Mauritius-toward-the-21st-century.pdf - World Bank Documents

154

UNDP-WORLD BANK TRADE EIPASION IPOGRAM COUNTRY REPORT 12 MAURITIUS Toward the 21st Century This country report is a product of the joint UNDP/World Bank Trade Expansion Program which provides technical and policy advice to countries intending to reform their trade regimes. The views contained herein are those of the authors and do not necessarily reflect those of the United Nations Development Program or the World Bank. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Mauritius-toward-the-21st-century.pdf - World Bank Documents

UNDP-WORLD BANK TRADE EIPASION IPOGRAM

COUNTRY REPORT 12

MAURITIUS

Toward the 21st Century

This country report is a product of the joint UNDP/World Bank Trade Expansion Program whichprovides technical and policy advice to countries intending to reform their trade regimes. The viewscontained herein are those of the authors and do not necessarily reflect those of the United NationsDevelopment Program or the World Bank.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

MAURITIUS

Toward the 21st Century

Trade Policy Division

Policy Research DepartmentWorld Bank

December 1993Wasbington, D.C.

This report was prepared for the Mauritian government in response to itsrequest for assistance from the joint United Natiocs Development Program/WorldBank Trade Expansion Program. The report was directed by Dominique Hachette(consultant, Universidad Catolica de Chile), with the participation of Mona Haddad(World Bank), Ron Hood (consultant, Louis Berger International), Ramon Lopez(consultant, University of Maryland). Patrick Messerlin (consultant, FondationNationale des Sciences Politiques), John Nash (World Bank), and Maurice Schiff(World Bank). The mission also received valuable input and assistance fromKapil Kapoor, Oey Astra Meesook and Brendan Horton (World Bank).

The mission visited Mauritius from 5 February - 21 February, 1992. Whilein Mauritius, the UNDP resident mission under the direction of Olubanke King-Ak6r616 provided both logistical support and valuable substantive input. Themission acknowledges with thanks the help of the many members of the public andprivate sectors who provided assistance and advice, particularly our counterpartsin the Ministry of Economic Planning and Development, Messrs. R. Bheenick(Director), D. Dusornth (Principal Economist) and their staff and Mr. P.Chundunsing and his staff in the Customs Service. This report was edited by Metade Coquereaumont and produced by Leonila Castillo (World Bank).

The report was discussed with the Mauritian authorities in March 1993 byMessrs. John Nash and Dominique Hachette.

The views and recommendations of the report are those of the authors anddo not necessarily reflect those of the United Nations Development Program or theWorld Bank.

Table of Contents

Page No.

Executive Sunnmary i

Chapter 1. Growth and Economic Development of the 1980s 1Growth in the 1980s 1Growth in the 1990s and beyond 6

Chapter 2. Exports and the External Environment 9Sugar 11Evolution and structure of export processing zones 23Textiles and apparel 31Trends in patterns of trade 39Regional agreements 40

Chapter 3. Regulations and Incentives in the Output Markets 45Trade policy 45Sales tax 56Hotel and restaurant tax 59Price controls 59Subsidies 62

Chapter 4. Factor Market Policies and Incentives 63Land 63Financial markets 66Investment incentives 71Labor markets 75Technical note: land use controls 87Technical note: tax credit for stock purchases 92

Chapter 5. Sectoral Summary of the Impact of Regulations and Incentives 93Export processing zones 98Emerging pioneer exports 100Sugar 104

Chapter 6. Conclusions and Recommendations 107Implications of the external environment for economic policy 108Goods and services markets and relative prices 109Sugar 117Price controls 122Recommendations for improving factor markets 122

Chapter 7. Timing, Sequencing and Quantitative Impact of Recommendations 129Impact on GDP 129Impact on the government budget 130Timing and sequencing 133

Appendix A. The Foreign Exchange 135Appendix B. The Impact of the Tariff Level on Exports 145

List of TablesPage No.

1.1 Some macroeconomic aggregates, 1970-90 21.2 Merchandise exports at current prices (f.o.b.), 1982-91 31.3 Merchandise imports at current prices (c.i.f.), 1982-91 41.4 Balance of payments 52.1 Main exports by product of Mauritius 1989-91 102.2 Main exports of Mauritius by country, 1989-91 112.3 Main exports of Mauritius by product and country, 1989-91 122.4 Production, exports, and prices for Mauritian sugar, 1985-90 132.5 Protection and world price volatility, 1979-89 averages 152.6 Effects of multilateral policy reform on world sugar prices 152.7 Indicators of internal forces working toward the

dismantling of the EC common sugar policy, 1985-91 182.8 Simulations of changes in the EC sugar policy 192.9 Basic statistics on export processing zones in Mauritius, 1983-90 242.10 Imports and exports of EPZ firms, 1977-90 242.11 EPZ imports and exports of Mauritius, by country, 1990 272.12 EPZ imports and exports by main commodity 282.13 Intermediate consumption of EPZ firms by industry group, 1985-1986 292.14 Production account of EPZ by product, 1989 302.15 The U.S. MFA quotas on Mauritian exports, 1985-89 342.16 Mauritian exports subject to the U.S. MFA, 1985-1990 372.17 The evolution of the Mauritian exports under U.S. MFA quotas, 1985-89 382.18 The existence of rents in Mauritian Apparel Exports to the U.S., 1991 39

3.1 Value of exports and import taxes, 1991 473.2 Customs collections and exemptions, 1991 493.3 Effective and statutory tariff rates, 1991 . 503.4 Protection in 1990 523.5 Customs collections and exemptions by class of goods 523.6 Customs tariff rates by class of goods 523.7 Sales tax revenues by category 583.8 Products subject to price controls in Mauritius 61

4.1 Land use in Mauritius 644.2 Sectoral distribution and interest rates of commercial

bank credit to the private sector, 1988-91 704.3 Employment in Mauritius, 1983, 1988, 1990 754.4 Wages and inflation, 1983, 1988, 1990 754.5 Sectoral employment in large firms; selected years 764.6 Job vacancy and employment growth 794.7 Real wages change by sector, 1984-90 804.8 Labor productivity and unit labor costs indexes in manufacturing, 1982-90 804.9 Public sector employment, 1989-91 854.10 Gross top salaries of certain grades in public sector/private sector 85

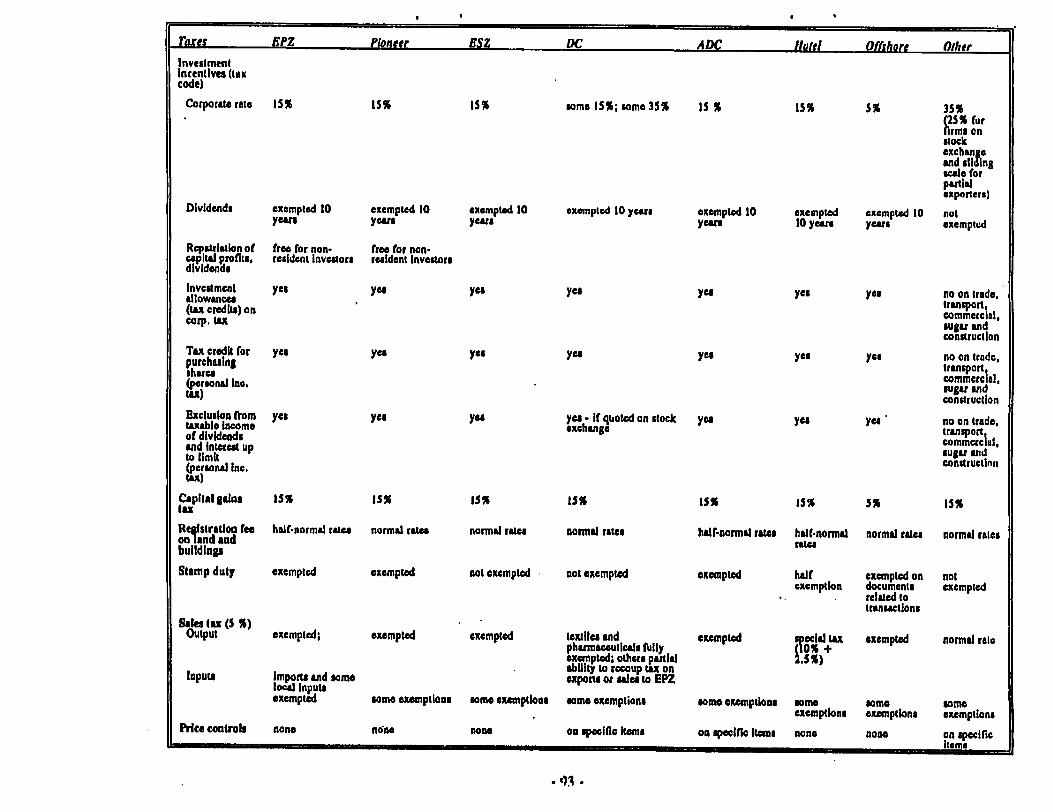

5.1- Sectoral incentive sStructure 945.2 A taxonomy of Mauritian 'other' exports 101

6.1 Composition of fiscal revenues, Mauritius and other selected countries,1972 and 1990 116

6.2 Personal income payable by employees and self-employed 1166.3 Estimates of production costs of sugar, 1974, 1981, 1989 118

7.1 Estimated revenue loss from import taxes reform 1307.2 Estimates of fiscal impacts of reform measures 131

. 7.3 Changes in taxes to generate or save Rs 100 million 132

A. I Real exchange rates 136A.2 Mauritius: bilateral real exchange rate 138A.3 Regression for the RER 141

List of Figures

2.1 Effects of making EC sugar quotas transferable 22

4.1 Vacancy rate and employment growth in Mauritius 794.2 Land use: demand and marginal value 904.3 Land use: optimal allocation 904.4 Land use: efficiency cost of restrictions . 914.5 Land use: increasing cost of restrictions over time 91

List of Boxes

3.1 Import taxes in Mauritius 456.1 The sugar sector in a rapidly growing economy 121

Executive Sumcary

Mauritius fared well during the 1980s. The economy grew at a rapid rate, and inflation and thefiscal and current account deficits were brought under control. Aided by a relatively well-developedhuman capital base, full employment and significant real wage increases improved the welfare of

much of the population. Mauritius maintained its exchange rate at a level attractive to exporters and

accumulated a comfortable volume of foreign exchange reserves. Trade taxes and restrictions were

relaxed and rationalized, price controls and subsidies diminished in importar . and incentives were

simplified. Exporters, especially firms in the export processing zones (EPZ -ook advantage of afavorable external and internal environment to propell exports into the forefront of economic growth.

The issues

Recently, however, clouds have begun to form above this rosy picture of strong, steady growth.

Full employment, while it has clearly brought many advantages, has in recent years become an

impediment to continued easy growth. Land and capital also seem to be fully employed. Natural

resources are scarce as well, and the country is already using them fully. The competitiveness of

Mauritian exports is diminishing with the rapid growth of real wages. And the export base remains

weak, with its heavy concentration on sugar and textiles and on particular markets.

It seems likely that Mauritius's comparative advantage no longer favors labor-intensive activities

as strongly as in the past. Consequently, growth will be tied to the development of sectors with

heavier requirements for education and training and based on more advanced technologies. Successful

development of these activities hinges on large investments in human capital, on the right market

. signals to direct productive factors to activities in which their productivity is highest, and on ease of

movement among sectors, activities, firms, and regions. Bringing idle factors into production will

contribute much less to growth than in the past. Growth will have to come instead from improvements

in the quality of productive factors and from a new framework of incentives and regulations for

encouraging better use of them.

Export-led growth depends crucially on the external environment as well. The 1990s are likely to

be much less predictable than the 1980s. Uncertainty is everywhere: in the results of the Uruguay

Round, revisions of the Common Agricultural Policy and of the Lom6 Convention in Europe,

modification or elimination of the Multifiber Agreement, changes in relative preferences granted to

Mauriius's two principal exports, increasing reliance on antidumping and safeguards-based protection

of textiles by industrial countries, and the emergence of new competitors. Whatever the outcomes,

one thing seems clear: diversification and flexibility will be required to meet the challenges of

unpredictable external markets. The days are numbered for a strategy of exportled development

based solely on sugar and textiles.

Availabiiy ofproducrive resources

The availability of productive factors will grow with the population and with savings and

investment. Labor and human capital remain the main source of growth. Population and human

development policies and improvements in the capital market are of paramount importance. Quality

improvements are equally critical. Human capital may become the binding factor in economic growth.

The experience of some East Asian countries is telling in this respect.

Beuner use of resources

These sources of growth have to be directed to the leading sectors of the economy as rapidly as

possible to take advantage of the benefits of factor availability and the external environment. What isneeded is a framework of incentives and regulations that will stimulate sectors with the highest

comparative advantage and increase the flexibility of the economy, improving economic performance

and reducing the costs of adjustment to fluctuations in the external environment.

The strateg

Amidst the chaos of signals created by a multitude of incentives and regulations, often working at

cross-purposes, the signals that reflect true relative prices and social costs and benefits of various

activities are nearly impossibLe to pick out. The thicket of regulations also impedes the movement of

factors of production. Under these conditions, switching resources to new areas of production is bothdifficult and costly.

A comprehensive review of incentives and regulations is required. Reforms should be directed at

reducing antiexport bias and removing the direct and indirect barriers to the development of the mostproductive sectors. A major overhaul of regulations is needed to improve the working of factor

markets (labor, land, and capital) so that resources are directed toward the best alternative uses, given

continuously changing external conditions.

Recommendations

The main recommendations of the report concern changes in overall incentives and taxes and

changes in factor markets.

Overall incemies and aes

a The composition of tax revenues needs to change so there is less reliance on trade taxes and

more reliance on taxes on domestic consumption. Harmonization of incentives is also needed, along

with greater simplicity, to reduce their bias. Eventually, if the proposals in this report are adopted,

there will be no more justification for special preferences and incentives.

-^n-

s Rationalizing and reducing import taxes would reduce the amiexport bias and other

distortions in the economy and lessen the need for special exemptions. A 10 percent flat tariff is

strongly recommended as a medium-term goal.

a Distributive and efficiency considerations call for a careful review of the level of the export

tax.

E For efficiency reasons, sugar cane growers should be paid the EC price (net of export tax

and other deductions) for the share of their output equivalent to the EC quota share of total output,and the world price (equal to the domestic price) for the rest of their production. This could be done

through a quota system. In the medium-to-long term, an auction system for the quotas could be

phased in.

* A broadening of the sales tax base should be undertaken to relieve the burden on tariffs, toreduce production distortions, and to strengthen linkages among different types of firms. This change

should not be expected to generate significant additional revenue without an increase in the rate. A

medium-term objective would be to move from the sales tax to a full value added tax with no more

than two to three rate levels. Whether a value added tax or a sales tax, this tax should become the

major tax base of the economy. High priority should be given to developing a workable scheme toallow direct and indirect exporters to get rebates of sales or value added taxes-on their exports.

a Any taxes on luxury items levied for distributive reasons should be excise, not import,

taxes.

a Tle corporate income tax rate needs to be uniform across all sectors. EPZs should not be

favored over other types of firms. Conditions have changed in Mauritins, making export

diversification an important priority. Also, tax rate setting should be considered from a fiscal revenue

perspective-rate reductions might increase tax revenues. Current income tax revenues are very low.

w Administrative improvements could also improve yields, but at least a year or two would be

required before results become noticeable.

* Administration of the duty drawback scheme needs to be considerably improved, to reduce

antiexport bias and stimulate domestic linkages with EPZs.

m Exemptions through the certificate programs could be phased out in a coordinated fashion as

rates are reduced and bases broadened.

a More general tax incentives (investment allowances, credit for stock purchases, etc.) should

be reformed along the lines described in this report.

i The economic and social conditions that may once have justified price controls and subsidies

have passed. Replacing them with targeted support programs would better meet distributive objectives

and could reap substantial efficiency gains.

- iii -

Factor markers

a Eliminating the land conversion tax and permit system for transfering land from one use

(primarily agriculture) to another would greatly expand the options for land use. Reducing registration

duties, fees, and taxes could also make a useful contribution to more flexible land use. Land titles

need to be made more secure. If land conversion permits continue to be required, institutional

responsibility should be assigned to an agency with an economywide perspective that weighs all

alternative uses of land. The objective of the permit process should be to prevent environmental

degradation or other negative externalities, not to obstruct the transfer of land out of agriculture.

a Eliminating credit allocations by sector, informal interest rate controls, and credit ceilings

would improve the flexibility and efficiency cf the capital market.

a Policy revisions in several areas-especially for the sugar industry-would make the labor

market more responsive to changing conditions: hiring and firing, sick leave, overtime pay, and the

attendance bonus.

a The banking sector should be made more competitive and efficient and long-term capital

made more readily available by allowing foreign banks to compete in domestic markets and locals to

deal with banks abroad.

a Wages and other incentives for public employees should be consistent with the goal of

reallocating labor to higher-productivity sectors.a Human development issues, such as technical and vocational training, need to be a top

priority. This issue assumes even greater than usual importance during a period of structural change

in the economy, such as Mauritius is likely to pass through in the near future. Improvements in

secondary education and greater private sector participation in training are advisable.

a Integration efforts based on regional trade policy coordination within the Preferential Trade

Area for Eastern and Southern African States (ETA) and the Indian Ocean Commission (IOC) should

not be given top priority, given the small size of the economies involved and their limited

differentiation. Attention within these regional arrangements should instead be directed toward ways

to eliminate barriers to the movement of labor and capital between Mauritius and neighboring

countries, which could be of great mutual benefit.

Exchange rate

a Mauritius' conservative fiscal and monetary policy has allowed it to maintain the real

exchange rate at a realistic and relatively stable level; these should remain high-priority goals.

* Exporters should be allowed to retain their foreign exchange earnings.

- iv -

Impacts and sequencng

Production in the economy could rise by 8 to 10 percent over a period of two to three years if

the proposed reforms in the labor market are carried out. Overall, the reforms recommended in the

report could bring about an increase in government revenue in the medium term-although that is not

their primary inten-but the composition of tax revenues will have to change significantly. In the

. short run, the reforms pose a r --blem of sequencing.

a With respect to sequencing, the first priority should be to improve the flexibility of factor

. markets. Administrative reforms to strengthen the weaker parts of the revenue generating machinery

should also be undertaken before any major shifting between taxes.

w Tariffs could be moved in stages toward the goal of a uniform rate of 10 percent. At each

stage, the highest tariffs would be reduced, the lowest ones raised, and exemptions eliminated (except

for inputs used in export production). The tariff reforms should be part &s a package of measures

designed to work together to avoid destabilizing the government's fiscal position. This could involve

reducing relatively unproductive public sector expenditures, increasing the coverage and rate of the

sales tax, cutting back investment incentives, eliminating subsidies, and making the income tax rate

more uniform, especially for enterprises. Earlier improvements in tax administration should also

improve the revenue picture.

-

Chapter 1. Growth and Economic Developments of the 1980s

Mauritius was a bright spot in the bleak landscape of developing countries during the 1980s.

After a difficult economic period at the beginning of the decade, Mauritius introduced a strong and

coherent package of policies that greatly improved the macroeconomic environment. Growth surged,fueled in part by appropriate monetary, fiscal, and wage policies. That period is over sw, however,and many of the policies of the 1980s, justified by the considerable idle capacity of the time, are no

longer appropriate. Labor, land, and capital seem to be fully employed, and growth will no longer

spring easily from idle resources. In the coming years, Mauritius will need to restrain demand and

seek new growth stimuli on the supply side.

Growth in the 1980s

Mauritius made many of the right policy choices in the 1980s. Inflation and the fiscal and current

account deficits were substantially reduced (table 1-1). International trade policies were rationalized,

price controls and subsidies reduced, and incentives simplified. Institutions became more efficient,

especially those involved in trade promotion (e.g., the Mauritius Export Development and Investmea

Authority, MEDIA). Sugar, the country's main export, retained its buoyancy in export markets.

Favorable external conditions helped, as did the burgeoning growth of export processing zones

(EPZs), spurred on by political and economic stability, relatively cheap and skilled labor, and easy

access to world markets. Investment and savings, particularly foreign, were stimulated by credible

policies and attractive conditions, thus expanding the country's growth capacity for the near future-

gross fixed capital formation grew from 182 percent of GDP in 1984 to 29.4 percent in 1990, two-

thirds of it in the private sector.

As a result of these factors, the country enjoyed a reasonably high and steady rate of growth.GDP grew at an average annual rate of 6.5 percent between 1986 and 1991. The share of

manufactures in GDP expanded substantially, reaching 25 percent in 1991 thanks largely to the

development of EPZs. The economy reached full employment, and steady real wage increases have

improved the welfare of a substantial portion of the population. While employment growth averaged

4.9 percent a year between 1986 and 1991, growth of the working age population never exceeded 1.4

percent a year.

Thus unemployment, which had been as high as 17.1 percent of the economically active

pcpulation in 1984, steadily declined, falling to 2.3 percent in 1990, which is probably below the

natural rate of unemployment'

1. Preliminay information indicates unWmployment figures for 1991 similar to that of I0-

-1-

Table 1.1 Some macronomi agregates, 1970-90

Year Irad. Trad Cas. Frcal Frdn. rn of GD? Readeict accm defdsr - lde p ak axdu-ge

deflca aes...Inda. me

WfMr.wu ssa 983-1J (pere) (1985-M)aGDP) f GD P GOP go GMP)I

1970 1.6 2.7 4.1 -53 13.5 105.9 -0.9 81.2

1971 0.3 -4.1 -2.5 -6.5 -2.1 104.6 4.5 83.4

1972 5.4 3.6 5.3 -5.2 21.4 117.5 3.0 30.5

1973 13.5 -1.4 0.1 -3.9 -3.2 105.3 11.2 30.5

1974 29.1 8.4 9.6 -6.5 633 161.2 3.0 30.2

1975 14.8 4.3 3.1 -4.2 5.0 187.4 1.3 73.3

1976 129 -7.1 -5.9 -3.9 -75.8 137.0 16.7 8339

1977 9.2 -7.3 -9.5 -7.4 -37.7 123.4 6.6 82.5

1978 8.5 -9.6 -11.5 -3.8 -69.3 113.9 3.8 74.6

1979 14.5 -8.3 -12.2 -9.4 -95.2 107.2 3.5 73.9

1930 42.0 -7.3 -10.5 -6.4 .27.9 101.3 -10.1 71.4

1981 14.5 -13.2 -13.7 -8.3 -133.4 102.4 5.9 79.3

1932 11.4 -2.3 -4.0 -9.5 460.6 91.7 5.5 92.9

1933 5.6 -1.6 -2.2 -6.1 -31.0 100.0 0.4 100.0

1934 7.4 -4.0 -5.4 -4.7 .40.2 99.2 4.3 117.5

1985 6.7 -2.4 -2.7 -5.3 -2.0 102.9 6.9 123.2

1986 1.6 4.0 6.4 -2.3 122.5 134.4 9. 30.9

1987 0.5 -0.9 3.4 0.5 213.8 145.3 10.2 79.9

198 9.2 -. 1 -3.1 -2.9 135.4 1413 6.8 30.2

1989 12.7 -10.1 -5.0 -20' 145.1 141.6 4.2 81.0

1990 13. -10.3 -3.6 -1.6 240.3 150.3 6.6 78.3

1991 7.0 -9.4 -5.2 -1.9" 199.4 151.3 4.7 79.9

Source: Inftrnatinal Faci Sbastics 1991; Governieqm Financial S tus Yarbool, 1989.

a. RER - (Nominal Excange/CPI) WPI- sgn means deficik

b. estimaesc. Bank of Mauritius. Annual Reparet

L. sa available

Foreign exchange reserves mounted to a comfortable level, and at the end of June 1992 reserves

were sufficient to meet import needs for about six months. At the same time, the exchange rate

remained favorable for exporters. External debt and debt service, which had been a major constaint

on economic recovery and external balance in the first half of the 1980s, were significantly reduced

through a combination of prudent management and international support.

-2-

Exports led the growth surge, expanding from 48 percent of GDP in 1978-80 to 67 percent in199(, at an average annual growth rate of 10 percent during the decade (table 1.2). Sugar, EPZproducts and tourism have been the main exports. Although EPZ exports exceeded sugar exports in

value terms, the high import content of EPZ exports (about 30 percent) meant that sugar including theEC aid, remained the largest net earner of foreign exchange. In 1991, sugar represented about 50

percent of goods exports (net of EPZ imports), EPZs about 40 percent.

* Table 1.2 Merchandise eq brts at current prices (f.o.b.), 19 91(millions of rupees)

1982 193 1984 INS 1986 1987 1988 1989 1990 199{

Sugar 2,463 2.679 2,523 2.367 3,553 4.310 4,467 4.946 5,104 5,133Molasses 67 63 62 89 90 73 92 66 102 29

Tea 67 97 249 173 104 90 U 87 34 67

Fish and 56 76 106 143 133 132 210 217 161 235Preparadons

Textila 91 67 79 90 123 169 239 433 594 630

Processed 52 49 39 127 176 192 317 335 363 395diamonds

Clothing 882 928 1,592 2.543 4,056 5.593 6.5382 7,205 9,192 9,793

Oracr 166 224 317 430 435 576 828 831 1163 n..manufacured

Odhr 53 40 so 61 188 200 397 417 421 n.a.

Toral 3,902 4.223 5,067 6.533 3,913 11,335 13,220 14,542 17,134 a.s.domesticexports

Re-port 85 123 134 106 145 162 245 507 384 U.a.

Total expors 3,987 4,346 5,201 6.639 9,063 11,497 13.465 15,049 17,56 8 13614

Source: Mauridus: Expanding Horinno and lauruauional Monetary Fund (1991).n.a. ot available

Export growth was not only rapid but steady. Fluctuations in sugar production were, to some

extent, compensated for by the high and stable prices for sugar (in ECU) in the European Community

(EQ. by far the country's largest export market. EPZ exports showed spectacular growth during mostof the period, rising at an average annual rate of 28.9 percent between 1982 and 1991. Increasing

concentration of production and markets accompanied the growth in EPZ exports. The share of

clothing jumped 8 percentage points between 1982 and 1991, and the EC absorbed an ever-larger

share of exports.

Imports followed the trends set by EPZ exports and aggregate consumption and investment

behavior, growing at an average annual rate of 11 percent during the 1980s. Inputs for EPZ

2. No comparaMble figure is avaiabic for 1991.

-3-

production accounted for 60 percent of imports. Other imports were influenced by the overheating of

the economy that accompanied the virtual elimination of unemployment and excessively expamsionaryfiscal, monetary, and wage policies. Appreciation of the rupee after 1985 induced a further surge in

imports. Imports also responded positively to changes in import duties designed to encouragediversification of exports beyond the EPZ firms, to improve living standards, to check inflationary

pressures, and to encourage housing construction. Imports of consumer goods, other than food and

beverages, grew at an annual rate of 28.9 percent between 1982 and 1991; imports of capital goods

grew at an even faster 32.8 percent (table 1.3).

Table 1.3 Merchandise iports at current price (c..f., 1982-91(milins of rupees)

1982 1983 1984 1985 198W 1987 1988 1989 1990 1991

Food and beverages 1,412 1,28 1,543 1.636 1,375 1,675 1,974 2.642 2916 2.921

Othcr conauer goods 322 343 429 Ot 733 1.040 1.30 1.684 1,864 2,262

Petroleum produce 907 954 1.024 1.096 707 978 1,009 1,509 1,939 893

Intermediarc goods 1.908 1,946 2.749 3.643 4,794 6.450 7,736 9.648 10.683 13.229

Capital goods 500 624 750 1.114 1,591 2,871 5,165 4,734 6,436 6.406

Total imports 5.049 5.155 6.495 81.20 9.200 13,014 17,247 20.217 23.843 25,716

Source: Mauriius: Expanding Horizns and lnutranional Monedary Fund.1991.

Tourism was exceptionally buoyant during most of the decade. Tourist arrivals rose by half

between 1987 and 1990, and receipts increased by more than 30 percent a year after 1985. Net

income from tourism was about half of export revenues for sugar.

Improving terms of trade and a favorable real exchange rate' helped fuel the export drive and

comributed to the accumulation of reserves and rising domestic investment. By the end of the decade,terms of trade were a third higher than at the beginning, while the real exchange rate was some 22percent higher in the 1980s than in the 1970s.

3. The echange ram is defined in iis report as the price of foreign currency cwpressd in units of domeic currency per unit offoreign currency.

-4-

/ � , � , � , �

ТеЫе 1. �1 Reance о[ peymeats � 1970�90(millions о( доll его )

l970 1971 /972 /97 Э /97 � 1975 /976 /977 197д 1979 19д0 /981 19 д? 19dJ 19 В� 19dS 19 дб l �д7 /98 д l98D /QA0

Oxparte 93 94 142 181 372 369 32S 401 440 512 S78 S01 307 301 S04 379 887 1209 1376 139 б 1668М егсhеп4l к 70 6¢ 108 139 31S ЭОЭ 261 306 312 383 438 317 366 369 371 4з3 673 891 998 993 1179Non �fecWr �,есг� �сее xs 28 э4 4t s7 бв 61 9э 11 е 1зо 14 о 174 141 1з8 1э0 146 21 г з1s з7в 4 оэ 489lгораае 9г 1а 1зs 189 ээ� збб 37s 489 s63 6s6 69 о в2а s38 s13 s4 г s99 7в8 1173 14 вв 1ss б 1869Merchandi к 6s 71 99 143� ?68 379 зо8 з68 419 4а3 s16 47а з97 3еб 41s 4s9 617 909 1166 12а 14s9Non �hctorк rvicee 27 30 36 46 бб 87 67 121 (/4 17Э 174 1S0 141 (27 127 (40 (71 264 322 352 401Reeourcaьыи се з � 1о 7 �8 з8 э -ю �Ве � 123 -144 -112 � 127 �з1 �б -з8 -20 99 эа .112 � 16о 19sNet Гасt осlпсоте 1 0 0 2 � 1 2 6 �3 �8 -16 -23 -46 �46 -41 -4S -4S �S4 �4l �44 �20 �31FвЧоггесеlрl а 3 3 3 S S 10 15 S 6 4 S 7 4 3 3 2 6 14 � 7 S 1 7р. сгогр. утЕаа 2 з 3 3 4 8 9 е 14 2о 28 sз so 44 4е 47 бо ss 71 71 э8Сипепt prlvetetгм даге 1 2 4 s s 6 4 4 s s 1о 12 14 16 19 гг 3о 4t 72 68 э8Сипепt ассоид!ьаlм се s �8 11 -1 44 11 -1о .е4 -126 � 1ss .12s -16t �бэ -э1 -б4 -43 7s зб �84 -111 �1е8

Direotlnveetment 2 1 1 0 4 б 4 э 3 4 1 1 2 2 3 8 7 17 24 ]6 33Oth п captW 9 2 S � t �2 32 �4а 27 31 47 6S 8 � 1? � 18 .1Э .72 � 12 12 101 16 31Епогем дот lи lом г о 1 �г 7 -э s 1t 11 2 24 1s -7 1д г4 s1 зз 96 122 199 � 19C+vE[dIЬеlм са 1� �2 21 �3 б4 SZ �76 �38 �70 �93 �26 � 133 �61 �31 ;40 -2 l23 219 186 14S 69

Ch и go 1n aetгекгvее' � !4 2 -21 Э -64 -S2 76 38 70 95 28 133 61 31 ,0 ? -!2 Э -219 -186 � 145 �69

Uw ofFund oredlt .4 .» ... ._ ... -- ... 13 12 37 4! 69 ц 13 �8 � 13 � =22 �33 ' -4l �37 32Olher reeervoсьеп8а. -1о г -г1 э �ы �s2 76 ц s8 s8 .1э ы эб 16 48 17 .1о1 � 18в .14s -108 -1 о 1

3 оигсе: lnk гnatlond FinancW SWiЧ1ce, Аппиаl Repo гt, ('.191.е. А т l пиееlргlndlceca и i дсга к ,Infonnatioa far 1991 i8 nat yet availa Ыв,

-5-

The capital account balance was positive but highly variable (table 1.4). Private direct investment,quite small before 1994, surged afkar diat, auracted by the potential of the EPZ . Today, private

investment accounts for a third of the capital account balance.

Growth in the 1990s and beyond

Following all this good news of the past decade are recent developments that can some doubt on

the economy's ability to maintain its rapid progress along The same growth path. Labor, land, and

capital seem to be fully employed. Consequently, growth cannot continue to flow from putting idle

resources to work. Full employment has yielded most of its positive benefits and now constitutes a

constraint to easy growth. Labor force participation is an already high 80 percent or more for men

and 43 percent for women- Natural resources are scarce, and the country is malrin fun use of dXW

it has. The rapid growth of real wages is reducing the competitiveness of Mauritim exports. Una

labor costs grew at an average annual rate of 10 percent between 1992 and 1991, while the real

exchange rate appreciated 14 percent (table 1.1).

The export base remains weak and too heavily concentrated on sugar and textiles, which accom3t

fbr some 80 percent of goods exports. International trade in these two commodities is highly

controlled and managed, and Mauritius remains constrained by the special feattizes of its major

foreign markets. Export market concentration is also undesirably high: 80 percent of sugar goes to

EC markets and 80 percent of EPZ exporm go to U.S. and EC markets. Furthermore, external

conditions in the 1990s are likely to be much less predictable than in the 1980s. Demand for textiles

is failing and internation2l competition is growing fierce, while the future of the Sugar Protocol is

uncertain. Tourism, another success story of the 1980s for Mauritius, which has earned a welL-

justified image as a luxury beach holiday destination, is creating unacceptable environmental and

social pressures that are damaging the potential far further growth.

The Mauritian authondes and the private sector are both aware of the constraints to fu*er

growth. Both are eager to find a strategy fbr casing those constraim or adapting efficiently to them

Growth will require some combination of increased availability and improved quality of productive

factors and a frainework of incentives and regulations for inducing a more efficient allocation of

productive factors and other resources.

The availability of productive factors will grow with the population and with savings and

investment. Improvements in capital markets will be important in that regard. Even more import;mt

will be humn resources development. The main source of growth in a natural resources and capital

scarce country is labor and human capital. Inadeqmdy developed humm capital may be the binding

factor on growdi in Mauritius. To have a substantial impact, these sources of growth need to support

the potentially leading sectors of the economy as fully and rapidly as possible. To help them to do

that requires a framework of incenaves that stimulates movement toward sectors with the gnm=

-6-

comparative advantage. And it requires an economy flexible enough to allow economic performance

to improve and to reduce the costs of adjusting to fluctuations in the external environment.

The main concern here is to eliminate all obstacles to the allocation of resources to their most

efficient uses, be that in activities directed to the domestic market or to foreign markets. To allow a

diversified export sector to emerge in Mauritius, it is important that the same regulations and

incentives apply to all export activities. In this context, the integration of EPZs with the local

economy is but one of many issues. Segregation of EPZs from the domestic economy is the result

either of natural economic causes or of artificial barriers. To the extent that artificial barriers are the

main cause, their elimination will not necessarily strengthen EPZs. It may rather be that new types of

firms will develop and attract resources away from EPZs. The result could be a healthier economy.

Efficient import substitution is as important as additional exports.

Mauritius's comparative advantages seem to be shifting toward less low-skilled labor-intensive

activities. Consequently, the economy's growth will be tied to the development of sectors in which.

technology, education, and training are far more important than they have been in the past. Again,

development of these activities will depend on large investments in human capital, on the right market

signals, and on easy movement between sectors, activities, firms, and regions.

Right now, however, the economy is not sending out the right signals to direct resources to

higher-productivity activities. A tangle of incentives and regulations has created numerous distortions,while many of the regulations constitute obstacles to the free movement of factors of production.

Incentives and regulations need to be thoroughly reviewed, with an eye toward identifying and

removing those that continue to create a bias against exports. Eliminating other direct and indirect

barriers to the development of the most productive sectors of the economy will require comprehensive

harmonization of incentives and major changes in regulations to significantly improve the working of

factor markets.

The rest of this report thus highlights the external environment, which constitutes the basic

framework for any export-led development of the Mauritian economy. The future of sugar and EPZ

markets receive special attention in light of proposals for major changes proposed in the ongoing

GATT negotiations and within the EC. The main domestic constraints to development are also

examined-first regulations, incentives, and sources of distortions affecting relative prices and then

regulations and sources of distortions related to factor markets. An attempt is made to classify relative

incentives by sectors of production and types of firms. The last part of the report presents

recommendations and some of their likely impacts.

-7-

Chapter 2. Exports and the External Environment

This chapter examines Mauritius's major exports-sugar, and textiles and apparel manufactured

in export processing zones (EPZs)--and the way the external environment affects them. It looks inparticular detail at the effect of European Community (EC) policies on Mauritian sugar productionand exports and at the development of EPZs, highlighting their strengths and weaknesses.

Muiritian exports are concentrated on a few products and countries. Sugar and apparel represent

roughly 80 percent of the value of Mauritian goods exports between 1989 a '91 (table 2.1).4 Few

other products have more than a 1 percent share of exports: fish, textile ya- ;earls and precious

stones, watches, and jewelry. The EC is by far the largest market for Mauritian products (table 2.2),with France and the United Kingdom dominating, although Germany has also become an important

market over the last few years. Outside the EC, the United States is the only other major market for

Mauritian exports.

This pattern has given rise to some concern about concentration and the need for greater

diversification. Indeed, 90 percent of Mauritian exports are concentrated on six well-defined products;

those products also represent 94 percent of Mauritius's exports to the EC (table 2.3). Ie only other

significant Mauritian exports were apparel exports to the United States, representing some 17 percentof exports. While concentration is clearly high, the argument for diversification must be weighed

against the fundamental economic principle of international specialization based on comparative

advantage.

Furthermore, the pattern of Mauritian exports (tables 2.1 to 2.3) is biased by several powerful

nonmarket phenomena. Prices paid for Mauritian sugar exports to the EC are 150 percent (on

average) higher than world prices would be if sugar prices were determined by free markets

worldwide. Thus if Mauritian exports of sugar to the EC were adjusted to accum for the effects of

the EC sugar policy on prices, the share of sugar in Mauritius's total exports and the share of export

markets represented by the EC would drop substantially and that of other products and markets would

rise accordingly. Apparel exports to the United States, and indirectly to the EC, are similarly

distorted by the Multifiber AgreementWhat this suggests is that foreign policy risks rather than concentration versus diversification is

the key issue for the future of Mauritian exports. It thus becomes important to consider to what extent

the structure of Mauritian exports depends on the trade policies of Mauritius's major trade partners.Risks related to large swings in foreign trade policies are less easy to forecast and protect against than

4. Esimars for 1991 are extrapolacd from the firk half of 1991.

-9-

Table 2.1 Main erports by product of Mauritius, 1989-91

19 1990 1991

Vatle SharC Valu .Shar Varm s1am(ft mia) (%) (ar mil0 (%) (Rs MilA (S)

0 Food&live animals 5413 36.0 5565 31.7 S76 31.0

03 fish 217 1-4 161 0.9 235 1.506 sugar 4946 32.9 5104 29.1 5133 27.606 molasses 66 0.4 102 0.6 39 0.507 tea 87 0.6 34 0.5 67 0.4

I Bcvmgcs & tobacco 2 0.0 12 0.1 20 0.1

2 Crud materisis 115 0.3 127 0.7 114 0.629 cut flowers 52 0.3 71 0.4 79 0.4

3 Miaca fuels 1 0.0 1 0.0 75 0.44 Oils& fat 1 0.0 2 0.0 2 0.0s Chemicals 135 0.9 161 0.9 206 1.1

6 Manufacurd goods 929 6.2 1063 6.1 1114 6.063 cork ad woodManuf 32 0.2 41 0.2 27 0.1

65 teunilc yam 433 2.9 594 3.4 630 3.4

andscnes 335 2.2 363 2.1 395 2.1

7 Machineryuansport 272 1.3 187 1.1 374 2.0

8 Miscellaneousmanuf. 3130 54.4 10444 59.4 10945 S3.383 travl bagsp 39 0.3 33 0.3 33 0.284 appazd 7205 47.9 9192 52.3 9793 52.688 Varchem 511 3.4 634 3.6 613 3.389 Toys A gane 92 0.6 129 0.7 136 0.78g jewllery 94 0.6 165 0.9 251 1.4

9 Others 3 0.0 2 0.0 0 0.0TaM! 15050 100.0 17563 100.0 13614 100.0

Source: Ministry of Economic P.anning ad Developmr, Central Stauisical Office-

risks associated with markets risks are also likely to be greater than market risks in the 1990s, whichalready seem to be marked byincreasing acrimony in international trade relations and the languishing

Uruguay Round negotiations. Flexibility is critical if Mauritius is to be prepared to respond to majorchanges in foreign trade policies. The rigid EC sugar policy has generated rigidities in the Mauritian

sugar sector, and the rigid U.S. quotas on apparel have had similar effects on Mauritian apparel

exporters. Assessing the extent of these rigidities and limiting their adverse effects on the economy as

a whole is a crucial goal for the Mauritian authorities in the years to come.

-10-

Table 21 Main exports of Mauritius by country, 1989-91

1919 1901991

VerA Shar Vde mbfre iVane Miare(RS JmI) (%) (Rr HM) () (r M) (%)

Prcfcrenial tariff 13.714 91.1 16,304 92.8 16.751 90.0countriec

European Community 11.583 77.0 13.997 79.7 14.438 73.3Bel.ium 307 2.0 396 2.3 323 1.6Britain 5,384 35.3 6,239 35.9 6,630 37.7France 2.9M6 19.8 3,981 22.7 3,727 18.6Gertmay 1.391 9.2 1,528 9.7 2.055 12.5Italy 570 3.8 793 4.5 916 4.9Nethdrlandn 349 3.3 298 1.7 363 1.Portugal 174 1-2 216 1-2 0 0.0Reunion 292 1.9 324 1.8 364 1.9

Other prefereanial countries 2,131 14.2 2.307 13.1 2,313 12.0United States of America 2.076 13.8 2,307 13.1 2,207 11.4

P.T.A.b 55 0.4 nO Rn 106 0.6

G=ncral tariff countries 1.336 3.9 1.274 7.3 1.863 10.0Total 15,050 100.0 17.S68 100.0 13.614 100.0

a. Estimared on the basis of firt half of 1991.b. Preferential Trade Area for Easterm and Sourhrn African States; caimared from von ICirchbach [1991].Source Ministry of Economic Planning & Development. Central Staistical Office.

Sugar

With roughly 80 percent of Mauritius's sugar production exported to EC markets, Mauritian sugar

production is highly dependent on EC sugar policy (table 2.4). As a signatory to the Lom6 Sugar

Protocol annexed to the African, Caribbean, and Pacific Accord (ACP), Mauritius benefits from the

largest EC sugar import quota and high prices for its sugar exports-nearly as high as subsidized ECdomestic prices, which averaged 150 percent above world prices during 1985-90. The future of

Mauritian sugar production will be affected by the outcome of the Uruguay Round of multilateraltrade negotiations. Successful conclusion of the round along the lines suggested by Arthur Dunkel's

proposal to the GATT negotiating parties will pave the road for liberalization of international trade in

agriculture. The effect is likely to be lower prices for sugar in OECD markets and higher prices in

world markets and a reduction in support to sugar production sufficient to generate noticeable price

changes in OECD importing markets (lower prices) and in other world markets (higher prices)

generally. Even failure of the Round will not mean business as usual, however. Strong forces are at

work that will inevitably bring about changes in the EC Common Agricultural :'olicy (CAP) and so in

EC prices and production quotas. However, in that case, reforms will not be supported by

international discipline under the GATT, so changes in sugar policy are likely to rely on a variety of

mechanisms-changes in production quotas as well as in prices.

- II -

Thus both outcomes for the Uruguay Round share common elements. Both will require fundamental

changes in Mauritius's sugar policy, to improve flexibility in sugar production. As in the EC, sugar

policy in Mauritius has significantly increased the value of land (and other inputs) used in sugar

production, and changes are needed that will make it easier to shift land from sugar production to

other productive activities.

Table 23 Main eKirt of auritius by product and country, 1989-91 (millions of rupees)

1989 190M9

SugarWorld 4,946 5.104 5.138European Community 4,961United States 115Rear of the world 63

FishWorld 217 161 25European Communiy 272United Stares 0Res of tbe world 13

Textile yarnWorld 438 594 630European Community 604United Stats 0Res of the world 26

Pearls and stoeWorld 335 363 395European Community 279United States 14Rest of the world 102

ApparelWorld 7.205 9,192 - 9,793European Community 7,348United Staies 1,721Rest of the world 723

WatchesWorld 511 634 613European Comunity 487United Stats 0Rea of the world 126

Total for the products concernedWorld 13.652 16,048 16.853European Community 13,950United statns 1,850Rest of the world 1,053

Total Mauritian export.World 15.050 17.568 18.614European Community 14.785United Stanes 2.151Rest of the world 1,671

Export shares of the products concerned (%)World 90.7 91.3 90.5European Community 944United States 86.0Rest of the world i2.8

Source- Minisry of Economic Planning and Development Cenral Statissical Oftws.

- 12 -

Table 2.4 Production, exports, and prices for Maurillan sugar, 1985-90

Thaw Donvelde &WL ~ EP Epo a EC-ACPkw QMVd £douImpo aggaL toIL th .onoit-EC d n-mo imal Offm "POAS) (Ots) M) (om) % of (o) ade adW Inserwnd i

tsal"xports

1980 34.0 27.3 22.1 10.2 64.91981 34,312 16.0 23.3 18.9 148,7 I1.31982 636,550 39,720 596,830 540,121 90.5 56709 11.2 22.9 11.1 205.1 162.51983 600,902 35,595 565,307 509,191 .00.1 S63l6 I.0 21.6 17.6 196.4 159.71984 576,203 38,663 537,54S Si1,997 95.2 25548 7.1 19.4 16.0 272.7 225.61985 639,713 36,379 602,839 SOS.656 83.9 96983 6.7 11.7 16.1 279.6 240.71986 669,713 44,834 624,949 504,803 30.1 120146 7.5 24.1 18.6 321.3 248.21987 68,721 32,404 656,317 507,200 77.3 149117 10.6 21.4 21.4 266.4 201.31988 687,145 34,693 652,452 505,000 77.4 147452 14.3 29.1 23.8 203.4 166.41989 672,203 36,003 636,200 505,357 79.4 130843 16.2 26.6 23.0 164.1 142.11990 616,420 38,420 578,000 11.7 30.6 26.7 261.0 227.81991 n1a. 1a. 584,000 n.s. Au.. n1. 0a.. al.1930-85 613,345 37,034 575,630 516,791 19.9 58839 14.3 22.3 18.2 197.1 162.01986.90 666,854 37,271 629,5384 505,590 78.7 136890 12.1 27.7 22.7 243.3 197.2

Source: Mauritius Ministry of Industry; Chamber of Agriculture; Sugar Syndicate; EC Commission; and Internalional Monetary Fund; authors' calculations.a. Sum of domestic consumption and total exports.b. World (o.I.f. Rotterdam) and Intervention prices were Initially expressed in European currency units (BCU) per ton, and then changed to US cents per pound by using averageaverage exchange rates.c. EC Import prices (In US cents per pound) as reported by the IMP.d. Respectively EC lntervertion and ACP Import prices In percent of world price.

-.1I3 -

SuccEss of the Uruguay Round

The European Community and the United States have high levels of protection for sugar in domestic

markets (table 2.5).s Sugar has the highest levels of protection on average in terms of producer

subsidy equivalents among the five most protected agricultural products in those markets-sugar,wheat, meat, soybeans, and rice. The comparatively large size of the world sugar market (asillustrated by a relatively high ratio of world imports to world consumption) has not been a strong

counterbalance to this high protection level. Prices in this protected market are relatively stable, as

are the quantities sold. Thus, any major shocks to supply are absorbed by the relatively small

unprotected market., with the result that sugar prices exhibit-by far-the highest degree of volatility

among the five products considered.

The high levels of protection have imposed high domestic prices in the protected markets The high

prices have induced high levels of production, as exemplified by the transformation of the EC from a

net importer of sugar before 1975 to a net exporter (17 to 19 percent of the world exports) in the late

1980s.' In turn, gluts of sugar exports from these protected markets have depressed sugar prices in

the world markets.

Trade liberalization is expected to reverse the evolution of domestic and world prices, lowering

prices in OECD countries and increasing world sugar prices. Econometric simulations of the impact

of trade liberalization on sugar prices suggest that world sugar prices are likely to rise only

moderately-most likely about 10 to 15 percent-even in the case of full liberalization (table 2.6).

Price volatility is expected to fall by one-third once the deep world price depressions associated with

interventionist sugar policies are eliminated

Several qualifications ought to be made about the projection of moderate price increases for sugar.

Not all the models project a moderate price increase. Some show a smaller increase (OECD) or a

larger increase (Borrell and Duncan, 1992). As Borrell and Duncan (1992) point out, the models are

based on data for initial periods that may underestimate price changes if world sugar prices were

relatively high during those base years, which would make measured levels of producer assistance

relatively low. Dynamic simulations that try to eliminate problems related to base periods tend to

suggest higher increases in the world price, at the upper level of the range of 10 to 15 percent and

even higher.

5. Producer subsidy equivalents measure the size of direct subsidy tiM vmuld be necesay to compensm producers for dhmiatioof Some ocher policy.

6. The EC Common Sugar Policy was introduced in 1968. However, it was not until 1975-76 tham he EC became a nt exporter, assupport prices were raised and production quotas increased to a level well above self-sufficiency (Borrell and Duncan 1990).

- 14-

Table 2.5 Pruminn and world price volatility, 1979-9 averag

(petentages)

Auripe prducern~di~ eamivalen~*'

Erope Un~rd Jp Canadn Au~wÅ k Vain f ramgfC4muiady Ar

Sugar 59 51 68 24 12 0.13 26.5Soybeana 51 8 98 10 13 0.26 25.4What 35 31 96 30 11 0.31 20.4

M~ai' 50 33 63 40 10 0.11 9.9Ricc 44 35 81 - 27 0.42 3.9Nom:a/ Ptocmion level am amnaed by OECD produczrubuidyequiva~nt (PSEs).b/ Enimend by m afwie= ofvaåis of(odd pgsggsi WMdd is~port m pernig of worl C0m00d~ Bef for thm PSEI.

S~urce: OECD (1991)

Table 2.6 Effectu of mUiMlerul polcy reform on world :.gar prcs

23pe of D~ag nerr..bea ~ i n

OECD(1991) partial" 1979.81 0.9 -Borl and Dunean (1990) p bria • 33.0 -28Vade & Zietz parial' 197941 6.7 -Wong. Sturgis. and Borell p - 7.6 -33Lord and Bay f 10-30 -Mahe and Traver partial' 1986 7.9 -

a. Ten perc~n reduc=ion in •••m-~e in OECD coumries.b. For the U.S.. EC ad apan only.c. Dynm~ic zimuanim ovr the period 1985-2004.d. Te= percmt minimum import ~wih domesic cling .. aaed.r. OECD con~me~ pny world pric~; som liberairia of marginalproductim -mang major exporæ.f. No foral economeiemdE.g. Support reduccion Iading to 40% (EC) and 30% (US) sugr pric= cut.

Source: OECD (1991)

- 15 -

Another concern is that economic forces that are difficult to take fully into account in

econometric models may make sugar substitutes more attractive. Alternate sweeteners have benefited

from the high domestic sugar prices in OECD markets imposed by OECD sugar policies (OECD,1991). For instance, the share of high fructose corn syrup in the U.S. caloric sweetener market grew

from virtually nothing in 1970 to 36 percent in the late 1980s. The large jumps in the growth path of

these alternate sweeteners have been clearly associated with the two world sugar price peaks of the

mid-1970s and early 1980s. The expiration of patents (aspartame) and the emergence of new

technologies and better sweeteners, such as acesulfame-k and sucralose, are likely to place a cap on

sugar price increases resulting 4om a freeing of trade.

Thus the upper range of the moderate price increases is the most likely in the long run, after the

full impact of a complete trade liberalization. However, trade liberalization is very likely to be

implemented through successive steps since OECD governments will have to counter opposition from

sugar interests. With the 15 percent reduction in support prices over 1991-96 proposed in GATT

negotiations, an increase of 7 to 10 percent in world sugar prices would be the most that could be

expected for the years to come.

Faiure of the Uruguay Round

Should the Uruguay Round fail, the EC sugar policy might remain unchanged. And, indeed, as

of April 1992 the latest Commission documents contained no official plan for the reform of the

common sugar policy. However, this outcome seems unlikely. The Common Agricultural Policy has

imposed such strong pressures on the EC and such high costs on national budgets that fundamental

reform is inevitable. It may be argued that sugar is a different case because the common sugar policy

imposes no direct budgetary costs since taxes on sugar production finance subsidies on sugar

exports.7 Yet that very self-financing mechanism leads to another argument for modifying the sugar

policy; the self-financing constraint tends to erode the benefits of the policy for farmers, who might

find a return to freer markets more beneficial, as shown below.

While the exact details of a reform of the common sugar policy cannot be predicted, there are

two crucial elements that will be part of any reform of the policy in the years to come. First, past

reforms of the EC sugar policy have exhausted all changes at the margin. Any further reform will

thus concern the core of the EC sugar system-that is, it will deal with both prices and production

quotas. And thus Mauritius and the other ACP countries will have to deal with changes in both prices

and import quotas.

7. However, this argument is only partially coect. Excluded from this self-inancig sysm is the suppor of the ACP sugar tha isconsidered by EC authorities as impored (under the high EC intervenzion prices) and exportd (under the low world prices). Inother words, the export subsidies associared with the ACP sugar are rnced by the EC budget

- 16 -

Second, improving the functioning of the quota system itself rather than merely reducing prices

and quotas is likely to be part of the reform. Allowing sugar production quotas to be transferred

among EC producers could improve the situation in the EC almost immediately, even without changes

in prices and global quotas. Were that to happen, markes for transferable sugar export quotas would

be likely to spring up in Mauritius and the other ACP countries.

Further reforms under nontransferable quotas. The ACP countries argue that the Lomd

Convention guarantees access for a certain duration to ACP sugar exporters. It is hard to believe,however, that EC governments will introduce drastic changes for their own sugar producers while

continuing to protect foreign producers. A sign of things to come: the reduc Jn of the EC

intervention price in 1989/90 applied to ACP sugar production as well.s A -cial concern for

Mauritius is forecasting how deep the sugar policy reform will bitm, since it seems likely that the

changes introduced since 1981 (under the pressures of GATr petitions and market evolution) have

exhausted the possibilities for painless changes.

EC sugar policy distinguishes three types of domestic sugar, A, B, and C. Type A sugar benefits

from both a large production quota (representing 70 to 75 percent of EC production between 1985

and 1990) and guaranteed intervention prices (table 2.7).9 Type B sugar also benefits from a

production quota and guaranteed prices, but the quotas are much smaller (15 to 18 percent of EC

production) and the intervention prices can be reduced by production levies used to finance export

subsidies, when necessary. Type C sugar has no quotas and is sold at world prices.Quotas for type A and B sugars are set at levels sufficient to guarantee self-sufficiency with a

large margin of safety; the self-sufficiency ratio (production/consumption, exciding stocks) averaged

129 percent between 1985 and 1990 (table 2.7). Any production of type A or B sugars over EC

consumption needs is exported. Export subsidies (export "restiutions") compensate for the differences

between the EC intervention prices and world prices. The high domestic prices have boosted

production levels, making the EC a large net exporter of all three types of sugar. The common sugar

policy's financial rule-levies on type B quotas finance subsidies on type A and B exports-reduce the

difference between the world price and the intervention price for the B sugar. If large amounts of type

A and B sugars are exported, the ner price (the intervention price minus the production levy) received

on the B sugar can equal the world price.' 0 Rough calculations show that the net price received for

8. The EC intervention price was reduced by 2 percent in 1989/90, and the ACP sugar price was reduced by the same amour. Therevenue loss for the ACP countries has been compenamed for by a direct transfer from the EC to the ACP countries. making Clear ashift from a sugsr policy to a direct id policy.

9. They are subject to a small corceponsibility tax of 2 percent, however.

10. As summarized by Lcuck and Neff (1991). the financial balance of the EC sugar symes can be written as:(1) IA(aPjl + [B(PrPb)] - (AZPrP.)lwhere the first expression in brackes represents the fiscal revenue from the type A quotas (based on the quota quantity A. acorcsponuibility lcvy of a percent. and intervention price Pj and the second expression the fiscal revenue from the B quotas (where

- 17-

Table 2.7 Indiesons of internal forces working toward the dimentling of the EC comnmn sar policy, 1985-91(thousamds of tens)

198546 1986-57 198745 195549 1959.0 1990-91 Avuge 85-91

EC ro2~

Toual 12.720 14,156 13.212 13,915 14.272 15.582 13,976C sugar 1.222 1.312 t19 1.591 2,273 2,138 1,559EC otherproduction 11.498 12.784 12.393 12,324 11.999 13.744 12.457

" ECeanm~ Mt

Variations of stock 223 89 -458 -374 -459 445 -8

Isoport 1.469 1.769 1,866 1,904 1.928 1.860 1.799Exports~ 3.348 3.557 3,870 3.716 3.115 3.310 3,486EC internl

consumption" 9.391 10.907 10.847 10.885 11,271 11.849 10.85

Mlafqr indicarors

Self-sufficiency rarté 135.4 129.8 121.8 127.8 126.6 131.5 128.8Toad expan~' 4.570 4,869 4.689 5,307 5,388 5.448 5,045EC xces prod.' 2,107 1,877 1.546 1.439 728 1.895 1.599A quota sugar 9,516 10.540 10,540 10.540 10.540 10.540 10,369B quom ugar 2.242 2.288 2.288 2.288 2,288 2.288 2,280

World prico (EcuPton)1 193.8 168.5 203.4 266.4 323.5 203.1 226.4Lx-y on A quota (%) 0.00 0.02 0.02 0.02 0.02 0.02 0.02Inurvendonpric= (Ecl~n) 541.8 541.8 541.8 541.8 531.0 530.1 538.1Exportrgiurins (Ecu mill.) 733.2 700.7 523.2 396.4 151.1 619.6 520.7

Exportrerimi(n. (Ecu mll.)' . 780.7 821.6 678.6 732.8 n.a. D.a. 753.4

Net price of

B ugar (Ecurony 193.6 182.7 245.2 221.5 n.a. a.a. 210.8an % worldprice 99.9 108.4 120.6 33.2 n.a. n.a. 103.0

a. Total produ~io mn C ugar aports.b. Exeluding C suger exporm.c. EC å~temna producon minus tocka and exprts plus impas.d. Total prdn~cin in permnt of EC imernal conum~ics.r. C suger prodction plus xports.f. EC intrnal production minm EC in~omal consumpion.g. (Cii) Ro~erdam ntil 1988. Pari and London uince then.h. EC ces producion im the difference be.en: rc world and intervention prices.i. As given by t-EC Cour den Comp~as (1991. pag 36).j. Intervenfion price minas xpo renwionm per t= of B sugar.Source: EC A~ma! Rpor on Agriculture EC Cour des Compes (1991); author' compu.inf.

P,, is the world price and P the ner prce received by producer of type B zugar). The right ide of the eq=ution gives th5 ea= ofthe export subsidies (PrP,, tioe X. the quaniy xpored) when the quan~riesproduced under type A and B qoarhs ueced ECcnemniptin. Equai I can be slved for P&:

(2) P, . (X/)P, + [I-( ]P, + (A~P,.

Table 2.8 Simulations of changes In the EC sugar policy (million tons)

EC oroduct EC consumption EC exports

EC Member 'US'Slais *A* Bare EMS EC-wide Free Base & Fre Bae EGIS EC-nie Free(EOES) queaso period quotq quota marei quota markets pedod quoe quote mareU

(a) markets marso [a) maaesb [al 1 moabs markef [a

Belgium-Luxembourg 680 893 752 764 773 380 233 513 372 384 540Denmark 328 484 328 331 337 202 231 282 126 129 106Germany (West) 1,990 3.128 2,40i 2,503 2,533 2,208 2.411 920 257 295 122France 2,996 4,452 3,932 3,971 4,003 2.017 2,394 2.435 1,915 1,954 1,609Ireland 182 195 182 92 99 .146 ISO 49 36 -54 -51Italy 1,320 1,372 1,320 192 233 1,547 1,722 .175 .227 .1,355 -1.489Netherlands 690 993 756 769 779 574 679 419 182 195 100United Kingdom 1,040 1,285 1,040 680 712 2,042 2,593 -757 -1,002 .1,362 -1,881Tho Community 9,226 12,802 10,775 9,302 9,469 9,116 10,413 3,686 1,659 186 -944

a. Case of complete world trade lIberalization.b. The base period chosen was 1982.86.

Source: Louck and Neff (1991).

- 19 -

B sugar (intervention price minus the export restitution levy per ton of B sugar produced) averaged

only a few percentage points above the world price between 1985 and 1988 (table 2.7).

Under these conditions and if net exports of type A and B sugars increase further, only two

solutions are possible (an unlikely third would be to finance export subsidies directly from the

budget): eliminating type B quotas, which are fast becoming meaningless as net prices paid for type B

sugar tend to equal world prices, and extending the levy mechanism to the A quotas-the core of the

EC system. In other words, any further reform of sugar policy means a reduction in the intervention

prices paid for type A sugar, further reducing the benefits of the policy for EC sugar producers.

Alternative solutions have the same impact. Reducing the quantities instead of the intervention price

for type A sugar quotas will have the same revenue-reducing effect on EC farmers as reducing the

export subsidies.

The import quotas granted to the ACP countries under the Lom4 Protocol have approximately the

same legal stams as the type A quotas. The ACP countries should thus be prepared for changes in

prices and import quotas that match the price and quantity changes imposed on type A sugar by any

further reform of the sugar policy.

Inroduction of transferable quotas. Cutting the intervention prices or quantities for type A

production quotas Ls a politically costly solution. A failure of the Uruguay Round, and the consequent

absence of international discipline, would make such changes even more difficult (and could increase

the danger that more of the burden would be shifted to the non-EC producers, a potential outcome

that should make the ACP countries and Mauritius active supporters of trade liberalization in

agriculture). Introducing transferable production quotas could avert such political pressures. Under the

current sugar policy, production quotas for type A and B sugars are granted to individual producers

and are not transferable." Making quotas transferable would improve the efficiency of EC sugar

producers and would tend to reduce net exports, thereby providing some relief for the EC's problems.

Type A sugar quotas are granted to efficient and inefficient producers alike. As diagrammed in figure

2.1 (from Leuck and Neff 1991), the situation of inefficient producers would improve if they could

sell their quotas (their rights to produce quantity MN) for a sum larger than the area enclosed by

points 1, 2, 3, and 4. This area demarcates the difference between the revenues received by Type A

producers based on the intervention price P, and their production costs. Efficient producers are likely

to be willing to buy quota rights in order to be allowed to produce more-as long as the amount they

pay to inefficient producers (area 1234) is less than the gain from producing and selling the quantity

OC (= MN) of additional sugar (area 56789).

11. As shown later, type C sugar is not subject to quotm. Since it does nor convey any special right with respect to wold prices, ithas no value beyond its rnarket value.

-20-

The sale of quota rights has the crucial advantage that it will reduce the EC exports. The

production abandoned by the inefficient producers (MN) is not totally made up by the efficient

producers. A world sugar price of P., would make it more profitable for efficient producers to divert

to EC markets the quantity they had been exporting (OX) before they purchased additional quota

rights-a welcome move since it means lower export subsidies.12

Markets for transferable quotas could be organized within each EC member state or for the EC

as a whole.13 Leack and Neff (1991) have estimated the impact of these two arrangements on EC

production and exports (table 2.8). As expected, quota markets have a much more powerful impact at

the EC level than at the national level, reducing production to the point at which the EC would no

longer be a net exporter of sugar. Leack and Neffs estimates suggest that the world price would

increase from a base rate of 11.6 US cents a pound to 12-5 cents a pound in the case of national

quota markets, 13.1 cents a pound in the case of an EC-wide quota market, and 13.5 cents a pound in

the case of global trade liberalization In sum, EC-wide quota markets would have almost the same

impact on world prices as a full-fledged llberalizationI

If markets for quota rights are organized on an EC basis, they are likely to cover imports from

ACP countries as well. These markets could be organized on a national basis (Mauritian quotas would

be sold only among Mauritian producers) among all ACP countries, or among EC and ACP

countries.

12. Note that since the quantity MN-OC (the quota ansferred). she quantity OX also measures the reduction in EC production.

13. There is a weil-known rc!a_ance ia the EC to introduce markets for transferable production quota. A strong argumer agaiRthat position is the fact thar, in the absence of mams in quom rights, the value af sugar quotas will merge in the increased valueof the land used for sugar production. In other words, quotas distar markets for land-with the additional disadvamageratransctions are much less numerous and their effccs last for longer periods, making mistakes much Irger and thus much more

PainfUL

14. Markets for quota rights will face two difficulties. The political argument has beca weaknd since coming up against the self-financing constraint, so that only the EC-wide versus national-level markets for quota rights remains as pounds for the politicalargumu. Another problem is that ncgotiable quotas could crease problems in matching processors with their suppliers, given theregional namure of production (BAE, 1985).

-21 -

vr,

� � � ��

�

оV и

N� ............................ Ф 1r

. л ................................. ......................................... s ��

�п_� '`т

�, N

� ; . а �`�С .........................».......».................»....» � ........_ � �

Z ............................................................»...........у р

�.

�.

�

D

.

�. . �

� 1

Evolution and shw1ure of aqxwt processing zmm

The EPZ sector in Mauritius has evolved through roughly four periods. Mw legislation

establishing the EPZ program was passed in 1969 and ushered in a period of rapid expansion of

manufactured exports, mostly textiles and garments. Investment was heavy baween 1970 and 1976,and the number of firms rose from 4 to 84. the mun er of employees from 640 to 17,400. In the next

period, from 1977 to 1982, investment and employment growth slowed, and the number of firms W1before picking up again- Between 1983 and 1999, there was a resurgence of investment and growth in

employment and output (table 2.9). Iben, affm 1998, growth tqxu-ed off again. -

Ihese four periods reflect changes in a number of underlying ftctors. Miere were shift in the

relative amou of foreign and domestic investment, the composition of outpm plant shm, labor

market conditions, export marixts, and dw exchange regime.

In the first paiod, domestic investors played a greater role in the development of EPZ Wastry

than in subsequent periods. Much of the financing for equity investments came from the sugar

industry, which had benefited from the sugar price boom of 1973-75. This som= of domestic

financing began to shrin'r however, with the end of the boom and the increase in the sugar cqxnt tax

after 1977. For a time, the sugar sector, once a traditional source of domestic finance, even became a

net borrower. The slowdown in EPZ growth during 1977-82 (Table 2.10) can also be attributed to the

gressive appreciation of the rupee, which tracked the rising doll= more closely than it did the

cmT=cies of Mauritius's more important trading partners.

Foreign investment played a more important role m die second surge of Jurvestment from 1983 to

1988. A recent survey (Lamusse) of firms operating in March 1987 finind that the foreign sham of

equity was 73 percent for firms established in 1984 and 1995; for firms established between 1970 and

1983, that share was only 53 percent.

The surge in investment after 1983 was dominated by Hong Kong interests. These investors put

their money almost exclusively into knitwear and garments. Fully 95 percent of the enterprises

established between 1983 and 1985 produced gloves, garments, and knitwear. French investors were a

distant second, and their investments were spread over a wider range of products, including toys and

leather goods as well as garments.

Ibe new firms established by the Hong Kong mvestors tend to be bigger than previously casting

firms. They are generally extensions of larger inwgrated production and marketing operations of dwk

Hong Kong p . 71hey focus on lower-end products that are simple and standardized and w.

labor- Wtensive production processes requiring little skill. 71he Mauritian portion of their operations is

usually restricted to the cut, sew, and trim activities. (Me AfWa po is an exception to this

pattern, with activities in spinning, weaving, and dyeing as well as assembly.) Design, finance, and

marketing decisions are made in Hong Kong. W-Rh the influx of these firms there has been a marked

increase in imports of inputs from Far Easteru sources.

-23-

Table 2.9 Basic stts on export procMsing zones ka Mauritius, 1983-90

1983 1954 1915 195 1957 195 198 9 1991

Number of nabli.mx,.r 129 179 244 365 469 559 571 528 586Number of employeea 23.424 33.751 47.842 67.938 82.554 37.392 87.035 89.906 90,361Average employme~tper eablii-n 182 189 196 136 176 156 153 170 155Valuc added (R. million) 543 365 1,333 1,900 2.515 3.125 3.450 3,975 4,400Valuc added per employce (rup~na) 23.395 25.629 27.363 27.967 31,313 35.758 39.616 44.213 43.425Companmrian of employeeu(Ra million) 263 406 661 975 1.275 1,580 1.765 2.075 D-a.Compmnrikn per empkys(rupeeM) 936 1.002 1.151 1.196 1,237 1,507 1.689 2,056 E.a.Exporu(Rs millon) 1,307 2,151 3.23 4,951 6.567 8.176 9.057 11.442 12,36Imporm(us milion) 847 1,651 1.530 3.863 4,801 5.890 7,502 7,389 7,067Net export. 460 500 1.753 1.08 1.766 2.286 1.555 4,053 5,069Nt expor0/expor(%) 35.2 23.2 53.4 22.0 26.9 28.0 17.2 35.4 42.0Iavemem(Rs million) 74 210 340 560 655 370 900 690 630Valuc adddexport(%) 41.9 40.2 40.6 38.4 39.4 38.2 38.1 34.7 36.3

rorh Rar

Number of ctablithm~mm 38.3 36.3 49.6 28.5 19.2 2.1 -7.5 11.0Numbr ofemploye 44.1 41.7 42.0 21.5 5.9 -0.4 3.2 1.1Aveage employmentper c=sablishuent 3.6 4.0 -5.1 -5.4 -11.2 -2.4 11.1 -8.8Valuo addd 57.8 54.1 42.5 36.1 20.9 10.4 15.2 10.7Compeminofemploye 54.4 62. 47.5 30.8 23.9 11.7 17.6 G..comnvu..ian per employe 7.1 144 3.9 7.6 17.1 12.1 21.7 EA..Export 64.6 52.6 50.8 32.6 24.5 10.8 26.3 6.1Impr 94.9 -7.3 152.5 24.3 22.7 27.4 -1.5 -4.4Invenment 183.8 61.9 64.7 17.0 32.8 3.4 -16.7 -3.7

Sourc: Diges of Industrial Stei.i~ Cenåral Suaiini Office.n.a. no available

Table 2,10 Imports and e~port of EPZ frm, 1977-90

1977 1978 199 1980 191 1982 1983 1984 195 195 1987 195 19 19 1991

Rsr miion

Totad export .(f.o.b.) 433 484 620 349 1,087 1.235 1,306 2.150 3.272 4,960 6.700 8.179 9,057 11.442 12,136Total import(e.i.f.) 301 340 395 658 681 742 846 1.650 2.524 3.337 4.801 5.390 7,502 7,389 7.067Net exports 132 144 225 191 406 493 460 500 748 1123 1.899 2.289 1.555 4.053 5.069

Exportas % ef GDP 8.0 7.7 8.1 9.3 10.6 10.5 10.2 15.0 19.7 25.2 28.4 29.4 28.6 31.3 28.4

Nec export.as % of GDP 2.4 2.3 2.9 2.2 4.0 4.2 3.6 3.5 4.5 5.7 8.1 3.2 4.9 11.1 11.9Nc export.as % oftotal export 30.5 29.3 36.3 22.5 37.4 39.9 35.2 23.3 22.9 22.6 23.3 28.0 17.2 35.4 27.2

Source: Quarriy Exrnal Trade Smrriem. Central Sra~rimi Office.

- 24 -

There is an important locally owned segment of the industry as well. Locally owned firms fall

into two groups. One includes a large number of small and medium-size firms with fairly low levels

of technical know-how, management, and marketing skills. They fill delivery orders for foreign

buyers in which the terms of the delivery (timing, volume, design) are tightly set by the buyer.

The second group consists of local firms that are similar in size to the Hong Kong firms.

However, their operations are different in scope. They produce some of the same low-end products,but they produce more sophisticated upmarket products as well. Bonair Knitwear, for instance, has its

ows iesigners and creates its own models, and these h.vc achieved some recognition in Europe.

Firms such as Floreal have developed their own marketing channels by keeping in close contact with

clients and minimizing the use of intermediaries. The larger local firms tend to be more verticallyintegrated than their Hong Kong counterparts. Spinning, weaving, dyeing, and garment production are

part of an overall process, although factory facilities are often separate.

Since 1988, all EPZ firms have experienced the effects of a tightening labor market and otherchanges whose influences are likely to persist for some time. There are complaints that firms are

raiding employees from other firms. Wages are rising, making the lower-value-added productsvulnerable to competition from lower-cost countries. The scope for contract production of standard

products for foreign buyers is being reduced. Firms that will be able to compete best are those that

can move upmarket, react quickly to delivery orders, and shift smoothly to new patterns and designs

as new fashion trends emerge and seasonal demand change. Staying ahead of the wave of change will

require investment in design, training, marketing, and more sophisticated automated production

technology.

Influence of vrade agrewnes

Trade agreements and regulations in importing countries have also influenced the development of

the export industry in Mauritius and the patterns that are likely to emerge in the future.

In the 1950s and 1960s, the newly industrializing countries of the Far East expanded rapidly into

the textile and garment industries. As trade-restricting measures such as the Multifiber Agreement