Making sense of complex industries

60

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Making sense of complex industries

Digitized by the Internet Archive

in 2011 with funding from

University of Illinois Urbana-Champaign

http://www.archive.org/details/makingsenseofcom1149mcge

FACULTY WORKINGPAPER NO. 1149

o<<&

«*P•&

Making Sense of Complex Industries

John McGeeHoward Thomas

College of Commerce and Business AdministrationBureau of Economic and Business ResearchUniversity of Illinois, Urbana-Champaign

BEBRFACULTY WORKING PAPER NO. 1149

College of Commerce and Business Administration

University of Illinois at Urbana-Champaign

May, 1985

Making Sense of Complex Industries

John McGeeLondon Business School

Howard Thomas, ProfessorDepartment of Business Administration

Paper originally presented as an invited paper at the Prince BertilSymposium on Global Strategies, held to celebrate the 75th anniversaryof the Stockholm School of Economics, in November 1984. A revisedversion is forthcoming in Strategies in Global Competition (eds. D.

Schendel, N. Hood, J. E. Vahlne) (John Wiley & Sons Ltd.).

Preliminary Draft: October 1984. Do not quote.

Address for Correspondence:

John McGeeLondon Business SchoolSussex PlaceLondon, NW1 4SAENGLANDTelephone Number: 01-262-5050

Making .Sense of Complex Industries

Abstract

Many strategic management models either ignore or severly

underestimate the complexity present in most strategic

situations. This paper identifies some of the key sources of

complexity and suggests some ways in which this complexity can be

handled. It argues for the importance of the fine-grained

historical industry study in identifying key strategic dimensions

and suggests that is should be supplemented with the more

fashionable strategic groups analysis.

Introducej on

During the last two decades, in particular, a substantialbody of literature has been developed in the fields of strategicmanagement, strategic planning,, corporate and business policy andrelated topics. This literature, which is admirably reviewed inSchendel and Hofer (1979), owes much to the prior writings ofAlfred Chandler [1962, 1977] and the decades of case writing andresearch undertaken at the Harvard Business School.

MOre recent ly strategic management has been subject toscrutiny through a wide variety of disciplinary -lenses" andmodels, including Porter's influential volume (Porter (1980)) oncompetitive strategy.

These "partial" models have been borrowed from suchdisciplines as industrial organization, organizational behavior,international business, and decision theory. However, many ofthese "partial" models either ignore or severely underestimatethe complexity present in most strategic situations.

A careful review of sources of strategic complexity (seeBower (1982), Porter (1980)) will almost always give priority tothe international context, technical change, the competitiveenvironment and government/political intersections at or near thetop of the list.

The examination of strategic complexity through manydifferent "lenses" provides strategists with a series ofopportunities with which to better understand complex strategicsituations. Yet the very diversity of these disciplinary per-spectives means that strategists have to assess the implications

of using each approach and judge between the often conflicting

conclusions offered by the set of "partial" models.

This paper argues that many constituencies try to "make

sense" of complex industry environments. These range from

industrial organization researchers (such as Porter (1980, 1982),

Caves (1980), Teece (1984), Nelson and Winter (1982), Rumelt

(1981), Williamson (1975, 1981) and Schmalensee (1982)) who

attempt to develop richer economic theory through to firm-level

strategists and governmental policy-makers (e.g. anti-trust) who

try to understand the bases for competition in particular

industry environments.

In a paper written for an anti-trust symposium Porter, (1981:

449-451) stresses the value of in-depth industry histories in

understanding industry environments and identifying firms 1

strategic interactions on a longitudinal basis. He recognizes

four main advantages: (Porter, 1981:. 450).

"First, its emphasis is longitudinal, built arounda careful re-creation of competitive moves and otherevents in the sequence in which they occurred. Second,it is broad and quite detailed in its coverage of firmbehavior and industry events rather than focusing onone or a few elements of competitive behavior such asinvestment or pricing. Third, it emphasizes theuncertainties present in predicting the future thatbear on the decisions facing firms. Fourth, it placesgreat emphasis on a full and complete description ofeach major competitor, including its full range ofactivities in all markets in which it competes, and agreat deal of emphasis on "internal" factors such asthe identity and backgrounds of management, theevolving organizational arrangements in place, etcetera.

In the same paper (1981: 474) Porter also points out that

there is an increasing incidence of industries in which strategic

interaction is global. Such global industries must also be

studied in depth since they change the rules of the competitiveenvironment (Gluck (1983)). Thus, if f irms more clearlyunderstand the nature of global competition then they should bebetter able to re-formulate their competitive strategies.

Porter's strong endorsement of the industry history approachsupports an important proposition in this paper, namely, thatfurther "rich", fine-grained (Harrigan (1983)), in-depth,industry studies should be carried out with the aim of developingricher hypotheses and theories about strategic interaction,competitive strategy and global competition. Such studies shouldattempt to make sense of the set of complex, competitive environ-ments by careful questioning of a number of issues. For example,,what analogies or experiences (Porter, 1980, Chapter 3) domanagements draw upon in addressing particular strategicproblems? Do they develop strategies from insights gainedthrough "personal" experience or from the examination ofstrategies borrowed from other firms? Alternatively, do theyidentify competitive concepts and approaches as shared byindustry members and base their strategies on competitive norms?What are the external forces such as technology which lead tochange in the bases of an industry competition? what are theappropriate units of analysis? What are the industry andenvironmental conditions which affect strategy formulation andshape the cost of changing position within an industry? Thus,with complexity better integrated into the analysis more insightcan then be gained about what constitutes a global industry andhow global strategies may be formulated.

.

The purpose of this paper is firstly to provide a review of

various definitions and important concepts (such as value-added

chains) which will be used in the paper. The authors argue thatricher industry studies need to be written and draw from theirown recent experience with major contemporary industry studies.

This includes such industries as personal computers, repro-graphics and automobiles. Generalizations and common factorsemerging from a study of the reprographics industry are thenidentified. Some implications for theory development, researchdesign, methodology and data base construction will complete thepaper.

o

o

Literature Review

Introductory

There has been much discussion in the recent literature ofindustrial organization about whether the firm or industry orsome other intra-industry group stratification (the so-calledstrategic group (Porter (1980: 129)) is the appropriate unit foranalysis. it is clear that most business firms are multi-product, sell in more than one market and have grown bydiversification. The industry as conventionally understoodproduces a range of different products all of which are not closesubstitutes, and uses a variety of technical productionprocesses. it, therefore, becomes unclear where the boundariesof the industry should be drawn. Many economists have concludedthat the concepts of market and industry should be viewed as

complementary and the emphasis employed should reflectthe problems under consideration. According to Joan Robinson

(1956):

"Questions relating to competition, monooolv andoligopoly must be considered in terms of MarketsProgresT Voc f 1f^??^"9 1

/b0r

'profits

' technicalprogress, localization and so forth have ^^ k=considered in terms of industries."

be

The newer concept of strategic groups focuses upon theimportance of intra-industry strategic groupings in understandingdifferences across firms within an industry. it fits neatlybetween the supply idea of an industry and the demand idea of amarket The defining characteristics of strategic groups arisefrom the nature of the mobility barriers (Caves and Porter(1977)) and i solating mechanisms (Rumelt, 1981) which protect thegroups. The~ three s^rTes of mobility barriers most commonlyadvanced (McGee and Thomas (1984)) are market related strategies,general supply characteristics of the industry, and theorganizational and boundary choices of the firm - each of thembeing decision variables for the firm.

Strategic groups offer an opportunity for business policyresearchers and business strategists to enrich theirunderstanding of the nature of industries and the. strategicinteractions amongst firms. m particular, the concept offers adistinctive slant on the identification of relative competitiveposition and suggests a systematic and comprehensive way ofassessing strategic capability in terms of the framework ofrelative competitive advantage.

The literature review which follows builds upon this notionof assessing f irm strategic capability by reference to theindustries and environments in which firms operate. First, theauthors review the rich tradition of research in industry-based

studies and industry histories and conclude, inter alia, that

there is a lack of established methodologies for treating

complexity. Second, key sources of industry complexity are

identified including notions of mobility barriers, value chains

and global industries. Third, research in other areas of social

science, notably organizational behavior and psychology is

briefly reviewed. This is attempted in order to provide further

insights into how strategists may reason by analogy or imitate

other firm strategies in the context of strategic decision-

making. It is possible that better industry sense-making willresult from examination of these alternative perspectives. As an

example, the discussion of alternative perspectives is focussed

around the strategic group concept, a device formulated by Porter

(1980) to make sense of competition and competitive advantage.

The findings of recent empirical grouping studies are reviewed to

determine whether they provide useful insights for firm conduct

and competitive strategic interaction in the context of complex

industries.

Industry Studies

Many different intellectual traditions are represented in

industry-level studies. These range from business history to the

domain of industrial organization economics and involve numerous

researchers and research approaches. Table I lists some of the

main features and perspectives of each approach and providesreferences to researchers whose work is most closely associated

with those perspectives.

TABLE I ABOUT HERE

The main differences in the conduct of alternative types ofindustry studies are shown in Table I. m particular, they varyin terms of the aims and purposes of each type of study and theresearch methodology used by the investigator. For example, morenarrowly defined data sets (drawn from government and industry-level sources, and more refined and sophisticated analyticalapproaches (often using econometric techniques) are used to gainanswers to specific questions concerning industry-levelprofitability, efficiency and monopoly power. This more narrowpurpose and focus has been extensively used in traditionalindustrial organization studies, some anti-trust analyses and inassessing the economic impacts of technology and research anddevelopment in different industries. More detailed, broaderpurpose studies have been developed for case study a„a teachingpurposes, and have been evident in some more recent anti-trustcases (Sullivan (1981)) and industrial policy debates (Lawrenceand oyer ,1983 ,). ?ese studies generally .^^ ^^ ^^analysis and allow the writer selectivity in the choice of datainsights and phenomena reported. An underlying aim of thesebroader studies is to reflect the contextual complexity ofindustry studies. Therefore, they report a wide range of firm-level phenomena includinq is<snec ^^ «-9 lssue s of organizational design,leadership, and strategy to achieve firm objectives. The focusof many of these studies is on the firm as the unit of analysis,and seeks to enrich understanding about the strategic interactionand rivalry between competitors and on the role of the general

TABLE I: DIFFERENT FORMS OF INDUSTRY 9TimTF«;

MAJOR INTELEECTUALTRADITION

IndustrialOrganizationEconomics

BusinessHistory

PublicPolicy

Strategy

Technology

_PURPOSE

Study of IndustryStructure,Behavior,Performance,Judgment ofCompetition,Profitability,Efficiency andMonopoly Power.

Mapping industry/business evolutionthrough time.Insight intohistoricalevolution ofbusiness organi-zations and therole of strategist/entrepreneur.

_DATA_BASE

Typically publishedgovernment orindustry sourcedata

UNIT OF.ANALYSIS

Industry Level

Monitoring ofCompetitionPolicy-Anti-Trust '

-Mergers

Development ofIndustrial PolicyOrations

Case Developmen t

-Teaching

Industry Analysis-Firm Strategies-GenericStrategies

Impacts ofTechnology onIndustry

,

Diffusion ofInnovations,Economics ofR&D, First/Second MoverAdvantages?

Mix of Sources-GovernmentStatistics

-Annual Reports-Newspapers-Biographies-Published Speeches

Mainly industry butalso business focus.

GovernmentStatistics,Industry LevelInvestigation

Focussed studiesof companies usingAnnual Reports,Speeches, etc.

Mainly industrylevel.

Mix of Sources-Statistics-Annual Reports-BusinessPeriodicals

-Company Visits

Use of Compustat,PIMS Data Base

Industry LevelData Basesof Economic,

Patent and ResearchActivityPhenomena

Usually TailorMade

Firm Level

Finn and industrylevel

Mainly industrylevel

RESEARCH.APPROACHES

Mainly statistical/econometric.

Some case studiesbut rich traditionof Europeanresearchers inindustry casestudies.

...REFERENCES

Porter (196

Scherer (19

Shepherd (1

LongitudinalAnalysis-History-Content Analysis-Analysis ofSpeeches

-Newer StatisticalAnalysis

Adams (1977Shaw andSutton ( i

Bateman (198

Chandler (19

197

Cole (1959)

Mainly statisticalanalysis.

Some richer mapping,industry historystudies involvingfirm/organizationconduct.

Case writerselectivityParticipantobservation

Rich case observa-tions with statis-tical, matrixmapping analysis.

Mainly statistical,econometric.

More process,firm-level in thediffusion ofinnovations

Porter (1981)

Salop (1981)Sullivan (198

Lawrence and

Dyer (1933)Reich (1983)

Andrews (1971

Christensen,Andrews et a.

(1980)Clueck (1980)

30,Porter (1930,

19S2)

Harrigan (1983

Freeman (1983)

Kantrow (1982)

Mansfield (196!

1977)

Schendel,Cooper (1977

i

manager as the architect of organizational direction and purpose.Clearly, these industry studies offer many different, but

not always synthesized insights into the analysis of competitive-

advantage in complex industry settings. However, some generalconclusions emerge for the conduct both of future studies and fortheory development. First, there seem to be a lack of bothestablished metholodologies, and rules of evidence, for handlingproblem complexity and reporting complex phenomena in asystematic fashion in order to allow replication by otherresearchers. Second, in the more finely defined studies there isoften a denial of complexity (and the role of other informationand evidence) in formulating particular relatively narrowhypotheses and in establishing or refuting the validity of thesehypotheses. Third, the theoretical and methodological crosscurrents from the different disciplines do not seem to beintegrated effectively and thus do not lead to richer investi-gations of complex phenomena.! As a result it appears thatcurrent industry studies of complex phenomena do not make clearcontributions to the development of theory in the specialistdisciplines and intellectual traditions. While this is „continuing difficulty in the management research field, thesearch for a useful measure of reconciliation and synthesisamongst the various forms of industry studies can have boththeoretical and practical advantages in regard to the advancementof strategic management. Perhaps themes such as policy dialogue«h»«U984>) and triangulation in research strategy to achieve

Notable exceptions are Porter (1982} * n ,q u=, •Cl \ ± y°*J and Hamgan (1983).

10

convergence of conclusions (Denzin (1978), Jick (1979) mayfacilitate the search for mechanisms to enrich the newer inter-

disciplinary theories such as Rumelt's (1981) Strategic Theory of

the Firm and Nelson and Winter's (1982) Evolutionary theory ofthe firm.

Sources £f Complexity

A number of writers, particularly Aldrich (1979), Caves andPorter (1977), Galbraith and Schendel (1982), HcGee and Thomas(1984), Porter (1980: 127-128) and Rumelt (1981) have addresseda wide range of economic, organizational and environmentalsources of complexity affecting strategic decision-making at thefirm level. Table 2 provides a listing of sources of complexitydrawn mainly from these references. For example, concepts suchas mabiliix barrie r s (Caves and Porter (1977) and iiisliULilia

mzzhznlzms. (Rumelt (1981)) together define from primarilyeconomic perspectives, key strategies available to firms, orgroups of firms within industries, and link them to unique firmadvantages and characteristics such as the possession of animportant financial resource or technological advantage. Aldrich(1979), Ackoff (1970) and others have stressed the difficultiesof organizations' adapting to their environments and matchingstrategies to changing circumstances. They argue that complexityinvolves both controllable or, at least partially controllablevariables such as marketing, financial and production decisionsand uncontrollable variables such as changes in technology andgovernmental policy. while the former endogenous variables are

11

largely controllable by management, uncontrollable (exogenous)

variables influence strategy formulation but cannot be directlyhandled. The organization's ability to handle environmentalchange is perhaps the key challenge to strategists in the 1980's.

TABLE 2 ABOUT HERE

Drucker (1980) in his book entitled ilajLiaiJia in Turbu lPnflimfiS suggests that the trend towards global competitionrepresents the most significant structural change facingbusinesses and governments today. Porter, like Drucker, makes a

distinction between international competition and globalcompetition. 'A global industry is one in which the strategicpositions of competitors in major geographic or national marketsare fundamentally affected by their overall global positions"(Porte

(

r, 1980: 275).

Globalization, therefore, can be examined as a majorenvironmental change. How should organizations confrontingglobalization seek to modify their strategic positions? Kogut(1984). and Williams (1984), amongst others, endorse the viewpointthat the concept of the "value-added- chain is a useful frameworkwith which to understand the bases of industry membership andglobal competition and thereby develop adaptive corporatestrategies. Williams (1984: 2) defines "value-added" in thefollowing terms: "Loosely put, -value-added' is defined as whatis added to the product during its production. The "value-added-influences productivity achieved by a firm and its cost structureover time. The impact of the value added is reflected incompetitive behavior, and, in turn, the formation of strategic

12

TABLE 2

KEY SOURCES OF COMPLEXITY

Endogenous Factors

Organization andManagement

Issues

Ownership Structure-Single Business v. Multi-Business

Capital Structure-Leverage, Relationship to Parent

Organization Structure-Design of Organizational Systemsand Procedures

Aims

Firm aims to develop firmembodied skills such asunique resources, reputationimage, development of patents,etc

Competitors and Markets Competitors : Number, Type,Geographic Position

Markets: Geographic Coverage ofMarkets: Global/NationalMarket SegmentationProduct-Line and MarketingMix

Firm aims to develop a senseof competition and of sourcesof competitive advantage inmarket niches.

Product Initiation andDevelopment

Value Added Chain Length

Substituation Patterns

Vertical Integration and Dependen

Horizontal Relatedness

Scale Effects

R&D Capability

Nature of Manufacturing Process

ce

Firm aims to capture rents, valueadded where appropriate

Exogenous Factors

International Trade

Technology

Government

Issues

Globalization

Competitive/Comparative Advantage

Aims

Firms aims to assess the effectson the value chain of the linkagebetween national base distinctiveskills and internationalization.

Firm aims to assess effect onvalue chain of changes intechnology. Clear effects oncompetitive advantage.

Firm aims to assess effect onvalue chain of government

m„..„ ^, intervention.Note. This Table adopted from Aldrich H97f» a «. c.

Porter (1980) "^ (197°^ **off. Calbraith and Schendel (1982), Hufsi and Thomas (1984).

Inventions, Innovation, Technological

Government as Policy Formulator,Rule Setter, Owner/Purchaser

13

groups within an industry."

TABLE 3 ABOUT HERE

In Table 3, a modified version of Williams categorization of

industries in terms of "value-added- is presented to throw lightupon the linkage between "value-added" and globalization. Kogut

(1984) provides additional important insights although definingthe value-added chain in terms of contribution to the marketvalue of the firm. He argues that a measure of economic rents is

needed which identifies excess return on investment for each linkof the value-added chain. Firm strategies in country-centeredmarkets are, typically, based on specialization in specific linksof the value-added chain. However, in global markets strategiesrest on the exploitation of economics captured along and betweenvalue-added chains - (Kogut (1984): 2). Kogut thus adds theconcept of economies of scope (Teece (1980)), the sharing ofresources to achieve synergy, to economies of scale and learningeffects in order to capture the process of exploitation ofeconomic advantage along multiple value-added chains.

It should be noted that the use of the term "value-chains-is associated with the firm's decision process in relation tobusiness-unit competition. Firms have a set of alternativ"value-chains" from which they can choose and this choice resultin different competition sets and strategic postures. The firm's

strategic aim is to match its distinctive skills (or strategiccapabilities) with one of the alternative competition setsavailable in the environment. Once this strategic choice is made

14

TABLE 3

Definition of IndustryTypes

TAXONOMY OF INDUSTRIES BY VALUE-ADDED/PROniTrTTVTTV BASE

Characteristics and Focusof Competitive Advantage Examples

i

Sensitivity toGlobalization

Class I - Value Added isConstrained From Achieve-ment of Significant Cost-Based Productivity IncreaseThrough Economies of Scaleor Learning by Doing

Fragmented IndustriesCompetition in Terms of:Geography, Reputation ofIndividuals, Regulation,Individualized Service,Creative Skills, CustomEngineering

Computer Software,Entertainment,Investment Banking,Consulting,EmbryonicTechnologies

Low

Resistant to Clobalizattbecause numerous barrierto consolidation of suppand demand

Class II - Value AddedCharacterized byModest Cost-BasedProductivity ThroughLearning by Doing andEconomies of Scale

Low Cost RivalryDifferentiated Rivalry(Premium Price)Focused Rivalry(Specialization in Small"ub-Segments)

ManufacturingAssembly BasedIndustries-Steel, Glass,Tire, Appliances,Chemicals,Automated Services

Moderately susceptibleAutos - yesSome, but not all heavymanufacturing

Class III - Value AddedWhich is Subject toExtremely Rapid Cost-BasedProductivity Gains ThroughLearning by Doing andEconomies of Scale

Rapid Technolog icalChange and InformationTransferRivalry-Product Technology-Process Technology-Commodity Technology

Serai-ConductorsFiber-OpticsConsumer ElectronicsTelecommunications

Vulnerable to

globalization-Few global or culturalbarriers

Transition - Value AddedShifting Permanentlyfrom One ProductivityBase to Another

Hybrid - Value AddedCoupled in Two or MoreProductivity Bases

Fundamental Changein Bases of CompetitionThrough Deregulation,Patents, ManufacturingInnovations, etc.

Identification ofof CompetitiveAdvantageDifficult

Retail Banking(I -> II)

Telecommunications(I -> II -» III)Biotechnology(I -> III)

CAD/ CAMRoboticsPersonal computers

Dependent onstage of transition

Not clear, situationspecific

I

15

the examination of the forces which drive the "value chain" leadsfirms towards an understanding and definition of an "industry"(whether global or country-centered) within which competitiontakes place. Close examination of the final customers for eachvalue chain leads to the definition of markets and allows morecomplex analyses of competition and market segmentation to beundertaken.

It is proposed here that the value-added chain concept is animportant means of organizing firm-level understanding of complexsituations, Table 3, using "value chain" ideas, provides a

.framework both for forming strategic groups within industrysettings and for analyzing the potential sensitivity of eachindustry setting to the threat of globalization. Table 2 showsclearly that strategy formulation can become more complex inenvironments of global competition. Factors such as theinfluence of distinctive firm skills in particular countrymarkets, and the role of government policies in setting the"rules of the game" in many countries can complicate firms-strategic choices. Governments often operate strategically ininternational trade through the formation of state-owned enter-prises as competitors (Hafsi and Thomas (1984)) and theestablishment of quota control or subsidy policies for "home-based" enterprises.

Kogut (1984: 38, 39) shows that full awareness ofinternational competition does not follow simply from anextension of the strategic analysis of competition in country-centered markets. He believPQ <-k=,4- ™~Deiieves that more research should becarried out on under stand ina srr a f „'oing strategic groups in the

16

international domain and on managing the environmental variance

of world competition. He concludes by identifying some of the

parameters which are important in making sense of globalization

and global markets:

"Global positioning consists, therefore, of threeelements. First, is the transferring of strategicassets between different markets which permit theexploitation of the economies of scale, scope, learningand real options. Second is the differentiation ofproducts to adapt to national arenas and to exploit up-stream competitive advantages. The third element isthe flexibility and bargaining strength that a multi-national network provides in managing stakeholders indiverse environments."

In summary, the argument in this section of the literaturereview promotes the importance of the "value chain" in

understanding the bases for industry competition in settingsinvolving complexity (as shown in Table 2). The majorenvironmental structural force of globalization and the resultingformation of global industries is discussed as an example ofcomplexity and the role of the value chain in aiding strategyformulation is assessed (see Table 3).

In the next section some alternative cognitive andorganizational perspectives for making sense of industrycomplexity are discussed using the strategic groups concept as an

example.

gense-Ma Kinn and gfciatfigjg r.r^r ^

The term "strategic groups" was originally coined by MichaelS. Hunt in his doctoral dissertation (1972) to contribute to hisexploration of the performance of the white goods industry in the1960's. Porter (1980: 129) provides the accepted definition of

17

a strategic group in terms of the similarity of competitivebehavior:

TABLE 4 ABOUT HERE

The main studies in the area of strategic groups aresummarized in Table 4. Most of these studies are "data-driven".That is, they identify a number of key strategic dimensions drawnfrom Porter's (1980: 127) or McGee and Thomas (1984) listing ofkey strategic variables and typically use cluster analysis withdata bases such as COMPUSTAT to form groups of firms who"cluster" together in terms of their observed strategic behavior.Yet despite ten years of research there remains confusion aboutthe concept and its linkage to the strategic management of firms.Criticisms have been voiced about whether the observed groupsmake sense to strategists or other interested parties. Littlefollow-up with industry participants has been reported except inthe case of the continuum of rich studies of the beer industrycarried out at Purdue (Batten (1974), Batten and Schendel (1977)and Hatten and Batten (1984)). We have little knowledge to tellus why some firms position their strategies close to those ofother firms. A study of strategists' beliefs and perceptionsabout competition and competitors in particular industries isclearly needed to identify the frameworks they use incompetitive positioning. This would provide an awareness of

18

TABLE 4

STRATEGIC GROiJPs=__PR£vioiJS STTOIES

Studv

Hunt (1972)

Industry

"White Goods

Basis for Strate gic££ou_pForcation

Newman (1973,1978)

Porter (1973)

34 4 digit"Producer GoodsIndustries:Chemical Pmr.c,^38 3 digit"Consumer Goods

u -, Industries

Schendel (1977)

Hatten, Schendel Brewing IndustTv""and Cooper (1978)industry

Caves and Pugel(1980)

Ryans andWittink (1982)

U »S. Manufacturing.Industry—Sample19 Consumer GoodsIndustries fromCompustatAirline Industry

Baird andSudharsan(1983)

Office Equipment/Electronic Computing

Primeaux (1983)

Howell andPrazier (1983)

TextilesPetroleumMedical Supplyand Equipment

i

- degree of productdiversification

- differences in productdifferentiation

- extent of vgrticaj IntegraHnnDecree of Vertjj^ — n

Integration

Relative Size of Firm~ Leader/Follower Classification

Manufacturing Variables~ Number, Age, Capital Intensic

of Plants.Marketing VariahTpg" Number of brands, price, and

receivables/salesItruc tural Variablpg

8-firB concentration ratio.." firm sizp.Manufacturing, Marketing ,nH "

Financial V_ariables. (Leverage,Merger/Acquisition BghavtorRelative Size of Firm

Product Strategy- Advertising/Sales Ratio

Financial StratPtnrClustering of Residuals fromCapital Asset Pricing Model.(Security Returns)Financial S trategy V^TTm- Leverage, Current Ratio,

Return on Assets, DividendPayment Ratio, Times Interest

. Earned, SizeSizi

.Investmen t BehaviorCustomer Groups ServedCustomer Needs Served-(due to Abell (1980))

I

19

those key controllable strategic dimensions which strategists-

perceive to be important in formulating competitive strategy in

the industry. Thus, adding the perceptual data drawn fromindividual decision-makers to the economic models of competitionprovided by industrial organization economics perspectives shouldenable a more general framework for identifying importantstrategic variables to be developed. •

Although Porter (1980: 127/8) lists thirteen variables assources of strategic differences and variability, he suggeststhat maybe two to four strategic dimensions should be selectedfor close attention and that group maps or graphs involving twovariables at a time should be drawn to make sense of theparticular strategic dimensions at hand. Such mapping processesare a means of getting the strategists to "frame" the problemcorrectly (McCaskey (1982)), to sense the existence of strategicgroupings and to simplify the problem around a number of keystrategic dimensions. According to Spender (1981) and Huff(1982), strategists may also borrow "recipes" for strategies fromother firms in the industry, particularly strategic groups, andalso from a wider set of firms. Through examining these recipesand reasoning by analogy to other sets of experience, strategistsmay develop other bases for grouping firm behavior.

The search for taxonomies of strategy 2(Hambrick (1984))

also suggests that strategists need such models of competitivebehaviorjo provide benchmarks for strategy positioning. Hervis

2 Examples of such taxonomies are Miles and q„ ftu t e M(nD ,

^^modei oTg^ ^.SSffi" "W^i^Z^l20

and Rosen (1981) and other researchers in experimental psychology

express this need as the search for protypical and stereotypical

behavior. The firm closest to the prototype or stereotype then

becomes the focal member of the perceived strategic group and

provides the "benchmark" for identifying and evaluating key

strategic dimensions.

It should be noted that the concepts of mapping, of

taxonomies and of industry recipes together with economic theory

should lead to the better, and more "grounded" identification of

the key strategic dimensions (and sources of dissimilarity

between firms) for strategic group formation. Yet even if this

objective were to, be fully achieved, many problems would still

remain in linking the strategic groups concept to firm conduct

and the evolution of complex industry settings. In particular,

each of the following issues raises questions about the role of

strategic groups in analyzing competitive advantage. First,

which concept of strategy operat ional i zes the concept of

strategic groups? Is it strategy as intentions or strategy as

realizations? In other words we need to question whether many of

the factors which identify groups are in fact purposivelymanipulated by the organization. Borrowing from a biologicalperspective and an adaptive strategy viewpoint (Boudling (1956),

Pondy and Mitroff (1979) and Chaffee (1983)) it can be arguedthat group membership is merely an observable manifestation of

viable niches in the environment and the organization's abilityto adapt to them. Organizations which exhibit certain survivaltraits which cannot be known completely in advance remain.

Second, do significant performance differences exist between

21

strategic groups? Third, do stable strategic groups exist or do

their characteristics change over time? What are the

determinants of change in the membership of strategic groups?

Fourth, which external environmental forces "trigger" changes in

the character of strategic groups and their membership?

While each of these issues is an area of future research, it

is argued in this section that the strategic group concept is an

important device for making sense of competition and competitive

advantage. While there is much conceptual and practical

ambiguity surrounding the strategic groups notion, it does add

usefully to the vocabulary of competitive strategy. Indeed,

examining notions of strategic groups and patterns of competitive

behavior from the widest possible set of viewpoints is clearly

valuable.

Overall, the importance of using multiple frameworks is

stressed through the general, literature review. It is concluded

that by using better frameworks for identifying complexity, we

should be better able to synthesize and make sense of complex

industry settings particularly those global industries reviewed

in Table 3.

In the next section we use the concepts developed through

the literature review to argue for many "richer" industry-level

studies. Indeed, as an example, we present some insights from a

recent study carried out with a co-researcher at London Business

School, namely Agha Ghazanfar.

22

The. Notion q£ a. "Rich" Industry Study:The. Example Ql Office Reorographi r.^

It has been argued during this paper that the discipline of

strategic management offers a number of partial models and

insights for formulating firm-level strategies in complex

industries. Since the entire complexity of the industry is

important, we have proposed that rich industry studies should be

carried out both for theory development and for identifying key

strategic dimensions and bases for competition within industries.

Our proposition is consistent with Porter's (1981) plea for

industry Case- histories and Porter's (1982) thorough and .rich set

of causes on competitive strategy.

In studying the office reprographics industry a number of

different research lenses were used. For example, the history of

the industry in the U.K. was reviewed for the last one hundredyears to show how the industry has undergone a series of changes

as a result mainly of the influence of technological innovation.

Also, the strategic positions of firms were assessed in terms of

strategic behaviors along key dimensions. Simple strategic maps

were also used to assess methods for analyzing competitiveadvantage and for forming strategic groups.

The aim of this study was to examine an industrycharacterized by technological change in which it would be

possible to examine relationships between:

(i) technological change and "industry" and "market"boundaries

(ii) technological change and the strategic response offirms

ThankQfllV\

e£??

t0 ^ha Ghazanfar from whose thesis (GhazanfarU984)) this section derives its empirical strength.

23

The first stage of the study, using methodologies common inthe fields of business and economic history, concentrated uponthe growth of firms and industries. m particular it examinedthe strategies of firms relative to industry development anddeveloped a typology of firms to categorize the differentstrategic positions taken by industy participants.

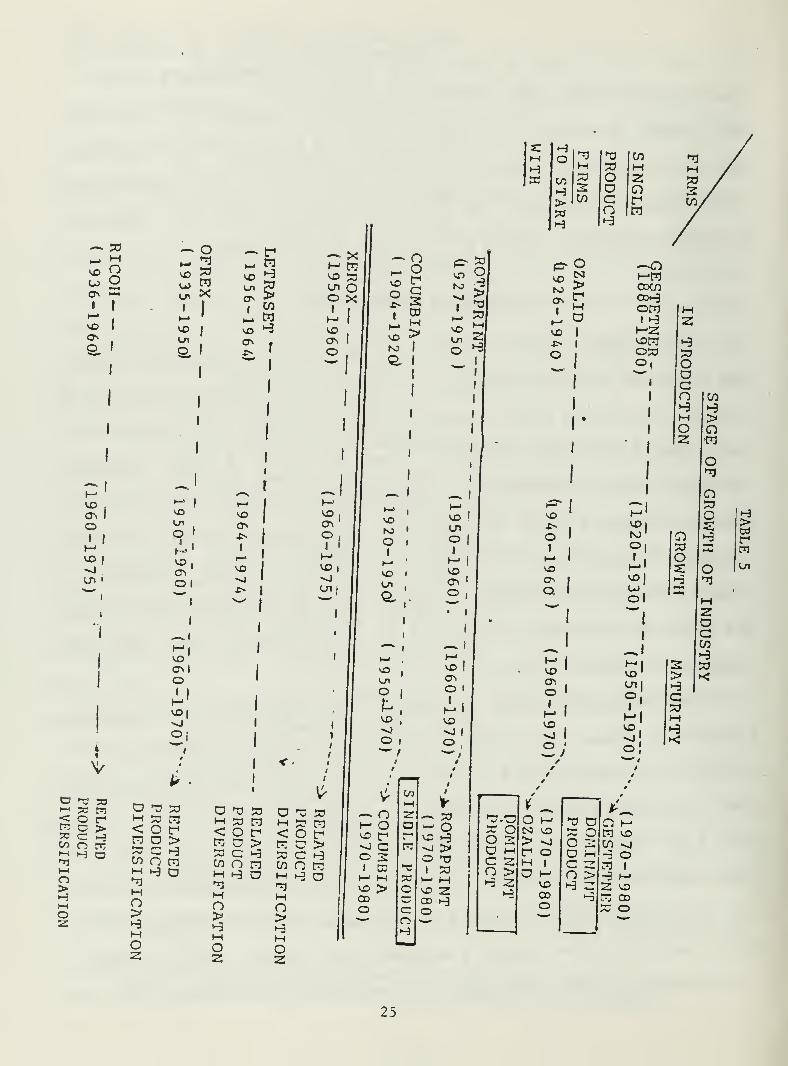

TABLE 5 ABOUT HERE

For example, Table 5 shows the movement of the eight firmswho entered the reprographics industry as single-technologyfirms, or created a new industry, at different periods of timeover the 1880-1980 period. Some of these firms, - Xerox,Letraset, Ofrex and Ricoh, - started diversifying out of theirbasic business whilst it was still g C ow j l t1 g and became "relatedproduct diversifiers" in terms of Rumelt's (1974) taxonomy ofdiversification strategies. others such as Gestetner and Ozaliddiversified in a small way out of reprographics but remained"dominant product" firms.

The companies shown in Table 5 all started out as single-technology firms within the office reprographics industry. Thiswas not the case with the next set of firms which diversifiedinto the reprographics market from adjacent industries. Therewere four "Dominant-Product " firms . IBM# 011yattlf A^ Mck ^A.M. - that entered the reprographics market at different stages.The most important of these was IBM entering in the early 1970'swhen the plain-paper copying business was growing very rapidly.

The third set of firms who entered the industry was the

24

^^ •AJ

1-^

VO

ON

MOol-l-t

1

h->

VOONo

ONO• I

VO|

Ln '

V

VO

V/»

oftftwX

ilvo

O

vo

O '

onOl

—.1

VOON I

o

VO|

°i

— ft

~ftvO<-n

On

Iw

vo ft

On .

X» '

voOv*>I

~ !

VO

X*

voUiOI

VOo%O

XP3ft

oX

-I

ONo,I '

MVO|

v-n|

—». o^» oVO ft-

OX^

Cs

1Da

t—t HVO >N> 1

a 1

I

voN> •

O I

I

t—

•

vo <

*-".

*,'I

vo

o

VO

o

o d 331—

<

X tn D ft S3 D ft S3 D ft S3<enoco>CD

<2

ftODC

raft>ft

<ft

S3Oa

ft

><n

S3o

ftft>

vO

H-

i

H aCO

S3 c ft c ft o"D CD ft CO n n CO o ft 1

o

l-l

o

MftMo>

3 a HftMo>

•-3 D MftMO>

ft ft h-1

vO

1g

z •-3

MO

ftMo

ftMo

II

2 2 z

—v; CO

•—1

o 2o aft

~c P3

2CO *CH TO

> C^^

co1

p"voro

I

t—

i

vo

o

S3o3>ftS3H

ft|

VO l

eno

|

Im|

voON '

o,

VO I

ONO 1

I

I

vo

o,

/ —J

^-^ S3t—

1

OVO i-3

-J >o ft1 S3(—

'

MVO 2oo •-3

o

HHoCO

H>33

H

e* O*>>ON "

VO I

X- I

O i

VOX*o1

I—

«

VOONCt

vo '

S<,!

2;

ft ft ICOM ft Ho 2S a CD

CO c fto 1 ft

votNJ

OI

ol

MlVO 1

o.I

r

If _ft.ft O M ft D» O CS3 VO ft OO 2 > >J O 21a h ft O O HC 2 H | C 2o > C3 M n >3 2 vo •-3 23

o»-3

^1

CD h-ft VO

h-ftcoco

OftI ftHZvonOS3

OI

CO

-a

ftft2 voft 00ft o

ftftOOGOftMo2

OS3oft

>ftGft(H

ft

CO

ft>CD•ft

Oft

CDS3Oft

oft

2OGCOftftk;

>ftw

25

^lated-Prodnrf Diversifies. Their diversification was relatedto their photo-chemical technology and the exploitation ofsynergistic links between the manufacture of optical equipment(cameras), photographic film or paper and'such supplies. Threeof these firms were American-based multi-national operations(Eastman Kodak, 3M and Nashua), one was European (Agfa-Gevaert)and three were Japanese (Canon, Minolta and Konishiroku).

The reprographics industry can be seen, thus, to havecomprised different kinds of firms. These are classified inTable 6. This classification suggests the following typology offirms:

(i) SINGLE TECHNOLOGY PIONEERS/INNOVATORS

(ii) SPECIALIZED SINGLE TECHNOLOGY FIRMS ENTERING LATEUii) DOMINANT-PRODUCT FIRMS ENTERING DURING GROWTH PERIODAND REMAINING DOMINANT-PRODUCT FIRMS °

WTH PERI0D

(IV) DOMINANT-PRODUCT FIRMS DIVERSIFYING FURTHER(V) RELATED PRODUCT FIRMS DIVERSIFYING ONLY RPfAncp nP

MARKET/TECHNOLOGY RELATEDNESSBECAUSE OF

(VI) UNRELATED PRODUCT FIRMS

TABLE 6 ABOUT HERE

in summary, it should be noted that there were three kindsof single technology firms: firstly, those which entered asPioneers and stuck to their technology. fiddly, those whoentered as pioneers but made strategic changes, and iMxdly thosethat tried to cater to a world market as specialized, low-costmanufacturers. The dominant category included a stable business(IBM) that had reached a settled position and those that were inthe process of diversifying further and were still groping for a

26

*1 |TJfChH 50 Z50 Oho2 o wc t-«

n >-3 1-3 •

TJ >0 50

s

27

final shape to their portfolio. Related Product Firms did notdiversify further, suggesting a settled strategy based ontechnology and market relatedness. These characteristics areshown in Table 7.

TABLE 7 ABOUT HERE

The next stage of the study involved an analysis of thecontent of strategy at different levels within firms. Inparticular, it examined whether there is any association betweenthis classification of strategic posture at the corporate leveland the operational strategies of firms.

TABLE 8 ABOUT HERE

Table 8 gives a preliminary classification of the types ofstrategies observed at the corporate level. The businessstrategies of these firms will now be discussed briefly. Inparticular, there will be a focus upon whether the study showsany symmetry or linkage between:

(i) the SCOPE of activities of firms and

(ii) the FUNCTIONAL strategies of firms.

TABLE 9 ABOUT HERE

Table 9 lists some of the strategic elements of firms thatstarted off as single technology f irms . It can be seen that ofthe firms that started as single-technology companies, there werethree types of business strategies found in the 1970 's.

(i) The hardwareStrate

cdware manufacturers who pursued a Monopolisinggy using four entry barriers based upon thei r

28

TABLE 7

SINGLE-TECHNOLOGYFIRMS

CHARACTERISTICS OF ENTRANT. TVTn ... „,.gm gJ

Timing of Entry Nature of Entry Strategic change Vertica._ „_ Intenrati'

(i) First-in :

Pioneers

(ii) First-in :

Pioneers

(iii) During

Innovation' Remain the same V.I.

1

Innovation Become Related- V.I.Product

growthBf ed

°n C ° St " Remai* th * sames °^ cn advantage Notnecessary

DOMINANT-PRODUCTFIRMS

(iv) Early-secondDuringgrowth

(v) Late entrant:Duringgrowth

Appeal of brand Remain the same V.I.name

Marketing network Diversify further Not fu 11

RELATED-PRODUCTFIRMS

(vi) Early-second:Duringgrowth

rTechnology ormarketrelatedness

Remain the same Notnecessary

29

TABLE 8

TYPES OF STRATEGIES OBSERVED AT THE CORPORA LEVE L

TYPE OF FIRM

1. Pioneer of thepast.

2. DynamicInnovators

SpecialisedLow-costproducers

Powerfulbrand-nameentrant

Other entrantsattempting to.exploitbrand names

Entrantsexploiting•synergy

CORPORATE STANCE (STRATEGY)Description

Single-Technology firms thatpioneered new products andremained single-technologyfirms or became Dominant-Product

Single-Technology pioneersthat attempted to becomeRelated Product firms sometime after their innovationsSpecialised Single-Technologyfirms entering the industryduring growth period

Dominant-Product firms enter-ing industry during growthperiod and remainingDominant -Product

Dominant-Product firms"

entering industry duringgrowth period and qoing infor further diversification

Related-Product firmsdiversifying into industrybecause of market/technologyrelatedness, and notdiversifying further.

FIRMS IN CATEGC

GestetnerOzalidRotaprintColumbia

XeroxLetrasetOfrexRicoh

Mita KogyoCopyer

IBM

AM.

A.B.DickOlivetti

Agfa GevaertCanonMinoltaKonishiroku3MNashua

30

>-3 enK —:*0 70m >

-9

WCDK

31

functional strategies (patents, marketing network,brand name, integration). This strategy was based onproduct differentiation. Those who had innovated newproducts were prone to following this strategy.

(ii) The low-cost manufacturers of hardware. This was astrategy of hardware. This was a strategy ofs^£cia_li2Linct in production and was not one ofdifferentiated marketing.

(iii) The suppliers of low-cost consumable products. Thiswas the siL2p_lle_s strategy in the pursuit of whichproduct differentiation could be important butmonopolizing posture was not adopted.

The next category of firms was that of the related productdiversifiers. These Related Product Firms diversified .into the

reprographics market because of marked and technology-relatedness. What distinguished them from the previous sets offirms was

££££&'. "" theY Were 2lready "lated-product(i)

(U).c^Slef "" "^ remained related product

(iii)

rtMbS'.that they did not follow the mon°P01 "i«g

The strategy of these firms was based on productdifferentiation, .and some of them (Canon, Minoita, Konishiroku)were also low-cost manufacturers. However, what distinguishedthem from the "monopolisers" was their policy towards

(i) patents

(ii) direct-selling networks

(iii) use of own-labels

(iv) vertical integration

(v) reliance on a single technology.

Along each of these strategic dimensions their policy wasdifferent from that of the single-technology firms discussed

32

earlier. This is shown in Table 10.

TABLE 10 ABOUT HERE

The discussion of content of strategy in the second stage of

the study can now be integrated to provide descriptors of firms:

a taxonomy of strategies. The taxonomy of firms (similar to

Vesper (1979)), and based mainly on supply-side characteristics);

that emerges from this industry is thus of:

(i) MONOPOLIZING - Eliminate competition, establishbarriers to entry, and controlresources.

(ii) COOPERATION - Join forces with competitor toensure survival and continuedeconomic performance.

(iii) SPECIALIZATION - Specialize in products and/orproduction process

(iv) SUPPLIES - supplier of low-cost consumableproducts

The taxonomy, which should help in identifying sensiblebases for strategic group formation is shown in Table 11.

TABLE 11 ABOUT HERE

The third stage of the study used both the historical

analysis and the strategy taxonomy to develop strategic maps, and

hence strategic groups of firms in the industry along important

strategic dimensions. Some of these maps are shown in Tables 12-

16.

TABLES 12 THROUGH 16 ABOUT HERE

In these strategic groups maps we have focussed upon

33

•-a

Kn

KXn

9nG

ooo<

2 rr-

•-a •ji

vn Hn Mxi n> >j fo2

Xo

o

CDX>CM

X so >r« XM *:o nk •-9

2

XI XI

O >H R

>

en

X>mMOo>X>nnxMco

|H

O

X

>

ai

xXoDGo

oo2:x>2:

IsCO

34

TABLE 11

A TAXONOMY OF FIRMS ACCORDING TO THEIR SCOPE OFACTIVATES AND PURSUIT OF BUSINESS STRATEGIES

STRATEGY CLASSIFTCATTnxr

LEVEL OF ANALYSIS

SCOPE SINGLE & DOMINANT PRODUCT RELATED PRODUCT

D £GENERIC^ DIFFERENTIATION DIFFERENTIATION

TYPE

LOW COST

Z_\A

1DIFFERENTIATION

MONOPOLISING SPECIALISATION SUPPLIES^ ±.

CO-OPERATION

FIRMS IBM GestetnerXerox Ozalid

Rotaprint

MitaCopyer

3MAgfaLetrasetOfrexColumbia

AgfaNashuaRicohKonishirokuMinolta

35

TABLE 12

COMMITMENTTO

~"X

.Sales

copy****,

'

)UPL\CftTiNG

/

WKueaddfd/salhs> £TxT£NT

OFVERTICALINTcG^^tioN

36

TABLE 13

SPECIALISATIONRftTlOA

3-0

•7

& i

•5-

VULNERABLEJ6 PRODUCTLIFE -CYCLEDECLINE

•3

'Xerox1975

Focu 5 StR3D

/

IBM/

^

i-

"5 ^ 5 g ^

f

VERyTHlMDispersal

R4D

>

37

TABLE 14

XEROA

MMUFfiCTuR^QMRRXZTINQ

MARKETING

L 1JJ Lji^t X J

AM3JTJOIX5

MANUFACTURING-

v!

MfiRKcTlNQ

MANUFACTURE

MARKETING

.'.»•.

'

39

TABLE 16

iXDDBX

P^TH

r

Ex/on I

BurroughsNCR

NCT;

-sAOctf^

40

TECHNOLOGICAL

COITH I,nj

"IMFOTECH"

strategic dimensions and competitive barriers that seem to

reflect the characteristics of the main types of strategies

identified in Tables 8 through 11.

For example, Table 12 shows the firms mapped in relation to

the extent of vertical integration (the length of the value-added

chain) and the degree of committment of the firm to office

reprographics (a variable which differentiates between single

product and related product firms). We have characterized the

positioning of firms in the mapping space in terms of opportunism

versus risk. It is apparent that some of the single-technologye

firms, - Xerox, Rotaprint, Ozalid and Gestetner - are adopting

risky strategies relative to the more opportunistic risk-balanced«

strategy of Canon.

Table 13, which maps the firm's specialization ratio against

its R&D capability shows the very traditional, single-technology

firms, e.g. Gestetner as being vulnerable to product life cycle

decline relative to the focussed R&D strategies adopted by Canon,

IBM and latterly Xerox.

Table 14 and" 15 together link the value-added dimensions to

the scope of product line and R&D capability. Indeed, Table 15

categorizes the groups according to the nature of technology (old

versus new e.g. Gestetner v. Xerox), marketing companies (e.g.

Nashua and Savin) and manufacturing oriented, process innovation

types of companies (e.g. Canon, Ricoh). The arrows on Table 15

show the problems faced by the old technology companies in

determining which strategic moves they should follow. Should

they target movement to a manufacturing grouping, a technology

grouping or define a new grouping based on cooperation and

41

focussedness of skills?

Table 16 is a more speculative mapping in that it seeks tocapture the potential behavior of new entrants and competitors(i.e., competition acx^ as well as H Jth in industries) from awider -industry" setting-information technology. An entry pathfor Kodak is drawn in order to show a direction of entry. WhatBurroughs or NCR might do, or the positioning of Sharp on thisspace, provides creative, insightful questions for the strategistin developing strategic posture.

These strategic group maps, therefore, provide usefulcognitive frames for making sense of the sets of current andfuture strategic positions which are possible as thereprographics industry evolves.

in summary, it is clear that this type of "rich" industrystudy, although limited mainly to Britain, provides a valuablelongitudinal analysis rather than a cross-sectional snapshot ofcorporate strategies. This allows strategic patterns to beidentified (see Table 5) and- throws light upon the strategiccharacteristics of first-movers in technology i„ comparison tolater, perhaps more product-diversified entrants. r„ addition,types of strategies and kev strata,,*,, a*Y snra tegic dimensions can beidentified which, in turn, means i-h^

'means that m°re relevant strategic

groupings can be formed.

This studv also l ph 4-^ *.w~ ^y *±so led to the formulation of conclusionsregarding the behavior of firms in rj^i^jnrms in declining businesses, the formof new entry competition and the* r»™^or, c • -,ana tne process of industry evaluation.These are summarized as follows:

42

(i) Behavior of Firms in Declining Industries

When the threat of technology change is perceived, thefirst response of firms is to improve their old products.As a result the old technology reaches its peak after theadvent of the new technology. The need, however, is forsuch firms to re-define their business. It emerges that thesingle-technology reprographics firms of half a century agowhich failed to do so found themselves relegated to aninsignificant position, while the successful firms are thosethat continually re-defined their concept of their businessacross industries.

(ii) The Forms of New Entry

The process of new entry in this study was analyzedwithin the framework of the firm's strategic decisions andthe strategic groupings within and across industries. It isfound that firms may enter one or more market segments andfirms operating in one segment may move to another.Movement in or out of segments may be determined not so muchby the - industry-wide barriers'as* by mobility barrierssurrounding particular segments. This also provides theopportunity for firms to make a gradual entry into anindustry, treating each investment stage as an incrementaldecision.

(iii) The Process q£ Industry Evolution

Step-changes in technology lead to changes in marketstructure and competitive conditions and to the formation ofnew sets of competitors. The entry strategy chosen by thesecompetitors is also important in determining the change inmarket structure. The height of entry barriers changes,cost conditions change and new ways of segmentation becomeavailable to suppliers as the extent and nature of productdifferentiation changes.

Although market structure does influence the conduct offirms, this structure is itself, to a great extent, theoutcome of the strategic decisions of firms. It is thesestrategic moves, together with the technological changescausing disturbances in market structure, that lead to theformation and re-formation of "strategic groups".

Conclusion ?

The concept of research based upon "rich" industry histories

has been explored in this paper. The premise is that insights

about strategic interaction and the formulation of competitive

43

strategy within industries should be based upon examination not

only of current strategic conduct but also of the evolution ofindustry structure. The reprographics study suggests that thestudy of sources of complexity within industries, of the processof industry evolution, of the emergence of new strategies andcompetitors and of strategic groupings illuminates our ability tomake sense of competitive strategy. y e t no study can be "rich-enough or exhaustive enough in scope (whether geographical oranalytical) to address all problems. But it can highlight thedynamic nature of industry evolution, the range of strategies «dpositions occupied by firms over time and the sometimes temporarynature of market leadership by -f irst-movers^ or pioneers inmarkets.

What is needed now is a consolidation of research themes andthe development of richer theory at the firm level. Singleindustry studies focussed on competitive strategy must requirethe use of existing economic .theory as a benchmark model and alsoengineer the incorporation of the richness of firm-level behaviorinto the newer "strategic theories of the firm". Porter (1980and 1982), Porter and Spence (1982), Caves (1980), Teece (1980)and Rumelt (1981) are "first-movers" in this endeavor. They willclearly be further aided by additional industry studiesincorporating the strengths of the industry history approach.

44

REFERENCES

Ackoff, R. L., A Concept oj; Corporate Planning, New York: JohnWiley and Sons f 1970.

Adams, W., The Structure of American Industry (5th ed ) NewYork: MacMillan, 1977. If

Aldrich, H., Organizations and Environments. Enqlewood CliffsN.J.: Prentice-Hall, 1979. '

Andrews, K. R., The Concept of Corporate Strategy, Homewood,111: Richard D. Irwin, Inc., 1971.

Bateman, F., "Business History in an Era of EconomicTransformation," Business and Economic History . 2nd SeriesVolume 12,. BEBR, (eJ. J. Atack) pp. 1-13, 1983.

Boulding, K. E., "General Systems Theory - The Skeleton ofScience," Management Science. 2, April 1956, 197-208.

Bower, J. L., "Business Policy in the 1980's," Academy ofManagement Review, Vol. 7, No. 4, 1982, pp. 630-638.

Caves, R. E., "Industrial Organization, Corporate Strategy andStructure: A Survey," Journal QL Economic LiteratnrP

r 1980,loll; , pp. o4-92.

Caves, R. E. and M. E. Porter, "From Entry Barriers to MobilityBarriers: Conjectural Decisions and Controlled DeterrenceQ? ™ o^PeoVoti0n '" Quai:terl y J° u^al QL Economics - 1977,

Chaffee, E. E , "Three Models in the Strategy Construct," Working. Paper, NCHEMS, Colorado, September 1983.

nvmang

Chandler A. D. Jr., fitxatfigg and Structure; Chapters in thfl

1>if«gY

?f*te IndugtCAal Enterprise, Cambridge, Mass: MITrress, ±yOZ.

Chandler, A. D. Jr., Ihs Visible Hand; ftg Managerial RevolutionAD amSXjlgan fiUSjJliLSS, Cambridge, Mass: Harvard University

Christensen, C, Andrews, K. R., Bower, J. L ., Hamermesh, R. andM. E. Porter, Business Policy: Text and Cases (5th ed.),Homewood, 111: Richard D. Irwin, 1980.

Cole, A., Business Enterprise in its Social Setting, Cambridge,Mass: Harvard, 1959.

Denzin N. R , The Research Act (2nd ed.), New York: McGraw-"111,1978.

45

DrUCkRow,

Pi98?.

a,m * ng ^ TWCb" 1ffnt H^' New Y°^: Harper and

•

Freernr?m'hr

CV

ThM

Economics of Industrial Innovation (2nd ed)Cambridge, Mass: MIT Press, 1983.

Galbraith, C. and D. E. Schendel, "An Empirical Analysis ofstrategy Types," stxatsais flanaafiiDfint JaiixnA, 4, 2Yf llelf

Ghazanfar, A., "Analysis of Competition in the Office Reorographics Industry in the n v » djT n mu •Repro-

Business School,' 1984.'

" "Thesis

- London

Gluck, P. w., "Global Competition -in the 1980's " Journal „fBminZZZ Stxatsgy, vol. 3, No. 4, Spring .1983Vppf^il. **

^"Mc'cr^-tfff^uf11^ "^ *t"^ flailMfiasflt, New York:

"^"sta^^l^ Thomas, "Understanding the Strategic Behayior offllintis 1mV?/"S' W° rking Paper

'BEBR

' diversity of

7 Hamb

|^^s^u«^Kana_qme n t, Vol. 10, No. 1, pp. 27-43.lssues

' ilojixjial Ql

Harrigan, K. R., "Research Methodo 1 oq i es for r rt «4-*Approaches to Business Strategy,-9AcIdi? ofContingency

SegilSK, 8, 3, July 1983, 398-40?!AcadeiW ^ ^a^emeni

Hatten, K. J., Strateqic Models i n *- v^ dUnpublished doctorai%is srtVtiU%u\Vun7y1e

nrgsit

I

yn

,

dUlS

974r

r-Hatte

sntrateg^c Marked: ^ITc'^T^^^ S^' I"

Hatten, K. J. and D. E. Schendel "h«*-^*.~

Huff

'^^"^SLi-iiSryo !". -aViV.? SfSiS!-'Hunt, M. S., Competition in the Ma-inr u^m« * -• •

s?^.9a

>

9

n7riished -<^»vx.i?tVffo

c.:"ees

J1C%^uS Ini

Actfo^1i^^^-f--iye Methods:

vol. 24, 1979, pd. 602-611 ^Qin^i^ti^ £cmmcj> Quarterly,

46

Kantrow, A., "The Technology/strategy Connection," HarvardBusiness Review , 1980. ' ^^^

Kogut, B., "Normative Observations on the International Value-Added Cham and Strategic Groups," WP-84-04, Reginald HJones Center, Wharton School, February 1984.

Lawrence, P. R. and D. Dyer, Renewing American Industry, NewYork: Free Press, 1983.

Mansfield, E., Industrial Research and Technological Innovation.Norton, 1968.

Mansfield, E., et al, The Production and Application of NewIndustrial Technology, Norton, 1977.

McCaskey, M. B., The Executive Challenge, Marshfield, Mass-Pitman, 1982.a

'wass.

McGee, J. and H. Thomas, "Strategic Groups: A Useful LinkageBetween Industry Structure and Strategic Management,"Working Paper, Center for Business Strategy, London Businessschool, (forthcoming in Strategic Management Journal)

Mervis, C. B. and E. Rosch, "Categorization of Natural Objects,"Annual Review of Psychology, 1981, 89-115.

Miles, R. E. and C. C. Snow, Organizationa l Strategy. Structure,

ajid Prices., New York: McGraw-Hill, 1978.*^^vufcs

Nelson, R. R. and S. G. Winter, An Evol utionary Theory of\ ^Qnonuc Change , Cambridge, Mass: Harvard University Press,

Pondy, L. R. and I. I. Mitroff, "Beyond Open Systems Models ofOrganizations," in B. M. Staw (ed.), R££e_a£c_n injrqan iLzatlon a l , gehavior., Greenwich, Ct: JAI Press, 1979, 3-

Porter, M. E., Competitiyp Strategy,. New York: Free Press, 1980.

Porter, M. E., "Strategic Interaction: Some Lessons From"H^y Histories for Theory and Anti-Trust Policy," pp.

Anti-Tr Uf

< S f-

inAn«i

eve " C--s5lop

,

(edJ ®*ates&* Predation f a^Anti Trust Ana l ysi s, Federal Trade Commission, Washington,D.C., September 1981.

Porter, M. E., Cases In Competitive. Strategy . New York: FreePress, 1982.

Porter, M. E and A. M. Spence, Capacity Expansion in the Corn-Wet Milling Industry in J. J. McCall (ed.) Economics o^Uncertainty, North-Holland, 1982.

**

47

ReiCh1983.

B" The N6Xt AmeriCan Front ier, New York: Times Books,

Robinson, ^Joan, "The Industry and the Market,- Economic Oournal,

Rumelt, R P., Strategy, Structure and Economic Performs™Cambridge, Mass: Harvard University Press, 1974.'

Rumelt, R. P., -Towards a Strategic Theory of the Firm » oanorprepared for a conference oh non-traditionll approache^toK^^^ff^. SCh001 ° f BUSlneSS'"SEES* S

Sal °PAnal

Sysi

Cs',. ^hing^D.'c!:' Ve^Ved^ ^"™September 1981.

Federal Trade Commission,

"atAii!*^.?: .222. Ho'rfJn^r^/— ^

scheifo-n- flf-^ia ess ^r-a^-ssK

^'MacMUl^, l^.8"" "' IndUStry

*nd Co-petition, London:

Shepherd, w. G., The Economics of Industrial (,„»„ .•Englewood Cliffs, N.j. : Prentice-Hall Inc., 1??I.

10B '

SPendper

r

eseJnte

Cd'at

BCon

nr S P ° liCy an<3 I»°™try Recipes," Paperpiebencea at Conference on Non-Tr^^ifi-An,! *^a^ci.

Policy Research, University" of"southern cSorSfa?^!! ^

^^ITsons' ft' z^^Ts^t^r^l Inte"=tion: somePolicy,'" in s c LL,„ ?k

£-

0t Theory and Anti-Trust*<•*» in s>. c. Salop (op-cit.), 1981, pp. 511-22

48

Thorny, H. f "Mapping Strategic Management Research," Journal ofSenega l MnmemmlL, Vol. 9, No. 4, Summer 1984, PP 55-7 2.

Vesper, K. (1979)

Williams JR., "The Productivity Base of Industries," W.P. 19-83-84, GSIA, Carnegie-Mellon University, May 1984.

Willpress,

n'i°9

C

75E:'

MiU*^ «* ^^Mes, New York, NY: Free

^^^u^'j^^a^S^^r' °riginS' solution,

et seq.jQMrnaI ** ^cojiomis Literature 19, 1981, pp. 4

49

HECKMANBINDERY INC.

JUN95Bound -To -Pica*? N.MANCHESTER

INDIANA 46962