Lifestyle and Tourism Industry - BKPM

121

Provided for Regional Investment Forum (RIF), Yogyakarta –Indonesia, 14-15 March 2018 Indonesia Investment Opportunities in Culinary & Cafe | Cinemas | Fashion | Spa & Sport Center | Digital Industry | 10 Tourism Destinations Supported by: Lifestyle and Tourism Industry

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Lifestyle and Tourism Industry - BKPM

Provided for Regional Investment Forum (RIF), Yogyakarta –Indonesia, 14-15 March 2018

Indonesia Investment Opportunities in

Culinary & Cafe | Cinemas | Fashion | Spa & Sport Center | Digital Industry | 10 Tourism Destinations

Supported by:

Lifestyle and Tourism Industry

INDONESIA ECONOMIC OUTLOOK

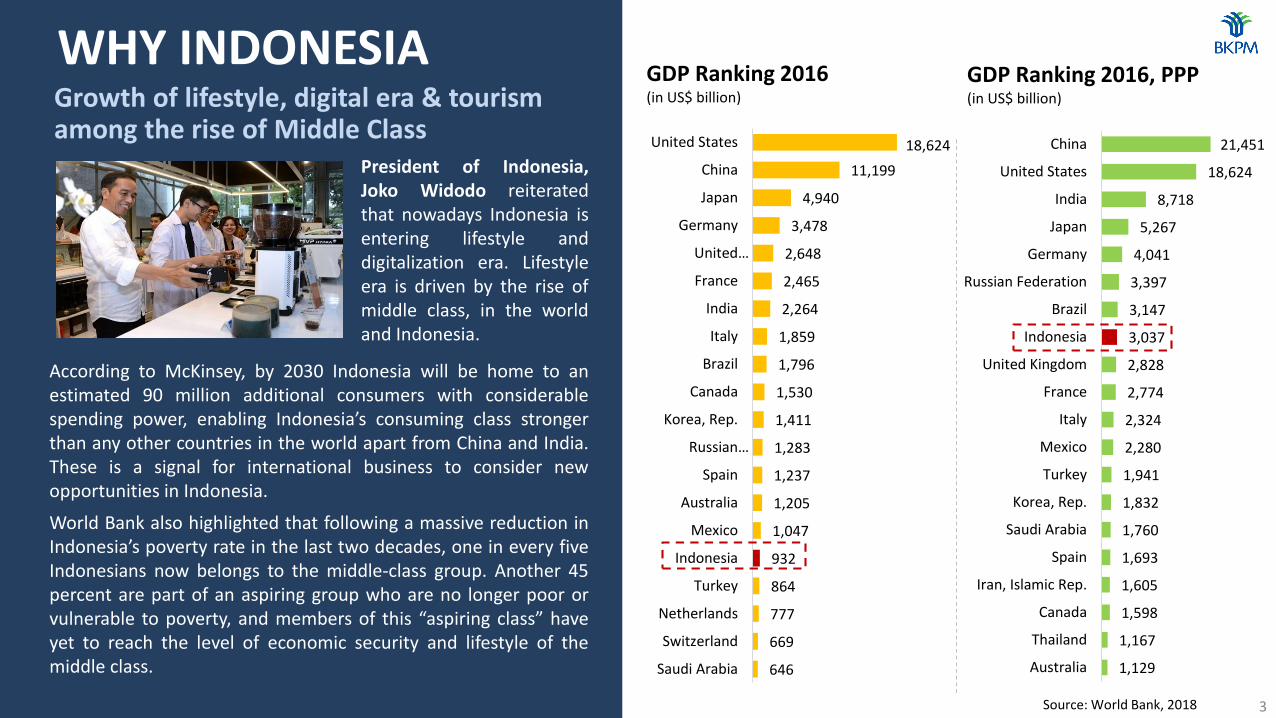

According to McKinsey, by 2030 Indonesia will be home to anestimated 90 million additional consumers with considerablespending power, enabling Indonesia’s consuming class strongerthan any other countries in the world apart from China and India.These is a signal for international business to consider newopportunities in Indonesia.

World Bank also highlighted that following a massive reduction inIndonesia’s poverty rate in the last two decades, one in every fiveIndonesians now belongs to the middle-class group. Another 45percent are part of an aspiring group who are no longer poor orvulnerable to poverty, and members of this “aspiring class” haveyet to reach the level of economic security and lifestyle of themiddle class.

President of Indonesia,Joko Widodo reiteratedthat nowadays Indonesia isentering lifestyle anddigitalization era. Lifestyleera is driven by the rise ofmiddle class, in the worldand Indonesia.

WHY INDONESIAGrowth of lifestyle, digital era & tourismamong the rise of Middle Class

646

669

777

864

932

1,047

1,205

1,237

1,283

1,411

1,530

1,796

1,859

2,264

2,465

2,648

3,478

4,940

11,199

18,624

Saudi Arabia

Switzerland

Netherlands

Turkey

Indonesia

Mexico

Australia

Spain

Russian…

Korea, Rep.

Canada

Brazil

Italy

India

France

United…

Germany

Japan

China

United States

1,129

1,167

1,598

1,605

1,693

1,760

1,832

1,941

2,280

2,324

2,774

2,828

3,037

3,147

3,397

4,041

5,267

8,718

18,624

21,451

Australia

Thailand

Canada

Iran, Islamic Rep.

Spain

Saudi Arabia

Korea, Rep.

Turkey

Mexico

Italy

France

United Kingdom

Indonesia

Brazil

Russian Federation

Germany

Japan

India

United States

China

GDP Ranking 2016(in US$ billion)

GDP Ranking 2016, PPP(in US$ billion)

Source: World Bank, 20183Source: World Bank, 2018

PPP Rank

2016 2030 2050

CountryGDP at PPP

(2016 US$bn)Country

Projected GDP at PPP(US$bn)

CountryProjected GDP at

PPP(US$bn)

1 China 21,269 China 38,008 China 58,499

2 United States 18,562 United States 23,475 India 44,128

3 India 8,721 India 19,511 United States 34,102

4 Japan 4,932 Japan 5,606 Indonesia 10,502

5 Germany 3,979 Indonesia 5,424 Brazil 7.540

6 Russia 3,745 Russia 4,736 Russia 7,131

7 Brazil 3,135 Germany 4,707 Mexico 6,863

8 Indonesia 3,028 Brazil 4,439 Japan 6,779

9United Kingdom

2,788 Mexico 3,661 Germany 6,138

10 France 2,737UnitedKingdom

3,638 United Kingdom 5,369

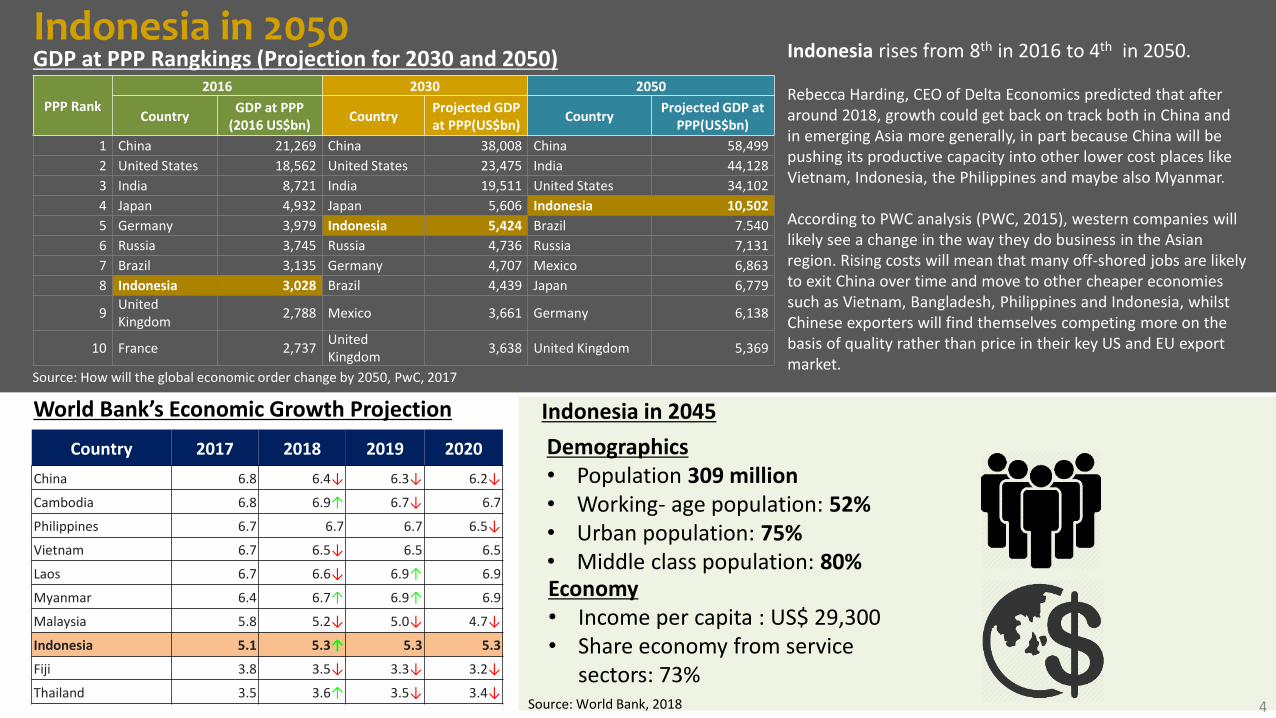

GDP at PPP Rangkings (Projection for 2030 and 2050) Indonesia rises from 8th in 2016 to 4th in 2050.

Rebecca Harding, CEO of Delta Economics predicted that after around 2018, growth could get back on track both in China and in emerging Asia more generally, in part because China will be pushing its productive capacity into other lower cost places like Vietnam, Indonesia, the Philippines and maybe also Myanmar.

According to PWC analysis (PWC, 2015), western companies will likely see a change in the way they do business in the Asian region. Rising costs will mean that many off-shored jobs are likely to exit China over time and move to other cheaper economies such as Vietnam, Bangladesh, Philippines and Indonesia, whilst Chinese exporters will find themselves competing more on the basis of quality rather than price in their key US and EU export market.

Source: How will the global economic order change by 2050, PwC, 2017

Indonesia in 2050

Country 2017 2018 2019 2020

China 6.8 6.4↓ 6.3↓ 6.2↓

Cambodia 6.8 6.9↑ 6.7↓ 6.7

Philippines 6.7 6.7 6.7 6.5↓

Vietnam 6.7 6.5↓ 6.5 6.5

Laos 6.7 6.6↓ 6.9↑ 6.9

Myanmar 6.4 6.7↑ 6.9↑ 6.9

Malaysia 5.8 5.2↓ 5.0↓ 4.7↓

Indonesia 5.1 5.3↑ 5.3 5.3

Fiji 3.8 3.5↓ 3.3↓ 3.2↓

Thailand 3.5 3.6↑ 3.5↓ 3.4↓

World Bank’s Economic Growth Projection

Demographics• Population 309 million• Working- age population: 52%• Urban population: 75%• Middle class population: 80%

Indonesia in 2045

Economy• Income per capita : US$ 29,300• Share economy from service

sectors: 73%Source: World Bank, 2018 4

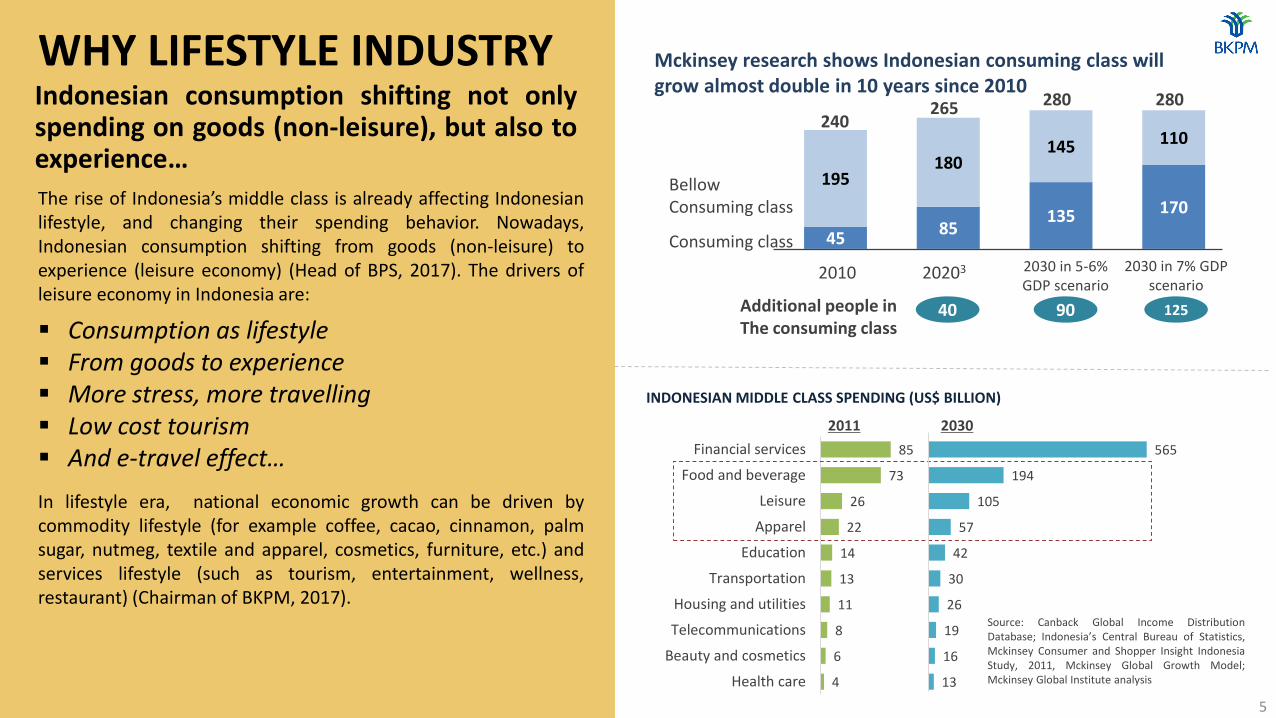

WHY LIFESTYLE INDUSTRYIndonesian consumption shifting not onlyspending on goods (non-leisure), but also toexperience…

The rise of Indonesia’s middle class is already affecting Indonesianlifestyle, and changing their spending behavior. Nowadays,Indonesian consumption shifting from goods (non-leisure) toexperience (leisure economy) (Head of BPS, 2017). The drivers ofleisure economy in Indonesia are:

Consumption as lifestyle From goods to experience More stress, more travelling Low cost tourism And e-travel effect…

In lifestyle era, national economic growth can be driven bycommodity lifestyle (for example coffee, cacao, cinnamon, palmsugar, nutmeg, textile and apparel, cosmetics, furniture, etc.) andservices lifestyle (such as tourism, entertainment, wellness,restaurant) (Chairman of BKPM, 2017).

4

6

8

11

13

14

22

26

73

85

Health care

Beauty and cosmetics

Telecommunications

Housing and utilities

Transportation

Education

Apparel

Leisure

Food and beverage

Financial services

13

16

19

26

30

42

57

105

194

565

2011 2030

Source: Canback Global Income DistributionDatabase; Indonesia’s Central Bureau of Statistics,Mckinsey Consumer and Shopper Insight IndonesiaStudy, 2011, Mckinsey Global Growth Model;Mckinsey Global Institute analysis

INDONESIAN MIDDLE CLASS SPENDING (US$ BILLION)

Additional people inThe consuming class

4585

135 170

195180

145 110

BellowConsuming class

Consuming class

2010 20203 2030 in 5-6% GDP scenario

2030 in 7% GDP scenario

240265 280 280

Mckinsey research shows Indonesian consuming class will grow almost double in 10 years since 2010

40 90 125

5

CREATIVE ECONOMY & LIFESTYLE INDUSTRY OUTLOOK

Yogyakarta

CREATIVE ECONOMY OUTLOOK

525.96581.54

638.39708.27

784.87852.56

922.59

2010 2011 2012 2013 2014 2015 2016

7,66%7,43%

7,41%

7,42%7,43%

7,39%7,44%

United States of America

11,12 % 8,67% 7,44% 6,06% 5,70% 4,92% 4,50%

South Korea Indonesia Russia Singapore Philippines Canada

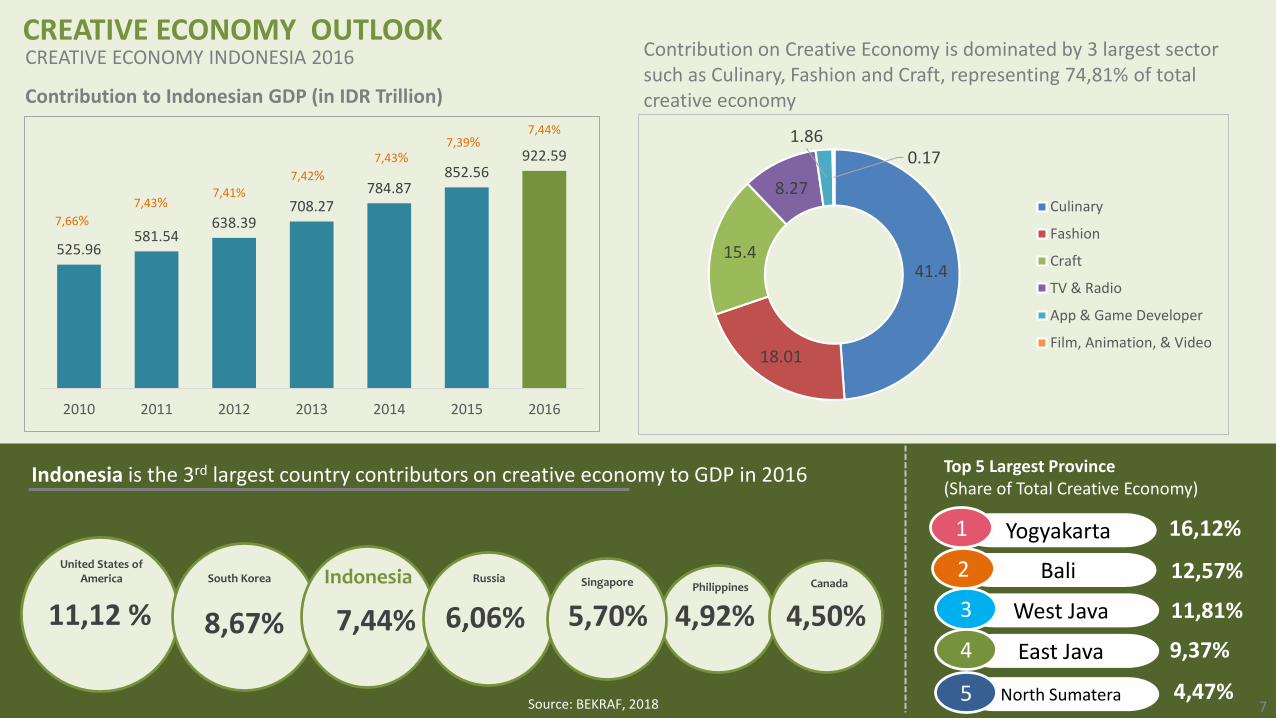

Indonesia is the 3rd largest country contributors on creative economy to GDP in 2016

Contribution to Indonesian GDP (in IDR Trillion)

41.4

18.01

15.4

8.27

1.860.17

Culinary

Fashion

Craft

TV & Radio

App & Game Developer

Film, Animation, & Video

Contribution on Creative Economy is dominated by 3 largest sector such as Culinary, Fashion and Craft, representing 74,81% of total creative economy

1

Bali2

West Java3

East Java4

North Sumatera5

16,12%

12,57%

11,81%

9,37%

4,47%

Top 5 Largest Province (Share of Total Creative Economy)

CREATIVE ECONOMY INDONESIA 2016

Source: BEKRAF, 2018 7

CREATIVE ECONOMY OUTLOOK

Sumatera17.94%

Java65,37%

Bali & Nusa Tenggara5,21%%

Sulawesi, Maluku & Papua6,53%Kalimantan

4,95%

CREATIVE ECONOMY INDONESIA 2016

Distribution of Creative Business in Indonesia (Total: 8,2 million creative business in 2016)

# CountryExport

(in US$ Billion)

1United States of America

6,04

2 Switzerland 2,08

3 Japan 1,35

4 Singapore 1,22

5 Germany 0,88

Top 5 Export Destinations

3,23%Export Growth

In 2016(US$ 20 billion)

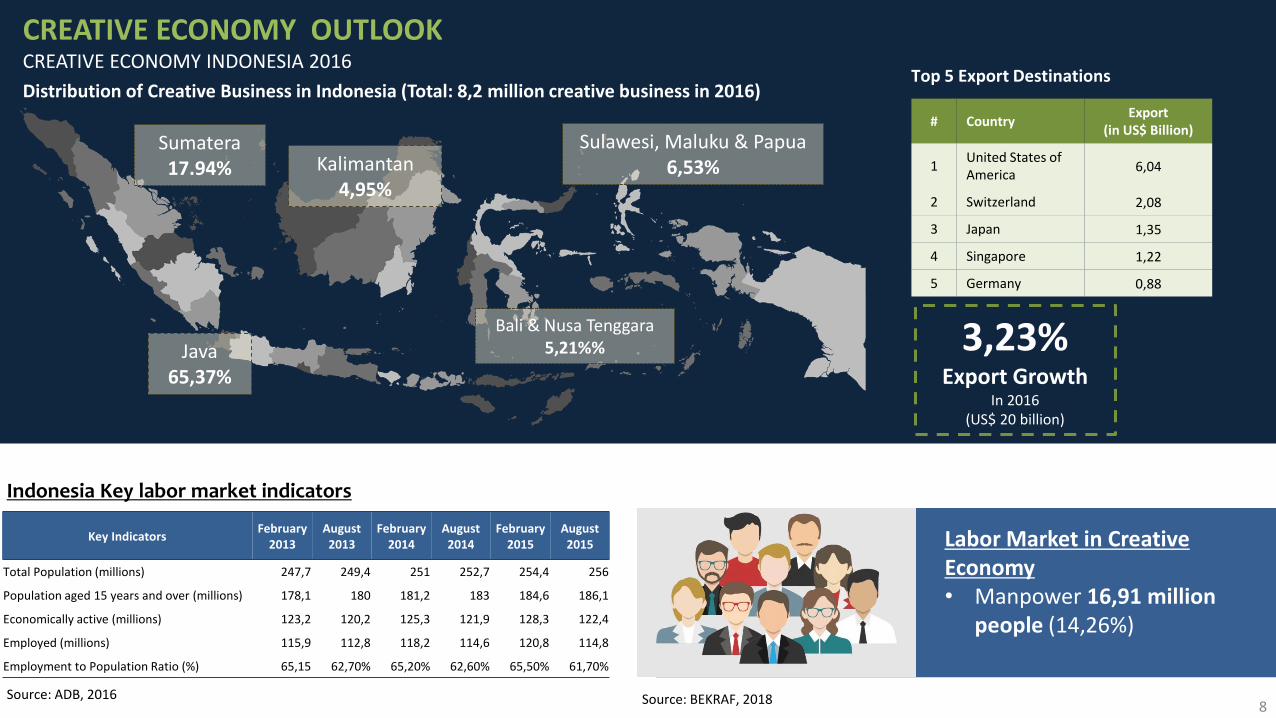

Labor Market in Creative Economy• Manpower 16,91 million

people (14,26%)

Source: BEKRAF, 2018 8

Key IndicatorsFebruary

2013August 2013

February 2014

August 2014

February 2015

August 2015

Total Population (millions) 247,7 249,4 251 252,7 254,4 256

Population aged 15 years and over (millions) 178,1 180 181,2 183 184,6 186,1

Economically active (millions) 123,2 120,2 125,3 121,9 128,3 122,4

Employed (millions) 115,9 112,8 118,2 114,6 120,8 114,8

Employment to Population Ratio (%) 65,15 62,70% 65,20% 62,60% 65,50% 61,70%

Indonesia Key labor market indicators

Source: ADB, 2016

Indonesia Abundant of

Lifestyle Commodity1

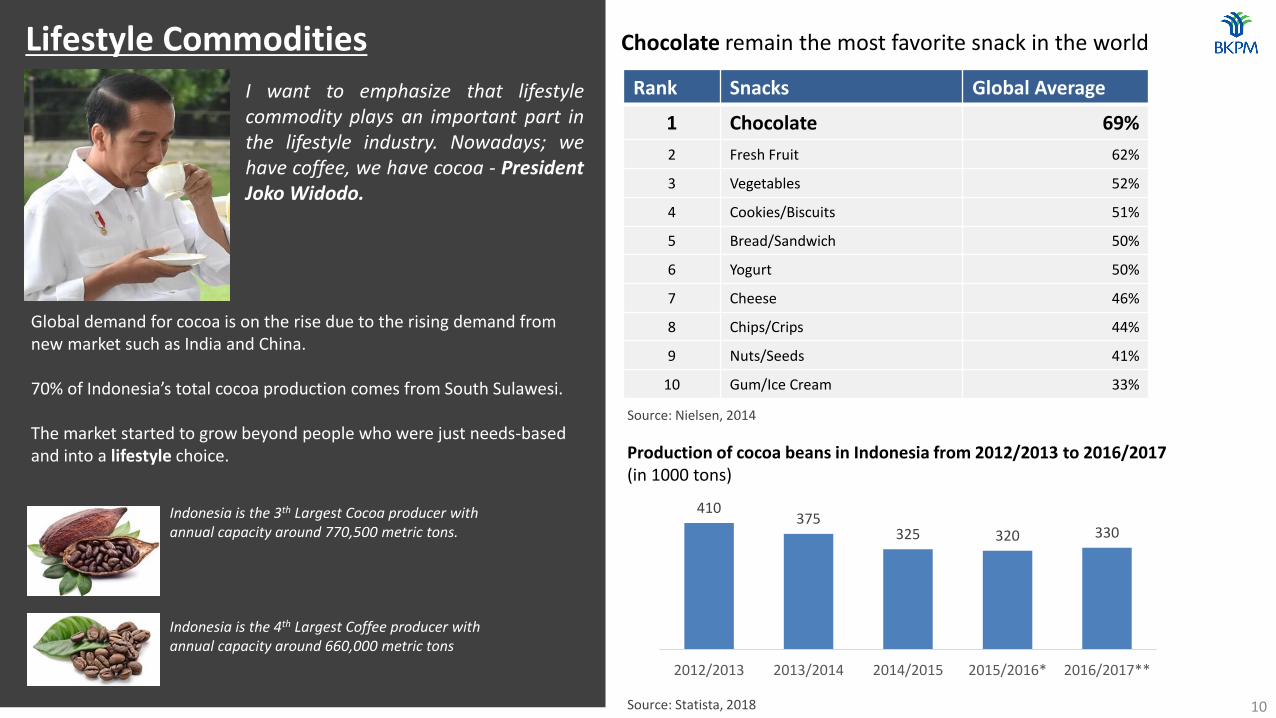

Indonesia is the 4th Largest Coffee producer with annual capacity around 660,000 metric tons

Indonesia is the 3th Largest Cocoa producer with annual capacity around 770,500 metric tons.

I want to emphasize that lifestylecommodity plays an important part inthe lifestyle industry. Nowadays; wehave coffee, we have cocoa - PresidentJoko Widodo.

Lifestyle Commodities

410375

325 320 330

2012/2013 2013/2014 2014/2015 2015/2016* 2016/2017**

Production of cocoa beans in Indonesia from 2012/2013 to 2016/2017 (in 1000 tons)

Source: Statista, 2018

Chocolate remain the most favorite snack in the world

Rank Snacks Global Average

1 Chocolate 69%

2 Fresh Fruit 62%

3 Vegetables 52%

4 Cookies/Biscuits 51%

5 Bread/Sandwich 50%

6 Yogurt 50%

7 Cheese 46%

8 Chips/Crips 44%

9 Nuts/Seeds 41%

10 Gum/Ice Cream 33%

Source: Nielsen, 2014

10

Global demand for cocoa is on the rise due to the rising demand from new market such as India and China.

70% of Indonesia’s total cocoa production comes from South Sulawesi.

The market started to grow beyond people who were just needs-based and into a lifestyle choice.

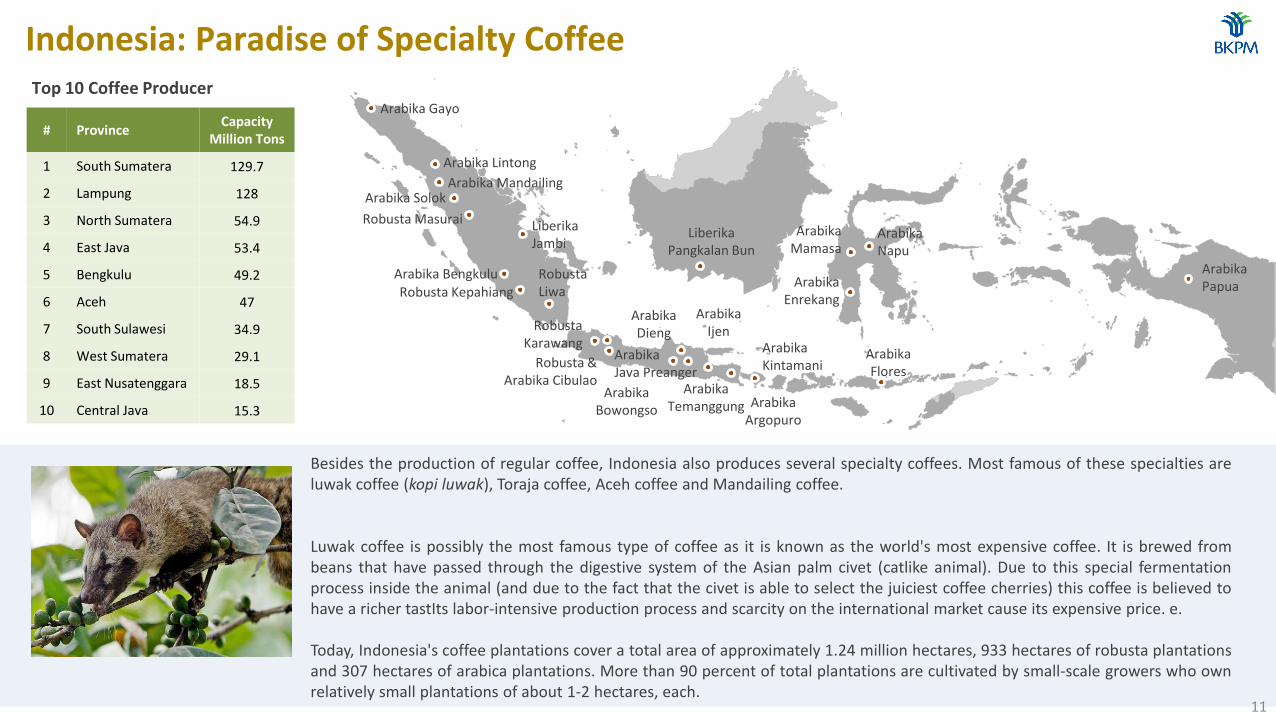

Indonesia: Paradise of Specialty Coffee

11

Arabika Gayo

Arabika Lintong

Arabika MandailingArabika Solok

Arabika BengkuluRobusta Kepahiang

RobustaLiwa

Robusta Masurai LiberikaJambi

LiberikaPangkalan Bun

ArabikaPapuaArabika

Enrekang

ArabikaKintamani

ArabikaFlores

ArabikaNapu

ArabikaMamasa

ArabikaIjen

Robusta & Arabika Cibulao

ArabikaJava Preanger

ArabikaBowongso

ArabikaDieng

ArabikaArgopuro

RobustaKarawang

ArabikaTemanggung

# ProvinceCapacity

Million Tons

1 South Sumatera 129.7

2 Lampung 128

3 North Sumatera 54.9

4 East Java 53.4

5 Bengkulu 49.2

6 Aceh 47

7 South Sulawesi 34.9

8 West Sumatera 29.1

9 East Nusatenggara 18.5

10 Central Java 15.3

Besides the production of regular coffee, Indonesia also produces several specialty coffees. Most famous of these specialties areluwak coffee (kopi luwak), Toraja coffee, Aceh coffee and Mandailing coffee.

Luwak coffee is possibly the most famous type of coffee as it is known as the world's most expensive coffee. It is brewed frombeans that have passed through the digestive system of the Asian palm civet (catlike animal). Due to this special fermentationprocess inside the animal (and due to the fact that the civet is able to select the juiciest coffee cherries) this coffee is believed tohave a richer tastIts labor-intensive production process and scarcity on the international market cause its expensive price. e.

Today, Indonesia's coffee plantations cover a total area of approximately 1.24 million hectares, 933 hectares of robusta plantationsand 307 hectares of arabica plantations. More than 90 percent of total plantations are cultivated by small-scale growers who ownrelatively small plantations of about 1-2 hectares, each.

Top 10 Coffee Producer

Investment opportunities

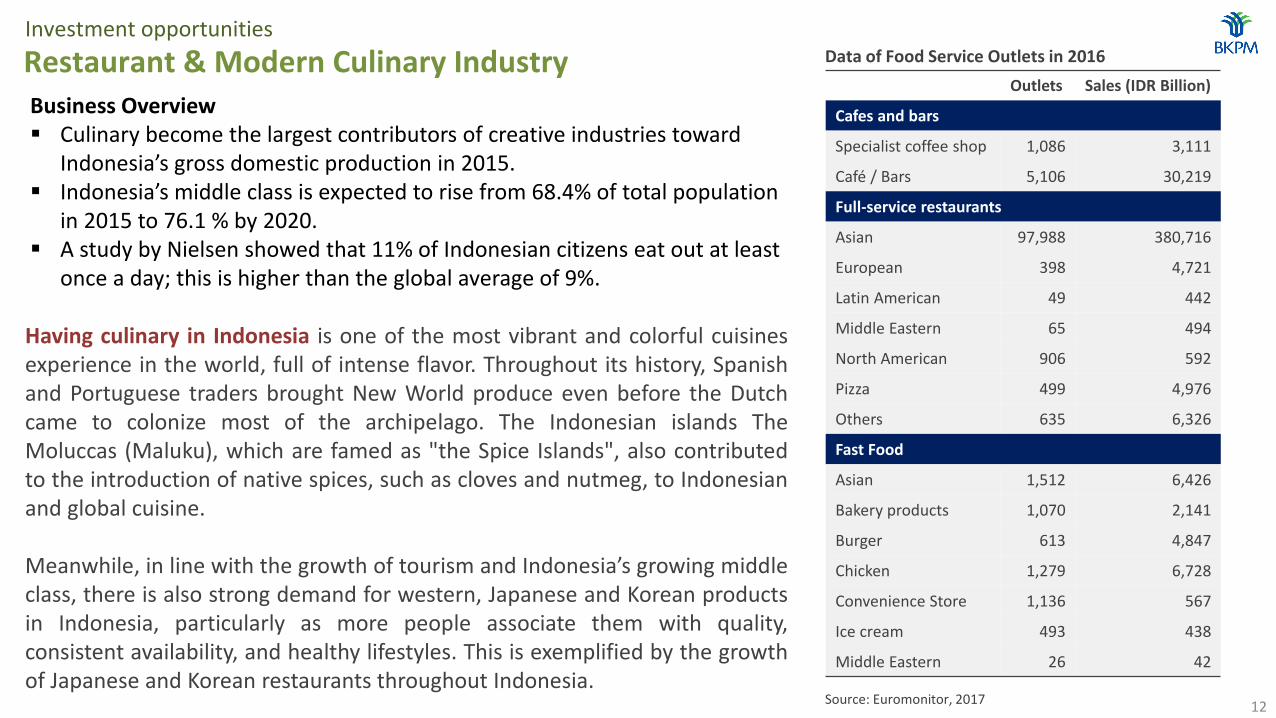

Restaurant & Modern Culinary IndustryOutlets Sales (IDR Billion)

Cafes and bars

Specialist coffee shop 1,086 3,111

Café / Bars 5,106 30,219

Full-service restaurants

Asian 97,988 380,716

European 398 4,721

Latin American 49 442

Middle Eastern 65 494

North American 906 592

Pizza 499 4,976

Others 635 6,326

Fast Food

Asian 1,512 6,426

Bakery products 1,070 2,141

Burger 613 4,847

Chicken 1,279 6,728

Convenience Store 1,136 567

Ice cream 493 438

Middle Eastern 26 42

Data of Food Service Outlets in 2016

Source: Euromonitor, 2017

Business Overview Culinary become the largest contributors of creative industries toward

Indonesia’s gross domestic production in 2015. Indonesia’s middle class is expected to rise from 68.4% of total population

in 2015 to 76.1 % by 2020. A study by Nielsen showed that 11% of Indonesian citizens eat out at least

once a day; this is higher than the global average of 9%.

Having culinary in Indonesia is one of the most vibrant and colorful cuisinesexperience in the world, full of intense flavor. Throughout its history, Spanishand Portuguese traders brought New World produce even before the Dutchcame to colonize most of the archipelago. The Indonesian islands TheMoluccas (Maluku), which are famed as "the Spice Islands", also contributedto the introduction of native spices, such as cloves and nutmeg, to Indonesianand global cuisine.

Meanwhile, in line with the growth of tourism and Indonesia’s growing middleclass, there is also strong demand for western, Japanese and Korean productsin Indonesia, particularly as more people associate them with quality,consistent availability, and healthy lifestyles. This is exemplified by the growthof Japanese and Korean restaurants throughout Indonesia.

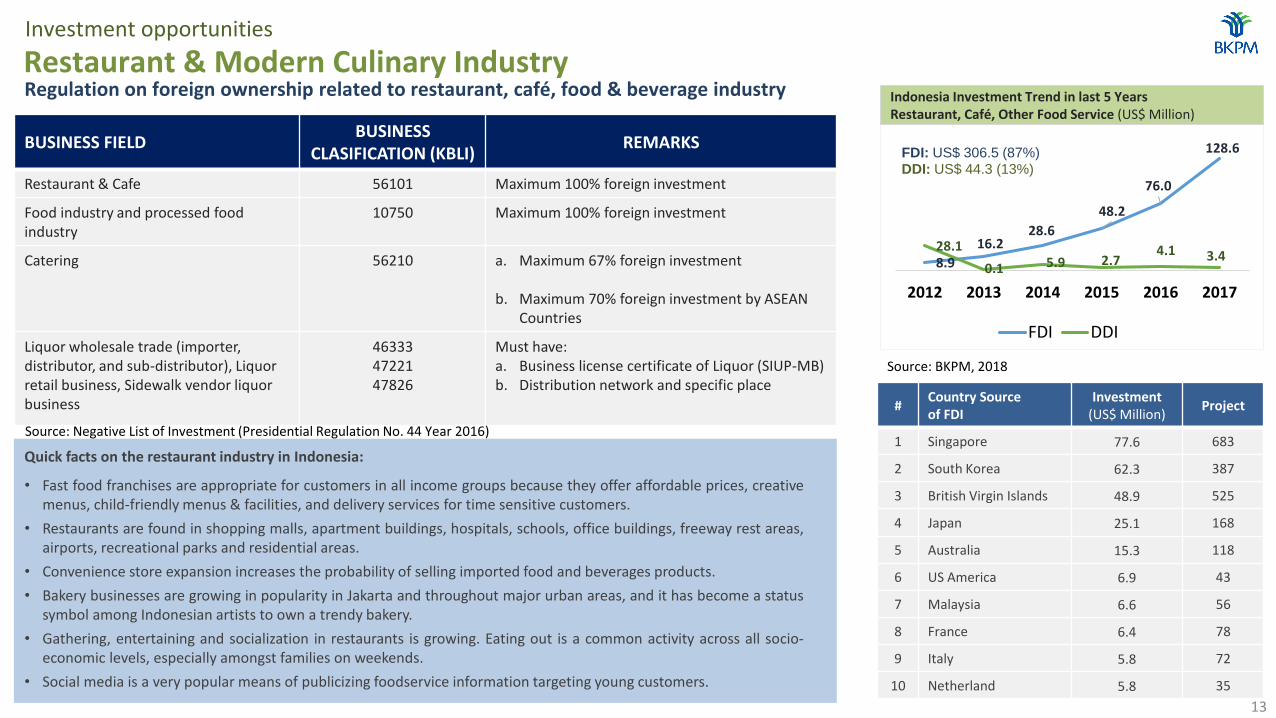

12

8.9

16.228.6

48.2

76.0

128.6

28.1

0.1 5.9 2.74.1 3.4

2012 2013 2014 2015 2016 2017

FDI DDI

Indonesia Investment Trend in last 5 Years Restaurant, Café, Other Food Service (US$ Million)

FDI: US$ 306.5 (87%)DDI: US$ 44.3 (13%)

#Country Sourceof FDI

Investment(US$ Million)

Project

1 Singapore 77.6 683

2 South Korea 62.3 387

3 British Virgin Islands 48.9 525

4 Japan 25.1 168

5 Australia 15.3 118

6 US America 6.9 43

7 Malaysia 6.6 56

8 France 6.4 78

9 Italy 5.8 72

10 Netherland 5.8 35

Investment opportunities

Restaurant & Modern Culinary Industry

BUSINESS FIELDBUSINESS

CLASIFICATION (KBLI)REMARKS

Restaurant & Cafe 56101 Maximum 100% foreign investment

Food industry and processed food industry

10750 Maximum 100% foreign investment

Catering 56210 a. Maximum 67% foreign investment

b. Maximum 70% foreign investment by ASEAN Countries

Liquor wholesale trade (importer, distributor, and sub-distributor), Liquor retail business, Sidewalk vendor liquor business

463334722147826

Must have:a. Business license certificate of Liquor (SIUP-MB)b. Distribution network and specific place

Quick facts on the restaurant industry in Indonesia:

• Fast food franchises are appropriate for customers in all income groups because they offer affordable prices, creativemenus, child-friendly menus & facilities, and delivery services for time sensitive customers.

• Restaurants are found in shopping malls, apartment buildings, hospitals, schools, office buildings, freeway rest areas,airports, recreational parks and residential areas.

• Convenience store expansion increases the probability of selling imported food and beverages products.

• Bakery businesses are growing in popularity in Jakarta and throughout major urban areas, and it has become a statussymbol among Indonesian artists to own a trendy bakery.

• Gathering, entertaining and socialization in restaurants is growing. Eating out is a common activity across all socio-economic levels, especially amongst families on weekends.

• Social media is a very popular means of publicizing foodservice information targeting young customers.

Source: Negative List of Investment (Presidential Regulation No. 44 Year 2016)

Source: BKPM, 2018

Regulation on foreign ownership related to restaurant, café, food & beverage industry

13

Fashion Industry2

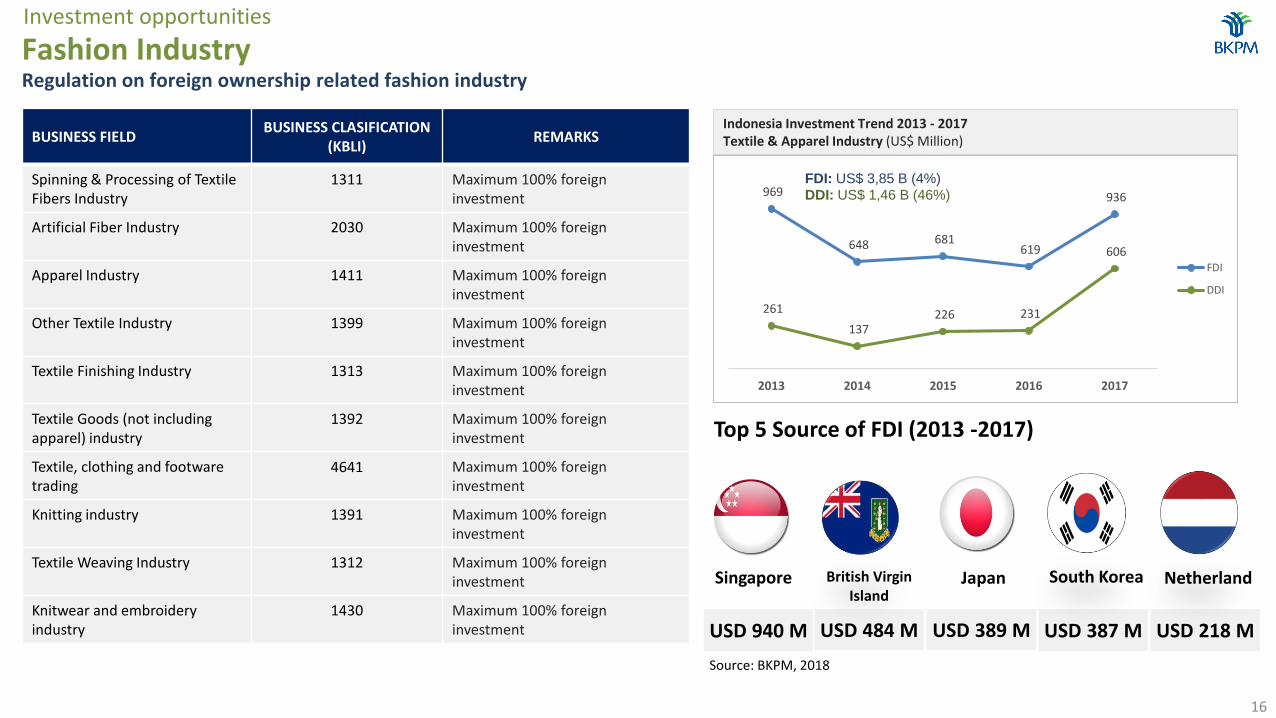

Investment opportunities

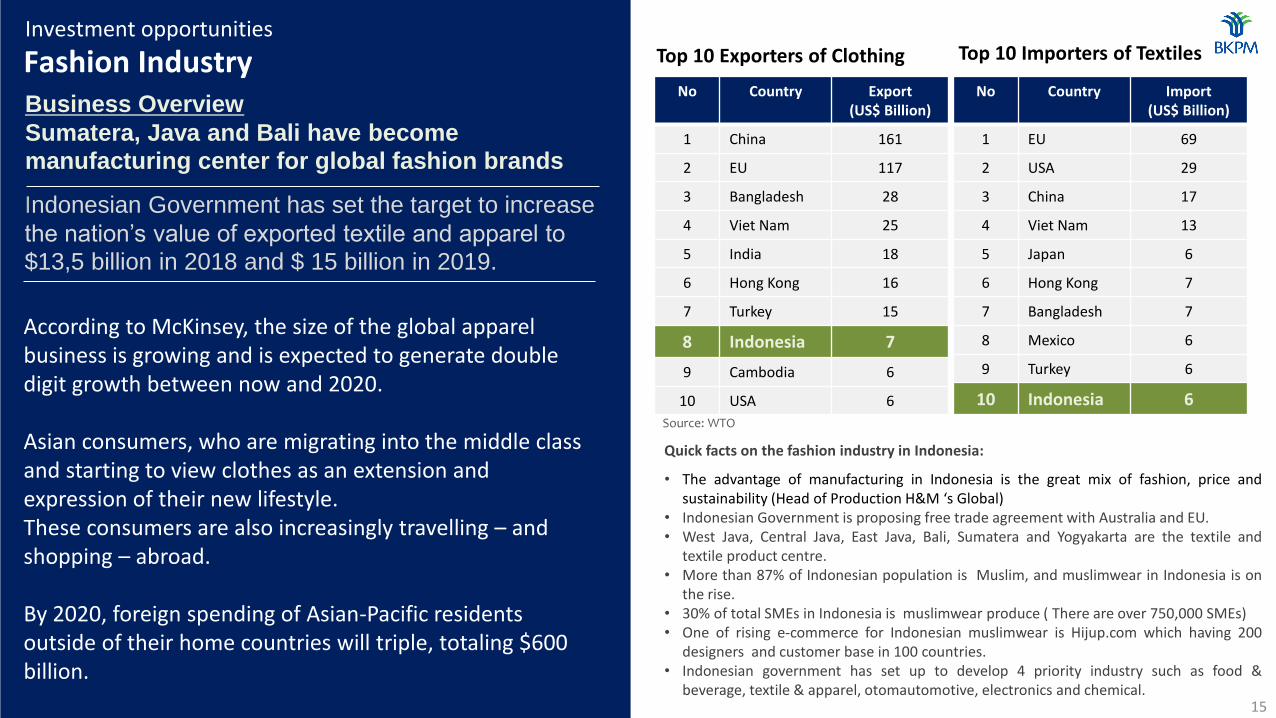

Fashion Industry

According to McKinsey, the size of the global apparel business is growing and is expected to generate double digit growth between now and 2020.

Asian consumers, who are migrating into the middle class and starting to view clothes as an extension and expression of their new lifestyle.These consumers are also increasingly travelling – and shopping – abroad.

By 2020, foreign spending of Asian-Pacific residents outside of their home countries will triple, totaling $600 billion.

Business Overview

Sumatera, Java and Bali have become

manufacturing center for global fashion brands

Indonesian Government has set the target to increase

the nation’s value of exported textile and apparel to

$13,5 billion in 2018 and $ 15 billion in 2019.

No Country Export (US$ Billion)

1 China 161

2 EU 117

3 Bangladesh 28

4 Viet Nam 25

5 India 18

6 Hong Kong 16

7 Turkey 15

8 Indonesia 7

9 Cambodia 6

10 USA 6

Top 10 Exporters of Clothing

Source: WTO

No Country Import(US$ Billion)

1 EU 69

2 USA 29

3 China 17

4 Viet Nam 13

5 Japan 6

6 Hong Kong 7

7 Bangladesh 7

8 Mexico 6

9 Turkey 6

10 Indonesia 6

Top 10 Importers of Textiles

15

Quick facts on the fashion industry in Indonesia:

• The advantage of manufacturing in Indonesia is the great mix of fashion, price andsustainability (Head of Production H&M ‘s Global)

• Indonesian Government is proposing free trade agreement with Australia and EU.• West Java, Central Java, East Java, Bali, Sumatera and Yogyakarta are the textile and

textile product centre.• More than 87% of Indonesian population is Muslim, and muslimwear in Indonesia is on

the rise.• 30% of total SMEs in Indonesia is muslimwear produce ( There are over 750,000 SMEs)• One of rising e-commerce for Indonesian muslimwear is Hijup.com which having 200

designers and customer base in 100 countries.• Indonesian government has set up to develop 4 priority industry such as food &

beverage, textile & apparel, otomautomotive, electronics and chemical.

Investment opportunities

Fashion Industry

BUSINESS FIELDBUSINESS CLASIFICATION

(KBLI)REMARKS

Spinning & Processing of Textile Fibers Industry

1311 Maximum 100% foreign investment

Artificial Fiber Industry 2030 Maximum 100% foreign investment

Apparel Industry 1411 Maximum 100% foreign investment

Other Textile Industry 1399 Maximum 100% foreign investment

Textile Finishing Industry 1313 Maximum 100% foreign investment

Textile Goods (not including apparel) industry

1392 Maximum 100% foreign investment

Textile, clothing and footware trading

4641 Maximum 100% foreign investment

Knitting industry 1391 Maximum 100% foreign investment

Textile Weaving Industry 1312 Maximum 100% foreign investment

Knitwear and embroidery industry

1430 Maximum 100% foreign investment

Singapore British Virgin Island

Japan South Korea Netherland

USD 940 M USD 218 MUSD 484 M USD 389 M USD 387 M

Top 5 Source of FDI (2013 -2017)

969

648 681 619

936

261

137 226 231

606

2013 2014 2015 2016 2017

FDI

DDI

Indonesia Investment Trend 2013 - 2017Textile & Apparel Industry (US$ Million)

FDI: US$ 3,85 B (4%)DDI: US$ 1,46 B (46%)

Regulation on foreign ownership related fashion industry

Source: BKPM, 2018

16

17

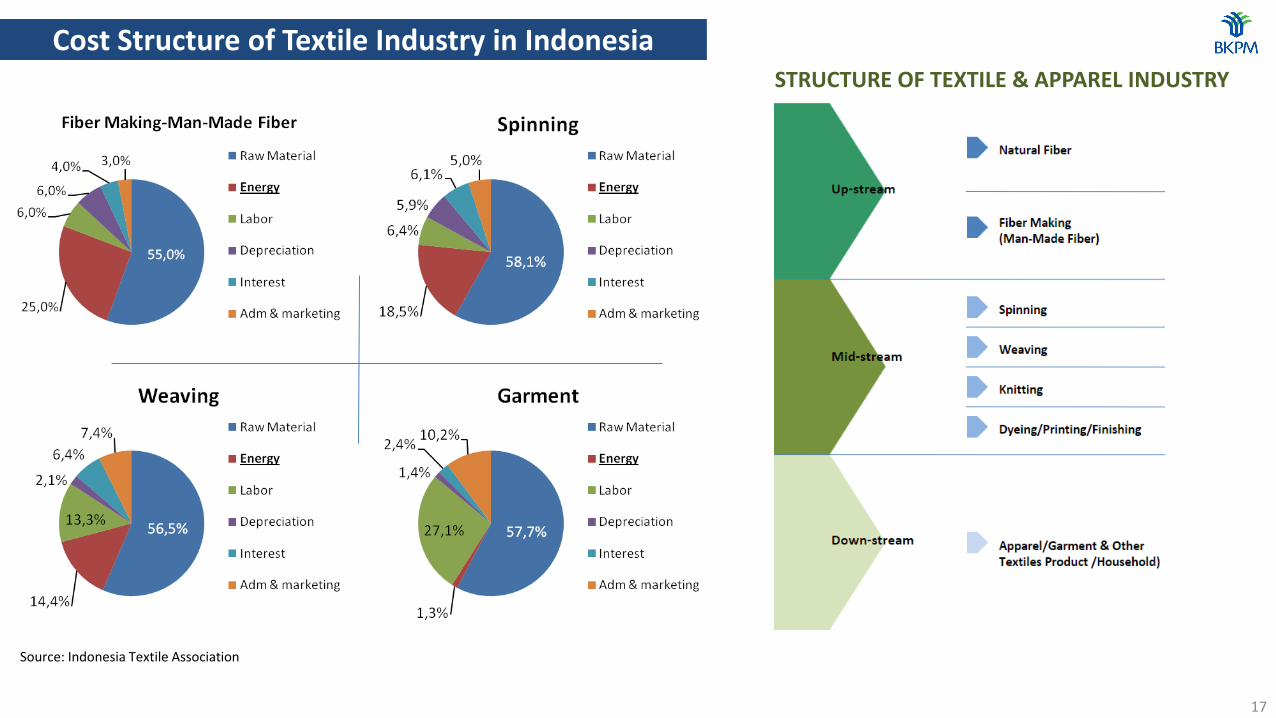

Cost Structure of Textile Industry in Indonesia

Source: Indonesia Textile Association

STRUCTURE OF TEXTILE & APPAREL INDUSTRY

18

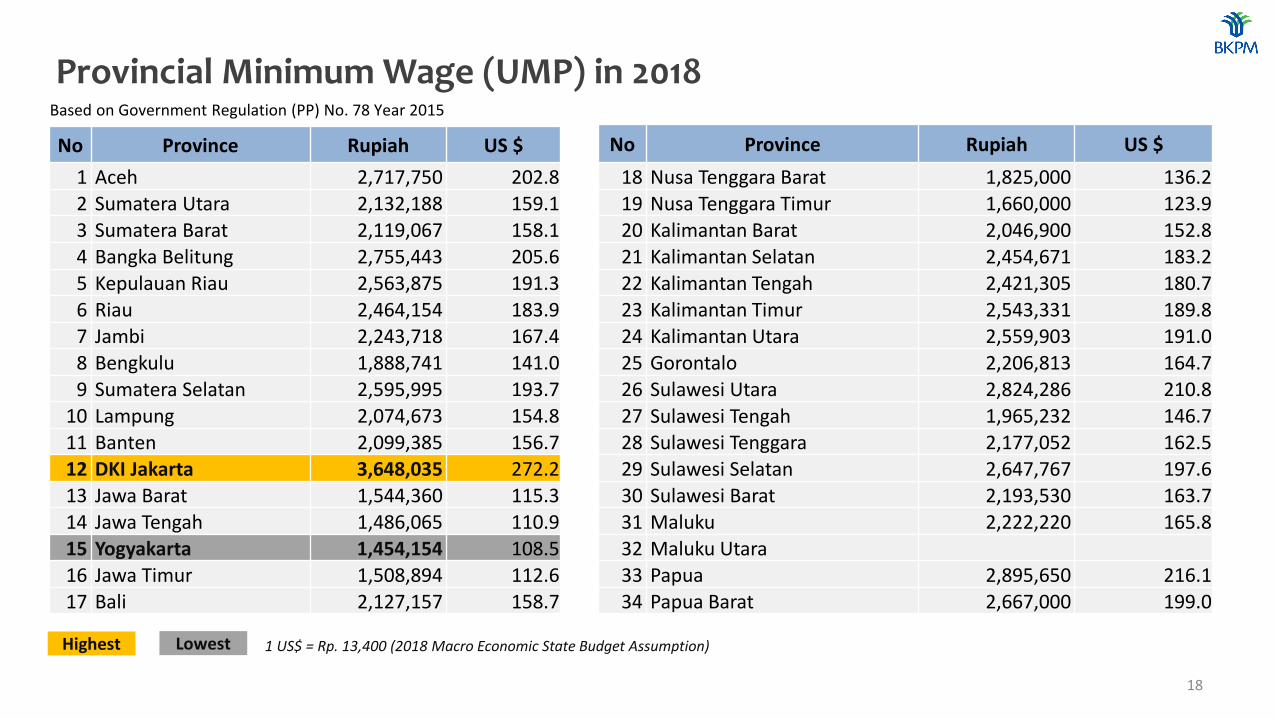

No Province Rupiah US $

1 Aceh 2,717,750 202.8

2 Sumatera Utara 2,132,188 159.1

3 Sumatera Barat 2,119,067 158.1

4 Bangka Belitung 2,755,443 205.6

5 Kepulauan Riau 2,563,875 191.36 Riau 2,464,154 183.97 Jambi 2,243,718 167.4

8 Bengkulu 1,888,741 141.0

9 Sumatera Selatan 2,595,995 193.7

10 Lampung 2,074,673 154.8

11 Banten 2,099,385 156.712 DKI Jakarta 3,648,035 272.213 Jawa Barat 1,544,360 115.314 Jawa Tengah 1,486,065 110.9

15 Yogyakarta 1,454,154 108.5

16 Jawa Timur 1,508,894 112.617 Bali 2,127,157 158.7

No Province Rupiah US $

18 Nusa Tenggara Barat 1,825,000 136.2

19 Nusa Tenggara Timur 1,660,000 123.9

20 Kalimantan Barat 2,046,900 152.8

21 Kalimantan Selatan 2,454,671 183.2

22 Kalimantan Tengah 2,421,305 180.723 Kalimantan Timur 2,543,331 189.824 Kalimantan Utara 2,559,903 191.0

25 Gorontalo 2,206,813 164.7

26 Sulawesi Utara 2,824,286 210.8

27 Sulawesi Tengah 1,965,232 146.7

28 Sulawesi Tenggara 2,177,052 162.529 Sulawesi Selatan 2,647,767 197.630 Sulawesi Barat 2,193,530 163.731 Maluku 2,222,220 165.8

32 Maluku Utara

33 Papua 2,895,650 216.134 Papua Barat 2,667,000 199.0

Provincial Minimum Wage (UMP) in 2018

Highest Lowest 1 US$ = Rp. 13,400 (2018 Macro Economic State Budget Assumption)

Based on Government Regulation (PP) No. 78 Year 2015

19

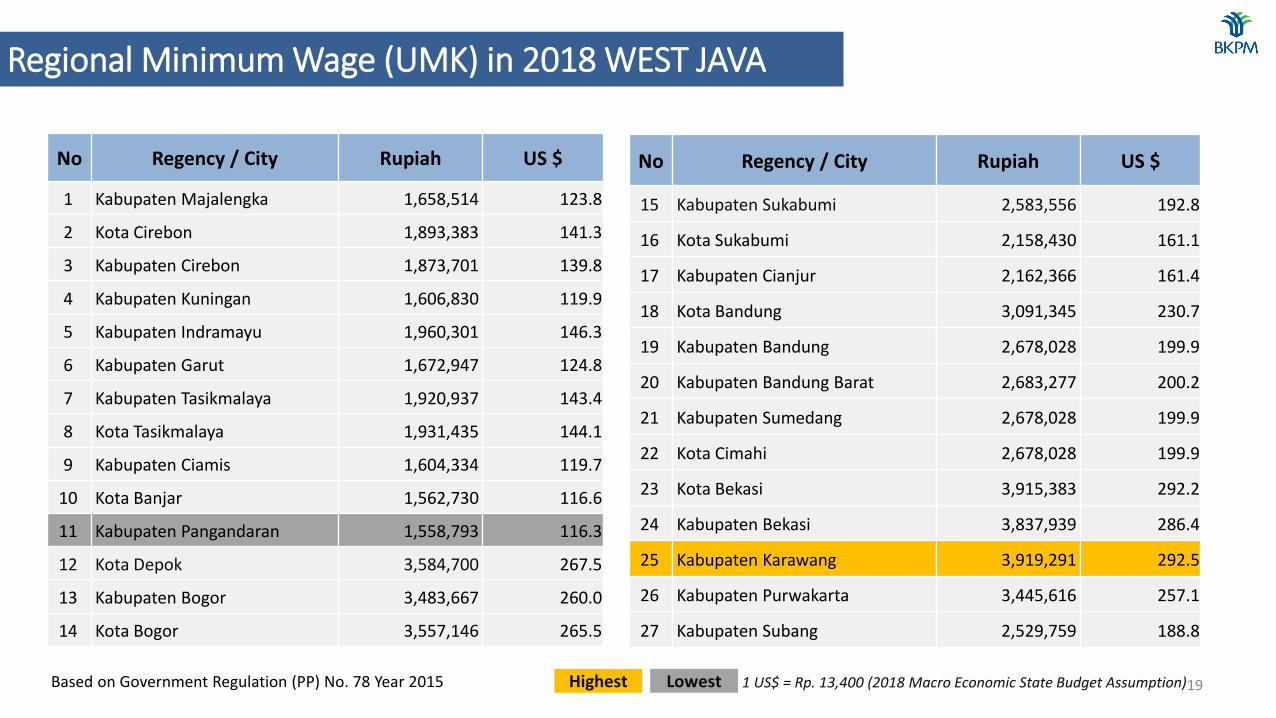

No Regency / City Rupiah US $

1 Kabupaten Majalengka 1,658,514 123.8

2 Kota Cirebon 1,893,383 141.3

3 Kabupaten Cirebon 1,873,701 139.8

4 Kabupaten Kuningan 1,606,830 119.9

5 Kabupaten Indramayu 1,960,301 146.3

6 Kabupaten Garut 1,672,947 124.8

7 Kabupaten Tasikmalaya 1,920,937 143.4

8 Kota Tasikmalaya 1,931,435 144.1

9 Kabupaten Ciamis 1,604,334 119.7

10 Kota Banjar 1,562,730 116.6

11 Kabupaten Pangandaran 1,558,793 116.3

12 Kota Depok 3,584,700 267.5

13 Kabupaten Bogor 3,483,667 260.0

14 Kota Bogor 3,557,146 265.5

No Regency / City Rupiah US $

15 Kabupaten Sukabumi 2,583,556 192.8

16 Kota Sukabumi 2,158,430 161.1

17 Kabupaten Cianjur 2,162,366 161.4

18 Kota Bandung 3,091,345 230.7

19 Kabupaten Bandung 2,678,028 199.9

20 Kabupaten Bandung Barat 2,683,277 200.2

21 Kabupaten Sumedang 2,678,028 199.9

22 Kota Cimahi 2,678,028 199.9

23 Kota Bekasi 3,915,383 292.2

24 Kabupaten Bekasi 3,837,939 286.4

25 Kabupaten Karawang 3,919,291 292.5

26 Kabupaten Purwakarta 3,445,616 257.1

27 Kabupaten Subang 2,529,759 188.8

Regional Minimum Wage (UMK) in 2018 WEST JAVA

Based on Government Regulation (PP) No. 78 Year 2015 Highest Lowest 1 US$ = Rp. 13,400 (2018 Macro Economic State Budget Assumption)

20

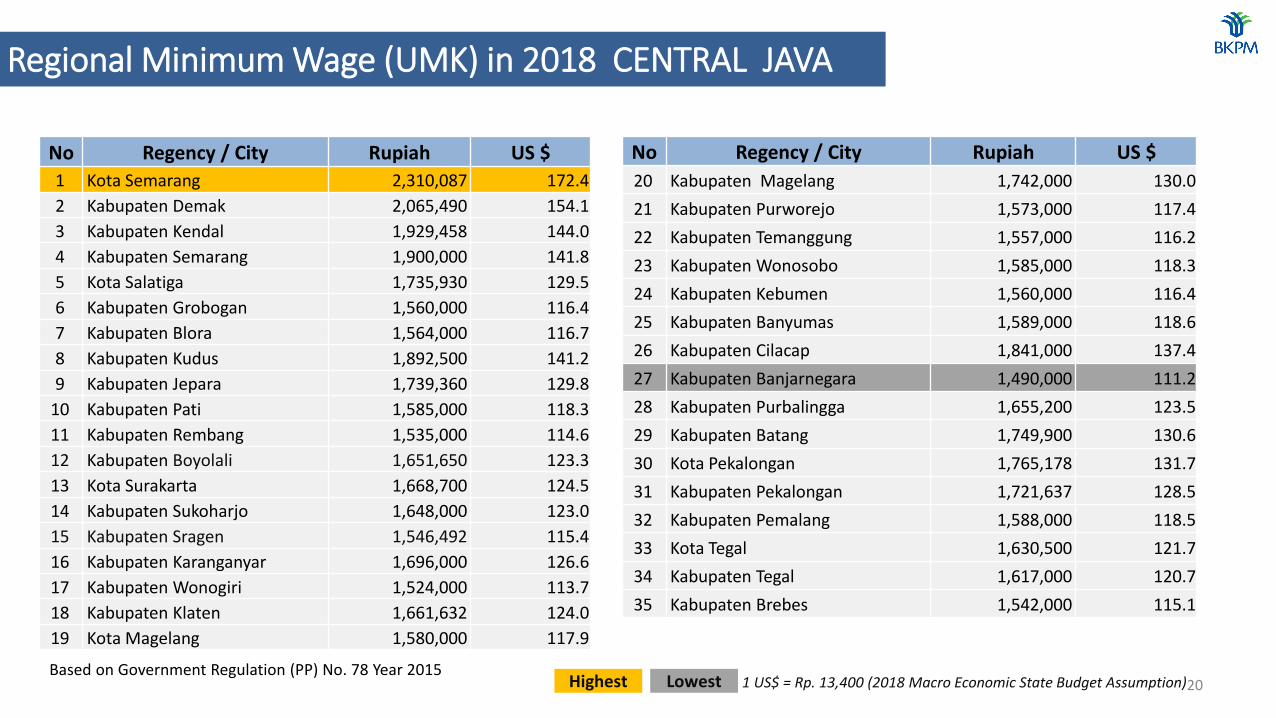

Regional Minimum Wage (UMK) in 2018 CENTRAL JAVA

Based on Government Regulation (PP) No. 78 Year 2015Highest Lowest 1 US$ = Rp. 13,400 (2018 Macro Economic State Budget Assumption)

No Regency / City Rupiah US $

1 Kota Semarang 2,310,087 172.4

2 Kabupaten Demak 2,065,490 154.1

3 Kabupaten Kendal 1,929,458 144.0

4 Kabupaten Semarang 1,900,000 141.8

5 Kota Salatiga 1,735,930 129.5

6 Kabupaten Grobogan 1,560,000 116.4

7 Kabupaten Blora 1,564,000 116.7

8 Kabupaten Kudus 1,892,500 141.2

9 Kabupaten Jepara 1,739,360 129.8

10 Kabupaten Pati 1,585,000 118.3

11 Kabupaten Rembang 1,535,000 114.6

12 Kabupaten Boyolali 1,651,650 123.3

13 Kota Surakarta 1,668,700 124.5

14 Kabupaten Sukoharjo 1,648,000 123.0

15 Kabupaten Sragen 1,546,492 115.4

16 Kabupaten Karanganyar 1,696,000 126.6

17 Kabupaten Wonogiri 1,524,000 113.7

18 Kabupaten Klaten 1,661,632 124.0

19 Kota Magelang 1,580,000 117.9

No Regency / City Rupiah US $

20 Kabupaten Magelang 1,742,000 130.0

21 Kabupaten Purworejo 1,573,000 117.4

22 Kabupaten Temanggung 1,557,000 116.2

23 Kabupaten Wonosobo 1,585,000 118.3

24 Kabupaten Kebumen 1,560,000 116.4

25 Kabupaten Banyumas 1,589,000 118.6

26 Kabupaten Cilacap 1,841,000 137.4

27 Kabupaten Banjarnegara 1,490,000 111.2

28 Kabupaten Purbalingga 1,655,200 123.5

29 Kabupaten Batang 1,749,900 130.6

30 Kota Pekalongan 1,765,178 131.7

31 Kabupaten Pekalongan 1,721,637 128.5

32 Kabupaten Pemalang 1,588,000 118.5

33 Kota Tegal 1,630,500 121.7

34 Kabupaten Tegal 1,617,000 120.7

35 Kabupaten Brebes 1,542,000 115.1

21

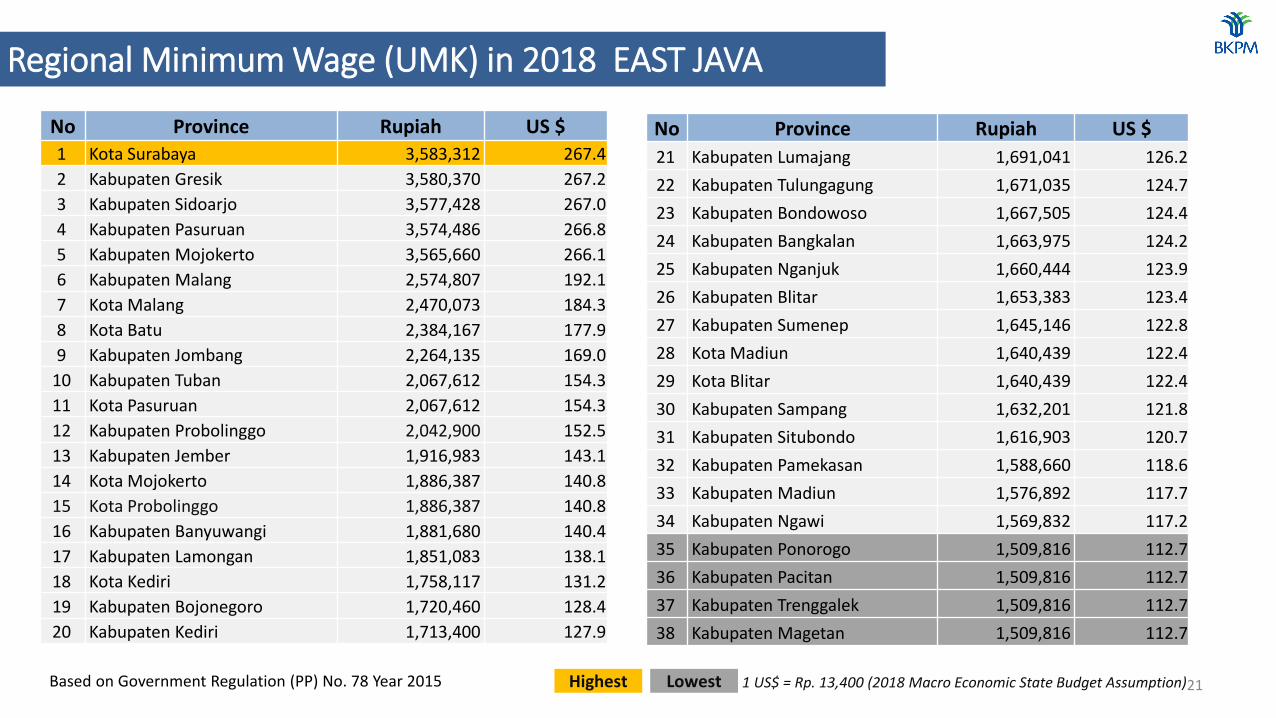

Regional Minimum Wage (UMK) in 2018 EAST JAVA

Based on Government Regulation (PP) No. 78 Year 2015 Highest Lowest 1 US$ = Rp. 13,400 (2018 Macro Economic State Budget Assumption)

No Province Rupiah US $

1 Kota Surabaya 3,583,312 267.4

2 Kabupaten Gresik 3,580,370 267.2

3 Kabupaten Sidoarjo 3,577,428 267.0

4 Kabupaten Pasuruan 3,574,486 266.8

5 Kabupaten Mojokerto 3,565,660 266.1

6 Kabupaten Malang 2,574,807 192.1

7 Kota Malang 2,470,073 184.3

8 Kota Batu 2,384,167 177.9

9 Kabupaten Jombang 2,264,135 169.0

10 Kabupaten Tuban 2,067,612 154.3

11 Kota Pasuruan 2,067,612 154.3

12 Kabupaten Probolinggo 2,042,900 152.5

13 Kabupaten Jember 1,916,983 143.1

14 Kota Mojokerto 1,886,387 140.8

15 Kota Probolinggo 1,886,387 140.8

16 Kabupaten Banyuwangi 1,881,680 140.4

17 Kabupaten Lamongan 1,851,083 138.1

18 Kota Kediri 1,758,117 131.2

19 Kabupaten Bojonegoro 1,720,460 128.4

20 Kabupaten Kediri 1,713,400 127.9

No Province Rupiah US $

21 Kabupaten Lumajang 1,691,041 126.2

22 Kabupaten Tulungagung 1,671,035 124.7

23 Kabupaten Bondowoso 1,667,505 124.4

24 Kabupaten Bangkalan 1,663,975 124.2

25 Kabupaten Nganjuk 1,660,444 123.9

26 Kabupaten Blitar 1,653,383 123.4

27 Kabupaten Sumenep 1,645,146 122.8

28 Kota Madiun 1,640,439 122.4

29 Kota Blitar 1,640,439 122.4

30 Kabupaten Sampang 1,632,201 121.8

31 Kabupaten Situbondo 1,616,903 120.7

32 Kabupaten Pamekasan 1,588,660 118.6

33 Kabupaten Madiun 1,576,892 117.7

34 Kabupaten Ngawi 1,569,832 117.2

35 Kabupaten Ponorogo 1,509,816 112.7

36 Kabupaten Pacitan 1,509,816 112.7

37 Kabupaten Trenggalek 1,509,816 112.7

38 Kabupaten Magetan 1,509,816 112.7

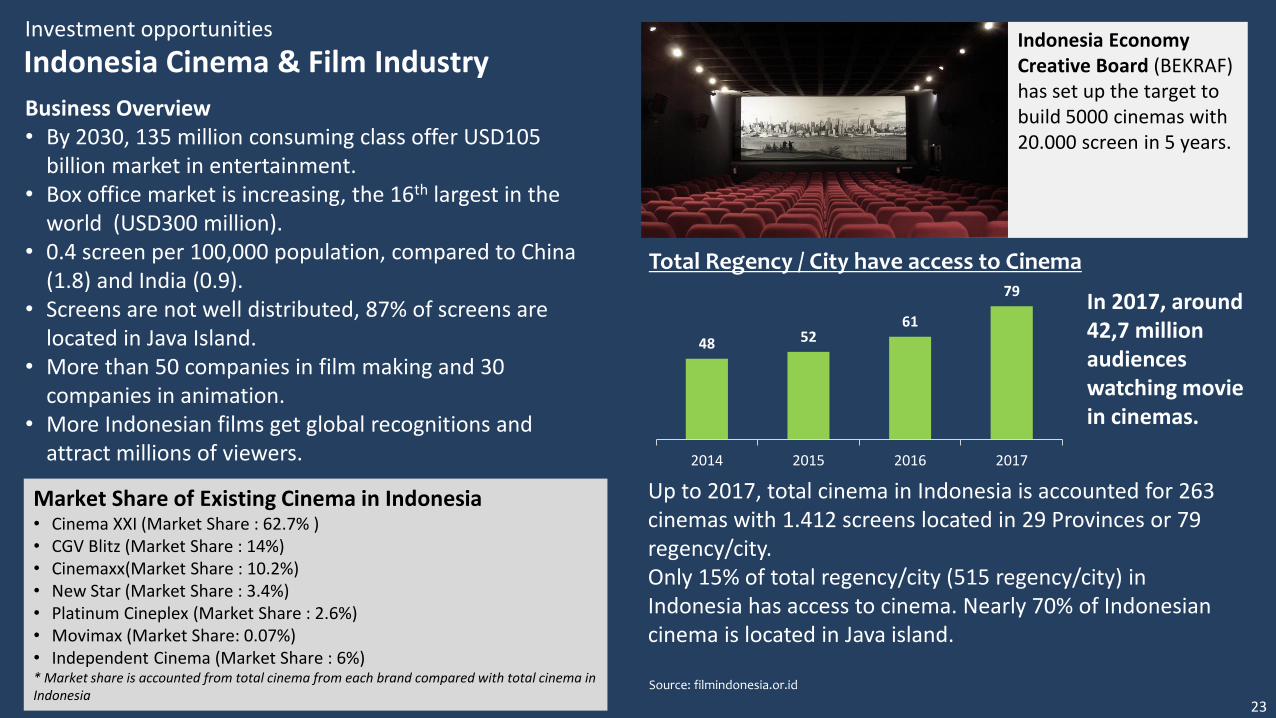

Indonesia Cinema & Film Industry

3

Business Overview• By 2030, 135 million consuming class offer USD105

billion market in entertainment.• Box office market is increasing, the 16th largest in the

world (USD300 million).• 0.4 screen per 100,000 population, compared to China

(1.8) and India (0.9).• Screens are not well distributed, 87% of screens are

located in Java Island.• More than 50 companies in film making and 30

companies in animation.• More Indonesian films get global recognitions and

attract millions of viewers.

Investment opportunities

Indonesia Cinema & Film IndustryIndonesia Economy Creative Board (BEKRAF) has set up the target to build 5000 cinemas with 20.000 screen in 5 years.

48 5261

79

2014 2015 2016 2017

Up to 2017, total cinema in Indonesia is accounted for 263 cinemas with 1.412 screens located in 29 Provinces or 79regency/city. Only 15% of total regency/city (515 regency/city) in Indonesia has access to cinema. Nearly 70% of Indonesian cinema is located in Java island.

Total Regency / City have access to Cinema

Source: filmindonesia.or.id

Market Share of Existing Cinema in Indonesia• Cinema XXI (Market Share : 62.7% )• CGV Blitz (Market Share : 14%)• Cinemaxx(Market Share : 10.2%)• New Star (Market Share : 3.4%)• Platinum Cineplex (Market Share : 2.6%)• Movimax (Market Share: 0.07%)• Independent Cinema (Market Share : 6%)* Market share is accounted from total cinema from each brand compared with total cinema in Indonesia

In 2017, around 42,7 million audiences watching movie in cinemas.

23

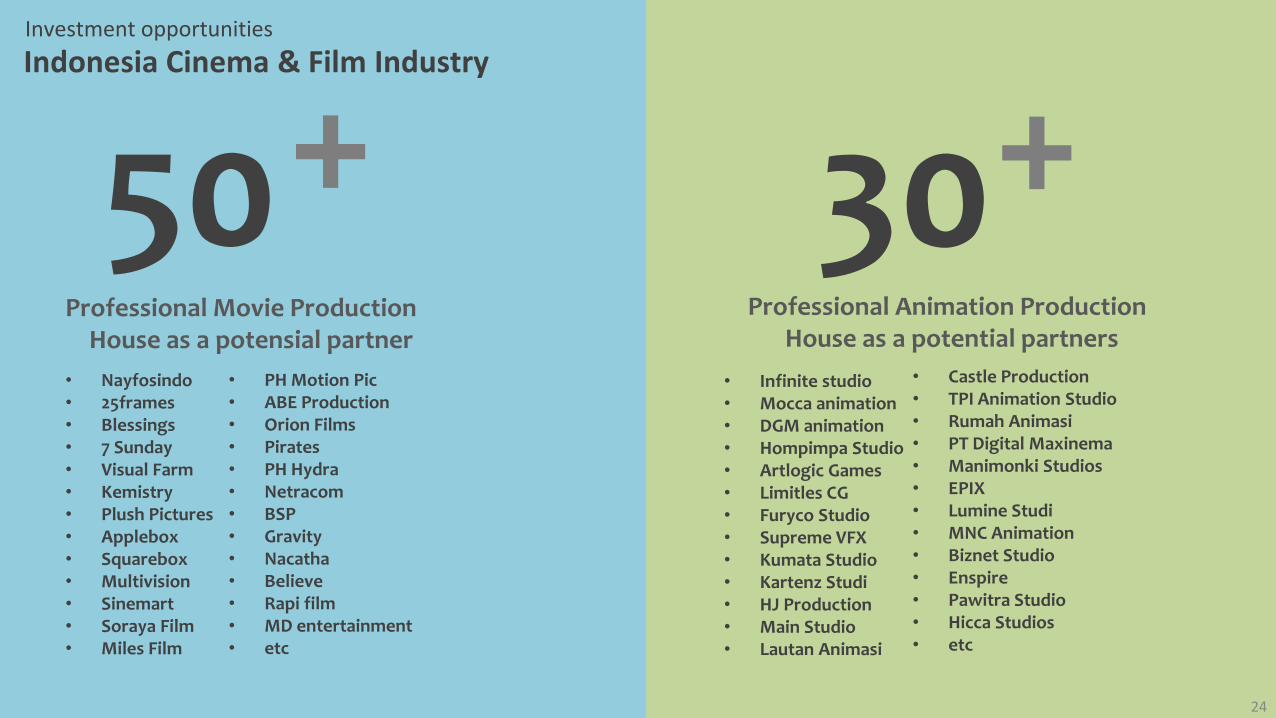

Investment opportunities

Indonesia Cinema & Film Industry

Professional Movie Production House as a potensial partner

Professional Animation Production House as a potential partners

• Castle Production• TPI Animation Studio• Rumah Animasi• PT Digital Maxinema• Manimonki Studios• EPIX• Lumine Studi• MNC Animation• Biznet Studio• Enspire• Pawitra Studio• Hicca Studios• etc

• Nayfosindo• 25frames• Blessings• 7 Sunday• Visual Farm• Kemistry• Plush Pictures• Applebox• Squarebox• Multivision• Sinemart• Soraya Film• Miles Film

• Infinite studio• Mocca animation• DGM animation• Hompimpa Studio• Artlogic Games• Limitles CG• Furyco Studio• Supreme VFX• Kumata Studio• Kartenz Studi• HJ Production• Main Studio• Lautan Animasi

3050+• PH Motion Pic• ABE Production• Orion Films• Pirates• PH Hydra• Netracom• BSP• Gravity• Nacatha• Believe• Rapi film• MD entertainment• etc

+

24

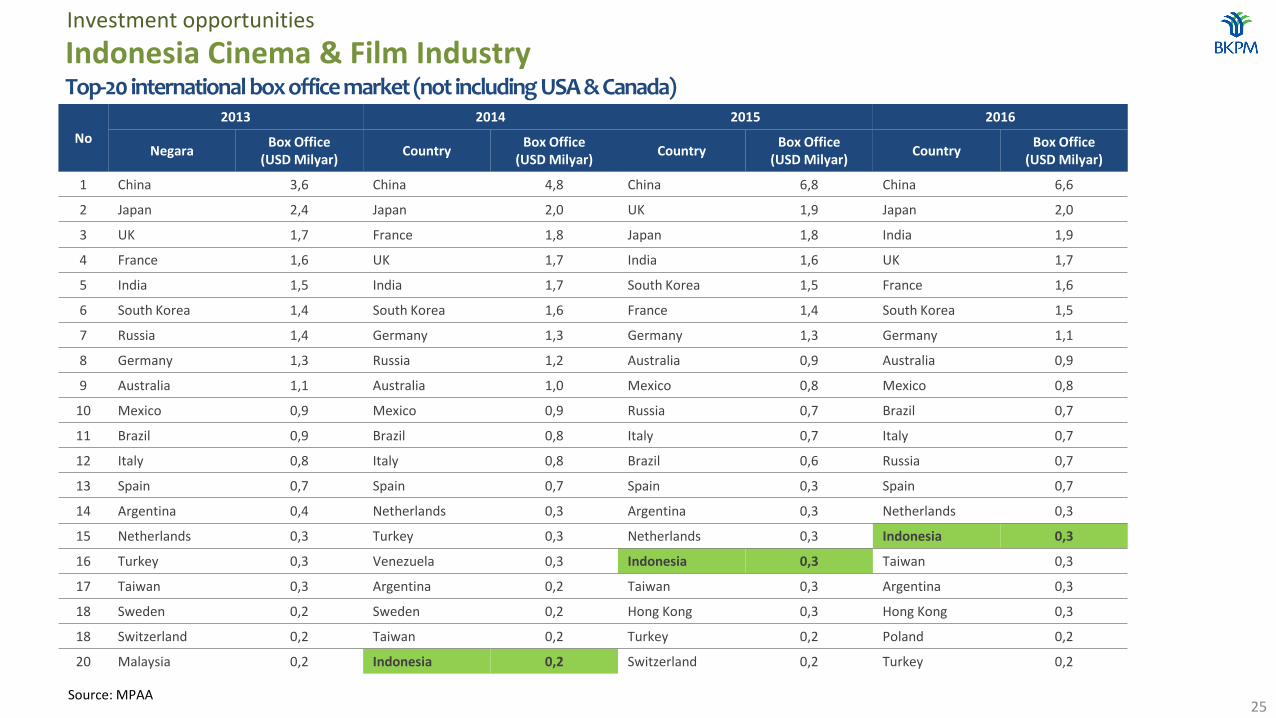

No

2013 2014 2015 2016

NegaraBox Office

(USD Milyar)Country

Box Office(USD Milyar)

CountryBox Office

(USD Milyar)Country

Box Office(USD Milyar)

1 China 3,6 China 4,8 China 6,8 China 6,6

2 Japan 2,4 Japan 2,0 UK 1,9 Japan 2,0

3 UK 1,7 France 1,8 Japan 1,8 India 1,9

4 France 1,6 UK 1,7 India 1,6 UK 1,7

5 India 1,5 India 1,7 South Korea 1,5 France 1,6

6 South Korea 1,4 South Korea 1,6 France 1,4 South Korea 1,5

7 Russia 1,4 Germany 1,3 Germany 1,3 Germany 1,1

8 Germany 1,3 Russia 1,2 Australia 0,9 Australia 0,9

9 Australia 1,1 Australia 1,0 Mexico 0,8 Mexico 0,8

10 Mexico 0,9 Mexico 0,9 Russia 0,7 Brazil 0,7

11 Brazil 0,9 Brazil 0,8 Italy 0,7 Italy 0,7

12 Italy 0,8 Italy 0,8 Brazil 0,6 Russia 0,7

13 Spain 0,7 Spain 0,7 Spain 0,3 Spain 0,7

14 Argentina 0,4 Netherlands 0,3 Argentina 0,3 Netherlands 0,3

15 Netherlands 0,3 Turkey 0,3 Netherlands 0,3 Indonesia 0,3

16 Turkey 0,3 Venezuela 0,3 Indonesia 0,3 Taiwan 0,3

17 Taiwan 0,3 Argentina 0,2 Taiwan 0,3 Argentina 0,3

18 Sweden 0,2 Sweden 0,2 Hong Kong 0,3 Hong Kong 0,3

18 Switzerland 0,2 Taiwan 0,2 Turkey 0,2 Poland 0,2

20 Malaysia 0,2 Indonesia 0,2 Switzerland 0,2 Turkey 0,2

Investment opportunities

Indonesia Cinema & Film IndustryTop-20 international box office market(not including USA & Canada)

Source: MPAA25

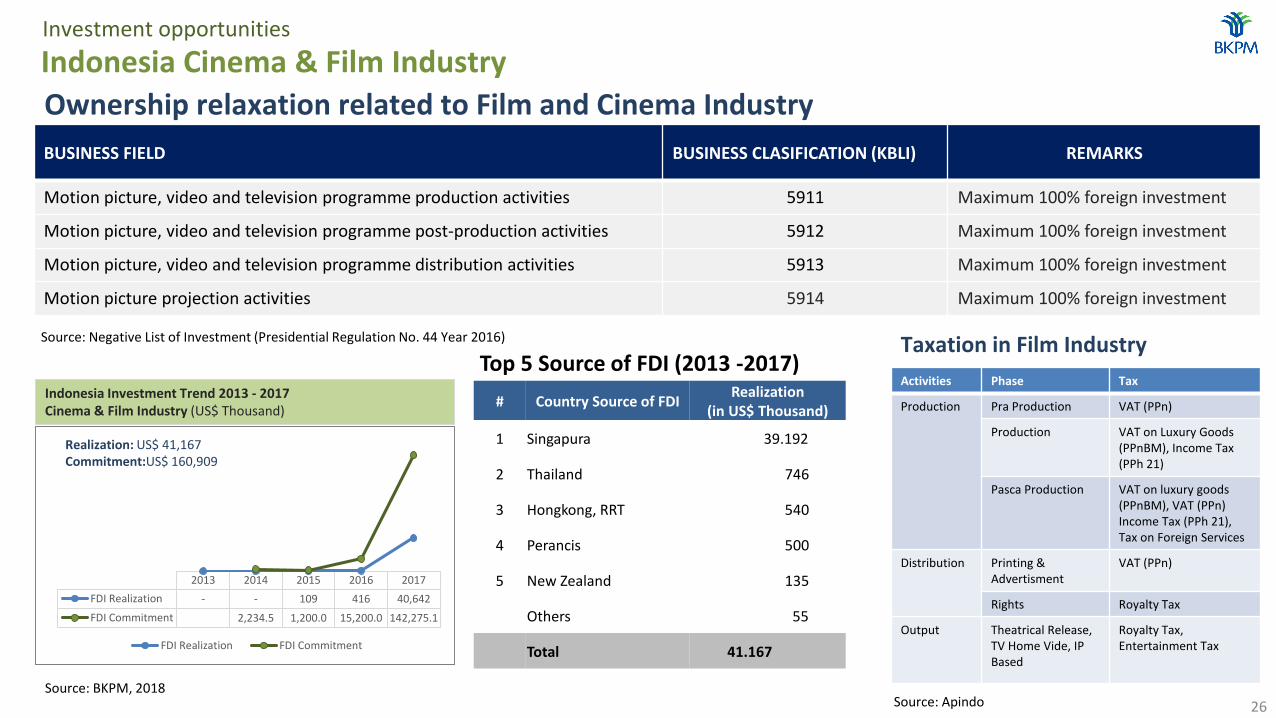

2013 2014 2015 2016 2017

FDI Realization - - 109 416 40,642

FDI Commitment 2,234.5 1,200.0 15,200.0 142,275.1

FDI Realization FDI Commitment

BUSINESS FIELD BUSINESS CLASIFICATION (KBLI) REMARKS

Motion picture, video and television programme production activities 5911 Maximum 100% foreign investment

Motion picture, video and television programme post-production activities 5912 Maximum 100% foreign investment

Motion picture, video and television programme distribution activities 5913 Maximum 100% foreign investment

Motion picture projection activities 5914 Maximum 100% foreign investment

Ownership relaxation related to Film and Cinema Industry

Source: Negative List of Investment (Presidential Regulation No. 44 Year 2016)

Investment opportunities

Indonesia Cinema & Film Industry

26

Indonesia Investment Trend 2013 - 2017Cinema & Film Industry (US$ Thousand)

Realization: US$ 41,167Commitment:US$ 160,909

# Country Source of FDIRealization

(in US$ Thousand)

1 Singapura 39.192

2 Thailand 746

3 Hongkong, RRT 540

4 Perancis 500

5 New Zealand 135

Others 55

Total 41.167

Top 5 Source of FDI (2013 -2017)Activities Phase Tax

Production Pra Production VAT (PPn)

Production VAT on Luxury Goods (PPnBM), Income Tax (PPh 21)

Pasca Production VAT on luxury goods (PPnBM), VAT (PPn) Income Tax (PPh 21), Tax on Foreign Services

Distribution Printing & Advertisment

VAT (PPn)

Rights Royalty Tax

Output Theatrical Release, TV Home Vide, IP Based

Royalty Tax, Entertainment Tax

Taxation in Film Industry

Source: ApindoSource: BKPM, 2018

Digital Industry and E-Commerce

4

Investment opportunities

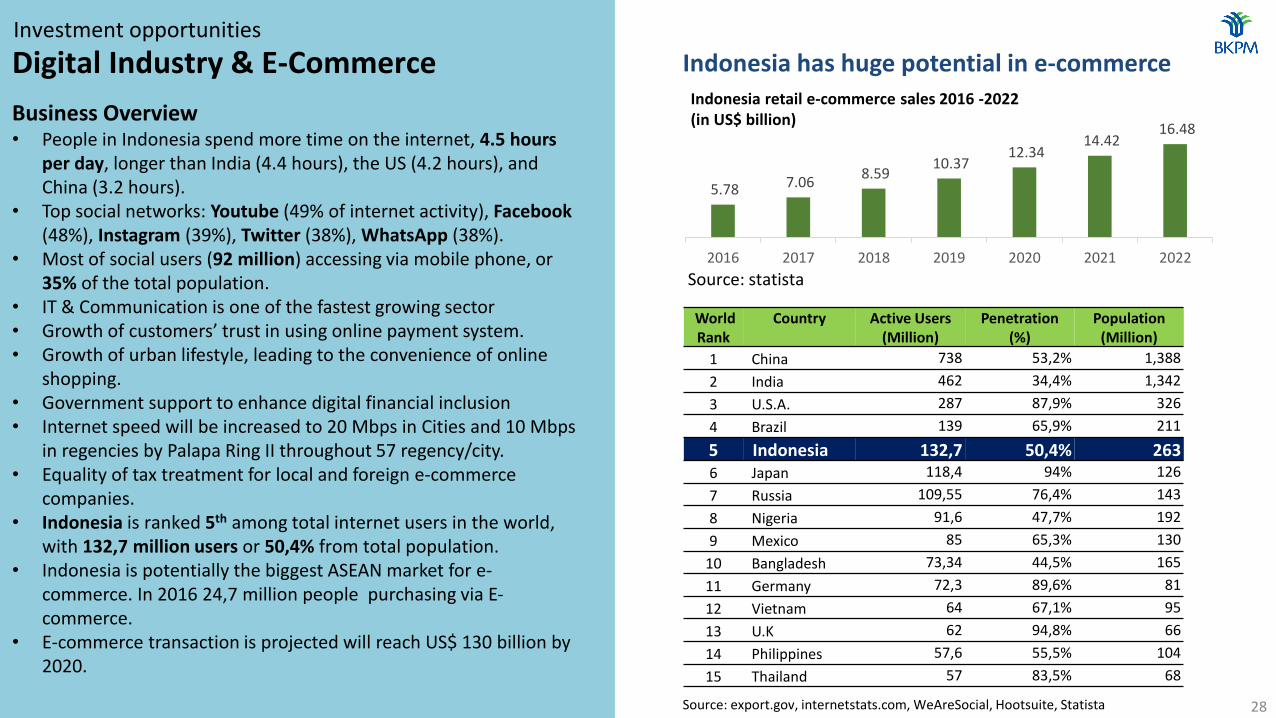

Digital Industry & E-Commerce

Business Overview • People in Indonesia spend more time on the internet, 4.5 hours

per day, longer than India (4.4 hours), the US (4.2 hours), and China (3.2 hours).

• Top social networks: Youtube (49% of internet activity), Facebook(48%), Instagram (39%), Twitter (38%), WhatsApp (38%).

• Most of social users (92 million) accessing via mobile phone, or 35% of the total population.

• IT & Communication is one of the fastest growing sector• Growth of customers’ trust in using online payment system. • Growth of urban lifestyle, leading to the convenience of online

shopping.• Government support to enhance digital financial inclusion• Internet speed will be increased to 20 Mbps in Cities and 10 Mbps

in regencies by Palapa Ring II throughout 57 regency/city.• Equality of tax treatment for local and foreign e-commerce

companies.• Indonesia is ranked 5th among total internet users in the world,

with 132,7 million users or 50,4% from total population.• Indonesia is potentially the biggest ASEAN market for e-

commerce. In 2016 24,7 million people purchasing via E-commerce.

• E-commerce transaction is projected will reach US$ 130 billion by 2020.

5.78 7.06 8.59

10.37 12.34

14.42 16.48

2016 2017 2018 2019 2020 2021 2022

Indonesia retail e-commerce sales 2016 -2022 (in US$ billion)

Source: statista

World Rank

Country Active Users(Million)

Penetration (%)

Population(Million)

1 China 738 53,2% 1,388

2 India 462 34,4% 1,342

3 U.S.A. 287 87,9% 326

4 Brazil 139 65,9% 211

5 Indonesia 132,7 50,4% 2636 Japan 118,4 94% 126

7 Russia 109,55 76,4% 143

8 Nigeria 91,6 47,7% 192

9 Mexico 85 65,3% 130

10 Bangladesh 73,34 44,5% 165

11 Germany 72,3 89,6% 81

12 Vietnam 64 67,1% 95

13 U.K 62 94,8% 66

14 Philippines 57,6 55,5% 104

15 Thailand 57 83,5% 68

Source: export.gov, internetstats.com, WeAreSocial, Hootsuite, Statista

Indonesia has huge potential in e-commerce

28

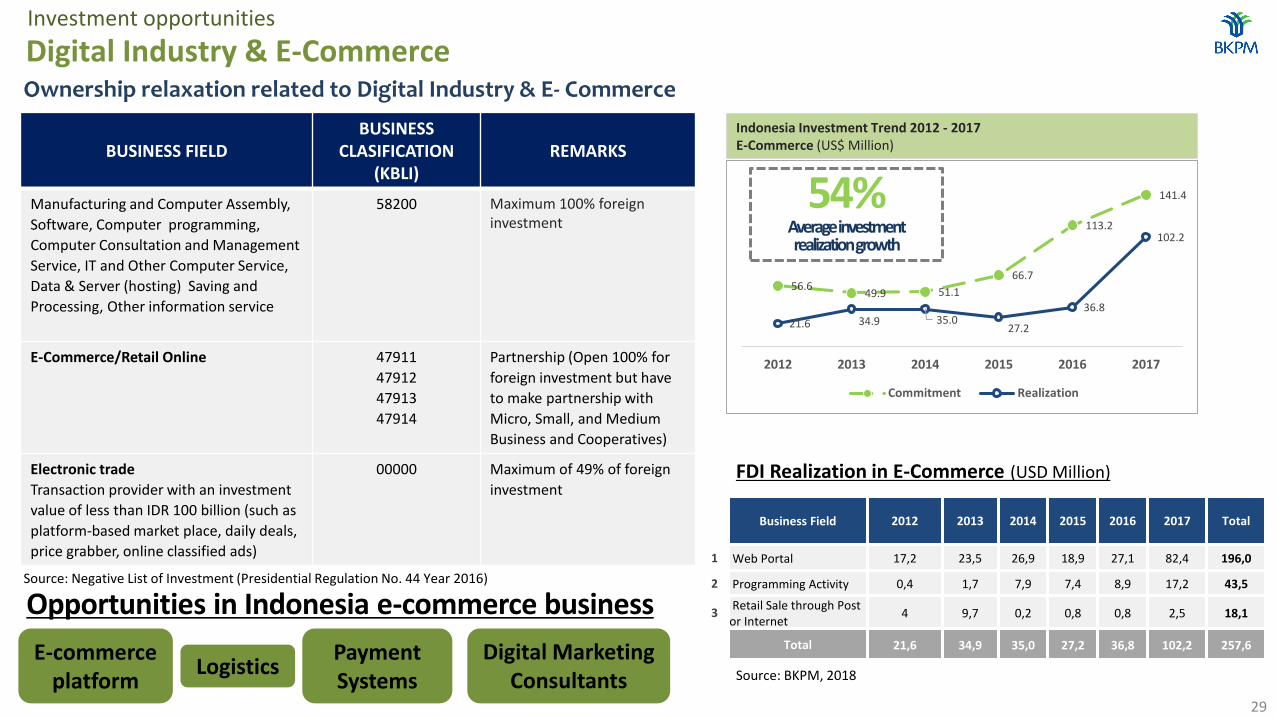

BUSINESS FIELDBUSINESS

CLASIFICATION (KBLI)

REMARKS

Manufacturing and Computer Assembly,

Software, Computer programming,

Computer Consultation and Management

Service, IT and Other Computer Service,

Data & Server (hosting) Saving and

Processing, Other information service

58200 Maximum 100% foreign investment

E-Commerce/Retail Online 47911

47912

47913

47914

Partnership (Open 100% for

foreign investment but have

to make partnership with

Micro, Small, and Medium

Business and Cooperatives)

Electronic trade

Transaction provider with an investment

value of less than IDR 100 billion (such as

platform-based market place, daily deals,

price grabber, online classified ads)

00000 Maximum of 49% of foreign

investment

Investment opportunities

Digital Industry & E-CommerceOwnership relaxation related to Digital Industry & E- Commerce

Source: Negative List of Investment (Presidential Regulation No. 44 Year 2016)

56.649.9 51.1

66.7

113.2

141.4

21.6 34.9 35.027.2

36.8

102.2

2012 2013 2014 2015 2016 2017

Commitment Realization

Opportunities in Indonesia e-commerce business

LogisticsPayment Systems

Digital Marketing Consultants

E-commerce platform

29

Indonesia Investment Trend 2012 - 2017E-Commerce (US$ Million)

54%Average investment realization growth

Business Field 2012 2013 2014 2015 2016 2017 Total

1 Web Portal 17,2 23,5 26,9 18,9 27,1 82,4 196,0

2 Programming Activity 0,4 1,7 7,9 7,4 8,9 17,2 43,5

3Retail Sale through Post

or Internet4 9,7 0,2 0,8 0,8 2,5 18,1

Total 21,6 34,9 35,0 27,2 36,8 102,2 257,6

FDI Realization in E-Commerce (USD Million)

Source: BKPM, 2018

30

7.5

9.5

11.1

5.4

8.2

46.0

87.7

0.4

0.5

0.9

1.0

1.0

1.7

5.5

Vietnam

Philippines

Thailand

Singapore

Malaysia

Indonesia

ASEAN

2015 2025

The E-Commerce roadmap 2017-2019 is created to support the development of local e-commerce industry in order to be the biggest digital economy nation in ASEAN by 2020.

ASEAN E-commerce market 2015-2025 (in USD billion)

Source:Katadata Indonesia, 2017

E-commerce platforms

Payment Services

Logistics

Investment opportunities

Digital Industry & E-Commerce

Types of E-commerce in Indonesia

Source: ecommerceiq

Wellness Industry5

32

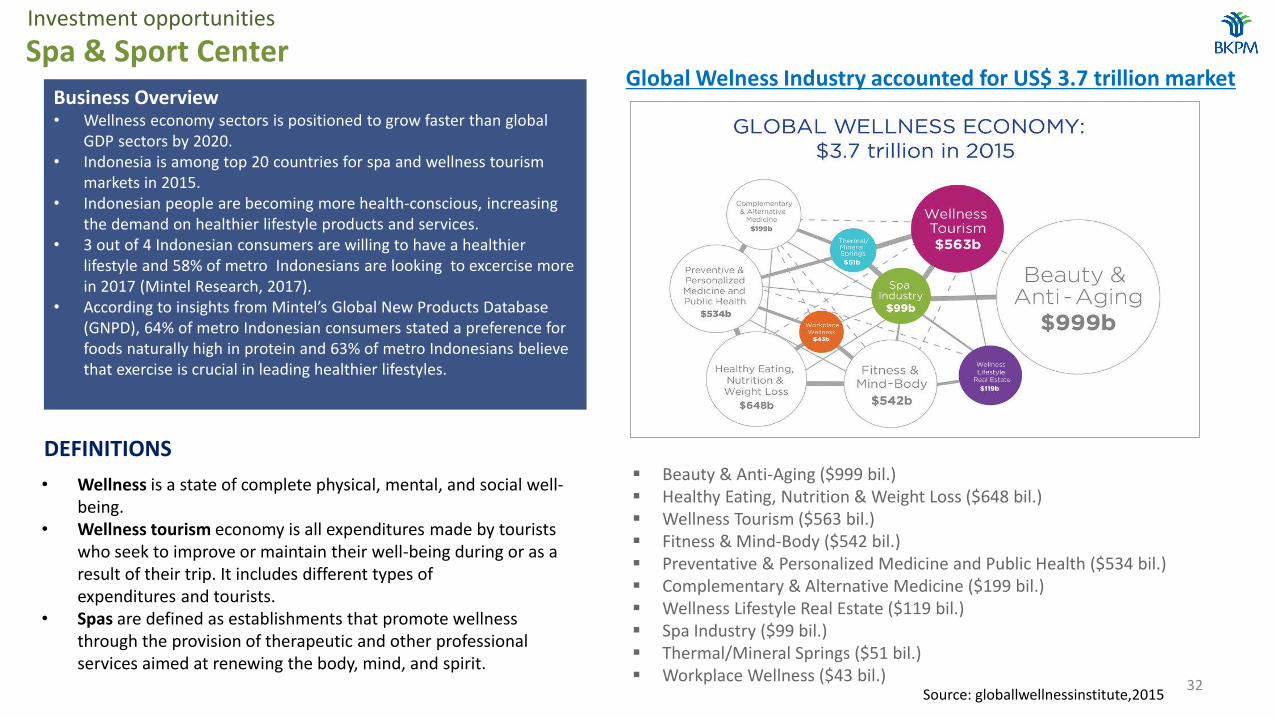

Investment opportunities

Spa & Sport Center

Business Overview• Wellness economy sectors is positioned to grow faster than global

GDP sectors by 2020.• Indonesia is among top 20 countries for spa and wellness tourism

markets in 2015.• Indonesian people are becoming more health-conscious, increasing

the demand on healthier lifestyle products and services.• 3 out of 4 Indonesian consumers are willing to have a healthier

lifestyle and 58% of metro Indonesians are looking to excercise more in 2017 (Mintel Research, 2017).

• According to insights from Mintel’s Global New Products Database (GNPD), 64% of metro Indonesian consumers stated a preference for foods naturally high in protein and 63% of metro Indonesians believe that exercise is crucial in leading healthier lifestyles.

• Wellness is a state of complete physical, mental, and social well-being.

• Wellness tourism economy is all expenditures made by tourists who seek to improve or maintain their well-being during or as a result of their trip. It includes different types of expenditures and tourists.

• Spas are defined as establishments that promote wellness through the provision of therapeutic and other professional services aimed at renewing the body, mind, and spirit.

Beauty & Anti-Aging ($999 bil.) Healthy Eating, Nutrition & Weight Loss ($648 bil.) Wellness Tourism ($563 bil.) Fitness & Mind-Body ($542 bil.) Preventative & Personalized Medicine and Public Health ($534 bil.) Complementary & Alternative Medicine ($199 bil.) Wellness Lifestyle Real Estate ($119 bil.) Spa Industry ($99 bil.) Thermal/Mineral Springs ($51 bil.) Workplace Wellness ($43 bil.)

DEFINITIONS

Source: globallwellnessinstitute,2015

Global Welness Industry accounted for US$ 3.7 trillion market

Investment opportunities

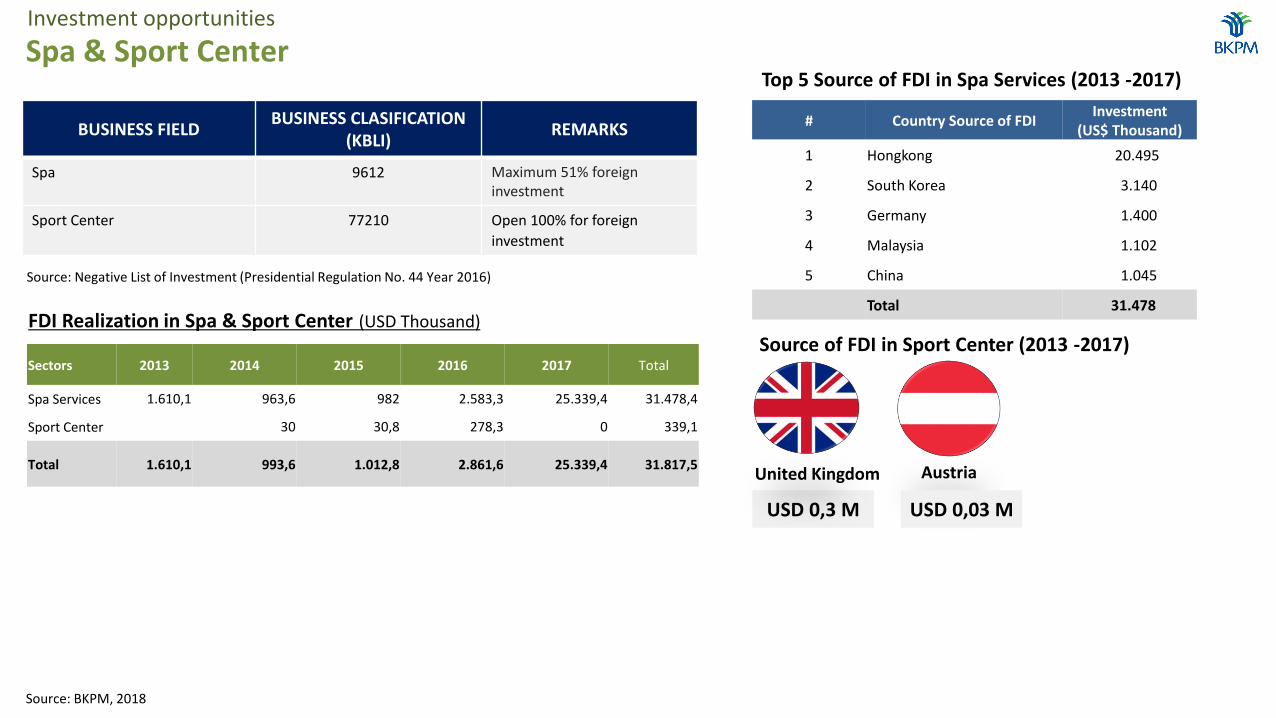

Spa & Sport Center

BUSINESS FIELDBUSINESS CLASIFICATION

(KBLI)REMARKS

Spa 9612 Maximum 51% foreign investment

Sport Center 77210 Open 100% for foreign

investment

Sectors 2013 2014 2015 2016 2017 Total

Spa Services 1.610,1 963,6 982 2.583,3 25.339,4 31.478,4

Sport Center 30 30,8 278,3 0 339,1

Total 1.610,1 993,6 1.012,8 2.861,6 25.339,4 31.817,5

Source: Negative List of Investment (Presidential Regulation No. 44 Year 2016)

FDI Realization in Spa & Sport Center (USD Thousand)

# Country Source of FDIInvestment

(US$ Thousand)

1 Hongkong 20.495

2 South Korea 3.140

3 Germany 1.400

4 Malaysia 1.102

5 China 1.045

Total 31.478

Source: BKPM, 2018

Top 5 Source of FDI in Spa Services (2013 -2017)

Source of FDI in Sport Center (2013 -2017)

United Kingdom

USD 0,3 M

Austria

USD 0,03 M

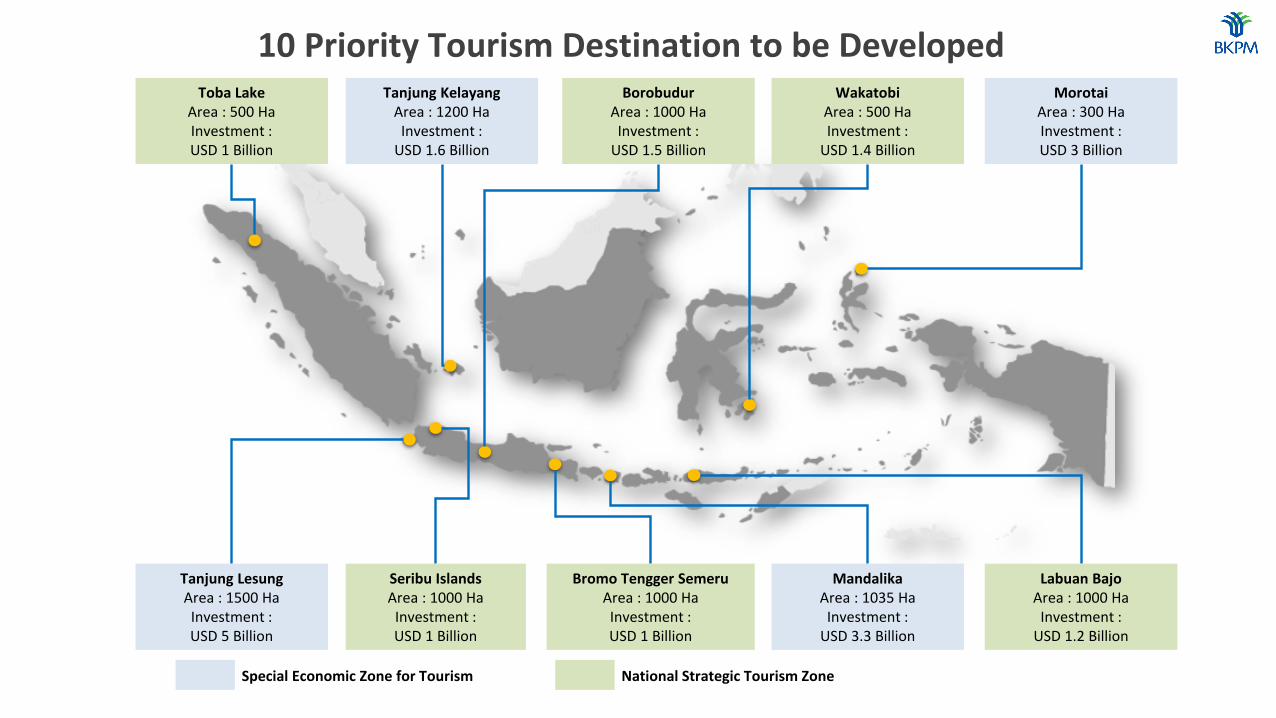

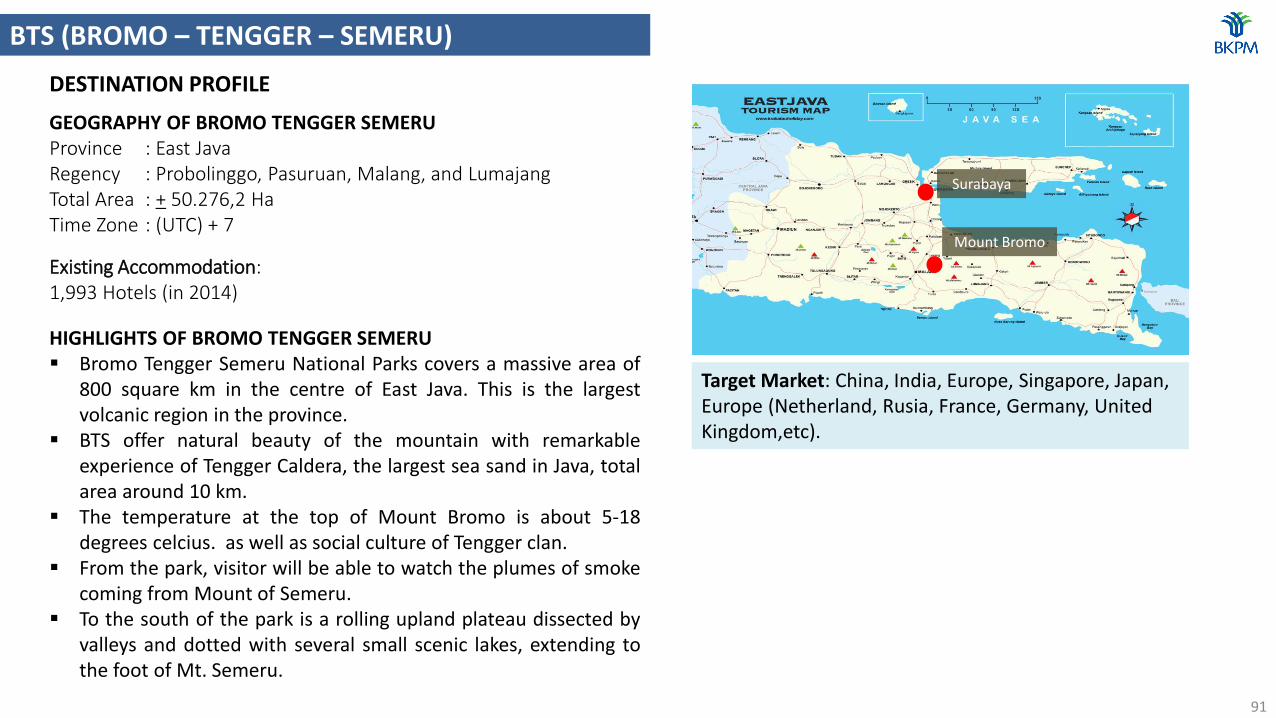

10 PRIORITY TOURISM DESTINATION

Toba LakeArea : 500 HaInvestment : USD 1 Billion

Tanjung KelayangArea : 1200 HaInvestment :

USD 1.6 Billion

BorobudurArea : 1000 HaInvestment :

USD 1.5 Billion

WakatobiArea : 500 HaInvestment :

USD 1.4 Billion

MorotaiArea : 300 HaInvestment : USD 3 Billion

Tanjung LesungArea : 1500 HaInvestment : USD 5 Billion

Seribu IslandsArea : 1000 Ha

Investment : USD 1 Billion

Bromo Tengger SemeruArea : 1000 HaInvestment : USD 1 Billion

MandalikaArea : 1035 HaInvestment :

USD 3.3 Billion

Labuan BajoArea : 1000 Ha

Investment : USD 1.2 Billion

10 Priority Tourism Destination to be Developed

Special Economic Zone for Tourism National Strategic Tourism Zone

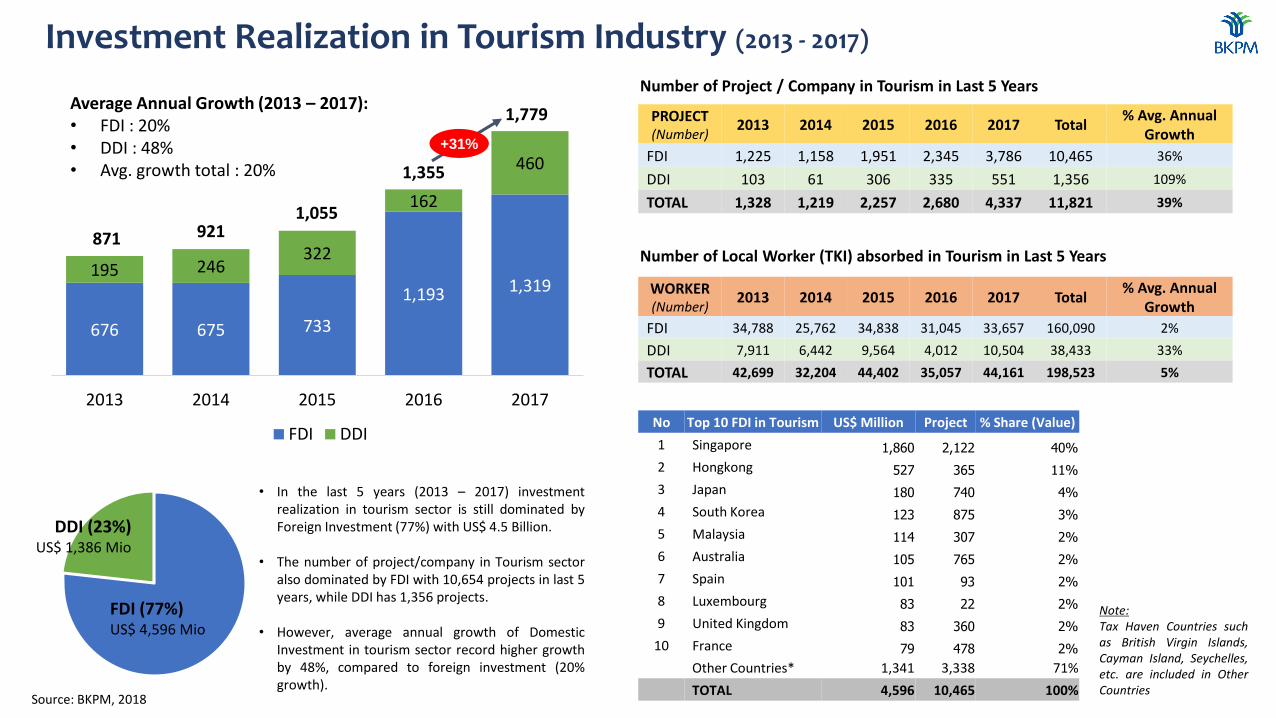

Investment Realization in Tourism Industry (2013 - 2017)

676 675 733

1,193 1,319195 246

322

162

460

2013 2014 2015 2016 2017

FDI DDI

871 9211,055

1,355

1,779

+31%

Average Annual Growth (2013 – 2017):• FDI : 20%• DDI : 48%• Avg. growth total : 20%

DDI (23%)US$ 1,386 Mio

FDI (77%)US$ 4,596 Mio

• In the last 5 years (2013 – 2017) investmentrealization in tourism sector is still dominated byForeign Investment (77%) with US$ 4.5 Billion.

• The number of project/company in Tourism sectoralso dominated by FDI with 10,654 projects in last 5years, while DDI has 1,356 projects.

• However, average annual growth of DomesticInvestment in tourism sector record higher growthby 48%, compared to foreign investment (20%growth).

PROJECT(Number)

2013 2014 2015 2016 2017 Total% Avg. Annual

Growth

FDI 1,225 1,158 1,951 2,345 3,786 10,465 36%

DDI 103 61 306 335 551 1,356 109%

TOTAL 1,328 1,219 2,257 2,680 4,337 11,821 39%

Number of Project / Company in Tourism in Last 5 Years

Number of Local Worker (TKI) absorbed in Tourism in Last 5 Years

WORKER(Number)

2013 2014 2015 2016 2017 Total% Avg. Annual

Growth

FDI 34,788 25,762 34,838 31,045 33,657 160,090 2%

DDI 7,911 6,442 9,564 4,012 10,504 38,433 33%

TOTAL 42,699 32,204 44,402 35,057 44,161 198,523 5%

No Top 10 FDI in Tourism US$ Million Project % Share (Value)

1 Singapore 1,860 2,122 40%

2 Hongkong 527 365 11%

3 Japan 180 740 4%

4 South Korea 123 875 3%

5 Malaysia 114 307 2%

6 Australia 105 765 2%

7 Spain 101 93 2%

8 Luxembourg 83 22 2%

9 United Kingdom 83 360 2%

10 France 79 478 2%

Other Countries* 1,341 3,338 71%

TOTAL 4,596 10,465 100%

Note:Tax Haven Countries suchas British Virgin Islands,Cayman Island, Seychelles,etc. are included in OtherCountries

Source: BKPM, 2018

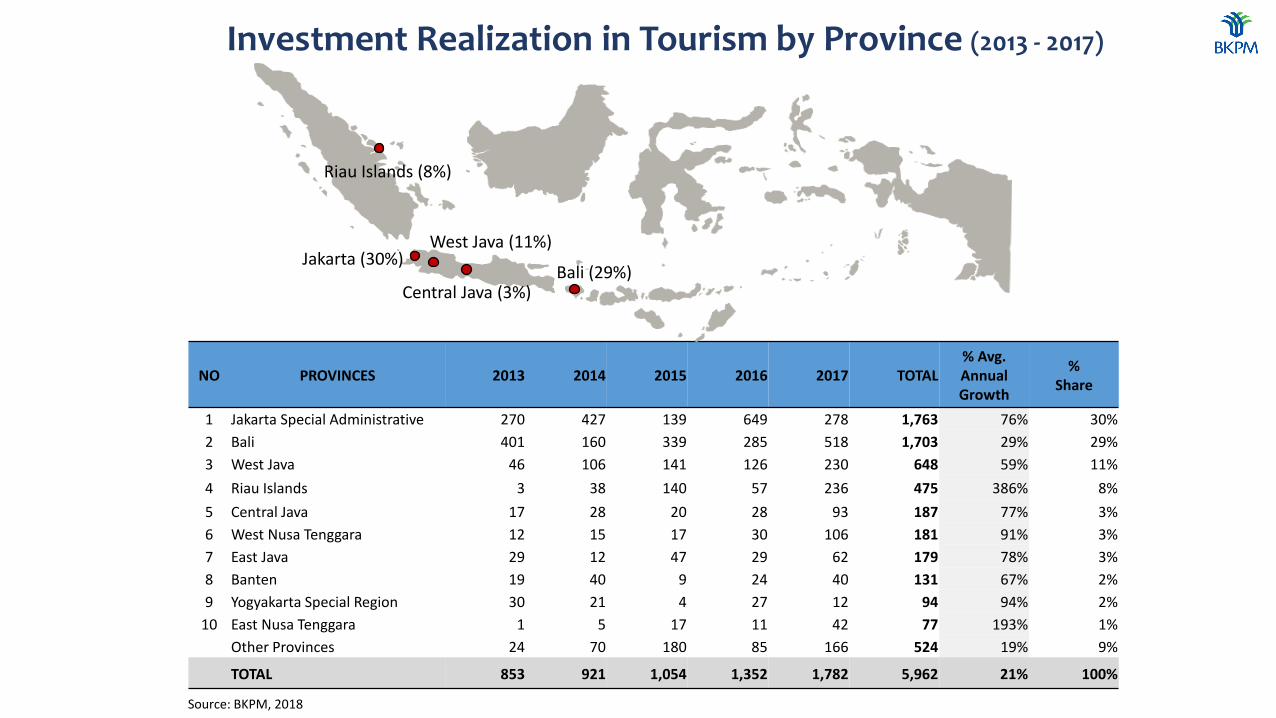

NO PROVINCES 2013 2014 2015 2016 2017 TOTAL% Avg. Annual Growth

%Share

1 Jakarta Special Administrative 270 427 139 649 278 1,763 76% 30%

2 Bali 401 160 339 285 518 1,703 29% 29%

3 West Java 46 106 141 126 230 648 59% 11%

4 Riau Islands 3 38 140 57 236 475 386% 8%

5 Central Java 17 28 20 28 93 187 77% 3%

6 West Nusa Tenggara 12 15 17 30 106 181 91% 3%

7 East Java 29 12 47 29 62 179 78% 3%

8 Banten 19 40 9 24 40 131 67% 2%

9 Yogyakarta Special Region 30 21 4 27 12 94 94% 2%

10 East Nusa Tenggara 1 5 17 11 42 77 193% 1%

Other Provinces 24 70 180 85 166 524 19% 9%

TOTAL 853 921 1,054 1,352 1,782 5,962 21% 100%

Jakarta (30%) West Java (11%)

Central Java (3%)Bali (29%)

Riau Islands (8%)

Investment Realization in Tourism by Province (2013 - 2017)

Source: BKPM, 2018

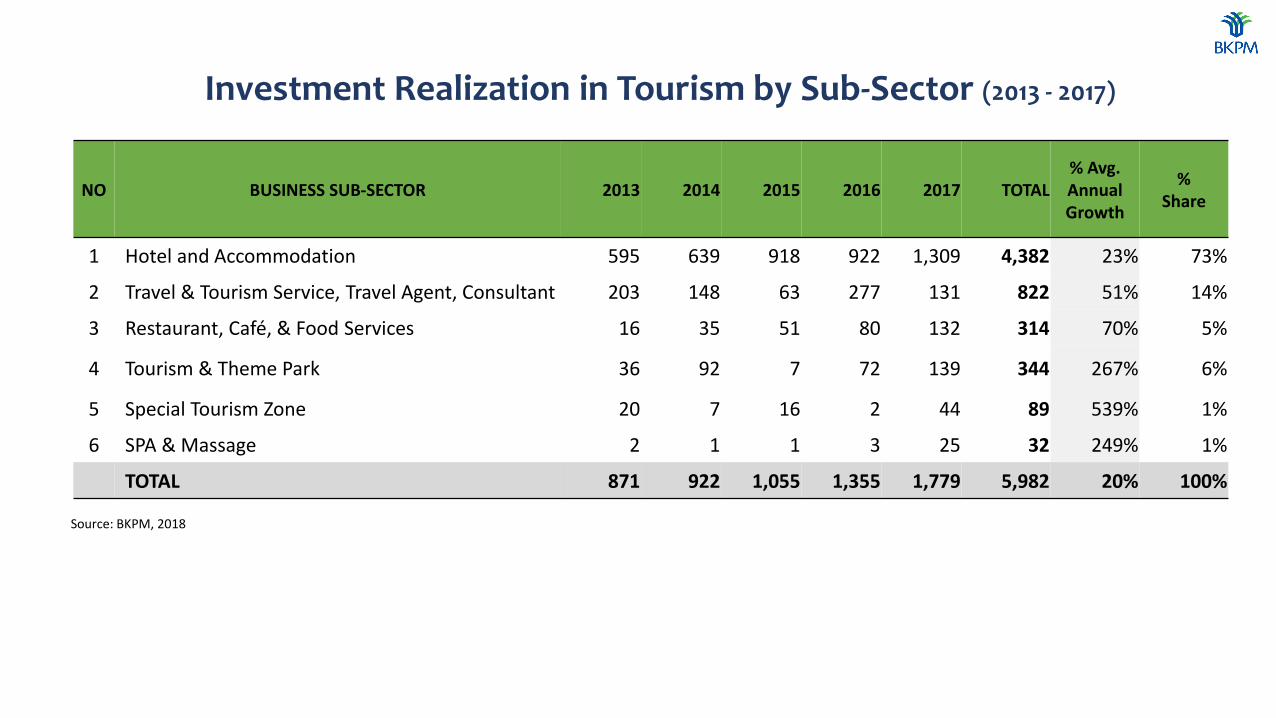

NO BUSINESS SUB-SECTOR 2013 2014 2015 2016 2017 TOTAL% Avg. Annual Growth

%Share

1 Hotel and Accommodation 595 639 918 922 1,309 4,382 23% 73%

2 Travel & Tourism Service, Travel Agent, Consultant 203 148 63 277 131 822 51% 14%

3 Restaurant, Café, & Food Services 16 35 51 80 132 314 70% 5%

4 Tourism & Theme Park 36 92 7 72 139 344 267% 6%

5 Special Tourism Zone 20 7 16 2 44 89 539% 1%

6 SPA & Massage 2 1 1 3 25 32 249% 1%

TOTAL 871 922 1,055 1,355 1,779 5,982 20% 100%

Investment Realization in Tourism by Sub-Sector (2013 - 2017)

Source: BKPM, 2018

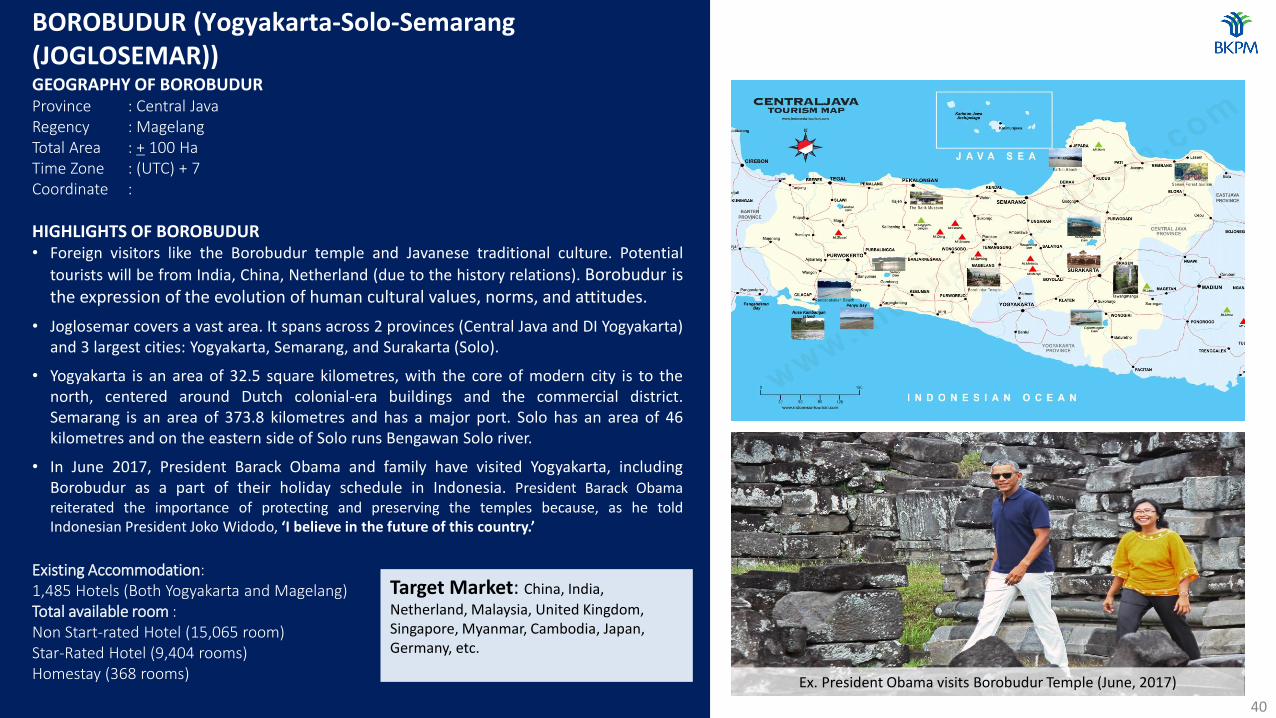

BOROBUDUR| CENTRAL JAVA

INTEGRATED TOURISM AREA1

GEOGRAPHY OF BOROBUDURProvince : Central JavaRegency : MagelangTotal Area : + 100 HaTime Zone : (UTC) + 7Coordinate :

HIGHLIGHTS OF BOROBUDUR• Foreign visitors like the Borobudur temple and Javanese traditional culture. Potential

tourists will be from India, China, Netherland (due to the history relations). Borobudur isthe expression of the evolution of human cultural values, norms, and attitudes.

• Joglosemar covers a vast area. It spans across 2 provinces (Central Java and DI Yogyakarta)and 3 largest cities: Yogyakarta, Semarang, and Surakarta (Solo).

• Yogyakarta is an area of 32.5 square kilometres, with the core of modern city is to thenorth, centered around Dutch colonial-era buildings and the commercial district.Semarang is an area of 373.8 kilometres and has a major port. Solo has an area of 46kilometres and on the eastern side of Solo runs Bengawan Solo river.

• In June 2017, President Barack Obama and family have visited Yogyakarta, includingBorobudur as a part of their holiday schedule in Indonesia. President Barack Obamareiterated the importance of protecting and preserving the temples because, as he toldIndonesian President Joko Widodo, ‘I believe in the future of this country.’

Ex. President Obama visits Borobudur Temple (June, 2017)

Existing Accommodation: 1,485 Hotels (Both Yogyakarta and Magelang)Total available room : Non Start-rated Hotel (15,065 room)Star-Rated Hotel (9,404 rooms)Homestay (368 rooms)

Target Market: China, India,

Netherland, Malaysia, United Kingdom,Singapore, Myanmar, Cambodia, Japan, Germany, etc.

BOROBUDUR (Yogyakarta-Solo-Semarang(JOGLOSEMAR))

40

ATTRACTIONCulture & HeritagesBorobudur Temple, Pawon Temple, and Mendut Temple (to a lesser extent Bukit Rhema and Punthuk Setumbu including chicken Church). Prambanan is thelargest Hindu Temple of ancient Java and the building was completed in the mid of 9th century. As a UNESCO World Heritage Site since 1991. Indonesia(Prambanan temple) is perfect place to watch Ramayana Ballet. You can watch the performance of Ramayana dance every Tuesday, Thursday, and Saturday.

Sunrise in PuthukSetumbu,

Yogyakarta

Mendut Temple

Prambanan Temple

Ratu Boko Temple

KeratonKasepuhan

Culinary

Malioboro Street

Royal servants

Culture, Culinary, and Fashion

Yogyakarta is renowned as a center of education, classical Javanese fine art, and fashion like batik. Despites Yogyakarta also offer many heritage sites and plenty of culinary option with great local recipes. In Solo you can also discover some culinary delight and batik with special motives.

BOROBUDUR (Yogyakarta-Solo-Semarang (JOGLOSEMAR))

41

ACCESIBILITIES

Existing Airport: Adisucipto International Airport, Yogyakarta Adisumarmo International Airport, Solo Achmad Yani International Airport, Semarang

Airport Under Development: Kulonprogo International Airport, Kulonprogo

Current Mode of Transport

Transport Mode Public Bus/Rail Taxi/Car Rental/ Tourist Bus/Van

Travel Time By Bus:Yogyakarta to Borobudur (40km): 2 hoursMagelang to Borobudur (17km): 1 hourBy Rail:Jakarta to Yogyakarta: 8 hoursSolo to Yogyakarta : 1 hour

Yogyakarta to Borobudur (40 km) : 1 to 1.5 hoursSemarang to Yogyakarta (100 km) : 2.5 to 3 hoursSolo to Borobudur (100 km) : 3 hours

BOROBUDUR (Yogyakarta-Solo-Semarang (JOGLOSEMAR))

42

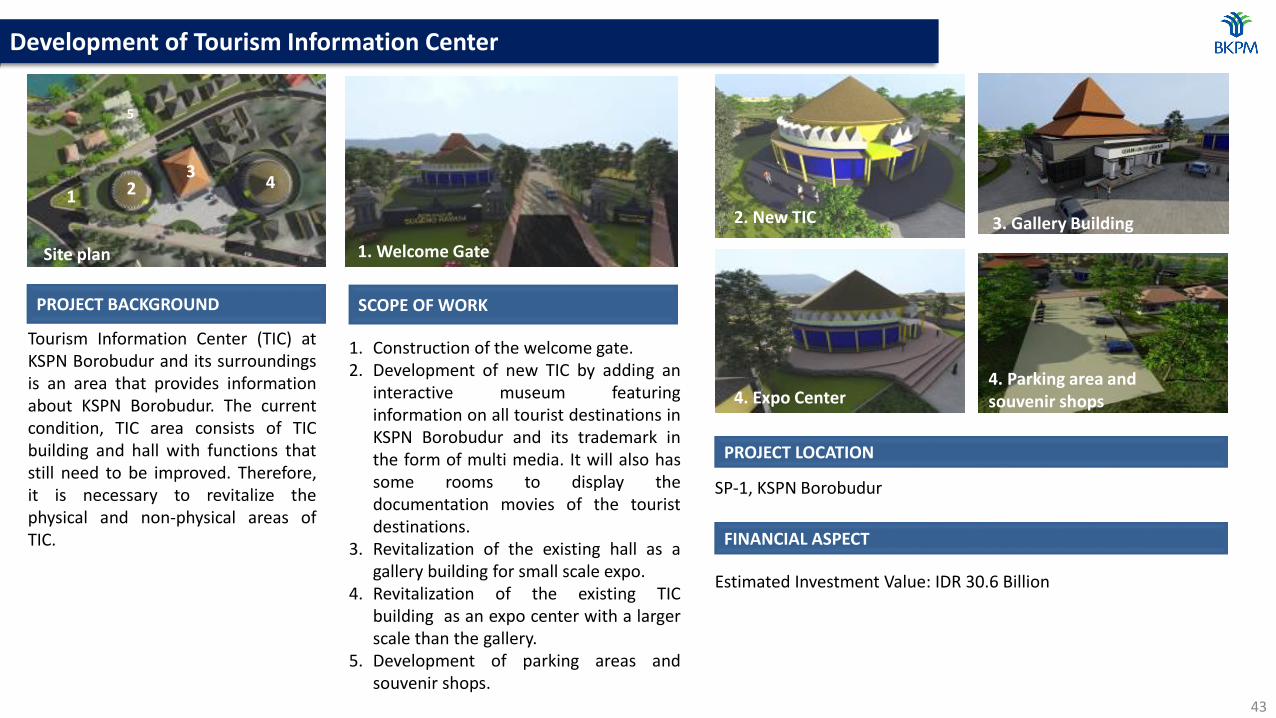

PROJECT LOCATION

SP-1, KSPN Borobudur

PROJECT BACKGROUND

Tourism Information Center (TIC) atKSPN Borobudur and its surroundingsis an area that provides informationabout KSPN Borobudur. The currentcondition, TIC area consists of TICbuilding and hall with functions thatstill need to be improved. Therefore,it is necessary to revitalize thephysical and non-physical areas ofTIC.

Estimated Investment Value: IDR 30.6 Billion

FINANCIAL ASPECT

Development of Tourism Information Center

SCOPE OF WORK

1. Construction of the welcome gate.2. Development of new TIC by adding an

interactive museum featuringinformation on all tourist destinations inKSPN Borobudur and its trademark inthe form of multi media. It will also hassome rooms to display thedocumentation movies of the touristdestinations.

3. Revitalization of the existing hall as agallery building for small scale expo.

4. Revitalization of the existing TICbuilding as an expo center with a largerscale than the gallery.

5. Development of parking areas andsouvenir shops.

Site plan

1 23

4

5

1. Welcome Gate

2. New TIC 3. Gallery Building

4. Expo Center4. Parking area and souvenir shops

43

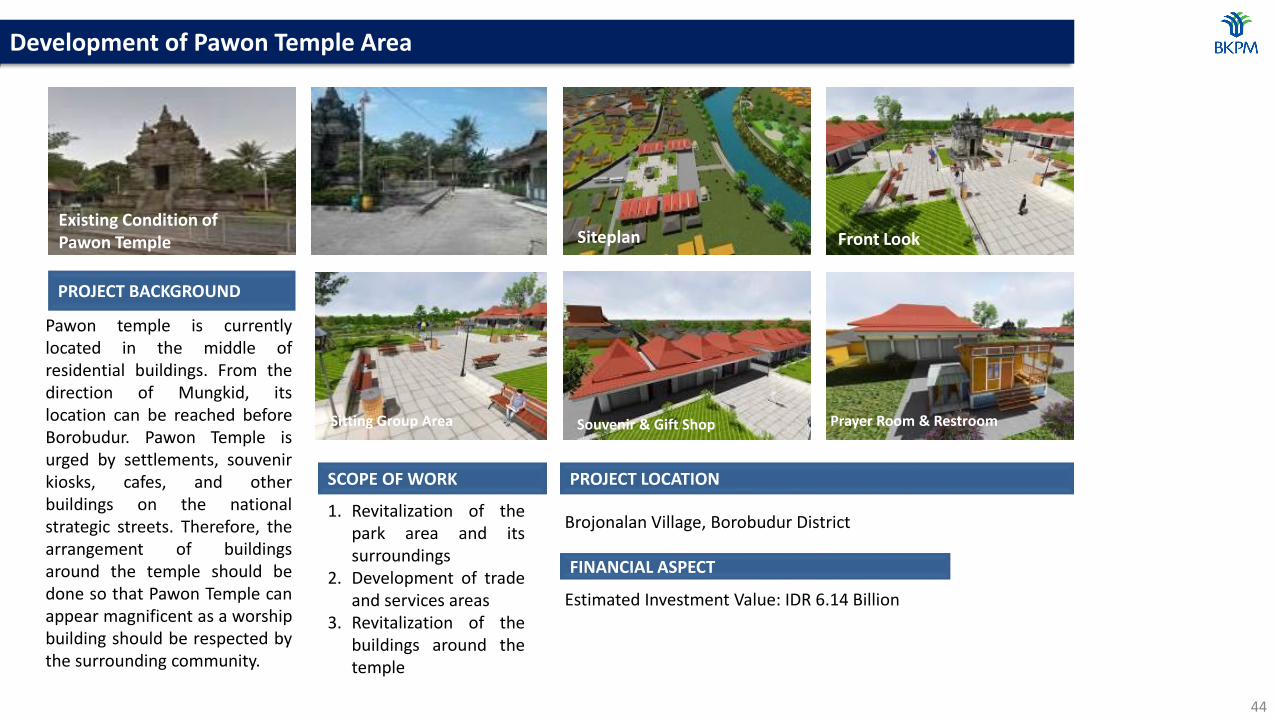

Development of Pawon Temple Area

Existing Condition of Pawon Temple Siteplan Front Look

PROJECT BACKGROUND

Pawon temple is currentlylocated in the middle ofresidential buildings. From thedirection of Mungkid, itslocation can be reached beforeBorobudur. Pawon Temple isurged by settlements, souvenirkiosks, cafes, and otherbuildings on the nationalstrategic streets. Therefore, thearrangement of buildingsaround the temple should bedone so that Pawon Temple canappear magnificent as a worshipbuilding should be respected bythe surrounding community.

Souvenir & Gift Shop Prayer Room & RestroomSitting Group Area

PROJECT LOCATION

Brojonalan Village, Borobudur District

Estimated Investment Value: IDR 6.14 Billion

FINANCIAL ASPECT

SCOPE OF WORK

1. Revitalization of thepark area and itssurroundings

2. Development of tradeand services areas

3. Revitalization of thebuildings around thetemple

44

PROJECT LOCATION

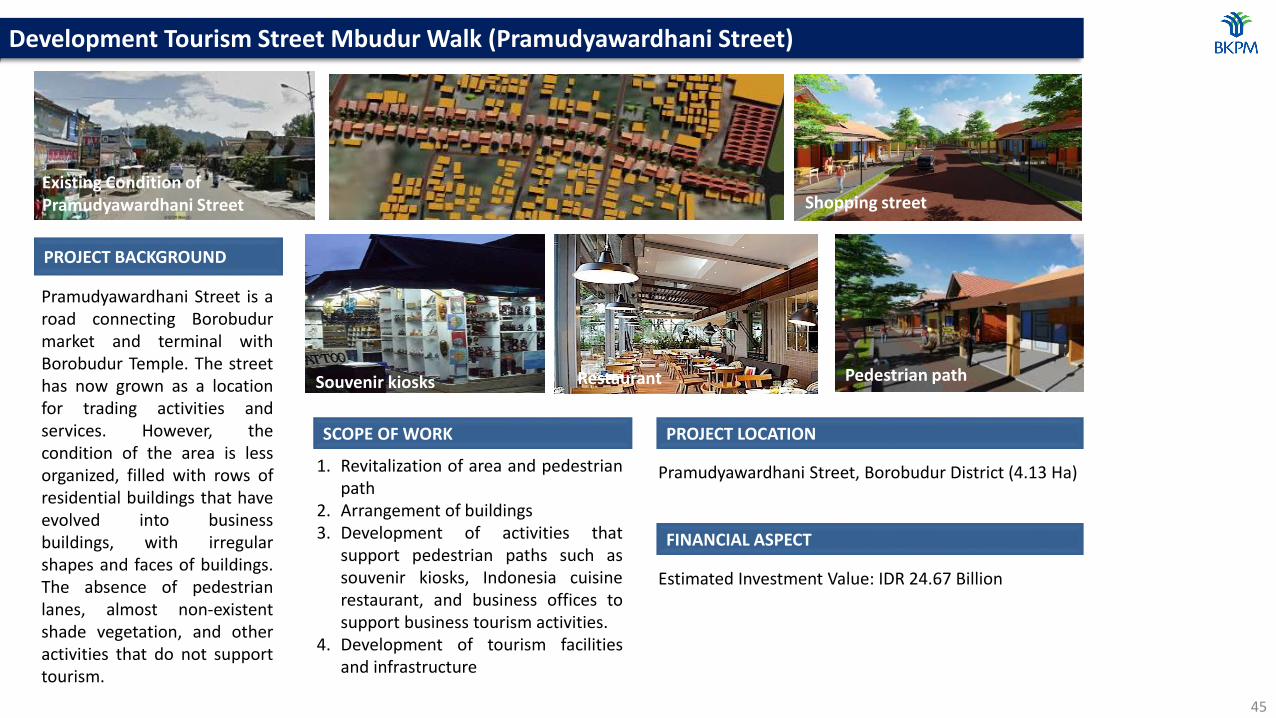

Pramudyawardhani Street, Borobudur District (4.13 Ha)

PROJECT BACKGROUND

Pramudyawardhani Street is aroad connecting Borobudurmarket and terminal withBorobudur Temple. The streethas now grown as a locationfor trading activities andservices. However, thecondition of the area is lessorganized, filled with rows ofresidential buildings that haveevolved into businessbuildings, with irregularshapes and faces of buildings.The absence of pedestrianlanes, almost non-existentshade vegetation, and otheractivities that do not supporttourism.

Estimated Investment Value: IDR 24.67 Billion

FINANCIAL ASPECT

Development Tourism Street Mbudur Walk (Pramudyawardhani Street)

SCOPE OF WORK

1. Revitalization of area and pedestrianpath

2. Arrangement of buildings3. Development of activities that

support pedestrian paths such assouvenir kiosks, Indonesia cuisinerestaurant, and business offices tosupport business tourism activities.

4. Development of tourism facilitiesand infrastructure

Shopping street

Pedestrian path

Existing Condition of Pramudyawardhani Street

RestaurantSouvenir kiosks

45

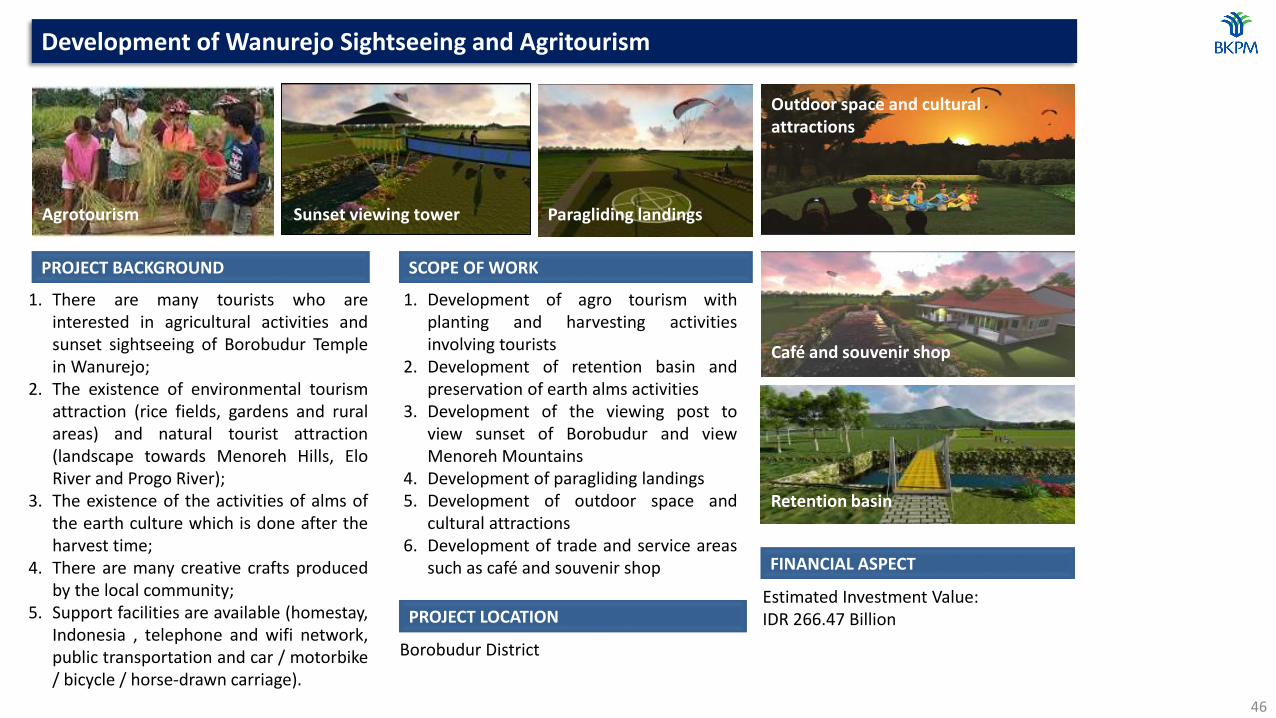

PROJECT BACKGROUND

1. There are many tourists who areinterested in agricultural activities andsunset sightseeing of Borobudur Templein Wanurejo;

2. The existence of environmental tourismattraction (rice fields, gardens and ruralareas) and natural tourist attraction(landscape towards Menoreh Hills, EloRiver and Progo River);

3. The existence of the activities of alms ofthe earth culture which is done after theharvest time;

4. There are many creative crafts producedby the local community;

5. Support facilities are available (homestay,Indonesia , telephone and wifi network,public transportation and car / motorbike/ bicycle / horse-drawn carriage).

Development of Wanurejo Sightseeing and Agritourism

SCOPE OF WORK

1. Development of agro tourism withplanting and harvesting activitiesinvolving tourists

2. Development of retention basin andpreservation of earth alms activities

3. Development of the viewing post toview sunset of Borobudur and viewMenoreh Mountains

4. Development of paragliding landings5. Development of outdoor space and

cultural attractions6. Development of trade and service areas

such as café and souvenir shop

Borobudur District

Estimated Investment Value: IDR 266.47 Billion

FINANCIAL ASPECT

Agrotourism Sunset viewing tower Paragliding landings

Outdoor space and culturalattractions

Café and souvenir shop

Retention basin

PROJECT LOCATION

46

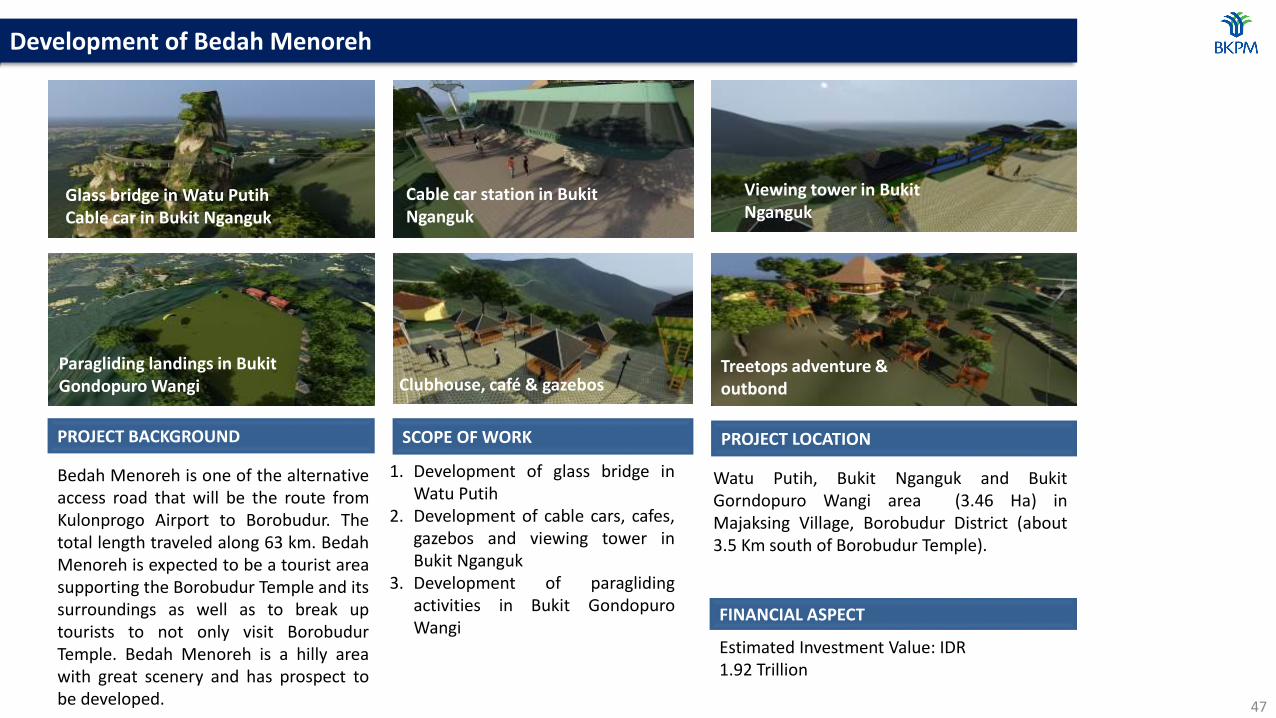

PROJECT BACKGROUND

Bedah Menoreh is one of the alternativeaccess road that will be the route fromKulonprogo Airport to Borobudur. Thetotal length traveled along 63 km. BedahMenoreh is expected to be a tourist areasupporting the Borobudur Temple and itssurroundings as well as to break uptourists to not only visit BorobudurTemple. Bedah Menoreh is a hilly areawith great scenery and has prospect tobe developed.

Development of Bedah Menoreh

SCOPE OF WORK

1. Development of glass bridge inWatu Putih

2. Development of cable cars, cafes,gazebos and viewing tower inBukit Nganguk

3. Development of paraglidingactivities in Bukit GondopuroWangi

PROJECT LOCATION

Glass bridge in Watu PutihCable car in Bukit Nganguk

Cable car station in Bukit Nganguk

Viewing tower in Bukit Nganguk

Treetops adventure & outbond

Gazebo

Paragliding landings in Bukit Gondopuro Wangi Clubhouse, café & gazebos

Watu Putih, Bukit Nganguk and BukitGorndopuro Wangi area (3.46 Ha) inMajaksing Village, Borobudur District (about3.5 Km south of Borobudur Temple).

Estimated Investment Value: IDR 1.92 Trillion

FINANCIAL ASPECT

47

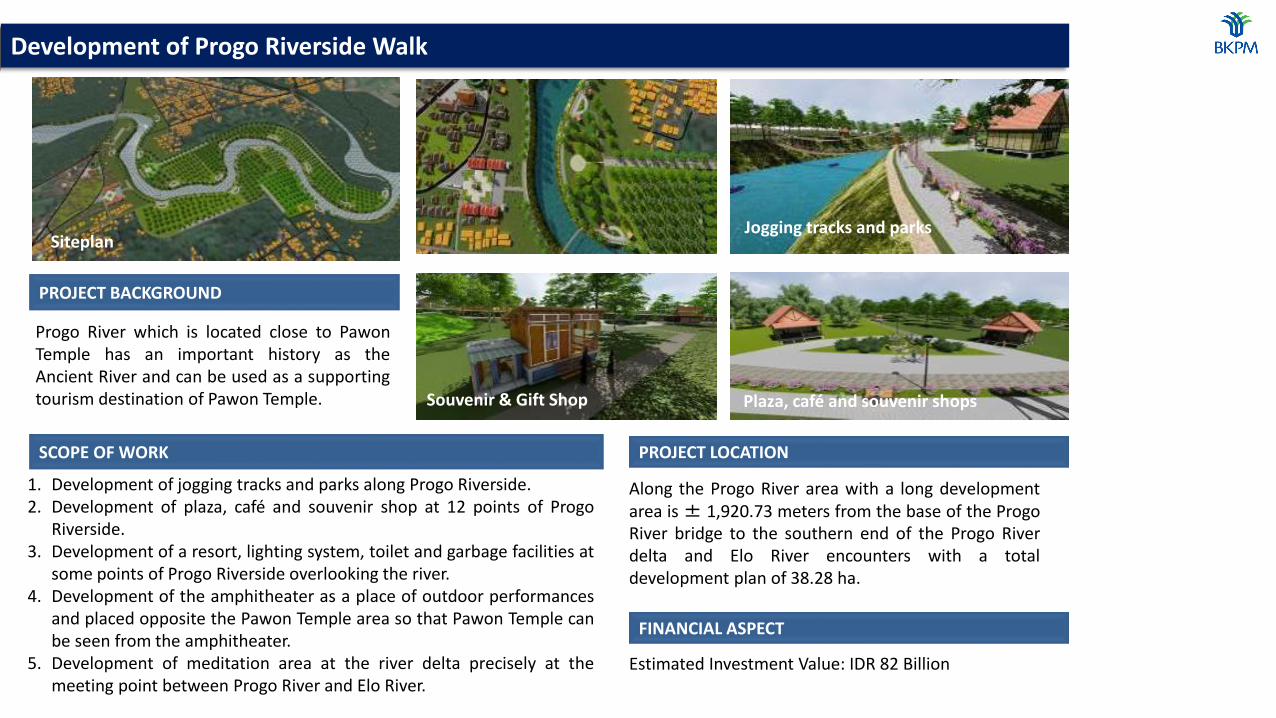

PROJECT LOCATION

Along the Progo River area with a long developmentarea is± 1,920.73 meters from the base of the ProgoRiver bridge to the southern end of the Progo Riverdelta and Elo River encounters with a totaldevelopment plan of 38.28 ha.

PROJECT BACKGROUND

Progo River which is located close to PawonTemple has an important history as theAncient River and can be used as a supportingtourism destination of Pawon Temple.

Estimated Investment Value: IDR 82 Billion

FINANCIAL ASPECT

Development of Progo Riverside Walk

SCOPE OF WORK

1. Development of jogging tracks and parks along Progo Riverside.2. Development of plaza, café and souvenir shop at 12 points of Progo

Riverside.3. Development of a resort, lighting system, toilet and garbage facilities at

some points of Progo Riverside overlooking the river.4. Development of the amphitheater as a place of outdoor performances

and placed opposite the Pawon Temple area so that Pawon Temple canbe seen from the amphitheater.

5. Development of meditation area at the river delta precisely at themeeting point between Progo River and Elo River.

Siteplan

Plaza, café and souvenir shopsSitting Group Area

Jogging tracks and parks

Souvenir & Gift Shop

PROJECT LOCATION

Bener District, Purworejo Regency

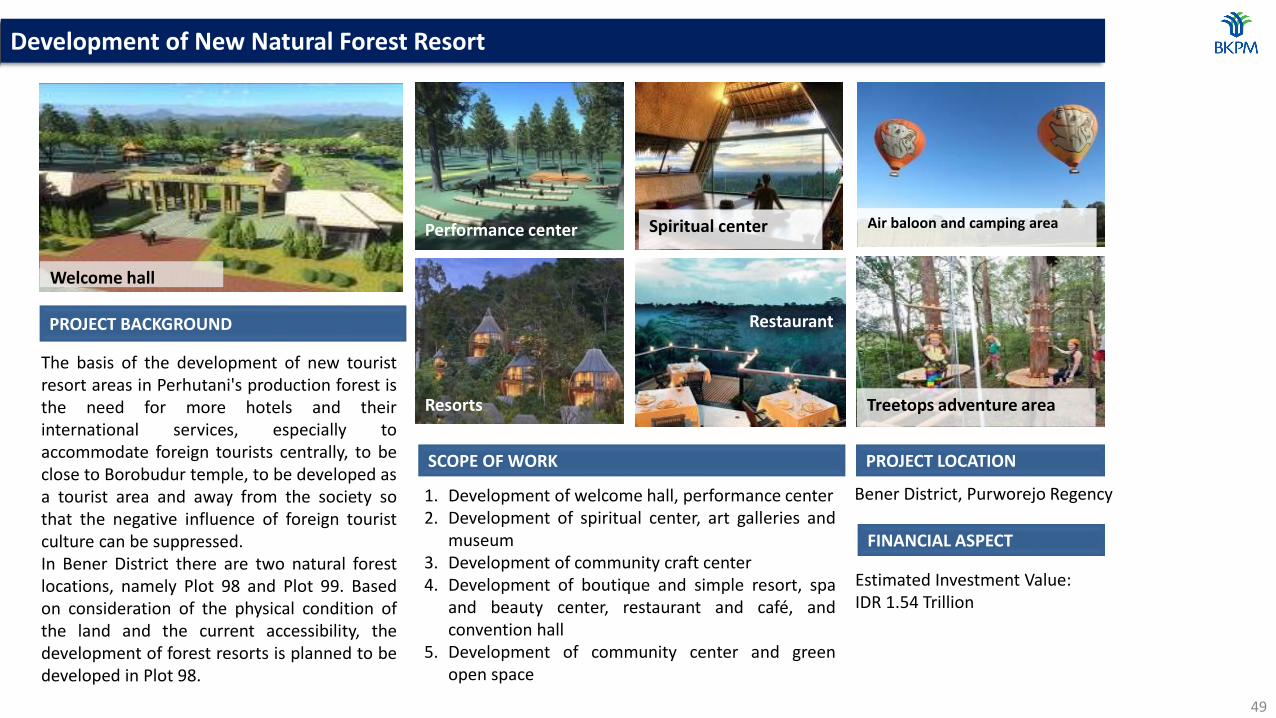

PROJECT BACKGROUND

The basis of the development of new touristresort areas in Perhutani's production forest isthe need for more hotels and theirinternational services, especially toaccommodate foreign tourists centrally, to beclose to Borobudur temple, to be developed asa tourist area and away from the society sothat the negative influence of foreign touristculture can be suppressed.In Bener District there are two natural forestlocations, namely Plot 98 and Plot 99. Basedon consideration of the physical condition ofthe land and the current accessibility, thedevelopment of forest resorts is planned to bedeveloped in Plot 98.

Estimated Investment Value: IDR 1.54 Trillion

FINANCIAL ASPECT

Development of New Natural Forest Resort

SCOPE OF WORK

1. Development of welcome hall, performance center2. Development of spiritual center, art galleries and

museum3. Development of community craft center4. Development of boutique and simple resort, spa

and beauty center, restaurant and café, andconvention hall

5. Development of community center and greenopen space

Welcome hall

Sitting Group Area

Performance center Spiritual center Air baloon and camping area

Resorts

Restaurant

Treetops adventure area

49

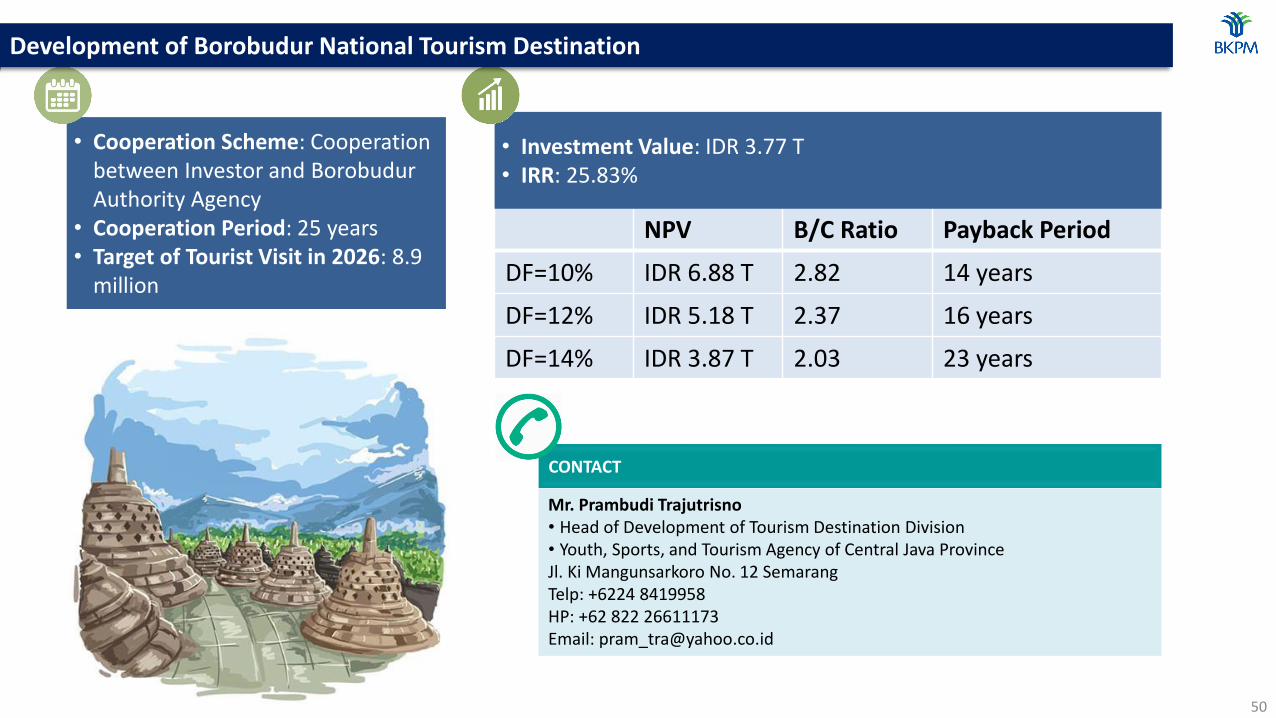

• Cooperation Scheme: Cooperation between Investor and Borobudur Authority Agency

• Cooperation Period: 25 years• Target of Tourist Visit in 2026: 8.9

million

NPV B/C Ratio Payback Period

DF=10% IDR 6.88 T 2.82 14 years

DF=12% IDR 5.18 T 2.37 16 years

DF=14% IDR 3.87 T 2.03 23 years

CONTACT

Mr. Prambudi Trajutrisno• Head of Development of Tourism Destination Division• Youth, Sports, and Tourism Agency of Central Java ProvinceJl. Ki Mangunsarkoro No. 12 SemarangTelp: +6224 8419958HP: +62 822 26611173Email: [email protected]

• Investment Value: IDR 3.77 T• IRR: 25.83%

Development of Borobudur National Tourism Destination

50

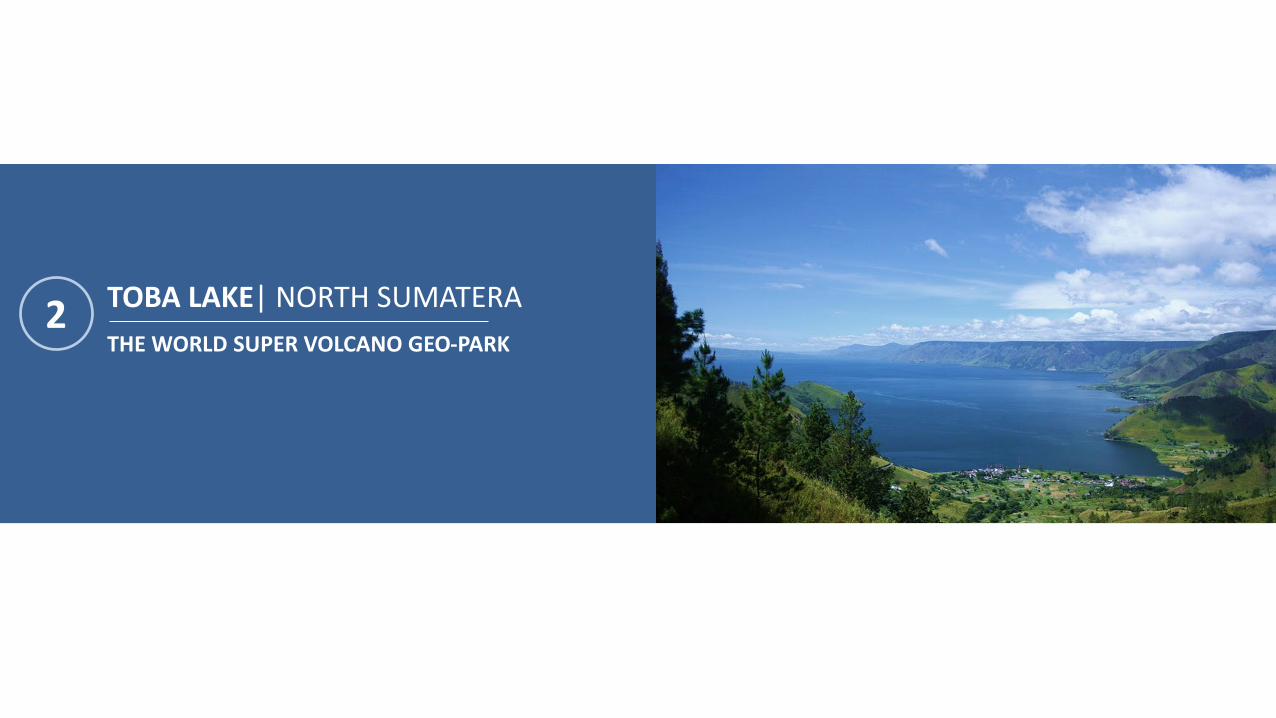

TOBA LAKE| NORTH SUMATERA

THE WORLD SUPER VOLCANO GEO-PARK2

HIGHLIGHTS OF TOBA LAKE

• Toba Lake is the largest volcanic lake in the world and the second largest lake in theworld after Lake Victoria in Africa.

• Toba Lake is one of the ten deepest lakes in the world, which reached a depth ofabout 500 meters.

• Toba Samosir Island in the middle of the Lake has an area of 64,000 hectares,equivalent to the state of Singapore.

• Toba Lake is formed by three major eruptions in the last 900,000 years, 500,000years ago and 75,000 years ago. Which then led to many historical records throughhuman evolution, flora and fauna.

• There are a total of 45 Geo - Trip in 4 Geo - Area among others Porsea Caldera,Caldera Haranggaol, Sibandang Caldera and Caldera Samosir.

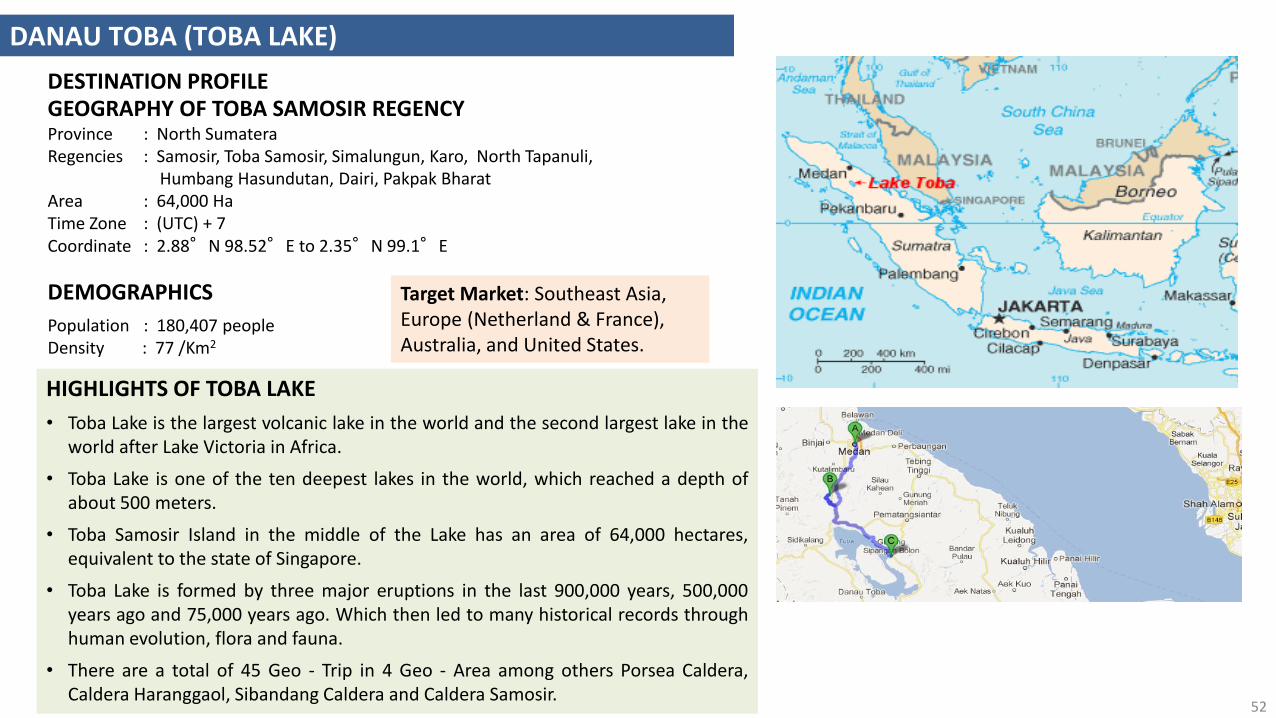

GEOGRAPHY OF TOBA SAMOSIR REGENCYProvince : North SumateraRegencies : Samosir, Toba Samosir, Simalungun, Karo, North Tapanuli,

Humbang Hasundutan, Dairi, Pakpak BharatArea : 64,000 HaTime Zone : (UTC) + 7Coordinate : 2.88°N 98.52°E to 2.35°N 99.1°E

DEMOGRAPHICS

Population : 180,407 peopleDensity : 77 /Km2

DANAU TOBA (TOBA LAKE)

DESTINATION PROFILE

Target Market: Southeast Asia, Europe (Netherland & France), Australia, and United States.

52

FESTIVAL & CULTURE

Annual Lake Toba Festival aroundSeptember, forest and lake cleaning,history telling, and Geo Park (geollogy -ecology - cultural) themed activites

CULLINARY

Lake Toba has a culinary peculiarities thatdiffer from other regions in Indonesia,especially in fish dishes. There is a populardish called sushi style Naniura known asBatak where raw fish served with herbsand spices.

NATURE

Mount hiking, water attraction (SpeedBoat, Water Skiing, Canoeing orKayaking), golf, fishing, sunset views.

ATTRACTION

53

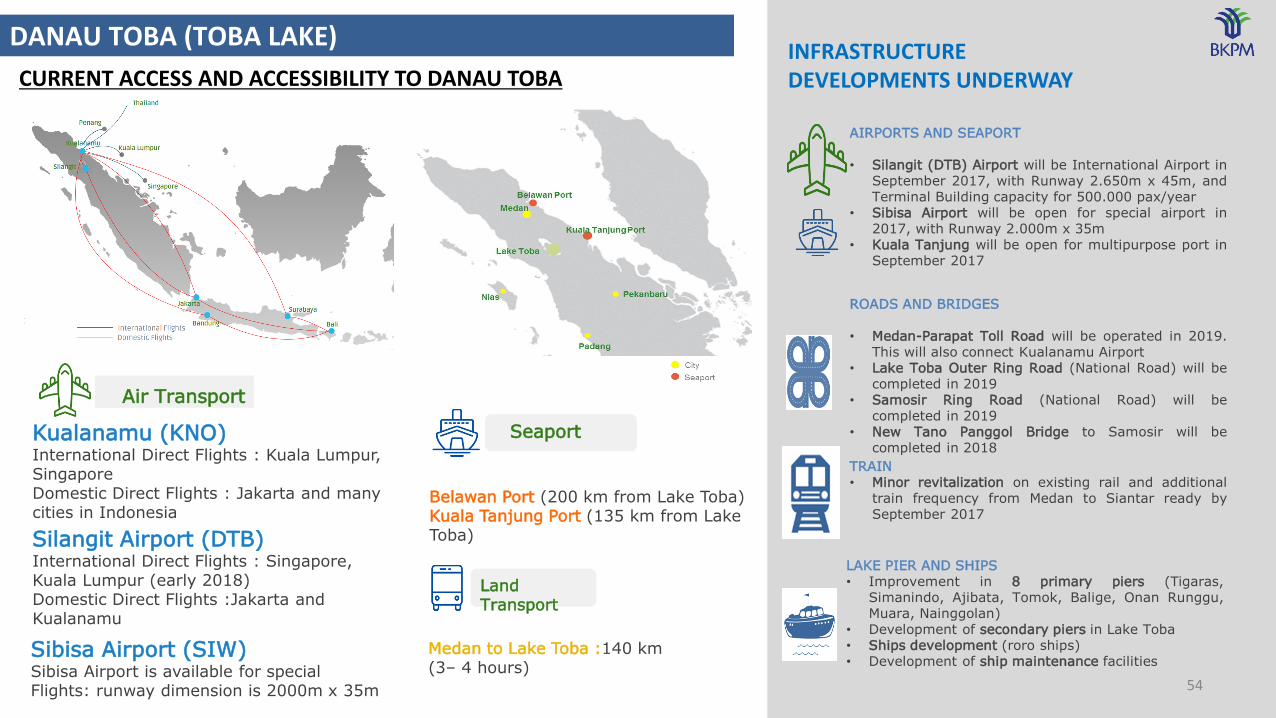

Air Transport

Kualanamu (KNO)International Direct Flights : Kuala Lumpur, SingaporeDomestic Direct Flights : Jakarta and many cities in Indonesia

Silangit Airport (DTB)International Direct Flights : Singapore, Kuala Lumpur (early 2018)Domestic Direct Flights :Jakarta and Kualanamu

Sibisa Airport (SIW) Sibisa Airport is available for special Flights: runway dimension is 2000m x 35m

DANAU TOBA (TOBA LAKE)

54

Air Transport

Kualanamu (KNO)International Direct Flights : Kuala Lumpur, SingaporeDomestic Direct Flights : Jakarta and many cities in Indonesia

Silangit Airport (DTB)International Direct Flights : Singapore, Kuala Lumpur (early 2018)Domestic Direct Flights :Jakarta and Kualanamu

Sibisa Airport (SIW) Sibisa Airport is available for special Flights: runway dimension is 2000m x 35m

Belawan Port (200 km from Lake Toba)Kuala Tanjung Port (135 km from Lake Toba)

Seaport

Medan to Lake Toba :140 km (3– 4 hours)

Land Transport

AIRPORTS AND SEAPORT

• Silangit (DTB) Airport will be International Airport inSeptember 2017, with Runway 2.650m x 45m, andTerminal Building capacity for 500.000 pax/year

• Sibisa Airport will be open for special airport in2017, with Runway 2.000m x 35m

• Kuala Tanjung will be open for multipurpose port inSeptember 2017

ROADS AND BRIDGES

• Medan-Parapat Toll Road will be operated in 2019.This will also connect Kualanamu Airport

• Lake Toba Outer Ring Road (National Road) will becompleted in 2019

• Samosir Ring Road (National Road) will becompleted in 2019

• New Tano Panggol Bridge to Samosir will becompleted in 2018

LAKE PIER AND SHIPS• Improvement in 8 primary piers (Tigaras,

Simanindo, Ajibata, Tomok, Balige, Onan Runggu,Muara, Nainggolan)

• Development of secondary piers in Lake Toba• Ships development (roro ships)• Development of ship maintenance facilities

TRAIN• Minor revitalization on existing rail and additional

train frequency from Medan to Siantar ready bySeptember 2017

INFRASTRUCTUREDEVELOPMENTS UNDERWAYCURRENT ACCESS AND ACCESSIBILITY TO DANAU TOBA

DANAU TOBA (TOBA LAKE)

55

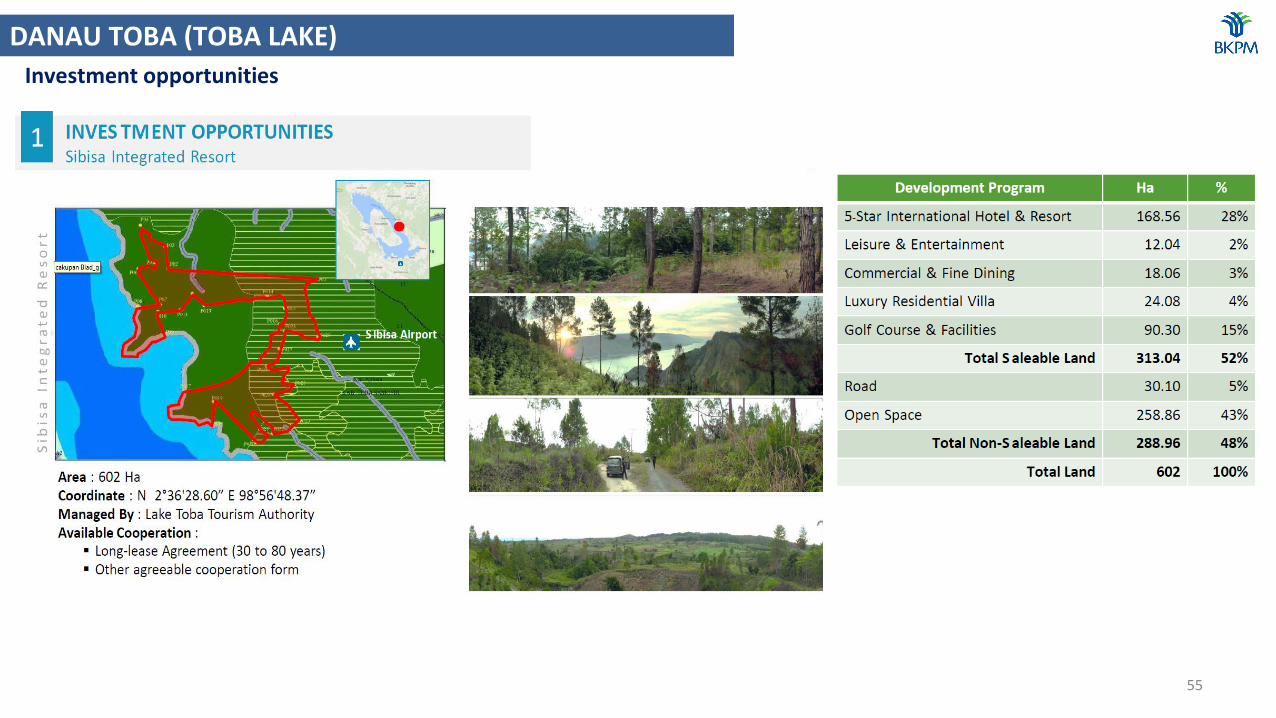

Investment opportunities

DANAU TOBA (TOBA LAKE)

56

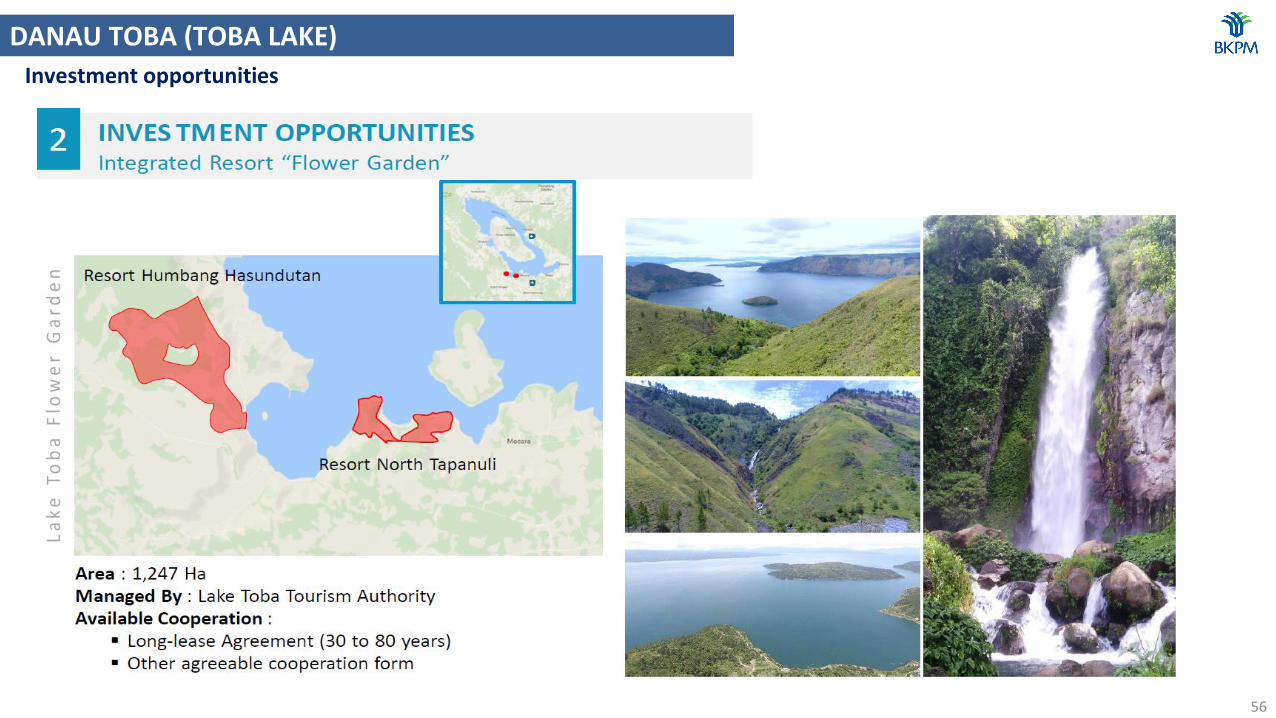

Investment opportunities

DANAU TOBA (TOBA LAKE)

57

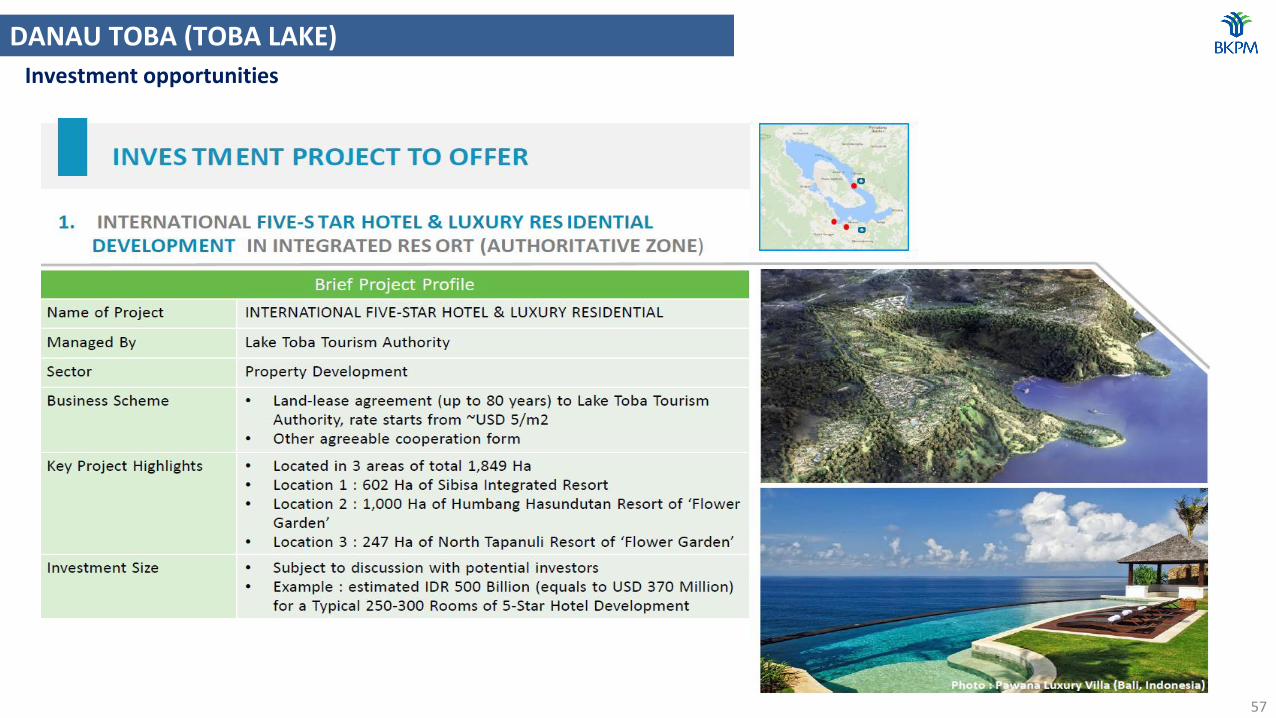

Investment opportunities

DANAU TOBA (TOBA LAKE)

Investment opportunities

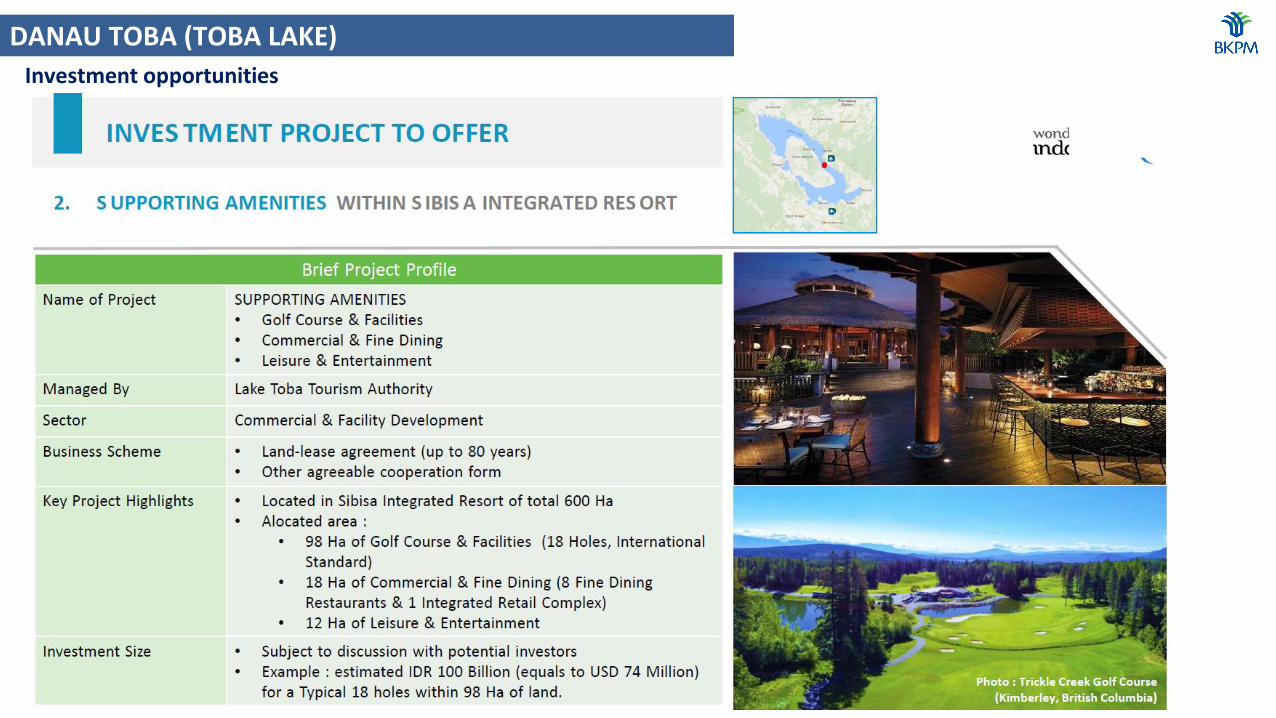

DANAU TOBA (TOBA LAKE)

Investment opportunities

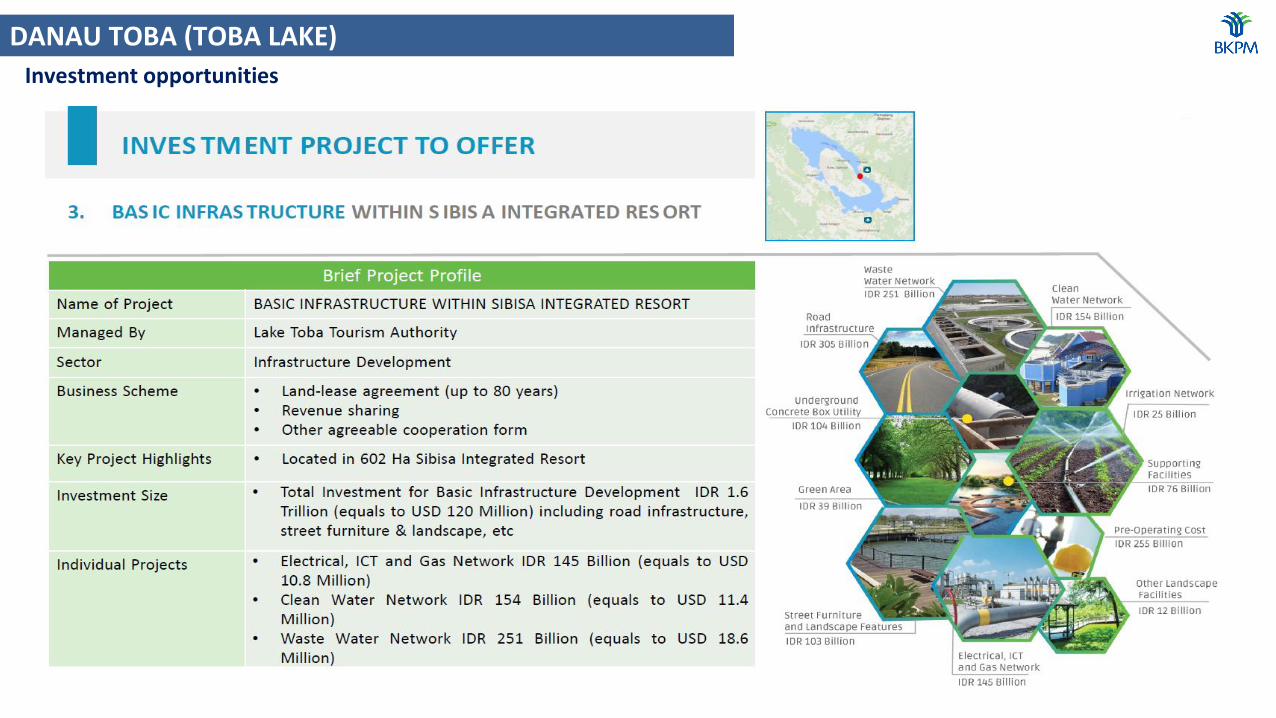

DANAU TOBA (TOBA LAKE)

60

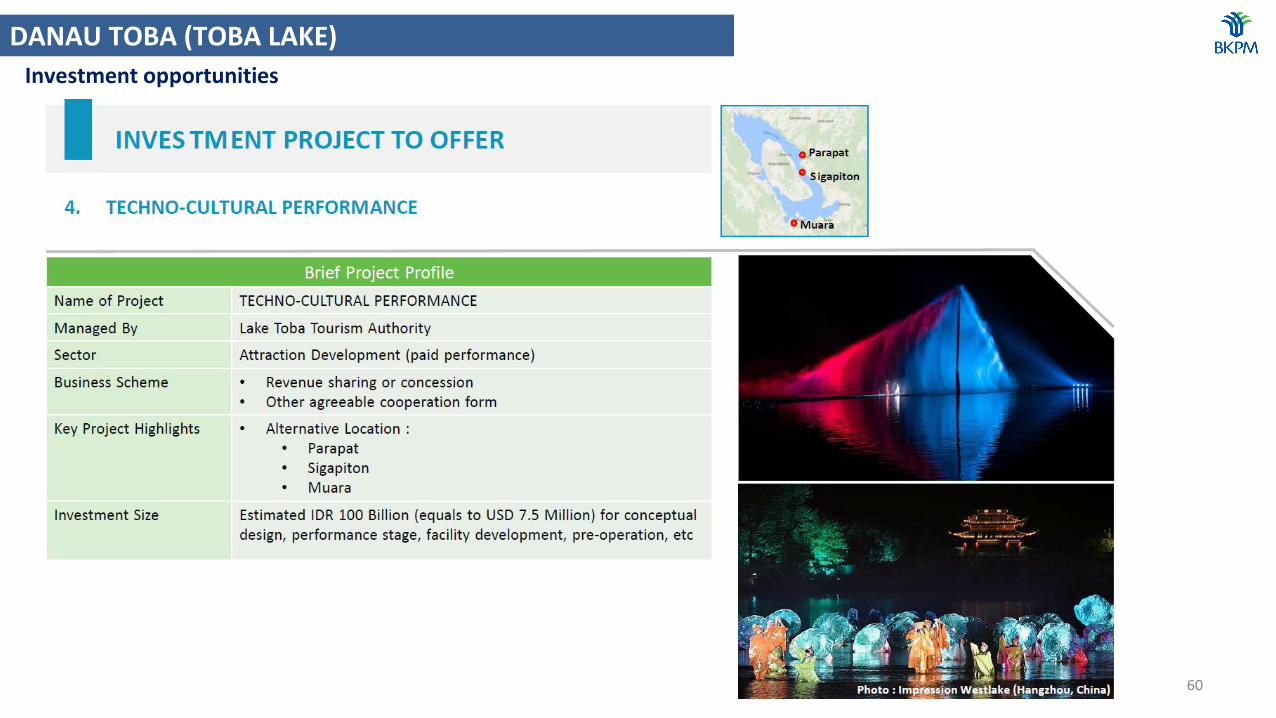

Investment opportunities

DANAU TOBA (TOBA LAKE)

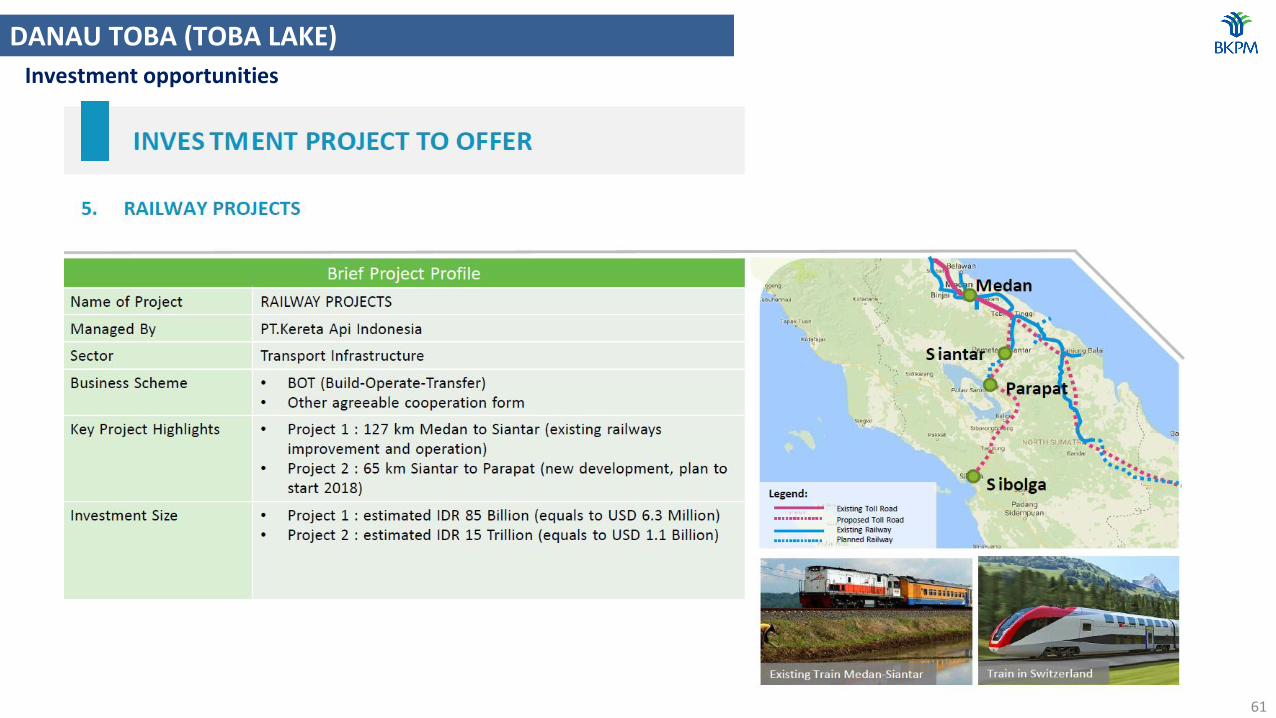

61

Investment opportunities

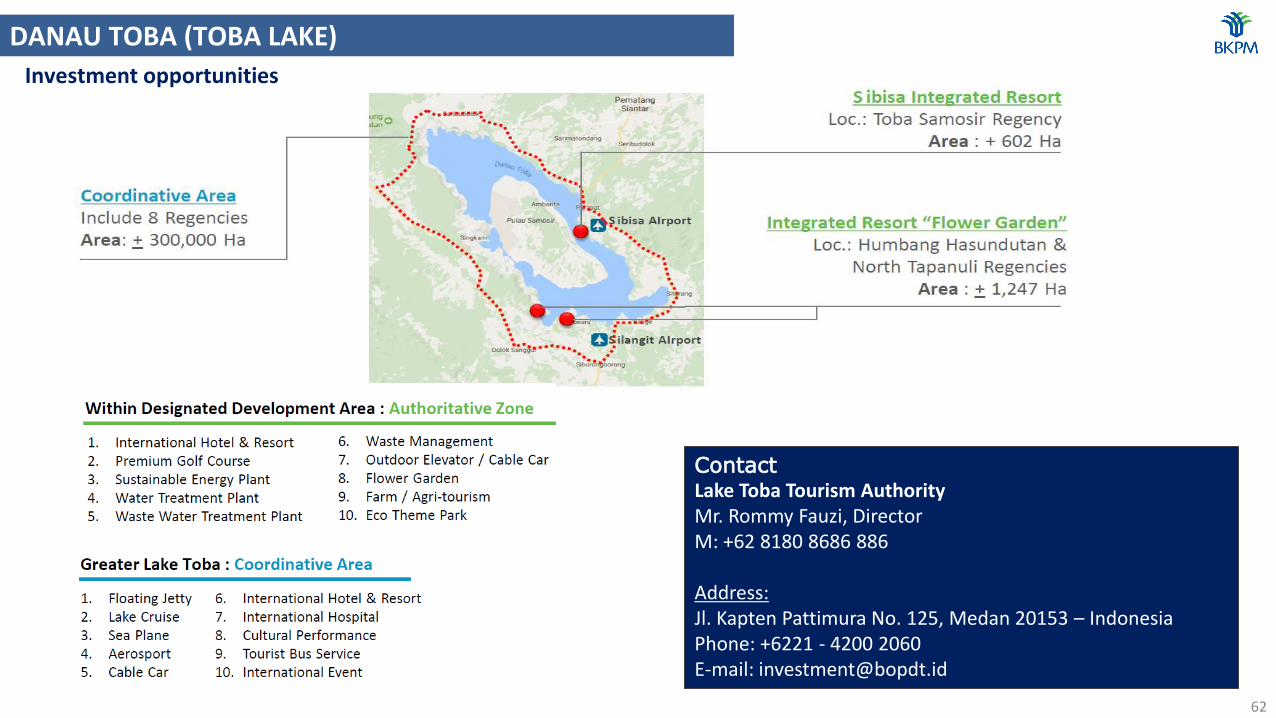

DANAU TOBA (TOBA LAKE)

ContactLake Toba Tourism AuthorityMr. Rommy Fauzi, DirectorM: +62 8180 8686 886

Address:Jl. Kapten Pattimura No. 125, Medan 20153 – IndonesiaPhone: +6221 - 4200 2060E-mail: [email protected]

62

Investment opportunities

DANAU TOBA (TOBA LAKE)

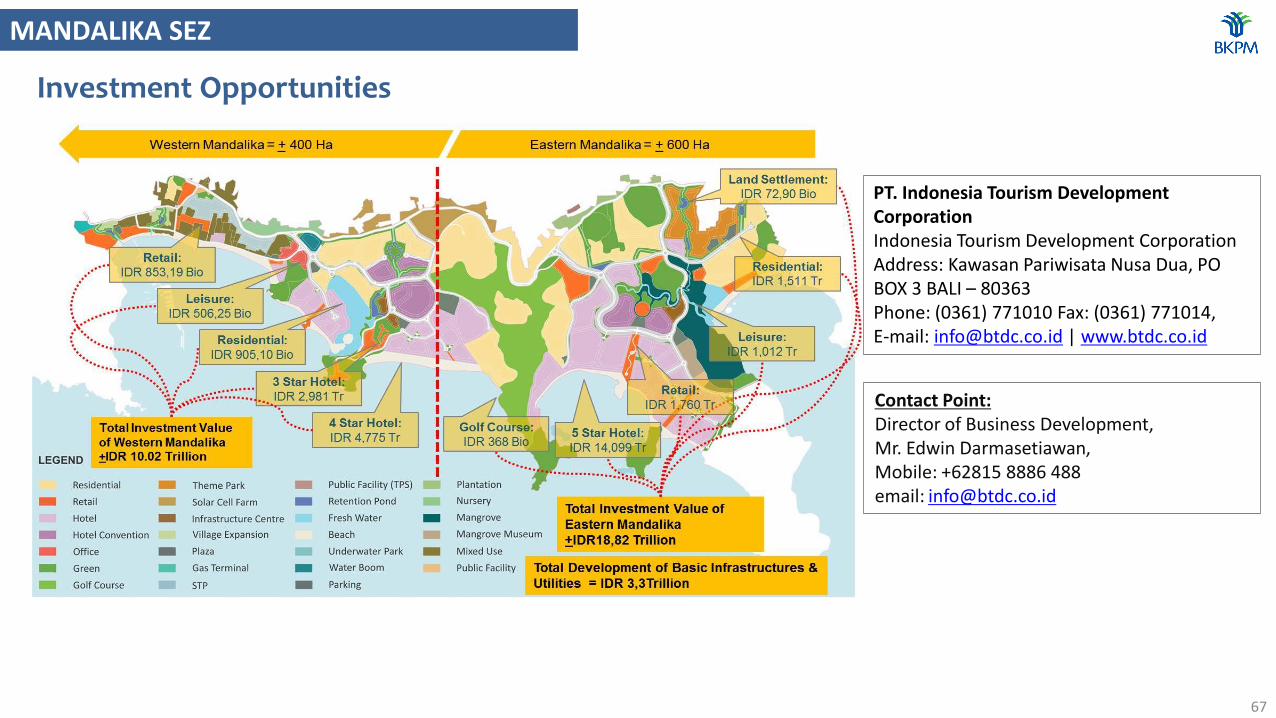

3 MANDALIKA| WEST NUSA TENGGARA

SPECIAL ECONOMIC ZONES

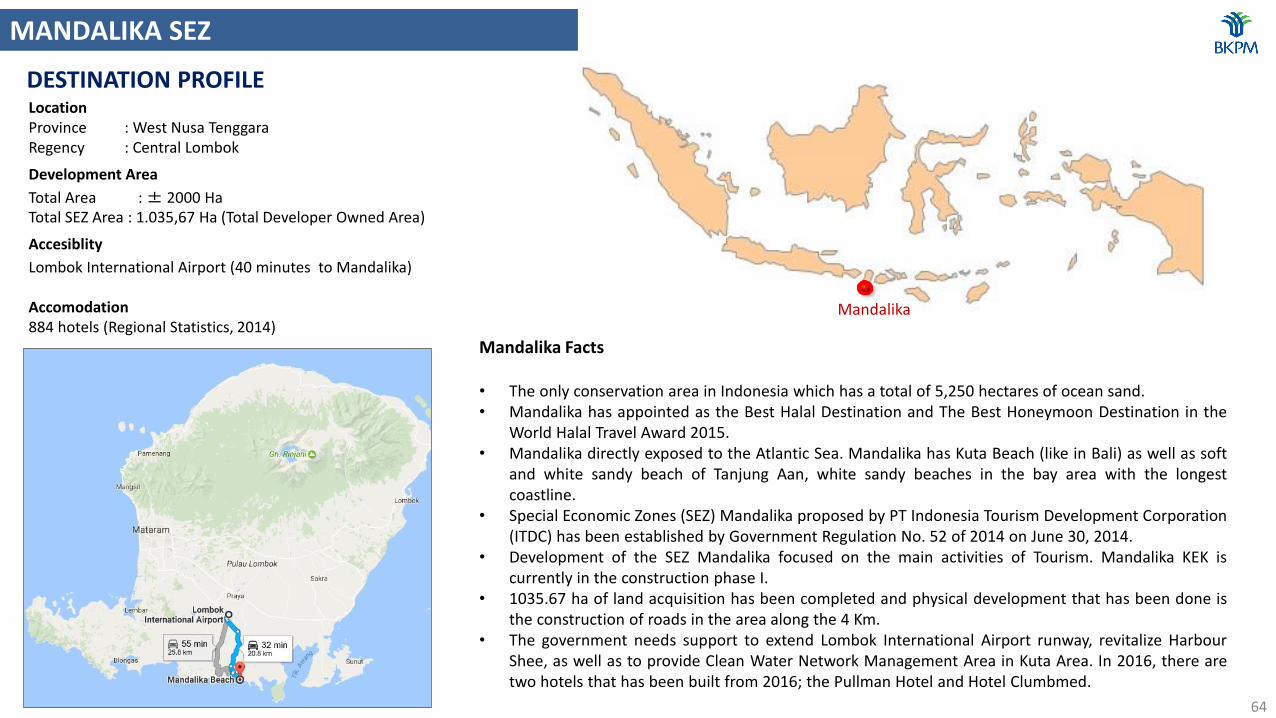

Mandalika

LocationProvince : West Nusa TenggaraRegency : Central Lombok

Development Area

Total Area : ± 2000 HaTotal SEZ Area : 1.035,67 Ha (Total Developer Owned Area)

Accesiblity

Lombok International Airport (40 minutes to Mandalika)

Accomodation884 hotels (Regional Statistics, 2014)

Mandalika Facts

• The only conservation area in Indonesia which has a total of 5,250 hectares of ocean sand.• Mandalika has appointed as the Best Halal Destination and The Best Honeymoon Destination in the

World Halal Travel Award 2015.• Mandalika directly exposed to the Atlantic Sea. Mandalika has Kuta Beach (like in Bali) as well as soft

and white sandy beach of Tanjung Aan, white sandy beaches in the bay area with the longestcoastline.

• Special Economic Zones (SEZ) Mandalika proposed by PT Indonesia Tourism Development Corporation(ITDC) has been established by Government Regulation No. 52 of 2014 on June 30, 2014.

• Development of the SEZ Mandalika focused on the main activities of Tourism. Mandalika KEK iscurrently in the construction phase I.

• 1035.67 ha of land acquisition has been completed and physical development that has been done isthe construction of roads in the area along the 4 Km.

• The government needs support to extend Lombok International Airport runway, revitalize HarbourShee, as well as to provide Clean Water Network Management Area in Kuta Area. In 2016, there aretwo hotels that has been built from 2016; the Pullman Hotel and Hotel Clumbmed.

DESTINATION PROFILE

64

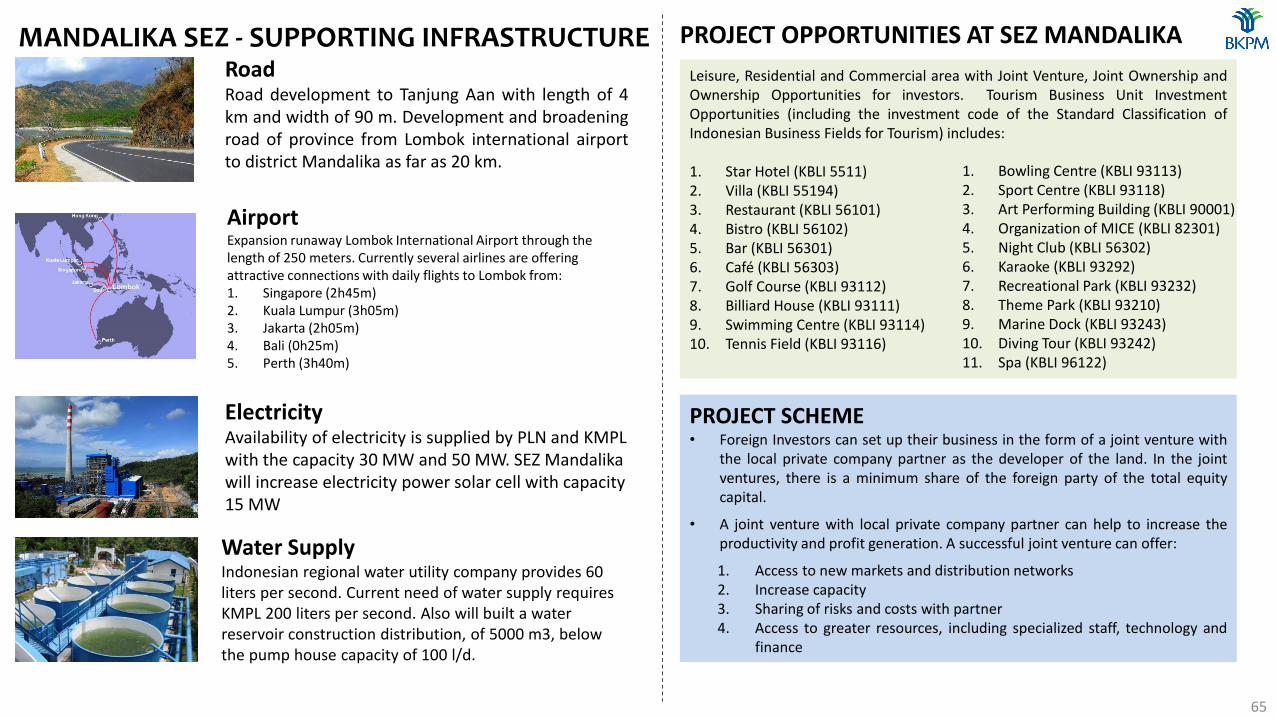

MANDALIKA SEZ

MANDALIKA SEZ - SUPPORTING INFRASTRUCTURERoadRoad development to Tanjung Aan with length of 4km and width of 90 m. Development and broadeningroad of province from Lombok international airportto district Mandalika as far as 20 km.

AirportExpansion runaway Lombok International Airport through the length of 250 meters. Currently several airlines are offering attractive connections with daily flights to Lombok from:1. Singapore (2h45m)2. Kuala Lumpur (3h05m)3. Jakarta (2h05m)4. Bali (0h25m)5. Perth (3h40m)

ElectricityAvailability of electricity is supplied by PLN and KMPL with the capacity 30 MW and 50 MW. SEZ Mandalikawill increase electricity power solar cell with capacity 15 MW

Water SupplyIndonesian regional water utility company provides 60 liters per second. Current need of water supply requires KMPL 200 liters per second. Also will built a water reservoir construction distribution, of 5000 m3, below the pump house capacity of 100 l/d.

65

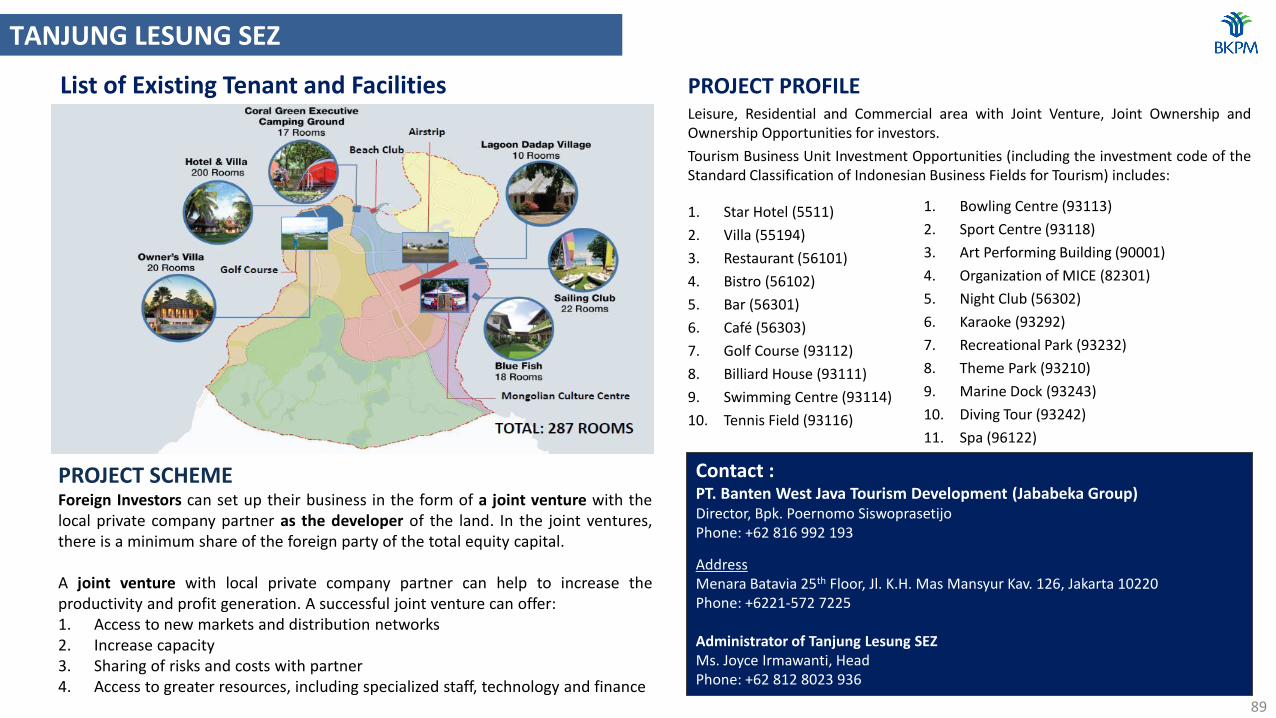

Leisure, Residential and Commercial area with Joint Venture, Joint Ownership andOwnership Opportunities for investors. Tourism Business Unit InvestmentOpportunities (including the investment code of the Standard Classification ofIndonesian Business Fields for Tourism) includes:

1. Star Hotel (KBLI 5511) 2. Villa (KBLI 55194)3. Restaurant (KBLI 56101)4. Bistro (KBLI 56102)5. Bar (KBLI 56301)6. Café (KBLI 56303)7. Golf Course (KBLI 93112)8. Billiard House (KBLI 93111)9. Swimming Centre (KBLI 93114)10. Tennis Field (KBLI 93116)

PROJECT OPPORTUNITIES AT SEZ MANDALIKA

PROJECT SCHEME• Foreign Investors can set up their business in the form of a joint venture with

the local private company partner as the developer of the land. In the jointventures, there is a minimum share of the foreign party of the total equitycapital.

• A joint venture with local private company partner can help to increase theproductivity and profit generation. A successful joint venture can offer:

1. Access to new markets and distribution networks2. Increase capacity3. Sharing of risks and costs with partner4. Access to greater resources, including specialized staff, technology and

finance

1. Bowling Centre (KBLI 93113)2. Sport Centre (KBLI 93118)3. Art Performing Building (KBLI 90001)4. Organization of MICE (KBLI 82301)5. Night Club (KBLI 56302)6. Karaoke (KBLI 93292)7. Recreational Park (KBLI 93232)8. Theme Park (KBLI 93210)9. Marine Dock (KBLI 93243)10. Diving Tour (KBLI 93242)11. Spa (KBLI 96122)

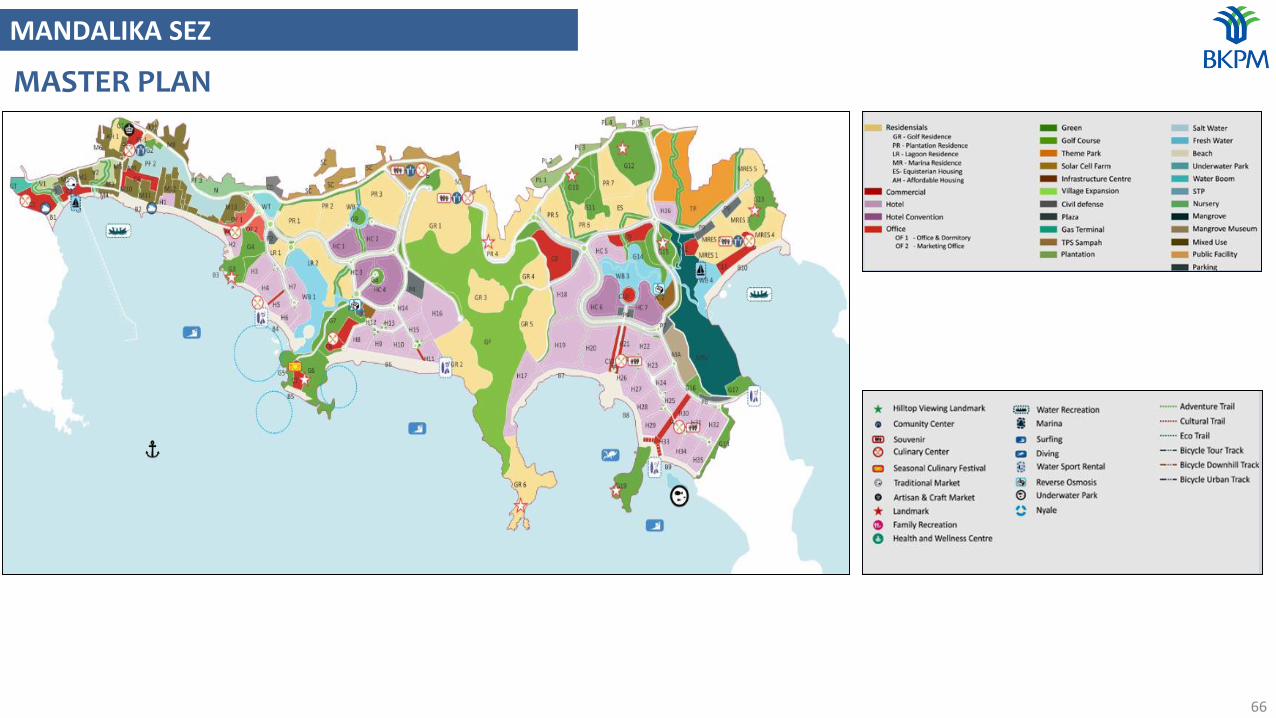

MASTER PLAN

66

MANDALIKA SEZ

PT. Indonesia Tourism Development CorporationIndonesia Tourism Development CorporationAddress: Kawasan Pariwisata Nusa Dua, PO BOX 3 BALI – 80363Phone: (0361) 771010 Fax: (0361) 771014, E-mail: [email protected] | www.btdc.co.id

Contact Point:Director of Business Development,Mr. Edwin Darmasetiawan, Mobile: +62815 8886 488 email: [email protected]

67

MANDALIKA SEZ

Investment Opportunities

1. Seger Beach

Located at Kuta Lombok Village, Pujut Sub-District, Central Lombok District, West Nusa Tenggara ProvinceCoordinate : S08°54’33.51” E116°17’54.17”

SEGER BEACH

68

SERENTING BEACH

Located at Kuta Lombok Village, Pujut Sub-District, Central Lombok District, West Nusa Tenggara ProvinceCoordinate : S08°54’27.26” E116°18’35.44”

2. Serenting Beach MANDALIKA SEZ

Investment Opportunities

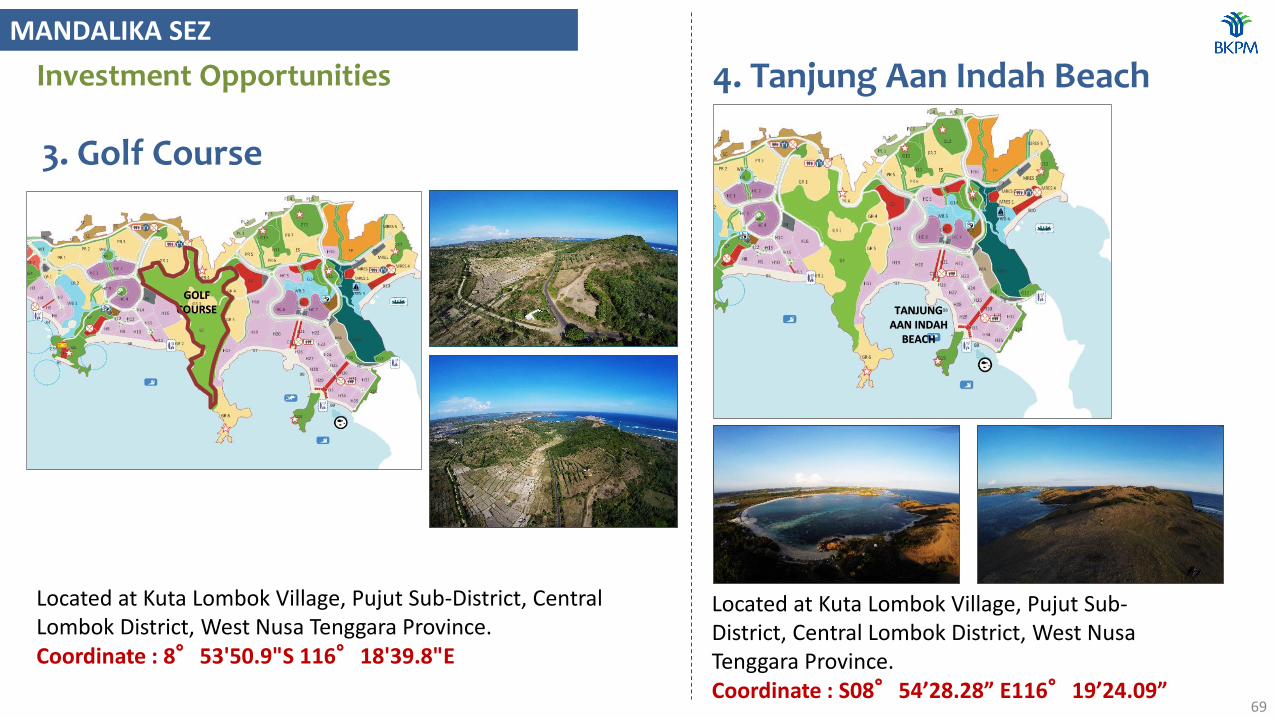

3. Golf Course

Located at Kuta Lombok Village, Pujut Sub-District, Central Lombok District, West Nusa Tenggara Province.Coordinate : 8°53'50.9"S 116°18'39.8"E

GOLF COURSE

69

TANJUNG AAN INDAH

BEACH

Located at Kuta Lombok Village, Pujut Sub-District, Central Lombok District, West Nusa Tenggara Province.Coordinate : S08°54’28.28” E116°19’24.09”

4. Tanjung Aan Indah Beach

MANDALIKA SEZ

Investment Opportunities

TANJUNG KELAYANG| BELITUNG ISLAND

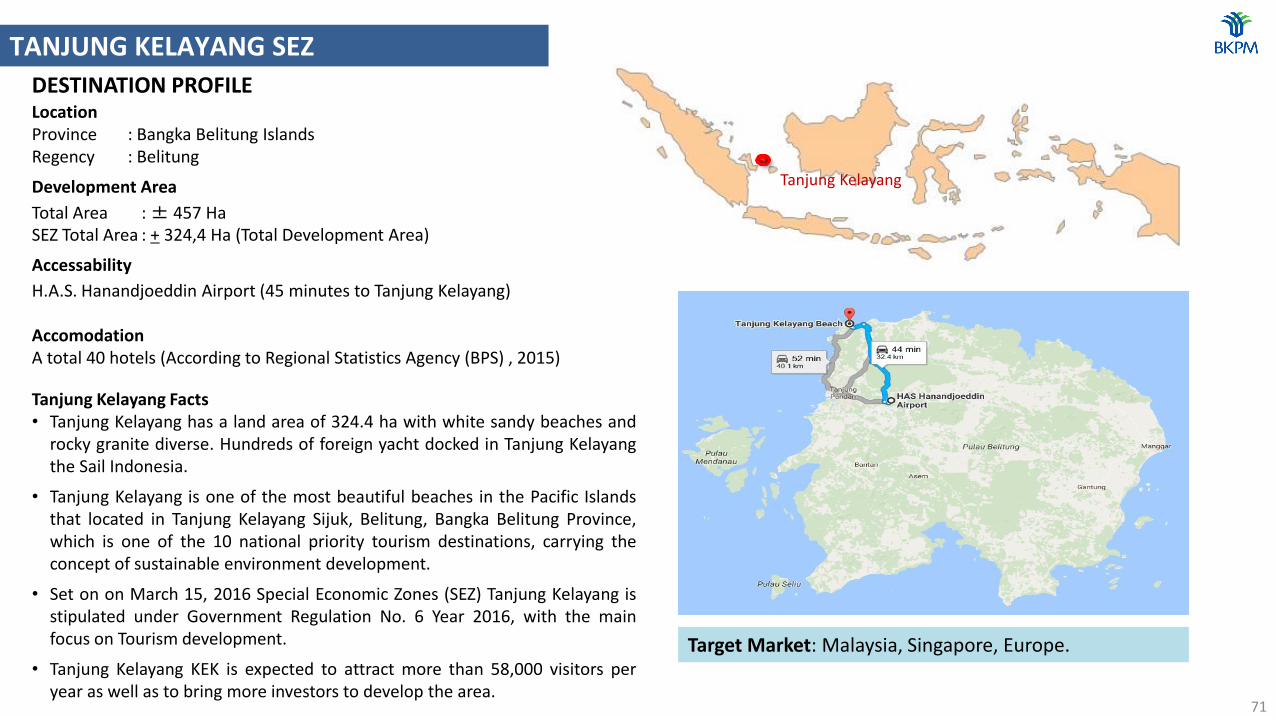

SPECIAL ECONOMIC ZONES4

LocationProvince : Bangka Belitung IslandsRegency : Belitung

Development Area

Total Area : ± 457 HaSEZ Total Area : + 324,4 Ha (Total Development Area)

Accessability

H.A.S. Hanandjoeddin Airport (45 minutes to Tanjung Kelayang)

AccomodationA total 40 hotels (According to Regional Statistics Agency (BPS) , 2015)

Tanjung Kelayang Facts• Tanjung Kelayang has a land area of 324.4 ha with white sandy beaches and

rocky granite diverse. Hundreds of foreign yacht docked in Tanjung Kelayangthe Sail Indonesia.

• Tanjung Kelayang is one of the most beautiful beaches in the Pacific Islandsthat located in Tanjung Kelayang Sijuk, Belitung, Bangka Belitung Province,which is one of the 10 national priority tourism destinations, carrying theconcept of sustainable environment development.

• Set on on March 15, 2016 Special Economic Zones (SEZ) Tanjung Kelayang isstipulated under Government Regulation No. 6 Year 2016, with the mainfocus on Tourism development.

• Tanjung Kelayang KEK is expected to attract more than 58,000 visitors peryear as well as to bring more investors to develop the area.

TANJUNG KELAYANG SEZ

DESTINATION PROFILE

Tanjung Kelayang

Target Market: Malaysia, Singapore, Europe.

71

NATURE

Panoramic Sightseeing of the lighthousetower built in 1882 (Dutch Colonial Era),sailing, snorkeling, beauty Granite stonesneatly arranged on the beach shaped eagle.

Total Solar Eclipse Festival , Rainbow TroopsFestival, Belitong Festival, Belitong Fair,Belitong Cultural Festival, Sail Indonesia/Wonderful Sail Indonesia/ Sail Karimata

FESTIVAL & CULTURE

Belitung is famous with traditional coffeeshop with a natural coffe processing. Itsfamous food called Gangan Soup is broththick yellow soup and its sour taste ascooked with pineapple.

FESTIVAL & CULTURE

ATTRACTION

72

ACCESIBILITIES & INFRASTRUCTURE

Existing regional infrastructure in Tanjung Kelayang SEZ, including:Road development to Tanjung Kelayang isaccordance to national road standard.Development and broadening road fromBelitung airport to Tanjung Kelayang as faras 41 km.

Regional infrastructure need to be improved:• Installation of Waste Water Management• Extension of runway airport Hanandjoeddin

H.A.S from 2250 m to 2500 m• Increasing power capacity of existing 41.5

MW of electricity• Improvement of national roads to the area• Power Plant Surge

Water SupplyReservoir Mount Sharp with productionwater capacity 400L/S will be availablesoon.

TANJUNG KELAYANG SEZ

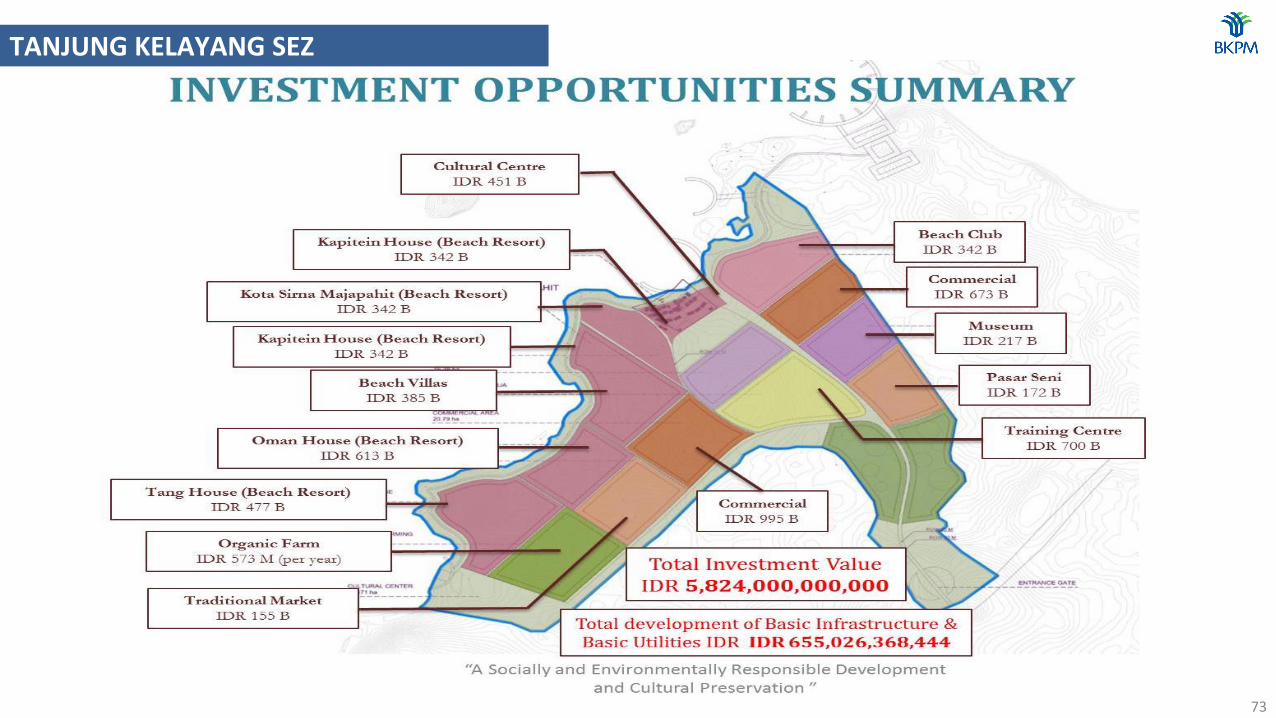

73

TANJUNG KELAYANG SEZ

74

TANJUNG KELAYANG SEZ

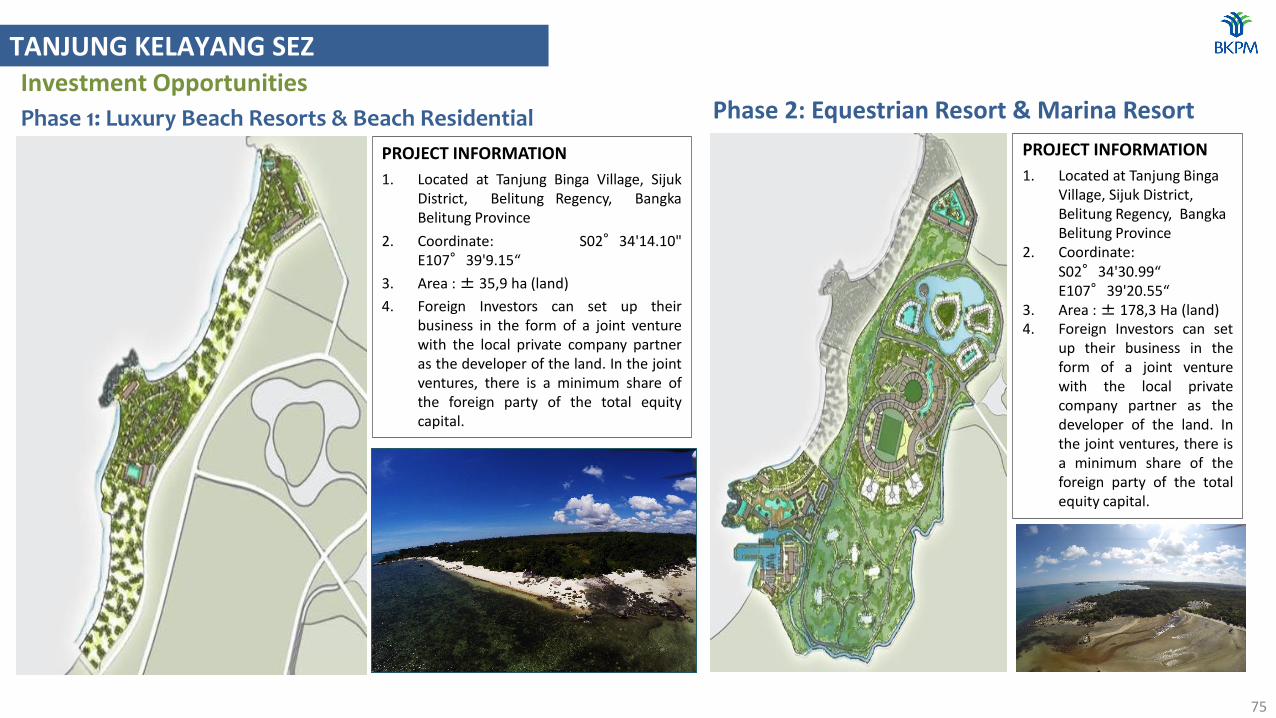

Phase 1: Luxury Beach Resorts & Beach Residential

PROJECT INFORMATION

1. Located at Tanjung Binga Village, SijukDistrict, Belitung Regency, BangkaBelitung Province

2. Coordinate: S02°34'14.10"E107°39'9.15“

3. Area :± 35,9 ha (land)

4. Foreign Investors can set up theirbusiness in the form of a joint venturewith the local private company partneras the developer of the land. In the jointventures, there is a minimum share ofthe foreign party of the total equitycapital.

75

Investment Opportunities

PROJECT INFORMATION

1. Located at Tanjung BingaVillage, Sijuk District, Belitung Regency, Bangka Belitung Province

2. Coordinate: S02°34'30.99“E107°39'20.55“

3. Area : ± 178,3 Ha (land)4. Foreign Investors can set

up their business in theform of a joint venturewith the local privatecompany partner as thedeveloper of the land. Inthe joint ventures, there isa minimum share of theforeign party of the totalequity capital.

Phase 2: Equestrian Resort & Marina Resort

TANJUNG KELAYANG SEZ

76

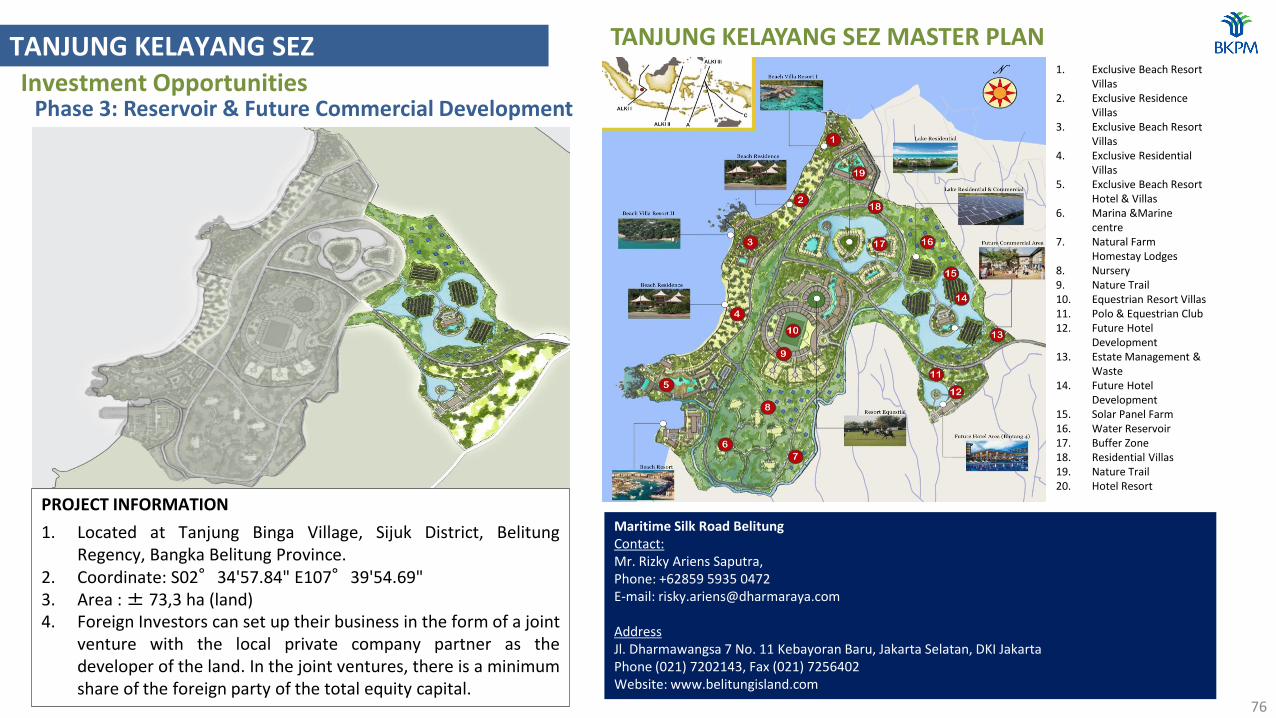

PROJECT INFORMATION

1. Located at Tanjung Binga Village, Sijuk District, BelitungRegency, Bangka Belitung Province.

2. Coordinate: S02°34'57.84" E107°39'54.69"3. Area :± 73,3 ha (land)4. Foreign Investors can set up their business in the form of a joint

venture with the local private company partner as thedeveloper of the land. In the joint ventures, there is a minimumshare of the foreign party of the total equity capital.

Phase 3: Reservoir & Future Commercial Development

1. Exclusive Beach Resort Villas

2. Exclusive Residence Villas

3. Exclusive Beach Resort Villas

4. Exclusive Residential Villas

5. Exclusive Beach Resort Hotel & Villas

6. Marina &Marine centre

7. Natural Farm Homestay Lodges

8. Nursery9. Nature Trail10. Equestrian Resort Villas11. Polo & Equestrian Club12. Future Hotel

Development13. Estate Management &

Waste14. Future Hotel

Development15. Solar Panel Farm16. Water Reservoir17. Buffer Zone18. Residential Villas19. Nature Trail20. Hotel Resort

TANJUNG KELAYANG SEZ MASTER PLAN

Maritime Silk Road BelitungContact:Mr. Rizky Ariens Saputra, Phone: +62859 5935 0472E-mail: [email protected]

AddressJl. Dharmawangsa 7 No. 11 Kebayoran Baru, Jakarta Selatan, DKI JakartaPhone (021) 7202143, Fax (021) 7256402Website: www.belitungisland.com

TANJUNG KELAYANG SEZInvestment Opportunities

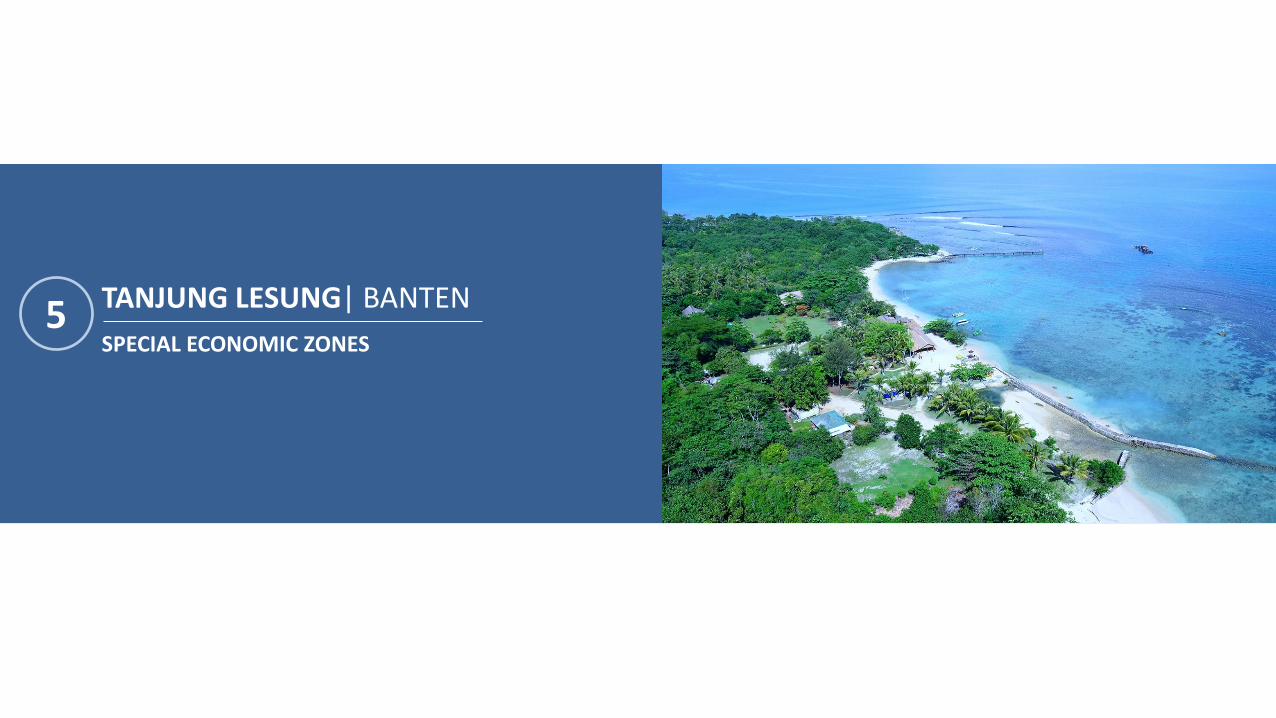

5 TANJUNG LESUNG| BANTEN

SPECIAL ECONOMIC ZONES

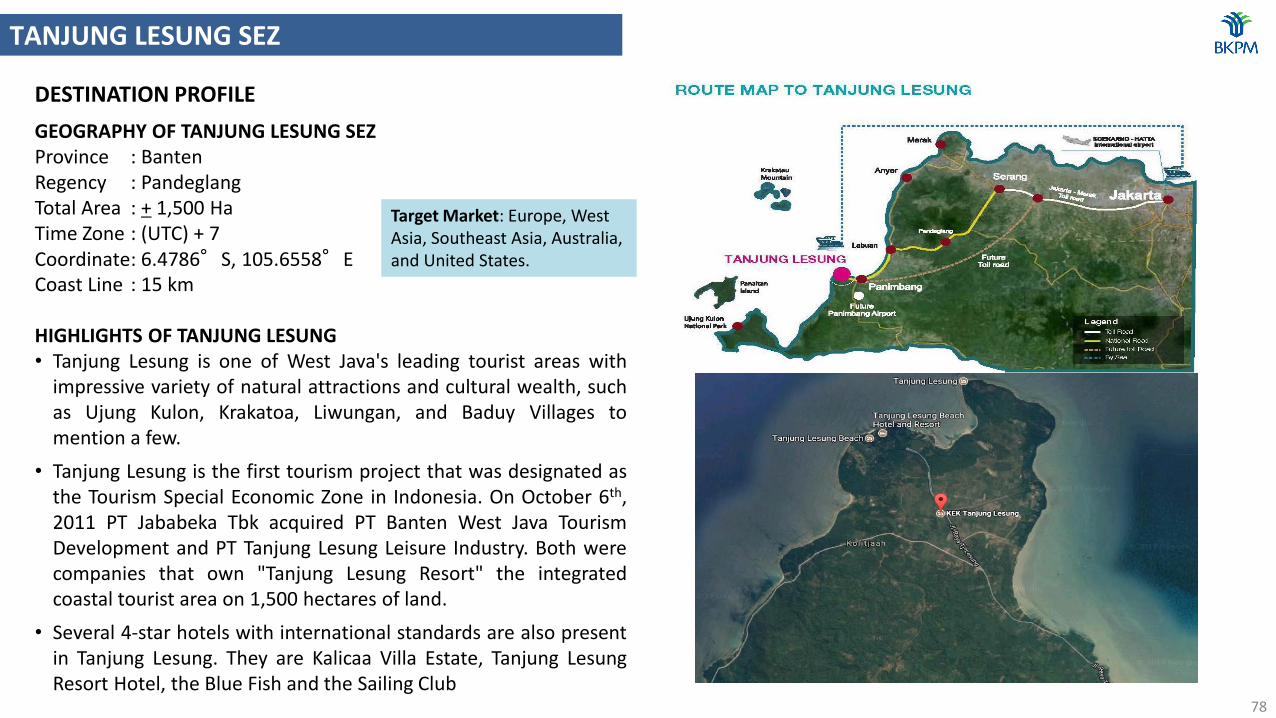

GEOGRAPHY OF TANJUNG LESUNG SEZProvince : BantenRegency : PandeglangTotal Area : + 1,500 HaTime Zone : (UTC) + 7Coordinate: 6.4786°S, 105.6558°ECoast Line : 15 km

HIGHLIGHTS OF TANJUNG LESUNG• Tanjung Lesung is one of West Java's leading tourist areas with

impressive variety of natural attractions and cultural wealth, suchas Ujung Kulon, Krakatoa, Liwungan, and Baduy Villages tomention a few.

• Tanjung Lesung is the first tourism project that was designated asthe Tourism Special Economic Zone in Indonesia. On October 6th,2011 PT Jababeka Tbk acquired PT Banten West Java TourismDevelopment and PT Tanjung Lesung Leisure Industry. Both werecompanies that own "Tanjung Lesung Resort" the integratedcoastal tourist area on 1,500 hectares of land.

• Several 4-star hotels with international standards are also presentin Tanjung Lesung. They are Kalicaa Villa Estate, Tanjung LesungResort Hotel, the Blue Fish and the Sailing Club

DESTINATION PROFILE

TANJUNG LESUNG SEZ

Target Market: Europe, West Asia, Southeast Asia, Australia, and United States.

78

79

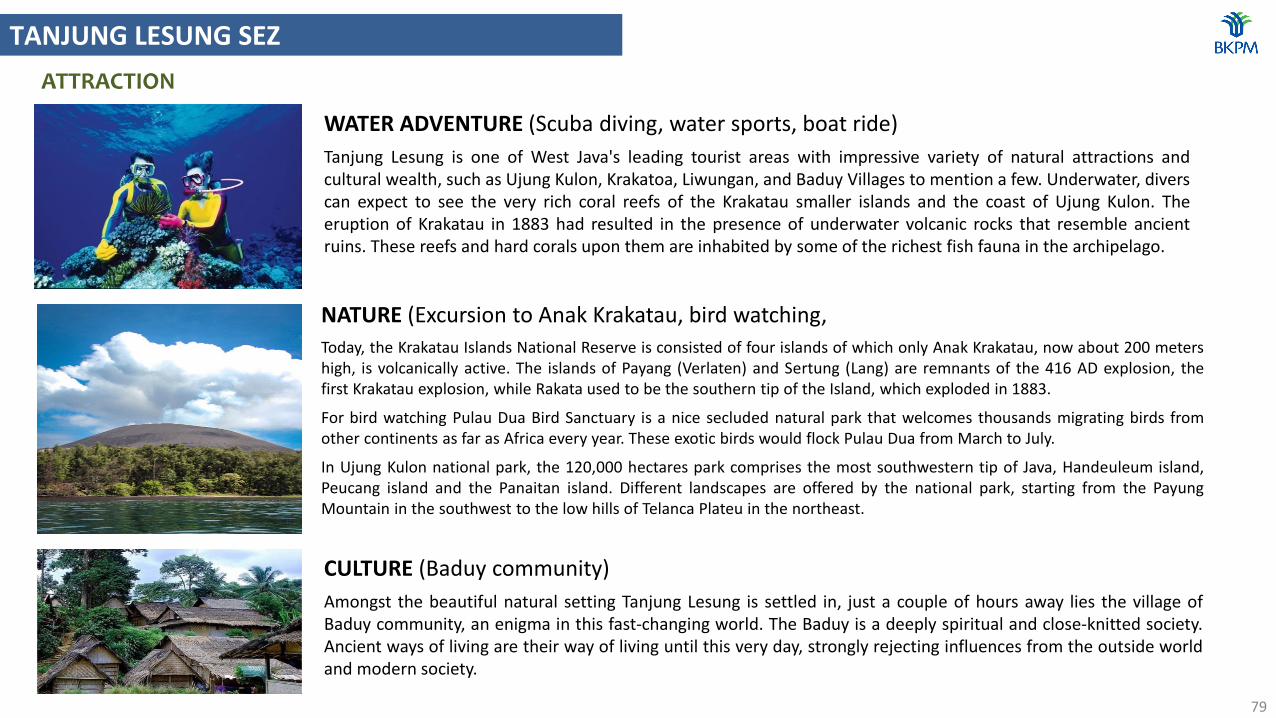

WATER ADVENTURE (Scuba diving, water sports, boat ride)

Tanjung Lesung is one of West Java's leading tourist areas with impressive variety of natural attractions andcultural wealth, such as Ujung Kulon, Krakatoa, Liwungan, and Baduy Villages to mention a few. Underwater, diverscan expect to see the very rich coral reefs of the Krakatau smaller islands and the coast of Ujung Kulon. Theeruption of Krakatau in 1883 had resulted in the presence of underwater volcanic rocks that resemble ancientruins. These reefs and hard corals upon them are inhabited by some of the richest fish fauna in the archipelago.

NATURE (Excursion to Anak Krakatau, bird watching,

Today, the Krakatau Islands National Reserve is consisted of four islands of which only Anak Krakatau, now about 200 metershigh, is volcanically active. The islands of Payang (Verlaten) and Sertung (Lang) are remnants of the 416 AD explosion, thefirst Krakatau explosion, while Rakata used to be the southern tip of the Island, which exploded in 1883.

For bird watching Pulau Dua Bird Sanctuary is a nice secluded natural park that welcomes thousands migrating birds fromother continents as far as Africa every year. These exotic birds would flock Pulau Dua from March to July.

In Ujung Kulon national park, the 120,000 hectares park comprises the most southwestern tip of Java, Handeuleum island,Peucang island and the Panaitan island. Different landscapes are offered by the national park, starting from the PayungMountain in the southwest to the low hills of Telanca Plateu in the northeast.

CULTURE (Baduy community)

Amongst the beautiful natural setting Tanjung Lesung is settled in, just a couple of hours away lies the village ofBaduy community, an enigma in this fast-changing world. The Baduy is a deeply spiritual and close-knitted society.Ancient ways of living are their way of living until this very day, strongly rejecting influences from the outside worldand modern society.

ATTRACTION

TANJUNG LESUNG SEZ

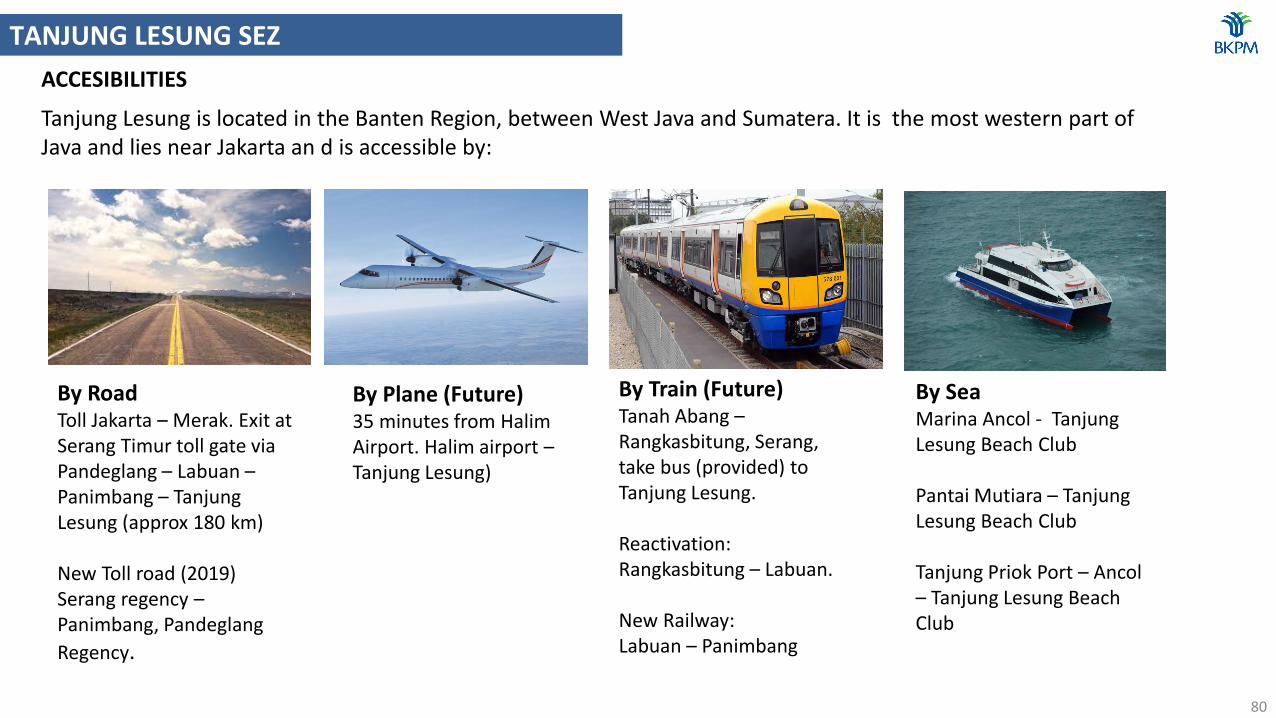

ACCESIBILITIES

Tanjung Lesung is located in the Banten Region, between West Java and Sumatera. It is the most western part of Java and lies near Jakarta an d is accessible by:

By RoadToll Jakarta – Merak. Exit at Serang Timur toll gate via Pandeglang – Labuan –Panimbang – Tanjung Lesung (approx 180 km)

New Toll road (2019)Serang regency –Panimbang, Pandeglang

Regency.

By Plane (Future)35 minutes from Halim Airport. Halim airport –Tanjung Lesung)

By Train (Future)Tanah Abang –Rangkasbitung, Serang, take bus (provided) to Tanjung Lesung.

Reactivation:Rangkasbitung – Labuan.

New Railway:Labuan – Panimbang

By SeaMarina Ancol - Tanjung Lesung Beach Club

Pantai Mutiara – Tanjung Lesung Beach Club

Tanjung Priok Port – Ancol – Tanjung Lesung Beach Club

80

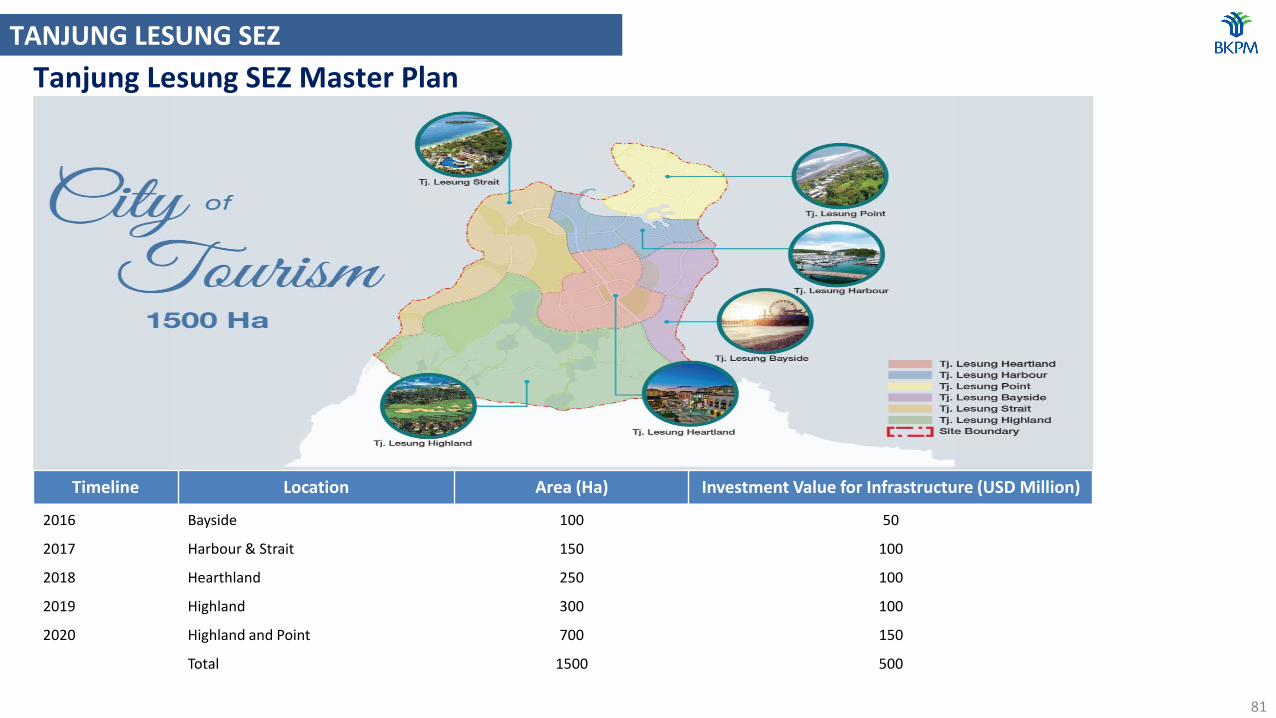

TANJUNG LESUNG SEZ

Tanjung Lesung SEZ Master Plan

Timeline Location Area (Ha) Investment Value for Infrastructure (USD Million)

2016 Bayside 100 50

2017 Harbour & Strait 150 100

2018 Hearthland 250 100

2019 Highland 300 100

2020 Highland and Point 700 150

Total 1500 500

81

TANJUNG LESUNG SEZ

Project Development Plant: Tanjung Lesung Bayside

District Character:1. Maritime Museum2. Banten Museum3. Water Themepark4. Residential/Villa5. Food Junction6. Hotel

82

TANJUNG LESUNG SEZ

Project Development Plant: Tanjung Lesung Harbour

83

TANJUNG LESUNG SEZ

Project Development Plant: Tanjung Lesung Strait

84

TANJUNG LESUNG SEZ

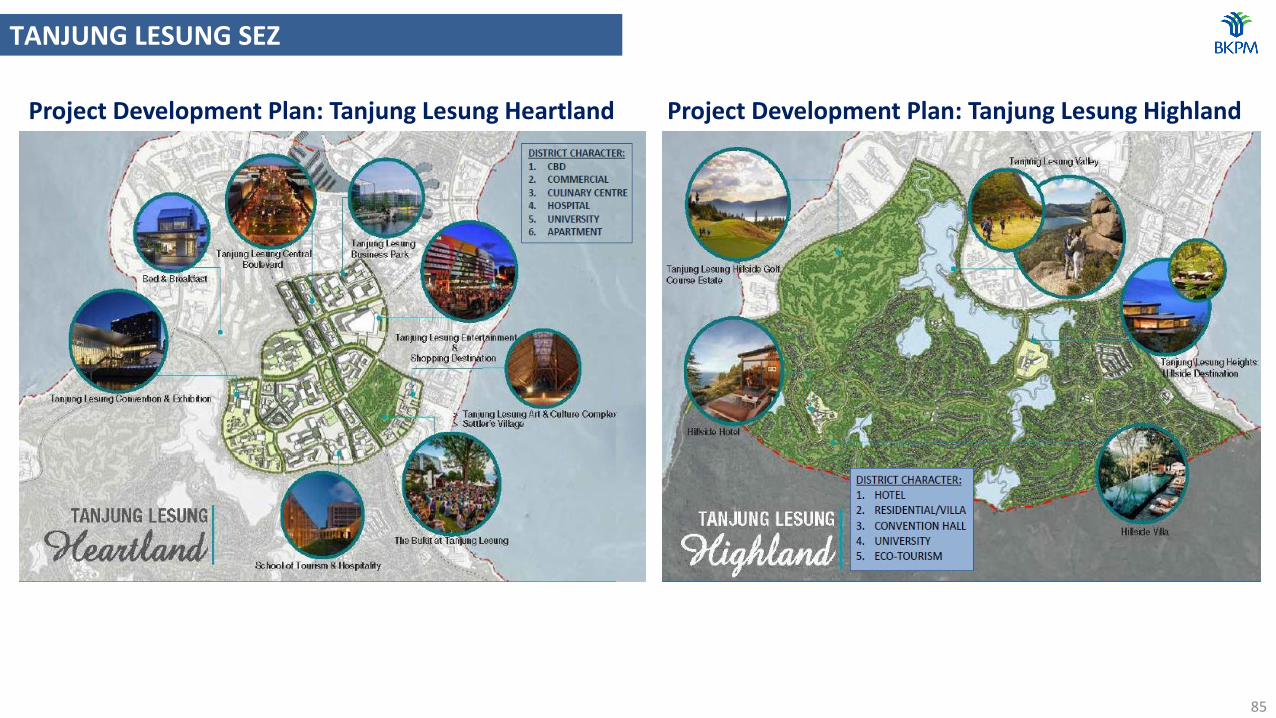

Project Development Plan: Tanjung Lesung Heartland

85

Project Development Plan: Tanjung Lesung Highland

TANJUNG LESUNG SEZ

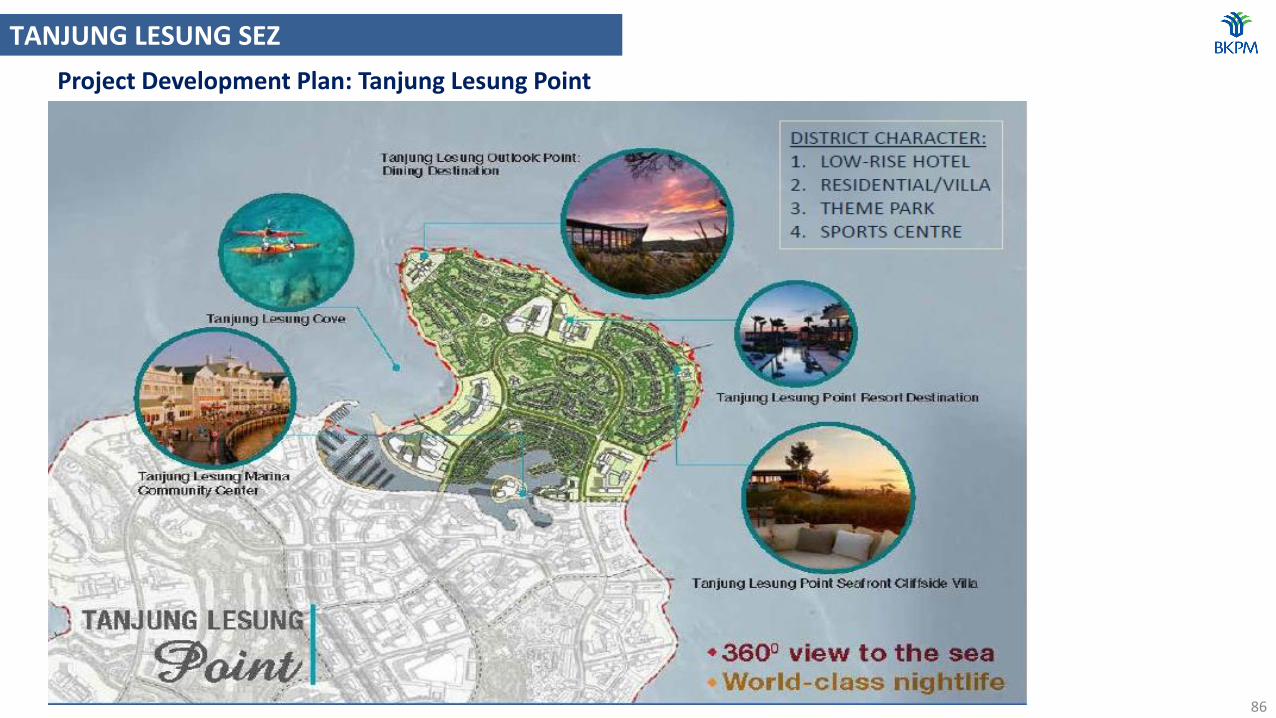

Project Development Plan: Tanjung Lesung Point

86

TANJUNG LESUNG SEZ

Tanjung Lesung Surrounding

87

TANJUNG LESUNG SEZ

Tanjung Lesung Future Development

88

TANJUNG LESUNG SEZ

List of Existing Tenant and Facilities

89