Management Principles for Engineering Managers Tutorial 10

16

Seg2510 – Management Principles for Engineering Managers Tutorial 10 The Chinese University of Hong Kong Systems Engineering and Engineering Management 2009/2010

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Management Principles for Engineering Managers Tutorial 10

Seg2510 – Management Principlesfor Engineering Managers

Tutorial 10

The Chinese University of Hong Kong Systems Engineering and Engineering Management 2009/2010

Depreciation

Reduction in the cost of an asset over the span of several years

Used for business purposes during certain amount of time Recorded as expenses on firm’s balance sheet and

income statement Their costs are distributed by subtracting them as

expenses from gross income – one part at a time over a number of periods

Depreciation

Things concerned for calculation of depreciation Cost basis of an asset

Total cost that is claimed as an expenses over an asset’s life

E.g. installation cost of a machine Salvage value Depreciable life Method of depreciation

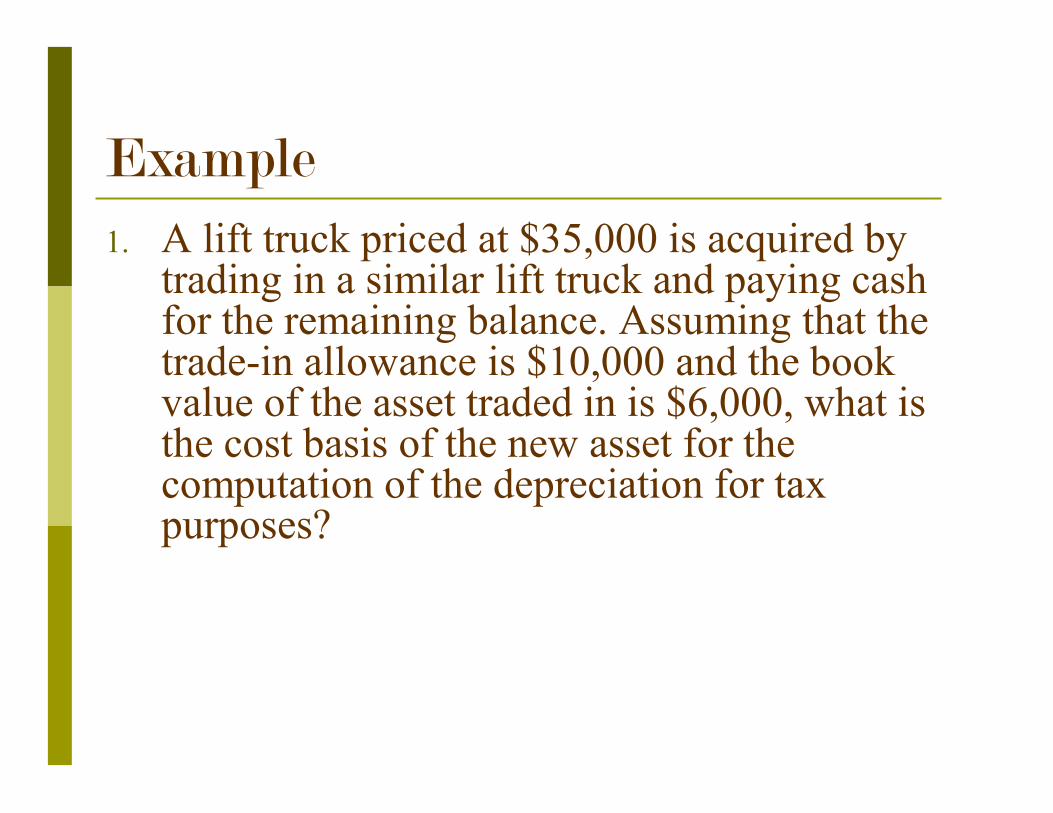

Example

1. A lift truck priced at $35,000 is acquired by trading in a similar lift truck and paying cash for the remaining balance. Assuming that the trade-in allowance is $10,000 and the book value of the asset traded in is $6,000, what is the cost basis of the new asset for the computation of the depreciation for tax purposes?

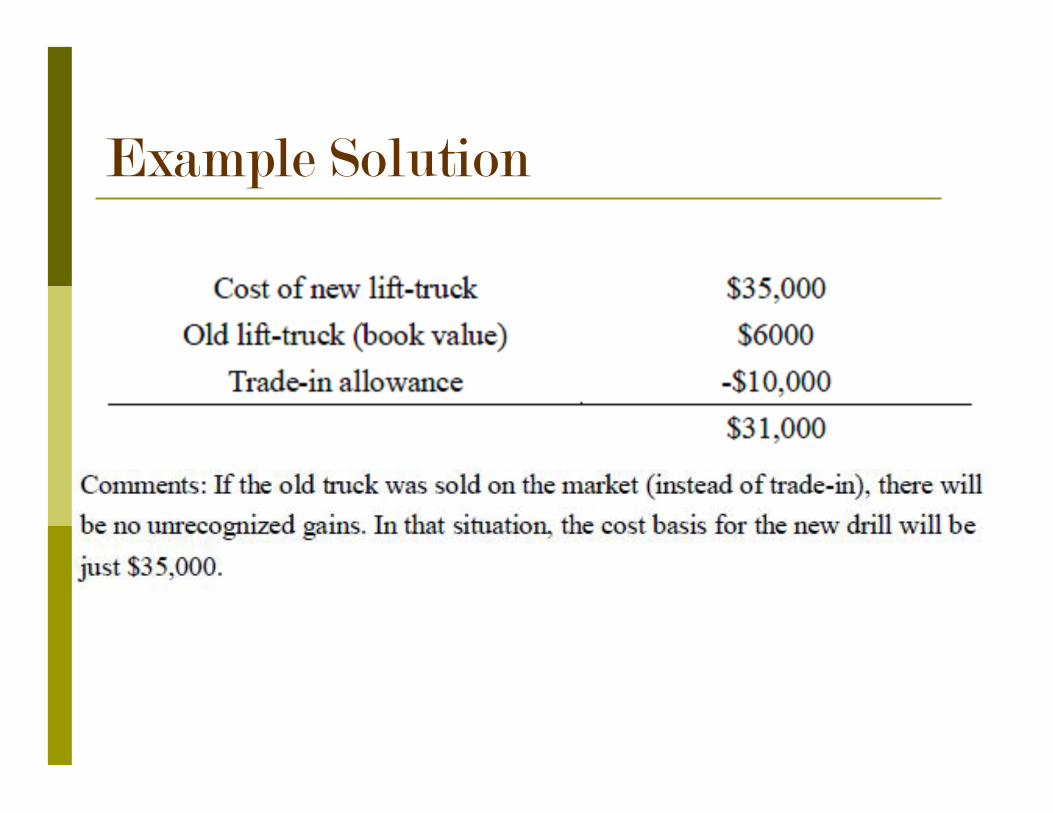

Example Solution

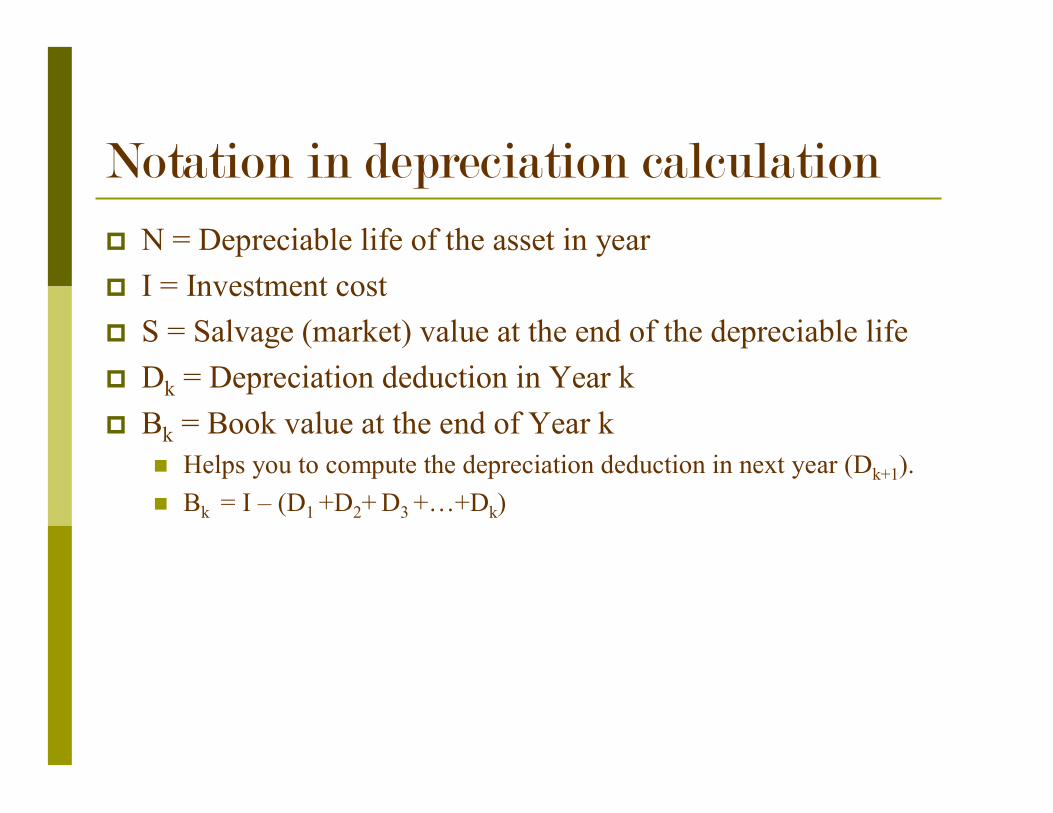

Notation in depreciation calculation

N = Depreciable life of the asset in year I = Investment cost S = Salvage (market) value at the end of the depreciable life Dk = Depreciation deduction in Year k Bk = Book value at the end of Year k

Helps you to compute the depreciation deduction in next year (Dk+1). Bk = I – (D1 +D2+ D3 +…+Dk)

Method of depreciation

Straight-line method

Declining-balance method

Unit-of-production method

1.5(150% DB)

2(200% DB)

Example

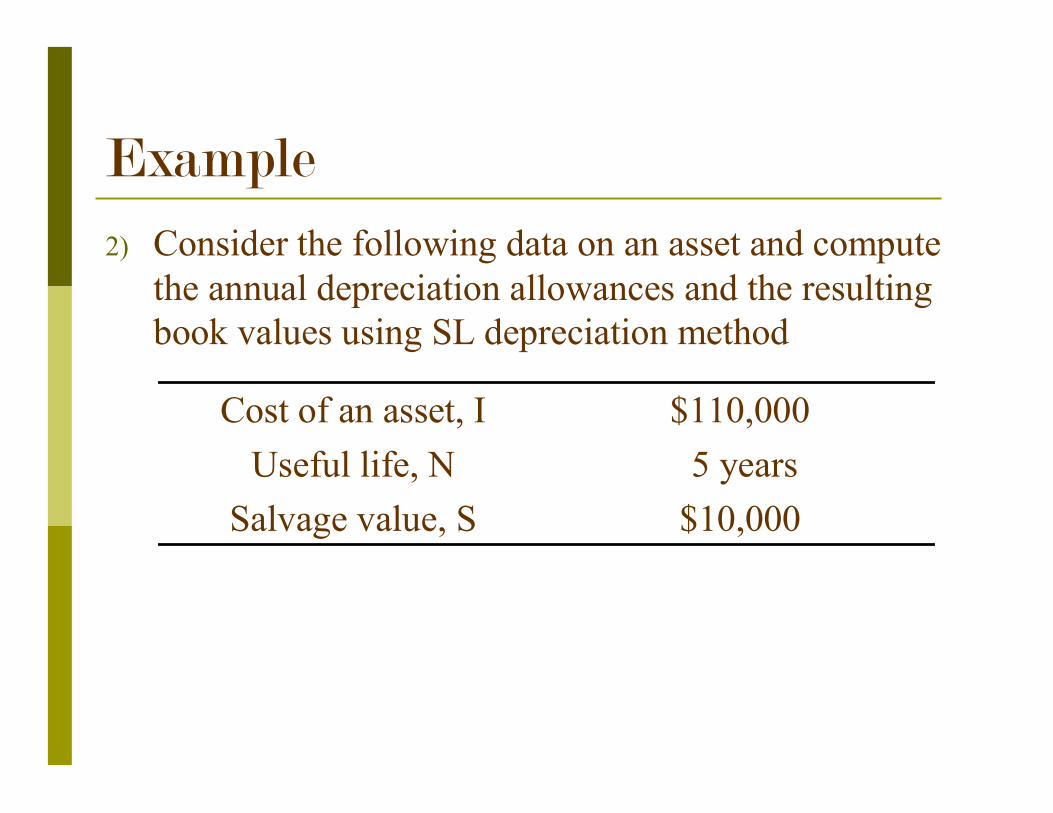

2) Consider the following data on an asset and compute the annual depreciation allowances and the resulting book values using SL depreciation method

$10,000Salvage value, S5 yearsUseful life, N

$110,000Cost of an asset, I

Example Solution

The SL depreciation rate = 1/5=20% The annual depreciation charge is

Dn = (0.20)($110,000 - $10,000) = $20000

30000 – 20000 = 10000200005

50000 – 20000 = 30000200004

70000 – 20000 = 50000200003

90000 – 20000 =70000200002

110000-20000 = 90000200001

BnDnn

Switching policy

Book value at the end of depreciable life of an asset will never reach 0 by DB method

Switch from DB to SL whenever SL allows a larger depreciation amount than DB

SL depreciation in any year n is calculated by:

Example

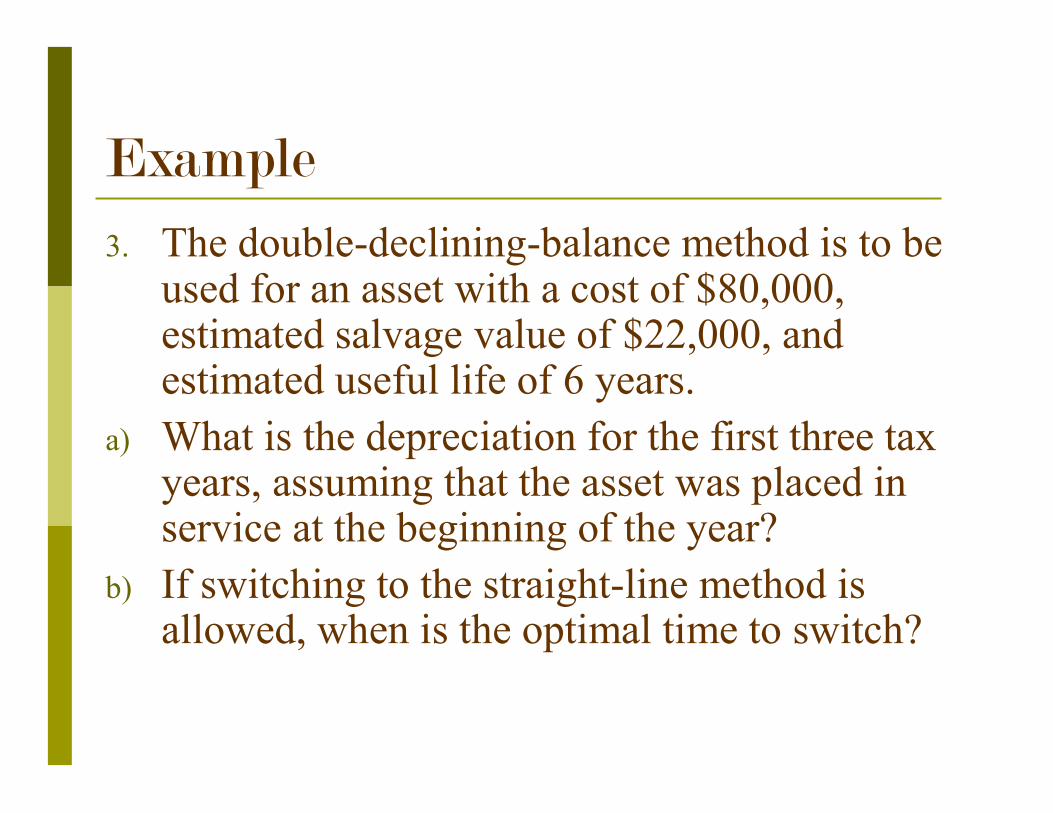

3. The double-declining-balance method is to be used for an asset with a cost of $80,000, estimated salvage value of $22,000, and estimated useful life of 6 years.

a) What is the depreciation for the first three tax years, assuming that the asset was placed in service at the beginning of the year?

b) If switching to the straight-line method is allowed, when is the optimal time to switch?

Example SolutionGiven: I = $80,000, S = $22,000, N = 6 years(a) α = (1/N)x2 = (1/6) x 2 = 1/3

(b)

Comments: If the regular DDB deduction is taken during the fourth year, B4 (23703 -7901.3) would be less than the salvage value. Therefore, it is necessary to adjust D4. The number in the box (1703) represents the adjusted value. No switching is common for this type of situation whenever the salvage value is high.

Example

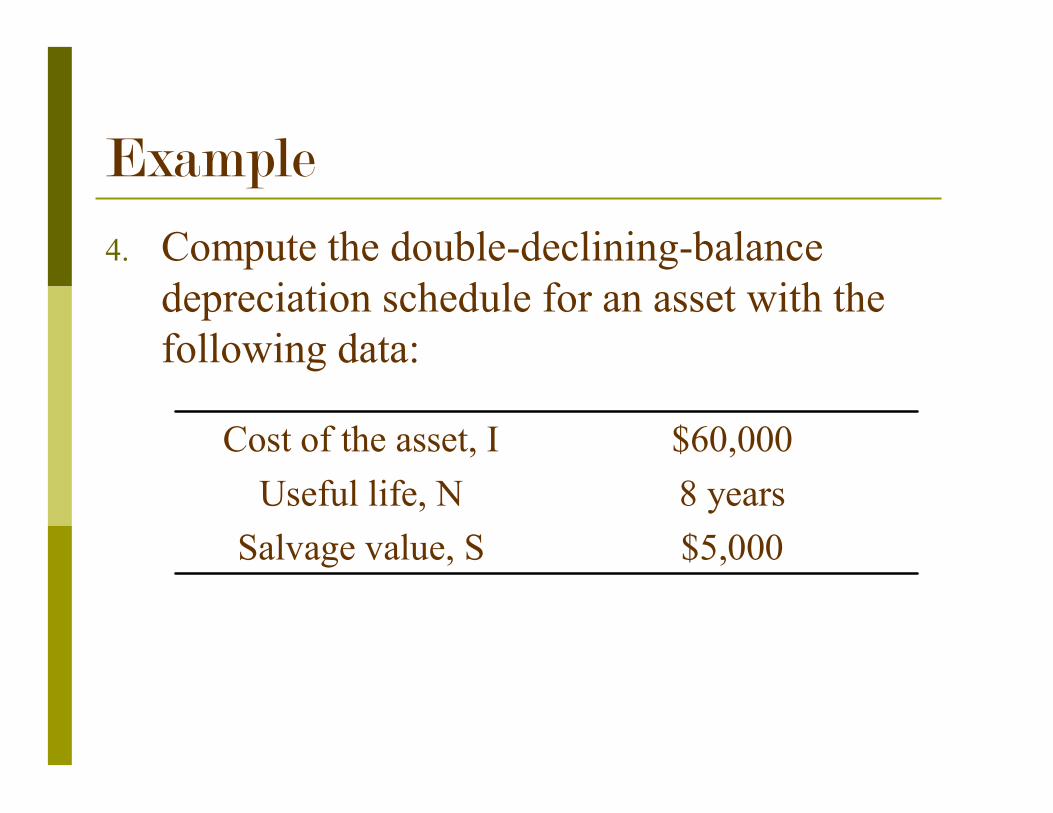

4. Compute the double-declining-balance depreciation schedule for an asset with the following data:

$5,000Salvage value, S8 yearsUseful life, N$60,000Cost of the asset, I

Example SolutionGiven: I = $60,000, S = $5,000, N = 8 years ,α = (1/N)x2 = (1/8) x 2 = 0.25

Example

5. A diesel-powered generator with a cost of $60,000 is expected to have a useful operating life of 50,000 hours. The expected salvage value of this generator is $8,000. In its first operating year, the generator was operating for 5,000 hours. Determine the depreciation for the year.

Example Solution