Teaching a Financial Planning Language as the Principal ...

29

Southern Methodist University Southern Methodist University SMU Scholar SMU Scholar Historical Working Papers Cox School of Business 1-1-1982 Teaching a Financial Planning Language as the Principal Teaching a Financial Planning Language as the Principal Computer Language for MBA's Computer Language for MBA's Thomas E. Perkins Southern Methodist University Paul Gray Southern Methodist University Follow this and additional works at: https://scholar.smu.edu/business_workingpapers Part of the Business Commons This document is brought to you for free and open access by the Cox School of Business at SMU Scholar. It has been accepted for inclusion in Historical Working Papers by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Teaching a Financial Planning Language as the Principal ...

Southern Methodist University Southern Methodist University

SMU Scholar SMU Scholar

Historical Working Papers Cox School of Business

1-1-1982

Teaching a Financial Planning Language as the Principal Teaching a Financial Planning Language as the Principal

Computer Language for MBA's Computer Language for MBA's

Thomas E. Perkins Southern Methodist University

Paul Gray Southern Methodist University

Follow this and additional works at: https://scholar.smu.edu/business_workingpapers

Part of the Business Commons

This document is brought to you for free and open access by the Cox School of Business at SMU Scholar. It has been accepted for inclusion in Historical Working Papers by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu.

Lo S ·2 ~~ :t·c l1 t e: .. . (~ ;::(L cf

- -~ --~{I ;~

Southern Methodist University Dallas, Texas 75275

TEACHING A FINANCIAL PLANNING LANGUAGE AS THE PRINCIPAL COMPUTER LANGUAGE FOR MBA'S

Working Paper 82-301*

by

Thomas E. Perkins

and

Paul Gray

Thomas E. Perkins Assistant Professor of Management Science and Computers

Edwin L. Cox School of Business Southern Methodist University

Dallas, Texas 75275

Paul Gray Professor of Management Science and Computers

Edwin L. Cox School of Business Southern Methodist University

Dallas, Texas 75275

*This paper represents a draft of work in progress by the authors and is being sent to you for information and review. Responsibility for the contents rests solely with the authors. This working paper may not be reproduced or distributed without the written consent of the authors. Please address all correspondence to Thomas E. Perkins.

TEACHING A FINANCIAL PLANNING LANGUAGE AS THE PRINCIPAL COMPUTER LANGUAGE FOR MBA'S

Thomas E. Perkins and Paul Gray Edwin L. Cox School of Business

Southern Methodist University Dallas, TX 75275

ABSTRACT

This paper de,scribes t,~e experiences at SMU in using a financial planning

language ( specific$l.lX, the Interactive Financial Planning System (IFPS)) as ' · ~ ,-~

the pri~ry computer language t_aught to MBA's. The language was introduced to

extend the students' ability to solve business problems. Experiences with

teaching the language, the extent of its use, and the results of a student

survey are discussed.

INTRODUCTION

For a number of years, incoming MBA students at Southern Methodist Uni-

versity (SMU) had been taught to program in BASIC and to use a sophisticated

calculator (such as the TI-58) as part of their first semester introductory

management science and computer course. Part of the reason for the use of

BASIC was that the SMU MBA program attracts large numbers of students with hu-

manities and social science backgrounds. When a new chairman was brought in

from outside the University at the end of the 1970's, he took the view that it

was no longer appropriate to give graduate credit for learning BASIC at a time

'\ when many were learning the language in high school. The problem then was to

redesign the computer portion of the course in a meaningful way.

It was, of course, clear that MBA students would be living in a computer

environment after graduation and that they had to be prepared for it. It was

also clear that the students should know more about computing than merely

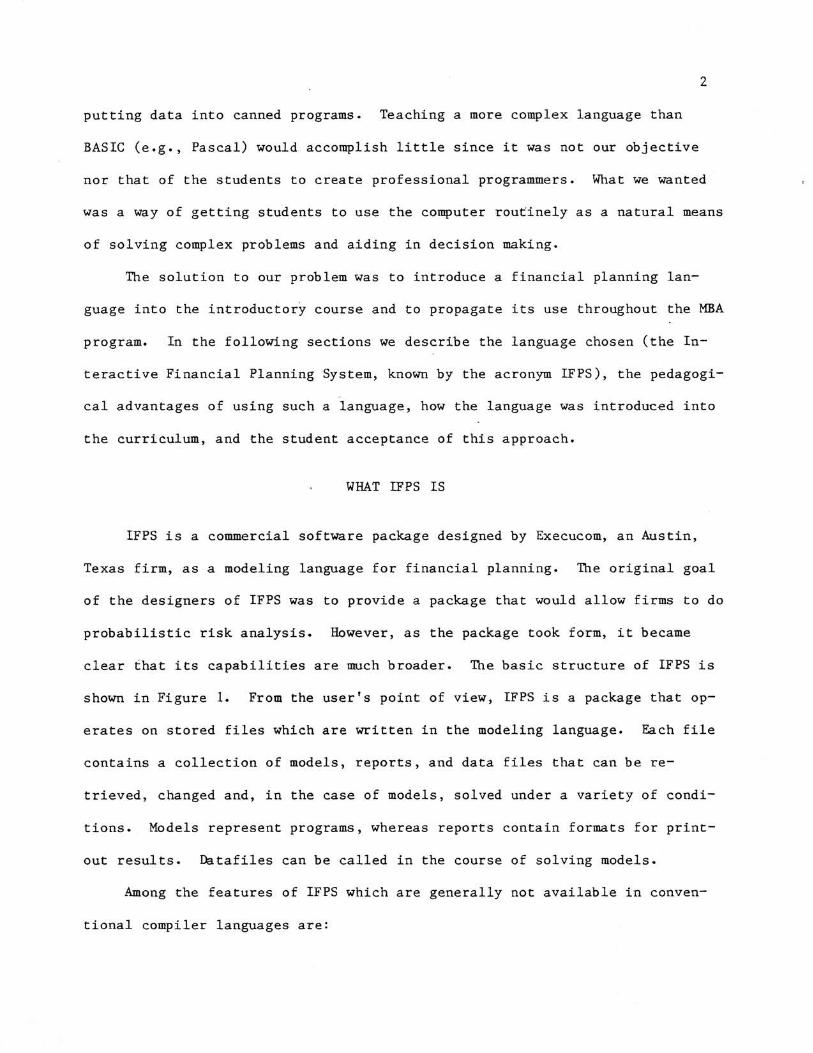

2

putting data into canned programs. Teaching a more complex language than

BASIC (e.g., Pascal) would accomplish little since it was not our objective

nor that of the students to create professional programmers. What we wanted

was a way of getting students to use the computer routinely as a natural means

of solving complex problems and aiding in decision making.

The solution to our problem was to introduce a financial planning lan

guage into the introductory course and to propagate its use throughout the MBA

program. In the following sections we describe the language chosen (the In

teractive Financial Planning System, known by the acronym IFPS), the pedagogi

cal advantages of using such a language, how the language was introduced into

the curriculum, and the student acceptance of this approach.

WHAT IFPS IS

IFPS is a commercial software package designed by Execucom, an Austin,

Texas firm, as a modeling language for financial planning. The original goal

of the designers of IFPS was to provide a package that would allow firms to do

probabilistic risk analysis. However, as the package took form, it became

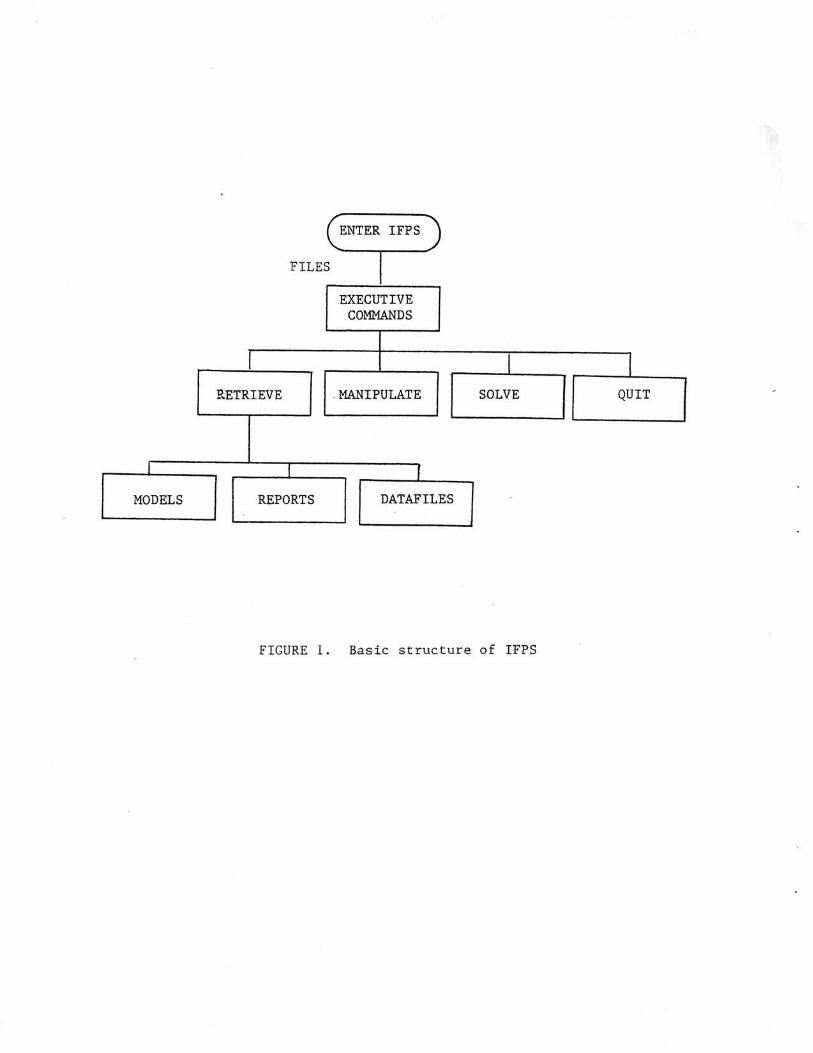

clear that its capabilities are much broader. The basic structure of IFPS is

shown in Figure 1. From the user's point of view, IFPS is a package that op

erates on stored files which are written in the modeling language. Each file

contains a collection of models, reports, and data files that can be re

trieved, changed and, in the case of models, solved under a variety of condi

tions. Models represent programs, whereas reports contain formats for print

out results. Datafiles can be called in the course of solving models.

Among the features of IFPS which are generally not available in conven

tional compiler languages are:

3

""' n&turll language. Otdlnary English names can be used with almost no

rur:r·fot:to'H•fon name lengths •

. . .... ',\' ' ' ;.,: ,'order d~il not matte-r. IFPS is a non-procedural language. Such lan-

guagu are no~ n•w (e.g., DYNAMO). The only restriction is that each variable

has to appea~ once on the left . side of a relation.

spread sheet format. The user perceives the internal world of IFPS as

consisting of a two-dimensiotlal mat:rix. The rows of this matrix are the vari-

ab les in the model; the columns represent the time pet"iods. IFPS places a

value in each cell to represent the value of the row variable during the col-

umn's time period.

forward and backward movement in time. Commands are available that

allow the use of values from previous and future time periods to be used in

the computation of values for individual cells.

"what if" capability. Built-in commands allow asking "what if" ques-

tions. These can be in the form of substituting alternative values or rela-

tions, sensitivity analysis, and goal seeking. The user thereby can quickly

explore the implications of decision alternatives.

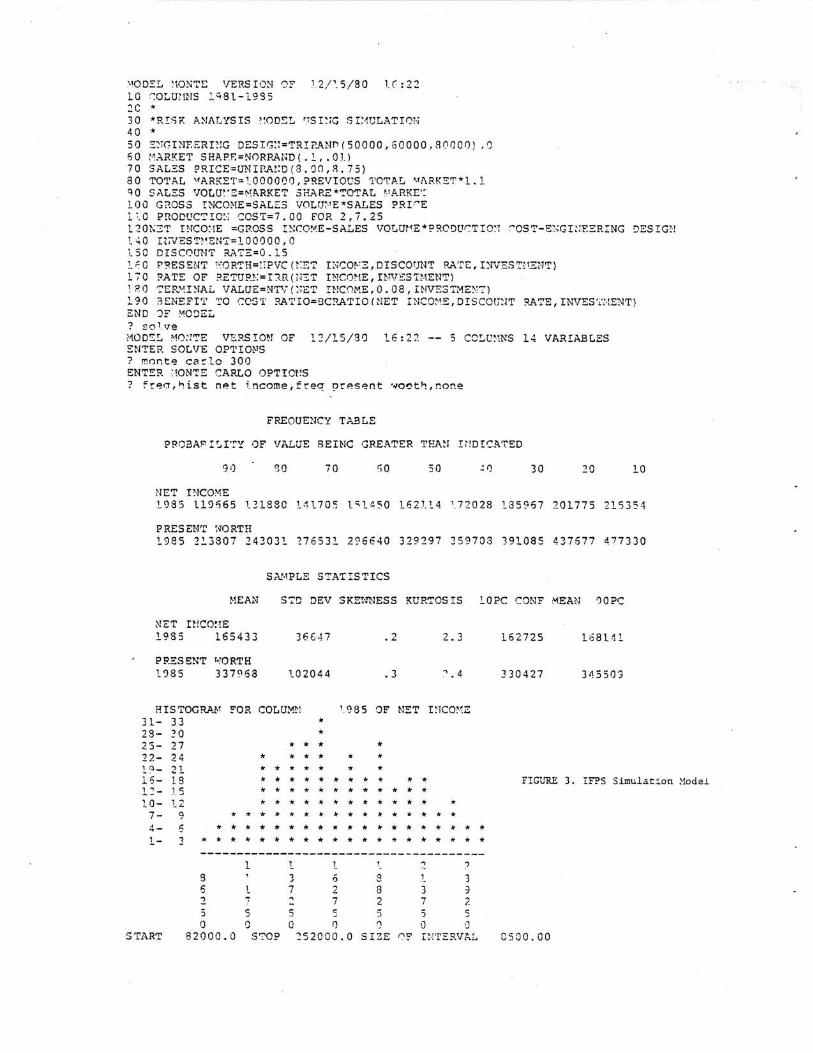

simulation analysis. IFPS can be run in simulation mode, with vari-

ables being defined in terms of probability distributions. Thus, because of

its column structure, IFPS is also a fixed-time interval simulation language.

built-in functions. IFPS relieves the user of programming many of the

tedious, repetitive calculations of finance and statistics by containing

built-in functions for net present value, internal rate of return, deprecia-

tion, trend extrapolation, and many more.

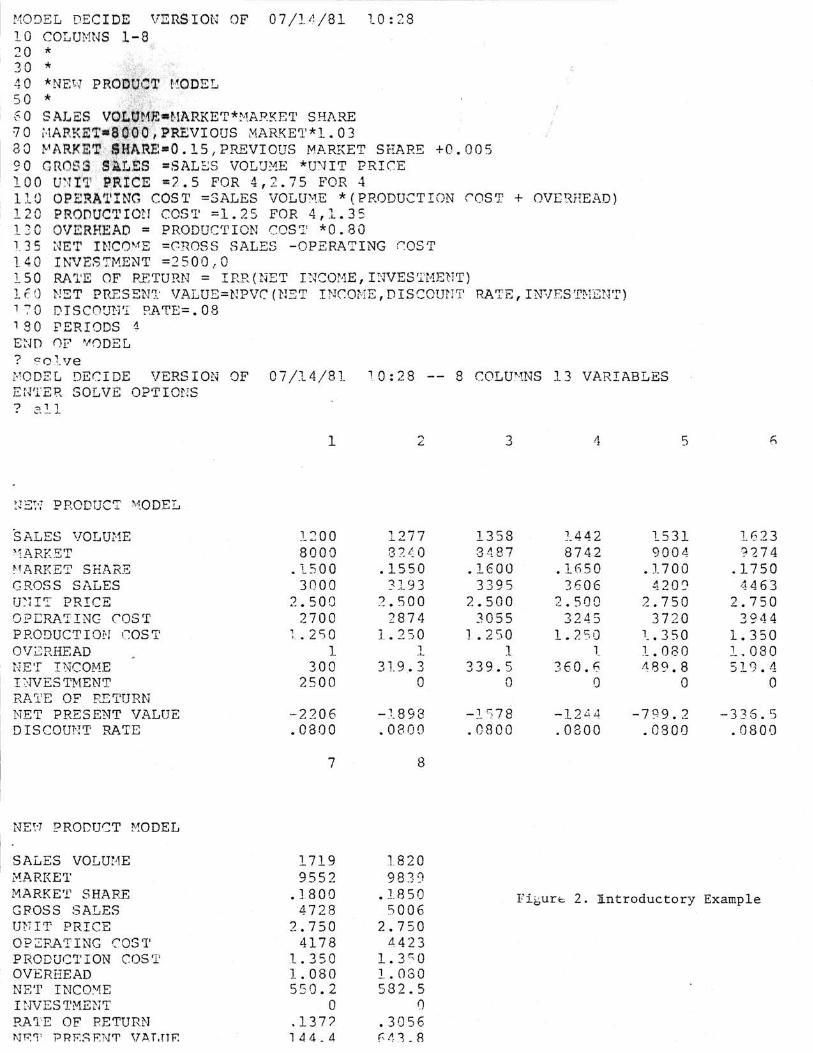

Figure 2 shows a simple deterministic IFPS model and its solution. The

decision problem being modeled involves introduction of a new product which

will require an initial investment and will have certain variable costs

4

associated with it. Estimates of the market, the firm's market share, and the

growth of these two quantities drive the values in the model. The financial

functions express the measures of effectiveness. (The model shown in Figure 2

serves as the example used to introduce our students to IFPS.)

WHY IFPS WAS INTRODUCED

As stated in the introduction of this paper, we were seeking a way of

getting students, particularly computer-naive students, to use the computer

routinely as a natural means of solving problems and aiding in decision mak

ing. We therefore sought a language which:

1. is as close to the language of business as possible,

2. is easy for the student to learn quickly and to achieve succes in

rapidly,

3. allows students to see and understand the underlying assumptions of

their models, and

4. is likely to be related to the languages they would see after

graduation.

We will now discuss each of these points in turn.

1. The many financial planning languages developed commercially during

the 1970's were aimed at financial analysts and other corporate staff people.

~ese people were interested in having the computer essentially speak the same

language that they do. The designers of the successful financial planning

languages understood that the style, format, and conventions of compiler lan

guages such as BASIC introduced a psychological barrier to the use of the com

puter and had to be eliminated as much as possible. By making the planning

languages conform to English and to the spread-sheets familiar from accounting

practice, they gained rapid and widespread acceptance. Since, in our opinion,

5

a large portion of the business school experience is learning the language of

business, financial planning languages are a natural choice to meet the first

criterion.

2. From an instructional point of view, one of the primary attractions

of the financial planning languages is the simplicity of the underlying con

ceptual model. This is particularly true for the financial planning languages

that are non-procedural. Since the student can write down expressions one af

ter the other in the order in which they occur in their thinking process, the

models become easy to formulate and write. The simplicity of the language

makes it possible for the student to write and solve a meaningful model after

a single class period. Students, particularly computer-naive students, gain

success quickly and, as a result, develop faith in their own ability to cope

with the computer. The ability of students to learn the language quickly

means that more class time can be devoted to the principles of modeling and to

applications, thereby increasing the content of the course for the students.

3. Financial planning languages allow students to express their modeling

assumptions clearly and explcitly. By stating their assumptions about input

values and relationships in a clear form in the model, students can understand

what the assumptions are. As G. R. Wagner states, they then "own" their as

sumptions (Ref.l).

4. Having decided on a financial planning language, we next sought to

find one that was being widely used in business and was available to univer

sities at reasonable cost with good support. We chose IFPS because it has a

very large users group (over 1,000 organizations) and is available on a time

sharing network commercially, as well as being used in over 60 universities

around the country.

6

HOW IFPS WAS INTRODUCED

IFPS became operational on the SMU CDC-6600 in February 1980. Because of

our MBA program's trimester schedule we were then in the middle of the second

semester. We therefore used IFPS initially as a supplementary language. The

130 full-time MBA students (in 4 sections) were taking the production and op

erations management course. We developed a full 2-hour lecture that intro

duced the deterministic features of the language including the "what if" capa

bilities. This initial lecture centered around the example shown in Figure 2.

Students were told to put this model up on the computer and to run a series of

"what if" cases. Without exception, students were able to do this without

difficulty. This lecture and assignment are now standard and give students

the initial success they need with a new language.

We followed up this initial assignment with one requiring the students to

write their own model. Toward the end of the semester, we brought IFPS in

again, this time as a way of teaching simulation, which is part of the produc

tion and operations management course. IFPS proved to be an efficient way of

getting students to write their own simulation models. One of the examples

used is shown in Figure 3. A limitation, of course, is that the IFPS struc

ture is set up for fixed time intervals and hence IFPS is not suitable for

modeling next event situations such as are encountered in queuing situations.

(But then, one can't have everything.)

Our initial success led the engineering school to introduce the language

in their engineering economy courses. It also encouraged several students to

undertake projects involving the use of the language and/or to do their home

work in other courses, particularly finance, in IFPS.

In the Summer 1980 trimester we introduced IFPS into the first (introduc

tory) course for the Executive MBA class and then into the first course for

7

the full-time group in the fall of 1980. These students received reinforce-

ment in the language throughout the semester and then through the following

semester as they took production and operations management. At this point, as

in any changeover, we continued to teach both BASIC and IFPS. However, the

student response we were receiving to IFPS was so enthusiastic that starting

in the summer of 1981, we dropped BASIC and offered IFPS only. (As a backup,

students were offered a separate 8--hour BASIC short course. Some 55 students

paid $25 to take it.)

Of particular help was the creation of the SMU Student's Guide to IFPS.

The IFPS Tutorial supplied by the vendor is designed more for commercial users

than students. We felt we needed a simple "how-to" set of instructions that

begin with how to get on the computer and obtain IFPS, how to write a simple

-model, how to use the editor to correct mistakes, how to get out of IFPS, et:c.

This initial portion of the wide is essentially a life-support system for the

beginning student. The second part of the Guide deals with the useful fea-

tures of the systems (what if, built-in functions and subroutines, and Monte

Carlo simulation). The third and final part covers special features (includ-

ing data files, formatted reports and some specialized examples) designed for

the students who wante~ to go into the language more deeply. Figure 4 shows

the table of contents of the Student Guide. Figure 5 shows the extremely sim-

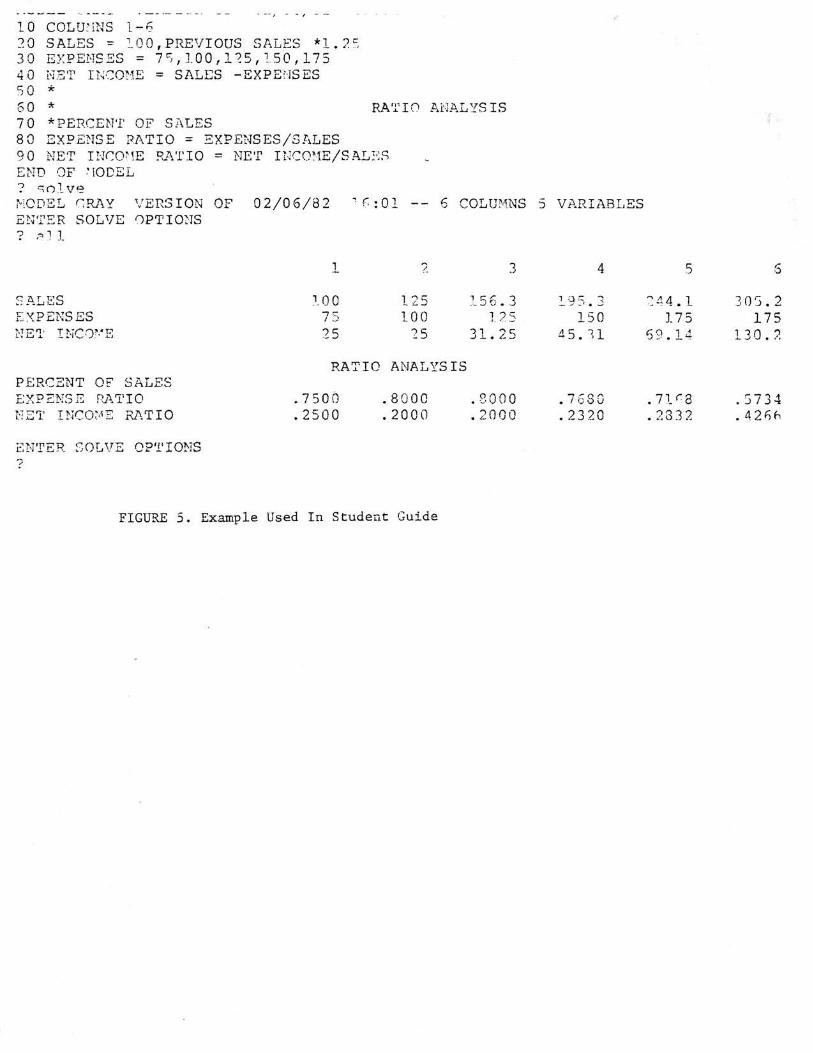

ple model that we used as an example throughout the Guide and ties the various

pieces together.

Today, all 350 MBA's (full-time, part-time, and executive) are taught on-

ly IFPS. At the undergraduate level, it is included in most management sci-

ence electives. In engineering it is used in all engineering economy and pro-

duction courses. During Fall 1981, IFPS was used for the first time in an

economics course.

8

In summary, we have moved from providing the language as a supplement to

relying on it as the primary way of teaching MBA students how to use the

computer.

SURVEY RESULTS

To evaluate the use of IFPS as a teaching tool, full-time and Executive

MBA students were surveyed at the end of the Fall 1981 semester. The ques

tionnaire used is shown in Figure 6. It asks students about such factors as

the student's background experience with computers prior to entering the MBA

program, the difficulty they experienced in learning IFPS, and how well they

had accepted IFPS as a tool which they could use outside the classes in which

it was taught.

Two groups of students were surveyed, each with a different amount of ex

posure to IFPS. The first group (117 students) consisted of four sections of

full-time and one section of part-time students who had just completed the

course in which the language was introduced. The second group (19 students)

were a section of Executive MBA students who had used the language for two

semesters, the same introductory course and the follow-on production course.

Student Background

As anticipated, the survey showed that an appreciable number of the stu

dents entering the MBA program have some experience with a computer language.

Of all the students surveyed, 60% indicated they had received instruction in

at least one computer language prior to the course in which IFPS was intro

duced. Of these, 81% had programmed in BASIC, 46% had programmed in FORTRAN,

and 11% had programmed in COBOL. Of the students with no prior programming

experience, over half (52%) recalled experiencing "computer anxiety" prior to

starting the program.

9

The !~~~~ng Experience ,. :,~!,'} ':~ i .

As· the students began to use IFPS as a modeling tool, 34% rated it "easy"

to l earn; 46% rated it "somewhat hard" to learn. Only 20% found it "hard" or

"very hard" to learn.

A common problem in the teaching of computer languages is that students

tend to become attached to the first language they learn and resist efforts to

introduce a second language. However, this phenomenon did not occur with the

students surveyed. Of the 99 students who were able to compare their learning

experience in IFPS with other languages, 6 7 indicated that IFPS was easier to

learn. TWenty-eight found the learning experiences comparable, and only 4

found IFPS more difficult to learn.

As we expected, students in the advanced section tended to perceive them-

selves as mc{re proficient in the language. In the group with two semesters of

experience with IFPS, 47% rated themselves as having "intermediate" language

skills; the remainder of this group rated themselves as a "novice. No stu-

dent in either group felt that their skills had yet reached the "expert" lev-

el. It is interesting to note that in the group with only one semesters of

exposure to IFPS, almost 25% described their IFPS language fluency level as

"intermediate. "

Most students (61%) felt that the IFPS Student Guide in its present form

provided sufficient support for IFPS learning outside the classroom. Others

expressed a need for more examples of the language features, possibly includ-

ing cases and related IFPS models as an appendix. Another common suggestion

was for more explanation of "what to do when you make a mistake." Some stu-

dents commented that the availability of an "IFPS expert" teaching assistant

in the terminal lab area would have been helpful.

IFPS Use Outside the Classroom

The survey showed that students with two semesters of exposure to IFPS

tended to use it more as a personal tool, both for other courses and outside

the classroom. In the group for which IFPS had just been introduced, only 9%

reported using IFPS for homework in another course. In the more advanced

group, however, over 52% used IFPS for other classes and projects.

A similar pattern was found in the students' use of IFPS as a tool for

personal calculations or in a work environment. Of the students in the intro

ductory course, 8% had used the language for personal use or on the job. In

t:he Executive MBA section, however, over 68% indicated they had used IFPS for

calculations other than classroom work.

IFPS versus Hand-held Calculators

When asked whether they felt instruction in the use of hand....;held calcula

tors or instruction in IFPS would be worth more t .o them for their short-term

MBA experience, the students responded overwhelmingly (85%) in favor of the

hand-held calculator instruction. We believe this to be a reflection of the

methods. of teaching in other courses in the program. When asked a similar

question regarding the anticipated relative value of the two tools for the

long term (in the next five years), 42% responded they felt the IFPS instruc

tion would prove more valuable.

Perceived Future Computer Use

Most of the students anticipate using the computer as an everyday tool

in the future. The survey showed that 80% plan to make use of the computer in

business once they graduate.

It is interesting to note the students' perception of computer availabil

ity. Rather than the difficult-to-get-to computing power of an isolated

11

main-frame environment, almost two-trirds of the students surveyed said they

plan to own a personal computer after graduation.

CONCLUSIONS AND FUTURE DIRECTIONS

This paper has reported the qualitative experiences with using a finan

cial planning language as the principal language for MBA's. Survey data indi

cates overall satisfaction with the language after the first semester, and the

ability of at least some students to use the language outside the course in

which it is taught.

Based on our experience, IFPS and similar financial planning languages

present a viable approach around which to .structure MBA student interaction

with the computer. Even students with no prior computer experience found the

language easy to learn and apply to a wide range of problems. Since students

can readily grasp the syntax of the language, instructional time can be better

spent dealing with the principles of business problem analysis and solution.

Less time is needed to describe how to represent the problem in a computer

language.

In addition to being easy to learn, financial planning languages provide

the student with a skill that he can apply directly upon graduation. Since

very few of our students plan to become systems analysts or professional pro

grammers, they generally have little need for procedural programming lan

guages.

In the future, we plan to broaden the base of courses at SMU which ·use

IFPS, including the required management science courses at the undergraduate

level. Within the introductory MBA course we plan to reinforce IFPS instruc

tion by including additional IFPS examples in the statistics and forecasting

portions of the course.

12

We plan to survey the full-time MBA student group again at the end of the

Spring semester and prior to graduation at the end of the summer semester. We

anticipate finding a larger and larger percentage of students making more use

of the computer as a problem-solving tool, both inside and outside of the

classroom.

In general, our experiences with IFPS have been positive. The develop

ment of the Student Guide combined with documentation provided by Execucom

(the software's creator) have made this a well-documented system. Students

grasped the language quickly; we met very little resistan~e, even from stu

dents who were "programming experts" in languages such as FORTRAN or COBOL.

Even that prodigious bastion of resistance to pedagogical change, the faculty,

had its foundations shaken. Instructors actually be~ame enthusiastic about

using the language in their classes.

13

REFERENCES

l. Wagner, G. R., "Decision Support Systems: Computerized Mind Support for Executive Problems," Managerial Planning, September/October , 1980.

ENTER IFPS

FILES

EXECUTIVE COMMANDS

I I RETRIEVE .MANIPULATE SOLVE QUIT

I I , MODELS REPORTS DATAFILES ~

FI GURE 1. Basic structure of IFPS

MODEL DECIDE VERSION OF 07/l A/81 l0:28 10 COLUMNS 1-8 20 * 30 * 40 50 *

~10DEL

6 0 SAJ .. ES V •NARKE'r*~·lAPSET SHJ\RE 7 0 i-lAF.KDJ'rill I PREVIous MARKET* l . 0 3 3 0 r-1ARI<Iil'lt · .. ~!fARE•O. 15 I PREVIOUS MP .. RKET SHARE +0. 0 0 5 9 0 GROSS S~LES =SAL.SS VOLU~E *U'HT PRICE l 0 0 D;·Yt'T P:~ICE =2. 5 FOR 4, 2. 7 5 FOR -1 110 OP ~~A'l'ING COS'l' =SALES VOLU~·m *(PRODUCTION C'OST + OVERHE.l\D) 120 PRODUC'l'IO!I COST =1.25 FOR 4,1.35 1 30 OV!!:RHEAD = PRODUCTION COST *0.80 1.35 ~ET INCOME =GROSS SALES -OPERATING rOST 140 INVESTMENT =2500,0 150 RATE OF RETURN = IRR(NET INCm·1E, INVES'..l'[ •lE~lT)

lfO NS T PRESEN':t VALUE=NPVC(l!:ST Il'Wm·IE,DISCOUn'I' RATE,INVEST~lEHT) 170 DISCOUNT PA'1'E=.08 130 PERIODS .1

EI·m 0F ¥()DEL ? ~o1. ve MODEL DECIDE VERSION OF 07/14/81 10:28 -- 8 COLUMNS 13 VARIABLES ENTER SOLVE OPTIONS ? 2.:_1

~J E~~; PPODUCT 'vtODEL

SALES VOLU.l-1£ '1ARK:ST ~ ·IARI\ET SHl\RE GROSS Si\LES U~J I'=' PRICE OPERATING COST PRODUCTION COST OVL:RHEAD 'l'.TP 1r l. .. .J-..J .4. INCOME I ~'NES Tr-1ENT RATE OF RETURN NET PRESENT Vi\LUE DISCOUNT RATE

NEW PRODUCT MODEL

SALES VOLU:,lE ~ARKET

1

1200 8000

. l5 00 3000

2.500 2700

l .2SO l

300 2500

-22 0 6 .0800

7

1719 9552

3 4 5

1 .., ... .., .1- ~ I I 1358 }_442 1531 3~ ~ 0 3487 8742 9004

.1550 .1600 . lf.SO .1700 3193 3395 3606 4209

2.SOO 2.500 2.500 2.750 2874 3055 3245 3720

l. 2SO 1.250 l. 250 l_. 3 50 1 1 l l. 080 ·'-

31. 9. 3 339.5 360 . 6 .189 .8 0 0 0 0

- _1_898 - lS78 -12~14 -799.2 .0300 .0800 .0800 .0300

8

1820 983 9

1.623 ?'274

.1750 4463

2.750 3944

1. 350 L 080 519.4

0

-336.5 .0800

MARKET SHARE GROSS SALES

.1800 4728

.1850 5006

Figure: 2. ]introductory Example

Ul'i IT PRICE OP2P.ATING COST PRODUCTION COST OVERHEAD NET INCO~'lE

I NVES 1'~1ENT RA 'lE OF PETUR.N N~'i ' PR F: ::;F.N'1' V,li..T.flF.

2.750 4178

l. 350 1.080 550.2

0 .137? 1 4 4- 4

2.750 Ll423

l.3r..o J . • 030 582.5

0 .3 056 F t.l_ 8

- ----------------------------------

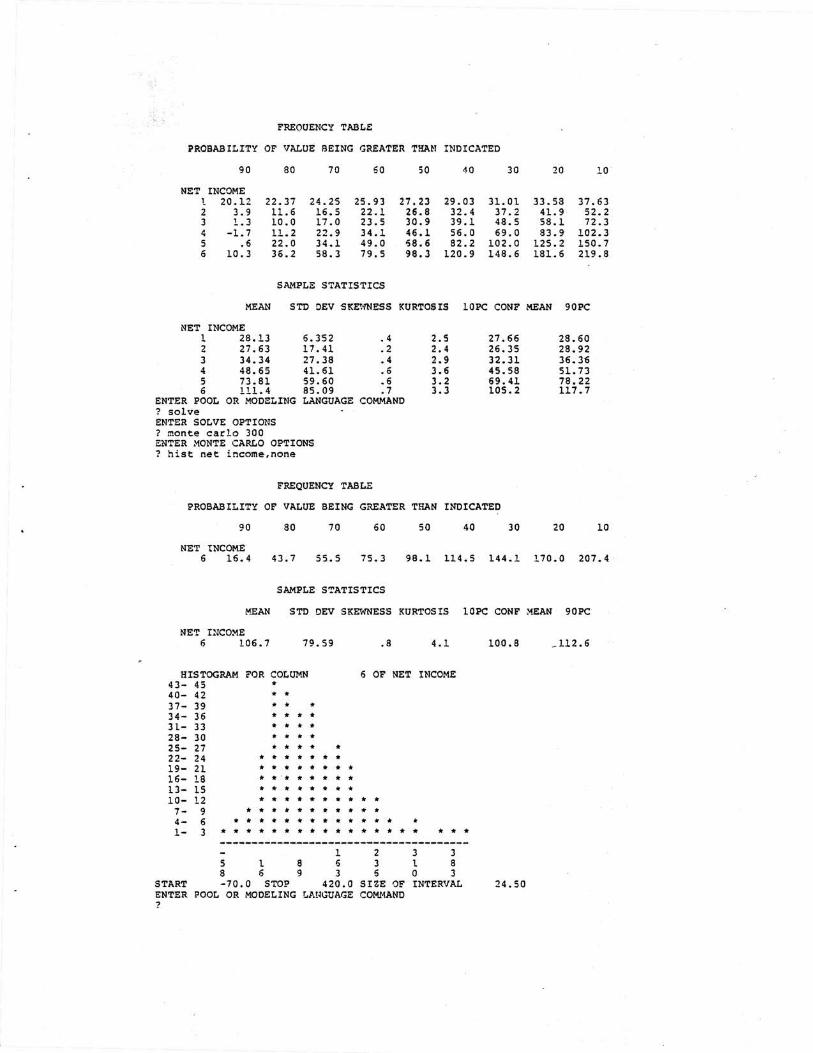

\ 1QD2L \10NTS VERSION 0!." 12 / '.5/80 H:22 1 o -:oL mms ;_:; Bl- ;_ 9 s s 2C * 3 0 *R!S K A~lALYS IS ':OD.SL 'TS I~iG S I :~ULATI0l·i

40 * 50 ':::clGI?-lF.ERI~!G DESIG~i='!'!U?_l\Nn ( 50000,60000, 80000 ) . 0 6 0 c·•.:;.RKET SH!I.P.E=~ORP.AND (.!., . 0 J. ) 7 0 SALES PRICE=UNIP.A~:D ( 8. 00, R. i 5) 80 TOTAL ~ARKET=tOOOOOO,PREVIODS TOTAL UARKET*l.l qo SALES VOLU''E=!-!?.RKET SHAP.E*~O'!'AL '·1ARKE': 100 G?.OSS INCO:'<lE=SALl:S 1/0LU:'E"'SALES PRFE l t O ?RODDC'!'IO~ COST=7.00 fOR 2,7.25 l2 0~~=~ E ·ICO: lE =GROSS E!CO!••E-SALES VOLUt'.E * PRCDUr.T I C:1 ~as T- E:·:G I:!F.ERING ::JES IG!·! l '-'0 I<<v'EST~·'EN7=1.00000, 0 150 DISCC'UNT RATE=O . 15 :. ;: 0 P.?ESENT '·'OR~H=::PVC (!:E7 INC0!-':7.:, DISCOUNT HATE, !)NES'I':\ENT) 170 ?ATE OF RETUP.!·: =D.R(li:::T I!'1CO~!E, IYV!::S'INENT) 1 ?0 ':'ER"!El~ . .L VALUE.=NTV(:·iET INC01'!E,0.08, INV!':ST;'-lE~:?) 190 ::!ENEFI'i' 'l'O COST ?.A'I'IO=GC?.ATIO(NET I;:oJC0~·1E,DISCOUclT :l..A,'I'E,INVES'i.' :-lE?~T) i::ND 'JF "O:JEL ? sol_ve 1100SI. ~10:1TE VERSION OF l::'/15 / 30 16:22 -- 5 CC!..l'~·!!I!S l~ VARIABLES SNTEP. SOLVE OP'l'Im1S 7 rnnnt• ca~lo 300 ENT!::R : !ONTE CARLO OPTIONS 7 f'r••:r,~ist nP.t i.ncome,freo: p~P.s•nt ·-roocth,none

FREOUENCY TABLE

PPCBAP. ISI'!'Y OF VALUE BEINC GREATER TEA~! D!DIC.l\TED

30 70 'iO 50 30 20

NET nco~~E

1.0

1985 ll9~65 l31BBC 141705 l~l450 l62l14 ' 72028 135957 201775 215354

PRESEN'l' lvORTil 1985 2~3807 143031 ~76531 2?6640 329297 359703 391085 437677 477330

SN·lPLE ST.l\TISTICS

~!EAN S?D DEV SKm·l'NESS KURTOSIS 10PC CONF :"'EAN ')QPC

NET 1985

H!CO~!E

165433

PRESENT r.;QRTH 1')85 337968

36647 • 2 2. 3

102044 • 3 ~. 4

HISTOGRAN :'OR COLUM~l 1.985 OF NET InC0'\2 31- 33 • 23- ?0 * 25- 27 * * *

* * * * * * * * * * * ~ • * * * * * * * * * * * *

* *

* *

* * * * * * * *

22- 24 l?- 21 16- 18 13- JS 10- 12 * * * * * ******* *

* * * * * * * * * * * * * * * * 7- 9 4- 6 * * * * * * * * * * * * * * * * * * * l- 3 • * * * * * * * * * * * * * * * * * * *

l '!.. 1. "' ?

8 3 ,:; 8 1_ 1 '5 7 2 8 3 :l 2 '

., 7 2 7 7. -5 5 5 5 5 s 5 0 IJ 0 () 0 0 •J

START 82000.0 S':'OP 252000.0 SIZE ~"'? I N .. rERVJ;.I~

162725 HBl-11

330427 3'\550'3

FIGURE 3. IFPS Simulation ~!odel

8500 . 00

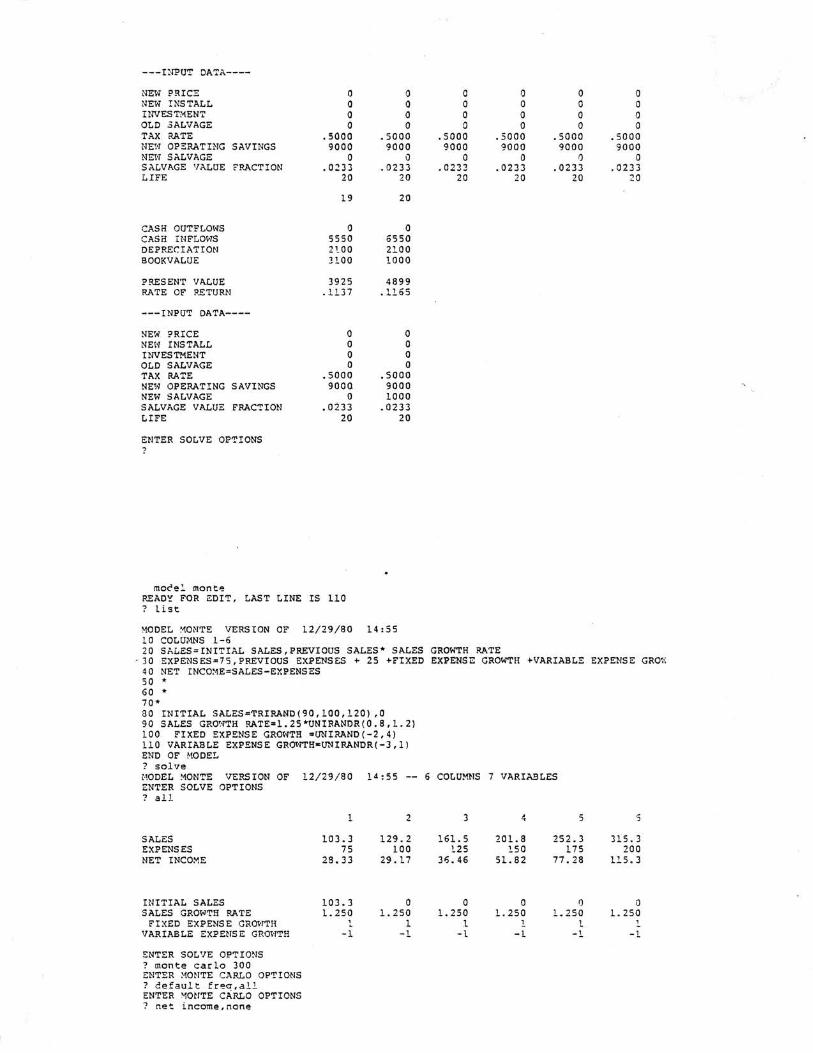

MODEL REPLACE 'lERSION OF 01/26/ 8 1 2l:31 10 COLUMNS 1-20 20 * 30 CASH OUTFLO,'lS=NEiq PRICE +NE;v INS TALL- {OLD SALVAGE'* { 1-TAX RATE)) 40 CASH INFLOWS = {NEW OPEP-ATING SAVINGS-DEPRECIATION) *{1-TAX ~ATE) +NEW SALVAGE + SOSTLINE DEPR { INVESTI1ENT ,SALVAGE VALUE FRACTION, LIFE, DEPRECIATION, 300KVALUE) 60 .. 70 !?RESENT VALUE=NPVC{CASH INFLOivS, .10 ,CASH OUTFLOHS) 80 RATE OF RETU~< = IRR(CASH INFLOWS,CASH OUTFLOWS) 90 * 100*---INPUT DATA----110* 120 NEW PRICE=40000,0 130 NEW INSTALL=3000,0 135 !NVESTMENT=NEH PRICE -+-NEW INSTALL 140 OLD SALVAGE=1000,0 l50 TAX RATE = .50 160 NE1ol OPERATING SAVINGS•9000 180 NE>•T SALVAGE=O FOR l 9, 80011: VALUE 1~0 SALVAGE VALUE FRACTION•l /43 20 0 LIFE=20 END OF ~10DEL ? solve ~!ODEL REPLACE VERSION ENTER SOLVE OPTIONS

OF 01 /2 6/ 81 21:31 -- 20 COLUMNS 15 VARIABLES

? all

CASH OUTFLOWS <::ASH INFLOWS DEPRECIATION BOOKVALUE

PRESENT VALUE RATE OF RETURN

---INPUT DATA----

NEN PRICE ~:EH INSTALL INVESTMENT OLD SALVAGE TAX PJI.TE NEN OPERI\TH!G SAVINGS NE,•T SALVAGE SALVAGE VALUE FRACTION LIFE

CASH OUTFLOWS CASH INFLOWS DEPRECIATION BOOKVALUE

PRESENT VALUE RATE OF P-ETURN

---INPUT DATA----

NEN PRICE NE~·r INSTALL INVESTilENT OLD SALVAGE TAX P-ATE NEH OPERATING SAVINGS NEW SALVAGE SALVAGE VALUE FRACTION LIFE

CASH OUTFLOI-TS CASH INFLO:-lS DEPRECIAT!Ot-: 300KVALUE

PRESENT VALUE RATE OF RETURN

1

42500 5550 2100

40900

-37455

4000 0 3000

43000 1000

.5000 9000

0 .0233

20

7

0 555 0 21 00

2830 0

-15480

0 0 0 0

. 5000 9000

0 .0233

20

13

0 3550 210 0

15700

-307<i .0858

2

0 5550 2100

38800

-32868

0 0 0 0

. 5000 9000

0 .0233

20

8

0 5550 210 0

26200

-12891 .0098

0 0 0 0

.5000 9000

0 .0 233

20

l4

0 5550 2100

1360 0

-1615 .093 0

3 4 5

0 0 0 5550 5550 5550 2100 2100 2100

36700 34600 32500

-28698 -24907 -21461

0 0 0 0 0 0 0 0 0 0 0 0

.5000 .5000 .50 00 9000 9000 9000

0 0 0 .0233 .0233 . 0233

20 20 20

9 1 0 11

0 0 0 5550 5550 5550 2100 2100 2100

24100 22000 19900

-10537 -8398 -6452 .0336 . 0517 .0658

0 0 0 0 0 0 0 0 0 0 0 0

.5000 . 5000 . 5000 9000 9000 9000

0 0 I)

.0233 .0233 .0233 20 20 20

1 5 16 17

0 0 0 5550 5550 5550 210 0 2100 210 0

11500 94 00 73 00

-2S S. J 921 . 6 20 2 0 . 0988 .1035 . 1076

6

0 5550 2100

30400

-18328

0 0 0 0

.5000 900 0

0 .0233

20

12

0 5550 2100

17800

-4684 .0769

0 0 0 0

.5000 90 0 0

0 .0 233

20

18

0 5550 2100 5 200

3018 .1 : 09

---E-lPUT DATA----

NEi; PRICE 0 NEW INSTALL 0 INVESTMENT 0 OLD 3ALVAGE 0 T."<X RATE .5000 NEW OP::RATING SAVINGS 9000 NEH SALVAGE 0 SALVAGE IJALUE FRACTION .0233 LIFE 20

19

CASH OUTFLONS 0 CASH INFLOt-TS '5550 DEPRECIATION 2~00

BOOKVALUE 3100

PRESENT VALUE 3925 RATE OF RETURN .1137

---INPUT DATA----

NEW ?RICE 0 NEI•T INSTALL 0 INVESTMENT 0 OLD SALVAGE 0 TAX RATE .5000 NEW OPERATING SAVINGS 9000 NEW SALVAGE 0 SALVAGE VALUE FRACTION .0233 LIFE 20

ENTER SOLVE OPTIONS ?

moCe.!. monte READY FOR EDIT, LAST LINE IS 110 ? list

0 0 0 0

.5000 9000

0 .0233

20

20

0 6550 2100 1000

4899 .1165

0 0 0 0

.5000 9000 1000

.0233 20

MODEL 'IONTE VERSION OF 12/29/80 14:55 10 COLUMNS l-6

0 0 0 0 0 0 0 0

.5000 .5000 9000 9000

0 0 .0233 .0233

20 20

20 SALES=INITIAL SALES,PREVIOUS SALES* SALES GROWTH RATE

0 0 0 0 0 0 0 0

.5000 .5000 9000 9000

a 0 .0233 . 0233

20 20

• 30 SXPENSESs75, PREVIOUS EXPENSES + 25 +FIXED EXPENSE GROWTH +VARIABLE EXPENSE GRO\·; 4 0 NET INC0~1E=SALES-EXPENSES

50 * 60 * 70* 80 INITIAL SALES=TRIRAND(90,100,120) ,0 90 SALES GRO~'ITH RATE=l.25*UN!RANOR(0.8,1.2) 100 FIXED EXPENSE GRONTH =UNIRAND(-2,4) 110 VARIABLE EXPENSE GRONTHcUNIRANDR(-3, 1) END OF ~IODEL

? solve 1·!0DEL ~10NTE VERSION OF 12/29/80 14:55 -- 6 COLUMNS 7 VARIABLES ENTER SOLVE OPTIONS ? all_

SALES EXPENSES NET INCOME

INITIAL SALES SALES GROWTH RATE

FIXED EXPENSE GRO~ITH VARIABLE EXPENSE GRO>•ITH

ENTER SOL'JE OPTIO~TS ? monte carlo 300 ENTER ~ONTE CARLO OPTIONS ? default fr~a,all ENTER MONTE CARLO OPTIONS ? net income,none

1

103.3 75

28.33

103.3 1. 250

-l

2

129. 2 100

29.17

0 1. 250

1 -1

3

161.5 t25

36.46

0 1. 250

1 -l

201. B :!.SO

51.82

0 1.250

-l

5

252.3 175

77.28

0 l. 250

l -l

s

315.3 200

115.3

0 l. 250

:!. -l

FREQUENCY TABLE

PROBABILITY OF VALUE BEING GREATER THA~l !NDICATED

90 80 70 60

NET INCOME l 20.12 22.37 24.25 25.93 2 3.9 3 1.3 4 -l.7 5 .6 6 10.3

MEAN

NET INCOME 1 28.13 2 27.63 3 34.34 4 48.65 5 73.81 6 111.4

11.6 16.5 22.1 10.0 17.0 23.5 11.2 22.9 34.1 22.0 34.1 49.0 36.2 58.3 79,5

SAMPLE STATISTICS

STD OEV SKE~·INESS

• 4 . 2 .4 • 6 .6 • 7

50 40 30

27. 23 29.03 31.01 26.8 32.4 37.2 30.9 39.1 48.5 46.1 56.0 69.0 o58.6 82.2 102.0 98.3 120.9 148.6

KURTOSIS lOPC CONF

2.5 2.4 2.9 3.6 3.2 3.3

27.66 26.35 32.31 45.58 69. 4l 105.2

ENTER POOL OR MODELING ? solve

6.352 17.41 27.38 41.61 59.60 85.09 LANGUAGE COMMAND

ENTER SOLVE OPTIONS ? monte carlo 300 ENTER MONTE CARLO OPTIONS ? hist net income,none

FREQUENCY TABLE

PROBABILITY OF VALUE BEING GREATER THAN INDICATED

20 10

33.58 37.63 41.9 52.2 58.1 72.3 83.9 102.3

125.2 150.7 181.6 219.8

MEAN 90PC

28.60 28 . 92 36.36 51.73 78.22 117.7

90 80 70 60 50 40 30 20 10

NET INCOME 6 16.4 43.7 55.5 75.3 98.1 114.5 144.1 170.0 207.4

SAMPLE STATISTICS

MEAN STD OEV SKE"..rNESS KURTOSIS 10PC CONF MEAN 90PC

NET INCO!'!E 6 106.7 79.59 • 8 4.1

HISTOGRAM 6 OF NET INCOME FOR COLUMN 43- 45 40- 42 37- 39 34- 36 31- 33 28- 30

* * * * * *

* * * * *

* * * * * * *

25- 27 * * * * * 22- 24 * * * * * * * 19- 21 * * * * * * * * 16- 18 * * * * * * * * LJ- 15 * * * * * * * * 10- 12 * * * * * * * * * * 7- 9 •• * •• * • * • * * 4- 6 •• * • * •• * • * ••• 1- 3 • * •• * * • * • * ••• * • * •• *

1 2 3 3 5 t 8 6 3 l 8 8 6 9 3 6 0 3

START -70.0 STOP 420.0 SIZE OF INTERVAL ENTER POOL OR MODELING LAHGUAGE COMNAND ?

100.8 _112. 6

24.50

CONTENTS

PART I. BASIC ELEMENTS OF IFPS

I. Introduction

II. Organization of IFPS

III. How to Obtain IFPS at Your Terminal and Begin Work

IV. A Simple IFPS Model

- Problem - IFPS Model - What You Type at the Terminal - Listing Your Program - Obtaining Answers (The use of SOLVE)

V. Getting out of IFPS (the QUIT Command)

VI. Correcting Mistakes (The EDIT Commands)

Misspellings While Typing Error in Complete Line Using the C Edit Command Retyping a Line Deleting a Line Inserting a Line Obtaining a Listing of a Single Line

VII. Obtaining a Listing on the Line Printer at the Computer Center

PAGE

1

2

5

8

8 9

10 11 12

13

14

14

15 16 17 17 17

(The RECORD Comand) 18

PART II. USEFUL FEATURES OF IFPS

VIII. Using IFPS to Ask Questions and Make Decisions (WHAT IF, SENSITIVITY, GOAL SEEKING, ANALY2E)

What If Sensitivity Goal Seeking Analyze

IX. Built-In Functions (Financial, Forecasting, Mathematical)

Financial Functions The Periods Statement Forecasting Functions Mathematical Functions

i

FIGURE if. TABLE OF CvNTENTS OF STUDENT GUIDE

20

20 22 24 24

25

26 28 28 30

PART II. CONT.

X. Built-in Subroutines (Depreciation, Amortization)

XI. Monte Carlo Simulation (Risk Analysis)

Built-In Probability Distributions (UNIRAND, TRIRAND, NORRAND)

Defining Your Own Probability Distribution Choosing the Same Random Number for All Periods

or a New Value for Each Period A Simple Monte Carlo Program Deterministic Solution of Monte Carlo Models (Best

Case/Worst Case/Most Likely Case) MONTE CARLO Simulation The STOP Command (What to do if you make an options

mistake) Interpreting Monte Carlo Results The POOL Command

PART III. SPECIAL CAPABILITIES AND SAMPLE PROBLEMS

XII. Solve Options

XIII. Plotting Results Graphically

XIV. Data Files

The Dummy Model The Data File Obtaining Answers Creating and Saving a New Data File Changing a Data File Storing the Output of a Model for Future Use as Data

XV. Generating Formatted Reports

Creating a New Report A Simple Example

XVI. Miscellaneous Features and Examples

Using Line Numbers Rather than Variable Names SUM Function IF Statements in IFPS Example: Using IFPS for Exponential Smoothing Example: Series Decomposition of Trends Example: Computing the Values in the Tables in Your

Finance Text

ii

PAGE

31

34

35 36

37 38

39 41

42 42 45

46

48

50

so so 51 51 52 52

53

53 54

59

59 60 60 62 62

63

10 COLU~lNS l-6 20 SALES = lOO,PREVIOUS SALES *1.75 30 EXPENSES = 7S,J.OO,l~S,l50,175 40 NBT INCOME = SALES -EXPENSES 50 ir::

60 * RA'l'IO Ai·LI\LYSIS 70 *PERCENT OF SALES 80 EXPE~lSE PATIO = EXPENSES/S.?\LES 90 NET IN~OnE P-..t-\TIO = NET INC0~1E/S.I\L~•:s

? solve iv!ODEL GRAY VERSION OF 02/06/82 "f. :01 -- 6 COLm.·mS 5 VARIABLES

SOLVE 0PTimJS ? ""1 l

E:<PENSES t·!E'l IL,iCt)!_.E

PERCENT OF Si\LES EXP2NSE P .. A'I'IO PET INCO~<•E RATIO

ENTER SOLVE OPTIONS ?

1

1. 00

?.

125 100

'25

RATIO Al:!ALYSIS

.7500

.2500 .8000 .2000

FIGURE j. Example Used In Student Guide

") . )

]_56. 3 1 ') c:: .i .• :. -·

31.25

.8000

.2000

4

:!..95.3 150

4 5. 11

.7630

.2320

5

~ !', 4. l 175

69.1~

. 71J8

.2332

6

30:).2 175

130.~

.:J73~

.42fih

Figure 6.

IFPS QUESTIONNAIRE

t.Te are surveying the t1BA class about its responses to the use of the IFPS in the MBA program. We would appreciate your filling out this brief questionnaire. Thanks for your help.

T.E. Perkins and P. Gray

Do you consider yourself a novice ____ intermediate ____ expert ____ in IFPS?

Did you find it easy ____ somewhat hard hard ____ very hard ____ to learn IFPS?

Was the IFPS Student Guide sufficient support for learning the language? Yes No

If not, please expl~on the back of this page.

Have you used IFPS 1n any course other than MS&C (e.g., homework, class project, case analysis)? Yes ___ NO ____ _

If yes, please describe on the back of this page what you used IFPS for and how often you have used it.

Have you ever created an IFPS model for personal use {e.g., personal finances, taxes) or as part of your job or as a research assistant to a professor? Yes ____ No __ __

!£ yes, please describe on the back of this page.

Have you received instruction in another computer language either at SMU or elsewhere (include BASIC short course)? Yes ___ No ___ I£ yes, which languages: BASIC __ FORTRAN __ SPSS __ OTHER(specify)

Did you find IFPS easier same as ____ harder ____ to learn than other computer languages? ----

Do you expect to be using a computer after you graduate? Yess ____ No __ __

Do you expect to own your own personal computer? Yes ____ No

As part of your MS&C course ~rk you received instruction in both the use of the MBA calculator and modeling in IFPS. Which of these do you believe is ~rth more to you:

in the short term (while at 51111) MBA IFPS in the long term {during next S years-)---MBA -IFPS ____ _

Answer the following questions only 1f you did not have computer experience prior to coming to SMU:

·otd you have "fear of computer" prior to coming to SMU? Yes ___ No __ __

If yes, have you overcome that fear? Yes ____ No __ __

Demographic Data:

Male ___ Female

Year of Bachelor.'s Degree'-------No. of units of mathematics/statistics as undergraduate ______ _ MBA concentration:

Acc:ounting ___ Finance ____ International _____ Market:f.ng ___ MS&C __ _ Organizational Behavior _____ Real Estate _____ Other __________ __

Pro-fessor: Aronofsky _____ Barr ___ Perkins ___ Sobol ____ _

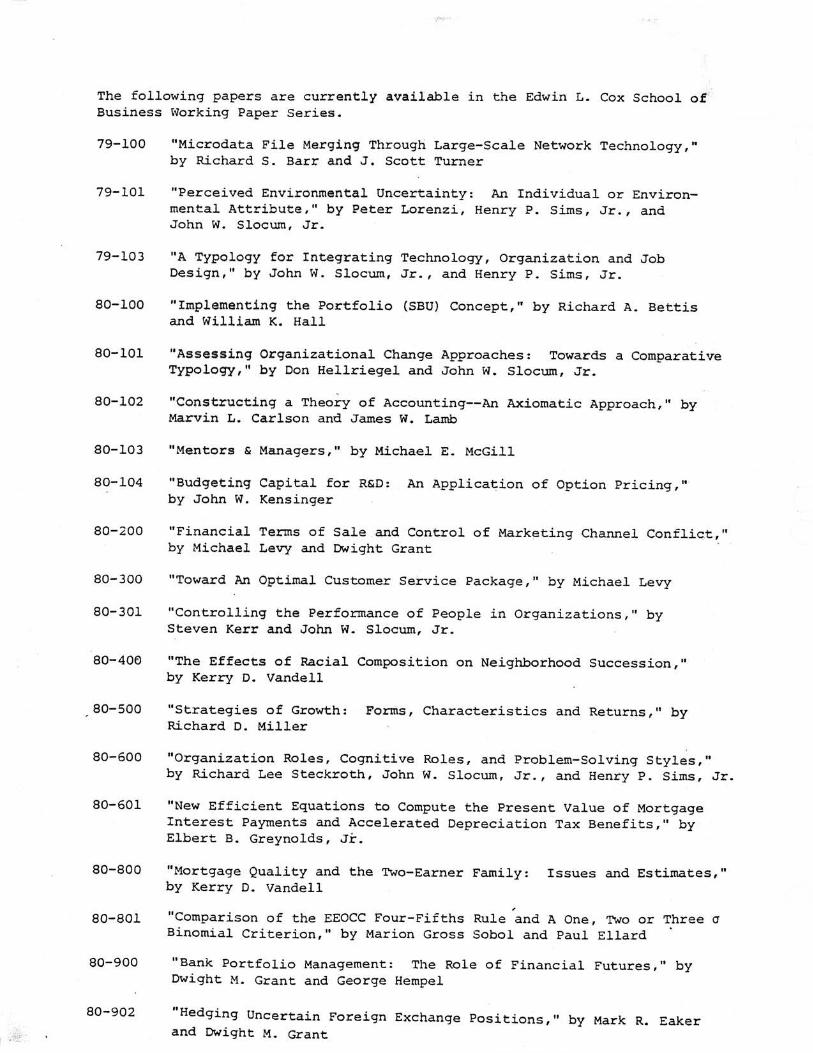

The following papers are currently available in the Edwin L. Cox School of Business ~iorking Paper Series.

79-100

79-101

79-103

80-100

80-101

80-102

80-103

80-104

80-200

80-300

80-301

80-405

80-500

80-600

80-601

80-800

80-801

80-900

80-902

"Microdata File Merging Through Large-Scale Network Technology," by RichardS. Barr and J. Scott Turner

"Perceived Environmental Uncertainty: An Individual or Environmental Attribute," by Peter Lorenzi, Henry P. Sims, Jr., and John W. Slocum, Jr.

"A Typology for Integrating Technology, Organization and Job Design," by John W. Slocum, Jr., and Henry P. Sims, Jr.

"Implementing the Portfolio (SBU) Concept," by Richard A. Bettis and William K. Hall

"Assessing Organizational Change Approaches: Towards a Comparative Typology," by Don Hellriegel and John w. Slocum, Jr.

"Constructing a Theory of Accounting--An Axiomatic Approach," by Marvin L. Carlson and James W. Lamb

"Mentors & Managers," by Michael E. McGill

"Budgeting Capital for R&D: An Application of Option Pricing," by John W. Kensinger

"Financial Terms of Sale and Control of Marketing Channel Conflict," by Michael Levy and Dwight Grant

"Toward An Optimal Customer Service Package," by Michael Levy

"Controlling the Performance of People in Organizations," by Steven Kerr and John W. Slocum, Jr.

"The Effects of Racial Composition on Neighborhood Succession," by Kerry D. Vandell

"Strategies of Growth: Forms, Characteristics and Returns," by Richard D. Miller

"Organization Roles, Cognitive Roles, and Problem-Solving Styles," by Richard Lee Steckroth, John W. Slocum, Jr., and Henry P. Sims, Jr.

"New Efficient Equations to Compute the Present Value of Mortgage Interest Payments and Accelerated Depreciation Tax Benefits," by Elbert B. Greynolds, Jr.

"Mortgage Quality and the Two-Earner Family: Issues and Estimates," by Kerry D. Vandell

, "Comparison of the EEOCC Four-Fifths Rule and A One, TWo or Three a Binomial Criterion," by Marion Gross Sobol and Paul Ellard

"Bank Portfolio Management: The Role of Financial Futures," by Dwight M. Grant and George Hempel

"Hedging Uncertain Foreign Exchange Positions," by Mark R. Eaker and Dwight M. Grant

90""-j . "Strategic Portfolio Management in the Multibusiness Firm: An , :ij::f;A Implementation Status Report," by Richard A. Bettis and William

::'" K. Hall

SQ;.;t;l,,J,.l "Sources of Performance Differences in Related and Unrelated Diversified Firms," by Richard A. Bettis

SO•ll2 "The Information Needs of Business With Special Application to Managerial Decision Making," by Paul Gray

90•113 "Diversification Strategy, Accounting Determined Risk, and Accounting Determined Return," by Richard A. Bettis and William K. Hall

80-114 "Toward Analytically Precise Definitions of Market Value and Highest and Best Use," by Kerry D. Vandell

80-115 "Person-Situation Interaction: An Exploration of Competing Models of Fit," by William F. Joyce, John W. Slocum, Jr., and Mary Ann Von Glinow

80-116 "Correlates of Climate Discrepancy," by William F. Joyce and John Slocum

80-117 "Alternative Perspectives on Neighborhood Decline," by Arthur P. Solomon and Kerry D. Vandell

80-121

80-122

80-..123

81-100

81- 200

81-201

81-300

81-400

81-500

"Project Abandonment as a Put Option: Investment Decision and Operating Risk Theory," by John W. Kensinger

Dealing with the Capital Using Option Pricing

"The Interrelationships Between Banking Returns and Risks," by George H. Hempel

"The Environment For Funds Management Decis i ons In Corning Years," by George H. Hempel

"A Test of Gouldner's Norm of Reciprocity In A Commercial Mark eting Research Setting," by Roger Kerin, Thomas Barry, and Alan Dubinsky

" Solution Strategies and Algorithm Behavi or in Large-Scale Network Codes, " by Richard S. Barr

"The SMU De cision Room Pro j ect," by Paul Gray, Juli us Arono fsk y , Nancy W. Berry, Olaf Helmer, Gerald R. Kane, and Thomas E. Perkins

"Cash Discounts To Retail Customers: An Alternative To Credit Ca r d Performance," by Michael Levy and Charles I ngene

"Merchandising Decis i ons: A Ne w View o f Planning a nd Measuri ng Per f orma nce ," b y Michael Levy and Charle; A. I ngene

"A Meth~dology For The Formulation a nd Ev a l uati on o f Energy Goals And ~ol~cy Alternatives For I s r ael," by Juli us Aronofsky, Reuven Karn~ , a nd Ha r ry Tankin

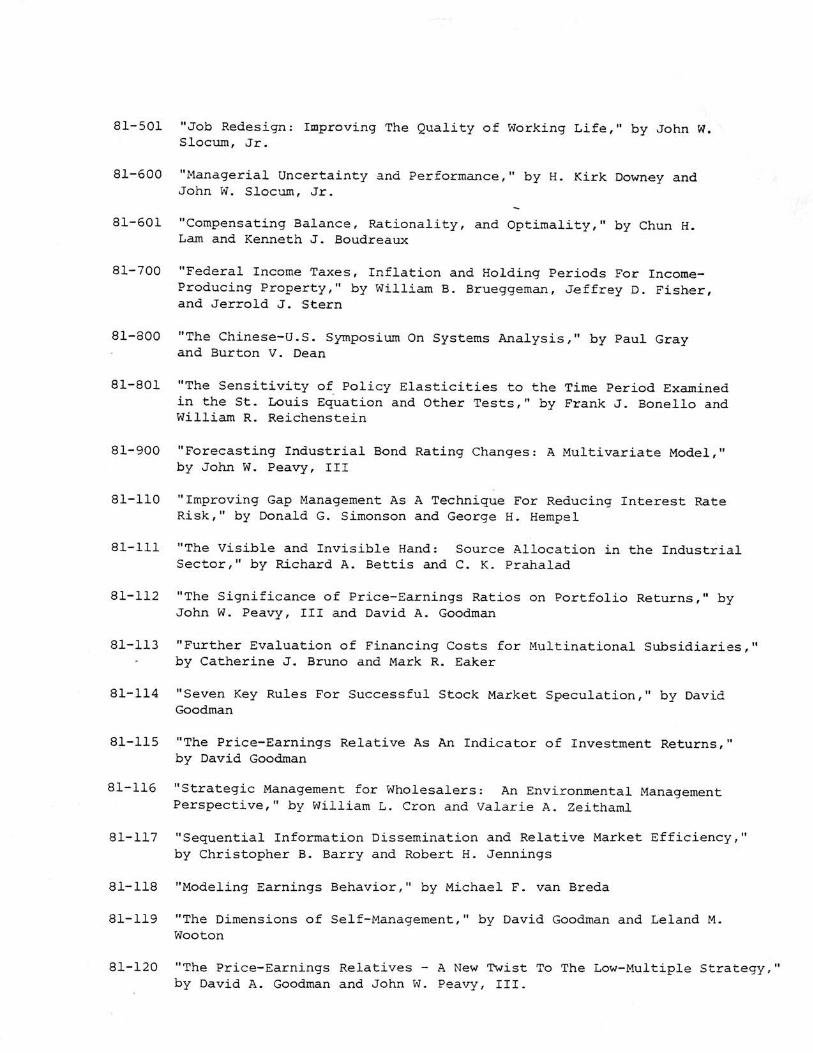

81-501 "Job Redesign: Improving The Quality of Working Life," by John W. Slocum, Jr.

81-600 "Managerial Uncertainty and Performance," by H. Kirk Downey and John W. Slocum, Jr.

81-601 "Compensating Balance, Rationality, and Optimality," by Chun H. Lam and Kenneth J. Boudreaux

81-700 "Federal Income Taxes, Inflation and Holding Periods For IncomeProducing Property," by William B. Brueggeman, Jeffrey D. Fisher, and Jerrold J. Stern

81-800 "The Chinese-U.S. Symposium On Systems Analysis," by Paul Gray and Burton V. Dean

81-801 "The Sensitivity of Policy Elasticities to the Time Period Examined in the St. Louis Equation and Other Tests," by Frank J. Bonello and William R. Reichenstein

81-900 "Forecasting Industrial Bond Rating Changes: A Multivariate Model," by John W. Peavy, III

81-110 "Improving Gap Management As A Technique For Reducing Interest Rate Risk," by Donald G. Simonson and George H. Hempel

81-lll "The Visible and Invisible Hand: Source Allocation in the Industrial Sector," by Richard A. Bettis and C. K. Prahalad

81-112 "The Significance of Price-Earnings Ratios on Portfolio Returns," by John W. Peavy, III and David A. Goodman

81-113 "Further Evaluation of Financing Costs for Multinational Subsidiaries," by Catherine J. Bruno and Mark R. Eaker

81-114 "Seven Key Rules For Successful Stock Market Speculation," by David Goodman

81-115 "The Price-Earnings Relative As An Indicator of Investment Returns," by David Goodman

81-116 "Strategic Management for Wholesalers: An Environmental Management Perspective," b y William L. Cron a n d Valari e A. Zeithaml

81-117 "Sequential Information Diss emination and Relative Market Efficiency," by Christopher B. Barry and Robert H. Jennings

81-118 "Modeling Earnings Be havior," by Mic hael F. van Breda

81-119 "The Dime n sions o f Se l f -Manageme nt, " by David Goodma n and Leland M. Wooton

81-120 "The Pric e-Earnings Relatives- A New Twist To The Low-Multiple Strategy," by David A. Goodman and John W. Peavy , III .

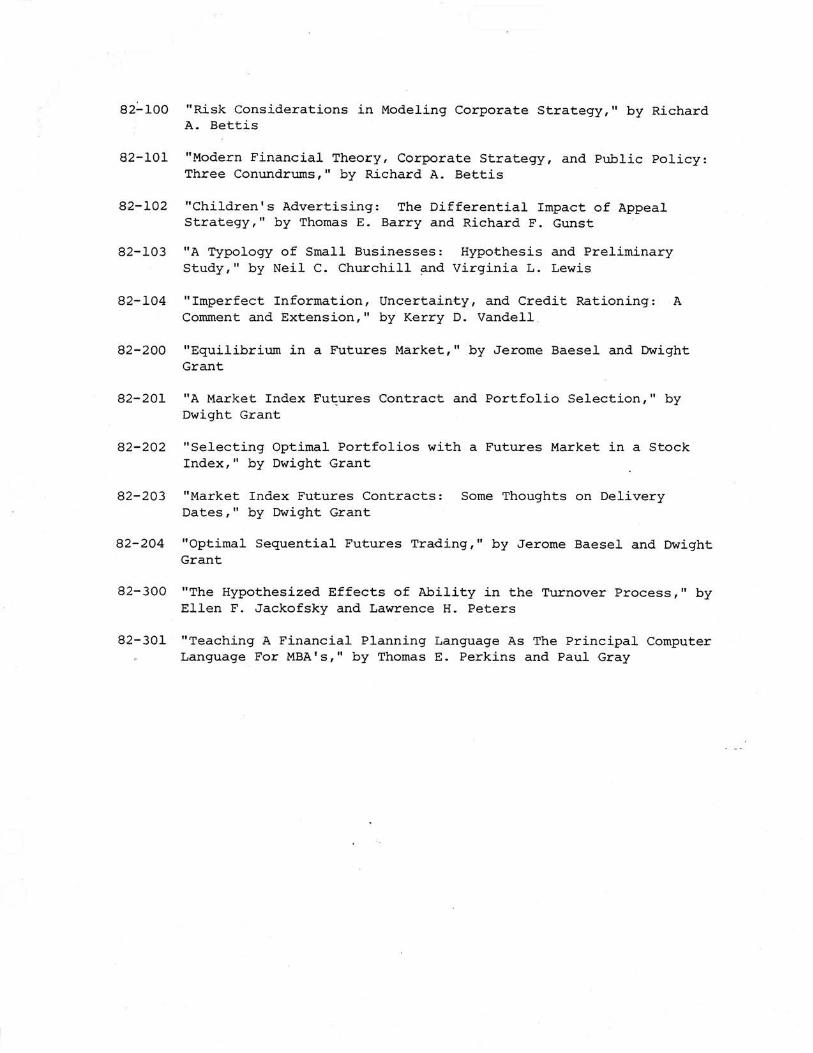

82:..100 "Risk Considerations in Modeling Corporate Strategy," by Richard A. Bettis

82-101 "Modern Financial Theory, Corporate Strategy, and Public Policy: Three Conundrums," by Richard A. Bettis

82-102 "Children's Advertising: The Differential Impact of Appeal Strategy," by Thomas E. Barry and Richard F. Gunst

82-103 "A Typology of Small Businesses: Hypothesis and Preliminary Study," by Neil C. Churchill and Virginia L. Lewis

82-104 "Imperfect Information, Uncertainty, and Credit Rationing: A Comment and Extension," by Kerry D. Vandell

82-200 "Equilibrium in a Futures Market," by Jerome Baesel and Dwight Grant

82-201 "A Market Index Futures Contract and Portfolio Selection," by Dwight Grant

82-202 "Selecting Optimal Portfolios with a Futures Market in a Stock Index," by Dwight Grant

82-203 "Market Index Futures Contracts: Some Thoughts on Delivery Dates," by Dwight Grant

82-204 "Optimal Sequential Futures Trading," by Jerome Baesel and Dwight Grant

82-300 "The Hypothesized Effects of Ability in the Turnover Process," by Ellen F. Jackofsky and Lawrence H. Peters

82-301 "Teaching A Financial Planning Language As The Principal Computer Language For MBA's," by Thomas E. Perkins and Paul Gray