Swinging For the Fences: The Effects of CEO Stock Options on Company Risk-Taking and Performance

53

Swinging For the Fences: The Effects of CEO Stock Options on Company Risk-Taking and Performance Wm. Gerard Sanders 790 TNRB Marriott School of Management Brigham Young University Provo, UT 84602 (801) 422-7607 [email protected] Donald C. Hambrick Smeal College of Business The Pennsylvania State University 414 Business Building University Park, PA 16802 (814) 863-0917 [email protected] This paper has benefited from the insights of Amy Hillman and three anonymous reviewers. For specific comments we thank Trevis Certo, Luis Gomez-Mejia Andrew Henderson, and Tim Pollock. © Academy of Management. All rights reserved. Content may NOT be copied, e-mailed, shared or otherwise transmitted without written permission. This non-copyedited article version was obtained from the Academy of Management InPress website and is intended for personal or individual use.

Transcript of Swinging For the Fences: The Effects of CEO Stock Options on Company Risk-Taking and Performance

Swinging For the Fences: The Effects of CEO Stock Options on Company

Risk-Taking and Performance

Wm. Gerard Sanders790 TNRB

Marriott School of ManagementBrigham Young University

Provo, UT 84602(801) 422-7607

Donald C. HambrickSmeal College of Business

The Pennsylvania State University414 Business Building

University Park, PA 16802(814) [email protected]

This paper has benefited from the insights of Amy Hillman and three anonymous reviewers. For specific comments we thank Trevis Certo, Luis Gomez-Mejia Andrew Henderson, and Tim Pollock.

© Academy of Management. All rights reserved. Content may NOT be copied, e-mailed, shared or otherwise transmitted without written permission. This non-copyedited article version was

obtained from the Academy of Management InPress website and is intended for personal or individual use.

1

Swinging For the Fences: The Effects of CEO Stock Options on Company Risk-

Taking and Performance

Abstract

We unpack the concept of managerial risk-taking, distinguishing among three of

its major elements: the size of the outlay; the variance of the potential outcomes; and the

likelihood of extreme loss. We then apply our framework in hypothesizing the effects of

CEO stock options on strategic behavior and company performance. We find that CEO

stock options engender high levels of investment outlays and bring about extreme

corporate performance (big gains and big losses), suggesting that stock options prompt

CEOs to make high-variance bets, not simply larger bets. Finally, we find that option-

loaded CEOs deliver more big losses than big gains.

2

It is an axiom of agency theory that managers tend to be more risk-averse than

shareholders would like them to be (Eisenhardt, 1989). Because CEOs have so much of

their economic wherewithal, as well as their reputations, tied to their focal firms, they are

relatively “underdiversified” and stand to lose a great deal if their companies stumble or

fail (Milgrom & Roberts, 1992). Thus, out of an overwhelming aversion to downside

outcomes, managers tend to avoid taking large risks. Shareholders, on the other hand, are

generally widely diversified in their holdings; hence they are risk-neutral and seek to

maximize returns. Because large gains tend to require that large risks be taken,

shareholders therefore favor more risk-taking than do CEOs. In this regard, agency

theorists draw on a central concept of financial economics – the correlation of risk and

return (Fama, 1976; Sharpe, 1964) – to argue that the two go hand in hand; you cannot

have big returns without taking big risks (Core, Guay, & Larcker, 2003).

Despite their zeal about risk-taking, however, agency theorists have been

generally ambiguous about just what they mean when they say they want managers to

take bigger risks.1 In some instances, agency theorists refer to the importance of placing

bigger bets, or making larger strategic outlays (Larcker, 1983). In other instances, they

refer to the importance of placing bets that have more extreme potential outcomes

(Jensen & Meckling, 1976; Wright, Kroll, Lado, & VanNess, 2002). And in still other

cases, agency theorists suggest that the main problem is that managers worry too much

about downside/losses which then prevents them from taking needed risks (Amihud &

Lev, 1983). It is due to this conceptual complexity, as well as other ambiguities, that

Wiseman & Gomez-Mejia (1998) described agency theory’s portrayal of risk as

“underdeveloped.”

1 Agency theorists want managers to join shareholders in being “risk-neutral,” which is defined as indifference between receiving a fixed sum and taking a chance on an uncertain action that has an expected value equal to the fixed sum (Milgrom & Roberts, 1992). Such a choice situation can be engineered in experimental settings, but its direct translation into managerial behavior is not straightforward.

3

But such limitations have not prevented agency theorists from making

prescriptions about how to promote managerial risk-taking. Among these prescriptions

has been the call for the heavy use of stock options to motivate CEOs, as when Hall &

Liebman (1998: 656) said that “the most direct solution to [the] agency problem is to

align the incentives of executives with the interests of shareholders by granting (or

selling) stock and stock options to the CEO.” Moreover, boards have largely followed

this advice. At their peak, in 2001, stock options (valued ex ante) accounted for over 50

percent of the pay of CEOs of major U.S. firms. In 2005, options were still the single

biggest element of CEO pay accounting for 41 percent (Lublin, 2006).

Oddly, the most vigorous discussions about stock options have been over whether

they should be expensed when they are granted, and over the practice of back-dating

options, rather than over the far more consequential question: Do stock options promote

constructive executive behavior, particularly sensible risk-taking? Studies have indicated

that stock options tend to induce managers to take bigger risks (e.g., Rajgopal & Shevlin,

2002), but have generally stopped short of examining whether these increased risk-taking

behaviors are value- and profit-enhancing or not. The central tension, to paraphrase the

arguments raised by Hanlon, Rajgopal, and Shevlin (2003), is whether stock options are

economically efficient, helping to enhance firm value, or whether they mostly create the

illusion of stimulating constructively aggressive behavior, while diverting windfalls to

executives. In this latter vein, only lately have some agency theorists conceded that stock

options may not resolve the agency problem in the way they had initially envisioned

(Jensen, Murphy, & Wruck, 2004).

In recent years, theorists have shown interest in how stock options shape

managerial perceptions and behaviors. For example, in an experimental setting, Devers,

Wiseman, and Holmes (in press) examined how option-holders revise their subjective

valuations of their options, depending on the interaction of the company’s recent stock

price trend and volatility. This finding leads to the important insight that managers

4

continuously update their assessment of the worth of their options, in ways that can be

expected to affect their strategic behaviors. Another recent study by Sanders (2001),

which is pivotal for our own inquiry, finds that stock options cause managers to engage in

risk-taking, as expected; but the form of risk-taking examined – acquisitions – is widely

believed to be value-destroying on average (Bruner, 2004; Jensen & Ruback, 1983;

Porter, 1987). The thrust of that study, then, is that stock options induce risk-taking, but

not necessarily wise risk-taking.

Our study attempts to make a theoretical contribution on two fronts. First, we

unpack the concept of managerial risk-taking. Specifically, we distinguish among three

elements of risk-taking: the size of the outlay or bet; the variance of the potential

outcomes; and the likelihood of extreme loss. As noted, prior research has tended either

to equate one of these elements with overall risk-taking or to speak about risk-taking

broadly without consideration of these distinct elements. Second, we apply our

framework of managerial risk-taking in examining the effects of stock options – a

favorite prescription for heightening executive risk-taking – on strategic behavior and

company performance. As noted above, relatively little is known about the inter-

connected consequences of CEO stock options for firm behavior and performance.

A brief overview of our line of argument is helpful at this point. First, we argue

that stock options encourage CEOs to place relatively large bets on uncertain investments

categories, such as R&D, capital expenditures, and acquisitions. Second, we argue that

stock options tend to bring about extreme corporate performance – big wins and big

losses. Moreover, we anticipate that the interaction of high levels of stock options and

high levels of investment spending will exacerbate performance extremeness, beyond the

simple additive effects of the two, indirectly indicating that option-loaded executives not

only make bigger investments but also (unobserved) higher-variance investments. Third,

and finally, we hypothesize that heavy use of CEO stock options will bring about more

big losses than big wins. This counterintuitive expectation is based upon the asymmetric

5

payoffs that CEOs experience when they hold large quantities of stock options: big

personal gains for performance improvements, but no losses for big company setbacks.

Based upon a multi-year analysis of over 800 companies, we find considerable support

for our hypotheses.

Before proceeding, we wish to note three limits to the scope of our study. First,

we focus specifically on CEO stock options, in keeping with the prevailing approach of

scholars of executive compensation, even though we recognize that many strategic

actions emanate from decision-making beyond the CEO. While we expect that CEO

compensation directly affects many strategic choices, we can also envision fruitful

research on how stock option allocations to entire top management teams might affect

organizational outcomes. Second, our empirical tests rely upon ex post evidence of risk-

taking, as reflected in corporate expenditures, performance extremes, and aggregate

financial ratios. Although this approach has been widely followed in research on

compensation and risk-taking (Carpenter, Pollock, & Leary, 2003; Eisenmann, 2002;

Wright et al., 2007), it does not allow examination of the ex ante risk profiles of the

choices made by the CEOs in our sample. Data allowing such insights are exceedingly

rare, and would almost always fall short of providing the fine detail required to directly

test our risk-taking framework. As a partial effort in this regard, however, we will report

a supplementary analysis of the characteristics of the acquisitions made by CEOs in our

sample. Third, an emerging stream of research suggests that executives continuously

update their subjective assessments of their option values, in ways that could influence

their strategic behaviors (Devers et al., forthcoming; Wiseman & Gomez-Mejia, 1998).

We do not attempt to develop our theory and hypotheses around this interesting line of

thought, but we do control for factors that should lead to this endowment effect.

6

Unpacking the Concept of Managerial Risk-Taking

Prior Literature

A voluminous literature on managerial risk-taking (dating back to Knight, 1921;

von Neuman & Morgenstern, 1947; and Arrow, 1965) has contributed greatly to our

understanding of a central feature of executive work (e.g., Bloom & Milkovich, 1998;

March & Shapira, 1987; Palmer & Wiseman, 1999; Shapira, 1995; Sitkin & Pablo, 1992;

Wiseman & Gomez-Mejia, 1998). Yet this literature carries some substantial

ambiguities, which pose difficulties for researchers who are concerned with fundamental

questions such as these: Just what do we mean when we say that a manager is taking a

risk? Is it possible that a given course of action is risky in some ways but not in others?

Namely, are there multiple elements or dimensions of risk?

Perhaps the main factor contributing to an over-aggregation of the risk-taking

construct in the management literature is that definitions generally have been abstract and

all-encompassing. For example, Wright, et al., (1996: 442) defined corporate risk-taking

as “the analysis and selection of projects that have varying uncertainties associated with

their expected outcomes.” Bloom & Milkovich (1998: 285) similarly defined risk as

“uncertainty about outcomes or events.”2 But because there is some uncertainty with

almost any managerial action, and because uncertainty itself begs explication, such

definitions leave the reader still puzzled as to just what constitutes risk-taking.3

In treating risk as a composite construct, prior researchers have not considered the

components, or elements, that comprise a risk; in turn, they have not examined the

possibility that a manager might make a decision that is risky when viewed on one

2 Much of the literature uses the terms risk and uncertainty interchangeably, or with one term being used to define the other. Knight (1921) defined the two as distinct constructs; risk being a condition to which a manager can assign probabilities to various possible outcomes, and uncertainty being a condition when outcomes are not knowable and thus void of assigned probabilities. In contrast, our study is specifically about “risk taking” (its antecedents and outcomes), which may involve both risk and uncertainty as Knight defined the terms. 3 It should be noted that we do not aim to provide a comprehensive elaboration of all forms of risk taking. Scholars from such diverse disciplines as political science, psychology, anthropology, and economics have varying epistemological notions of what constitutes taking a risk (Althaus, 2005).

7

dimension but not so risky on another. Indeed, the foundational work on risk and

uncertainty in economics clearly notes that the construct is multidimensional (Rothschild

& Stiglitz, 1970). In a managerial decision-making context, March and Shapira (1987)

(and later Shapira, 1995) made a step toward disaggregating the concept of managerial

risk-taking, proposing that “likelihood of outcomes and their values enter into

calculations of risk independently, rather than as their product” (p. 1405), and when they

observed that managers hold a special concern for “the worst outcomes” in weighing

choice alternatives. So far, however, these insights have generally not been systematized

or put to use in theory or research on incentives and managerial risk-taking.

The Elements of Risk

In this section, we seek to address the ambiguities just noted, by presenting a

framework for assessing the amount of risk associated with a managerial decision. We

define risk as the degree to which potential outcomes associated with a decision are

consequential, vary widely, and include the possibility of extreme loss. To elaborate,

potential outcomes are deemed consequential to the extent they have the potential to alter

– positively or negatively – the health and vitality of the firm; potential outcomes vary

widely to the extent there is a large spread in the possible results; and the possibility of

extreme loss exists when one of the potential outcomes is a loss of most or all of the

outlay made (which we discuss again below).

In our conceptualization, then, the riskiness of a managerial decision can be

decomposed into three conceptually distinct, but inter-related elements: 1) the size of the

outlay, or the amount at stake; 2) the variance of probabilistic outcomes; and 3) the

likelihood of losing most or all of the investment. These three elements can be thought of

as “dimensions” of risk. Thus, even though we have offered a single definition of risk, a

given choice alternative might be very risky on one dimension but not so risky on

another.

8

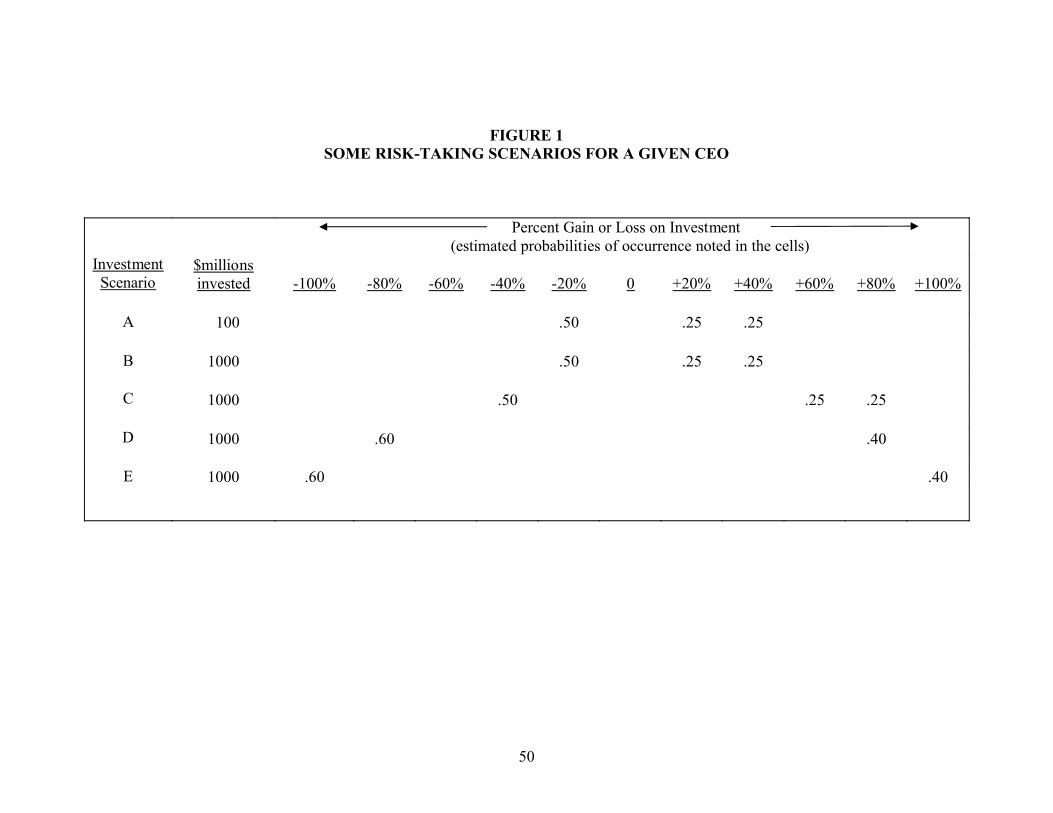

Figure 1 helps to illustrate the three elements of risk, by showing the potential

outcomes associated with several alternative risk-taking scenarios (A through E) for a

given manager. The figure depicts three main characteristics of each scenario: the size

of the investment being considered, the probabilistic distribution of alternative outcomes,

and the possible gains and losses. For example, Scenario A involves an investment of

$100 million; and, the manager estimates that there is a 25% chance of a 40% profit, a

25% chance of a 20% profit, and a 50% chance of a 20% loss. Obviously, this figure is a

simplification of managerial alternatives, for ease of presentation and discussion. For

example, it omits consideration of timing, including the possibility that an investment can

be made in stages, so as to minimize risk (Miller & Folta, 2002). More significantly, the

figure implies that the probabilities associated with the various alternatives are knowable

– when in actuality, such is almost never the case. It is reasonable to speak of the

probability of “heads” in a coin toss, but far less reasonable to speak of the probability of

a given outcome in a complex business situation. Indeed, March and Shapira (1987)

found in field research that managers generally do not think in terms of probabilities of

outcomes, but instead view risk subjectively or according to the likelihood of a large loss.

These complications do not negate the basic logic of our figure, but rather reaffirm that it

is a simplified depiction of managerial choice alternatives.-----------------------------------

Insert Figure 1 about Here-----------------------------------

We can use the figure to explicate the three inter-related elements of risk. First,

ceteris paribus, the bigger the investment (for a given firm), the bigger the exposure and

hence the bigger the risk. (We assume that, in business, almost all investments have

some likelihood of some loss; if no loss is possible, then the size of investment does not

matter – at least on the downside). Small investments (again ceteris paribus) tend not to

yield very consequential outcomes; or worded conversely, for a given distribution of

payoff probabilities, a small investment will yield less consequential outcomes – in terms

9

of both gains or losses – than a large investment. Thus, for the manager facing the

scenarios in Figure 1, Scenario B is riskier than Scenario A. The potential distribution of

outcome probabilities is identical for the two scenarios, but the stakes are ten times

greater for B than for A. Interestingly, most researchers omit any consideration of “the

size of the bet” in conceptualizing risk-taking, while others treat it as a relatively

complete indicator of risk-taking (Larker, 1983; Hoskisson, Hitt, & Hill, 1993; Lee &

O’Neill, 2003). But, the size of the outlay is just one element of risk-taking.4

The second element of risk-taking is the variance of potential outcome

probabilities. (We should note that the term “variance” is used in two very different ways

in the literature on managerial risk-taking. The first way, and the one we adopt here, is to

refer to the dispersion of possible outcomes from a given action. The second way is to

refer to the intertemporal volatility of company performance.) A decision that can lead to

a wide range of possible results is riskier than one that can lead to a narrow, tightly-

bounded array of possible outcomes (Rothschild & Stiglitz, 1970). Thus, returning to

Figure 1, Scenario C is riskier than Scenario B. Although the two involve identical

outlays, the possible outcomes for C are much more extreme (ranging from the possibility

of a 40% loss to the possibility of an 80% gain). Scenario C might represent, for

example, the alternative of spending a billion dollars to build a facility to produce a

potentially high-margin product with unproven demand, whereas Scenario B involves an

outlay of the same amount to expand capacity to meet predictable demand for the

company’s existing low-margin products.

We do not wish to propose a precise quantification of this second element of risk-

taking – variance, or range, in possible outcomes – but rather are content to describe it

conceptually. What is useful to point out (and presaging our eventual empirical analysis)

4 We acknowledge that executive investment actions are not literally “bets,” and that executives do not like for gambling terminology to be applied to their behaviors (Shapira, 1995); still, such expressions as “the size of the bet” allow a convenient shorthand for some of our descriptions.

10

is that if two sets of companies make identical levels of investment (or their levels of

investment are otherwise statistically controlled for), but they differ in how extreme their

subsequent performance is, then there is a good chance that those companies with the

more extreme performance took courses of action that had widely varying potential

outcomes (as in Scenario C), while the other companies pursued actions that had less

extreme potential outcomes (as in Scenario B).

The third element of risk – and the one closest to the connotation among

managers – is the likelihood that most or all of the investment will be lost. Among the

few theorists who have pointed to this specific element of risk are Sitkin and Pablo

(1992:10), who defined risk as “uncertainty about whether potentially significant and/or

disappointing outcomes…will be realized.” Shapira (1986) also concluded that extreme

loss is a distinct aspect of risk, particularly in the eyes of executives. Most of his

interviewees, when asked how they think about risk, referred to concern for “worst

outcome” or “maximum loss.” If the only possible negative outcome is just mildly

negative – as when an asset can be readily re-sold at close to its purchase price – then the

risk is far more limited than if the potential negative outcomes include, say, loss of half or

all of the investment. We are not proposing a universal threshold for what constitutes the

likelihood of extreme loss, for it depends on the practical matters involved, as well as the

researcher’s specific interest. But, for the sake of discussion, let us assume this condition

exists for any investment that has at least a 10% chance of resulting in a loss of 50% or

more. Under this conception, Scenarios D and E in Figure 1 contain this third element of

risk, while A, B, and C do not. (Likelihood of a major loss could obviously be

operationalized in other ways).

It is important to note that the first two dimensions of risk are not fully

determinative of the third. For example, Scenario B in Figure 1 involves a large

investment that has a narrow band of potential outcomes and no possibility of extreme

loss. Now consider a slightly modified scenario, in which the downside consists of a

11

40% chance of a 20% loss, as well as a 10% chance of a total 100% loss. The outlay is

the same; the variance of probabilistic outcomes has changed only slightly (and is still

smaller than in Scenario C, D, or E); but now the possibility of extreme loss exists. We

could also envision a situation in which a large investment is made, and the payoffs

consist of the possibility of modest loss and extraordinary upside; hence great variance

exists, but there is no likelihood of extreme loss. Thus, the three dimensions of risk are

somewhat interdependent but not conceptually redundant.

In sum, we have presented a framework for dimensionalizing managerial risk.

When an executive faces an investment decision, he or she will consider – implicitly or

explicitly – three aspects of each alternative: How big of an outlay is involved? How

much variance is there in the possible outcomes? And what is the likelihood that I will

lose most or all of my investment? These three dimensions of risk allow an unpacking of

this important construct, which may yield new theoretical, empirical, and practical

insights beyond those that have arisen from more aggregated portrayals. Returning to

Figure 1, we can say that the overall riskiness of the scenarios increases monotonically

from A through E. Scenario A involves a small bet, with a relatively narrow range of

potential outcomes. B is a big bet, with a narrow range of possible outcomes. C is a big

bet, with a moderate range of outcomes. And D and E involve even more extreme

potential outcomes, including the possibility of extreme loss.5

According to agency theorists, managers who lack appropriate incentives will be

timid and risk-averse, favoring investments such as in Scenario A. But because investors

are widely-diversified and risk-neutral, they want managers to be more aggressive;

specifically they want managers to take the highest expected-value actions among all

those available. In Figure 1, that is Scenario C. In our framework, Scenario C (compared

5 We have constructed the scenarios in Figure 1 so as to yield monotonic increases in aggregate risk. Other, more complex combinations could be imagined which would make it difficult to rank scenarios in terms of overall risk.

12

to the others) happens to involve a major investment, with a wide range of outcomes

(including a possible 80% gain), and no apparent chance of extreme loss.

Agency theorists have argued that one way of getting executives to overcome

their risk-aversion, and to see investment alternatives as shareholders do, is to pay them

heavily with stock options. But what the architects of such plans fail to anticipate is that

a very high level of stock option pay may induce executives to surpass the level of

riskiness that is prudent for shareholders. The executives may become “risk-lovers”

(Wiseman & Gomez-Mejia, 1998) and gravitate to whichever alternative carries the

greatest expected value of upside outcomes, even if that value is exceeded by the

possibility of substantial loss. Option-loaded CEOs will be inclined to pursue Scenario

E.6

CEO Stock Options and Risk-Taking

According to agency theory, the ideal instrument for rewarding CEOs will

overcome three major problems that arise when relying on base salary alone: shirking,

short-sightedness, and risk aversion (Haugen & Senbet, 1981; Jensen & Murphy, 1990).

Stock options are thought to address all three of these problems. First, stock options help

to ameliorate problems of shirking, by aligning CEO payoffs with shareholder payoffs.7

To the extent that CEO effort brings about high levels of company performance, those

CEOs whose rewards are tied to company performance will exert themselves in their jobs

(Eisenhardt, 1989). Second, stock options should help overcome the problem of short-

sightedness. If paid as bureaucrats, CEOs will under-invest in the future (Hall &

Liebman, 1998). They have little incentive to undertake projects that will benefit only

6 We thank an anonymous reviewer for pointing out that a related factor that likely affects the choices among risky alternatives is the difference between objective properties of risk and subjective perceptions of it. Moreover, CEOs might impose decision weights that vary from what objective data might suggest. Cumulative prospect theory (Tversky & Kahneman, 1992) might shed some light on how decision weighting affects the relationship between stock option incentives and the choice of risky investments. However, because our data do not allow us to assess CEOs’ subjective risk assessments, we defer this for future research. 7 Shirking is a generalizable label that encompasses all forms of self-serving behavior.

13

their successors, even if those projects might improve the strategic health, and hence the

value, of the firm. Stock options help to overcome this problem by making the CEO

eligible to participate in future gains of the company’s share price. Because there is

typically a vesting period before options can be exercised, CEOs who are paid with stock

options have an incentive to take the long view in their decisions about investments.

Stock options also help to solve the third basic challenge of CEO compensation,

by encouraging CEOs to take greater risks on behalf of shareholders (Haugen & Senbet,

1981; Rajgopal & Shevlin, 2002; Sanders, 2001; Tufano, 1996). Stock options are

thought to help overcome the CEO’s risk aversion, by allowing the CEO to participate in

upside gains without limit, while providing a floor to avoid losses. With enough stock

options, risky projects that work out well can make the CEO very wealthy. If the projects

fail, and the company’s shares drop, the CEO neither gains nor loses – at least not from

the stock options. It is this supposed feature of CEO stock options – increasing

managerial risk-taking – to which we turn momentarily, organizing our hypotheses in line

with our earlier discussion of the elements of risk-taking.

An emerging stream of research provides evidence that stock option pay may

affect managerial decision making. For instance, scholars have found that stock option

pay is negatively associated with the use of derivatives to hedge financial risk (Rajgopal

& Shevlin, 2002; Tufano, 1996). Others have linked stock option pay to specific

investment choices, such as the number of acquisitions firms make (Sanders, 2001), and

the riskiness of acquisitions (Wright et al., 2002). Very few studies have gone the extra

step by attempting to find a link between stock option pay and subsequent firm

performance. Exceptions include recent studies which have reported that executive stock

option plans are associated with increases in operating performance (Hanlon, Rajgopal, &

Shevlin, 2003; Kato, Lemmon, Luo, & Schallheim, 2005). Notwithstanding these recent

strides to examine the effects of stock option pay, essentially all of this early work has

significant limitations. First, few studies link stock option pay to substantive strategic

14

decisions, or they focus on only one type of investment (e.g., acquisitions). Second, most

research on the effects of stock option pay is highly vulnerable to the analytic problem of

endogeneity (Rajgopal & Shevlin, 2002). Specifically, prior studies that have tried to

link stock option pay to risk-taking have largely failed to account for the fact that firm

characteristics such as risk and investment behavior are also antecedents of stock option

pay (Beatty & Zajac, 1994; Henderson & Fredrickson, 1996; Zajac & Westphal, 1994).

Effects of CEO Stock Options on Investment Magnitude

The first element of risk-taking is the size of the bet, or, for CEOs, the magnitude

of investment outlays they make. The idea that incentives can cause CEOs to make large

investments is supported by Larcker’s (1983) study, which found that the adoption of

long-term incentive programs (LTIPs) for CEOs was associated with increases in capital

spending levels. According to Larcker, these LTIPs – which provided payoffs for multi-

year performance improvements – prompted CEOs to invest more in fixed assets, which

by their very nature tend to deliver the bulk of their returns in future years rather than

currently. In the absence of such incentives, Larcker asserted, CEOs were reluctant to

sacrifice current earnings for initiatives that had uncertain returns only in the future.

So far, evidence that stock options prompt larger investment spending is only

indirect. In an early study, Lambert et al. (1989) found that option pay adoption was

associated with a reduction in dividend payouts. This result logically follows from the

fact that options only give executives rights to share price appreciation, but not to income

distributions; therefore option-loaded executives prefer to retain earnings, so that they can

be applied toward long-term investment that might help push up future share prices. In a

more recent study, Sanders (2001) found that CEO stock option pay was positively

related to the number of acquisitions that companies made; although data on the scale of

the acquisitions were not reported, the results suggest that stock options promote

investment spending.

15

Bearing in mind that option-loaded CEOs are aiming for large share-price

increases, and that consequential outcomes tend to require large investment spending, we

anticipate that stock options will increase a CEO’s willingness to make large outlays on

uncertain projects, such as R&D, capital expenditures, and acquisitions. Modest

investment spending will tend to have little potential to dramatically alter the company’s

share price. Large spending, however, will have much greater chance to substantially

affect company performance, including in the upward direction that the option-loaded

CEO is hoping for. This line of thought leads to our first hypothesis:

Hypothesis 1: The more that CEO compensation consists of stock options, the greater the magnitude of investments made by the firm.

We should acknowledge at this point that our empirical analysis examines

aggregate investment outlays (as Larcker (1983) did in his study of LTIPs), even though

we would ideally like to examine the size of individual investment projects. In line with

our earlier argument (reflected in Figure 1), option-loaded executives are expected to

invest heavily in uncertain projects, but they are especially expected to invest in big

projects rather than spread modest investments over many projects. We will revisit this

distinction in our discussion.

Performance Extremeness and the High-Variance Nature of Investments

Stock options not only stimulate CEOs to make large strategic investments, but

also encourage them to direct such spending to high-variance initiatives. As envisioned

by agency theorists, CEOs who are loaded-up with stock options will undertake more

extreme, high-variance risks than those who are not (Agrawal & Mandelker, 1987;

Wright et al., 2002). For example, we can anticipate that they will be more likely to

invest in the development of radical new products instead of safer product-line

extensions; they will be more likely to build new plants in anticipation of uncertain

demand, instead of only after demand has materialized; and so on. Because option-

loaded CEOs stand to gain substantially from every upward increment in the company’s

16

share price, but are buffered from any downward movement, they are relatively willing to

engage in what we earlier referred to as the second element of risk-taking: high-variance

investing. Option-loaded CEOs will “swing for the fences,” hoping to hit home runs but

knowing that they also have an increased likelihood of striking-out.

To date, evidence that stock options lead to high-variance investments is limited.

Tufano (1996) and Rajgopal and Shevlin (2002) reported that, in raw material extraction

industries (gold mining and oil and gas, respectively), CEOs who were paid with stock

options were less likely to hedge their risks with derivatives, inferring that option-loaded

CEOs were willing to accept more exploration risk. Wright et al., (2002) reported that,

among firms completing large acquisitions, stock option pay was positively associated

with riskier acquisitions, as measured by the degree of ex ante covariance of stock returns

(of the acquirer and target firms). The authors reasoned that stock options motivate

executives to make riskier acquisitions than they would otherwise.

In a related vein, Agrawal and Mandelker (1987) investigated the stock price

variance, or intertemporal volatility, of firms that completed acquisitions and divestitures.

They divided their sample of firms into those that had an increase in stock price volatility

following the acquisition or divestiture and those that experienced a decrease in stock

price volatility. They then examined the mean level of option pay and ownership (these

two variables were collapsed into a single measure) of these two groups and found that

the combined value of CEO stock options and ownership was significantly higher in the

variance-increasing group than in the variance-decreasing group. The interpretation was

that options and equity holdings prompted CEOs to take riskier initiatives.

What has not been directly considered, although it follows logically from prior

work, as well as from the basic rationale of stock options, is that CEOs who are paid

heavily with stock options will tend to generate extreme performance. Because stock

options increase the propensity of executives to make large and high-variance bets, stock

options should also be associated with a greater propensity to both “hit home runs” and to

17

“strike out.” That is, option pay should lead to performance extremes, defined as

performance that deviates widely from neutral or moderate levels. Large high-variance

bets, as undertaken by option-loaded CEOs, are likely to either pay off handsomely or to

lead to large losses. In contrast, decision makers who are without such incentives are

likely to make smaller and lower-variance bets, and their firms will be more likely to

achieve moderate, relatively neutral performance. This logic leads to the following

hypothesis:

Hypothesis 2: The more that CEO compensation consists of stock options, the more extreme will be the firm’s subsequent performance.

If the extreme performance (big wins and big losses) of option-loaded CEOs is

due, as we have argued, to bets that are both big and of high-variance, then both of these

elements of risk-taking should be detectable in empirical analysis, even though only one

– the size of the bet – is directly observable. If option-loaded CEOs not only make bigger

investments, but also investments with high-variance (which is unobservable), then we

can expect that the interaction of CEO stock options and investment magnitude will be

positively associated with performance extremeness – beyond the independent, additive

effects of the two. We anticipate that the combination of heavy use of CEO stock options

and large levels of investment spending tend to generate extraordinarily extreme

performance – very big wins and losses – due to the (unobserved) high-variance nature

of the investments made. Put another way, high levels of stock options and investment

spending are like a “combustible combination” that leads to even greater performance

extremeness than the additive effects of stock option pay and investment magnitude do

on their own. Thus:

Hypothesis 3: The interaction between CEO stock options and magnitude of investments will be positively related to performance extremeness.

We can expect to observe suggestive evidence of the distinct effects of investment

magnitude and investment outcome-variance on extreme performance in yet one more

way. If it were the case that stock options cause CEOs to make large investments, but not

18

higher-variance investments, then investment magnitude would fully mediate the

relationship between stock options and performance extremeness. If, on the other hand,

and as we have argued, stock options lead CEOs not only to make bigger bets, but also

high-variance bets, then investment magnitude will not fully explain the extreme

performance of option-loaded CEOs. If CEOs who are paid heavily with stock options

undertake systematically, higher-variance projects – or otherwise engage in an

investment style that brings about extreme performance – then investment magnitude will

not be a full mediator of the relationship between CEO stock options and performance

extremeness. Instead, the high-variance nature of the projects undertaken is an

additional, but unobserved, causal mechanism leading to extreme performance outcomes.

Because an absence of full mediation does not provide any direct insight as to

what the unobserved operative mechanism actually is, we do not posit this line of thought

as a formal hypothesis. Still, we will empirically assess whether the magnitude of

investment spending fully accounts for the association between CEO stock options and

performance extremeness.

Performance Asymmetry

In espousing the use of stock options, agency theorists not only anticipate that

such incentives will bring about greater managerial risk-taking, but also that such risk-

taking will be beneficial to company performance and shareholder interests (Jensen &

Murphy, 1990; Mehran, 1995). Some prior studies indicate that shareholders seem to

subscribe to these beliefs. For instance, Brickley, Bhagat, and Lease (1985) reported a

positive abnormal return for firms upon adoption of stock-based compensation plans, and

Yermack (1997) and Morgan and Poulsen (2001) similarly found that stock prices

increased upon adoption of executive stock option plans. Thus, it appears that investors

believe that stock options will have positive performance effects.

In our preceding discussion, we argued that high levels of stock option pay tend to

bring about extreme performance – big wins and big losses. In responding favorably to

19

stock option pay, investors seem to believe there will be more of the former than the

latter. But other scenarios are possible. For instance, it could be that the extreme

performance levels delivered by CEOs who are under aggressive stock option plans will

be centered on zero, evenly divided between big wins and big losses. This performance

symmetry would occur if stock options prompt CEOs to be more aggressive but not

necessarily smarter or luckier. It is also possible that CEOs who are paid largely with

stock options will generate more big losses than big wins. That is our expectation, and

we shall now develop this as a formal hypothesis.

Managers generally tend to be very concerned – too concerned, according to

agency theorists – with the potential downside, especially the maximum possible loss, of

the alternatives they consider (Amihud & Lev, 1983; Shapira, 1996). But with enough

stock options, CEOs have significant incentive to focus on possible gains but little reason

to be concerned with the possibility of big losses. This shift of attention is due to the

asymmetric payoffs from stock options: unlimited upside but no downside (Sanders,

2001). As a result, option-loaded CEOs are more likely to prioritize their alternatives

according to the expected value of the upside outcomes, rather than the expected value of

the full range of all possible outcome possibilities. If we acknowledge the premise

(which originated in financial economics and is now central to agency theory) that the

possibility of big payoffs is typically accompanied by the possibility of big losses

(Milgrom & Roberts, 1992), and then couple that premise with the fact that option-loaded

CEOs are oriented toward ignoring or downplaying the potential magnitude and

likelihood of those losses, then it becomes straightforward to see how such CEOs will

often pursue projects in which the chances of major loss are substantial. Returning to our

earlier Figure 1, which laid out several investment scenarios, we can anticipate that the

option-loaded CEO would pursue Scenario E, because it has the greatest expected value

for gains, even though it has a negative expected value overall and carries a 60% chance

20

of generating a extreme loss. With enough stock options, CEOs lose sight of the

downside and become “risk-lovers” (Wiseman & Gomez-Mejia, 1998).

The asymmetric payoff from stock options encourages risk-taking that is more

careless and uncontrolled than envisioned by the theoretical models justifying stock

options. Indeed, it is not difficult to imagine a CEO who derives a large portion of his

compensation in stock options, and stands to make millions from those stock options,

who undertakes a spate of far-fetched, exceedingly long-shot initiatives – in hopes of the

big win that will push the company’s share price greatly upward. Concerns about failure

are minimized not only because of the floor-effect of the stock options, but also possibly

by other forms of protection, including a co-opted or congenial board (Mace, 1971;

Westphal, 1998; 1999), the CEO’s ability to create the impression that he or she was

acting in an appropriate entrepreneurial fashion (Davidson et al., 2004), and even a

handsome severance agreement (Almazan & Suarez, 2003; Dalton, Daily, and Kesner,

1993).8 Thus, not only do we expect that option-loaded CEOs will generate more large

losses than large gains, but we can place this idea in a more rigorous, comparative

hypothesis:

Hypothesis 4: Large losses will constitute a greater percentage of all instances of extreme performance (large losses and large gains combined) when stock options are a large part of CEO pay than when stock options are a small or moderate part of CEO pay.

RESEARCH METHOD

Our sample frame included all firms listed on the Standard & Poor’s 500, Mid-

Cap, and Small-Cap indices in 1998. We randomly selected 1,000 of these firms and

collected data for them over the period 1993 to 2000. Not all firms were observed in

8 Anecdotal evidence suggests that CEOs who are under stock option plans are sometimes additionally buffered from downside penalties – in two ways. First, in some cases their existing options are “re-priced” to accommodate the fact that the company’s share price has dropped; this repricing of course sets a new, lower floor from which the CEO “tries again” (Pollock, Fischer, & Wade, 2002). Second, and less well known, some boards perversely reward CEOs who have not performed well under an option plan, by giving them new rounds of even more options – out of a belief that the original amount must not have been sufficiently motivating.

21

each year, due to mergers or missing compensation data. We dropped 50 firms because

of too much missing data, reducing the number of unique firms to 950 (the mean values

of the independent and dependent variables for the dropped firms did not differ from

those of the retained firms).

Because the hypotheses deal with the effects of stock option incentives on

subsequent investments and performance, a lagged model structure was in order

(described in detail below). Various model designs were tested, but we adopted an

approach that uses information on CEO stock options measured over a three-year period

(t-3, t-2, and t-1) to predict investments in the fourth year (t); these were then used to

predict performance extremeness in the fifth year (t+1). Thus, the lag design resulted in

the pooling of five four-year data panels to predict investment spending, and four five-

year data panels to predict performance extremeness. There were 3,820 firm-years in the

models predicting investment spending, and 2,862 firm-years in the performance models

(the fewer observations being largely due to one more lagged year).

Financial data were drawn from COMPUSTAT. Acquisition data came from the

Securities Data Corporation (SDC) merger and acquisitions database. Compensation data

were collected from Execucomp.

Measures

Dependent variables. We examined three distinct types of investment spending:

R&D investment, capital investment, and acquisition investment. These three measures

have been used as indicators of risky and uncertain long-term investment behavior in

prior research (Beckman & Haunschild, 2002; Hoskisson et al., 1993; Larcker, 1983).

R&D and capital expenditures were coded as reported in Compustat. Acquisition

expenditures were measured as the sum of the transaction values for all acquisitions

completed during the year, as reported in SDC. The values were all log transformed

(after adding the constant 1 to all cases). We also estimated the models using the sum of

22

all three types of expenditures. As a way to allow parsimonious tests of our interaction

hypothesis, we used this summed aggregate measure of long-term investment.

Performance extremeness was assessed by transforming two common indicators

of firm performance: total shareholder returns (TSR) and return on assets (ROA). TSR, a

stock market measure, is calculated as year-end stock price minus year-start stock price,

plus dividends paid, all divided by year-start stock price. ROA, a common accounting-

based indicator of performance, is net income divided by year-end assets. Both of these

measures of performance have been widely used in compensation studies (Bloom &

Milkovich, 1998; David et al., 1998; Finkelstein & Boyd, 1998; Henderson and

Fredrickson, 1996; 2001; Sanders & Carpenter, 1998).

To derive our theoretical variable of interest, performance extremeness in t+1, we

applied a two-step process. First, we estimated “predicted performance” by regressing

performance on all control variables discussed below.9 These models generated expected

performance levels, based on information from a comprehensive set of control variables

known to affect firm performance; they had χ2s of 1,259 (p<.0001) for TSR and 485

(p<.0001) for ROA. Next, we took the residual from the first regression (i.e., the

difference between the firm’s actual performance and predicted performance calculated

in the first step). We then calculated the absolute difference score (i.e., the absolute value

of the residual), to indicate how divergent, or extreme, the firm’s performance was in t+1,

relative to a best estimate of what the firm’s performance was expected to be. The

absolute value of the residual, then, is an indicator of how much actual performance

deviated from what might have been reasonably expected (without regard for the

direction of that extremeness). We will describe below our approach for operationalizing

“large losses” and “large gains” (for testing Hypotheses 4).

9 One of these controls is prior performance, which will likely be correlated with the error term. To avoid this problem, we used the well known instrumental variable technique (Johnston & DiNardo, 1997) to create an instrument that is correlated with prior performance but not with the error term.

23

Independent variables. Consistent with our hypotheses and prior research, we

measured stock option pay as the proportion of total compensation paid as stock options

(which could theoretically range from zero to 100 percent). We repeated all analyses

using a second operationalization – the natural log of the dollar value of stock option pay

– and the results (not shown) were essentially identical to those we report here. Stock

option values, based upon the Black-Scholes method, were calculated by Execucomp.

Because some firms award stock options periodically rather than annually, and because

incentives carry motivational effects over multiple years, we used a lagged model design.

We experimented with two alternative methods for creating this lag. First, we estimated

a model that used the simple average percentage of stock option pay for the prior three

years ((t-1 + t-2 + t-3) / 3). Second, we used a distributed lag model that included as

variables the percentage of stock option pay for each of the prior three years in the model

(t-1, t-2, and t-3) (e.g., Ahuja, 2000). These two lag structures produced substantially

similar results. For ease of presentation, we report results only for the first approach, in

which we used the three-year average of stock option pay as a percentage of total pay.

While our theory focuses on CEO incentives, it might be reasonable to ask whether stock

option pay measured at the level of the TMT would result in similar or different results

(Carpenter & Sanders, 2004). In supplementary analysis not reported in the tables, we

found that the average level of TMT stock option pay produced results very similar to

those we report.

Control variables. We included several control variables, all measured one year

prior to whichever dependent variable was under examination. Firm size, measured as

the natural log of revenues, was included because it affects investment levels and

performance. We included measures of firm diversification (entropy measure) and

international scope (foreign sales as a percentage of total sales) (Finkelstein & Boyd,

1998; Henderson & Fredrickson, 1996; Sanders and Carpenter, 1998), because firms

facing different institutional and competitive dynamics face distinct investment

24

opportunities and imperatives. Since investments and performance are likely to be

strongly affected by industry context, we included dummy variables for each 2-digit SIC

represented in the sample. There were 59 separate two-digit industries in the sample;

therefore, all analyses include 58 industry dummies as controls. In addition, we included

dummy variables to account for the calendar year of observation (year t). In models

predicting investment spending, we also controlled for prior year performance, measured

as TSR(t-1). Using ROA instead of (or in addition to) TSR yielded the same results.

Recent research suggests executives continuously reassess the subjective value of

their stock options, depending on the firm’s stock price volatility and stock price trend

(Devers, Wiseman, & Holmes, forthcoming). Therefore, we included these as control

variables. Stock price volatility was measured using the Black-Scholes volatility factor

(60 month). Stock price trend was measured as the percentage change in stock price

between the beginning of the year in which options were awarded to the end of t-1.

Because we measured stock option incentives over the prior three years, and the price

trend that is most relevant to executives is that which coincides with the period between

the grant date and the current time, we used a weighted average stock price trend. This

price trend was calculated by weighting each year’s grants (as a percentage of all grants

during the three years) by the change in stock price between the year of the grant and the

end of year t-1. Illustratively, if an executive was awarded 100,000 options in t-3 and no

options in t-2 and t-1, and the change in stock price from the beginning of t-3, t-2, and t-1

to the end of t-1 was 30%, 20%, and 10%, respectively, the weighted average stock price

trend would be 30% (30%*100%+20%*0%+10%*0%). Alternatively, if the executive

was granted 25,000 options in t-3, 25,000 in t-2 and 50,000 in t-1, the weighted average

stock price trend would be 17.5% (30%*25% + 20%*25% + 10%*50%).

Because stock options represent only one form of incentive, we also controlled for

CEO stock ownership, measured as the natural log of the value of the CEO’s equity

ownership. Stock ownership values are highly inertial, so there was no need to include

25

three years’ values; we thus included the value of stock ownership for t-1. Finally, to

control for the possibility that high levels of stock option pay could be offset, or

outweighed, by high levels of other forms of pay, we included a control for the total value

of all other forms of CEO compensation (excluding stock options). Total other

compensation was measured as the natural logarithm of the dollar value of all forms of

compensation (except stock options) awarded in t-1.

Endogeneity control. Finally, although we aim to examine the effects of stock

option pay on investment and performance, it is quite likely that option pay is itself

partially determined by firm investment patterns and performance. In other words, this is

a classic problem of endogeneity. Most of the prior empirical work on CEO pay suffers

from the threat of endogeneity, and very few studies account for this problem (Rajgopal

& Shevlin, 2002). We experimented with several techniques to control for endogeneity

(Hamilton & Nickerson, 2003), all with similar results. The endogeneity control we used

is a parameter that was created by regressing CEO stock option pay in t-1 on firm and

executive characteristics in t-2, and industry and year dummies. From that initial

regression, we retained all predictors that were significant. The significant predictors that

were positive included R&D intensity, capital intensity, prior performance, stock price

volatility, and firm size, while CEO stock ownership was negative and significant. In

addition, several industry dummies and all year dummies were significant. These results

are consistent with prior research on the antecedents of CEO incentive pay. Using these

regression results, we calculated the “predicted” level of CEO stock option pay, which

was then included as an endogeneity control in all our analyses.

Estimation Method

Our data consists of multiple, unbalanced panels of observations. As a result,

ordinary least squares regression would result in correlated error terms, understated

standard errors, and inflated t-statistics. Fortunately, there are several models appropriate

for pooled cross sectional panel data. We settled on using the cross-sectional time series

26

regression with random-effects models and generalized least square (GLS) estimators

with controls for autocorrelation (xtregar in STATA). This procedure estimates cross-

sectional time-series regression models that have a first-order autoregressive disturbance

term and it accommodates unbalanced panels with unequally spaced observations over

time. Our findings were also robust to using a relatively new class of robust estimators

known as generalized estimating equations, using the XTGEE procedure in STATA. Our

results were robust to this specification.10 In both instances, we corrected for

autoregressive disturbance (to conserve space, the latter method is not shown in the

tables). The results were substantially similar; all signs were the same and the levels of

significance were similar in both models. We tested Hypotheses 4 in several ways,

including a Kolmogorov-Smirnov test of the homogeneity of distributions of performance

across different levels of CEO stock option pay, z-ratio tests for the equality of

proportions of cases of big losses and big gains, and polynomial logistic regression

predicting the incidence of big losses and big gains.

RESULTS

Descriptive statistics and correlations are reported in Table 1. Statistics for

industry and year dummy variables are not shown.

-----------------------------------Insert Table 1 about Here

-----------------------------------

10 Our use of random-effects models follows prior research studying similar strategy initiatives (Beckman, 2006; Beckman, Haunschild, & Phillips, 2004, Gulati, 1995, & Lavie & Rosenkopf, 2006). Random-effects models are efficient while fixed-effects models reduce degrees of freedom and are especially problematic and unstable when estimating models where n is large and T is small. In our sample, we have over 900 firms with a maximum number of observations per firm of five years. Moreover, fixed-effects models predict the annual change in the dependent variable, while we are more interested in the explaining the variance across firms in risk-taking and performance. Fixed-effects models also preclude the use of any control variable that invariant over time, such as industry membership. Finally, random-effects estimators are preferred when there is reason to believe that Xit and Xit-1 are correlated, which they are in our case (Johnston & DiNardo, 1997).

27

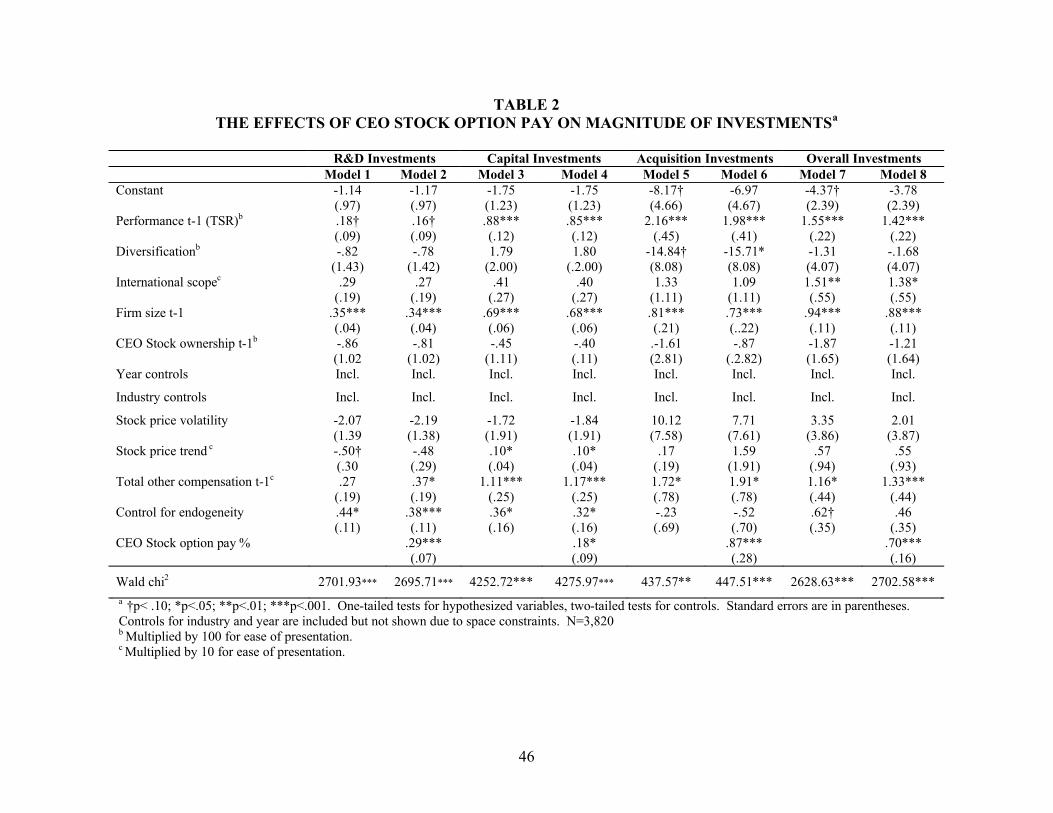

Stock Options and Investment Behavior

Table 2 reports the results of the analysis of CEO stock options on investment

spending. Models 1 and 2 examine R&D investment, Models 3 and 4 examine capital

investment, Models 5 and 6 examine acquisition investment, and finally Models 7 and 8

examine the aggregate measure of overall long-term investment. Industry and year

dummies are not shown, but many were significant; moreover, several of the reported

control variables were significant in explaining each measure of investment spending.

The base models, which regressed the four dependent variables on all control variables

(1, 3, 5, and 7), were highly significant (by Wald Chi-squared test).

CEO stock option pay was significantly positively related to all four investment

spending measures (as show in Models 2, 4, 6, and 8). In support of Hypothesis 1, then,

high levels of stock options engendered high levels of investment spending.

-----------------------------------Insert Table 2 about Here

-----------------------------------

Stock Options and Extreme Performance

Hypothesis 2 predicted that CEO stock option pay would be positively associated

with extreme levels of subsequent performance. Table 3 presents the results for

regressions predicting performance extremeness. Models 1-4 report the results for TSR

extremeness, while Models 5-8 report the results for ROA extremeness. Recall that our

measures of performance extremeness were the absolute value of the residuals from an

initial regression (not shown) in which the dependent variable was the respective

performance indicator (in year t+1), and the independent variables were: industry

dummies and year dummies; performance, diversification, international scope, firm size,

stock price volatility, and stock price trend (all in t). In Models 1 and 5, we enter the

controls for total CEO pay, stock ownership and the endogeneity control. CEO stock

ownership was positively related to both measures of performance extremeness.

28

In Models 2 and 6 we add stock option pay. Consistent with Hypothesis 2, the

coefficients for stock option pay were significantly positive predictors of performance

extremeness for both TSR and ROA. Thus, higher levels of CEO stock option pay were

associated with more extreme levels of subsequent firm performance.

-----------------------------------Insert Table 3 about Here

-----------------------------------

Models 3 and 7 include the magnitude of overall investment spending, and

Models 4 and 8 then add the interaction of CEO stock option pay and overall investment

spending. The first pattern worth noting is that the magnitude of investment spending did

not at all mediate the relationship between CEO stock options and performance

extremeness, inasmuch as the addition of investment spending (in Models 3 and 7) did

not diminish the coefficients or significance of CEO stock options. Thus, even though

CEO stock options engender large levels of spending (as seen above), it is not this high

level of investment spending that causes performance extremeness. From our data, we

have no way of knowing what the unobserved mechanism might be, but the results

clearly point away from investment magnitude and more toward what might be called

“investment style,” possibly including the tendency to engage in long-odds projects.

In this same vein, we now turn to results for Hypothesis 3, which posited that

stock options and investment spending would have an interactive effect on performance

extremeness. Table 3 indicates strong support for this hypothesis for TSR extremeness

(Model 4) but no support for ROA extremeness (Model 8). Thus, for one of the

performance indicators there is evidence that large levels of CEO stock options and large

levels of investment spending bring about very extreme outcomes; we have no way of

knowing why this is a “combustible combination,” but our theory points to the likelihood

that option-loaded CEOs undertake big projects that are long-odds in nature.

29

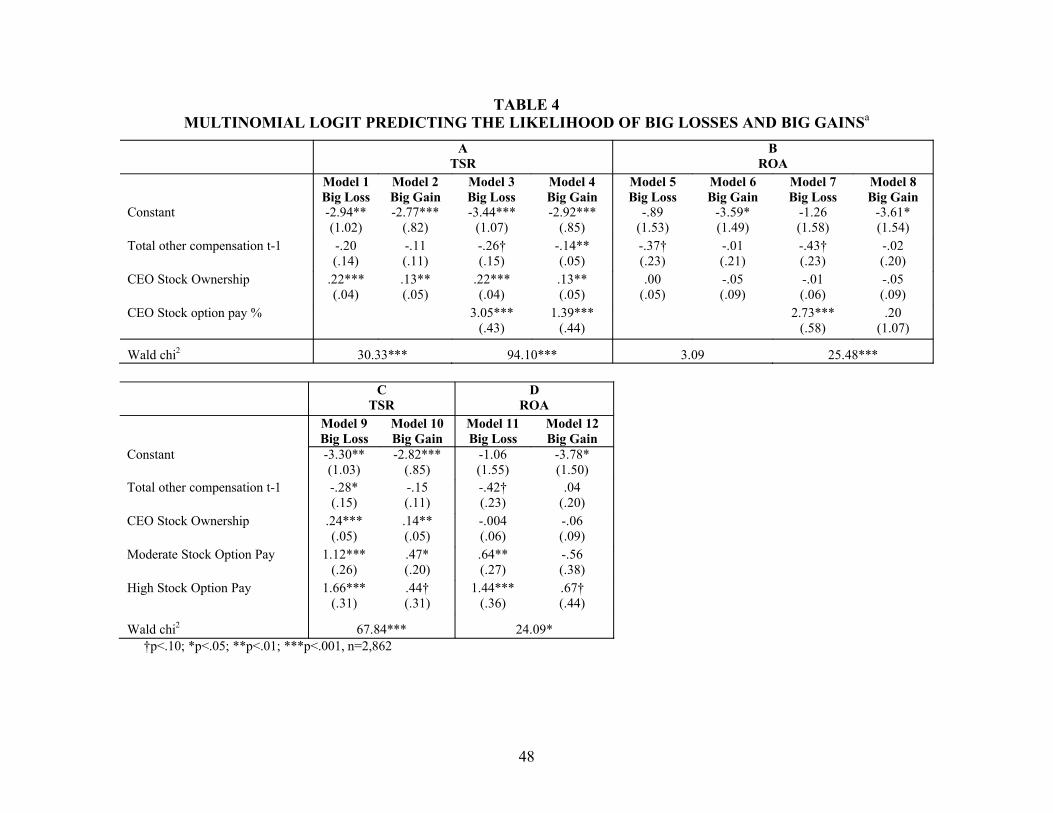

Stock Options, Big Losses, and Big Gains

Our remaining hypothesis predicted that when stock options constitute a large part

of CEOs’ pay packages, large losses will be more prevalent than large gains. To test this

hypothesis, we examined the distribution of performance outcomes (in year t+1) for three

subsamples of observations, divided into roughly equal thirds based on the CEO’s

percentage of stock option pay. Cases in which stock options accounted for less than 20

percent of CEO pay were considered “low stock option pay;” cases between 20 and 49

percent were considered “medium;” and cases of 50 percent or more were conditions of

“high stock option pay.” Our results remain robust across other categorization cutpoints.

We first examined the distribution of performance outcomes under the three

different levels of CEO stock option pay, shown in Figure 2 (for both TSR and ROA).

To calculate performance outcomes, we used the residuals described above (e.g., the

residual from a regression in which performance was the dependent variable, and all

control and predictor variables except stock options were the independent variables) – but

now we retain the directionality of these residuals. The measure thus indicates the degree

to which performance was higher or lower than estimated by all the available predictors

(except CEO stock options). For both performance measures, we show brackets of

outcomes in increments of half standard deviations, centered on zero (or the outcome in

which a firm’s performance was exactly what would be predicted from all controls). To

aid visual interpretation, we also show curves fitted to the bracket outcomes. -----------------------------------

Insert Figure 2 about Here------------------------------------

Two primary conclusions can be drawn from Figure 2. First, reaffirming our

earlier results in Table 3, performance was much more likely to be neutral, or

nonextreme, under conditions of low and medium stock options than under conditions of

high CEO stock options. For example, if we look at the brackets that are within half a

standard deviation either side of zero, the frequencies (for both performance measures)

30

are substantially greater for the low and medium stock option subsamples than for the

high stock option subsample. As a systematic test for whether these distributions

differed, we applied the Kolmogorov-Smirnov test for homogeneity between sample

distributions. Various iterations of this test confirmed that the distribution of

performance outcomes (for both TSR and ROA) under conditions of high CEO stock

option pay was significantly different (p<.001) from the distribution for all other firms

combined, as well as from both the low and medium stock option firms separately.

Second, big losses were more common than big gains under high levels of stock

option pay. If we define extreme performance as greater than 1.5 standard deviations

away from zero, then among those firms with high stock option pay, the percentage of

cases with big TSR losses was 10.1 percent, while only 6.8 percent of the cases were of

big gains, a significant difference (by z-ratio test, p<.001). For ROA, the corresponding

proportions were 6.9 percent extreme losses and 3.9 percent extreme gains, again a

significant difference (p<.001).

Hypothesis 4 was more rigorous in proposing that large losses would constitute a

greater percentage of extreme outcomes (large losses and large gains combined) among

firms with high levels of stock option pay than among firms with low and moderate

levels. To test this hypothesis, we calculated the ratio of large losses to total cases of

extreme performance (large gains and large losses combined) for the high stock option

category and compared it with the same ratio for all other firms. For TSR, this ratio was

.60 for high stock option firms and .40 for all other firms, a significant difference

(p<.001). The difference was starker in the comparison of high and low stock option

firms: .60 vs. .32 (p<.001). For ROA, the ratios were .63 and .62 for high stock option

firms versus all other firms, which was not a significant difference. The difference in the

ratio for high stock option firms (.63) and low stock option firms (.48) was significant

(p<.05). Thus, there was considerable evidence that the extreme performance delivered

by high stock option CEOs was more lopsidedly negative than for other CEOs.

31

It might reasonably be asked whether our results were sensitive to where we drew

the cutoff for defining a “high level” of CEO stock options. Accordingly, we conducted

extensive sensitivity analyses (not shown), in which we varied our definition of high

stock option pay, using seven different cutoffs (ranging from 30 to 60 percent of pay).

We found substantial support for Hypothesis 4 across almost all these operationalizations.

Only when “high” was defined as above 30 percent of pay, did support for Hypothesis 4

disappear. Thus, the support we found for Hypothesis 4 was generally robust, not an

artifact of our specific cutoff for defining high stock option CEOs.

As a final test of performance asymmetry (i.e., Hypothesis 4), we conducted

multinomial logit on our sample, in which we sought to predict three alternative

outcomes: a big loss, a big gain, or neither (neutral performance). Big losses and big

gains were defined as performance that was 1.5 standard deviations below or above,

respectively, the value that was predicted from all control variables. Results are reported

in Table 4.

-----------------------------------Insert Table 4 about Here

-----------------------------------

In analyses A and B, we assess the effect of CEO stock option pay (as a

continuous variable) in predicting big losses, big gains, or neither (the omitted outcome),

for TSR and ROA, respectively. For TSR, CEO stock option pay was positively related

to the incidence of big losses and big gains; but the coefficient was more than two times

greater for big losses (coefficients differed at p<.01). For ROA, stock options were

highly predictive of big losses but were not predictive of big gains (difference of p<.01).

In analyses C and D, we used our stock option categories instead of the

continuous measure. Low stock option pay (under 20% of pay) was the omitted category.

Moderate stock option pay (20 – 49% of pay) was somewhat more positively related to

big losses than big gains, for both TSR and ROA. But differences were especially

pronounced under high stock option pay. High stock option pay was positively

32

associated with both big losses and big gains in TSR, but the coefficient for big losses

was about four times that for big gains (differing at p<.01). And, high stock option pay

was related to big losses and big gains in ROA, but the coefficient for losses was twice as

for gains (differing at p<.01).

In sum, the multinomial logit analysis strongly supports our earlier results. We

find robust evidence of two interrelated patterns: The more that a CEO is paid in stock

options, the more extreme the firm’s subsequent performance, and the greater the

likelihood that the extreme performance will be a big loss rather than a big gain.

DISCUSSION

CEO Stock Options and Three Elements of Risk-Taking

Our study was motivated by a desire to unpack and clarify the concept of

managerial risk-taking and to examine how a CEO’s financial incentives can influence

different dimensions of risk-taking and performance. We focused specifically on the

effects of CEO stock options, because 1) they have been the most vigorously-espoused

tool for encouraging CEOs to take bigger risks, and yet, 2) in sufficient quantities, stock

options can be expected to bring about imprudent risk-taking.

Perhaps the most basic element of managerial risk-taking is the size of the outlay

made (Larcker, 1983). We found, as expected, that stock options stimulate investment

spending. The more that CEOs were paid in stock options, the more aggressive they

were in their outlays in three major investment categories: R&D, capital spending, and

acquisitions (as well as in an aggregate index of all three).

The second element of managerial risk-taking is the variance, or range, of

potential outcomes. One of the objectives of stock options is to encourage CEOs to take

more extreme risks, which carry the prospect of greater payoffs, and which risk-neutral

shareholders prefer (Wright et al., 2002). We were not able to observe the a priori

probability distributions of the actions taken by the CEOs in our sample, but we used a

33

two-step analysis to infer that stock options were associated not only with large

investments, as just discussed, but also with high-variance investments.

We first demonstrated that CEO stock options were associated with subsequently

extreme company performance. Then we showed that investment spending did not at all

mediate the relationship between CEO stock options and extreme performance. Thus,

option-loaded executives delivered extreme performance for reasons other than their

large investments. From our data, we cannot be sure of what the unobserved

mechanism(s) might be. But we surmise that the undertaking of high-variance projects,

along with possibly other factors (such as hubris, impatience, and noncomprehensive

decision-making) contribute to the extreme performance of option-loaded CEOs. We

explored this idea of (unobserved) high-variance projects in one additional way, by

examining the interactive effect of CEO stock options and investment spending levels on

performance extremeness. This effect was highly positively significant for TSR

extremeness (but not for ROA extremeness), thus suggesting that large investments made

by option-loaded CEOs deliver more extreme performance than do investments (of the

same magnitude) made by CEOs who are not heavily paid with options. In hindsight, the

strong effect for TSR, but lack of effect for ROA extremeness, may not be surprising

given that stock option payoffs are tied to stock prices rather than operational

performance. Again, we cannot be sure of how option-loaded CEOs differ in their

investment styles from other CEOs, but our interpretation is that they invest in riskier

projects – presumably in more uncertain markets, with newer technologies, ahead of

competitors – all in hopes of greatly pushing up their companies’ share prices, so they

can exercise their options for a large gain.

The third element of managerial risk-taking is the likelihood of a major loss. And

this is where CEO stock options have their most provocative effect. Because option-

loaded CEOs benefit from share price increases but lose nothing if share prices drop, they

can be expected to sort investment alternatives according to the expected values of gains

34

while paying little attention to the likelihoods or magnitudes of losses (Sanders, 2001). If

we accept the commonsense idea that the projects with the biggest possible upside are

likely to also have the biggest possible downside, and then couple it with the assumption

that option-loaded CEOs have little concern with the size or probabilities of downside

outcomes, it is straightforward to expect that option-loaded CEOs have a relatively high

likelihood of delivering big losses.

Our results in this regard were strong. In our sample, those CEOs who derived a

high level of their pay from stock options generated more big losses than big gains (as

measured both by market and accounting metrics); and their ratio of big losses to big

gains was greater than the corresponding ratios for CEOs who derived less of their pay

from stock options. This result held over a wide range of cutpoints for defining a “high”

level of stock option pay.

In sum, high levels of stock options appear to motivate CEOs to take big risks, or