Handsets/Components - Monthly InsighT

37

December 2020 Handsets/Components Monthly InsighT Seize the day Wonjae Park +822-3774-1426 [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Handsets/Components - Monthly InsighT

De c e m b e r 2 0 2 0

Handsets/Components

Monthly InsighTSeize the day

Wonjae Park [email protected]

Mirae Asset Daewoo Research2 | Monthly InsighT

I. Investment strategy

II. Sector view

III. Spotlight stocks & other notable stocks

IV. Pioneer: Company visits/IR/NDRs/IPOs

V. Global IT navigation

Mirae Asset Daewoo Research3 | Monthly InsighT

Cumulative returns

November

Monthly InsighT returnsNovember: +4.1% for spotlight stocks vs. +19.4% for other notable stocks

Mirae Asset Daewoo IT universe share performance

I. Investment strategy

Note: Mar.-Nov. 2020 data

11.8

14.3

19.4

4.1

0 10 20 30

KOSDAQ

KOSPI

Avg. of other notable stocks

Avg. of spotlight stocks

(%)

45.1

30.9

29.0

64.1

0 20 40 60 80

KOSDAQ

KOSPI

Avg. of other notablestocks

Avg. of spotlight stocks

(%)

16.9

22.0

19.4

1.8

2.0

5.2

7.4

4.1

0 5 10 15 20 25

SEMCO

LS

Avg. of other notable stocks

LGE

LG Innotek

Hanwha Aerospace

SSC

Avg. of spotlight stocks

(%)

Mirae Asset Daewoo Research4 | Monthly InsighT

Share performance and 2020F P/E for Korean IT large caps

Key handsets/components stocks

Company RatingTP

(W)

Current price

(11/30/20)

Upside(%)

Share performance (%)

P/E (x) P/B (x) ROE (x)

1W 1M 20F 21F 20F 21F 20F 21F

SEMCO Buy 196,000 156,000 25.6 2.6 16.9 20.9 16.2 2.1 1.9 10.3 12.0

LG Innotek Buy 221,000 155,000 42.6 -4.9 2.0 11.5 8.0 1.5 1.2 13.3 16.7

LS Buy 80,000 63,200 26.6 0.3 22.0 14.9 10.0 0.6 0.6 3.9 5.6

MCNEX Buy 47,000 36,450 28.9 1.0 11.0 7.7 6.5 1.9 1.5 27.2 25.4

LGE Buy 125,000 85,500 46.2 -4.1 1.8 8.0 7.4 1.0 0.9 12.1 12.0

HAS Buy 39,000 26,400 47.7 -3.6 5.2 12.4 10.0 0.5 0.5 4.2 4.9

SSC Buy 23,100 18,750 23.2 -2.1 7.4 27.8 18.9 1.5 1.5 5.6 7.7

I. Investment strategy

Smartphone components suppliers deserve attention in 2021

Source: WISEfn, Mirae Asset Daewoo Research

■ IT industry update- COVID-19 continues to weigh on the economy, but IT players have benefited from

pandemic effects. 1) Spread of contactless culture: Remote work, e-learning, online games, etc.2) Channel inventory shortages in 1H20 and economic recovery expectations for 2021

� Stockpiling demand3) China backlash (trade war with US, territorial conflict with India): Favorable to Korean IT firms

- Smartphones: The market has normalized, and SEC’s M/S expansion strategy has yielded positive results; Huawei posted weak results, while Xiaomi benefited from Huawei’s predicament.

- TVs/home appliances: Margins have improved on solid demand and lower marketing spending.

- Components: Prices are stable, and stockpiling demand is picking up due to concerns over supply disruptions; F/X rate movements are worrisome.

■ Strategy1) We recommend focusing on companies with strong competitiveness, decent results, and

a robust 2021 outlook, but note that expectations have reached burdensome levels. 2) Amid an increase in uncertainties (F/X rates and COVID-19 resurgence), we recommend a

short-term trading strategy.3) SEC’s smartphone sales likely to expand in 2021 � Overweight components suppliers

■ Spotlight stocks- SEMCO, LG Innotek, LS, MCNEX

■ November company visits/IR/NDRs (small/mid-caps)- SEMCO, SSC, Spigen Korea, Shinsung E&G, Everybot, SD Optics, Optrontec, INNO

Instrument, Innox Advanced Materials, Intellian, JNTC, Park Systems, Point Mobile, LGInnotek, LGE, LS

0

9

18

27

36

-18

-6

6

18

30Price (1M, L) 2020F P/E (R)

(%) (x)

(20.6, 63.0)

Note: Market cap of W1tr+Source: WISEfn, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research5 | Monthly InsighT

Earnings forecast revisions for large-cap handsets/components plays

I. Investment strategy

(Wbn, %)

Source: Mirae Asset Daewoo Research

Previous Revised % chg.Notes

4Q20F 2020F 2021F 4Q20F 2020F 2021F 4Q20F 2020F 2021F

SEMCO Revenue 2,040.6 8,365.2 9,214.2 2,040.6 8,365.2 9,214.2 0.0 0.0 0.0

OP 218.3 781.3 903.6 218.3 781.3 903.6 0.0 0.0 0.0

NP 156.4 557.8 652.4 156.4 557.8 652.4 0.0 0.0 0.0

LG Innotek Revenue 3,483.5 9,264.2 9,299.6 3,483.5 9,264.2 9,299.6 0.0 0.0 0.0

OP 314.9 585.2 660.9 314.9 585.2 660.9 0.0 0.0 0.0

NP 230.8 345.8 450.6 230.8 345.8 450.6 0.0 0.0 0.0

LS Revenue 2,624.7 10,275.3 10,454.2 2,624.7 10,275.3 10,454.2 0.0 0.0 0.0

OP 115.2 426.6 461.8 115.2 426.6 461.8 0.0 0.0 0.0

NP 57.8 129.5 223.4 57.8 129.5 223.4 0.0 0.0 0.0

MCNEX Revenue 322.6 1,349.6 1,478.4 322.6 1,349.6 1,478.4 0.0 0.0 0.0

OP 17.9 64.6 97.3 17.9 64.6 97.3 0.0 0.0 0.0

NP 13.9 55.1 71.9 13.9 55.1 71.9 0.0 0.0 0.0

LGE Revenue 18,320.7 62,801.9 68,272.8 18,320.7 62,801.9 68,272.8 0.0 0.0 0.0

OP 597.6 3,142.4 3,731.2 597.6 3,142.4 3,731.2 0.0 0.0 0.0

NP 299.7 2,007.7 2,222.4 299.7 2,007.7 2,222.4 0.0 0.0 0.0

Hanwha Revenue 1,690.6 5,287.8 5,969.6 1,690.6 5,287.8 5,969.6 0.0 0.0 0.0

Aerospace OP 70.2 237.9 253.4 70.2 237.9 253.4 0.0 0.0 0.0

NP 42.4 107.3 153.8 42.4 107.3 153.8 0.0 0.0 0.0

SSC Revenue 309.8 1,152.3 1,256.2 309.8 1,152.3 1,256.2 0.0 0.0 0.0

OP 19.4 64.5 81.0 19.4 64.5 81.0 0.0 0.0 0.0

NP 10.7 32.7 54.1 10.7 32.7 54.1 0.0 0.0 0.0

Seoul Viosys Revenue 116.9 427.7 507.7 116.9 427.7 507.7 0.0 0.0 0.0

OP 6.0 24.2 35.0 6.0 24.2 35.0 0.0 0.0 0.0

NP 2.0 11.3 13.0 2.0 11.3 13.0 0.0 0.0 0.0

Partron Revenue 265.2 1,111.3 1,148.6 265.2 1,111.3 1,148.6 0.0 0.0 0.0

OP 12.7 45.1 70.7 12.7 45.1 70.7 0.0 0.0 0.0

NP 11.3 28.6 61.2 11.3 28.6 61.2 0.0 0.0 0.0

Spigen Korea Revenue 104.5 398.4 370.2 104.5 398.4 370.2 0.0 0.0 0.0

OP 15.8 80.3 61.4 15.8 80.3 61.4 0.0 0.0 0.0

NP 13.5 70.1 51.4 13.5 70.1 51.4 0.0 0.0 0.0

Amotech Revenue 55.0 217.5 271.2 55.0 217.5 271.2 0.0 0.0 0.0

OP -0.3 -2.7 14.3 -0.3 -2.7 14.3 0.0 0.0 0.0

NP -3.1 -12.5 10.2 -3.1 -12.5 10.2 0.0 0.0 0.0

Mirae Asset Daewoo Research6 | Monthly InsighT

Consensus vs. Mirae Asset Daewoo estimates

I. Investment strategy

(Wbn, %)

Source: WISEfn, Mirae Asset Daewoo Research

Mirae Asset Daewoo Consensus Diff.Notes

4Q20F 2020F 2021F 4Q20F 2020F 2021F 4Q20F 2020F 2021F

SEMCO Revenue 2,040.6 8,365.2 9,214.2 2,152.5 8,479.2 9,397.1 -5.2 -1.3 -1.9

OP 218.3 781.3 903.6 256.9 820.6 1,029.6 -15.0 -4.8 -12.2

NP 156.4 557.8 652.4 173.9 586.6 734.6 -10.1 -4.9 -11.2

LG Innotek Revenue 3,483.5 9,264.2 9,299.6 3,512.3 9,282.0 10,073.1 -0.8 -0.2 -7.7

OP 314.9 585.2 660.9 318.3 592.5 743.9 -1.1 -1.2 -11.2

NP 230.8 345.8 450.6 167.9 304.1 468.2 37.5 13.7 -3.8

LS Revenue 2,624.7 10,275.3 10,454.2 2,701.1 10,322.1 10,844.3 -2.8 -0.5 -3.6

OP 115.2 426.6 461.8 116.0 410.6 467.0 -0.7 3.9 -1.1

NP 57.8 129.5 223.4 60.5 115.8 186.5 -4.5 11.9 19.8

MCNEX Revenue 322.6 1,349.6 1,478.4 319.8 1,345.2 1,547.1 -0.9 -0.3 4.6

OP 17.9 64.6 97.3 16.5 62.8 98.6 -7.8 -2.8 1.3

NP 13.9 55.1 71.9 12.9 53.9 77.0 -7.2 -2.2 7.1

LGE Revenue 18,320.7 62,801.9 68,272.8 17,668.1 62,538.0 67,290.4 3.7 0.4 1.5

OP 597.6 3,142.4 3,731.2 576.7 3,152.6 3,593.7 3.6 -0.3 3.8

NP 299.7 2,007.7 2,222.4 263.2 1,887.9 2,122.4 13.9 6.3 4.7

Hanwha Revenue 1,690.6 5,287.8 5,969.6 1,736.1 5,290.7 5,718.3 -2.6 -0.1 4.4

Aerospace OP 70.2 237.9 253.4 67.0 217.5 244.3 -4.8 9.4 3.7

NP 42.4 107.3 153.8 41.1 102.5 131.0 -3.2 4.7 17.4

SSC Revenue 309.8 1,152.3 1,256.2 314.0 1,155.8 1,267.6 -1.3 -0.3 -0.9

OP 19.4 64.5 81.0 20.7 65.4 88.5 -6.3 -1.4 -8.5

NP 10.7 32.7 54.1 14.3 37.7 58.1 -25.2 -13.3 -6.9

Seoul Viosys Revenue 116.9 427.7 507.7 116.0 426.8 490.7 -0.8 -0.2 -3.3

OP 6.0 24.2 35.0 7.9 26.1 38.3 31.7 7.9 9.4

NP 2.0 11.3 13.0 3.5 14.3 16.9 75.0 26.5 30.0

Partron Revenue 265.2 1,111.3 1,148.6 279.0 1,109.7 1,284.7 -4.9 0.1 -10.6

OP 12.7 45.1 70.7 12.1 45.4 80.1 5.0 -0.7 -11.7

NP 11.3 28.6 61.2 10.7 27.6 57.9 5.6 3.6 5.7

Spigen Korea Revenue 104.5 398.4 370.2 106.3 400.2 405.3 -1.7 -0.4 -8.7

OP 15.8 80.3 61.4 16.5 80.9 68.2 -4.2 -0.7 -10.0

NP 13.5 70.1 51.4 12.6 68.7 56.5 7.1 2.0 -9.0

Amotech Revenue 55.0 217.5 271.2 56.9 219.4 311.3 -3.3 -0.9 -12.9

OP -0.3 -2.7 14.3 0.3 -2.1 26.4 TTR RR -45.8

NP -3.1 -12.5 10.2 -0.8 -8.4 19.3 RR RR -47.2

Mirae Asset Daewoo Research7 | Monthly InsighT

I. Investment strategy

II. Sector view

III. Spotlight stocks & other notable stocks

IV. Pioneer: Company visits/IR/NDRs/IPOs

V. Global IT navigation

Mirae Asset Daewoo Research8 | Monthly InsighT

Huawei rapidly losing ground; SEC’s smartphone sales to expand in 2021; time to accumulate top-tier parts makers

SEC smartphone sales and M/S

Check point

II. Sector view

Apple iPhone shipments and M/S

Source: SEC, Counterpoint, Mirae Asset Daewoo Research

Source: Apple, FactSet, Mirae Asset Daewoo Research

■ Shipment data

- October shipments (Counterpoint): 146mn handsets (-12.4% YoY, +5.9% MoM)

125mn smartphones (-8.6% YoY, +5.3% MoM)

- October shipments and M/S of top five smartphone makers (Counterpoint)

1. SEC: 25.9mn units (-1.1% YoY, +1.2% MoM), 20.8%

2. Apple: 17.4mn units (-23.8% YoY, +44.4% MoM), 14.0%

3. Xiaomi: 15.5mn units (+29.7% YoY, +0.5% MoM), 12.5%

4. Vivo: 11.1mn units (+9.6% YoY, +3.5% MoM), 8.9%

5. Oppo: 11.0mn units (+5.0% YoY, +7.3% MoM), 8.8%

[9. LGE: 2.5mn units (+1.8% YoY, +21.6% MoM), 2.0%]

- Shipments by market: US: 12mn units (-15.1% YoY, +17.1% MoM)

China: 25.9mn units (-22.4% YoY, +1.8% MoM)

India: 20mn units (+0.0% YoY, +2.6% MoM)

■ Key takeaways

1. Global smartphone shipments contracted 8.6% YoY; -15.1% YoY in the US, -22.4% YoY in China, and +0.0% YoY in India

2. SEC: Largest smartphone vendor based on monthly M/S (20.8%; +1.6%p YoY, -0.8%p MoM)- Second-largest vendor in India with a M/S of 22.5%

3. Apple: Delays to new model releases (M/S of 14.0%; -2.8%p YoY, +3.8%p MoM)

4. Huawei: Down to 6th place (M/S of 7.8%; -7.0%p YoY, -4.9%p MoM) following the sale of the Honor brand (M/S of 3.0%; -0.6%p MoM)

5. LGE: Shipments surpassed 2mn units for the fourth straight month (2.5mn units), and M/S increased 0.3%p MoM to 2.0% (9th place).

6. Xiaomi: Third-largest smartphone maker based on monthly M/S; benefited from the US ban on Huawei products and retained its top spot in India with a M/S of 26.3%

* Huawei is rapidly losing ground, which should benefit Xiaomi and SEC.* SEC’s smartphone sales are projected to expand in 2021. For components plays,

performances are likely to diverge. We advise investors to accumulate shares of top-tier components makers.

-15

0

15

30

45

0

25

50

75

100

1Q11 1Q13 1Q15 1Q17 1Q19

(%)(mn units) iPhone shipments (L)

YoY (R)

Apple M/S (R)

-15

0

15

30

45

0

25

50

75

100

1Q11 1Q13 1Q15 1Q17 1Q19

(%)(mn units) Smartphone shipments (L) YoY (R) SEC M/S (R)

Mirae Asset Daewoo Research9 | Monthly InsighT

II. Sector view

Key charts

Global monthly smartphone M/S trends

China monthly smartphone M/S trends

Huawei smartphone shipments and M/S

India monthly smartphone M/S trends

Note: Huawei sold off its Honor business in October.Source: IDC, Mirae Asset Daewoo Research

Source: Counterpoint, Mirae Asset Daewoo Research

Note: Huawei sold off its Honor business in October.Source: Counterpoint, Mirae Asset Daewoo Research

Source: Counterpoint, Mirae Asset Daewoo Research

-15

0

15

30

45

0

25

50

75

100

4Q13 4Q14 4Q15 4Q16 4Q17 4Q18 4Q19

(%)(mn units) Smartphone shipments (L) YoY (R) Huawei M/S (R)

0

10

20

30

40

4/14 10/14 4/15 10/15 4/16 10/16 4/17 10/17 4/18 10/18 4/19 10/19 4/20 10/20

SEC Apple Huawei Xiaomi Oppo Vivo

(%)

0

15

30

45

60

4/16 10/16 4/17 10/17 4/18 10/18 4/19 10/19 4/20 10/20

Oppo + Vivo Huawei Apple Xiaomi SEC

(%)

0

15

30

45

60

4/16 10/16 4/17 10/17 4/18 10/18 4/19 10/19 4/20 10/20

SEC Xiaomi Huawei + Vivo + Oppo Micromax + Lava

(%)

Mirae Asset Daewoo Research10 | Monthly InsighT

Forecasts vs. actual handset shipment data during IT bubble and financial crisis (mn units)

Oppo + Vivo smartphone shipments and M/S

US monthly smartphone M/S trends

Xiaomi smartphone shipments and M/S

Key charts

Source: IDC, Mirae Asset Daewoo Research Source: Counterpoint, Mirae Asset Daewoo Research

Source: Counterpoint, Mirae Asset Daewoo Research Source: Counterpoint, Mirae Asset Daewoo Research

II. Sector view

-15

0

15

30

45

0

20

40

60

80

3Q11 3Q13 3Q15 3Q17 3Q19

(%)(mn units)Oppo + Vivo shipments (L) YoY (R) Oppo + Vivo M/S (R)

-15

0

15

30

45

5

15

25

35

45

4Q13 4Q14 4Q15 4Q16 4Q17 4Q18 4Q19

(%)(mn units)Smartphone shipments (L) YoY (R) Xiaomi M/S (R)

0

15

30

45

60

4/16 10/16 4/17 10/17 4/18 10/18 4/19 10/19 4/20 10/20

(%)SEC Apple LGE ZTE Motorola

Mirae Asset Daewoo Research11 | Monthly InsighT

Global and China handset market trends China monthly smartphone shipments

2015 2016 2017 2018 2019

Global (mn units) Feature phones 542 501 512 489 422

Smartphones 1,438 1,469 1,465 1,403 1,372

Total 1,980 1,971 1,978 1,891 1,794

Global (US$bn) Feature phones 13 10 10 9 7

Smartphones 426 416 458 483 458

Total 439 426 468 492 465

China (mn units) Feature phones 43 34 24 21 18

Smartphones 430 467 444 397 367

Total 473 501 469 417 385

China (US$bn) Feature phones 1 1 0 0 0

Smartphones 112 120 133 127 118

Total 113 121 134 127 118

China proportion (%, volume) Feature phones 7.9 6.8 4.7 4.2 4.2

Smartphones 29.9 31.8 30.3 28.3 26.7

Total 23.9 25.4 23.7 22.1 21.4

China proportion (%, US$ value) Feature phones 5.9 5.3 4.7 5.4 5.2

Smartphones 26.3 28.9 29.1 26.2 25.8

Total 25.6 28.3 28.6 25.8 25.5

II. Sector view

Key charts

Source: IDC, Mirae Asset Daewoo Research Source: CAICT, Mirae Asset Daewoo Research

Note: Huawei sold off its Honor business in October.Source: Counterpoint, Mirae Asset Daewoo Research

0

20

40

60

80

-60

-30

0

30

60

3/16 9/16 3/17 9/17 3/18 9/18 3/19 9/19 3/20 9/20

(%) (mn units)Shipments (L) YoY (R) MoM (R)

China M/S (total) 10/19 11/19 12/19 1/20 2/20 3/20 4/20 5/20 6/20 7/20 8/20 9/20 10/20

SEC 0.7 0.8 0.5 0.6 0.5 0.7 0.7 0.6 0.7 0.5 0.5 0.6 0.6

Apple 13.6 11.8 12.3 11.2 9.1 7.7 9.5 9.2 8.4 7.7 7.8 7.3 9.6

Huawei 37.4 34.9 34.9 34.7 37.7 41.6 43.0 45.7 45.8 47.1 44.4 39.4 25.7

Oppo + Vivo 30.5 32.3 33.1 34.7 34.9 33.6 31.1 30.6 28.6 29.7 30.8 33.6 35.1

China M/S(smartphones)

10/19 11/19 12/19 1/20 2/20 3/20 4/20 5/20 6/20 7/20 8/20 9/20 10/20

SEC 0.7 0.8 0.6 0.6 0.5 0.7 0.7 0.6 0.7 0.5 0.5 0.6 0.6

Apple 14.1 12.2 12.7 11.5 9.5 8.0 9.8 9.4 8.6 7.8 7.9 7.5 9.9

Huawei 38.7 36.2 36.2 35.7 39.4 43.1 44.4 46.8 46.8 47.9 45.2 40.3 26.3

Oppo + Vivo 31.5 33.5 34.3 35.8 36.5 34.8 32.1 31.3 29.2 30.2 31.3 34.3 35.9

China smartphone M/S trends (%) India smartphone M/S trends (%)

India M/S (total) 10/19 11/19 12/19 1/20 2/20 3/20 4/20 5/20 6/20 7/20 8/20 9/20 10/20

SEC19.0 19.8 16.6 16.3 17.1 19.1 7.5 14.8 24.2 25.2 24.1 22.9 22.9

Xiaomi 18.4 16.5 15.9 15.1 18.6 21.7 37.5 24.1 18.6 18.1 17.5 18.8 18.1

Oppo + Vivo 15.7 18.1 19.4 18.0 15.6 15.1 15.0 17.3 22.7 21.2 19.3 18.3 17.3

Realme 8.8 4.5 4.6 5.9 6.5 7.1 5.0 8.1 9.3 9.2 9.6 12.8 10.7

India M/S(smartphones)

10/19 11/19 12/19 1/20 2/20 3/20 4/20 5/20 6/20 7/20 8/20 9/20 10/20

SEC 19.0 20.2 17.1 17.3 17.6 18.9 8.6 17.5 26.2 27.4 26.2 23.6 22.5

Xiaomi 29.8 28.7 27.7 27.2 32.1 35.2 51.7 34.9 24.4 23.8 23.7 25.2 26.3

Oppo + Vivo 25.4 31.4 33.7 32.4 27.0 24.6 20.7 25.0 29.8 27.8 26.2 24.5 25.1

Realme 14.3 7.9 7.9 10.6 11.2 11.6 6.9 11.8 12.2 12.1 13.0 17.2 15.5

Source: Counterpoint, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research12 | Monthly InsighT

I. Investment strategy

II. Sector view

III. Spotlight stocks & other notable stocks

IV. Pioneer: Company visits/IR/NDRs/IPOs

V. Global IT navigation

Mirae Asset Daewoo Research13 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

781

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSPI

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 6,838 8,002 8,041 8,365 9,214 10,278

Free float (%) OP (Wbn) 306 1,150 734 781 904 1,112

Foreign ownership (%) OP margin (%) 4.5 14.4 9.1 9.3 9.8 10.8

Beta (12M) NP (Wbn) 162 656 514 558 652 814

52-week low (W) EPS (W) 2,084 8,457 6,627 7,188 8,407 10,496

52-week high (W) ROE (%) 3.8 14.5 10.2 10.0 10.7 12.1

(%) 1M 6M 12M P/E (x) 48.0 12.2 18.9 21.7 18.6 14.9

Absolute 16.9 24.8 40.5 P/B (x) 1.8 1.6 1.8 2.0 1.9 1.7

Relative 2.2 -2.3 13.2 Div. yield (%) 0.8 1.0 0.9 0.8 0.8 0.9

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: Samsung Electro-Mechanics, Mirae Asset Daewoo Research estimates

Buy

196,000

156,000

Expected return 26%

85,700

158,500

21.7

17.7

2,591.34

11,652

78

73.4

8.5

OP (20F, Wbn)

821

34.5

1.04

70

80

90

100

110

120

130

140

150

19.11 20.2 20.5 20.8 20.11

Samsung Electro-Mechanics

KOSPI

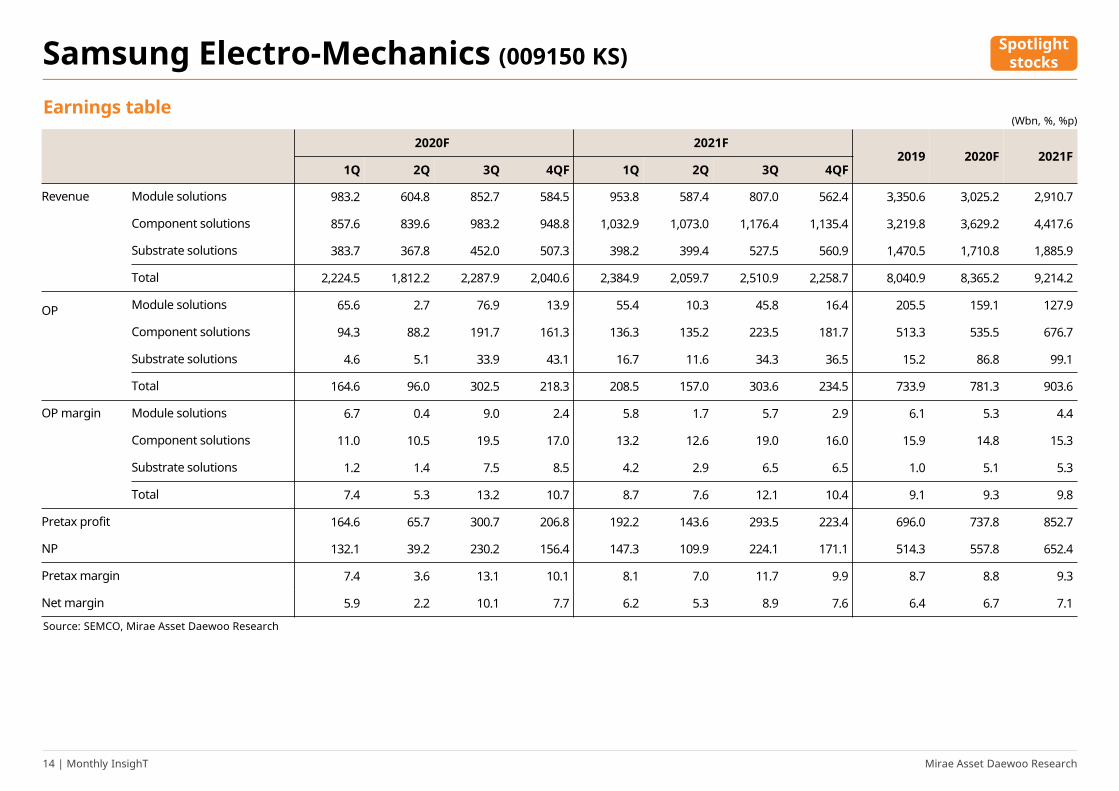

Samsung Electro-Mechanics (009150 KS)

Aiming high for 2021

■ 2020 preview: Decent OP of W781.3bn (+6.5% YoY) expected

- For 2020, we forecast SEMCO to deliver revenue of W8.37tr (+4.0% YoY) and operating profit of W781.3bn (+6.5% YoY).

- IT demand has been stronger than feared, and sales of MLCCs have been decent.

- Moreover, substrate profitability has improved following business streamlining efforts, and SEC’s smartphone volume growth

has had a favorable impact on SEMCO’s earnings.

■ 2021 outlook: OP to expand 15.7% YoY to W903.6bn

- For 2021, we anticipate revenue of W9.21tr (+10.1% YoY) and operating profit of W903.6bn (+15.7% YoY). We think operating

profit could surpass W1tr if market conditions and currency effects turn more favorable.

- We expect SEMCO to benefit from: 1) solid sales of MLCCs for PC/game console applications; 2) improving business

conditions for semiconductor substrates; and 3) a recovery in automotive demand.

■ Reiterate Buy and target price of W196,000

- While the falling USD/KRW rate is worrisome, we note that market conditions are becoming more favorable.

- We maintain our Buy rating and target price of W196,000 (P/B of 2.35x; 10% premium to the three-year upper band average),

in light of solid MLCC sales and the upside potential of the substrate business.

Spotlightstocks

Mirae Asset Daewoo Research14 | Monthly InsighT

2020F 2021F2019 2020F 2021F

1Q 2Q 3Q 4QF 1Q 2Q 3Q 4QF

Revenue Module solutions 983.2 604.8 852.7 584.5 953.8 587.4 807.0 562.4 3,350.6 3,025.2 2,910.7

Component solutions 857.6 839.6 983.2 948.8 1,032.9 1,073.0 1,176.4 1,135.4 3,219.8 3,629.2 4,417.6

Substrate solutions 383.7 367.8 452.0 507.3 398.2 399.4 527.5 560.9 1,470.5 1,710.8 1,885.9

Total 2,224.5 1,812.2 2,287.9 2,040.6 2,384.9 2,059.7 2,510.9 2,258.7 8,040.9 8,365.2 9,214.2

OP Module solutions 65.6 2.7 76.9 13.9 55.4 10.3 45.8 16.4 205.5 159.1 127.9

Component solutions 94.3 88.2 191.7 161.3 136.3 135.2 223.5 181.7 513.3 535.5 676.7

Substrate solutions 4.6 5.1 33.9 43.1 16.7 11.6 34.3 36.5 15.2 86.8 99.1

Total 164.6 96.0 302.5 218.3 208.5 157.0 303.6 234.5 733.9 781.3 903.6

OP margin Module solutions 6.7 0.4 9.0 2.4 5.8 1.7 5.7 2.9 6.1 5.3 4.4

Component solutions 11.0 10.5 19.5 17.0 13.2 12.6 19.0 16.0 15.9 14.8 15.3

Substrate solutions 1.2 1.4 7.5 8.5 4.2 2.9 6.5 6.5 1.0 5.1 5.3

Total 7.4 5.3 13.2 10.7 8.7 7.6 12.1 10.4 9.1 9.3 9.8

Pretax profit 164.6 65.7 300.7 206.8 192.2 143.6 293.5 223.4 696.0 737.8 852.7

NP 132.1 39.2 230.2 156.4 147.3 109.9 224.1 171.1 514.3 557.8 652.4

Pretax margin 7.4 3.6 13.1 10.1 8.1 7.0 11.7 9.9 8.7 8.8 9.3

Net margin 5.9 2.2 10.1 7.7 6.2 5.3 8.9 7.6 6.4 6.7 7.1

Earnings table

Samsung Electro-Mechanics (009150 KS)

Source: SEMCO, Mirae Asset Daewoo Research

(Wbn, %, %p)

Spotlightstocks

Mirae Asset Daewoo Research15 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

585

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSPI

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 7,641 7,982 8,302 9,264 9,300 9,633

Free float (%) OP (Wbn) 296 264 403 585 661 684

Foreign ownership (%) OP margin (%) 3.9 3.3 4.9 6.3 7.1 7.1

Beta (12M) NP (Wbn) 175 163 102 346 451 471

52-week low (W) EPS (W) 7,385 6,891 4,323 14,613 19,039 19,915

52-week high (W) ROE (%) 9.4 8.0 4.7 14.5 16.3 14.6

(%) 1M 6M 12M P/E (x) 19.5 12.5 32.4 10.6 8.1 7.8

Absolute 2.0 5.1 27.0 P/B (x) 1.7 1.0 1.5 1.4 1.2 1.1

Relative -10.8 -17.7 2.4 Div. yield (%) 0.2 0.3 0.2 0.2 0.2 0.2

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: LG Innotek, Mirae Asset Daewoo Research estimates

Buy

221,000

155,000

Expected return 43%

76,300

179,500

10.6

17.7

2,591.34

3,668

24

59.2

238.1

OP (20F, Wbn)

593

34.5

0.99

70

80

90

100

110

120

130

140

150

19.11 20.2 20.5 20.8 20.11

LG Innotek

KOSPI

LG Innotek (011070 KS)

Strong performance to continue into 2021

Spotlightstocks

■ 2020 preview: OP of W585.2bn (+45.2% YoY) expected

- For 2020, we expect LG Innotek to report record-high revenue of W9.26tr (+11.6% YoY) and operating profit of W585.2bn

(+45.2% YoY).

- The strong performance should be attributable to record results at the optical solutions unit (camera modules and 3D

sensing modules) and the effects of Apple’s new product releases.

■ Anticipating a quarterly record in 4Q20 followed by a record year in 2021

- For 4Q20, we look for revenue of W3.48tr (+17.5% YoY, +56.2% QoQ) and operating profit of W314.9bn (+50.5% YoY, +252.1%

QoQ).

- In 2021, we forecast LG Innotek to break records again, with revenue of W9.30tr (+0.4% YoY) and operating profit of

W660.9bn (+12.9% YoY).

- The substrates/materials unit (semiconductor/tape substrates, photomasks, and touch windows) is anticipated to deliver

top- and bottom-line growth, and Apple is expected to adopt ToF modules on a broader scale.

■Maintain Buy and target price of W221,000

- The sale of the LED business should remove W100bn in operating losses annually.

Mirae Asset Daewoo Research16 | Monthly InsighT

Earnings table

2020F 2021F2019 2020F 2021F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue Total 2,010.9 1,539.9 2,229.9 3,483.5 2,133.1 1,727.1 2,491.8 2,947.5 8,302.0 9,264.2 9,299.6

Optical solutions 1,334.3 929.6 1,458.4 2,757.8 1,423.7 1,037.0 1,697.6 2,140.0 5,425.8 6,480.1 6,298.3

Substrates & materials 289.7 295.7 319.2 312.4 322.4 326.4 346.7 336.2 1,126.0 1,217.0 1,331.8

LED 283.3 232.9 328.2 345.2 335.3 321.7 386.9 420.7 1,131.9 1,189.6 1,464.7

Automotive components 103.6 81.7 124.1 68.1 51.7 42.0 60.7 50.5 618.3 377.5 204.9

OP Total 138.0 42.9 89.4 314.9 143.3 84.5 204.7 228.3 403.1 585.2 660.9

Optical solutions 113.4 12.1 29.2 262.0 85.4 20.7 118.8 149.8 361.0 416.7 374.8

Substrates & materials 42.1 71.4 76.8 70.5 61.7 72.9 87.4 80.3 185.6 260.9 302.3

LED 2.0 -29.0 1.2 2.2 -5.5 -9.4 -1.1 -1.3 -52.9 -23.6 -17.3

Automotive components -19.6 -11.5 -17.8 -19.8 1.7 0.3 -0.5 -0.5 -90.6 -68.7 1.1

OP Total 6.9 2.8 4.0 9.0 6.7 4.9 8.2 7.7 4.9 6.3 7.1

margin Optical solutions 8.5 1.3 2.0 9.5 6.0 2.0 7.0 7.0 6.7 6.4 6.0

Substrates & materials 14.5 24.1 24.1 22.6 19.1 22.3 25.2 23.9 16.5 21.4 22.7

LED 0.7 -12.5 0.4 0.6 -1.6 -2.9 -0.3 -0.3 -4.7 -2.0 -1.2

Automotive components -18.9 -14.1 -14.3 -29.2 3.4 0.7 -0.8 -1.0 -14.7 -18.2 0.5

Pretax profit 109.3 14.6 34.7 298.0 129.6 70.7 187.9 213.1 158.2 456.5 601.2

NP 80.6 7.6 26.9 230.8 97.1 53.0 140.8 159.7 102.3 345.8 450.6

Pretax margin 5.4 0.9 1.6 8.6 6.1 4.1 7.5 7.2 1.9 4.9 6.5

Net margin 4.0 0.5 1.2 6.6 4.6 3.1 5.7 5.4 1.2 3.7 4.8

LG Innotek (011070 KS)

(Wbn, %, %p)

Source: LG Innotek, Mirae Asset Daewoo Research

Spotlightstocks

Mirae Asset Daewoo Research17 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

339

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSPI

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 9,418 10,093 10,176 10,275 10,454 10,689

Free float (%) OP (Wbn) 402 360 272 339 355 373

Foreign ownership (%) OP margin (%) 4.3 3.6 2.7 3.3 3.4 3.5

Beta (12M) NP (Wbn) 297 404 25 130 223 239

52-week low (W) EPS (W) 9,219 12,551 787 4,023 6,939 7,428

52-week high (W) ROE (%) 11.5 13.7 0.8 4.0 6.6 6.7

(%) 1M 6M 12M P/E (x) 7.9 3.9 60.8 15.7 9.1 8.5

Absolute 22.0 69.0 43.1 P/B (x) 0.8 0.5 0.5 0.6 0.6 0.5

Relative 6.7 32.4 15.3 Div. yield (%) 1.7 2.5 3.0 2.3 2.3 2.3

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: LS, Mirae Asset Daewoo Research estimates

Buy

80,000

63,200

Expected return 27%

24,100

64,700

15.7

17.7

2,591.34

2,035

32

50.9

411.4

OP (20F, Wbn)

412

11.9

1.27

70

80

90

100

110

120

130

140

150

160

19.11 20.2 20.5 20.8 20.11

LS KOSPI

LS (006260 KS)

Favorable market conditions and recovery of subsidiaries

■ 2020 earnings to be better than feared

- For 3Q20, LS announced revenue of W2.57tr (+3.3% YoY, +2.8% QoQ) and operating profit of W123.8bn (+25.9% YoY, +31.4%

QoQ; including equity-method gains of W23.1bn).

- Revenue and operating profit exceeded our estimates by 3.2% (vs. W2.49tr) and 31.9% (vs. W93.9bn), respectively.

- For 2020, we look for revenue of W10.3tr (+1.0% YoY) and operating profit of W426.6bn (+21.2% YoY; including equity-

method gains of W87.7bn).

■ 2021 outlook: OP to grow 8.3% to W461.8bn (including equity-method gains of W107.1bn)

- Looking ahead to 2021, we see revenue rising 1.7% to W10.45tr and operating profit growing 8.3% to W461.8bn (including

equity-method gains of W107.1bn).

- At LS Cable & System (LSCS), margins are improving thanks to increasing orders for high-end products, while LS-Nikko

Copper looks poised to benefit from higher copper prices.

- LS I&D and LS Mtron should also continue to improve—the former due to Superior Essex’s improvements and the latter due

to increasing electronic parts revenue.

■ Reiterate Buy and lift TP to W80,000

- We reiterate our Buy call on LS and lift our target price to W80,000, applying a P/B of 0.73x (10% premium to the five-year

average) to our 12-month forward BPS of W109,635.

- Assuming a DPS of W1,450, the stock offers a dividend yield of 2.4% based on the current share price.

Spotlightstocks

Mirae Asset Daewoo Research18 | Monthly InsighT

Earnings table

LS (006260 KS)

2020F 2021F2020F 2021F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

LS Revenue 2,581.5 2,499.4 2,569.8 2,624.7 2,626.3 2,593.6 2,574.8 2,659.5 10,275.3 10,454.2

Equity-method 21.4 12.3 23.1 30.9 27.2 17.7 31.0 31.3 87.7 107.1

OP 93.3 94.2 123.8 115.2 102.9 105.2 134.4 119.3 426.6 461.8

Pretax profit 30.0 52.3 87.3 105.7 78.7 88.9 121.9 106.7 275.3 396.2

NP -7.2 31.1 47.8 57.8 44.3 50.1 69.1 60.0 129.5 223.4

EPS -222 965 1,485 1,795 1,374 1,555 2,145 1,864 4,023 6,939

OP margin 3.6 3.8 4.8 4.4 3.9 4.1 5.2 4.5 4.2 4.4

Pretax margin 1.2 2.1 3.4 4.0 3.0 3.4 4.7 4.0 2.7 3.8

Net margin -0.3 1.2 1.9 2.2 1.7 1.9 2.7 2.3 1.3 2.1

LSCS Revenue 1,155.7 1,216.7 1,171.3 1,162.4 1,250.8 1,230.3 1,157.9 1,169.5 4,706.1 4,808.5

(consolidated) OP 40.9 42.9 42.1 36.0 48.7 47.7 45.8 36.3 161.9 178.4

Pretax profit 23.1 30.5 20.7 45.2 50.6 48.5 54.0 44.0 119.5 197.0

LS I&D Revenue 559.3 464.9 594.6 572.1 564.9 469.5 600.5 577.8 2,190.9 2,212.8

(consolidated) OP -10.6 -0.9 26.0 8.8 -9.6 3.8 20.3 10.1 23.3 24.5

Pretax profit -21.5 -11.6 16.2 6.7 -6.1 2.3 14.5 7.4 -10.2 18.2

LS Mtron Revenue 208.6 204.7 226.2 204.6 232.8 263.9 247.4 233.9 844.1 978.0

(consolidated) OP 0.2 1.6 6.1 6.4 1.8 -9.5 -0.7 1.9 14.3 -6.5

Pretax profit -34.8 -8.0 -8.5 34.1 0.2 4.0 37.5 30.9 -17.2 72.6

LSIS Revenue 635.6 598.3 558.6 685.6 577.8 629.9 568.9 678.3 2,478.1 2,454.8

(consolidated) OP 40.5 38.8 21.8 33.1 34.8 45.5 38.1 39.8 134.2 158.2

Pretax profit 33.0 31.6 28.9 26.5 27.8 36.4 30.5 31.8 120.0 126.6

LS-Nikko Revenue 1,884.7 1,827.1 2,105.5 1,959.3 1,903.5 1,845.4 2,126.6 1,978.9 7,776.6 7,854.4

(consolidated) OP 83.4 44.6 63.7 74.5 84.2 45.0 64.3 75.2 266.2 268.8

Pretax profit 71.1 45.8 79.9 81.0 71.3 46.3 81.3 82.0 277.8 281.0

Source: LS, Mirae Asset Daewoo Research

(Wbn, W, %, %p)

Spotlightstocks

Mirae Asset Daewoo Research19 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

65

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSDAQ

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 668 697 1,268 1,350 1,478 1,609

Free float (%) OP (Wbn) 20 41 113 65 97 114

Foreign ownership (%) OP margin (%) 3.0 5.9 8.9 4.8 6.6 7.1

Beta (12M) NP (Wbn) -1 30 85 55 72 85

52-week low (W) EPS (W) -66 1,767 4,787 3,087 4,022 4,767

52-week high (W) ROE (%) -1.1 26.2 47.7 22.2 23.6 22.9

(%) 1M 6M 12M P/E (x) - 7.3 7.9 11.8 9.1 7.6

Absolute 11.0 13.9 35.3 P/B (x) 2.3 1.7 3.0 2.4 1.9 1.6

Relative -0.7 -8.3 -3.4 Div. yield (%) 1.3 2.3 1.3 1.4 1.9 2.2

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: MCNEX, Mirae Asset Daewoo Research estimates

Buy

47,000

36,450

Expected return 29%

21,750

43,350

11.8

17.7

886.11

651

18

70.7

-35.5

OP (20F, Wbn)

63

10.3

0.99

70

80

90

100

110

120

130

140

150

160

170

19.11 20.2 20.5 20.8 20.11

MCNEX KOSDAQ

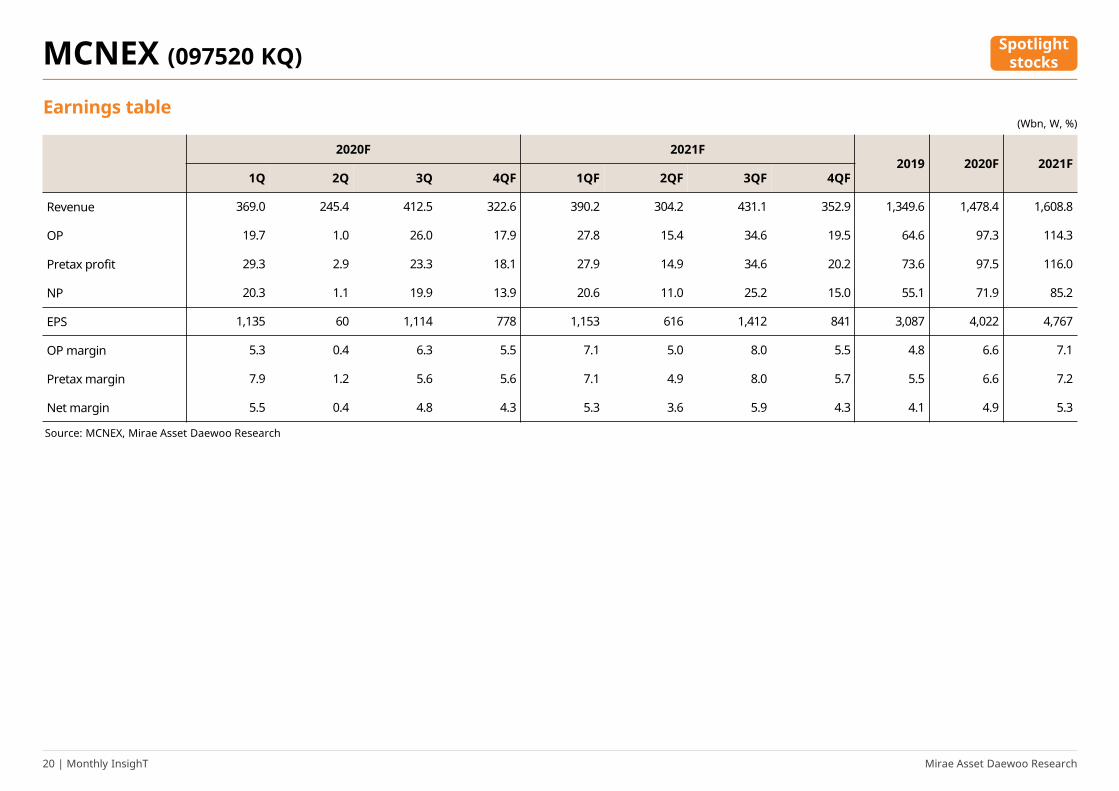

MCNEX (097520 KQ) Spotlight

stocks

A leading smartphone component supplier

■ Revenue to hit a record high in 2020; outstanding risk management capability

- For 2020, we forecast MCNEX to post revenue of W1.35tr (+6.5% YoY) and operating profit of W64.6bn (-42.9% YoY).

- We would view such results as solid, given the sharp deterioration of the smartphone market due to COVID-19.

- We expect revenue to hit a record high on the normalization of SEC’s smartphone sales from 3Q20. However, we see OP

margin contracting 4.1%p YoY to 4.8% due to an unfavorable cost structure.

■ OP to improve to W97.3bn (+50.6% YoY) in 2021

- Looking ahead to 2021, we expect revenue of W1.48tr (+9.5% YoY) and operating profit of W97.3bn (+50.6% YoY).

- We anticipate another year of record-breaking revenue, driven by: 1) SEC’s smartphone sales volume growth; and 2) an

increase in actuator revenue.

- We forecast OP margin to improve 1.8%p YoY to 6.6% (though still lagging behind the 2019 level), fueled by top-line growth

and better automotive camera module margins.

■ Retain Buy and TP of W47,000

- We believe 1) MCNEX’s ability to mass produce smartphone camera modules and 2) the growth potential of its automotive

camera module business deserve attention.

- We derived our target price of W47,000 by applying a P/E of 12x to our 12-month forward EPS of W3,944.

Mirae Asset Daewoo Research20 | Monthly InsighT

Earnings table

2020F 2021F2019 2020F 2021F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue 369.0 245.4 412.5 322.6 390.2 304.2 431.1 352.9 1,349.6 1,478.4 1,608.8

OP 19.7 1.0 26.0 17.9 27.8 15.4 34.6 19.5 64.6 97.3 114.3

Pretax profit 29.3 2.9 23.3 18.1 27.9 14.9 34.6 20.2 73.6 97.5 116.0

NP 20.3 1.1 19.9 13.9 20.6 11.0 25.2 15.0 55.1 71.9 85.2

EPS 1,135 60 1,114 778 1,153 616 1,412 841 3,087 4,022 4,767

OP margin 5.3 0.4 6.3 5.5 7.1 5.0 8.0 5.5 4.8 6.6 7.1

Pretax margin 7.9 1.2 5.6 5.6 7.1 4.9 8.0 5.7 5.5 6.6 7.2

Net margin 5.5 0.4 4.8 4.3 5.3 3.6 5.9 4.3 4.1 4.9 5.3

(Wbn, W, %)

Source: MCNEX, Mirae Asset Daewoo Research

SpotlightstocksMCNEX (097520 KQ)

Mirae Asset Daewoo Research21 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

3,142

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSPI

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 61,396 61,342 62,306 62,802 68,273 74,000

Free float (%) OP (Wbn) 2,469 2,703 2,436 3,142 3,731 4,062

Foreign ownership (%) OP margin (%) 4.0 4.4 3.9 5.0 5.5 5.5

Beta (12M) NP (Wbn) 1,726 1,240 31 2,008 2,222 2,587

52-week low (W) EPS (W) 9,543 6,858 173 11,103 12,290 14,308

52-week high (W) ROE (%) 13.7 9.0 0.2 13.2 13.0 13.3

(%) 1M 6M 12M P/E (x) 11.1 9.1 416.8 7.7 7.0 6.0

Absolute 1.8 44.2 22.3 P/B (x) 1.4 0.8 0.9 1.0 0.8 0.7

Relative -10.9 12.9 -1.4 Div. yield (%) 0.4 1.2 1.0 0.9 0.9 0.9

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: LG Electronics, Mirae Asset Daewoo Research estimates

Buy

125,000

85,500

Expected return 46%

41,850

96,100

7.7

17.7

2,591.34

13,992

181

65.6

6,317.6

OP (20F, Wbn)

3,153

35.6

0.88

70

80

90

100

110

120

130

140

19.11 20.2 20.5 20.8 20.11

LG Electronics

KOSPI

LG Electronics (066570 KS)

Recovery in auto components; expectations for improvement in smartphones

■ Above-consensus OP of W3.14tr (+29.0% YoY) expected in 2020

- For 2020, we forecast LGE to deliver revenue of W62.80tr (+0.8% YoY) and operating profit of W3.14tr (+29.0% YoY).

- The strong results should be attributable to robust sales of home appliances and TVs amid the COVID-19 pandemic.

■ 2021 outlook: Record OP of W3.73tr (+18.7% YoY)

- For 4Q20, we expect revenue of W18.32tr (+14.1% YoY, +8.3% QoQ) and operating profit of W597.6bn (+487.6% YoY, -37.7%

QoQ).

- Looking to 2021, we anticipate record-high revenue of W68.27tr (+8.7% YoY) and operating profit of W3.73tr (+18.7% YoY).

- Excluding LG Innotek, we expect LGE to post operating profit of W3.07tr, surpassing the record set in 2009 (W2.68tr),

supported by strong home appliance/TV sales.

- The automotive electronics business is projected to swing to profit.

■ Retain Buy and target price of W125,000

- LGE boasts the world’s strongest competitiveness in home appliances and TVs, and the automotive electronics business—a

key growth engine—is improving. Opportunities could also open up for the smartphone business.

- We see no reason for LGE to trade at a P/B of 1x or less. We believe now is the time to aggressively overweight the stock.

Notable stocks

Mirae Asset Daewoo Research22 | Monthly InsighT

2020F 2021F2019 2020F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QFMC Revenue 998.6 1,308.7 1,524.8 1,572.6 1,168.2 1,489.9 1,700.3 1,805.0 5,404.7 6,163.4

(Mobile OP -237.8 -206.5 -148.4 -188.7 -116.8 -164.6 -170.0 -151.6 -781.4 -603.0

Communications) OP margin -23.8 -15.8 -9.7 -12.0 -10.0 -11.0 -10.0 -8.4 -14.5 -9.8

HE Revenue 2,970.7 2,256.7 3,669.4 4,125.0 3,348.1 2,808.0 4,170.6 4,762.8 13,021.8 15,089.5

(Home OP 325.8 112.8 326.6 218.6 300.2 238.6 350.4 252.4 983.8 1,141.6

Entertainment) OP margin 11.0 5.0 8.9 5.3 9.0 8.5 8.4 5.3 7.6 7.6

H&A Revenue 5,418.0 5,155.1 6,155.8 5,308.5 5,394.3 4,754.8 6,346.4 5,388.1 22,037.4 21,883.6

(Home Appliance OP 753.5 628.0 671.5 238.9 675.2 579.2 623.1 218.2 2,291.9 2,095.7

& Air Solutions) OP margin 13.9 12.2 10.9 4.5 12.5 12.2 9.8 4.1 10.4 9.6

VS Revenue 1,319.3 912.2 1,655.4 2,069.3 2,014.4 2,115.2 2,326.7 2,443.0 5,956.2 8,899.3

(Vehicle OP -96.8 -202.5 -66.2 -41.4 -40.3 -21.2 65.1 68.4 -406.9 72.1

Components) OP margin -7.3 -22.2 -4.0 -2.0 -2.0 -1.0 2.8 2.8 -6.8 0.8

BS Revenue 1,709.1 1,307.1 1,482.8 1,408.6 1,686.0 1,269.6 1,448.8 1,372.7 5,907.6 5,777.1

OP 212.2 98.3 77.0 63.4 125.6 85.9 75.2 61.8 450.9 348.5

OP margin 12.4 7.5 5.2 4.5 7.4 6.8 5.2 4.5 7.6 6.0

Internal & other Revenue 301.2 354.1 201.6 353.2 273.2 307.2 221.2 358.7 1,210.1 1,160.4

OP -4.5 22.4 9.1 -8.1 -4.3 18.7 8.9 -8.0 18.9 15.4

OP margin -1.5 6.3 4.5 -2.3 -1.6 6.1 4.0 -2.2 1.6 1.3

LG Innotek Revenue 2,010.9 1,539.9 2,229.8 3,483.5 2,133.1 1,727.1 2,491.8 2,947.5 9,264.1 9,299.6

OP 138.0 42.9 89.4 314.9 143.3 84.5 204.7 228.3 585.2 660.9

Total Revenue 14,727.8 12,833.8 16,919.6 18,320.7 16,017.3 14,471.8 18,705.8 19,077.9 62,801.9 68,272.8

OP 1,090.4 495.4 959.0 597.6 1,083.0 821.3 1,157.3 669.6 3,142.4 3,731.2

OP margin 7.4 3.9 5.7 3.3 6.8 5.7 6.2 3.5 5.0 5.5

LGE(excludingLG Innotek)

Revenue 12,860.4 11,441.8 14,916.3 15,014.9 14,046.7 12,929.4 16,412.3 16,291.9 54,233.4 59,680.4

OP 951.2 453.8 872.1 280.2 938.3 741.3 955.1 438.8 2,557.3 3,073.6

OP margin 7.4 4.0 5.8 1.9 6.7 5.7 5.8 2.7 4.7 5.2

Pretax profit 1,389.4 147.9 771.6 390.3 983.6 736.9 1,025.7 457.2 2,699.1 3,203.4

Pretax margin 9.4 1.2 4.6 2.1 6.1 5.1 5.5 2.4 4.3 4.7

NP 1,025.4 56.5 626.1 299.7 735.4 490.6 657.2 339.2 2,007.7 2,222.4

Net margin 7.0 0.4 3.7 1.6 4.6 3.4 3.5 1.8 3.2 3.3

Handset sales volume 5,900 6,300 7,400 7,590 6,195 6,930 7,770 7,970 27,190 28,865

- Smartphones 5,800 6,200 7,300 7,505 6,113 6,850 7,694 7,897 26,805 28,554

TV sales volume 6,500 4,500 7,500 8,385 6,672 5,433 8,000 8,701 26,885 28,806

- OLED TV 370 330 500 800 481 429 650 1,040 2,000 2,600

Earnings table

Source: LGE, Mirae Asset Daewoo Research

LG Electronics (066570 KS) Notable stocks

Mirae Asset Daewoo Research23 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

238

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSPI

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 4,215 4,453 5,264 5,288 5,970 6,341

Free float (%) OP (Wbn) 83 53 165 238 253 294

Foreign ownership (%) OP margin (%) 2.0 1.2 3.1 4.5 4.2 4.6

Beta (12M) NP (Wbn) -48 32 132 107 154 180

52-week low (W) EPS (W) -913 619 2,555 2,111 3,038 3,552

52-week high (W) ROE (%) -2.1 1.4 5.4 4.2 5.8 6.4

(%) 1M 6M 12M P/E (x) - 52.5 13.7 12.5 8.7 7.4

Absolute 5.2 8.6 -31.3 P/B (x) 0.9 0.7 0.7 0.5 0.5 0.5

Relative -8.0 -14.9 -44.7 Div. yield (%) 0.0 0.0 0.0 0.0 0.0 0.4

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: Hanwha Aerospace, Mirae Asset Daewoo Research estimates

Buy

39,000

26,400

Expected return 48%

15,000

38,450

12.5

17.7

2,591.34

1,337

51

66.0

-17.4

OP (20F, Wbn)

217

16.7

1.48

70

80

90

100

110

120

130

19.11 20.2 20.5 20.8 20.11

Hanwha Aerospace

KOSPI

Hanwha Aerospace (012450 KS)

Unfairly undervalued

■ 2020F OP of W237.9bn (+44.0% YoY)

- For 2020, we forecast Hanwha Aerospace to post revenue of W5.29tr (+0.5% YoY) and operating profit of W237.9bn (+44.0%

YoY).

- While our revenue forecast would mark a record high, our operating profit forecast is shy of the historical high of W250.7bn

posted in 2011.

- We estimate risk and revenue sharing program (RSP) expenses at W88.4bn.

■ Record-breaking OP of W253.4bn (+6.5% YoY) expected in 2021

- Looking ahead to 2021, we expect the company to deliver record-breaking revenue and operating profit of W5.97tr (+12.9%

YoY) and W253.4bn (+6.5% YoY), respectively.

- The security camera business (Hanwha Techwin) and chip mounter business (Hanwha Precision Machinery) should deliver

robust earnings, while Hanwha Systems should also see stable earnings.

■ Reaffirm Buy and target price of W39,000

- Currently trading at a 2021F P/E of 8.7x and P/B of 0.5x, Hanwha Aerospace’s stock appears excessively undervalued, given

steadily improving earnings.

- We reaffirm our Buy rating and target price of W39,000 and advise investors to start accumulating the stock.

Notable stocks

Mirae Asset Daewoo Research24 | Monthly InsighT

Hanwha Aerospace (012450 KS)

(Wbn, %, %p)Earnings table

2020F 2021F2019 2020F 2020F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue Hanwha Aerospace 346.9 264.4 310.7 352.8 364.2 277.6 326.2 370.4 1,265.8 1,274.8 1,338.5

Hanwha Techwin 136.3 125.1 129.7 181.2 147.4 101.0 142.7 218.8 580.1 572.3 609.9

Hanwha Power Systems 18.3 61.0 58.9 80.6 19.2 64.2 62.1 85.2 227.1 218.8 230.8

Hanwha Precision Machinery 63.6 75.6 94.9 90.2 81.1 121.7 109.5 104.1 359.9 324.3 416.4

Hanwha Systems 282.2 323.1 379.6 474.5 332.2 365.8 417.0 469.2 1,546.0 1,459.4 1,584.2

Hanwha Defense 212.5 377.1 435.2 545.3 381.7 425.6 481.2 633.4 1,462.6 1,570.1 1,921.9

Adjustments -32.4 -33.6 -31.9 -33.9 -33.0 -33.1 -33.0 -33.2 -177.5 -131.8 -132.2

Total 1,027.4 1,192.7 1,377.1 1,690.6 1,293.0 1,322.9 1,505.9 1,847.8 5,264.0 5,287.8 5,969.6

OP Hanwha Aerospace -9.1 -5.2 0.0 -3.5 -9.0 -4.0 -3.6 -3.8 -56.2 -17.8 -20.3

Hanwha Techwin 6.0 5.7 7.8 8.2 5.8 6.9 6.7 9.2 29.5 27.7 28.6

Hanwha Power Systems -6.3 4.5 3.4 4.0 -1.0 4.7 1.6 8.3 13.1 5.6 13.6

Hanwha Precision Machinery -6.1 -0.3 8.5 7.2 -4.1 9.6 3.0 2.4 14.0 9.3 10.8

Hanwha Systems 10.9 18.2 44.7 33.2 13.9 21.2 37.6 28.5 85.8 107.0 101.2

Hanwha Defense 11.7 50.6 32.8 24.5 12.9 41.5 49.6 29.4 92.9 119.6 133.4

Adjustments -3.9 -3.3 -2.9 -3.5 -3.4 -3.4 -3.5 -3.7 -13.9 -13.6 -14.0

Total 3.2 70.2 94.3 70.2 15.1 76.6 91.5 70.3 165.2 237.9 253.4

OP margin 0.3 5.9 6.8 4.1 1.2 5.8 6.1 3.8 3.1 4.5 4.2

Pretax profit -9.4 61.0 75.6 62.3 7.0 69.8 84.1 64.5 156.3 189.5 225.4

NP -13.1 36.9 41.1 42.4 4.6 48.9 56.1 44.2 132.2 107.3 153.8

Pretax margin -0.9 5.1 5.5 3.7 0.5 5.3 5.6 3.5 3.0 3.6 3.8

Net margin -1.3 3.1 3.0 2.5 0.4 3.7 3.7 2.4 2.5 2.0 2.6

Source: Hanwha Aerospace, Mirae Asset Daewoo Research

Notable stocks

Mirae Asset Daewoo Research25 | Monthly InsighT

(Maintain)

Target price (12M, W)

Current price (11/30/20, W)

65

Consensus OP (20F, Wbn)

EPS growth (20F, %)

P/E (20F, x)

Market P/E (20F, x)

KOSDAQ

Market cap (Wbn) (Dec.) 2017 2018 2019 2020F 2021F 2022F

Shares outstanding (mn) Revenue (Wbn) 1,110 1,194 1,130 1,152 1,256 1,380

Free float (%) OP (Wbn) 98 95 50 65 81 98

Foreign ownership (%) OP margin (%) 8.8 8.0 4.4 5.6 6.4 7.1

Beta (12M) NP (Wbn) 40 63 34 33 54 65

52-week low (W) EPS (W) 692 1,077 592 560 928 1,121

52-week high (W) ROE (%) 6.7 10.1 5.3 4.8 7.5 8.6

(%) 1M 6M 12M P/E (x) 40.3 18.0 27.5 33.5 20.2 16.7

Absolute 7.4 34.9 41.5 P/B (x) 2.7 1.7 1.4 1.5 1.4 1.4

Relative -3.9 8.6 1.1 Div. yield (%) 0.7 1.5 1.0 1.6 1.6 0.5

Notes: Under consolidated K-IFRS; NP is attributable to owners of the parent

Source: Seoul Semiconductor, Mirae Asset Daewoo Research estimates

Buy

23,100

18,750

Expected return 23%

10,000

20,150

33.5

17.7

886.11

1,093

58

66.5

-5.3

OP (20F, Wbn)

65

10.7

1.04

70

80

90

100

110

120

130

140

150

19.11 20.2 20.5 20.8 20.11

Seoul Semiconductor

KOSDAQ

Seoul Semiconductor (046890 KQ)

Potential end-market improvements and efficient cost management

■ Better-than-feared 2020F OP of W64.5bn (+30.2% YoY)

- For 2020, we expect SSC to deliver revenue of W1.15tr (+2.0% YoY) and operating profit of W64.5bn (+30.2% YoY).

- We believe the company has benefited from IT product demand related to remote work and distance learning amid COVID-

19; sales of backlight units (BLUs) for TV, notebook, and monitor applications came in better than expected.

- In particular, we estimate that BLU earnings related to TV/laptop/monitor applications will exceed our expectations.

■ 2021F OP of W81.0bn (+25.6% YoY)

- For 4Q20, we anticipate revenue of W309.8bn (+10.3% YoY, -6.5% QoQ) and operating profit of W19.4bn (+40.2% YoY, -23.5%

QoQ).

- Looking ahead to 2021, we expect revenue and operating profit to improve to W1.25tr (+9.0% YoY) and W81.0bn (+25.6%

YoY), respectively.

- We expect: 1) the strong performance of TV/monitor BLUs to continue; 2) automotive LED revenue to gradually pick up; and

3) Seoul Viosys’s UV LED sales to grow.

■ Reaffirm Buy and target price of W23,100

- SSC is further strengthening its competitiveness on the back of its strong technology and patents.

- We expect the mini-LED BLU TV market to expand in 2021.

- Bullish expectations on UV LED and micro-LED are also positive to the company’s stock.

Notable stocks

Mirae Asset Daewoo Research26 | Monthly InsighT

Earnings table

2020F 2021F2019 2020F 2021F

1Q 2Q 3Q 4QF 1QF 2QF 3QF 4QF

Revenue 243.2 268.1 331.2 309.8 297.5 310.5 324.0 324.2 1,129.4 1,152.3 1,256.2

OP 6.0 13.7 25.4 19.4 13.0 17.1 28.4 22.6 49.5 64.5 81.0

Pretax profit 10.1 13.0 18.5 15.7 12.6 16.4 28.0 22.5 47.7 57.4 79.6

NP 6.3 5.0 10.7 10.7 8.6 11.2 19.1 15.3 34.5 32.7 54.1

EPS 108 86 184 183 147 192 327 263 592 560 928

OP margin 2.5 5.1 7.7 6.3 4.4 5.5 8.8 7.0 4.4 5.6 6.5

Pretax margin 4.2 4.9 5.6 5.1 4.2 5.3 8.6 6.9 4.2 5.0 6.3

Net margin 2.6 1.9 3.2 3.4 2.9 3.6 5.9 4.7 3.1 2.8 4.3

Seoul Semiconductor (046890 KQ)

(Wbn, W, %)

Source: SSC, Mirae Asset Daewoo Research

Notable stocks

Mirae Asset Daewoo Research27 | Monthly InsighT

I. Investment strategy

II. Sector view

III. Spotlight stocks & other notable stocks

IV. Pioneer: Company visits/IR/NDRs/IPOs

V. Global IT navigation

Mirae Asset Daewoo Research28 | Monthly InsighT

(Wbn)

Consensus (Wbn)Share performance

(%)2020F (x, %)

Notes

4Q20F 2020F 2021F 1W 1M 1Y P/E P/B ROE

Shinsung E&G Revenue - - - 7.3 35.3 333.1 - - - Established in Jan. 1977; went public in Jul. 1996

Market cap: OP - - -Businesses: Clean environment solutions (clean room) and renewable energy (solar cells/modules)

811.5 NP - - -3Q20 results: Revenue of W138.6bn (+18% YoY, +9% QoQ) and OP of W3.5bn (+60% YoY, +2% QoQ)

Everybot Revenue - - - 11.8 55.6 1,478.6 - - - Established in 2015 and listed on the KONEX in Jul. 2017

Market cap: OP - - -Launched the world’s first dual-spin mopping robot in 2016; cumulative sales of over 420,000 units as of Jun. 2020

124.1 NP - - -Sales volume: 142,000 units in 2017, 83,000 units in 2018, 89,000 units in 2019, 77,000 units in 1H20

SD Optics Revenue - - - - - - - - -

Established in 2010

Businesses: Manufacture of optical modules and inspection systems based on Micro-mirror Array Lens System (MALS™)

Market cap: OP - - - Products: MALS lenses (the world’s first ultra-fast varifocal lenses; based on the MEMS technology)

Unlisted NP - - -

Optrontec Revenue 55.2 215.0 245.5 9.8 23.2 -3.3 17.5 1.5 9.2Established in May 1999; listed on the KOSDAQ in Jun. 2005; merged with Havit Information in Feb. 2009

Market cap: OP 5.1 17.4 23.1Products: Optical filters/lenses/zoom and variable aperture lenses

178.5 NP 3.0 8.7 12.4

INNO Instrument Revenue 14.1 45.0 - 2.9 15.4 -23.5 16.0 - 9.3Established in Feb. 2007; completed a merger with NH Special Purpose Acquisition 5 in Apr. 2017 (SPAC)

Market cap: OP 1.7 3.2 - Business: Manufacture/sale of fusion slicers

78.6 NP 1.3 4.2 - A potential beneficiary of 5G market expansion

November company visits/IR/NDRs

IV. Pioneer

Source: Company data, Bloomberg, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research29 | Monthly InsighT

Source: Company data, Bloomberg, Mirae Asset Daewoo Research

November company visits/IR/NDRs

IV. Pioneer

(Wbn)

Consensus (Wbn)Share performance

(%)2020F (x, %)

Notes

4Q20F 2020F 2021F 1W 1M 1Y P/E P/B ROE

Innox AdvancedMaterials

Revenue 94.2 341.5 430.7 -0.4 2.2 -5.6 14.5 2.0 15.1 Spun off from Innox in Jun. 2017 and listed on the KOSDAQ in Jul. 2017

Market cap: OP 12.9 42.6 59.7Businesses: Development/manufacture of materials for FPCBs, semiconductor packages, and OLEDs based on polymer synthesis/compounding technology

428.6 NP 8.1 29.3 43.23Q20 results: Revenue of W105.9bn (+10% YoY, +43% QoQ), OP of W19.4bn (+48% YoY, +178% QoQ)

Intellian Technologies

Revenue - 119.2 141.4 -1.1 13.0 1.4 44.9 4.3 6.0Businesses (established on Feb. 5, 2004): Development/manufacture/distribution of satelliteantennas

Market cap: OP - 6.9 12.2 Key products: Very-small-aperture terminal (VSAT) antennas (C-/Ku-/Ka-bands), fleet broadband (FBB) antennas (L-band), television receive-only (TVRO) antennas, flyaway antennas, etc.246.9 NP - 5.5 10.8

JNTC Revenue 75.4 365.9 376.2 2.7 4.7 - 7.5 1.5 23.7 Established as Hyupjin Industries in Nov. 1996 and renamed JNTC in Apr. 2012

Market cap: OP 12.6 89.5 73.7 Businesses: Development/manufacture of tempered glass and handset-use connectors

650.8 NP 11.3 87.0 68.9 3Q20 results: Revenue of W87.7bn (-6% YoY, -7% QoQ), OP of W17.1bn (-47% YoY, -24% QoQ)

Park Systems Revenue - 68.6 78.2 9.8 22.6 110.3 28.2 - 33.1 Established in Apr. 1997 and listed on the KOSDAQ in Dec. 2015

Market cap: OP - 19.4 24.1 Businesses: Development/manufacture of atomic force microscopes

492.1 NP - 17.4 19.2 3Q20 results: Revenue of W16.4bn (+60% YoY, -12% QoQ), OP of 4bn (+1,417% YoY, -0.5% QoQ)

Point Mobile Revenue - - - - - - - - -Businesses: Development/manufacture of industrial-use PDAs and peripherals (established in 2006)

Market cap: OP - - - No. 1 share in domestic market; products available in 79 countries

IPO NP - - - IPO scheduled for Dec. 2020 at an IPO price of W15,000

Mirae Asset Daewoo Research30 | Monthly InsighT

I. Investment strategy

II. Sector view

III. Spotlight stocks & other notable stocks

IV. Pioneer: Company visits/IR/NDRs/IPOs

V. Global IT navigation

Mirae Asset Daewoo Research31 | Monthly InsighT

IV. Global IT navigation

Stock market remained strong despite resurgence of COVID-19

Global IT index performance table (11/30)

Global IT shares: Top/bottom 15 performers in NovemberDomestic IT shares: Top/bottom 10 performers in November

IndexPerformance (%)

1W 1M 3M 6M 12M

Dow Jones 29,910 1.4 12.9 5.2 17.8 6.6

S&P 500 3,638 1.6 11.3 3.9 19.5 15.8

NASDAQ 12,206 2.5 11.9 3.7 28.6 40.9

KOSPI 2,591 -0.4 14.3 11.4 27.7 24.1

KOSDAQ 886 1.5 11.8 4.5 24.2 40.0

MSCI IT

World 417 2.6 11.8 1.2 26.9 39.7

Korea 1,743 1.0 20.9 26.2 33.6 37.8

US 501 1.3 11.1 0.3 27.2 41.8

Japan 205 5.5 16.4 19.9 24.2 20.3

Taiwan 329 -0.8 12.1 14.6 49.1 43.2

China 1,078 -1.5 9.5 8.3 56.8 69.4

Source: Bloomberg, Mirae Asset Daewoo Research

Source: Bloomberg, Mirae Asset Daewoo ResearchSource: Bloomberg, Mirae Asset Daewoo Research

■ Global industry performance- MSCI IT World (+11.8%), MSCI IT Korea (+20.9%), MSCI IT US (+11.1%), MSCI IT China

(+9.5%), and MSCI IT Taiwan (+12.1%) all posted MoM gains. - IT product demand has increased since the COVID-19 outbreak. - Korean IT plays deserve attention.

■ Sector performance- IT companies (semiconductor, etc.) reported decent earnings, as IT product sales

have increased amid the rise of the contactless culture. - Green/renewable energy stocks that are expected to benefit from the Biden

presidency advanced. - Share performances diverged by downstream industry.

■ Company performance- Lyft (LYFT US, +71.0%): California Assembly Bill 5 (AB5) extended employee

classification status to gig workers (including Uber/Lyft drivers).- Nikola (NKLA US, +52.5%): GM, Nikola’s strategic partner, pulled out of the California

emissions litigation (spearheaded by the Trump administration) in favor of President-elect Joe Biden’s eco-friendly energy policies.

- Tesla (TSLA US, +51.0%): Addition to the S&P 500 and favorable renewable energy policies of the upcoming administration

0

10

20

30

L&F

Won

ik IP

S

Eug

ene

Won

ik M

ater

ials

SK

Hyn

ix LS

Sam

sung

SD

I

TE

S

SE

C

SK

Mat

eria

ls

Han

wha

Aer

ospa

ce KC

Am

otec

h

Par

tron

Sili

con

Wor

ks

Spi

gen

Kor

ea

Inno

x A

MC

LG In

note

k

LGE

Sou

lbra

in

(%)

-40

0

40

80

Lyft

Nik

ola

Ube

r

Tes

la

3D S

yste

ms

Boe

ing

Cre

e

Com

mS

cope

AM

AT

GS

Yua

sa

Bla

ckB

erry

Glo

bal W

afer

s

Lam

Res

earc

h

SU

MC

O

Vee

co

Japa

n D

ispl

ay

Eve

rligh

t

Ten

cent

Ace

r

Sky

wor

ks

Coh

eren

t

SM

IC

Wiw

ynn

TP

K

Alib

aba

Pre

cise

Bio

met

rics

Cal

-Com

p E

lect

roni

cs

His

ense

Alp

s E

lect

ric

Goe

rtek

(%)

Mirae Asset Daewoo Research32 | Monthly InsighT

IV. Global IT navigation

Key charts

Source: Bloomberg, Mirae Asset Daewoo Research Source: Bloomberg, Mirae Asset Daewoo Research

Source: Bloomberg, Mirae Asset Daewoo Research Source: Bloomberg, Mirae Asset Daewoo Research

MSCI World and MSCI World IT

IT sector P/E comparison (2020)

MSCI IT performance by country

IT sector P/B-ROE comparison (2020)

80

120

160

200

240

280

320

360

400

440

480

520

1/12 1/13 1/14 1/15 1/16 1/17 1/18 1/19 1/20

MSCI World MSCI World IT(1/1/12=100)

80

140

200

260

320

380

440

500

560

620

1/12 1/13 1/14 1/15 1/16 1/17 1/18 1/19 1/20

MSCI US IT MSCI Korea IT

MSCI Japan IT MSCI Taiwan IT

(1/1/12=100)

31.9

27.8 29.9 29.6

20.8 18.2

0

10

20

30

40

China Japan World US Taiwan Korea

(x)

0

2

4

6

8

10

12

0 10 20 30 40 50 60 70

ROE (%)

P/B (x)

World

US

China

TaiwanJapan

Korea

Mirae Asset Daewoo Research33 | Monthly InsighT

Important disclosures and disclaimers

Two-year rating and TP history

Company Date Rating TP (W) Company Date Rating TP (W)

Samsung Electro-Mechanics (009150) 11/14/18 Buy 80,000

11/18/20 Buy 196,000 MCNEX (097520)

07/29/20 Buy 178,000 11/18/20 Buy 47,000

07/01/20 Buy 159,000 LG Electronics (066570)

06/01/20 Buy 152,000 10/05/20 Buy 125,000

04/01/20 Buy 143,000 09/01/20 Buy 105,000

01/29/20 Buy 160,000 07/31/20 Buy 91,700

01/01/20 Buy 151,000 04/01/20 Buy 82,000

10/24/19 Buy 143,000 01/30/20 Buy 87,400

03/25/19 Buy 133,000 07/30/19 Buy 89,900

01/01/19 Buy 150,000 03/29/19 Buy 99,500

09/30/18 Buy 195,000 03/03/19 Buy 89,100

LG Innotek (011070) 02/01/19 Buy 86,000

07/01/20 Buy 221,000 01/01/19 Buy 89,000

01/29/20 Buy 201,000 09/30/18 Buy 99,000

11/25/19 Buy 171,000 Hanwha Aerospace (012450)

10/29/19 Buy 166,000 08/12/20 Buy 39,000

10/01/19 Buy 147,000 08/03/20 Buy 35,000

06/30/19 Buy 139,000 05/13/20 Buy 33,000

04/23/19 Buy 156,000 04/01/20 Buy 34,100

03/20/19 Buy 139,000 08/12/19 Buy 44,700

01/27/19 Buy 122,000 02/20/19 Buy 43,000

01/01/19 Buy 126,000 01/17/19 Buy 47,000

09/30/18 Buy 177,000 11/13/18 Buy 42,000

LS (006260) Seoul Semiconductor (046890)

12/01/20 Buy 80,000 10/27/20 Buy 23,100

11/18/20 Buy 72,300 10/05/20 Buy 23,000

10/05/20 Buy 63,600 07/30/20 Buy 21,000

09/01/20 Buy 56,900 07/01/20 Buy 17,000

08/03/20 Buy 53,400 04/01/20 Buy 16,700

04/01/20 Buy 48,800 01/01/20 Buy 21,300

02/11/20 Buy 51,700 11/01/19 Buy 18,300

08/15/19 Buy 57,300 10/01/19 Buy 18,600

05/15/19 Buy 65,900 08/01/19 Buy 21,300

Mirae Asset Daewoo Research34 | Monthly InsighT

Company Date Rating TP (W) Company Date Rating TP (W)

06/30/19 Buy 24,500 10/26/18 Buy 9,900

04/29/19 Buy 29,500 Amotech (052710)

04/08/19 Buy 29,100 08/18/20 Hold 31,800

01/30/19 Buy 30,500 05/18/20 Hold

01/18/19 Buy 27,300 04/20/20 Trading Buy 25,900

01/01/19 Buy 26,700 02/20/20 Buy 37,400

09/30/18 Buy 26,000 10/21/19 Buy 27,700

Seoul Viosys (092190) 08/01/19 Buy 23,500

11/18/20 Buy 23,000 04/10/19 Buy 29,000

Partron (091700) 02/11/19 Buy 26,300

11/03/20 Buy 12,900 11/01/18 Buy 28,200

07/31/20 Hold 11,400 Spigen Korea (192440)

05/04/20 Hold 10/05/20 Buy 90,000

04/20/20 Trading Buy 10,000 08/18/20 Buy 87,000

02/23/20 Buy 14,600 07/01/20 Buy 78,000

10/21/19 Buy 18,000 05/18/20 Buy 63,000

08/15/19 Buy 20,000 04/20/20 Buy 60,000

06/17/19 Buy 22,700 10/21/19 Buy 78,000

05/02/19 Buy 19,000 08/15/19 Buy 76,000

03/21/19 Buy 17,000 01/28/19 Buy 79,000

02/07/19 Buy 12,500 08/01/18 Buy 74,000

Mirae Asset Daewoo Research35 | Monthly InsighT

Ratings distribution and investment banking services

Buy Trading Buy Hold Sell

Ratings distribution 73.62% 14.11% 11.04% 1.23%

Investment banking services 72.22% 11.11% 16.67% 0.00%

* Based on recommendations in the last 12-months (as of September 30, 2020)

Stock ratings Sector ratings

Buy Expected 12-month performance: +20% or greater Overweight Expected to outperform the market over 12 months

Trading Buy Expected 12-month performance: +10% to +20% Neutral Expected to perform in line with the market over 12 months

Hold Expected 12-month performance: -10% to +10% Underweight Expected to underperform the market over 12 months

Sell Expected 12-month performance: -10% or worse

Rating and TP history: Share price (─), TP (▬), Not Rated (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆)

* Our investment rating is a guide to the expected return of the stock over the next 12 months.

* Outside of the official ratings of Mirae Asset Daewoo Co., Ltd., analysts may call trading opportunities should technical or short-term material developments arise.

* The TP was determined by the research analyst through valuation methods discussed in this report, in part based on estimates of future earnings.

* TP achievement may be impeded by risks related to the subject securities and companies, as well as general market and economic conditions.

0

50,000

100,000

150,000

200,000

250,000

Dec 18 Dec 19 Dec 20

(W) Samsung Electro-Mechanics

0

50,000

100,000

150,000

200,000

250,000

Dec 18 Dec 19 Dec 20

(W) LG Innotek

0

20,000

40,000

60,000

80,000

100,000

Dec 18 Dec 19 Dec 20

(W) LS

0

10,000

20,000

30,000

40,000

50,000

Dec 18 Dec 19 Dec 20

(W) MCNEX

0

50,000

100,000

150,000

Dec 18 Dec 19 Dec 20

(W) LG Electronics

0

10,000

20,000

30,000

40,000

50,000

Dec 18 Dec 19 Dec 20

(W) Hanwha Aerospace

0

10,000

20,000

30,000

40,000

Dec 18 Dec 19 Dec 20

(W) Seoul Semiconductor

0

5,000

10,000

15,000

20,000

25,000

30,000

Dec 18 Dec 19 Dec 20

(W) Seoul Viosys

0

5,000

10,000

15,000

20,000

25,000

Dec 18 Dec 19 Dec 20

(W) Partron

0

10,000

20,000

30,000

40,000

Dec 18 Dec 19 Dec 20

(W) Amotech

0

20,000

40,000

60,000

80,000

100,000

Dec 18 Dec 19 Dec 20

(W) Spigen Korea

Mirae Asset Daewoo Research36 | Monthly InsighT

Disclosures

As of the publication date, Mirae Asset Daewoo Co., Ltd. has acted as a liquidity provider for equity-linked warrants backed by shares of Samsung Electro-Mechanics, LG Innotek, Hanwha Aerospace, LG Electronics as an underlying asset; other than

this, Mirae Asset Daewoo has no other special interests in the covered companies.

As of the publication date, Mirae Asset Daewoo Co., Ltd. is acting as a financial advisor to Seoul Semiconductor for its treasury share buyback and cancellation.

Analyst certification

The research analysts who prepared this report (the “Analysts”) are registered with the Korea Financial Investment Association and are subject to Korean securities regulations. They are neither registered as research analysts in any

other jurisdiction nor subject to the laws or regulations thereof. Each Analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the personal views of the Analyst about any

and all of the issuers and securities named in this report and (ii) no part of the compensation of the Analyst was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report. Mirae Asset

Daewoo Co., Ltd. (“Mirae Asset Daewoo”) policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director, or

advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and have not been

promised the same in connection with this report. Like all employees of Mirae Asset Daewoo, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from, among other business units,

the institutional equities, investment banking, proprietary trading, and private client divisions. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the

Analyst or Mirae Asset Daewoo except as otherwise stated herein.

Disclaimers

This report was prepared by Mirae Asset Daewoo, a broker-dealer registered in the Republic of Korea and a member of the Korea Exchange. Information and opinions contained herein have been compiled in good faith and from

sources believed to be reliable, but such information has not been independently verified and Mirae Asset Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness, or

correctness of the information and opinions contained herein or of any translation into English from the Korean language. In case of an English translation of a report prepared in the Korean language, the original Korean language

report may have been made available to investors in advance of this report.

The intended recipients of this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its common practices, laws, and accounting principles, and no person whose receipt or

use of this report would violate any laws or regulations or subject Mirae Asset Daewoo or any of its affiliates to registration or licensing requirements in any jurisdiction shall receive or make any use hereof.

This report is for general information purposes only and is not and shall not be construed as an offer or a solicitation of an offer to effect transactions in any securities or other financial instruments. The report does not constitute

investment advice to any person, and such person shall not be treated as a client of Mirae Asset Daewoo by virtue of receiving this report. This report does not take into account the particular investment objectives, financial situations,

or needs of individual clients. The report is not to be relied upon in substitution for the exercise of independent judgment. Information and opinions contained herein are as of the date hereof and are subject to change without notice.

The price and value of the investments referred to in this report and the income from them may depreciate or appreciate, and investors may incur losses on investments. Past performance is not a guide to future performance. Future

returns are not guaranteed, and a loss of original capital may occur. Mirae Asset Daewoo, its affiliates, and their directors, officers, employees, and agents do not accept any liability for any loss arising out of the use hereof.

Mirae Asset Daewoo may have issued other reports that are inconsistent with, and reach different conclusions from, the opinions presented in this report. The reports may reflect different assumptions, views, and analytical methods of

the analysts who prepared them. Mirae Asset Daewoo may make investment decisions that are inconsistent with the opinions and views expressed in this research report. Mirae Asset Daewoo, its affiliates, and their directors, officers,

employees, and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time

to time in the open market or otherwise, in each case either as principals or agents. Mirae Asset Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to provide

investment banking, market-making, or other financial services as are permitted under applicable laws and regulations.

No part of this document may be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset Daewoo. For further information regarding company-

specific information as it pertains to the representations and disclosures in this Appendix 1, please contact [email protected] or +1 (212) 407-1000.

Distribution

United Kingdom: This report is being distributed by Mirae Asset Securities (UK) Ltd. in the United Kingdom only to (i) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial

Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as

“Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its contents.

United States: Mirae Asset Daewoo is not a registered broker-dealer in the United States and, therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This report is

distributed in the U.S. by Mirae Asset Securities (USA) Inc., a member of FINRA/SIPC, to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6(b)(4) under the U.S. Securities Exchange Act

of 1934, as amended. All U.S. persons that receive this document by their acceptance hereof represent and warrant that they are a major U.S. institutional investor and have not received this report under any express or implied

understanding that they will direct commission income to Mirae Asset Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact and place orders with

Mirae Asset Securities (USA) Inc. Mirae Asset Securities (USA) Inc. accepts responsibility for the contents of this report in the U.S., subject to the terms hereof, to the extent that it is delivered to a U.S. person other than a major U.S.

institutional investor. Under no circumstances should any recipient of this research report effect any transaction to buy or sell securities or related financial instruments through Mirae Asset Daewoo. The securities described in this

report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration

requirements.

Hong Kong: This report is distributed in Hong Kong by Mirae Asset Securities (HK) Limited, which is regulated by the Hong Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory

authority in Hong Kong. This report is for distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and any rules made

thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All other jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae Asset Daewoo or its affiliates only if distribution to or use by such customer of this

report would not violate applicable laws and regulations and not subject Mirae Asset Daewoo and its affiliates to any registration or licensing requirement within such jurisdiction.

Mirae Asset Daewoo Research37 | Monthly InsighT

Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd.

One-Asia Equity Sales Team

Mirae Asset Center 1 Building

26 Eulji-ro 5-gil, Jung-gu, Seoul 04539

Korea

Units 8501, 8507-8508, 85/F

International Commerce Centre

1 Austin Road West

Kowloon

Hong Kong

41st Floor, Tower 42

25 Old Broad Street,

London EC2N 1HQ

United Kingdom

Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000

Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM

810 Seventh Avenue, 37th Floor

New York, NY 10019

USA

555 S. Flower Street, Suite 4410,

Los Angeles, California 90071

USA

Rua Funchal, 418, 18th Floor, E-Tower Building

Vila Olimpia

Sao Paulo - SP

04551-060

Brazil

Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100

PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC

Equity Tower Building Lt. 50

Sudirman Central Business District

Jl. Jend. Sudirman, Kav. 52-53

Jakarta Selatan 12190

Indonesia

6 Battery Road, #11-01

Singapore 049909

Republic of Singapore

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 62-21-515-3281 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110)

Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

2401B, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022

China

2401A, 24th Floor, East Tower, Twin Towers

B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022

China

Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300)

Shanghai Representative Office Ho Chi Minh Representative Office

38T31, 38F, Shanghai World Financial Center

100 Century Avenue, Pudong New Area

Shanghai 200120

China

7F, Saigon Royal Building

91 Pasteur St.

District 1, Ben Nghe Ward, Ho Chi Minh City

Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-7715