LightCastle Business Confidence Index 2017-18

48

LightCastle Business Confidence Index 2017-18 Volume 2

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of LightCastle Business Confidence Index 2017-18

LightCastleBusinessConfidenceIndex

2017-18

Volume 2

About LightCastle Partners

At LightCastle Partners, we aspire to work towards creating a data- and knowledge-driven economy. Our unique approach to combining data, analytics and technology allows us to design and implement research and interventions quickly, efficiently and objectively. Till date, we have collaborated with 100+ local and international clients in 150+ projects spanning 40+ industries to help deliver lasting impact in Bangladesh and beyond.

Acknowledgments

We would like to thank the 102 CxO members across a range of private industries in Bangladesh for partaking in our study by giving their valuable time and responding to our data requests. This piece of research could not have been possible without them graciously sharing their views with us. For that and more, we are deeply humbled and grateful.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 1

LightCastleBusinessConfidenceIndex

2017-18

Strategic Partner

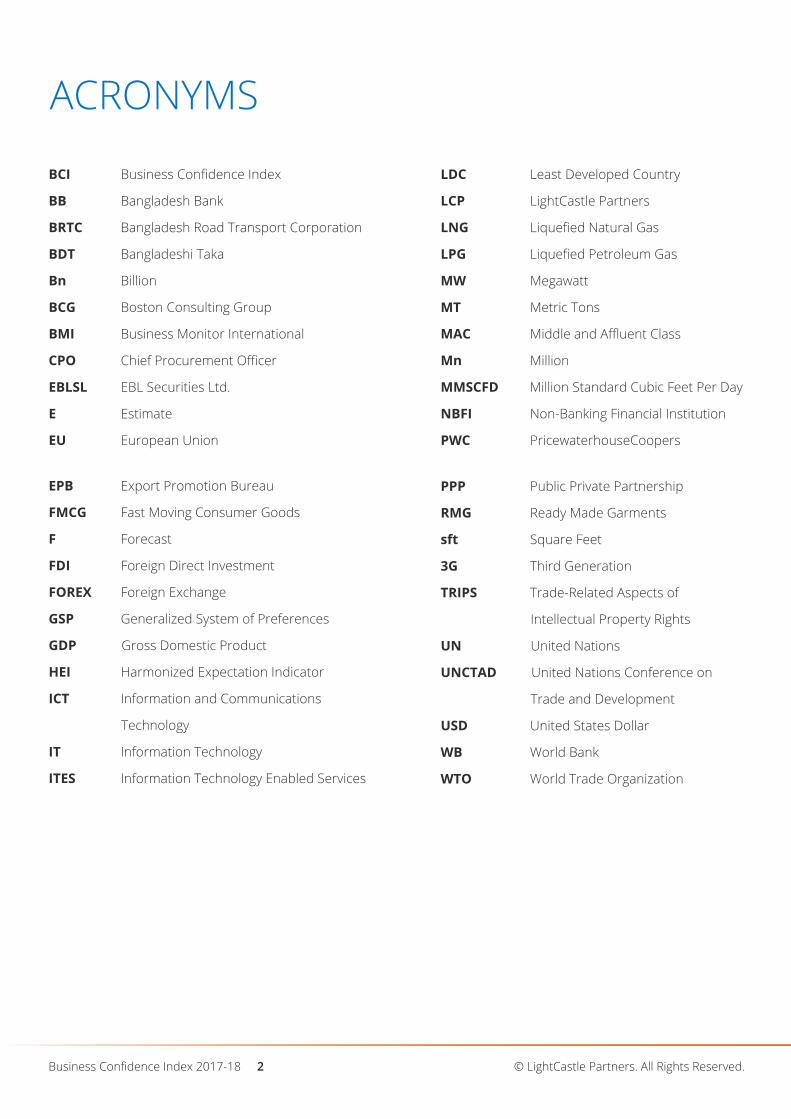

BCI Business Confidence Index

BB Bangladesh Bank

BRTC Bangladesh Road Transport Corporation

BDT Bangladeshi Taka

Bn Billion

BCG Boston Consulting Group

BMI Business Monitor International

CPO Chief Procurement Officer

EBLSL EBL Securities Ltd.

E Estimate

EU European Union

ACRONYMS

EPB Export Promotion Bureau

FMCG Fast Moving Consumer Goods

F Forecast

FDI Foreign Direct Investment

FOREX Foreign Exchange

GSP Generalized System of Preferences

GDP Gross Domestic Product

HEI Harmonized Expectation Indicator

ICT Information and Communications

Technology

IT Information Technology

ITES Information Technology Enabled Services

LDC Least Developed Country

LCP LightCastle Partners

LNG Liquefied Natural Gas

LPG Liquefied Petroleum Gas

MW Megawatt

MT Metric Tons

MAC Middle and Affluent Class

Mn Million

MMSCFD Million Standard Cubic Feet Per Day

NBFI Non-Banking Financial Institution

PWC PricewaterhouseCoopers

PPP Public Private Partnership

RMG Ready Made Garments

sft Square Feet

3G Third Generation

TRIPS Trade-Related Aspects of

Intellectual Property Rights

UN United Nations

UNCTAD United Nations Conference on

Trade and Development

USD United States Dollar

WB World Bank

WTO World Trade Organization

Business Confidence Index 2017-18 2 © LightCastle Partners. All Rights Reserved.

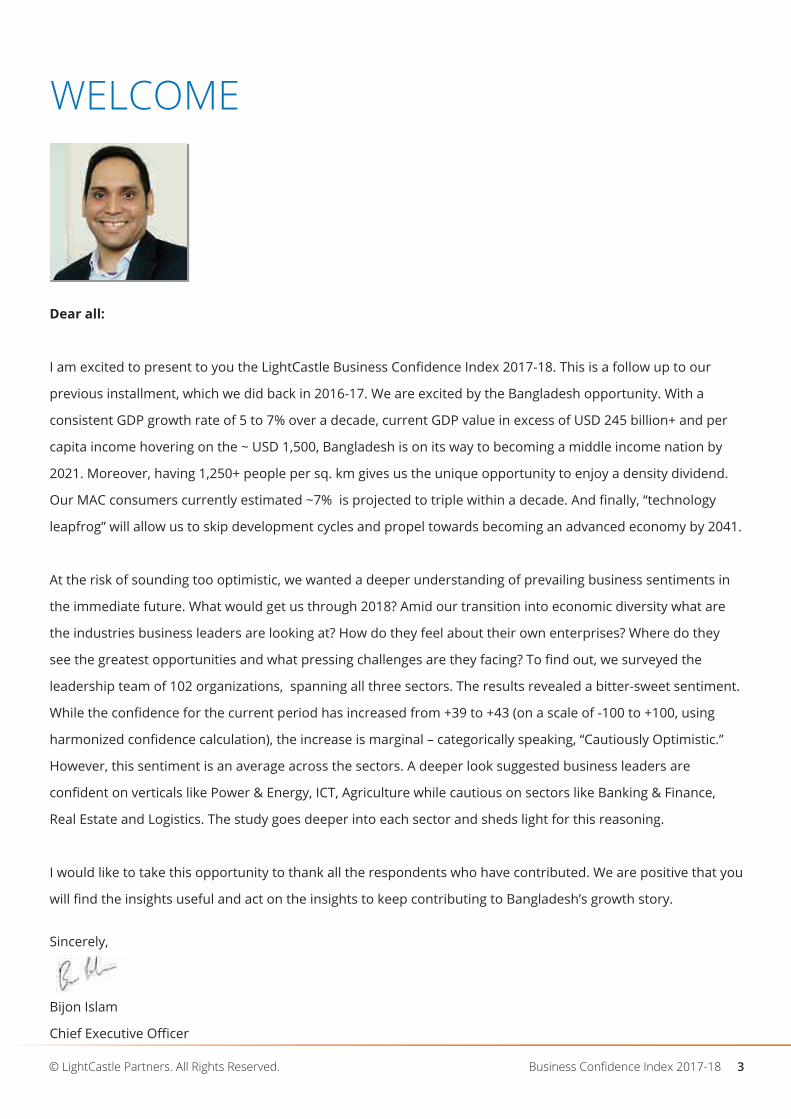

WELCOME

Dear all:

I am excited to present to you the LightCastle Business Confidence Index 2017-18. This is a follow up to our

previous installment, which we did back in 2016-17. We are excited by the Bangladesh opportunity. With a

consistent GDP growth rate of 5 to 7% over a decade, current GDP value in excess of USD 245 billion+ and per

capita income hovering on the ~ USD 1,500, Bangladesh is on its way to becoming a middle income nation by

2021. Moreover, having 1,250+ people per sq. km gives us the unique opportunity to enjoy a density dividend.

Our MAC consumers currently estimated ~7% is projected to triple within a decade. And finally, “technology

leapfrog” will allow us to skip development cycles and propel towards becoming an advanced economy by 2041.

At the risk of sounding too optimistic, we wanted a deeper understanding of prevailing business sentiments in

the immediate future. What would get us through 2018? Amid our transition into economic diversity what are

the industries business leaders are looking at? How do they feel about their own enterprises? Where do they

see the greatest opportunities and what pressing challenges are they facing? To find out, we surveyed the

leadership team of 102 organizations, spanning all three sectors. The results revealed a bitter-sweet sentiment.

While the confidence for the current period has increased from +39 to +43 (on a scale of -100 to +100, using

harmonized confidence calculation), the increase is marginal – categorically speaking, “Cautiously Optimistic.”

However, this sentiment is an average across the sectors. A deeper look suggested business leaders are

confident on verticals like Power & Energy, ICT, Agriculture while cautious on sectors like Banking & Finance,

Real Estate and Logistics. The study goes deeper into each sector and sheds light for this reasoning.

I would like to take this opportunity to thank all the respondents who have contributed. We are positive that you

will find the insights useful and act on the insights to keep contributing to Bangladesh’s growth story.

Sincerely,

Bijon Islam

Chief Executive Officer

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 3

SNAPSHOT: BANGLADESH BY THE NUMBERS

GDP

248.8Bn USD

(FY 16-17)

© LightCastle Partners. All Rights Reserved.

GDP PER CAPITA

1480USD

(FY 16-17)

GDP GROWTH RATE

7.3%

(E, FY 16-17)

POPULATION

164.8 Mn

(2017)

POPULATION DENSITY

1252people per sq. km of land area

(FY 15-16)

MAC POPULATION

15 Mn

(F, 2017)

FOREX RESERVE

33.5Bn USD

(2017)

TOTAL EXPORTS FY

34.8Bn USD

(FY 2016-2017)

RMG EXPORTS

28.2Bn USD

(FY 16-17)

IT EXPORTS

800Mn USD

(FY 16-17)

FDI

2.5 Bn USD

(F, 2017)

MOBILE SUBSCRIBERS

145.1 Mn

(Dec 2017)

INTERNET SUBSCRIBERS

80.2 Mn

(Dec 2017)

MOBILE INTERNET SUBSCRIBERS

75Mn

(Dec 2017)

MP GROWTH RATE

7.3%

(F, 2017)

Business Confidence Index 2017-18 4

Sources: World Bank, United Nations, BCG, LightCastle Partners, EPB, ICT Ministry, BTRC

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY

2 METHODOLOGY

3 THE MACROECONOMY: THE EMERGENCE

4 INDUSTRY SPECIFIC INSIGHTS: VOICES OF THE LEADERS

5 PROBLEM AREAS: BOTTLENECKS TO OVERCOME

6 FUTURE PROSPECTS: THE ROYAL BENGAL TIGERS OF THE NEXT DECADE

7 CONCLUDING REMARKS: THE WAY FORWARD

8 CONTRIBUTORS

6

9

11

19

35

39

42

45

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 5

EXECUTIVESUMMARY & METHODOLOGY

EXECUTIVE SUMMARY

Business Operational Challenges: Raw material import dependency, especially

in the cement and pharmaceutical industries, per unit fall in value in RMG prices

and working capital management in ICT.

Business leaders cited five key factors that contributed to the rise in confidence.

These are: increased investment in power generation, green revolution &

mechanization in the agriculture sector, higher disposable income and

consumer spending, growing health awareness, and the government’s increased

focus on ICT.

However, some concerns still remain in regards to creation of fault lines by the

classified loans condition, bureaucratic red tapes in opening and conducting

businesses, recent slump in RMG prices, transportation & logistical hassles and

infrastructure bottlenecks such as port congestions.

From low to moderate

confidence of +39 in 2016,

the score in 17-18 signifies

a cautiously optimistic

confidence of +43

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 7

The findings further suggest that Bangladesh’s top business professionals agree

on the following issues, which impede progress:

As rapid technological advancements and the threat of looming uncertainty –

with the upcoming election in 2019 – shape the business landscape,

Bangladesh’s top executives continue to have a moderately high level of

confidence in their outlook to the economy. However, they also voice specific

concerns, which if addressed, can help them play an even greater role in

effective economic contribution.

LightCastle Business Confidence Index 2017-18 analyzed survey findings of 102

CXO members across a myriad of industries and found the overall business

sentiment in the country to be +43. This marks a 4 points increase from last

year’s score of +39. In other words, the score sends out a cautiously optimistic

vibe among the business community.

+430-100 +100

Overwhelmingly pessimistic Overwhelmingly optimistic

Regulatory Challenges: Government bureaucracy and lack of unity among

public entities.

Infrastructure/Logistics: Port congestion is a major barrier to shortening lead

times. Moreover, power outages have increased production costs and final

prices as manufacturers have to rely on backup captive power generation.

Industry experts opine the following set of actions will help improve the current

drawbacks – along with investor confidence:

Diversifying export basket and reducing dependence on RMG

Facilitating the ease of starting and conducting business

Improving infrastructure and logistics

Enhancing the skill of human resources

Streamlining the financial sector and scaling up the use of alternative

capital avenues

When asked to rank the top sectors in the coming decade, business leaders – by

and large – again painted an unanimous picture. According to them, the

following industries will have the highest possibility to drive larger impacts in

Bangladesh:

• ICT & ITES

• Pharmaceuticals

• Agro-Processing

• Power & Energy

• Footwear

• Ready Made Garments (RMG)

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.8

Business Confidence =

√[(Situation+200) × (Expectations+200)] - 200

METHODOLOGY

Harmonized Business Confidence Index: The indicator was later examined for

differences between the percentages of favorable and unfavorable responses

with respect to business confidence. The subsequent score can fluctuate

between -100 (all respondents carrying negative expectations for the coming

year) and +100 (all respondents carrying positive expectations for the coming

year). Built using a conveniently standardized geometric average between

Situation and Expectations, the BCI score induced from the HEI method supplied

an accurate scenario of the prevailing business confidence. It is defined as the

average between Situation and Expectations.

Sampling: The BCI was calculated by surveying 102 C-Suite level executives –

CEOs, CFOs, COOs and MDs including immediate pipeline – spanning a wide

range of industries. Interviews have been carried out between September 26

and November 12, 2017. Nearly 90% of the interviews were conducted in person

while the remaining 10% were collected online.

For this research, we took an approach to select only those industries that have

the highest level of contribution to the country’s GDP. The industries have been

further segregated into three categories – namely Primary, Secondary and

Tertiary. Primary sector incorporates agriculture and commodities. Secondary

includes manufacturing and processing while Tertiary encompasses services.

The index was constructed from the Harmonized Expectation Indicator (HEI)

methodology. This approach evaluates business performance reviews for the

foregone year in combination with both the present and expectations for the

upcoming year.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 9

53%42%5%

Primary( agriculture/commodities )

Secondary( manufacturing/processing )

Tertiary( services )

Exhibit 1: Sector-wise Representation of Sampling

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 10

* Grouped into three categories – Foreign banks, local banks and non-bank financial institutions.

Primary: Agro Inputs, Agro Commodities, Fisheries, Tea and Oil

Secondary: RMG & Textiles, Pharmaceuticals, Power, Cement, Steel,

Electronics, Agro-Processing, Footwear, Ship Building, Ceramic,

Plastic and FMCG

Tertiary: Financial Institutions*, Information Technology, Logistics,

Real Estate, Business Services/Consulting, Advertising, Automobile,

Hotels, Telecom, Architecture, Print & Digital Media, Retailer Chain,

Healthcare, Insurance and Money Transfer Networks

Finally, firm representation was carefully calculated to be reflective

of their respective industries. Overall, we hoped to capture the

entire spectrum of enterprises by covering small, medium and

large-sized firms, considering a blend of both local and foreign

entities.

THEMACROECONOMY:THE EMERGENCE

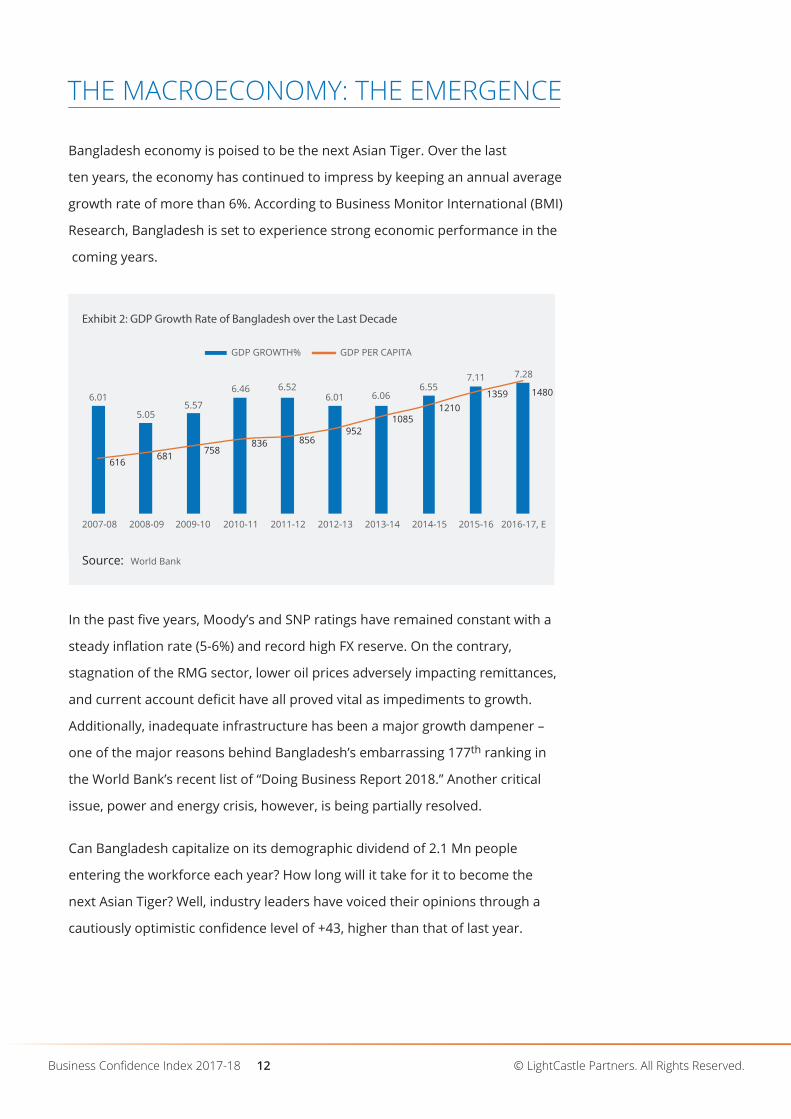

THE MACROECONOMY: THE EMERGENCE

Bangladesh economy is poised to be the next Asian Tiger. Over the last

ten years, the economy has continued to impress by keeping an annual average

growth rate of more than 6%. According to Business Monitor International (BMI)

Research, Bangladesh is set to experience strong economic performance in the

coming years.

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 12

Exhibit 2: GDP Growth Rate of Bangladesh over the Last Decade

GDP GROWTH% GDP PER CAPITA

6.01

5.05

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17, E

5.57

6.46 6.526.01 6.06

6.557.11 7.28

1480

616681 758

836 856952

10851210

1359

Source: World Bank

In the past five years, Moody’s and SNP ratings have remained constant with a

steady inflation rate (5-6%) and record high FX reserve. On the contrary,

stagnation of the RMG sector, lower oil prices adversely impacting remittances,

and current account deficit have all proved vital as impediments to growth.

Additionally, inadequate infrastructure has been a major growth dampener –

one of the major reasons behind Bangladesh’s embarrassing 177th ranking in

the World Bank’s recent list of “Doing Business Report 2018.” Another critical

issue, power and energy crisis, however, is being partially resolved.

Can Bangladesh capitalize on its demographic dividend of 2.1 Mn people

entering the workforce each year? How long will it take for it to become the

next Asian Tiger? Well, industry leaders have voiced their opinions through a

cautiously optimistic confidence level of +43, higher than that of last year.

BREAKING DOWN THE CONFIDENCE

+43 - The overall confidence level is an accumulation of confidence levels of various industries:

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 13

+43+39

Power and Energy :

Agriculture and Agro-Processing :

FMCG :

Pharmaceuticals :

ICT and ITES :

Banking and Finance :

RMG and Textiles :

Logistics :

Real Estate :

Cement :

Exhibit 3: Vertical Wise Business Confidence Index

Source : LCP Survey of 102 CXOs of Bangladesh based companies

Overall Confidence (2017-18)2017-18 Overall Confidence 2016-17

( Values are on a scale of -100 to +100 )

+83.28

+69.92+60.87

+56.44

+46.22

+37.52 +37.06+32.74

+28.83+23.61

LOWER ENERGY; DIFFICULT DUE TO INCREASED INVESTMENT ON POWER GENERATION

GREEN REVOLUTION IN THE AGRICULTURE SECTOR

HIGHER DISPOSABLE INCOME & CONSUMER SPENDING ON FMCG

GROWING HEALTH AWARENESS

ICT BEING THE THURST SECTOR THROUGH MAJOR POLICY DISCOURSE

CLASSIFIED LOANS CONDITION

SLUMP IN RMG PRICE

INFRASTRUCTURE ISSUES SUCH AS PORT CONGESTIONS & PROBLEM RELATED TO TRANSPORTATION

OVERSUPPLY OF APARTMENTS & STRICTER BANK LOAN REGULATIONS

OVER CAPACITY IN CEMENT SECTOR

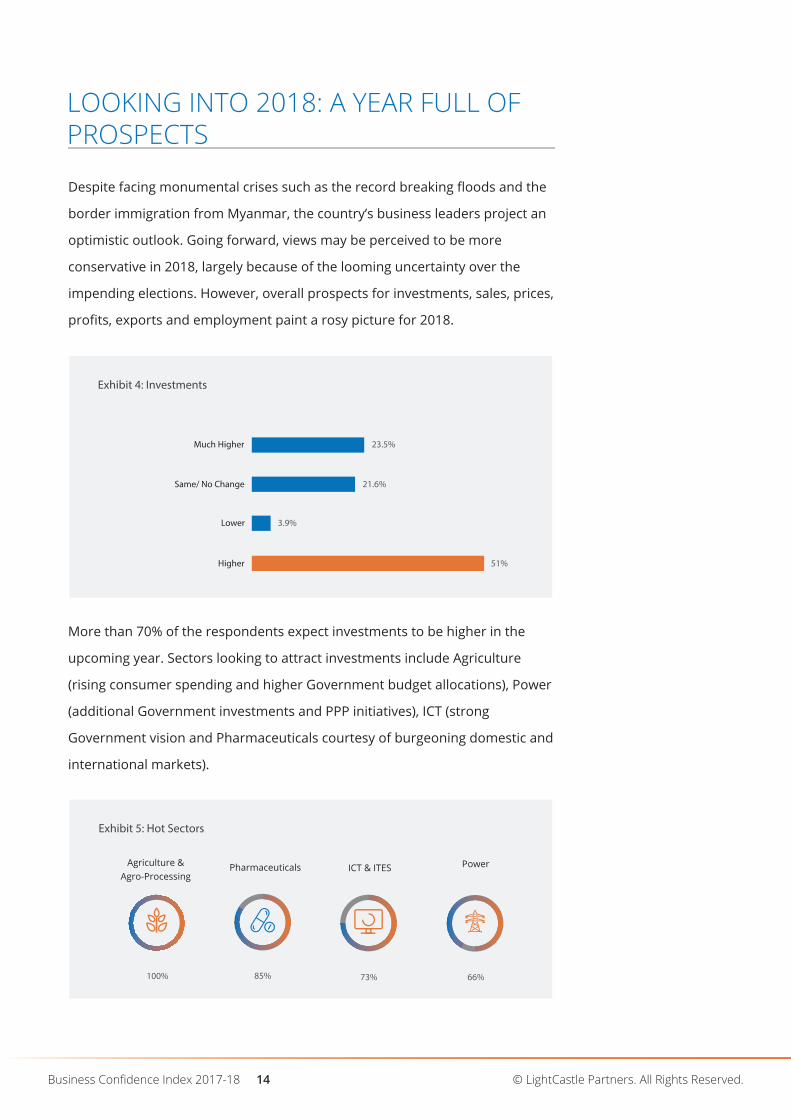

LOOKING INTO 2018: A YEAR FULL OFPROSPECTS

Despite facing monumental crises such as the record breaking floods and the

border immigration from Myanmar, the country’s business leaders project an

optimistic outlook. Going forward, views may be perceived to be more

conservative in 2018, largely because of the looming uncertainty over the

impending elections. However, overall prospects for investments, sales, prices,

profits, exports and employment paint a rosy picture for 2018.

Same/ No Change 21.6%

Much Higher 23.5%

Higher 51%

Lower 3.9%

Exhibit 4: Investments

Exhibit 5: Hot Sectors

More than 70% of the respondents expect investments to be higher in the

upcoming year. Sectors looking to attract investments include Agriculture

(rising consumer spending and higher Government budget allocations), Power

(additional Government investments and PPP initiatives), ICT (strong

Government vision and Pharmaceuticals courtesy of burgeoning domestic and

international markets).

PowerAgriculture &Agro-Processing

Pharmaceuticals

100%

ICT & ITES

85% 66%73%

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.14

Over 63% of respondents anticipate sales to be higher in the coming year –

which is conducive to Bangladesh’s growth potential. Among the industries,

100% from the Pharmaceutical and Agro industry expect to generate higher

sales. Surprisingly enough, respondents from the Real Estate also exhibited

upbeat vibes.

Exhibit 6: Sales

Exhibit 7: Hot Sectors

Same/ No Change 15.7%

Much Higher 17.6%

Higher 63.7%

Lower 2.9%

Agriculture &Agro-Processing

Pharmaceuticals

100%

ICT & ITES

100% 93%

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 15

15.7%

24.5%

Exhibit 8: Selling Prices

Same/ No Change 58.8%

Much Higher 1%

Higher

Lower

FMCG ICT & ITES

66%

Pharmaceuticals

71% 53%

Half of the respondents predict selling prices will remain unchanged. Power

sector leaders maintain that prices will go up due to a pass-through effect

from natural gas and oil prices globally. On the flip side, majority of the RMG

industrialists posit that prices will drop in the coming year amid increasing

competition in the international apparel market.

100% 54%

Power RMG

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.16

Nearly half of the respondents claim profits will soar in 2018. ICT & ITES,

FMCG and Pharmaceutical industries are expected to be the most profitable,

chiefly due to increasing consumer spending on FMCG, and higher projected

export in Pharmaceuticals.

29.4%

8.8%

16.7%

45.1%

Exhibit 10: Pro�ts

Same/ No Change

Much Higher

Higher

Lower

Exhibit 13: Hot Sectors

Agriculture &Agro-Processing

Pharmaceuticals

66%80%

ICT & ITES

83%

Export expectations in the Agriculture, ICT & ITES and Pharmaceutical

industries are substantially higher compared to the rest. Leaders in

Agriculture believe exporting is the way forward while the ICT & ITES industry

anticipates larger outsourcing tasks. Moreover, Pharmaceutical leaders expect

new export frontiers to emerge very soon.

Exhibit 12: Exports

Same/ No Change

Much Higher

Higher

Lower

23.1%

7.7%

5.1%

64.1%

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 17

Exhibit 14: Employment

Same/ No Change

Much Higher

Higher

Lower

34.3%

8.8%

3.9%

52.9%

Exhibit 15: Hot Sectors

Power & Energy sector is on the rise with the establishment of multiple power

plants. Therefore, higher employment generation is predicted. The ICT & ITES

industry is poised to generate significantly higher employment owing to

growing investor optimism and favorable government policies. RMG sector

participants, however, fear that employment will maintain status quo in the

near future.

Power Pharmaceuticals

100%

ICT & ITES

86% 71%

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 18

INDUSTRY SPECIFICINSIGHTS:VOICES OF THE LEADERS

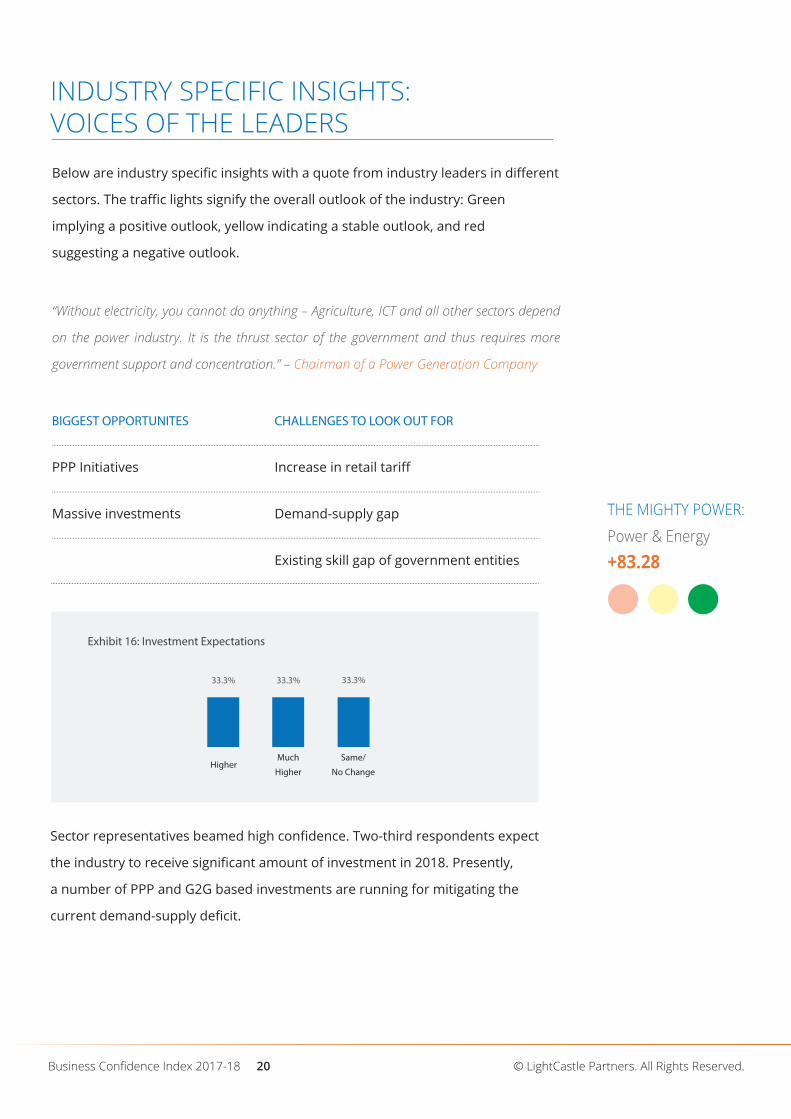

INDUSTRY SPECIFIC INSIGHTS:VOICES OF THE LEADERS

Below are industry specific insights with a quote from industry leaders in different

sectors. The traffic lights signify the overall outlook of the industry: Green

implying a positive outlook, yellow indicating a stable outlook, and red

suggesting a negative outlook.

“Without electricity, you cannot do anything – Agriculture, ICT and all other sectors depend

on the power industry. It is the thrust sector of the government and thus requires more

government support and concentration.” – Chairman of a Power Generation Company

THE MIGHTY POWER:

Power & Energy

+83.28

BIGGEST OPPORTUNITES

PPP Initiatives

Massive investments

CHALLENGES TO LOOK OUT FOR

Increase in retail tariff

Demand-supply gap

Existing skill gap of government entities

Exhibit 16: Investment Expectations

33.3% 33.3% 33.3%

Much

HigherHigher

Same/

No Change

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.20

Sector representatives beamed high confidence. Two-third respondents expect

the industry to receive significant amount of investment in 2018. Presently,

a number of PPP and G2G based investments are running for mitigating the

current demand-supply deficit.

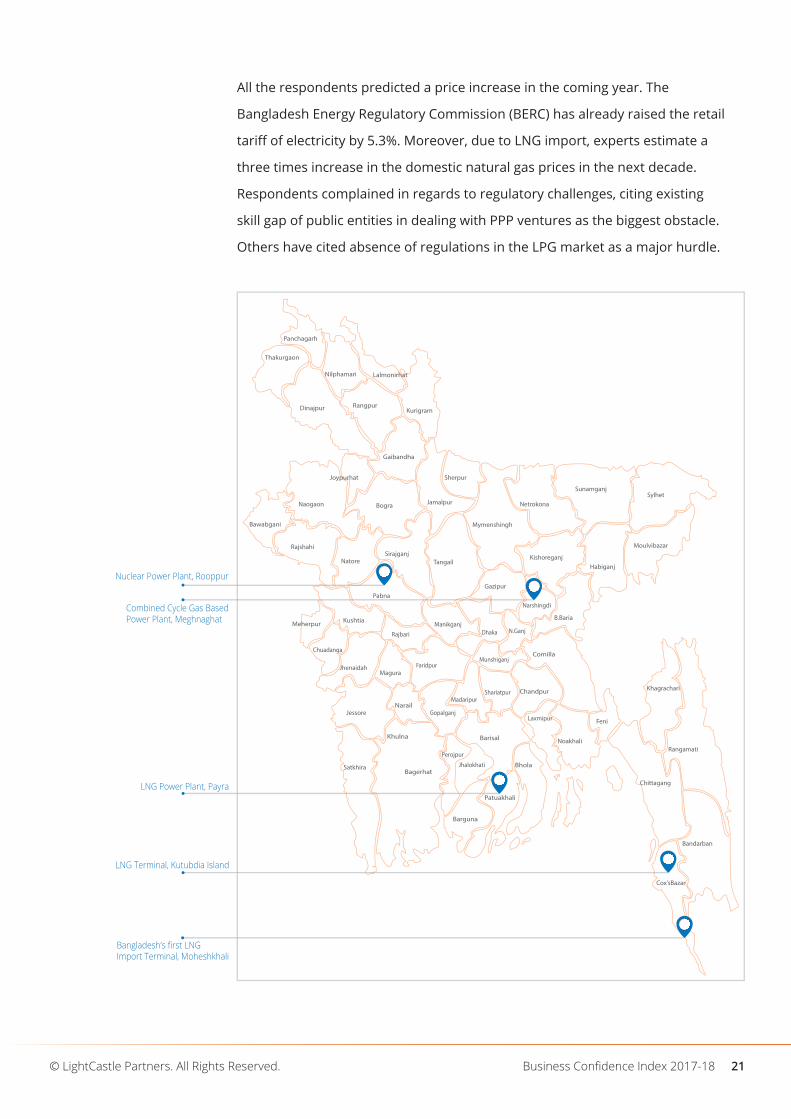

All the respondents predicted a price increase in the coming year. The

Bangladesh Energy Regulatory Commission (BERC) has already raised the retail

tariff of electricity by 5.3%. Moreover, due to LNG import, experts estimate a

three times increase in the domestic natural gas prices in the next decade.

Respondents complained in regards to regulatory challenges, citing existing

skill gap of public entities in dealing with PPP ventures as the biggest obstacle.

Others have cited absence of regulations in the LPG market as a major hurdle.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 21

Combined Cycle Gas Based Power Plant, Meghnaghat

LNG Power Plant, Payra

LNG Terminal, Kutubdia Island

Bangladesh’s first LNGImport Terminal, Moheshkhali

Nuclear Power Plant, Rooppur

Bandarban

Cox’sBazar

Khagrachari

Rangamati

Chittagang

Feni

Noakhali

Laxmipur

Chandpur

Comilla

B.Baria

Habiganj

Moulvibazar

SylhetSunamganj

Bhola

Barisal

BagerhatJhalokhati

Perojpur

Khulna

NarailJessore

MaguraJhenaidah

Chuadanga

KushtiaMeherpur

Patuakhali

Barguna

Satkhira

Sherpur

Jamalpur

Tangail

Pabna

NatoreSirajganj

Rajshahi

Naogaon

Bawabgani

Bogra

Joypurhat

Gaibandha

Rangpur

LalmonirhatNilphamari

Thakurgaon

Panchagarh

KurigramDinajpur

Kishoreganj

Gazipur

Narshingdi

Manikganj

Rajbari

FaridpurMunshiganj

ShariatpurMadaripur

Gopalganj

Dhaka N.Ganj

Netrokona

Mymenshingh

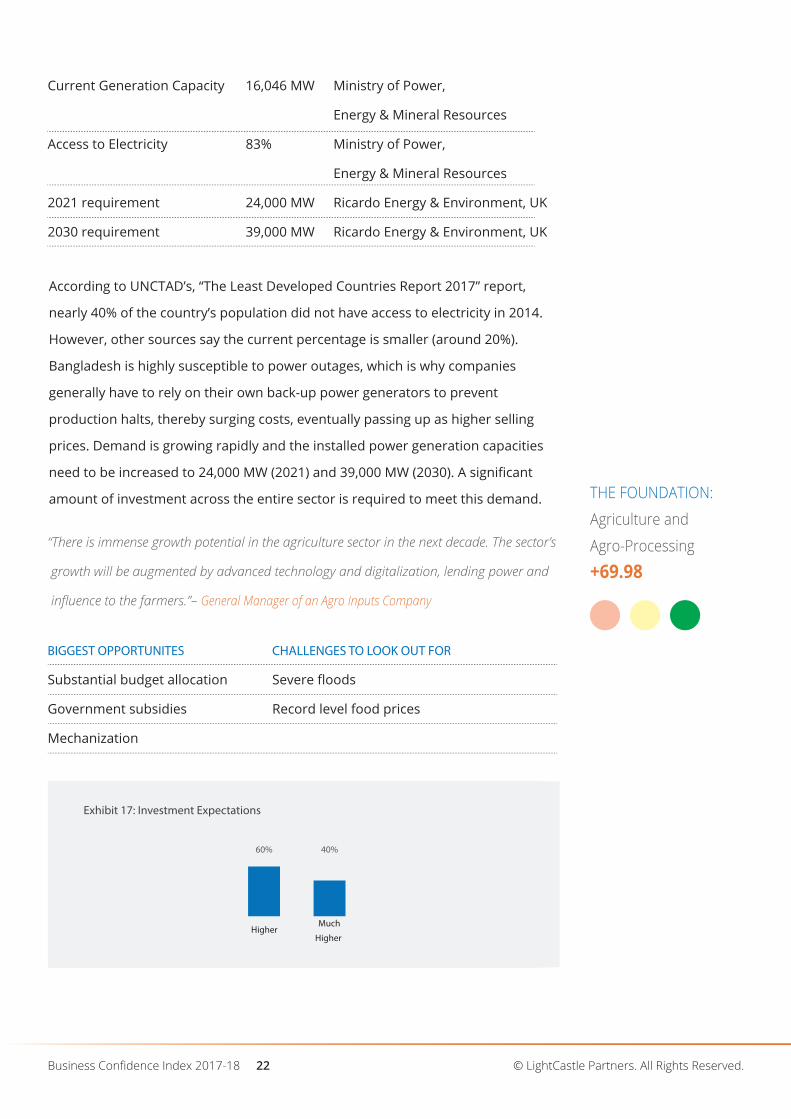

Current Generation Capacity

Access to Electricity

2021 requirement

2030 requirement

16,046 MW

83%

24,000 MW

39,000 MW

Ministry of Power,

Energy & Mineral Resources

Ministry of Power,

Energy & Mineral Resources

Ricardo Energy & Environment, UK

Ricardo Energy & Environment, UK

THE FOUNDATION:

Agriculture and

Agro-Processing

+69.98“There is immense growth potential in the agriculture sector in the next decade. The sector’s

growth will be augmented by advanced technology and digitalization, lending power and

influence to the farmers.”– General Manager of an Agro Inputs Company

BIGGEST OPPORTUNITES

Substantial budget allocation

Government subsidies

Mechanization

CHALLENGES TO LOOK OUT FOR

Severe floods

Record level food prices

Exhibit 17: Investment Expectations

40%60%

HigherMuch

Higher

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.22

According to UNCTAD’s, “The Least Developed Countries Report 2017” report,

nearly 40% of the country’s population did not have access to electricity in 2014.

However, other sources say the current percentage is smaller (around 20%).

Bangladesh is highly susceptible to power outages, which is why companies

generally have to rely on their own back-up power generators to prevent

production halts, thereby surging costs, eventually passing up as higher selling

prices. Demand is growing rapidly and the installed power generation capacities

need to be increased to 24,000 MW (2021) and 39,000 MW (2030). A significant

amount of investment across the entire sector is required to meet this demand.

Exhibit 18: Sales Expectations

20%

80%

HigherMuch

Higher

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 23

In spite of remaining extremely vulnerable to climate changes, Agriculture has

largely contributed to poverty alleviation in Bangladesh. Industry leaders

voiced satisfaction towards government support with respect to budget

allocation (BDT 244.3 Bn in FY 2017-18), subsidies and measures to promote

mechanization of agriculture such as soilless agriculture and drip water

irrigation. All the respondents expect investments and sales to soar in the

coming year.

This year, floods caused severe damages, triggering prices of food

commodities to reach record levels in September. As a result, the government

reduced the import duty of rice to 5% and was compelled to import 3.5 lac

tonnes of rice. Furthermore, classified loans rose by more than 14% (BDT 6.08

Bn) in 2017. Finally, participants also mentioned stringent regulations,

government bureaucracy and power crisis as leading obstacles to growth.

THE CONVENIENCE STORE:

FMCG

+60.87

BIGGEST OPPORTUNITES

Density dividend

Increasing consumer spending

Changing consumer lifestyle

CHALLENGES TO LOOK OUT FOR

Threat of imports

Compliance issues

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.24

“We have a huge market and growing spending power. Consumer income and

spending are both ever-increasing and consumers are now more conscious of

quality than ever.”– Executive Director of an FMCG Company

100

150

7.9% 10.5% 11.8% 6.4% 4.9% 7.8%

0

MAC Populationin millions

5.8 8.511.7

19.3 18.7

33.245.4

38.9

49.4

96.7

140.9

32.7

Mac % of populations

Myanmar Bangladesh Vietnam Philippines Thailand Indonesia

11% 15% 7% 12% 21% 34% 33% 42% 69% 72% 38% 53%

2020 2015

CAGR 2015 - 2020

Exhibit 18: MAC Population

Source: BCG Analysis

Sector leaders assert the industry is growing on the backdrop of new,

innovative product categories (e.g., yogurt drinks) gaining traction among

consumers. Due to changing lifestyle, taste and fashion, consumers are

becoming more quality conscious. The Bangladesh market has the advantage

of a huge population remaining concentrated in small geographic locations.

Looked another way, the country is enjoying a “density dividend.” The total

MAC population is expanding rapidly at 10.5% annually and at this pace, the

population segment is expected to triple to 34 million by 2025. Furthermore,

the figure is estimated to expand across different territories. Millions of

households are approaching an income level at which they can afford to

move beyond basic necessities – lending higher affordability leading to better

convenience, comfort, and luxury.

Major challenges include threat of imports (for local firms), rising raw material

costs, and lack of human talent in the middle and top management.

Inadequate government support, compliance related issues and open-ended

regulations in marketing certain products cause additional barriers to growth.

DOCTOR TO THE

ECONOMY:

Pharmaceuticals

+56.44

“With an increasing life expectancy, 5,000 new local doctors and Pharma patent waiver

period extended till 2032, we can be certain of massive opportunities in the

Pharmaceutical sector.”– General Manager, Marketing of a Pharmaceutical Company

BIGGEST OPPORTUNITES

Increasing ageing population

FDA approvals

TRIPS extension to 2032

CHALLENGES TO LOOK OUT FOR

Raw material import dependency

Lack of skilled human resources

The industry is currently catering to 98% of local market demand and exporting

to over 125 countries. All the industry leaders surveyed expect an upsurge in

sales in the coming year. 71% and 80% are hopeful about increase in profits

and exports respectively. Respondents attribute such short (and long-term)

aspirations to:

Rising income levels among the poorest socio-economic groups

Change in the country’s disease profile in terms of the rise of

non-communicable diseases and a gradual move from acute to chronic

diseases

Increasing ageing population (25% will be above 50 by 2036)

FY10FY11FY12FY13FY14FY15FY16

FY17, E

36.24144.3

48.359.8

72.681.2

89

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 25

Exhibit 19: Pharma Exports, USD Mn (EPB)

Source: Export Promotion Bureau of Bangladesh

FDA approvals for Beximco Group and Square Pharma, opening up to the

world's largest pharmaceuticals market

Growing endorsement of generic drugs in international markets;

Valuation of global generic drugs is estimated at USD 380 Bn by 2021

Emerging markets’ spending on pharmaceutical products, expected to reach

USD 345-375 Bn by 2020.

THE CROSS-CUTTING

AGENT OF CHANGE:

ICT & ITES

+46.42

“Bangladesh’s domestic market is growing and local companies are going digital. Even

mid-tier organizations are going for technology transformations as it is now deemed to be

an investment instead of expense. To leverage proper opportunities, we need greater

customer education and professionalism from IT firms.”– CEO of a Software Firm

BIGGEST OPPORTUNITES

Government support

Establishment of IT parks

CHALLENGES TO LOOK OUT FOR

Difficulty in collection of payments

Logistical challenges (e.g., internet services in rural areas)

Exhibit 20: Employment Expectations (Upcoming 6 months)

66.7%

6.7%20%

LowerHigherMuch

Higher

6.7%

Same/

No Change

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.26

Respondents have also credited policies – Drug Control Ordinance, 1982, which

prohibits foreign pharmaceuticals from selling imported drugs and the WTO’s

agreement on TRIPS, which permits Bangladesh to reverse engineer patented

generic drugs – for contributing to the sector’s success.

Rising raw material costs, power crises and lack of skilled human resources

surface as primary challenges. The standard of Pharma education system is

relatively poor while “brain drain” is also quite prevalent. However, the

government is taking initiatives such as the Active Pharmaceutical Ingredients

(API) industrial park to reduce raw material import dependency. With 41 plots

allotted to 27 pharmaceutical firms and expected to be operational by 2018, the

park will allow companies to source at least half of their raw materials locally.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 27

ICT & ITES industry is getting maximum exposure through the lens of policy

favors. In fact, it is being touted as the “next RMG sector” of Bangladesh. Roughly

40% of the industry leaders said investments will rise substantially in 2018 and

more than 85% expect greater ICT based jobs. Respondents showed optimism

towards the emergence of special ICT focused zones such as establishment of 25

IT and Hi-tech parks in regions including Khulna, Barisal, Rangpur, Natore,

Chittagong, Comilla, Cox's Bazar, Mymensingh, Jamalpur, Gopalganj, Dhaka and

Sylhet from where the government hopes to export software and IT services

worth USD 10 Bn by 2030. Additionally, to encourage entrepreneurship in this

sector, 100% corporate tax exemption has been accorded and various startup

projects, such as “Innovation Design and Entrepreneurship Academy,” have been

established. The government aims to transform Bangladesh into a middle

income nation through the success of ICT & ITES industry. Finally, industry

leaders have also expressed satisfaction with the rise in Venture Capital (VC)

firms’ growing interest in tech startups.

The difficulty in payment collections or yields is a challenge particular to the ICT &

ITES industry. Other confronted challenges are financing difficulties due to high

cost of credit and the need for physical assets as collateral, regulatory challenges

such as corruption, open ended regulations, government bureaucracy, and

human capital challenges in terms of employee incompetency and attrition.

However, the government’s efforts in solving such problems can be seen through

collaborations with international consulting firms such as BCG, where BCG will

work for international B2B development. Initiatives such as the CEO Outreach

Programme will help boost investment and create more job opportunities.

THE CAPITAL ENGINE:

Banking & Finance

+37.52

BIGGEST OPPORTUNITES

High competition

Banks are more confident than NBFIs

FinTech, Mobile Financial Services

CHALLENGES TO LOOK OUT FOR

Upsurge in classified loans

Inadequate credit analysis

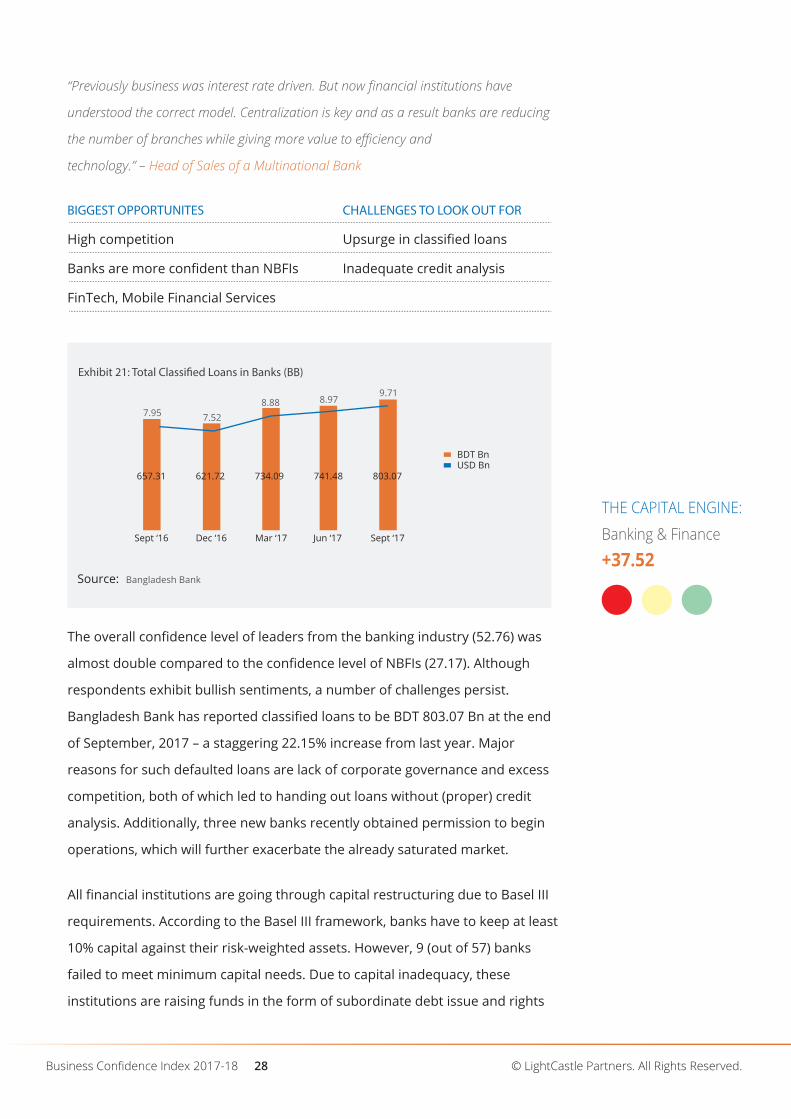

The overall confidence level of leaders from the banking industry (52.76) was

almost double compared to the confidence level of NBFIs (27.17). Although

respondents exhibit bullish sentiments, a number of challenges persist.

Bangladesh Bank has reported classified loans to be BDT 803.07 Bn at the end

of September, 2017 – a staggering 22.15% increase from last year. Major

reasons for such defaulted loans are lack of corporate governance and excess

competition, both of which led to handing out loans without (proper) credit

analysis. Additionally, three new banks recently obtained permission to begin

operations, which will further exacerbate the already saturated market.

All financial institutions are going through capital restructuring due to Basel III

requirements. According to the Basel III framework, banks have to keep at least

10% capital against their risk-weighted assets. However, 9 (out of 57) banks

failed to meet minimum capital needs. Due to capital inadequacy, these

institutions are raising funds in the form of subordinate debt issue and rights

Sept ‘16 Dec ‘16 Mar ‘17 Jun ‘17 Sept ‘17

7.95 7.528.88 8.97

9.71

657.31 621.72 734.09 741.48 803.07

BDT BnUSD Bn

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.28

“Previously business was interest rate driven. But now financial institutions have

understood the correct model. Centralization is key and as a result banks are reducing

the number of branches while giving more value to efficiency and

technology.” – Head of Sales of a Multinational Bank

Exhibit 21: Total Classi�ed Loans in Banks (BB)

Source: Bangladesh Bank

Exhibit Source: World Bank

share issue. The surge in risky financing raised these banks’ risk-weighted assets

and dipped capital base.

Industry leaders, from both bank and NBFIs, quoted regulatory challenges such as

government bureaucracy, open ended regulations and unfavorable taxation

regime to be the primary hurdles. The next big difficulty is employee

incompetency due to lack of specialized training and brain drain from the country.

Respondents opine better corporate governance as a necessity to solving the

problem of classified loans.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 29

STANDING IN MOTION:

RMG & Textiles

+37.06

“Globally, after China, Bangladesh is the second largest garments exporter. China is getting

more expensive, which opens many doors for us. We need to go after product and market

diversification. Locally, RMG sector is the highest contributor to the economy and the

no. 1 employment generator.”– Director of a Premium Denim Jeans Manufacturer

BIGGEST OPPORTUNITES

Over 80% of total exports

‘China plus one’ policy

Heavy investment in high class facilities

CHALLENGES TO LOOK OUT FOR

Fall in benchmark prices

Port congestions & power crisis

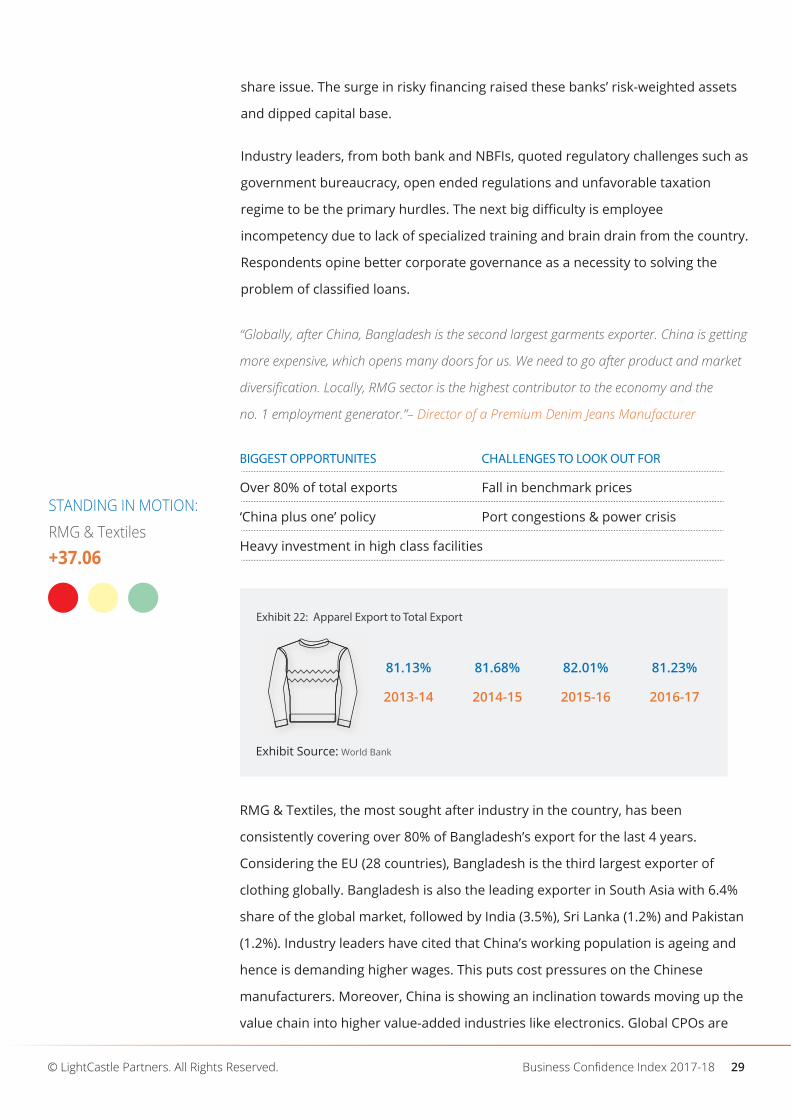

RMG & Textiles, the most sought after industry in the country, has been

consistently covering over 80% of Bangladesh’s export for the last 4 years.

Considering the EU (28 countries), Bangladesh is the third largest exporter of

clothing globally. Bangladesh is also the leading exporter in South Asia with 6.4%

share of the global market, followed by India (3.5%), Sri Lanka (1.2%) and Pakistan

(1.2%). Industry leaders have cited that China’s working population is ageing and

hence is demanding higher wages. This puts cost pressures on the Chinese

manufacturers. Moreover, China is showing an inclination towards moving up the

value chain into higher value-added industries like electronics. Global CPOs are

Exhibit 22: Apparel Export to Total Export

81.13%

2013-14

81.68%

2014-15

82.01%

2015-16

81.23%

2016-17

China EU (28 Vietnam India Hongkong Turkey Indonesia Cambodia USAcountries)

25 18 16 15 7 6 6

Exhibit 23: Top 10 Exporters of Clothing161

117

Bangladesh

28

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.30

Source: WTO 2016

adopting a ‘China plus one’ policy in order to diversify away from China and

looking for cheaper alternatives such as Bangladesh.

Bangladesh has captured almost two thirds of China’s low-end manufacturing

market share in Europe. In addition, Bangladesh is now the top denim exporter

to EU with a market share of 21.18%. This has come about as a result of heavy

investment in high quality facilities, leading to products with better quality,

competitive prices and shorter lead times. As an LDC, Bangladesh enjoys duty

and quota free access to the EU market under provision of GSP. However,

as soon as Bangladesh becomes a middle-income country (potentially by 2024)

it will lose this provision. Over 50% of the respondents claimed poor

infrastructure as a major challenge. One participant from a woven factory

also mentioned that due to a dip in demand, many players are taking orders

below costs to run their lines, which are lowering the benchmark price. Nearly

55% of the industry leaders anticipate prices to reduce further in 2018.

China

41% 1.2%

Sri Lanka

6.4%

Bangladesh

3.5%

India

1.2%

Pakistan

46%

Others

Source: World Bank

Exhibit 24: Market Share among Key RMG Exporters

COMPLETING THE

LAST MILE:

Logistics

+32.74

“The RMG sector, in particular, has recovered from shocks such as the Rana Plaza

catastrophe. Additionally, we have several green factories currently operating. The world

does not see us as non-compliant anymore. This implies RMG business is back on track,

which in turn, benefits the Logistics industry.”– Head of Ocean Freight at Multinational

Logistics Firm

BIGGEST OPPORTUNITES

Government initiatives (Payra port)

CHALLENGES TO LOOK OUT FOR

Port congestions

Lack of operation space

“Long lead time” is a phrase prevalent in the trade sector of Bangladesh. The

logistics industry, a support system for all other industries, plays a vital role in

shortening such lead times. Majority of the leaders in the other industries have

complained about the infrastructure and logistics of the country. Leaders of the

logistics industry do not disagree either. They complain port congestion to be the

biggest challenge of 2017, when vessels in Chittagong port had to wait up to even

10 days at the outer anchorage due to an accident. They even said the existing

ports have run out of sufficient operations space.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 31

On the positive side, the government is taking initiatives to tackle this problem.

They are investing time and resources on the development of Payra port, which

will have direct rail, road, and waterway linkages with Dhaka. The government is

also taking several internal city development initiatives such as the construction

of flyovers, the metro rail in Dhaka, and the improvement of the

Chittagong-Cox's Bazar highway. Furthermore, a program of Authorized

Economic Operators (AEO) is being introduced within the next year to cut down

on congestion in ports and highways. In order to hasten the release of goods

from the ports, the program will involve almost no physical check of import and

export containers, nominal bank guarantee submission, deferred payment, etc.

Firms will have to invest in supply chain security and comply with specific

customs requirements in return for the benefits from this fast-track program.

HEART IS WHERE

THE HOME IS:

Real Estate

+28.83

The real estate bubble in Bangladesh has burst and now the competition is very high.

Customers are more informed. Profit margin is low. There is a need for decentralization

from Dhaka.”– CEO of a Real Estate Company

BIGGEST OPPORTUNITES

Decentralization from Dhaka

CHALLENGES TO LOOK OUT FOR

Oversupply of apartments

Stricter home loan regulations

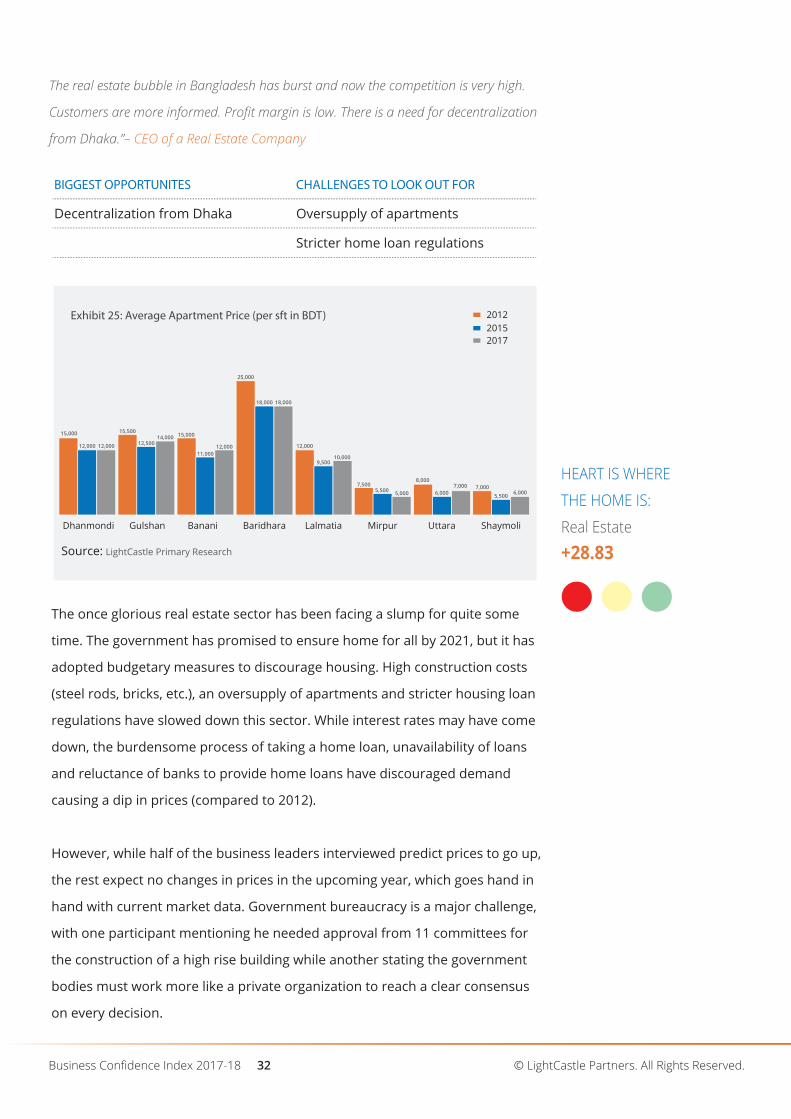

15,000 15,500

12,50014,000 15,000

11,00012,000

25,000

18,000 18,000

12,000

9,50010,000

7,5005,500 5,000

8,000

6,0007,000 7,000

5,500 6,000

12,000 12,000

Dhanmondi Gulshan Banani Baridhara Lalmatia Mirpur Uttara Shaymoli

201220152017

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 32

Exhibit 25: Average Apartment Price (per sft in BDT)

Source: LightCastle Primary Research

The once glorious real estate sector has been facing a slump for quite some

time. The government has promised to ensure home for all by 2021, but it has

adopted budgetary measures to discourage housing. High construction costs

(steel rods, bricks, etc.), an oversupply of apartments and stricter housing loan

regulations have slowed down this sector. While interest rates may have come

down, the burdensome process of taking a home loan, unavailability of loans

and reluctance of banks to provide home loans have discouraged demand

causing a dip in prices (compared to 2012).

However, while half of the business leaders interviewed predict prices to go up,

the rest expect no changes in prices in the upcoming year, which goes hand in

hand with current market data. Government bureaucracy is a major challenge,

with one participant mentioning he needed approval from 11 committees for

the construction of a high rise building while another stating the government

bodies must work more like a private organization to reach a clear consensus

on every decision.

Exhibit 26: Selling Price Expectations

50%50%

HigherSame/

No Change

Industry experts further recommended a low-cost credit support to middle

income people (to purchase flats) and decentralization away from Dhaka

are necessary factors to pull the industry out of its current sorry state.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 33

“Cement use is multi-dimensional. Currently the profit margin is low but the business is

based on volume. Economies of scale is the only way to sustain and in the long run big

players will survive.”– CFO of a Local Cement Company

BIGGEST OPPORTUNITES

Rise in construction projects

Recent fall in clinker prices

CHALLENGES TO LOOK OUT FOR

Slump in the real estate sector

Seasonal demand

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

20.021.0

22.025.0

28.0

38.040.0

69.5% 69.0% 68.2%

64.0% 62.5%

73.7%

80.0%

Exhibit 27: Production Capacity and Utilization

Production , Mn MTProduction Capacity, Mn MT Utilization

Source: Industry Players' Estimate and EBLSL Research and The Daily Star

A STICKY SITUATION:

Cement

+23.61

Source: Industry Players' Estimate and EBLSL Research and The Daily Star

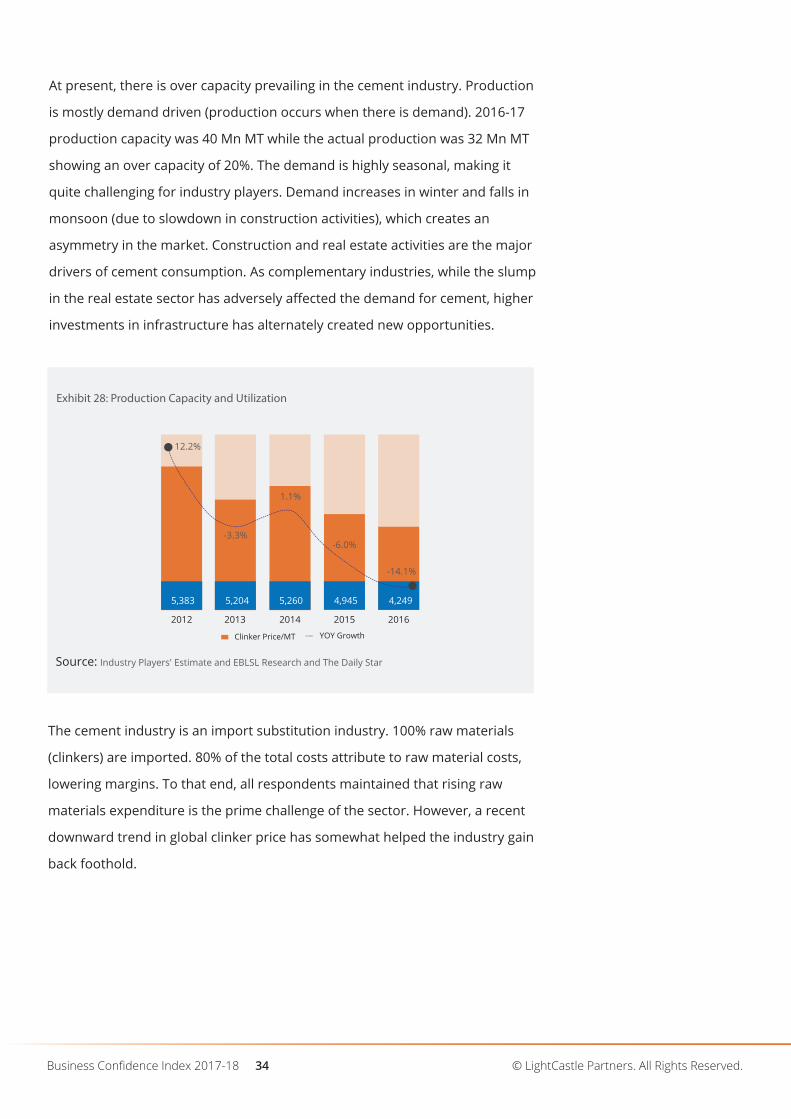

At present, there is over capacity prevailing in the cement industry. Production

is mostly demand driven (production occurs when there is demand). 2016-17

production capacity was 40 Mn MT while the actual production was 32 Mn MT

showing an over capacity of 20%. The demand is highly seasonal, making it

quite challenging for industry players. Demand increases in winter and falls in

monsoon (due to slowdown in construction activities), which creates an

asymmetry in the market. Construction and real estate activities are the major

drivers of cement consumption. As complementary industries, while the slump

in the real estate sector has adversely affected the demand for cement, higher

investments in infrastructure has alternately created new opportunities.

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 34

The cement industry is an import substitution industry. 100% raw materials

(clinkers) are imported. 80% of the total costs attribute to raw material costs,

lowering margins. To that end, all respondents maintained that rising raw

materials expenditure is the prime challenge of the sector. However, a recent

downward trend in global clinker price has somewhat helped the industry gain

back foothold.

2012 2013 2014 2015 2016

Clinker Price/MT YOY Growth

5,383 5,204 5,260 4,945 4,249

12.2%

-14.1%

-3.3%-6.0%

1.1%

Exhibit 28: Production Capacity and Utilization

PROBLEM AREAS:BOTTLENECKS TOOVERCOME

PROBLEM AREAS: BOTTLENECKS TO OVERCOME

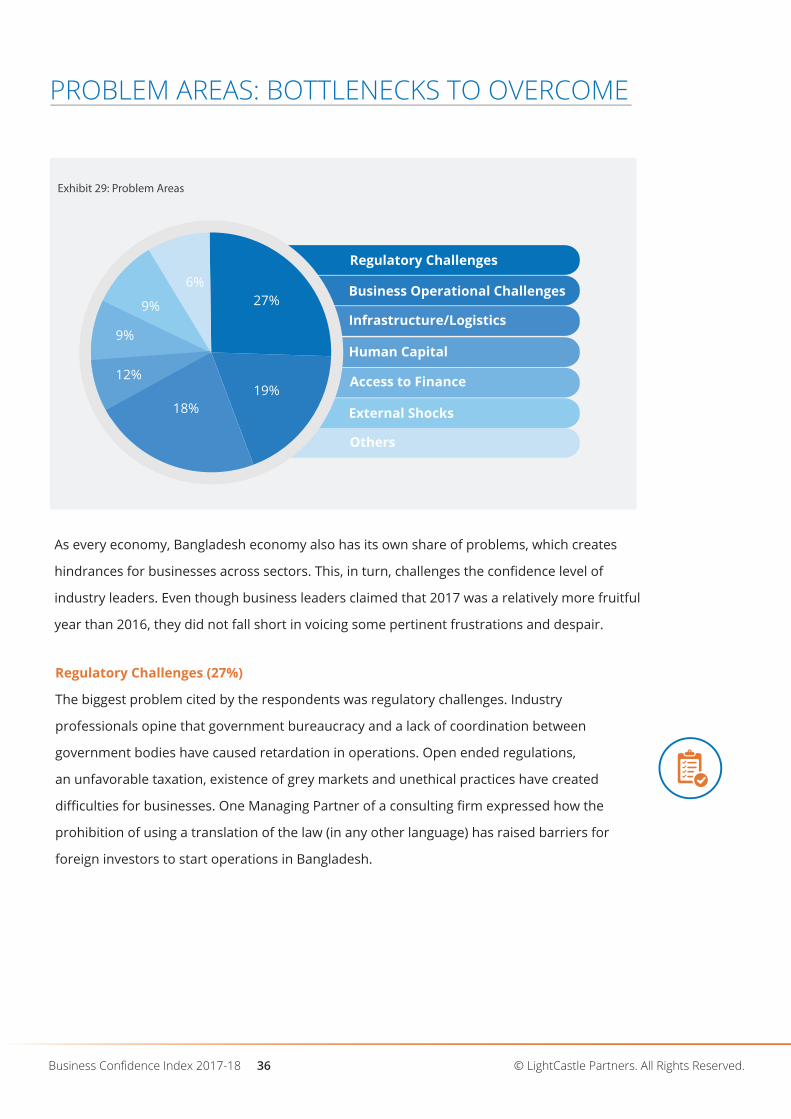

As every economy, Bangladesh economy also has its own share of problems, which creates

hindrances for businesses across sectors. This, in turn, challenges the confidence level of

industry leaders. Even though business leaders claimed that 2017 was a relatively more fruitful

year than 2016, they did not fall short in voicing some pertinent frustrations and despair.

27%

19%18%

12%

9%

9%

6%Regulatory Challenges

Business Operational Challenges

Infrastructure/Logistics

Human Capital

Access to Finance

External Shocks

Others

© LightCastle Partners. All Rights Reserved. Business Confidence Index 2017-18 36

Regulatory Challenges (27%)

The biggest problem cited by the respondents was regulatory challenges. Industry

professionals opine that government bureaucracy and a lack of coordination between

government bodies have caused retardation in operations. Open ended regulations,

an unfavorable taxation, existence of grey markets and unethical practices have created

difficulties for businesses. One Managing Partner of a consulting firm expressed how the

prohibition of using a translation of the law (in any other language) has raised barriers for

foreign investors to start operations in Bangladesh.

Exhibit 29: Problem Areas

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 37

Business Operational Challenges (19%)

Business operational challenges adversely affect profits in the form of rising raw

material costs especially in the cement and pharmaceutical industries. The per unit

fall in value and increase in volume in the RMG sector is another difficulty. Other

problems include the struggles in handling working capital especially in the ICT & ITES

sector.

Infrastructure/Logistics (18%)

Port congestions, mainly in the export-import oriented industries, and power &

energy crisis, especially in the manufacturing industries, have snatched away the

price competitiveness of Bangladeshi companies. Customs inefficiency and

transportation problems also add to the woes relating to infrastructure and logistics.

Human Capital (12%)

Although 2.1 million young people enter the job market each year, respondents

complain a stark gap between employees’ level of competence and professional

requirements. Dearth of competent middle management and persistent “brain drain”

surface as poignant challenges.

Access to Finance (9%)

While many industry leaders were satisfied by lower interest rates, mostly ICT & ITES

sector respondents complained about the high cost of credit and difficulties faced in

availing finance, especially the need for physical assets as collateral for loans.

External Shocks (9%)

Threat of imports in the FMCG industry and threat of foreign players in the ICT & ITES

sector are external shocks that industry leaders want to mitigate.

Others (6%)

Respondents have cited some other challenges which cannot be clubbed into any of

the aforementioned problems. These include a lack of collaboration among industry

peers and inadequate support system for startups.

Problem-Industry matrixBelow is a summary of the major problems cited by industry leaders in their

respective industries.

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.38

Industries

Regulatory Challenges

Business Operational Challenges

Infrastructure/Logistics

Human Capital

Access to Finance

External Shocks

Prob

lem

s

Power and Energy

Agriculture and Agro-Processing

FMCG

Pharmaceuticals

ICT and ITES

Banking and Finance

RMG and Textiles

Logistics

Real Estate

Cement

FUTURE PROSPECTS:THE ROYAL BENGALTIGERS OF THE NEXT DECADE

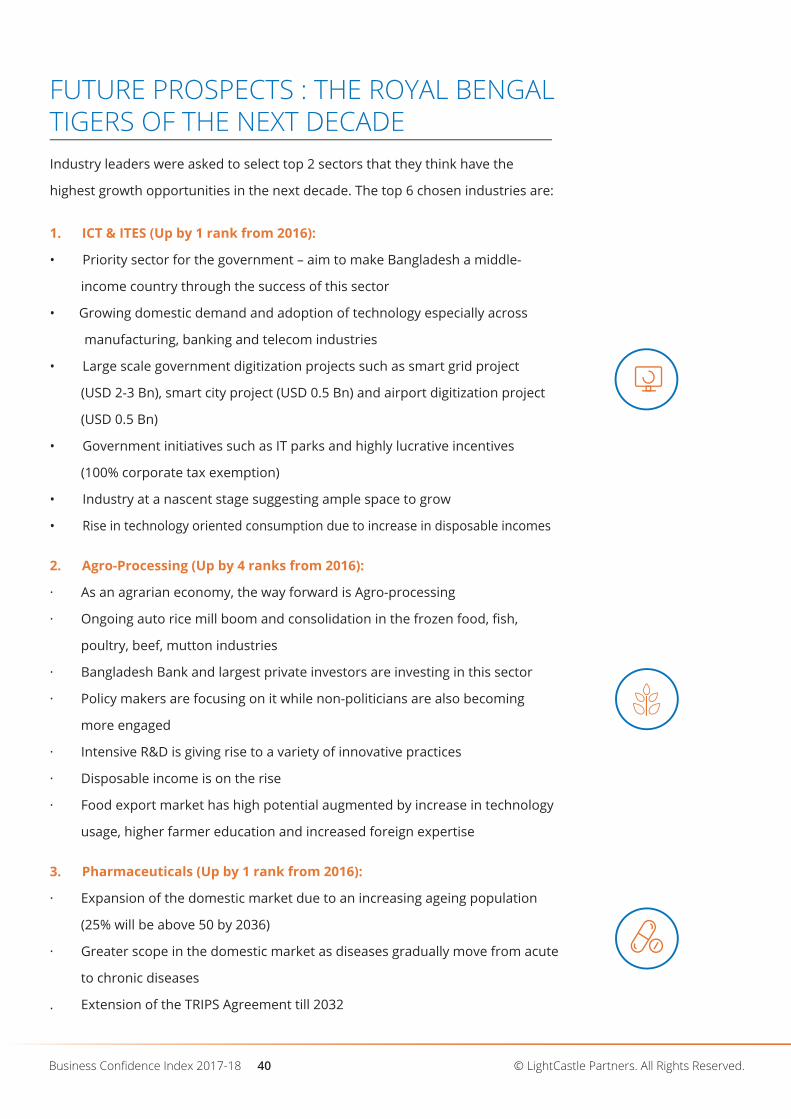

FUTURE PROSPECTS : THE ROYAL BENGALTIGERS OF THE NEXT DECADE Industry leaders were asked to select top 2 sectors that they think have the

highest growth opportunities in the next decade. The top 6 chosen industries are:

1. ICT & ITES (Up by 1 rank from 2016):

• Priority sector for the government – aim to make Bangladesh a middle-

income country through the success of this sector

• Growing domestic demand and adoption of technology especially across

manufacturing, banking and telecom industries

• Large scale government digitization projects such as smart grid project

(USD 2-3 Bn), smart city project (USD 0.5 Bn) and airport digitization project

(USD 0.5 Bn)

• Government initiatives such as IT parks and highly lucrative incentives

(100% corporate tax exemption)

• Industry at a nascent stage suggesting ample space to grow

• Rise in technology oriented consumption due to increase in disposable incomes

2. Agro-Processing (Up by 4 ranks from 2016):

· As an agrarian economy, the way forward is Agro-processing

· Ongoing auto rice mill boom and consolidation in the frozen food, fish,

poultry, beef, mutton industries

· Bangladesh Bank and largest private investors are investing in this sector

· Policy makers are focusing on it while non-politicians are also becoming

more engaged

· Intensive R&D is giving rise to a variety of innovative practices

· Disposable income is on the rise

· Food export market has high potential augmented by increase in technology

usage, higher farmer education and increased foreign expertise

3. Pharmaceuticals (Up by 1 rank from 2016):

· Expansion of the domestic market due to an increasing ageing population

(25% will be above 50 by 2036)

· Greater scope in the domestic market as diseases gradually move from acute

to chronic diseases

. Extension of the TRIPS Agreement till 2032

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.40

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 41

· Capitalize on the global market as the size of global generic drugs is

estimated at USD 380 Bn by 2021

· Expand the international markets as emerging markets’ spending on

pharmaceutical products is expected to reach USD 345-375 Bn by 2020

4. Power & Energy (Down by 4 ranks from 2016):

· Significant mismatch in demand and supply

· Numerous LNG and LPG players will enter the market

· Private sector players are heavily investing in this sector

· Government is heavily involved in the establishment of power plants in

Mongla, Rooppur, Meghnaghat, etc.

· LNG will be sourced globally by mid-2018

5. Footwear (Same as 2016):

· Local consumer base is on the rise

· 35% of tanneries have been shifted from Hazaribagh to Savar Tannery

Estate

· Government is incentivizing production of synthetic footwear

· China (57% of global market share) is shifting focus towards technology

oriented industries – opening new windows

· Piqued interest in the sector – Increase in foreign investor inquiries

6. RMG & Textiles (Down by 3 ranks from 2016):

· ‘China plus one’ policy: Bangladesh can capture China’s loss in market

share with almost two-thirds of low-end manufacturing market share in

Europe

· Government offers packages for exploring new destinations such as Japan,

China and India

· Emergence of high value items such as intimate wears and jackets (product

diversification)

· Top denim exporter to EU with a market share of 21.18%

· Players heavily investing in high quality facilities, leading to products with

better quality, competitive prices and shorter lead times

· Leading exporter in South Asia

· Delivering better standard levels than other South Asian countries

CONCLUDING REMARKS:THE WAY FORWARD

CONCLUDING REMARKS:THE WAY FORWARDBangladesh has shown an immense potential to recover from the biggest crises. Business representatives

believe the public and private sectors can work in coordination with each other for the economy to achieve

higher growth in the near future. Key agreed upon recommendations are presented below:

Shifting export dependency from the RMG sector

When it comes to exports, it is high time the government shifts its focus from the RMG sector to other industries

such as Footwear and ICT. Other industries need to be incentivized to level the playing field. Formulating and

adopting strategies for trade in services will help uplift the ICT sector. The World Bank has recently approved

USD 100 Mn to support the country in diversifying exports in labor and skill intensive industries beyond the

RMG sector. In order to increase competitiveness, the government should come forward to increase non-RMG

firms’ access to international markets, and enhance their ability to conform to global standards.

Facilitating the ease of starting and conducting business

Private sector leaders claim government entities require capacity building to reduce sluggishness in operations.

Leaders have suggested such government entities must work like private sector organizations and with greater

unity to improve efficiency. Red-tapes need to be removed to speed up the process of starting a business.

Construction permits need to be issued faster while the time taken for a company to be connected to the

national grid needs to be lessened. Simplifying property registration process and fully digitizing tax submission

will further ease the way of doing business in Bangladesh.

Improving infrastructure and logistics

Port congestions must be addressed by increasing the number of ports and modernizing the existing ones in

order to shorten lead times. Additionally, customs efficiency must be enhanced. National highways need to be

upgraded to 4 or more lanes and road safety must be improved. New bridges to ensure undisturbed traffic flow

have to be constructed and old ones replaced or repaired.

Business Confidence Index 2017-18© LightCastle Partners. All Rights Reserved. 43

Enhancing the skill of human resources

To develop capacity of human resources, skill development has become a necessity. This will not only enhance

the quality of final goods but also reduce waste and increase labor income. A comprehensive strategy for talent

development needs to be formulated. This involves formal and informal training along with improvements in

the quality standards of basic education.

Streamlining the Financial Sector and scaling up the use of alternative capital avenues

The financial sector must be regulated and supervised properly by an independent body such as the central

bank to reduce the struggle with loan defaults. Government must strengthen corporate governance which

would help strengthen the lending processes in different commercial banks. Additionally, the government

should promote opportunities that can be availed from venture capital, impact investments, private equity and

accelerator programs.

The good news is that the overall optimism in the country’s business world is higher than last year. The

cautiousness reflected in the score can be overcome by mitigating the challenges mentioned. With an average

annual economic growth of 6% over the last decade, Bangladesh has the potential to be the 28th largest econo-

my by 2030 as projected by PwC. By integrating information technology in every industry, lowering power

deficit, enabling infrastructural improvements and lessening regulatory challenges to facilitate more commerce,

the country can generate higher employment – giving rise to one of the most important economies of the world.

Business Confidence Index 2017-18 © LightCastle Partners. All Rights Reserved.44

Floor 01 | House 134 | Road 03 | Block ANiketan | Gulshan-1 | Dhaka 1212 | Bangladesh

Mobile: +88 01711 385 988 | +88 01747 353 438Web: www.lightcastlebd.com

Real Time Consumer Research: www.lightcastledata.comReal Time Reports: www.lightcastledata.com/drive

All information contained herein is obtained by LightCastle from sources believed by it to be accurate and reliable.

Because of the possibility of human or mechanical error as well as other factors, however, all information contained

herein “As IS” without warranty of any kind. LightCastle adopts all necessary measures so that the information it uses

is of sufficient quality and from sources LightCastle considers to be reliable including, when appropriate, independent

third-party sources. However, LightCastle is not an auditor and cannot in every instance independently verify or

validate information received in preparing publications.