Prospectus Initial Public Offering - Sphera Franchise Group

472

IMPORTANT NOTICE IMPORTANT: You must read the following disclaimer before continuing. This Document is not a prospectus. This Document is an unofficial translation of the Prospectus approved by the FSA for the initial public offering of shares in the Company by the Selling Shareholders. Neither the Company, nor the Managers makes any representation as to the accuracy, completeness or reliability of the information included in this Document and the Company cautions investors to take their investment decision exclusively based on the information included in this Prospectus and any supplement thereto, if published, as approved by the FSA in the Romanian language. The following disclaimer applies to the electronic version of the English translation of the Prospectus attached to this notice (the "Document"), received via email, accessed from an internet page or otherwise received as a result of electronic communication, and you are therefore advised to read this notice carefully before reading, accessing or making any other use of the attached Document. In accessing the Document, you agree to be bound by the following terms and conditions and in particular restrictions set out in the Prospectus, including any modifications to them from time to time, each time you receive any information from WOOD & Company Financial Services, a.s., Raiffeisen Bank S.A. and Alpha Finance Romania S.A. (the "Managers"), Sphera Franchise Group S.A. ("Sphera" or the "Company") and Lunic Franchising and Consulting Ltd and M.B.L. Computers S.R.L. (the "Selling Shareholders") as a result of such access. You acknowledge that this electronic transmission and the delivery of the attached Document is confidential and intended only for you and you agree you will not forward, reproduce or publish this electronic transmission or the attached Document (or any copy of it or part thereof) in any manner whatsoever to any other person. The document and the offer when made are only addressed to and directed at persons in member states of the European Economic Area ("EEA"), other than Romania, who are "qualified investors" within the meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC) (the "Prospectus Directive") ("Qualified Investors"). Any investment or investment activity to which this document relates is available only to (i) the public in Romania, and (ii) in any member state of the EEA other than Romania, to Qualified Investors, and will be engaged in only with such persons. THIS DOCUMENT AND THE SECURITIES REFERENCED HEREIN MAY ONLY BE DISTRIBUTED IN "OFFSHORE TRANSACTIONS" AS DEFINED IN, AND AS PERMITTED BY, REGULATION S UNDER THE US SECURITIES ACT OF 1933, AS AMENDED (THE "SECURITIES ACT"). ANY FORWARDING, REDISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS NOTICE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. NOTHING IN THIS ELECTRONIC TRANSMISSION OF THE ATTACHED DOCUMENT CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND MAY NOT BE OFFERED OR SOLD IN THE UNITED STATES. Confirmation of your representation: The attached document is delivered to you at your request and on the basis that you have confirmed, and by accessing this Document you shall be deemed to have represented, to each of the Managers, the Company and the Selling Shareholders that (i) you are in Romania or (ii) you and the electronic mail address that you have provided are located outside United States (as defined in Regulation S under the Securities Act); or (iii) if you are in any member state of the EEA other than Romania, you are a Qualified Investor; or (iv) if you are acting as financial intermediary (as that term is used in Article 3(2) of the Prospectus Directive), the securities acquired by you as a financial intermediary in the offer have not been acquired on a non-discretionary basis on behalf of, nor have they been acquired with a view to their offer or resale to, any person in circumstances which may give rise to an offer of any securities to the public other than their offer or resale to Qualified Investors (as defined in the Prospectus Directive) in any member state of the EEA which has implemented the Prospectus Directive; or (v) you are outside the EEA (and the electronic mail addresses that you gave us and to which this document has been delivered are not located in such jurisdictions) or (vi) you are a person into whose possession this document may lawfully be delivered in accordance with the laws of the jurisdiction in which you are located. In addition, by accessing this Document you have confirmed to

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Prospectus Initial Public Offering - Sphera Franchise Group

IMPORTANT NOTICE

IMPORTANT: You must read the following disclaimer before continuing.

This Document is not a prospectus. This Document is an unofficial translation of the Prospectus approved

by the FSA for the initial public offering of shares in the Company by the Selling Shareholders. Neither

the Company, nor the Managers makes any representation as to the accuracy, completeness or reliability

of the information included in this Document and the Company cautions investors to take their investment

decision exclusively based on the information included in this Prospectus and any supplement thereto, if

published, as approved by the FSA in the Romanian language.

The following disclaimer applies to the electronic version of the English translation of the Prospectus attached to

this notice (the "Document"), received via email, accessed from an internet page or otherwise received as a

result of electronic communication, and you are therefore advised to read this notice carefully before reading,

accessing or making any other use of the attached Document.

In accessing the Document, you agree to be bound by the following terms and conditions and in particular

restrictions set out in the Prospectus, including any modifications to them from time to time, each time you

receive any information from WOOD & Company Financial Services, a.s., Raiffeisen Bank S.A. and Alpha

Finance Romania S.A. (the "Managers"), Sphera Franchise Group S.A. ("Sphera" or the "Company") and

Lunic Franchising and Consulting Ltd and M.B.L. Computers S.R.L. (the "Selling Shareholders") as a result of

such access. You acknowledge that this electronic transmission and the delivery of the attached Document is

confidential and intended only for you and you agree you will not forward, reproduce or publish this

electronic transmission or the attached Document (or any copy of it or part thereof) in any manner

whatsoever to any other person.

The document and the offer when made are only addressed to and directed at persons in member states of the

European Economic Area ("EEA"), other than Romania, who are "qualified investors" within the meaning of

Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC) (the "Prospectus Directive") ("Qualified

Investors"). Any investment or investment activity to which this document relates is available only to (i) the

public in Romania, and (ii) in any member state of the EEA other than Romania, to Qualified Investors, and will

be engaged in only with such persons.

THIS DOCUMENT AND THE SECURITIES REFERENCED HEREIN MAY ONLY BE DISTRIBUTED IN

"OFFSHORE TRANSACTIONS" AS DEFINED IN, AND AS PERMITTED BY, REGULATION S UNDER

THE US SECURITIES ACT OF 1933, AS AMENDED (THE "SECURITIES ACT"). ANY FORWARDING,

REDISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS

UNAUTHORISED. FAILURE TO COMPLY WITH THIS NOTICE MAY RESULT IN A VIOLATION OF

THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS.

NOTHING IN THIS ELECTRONIC TRANSMISSION OF THE ATTACHED DOCUMENT CONSTITUTES

AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION

WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN AND WILL NOT BE

REGISTERED UNDER THE SECURITIES ACT OR WITH ANY SECURITIES REGULATORY

AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND MAY NOT BE

OFFERED OR SOLD IN THE UNITED STATES.

Confirmation of your representation: The attached document is delivered to you at your request and on the

basis that you have confirmed, and by accessing this Document you shall be deemed to have represented, to each

of the Managers, the Company and the Selling Shareholders that (i) you are in Romania or (ii) you and the

electronic mail address that you have provided are located outside United States (as defined in Regulation S

under the Securities Act); or (iii) if you are in any member state of the EEA other than Romania, you are a

Qualified Investor; or (iv) if you are acting as financial intermediary (as that term is used in Article 3(2) of the

Prospectus Directive), the securities acquired by you as a financial intermediary in the offer have not been

acquired on a non-discretionary basis on behalf of, nor have they been acquired with a view to their offer or

resale to, any person in circumstances which may give rise to an offer of any securities to the public other than

their offer or resale to Qualified Investors (as defined in the Prospectus Directive) in any member state of the

EEA which has implemented the Prospectus Directive; or (v) you are outside the EEA (and the electronic mail

addresses that you gave us and to which this document has been delivered are not located in such jurisdictions)

or (vi) you are a person into whose possession this document may lawfully be delivered in accordance with the

laws of the jurisdiction in which you are located. In addition, by accessing this Document you have confirmed to

the Managers, the Company and the Selling Shareholder, that (i) you have understood and agree to the terms set

out herein, (ii) you consent to delivery by electronic transmission, (iii) you acknowledge that you will make your

own assessment regarding any legal, taxation or other economic considerations with respect to your decision to

purchase shares subject to the offering under the Prospectus.

This document has been made available to you in an electronic form. You are reminded that documents

transmitted via this medium may be altered or changed during the process of electronic transmission and

consequently none of the Company, the Selling Shareholders, the Managers, persons that control the Managers

or any director, officer, employee or agent of them or affiliate of any such person accepts any liability or

responsibility whatsoever in respect of any difference between the document distributed to you in electronic

format and the hard copy version.

You are reminded that this Document has been delivered to you and you have accessed it on the basis that you

are a person into whose possession this Document may be lawfully delivered in accordance with the laws of the

jurisdiction in which you are located and you may not nor are you authorized to deliver this document,

electronically or otherwise, to any other person and in particular to any U.S. address.

Restriction: Nothing in this electronic transmission constitutes an offer of securities for sale to persons other

than the public in Romania or the specified qualified institutional buyers described above and to whom it is

directed and access has been limited so that it shall not constitute a general solicitation. If you have gained

access to this transmission contrary to the foregoing restrictions, you will be unable to purchase any of the

securities described therein.

The Managers are acting exclusively for the Selling Shareholders and no one else in connection with the offer.

They will not regard any other person (whether or not a recipient of this document) as its client in relation to the

offer and will not be responsible to anyone other than the Selling Shareholders and the Company, in accordance

with the specific contractual terms agreed between them, for providing the protections afforded to its clients nor

for giving advice in relation to the offer or any transaction or arrangement referred to herein.

You are responsible for protecting against viruses and other destructive items. Your receipt of the electronic

transmission is at your own risk and it is your responsibility to take precautions to ensure that it is free from

viruses and other items of a destructive nature.

Sphera Franchise Group S.A.

(A joint stock company incorporated under the laws of Romania)

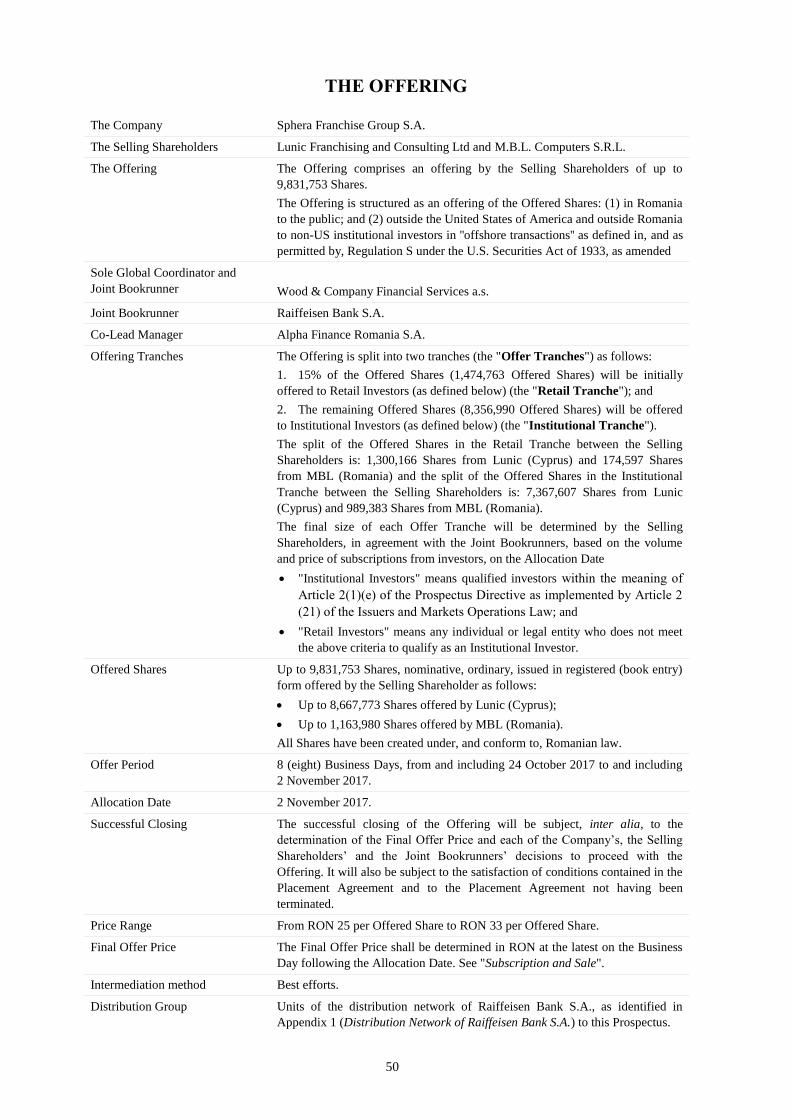

Offering of up to 9,831,753 existing shares in Sphera Franchise Group S.A.

by Lunic Franchising and Consulting Ltd and by M.B.L. Computers S.R.L.

Price Range: RON 25/Share to RON 33/Share

This document has been approved by way of Decision 1508/20.10.2017 by the Romanian Financial Supervisory Authority (the "FSA"), which is the Romanian

competent authority for the purposes of Directive 2003/71/EC, as amended (the "Prospectus Directive") and relevant implementing measures in Romania, as a

prospectus (the "Prospectus") in accordance with Law no. 24/2017 on issuers of financial instruments and market operations (the "Issuers and Markets

Operations Law"), Regulation no. 1/2006 on issuers and operations with securities issued by the Romanian National Securities Commission (currently, the FSA)

and Commission Regulation (EC) No 809/2004 of 29 April 2004 implementing the Prospectus Directive as regards information contained in prospectuses as well as

the format, incorporation by reference and publication of such prospectuses and dissemination of advertisements, as amended (the "Prospectus Regulation").

This Prospectus relates to an offering (the "Offering") of an aggregate number of up to 9,831,753 nominative, ordinary shares ("Offered Shares") in Sphera

Franchise Group S.A., a joint stock company incorporated under the laws of Romania, registered with the Bucharest Trade Registry under number J40/7126/2017,

sole registration code 37586457, with registered seat in 239 Calea Dorobanți str., 2nd floor, office 4, district 1, Bucharest, Romania (the "Company"). The Company

has a share capital of RON 581,990,100 divided into 38,799,340 nominative, ordinary, book entry form shares, each of which is issued, fully paid with a par value of

RON 15 and carrying one vote in the Company's general meetings of shareholders (the "Shares"). The Offered Shares are offered in the Offering as follows: (1) up

to 8,667,773 ordinary shares in the Company by Lunic Franchising and Consulting Ltd, a company organized and existing under the laws of Cyprus, registered

under no. HE 80898, with registered office at Riga Feraiou nr. 2, Limassol Center, Block B, 4th floor, office 406, 3095 Limassol, Cyprus ("Lunic (Cyprus)"); and

(2) up to 1,163,980 ordinary shares in the Company by M.B.L. Computers S.R.L., a company organized and existing under the laws of Romania, registered with the

Bucharest Trade Registry under No. J40/6119/1991, having its registered office at 15 Fabrica de Glucoză street, Bucharest, Romania ("MBL (Romania)") (Lunic

(Cyprus) and MBL (Romania) are hereinafter referred to as the "Selling Shareholders").

The final offer price (the "Final Offer Price") of each Offered Share will be calculated based on the mechanics set out in "Subscription and Sale". After the

successful closing of the Offering, the Company intends to apply for admission of the Shares to trading on the spot regulated market operated by Bursa de Valori

Bucuresti S.A. (the Bucharest Stock Exchange) (the "BSE"), premium tier, under market symbol "SFG". The BSE is a regulated market in the European Economic

Area (the "EEA") for the purposes of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and

amending Directive 2002/92/EC and Directive 2011/61/EU (the "Directive on Markets in Financial Instruments"). Prior to the Offering, there has been no public

market for the Shares.

In connection with the Offering, the Selling Shareholders have agreed that the Stabilising Managers will retain 10% of the gross proceeds obtained by the Selling

Shareholders from the Offering (the "Stabilisation Proceeds") and will use such Stabilisation Proceeds for the purposes of conducting stabilisation activities, if any,

in the Shares, during the period of not more than 30 calendar days after the commencement of trading of the Shares on the BSE (the "Stabilisation Period"),

provided that the aggregate amount of Shares acquired by the Stabilising Managers in connection with such activities shall not exceed 983,175 Shares. Such

stabilisation activities, if commenced, may be discontinued at any time and may be commenced from time to time on one or more occasions. The Stabilising

Managers will not be required to take any stabilisation actions. No assurance may be given that such stabilisation actions, if taken, will bring the expected results.

The Offering is structured as an offering of Offered Shares: (1) in Romania to the public; and (2) outside the United States of America and outside Romania to non-

US institutional investors in ''offshore transactions'' as defined in, and as permitted by, Regulation S ("Regulation S") under the U.S. Securities Act of 1933, as

amended (the "Securities Act").

An investment in the Shares involves a high degree of risks and uncertainties. Prospective investors should read the entire document, and, in particular, should see

"Risk Factors" beginning on page 22 for a discussion of certain matters investors should consider prior to making an investment in the Shares. Prospective investors

must be able to bear the economic risk of an investment in the Shares and should be able to sustain a partial or total loss of their investment.

THIS PROSPECTUS HAS BEEN APPROVED BY THE ROMANIAN FINANCIAL SUPERVISORY AUTHORITY. THE APPROVAL VISA APPLIED ON

THIS PROSPECTUS DOES NOT CONSTITUTE A GUARANTEE OR ANY KIND OF ASSESSMENT BY THE ROMANIAN FINANCIAL SUPERVISORY

AUTHORITY WITH REGARD TO THE OPPORTUNITY, ADVANTAGES OR DISADVANTAGES, PROFIT OR RISKS INVOLVED IN TRANSACTIONS

TO BE EXECUTED FOLLOWING THE ACCEPTING OF THE OFFERING, OBJECT OF THE APPROVAL DECISION; THE APPROVAL CERTIFIES ONLY

THE CONFORMITY OF THIS PROSPECTUS WITH THE LEGAL REQUIREMENTS AND THE RULES ADOPTED FOR THE APPLICATION THEREOF.

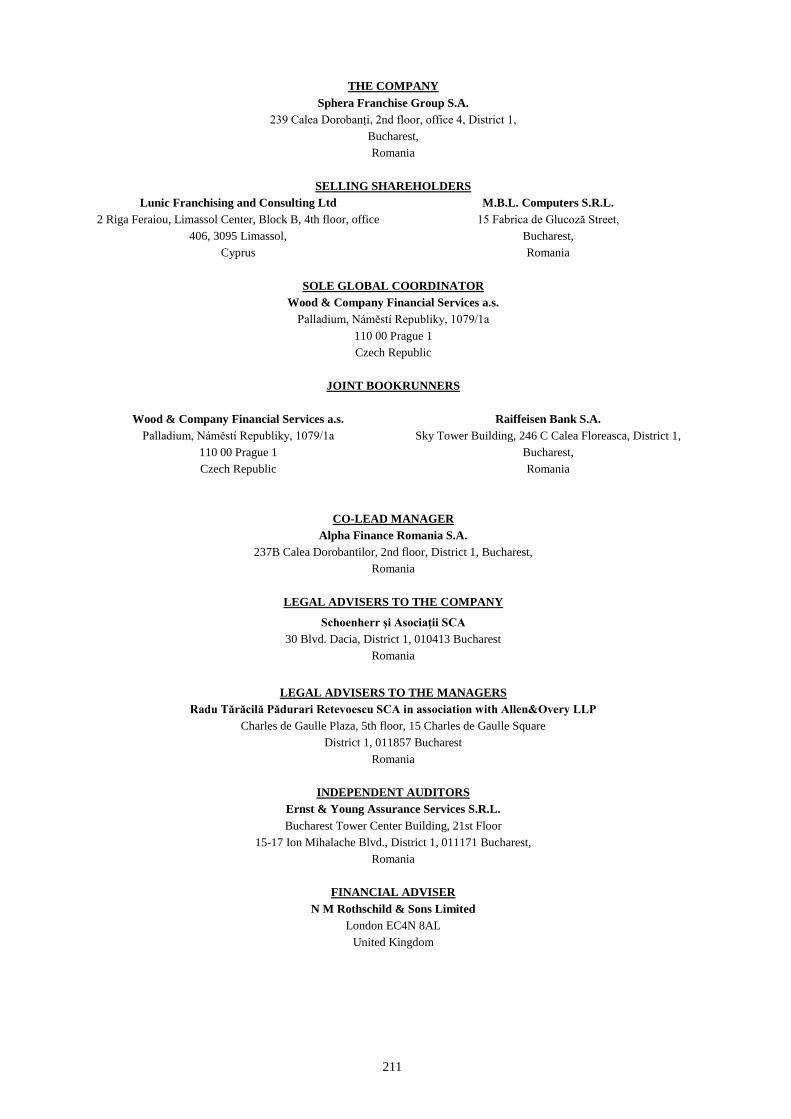

Sole Global Coordinator and Joint Bookrunner

WOOD & Company

Joint Bookrunner Co-Lead Manager

Raiffeisen Bank Alpha Finance Romania

Financial Adviser

Rothschild

The date of this Prospectus is 20 October 2017.

1

CONTENTS

Page

SUMMARY ............................................................................................................................................................... 2

IMPORTANT INFORMATION ABOUT THIS PROSPECTUS ........................................................................... 17

RISK FACTORS ..................................................................................................................................................... 21

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS ................................................ 42

SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES ........................................................ 43

PRESENTATION OF FINANCIAL AND OTHER INFORMATION ................................................................... 45

EXCHANGE RATE INFORMATION.................................................................................................................... 49

THE OFFERING ..................................................................................................................................................... 50

USE OF PROCEEDS ............................................................................................................................................... 54

DIVIDEND POLICY ............................................................................................................................................... 55

CAPITALIZATION AND INDEBTEDNESS......................................................................................................... 57

SELECTED FINANCIAL AND OPERATING INFORMATION .......................................................................... 58

PRO FORMA FINANCIAL INFORMATION........................................................................................................ 63

OPERATING AND FINANCIAL REVIEW ........................................................................................................... 73

FOODSERVICE SECTOR .................................................................................................................................... 107

BUSINESS ............................................................................................................................................................. 124

LEGAL PROCEEDINGS ...................................................................................................................................... 157

MANAGEMENT ................................................................................................................................................... 158

PRINCIPAL SHAREHOLDERS ........................................................................................................................... 165

DESCRIPTION OF SHARE CAPITAL AND CORPORATE STRUCTURE ...................................................... 166

RELATED PARTY TRANSACTIONS ................................................................................................................ 176

MATERIAL CONTRACTS .................................................................................................................................. 177

REGULATORY MATTERS ................................................................................................................................. 180

TAXATION ........................................................................................................................................................... 184

SUBSCRIPTION AND SALE ............................................................................................................................... 188

SELLING AND TRANSFER RESTRICTIONS ................................................................................................... 201

LEGAL MATTERS ............................................................................................................................................... 203

INDEPENDENT AUDITORS ............................................................................................................................... 204

GENERAL INFORMATION ................................................................................................................................ 205

DEFINITIONS AND GLOSSARY OF SELECTED TERMS .............................................................................. 207

APPENDIX 1 - DISTRIBUTION NETWORK OF RAIFFEISEN BANK S.A. ................................................... 213

APPENDIX 2 - GROUP FINANCIAL STATEMENTS ....................................................................................... 223

2

SUMMARY

Summaries are made up of disclosure requirements known as "Elements". These Elements are numbered in Sections A-

E (A.1–E.7).

This summary contains all the Elements required to be included in a summary for this type of securities and issuer.

Because some Elements are not required to be addressed, there may be gaps in the numbering sequence of the

Elements.

Even though an Element may be required to be inserted in the summary because of the type of securities and issuer, it is

possible that no relevant information can be given regarding the Element. In this case, a short description of the

Element is included in the summary with the note "not applicable".

Section A—Introduction and warnings

A.1 Warning. This summary should be read as introduction to this prospectus (the "Prospectus");

Any decision to invest in the shares the offering of which is the subject to this Prospectus (the "Offered

Shares") should be based on consideration of the Prospectus as a whole by the investor;

Where a claim relating to the information contained in the Prospectus is brought up before a court, the

plaintiff investor might, under the national legislation of the Member States ("Member States") of the

European Economic Area ("EEA"), have to bear the costs of translating the Prospectus before the legal

proceedings are initiated;

Civil liability attaches only to those persons who have tabled the summary, including any translation

thereof, but only if the summary is misleading, inaccurate or inconsistent when read together with the

other parts of the Prospectus or it does not provide, when read together with the other parts of the

Prospectus, key information in order to aid investors, when considering whether to invest in the Offered

Shares.

A.2 Consent by

the issuer or

person

responsible

for drawing

up the

prospectus to

the use of the

prospectus

for

subsequent

resale or

final

placement of

securities by

financial

intermediari

es.

Not applicable. Sphera Franchise Group S.A. (the "Company" or "Sphera") did not and does not

consent to the use of the Prospectus for subsequent resale or final placement of the shares issued by the

Company (the "Shares") by financial intermediaries or by any other third party.

Section B—Issuer and any guarantor

B.1 The legal

and

commercial

name of the

issuer.

The legal and commercial name of the issuer is Sphera Franchise Group S.A..

B.2 The domicile

and legal

form of the

issuer, the

legislation

under which

The Company is a joint stock company incorporated in Romania, registered with the Bucharest Trade

Registry under number J40/7126/2017, sole registration code 37586457, with registered seat in 239

Calea Dorobanți str., 2nd floor, office 4, district 1, Bucharest, Romania. The Company operates in

accordance with Romanian law and the Company's articles of association (the "AoAs").

3

the issuer

operates and

its country of

incorporatio

n.

B.3 A description

of, and key

factors

relating to,

the nature of

the issuer’s

current

operations

and its

principal

activities,

stating the

main

categories of

products sold

and/or

services

performed

and

identification

of the

principal

markets in

which the

issuer

competes.

Sphera is the holding company for the Group companies that hold rights to operate KFC branded

restaurants in Romania, Republic of Moldova and certain regions in Northern Italy, and Pizza Hut

branded restaurants and Taco Bell branded restaurants in Romania. As of 1 September 2017, it also

provides to the benefit of its subsidiaries USFN (Romania) and ARS (Romania) services with respect

to: finance and accounting, marketing, development, operational, and human resources activities.

The Group (as defined in B.5 below) operates in three segments of the foodservice sector: quick-service

restaurants (through the KFC brand), full-service restaurants (through the Pizza Hut Dine-In brand) and

home delivery (through the Pizza Hut Delivery brand).

In the KFC restaurants, we sell food and beverage products either individually or as a part of a price-

attractive bundle labelled "menu". Generally, the menus include three main components: a portion of a

chicken-based product (sandwiches, wrappers or pieces of chicken meat), a medium-sized portion of

French fries and a medium-sized non-alcoholic drink. A dipping sauce is also offered in some menu

offers. Whereas menus are normally sized for one person, we also offer products, called Buckets, that

are targeted for group consumption (normally, up to four people) and which consist of higher number of

chicken meat pieces and some include portions of French fries and non-alcoholic drinks.

In Pizza Hut restaurants, we sell pizza, pasta, side dishes, deserts and beverage products.

The food offered in our restaurants includes proprietary menu items, the recipes of which are generally

sourced from the Yum! restaurants across the world or developed in-house.

The first Taco Bell restaurant was opened on 12 October 2017.

B.4a A description

of the most

significant

recent trends

affecting the

issuer and

the industries

in which it

operates.

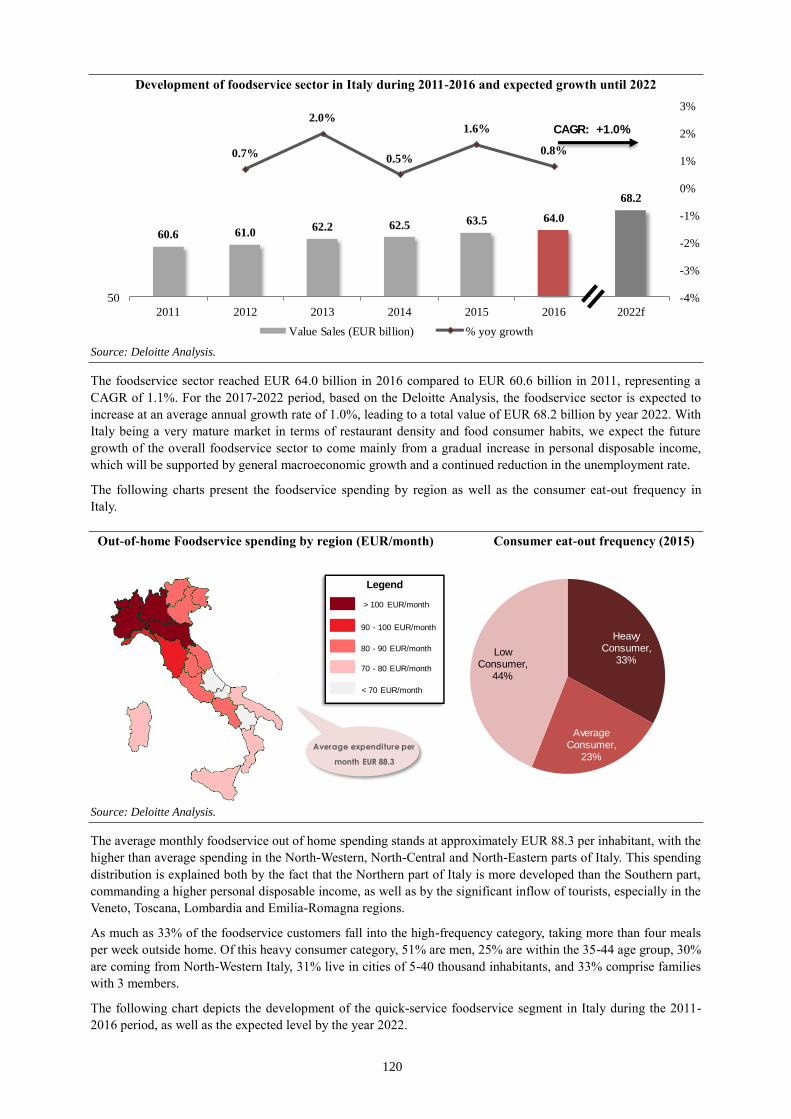

Sales in modern retailing have surpassed traditional retail throughout the country, leading to changes in

shopping habits, as well as in foodservice consumption generally. The main attraction of modern

shopping centres is easy access to both entertainment and shopping facilities in close proximity to food

courts that offer meals. With investors continuing to develop large shopping centres across major cities

whilst tracking shopping galleries around hypermarkets, this trend has significantly contributed to the

strong development of consumer foodservice through retail units, which increased by over 12% in value

terms and 10% in transaction terms in 2016 compared with the previous year (Euromonitor, Consumer

Foodservice in Romania, May 2017).

We believe that the following main factors that have supported the foodservice sector’s growth in recent

years will continue to play a key role in the sector’s development over the next few years:

• On average, the Romanian population eats out of home less frequently than in more developed

countries and we expect the Romanian average to move towards the international trend;

• Expected growth of disposable income and continuously increasing levels of female employment

will further support the trend of eating out;

• Romania remains underpenetrated in terms of foodservice restaurants per capita; and

• Strong minimum wage and average salary increase since 2014 resulted in strong price increase

across all foodservice formats; furthermore, the current Romanian Government has indicated its

intention to continue the policy of increasing the minimum wage at rates that are significantly

higher than overall economic growth and consumer price inflation, leading to further increases in

the purchasing power of the population. At the same time, the increases of the minimum wage and

average salary have also resulted in the increase of our labour costs.

B.5 If the issuer

is part of a

group, a

description

of the group

and the

issuer’s

position

Sphera is the parent company of:

• US Food Network S.A., Romania (USFN (Romania)) holding franchise rights to operate KFC

branded restaurants in Romania;

• American Restaurant System S.A., Romania (ARS (Romania)) holding franchise rights to operate

Pizza Hut branded restaurants in Romania;

• US Food Network S.A., Italy (USFN (Italy)) holding franchise rights to operate KFC branded

restaurants in certain northern regions of Italy;

4

within the

group. • US Food Network S.R.L., Republic of Moldova (USFN (Moldova)) operating KFC branded

restaurants in the Republic of Moldova;

• California Fresh Flavors S.R.L., Romania (California Fresh Flavors (Romania)) holding franchise

rights to operate Taco Bell restaurants in Romania.

Sphera together with its subsidiaries listed above are referred to in this Summary as the "Group".

The shareholders of Sphera are:

• Lunic Franchising and Consulting Ltd (Cyprus) ("Lunic (Cyprus)");

• M.B.L. Computers S.R.L. (Romania) ("MBL (Romania)");

• Tatika Investments Ltd. (Cyprus) ("Tatika (Cyrpus)");

• Anasa Properties S.R.L. (Romania) ("Anasa Properties (Romania)");

• Wellkept Group S.A. (Romania) ("Wellkept (Romania)").

Ultimately, Lunic (Cyprus) and Anasa Properties (Romania) are owned by Mr. Lucian Vlad, MBL

(Romania) is owned by Mr. Nicolae Badea and Tatika (Cyprus) and Wellkept (Romania) are owned by

Mr. Radu Dimofte.

B.6 In so far as is

known, the

name of any

person who,

directly or

indirectly, has

an interest in

the issuer’s

capital or

voting rights

which is

notifiable

under the

issuer’s

national law,

together with

the amount of

each such

person’s

interest.

Whether the

issuer’s

major

shareholders

have different

voting rights

if any. To the

extent known

to the issuer,

state whether

the issuer is

directly or

indirectly

owned or

controlled

and by whom

and describe

the nature of

such control.

On the date of the Prospectus, no voting rights in Sphera are notifiable according to the Romanian law.

The shareholders structure of Sphera on the date of the Prospectus is the following:

Shareholder Number of shares Percentage of

voting rights

Tatika Investments Ltd. 10,603,860 27.33%

Wellkept Group S.A. 6,339,812 16.34%

Lunic Franchising and Consulting Ltd. 8,667,773 22.34%

Anasa Properties S.R.L. 4,264,047 10.99%

M.B.L. Computers S.R.L. 8,923,848 23.00%

Total 38,799,340 100.00%

After the admission of the Shares to trading on the spot regulated market operated by the Bucharest

Stock Exchange ("BSE"), if following the acquisition or sale of or other operations in Shares, the

proportion of voting rights held by a person reaches, exceeds or falls below one of the thresholds of 5%,

10%, 15%, 20%, 25%, 33%, 50% or 75% of the total voting rights, that person must notify the

Company of the proportion of the voting rights held promptly, but not later than 4 trading days.

The shareholders of the Company have equal voting rights.

None of the shareholders listed above exercises control or common control over the Company.

B.7 Selected

historical key

financial

information

regarding

the issuer,

The following have been identified as the Group's historical financial statements for the purpose of this

Prospectus:

• US Food Network S.A. Consolidated Financial Statements prepared in accordance with the

International Financial Reporting Standards as adopted by the European Union for the years ended

31 December 2014, 31 December 2015 and 31 December 2016, respectively, audited ("USFN

5

presented for

each

financial

year of the

period

covered by

the historical

financial

information,

and any

subsequent

interim

financial

period

accompanied

by

comparative

data from the

same period

in the prior

financial

year except

that the

requirement

for

comparative

balance

sheet

information

is satisfied

by presenting

the year-end

balance

sheet

information.

This should

be

accompanied

by a

narrative

description

of significant

change to the

issuer’s

financial

condition

and

operating

results

during or

subsequent

to the period

covered by

the historical

key financial

information

(Romania) Annual Financial Statements");

• American Restaurant System S.A. Financial Statements prepared in accordance with the

International Financial Reporting Standards as adopted by the European Union for the years ended

31 December 2014, 31 December 2015 and 31 December 2016, respectively, audited ("ARS

(Romania) Annual Financial Statements");

• American Restaurant System S.A. Interim Consolidated Financial Statements prepared in

accordance with the International Financial Reporting Standards as adopted by the European

Union for the period ended 30 June 2017, unaudited ("ARS (Romania) Interim Financial

Statements"); and

• Sphera Franchise Group S.A. Interim Consolidated Financial Statements prepared in accordance

with the International Financial Reporting Standards as adopted by the European Union for the

period ended 30 June 2017, unaudited ("Sphera Interim Financial Statements").

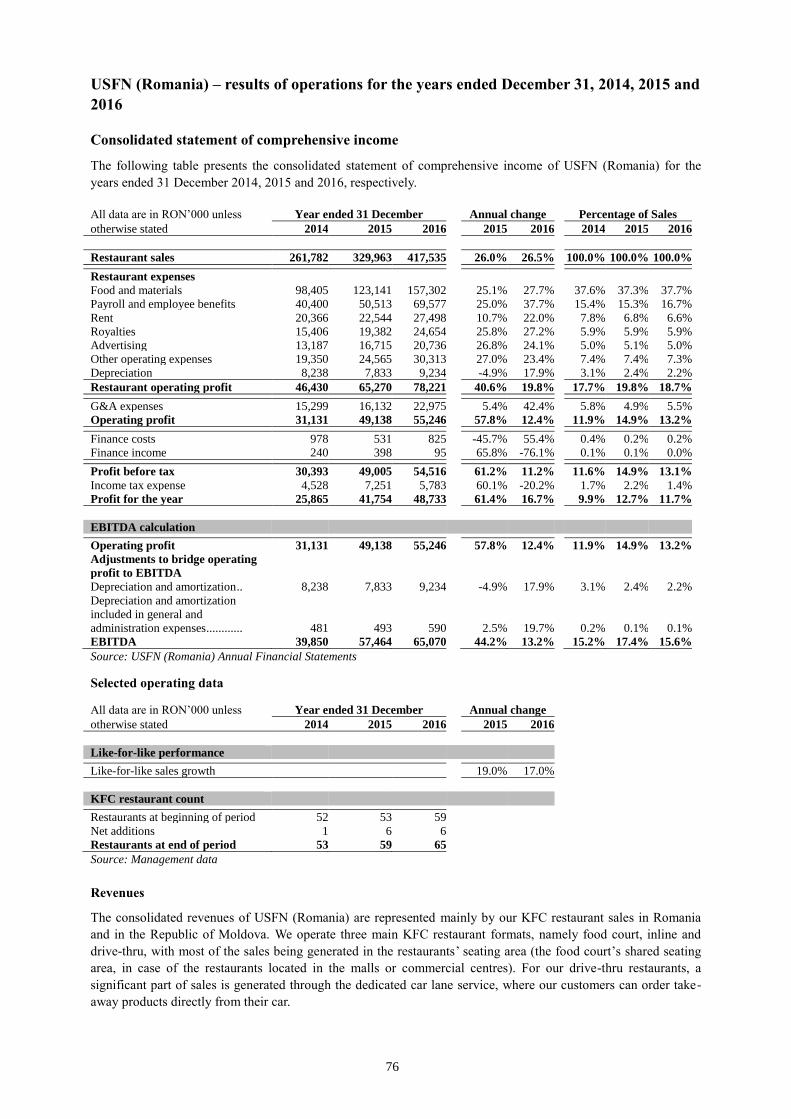

Summary of the consolidated statement of comprehensive income of USFN (Romania) and

of Sphera

Year ended 31 December

Six months ended 30

June

All data are in RON thousand

unless otherwise stated 2014 2015 2016

2016 2017

Unaudited

Restaurant sales 261,782 329,963 417,535

193,220 242,204

Restaurant expenses 215,352 264,693 339,314

156,197 197,650

Food and materials 98,405 123,141 157,302

74,225 87,944

Payroll and employee benefits 40,400 50,513 69,577

30,623 43,430

Rent 20,366 22,544 27,498

12,984 17,001 Royalties 15,406 19,382 24,654

11,380 14,125

Advertising 13,187 16,715 20,736

8,457 11,724

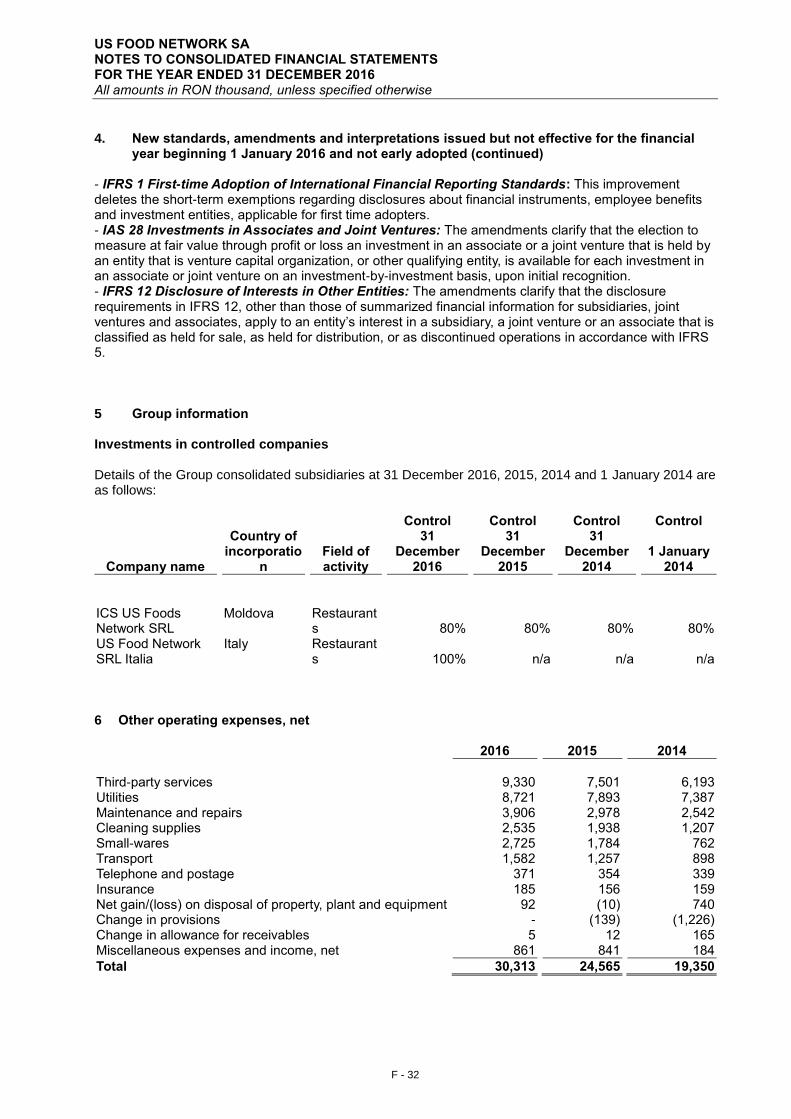

Other operating expenses, net 19,350 24,565 30,313

14,330 18,474 Depreciation and amortization 8,238 7,833 9,234

4,198 4,952

Restaurant operating profit 46,430 65,270 78,221

37,023 44,554

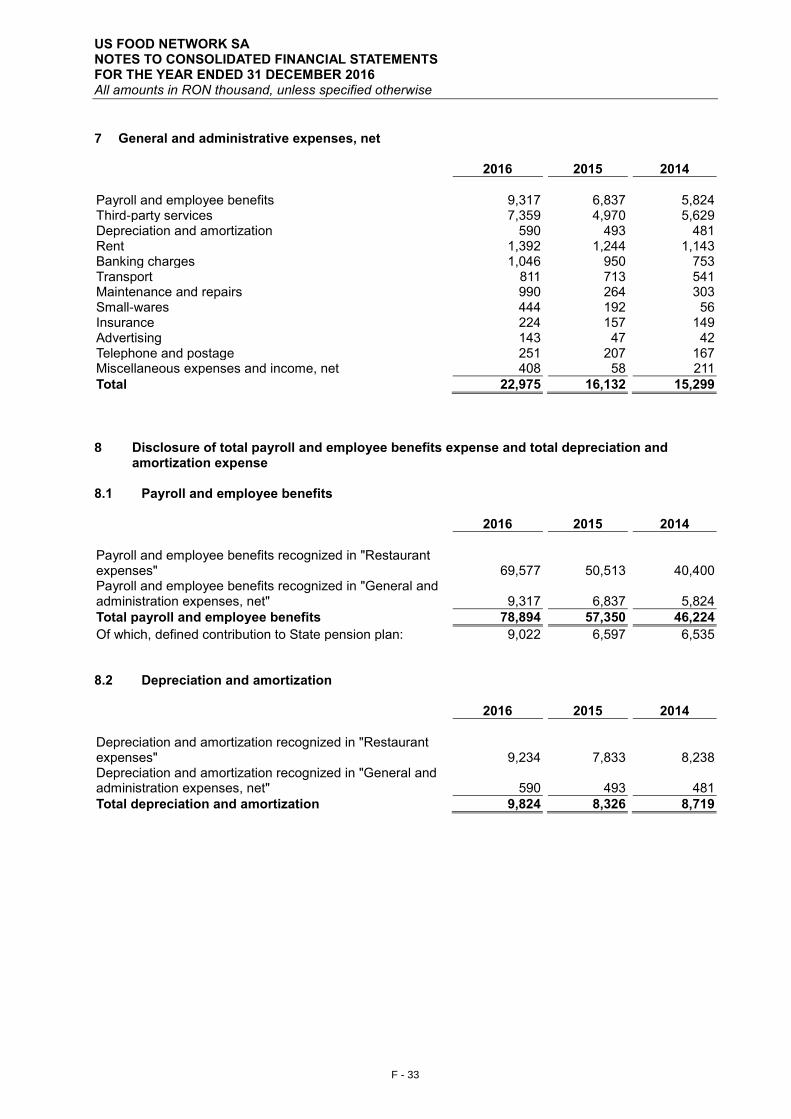

General and administration expenses, net 15,299 16,132 22,975

10,625 15,832

Operating profit 31,131 49,138 55,246

26,398 28,722

Finance costs 978 531 825

978 440

Finance income 240 398 95

125 109

Profit before tax 30,393 49,005 54,516

25,545 28,391

Income tax expense/(credit) 4,528 7,251 5,783

3,315 1,189

Profit for the period 25,865 41,754 48,733

22,230 27,202

Attributable to:

Equity holders of the parent 25,716 41,597 48,693

22,216 27,090

Non-controlling interests 149 157 40

14 112

Other comprehensive income

Other comprehensive income to be

reclassified to profit or loss in subsequent periods (net of tax): 0 0 0

(21) (30)

Exchange differences on translation

of foreign operations (10) (92) 83 Total comprehensive income for

the period, net of tax 25,855 41,662 48,816

22,209 27,172

Attributable to:

Equity holders of the parent 25,708 41,513 48,774

22,198 27,060

Non-controlling interests 147 149 42

11 112

Source: USFN (Romania) Annual Financial Statements; Sphera Interim Financial Statements,

unaudited

Summary of the consolidated statement of financial position of USFN (Romania) and of

Sphera

31 December

All data are in RON thousand unless

otherwise stated 2014 2015 2016

30-Jun-17

Unaudited

Assets

Non-current assets 41,658 45,562 54,246

143,055

Property, plant and equipment 37,779 41,084 47,551

81,159

Intangible assets 3,765 4,298 6,365

60,475

Trade and other receivables

285

6

Deposits for rent guarantee 95 163 290

668

Deferred tax assets 19 17 40

468

Current assets 38,275 55,497 65,399

51,769

Inventories 4,161 5,717 5,744

7,458 Trade and other receivables 3,473 4,438 8,780

5,077

Prepayments 1,729 1,743 1,907

3,418

Cash and short-term deposits 28,912 43,599 48,968

35,816

Assets held for sale

195

Total assets 79,933 101,059 119,645

195,019

Equity and liabilities

Total equity 33,456 50,482 58,253

100,342

Equity attributable to equity holders

of the parent 33,449 50,479 58,292

100,339

Issued capital 190 190 190

581,990

Share premium

(520,557)

Other capital reserves 19 19 19

- Retained earnings 33,278 50,392 58,124

38,977

Foreign currency translation reserve (38) (122) (41)

(71)

Non-controlling interests 7 3 (39)

3

Non-current liabilities 12,010 15,349 16,304

33,223

Interest-bearing loans and

borrowings 8,773 11,787 14,630

31,227

Trade and other payables 1,597 1,827 1,674

1,996

Deferred tax liabilities 1,640 1,735 -

Current liabilities 34,467 35,228 45,088

61,454

Trade and other payables 27,950 28,594 37,292

45,650

Interest-bearing loans and borrowings 6,378 6,634 7,796

15,804

Provisions 139 - -

Total liabilities 46,477 50,577 61,391

94,677

Total equity and liabilities 79,933 101,059 119,645

195,019

Source: USFN (Romania) Annual Financial Statements; Sphera Interim Financial Statements,

unaudited

Summary of the consolidated statement of cash flows of USFN (Romania) and of Sphera

Year ended 31 December

Six months ended 30 June

All data are in RON thousand

unless otherwise stated 2014 2015 2016

2016 2017

Unaudited

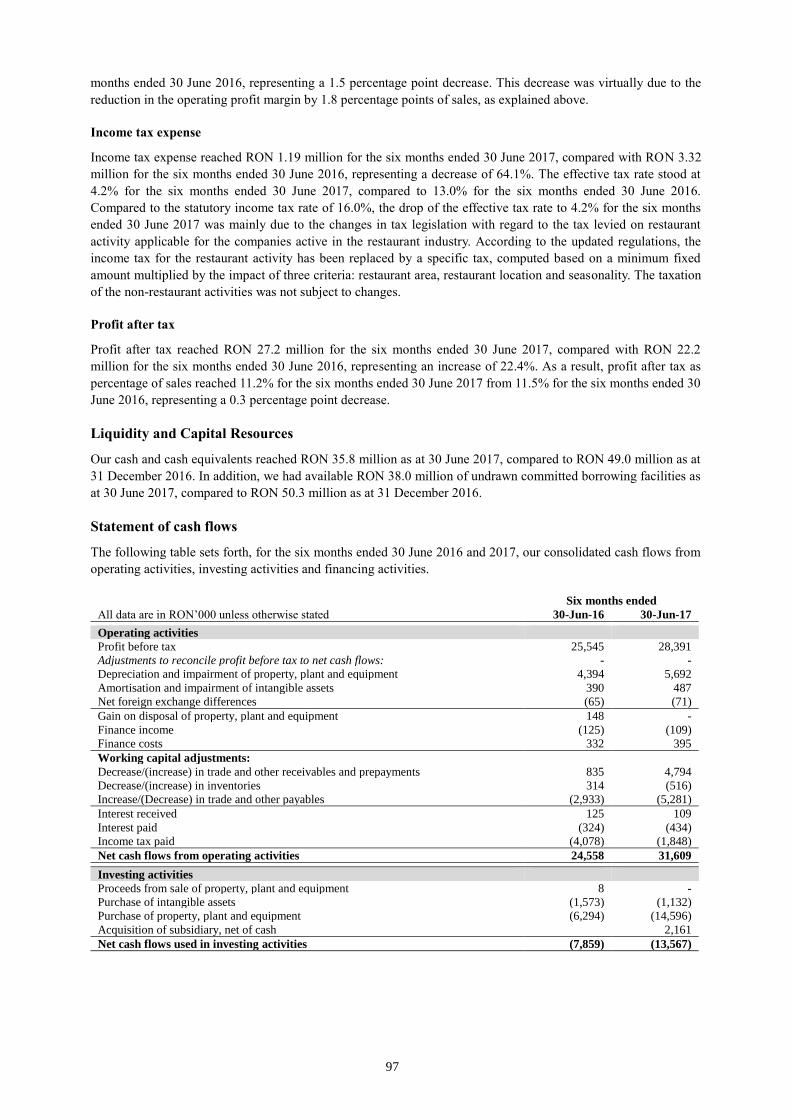

Operating activities

Profit before tax 30,393 49,005 54,516

25,545 28,391 Adjustments to reconcile profit

before tax to net cash flows:

Depreciation and impairment of property, plant and equipment 8,044 7,628 8,977

4,394 5,692

Amortisation and impairment of

intangible assets 675 698 847

390 487 Net foreign exchange differences (116) 181 60

(65) (71)

Gain on disposal of property, plant

and equipment 740 (10) 92

148 - Finance income (240) (398) (95)

(125) (109)

Finance costs 555 424 536

332 395

Movement in current assets

allowances 165 12 5 Movements in provisions, pensions

and government grants (1,226) (139) 0

Working capital adjustments:

Decrease/(Increase) in trade and

other receivables and prepayments (553) (989) (4,574)

835 4,794

Decrease/(Increase) in inventories (652) (1,570) (27)

314 (516) Increase/(Decrease) in trade and

other payables 8,035 459 8,655

(2,933) (5,281)

Interest received 192 342 31

125 109

Interest paid (561) (453) (561)

(324) (434) Income tax paid (3,452) (6,698) (7,619)

(4,078) (1,848)

Net cash flows from operating

activities 41,999 48,491 60,843

24,558 31,609

Investing activities

Proceeds from sale of property, plant

and equipment 2 27 0

8 - Purchase of intangible assets (430) (1,246) (2,916)

(1,573) (1,132)

7

Purchase of property, plant and

equipment (4,108) (10,935) (15,536)

(6,294) (14,596)

Acquisition of subsidiary, net of cash

- 2,161

Net cash flows used in investing

activities (4,536) (12,154) (18,452)

(7,859) (13,567)

Financing activities

Capital contribution from shareholders of Sphera on set up, net

of transaction costs paid

- 1,151

Proceeds from borrowings 3,382 10,993 11,704

3,552 19,225 Repayment of borrowings (7,531) (7,730) (7,480)

(3,678) (5,051)

Payment of finance lease liabilities (155) (185) (284)

(156) (134) Dividends paid to equity holders of

the parent (12,664) (24,483) (40,961)

(40,961) (46,237)

Dividends paid to non-controlling interests (133) (153) (84)

- (70)

Net cash flows from/(used in)

financing activities (17,101) (21,558) (37,105)

(41,263) (31,116)

Net increase/(decrease) in cash and cash equivalents 20,362 14,779 5,286

(24,564) (13,074)

Net foreign exchange difference (10) (92) 83

(18) (78)

Cash and cash equivalents at 1 January 8,560 28,912 43,599

43,599 48,968

Cash and cash equivalents at end

of period 28,912 43,599 48,968

19,017 35,816

Source: USFN (Romania) Annual Financial Statements; Sphera Interim Financial Statements,

unaudited

Summary of the statement of comprehensive income of ARS (Romania)

Year ended 31 December

Six months ended 30

June

All data are in RON thousand

unless otherwise stated 2014 2015 2016

2016 2017

Unaudited

Restaurant sales 63,130 75,867 96,940

46,398 54,210

Restaurant expenses 51,952 59,962 82,329

37,684 46,486

Food and materials 16,881 19,718 26,107

12,606 14,830

Payroll and employee benefits 12,001 14,622 22,383

9,608 13,690 Rent 6,081 6,476 8,027

3,672 4,692

Royalties 3,697 4,448 5,702

2,721 3,166

Advertising 3,590 4,245 5,785

2,727 2,973

Other operating expenses, net 7,514 8,339 11,659

5,234 5,386

Depreciation and amortization 2,188 2,114 2,666

1,116 1,749

Restaurant operating profit 11,178 15,905 14,611

8,714 7,724

General and administration

expenses, net 6,094 7,751 8,982

4,338 5,732

Operating profit 5,084 8,154 5,629

4,376 1,992

Finance costs 309 482 213

81 187

Finance income 7 19 127

93 6

Profit before tax from continuing

operations 4,782 7,691 5,543

4,388 1,811

Income tax expense 667 1,170 361

626 772

Profit for the period from

continuing operations 4,115 6,521 5,182

3,762 1,039

Discontinued operations

Profit/(loss) after tax for the year from discontinued operations (595) (397) (1,953)

293 -

Profit for the period 3,520 6,124 3,229

4,055 1,039

Source: ARS (Romania) Annual Financial Statements; ARS (Romania) Interim Financial Statements,

unaudited.

Summary of the statement of financial position of ARS (Romania)

31 December

8

All data are in RON thousand unless

otherwise stated 2014 2015 2016

30-Jun-17

Unaudited

Assets

Non-current assets 10,777 15,262 21,374

22,799

Property, plant and equipment 9,653 13,265 18,201

19,511

Intangible assets 1,007 1,749 2,917

2,757 Trade and other receivables

285

Deposits for rent guarantee 117 248 256

246

Current assets 14,806 18,562 11,612

6,225

Inventories 6,986 6,758 1,111

1,206 Trade and other receivables 5,849 5,363 6,089

1,513

Prepayments 665 867 1,118

1,186 Cash and short-term deposits 1,306 5,574 3,294

2,320

Assets held for sale 0 0 195

195

Total assets 25,583 33,824 33,181

29,219

Equity and liabilities

Total equity 6,607 8,781 5,980

3,651

Issued capital 1,644 1,644 1,644

1,644

Share premium 0 0 0 Other capital reserves 21 21 21

21

Retained earnings 4,942 7,116 4,315

1,986

Non-current liabilities 1,243 4,448 7,865

7,273

Interest-bearing loans and borrowings 492 3,692 7,536

6,950

Trade and other payables 307 302 329

323 Deferred tax liabilities 444 454 0

Current liabilities 17,733 20,595 19,336

18,295

Trade and other payables 16,298 18,477 15,401

13,967

Interest-bearing loans and borrowings 1,435 2,118 3,935

4,328

Total liabilities 18,976 25,043 27,201

25,568

Total equity and liabilities 25,583 33,824 33,181

29,219

Source: ARS (Romania) Annual Financial Statements; ARS (Romania) Interim Financial Statements,

unaudited

Summary of the statement of cash flows of ARS (Romania)

Year ended 31 December Six months ended 30 June

All data are in RON thousand unless

otherwise stated 2014 2015 2016

2016 2017

Unaudited

Operating activities

Profit before tax from continuing

operations 4,782 7,691 5,543

4,388 1,811

Profit/(loss) before tax from discontinued operations (708) (477) (2,141)

349 -

Profit before tax 4,074 7,214 3,402

4,737 1,811

Adjustments to reconcile profit before tax to net cash flows:

Depreciation and impairment of

property, plant and equipment 2,268 2,208 2,862

1,294 1,609 Amortisation and impairment of

intangible assets 202 210 323

147 207

Impairment allowance of property, plant and equipment - - 966

Net foreign exchange differences (129) 3 54

2 (8)

Gain on disposal of property, plant and equipment 391 (56) 115

6 (4)

Finance income (7) (19) (18)

(15) (6)

Finance costs 100 97 213

81 157 Movements in current asset allowances 2 19 -

- (63)

Working capital adjustments:

Decrease/(increase) in trade and other

receivables and prepayments (2,146) 153 (985)

2,187 4,233 Decrease/(increase) in inventories (673) 209 5,647

(2,420) (32)

Increase/(Decrease) in trade and other

payables 1,828 1,896 (2,489)

(483) (2,212)

Interest received 7 19 18

15 6

Interest paid (100) (119) (240)

(96) (162)

Income tax paid (592) (801) (1,186)

(928) -

Net cash flows from operating 5,225 11,033 8,682

4,527 5,536

9

activities

Investing activities

Proceeds from sale of property, plant

and equipment 15 56 33

- 8 Purchase of intangible assets (44) (953) (1,491)

(496) (47)

Purchase of property, plant and

equipment (1,119) (5,819) (9,107)

(4,139) (2,923)

Net cash flows used in investing

activities (1,148) (6,716) (10,565)

(4,635) (2,962)

Financing activities

Proceeds from borrowings - 6,359 8,603

3,762 1,838

Repayment of borrowings (2,151) (2,458) (2,769)

(1,297) (1,920)

Payment of finance lease liabilities (107) - (201)

(81) (98) Dividends paid to equity holders (1,800) (3,950) (6,030)

(6,030) (3,368)

Net cash flows from/(used in)

financing activities (4,058) (49) (397)

(3,646) (3,548)

Net increase in cash and cash equivalents 19 4,268 (2,280)

(3,754) (974)

Cash and cash equivalents at 1 January 1,287 1,306 5,574

5,574 3,294

Cash and cash equivalents at end of

period 1,306 5,574 3,294

1,820 2,320

Source: ARS (Romania) Annual Financial Statements; ARS (Romania) Interim Financial Statements,

unaudited

Since 30 June 2017, the reference date of Sphera Interim Financial Statements, there has been no

significant change in the financial or trading position of the Group.

B.8 Selected key

pro forma

financial

information,

identified as

such.

The selected

key pro

forma

financial

information

must clearly

state the fact

that because

of its nature,

the pro

forma

financial

information

addresses a

hypothetical

situation

and,

therefore,

does not

represent the

company’s

actual

financial

position or

results

The Pro forma Financial Information was prepared to illustrate the consolidated operational

performance of the Group for the twelve months periods ended 31 December 2014, 31 December 2015

and 31 December 2016 and for the six-month period ended 30 June 2017, respectively, as if the

incorporation of the Company and the contribution of USFN (Romania) shares and of ARS (Romania)

shares to the Company's share capital took place on 1 January 2014, 1 January 2015 and 1 January

2016, and 1 January 2017, respectively. The acquisition by the Company of the shares in USFN (Italy)

and in USFN (Moldova) from USFN (Romania), which has no impact on the consolidated financial

statements of the Company, and the incorporation of California Fresh Flavors (Romania) are not

adjusted for in the Pro forma Consolidated Financial Information.

USFN (Romania) and ARS (Romania) had identical shareholder structures and also their key

management personnel was preponderantly the same since 2012. Therefore, although from an IFRS

perspective the criteria to qualify as being "under common control" are not met (since none of the

shareholders had control or common control), the presentation of the Pro forma Information is reflective

of the manner in which the two business segments (KFC operated by USFN (Romania) and Pizza Hut

operated by ARS (Romania)) were managed together.

Because of its nature, the Pro forma Financial Information describes a hypothetical situation and

has been prepared for illustrative purposes only and does not purport to represent the

Company’s actual financial position or results, nor are they necessarily indicative of future

consolidated operational results.

In addition, the statements are based on available information and various assumptions that

management believes to be reasonable. The actual results may differ from those reflected in the Pro

forma Financial Information for a number of reasons, including, but not limited to, differences between

the assumptions used to prepare the Pro forma Financial Information and actual amounts.

The Pro forma Financial Information only consists of the pro forma consolidated statement of

comprehensive income for the twelve-month period ended 31 December 2014, 31 December 2015 and

31 December 2016 and for the six months period ended 30 June 2017, respectively, and selected notes.

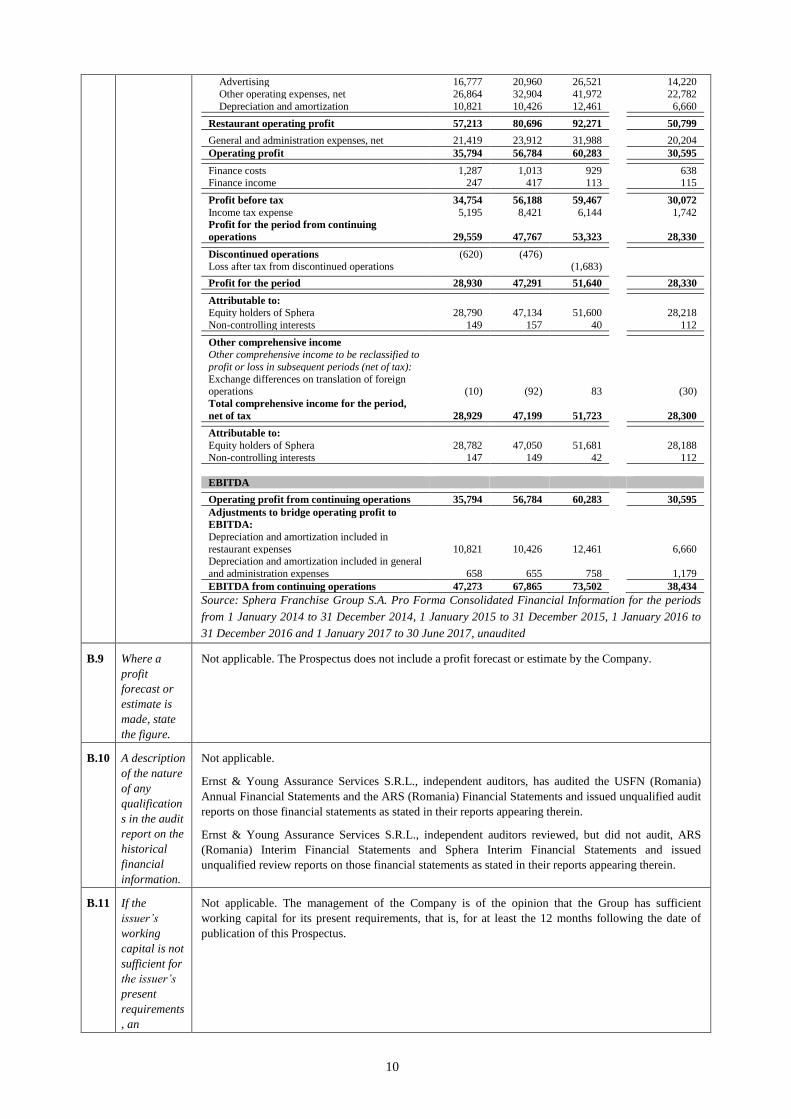

Summary of Pro forma consolidated statement of comprehensive income for the years ended 31

December 2014, 2015 and 2016 and for six months ended 30 June 2017

Year ended 31 December

Six months

ended 30

June

2014 2015 2016

2017

Unaudited

Restaurant sales 324,912 405,830 514,475

287,833

Restaurant expenses 267,699 325,134 422,204

237,034

Food and material expenses 115,286 142,859 183,409

100,472

Payroll and employee benefits 52,401 65,135 91,960

55,195

Rent 26,447 29,020 35,525

20,898 Royalties 19,103 23,830 30,356

16,807

10

Advertising 16,777 20,960 26,521

14,220

Other operating expenses, net 26,864 32,904 41,972

22,782

Depreciation and amortization 10,821 10,426 12,461

6,660

Restaurant operating profit 57,213 80,696 92,271

50,799

General and administration expenses, net 21,419 23,912 31,988

20,204

Operating profit 35,794 56,784 60,283

30,595

Finance costs 1,287 1,013 929

638 Finance income 247 417 113

115

Profit before tax 34,754 56,188 59,467

30,072

Income tax expense 5,195 8,421 6,144

1,742 Profit for the period from continuing

operations 29,559 47,767 53,323

28,330

Discontinued operations (620) (476)

Loss after tax from discontinued operations

(1,683)

Profit for the period 28,930 47,291 51,640 28,330

Attributable to: Equity holders of Sphera 28,790 47,134 51,600 28,218

Non-controlling interests 149 157 40 112

Other comprehensive income Other comprehensive income to be reclassified to

profit or loss in subsequent periods (net of tax):

Exchange differences on translation of foreign operations (10) (92) 83 (30)

Total comprehensive income for the period,

net of tax 28,929 47,199 51,723 28,300

Attributable to:

Equity holders of Sphera 28,782 47,050 51,681 28,188

Non-controlling interests 147 149 42 112

EBITDA

Operating profit from continuing operations 35,794 56,784 60,283 30,595

Adjustments to bridge operating profit to

EBITDA:

Depreciation and amortization included in

restaurant expenses 10,821 10,426 12,461 6,660 Depreciation and amortization included in general

and administration expenses 658 655 758 1,179

EBITDA from continuing operations 47,273 67,865 73,502 38,434

Source: Sphera Franchise Group S.A. Pro Forma Consolidated Financial Information for the periods

from 1 January 2014 to 31 December 2014, 1 January 2015 to 31 December 2015, 1 January 2016 to

31 December 2016 and 1 January 2017 to 30 June 2017, unaudited

B.9 Where a

profit

forecast or

estimate is

made, state

the figure.

Not applicable. The Prospectus does not include a profit forecast or estimate by the Company.

B.10 A description

of the nature

of any

qualification

s in the audit

report on the

historical

financial

information.

Not applicable.

Ernst & Young Assurance Services S.R.L., independent auditors, has audited the USFN (Romania)

Annual Financial Statements and the ARS (Romania) Financial Statements and issued unqualified audit

reports on those financial statements as stated in their reports appearing therein.

Ernst & Young Assurance Services S.R.L., independent auditors reviewed, but did not audit, ARS

(Romania) Interim Financial Statements and Sphera Interim Financial Statements and issued

unqualified review reports on those financial statements as stated in their reports appearing therein.

B.11 If the

issuer’s

working

capital is not

sufficient for

the issuer’s

present

requirements

, an

Not applicable. The management of the Company is of the opinion that the Group has sufficient

working capital for its present requirements, that is, for at least the 12 months following the date of

publication of this Prospectus.

11

explanation

should be

included.

Section C—Securities

C.1 A description

of the type

and the class

of the

securities

being offered

and/or

admitted to

trading,

including

any security

identification

number.

The Offering consists in an offering of an aggregate number of up to 9,831,753 nominative, ordinary

shares in the Company, offered as follows: (1) up to 8,667,773 ordinary shares in the Company by

Lunic (Cyprus); and (2) up to 1,163,980 ordinary shares in the Company by MBL (Romania).

In case of successful closing of the Offering, application will be made for the admission of the Shares to

trading on the spot regulated market operated by the BSE.

The security identification numbers of the Shares are:

ISIN: ROSFGPACNOR4;

CFI: ESVUFR;

LEI: 315700GSVZ0HSS7J1457;

BSE market symbol: SFG.

C.2 Currency of

the securities

issue.

The currency of the Shares is RON.

C.3 The number

of shares

issued and

fully paid

and issued

but not fully

paid. The par

value per

share, or that

the shares

have no par

value.

As at the date of the Prospectus, the issued, subscribed and paid-up share capital of the Company is

divided into 38,799,340 nominative, ordinary, book entry form shares, each of which is issued, fully

paid with a par value of RON 15 and carrying one vote in the Company's general shareholders

meetings.

C.4 A description

of the rights

attached to

the

securities.

Each Offered Share is an ordinary share of par value RON 15 carrying similar rights.

All shareholders are to be treated equally to other shareholders that own the same type of Shares, with

the material rights set forth below:

• the pre-emptive right of the shareholders to subscribe for any issue of new shares on a pro rata

basis, unless such pre-emptive right is limited by the general shareholders meeting in accordance

with the law and the articles of association;

• the right to vote and participate in the general meetings of the shareholders;

• the right to receive dividends, if declared;

• the right to information (e.g. to be informed about the activity of the Company in line with and

subject to the applicable law, to obtain any information regarding the exercise of voting rights and

information regarding the voting results in the general shareholders meetings);

• the right to add new items on the agenda of the meeting or propose draft resolution, in case of

shareholders holding severally or jointly at least 5% of the share capital;

• the right to withdraw from the Company and to request the Company to acquire their shares, in

case the shareholders did not vote in favour of a certain decision in the general meeting of

shareholders;

• the rights to proceeds derived from the liquidation of the Company, when applicable;

• the right to challenge the decisions of the general meeting of shareholders; and

• other rights provided under the Company’s articles of association, by-laws and applicable law.

C.5 A description

of any

restrictions

on the free

transferabilit

Starting with the first trading date on the BSE, the Shares will be freely transferable subject to the rules

of the regulated spot market operated by the BSE, and clearing and settlement rules of Depozitarul

Central S.A. (the "Romanian CSD").

12

y of the

securities.

C.6 An indication

as to whether

the securities

offered are

or will be the

object of an

application

for

admission to

trading on a

regulated

market and

the identity

of all the

regulated

markets

where the

securities are

or are to be

traded.

After the Offering is successfully closed in accordance with the provisions of the Prospectus and the

transactions in the Offered Shares are settled, the Company intends to apply for the admission of the

shares issued by the Company to trading on the spot regulated market operated by the BSE.

C.7 A description

of dividend

policy.

The Company's ability to pay dividends is based, among other things, on the Company's future profits,

including the distributable profits obtained by the Company's consolidated subsidiaries, as recorded in

the Company's financial statements. Dividends (if any) may only be declared and paid from the current

year’s statutory profit and accumulated profit from previous years, as recorded in the Company's annual

financial statements as approved by the ordinary general shareholders meeting ("OGSM") on the basis

of the report presented by the Company's board of directors ("BoD"). In determining the amount

available for distribution as dividends, the current year’s statutory profit and accumulated profit from

previous years will be adjusted to account for the creation of the required statutory reserves. In absence

of exceptional market conditions or circumstances, for future years the BoD intends to recommend to

the OGSM that the Company distributes 100% of its distributable profits each year, subject to any

restrictions due to Romanian legal and taxation regulation. Furthermore, the BoD may from time to

time propose to the shareholders cash distributions by way of restitution of capital to the shareholders, if

it finds that such distribution is appropriate and sustainable in the context of the Group's growth strategy

and provided that such distribution may be carried out in compliance with the applicable law.

Section D—Risks

D.1 Key

information

on the key

risks that are

specific to

the issuer or

its industry.

Risks Relating to the Group's Business and Industry

• Our rights to operate KFC, Pizza Hut and Taco Bell branded units are dependent on the Franchise

Agreements concluded with Yum!

• Our business depends on our relationship with Yum! and on our ability to comply with Yum!

requirements

• We may not be able to comply with the minimum roll-out of restaurants imposed by Yum!

• Failure by Yum! to protect its intellectual property rights, including its brands, could harm our

results of operations

• We operate in a highly competitive market, and competition is expected to increase in the coming

years

• We are dependent on our suppliers and the supply chain may be materially disrupted

• Increases in commodity prices or other operating costs could decrease our operating profit margins

• Product liability claims or poultry related health pandemics could have a negative impact on

consumers' confidence in the safety and quality of our products

• We may be unable to attract or retain sufficient qualified personnel, including due to increased

labour costs

• We are dependent on our management and key personnel

• We may not be able to implement our expansion strategy

• We have recently entered the Italian market by opening KFC restaurants in cities where the KFC

brand is novel

13

• We have launched and are further planning to develop Taco Bell brand in the Romanian market

• Failure to secure sub-franchisees may have an impact on the Pizza Hut Delivery business

• We operate in a sector where a number of approvals, licences and permits need to be in place for

each restaurant

• Our operational authorisations and permits may be deficient

• Fire safety permits are required for all our restaurants

• Operating and leasing a broad portfolio of locations exposes us to potential losses and liabilities

• Covenants and events of default in the agreements governing our outstanding indebtedness could

limit our ability to undertake certain types of transactions and adversely affect our liquidity

• We are exposed to fluctuations in foreign exchange rates

• We are exposed to fluctuations of the interest rate

• We may be exposed to claims or disputes in the ordinary course of business

• A potential failure to protect the integrity and security of personal information of our customers

and employees could result in substantial costs, expose us to litigation and damage our reputation

• We may not be able to ensure the traceability of the recovered/recycled package waste

• A number of insurance policies need to be in place to cover for a wide range of potential liabilities

• A strike or other labour disruption may have a material adverse effect on our business

• Poor maintenance of the road network in Romania may adversely affect our Pizza Hut Delivery

business

• Our information systems and the implementation of an Enterprise Resource Planning (ERP), may

fail or be damaged, which could harm our operations and our business

• Any changes to the current food law regime in Romania and in other countries in which we

operate may require engagement of significant costs to ensure compliance

• Any tax increase or change in tax legislation may adversely affect our operational results

• We may not be able to always comply with the transfer pricing rules

• Deductibility of expenses and VAT may be limited

• We may have to implement IFRS 16 (Leases) starting on or after 1 January 2019

• Our management team and the BoD members have limited experience in managing and governing

a public company, and regulatory compliance may divert our attention from the administration of

our business

• Our restaurants and the equipment in our restaurants may get damaged or destroyed as a result of

events or factors that are beyond our control

• We are exposed directly or indirectly to reputational risk

Country-Specific and Regional Risks

• Investor confidence in emerging economies, including Romania, may further decline due to

uncertainty regarding the global macroeconomic environment

• Recent political and social unrest risks weakening market confidence

• Deterioration in fiscal policies threatens growth in Romania

• Financing opportunities from internal and external sources are under-exploited which hinders

growth

• The Romanian national currency may register high levels of volatility

• Deficient and poor-quality infrastructure in Romania limits investments

• EU may apply sanctions if Romania fails to meet its post-accession obligations

• Law making processes often skip public consultation or impact study stages and adopted

legislation is not applied consistently by public authorities and courts and frequently lacks

transitional norms, which endangers competitiveness

• The European Commission has initiated infringement proceedings against Romania in a number

of areas, including waste management

• Corruption could create a difficult business climate

D.3 Key

information

Risks relating to the Shares

• The Offering may not result in an active or liquid trading market and investors may be unable to

14

on the key

risks that are

specific to

the

securities.

resell their Shares at or above the Final Offer Price

• The current shareholders of the Company will continue to have significant influence over the

Company after the Offering, and their interests may not be aligned with those of the other

shareholders of the Company

• The Shares may not be admitted to trading on the BSE or may be de-listed from the BSE

• As a holding company, the Company’s operating results, financial condition and ability to pay

dividends or other distributions are mainly dependent on dividends and other distributions

received from its subsidiaries

• Exchange rate variations may have an adverse impact on the value of non-Romanian holders of

Shares

• The price of the Shares may generally fluctuate

• Future sales of substantial amounts of our ordinary shares, or the perception that such sales could

occur, could adversely affect the market value of the Shares

• Due to a gap of five days between the pricing and the prospective first date of trading in the

shares, the initial trading price may be lower than the Final Offer Price

• Financing subscriptions in Offered Shares may create a misleading appearance with respect to

interest in the Offering

• There is no central counterparty for the spot market in Romania

Section E—Offer

E.1 The total net

proceeds and

an estimate

of the total

expenses of

the

issue/offer,

including

estimated

expenses

charged to

the investor

by the issuer

or the

offeror.

The Company will not receive any proceeds from the Offering.

The total estimated net proceeds obtained by the Selling Shareholders from the sale of the Offered

Shares in the Offering, after deduction of all fees, and charges incurred with the Offering, will be of

approximately RON 311,014,220 (assuming that all Offered Shares will be sold at the maximum price

of the Price Range and no proceeds will be used for stabilisation activities).The total estimated fees, and

charges payable by the Selling Shareholders in connection with the Offering are expected to be in the

range of RON 13,433,629 (assuming that all Offered Shares will be sold at the maximum price of the

Price Range).

The total fees and charges payable by the Company in connection with the Offering are expected to be

in the range of RON 424,769.

No commissions, fees or expenses in connection with the Offering will be charged to investors by the

Company or by any Selling Shareholder. However, the investors shall be charged costs (if any)

associated with opening and maintaining a securities account (unless such investor already has an

account) and any brokerage commissions payable by the institutional investors under any relevant

agreements or pursuant to the regulations of the entity accepting such purchase orders.

E.2a Reasons for

the offer, use

of proceeds,

estimated net

amount of

the proceeds.

The Offering is being conducted in order to allow the Selling Shareholders to dispose of a portion of

their shareholdings, while raising Sphera’s profile with the international investment community and

establishing a market for the Shares, which may benefit Sphera if it desires to access the equity markets

in the future.

The total estimated net proceeds obtained by the Selling Shareholders from the sale of the Offered

Shares in the Offering, after deduction of all fees, and charges incurred with the Offering, will be of

approximately RON 311,014,220 (assuming that all Offered Shares will be sold at the maximum price

of the price range and no proceeds will be used for stabilisation activities).

E.3 A description

of the terms

and

conditions of

the offer.

The Offer Shares will be offered at the Offer Price Range that is RON 25 to RON 33(the "Offer Price

Range") and will be sold at the final offer price determined in RON (the "Final Offer Price").

Subscriptions for Offered Shares can be made from 24 October 2017 to 2 November 2017 inclusively,

namely 8 (eight) Business Days (the "Offer Period"), unless extended or otherwise changed. The price

of the Offered shares is denominated in RON.

The Offering is split into two tranches (the "Offer Tranches") as follows:

• 15% of the Offered Shares (1,474,763 Offered Shares) will be initially offered to Retail Investors

(the "Retail Tranche"); and

• the remaining Offered Shares (8,356,990 Offered Shares) will be offered to Institutional Investors

(the "Institutional Tranche").

Retail Investors must subscribe for Offered Shares at the fixed price of RON 33 (i.e. the top of the Offer

Price Range).

15

Institutional Investors may validly subscribe for Offered Shares at any price within the Offer Price

Range (including the bottom and the top of the price range). The price tick for the subscription of

Offered Shares by Institutional Investors is RON 0.1.

In case of oversubscription in the Retail Tranche, the allocation shall be done pro-rata. The Selling

Shareholders will determine, in close consultation with Wood & Company Financial Services a.s., and

Raiffeisen Bank S.A., as Joint Bookrunners, the number of Offered Shares allocated to each

Institutional Investor, based on certain qualitative criteria.

The allocation factor for the Retail Tranche, together with the final number of allocated Offered Shares,

will be publicly announced on the last day of the Offer Period (the "Allocation Date").

The Final Offer Price for Retail Investors is equal to the Final Offer Price for Institutional Investors.

The Final Offer Price will be determined based on the expressions of interest made by the Institutional

Investors during the bookbuilding process. The Final Offer Price will be publicly announced no later

than one Business Day following the Allocation Date.

The transaction related to the Offered Shares will take place on the transaction date and the transfer of

the Offered Shares will be settled through the Romanian CSD's system within two business days from

the transaction date.

E.4 A description

of any

interest that

is material to

the

issue/offer

including

conflicting

interests.

The Managers and their respective affiliates may have engaged in transactions with, and performed

various investment banking, commercial banking, financial advisory and other services for, the

Company and the Selling Shareholders and their respective affiliates, for which they received

customary fees. The Managers and their respective affiliates may provide such services for the

Company and the Selling Shareholders and their respective affiliates in the future.

In connection with the Offering, each of the Managers and any affiliate, acting as an investor for its own

account may take up the Offered Shares and in that capacity may retain, purchase or sell for its own

account such Offered Shares and any related investments and may offer or sell such Offered Shares or

other investments otherwise than in connection with the Offering. Accordingly, references in this

Prospectus to the Offered Shares being offered or placed should be read as including any offering or

placement of Offered Shares to the Managers and any affiliate acting in such capacity. None of the

Managers intend to disclose the extent of any such investment or transactions otherwise than in

accordance with any legal or regulatory obligation to do so. In addition, in connection with the

Offering, certain of the Managers may enter into financing arrangements with investors, such as share

swap arrangements or lending arrangements where securities are used as collateral, which could result

in such Managers acquiring shareholdings in the Company.

E.5 Name of the

person or

entity

offering to

sell the

security.

Lock-up

agreements:

the parties

involved;

and

indication of

the period of

the lock up.