RESEARCH SYNOPSIS ON FINANCE BCOM Honours By Akash ...

395

RESEARCH SYNOPSIS ON FINANCE BCOM Honours By Akash Raghuvanshi to the DEPARTMENT OF COMMERCE BHOPAL SCHOOL OF SOCIAL SCIENCES May 2021 Submitted by Akash raghuvanshi Bcom (Hons) 3 rd year Guided by Dr Mrs Smitha Pillai Associate Professor Department of Commerce

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of RESEARCH SYNOPSIS ON FINANCE BCOM Honours By Akash ...

RESEARCH SYNOPSIS ON FINANCE

BCOM Honours

By

Akash Raghuvanshi

to the

DEPARTMENT OF COMMERCE

BHOPAL SCHOOL OF SOCIAL SCIENCES

May 2021

Submitted by

Akash raghuvanshi

Bcom (Hons) 3rd year Guided by

Dr Mrs Smitha Pillai

Associate Professor

Department of Commerce

CERTIFICATE

It is certified that the work contained in the project report titled Corporate

finance by Akash raghuvanshi has been carried out under my/our supervision and

that this work has not been submitted elsewhere for a degree*

Signature of Supervisor: …………….

Name : Dr MRS Smitha Pillai , Associate Professor

Department : Commerce

Bhopal School of Social Sciences

May, 2021

DECLARATION

I hereby declare that this project report entitled “- Corporate finance was carried

out by me for the degree of BCOM Honours under the guidance and supervision

of MRS Smitha Pillai of Department of Commerce, BSSS College. The

interpretations put forth are based on my reading and understanding of the

original texts and they are not published anywhere in any form. The other books,

articles and websites, which I have made use of are acknowledged at the

respective place in the text. This research report is not submitted for any other

degree or diploma in any other University.

Place: Bhopal

Name of the Student: Akash Raghuvanshi

Class & Section: BCOM (HONS) 3rd year

Date: 27/05/2021

ACKNOWLEDGEMENT

I would like to thank our Principal Dr. Fr. John P.J. and Vice Principal Dr Sr

Sonia Kurien for their immense support and blessings. I thank our HOD Dr Amit

Kumar Nag for his support. I would like to express my special thanks of gratitude

to my research guide Dr. MRS Smitha Pillai Associate Professor of Department

of Commerce for her valuable suggestions and guidance and for giving me the

golden opportunity to do this wonderful research project on the topic Consumer

behaviour towards electronic production online shopping Without her help it

would have been difficult for me to have reached this state of completion of my

project report. Also, I would like to thank my parents and friends who helped me

a lot in the preparation of this project.

I wish to acknowledge the help of all those who have provided me information,

guidance and other help during my research period.

Chapter 1 INTRODUCTION

Corporate finance is the area of finance that deals with sources of funding, the capital structure of corporations, the actions that managers take to increase the value of the firm to the shareholders, and the tools and analysis used to allocate financial resources. The primary goal of corporate finance is to maximize or increase shareholder value.

Correspondingly, corporate finance comprises two main sub-disciplines Capital budgeting corporate financier is concerned with the setting of criteria about which value-adding projects should receive investment funding, and whether to finance that investment with equity or debt capital. Working capital management is the management of the company's monetary funds that deal with the short-term operating balance of current assets and current liabilities; the focus here is on managing cash, inventories, and short-term borrowing and lending (such as the terms on credit extended to customers).

The terms corporate finance and are also associated with investment banking. The typical role of an investment bank is to evaluate the company's financial needs and raise the appropriate type of capital that best fits those needs. Thus, the terms "corporate finance" and "corporate financier" may be associated with transactions in which capital is raised in order to create, develop, grow or acquire businesses. Recent legal and regulatory developments in the U.S. will likely alter the makeup of the group of arrangers and financiers willing to arrange and provide financing for certain highly leveraged transactions.

Although it is in principle different from managerial finance which studies the financial management of all firms, rather than corporations alone, the main concepts in the study of corporate finance are applicable to the financial problems of all kinds of firms. Financial management overlaps with the financial function of the accounting profession. However, financial accounting is the reporting of historical financial information, while financial management is concerned with the deployment of capital resources to increase a firm's value to the shareholders.

Bajaj Finance Limited a subsidiary of Bajaj Finserv, is an Indian non-banking financial company (NBFC). The company deals in consumer finance, SME (small and medium-sized enterprises) and commercial lending, and wealth management. Headquartered in Pune, Maharashtra, the company has 294 consumer branches and 497 rural locations with over 33,000+ distribution points. The company reported a pre-tax profit of Rs.626 crores and a post-tax profit of Rs.408 crores

Muthoot Finance Ltd. is an Indian financial corporation and the largest gold loan NBFC in the country.[3] In addition to financing gold transactions, the company offers foreign exchange services, money transfers, wealth management services, travel and tourism services, and sells gold coins. The company's headquarters are located in Kerala, India, and it operates over 4,400 branches throughout the country. Outside India, Muthoot Finance is established in the UK, the US, and the United Arab Emirates.The company falls under the brand umbrella of the Muthoot Group. Its stocks are listed on the Bombay Stock Exchange (BSE) and NSE. As of March 2012, revenue (after expenditure) stood at more than ₹23,000 crore (US$4.2 billion).[4] The target market of Muthoot Finance includes small businesses, vendors, farmers, traders, SME business owners, and salaried individuals.

Mahindra & Mahindra Financial Services Limited (MMFSL) is a rural NBFC headquartered in Mumbai, India.[4] It is amongst the top tractor financers in India and offers a wide range of financial products to address varied customer requirements.[5] The NBFC has 1000+ offices spread over 1 in every 3 villages across India with a total of more than 4.7 million customers to date.Mahindra Finance started on 1 January 1991, as Maxi Motors Financial Services Limited.[6] They received the certificate of commencement of business on 19 February 1991. On 3 November 1992, Mahindra Finance changed their name to Mahindra & Mahindra Financial Services Limited.[7] Mahindra Finance is registered with the Reserve Bank of India as an asset finance, deposit taking NBFC

Chapter 2:

Review of Literature

International Review

Williamson(1998)

Williamson in his article, “Corporate Finance and Corporate Governance”,

analyzed the effects of tangible assets and probability of bankruptcy on the

relationship between capital structure, leverage, and asset liquidity. He predicted

that asset liquidity will increase optimal leverage, which means he concluded

positive relationship between asset liquidity and capital structure.

Shleifer and Vishny (1992)

Shleifer and Vishny (1992) in their article, “Liquidation Values and Debt

Capacity: A Market Equilibrium Approach”, discussed about asset liquidity and

optimal leverage. They argue that in costs of financial distresses, asset liquidity

plays an important role as a determinant. Their paper is focused on industry and

economy wide determinants of liquidity.

Rajan and Zingales (1995)

Rajan and Zingales (1995) analyzed Germany market to explain relationship

between capital structure and its components. Their result can be an explanation

of the empirical finding which firm size is negatively related to leverage in

Germany. This negative effect is for German capital markets which are less

developed and just large firms are traded in public.

Weiss and Wruck (1998)

Weiss and Wruck (1998) believe in their paper “Information problems, conflicts

of interest, and asset stripping” that relationship between asset liquidity and

leverage is negative. They say that distressed companies selling assets are

probably to face a less liquid or illiquid market because their industry companions

are also distressed. Thus companies can sell assets only at minimum price which

is “fire sale”. They find that this illiquidity will decrease a company’s leverage

level or debt capacity. As it is mentioned in Eastern’s case definition of asset

liquidity will be “what allows value-destroying asset stripping to occur”. Less

liquid assets would provide creditors with defense of

such operations. “Unless a credible promise can be made not to engage in asset

stripping, asset liquidity will reduce, not increase, a firm’s ability to issue debt

securities”. They say that if development of capital market is continuing and

provision of liquidity is increasing in a sort of asset markets, the asset stripping

problem will importantly increase.

National Reviews

Chatterjee Debabrata (2010) did a comparative study on Corporate Governance

and Corporate Social Responsibility – The case of Three Indian Companies ITC

Ltd., Reliance Industries Ltd., and Infosys Technologies Ltd. He concluded that

though the corporate governance practices are exemplary, there exist differences

in the way the companies adopt the corporate governance practices. He rated

Infosys better than the other two companies.

Mohamad Wan Adilah Wan Izyani , Sulong Zunaidab (2010) did a

comprehensive study on Corporate Governance Mechanisms and Extent of

Disclosure: Evidence from listed companies in Malaysia has revealed that

companies with a higher percentage of family members, on the board,

significantly have lower level of disclosure in annual report. It has been suggested

that regulators like Bussa Malaysia and Securities Commission should review and

impose a minimum level of family members on the board and Malaysian

regulators should implement the same guidelines.

Thrikawala Sujani, et. al (2011) in their research Corporate Governance –

erformance relationship in Microfinance Institutions suggested that it is important

to determine those corporate governance practices that have great impact on MFI

performance. It has also made an advanced contribution to the understanding of

corporate governance practices in MFI, identifying and developing an appropriate

governance structure. It has also provided guidance for selecting directors for

MFI Boards based on their academic and professional qualifications.

. Kajanathan Rajendran (2012) did a study in Sri Lanka titled Effect of corporate

Governance on Capital Structure. Investigation was made on the impact of

corporate governance on capital structure of Sri Lankan manufacturing firms. It

was concluded that corporate governance has important implications on the

financing decisions of Sri Lankan manufacturing firms.

Bihari Suresh Chandra (2012) conducted the study Corporate Governance is key

to Better Corporate Image: A study in the Banking Sector in India. It has been

concluded that there is a need for a strong culture of compliance at the top of the

organization and necessary to consider how management can respond to ethical

or reputation concerns. The biggest challenge in India is to implement the rules

of corporate governance at the ground level. It is required to extend the principles

of good corporate governance practices to co-operatives, Non-banking Private

Companies and other financial institutions.

Chapter 3 :

Research Methodology

Scope Corporate Finance:

Corporate finance is the area of finance dealing with the sources of funding and

the capital of corporations and the actions that managers take to increase

the value of the firm to the shareholders, as well as the tools and analysis used to

allocate financial resources. The primary goal of corporate finance is

to maximize or increase shareholder.

1. Corporate Finance broadly speaking business finance can be defined as the

activity concerned with the raising and administering of funds used in business.

2. Precedents: Corporate finance deals with precedents, practice and policies

based or experience, accident or anticipation,

3. Financial Problem: Corporate finance deals with the financial problems

of corporate. Also deal with distinction between capital and Income.

4. Capital required: It examine the extent form of Capital required by

Corporate.

5. Income: It scrutinizes the practice and policies of administering corporate

Income.

6. Dividend: It looks into propriety of Dividend, Depreciation and reserve

policies of the companies.

7. Financial Institution: It studies the importance of financial institutions

Insurance, stock exchanges, investment bankers etc

.

8. Role of State: It examine the role of state in regulating and controlling the

financial Practices and policies of Corporate.

9. Divorce ownership and Management: Management is provided with a

number of opportunities to manipulate the financial statements. Corporate finance

separate between ownership and management.

10. Protector of share holders: Corporate finance is likely to stand as a

protector of shareholders.

Objective of Corporate Finance:

A firm is a group of claimants of share holders, creditors, suppliers, customers

and employees. The shareholders appoint a Board of directors to see the

functioning and directing the company. The directors will act in the interest of

the claimant not act in their own interest. In corporate finance theory generally

agrees that the objective of a firm is to maximize the profit and wealth

maximization. Wealth maximization rules require managers to work towards a

sustainable increase in the price of the firm’s stock.

I Profit maximization: Profit is the excess of revenue over expenses. Profit

maximization requires manager to keep low expenses.

ii. Social welfare: Business persons are supposed to be socially responsible.

Iii Corporate Growth:

Chapter 4 :

Data representation & Analysis

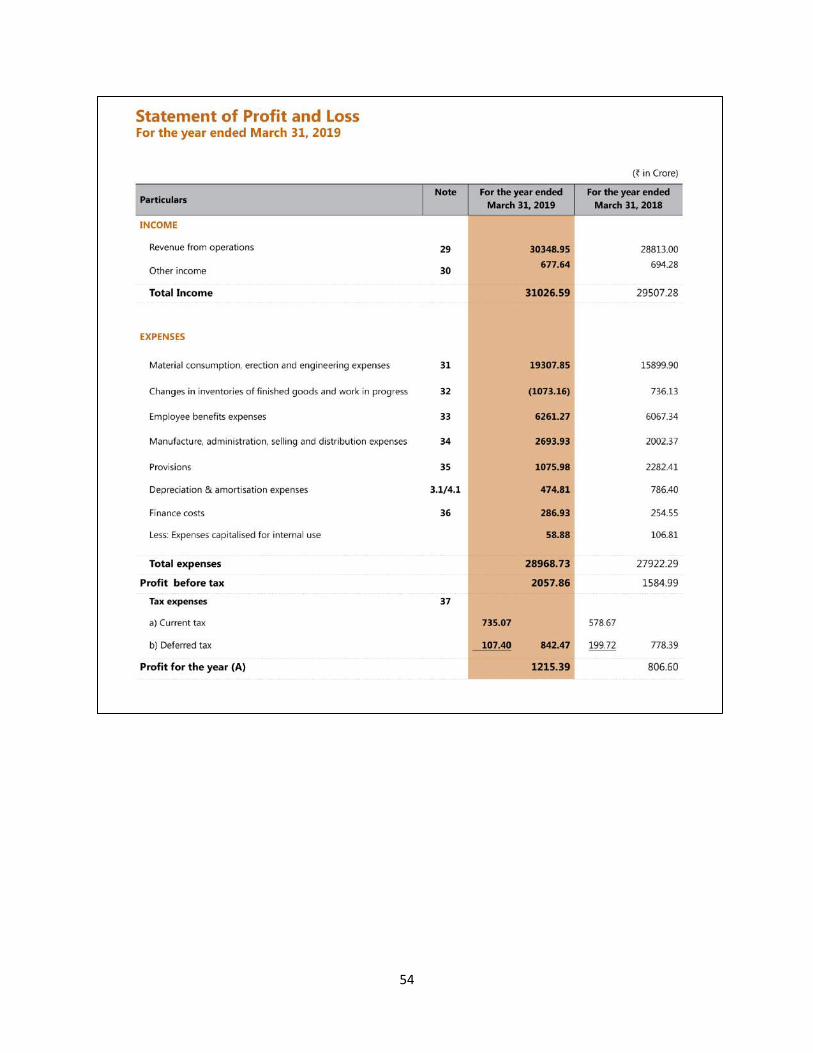

PROFITABILITY RATIOS

1. Net Profit Ratio-This ratio establishes the relationship in terms of percentage between net profit and net sales.

Net profit ratio= Net profit / Net sales *100

Table – 1

Bajaj Finance Limited

Muthoot Finance Ltd Years

Net Profit Net sales

Ratio

Net Profit Net sales

Ratio

2016 1,964.57 7304.31 26.89 1,316.75 4,800.67 24.42 2017 2,817.52 9963.02 28.27 1,920.98 5,639.55 34.062018

4,056.36

13287.7730.52 2,844.69 6,161.83 46.1

2019 6,035.30 17386.02 34.7 3,076.82 6,878.21 44.7 2020 6,808.13 23822.53 28.57

4,057.418,714.64 46.55

AVERAGE 29.79 AVERAGE 39.27

Operation profit Ratio – The difference between net profit ratio and net operating profit ratio is that net operating profit is calculated without considering

non-operating expenses and non-operating incomes. If we deduct this ratio from 100, the result will be operating ratio. Higher operating profit ratio enables the organization to recoup non-operating expenses out of operating profits and provide reasonable return.

Operating Profit Ratio = Operating Profit / Net Sales *100

Table - 2

Bajaj Finance Limited Muthoot Finance LtdYearsOperating

Profit Net sales

RatioOperating

ProfitNet sales

Ratio

2016 242.32 7304.31 3.31 4,861.40 4,800.67 101.22017 153.90 9963.02 1.54 5,728.63 5,639.55 101.572018

241.9013287.77

1.813 6,266.526,161.83 101.6

2019 423.05 17386.02 2.433 6,878.21 6,878.21 1002020

779.8623822.53 3.27

8,714.648,714.64 100

AVERAGE 2.47 AVERAGE 100.87

1.2.3. Earnings per share (EPS) - Earnings per share (EPS) is calculated as a

company's profit divided by the outstanding shares of its common stock. The resulting number serves as an indicator of a company's profitability. It is common for a company to report EPS that is adjusted for extraordinary items and potential share dilution. The higher a company's EPS, the more profitable it is considered to be.

Table - 4

Bajaj Finance Limited

Muthoot Finance LtdYears

Net Profit

No. of Equity share

Ratio

Net Profit

No. of Equity share

Ratio

2016 -5395.54 462.09 -23.89 9726.29 1163.17 16.732017 1383.14 462.09 6.00 9801.09 1165.11 16.832018 -2431.81 530.36 -9.17 6777.42 1285.81 10.542019 433.52 530.36 1.64 3363.30 1289.46 5.222020 546.19 925.37 1.18 7930.81 1294.76 12.25

AVERAGE -4.84 AVERAGE 12.31

IMPACT OF COVID-19 ON EDUCATION

Research Project Submitted in Partial Fulfilment of the Requirements for

Degree of

BCOM Honours

by

AKRAM KHAN

to the

DEPARTMENT OF COMMERCE

BHOPAL SCHOOL OF SOCIAL SCIENCES

APRIL,2021

Submitted by Guided by

AKRAM KHAN Dr. Smitha Pillai

Associate Professor

Department of Commerce

CERTIFICATE

It is certified that the work contained in the project report titled “Impact of Covid-

19 on Education”, by “Akram Khan”, has been carried out under my supervision

and that this work has not been submitted elsewhere for a degree.

Signature of the supervisor: ……………

Name : Dr. Smitha Pillai, Associate Professor

Department : Commerce

Bhopal School of Social Sciences

April, 2021

DECLARATION

I hereby declare that this project report entitled “Impact of Covid-19 on

Education” was carried out by me for the degree of BCOM Honours under the

guidance and supervision of Dr. Smitha Pillai, Associate Professor of Department

of Commerce, BSSS College. The interpretations put forth are based on my

reading and understanding of the original texts and they are not published

anywhere in any form. The other books, articles and websites, which I have made

use of are acknowledged at the respective place in the text. This research report

is not submitted for any other degree or diploma in any other University.

Place: Bhopal

Name of the Student: Akram Khan

Class & Section: BCOM HONOURS 3A

Date: 15th April, 2021

ACKNOWLEDGEMENT

I would like to thank our Principal Dr.Fr.John P.J. and Vice Principal Dr. Sr.

Sonia Kurien for their immense support and blessings. I thank our HOD Dr. Amit

Kumar Nag for his support. I would like to express my special thanks of gratitude

to my research guide Dr.Smitha Pillai, Associate Professor of Department of

Commerce for her valuable suggestions and guidance and for giving me this

opportunity to do this wonderful research project on the topic: Impact of Covid-

19 on Education, Without her help it would have been difficult for me to have

reached this state of completion of my project report. Also, I would like to thank

my parents and friends who helped me a lot in the preparation of this project.

I wish to acknowledge the help of all those who have provided me information, guidance and other help during my research period.

Chapter 1: Introduction of the Topic

1.1 Rationale of the study

1.2 Introduction to the Industry

1.3 Introduction to the Company

1.4 Justification of the Topic

Chapter 2: Review of Literature

2.1 International Review

2.2 National Review

Chapter 3: Research Methodology

3.1 Objective of the study

3.2 Scope of Study

3.3 Data Collection

3.4 Limitation of the study

Chapter 4: Data representation & Analysis

4.1 Data representation & Interpretation

Chapter 5: Results & Discussion

5.1 Major Findings

5.2 Discussion & Suggestions

5.3 Conclusion

REFRENCES

ANNEXURE

CHAPTER – 1

INTRODUCTION TO THE TOPIC

1.1 Rationale of the Study

What impact did covid-19 have on education? The impact of pandemic COVID-19 is observed in every

sector around the world. The education sectors of India as well as world are badly affected by this. It

has enforced the world wide lock down creating very bad effect on the students' life. Around 32 crore

learners stopped to move schools/colleges, all educational activities halted in India. The outbreak of

COVID-19 has advised us that change is inevitable. It has worked as a catalyst for the educational

institutions to grow and opt for platforms and techniques, which have not been used before. The

education sector has been fighting to survive the crises with a different approach and digitising the

challenges to wash away the threat of the pandemic. This paper highlights some measures taken by

Govt. of India to provide seamless education in the country. Both the positive and negative impacts of

COVID-19 are discussed and some fruitful suggestions are pointed to carry out educational activities

during the pandemic situation.

1.2 Introduction to the Topic

The pandemic Covid-19 has spread over whole world and compelled the human society to maintain

social distancing. It has significantly disrupted the education sector which is a critical determinant of a

country’s economic future. February 11, 2020, the World Health Organisation (WHO) proposed an

official name of the virus as COVID acronym for Coronavirus disease 2019. It was first identified in

Wuhan, China on December 31, 2019. First death by COVID 19 was the 61-year old man in Wuhan,

China on January 11, 2020. WHO declared COVID-19 as a pandemic on March 11, 2020. The first case

of the COVID-19 pandemic reported on 30 January 2020 in the state of Kerala and the affected had a

travel history from Wuhan, China (Wikipedia). The first death due to COVID-19 was reported in India

on March 12, 2020. It has affected more than 4.5 million peoples worldwide (WHO). According to the

UNESCO report, it had affected more than 90% of total world’s student population during mid-April

2020 which is now reduced to nearly 67% during June 2020. Outbreak of COVID-19 has impacted

more than 120 crores of students and youths across the planet. In India, more than 32 crores of students

have been affected by the various restrictions and the nationwide lockdown for COVID-19. As per the

UNESCO report, about 14 crores of primary and 13 crores of secondary students are affected which are

two mostly affected levels in India.

After observing the corona virus pandemic situation, the WHO advised to maintain social distancing as

the first prevention step. So, every country started the action of lockdown to separate the contaminated

people. The education sectors including schools, colleges and universities became closed. Classes

suspended and all examinations of schools, colleges and universities including entrance tests were

postponed indefinitely. Thus, the lockdown destroyed the schedules of every student. Though it is an

exceptional situation in the history of education, COVID-19 has created many opportunities to come

out of the rigorous classroom teaching model to a new era of digital model.

The lockdown has compelled many educational institutions to cancel their classes, examinations,

internships etc. and to choose the online modes. Initially, the educators and the students were quite

confused and didn’t understand how to cope up with the situation of this sudden crisis that compelled

closure of the educational activities. But latter on all realized that the lockdown has taught so many

lessons to manage with the emergence of such pandemics. Thus, COVID-19 has created many

challenges and opportunities for the educational institutes to strengthen their infrastructure. The

lockdown has given them a ray of hope for teachers and students to continue their educational activities

through online. The teachers assigned work to students via internet, delivered lectures video

conferencing using different Apps like Zoom, Google meet, Facebook, YouTube, and Skype etc. There

are WhatsApp groups of guardians, teachers, students and parents for affective communication through

which they are always in touch to share their difficulties through this e-medium. In a nation like China

that practices a considerably more centralization system, a change to digital learning may be simpler.

Even in a nation like the U.S.A, there are some low pay students who don’t approach broad bands and

unable to use computerized learning arrangement (Study Abroad Life). The same is the situation that

happens with India where not every student is well equipped with the high-speed internet and digital

gadgets and are along these lines of suffer. Numerous advanced educational institutions in India are not

also equipped with digital facilities right now to cope up with sudden change from traditional education

set up to the online education system. (Covid-19 Educational Disruption and Response, 2020)

(UNESCO, 2020)

1.3 Justification of the Topic

The present research report is focusing on quantifying the impact of Covid-19 on Education, which

helps to understand is online teaching mode effective in providing knowledge to students or not in the

pandemic. The primary data on the field is collected through questionnaire and responses are analyses

on percentage basis.

CHAPTER-2

REVIEW OF LITERATURE

2.1 International Reviews

2.1.1 Online Distance Learning versus Face-to-Face Comparative Studies

A large number of studies, before pandemic, compared face-to-face with online distance courses in

terms of university student performance, as well as many other academic and demographic variables of

students. For example, Soesmanto and Bonner evaluated a dual mode design in which students of year

one of a business school at the Griffith University in Australia have the option to undertake the same

statistics course in a face-to-face mode and/or an online mode. The comparative analysis suggested no

significant differences in learning satisfaction and academic performance of the two cohorts within the

dual mode system. In a similar study done in California State University, Tan suggested that, with

proper training and support of technology, university instructors are delivering both the on-ground and

online sections of a business technology course with the same effectiveness as measured by students’

grade points.

For a different type of courses, Lorenzo-Alvarez et al. found that a radiology course taught online at a

university in Australia resulted in similar academic outcomes to F2F learning. In their online vs. face-

to-face comparative study, Cavanaugh and Jacquemin compared grade-based learning outcomes

between online and face-to-face course taught at Ohio University, using a large dataset of 5,000 courses

taught by over 100 faculty members over a period of ten academic terms at a large, public, four-year

university. Given the large scale of the study, the results suggest no difference in grade-based student

performance between instructional modes for courses where both modes are applicable. According to

the regression analysis of the study, the primary influence on individual course grades was student GPA.

Students with higher GPAs performed better in online courses, and students with lower GPAs

performed worse when taking courses in an online format compared to a face-to-face format.

Nyer investigated effective ways of quickly offering an online lecture in a course that is otherwise

taught using traditional face-to-face lectures at Chapman University in California. The study compared

student learning outcomes (using test scores) across three modes of delivering lectures: using a

traditional face-to-face lecture, using online instruction where the lecture was delivered using a video

recording of the classroom lecture, and using online instruction where the lecture was delivered using

a static document created from an edited transcript of the classroom lecture embedded with charts,

graphs, etc. The results showed that quickly created online instruction methods scored lower in

engagement compared to the traditional face-to-face lecture. Students who were exposed to the online

lecture delivered using a static document and students attending the face-to-face lecture both reported

having higher quality of notes compared to students exposed to the video recording. Finally, the effect

of the different instructional material on student test scores was found to be mediated by student

engagement and perceived note quality.

2.1.2 Online Distance Learning and the COVID-19 Lockdown

The research of Bozkurt et al. is one of the early studies reporting the impact of the interruption

of education due to COVID-19 pandemic in 31 countries. In addition to the assessment of each

case by country, the study highlighted major themes that have commonly arisen in these

countries from the interruption of education during COVID-19, such as the inequity and the

digital divide which have been aggravated during the pandemic, the need for alternative

assessment and evaluation methods and the needed switch to formative assessments through

both synchronous and asynchronous means, and the use of online proctoring services as a way

to control for cheating and academic dishonesty.

The research by Hjelsvold et al. is also one of the first studies which investigated educators’

feedback on the distance learning during the COVID-19 lockdown, as a result of a survey

conducted on 303 university students and 56 educators in Norway. The study reported that

short time and lack of ready resources were important barriers to sudden shift to distant

learning. Even though learners and educators report a lack of practice in online education, the

study declared that they both adapted fast, showing a positive attitude towards the change.

According to the results of the survey, key factors affect the online experience during the first

weeks of distance learning, and these are as follows: from learners’ side: feedback to

instructors, engagement in discussion forums, use of online tutorials, and participation in group

work; from educators’ side: timely communication and clear instructions about formative and

summative assessments, exams, quizzes and assignments, informing learners of how to get

help, providing support using synchronous and asynchronous tools, ensuring virtual place for

students-to-students and students-to-instructor online interaction, and giving advice to students

to set their study place and schedule for an effective study-at-home experience; from leaders

and administrators’ side: timely communication with students especially with exam regulations

and petitions, supporting learners in preparing new pedagogical approaches to teaching as well

as learning new tools, and providing a more collective approach to the coordination of activities

and collaboration between educators.

2.1.3 Distant Learning and Higher Education Plans in Egypt after COVID-19

Egypt has the largest education system in the Middle East and North Africa region with 52,000

schools, accommodating 20 million school students, and 44 universities with 830 higher

education institutions, accommodating 3 million higher education students. In March 2020, the

Egyptian government made a set of immediate precautionary decisions to confront the dangers

of the emerging Corona virus, the most important of which was the closure of all schools,

universities, and higher education institutions. The Egyptian Ministry of Higher Education and

Scientific Research, to ensure the continuation of the educational process, urged higher

education institutions to apply distance education as a modality during the lockdown.

In May 2020, four nation-wide surveys were administered to assess the Egyptian experience of distance

education in Egyptian universities and higher institutes, to measure the satisfaction of educational

leaders, professors, administrators, and students, and to set an integrated vision of the future of distance

learning in higher education in Egypt. The data collection was based on the crowdsourcing approach,

whereby surveys were placed on various portals. A total of 106,897 participants filled the survey: 1,041

educational leaders, 11,100 faculty members, 1,258 administrative staff, 89,867 Egyptian students, and

3,631 international students.

The results of the four surveys included the following: the majority of educational leaders endorsed

online distant learning in higher education; Internet connectivity and weak IT skills are the most

prominent difficulties of distance education in Egypt; and recorded lectures are the most plausible ways

to deliver educational materials [16]. Based on the recommendations of these nation-wide surveys, the

government of Egypt decided to integrate face-to-face with online distant learning in all future higher

education plans. This plan for merging on-campus and online distant learning will not only put the

Egyptian universities in a state of movement for any urgent conditions such as COVID-19, but most

importantly achieve vital educational objectives, such as reducing student density, making the best use

of the expertise of professors and technological infrastructure of universities, and making a gradual

transformation of students to lifelong learners.

This study investigates the overall learning experience after the sudden shift from face-to-face to online

distance learning due to COVID-19 lockdown at one of the universities in Egypt. Since Egypt decided

to integrate online distant learning into all future higher education plans, the main aim of this study is

to provide recommendations for future application of this mode of learning in the Egyptian higher

education institutions. The main research question of the current study is to determine if there was a

statistically significant difference in terms of academic performance between face-to-face learners of

an undergraduate course taught on-campus in Spring 2019 and learners who completed the same course

but fully online via long distance learning during the COVID-19 lockdown in spring 2020 semester.

The study also assesses professors’ feedback and students’ satisfaction concerning the online distance

learning experience during the lockdown.

2.2 National Reviews

2.2.1 Cancellation of Exams

In India, all academic activities were suspended after the announcement of the University Grants

Commission (UGC) on 19 March to postpone examinations in all universities until the end of March.

All the central universities like the University of Hyderabad announced to defer all academic activities

and close their hostels, and even private universities the SRM Institute of Science and Technology and

VIT, Vellore declared the summer vacation for students (Crawford et al., 2020).

2.2.2 Change in online teaching for upliftment

An Indian national newspaper, The Hindu (April 14, 2020 ) reports that during the most significant

months of February to April, which includes activities around the curriculum and assessments, around

60 million students around the world are restricted to home. Both students and teachers are under the

pressure of not losing the academic time and are trying to re-design the teaching-learning techniques

by changing it to an online mode, which is the only possible alternative at the moment (The Hindu,

April 14, 2020). However, the bigger question is why the online mode of teaching-learning has not been

adopted (by replacing the face-to-face mode of teaching-learning) before the pandemic when other

activities or industries have changed from offline mode to online? The Hindu (April 14, 2020) states

that online learning is an amalgamation of various pedagogical models instead of anyone single model

as it is a specialized learning science that includes delivery of content, behavioural analytics, learning

psychology and assessments. This enables to measure the learning progress of individuals and therefore,

having a ‘hand-stitched’ mechanism of delivery is the need of the hour. Through interactions and

discussion in the face-to-face classes, the teachers get an idea of the prior knowledge and the collective

ability of the students based on which they can customize the teaching-learning techniques and lesson

plans. However, this becomes difficult in the digital platform. The focus is not on delivering the content

but ensuring effective opportunities for learning. The shift is, thus, from a teacher-centric approach to

a learner-centric one. The aim is always to impact learners in such a manner that they are able to

understand concepts better, think effectively and apply them practically. Thus, it becomes extremely

essential for facilitators to further orient themselves to become efficient disseminators of knowledge on

digital platforms.

2.2.3 Difficulties to opt for online Teaching

According to the Key Indicators of Household Social Consumption on Education in India report, based

on the 2017-18 National Sample Survey, less than 15% of rural Indian households have Internet (as

opposed to 42% urban Indian households). A mere 13% of people surveyed (aged above five) in rural

areas — just 8.5% of females — could use the Internet. The poorest households cannot afford a

smartphone or a computer The Indian Express (June 8, 2020).

The digital divide has not only led to the exclusion of students from poor and m arginalized backgrounds

from digital learning but also pushed many underprivileged students towards depression and death. For

instance, In the Indian state of Kerala, a 14-girl committed suicide as she was unable to join online

classes The Hindu (June 11, 2020). A 16-year-old boy (class 10 student), from a very poor family, took

his life because he did not have a smartphone to attend online classes and examinations organized by

his school in the Chirang district of Assam in India (The Hindustan Times, June 24, 2020).

CHAPTER – 3

RESEARCH METHODOLOGY

3.1 Objectives of the Study

1. To find impact pandemic on education sector.

2. Finding strategies to counter impact of pandemic in this sector

3.2 Scope of the Study

3.2.1 The purview of the study is to analyse the impact of pandemic on education sector.

3.2.2 For analysis primary data is collected through the means of questionnaire and analysed and

based on that results are been stated.

3.2.3 The standard population size of people of age group between 19-35 years is taken.

3.2.4 The duration of the study is of 2 months.

Topics discussed under this study are:

• Enlightenment of various measures taken by Govt. of India for education sector during

this Pandemic.

• Highlights of various measures taken by Govt. of India for education sector during this

Pandemic.

• Enlisting of some negative impacts of COVID-19 and some effective suggestions for

continuing education during the pandemic situation.

3.3 Data Collection

For conducting this research, primary data was collected through the means of questionnaire.

Data collection done through this has been analysed and method use to interpret the data is percentage

method of data collection.

The data collected here is from different working age groups in the education sector to understand its

impact better.

3.4 Limitation of the Study

1) The main limitation for this study was due to pandemic that struck all over the world. Due to the

social distancing norms and prevention methods, the data which could have been collected in person

more accurately was all collected online.

2) Data collected under the “maybe” or “other” section in the questionnaire was interpreted in a manner

which helped the study and could be interpreted differently.

3) The sample size is only confined to 36 people of Bhopal.

CHAPTER – 4

DATA INTERPRETATION AND ANALYSIS

4.1 Data Representation and Interpretation

The data collection was done through a structured questionnaire. The designed questionnaire had two

parts.

• The first part focused on the data related to demographic characteristics of the respondents: this

covered gender, age, education.

• The second part of the questionnaire measures the model variables.

4.1.1 A total of 36 respondents were collected in this study and the gender classification was as under:

• From the above pie-chart it is clearly visible that males are more than females i.e. 55.6% in the total respondents.

4.1.2 The Age and Qualification of the respondents us shown under via pie charts:

• It is clear from the information given in this pie chart that the most popular age range taking this survey was “Under 20” years old comprising of 52.8% of the total respondents, the other ranges did take the survey however “Under 20” was by far the most popular category, this shows the age range in which the Impact of pandemic on Education in this survey applies to.

• The maximum no. of qualification of people lie in the “Under-Graduate” section , 47.2% while “High School”, “Post-Graduate” and “Other” qualification of people are close to each other in group.

4.1.3 Following are the model variable collected in this survey for the study:

• Most of the people in the survey conducted were familiar with the concept of online classes i.e. 75% while the rest 25% were all new to this online teaching system.

• Most of the people had facilities like mobile phone or laptop for joining online classes i.e. 86.1% while the other 13.9% troubled getting any means to have facilities to attend online classes.

• It is to pay emphasis that the 47.2% of the people say that workload has been significantly been smaller or reduced during the pandemic because of online classes and online submission of assignments which is much easier for the students to submit, while people also state that the workload has been same i.e. 33.3% of the group while the rest 19.4% face to be greater due to inaccessibility of online submission materials.

• Here 55.6% people have Completely different experience as they have never been into online mode of teaching

• 19.4% people find online teaching to be similar with offline as they have been thorough with the concept of it.

• While 25% people found it to have a slightly different experience.

• There is no clear justification of are people happy or satisfied with current online classes as freedom and personal teaching in onsite lectures or comfort and efficient time utilisation may be the factor.

• From the given information in this pie chart it is not really obvious what people prefer as to going back to onsite classes, however it can be seen that most people are in the dilemma as to what to choose.

CHAPTER – 5

RESULTS AND DISCUSSION

5.1 Major Findings

Basic statistical methods are applied for data analysis, like frequency and percentages of replies in

favour and against online education to understand how Covid -19 has affected education. After

evaluating, organizing, tabulation and interpreting data, the conclusions are carried away. Roughly,

55.6% people have completely different experience in online classes as they have never been into online

mode of teaching, according to 25% it was similar to offline mode and 19.4% told that they had a

slightly different experience. While roughly 41.7% of the total respondents are not sure whether they

are happy or not of the current concept of online classes, the other 33.3% feel it much better than offline

classes and the rest 25% are not happy with this concept. By this it can be drawn out that, most

respondents face completely different experience and they are not even sure of going back to offline

mode as both way of teaching i.e. online and offline has their own pros and cons.

5.2 Discussions and Suggestions

• India should develop creative strategies to ensure that all children must have sustainable access

to learning during pandemic Covid-19. The Indian policies must include various individuals

from diverse backgrounds including remote regions, marginalised and minority groups for

effective delivery.

• Immediate measures are required to lessen the effects of the pandemic on job offers, internship

programs, and research projects.

• Many online learning platforms offer multiple programmes on the same subjects with different

levels of certifications, methodology and assessment parameters. So, the quality of programmes

may differ across different online learning platforms. Therefore, establishment of quality

assurance mechanisms and quality benchmark for online learning programmes must be

developed and offered by Higher Education Institutions (HEIs) in India keeping in view of

rapid growth of the online learning platforms.

• Across the globe, Indian traditional knowledge is well known for its scientific innovations,

values and benefits to develop sustainable technologies and medicines and this knowledge

systems in different fields should be integrated with a present-day mainstream higher education

system.

• Govt and educational institutes should plan to continue the educational activities maintaining

social distancing. 30-40% students and teachers may attend schools/colleges in two shifts per

day to carry on educational activities by obeying guidelines for Covid-19.

• At current times, access to technology and internet is an urgent requirement. So, the digital

capabilities and the required infrastructure must reach to the remotest and poorest communities

to facilitate the students to continue their education during the pandemics. There is a need to

deploy public funds to fix the internet gap and ensure that students continue to learn digitally.

The state governments/private organisations should come up with ideas to address this issue of

digital education.

• Some significant issues associated with distance learning strategies like the availability and

access to digital devices with internet connectivity, the need for safe learning spaces, creating

capabilities for teachers, families and students to operate and navigate digital devices, and

engaging lesson plans for disabled students and other marginalised groups should be addressed

by Govt. and the stakeholders.

5.3 Conclusion

COVID-19 has impacted immensely to the education sector of India. Though it has created many

challenges, various opportunities are also evolved. The Indian Govt. and different stakeholders of

education have explored the possibility of Open and Distance learning (ODL) by adopting different

digital technologies to cope up with the present crisis of COVID-19. India is not fully equipped to make

education reach all corners of the nation via digital platforms. The students who aren’t privileged like

the others will suffer due to the present choice of digital platforms. But universities and the government

of India are relentlessly trying to come up with a solution to resolve this problem. The priority should

be to utilise digital technology to create an advantageous position for millions of young students in

India. It is need of the hour for the educational institutions to strengthen their knowledge and

Information Technology infrastructure to be ready for facing COVID-19 like situations. Even if the

COVID-19 crisis stretches longer, there is an urgent need to take efforts on maximum utilisation of

online platforms so that students not only complete their degree in this academic year but also to get

ready for the future digital oriented environment. The concept of “work from home” has greater

relevance in such pandemic situation to reduce spread of COVID-19. India should develop creative

strategies to ensure that all children must have sustainable access to learning during pandemic COVID-

19. The Indian policies must include various individuals from diverse backgrounds including remote

regions, marginalised and minority groups for effective delivery of education. As online practice is

benefitting the students immensely, it should be continued after the lockdown. Further detailed

statistical study may be undertaken to explore the impact of COVID-19 on education system of India.

BIBLIOGRAPHY

(April 14, 2020 ). The Hindu.

Covid-19 Educational Disruption and Response. (2020). Wikipedia.

(June 11, 2020). The Hindu.

(June 8, 2020). The Indian Express.

The Hindustan Times. (June 24, 2020).

UNESCO. (2020). Covid-19 Educational Disruption and Response.

ANNEXURE1. Copy of blank Questionnaire:

Personal Details –

• Name:

• Mobile Number:

• Address: ________________________________________________________________

• Occupation:

• Age:

Please select an appropriate option for the asked question

1) Were you familiar with the concept of online Classes?

• Yes

• No

2) Did you had the proper facilities to join the online classes?

• Yes

• No

3) On average, compared to the workload before on-site classes were cancelled, would you say that your study workload over the last year has been?

• Smaller.

• The same.

• Larger

4) How was the teaching/learning experience compared to before?

• Completely Different

• Similar

• Slightly Different

5) Are you happy with the current Concept of Online Classes?

• Yes

• No

• Maybe

6) Are you willing to take proper precautionary methods and try to go back to onsite Classes?

• Yes

• No

• Maybe

7) According to you, how did Covid 19 affected your Studies?

________________________________________________________________

Future of Electric Vehicles in Indian Markets

Research Project Submitted in Partial Fulfillment

Of

the Degree of BCOM Honors

By Akshat Shrivastava to the

DEPARTMENT OF COMMERCE

BHOPAL SCHOOL OF SOCIAL SCIENCES

April 2021

Guided by:-

Dr Smitha Pillai

Associate Professor

Department of Commerce

DECLARATION

I hereby declare that this project report entitled “Future of Electric Vehicles in Indian Markets“ was carried out by me for the degree of BCOM (Honors) under the guidance and supervision of Dr Smitha Pillai of Department of Commerce, BSSS College. The interpretations put forth are based on my reading and understanding of the original texts and they are not published anywhere in any form. The other books, articles and websites, which I have made use of are acknowledged at the respective place in the text. This research report is not submitted for any other degree or diploma in any other University.

Place: Bhopal

Name of the Student: Akshat Shrivastava

Class & Section: BCOM {Honors} – 3 'A'

Date: April 2021

CERTIFICATE

It is certified that the work contained in the project report titled “Future of Electric Vehicles in Indian Markets” by “Akshat Shrivastava” has been carried out under my/our supervision and that this work has not been submitted elsewhere for a degree.

Signature of Supervisor: …………….

Name : Dr Smitha Pillai, Associate Professor

Department : Commerce

Bhopal School of Social Sciences

April, 2021

ACKNOWLEDGEMENT

I would like to thank our Principal Dr. Fr. John P.J. and Vice Principal Dr Sr Sonia Kurien for their immense support and blessings. I thank our HOD Dr Amit Kumar Nag for his support. I would like to express my special thanks of gratitude to my research guide Dr. Smitha Pillai, Associate Professor of Department of Commerce for her valuable suggestions and guidance and for giving me the golden opportunity to do this wonderful research project on the topic: Future of Electric Vehicles in Indian Markets, without her help it would have been difficult for me to have reached this state of completion of my project report. Also, I would like to thank my parents and friends who helped me a lot in the preparation of this project.

Contents

• Declaration

• Certificate

• Acknowledgement

• Chapter 1: Introduction of the Topic

• 1.1 Rationale of the Study

• 1.2 Introduction to the industry

• 1.3 Introduction to the company

• 1.4 Justification of the topic

• Chapter 2: Review of Literature

• Chapter 3: Research Methodology

• 3.1 Objectives of the Study

• 3.2 Research Hypothesis

• 3.3 Scope of the Study

• 3.4 Data collection

• 3.5 Limitations of the study

• Chapter 4 : Data representation & Analysis

• 4.1 Data representation & Interpretation

• 4.2 Hypothesis Testing

• Chapter 5. Results & Discussion

• 5.1 Major Findings

• 5.2 Discussions & Suggestions

• 5.3 Conclusion

• Copy of questionnaire

• Reference

1. INTRODUCTION

1.1 Rationale of Study

Electric Vehicles are those vehicles that uses one or more electric motors for propulsion. These vehicles are generally self-contained i.e. they use batteries as their energy source. Electric vehicles first came into existence at around mid-19th century and since then we have been in a race to develop these more.

India being an economy of around 130 crore people, our daily activities cannot be imagined without the use of vehicles. There has been a duopoly of petrol and diesel as our main source of fuel for the vehicles. This not only causes air pollution, but is also hard on our pockets. Petrol prices hiking as much as up to 98 rupees liter, we are eagerly looking for a substitute.

Commonly, the term EV is used to refer to an electric car. In the 21st century, EVs have seen a resurgence due to technological developments, and an increased focus on renewable energy and the potential reduction of transportation's impact on climate change and other environmental issues. Project Drawdown describes electric vehicles as one of the 100 best contemporary solutions for addressing climate change.

The main reason for taking up this topic for research is to make people more aware about the

Electrical vehicle Industry and it’s comparison with the fuel operated vehicles so that people are

made aware about the benefits of eco-friendly vehicles that go an extra mile to look out for

environment.

1.2 Introduction to the industry

Government incentives to increase adoption were first introduced in the late 2000s, including in the United States and the European Union, leading to a growing market for the vehicles in the 2010s. Increasing public interest and awareness and structural incentives, such as those being built into the green recovery from the COVID-19 pandemic, is expected to greatly increase the electric vehicle market. A pre-COVID 2019 analysis projected that Electric vehicles are expected to increase from 2% of global share in 2016 to 22% in 2030. Much of this market growth is expected

in markets like North America and Europe; a 2020 literature review suggested that growth in use of electric vehicles, especially electric personal vehicles, currently appears economically unlikely in developing economies.

As of yet, 50% of the EV's belong in china and rest is in North America and European countries and India lacks behind by a wider margin in this field.

A giant in the industry of electric vehicles, Tesla, has recently shown interest in introducing their vehicles in India as well.

Tata Nexon , MG gloster are some popular electric vehicles these days

Electric motive power started in 1827, when Hungarian priest Ányos Jedlik built the first crude but viable electric motor, provided with stator, rotor and commutator; the next year, he used it to power a tiny car. In 1835, professor Sibrandus Stratingh of the University of Groningen, the Netherlands, built a small-scale electric car, and between 1832 and 1839 (the exact year is uncertain), Robert Anderson of Scotland invented the first crude electric carriage, powered by non-rechargeable primary cells. American blacksmith and inventor Thomas Davenport built a toy electric locomotive, powered by a primitive electric motor, in 1835. In 1838, a Scotsman named Robert Davidson built an electric locomotive that attained a speed of four miles per hour (6 km/h). In England a patent was granted in 1840 for the use of rails as conductors of electric current, and similar American patents were issued to Lilley and Colten in 1847.

The first mass-produced electric vehicles appeared in America in the early 1900s. In 1902, the Studebaker Automobile Company entered the automotive business with electric vehicles, though it also entered the gasoline vehicles market in 1904. However, with the advent of cheap assembly line cars by Ford, the popularity of electric cars declined significantly.

Due to the limitations of storage batteries at that time, electric cars did not gain much popularity; however, electric trains gained immense popularity due to their economies and achievable speeds. By the 20th century, electric rail transport became commonplace due to advances in the development of electric locomotives. Over time their general-purpose commercial use reduced to specialist roles as platform trucks, forklift trucks, ambulances, tow tractors and urban delivery vehicles, such as the iconic British milk float; for most of the 20th century, the UK was the world's largest user of electric road vehicles.

Electrified trains were used for coal transport, as the motors did not use precious oxygen in the mines. Switzerland's lack of natural fossil resources forced the rapid electrification of their rail network. One of the earliest rechargeable batteries – the nickel-iron battery – was favored by Edison for use in electric cars.

EVs were among the earliest automobiles, and before the preeminence of light, powerful internal combustion engines, electric automobiles held many vehicle land speed and distance records in the early 1900s. They were produced by Baker Electric, Columbia Electric, Detroit Electric, and others, and at one point in history out-sold gasoline-powered vehicles. In 1900, 28 percent of the cars on the road in the US were electric. EVs were so popular that even President Woodrow Wilson and his secret service agents toured Washington, D.C. in their Milburn Electrics, which covered 60–70 mi (100–110 km) per charge.

Types of Electric Vehicles

There are two main types of electric vehicles (EVs), defined by the degree that electricity is used as their energy source.

1. Battery Electric Vehicles (BEVs)

BEVs are fully electric vehicles, meaning they are only powered by electricity and do not have a petrol engine.

BEVs are quiet, cost-efficient to run and eco-friendly, but are more expensive to buy than a comparable petrol fueled car. However, when the total cost of ownership over the time you’re likely to own the car is considered, EVs compare quite favorably, and may even cost less overall.

2. Plug-in Hybrid Electric Vehicles (PHEVs)

This type of EV is powered by both petrol and electricity. The amount of driving that can be done in ‘electric’ mode depends on the capacity of the battery.

The advantage of PHEVs over BEVs is that if you can’t get to a charging point, you can keep driving using fuel alone. The downsides are that the car needs two systems – fuel and electric – so maintenance costs can be higher than for a BEV. Also, once your relatively small battery runs flat, you lose the financial and environmental benefits of an EV until you recharge.

1.3 Company Selected for research

Mahindra Electric

Mahindra Electric is the first major EV manufacturer in India. Mahindra Electric Mobility Limited, formerly known as the Reva Electric Car Company, is an Indian company based in Bangalore, involved in designing and manufacturing of compact electric vehicles. Mahindra Electric started their journey in to the EV space in 2001 by launching Mahindra Reva, India’s first electric car. They subsequently launched Mahindra E20, the current version on roads in India. Some key features of this firm are: • The first and pioneer in the Electric Vehicles in India • The company is selling around 180-200 units per month across India in all models. • Recently, launched a new EV model, eVerito and expecting sales of 350-400 per month • Mahindra has a dedicated R&D centre in Bengaluru where over 200 engineers are working on e-vehicle technology and refinements. • Since 2010, Mahindra electric has 7000+ customers under EV segment and has completed over 50 million miles of Electric vehicle driving in India • Mahindra Electric has partnered with a Corporate Fleet firm - Lithium and provides Electric Corporate fleet services in Bengaluru. • Partnered with OLA to launch 300 EVs in Nagpur

• It has participated in the EESL and has supplied over 150 eVerito in the first EV tender in India • Partnered with NTPC to launch charging stations in Noida and Delhi

• The company is boosting capacity at its Bengaluru facility to make battery packs from 500 per month to 800 -1000 per month in the next two to three months. (two facilities can assemble 5,000 battery packs per month)

• All the EVs have a battery packed by Mahindra, while importing cells from China – typically a battery of 48Volts (or 76 volts) will have about 16 cells and each cell would have 3 modules

• It has tied up with Zoom Car to sell 200 cars (e2o Plus) • They are planning to increase the production capacity that can help them to sell over

5000 units per month over the next 2 years in all category vehicles • Currently they are in discussion with all the fleet operators as most traction in future will

come from commercial operators

1.4 Justification of the study

Mahindra Electric Mobility is the pioneer of electric vehicle technology in the country. Their mission is to bring tomorrow’s movement, today. They have a wide variety of electric vehicles, and will be increasing this range even further, under the brand - Mahindra Electric. Their products span personal and commercial segments and are designed to support the new paradigm of shared, electric and connected mobility.

• Their vision is to become a leading brand in providing customized electric mobility experiences through cutting edge technology.

• In view of this, they have created a comprehensive roadmap to establish a robust EV ecosystem by investing in next generation technology solutions and globally competitive products, to drive adoption of sustainable mobility.

• EV 2.0 will see the company make investments to ramp up manufacturing and to develop new, high-end electric powertrains, motor controllers, systems integration and battery technology. The next generation of EVs will now deliver longer range, higher speeds and futuristic connected car technologies to enable contemporary mobility solutions.

• They are actively engaging with ecosystem stakeholders, both private and public, to drive faster adoption of electric vehicles and ensure a progressive and greener future in the mobility system of the country, together.

2 Review of Literature

Extensive literature searching has been done before and during the work process, mainly on the

websites such as Times of India, Niti Ayog, Mahindra Electric, Department of Heavy Industry,

etc. When Internet has been used for literature searching Google has been the main search engine.

The search for suitable information has been time-consuming since the quality of the information

varies and the hits have been numerous. Therefore, an important part of the work of finding

information has been to separate essential information from unessential.

The literature in this thesis is considered to fulfil the requirements of high reliability.

A huge quantity of academic literature addresses the topic of Future of Electric Vehicles in Indian

Markets. Various Government policies have been criticized to look at positive as well as negative

aspects through high intellectual research methods. The behavior of consumer has been analyzed

and evaluated through various procedures and research work.

3 Research Methodology

3.1OBJECTIVES OF THE PROJECT:

❖ To get an insight knowledge about future of Electric Vehicles in Indian Markets

❖ Understanding the different aspects of the Electric Vehicle Industry and its working

❖ To know the behavior of customers towards the Electrification of the vehicles.

❖ To analyze the comparative study between Electric and fuel operated vehicles.

❖ To gain knowledge about the various policies launched by government towards Electrification of the Vehicles.

3.2 Research Hypothesis

Null Hypotheses:

1. The decision to switch a vehicle from petrol and diesel vehicles to Electric Vehicles is not depends on one’s knowledge and awareness about the pollution caused by fuel emissions.

2. Ability to switch to Electric vehicles is not depends on the income of a consumer as one looks for a mid-range vehicle but EV’s cost a tad higher on the costing spectrum.

3.3 Scope of Study

Shifting modes of mobility could launch new business opportunities. These would emerge in areas such as charging and swapping infrastructure, service, or integrated transport. In India, energy players have entered the mobility industry, while some traditional power companies are exploring possibilities in charging infrastructure, and infrastructure companies are seen entering the battery business. An important task that needs attention is transforming and up-scaling small and medium sub-system and auto-component industries. A large number of such mini-micro industries are auto-ancillary companies for diesel/petrol vehicles. They provide large number of jobs. Many of them will not survive as EV replaces petrol/diesel vehicles. A careful plan to hand-hold such industries and help them during the transition to EV components manufacturing is required.

Expansion of transport fleets based on IC engines negatively impact the economy considerably, apart from their negative health contributions. Crude oil price volatility adds uncertainty to an already burgeoning import bill, while also needing huge investments in oil refineries and related distribution infrastructure. There are several studies that suggest overall positive impact on GDP on introduction of EVs in fuel importing service dominated economies. One study has estimated that driving the shift to electric vehicles would lead to a 1% increase in EU GDP. In another study, net private and social benefits are estimated between $300 and $400 per EV. Coupled with generation of renewable power, the battery manufacturing industry in India can become bigger than the total amount spent on import of crude oil. This would provide a huge boost to the Indian

economy. The revenue loss for governments from the taxes on the oil sector is expected to be replaced by higher tax revenues in other economic sectors.

IMPACT ON EMPLOYMENT

European Climate Foundation has estimated that through reducing oil demand by more efficient electric cars, employment will increase by 5,00,000 to 8,50,000 by 2030. Another report estimates that about 2 million additional jobs will be created by EVs by 2050. The report further adds that oil production and distribution has very low employment intensity of just four jobs per million Euros value added compared to 24 jobs per million Euros in the general economy. Therefore, any shift in expenditure from buying imported oil to other expenditure choices would generate additional employment. Further, as imported oil is replaced by electricity and batteries, large employment is possible in enhancing power-generation and distribution, and in battery manufacturing, including battery-recycling.

As far as the automotive sector is concerned, a large part of the supply chain will get transformed in the power train segment. Traditional suppliers will move from supplying parts such as exhaust pipes and ICEs to perhaps battery materials, electric motors, and regenerative braking systems. EVs will create opportunities in durable and lightweight thermoplastics, higher demand for electricity, storage and many others. The net impact on employment would perhaps be balanced out. In addition, EV battery charging and swapping would create a large number of jobs throughout the country

IMPACT ON ENVIRONMENT AND HEALTH

ICEs are one of the main sources of air pollution globally. They negatively affect both human health and ecology. Emissions from ICE powered motor vehicles are responsible for about two-thirds of air pollution in urban areas. The current ban on older fuel cars in some Indian cities already shows a positive influence on air quality, and this can only further improve with the large scale introduction of EVs.

LAST-MILE CONNECTIVITY AND RURAL TRANSPORT

Some Indian cities today have metros as public transport and others have bus services. Many other cities and most towns do not have either. The last-mile connectivity in cities which have metros/buses is provided by rickshaws/autos. In cities and towns which do not have metros or buses, the only public transport available are rickshaws and autos. Early conversion of these vehicles to electric vehicles using Lithium-ion batteries will provide clean transport to a large number of people.

Today the primary transport for villages, taking people to bus-stops on the highways or train-stations, is ICE three-wheelers. It is possible to quickly convert them to electric, providing clean transport in villages. Further, battery-charging and swapping outlets may be operated in larger villages, creating jobs in rural areas. Specifications must ensure that these vehicles do not pose an inconvenience to other users of public roads and highways.

Freight movement in the rural areas, and for transport connecting farms to cities, are primarily handled by smaller transport vehicles (like rickshaws, autos and tempos). These vehicles are eminently suited for replacement by EVs. Sustainable mobility would require that small freight vehicles are enabled by aggregators to be made available on request, just as Uber or Ola cabs for city commuters. This would cut farm to market costs for the farmers, and also result in better fleet utilization. The electronic platforms to enable such operations need to be developed.

Market behavior towards electrification of vehicles

Electric vehicles will incite crucial changes in the Indian automobile market, and their growing

adoption will lead to more futuristic business models. The global environment seems to favour

electric vehicles, and with time the world seems to be getting serious about them. A large number

of EVs are selling across the globe, and even though China, the US, and Europe are contributing

to a significant chunk of the sales, industry leaders consider India to be a promising player with a

receptive market.

EVs operate at a fundamentally lower cost, and in the last few years, the trends suggest that there

has been a steady interest among the Indian masses for electric cars as well as two-wheelers.

Understanding Consumer Behaviour

Buying a vehicle is a time-consuming process with various internal and external factors

influencing the decision. Particularly in India, the decision-making process is particularly

complicated as the buyers often face an information overload. Market research indicates that

female automobile buyers consider features such as safety, affordability, and efficiency, whereas

male buyers focus on performance, features, and aesthetics such as interiors and style. Also, male

audiences express more interest in electric vehicles.

Viability

In a consumer-based market, the viability of the E.V. industry is affected by factors like incentives

on scrapping used vehicles, favourable government policies, and reducing GST. Consumers also

believe that E.V. manufacturers need a more proactive marketing approach rather than playing

safe.

Fuel Efficiency

Because petrol and diesel prices are always on the rise, consumers are keenly interested in how

much would they save by switching to an electric vehicle from an ICE vehicle. Marketing an

estimated long-term fuel savings are the key to a consumer’s heart.

Technology

Most electric vehicle buyers are early adopters of innovation, green technology, and take pride in

being an environmental ambassador. Consumers applaud EVs as an environment-friendly

technology and are enthusiastic about switching to vehicles that will have zero emissions.

Driving Demand

To understand the factors that drive demand, we first need to know how consumers make

decisions. Even though industry leaders consider EVs to be a promising option for Indian

audiences, just price incentives alone are not enough to drive the demand.

We need to consider the massive impact of charging infrastructure that will be felt in metropolitan

cities, particularly since the pollution levels have reached disastrously high. Close cooperation

among manufacturers, dealers, government, and marketers will also lead to a more progressive

adoption of electric vehicles, mainly if EVs are pushed in the commercial and public transport

segments.

The modern generation runs on innovation, sustainability, and environmental conservation – and

electric vehicles fit the bill perfectly. The indigenous availability of vehicles, batteries, and spare

parts will also impact the consumer mindset.

EVs are definitely the future!

We are at a critical crossroads where electric vehicles and the decisions taken by key players will

shape the future of transportation either for better or for worse. Now is the time, auto experts will

look back to as a stepping stone to a brighter future for not just electric vehicles, but for the auto

industry as a whole. This phase is the beginning of a steady climb to a more extensive electric-

vehicle adoption.

The market and consumer sentiments toward electric vehicles are principally positive. The

consumer mindset is evolving, which will ultimately lead to healthy growth for the electric

vehicles. It is being said that EVs will become mainstream in less than a decade and can be taken

as a sign of markets being aggressively ready for a product launch and marketing by automobile

companies.

Backbone of Electrification of vehicles: Charging Stations

The rate at which electric vehicles (EV) can be charged is becoming a key differentiator in this rapidly developing market, for a very straightforward reason: charging an EV’s battery is currently a lot slower than refilling a tank with petrol to go the same distance.

Take a generic EV with a battery capacity of 60kWh. Charging this battery from zero to 100%, using a cable plugged in to a standard UK 240V, 13A socket, will take about 20 hours. This isn’t practical for a daily driver, much less for a long-distance traveller.

In practice, most EV owners rely on dedicated chargers, often wired in at home to higher-current ring mains. UK energy supplier E-On, for example, will wire a 7.4kW wall-mounted charger, with either a tethered charging cable or a universal socket for a charging cable, into a 32A ring main. With this charger, our generic 60kWh EV can be charged in more like eight and a half hours.

A widespread, accessible public charging infrastructure network is needed to support a robust Indian EV market. And a healthy ratio between the number of EVs to charging stations is important to encourage early adopters and relieve drivers of range anxiety. A technical committee (part of the state-level EV Steering Committee) recently met in Hyderabad to discuss including provisions to the existing building codes and government regulations to set up charging infrastructure in buildings in Telangana. Administrative Staff College of India (ASCI) and NRDC presented on how to regulate the EV policy and make it easier for the charging service providers and manufacturers to operate. There are a number of considerations when it comes to location and siting, the more specific position within a location, for EV charging stations. These include economics and utilization, maintenance, charger type, and interoperability.

Industry Structure in India Existing suppliers

• ~15 firms currently supplying EV Chargers in India

• Only 3 firms in 4W, AC Chargers so far in India

• 4 Wheelers – AC Chargers - RRT Electro Power, Chennai; Mass Tech Controls, Mumbai; Exicom, New Delhi

• These are mostly Power Electronics & Battery Charger manufacturers who have diversified into EV Chargers