RBFI Termpaper 1211247

-

Upload

iimbangalore -

Category

Documents

-

view

0 -

download

0

Transcript of RBFI Termpaper 1211247

2013

Critically Analyzing Policy

Framework for Financial

Inclusion through Microfinance

Institutions in India

Final SubmissionAniket Karde (1211247)

RBFI TERM PAPER

ContentsIntroduction.........................................................2

Financial inclusion as a driver of economic growth and poverty alleviation.........................................................2

Introduction to MFIs in India........................................31. Self Help Group-bank linkage model..............................4

2. MFI model.......................................................4Evolution of regulatory framework for MFIs in India..................5

1. Prior to the Andhra Pradesh MFI crisis of 2010..................52. Andhra Pradesh Crisis and the cracks in the Regulatory framework 6

3. Post AP crisis: Malegam Committee response & present regulations 74. Pending Regulation: Micro Finance Institutions (Development and Regulations) Bill 2011..............................................9

How is regulating microfinance different from other forms of finance?....................................................................10 Unique features of the credit risk faced by MFIs.................11

Critical analysis of existing policy documents......................13 Malegam Committee report.........................................13

MFI Bill 2012....................................................13Which agency should enforce the law?................................14

Conclusion..........................................................15Transcript of interview with Mr. Chandrashekar Ramaiah..............17

Appendix............................................................19References..........................................................20

Introduction

According to Rangarajan Committee’s report (2008) on financial

inclusion, financial inclusion is defined as the process of access to

financial services and timely and adequate credit where needed by

vulnerable groups such as weaker section of the society and low income

groups at an affordable prices. The importance of financial inclusion,

based on the principle of equity and inclusive growth, has been the

center of attention of policy makers globally; however in India it has

been a recent story. In India more than half of the population does

not have access to mainstream banking services, even though growth

with equity was the main objective right from the inception of

planning process. This financially excluded population mainly

comprised of marginal farmers, landless laborers, self-employed

unorganized sector enterprises, urban slum dwellers, migrants, ethnic

minorities, socially excluded groups, senior citizens and women.

Government of India’s has always developed its strategies taking into

consideration the causality between economic growth, financial

deepening and financial inclusion, particularly since early 1990s

reforms. It had further re-emphasized the need for financial inclusion

in its 11th Five year plan by opening nearly 100 million bank/ post

office accounts for the poorest segment of the population who

comprised of MNREGA workforce. Subsequent efforts are being made by

the government and banking sector to achieve financial inclusivity at

large. Some of the policy initiatives initiated by RBI for financial

inclusion involves opening of frill accounts, relaxation of know your

customer (KYC) norms, engaging Business Correspondents (BCs), use of

IT, adoption of Electronic benefit transfer (EBT), general purpose

FINANCE FOR ALL Access to financial services for poor people, reduces vulnerability and improves welfare

They are mutually

reinforcing

Inclusive financial sector development reduces poverty in two ways

FINANCE FOR GROWTH The financial sector mobilizing savings, building institutions and investing in growth of the productive sector

credit card (GCC). Thus the planning strategy has recognized the

critical role played by financial inclusion in holistic development of

the country. Accordingly, the authorities have modified the policy

framework from time to time to satisfy the financial needs of the

various segments of the society.

Financial inclusion as a driver of economic growth and poverty

alleviationFinancial inclusion provides two complementary contributions to

poverty alleviation. They are as follows:

It drives economic growth which indirectly reduces poverty and

inequality

It provides appropriate, affordable, financial services for poor

people which can improve their welfare

The above two contributions are complementary to each other because

financial inclusion brings about the inclusion of the previously

excluded to connect to the formal economy and contribute to economic

growth, this in turn facilitates the inclusion of more people in the

economy and in the financial system.

Inclusiv

Introduction to MFIs in India MFIs have become one of the primary means through which much required

financial services are made available to small traders and craftsmen

working in the informal sector. MFIs through its thrift, credit and

other financial services and products of very small amount to the poor

in rural, semi-urban and urban areas provide them with an opportunity

to raise their income levels and improve their living standards.

Microfinance has been high on the public agenda after the UN Year of

Microcredit in 2005 and since the Nobel Peace Prize went to Mohammed

Yunus and Grameen Bank in 2006. The primary reason behind the success

of the model of Grameen Bank is its existence as primarily a non-

profit organization.

In India, microfinance sector has assumed a lot of importance for the

Reserve Bank of India (RBI) which has identified the growth of the

microfinance sector as an important avenue for achieving the national

goal of financial inclusivity of increasing proportion of the

population (usually referred to as financial inclusion goal) . In

addition, the RBI considers lending by banks to the microfinance

sector as a part of their priority sector lending requirements.

Considering all these aspects there is a need to ensure orderly

development and sound governance and regulatory structures for the

microfinance sector.

The regulation of MFIs in India has always been a subject of

controversy. SKS Microfinance Limited, the largest provider of micro-

finance services in India, was in controversy in 2010 due to alleged

violent recovery practices from the farmers which led to a number of

farmer suicides. All these farmers committed suicide because of their

inability to pay back high-interest loans. Owing to this, in 2011, the

Ministry of Finance proposed a comprehensive new Bill for the

regulation of MFIs.

There are some fundamental questions about the regulation of this

sector which need to be answered in going forward with these changes.

Should MFIs be allowed to be run as profit making organization or as

not-for profit institutions as envisaged under 25 of the Companies

Act? What kind of regulation is best suited to ensure that microfi-

nance is able to achieve financial inclusion, and who should be this

regulator?

In India basically there are two models of microfinance

1. Self Help Group-bank linkage model

As per this model, NGOs and banks collectively communicate with

potential clients to form small homogenous groups. The most

significant aspect of this system is that it provides for opening of

bank accounts in the name of the entire group thus reducing the cost

per transaction to a large extent. Recovery of loans is based on peer

review, the returns are empirically found to be higher. In addition to

this system protects the members from usurious debt traps and

strengthens decision-making and fund management within their groups.

As the pooled thrift grows the group is eligible for getting more

funds in multiples of their group savings. At present, Regional Rural

Banks (RRBs), co-operative banks and commercial banks are linked to

this model. As on March 31, 2007, 50 commercial banks, 96 RRBs and 352

co-operative banks were participating in the programme. The number of

bank branches (as per the last available data) lending to SHGs was

35,294 at end-March 2006 and the number of participating NGOs and

other agencies was 3,024.

2.MFI modelIn India, MFIs has some severe semantic difficulties. Definition of

MFIs is based on the intent of the lender not by its form. If a market

intermediary lends loan to a small borrower, it is not microfinance;

however if an institution whose constituent intent is the distribution

of such loans gives a similar loan, it is treated as microfinance.

Such institutions can be constituted as a society, NGO or a company

(profit or not for profit).

There are several MFI models, some of which are state initiatives and

some of them are private ones. National Bank for Agriculture and Rural

Development (‘NABARD’) and Small Industries Development Bank of India

(‘SIDBI’) are examples of state run MFIs. Besides, supporting small-

scale financial institutions, commercial banks, RRBs, and co-operative

banks provide separate retail services as well. The last decade has

seen the emergence of several private players like SKS Microfinance

Limited, which are solely dealing with microfinance. Both the private

and state players provides the same services and governed by the

existing legal and regulatory framework for private sector rural and

microfinance operators.

Evolution of regulatory framework for MFIs in India

Microfinance institutions in India are registered as one of the

following five entities:

Non- Government Organizations engaged in microfinance (NGO-MFIs),

comprised of Societies and Trusts

Cooperatives registered under the conventional state-level

cooperative acts, the national level multi-state cooperative

legislation Act (MSCA 2002 ), or under the new state-level

mutually aided cooperative acts (MACS Act)

Section 25 Companies (not-for-profit)

For-profit Non-Banking Financial Companies (NBFCs)

NBFC-MFIs

There are four distinct phases of the evolution of regulatory

framework for MFIs

1. Prior to the Andhra Pradesh MFI crisis of 2010Prior to major crisis in AP, the process of registration involved

would decide the kind of legislation and regulatory rules to govern

the MFIs. There was multitude of ways to form and register a private

MFI. MFI registering under each of the categories had to follow

different legislations. Even though all these MFIs were providing the

same set of services, there was an inconsistency with the regulations

governing the bodies. The table below provides the seven categories

Prior to the Andhra Pradesh MFI crisis of

2010

Andhra Pradesh Crisis and the cracks in the Regulatory framework

Post AP crisis: Malegam Committee response & present

regulations

Pending Regulation: Micro Finance Institutions (Development

and Regulations) Bill 2012

Evolution of regulatory framework for MFIs

recognised by the RBI and the legal framework that governed their

activities:

S.

no

Categories of providers Legal Framework governing their

activities

1 Domestic Commercial

Banks:

Public Sector Banks;

Private Sector Banks &

Local Area Banks

RBI Act 1934

BR Act 1949

SBI Act

SBI Subsidiaries Act

Acquisition & Transfer of Undertakings

Act 1970 & 1980

2 Regional Rural Banks RRB Act 1976

RBI Act 1934

BR Act 1949

3 Co-operative Banks Co-operative Societies Act

BR Act 1949 (AACS)

RBI Act 1934 (for sch. banks)

4 Co-operative

Societies

State legislation like MACS

5 Registered NBFCs RBI Act 1934

Companies Act 1956

6 Unregistered NBFCs NBFCs carrying on the business of a

financial institution prior to the

coming into force of RBI Amendment Act

1997 whose application for CoR has not

yet been rejected by the Bank

Sec. 25 of Companies Act

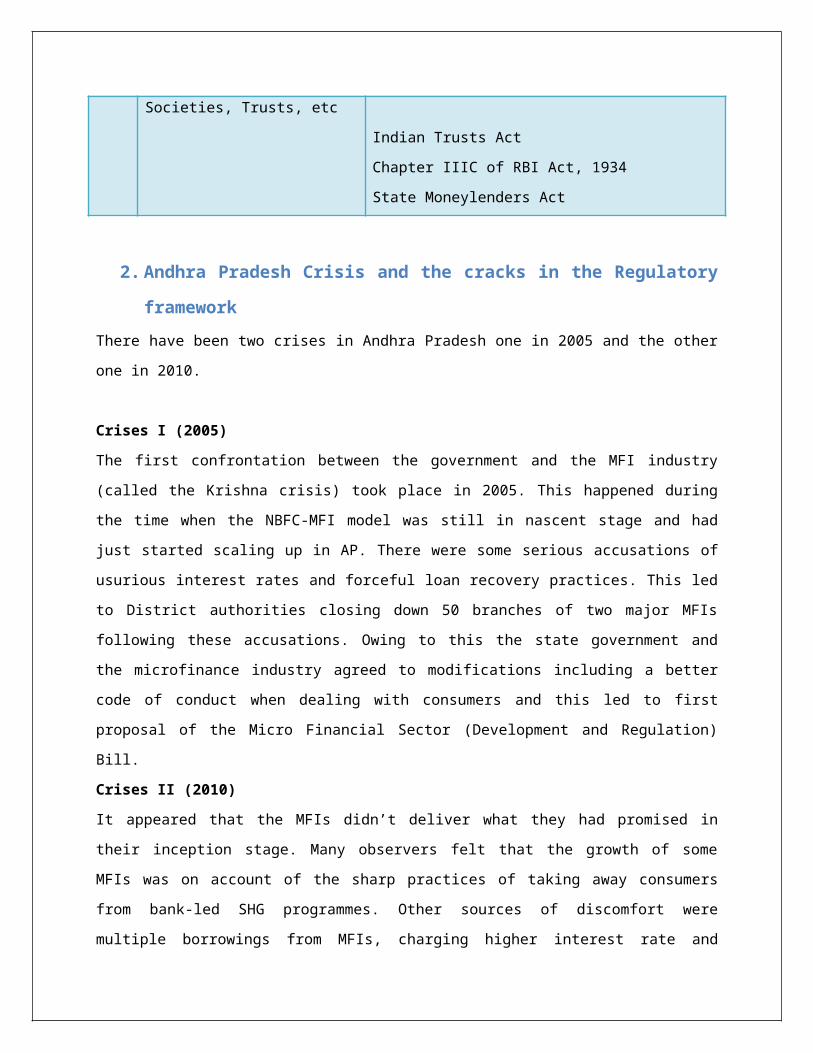

7 Other providers like Societies Registration Act, 1960

Societies, Trusts, etc

Indian Trusts Act

Chapter IIIC of RBI Act, 1934

State Moneylenders Act

2. Andhra Pradesh Crisis and the cracks in the Regulatory

frameworkThere have been two crises in Andhra Pradesh one in 2005 and the other

one in 2010.

Crises I (2005)

The first confrontation between the government and the MFI industry

(called the Krishna crisis) took place in 2005. This happened during

the time when the NBFC-MFI model was still in nascent stage and had

just started scaling up in AP. There were some serious accusations of

usurious interest rates and forceful loan recovery practices. This led

to District authorities closing down 50 branches of two major MFIs

following these accusations. Owing to this the state government and

the microfinance industry agreed to modifications including a better

code of conduct when dealing with consumers and this led to first

proposal of the Micro Financial Sector (Development and Regulation)

Bill.

Crises II (2010)

It appeared that the MFIs didn’t deliver what they had promised in

their inception stage. Many observers felt that the growth of some

MFIs was on account of the sharp practices of taking away consumers

from bank-led SHG programmes. Other sources of discomfort were

multiple borrowings from MFIs, charging higher interest rate and

unfair debt collection pratices from micro- borrowers. Charging higher

interest rate was harshly opposed as the MFIs were able to borrow from

banks that are intended to deliver subsidised bank loans to the poor,

at much lower PSL rates. This discomfort of the policymakers reached

its climax in December, 2010 when SKS Microfinance, one of the largest

NBFCs in AP, went for IPO. For many policymakers it was self-evident

that earning profits and valuations from serving the poor was wrong.

This led to the second crises in October 2010. This time AP government

responded with an ordinance which became law in December 2010. As per

the new law collections on existing loans were stopped and any new

microcredit was prevented from originating in the state of AP by

intervening in the business processes of the microfinance firms.

While passing the legislation AP government made no distinction

between the errant institutions and the rest. Such heavy handedness

shown by AP government created an undesired competitive barrier to MFI

model. With such action taken up by the state authorities the MFIs

were caught between the existing norms of the RBI and the ones placed

by the state government. Thus there was a sense of ambiguity in

regulatory framework designed for MFI’s functioning.

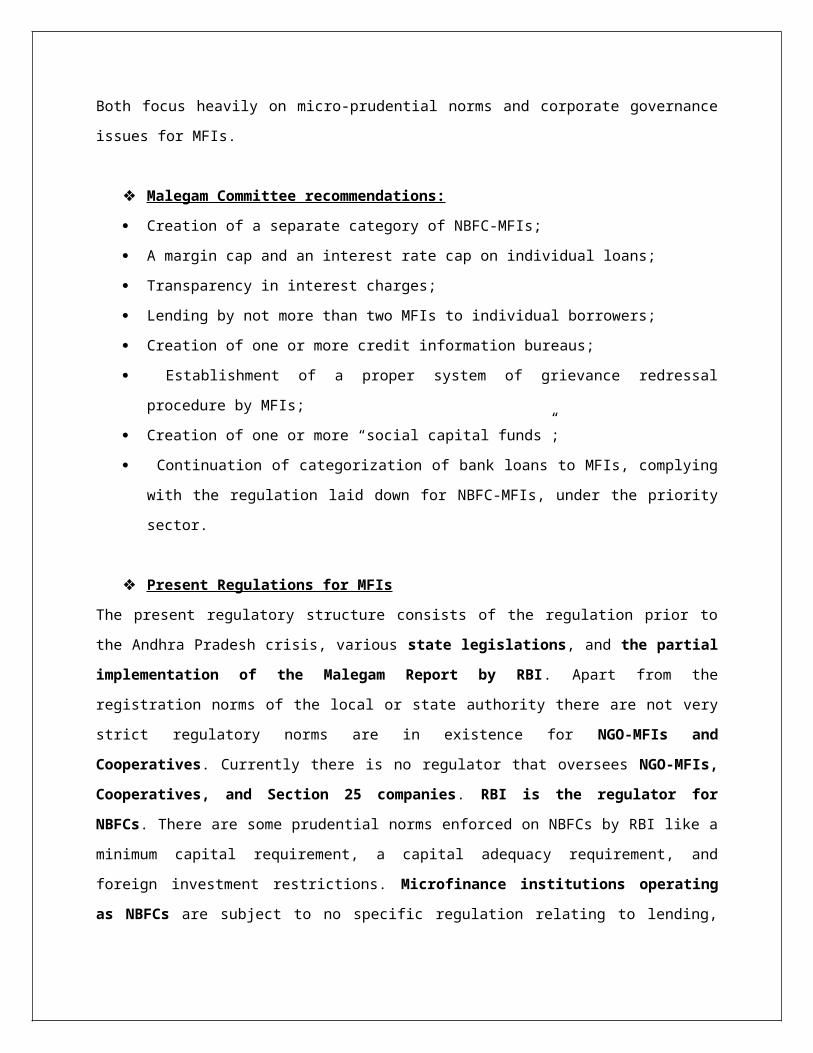

3. Post AP crisis: Malegam Committee response & present

regulations Post Andhra Pradesh microfinance crisis of 2010 there was an immediate

need for more rigorous regulation of NBFCs functioning as MFIs. After

the 2010 AP legislation was passed, two efforts are made in

formulating the regulatory framework for the Indian microfinance

industry. These efforts were in the form of Malegam Report (2011) and

the Microfinance Institutions (Development and Regulation) Bill, 2012.

Both focus heavily on micro-prudential norms and corporate governance

issues for MFIs.

Malegam Committee recommendations:

Creation of a separate category of NBFC-MFIs;

A margin cap and an interest rate cap on individual loans;

Transparency in interest charges;

Lending by not more than two MFIs to individual borrowers;

Creation of one or more credit information bureaus;

Establishment of a proper system of grievance redressal

procedure by MFIs;

Creation of one or more “social capital funds”;

Continuation of categorization of bank loans to MFIs, complying

with the regulation laid down for NBFC-MFIs, under the priority

sector.

Present Regulations for MFIs

The present regulatory structure consists of the regulation prior to

the Andhra Pradesh crisis, various state legislations, and the partial

implementation of the Malegam Report by RBI. Apart from the

registration norms of the local or state authority there are not very

strict regulatory norms are in existence for NGO-MFIs and

Cooperatives. Currently there is no regulator that oversees NGO-MFIs,

Cooperatives, and Section 25 companies. RBI is the regulator for

NBFCs. There are some prudential norms enforced on NBFCs by RBI like a

minimum capital requirement, a capital adequacy requirement, and

foreign investment restrictions. Microfinance institutions operating

as NBFCs are subject to no specific regulation relating to lending,

pricing, or operations as they encompass many types of financial

institutions.

RBI has broadly accepted the Malegam Committee’s recommendations. The

new regulation from RBI, currently, only applies to the newly created

NBFC-MFI category. Microfinance institutions operating under other

legal structures face minimal regulatory requirements, aside from

registration. However the pending Micro Finance Institutions

(Development and Regulations) Bill 2011 has put all microfinance

institutions under the jurisdiction of RBI.

Microfinance institutions self-regulation:

Most of the MFIs often join an industry association which guides them

in adopting code of conduct, lending methods, collection practices,

institutional transparency, and training practices. Currently, the two

biggest industry associations in India are the Microfinance

Institutions Network (MFIN) and Sa-dhan. Both these industry

associations offer their guidance to their member MFIs so that the so

that the most pressing issues facing the industry can be collectively

addressed.

State Level Regulation:

There are several state level legislations which are enacted to

control MFIs in the state. Money Lending Act and the Andhra Pradesh

Micro Finance Institutions Ordinance, 2010, are some of the prominent

state level regulations.

The Money Lending Act: This act was originally formulated to

prevent moneylenders from charging exorbitant interest rates.

However this has been applied to control MFIs in some states.

The Andhra Pradesh Ordinance, 2010: this ordinance was enacted

in 2010 during the repayment crisis in Andhra Pradesh (AP). Its

enactment led to large amount of restrictions on the MFI’s

operations in AP, such as district by district registration,

required collection near local government premises, and forced

monthly repayment schedules.

4. Pending Regulation: Micro Finance Institutions

(Development and Regulations) Bill 2011The first draft of Micro Finance Institutions (Development and

Regulations) Bill was drafted in 2007. The latest Micro Finance

Institutions (Development and Regulations) Bill, 2012 is an updated

version of an earlier bill. This bill has been re-drafted several

times and its latest draft was released in 2012 which is under the

scrutiny of Parliament Standing Committee and would then be brought to

parliament for passage. Government of India is of the view that once

the bill is passed, it will provide an adequate legislative framework

for the entire gamut of micro-finance services. The bill addresses all

legal forms of microfinance institutions, providing a comprehensive

legislation for the sector. New regulation includes:

Designation of RBI as the sole regulator for all microfinance

institutions,

Power to regulate interest rate caps, margin caps, and

prudential norms

All microfinance institutions must register with RBI

Formation of a Micro Finance Development Council, which will

advise the central government on a variety of issues relating to

microfinance

Formation of State Advisory Councils to oversee microfinance at

the state level

Creation of Micro Finance Development Fund for investment,

training, capacity building, and other expenditures as determined

by RBI.

If the bill passes, RBI must effectively regulate and monitor a great

number of microfinance institutions that have previously been subject

to very little regulation.

How is regulating microfinance different from other

forms of finance?

In this section I have tried to explain the two features of micro-

finance which call for unique treatment in policy considerations as

compared to policy making in the mainstream body of financial law.

These features are credit recovery and the credit risk of the MFI,

when credit access is enabled through the structure of the joint

liability group (JLG)

Majority of the legislations in India on the business of credit

provision rests in the domain of debt of firms or individuals. As in

the case of standard credit contracts, legislation are mainly designed

to constrain the manner in which the lender can collect on the loan,

or the process for recovery in the case of default. Also in the case

of companies taking credit, contract enforcement was strengthened by

the SARFAESI Act. And in the case of loans by individuals, RBI

mandates best practices for debt collection and recovery by banks.

However, microfinance form of credit (Micro-credit) involves facets

that are different compared to the credit processes that the formal

financial sectors like the banks are used to. In case of micro-credit,

the contract that the MFI signs with an individual involves a two-tier

obligation: the first is with the individual and the second is with

the JLG (Joint Liability Group), without which the individual cannot

become a customer of the MFI. This second layer is the critical

feature that makes micro-credit different from general credit to

retail customers, rather than any specific size of the loan.

The confidence of the lender is strengthened by this two-tier

structure when a loan is made. The second level of the JLG guarantee

provides a positive adjustment for the lack of collateral, or

certainty of income, that is typical in standard individual credit

contracts. The probability of default is lower in case of MFI, since

the group offers an implicit guarantee to repay the loan even if the

individual failed do so. Thus in absence of this intangible group

guarantee, the individual would be unable to access the loan. JLG

therefore offers a mechanism through which individuals, who are not

otherwise able to access credit at rates they can afford, are able to

obtain loans. Unique problems of credit recovery in micro-credit

The enforcement of regulation becomes fairly easy when there is clear

demarcation between those who have the rights and those who have the

obligations. In case of a standard financial contract, the customer

has the rights while the service provider has the obligations. While

in case of credit, the customer (borrower) has the obligations and the

service provider (the lender) has the rights. All over the world for

consumer credit the legislations are put in place to define the rights

of the borrower. And then regulations are enforced to define a code of

conduct and practice under which debt collection can be undertaken,

and how recovery can be done when the borrower defaults.

However it is far more complicated in case of micro-credit where

credit is given through a JLG structure. Here, the code of conduct

needs to account for more than just the link between the service

provider (the MFI as the lender) and the customer (member of group).

Additionally two more links have to be taken into account here:

1. The link between the member of the JLG and the JLG itself.

2. The link between the MFI and the other members of the JLG, when

one member defaults.Unlike in case of formal credit, MFIs credit is given based on the

strength of credit quality of the group. Therefore there needs to be

legal clarity on what are the rights of the lender and the obligations

of the JLG when a member of the group defaults. In addition to this

there is one other unique concern for regulation is the link between

JLG member and other members of JLG. Group leaders or other members of

the JLG have far greater access to the borrower member than the MFI

does. There is always a concern for consumer protection because group

could more efficiently inflict damage in the process of debt

collection or debt recovery than the MFI or their employees. The

consumer protection mandate of the regulation must, therefore, have

provision for grievance redressal for the individual borrower against

the MFI as well as the JLG or any other member of the JLG through

which they obtained the loan. Thus the regulation has to take care of

the rights of the borrower against the MFI, rights of the JLG against

the MFI, and rights of the individual borrower against the JLG.

Unique features of the credit risk faced by MFIsMFIs are the conduit for the flow of credit from the formal financial

sector to those who are otherwise credit constrained. However this

group lending approach in the form of JLG is also the source of risk

for the lenders. These risks to the lenders arise in two ways as

follows:

1. Correlated defaults associated with homogenous credit

quality:

There is every possibility that there will always be a higher degree

of homogeneity when lending to different members in a group, whether

the members are from the same cultural background, physical location,

risk preferences, political preference etc. such common factors within

a group can lead to correlated changes in the level of default.

Willful defaults among micro-borrowers of the same community in the

Kolar district in 2007 is a testimony to the existence of such risks.

Those defaults caused a rise simultaneously in all the MFIs that were

operating in that district at the time. After such incidents MFIs have

made changes in their business models to account for same factor

concentration risk in their credit evaluation of JLGs. However, not

all factors of homogeneity can be directly observed. In case of JLGs

there is a need to track the history of default performance at the

level of groups (as defined by a known set of individuals rather than

just one individual). As of now the credit information bureaus collect

repayment history at the level of individuals, but do not collect

these at the level of groups. If there are different groups dealing

with different MFIs who share some similar members, here there is very

possibility that a default of a member or a set of members can

generate default across different groups. This, in turn, may adversely

impact the default performance across MFIs, depending upon the

contractual implications of member default and JLG default to the MFI.

Thus the regulator should understand how the default of one or more of

group members may simultaneously affect the credit performance of one

or more MFIs together. For this understanding, credit information

bureaus must need to track not only the credit history of individual

borrowers but also the credit history of the JLG which they are a part

of.

2. Systemic risk

The business of lending to the poor is fraught with political risk

given the governance problems of India. While the business of MFIs is

national, the business is vulnerable to political risk emanating from

any one State Government. Most of the previous episodes in the history

of MFIs have shown that the greatest source of vulnerability of the

MFI industry is the political risk that is faced by firms working with

the poor. A group is always an effective channel for deploying

political actions, which enhances the systemic risk for the MFI

industry which deals with its customers in the form groups. Political

action has been known to influence the micro-borrower to default on

their repayments without fear of action from the MFI. JLG approach can

lead to a better credit behaviour from their members; however at the

same time the structure can be equally effective in encouraging group-

level default. This is a core risk that the MFI industry will

inevitably face, and needs to be monitored through JLG level tracking

by the regulator using data from the credit information bureaus.

Thus from the above issues we can say that there are new and different

concerns which are not addressed by the existing legislation when the

customer is a borrower with no collateral or guarantee other than the

structure of a joint liability group (or JLG). Also, MFIs are highly

exposed to banks and banking regulation, given the predominance of

banks amongst lenders to MFIs. However the above mentioned risks

related to MFIs tells us that this sector does require new and

different legislative and regulatory considerations as compared to the

mainstream financial sector (Banks and NBFCs) regulatory framework.

“Time and again there has been some controversy about microfinance in India. The controversy

was created when MFIs turned to profit-making rather than their original social goal of

supporting self-employment and job creation. This is the reason why a special legal framework

is needed to support microfinance. Microfinance cannot operate in a vacuum; it has to be

regulated. But the regulatory authority needs to be separate from the central bank because

regulating microfinance is different from regulating conventional banks. Microfinance is about

“social business”, not profit-making business. Traditional banking regulation deals with banking

as a profit-making business. It is not equipped to regulate microfinance”- Mr. Mohammad

Yunus, Founder Grameen Bank

Critical analysis of existing policy documents

Malegam Committee reportIn this report a significant emphasis was given on framing and

defining micro prudential norms for the NBFC MFIs with a view to

address the high failure probability of MFIs and was a way to control

the systemic risk posed by MFIs. However, a high probability of

failure of the MFI was not the essence of the Andhra Pradesh crisis.

MFIs are also too small to present systemic risk. The report also

proposed that the norms for MFIs should be similar to banks even

though the business of microfinance differs from the business of banks

in fundamental ways as stated in the previous section. Many industry

personnel are of the opinion that the key reason why MFIs have

succeeded in delivering credit to poor people, to a greater extent

that banks in India have, lies in the fact that MFIs operate

differently from banks.

The recommendations of the report seem to worry more about ensuring

that bank-lending under priority sector lending targets is done

effectively without any special emphasis in providing an enabling

framework for microcredit as a whole.

MFI Bill 2012The MFI (D&R) Bill is a more holistic attempt at MFI regulation, as it

is applicable to a more diverse set of organizational forms of

microfinance as opposed to banks. However, a basic problem with the

Bill is that it treats microfinance companies as extended arms of

banks and financial services. The bill lacks a clear regulatory

philosophy and consists of a diverse array of initiatives, some of

which are internally inconsistent with each other.

The bill envisages deposit-taking by MFIs. Taking deposits has its own

merits and risks which has to be weighed by the regulator.

Merit: This would create an additional source of funding for MFIs, and

also enable clients to have an option to save. MFI is in constant

contact with its customers and has a good network so it makes immense

sense to provide this service to the poor. Further it will help MFI in

diversifying its funding sources and will make it more independent,

thereby making it less vulnerable to the whims of the commercial banks

and will provide them with a greater opportunity to tide over any

difficult periods such as the Andhra episode after which banks

stopped funding MFIs

Risk: Deposits will be taken from the micro-borrowers who would be

borrowing themselves. This means that the savings of the poor would be

going into risky credit products. And if a certain MFI happens to be

going into a bankruptcy, the savings of large numbers of micro-

borrowers would be under threat. Thus, it would further escalate the

problem of political risk of the microfinance industry, which in turn

would induce an implicit fiscal burden of bailing out such failing

MFIs.

Furthermore, the bill calls for the mandate for all MFIs including

NBFCs to obtain a certificate of registration from RBI before they

start providing services. These NBFCs have to comply with both the

terms and conditions of registration and other directions issued by

the RBI under the Reserve Bank of India Act, 1934 and those issued by

the RBI under the Bill. Prerequisite for registration of MFIs is that

they should have a minimum capital requirement of INR 5 lakh, as

opposed to the Malegam Committee recommendation of Rs. 5 crore.

It has given power to RBI to cease-and-desist MFIs if they operate in

a manner which is detrimental to clients or depositors or the MFIs

interests. Thus we can conclude that the bill has vested enormous

power in RBI to ensure smooth monitoring of operational risks

involved. However there are some issues of rule of law which may raise

concerns. According to bill any violation is a criminal offence and

consumers are visualized as having no recourse to civil or criminal

courts without RBI’s permission. There is no provision for a skilled

judicial appeals mechanism where orders can be appealed.

Current flow of credit and regulation in Indian micro finance

The bill has also proposed a mechanism for the redressal of disputes

between clients and MFIs by “Microfinance Ombudsmen”. Such measure may

curtail the profit seeking behavior exhibited by most MFIs.

Furthermore, the bill calls for a single central regulator and so the

state control over organizations registered under a state law would

cease in favor of this single central regulator, thereby, creating a

huge jurisdictional challenge.

Which agency should enforce the law?

If the MFI bill passes, RBI would effectively regulate and monitor a

great number of microfinance institutions that have previously been

subject to very little regulation. However this can be problematic.

There is the possibility of RBI being oriented towards banks, and thus

forcing MFIs to become more like banks. This will demolish the very

essence of existence of the MFI industry, which lies in new and

innovative ways to structure the credit process, in ways which differ

from those of banks. Furthermore RBI is more accustomed in dealing

with affluent borrowers and so it does not have the organization

structure and skillsets required in undertaking supervisory

responsibilities about the interaction between lenders and poor

people.

As per the series of reports by various committees in recent years

(The High Powered Expert Committee on Making Mumbai an International

Financial Centre, 2007; The Internal Working Group on Debt Management,

2008; Planning Commission Committee on Financial Sector Reforms, 2009;

Committee on Investor Awareness and Protection, 2010), the main

problem identified has been that the focus of existing financial

regulation on the service provider rather than the service provided.

The problem seems to be that there are too many regulators as there

are varied ways to initiate a MFI in India. Due to such fragmentation

of regulation there is a lack of a level playing field for different

providers of a common service, which in turn creates confusion about

consumer rights for the customers of different financial products.

Conclusion

After the start of December 2010 crisis in MFI industry, policymakers

have been unanimous in putting into place a regulatory framework that

would resolve such crisis. But even then crisis is still there and MFI

industry is still facing the problem of shortage of funds. This

suggests that neither of the policy initiatives taken so far by the

government has been instrumental is tackling these problems. MFI Bill

2012 has answered in some ways the challenges put forth by Andhra

Crisis. But there is one problem with the bill. It has simply vested

all the regulatory powers within the RBI. The threat of being

regulated by a completely banking centric regulator would raise

concerns within the industry as such a move is likely to curb sector’s

growth.

There are some main concerns which continue to persist for MFI

industry on the regulatory front which needs to be addressed by

regulatory framework in future. They are as follows:

Lack of clarity on regulation that is uniform across all forms of

micro-credit organization forms

Lack of clarity on a single regulator to regulate, monitor and

supervise, and enforce regulations in the area of micro-credit

business

Lack of clarity on how the new proposed regulations are distinct

and different from existing regulations targeting credit given to

firms and other individuals.

Unique thing about the micro-credit given by MFIs which differentiates

it from every other business providing credit is that micro-credit is

given to individuals based on their being part of a joint liability

group. Though this brings in a new concept of credit delivery to

previously neglected population, it also brings with it a new set of

concerns of customer protection, risks in the business of delivering

credit, and risks that an industry based on delivering credit through

groups could pose to the entire financial system.

From the primary research and interaction with the industry personnel,

I feel that a regulatory framework should be designed to take care of

both prudential and non-prudential norms. Thus a dual model having two

regulators for the sector (consisting of RBI and an Oversight Board,

which would report to RBI) may be a good model to tackle the present

issues. RBI would be the regulator for MFI banks permitted to offer

savings and mobile based remittance services and the Oversight Board

will be the one deciding upon the industry norms to safeguard consumer

interests.

However, MFI sector in India is highly heterogeneous and only a few of

the MFIs have significant outreach with substantial volumes of credit.

Many of these MFIs are already regulated as NBFCs but the remaining

MFIs that constitute the bulk are generally very small in size and

operate in a small geographical area. These MFIs are not financially

stable and require huge capacity-building efforts before they can be

subjected to effective supervision and regulation. Hence, a move to

regulate these MFIs presently is likely to hamper their growth

prospects and throttle their slender development initiatives. Need of

the hour is to adopt a more developmental framework rather than a

regulatory framework. Thus, a larger effort is required to put the

financial regulatory architecture in India on a sound footing wherein

the field of microfinance needs to be placed correctly

Transcript of interview with Mr. Chandrashekar Ramaiah

Mr. Chandrashekar Ramaiah

Sr. Branch Head

Retail Assets

Janalakshmi Financial Services Pvt. Ltd

1. What are your views on the present regulatory environment for

MFIs in India?

Mr. Chandrashekar: Micro credit has come a long way since its

inception and still now it has a long way to go in future. Micro-

credit institutions have failed to succeed to their fullest

potential due some inherent weaknesses in our regulatory framework.

Speedy actions are needed to remove the obstacles to microcredit’s

development. Inadequate regulation is one of the factors which is

hampering the growth of this sector. This sector has such a huge

potential and to tap this potential some rectifications have to be

made in the Bill.

2. Can the existing regulatory framework for NBFCs work for MFI

sector?

Mr. Chandrashekar: Regulating microfinance is different from

regulating conventional banks and NBFCs. Microfinance is about

social business, not profit-making business. So I think a special

legal framework is needed to support microfinance. Traditional

banking regulation deals with banking as a profit-making business.

It is not equipped to regulate microfinance.

3. Should regulation of MFIs differ from regulating a commercial

bank? Who should supervise microfinance institutions if not the

central bank or the government?

Mr. Chandrashekar: Yes, the regulations of MFIs should differ from

commercial banks. There are some unique features of credit risk and

credit recovery involved in micro-credit, which are not there in

commercial lending. Microfinance has to be regulated, but the

regulatory authority needs to be separate from the central bank. One

needs a separate institution, where people with different skills and

a different mindset work. It should work as a fully separate entity.

Central banks are not used to the concept of lending without

collateral. It can have separate management consisting of the former

officials working under central bank governor’s direction. In some

countries like Bangladesh, the central bank governor heads the

authority for regulating microfinance. But this institution is

outside the central bank.

4. How micro-credit is different from lending to small and medium

sized enterprises?

Mr. Chandrashekar: Well, Microfinance is all about poor people.

Small and medium sized enterprises are not at all the target of

MFIs. We lend to poor some 1000-1500 Rs. On an average microfinance

loan does not exceed 10,000 to 12,000 Rs. It is for the people at

the bottom of the pyramid. It is about eradication of poverty using

the potential that people have.

5. Is a single regulator the answer?

Mr. Chandrashekar: The problem is that there are too many regulators

as there are multiple ways to start a MFI in India. This

fragmentation of regulation causes an absence of a level playing

field for different providers of a common service, and results in

confusion. Any approach to regulation and supervision of MFIs needs

to recognize their heterogeneity, and accommodate the flexibility

and scope for development that MFIs need. These institutions are

highly specialized and they need sound and unique regulatory

environment for their growth. I think there has to be two separate

regulators. RBI should be the regulator for MFI banks which accept

deposits and an oversight board which can safeguard the consumer

interests. This can address problem of conflict of interest between

a service provider and a regulator. It would also provide for good

governance and orderly development.

6. What should be the role of central bank in functioning of MFIs?

Mr. Chandrashekar: Like I said earlier, central banks are not fully

equipped to deal with this sector. Central Bank can help in drafting

and passing microfinance legislations. But they are not well placed

to regulate microfinance. One needs a separate institution, where

people with different skills and a different mindset work.

Appendix

Exhibit 1: Overview of financial inclusion services

Exhibit 2: MFI and Self Help Group Penetration among Women population

Exhibit 3: MFI and Self Help Group Penetration among total

Population

Exhibit 4: Key differences in the organization and operation of

those different institutions

References Microfinance India 2012- State of the sector report

Microfinance in India: A New Regulatory Structure by Kenny

Kline, Senior Policy Researcher, Centre for Microfinance &

Santadarshan Sadhu, Research Manager, Centre for

Microfinance

Financial inclusion in India: An analysis by Dr. Anurag B

Singh and Priyanka Tondon

IFMR research report on Financial Inclusion: Government

Promoted Initiatives by Deepti KC

G20 Financial Inclusion Experts Group—ATISG Report

M-CRIL Microfinance Review 2012: MFIs in a Regulated

Environment

Regulating Microfinance Institutions by Renuka Sane, Susan

Thomas

Malegam Committee on Microfinance (January 2011)

Should we pick the Microfinance Bill?- Article in Economic

Times by Mr. M.S Sriram

How is financial regulation different for micro-finance?-M.

Sahoo, Renuka Sane, Susan Thomas (Indira Gandhi Institute of

Development Research, Mumbai January 2012)

Regulatory Framework for MFIs in India by Krishan Jindal

Microfinance and the Cooperatives: Can the Poor Gain from

Their Coming Together? by H.S. Shylendra (Institute of

Rural Management Anand (IRMA))

Existing Legal and Regulatory Framework for the Microfinance

Institutions in India: Challenges and Implications by Sa-

Dhan