MSME - CBOA

54

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of MSME - CBOA

MSME INTERNATIONAL MSME DAY – 27th June

Introduction of “Simplified Common Appraisal Memorandum for MSMEs”

Loans above Rs. 5 Cr to Rs. 25 C –NF 1023 Loans above Rs. 10 lakhs to Rs. 1 Crore NF1028

Loans above Rs. 1 Crore to Rs. 5 Crore -NF 1029

889/20 24.11.20 : No collateral/third party guarantees to be stipulated for loan amounts uptoRs. 10 lakhs extended to MSEs

Under BAM83

820/20 : INTRODUCTION OF GST RETURNS SUBMISSION

All business entities whose aggregate T/O in a FY exceeds Rs 40 lakhs has to mandatorily register under GST This limit is set at Rs 10 lakhs for North Eastern and hilly states flagged as special category states]

The enterprise whose turnover is less than Rs. 1.50 Crore during the Financial Year 2019-20 can file their GST Returns on Quarterly basis

GST format to be submitted by all the borrowers with working capital exposure (fund/non-fund based) (Rs.5 crore) and above whose gst is fully/partially applicable wef 1.10.20

819/20 : FIXATION OF QUICK RATIO AS FINANCIAL BENCHMARK FOR VARIOUS INDUSTRIES

In respect of MSME borrowers with total exposure above Rs.10 crore(FB+NFB) from our Bank.

In respect of Corporate other than MSME borrowers with total exposure above Rs.50 crore (FB+NFB) from our Bank.

818/20 27.10.20 : INTRODUCTION OF MONITORING OF CROSS DEFAULT AND OTHER FINANCIAL COVENANTS – (PSB EASE 2.0 reforms).

Cross Default can be defined as default with one lender that may trigger default with another lender.

Default (overdues) by the borrower to any other lender for more than 30 days will be treated as Cross Default.

Applicable : Listed Corporate with exposure (FB+NFB) Rs.50.00 cr& above

MSME borrowers with exposure of Rs 1.00 Crore from our Bank.

P&L covenants and Balance Sheet covenants for the eligible listed companies are to be monitored on quarterly basis and annual basis respectively to ascertain deviation from the sanction/ accepted levels, if any.

Deterioration of more than 10% in the actual level, vis-à-vis sanction level /last reviewed level, will be treated as breach of financial covenants.

The cross default will be monitored on quarterly basis from the CRILIC reports for accounts above CRILIC threshold and from CIC reports for other account

223/2021 07.04.2021 : Introduction of “PARTIAL RISK SHARING FACILITY (PRSF)” scheme launched by SIDBI for certain eligible sectors to promote energy efficiency projects.

To promote Energy Efficiency projects implemented by ESCOs (Energy Service Companies) in the unit premises of Host Entities, that offer energy efficiency improvement services which may also include guarantee of savings.

Our Bank has been registered as a Participating Financial Institution (PFI) under the scheme by entering into an MOU and executing an MGA (Master Guarantee Agreement) with M/s. SIDBI, the Project Execution Agency (PEA).

M/s. SIDBI, provides credit guarantee upto 75% of the loans granted by PFI for energyefficiency projects sanctioned for eligible sectors such as MSMEs, Municipalities, Building Discoms and Large Industries.

However, loans shall be sanctioned under PRSF scheme to either the ESCO OR THE Host entity, falling within the MSME

CONTINUED………

223/2021 07.04.2021 “PARTIAL RISK SHARING FACILITY (PRSF)” scheme

Loan quantum : TERM LOAN ONLY Minimum (per project) :- Rs. 10 lakhs Maximum (per project) :- Rs. 15 crore Maximum exposure to a single Host/ESCO rated grades 1-4:- Rs. 60 Crore (Hence, a

maximum of 4 projects can be considered for financing under the scheme per ESCO/Host)

Maximum exposure to a single Host/ESCO rated grade 5 :- Rs. 53.33 Crore.

MARGIN : Minimum 25% of the project cost

Loan Tenor : Maximum 5 years (inclusive of Moratorium, if any). In exceptional cases, loan may be recommended for 7 years tenor (inclusive of Moratorium, if any).

However, SA to take prior permission from SIDBI through Energy Efficiency Cell, for sanction of loans above 5 years tenor (and upto 7 years including moratorium).

74/21 : Compressed Bio-Gas (CBG) plants loan scheme – Tripartite agreement between Bank, Borrower (LOI holder) and Oil & Gas Marketing

Companies (OMC).

To be insisted for receipt of sale proceeds to “Escrow account” with our Bank. If Tripartite agreement available, Collateral minimum 25% of Sanctioned limit to be

obtained. In other cases, collateral value of minimum 50% of Sanctioned limit to be obtained

475/21 02.07.21 : Modifications under Security norms for financing Compressed Bio-Gas (CBG) plants initiative of Ministry of Petroleum & Natural Gas (MoPNG), GOI

Post development security (Prime Security) value of minimum 133% of the limit, including the mortgage of land where the CBG plant is established.

Exclusive charge on entire project assets including immovable assets, movable assets, cash flow, Commercial Agreement and Escrow Account.

123/21 : EMPANELMENT OF CS for PREPARATION AND CERTIFICATION OF DILIGENCE REPORT FOR LENDING UNDER CONSORTIUM ARRANGEMENT /MULTIPLE BANKING ARRANGEMENTS OR ANY OTHER STATUTORY REPORTS.

Discontinuation of the existing practice of obtaining Diligence Report on H/Y basis from the borrower’s Company Secretary / Chartered Accountant.

Empanelment shall be for a period of 3 years Payment of charges Rs 20000 + GST (borrower to pay)

706/21 30.10.21 : DAF-SDSM Credit Guarantee Scheme for Subordinate Debt (CGSSD), launched by CGTMSE – extension of scheme validity till March 31, 2022.

Duration of the Scheme: All credit facilities sanctioned under CGSSD for a maximum period of 10 years from the guarantee availment date or March 31, 2022 whichever is earlier, or till an amount of Rs 20,000 crore of guarantee amount is approved.

Repayment : The sub-debt facility shall have a maximum tenor of 10 years from the guarantee availment date or March 31, 2022, whichever is earlier

Accounts opened after 31.03.2018 and which are fulfilling other terms and conditions of the Scheme are eligible for coverage. (HO CIR 628/21)

231/2021 12.04.21 : Modification in Service charges for Credit related transactions

Pre payment penalty shall be collected for floating rate term loans sanctioned for business purposes, to individual borrowers other than MSE category.

Secured NFB, minimum margin requirement shall be 15% as TDR.

In case of Clean NFB limits minimum margin requirement shall be 25% as TDR.

Additional commission of 0.25% shall be stipulated in respect of Secured NFB limits where minimum margin of 15% is not maintained.

Additional commission of 0.25% shall be stipulated in respect of Clean NFB limits where minimum margin of 25% is not maintained.

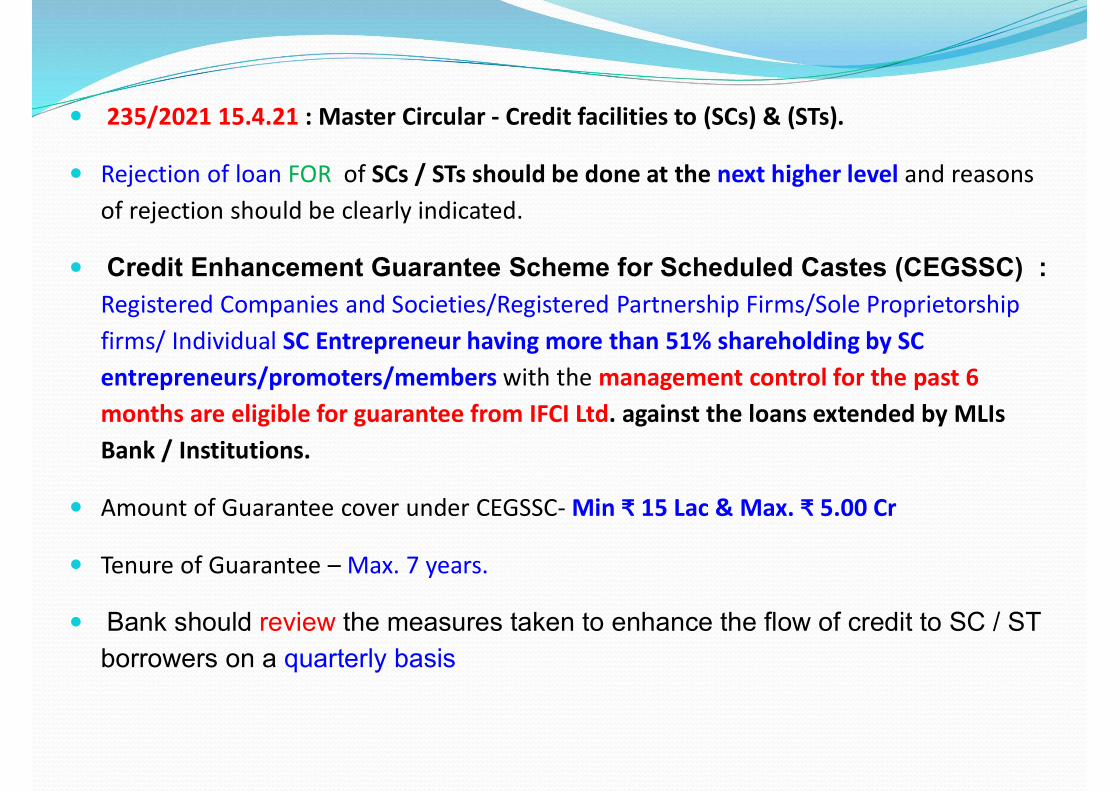

235/2021 15.4.21 : Master Circular - Credit facilities to (SCs) & (STs).

Rejection of loan FOR of SCs / STs should be done at the next higher level and reasons of rejection should be clearly indicated.

Credit Enhancement Guarantee Scheme for Scheduled Castes (CEGSSC) : Registered Companies and Societies/Registered Partnership Firms/Sole Proprietorship firms/ Individual SC Entrepreneur having more than 51% shareholding by SC entrepreneurs/promoters/members with the management control for the past 6 months are eligible for guarantee from IFCI Ltd. against the loans extended by MLIs Bank / Institutions.

Amount of Guarantee cover under CEGSSC- Min ₹ 15 Lac & Max. ₹ 5.00 Cr

Tenure of Guarantee – Max. 7 years.

Bank should review the measures taken to enhance the flow of credit to SC / ST borrowers on a quarterly basis

238/2021 15.4.21 : “Stand-Up India” for financing SC/ST and/or Women Entrepreneurs

Purpose: For setting up a New Enterprise (Green Field Project) in Manufacturing, Trading or Services Sector by SC/ST/Women Entrepreneur.

‘Activities allied to agriculture’ e.g. pisciculture, beekeeping, poultry, livestock, food & agro-processing, etc. (Excluding crop loans, land improvement such as canals, irrigation, wells) and services supporting these, shall be eligible for coverage under this scheme.

Minimum: Above Rs.10 Lakhs & Maximum: Rs.100 Lakhs. Quantum : 85 % OF PC Margin : 15% of the Project Cost

Margin money can be provided in convergence with eligible Central/State schemes. While such schemes can be drawn upon for availing admissible subsidies or for meeting margin money requirements (In all cases, the borrower shall be required to bring in minimum of 10% of the project cost as own contribution.)

Collateral security/ Third party guarantee : CGTMSE/(CGSSI) OR 100 % COLLATERAL

REPAYMENT : 7 YEARS (MORATORIUM 6 MONTHS)

Classification : MSME (MFG/Services) or Agriculture (in case of loans granted to finance activities allied to agriculture)

283/21 & 485/21 : PM SVANIDHI- TIMELINE FOR UPDATING DISBURSEMENT DETAILS FOR ISUSSING GUARANTEE COVER BY CGTMSE AND RELEASE OF INTEREST SUBSIDY BY MOHUA.

Disbursement for any subsequent quarters to be updated on the PMS portal by Branches latest by 15th of the month following the quarter after which disbursement updation will not be permitted.

Interest Subsidy Claim and processing thereof

Branches shall update disbursement details to enable MSME Wing HO to submit the interest subsidy claim within a month of the close of the quarter i.e., by July 31 for the quarter ending June 30 and so on.

92/2021 06.05.21 : (PMEGP) – Reiteration of guidelines with respect to time norms

and rejection of applications.

Disposal of loan applications under PMEGP : UPTO 5 LACS – 15 DAYS ABOVE 5 LACS : 30 DAYS

REJECTION OF CREDIT PROPOSALS :

SC / ST customers shall be rejected by the NHA .

Govt. sponsored schemes are rejected by the BM for valid reasons, the same has to be recorded in a register maintained to this effect which shall be examined by the controlling authorities during their branch visits

MSMEs is subject to concurrence of the NHA

302/21 13.05.21 : Deendayal Antyodaya Yojana-National Urban Livelihoods Mission (DAY-NULM) - Modification in existing guidelines

A special provision of 5 % reservation should be made for the differently-abled under this program with priority to women.

313/21 17.05.21 : Bank has entered into an MoU with NSIC valid for 3 years till 22.03.2024) for arranging credit support (FB and NFB ) from the Bank to the (MSME ENTERPRISES) under NSIC-Bank Credit Facilitation Scheme.

NSIC provides integrated support services to MSMEs under marketing, credit, technology and other support services such as raw material assistance, exhibition, buyer-seller meets, export facilitation, government stores purchase programme, financing for marketing, financing for procurement of raw materials, training/skill upgradation, performance and other support services

Upon sanction of a loan forwarded by NSIC : Bank branch shall pay within 30 days, 50% of the processing fee received from applicants to NSIC for each application so forwarded

366/21 01.06.21 : (PMEGP)- Acceptance of pre-sanction EDP training certificates through online portal (Samadhan portal) as a valid proof of EDP training.

Online EDP training has been introduced from October, 2019 through Samadhan portal and PMEGP beneficiaries can opt for either pre-sanction EDP or post-sanction EDP training either through online or offline mode.

368/21 02.06.21 : Introduction of Legal Entity Identifier (LEI) for Large Value Transactions in Centralised Payment Systems

RBI has notified requirement of sender and beneficiary Legal Entity Identifier (LEI) for all inward and outward NEFT/RTGS transaction of Rs.50 crores and above initiated or received by all non-individual entities.

Legal Entity Identifier (LEI) under CIM17 option has been enabled.

The LEI is a 20-digit number used to uniquely identify parties to financial transactions worldwide. The structure of the global LEI is determined in detail by ISO Standard 17442and takes into account Financial Stability Board (FSB) stipulations.

371/21 04.06.21 : Process of release of credit linked subsidy under PM FME (Pradhan Mantri Formalisation of Micro food processing Enterprise) Scheme

Branches can claim the credit-linked capital subsidy based on the first disbursement of the loan amount through PM FME portal.

The subsidy will be received in the Transient GL Account 209272957

After receipt of subsidy , Branch acknowledge, updated in portal regarding the date of receipt and date of deposit (ZERO ROI) – LNM 83 OPTION

CBS OPTION LNM95 TO LINK TO LOAN A/C

The scheme mainly envisages support to Individual Micro Enterprises as under:

Credit-linked capital subsidy @35% of the eligible project cost, maximum ceiling Rs.10 lakhs per unit

Beneficiary contribution - Minimum of 10% of the eligible project cost BANK LOAN : 90% of the project cost including 35% back end subsidy

After 3 years if account is standard , subsidy adjusted to loan account

If the account becomes NPA within 3 years subsidy would be adjusted towards repayment.

402/21 09.06.21 : PREPACKAGED INSOLVENCY RESOLUTION PROCESS (PIRP) IBC 2016

Pre-Packaged Insolvency Resolution Process means Insolvency Resolution Process of Corporate Debtors classified as MSMEs with minimum default of Rs.10.00 lacs. Central Government may, by notification, specify such minimum amount of default of higher value, which shall not be more than Rs.1.00 Crore.

PIRP commences in an informal manner firstly, when the Corporate Debtor (CD) being a corporate person and is classified as MSME under the MEMED Act; with the consent of their Directors or partners decide to invoke the PIRP and seek the approval of atleast66% of the Financial creditors (who are not related to CD) and appoint the IP/RP with consent of FCs.

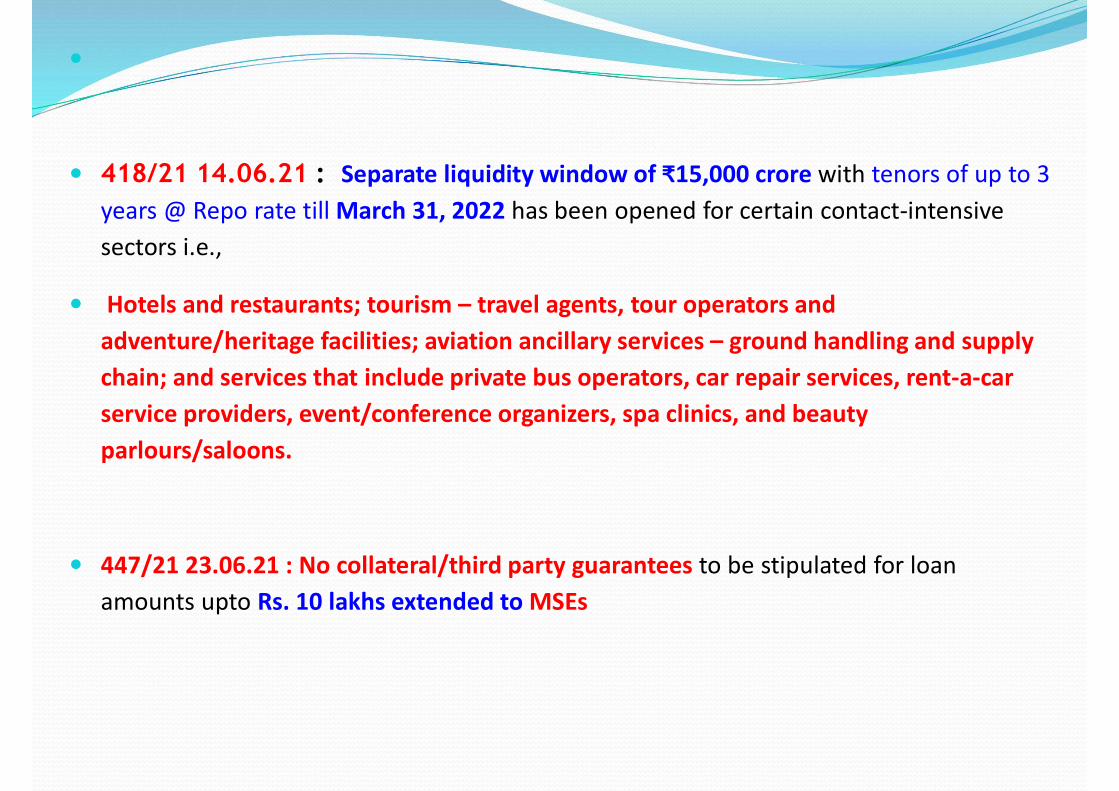

418/21 14.06.21 : Separate liquidity window of ₹15,000 crore with tenors of up to 3 years @ Repo rate till March 31, 2022 has been opened for certain contact-intensive sectors i.e.,

Hotels and restaurants; tourism – travel agents, tour operators and adventure/heritage facilities; aviation ancillary services – ground handling and supply chain; and services that include private bus operators, car repair services, rent-a-car service providers, event/conference organizers, spa clinics, and beauty parlours/saloons.

447/21 23.06.21 : No collateral/third party guarantees to be stipulated for loan amounts upto Rs. 10 lakhs extended to MSEs

452/21 25.06.21 : Modification in fee structure payable to Stock Auditors / Chartered Engineers / Lenders’ Independent Engineers and Techno Economic Viability consultants.

Stock Audit Fee (exclusive of admissible taxes) :

MAXIMUM FEE PER BORROWER : Not exceed Rs. 2.0 lakhs.

LPD/NPA account fee payable is 50% of the above and subject to MAX Rs.50,000/-.

The above charges shall be borne by the borrowers.

CONTD……

Manufacturing Concern Rs. 500/- per Rs. 1 crore value of stock & BD MIN of Rs.10,000/- and MAX Rs.1,00,000/.

Other Than Manufacturing Concerns

Rs. 300/- per Rs. 1 crore value of stock and BD Minimum of Rs. 7,500 /- and Max Rs.1,00,000/-.

Modifications in respect of fees payable to Fixed Asset Valuers :

Minimum is Rs.2, 000/- & Maximum fee payable will be Rs. 50,000/-

LPD/NPA account, the fee is 50% of the above and subject to MAX Rs. 25,000/-

In respect of vacant land, the fee payable shall be 25% of the above and subject to maximum of Rs. 12,500/-

The entire fee inclusive of all expenses to be incurred by Valuer of one borrower including travelling, boarding, lodging etc. will not exceed Rs. 75,000/-. However, Circle Heads & above s may consider payment of charges over & above the ceiling of Rs. 75,000/- on case to case basis.

The above charges shall be borne by the borrowers.

Value of the Security Maximum Fee (exclusive of admissible taxes)

Upto Rs.5 lacs of the assets valued 0.25%

Next Rs.10 lacs of the assets valued 0.20%

Next Rs.35 lacs of the assets valued 0.10%

Next Rs.50 lacs of the assets valued 0.05%

The Indicative fee structure payable for Lender’s Independent Engineer (LIE) :

The indicative fee structure payable for TEV Studies

463/21 30.06.21 : Weavers Mudra Loan Scheme under (PMMY), with pricing linked to RLLR, applicable for the amalgamated entity.

Rate linked to RLLR as applicable i.e. ROI for

Working capital – RLLR + 1.05% and

Term loan – RLLR + 1.30% (as per Cir. 501/2019 dt. 30.09.2019).

Project outlay % of Project Outlay

Minimum maximum

More than Rs 1.50 Crores to Rs 10.00 Crores 0.075 Rs. 20,000 Rs 60, 000

More than Rs. 10.00 Cr to Rs. 25.00 Crores 0.050 Rs. 70,000 Rs. 1,00,000

More than Rs. 25.00 Crores 0.040 Rs. 1,00,000 Negotiable

453/21 25.06.21 : Capital subsidy under Swachhta Udyamai Yojana (SUY) scheme of National Safai Karamacharis Finance and Development Corporation (NSKFDC).

NSKFDC providing the capital subsidy under Swachhta Udyami Yojana (SUY) scheme from SRMS funds for procurement of mechanised cleaning equipments /vehicles as per the details given below

After receiving the Subsidy (Front ended) the branch can disburse the loan amount along with subsidy and make 100% payment as per quotation to the supplier of the machinery.

Unit Cost (INR) CAPITAL SUBSIDY Loan

Up to Rs.5 Lac 50% of the unit cost There will be no beneficiary contribution (Margin) and the balance amount other than the capital subsidy will be provided as loan. As the subsidy is front ended, the loan amount has to be arrived excluding the subsidy from total unit cost

5-10 Lacs Rs.2.00 Lacs + 25% of unit cost between Rs. 5-10 Lac maximum up to Rs.3.25 Lacs

10-15 Lacs Rs.3.25 Lacs

492/21 07.07.21 : Revised Definition of MSME- existing guidelines.

The existing EM Part II and Udyog Aadhar Memorandum (UAMs) of the MSMEs obtained till June 30, 2020 shall remain valid till 31.12.2021

497/21 08.07.21 : Central Sector Scheme of Self Employment Scheme for Rehabilitation of Manual Scavengers (SRMS) - Continuation of the scheme with revisions.

National Safai Karmacharis Finance & Development Corporation (NSKFDC) which is the nodal agency of Government of India for implementing the SRMS Scheme.

SRMS continued for 5 years from 2021-22 to 2025-26 with revisions.

Credit linked capital subsidy will be provided upfront to the beneficiaries in a scaled manner

Projects of SHG/Groups costing up to Rs.50.00 lakh would be admissible for assistance

Range of Project Cost (Rs.) Rate of Subsidy

i) For Individuals:

Up to Rs.5,00,000/- 50% of project cost

Rs.5,00,000/- to Rs.15,00,000/- Rs.2.5 lakh + 25% of remaining project cost.

ii) For Group Projects:

Up to Rs.10.00 lakh per beneficiary maximum project cost up to Rs.50.00 lakh

same as admissible to Individuals subject to maximum Rs. 3.75 lakh per beneficiary.

469/21 01.07.21 : Exposure to Short Term Corporate Loans (STCLs) - Ceiling for the FY 21-22.

Exposure ceiling of Rs. 40000 Crores to Short Term Corporate Loans for FY 21-22.

501/21 12.07.21 : Revised Definition of MSME Addition of Retail and Wholesale Trade.

Retail and Wholesale Trade shall be classified as MSMEs for the limited purpose of Priority

Udyam Registration Portal for the following NIC Codes and activities :

45 Wholesale and Retail Trade and Repair of motor vehicles and motorcycles

46 Wholesale trade Except of motor vehicles and motorcycles

47 Retail trade Except of motor vehicles and motorcycles

Enterprises having UAM under this 3 NIC Codes are now allowed to migrate to URC.

523/21 28.07.21 : RENEWAL OF MOU WITH M/s TATA MOTORS LTD. FOR FINANCING UNDER CANARA VEHICLE LOAN SCHEME. till 26.12.22

524/21 & 549/21 : Implementation of Credit Guarantee Scheme for NBFC- MFI or (MFIs).

The Scheme shall cover funding provided to NBFC-MFIs/MFIs till March 31, 2022 or till guarantees for an amount of Rs.7,500 crore are issued, whichever is earlier.

ROI by MLIs shall be capped at 1 year MCLR Rate + 2% per annum.

At least 50% of the funding made and covered under the scheme goes to lower rated/graded NBFC-MFIs/MFIs i.e.: MFR 2 or below.

Guarantee coverage : By NCGTC upto 75% of the amount in default.

Tenor of NCGTC’s guarantee would be for a maximum period of 3 years

Guarantee shall be available only on the uncovered portion of the loan (FD Margin to be netted off).

No Guarantee Fee

Lock in period : 1 year from the date of issue of guarantee or last date of disbursement out of the sanctioned amount, whichever is later. CONT…..

The funding so provided by the MLIs to the MFIs/NBFCMFIs shall be utilized for on-lending to eligible small borrowers. MFIs/NBFC-MFIs should ensure that:

80% of the assistance so extended is utilized for creation of fresh loan assets.

These assets should be created within 4 months from the date of disbursement of each tranche of loans

ROI charged on these loans is at least 2% below the maximum rate prescribed by RBI on such loans.

A separate account is opened for credit facility extended to the eligible small borrowers under the Scheme

NBFC-MFI/MFI should submit a Statutory Auditor certificate to its MLI confirming compliance with the above within 4 months from the date of disbursement of each tranche of loan

Upon submission of the claim the eligible amount shall be paid within 30 days

526/21 29.07.21 : Delegation of Powers for OTS in Wilful & Fraud accounts -

Write Off for willful defaulters (other than fraud cases) and Write Off for Fraud cases/quick mortality accounts: Powers vested with MC of the Board.

552/21 12.08.21 : Financing to Aviation and Gems & Jewellery Sectors – obtention of prior approval from Management Committee of the Board. (EXEMPTED FOR GECL- 725/21)

553/21 12.08.21 : : Clarification in Review Mechanism/Review Authority, in respect of Circle power accounts under IBC 2016

Consolidated monthly note on the decision of circles shall be placed

by IBC Monitoring Section and RAD (Resolution Review), of SAM Wing, HO Bengaluru

before CGM/GM-HO-RC [Review Committee] for review/noting

533/21 05.08.21 : “End to end digitization of Shishu Mudra Loans” for existing customers, as per EASE 3.0 PSB Reforms.

End to End (E2E) digitization of Shishu Mudra loans under (STP) mechanism for existing customers of the Bank.

Online validation of KYC and Udyam Registration Certificate.

Sanction of loans up to Rs50,000/- based on pre-defined business rule engines.

Digital Document Execution (e-stamping and e-signing) by the borrower.

System has the following capabilities:

KYC validation. URC verification. Eligibility Check based on the set of business rule engines. End to end processing of loan Digital document execution (e- stamping & e-signing)

Charges : Digital verification charges Rs.100 + Applicable Taxes. e-Signing of Document (Per Signature) Rs. 7 + Applicable Taxes Processing / Documentation / Other charges As applicable Cont…….

.

MAJOR ELIGIBILITY CRITERIA CONSIDERED FOR SHISHU LOANS UNDER STP

Applicant should active account with our Bank for the last 6 months

Joint Accounts are not eligible under this process.

Only Individual/ Proprietorship are eligible.

Maximum loan : 4 times of average monthly balance of the last 6 months (in SB/CA) subject to a maximum of Rs. 50,000/-.

NO cheque return due to insufficient fund.

Should not be more than 3 cheque returns due to any reason other than insufficient fund.

Registration with Udyam portal is mandatory.

CIBIL score of individual App/prop/promoter should not be less than 700.

Business turnover will be captured on declaration basis.

Loans will be form of term loan only for a period of 12 to 36 months

567/21 19.08.21 : Deendayal Antyodaya Yojana – National Rural Livelihoods Mission (DAY-NRLM)- Enhancement of collateral free loans to SHGs) under DAYNRLM from Rs 10 lakh to Rs 20 Lakh.

For loans to SHGs up to Rs 10.00 lakh, No collateral and No margin will be charged.

No lien should be marked against SB account of SHGs and

NO deposits should be insisted upon while sanctioning loans.

Eligible for coverage under Credit Guarantee Fund for Micro Units (CGFMU)

577/21 30.08.21 : Renewal of MoU with the following agencies for entrusting Due Diligence Services for MSME : valid upto 02.08.2024

External Due Diligence from such agencies has been made Mandatory for MSME who approach our Bank for the first time seeking credit facility requirement of above Rs. 10 lakhs and are eligible to be covered under CGTMSE

Agency Amount Bracket Charges

M/s. Brickworks Analytics Pvt. Ltd.(wholly owned subsidiary of Brickwork Ratings India Pvt Ltd

Upto Rs.25 lakhs Rs 6,500

Rs.25 lakhs upto Rs.75 lakhs Rs 8,500

Above Rs.75 Lakhs Rs 10,500

M/s. Acumen Business Consultancy Pvt. Ltd. Upto Rs.2 Crore Rs 5,000

Rs.2 Crore upto Rs.10 Crore Rs 7500

Above Rs.10 Crore Rs 10000/-

M/s. SMERA Gradings &Ratings Pvt. Ltd Irrespective of Loan amount Rs 12000/-

579/21 31.08.21 : Revision of charges for MSME loans through “PSB Loans in 59 Minutes”online platform – Charges to be collected from customers.

Details of revised additional processing fees to be collected from borrower :Market Place URL: Charges are inclusive of GST

Bank specific URL :

S No. Particulars Charges per proposal payable to M/s Online PSB loans Ltd.**MSME MUDRA (10 lacs)

1 For eligible (online) proposals Rs.3900/- (ANY AMT) Rs 1300/-

2 Offline Proposal Rs 1950 Rs 975

S No. Particulars Charges per proposal payable to M/s Online PSB loans Ltd.**MSME MUDRA (10

lacs)1 New Customers/Fresh TL or WC Rs.3500/- (Up to Rs.1 Cr) Rs 1300/-

2 Renewal (With enhancement) Rs.1950/- (Up to Rs.1 Cr) Rs 650

3 Renewal (Same limits) Rs 650 (Up to Rs.1 Cr Rs 300

4 For Eligible proposal(New/Fresh TL or WC/Renewal

With or without enhancement)

Rs.3900/- (Above Rs.1 Cr) NA

586/21 MASTER POLICY ON CREDIT RISK MANAGEMENT CREDIT DELIVERY TAT : Loan applications shall be verified within a period of 7 days. If additional documents are required, the applicants shall be intimated immediately.

The applicant shall provide the additional required documents with in a period of 7 days from the date of communication.

In case of non receipt of required documents from the applicant within 7 days from the date of communication, the proposal can be rejected and communicated to borrower as per the extant norms

Bank should not grant loans aggregating to 25 lakhs and above to Directors (including the Chairman / MD & CEO) of other banks. In case of Personal Loans, the threshold is Rs 5 Crores

Bank shall not grant loans and advances aggregating to Rs.5 Crores and above to : Any relative other than spouse and minor children/dependent children of Bank’s Chairman /Managing Director & CEO or other Directors of our Bank/Other bank

(SA : Board of Directors / Management Committee) Less than Rs 25 lakh or Rupees 5 crores may be sanctioned by the appropriate sanctioning

authority but Report to Board of Directors

236/2021 15.4.21 : Master Circular - Credit facilities to Minority Communities

A company has a separate legal entity : Hence advances granted to it cannot be classified as advances to the specified minority communities.

GOI of India has also forwarded a list of 121 minority concentration districts having at least 25% minority population, excluding those States / UTs where minorities are in majority (J & K, Punjab, Meghalaya, Mizoram, Nagaland and Lakshadweep)

National Minorities Development and Finance Corporation (NMDFC) : NMDFC is operating, inter-alia, the Margin Money Scheme.

60 % Bank finance 25 % shared by NMDFC, 10 % by the State channelising agency and 5 % beneficiary

587/21 03.09.21 : NATIONAL MINORITIES DEVELOPMENT & FINANCE CORPORATION (NMDFC) - SCHEME GUIDELINES

Our Bank has entered into (MoA) with M/s NMDFC to implement the schemes of NMDFC through our Bank.

NMDFC provides concessional finance to the Minorities for self-employment/ income generation activities.

As per the National Commission for Minorities Act, 1992, the notified Minorities are Muslims, Christians, Sikhs, Buddhists, Parsis & Jain community

Loans for the target group of NMDFC will come under Priority Sector Lending.

Credit Line 1:- Concessional credit available for beneficiaries with annual family income of Rs.1.20 lacs in Urban areas & Rs.98,000/- in Rural areas

Credit Line 2:- Concessional credit is provided to “Creamy Layer” criterion of OBC, i.e., with household income of Rs.8.00 lacs p.a.

Schemes costing up to Rs.30.00 lac for self-employment venture on concessional ROI ranging between 3% to 10% from the beneficiaries.

Interest margin of 2% -3% for the Channelizing Agencies (CAs) of NMDFC to meet their operation and administrative costs.

Self declaration/certification by the applicant would suffice for a Religion Certificate.

For annual Family Income, a certificate from Revenue Authorities duly self-certified by the applicant would be required.

The fund provided to Bank by NMDFC is neither grant nor subsidy for disbursement to the beneficiaries. The funds so received shall be repaid to NMDFC as per terms of Letter of Intent.

Term Loan Scheme : This scheme is for individual beneficiaries. Projects costing up to Rs.30.00 lacs are considered for financing with NMDFC providing

90% of the loan amounting to Rs.27.00 lacs. Remaining cost is to be borne by Bank& beneficiary.

Assistance is available for any commercially viable & technically feasible venture, which for the purpose of convenience, are classified into following sectors:-

(a) Agriculture & Allied (b) Retail Trade business (c) Small business (d) Artisan & traditional occupations (e) Transport & Service Sector

SI NO PARTICULARS Scheme DetailsCredit Line-1 Credit Line-2

1 Loan Amount Up to Rs.20.00 Lakhs Up to Rs.30.00 Lakhs

2 Rate of Interest 6% p.a 8% p.a. for males 6% p.a. for females

3 Rate of Interest payable by BANKs to NMDFC

3% p.a. 5% p.a. for males 3% p.a. for females

4 Moratorium period 6 months 6 months

5 Repayment period for beneficiarie 5 years 5 years

6 Repayment period for the BANKs 8 years 8 years

7 Pattern of Financing NMDFC:BANK:Benf.contribution

90:5:5 90:5:5

8 Utilization Period 3 Months 3 Months

Micro-Finance Scheme : Beneficiaries are organized into SHGs . NMDFC allows financing of SHGs with 75% members Minority and Rest from other community Exceptional cases, SHGs with 60% members from Minority community and Rest from sc/st/obc

SI NO

PARTICULARS Scheme DetailsCredit Line-1 Credit Line-2

1 Loan Amount Up to Rs. 1.00 lac per member of SHG and Up to Rs.20.00 lacs for a group of 20 members in one SHG

Up to Rs.1.50 lacs per member of SHG and Up to Rs.30.00 lacs for a group of 20 members in one SHG

2 Rate of Interest 7% p.a 10% p.a. for males.8% p.a. for females.

3 Rate of Interest payable by BANK/NGO to NMDFC

1% p.a. 4% p.a. for males2% p.a. for females

4 Rate of Interest charged by BANK from NGO 2% p.a 5% p.a. for Males 3% p.a. for females

5 Moratorium period 3 months 3 months

6 Delegated authority to BANK to sanction loan to NGOs/Federation

Limit of Rs.25.00 Lakhs per NGO/Federation. This limit is increased to Rs.50.00 lakhs for BANKs with 100% repayment record for last 2 years.

Limit of Rs.30.00 Lakhs per NGO/Federation. This limit is increased to Rs.50.00 lakhs for BANKs with 100% repayment record for last 2 years

7 Repayment period for beneficiarie 3 years 3 years

8 Repayment period for the BANKs/NGOs 4 years/3 years 4 years/3 years

9 Utilization Period for the BANKs/NGOs 3 months/1 month 3 months/1 month

10 Pattern of FinancingNMDFC:BANK:Beneficiary 90:5:5 90:5:5

VIRASAT SCHEME : objective to meet credit requirements of the Artisans, both in terms of WC & Fixed capital requirement for purchase of equipment/tools/machineries.

.

SI NO Parameters SCHEME DETAILS1 Loan Amount Up to Rs.10.00 Lakhs

2 Rate of Interest for Artisans 5% p.a. for males &4% p.a. for females

3 Rate of Interest payable by BANKs to NMDFC

3% p.a. for males &2% p.a. for females

4 Moratorium period 6 months

5 Repayment period for Artisans 5 years

6 Repayment period for the BANKs 8 years

7 Pattern of Financing NMDFC:BANK:Benf.contribution

90:5:5

8 Utilization Period 3 months

593/21 06.09.21 : Renewal of MoU with M/s National Bulk Handling Corporation Private Limited (NBHC) to finance the produce loans. 3 year from 17.8.2021

Fees Payable to M/s NBHC : 1.25% per annum (exclusive of all taxes) on the Loan Outstanding amount.

594/21 06.09.21 : Renewal of MoU with M/s National Commodities Management Services Limited (NCML) to finance the produce loans. 3 year from 02.08.2021.

FEES : Bank will pay fee/charges @ 1.20% p.a on Loan Outstanding amount, exclusive of taxes at any point of time payable on monthly basis and calculated on daily product

603/21 14.09.21 : : LOANS AND ADVANCES AGAINST SHARES/DEBENTURES: REVISED LIST OF COMPANIES

NO fresh loans/advances shall be granted against the securities held in materialized form.

Companies with external rating of “A” and above are only considered in the approved list.

In the cases where loans are outstanding against the security of shares/ debentures of those companies which are not appearing in the present consolidated list , branches shall initiate steps to get the related accounts regularized either by way of substitution with shares/debentures of Companies (As per Annexures) of adequate value or by way of recovery within 3 months from the date of this circular.

Further, Circle head level CACs i.e., CGM/GM-CO-CAC/DGM-CO-CAC is empowered to permit further extension of time of not more than 3 months for the substitution, if required.

Branches to review the loans against shares/debentures at least on a fortnightly basis to ensure adequacy of margin

609/21 15.09.21 : “PM Street Vendor’s AtmaNirbhar Nidhi (PM SVANidhi)” scheme Eligible street vendors are considered WCDL loans of upto Rs. 10,000/- repayable in

monthly instalments for a maximum tenure of 1 year. “On timely/ early repayment of loan of initial WC , a vendor becomes eligible to avail a

higher tranche of loan in next cycle and NO prepayment penalty will be charged Documents defined for the subject scheme : NF546 & NF 481 & Undertaking letter Eligibility Criteria

Bank shall ensure marking of the 1st loan as closed, for processing the 2nd loan. Loans which are settled by CGTMSE are not eligible for the 2nd loan and shall not be closed on the portal by the Bank

Loan Amount Minimum: Rs. 15000/- Maximum: Rs. 20000/

Loan Tenor Upto 18 months

Interest Subsidy @ 7% upto March 31, 2022

Cashback Cashback on digital transactions shall be available for the beneficiaries of 2nd loans

Credit Guarantee by CGTMSE

Available on all the 2nd tranche loans disbursed upto March 31, 2022

Scheme Code 104600 (Product code – 711 ; for both 1st and 2nd tranche loans)

Rate of Interest RLLR+1.05%

617/21 17.09.21 : CANARA MSME CAP (CREDIT AGAINST PROPERTY) SCHEME FOR FINANCING MSME – MODIFICATIONS IN SCHEME GUIDELINES.

Target Group MSME (Manufacturing/Service) (Excluding Educational /SHG/JLG )

ELIGIBILITY Individuals/Proprietary/Traders/Professionals or self employed Partnership firm(other than partnership firms where HUF is a partnerCompany (excluding NBFC)

Minimum loan Rs 10 LACS

MAX LOAN RS 20 CRORES (MANUFACTURING)RS 10 CRORES (SERVICE)

MARGIN 20 % FOR WC AND TERM LOAN25% FOR NFB

Repayment Working Capital – Tenable for one year. Term Loan- Maximum 10 years including moratorium

Valuation Report

1 panel valuer to be obtained for loans extended upto Rs. 2 Cr. and2 panel valuers for loans extended above Rs. 2 Cr.

No liquidity premium is applicable for term loans under the scheme.50% of the applicable upfront fee/ processing charges.Fresh valuation once in 3 yearsVacant land shall not be accepted as securitySubmission of Stock Statement and Inspection of stocks : QuarterlySTOCK AUDIT : Low & Normal Risk Rated Accounts: Waived upto Rs. 5 CrModerate Risk Rated Accounts: Every Year

MSME CAP : SECURITY

Urban & Metro Properties 100% of the loan amount for MFG units 125% of the loan amount for service sector units

Semi-Urban Properties 125% of the loan amount for MGF units 150% of the loan amount for service sector units

Select Rural Properties located close to Metro/Urban/Semi Urban centres:At least 150% of the loan for both MFG units and service sector units subject to :

Located within 20 kms radius from nearby Metro/Urban city.

Located within 10 kms radius from nearby Semi-Urban city

Unit should be functioning in that property or used for the said business

Approvals relating to conversion as industrial area/commercial land to be available

Enforceability of underlying security has to be confirmed

Clearance from Circle Head CO CAC

DOP : Beyond Rs 25.00 Lakh or branch DOP whichever is less (i.e. in case of Small, Medium, Large and VLB branches) shall be handled by MSME Sulabhs. (620/21)

In respect of properties which are less than 1 year old, valuation of the property shall be taken as “Sale deed value” or “Guideline value” whichever is less.

656/21 04.10.21 : CANARA MSME CAP –DOP

722/21 06.11.21 : ROI ON RUPEE LOANS AND ADVANCES (MCLR, RLLR, Base Rate, STRLLR, EBLR1) w.e.f. 07.11.21.

Overnight MCLR : 6.55 % 1 Month MCLR : 6.55 % 3 Month MCLR : 6.85 % 6 Month MCLR : 7.20 % 12 MONTHS MCLR : 7.25 % REPO LINKED LENDING RATE (01.10.2019) (RLLR) : 6.9 % SHORT TERM REPO LINKED LENDING RATE (STRLLR): 4 % EXTERNAL BENCHMARK LENDING RATE (EBLR1) : 6.30 %

DM-CAC at CircleDM-CAC at RODM-CAC at MSME SulabhMaximum sanctioning powers for both FB & NFB limits.

500.00 LAKHS

Low Risk 500.00 LAKHS

Normal Risk 500.00 LAKHS

Moderate Risk 400.00 LAKHS

Term Loan # 250.00 LAKHS

618/21 18.09.21 : CANARA GST scheme - Modifications in scheme guidelines

Target Group MSME (Manufacturing/Service)

ELIGIBILITY New customers with minimum business operation of 6 months and existing customers shall be brought under the schemeGST Return of minimum for the past 6 months.At least 75% of turnover reflected in GST return should have been routed through the Bank account

Minimum loan Rs 10 lacs

MAX LOAN Rs.5 Crores

MARGIN NIL Current Ratio: Minimum 1

Assessment : Maximum of 25% of the annual turnover as per GST Return with NIL Margin.

In case of non-availability of preceding year annual GST Return, past 6 months returns shall be considered to arrive annual turnover (2 times of the past 6 months turnover).

Assessment of the WC limit is based on GST return and not based on financial papers

Collateral 75% of the loan amount for Low & Normal Risk (100% for Moderate)

Proc charges 50% of the applicable processing charges

Penal Interest

If T/O is between 50% to 74% compared to GST return : 0.25%If T/O is less than 50 % compared to GST return : 0.50 %

GST : RURAL SECURITY

Select Rural Properties located close to Metro/Urban/Semi Urban centres:At least 150% of the loan for both MFG units and service sector units subject to :

Located within 20 kms radius from nearby Metro/Urban city.

Located within 10 kms radius from nearby Semi-Urban city

Unit should be functioning in that property or used for the said business

Approvals relating to conversion as industrial area/commercial land to be available

Enforceability of underlying security has to be confirmed

Clearance from Circle Head CO CAC

629/21 22.09.21 : Mandatory obtention and updation of ‘Udyam Registration Certificate’ details in CBS (under CIM22 option) in respect of all eligible MSMEs –

URC details of all the eligible MSMEs for strict adherence and accomplish completion of the same on or before 31.10.2021

679/21 13.10.21 : Weavers Mudra Scheme–Prompt and timely sanctioning, claiming of Margin Money subsidy, Interest Subsidy and Guarantee Fees/Annual Service Fees of CGTMSE/CGFMU through online “Handloom Weavers Mudra Portal”

MSME proposals upto Rs. 5.00 lakhs is to be sanctioned within 15 days

689/21 21.10.21 : Priority Sector Lending– Banks’ lending to NBFCs for On-Lending - Bank credit to registered NBFCs (other than MFIs) for on-lending will be eligible for

classification as Priority Sector under Agriculture and MS Enterprises extended till 31.3.22

630/21 22.09.21 : MSME SUGAM scheme for lending under Origination Tie-ups Target Group Micro and Small Enterprises (Manufacturing/Service)

ELIGIBILITY

NOT ELIGIBLE

Individuals, Proprietorship, Partnership Concerns, LLP, Pvt Ltd Company are eligible. GST registered borrower (where ever applicable)New/Existing Customer with Business operation for minimum 1 year.Individuals/units whose risk rating is upto Moderate Risk under IRR

Partnership Firms with HUF as one of the Partners, Educational institutions, SHG, JLG are not eligible.Existing customer with SMA 2 during the last FY are not eligible.WC facility under the scheme may not be extended to customers who are already enjoying WC Facilities in any form with our Bank or other Banks

Purpose To meet WC/Asset creation requirements

Nature of Facility

WCTL (to finance WC requirements/cash flow mismatch) Term Loan (to finance new asset creation)

QUANTUM WCTL – Maximum upto Rs. 5 lakhsTerm loan – Maximum upto Rs. 10 lakhsAgg. exposure per borrower under the scheme not to exceed Rs10 lakh

SECURITY CGTMSE coverage Applicable

630/21 22.09.21 : MSME SUGAM scheme for lending under Origination Tie-ups REPAYMENT WCTL: Minimum - 12 months; Maximum - 60 months

Term Loans: Minimum - 12 months; Maximum - 84 months (including maximum moratorium period of 3 months)All loans under the scheme to be repaid in EMI

ROI RLLR + 2.50% p.a. (No Liquidity Premium to be added additionally)

MARGIN 20%

Assessment For WCTL : LOWER of the following may be permitted

3 Times of the Cash accrual as per the latest Financial Statement/ ITR, subject to DE Ratio Not more than 4:1 , DSCR Should not be below 1 during the tenure of the loan

ORWorking Capital requirement as assessed under Turnover method.

For Term Loan : 3 times of the cash accrual as per the latest Financial Statement/ ITR, subject to DE Ratio Not more than 4:1 DSCR Should not be below 1 during the tenure of the loan

Disbursement In lump sum or in Maximum 3 tranches

Product Code 753- For loans under Fin-tech arrangement

669/21 08.10.21 : Restrictions on number of layers for Holding Company as per Companies Act 2013

No Holding Company shall have more than 2 layers of subsidiaries.

Provisions of this rule shall not affect a Company from acquiring a Company incorporated outside India.

The restrictions on having more than 2 layer of subsidiaries is not applicable for the following companies,

a) Banking Company as per BR Act, 1949 (10 of 1949); b) NBFC registered with RBI c) An insurance Company d) A Government Company

If any Company contravenes any provision of these rules the Company and every officer of the Company who is default shall be punishable with fine which may extend to RS 10000and where contravention is a continuing one, with a further fine which may extend to Rs 1000 for every day after the first during which such contravention continues.

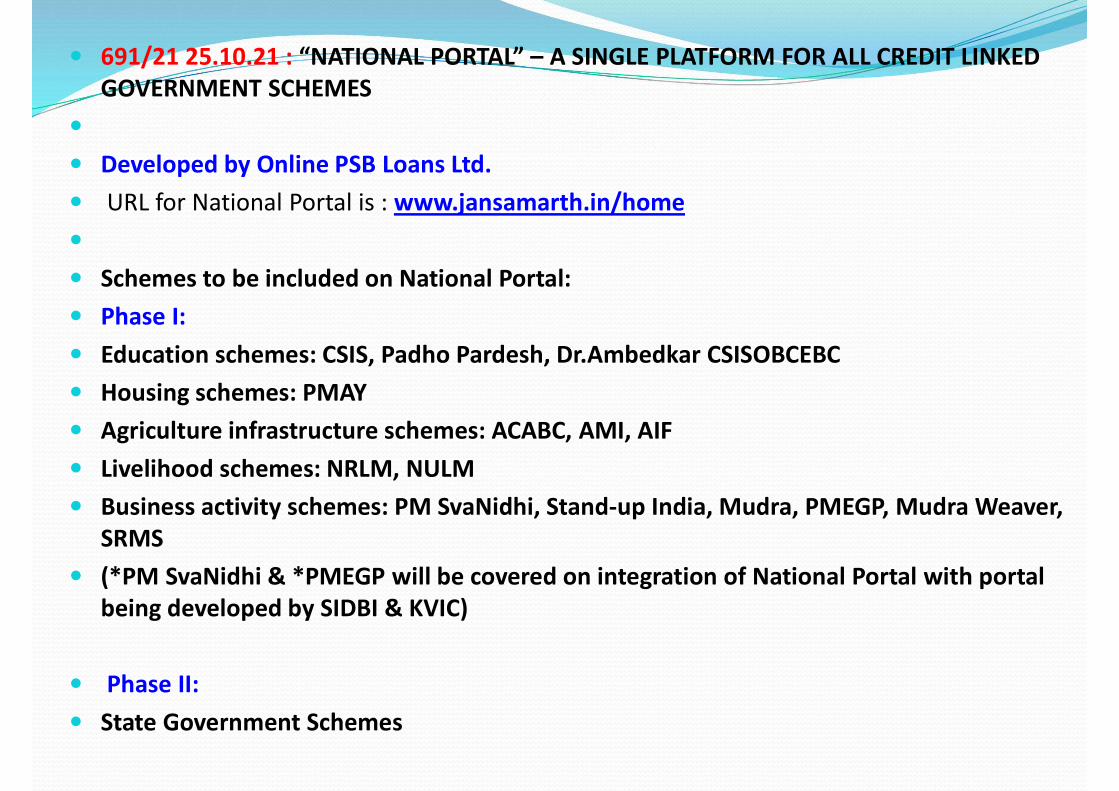

691/21 25.10.21 : “NATIONAL PORTAL” – A SINGLE PLATFORM FOR ALL CREDIT LINKED GOVERNMENT SCHEMES

Developed by Online PSB Loans Ltd. URL for National Portal is : www.jansamarth.in/home

Schemes to be included on National Portal: Phase I: Education schemes: CSIS, Padho Pardesh, Dr.Ambedkar CSISOBCEBC Housing schemes: PMAY Agriculture infrastructure schemes: ACABC, AMI, AIF Livelihood schemes: NRLM, NULM Business activity schemes: PM SvaNidhi, Stand-up India, Mudra, PMEGP, Mudra Weaver,

SRMS (*PM SvaNidhi & *PMEGP will be covered on integration of National Portal with portal

being developed by SIDBI & KVIC)

Phase II: State Government Schemes