LIVE d-MOVI~ - NSE

60

5 th August, 2019 The Secretary BSE Limited P J Towers Dalal Street Mumbai – 400 001 Scrip Code: 532706 The Manager National Stock Exchange of India Limited Exchange Plaza, 5th Floor, Plot No C/1 G Block, Bandra-Kurla Complex Bandra (East), Mumbai – 400 051 Scrip Code: INOXLEISUR Dear Sir / Madam, Sub: Disclosure of Material Events / Information under Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 - Schedule of Analysts / Investors Meetings. Pursuant to Regulation 30 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, we would like to inform you that the Company has scheduled Analysts / Investors Meetings as per details given below: Date Event Interaction with Type of Meeting City August 6, 2019 – August 8, 2019 Non-Deal Road Show with HSBC Various Analysts / Investors One on One / Group Meetings Hong Kong / Singapore Please note that no unpublished price sensitive information is proposed to be shared during the meeting(s). A copy of the Investor Presentation prepared by the Company which we propose to make to the Analysts / Investors during the above Investor Conference is enclosed and the said Investor Presentation has also been uploaded on the Company’s Website at https://www.inoxmovies.com/Corporate.aspx?Section=3 Note: The above schedule may undergo changes due to exigencies on the part of the Analysts / Investors or the Company. You are requested to take the same on record. Thanking you, Yours faithfully, For INOX Leisure Limited Parthasarathy Iyengar Company Secretary INOXLEISURE LTO. 51!1Floor,VW11j1-1;,Nu1t1Ardllllflyower.Wft1em~H,gllwlyAnttolri(Eall~J.tJml:ial "IXI093,lnl;l,a. Titl(9122}40626900 · Fa (ll122).Wll999 · E. ~.oom•-Jnomo,,,N.oom it.gillel'l'CIOlfic• :"8STOW9tl,OldP..:l,.Ro.d,'hdoda'IIJ90007•Ttll(91265}61911111 • Fa(ll1265)Z310312 • CIN. l921119GJ11199Plco,i..o.&5 LIVE d- MOVI~

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of LIVE d-MOVI~ - NSE

5th August, 2019 The Secretary BSE Limited P J Towers Dalal Street Mumbai – 400 001

Scrip Code: 532706

The Manager National Stock Exchange of India Limited Exchange Plaza, 5th Floor, Plot No C/1 G Block, Bandra-Kurla Complex Bandra (East), Mumbai – 400 051 Scrip Code: INOXLEISUR

Dear Sir / Madam, Sub: Disclosure of Material Events / Information under Regulation 30 of

SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 - Schedule of Analysts / Investors Meetings.

Pursuant to Regulation 30 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, we would like to inform you that the Company has scheduled Analysts / Investors Meetings as per details given below:

Date Event Interaction with

Type of Meeting

City

August 6, 2019 – August 8, 2019

Non-Deal Road Show with HSBC

Various Analysts / Investors

One on One / Group Meetings

Hong Kong / Singapore

Please note that no unpublished price sensitive information is proposed to be shared during the meeting(s). A copy of the Investor Presentation prepared by the Company which we propose to make to the Analysts / Investors during the above Investor Conference is enclosed and the said Investor Presentation has also been uploaded on the Company’s Website at https://www.inoxmovies.com/Corporate.aspx?Section=3 Note: The above schedule may undergo changes due to exigencies on the part of the Analysts / Investors or the Company. You are requested to take the same on record. Thanking you, Yours faithfully, For INOX Leisure Limited

Parthasarathy Iyengar Company Secretary

INOXLEISURE LTO. 51!1Floor,VW11j1-1;,Nu1t1Ardllllflyower.Wft1em~H,gllwlyAnttolri(Eall~J.tJml:ial "IXI093,lnl;l,a. Titl(9122}40626900 · Fa (ll122).Wll999 · E.~.oom•-Jnomo,,,N.oom ~

it.gillel'l'CIOlfic• :"8STOW9tl,OldP..:l,.Ro.d,'hdoda'IIJ90007•Ttll(91265}61911111 • Fa(ll1265)Z310312 • CIN. l921119GJ11199Plco,i..o.&5

LIVE d-MOVI~

I nve st or

P re se nt at ion

August 2019

Disclaimer

2

This presentation and the following discussion may contain “forward looking statements” by Inox Leisure Limited (“ILL” or “theCompany”) that are not historical in nature. These forward looking statements, which may include statements relating to future stateof affairs, results of operations, financial condition, business prospects, plans and objectives, are based on the current beliefs,assumptions, expectations, estimates, and projections of the management of ILL about the business, industry and markets in which ILLoperates.

These statements are not guarantees of future performance, and are subject to known and unknown risks, uncertainties, and otherfactors, some of which are beyond ILL’s control and difficult to predict, that could cause actual results, performance or achievementsto differ materially from those in the forward looking statements.

Such statements are not, and should not be construed, as a representation as to future performance or achievements of ILL. Inparticular, such statements should not be regarded as a projection of future performance of ILL. It should be noted that the actualperformance or achievements of ILL may vary significantly from such statements.

Due to rounding-off, figures presented throughout this document may not add up precisely to the totals provided and percentagesmay not precisely reflect the rounded-off figures.

FY15 financial figures are as per IGAAP and for FY16 and thereafter are as per IND-AS. Revenues for FY15 are shown net ofentertainment tax, to be consistent with the revenues under IND-AS for FY16 onwards

3

D I S C U S S I O N S U M M A R Y

I N D U S T R Y O V E R V I E W

C O M P A N Y O V E R V I E W

C O M P E T I T I V E A D V A N T A G E & O U T L O O K

A N N E X U R E

1Ne ·x BRINGS TO YOU

SPECTACULAR CINEMA FORMATS

4

INDUSTRY OVERVIEW

Strong Fundamentals & Huge Growth Potential

5

125

95 80

60 57 40 37

26 25 12 10 8

US France Spain UK Germany South Korea China Japan Taiwan Thailand Brazil India

H o w e v e r , I n d i a ’ s S c r e e n D e n s i t y i s O n e o f t h e L o w e s t

Screens / Million population

Source: CRISIL Report, http://uis.unesco.org/en/news/cinema-data-release (2015), Industry sources and internal calculations

2,178 1,930

1,364

208 197 176 171 169 156 146

China India US France Mexico UK Japan S. Korea Germany Russia

2 n d H i g h e s t N u m b e r O f T h e a t r e F o o t f a l l s i n t h e W o r l d

Footfalls in Million2,000

791686

581

300 298 269 255 226 185

-4 00

100

600

1,10 0

1,60 0

2,10 0

India US China Japan France UK S. Korea Spain Germany Italy

H i g h e s t N u m b e r o f F i l m P r o d u c e d i n t h e W o r l d

.,1 .I .1 I : , ____ .,

,l ,I

1 .• , ■ , • . • . •

1 . ■ . ■ . ■ . ■ - r -

• r •

I I I I I I , ____ .,

Steady Performance and Resilience

6

96.3 102.1 110.0130.0

155.5174.5

194.2

236.1

0.0

50.0

100.0

150.0

200.0

250.0

2017 2018 2019E 2021EDomestic Theatrical Overseas Theatrical Broadcast rights Digital/OTT rights In-cinema advertising Home Video

In Rs. Billion

I n d i a n F i l m I n d u s t r y D i s p l a y s S t e a d y P e r f o r m a n c e T r e n d s

D o m e s t i c T h e a t r i c a l s C o n s t i t u t e s 5 9 % O f T o t a l F i l m I n d u s t r y

Source: FICCI-EY 2019 Report

59%

17%

12%

8% 4% 0%

Domestic Theatrical

Overseas Theatrical

Broadcast rights

Digital/OTT rights

In-cinema advertising

Home Video

2018

■

IN

_________________________________ CA.GB~1% -------------------------------+ --■

■

■

■

■

■

X

Multiplexes Witnessing Rapid Growth

7

FACTORS DRIVING GROWTH IN

MULTIPLEXES:

Strong demographics, rising disposable

incomes and discretionary spends.

Superior location, destination and

parking facilities.

Multiple screens in one location offer a

wider variety of content to the patrons.

Different screen sizes provide

programming flexibility. This results in

higher occupancy ratios.

State of art equipment (high quality

video and audio), superior interiors,

ambience and service.

Source: FICCI-EY Report 2018 & 2019

M u l t i p l e x e s c u r r e n t l y a c c o u n t f o r ~ 3 1 % m a r k e t s h a r e o f t h e s c r e e n s ,

h o w e v e r t h e y a c c o u n t f o r ~ 5 5 % o f b o x o f f i c e c o l l e c t i o n s

Number of Screens

9,710 9,121 8,451 7,400 7,031 6,780 6,651

925 1,225

1,500 2,100 2,450 2,750 2,950

10,635 10,346 9,951 9,500 9,481 9,530 9,601

-

2,00 0

4,00 0

6,00 0

8,00 0

10,0 00

12,0 00

14,0 00

16,0 00

2009 2011 2013 2015 2016 2017 2018

Single Screens Multiplexes

T T T

■

Increasing Number Of INR 1bn + Movies

8

1,000 1,598

2,065 2,101 2,638

3,014 3,446 3,359

5,200 4,500

5,300

6,500

4,500

6,900

-

1,00 0

2,00 0

3,00 0

4,00 0

5,00 0

6,00 0

7,00 0

8,00 0

3 Idiots(2009)

Dabaang(2010)

Bodyguard(2011)

Ek Tha Tiger(2012)

Dabaang 2(2012)

ChennaiExpress(2013)

Dhoom 3(2013)

Kick(2014)

P.K(2014)

BajrangiBhaijaan(2015)

Dangal(2016)

Bahubali 2 -The

Conclusion(2017)

Tiger ZindaHai (2017)

2.0 (2018)

1 2

5 9

6 7 5

8 7 10

5

1

2 1 1

- 1

2

3

- --

-

-- 1

1

2 2

3

1

-

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Jul-19

INR 1Bn to 1.99Bn INR 2Bn to 2.99 Bn INR 3Bn and above

Wider Screen Releases

Higher Number Of INR 1 Bn + MoviesINCREASING NUMBER OF

MOVIES ARE GENERATING

MORE THAN RS 1 BN IN NET

BOX OFFICE COLLECTIONS

DRIVEN BY WIDER SCREEN

RELEASES AND FACILITATED BY

DIGITISATION OF CONTENT

DELIVERY

Source: Industry

■ ■ ■

I n d i a ’ s C o n s u m p t i o n S t o r y

9Source: Mckinsey - Tracking the growth of Indias Middle Class - 2017

6148 39 30

3952 61 70

1995 2005 2015 2025

Necessities Discretionary

%Share of Average Annual Household Consumption

%Share of Population by Income Bracket

9380

54

3522

618

41

43

36

1 25

22

42

0

10

20

30

40

50

60

70

80

90

100

1985 1995 2005 2015 2025

Lower Class Lower Middle Class Middle & Affluent Class

755 928

1,107 1,278

1,429

-

200

400

600

800

1,00 0

1,20 0

1,40 0

1,60 0

1985 1995 2005 2015 2025

Population of India (Million)

Based on Annual Household Income: Lower Class: < Rs.90,000 , Lower Middle Class: Rs.90,000 to Rs.199,999 , Middle & Affluent Class: > Rs.200,000

702 742 598

447 314

45 167 454

550

514

8

19

55 281 600

-

200

400

600

800

1,000

1,200

1985 1995 2005 2015 2025

Lower Class Lower Middle Class Middle & Affluent Class

Share of Population by Income Bracket (Million)

■ ■ ■

■ ■ ■

■ ■

IN

.------.

-----.

t •= I I

it I --1 -I I I I

X

10

Company Overview

INOX Nehru Place, Delhi

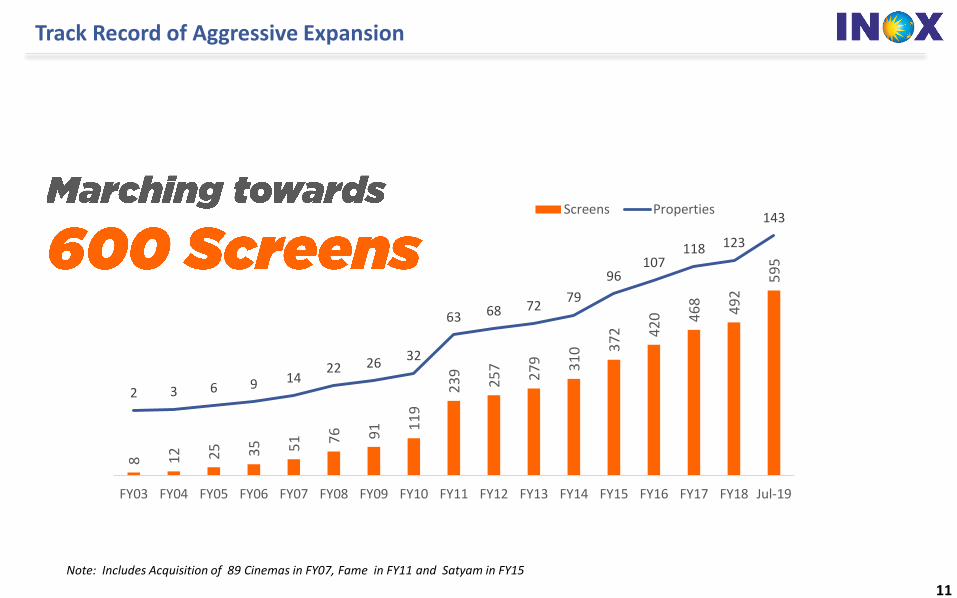

Track Record of Aggressive Expansion

11

Note: Includes Acquisition of 89 Cinemas in FY07, Fame in FY11 and Satyam in FY15

8 12 25 35 51 7

6 91 1

19

23

9

25

7

27

9 31

0 37

2 42

0 46

8

49

2

59

5

2 3 6 9 1422 26

32

63 68 7279

96107

118 123

143

-50

0

50

100

150

200

0

100

200

300

400

500

600

700

800

900

1000

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 Jul-19

Screens PropertiesMarching towards - -600Screens

- - - ■ ■ I I I I I

PAN India Presence

12

ONE OF THE LARGEST MULTIPLEX CHAIN OPERATOR IN INDIA

* Includes 8 management properties with 29 screens and 7,370 seats

KERALA |1 Property | 6 Screens

19States

67Cities

143Properties

595Screens

139,797Seats

JHARKHAND | 1 Property | 4 Screens

WEST BENGAL | 15 Properties | 59 Screens

ODISHA | 4 Property | 14 Screens

CHHATTISGARH | 2 Properties | 8 Screens

TELANGANA | 3 Properties | 19 Screens

ANDHRA PRADESH | 8 Properties | 33 ScreensKARNATAKA |12 Properties | 49 Screens

GOA | 4 Properties | 14 Screens

MAHARASHTRA | 28 Properties | 130 Screens

GUJARAT | 20 Properties | 81 Screens

MADHYA PRADESH | 5 Properties | 22 Screens

RAJASTHAN | 13 Properties | 47 Screens

HARYANA | 6 Properties | 19 Screens

TAMIL NADU | 5 Properties | 31 Screens

UTTAR PRADESH | 8 Properties | 31 Screens

DELHI | 5 Properties | 16 Screens

PUNJAB | 2 Property | 10 Screens

Assam | 1 Property | 2 Screens

IN X

13

INSIGNIA – LUXURY MOVIE

WATCHING EXPERIENCE

R-City Ghatkopar, Mumbai

14

Atria, Worli, Mumbai

15

CR2, Nariman Point, Mumbai

16

Atria, Worli, Mumbai

17

R-City, Ghatkopar, Mumbai

18

Palm Beach, Navi Mumbai

19

INOX Epicuria, Delhi

20

INOX Metro, Mumbai

21

INOX GT Central, Jaipur

22

INOX Malad, Mumbai

23

INOX Marina Mall, Chennai

24

IN• :X L I V E IAt M O V I E

~ -x~eeclf.#t; expectationsc' ..

MOST AWARDED MULTIPLEX OF THE YEAR INOX LEISURE

ET BEST BRANDS

2018-19

BEST TECHNOLOGY OFTHEYEAR

t IMAX BIG CINE AWARDS

2018

POPULAR MULTIPLEX

TIMES RETAIL ICON AWARDS

2018-19

BEST MARKETED

BRAND KOTLER AWARD OF EXCELLENCE

2018-19

MULTIPLEX CHAIN OFTHEYEAR

AT IMAX BIG CINE AWARDS

2018

HIGHEST LUXURY STANDARDS

AT INTERNATIONAL FILM BUSINESS AWARDS2018

MOST ADMIRED MULTIPLEX OF THE

YEAR AT ET NOW GLOBAL AWARDS

FOR RETAIL EXCELLENCE

BEST EMPLOYER OFTHEYEAR

AT EMPLOYER BRANDING AWARDS 2018-19

25

Highest “EBITDA to Capital

Invested” Ratio in the Industry

Highest PAT Margin

in the Industry - Q1FY20

Highest Ad Revenue Growth

Rate in the Industry for

Highest Q1FY20 Footfalls

Growth in the Industry

First National Chain

in the Industry to be

Excludes Ind AS 116 impact

8%

9 Consecutive Quarters

Net Debt Free

CORDS CONSISTENTLY

26

Revenue

Rs.493crs

19%YoY

EBITDA

Rs.89crs

6%YoY

PAT

Rs.41crs

11%YoY

Footfalls

1.73crs

11%YoY

SPH

Rs.816%YoY

Excludes impact of Ind AS 116 Excludes impact of Ind AS 116

Ad Sales

Rs.47crs

18%YoY

27

INHGNIA ,~ors SIi.NATURE

EXPERIEIICE

BRINGS YOU

SCAEEN:xt: Onyx 'Di11ef WOltUl'S MOST IIIMfRSl'IE

MOVIE EnRAVAGANZA! IKlll.l'S FIRST M:UO CINEl\lA

ntAT 5nMULATES All YOUR SENSES

LASER 30if., BRIGHTER

IIIDIA'S FIRST 270 DE~REE l'Jl1'01tAM-IC

MOYIE WATCIUKG EXPERIENCE

AFFDROAlllf LUXURY ntf LARC.E SCREEN EXPERIENCE

ANO SHARPER Pi<OJECTlON FOIi THE $MARTIR GENERATION DEDICATEll llD'S

P\AY ZONE

MUllll.til'S FIRST LED SPECJACIJLAl'I SCREEN

Overview of IND AS-116 “Leases”

28

New Accounting Standard-116 on Leases is effective from 1st April 2019

No Distinction between Finance and Operating Lease now.

All Leases to be recognised in financials as assets and liabilities (No off-BalanceSheet Rights/Obligations) with exceptions available for immaterial leases andshort term leases (less than 12 month)

Calculation of Assets (Rights) and Liabilities (Obligations)- Lease liability- Calculates Net Present Value (NPV) of lease rent

payment over full lease tenure (discounted at incremental borrowingrate ).

Right of use (ROU)-Initially measured at the amount of lease liabilityadjusted for lease prepayments if any. ROU is depreciated over leaseterm on straight line basis.

Lease liability and ROU will be NIL at the end of the Lease term.

Impact on Profit and Loss Statement - Operating lease expense (fixed part) willbe replaced by depreciation and interest cost, impacting EBITDA, EBIT, PBT andPAT.

Transitional Approach- Company has followed Modified Retrospective approachfor transition to IND AS-116. This approach does not require restatement ofcomparative information for earlier period. The cumulative effect of initiallyapplying the standard is recognized as an adjustment in retained earnings netof deferred taxes.

Ind AS 116 Transitional Impact on Balance SheetAs on 1st April 2019

Right of Use - Assets Rs.1,663Crs.

Lease Liability Rs.2,192Crs.

Impact on Retained EarningsRs.344Crs.

Impact on Deferred Tax AssetRs.185Crs.

LIVE l'/4 MOVIE

Q1FY20 P&L Impact Analysis of Ind AS 116

29

INR Crs.

ParticularsQ1FY20

Reported

Ind AS 116

Impact

Q1FY20

Without

Ind AS 116

Q1FY19 YoY%

Revenue from Operations 493 493 415 19%

Total Expenses * 343 61 404 331 22%

EBITDA 150 -61 89 83 6%

EBITDA Margin(%) 30% 18% 20% -2%

[-]Depreciation 61 -35 26 23 14%

EBIT 89 -26 63 61 3%

[-]Interest 51 -48 3 7 -62%

[+]Other Income 3 3 3 10%

PBT 42 22 63 57 12%

[-] Tax 15 8 22 20 12%

PAT 27 14 41 37 11%

PAT Margin(%) 5% 8% 9% -1%

Basic EPS (Rs.) 2.75 1.45 4.19 4.03 4%

*Ind AS 116 - Rent Impact

IN LIVE l'/4 MOVIE

30

ICC WORLD CUP LIVE SCREENING

AT INOX

INOX PARTNERS WITH IPL RAJASTHAN

INOX ROYALS TEAM PARTNERS WITH INDIAN NATIONAL

RALLY CAMPIONSHIP lFMSCIJ

INOX PARTNERS WITH

RP-SG MAVERICKS FOR

ULTIMATE TABLE TENNIS

R e v e n u e f r o m O p e r a t i o n s

31

All figures in INR Crs., unless specified

415 493

-

100

200

300

400

500

600

Q1FY19 Q1FY20

19%

26%

1,348 1,692

-

200

400

600

800

1,00 0

1,20 0

1,40 0

1,60 0

1,80 0

FY18 FY19

895

1,161 1,221 1,348

1,692

FY15 FY16 FY17 FY18 FY19

t

t

E a r n i n g s B e f o r e I n t e r e s t , Ta x ,D e p r e c i a t i o n a n d A m o r t i z a t i o n [ E B I T D A ]

32

All figures in INR Crs., unless specified

123

189

146

210

309

14%

16%

12%

16%

18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY15 FY16 FY17 FY18 FY19

EBITDA EBITDA Margin %

83 89

20% 18%

0%

5%

10%

15%

20%

25%

-

10

20

30

40

50

60

70

80

90

100

Q1FY19 Q1FY20

EBITDA EBITDA Margin

210 309

16%

18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

50

100

150

200

250

300

350

FY18 FY19

EBITDA EBITDA Margin

47%

Note: EBITDA excludes Other Income (non-operating)

6%

Excludes Ind AS 116

__ .. GO "'lf,0/o --------

c~ I''"----------------

---

-t

- -

P r o f i t a f t e r t a x [ PAT ]

33

20

81

31

115

133

2%

7%

3%

9%8%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-

20

40

60

80

100

120

140

FY15 FY16 FY17 FY18 FY19

PAT PAT Margin %

37 41

9% 8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

-

5

10

15

20

25

30

35

40

45

50

Q1FY19 Q1FY20

PAT PAT Margin

16%

115 133

9% 8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-

20

40

60

80

100

120

140

160

FY18 FY19

PAT PAT Margin

All figures in INR Crs., unless specified# Includes tax write back of Rs.54crs (FY18) and Rs.5crs (FY19)

11%

# #

Excludes Ind AS 116

.,,.. .,,. .,,,. .,,.. --- -

-

,:_'I ol - - ... c~GR u.1.70 - - - - - - - - - -- ---.,,...,.,..,,.--

-

IN

-t =

-t

R e v e n u e s - S e g m e n t B r e a k u p

34

All figures in INR Crs., unless specified

552 713 748 802

975 191

266 284

306

436

81

91 96

139

176

71

91 92 101

105

895

1,161 1,221

1,348

1,692

-

200

400

600

800

1,00 0

1,20 0

1,40 0

1,60 0

1,80 0

2,00 0

FY15 FY16 FY17 FY18 FY19

NBOC F & B Advertising Others

242287

111

13240

4722

26415

493

0

100

200

300

400

500

600

Q1FY19 Q1FY20

802975

306

436139

176

101

105

1348

1692

0

200

400

600

800

100 0

120 0

140 0

160 0

180 0

200 0

FY18 FY19

3%

27%

42%

22%

22%

18%

19%

19%

ol - -Go \11° ____ _

c.~ ·" --------

■ ■ ■ ■

• • • •

• • • •

F o o t f a l l s a n d O c c u p a n c y R a t e

35

All figures in Lakhs, unless specified

156 173

29% 30%

3%

8%

13%

18%

23%

28%

33%

80

100

120

140

160

180

200

Q1FY19 Q1FY20

533 625

26%28%

3%

8%

13%

18%

23%

28%

33%

-

100

200

300

400

500

600

700

FY18 FY19

11%

17%

411

534 537 533625

25%

29%28%

26%

28%

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

800

FY15 FY16 FY17 FY18 FY19

Footfalls Occ%

__ .,. ol -----

Go" 'l,:10 _ - - - -c~ "~-----

~ --- ----- I ----------t

- t

A v e r a g e T i c k e t P r i c e [ AT P ]

36

164 170 178193 197

FY15 FY16 FY17 FY18 FY19

All figures in INR, unless specified

199 198

-

20

40

60

80

100

120

140

160

180

200

Q1FY19 Q1FY20

193 197

-

20

40

60

80

100

120

140

160

180

200

FY18 FY19

-0.4%

2%

*W.e.f 1st Jan 2019, GST rate on tickets is reduced from 28%/18% to 18%/12%, thereby affecting the YoY ATP growth.

-_,. 0 so/o - - - - - - - -

c~G"_ ---------------------

t

S p e n d P e r H e a d [ S P H ]

37

55 58 62 6674

FY15 FY16 FY17 FY18 FY19

All figures in INR, unless specified

76 81

-

10

20

30

40

50

60

70

80

90

100

Q1FY19 Q1FY20

66 74

-

10

20

30

40

50

60

70

80

FY18 FY19

6%

11%

-~

t

t

F & B C o n t r i b u t i o n

38

41 44

47 50

55 74.1% 75.0% 76.0% 75.7%74.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

-

10

20

30

40

50

60

FY15 FY16 FY17 FY18 FY19

SPH Contribution (Rs.)

F & B Contribution (%)

57 61

75.6% 74.9%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

80. 0%

-

10

20

30

40

50

60

70

Q1FY19 Q1FY20

50 55

75.7% 74.2%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

80. 0%

-

10

20

30

40

50

60

FY18 FY19

5%

9%

All figures in INR, unless specified

SPH Contribution (Rs.) = SPH (Rs.) x F&B Contribution (%)

c~GRS°lo ---------~

------------------------------

•---

t

- t -+-

A d v e r t i s e m e n t R e v e n u e

39

81 91 96

139

176

25 2522

30

34

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

FY15 FY16 FY17 FY18 FY19

Advertising Rev (Rs Crs)

Advertising Rev Per Screen (Rs Lakhs)

40 47

8 8

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

-

10

20

30

40

50

60

70

Q1FY19 Q1FY20

18%

139

176

30

34

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

20

40

60

80

100

120

140

160

180

200

FY18 FY19

27%

IN X

t

t

e

O t h e r O p e r a t i n g I n c o m e P e r S c r e e n

40

21.9 24.6

22.7 23.1 21.3

FY15 FY16 FY17 FY18 FY19

All figures in INR Lakhs, unless specified

4.7 4.8

-

1.0

2.0

3.0

4.0

5.0

6.0

Q1FY19 Q1FY20

23.1 21.3

-

5.0

10.0

15.0

20.0

25.0

FY18 FY19

2%

-8%

t

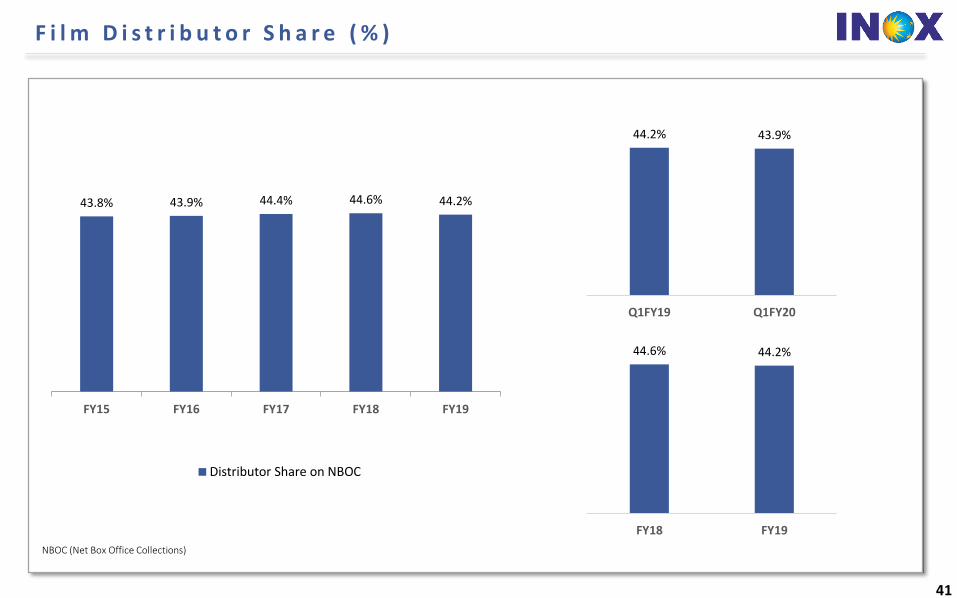

F i l m D i s t r i b u t o r S h a r e ( % )

41

43.8% 43.9% 44.4% 44.6% 44.2%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

FY15 FY16 FY17 FY18 FY19

Distributor Share on NBOC

NBOC (Net Box Office Collections)

44.2% 43.9%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

Q1FY19 Q1FY20

44.6% 44.2%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

35. 0%

40. 0%

45. 0%

50. 0%

FY18 FY19

■

O t h e r O v e r h e a d s P e r O p e r a t i n g S c r e e n

42

20.3 20.1 21.2 22.1 23.5

41.3 44.0 45.6 46.7 50.8

40.8 45.5 42.9 43.1 43.2

43.447.5 52.7 47.5

50.9

145.8157.1 162.4 159.4

168.3

FY15 FY16 FY17 FY18 FY19

Employee BenefitsLease Rental & Hire ChargesCAM, Power & Fuel, R&MOther Overheads

All figures in INR Lakhs, unless specified

22.0 23.5

46.6 50.8

43.1 43.2

47.5 50.9

159.3 168.3

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

FY18 FY19

5.7 6.4

12.6 12.7

11.6 11.9

12.6 13.0

42.6 44.0

(5.0)

5.0

15.0

25.0

35.0

45.0

55.0

Q1FY19 Q1FY20

3.5%

2.3%

0.5%

11.4%

7.1%

0.2%

8.9%

6.4%

Excludes Ind AS 116

-- - ----- ----

■

■

■

■

----CAGR4% -------------► --------- t

t t t

t t t t

43

Compet i t ive Advantage• R e c o g n i s e d A n d T r u s t e d C o r p o r a t e

G r o u p

• W e l l D i v e r s i f i e d P r e s e n c e A c r o s s I n d i a

• S t r o n g N e w S c r e e n s P i p e l i n e

• S t r o n g B r a n d P a r t n e r s h i p s

• S t r o n g B a l a n c e S h e e t

• S t a t e O f T h e A r t T e c h n o l o g y , U n m a t c h e d

S e r v i c e A n d A m b i e n c e

INOX Nehru Place, Delhi

44

•

•

•

•

Erstwhile INOX

Fluorochemicals Limited

Largest producer of

Chloromethanes,

refrigerants and

Polytetrafluoroethylene in

India.

Fully integrated player in

the wind energy market

State-of-the-art

manufacturing plants near

Ahmedabad (Gujarat), Una

(Himachal Pradesh) and

Barwani (Madhya Pradesh).

Our Madhya Pradesh

facility is one of the largest

in Asia

Ability to provide end-to-end

turnkey solutions for wind

farms

One of the largest

multiplex chains in India

In the business of setting

up, operating and

managing a national

chain of multiplexes

under the brand name

‘INOX’

Present in 67 cities with

143 multiplexes and 595

screens

Largest producer of

cryogenic liquid storage

and transport tanks in

India

Offers comprehensive

solutions in cryogenic

storage, vaporization and

distribution engineering

Has operations in India,

USA, Netherlands and

Brazil

50:50 joint venture with

Air Products Inc., USA

Largest producer of

industrial gases in

India

40 plants spread

throughout the

country

Erstwhile Gujarat

Fluorochemicals

Limited

Holding company of

INOX Wind and INOX

Leisure Ltd.

INOX Wind Limited INOX Leisure Limited Gujarat Fluorochemicals

Limited

INOX Air Products

Private LimitedINOX India

Private Limited

ANNEXURE: RECOGNISED AND TRUSTED CORPORATE GROUP

LISTED COMPANIES

GFLLimited IN X LIVE b'w MOVIE

90 Year track record of consistent business growth USO $3 Billion lnox Group diversified across 7 different businesses

OTHER KEY COMPANIES

Q INOXAIR ✓,:.. ~ PRODUCTS~ INOX:CVA

10,000+ employees at 150+ business units across India Distribution network spread over 50+ countries

W e l l D i v e r s i f i e d P r e s e n c e A c r o s s I n d i a

45

East; 23; 16%

West, 57, 40%

North, 34, 24%

South, 29, 20%East; 10; 15%

West, 23, 34%

North, 20, 30%

South, 14, 21%

East; 87; 15%

West, 247, 41%North, 123, 21%

South, 138, 23%

East, 21,702 , 15%

West, 57,819 , 41%North; 28,783 ; 21%

South; 31,493 ; 23%

Well DiversifiedDistribution of

Multiplexesacross India

Access toWide Variety of

Regional Content

Lower Dependencyon Hindi and English

Content

Includes 8 management properties with 29 screens and 7,370 seats

143 Properties 67 Citiess

595 Screens 139,797 Seat

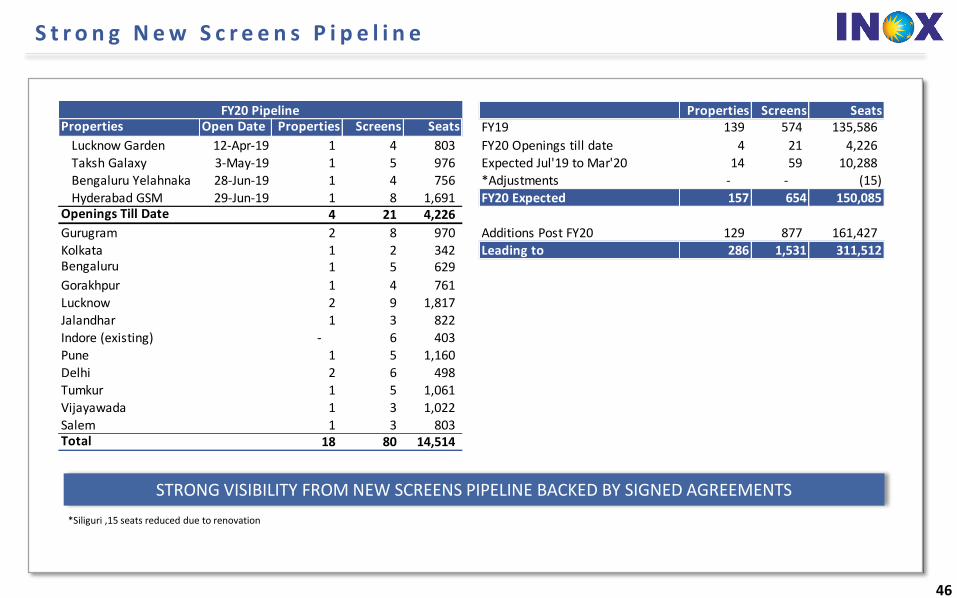

S t r o n g N e w S c r e e n s P i p e l i n e

46

STRONG VISIBILITY FROM NEW SCREENS PIPELINE BACKED BY SIGNED AGREEMENTS

Properties Screens SeatsProperties Open Date Properties Screens Seats FY19 139 574 135,586

Lucknow Garden 12-Apr-19 1 4 803 FY20 Openings till date 4 21 4,226

Taksh Galaxy 3-May-19 1 5 976 Expected Jul'19 to Mar'20 14 59 10,288 Bengaluru Yelahnaka 28-Jun-19 1 4 756 *Adjustments - - (15)

Hyderabad GSM 29-Jun-19 1 8 1,691 FY20 Expected 157 654 150,085 Openings Till Date 4 21 4,226

Gurugram 2 8 970 Additions Post FY20 129 877 161,427 Kolkata 1 2 342 Leading to 286 1,531 311,512 Bengaluru 1 5 629

Gorakhpur 1 4 761

Lucknow 2 9 1,817 Jalandhar 1 3 822

Indore (existing) - 6 403 Pune 1 5 1,160

Delhi 2 6 498 Tumkur 1 5 1,061

Vijayawada 1 3 1,022 Salem 1 3 803 Total 18 80 14,514

FY20 Pipeline

*Siliguri ,15 seats reduced due to renovation

---------

CONSUMER DURABLES GEC

BFSI

17%

OTHERSAUTOMOBILESECOMMERCE &TELECOMM.FMCG

S t r o n g B r a n d P a r t n e r s h i p s

I.~ l'T• J I

P&G

" HAVELLS

IDFC LIMITED

Rojoigaodbo

HONDA

TOYOTA

~

'~ ◄

He a

TATA ~ aaTTeries -·-~ svGAsA ,. ... ~

INOIA Kl BATTERY

£airbnb

STAR * PaY1'm

JJw,cK~ colors

v 1ac0M i!J - ,, HUAWEI

aiPhone

@l xiaomi (;) PhonePe H><b'sPsy-~IOApp

Justdial

h!HN,i

e Lufthansa

IN X

TURKISH f'i'\ AIRLINES ~

~c Ill Emirates •• _..,_

ft R iance 1 ... ... ... . , -. r .• i1 ■ , i1 .. ,I

Khadlm·s 1.11:x:® INNERWEAR

.x. WROGN

~ Tim Tl~IF,S OF INl)IA Kaj~rla

Siyarams·

S t r o n g B a l a n c e S h e e t

48

Potential To Grow Aggressively Without Any

Stress On Balance Sheet

Particulars (INR Crs.) Mar-19 Mar-18

Share Capital 102.6 96.2

Other Equity 893.9 606.1

Interest in Inox Benefit Trust, at cost (32.7) (32.7)

Total Shareholder funds 963.8 669.6

Non-Controlling Interest 0.01 0.01

Total Equity 963.8 669.6

Total Debt 110.0 291.9

Other Non-Current Liabilities 90.7 88.9

Total Sources of Funds 1,164.5 1,050.4

Fixed Assets 986.1 825.7

Other Non-Current Assets 341.3 315.8

Current Assets 137.6 116.5

Cash & Cash Equivalents 13.7 26.9

Less: Current Liabilities 314.3 234.6 Net Current Assets (163.0) (91.1)

Total Assets 1,164.5 1,050.4

Key Balance sheet Ratios Mar-19 Mar-18

Net Debt : Equity 0.10 0.40

Return on Equity (ROE)# 16.3% 18.8%

Return on Capital Employed (ROCE) 20.9% 13.2%

Low Leverage Net D/E:

Treasury Stock in Inox Benefit Trust

Promoters Stake

Strong Balance Sheet

Real Estate on Balance Sheet

INR 350 Crs.

128 INR Crs.As on 31-Jul-19

0.10x

51.9%

ROE (TTM): PAT/Avg. Equity, ROCE (TTM): EBIT/Avg. Capital Employed (Capital Employed = Equity + Total Debt)#Includes Tax write back pertaining to earlier years of Rs.53.7 crs.(FY18) and Rs.4.6crs (FY19)

--

S t a t e o f t h e A r t Te c h n o l o g y, U n m a t c h e d S e r v i c e & A m b i e n c e

49

Focus On Technology

ILL is the first multiplex chain to implement SAP HANA with all integrated functions

Focus on ensuring transparency with regulatory agencies and distributors through daily performance analysis reports

The Network Operations Centre (NOC) in Mumbai enables continuous monitoring, control and reporting of information on all digital systems across the

country. Advertisers can track their advertisement screening at various multiplexes on real-time basis leading to improved transparency and higher advertising

revenues for ILL

ILL stands for the best in LUXURY, SERVICE and TECHNOLOGY and keeping this core in mind; INOX has tied up with IMAX for the best in cinema viewing

experience for 10 screens.

ILL has pioneered Laser projection across the country including India’s first Laserplex.

ILL has tied up with Samsung for its ONYX Cinema LED screen technology.

ILL has tied up with MX4D for providing exciting in-cinema 4D effects to its Patrons.

ILL has tied up with ScreenX to provide a 270 degree viewing experience on 3 walls of the theatre enabled through multi-projection system.

Focus on high quality video and audio

ILL operates high quality DCI Compliant 2K & 4K Digital Projection Systems across all the screens in India

High-definition picture quality, strong 3D capabilities and high frame rate (HFR) (can go up to 60 fps)

ILL has been one of the early adopters of Dolby ATMOS sound technology. Excellent acoustic systems and distortion free sound

Focus on service and ambience:

Focus on providing world class ambience.

ILL with its in-app F&B ordering and Qbuster service, is able to considerably reduce its queue size and transaction time

Emphasis on safety, comfort and convenience

Focus On Strong Technology, Unmatched Service And Ambience

Content pipeline Aug 2019

50

Batla House

Release Date:15th August 2019Cast: John Abraham, Mrunal ThakurDirector: Nikhil AdvaniBanner: T-Series Super Cassettes Industries Ltd., Emmay Entertainment Pvt. Ltd, JA Entertainment Pvt. Ltd.

Hobbs & Shaw

Release Date: 2nd August 2019Cast: DwayneJohnson, Idris Elba, Eiza GonzálezDirector: David LeitchBanner: Universal Pictures

Made in China

Release Date:30th August 2019Cast: RajKummar Rao, Mouni RoyDirector: MikhilMusaleBanner: Maddock Films

Mission Mangal

Release Date:15th August 2019Cast: Akshay Kumar, Vidya Balan, TaapseePannuDirector: Jagan ShaktiBanner: Cape of Good Films, Fox Star Studios

Saaho

Release Date:30th August 2019Cast: Prabhas, Shraddha KapoorDirector: SujeethBanner: UV Creations, T-Series, Dharma Productions

Jabariya jodi

Release Date:9th August 2019Cast: SidharthMalhotra, ParineetiChopraDirector: PrashantSinghBanner: BalajiTelefilms, Karma Media

IN X

Hp1ss _.'HAW

Content pipeline Sep 2019

51

Commando 3

Release Date: 6th September 2019Cast: Vidyut Jammwal, Adah SharmeDirector: Aditya DattBanner: RelianceEntertainment

IT - Chapter 2

Release Date: 6th September 2019Cast: James McAvoy , Jessica Chastain Director: Andy MuschiettiBanner: KatzSmithProductions, Lin Pictures, New Line Cinema

Ad Astra

Release Date:20th September 2019Cast: Brad Pitt, Tommy Lee Jones, Liv TylerDirector: James GrayBanner: Maddock Films

Dream Girl

Release Date:13th September 2019Cast: AyushmannKhurrana, NushratBharuchaDirector: RaajShaandilyaaBanner: Balaji Motion Pictures, ALT Entertainment,Mangl Murti Films

The Zoya Factor

Release Date:20th September 2019Cast: Sonam Kapoor, Dulquer SalmanDirector: AbhishekSharmaBanner: Fox Star Studios, Adlabs Films Ltd

Chhichhore

Release Date: 6th September 2019Cast: Sushant Singh Rajput, Shraddha KapoorDirector: Nitesh TiwariBanner: Fox Star Studios, Nadiadwala GrandsonEntertainment

IN

Content pipeline Oct 2019

52

JokerRelease Date:4th October 2019Cast: Robert De Niro, Joaquin PhoenixDirector: Todd PhillipsBanner: BRON Studios, Creative Wealth Media Finance, DC Comics

Marjaavaan

Release Date: 2nd October 2019Cast: Sidharth Malhotra, Riteish Deshmukh, Tara Sutaria, Rakul Preet Singh, Nushrat BharuchaDirector: Milap ZaveriBanner: T-Series Super Cassettes Industries Ltd., Emmay Entertainment Pvt. Ltd.

War

Release Date: 2nd October 2019Cast: Hrithik Roshan, Tiger Shroff, VaniKapoorDirector: SiddharthAnandBanner: Yash Raj Films

Housefull 4

Release Date:25th October 2019Cast: Akshay Kumar, Riteish Deshmukh, Abhishek BachchanDirector: Farhad SamjiBanner: NadiadwalaGrandson Entertainment

The Sky is Pink

Release Date:11th October 2019Cast: Priyanka Chopra Jonas, Farhan AkhtarDirector: Shonali BoseBanner: RSVP, Roy Kapur Films, Ivanhoe Pictures

Gemini Man

Release Date:11th October 2019Cast: Will Smith, Mary Elizabeth Winstead, Clive OwenDirector: Ang LeeBanner: Fosun Group Forever Pictures, Jerry Bruckheimer Films

IN X

Content pipeline Nov 2019

53

BHOOT: Part One –The Haunted Ship

Release Date:15th November 2019Cast: Vicky Kaushal, Bhumi PednekarDirector: Bhanu PratapSinghBanner: Dharma Productions

Pagalpanti

Release Date: 8th November 2019Cast: John Abraham, Ileana D'CruzDirector: Anees BazmeeBanner: Panorama Studios, T-Series Super Cassettes Industries Ltd

Terminator: Dark Fate

Release Date: 1st November 2019Cast: Mackenzie Davis, Arnold Schwarzenegger, Linda HamiltonDirector: Tim MillerBanner: Paramount Pictures, Twentieth Century Fox, SkydanceMedia

Frozen 2

Release Date:29th November 2019Cast: Kristen Bell, Evan Rachel Wood, Jonathan GroffDirector: Chris Buck, Jennifer LeeBanner: Walt Disney Animation Studios, Walt Disney Pictures

Bala

Release Date:22nd November 2019Cast: AyushmannKhurrana, BhumiPednekarDirector: Amar KaushikBanner: Jio Studios,Maddock Films

Dil Bechara

Release Date:29th November 2019Cast: Sushant Singh Rajput, Sanjana SanghiDirector: MukeshChhabraBanner: Fox Star Studios

---DINESHVIJAN'S------i

AIIISHMANNKIIURRAMA , BHUMI PEDNEKAR , !AMI GAUTAM SAURABH SHUKLA • JAVED IAFIREY • SIEMA PAIIWA

lllfm11AMARKAUSHIK

IN X

·' --"? FY7F.:" N ' • I

NOVEMDER 201<> I I N .Nl,\ l \11 , III N~: T::,~~ ANO I IIU(,U

I

54

Annexure

INOX Metro, Mumbai

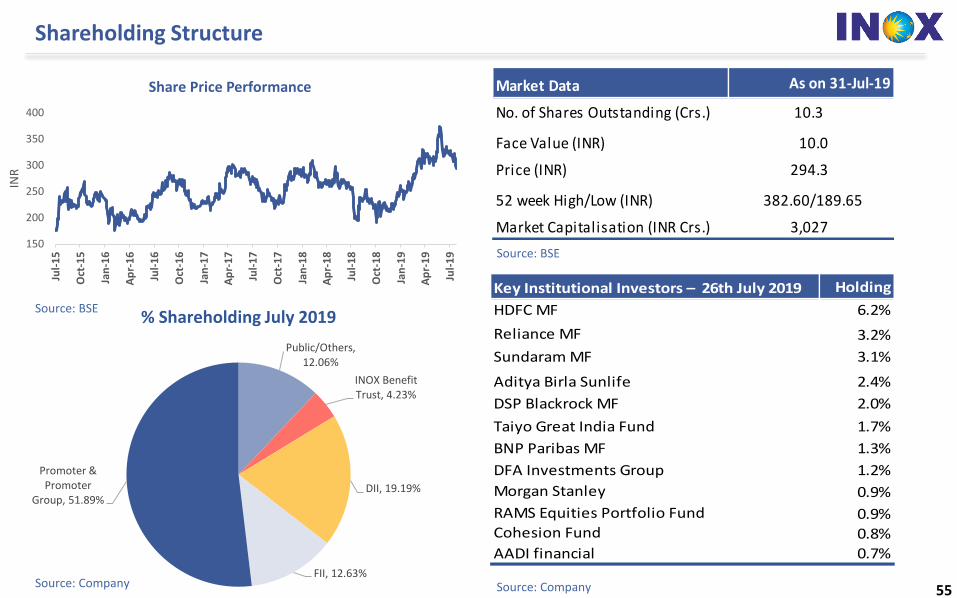

Shareholding Structure

55

Source: BSE

Source: Company Source: Company

Source: BSE

Market Data As on 31-Jul-19

No. of Shares Outstanding (Crs.) 10.3

Face Value (INR) 10.0

Price (INR) 294.3

52 week High/Low (INR) 382.60/189.65

Market Capitalisation (INR Crs.) 3,027

Key Institutional Investors – 26th July 2019

%

Holding

HDFC MF 6.2%

Reliance MF 3.2%

Sundaram MF 3.1%

Aditya Birla Sunlife 2.4%

DSP Blackrock MF 2.0%

Taiyo Great India Fund 1.7%

BNP Paribas MF 1.3%

DFA Investments Group 1.2%

Morgan Stanley 0.9%

RAMS Equities Portfolio Fund 0.9%Cohesion Fund 0.8%

AADI financial 0.7%

150

200

250

300

350

400

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Jul-

19

INR

Share Price Performance

Public/Others, 12.06%

INOX Benefit Trust, 4.23%

DII, 19.19%

FII, 12.63%

Promoter & Promoter

Group, 51.89%

% Shareholding July 2019

r r r r r r r

-

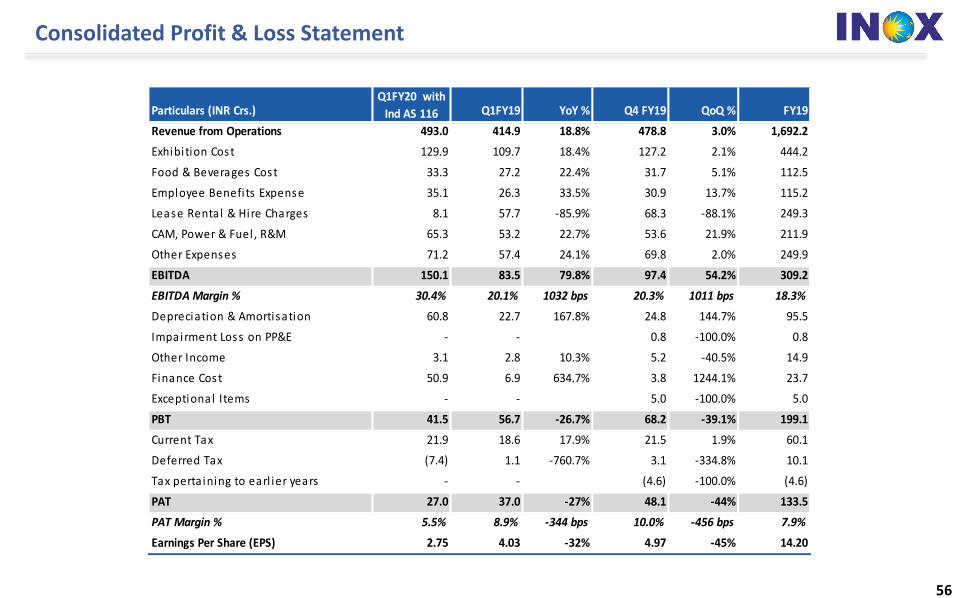

Consolidated Profit & Loss Statement

56

Particulars (INR Crs.)Q1FY20 with

Ind AS 116 Q1FY19 YoY % Q4 FY19 QoQ % FY19

Revenue from Operations 493.0 414.9 18.8% 478.8 3.0% 1,692.2

Exhibi tion Cost 129.9 109.7 18.4% 127.2 2.1% 444.2

Food & Beverages Cost 33.3 27.2 22.4% 31.7 5.1% 112.5

Employee Benefi ts Expense 35.1 26.3 33.5% 30.9 13.7% 115.2

Lease Rental & Hire Charges 8.1 57.7 -85.9% 68.3 -88.1% 249.3

CAM, Power & Fuel , R&M 65.3 53.2 22.7% 53.6 21.9% 211.9

Other Expenses 71.2 57.4 24.1% 69.8 2.0% 249.9

EBITDA 150.1 83.5 79.8% 97.4 54.2% 309.2

EBITDA Margin % 30.4% 20.1% 1032 bps 20.3% 1011 bps 18.3%

Depreciation & Amortisation 60.8 22.7 167.8% 24.8 144.7% 95.5

Impairment Loss on PP&E - - 0.8 -100.0% 0.8

Other Income 3.1 2.8 10.3% 5.2 -40.5% 14.9

Finance Cost 50.9 6.9 634.7% 3.8 1244.1% 23.7

Exceptional Items - - 5.0 -100.0% 5.0

PBT 41.5 56.7 -26.7% 68.2 -39.1% 199.1

Current Tax 21.9 18.6 17.9% 21.5 1.9% 60.1

Deferred Tax (7.4) 1.1 -760.7% 3.1 -334.8% 10.1

Tax perta ining to earl ier years - - (4.6) -100.0% (4.6)

PAT 27.0 37.0 -27% 48.1 -44% 133.5

PAT Margin % 5.5% 8.9% -344 bps 10.0% -456 bps 7.9%

Earnings Per Share (EPS) 2.75 4.03 -32% 4.97 -45% 14.20

------

------------

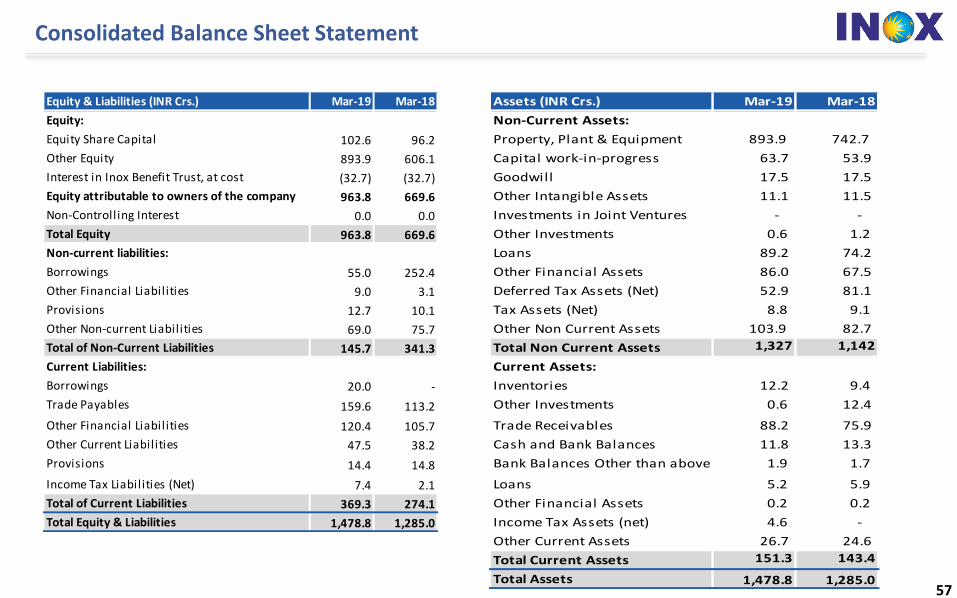

Consolidated Balance Sheet Statement

57

Equity & Liabilities (INR Crs.) Mar-19 Mar-18

Equity:

Equity Share Capital 102.6 96.2

Other Equity 893.9 606.1

Interest in Inox Benefit Trust, at cost (32.7) (32.7)

Equity attributable to owners of the company 963.8 669.6

Non-Controlling Interest 0.0 0.0

Total Equity 963.8 669.6

Non-current liabilities:

Borrowings 55.0 252.4

Other Financial Liabilities 9.0 3.1

Provisions 12.7 10.1

Other Non-current Liabilities 69.0 75.7

Total of Non-Current Liabilities 145.7 341.3

Current Liabilities:

Borrowings 20.0 -

Trade Payables 159.6 113.2

Other Financial Liabilities 120.4 105.7

Other Current Liabilities 47.5 38.2

Provisions 14.4 14.8

Income Tax Liabilities (Net) 7.4 2.1

Total of Current Liabilities 369.3 274.1

Total Equity & Liabilities 1,478.8 1,285.0

Assets (INR Crs.) Mar-19 Mar-18

Non-Current Assets:

Property, Plant & Equipment 893.9 742.7

Capital work-in-progress 63.7 53.9

Goodwill 17.5 17.5

Other Intangible Assets 11.1 11.5

Investments in Joint Ventures - -

Other Investments 0.6 1.2

Loans 89.2 74.2

Other Financial Assets 86.0 67.5

Deferred Tax Assets (Net) 52.9 81.1

Tax Assets (Net) 8.8 9.1

Other Non Current Assets 103.9 82.7

Total Non Current Assets 1,327 1,142

Current Assets:

Inventories 12.2 9.4

Other Investments 0.6 12.4

Trade Receivables 88.2 75.9

Cash and Bank Balances 11.8 13.3

Bank Balances Other than above 1.9 1.7

Loans 5.2 5.9

Other Financial Assets 0.2 0.2

Income Tax Assets (net) 4.6 -

Other Current Assets 26.7 24.6

Total Current Assets 151.3 143.4

Total Assets 1,478.8 1,285.0

-- ------ --

Financial Summary

58

895

1,161 1,221 1,348

1,692

FY15 FY16 FY17 FY18 FY19

123

189 146

210

309 13.7% 16.3% 12.0% 15.6% 18.3%

FY15 FY16 FY17 FY18 FY19

EBITDA EBITDA Margin %

20

81

31

115 133

2.2%7.0%

2.5%

8.5% 7.9%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0 %

5.0 %

10. 0%

-

20

40

60

80

100

120

140

FY15 FY16 FY17 FY18 FY19

PAT PAT Margin %

241 267 317 292 110

676 522 553 670 964

0.3 0.4 0.5 0.4 0.1

FY15 FY16 FY17 FY18 FY19

Equity Debt Net Debt to Equity

61.6% 61.4% 61.3% 59.5% 57.6%

21.3% 22.9% 23.3% 22.7% 25.8%

9.1% 7.8% 7.9% 10.3% 10.4%

8.0% 7.8% 7.6% 7.5% 6.2%

FY15 FY16 FY17 FY18 FY19

NBOC F & B Advertising Others

ROE: PAT/Avg. Equity, ROCE: EBIT/Avg. Capital Employed [(Capital Employed = Equity + Total Debt)Net Debt = Total Debt – Cash –Bank – Liquid MF Investments

REVENUES EBITDA PAT

REVENUES - SEGMENT BREAKUP LEVERAGE ANALYSIS RETURN METRICS

All figures in INR Crs., unless specified

6.1

%

14

.9%

7.3

%

13

.2%

20

.9%

3.8

%

16

.8%

5.7

%

18

.8%

16

.3%

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

FY15 FY16 FY17 FY18 FY19

ROCE % ROE %

IN X

- - - -

■ ■ ■ ■ - - - ■ ■

59

Thank YouBalesh Talapady

AVP – Business Analysis

INOX Leisure Ltd.

Contact+91-22-4062 6927

Email: [email protected]