Role of Social Security Schemes in Tanzania. Challenges Facing NSSF and Members amid Government...

85

Role of Social Security Schemes in Tanzania. Challenges Facing NSSF and Members amid Government Failure to Confine Withdrawal. By: Mohamed Juma Mwerinde. UB No. 11 031 946 A Dissertation submitted to the Department of Development & Economic Studies (DDES) University of Bradford in partial fulfilment of the requirements for the award of the MSc in Economic and Finance for Development, March 2013 School of Social and International Studies Department of Development and Economic Studies University of Bradford Bradford, West Yorkshire BD7 1LP The United Kingdom Word Count: The length of this dissertation is 12,932 words 11

Transcript of Role of Social Security Schemes in Tanzania. Challenges Facing NSSF and Members amid Government...

Role of Social Security Schemes in Tanzania. Challenges Facing

NSSF and Members amid Government Failure to Confine

Withdrawal.

By:

Mohamed Juma Mwerinde.

UB No. 11 031 946

A Dissertat ion submitted to theDepartment of Development & Economic Studies (DDES)

University of Bradford

in part ial fulf i lment of the requirements for the award of the MSc inEconomic and Finance for Development,

March 2013

School of Social and Internat ional Studies Department of Development and Economic Studies University of Bradford Bradford, West Yorkshire BD7 1LP The United Kingdom

Word Count: The length of this dissertation is 12,932 words

11

CERTIFICATION

The undersigned certi f ies that, he has read and hereby recommends

for acceptance by the University of Bradford, a Dissertation ti t led

“Role of Social Security Schemes in Tanzania: Challenges Facing

NSSF and Members amid Government Failure to Confine

Withdrawal” in partial fulf i lment of the requirements for the degree of

Masters of Science (Economic and Finance for Development) of the

University of Bradford.

…………………………………………………………………………

Dr Andrew Mushi

(Supervisor)

Date ………………………………………………………..

22

DECLARATION AND COPYRIGHT

© Mohamed Juma Mwerinde

No part of this dissertation may be reproduced without the permission

of the author.

I declare that this dissertation is substantial ly my own original work

and has not been submitted in any form for an award at any other

academic institution. Where material has been drawn from other

sources, this has been fully acknowledged.

Signature ………………………………….

Date…………………………………

33

ACKNOWLEDGEMENT

It is my confession that this thesis report could not be completed without the clutch

up of a number of peoples around me. It is not easy to mention all who contributed,

but let it suffice to say that I appreciate all and the contributions made. Owing to

space constraints, allow me to mention a few of them; My heartfelt appreciation to

my principal Supervisor, Dr A. Mushi for his encouragement, intellectual support,

constructive criticism and tolerance from which production of this quality thesis

report have been able to achieve. I also recognize with gratitude the contributions

of all MSc. Economics and Finance for Development lecturers at Mzumbe

University and University of Bradford. They made me build confidence in critical

writings and thinking.

I as well lengthen my gratitude to NSSF management for allowing me to attend

classes and conduct study in their organization. I thank all NSSF staff especially

ones at the Head Office for their valuable contributions in getting data and annual

reports for supporting my research.

Last but not least, I recognize and appreciate the suffering my family and relatives

which experienced during the entire period of my study when they missed my

presence, love and care. I highly appreciate the patience, understanding,

emotional support and encouragement of my beloved wife Rachel Jonathan

together with my lovely children, Rebecca and Kiangi.

I remain fully responsible for any shortcomings in this work.

44

DEDICATION

I dedicate this work to my Heavenly Father who gave me the ability to do

everything through his strength and willingness. I also dedicate this work to my

loving and caring parents, the late Mr and Mrs Mwerinde, as I have achieved my

success behind their care, love, courage and prayers, what they did continues to

make me prosper in my life. Finally, I dedicate this work to my loving wife, my

children, my brothers and sisters whose prayers, encouragement and support

made possible completion of this work may the Almighty God bless them all!

55

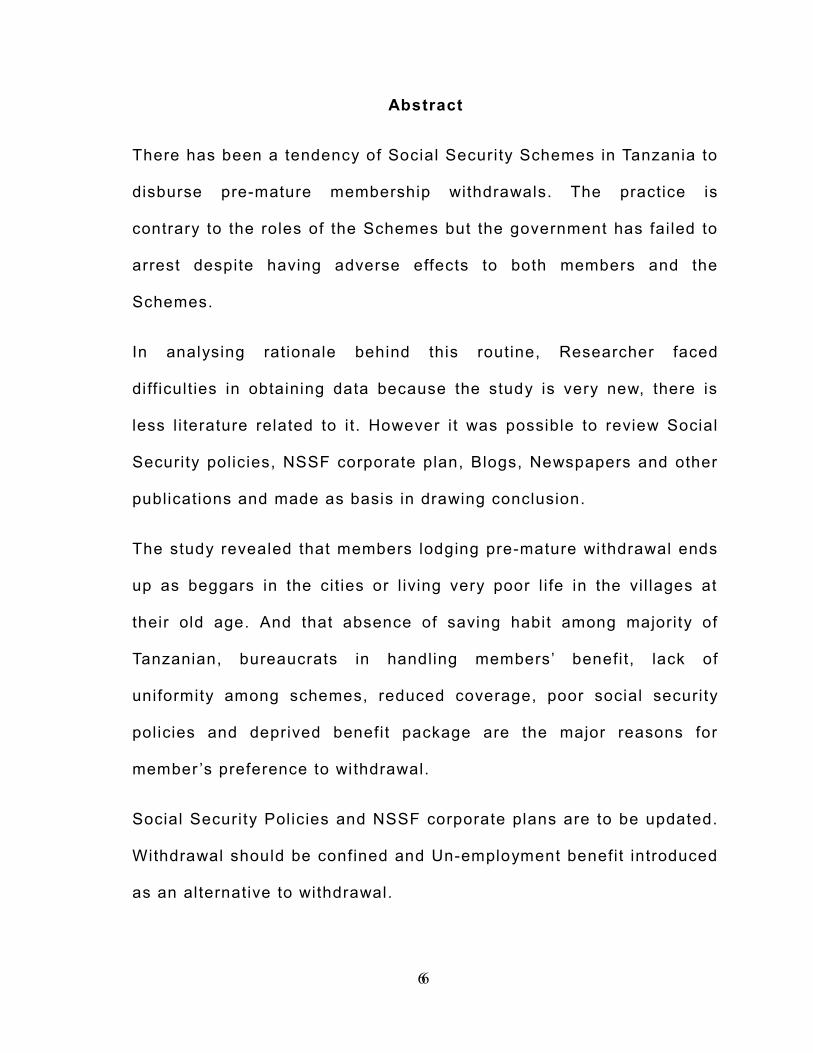

Abstract

There has been a tendency of Social Security Schemes in Tanzania to

disburse pre-mature membership withdrawals. The practice is

contrary to the roles of the Schemes but the government has fai led to

arrest despite having adverse effects to both members and the

Schemes.

In analysing rationale behind this routine, Researcher faced

diff icult ies in obtaining data because the study is very new, there is

less l i terature related to it. However it was possible to review Social

Security policies, NSSF corporate plan, Blogs, Newspapers and other

publications and made as basis in drawing conclusion.

The study revealed that members lodging pre-mature withdrawal ends

up as beggars in the cit ies or l iving very poor l i fe in the vi l lages at

their old age. And that absence of saving habit among majority of

Tanzanian, bureaucrats in handling members’ benefit, lack of

uniformity among schemes, reduced coverage, poor social security

policies and deprived benefit package are the major reasons for

member ’s preference to withdrawal.

Social Security Policies and NSSF corporate plans are to be updated.

Withdrawal should be confined and Un-employment benefit introduced

as an alternative to withdrawal.

66

CONTENTS;

Page

Certif ication ………………………………………………..……….……..…. i i

Declaration and Copyright …………………………………………………...i i i

Acknowledgement ……………………………………….………..….………. iv

Dedication ………………………………………………………..…………….. v

Synopsis …………………….……………………………………..…….…….. vi

List of Tables and Figures …………………..………………..………..….. ix

List of Abbreviations /Acronyms …………………………………………... xi

CHAPTER ONE: Overview of the Study

1.1.0 Introduction ………………………………………………………..….. 01

1.1.1 Background to the study…..... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... 03

1.4.3 Research question …………………………………………………... 07

1.4.0 Research Objectives ………………………………………………... 07

1.2.0 Statement of the Research Problem …………………………….. 08

1.3.0 Significant of the Study……………………………………………... 09

1.5.0 Scope of the Study …………………….…………………...... ... ... . 10

1.5.1 Organization of the Study ….... ... ... ... ... ... ... ... ... ... ... ... ... ... ... . 11

1.5.2 Limitation of the Study ………………………………………….…... 11

1.6.0 Research Methodology …………………………………………..…. 12

1.6.1 Data collection ……………………………………………………………...…. 13

77

CHAPTER TWO: Literature review.

2.1.0 Introduction ……………………………………………..……………………….. 14

2.2.1 Roles of Social Security institutions ……………………………….....14

2.3.0 Social Security Scheme in Tanzania and Problems

associated with ………………………………………………………… 18

2.4.0 Adequacy of Social Security in Tanzania and destines of pre-mature

membership withdrawers …..... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... . 28

CHAPTER THREE: Review of Social Security Policies.

3.1. Introduction…………………………………………………………….....34

3.1 Review of Global Social protection floor policy …………………...34

3.2 Review of Tanzania social security policy (2003)…………….…...36

3.3 Review of Tanzania National Ageing Policy………………………...38

3.4 Overall Challenges facing Social security sector in Tanzania………………………………………………………………....40

CHAPTER FOUR; Impact and Challenge of Withdrawal Benefit toNSSF

4.0Introduction ………………………………………………………….….... 42

4.1 Roles and Functions of NSSF ..... ... ... ... ... ... ... ... ... ... ... ... ... ... ... .…... 42

4.2 Adequacy of Benefits paid by NSSF…….………..….…………..... 44

4.3 Review of NSSF corporate plan 2009/10- 2012/13 …….…………48

88

4.4. NSSF and the Challenge of withdrawal benefit …….…….…..….51

4.5 Trends in withdrawal benefits in NSSF ……………………………..56

4.6 High membership withdrawal... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ..56

4.7 Members’ complaints on barred withdrawal benefit …...... ... ... ...57

4.8 Why members prefer withdraw benefit ……………………………. 62

4.9 Provision of insufficient benefits to members ………………..... . 63

4.10 Provision of regular training to Employees and members …....65

4.11 Sufficient system of collecting members’ complaints..……..… 66

4.12 Whether there is di lemma in confining withdrawal…………..... 66

CHAPTER FIVE; Conclusions

5.0 Conclusions……………………………………………………………... 69

5.1 Recommendations for further research ………………………..…. 70

List of References ……………………………………………………..…... 70

List of Tables and Figures;

Graph No.1 Global Pension coverage by 2010…………………….………….…....16

Table No. 1 Global population coverage of social security………………………..17

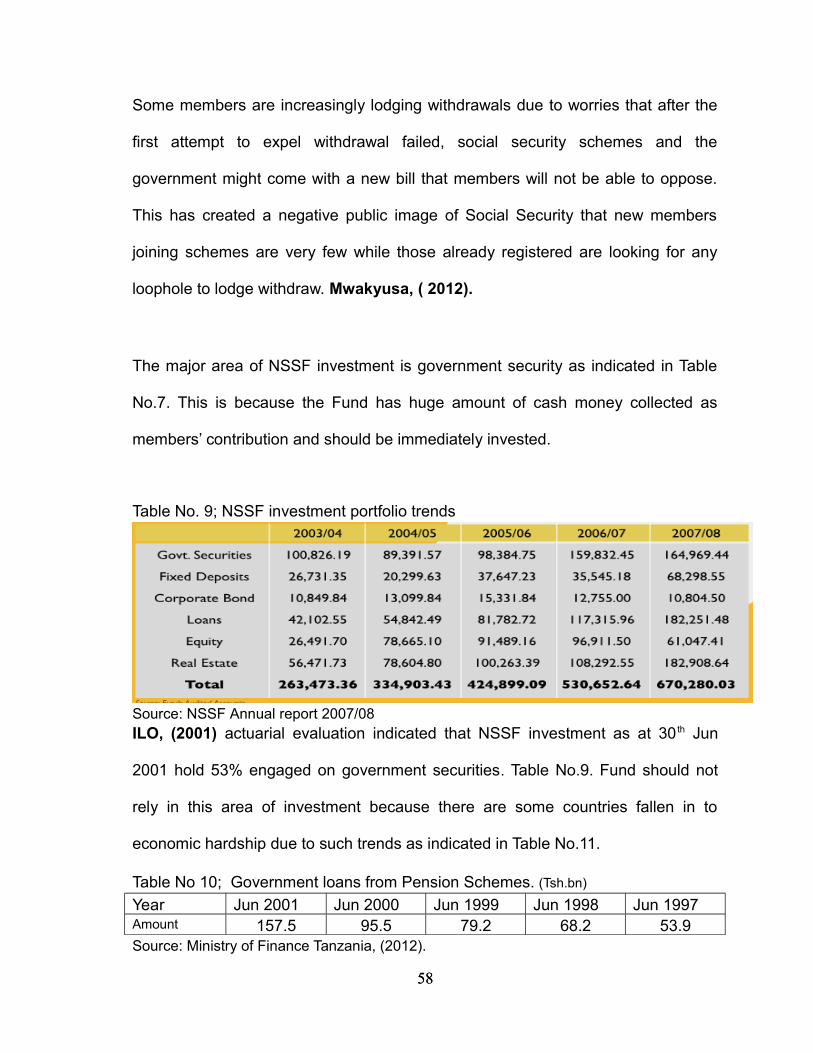

Table No. 2 Tanzania Social security investments at 2009 …………………....… 21

99

Table No. 3 Variations among social security in Tanzania …………….…...….…..23

Graph No. 2 Social security coverage in Sub Sahara Africa ……………………… 29

Picture No.2 Elders Caring Extended Family …………………………………...….. 32

Table No. 4 Trends of NSSF membership and benefit payments …………..…… 32

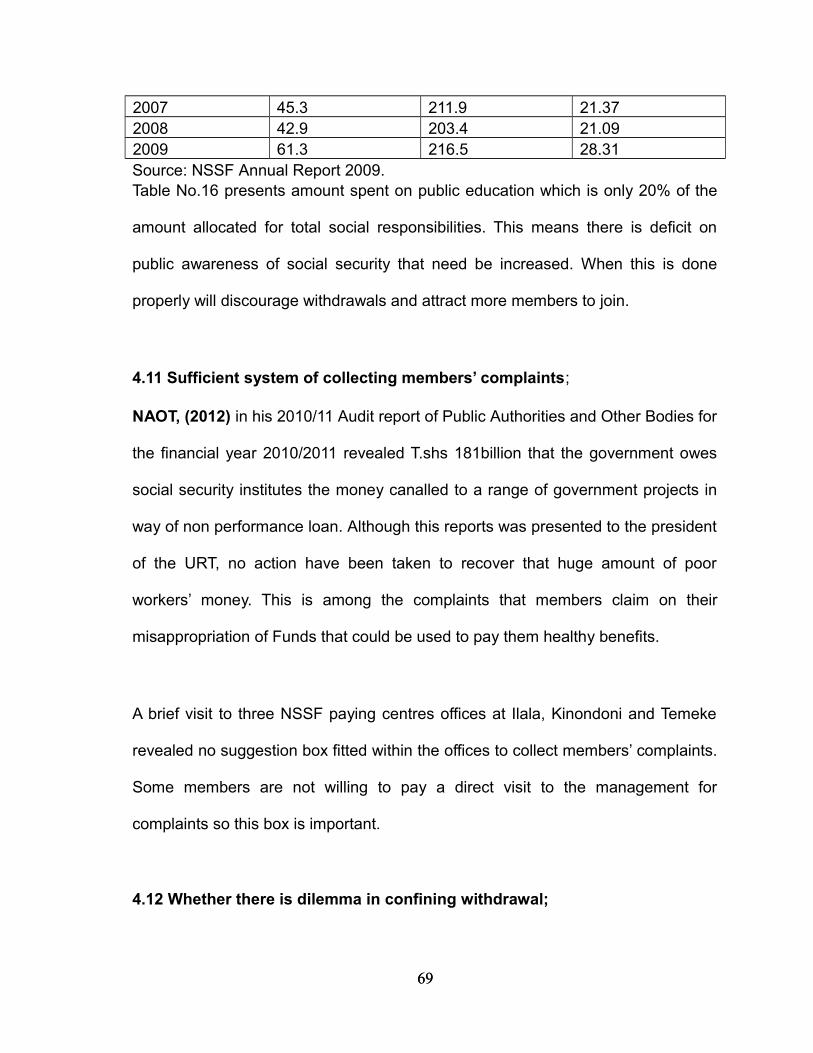

Graph No.5 Stages of social protections ……….…………………………….….…. 35

Diagram No 1 How Social protection Invests in Human Infrastructure ……....….. 35Table No 5. Position of NSSF among other schemes in Tanzania……………..… 42Table No 6. Number of members and amount of pensions by each scheme……………. 43Table No. 7 NSSF Financial Position at 2008 …………………………………...…. 43Graph No. 3; World Un-employment benefits payments……………. 45Graph No 4; World Social security expenditure ………………………….......……. 46Picture No. 1; Retiree awaiting pension computation …………………………..…. 47Table No.8 Benefit Processing Period Performance ……………………….…… 48Table No. 12; Corporate plan 2009/10 – 2010/12 performance summary………. 49Table No. 9; NSSF investment portfolio trends ……………………………….……. 54Table No 10; Government loans from Pension Schemes ………………………… 54Table No 11; Countries with huge National Debt led to economic hardship …….55Table No. 13; Total benefits paid by NSSF 2002 to 2009 …………………...……. 56Graph No.6 Five Years Trend of Benefit Payments …..….…………………..……. 56Map No.1; Tanzania Social security survey …………………………………..……. 60Table No. 14; Social security coverage in Tanzania ……….………… 64Table No.15; Amount spent on employee training ………………………………… 65Table No16; Amount spent on Public Education vs corporate social responsibility……………………………..…………….…………. ……………….……65

List of Abbreviations /Acronyms;

CAG …………………..…………………………..…….. Controller and Audit GeneralCCK ………………..……………………………………....………. Chama Cha KijamiiCESCR …….……....…………. Committee on Economic, Social and Cultural RightsCUF ……….………..…………..………………..………………….. Civic United FrontGDP …………………………..……………………………….. Gross Domestic ProductGEPF ……………………..……...….. Government Employees Pension FundILFS ……………………….....……………….…..….. Integrated Labour Force SurveyILO …………………………..…………..…. International Labour Organization

ISSA …………………….....…...... International Social Security Association

1010

LAPF ………..………………………………..…….…… Local Authority Pension FundLHRC ……………………………..………..….. Legal and Human Right CommissionMKUKUTA ……… Mkakati wa Kukuza Uchumi na Kupunguza Umaskini TanzaniaNAOT …………............................................................... National Audit of Tanzania

NHIF ……………………...……..………..…... National Health Insurance Fund

NPF ……………………..….…………………..……………… National Provident Fund

NSSF ……………………………...………...…... National Social Security Fund

POAC ……..…..…….... Parliamentary Public Organizations Accounts Committee

PPF …………….……………………………..….…..…..…… Parastatal Pension Fund

PSPF …………….………………………….…………….. Public Sector Pension FundREPOA ……………..…..……………………………. Research on Poverty AlleviationSATF ………………………..……………………..…….…… Social Action Trust FundSPSS …………..……..………..…. Statistic Package for Social Scientist

SSRA …………………………….......… Social Security Regulatory AuthorityTAMWA ……………………………..……..….. Tanzania Media Women AssociationTASAF ……………………………….….………………. Tanzania Social Action FundTUCTA ………………………….…..……..…….. Trade Union Congress of Tanzania

UDHR ........................................................ Universal Declaration of Human Rights

UN ………………………………..…….………….……………..………... United NationURT ………………………………….…….……..………. United Republic of TanzaniaWDI ……………………………………..……………….. World Development Indicator

ZSSF …………………………...…..…………… Zanzibar Social Security Fund

1111

CHAPTER ONE Overview of the Study

1.0 Introduction;

Social security is a program designed to offer social protections

amongst members in a society. I ts history goes back from the

Palaeolithic era from which men l ived in groups known as Bands

formed for the purpose of social and economical protections. Due to

challenges and contingencies faced by these groups in search of

development, members of the bands assisted themselves by means of

physical and economical well beings. Kathy,(2007). The social groups

formed went through various reformations and adaptations until when

United Nation in i ts General assembly on 10 t h Dec 1948 adopted

Universal Declaration of Human Rights. Article 22 of this declaration

required everyone in a society to be protected, i t insists that;

“ Everyone, as a member of any society, has the right to social security and entitled

to realization, through national effort and international co-operation in accordance

with the organization and resources of each State from social and economical

contingencies”. UN (CESCR), (2008).

Following this declaration, International Labour Organization, (ILO) set Social

Security Convention No. 102 at its 35th conference 1952 which pointed out nine

minimum benefits to be paid by social security schemes as; Old Age, Invalidity,

Survivorship, Employment Injury, Maternity, Medical Care, Sickness,

Unemployment and Death. These benefits lock up social security functions to;

Provisions of Social safety,

1212

Redistribution of income, Diversification of risks, Social and economic stability,

There are three main types of social security programs depending on the country’s

economic capability. One is a protection to all by the government which is mainly

practiced by high income countries and the other two are insurance programs by

members contributing certified amount. All three, despite offering short terms

benefits majors in old age protection when members has undergone economical

inactive and became more vulnerable.

This study investigates role of Social Security Funds in Tanzania and

reveals consequences of government failure to confine withdraw. It

looks on destines of members of social security following increasing

tendency of withdrawals after government consent to members wil l ing

to quite protection and further tables out status of social security

coverage in Tanzania to see how ILO declaration No. 102 of social

security for all is achieved behind Schemes competing to pay

withdrawal.

Researcher reviewed various li teratures and publications which

guided him on conceptual frame work to build his own theoretical

views and analysis. Citing from Magazines, News Papers, Brochures,

previous researches, Annual reports from NSSF, SSRA publications,

Blogs, Government Bureau of Statistics together with Tanzanian

1313

Parliamentary discussions and presentations made it possible and

basis in drawing conclusion of this study.

1.1 Background to the study;

Following increasingly trends of pre-mature membership withdrawal from social

security schemes in Tanzania, the government passed a law to confine this benefit

but few days after the law enacted, members, activists, scholars and some

politicians revoked over it to the extent that the government detach the amendment

and allowed payments to members retrenched and wishes to terminate

membership with the Scheme to continue. Parliament of Tanzania (2012) and

The Citizen (26 July 2012).

A survey of all Schemes in Tanzania portrayed that it is only Parastatal

Pension Fund (PPF) that has withdrawal benefit clause il lustrated in

its Act. Baruti, (2011) identif ied. However, all other schemes un-

officially adopted this benefit without amending their Laws simply

because members prefer i t. Schemes without such an opportunity are

losing members from the very beginning during membership

registration. This is puzzling, i t means members are registering

themselves eye-marking withdraw in a near future. This compels

Social Security Schemes to compete for members just like any other trading

institutions. According to Barya, (2011) in Tanzania, schemes attract members by

assuring issuance of withdrawals. This is funny and contrary to roles of social

security schemes which advocates for lifetime members’ protection. Competitions

1414

in these Schemes should be in quality provision of benefits and efficiency rather

than entertaining withdraws. If this habit is not monitored, sooner all Schemes will

run without members to protect and the meaning of social protection in the country

will be lost.

NSSF Corporate plan (2007/08 – 2009/10) revealed the Fund to have an

increase of 162% in members’ premature withdraw from 2003 to 2007. This trend

is very high and dangerous to NSSF and members but unfortunately, the

government is comfortable to the extent of allowing withdrawal to continue.

Researcher is interested to know whose burden is it when members withdrawing

today become old and vulnerable! Will the government come back to Social

Security Schemes for a help or will offer them protection? Who will bear the costs?

Does the situation mean that government wants to make people happy today by

enjoying withdrawal benefit which ruins their old age life plan? It is learned that if

the government decide to offer coverage to all the elders in the country it will

spend 11.2% of its Gross Domestic Product by 2050. Help Age, (2011)

Schemes must portray to members and the government on the consequences of

pre-mature withdrawals. Members must be educated on how to maintain their

membership despite all the difficulties they are going through, for the betterment of

tomorrow during when their earning capacity will be lost. A good example is cited

from elders seen today begging in streets simply because they lost or did not

bother to join Social Security Schemes during their employment period as a result

are now living horrible and begging life around.

1515

Social Security Act No. 5 of 2012 restricts members of all pension funds

accessing their terminal benefits before reaching voluntary retirement age of 55

years or 60 compulsory. Immediately after Social Security Institutions started

implementing this Law, some employees in the private sector reacted harshly to

the new legislation. Some workers say the legislation is oppressive and are now

quitting jobs in protest. The Citizens 05 Aug (2012) presented this matter.

Report issued in the parliament revealed that population aged 65 years and above

in Tanzania are 1.4 million (3.2% of Tanzanian population) but only 4% are covered

by one of the scheme available leaving 96% of them distressed, begging and living

poor life around. Parliament of Tanzania Report, (2012). Following this report in

the parliament it was found necessary to confine pre mature withdrawal with

expectation of arresting the problem of old age protection in future. Now that the

move has failed it is expected that there will be more vulnerable elders than it is

today in the near future which will be a burden and shame to the government.

Allowing pre-mature membership withdraw has possibly produced attitudes that

National Social Security Fund (NSSF) is still a continuity of the previous National

Provident Fund (NPF) which members can treat their pension contributions like

savings in a Bank that can be accessed at any time according to members wish.

Mwakyusa (2012) presented NSSF Chief in the Daily-Newspaper addressing

Parliamentary Public Organizations Accounts Committee, (POAC) that the habit of

social security membership withdrawals though advocated by majority of

parliamentarians is not practised anywhere in the world. He insisted that is

1616

contrary to the basic intention of social security which invests money collected and

pay benefits from investment returns but mainly focuses on provision of pensions.

1.2 Research question;

Does government fai lure to expel withdrawal benefit in social security

a privi lege or thrashing to members and the Scheme?

1.3 Research Objectives;

This study reveals how roles of social security schemes in Tanzania

are achieved behind increasing membership withdrawals and

government fai lure to confine the situation. Following increasing

numbers of vulnerable elders in the country the government is

planning to set aside amounts in the main budget that wil l take care

of the unprotected elderes. Parliament report, (2012/13 ). However,

this study reveals a better way of strengthen Social Security benefits

and coverage than setting amount from the government budget which

all the years has a deficit ! Specific Objectives;

To identify reasons behind members of NSSF’s preference to

withdrawal. Tracing adequacy in coverage and benefits paid by NSSF if are the

reason behind increasing membership withdrawal. To discover destines of members of social security in Tanzania

following government failure to expel withdrawal benefit.

1.4 Statement of the Research Problem;

1717

Withdrawal benefit has been practised by all social security Funds in Tanzania

ever since their establishment. In reality, this is contrary to the roles of social

security schemes where protection is extended over the members’ life time.

Recently the government barred pre-mature withdrawal benefit from

these Schemes a case which raised strong arguments from Members,

Activists, Scholars and Some political leaders who objected that the move violates

human rights. TUCTA July 26, 2012. At last the government reverted to the

original state and allowed Schemes to continue paying withdrawal benefit to

members retrenched. SSRA, (2012)

Currently, not much has been researched to reveal the consequences of pre-

mature membership withdrawal in Social Security Schemes. The problem has

grown to the extent that government has planned to set amount in the 2012/13

budget that would take care of the vulnerable elders who are not protected by any

of the available Schemes.. Parliament report, (2012). This study intends to

identify the extent of the problem and suggests long lasting solution.

1.5 Significant of the Study;

This study criticizes government decision in reverting laws passed to expel pre-

mature membership withdrawal in Social Security Schemes. It explains the

extreme that poverty is exploding among members quitting the Schemes early

before they become old and enjoy their old age benefits from social security

schemes. Section 2.6 of the National Strategy for Poverty Reduction in Tanzania

2011-2015 (MKUKUTA) promised provision of social protection and rights of the

vulnerable with basic needs. This goal will never be achieved under pre-mature

1818

withdrawal environments. Sooner our elders will be distressed looting the streets

begging following lack of protection and loss of ability to generate income for their

basic needs.

Help Age, (2011) revealed that there are 2 million elders in the country today and

73% of them still engages in economic activities in small agricultural to generate

income due to lack of protection by any of the social security scheme. The elders

also carry a burden of HIV relative orphans and labour immigrants as a result

poverty. Destitution are common in this group, see Picture No.2.

ILO, (2011) urged Social Security Sector in the country to offer improved benefits

and extend coverage. This could well be done after barring pre mature withdraws,

now that the government has intervene and failed to confine it, obviously our

Schemes will continue covering less members and difficult to offer good benefit

packages as required.

1.6 Scope of the Study;

This study is confined to National Social Security Fund. It reviews

Annual Reports, Social policies, corporate plans, Publications and

Brochures available at the head office in Dar es Salaam Tanzania and

other publications related to this study. Research question of social

security members’ destine following government fai lure to confine

pre-mature membership withdrawal, is given a primary concern.

The study abided to NSSF following the reason that i t is the giant

social security provider in the country; i t holds 51% of the market

1919

share social security schemes in the country. NSSF corporate plan

(2009/10-2012/13).

1.7 Organization of the Study; This study is divided into three chapters. Chapter one begins with an

introductory part highlighting points which the Researcher intends to

cover. It also tackles the historical background of social security

worldwide and Tanzania in particular. The Second Chapter depicts the

literature review related to this study. Chapter Three is review of

NSSF operations, policies and presentation. Chapter Four is

interpretation of the study findings while Chapter f ive concludes and

recommends further studies of this research.

1.8 Limitations of the Study;

The study area on this research is something very new, no l i terature

has been presented directly concerning the government di lemma in

confining withdrawal benefit and destines of social security members

withdrawing today. For that matter Researcher abided to News,

Magazines, Flayers, Blogs, Reports, own experience of NSSF,

Discussions in the Parliament and review of Social policies available.

There is also a bureaucrat problem in issuance of documents at NSSF

offices. Most documents are treated as confidential and what is

revealed to the public cannot be used to retrieve enough data for

judgement. At the same time some of the reports are contradicting on

2020

same information that i t was so diff icult for Researcher to decide

which was true and which was not.

It was also so diff icult to use SPSS and STATA in interpretation of

data collected from this study fol lowing type of data used and

unfamiliarity of the software.

1.9 Research Methodology;

The approach to this study was to review information from customers,

the Fund and Activists as presented by news agencies, blogs,

publications, scholars and social securit ies’ reports.

As defined by Kothari, (2004). Research is an original or additional finding to

the already obtainable stock of knowledge collected for further development. But

Greenfield, (1996) put it as an arrangement for exploring collected data

in a way that i t wil l be relevant to the study in question. It is a

structure of the research conducted, measurements, collections and

analysis of research data.

There are three main types of research design;

1. Exploratory; Deals with discovery idea from l i terature survey,

experience survey and analysis of insight2. Descriptive; Describing a certain group or individual by means

of predictions on fact characters .3. Experimental; This are studies focused on determination of

causes and effects of a certain phenomenon.

2121

In this study Researcher chose exploratory type of research because

it is able to clearly define what he wanted and had adequate of

li terature.

1.10 Data Collection;

In this study only secondary data was collected and used. This

technique was preferred due to limited time available to the study

(three months only) and cheapness in collecting and availabil i ty of

data taking in to mind that the study was self sponsorship.

CHAPTER TWO Literature Review

2.1. Introduction;

The role and experience of Social Security in Tanzania is reviewed in

this Chapter. Weakness in practices that might be fuell ing upward

trends of withdrawals and reasons for government failure to expel i t,

is hereby tacked. Adequacy of Social security in terms of coverage

and benefit provision in the country is covered in this Chapter.

2.2. Role of Social Security institutions;

ISSA defines social security as an insurance programs and social assistance that

offers mutual benefit to qualifying members. It embraces national provident funds,

pension schemes and other social arrangement schemes that, according to the

respective country policies they form part of strategy on social protection program

for that country. ISSA 1927 Constitution, (2007).

2222

There are three types of social security schemes worldwide;

Social Insurance, a system where its members obtain benefits in respect

of contributions made to the scheme (pension, disability and unemployment

payments). It is most practiced by developing countries. Services scheme, one which provides social protections to the needy only. Basic security scheme, assistance by the government of basic needs to

the needy like poor people, refugees or havoc sufferers.

In Tanzania the dominant scheme is social insurance due to low economic

capability of the government to issue free coverage to all its citizens, however

there are some basic steps that the government is taking care of like free primary

education and health care to the elders though it is not practised adequately.

One of the major roles of Social security schemes is provision of social protection

and income security for members and basic needs for all the citizens. In African

countries this has not been possible. Ackson,(2010) revealed that in Tanzania it is

only 6% of the working force that are covered. In Global statistics, ILO, (2010/11)

presented that by the year 2010 coverage was 50% of the entire world population.

However, from that group only 20% enjoy adequate coverage. The main reason for

this poor coverage is said to be recession of informal sector which is the majority in

all countries especially developing ones. While attending these challenges, other

issues like poor country policies, increasing demographic of the ageing, extended

family structures, economic globalization and environmental developments raises

more challenges to social security schemes.

2323

Increasing demographic of the elders is indeed a challenge to Social Security

Schemes especially in developing countries whose economies are poor.

Worldwide, people aged 60 years and above by 2009 were 8% of the entire

population. The figure is rising fast that by the year 2050 Scardino, (2009)

projected it to hit 16%. Clause 22 of the declaration of human rights 1952, requires

all human being in any society to be covered by at least with the basic needs. This

makes Schemes to have an extra task of caring this group regardless that were

not contributing members. The issue is more challenging in Tanzania where none

of these schemes have not managed to pay the nine benefits stipulated in ISSA’s

recommendations, yet are now required to increase coverage to the entire society

who were initially not contributing members, at the same time handle high rate of

pre-mature membership withdrawals ILO,(2010).

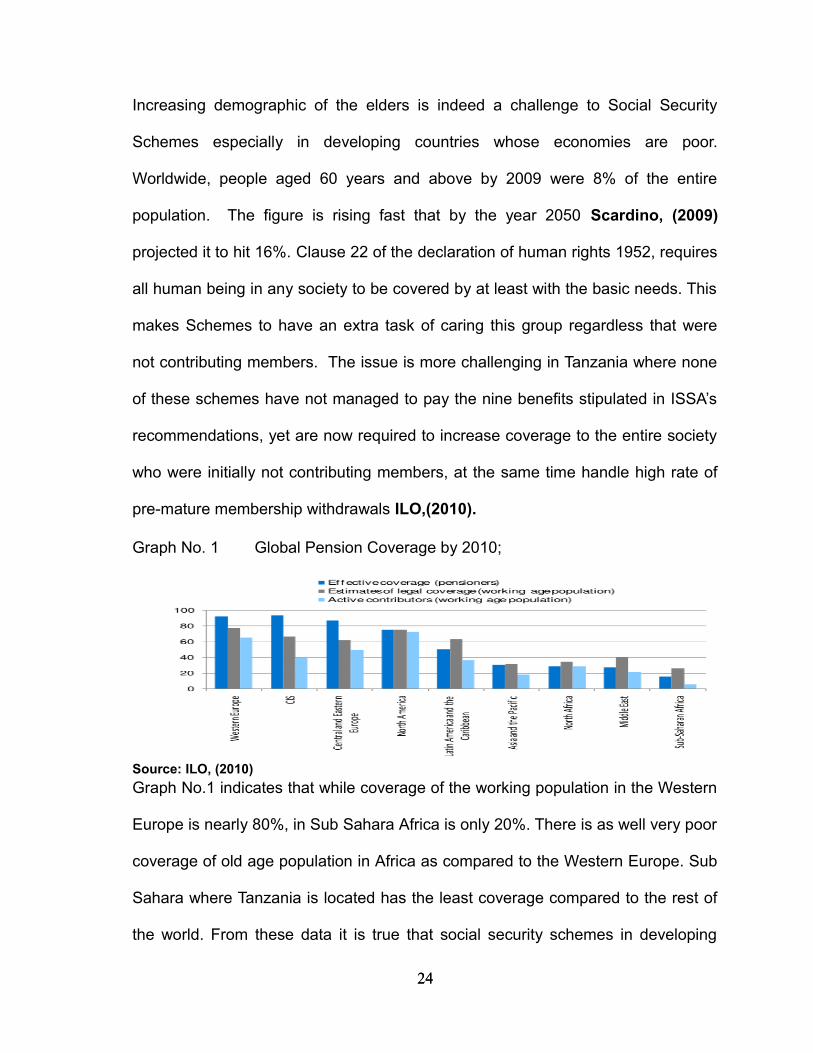

Graph No. 1 Global Pension Coverage by 2010;

Source: ILO, (2010)

Graph No.1 indicates that while coverage of the working population in the Western

Europe is nearly 80%, in Sub Sahara Africa is only 20%. There is as well very poor

coverage of old age population in Africa as compared to the Western Europe. Sub

Sahara where Tanzania is located has the least coverage compared to the rest of

the world. From these data it is true that social security schemes in developing

2424

countries have extra tasks in extending coverage. Pre-mature withdrawal should

totally be banished.

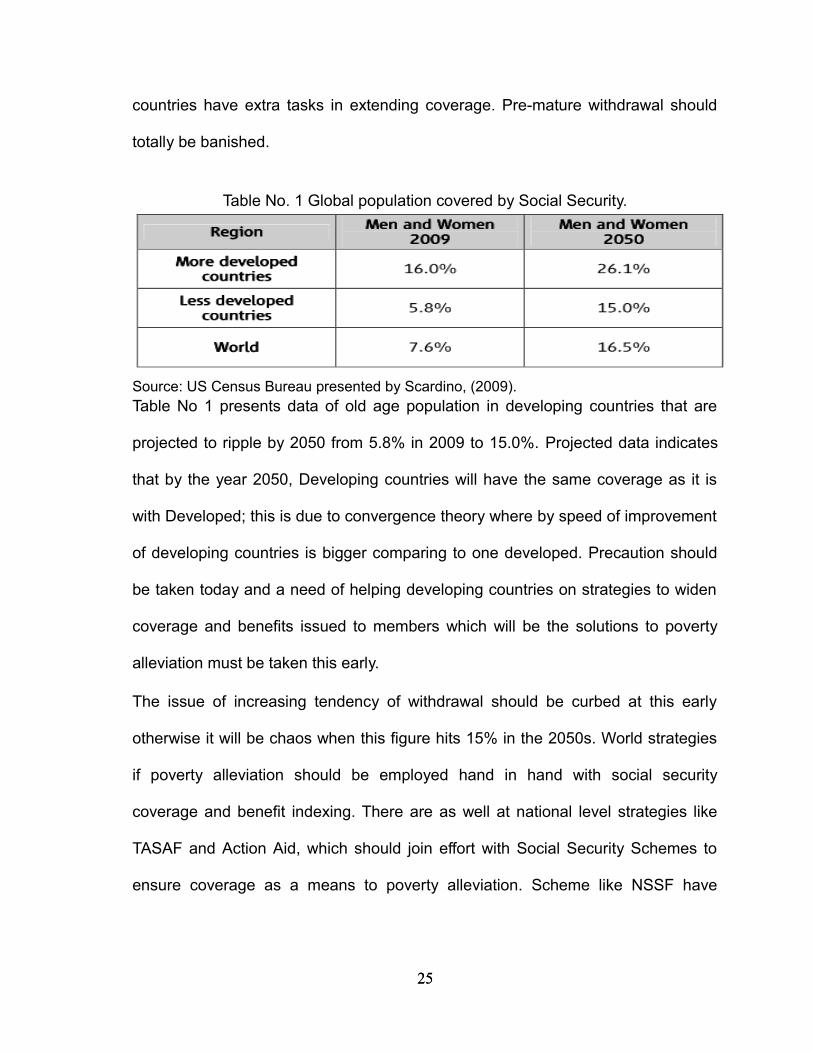

Table No. 1 Global population covered by Social Security.

Source: US Census Bureau presented by Scardino, (2009). Table No 1 presents data of old age population in developing countries that are

projected to ripple by 2050 from 5.8% in 2009 to 15.0%. Projected data indicates

that by the year 2050, Developing countries will have the same coverage as it is

with Developed; this is due to convergence theory where by speed of improvement

of developing countries is bigger comparing to one developed. Precaution should

be taken today and a need of helping developing countries on strategies to widen

coverage and benefits issued to members which will be the solutions to poverty

alleviation must be taken this early.

The issue of increasing tendency of withdrawal should be curbed at this early

otherwise it will be chaos when this figure hits 15% in the 2050s. World strategies

if poverty alleviation should be employed hand in hand with social security

coverage and benefit indexing. There are as well at national level strategies like

TASAF and Action Aid, which should join effort with Social Security Schemes to

ensure coverage as a means to poverty alleviation. Scheme like NSSF have

2525

offices in at district and sub district level which could be easier to reach all the poor

in the country. This could be a good start off.

2.3. Social Security Scheme in Tanzania and Problems associated with;

The history of Social Security Scheme in Tanzania goes back beyond

the colonial era. Msalangi, (2003) identif ied presence of certain form

of social protection even before the coming of Colonial system that

were organized by customary laws and norms. The informal and

traditional social protections practiced were based on family and

community assistance. There were assistances during the time of

festivals and contingencies like famine, diseases, death and old age. People

were depending on family and clan members for communal assistance in form of

cash, food or sort of a kind. The formal social security schemes seen today are

revealed by Eckert, (2004) who says are a product of colonialism introduced to

save the interests of some Europeans and few elite Tanzanians working for the

colonial Government.

However, Barya, (2011) learned that Tanzania, Kenya and Uganda did not change

much the social security system inherited from colonial despite all the shortfalls

these schemes embraced! He further learned that this is the main reason why

schemes we have today have many shortfalls. I agree with Barya, (2011) that it

was necessary to change these Schemes to fit our environment that could take

challenges of our present society needs. However, it was difficult to have a

2626

universal scheme by the government due to poor economic capability of our

country.

Currently there is National Social Security Policy of 2003 which considers social

and economic changes occurring in the country and liberalizes this sector in

Tanzania. The reformation re-organized activities of social security providers to act

in response to the market demands considering free market economy.

Currently, present Social security institutions in Tanzania are;

• National Social Security Fund, (NSSF)

• Parastatal Pension Fund, (PPF)

• Local Authorities Provident Fund, (LAPF)

• Public Service Pensions Fund, (PSPF)

• Government Employees Provident Fund (GEPF)

• Public Service Retirement Benefit Scheme (PSRB)

• National Health Insurance Fund (NHIF)

• Tanzania Social Action Fund - TASAF)

• Social Action Trust Fund, (SATF)

• Zanzibar Social Security Fund, (ZSSF)

It is believed that despite a number of available Social Security Schemes,

coverage is still very poor. Baruti,(2007) sees that Tanzanian have potential

opportunities to be covered by Schemes available! However it is only of recent

2727

efforts the government has intervened to extend coverage with informal sectors

which is considered green pastures for all Schemes. Although Baruti, (2007)

advocates on this potential opportunities, he is not mentioning strategies to be

employed to add the omitted ones. He also has not identified how people in the

informal sector could be handled with matters concerning compliances. This group

is so difficult to maintain due to nature of their business and none existence of

permanent business place. Indeed this sector is potential but needs care on how

to handle.

Maghimbi at el, (2002) recognized that opportunities available for Social Security

have not been covered well by any of the Schemes in the country. He further

identified that Social Security Schemes in the country have failed to contribute

equitable economic growth and are there to flourish the rich out of the sweat of the

poor members of these schemes. He is eye marking things like credits granted to

some of the business people from contributions made by the poor members and

other investments made which are utilized by well off people leaving the poor

members not enjoying their sweats. The above statement is true to some extent

however, investment made by these schemes apart from offering employments

they are also contribute to the GDP and thus contributs to the economic growth of

the country. Beautiful buildings erected attract investments and more business at

the same time offers employment during constructions. Maghimbi at el, (2002)

suggests that members should be given first priority when it comes to credit

facilities.

2828

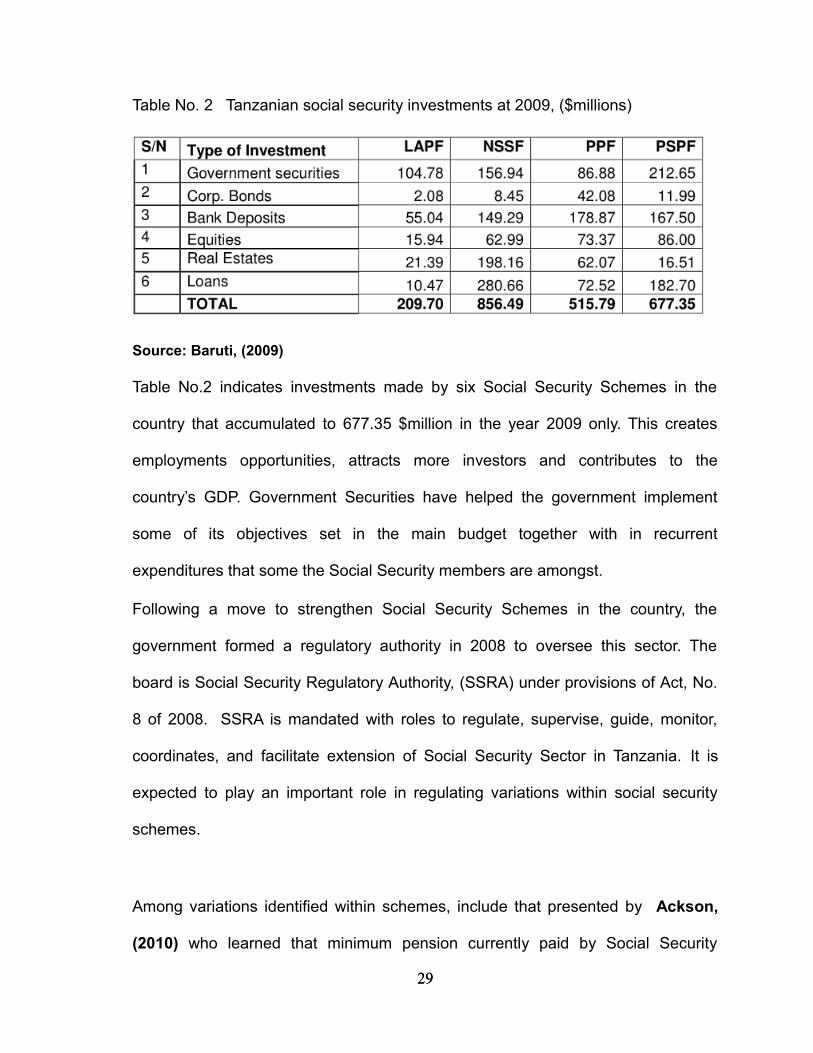

Table No. 2 Tanzanian social security investments at 2009, ($millions)

Source: Baruti, (2009)

Table No.2 indicates investments made by six Social Security Schemes in the

country that accumulated to 677.35 $million in the year 2009 only. This creates

employments opportunities, attracts more investors and contributes to the

country’s GDP. Government Securities have helped the government implement

some of its objectives set in the main budget together with in recurrent

expenditures that some the Social Security members are amongst.

Following a move to strengthen Social Security Schemes in the country, the

government formed a regulatory authority in 2008 to oversee this sector. The

board is Social Security Regulatory Authority, (SSRA) under provisions of Act, No.

8 of 2008. SSRA is mandated with roles to regulate, supervise, guide, monitor,

coordinates, and facilitate extension of Social Security Sector in Tanzania. It is

expected to play an important role in regulating variations within social security

schemes.

Among variations identified within schemes, include that presented by Ackson,

(2010) who learned that minimum pension currently paid by Social Security

2929

Schemes in the country are; NSSF - 47US.$, PSPF- 14US.$ and PPF - 37US.$

for members with the same credits but enrolled in different Schemes. Current

minimum wage of formal sectors in Tanzania is 59US.$. The summary revels that it

is only NSSF paying pension close to the minimum wage and at slightly

reasonable amount. However, the amount is still a challenge to the actual cost of

living which Kanywanywi, (2005) shows that a normal cost of living of five people

in Tanzania by 2004 was about 105 US.$, per month which is twice the amount

paid by highly paying pension fund in the country. In that matter amount paid to

retiree is vastly inadequately.

Another issue to be addressed by SSRA is coverage gap of the vast majority who

are engaged in the informal sector like agriculture, fisheries and traders. Efforts to

extend coverage to them are so little that researcher worries if they will be reached

at all. Since the economic backbone of Tanzania is agriculture, where ILSF (2006)

noted that 80% of the working force is in this sector, then there is a need of

extending social protection to this sector which dominates the backbone of the

country.

Another problem facing social security sector in Tanzania is variation in terms of

benefit paid, coverage category and contribution made between one scheme and

the other, Table No.3 summarises these variations. Dau, (2006) and Rutinwa at

el, (2008)

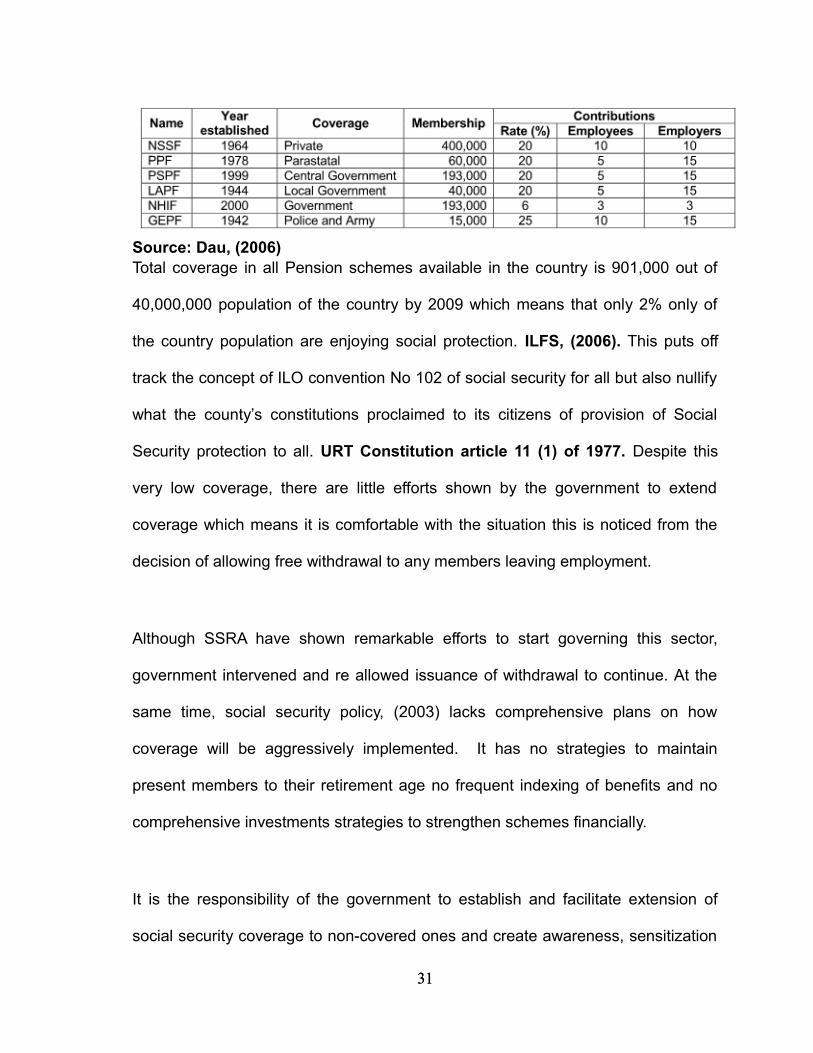

Table No 3. Variation among Social security schemes in Tanzania.

3030

Source: Dau, (2006)Total coverage in all Pension schemes available in the country is 901,000 out of

40,000,000 population of the country by 2009 which means that only 2% only of

the country population are enjoying social protection. ILFS, (2006). This puts off

track the concept of ILO convention No 102 of social security for all but also nullify

what the county’s constitutions proclaimed to its citizens of provision of Social

Security protection to all. URT Constitution article 11 (1) of 1977. Despite this

very low coverage, there are little efforts shown by the government to extend

coverage which means it is comfortable with the situation this is noticed from the

decision of allowing free withdrawal to any members leaving employment.

Although SSRA have shown remarkable efforts to start governing this sector,

government intervened and re allowed issuance of withdrawal to continue. At the

same time, social security policy, (2003) lacks comprehensive plans on how

coverage will be aggressively implemented. It has no strategies to maintain

present members to their retirement age no frequent indexing of benefits and no

comprehensive investments strategies to strengthen schemes financially.

It is the responsibility of the government to establish and facilitate extension of

social security coverage to non-covered ones and create awareness, sensitization

3131

and capacity building to the Schemes. According to Ackson, (2010), 10.5% of the

population in Tanzania is employed but its only 1.8% that are in a formal sector

with social protection, the rest 91.2 % are self employed which social security

sector have not covered. The coverage should be extended to farmers,

pastoralists, Traders and rural-based populations which are the majority and

currently neglected by all Schemes. BARUTI, (2008) See this as a golden

opportunities of Social Security sector in the country to extend their converage.

Perception of Social security in developing countries like Tanzania is

a di ff icult task following lack of f inancial capacityl, poor development

of insurance concept, government budget constraints, higher poverty

ratio and narrow coverage. Justino, (2003) in His working paper

traced the state of social security in developing countries giving the

case of India in which He identif ied well managed, endogenous

policies and wider coverage to have significant contribution in

development of social protections which helped positively in poverty

reduction among societies of developing countries. Countries with bad

social security policy have not achieved well in the case of poverty

reduction.

According to SSRA, (2011), confining membership withdraw in the

country was made with a good reason to strengthen pension benefit

and protecting members in wide adequacy at old age than it is today.

3232

This policy could not win majorit ies acceptance that researcher is

interested to know if the policy was really in favours of members,

social security schemes or the government. Dau, (2006) worked on

sustainabil i ty of benefits paid by Social Security Schemes in Tanzania

and noticed that are not adequate. In Researcher ’s view this could be

the reason for members’ restrain for barred pre mature withdraw. ISSA

Convention, (1952) (No. 102) requires Social Security Schemes to pay nine

benefits but none of Tanzanian Scheme has managed to pay all, it is only NSSF

that is currently paying seven others are paying even less.

Population aged 60 years and above in the country that are getting

pension are very few (4%) the reasons is depicted by ILO, (2010) that

is due to increasing numbers of pre mature withdrawals during loss of

employment. With this observation, i t is necessary for the government

in Tanzania to employ barred pre mature withdraw otherwise the

burden wil l l ie to the government when these member become old and

has no other means to support themselves. I t is true that members

are aware of the consequences of pre-mature withdrawal, but are

neglecting thinking that they wil l be taken care by the government in

time of their old age. There must be deliberate effort to let members

maintain their membership to the retirement age.

3333

Tanzania is not alone in challenges associated with Social Security

reformations, King and Cecil, (2006) presented challenges faced by Social

Security in United States when introducing changes to curb the financial crisis and

other difficulties over 70 years of its existence. In His brief history of Social

Security in the U.S a giant country, various reformations and changes were made

to the current Scheme yet are not complete. Barbone and Luis, (1999) revealed

reasons for failure of reformation on social security in Sub Sahara Africa as being

participation of minor formal sector leaving the vast majority who are the upper and

lower class within the country uncovered. They further noted un-improved

governance and poor social security policies to hinder reformation.

Premature membership withdraws have the following effects;

Reduce or nullify completely old age pension benefit package. Withdraw payments is amount without earned interest since the money is

drawn soon before invested. It also affects investment plans of the respective Schemes following drawn

of money already assigned to a certain project.

It is advised that members maintain their membership status even after laid off

from works. For contractual employees should stay in while seeking another

employment and still enjoy some short term benefits, in case of total failure to

secure any of the employment they should engage themselves in other economical

activities that will allow them earn some income and continue contributing as

voluntary members. This will let them accumulate their credits to qualify for

pension benefit at old age.

3434

2.4. Adequacy of Social Security in Tanzania and destines of pre-mature

membership withdrawers;

Social security schemes are vastly used as a means and strategy to poverty

alleviation; if well monitored, it is the road to sustainable development. WDI, (2001)

depicted that, 46.4% of the population in sub Sahara Africa are living in severe

poverty with no proper social protection planned to rescue them. According to

REPOA, (2005) income of a common Tanzanian in rural area where Social

protection is not provided at all is characterised of a sharp poverty increase as

compared to ones in the urban with Social protection. The report further revealed

a tendency of increasing inequality and vulnerability when one is talking of issues

associated with social security. One role of Social security scheme is redistribution

of income, so when there is an increasingly trend of income inequality it means

social security has not worked adequately in that area. A well designed Social

Security Program should assign the money contributed by rich to offer protection to

the poor. The program could be a mandatory one otherwise it should work in a

form of tax where by a certain tax is imposed to the rich or to the luxurious goods

which in turn the collected money is used to offer protection to the poor.

Poor coverage of Social security in the country, is well explained by Watson et al ,

(2005) who identified that only 3% of the Tanzanian labour force is covered leaving

out 97% of the population. This poor coverage is not in Tanzania alone; Graph

No.2 signifies that all of the Sub Sahara African countries are facing this problem.

3535

With exception of Mauritius whose 35% of its population is covered. World Bank,

(2012), other African countries has less than 19.5% of their working population

coverage.

Graph No. 2 Percentage Coverage of Social security in Sub-Sahara Africa

Source: World Bank, (2012), compiled by researcher.

Low coverage of Social Security in Developing countries is mainly due to poor

financial capabilities and lack of good co-ordinations of the Schemes. In his

findings Baruti (2008), revealed that social security istitutions are able to aleviate

poverty only if there are good policy and well monitored investments of these

institutions.

Due to limited coverage of social security in the country, some people have joined

effort and formed their own groups of social assistance amongst. Example of

some of them are; Christian group at Mabibo Dar es salaam launched a program

known as Development Entrepreneurship for Community Initiative (DECI) this,

aimed at offering assistance among members but was terminated by the

government following lack of financial procedure. Village Community Banking,

(VIKOBA) is another example of social protection, it was formed within women

employed in the informal sector where by members are loaned money for small

business establishment and offered assistances of other social needs at times.

There is also another group very familiar in Tanzania which loans members at a

time in a system known as “Money-go-round” group known as UPATU in Kiswahili.

There is also (Umoja wa Matibabu sekta Isiyo rasmi Dar-es-Salaam) UMASIDA

3636

offering health assistance to members and the last is umbrella society for small

businesses (VIBINDO). baso.blogspot, (June 12, 2012)

Income Security Recommendation No. 67, (1944) insists on compulsory

national social insurance schemes, which cover all service servants self-employed

that should be included in the social assistance. In Tanzania this recommendation

has not been practiced perfectly since ILFS, (2007) noted that there is 1,362,559

employees in the formal sector but only 900,000 are members of social security

schemes. Furthermore, ILO and the UN asserted that every human being has the

right to social security. In this case the country is off track. In the Declaration of

Philadelphia, (1944), Income Security Recommendation No. 67, (1944)

recognized major task of social security ahead being extension of protection to all.

Paragraph 17 requires that “social insurance should offer protection, of

contingencies facing all employed and self-employed persons, including their

dependants.

Universal Declaration of Human Rights, 1948, in its part requested everyone as a

member of society to have the right of social security (article 22). This refers to the

right of health care and basic social services needs in the event of sickness,

disability, widowhood, old age and unemployment, and to special care and

assistance for motherhood and childhood (article 25). International Covenant on

Economic, Social and Cultural Rights, 1966, identifies “the right of all people to

social protection, with social insurance, (article 9).

3737

These international organizations had in mind that there is a need of provision of

social protection to all since it is too difficult for individuals to fight for contingencies

alone. For social security members seeking withdrawals today, there is a danger of

becoming beggars at their old age. NSSF has to extend social security to all

according to ILO, (2010) nevertheless, more members are lodging pre-mature

withdrawal and the government has failed to expel. These are two challenging

issues with NSSF, there should be means to retain members and discourage them

from withdrawal otherwise ILO effort of reaching all will be a nightmare.

When Mboghaina and Osberg, (2010) worked on the welfares of the elderly in

Tanzania they revealed that in 2010 number of the elders over 60 years of age

were 2.95 million but estimation confirmed that the number will triple to 8.39

between 2020 and 2050. With the current poor mechanism of elderly protection in

the country the situation will be worse in the future unless measures are taken this

early.

Picture No. 2; Elders caring extended family in Tanzania;

Source: Help age International, (2004)

3838

Picture No.2 is a common family size of many Tanzanian that retirees do take care

of. When this is taken as an example there are 10 persons to be cared by one

elder while it was supposed to be vice versa.

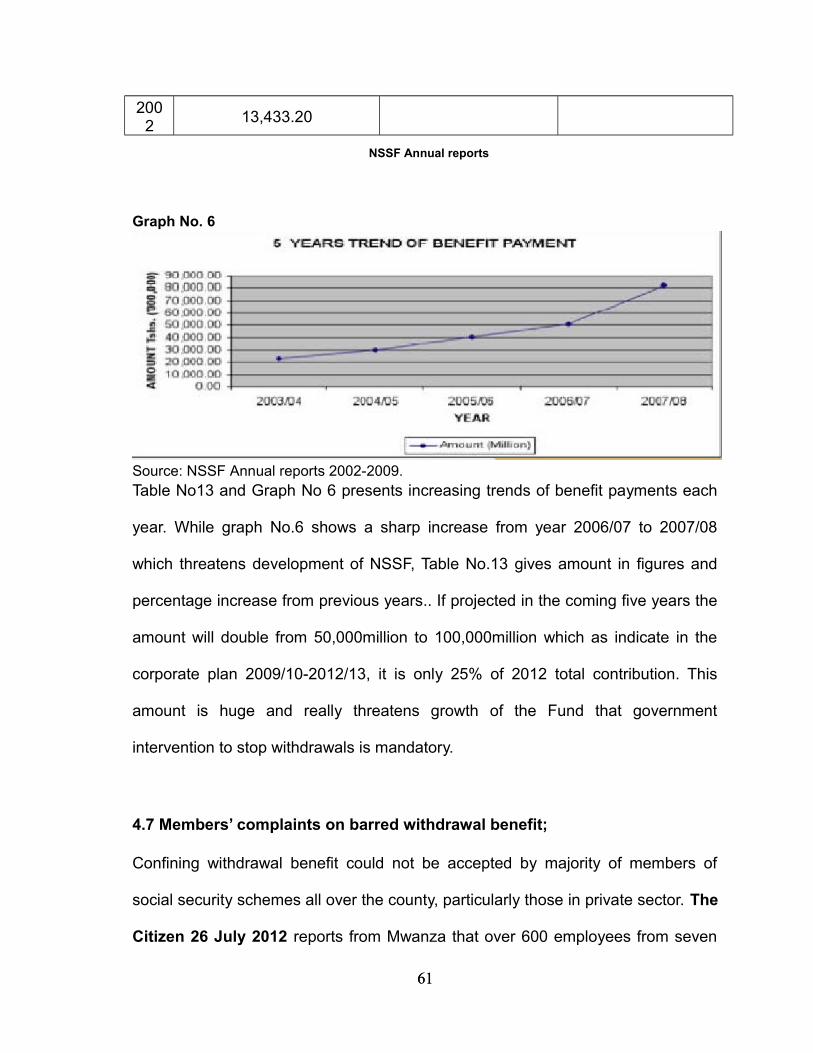

Table No 4. Trends of NSSF Membership size and Benefit payments.

Year Total Employer Total MembersBenefit paid(tshs.mill)

2001/02 15,535 351,975 13,433.202002/03 15,097 327,609 20,735.602003/04 15,970 353,835 23,416.002004/05 14,817 356,070 29,775.272005/06 14,465 380,693 40,183.89

Source: NSSF Annual report, (2005/06) compiled by researcher.

Table No.4 shows huge amount of money paid to members departing the scheme

as compared to the contributions received. There is a slightly increase of members

joining which is only 5% each year while amount paid to members leaving the

scheme increased by 25% each year. This is a challenge to the Funds income

which means amount paid to members leaving the Scheme will soon deplete the

available funds for investments and other Fund’s activities. The scheme will be in

crisis unless stern measures are taken.

Dimoso P at el, (2011) in their Global journal of Human science, identified

increasing trends of demographic beggary in the Urban of Tanzania that the

situation is alarming and calls for immediate redress. In their recommendations the

solution is to increase social security coverage. With the government allowed pre

mature withdrawal this situation calls for actions and government reversal of the

decision for the benefit of people. Dimoso P at el (2011) says that begging is

humiliating, harsh and demeaning to themselves, the media, leaders and visitors of

the country.

3939

Increasing trends of withdrawals in NSSF if not blocked will lead to increased

poverty amongst society since there will be more unprotected elders who had

opportunity to be protected but left to decide otherwise. This will be a shame to the

government when these elders begin to beg in the streets.

CHAPTER THREE Review of Social Security Policies

3.1. Introduction;

Social security policies in international and countrywide levels are herby reviewd in

this Chapter. NSSF Corporate plan and annual reports are scrutinized with the

aim of identifying loopholes leading to increasing membership withdrawal. At the

Ageing National Policy will also be reviewed and illustrate elders destine following

increasing trends of pre-mature membership withdrawals from Pension Schemes.

The chapter presents findings of the entire study which is the basis for drawing

conclusions in the fifth Chapter.

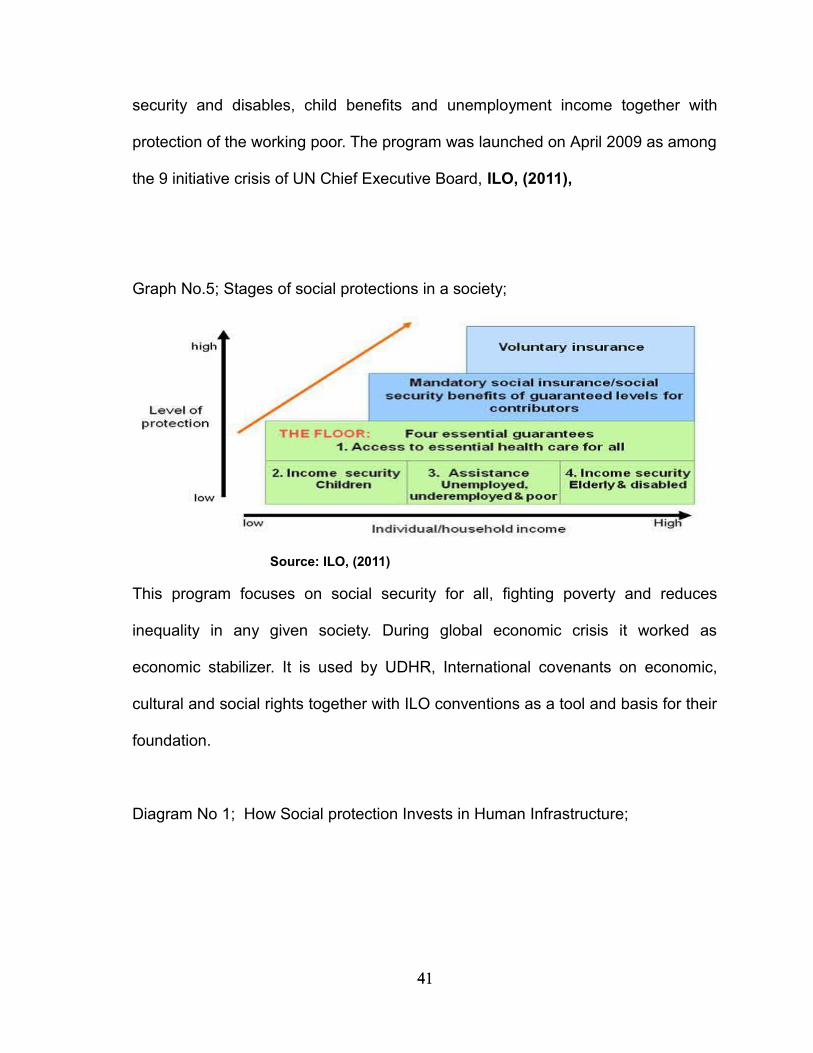

3.1 Review of Global Social protection floor policy;

This is a global agreement on percentage spent from the country’s GDP for social

protection. The protection is supposed to cover basic health care, elder’s income

4040

security and disables, child benefits and unemployment income together with

protection of the working poor. The program was launched on April 2009 as among

the 9 initiative crisis of UN Chief Executive Board, ILO, (2011),

Graph No.5; Stages of social protections in a society;

Source: ILO, (2011)

This program focuses on social security for all, fighting poverty and reduces

inequality in any given society. During global economic crisis it worked as

economic stabilizer. It is used by UDHR, International covenants on economic,

cultural and social rights together with ILO conventions as a tool and basis for their

foundation.

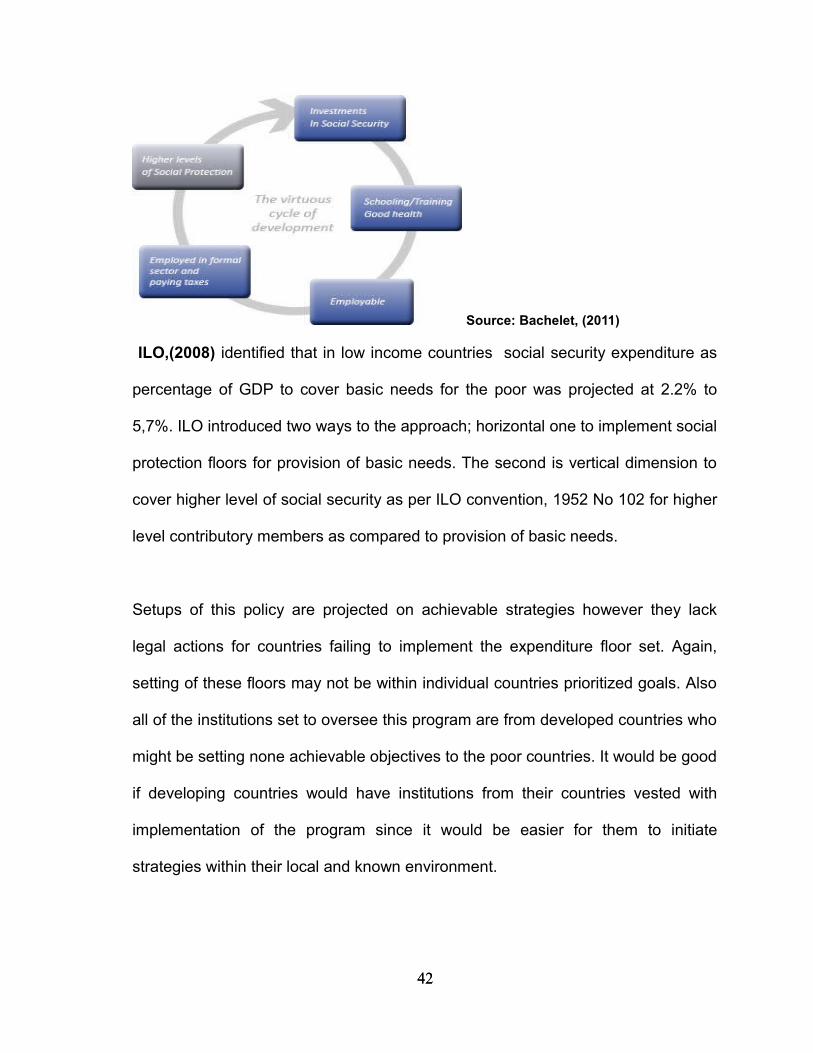

Diagram No 1; How Social protection Invests in Human Infrastructure;

4141

Source: Bachelet, (2011)

ILO,(2008) identified that in low income countries social security expenditure as

percentage of GDP to cover basic needs for the poor was projected at 2.2% to

5,7%. ILO introduced two ways to the approach; horizontal one to implement social

protection floors for provision of basic needs. The second is vertical dimension to

cover higher level of social security as per ILO convention, 1952 No 102 for higher

level contributory members as compared to provision of basic needs.

Setups of this policy are projected on achievable strategies however they lack

legal actions for countries failing to implement the expenditure floor set. Again,

setting of these floors may not be within individual countries prioritized goals. Also

all of the institutions set to oversee this program are from developed countries who

might be setting none achievable objectives to the poor countries. It would be good

if developing countries would have institutions from their countries vested with

implementation of the program since it would be easier for them to initiate

strategies within their local and known environment.

4242

Another challenge is the high number of unprotected poor people in developing

countries. Poor economic performance of government of developing countries

hinders them to allocate enough amounts from the main budget to take care of the

vulnerable poor in these countries.

3.2 Review of Tanzania social security policy (2003);

This is a government document issued to address social, economic and political

changes occurring in the country. It accounts in extending social security to benefit

the citizens and ensure harmonized activities. The policy began in 2001 and

adopted in 2003.

This policy has some shortfalls to be addressed so as to help in boosting social

security institutes in the country. First of all the policy does not recognize tax

financed social security schemes, while one of the functions of social security

schemes is redistribution of income. The best means to do this is by tax system.

There should be scheme based on tax that will take care of the old aged people

who could not be able to be covered at their working period or for one reason have

happened to fall in problems like one of collapsed East African Community and its

employee who are now suffering in streets with no help.

This policy, though mentioning some informal social security groups do not say

how and when they will be recognized and given priorities by the government as it

is for the formal schemes. These are initiatives by peoples in the informal sector

4343

thus if given government shield would not face challenges like the formal schemes

that many takes them like a burden and extra costs to them. There should be a

policy clearly mentioning how these groups will be helped. Some of them are

UPATU, VIBINDO and UMASIDA elaborated in detail in page 30 of this study.

Investment portfolio of social security schemes are commercial loans, government

bonds and real estate. The policy does not guide clearly how these portfolios

should be organized and it should restrict government loan like that of building

Bunge house and University of Dodoma in Dodoma which are non performing

projects. This is pensioners’ money which must be invested in viable projects only

which will yield good profit to cover protection of retired and not used in pompous

investments.

3.3 Review of Tanzania National Ageing Policy;

Tanzania is the second country in Africa to prepare the National Ageing Policy after

Mauritius. Aged people are those in 60years and above. According to Help Age

International, (2011), this group was 2million by 2010 in Tanzania and is

expanding very fast despite the fact that is more vulnerable in terms of income

security, diseases and general health.

4444

ILFS, (2011) revealed that due to lack of social protections to old people in

Tanzania, majority are forced to continue working at that age mostly in the poor

agricultural works. This group also takes a major role of caring orphans for HIV

and Labour migration victims, see picture No.2. It is estimated that 53% of

Tanzanian orphans are under care of the old people. Help Age International,

(2011), presented that only 6.5% of old people are covered by formal social

security scheme and that 82% of them are living in the rural. It is learned that if a

universal social security is extended to this group, it will result into decrease of

national poverty by 12%. It is difficult for the government to offer social protection

to this group at a go due to poor economic capabilities of the country, however all

things starts by daring so it can be employed slowly and as time goes on will be

improved.

The National Ageing Policy was implemented in the country since 2003 by the

government after identifying existing gap in old age social protection. The policy

has various shortfalls like presence of too general provisions that are difficult to

implement. It also lacks legal bindings that majority contempt it. One provision

requires provision of social coverage to elders but at the same time the

government has allowed pre-mature withdrawals from these schemes.

The policy does not state clearly what are the provisions to be made to elders and

by what means. It would be easier to make means of identifying them by opening

4545

office or individual bank accounts before making other means to help. The policy in

sec. 3.12 of this policy, warns insists that there is a tendency of the majority to

enter old age unprepared and become a burden to the community. This is contrary

since allowing pre-mature membership withdrawal is the main source of

unprepared for old age. Sec. 3.12 (iii) said Ageing will be taught in schools as

Civics subject, unfortunately since 2003 8years passed without implementation.

3.4 Overall Challenges facing Social security sector in Tanzania;

Overall management and administration of social security funds are vested to the

board of trustees and the Director General all appointed by the government

through the responsible ministry. Due to this there is excessive government control

over the schemes in issues relating to investment decisions and expenditures

NSSF Act No.28 1997. Grandiose investments made by this sector in favour of

government interest can be seen in University of Dodoma, Machinga complex in

DSM, Police and Military Houses all are none performing projects as revealed by

CAG Report, (2012)

Actuarial evaluation made by ILO(2004) in respect of NSSF for the year 2002

depicted very high administrative expenditure 22% of the Fund’s income whereby

required amount is less than 15%. This problem could be arrested by merging

some of NSSF Departments with similar functions, reducing number of offices at

district level and investing heavily on computerization to enhance efficiency and

increase control. This will strengthen services delivery and attract more members

4646

that would increase Funds financial position and arrest the problem of poor record

keeping that causes dalliance on benefit provision which discourage members.

There is lack another problem of interactions between schemes. Members cannot

shift from one scheme to another. This is really a problem since there are

members like non pension government employee who are members of NSSF

cannot shift their money and credits to PSPF when qualified for registration with

PSPF.

The last identified challenge is that of pension schemes in Tanzania saving only

the working elite leaving the majority in the informal sector uncovered. There are

no strategies for substantial public campaign on understanding importance of

Social Security and formalization of informal sector so that could be easily taken in

the Scheme. These if taken inn are the majority and could flourish the Scheme.

Researcher identified that there is a need of NSSF to maintain future financial

sustainability of the schemes. In doing this it is mandatory to increase retirement

age, increase contribution amount, put inn aggressive means to register informal

sector and invest only on viable projects with high yield but of short terms to cover

short terms liquidities and priories given to members who are the primary focus.

CHAPTER FOUR Impact and Challenge of Withdrawal Benefit to NSSF

4747

4.0 Introduction;

This Chapter reveals the extent and consequences of withdrawal benefit to NSSF.

The benefit contradicts with the role of NSSF of offering members protection

during and after work as per NSSF Motto “NSSF BUILDS YOUR FUTURE”

4.1 Roles and Functions of NSSF;

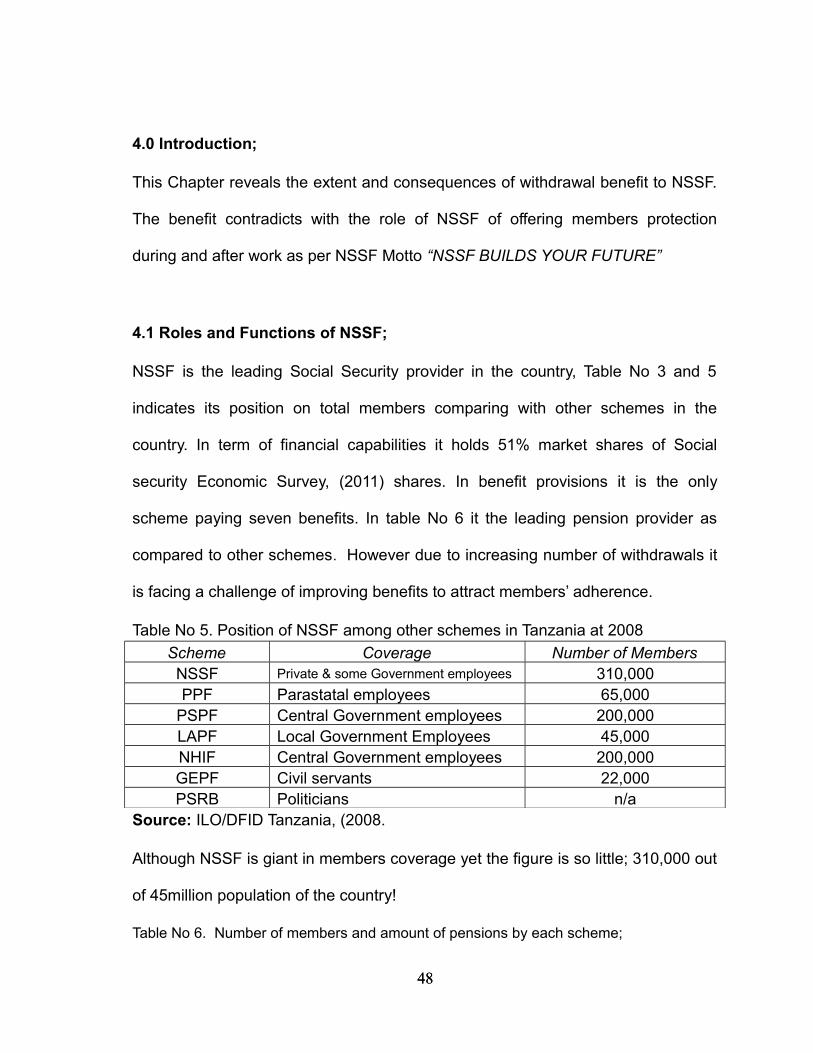

NSSF is the leading Social Security provider in the country, Table No 3 and 5

indicates its position on total members comparing with other schemes in the

country. In term of financial capabilities it holds 51% market shares of Social

security Economic Survey, (2011) shares. In benefit provisions it is the only

scheme paying seven benefits. In table No 6 it the leading pension provider as

compared to other schemes. However due to increasing number of withdrawals it

is facing a challenge of improving benefits to attract members’ adherence.

Table No 5. Position of NSSF among other schemes in Tanzania at 2008

Scheme Coverage Number of MembersNSSF Private & some Government employees 310,000PPF Parastatal employees 65,000

PSPF Central Government employees 200,000LAPF Local Government Employees 45,000NHIF Central Government employees 200,000GEPF Civil servants 22,000PSRB Politicians n/a

Source: ILO/DFID Tanzania, (2008.

Although NSSF is giant in members coverage yet the figure is so little; 310,000 out

of 45million population of the country!

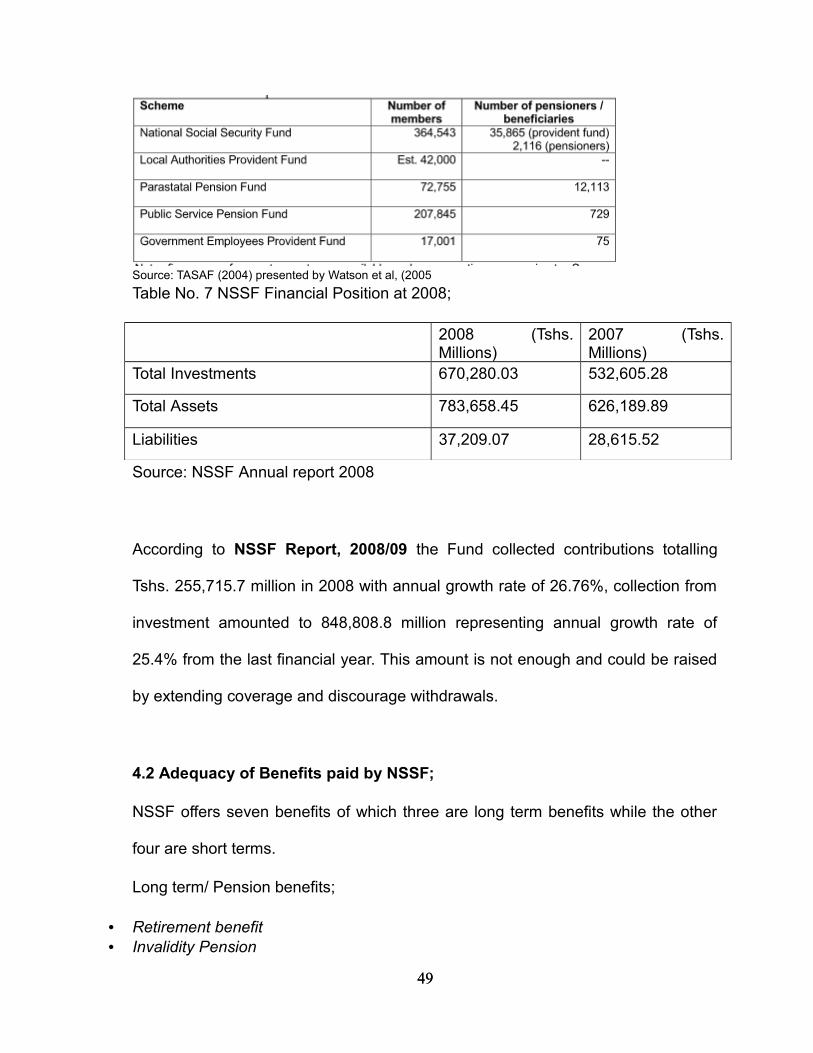

Table No 6. Number of members and amount of pensions by each scheme;

4848

Source: TASAF (2004) presented by Watson et al, (2005

Table No. 7 NSSF Financial Position at 2008;

2008 (Tshs.Millions)

2007 (Tshs.Millions)

Total Investments 670,280.03 532,605.28

Total Assets 783,658.45 626,189.89

Liabilities 37,209.07 28,615.52

Source: NSSF Annual report 2008

According to NSSF Report, 2008/09 the Fund collected contributions totalling

Tshs. 255,715.7 million in 2008 with annual growth rate of 26.76%, collection from

investment amounted to 848,808.8 million representing annual growth rate of

25.4% from the last financial year. This amount is not enough and could be raised

by extending coverage and discourage withdrawals.

4.2 Adequacy of Benefits paid by NSSF;

NSSF offers seven benefits of which three are long term benefits while the other

four are short terms.

Long term/ Pension benefits;

• Retirement benefit• Invalidity Pension

4949

• Survivors’ Pension

Short term benefits are;

• Funeral grants• Maternity benefit• Employment injury benefit• Health insurance benefit.

Although there are benefits adjustments reviewed periodically by the

Board of the National Social Security Fund, the Fund has only

managed to pay seven benefits leaving two more (un-employment and

family care) as stipulated in UDHR 1942 not yet implemented. The

seven benefits are tuned according to the current economic situation

and actuarial valuation of the fund. They also adjusted according to

changes in the legal minimum wage set by the government. The

current minimum pension of NSSF today, is 80% of the legal minimum

wage which is about (43US.$) to (230USD). Baruti(2010).

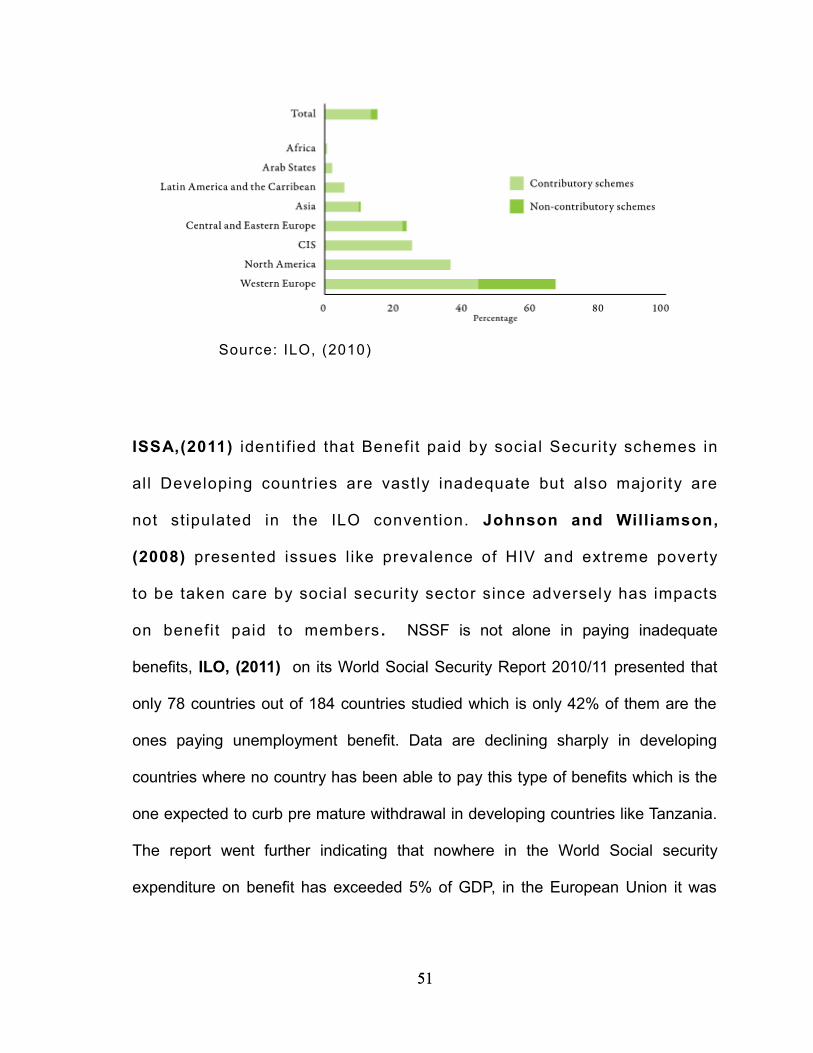

Unemployment benefit is almost not there in all African countries it is

only Maurit ius that managed to launch it in 2008.

Graph No. 3; World Un-employment benefits payments.

5050

Source: ILO, (2010)

ISSA,(2011) identif ied that Benefit paid by social Security schemes in

all Developing countries are vastly inadequate but also majority are

not stipulated in the ILO convention. Johnson and Williamson,

(2008) presented issues l ike prevalence of HIV and extreme poverty

to be taken care by social security sector since adversely has impacts

on benefit paid to members . NSSF is not alone in paying inadequate

benefits, ILO, (2011) on its World Social Security Report 2010/11 presented that

only 78 countries out of 184 countries studied which is only 42% of them are the

ones paying unemployment benefit. Data are declining sharply in developing

countries where no country has been able to pay this type of benefits which is the

one expected to curb pre mature withdrawal in developing countries like Tanzania.

The report went further indicating that nowhere in the World Social security

expenditure on benefit has exceeded 5% of GDP, in the European Union it was

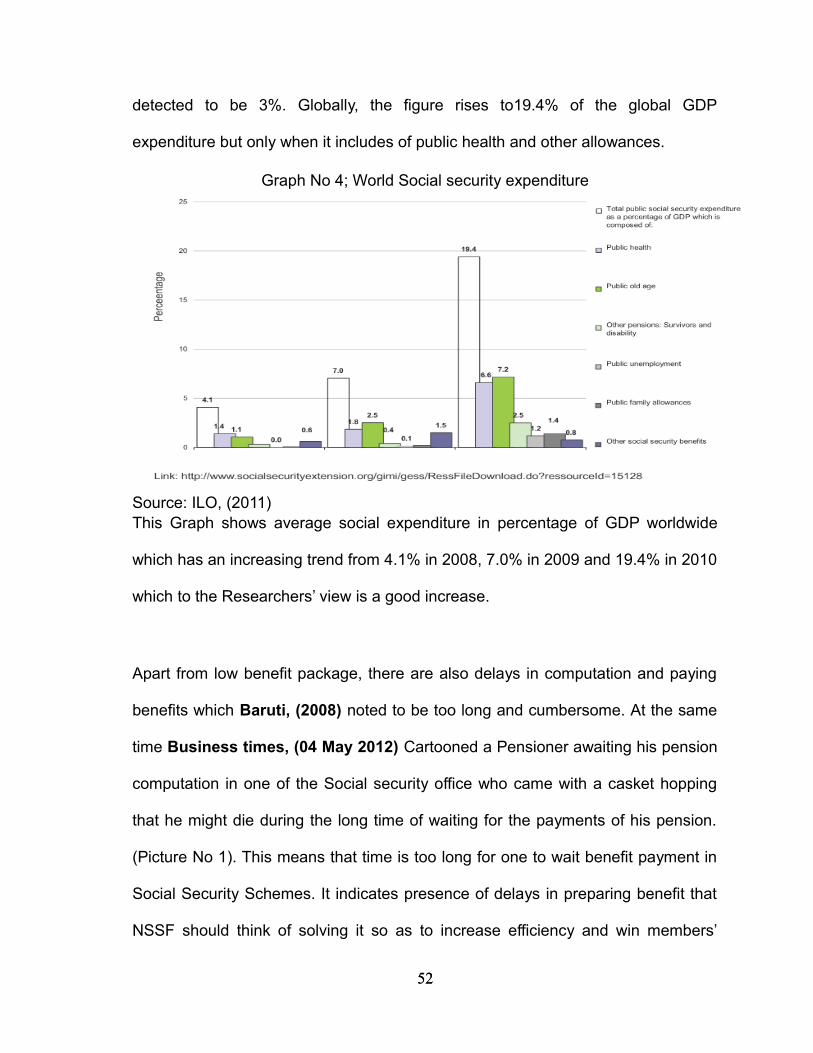

5151

detected to be 3%. Globally, the figure rises to19.4% of the global GDP

expenditure but only when it includes of public health and other allowances.

Graph No 4; World Social security expenditure

Source: ILO, (2011) This Graph shows average social expenditure in percentage of GDP worldwide

which has an increasing trend from 4.1% in 2008, 7.0% in 2009 and 19.4% in 2010

which to the Researchers’ view is a good increase.

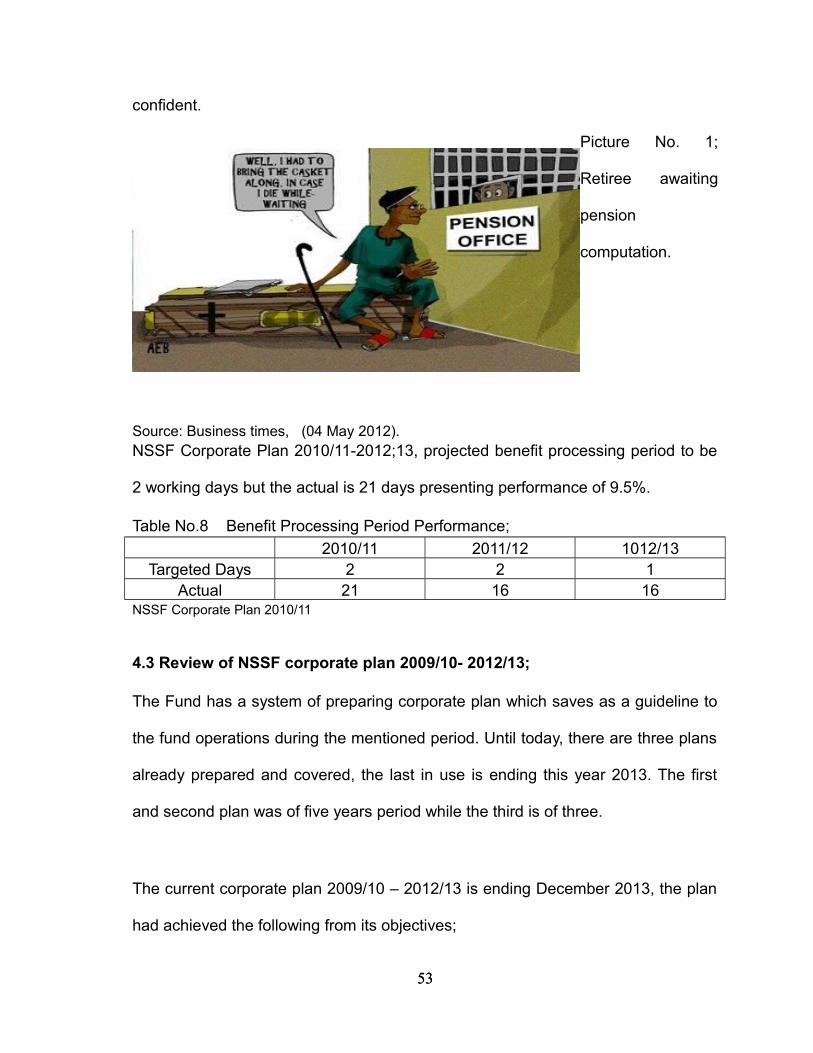

Apart from low benefit package, there are also delays in computation and paying

benefits which Baruti, (2008) noted to be too long and cumbersome. At the same

time Business times, (04 May 2012) Cartooned a Pensioner awaiting his pension

computation in one of the Social security office who came with a casket hopping

that he might die during the long time of waiting for the payments of his pension.

(Picture No 1). This means that time is too long for one to wait benefit payment in

Social Security Schemes. It indicates presence of delays in preparing benefit that

NSSF should think of solving it so as to increase efficiency and win members’

5252

confident.

Picture No. 1;

Retiree awaiting

pension

computation.

Source: Business times, (04 May 2012).NSSF Corporate Plan 2010/11-2012;13, projected benefit processing period to be

2 working days but the actual is 21 days presenting performance of 9.5%.

Table No.8 Benefit Processing Period Performance;

2010/11 2011/12 1012/13Targeted Days 2 2 1

Actual 21 16 16NSSF Corporate Plan 2010/11

4.3 Review of NSSF corporate plan 2009/10- 2012/13;

The Fund has a system of preparing corporate plan which saves as a guideline to

the fund operations during the mentioned period. Until today, there are three plans

already prepared and covered, the last in use is ending this year 2013. The first

and second plan was of five years period while the third is of three.

The current corporate plan 2009/10 – 2012/13 is ending December 2013, the plan

had achieved the following from its objectives;

5353

Table No. 12; Corporate plan 2009/10 – 2010/12 performance summary.

Category 2009/10 2010/11 2011/12 2012/13Membership size 506,218 521,629 543,685 666,641*

Contributioncollection

Tshs(000,000)300,089.54 348,504.64 404,415.787 594,055.25*

Total Investments.Tshs.(000,000)

1,029,206.18 1,216,624.641,452,085.5

72,085,426.44

*Total Benefit

payments Tshs.(000,000)

110,135.31 136,596.51 174,616.16 134,006.05*

Withdraw benefitpayments Tshs.

(000,000)89,814.59 106,221.07 136,309.60 107,690.01*

* projected. Source: NSSF Corporate plan 2009/10-2012/13 compiled by Researcher

The Fund had objective of increasing membership size to attain 15% from 6.8% of

the previous corporate plan 2004/5 – 2009/10. Table No.12 indicates increasing

trend of an average of 3.6% meaning that this objective had failed to be achieved.

The possible reason for this failure could be lack of aggressive means to attract

new members as well as high rate of withdrawals.

The Fund should employ a comprehensive strategy to register members from

informal sector, fisheries and agricultural sectors. ILFS, (2011) identified that

among the 1,362,559 people employed in the country by 2011 1,096,360

employed in the formal sector. This sector is not covered by any of social security

scheme available in the country. If there were comprehensive strategy and

attractive packages to social security schemes, this group could join one of the

5454

schemes voluntarily. There is as well 12,485,516 people employed in agriculture

sector ILFS, (2007) but none of these are registered with any of the schemes.

There are also government projects implemented already while others are on final

preparation to start. To mention a few, there is 3960 trunk road and 14 bridges in

Dar es Salaam under progress, there is 100kms Dar es salaam-Chalinze

expressway all of them to be completed by June 2017, none of the Schemes have

shown efforts to register casual labours in these projects.

The second objective was increasing contribution collection from 25.5% to 30%.

Result from table No.12 indicates an average increase trend of 26.3% which is

less than the projected 30%. The main reason for this failure is lack of identified

potential areas to tap new members. Operation department dealing with

registration of new members should be strengthen and equipped with modern

tools. There should be a means of indentifying new employers from registrar of

company and investment centre. The team should be knowledgeable with

customer care and able to convince customers on their products.

The third plan was increasing investment income from 19.9% growth rate from last

corporate plan to 30%. This grew from Tshs.1,029,206,180,000 in 2009/10 to

1,582,337,000,000 at 2012/13. Which is an averaged of 15.8% the target could not

be achieve. In reviewing this failure Researcher noted some shortfalls like non

performing government projects, CAG Report, (2012). There is also a problem of

economic recession during the 2009s that affected this area. The Fund should

5555

diversify its investment so that in time of economic difficulties like that of 2009s the

impact could be minimized.

The Fund could meet members’ expectation and set free complains and reasons

for increasing tendency of withdrawal had the entire corporate plan achieved at

least up to 75%. It is believed that increasing withdrawal is to some extent

engineered by members’ dissatisfactions on service and benefits offered. There

must be efforts of improving benefits issuance and quality service. Benefit

indexation should be done on a regular basis.

4.4. NSSF and the Challenge of withdrawal benefit;

NSSF corporate plan 2009 revealed number of withdrawals increasing by 150% in

2009 only. This benefit is not common within social security schemes in any of the

African country neither in Developed advocating as such, Dau, (2012) warned that

this practice is to escort members into poverty. Failure of government to expel this

benefit has a negative impact to members in a very near future when Social

Security Schemes will no longer be there to take care of members withdrawn

earlier who are now old and have no income security. But it also affect the Scheme

by failing to offer better services to present members following huge payments to