THE EFFECTS OF ACCOUNTING CONCEPTS ON THE FINANCIAL ...

59

THE EFFECTS OF ACCOUNTING CONCEPTS ON THE FINANCIAL STATEMENTS (A CRITIQUE) A Case Study of CPAR Uganda and other organizations like; UNICEF, UNHCR, UN, UNAIDS By: Adupa Richard BBA/6044/41/DU Supervisor: Dr. Sunday Nicholas Olwor A Research Report Submitted in partial fulfillment of a Bachelor Degree in Business ·Administration and Management of Kampala International University July, 2006

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of THE EFFECTS OF ACCOUNTING CONCEPTS ON THE FINANCIAL ...

THE EFFECTS OF ACCOUNTING CONCEPTS

ON THE

FINANCIAL STATEMENTS (A CRITIQUE)

A Case Study of CPAR Uganda and other organizations

like; UNICEF, UNHCR, UN, UNAIDS

By:

Adupa Richard

BBA/6044/41/DU

Supervisor: Dr. Sunday Nicholas Olwor

A Research Report Submitted in partial fulfillment

of

a Bachelor Degree in Business ·Administration and

Management

of

Kampala International University

July, 2006

BBA (Accounting)

DECLARATION

I Adupa Richard declare that this piece of work is original and has not

been submitted to any institution or university for any award

whatsoever.

Signed \., (Ad pa Richard

Date

Signed u (Dr. Sunday Nicho as Olwor)

Date

BBA (Accounting)

EBA (Accounting)

APPROVAL

The following research by Mr. Adu pa Richard was carried out under the

title, 'The Effects of Accounting Concepts on the Financial Statements,'

A case study of CPAR Uganda has been under my supervision until it

was ready for submission at Kampala international university with my

approval.

Signed

(Dr. Sunday Nicholas Olwor)

Date

11 EBA (Accounting)

BBA (Accounting)

DEDICATION

This piece of work is dedicated to my belated dad whom I miss so

much, my mum, Imat Coney who acted both as a father and mother

and tirelessly endeavored to bring me up, educated me and groomed

me to be a polite boy, not forgetting my beloved brothers and sisters;

the source of my consolation.

I also dedicate this work to Mr. Eliot Thomas Masters and Ms. Carmen

Jaquez. I respect you so much because you are my foundation of

exposure to the world, a source of hard work and tasks management.

iii BBA (Accounting)

BBA (Accounting)

ABSTRACT

The study sought to establish and understand the effects of accounting

concepts on the financial statements. It mainly looked at CPAR

Uganda, a non-profit making organization.

The researcher utilized both quantitative and qualitative methods for

data analysis. Respondents included Financial Managers, Accounts

Assistants and other employees of the organization.

The findings of the research revealed that Accounting Concepts are

used by organizations (CPAR Uganda) in the preparation of financial

statements and they are supplemented by accounting standards

(IAS)/financial reporting standards. The Accounting Bodies have

played great roles in the effectiveness of financial statements by

ensuring use of accounting concepts, the legal framework and financial

reporting standards. This is revealed by over 75% of the respondents

who strongly confirmed the above statement. However, there are also

some challenges faced in the process of such efforts by accounting

bodies.

The study concludes that there is continuous improvement on the use

of accounting concepts and financial reporting standards. Though there

is still need for increased concerted efforts from the accounting bodies

and all the users of accounting information to help put hands together

so as to enable effective financial reporting, and produce accurate

reports for better decision making.

V BBA (Accounting)

BBA (Accounting)

TABLE OF CONTENTS

Contents Page DECLARATION ............................................................................................................ i APPROVAL ................................................................................................................... ii DEDICATION ............................................................................................................. iii ACKNOWLEDGEMENTS .......................................................................................... iv ABSTRACT ................................................................................................................... v TABLE OF CONTENTS ............................................................................................ vi LIST OF TABLES ..................................................................................................... viii LIST OF FIGURES .................................................................................................... ix LIST OF SELECTED ABBREVIATIONS ............................................................... x OPERATIONAL DEFINITION OF TERMS ........................................................... xi CHAPTER ONE ......................................................................... 1 1.0 Introduction ..................................................................................................... 1 1.1 Background to the study ............................................................................ 3 1.2 Statement of the Problem .......................................................................... 5 1.3 Purpose of the study .................................................................................... 6 1.4 Research questions ....................................................................................... 6 1.5 General Objectives ........................................................................................ 6 1.6 Specific Objectives ........................................................................................ 6 1. 7 Significance /justification of the study ................................................. 7 1.8 Theoretical/conceptual framework of the study ............................... 8 1.9 The scope of the study ................................................................................ 8 1.10 Hypotheses ...................................................................................................... 9

CHAPTER TWO ...................................................................... 10 2.0 Review of related Literature .................................................................... 10 CHAPTER THREE ................................................................... 24 METHODOLOGY ....................................................................................................... 24 3.0 Introduction ................................................................................................... 24 3.1 Research Design .......................................................................................... 24 3.2 Research Procedures .................................................................................. 25 3.3 Sample size ................................................................................................... 25 3.4 Sources of Data ........................................................................................... 25

3.4.1 Primarydata ......................................................................................... 25 3.4.2 Secondary Data ................................................................................... 26

3.5 Methods and Tools of Data Collection ................................................. 26 3.5.1 Questionnaire ....................................................................................... 26 3.5.2 Interview ................................................................................................ 26

3.6 Data Analysis ................................................................................................ 27 3. 7 Limitations/ Anticipated Problems ........................................................ 27

CHAPTER FOUR ..................................................................... 29 DATA PRESENTATION AND ANALYSIS OF FINDINGS .............................. 29 4.0 Introduction ................................................................................................... 29

VI BBA (Accounting)

EBA (Accounting)

4.1 Categorization of respondents ............................................................... 29 4.2 Response on whether Accounting concepts are followed ............ 30 4.3 Response on whether a change accounting concepts could lead

to accurate financial statements .............................................................. 31 4.4 Response on whether various organizations use the same

accounting concepts ...................................................................................... 33 4.5 Response on whether Accounting Standards (IASs) and Financial

Reporting Standards (FRSs) are used to supplement accounting concepts ............................................................................................................. 34

4.6 Problems faced by CPAR Uganda while using the accounting concepts ............................................................................................................. 35

4.7 Solution to Problems faced by CPAR Uganda while using Accounting Concepts ..................................................................................... 36

CHAPTER FIVE ...................................................................... 37 5.0 Introduction ................................................................................................... 37 5.1 Summary of the Findings ......................................................................... 37 5.2 Recommendation ......................................................................................... 39 5.3 Conclusions .................................................................................................... 39 REFERENCES ............................................................................................................ 41 APPENDICES ................................................................................................................ ! I Introductory Letter ........................................................................................ 1 II Study Questionnaire .................................................................................... II III Map of Uganda .............................................................................................. V IV Map of Kampala ........................................................................................... VI

Vil BBA (Accounting)

BBA (Accounting)

Table 1

Table 2

LIST OF TABLES

List of Core Standards and Each Standard's Effective Date

showing categories of respondents

Table 3 showing the response on whether the accounting concepts

are followed

Table 4 a change in accounting concepts could lead to accurate

financial statements

Table 5

concepts

whether various organizations use the same accounting

Table 6 Showing whether Accounting Standards are used to supplement accounting concepts

vm BBA (Accounting)

BBA {Accounting)

LIST OF FIGURES

Figure 1 showing the response on whether accounting concepts are

followed.

Figure 2 showing whether a change in accounting concepts could lead

to accurate financial statements.

Figure 3 showing whether various organizations use the same

accounting concepts.

Figure 4 Showing whether Accounting Standards are used to

supplement accounting concepts.

IX BBA {Accounting)

BBA (Accounting)

AICPA

AIDS

ASB

ASC

Co.

CPAR

FASB

FRSs

FRSSE

FSB

GAAP

HIV

IASs

IASB

IFRSs

Ltd

No.

SSAPs

UITFs

UK

UN

UNAIDS

UNHCR

UNICEF

LIST OF SELECTED ABBREVIATIONS

According to the American Institute of Certified Public

Accountants

Acquired Immune Deficiency Syndrome

Accounting Standards Board

Accounting Standards Committee

Company

Canadian Physicians for Aid and Relief

Financial Accounting Standards Board

Financial Reporting Standards

Financial Reporting Standard for Smaller Entities

Financial Standards Board

Generally Accepted Accounting Principles

Human Immune Virus

International Accounting Standards

International Accounting Standards Board

International Financial Reporting Standards

Limited

Number

Statements of Standard Accounting Practice

Urgent Issue Task Force Abstracts

United Kingdom

United Nations

United Nations program on HIV/AIDS

United Nations High Commissioner for Refugees

United Nations International Children's Emergency Fund

X BBA (Accounting)

BBA {Accounting)

OPERATIONAL DEFINITION OF TERMS

Concepts

These are used interchangeably with conventions/principles to mean

generalized ideas/rules derived from observations. The accounting

concepts/conventions are the most important ideas in accounting

theory.

Financial Accounting

This refers to the identification, recording, analyzing, summarizing and

interpreting economic transactions of a business to the users of

accounting information such as the shareholders, creditors, managers,

employees, government agent and the general public.

Manager

This is a person who is responsible for the general activities of the

organization. He/she is a person that takes the general operational

decisions of the organization.

Financial Statement

It is the summary form of report on the economic activities of an

organization/business.

Accounting Standards

These are rules/regulations that are used to govern the operations of

the accountants. They act as a guide to the accountants.

XI BBA (Accounting)

BBA (Accounting)

CHAPTER ONE 1.0 Introduction

Concepts are generalized ideas derived from observations. The

accounting concepts/conventions are the most important ideas in

accounting theory. They are the ground rules and basic

assumptions that govern the preparation and presentation of

financial accounts. It is, however, the responsibility of the

enforcing or overseeing institutions to spell out in the accounting

standards the fundamental concepts/principles to compel

practicing accountants under their jurisdiction to observe.

The basic objective of accounting is to provide information about

an enterprise/organization; information that helps users to make

economic decisions. Whereas, accounting is the language of

business and through the medium of this language, the business

enterprise communicates information about their profitability and

financial position to people interested in this information. To

make the language convey the same meaning to all interested

people, it is of vital importance that the information contained in

the medium be highly reliable and clearly understood. The

owners, managers, creditors, employees, government

administrators, all rely upon the financial statements and other

accounting reports in making their decisions which shape the

economy of a country.

In order that the financial statements may convey the same

meaning to all the users and that they understand in the same

way, it is very important that a body of principles be well-defined

to guide the accountants in preparing the financial statements

1 BBA (Accounting)

BEA (Accounting)

with the characteristics of reliability, understandability and

comparability.

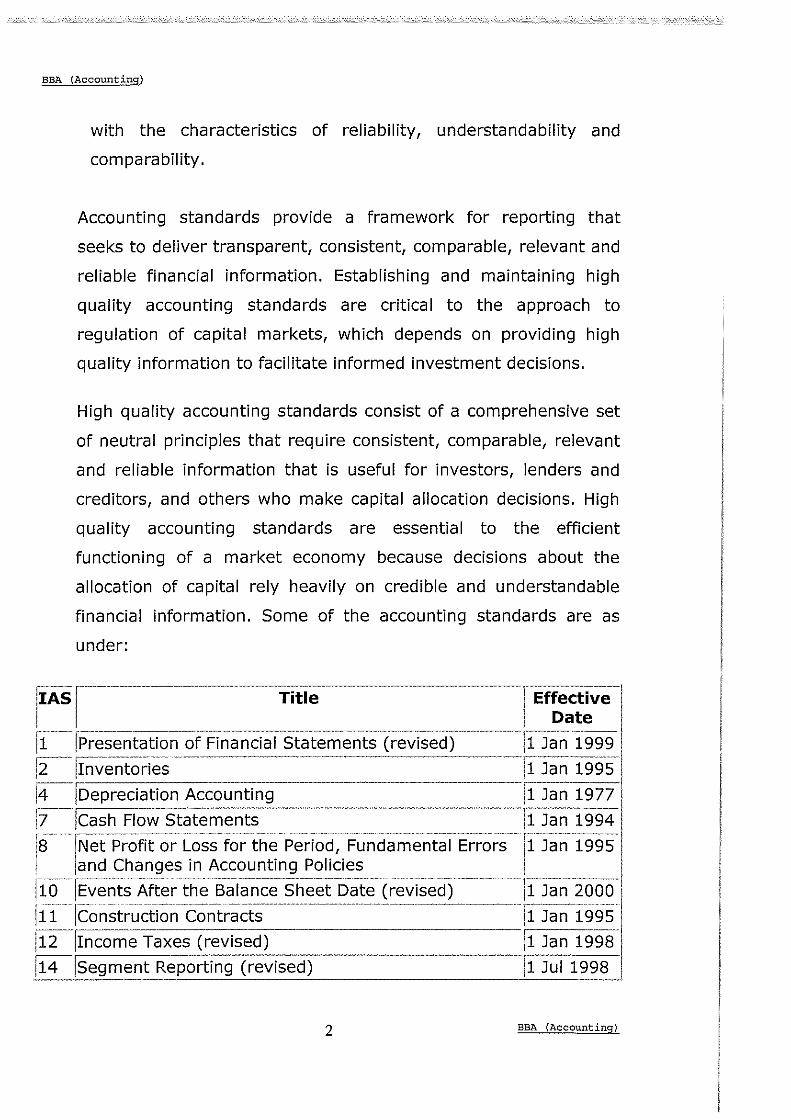

Accounting standards provide a framework for reporting that

seeks to deliver transparent, consistent, comparable, relevant and

reliable financial information. Establishing and maintaining high

quality accounting standards are critical to the approach to

regulation of capital markets, which depends on providing high

quality information to facilitate informed investment decisions.

High quality accounting standards consist of a comprehensive set

of neutral principles that require consistent, comparable, relevant

and reliable information that is useful for investors, lenders and

creditors, and others who make capital allocation decisions. High

quality accounting standards are essential to the efficient

functioning of a market economy because decisions about the

allocation of capital rely heavily on credible and understandable

financial information. Some of the accounting standards are as

under:

r-AS1 Title Effective Date

1 [Presentation of Financial Statements (revised) !1 Jan 1999

~· lrnventories !1 Jan 1995 ' !Depreciation Accounting 11 Jan 1977 14

17 leash Flow Statements 11 Jan 1994

rs !Net Profit or Loss.for the-Pe-rioci;i=-undamental Errors--· ·--

1 Jan 1995

' 1and Changes in Accounting Policies

[10 JEvents After the-Balance SheetD-ate-(revised) J1 Jan- 2000

[ii-Jconstructio_n_coni:racts - 11 Jan 1995

12 Jrncome Taxes (revised) 11 Jan 1998

114 [Segment Reporting (revised) 11 Jul 1998

2 EBA (Accounting)

BBA (Accounting)

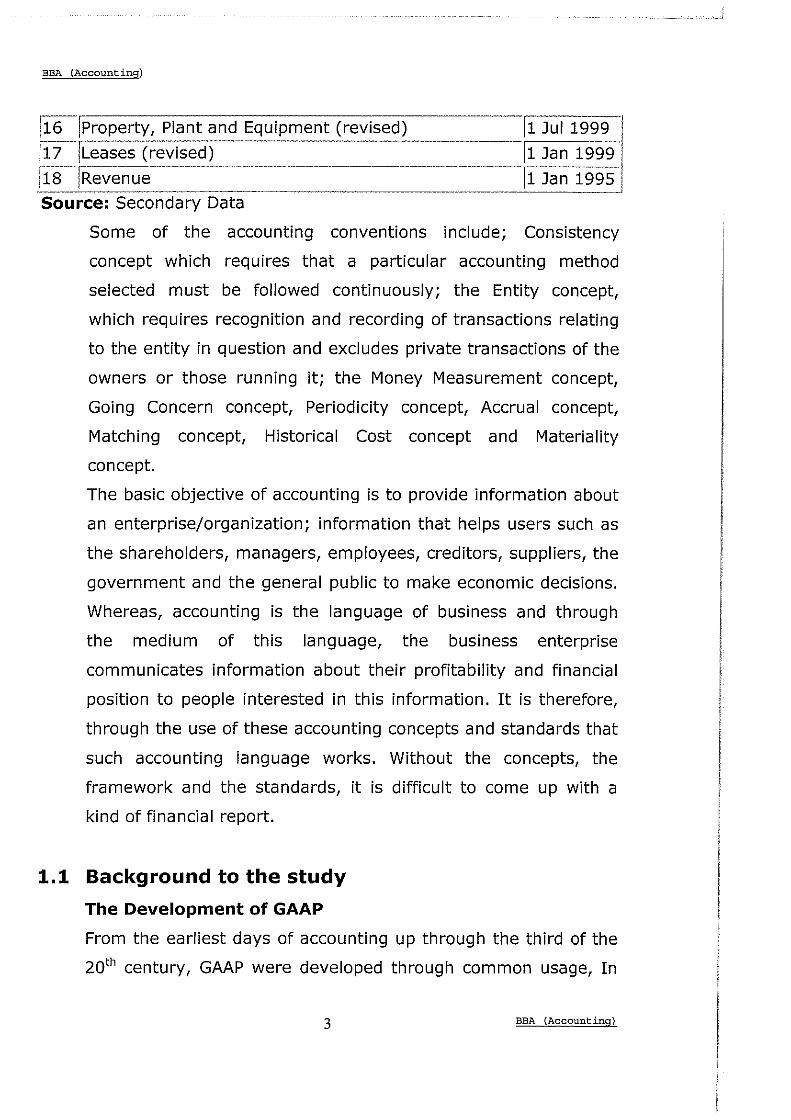

116 !Property, Plant and Equipment (revised)

/l?!Leases (revised)

18 !Revenue Source: Secondary Data

!1 Jul 1999

11 Jan 1999 ----11 Jan 1995

Some of the accounting conventions include; Consistency

concept which requires that a particular accounting method

selected must be followed continuously; the Entity concept,

which requires recognition and recording of transactions relating

to the entity in question and excludes private transactions of the

owners or those running it; the Money Measurement concept,

Going Concern concept, Periodicity concept, Accrual concept,

Matching concept, Historical Cost concept and Materiality

concept.

The basic objective of accounting is to provide information about

an enterprise/organization; information that helps users such as

the shareholders, managers, employees, creditors, suppliers, the

government and the general public to make economic decisions.

Whereas, accounting is the language of business and through

the medium of this language, the business enterprise

communicates information about their profitability and financial

position to people interested in this information. It is therefore,

through the use of these accounting concepts and standards that

such accounting language works. Without the concepts, the

framework and the standards, it is difficult to come up with a

kind of financial report.

1.1 Background to the study

The Development of GAAP

From the earliest days of accounting up through the third of the

20th century, GAAP were developed through common usage, In

3 BBA (Accounting)

BBA (Accounting)

other words, a practice was considered good if it was acceptable

to the most accountants. This history is still reflected in the

phrase, generally accepted. A principle became generally

accepted as accountants came to agree that it wound provide

useful and dependable information. However, as the accounting

profession grew and the world of business became more

complex, many people were not satisfied with the rate of

progress towards improved financial reporting

Many professional accountants, managers, and the government

wanted to bring more uniformity to the practice. Thus, in the

1930,s, they began to give authority for defining accepted

principles to small groups of experienced people. Since then,

there have been several authoritative bodies with different

structures and procedures. The power to prescribe acceptable

principles also has been greatly increased. Shortly, we describe

the present arrangement for establishing GAAP.

It is believed that accounting concepts/conventions are most

needed by accountants in preparation of financial statements. As

said by many scholars like Frank Wood and Allan Sangster

(2002), through practice, it has been confirmed that accounting

conventions are normally used when making accounting records,

and also, in practice especially when transacting business. There

are quite a number of concepts (conventions) handled in

different ways by different scholars (M.A Wahab). Some of these

accounting concepts are; the Money Measurement concept which

requires that all transactions must be quantified in monetary

terms; Going Concern concept, that business exist in the

4 BBA {Accounting)

BBA {Accounting)

foreseeable future; Periodicity concept that makes financial

reporting mandatory; Accrual concept, that income is recognized

as earned even though it might have not been received in cash

provided there is right to income; Matching concept, that all

expenses should be matched against revenue of that same

accounting period; Historical Cost concept, that assets and

liabilities should be recorded at historical costs of their

acquisitions, and Materiality concept, which requires that only

material items should be recorded and exclude immaterial items.

Some of these scholars keep criticizing the use of some

conventions/concepts; saying that some of them conflict with

one another, which makes them unreliable for the preparation of

financial statements and financial reports.

1.2 Statement of the Problem

The accounting bodies have always tried their best to see that

financial statements/financial reports are presented in a way that

it is easy to rely upon, comparable and understood by various

users; the managers, creditors, shareholders among others.

Perhaps their efforts have always been successful, though in

some cases there are still doubts. Some of the concepts are seen

to be unrealistic in the way they are considered. Due to lack of

reliability in some of the concepts used, there is need for further

investigation on the truthness of these concepts. This study

seeks to examine how confidence and hope can be restored to

5 BBA {Accounting)

BBA {Accounting)

the users of the accounting information and the accountants who

prepare these reports.

1.3 Purpose of the study

The aim of the study was to examine the relationship between

accounting concepts and the financial reports prepared by

accountants.

1.4 Research questions

The following research questions were used in this study:

1. What are the accounting concepts used in financial reporting?

2. Are these concepts dynamic enough to cope up with the changing

accounting environment?

3. What are the attitudes of the accounting information users towards

the reports prepared by the accountants?

1.5 General Objectives

The purpose of this study was to examine the relationship

between accounting concepts and financial statements.

1.6 Specific Objectives

Basing on the time period 2004/2005 and in respect to CPAR

Uganda, the specific objectives of this study are the following:

6 BBA {Accounting)

BBA (Accounting)

¢ To identify accounting concepts/conventions which enable

accountants to prepare financial statements/financial reports

that are relied upon, clearly understandable and can be

compared for reliability to the accounting information users.

¢ To examine whether a change in accounting

concepts/conventions could lead to accurate financial

statements/financial reporting.

¢ To scrutinize whether various organizations use the same

accounting concepts/conventions.

¢ To find out whether some of the accounting standards (IASs)

and Financial Reporting Standards (FRSs) used to supplement

the accounting concepts.

¢ To make recommendations for action and for future studies. This

would help in improving on Financial Reporting in any

organization in Uganda and those outside since accounting

environment is never static.

1.7 Significance /justification of the study

This study was carried out with the following justifications:

¢ The investigation will help in bringing increased awareness and

understanding about the reliability of financial statements

¢ The research was to help the accountants use accounting

conventions that are reliable and can lead to accurate financial

statements.

¢ The study will help in partial fulfillment of a bachelor's degree in

Business Administration and Management at Kampala

International University. One thing that remains certain here is;

the researcher was exposed to the practical realities of

procedures and the need to follow accounting principles.

7 BBA (Accounting)

BBA (Accounting)

¢ It is hoped that the research findings will be an added source of

information to the Accounting Regulatory Body as well as to the

accounting information users for further efforts to mark an end

to the doubts on financial statements.

¢ The study will create more avenues for future research and will

be a reliable source of literature for the people who will be

interested in the same area on related issues since important

areas were tackled.

1.8 Theoretical/conceptual framework of the study

The researcher found out that most of the organizations use the

same accounting concepts and they generally have the same

problem with these concepts and that the fairness of financial

statements greatly relies on the accounting conventions used.

When the accounting concepts are wrongly used or

misinterpreted, then the financial statements produced are

inaccurate.

1.9 The scope of the study

The study focused on the effects of accounting concepts on

financial statements, taking a case study of CPAR Uganda. CPAR

Uganda is an NGO with its head office located in Kansanga,

Makindye Division, Kampala City. CPAR Foundation works in

partnership with vulnerable communities and diverse

organizations to overcome poverty and build healthy

communities in Africa.

However, ten (10) copies of the questionnaires were also sent to

accountants from different organizations especially Non

8 BBA (Accounting)

BBA {Accounting)

1.10

Governmental Organizations within Kampala as part of the study

respondents. The researcher focused his investigation on the

accountants of these organizations and the sample was taken.

The study took three months.

Kampala city is located to the central region of Uganda. It's

comprised of different races and nationalities. It's

administratively divided into four divisions; Makindye, Kawempe,

Nakawa and Central divisions. There are quite a number of

organizations in Kampala, of which the researcher chose as

stated earlier.

Hypotheses

The study was about investigating the effects of the accounting

concepts on the financial statements/reports. The following

hypotheses were used as a guide to this investigation:

c:> Accounting concepts/conventions are rigid and therefore, their

use has lead to preparation of inaccurate financial statements.

c:> Strict adherence to accounting concepts/conventions has lead to

misleading financial statements.

c:> Due to inadequacy and rigidity of accounting

concepts/conventions, shareholders and other users of

accounting information are reluctant to use financial statements

which are not audited.

c:> Accounting concepts/conventions has lead to preparation of

financial statements which are outdated. Financial statements do

not contain current information since they involve only past

information.

9 BBA {Accounting}

BBA (Accounting)

CHAPTER TWO 2.0 Review of related Literature

Generally accepted principles may be defined as those rules of

action or conduct which are derived from experience and

practice and which prove useful, they became accepted as

principles of accounting. According to the American institute of

certified Public Accountants (AICPA), the principles which have

substantial authoritative support become apart of the generally

accepted accounting principles.

THE DEVELOPMENT OF GAAP

From the earliest days of accounting up through the first third of

the 20th century, GAAP were developed through common usage.

In other words, a practice was considered good if it was

acceptable to the most accountants. This history is still reflected

in the phrase, generally accepted. A principle became generally

accepted as accountants came to agree that it would provide

useful and dependable information. However, as the accounting

profession grew and the world of business became more

complex, many people were not satisfied with the rate of

progress towards improved financial reporting

Many professional accountants, managers, and the government

wanted to bring more uniformity to practice. Thus, in the 1930,s,

they began to give authority for defining accepted principles to

small groups of experienced people. Since then, there have been

several authoritative bodies with different structures and

procedures. The power to prescribe acceptable principles also

has been greatly increased. Shortly, we describe the present

10 BBA (Accounting)

BBA (Accounting)

arrangement for establishing GAAP. The primary source of GAAP

is the Financial Accounting Standards Board. The FASB is a

nonprofit organization established to regulate GAAP.

Understanding GAAP

The function of accounting is to provide useful information to

people who make rational investment, credit, and similar

decision. In fact, this description of the function of accounting

comes from a FASB project called the conceptual frame work.

This framework also defines number of terms used by

accountants. For example, we relied on the conceptual frame

work when we defined revenue, expense, asset liability, and

equity.

It is believed that accounting concepts/conventions are most

needed by accountants in preparation of financial statements. As

said by many scholars like Frank Wood and Allan Sangster and

through practice, it has been confirmed that accounting

conventions are normally used when making accounting records,

and also, in practice especially when transacting business. There

are quite a number of them (the concepts/conventions) handled

in different ways by different scholars (M.A Wahab). Some of

these scholars keep criticizing the use of some

conventions/concepts; saying that some of them conflict with

one another, which makes them unreliable for the preparation of

financial statements and financial reporting. For instance

Omonuk writes that the business entity concept/convention has

some limitations which can be appreciated from the perspective

of a humble business man/woman like a sole trader or a family

11 BBA (Accounting)

BBA {Accounting)

run business. The owner and the business are actually

inseparable. For example if a sole trader sells but also

dwells/lives in the same premise, rent and utilities paid on those

premises will be difficult to apportion between the owner and the

business especially if there are no clear apportionment bases.

He (Omonuk) further goes ahead and said that materiality

concept/convention has to be applied with some caution because

there is no threshold or quantitative guidelines for judging

whether an asset is material or not. "Materiality is a matter of

opinion and judgment, abuses should be guarded against."

Omonuk (1999) also goes on to say that prudence

concept/convention, other than being inconsistent with the

historical cost concept/convention, has also been criticized for

discourages optimism, ambition, creativity and innovation

because it requires accountants to behave in a conservative

manner.

M.A Wahab (2000) in his book "A Straight Approach to

Accounting" criticized the money measurement

concept/convention that though accountants use money as a

basic unit in identifying, recording, classifying, reporting and

interpreting business transactions on the assumption that money

is a stable unit of value just as mile is a stable unit of distance

and a litre is a stable unit of weighing some liquid, but money is

not a stable unit of value. The prices of goods and services are

changing over time be4cause the purchasing power of money is

changing.

12 BBA {Accounting)

BBA (Accounting)

Relying on this short background, the researcher will therefore

put much emphasis on the negative effects of accounting

concepts/conventions on the financial statements. However, all

these concepts/conventions also have positive effects as

mentioned by these book writers; though not indicated in this

background, but shall be seen in the literature review. And

actually some of them is believed to have got not negative

effects as stated by Omonuk that the consistency

concept/convention is one of the fundamental

concepts/conventions required by United Kingdom and

international accounting standards.

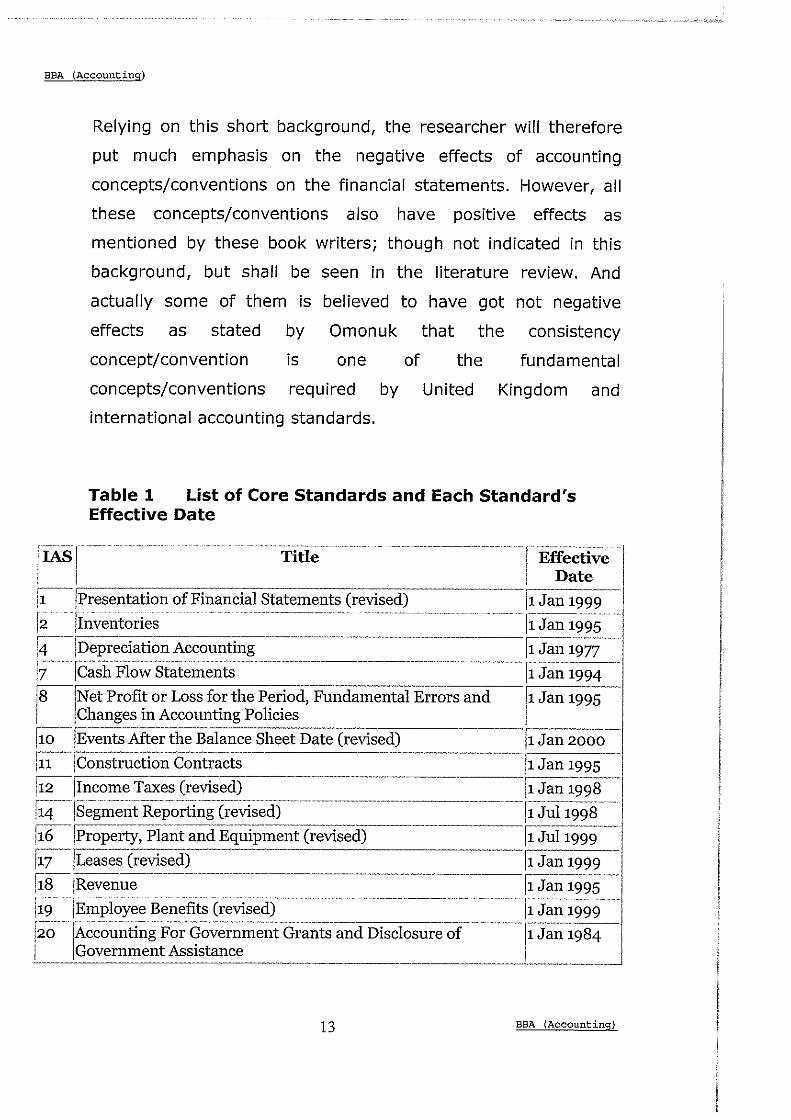

Table 1 List of Core Standards and Each Standard's Effective Date

I IASf- Title -· 1 Effective I I Date

:------------------------:-----1 ~--!Presentation of Financial Statements (revised) 11 Jan 1999 [2 · [In~entories ·· ··· ----- ········ 11 Jan 1995- ·

14 !Depreciation Accounting 11 Jan 1977

~ leash Flow Statements 11 Jan 1994

rs-- Net Profit or Loss for the Period, Fundamental Errors and Ji Jan 1995 I Changes in Accounting Policies

[10 !Events After the Balance Sheet Date (revised) j1 Jan 2000

ri:;:-·· · !construction Contracts 11 Jan 1995

112 !Income Taxes (revised) 11 Jan 1998 il4 !Segment Reporting (revised) 11 Jul 1998 · -r---;----------------------116 !Property, Plant and Equipment (revised) 11 Jul 1999 ;___;_-=-_..:..:._ ___ __::..._::__ ____ _:._ ______ _

117 !Leases (revised) 11 Jan 1999 __ ; _____________________ _ [18 !Revenue 11 Jan 1995 !19 · [Einploy;~Ben:~fiti(ievised) ··· ---······-······ ---11 Jan 1999 -;___;_..::__:_ ____ :__ _____________ _ /20 Accounting For Government Grants and Disclosure of 11 Jan 1984 i Government Assistance

13 BBA (Accounting)

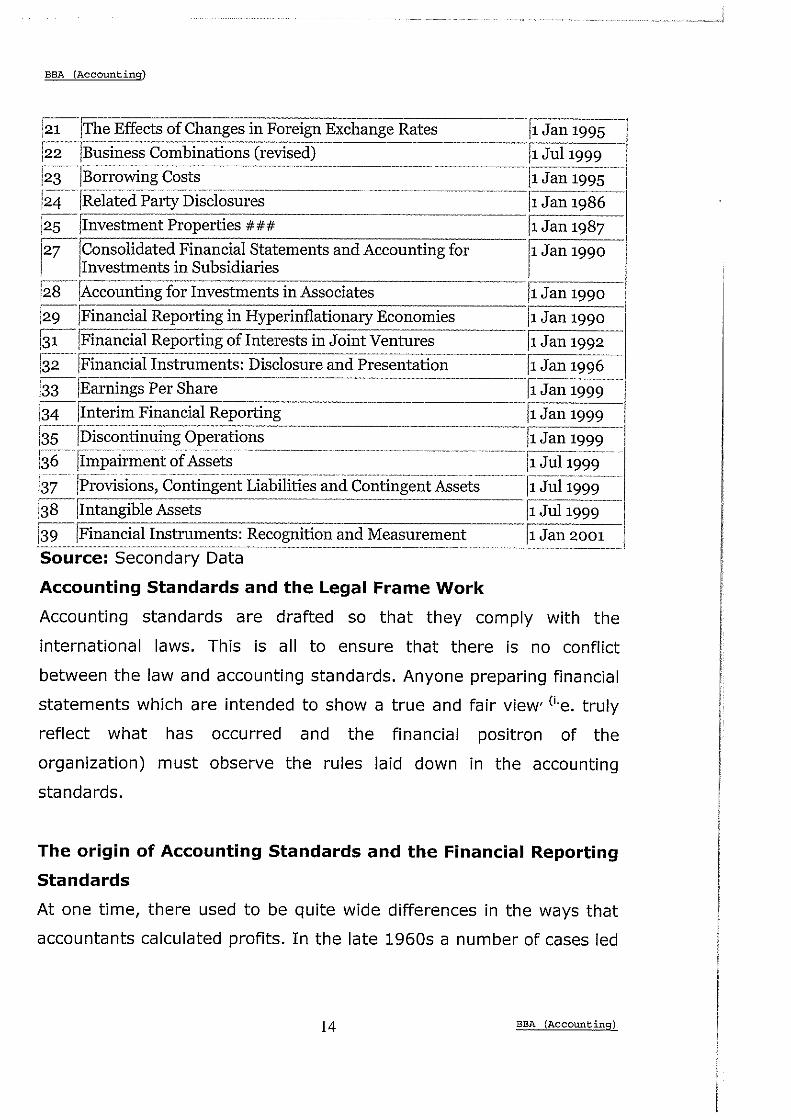

EBA (Accounting)

r;;:-JThe Effects of Changes in Foreign Exchange Rates J1Jan 1995 122 I !Business Combinations (revised) J1 Jul 1999 [23 JBorrowing Costs j1Jan 1995

...

j24 . [Relateif P;rty·Di;;1;;;11res ·--.----·-·--·---

J1Jan1986

i25 !Investment Properties### J1Jan 1987 ,---

Consolidated Financial Statements and Accounting for 11Jan 1990 !27 I

Investments in Subsidiaries I 128 !Accounting for Investments in Associates J1Jan 1990 I

JFinancial Reporting in Hyperinflationary Economies J1Jan 1990 129 ~ !Financial Reporting of Interests in Joint Ventures J1Jan 1992 !32 . JFinancial Instruments: Disclosure and Presentation J1Jan 1996

133 !Earnings Per Share J1Jan 1999 I

!Interim Financial Reporting J1Jan 1999 134 )35 JDiscontinuing Operations J1Jan 1999 136 ·rimpairment of Assets

---~--- . ··--·-·-··--··-·

J1 Jul 1999

/37 !Provisions, c;;ii.1:iiigeiit Liabilities aiidContingent Asset~ 11 Jul 1999 ~!Intangible Assets J1 Jul 1999 ~!Financial Instruments: Recognition and Measurement J1Jan 2001 Source: Secondary Data

Accounting Standards and the Legal Frame Work

Accounting standards are drafted so that they comply with the

international laws. This is all to ensure that there is no conflict

between the law and accounting standards. Anyone preparing financial

statements which are intended to show a true and fair view· (i.e. truly

reflect what has occurred and the financial positron of the

organization) must observe the rules laid down in the accounting

standards.

The origin of Accounting Standards and the Financial Reporting

Standards

At one time, there used to be quite wide differences in the ways that

accountants calculated profits. In the late 1960s a number of cases led

14 EBA (Accounting)

BBA (Accounting)

to a widespread outcry against this lack of uniformity in accounting

practice.

In response, the accounting bodies formed the Accounting Standards

Committee. It issued a series of accounting standards, called

Statements of Standard Accounting Practice (SSAPs). The ASC was

replaced in 1990 by the Accounting Standards Board, which also

issued accounting standards, this time called Financial Reporting

Standards (FRSs). Both forms of accounting standards are compulsory,

enforced by company law.

By the end of 2001, nineteen FRSs had been issued and ten of the

SSAPs were still in force. From time to time, the ASB also issued

Urgent Issue Task Force Abstracts (UITFs). These are generally

intended to be in force only while a standard is being prepared or an

existing standard amended to over the topic dealt with in the UITF. Of

course, some issues do not merit a full standard and so most of the

thirty UITFs issued to date are still in force. UITFs carry the same

weight as accounting standards and their application is compulsory.

In November 1997, the ASB issued a third category of standard - the

Financial Reporting Standard for Smaller Entities (FRSSE). SSAPs and

FRSs had generally been developed with the larger company in mind.

The FRSSE was the FSB's response to the view that smaller entities

should not have to apply all the cumbersome rules contained in the

SSAPs and FRSs. It is, in effect, a collection of some of the rules from

virtually all the other accounting standards. Small entities can choose

whether to apply it or, as seems unlikely, continue to apply all the

other accounting standards.

15 BBA (Accounting)

BBA {Accounting)

The authority, scope and application of each document issued by the

ASB is announced when the document is issued. Thus, even though

each accounting standard and UITF must be applied by anyone

preparing financial statements, in some cases certain classes of

organizations are exempted from applying some or all of the rules

contained within them.

The use of accounting standards does not mean that two identical

businesses will show exactly the same revenue, expenditure and

profits year by year in their financial statements. It does, however,

considerably reduce the possibilities of very large variations in financial

reporting.

FUNDAMENTAL ACCOUNTING CONCEPTS

These comprise a set of concepts considered so important that they

have been enforced through accounting standards and/ or through the

companies Acts. Five have been enforced through the Companies Act

1985, and a sixth through an accounting standard, FRS 5, (Reporting

the subsistence of transactions).

The five enforced through the companies Act are the going concern

concept, the consistency concept, the prudence concept, accruals

concept, and the separate determination concept.

Generally accepted accounting principles (GAAP)

The principles which constitutes the "ground rules" and which are

Used in business entities in preparing financial statements are called

Generally Accepted Accounting principles. These principles have been

developed by the accounting profession over many years in an attempt

16 BBA {Accounting}

EBA (Accounting)

to provide consistent system of financial reporting in a constantly

changing business environment.

Accounting principles are not like physical sciences, where natural laws

are universally and externally true. Rather, accounting principles are

developed in relation to what we consider to be the most important

objectives of financial reporting. What may have been adequate

several years ago may not be adequate today.

Although various terms, such as principles, standards, assumptions,

and concepts are often used to describe the general guidelines which

underlie the preparation of financial statements, a distinction among

these terms is not essential to an understanding of the guidelines. At

this point, a clear grasp of these concepts is useful in understanding

the structure of the accounting process. There is no authoritative list of

the concepts, but the following are important in accounting:

Business Entity: - this concept requires recognition and recording of

transactions relating to the entity in question and excludes private

transaction of the owners or those running it. Record is only made for

what the entity owes the owner (capital) and what the owner owes the

entity (drawings). When an organization is set up and is fully

incorporated under the law, it becomes a separate legal person

(entity) capable of transacting on its own including the power to

borrow and lend (sue or be sued). In writing or preparation of

accounts this concept is important because it filters transactions by

isolating business from non-business private transactions. However,

this concept has some limitations which can be appreciated in from the

perspective of a humble business man like a sole trader or w family

17 EBA (Accounting}

BBA (Accounting)

run business. The owner and the business are actually inseparable. For

instance if a sole trader sells but also dwells in the same premises,

rent and utilities paid on those premises will be difficult to apportion

between the owner and the business especially if there are no clear

apportionment basis.

Money Measurement Concept: - according to this concept all

transaction to be recorded must be quantified in monetary terms.

Money is a common denominator for all transactions. Let alone being

an objective measure, money is also a unit of account and store of

value. This convention assumes money has stable value over time and

it is a source for one of its criticisms. This concept limits recognition of

business transactions to those that can be expressed in monetary

terms. Even where goods are exchanged for goods, value must be

attached to the items in question. Whatever cannot be monetized is

not recorded. This concept has some shortcomings; the assumption

that money is a stable value is not true. It is a common knowledge

that money losses value with time a phenomenon referred to as

inflation.

Going Concern Concept: - this concept states that the business

entity is assumed to continue in operational existence in the

foreseeable future. The business is not on the verge of collapse unless

there are indications to suggest so this assumption is very

fundamental to preparation of accounts. Omonuk says that there is

almost no challenge against the going concern assumption and have

been embraced and enshrined in accounting standards of many

counties as a fundamental assumption or concept.

18 BBA (Accounting)

BBA (Accounting)

Consistency Concept: - it states that once a particular accounting

method or base has been selected and has become accounting policy,

it must be applied continuously or consistently from year to year.

Changes in accounting methods or policies are permitted only if there

are justifiable reasons for doing so for instance if old ones have

become inappropriate for the present circumstances. When a change is

made, the effect of the change on the reported net profit and balance

sheet position if material must be disclosed as foot noted in the

accounts. Consistency is one of the most fundamental concepts

required by UK and international accounting standards. There is no

serious challenge of this concept.

Prudence Concept: - preparation of accounts involves estimation,

measurements and valuations, according to the conservatism or

prudence concept it is good practice to follow a procedure that tends

to understate things. Other than being inconsistent with the historical

cost concept, conservatism concept has also been criticized for

discourages optimism, ambition, creativity and innovation because it

requires accountants to behave in a conservative manner.

Accrual Concept: - according to this concept, income is recorded as

earned even though it might have not been received in cash provided

there is right to income. There is no major criticism of this concept just

like the realization concept, however when preparing a cash flow

statement which shows the actual or expected cash flow position of

the enterprise, accrual items should be eliminated. Investment

decisions are based on the available or expected cash, accrued items

will falsify the actual cash position.

19 BBA (Accounting)

BBA {Accounting)

The Matching Concept: - this requires accurate matching of

expenses against incomes by writing off only those costs or expenses

that were incurred in generating specific income for the period ended.

Cost or expenses paid should be adjusted for any part-period that does

not relate to the overall period. The matching concept and indeed the

accrual concept are very important in the preparation of the income

statement.

Historical Cost Concept: - this concept requires accountants to

record assets and liabilities at historical costs of their acquisitions.

Assets are recorded at their acquisition costs even if the value today is

more than the historical cost. Likewise, liabilities are recorded at

amounts they were incurred though the true value of the liability might

have changed due to foreign exchange fluctuations and other macro

economic issues such as inflation, devaluation and currency reform.

Realization Concept: - this concept requires that accountants

recognize income as earned only when a sale has been made and the

goods have been accepted by the customer or services have been

offered and enjoyed by the customer or when value has been created

by a transaction and legal rights and obligations have resulted. There

is no major problem with the realization concept; however question

debated is at which point in time income should be recognized as

earned. The majority argue that income should be recognized when

sale has been mad and title has passed.

Periodicity Concept: - this concept makes financial reporting

mandatory and is enshrined in the Companies Act of Uganda and of

many other countries. At the end of an accounting or financial year, a

20 BBA (Accounting)

BBA {Accounting)

company must prepare and disclose financial statements. Publishing

annual accounts is made an obligation by this concept. Disclosure can

be made more than once a year if the accountant so wishes. If interim

accounts are to be published, it is not discouraged. Non disclosure

even once a year is illegal. All material information must be disclosed,

an accountant must not be seen to be hiding some vital information.

Materiality Concept: - this requires recognition of only material

items and excluding immaterial or trivial items or matters. Information

is material if it is able to influence the decision. For instance, if the

cost of recording certain items is not justifiable, then they should be

lelt out. Take an example of buying a razorblade at shs. 50 for the

business from your own money; it is immaterial to record that amount

in the cash book or as your asset. Some assets like goodwill and some

low value assets are written off in the profit and loss account rather

than being included as assets in the balance sheet because of

materiality consideration, departures from good accounting practice

that are not material should also be ignored. This concept has to be

applied with some caution because there is no threshold or

quantitative guidelines for judging whether an asset is material or not.

Materiality is a matter of opinion and judgment, abuse should be

guarded against.

Objectivity Concept: - it states that whatever figure is recorded in

accounting books and financial statements must have a basis for

arriving at them but not simply planted into financial statements.

Accountants must be able to defend figures in financial statements

using objective evidence, empirical or otherwise. This concept aims at

eliminating subjectivity and free accounting information from bias. The

21 BBA {Accounting)

BBA (Accounting)

entire regulatory framework of accounting aims at emphasizing

objectivity of accounting information this concept is reflected in all the

others and other forms of accounting regulations. The preparation of

accounting statements however involves a considerable amount of

individual discretion especially on judging the materiality of amounts

or issues. While personal discretion cannot do away completely,

accounts should be prepared with minimum amount of personal bias

and the maximum amount of overall objectivity.

Relevance Concept: - according to this concept the overall message

that the accounts are trying to relay may be obscured if too much

information is presented. Accounting statements should contain only

information that complies strictly with the specific requirements of the

user. This concept is at times combined with materiality concept.

Substance over Form: - it states that transactions and other events

should be accounted for and presented in accordance with their

substance and financial reality and not merely with their legal form.

For instance if you buy a motor vehicle for your business on hire

purchase, when you make a down payment you can be given the

vehicle to sue as you continue making installment payments the

registration book, which is evidence of ownership, will not be released

to you until you make the last installment payment. The lawyer says

that title passes on fully paying up. The question then is, how do you

account for such a vehicle, should you make it off-balance sheet that is

not to record in your balance sheet? Substance over form gives the

answer as follows. The substance and reality is that you are using the

vehicle in your business so it is a business asset and should be

recorded in its books and statements. You should stop worrying about

22 BBA (Accounting)

BBA (Accounting)

legalities of title passing after all you will complete installment

payments and documents of ownership will be rendered to you.

Duality (Dual Aspect) Concept: - it requires a transaction to be

recorded twice. The dual aspect rule is recognition that every

transaction involves giving and receiving effect. When somebody gives

something, another must receive it.

23 BBA (Accounting)

BBA {Accounting)

3.0 Introduction

CHAPTER THREE METHODOLOGY

This chapter describes how the research was conducted. It

includes the methods that were employed in the analysis of the

effects of accounting concepts on the financial statements. It

gives an explicit description of the Research design, Research

procedures, sample size and selection, methods of data

collection, data analysis as well as limitation of the study.

3.1 Research Design

The study was conducted through use of both quantitative and

qualitative designs. The quantitative design was got from

Discussion as well as questionnaires.

In the qualitative study, the researcher intended to find out the

numerical points like the number of accounting concepts used in

the organization, with a greater focus on the ones that are

frequently used.

The observation of subjects was done qualitatively, with

sampling and documentation, the researcher used the survey

techniques using cross sectional survey that is interviewing

different accountants at the same time and their trend survey

24 BBA (Accounting)

BBA {Accounting)

where the researcher interviewed individuals which included in

depth interviews with managers, and some other employees.

3.2 Research Procedures

The researcher began by formulating a topic which was approved

by the supervisor, after which, the researcher wrote a proposal

and formulated a questionnaire. Before leaving for the field a

letter of introduction was obtained from the School of Business

and Management, Kampala International University which was

presented to the authority of the organization for permission

after which the researcher distributed questionnaires and

conducted interviews with the relevant respondents.

3.3 Sample size

The sample size consisted of the accountants/managers of the

accounting department of the chosen organizations. This

involved a selection of two accountants from each organization.

3.4 Sources of Data

The source of data was both primary and secondary data which

assisted the researcher to make a thorough analysis of the study

problem.

3.4.1 Primary data Primary data refers to raw data collected through personal

interviews, through questionnaires. Primary data was collected

from personal interviews, questionnaires as well as Discussions.

25 BBA (Accounting)

BBA (Accounting)

3.4.2 Secondary Data Secondary data refers to the data obtained through the existing

literature from libraries, data from published bulletins and news

papers. This data was largely obtained from Bulletins, News

papers, Text books, Journals, internet and performance Records

of CPAR.

3.5 Methods and Tools of Data Collection

The following are the techniques and instruments that were used

to collect data:

3.5.1 Questionnaire This refers to the collection of items to which the respondent is

required to fill in the questions asked by the researcher. This

technique helped the researcher in collection of primary data.

The questionnaires were self-administered with both open and

close ended questions to employees of CPAR and other

organizations like; UNICEF, UNHCR, UN, UNAIDS.

3.5.2 Interview Interview method refers to where there is person to person

verbal communication in which one person or a group of persons

26 BBA (Accounting)

BEA (Accounting)

asks the questions intended to obtain information. Interview

schedules were used. The main respondents were the

accountants, accounts assistants/cashiers and managers.

3.6 Data Analysis

Data was analyzed before, during and after data collection.

Before data collection the researcher identified the themes

according to which data would be analyzed. During data

collection questionnaires were distributed to the respondents,

and after data collection the investigator further analyzed the

data descriptively; through use of tables, pie charts and

Computer packages were used as well as SPSS to present the

existing relationship.

3.7 Limitations / Anticipated Problems

As anticipated, the following problems were encountered by the

researcher during data collection:

c) There were difficulties in getting information from some

members of management/the accounting department since

some of them claimed to have no time for the researcher due to

workload. However, such problem was minimized by proper

timing. For instance, interviews were conducted on special

arrangements over weekends.

c) There was some information that the accountants are not

allowed to display. Therefore, access to such information was

denied. Such information could have been very vital in this

study.

27 EBA (Accounting)

EBA (Accounting)

¢ Due to poor record keeping of accounting data by accountants.

There was a problem of gathering of wrong data, hence wrong

report. However, this problem was solved by taking only

information which had better records.

¢ There was also a problem of tight academic work on the side of

the researcher because there was a busy schedule for lectures

and yet the researcher work had to be carried out; this was also

a hindrance to giving proper attention to other subjects. To solve

this problem of tight academic work, the researcher had to wait

till the second semester holiday so as to get some time to carry

out the research.

28 EBA (Accounting)

BBA (Accounting)

CHAPTER FOUR DATA PRESENTATION AND ANALYSIS OF FINDINGS

4.0 Introduction

This chapter contains the presentation, analysis and discussion

of the findings made by the researcher. The researcher followed

the objectives of the study to help in making a thorough

analysis. The researcher used tables, pie charts and bar graphs

to present and analyze the findings.

4.1 Categorization of respondents

Table 2 showing categories of respondents

Categories Number of respondents Percentages

Financial Managers 10 20

Accounts Assistants 20 40

General managers 5 10

Other employees 15 30

Total 50 100

Source: primary data

From table 1 above, the findings of the study revealed that 20%

of the total respondents were financial managers. These were

sampled from CPAR Uganda and other financial managers from

other organizations. The findings of the study further revealed

that 40% of the total respondents were accounts assistants from

CPAR and other organizations, 10% of the respondents were

General Managers, 30% were other employees both from CPAR

Uganda and other organizations. The findings of the study

confirmed that the largest numbers of the respondents were

29 BBA (Accounting)

BBA (Accoun ting)

willing to respond and they gave the appropriate required

information of the study.

4. 2 Response on whether Accounting concepts are

followed

Table 3 showing the response on whether the accounting

concepts are followed

Response Number of respondents Percentage

Strongly agree 40 80

Agree 5 10

Disagree 2 4

Strongly disagree - -

Not sure 3 6

Total so 100

Source: Primary data

Figure 1 showing the response on whether accounting concepts are followed

Source: Primary data

o Strongly agree

■ Agree

o Disagree

□ Not sure

From the table2 and figure 1 above, the findings of the study

revealed that accounting concepts are always followed while

preparing the financial statements in CPAR Uganda. 80% of the

respondents strongly agreed that GAAP are followed in almost all

30 BBA (Accounting)

BBA (Accounting)

the organizations. 10% agreed that accounting concepts are

followed. However, the findings of the study revealed that 6% of

the respondents were not sure whether accounting concepts are

always followed while preparing financial statements. The

financial statements include balance sheet, income statement,

cash flow statement and statement of changes in equity. Thus

the researcher confirmed that CPAR Uganda and other

organizations in the sample always follow the GAAP while

preparing their financial statements.

4.3 Response on whether a change accounting

concepts could lead to accurate financial

statements

Table 4 a change in accounting concepts could lead to

accurate financial statements

Response Number of respondents Percentage

Strongly agree 30 60

Agree 10 20

Disagree 4 8

Strongly disagree - -Not sure 6 12

Total 50 100

Source: Primary data

31 BBA {Accounting)

BBA (Accounting)

Figure 2 showing whether a change in accounting concepts could lead to accurate financial statements

Source: Primary data

□ Strongly agree

■ Agree

□ Disagree

□ Not sure

From table 3 and figure 2 above, the findings of the study

revealed, a change in accounting concepts could lead to

preparation of accurate financial statements. This was because

60% of the total respondents strongly agreed that the change

would yield accurate reports. The findings of the study further

revealed that the current accounting principles have some

limitations, of which if they could be changed, then accurate

financial statements would be yielded by different organizations.

The findings of the study further revealed that 8% of the

respondents were pessimistic that there is no need to change the

accounting concepts since it may affect the standards of the

financial statements. The study also revealed that 12% of the

total respondents were not sure of whether a change in

accounting concepts would lead to preparation of accurate

financial statements.

32 BBA (Accounting}

BBA (Acc ount ing)

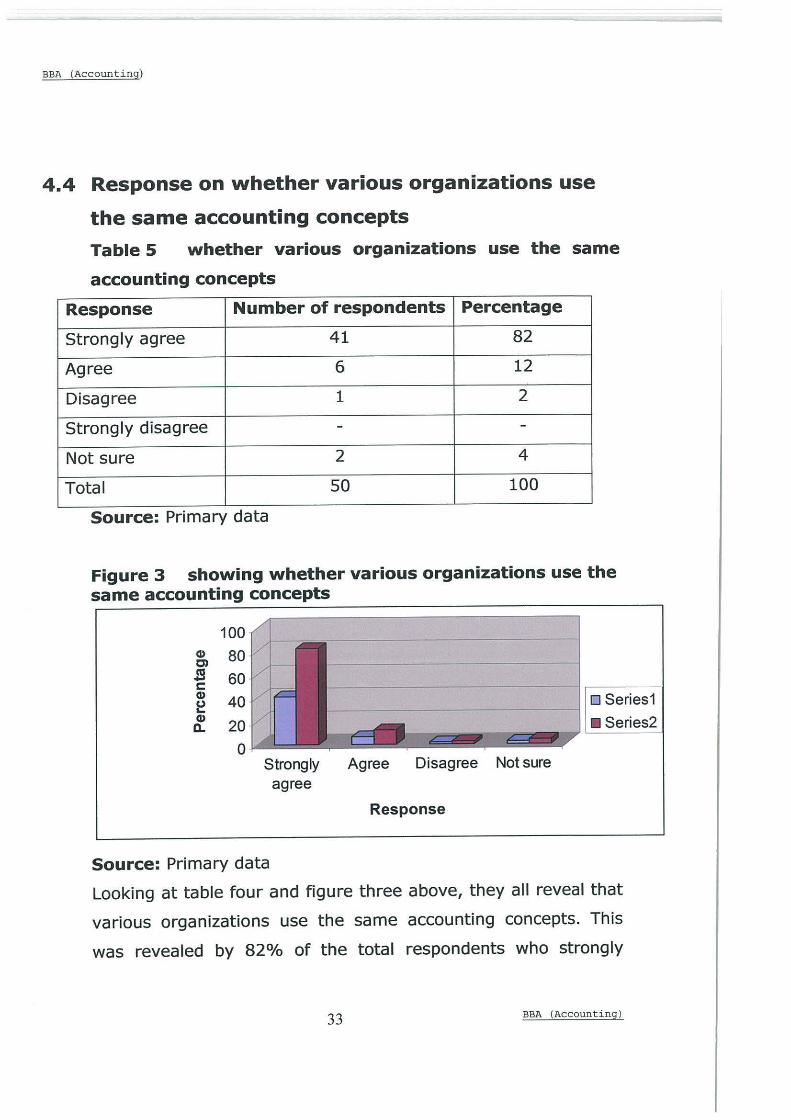

4.4 Response on whether various organizations use

the same accounting concepts

Table 5 whether various organizations use the same

accounting concepts

Response Number of respondents Percentage

Strongly agree 41 82

Agree 6 12

Disagree 1 2

Strongly disagree - -

Not sure 2 4

Total 50 100

Source: Primary data

Figure 3 showing whether various organizations use the same accounting concepts

100 C1) 80 C)

s 60 C: C1)

40 ~ C1)

20 £l.

0 Strongly agree

Source: Primary data

Agree Disagree Not sure

Response

□ Series1

■ Series2

Looking at table four and figure three above, they all reveal that

various organizations use the same accounting concepts. This

was revealed by 82% of the total respondents who strongly

33 BBA (Accountin g)

BBA (Accounting)

agreed that various organizations use the same accounting

concepts. Although the study further revealed that there could

be a few organizations that do not use some of these concepts.

However, the study also revealed that 4% of the respondents

were not sure whether the accounting concepts are used by

different organizations.

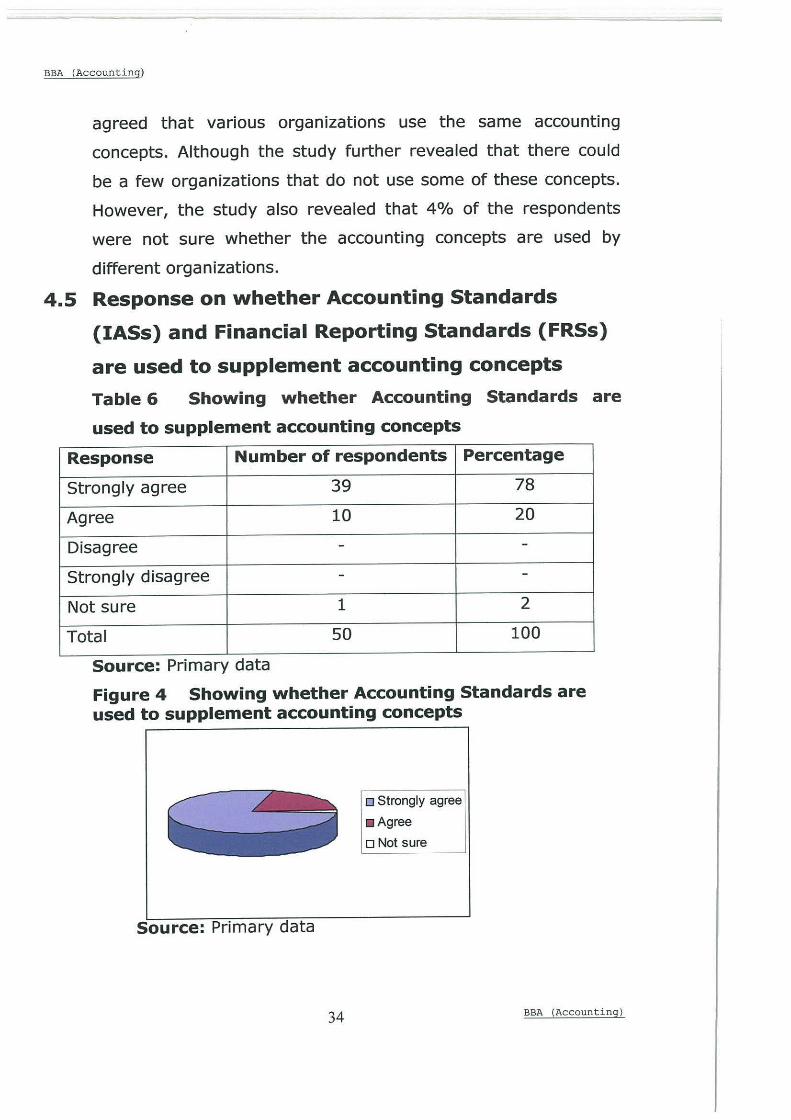

4.5 Response on whether Accounting Standards

(IASs) and Financial Reporting Standards (FRSs)

are used to supplement accounting concepts

Table 6 Showing whether Accounting Standards are

used to supplement accounting concepts

Response Number of respondents Percentage

Strongly agree 39 78

Agree 10 20

Disagree - -

Strongly disagree - -

Not sure 1 2

Total so 100

Source: Primary data

Figure 4 Showing whether Accounting Standards are used to supplement accounting concepts

Source: Primary data

34

□ Strongly agree

■ Agree

□ Not sure

BBA (Accounting)

BBA (Accounting)

From the table 5 and figure 4 above, the findings of the study

revealed that accounting concepts are supplemented by

accounting standards/financial reporting standards in

preparation of financial statements in CPAR Uganda and other

organizations. 78% of the respondents strongly agreed that

accounting standards are followed in almost all the

organizations. 20% agreed that accounting standards are

followed. However, the findings of the study revealed that 2% of

the respondents were not sure whether accounting standards are

always followed while preparing financial statements. The

financial statements include balance sheet, income statement,

cash flow statement and statement of changes in equity. Thus

the researcher confirmed that CPAR Uganda and other

organizations in the sample always supplement GAAP with

accounting standards while preparing their financial statements.

4.6 Problems faced by CPAR Uganda while using the

accounting concepts

There has been difficulty in determining the scrap value of used

assets due to the adherence to the historical cost concept that

assets should and liabilities should be valued at their historical

cost prices. At the end of it all, these assets depreciate and lose

value and therefore make it difficult to allocate a scrap price

when disposing these assets off.

There are other organizational benefits that are sometimes given

to staff but cannot be measured in monetary terms. Such

benefits are study leaves, sick leaves, maternity leaves and a

word of thanks for the good work done by a staff member. Yet

35 BBA (Accounting)

EBA {Accounting)

considering the money measurement concept, it's only those

items that can attach a money value that can be included in the

financial reporting. Effectiveness on the part of some staff, say

when they meet the organizational target on time, therefore

enabling effectiveness of the organization, but these efforts are

difficult to measure in terms of money.

4.7 Solution to Problems faced by CPAR Uganda while

using Accounting Concepts

CPAR now predetermines the scrap value of its assets so that

when the time period in use elapses, the asset is disposed at the

predetermined scrap value/price.

To overcome the problem of attaching money value on other

benefits like study leaves, sick leaves and maternity leaves,

CPAR makes a full payment of salary irrespective of such leaves.

In terms of appreciation for the work well-done, CPAR uses what

it calls "Hospitality" as a thanks giving for the good work

performed by the staff.

36 EBA (Accounting)

BBA (Accounting)

CHAPTER FIVE 5.0 Introduction

This chapter presents a summary of the main findings of the study and

it attempts to find out the extent to which the objectives were

achieved. It further presents the conclusions drawn by the researcher

from the findings of the study and recommendations.

5.1 Summary of the Findings

The study was on the effects of accounting concepts on the financial

statements, with a case study of CPAR Uganda.

CPAR Foundation works in partnership with vulnerable communities

and diverse organizations to overcome poverty and build healthy

communities in Africa.

In 1992, CPAR was invited by the Ugandan government to work with

northern communities and local authorities on health and development

initiatives. CPAR is one of the only NGOs implementing peacebuilding

programs in the rural communities of Northern Gulu.

Today, CPAR-Uganda undertakes the following initiatives:

Disaster Preparedness, Income generation, Natural Resource

Management, Food Security, Water and Sanitation, Peacebuilding, and

Emergency Relief.

The study constituted of 50 respondents of which 20% were financial

managers, 40% were accounts assistants from CPAR and other

organizations, 10% of the respondents were General Managers and

30% were other employees both from CPAR Uganda and other

organizations. The findings of the study confirmed that the largest

37 BBA (Accounting)

EBA (Accounting)

numbers of the respondents were willing to respond and they gave the

appropriate required information on the study.

The findings of the study revealed that accounting concepts are always

followed while preparing the financial statements in CPAR Uganda and

other organizations. This was revealed by 80% of the respondents who

strongly agreed that GAAP are followed in all organizations. 10%

agreed that accounting concepts are followed. However, 6% of the

respondents were not sure whether accounting concepts are always

followed while preparing financial statements. The financial statements

include balance sheet, income statement, cash flow statement and

statement of changes in equity. Thus, the researcher confirmed that

CPAR Uganda and other organizations always follow the GAAP while

preparing financial statements.

A change in accounting concepts could lead to preparation of accurate

financial statements. This was because 60% of the total respondents

strongly agreed that the change would yield accurate financial reports.

Accounting principles have some limitations, of which if they could be

changed, then accurate financial statements would be capitulated by

different organizations. The findings of the study also revealed that

8% of the respondents were pessimistic that there is no need to

change the accounting concepts since it may affect the standards of

the financial statements. This is a very small percentage that could not

be regarded as something so serious. And of course 12% of the total

respondents were not sure of whether a change in accounting concepts

would lead to preparation of accurate financial statements.

38 EBA (Accounting)

BBA (Accounting)

Various organizations use the same accounting concepts. This was

revealed by 82% of the total respondents who strongly agreed that

various organizations use the same accounting concepts. However

there could be a few organizations that do not use some of these

concepts.

Accounting concepts cannot work alone. They are supplemented by

accounting standards/financial reporting standards in preparation of

financial statements. 78% of the respondents strongly agreed that

accounting standards are followed in almost all the organizations. 20%

agreed that accounting standards are followed. Combining 78% and

20% gives 98%, which means that account concepts do not work

alone; they are supported by financial reporting accounting standards.

5.2 Recommendation

NGOs and other organizations/companies should continue using

accounting concepts in supplement with financial reporting standards

so as to produce fairly accurate financial statements. This is because,

without the use of GAAP, it would be difficult to record, analyze,

summarize and produce financial information in form of financial

statements. Therefore, it is very vital for both accountants and

financial information users to take note of this as this would ensure

reliability on such financial reports.

5.3 Conclusions

To end with, in 1992, CPAR was invited by the Ugandan government to

work with northern communities and local authorities on health and

development initiatives. CPAR is one of the only NGOs implementing

peacebuilding programs in the rural communities of Northern Gulu.

39 BBA (Accounting)

BBA (Accounting)

CPAR among other organizations also uses accounting concepts

as an aid to financial reporting. The findings of the study

indicated that CPAR has always used the fundamental accounting

concepts and accounting standards (IASs)/financial reporting

standards (FRSs) while preparing its financial statements. The

study further revealed that different organizations use

accounting concepts and financial reporting standards (FRSs) to

produce financial statements and other financial repots. However

there is still need for further improvements on the financial

statements/reports for reliability by the accounting information

users.

40 BBA (Accounting)

BBA {Accounting)

REFERENCES 1. ACCA (2004), Financial Reporting, Paper 2.5, Foulks and Lynch

Publications Ltd, Middlesex.

2. ACCA (2004, Financial Reporting, Paper2.5, Foulks and Lynch

Publication Ltd, Middlesex.

3. Bendry (1996), Accounting and Finance in Business, Fourth Edition,

Ashford.

4. Fess E.P (1993), Financial and Management Accounting, Fourth

Edition, SW Publishing Company- Ohio.

Fourth Edition.

5. Frank Wood & Alan Sangster (2002), Business Accounting 1, Ninth

Edition, British Library Cataloging-in-Publication Data

6. IASB (Jan 2006-July 2006), Board Decisions on International

Financial Reporting Standards-Update.

7. J B Omonuk, A Guide for Excelling in Fundamental Accounting

Principles, Accounting 1, Makerere University Business School

8. Kakuru J. (2003), Financial Decision and Business, Second Edition,

Business Publishing Group- Kampala.

9. Kermit D. Larson and Paul B.W. Miller (1992), Financial Accounting,

Fifth Edition, Irwin-McGraw Hill.

10. Kermit D. Larson, Essentials of Financial Accounting, A

Multimedia Approach, Information for Business Decision, Seventh

Edition, McGraw Hill Companies, Inc.

11. Kermit D. Larson, John J. Wild and Barbara Chiappetta (2002),

Fundamental Accounting Principles, Sixteenth Edition, McGraw Hill

Irwin.

41 BBA {Accounting)

BBA (Accounting)

Library of congress Cataloging-in-Publication Data

12. M.A Wahab (2000), A Straight Approach to Accounting Volume

1, M.A Wahab T & E Publishers, 2nd Edition

13. PC Tulisian (2001), Accountancy for CA Foundation, Third

Edition, McGraw Hill Publishing Company.

14. Peter J. Eisen (2000), Accounting, Business Review Books

15. Robert M. Swanson, Kenton E. Ross, Robert D. Hanson and

Lewis D. Boynton (1982), Century 21 Accounting, Third Edition,

South-western Publishing Company.

16. Securities and Exchange Commission (February 2000), !AS, SEC

Concept Release.

42 BBA (Accounting)

BBA (Accounting)

APPENDICES

I Introductory Letter

April 22, 2006

Dear Respondent,

Kampala Interantional Univerity P.O. Box 20000 Kampala

RE: Questionnaire for Data Collection

I am a student of Kampala International University, School of Business and Management, pursuing a Bachelor of Business Administration and Management majoring in Accounting Option.

This is to kindly request you to sacrifice some time, respond and contribute to the ongoing study with the title "The Effects of Accounting Concepts on the Financial Statements" a case study of CPAR Uganda.

Your absolute participation will be of great academic value and for that reason a major determinant to the success of this study.

Your participant and response will be treated with strictest privacy.

Thank you.

Yours faithfully,

Mr. Adupa Richard.

I BBA (Accounting)

BBA (Accounting)

II Study Questionnaire

PERSONAL DATA

Please tick in the appropriate box

1. Respondent Finance Manager

Accounts Assistant

General Manager

Other Employee

2. Sex Male

Female

D D D D

D D

3. Do accountants use financial accounting concepts while preparing

financial statements?

Yes D No,D If yes, please mention the concepts used .

........................................................................................................................... , ..

······························································································································

······························································································································

······································································································· ...................... .

4. What are the challenges faced by accountants while using

accounting concepts?

..............................................................................................................................

..............................................................................................................................

······························································································································

II BBA {Accounting)

BBA (Accounting)

5. How often are the concepts used in recording accounting

information, analyzing and reporting financial information/financial

statements?

Always daily D When preparing monthly report D When preparing quarterly repot D At the end of the financial year D

6. What are the contributions of International Accounting Standards

Board (IASB) and Financial Institutions on Financial Reporting?

Please tick.

Regulate use of accounting concepts D Regulate financial reporting D Recommends use of accounting concepts D Identification of new concepts D Improvement on reporting standards D Other, please mention ................................................................................... .