Factors Affecting performance of Income generating units in public universities.

67

i DECLARATION I, declare that this is my original work and has not been presented for a degree in any other university other than Jomo Kenyatta University of Agriculture and Technology Mombasa campus. Agnes Nyamvula Tsuma, HD333-COO5-0360/2010 …………………. ………………… Signature Date This project has been submitted for examination with my approval as University Supervisor DR. FRED MUGAMBI ……………… ………………. Signature Date

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Factors Affecting performance of Income generating units in public universities.

i

DECLARATION

I, declare that this is my original work and has not been presented for a degree in anyother university other than Jomo Kenyatta University of Agriculture and TechnologyMombasa campus.

Agnes Nyamvula Tsuma,

HD333-COO5-0360/2010

…………………. …………………Signature Date

This project has been submitted for examination with my approval as UniversitySupervisor

DR. FRED MUGAMBI

……………… ……………….Signature Date

ii

ACKNOWLEDGEMENT

I would first like to thank Almighty for giving me the grace to undertake the project. My

sincere gratitude is to Dr. Fred Mugambi for his consistent support throughout the

project, and my parents and husband who have been pillars of strength throughout.

iii

ABSTRACT

Low funding has been one of the major problems facing public institutions. The

government is finding it more difficult to meet the vast needs of the society hence

institutions are facing shortages intensively. In an attempt to bridge the gap between the

budgetary allocations and actual expenditures most universities have started income

generating units with the aim of boosting their operational expenses. This study seeks to

determine the factors that contribute to the performance of income generating units in

public universities and specifically a case study of Technical University of Mombasa.

This project outlined are four main objectives which were to determine the effect of;

allocation of resources, internal controls, management capacity and work culture on

performance of income generating units in the university.

The perception of universities as merely institutions of higher learning has gradually

given way to the view that universities are important engines of economic growth and

development. History has shown that the higher the success, the tougher the demands that

are placed on institutions as well as on individual players. Various issues were

highlighted the need for diversification of business areas; consolidation and expansion of

existing programmes; relationships with various university organs, corporate governance

and image, and human resource-related issues hence literature was reviewed in relation to

the variables identified in this research to determine what other scholars have written

with regards to the study. The target population identified was from TUM staff from the

specific departments and the management. Purposive sampling technique and random

sampling technique were used in the study due to its uniqueness and convenience. Data

collection was done using the questionnaire and interview guide to ensure sufficient data

is collected from the respondents. Data analysis was done using SPSS and presentations

made in pie charts, distribution graphs, diagrams and figures to clearly show the response

from the respondents according to the different variables in form of tables.

iv

The findings of this study suggest that in determining how allocation of resources

affected performance of IGU’s majority of the respondents agreed that funds allocated to

the various votes do not sufficiently meet the needs of the IGU’s. It was noted that

internal controls have a great effect on the reliability of financial reports. In investigating

the management capacity effect on performance of IGU’s respondents strongly believe

management styles influence performance of IGU’s. Respondents agree that employee

attitude can have a positive or negative influence on the performance of the units. It was

found that all the independent variables have a significant influence on the dependent

variable.

It was concluded that performance of income generating units in public universities is

majorly influenced by funds available and the work culture of the employees due to the

high response rate on the two variables.

v

TABLE OF CONTENTS

DECLARATION……………………………………………………………………........i

ACKNOWLEDGEMENT……………………………………………………………....ii

ABSTRACT……………………………………………………………………………..iii

LIST OF TABLES………………………………………………………………............vi

LIST OF FIGURES…………………………………………………………………....viii

ACRONYMS……………………………………………………………………….…....ix

CHAPTER ONE……………………………………………………………………....x

INTRODUCTION……………………………………………………………….............1

1.1 Background of the study……………………………………………………....11.2 Statement of the problem………………………………………………….......41.3 General Objective…………………………………………………………......51.4 Specific Objective………………………………………………………….....51.5 Research Questions…………………………………………………………...61.6 Justification of the study……………………………………………………...61.7 Scope of the study………………………………………………………….....71.8 Limitation of the Study…………………………………….……………….....7

CHAPTER TWO………………………………………………………………………...8

LITERATURE REVIEW……………………………………………………………….8

2.1 Introduction…………………………………………………………………...82.3 Conceptual framework……………………………………………………....112.3.1 Performance of Income Generating Units…………………………..……….122.3.2 Allocation of Resources……………………………………………………....122.3.3 Internal Controls……………………………………………………………..142.3.4 Management Capacity…………………………………………………….....162.3.5 Work Culture…………………………………………………………….......172.4 Critique of the Existing Literature Relevant to the Study…………………...192.5 Summary…………………………………………………………………......192.6 Research Gaps…………………………………………………………….....19

CHAPTER THREE……………………………………………………………........…20

vi

METHODOLOGY………………………………………………………………….....20

3.1 Introduction………………………………………………………………....203.2 Research Design……………………………………………………………..203.3 Population…………………………………………………………………....203.4 Sampling Frame……………………………………………………………...213.5 Sample and Sampling Technique…………………………………………....213.6 Research Instruments………………………………………………………...233.7 Data Collection……………………………………………………………....233.9 Data Processing, Analysis and Presentation of Findings………………........24

CHAPTER FOUR………………………………………………………………...........25

DATA PRESENTATION, ANALYSIS AND INTERPRETATION………………..25

4.2 Respondent Demographics………..………………….....…….......................254.3 Allocation of resources………………...………………………………….....304.4 Internal controls on the performance of income generating units...………....324.5 Management Capacity………………………………………………..…......344.6 Culture on the performance of income generating units……………………..36

CHAPTER FIVE……………………………………………….....................................38

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATION……...38

5.1 Introduction…………………………………………………………..……....385.2 Summary of Findings…………………………………………………..…….385.3 Conclusions……………………………………………………………..…....395.4 Recommendations……………………………………………………..……..405.5 Suggestions for further Research……………………………………..……..42

REFERENCES……………………………………………………….…………………43

APPENDICES…………………………………………………………………………..46

LETTER TO RESPONDENTS…………….………………………………………46INTERVIEW GUIDE……………………………………………………………...47QUESTIONNAIRE………………………………………………………………..49WORK PLAN……………………………………………………………………...55BUDGET…………………………………………………………………………...57

vii

LIST OF TABLES

Table 3.1 Target Population ………………………………………………………..…21

Table 3.2 Sample Size …………………………………………………………………22

Table 4.1 Gender ………………………………………………………………………26

Table 4.2 Age bracket…………………………………………………………………27

Table 4.3 Level of Education …………………………………………………………28

Table 4.4 Years of service with employer……………………………………………..29

Table 4.5 Allocation of resources……………………………………………………...30

Table 4.5 Budget fund and planning effect on performance………………………… 32

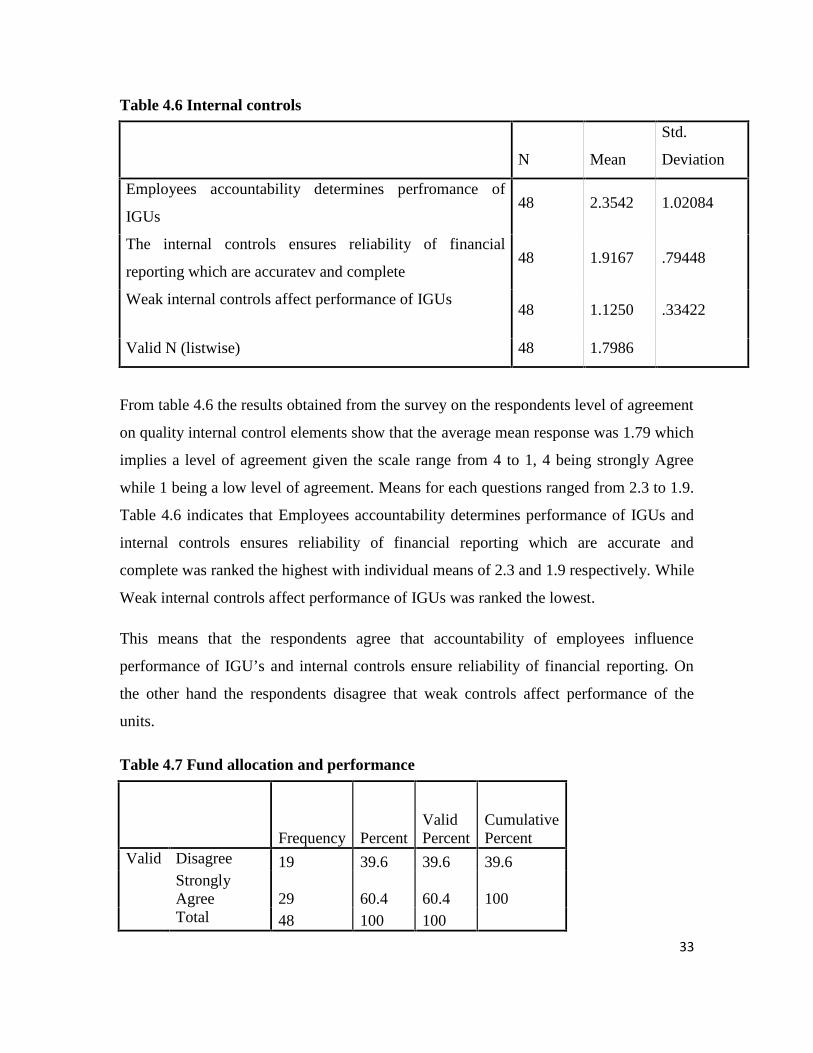

Table 4.6 Internal controls…………………………………………………………....33

Table 4.7 Fund allocation and performance………………………………………….33

Table 4.8 Management capacity………………………………………………………34

Table 4.9 Manager and decision making……………………………………………..35

Table 4.10 Culture and performance……………………………………………………36

viii

LIST OF FIGURES

Figure 2.1 Conceptual framework…………………………………………………….11

Figure 4.1 Response Rate……………………………………………………………..25

Figure 4.2 Respondent’s age bracket……………………………………………….....26

Figure 4.3 Level of education……………………………………………………….. 28

Figure 4.4 Distribution of respondent’s year of service……………………………….30

ix

ACRONYMS

MIOME - Mombasa Institute of Muslim Education

TUM - Technical University of Mombasa

MTI - Mombasa Technical Institute

IGU - Income Generating Unit

PC - Pure consultancies

SBPU - Specialist-Based Production Units General Production Units GPU

MIIP - Module II Programmes

SWSC - Seminars, Workshops and Short Courses

AICPA - American Institute of Certified Public Accountants

UNES - University of Nairobi Enterprises and Services

x

DEFINITION OF TERMS

Accountability The obligation of an individual or organization to account for its

activities, accept responsibility for them, and to disclose the results in a

transparent manner.

Budgets An estimation of the revenue and expenses over a specified future period

of time. A budget is a microeconomic concept that shows the tradeoff

made when one good is exchanged for another.

Compliance The act of conforming, acquiescing, or yielding. An employee whose

responsibilities include ensuring that the company complies with its

outside regulatory requirements and internal policies.

Diversification A risk management technique that mixes a wide variety of investments

within a portfolio. The rationale behind this technique contends that a

portfolio of different kinds of investments will, on average, yield higher

returns and pose a lower risk than any individual investment found

within the portfolio.

Forecasting A planning tool that helps management in its attempts to cope with the

uncertainty of the future, relying mainly on data from the past and

present and analysis of trends.

Organizations culture The values and behaviors that contribute to the unique social and

psychological environment of an organization.

Reliability Is the ability of a person or system to perform and maintain its functions

in routine circumstances, as well as hostile or unexpected circumstances.

.Requisition Written order or a formal demand by the user(s) of a good or service(which is not made available without a specific request) to theorganization's purchase (or stores) department

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Income generating units comprise of units that are a means for gaining or increasing

income. They have been sort as a means of livelihood not just in organizations but even

so in community development areas. According to Bruce (1998), income Generating

Activities serve as a cushion/support kitty for funds received such as Constituency

Development Funds where there are restrictions that control the utilization of these funds,

for instance it is stipulated that Constituency Development Funds’ money should be

utilized only on purchasing component materials of the project and cannot be used to pay

off debts of any kind, transport or labor charges.

Most African higher education institutions rely greatly on the state for funding as well as

for policy-making as far as the public sector are concerned. However, most states do not

apportion a sufficient amount of their financial resources to the education sector. From

the little provision that is made for education, the greater portion is assigned to basic and

secondary education, (Bloom, 2005).

Odebiyi and Aina et al (1999), the inadequate funding of the Universities and other

tertiary institutions has had calamitous effect on teaching and research and universities

themselves have been forced to embark on income generating projects in order to source

for funds. Therefore, the available revenue is spent on capital projects, administration,

teaching and research and students welfare. Capital Projects and salaries reportedly take a

bulk of the total revenue while teaching and students’ welfare tend to be given less

priority.

Over the past ten years public corporations have continuously received less financial

allocation by the Government than the estimated expenditure as forecasted by the

institution. According to Kiamba (2003), the government made it clear that it will no

longer be able to fully finance public universities. A notable observation in the Kenya

1994/1998 development plan was that “the central thrust of the new policies is to rely on

2

market forces to mobilize resources for growth and development with the role of the

Government increasingly confined to providing an effective regulatory framework and

essential public infrastructure and social services. The Government will limit direct

participation in many sectors and instead promote private sector activity”. As a result

most public universities had to explore other means of generating income to finance the

university programmes. The income generating activities, currently being undertaken by

universities in Africa, can be generally classified in two groups, namely; teaching

(parallel degree) programs and non-teaching income generating activities.

Technical University of Mombasa (TUM) is one of the National Polytechnics recently

elevated to status of University in Kenya. It encompasses the many benefits of a small

university in the nation's Island city bordering the great Indian Ocean. For several

decades TUM has been offering technical education to students pursuing professional

courses in the various fields Engineering, Applied Sciences and Business studies

culminating in the recent elevation to University status giving it the opportunity to offer

Degree programs currently under the tutelage of Jomo Kenyatta University of Agriculture

and Technology.

The origin of the Mombasa Polytechnic can be traced back to the late 1940’s as a

consequence of the consultations pioneered by Sir Philip Mitchell in 1948 between The

Aga Khan, the sultan of Zanzibar, The Secretary of State for the colonies, Sir Bernard

Reilly and H.M. Treasury, Mombasa Institute of Muslim Education (M.I.O.M.E) was

founded from capital raised by means of gifts of £100,000 from Sultan of Zanzibar. A

further £50,000 was raised by the Bohora Community of East Africa at the insistence of

Doctor Sayedna Taher Saifuddin , the high priest of the community. On 22nd June 1948,

the then Governor of Kenya signed the charter bringing the Mombasa Institute of Muslim

Education into being to be managed by board governors. On its inception, M.I.O.M.E

was charged with the prime objective of providing adequate technical education to

Muslim students of East Africa.

It was on this basis that in 1966 M.I.O.M.E became Mombasa Technical Institute (M.T.I)

and started to admit any qualified Kenyan regardless of their religious backgrounds.

3

M.T.I became The Mombasa Polytechnic in 1972, this being the second National

Polytechnic. Since then, the Polytechnic has expanded its operations in all directions and

dimensions.

By 1985, The Polytechnic had five fully-fledged departments namely; Business Studies,

Electrical and Electronics Engineering, Building and Civil Engineering, Mechanical

Engineering and Applied Sciences.On the 23rd August 2007, the Mombasa Polytechnic

was upgraded to become the Technical University of Mombasa under the legal notice no.

160 as a constituent college of the Jomo Kenyatta University of Agriculture and

Technology so as to be a degree awarding institution.

Technical University of Mombasa is famous for its hands on graduates with a touch of

creativity and innovation, this comes out clearly whenever they participated in

technological exhibitions and other related events where its students always come out

tops a good example is the National Robot Contest where for two years in row they have

been tops trouncing even the better equipped and well established institutions of higher

learning. TUM offers academic programmes at the undergraduate, Diploma and

Certificate levels with strong focus on technological, scientific and vocational areas of

study. As a University College TUM boasts of three campuses, the main campus which is

based in the coastal city of Mombasa Island, Lamu Satellite campus and Ukunda

Campus. The TUM has got three faculties vis Faculty of Engineering and Technology,

Applied and Health Sciences, and the third one is the Business and Social Studies faculty.

It also has two Directorates that is the Directorate of Information Technology

Communication Services, and the Directorate of Research. TUM's over sixty departments

offer a variety of degree, higher Diploma, Diploma and Certificate courses.

As an institution of higher learning under the Ministry of Higher Education, Science and

Technology, Technical University of Mombasa is currently undergoing a transition from

a National Polytechnic to a University through the mentorship of Jomo Kenyatta

University of Agriculture and Technology. Income generating units have been a great

source of income for the University since it started its transition due to high demand of

funds for operational purposes.

4

The university has employed more staff to facilitate the increased demand by its clients

hence increasing the expenses of the University. The income generating units have

played a major role in the growth and development of the institution. There are various

factors that determine the performance of these income generating units in the institution.

This paper will explore the various factors that determine the performance of IGU’s.

There are four main units that the university has set up in which three are mainly in the

hospitality field: the Kiziwi Guest House, Catering Unit and the Training restaurant and

the Module II programme. These units are separately managed and all funds generated

channeled to one central account.

The researcher will therefore seek to analyze the said factors influencing the performance

of the income generating units. This will assist the management in decision making and

eventually realize better returns.

1.2 Statement of the Problem

Universities in developed countries have shown that significant funds can be generated

through income generating units. This has been possible through the use of university

facilities and expertise to generate more funds. Whereas the potentials for income

generation through innovation and inventions are there for most universities in African

countries, these have not been adequately utilized and full realization of these potentials

may not be possible due to several bottlenecks (Ogada, 2000). The management of

income generating units has been difficult due to various factors hence affecting its

performance.

Technical University of Mombasa which is situated at the coast has taken much interest

in the hotel industry. It is currently running a hotel and restaurant and a catering unit.

These two main units have been a source of income to the university since it

accommodates people from different parts of the country. However the units have been

facing challenges which have affected its growth and development. Allocation of

resources has been a great battle within the institution whereby most resources realized

are not necessarily ploughed back into the business hence operations are not efficiently

5

met. Due to low funding by the government most of the resources are allocated to

university development and very little is allocated to the IGU’s.

Internal controls put in place are not adhered to hence the operations of the unit are

interfered due to high management override which has affected the overall performance

of the units. The unit being part of the university and a public corporation has played a

big role in influencing the performance of the employees. The organizational culture has

a great impact on the performance of the IGU’s. Work culture in public corporations has

been a challenge in achieving organizational goals. Employees are not result oriented and

working without targets has made it quite difficult to meet the competitive edge. This is

due to negligence by the staff since they believe that whether there is production or not

they are still entitled to remunerations. This notion has brought about conflict of interest

and highly affected the unit’s performance.

On the other hand management has a mandate to oversee the operations of the income

generating units. This may be in their docket but without the necessary capacity and

ability it is becoming a challenge for the management to make the necessary decisions in

the operations of the income generating units.

It is for this reasons the researcher seeks to explore the factors and look at possible ways

of improving operations and performance of IGU’s in public corporations.

The purpose of this study therefore was to investigate the effects of these factors on the

performance of income generating units in public universities. These factors contribute

numerously to the income of the universities hence with this critical study it will help

improve the performance of the IGU’s.

1.3 General Objective

The general objective of the study is to analyze the factors influencing the performance of

income generating units in public universities.

1.4 Specific Objective

The specific objectives of the study are:

6

i. To investigate the effect of allocation of resources on performance of income

generating units at the Technical University of Mombasa.

ii. To evaluate the effect of internal controls on the performance of income

generating units at the Technical University of Mombasa.

iii. To investigate the effect of management capacity on the performance of income

generating units at the Technical University of Mombasa.

iv. To examine the effect of work culture on the performance of income generating

units at the Technical University of Mombasa.

1.5 Research Questions

This study will be motivated by the following questions:

i. How does the allocation of resources at the Technical University of Mombasa

affect the performance of its income generating units?

ii. What is the effect of internal controls on the performance of income generating

units at the Technical University of Mombasa?

iii. How does the management capacity of the Technical University of Mombasa

affect the performance of its income generating units?

iv. What is the effect of work culture on the performance of income generating units

at the Technical University of Mombasa?

1.6 Justification of the study

Based on the problem stated, it is realized that various aspects on the operations of

income generating units have not been explored to have a clear understanding on the

variance between the operations in public corporations unlike private ones. This research

will therefore enlighten the readers on how the stated factors can be used effectively to

improve the performance of the income generating units. The parties that will benefit

from the study are as follows:

i. The Top Management at the Technical University of Mombasa who shall use the

study findings in policy formulation and review.

ii. The Managers in the different income generating units.

7

iii. Other institutions operating the income generating units can apply what has been

recommended

iv. It will assist future researchers in the field of study.

1.7 Scope of the study

The study is to be undertaken at the Technical University of Mombasa this being my

target population. Information will be gathered through the use of questionnaires and

interview. The extent of the study is confined within the stated objectives.

1.8 Limitation of the Study

During the study, the following limitations were encountered:

The major limitation encountered by the researcher was inadequate financial resources. It

was very expensive to get internet access for purposes of the research, print several

copies of the research, use of airtime and transport costs to get in touch with the

supervisor.

The researcher encountered problems of limited time as the research was to be taken in a

short period which limits time for doing a wider research so as to submit the report on

time. However the researcher over came this limitation by carrying out the research

across all the departments and management levels in the organization to enable a

generalization of the study findings.

The respondents were reluctant in giving information fearing that the information asked

may be used to intimidate them or print a negative image about them. The researcher

handled this problem by carrying with her an introduction letter from the University in

order to assure the respondents that the information they give will be treated with

confidentiality and it will be used purely for academic purposes.

8

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter will present the conceptual framework, related literature on the allocation of

resources for income generating units, the management capacity in running the operations

of the income generating units, performance contracting in public corporations and the

effect of internal controls on performance of income generating units.

2.1.1 Categories of Income Generating Units

According to Kiamba (2003), at present the following major categories of IncomeGenerating Units have been recognized based on the value of respective input by theparticipants (members of staff) and the University:

a) Pure consultancies (PC): In this category the investment is greater on the part of the

participants than it is on the part of the University due to the high intellectual input from the

participants.

b) Specialist-Based Production Units (SBPU): This category includes production units whose

survival requires specialized or technical human resources at the teaching departments. It is

assumed that the initial and any subsequent physical and material investments have been or

are to be provided by the University

c) General Production Units (GPU): This category includes income generating activities

which are artisan-based without heavy dependence on specialized human resources of a

professional nature.

Ideally the cost of employment is met as part of production cost.

d) Module II Programmes (MIIP): These programmes, also referred to as “Parallel

Programmes”, refer to the academic programmes in which the registered students are

privately sponsored and therefore paying full tuition fees as distinct from the “Regular” or

“Module I” Programmes in which students are sponsored by the Government under a some

cost-sharing arrangement in where about 80% of the tuition fees is paid by the Government.

It was clear early in the initiation of the programmes that there was need to consider this as a

special category in the distribution formula largely because the Service Providers (those

9

members of staff directly teaching the academic programmes) involved spread across the

entire University.

e) Seminars, Workshops and Short Courses (SWSC): This category includes Workshops

and Seminars conducted by the various units and/or individuals in which the corporate

name of the University is used. Also included in this category are short certificate courses

whose duration does not exceed three months.

2.2 Theoritical Framework

2.2.1 Financing Universities in Other African Countries

The financing of higher education is an area of discussion all over the world. In Africa, it

has become a major problem for Governments because of limited financial resources

coupled with urgent and competing demands. In the past decades numerous reports

dealing with this issue have been presented.

At a Senior Policy Workshop on the theme "Resource Mobilisation and Financing of

African Universities" from 2 to 6 December, 1991 in Accra, Ghana, Professor Sawyer

(1991, p. 5) observed that drastic reduction of financial outlay to Universities had several

adverse effects. These included lowering of standards of research and teaching; insecurity

for University staff; lack of freedom to innovate and explore new areas; and reduction of

indigenous knowledge generation.

At the same workshop the participants also observed that the Universities in Africa

remain by and large in the hands of the state. Unlike the earlier decades following

independence when Universities were major beneficiaries of government support, recent

trends suggest a steady decline in such support. Studies indicate that capital and recurrent

funding to African Universities has declined substantially in real terms and were

inadequate to meet the needs of the universities. Funding levels to the universities in

1988/89 was around 50% of the real value of 1980/81.

During the 1980's, the capacity of African Governments to finance public services fell

sharply (Saints 1992, p. 8). By 1990 the income per person in Africa as measured in

constant 1980 US Dollars, was 20% lower than it was in 1980. Government expenditures

10

on education suffered accordingly. Although the average share of governmental budgets

allocated to the education sector increased slightly from 16.3 to 16.6 percent between

1980 and 1990, it declined to 15.2 percent during the following decade. Saint (1992)

further says that in per capita expenditure terms, this decline was even more precipitous.

Public spending on education in Africa, measured in constant US Dollars per person,

plunged by 55% over 1980-86, even as it increased in all other regions of the world

except Latin America (Woodhall 1991, p. 14).

Governments' commitment to education is reflected in education expenditures as a

proportion of GNP. Here a similar pattern is apparent. On average, this share increased

from 3.4% in 1970 to 4.3% in 1980, but slid back to 4.0 by 1988. Here it should be

remembered that GNP was also falling at the same time, thus accentuating this negative

trend.

The Government allocations to education have remained as high as they have in the face

of sharply constricted possibilities in witness to the high priority that the Governments

attach to investment in education. The countries of Sub-Saharan Africa have, over the

past two decades, consistently favoured education often at the expense of military

expenditures (Saint 1992, p. 10).

In its 1988 policy paper, Education in Sub Saharan Africa, the World Bank expressed

concern with higher education's rising share of education budgets and prescribed that "the

share of stagnant real public education cannot expand further and in some cases may have

to contract". To achieve this goal, it proposed savings through improvements in

efficiency, increases in private contributions, and constraints on the growth of output.

Since this report was released, progress in these latter areas has been spotty. As a result,

the predicted budget cuts have materialised.

Higher education's share of nation education budgets initially increased as real education

spending fell in the early 1980s. It grew from an average 15.5 percent during 1970-74

to18.3 in 1975-79 and 19.1 percent in 1980-84. It then gave ground with its average share

for 1985-88 declining to 17.6 percent. As a result, higher education expenditures as a

11

portion of education budgets were lower at the end of the 1980s than they had been a

decade earlier, Sherman (1989).

2.3 Conceptual Framework

Figure 2.1 Conceptual framework

Independent Variable Dependent Variable

Source: Researcher (2012)

The above diagram illustrates the conceptual framework of the study. This conceptual

framework has been adopted from previous work of Blumerg 1982, with some

modification to suit the case of income generating units at the Technical University of

Mombasa. In the course of study the researcher seeks to investigate the relationship

between the stated independent variables and the dependent variable.

Allocation ofResources

Performance of IncomeGenerating Units

Internal Controls

ManagementCapacity

Work Culture

12

2.3.1 Performance of Income Generating Units

In times of financial crisis and tight public budgets the pressure on universities and

research institutions to find new funding sources is rising. Public funding for universities

and research institutions is decreasing. At the same time, competition between

universities is increasing and they become more commercially orientated. Every

institution needs to define its own strategy for altering its income sources apart from

public funding. Several options such as cooperating with industry or funding are

available. Commercialization of research can also be a major factor in this regard. Higher

education and research institutions are required to prove that their research has an impact

outside their institution and that it is of interest for industry. Both the institutions research

status and reputation is more and more dependent on research commercialization.

Therefore, it is ever more important to ensure its success in order to attract students,

researchers, private companies and external partners – who in turn contribute to the

institution’s overall income generation themselves again. Furthermore, universities,

faculties and institutes act in their own interest when increasing knowledge and

technology income as they assure a high quality of their research and raise their own

budgets.

However, the diversification of income streams is a very complex process. It involves

various different units that need to collaborate. This affects also staff that is not used to

deal with private funding and business co-operations including researchers. They are

required to turn to business and launch spin-out companies while still having to fulfill

their core tasks and ensuring quality of teaching and research. In addition, the

institutions’ funding models have become more risky as the budget cannot be foreseen

and planned for many years anymore.

2.3.2 Allocation of Resources

According to the economic glossary, Allocation of resources is the process of dividing up

and distributing available, limited resources to competing, alternative uses that satisfy

unlimited wants and needs. Choices have to be made. These choices, these decisions are

the resource allocation process. Ogada (2000) states that, following the launching of the

13

Economic Reforms of 1996 - 1998: Policy Framework Paper, the Kenyan Government’s

position on financing of Education is that the public expenditure is to concentrate on

primary and secondary education. This implies that the funds available for university

education has been reduced and Kenyan universities have been urged to put in place

strategies which can enable them generate income using internal resources to finance the

shortfalls. All public universities have been facing this crisis of resource allocation due

to limited funds provided by the government such that allocating these little resources

becomes a challenge. The management of the university has to make difficult choices on

what project is to be allocated what amount and hence interfering with the growth of the

income generating units.

Financial regulations governing the operation of most public corporations are

cumbersome, each financial transactions requires several stages. Particularly the

processing of payment and purchase are so tedious that they cannot stimulate the business

activities of the units and some units have lost customers for not delivering services in

time. This has occurred due to poor allocation of funds such that most of the vote heads

are exhausted before the financial year is half way thus all financial transactions needing

approval for processing.

Getange et al., (2005) lack of sufficient funding is a major challenge especially

considering the fact that some of the public corporations initiate new units and expand

existing ones. Therefore they depended on funds from other vote heads. This dependency

has had a great influence on the performance of the income generating units.

The European University Association et al (2008) explains that inadequate funding

modalities may have a negative effect and create powerful disincentives for universities

to seek additional funding sources. An excessive administrative burden and uncertainty

associated with these sources – whether public or private – is one hurdle, which is

especially relevant in the context of competitive funding schemes. The Association

suggests the simplification of administrative processes and requirements associated with

funding programmes .Simplification of rules will ensure that both financial and human

14

resources are released for the primary objectives of excellent teaching and research. This

should be underpinned by proportionate accountability measures as well as consistent

rules and terminology across programmes.

Many governments have tried to square the circle through tighter management, but

management cannot make up for lack of resources. Ajayi et al., (1996) “…funds available

to run higher education institutions in Africa are grossly inadequate, making them subsist

on a ‘starvation diet’.” They insist that the contraction of resources to the universities,

coupled with an increase in demand, constitutes the most critical problem and greatest

challenge of Africa’s higher education. Indeed, the unavailability of enough financial

resources has led to the inability to sustain growth of enrolment and improve quality

Nigel Thrift, Vice-Chancellor of the University of Warwick, stressed that income

generation and diversification helps the academic enterprise, rather than hindering it.

Knowledge transfer, commercial operations, public-private partnerships and

philanthropic giving are four main areas of diversified income for his institution. It also

helps the university to reduce dependency towards public authorities in relation to its

internal management. He outlined three key success factors to income diversification – a

flat management structure, an entrepreneurial attitude and an outward looking mindset.

2.3.3 Internal Controls

Internal control is a process designed to provide reasonable assurance regarding the

achievement of objectives in the following categories:

I. Effectiveness and efficiency of operations

II. Reliability of financial reporting

III. Compliance with applicable laws and regulations

According to Whittington (2004), one of the important reasons of financial fraud is the

failure of internal control and the lack of related information disclosure. Effective internal

15

control system can ensure the truthfulness and reliability of financial information.

Information disclosure can contribute to the constant improvement of internal control,

offering data for decision making to information users. The establishment and effective

implementation of internal control system can assure the corporate continuing operating

and developing healthily. The quality of internal control disclosure reflects the situation

of the system, which is vital to regulators and investors.

Ogada(2000) states that although business units have been established in various

departments, IGUs have been operating without clear and comprehensive guidelines

being in place, to govern the day to day operations of the units.

From the reference guide for managing University Business Practices, University

employees use a variety of information systems: mainframe computers, local area and

wide area networks of minicomputers and personal computers, single-user workstations

and personal computers, telephone systems, video conference systems, etc. The need for

internal control over these systems depends on the criticality and confidentiality of the

information and the complexity of the applications that reside on the systems. There are

basically two categories of controls over information systems: General Controls and

Application Controls.

I. General Controls

General controls apply to entire information systems and to all the applications that reside

on the systems.

II. Application Controls

Application controls apply to computer application systems and include input controls

(e.g., edit checks), processing controls (e.g., record counts), and output controls (e.g.,

error listings), they are specific to individual applications.

Statement on Auditing Standards issued by the American Institute of Certified Public

Accountants (AICPA) stipulates that the purpose of internal control in reliability of

financial reporting is generating monthly financial statements that are accurate and

complete. Effective and efficient operations ensure that the University can continuously

16

progress toward its mission with limited setbacks. Compliance with applicable laws and

regulations will help the University avoid fines, penalties, unrecorded liabilities, and

reputational damage.

2.3.4 Management Capacity

Managerial capacity refers to the specialized financial and managerial expertise to

finance, develop, manage and operate infrastructure assets (Sommerfield, 1995).

Results-based management is currently being instilled into the Public Service

through performance contracts. A performance contract is an agreement between

two parties that clearly specifies their mutual performance obligations, intentions

and responsibilities. Simply stated, a performance contract comprises the two major

components of determination of mutually agreed performance targets and review

and evaluation of periodical and terminal performance. The two components also

constitute the hub of an implementable strategic plan.

According to the UNES Strategic Plan (2005-2010), it was formulated in such a way

that it reflects the key elements of results-(performance-) based management, namely the

mission, objectives, performance criteria and indicators, and targets. This has greatly

influenced the performance of their IGU’s. With a result based management the

management capacity and abilities are maintained at high standard hence promoting good

governance and performance of the IGU’s.

One major prerequisite to be met is necessary skills and expertise that is needed in the

institution in the shape of professional leadership and management. Income

diversification needs skilled management at all levels of the institution and may require

new staff profiles, such as professional research administrators and fundraisers. These

need to be included in the design of the university’s strategy and must operate within

adapted structures. Leadership may also need to take on new tasks, especially in relation

to fundraising. It is clear that to engage philanthropists with the university, the leadership

must be committed to these activities. Therefore it is crucial that training and support

17

programmes are provided for the different levels of leadership in the university

(European University Association conference, 2008).

2.3.5 Work Culture

Culture in an organization evolves out of collective perceptions of employees on various

aspects of the organizational work life. It is shaped through their day-to-day experiences

while dealing with various facets of the organizational realities such as its goals and

objectives, policies and practices, leadership, structure, work design, technology adopted,

people, dominant modes of communication, motivational and reward mechanisms,

working conditions, etc. It provides dynamic interface to the employees in the

organization in the form psychologically meaningful and behaviorally pertinent

perceptions, which impels them to think, feel and act in consistently similar ways

(Schneider, 1975). Numerous studies have shown organizational culture as undisputedly

a major contributing factor for changing employees’ attitudes and behavior towards

superior job performance and satisfaction. Several measured aspects of culture such as

communication flow, decision-making practices, relationship with colleagues, work

design and supervisory support have shown significant positive relationship with many

out come variables like organizations’ financial performance (Dennison, 1990; Ryan,

Schmit & Johnson, 1996; Kangis &Williams, 2000) employees’, productivity and

satisfaction (Schneider et al., 1998; Rogg, et al., 2001).

University staffs, just like most other civil servants have civil service work culture of low

productivity, insensitivity to deadlines and quality of service, etc. This culture is not

conducive for efficient and profitable to business operations. During a workshop with

managers from industries, pointed out that the civil service culture and bureaucracy are

the two major impediments to doing business with universities (Ogada, 2000).

For Pettigrew (1979), organizational culture consists of "a system of public and collective

meanings accepted by a given group over a certain period of time. This system of terms,

forms, categories and images interpret for people their own situations". However, for

Schein (1992), organizational culture is to be understood as "the pattern of shared basic

18

assumptions that a given group has invented, discovered, or developed in learning to cope

with its problems of external adaptation and internal integration -- a pattern of

assumptions that has worked well enough to be considered valid and, therefore, to be

taught to new members as the correct way to perceive, think and feel in relation to those

problems". According to Trice and Beyer (1993), culture involves conceptions, norms

and values that are inculcated during the life of an organization.

Nevertheless, according to Riley (1983), although theoretical conceptions on

organizational culture are polarized with regard to the two perspectives mentioned above,

empirical studies in this area have opted for the integration of both conceptions.

Consequently, Alvesson (1993), though acknowledging Smircich’s reference (1983) as

being crucial to regulate the study area in organizational culture, comments that it has not

exhausted the various analyses made possible by a particular theory.

Public corporations emphasis is on valuing a centralized and authoritarian system of

authority that makes it difficult to increase professional development and to acknowledge

the human element (rigid hierarchical power structure). In as much as the public

companies emphasize individual competence and efficiency as a way to achieve the

highly desired personal objectives, they implicitly stimulate the necessity of "passing

over" colleagues who have longed for similar objectives (competitive professionalism).

Such values manifest themselves through practices that aim at the implementation of

interpersonal communication strategies and decision-making tactics that enhance the

aforementioned power structure. In other words, the culture of the public companies that

have taken part in this research can be fundamentally defined by valuing authority and

competition, detrimental to the human element and to interpersonal relations, as a means

of climbing the hierarchy (Heleena, 2000).

This in turn has led to a conflict of interest and decline in performance of income

generating units in public corporations. There is no vigilance on the part of the employee

therefore low productivity in the market is experienced.

19

2.4 Critique of the Existing Literature Relevant to the Study.

There are many studies relating to the Income Generating Units in corporations, but very

few have looked in to the area of the issues surrounding the IGU’s performance

specifically in public corporations. However, the myriad of articles, journals, web

publications, and books on Income generating units formed the foundation for my

research. This study helped theoretically and empirically in providing answers to the

research problems and therefore getting meaningful conclusions.

2.5 Summary

The various studies explored in this area have had a focus on operations generally in

income generating units. It is further realized that less information is found on specific

areas concerning work culture since most corporations are privatized hence have their

organizational culture concentrating on the customers’ needs.

Most studies have dwelt on the issue of allocation of resources though no definite

solution has been found as to how resources may be allocated in public corporations to

improve its performance.

2.6 Research Gaps

Based on the literature presented by the research, the study has not been fully exhausted

to meet the need in the market. Most public universities are still facing challenges in

these areas since most of the studies identified have been looking at factors generally

affecting income generating units in organizations. The researcher will take time to

explore the issues relating particularly to public universities.

20

CHAPTER THREE

METHODOLOGY

3.1 Introduction

This chapter presents the methods that were used to conduct the study. It specifically

dealt with the research design, sampling frame, sample and sampling technique, the

research instruments, data collection procedures and data analysis techniques. This

research was conducted at the Technical University of Mombasa because of its

accessibility to the researcher.

3.2 Research Design

The study took a descriptive approach as it explained the factors influencing operations

of income generating units in public universities. Descriptive research was used to obtain

information concerning the current status of the phenomena to describe "what exists"

with respect to variables or conditions in a situation (Key, 1997). The study also used

quantitative design since the researcher aimed at determining the relationship between the

independent variables and the dependent variable. Purposive sampling is the use of cases

that have the required information with respect to the objectives of the study (Mugenda

and Mugenda, 2003).

3.3 Population

The target population comprised of the management board members who included: the

University Principal, the University Enterprise Manager, the Finance officer, Deputy

Principal Administration Finance and planning, Registrar administration and planning. It

also included the respective unit managers and staff in the respective income generating

units. From the statistics obtained at the university Human Resource department there are

a three main categories as presented below:

21

Table 3.1 Target Population

CATEGORY POPULATION % OF TARGET

POPULATION

Board Members 12 17%

Unit Managers 6 9%

Other staff 50 74%

Total 68 100%

3.4 Sampling Frame

According to Bennet 1993, a sampling frame is the set of source materials from which

the sample is selected. The definition also encompasses the purpose of sampling frames,

which is to provide a means for choosing the particular members of the target population

that are to be interviewed in the survey.

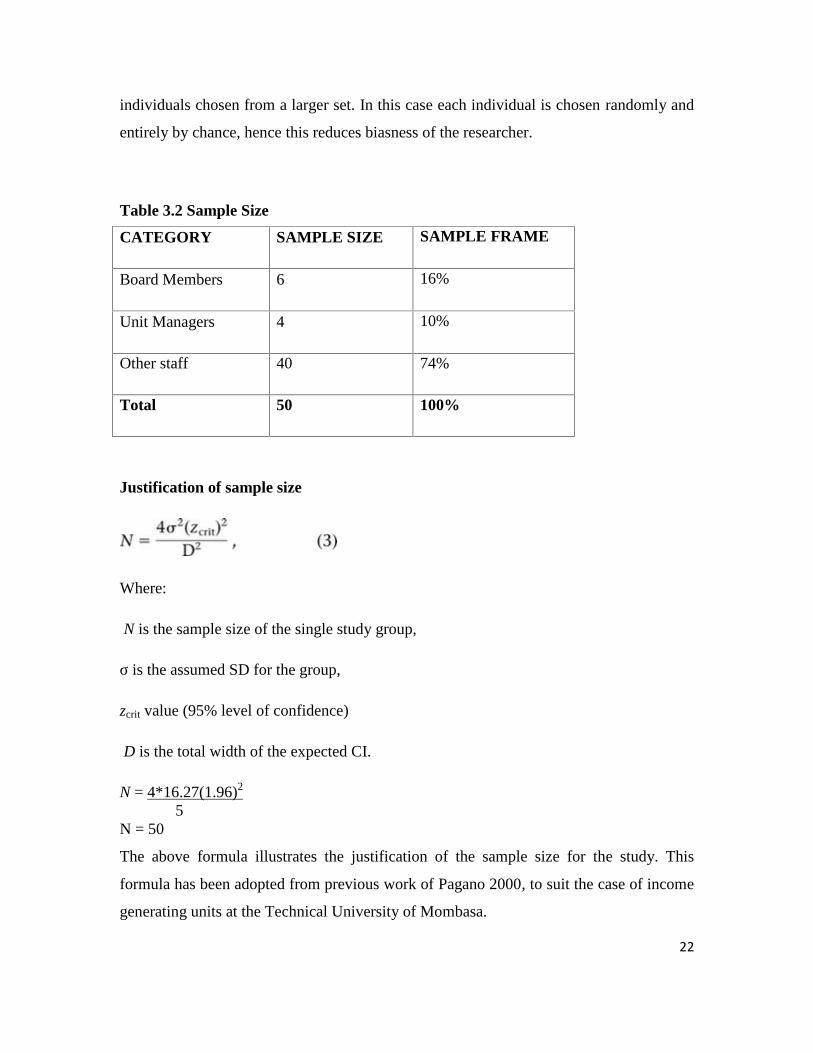

3.5 Sample and Sampling Technique

Ross (2005) argues that sampling in research is generally conducted in order to permit the

detailed study of part, rather than the whole, of a population. The information derived

from the resulting sample is customarily employed to develop useful generalizations

about the population. These generalizations may be in the form of estimates of one or

more characteristics associated with the population, or they may be concerned with

estimates of the strength of relationships between characteristics within the population.

Purposive sampling technique was used to interview the management board and the unit

managers since they are already known to the researcher whereas for the other staff,

simple random sampling technique was used. A simple random sample is a subset of

22

individuals chosen from a larger set. In this case each individual is chosen randomly and

entirely by chance, hence this reduces biasness of the researcher.

Table 3.2 Sample Size

CATEGORY SAMPLE SIZE SAMPLE FRAME

Board Members 6 16%

Unit Managers 4 10%

Other staff 40 74%

Total 50 100%

Justification of sample size

Where:

N is the sample size of the single study group,

σ is the assumed SD for the group,

zcrit value (95% level of confidence)

D is the total width of the expected CI.

N = 4*16.27(1.96)2

5N = 50

The above formula illustrates the justification of the sample size for the study. This

formula has been adopted from previous work of Pagano 2000, to suit the case of income

generating units at the Technical University of Mombasa.

23

3.6 Research Instruments

The study employed the use of questionnaire as the main instrument for carrying out the

survey as well as interviews to the keys respondents since they were in a position to give

further clarification to any detailed information needed. Structured questions in an

interview guide were used to gather the required information from the key respondents

who include the University Principal, Deputy Principal, the Registrar, the Finance officer

and the University Enterprise Manager. From preliminary investigations done all the

respondents in the target population had adequate educational background hence in a

position to respond to questionnaires’ favorably. Therefore questionnaires’ were also

used collect the necessary data from the staffs that were randomly identified amidst the

total population.

3.7 Data Collection

The study used both primary and secondary data. Primary data was collected directly

from the University employees through the use of questionnaires and interviews were

conducted especially to senior staff like the management board. Secondary data included

information from documents such as brochures, strategic plans, charters, legislations,

statutes and journals obtained from the university. The researcher dropped the

questionnaires physically at the respondents’ place of work. The researcher left the

questionnaires with the respondents and picked them up later. Each questionnaire was

coded and only the researcher knew which person responded. The coding technique is

only used for the purpose of matching returned, completed questionnaires with those

delivered to the respondents.

3.8 Pilot Testing

The researcher carried out a pilot study to pretest the validity and reliability of data that

was to be collected using the questionnaire and interview guide. According to Key

(1997), validity can be defined as the degree to which a test measures what it is supposed

to measure. On the other hand reliability of a research instrument concerns the extent to

which the instrument yields the same results on repeated trials. Although unreliability is

always present to a certain extent, there will generally be a good deal of consistency in

24

the results of a quality instrument gathered at different times. The tendency toward

consistency found in repeated measurements is referred to as reliability (Carmines &

Zeller, 1979).

The researcher selected a pilot group of 3 individuals from the target sample of the staff

working in the TUM to test the reliability of the research instrument. The pilot study was

allowed for pre-testing of the research instrument. The clarity of the instrument items to

the respondents was necessary so as to enhance the instrument’s validity and reliability.

The aim was to correct inconsistencies arising from the instruments, which were to

ensure that they measure what is intended. The pilot data was not included in the actual

study.

3.9 Data Processing, Analysis and Presentation of Findings

Quantitative data collected was analyzed with the Statistical Package for Social Sciences

(SPSS). SPSS is commonly used in survey research and deployment especially of

statistical analysis. Data analysis was also done using regression analysis to analyze the

relationship between the independent and dependent variables. Regression analysis is a

statistical measure that attempts to determine the strength of the relationship between one

dependent variable (usually denoted by Y) and a series of other changing variables

(known as independent variables). Regression is often used to determine how many

specific factors for example the price of a commodity; interest rates, particular industries

or sectors influence the price movement of an asset.

The findings of the study have been presented in pie charts, distribution graphs, diagrams

and frequency polygons to clearly show the response from the respondents according to

the different variables. The variables used in the study are the reference points used in

order for the researcher to find out if the objectives are achieved from conducting the

study.

25

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION4.1.1 Introduction

This chapter discusses the analysis of data collected from respondents. It involves

scrutinizing the acquired information from the survey and making inferences. The

findings are represented based on the objectives of the study as presented in section 1.4;

these are presented in the form of tables and others graphs showing frequencies and

percentages. The results are then discussed in relation to the existing literature on

findings of the related studies.

4.2 Respondent Demographics

In this section the researcher sought to establish the demographics of the respondent’s in

terms of gender, age, level of education and years of service. This being a sample study,

all the views from respondents were merged.

4.2.1 Respondent’s Organization

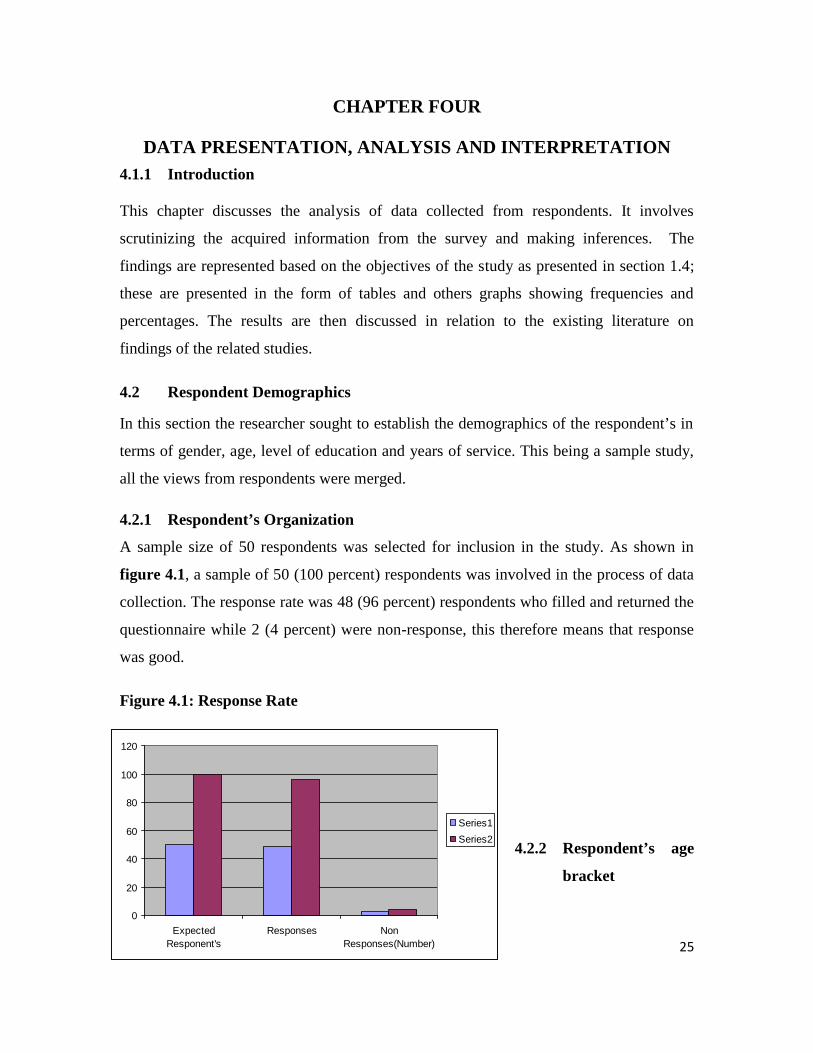

A sample size of 50 respondents was selected for inclusion in the study. As shown in

figure 4.1, a sample of 50 (100 percent) respondents was involved in the process of data

collection. The response rate was 48 (96 percent) respondents who filled and returned the

questionnaire while 2 (4 percent) were non-response, this therefore means that response

was good.

Figure 4.1: Response Rate

4.2.2 Respondent’s age

bracket

0

20

40

60

80

100

120

ExpectedResponent's

Responses NonResponses(Number)

Series1Series2

26

Section ABackground Information

Table 4.1 Gender

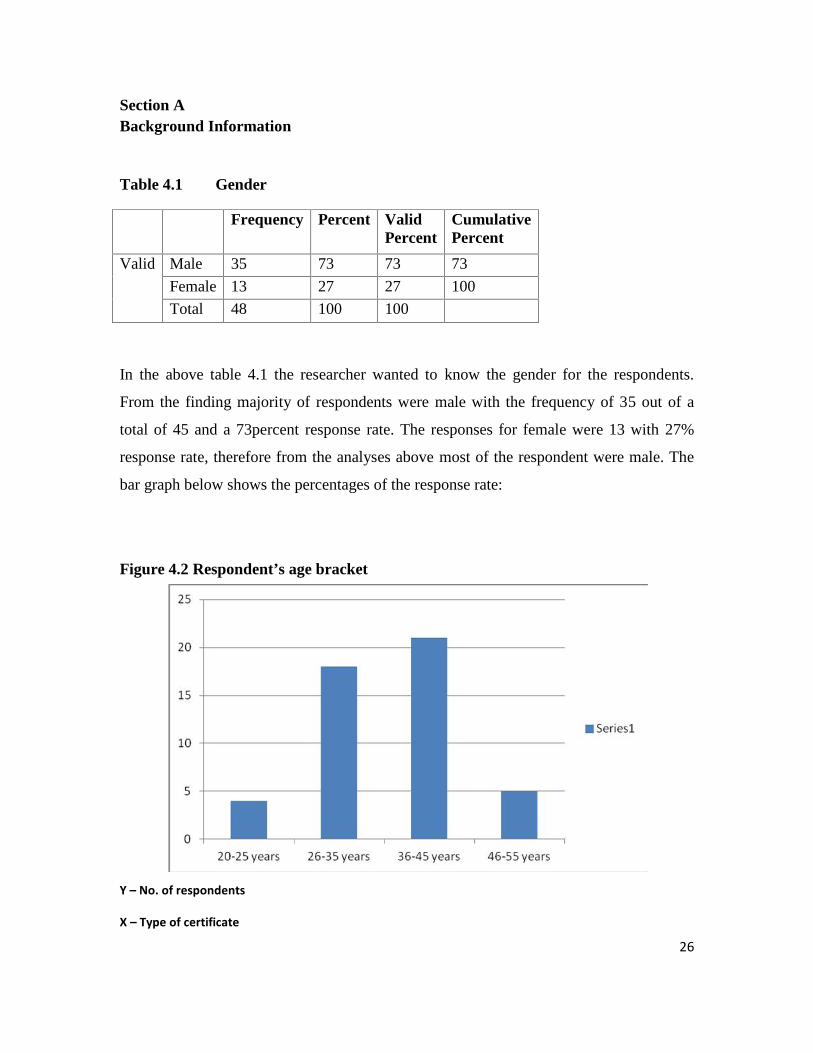

In the above table 4.1 the researcher wanted to know the gender for the respondents.

From the finding majority of respondents were male with the frequency of 35 out of a

total of 45 and a 73percent response rate. The responses for female were 13 with 27%

response rate, therefore from the analyses above most of the respondent were male. The

bar graph below shows the percentages of the response rate:

Figure 4.2 Respondent’s age bracket

Y – No. of respondents

X – Type of certificate

Frequency Percent ValidPercent

CumulativePercent

Valid Male 35 73 73 73

Female 13 27 27 100

Total 48 100 100

27

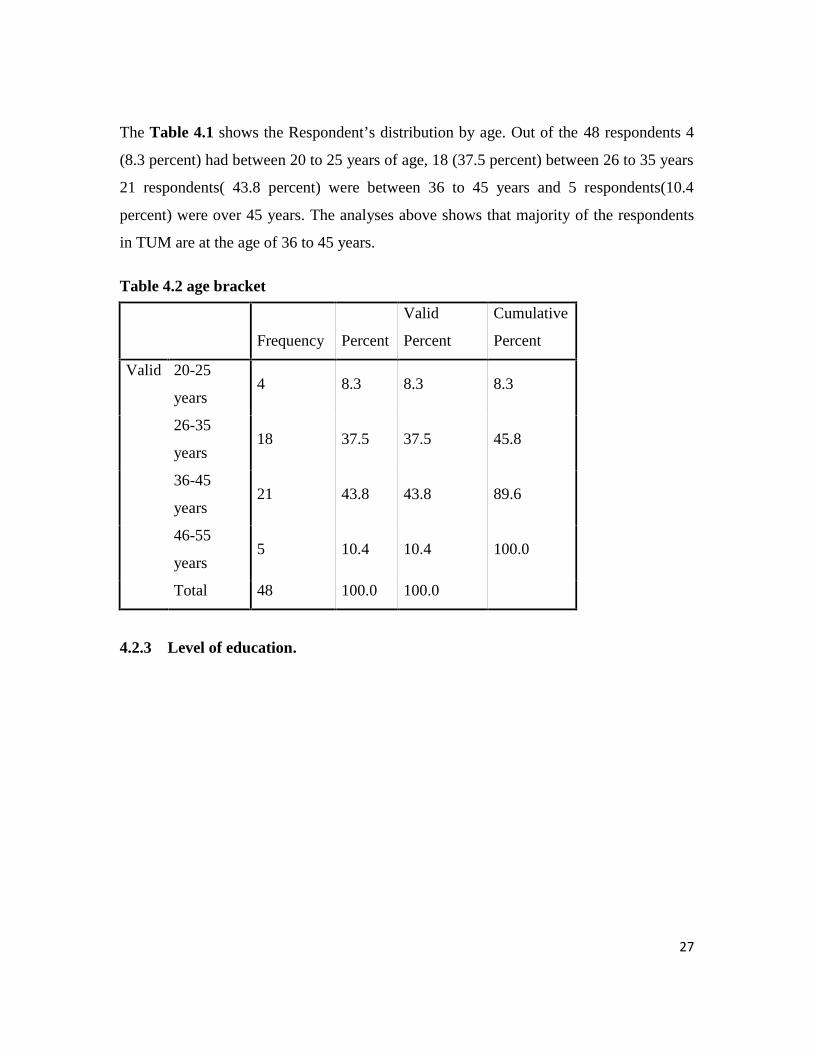

The Table 4.1 shows the Respondent’s distribution by age. Out of the 48 respondents 4

(8.3 percent) had between 20 to 25 years of age, 18 (37.5 percent) between 26 to 35 years

21 respondents( 43.8 percent) were between 36 to 45 years and 5 respondents(10.4

percent) were over 45 years. The analyses above shows that majority of the respondents

in TUM are at the age of 36 to 45 years.

Table 4.2 age bracket

Frequency Percent

Valid

Percent

Cumulative

Percent

Valid 20-25

years4 8.3 8.3 8.3

26-35

years18 37.5 37.5 45.8

36-45

years21 43.8 43.8 89.6

46-55

years5 10.4 10.4 100.0

Total 48 100.0 100.0

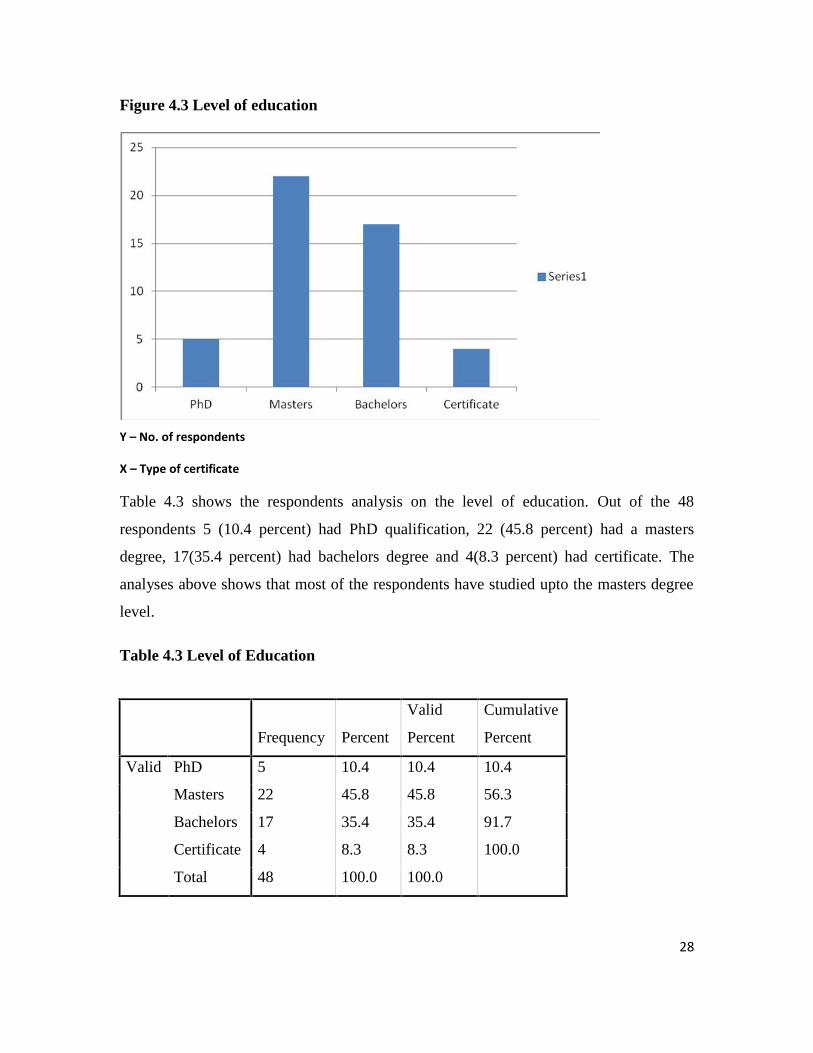

4.2.3 Level of education.

28

Figure 4.3 Level of education

Y – No. of respondents

X – Type of certificate

Table 4.3 shows the respondents analysis on the level of education. Out of the 48

respondents 5 (10.4 percent) had PhD qualification, 22 (45.8 percent) had a masters

degree, 17(35.4 percent) had bachelors degree and 4(8.3 percent) had certificate. The

analyses above shows that most of the respondents have studied upto the masters degree

level.

Table 4.3 Level of Education

Frequency Percent

Valid

Percent

Cumulative

Percent

Valid PhD 5 10.4 10.4 10.4

Masters 22 45.8 45.8 56.3

Bachelors 17 35.4 35.4 91.7

Certificate 4 8.3 8.3 100.0

Total 48 100.0 100.0

29

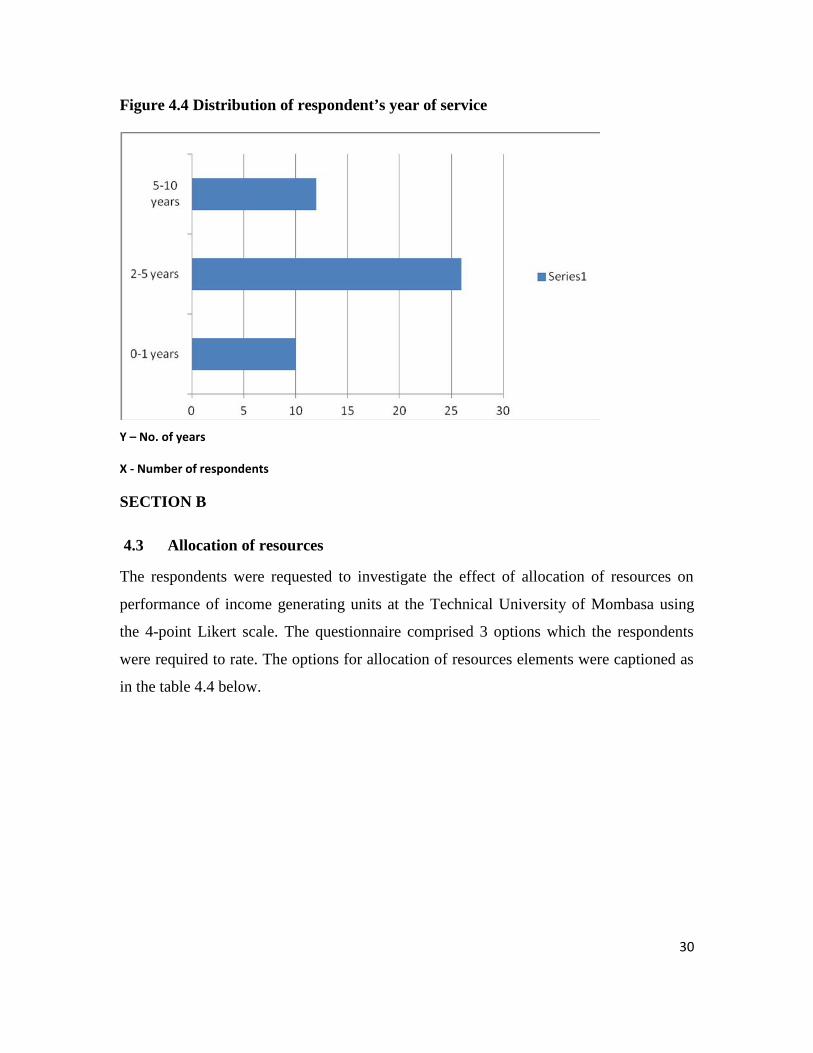

4.2.4 Respondent’s years of service with their employer

The table 4.4 shows the years of service by the same employer. Out the 48 respondents

10 (21percent) respondents had served below 1 year, 26 (54 percent) had served for 1 to 5

years, and 12 (25 percent) had served for more than 5 years.

Table 4.4 Years of service with employer

Frequency Percent ValidPercent

Cumulativepercent

0-1 years 10 21 21 212-5 years 26 54 54 755-10 years 12 25 25 100

48 100 100

Based on the table above, majority of the respondents 54 percent have served for more

than 1 year but not less than 5 years while 25 percent have served for more than 5 years.

This therefore indicates that a majority of the respondents had served for almost five year

hence their views were current and factual.

30

Figure 4.4 Distribution of respondent’s year of service

Y – No. of years

X - Number of respondents

SECTION B

4.3 Allocation of resources

The respondents were requested to investigate the effect of allocation of resources on

performance of income generating units at the Technical University of Mombasa using

the 4-point Likert scale. The questionnaire comprised 3 options which the respondents

were required to rate. The options for allocation of resources elements were captioned as

in the table 4.4 below.

31

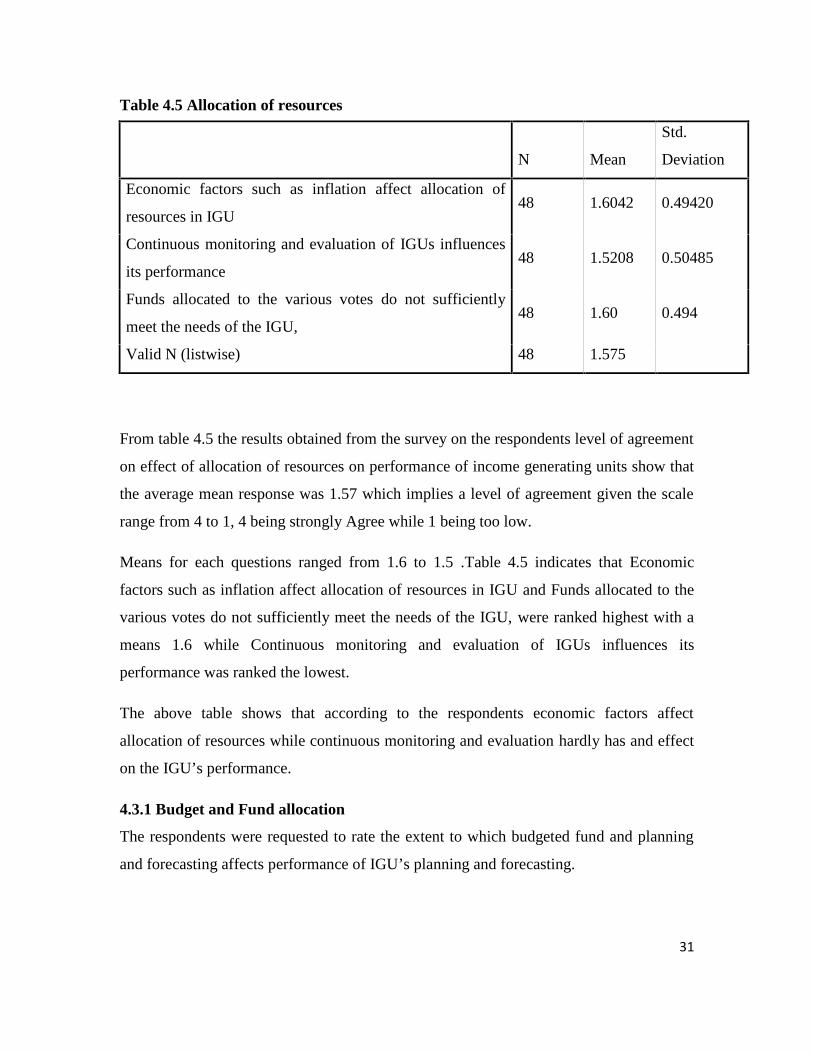

Table 4.5 Allocation of resources

N Mean

Std.

Deviation

Economic factors such as inflation affect allocation of

resources in IGU48 1.6042 0.49420

Continuous monitoring and evaluation of IGUs influences

its performance48 1.5208 0.50485

Funds allocated to the various votes do not sufficiently

meet the needs of the IGU,48 1.60 0.494

Valid N (listwise) 48 1.575

From table 4.5 the results obtained from the survey on the respondents level of agreement

on effect of allocation of resources on performance of income generating units show that

the average mean response was 1.57 which implies a level of agreement given the scale

range from 4 to 1, 4 being strongly Agree while 1 being too low.

Means for each questions ranged from 1.6 to 1.5 .Table 4.5 indicates that Economic

factors such as inflation affect allocation of resources in IGU and Funds allocated to the

various votes do not sufficiently meet the needs of the IGU, were ranked highest with a

means 1.6 while Continuous monitoring and evaluation of IGUs influences its

performance was ranked the lowest.

The above table shows that according to the respondents economic factors affect

allocation of resources while continuous monitoring and evaluation hardly has and effect

on the IGU’s performance.

4.3.1 Budget and Fund allocation

The respondents were requested to rate the extent to which budgeted fund and planning

and forecasting affects performance of IGU’s planning and forecasting.

32

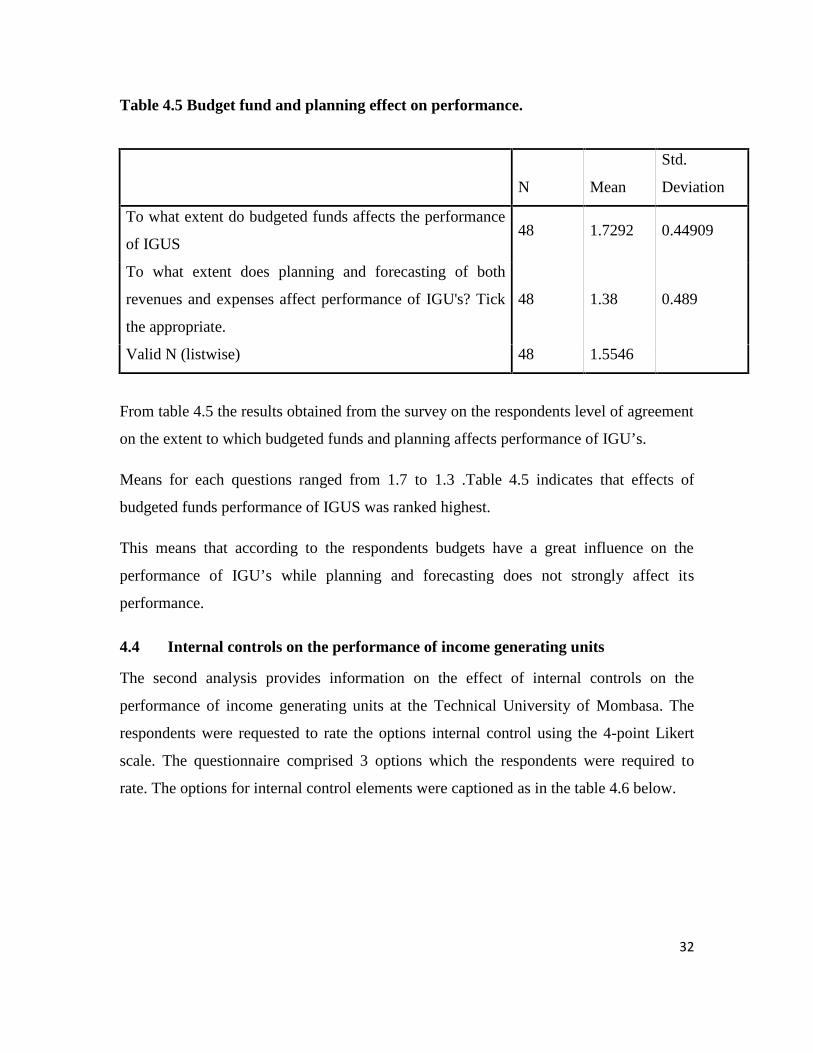

Table 4.5 Budget fund and planning effect on performance.

N Mean

Std.

Deviation

To what extent do budgeted funds affects the performance

of IGUS48 1.7292 0.44909

To what extent does planning and forecasting of both

revenues and expenses affect performance of IGU's? Tick

the appropriate.

48 1.38 0.489

Valid N (listwise) 48 1.5546

From table 4.5 the results obtained from the survey on the respondents level of agreement

on the extent to which budgeted funds and planning affects performance of IGU’s.

Means for each questions ranged from 1.7 to 1.3 .Table 4.5 indicates that effects of

budgeted funds performance of IGUS was ranked highest.

This means that according to the respondents budgets have a great influence on the

performance of IGU’s while planning and forecasting does not strongly affect its

performance.

4.4 Internal controls on the performance of income generating units

The second analysis provides information on the effect of internal controls on the

performance of income generating units at the Technical University of Mombasa. The

respondents were requested to rate the options internal control using the 4-point Likert

scale. The questionnaire comprised 3 options which the respondents were required to

rate. The options for internal control elements were captioned as in the table 4.6 below.

33

Table 4.6 Internal controls

N Mean

Std.

Deviation

Employees accountability determines perfromance of

IGUs48 2.3542 1.02084

The internal controls ensures reliability of financial

reporting which are accuratev and complete48 1.9167 .79448

Weak internal controls affect performance of IGUs48 1.1250 .33422

Valid N (listwise) 48 1.7986

From table 4.6 the results obtained from the survey on the respondents level of agreement

on quality internal control elements show that the average mean response was 1.79 which

implies a level of agreement given the scale range from 4 to 1, 4 being strongly Agree

while 1 being a low level of agreement. Means for each questions ranged from 2.3 to 1.9.

Table 4.6 indicates that Employees accountability determines performance of IGUs and

internal controls ensures reliability of financial reporting which are accurate and

complete was ranked the highest with individual means of 2.3 and 1.9 respectively. While

Weak internal controls affect performance of IGUs was ranked the lowest.

This means that the respondents agree that accountability of employees influence

performance of IGU’s and internal controls ensure reliability of financial reporting. On

the other hand the respondents disagree that weak controls affect performance of the

units.

Table 4.7 Fund allocation and performance

Frequency PercentValidPercent

CumulativePercent

Valid Disagree 19 39.6 39.6 39.6StronglyAgree 29 60.4 60.4 100Total 48 100 100

34

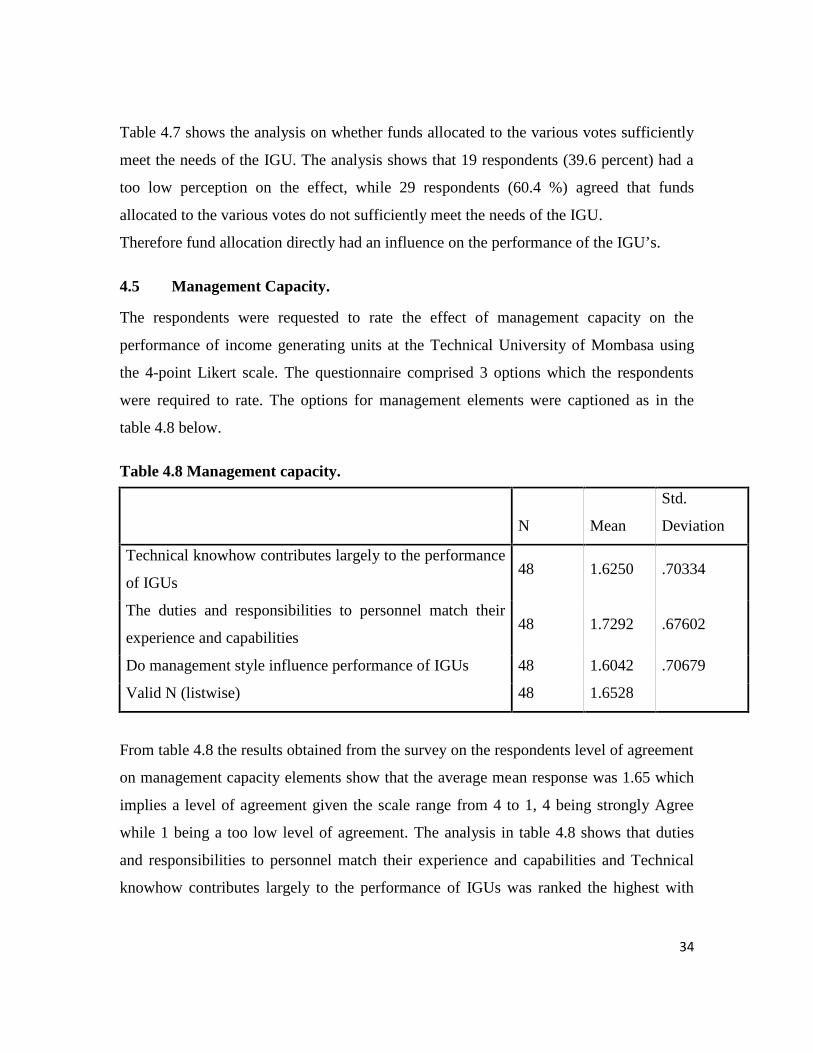

Table 4.7 shows the analysis on whether funds allocated to the various votes sufficiently

meet the needs of the IGU. The analysis shows that 19 respondents (39.6 percent) had a

too low perception on the effect, while 29 respondents (60.4 %) agreed that funds

allocated to the various votes do not sufficiently meet the needs of the IGU.

Therefore fund allocation directly had an influence on the performance of the IGU’s.

4.5 Management Capacity.

The respondents were requested to rate the effect of management capacity on the

performance of income generating units at the Technical University of Mombasa using

the 4-point Likert scale. The questionnaire comprised 3 options which the respondents

were required to rate. The options for management elements were captioned as in the

table 4.8 below.

Table 4.8 Management capacity.

N Mean

Std.

Deviation

Technical knowhow contributes largely to the performance

of IGUs48 1.6250 .70334

The duties and responsibilities to personnel match their

experience and capabilities48 1.7292 .67602

Do management style influence performance of IGUs 48 1.6042 .70679

Valid N (listwise) 48 1.6528

From table 4.8 the results obtained from the survey on the respondents level of agreement

on management capacity elements show that the average mean response was 1.65 which

implies a level of agreement given the scale range from 4 to 1, 4 being strongly Agree

while 1 being a too low level of agreement. The analysis in table 4.8 shows that duties

and responsibilities to personnel match their experience and capabilities and Technical

knowhow contributes largely to the performance of IGUs was ranked the highest with

35

individual means of 1.72 and 1.62 respectively, while management style influencing

performance of IGUs was ranked lowest.

This shows that in the respondents view technical knowhow is very important in overall

development of IGU’s thus ranked highest while management style lowly influencing its

performance.

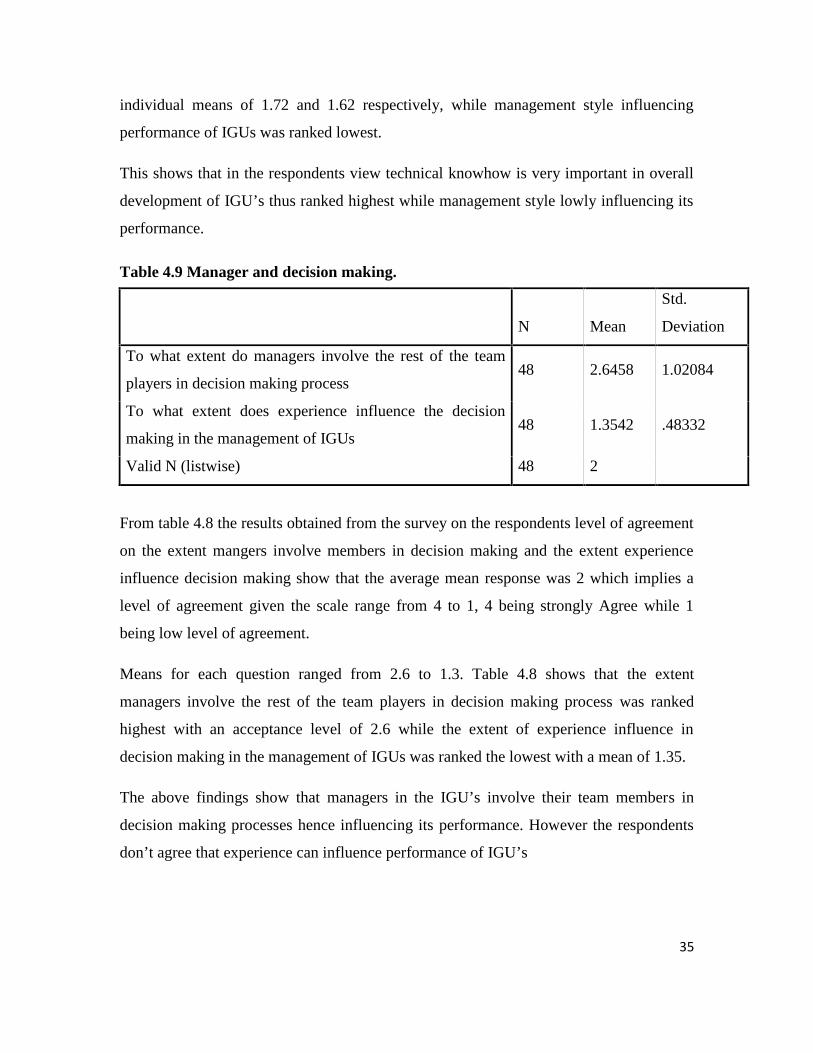

Table 4.9 Manager and decision making.

N Mean

Std.

Deviation

To what extent do managers involve the rest of the team

players in decision making process48 2.6458 1.02084

To what extent does experience influence the decision

making in the management of IGUs48 1.3542 .48332

Valid N (listwise) 48 2

From table 4.8 the results obtained from the survey on the respondents level of agreement

on the extent mangers involve members in decision making and the extent experience

influence decision making show that the average mean response was 2 which implies a

level of agreement given the scale range from 4 to 1, 4 being strongly Agree while 1

being low level of agreement.

Means for each question ranged from 2.6 to 1.3. Table 4.8 shows that the extent

managers involve the rest of the team players in decision making process was ranked

highest with an acceptance level of 2.6 while the extent of experience influence in

decision making in the management of IGUs was ranked the lowest with a mean of 1.35.

The above findings show that managers in the IGU’s involve their team members in

decision making processes hence influencing its performance. However the respondents

don’t agree that experience can influence performance of IGU’s

36

4.6 Culture on the performance of income generating units.

The respondents were requested to examine the effect of work culture on the performance

of income generating units at the Technical University of Mombasa using 4-point Likert

scale. The questionnaire comprised 3 options which the respondents were required to

rate. The options were captioned as in the table 4.10 below.

Table 4.10 Culture and performance

N Mean

Std.

Deviation

Do employees adhere to the code of ethics on service

delivery in the university48 1.8958 .62704

Does staff working attitude affects performance of IGUs 48 1.3542 .48332

Does bureaucratic form of organization affect performance

of IGUcs48 1.6042 .49420

Valid N (listwise) 48 1.6181

The analysis in table 4.10 show that the average mean response was 1.61 which implies a

level of agreement given the scale range from 4 to 1, 4 being strongly Agree while 1

being a low level of agreement.

This indicates that respondents agree that employee adhere to the code of ethics on

service delivery and that staff working attitude does not affect performance of IGU’s. It

further indicates that the bureaucratic form of organization has an influence on the

performance of the units.

The university operates on a standard budget which has equally distributed the funds to

the various votes hence a procurement plan is drawn to facilitate efficient acquisition of

materials. All materials purchased are through a clear procurement procedure outlined by

the supplies department. Individual departments make requisition for materials and send

to the central stores where they get the necessary materials. If the materials are not

available in the central stores, the supplies officer can make local purchase order from the

37

existing pre-qualified suppliers whereby they procure the products which are then

received in the presence of the chairperson of the department requesting for the materials.

Thereafter the payment process is initiated after the necessary documents have been

presented by the supplier to the central stores.

38

CHAPTER FIVE

SUMMARY OF FINDINGS, CONCLUSION ANDRECOMMENDATIONS

5.1 Introduction

This chapter discusses summary of findings in relations to the research objectives. It also

draws the conclusions, recommendations and suggested areas for further study.

5.2 Summary of Findings

The research study sought to evaluate the factors determining performance of income

generating units in public universities, specifically the study explored the research

objectives provided in chapter one.

The study employed descriptive data analysis. The sample under study comprised 48

respondents. The study used primary and secondary data that was collected using

questionnaire that was served on the respondents and findings presented using tables.

The first part of the objective was to investigate the effect of allocation of resources on

performance of income generating units at the Technical University of Mombasa.

Majority of the respondents agreed that allocation of resources had a high effect on

performance of income generating units. There was a high level of acceptance that

Economic factors such as inflation affect allocation of resources in IGU and Funds

allocated to the various votes do not sufficiently meet the needs of the IGU.

The second part of analysis was to evaluate the effect of internal controls on the

performance of income generating units at the Technical University of Mombasa.

Majority of the respondents agreed that employees’ accountability determines

performance of IGUs and internal controls ensures reliability of financial reporting which

are accurate and complete. There was a level of acceptance that funds allocated to the

various votes sufficiently meet the needs of the IGU.

39

The third part of the analysis was to investigate the effect of management capacity on the

performance of income generating units at the Technical University of Mombasa. There

was a high level of acceptance that duties and responsibilities to personnel matching their

experience and capabilities and Technical knowhow contributes largely to the

performance of IGUs. Majority of the respondents rated high managers involving the rest

of the team players in decision making process.

The last part of the analysis was to examine the effect of work culture on the performance

of income generating units at the Technical University of Mombasa. Majority of the

respondents rated highly employee’s adherence to the code of ethics on service delivery

in the university, while staff working attitude affects performance of IGUs was rated the

least.

5.3 Conclusions

The broad research questions relating factors determining performance of income

generating units in public universities, was studied and the finding analyzed so as to draw

conclusions.

In investigating the effect of allocation of resources on performance of income generating

units at the university, economic factors affect the allocation of resources. With the