procedure.

Audit Risk and Materiality

Risk is anything that serves a hindrance to corporate objective. Entities pursue strategies to

achieve objectives and depending on the nature of the operations, environments in which they

operate, the size and complexity of their work they face a business risk.

Any risk that the auditors encounter put limitation on their ability to express independent opinion

on the financial statements. The concept of reasonable assurance acknowledged that there is risk

that auditor’s opinion might not be appropriate. When auditors are not able to express their

15

independent audit opinion on the financial statement as a result of material misstated is known as

audit risk.

According to (IASB), financial information is material if it omission or misstatement could

influence the economic decision of the users taken on the bases of the financial statement. The

application on materiality during the planning stage helps us to identify potential risk areas like

trade receivables, payables, invoice and fixed assets.

Accumulating and Evaluating Audit Evidence

Evidence is any information used by the audit to determine whether or not the financial

statement represent true and fair view and prepared in accordance with the established criteria.

Evidence takes many different forms including: oral, testimony of the clients, written

communication with outsiders, observation by the auditor and electronic data about transactions.

It is important to obtain a sufficient quality and volume of evidence to satisfy the purpose of the

audit. Determining the type and amount of evidence and evaluating whether the information

correspond to the establish criteria is critical in every audit.

Auditors Reports

Auditors report is a formal opinion or disclaimer there off issued by either an internal auditor or

an independent external auditor as a result of his/her evaluation perform on a legal entity or

subdivision there off. The report is subsequently provided to the users such as an individual,

group of persons, a government, and the general public and among others. Audit report is

considered an essential tool when reporting financial information to the users, particular in

business since many third parties prefer or even require financial information to be satisfied by

an independent external auditor, many organisations rely on the auditor’s report to certify the

information in order to attract investors, obtain loans, boost public confidence. Some have even

stated that financial information without an auditor’s report is “essentially worthless” for

investigating purposes.

16

Auditors report may take many different forms and below are some of the forms are;

Unqualified Opinion, an opinion is said to be unqualified when the auditor conclude that the

financial statement give true and fair view in accordance with financial reporting frame work

used for the preparation and presentation of the financial statement. This type of report issued by

an auditor where financial statement presented are free from material misstatement and

represented fairly in accordance with the Generally Accepted Accounting principle(GAAP) or

that the company financial condition, position and operations are fairly presented in a financial

statement. It is the best report an external may issue to the organisation been audited. An Auditor

will issue unqualified report when the financial statement portrays the following:

Financial statement has been prepared using the generally accepted accounting principles which

has been consistently applied.

Financial statement follows relevant statutory requirement and regulation. There is an adequate

disclosure of all material matters relevant to the proper presentation of financial statement

subject to statutory requirement where applicable.

Any changes in the accounting principles or in the method of their application and effect there

off have been properly determined and disclosed in the financial statement.

Qualified opinion report, is issued when the auditor encounter one of the two types of situations

which does not comply with the generally accepted accounting principles, however financial

statement is fairly presented. This type of opinion is very similar to the unqualified “clean

opinion”, but the report state that the financial statement is fairly presented with certain

exception which is otherwise misstated.

Single deviation from GAAP: this type of qualification occurs when one or more areas of a

financial statement do not conform to GAAP.

Limitation of scope: this type of qualification occurs when the auditor could not audit one or

more areas of financial statement.

17

Adverse opinion, is when the auditor determines that financial statement are materially

misstated and when considered as a whole do not conform with GAAP, it is considered the

opposite of an unqualified or clean opinion.

Generally an adverse opinion is only given when the financial statement seem to be pervasive

and different from GAAP.

Disclaimer of opinion is commonly referred to as disclaimer and it is issued when the auditors

could not form an opinion and consequently refuses to present an opinion on the financial

statement. Statement of auditing standard provides certain situations where a disclaimer of

opinion may be appropriate:

When there is lack of independence or conflicts of interest exist between the auditor and the

management of organisation been audited (SAS NO 26).

There are significant scope of limitation whether intentional or not which hinders the auditor

work in obtaining evidence and performing procedures (SAS No 36). There is a substantial doubt

about the organisations audited on their ability to continue as a going concern (SAS NO59).

Auditing and Accounting

Many users of financial information and the general public find it very difficult to distinguish

between auditing and accounting. This is because most auditing activities are usually concern

with accounting information and many auditors have more experience in accounting issues.

Accounting is based on recording, classifying summarizing of economic events in a logical

manner for the purpose of providing financial information for decision making. The function of

accounting is to provide a certain type of qualitative information that management and auditors

can use to make a decision to provide relevant information, accountant must have a thorough

understanding of the principles and rules that provide the basis for preparing the accounting

information.

Besides, accountant must develop a system to make sure that entity’s economic events are

properly recorded and timely basis and at a reasonable cost.

18

In auditing accounting data, the concern is with determining whether the recorded information is

properly reflects the events rules that occur during the accounting period. Because accounting

rules are the criteria for evaluating whether the accounting information properly recorded, any

auditor should thoroughly understand those rules in context of the audit of financial statement,

the rules and generally accepted accounting principles. Through this text the assumption is made

that the reader has knowledge in generally accepted accounting principles.

In addition to understanding accounting the auditor must possess the expertise in accumulation

and interpretation of audit evidence. It is the expertise that distinguishes auditors from

accountant. Determining the proper audit procedures, deciding the number and type of items to

test and evaluating the result are problems unique to the auditor.

Basically there are two types of audit activities and they are:

Statutory Audit

It is an independent opinion and expression of opinion on financial statement by an appointed

auditor in pursuance of that appointment and in compliance with relevant statutory obligation.

The Ghana company codes, 1963 Act179 makes it mandatory for any company incorporated

under the act to appoint auditors within three months of the incorporation of the company or the

ministry. It also states that every existing company shall unless it already had duly qualified

auditors, appoints auditors within three months after the commencement of this code (section

134). The purpose of statutory audit is to determine whether an organisation is providing affair

and accurate presentation of its financial position by examining information such as bank

balances, bookkeeping records and financial transactions.

Internal Audit

There are three types of internal audit:

Financial Statement Audit.

Operational Audit.

19

Compliance Audit.

Financial Statement Audit

It is conducted to determine whether the overall financial statements are stated in accordance

with the specified criteria. Normally the criteria are generally accepted Principles, although it is

also common to conduct audits of financial statements prepared using cash basis or some other

basis of accounting appropriate for the organisation. The financial statements most often

included are the statement of financial position, income statement, and statement of cash flows,

including accompanying footnotes. In determining whether financial statements are fairly stated

in accordance with accounting principles, the auditor performs appropriate test to determine

whether the statement contains numerical errors or other misstatements.

The financial statements audit has never been more important. In today’s business Environment

there is more scrutiny and scepticism of a company’s financial statement than ever before.

Investors have lost faith in corporate governance and reporting, and they expect greater

reliability, more oversight and clear evidence of control.

Corporate management, board and audit committee, internal auditors, analyst and other

investment professionals all have important roles play in rebuilding investors trust by executing

their respective responsibilities keeping in mind both legal obligations and heightened

expectations of investors. Meeting investor’s expectation begins with completeness and accuracy

of information contained in the financial statements.

Compliance Audit

Compliance audit is the comprehensive review of organisation adherence to regulatory

guidelines, independent accounting security or consultant evaluates the strength and

thoroughness of compliance procedures. Auditors review compliance procedure, user access

control and risk management procedures over the course of compliance audit.

20

What precisely is examined in the compliance audit will vary depending upon whether an

organisation is public or private company, what kind of data it handles and if it transmits or store

sensitive financial data.

Operational Audit

An operational audit test a company’s internal systems and procedure used to produce its goods

and service sold to consumers. These audits test production operations efficiency and

effectiveness. Audits may be conducted by internal employees or external employees or external

auditors with business experience relating to the company’s operational procedures. Operational

auditors are usually conduct deeper review of company operations than a financial audit, which

is conducted after the fact audit process. Benefits from operational audits include objective

opinions, improved work flow or cost allocation processes and quicker turnaround times.

Accountants from public accounting firms usually conduct operational audit to allow companies

to have an objective opinion, on how well the company is using their business resources.

Department managers may have a tendency to fudge their audit figures since they often receive

compensation bonus or pay increment from improved performance. Public accounting firms

sometimes are used for operational audits to inform outside stakeholders on operational strength

of a company’s operations. Objective audit opinions may lead companies to increase production

cost.

Functions of Internal Auditors

Help the organisation to ascertain whether or not the quality management system is

working effectively.

Determine the adequacy of the system of internal control.

Report findings to management and recommend corrective action where necessary.

Investigate compliance with company policies and procedures.

For internal auditors to perform effectively to assist unrestricted evaluations of management

activities and the personnel, it requires organization independence from management. Activities

21

of internal auditors can be facilitated based on adequate internal control policies that

management and board have put in place in the organization. Therefore with proper internal

control, internal audit function can be executed effectively and efficiently

Definition of Internal control

Internal control is defined by COSO as a process effect by an organisation’s structure, work and

authority flow, people and management information system, designed to help the organisation

accomplish a specific goal or objective. It is a means by which organizations resources are

directed, monitored and measured.

It plays an important role in preventing and detecting fraud and protecting the organisation’s

resources both physical (machinery and property) and intangible (example reputation or

intellectual property such as trademarks).

At organisational level internal control objectives relate to the reliability of financial reporting,

timely feedback on the achievement of operational or strategic goals and compliance with laws

and regulations. At the specific transaction level internal control refers to the action taken to

achieve specific objective (e.g. how to ensure the organisation payment made to third parties are

for valid services rendered).

Internal control procedures reduce process variations, leading to more predictable outcomes.

Internal control is a key element of Falling Corrupt Practices (FCPA) of 1977 in public Co –

operations which was termed as operational controls. The framework designed by COSO broadly

defines internal control as process affected by an entities’ board of directors’ management and

other personnel, designed to provide reasonable assurance regarding the achievement of

objectives in the following categories:

Effectiveness and efficiency of operations.

Reliability of financial reporting.

Compliance with laws and regulations.

22

According to COSO effective internal controls must have the following five components:

Control environment – Set the tone for the organisation which influences the control

consciousness of its people. It is the foundation for all other components of internal control.

Risk Assessment – It identifies and analysis relevant risk to the achievement of objectives,

forming a basis for how the risk should be managed.

Information and communication – system of processes which support the identification, capture

and exchange of information in a form and time frame that enable people to carry out their

responsibilities.

Control Activities – It lays down policies and procedures that help ensure management directives

are carried out.

Monitoring – Process use to assess the quality of internal performance over a time

The concept of cooperate governance also heavily rely on the necessity of the internal controls.

Internal controls helps ensure that processes operate as designed and that risk response (risk

treatment) and risk management are carried out. In addition, there are the needs to put in place

mechanism that ensure the aforementioned procedures will be performed as intended and the

right attitudes, integrity, competence, and others are been monitored by managers.

Control procedures are defined by SEC as specific set of policies, procedures and activities

designed to meet an objective. A control may exist within a designated function or activity in a

process. A control procedure may be designed to cover a specific area such as an account

balance or class of transactions, reconciliation, segregation of duties and authorisation,

safeguarding and accountability of assets, preventing or detecting of error or fraud. Control may

consist of financial reporting controls and operational controls (that is design to achieve

operational objectives). Internal control is the integration of the activities, plans, attitudes,

policies, and efforts of the people of an organization working together to provide reasonable

assurance that the organization will achieve its objectives and mission. Thomas P. DiNapoli

(2007)

23

Internal control is a process designed, implement and maintain by those charged with

governance, management and other personnel to provide reasonable assurance about the

achievement of an entity’s objective with regard to reliability of financial reporting, effectiveness

and efficiency of operation, safe guarding of assets and compliance with the applicable laws and

regulations.

Generally, setting objectives, budget plans and other expectations establish criteria for control,

control itself exist to keep performance or a state of affairs within what is expected, allowed or

accepted. Control built within a process is internal in nature. It takes place with a combination of

inter-related components – such as social environment effecting behaviour of employees,

information necessary in control, polices and procedure.

The purpose of internal control is to provide assurance that the entire organization operates in

accordance with management plans and policies. Meigs and Meigs (1987)

The overall purpose of internal control is to help an organization achieve its mission; internal

control also helps an organization to:

Promote orderly, economical, efficient and effective operations, and produce quality

products and services consistent with the organization's mission.

Safeguard resources against loss due to waste, abuse, mismanagement, errors and fraud.

Promote adherence to laws, regulations, contracts and management directives.

Develop and maintain reliable financial and management data, and accurately present that

data in timely reports. Thomas P. DiNapoli (2007)

Types of Internal Control

24

The modern audit encompasses the reliance on the internal control of the client to the amount of

testing of final balances. The types of internal controls which auditors seek to rely on to seek

some degree of reliance according ACCA study guide (1989) are as follows:

Organisation

Basically, it looks at the plan of the organisation concerned. An organisation should define and

allocate responsibilities as well as identifying lines of reporting for all aspect of the organisation

operation including the controls. Delegation of authority within the organisation and

responsibilities should be clearly specified. One of the basic means of control is the separation of

those responsibilities or duties which would be maintained to enable an individual to record and

process a complete transaction.

Segregation of Duty

Segregation of duties reduces the risk of intentional manipulation and increase the element of

checking on the work of those in charge of controls. Authorisation, execution, custody, recording

and accounting system, system development and daily operation in the case of computer based

are the function which should be separated.

Physical Control

Physical control mainly concerns the custody of assets and involves procedures and security

measures designed to ensure that access assets such as warehouse and documents are limited to

authorised personnel.

Authorisation and Approval

This requires that all transaction should be properly authorised or approved by the appropriate

responsible person. The limit for this authorisation should be clearly specified.

Arithmetic of Accounting:

25

These are the control within the recording function which seek to check that transactions need to

be recorded and processed have been authorised, they are all included, correctly recorded and

accurately processed. Such controls include checking of totals, reconciliatory control account

and trial balances and accounting for documents, checking arithmetical accuracy of records and

maintenance.

There should exist in every enterprise procedures to ensure that personnel have capabilities that

commensurate with their responsibilities. It is the clear that the proper functioning of the systems

depends on the competence and integrity of those operating it. In setting up any control system,

important features such as qualification, selection and training as well as the innate personal

characteristics of the personnel involved.

Any system of internal control should include the supervision by responsible officials of the day-

to-day transaction and recording thereof. The responsibility for supervision should be clearly laid

down and communicated to the persons being supervised.

Management

Controls are exercise by management outside the day-to-day routine of the system. They include

the overall supervisions; control exercised by management, the review of management accounts

and the comparison thereof, with budgets, the internal function of any other special review

procedures.

Personnel

There should be procedures to ensure that personnel have capabilities commensurate with their

responsibilities. Inevitably, proper functioning of any system depends on the competence and

integrity of those operating it.

Public service organizations may be defined as commercial undertaking owned and managed by

the government with a view to maximize social welfare and uphold public interest. Public

service can take the forms like statutory corporation, direct administration funded by taxation,

partially or completely outsourcing organizations.

26

Public organizations are accountable to legislature, follow excessive formalities in their

operation, welfare oriented, funded by government, owned, managed and controlled by

government. With the help of public service organization economics inequalities can be

minimized, public welfare could be improved, regional development can be achieved, monopoly

of private sector will be reduced, and price can be controlled in the country and boost the basic

industry of an economy. All these dreams can be materialised based on effective internal control

policies instituted by management of the public service organisations.

Auditing in Specific Areas

With regard to specific study, audit specific areas of cash or bank, payroll security of assets,

legitimacy of income and expenditure, management information and computer operation are the

focus area in this section which of course, if followed will help achieve the desire objectives.

Auditing of Cash / Cheque

The major objectives of auditing of cash or cheque are to ensure that all cash and cheques

received are accounted for and accurately recorded in the book and that all such receipts are

prepared. Measures to be adopted include.

Ensuring that all cash, cheque and other negotiable instruments are recorded and immediately

giving details of receipts signed by both parties present.

Ensuring regular dependent comparison of the list of cash/cheque receipts with banking records

Prescribing and limiting the number of persons who are authorized to receive cash.

Establishing means of evidencing cash and cheque receipts to ensure payment are not made into

wrong hands.

Auditing of Wages and Salaries

27

The basic concern of auditing in this area is to ensure that wages and salaries are paid only to the

actual employees at authorised rates of pay as well as ensuring that payrolls are correctly

calculated and that payments are made to only deserving employees. In the view of mill champ

(1996) the following measures are to be adopted in achieving the above objectives.

The payroll should be checked by the independent personnel. All work on the preparation and

the checking of payroll is initiated.

The payroll should be prepared by the personnel unconnected with wages duties.

There should be separate records kept for each employee. The records contain such matters as

date of engagement, age, skills department and specimen signature.

Regular independent comparisons between personal records and wage records

Regular independent comparison of payroll at different dates

Security of Assets:

Assets of an organisation should be kept in proper custody and any misclassification either by

error or intent should be corrected. The internal auditor should ensure that proper stock or asset

register are kept in accordance with the regulation 295 of the financial Accounting Regulation

(LI 1234).

Auditor and Internal control

Effectiveness of the internal control system of an organisation is influenced considerably by an

audit conducted by the auditor. COSO Report (1992) emphasized that auditor or accountant

being familiar with the internal controls as they relate to the audit of the financial statement is an

obvious choice in examining the appropriateness of the design of the internal control system or

the operating effectiveness of the internal control system.

The auditor has to evaluate and set the internal control so as to determine the degrees of reliance

that may be placed on the information in the accounting records. Where he obtained reasonable

assurance by means of compliance test and procedure that internal control are effective in

ensuring completeness and accuracy of accounting records, and the validity of entries therein, he

28

may limit the extent of its substantive test and procedure. If on the other hand the test disclosed

that controls are virtually nonexistent or they are not operated properly, the auditor should

ascertain reasonable assurance for such expectations.

In determine the success, the auditor will assess whether it raises the presumption of possible

existence of fraud or errors in accounting records. If the explanations he receives suggest that the

exception is only an isolated departure, then he must confirm the validity of explanation for

example, carrying on further test. The control can be relied on if there is a confirmation as a

result of further test that the internal control tested was being improperly operated. Under this

circumstance the auditor will increase the level of his substantive test unless there are alternative

controls.

Despite the numerous contribution of internal control towards the achievement of operational

efficiency, they have their own limitation. Paragraph four (4) of National Standard Auditing

states that “internal control can only provide reasonable assurance that management objectives

are not reached because of inherent limitations”.

Therefore no internal control system can by itself guarantee efficient administration and

reliability of records nor can it be proved against fraudulent collusion especially internal control

which depends on separation of duties can be avoided by collusion of those involved.

Authorisation of control can be abused by person or official in whom authority is rested. Pressure

exerted from both within and outside the organisation may also influence the competence and

integrity of personnel operating controls.

The potential of human error in operation of internal control due to carelessness, fatigue,

distraction, misunderstanding, errors of judgement are among numerous factors likely to

undermine effective operation of internal control.

Conclusion on literature Review

29

As it has been clearly stated by writers, concerning the definition of internal auditing and internal

control, one could clearly see that both internal audit and internal control system work together

as no auditor can help to achieve the objective of any organisation without implementation of

proper internal control measures. The objective of an audit is to enable the auditor to express

opinion whether the financial statements are prepared in all material respect in accordance with

an identified financial recording frameworks. This objective could be realised based on

formulating and implementation of effective internal control systems that ensure wastages, fraud

and errors are minimized as well as to establish responsibility for various actions. According to

Anderson and Bragg, the existence of qualified internal audit department or unit, certainly is the

medium to a large organisation is an important element of the system of internal control.

It is obvious that one cannot rule out the appreciable contribution that have made by these writers

on the importance of internal auditors in helping to implement a proper internal control system

which enable organisation to achieve its vision and missions. From the literature review, it is

clear that management and employees of public service organisation do not attach any

seriousness to recommendation made by internal auditors which has led to failure of many

organisations to attain value for money. Besides this, many public service organisations have

suffered immense financial losses through misappropriation, embezzlement, falsification of

document and the like whereas these organisations have internal audit unit. It is therefore against

this background that this study is conducted in Ghana Education Service in Kumasi to assess

their internal audit practices and policies regarding internal control system.

30

CHAPTER THREE

METHOLOGY

This chapter deals with the method used for the study. These are research design, population,

sample and sampling procedures, data collection techniques, research instrument and data

analysis.

Research Design

The review of literature and the analysis of the study on the impact of internal audit on public

service organization can be well assessed using descriptive survey.

Similar studies made the great use of research’s designed questionnaires for data collection. The

following data collection techniques were adopted; questionnaires, interview and a lot of

interactions were used to collect information from people who matter in the study. The relevance

of the descriptive survey to this study is that, it describes how internal auditor’s

recommendations are adhered to at management level and all relevant department of the

organization.

It is the researcher’s intention to do the survey of the study based on the objectives of the

research in order to get various responses that will help to draw a comprehensive analysis to the

study. In this survey it is the researcher’s aim to conduct an examination into the implementation

of the internal control recommendation made by internal auditors and its relation to the

administrative efficiency in public service organizations and for that matter Ghana Education

Service in Ashanti.

In order to obtain accurate information for our research, five areas were selected for the study

from the various areas of the public service organisations. The objective of the researcher is to

assess the internal audit practices that are carried out in these selected areas of public service

organisation in Ashanti region. The five areas are finance section, procurement department,

library, stores and accounts departments. The aim of selecting these areas is to assess whether or

not the public perception of fraudulent activities carry on by people in these areas are true or

false.

31

Population

The term population refers to a complete set of individuals (subject), objects or events having

common observable characteristics in which the researcher is interested in studying. It can also

be defined as the total collection of elements about which we want to make references.

The interests of our study concern the management, staff of internal audit units, and basic head

teachers of Ghana Education Service in Kumasi. The population for the study is one hundred

people including management, staff of internal audit and basic school head teachers. These were

officials who were directly related to policy formulation, implementation, monitoring, and

evaluation of internal control measures as well as record keeping in Ghana Education service in

Kumasi. Management constitutes 20% of the respondents, staff of internal audit 40% and basic

school head teachers 40%.

Sample and Sampling Procedures

The sample population is exactly 100% of the study. According to Cohen and Manion (1995), a

sample is a collection of information from a smaller group or subset of the population in such a

way that knowledge gain is representative of total population under study.

A sample is thus a subset of the population and consists of individuals, objects or events that

form the population. The two methods of sampling are probability sampling and non –probability

sampling. The two basic types of sample selection procedures are random sampling and non-

random sampling.

Instead of involving the entire population in the study, the researchers chose a representative

sample that exhibits characteristics typically of those possessed by the target population and

generalize the findings to the larger population. In order to guarantee a representative sample, the

researchers ensured that a random sample is chosen for the study. This method ensures that every

possible element of the population has an equal chance of being selected for the study.

32

Research Instrument

In collecting the data for the study, the researchers made use of questionnaire and interview. A

Questionnaire is a written instrument that contains a series of questions or statement called items,

which attempt to collect information on a particular topic. (Agyedu, G.O.Donkor, F and Obeng,

S. B. Ansah 2007).

According to Agyedu, G.O. Donkor, F and Obeng, S. B. Ansah 2007, interview is face to face

meeting between a questioner and respondents, or an oral representation of an opinion or attitude

scale. It is often used in collecting data for descriptive studies, action research, evaluation and

sometime co relational studies. The benefit of interview is that the response rate is high and

issues can be clarified.

The major item types for interview schedule included dichotomous response and multiple

choices.

Data Collection Procedure

The researchers administered hundred questionnaires and handed over personally to an

assembled group or persons. This method afforded the researchers the opportunity of

establishing a rapport, to explain the purpose of the study and to explain the meaning of items

that were not clear.

Out of hundred questionnaires distributed, 75% were received within two weeks. The rest of

25% were received after two weeks.

Interview was also adopted alongside the questionnaire guide to collect data from the

respondents for further clarification. The questionnaires consist of open and closed ended to

enable the respondent to air their view on the topic. Group discussions held by ten workers of

each service organisation provided another platform to ascertain information to facilitate the

research work.

33

Business journal, library material such as text books and other business magazines, articles and

internet assist us to obtain secondary data. Descriptive presentation data help us to have a clear

analysis of available information.

Data Analysis

The study design adopts the single method and therefore quantitative data collection

techniques. The deductive- approach was applied in the data analysis. Under this method,

hypothesis generated from the study objectives were expressed in operational terms and

tested. Computer software such as Microsoft excel spread sheet was used to analyse the

data, table and chart generated to explain the quantitative data. Table and chart were used

to display the result of the study to ensure maximum clarity and objectivity. Furthermore,

analyses of descriptive information from the field group discussion were made to obtain

further confirmation of the findings made.

34

CHAPTER FOUR

THE RESULT OF THE STUDY

Introduction

This chapter focuses attentions on the analysis and the results of data received from the

interviews, questionnaires and group discussions. The details included identification and

grouping of questionnaire items, finding the aggregate and striking the percentages from the

respondents to give answers to research questions raised in previous chapter.

Background Analysis of Data

One hundred questionnaires were distributed to some selected schools in Kumasi and were all

returned. The questionnaires were designed into three phases. The phase one was for internal

audit unit to respond since they were the main focus of this research, the phase two was designed

to management while the last phase was for head teachers of selected schools. Seventy four of

the respondents were males and twenty six were females. Nineteen (19%) of the entire

respondents were above the age of fifty (50], forty nine (49%] of them were between the age of

thirty and fifty and thirty two (32) were below the thirty years. Sixty nine (69) of responded were

married whiles the remaining thirty (31%) were single.

Data Analysis

Editing was made to the data obtained to assess the consistency of the responses and to ensure

that all the questionnaire items had been responded to. Grouping and quantification of responses

to questionnaires, interviews and group discussion were made. Documentary source and statics

techniques were also used to decide whether any variations to the responses were significant or

merely due to random selections. Below are the details of the results

35

Auditors are generally appointed by shareholders in general meeting by ordinary resolutions. It is

also permissible for the directors to appoint auditors for a company and fill any vacancy in the

office of the auditor. The registrar of companies can also appoint auditors of the company if the

company shall have not had auditors for a continuous period of three months. In most of public

service organization is the government who appoint these auditors.

The research question put up to find out the views on qualification and expertise of internal

auditors in helping to improve the activities of public service organisation.

“Do the auditors have the required qualification, expertise and resources that facilitate their

work?”

Through the findings disclosed by this study and examining the qualification of an auditor, it was

realised that for one to be appointed as an auditor the person should be a member of Institute of

Chartered Accountants and must not be disqualified from acting as auditor by any legislative

instruments issued by the Registrar

People perception as to internal auditors possess right qualification to achieves their objectives

seems to be varies.

36

From the diagram in Fig 1.1above the respondents who said degree are minimum were 38%,

professional 27%, HND constitute 31% and others who do not fall within these criteria were 4%.

Even though the respondents gave different answers, they accepted the fact that the performance

of the unit could have been great if they were all holding professional certificate as their

knowledge on the job would have enhanced very well. The respondents therefore advised the

appointment authority to ensure that the head of audit unit in national and region is given to the

person who has acquired professional knowledge in the field.

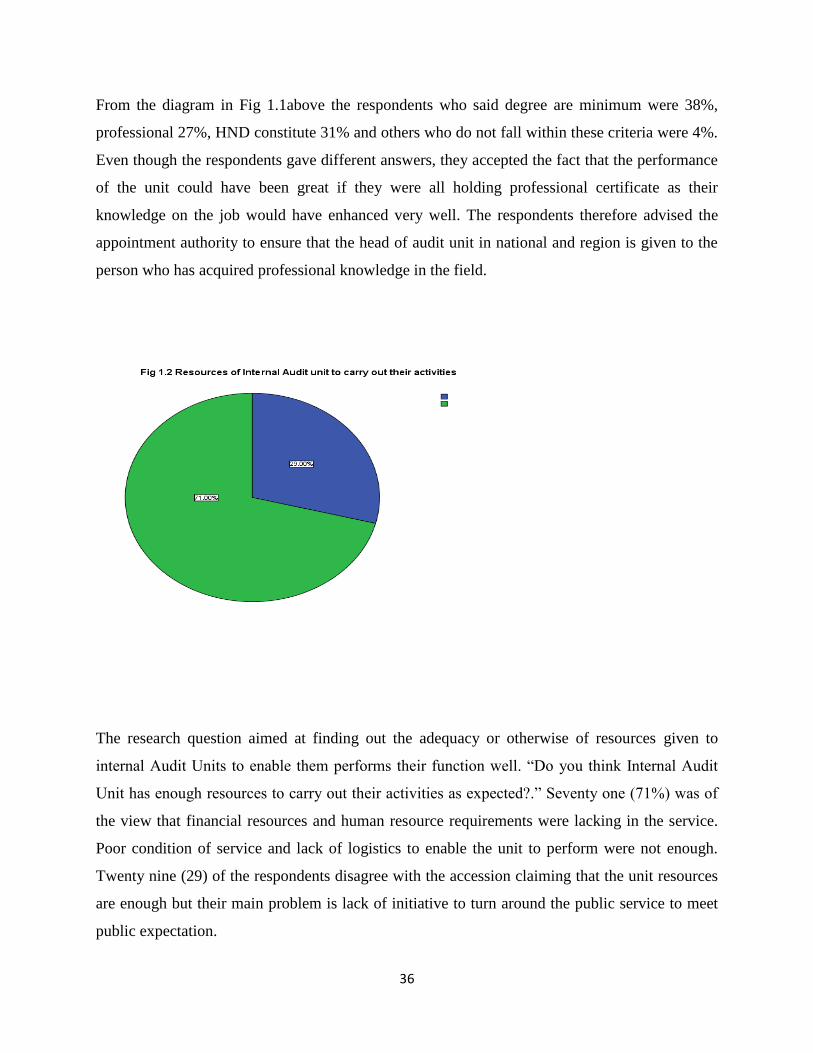

The research question aimed at finding out the adequacy or otherwise of resources given to

internal Audit Units to enable them performs their function well. “Do you think Internal Audit

Unit has enough resources to carry out their activities as expected?.” Seventy one (71%) was of

the view that financial resources and human resource requirements were lacking in the service.

Poor condition of service and lack of logistics to enable the unit to perform were not enough.

Twenty nine (29) of the respondents disagree with the accession claiming that the unit resources

are enough but their main problem is lack of initiative to turn around the public service to meet

public expectation.

37

Auditor’s reports disclose to managements and shareholders to assess whether the financial

statement give a true and fair view or presented fairly, in all material respects in accordance with

the applicable financial reporting frameworks. The report evaluate the accounting policies to

verify whether they are reliable, understandable and relevant and how consistent the policies are

been used to achieve the objective of the organisations. The report convey to managements and

government who happen to be a major shareholder in public service organisations to assess

overall presentation, structure and content of the financial statements to identify strength and

weakness of the various departments of organisation. When the reports are presented, it is the

duty of managements and government to take necessary actions to rectify all material

misstatements and other inefficiencies which the auditors pointed out to ensure smooth running

of the organisations. We want to assess how managements and government give priority to

reports issued by auditors.

Do the recommendation and advisory service provided by internal auditors accepted and

implanted by management and government?

From diagram, most of the respondents respond that recommendation from audit report are

implement as soon as practicable constitute 60% and 40% did agree indicating that management

38

do not comply with the laid procedures and sanctions which enhance the growth of the

organisations because they see auditors as hindrance to their progress.

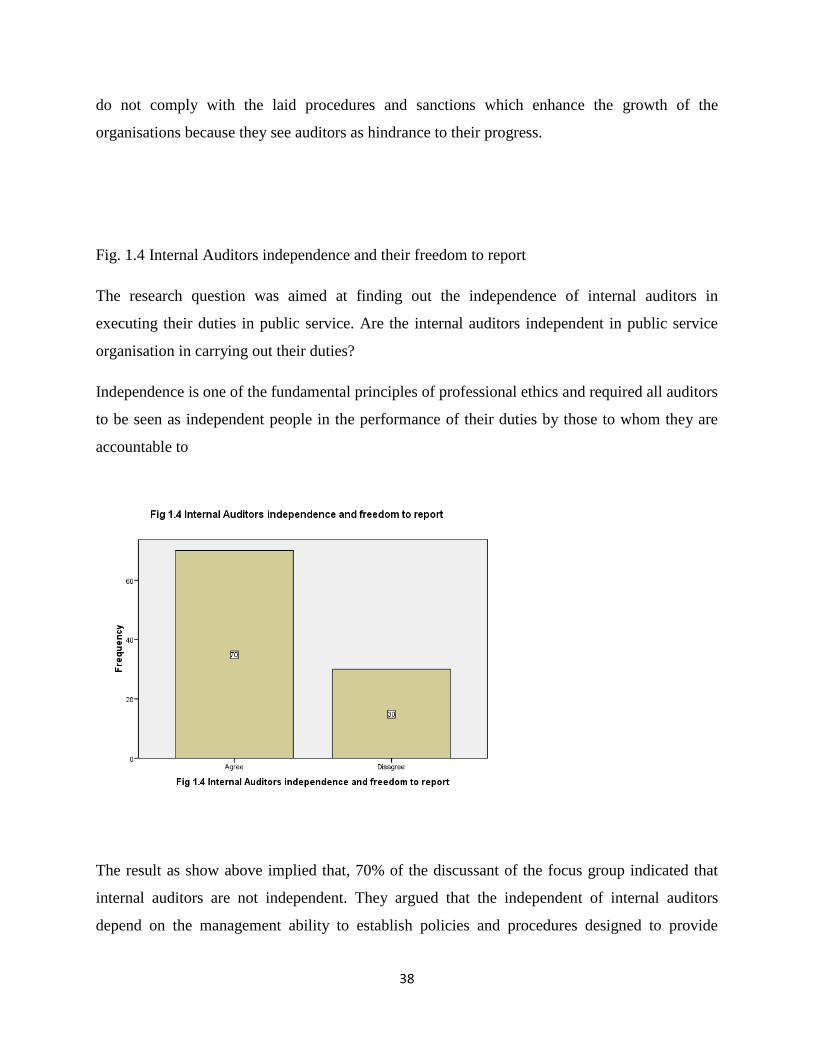

Fig. 1.4 Internal Auditors independence and their freedom to report

The research question was aimed at finding out the independence of internal auditors in

executing their duties in public service. Are the internal auditors independent in public service

organisation in carrying out their duties?

Independence is one of the fundamental principles of professional ethics and required all auditors

to be seen as independent people in the performance of their duties by those to whom they are

accountable to

The result as show above implied that, 70% of the discussant of the focus group indicated that

internal auditors are not independent. They argued that the independent of internal auditors

depend on the management ability to establish policies and procedures designed to provide

39

reasonable assurance that the firm and its personnel are subject to independence requirements .It

is the duty of managements to identify and evaluate circumstances and the relationship that

create threat to independence, and to take appropriate action to eliminate those threats or reduce

them to barest minimum level by applying adequate safeguards. But in most organisations

management do ignore these policies because they see the auditors as a rather threat to their

personal advancement and for that reasonable adequate support and resources are not given to

them. They doubt the independent of internal auditors in the area of finance, decision making

and expressing of their independent opinion as they always influence by managements and

government to hide certain vital information’s which when exposed will affect their reputation.

The result gathered from questionnaire majority of them conceded the fact that, lack of financial

independence and threat from management was a major operational bottleneck of auditors to put

measures in place to promote good governance in public service whiles 30% disagree

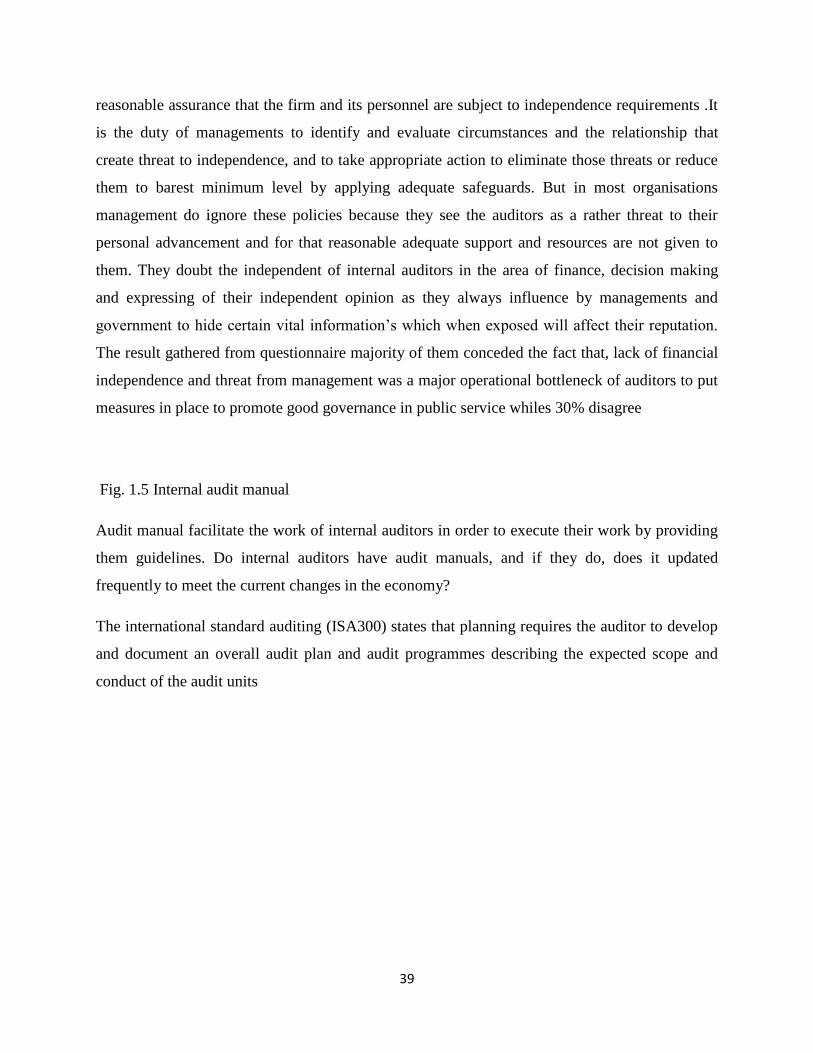

Fig. 1.5 Internal audit manual

Audit manual facilitate the work of internal auditors in order to execute their work by providing

them guidelines. Do internal auditors have audit manuals, and if they do, does it updated

frequently to meet the current changes in the economy?

The international standard auditing (ISA300) states that planning requires the auditor to develop

and document an overall audit plan and audit programmes describing the expected scope and

conduct of the audit units

40

From the data above, a small percentage (18%) of the respondents claimed that internal auditors

do not have manual but 82 debunk the claim and said that audit manuals are always available at

the office of the unit and help facilitate their in order achieve the required result. They also

argued that these manuals are frequently updated to meet current economy situations. The

revisions of these manuals are normally done in annually to prepare them into subsequent year.

41

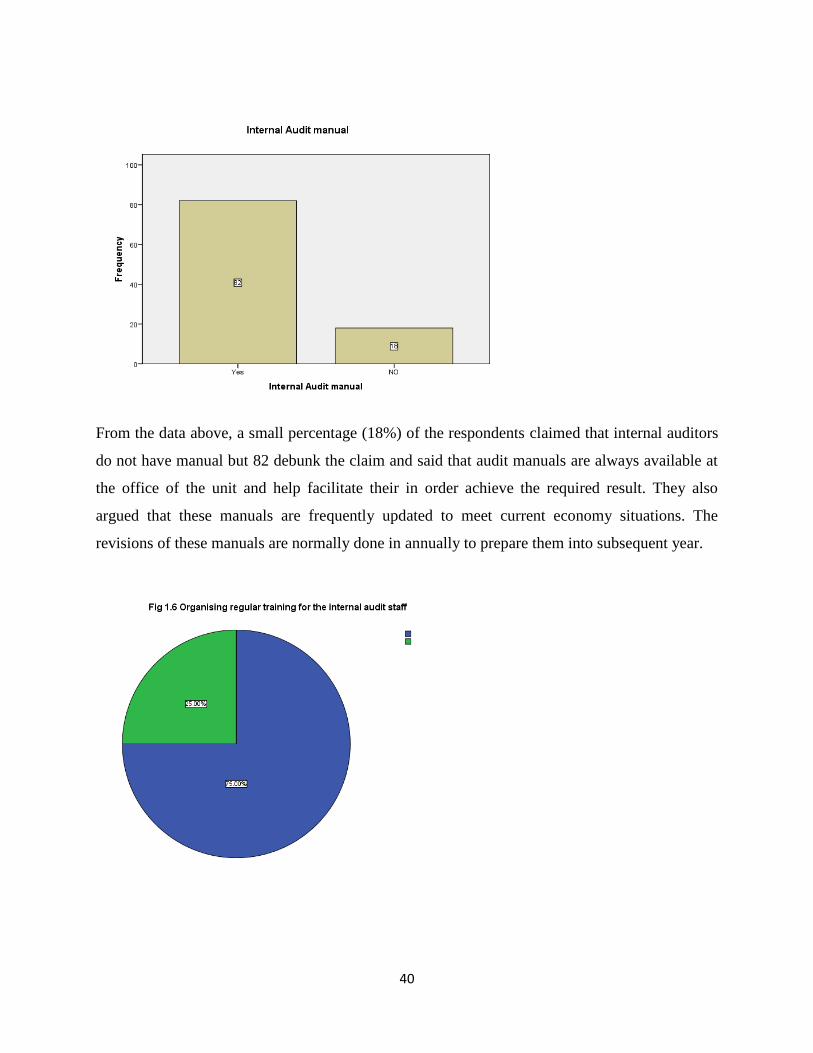

The respondents given show a greater concern of organisation of regular training for internal

audit staff.

From the above pie chart it can be recognized that seventy per cent (75%) of the respondents

answered yes indicating that the internal audit units normally organise training to update their

knowledge in the professional work. While about twenty five (25%) of the respondents answered

no, attributing that the internal audit unit seldom organised training which normally affect their

ability to detect fraud and irregularities within organisation.

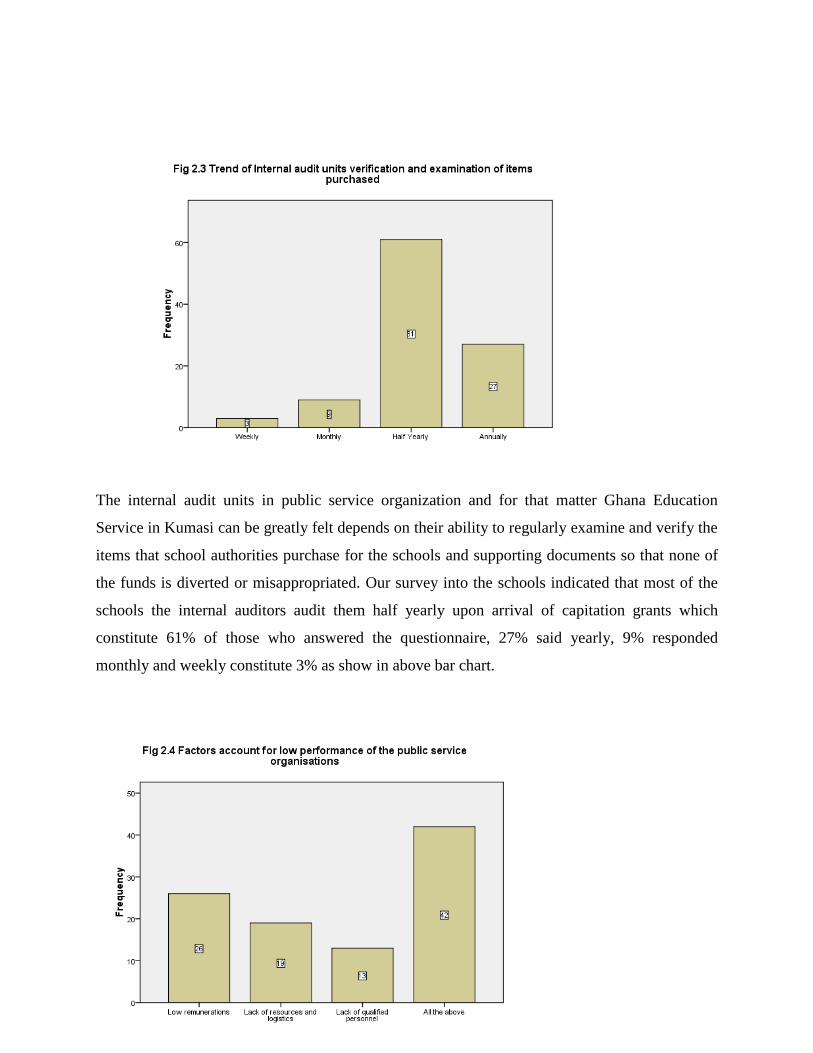

As to the trend of training they do organise in the year, the respondents attributed 8% as

monthly training, 26% of the respondents also gave their consent that regular training takes place

every month to the international audit units while overwhelming percentages of 34% argued that,

regular training organise for the internal audit units every half yearly while 16% also sees that

their audit unit only upgrade their knowledge yearly and those who did answered them were

16%.

42

Accountability required officials to be transparent, responsive and accountable for their actions.

Management is responsible for the prevention and detection of fraud and errors through the

implementation of proper policies and procedures to ensure adequate accounting and internal

control system of the public service organization. Management should also protect the

organization’s equipment, document and other resources that could be wrongfully used, damage

or stolen. Management can protect these resources by limiting access to authorized individual

only. Access can limited by various means such as locks, passwords, electronics firewalls and

encryption.

Employees are also responsible to ensure that the policies and procedures put in place by

management are adequately adhering to ensure that all the department of the organisation work

effectively and efficiently. The question that one has to ask is does managements and employees

of public service are ensuring that public resources are not wasted and any offender of the rules

are been asked to account for his or her action which result in fraud and embezzlement.

From the selected public service organization interviewed and the discussants of focus group all

responded that officials of the service should be made to account for their stewardship for using

public resources and failure to give proper account the culprit must be dealt with. They accepted

the fact that people misused the state resources with impunity and if such people are compelled

to render account on how the resources given them were used, they will realised the need to

safeguard the properties that belong to the state.

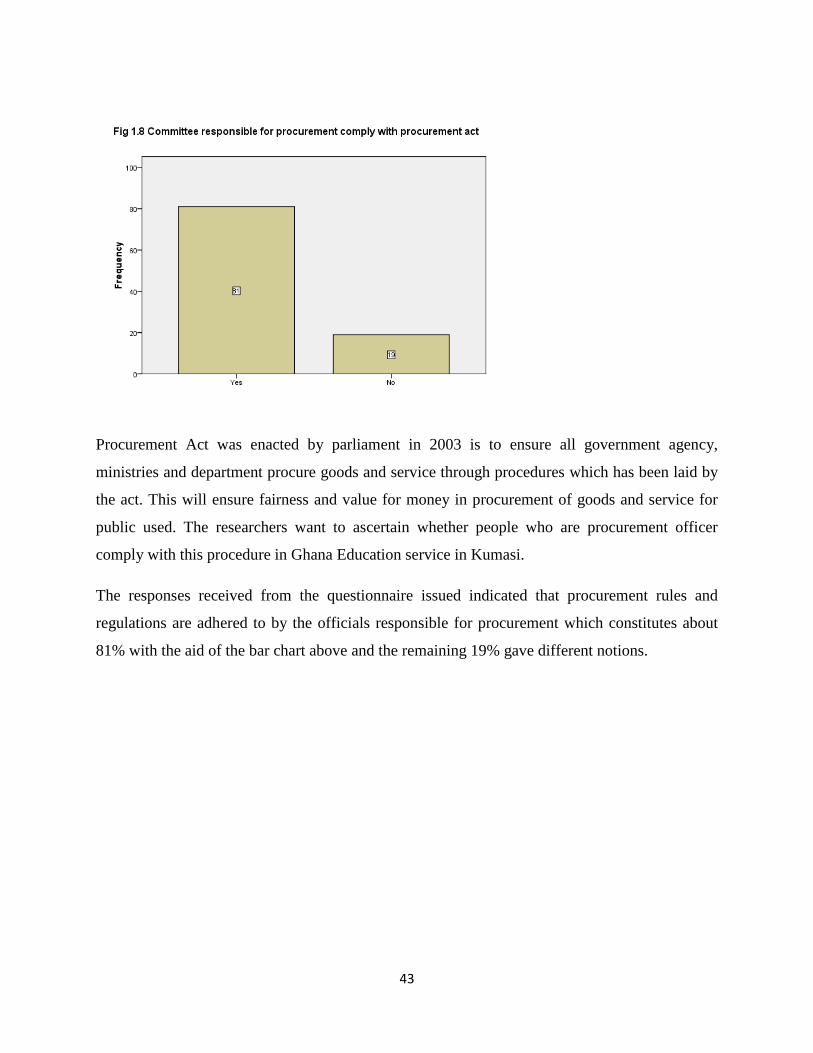

43

Procurement Act was enacted by parliament in 2003 is to ensure all government agency,

ministries and department procure goods and service through procedures which has been laid by

the act. This will ensure fairness and value for money in procurement of goods and service for

public used. The researchers want to ascertain whether people who are procurement officer

comply with this procedure in Ghana Education service in Kumasi.

The responses received from the questionnaire issued indicated that procurement rules and

regulations are adhered to by the officials responsible for procurement which constitutes about

81% with the aid of the bar chart above and the remaining 19% gave different notions.

44

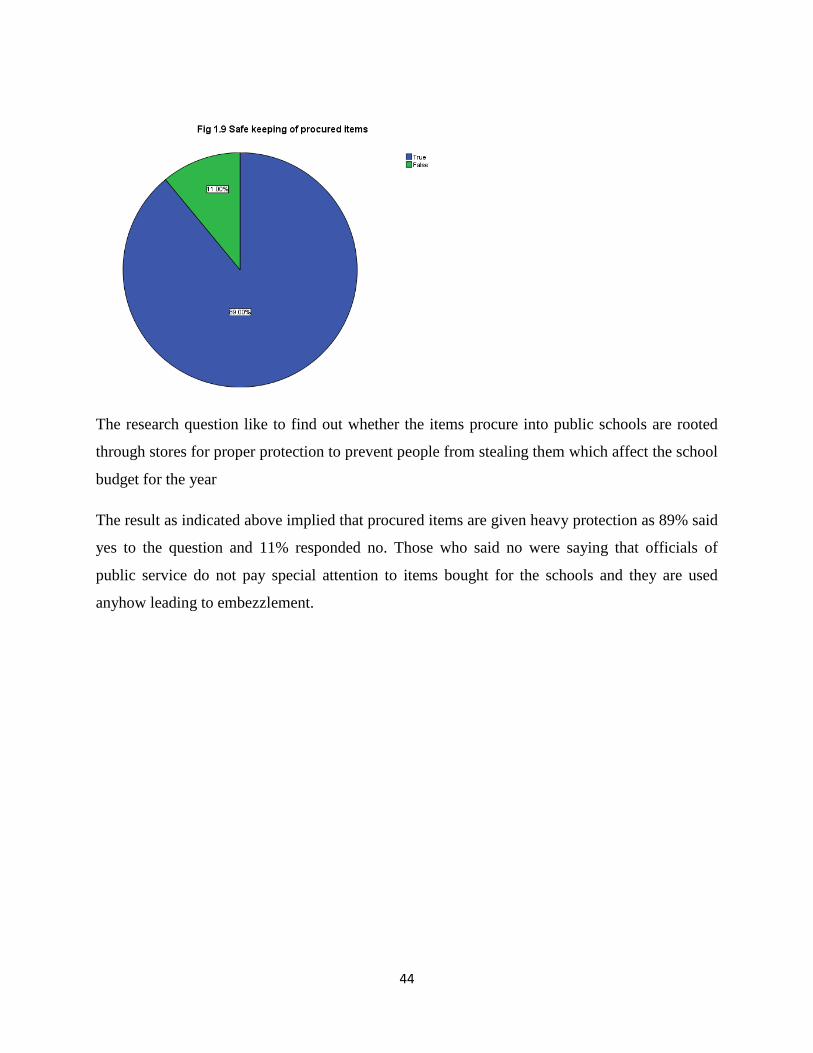

The research question like to find out whether the items procure into public schools are rooted

through stores for proper protection to prevent people from stealing them which affect the school

budget for the year

The result as indicated above implied that procured items are given heavy protection as 89% said

yes to the question and 11% responded no. Those who said no were saying that officials of

public service do not pay special attention to items bought for the schools and they are used

anyhow leading to embezzlement.

45