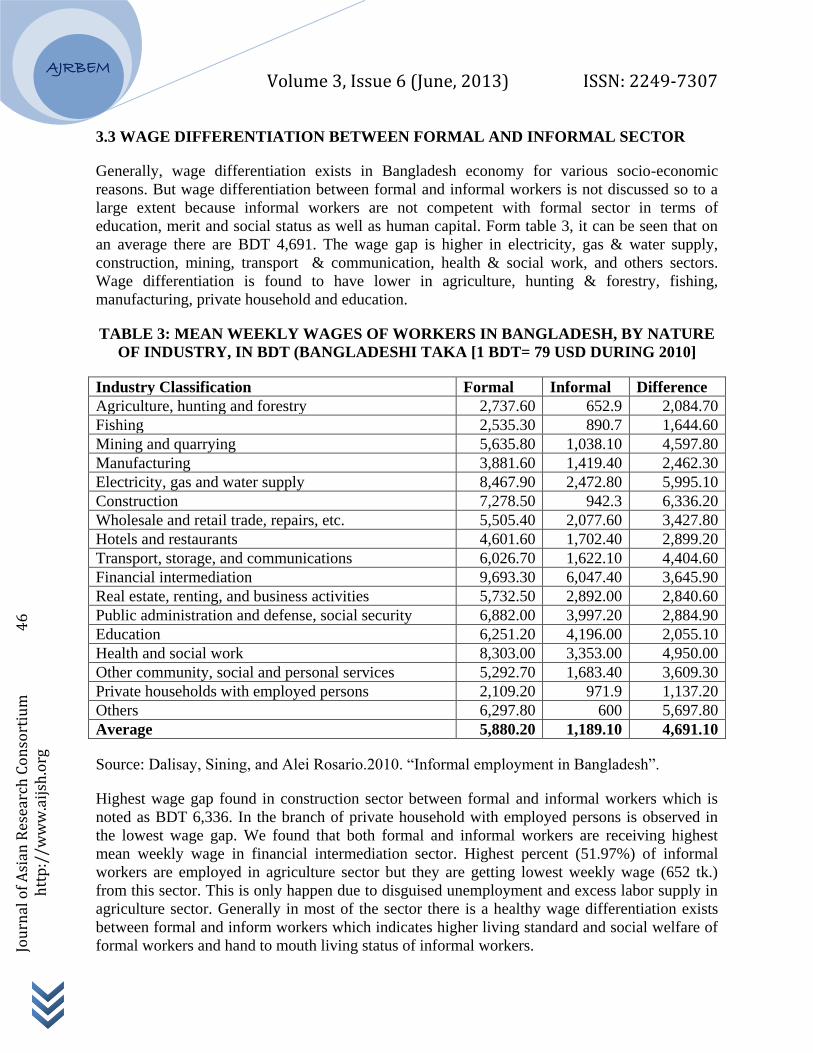

POST HARVEST MANAGEMENT \u0026 AGRO-FOOD RETAIL MARKET DEVELOPMENT IN DIFFERENT ALLIED SECTORS IN...

197

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of POST HARVEST MANAGEMENT \u0026 AGRO-FOOD RETAIL MARKET DEVELOPMENT IN DIFFERENT ALLIED SECTORS IN...

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l

o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F

R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D

M A N A G E M E N T

IMPACT FACTOR(GLOBAL)=0.376

Visit www.globalimpactfactor.com for verification

INDEX COPERNICUS VALUE (2011)=5.09

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l

o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F

R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D

M A N A G E M E N T

SR.

NO. P A R T I C U L A R

PAGE NO.

1.

RELATIONSHIP BETWEEN POST PURCHASE SERVICES BY PRIVATE

COMPANIES AGENTS AND FIRST YEAR POLICY LAPSATION RATE

IN LIFE INSURANCE SELLING

PROF. MITESH JAYSWAL

[PDF]

1-13

2.

A CONCEPTUAL FRAMEWORK OF EMPLOYEES’ CONTINUANCE

INTENTION TO USE E-LEARNING SYSTEM

DR. A. THIRUCHELVI, S. KOTEESWARI

[PDF] 14-20

3. PERFORMANCE OF INDEX FUNDS IN INDIA

DR. (MRS.) PRASHANTA ATHMA, MS. B. MAMATHA

[PDF] 21-29

4.

DEMOGRAPHIC DIFFERENCES & SHOPPING BEHAVIOR OF INDIAN

MIDDLE INCOME GROUP USERS WITH DEBIT CARDS:

AN EMPIRICAL ANALYSIS

VIVEK KUMAR TRIPATHI, TANU MARWAH

[PDF]

30-41

5.

INFORMAL WORKERS IN BANGLADESH: AN ANALYSIS FROM

SOCIO-ECONOMIC PERSPECTIVE

ABDUR RAZZAQUE SARKER

[PDF] 42-48

6.

IMPACT OF CREATIVE ADVERTISING STRATEGIES ON DOCTORS

BY MEDICAL REPRESENTATIVES FOR PHARMACEUTICAL

PRODUCTS

DR. P. T. CHAUDHARI, ABHIJEET HARIDAS GAHUKAR

[PDF]

49-60

7.

PROFITABILITY IN INLAND FISHERY SECTOR – A CASE STUDY IN

THE DISTRICT OF MIDNAPORE (EAST & WEST)

PRADIP KUMAR DASH

[PDF] 61-75

8.

A STUDY ON QUALITY OF WORK LIFE AT A GARMENT

MANUFACTURING UNIT IN PERNDURAI – A CASE STUDY

D. ANBUGEETHA

[PDF] 76-87

9.

EXPERIENCE IS A KEY TO SUCCESS IN POULTRY INDUSTRY

DR. S. C. VETRIVEL, DR. R. SOMASUNDARAM

[PDF] 88-95

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

10.

A STUDY ON FACTORS INFLUENCING FOR NON MIGRATION TO

URBAN AREA WITH SPECIAL REFERENCE TO KANCHEEPURAM

TALUK

DR. K. S. MEENAKSHISUNDARAM, DR. N. PANCHANATHAM

[PDF]

96-100

11.

MINOR IRRIGATION DEVELOPMENT AND POLOCIES IN MODERN

SYSTEMS UNDER DIFFERENT SOURCES IN ANDHRA PRADESH

DR. RADHA RANI KOTHAKALLA

[PDF] 101-107

12.

CORPORATE SOCIAL RESPONSIBILITY AND PHILANTHROPY –

ESSENTIAL TOOLS FOR BUILDING STRONG BRANDS;

A MARKETING PERSPECTIVE

M V A L NARASIMHA RAO, S RAMESH BABU, DR. M KISHORE BABU

[PDF]

108-121

13.

NETWORKED READINESS INDEX IN BRICS – COMPARATIVE

ANALYSIS

DR. L. KRISHNA VENI

[PDF] 122-135

14.

HIGH WORLD FOOD PRICES-CAUSES AND CONSEQUENCES

DR. U. JAYALAKSHMI SRIKUMAR

[PDF] 136-146

15.

POST HARVEST MANAGEMENT & AGRO-FOOD RETAIL MARKET

DEVELOPMENT IN DIFFERENT ALLIED SECTORS IN INDIA

MRK MURTHY, V MURALI

[PDF] 147-159

16.

TOWARD HIGHER STUDIES IN BUSINESS SCHOOLS

DR. RUKHSAR AHMED

[PDF] 160-176

17. PROFIT RE-ENGINEERING FOR BUSINESS PROGRESS

K. V. MURALI

[PDF] 177-189

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l

o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F

R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D

M A N A G E M E N T

RELATIONSHIP BETWEEN POST PURCHASE SERVICES BY PRIVATE

COMPANIES AGENTS AND FIRST YEAR POLICY LAPSATION RATE

IN LIFE INSURANCE SELLING

PROF. MITESH JAYSWAL*

*Associate Professor,

S.V. Institute of Management,

Kadi, Gujarat. India.

ABSTRACT

PURPOSE: The purpose of this paper is to study the relationship between first year

policy lapsation rate and service quality provided by agents of private life insurance

companies. It check, whether first year policy lapsation rate differences is significant

on post purchase services of intermediary.

DESIGN/METHODOLOGY/APPROACH: The paper presents a survey of the

agents of private life insurance companies of Gujarat under descriptive- cross

sectional design. The statistical tools like exploratory factor analysis, confirmatory

factor analysis and MANOVA have been used.

MAJOR FINDINGS: First year policy lapsation rate differences of Private

Companies Agents is not found significant on post purchase services. It is significant

for exceptional services only.

ORIGINALITY/VALUE: The paper will be of value to those interested in insurance

distribution and specifically about agents performance of private life insurance

companies. It is suitable for academics and practitioners alike.

KEYWORDS: Service Quality, Policy Lapsation.

_____________________________________________________________________________

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

INTRODUCTION

An agency relationship is defined as: a contract under which one or more persons (the

principal(s) engage another person (the agent) to perform some service on their behalf which

involves delegating some decision making authority to the agent (Jensen and Meckling, 1976).

Emphassing the importance of further bifarcation on this traditional meaning Lowry, Avila, &

Baird (1999) says that with increasing competition among agencies for the same clients, the need

for a strategy to differentiate one agency from another is critical. By focusing efforts on a niche

market, an agency can benefit by being the one of choice for consumers in the niche. Further

adding to marketing system Machiraju (2004) says that the job of marketing life insurance has

always been of a hybrid nature. The fact-finding and advice-giving phase at the contact level

may be considered as the work of counselor; the persuading phase as the work of a salesman.

Adding to this Cummins & Doherty (2005) specify the duty of an agent by saying that in

addition to placement of insurance, insurance intermediaries also help their clients understand

and measure their risk, advice them on how insurance can alleviate the costs of risk, help design

insurance coverage programs, and assist with claims settlement.

Emphasizing on latest change in insurance market article titled “Change Agents” (2008) mention

that the onset of competition also means that the role of the ubiquitous life insurance agent is

evolving, expanding and, in some cases, witnessing a complete turnaround. Increased

competition and proliferation of products are compelling agents to innovate and spend greater

amount of time understanding competing products. With new products from mutual funds and

insurance companies hitting the market every other day, the new-age agent is armed with

knowledge not just about his own portfolio, but also about financial products from competing

firms. Adding to this about Indian life insurance agents, Singhvi & Bhatt (2008) says that the

greater relationship and more face to face contact, consumers are used to the channel, experience

and greater knowledge of industry and cross selling ability are the strength of the agents while

higher cost for insurer and consumer because of higher commission rates, not as convenient as

other channels, old fashioned channel, not fully updated with latest technologies are the

weakness of the agent system. Not only emphasizing the role of agent in customer loyalty a

study finds evidnces that headquarters’ contribution to customer loyalty is significantly stronger

through the image path than through the delivery path (Andreassen & Lanseng, 1997).

ETHICAL ISSUES

An illuminating research by Banumathy & Manickam (2004) concludes that agents offer good

services before the policy is issued and while it is in operation but don’t offer good services at

the stage of maturity when a customer approaches them for settlement of claims. It, therefore,

makes sense to look at well-balanced, alternative channels of distribution. Talking on unethical

practices by agents Cummins & Doherty (2005) says that there is empirical evidence that most of

the contingent commissions is passed on to policyholders in the premium. On the bases of the

survey of LIC agents from Madurai district Arulsuresh & Rajamohan (2010) suggetsed that the

percentage of commission given to the agent should be the same for all policies because when

there is any differentiation between the rates of the commission of policies sold, the agent will be

attracted to policies which are giving higher rate of commission to them.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

3

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

RECRUITMENT OF AGENTS

In India where LIC a dominating players getting more than ninety percent of its market through

exclusive agents Machiraju (2004) commented on the prosess of recruitment of agents by saying

“LIC has adopted the rather crude process of recruiting a large number of agents and waiting for

a few successful ones to emerge. By this process, the calling of the agent was stamped almost

from the beginning as one that just anybody could follow, at least for a while.” According to

Shettewar & Dixit (2009) older agents and male agents would take lesser duration to get the

license as compared to duration taken by younger agents and female agents. It is also found that

the offline mode training would reduce the duration of licensing. It may be because of offline

mode of training is more accessible and convenient to the agents from different regions.

SHRINKING BUSINESS BY AGENTS

While World wide more than ninty percent of premium was procured by the individual agents

and brokers (Naga Raja Rao, 2004), evidence is found in the decrease of life insurers operating

in the U.S., industry demutualization, and the decreased number of affiliated agents combined

with the emergence and growth of direct and independent advisor distribution channels. Such

trends signal a fundamental restructuring of how life products are structured and delivered1.

According to Verma (2004) the life insurance players need to develop alternative distribution

channels, as the traditional channels alone are not financially viable. India Infoline article,

(August 2004) maintains that insurance agents are still the main vehicles through which

insurance products are sold but in a huge country like India, one can never be too sure about the

levels of penetration of a product. Insurers in a top-down product development approach create

products with features attractive to agents. Fleming, John D; President Fleming Advisor

International (2008) Observes a disturbing trend in North American Life insurance industry that

the number of people providing face to face advice to consumer is shrinking. More important, he

notes that new blood is being infused at an alarmingly slow rate. He also added that the company

leaders are aware of this situation; there are few concrete signs of companies doing something to

address this problem. In India nearly three fourth of the agents are about to go out from business

because of change in policy about Unit link Life insurance in September 2010 (New ULIP norms

may throw 1.2 million agents out of work, 2010).

Using primary data from two hundred fifty five insurance agent-insurance provider dyads Ross,

Anderson, & Weitz (1995) conclude that the Perceivers rate their performance outcomes from

the dyad (i.e. harmony and profit) highest when they believe they are less committed than their

counterpart. Conversely, they rate their own performance outcomes lowest when they believe

they are more committed than the other party.

POLICY LAPSATION & INTERMEDIARY SERVICE QUALITY

A life insurance policy lapses when the subscriber does not pay the premium within the grace

period. When a policy lapses, the holder forfeits the premium paid and the insurance cover. The

1 Report in TIAA-CREF Institute’s, Trends & Issues, December 2008 titled “Product and Distribution Evolution In

the Life Insurance Industry”.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

4

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

agent loses the renewal commission. It also impacts the growth of the insurance business and

solvency margins of the insurer. Lapsation of a life insurance policy is discontinuation of

premium payment by the policyholder during the period of operation of the policy, due to any

reason other than the death of the policyholder. The length of life of a lapsed policy can be

defined as the period between the month when the last premium installment was paid and the

month the policy was issued. According to Gummarra (2008) a cancelation of insurance contract

during the first year demonstrates the probable customer dissatisfaction and is an indicator of

lower level services by intermediary. Policyholders who had repeated unpleasant experience with

the services of an insurance company or the advisor, most typically, would prefer to end their

relationship with the company (Mallela at al. 2008). Reasons for lapsation are wrong selling,

forced selling, over selling, bogus selling, effect of competition, introduction of new plans, bad

service, awareness levels of customers, non-receipt of notices, no follow-up by agents,

requirement of medical check-ups, change of address, inadequate explanation of the product

riders, repayment of house finance, malpractice of agents an field force (Subramanian, 2008).

From search theory a number of factors that affect the service quality provided by insurance

intermediaries can be identified (Posey/ Yavas 1995; Posey/ Tennyson 1998; Seog 1999, 2005;

Eckardt 2007). On the demand side, consumers’ preferences in regard to insurance related

information and other transaction services and their transaction costs influence their make-or-buy

decision. Besides, many information services depend on privately held information by

consumers. Thus intermediation service quality depends also on the collaboration between

consumers and intermediaries. On the supply side, the distribution of the relevant information as

well as the search technology used are important factors that affect the search costs which have

to be incurred for producing information and other services of a certain quality level (Rose 1999;

Eckardt 2007). Most important inputs are the time spent for searching, processing and evaluating

information and investment in specific insurance-related human capital (knowledge and skills).

Since consumers act either under a “free price”-illusion or simply do not know about what

percentage of the premiums they pay go to insurance intermediaries, price competition is quasi

not existent in the market for insurance intermediation (Cummins and Doherty 2006). Thus,

insurance intermediary markets are characterized by monopolistic competition (Cummins and

Doherty 2006; Eckardt 2007). Insurance intermediaries compete for customers both by

horizontal and vertical product differentiation. In the former case they offer different kinds of

services, while in the latter they offer different quality levels.

LITERATURE GAP

An article by Arnold (2000) contains a survey of 750 executives, which found that the

distribution effectiveness and technological preparedness are the big concern for the life

insurance CEOs in Europe and North America. In lately liberalized Indian market where

alternate channels are having combine share of twenty two per cent of new premium it is need to

study the reasons for reduction in adoption rate of traditional channel. For Individual Agents

(having a share of 78.69 per cent in new business, 44.05 for private companies and 96.56 per

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

5

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

cent for LIC)2, this is a pathetic situation for the industry experts who notice the consistently

shrinking share in last ten years.

While the key success factors for distribution are Productivity, Control, Turn Over and Customer

relationship (Shelton ,1995), the literature indicates that, In India the focus has been finding out

on getting new business only. Most of the problems and issues confronting the Indian life

insurance business in today’s situation are of because of more marketing orientation less focus

on the issues like recruitment and selection of intermediaries, retention, education and training,

productivity and morale, market conduct issues and research (Machiraju, 2003). The marketing

orientation is not only limited to insurer but also associated with intermediary. Like rebating in

the insurance industry has remained a bone of contention right from the colonial era.

Rajagopalan (2008) expects the variations in the lapse experience of the business transacted

through the channels and mention that it needs to be investigated separately. As there is no

attempt found to study the service quality of private life insurance agents in Indian market, the

study to relate the first year lapsation rate with service quality is novel phenomenon in Indian

context. So it is interesting to study the relationship between first year policy lapsation rate and

post purchase service quality of Individual Agents of private Life insurance companies and fulfill

this literature gap up to some extent.

STUDY OBJECTIVE

The broad aim of the proposed study is to know that whether there is a significant difference

among first year policy lapsation rate and post purchase services of the intermediary3. The

researcher believes that the intermediaries giving more importance to post purchase services

having low first year policy lapsation rate. The researcher would also like to explore the

categories of post purchase service variables on which the first year lapsation rate differs.

HYPOTHESIS

H1: Cancellation of policy due to first year leapsation is significant on post purchase services of

intermediary

H1a: Cancellation of policy due to first year leapsation is significant on Revival Services

H1b: Cancellation of policy due to first year leapsation is significant on Routine & Alteration

Services

H1c:Cancellation of policy due to first year leapsation is significant on Exceptional services

RESEARCH METHODOLOGY

An insurance market is characterized by incomplete and asymmetric information between

insurance companies and consumers (Cummins & Doherty 2006; Eckardt 2007). Insurance

2 IRDA Annual Report 2012 3 In this paper, the word Intermediary is used for individual agents of private life insurance companies.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

6

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

intermediary market is also characterized by incomplete and asymmetric information.

Information and counseling services are complex and long-term insurance purchase decisions

having experience and credence goods (Nelson 1970; Darby & Karni 1973; Hirshleifer 1973).

According to principal-agent theory this information asymmetry leads to low quality provision

due to differing objectives between principals and agents. Consumers as principals have only

incomplete information about an intermediary’s characteristics, knowledge and experience

before contract conclusion as well as about the intermediary’s proper intentions and actions after

contract conclusion. Therefore the performance of the intermediary can be only incompletely

assessed by the principal. So the service quality of life insurance intermediary can better assess

through survey of intermediaries than customers. This research begins with exploratory research

design as its immediate purpose is to develop hypothesis and questions for further research. The

formal study begins after the exploration leaves off. For making the study conclusive after

exploratory research, descriptive research design is used. Post purchase services include number

of activities carried out by the intermediary after conclusion of the contract. A list of different

activities is prepared on the bases of interaction with insurance professionals. In this case the list

of intermediaries is not available, so it is decided to go with non probability sampling methods

under which convenience sampling method is used.

EXPLORATORY FACTOR ANALYSIS (EFA)

To identify sources underlying the prepurchase services of intermediary, an exploratory factor

analysis was carried out. EFA is a technique aimed to identify number of latent constructs form

set of interrelated variables. Principle components method was used to extract the factors. The

KMO Measure of Sampling Adequacy was 0.771 indicating analysis results are meritorious

(Kaiser, 1970).Bartlett’s test of sphericity was significant at 0.000 levels demonstrating that a

high elevated degree of correlation between the variables exists (Hair et al., 1998) (Table 1).

TABLE 1: KMO, BARTLETT’S TEST OF SPHERICITY AND SIGNIFICANT LEVEL

Kaiser-Meyer-Olkin Measure of Sampling Adequacy 0.771

Bartlett's Test of Sphericity

Approx. Chi-Square 1063

Df 66

Sig. 0.000*

*significant at 0.001 level

In total, there were twelve (12) variables in the data. Items with higher cross loadings (more

than 0.20) and those with lower than 0.5. Varimax rotation method was used with factors

extraction with Eigen value over 1. It resulted into extraction of three factors, which explained

51.76 per cent of variance. The minimum factor loading observed was 0.499 and the maximum

loading was seen to be 0.852.The factors, their respective items with the numbers and their

corresponding factor loading are given in Table 2 and 3.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

7

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

TABLE 2: DESCRIPTION OF FACTORS

Factors Description % of

Variance

% of

Cumulative

variance

Routine & Alteration

Services

Services which are used by more number of

clients & Alteration Services

19.422 19.422

Exceptional Services Services which are used by very few clients 17.268 36.691

Revival Services Services related to non-commitment by clients 15.077 51.767

TABLE 3: COMPOSITION OF EACH FACTOR IDENTIFIED IN FACTOR ANALYSIS

Factor Items Factor

loadings

Routine & Alteration

Services

Grant of loan (V7) 0.762

Assignment (V6) 0.675

Settlement of surrender value (V9) 0.574

Settlement of claims (V11) 0.519

Payment of survival benefit (V8) 0.512

Alteration in policy terms (V10) 0.499

Exceptional Services Collection of premium (V2) 0.739

Policy delivery (V1) 0.695

Change in personal information (V12) 0.612

Nomination (V5) 0.512

Revival Services Revival / reinstatement of paid up policies (V3) 0.852

Revival / reinstatement of lapsed policies (V4) 0.838

CONFIRMATORY FACTOR ANALYSIS

The first order confirmatory factor analysis model fit indices are x2 = 183.740, x

2 / df = 3.603,

df = 51, GFI = 0.933, RMSEA = 0.082, PCLOSE = 0.000, NFI = 0.829, CFI = 0.869, TLI =

0.830, RMR = 0.051, AGFI = 0.897.

From table 4 it is easy to see that the regression weights of all variable loading on their

respective factors. All critical ratios are statistically significant at the 99 per cent confidence

level. The factor intercorrelations for the three first-order factors are presented in Table 4 and are

statistically significant at 99 per cent. The moderate correlation between factors suggests

adequate discriminant validity between these related aspects of temperament. In other words, as

specified by the theory, the scale measures related but still separate aspects of temperament.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

8

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

TABLE 4: LOADING OF THE FIRST ORDER CONFIRMATORY ANALYSIS FOR

POST SELLING SERVICE QUALITY

Standard first – order loading a

Variables R2 Routine &

Alteration Services

Exceptional

Services

Revival Services

posgrnloan7 0.237 0.487c

posassig6 0.312 0.559 (7.169)

possurrval9 0.245 0.495 (6.690)

posclaim11 0.325 0.570 (7.246)

possurvben8 0.316 0.562 (7.192)

posaltpol10 0.318 0.564 (7.204)

Routine

&Alteration

Servicesb

--- 0.714

0.566

poscollprem2 0.294 0.542c

pospoldel1 0.355 0.596 (7.441)

posperinf12 0.377 0.614 (7.542)

posnomi5 0.176 0.420 (5.986)

Exceptional

Servicesc

--- 0.486

posrevPUpo3 0.586 0.765 c

posrevLPpo4 0.711 0.843 (9.546)

Revival Servicesc ---

Notes: aStandard first order loading is the standard regression weight of the individual variables’

loading on to one of the component factors. Figures in parentheses are critical ratios from the

unstandardized solution; b Standard first order loading for component factors (i.e. Routine &

Alteration Services, Exceptional Services, Revival Services) is the covariance between any two

of these component factors; c The critical ratio is not available, because the regression weight of

the first variable of each component factor is fixed at 1; x2 = 183.740, x

2 /df= 3.603, df = 51, GFI

= 0.933, RMSEA = 0.082, PCLOSE = 0.000, NFI = 0.829, CFI = 0.869, RMR = 0.051, AGFI =

0.897.

The graphical presentation of the model is as under.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

9

htt

p:/

/ww

w.a

ijsh

.org

AJRBEM

LOADING OF THE FIRST ORDER CONFIRMATORY ANALYSIS FOR POST

SELLING SERVICE QUALITY

RELATING CANCELLATION OF POLICY DUE TO FIRST YEAR LEAPSATION TO

POST PURCHASE SERVICES OF INTERMEDIARY

The major objective of this research paper is to establish the relationship between cancellation of

policy due to first year leapsation and post purchase services of intermediary. Considering this,

Cancellation of policy due to first year leapsation is taken as independent variable while post

purchase service of intermediary is dependent variable. For this, MANOVA is administered

because MANOVA is a multivariate extension of the univariate techniques used for measuring

the differences between group means. As stated by Hair et al. (1998, p.14), MANOVA ‘…is a

statistical technique that can be used to simultaneously explore the relationship between several

categorical independent variables (usually referred to as treatments) and two or more metric

variables.’

To measure significant difference related to the independent variables, one Multivariate Analysis

of Variance (MANOVA) test with repeated measures were conducted. The MANOVA and

subsequent ANOVA results are shown in Table 5, and it was found that there is statistically

insignificant difference between cancellation of policy due to first year leapsation(i.e. 0 to 20, 21

.24

posgrnloan7

.31

posassig6

.24

possurrval9.33

posclaim11.32

possurvben8.32

posaltpol10.29

poscollprem2.35

pospoldel1.38

posperinf12.18

posnomi5.59

posrevPUpo3.71

posrevLPpo4

Rout_Alt_Ser

Excep_ser

Revival ser

e1

e2

e3

e4

e5

e6

e7

e8

e9

e10

e11

e12

.49

.56

.49

.57

.56

.56

.54

.60

.61

.42

.77

.84

.71

.57

.49

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

0

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

to 40, 41 to 60 and 61 to 80) for the four dependent variables of post purchase services of

intermediary i.e. Routine & Alteration Services, Exceptional Services and Revival services

(Wilk’s Lamda = 0.847; Significance: p =0.055> 0.05).

As indicated in Table 5, the univariate F-ration were also significant for the one dependent

variables i.e. Exceptional Services (F=2.987, Sign. = 0.035) but statistically cancellation of

policy due to first year leapsation was non – significant on Calculation of Revival Services

(F=1.206, Sign. =0.312), Routine & Alteration Services (F=0.917, Sign. =0.435), In addition to

this, the means score of all the three dimensions of post purchase services of intermediary

(aggregate score) were checked and it was found that Cancellation of policy due to first year

leapsation of 0 to 20 per cent have more importance compare to other prospect in post purchase

services of intermediaries. Henceforth, overall results support H1c but H1, H1a, H1b, were not

supported (Table 5).

TABLE 5: MANOVA RESULTS FOR CANCELLATION OF POLICY DUE TO

FIRST YEAR LEAPSATION TO POST PURCHASE SERVICES OF INTERMEDIARY

(OVERALL) Effect Value F Significance

Multivariate tests

First year policy

lapsation rate

Pillai’s Trace 0.157 1.862 0.057

Wilks’ Lambda 0.847 1.886 0.055

Hotelling’s Trace 0.175 1.896 0.052

Roy’s Largest Root 0.136 4.580 0.005

ANOVA tests

Revival Services ----- 1.206 0.312

Routine & Alteration

Services

----- 0.917 0.435

Exceptional Services ----- 2.987 0.035

Cancellation of policy due to first

year leapsation

Revival Services Routine &

Alteration

Services

Exceptional Services

0 to 20 (n=79) 2.14 1.67 1.83

21 to 40 (n=21) 1.96 1.48 2.11

41 to 60 (n=14) 1.45 1.50 1.50

61 to 80 (n=10) 2.00 1.50 3.00

Note: * p < 0.05

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

1

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

LIMITATION AND FUTURE RESEARCH

There are three limitations of this study. First, the survey has been conducted in Gujarat only so

the results may not be applicable to country wide. Second, the sampling method is of non

probability type so the sample’s representation about the population is questioned. And third,

Comrey and Lee (1992) (see Tabachnick & Fidell, 1996) say the sample size is 124 only, it is

poor for factor analysis.

This research is limited to the post purchase services only but further research can be done by

considering pre-selling services of intermediaries. That is interaction on various issues before

execution of insurance contract. Such study has been conducted in Germany but not in India

(Eckardt & Doppner, 2008). Guiding results can also be obtained by comparing the results of

various insurance intermediary namely agents, brokers, direct marketing and bancassurance. The

first year policy lapsation ratio can also be replaced with other positive variables like repeat

purchase and referral sales.

REFERENCES

Anderson, E., Ross, W. T., & Weitz, B. (1998). Commitment and Its Consequences in the

American Agency System of Selling Insurance. Journal of Risk and Insurance (65), 637-669.

Andreassen, T. W., & Lanseng, E. (1997). The principal’s and agents’ contribution to customer

loyalty within an integrated service distribution channel: An external perspective. European

Journal of Marketing, , 31 (7), 487-503.

Arnold, C. (2000, December 4). Life CEOs: Distribution, Technology are Key. National

Underwriter , pp. 6.

Arulsuresh, J., & Rajamohan, S. (2010). Attitude of the Agents Towards the Marketing of

Insurance Services by the LIC of India. The IUP Journal of Risk & Insurance , VII (4), 47-71.

Banumathy, S., & Manickam, S. (2004, June). Customer services provided by Life Insurance

Corporation of India- A case study. The Insurance Times , 30-33.

Change Agents. (2008, October 19). Business Today .

Comrey, A. L., & Lee, H. B. (1992). A first course in factor analysis (2nd Edition ed.). Hillsdale,

NJ: Erlbaum.

Cummins, J. D., & Doherty, N. A. (2005). The Economics of Insurance Intermediaries. Wharton

School, University of Pennsylvania.

Cummins, J. D., & Doherty, N. A. (2005). The Economics of Insurance Intermediaries. Wharton

School, University of Pennsylvania.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

2

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

Cummins, J. D., & Doherty, N. A. (2006). The Economics of Insurance Intermediaries. Journal

of Risk & Insurance , 73: 359-396.

Darby, M. R., & Karni, E. (1973). Free Competition and the Optimal Amount of Fraud. Journal

of Law and Economics , 16: 67-88.

Eckardt, M. (2007). Insurance Intermediation: An Economic Analysis of the Information

Services Market. (Berlin, Heidelberg: Physica-Verlag) .

Eckardt, M., & Doppner, S. R. (2008). The Quality of Insurance Intermediary Services –

Empirical Evidence for Germany. Andrássy Working Paper Series No. XXV . Andrássy Gyula

University, Budapest.

Fleming, John D; President Fleming Advisor International. (2008). The plight of Face to Face

Insurance Distribution. LIMRA's MarketFacts Quarterly , 27 (3), pg 64.

Gummarra, L. T. (2008). Reason for coexistance of diffrent distribution channels: An Empirical

test for the German Insurance Market. The Geneva Papers on Risk and Insurance- Issues and

Practice , 389-407.

Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate Data Analysis

(5th Edition ed.). New Jersey: Prentice-Hall.

Hirshleifer, J. (1973). Where are we in Theory of Information? American Economic Review , 63:

31-39.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: managerial behavior, agency costs

and ownership structure. Journal of Financial Economics , 3, 305-60.

Kaiser, H. F. (1970). A second generation little jiffy. Psychometrica , 35,401-415.

Lowry, J. R., Avila, S. M., & Baird, T. R. (1999, Summer ). Developing a Niching Strategy for

Insurance Agents. CPCU Journal , 74-83.

Machiraju, A. (2003, March). Training Life Agents to Serve. IRDA Journal , 22-24.

Machiraju, A. (2004, December). A Noble Pro Called An Agent. IRDA Journal , 21-24.

Naga Raja Rao, P. (2004, January). Distribution Channels in Insurance Industry -New Trends.

Bima Vidya , 15-18.

Nelson, P. (1970). Information and Consumer Behavior. Journal of Political Economy , 78:

311-329.

Posey, L. L., & Tennyson, S. (1998). The Coexistence of Distribution Systems Under Price

Search: Theory and Some Evidence from Insurance. Journal of Economic Behavior and

Organization , 35: 95-115.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

3

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

Posey, L. L., & Yavas, A. (1995). A Search Model of Marketing Systems in Property-Liability

Insurance. Journal of Risk and Insurance , 62: 666-689.

Rajagopalan, V. (2008). Lapsation of Life Insurance Policies. IRDA Journal , 8-12

Rose, F. (1999). The Economics, Concept, and Design of Information Intermediaries.

(Heidelberg:Physica Verlag).

Seog, S. H. (1999). The Coexistence of Distribution Systems When Consumers Are Not

Informed. The Geneva Papers on Risk and Insurance Theory , 24: 173-192.

Seog, S. H. (2005). Distribution Systems and Operating Leverage. Asia-Pacific Journal of Risk

and Insurance , 1: 45-61.

Shelton, D. (1995). Distribution strategy in the life and pensions market. International Journal of

Bank Marketing , 13 No. 4, 41-44.

Shettewar, R., & Dixit, S. (2009). Life Insurance Agent Profiling: Leading Indicators to Growth.

Journal of Insurance & Risk Management , VII (14), 21-29.

Singhvi, N., & Bhatt, P. (2008). Distribution Channesl in Life Isurance. Bimaquest , VIII (1),

20-40.

Varma, V. (2004, July-December). Insurance Broking In India : Scope Challenges and Prospects.

The Journal of Insurance Institute of India , 106-116.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

4

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l

o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F

R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D

M A N A G E M E N T

A CONCEPTUAL FRAMEWORK OF EMPLOYEES’ CONTINUANCE

INTENTION TO USE E-LEARNING SYSTEM

DR. A. THIRUCHELVI*; S. KOTEESWARI**

*Faculty,

Department of Management Studies,

CEG Campus, Anna University,

Chennai, India.

**Student,

Department of Management Studies,

CEG Campus, Anna University,

Chennai, India.

ABSTRACT

We are now in an era where all organizations are orienting themselves towards

strategic human resource management initiatives. One such an initiative is the use of

Virtual Learning Environment (VLE) that enables the organizations to offer

consistent and convenient training to their employees at low cost. The investments

made in implementing VLE can have fruitful returns only when there is continuous

usage by the employees which is determined by satisfaction derived from it. Though

many studies have attempted to test the relationship between perceived usefulness,

perceived ease of use, self efficacy, learning style, technical know-how, interaction

with instructor & interaction with other learners and the e- learner satisfaction, no

study has holistically tested the relationship. This paper tries to fill the gap by

proposing a single conceptual framework depicting the relationship between all such

employee related variables and e-learning satisfaction which in turn influences the

continuance intention to use. The proposed framework will help organizations in

formulating strategies to enhance employees’ satisfaction towards e-learning and

thereby increasing their intention to use the e-learning system.

KEYWORDS: e Learning, e learner Satisfaction, continuance intention.

______________________________________________________________________________

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

5

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

1 INTRODUCTION

The organizations consider training and improving the human resources as the crucial points of

development and put them on the top of their programs due to the rapid changes in technology

and knowledge raise (Hassan, Shahidi, Hosseini, & Nahad, 2011).The process of providing

consistent training to all employees spread across the world is a challenge for global firms. And

also the training and development department is highly responsible for returns on the

investments made in training the employees.

Information and Communication Technology (ICT) has become the saviour for

organisations to overcome these challenges. ICT has driven the evolution of e-learning as a

strategic initiative for training the employees (Schneckenberg, 2010). The number of e-learning

programs implemented in a corporate setting has increased dramatically over the last few years

and e-learning has become a major form of training and development within organizations (Ho &

Kuo, 2010).

There had been many research conducted on assessing success of e learning in

organisations. Though the initial acceptance of e learning is highly essential, real success can be

measured only with the continuance intentions among employees to undergo the courses through

e learning system. The Theory of Reasoned Action (TRA) and Theory of Planned Behaviour

(TPB) explain how attitudes of individuals lead to intentions. The Technology Acceptance

Model (TAM) applies TRA and TPB and explains how attitudes lead to actual usage of

information systems. The expectancy confirmation model says that satisfaction leads to

continuance intentions. Many works in the literature have used the above mentioned theories in e

learning context and have identified the measures of individual attitudes about e-learning system

resulting in satisfaction which in turn influences the continuance intention.

The purpose of this paper is to conceptualise a holistic model which brings together all

attributes that influences e learner satisfaction which leads to continuance intentions.

2 THEORETICAL DEVELOPMENT

2.1 E-LEARNING

E-Learning is the use of telecommunication technology to deliver information for education and

training (Sun, Tsa, Finger, Chen, & Yeh, 2008).

E-Learning systems include: web-based learning, computerized learning, virtual

classrooms, and digital cooperation. In an e-learning environment, learners are supplied with

learning materials via media, making e-learning systems a cost and time-effective approach to

train employees (Chen, 2010).

The shift from a product-based economy to a knowledge-based economy has resulted in

an increased demand for knowledge workers who are capable of higher-order thinking and

reasoning to solve intricate problems in the work place. There arises the need to build more cost-

effective and efficient learning environments in the workplace to meet both individual and

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

6

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

organizational objectives. This requires organizations to educate and train employees at multiple

sites and times (Govindasamy, 2002).

Organizations are using technology to offer training programs for their employees due to

its beneficiary effects such as cost reduction in travel expenses and training time, flexibility in

pace and delivery of training, variety of available content, standardized and consistent course

delivery, permanent use of material within the company, boost worker productivity, increase in

number of people trained, stay competitive, etc (Ozturan & Kutlu, 2010).

2.2 ATTITUDES, SATISFACTION AND INTENTION

An attitude is a disposition to respond favourably or unfavourably to an object, person, intuition

or event. Attitudes are evaluative in nature. TRA argues that attitudes and subjective norms are

determinants of intention. TPB which is an extension of TRA depicts that there are three major

antecedents of intention towards behaviour. First is the attitude towards a behaviour, which is

determined by the beliefs about the consequences of the behaviour, termed as behavioural beliefs

and the evaluation of its outcome. Second is the subjective norm, which is determined by the

beliefs about approval or disapproval of performing the behaviour by social referents, termed as

normative beliefs and the individual’s motivation to comply with the referents. Third is the

perceived behavioural control, which is determined by the beliefs about the factors that facilitate

or obstructs the performance of the behaviour termed as control beliefs and the power of the

factor to assist or inhibit the performance of the behaviour (Ajzen, 2010).

The Expectancy Confirmation Theory (ECT) states that confirmations with expectations

about an object or event after experiencing it, results in satisfaction leading to continuance

intentions (Oliver, 1980). Thus combining the TPB and ECT it is inferred that behavioural belief

on outcome, evaluation of outcome, concerned normative belief, individual’s motivation, control

belief on resources and power to facilitate the behaviour influences satisfaction which in turn

influences continuance intention (Roca, Chiu, & Martinez, 2006).

2.3 CONTINUANCE INTENTION TO USE E-LEARNING SYSTEM

Organisations take great efforts to develop and implement e-learning program for their

employees. Although initial acceptance of e-learning is an important first step toward achieving

e-learning success, actual success still needs continued usage. Continuance intention is the

intention of employees to use the e learning system continuously after initial usage. Intentions

often predict behaviour. People do what they intend to do. To understand their behaviour we

must identify the determinants of intentions (Ajzen, 2010). Understanding the factors affecting

employees’ intention to continue using e-learning system helps in designing strategies that are

most likely to increase the use of e learning (Lee, 2010).

2.4 SATISFACTION ON E-LEARNING SYSTEM

The organizations should make sure that the employees are satisfied with e-learning courses,

only then they will have the intention to continually undergo more courses and also encourage

their peers to use e-learning setup. After taking up e learning courses employees should be glad

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

7

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

about their decision and feel that the courses have satisfied their needs (Sun, Tsa, Finger, Chen,

& Yeh, 2008). Users’ satisfaction has a positive effect on e-learning continuance intention (Roca,

Chiu, & Martinez, 2006; Lee, 2010). Hence it is inferred that e- learner satisfaction influences

continuance intention to use e learning system.

Previous works in literature have measured e-learning success from many dimensions

like individual dimension, course dimension, technical dimension and environmental dimension,

of which individual dimension is the most important one, as the success of any system depends

on the user. Following independent variables are said to have influence on e-learning

satisfaction: perceived usefulness, perceived ease of use, self efficacy, learning style and

interaction. Apart from these variables motivation is proposed as an influential determinant of e-

learning satisfaction the framework.

2.5 PERCEIVED USEFULNESS

Davis (1989) has defined perceived usefulness as the degree to which a person believes that

using a particular system would enhance his/her job performance. Positive behavioural beliefs

help in deriving satisfaction resulting in positive intentions. The employees will be satisfied with

the e-learning system only if they perceive that it helps them to improve their job performance.

Realising that e-learning system increases their productivity and usefulness induces the

employees to derive satisfaction from it (Ong & Lai, 2006). Perceived usefulness while using the

e-learning system has a positive effect on satisfaction (Roca, Chiu, & Martinez, 2006; Lee, 2010;

Johnson, Hornik, & Salas, 2008). Hence it is inferred that perceived usefulness has influence on

e-learner satisfaction.

2.6 PERCEIVED EASE OF USE

Davis (1989) has defined perceived ease of use as the degree to which a person believes that

using a particular system would be free of physical and mental effort. Attitude towards behaviour

highly affects the level of satisfaction after performing the behaviour. Employees should believe

that the system is easily understandable and that they can easily get familiarized with the e

learning system which enables them to be satisfied with the e- learning system (Lee &

Lee, 2008).Perceived ease of use while using the e-learning system has a positive effect on

satisfaction (Roca, Chiu, & Martinez, 2006; Sun, Tsa, Finger, Chen, & Yeh, 2008). Hence it is

inferred that perceived ease of use has a role to play in e-learner satisfaction.

2.7 SELF EFFICACY

Roca (2006) has defined self efficacy as the degree to which an individual is confident that

he/she can perform a specific task or achieve a specific goal. Control beliefs of an individual

influences intentions through satisfaction. Employees should feel confident to use the e-learning

system. They should trust themselves that they have the ability to access and complete the

courses, only then they can gain satisfaction from the system. Perceived satisfaction in e-learning

will be influenced by the perceived self-efficacy (Liaw & Huang, 2013; Sun, Tsa, Finger, Chen,

& Yeh, 2008; Johnson, Hornik, & Salas, 2008). Hence it is inferred that Self Efficacy influences

the e-learner satisfaction noticeably.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

8

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

2.8 INTERACTION

Johnson (2008) has defined interaction as the exchange of information between the various

stakeholders in the course (e.g. peers, instructors, and other support staff). The e-learning system

should facilitate employees to share knowledge with other participants and encourage them to

get the doubts clarified from the course instructor, only then the employees can attain satisfaction

(Choi, Kim, & Kim, 2007).Learner perceived interaction with others will positively influence

perceived e-Learner satisfaction with e-Learning (Liaw & Huang, 2013; Sun, Tsa, Finger, Chen,

& Yeh, 2008; Johnson, Hornik, & Salas, 2008). Hence it is inferred that Interaction has

considerable influence on e-learner satisfaction.

2.9 LEARNING STYLE

For instructor based learning, learning style is irrelevant but for web based learning, learning

style is significantly important. Learners who learn through thinking and watching and thinking

would better learn with e-learning. There is statistically significant difference among those with

different learning styles (Lu, Yu & Liu, 2003). Hence it is inferred that learning style is an

inevitable factor on E-Learner Satisfaction. But many existing works do not include learning

style in the models that are used to judge whether employees are interested in the e-learning

system. This paper proposes a model for employees’ continuance intention to use e-learning

system that includes learning style as one of its parameters.

2.10 MOTIVATION

Motivation is defined as the process that accounts for an individual’s intensity, direction, and

persistence of effort toward attaining a goal. Motivation is a part of subjective norm which

greatly influences intention through satisfaction. Porter Lawler theory of motivation (1968)

explains the process of how employee motivation helps in attaining satisfaction in workplace. In

the flow of motivation process it is well explained that extrinsic and intrinsic rewards help an

individual to attain satisfaction. Hence this paper includes motivation as a major parameter in the

model of employees’ continuance intention to use e-learning system. E-learner satisfaction is

influenced by their level of motivation with rewards as their drive. Self motivation drives

employees to have a strong desire to take-up the e-learning courses. When employees are given

rewards like credit points for the e-learning courses, their satisfaction level will be enhanced.

Hence it is inferred that motivation as an additional parameter helps to improve e-learner

satisfaction.

2.11 THE CONCEPTUAL MODEL

A framework of employees’ continuance intention to use e-learning system is conceptualized as

shown in figure 1. This framework gives a holistic view of how perceived usefulness, perceives

ease of use, self efficacy, interaction, learning style and motivation influences the satisfaction

derived from e-learning which in turn influences intention to use the e-learning system. The

major contribution of this paper is that the independent variables – learning style and motivation

are included to study about employees’ satisfaction and continuance intention towards e-learning

systems used in the organisations.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

1

9

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

FIGURE 1. THE CONCEPTUAL FRAMEWORK OF EMPLOYEES’ CONTINUANCE

INTENTION TO USE E-LEARNING SYSTEM

3 CONCLUSION

To improve the continuance intention to use e-learning system among employees all factors that

have influence on e-learning satisfaction should be considered. Employees should be made to

perceive that E-Learning will be useful for improving their performance. They should also be

made to perceive that the system can be used without much effort. Organization should give

them the confidence that they can successfully learn from the system. Interaction among

employees and with instructor should be facilitated. Learning Style of employees should be

oriented towards field independence. Motivation of employees to undergo e-learning courses

should be seriously considered to improve e-learning satisfaction.

To reap the fruits of E-Learning, organizations should concentrate on all the employee

attributes as mentioned in the framework.

REFERENCES

Ajzen, I. (2010). Attitudes, personality and behaviour. Tata McGraw Hill education private

limited.

Chen, H.J. (2010). Linking employees’ e-learning system use to their overall job outcomes:

An empirical study based on the IS success model. Computers & Education, 55, 1628-1639.

Choi, D.H., Kim, J., & Kim, S.H. (2007). ERP training with a web-based electronic learning

system: The flow theory perspective. Int. J. Human-Computer Studies 65, 223–243.

E- Learning satisfaction

Learning style

Interaction

Self efficacy

Perceived ease of use

Perceived usefulness

Motivation

Intention to use

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

0

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

Govindasamy, T. (2002). Successful implementation of E-Learning: Pedagogical considerations.

Internet and Higher Education 4, 287–299.

Hassan, M., Shahidi, M.R., Hosseini., & Nahad, R.F. (2011). Classroom Training rather than

ETraining Effectiveness for Promotion Managerial Skills in Iran: A Comparative

Study.International Conference on E business, Management and Economics IPEDR vol.3.

Ho, L.A., & Kuo,T.S. (2010). How can one amplify the effect of e-learning? An examinationof

high-tech employees’ computer attitude and flow experience. Computers in Human Behavior 26,

23–31.

Johnson, R.D., Hornik,S., & Salas,E. (2008). An empirical examination of factors contributingto

the creation of successful e-learning environments. Int. J. Human-Computer Studies 66,

356–369.

Lee, J.K., & Lee, W.K. (2008). The relationship of e-Learner’s self-regulatory efficacy

andperception of e Learning environmental quality. Computers in Human Behavior 24, 32–47.

Lee, M.C. (2010). Explaining and predicting users’ continuance intention toward e-learning:

An extension of the expectation–confirmation model. Computers & Education 54, 506-516.

Liaw, S.S., & Huang, H.M. (2013). Perceived satisfaction, perceived usefulness and

interactivelearning environments as predictors to self-regulation in e-learning environments.

Computer & Education 60, 14–24.

Lu, J., Yu,C.S., & Liu, C. (2003). Learning style, learning patterns, and learning performance in

a WebCT-based MIS course. Information & Management 40, 497–507.

Oliver, R.L. (1980). A Cognitive Model of the Antecedents and Consequences of Satisfaction

Decisions. Journal of Marketing Research, 17, No. 4, 460-469.

Ong, C.S., & Lai, J.Y. (2006). Gender differences in perceptions and relationships among

dominants of e learning acceptance. Computers in Human Behavior, 22, 816–829.

Ozturan, M., & Kutlu, B. (2010). Employee satisfaction of corporate e-training programs.

Procedia Social and Behavioral Sciences 2, 5561–5565.

Rocaa, J.C., Chiu, C.M., & Martinez, F.J. (2006). Understanding e-learning continuance

intention: An extension of the Technology Acceptance Model. Int. J. Human Computer

Studies 64, 683–696.

Schneckenberg, D. (2010). Overcoming barriers for eLearning in universities—portfolio models

for e Competence development of faculty. British Journal of Educational Technology 41 No.6,

979–991.

Sun, P.C., Tsai, R.J., Finger, G., Chen, Y.Y., & Yeh, D. (2008). What drives a successful

e Learning? An empirical investigation of the critical factors influencing learner satisfaction.

Computers & Education 50, 1183-1202.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

1

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

A P e e r R e v i e w e d I n t e r n a t i o n a l J o u r n a l

o f A s i a n R e s e a r c h C o n s o r t i u m

AJRBEM:

A S I A N J O U R N A L O F

R E S E A R C H I N B U S I N E S S

E C O N O M I C S A N D

M A N A G E M E N T

PERFORMANCE OF INDEX FUNDS IN INDIA

DR. (MRS.) PRASHANTA ATHMA*; MS. B. MAMATHA**

*Professor,

Department of Commerce,

Osmania University,

Hyderabad, A.P., India.

**Research Scholar,

Department of Commerce,

Osmania University,

Hyderabad, A.P., India.

ABSTRACT

Mutual Fund is a trust that pools money from a group of investors (sharing common

financial goals) and invest the money thus collected into asset classes that match the

stated investment objectives of the scheme. Index Funds (IFs) focuses on the

performance of specific stock indices, as opposed to other types of ETFs that are

based on oil or other commodities. Index funds spread the risk factor over the entire

index, As such; large institutional investors like pension funds as well as older

individual investors who are looking to reduce the risk in their portfolios often find

Index Funds a preferable alternative to buying stock of individual companies.

The study is based on secondary data covering a period of 14 years for Index Funds

i.e. 1999 to 2012 to reflect upon the growth of Index Funds over a period of time

since their inception.

The parameters for evaluating the performance are Net Asset Value, standard

deviation, Return, Beta, Reward to Variability (Sharpe) and Treynors Performance

Evaluation Ratio. The statistical tools like Standard Deviation, Beta, Sharpe Ratio,

and Treynors Ratio are used for data analysis.

______________________________________________________________________________

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

2

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

INTRODUCTION

Mutual Fund is a trust that pools money from a group of investors (sharing common financial

goals) and invest the money thus collected into asset classes that match the stated investment

objectives of the scheme.

The Fund Manager manages the Mutual Fund and uses his investment management skills and

necessary research works and ensures much better return than what an investor can manage on

his own. The capital appreciation and other incomes earned from these investments are passed on

to the investors (also known as unit holders) in proportion to the number of units an investor

owns.

Mutual Fund was introduced in the year 1963 in India. From an historical point of view, Mutual

Funds have been around four hundred years, but they are a relatively new investment

phenomenon to the novice investors. Mutual Funds are a conglomeration of stocks, bonds,

securities and even real estate, put together by a smart Fund Manager who hand-picks winners

for a winning combination.

INDEX FUND

An Index Fund is a Mutual Fund that aims to replicate the movements of an index of a specific

financial market. An Index Fund follows a passive investing strategy called Indexing. It involves

tracking an index say for example, the Sensex or the Nifty and builds a portfolio with the same

stocks in the same proportions as the index. The Fund makes no effort to beat the index and in

fact it merely tries to earn the same return. Index Funds, an instrument of Mutual Fund, came in

to existence in India in the year 1998.

REVIEW OF LITERATURE

Philippe Jorion (2003)1 in his article explored the risk and return relationship of active portfolios

subject to a constraint on tracking-error volatility (TEV), which can also be interpreted in terms

of value at risk. Such a constrained portfolio is the typical setup for active managers who are

given the task of beating a benchmark. The problem with this setup is that the portfolio manager

pays no attention to total portfolio risk, which results in seriously inefficient portfolios unless

some additional constraints are imposed. The study reflected that TEV-constrained portfolios are

described by an ellipse on the traditional mean–variance plane. This finding yields a number of

new insights. Because of the flat shape of this ellipse, adding a constraint on total portfolio

volatility can substantially improve the performance of the active portfolio. In general, plan

sponsors should concentrate on controlling total portfolio risk.

Manuel Ammann, Stephan Kessler and Jurg Tobler (2006)2 stated that for investors, it is

important to know what trading strategies an asset manager pursues to generate excess returns. In

this paper, they proposed an alternative approach for analyzing trading strategies used in active

investing. They used tracking error variance (TEV) as a measure of activity

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

3

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

Benchmark Funds Asset Management Company(2008)3 research department did research in

early 2008 on the topic of “Myth of Eternal Alpha” It has often been argued that individual

active fund managers are consistently able to exploit anomalies and aberrations that may exist in

the market and while considering out performance/ under performance one should look at longer

periods.

J. Christopher Hughen, Prem G. Mathew (2009)4 “The efficiency of international information

flow: Evidence from the ETF and CEF prices” stated that closed-end funds (CEFs) and

exchange-traded funds (ETFs) differ in their liquidity and ease of arbitrage. We compare their

price transmission dynamics using a sample of funds that invest in foreign securities and are

most likely to show the deficiencies in the manner in which they process information. Our

analysis shows that ETF returns are more closely related to their portfolio returns than are CEF

returns. However, both fund types under react to portfolio returns but overreact to domestic stock

market returns. A simple trading strategy using these results is profitable with roundtrip trading

costs less than 1.38% for CEFs and 0.71% for ETFs.

Sangheon Shin, Gökçe Soydemir (2010)5 “ Exchange- Traded Funds, persistence in tracking

errors and information dissemination” stated that tracking errors from 26 exchange-traded funds

(ETFs) utilizing three different methods and test their relative performance using Jensen's model.

We find that tracking errors are significantly different from zero and display persistence. Based

on Jensen's alpha, risk adjusted returns are significantly inferior to benchmark returns for all

ETFs with two exceptions at conventional significance levels revealing that passive investment

strategy does not outperform market returns. We then examine the degree to which frequently

used factors such as expense ratio, dividends, exchange rate and spreads of trading prices may be

underlying sources of tracking errors causing this underperformance.

RESEARCH GAP

The above review of literature points out that the studies are based on tracking errors, risk

returns, price Transmission etc. Though the Index Funds came in to existence in 1988 in US, and

growth over a period of time is not reflected. Hence, the study is undertaken to reflect upon the

growth of Index Funds over a period of time since their inception and evaluate its performance in

terms of risk and return.

OBJECTIVES OF THE STUDY

The objectives of the study are

To present the trends and progress of Index Funds in India and

To evaluate the performance of Index Funds in India.

SOURCES OF DATA

The study is based on secondary data. The Secondary data sources include Fact sheets of Mutual

Funds, Articles, News papers, SEBI Manuals, AMFI Reports and Websites.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

4

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

PERIOD OF THE STUDY

The study covers a period of 14 years from 1999 to 2012 i.e. since their inception to study the

trends and evaluate the performance.

SAMPLE SIZE

There are 44 Index Funds in India. Data with regard to all the parameters selected for the

evaluation of performance are available only for 23 Index funds which were operating between

the period of 1999 – 2012. Hence, the study is made only for 23 Index Funds.

PARAMETERS

The parameters for evaluating the performance are Net Asset Value, standard deviation, Return,

Beta, Reward to Variability (Sharpe) and Treynors performance evaluation Ratio.

STATISTICAL TECHNIQUES

The data are analyzed with the help of statistical tools like Standard Deviation, Sharpe Ratio,

Treynors Ratio and Beta.

GROWTH OF INDEX FUNDS

The growth of Index Funds in terms of the number of Funds and NAV is given in Table-1.

Starting with 1 Index Fund in the year 1999 viz., Principal Index Funds the number of IFs

increased to 24 by the end of the year 2012 registering a CAGR of 25.48%.The awareness and

popularity of the Mutual Fund Schemes is reflected in the addition of 20 more Mutual Funds

Schemes in the year 2013 in addition to the existing 24 schemes, which is a welcome sign. The

same is provided in Table -2.

TABLE-2 NEWLY INTRODUCED MUTUAL FUND SCHEMES DURING 2013

S.No Name of the Fund Launch Date

1 FRANKLIN INDIA INDEX BSE SENSEX DIRECT Jan 2013

2 FRANKLIN INDIA INDEX NSE NIFTY DIRECT Jan 2013

3 HDFC INDEX NIFTY DIRECT Jan 2013

4 HDFC INDEX SENSEX DIRECT Jan 2013

5 ICICI PRUDENTIAL INDEX DIRECT Jan 2013

6 ICICI PRUDENTIAL NIFTY JUNIOR INDEX DIRECT Jan 2013

7 IDBI NIFTY INDEX DIRECT Jan 2013

8 IDBI NIFTY JUNIOR INDEX DIRECT Jan 2013

9 IIFL DIVIDEND OPPORTUITIES INDEX DIRECT Jan 2013

10 LIC NOMURA MF INDEX NIFTY DIRECT Jan 2013

11 LIC NOMURA MF INDEX SENSE X DIRECT Jan 2013

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

5

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

12 PRINCIPAL INDEX DIRECT Jan 2013

13 RELIANCE INDEX NIFTY DIRECT Jan 2013

14 RELIANCE INDEX SENSEX DIRECT Jan 2013

15 TATA INDEX NIFTY PLAN A DIRECT Jan 2013

16 TATA INDEX SENSEX PLAN A DIRECT Jan 2013

17 UTI NIFTY INDEX DIRECT Jan 2013

18 CANARA ROBACCA NIFTY INDEX DIRECT Jan 2013

19 GOLDMAN SACHS S&P 500 INDEX FUND DIRECT Jan 2013

20 BIRLA SUN LIFE INDEX DIRECT Jan 2013

Source: www.valueresearch.com

Net Asset Value (NAV) is a term used to describe the value of an entity’s assets less the value of

its liabilities. The term is most commonly used in relation to Mutual Funds due to the fact that

shares of such funds are redeemed at their Net Asset Value. It may represent the value of the

total equity, or it may be divided by the number of shares outstanding and, thereby, represent the

per share Net Asset value.

NAV as per IRDA is calculated as follows:

NAV = (Market Value of the Investment held by the Fund + Value of Current Assets-Value of

Current Liabilities and provisions) /Number of units existing on valuation date (before creation

/redemption of units)

The Table-1 shows NAV per share over a period of time for the various IFs .The overall CAGR

during the period is 42.42%. It can be observed that the Principal Index Fund and Birla Sun Life

Index Fund have a growth rate more than the overall growth rate. It is Birla Sun Life IFs which

Rank 1st with a CAGR of 84.56% followed by Principal IFs with 80.93%, TATA Index Sensex

Plan –A with 16.37% and HDFC sensex Index Fund with 15.99%.

The last five ranks were scored by Taurus Nifty, Reliance Index nifty, Quantum Index Fund,

Reliance Index Sensex and GOLDMAN SACHS S&P 500 Index Fund. Out of these 5 IFs,

excepting Quantum Index Fund, GOLDMAN SACHS S&P 500 Index Fund all other IFs are just

2 years old. Though HDFC Index Nifty .Franklin India Index BSE Sensex, Franklin India Index

NSE Sensex IFs entered early in IF Market, their ranks are in the middle order viz., 11,12,13

respectively reflecting upon the fact that it is not the age of the Fund but their efficiency level

that yields better results.

ANNUAL RETURNS OF INDEX FUNDS

One of the parameters for the evaluation of the IFs is the annual returns, which is presented in

Table-4. The Fund is rank based on the average returns which is the simple average of the returns

over a period of time. Higher the ratio better the performance of the Fund compare to the Other

IFs.

Volume 3, Issue 6 (June, 2013) ISSN: 2249-7307

Jou

rnal

of

Asi

an R

esea

rch

Co

nso

rtiu

m

2

6

h

ttp

://w

ww

.aij

sh.o

rg

AJRBEM

On the basis of average returns, TATA Index Sensex PLAN A occupied the Rank 1st with a

average return of 23.92% followed by HDFC Index Fund with 23.81%, SBI MAGNUM Index

Fund with 21.64%, LIC NOMURA MF INDEX Fund with 19.50%, TATA Index Fund with

19.24%

RISK ANALYSIS OF INDEX FUNDS

The variability in the returns is called as risk and the same is measured with the help of Standard

Deviation and Beta. Standard deviation is a measure of the deviation in the returns of the Fund.

A volatile stock would have a high standard deviation. It tells us how much the return on a Fund

is deviating from the expected returns based on its historical performance.

The below tables give the details relating to Standard deviation, Sharpe ratio, Beta and Treynors

Ratio.

TABLE – 4 RISK ANALYSIS OF INDEX FUNDS

S.No.

Name of the Fund

Standard

Dev (%)

Sharpe

Ratio (%) Beta

Treynors

Ratio (%)

1 Principal Index 34.14 15.78 (12) 0.59 1.81(11)

2 Birla Sun Life Index 39.01 14.82 (14) 0.51 -1.37( 12)

3 Franklin India Index Bse Sensex 48.66 11.73 ( 17) 0.27 -19.46(17)

4 Franklin India Index Nse Nifty 41.05 16.59 ( 8 ) 0.65 3.82(13)

5 HDFC Index Nifty 41.58 18.00 ( 6 ) 0.76 7.13(8)

6 UTI Nifty Index 39.03 17.87 ( 10 ) 0.75 6.85(9)

7 HDFC Index Sensex 40.53 23.61 ( 2 ) 1.20 16.78(4)

8 ICICI Prudential Index Reg 25.46 13.41 ( 19 ) 0.29 -15.74(17)

9 LIC Nomura Mf Index Nifty 34.56 15.79 ( 11 ) 0.41 -4.538 (-15)

10 LIC Nomura Mf Index Sensex 39.28 19.29 ( 4 ) 0.59 5.38( 10)

11 SBI Magnum Index 39.24 21.43 ( 3 ) 0.71 9.82( 6)

12 Tata Index Nifty Plan A 36.39 19.02 ( 5 ) 0.80 8.79( 7)

13 Tata Index Sensex Plan A 37.83 23.70 ( 1) 1.15 16.63( 5)

14 Canara Robecca Nifty Index Reg 38.94 14.60 ( 16 ) 0.43 -4.40( 14)

15 Quantum Index 49.01 10.98 ( 20 ) 0.18 -35.47( 21)

16 Goldman Sachs S&P 500 Index Fund 54.48 4.11 ( 23 ) -0.29 32.56( 3)

17 ICICI Prudential Nifty Junior Index 22.3 8.36 ( 21 ) -0.03 238.49( 1)

18 IDBI Nifty Index 22.36 6.03 ( 22) 0.25 -26.42( 19)

19 IDBI Nifty Junior Index 13.39 15.78 ( 12 ) 0.17 -40.40( 22)

20 Reliance Index Nifty 18.89 14.82 ( 14 ) 0.43 -14.60( 16)

21 Reliance Index Sensex 0.249 11.73 ( 17 ) -0.09 101.41( 2)

22 Tauras Nifty Index 23.55 16.59 ( 8 ) 0.23 -28.96( 20)

23 IDFC Nifty Index Fund 20.80 18.00 ( 6 ) 0.09 -85.28( 23 )

Source: www.valueresearch.com