Solapur University, Solapur MBA Part II Syllabus (CBCS) w.e.f. ...

28/9/2014

1

بسم هللا الرحمن الرحیموبھ نستعین

Welcome to

Business Administration Training Program

Trainer

Ass.Prof Dr. Omaima El Tahir Babikir Mohamed [email protected]/ [email protected]

+60163430273

Park Royal Hotels

Kuala Lumpur

18-27 March 2013

2

28/9/2014

2

Dr. Omaima’s Profile

Dr. Omaima El Tahir Babikir Mohamed, PhD, Received herPhD in Islamic Finance from International Centre forEducation in Islamic Finance (INCEIF) in 2012. She iscurrently a professional Consultant trainer at Salam MalaysiaSdn. Bhd. She worked at the National Bank of Sudan as anexecutive banker; also she worked as a professional trainingconsultant for the period 2005-2012 with Alibdaa Regionalconsultant (Malaysia) and Yataka Legend Sdn. Bhd. The twocompanies are providing Training and Development and bothcompanies are based in Malaysia. She presented a numberof papers at international conferences. Omaima also haspublished in International Journal of Excellence in IslamicBanking and Finance (IJEIBF), and currently she is writing abook from six Chapters in Takaful.

2-

Course OBJECTIVES� To provide concise, comprehensive coverage of

vital business topics & important concepts.

� To grasp the essential ingredients of:� Personal success� Management success� Business success

� To help non business-trained professionals understand fundamental business principles.

� To ensure that attendees are abreast of the latest thinking in management and leadership as well as business strategies.

4

28/9/2014

3

Part II: Management Accounting

� Concept of Management Accounting

� Classification of Costs

� Job costing

� Process costing

� Backflush Costing

� Planning and Techniques

� Business strategy and Management Accounting

� Excellent Strategic Thinking & Planning

5

Concept of Management Accounting

Management Accounting (managerial accounting) isconcerned with the provisions and use of accountinginformation to provide the basis of making businessdecisions in order to be better equipped in managementand control functions.

6

28/9/2014

4

Financial accounting is used to present the financial position of an organization to: Board of directors, stockholders, financial institutions and other investors are the audience for financial accounting reports. Financial accounting presents a specific period of time in the past and enables the audience to see how the company has performed. Financial accounting reports must be filed on an annual basis, and for publically traded companies, the annual report must be made part of the public record.

Management accounting is used by managers to make decisions concerning the day-to-day operations of a business. It is based not on past performance, but on current and future trends, which does not allow for exact numbers. Because managers often have to make decisions in a short period of time in a fluctuating environment, management accounting relies heavily on forecasting of markets and trends.

7

Focus

Stage

CostDetermination

Controland Financial

Transformation

Informationfor

Planning andControl

Management

Transformation

Reduction ofWaste ofResources in

ProcessesBusiness

Transformation

Creation of Value

Resource Usethrough Effective

Transformation

The Evolution of Management Accounting

8

1990s

1980s

1950s

1910s

28/9/2014

5

Key Financial Players

9

President and

Chief Executive Officer

Finance Vice-President (CFO)

Treasurer

Controller

ManagementAccounting

FinancialReporting

Tax Reporting

Internal Audit

OtherVice-Presidents

Part II: Management Accounting

� Concept of Management Accounting

� Classification of Costs

� Job costing

� Process costing

� Backflush Costing

� Planning and Techniques

� Business strategy and Management Accounting 1

0

28/9/2014

6

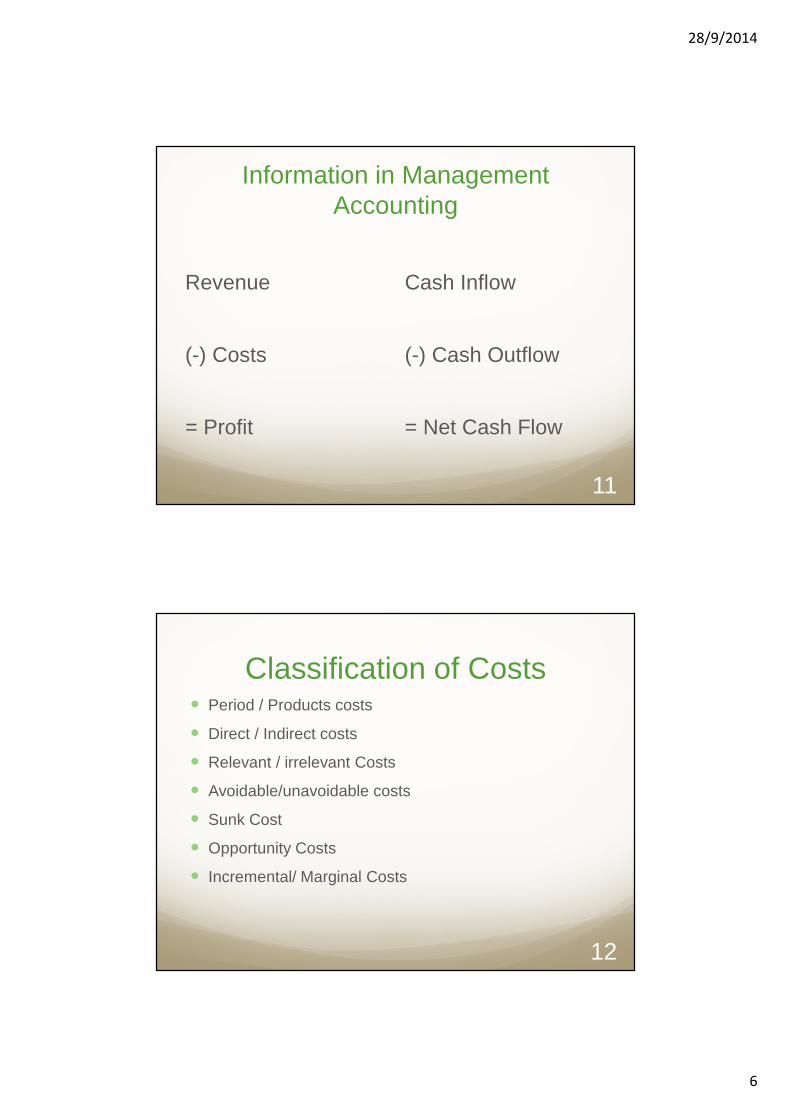

Information in Management Accounting

Revenue

(-) Costs

= Profit

Cash Inflow

(-) Cash Outflow

= Net Cash Flow

11

Classification of Costs� Period / Products costs

� Direct / Indirect costs

� Relevant / irrelevant Costs

� Avoidable/unavoidable costs

� Sunk Cost

� Opportunity Costs

� Incremental/ Marginal Costs

12

28/9/2014

7

Nature of Fixed & Variable CostsVariable, Fixed Semi- variable or Semi-fixed “show ho w

cost react to changes in activity”

Variable costs - change in total as the level of activity changesThere is a definitive physical relationship to the activity measure

Fixed costs - do not change in total with changes in activity levels

Accounting concepts of variable and fixed costs are short run concepts

Apply to a particular period of time Relate to a particular level of production

Relevant range is the range of activity over which the firm expects cost behavior to be consistentOutside the relevant range, estimates of fixed and variable costs may not be

valid 13

Types of Fixed Costs Capacity costs - fixed costs that provide a firm with the

capacity to produce and/or sell its goods and servicesAlso know as committed costs and typically relate to a firm’s

ownership of facilities and its basic organizational structure

Capacity costs may cease if operations shut down, but continue in fixed amounts at any level of operations

Examples: property taxes, executive salaries

14

28/9/2014

8

Types of Fixed Costs Discretionary costs - need not be incurred in the short run

to operate the business, however, usually they are essential for achieving long-run goals. Also referred to as programmed or managed costs

Examples: research and development costs, advertising

15

Semi-Fixed CostsSemi-fixed cost is a defined level of cost

that can increase or decrease when activity reaches upper and lower levels .Example: A quality-control inspector can

examine 1,000 units per day. Inspection costs are semi fixed with a step up for every 1,000 units per day

16

28/9/2014

9

Cost ObjectsA cost object is a tangible input for a

product manufactured. a.k.a. Prime Cost

Labor is a cost object as it can be directly associate cost of production.

Raw material such as cotton or threads can be another cost object

17

Direct CostA cost of an activity that is used by a single cost object

Cost object = A dining room tableCost of the wood that went into the dining room table

Cost object = Line of dining room tablesA manager’s salary would be a direct cost if a manager were hired to supervise the production of dining room tables and only dining room tables

Direct cost

Direct materials Direct labor

18

28/9/2014

10

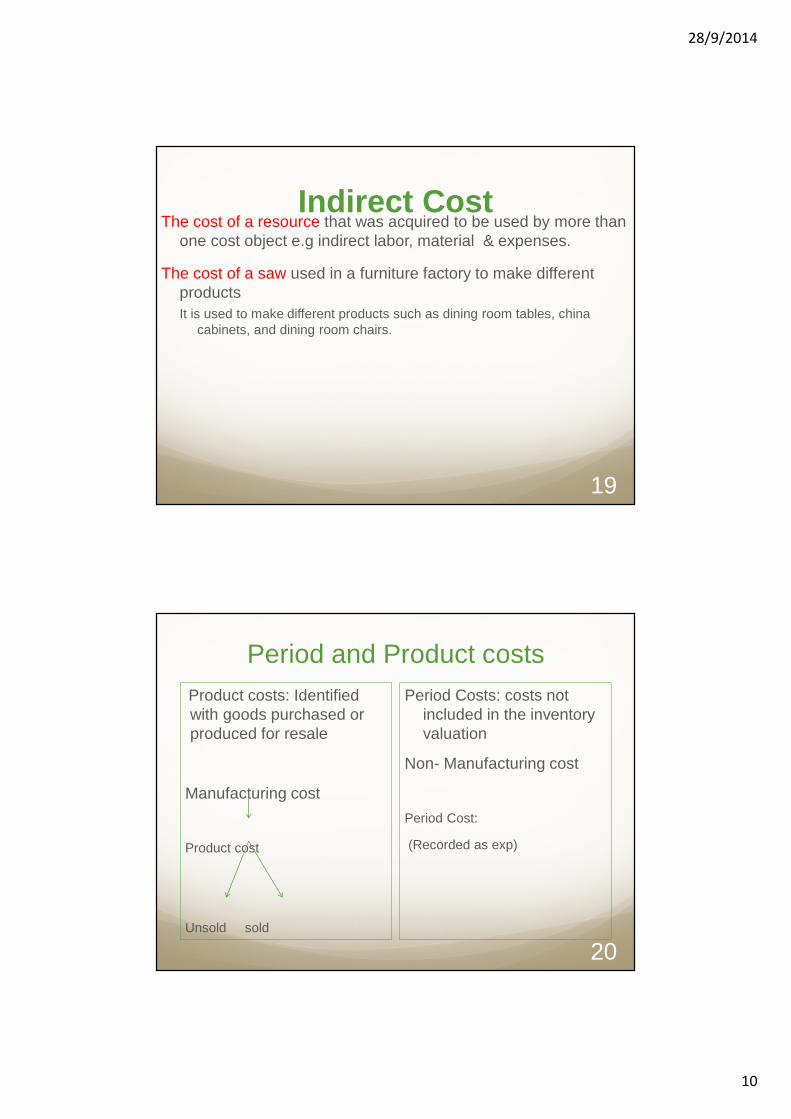

Indirect CostThe cost of a resource that was acquired to be used by more than

one cost object e.g indirect labor, material & expenses.

The cost of a saw used in a furniture factory to make different productsIt is used to make different products such as dining room tables, china

cabinets, and dining room chairs.

19

Period and Product costsProduct costs: Identified with goods purchased or produced for resale

Manufacturing cost

Product cost

Unsold sold

Period Costs: costs not included in the inventory valuation

Non- Manufacturing cost

Period Cost:

(Recorded as exp)

20

28/9/2014

11

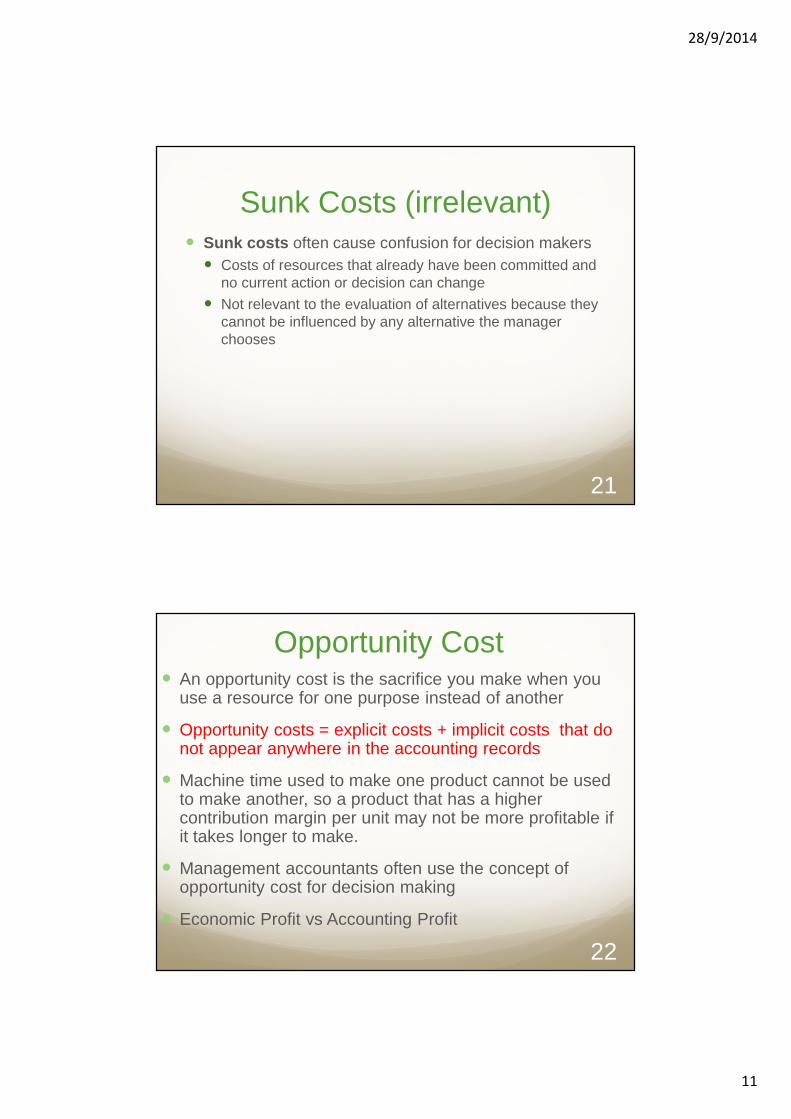

Sunk Costs (irrelevant)� Sunk costs often cause confusion for decision makers

� Costs of resources that already have been committed and no current action or decision can change

� Not relevant to the evaluation of alternatives because they cannot be influenced by any alternative the manager chooses

21

Opportunity Cost� An opportunity cost is the sacrifice you make when you

use a resource for one purpose instead of another

� Opportunity costs = explicit costs + implicit costs that do not appear anywhere in the accounting records

� Machine time used to make one product cannot be used to make another, so a product that has a higher contribution margin per unit may not be more profitable if it takes longer to make.

� Management accountants often use the concept of opportunity cost for decision making

� Economic Profit vs Accounting Profit

22

28/9/2014

12

Types of Production Activities� The allocation of manufacturing overhead to products on

the basis of a volume metric such as direct labor hours or production machine hours.

� A new classification system, developed originally for manufacturing operations, gives a broader framework for classifying an activity and its associated costs

23

Costs AllocationsCost allocation is the process of assigning costs when direct measure does not exist.

Traditional cost accounting systems assign indirect costs to products with a two-stage procedure:

� Indirect costs are assigned to production departments

� Production department costs are assigned to the products

24

28/9/2014

13

New Classification System� The new classification system places activities and

their associated costs into one of the following categories:� Unit related

� Batch related

� Product sustaining

� Customer sustaining

� Business sustaining

25

Cost Driver Rates� A cost driver is a factor that causes or “drives” an activity’s

costs

� All costs associated with a cost driver, such as setup hours, are accumulated separately

� Each cost pool has a separate cost driver rate

� The cost driver rate is the ratio of the cost of a support activity accumulated in the cost pool to the level of the cost driver for the activity

Activity cost driver rate = Cost of support activity / Level of cost driver

26

28/9/2014

14

Number of Cost Pools� The number of cost pools can vary

� Some German firms use over 1,000� Henkel-Era-Tosno

� The general principle is to use separate cost pools if the cost or productivity of resources is different and if the pattern of demand varies across resources

� The increase in measurement costs required by a more detailed cost system must be traded off against the benefit of increased accuracy in estimating product costs� If cost and productivity differences between resources are small,

having more cost pools will make little difference in the accuracy of product cost estimates

27

Two-Stage Cost Allocation (1)

� Conventional product costing systems assign indirect costs to jobs or products in two stages

1. In the first stage:� System identifies indirect costs with various production

and service departments

� Service department costs are then allocated to production departments

2. The system assigns the accumulated indirect costs for the production departments to individual jobs or products based on predetermined departmental cost driver rates

28

28/9/2014

15

Life-Cycle Costs� Life-cycle costing is a relatively new perspective that

argues, organizations should consider a product’s costs over its entire lifetime when deciding whether to introduce a new product

� There are five distinct stages in a typical product’s life cycle� Not all products will follow this pattern� Some products will fail early and have a shortened life

cycle

29

Product Life Cycle (1)

Product development and planning

� The organization incurs significant research and development costs and product testing costs

� Because of the increasing costs of launching products, organizations are devoting more effort to the product development and planning phase

� The nature and magnitude of these costs should be identified so that when products are initially proposed, planners have some idea of the cost that new product development will inflict on the organization

� Shorter life cycles provide less time to recover costs

30

28/9/2014

16

Product Life Cycle (2)

� Introduction phase� The organization incurs significant promotional costs as

the new product is introduced to the marketplace

� At this stage the product’s revenue will often not cover the flexible and capacity-related costs that it has inflicted on the organization

31

Product Life Cycle (3)

� Growth phase� The product’s revenues finally begin to cover the flexible

and capacity-related costs incurred to produce, market, and distribute the product

� There is often little or no price competition

� The focus of attention is on developing systems to deliver the product to the customer in the most effective way

32

28/9/2014

17

Product Life Cycle (4)

� Product maturity phase� Price competition becomes intense and product margins

begin to decline

� While the product is still profitable, profitability is declining relative to the growth phase

� The organization undertakes intense efforts to reduce costs to remain competitive and profitable

33

Product Life Cycle (6)

� Product-related costs occur unevenly over the product’s lifetime

� The motivation for considering total life cycle costs before the product is introduced is to ensure that the difference between the product’s revenues and its manufacturing and distribution costs cover the other costs associated with developing, supporting, and abandoning the product

� Life-cycle costing is a good example of a costing system designed for decision making that has little or no practical relevance in external reporting

34

28/9/2014

18

Direct costingand short-term decisions

Cost-Volume-Profit Analysis� Decision makers often like to combine information about

flexible and capacity-related costs with revenue information to project profits for different levels of volume

� Conventional cost-volume-profit (CVP) analysis rests on the following assumptions:� All organization costs are either purely variable or fixed

� Units made equal units sold

� Revenue per unit does not change as volume changes

36

28/9/2014

19

CVP Model� Cost-volume-profit (CVP) model summarizes the

effects of volume changes on a firm’s costs, revenues, and profit� Analysis can be extended to determine the impact on

profit of changes in selling prices, service fees, costs, income tax rates, and the mix of products and services

� Break-even point is the volume of activity that produces equal revenues and costs for the firm� No profit or loss at this point

37

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

- 100 200 300 400 500 600 700 800

Cost Volume -Profit Graph (CVP) Graph

38

Fixed expenses

Units

Total Expenses

Total Sales

28/9/2014

20

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

- 100 200 300 400 500 600 700 800

Units

Cost Volume -Profit Graph

39

Break-even point

Equation Method

40

Profits = Sales – (Variable expenses + Fixed expen ses)

Sales = Variable expenses + Fixed expenses + Prof its

OR

At the break-even point profits equal zero.

28/9/2014

21

Activity Based Costing (ABC)

ABC is designed to provide managers with cost information for strategic and other decisions that potentially affect capacity and therefore “fixed” costs.

ABC is agood supplementto our traditional

cost systemI agree!

42

28/9/2014

22

Break-even Volume� Using the CVP profit equation, break-even volume is

determined by calculating the volume where profit = 0

� 0 = (Units sold x Contribution margin per unit) - Fixed costs

� Units sold to break even =

Fixed costs÷ Contribution margin per unit

43

Target Profit� Cost Volume Profit analysis can be used to determine

the sales volume required to achieve a specified target profit� Note that the previous break-even analysis was used to

determine the unit sales required to achieve a target profit of $0

44

28/9/2014

23

Margin of Safety

� Margin of safety - excess of projected sales units over break-even sales level, calculated as follows:

Sales Units - Break-Even Sales Units = Margin of Safety

� Provides an estimate of the amount that sales can drop before the firm incurs a loss

45

Relevant Costs and Revenues

� Whether particular costs and revenues are relevant for decision making depends on the decision context and the alternatives available

� When choosing among different alternatives, managers should concentrate only on the costs and revenues that differ across the decision alternatives� These are the relevant cost/revenues

� Opportunity costs by definition are relevant costs for any decision

� The costs that remain the same regardless of the alternative chosen are not relevant for the decision

46

28/9/2014

24

Replacement of A Machine (1)

� A Company purchased a new drilling machine for $180,000 on September 1, 2003� They paid $30,000 in cash and financed the remaining $150,000

with a bank loan� The loan requires a monthly payment of $5,200 for the next 36

months

� On September 27, 2003, a sales representative from another supplier of drilling machines approached the company with a newly designed machine that had only recently been introduced to the market and offered special financing arrangements� The new supplier agreed to pay $50,000 for the old machine,

which would serve as the down payment required for the new machine

� In addition, the new supplier would require monthly payments of $6,000 for the next 35 months

47

Replacement of A Machine (2)

� The new design relied on innovative computer chips, which would reduce the labor required to operate the machine� The company estimated that direct labor costs would decrease by

$4,400 per month on the average if it purchased the new machine

� In addition it had fewer moving parts than the current machine� The new machine would decrease maintenance costs by $800 per

month

� The new machine has greater reliability� This would allow the company to reduce materials scrap cost by

$1,000 per month

� Should the company dispose of the machine it just purchased on September 1 and buy the new machine?

48

28/9/2014

25

Analysis Of Relevant Costs (1)

� If the company buys the new machine, it will still be responsible for the monthly payments of $5,200 committed to on September 1� Therefore, the $30,000 that it paid in cash for the old

machine and the $5,200 it is committed to pay each month for the next 36 months are sunk costs

� The company already has committed these resources, and regardless if it decides to buy the new machine, it cannot avoid any of these costs

� None of these sunk costs are relevant to the decision

49

Analysis of Relevant Costs (2)

� What costs are relevant?

� The 35 monthly payments of $6,000 and the down payment of $50,000 are relevant costs, because they depend on the decision

� Labor, materials, and machine maintenance costs will be affected if the company acquires the new machine� The relevant expected monthly savings are:

� $4,400 in labor costs� $1,000 in materials costs� $ 800 in machine maintenance costs

� The revenue of $50,000 expected on the trade-in of the old machine is also relevant, because the old machine will be disposed of only if the company decides to acquire the new machine

50

28/9/2014

26

Analysis of Relevant Costs (3)

� In a comparison of the cost increases/cash outflows to cost savings/cash inflows� The down payment required for the new machine is

matched by the expected trade-in value of the old machine

� The expected savings in labor, materials, and machine maintenance costs each month ($6,200) are more than the monthly lease payments for the new machine ($6,000)

� Thus, it is apparent that the company will be better off trading in the old machine and replacing it with the new machine

51

Part II: Management Accounting

� Define the basic tools of management accounting

� Classification of Costs

� Job costing

� Process costing

� Backflush Costing

� Planning and Techniques

� Business strategy and Management Accounting

� Excellent Strategic Thinking & Planning52

28/9/2014

27

Job-Costing and

Process-Costing Systems

53

Job -Order Costing and Process Costing

54

Job-order costing allocates costs

to products that are identified by

individual units or batches.

Process costing averages costs

over large numbers of nearly

identical products.

28/9/2014

28

Job-Order Costing Basic Records

55

Job-cost records contain all costs for a particular

product, service, or batch of products.

Materials requisitions are records of

materials used in particular jobs.

Labor time cards record the time a

particular direct laborer spends on each job.

Date Started: 1/7/20X7 Job Number: 963

Date Completed: 1/14/20X7 Units completed: 12

Cost Date Ref. Quantity Amount Summary

Direct Materials:

6” Bars 1/7 N41 24 120.00

Casings 1/9 K56 12 340.00 460.00

Direct Labor:

Drill 1/8 7Z4 7.0 105.00

1/9 7Z5 5.5 82.50

Grind 1/13 9Z2 4.0 80.00 267.50

Overhead:

Applied 1/14 9.0 mach. hrs. 180.00 180.00

Total cost 907.50

Unit cost 75.625

Job-Cost Record

56

28/9/2014

29

Job-Costing System Example

57

Beginning

Direct Materials

inventory $110,000

Purchases

$1,900,000+

=

Ending

Direct Materials

Inventory

$120,000

Direct Materials

requisitioned

$1,890,000

–

Enriquez Machine Parts Company

Beginning

WIP

inventory $0

Direct materials

used

$1,890,000

+

Direct labor

and applied

overhead

$765,000

=

Ending WIP

inventory

$155,000

Cost of goods

manufactured

$2,500,000

–

Job-Costing System Example

58

28/9/2014

30

Beginning

Finished Foods

inventory $12,000

Cost of Goods

Available for

Sale $2,512,000

Cost of Goods

Manufactured

$2,500,000

+

=

Ending

Finished Goods

inventory

$32,000

Cost of

Goods Sold

$2,480,000

–

Job-Costing System Example

59

Materials Cost Journal Entry

60

Direct-Materials Inventory 1,900,000

Accounts Payable 1,900,000

To record purchase of direct materials

Work-in-Process Inventory 1,890,000

Direct-Materials Inventory 1,890,000

To record usage of direct materials

28/9/2014

31

Actual Overhead Costs Journal Entry

61

Factory Department Overhead Control 392,000

Cash, Accounts Payable, Various Accounts 392,000

To record actual factory overhead incurred

Work-in-Process Inventory 390,000

Accrued Payroll 390,000

To record actual labor costs incurred

Applying Factory Overhead to Products

62

Enriquez Machine Parts Company’s

budgeted manufacturing overhead for

the assembly department is $103,200.

Budgeted direct labor cost is $206,400.

$103,200 ÷ $206,400 = 50%

28/9/2014

32

Applying Factory Overhead to Products

63

Suppose that at the end of the year

Enriquez had used 70,000 machine

hours in assembly and incurred

$190,000 in direct-labor costs.

How much overhead was

applied to assembly?

Applying Factory Overhead to Products

64

70,000 machine hours X $4 = $280,000

Actual direct-labor cost of $190,000 X .5 = 95,000

Total factory overhead applied $375,000

Work-in-Process Inventory 375,000

Factory Department Overhead Control 375,000

To record overhead applied

28/9/2014

33

Finished Goods, Sales, and Cost of Goods Sold

65

Finished Goods Inventory 2,500,000

WIP Inventory 2,500,000

To record the cost of goods completed

Finished Goods Inventory 2,500,000

WIP Inventory 2,500,000

To record the cost of goods completed

Accounts Receivable 4,000,000

Sales 4,000,000

To record the sales on account

Accounts Receivable 4,000,000

Sales 4,000,000

To record the sales on account

Cost of Goods Sold 2,480,000

Finished Goods Inventory 2,480,000

To record the cost of goods sold

Cost of Goods Sold 2,480,000

Finished Goods Inventory 2,480,000

To record the cost of goods sold

Actual and Applied Overhead Journal Entry

66

Actual overhead = $392,000

Applied overhead = $375,000

$392,000 – $375,000 = $17,000 underapplied

Cost of Goods Sold 17,000

Factory Department Overhead Control 17,000

To dispose of underapplied overhead

28/9/2014

34

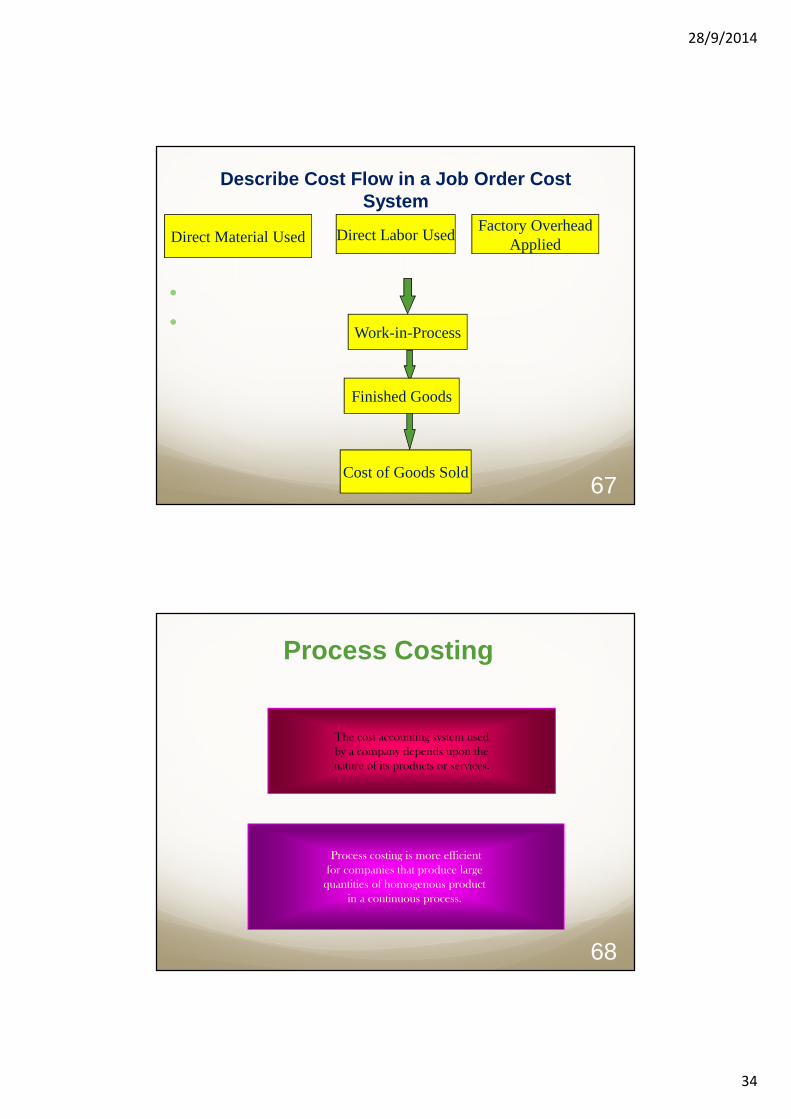

Describe Cost Flow in a Job Order Cost System

�

�

67

Direct Labor UsedFactory Overhead

AppliedDirect Material Used

Work-in-Process

Cost of Goods Sold

Finished Goods

Process Costing

68

Process costing is more efficient

for companies that produce large

quantities of homogenous product

in a continuous process.

The cost accounting system used

by a company depends upon the

nature of its products or services.

28/9/2014

35

Process Costing Compared With Job Costing

69

It accumulates costs for

a period and divides

them by quantities produced

during the period to get

broad, average unit costs.

Process costing can

be applied to non-

manufacturing and

manufacturing

activities.

Process-costing does not

distinguish among

individual units of product.

Backflush Costing

70

What is backflush costing?

It is an accounting system thatapplies costs to products only

when the production is complete.

28/9/2014

36

Principles of Backflush Costing

71

Backflush costing has onlytwo categories of costs:

Materials Conversion

There is no work in process account.

Backflush Costing Example

72

Speaker Technology, Inc., recentlyintroduced backflush costing and JIT.

Model AX27 Standard material cost:$14Standard conversion cost: $21

Actual production for the month: 400 unitsActual materials purchased: $5,600Actual conversion costs: $8,400

28/9/2014

37

Backflush Costing Example

73

Materials Inventory 5,600Accounts Payable or Cash 5,600

To record material purchases

Conversion Costs 8,400Accrued Wages 8,400

To record conversion costs incurred

Backflush Costing Example

74

Finished Goods Inventory 14,000Material Inventory 5,600Conversion Costs 8,400

To record costs of completed production

Cost of Goods Sold 14,000Finished Goods Inventory 14,000

To record costs of 400 units sold

28/9/2014

38

Backflush Costing Example

75

Cost of Goods Sold 14,000Material Inventory 5,600Conversion Costs 8,400

Cost of Goods Sold 200Conversion Costs 200

To recognize underapplied conversion costs

The Finished Goods Account can be eliminated.

Part II: Management Accounting

� Define the basic tools of management accounting

� Classification of Costs

� Job costing

� Process costing

� Backflush Costing

� Planning and Techniques

� Business strategy and Management Accounting76

28/9/2014

39

Cost & Management Accounting Techniques

Must for Effective Decision Making

INSTITUTE OF COST & MANAGEMENT ACCOUNTANTS OF PAKISTAN77

Cost & Management Accounting

The Process of � Identifying�Measuring�Analyzing� Interpreting�Communicating Information

78

28/9/2014

40

Techniques� The Make or Buy Decision

� Just-In-Time

� Inventory Management

� Budgeting

� Variance Analysis

� Const-Volume-Profit Analysis

� Activity Based Costing

� Linear Programming79

The Make or Buy DecisionA decision concerning whether an item should

be produced internally or purchased from an outside supplier is called a “Make or Buy”

decision.

E.g in computer companies some of the parts to be bought from suppliers much cheaper

80

28/9/2014

41

The Make or Buy Decision� XXX manufactures part 4A that is used in one

of its products.

� The unit product cost of this part is:

81

Direct materials $ 9 Direct labor 5 Variable overhead 1 Depreciation of special equip. 3 Supervisor's salary 2 General factory overhead 10 Unit product cost 30$

Direct materials $ 9 Direct labor 5 Variable overhead 1 Depreciation of special equip. 3 Supervisor's salary 2 General factory overhead 10 Unit product cost 30$

The Make or Buy Decision� Equipment used to manufacture part 4A has no resale value.

� Total general factory overhead, which is allocated on the basis of direct labor hours, would be unaffected by this decision.

� The $30 unit product cost is based on 20,000 parts produced each year.

� An outside supplier has offered to provide the 20,000 parts at a cost of $25 per part.

Should we accept the supplier’s offer? 82

28/9/2014

42

Cost Per Unit Cost of 20,000 Units

Make BuyOutside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000 Direct labor 5 100,000 Variable overhead 1 20,000 Depreciation of equip. 3 - Supervisor's salary 2 40,000 General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

8320,000 × $9 per unit = $180,000

Cost Per Unit Cost of 20,000 Units

Make BuyOutside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000 Direct labor 5 100,000 Variable overhead 1 20,000 Depreciation of equip. 3 - Supervisor's salary 2 40,000 General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

84

The special equipment has no resale value and is a sunk cost.

28/9/2014

43

Cost Per Unit Cost of 20,000 Units

Make BuyOutside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000 Direct labor 5 100,000 Variable overhead 1 20,000 Depreciation of equip. 3 - Supervisor's salary 2 40,000 General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

The Make or Buy Decision

85

Not avoidable; irrelevant. If the product is dropped, it will be reallocated to other products.

The Make or Buy Decision

86Should we make or buy part 4A?

Cost Per Unit Cost of 20,000 Units

Make BuyOutside purchase price $ 25 $ 500,000

Direct materials 9$ 180,000 Direct labor 5 100,000 Variable overhead 1 20,000 Depreciation of equip. 3 - Supervisor's salary 2 40,000 General factory overhead 10 - Total cost 30$ 340,000$ 500,000$

28/9/2014

44

The Make or Buy Decision

DECISION RULE

In deciding whether to accept the outside supplier’s offer, XXX isolated the relevant costs of making the part by eliminating:

� The sunk costs.� The future costs that will not differ between making or

buying the parts.

87

Impact of Just in Time ( JIT)Inventory Methods

88

In a JIT inventory system . . .

Productiontends to equalsales . . .

So, the difference between variable andabsorption income tends to disappear.

28/9/2014

45

Inventory Management

89

Budgeting

Define goaland objectives

Uncover potentialbottlenecks

Coordinateactivities

Communicatingplans

Think about andplan for the future

Means of allocatingresources

90

28/9/2014

46

Part II: Management Accounting

� Define the basic tools of management accounting

� Classification of Costs

� Job costing

� Process costing

� Backflush Costing

� Planning and Techniques

� Strategic Management

91

Strategic ManagementStrategic planning is a continuous andsystematic process where people makedecisions about intended future outcomes, howoutcomes are to be accomplished, and howsuccess is measured and evaluated

In essence, the strategic plan is a

company’s game plan

92

28/9/2014

47

93Strategic Planning Cycle

Purpose of Strategic Management

To exploit and create new and different opportunities for tomorrow

94

28/9/2014

48

Key Terms in Strategic Management

� Competitive advantage

� Strategists

� Vision and mission statements

� External opportunities and threats

� Internal strengths and weaknesses

� Long-term objectives

� Strategies

� Annual objectives

� Policies

95

96

Vision & Mission

Strategy Formulation

External Opportunities & Threats

Internal Strengths & Weaknesses

Long-Term Objectives

Alternative Strategies

Strategy Selection

28/9/2014

49

97

Strategy Implementation

Annual Objectives

Policies

Employee Motivation

Resource Allocation

98

Strategy Evaluation

Internal Review

External Review

Performance Measurement

Corrective Action

28/9/2014

50

Benefits of Strategic Management

� Nonfinancial Benefits� Enhanced awareness of threats� Improved understanding of competitors’ strategies� Increased employee productivity� Reduced resistance to change� Clearer understanding of performance-reward

relationship� Enhanced problem-prevention capabilities

99

Why Some Firms Do Not have Strategic Planning

�Lack of knowledge of strategic planning

�Poor reward structures

�Fire fighting

�Waste of time

�Too expensive

�Laziness100

28/9/2014

51

Why Some Firms Do Not have Strategic Planning

� Fear of failure

� Overconfidence

� Prior bad experience

� Self-interest

� Fear of the unknown

� Honest difference of opinion

� Suspicion101

Pitfalls in Strategic Planning

Strategic planning is an involved and complex process that takes an organization into uncharted territory

102

28/9/2014

52

Effective Strategic Planning is:

� A people process more than a paper process

� A learning process

� Words supported by numbers

� Simple and nonroutine

� Varying assignments, team membership, meeting formats, and planning calendars

� Challenging assumptions underlying corporate strategy

103

Effective Strategic Planning continued� Welcomes bad news

� Requires open-mindedness and a spirit of inquiry

� Is not a bureaucratic mechanism

� Is not ritualistic or stilted

� Is not too formal, predictable, or rigid

� Does not contain jargon or arcane language

104

28/9/2014

53

Effective Strategic Planning continued

� Is not a formal system for control

� Does not disregard qualitative information

� Is not controlled by “technicians”

� Does not pursue too many strategies at once

� Continually strengthens the “good ethics is good business” policy

105

Comparing Business and Military Strategy

� Strategic planning started in the military

� Similarity � Both business and military organizations must

adapt to change and constantly improve

� Difference � Business strategy assumes competition� Military strategy assumes conflict

106

28/9/2014

54

Benefits of Strategic Management

� Nonfinancial Benefits� Enhanced awareness of threats� Improved understanding of competitors’ strategies� Increased employee productivity� Reduced resistance to change� Clearer understanding of performance-reward relationship� Enhanced problem-prevention capabilities

107

End of Slides� ANY QUESTIONS PLEASE?

� Thank You Wasalam

108

Copyright © 2022 FDOKUMEN