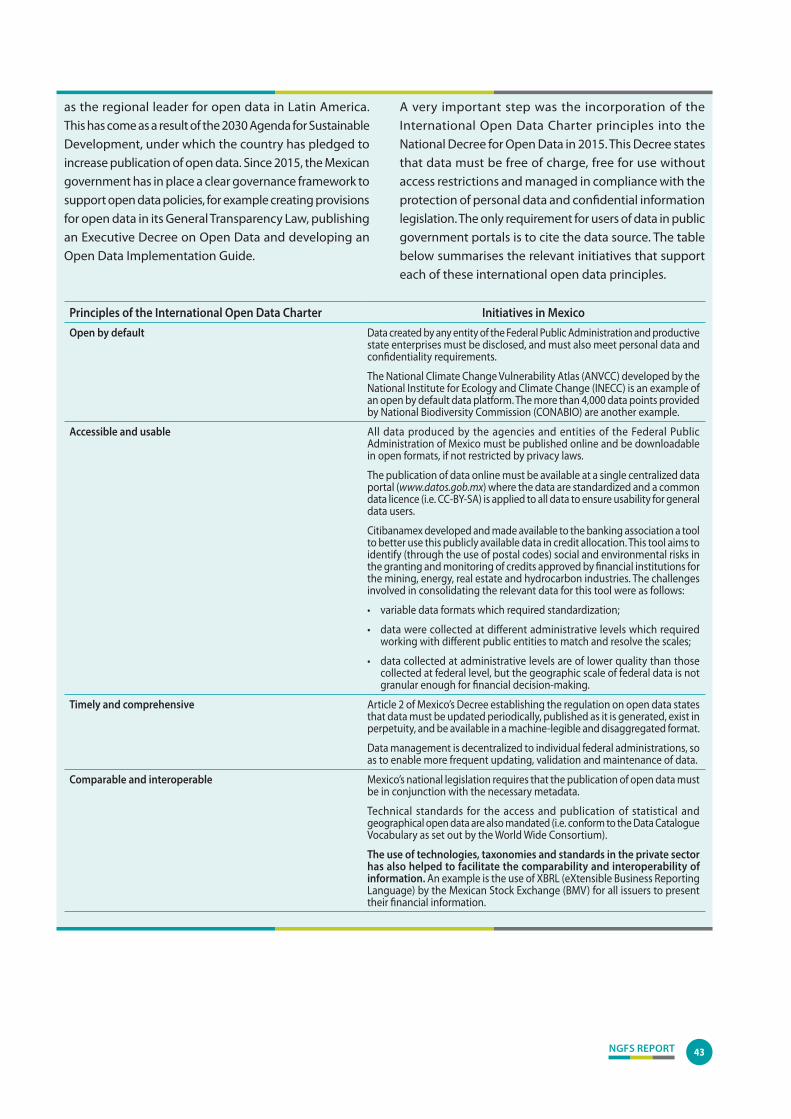

Progress report on bridging data gaps - NGFS

52

Network for Greening the Financial System Technical document Progress report on bridging data gaps May 2021

-

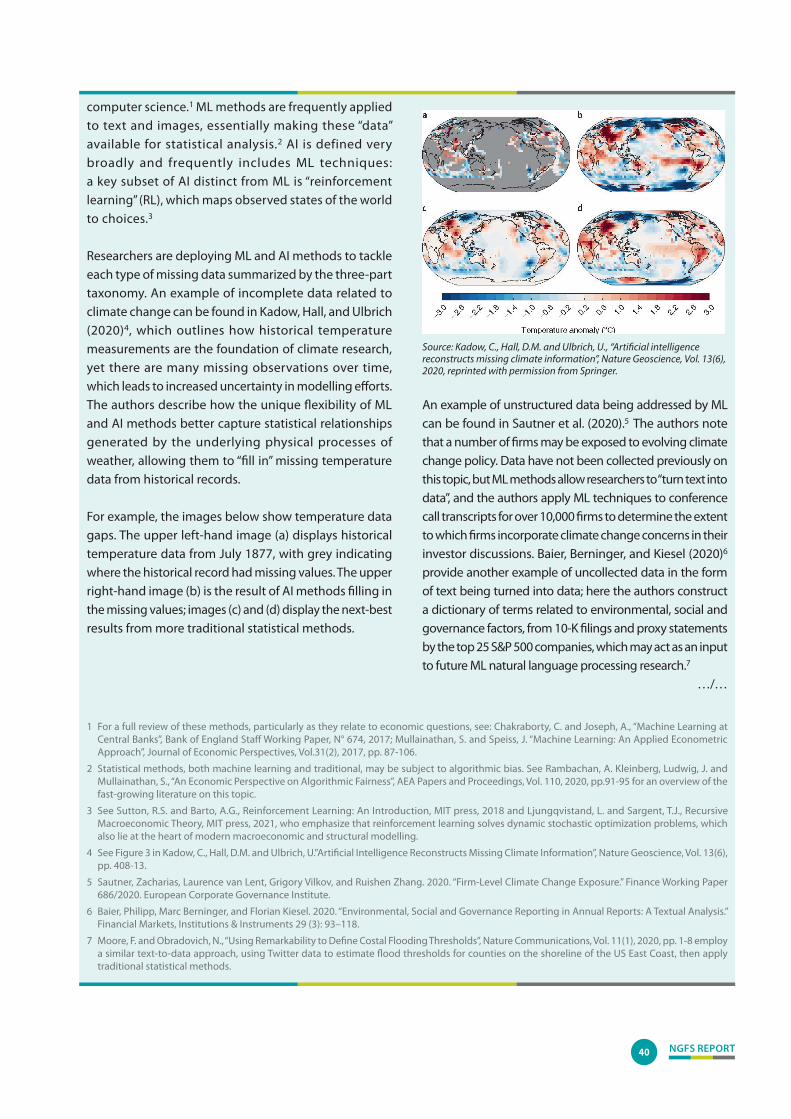

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Progress report on bridging data gaps - NGFS

Network for Greening the Financial System Technical document

Progress report on bridging data gapsMay 2021

NGFS REPORT2

Climate change poses a fundamental threat to our prosperity and collective well-being. As extreme weather events increase sharply and biodiversity declines at an alarming rate around the globe, devising effective means to address climate-related and environmental risks becomes more urgent by the second.

The Network for Greening the Financial System (NGFS) aims to contribute to this effort. From our inception in 2017, we have worked to strengthen the global response required to meet the goals of the Paris Agreement. Policymakers need to act urgently to strengthen the role that the financial system can play in managing climate-related risks and mobilizing capital for green and low-carbon investments.

Over the years, the lack of good quality and readily accessible climate-related data has posed a challenge for central banks, supervisors and financial sector participants alike. Against this backdrop, in 2020 the NGFS set up a Workstream dedicated to more systematically mapping such data gaps and proposing ways to bridge them. This report lays the groundwork for a comprehensive stock-take of the data needs, objectives and activities of stakeholders across the financial sector, and identifies ways to further bridge gaps.

Better data does not simply mean more data. Both the public sector and the private sector need high-quality, granular, reliable and comparable climate-related data. The findings of this report suggest that we need to foster convergence towards more consistent and more easily accessible data, and ultimately build up a global climate information architecture in a series of steps. First, we must promote rapid convergence towards a common and consistent set of global sustainability disclosure standards. Second, we must support efforts towards a minimally accepted global taxonomy. Third, we must develop clear metrics and methodologies for climate-related and environmental risks that help decision-making by organizations and individuals in the financial sector.

Importantly, we – financial institutions, investors, supervisors and central banks – need to act urgently. As this report shows, there is significant scope to already start leveraging available data and approaches.

The NFGS will continue its work to identify and prioritize data needs, enhance the availability, reliability and comparability of climate-related data, and develop policy recommendations to bridge the data gaps identified. A final report will be published towards the end of the year.

We are grateful to all NGFS members and observers for their ongoing contributions to this work. Our special thanks go to the lead authors of this progress report and its contributors, as well as the NGFS Secretariat. Their tireless efforts continue to make it possible for us to carry forwards the mission of the NGFS and promote a more sustainable and climate-conscious financial system.

Patrick Amis

Co-Chair of the Workstream on bridging the data gaps

Fabio Natalucci

Co-Chair of the Workstream on bridging the data gaps

Frank Elderson

Chair of the NGFS

Joint foreword by Frank Elderson, Patrick Amis and Fabio Natalucci

NGFS REPORT 3

Table of Contents

Executive summary 4

1. Introduction 101.1. Climate change and the data challenge 10

1.2. Mandate and work programme of the NGFS Workstream on bridging the data gaps (WS BDG) 10

2. A repository of data needs 132.1. Taking stock of stakeholders’ needs 14

2.2. Identifying common metrics 15

2.3. Deriving the raw data items needed 18

3. Key issues related to data availability, reliability and comparability 213.1. Issues related to data availability 21

3.2. Issues related to data reliability and comparability 23

3.3. Key findings from the workshops 25

4. Building blocks to bridge the data gaps 274.1. Disclosure standards 28

4.2. Taxonomies 31

4.3. Metrics, labels and methodological standards 32

4.4. Existing sources and approaches 36

Acknowledgements 45

List of acronyms 46

List of boxes and figures 48

Annex: Glossary of use cases 49

NGFS REPORT4

Climate change and the data challenge

Reliable and comparable climate-related data are crucial for financial institutions (including central banks and supervisors), investors and policymakers to assess financial stability risks, properly price and manage climate-related risks, and take advantage of the opportunities arising from the transition to a low-carbon economy. Such climate-related data are key for microprudential and macroprudential supervision. They also enable financial institutions and investors to gauge the financial repercussions of climate change and increase their resilience to climate-related risks. Moreover, they enable financial institutions to ensure that

Executive summary

• Reliable and comparable climate-related data are crucial in order for financial sector stakeholders to assess financial stability risks, properly price and manage climate-related risks, and take advantage of the opportunities arising from the transition to a low-carbon economy.

• Persistent gaps in climate-related data hinder the achievement of these objectives. Stakeholders report the need for more forward-looking data (for example targets or emissions pathways) and granular data (for example geographical data at entity and asset-levels). Stakeholders are also calling for assurance about the quality of climate-related data through verification and audit mechanisms, as well as improvements in data accessibility.

• A mix of policy interventions is needed to catalyse progress towards better data, based on the following three building blocks: i. rapid convergence towards a common and consistent set of global disclosure standards;ii. efforts towards a minimally accepted global taxonomy;iii. the development and transparent use of well-defined and decision-useful metrics, certification labels

and methodological standards.

• Global progress on the building blocks that the NGFS is calling for should not prevent better leveraging of already available data sources and approaches (such as proxies and estimates, qualitative approaches and capacity building), as well as the promotion of new data tools.

• The NGFS will continue its evidence-based identification of the most prevalent data gaps – including by further engaging with other stakeholders such as non-financial corporates, data providers and ratings agencies – and issue recommendations on how to bridge them.

Key messages

sufficient capital is made available for the investments needed to achieve the goals of the Paris Agreement.

Persistent gaps in climate-related data hinder the achievement of these objectives. The need to find solutions for data gaps has garnered significant attention and led to a renewed sense of urgency, as pressure continues to grow to address climate change from investors, researchers, regulators and policymakers, as well as NGOs and the general public. These data gaps have multiple causes, which include the time horizon for climate-related risks, the widespread nature of their impact and the high degree of uncertainty surrounding them, as well as the need to translate climate-related risks into financial impacts.

NGFS REPORT 5

Mandate and work programme of the Workstream on bridging the data gaps (WS BDG)

The Network for Greening the Financial System (NGFS) set up the Workstream on bridging the data gaps (WS BDG) in July 2020 to identify climate-related data needs and data gaps and to propose policy recommendations to bridge such gaps. The WS BDG represents the implementation of Recommendation n° 3 “Bridging the data gaps” issued in April 2019 in the First comprehensive report by the NGFS. More specifically, in line with its mandate, the work of the WS BDG is structured according to the following three-phase approach:i Identify data items needed by the financial sector –

including central banks and supervisors – for the purpose of climate-related risk analysis and the scaling up of green finance.

ii Determine whether the data items are available, and if so, identify their data sources and limitations for accessing them.

iii Provide guidance and recommendations on how to bridge the data gaps identified.

This Progress report forms part of the first phase of the Workstream’s work programme and, in setting out the issues that need to be considered going forward, lays the groundwork for a comprehensive assessment of climate-related data needs and gaps. The Workstream completed a systematic literature review, undertook outreach to a variety of international organizations and other relevant stakeholders, and conducted a survey and two closed-door workshops with banks and buy-side firms. Given the breadth and magnitude of climate-related risks, and the urgent need for action, this report is narrowly focused on climate-related data issues, both at a granular

level (such as firm-level data and asset-level exposures) and at an aggregate level (such as data on the incidence of natural disasters at the regional or country level). Broader environmental data issues, for example those related to biodiversity, may be addressed in the future. It should be noted that climate change research, methodologies and metrics for application in the financial sector are evolving quickly and further data needs will continue to emerge over time.

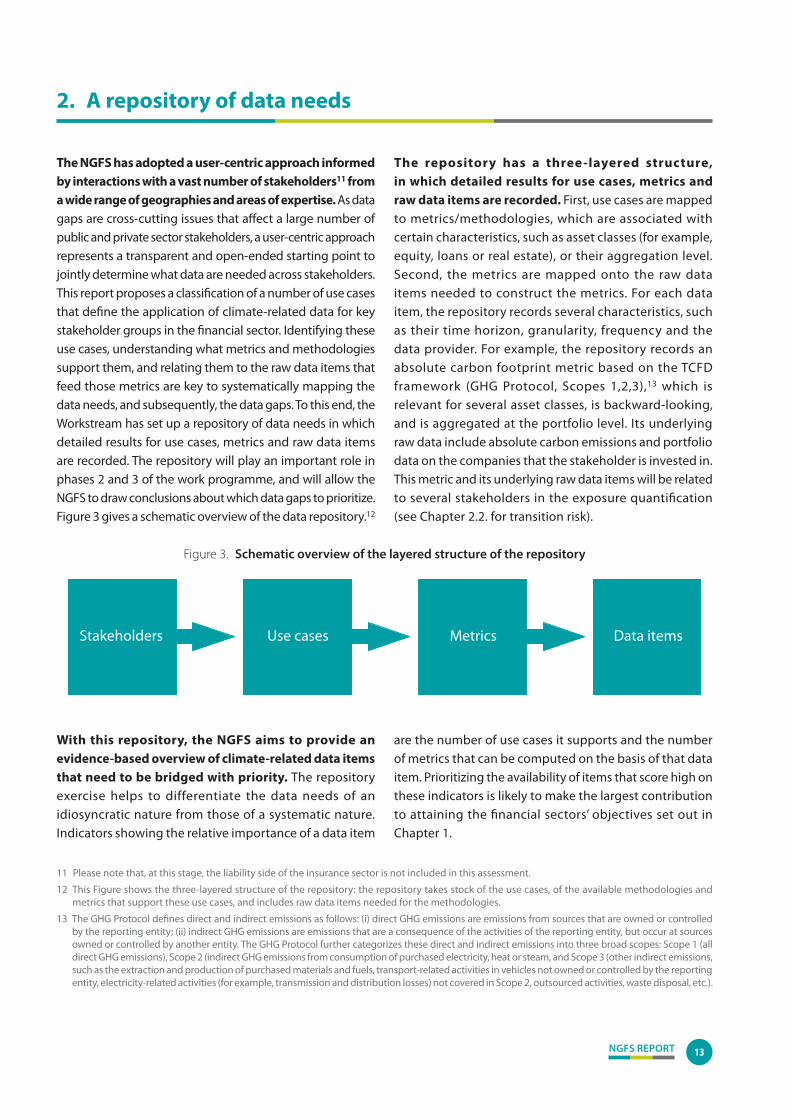

A repository of data needs

The NGFS has adopted a user-centric approach informed by interactions with a vast number of stakeholders1 from a wide range of geographies and areas of expertise. As data gaps are cross-cutting issues that affect a large number of public and private sector stakeholders, a user-centric approach represents a transparent and open-ended starting point to jointly determine what data are needed across stakeholders. This report proposes a classification of a number of use cases that define the application of climate-related data for key stakeholder groups in the financial sector. Identifying these use cases, understanding what metrics and methodologies support them, and relating them to the raw data items that feed those metrics are key for systematically mapping the data needs, and subsequently, the data gaps. To this end, the Workstream has set up a three-layered repository of data needs in which detailed results for use cases, metrics, and raw data items are recorded. The repository will play an important role in phases 2 and 3 of the work programme and will allow the NGFS to draw conclusions about which data gaps to prioritize. A schematic overview of the data repository is presented in Figure 1.2

1 Note that, at this stage, the liability side of the insurance sector is not included in this assessment.

2 This figure gives a schematic overview of the data repository: from left to right, it shows the six stakeholder categories, their use cases for climate-related data, the metrics required to support the use cases, and the raw data items that feed the metrics.

NGFS REPORT6

Key issues related to data availability, reliability and comparability

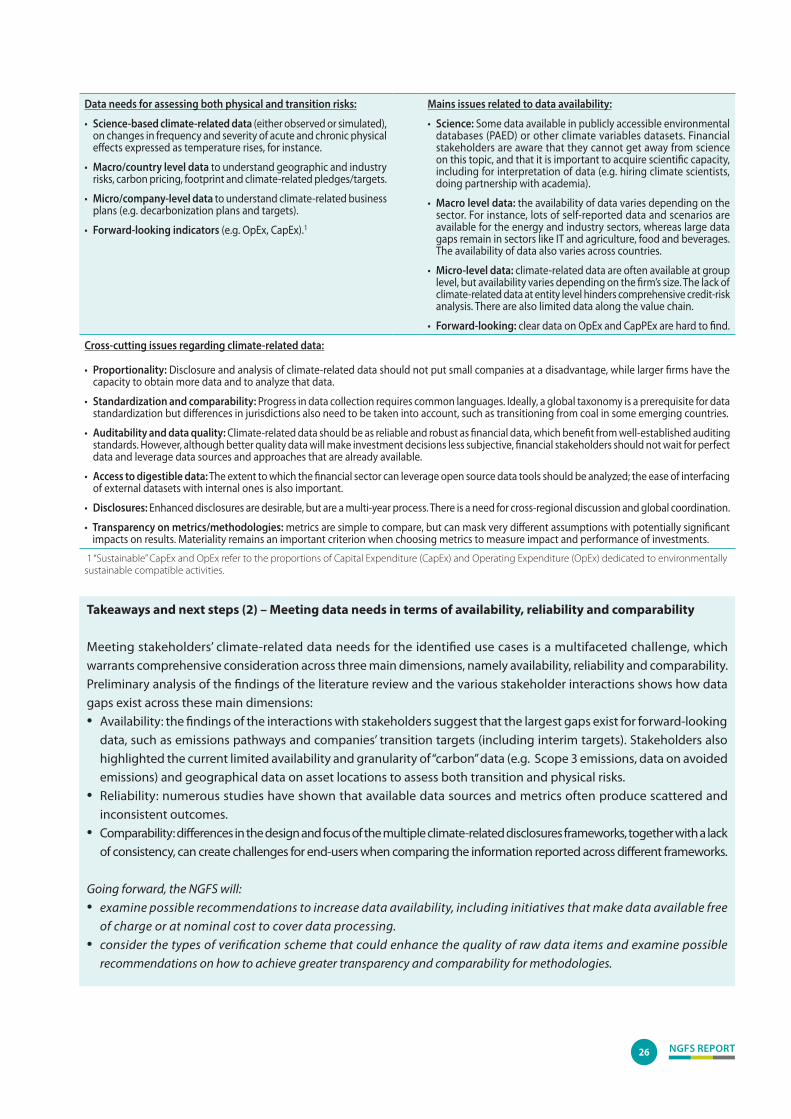

Meeting stakeholders’ climate-related data needs for the identified use cases is a multifaceted challenge, which warrants comprehensive consideration across three dimensions: availability, reliability and comparability.

With regard to availability, stakeholders need climate-related data across asset classes, sectors and geographies, and over different timeframes. In some instances, relevant data sources lack the appropriate granularity, and/or the geographical or sectoral coverage. In other instances, relevant data sources exist, but are not collected in a consistent manner, are not directly accessible, cannot be easily compared or may produce varying outcomes. As for reliability, numerous studies3 have shown that the available data sources and metrics generally produce scattered and inconsistent outcomes. Reliability depends on the quality of the raw data, as well as the auditability and transparency of the providers. For example, more transparency about how ESG scores

are determined would enable the sometimes large differences in the scores of different data providers to be better understood. Lastly, with regard to comparability, differences in the design and focus of the multiple frameworks for climate-related disclosures, as well as a lack of consistency, can make it challenging for end-users when they need to compare the information reported across different frameworks.

The findings of the interaction with stakeholders suggest that the largest data gaps exist for forward-looking data, such as emissions pathways and companies’ transition targets (including interim targets). Given the importance of forward-looking assessments of both physical and transition risks, the current reliance on mostly backward-looking data is unsatisfactory. Stakeholders reported that they need to understand the point-in-time performance of an exposure against a transition pathway – hence the need for firms to disclose their transition plans – as well as the impact of adaptation and mitigation measures on the evolution of the risks.

3 For more information, see Box 3 on “Comparability and transparency issues in practice”.

Figure 1. Interconnectedness of use cases, metrics and raw data items by stakeholder category in the repository

NGFS REPORT 7

Stakeholders also highlighted the currently limited availability and granularity of “carbon” data (such as Scope 3 emissions, data on avoided emissions) and geographical data on asset locations, to assess both transition and physical risks. Since there are large geospatial differences in the manifestation and evolution of physical risks, it is critical to make asset location data available to determine the variety and severity of the physical threats of climate change.

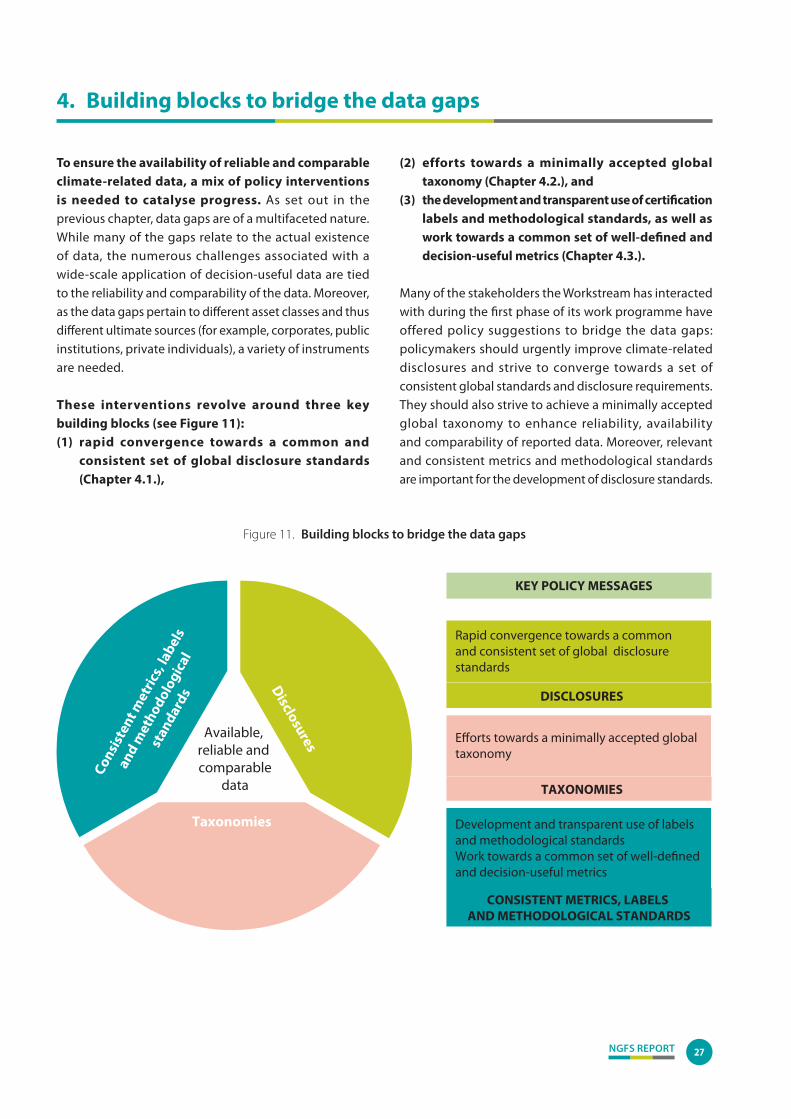

Building blocks to bridge the data gaps

To ensure the availability of reliable and comparable climate-related data, a mix of policy interventions is needed to catalyse progress. Three building blocks are paramount: 1) rapid convergence towards a common and consistent

set of global disclosure standards, 2) efforts towards a minimally accepted global taxonomy,

and 3) the development and transparent use of well-defined

and decision-useful metrics, certification labels and methodological standards.

Many of the stakeholders with which the Workstream has interacted during the first phase of its work programme have made policy suggestions for bridging the data gaps: policymakers should take urgent steps to improve climate-related disclosures and strive to converge towards a set of consistent global standards and disclosure requirements. They should also aim to achieve a minimally accepted global taxonomy to enhance reliability, availability and comparability of reported data. Moreover, relevant and consistent metrics and methodological standards are important for the development of disclosure standards.

1. Disclosure frameworks

While some progress has been made in recent years, climate-related disclosures by financial and non-financial companies are still limited, fragmented and inconsistent across economic sectors. Financial institutions stress the degree to which they rely on disclosures from the wide range of corporates that they invest in, lend to or insure. It is essential

for them to have access to information regarding the climate risks and opportunities faced by the corporates they are exposed to. Meanwhile, corporates also face challenges in providing climate-related data to their stakeholders amid a fragmented landscape of still largely voluntary disclosure frameworks. The main issues identified relate to the voluntary nature of disclosure frameworks, the fragmentation in the landscape, the absence of technical guidance and independent verification, and the lack of a common approach to materiality. Moreover, different definitions and thresholds for materiality with respect to climate issues also affect the availability of climate-related data.

Convergence towards a global disclosure framework, alongside progress towards a globally consistent set of minimal climate disclosure standards and requirements is likely to improve the availability and comparability of climate-related data. A stronger push for consistency across sectors and regions, and an appropriate scope for disclosures is a prerequisite for an adequate disclosure framework for the financial sector. Notably, at the beginning of 2021 the IFRS Foundation announced a plan to establish a sustainability standards board with support from IOSCO and building on existing frameworks, such as the Task Force on Climate-related Financial Disclosures (TCFD) and the prototype developed by the “group of five”, namely the Carbon Disclosure Project (CDP), Climate Disclosure Standards Board (CDSB), Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board(SASB).4

This will pave the way for greater consistency and the convergence of sustainability-related financial reporting standards, with climate standards being prioritised.

Mechanisms for verifying and auditing climate-related financial disclosures are essential to make data reliable and comparable. The development of sufficiently granular methodological standards that prescribe how data items are defined and how metrics are to be computed is a precondition for assuring the quality of disclosures. In turn, external assurance of such information facilitates the appropriate application of standards and definitions. Some stakeholders have called for an assurance framework similar to the one for financial statements and its integration in mainstream financial reporting.

4 For information on the prototype developed by the “group of five“, see Reporting on enterprise value, Illustrated with a prototype climate-related financial disclosure standard, December 2020.

NGFS REPORT8

2. Taxonomies

Taxonomies are another building block in improving data reliability and comparability, and therefore providing financial institutions and investors with relevant information. Many stakeholders consider developing taxonomies as a prerequisite for consistent collection of data and comparable analysis based on these data. Currently, different jurisdictions are establishing different, separate taxonomies for green finance, including pathways and targets that are relevant in their regional context. Many stakeholders point to the need to recognize transition pathways in taxonomies, as a way of catering for differences in regional starting points and facilitating transition financing for companies and other economic players that aim to improve their environmental impact. Other stakeholders questioned the added complexity this would bring to the task of developing a minimally accepted harmonized taxonomy and suggested that disclosing the pathways and distance to targets would be an easier way forward. There is therefore a need for cross-regional discussion on taxonomies. Efforts towards developing a globally agreed upon taxonomy could help ensure worldwide comparability of raw data. The convergence of different taxonomies over time will be important in ensuring consistency in climate-related disclosures.

There is a need to intensify and coordinate the development of taxonomies across the globe, and to examine the possibility of harmonizing them over time. Such efforts need to be intensified and well-coordinated, especially in regions where taxonomies do not yet exist. These are important steps towards the development of a global taxonomy. Limiting the scope to that of a climate-related taxonomy first (as opposed to including issues such as biodiversity which could well be added as a next step) may be a pragmatic way forward. For example, the International Platform on Sustainable Finance has created a dedicated working group on taxonomies to comprehensively compare existing European and Chinese taxonomies for environmentally sustainable investments and identify commonalities and differences in their respective approaches, criteria and outcomes.

3. Certification labels, methodological standards and consistent metrics

Certification labels5 and harmonized methodological standards are key to improving data reliability and comparability. They can make it easier to identify climate-related data and construct datasets (for example, energy efficiency certificates). Certification labels should be harmonized across regions and the information they certify should be made comparable, homogeneous and easily available.

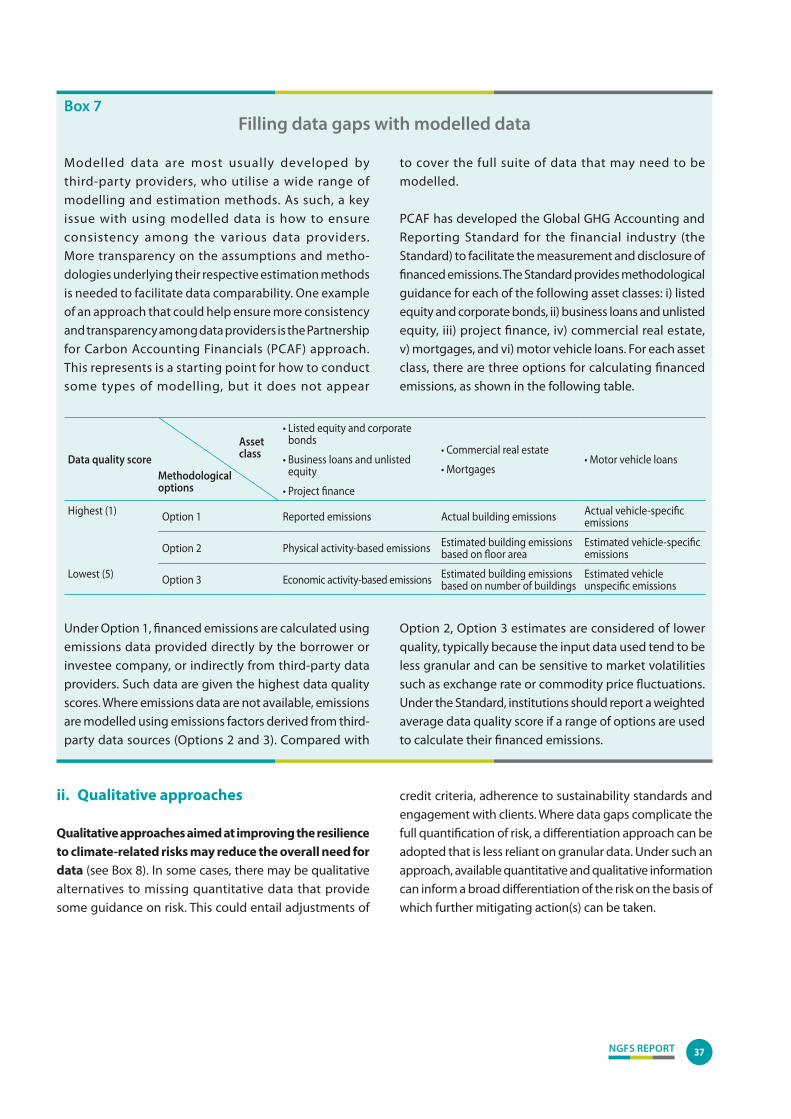

Data comparability is also enhanced when financial market participants harmonize their approaches. The methodologies and disclosure frameworks observed by the NGFS often rely on different computation methods, even for key metrics used across stakeholders and geographies. Such divergences can hinder the comparability of climate-related data, with a profound effect on the outcomes of analyses, especially as transparency regarding the methods adopted is limited. For example, De Nederlandsche Bank has recently shown that inflation and exchange rate effects can have a substantial impact on the outcomes of relative carbon footprint metrics.6 If financial market participants adopt harmonized approaches, this supports the comparability of data. It is worth noting that a number of initiatives have led to open source methodologies and voluntary methodological standards being produced which are then widely used. For example, one such methodological standard is the attribution methodology for the computation of financed emissions by the Partnership for Carbon Accounting Financials (PCAF), which has been embraced by the Greenhouse Gas (GHG) Protocol.

Leveraging existing data sources and approaches

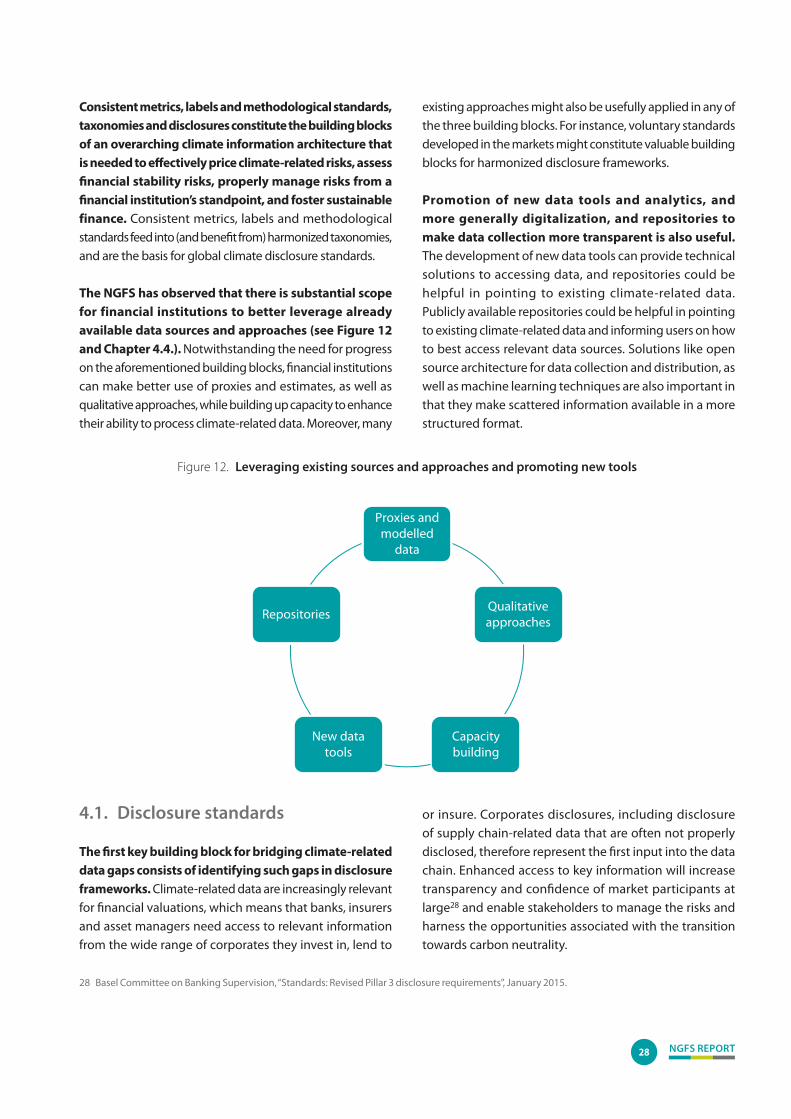

The NGFS notes that there is substantial scope for financial institutions to better leverage already available data sources and approaches. Notwithstanding the need to make progress on the three aforementioned building blocks, financial institutions can also make better use of

5 A certification label is a label or symbol indicating that compliance with standards has been verified. Use of the label is usually controlled by the standard-setting body. Where certification bodies certify against their own specific standards, the label can be owned by the certification body. Examples are Energy Performance Certificates or ISO standards.

6 See Janssen, A., Dijk, J. and Duijm, P., “Misleading Footprints, Inflation and exchange rate effects in relative carbon disclosure metrics”, DNB Occasional Paper, Vol. 19(1), 28 January 2021.

NGFS REPORT 9

Identifying and prioritizing data needs: use cases, metrics that serve the use cases and the raw data items needed for those metrics

The NGFS will further expand its engagement with stakeholders and, using the data repository, aims to draw evidence-based conclusions about which data needs should be prioritized. To this end, the NGFS will: • engage with a broad set of stakeholders, including non-financial corporates (which constitute the first input in the

data chain), central banks and international financial institutions (whose statistical functions are key to help bridge the gaps), data providers and rating agencies, in order to determine whether the data needs identified can be addressed and, if not, how the gaps can be bridged;

• further assess the types of metrics that are most suited to support the different use cases identified in the first phase.

Meeting data needs across three main data dimensions: availability, reliability and comparability

Going forward, the NGFS will:• examine possible recommendations for increasing data availability, including initiatives that make data available

free of charge or at nominal cost to cover data processing; • consider the types of verification scheme that could enhance the quality of raw data items, and issue

recommendations for achieving greater transparency and comparability on methodologies.

Developing policy recommendations to help bridge data gaps

The NGFS will, in liaison with relevant stakeholders:• identify how the progressive harmonization of metrics and methodological standards, certification labels and

taxonomies can contribute to the reliability and comparability of data, together with a wider implementation of mandatory disclosures in financial statements. In doing so, the NGFS will engage with relevant stakeholders, including non-financial corporates and methodologies providers;

• examine how publicly accessible databases can improve data availability and comparability. In doing so, the NGFS will reach out to initiatives that pool climate-related raw data in a single point and to relevant stakeholders in the field of geospatial data, paying specific attention to the use of new technologies (such as artificial intelligence).

Next steps

proxies and estimates, as well as qualitative approaches, while they build up capacity to enhance their ability to process climate-related data. Moreover, many existing approaches might be usefully applied in any of these building blocks. For instance, voluntary standards developed in the markets might provide to be valuable building blocks for harmonized disclosure frameworks.

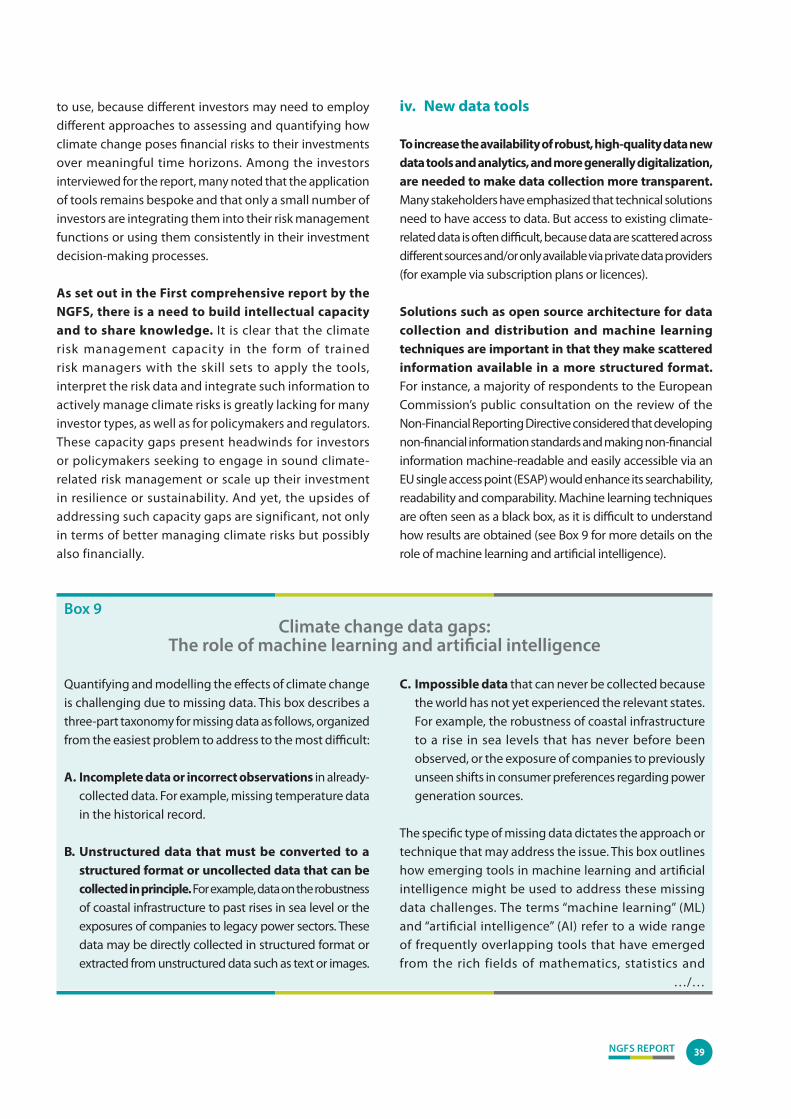

The promotion of new data tools and analytics, and more generally digitalization, as well as repositories to make data collection more transparent are also useful. The development of new data tools can provide technical solutions for accessing data, and repositories could be helpful in pointing to existing climate-related data. Indeed, many stakeholders emphasized that they often face technical obstacles when working with climate-related data.

Access to existing climate-related data is often difficult, because data are scattered across different sources and/or only available via private data providers. Publicly available repositories could be helpful as a way of pointing to existing climate-related data and informing users on how best to access relevant data sources. Solutions such as open source architecture for data collection and distribution and machine learning techniques may also play a role in making scattered information available in a more structured format. However, more work needs to be done to make existing data more broadly available to policymakers and investors. To date, several initiatives have been launched with a view to pooling climate-related raw data in a single point (see Box 10 for a case study in Mexico). It would be worth examining how these can improve data availability and comparability.

NGFS REPORT10

1.1. Climate change and the data challenge

Measures are being taken urgently, including by central banks and supervisors, to prepare the economy and the financial system for the anticipated consequences of climate change, both in terms the risks (i.e. physical and transition risks) and opportunities arising from the transition to a low-carbon economy. To address these unprecedented challenges, more than 80 central banks and supervisors have joined forces in the NGFS to pool their analytical and methodological capabilities and to build up a meaningful information base.

Reliable and comparable climate-related data are crucial for financial institutions, including central banks and supervisors, as well as for investors and policymakers to assess risks to financial stability, properly price and manage climate-related. Such climate-related data are key for microprudential and macroprudential supervision. They also enable financial institutions and investors to gauge the financial repercussions of climate change and thereby increase their resilience to climate-related risks. Moreover, climate-related data enable financial institutions to ensure that sufficient capital is made available for the investments needed to achieve the goals of the Paris Agreement.

Persistent gaps in climate-related data hinder the achievement of these objectives. These data gaps have multiple causes, which include the time horizon for climate-related risks, the widespread nature of their impact and the high degree of uncertainty surrounding them, as well as the need to translate climate-related risks into financial impacts. There is increasing demand for forward-looking data,

since past trends do not typically reflect the nature and extent of climate-related risks. A large amount of information at a very granular level is also required. In particular, there is a growing need for detailed geographical data on asset locations in order to assess physical risks, and for more details on the emissions along the value chains across countries and sectors. The need to find solutions for data gaps has garnered significant attention and led to a renewed sense of urgency as pressure to address climate change continues to grow from investors, researchers, regulators and policymakers as well as NGOs and the general public.

1.2. Mandate and work programme of the NGFS Workstream on bridging the data gaps (WS BDG)

The NGFS set up the Workstream on bridging the data gaps (WS BDG) in July 2020 to identify data needs and data gaps and to propose policy recommendations to bridge such gaps. The WS BDG represents the implementation of Recommendation n°3 “Bridging the data gaps” issued in the April 2019 First comprehensive report by the NGFS.7 In accordance with its mandate, the work of the WS BDG is structured according to the following three-phase approach:i. Identify data items needed by the financial sector –

including central banks and supervisors – for the purpose of climate-related risk analysis and the scaling up of green finance.

ii. Determine whether the data items are available, and if so, identify their data sources and limitations for accessing them.

iii. Provide guidance and recommendations on how to bridge the data gaps identified.

1. Introduction

7 NGFS, “A call for action: Climate change as a source of financial risk”, First comprehensive report, April 2019.

NGFS REPORT 11

As part of phase 1 of its work programme, the Workstream carried out the following initiatives (see Figure 2):• A literature review to identify use cases, methods, data items

and data gaps (of approximatively 150 relevant papers). • Bilateral outreach sessions with:

– the other NGFS workstreams8, as the metrics, data needs and data gaps are those previously identified by the existing workstreams of the NGFS (see Box 1);

– international organizations9, given that many initiatives on the analysis of climate-related or environmental data are ongoing in various international fora. The main objectives were to identify potential overlaps and synergies and to align the respective work programmes as much as possible;

– relevant stakeholders10 (such as NGOs, industry groups and market driven initiatives), in order to learn about and possibly build on ongoing work outside the NGFS.

A survey aimed at gathering high-level input on the work of the stakeholders on data issues (with a focus on identifying data items and their availability) was circulated ahead of each session.

• Two closed-door workshops dedicated to climate-related data gaps were organized by the Workstream with around 20 representatives from major banks and 20 representatives from major buy-side firms, covering four continents.

This progress report forms part of the first phase of the Workstream’s work programme and, in setting out the issues that need to be considered going forward, lays the groundwork for a comprehensive assessment of data needs and data gaps. Given the breadth and magnitude of climate-related risks, and the urgent need for action, this report is narrowly focused on climate-related data issues, both at a granular level (such as firm-level data and asset-level exposures) and at an aggregate level (such as data on the incidence of natural disasters at the regional or country level). Broader environmental data issues, for example those related to biodiversity, may be addressed in the future. It should be noted that climate change research, methodologies and metrics for application in the financial sector are evolving quickly and further data needs will continue to emerge over time.

Figure 2. Overview of the steps taken, the stakeholders involved and the way forward

• An extensive literature review• Bilateral outreach sessions

• Workshop with banks• Workshop with buy-side firms• Methodology and data providers• Non-financial corporates• Rating agencies…

• This progress report• The definition of relevant solutions to bridge the data gaps

Identification of relevant

stakeholdersand use cases

Input findings in the data repository and discussing

pathways of closing data gaps, improving availability,

reliability and comparability

Using resultsfrom repository

and collection oftakeaways for:

8 Workstream on microprudential and supervision, Workstream on macrofinancial and Workstream on scaling up green finance.

9 FSB/AGV, IAIS, IOSCO, OECD, World Bank, BIS, Irving Fisher Committee, Basel Committee on Banking Supervision, TCFR, ESCB STC Expert Group.

10 OMFIF, IIF, Climate Bonds Initiative, PRI, Sustainability Accounting Standards Board, WWF, TCFD and International Platform on Sustainable Finance.

NGFS REPORT12

Box 1Work by NGFS Workstreams on determining data needs

and data availability, and suggestions for bridging data gaps

Since the launch of the NGFS, all NGFS Workstreams have experienced data issues: limited coverage (geographic, sectoral, companies), insufficient granularity, comparability and quality of data.

The Workstreams highlighted that there is a growing number of private data providers but pointed to the issue of the lack of transparency and access as well as the lack of databases that are open source1. In addition, their work also provides examples of how data availability can be improved by means of public databases and offers some suggestion on how to possibly bridge data gaps.

The Workstream on microprudential and supervision’s work on financial institutions’ practices with respect to risk differential between green, non-green and brown financial assets and a potential risk differential2 pointed to various data challenges: • the absence of a taxonomy and a harmonised

classification system for green and brown assets affects data consistency and comparability;

• the horizon mismatch between the materialization of climate-related risks (full impact only in the medium to long term) and the time horizons of the existing institutions’ risk management methods and the prudential frameworks;

• the need for material adjustments to financial institutions’ existing stress-testing models, including the horizon considered, as some banks’ existing top-down stress-testing models may not have taken into account environmental risk factors or may be configured for a given set of geographies and sectors, that may not include those vulnerable to environmental risks;

• technical difficulties in tagging climate and environmental data in the IT systems.

The Workstream on macrofinancial’s work on scenario analysis produced in 20203 a set of climate scenarios in partnership with an academic consortium. This includes one dataset

with transition pathways and data on macro-economic impacts from physical risks and one dataset with the physical impact data collected by the Inter-Sectoral Impact Model Intercomparison Project (ISIMIP). These datasets are generated with a suite of models and are complemented by links to other resources with more detailed information. They are an example of how to make new data publicly available along with the associated methodology. This Workstream is currently upgrading its scenarios and datasets to include a larger set of macroeconomic variables, as well as more granular outputs for individual countries.

The Workstream on scaling up green finance’s subgroup on market dynamics has worked on a concise/decision helpful dashboard to monitor green finance. The Dashboard on scaling up green finance4, available on the NGFS Website, displays a set of 21 indicators. It is a first attempt at compiling a catalogue of desirable data series that allow for the analysis of how green finance is evolving over time, with a focus on trends rather than absolute levels. Furthermore, the Dashboard is intended for use at jurisdiction level. To this end, the metadata describe the country coverage and where these data can be found. The Dashboard is another example of how to make data and the underlying methodology publicly available. The sub-group has also defined further “must-have” indicators, for which no (publicly available) sources have been identified yet. Closing the Data Gaps outlined in that work may take a long-term approach. The lack of statistics covers a wide range of diverse information systems. It may be national financial regulators (central banks and supervisors), standard-setting bodies, or international organizations, who are best prepared to tackle the challenges in front of us. For some already available indicators, one approach might be the gradual expansion of existing statistical frameworks, including their implementation in jurisdictions. For certain unavailable indicators, in particular those concerned with (total assets of) financial institutions, surveys could be issued, e.g. by supervisors. For other indicators: relying on commercial data providers should be considered as a viable option, at least in the short to medium term.

1 Open source means openness of data access, use and share, in line with the Open Data Charter (ODC) and the ODC Principles, for example.

2 NGFS, A Status Report on Financial Institutions’ Experiences from working with green, non-green and brown financial assets and a potential risk differential, May 2020.

3 NGFS, Climate scenarios for central banks and supervisors, and Guide to climate scenario analysis for central banks and supervisors, June 2020.

4 NGFS, Dashboard on scaling up green finance, March 2021.

NGFS REPORT 13

The NGFS has adopted a user-centric approach informed by interactions with a vast number of stakeholders11 from a wide range of geographies and areas of expertise. As data gaps are cross-cutting issues that affect a large number of public and private sector stakeholders, a user-centric approach represents a transparent and open-ended starting point to jointly determine what data are needed across stakeholders. This report proposes a classification of a number of use cases that define the application of climate-related data for key stakeholder groups in the financial sector. Identifying these use cases, understanding what metrics and methodologies support them, and relating them to the raw data items that feed those metrics are key to systematically mapping the data needs, and subsequently, the data gaps. To this end, the Workstream has set up a repository of data needs in which detailed results for use cases, metrics and raw data items are recorded. The repository will play an important role in phases 2 and 3 of the work programme, and will allow the NGFS to draw conclusions about which data gaps to prioritize. Figure 3 gives a schematic overview of the data repository.12

The repository has a three-layered structure, in which detailed results for use cases, metrics and raw data items are recorded. First, use cases are mapped to metrics/methodologies, which are associated with certain characteristics, such as asset classes (for example, equity, loans or real estate), or their aggregation level. Second, the metrics are mapped onto the raw data items needed to construct the metrics. For each data item, the repository records several characteristics, such as their time horizon, granularity, frequency and the data provider. For example, the repository records an absolute carbon footprint metric based on the TCFD framework (GHG Protocol, Scopes 1,2,3),13 which is relevant for several asset classes, is backward-looking, and is aggregated at the portfolio level. Its underlying raw data include absolute carbon emissions and portfolio data on the companies that the stakeholder is invested in. This metric and its underlying raw data items will be related to several stakeholders in the exposure quantification (see Chapter 2.2. for transition risk).

2. A repository of data needs

11 Please note that, at this stage, the liability side of the insurance sector is not included in this assessment.

12 This Figure shows the three-layered structure of the repository: the repository takes stock of the use cases, of the available methodologies and metrics that support these use cases, and includes raw data items needed for the methodologies.

13 The GHG Protocol defines direct and indirect emissions as follows: (i) direct GHG emissions are emissions from sources that are owned or controlled by the reporting entity; (ii) indirect GHG emissions are emissions that are a consequence of the activities of the reporting entity, but occur at sources owned or controlled by another entity. The GHG Protocol further categorizes these direct and indirect emissions into three broad scopes: Scope 1 (all direct GHG emissions), Scope 2 (indirect GHG emissions from consumption of purchased electricity, heat or steam, and Scope 3 (other indirect emissions, such as the extraction and production of purchased materials and fuels, transport-related activities in vehicles not owned or controlled by the reporting entity, electricity-related activities (for example, transmission and distribution losses) not covered in Scope 2, outsourced activities, waste disposal, etc.).

Figure 3. Schematic overview of the layered structure of the repository

Stakeholders Use cases Metrics Data items

With this repository, the NGFS aims to provide an evidence-based overview of climate-related data items that need to be bridged with priority. The repository exercise helps to differentiate the data needs of an idiosyncratic nature from those of a systematic nature. Indicators showing the relative importance of a data item

are the number of use cases it supports and the number of metrics that can be computed on the basis of that data item. Prioritizing the availability of items that score high on these indicators is likely to make the largest contribution to attaining the financial sectors’ objectives set out in Chapter 1.

NGFS REPORT14

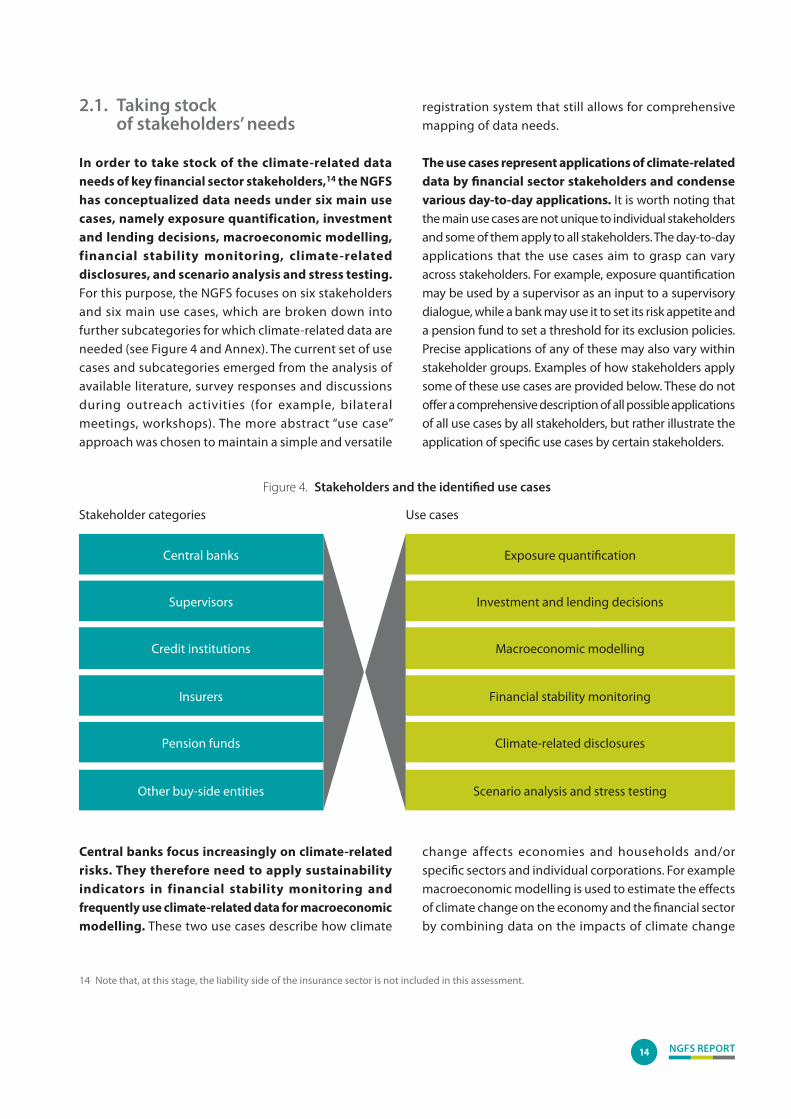

2.1. Taking stock of stakeholders’ needs

In order to take stock of the climate-related data needs of key financial sector stakeholders,14 the NGFS has conceptualized data needs under six main use cases, namely exposure quantification, investment and lending decisions, macroeconomic modelling, financial stability monitoring, climate-related disclosures, and scenario analysis and stress testing. For this purpose, the NGFS focuses on six stakeholders and six main use cases, which are broken down into further subcategories for which climate-related data are needed (see Figure 4 and Annex). The current set of use cases and subcategories emerged from the analysis of available literature, survey responses and discussions during outreach activities (for example, bilateral meetings, workshops). The more abstract “use case” approach was chosen to maintain a simple and versatile

14 Note that, at this stage, the liability side of the insurance sector is not included in this assessment.

Figure 4. Stakeholders and the identified use cases

Central banks

Supervisors

Credit institutions

Insurers

Pension funds

Other buy-side entities

Exposure quantification

Stakeholder categories Use cases

Investment and lending decisions

Macroeconomic modelling

Financial stability monitoring

Climate-related disclosures

Scenario analysis and stress testing

registration system that still allows for comprehensive mapping of data needs.

The use cases represent applications of climate-related data by financial sector stakeholders and condense various day-to-day applications. It is worth noting that the main use cases are not unique to individual stakeholders and some of them apply to all stakeholders. The day-to-day applications that the use cases aim to grasp can vary across stakeholders. For example, exposure quantification may be used by a supervisor as an input to a supervisory dialogue, while a bank may use it to set its risk appetite and a pension fund to set a threshold for its exclusion policies. Precise applications of any of these may also vary within stakeholder groups. Examples of how stakeholders apply some of these use cases are provided below. These do not offer a comprehensive description of all possible applications of all use cases by all stakeholders, but rather illustrate the application of specific use cases by certain stakeholders.

Central banks focus increasingly on climate-related risks. They therefore need to apply sustainability indicators in financial stability monitoring and frequently use climate-related data for macroeconomic modelling. These two use cases describe how climate

change affects economies and households and/or specific sectors and individual corporations. For example macroeconomic modelling is used to estimate the effects of climate change on the economy and the financial sector by combining data on the impacts of climate change

NGFS REPORT 15

15 NGFS, “Overview of Environmental Risk Analysis by Financial Institutions”, Technical document, 2020; UNEP FI reports.

16 NGFS, Dashboard on scaling up green finance, March 2021; IMF, Climate Change Indicators Dashboard.

17 See Nicol, M. and Cochran, I., “How should financial actors deal with climate-related issues in their portfolios today”, Institute for Climate Economics brief, N° 46, April 2017 for an analysis of families of climate-related indicators, their advantages and disadvantages, as well as the associated data availability issues.

with (financial) data related to a specific country, sector, portfolio or company. These models not only describe the effect of climate change, but sometimes also describe the effects of mitigating or adapting to the effects of climate change. Another example is the use of input-output models to model countries’ consumption productivity and pricing data together with emissions across the value chain of specific industries.

To gauge the potential impact of climate-related risks on financial institutions, supervisors use exposure quantification, as well as scenario analysis and stress testing. Scenario analysis and stress testing is applied to capture the size and scale of climate-related risks and assess resilience to climate-related risks, taking into account the forward-looking nature of the risks and inherent uncertainty associated with climate-related risks. The results could serve as a basis for supervisory policy development, i.e. macroprudential supervision, and for dialogues with financial institutions, i.e. microprudential supervision.

Banks, insurers (asset side), pension funds and other buy-side entities (e.g. asset managers, hedge funds) also apply scenario analyses and stress testing in order to analyse climate-related risks at both the portfolio level and at corporate level together with credit rating. Scenario analyses and stress testing can be applied once the vulnerable exposures to climate-related risks are identified (at sector, company, household and sovereign level) and the determinants of physical risks (for example, climate sensitivity of sectors, geographical location) and transition risks (for example, policy sensitivity) are assessed.

Finally, banks, insurers (asset side), pension funds and other buy-side entities (e.g. asset managers, hedge funds) also need climate-related data to make well-informed investment and lending decisions and to quantify risk exposures. For example, information on the

exposure to current and potential future climate-related risks is used in the risk management cycle of credit institutions, i.e. risk identification, risk assessment, risk mitigation and risk monitoring, and strategic decision-making. The outcome of such analyses could feed into credit models and affect pricing and investment/divestment decisions. In particular, for the use cases exposure quantification and investment and lending decisions, transition and physical risk metrics are often applied.

2.2. Identifying common metrics

Metrics are central to translating the complex impacts of climate change on the financial system into decision-useful, comparable measurements. They will ultimately enable governments, companies and individuals to better understand the risk that a changing climate poses to the financial system and how best to ensure the resilience of these systems. In recent years, a growing number of methodologies have emerged for assessing climate-related risks15 and measuring the greening of the financial system at large16. While these methodologies differ substantially in terms of modelling complexity, time horizons, scenario use, assumptions and attribution approaches, the NGFS postulates that they are ultimately based on a much smaller number of metrics. For that reason, the NGFS has endeavoured to classify the most commonly used metrics and register their use in the repository.

Establishing a system to classify metrics is key to systematically mapping climate-related data needs by different stakeholders in the financial sector (see Figure 5).17 Given the sheer number of metrics available for use in measuring climate risks, climate change impacts and the scaling up of green finance, establishing a method to classify metrics is central to understanding their features, advantages and disadvantages. It will allow the NGFS to offer more structured guidance on sets of metrics in the future and ways of improving related data availability.

NGFS REPORT16

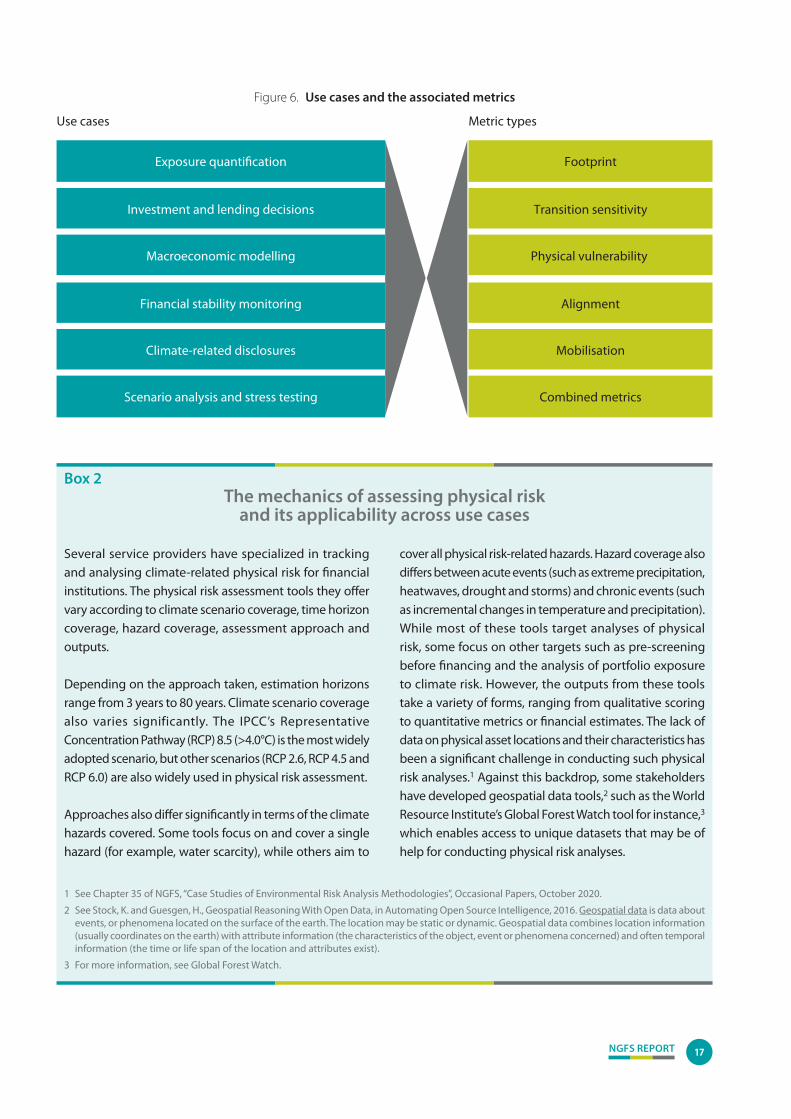

This Progress report offers a first classification into six categories of metrics, namely footprint, transition sensitivity, physical vulnerability, alignment, mobilisation (i.e. scaling up green finance) and combined metrics. Footprint metrics refer to GHG emissions caused directly or enabled by an individual, event, organisation, service or product. Transition risk refers to the disruption caused by adjusting to a low-carbon economy, which may be the result of policy changes, technological innovation or social adaptation. Physical risk refers to the direct damage to assets or property that may come about owing to a changing climate (for example rise in sea levels) or extreme weather events. Alignment metrics18 track progress towards a 2°C world, while mobilisation metrics capture growth in green financing.

For all registered use cases, the repository registers the associated metrics used, along with a classification into one of the metric types (see Figure 6). Some use cases, such as subcategories of exposure quantification, require information from a single metric type, such as physical or

transition risk, while other use cases, like stress testing or scenario analysis, require a combination of inputs across a number of different metrics. Metrics are important for understanding the implications of climate on all of the listed use cases, because it is through metrics that inputs can be changed and the impact of different conditions understood.

Looking at a case study on the impact of physical risk on a financial institution’s portfolios gives an understanding of the wide range of inputs that must be considered in order to produce metrics that are useful for a wide variety of applications (see Box 2). It is clear that, when many metrics are necessary to apply a particular (subcategory of a) use case, the metrics will also require more raw data items (across several asset classes) (see Chapter 2.3.). The layered structure of the repository can thus facilitate identification of data-heavy and less data-heavy use cases and offers an evidence-based approach to identify for which use cases and stakeholders the data needs are more prevalent.

Figure 5. Preliminary classification of available metrics

Type Subtype Example of metrics Footprints Carbon footprint indicators Financed emissions of a portfolio (PCAF)

Transition sensitivity Policy sensitivity indicators Exposures to economic activities according to the classification “Climate Policy Relevant Sectors” (CPRS, Battiston et al. 2017)1

Technology indicators Financed technology mix (e.g. percentage of coal-fired power plants in energy portfolio)

Physical vulnerability Vulnerability to chronic hazards indicators Geospatial vulnerability of business facilities to water stress

Vulnerability to acute hazards indicators Geospatial vulnerability of business facilities to flood risk

Alignment Technology pathway indicators Percentage deviation from the International Energy Agency Sustainable Development Scenario for the share of electric vehicles in car manufacturing portfolio

Temperature increase indicators Implied portfolio temperature increase or (mis)alignment with a sustainable policy scenario (e.g. Paris Agreement Capital Transition Assessment or PACTA)

Emissions intensity indicators Percentage deviation from the International Energy Agency Sustainable Development Scenario for the tailpipe emissions intensity of vehicles in car manufacturing portfolios

Mobilization (scaling up green finance)

Volumes of products indicators Share of green bonds as a percentage of total issuance

Reporting-based indicators Share of corporates that commit to Paris alignment

Standards-based indicators Share of the portfolio that is EU Taxonomy-aligned

Combined metrics ESG ratings A metric aggregating a combination of the above metrics to provide insight on the extent to which a firm manages environmental, social and governance issues

1 Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., & Visentin, G. (2017). A Climate stress-test of the financial system. Nature Climate Change, 7(4), 283–288.

18 Temperature alignment is a forward-looking metric that attempts to convey the future trajectory of GHG emissions of a given entity or portfolio in terms of its estimated global temperature rise. It is designed to convey a simple story: whether the planned pathway is aligned with the goals of the Paris climate accord, for example below 2°C or a more damaging climate pathway such as 4°C. Temperature alignment is an emerging concept, and an industry-wide standard on the methodology is still evolving.

NGFS REPORT 17

Figure 6. Use cases and the associated metrics

Footprint

Transition sensitivity

Physical vulnerability

Alignment

Mobilisation

Combined metrics

Exposure quantification

Investment and lending decisions

Macroeconomic modelling

Financial stability monitoring

Climate-related disclosures

Scenario analysis and stress testing

Use cases Metric types

Box 2The mechanics of assessing physical risk

and its applicability across use cases

Several service providers have specialized in tracking and analysing climate-related physical risk for financial institutions. The physical risk assessment tools they offer vary according to climate scenario coverage, time horizon coverage, hazard coverage, assessment approach and outputs.

Depending on the approach taken, estimation horizons range from 3 years to 80 years. Climate scenario coverage also varies significantly. The IPCC’s Representative Concentration Pathway (RCP) 8.5 (>4.0°C) is the most widely adopted scenario, but other scenarios (RCP 2.6, RCP 4.5 and RCP 6.0) are also widely used in physical risk assessment.

Approaches also differ significantly in terms of the climate hazards covered. Some tools focus on and cover a single hazard (for example, water scarcity), while others aim to

cover all physical risk-related hazards. Hazard coverage also differs between acute events (such as extreme precipitation, heatwaves, drought and storms) and chronic events (such as incremental changes in temperature and precipitation). While most of these tools target analyses of physical risk, some focus on other targets such as pre-screening before financing and the analysis of portfolio exposure to climate risk. However, the outputs from these tools take a variety of forms, ranging from qualitative scoring to quantitative metrics or financial estimates. The lack of data on physical asset locations and their characteristics has been a significant challenge in conducting such physical risk analyses.1 Against this backdrop, some stakeholders have developed geospatial data tools,2 such as the World Resource Institute’s Global Forest Watch tool for instance,3 which enables access to unique datasets that may be of help for conducting physical risk analyses.

1 See Chapter 35 of NGFS, “Case Studies of Environmental Risk Analysis Methodologies”, Occasional Papers, October 2020.

2 See Stock, K. and Guesgen, H., Geospatial Reasoning With Open Data, in Automating Open Source Intelligence, 2016. Geospatial data is data about events, or phenomena located on the surface of the earth. The location may be static or dynamic. Geospatial data combines location information (usually coordinates on the earth) with attribute information (the characteristics of the object, event or phenomena concerned) and often temporal information (the time or life span of the location and attributes exist).

3 For more information, see Global Forest Watch.

NGFS REPORT18

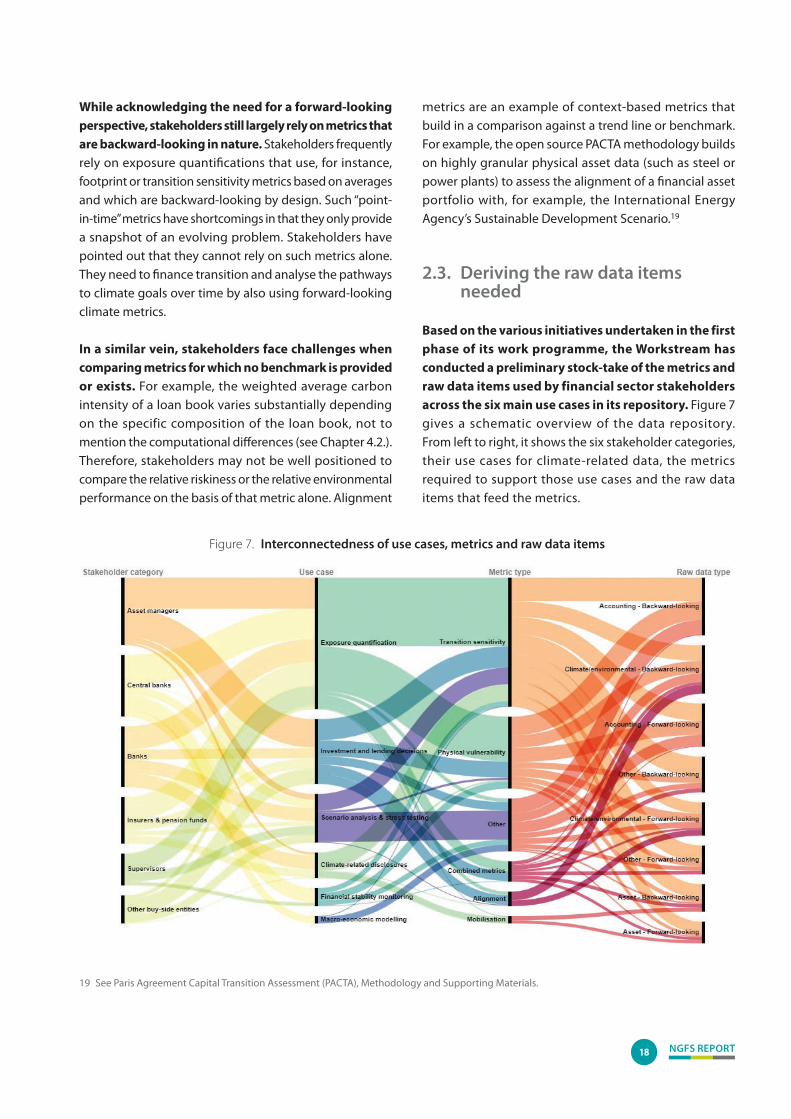

While acknowledging the need for a forward-looking perspective, stakeholders still largely rely on metrics that are backward-looking in nature. Stakeholders frequently rely on exposure quantifications that use, for instance, footprint or transition sensitivity metrics based on averages and which are backward-looking by design. Such “point-in-time” metrics have shortcomings in that they only provide a snapshot of an evolving problem. Stakeholders have pointed out that they cannot rely on such metrics alone. They need to finance transition and analyse the pathways to climate goals over time by also using forward-looking climate metrics.

In a similar vein, stakeholders face challenges when comparing metrics for which no benchmark is provided or exists. For example, the weighted average carbon intensity of a loan book varies substantially depending on the specific composition of the loan book, not to mention the computational differences (see Chapter 4.2.). Therefore, stakeholders may not be well positioned to compare the relative riskiness or the relative environmental performance on the basis of that metric alone. Alignment

metrics are an example of context-based metrics that build in a comparison against a trend line or benchmark. For example, the open source PACTA methodology builds on highly granular physical asset data (such as steel or power plants) to assess the alignment of a financial asset portfolio with, for example, the International Energy Agency’s Sustainable Development Scenario.19

2.3. Deriving the raw data items needed

Based on the various initiatives undertaken in the first phase of its work programme, the Workstream has conducted a preliminary stock-take of the metrics and raw data items used by financial sector stakeholders across the six main use cases in its repository. Figure 7 gives a schematic overview of the data repository. From left to right, it shows the six stakeholder categories, their use cases for climate-related data, the metrics required to support those use cases and the raw data items that feed the metrics.

19 See Paris Agreement Capital Transition Assessment (PACTA), Methodology and Supporting Materials.

Figure 7. Interconnectedness of use cases, metrics and raw data items

NGFS REPORT 19

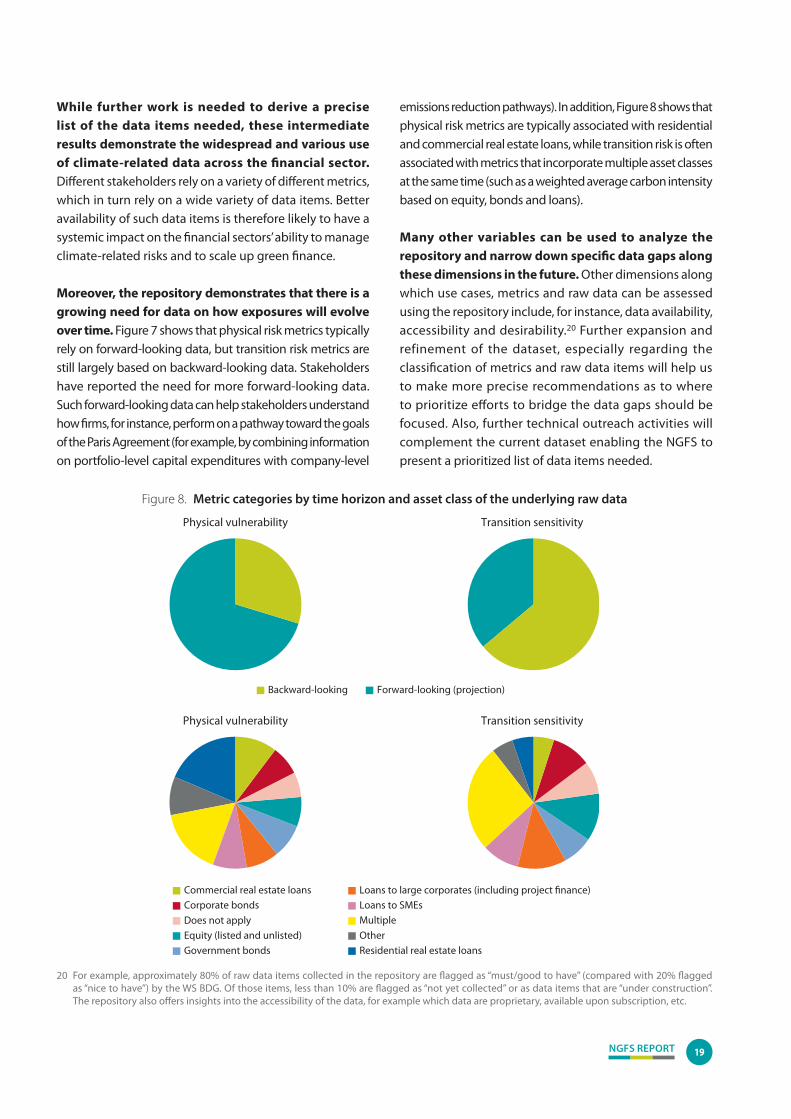

While further work is needed to derive a precise list of the data items needed, these intermediate results demonstrate the widespread and various use of climate-related data across the financial sector. Different stakeholders rely on a variety of different metrics, which in turn rely on a wide variety of data items. Better availability of such data items is therefore likely to have a systemic impact on the financial sectors’ ability to manage climate-related risks and to scale up green finance.

Moreover, the repository demonstrates that there is a growing need for data on how exposures will evolve over time. Figure 7 shows that physical risk metrics typically rely on forward-looking data, but transition risk metrics are still largely based on backward-looking data. Stakeholders have reported the need for more forward-looking data. Such forward-looking data can help stakeholders understand how firms, for instance, perform on a pathway toward the goals of the Paris Agreement (for example, by combining information on portfolio-level capital expenditures with company-level

emissions reduction pathways). In addition, Figure 8 shows that physical risk metrics are typically associated with residential and commercial real estate loans, while transition risk is often associated with metrics that incorporate multiple asset classes at the same time (such as a weighted average carbon intensity based on equity, bonds and loans).

Many other variables can be used to analyze the repository and narrow down specific data gaps along these dimensions in the future. Other dimensions along which use cases, metrics and raw data can be assessed using the repository include, for instance, data availability, accessibility and desirability.20 Further expansion and refinement of the dataset, especially regarding the classification of metrics and raw data items will help us to make more precise recommendations as to where to prioritize efforts to bridge the data gaps should be focused. Also, further technical outreach activities will complement the current dataset enabling the NGFS to present a prioritized list of data items needed.

20 For example, approximately 80% of raw data items collected in the repository are flagged as “must/good to have” (compared with 20% flagged as “nice to have”) by the WS BDG. Of those items, less than 10% are flagged as “not yet collected” or as data items that are “under construction”. The repository also offers insights into the accessibility of the data, for example which data are proprietary, available upon subscription, etc.

Figure 8. Metric categories by time horizon and asset class of the underlying raw data

Backward-looking Forward-looking (projection)

Physical vulnerability Transition sensitivity

Equity (listed and unlisted)

Government bonds

Does not apply

Corporate bonds

Commercial real estate loans Loans to large corporates (including project finance)

Residential real estate loans

Other

Multiple

Loans to SMEs

Physical vulnerability Transition sensitivity

NGFS REPORT20

Takeaways and next steps (1) – Identifying and prioritizing data needs: use cases, metrics that serve the use cases and the raw data items required for the metrics

The user-centric approach adopted by the NGFS represents a transparent and open-ended starting point to jointly determine what data are needed across stakeholders. Identifying the main use cases, understanding which metrics and methodologies support them, and relating them to raw data items are all key to systematically mapping data needs and, subsequently, data gaps. To this end, the Workstream has set up a repository of data needs that will play an important role in phases 2 and 3, which will allow it to draw conclusions about which data gaps to prioritize.

The results from the repository show that:• financial sector stakeholders report an urgent need for climate-related data across a variety of use cases;• financial stakeholders are increasingly using methodologies and metrics for the measurement of climate-related

risks and scaling up of green finance;• most raw data items that support the wide range of metrics and use cases are unavailable, with the result that

stakeholders have often resorted to measurement proxies, aggregates or estimates.

Going forward, the NGFS plans to use the data repository to further expand its engagement with stakeholders with a view to drawing evidence-based conclusions about the prioritization of data needs. To this end, the NGFS will: • engage with a broad set of stakeholders, including non-financial corporates (which represent the first input into the

data chain), as well as central banks and international financial institutions (whose statistical functions are key to help bridge the gaps), data providers and rating agencies, in order to determine whether the data needs identified can be addressed and, if not, how any gaps can be bridged;

• further assess the types of metric that are best suited to support the different use cases identified during the first phase.

NGFS REPORT 21

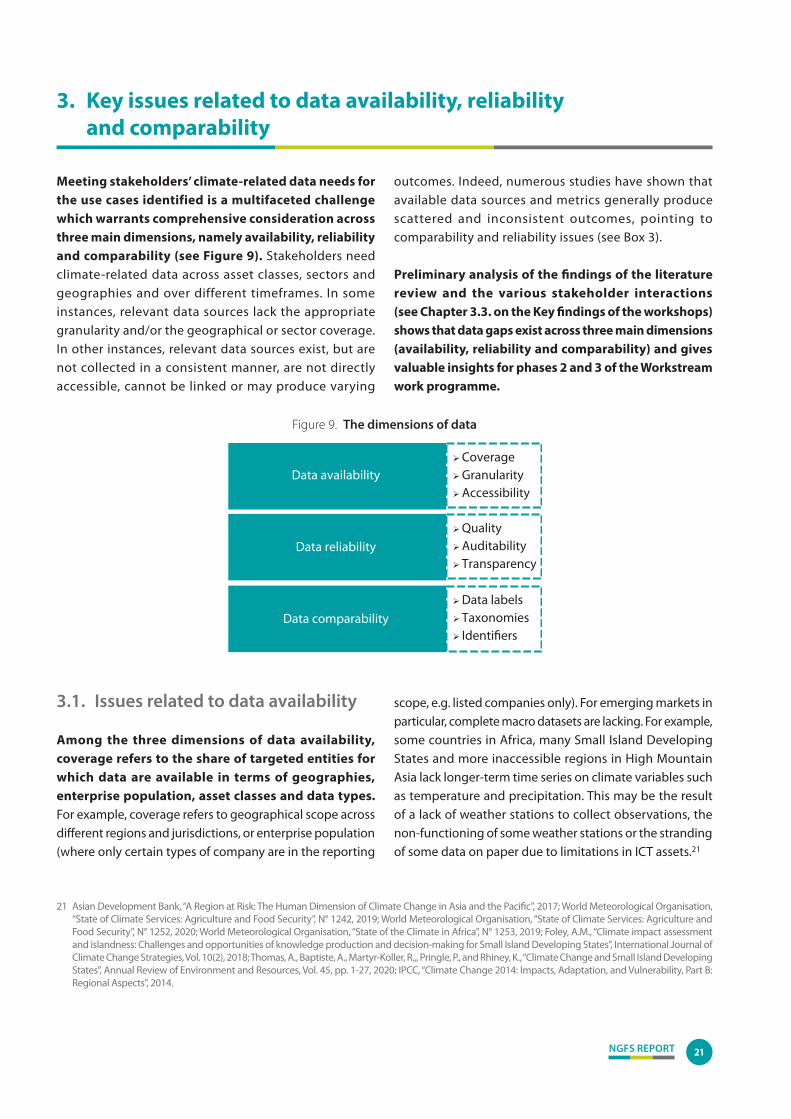

Meeting stakeholders’ climate-related data needs for the use cases identified is a multifaceted challenge which warrants comprehensive consideration across three main dimensions, namely availability, reliability and comparability (see Figure 9). Stakeholders need climate-related data across asset classes, sectors and geographies and over different timeframes. In some instances, relevant data sources lack the appropriate granularity and/or the geographical or sector coverage. In other instances, relevant data sources exist, but are not collected in a consistent manner, are not directly accessible, cannot be linked or may produce varying

outcomes. Indeed, numerous studies have shown that available data sources and metrics generally produce scattered and inconsistent outcomes, pointing to comparability and reliability issues (see Box 3).

Preliminary analysis of the findings of the literature review and the various stakeholder interactions (see Chapter 3.3. on the Key findings of the workshops) shows that data gaps exist across three main dimensions (availability, reliability and comparability) and gives valuable insights for phases 2 and 3 of the Workstream work programme.

3. Key issues related to data availability, reliability and comparability

21 Asian Development Bank, “A Region at Risk: The Human Dimension of Climate Change in Asia and the Pacific”, 2017; World Meteorological Organisation, “State of Climate Services: Agriculture and Food Security”, N° 1242, 2019; World Meteorological Organisation, “State of Climate Services: Agriculture and Food Security”, N° 1252, 2020; World Meteorological Organisation, “State of the Climate in Africa”, N° 1253, 2019; Foley, A.M., “Climate impact assessment and islandness: Challenges and opportunities of knowledge production and decision-making for Small Island Developing States”, International Journal of Climate Change Strategies, Vol. 10(2), 2018; Thomas, A., Baptiste, A., Martyr-Koller, R.,, Pringle, P., and Rhiney, K., “Climate Change and Small Island Developing States”, Annual Review of Environment and Resources, Vol. 45, pp. 1-27, 2020; IPCC, “Climate Change 2014: Impacts, Adaptation, and Vulnerability, Part B: Regional Aspects”, 2014.

Figure 9. The dimensions of data

Data availability CoverageGranularityAccessibility

Data reliability

QualityAuditabilityTransparency

Data comparability

Data labelsTaxonomiesIdentifiers

3.1. Issues related to data availability

Among the three dimensions of data availability, coverage refers to the share of targeted entities for which data are available in terms of geographies, enterprise population, asset classes and data types. For example, coverage refers to geographical scope across different regions and jurisdictions, or enterprise population (where only certain types of company are in the reporting

scope, e.g. listed companies only). For emerging markets in particular, complete macro datasets are lacking. For example, some countries in Africa, many Small Island Developing States and more inaccessible regions in High Mountain Asia lack longer-term time series on climate variables such as temperature and precipitation. This may be the result of a lack of weather stations to collect observations, the non-functioning of some weather stations or the stranding of some data on paper due to limitations in ICT assets.21

NGFS REPORT22

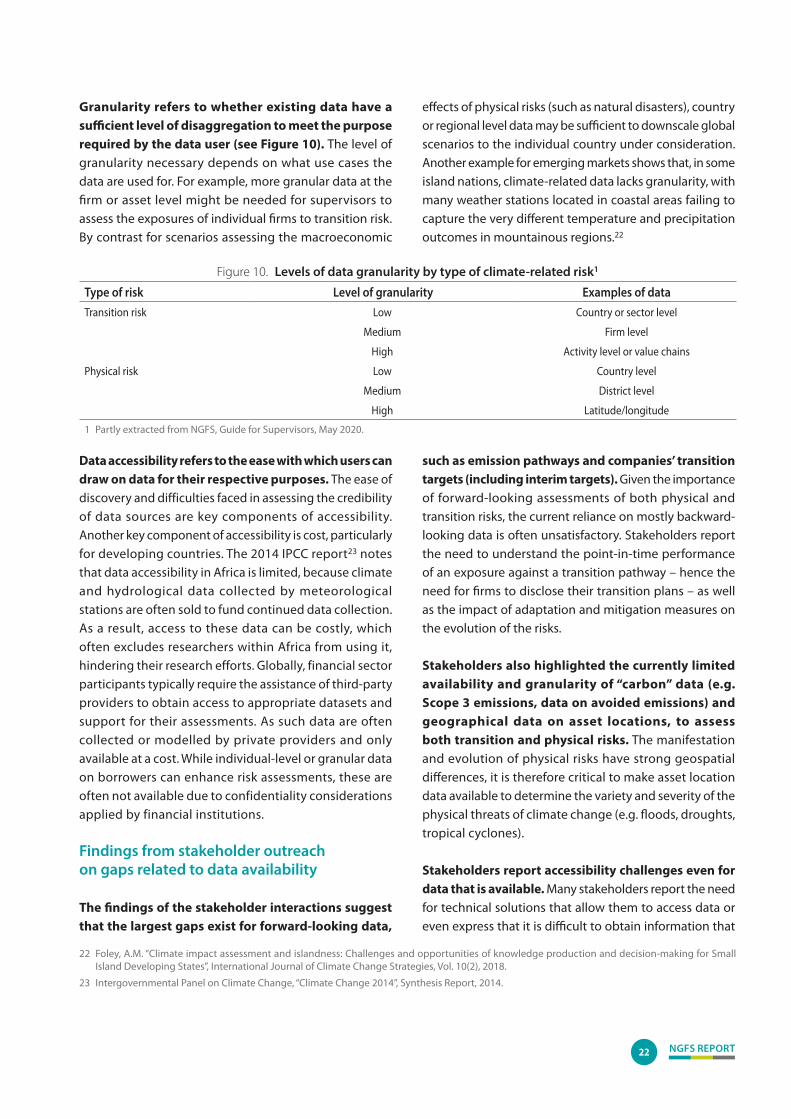

Granularity refers to whether existing data have a sufficient level of disaggregation to meet the purpose required by the data user (see Figure 10). The level of granularity necessary depends on what use cases the data are used for. For example, more granular data at the firm or asset level might be needed for supervisors to assess the exposures of individual firms to transition risk. By contrast for scenarios assessing the macroeconomic

effects of physical risks (such as natural disasters), country or regional level data may be sufficient to downscale global scenarios to the individual country under consideration. Another example for emerging markets shows that, in some island nations, climate-related data lacks granularity, with many weather stations located in coastal areas failing to capture the very different temperature and precipitation outcomes in mountainous regions.22

22 Foley, A.M. “Climate impact assessment and islandness: Challenges and opportunities of knowledge production and decision-making for Small Island Developing States”, International Journal of Climate Change Strategies, Vol. 10(2), 2018.

23 Intergovernmental Panel on Climate Change, “Climate Change 2014”, Synthesis Report, 2014.

Figure 10. Levels of data granularity by type of climate-related risk1

Type of risk Level of granularity Examples of dataTransition risk Low Country or sector level

Medium Firm level

High Activity level or value chains

Physical risk Low Country level

Medium District level

High Latitude/longitude

1 Partly extracted from NGFS, Guide for Supervisors, May 2020.

Data accessibility refers to the ease with which users can draw on data for their respective purposes. The ease of discovery and difficulties faced in assessing the credibility of data sources are key components of accessibility. Another key component of accessibility is cost, particularly for developing countries. The 2014 IPCC report23 notes that data accessibility in Africa is limited, because climate and hydrological data collected by meteorological stations are often sold to fund continued data collection. As a result, access to these data can be costly, which often excludes researchers within Africa from using it, hindering their research efforts. Globally, financial sector participants typically require the assistance of third-party providers to obtain access to appropriate datasets and support for their assessments. As such data are often collected or modelled by private providers and only available at a cost. While individual-level or granular data on borrowers can enhance risk assessments, these are often not available due to confidentiality considerations applied by financial institutions.

Findings from stakeholder outreach on gaps related to data availability

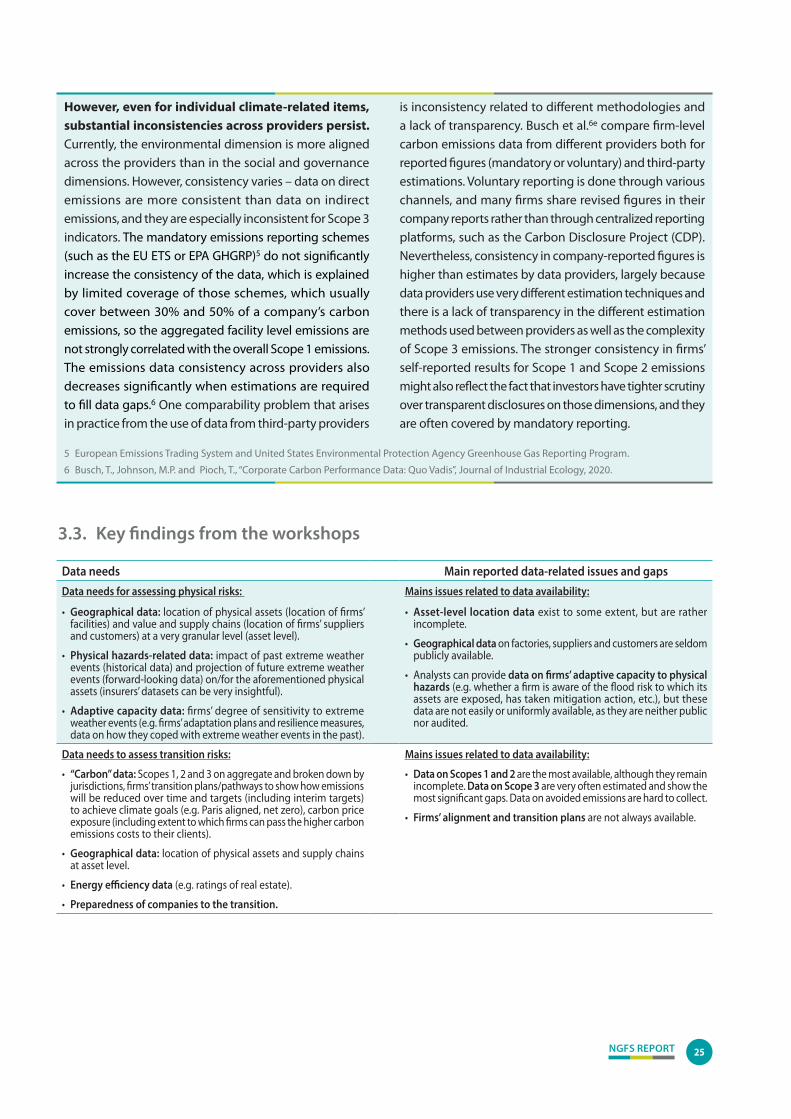

The findings of the stakeholder interactions suggest that the largest gaps exist for forward-looking data,

such as emission pathways and companies’ transition targets (including interim targets). Given the importance of forward-looking assessments of both physical and transition risks, the current reliance on mostly backward-looking data is often unsatisfactory. Stakeholders report the need to understand the point-in-time performance of an exposure against a transition pathway – hence the need for firms to disclose their transition plans – as well as the impact of adaptation and mitigation measures on the evolution of the risks.

Stakeholders also highlighted the currently limited availability and granularity of “carbon” data (e.g. Scope 3 emissions, data on avoided emissions) and geographical data on asset locations, to assess both transition and physical risks. The manifestation and evolution of physical risks have strong geospatial differences, it is therefore critical to make asset location data available to determine the variety and severity of the physical threats of climate change (e.g. floods, droughts, tropical cyclones).

Stakeholders report accessibility challenges even for data that is available. Many stakeholders report the need for technical solutions that allow them to access data or even express that it is difficult to obtain information that

NGFS REPORT 23

24 World Resources Institute, UNEP Finance Initiative and 2° Investing Initiative, “Portfolio Carbon Initiative: Exploring metrics to measure the climate progress of banks”, May 2018.

25 Liesen, A., Hoepner, A.G., Patten, D.M. and Figge, F., “Does stakeholder pressure influence corporate GHG emissions reporting? Empirical evidence from Europe”, Accounting, Auditing & Accountability Journal, Vol. 28, N° 7, pp. 1047-1074; Hoepner, A.G.F. and Yu, P.S., “Science Based Targets Without Science Based Disclosure? Towards a Complete Carbon Data Science”, Centre for Social and Environmental Accounting Research paper, 2017.

already exists. The root causes of this seem to be that the data are not collected in a systematic manner, because their proprietary nature creates barriers to transparency and to uses other than those for which the data have been initially collected (in particular, administrative data). Another obstacle to accessing and making use of existing climate-related data is the lack of unique identifiers, which are crucial for interlinking climate-related data and financial data. Data are thus scattered across different sources and/or only available via private data providers (for example, subscription plans, licences). Moreover, in some cases and especially for data derived from administrative sources, information is not immediately serviceable for statistical/analytical uses, as a clear understanding of the contents and rules that govern data collection (for example, in terms of periodicity, timeliness, methodology, etc.) is required to effectively bridge the gap between the administrative data and needs of statisticians or analysts.

3.2. Issues related to data reliability and comparability

Reliable and comparable data is a prerequisite for ensuring trust in climate-related data and avoiding greenwashing. There is therefore a preference for raw data as opposed to metrics to support investment decisions. Currently, poor quality and unaudited data, alongside non-transparent methodologies, continue to pose significant limitations to the usability of climate-related data.

Reliability depends on the quality of the raw data, as well as the auditability and transparency of the providers. The assessment of quality consists of assessing the plausibility of information, checking its internal consistency (such as emissions reported under Scopes 1, 2 and 3) and benchmarking it to external data sources (for example, aggregated emissions at the sectoral and national level based on official statistics). Data auditing is the process by which data quality or usability for a specific purpose is assessed. However, currently climate-related data are often not subject to audits, which negatively impacts their reliability. Moreover, a lack of transparency on the

methodologies, definitions and criteria used acts as an obstacle to assessing the reliability of available data, whether from external providers or firms’ disclosures.

Currently, comparison of data across data sources is made extremely difficult by the widely varying methods used and the difficulties involved in linking and combining the disparate data available. The lack of common definitions and technical standards, such as taxonomies and certification labels (see Chapter 4) is a major obstacle to data comparability. Comparability consists of checking the consistency of information sourced from different providers or reported for distinct purposes, where discrepancies might stem from different coverage, timing, aggregation methods, estimation of missing information and other methodological issues.

Common identifiers are crucial for linking financial and non-financial information, which are often reported separately. In this context, the availability of unique identifiers at the company level (such as a legal entity identifier or LEIs) and the security level (such as an international securities identity number or ISIN) would allow the consistency of individual information to be checked across different data providers.

Findings from stakeholder outreach on gaps related to data reliability and comparability

Attendees at the workshops highlighted persistent gaps in data reliability, in that they are faced with poor quality, unaudited and non-transparent data. This scepticism toward climate-related data may be due to the perception that much reporting in this area is incomplete or biased. This is not entirely unfounded: for example, a joint report by the World Resources Institute24 found that some banks took advantage of the flexible nature of climate risk metrics by reporting on green activities yet providing little disclosure on more carbon-intensive business activities. Moreover, some studies on carbon emissions reporting have warned about incomplete, inaccurate or missing data in corporate disclosure.25 Data vendors tend to refer to

NGFS REPORT24

companies’ disclosure to collect carbon emissions and in case of missing data they complete their database with estimations using their proprietary models26. Studies that compared carbon emissions data from different providers observed that data on direct emissions are more consistent than data on indirect emissions, while Scope 3 emissions data seem to be inconsistent.27