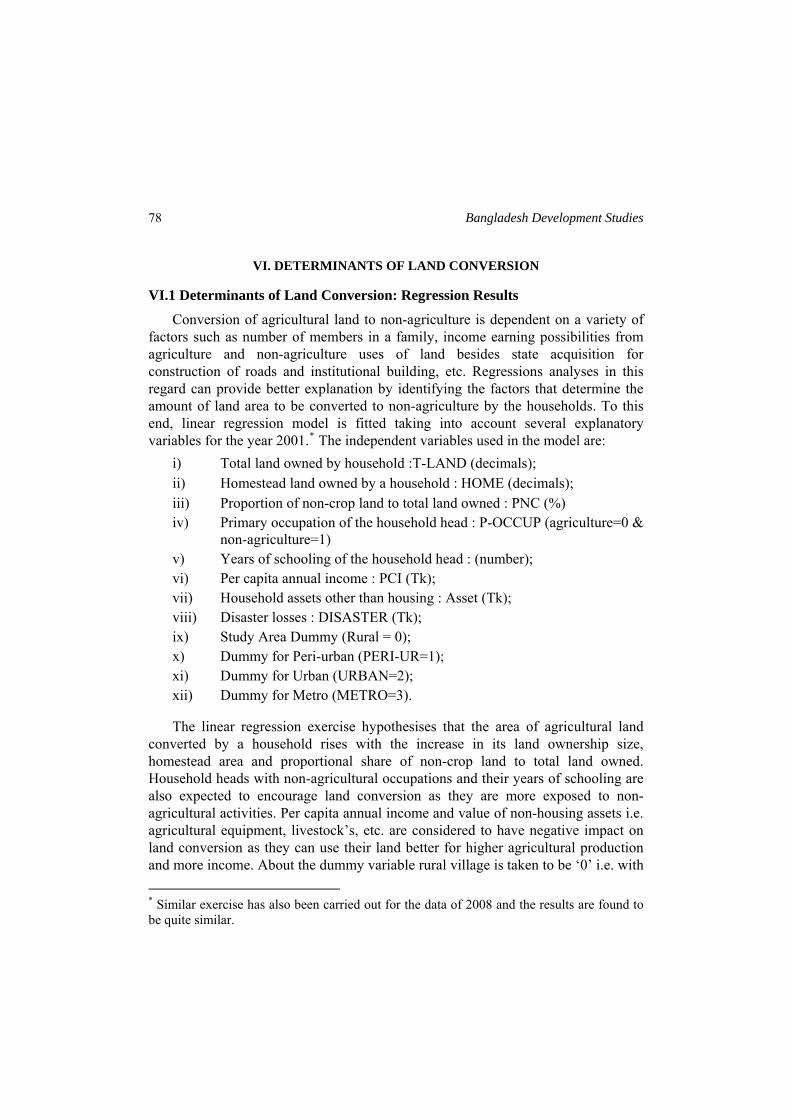

The Bangladesh Development Studies

109

BANGLADESH UNNAYAN GOBESHONA PROTISHTHAN (BANGLADESH INSTITUTE OF DEVELOPMENT STUDIES) E-17, AGARGAON, SHER-E-BANGLA NAGAR DHAKA-1207, BANGLADESH The Protishthan carries out basic research studies on the problems of development in Bangladesh. It also provides training in socio-economic analysis and research methodology for the professional members of its staff and for members of other organisations concerned with development problems. BOARD OF TRUSTEES Chairman: The Minister for Planning, ex-officio Trustees: A Member of the Planning Commission to be nominated by the Chairman The Director General of the Protishthan, ex-officio The Chairman or a Member of the University Grants Commission to be nominated by it The Governor, Bangladesh Bank, ex-officio The Secretary, Ministry of Finance, ex-officio The Secretary, Ministry of Education, ex-officio Two Senior Fellows of the Protishthan Three Senior Staff Members of the Protishthan Director General, Bangladesh Rural Development Board, Ex-officio One Trustee to be appointed by the President DIRECTOR GENERAL: Mustafa K Mujeri Manuscript in duplicate and editorial correspondence should be addressed to the Executive Editor, The Bangladesh Development Studies, BIDS, E-17, Agargaon, Sher-e-Bangla Nagar, Dhaka, G.P.O. Box No. 3854, Bangladesh, Fax: 880-2- 8113023,Website: www.bids.org.bd. Style Instructions for guidance in preparing manuscript in acceptable form is appended and may also be provided upon request. All business correspondence should be addressed to the Chief Publication Officer at the above address. Annual Subscriptions (Four issues per year): Inland: Individuals: Tk.500 Institutions: Tk.600 Foreign (By Air Mail): Individuals: US$100 Institutions: US$200

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of The Bangladesh Development Studies

BANGLADESH UNNAYAN GOBESHONA PROTISHTHAN (BANGLADESH INSTITUTE OF DEVELOPMENT STUDIES)

E-17, AGARGAON, SHER-E-BANGLA NAGAR DHAKA-1207, BANGLADESH

The Protishthan carries out basic research studies on the problems of development in Bangladesh. It also provides training in socio-economic analysis and research methodology for the professional members of its staff and for members of other organisations concerned with development problems.

BOARD OF TRUSTEES Chairman: The Minister for Planning, ex-officio Trustees: A Member of the Planning Commission to be nominated by the Chairman The Director General of the Protishthan, ex-officio The Chairman or a Member of the University Grants Commission to be nominated by it The Governor, Bangladesh Bank, ex-officio The Secretary, Ministry of Finance, ex-officio The Secretary, Ministry of Education, ex-officio Two Senior Fellows of the Protishthan

Three Senior Staff Members of the Protishthan Director General, Bangladesh Rural Development Board, Ex-officio One Trustee to be appointed by the President

DIRECTOR GENERAL: Mustafa K Mujeri

Manuscript in duplicate and editorial correspondence should be addressed to the Executive Editor, The Bangladesh Development Studies, BIDS, E-17, Agargaon, Sher-e-Bangla Nagar, Dhaka, G.P.O. Box No. 3854, Bangladesh, Fax: 880-2-8113023,Website: www.bids.org.bd. Style Instructions for guidance in preparing manuscript in acceptable form is appended and may also be provided upon request.

All business correspondence should be addressed to the Chief Publication Officer at the above address.

Annual Subscriptions (Four issues per year): Inland: Individuals: Tk.500 Institutions: Tk.600

Foreign (By Air Mail): Individuals: US$100 Institutions: US$200

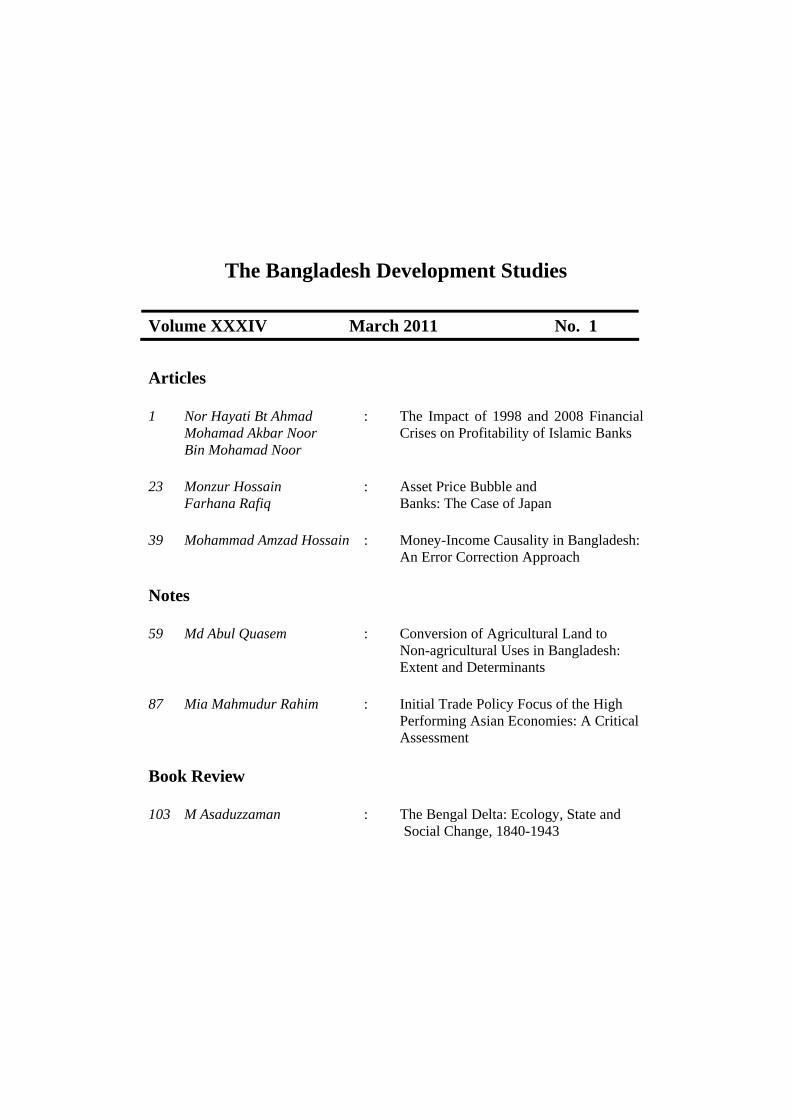

The Bangladesh Development Studies

Volume XXXIV March 2011 No. 1

Articles

1 Nor Hayati Bt Ahmad : The Impact of 1998 and 2008 Financial Mohamad Akbar Noor Crises on Profitability of Islamic Banks Bin Mohamad Noor

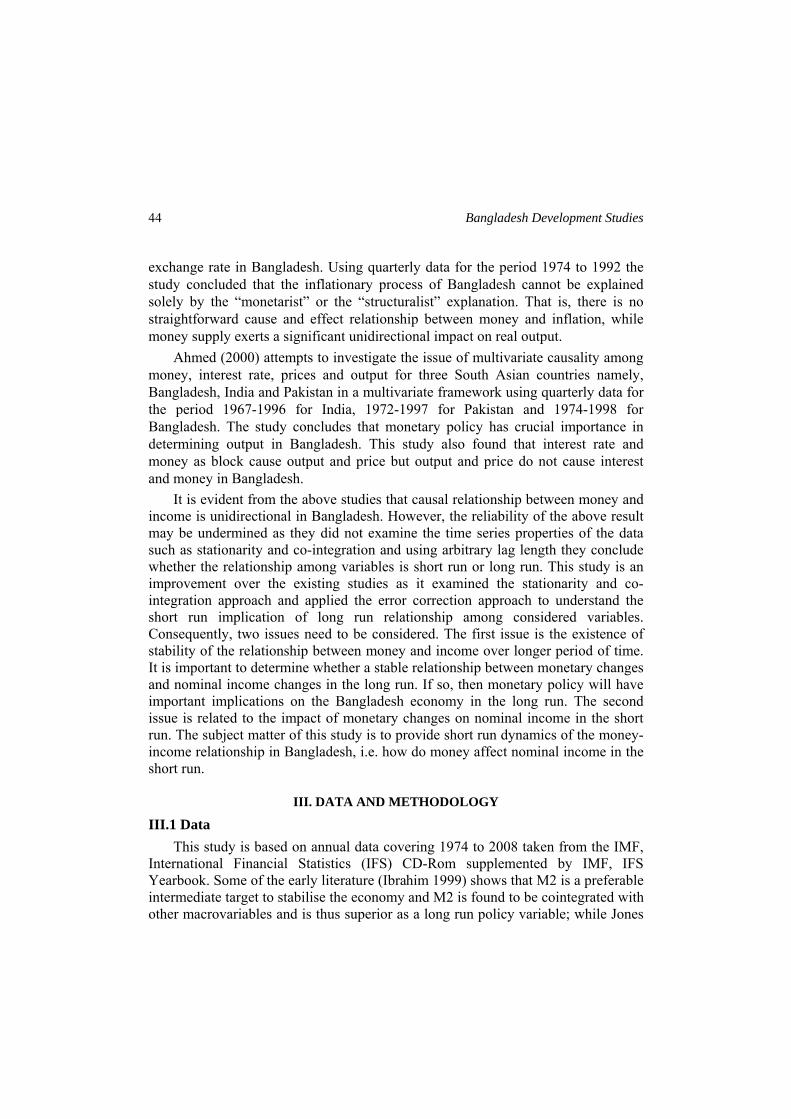

23 Monzur Hossain : Asset Price Bubble and Farhana Rafiq Banks: The Case of Japan

39 Mohammad Amzad Hossain : Money-Income Causality in Bangladesh: An Error Correction Approach

Notes

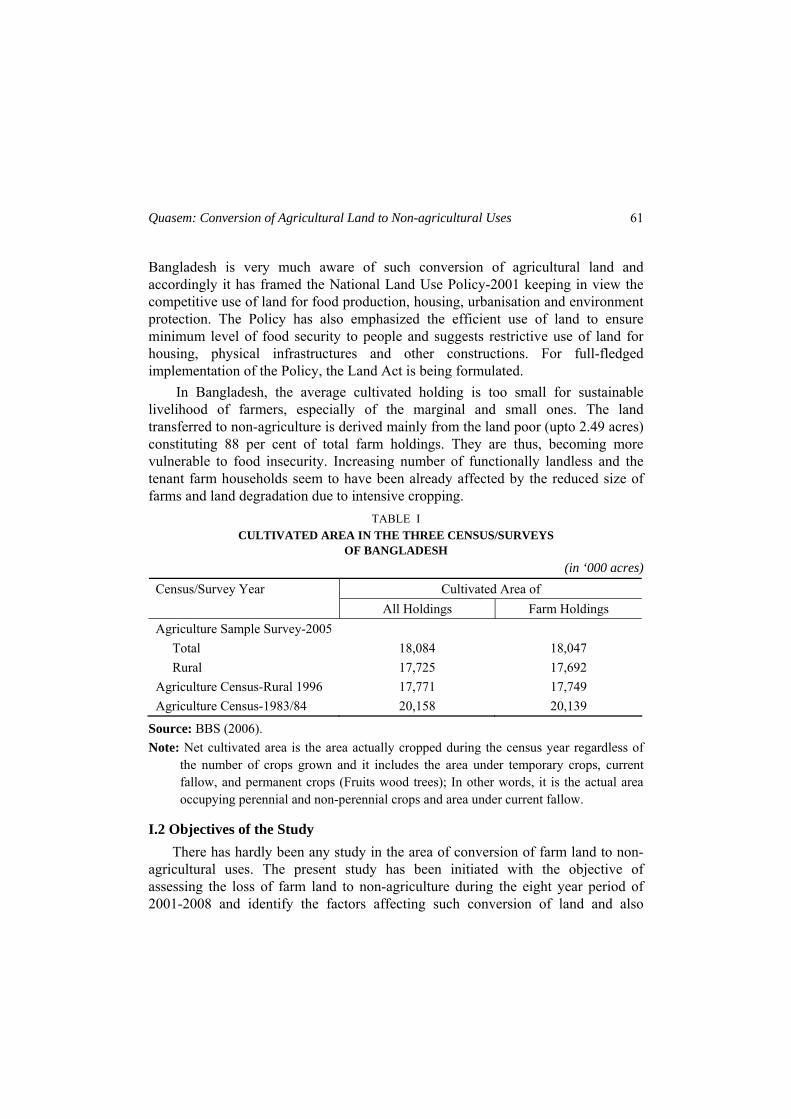

59 Md Abul Quasem : Conversion of Agricultural Land to Non-agricultural Uses in Bangladesh: Extent and Determinants

87 Mia Mahmudur Rahim : Initial Trade Policy Focus of the High Performing Asian Economies: A Critical Assessment

Book Review

103 M Asaduzzaman : The Bengal Delta: Ecology, State and Social Change, 1840-1943

EDITORIAL BOARD : Mustafa K Mujeri Chairman & Executive Editor : Binayak Sen Associate Editor : M Asaduzzaman Member : Zaid Bakht Member : Rushidan Islam Rahman Member

EDITORIAL ADVISORY BOARD: Rehman Sobhan : Nurul Islam : Mosharaff Hossain

CHIEF PUBLICATION OFFICER : Mohammad Meftaur Rahman

International Editorial Advisory Board Amartya Sen Harvard University

Salim Rashid University of Illinois, Urbana- Champaign

Keith B Griffin Professor Emeritus University of California, Riverside

J B Parkinson Professor Emeritus Nottingham University

Nurul Islam IFPRI, Washington, D.C.

Just Faaland Chr. Michelsen Institute, Bergen

A R Khan Professor Emeritus University of California, Riverside

Kaushik Basu Chief Economic Advisor Ministry of Finance North Block, New Delhi

Frances Stewart University of Oxford

S R Osmani University of Ulster

Copyright BIDS, March 2011

Bangladesh Development Studies Vol. XXXIV, March 2011, No. 1

The Impact of 1998 and 2008 Financial Crises on Profitability of Islamic Banks

NOR HAYATI BT AHMAD*

MOHAMAD AKBAR NOOR BIN MOHAMAD NOOR**

The paper investigates the profitability of 78 Islamic banks in 25 countries for the period of 1992-2009. The Fixed Effect Model (FEM) used to analyse profitability shows that profit efficiency is positive and statistically significant with operating expenses against asset, equity, high income countries and non-performing loans against total loans. Interestingly, the empirical results show that more profitable banks are those that have higher operating expenses against asset, more equity against asset and concentrated at high income countries demonstrating close relationship between monetary factors in determining Islamic banks profitability. The findings for 1998 Asian Financial Crisis and 2008 Global Financial Crisis are negative and imply that Islamic banks’ profitability has not been impacted during Asian and Global Financial crises.

I. INTRODUCTION

Islamic banks today exist in all parts of the world, and are looked upon as a viable alternative system which has many things to offer. While it was initially developed to fulfill the needs of Muslims, Islamic banking has now gained universal acceptance. Islamic banking is recognised as one of the fastest growing areas in banking and finance. Since the opening of the first Islamic bank in Egypt in 1963, Islamic banking has grown rapidly all over the world. The number of Islamic financial institutions worldwide has risen to over 300 today in more than 75 countries concentrated mainly in the Middle East and Southeast Asia (with Bahrain and Malaysia the biggest hubs), but are also appearing in Europe and the United States. The Islamic banking total assets worldwide are estimated to have exceed $250 billion and are growing at an estimated pace of 15 per cent a year. Zaher and * Professor of Banking and Risk Management, College of Business, Universiti Utara Malaysia. ** Supply Chain Management Department, PETRONAS Carigali Sdn Bhd, Malaysia and College of Business, Universiti Utara Malaysia.

Bangladesh Development Studies

2

Hassan (2001) suggested that Islamic banks are set to control some 40-50 per cent of Muslim savings by 2009/10.

The Islamic resurgence in the late 1960s and 1970s, further intensified by the 1975 oil price boom, which introduced a huge amount of capital inflows to Islamic countries, has initiated the call for a financial system that allows Muslim to transact in a system that is in line with their religious beliefs. Muslims throughout the world has only conventional financial system to fulfill their financial needs before the re-emergence of the Islamic financial system as an alternative and comply with Islamic principles (Sufian and Noor 2008).

Islamic financial products are aimed primarily to the investors who want to comply with the Islamic laws (Syaria’) that govern Muslim's daily life. The Syaria’ law forbids giving or receiving riba’1 because earning profit from an exchange of money against money is considered immoral and mandate that all financial transactions to be based on real economic activity; and prohibit investment in sectors such as tobacco, alcohol, gambling, and armaments. Despite that, Islamic financial institutions are providing an increasingly broad range of financial services, such as fund mobilisation, asset allocation, payment and exchange settlement services, and risk transformation and mitigation. Despite the growing interest and the rapid growth of the Islamic banking and finance industry, analysis of Islamic banking at a cross-country level is still at its infancy. This could partly be due to the unavailability of data, as most of the Islamic financial institutions, particularly in the Asian region, are not publicly traded.

The aim of this paper is to fill a demanding gap in the literature by providing the latest empirical evidence on the profit performance of Islamic banks in the World during the period 1992 to 2009. The profit efficiency estimate of each Islamic bank is computed by using the least square method of Fixed Effects Model (FEM) to control for bank-specific effects. This paper also seeks to provide clear empirical evidence on the impact of various explanatory variables on the World Islamic banking profitability performance sector that touch several interesting issues, primarily 1998 Asian Financial Crisis and 2008 Global Financial Crisis. To

1 Riba’ the English translation of which is usury is prohibited in Islam and is acknowledged by all Muslims. The prohibition of riba’ is clearly mentioned in the Quran, the Islam's holy book and the traditions of Prophet Muhammad (sunnah). The Quran states: "Believers! Do not consume riba’, doubling and redoubling…" (3.130); "God has made buying and selling lawful and riba’ unlawful… (2:274).

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 3

list a few, the impact of total assets, deposit, inflation and country income level towards Islamic banks profit efficiency.

Since the countries of coverage are span across 25 countries, we will also study the profitability result based on the Islamic bank country of origin. The countries are diversified in terms of the economic activity; we divided the classification by using 2003 Gross National Income (GNI) published by World Bank. According to 2003 GNI per capita, calculated using the World Bank Atlas method2, the income groups are: low income, $765 or less; middle income, $766–$9,385; and high income, $9,386 or more.

Based on 2003 GNI report, some high income countries may also be developing countries. Our samples in the paper will include this particular country and study the differences of country background into the profitability of Islamic Banks. The Gulf Cooperation Council (GCC), for example, are classified as developing high–income countries. This paper unfolds as follows. Section II provides an overview of the related studies in the literature, followed by a section that outlines the method used and choice of input and output variables for the efficiency model. Section IV reports the empirical findings. Section V concludes and offers avenues for future research.

II. REVIEW OF THE LITERATURE

While there have been extensive literatures examining the profit efficiency features of the contemporary banking sector, particularly the U.S. and European banking markets, the work on Islamic banking is still in its infancy. Typically, studies on Islamic bank efficiency have focused on theoretical issues and the empirical work has relied mainly on the analysis of descriptive statistics rather than rigorous statistical estimation (El-Gamal and Inanoglu 2004). However, this is gradually changing as a number of recent studies have sought to apply various frontier techniques to estimate the efficiency of Islamic banks. Hassan (2005) examined the relative cost, profit, X-efficiency, and productivity of the world Islamic Banking industry. The results also show that all five efficiency measures are highly correlated with ROA and ROE, suggesting that these efficiency measures can be used concurrently with the conventional accounting ratios in determining Islamic banks’ performance.

2Atlas conversion factor, calculating gross national income (GNI—formerly referred to as GNP) and GNI per capita in U.S. dollars for certain operational purpose’s, the World Bank uses the Atlas conversion factor. The purpose of the Atlas conversion factor is to reduce the impact of exchange rate fluctuations in the cross-country comparison of national incomes.

Bangladesh Development Studies

4

The empirical studies on the performance of banking sectors have focused on the Returns On Assets (ROA), Returns On Equity (ROE), and net interest margins. It has traditionally explored the impact of bank-specific factors such as risk, market power, size and capitalisation on bank performance. More recently, research has focused on the impact of macroeconomic factors on bank performance.

To date, empirical researches have focused mainly on a specific country mainly the US banking system (Angbazo 1997, DeYoung and Rice 2004, Bhuyan and Williams 2006) and the banking systems in the western and developed countries such as New Zealand (Ho and Tripe 2002), Australia (Williams 2003), UK (Kosmidou et al. 2008) and Greece (Pasiouras and Kosmidou 2007). On the other hand, fewer studies have looked at bank performance in developing economies. Guru, Staunton and Balashanmugam (2002) examine the determinants of bank profitability in Malaysia. They employ a sample of 17 commercial banks during the 1986–1995 periods. The profitability determinants were divided into two main categories, namely the internal determinants (liquidity, capital adequacy and expenses management) and the external determinants (ownership, firm size and economic conditions). The findings revealed that efficient expenses management was one of the most significant in explaining high bank profitability. Among the macro indicators, high interest ratio was associated with low bank profitability and inflation was found to have a positive effect on bank performance.

Heffernan and Fu (2008) examine the performance of different types of Chinese banks during the period 1999–2006. The results suggest that economic value added and the net interest margin do better than the more conventional measures of profitability, namely Return On Average Assets (ROAA) and Return On Average Equity (ROAE). Some macroeconomic variables and financial ratios are significant with the expected signs. Though the type of bank is influential, bank size is not. Neither the percentage of foreign ownership nor bank listings has a discernable effect.

Ben Naceur and Goaied (2008) examine the impact of bank characteristics, financial structure and macroeconomic conditions on Tunisian banks’ net-interest margin and profitability during the period of 1980–2000. They suggest that banks that hold a relatively high amount of capital and higher overhead expenses tend to exhibit higher net-interest margin and profitability levels, while size is negatively related to bank profitability. During the period under study, they find that stock market development has positive impact on banks’ profitability. The empirical findings suggest that private banks are relatively more profitable than their state-

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 5

owned counterparts. The results suggest that macroeconomic conditions have no significant impact on Tunisian banks’ profitability.

Ben Naceur and Omran (2008) examine the influence of bank regulations, concentration, financial and institutional development on Middle East and North Africa (MENA) countries commercial banks’ margin and profitability during the period 1989–2005. They find that bank-specific characteristics, in particular bank capitalisation and credit risk, have positive and significant impact on banks’ net interest margin, cost efficiency and profitability. On the other hand, macroeconomic and financial development indicators have no significant impact on bank performance. More recently, Sufian and Habibullah (2009) examine the determinants of the profitability of the Chinese banking sector during the post-reform period of 2000–2005. The empirical findings suggest that all the determinant variables have statistically significant impact on China banks profitability. However, the impacts are not uniform across bank types. They find that liquidity, credit risk and capitalization have positive impacts on the State-Owned Commercial Banks (SOCBs) profitability, while the impact of cost is negative. Similar to their SOCB counterparts, they find that Joint Stock Commercial Banks (JSCBs) with higher credit risk tend to be more profitable, whereas higher cost results in a lower JSCB profitability level. During the period under study, the empirical findings suggest that size and cost results in a lower city commercial banks (CITY) profitability, whereas the more diversified and relatively better capitalised CITY tend to exhibit higher profitability levels. The impact of economic growth is positive, while growth in money supply is negatively related to the SOCB and CITY profitability levels.

More recently Sufian (2010) suggest that overall economic freedom and business freedom exerts positive impacts on the profitability of the Malaysian banking sector. The positive sign of the coefficient indicates that higher (lower) freedom on the activities that banks can undertake increases (reduces) banks’ profitability, which is consistent with the view that less regulatory control allows banks to engage in various activities enabling banks to exploit economies of scale and scope and generate income from non-traditional sources. Furthermore, higher freedom on entrepreneurs to start businesses is conducive to job creation and consequently increases banks’ profitability. He also find that freedom from corruption has a significant positive impact on Malaysian banks’ profitability.

Bangladesh Development Studies

6

III. METHODOLOGY To test the relationship between bank profitability and the bank-specific and

macroeconomic determinants described earlier, we estimate a linear regression model in the following form:

yit = b0it + bijt Xijt + bejt Xejt + εit (1)

where i refers to an individual bank; t refers to year; yjt refers to the ROE and is the observation of a bank i in a particular year t; Xi represents the internal factors (determinants) of a bank; Xe represents the external factors (determinants) of a bank; εit is a normally distributed variable disturbance term. We apply the Ordinary Least Square (OLS) method, while the standard errors are calculated by using White’s (1980) transformation to control for cross-section heteroskedasticity. As a robustness checks, the empirical setting is also performed by using the least square method of Fixed Effects Model (FEM) to control for bank-specific effects. The opportunity to use a fixed effects rather than a random effects model has been tested with the Hausman test. Extending equation (1) to reflect the numbers of explanatory variables as described in Table 1, the baseline model is formulated as follows:

φjt = α + β1OE/TA + β2EQUITY/TA + β3LNTA

+ β4LOANS/TA + β5LNDEPO+ β6NPL/TL

+ β7LNGDP+ β8INFLATION + β9MARKET+

β10ΣDUMMY (AFC, GFC, MENA, ASIA, LOW, MEDIUM, HIGH)+ εj

The dependent variable is ROE; ROE is proxy measure of bank’s profitability calculated as net income after tax divided by total shareholders’ equity; OE/TA is a measure of bank operating expenses against total asset; EQUITY/ TA is a measure of bank leverage intensity measured by banks’ total shareholders’ equity divided by total assets; LNTA is the size of the bank’s total asset measured as the natural logarithm of total bank assets; LOANS/TA is a measure of bank’s loans intensity calculated as the ratio of total loans to bank total assets; LNDEPO is a measure of bank’s market share calculated as a natural logarithm of total bank deposits;

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 7

NPL/TL is a measure of banks risk calculated as non performing loans divided by total loans; LNGDP is country gross domestic product of the country’s measured as the natural logarithm of gross domestic product; INFLATION is country inflation rates; MARKET is overall stock market capitalization size of the country’s bank operated; DUMMY is a dummy variables which takes a value of 1 for AFC, 0 otherwise; same apply for GFC, MENA, ASIA, LOW, MEDIUM, and HIGH where each variable takes a value of 1, 0 otherwise.

III.1 Performance Measure

In the literature, bank profitability, typically measured by the ROA and the ROE, is usually expressed as a function of internal and external determinants. Internal determinants are factors that are mainly influenced by a bank’s management decisions and policy objectives. Such profitability determinants are the level of liquidity, provisioning policy, capital adequacy, expenses management and bank size. On the other hand, the external determinants, both industry and macroeconomic related, are variables that reflect the economic and legal environments where the financial institution operates. Following Pasiouras and Kosmidou (2007), Ben Naceur and Goaied (2008), Kosmidou (2008), and Sufian and Habibullah (2009), among others, the dependent variable used in this study is ROA while our study adopted ROE as our dependent variables. ROE reflects how effectively a bank management utilising its shareholders funds in providing returns. Since ROA tends to be lower for financial intermediaries, most banks utilise financial leverage heavily to increase ROE to competitive levels.

III.2 Definition and the Choice of Variables Due to entry and exit factor, the efficiency frontier is constructed by using an

unbalanced sample of Islamic banks operating in the World during the period 1992-2009 (see Appendix 1). We collected our bank-specific variables from the financial statements of a sample of World Islamic banks operating over the period 1992–2009 available in the Bankscope database by IBCA and sourced from individual Islamic bank’s annual balance sheet and income statements. The BankScope database converts the data to common international standards to facilitate comparisons and all financial information is reported both in local currency and in US dollar. We also convert local currency that not US dollar into US dollar for data sourced directly

Bangladesh Development Studies

8

from the Islamic banks. We are able to collect several internal and external determinants as listed in Table I that stated internal as bank characteristic and external as economic condition.

III.3 Internal Determinants The bank characteristic variables included in the regressions are Total Loans

divided by Total Assets (LOANS/TA), Log of Total Assets (LNTA), Non Performing Loans divided by Total Loans (NPL/TL), Log of Total Deposit (LNDEPO), Operating Expenses divided by Total Assets (OE/TA) and book value of stockholders’ equity as a fraction of total assets (EQUITY/ TOTAL ASSET).

Liquidity risk, arising from the possible inability of banks to accommodate decreases in liabilities or to fund increases on the assets’ side of the balance sheet, is considered an important determinant of bank profitability. The loans market, especially credit to households and firms, is risky and has a greater expected return than other bank assets, such as government securities. Thus, one would expect a positive relationship between liquidity (LOANS/TA) and profitability (Bourke 1989). It could be the case, however, that the fewer the funds tide up in liquid investments, the higher we might expect the profitability to be (Eichengreen and Gibson 2001). The LNTA variable is included in the regression as a proxy of size to capture the possible cost advantages associated with size (economies of scale). This variable controls for cost differences and product and risk diversification according to the size of the bank. The first factor could lead to a positive relationship between size and bank profitability if there are significant economies of scale (Akhavein, Berger and Humphrey 1997, Bourke 1989, Molyneux and Thornton 1992, Bikker and Hu 2002, Goddard,Molyneox and Wilson 2004), whereas the second to a negative one, if increased diversification leads to lower credit risk and thus lower returns.

Other researchers, however, conclude that marginal cost savings can be achieved by increasing the size of the banking firm, especially as markets develop (Berger et al. 1995, Boyd and Runkle 1993). In essence, LNTA may lead to positive effects on bank profitability if there are significant economies of scale. On the other hand, if increased diversification leads to higher risks, the variable may exhibit negative effects.

The ratio of Operating Expenses to Total Assets (OE/TA) is used to provide information on the variations of bank operating costs. The variable represents total amount of wages and salaries, as well as the costs of running branch office facilities. For the most part, the literature argues that reduced expenses improve the efficiency and hence raise the profitability of a financial institution, implying a negative

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 9

relationship between operating expenses ratio and profitability (Bourke 1989). However, Molyneux and Thornton (1992) observed a positive relationship, suggesting that high profits earned by banks may be appropriated in the form of higher payroll expenditures paid to more productive human capital. In any case, it should be appealing to identify the dominant effect in a developing banking environment like Malaysia. EQUITY/TA is included in the regressions to examine the relationship between profitability and bank capitalisation. Even though leverage (capitalisation) has been demonstrated to be important in explaining the performance of financial institutions, its impact on bank profitability is ambiguous. As lower capital ratios suggest a relatively risky position, one might expect a negative coefficient on this variable (Berger 1995). However, it could be the case that higher levels of equity would decrease the cost of capital, leading to a positive impact on bank profitability (Molyneux 1993). Moreover, an increase in capital may raise expected earnings by reducing the expected costs of financial distress, including bankruptcy (Berger 1995).

III.4 External Determinants The economic condition variables included in the regressions are Total Loans

divided by Total Assets (LOANS/TA), Log of Total Assets (LNTA), Non Performing Loans divided by Total Loans (NPL/TL), Log of Total Deposit (LNDEPO), Operating Expenses divided by Total Assets (OE/TA) and book value of stockholders’ equity as a fraction of total assets (EQUITY/ TOTAL ASSET).

Bank profitability is sensitive to macroeconomic conditions despite the trend in the industry towards greater geographic diversification and larger use of financial engineering techniques to manage risk associated with business cycle forecasting., Higher economic growth generally encourages bank to lend more and permits them to charge higher margins, as well as improving the quality of their assets. Neely and Wheelock (1997) use per-capita income and suggest that this variable exerts a strong positive effect on bank earnings. Demirguc-Kunt and Huizinga (2001) and Bikker and Hu (2002) identify possible cyclical movements in bank profitability, i.e. the extent to which bank profits are correlated with the business cycle. Their findings suggest that such correlation exists, although the variables used were not direct measures of the business cycle. To measure the relationship between economic and market conditions and bank profitability, Natural Log of Gross Domestic Product (LNGDP) and INFL (the inflation rate) are used. Bank performance is expected to be sensitive to macroeconomic control variables. The impact of macroeconomic variables on bank performance has recently been highlighted in the literature. We use the log of GDP as a control for cyclical output

Bangladesh Development Studies

10

effects, which we expect to have a positive influence on bank profitability. As GDP growth slows down, in particular during recessions, credit quality tends to deteriorate and default rate increases, thus reducing bank profitability. We also account for macroeconomic risk by controlling for the rate of inflation (INFL). The extent to which inflation affects bank profitability depends on whether future movements in inflation are fully anticipated, which in turn depends on the ability of banks to accurately forecast its future movements. An inflation rate that is fully anticipated raises profits as banks can appropriately adjust interest rates to increase revenues, while an unanticipated change could raise costs due to imperfect interest rate adjustment (Perry 1992). Earlier studies by among others Bourke (1989), Molyneux and Thornton (1992), Demirguc-Kunt and Huizinga (1999) have found a positive relationship between inflation and bank performance.

To examine the impact of market capitalisation on bank profitability, an overall index, MARKET has been added to the variables list. We introduce 2 variables AFC and GFC to identify the impact of 1998 Asian Financial Crisis and 2008 Global Financial Crisis towards Islamic banks profitability. It has been entered in regression models 2, 4 and 6 and 3, 5 and 7 respectively. To further examine the Islamic banks origin impact on bank profitability, we introduce region index, namely MENA and ASIA, to represent banks origin from Middle East and North Africa (MENA) and Asian countries (ASIA) is entered in regression models 4 and 5 and 6 and 7 respectively. Finally, to test impact of country income level towards Islamic bank profitability, we introduce LOW, MEDIUM and HIGH as variables and been entered in regression models 8, 9 and 10 respectively.

IV. RESULTS

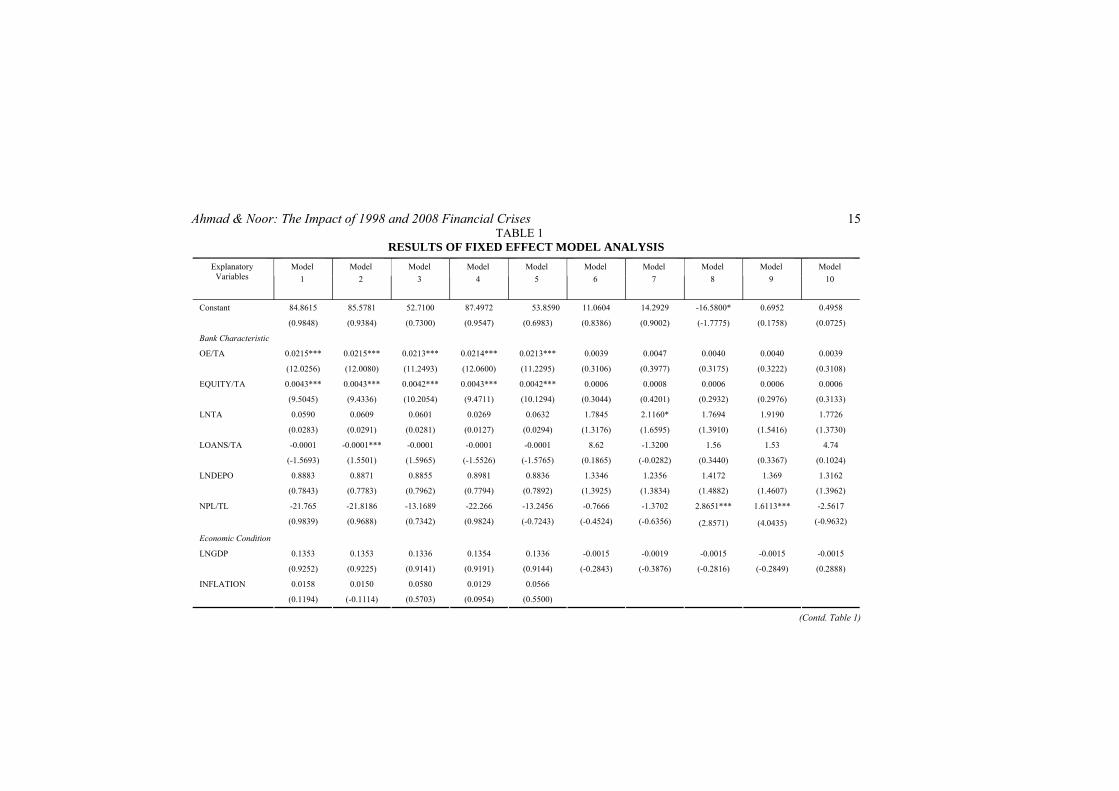

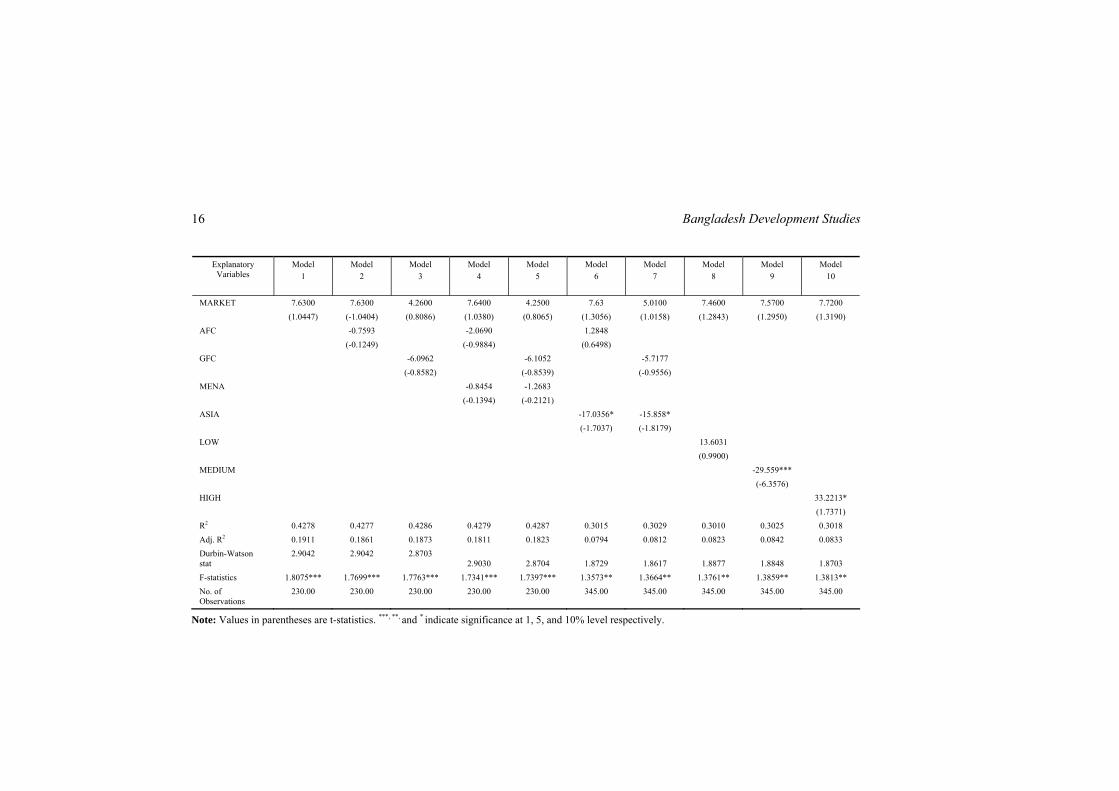

In this section, we will discuss the performance profitability of the World Islamic banking sectors, measured by the Fixed Effect Model (FEM). The regression results focusing on the relationship between bank profitability and the explanatory variables are presented in Table 1.

IV.1 The Islamic Banks’ Profitability Performance Based on literature, bank profitability is typically measured by return on equity

(ROE) and/ or return on asset (ROA) and usually expressed as a function of internal and external determinants.

Internal determinants are factors that are mainly influenced by a bank’s management decisions and policy objectives. Such profitability determinants are the level of liquidity, provisioning policy, capital adequacy, expenses management, and

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 11

bank size. On the other hand, the external determinants, both industry and macroeconomic related, are variables that reflect the economic and legal environments where the financial institution operates (Sufian and Habibullah 2009).

We will select ROE as dependent variable based on several reasons. Of all the fundamental ratios that measure profitability, one of the most important is return on equity. It is a basic test of how effectively a company's management uses investors' money. By measuring how much earnings a company can generate from assets, ROE offers a gauge of profit-generating efficiency. Firms that do a good job of milking profit from their operations typically have a competitive advantage, a feature that normally translates into superior returns for investors. The other factor as to why ROE has been selected is due to DuPont analysis3 that breaks down ROE into three distinct elements. This analysis will enable details analysis to understand the source of superior (or inferior) return by comparison with companies in similar industries (or between industries). DuPont analysis tells us that ROE is affected by three things: Operating efficiency, which is measured by profit margin; Asset use efficiency, which is measured by total asset turnover; and Financial leverage, which is measured by the equity multiplier.

The regression results focusing on the relationship between bank profitability and the explanatory variables are presented in Table 1. The model performs reasonably well with most variables remaining stable across the various regressions tested. The explanatory power of the models is reasonably high, while the F-statistics for all models is significant at the 1% level for model 1 to model 5 and 5% level for model 6 to model 10. The adjusted R2 is 18% for model 1 to 5 and 8% for model 6 to 10, this is more lower compared to Kosmidou et al. (2008) at 92% and Sufian (2010) at 75%.

The ratio of Operating Expenses to Total Assets (OE/TA) is used to provide information on the bank operating costs against asset have. The variable represents total amount of overhead expenses, wages and salaries, as well as the costs of running branch office facilities inclusive utilities, stationary, etc. against bank assets. For the most part, the literature argues that reduced expenses improve the efficiency and hence raise the profitability of a financial institution, implying a negative relationship between operating expenses ratio and profitability (Bourke

3 A method of performance measurement that was started by the DuPont Corporation in the 1920s. With this method, assets are measured at their gross book value rather than at net book value in order to produce a higher return on equity (ROE). It is also known as “DuPont identity.”

Bangladesh Development Studies

12

1989). The result exhibits positive relationship with bank profitability at all 10 models with 5 models is statistically significant at the 1% level. The result justification that talent is attracted to benefit and financial returns offered by organisation in working environment is also applicable in Islamic bankings on justifying strong positive relationship between bank profitability with OE/TA ratio. This is consistent with Molyneux and Thornton (1992) who observed a positive relationship, suggesting that high profits earned by banks may be appropriated in the form of higher payroll expenditures paid to more productive human capital.

Referring to the impact of capitalisation, it is observed from Table 1 that EQUITY/TA exhibits positive relationship with profitability and is statistically significant at 1% level. But when we control for GNI country income, the result is still positive but not significant. This is consistent with previous studies (Isik and Hassan 2003, Staikouras and Wood 2003, Sufian and Habibullah 2009) providing support to the argument that well capitalised banks face lower costs of going bankrupt, thus lowers their funding cost, or that they have lower needs for external funding resulting in higher profitability. Nevertheless, strong capital structure is essential for banks in emerging economies since it provides additional strength to withstand financial crises and increased safety for depositors during unstable macroeconomic conditions.

The LNTA variable is included in the regression models as a proxy of size to capture the possible cost advantages associated with size (economies of scale). This variable controls for cost differences and product and risk diversification according to the size of the bank. The findings indicate that LNTA, as a proxy of bank’s size, shows positive sign, suggesting larger banks tend to be more profitable. Concerning the liquidity results, LOANS/TA has a negative relationship with profit efficiency levels. There may be decreasing returns to scale through the allocation of fixed costs (e.g. research or risk management) over a higher volume of services or from efficiency gains from a specialised workforce, while LNDEPO reveals positive relationship with profit efficiency. Although it is not statistically significant at the considered levels, it is perceived that the more deposit the bank’s receive, higher will be loan disbursement that is positively correlated with bank revenue translating into higher profits.

For credit risk result, the impact of credit risk (NPL/TL) has a negative relationship with bank profitability, this generally suggesting that banks with higher credit risk exhibit lower profitability levels. The results imply that World Islamic banks should focus more on credit risk management, which has been proven to be problematic in the recent past. Sufian and Habibullah (2009) also find similar result

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 13

and stated that serious banking problems have arisen from the failure of financial institutions to recognise impaired assets and create reserves for writing off these assets. An immense help towards smoothing these anomalies would be provided by improving the transparency of the banking sector, which in turn will assist banks to evaluate credit risk more effectively and avoid problems associated with hazardous exposure.

The results about the impact of macroeconomic conditions of Malaysian banks’ profitability are mixed. The empirical findings suggest that LNGDP has a positive relationship with bank profitability when we run for model 1 to model 5. But once we remove inflation from model 6 to model 10 because of multicollinearity problem, it becomes negative relationship. On the other hand, INFLATION exhibits positive sign for model 1 to model 5, for model 6 to model 10 the inflation variable has been dropped from the regression due to multicollinearity problem with GNI variables (LOW, MEDIUM AND HIGH). While market capitalisation represents by MARKET exhibits positive relationship for all 10 models.

As a robustness check, a binary dummy variable AFC, which takes a value of 1 for the year 1998 where Asian Financial Crisis happened, and 0 otherwise is included in models 2, 4 and 6 regressions. The regression result in Table 1 stated negative relationships between AFC and bank profitability for all 3 models. The same procedure repeated for GFC where value of 1 for the year 2008 represented Global Financial Crisis happened, and 0 otherwise is included in models 3, 5 and 7 regressions. The GFC result is consistent with AFC that has negative relationship with bank profitability for all 3 models.

Since the coverage of studied is from the whole world, we extend dummy variables for identifying impact on regions where Islamic banks concentrated the most, which takes a value of 1 for banks from the Middle East and North Africa (MENA) region, and 0 otherwise is included in models 4 and 5 of the regression. The results are presented Table 1, which stated negative relationship between MENA and profitability. Then we test the same method for bank originated from Asian, value of 1 for banks from the Asian (ASIA) region and 0 otherwise is included in model 6 and 7 of the regression. The result exhibits negative relationship with profitability and is statistically significant at 10% level. The result

Bangladesh Development Studies

14

is interesting since Asian Islamic banks are less profitable than MENA Islamic banks.

Finally we test the impact of country income classification where the Islamic banks operated with profitability. The three GNI country incomes classify as LOW, MEDIUM and HIGH in the regression models 8, 9 and 10 of Table 1. Each model starts with LOW will take value of 1 for Islamic banks originated from World Bank GNI classification as low income country and 0 otherwise. The same procedure applies for MEDIUM and HIGH income countries. Model 8 represents regression with LOW income countries and the result in Table 1 stated positive relationship with profitability. On the other hand, MEDIUM income countries in model 9 have a negative relationship and significant at 1% level. The result implies that Islamic banks originated from MEDIUM income countries have negative relationship with profitability. This contradicts with basic understanding that when people have money, banking sector will benefit from it via higher deposits, more subscribers in financial product, etc. It may be the result of consumers in middle income countries not engaging with banking product and facility that contribute to these negative relationships with bank profitability. Based on Table 1, result for HIGH income countries found positive relationship and statistically significant at 10% level. This is interesting since MEDIUM and HIGH income countries have different results finding between one and another. The result supports, Pareto rules of 80/20 where 20 per cent population will contribute 80 per cent of profitability; most of HIGH income countries in the study are relatively smaller in population. We may stated that profitability of HIGH income countries is correlated with understanding that people or organisation will engage more with banking product that can lead towards profitability of the Islamic banks.

The results above seem to suggest that most of the bank trait variables continued to remain robust in the directions and significance level. Favourable economic conditions during the period of study may have fuelled higher demand for Islamic banking products and services, reduced default loan probabilities, and thus resulting in profitability.

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 15TABLE 1

RESULTS OF FIXED EFFECT MODEL ANALYSIS Explanatory

Variables Model

1 Model

2 Model

3 Model

4 Model

5 Model

6 Model

7

Model 8

Model 9

Model 10

84.8615 85.5781 52.7100 87.4972 53.8590 11.0604 14.2929 -16.5800* 0.6952 0.4958 Constant

(0.9848) (0.9384) (0.7300) (0.9547) (0.6983) (0.8386) (0.9002) (-1.7775) (0.1758) (0.0725)

Bank Characteristic

0.0215*** 0.0215*** 0.0213*** 0.0214*** 0.0213*** 0.0039 0.0047 0.0040 0.0040 0.0039 OE/TA

(12.0256) (12.0080) (11.2493) (12.0600) (11.2295) (0.3106) (0.3977) (0.3175) (0.3222) (0.3108)

0.0043*** 0.0043*** 0.0042*** 0.0043*** 0.0042*** 0.0006 0.0008 0.0006 0.0006 0.0006 EQUITY/TA

(9.5045) (9.4336) (10.2054) (9.4711) (10.1294) (0.3044) (0.4201) (0.2932) (0.2976) (0.3133)

0.0590 0.0609 0.0601 0.0269 0.0632 1.7845 2.1160* 1.7694 1.9190 1.7726 LNTA

(0.0283) (0.0291) (0.0281) (0.0127) (0.0294) (1.3176) (1.6595) (1.3910) (1.5416) (1.3730)

-0.0001 -0.0001*** -0.0001 -0.0001 -0.0001 8.62 -1.3200 1.56 1.53 4.74 LOANS/TA

(-1.5693) (1.5501) (1.5965) (-1.5526) (-1.5765) (0.1865) (-0.0282) (0.3440) (0.3367) (0.1024)

0.8883 0.8871 0.8855 0.8981 0.8836 1.3346 1.2356 1.4172 1.369 1.3162 LNDEPO

(0.7843) (0.7783) (0.7962) (0.7794) (0.7892) (1.3925) (1.3834) (1.4882) (1.4607) (1.3962)

-21.765 -21.8186 -13.1689 -22.266 -13.2456 -0.7666 -1.3702 2.8651*** 1.6113*** -2.5617 NPL/TL

(0.9839) (0.9688) (0.7342) (0.9824) (-0.7243) (-0.4524) (-0.6356) (2.8571) (4.0435) (-0.9632)

Economic Condition

0.1353 0.1353 0.1336 0.1354 0.1336 -0.0015 -0.0019 -0.0015 -0.0015 -0.0015 LNGDP

(0.9252) (0.9225) (0.9141) (0.9191) (0.9144) (-0.2843) (-0.3876) (-0.2816) (-0.2849) (0.2888)

0.0158 0.0150 0.0580 0.0129 0.0566 INFLATION

(0.1194) (-0.1114) (0.5703) (0.0954) (0.5500)

(Contd. Table 1)

Bangladesh Development Studies

16

Explanatory Variables

Model 1

Model 2

Model 3

Model 4

Model 5

Model 6

Model 7

Model 8

Model 9

Model 10

7.6300 7.6300 4.2600 7.6400 4.2500 7.63 5.0100 7.4600 7.5700 7.7200 MARKET (1.0447) (-1.0404) (0.8086) (1.0380) (0.8065) (1.3056) (1.0158) (1.2843) (1.2950) (1.3190)

-0.7593 -2.0690 1.2848 AFC (-0.1249) (-0.9884) (0.6498) -6.0962 -6.1052 -5.7177 GFC (-0.8582) (-0.8539) (-0.9556) -0.8454 -1.2683 MENA (-0.1394) (-0.2121) -17.0356* -15.858* ASIA (-1.7037) (-1.8179) 13.6031 LOW (0.9900) -29.559*** MEDIUM (-6.3576) 33.2213* HIGH (1.7371)

R2 0.4278 0.4277 0.4286 0.4279 0.4287 0.3015 0.3029 0.3010 0.3025 0.3018 Adj. R2 0.1911 0.1861 0.1873 0.1811 0.1823 0.0794 0.0812 0.0823 0.0842 0.0833 Durbin-Watson stat

2.9042 2.9042 2.8703 2.9030 2.8704 1.8729 1.8617 1.8877 1.8848 1.8703

F-statistics 1.8075*** 1.7699*** 1.7763*** 1.7341*** 1.7397*** 1.3573** 1.3664** 1.3761** 1.3859** 1.3813** No. of Observations

230.00 230.00 230.00 230.00 230.00 345.00 345.00 345.00 345.00 345.00

Note: Values in parentheses are t-statistics. ***, **, and * indicate significance at 1, 5, and 10% level respectively.

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 17

V. CONCLUSIONS AND DIRECTIONS FOR FUTURE RESEARCH

By using an unbalanced bank level panel data, the present study attempts to examine World Islamic Banks performance profitability during the period 1992-2009. We find that the larger, more diversified, and better capitalized banks are relatively more profitable. The empirical findings seem to support the expense preference theory, which could be explained by the more highly qualified and professional management that requires higher remuneration packages. On the other hand, we find that higher credit risk has negative impact on bank profitability.

In this paper, we examine the profitability performance of the World Islamic banks that consist of 25 countries namely Bahrain, Bangladesh, Brunei, Egypt, Gambia, Indonesia, Iran, Iraq, Jordan, Kuwait, Malaysia, Mauritania, Pakistan, Palestine, Saudi Arabia, Singapore, Syria, Thailand, Turkey, United Arab Emirates, Qatar, Yemen, South Africa, Sudan and Yemen during the period of 1992-2009 with 78 Islamic banks involved. The profitability performance of individual banks is evaluated using Fixed Income Model (FEM) against a set of bank specific variables.

The Fixed Effect Model (FEM) result that has been used for analysing profitability proposed that profit efficiency is positively and significantly associated with operating expenses against asset, equity, HIGH income countries and non performing loans against total loans specifically for models 8 and 9 that positively significant at 1 per cent level. The empirical results show that more profitable banks are those that have higher operating expenses against asset, more equity against asset and concentrated at high income countries. The results also suggest that favourable economic conditions exhibit positive relationship with profit efficiency. The impact of 1998 and 2008 financial crises have been examined in the study. The finding for both crises is negative and non significant. It implies that world Islamic banks’ profitability does not impacted during Asian and Global Financial crises.

Due to its limitations, the paper could be extended in a variety of ways. Firstly, the scope of this study could be further extended to investigate other variables such as taxation and regulation indicators. Secondly, it is suggested that further analysis into the investigation of the Islamic banking sector efficiency to consider risk exposure factors. Finally, investigation of changes in productivity over time as a result of technical change or technological progress or regress by employing the Malmquist Total Factor Productivity Index could yet be another extension to the paper.

Despite these limitations, the findings of this study are expected to contribute significantly to the existing knowledge on the operating performance of the World Islamic banking industry. Nevertheless, the study has also provided further insight

Bangladesh Development Studies

18

to bank specific management as well as the policymakers with regard to attaining optimal utilisation of capacities, improvement in managerial expertise etc. This may also facilitate directions for sustainable competitiveness of World Islamic banking operations in the future.

REFERENCES

Akhavein, J., A.N. Berger and D.B. Humphrey. 1997. “The Effects of Megamergers on Efficiency and Prices: Evidence from a Bank Profit Function.” Review of Industrial Organization, 12(1):95–139.

Angbazo, L. 1997. “Commercial Bank Net Interest Margins, Default Risk, Interest Rate Risk, and Off Balance sheet Banking.” Journal of Banking and Finance, 21:55–87.

Berger, A.N. 1995. “The Relationship between Capital and Earnings in Banking.” Journal Money, Credit and Banking, 27:432–456.

Berger, A.N. and D.B.Humphrey.1997. “Efficiency of Financial Institutions: International Survey and Directions for Future Research.” European Journal of Operational Research, 98 (2): 175-212.

Ben Naceur, S. and M.Goaied.2008. “The Determinants of Commercial Bank Interest Margin and Profitability: Evidence from Tunisia.” Frontiers in Finance and Economics. 5 (1):106–130.

Ben Naceur, S. and M.Omran.2008. “The Effects of Bank Regulations, Competition and FinancialReforms on Mena Banks’ Profitability.” Working Paper, Economic Research Forum,Cairo, Egypt.

Berger, A.N., A.K. Kashyap and J.M. Scalise.1995. “The Transformation of the U.S. Banking Industry: What a Long, Strange Trip It’s Been.” Brookings Papers on Economic Activity, 2: 55-218.

Bhuyan, R. and D.L. Williams. 2006. “Operating Performance of the US Commercial Banks after IPOs: An Empirical Evidence.” Journal of Commercial Banking and Finance, 5 (1–2):68–95.

Bikker, J. and H. Hu. 2002. “Cyclical Patterns in Profits, Provisioning and Lending of Banks and Procyclicality of the New Basel Capital Requirements.” BNL Quarterly Review, 221:143–175.

Bourke, P. 1989. “Concentration and Other Determinants of Bank Profitability in Europe, North America and Australia.” Journal of Banking and Finance, 13:65–79.

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 19

Boyd, J. and D. Runkle.1993. “Size and Performance of Banking Firms: Testing the Predictions Theory.” Journal of Monetary Economics, 31:47–67.

Demirguc-Kunt, A. and H.Huizinga.1999. “Determinants of Commercial Bank Interest Margins and Profitability: Some International Evidence.” World Bank Economic Review, 13:379–408.

Demirguc-Kunt, A. and H. Huizinga. 2001. “Financial Structure and Bank Profitability.” In Demirguc-Kunt, A. and Levine, R. (eEds.), Financial Structure and Economic Growth: A Cross Country Comparison of Banks, Markets and Development. Cambridge, MA :MIT Press.

DeYoung, R. and T. Rice.2004. “Non-interest Income and Financial Performance at US Commercial Banks.” Financial Review, 39(1):101–127.

Eichengreen, B. and H.D. Gibson. 2001. “Greek Banking at the Dawn of the New Millennium.” Discussion Paper, Centre of Economic and Policy Research, London, UK.

Goddard, J., P. Molyneux and J. Wilson. 2004. “Dynamic of Growth and Profitability in Banking.” Journal Money, Credit and Banking, 36:1069–1090.

Guru, B.K., Staunton, J. and B. Balashanmugam.2002. “Determinants of Commercial Bank Profitability in Malaysia.” Multimedia University Working Paper, Cyberjaya, Malaysia.

Hassan, M.K. 2005. “The Cost, Profit and X-Efficiency of Islamic Banks.” Paper presented at the 12th ERF Annual Conference, 19th-21st December, Egypt.

Heffernan, S. and M. Fu. 2008. “The Determinants of Bank Performance in China.” EMG Working Paper Series.

Ho, M.T. and D. Tripe.2002. “Factors Influencing the Performance of Foreign Owned Banks in New Zealand.” Journal International Financial Markets, Institutions and Money, 12:341–357.

Isik, I. and M.K. Hassan. 2003. “Efficiency, Ownership and Market Structure, Corporate Control and Governance in the Turkish Banking Industry.” Journal of Business Finance and Accounting ,30 (9-10):1363-1421.

Kosmidou, K. 2008. “The Determinants of Banks’ Profits in Greece during the Period of EU Financial Integration.” Managerial Finance, 34 (3):146–159.

Molyneux, P. 1993. Structure and Performance in European Banking. University of Wales Bangor, Bangor, UK. Mimeo.

Molyneux, P. and J. Thornton. 1992. “Determinants of European Bank Profitability: A Note.” Journal Banking and Finance, 16:1173–1178.

Bangladesh Development Studies

20

Neely, M. and D. Wheelock.1997. “Why Does Bank Performance Vary Across States?” Federal Reserve Bank St. Louis Review, March:27–38.

Pasiouras, F. and K.Kosmidou. 2007. “Factors Influencing the Profitability of Domestic and Foreign Commercial Banks in the European Union.” Research in International Business and Finance, 21:223–237.

Perry, P. 1992. “Do Banks Gain or Lose from Inflation.” Journal Retail Banking, 14 (2): 25–40.

Staikouras, C. and G.Wood. 2003. “The Determinants of Bank Profitability in Europe.” Paper presented at the European Applied Business Research Conference, Venice, 9-13 June.

Sufian, F. and M.A.N.M. Noor. 2009. “The Determinants of Islamic Bank’s Efficiency Changes: Empirical Evidence from the MENA and Asian Countries Islamic Banking Sectors.” International Journal of Islamic and Middle Eastern Finance and Management, 2(2):120-138

Sufian, F. and M.S. Habibullah. 2009. “Bank Specific and Macroeconomic Determinants of Bank Profitability: Empirical Evidence from the China Banking Sector.” Frontiers of Economics in China, 4 (2):274–291.

Sufian, F., M.S., Habibullah. 2010. “Does Economic Freedom Fosters Banks’ Performance? Panel Evidence from Malaysia.” Journal of Contemporary Accounting & Economics, doi: 10.1016/j.jcae.2010.09.003

Sufian, F. 2010. “Developments in the Performance of the Malaysian Banking Sector: Opportunity Cost of Regulatory Compliance.” Int. J. Business Competition and Growth, 1 (1):85–103.

White, H.J. 1980. “A Heteroskedasticity-consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity.” Econometrica, 48:817–838.

Williams, B. 2003. “Domestic and International Determinants of Bank Profits: Foreign Banks in Australia.” Journal of Banking and Finance, 27:1185–1210.

Zaher, T.S. and M.K. Hassan. 2001. “A Comparative Literature Survey of Islamic Finance and Banking.” Financial Markets, Institutions & Instruments ,10 (4): 155-199.

Ahmad & Noor: The Impact of 1998 and 2008 Financial Crises 21

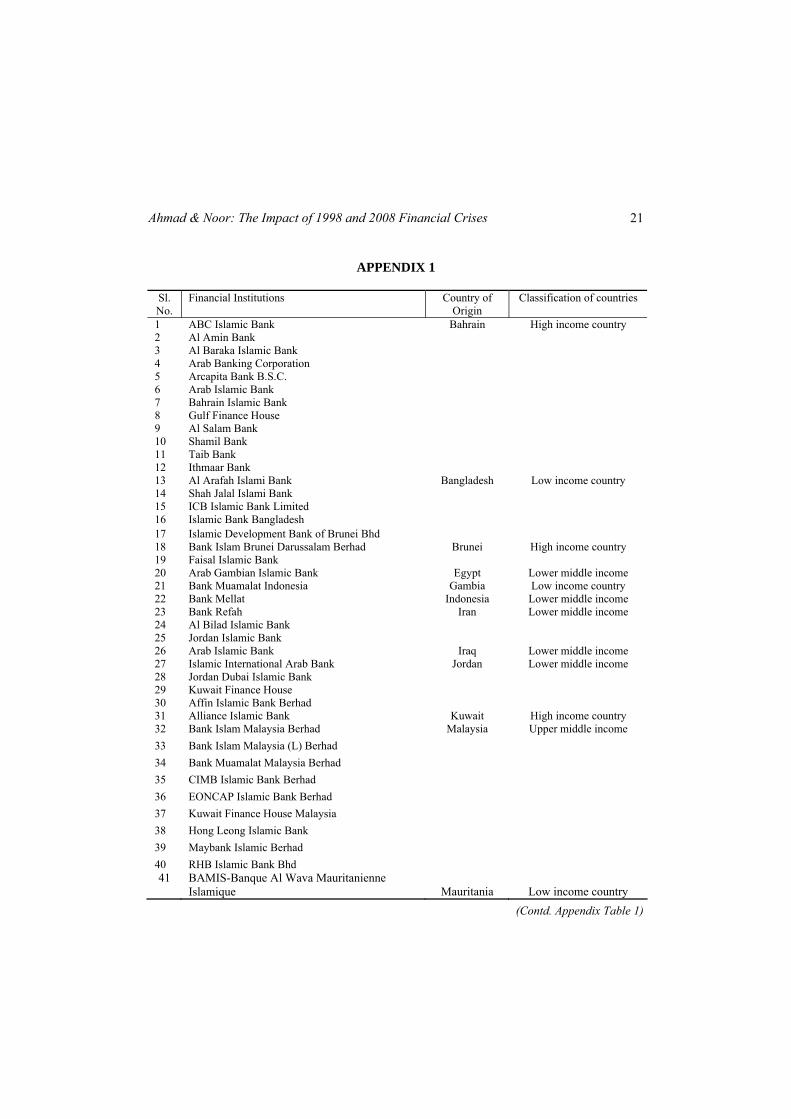

APPENDIX 1

Sl. No.

Financial Institutions Country of Origin

Classification of countries

1 ABC Islamic Bank Bahrain High income country 2 Al Amin Bank 3 Al Baraka Islamic Bank 4 Arab Banking Corporation 5 Arcapita Bank B.S.C. 6 Arab Islamic Bank 7 Bahrain Islamic Bank 8 Gulf Finance House 9 Al Salam Bank 10 Shamil Bank 11 Taib Bank 12 Ithmaar Bank 13 Al Arafah Islami Bank Bangladesh Low income country 14 Shah Jalal Islami Bank 15 ICB Islamic Bank Limited 16 Islamic Bank Bangladesh 17 Islamic Development Bank of Brunei Bhd 18 Bank Islam Brunei Darussalam Berhad Brunei High income country 19 Faisal Islamic Bank 20 Arab Gambian Islamic Bank Egypt Lower middle income 21 Bank Muamalat Indonesia Gambia Low income country 22 Bank Mellat Indonesia Lower middle income 23 Bank Refah Iran Lower middle income 24 Al Bilad Islamic Bank 25 Jordan Islamic Bank 26 Arab Islamic Bank Iraq Lower middle income 27 Islamic International Arab Bank Jordan Lower middle income 28 Jordan Dubai Islamic Bank 29 Kuwait Finance House 30 Affin Islamic Bank Berhad 31 Alliance Islamic Bank Kuwait High income country 32 Bank Islam Malaysia Berhad Malaysia Upper middle income 33 Bank Islam Malaysia (L) Berhad 34 Bank Muamalat Malaysia Berhad 35 CIMB Islamic Bank Berhad 36 EONCAP Islamic Bank Berhad 37 Kuwait Finance House Malaysia 38 Hong Leong Islamic Bank 39 Maybank Islamic Berhad 40 RHB Islamic Bank Bhd 41 BAMIS-Banque Al Wava Mauritanienne

Islamique Mauritania Low income country (Contd. Appendix Table 1)

Bangladesh Development Studies

22

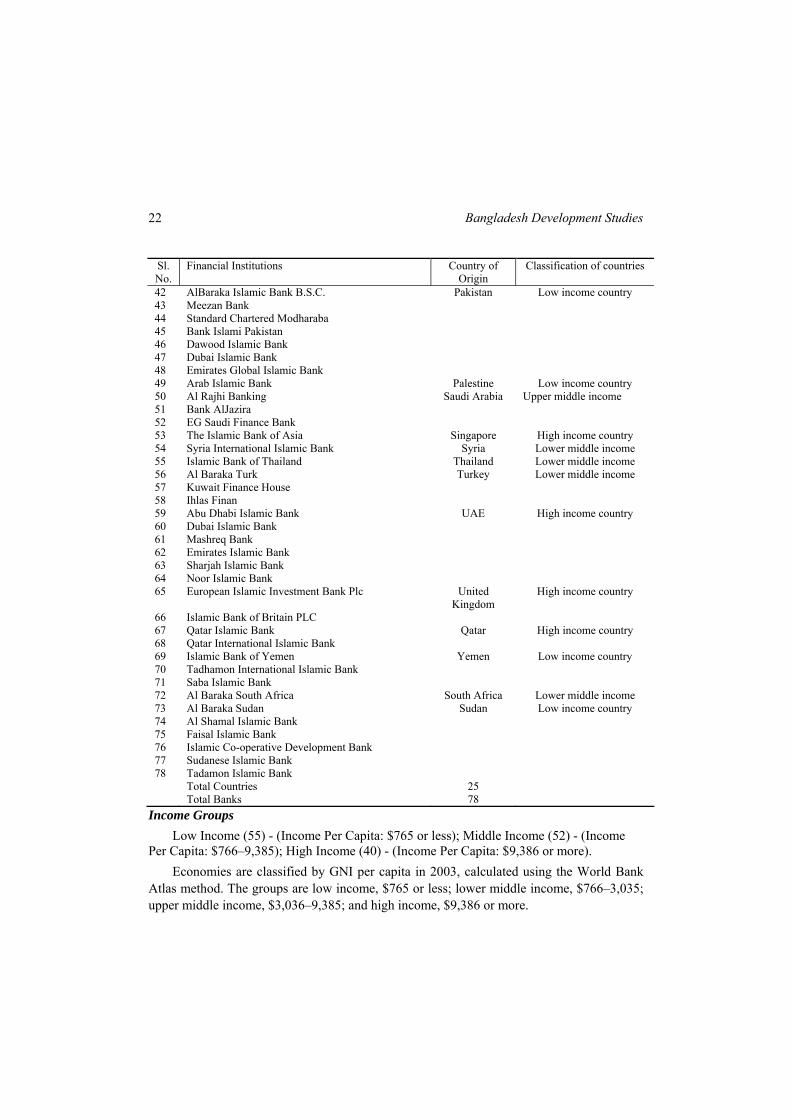

Sl. No.

Financial Institutions Country of Origin

Classification of countries

42 AlBaraka Islamic Bank B.S.C. Pakistan Low income country 43 Meezan Bank 44 Standard Chartered Modharaba 45 Bank Islami Pakistan 46 Dawood Islamic Bank 47 Dubai Islamic Bank 48 Emirates Global Islamic Bank 49 Arab Islamic Bank Palestine Low income country 50 Al Rajhi Banking Saudi Arabia Upper middle income 51 Bank AlJazira 52 EG Saudi Finance Bank 53 The Islamic Bank of Asia Singapore High income country 54 Syria International Islamic Bank Syria Lower middle income 55 Islamic Bank of Thailand Thailand Lower middle income 56 Al Baraka Turk Turkey Lower middle income 57 Kuwait Finance House 58 Ihlas Finan 59 Abu Dhabi Islamic Bank UAE High income country 60 Dubai Islamic Bank 61 Mashreq Bank 62 Emirates Islamic Bank 63 Sharjah Islamic Bank 64 Noor Islamic Bank 65 European Islamic Investment Bank Plc United

Kingdom High income country

66 Islamic Bank of Britain PLC 67 Qatar Islamic Bank Qatar High income country 68 Qatar International Islamic Bank 69 Islamic Bank of Yemen Yemen Low income country 70 Tadhamon International Islamic Bank 71 Saba Islamic Bank 72 Al Baraka South Africa South Africa Lower middle income 73 Al Baraka Sudan Sudan Low income country 74 Al Shamal Islamic Bank 75 Faisal Islamic Bank 76 Islamic Co-operative Development Bank 77 Sudanese Islamic Bank 78 Tadamon Islamic Bank Total Countries 25 Total Banks 78

Income Groups Low Income (55) - (Income Per Capita: $765 or less); Middle Income (52) - (Income

Per Capita: $766–9,385); High Income (40) - (Income Per Capita: $9,386 or more). Economies are classified by GNI per capita in 2003, calculated using the World Bank

Atlas method. The groups are low income, $765 or less; lower middle income, $766–3,035; upper middle income, $3,036–9,385; and high income, $9,386 or more.

Bangladesh Development Studies Vol. XXXIV, March 2011, No. 1

Asset Price Bubble and Banks: The Case of Japan

MONZUR HOSSAIN*

FARHANA RAFIQ**

This paper analyses the behaviour of the Japanese banks at the outset of the asset price bubble in the late 1980s. The paper argues that with the advent of financial deregulations, the declining trend of profitability forced the banks to exhibit speculative behaviour during the asset price bubble period (mid-1980s) to increase short term profit. This has ultimately led to the banking crisis after the burst of the bubble in 1989. Our empirical results support this argument. The paper also attempts to provide a comprehensive description of a number of interrelated structural changes in the financial system of Japan during 1977-2003 that opens up the domain of possibility for rethinking the issues related to change in policies. The case of Japan in the context of the rise and burst of the asset price bubble and subsequent banking crisis could be instructive for many countries including Bangladesh that are facing the asset price bubble situation. Japanese experience suggests that monetary policy should respond to asset bubbles in a cautious and moderate manner in order to avoid economic distortions. The lessons that can be learned from the Japanese experience are: (i) central bank’s role to burst bubbles must depend on the degree of efficiency of the financial sector, and (ii) the speed to burst the bubble must be based on the overall economic situation.

I. INTRODUCTION

The emergence and burst of the bubble economy in Japan in the late 1980s were mostly characterised by the commercial banks’ aggressive behaviour, collapse of some banks and debtor companies with a huge burden of non-performing loans (NPL). About 180 banks were failed in the 1990s and subsequently a prolonged

* Research Fellow, Bangladesh Institute of Development Studies. ** Lecturer, Department of Economics, American International University, Dhaka, Bangladesh.

Bangladesh Development Studies

24

stagnant period for the Japanese economy started. Naturally, the question arises: were the banks responsible for creating the bubble that subsequently led to the banking crisis of the 1990s? This also raises curiosity as to why the most successful banking system of the 1960s and the 1970s has failed? Did the deregulatory measures indicate any structural changes in the financial system that contributed to the failure of the banks? The paper attempts to shed some insights into these questions.

Many authors have tried to analyse the situation from various aspects (see, Aoki and Patrick 1994, Okina et al. 2001, Hossain 2005, Aoki and Patrick 1994) expressed concern about the structural changes that occurred in the financial system of Japan. They argued that the asset-price bubble in the late 1980s was partially created by the erosion of the coherence and integrity of the regulatory framework. According to them, with diminishing opportunity for traditional lending and limited access to bond-related services during the protracted monetary easing of the mid 1980s, banks started to increase lending to real estate companies and non-banks. This also revealed the banks’ weak monitoring capacity in the newly emerged market environment.

Okina et al. (2001) identified some other reasons for the emergence of the bubble in the late 1980s and the subsequent banking crisis. These are aggressive bank behaviour, protracted monetary easing, taxation and regulation on land, weak mechanism to impose discipline on economic agents, self confidence of economic agents, etc. In line with the views of Okina et al. (2001), Hossain (2005) argued that weaknesses in the corporate governance of banks were crucial for the banking crisis in the 1990s, rather than asset price bubble and financial deregulations.

In this paper we take the view that financial liberalisation was started in the early 1980s without making financial institutions prepared properly for the changing situation. As a result, financial institutions could not cope with the situation instantly and indulged in some speculative behaviour. Of course, such behaviour may be associated with corporate governance problem, as Hossain (2005) argued. Therefore, analysis of banks’ profitability is important as this has led to a sharp response from banks to the structural changes that occurred in the Japanese banking system in the 1980s. Although the deregulatory measures were partial in nature, these measures created problems in functioning of the banks as they were not fully prepared for moving toward competitiveness. Thus the paper analyses the behaviour of the financial institutions by taking their profitability issue into consideration. We use aggregate data for the period 1977-2003 to analyse bank profitability. Since the data resembles time-series properties, ordinary least square regression is not appropriate. Therefore, we apply Vector Error Correction Model (VECM) to assess

Hossain & Rafiq : Asset Price Bubble and Banks 25

the long run and short run relationship between bank profitability and other macroeconomic and monetary variables.

The paper is organised as follows. After introduction, Section II provides an overview of the Japanese financial system. Section III highlights various aspects of banks behaviour during the asset price bubble. Section IV describes methodology and data and Section V discusses empirical results on bank profitability. Section VI concludes the paper.

II. JAPANESE FINANCIAL SYSTEM: AN OVERVIEW

II.1 The Main-bank System The Japanese financial system is predominantly bank-based. Post-war Japanese

financial system was highly regulated and banks were heavily dependent on Bank of Japan’s (BOJ) subsidies (window guidance) and borrowings of enterprise groups. The characteristics of Japanese model of financial system during post-war period included high debt/equity ratios, greater reliance on bank loans than securities markets, closer relationship between banks and borrowers, extensive corporate cross-shareholding, greater guidance from the government in credit allocation, etc. The system is well known as the “main bank” system. It is evident from many research works that this “main bank” system contributed greatly to the post-war economic growth of Japan although the varieties of functions played by the main bank were not associated with the usual concept of commercial banking. This type of Japanese banking system is characterised by clearly defined structural policy of the government for stimulating and maintaining specialisation among financial institutions. The changes were not made to achieve maximum competition in a free market (Wallich and Wallich 1976).

There is a vast literature on how the main bank system played a very important role in Japanese economy and financial system. The core of an enterprise group is usually a bank that is called Main Bank. Pre-war Zaibatsu and post-war Keiretsu are examples of such types of enterprise groups, with the big six being Mitsui, Mitsubishi, Sumitomo, Fuyo, Sanwa and Ikkan. Group affiliation interlocks stock shares among industrial enterprises, banks and other financial institutions. The arrangements between main bank and group involved both financial and non-financial aspects. The financial arrangements included the sharing of financial risk through mutual support, preferential loans from the financial institutions and the control of stock voting power through ownership within the group. The non-financial arrangements included joint sale and purchase arrangements, assured markets and sources of supply, technological affinity, combined research, and cooperative planning. This structure of Japanese banks might be relevant to the so-

Bangladesh Development Studies

26

called “Industrial bank” (also available in Germany as House bank) rather than modern commercial bank.

Unlike American and many other countries’ banks, Japanese banks were allowed to own equity in other corporations. The shares of group member firms owned by banks form an important link in the interlocking structure of enterprise groups. In addition to interlocking shares, banks provide preferential loans and board members to the group affiliated firms. A group bank serves as a screening agent for the investment projects of the group firms and stands ready to lend funds whenever they are needed (Hoshi, Kashyap and Scharfstein 1991). Table I demonstrates that despite efforts to change the main banking system, each enterprise group consisted of at least 3 banks or insurance companies in 1987. This indicates that all the characteristics of the main banking system have not been completely eliminated during the liberalised period.

TABLE I ECONOMIC SIZE OF THE BIG COMPANIES (FY1987)

No. of member

firms

Total Bank/Insurance

Average interlocking

Shares

Average intra-group loans

Total assets (billion Yen)

Loan share1

(FY1989)

Board of directors

share2

(FY1989)

Mitsui 24 4 17.1 21.94 238,447 5.96 6.69 Mitsubishi 29 4 27.8 20.17 241,846 7.17 7.08 Sumitomo 20 4 24.22 24.53 153,202 6.75 6.58 Fuyo 29 4 15.61 18.20 322,798 6.03 9.38 Sanwa 44 3 16.47 18.51 377,622 7.30 8.97 Ikkan 47 5 12.49 11.18 466,250 4.44 12.44

Source: Ito (1992). Note:1Outstanding loans lent by group financial companies/ Total outstanding loans.

2No. of directors sent from group companies/Total outside board members.

Literature review suggests that a policy shift toward a greater emphasis on competition was induced in the late 1960s. Amongst other measures, an effort has been made to make banks more profit-oriented by easing the dividend restrictions (Wallich and Wallich 1976). As a part of intensive and continuous effort to improve the competitive structure, the Certificates of Deposits (CDs) became available in May 1979; Gensaki1 transactions with CDs (unregulated interest rate) became

1 The “Gensaki market” means repurchase agreement market established in 1949 by securities houses. It became important in 1970 when FIs and large companies began to participate.

Hossain & Rafiq : Asset Price Bubble and Banks 27

increasingly popular, as there is no transaction tax on CDs. The Tegata2 market, freed from interest rate regulation, also grew in the 1980s. During this period, restrictions on fund-raising in the securities market by firms were removed and major firms became less dependent on bank borrowing. These deregulations were aimed at strengthening capital market. The decade of 1980 might be termed as undirected deregulations as like a “boat without sail.” Aoki and Patrick (1994) termed the banking system of that time as “market-embedded main bank system” since some elements of the main bank system remained valid. Such untargeted liberalisation policies created many problems for the economy and the financial sector while switching from regulated regime to a complex partially liberalised regime.

As a compensation for reduced dependency of enterprise groups by these regulatory frameworks, banks are allowed to expand their businesses in risk market (security and insurance), capital market (investment banking) as well as money market. In fact, this model follows universal banking system although economists have no consensus on the economies of scale of universal banking (Caprio 1994). One of the counter arguments is that commercial banking activities are less risky than the security operations, so risky security business may affect the commercial banking activities.

II.2 Financial Liberalisation The structural changes in the Japanese financial system have been started from

the mid–1970s (Sujuki 1987). The main features of these deregulations were interest rate deregulation, relaxation of regulation to raise funds in the securities and investment market by firms, initiation of freely floating exchange rate and allowing banks and firms to participate in the capital market, etc. to increase the ability of the Japanese banking system to meet international competition. These deregulations also targeted the dissolution of cross-shareholdings.3 Many have attributed that financial liberalisation policies were also needed to finance government budget deficit through allowing banks to participate in the bond market. There was a sharp increase in government budget deficits in the late 1970s and to finance the deficit,

2 The Tegata (bill discount) market is a short-term financing market for two-weeks to six-weeks. It was spun off from the call market in 1971. 3The Anti Monopoly Law Reform, 1977 was one-step forward in reducing cross-shareholding. Okabe (2001) shows that cross-shareholding is gradually reducing in the Japanese financial system.

Bangladesh Development Studies

28

there was a need to sell large amounts of government bonds (see Cargill and Royama 1988).

The developments in regulatory frameworks after 1990 allowed banks to do business in both the capital and risk market. Under these regulatory frameworks, Japanese banks were given license to do conventional non-banking activities like lease financing, investment and merchant banking, underwriting, insurance business, etc. Thus, these types of regulatory frameworks allowed banks to expand their businesses in risk market (security and insurance), capital market (investment banking) as well as money market. This model follows universal banking-type system rather than modern commercial banking.

Some of the deregulatory measures are noteworthy. The interest rates for large-amount time deposits (LTDs) were deregulated in 1985, thus the share of these deposits in the money supply had skyrocketed. The lowering of the minimum deposit amount for money market certificates (MMCs) to 10 million yen in October 1987 made those certificates more popular among households. The Anti-Monopoly Law Reform of 1977 specified that all financial institutions must reduce their share holdings from 10 per cent to below 5 per cent by December 1987.4 Although this law was aimed at dissolution of cross-shareholdings, there was no limit on the total number of different stocks a bank can hold. By this law, a bank’s holding of different stocks can exceed its total capital, which might carry risk for the banking business. Since bank’s money are the depositors short-term money, share holding in equity of its enterprise groups sometimes may create mismatch in maturity and loan portfolio.5

After the collapse of the bubble, the important structural changes started by the Financial System Reform Act, 1992 (enforced in April 1993) that has allowed banks to conduct trust businesses either through trust bank subsidiaries or by themselves and securities business through securities subsidiaries subject to the permission of the Prime Minister. Later, the Financial System Reform Law of 1998 was enacted which allows banks to conduct insurance businesses through subsidiaries from 4 By this reform the policy of 1951 again revived. 5 It is widely argued that Ministry of Finance (MOF) has been very deliberate in asserting authority over banks, merging banks, and controlling the system. Moreover, Japanese socio-cultural activities have been rooted in the form of “group” activities or “joint” decision; Zaibatsu, Keiretsu, and the main bank system were a reflection of this “group” phenomenon. With the financial deregulations, is the authoritarian role of MOF shrinking or is the “group phenomenon” of Japanese culture getting eliminated? The interesting thing is that the structural changes in the financial system can be explained as the two sides—industrial banking and universal banking, of the same coin “convoy system.”

Hossain & Rafiq : Asset Price Bubble and Banks 29

October 2000. Since March 1998, banks are allowed to establish bank-holding companies that can own a securities subsidiary. Banks were allowed to sell investment trusts at their counter from December 1998. This policy shift was necessary as the bad loans consequences of the bursting bubble result in a weaker banking system that needs further deregulations, particularly permitting banks to engage in bond underwriting and related services more liberally.

Non-bank financial institutions (NBFIS), consumer-financing institutions, insurance companies, etc. are mostly working as a subsidiary company of the banks. They are heavily dependent on banks for their funding. However, the scope of business has opened up a wide range of business possibility for the banks that indicates a significant change in their structure compared to the structure before 1980.

III. ASSET PRICE BUBBLE (1987-89) AND BANKS’ BEHAVIOUR

With the advent of liberalisation in the 1970s and 1980s, market forces unleashed on the hitherto regulated environment. In this market upheaval, banks lost their big customers as they were shifted away from bank borrowing towards other financing methods including retained profits, corporate bonds, international financial market, etc. Due to decrease of the large firms’ dependency on banks borrowing, banks shifted aggressively their mode of investment to the small and medium enterprises (SMEs), NBFIs and real estate businesses.

Along with the structural changes in the Japanese financial system, the “monetary phenomenon” made the situation more critical. In order to counter the recession brought about by the rapid appreciation of the yen after the Plazza Accord in 1985, the BoJ lowered discount rate five times as part of monetary easing between 1986 and 1987. At that time, money supply was increased by more than 10 per cent. The commercial banks took this opportunity of protracted monetary easing to lend aggressively to the SMEs and real estate market in order to increase their short term profit. This has been possible due to lack of prudential regulations. Also, lower tax on holding of land and higher tax on transaction of land created demand and supply gap in the real estate sector, which contributed to rapid rise of asset prices. With these favourable situations, banks lent aggressively to the SMEs and contributed in creating asset price bubble and transmitting the shocks to the economy after collapse of the bubble.

Here it might be important to note the way the bubble had burst. As part of BoJ’s monetary tightening and government’s effort to curb land prices, the bubble started to burst in 1990, leading to asset prices falling sharply, many debtor

Bangladesh Development Studies

30

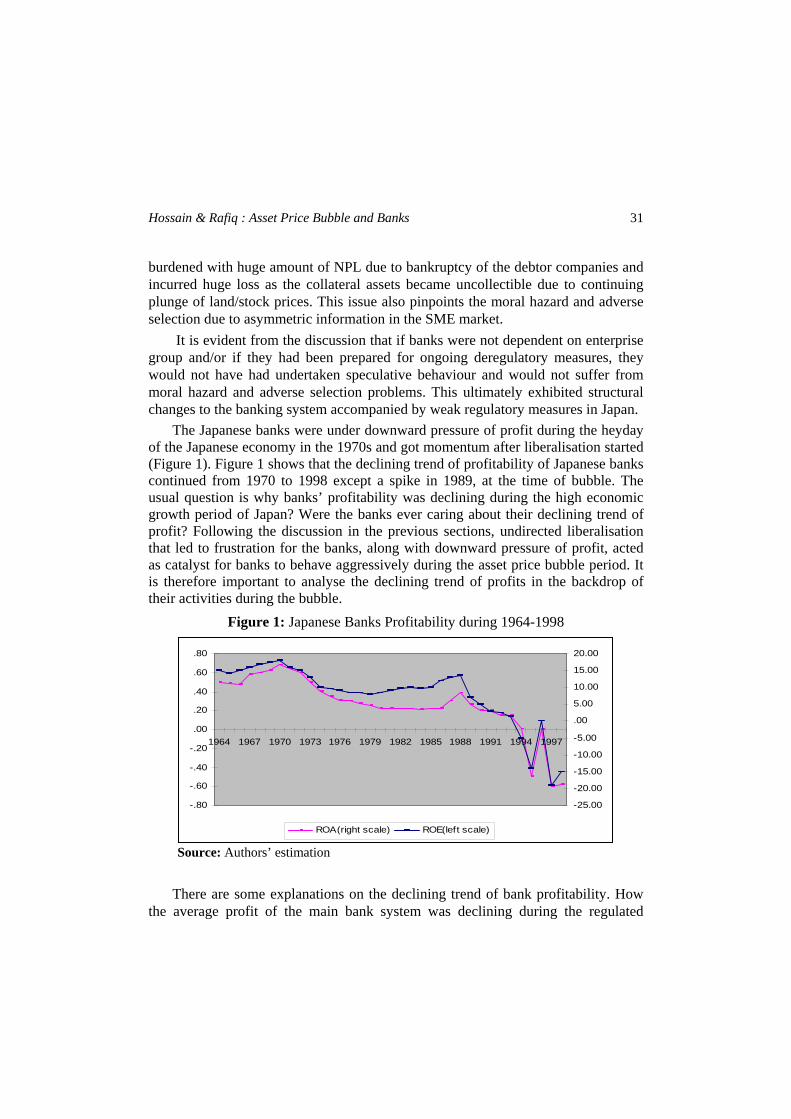

companies becoming bankrupt, and creditor companies having a huge burden of non-performing loan (accumulated direct write-offs stood around 9 per cent of GDP in 1999; Okina et al. 2001).

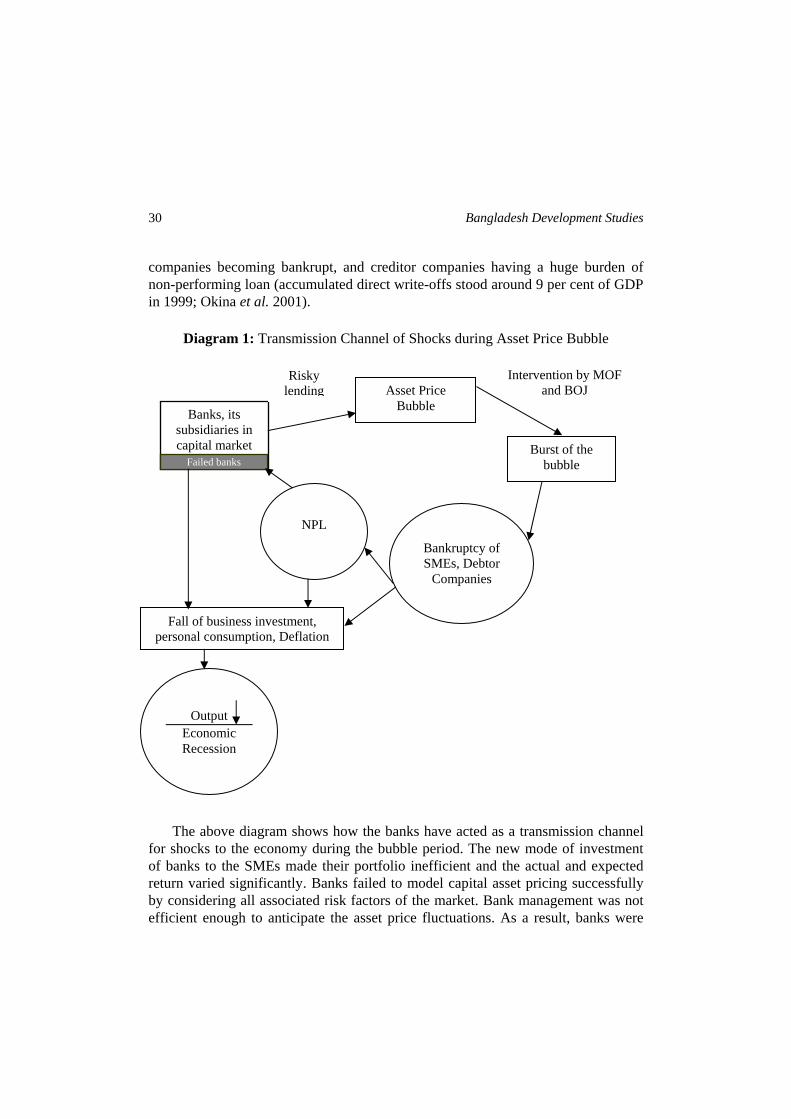

Diagram 1: Transmission Channel of Shocks during Asset Price Bubble

Banks, its subsidiaries in capital market

Failed banks

Asset Price Bubble

Burst of the bubble

Bankruptcy of SMEs, Debtor

Companies

NPL

Fall of business investment, personal consumption, Deflation

Output

Economic Recession

Risky lending

Intervention by MOF and BOJ

The above diagram shows how the banks have acted as a transmission channel

for shocks to the economy during the bubble period. The new mode of investment of banks to the SMEs made their portfolio inefficient and the actual and expected return varied significantly. Banks failed to model capital asset pricing successfully by considering all associated risk factors of the market. Bank management was not efficient enough to anticipate the asset price fluctuations. As a result, banks were

Hossain & Rafiq : Asset Price Bubble and Banks 31

burdened with huge amount of NPL due to bankruptcy of the debtor companies and incurred huge loss as the collateral assets became uncollectible due to continuing plunge of land/stock prices. This issue also pinpoints the moral hazard and adverse selection due to asymmetric information in the SME market.

It is evident from the discussion that if banks were not dependent on enterprise group and/or if they had been prepared for ongoing deregulatory measures, they would not have had undertaken speculative behaviour and would not suffer from moral hazard and adverse selection problems. This ultimately exhibited structural changes to the banking system accompanied by weak regulatory measures in Japan.