It's a small world: managing human resources in small businesses

19

This article was downloaded by: [Library Services City University London] On: 01 April 2015, At: 11:16 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK West European Politics Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/fwep20 Re‐casting the politics of steel in Europe: The impact on trade unions Nicolas Bacon a & Paul Blyton b a Lecturer in management , Nottingham University , b Professor of Industrial Relations and Industrial Sociology , University of Wales , Published online: 03 Dec 2007. To cite this article: Nicolas Bacon & Paul Blyton (1996) Re‐casting the politics of steel in Europe: The impact on trade unions, West European Politics, 19:4, 770-786, DOI: 10.1080/01402389608425164 To link to this article: http://dx.doi.org/10.1080/01402389608425164 PLEASE SCROLL DOWN FOR ARTICLE Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) contained in the publications on our platform. However, Taylor & Francis, our agents, and our licensors make no representations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of the Content. Any opinions and views expressed in this publication are the opinions and views of the authors, and are not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon and should be independently verified with primary sources of

Transcript of It's a small world: managing human resources in small businesses

This article was downloaded by: [Library Services City UniversityLondon]On: 01 April 2015, At: 11:16Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number:1072954 Registered office: Mortimer House, 37-41 Mortimer Street,London W1T 3JH, UK

West European PoliticsPublication details, including instructions forauthors and subscription information:http://www.tandfonline.com/loi/fwep20

Re‐casting the politics ofsteel in Europe: The impacton trade unionsNicolas Bacon a & Paul Blyton ba Lecturer in management , NottinghamUniversity ,b Professor of Industrial Relations and IndustrialSociology , University of Wales ,Published online: 03 Dec 2007.

To cite this article: Nicolas Bacon & Paul Blyton (1996) Re‐casting the politicsof steel in Europe: The impact on trade unions, West European Politics, 19:4,770-786, DOI: 10.1080/01402389608425164

To link to this article: http://dx.doi.org/10.1080/01402389608425164

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of allthe information (the “Content”) contained in the publications on ourplatform. However, Taylor & Francis, our agents, and our licensorsmake no representations or warranties whatsoever as to the accuracy,completeness, or suitability for any purpose of the Content. Anyopinions and views expressed in this publication are the opinionsand views of the authors, and are not the views of or endorsed byTaylor & Francis. The accuracy of the Content should not be reliedupon and should be independently verified with primary sources of

information. Taylor and Francis shall not be liable for any losses, actions,claims, proceedings, demands, costs, expenses, damages, and otherliabilities whatsoever or howsoever caused arising directly or indirectlyin connection with, in relation to or arising out of the use of the Content.

This article may be used for research, teaching, and private studypurposes. Any substantial or systematic reproduction, redistribution,reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of accessand use can be found at http://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

Re-casting the Politics of Steel in Europe:The Impact on Trade Unions

NICOLAS BACON and PAUL BLYTON

In this article we explore the response of European trade unions to the1990s steel crisis. Trade unions have faced wide ranging challengesincluding: the globalisation of the industry; steel companies becomingincreasingly international; privatisation; the eastern European steelmarket; the liberalisation of world trade; the new emerging priorities ofthe EU and internal company reorganisation. Our key argument is thattheir response has been highly traditional and unsuited to the newchallenges. When we consider the more progressive responses they havemade, there is little sign that these alternatives will be anymore successful.

Due to the cyclical nature of the steel industry steel companies routinelyexperience periods of boom followed by periods of crisis. The steel crisisstretching from the 1970s into the 1980s was deeper and more prolongedthan any since World War II. A period of relative stability in the latter halfof the 1980s was predictably followed in the first half of the 1990s by renewedtrauma as steel demand and prices collapsed. The downturn of the 1990sreproduced the traditional features of the 1980s crisis.1 Steel companiesverging on bankruptcy cut excess capacity making workers redundant. Inresponse, governments intervened to support national steel companies.There are many implications of the 1990s crisis, but in this article we willspecifically explore the impact on the trade unions. Our key argument isthat in the 1990s we have not witnessed the demise of traditional unionism.2

The response of the unions remains traditional even though an increasinglyhostile economic and political context demands new and innovative tacticsto deal with the threats they face. These threats are wide ranging and include:the globalisation of the industry; steel companies becoming increasinglyinternational; privatisation; the eastern European steel market; the liberali-sation of world trade; the new emerging priorities of the EU and internalcompany reorganisation. In the absence of new strategies, trade unions facecontinued marginalisation, resorting to appeals for social partnership atcompany, national and European levels at a time when there is no receptiveaudience for such appeals. Their response has been flawed in many respects:they have been unable to prevent plant closures or influence mergers; theyhave been unable to address relocation in the developing world; prior to

West European Politics, Vol.19, No.4 (October 1996), pp.770-786PUBLISHED BY FRANK CASS, LONDON

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 771

privatisation, unions have been roundly defeated; there has been littleeffective solidarity shown with eastern European steel workers; liberalisedworld trade has not been accompanied by any greater social protection forworkers; private steel makers have dominated EU steel policy; and unionshave played little part in internal company reorganisation.

To make this case in this article we will initially outline the externalaspects of the crisis. The first section considers the changing global steelmarket, while the second outlines the internationalisation of steel companies.The third then outlines the privatisation of the industry and the fourth thechallenge posed by eastern Europe. The fifth considers developments inworld trade and the sixth section examines the response of the EuropeanCommission to this crisis. The seventh section explores the implications forthe labour movement of industrial relations and work organisation develop-ments before reaching some conclusions.

TRADE UNIONS FACE CONTINUED STRUCTURAL CHANGES IN THE GLOBAL

STEEL MARKET

Competition in the steel industry has intensified as the world steel markethas become increasingly global and international trade in steel hasexpanded.3 There has been a changing geography of steel consumption withthe developing world becoming an increasingly important consumer ofsteel. World-wide structural over-capacity4 has been exacerbated by thesubsequent mismatch between increasing production and demand in thedeveloping world and the traditionally dominant steel-producing regionssituated in the developed world. Developing countries accounting for 20per cent of world output in 1988 had increased their share to 30 per centby 1994. This share will rise further because of high economic growth ratesin developing countries and a relatively low per capita consumption of steel.

TABLE 1

WORLD CRUDE STEEL PRODUCTION (MILLION TONNES):SELECTED COUNTRIES

Country 1988 1989 1990 1991 1992 1993 1994(1)

Germany (2)ItalyFranceUK

41.023.819.119.0

41.125.219.318.7

38.425.519.017.8

42.225.118.416.5

39.724.818.016.2

37.625.717.116.6

40.826.118.017.4

(1) 1994 figures are provisional(2) Includes the former East Germany

Source: International Iron and Steel Institute (Baxter, 1995; House of Commons, 1994: p.40).

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

772 WEST EUROPEAN POLITICS

The cycle of boom followed by bust in the steel industry reflects theindustry's dependence on manufacturing and construction for its mainmarkets. Correspondingly, the demand for steel products in OECDcountries declined for three years from 1991. The effect in western Europeis displayed in Table 1. In 1994, demand then improved by 6.8 per cent to326 million tonnes. Comprehensive figures to show the subsequent declineof steel trade unions in western Europe are not available but single casesillustrate the overall trend. In 1974, the Iron and Steel Trades Confederation(ISTC) in Britain had 120,000 members in 854 branches administered by31 full-time officers. In 1994, it had 34,000 members with 480 branches andonly 20 full-time officers.5

THE INCREASING MOBILITY OF CAPITAL: INTERNATIONALISING STEELCOMPANIES

The steel industry is not yet truly global. There are no significant multi-national steel companies as national steel companies still largely dominateand supply home markets.6 To give one example, in 1995 British Steel pro-duced 84 per cent of all UK crude steel.7 However, companies export almostone half of steel produced in the EU to other EU states. The steel industryis nationally based because of the historical economic and militaryimportance of steel to nation states. Investment overseas is also discouragedby the enormous sunk costs in this capital intensive industry that make itdifficult to exit from foreign operations.8 Traditionally, these factors haveshaped the politics of the industry providing steel unions with a strongnational political voice. However, the recent trend is for steel companiesto become international operations. This has made steel capital increasinglymobile accelerating the pace of structural change. Steel compan ies are seekingmarket solutions to their long-term structural problems through innovativetrans-national alliances, aggressive purchasing, overseas investment andmergers to create a less nationally based steel industry. For instance, a three-way venture involving Vallourec (France), Mannesman (Germany) and Ilva(Italy) led to a new company that accounted for 70 per cent of the EU steeltubes market.' In part, the ownership structure in the European steelindustry has also changed as companies have pursued aggressive accumu-lation strategies. The Italian company Riva became the second largestEuropean steel producer in 1995 after seven years spent buying parts ofthe Italian, French, East German and Belgian public steel sectors.10 Duringthis time Riva increased its turnover from 3,000 billion lira to 12,000 billionlira.

The growth of the steel market in the developing world is an important

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 773

factor forcing Western steel makers to step outside their national marketsto exploit these new opportunities. As transport costs from home facilitiesmake many traditional steel producing areas in western Europe un-competitive in the new markets, companies have relocated production todeveloping countries where demand growth is highest. Steel companieshave also sought to escape the more restrictive European market. BritishSteel, for instance, invested £210m in the US in the four months to January1995. This involved a joint venture called Trico with LTV (US) andSumitomo (Japan)," and the purchase of a steel mill in Tuscaloosa,Alabama. The company relocated two direct reduced iron units fromHunterston (Scotland) to service the latter.12 The number of mergers in theEuropean steel industry has also increased. Krupp and Hoesch, the secondand third largest steel producers in Germany, merged in 1992 and closedthe Rheinhaussen plant in 1993 as part of plans to shed 25,000 jobs (onein four). German steel companies have increasingly diversified away fromsteel and, as we explain later, consequently away from traditionally strongtripartite links with the trade unions. For instance, by 1994 Klockner Werkehad moved largely out of steel, transforming itself into a plastics andengineering group with a residual interest in Bremen's Klockner steelplant."

These moves towards a more global industry directly challenge nationalunions formed in response to national steel companies. However, in theface of such changes trade unions have become increasingly unable toinfluence events. Whereas the protests of west German steel workerssuccessfully won a reprieve for the Rheinhaussen plant in Duisburg in 1988,a march of 10,000 in 1993 failed to prevent the closure of the works. Thethousands of workers who marched in Dortmund in 1991 failed to preventthe merger of Krupp and Hoesch that resulted in the large number ofredundancies described above.14 Despite occupying the Bagnoli plant inNaples for two years, Italian steel-workers failed to prevent its closure.15

There is every indication that when faced with capital restructuring thispattern of trade-union failure will continue. Increased internationalisationalso has broader implications for the steel trade unions of western Europein that they need to develop a much closer relationship with other steel-worker unions in Asia. In addressing the ISTC, David Fowler, GeneralSecretary of the International Metalworkers Federation has pointed outthat 'our colleagues in the developing countries will be looking to you foryour experience and leadership'.16 The unions of western Europe have beenslow in meeting this call. A further implication is the need for closer co-operation between steel unions in Europe, an issue we address towards theend of this article.

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

774 WEST EUROPEAN POLITICS

TRADE UNIONS FACE PRIVATISATION IN THE EUROPEAN STEEL INDUSTRY

The trend towards privatisation across the steel industry is the most signifi-cant development re-shaping the politics of steel and the influence of tradeunions. As privatisation weakens the national nature of steel companies17

it directly reduces the channels of political influence open to trade unions.In 1986, more than one half of steel capacity in the EU was state-owned.Between 75 and 80 per cent of the industry was in the private sector by theend of 1995.18 The list of privatisations includes British Steel in 1988, EkoStahl in 1994, Ilva, Usinor Sacilor and Freital in 1995 (see Table 2). By theend of 1995, state-owned companies were concentrated in the Beneluxcountries, the Iberian Peninsular and regional government involvement inGermany. This includes partial state ownership of Hoogovens in the Nether-lands, Sidmar and Cockerill Sambre in Belgium, Arbed in Luxembourg,Klockner Stahl and Saarstahl in Germany, and CSI in Spain.

TABLE 2

PRIVATISATION IN THE EUROPEAN STEEL INDUSTRY

Company

British SteelEko StahlUsinor SacilorFreitalIlva

Country

UK(East) GermanyFrance(East) GermanyItaly

Date

19881994199519951995

Form of Privatisation

FloatationSold to Cockerill SambreFloatationSold to German company BGHSplit into 3. ILP sold to Riva, AST toGerman/Italian consortium

Thus far, campaigns by steel-workers against privatisation have beenspectacularly unsuccessful. When faced with determined governments mostworkers' campaigns have concentrated on job security rather than owner-ship. The form of privatisation and its political sensitivity help to explainthe lack of trade union influence upon this process. Where governmentshave used public floatations, unions have been unable to use political influenceto place restrictions upon the new companies. In the case of British Steel,the company emerged 'aggressively' from privatisation, closing theRavenscraig works. Usinor Sacilor appeared to be following a similar pathin France, but political instability has led Prime Minister Alain Juppe toconsult with the unions about privatisation.19 When governments have soldsteel companies to private companies, then the issues have been moredelicate. This is because these steel companies were located in politicallysensitive regions and have required further state aid in the privatisationprocess to secure the future of sensitively located plants. For example, thesale of Eko Stahl to Cockerill Sambre involved £370 million of state aid to

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 775

modernise the plant. In another case, to privatise the Italian steel companyIlva, the Italian state holding company (IRI) had to assume a debt of 4.8trillion lira.

In most instances, governments and managers had already overcometrade union opposition prior to privatisation. Undoubtedly, in some countries,though not all,20 the commercial pressures involved in privatisation haveaccelerated restructuring in nationalised companies. It is less certain,however, that privatisation will lead to further sudden rationalisations orimproved productivity.21 As with the case of British Steel,22 privatisationdoes not herald the start of restructuring, rather a return to profitability isa precondition for privatisation. When Ilva Laminati Piani (ILP) made aprofit of 700 billion lira in 1994, the government sold it to Riva - endingsix decades of Italian state involvement in steel.23 A key factor contributingto increased productivity and profitability was ILP's restructuringprogramme. This had reduced the workforce from 12,000 to 9,000 at theTaranto steelworks (Europe's largest) by the end of 1996.24 The sale ofEurope's largest producer Usinor Sacilor by the French government followsa similar return to a profit of 1.5 billion French francs ($282.2 million) in1994. Managers had reduced the work-force from 95,750 in 1989 to 62,000in 1995. Over the same period, productivity improved from 5.1 to less thanthree man hours per tonne.25 Consequently, managers of privatised steelcompanies have not begun attacking trade unions, they have continued anexisting process.

EASTERN EUROPEAN STEEL MARKETS CHALLENGE TRADE UNIONS

The fall of communism has also brought change for the steel industry inwestern Europe. Steel demand in the former communist economiescollapsed from the late 1980s, creating a massive capacity surplus alongsidethe desire for hard currency earnings from exports. Imports from centraland eastern Europe have challenged European political and economicunion. Between 1989 and 1992, imports of rolled steel from the formerSoviet Union had increased from a monthly average of 44,619 tonnes to112,488 tonnes. From Poland they had increased from 38,529 to 68,810tonnes, and from Czechoslovakia from 53,424 to 120,253 tonnes. Ministersand officials of EU countries have wished to support the economies ofcentral and eastern Europe and the former Soviet Union. However, theyhave tempered this desire, given the potential economic impact of theseimports on the European steel market. More immediate practical problemshave confronted the trade unions, as working conditions in eastern Europethreaten to undermine standards in western Europe and attract companiesto relocate into cheaper labour markets. German trade unions have been

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

776 ' WEST EUROPEAN POLITICS

at the forefront of this battle in seeking to upgrade working conditions inthe former East Germany. IG Metall conducted a three-week campaign ofindustrial action following the refusal of employers in East Germany toimplement an agreed pay increase. The outcome of the dispute was anagreement to postpone wage parity with West Germany until 1 April 1996.26

However, workers in eastern Europe have felt isolated and critical of steelunions and companies in the West. When it appeared that the EU wouldallow state aid to help privatise the east German plant Ekostahl one workerexplained: 'We fought hard for these subsidies. The steel producers over inWest Germany never showed the slightest bit of solidarity with us. And Iknow why. They were afraid that if we managed to get the subsidies, wewould really become competitive.'27

Although IG Metall has tried to help workers, after privatisation eachcompany pursued its own policy seeking Western partners and diversifyingout of steel. Other steel unions have been more eager to protect theirdomestic markets. Consequently, they have backed the lobbying agenda ofthe private steel companies to prevent import competition and state aidsthat modernise the uncompetitive plants of eastern Europe. Solidarity witheastern Europe's steel workers has been notable for its absence.

TRADE UNIONS FACE THE FREE MARKET OF LIBERALISED WORLD TRADE

Traditionally, national companies, trade barriers and state subsidies havedominated the political agenda of steel trade. Trade barriers and stateinvolvement in the industry had become closely linked as productioncapacity, built or maintained with state subsidies, distorted the market.28

The political and geographical concentration of steel plants and their largesize creates strong lobbying groups that have made the industry highlysensitive to politics. The trend towards a more global privatised industryhas improved the prospects for free trade in an industry affected by tradedisputes throughout the 1980s. The USA and Europe have fought the majorpolitical battle over trade as the US steel crisis forced North Americancompanies to seek protection.29 However, by the mid-1990s, the MultilateralSteel Agreement (MSA) appeared to offer a new global agenda for theindustry. North American steel-makers have already established new liberalcredentials by supporting the free trade agreement between the US andCanada.30 The MSA will bring the political influence of the World TradeOrganisation to impose disciplines on subsidies world-wide and eradicatethe succession oiadhoc Voluntary Restraint Agreements (VRAs) that havebedevilled steel trade. As such, it will further encourage the developmentof multinational steel companies and move the industry farther away fromstate involvement. The gap between neo-liberal rhetoric and protectionist

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 777

reality narrowed significantly in the early 1990s. As a result, the economicand political framework will increasingly proscribe the ability of tradeunions to seek trade protection in the future. In recognition of this 'newworld' the main mover to revise trade union strategies has been theInternational Metalworkers Federation. At its 1993 Centenary Congress itabandoned all previous resolutions adopting an action programme and in1994 a metalworkers' charter. This new strategy insists that free trade bebased upon international standards of 'what is right, fair and decent, andtrade union rights to organise and bargain as ... laid down in the ILOconventions'.31 However, to date no sanctions back this threat after the WorldTrade Organisation rejected the idea of a social clause in a new agreementon GATT.

EU CRISIS MANAGEMENT MARGINALISES TRADE UNIONS

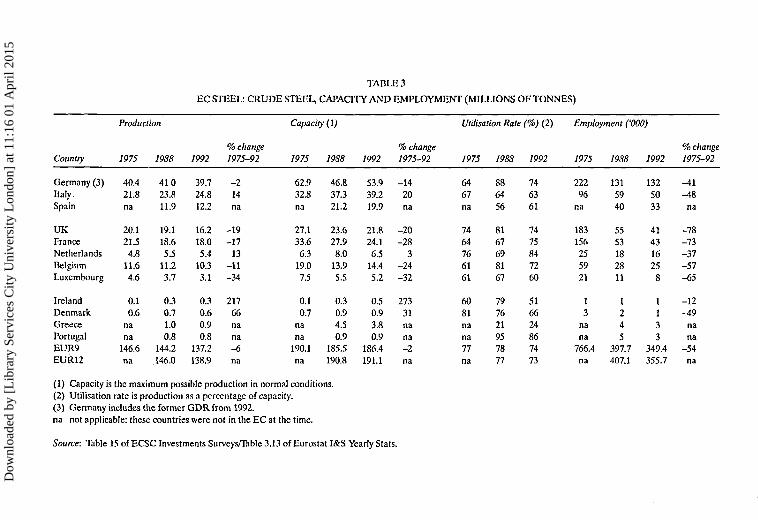

In the 1990s the impact of European trade unions upon the process of EUcrisis management has become slight. In 1992, the collapse of steel pricesled to a combined loss of £3 billion for European steel companies.32 Despitewaves of job losses and plant closures in the 1980s, over-capacity in Europeremained endemic. Capacity utilisation rates dropped below their 1988levels in many countries (Table 3).

The EU has sought laissez-faire market solutions and the agenda becameincreasingly dominated by aggressive newly privatised companies seekingmarket solutions to the industry's problems. For instance, British Steel hasstrongly opposed aid throughout and took the European Commission tothe European Court of Justice for breaking its own subsidy rules. It has alsopressurised the UK government to the point that the Department of Tradeand Industry created a Steel Subsidies Monitoring Committee to checkstate aids throughout Europe.33 German steel companies have repeatedlythreatened to withdraw any support for EU action as the Commission failedfully to address the issue of state subsidies. The only exceptions to this neo-liberal agenda have been re-adaptation packages for redundant steel-workersand state aid that owed more to the concerns of national sovereignty thansteel-workers.

In 1992, the European steel companies requested an EU actionprogramme to help the industry restructure.34 Community intervention hadpreviously escalated from the 1970s onwards, with each successiveCommission plan (the Spinelli, Simonet and two Davignon plans) provingto be increasingly interventionist.35 Under the second Davignon Plan theCommission had declared a 'manifest crisis' in the steel industry. It directlyintervened in the market, dictated the production quotas of individualcompanies, introduced protectionist trade measures and endorsed subsidies

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

TABLE 3

EC STEEL: CRUDE STEEL, CAPACITY AND EMPLOYMENT (MILLIONS OF TONNES)

Country

Germany (3)Italy.Spain

UKFranceNetherlandsBelgiumLuxembourg

IrelandDenmarkGreecePortugalEUR9EUR12

Production

1975

40.421.8na

20.121.5

4.811.64.6

0.10.6

nana

146.6na

19SS

41.023.811.9

19.118.65.5

11.23.7

0.30.71.00.8

144.2146.0

7992

39.724.812.2

16.218.05.4

10.33.1

0.30.60.90.8

137.2138.9

% change1975-92

-214na

-19-17

13-11-34

21766nana-6na

Capacity (1)

1975

62.932.8na

27.133.6

6.319.07.5

0.10.7

nana

190.1na

1988

46.837.321.2

23.627.98.0

13.95.5

0.30.94.50.9

185.5190.8

1992

53.939.219.9

21.824.16.5

14.45.2

0.50.93.80.9

186.4191.1

% change1975-92

-1420na

-20-28

3-24-32

27331nana_2

na

Utilisation Rate (%) (2)

1975

6467na

7464766161

6081nana77na

1988

886456

8167698167

797621957877

1992

746361

7475847260

516624867473

Employment ('000)

1975

22296

na

183156255921

13

nana

766.4na

1988

1315940

5553182811

1245

397.7407.1

1992

1325033

414316258

1133

349.4355.7

% change1975-92

-41^t8

na

-78-73-37-57-65

-12-49

nana

-54na

(1) Capacity is the maximum possible production in normal conditions.(2) Utilisation rate is production as a percentage of capacity.(3) Germany includes the former GDR from 1992.na not applicable: these countries were not in the EC at the time.

Source: Table 15 of ECSC Investments Surveys/Table 3.13 of Eurostat I&S Yearly Stats.

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 779

and price cartels. However, political views on state intervention hadchanged significantly by the 1990s. The steel companies, national govern-ments and the Commission agreed upon new plans in February 1993.Although it identified potential capacity cuts of between 19 and 25 milliontonnes the Commission reversed the previous trend of escalating inter-vention with each crisis. In return for a minimum capacity reduction acrossthe EU of 19 million tonnes, it offered a series of measures to help companiesrestructure: quarterly market forecasts on production and delivery volumesas 'guidance'; an increase by 240 million Ecu in the financial assistanceavailable from ECSC funds for employees made redundant as a result ofclosures; authorisation for ECSC companies to form groups to 'buy out'and close capacity; limited protection from imports through a surveillancesystem of certain eastern European and former Soviet Union countries;and a stronger line on state subsidies.

However, the agreement repeatedly faltered, as governments sought adhoc derogations to allow state aid. In December 1993, the Council ofMinisters agreed six ad hoc derogations for Eko Stahl and Freital inGermany, CSI and Sidenor in Spain, Ilva (Italy) and Siderurgia Nacional(Portugal).36 In return for the aid totalling £5.1 million (6.7 million Ecu)companies promised capacity reductions totalling 5.4 million tonnes. Inthese decisions regional political issues were to the fore in the Europeansteel industry. The German Government insisted that it needed to provideaid to privatise the former GDR companies Freital and Eko Stahl. At theend of 1994 the EU approved DM910 million (£370 million) aid for EkoStahl for new installations and modernisation. This allowed an eventualprivatisation when the Belgian steel company, Cockerill Sambre, boughtthe company.37-38 In Spain, Prime Minister Felipe Gonzalez closed capacityin the Basque country only after winning approval from Brussels toconstruct a modern steel plant at Sestao.39 The Commission, eager not toundermine a reform-minded Italian Government, allowed it to slow cutsin 1993. Efforts to eliminate steel mills in the northern Brescian region in1994 were sensitive to the new Berlusconi government and its NorthernLeague coalition partners.40 The more exceptional case of trade union influ-ence was in November 1993 when a powerful local campaign prevented theclosure of Klockner Works near Bremen in Germany. This continued thetradition of the German approach to crisis management.41 A consortium ofEuropean steel companies planned to buy the works for DM1 billion (£300million) and then close it. They were frustrated in this when a consortiumled by Bremen city state and public companies purchased a 75 per centstake for DM4 (£1.50).42

By October 1994 companies had volunteered only 16 million tonnes ofcapacity reductions and the European Commission pronounced the plan

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

780 WEST EUROPEAN POLITICS

'dead'. The Commission withdrew all aspects of the plan except for thealready approved subsidies and the aid offered to redundant steel-workers.43 As the recession in Europe ended and steel companies returnedto profitability there was little incentive for them to proffer further cuts incapacity. Throughout, the role of the unions was marginal.

THE INCREASING PACE OF INTERNAL COMPANY REORGANISATION

The marginalisation of the unions at national level and international levelsmirror attempts by managers to weaken the influence of unions in steelcompanies. Whereas job losses dominated the 1980s and continue to thepresent, in the 1990s trade unions have also had to deal with managersforcing the pace of industrial relations and organisational changes.European steel companies face a paradox with their own internalrestructuring. As managers have reduced capacity the resulting large-scalejob cuts have inevitably led to conflict with trade unions. However, the pan-European technological and organisational modernisation towards'diversified quality production' has increased the need for workforce co-operation with management.44 The industry is changing from a high volume,standardised, price competitive production pattern towards a high-volume,customised, quality-competitive production pattern.45 Consequently, aprocess of change is occurring involving product innovation and speciali-sation, new technologies of production control, the organisation of workinto multi-skilled teams and improvements in the system of vocational andskills training.46 Steel companies across Europe are slowly transformingestablished work patterns and arrangements47 some of which have been inplace for nearly a century.48 An outstanding question remains whether steelcompanies will generate commitment and motivation from steelworkers asindividuals or whether they will continue to attribute a strong role to thetrade unions in the workplace.

Initial 'cutting edge' experiments offering trade unions arole in the processof change have given way more recently to a more unitarist scenario in whichmanagers enforce their prerogative in reorganising work. Developments inGermany illustrate this shift. In the German steel industry, a works councilin 1983 had initiated group working arrangements at Hoesch Stahl AG coldrolling mills of Westfalenhutte (Dortmund) which then spread to otherplants.49 Similarly, at Saarstahl Volkingen the survival plan of the IG Metallunion involved widespread multi-skilling and job rotation.50 However, thecrisis of the 1990s, while increasing the speed of rationalisation, has seen thetrade unions become more marginalised. In 1994, both Thyssen Stahl andKrupp Hoesch moved away from co-determination, diluting workers' rightsto increase the pace of restructuring and redundancies. The steel form of

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 781

co-determination only applies when a company employs a majority of itsemployees in steel-making. Thyssen Stahl split its long products and wiredivisions into separate companies that will not be subject to the steel industry'sparticular version of the German system of co-determination {Montamit-bestimmung).51 Krupp Hoesch broke down its steel division with the newcompanies escapingMontamitbestimmung.52 These moves followed extensiveunion protests over the merger of Krupp and Hoesch and the subsequentclosure of the Rheinhausen works described above. In Germany, bothThyssen Stahl and Krupp Hoesch have since gone further in announcingmoves away from social measures and generous redundancy payments.53

These moves towards deregulation indicate that European steelcompanies may be following a path of marginalising the unions similar tothat pioneered by British Steel.54 At British Steel the decentralisation ofcollective bargaining has left the unions with a reduced central role. Never-theless, in some EU countries trade unions remain influential, althoughthey have conceded certain principles. In Italy, companies made redund-ancies after the unions compromised their traditional opposition andaccepted the case for closures in return for social measures to ease theimpact upon workers. Italian law provides for a Cassa d'Integrazione underwhich workers who have been Iaid-off receive a negotiated percentage oftheir salary for a negotiated time.55 Under 'solidarity contracts' jobs havebeen saved by work-sharing agreements, workers have been transferred toother companies and employed on community work projects.56 Never-theless, this did represent 'ardent reformism' in the steel unions and anacceptance that the unions had to deal with the crisis facing the industryirrespective of the views they held about management.

When faced with the threat of marginalisation, European steel unionshave been slow to respond. There are, however, seeds of alternativestrategies emerging. Two of the key themes in this response are the pushfor greater union involvement in decision making and a new bargainingagenda. In Spain, a landmark agreement between state-controlled steelcompanies and the major trade unions provided for inflation-linked payincreases and union participation in management in return for productivityincreases and a restructuring of grades.57 In Germany, building upon theradical new bargaining agenda Tarriff Reform 2000, IG Metall entered the1994 bargaining round without a pay demand but with a range of proposalson working time aimed at preserving employment.58 In advanced negotia-tions for 1997, in a document 'Alliance for Work', IG Metall has furtheroutlined plans to limit wage demands in line with inflation in return for jobcreation.59 In the early 1990s, the steel unions in France signed a paymentfor skills deal aimed at up-skilling the labour force. Although this newagenda for the steel unions is somewhat tentative and unsecured, it does

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

782 WEST EUROPEAN POLITICS

follow some global trends. Managers and unions in the US steel industryhave developed new forms of production organisation and new co-operative relations with workers.60 By 1993, five of the six large integratedsteel companies had concluded six year agreements with the UnitedSteelworkers of America union to allow union representatives onto theirboards.61 This represents the most far-reaching experiment in employeeinvolvement by any US industry and it breaks markedly from the traditionof adversarial labour relations in the US steel industry.62

It is unlikely that European works councils will be of much help to theEuropean steel unions. In the UK the social chapter of the MaastrichtTreaty would cover British Steel, Johnson Matthey and Delta. Of these,Johnson Matthey has de-recognised unions in its UK steel operations andin the 1980s British Steel abolished its worker directors and decentralisedcollective bargaining. As other European companies appear to be followingaspects of the British Steel model, there is little enthusiasm for the newforums in the rest of Europe. As described above, companies in Germanyappear to be weakening co-determination and European works councilsare a poor substitute to Montamitbestimmung as they offer only consultationand not negotiation rights.. The second largest European steel companyRiva pulled out of its planned purchase of Eko Stahl due to the system ofGerman co-determination and the rights it provided steel-workers.63 BritishSteel has signalled its intent in declining to participate in seminars onEuropean works councils. These seminars have brought together unionofficials from Skinningrove and works council members from its sister plantMannstaedt works in Germany. As one Skinningrove union representativeoutlined the continuing experience of industrial relations in British Steelis one where trade unions are marginalised:

British Steel managers are keen on promoting Total QualityPerformance through joint working parties of the work-force andthemselves. The working parties are set up to get ideas from theworkers but when it comes to the subject of people's employment,the work-force has very little voice. The usual outcome of discussionson this topic is a proposal by management without pre-discussion,then a rejection by the union, and a disagreement which drags on formonths so everyone loses out.64

The prevailing evidence indicates that this is more likely to become theexperience for the unions across Europe. In response there are signs thaton a more regular basis steel unions are starting to exchange informationon health and safety, pay and the way employers threaten unions aroundthe world. At a World Steel Conference in 1995 steel union delegates from42 countries met with leading steel makers, politicians and experts to discuss

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 783

the industry. However, there is little hope that European trade unions willbe able to extend workers' rights across Europe in the current economicand political climate. In eastern Europe governments have sided withemployers in disputes. In 1994, 3,400 Polish steel-workers in Warsawembarked upon a seven-week sit-in strike over wages during which theythreatened to take over production. The workers felt the company forcedthem into a neo-colonial situation with foreign owners (the Italian companyLucchini) showing them little respect. The strikers had erected a sign onthe gates reading 'Welcome to the white blacks at Lucchini'. The Polishgovernment, eager not to deter foreign investment backed the company,put pressure on the workers to go back to work before talks could take placeand the dispute be resolved.65 In such a climate, it is difficult to see how theInternational Metalworkers Federation can have much effect.

CONCLUSION

Reflecting upon the predictions of those who have studied the steel industryin the past should counsel caution in predicting the future. In the currentclimate the politics of steel are undergoing a profound change from regionalprotectionism towards liberalisation. Rather than further escalating EUinvolvement in the 1990s there has been a step back from direct inter-vention. The extent to which this metamorphosis of the politics of steeldevelops will depend upon how successfully companies can rationalisethemselves and in this many have a historically poor track record. The steelindustry in Europe remains fragmented. Europe has 15 main producerscompared with five in Japan. What is clear is that the technical andorganisational changes that have occurred in the steel industry in recentyears only go some way to reconciling the gap between the nature of steelproduction and the changing demands of an increasingly sophisticated anddiverse market for steel products. Already these changes have had majorquantitative and qualitative implications for the labour force within theindustry. Indeed, whether the transformation is slow or sudden the crisisfor the labour movement looks set to continue and the urgency for a newagenda for European trade unions under liberalised trade is pressing.However, the current strategy of the European steel unions appears to beweak. There is little chance that the International. Metalworkers Federationwill impose social conditions upon international trade, the EU has movedin an avowedly free-market direction, and European works councils offera poor alternative even if they were welcomed by steel companies. Thelikely alternative is an increasingly marginalised position, with employersadopting individualised approaches to gain the work-force consentnecessary to achieve the more exacting performance requirements.

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

784 WEST EUROPEAN POLITICS

NOTES

1. F. Yachir The World Steel Industry Today (London: Zed Books 1988). Yves Meny andVincent Wright (eds.) The Politics of Steel (Berlin and London: Walter de Gruyter 1987).

2. Martin Rhodes and Vincent Wright, 'The European Steel Unions and the Steel Crisis,1974-84: A Study in the Demise of Traditional Unionism', British Jnl of Political Science18/2 (April 1988) pp.171-95.

3. F. Yachir The World Steel Industry Today (London: Zed Books 1988).4. A.P. Dcosta, 'State, Steel and Strength - Structural Competitiveness and Development

in South Korea',/«/of 'DevelopmentStudies 31/1 (Oct. 1994) pp.44-81. L.T Feng, 'China'sSteel Industry - Its rapid expansion and influence on the international steel industry',Resources Policy 20/4 (1994) pp.219-34. R.R. Miller, 'The Changing Economics of Steel',Finance and Development (June 1991) pp.38-40.

5. ISTC Phoenix, 'ISTC Membership' (Dec. 1994) p.6.6. P.A. Messerlin, 'The European Iron and Steel Industry and the World Crisis', in Meny

and Wright (note 1) pp.111-36.7. ISTC Today, 'British Steel makes 84% of UK crude steel' (June 1995) p.l.8. Jonathan Aylen, 'Privatisation of the British Steel Corporation', Fiscal Studies 9/3(1988)

pp.1-25.9. Financial Times, 'EU Commission allows Mannesmann, Valourec and Ilva unit, Dalmine,

to form DMV joint venture despite opposition of Competition Commissioner', 27 Jan.1994, p.24b.

10. Ibid. 'Riva Finanziaria plans to acquire', 14 March 1995, p.28a.11. Iron Age Steel News, 'LTV, British Steel and Sumitomo form minimill joint venture' 11/

2 (Feb. 1995) p.8.12. Financial Times, 'BS to spend £87m on two projects in USA and South Wales', 12 Jan.

1995, p.20d.13. Ibid. 'Klockner-Werke moves out of steel', 17 March 1994.14. Ibid. 'Largest steel producer to shed jobs', 14 Nov. 1991, p.2b.15. Ibid. 'Report on EU agreement to cut steel capacity while approving state subsidies for

German, Italian, Spanish and Portuguese producers', 20 Dec. 1993, p.26.16. ISTC Phoenix, 'Bridging the Differences Between Countries: Fraternal Address to ISTC

Annoual Conference by David Fowler' (Dec. 1994) p.24.17. Heidrun Abromeit, British Steel: An Industry Between the State and the Private Sector,

(Leamington Spa: Berg 1986).18. Financial Times, 'Steeled for Global Action', 22 March 1995, p.17.19. The Economist, 'France's New Prime Minister to Consult Trade Unions About

Privatisation', 335/7916,7 May 1995, pp.68.20. Nicolas Bacon, Paul Blyton, and Jonathan Morris, 'Steel, State and Industrial Relations:

Restructuring Work and Employment Relations in the Steel Industry', in Tom Clarke(ed.) International Privatisation: Strategies and Practices (London and Berlin: Walter DeGruyter 1994) pp.139-52.

21. D. Parker, and S. Martin, The Impact of UK Privatisation on Labour and Total FactorProductivity Working Paper in Commerce 93/14 (U. of Birmingham 1993).

22. Bacon, Blyton, and Morris, 'Steel, State and Industrial Relations', in Clarke (note 20)pp.139-52. Paul Blyton, 'Steel: A Classic Case of Industrial Relations Change in Britain',M of Management Studies 29/5 (1992) pp.635-50. Ralph Fevre, 'Subcontracting in Steel',Work, Employment and Society 1/4 (Dec. 1987) pp.509-27.

23. Financial Times, 'IRI agrees to sell Ilva Laminati Piani flat steel producer to RivaFinanziaria', 2 March 1995, p.24a.

24. Ibid., 'Riva Finanziaria expected to acquire Ilva Laminati Piani steel producer from IRI',14 March 1995, p.28a.

25. Ibid. 'Prospects for privatisation of Usinor Sacilor', 20 March 1995, p.25f.26. IDS European Report, 'Steel Agreement in East', Issue 378 (June 1993) p.6.27. Financial Times, 'Aid Lifeline for EkostahP, 20 Dec. 1993, p.2g.28. E. Abe, and Y. Suzuki, Changing Patterns of International Rivalry - Some Lessons From

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

THE POLITICS OF STEEL IN EUROPE 785

the Steel Industry (U. of Tokyo Press 1991).29. H. Van Der Ven, and Thomas Grunert, 'The Politics of Transatlantic Steel Trade', in

Meny and Wright (note 1) pp.137-85. J.P. Hoen, And the Wolf Finally Came: The Declineof the American Steel Industry (U. of Pittsburgh Press 1988).

30. R. Storey, 'Making Steel Under Free Trade', Relations Industrielles - Industrial Relations48/4 (1993) pp.712-31.

31. ISTCPhoenix, 'Bridging the Differences Between Countries: Fraternal Address to ISTCAnnual Conference by David Fowler' (Dec. 1994) p.24.

32. Financial Times, 'BS Chairman expounds on EU steel package', 12 Jan. 1994, p.27c.33. Ibid. 'DTI Launches Steel Subsidies Committee', 17 Feb. 1995, p.lOh.34. The institutional setting of industrial policy-making and the general style of decision-

making were similar to those in the 1980s. The European steel industry is a special casein that it is subject to the ECSC Treaty of Paris (1951). This gives the EuropeanCommission a stronger role than it enjoys vis-à-vis other industries subject to the Treatyof Rome. Article 95 of the Treaty of Paris allows the Commission to assent to state aidsto achieve the objectives of the Treaty. This framework is well covered by ThomasGrunert, 'Decision-Making Processes in the Steel Crisis Policy of the EEC', in Meny andWright (note 1) pp.222-307.

35. L. Tsoukalis, and R. Strauss, 'Community Policies on Steel 1974-'82', in ibid.36. House of Commons, The UK Steel Industry, Trade and Industry Committee Report, House

of Commons Paper HC84, HMSO (1994) p.26.37. Financial Times, 'EU ministers expected to approve state aid for Eko Stahl', 8 Dec. 1994,

p.2f.38. The social and political consequences of closure proved too important for the

Commission to ignore. Without this support the 50,000 workers of Eisenhuttenstadt(literally translated as Iron Works City) who were dependent upon the mill for theirlivelihood, faced a bleak future. Unemployment in the town was 15 per cent, a further15 per cent were on government-supported schemes and 5,000 of its' young people hadalready fled to West Germany.

39. Financial Times, 'EU steel rescue plan possible', 7 June 1994, p.l9c.40. Ibid., 'EU resurrects steel rescue plan', 16 June 1994, p.22a.41. J. Esser, and W. Fach, 'Crisis Management "Made in Germany": The Steel Industry', in

Peter Katzenstein (ed.) Industry and Politics in West Germany (Ithaca, NY: Cornell UP1989). K. Thelen, 'Codetermination and Industrial Adjustment in the German SteelIndustry: A Comparative Interpretation', California Management Review 24/3 (1987)pp.134-48. A.L. Thimm, 'Codetermination and Industrial Policy: The Special Case ofthe German Steel Industry', ibid. (1987) pp.115-33. Trevor Bain, 'German Codeter-mination and Employment Adjustments in the Steel and Auto Industries', Columbia Jnlof World Business 18/2 (1983) pp.40-7.

42. Financial Times, 'BS warns EU Commission's plan to restructure the steel industry couldcollapse if Kloeckner-Werke mill allowed to accept subsidies from Bremen', 11 Jan. 1994,p.2a.

43. Ibid. 'EU poised to abandon plan', 25 Oct. 1994, p.20d.44. Hans Werner Franz, 'Do it right the first time- quality as the crucial change agent in the

European steel industries', Int. Jnl of Human Factors in Manufacturing 5/2 (1995)pp.211-24.

45. Hans Werner Franz, 'Quality Strategies and Workforce Strategies in the European Ironand Steel Industry', in Paul Blyton, and Jonathan Morris (eàs)A Flexible Future? Prospectsfor Employment and Organisation (Berlin and NY: De Gruyter 1991) pp.259-73.

46. Paul Blyton, Hans Werner Franz, Jonathan Morris, Nicolas Bacon and Rainer LichteChanges in Work Organisation in the UK and German Steel Industries: Implications forTrade Unions and Industrial Relations (Anglo-German Foundation Report 1994).

47. Hans Werner Franz Occupational Profiles in the European Steel Industry, (Berlin,European Centre for the Development of Vocational Training 1992).

48. B. Elbaum, and Frank Wilkinson, 'Industrial Relations and Uneven Development: AComparative Study of the American and British Steel Industries', Cambridge Jnl of

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15

786 WEST EUROPEAN POLITICS

Economics 3/3 (Sept. 1979) pp.275-303. K. Stone, 'The Origins of Job Structures in theSteel Industry', Review of Radical Political Economics 6/2 (1973) pp.113-73.

49. Jonathan Morris, Paul Blyton, Nicolas Bacon and Hans Werner Franz, 'Beyond survival:the implementation of new forms of work organisation in the UK and German steelindustries', Int. Jnl of Human Resource Management 3/2 (1992) pp.307-29.

50. Blyton et al. (note 46).51. Financial Times, 'Thyssen Stahl splits divisions', 6 Oct. 1994, p.29f.52. Ibid. 'BS must develop markets outside UK and Europe', 21 June 1994, p.22e.53. Ibid. 'Thyssen Stahl to cut 1,250 jobs', 15 Jan. 1994, p.2b. Ibid. 'Plans to cut a further

1,100 jobs', 25 Jan. 1994, p.3b.54. Nicolas Bacon, Paul Blyton and Jonathan Morris, 'Among the Ashes: Trade Union

Strategies in the UK and German Steel Industries', British Jnl of Industrial Relations,forthcoming. Paul Blyton, 'Steel: A Classic Case of Industrial Relations Change inBritain', Jnl of Management Studies 29/5 (1992) p.635-50. Bob Avis, 'British Steel: A Caseof Decentralisation of Collective Bargaining', Int. Jnl of Human Resource Management1/1 (Aut. 1990) pp.90-9.

55. The Guardian, 'Steeled for Survival', 24 Jan. 1992, p.26.56. Financial Times, 'Government agrees to early retirement programme for 10,450 Ilva

workers', 14 March 1994, p.2a.57. IDS European Report, 'Steel Replaces Labour Ordinance', Issue 379 (July 1993) p.7.58. Ibid. 'Steel Deal aims to Save Jobs', Issue 389 (May 1994) p.5.59. Financial Times, 'IG Metall makes pay-for-jobs offer', 2 Nov. 1995, p.2a.60. C. Scherrer, 'Seeking a Way out of Fordism: The US Steel and Auto Industries', Capital

and Class No.44 (Summer 1991) pp.93-120.61. Financial Times, 'US steel industry's experiment to improve competitiveness through

union involvement on company boards', 27 Oct. 1993, p.l4a.62. Hoerr, And the Wolf Finally Came (note 29). P.A. Tiffany, The Decline of American Steel-

How Management, Labour and Government Went Wrong (NY: OUP 1988). A.J. Stritch,'State Autonomy and Societal Pressure - The Steel Industry and United States ImportPolicy', Administration and Society 23/3 (1991) pp.288-309.

63. Financial Times, 'Krupp Hoesch Breaks Down Steel Division', 21 June 1994,64. ISTC Today, Letter from Colin Hart, Skinningrove Special Sections (June 1995).65. Financial Times, 'Compromise Offer in Polish Strike', 18 June 1994, p.2c.

Dow

nloa

ded

by [

Lib

rary

Ser

vice

s C

ity U

nive

rsity

Lon

don]

at 1

1:16

01

Apr

il 20

15