Front-cover National government 18-19fy - Office of the ...

740

REPORT OF THE AUDITOR-GENERAL FOR THE NATIONAL GOVERNMENT FOR THE YEAR 2018/2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Front-cover National government 18-19fy - Office of the ...

REPORT

OF THE

AUDITOR-GENERAL

FOR THE

NATIONAL GOVERNMENT

FOR THE

YEAR 2018/2019

Enhancing Accountability

i

Table of Contents

Vote

Foreword ......................................................................................................... iv

Introduction...…………………………………………………………………………vi

1071 The National Treasury ...................................................................................... 1

1072 State Department for Planning ........................................................................ 68

1011 The Presidency ............................................................................................ 103

1021 State Department for Interior ........................................................................ 105

1023 State Department for Correctional Services .................................................. 114

1024 State Department for Immigration and Citizen Services ................................ 119

1032 State Department for Devolution ................................................................... 121

1035 State Department for Development of the Asals ........................................... 141

1041 Ministry of Defence ....................................................................................... 146

1052 Ministry of Foreign Affairs ............................................................................. 148

1064 State Department for Vocational and Technical Training .............................. 150

1065 State Department for University Education ................................................... 157

1066 State Department for Early Learning and Basic Education ........................... 169

1068 State Department for Post-Training and Skills Development ........................ 182

1081 Ministry of Health…………………………………………………………………..183

1091 State Department for Infrastructure............................................................... 218

1092 State Department for Transport .................................................................... 257

1093 State Department for Shipping and Maritime ................................................ 270

1094 State Department for Housing and Urban Development .............................. 272

1095 State Department for Public Works ............................................................... 296

1096 State Department for Housing, Urban Development and Public Works ........ 304

1107 Ministry of Water and Sanitation ................................................................... 305

1108 Ministry of Environment and Forestry ........................................................... 345

1112 Ministry of Lands and Physical Planning ....................................................... 368

1122 State Department for Information Communication Technology ..................... 383

1123 State Department for Broadcasting and Telecommunications....................... 394

1132 State Department for Sports ......................................................................... 400

1134 State Department for Culture and Heritage ................................................... 412

ii

1152 State Department for Energy ........................................................................ 418

1162 State Department for Livestock ..................................................................... 443

1165 State Department for Crop Development ...................................................... 455

1166 State Department for Fisheries, Aquaculture and the Blue Economy ............ 511

1167 State Department for Irrigation ...................................................................... 517

1168 State Department for Agricultural Research .................................................. 525

1173 State Department for Co-operatives ............................................................. 527

1174 State Department for Trade .......................................................................... 528

1175 State Department for Industrialization ........................................................... 532

1184 State Department for Labour ........................................................................ 537

1185 State Department for Social Protection ......................................................... 547

1192 State Department for Mining ......................................................................... 554

1193 State Department for Petroleum ................................................................... 560

1202 State Department for Tourism ....................................................................... 565

1203 State Department for Wildlife ........................................................................ 569

1204 Ministry of Tourism and Wildlife .................................................................... 574

1211 State Department for Public Service and Youth ............................................ 576

1212 State Department for Gender........................................................................ 588

1213 State Department for Public Service ............................................................. 600

1214 State Department for Youth .......................................................................... 610

1221 State Department for East African Community ............................................. 636

1222 State Department for Regional nd Northern Corridor Development .............. 640

1252 State Law Office and Department of Justice ................................................. 644

1261 The Judiciary ................................................................................................ 654

1271 Ethics and Anti-Corruption Commission ....................................................... 668

1281 National Intelligence Service ........................................................................ 671

1291 Office of the Director of Public Prosecutions ................................................. 673

1311 Office of the Registrar of Political Parties ...................................................... 674

1321 Witness Protection Agency ........................................................................... 676

2011 Kenya National Commission on Human Rights ............................................ 677

2021 The National Land Commission .................................................................... 678

2031 Independent Electoral and Boundaries Commission ..................................... 683

2041 Parliamentary Service Commission .............................................................. 686

2042 National Assembly ........................................................................................ 691

2051 Judicial Service Commission ......................................................................... 692

iii

2061 Commission on Revenue Allocation ............................................................. 694

2071 Public Service Commission .......................................................................... 696

2081 Salaries and Remuneration Commission ...................................................... 697

2091 Teachers Service Commission ..................................................................... 698

2101 National Police Service Commission ............................................................ 701

2121 Office of the Controller of Budget .................................................................. 702

2131 Commission on Administrative Justice .......................................................... 704

2141 National Gender and Equality Commission ................................................... 705

2151 Independent Policing Oversight Authority ..................................................... 706

iv

Foreword

The Auditor-General is mandated by the Constitution of Kenya, under Article 229,

to audit and report on the use of public resources by all entities funded from public

funds. These entities include the National Government, County Governments, the

Judiciary, Parliament, Statutory Bodies/State Corporations, Commissions,

Independent Offices, Public Debt, Political Parties funded from public funds, other

government agencies and any other entity funded from public funds. The mandate

of the Auditor-General is further expounded by the Public Audit Act, 2015.

Article 229 (7) of The Constitution requires the Auditor-General to audit and submit reports to Parliament or the relevant County Assembly within six (6) months after the end of the financial year. However, Section 81(4) of the Public Finance Management Act, 2012, reduces the timeline to three (3) months by giving entities leeway up to the end of September to prepare and submit financial statements for audit.

Further, an effective mechanism for follow up on implementation of audit recommendations is lacking and as such most audit queries recur in subsequent audit reports due to lack of adequate action. Section 204(1) (g) of the Public Finance Management Act, 2012 provides that the Cabinet Secretary for The National Treasury may apply sanctions to a national government entity that fails to address issues raised by the Auditor-General, to the satisfaction of the Auditor-General. However, lack of requisite sanctions has led to perennial failure by some Accounting Officers to adequately account for the management and use of public resources. It has also led to fiscal indiscipline including misallocations, wastage of resources and lack of value for money in implementation of projects, thereby affecting development programmes in various entities, which in turn threatens sustainability of service delivery to citizens. There is also lack of adequate preparation for audit by some Accounting Officers which is exhibited by lack of requisite supporting documents and in some cases reluctance to cooperate with the auditors during the audit process. A summary highlighting the key cross-cutting audit findings is submitted separately.

An effective and quality audit process ensures that the results of audit and the

recommendations given are credible, relevant, reliable and value adding. This

influences improved decision making and positive change which impacts the lives

and livelihoods of citizens and other stakeholders. Provision of quality and effective

audit services and confirmation of lawfulness and effectiveness of implemented

programmes, requires comprehensive scrutiny and evaluation of documents. Most

critical is the physical confirmations of the existence and utilization of projects or

programs implemented throughout the country. This, therefore, requires an

independent and well-resourced audit Office with guaranteed availability of

v

resources to enable efficient and effective execution of the audit cycle and optimal

staffing to ensure continuous and sustainable audit operations.

The Office continues to seek support from Parliament and The National Treasury

for enhancement of resources to enable it build technical capacity, expand its

presence in the counties, widen the scope and comprehensiveness of audit and

motivate staff. We continue to devolve our services closer to the people through

creation and construction of regional offices to accommodate our staff in order to

address the audit needs at the county level. We have so far constructed regional

offices in Garissa, Kakamega and Eldoret, while construction works in Embu is

ongoing as the Office strives to enhance its presence in the counties for efficient,

effective and economic delivery of audit services. Plans for construction of our

Headquarters in Nairobi have, however, been delayed due to lack of funding. The

Office will continue to make appeals to Parliament and The National Treasury for

resources to enable enhancement of accountability across government.

During the period under review, the Office of the Auditor-General made great

strides in enhancing service delivery to the people of Kenya. The Office has

enhanced partnerships with other Supreme Audit Institutions (SAIs), oversight

institutions such as the Ethics and Anti-Corruption Commission (EACC), State

Corporations Advisory Committee (SCAC) among other organizations, as we

strive to increase the impact of audit through learning, knowledge sharing,

innovation and collaboration.

This report is the compilation of National Government Ministries and State

Departments including their respective Funds and Donor Funded Projects,

popularly referred to as the Blue Book. A separate Report will be submitted for the

forty-seven (47) county governments.

vi

1.0 Introduction

1.1 Constitutional Mandate of the Auditor-General The Auditor-General is mandated by the Constitution of Kenya, under Article 229, to audit and report on the use of public resources by all entities funded from public funds. These entities include; the National Government, County Governments, the Judiciary, Parliament, Statutory Bodies/State Corporations, Commissions, Independent Offices, Public Debt, Political Parties funded from public funds, other government agencies and any other entity funded from public funds. The mandate of the Auditor-General is further expounded by the Public Audit Act, 2015.

The Constitution requires the Auditor-General to audit and submit the audit reports of the public entities to Parliament and the relevant County Assemblies by 31st December, every year. In carrying out the mandate, the Auditor-General, is also required, under Article 229 (6) to assess and confirm whether the public entities have used the public resources entrusted to them lawfully and in an effective way.

Further, the objects and authority of the Auditor-General, as outlined in Article 249 of the Constitution, are: to protect the sovereignty of the people; to secure the observance by all State Organs of democratic values and principles; and to promote constitutionalism. The Auditor-General has also been given powers by the Constitution, under Article 252, to conduct investigations, conciliations, mediations and negotiations and to issue summons to witnesses for the purpose of investigations.

1.2 Responsibilities of Management and those Charged with Governance

Management is responsible for the preparation and fair presentation of the financial statements in accordance with the International Public Sector Accounting Standards (IPSAS)-Cash Basis, as prescribed by the Public Sector Accounting Standards Board (PSASB), and for the submission of the financial statements to the Auditor-General in accordance with the provisions of Section 47 of the Public Audit Act, 2015. Management is also responsible for maintaining effective internal control environment necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error, and for the assessment of the effectiveness of internal control, risk management and governance. Further, Management is required to ensure that the activities, financial transactions and information reflected in the financial statements are in compliance with the law

vii

and other relevant or applicable authorities, and that public resources are applied in an effective way. Those charged with governance are responsible for overseeing the financial reporting process, reviewing the effectiveness of how each entity monitors compliance with relevant legislative and regulatory requirements, ensuring that effective processes and systems are in place to address key roles and responsibilities in relation to governance and risk management, and ensuring the adequacy and effectiveness of the control environment.

1.3 Auditor-General’s Responsibility

My responsibility is to conduct an audit of the financial statements in accordance with the International Standards of Supreme Audit Institutions (ISSAIs), and to issue an auditor’s report. The audit report includes my opinion as provided by Section 48 of the Public Audit Act, 2015, and the report is submitted to Parliament in compliance with Article 229(7) of the Constitution.

In addition, Article 229(6) of the Constitution requires me to express a conclusion on whether or not, in all material respects, the activities, financial transactions and information reflected in the financial statements are in compliance with the law and other authorities that govern them, and that public resources are applied in an effective way. I also consider the entities’ control environment in order to give an assurance on the effectiveness of internal controls, risk management and governance processes and systems, in accordance with the provisions of Section 7 (1) (a) of the Public Audit Act, 2015.

I am independent in accordance with Article 249(2) of the Constitution of Kenya and ISSAI 130 on the Code of Ethics. I have fulfilled other ethical responsibilities in accordance with the ISSAI and in accordance with other ethical requirements applicable to performing audits of public entities in the Republic of Kenya.

1.4 Reporting Structure The new reporting structure of my report address the reporting requirements of Article 229(6) of the Constitution of Kenya, which requires that an audit report shall confirm whether or not public money has been applied lawfully and in an effective way. Section 7(1) (a) of the Public Audit Act, 2015 also requires that I provide assurance on the effectiveness of internal controls, risk management and overall governance in national and county governments entities. In addition, the International Standards of Supreme Audit Institutions (ISSAIs), require the incorporation of Key Audit Matters in the report on the financial statements, which are those matters that I determine in my professional judgment,

viii

are of most significance in the audit of the financial statements as a whole, for the year under review. In order to address these requirements, my audit reports contain the following:

i. Report on Financial Statements, in which I give an audit opinion on whether the financial statements present fairly, in all material respects the financial position and performance of the entity.

ii. Report on Lawfulness and Effectiveness in Use of Public Resources, in which I give a conclusion on whether or not public money has been applied lawfully and in effective way.

iii. Report on Effectiveness of Internal Controls, Risk Management and Governance, in which I give a conclusion on whether internal controls, risk management and overall governance were effective.

iv. Report on Other Legal and Regulatory Requirements is included where applicable, especially for the entities that are registered under the Companies Act, 2015 and any other enabling legislation or authorities that require such disclosure.

1.5 Audit Opinions

I have expressed different types of audit opinions based on the following criteria:

a) Unmodified/ Unqualified Opinion The books of accounts and underlying records agree with the financial statements and no material misstatements were found. The financial statements present fairly, in all material respects the operations of the entity. The financial statements with unqualified opinion are listed in Appendix A.

b) Qualified Opinion

Financial transactions were recorded and are to a large extent in agreement with the underlying records, except for cases where I noted material misstatements or omissions in the financial statements. The issues though material, are not widespread or persistent. The financial statements with qualified opinion are listed in Appendix B.

c) Adverse Opinion

The financial statements exhibit significant misstatements with the underlying accounting records. There is significant disagreement between the financial

ix

statements and the underlying books of accounts and/or standards. These problems are widespread, persistent and require considerable interventions by the management to rectify. The financial statements with adverse opinion are listed in Appendix C.

d) Disclaimer of Opinion

The financial statements exhibit serious and significant misstatements that may arise from inadequate information, limitation of scope, inadequacy or lack of proper records such that I was not able to form an opinion on the financial operations. The financial statements with disclaimer of opinion are listed in Appendix D.

The key findings noted during the audit of the financial statements for the year ended 30 June, 2019 are highlighted in the ensuing pages.

1

THE NATIONAL TREASURY-VOTE 1071

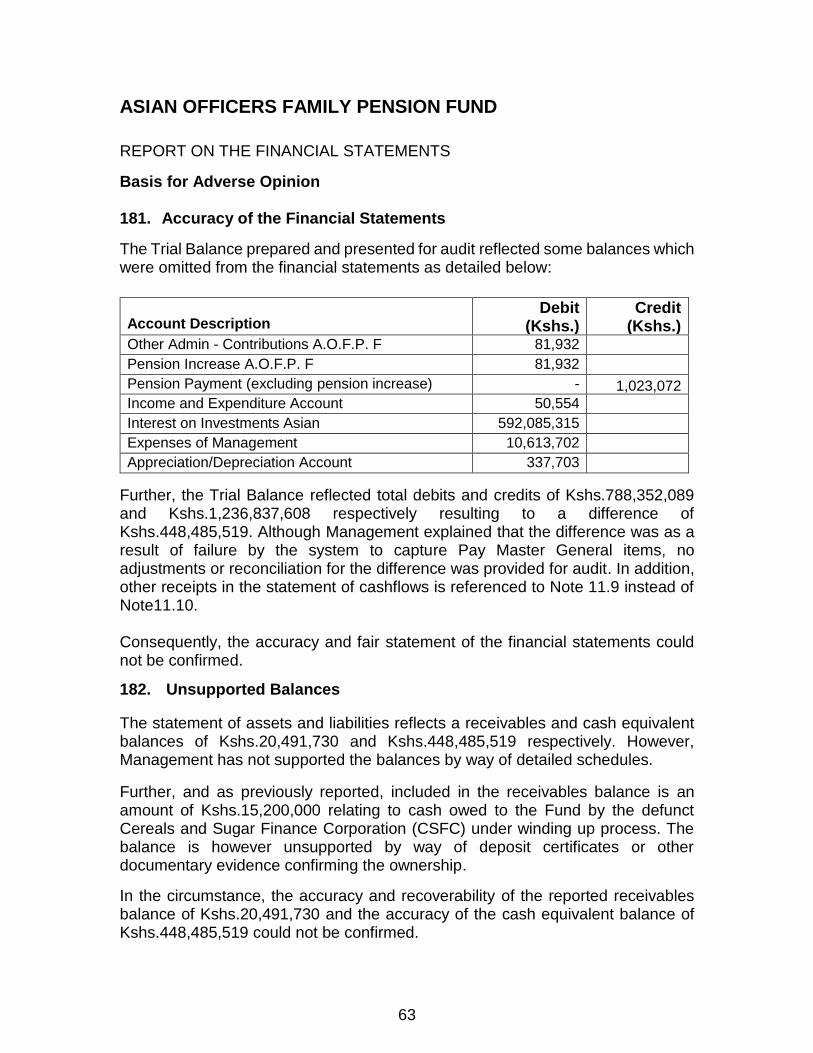

REPORT ON THE FINANCIAL STATEMENTS

Basis for Qualified Opinion

1. Variance Between Financial Statements and IFMIS Balances

The financial statements presented for audit and the Integrated Financial Management Information Systems (IFMIS) Trial Balance presented in their support had variances as detailed below: -

Component

Financial Statements

Balance (Kshs.)

IFMIS Balance (Kshs.)

Variance (Kshs.)

Bank Balances 2,248,780,788 116,580,445,030 (114,331,664,242)

Cash Balances 1,020,917 5,066,314 (4,045,397)

Accounts Receivable 899,585,508 902,182,669 (2,597,161)

Accounts Payable 80,200,064 173,301,104,441 (173,220,904,377)

Fund Balance b/fwd 2,056,688,154 (290,027,754,295) 292,084,442,449

Prior Year Adjustments (32,282,003) 0 (32,282,003)

Further, the reported accounts payable balance of Kshs.80,200,064 includes returned payments under the development vote of Kshs.6,913,831. This differs with IFMIS report balances of Kshs.8,085,150 resulting to an unexplained variance of Kshs.1,171,319.

In the circumstances, the accuracy and completeness of the financial statements for the year ended 30 June, 2019 could not be confirmed.

2. Compensation to Employees

As disclosed under Note 5 to the financial statements, the statement of receipts and payments reflects compensation to employees of Kshs.2,524,328,336;(2018- Kshs.2,308,812,613). However, the IFMIS payroll report in support of the balance reflects an amount of Kshs.2,275,019,969 resulting to an unexplained variance of Kshs.249,308,367. Similarly, payment vouchers supporting the expenditure on compensation to employees reflects an amount of Kshs.2,287,104,986 resulting to a variance of Kshs.237,223,350. The variances between the three (3) sets of records have not been reconciled. Other Matter

3. Budgetary Control and Performance The summary statement of appropriation- recurrent and development combined reflects final receipts budget and actual on comparative basis of

2

Kshs.64,865,387,441 and Kshs.56,209,005,073 respectively resulting to an underfunding of Kshs.8,656,382,368 or 13% of the approved budget. Of the underfunding, Kshs.6,508,245,168 and Kshs.2,148,137,200 relate to recurrent and development votes respectively. Further, of the realized budget receipts of Kshs.56,209,005,073 only Kshs.55,164,224,075 was absorbed resulting to an under absorption of Kshs.1,044,780,998. The underfunding and failure to absorb the realized receipts affected the planned activities and projects which may have impacted negatively on service delivery for the citizens.

4. Pending Bills

Note 18.1 to the financial statements reflects pending bills amounting to Kshs.241,957,497; (2018-Kshs.563,474,303). The balance comprises of opening balance of Kshs.2,035,366 and bills incurred during the year of Kshs.239,922,131. Failure to settle bills during the year in which they relate to adversely affects the provisions of the subsequent year to which they have to be charged. REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Basis for Conclusion

5. Contracts for Renovation of the Treasury Building, Bima and Herufi House

The National Treasury entered into a contract for rehabilitation, plumbing, drainage and sanitary appliances, amongst others, at the Treasury Building, Bima and Herufi Houses following tendering during the 2016/2017 financial year vide tender number TNT/012/2015-2016. The contract was awarded for a sum of Kshs.88,956,951 with the contractor taking possession of the site on 5 April, 2017. As at December, 2018 and more than one and half years later, no significant progress had been made due a number of reasons, amongst them, the need for the contractor to undertake additional works. This occasioned an additional contract to be awarded to the same contractor using direct procurement method. As at 22 May, 2019 two (2) years into the contract and after its expiry, progress was at 4.17% of the total contract works. The contractor has subsequently been granted multiple extension of time contracts but had not completed the renovation works as at the time of the audit. Available information indicates that three (3) other contracts were subsequently awarded to other contractors with total value of Kshs.90,644,783 and which are related to some of the works under the above initial contract. This could be indicative of duplicate awards. No explanation has been given on the subsequent awards and actions being taken against the first contractor to fully discharge the contract as per the contract terms.

3

Under the circumstances, it has not been possible to confirm if value for money will be realized from the four contracts valued at Kshs.179,621,734.

6. Consultancy Contracts

On 12 September, 2016, The National Treasury contracted three (3) professional accounting firms for consultancy services on the preparation of financial reports of National Government entities, State Agencies and County Governments at total cost of Kshs.425,100,219. As at 30 June, 2019 a sum of Kshs.403,617,347 had been paid out to the three (3) firms from the contract price of Kshs.425,100,219. However, the audits of the National Government entities, State Agencies and County Governments financial statements for the financial years 2017/2018 and 2018/2019 reported numerous gaps on accounting, disclosures and presentation of financial statements. Under the circumstances, it has not been possible to confirm whether value for money has been realized from the award of contract and payment totalling Kshs.425,100,219 for consultancy services to the three (3) professional firms. REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion

7. There were no material issues relating to effictiveness of internal controls, risk management and governance.

NATIONAL EXCHEQUER ACCOUNT

REPORT ON THE FINANCIAL STATEMENTS

Unqualified Opinion 8. There were no material issues noted during the audit of the financial statements

of the National Exchequer Account.

Other Matter 9. Budget Control and Performance

The statement of comparison of budget and actual performance reflects revised revenue estimates of Kshs.2,617,207,172,439 and total revenue collections of Kshs.2,497,637,419,575 resulting to an under collection of Kshs.127,337,194,547 or 5% of the budget. The statement also reflects budget realization on Exchequer transfers to National Government; Recurrent and Development Votes, County

4

Governments and Consolidated Fund Services of 97%, 88%, 98% and 96% of the budgets respectively. However, as reflected under Annex I to the financial statements: detailed analysis of transfers, four (4) Ministries, Departments and Agencies (MDAs) received transfers that were significantly low - ranging between 41% and 80% with some not receiving any funding under the development vote despite having budgets.

Consequently, service delivery to the citizens by the affected entities could have been negatively affected.

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Basis for Conclusion

10. Excess Exchequer Releases Two (2) MDAs received Exchequer issues in excess of the approved budget as detailed out below:

MDA

Approved Estimates

(Kshs.)

Actual Issued (Kshs.)

Excess Amount (Kshs.)

Salaries and Remuneration Commission (Recurrent)

483,196,637 512,506,930 29,310,293

State Department for Public Service and Youth (Development)

1,391,478,885 1,541,219,720 149,740,835

This is contrary to the provisions of Article 206 (2) (a) of the Constitution of Kenya which provides that money may be withdrawn from the Consolidated Fund only in accordance with an appropriation by an Act of Parliament. The National Exchequer Account Management was, therefore, in breach of the law. REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE Conclusion 11. There were no material issues relating to effictiveness of internal controls, risk

management and governance.

5

CONSOLIDATED FUND SERVICES - PUBLIC DEBT

REPORT ON THE FINANCIAL STATEMENTS Basis for Adverse Opinion 12. Public Debt -Outstanding Balance

The summary statement of public debt reflects an outstanding loan balance of Kshs.5,451,153,803,416; (2018-Kshs.4,801,416,851,482) representing an increase of Kshs.649,736,951,934 or (13.5%) of the public debt. The statement also reflects loan repayments of Kshs.1,648,856,675,693 during the year but does not expressly indicate the amount procured during the year. However, review of the opening and closing balances and adjusted for the repayments during the year results in borrowings of Kshs.2,298,593,627,627 which have not been supported.

Further, out of the twenty-four (24) loans sampled and reviewed, eleven (11) had total balances different from those reflected in the summary statement of public debt prepared by The National Treasury. The total variance between the two sets of records amounted to Kshs.95,241,461,497. The causes of the variances have not been explained.

Under the circumstances, the accuracy of the outstanding loan balance of Kshs.5,451,153,803,416 as at 30 June, 2019 could not be confirmed.

13. Inaccuracies in the Cash and Cash Equivalents

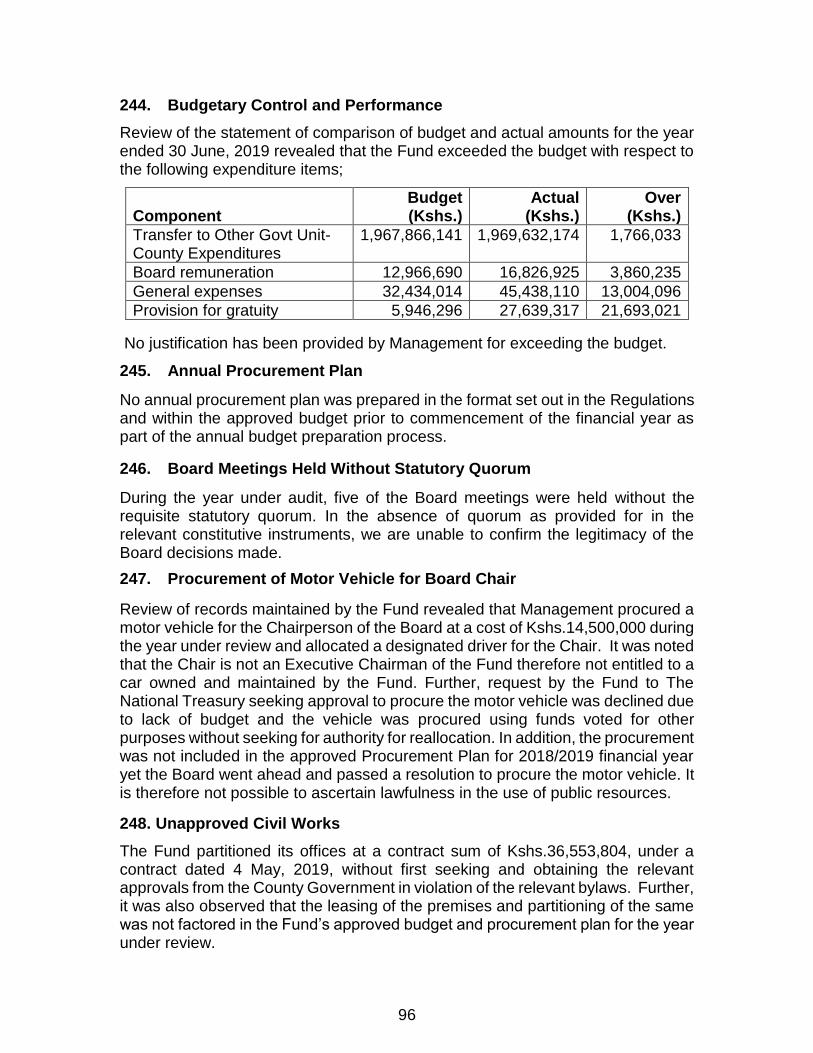

As disclosed in Note 5 to the financial statements, the statement of assets and liabilities reflects bank balances of Kshs.249,080,863 as at 30 June, 2019. On the other hand, the Trial Balance reflects bank balances of Kshs.1,064,098,739 resulting in a variance of Kshs 815,017,876 which has not been explained or reconciled. Further, the Board of Survey Report on the bank balance as at 30 June, 2019 was not availed for audit review. Under the circumstances, the accuracy of the reported bank balances of Kshs.249,080,86 as at 30 June, 2019 could not be confirmed Emphasis of Matter 14. Unauthorized Over-Expenditure - Finance Costs and Loan Interest The summary statement of appropriation reflects a final expenditure budget and actual on comparable basis of Kshs.848,303,865,142 and Kshs.826,202,867,839 respectively, resulting in under expenditure of Kshs.22,100,997,303 or 3% of the budget. However, detailed analysis of the individual expenditure items revealed

6

that an over-expenditure was incurred on Interest on Treasury Bonds (TB) and Foreign Borrowing (FB) of Kshs.50,247,591,640 and Kshs.76,011,232,922. Although Management has explained that part of the over expenditure on interest on Treasury Bonds of Kshs.28,915,693,668 related to pending bills for the financial year 2017/2018, the amount had not been disclosed in the financial statements for that year. The over expenditure has not been authorized.

Other Matter

15. Unresolved Prior Year Matters

15.1 Unsupported Balances

As previously reported, the statement of assets and liabilities for the year ended 30 June, 2018 reflected a prior year adjustment balance of Kshs.27,251,420,599 which was not supported by a journal voucher or Notes to the financial statements. In addition, the general ledger under payments reflected a balance of Kshs.516,547,493,884 which included a credit balance of Kshs.1,244,520,000 under Debut International SVRNG Bond (USD 2.75 BN). The balance was not supported by any documentary evidence. Further, the ledger reflected expenditure for new loans and new administrative costs of Kshs.7,919,757,971 and Kshs.59,894,313,393 respectively but details of these payments were not provided. Consequently, the accuracy and completeness of these balances could not be confirmed.

15.2 Accuracy of the Financial Statements

As reported in the previous year, a comparison of the statement of receipts and payments and the ledger for the year ended 30 June, 2018 reflected different accounts balances in respect to the same items as indicated:

Item Description

Financial Statement Balance (Kshs.)

Ledger Balance (Kshs.)

Variance (Kshs.)

Interest Payments on Foreign Borrowings

84,357,487,111 84,725,600,971 368,113,860

Principal Repayment on Domestic Loans

111,700,845,296 294,836,376,343 183,135,531,047

CBK -Pre-1997 Loans 1,110,000,000 2,220,000,000 1,110,000,000

Repayment of Principal from Foreign Lending and On-Lending

141,532,524,729 141,360,882,966 171,641,763

Exchequer Releases 517,161,876,534 - 517,161,876,534

7

Management has however not provided any analysis and supporting documents to support the adjustments.

The accuracy of the balances reflected in the financial statements could therefore not be confirmed.

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Conclusion

16. There were no material issues relating to lawfulness and effectiveness in use of public resources.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion

17. There were no material issues relating to effectiveness of internal controls,

risk management and governance.

REVENUE STATEMENTS (RECURRENT)

REPORT ONTHE REVENUE STATEMENTS Basis for Qualified Opinion 18. Cash Book Balance

18.1 Unsupported Adjustments

During the year under review adjustments were made to the cash book on account of the long outstanding reconciling items as detailed out below: -

Reconciling Item Amount (Kshs.)

Payments in bank not in cash book 15,723,735,928

Receipts in bank not in cash book 34,524,942,523

Receipts in cash book not in bank 16,240,834,531

Payments in cash book not in bank 605,746,618

However, the adjustments were unsupported by way of authorized journal entries.

8

18.2 Long Outstanding Reconciling Items

The bank reconciliation statement in support of the cash book as at 30 June, 2019 reflects long outstanding receipts in bank statement but not recorded in cash book of Kshs.164,731,174 dating back to June, 2000. No satisfactory explanation has been rendered for failure to reconcile the items.

From the foregoing, it is not possible to confirm the accuracy and fair statement

of the reported nil cash book balance as at 30 June, 2019.

19. Variance in Tax Receipts

The statement of revenues and transfers reflects tax revenues receipts of Kshs.1,440,830,331,255. However, the Kenya Revenue Authority accountability statement for the period reflects tax income receipts transfers of Kshs.1,338,169,499,540 resulting to an unexplained net variance of Kshs.102,660,831,716.

No satisfactory explanations have been rendered for the discrepancies between the two sets of records.

Consequently, it is not possible to confirm the accuracy and completeness of the reported tax revenue receipts of Kshs.1,440,830,331,256 for the year ended 30 June, 2019.

20. Unsupported Non-Tax Revenues

The statement of revenue and transfers reflects non-tax revenue receipts of Kshs.39,056,195,610; (2018-Kshs.39,440,753,231) comprising of fees on use of goods and services (PDL / traffic), social security contributions, property income, other receipts (miscellaneous), proceeds from domestic borrowings and proceeds from foreign grants. However, they were unsupported by way of detailed ledgers.

In the circumstances, the accuracy and completeness of the reported non-tax revenue receipts of Kshs.39,056,195,610 for the year ended 30 June, 2019 could not be confirmed.

21. Variances Between Revenue Statements and the General Ledger

The statement of revenue and transfers reflects tax revenues receipts that were at variance with the ledgers presented in support as detailed out below: -

9

]

No explanations have been rendered for the variances.

Consequently, the accuracy and completeness of the reported tax revenue receipts of Kshs.1,440,830,331,055 for the year ended 30 June, 2019 could not be confirmed.

Other Matter

22. Budgetary Control and Performance

The statement of comparison of budget and actual amounts reflects final proceeds from foreign grants (AMISOM) budget and actual on comparable basis of Kshs.6,500,000,000 and Kshs.575,433,441 respectively resulting to under collection of Kshs.5,924,566,559 or 91% of the budget. No satisfactory explanation has been rendered for the under collection and measures being put in place to avoid recurrence. REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES Basis for Conclusion 23. Incomplete Reporting on Waivers/Exemptions

The report on waivers/exemptions made available for audit review was incomplete and lacked crucial information such as names of the beneficiary, tax amount waived, reason(s) for the waiver and the applicable law for the waiver as required in law.

Revenue Item

Revenue Statements

(Kshs.) General Ledger

(Kshs.) Variance

(Kshs.)

Taxes on Individuals (PAYE)

393,439,728,378 393,361,503,751 78,224,627

Corporation Tax 294,841,466,811 294,979,065,094 (137,598,283)

(Land Rent) 610,032,875 617,606,996 (7,574,121)

Vat on Domestic Goods/Services

230,775,544,313 234,058,961,044 (3,283,416,731)

Vat on Imports 183,367,863,463 182,586,223,952 781,639,511

Excise Duty 196,608,900,149 196,588,499,134 20,401,015

Custom Duties 106,874,931,944 107,701,825,385 (826,893,441)

Import Declaration Fees 24,196,727,815 24,182,047,020 14,680,795

Stamp Duty 10,115,135,308 10,213,854,991 (98,719,683)

Total 1,440,830,331,055 1,444,289,587,367 (3,459,256,311

10

The National Treasury is in breach of the law to this extent. REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE Conclusion 24. There were no material issues relating to effictiveness of internal controls,

risk management and governance.

REVENUE STATEMENTS (DEVELOPMENT)

REPORT ON THE REVENUE STATEMENTS

Unqualified Opinion 25. There were no material issues noted during the audit of the development

revenue statements.

Other Matter

26. Budgetary Controls and Performance

The statement of comparative budget and actual amounts reflect final revenue budget and actual on comparable basis of Kshs.67,668,743,001 and Kshs.50,118,804,547 respectively resulting to under performance of Kshs.17,549,938,454 or 26% of the budget. Management has attributed the under collection to; requirement of the implementing units to exhaust funds released in the prior periods before accessing new disbursements, stringent conditions from the development partners on meeting AIA payments before accessing funding and partner delays in releasing no objection for projects not funded using Country systems.

Consequently, there was under funding of the planned development activities which may have impacted negatively on service delivery to the citizens. REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES Conclusion

27. There were no material issues relating to lawfulness and effectiveness in use of public resources.

11

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion 28. There were no material issues relating to effectiveness of internal controls,

risk management and governance.

REVENUE STATEMENTS - GOVERNMENT INVESTMENT AND PUBLIC ENTERPRISES

REPORT ON THE REVENUE STATEMENTS

Basis for Adverse Opinion

29. Accuracy of Schedule of Outstanding Loans

The summary schedule of outstanding loans reflects an outstanding loans balance of Kshs.809,988,920,916 as at 30 June, 2019. However, circularization of sample debtors for the loan balances revealed significant discrepancies between the reported book balances and the amounts confirmed as owing by the respective institutions as detailed below:

No

Entity

Balance as per Financial

Statement (Kshs.)

Confirmed Balance (Kshs.) Variance

(Kshs.)

1 Kenya Civil Aviation Authority

1,710,514,701 2,343,070,698 632,555,997

2 South Nyanza Sugar Company Limited

199,027,420 794,628,045 595,600,625

3 Agro Chemical and Food Company Limited

2,846,884,000 9,351,809,235 6,504,925,235

4 Moi University 231,250,000 257,765,332 26,515,332

5 Kenya Utalii College 127,000,000 140,125,028 13,125,028

6 IDB Capital Ltd 1,555,675,500 212,979,779 1,342,695,721

7 Kenya Railways Corporation 473,210,691,342 435,466,126,847 37,744,564,496

8 Cooperative Bank 402,151,336 351,857,512 50,293,824

9 Water Resources Authority 362,612,300 372,705,009 (10,092,709)

10 Equity Bank 421,332,807 100,282,010 321,050,797

11 Industrial and Commercial Dev’t Corp. (ICDC)

371,848,560 891,848,560 (520,000,000

12 Kenyatta University 10,857,620,656 85,988,783 10,771,631,873

13 SMEP Bank 79,037,111 69,157,472 9,879,639

14 Northern Water Works Dev’t Agency

5,389,000,000 2,757,697,547 2,631,302,453

15 Faulu Micro Finance Ltd 137,415,056 - 137,415,056

12

The discrepancies between the two sets of records was not explained or reconciled.

Under the circumstances, the accuracy of the reported outstanding loans balance of Kshs.809,988,920,916 as at 30 June, 2019 could not be confirmed. Other Matter

30. Unresolved Prior Year Matter

30.1 Dormant Loans

Loans amounting to Kshs.84,284,132,909 representing 10.4% of the total loan portfolio of Kshs.809,988,920,916 as at 30 June, 2019 had no movement and as previously reported, have remained unpaid over a significant period of time casting doubts on their recoverability. The loan details are as tabulated below:

No

Institution

Balance as at 30 June, 2019

(Kshs.)

1 Coast Water Service Board 12,241,117,290

2 East African Sugar Industries Limited, Muhoroni 177,123,100

3 Halal Meat Products 27,701,420

4 Kenya Meat Commission 940,241,100

5 Kenya Urban Transport Various Towns 40,706,140

6 Lake Victoria North Water Services Board 7,593,445,499

7 Lake Victoria South Water Services Board 13,121,785,606

8 Miwani Outgrowers Mills Limited 6,600,000

9 Miwani Sugar Company (1989) Ltd 16,000,020

10 Miwani Sugar Mills Limited 78,088,180

11 Mumias Sugar Company Limited 3,000,000,000

12 National Irrigation Board 2,262,036,544

13 National Water Conservation and Pipeline Corporation

2,460,874,897

14 Tana Water Services Board 7,543,116,143

15 Tanathi Water Services Board 9,713,565,506

16 Water Resource Management 362,612,300

17 Agricultural Finance Corporation 475,119,163

18 Kenya Airways 24,224,000,000

Total 84,284,132,908

No evidence of the measures taken by Management to recover the outstanding amounts was provided for audit.

13

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Basis for Conclusion

31. Supporting Documents and Management of Loan Portfolio

As previously reported, Management has not been able to confirm its active role in the management of existing loan portfolio and issuance of new loans through annual work plans and periodic monitoring and evaluation reports. In the absence of budgets, annual work plans, assessment or evaluation and performance reports of the loaning portfolios, the propriety on the utilization of public funds could not be ascertained. There is also risk of non-servicing of the loans leading to continued write offs as bad debts which is a cost to the public.

32. Long Outstanding Loans (Arrears)

The statement of arrears of receipts reflects total amount in arrears of Kshs.39,165,038,029 as at 30 June, 2019 (2018-Kshs.37,606,213,925) representing an increment of Kshs.1,558,824,104 during the year under review. Management has attributed the default to the fact that most of the entities were experiencing financial difficulties. However, Management has not provided evidence of measures taken to obtain payments or reports to the Cabinet Secretary explaining specific difficulties experienced in collecting the debts as required under Regulation 64 of the Public Finance Management (National Government) Regulations, 2015.

Consequently, Management is in breach of the Regulations.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion 33. There were no material issues relating to effectiveness of internal controls,

risk management and governance.

14

STATEMENT OF OUTSTANDING OBLIGATIONS GUARANTEED BY THE GOVERNMENT OF KENYA

REPORT ON THE FINANCIAL STATEMENTS

Basis for Disclaimer of Opinion

34. Presentation and Disclosure

The statement of outstanding obligations guaranteed by the Government of Kenya reflects outstanding balance of Kshs.152,317,825; (2018-Kshs.164,132,745) being Capital and Interest owed by Cereals and Sugar Finance Company. However, the Consolidated National Government Investment Report for the year 2018/2019, prepared by The National Treasury in accordance with Section 89 of the Public Finance Management Act, 2012, indicates that the total outstanding Government guaranteed debt stood at Kshs.159,405,000,000 as at 30 June, 2019 as shown below:

Agency

Outstanding Government

Guaranteed Debt as at 30 June, 2019

(Kshs.)

Kenya Broadcasting Corporation (KBC) 357,000,000

Tana and Athi River Development Authority 279,000,000

East African Portland Cement PLC 346,000,000

Kenya Electricity Generating Company PLC 43,035,000,000

Kenya Ports Authority 34,061,000,000

Kenya Railways Corporation 4,603,000,000

Kenya Airways 76,724,000,000

Total 159,405,000,000

The total outstanding Government guaranteed debt of Kshs.159,405,000,000 does not include the balance of Kshs.152,317,825 reflected in the statement of outstanding obligations guaranteed by the Government of Kenya prepared and submitted for audit by The National Treasury, which is indicated as relating to Capital and Interest owed by Cereals and Sugar Finance Company. Further, the parent Ministries for the Agencies mentioned above did not prepare and submit for audit their respective statements of outstanding obligations guaranteed by the Government of Kenya as at 30 June, 2019. No explanations have been provided for the omissions.

Under the circumstances, the completeness and accuracy of the outstanding balance of Kshs.152,317,825 reflected in the statement of outstanding obligations guaranteed by the Government of Kenya as at 30 June, 2019 could not be ascertained.

15

35. Decrease in Guaranteed Obligations

The statement indicates that obligations guaranteed decreased from Kshs.164,132,745 reported as at 30 June, 2018 to Kshs.152,317,825 as at 30 June, 2019. Although Note 2 to the financial statements explains the reasons for the decrease in balance, Management did not avail documentary evidence to support the explanation.

Consequently, the accuracy of the reported decrease of Kshs.11,814,920 could not be confirmed.

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Conclusion

36. Because of the significance of the matters described in the Basis for Disclaimer of Opinion section of my report, I have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit conclusion.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion

37. Because of the significance of the matters described in the Basis for Disclaimer of Opinion section of my report, I have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit conclusion.

CONSOLIDATED FUND SERVICES - SUBSCRIPTIONS TO INTERNATIONAL ORGANIZATIONS

REPORT ON THE FINANCIAL STATEMENTS

Unqualified Opinion

38. There were no material issues noted during the audit of the financial statements of the Fund

Other Matter

39. Dormancy of Consolidated Fund Services - Subscriptions to International Organizations

The financial statements of the CFS- Subscriptions to International Organizations for 2016/17, 2017/18 and 2018/19 financial years reflects no activity for the three

16

years period. Although a budget of Kshs.500.000 has been allocated under CFS - Subscriptions to International Organizations every year, no activities have been reported during the three (3) years period. The relevance of the CFS- Subscriptions to International Organizations is, therefore, not clear especially in view the Public Finance Management Regulations (African Union (AU) and Other International Organizations Subscription Fund) Regulations, 2017 which established the AU and Other International Organizations Subscription Fund from which Kenya’s contributions to AU and Other International Organizations should be paid from.

40. Unresolved Prior Year Audit Matters

The following prior year audit matters remained unresolved as at the end of the financial year:

40.1 Comparison of Expenditure with the Appropriation Account

As reported in 2017/2018 financial year, The National Treasury financial statements reflected payments as grants and transfers amounting to Kshs.1,069,476,595. Included in the amount were membership dues and subscriptions to unspecified international organizations totalling to Kshs.48,779,790 while the remaining balance of Kshs.1,020,696,805 was indicated to have been paid to four organizations as detailed out below: -

Organization Amount (Kshs.)

Africa Capacity Building Foundation 42,333,304

Shelter Afrique 355,000,000

MEFMI 81,363,501

International Bank for Reconstruction and Development, IBRD

542,000,000

Total 1,020,696,805

There is a risk of duplicate payments of expenditure where The National Treasury makes payments without authenticating with organizations responsible for the payments and more specifically where payments are not adequately disclosed as is the case of Kshs.48,779,790. From the foregoing, The National Treasury has not drawn a distinction between subscriptions and grants and hence the pay points of CFS - Subscription to International Organizations and The National Treasury main account respectively. 40.2 Unsupported Balances

In the audit report of 2015/2016, the detailed statement of Kenya Government share subscriptions and capital contribution to international organizations under Note 5 of the financial statements had reflected local value of subscriptions totalling Kshs.51,403,651,783 against various amounts in foreign currencies as at 30 June, 2016. However, an independent circularization to twelve (12) reported

17

recipient organizations yielded only four (4) confirmations. Further, amounts confirmed by two (2) of the four (4) organizations differed significantly with the reported amounts as per The National Treasury records.

Further, subscription for 2014/15 amounting to Kshs.116,813,106,919 in respect of ten (10) organizations were restated to Kshs.49,750,957,607 and attributed to foreign exchange rate fluctuations. However, the huge discrepancies attributed to foreign exchange losses have not been explained.

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Conclusion

41. There were no material issues relating to lawfulness and effectiveness in use of public resources.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE. Conclusion 42. There were no material issues relating to effectiveness of internal controls, risk

management and governance.

EAST AFRICA TOURIST VISA FEE COLLECTION ACCOUNT

REPORT ON THE FINANCIAL STATEMENTS

Basis for Disclaimer of Opinion 43. Inappropriate Financial Reporting Framework

Section 81(3) of the Public Finance Management Act, 2012 requires an Accounting Officer to prepare the financial statements in a form that complies with the relevant accounting standards prescribed and published by the Public Sector Accounting Standards Board (PSASB). The Board has prescribed the Accrual Basis of accounting method for accounts that carry forward and do not surrender balances at the end of financial year with the following elements; the statement of financial position, statement of financial performance, statement of changes in net assets, statement of cash flows and comparative statement of budget and actual expenditure.

However, the financial statements presented for audit have been prepared in accordance with the Cash Basis of accounting method under the International Public Sector Accounting Standards (IPSAS) which comprise of; the statement of

18

assets and liabilities, statement of receipts and payments, statement of cash flows and comparative statement of budget and actual amounts. In the circumstances, the financial statements as prepared and presented do not comply with the provisions of Section 81(3) of the Public Finance Management Act, 2012.

44. Completeness of Statement of Budget Versus Actual Performance

The statement of budget versus actual performance reflects receipts as a consolidated amount from East Africa Tourist Fee whereas the statement of receipts and payments disaggregates receipts into; receipts from sale of EATV stickers by Kenya, share of EATV revenue from partner states and foreign exchange gain. The Statement does not also disclose the budgeted transfers. Consequently, the statement of budget versus actual performance as prepared and presented is not IPSAS cash basis compliant.

45. Poor Maintenance of Accounting Records and Supporting Documents

The financial Statements prepared and presented for audit were not adequately supported with the underlying source documents including the Trial Balance, Ledgers and Visa Registers. Furthermore, the cashbook presented had no evidence of having been reviewed. No monthly bank reconciliation statements were prepared and board of survey reports were not carried out as part of the end of year procedures. The Joint verification report balances are at variance with those reported in the financial statements.

In absence of proper accounting records and supporting documents, no reliance

can be placed on the financial statements as prepared and presented.

46. Non-Compliance with the EATV MOU

Article 7 of the MOU outlines the modalities for sharing out revenues raised on EATV fees amongst the partner states with ten percent (10%) being retained by each member country issuing the sticker for its administration costs, including accrued bank charges, and the remaining 90% to be shared equally among the three partner states each receiving 30%. The MOU also indicates the departments with the responsibilities to implement the MOU, the timeframe for effecting the transfers to the member states and further defines the amounts for administration costs or bank charges. However, the statement of receipts and payments reflects receipts from sale of EATV stickers by Kenya of Kshs.100,775,998 resulting to equitable share to the partner countries of Kshs.60,465,599. However, actual transfers total to the partner countries amounted to Kshs.66,574,248 resulting an overpayment of Kshs.6,108,649. Management has not provided the reasons for the overpayment. In the circumstances, Management is in breach of the MOU.

19

47. Limited Segregation of Duties

The financial transactions for the Account were prepared and recorded by one officer. The officer solely undertook recordings in the cashbook and other books of original entry. Further, the officer was responsible for the preparation of financial statements and provision of supporting records and documents. Consequently, there is limited segregation of duties which makes the process susceptible to errors and manipulation.

48. Unresolved Prior Year Audit Matters

The following prior year audit matters remained unresolved as at 30 June, 2019: -

48.1 Receipts from Issue of Stickers in Kenya

As disclosed under Note 10.1 to the financial statements, the statement of receipts and payments for the year ended 30 June, 2017 reflected receipts from issue of stickers by Kenya of Kshs.72,459,424. However, Management did not avail the Trial Balance, Ledgers, and the Register for Visa Stickers Register in support of the reported revenue. Further, there is no reconciliation between receipts issued out by the agencies and the reported revenue receipts. A review of stickers under the custody of two revenue collecting agencies; Ministry of Foreign Affairs and the Directorate of Immigration and Registration of persons revealed that five thousand seven hundred and fifty (5,750) and five thousand and thirty-six (5,036) stickers were issued respectively. With each sticker selling at USD 100, the total receipts amounted to USD 1,078,600 or approximately Kshs.107,860,000. From the foregoing, the accuracy and completeness of the reported receipts from issue of stickers by Kenya of Kshs.72,459,424 for the year ended 30 June, 2017 could not be confirmed.

48.2 Non-Submission of Financial Statements

As previously reported, the financial statements prepared and presented for audit for the year ended 30 June, 2016 had comparative balances for the year ended 30 June, 2015. However, the financial statements for the year ended 30 June, 2015 were not prepared and presented for audit. Consequently, the comparative balances were for an unaudited financial statement. A review of the East African Tourist Visa (EATV) Memorandum of Understanding (MOU) indicates that it was signed on 27 October, 2013 with the collection of fees commencing in the financial year ended 30 June, 2014. The first set of financial statements should have covered the year ended 30 June, 2014 and subsequently to 30 June, 2015.

Consequently, the accuracy of the unaudited comparative figures could not be established.

20

48.3 Non-Adherence to MOU Provisions on Sharing of Receipts

As previously reported, the statements of receipts and payments reflected receipts from issue of stickers by Kenya of Kshs.70,883,521 for the year ended 30 June, 2016. However, the sharing out was not equitable as per the MOU which entitles the issuing party to retain 10% of the amount or Kshs.7,088,352 and the balance to be shared equally by the parties each receiving 30% or Kshs.21,265,056. Instead, each partner state received Kshs.15,934,153 which was an understatement by Kshs.5,330,903 as per the signed MOU. No satisfactory explanation has been provided for the breach of the agreement. Management has also not provided proof of remittance of its share of receipts of Kshs.28,353,408 to the Exchequer.

48.4 Discrepancies Between Financial Statements and Supporting Records

As previously reported, a review of records in support of the financial statements revealed that The National Treasury maintains two EATV fee operating bank accounts, account number 1000227257 denominated in Kenya Shillings and account number 1000239026 denominated in US dollars. Review of the Kenya Shillings account revealed that Kshs.51,182,218 EATV fees collected and recorded in the cashbook during the year was omitted from the 2015/2016 financial statements.

Further, receipts from share of revenue from partner states, Uganda and Rwanda amounting to Kshs.16,236,859 and Kshs.16,818,866 respectively deposited in the Kenya shillings bank account was not reported in the financial statements for the year.

In addition, the Kenya Shillings cashbook reflected a closing balance of Kshs.39,898,521 as at 30 June, 2016 which was not incorporated in the financial statements. Further, the transfers made to the partner states from the Kenya Shillings bank account were omitted from the reported share of EATV revenue to partner states in the statement of receipts and payment.

Consequently, it has not been possible to confirm the accuracy and completeness of the financial statements as prepared and presented.

48.5 Accountability for EATV Stickers

As previously reported, Article 6 of the MOU sets the modalities for issuance of the EATV stickers with the sticker issued to a tourist upon payment of USD100 or its equivalent in the local currency. The stickers issued to tourists are accountable documents and hence records of how they are procured, distributed and issued are critical for accountability. However, the management does not have in place registers of all stickers received from the partner states and issued out for the year.

21

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Conclusion

49. Because of the significance of the matters described in the Basis for Disclaimer of Opinion section of my report, I have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit conclusion.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion

50. Because of the significance of the matters described in the Basis for Disclaimer of Opinion section of my report, I have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit conclusion.

CONSOLIDATED FUND SERVICES (CFS) - SALARIES ALLOWANCES AND MISCELLANEOUS SERVICES

REPORT ON THE FINANCIAL STATEMENTS

Basis for Qualified Opinion

51. Unsupported Prior Year Adjustments

As disclosed under Note 10 to the financial statements, the statement of assets and liabilities reflects a prior year adjustment of Kshs.158,249,113;(2018- Kshs.18,420,097). However, the disclosures are inadequate as they are not supported by way of an itemized breakdown of the adjustment.

Consequently, the accuracy of the prior year adjustment of Kshs.158,249,113 as at 30 June, 2019 could not be confirmed. Other Matter

52. Budgetary Provisions and Performance

The summary statement of appropriation: recurrent and development combined reflects final miscellaneous services budget and actual on comparable basis of Kshs.128,000,000 and Nil respectively. As similarly reported in 2017/2018, the planned activities and programmes on the budgetary provision have not been disclosed.

22

53. Prior Year Issues

The following prior year audit matters remained unresolved as at 30 June, 2019;

53.1 Accuracy of the Financial Statements and Records

A review of various balances reflected in the financial statements for the year ended 30 June, 2018 revealed that records maintained by Management reflected different balances though relating to the same items as highlighted below:

i) The statement of receipts and payments reflected an expenditure of Kshs.2,685,214,290 under compensation of employees. The Trial Balance reflected a credit balance of Kshs.3,217,869,377 on the same item while the payroll and payment vouchers showed a total expenditure of Kshs.2,675,257,162. The differences between the three sets of records have not been reconciled.

ii) An analysis of the ‘off payroll’ payments reflected an expenditure of Kshs.256,036,689 while the physical vouchers availed and examined for the period indicate a total expenditure of Kshs.254,479,596. An expenditure of Kshs.1,557,093 could not therefore be vouched or explained.

iii) The expenditure on Teachers Service Commissioners as per the supporting schedules was Kshs.70,500,744 while the Ledger reflected a balance of Kshs.55,586,543 for the same period. The difference of Kshs.14,914,201 was not explained.

iv) Examination of schedules supporting the expenditure for the Independent Electoral and Boundaries Commission in the statement of receipts and payments reflected a closing balance of Kshs.61,788,248 while the payroll reflected an amount of Kshs.51,679,730 The difference of Kshs.10,108,518 was not explained. In addition, the amount was not recorded in the Ledger and Trial Balance.

v) Examination of payment vouchers revealed that an amount of Kshs.23,705,121 paid to two retired officers of the National Gender and Equality Commission (NGEC) was wrongly charged to the National Police Service Commission (NPSC) expenditure item. No adjustment has been made to correct the anomaly.

vi) The ledger reflected an expenditure of Kshs.100,210,801 for the National Cohesion and Integration Commission while the payment vouchers examined indicates a total of Kshs.97,017,530. The difference of Kshs.3,193,271 was not explained or reconciled.

vii) The Trial Balance provided for audit included balances which had not been identified as either debits or credits. Whereas the Trial Balance represents

23

a prima facie evidence on the accuracy of recording of all the transactions affecting an entity, it was difficult to establish whether the two sides of the Trial Balance balanced as at 30 June, 2018. The accuracy of the financial statements’ figures cannot therefore be ascertained without confirming the balancing of the Trial Balance.

In absence of an accurate Trial Balance, the resultant financial statements could have been grossly misstated and may not have reflected a true and fair view of the operations of the Consolidated Fund Service - Salaries, Allowances and Miscellaneous Services for the year ended 30 June, 2018.

53.2 Unsupported Prior Year Adjustments

The statement of assets and liabilities as at 30 June, 2018 reflected prior year adjustment of Kshs.18,420,097 (2017: Kshs.26,919,334) which was not supported. As reported similarly in the previous years’ audit reports, Management has not explained the genesis for the adjustments or provided any records by way of journal vouchers or entries in the ledger. It appears Management may have used the ‘prior year adjustments’ as a way of balancing inaccuracies and inconsistencies in the financial records. In absence of sufficient verifiable supporting documents and records, the authenticity of such adjustments in the financial statements cannot be ascertained.

53.3 Account Balances Not Recorded in Ledger

The financial statements for the year 2016/2017 reflected balances of individual items that were not reflected in the ledger of the Consolidated Fund Services - Salaries, Allowances and Miscellaneous Services as indicated below; -

Account

Amount (Kshs.)

Exchequer Releases 3,905,744,684

Transfers from Other Government Entities 362,830,853

Other Receipts 18,420,097

The figures in the financial statements in respect to the specific items could not be authenticated.

53.4 Unsupported Restatement of Balances

The financial statements for the year ended 30 June, 2016 reflected balance brought forward amounts under Fund balance, compensation of employees and accounts receivables of Kshs.8,566,405,035, Kshs.2,416,693,457 and nil which had been re-stated from Kshs.397,382,932, Kshs.2,418,352,317 and 8,663,621,032 respectively, reflected in the audited financial statements for 2014/2015. The statement of financial position also showed clearance of

24

outstanding items of Kshs.11,980,334. This has not been explained nor details of the adjustments provided.

Consequently, the accuracy of the balances reflected in the financial statements cannot be confirmed.

53.5 Unexplained Balance

The statement of assets and liabilities as at 30 June, 2017 reflected a balance of Kshs.4,456,673 referred to as “difference”. Management has not explained what this amount related to. Further the item does not appear in the subsequent financial statements and there is no disclosure on how it was dealt with.

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES

Conclusion

54. There were no material issues relating to lawfulness and effectiveness in use of public resources.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE

Conclusion

55. There were no material issues relating to effectiveness of internal controls, risk management and governance.

CONSOLIDATED FUND SERVICES - PENSIONS AND GRATUITIES

REPORT ON THE FINANCIAL STATEMENTS

Basis for Adverse Opinion

56. Inaccuracies in the Financial Statements

56.1 Discrepancies Between the Financial Statements and the Ledger Balances

The financial statements prepared and presented for audit had the following unexplained and unreconciled variances with the ledger as indicated below:

25

Item

Financial Statements

Balance (Kshs.)

Ledger Balance (Kshs.)

Variance (Kshs.)

Military Gratuity Payments 2,365,015,733 2,580,880,386 (215,864,653)

Returned Pensions 341,468,825 438,896,156 (97,427,331)

Re-credited Cheques 121,791,362 390,937,784 (269,146,422)

Commuted Pension and Gratuities

22,808,826,537 25,095,813,221 (2,286,986,684)

The differences between the two sets of records have not been reconciled or explained.

56.2 Misstated Payment of Pensions Balances

As disclosed in Note 13.3 to the financial statements, the statement of receipts and payments reflects a balance of Kshs.66,917,302,195 under payment of pensions. However, this balance varies with the casted amount of Kshs.66,119,310,602 reflected in Note 13.3 to the financial statements, by Kshs. 797,991,593. Further, included in the military pensions payments of Kshs.4,658,469,029 is an amount of Kshs.132,892,687 which was paid in the financial year 2019/2020. In addition, payments of civil pensions amounting to Kshs.29,820,146,295 was not properly supported as the payrolls and payment vouchers reflected an expenditure of Kshs.30,271,871,789 and Kshs.26,586,806,355 respectively as at 30 June, 2019.

From the foregoing, the accuracy of the financial statements prepared and presented for audit for the year ended 30 June, 2019 could not be confirmed.

56.3 Comparative Balances Differing with Audited 2017/18 Balances

The following comparative balances differed with the balances reflected in the audited 2017/18 financial statements:

Statement

Component

Comparative Balance as Per

2018/2019 Financial Statements

Balance as Per the Certified 2017/18

Financial Statements

Statement of Assets and Liabilities

Bank Balance 572,446,864 (572,446,864)

Statement of Assets and Liabilities

Net Financial Assets

4,633,699,481 (4,633,699,481)

Statement of Assets and Liabilities

Fund Balance b/f

3,876,911,341 (3,876,911,341)

Statement of Assets and Liabilities

Deficit for the period

756,788,140 (756,788,140)

26

Statement

Component

Comparative Balance as Per

2018/2019 Financial Statements

Balance as Per the Certified 2017/18

Financial Statements

Note 13.1 Exchequer Releases

63,170,121,740 62,413,333,600

Note 13.3 Civil gratuity Nil 1,219,455,965

In addition, the statement of assets and liabilities reflects a fund balance brought forward of Kshs.4,037,848,812 while the audited 2017/18 financial statements reflected a closing balance of Kshs.4,633,699,481 resulting into an unexplained difference of Kshs.595,850,669.

57. Accuracy of the Financial Statements

The statement of receipts and payments reflects balances of Kshs.1,706,000,086 and Kshs.1,270,867,275 under other receipts and other payments respectively. The balances are however, not reflected in the summary statements of appropriation. In the circumstances, the accuracy of the financial statements as presented could not be confirmed.

58. Unbalanced Trial Balance The Trial Balance in support of the financial statements presented for audit reflects total debits and credits of Kshs.64,242,772,210 and Kshs.63,699,446,337 respectively resulting to an unreconciled variance of Kshs.543,325,873. Further, the Trial Balance includes items with balances that have not been incorporated in the financial statements as detailed below:

Account Description Debit

(Kshs.) Credit

(Kshs.)

0-962-0900-2710102 Service and compassionate gratuities

15,267,436

0-962-0901-2710102 Marriage gratuities 16,059,357

0-962-0902-2710102 Civilian death gratuities 821,187,130

9-808-0000-9910201 Provision for encumbrance 151,553,515

9-808-0000-9910201 Provision for encumbrance 18,709,786

9-808-0001-9910201 Provision for encumbrance 2,323,457,922

9-808-0001-9910201 Provision for encumbrance 2,360,628

9-808-0001-9910201 Provision for encumbrance

727,459

9-808-0001-9910201 Provision for encumbrance 543,325,873

27

Consequently, it has not been possible to confirm the completeness and accuracy of the financial statements for the year ended 30 June, 2019 as prepared and presented.

59. Unsupported Expenditure The statement of receipts and payments for the year ended 30 June, 2019 reflects pension payments of Kshs.66,917,302,195. Included in this balance is Kshs.61,995,510 (2017/2018-Kshs 58,656,973) paid through the pension payroll to Asian and European Pensioners who retired due to Africanization of public sector after independence in 1963. However, no evidence was provided that the pensioners’ personal files and life certificates were submitted before payments were effected as required by the Pension Department’s internal controls. Consequently, the propriety of the expenditure of Kshs.61,995,510 could not be confirmed.

60. Returned Pensions and Unsupported Accounts Payables

As previously reported, the statement of assets and liabilities and as disclosed in Note 13.6 to the financial statements, reflects accounts payable of Kshs.4,183,043,979 (2018 - Kshs.4,061,252,617). Analysis of the figure revealed that Kshs.1,189,930,008 related to pensions payments returned during the year while Kshs.372,222,595 was paid back to pensioners on account of 2017 returns resulting in the net movement for the year of Kshs.817,707,413. However, detailed listing by individual pensioners in support of the accounts payables balance of Kshs.4,183,043,979 was not provided. Other Matter

61. Unresolved Prior Year Matter

The following prior year audit matter remained unresolved as at 30 June, 2019: 61.1 Unsupported Expenditure

As previously reported, included in the pensions expenditure of Kshs.63,170,121,740 as at 30 June, 2018 is an amount of Kshs.20,294,340 paid to an international development company. Although Management explained that the payment was on account of pre- independence and post - independence pensioners who worked in Kenya and currently residing in the United Kingdom, the expenditure was not adequately supported by way of payrolls detailing out the beneficiaries. Consequently, the propriety of the expenditure could not be confirmed.

28

REPORT ON LAWFULNESS AND EFFECTIVENESS IN USE OF PUBLIC RESOURCES Conclusion

62. There were no material issues relating to lawfulness and effectiveness in use of public resources.

REPORT ON EFFECTIVENESS OF INTERNAL CONTROLS, RISK MANAGEMENT AND GOVERNANCE Conclusion 63. There were no material issues relating to effectiveness of internal controls,

risk management and governance.

REVENUE STATEMENTS – PENSIONS DEPARTMENT

REPORT ON THE REVENUE STATEMENTS

Basis for Qualified Opinion

64. Discrepancies Between Budget Statement and the Printed Estimates

The statement of comparison of budget and actual amounts reflects total budget of non-tax receipts of Kshs.309,398,233 being contribution by government employees to social welfare which differs from the 2018/2019 printed revenue estimates of Kshs.894,349,041 resulting to an unexplained and unreconciled variance of Kshs.584,950,808.

Consequently, the accuracy and completeness of the revenue statements could not be confirmed.

65. Variance Between the Revenue Statement and Trial Balance Figures

The statement of revenues and transfers reflects total non-tax receipts of Kshs.262,230,402; (2018 – Kshs.308,019,086) comprising of receipts from MDAs and other receipts of Kshs.262,091,309 and Kshs.211,093 respectively. However, the Trial Balance and revenue analysis availed for audit reflected a total of non-tax receipts balance of Kshs.270,789,739 resulting to an unexplained variance of Kshs.8,559,337.

In the circumstance, the accuracy and completeness of the reported total non-tax receipts balance of Kshs.262,230,402 cannot be ascertained.

29

66. Incomplete Progress Report on Follow Up of Auditor’s Recommendations

As reported in the 2017/18 audit report, there is an unresolved matter of an unexplained difference of Kshs.1,379,147 between the total revenue collected and transferred to the Exchequer and transfers of receipts reflected in the bank statement. In addition, the receiver of revenue failed to provide a budget of the estimated revenue collections. These issues have not been captured under progress on follow up of auditor’s recommendation section of the financial statements.

In the circumstances, the financial statements have not been prepared in compliance with IPSAS.

Other Matter

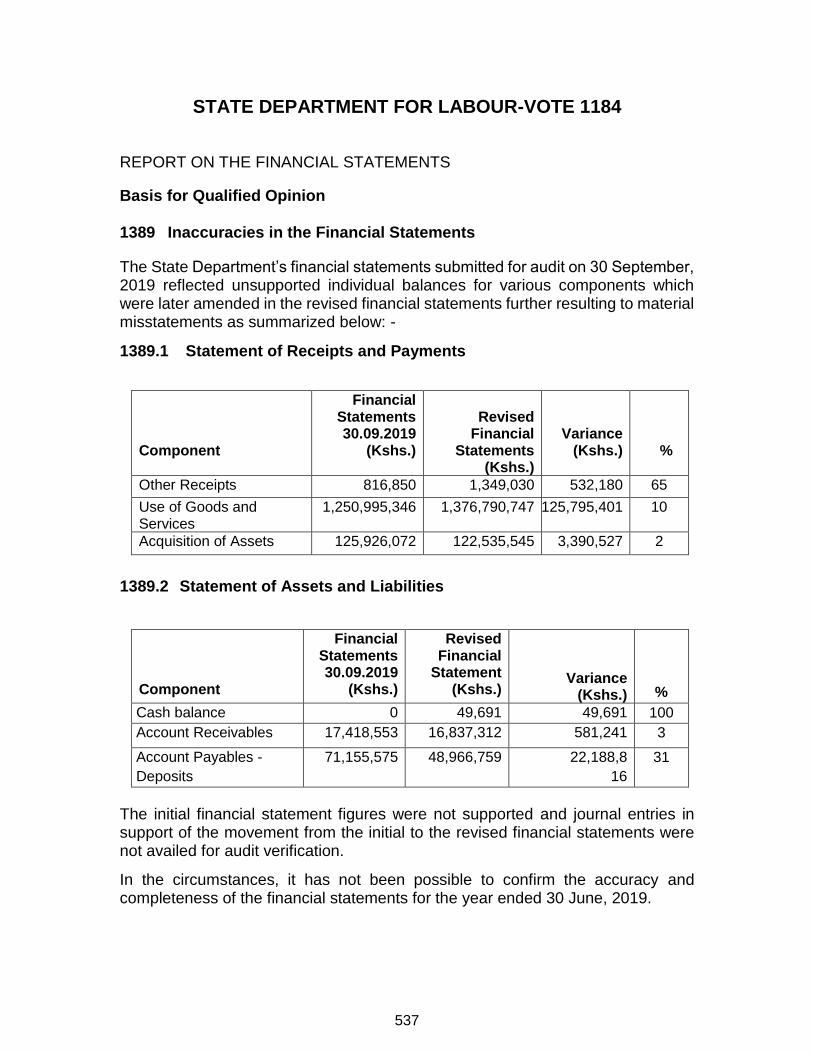

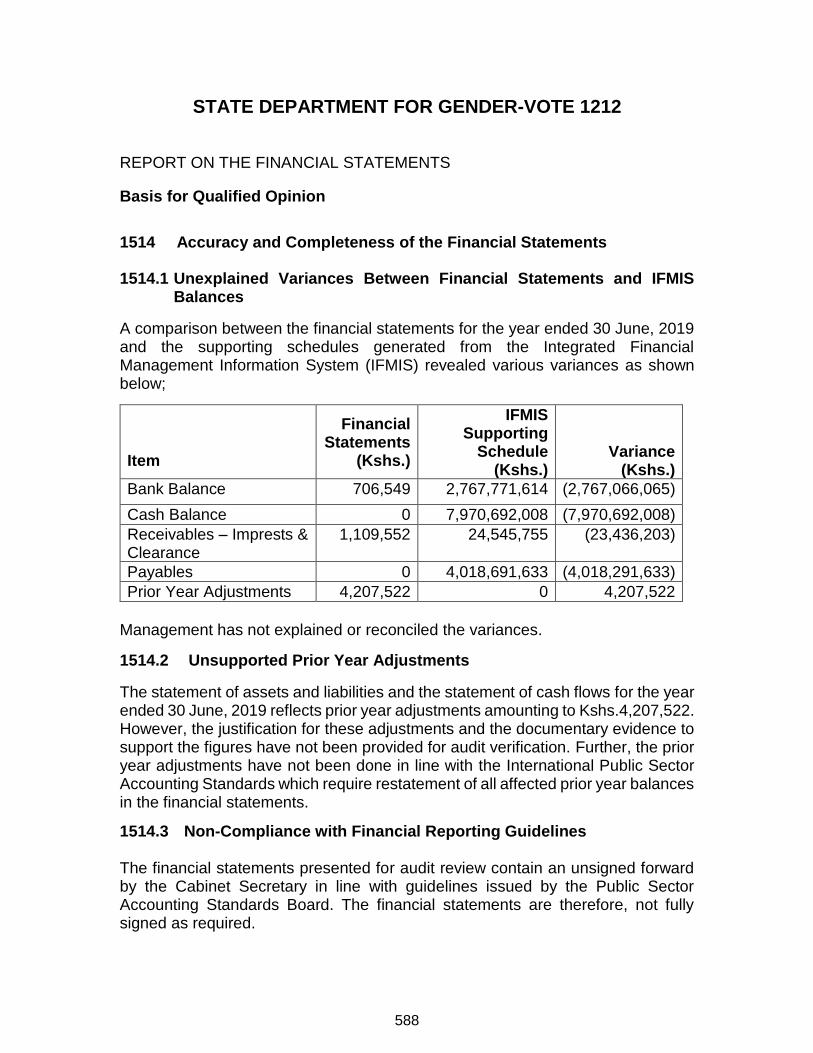

67. Under Collection of Receipts