Intermediate Accounting IFRS Edition Chapter 18 Revenue

10

18-1 Volume 2

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Intermediate Accounting IFRS Edition Chapter 18 Revenue

18-1

Volume 2

18-2

C H A P T E R 18

REVENUE

Intermediate Accounting

IFRS Edition

Kieso, Weygandt, and Warfield

18-3

1. Apply the revenue recognition principle.

2. Describe accounting issues for revenue recognition at point of

sale.

3. Apply the percentage-of-completion method for long-term

contracts.

4. Apply the cost-recovery method for long-term contracts.

5. Identify the proper accounting for losses on long-term contracts.

6. Describe the accounting issues for service contracts.

7. Identify the proper accounting for multiple-deliverable

arrangements.

Learning Objectives

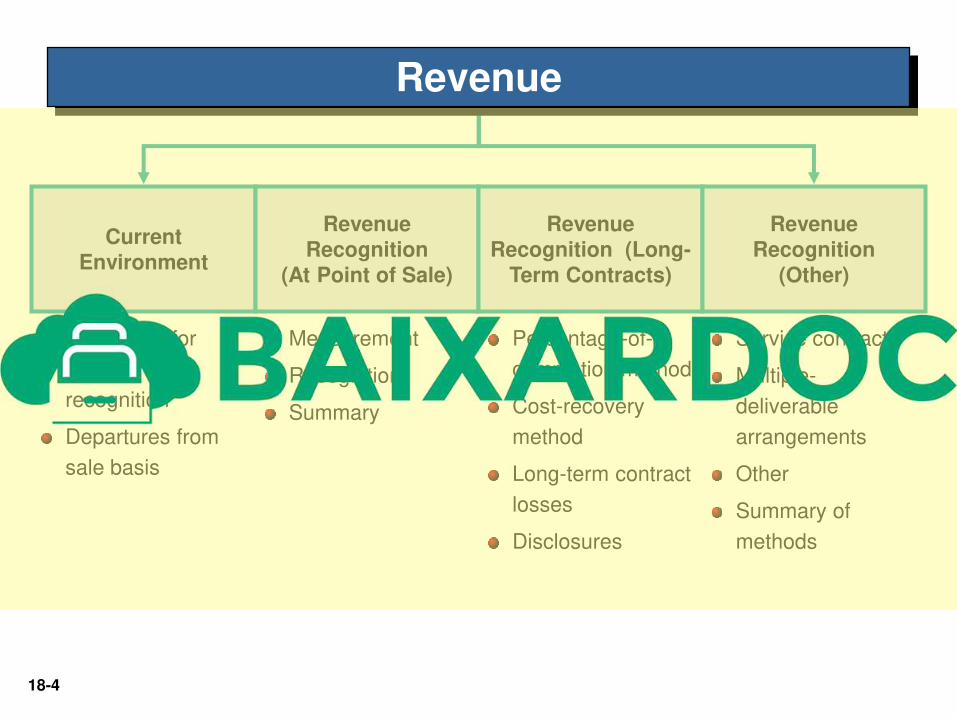

18-4

Current

Environment

Guidelines for

revenue

recognition

Departures from

sale basis

Revenue

Recognition

(At Point of Sale)

Revenue

Recognition (Long-

Term Contracts)

Revenue

Recognition

(Other)

Measurement

Recognition

Summary

Service contracts

Multiple-

deliverable

arrangements

Other

Summary of

methods

Percentage-of-

completion method

Cost-recovery

method

Long-term contract

losses

Disclosures

Revenue

18-5

Restatements for improper revenue recognition are

relatively common and can lead to significant share price

adjustments.

Revenue recognition is a top fraud risk and regardless

of the accounting rules followed (IFRS or U.S. GAAP),

the risk or errors and inaccuracies in revenue reporting is

significant.

The Current Environment

18-6

Revenue recognition principle: Revenue is recognized

Guidelines for Revenue Recognition

The Current Environment

LO 1 Apply the revenue recognition principle.

(1) when it is probable that the economic benefits will

flow to the company and

(2) when the benefits can be measured reliably.

18-7

Sale of product from inventory

Type of

Transaction Rendering a

service Permitting use

of an asset

Sale of asset other than inventory

Date of sale (date of delivery)

Services performed and

billable

As time passes or assets are

used

Date of sale or trade-in

Gain or loss on disposition

Revenue from interest, rents, and royalties

Revenue from fees or services

Revenue from sales

Description

of Revenue

Timing of

Revenue

Recognition

The Current Environment

LO 1 Apply the revenue recognition principle.

Illustration 18-1

Revenue Recognition Classified by Nature of Transaction

18-8

Earlier recognition is appropriate if there is a high degree of

certainty about the amount of revenue earned.

Delayed recognition is appropriate if the

degree of uncertainty concerning the amount of revenue

or costs is sufficiently high or

sale does not represent substantial completion of the

earnings process.

Departures from the Sale Basis

The Current Environment

LO 1 Apply the revenue recognition principle.

18-9

Revenue should be measured at the fair value of

consideration received or receivable.

Trade discounts or volume rebates should reduce

consideration received or receivable and the related

revenue.

If payment is delayed, seller should impute an interest

rate for the difference between the cash or cash

equivalent price and the deferred amount.

Measurement of Sale Revenue

Revenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

18-10

Revenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

Illustration 18-2