EU-Turkey-Russia Energy Triangle and Turkey's Energy Policy

62

EU-TURKEY-RUSSIA ENERGY TRIANGLE AND TURKEY’S ENERGY POLICY 1

Transcript of EU-Turkey-Russia Energy Triangle and Turkey's Energy Policy

EU-TURKEY-RUSSIA ENERGY TRIANGLE AND TURKEY’S ENERGY POLICY

1

‘Each member state should decide its own energy policy’1

Jose Manuel Barosso

President of the European Commission

1 Speech delivered at the ‘Energy For Europe’ Strategy Announcement, Brussels, 19 March 2007

2

TABLE OF CONTENTS

1. INTRODUCTION

1.1. Background

1.2. Argument

1.3. Outline

2. RUSSIAN ENERGY POLICY

2.1. Russia as a Global Actor

2.2. Russian Energy Interests in EU market

3. EU ENERGY INTERESTS

3.1. EU Energy Outlook

3.2. EU’s Energy Dependency and Russia

4. TURKISH ENERGY STRATEGY

3

4.1. Turkish Energy Outlook

4.2. Turkey’s New Foreign Policy Vision and Its

Energy Policy

4.3. Turkey-EU Energy Relations

4.4. Turkey-Russia Energy Relations

5. DISCUSSION

6. CONCLUSION

BIBLIOGRAPHY

I. INTRODUCTION

1.1. Background

By 2030, the world population will need 45% more energy than

today (Luft and Korin 2009:7). It is difficult to predict

how long existing resources will last. It is certain that

there is little investment in producer countries to energy

fields. At the same time, national energy companies have

become more powerful since the vast share of resources rest

in their hands. Given the resultant race for securing energy

supplies by less endowed states, there has been increased

4

concern regarding Russia’s reliability as an energy partner

in the aftermath of the Ukraine-Russia gas dispute in 2006,

the 2008 Georgia War and the repeated gas price

disagreements with the Ukraine in 2009.

The need to ensure energy security became a key policy

priority for European Union (EU) leaders following the

Russian-Ukrainian gas dispute in 2006 and Georgian War in

2008 in particular. In the EU, which is Russia’s biggest

customer, energy demand is increasing while its production

is declining. As a major actor in energy sector, Russia is

trying to control international energy markets by using its

energy companies. Despite the interdependency between Russia

and EU, conflicting aims and interests have presented an

obstacle to cooperation. While the EU targeted diversity of

supply, ‘Russia put energy in the centre of Russia’s foreign

policy’ (Sleivyte 2010: 89) and has used its assets to exert

political power (Lucas 2008: 211). Europe wants to access

East more; Russia wants to access West more. Within this

context, Turkey plays an important role in terms of bridging

the conflicting agendas of these two sides.

Turkey, as a country that is surrounded by the world’s

energy-rich regions, wants to transform its geopolitical

advantage to much more power. This vision also overlaps with

5

Turkey’s new foreign policy doctrine that aims at being a

regional power (Davutoglu 2007: 77). Turkey desires not only

to be a transit country but also an energy hub. Turkey has

played an active role in the region for proposed pipelines

and has announced its willingness to be in the EU’s fourth

corridor after Russia, Algeria and Norway. EU officials

emphasize Turkey’s importance as an energy partner and

Turkey points out its willingness to support the EU’s

diversification of supply strategy. Turkey is also now

carrying Caspian gas to the EU by the Interconnector Turkey-

Greece and Caspian oil by Baku-Tblisi-Ceyhan oil pipeline.

In addition, Turkey is one of the partners of the EU’s

flagship pipeline project Nabucco.

Still, on the one hand Turkey is the forerunner of the EU-

backed pipeline projects but on the other it remains a

supporter of Russian projects that would risk the EU’s aims

to diversify its energy resources. Essentially, Turkey

remains highly dependent on Russian energy for around 65% of

its energy needs. Turkey gave permission to Russia to use

Turkey’s territory in the Black Sea for exploration studies

of the South Stream that is analyzed by a rival to Nabucco

(Baran 2008: 8, Truscott 2009: 34). This raises the question

of whether or not heavily energy dependent Turkey’s energy

security requirements can align with the EU’s energy

6

interests and whether Turkey’s new foreign policy vision

that aims at a ‘zero problems with its neighbours’, will

affect its energy relations with Russia and the EU. In this

regard, a greater exploration of the key drivers of Turkey’s

energy policy could aid our understanding in terms of

reconciling the conflicting interests of different actors.

It is necessary to draw a picture of Turkey’s energy

considerations, taking into account the policies and

interests of important surrounding actors in the game.

However, debates within the media and existing academic

studies have tended to revolve around the practical

developments in Turkey’s energy sector and there has been

little focus on Turkey’s role in respect to the EU and

Russia’s policy interests. This is the gap in the literature

that this study aims to fill.

1.2. Argument

This study aims to shed light on Turkey’s energy policy

design within the triangle of the EU, Russia and Turkey. It

is argued that there is a certain need to build a link

between energy considerations of these three actors in order

to understand Turkey’s emerging policies since it will be

7

incomplete to analyze Turkey’s policy making and policy

outputs without fully understanding the other two key

actors. With this concern in mind, this study assesses

Russian and EU energy interests in the regional context and

their effects on Turkish energy policy. Within this context

my central argument is that Turkey’s energy policy is

conducted in line with the main principals of Turkey’s

foreign policy vision. This means that Turkey’s energy

interests are driven by its national interests while the EU

and Russia’s energy interests have a direct impact in

shaping Turkish energy decisions, also overlapping with

Turkey’s new foreign policy aim of being a regional power.

The paper will seek to answer these core questions by

providing a review of the most recent literature on the

subject area, and by assessing the available material that

has appeared in the local and international media.

1.3. Outline

In analysing the energy relationship between Turkey-Russia-

EU and the dynamics of Turkish energy policy making, this

study consists of four main sections. In the first two

sections, the study will explore the two dominant actors

that shape Turkish energy policy. In the first section, it

will illustrate Russia’s importance as a global energy actor

8

with a special emphasis on its interests in the European

market. The second section focuses on the EU’s energy

interests with a special focus on the concept of energy

security. It starts with the EU’s energy needs and Russia’s

importance in its energy mix; then expands on the EU’s

energy interests and aims in terms of its energy needs.

Upon exploring the positions of these two important external

actors, Turkey’s energy policy and its principles will be

analyzed. Firstly, Turkey’s energy outlook is examined.

Secondly, Turkey’s new foreign policy vision and its effects

on foreign policy will be discussed. After this general

outlook, Turkey’s energy relations with the EU and Russia

will be dealt with respectively. In the last chapter,

Turkey’s energy policy design will be focused on in respect

to Russia-EU energy interests and conclusion will be given.

2. Russian Energy Policy and European Market

2.1. Russia as a Global Energy Actor

With its top ranking in the world’s gas reserves and second

place in world oil reserves, Russia is a key player in the

9

global energy sector. Russia sits on 9% of the world’s

proven reserves and 30% of global gas reserves and its

production meets 11,5% of global energy demand (Mitrova

2010: 19). The Russian economy is fuelled by energy revenues

where one third of Russian GDP is accounted by the energy

sector and oil and gas provides almost half of government

revenues (European Commission 2007b, 33).

Russia’s most important export products are oil and gas.

Russia’s biggest trading partner is Europe. Around two

thirds of oil and gas exports go to the EU member states,

the rest heads to non-EU countries and CIS countries

(Perovic and Orttung 2009: 134). 56.2%of Russian exports

went to the EU in 2005 (Ibid: 134). The EU accounted for

44.8% of Russian imports. Conversely, Russia accounted for

only 10.1%of the EU’s overall imports and is responsible for

only6.2%of EU exports (European Commission 2007: 13 and 26-

31). Russia depends more on Europe where its consumers are

located (Sleivyte 2010: 89). Hence, Russia’s energy

relations with Europe need to be understood against the

background of economic dependencies as well as general

political trends (Perovic and Orttung 2009: 133)

Under Putin’s presidency, Russia wanted an active role in

the international arena. The exploitation of its vast energy

10

resources was a means by which this could be achieved

following the unfolding of economic crises and military

weakness. This was made possible by the increase in global

energy prices. The energy sector came to be increasingly

managed by the Kremlin as a strategic asset which could be

used to assert Russia on the world stage (Monaghan and

Kankovski: 2006: 21) When Russia became stronger, it started

to expand its room for manoeuvre to reach its objectives. In

2003, Russia initiated a new energy policy called the

“Energy Policy for 2020” whereby energy was placed at the

centre of diplomacy (Kohen, 2009: 93). In explaining this

vision Prime Minister Putin has remarked that, ‘Russia

enjoys vast energy and mineral resources which serve as a

basis to develop its economy; as an instrument to implement

domestic and foreign policy. The role of the country on

international energy markets determines, in many ways its

geopolitical influence’ (Kuchinsky 2009).

2.2. Russian Energy Strategy and European Market

As a powerful player within the energy arena, Russia’s

reliability was never questioned as much as until 2006

(Smith 2008: 15). The 2006 Ukraine-Russian gas dispute,

problems with Belarus, the 2008 Georgian War and the 2009

Ukrainian gas crisis have been critical in shifting

11

attitudes towards Russia in international relations.

Ukraine, Georgia and Belarus were three transit countries

for Russian gas towards Europe. According to Morozov (2008:

54) crises in Russia’a relations with its neighbours have

led to the deployment of the energy weapon which sometimes

affects European customers. In the 1990’s, 90% of Russian

gas was routed on Ukraine now it has decreased to 70% and

Russia plans to decrease it more (Pomfret 2009: 2) During

the gas dispute eleven importers of Russian gas were shut

out and major importers such as Germany, Italy and France

found their supplies sharply reduced (Ebel 2009: 10).

Russia’s use of energy assets as a foreign policy tool has

been widely analyzed by many scholars (Ebel 2009: 9; Youngs

2009: 98; Lucas 2008: 211). Although Russia has not accepted

the claim that it uses energy as a ‘political weapon’,

Russia’s President Vladimir Putin (from 2000-2008) signalled

this strategy in his doctoral thesis in 1997 where he

addressed “raw materials” as a tool for attaining great

power for Russia (Balzer, 2006: 48-54). Following his

elevation to the presidential office in 2000, Putin started

the implementation of this strategy. As a former KGB agent,

Putin appointed his friends or high-level bureaucrats to

manage energy companies (Kefferputz 2009: 98). Russia

expanded its power by using state-backed energy giants:

12

Gazprom and Rostneft. Gazprom is world’s largest gas

producer and Rostneft is one of the EU’s main oil suppliers.

Energy companies therefore became the key instrument of his

foreign policy vision. He gave special attention to Gazprom

and met with the CEO three times a month (Roberts 2009:

249). Putin’s successor Medvedev was also a former CEO of

Gazprom.

‘Since the early 2000s, the Russian government has tended to

understand the context of its energy business in Europe

better than Europeans understand Russia’ (Classon, 2010:90).

According to Lucas (2008: 211) Russia wanted to control

international energy market. There were two ways in which

this could be achieved; by controlling pipelines and the

European downstream market. Europe is expected to import two

thirds of its energy needs in 2020. Russia plans

alternatives for European energy security for its increasing

energy needs and finds European partners for these projects.

Russia’s major pipeline projects are South Stream and Nord

Stream gas pipeline projects. For South Stream Russia’s

partners are Italian ENI and French Gaz de France. For Nord

Stream Russia’s partner is Germany. Russia is creating blocs

in the European Union by bilateral agreements.

13

The South Stream project was announced on 23 June 2007. The

project was supported by Romania, Serbia, Hungary, Greece,

Turkey and Austria. According to Gazprom CEO Alexey Miller,2

the ‘South Stream is Gazprom’s top-priority project and its

implementation will testify Russia will remain a key

EU partner in the gas industry for decades ahead’. The South

Stream is seen by some analysts’ a direct competitor with

the EU and US-backed Nabucco project (Cohen 2009: 97). Baran

(2008: 8) gives greater chances for the South Stream project

because it is backed by the state-owned Gazprom that

supports projects according to their strategic goals.

Truscott (2009: 34) believes if South Stream is built first,

Nabucco may falter because Caspian producers who are also

proposed suppliers for the Nabucco project may prefer South

Stream as a gateway to the European market. Gazprom CEO

Alexey Miller has stated that South Stream will be

operational in 2015 and this will be earlier than Nabucco

(Yinanc, 2010). In addition, Truscott (2009:34) adds that

three of the five countries on Nabucco’s route are also part

of the South Stream project’s route. Russia has also signed

an agreement with Austria - which is a partner for Nabucco -

to join the South Stream project. During the ceremony the

current Russian Prime Minister Vladimir Putin called Nabucco

a risky and dangerous project and asked ‘can they show even2 Gazprom CEO Alexey Miller, Speech delivered at the “South Stream Project Presentation”, Moscow, July 19, 2010, available via www http://www.gazprom.com/press/miller-journal/513241/, accessed 22 July 2010

14

one supply contract? I cannot see any willing supplier

there. We can conclude contracts to supply South Stream any

time’ (Socor: 2010a).

In 2005 Germany and Russia signed a deal to bring Russian

gas to Europe via Germany. Moscow’s persistence in

advancing the Nord Stream gas pipeline project is also to a

large extent explained by the desire to decrease Russia’s

dependence on the transit states (Mozorov 2008: 54). Poland

and Baltic states have strongly opposed this project and did

not want to decrease Russia’s dependence on these countries

as a transit state. Former Polish Defence Minister Rodoslaw

Sikorski (2005-2007), compared the project with 1939

Soviet-Nazi pact that carved up Eastern Europe between

Germany and Russia (Shaffer 2009: 130). Nord Stream is seen

as the crown of the personal relationship between German

Chancellor Schroder and Russian Prime Minister Putin.

According to Westphal (2008: 107) the pipeline deal is

problematic because it will increase Germany’s dependence on

Russia by up to 40%.

Stuermer argues (2008: 202) that the Kremlin wanted to make

sure pipelines were under Russian control. Russia is also

interested in the long-term availability of Central Asian

gas (Cohen 2009: 97). Russia has quickly responded to EU

15

diversification plans and guaranteed not only EU partners

but also alternative suppliers in the Caspian. While the EU

was pursuing Nabucco, Russia was signing agreements with

Kazakhstan, Turkmenistan and Uzbekistan. ‘In 2007, at the

Summit of the Shanghai Cooperation Organization, the

presidents of Kazakhstan and Russia called for establishing

an “Asian energy club” to extend energy ties between the

member states’ (Ibid. 98). Given the weaknesses of the EU

Energy Policy and different energy mixes in each country,

Russia’s tactics found ground in Europe.

Russia is the ‘regulator, landlord and investor’ (Schaffer

2009: 123). In July 2005 Gazprom CEO Alexei Miller told the

Financial Times (Crooks 2008) that ‘the company wanted to

become one of the largest integrated energy companies in the

world, spanning oil, gas and electricity’.

Gazprom, the biggest company in Russia, controls 85% of

Russian energy production, and over a quarter of the world’s

reserves of natural gas. Gazprom expanded its influence by

acquiring shares in European companies. ‘If it wanted to

maintain its position as Western Europe’s primary supplier

of hydrocarbons, Moscow would need to increase the amount of

oil and gas flowing through Central Europe’ (Orban 2008:

166). Gazprom has 48 partnerships in different 25 European

16

countries from gas distribution to marketing (Vantra 2009:

162). In addition, the Baltic Sea Region and South Balkans

are at the core of major infrastructure projects by Russian

energy companies. (Vahtra 2009: 160).

2. EU Energy Interests

2.1.EU Energy Outlook

17

The EU is the third largest energy consumer in the world

after the USA and China. The EU is not an energy-sufficient

region. The EU was 60%self-sufficient in the 1990s but in

2008 this decreased to less than 40% (Pomfret 2009: 2). The

EU’s proven oil reserves are only 0.5% of the world total

and 1.6% for gas, although it consumes 17.9% of oil and

16.2% of gas (BP 2009: 13-24). Russia is the major foreign

supplier of oil accounting for 26%of oil followed by Norway

(13%), Saudi Arabia(9%), Libya (8%), Iran (5%) (Mangott and

Westphal, 2009: 149). For natural gas Europe produces two

fifths of its needs where 42% comes from Russia, 24% Norway,

18% Algeria and 5% Nigeria (Roberts, 2009: 248).

The EU announced its new energy policy aims in its ‘Green

Paper’ (European Commission 2006a) which targets

sustainability, competitiveness and security of supply. It

plans to increase the share of energy efficiency and

renewable energy to 20%. Although this has been reached,

figures show that it will not meet the EU’s energy demand.

The EU will probably rely on imports to meet over 80% and

90% of its collective natural gas and oil needs,

respectively, in the next two decades (European Commission

2007a: 3).

18

More imports also mean increased importance of efforts to

attain energy security within a changing world energy

outlook. Globally there are two trends that affect energy

relations from now on: resource-nationalism and location in

energy production (Orttung et al., 2009: 3). Focus is on the

producers and when national energy companies become more

influential, it becomes necessary to improve relations with

national suppliers. The Middle East, Caspian and Gulf region

are in the radar of EU energy policy but there are obstacles

for the body’s attempts to diversify its resources. It can

be summarized as the EU’s challenge in formulating a

‘single voice’ for energy policy; bilateral relations

between Russia and EU member states, and the different

energy mixes within the EU. ‘The new developments require

the EU member states to consider how and to what extent

their external policies should also be merged into a more

EU-wide approach, if they agree on the common risks that

need to be averted and the common benefits gained, and if an

how a crisis mechanism for fuels other than oil is needed to

manage the perceived increased security of supply risks’

(Jong and Linde, 2008: 1).

2.2. European Energy Dependency and Russia

19

In December 2005 and December 2006 Russia cut or threatened

to cut gas supplies to Ukraine and Belarus to demand higher

prices (Baghat 2010: 337). ‘Moscow’s attempts to set limits

to the national security policies of Georgia and Ukraine are

only the latest manifestation of Russian insecurities and

the short-sightedness of its foreign policies’ (Smith 2008:

1 ). When the EU tried to find alternatives to Russian

dependence, Russia made counter-attacks to thwart such

efforts. According to Baghat (2010:337) these attempts

reshaped the EU-Russian relationship and have given birth to

a number of pipeline projects.

The Nabucco gas pipeline is the EU’s centre-piece project to

bring as an alternative to Russian gas via Turkey, Bulgaria,

Romania and Hungary. Iran, Iraq, Caspian region and Egypt

are potential suppliers for Nabucco. Former EU Energy

Commissioner Andris Piebalgs noted ‘Nabucco is more than

just a pipeline. It is embodiment of the existence of a

common European energy policy’(Econews 2007). In reaction to

attempts to circumnavigate Nabucco, Russia has presented its

own project: South Stream. (Truscott, 2009: 33). According

to the plans, South Stream will be built under the Black

Sea with a European partner, Italian ENI, and Russia’s

Gazprom. When Turkey announced the Samsun-Ceyhan oil

20

pipeline that would bring Caspian oil to Europe, Russia

declared that the Burgas Alexandropoulis oil pipeline with

Bulgaria and Greece that could bypass Samsun-Ceyhan.

With competing projects being announced, the problem is how

to finance and how to fulfil these ambitions. Aside from

fears over Russia’s use of its energy for political

leverage, the EU is also concerned with the possibility that

Russia may not to make sufficient investments in developing

fields and therefore may not be able to meet the EU’s

growing needs (Roberts, 2009: 245). This is because

Gazprom’s revenues were used to buy up other sectors rather

than investing for modernization of energy infrastructure or

new fields (Youngs, 2009: 91). Russia has fallen behind in

its efforts to modernize its domestic capacity but it has

attempted to improve relations with energy-rich countries

for ‘diversification of supply’ (Russian Energy Ministry

2009: 12). Russia has strengthened cooperation with Africa

and Central Asia And also reached a pipeline deal with

Kazakhstan and Turkmenistan that would bring gas to Russia.

In 2008, Russia signed a memorandum of understanding with

Nigerian National Petroleum for cooperation in oil and gas

exploration. Russia is also interested in building a

pipeline between Libya and Europe (Buckley 2008) and is

considering potential partnerships with Iran.

21

Lacking a “common energy policy” the EU has been left

behind in comparison with Russia’s momentum of expanding

energy agreements. ‘Striking a balance between the

priorities of energy policy is difficult in EU where a wide

diversity of energy mixes and import dependencies prevails

and where foreign policy and security approaches are even

more diverse.(Jong and Linde, 2008: 1). ‘Although member

countries showed willingness to cooperate for an energy

policy, paradoxically this broad consensus over the need for

a more integrated energy policy ran parallel with the EU

member states’ reinforced trend to affirm their own national

policies’ (Natorski and Surralles,2008: 72).

Within the EU dependency on Russia differs from country to

country. Countries of the former Soviet bloc and Finland

are the most dependent countries. This is affecting

countries’ foreign policy attitudes as one Finnish policy

maker admitted: ‘We import one country through one pipeline’

(Youngs, 2009: 93). France, Germany, Italy are in the middle

while UK, Sweden, Spain, Portugal, Netherlands are less

dependent to Russia. According to Youngs (2009:80) besides

high dependent countries, also less dependent ones were

affected indirectly given the impact upon international

prices and the broader climate of international energy.

22

EU energy companies’ bilateral relations with Russia is

creating different understandings in Europe toward a common

energy policy. Companies are seeking profit and Russia as a

major player in the sector that has the resources and

revenues is a suitable partner for this.

3. TURKEY AND EU-RUSSIA ENERGY RELATIONS

3.1. Turkish Energy Outlook

Turkey is not an energy producer and while possessing

significant hydroelectric and lignite resources, it is

heavily dependent on oil and gas. Turkey imports 92% of its

oil needs and 98% of its gas (Pamir, 2010: 250). For oil,

Iran, Iraq, Saudi Arabia, Syria, Libya, Algeria and Russia

are Turkey’s main suppliers. In addition, with the

construction of US backed Baku-Tiblisi-Ceyhan pipeline,

Turkey is delivering Azerbaijani oil to world markets. For

gas Turkey is heavily dependent to Russia. Russia provides

nearly 70% of Turkey’s gas needs. After Russia; Turkey

imports 20 percent from Iran, 13 percent from Azerbaijan and

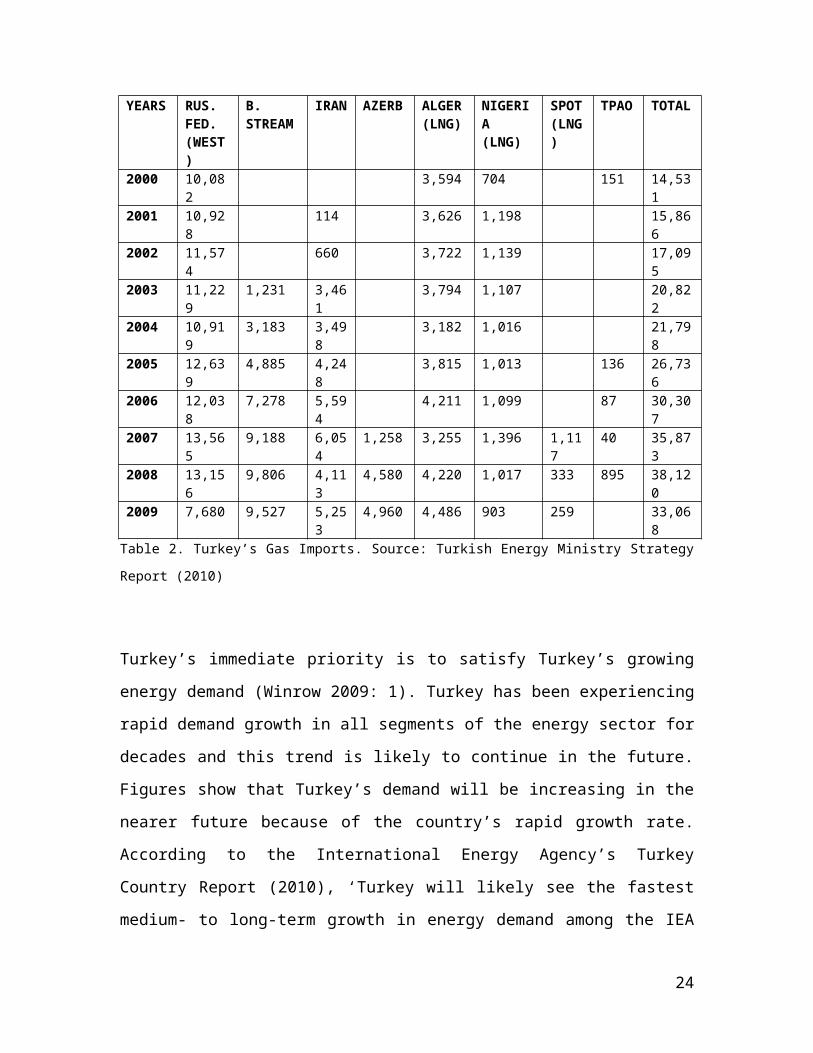

the remaining imports from Algeria and Nigeria (Table 2.)

(Turkish Energy Ministry 2010: 12).

23

YEARS RUS.FED.(WEST)

B.STREAM

IRAN AZERB ALGER(LNG)

NIGERIA(LNG)

SPOT(LNG)

TPAO TOTAL

2000 10,082

3,594 704 151 14,531

2001 10,928

114 3,626 1,198 15,866

2002 11,574

660 3,722 1,139 17,095

2003 11,229

1,231 3,461

3,794 1,107 20,822

2004 10,919

3,183 3,498

3,182 1,016 21,798

2005 12,639

4,885 4,248

3,815 1,013 136 26,736

2006 12,038

7,278 5,594

4,211 1,099 87 30,307

2007 13,565

9,188 6,054

1,258 3,255 1,396 1,117

40 35,873

2008 13,156

9,806 4,113

4,580 4,220 1,017 333 895 38,120

2009 7,680 9,527 5,253

4,960 4,486 903 259 33,068

Table 2. Turkey’s Gas Imports. Source: Turkish Energy Ministry Strategy

Report (2010)

Turkey’s immediate priority is to satisfy Turkey’s growing

energy demand (Winrow 2009: 1). Turkey has been experiencing

rapid demand growth in all segments of the energy sector for

decades and this trend is likely to continue in the future.

Figures show that Turkey’s demand will be increasing in the

nearer future because of the country’s rapid growth rate.

According to the International Energy Agency’s Turkey

Country Report (2010), ‘Turkey will likely see the fastest

medium- to long-term growth in energy demand among the IEA

24

member countries Closely intertwined with economic growth,

energy use in Turkey is expected to roughly double over the

next decade, and electricity demand is likely to increase

even faster’.

According to Turkish Energy Ministry’s (2010) new “Strategic

Plan until 2014”, Turkey’s top priority is diversification

of energy. Turkey will give more attention to its domestic

resources and will seek to develop partnerships with

suppliers. Turkey’s role as a bridge between west and east

seem to provide additional benefits for its energy policy.

In terms of its domestic resources Turkey will seek to

develop hydroelectric, coal, wind, geothermal and solar

power(Turkish Energy and Natural Resources Ministry, 2010:

3). There are also projections that Turkey could be self-

dependent in 2023. Turkish Petroleum Corporation General

Manager Mehmet Uysal noted that estimates that there could

be at least 10 billion barrels of oil reserves beneath the

Black Sea and it would be enough to meet Turkey's needs for

the coming 40 years (Bozkurt, 2009). Uysal has also

announced that Black Sea Oil made them hopeful that Turkey

could gain energy independence for 40 years (Ibid). However,

this confidence may yet be misplaced given that there are no

exploration results for the Black Sea yet.

25

3.2. Turkish Foreign Policy and Energy Security Strategy

Turkey is surrounded by states that have 71.8% of the

world’s gas reserves and 72.7% of the world’s proven oil

reserves.3 The United Nations Economic Commission for Europe

(2006:9) estimated that Turkey may host 6-7%of world oil

transport by 2012. After the Cold War, Turkey concentrated

more on its geographical advantage and tried to strengthen

its position in the region. Energy presented opportunities

and Turkey has been active in building new pipeline

projects. Pipelines would enable Turkey not only to meets

its domestic demand but also empowers its geo-strategic

position by linking producers to suppliers. Moreover,

pipelines could also bring new revenues as transit fees,

refineries, LNG terminals or trading opportunities (Barysch

2007: 2). In addition, constructing pipelines would open new

ways for new contracts for Turkish businessmen. As an

example, 65% of the Nabucco gas pipeline project will be

built within Turkey and that means $4.5 billion investment3 Turkish Energy and Natural Resources Minister Hilmi Guler (2002-2009),Speech delivered at the “Bosphorus Conference”, İstanbul, October 6, 2007, available via www.britishcouncil.org/turkey-society-governance-bosphorus-speeches-hilmiguler.doc - , accessed 12 July 2010

26

for Turkey; new business agreements for construction firms

and new jobs for fifteen thousand people (Erdil 2009).

Turkey aims to be the fourth corridor for Europe after

Russia, Norway and Algeria. Turkey is attempting find

alternative channels to deliver gas to Europe by negotiating

with Iraq, Iran, Kazakhstan, Turkmenistan, Egypt and Syria.

In addition to that Turkey is increasing partnerships with

Russia. Turkey wants to be an energy corridor and also a

crucial energy hub as a trade centre for supplies from the

producer regions (Turkish Energy Ministry 2010: 3). In this

context, ‘Turkey uses its energy policy as an active tool

and this policy is a continuation of its foreign policy’

(Cetinoglu 2010: 106). When AKP won the 2002 general

elections in Turkey, Turkish foreign policy was in a period

of deep Europeanization (Onis and Yilmaz 2009). After 2005,

Turkey’s foreign policy stance deviated from an

Europeanization drive to a kind of “loose Europeanization”

or “soft Euro-Asianism” strategy (Oguzlu 2008). According to

Onis and Yilmaz (2009: 16) during both periods

Europeanization and Euro-Asian elements in Turkish foreign

policy coexisted but there is a swing of the pendulum in the

direction of Euro-Asianism in periods of disappointment and

weakening of relations with the EU. Turkish Foreign Minister

Ahmet Davutoglu who took office in 2008 was the architect of

this foreign policy activism. Before being appointed as

foreign minister, he was the foreign policy adviser of Prime

27

Minister Recep Tayyip Erdogan. Davutoglu perceived foreign

policy as a series of mutually reinforcing and interlocking

processes (Onis & Yilmaz 2009: 9). Davutoglu (2007: 81)

believes’ Turkey’s foreign policy needs a new orientation in

light of the new regional and global developments’.

Davutoglu (2007: 77) says:

‘In terms of its sphere of influence, Turkey is Middle

Eastern, Balkan, Caucasian, Central Asian, Caspian,

Mediterranean, Gulf and Black Sea country all at the

same time. Turkey’s engagements from Africa to Central

Asia and from the European Union to Organization of

Islamic Countries are parts of new foreign policy

vision. The initiatives will make Turkey a global actor

as we approach 2023, the hundredth anniversary of the

establishment of the Turkish Republic.’

Although there is no clear turning point from the European

side, changing governments in the core European countries-

France and Germany, continuing dispute over Cyprus, and the

EU’s internal problems as ratification of a constitution,

changed the mood between both sides. Merkel and Sarkozy

proposed privileged membership to Turkey. In November 2006,

the EU froze talks on 8 chapters with Turkey after Turkey’s

decision not to open Turkish ports to traffic from Republic

28

of Cyprus until the EU eases its embargo on Turkish-

controlled northern Cyprus. As a result the EU Commission

stated that no chapters would be closed until a resolution

is found. After the EU’s decision German Chancellor Merkel

stated ’Turkey could be in deep, deep trouble when it comes

to its aspirations to join the European Union’ (Der Spiegel

2006). Up to mid-2010 there have only opened 13 chapters out

of 33. There has been a strong decline in public support

towards the EU within Turkey. In 2002 public support for the

European Union membership was 74%but dropped to around 50%in

2007. (Yılmaz 2008: 12).

With ascending star of the European Union and the vision of

Davutoglu, Turkey’s relations with the Middle East, Africa,

Caspian Region and Gulf countries gained a new impetus.

While Turkey is seeking stability and security in the

region, the area’s energy-rich nature has brought new

agreements followed by rapprochement with Russia, Iran and

the Middle East.

3.3. Turkish-EU Energy Relations

For the EU, diversifying resources is a priority but without

a “single voice” on energy policy, increasing bilateral

29

relations of EU countries with Russia and Russia’s ambitions

plans on EU energy markets, the EU has not succeeded in

being pro-active in its energy diplomacy. Turkey with its

unique position-surrounded by energy-rich regions- seems to

be a proper address for Europe’s aims. When the EU’s energy

concerns increased, Turkey’s candidacy gained a different

meaning. The European Union’s search for energy security

adds impetus to Turkey’s potential as an energy hub

(Saivetz, 2009: 1). In the 1997 Luxembourg Summit, the EU

rejected Turkey’s candidacy for membership. In contrast, in

1999 Helsinki Summit Turkey got what it wanted: official

candidacy. According to Tekin and Williams (2009: 12) after

1997, in EU’s internal debates Turkey’s geopolitical

advantages have been explicitly cited. In 2004 Helsinki

Summit EU decided to open accession talks with EU by 2005.

In 2004 Swedish Foreign Minister Carl Bildt and Italian

Foreign Minister Massimo D’Alema wrote an article and

emphasised Turkey’s role as a key actor for energy security:

“Given the uncertain state of energy markets, and the stakes

involved, it is our shared interest to incorporate Turkey in

a functioning integrated system” (Bildt and D’Alema, 2004).

The EU’s increased energy considerations gave more

importance to relations with producers. The EU has been more

aware of how relationships between producers and transit

30

countries are important for energy security since Russia-

Ukraine gas dispute in 2006. According to Truscott (2009:

36) there are only two alternatives for delivering gas to

Europe to bypass Russia: Georgia and Turkey. Following the

Russian-Ukrainian energy dispute in 2006, Turkey’s

significance for the EU as a relatively secure and

independent actor became more obvious (Tekin and Walterova,

2007: 87) Former EU Energy Commissioner Andris Piebalgs4

stated that Turkey and the EU both have much to gain from

closer energy co-operation.

The EU’s Green Paper(2006a: 16) stresses Turkey’s importance

as a strategic energy partner and recent documents prepared

by the Commission gave more emphasis on Turkey’s role for

EU’s policy objectives (Tekin and Williams, 2009: 13).

Within the European Commission’s 2004 Progress Report

(European Commission 2004:115), Turkey’s role for

strengthening its position as a transit country and efforts

for the Nabucco project was appreciated and Turkey was

expected to play a pivotal role for the EU. The European

Commission’s 2006 Turkey Progress Report (European

Commission 2006b: 49) and 2007 Turkey Progress Report

4 Joint Press Release, ‘Turkey and the EU: Together for a European Energy Policy’—High Level Conference in Istanbul, 5 June 2007, item 11, available at: http://ec.europa.eu/enlargement/pdf/european_energy_policy/conference_statement_final_en.pdf, accessed 11 July 2010.

31

(European Commission 2007b: 55) also stated Nabucco

project’s priority for EU and Turkey was encouraged to

support the project. The 2008 Progress Report (European

Commission 2008:57) pointed out Turkey-Greece Gas Pipeline’s

continuity. The 2009 Progress Report (European Commission

2009: 67) underlined the Intergovernmental Agreement for

Nabucco in July 2009. The report (Ibid) continues that ‘This

project is an important strategic step towards closer energy

cooperation between the EU, Turkey and other States in the

region as well as towards the diversification of energy

sources. The timely completion of the Southern Gas corridor,

through notably the swift implementation of the Nabucco

Intergovernmental Agreement, remains one of the EU's highest

energy security priorities’.

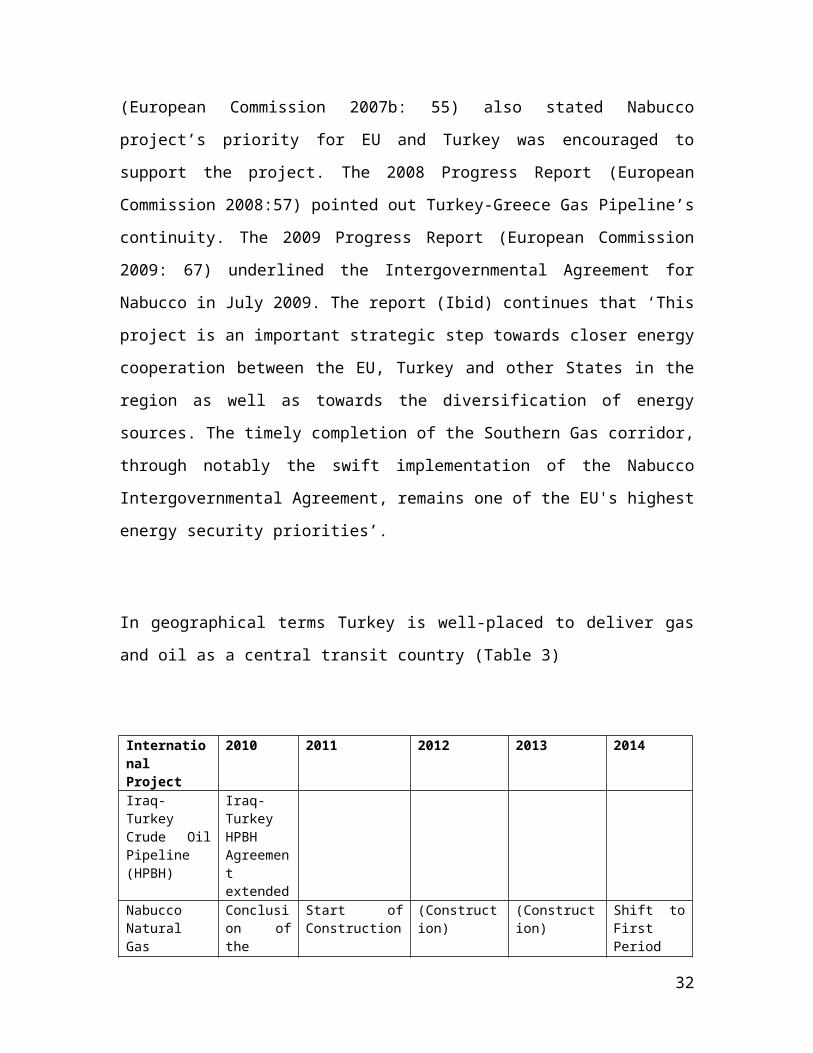

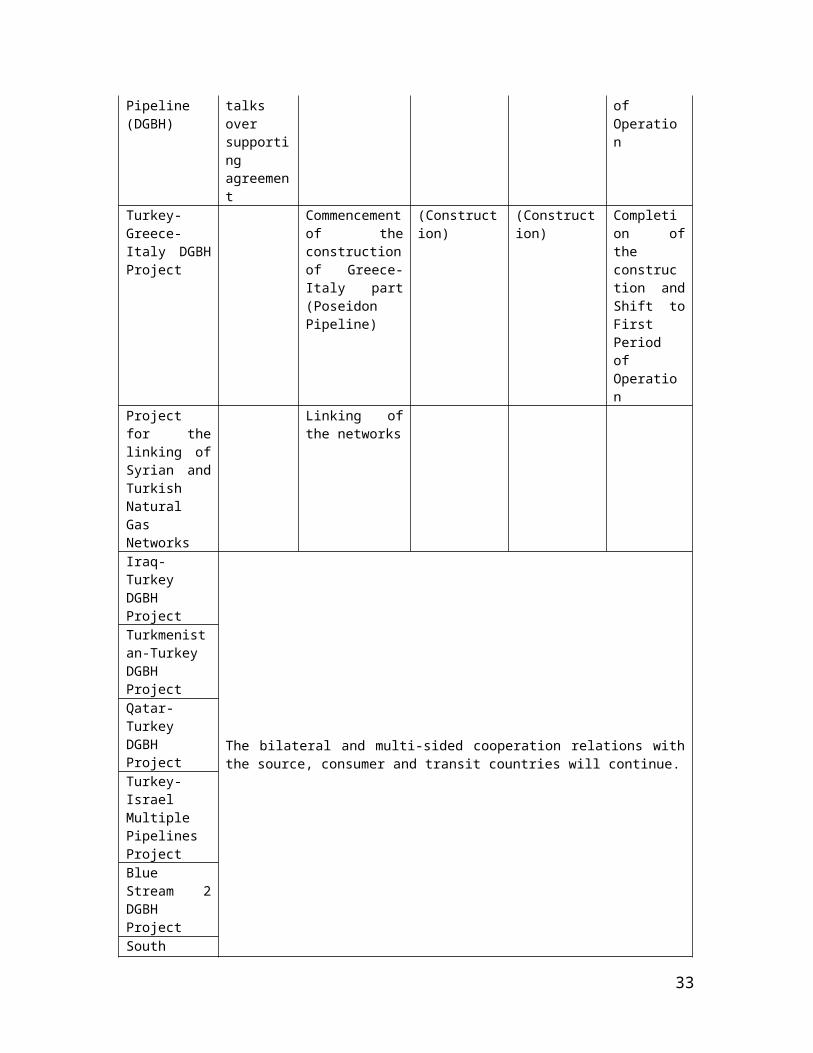

In geographical terms Turkey is well-placed to deliver gas

and oil as a central transit country (Table 3)

InternationalProject

2010 2011 2012 2013 2014

Iraq-TurkeyCrude OilPipeline(HPBH)

Iraq-TurkeyHPBHAgreementextended

NabuccoNaturalGas

Conclusion ofthe

Start ofConstruction

(Construction)

(Construction)

Shift toFirstPeriod

32

Pipeline(DGBH)

talksoversupportingagreement

ofOperation

Turkey-Greece-Italy DGBHProject

Commencementof theconstructionof Greece-Italy part(PoseidonPipeline)

(Construction)

(Construction)

Completion oftheconstruction andShift toFirstPeriodofOperation

Projectfor thelinking ofSyrian andTurkishNaturalGasNetworks

Linking ofthe networks

Iraq-TurkeyDGBHProject

The bilateral and multi-sided cooperation relations withthe source, consumer and transit countries will continue.

Turkmenistan-TurkeyDGBHProjectQatar-TurkeyDGBHProjectTurkey-IsraelMultiplePipelinesProjectBlueStream 2DGBHProjectSouth

33

StreamDGBHProjectSamsun-CeyhanHPBHProjectTable 3. Projects that will transit Turkey Source: Turkish EnergyMinistry

Presently Turkey is the transit country of existing

pipelines as Baku-Tblisi-Ceyhan (BTC); Romania, Bulgaria,

Turkey; Shahdeniz and Turkey-Greece. Turkey is the country

that transfers Caspian oil to Europe via BTC and Caspian Gas

via Turkey-Greece Pipeline. As an exporter of gas and oil to

the EU through its pipelines Turkey wants to empower its

role as a transit country and energy hub. There are some

proposed projects to deliver gas and oil to Europe and

Turkey is in the center of these projects. Nabucco, South

Stream, Samsun-Ceyhan, Turkey-Greece-Italy are the expected

pipelines to transfer gas and oil to Europe.

Nabucco is the one of the biggest projects that will bring

Caspian gas to Europe via Turkey, Bulgaria, Romania, Hungary

and Austria. Nabucco will cost 8 billion euros and is

expected to be operational in 2013. EU Commissioner for

Enlargement Olli Rehn5 has stated that ‘The Nabucco pipeline5 Joint Press Release, ‘Turkey as an energy hub for Europe:prospects andchallenges’ Policy’—High Level Conference in Brussels, 4 March 2009, available at:

34

is a key issue in EU - Turkey energy relations’. Rehn

believes for ‘Nabucco The EU has the market, Turkey has the

geography and only together can they achieve this’

Nabucco is the centre-piece project of European Union. US

backed Baku-Tblisi Ceyhan project succeeded against Russian

opposition and now delivers Caspian oil to Europe. It is

aimed for Nabucco to do the same for gas: alleviate EU’s

concerns regarding Russian gas by providing an alternative

for European energy needs. However as Azeri gas cannot

fulfil the whole pipeline, Kazakh and Turkmen gas are on the

table. Egypt, Iraq, Iran and also Russia explained their

willingness to give gas to Nabucco. The region is not stable

and political constraints may be an obstacle for the

project. Turkey’s involvement in Nabucco negotiations could

strengthen the EU’s aims. Yet, slow progress in EU-Turkey

relations affect strengthening of the partnership between

the two sides. Until the Intergovernmental Agreement was

reached, misunderstandings and conflicting messages were on

the scene between Turkish side and EU officials. According

to Winrow (2009: 2), the problems relating to Turkey’s EU

membership have had a direct effect on discussions regarding

Nabucco. During negotiations for Intergovernmental Agreement

for Nabucco, the Turkish side wanted to reach Nabucco gas

europa.eu/rapid/pressReleasesAction.do?reference=SPEECH/09/89&format=PDF&aged=0&language=EN&guiLanguage=en, accessed 15 July 2010.

35

with lower cost, and offered to buy Nabucco gas with 15%

discount. Furthermore, before the agreement was signed the

EU Commissioner Andris Piebalgs announced that Turkey gave

up its demands (Traynor 2009) Turkish Energy Minister Taner

Yildiz stated ‘all the alternatives were on the table’

(Radikal 2009). Although all these misunderstandings and

frustrations, the Intergovernmental Agreement was signed in

July 2009 in Ankara.

After the EU opened negotiations to Turkey in 2005,

perceptions towards Turkey’s membership started to change.

Leaders in France and Germany have opposed Turkey’s

membership during their election campaigns and suggested a

‘privileged partnership’ to Turkey. Turkey criticized this

as ‘unacceptable’. The EU froze talks on eight chapters in

2006 because of Turkey's refusal to open its ports and

airports to Cypriot vessels and aircraft. The ‘Energy’

chapter has been successfully screened and is ready to open

(Kilic 2010) but cannot be opened as it has been blocked by

the Republic of Cyprus. . During a conference in Brussels in

2009 the EU Commissioner Olli Rehn6 acknowledged that Turkey

was prepared for this chapter then concluded: ‘… for some

6 Joint Press Release, ‘Turkey as an Energy Hub for Europe: Prospects and Challenges’ Policy’—High Level Conference in Brussels, 4 March 2009,available at: europa.eu/rapid/pressReleasesAction.do?reference=SPEECH/09/89&format=PDF&aged=0&language=EN&guiLanguage=en, accessed 15 July 2010

36

time now it has not been possible to establish a consensus

among all EU Member States that would allow us to open the

energy chapter’. In the same conference, Turkish PM Tayyip

Erdogan stated “If we are faced with a situation where the

energy chapter is blocked, we would of course review our

position for Nabucco” (Barber: 2009). There is a general

sense in Ankara that Europeans are demanding without

offering anything in return (Winrow: 2009, 23).

3.4. Turkish Russian Energy Relations

Turkey’s growing economy, new foreign policy vision,

Russia’s interest for full-control of energy routes and

Turkey’s loosening relations with the EU created new

opportunities for Russian-Turkish relations. Russian Energy

Minister Sergey Shimatko has stated that he believes that

relations are showing great improvement (Karabulut 2010).

After the collapse of communism, the emergence of the

Russian Federation gave an opportunity for Turkey and Russia

to normalize their relationship. On 16 November 2001 both

sides signed ‘The Action Plan of Cooperation Between Turkey

and the Russian Federation in Eurasia’ that opened a new

page for the relations. Furthermore two leaders Vladimir

Putin and Erdogan has met ten times in five years (Meister

2010: 23). On June 28-29, 2006, Sezer became the first

37

Turkish President to visit Russia7. Two countries are

increasing partnerships on the energy sector. When Putin

visited Turkey in August 2009 after Turkey hosted Nabucco’s

Intergovernmental Agreement ceremony, Russia’s priority was

South Stream. Putin asked Turkey to let Russia use Turkey’s

territorial water for construction of Nabucco’s rival South

Stream. In return, Russia would give oil to Turkey’s Samsun-

Ceyhan project which is planned to be an alternative to

Russian oil. When Turkey announced the Samsun-Ceyhan oil

pipeline project, Russia announced a counter project Burgaz-

Alexandropoulis which would bypass Samsun-Ceyhan and deliver

oil to Europe. Turkey accepted Russia’s offer for South

Stream and Samsun-Ceyhan.

Aside from pipelines Russian companies are increasing their

shares in the Turkish market. Gazprom has announced

partnership with Turkish Calik Group to build a refinery in

Ceyhan where Turkey is planning to create an energy hub.

Gazprom also signed an agreement with Turkish Aksa Group to

expand in power plants in Turkish market. In addition Lukoil

entered the Turkish market and has bought companies in the

downstream area. Moreover, Russia will construct the first

nuclear energy power plan of Turkey.

7 News Release, ‘President Sezer Visit to Russia’ Turkish Embassy, Moscow, 29 June 2006.

38

Not only energy but also in other areas cooperation is

increasing. Russia has become Turkey’s biggest trade partner

in 2007 by overtaking Germany’s leadership (Babali 2009:

26). Turkish companies’ investments are exceeding $2 billion

in Russia, especially Turkish construction firms are very

powerful in Russia. In 1990, Turkish-Soviet trade was $1.7

billion, it exceeded $35 billion in 2008 and it is aimed to

reach $100 billion within five years.

4. DISCUSSION

For the EU-Russia-Turkey relationship the issue of energy

policy is of vital importance. The EU is the world’s third

largest customer, Russia is a major energy producer in the

world. Turkey which sits in the middle of these two actors,

is a country that is both heavily dependent on Russian

energy and also places the ‘EU as a top priority’ (Khalaf

&Gardner 2010).

As it is shown in previous chapters every actor has

converging and diverging interests in this triangle. One

common thing for the three actors is diversification of

supply. The EU is looking for alternatives to Russian

imports; Turkey is increasing its relations with energy rich

countries while aiming to decrease Russian imports from

39

70%to 40% (Turkish Energy and Natural Resources Ministry

2010: 3) and Russia is aiming to expand in Western markets

while considering Asian market opportunities more than

before (Russian Energy Ministry 2009: 25). ‘Diversification’

therefore is a common aim of all of the actors of the EU-

Russia-Turkey relationship.

Russia wants to augment its power and use energy as a tool

to implement its foreign policy objectives. After the Cold

War, pipelines have become Russia’s new missile to use or

threaten over countries. Russia has quickly been with its

‘project package’ or ‘agreement files’ where the European

Union aims or policies are weak and has no influence. Russia

is signing bilateral agreements with energy giants, buying

assets to hold international markets in its hand and

planning projects that eliminate transit countries which can

create problems (Lucas 2008: 211, Mozorov 2008: 54).

Although the EU wants to implement policies to diversify its

resources, the difficulties of creating a a common energy

policy has given Russia room to maneuvre.

‘Ensuring reliable and affordable supply will be a

formidable challenge’ (International Energy Agency 2007).

Given this reality, both energy companies which want to make

more profit but also governments accept Russia’s proposals.

Energy demand is increasing and resources are limited. To

guarantee themselves, governments sign any agreement that

40

proposes energy for their domestic needs. The EU is trying

to create a single voice in its energy policy but it has

been difficult to synchronise different national energy

interests. Still, a key policy goal remains finding

alternatives to Russian gas. EU policy documents (see

European Commission 2000 and 2006) indicate efforts to forge

new relationships with energy rich regions and special

importance is given to the EU candidacy of Turkey for the

pursuit of EU energy security. As has been discussed in

previous sections, the EU’s geopolitical considerations,

including energy, have played an important role for the

decisions over Turkey’s EU membership.

Turkey as a country between main energy suppliers and

producers, wants to use its geographical advantage to be

more powerful in its neighbourhood. There are not many

alternatives to bring gas to Europe to deliver energy

supplies securely especially for gas. Delivering gas is more

difficult compared to oil. Oil can be imported from anywhere

in the world by tankers (Lucas 2008: 212). It can be traded

in the spot market and is therefore more flexible to reach

(Pomfret 2009: 3). Transporting gas requires pipelines. As a

result, the political relations between suppliers and

consumers and also relations with transit countries become

important (Shaffer 2009: 130). In this context, Turkey wants

to be a powerful actor for energy interest of the regions

around its neighbourhood. Turkey is committed to become the

41

forth artery of Europe. On the other hand Turkey is a

heavily energy dependent country and 65%of its energy

imports come from Russia. In the EU-Turkey-Russia triangle,

Turkey shapes its policy objectives according to its

national interests, national interests draw its foreign

policy and energy policy uses principles of its foreign

policy.

Between 2002 and 2005, Turkey was in a period of ‘deep

Europeanisation’ (Onis and Yilmaz: 2009: 10). EU dynamism

shaped each policy structuring in Turkey. Implementations of

reforms and encouragement of Turkey’s membership reflected

Turkey’s energy relations with the EU. Turkey has been a

supporter of the EU’s diversification projects. Turkey

planned additional projects like the Samsun-Ceyhan oil

pipeline that would bring Caspian oil both for the EU’s and

Turkey’s interests. Turkey started to export Caspian oil

with US-backed Baku-Tblisi-Ceyhan project to the EU from the

Ceyhan hub in 2005. On the other hand, any project that

Turkey supported for the EU’s diversification of supply was

followed by the support of conflicting projects by from

Russia. Russia announced Nabucco’s rival South Stream after

it gained momentum in the EU. When Turkey announced Samsun-

Ceyhan project, Russia replied with Burgas Alexandropolis

that would bypass Turkish one. During these developments,

Turkey has always underlined the necessity for EU’s

diversification of supply. Although its dependence to

42

Russian energy resources, positioned itself closer to the

European angle in this relationship. Furthermore, Turkey,

which is Gazprom’s second largest customer, was

strengthening its hand. In addition, when Turkish-EU

relations were living its spring in the beginning of 2000s,

there was less concerns on Russian reliability.

When the dynamism between Turkish-EU relations slowed down

because of the interrelated developments that is shown in

the third section, Russia’s reliability was questioned after

the 2006 Ukranian gas dispute and Turkey came with a new

foreign policy vision with Ahmet Davutoglu’s ministry,

Turkey’s national interests and naturally energy policy was

rewritten. Davutoglu came with a vision claiming a

leadership role for the Turkey in the region. According to

Davutoglu (2007: 77) Turkey is ‘Eastern in the East, Western

in the West’. Accession to the EU is still Turkey’s most

important goal (Matthews 2010, Khalaf and Gardner 2010) but

Turkey is also concentrating on more increasing partnerships

in its neighbourhood. It is surrounded by energy-rich

regions so when a partnership is considered, energy has

become top on the agenda. Turkey wants to improve its

relations with Russia, Iran, Iraq, Caspian region and the

Gulf countries. As a rapidly growing economy, increasing

partnerships with energy suppliers are crucial for Turkey

43

and Turkey’s new agreements in the region are beneficial for

both Europe and Russia. When Turkey signed a memorandum of

understanding with Iran in 2007 for energy cooperation while

the UN Security Council was seeking sanctions on Iran,

Davutoglu defended Turkey’s position by arguing that

‘Turkey needs Iranian energy as a natural extension of its

natural interests. Therefore, Turkey’s energy agreements

with Iran can not be dependent upon its relations with other

countries’ (Davutoglu 2007: 91). Moreover, Turkey’s

improving relations with Iran increased the possibility of

Iranian gas supplies for the Nabucco which is lacking enough

gas to fulfill the project (Kreyanbuhl 2007). Although

Nabucco’s Intergovernmental Agreement was delayed because of

the misunderstandings between EU and Turkey due to

downgraded relations (Winrow 2009: 15) Turkey is still

attempting to achieve agreements to bring gas from the

Middle East and the Caspian Region. Turkey’s gas deal with

Azerbaijan in June 2007 also includes Nabucco (Euractiv

2010).

Increasing relations between Russia and Turkey are also an

example the changing environment after 2005. Russian Prime

Minister Vladimir Putin and Turkish Prime Minister Erdogan

have encouraged the deepening of bilateral relations (Babali

2009: 26). Russia found more room for manoeuvre when

44

Turkish-EU process slowed down. Russia’s interests overlap

with Turkey’s new foreign policy vision. In August 2009,

Putin visited Turkey and Turkey allowed Russia to use its

exclusive water in the Black Sea for Nabucco’s potential

rival South Stream. Russia has also guaranteed Turkey can

fulfill the Samsun-Ceyhan pipeline that will allow the

bypassing of Russia. In 2010, during the Russian President

Medvedev’s visit to Turkey, both sides signed new agreements

and Medvedev stated how relations between two sides gained a

strategic dimension. While Turkey is making more agreements

with Russia, looking for new ways for its security of

supply, the Turkish Energy Ministry wants to also make

greater use of Turkey’s own natural resources while

decreasing dependency to Russia from 70% to 40% in 2014

(Turkish Energy Ministry 2010: 15).

In this picture, Turkey is trying to use its geopolitical

position as an asset for its national interest regarding

energy policy. With Davutoglu’s new foreign policy vision

and the changing dynamics of Turkey-EU relations, Turkey is

likely to increase its relations within its neighbourhood to

maximise its national interest. Turkish energy policy takes

its principals from Turkish foreign policy. In this regard

it seems it is not easy for Turkey to act directly according

to EU’s security of supply considerations. Turkey continues

to support the EU’s energy aims while improving relations in

the region to secure its own security of supply. During the

45

times when Turkey-EU relations were at its peak, Turkey

seemed to be more supportive of EU interests. Yet, changing

balances in the EU-Russia-Turkey triangle have shifted

Turkey closer to Russia. Before any improvement in EU-Turkey

relations, it is not easy for Turkey to position itself

closer to the EU side of the triangle.

5.CONCLUSION

Energy security has been a priority for net energy

importing countries especially in the aftermath of the

Russian-Ukrainian gas dispute in 2006. This resulted in the

EU revising its energy policy to place diversification of

supplies as a main pillar of its strategy. As the EU’s

biggest energy supplier Russia is keen not to lose its best

customer and is working towards full-control over the

European pipeline network at the same time as the EU is

searching for alternative sources. Turkey, as a bridge

between west and east, plays a vital role in terms of these

divergent interests.

Energy policy has always been among the top issues within

Turkey’s political and economic agenda and accordingly it

has been important consideration in its foreign policy in

general and its bilateral relations with Russia, EU, Middle

46

East countries in particular. Especially in the last decade

Turkey’s political and economic agenda have thoroughly

undergone a structural transformation because of the

accelerated accession process with the EU on the one hand,

and the new paradigm called “The Davutoglu Strategic Depth

Doctrine” which dictates an active engagement with all of

the surrounding regions of Turkey on the other hand.

Turkey’s energy policy also has been influenced by this twin

transformation, though with varying degrees in certain

periods.

Energy is not only an asset with economic value but it is a

vital component of security for states in our age. This

functional significance of energy render it a sine qua non

factor in the designation of states’ domestic and foreign

policies. Thus, Turkey, as a country which is at the

intersection point of world’s major energy producers and

major energy consumer markets, has to take into account the

energy card in order to maximise its national interests.

Being aware of both its strategic position on energy transit

routes as well as its own energy needs, Turkey is attempting

to design its energy policy in a way that augments its

position as a regional power but its policy options are at

the same time constrained by its relations with the EU and

Russia. As explained above, these three actors are very much

47

interrelated in terms of their energy policies and therefore

have to consider each other’s position while shaping their

policies. The EU which is the third major energy consumer in

the world is attempting to secure its energy supply and

diversify its energy sources while Russia, on the other

hand, is aware of its power stemming from its huge energy

resources and thus is strengthening its position within the

international energy market through controlling pipelines as

well as European downstream market which holds the biggest

share in the destination of Russia’s exports.

Within such a context, Turkey has been wisely trying to

design its energy strategies considering the concerns and

strategies of these two important actors. Although Turkey

has been striving for immediate and full accession with the

EU, it cannot design its energy policies through fully

aligning itself with the EU, as is the case in many other

sectors such as trade policy. Since membership still appears

a distant and uncertain prospect, it has to pursue its own

national security interests while dealing with energy

issues. On the other hand, given the EU’s inability to

establish a real single voice on energy issues, there is no

coherent policy for Turkey align with. Besides, Turkey with

its new foreign policy doctrine struggles to be an important

regional actor besides its strong ambition to be a EU

48

member. Some analysts have interpreted this is as a move

towards Euro-Asianism from Europeanism which means a shift

in Turkey’s foreign policy orientation, though this argument

has been strictly rejected by Turkish policy makers. As

explained above, Turkey does not disregard the European

factor while making its energy policy, indeed it wisely uses

its energy potential in order to increase its attractiveness

to the EU, such as the Nabucco project. However, it has to

build strong relations with major energy producers like

Russia, even when this clashes with the expectations of the

EU from Turkey. Therefore, Turkey is trying to balance its

bilateral relations with its EU membership bid. As seen

above, while Turkey’s relations with EU develop smoothly and

closely, Turkey moves more towards the European side in the

energy policies. However, when Turkey is somehow sidelined

by the EU, it considers its pure national interests and can

approach to other actors, which is very understandable from

a realist perspective.

49

BIBLIOGRAPHY

Aalto P. (2008) 'The EU-Russia Energy Dialogue and theFuture of European Integration: From Economic to Politico-Normative Narratives' in P. Aalto (ed.) The EU-Russian EnergyDialogue: Europe’s Future Energy Security, Ashgate: Hampshire.

Aalto P. and Westphal K. (2008) 'Introduction' in P. Aalto(ed.) The EU-Russian Energy Dialogue: Europe’s Future EnergySecurity, Ashgate: Hampshire.

Babali, T. (2009) 'Turkey at the Energy Crossroads', MiddleEast Quarterly, 16 (2), pp. 25-33

50

Bahgat, G. (2010) ‘Iran’s Role in Europe’s Energy Security:An Assessment’ Iranian Studies, 43: 3, p.333 – 347

Balzer (2005) 'The Putin Thesis and Russian Energy Policy',Post-Soviet Affairs, 21 (3), pp. 210-225.

Baran, Z. (2008) Security Aspects of the South Stream Project,Brussels: European Parliament

Barber, T. (2009) ‘Turkey Links Pipeline to EU MembershipTalks’ Financial Times, January 19.

Barysch, K. (2007) Turkey’s role in European energy security, London:Center for European Reform.

Beaudreau, B. C. (1999) Energy and the Rise and Fall of PoliticalEconomy, Wesport: Greenwood Press.

Bildt, C. and D’Alema, M. (2004) ‘It is Time For a FreshEffort’, International Herald Tribune, August 31.

Bilgin, M. (2007) 'New prospects in the political economy ofinner-Caspian hydrocarbons and Western energy corridorthrough Turkey', Energy Policy, Volume 35, pp.6383-6394.

Bozkurt, H. (2009) Black Sea Oil to Meet Turkey’s Needs for40 Years, Today's Zaman, 4 March 2009,http://www.todayszaman.com/tz-web/detaylar.do?load=detay&link=168584 (accessed 20 August 2010)

51

BP (2009), BP Statistical Review, June 2009.

Buckley, N. (2008), ‘Gazprom Signs Fuel Supply Deal withLibya’ Financial Times, April 17.

Cetinoglu, N. (2010) ‘In The Search of Lost Time: Turkey andIts Current Energy Politics', Turkish Policy Quarterly, 8 (4), pp.105-114.

Crooks, E. (2008), ‘Gazprom chief sets out vision as biggestpower in world energy’, Financial Times, 27 June 2008.

Chevalier, J. M. (2009) The New Energy Crisis: Climate, Economics andGeopolitics, New York: Palgrave Macmillan.

Closson, S. (2009) 'Russia's key customer: Europe' in J.Perovic, R. W. Orttung, A. Wenger (eds.) Russian Energy Powerand Foreign Relations, New York: Routledge, ch. 5, pp. 89-108

Davutoğlu, A. (2007) 'Turkey's Foreign Policy Vision: AnAssessment of 2007', Insight Turkey, (10) 1, pp. 77-96

Der Spiegel (2006) 'Merkel Worried about Turkey SituationIs “Very, Very Serious”', Der Spiegel Online, 11 June 2006,http://www.spiegel.de/international/0,1518,446747,00.html(accessed 20 August 2010)

Ebel, R. E. (2009) The Geopolitics of Russian Energy: Looking Back,Looking Forward, A Report of the CSIS Energy and National Security Program,Washington: Center for Strategic and International Studies.

52

Econews, (2007) ‘EU and Nabucco’ 18 September.

Ehrstedt, S. and Vahtra, P. (2008) Russia Energy Investments inEurope, Electronic Publications of Pan-European Institute4/2008,http://www.tse.fi/FI/yksikot/erillislaitokset/pei/Documents/Julkaisut/Ehrstedt_Vahtra_42008.pdf (accessed 20 August2010)

Erdil, M. (2009) 'Nabucco’da İmzalar Atılıyor, Türkiye 300Milyar Doların Köprüsü Oluyor' ('Turkey bridges 300 billiondollars with the signing of Nabucco'), Hürriyet, 13 July2009, http://www.hurriyet.com.tr/ekonomi/12057240.asp(accessed 20 August 2010)

Euractiv (2010) 'Turkey brokers key gas supply deals forNabucco', Euractiv Website, 8 June 2010,http://www.euractiv.com/en/energy/turkey-brokers-key-gas-supply-deals-nabucco-news-494988 (accessed 21 June 2010)

European Commission (2009) Turkey 2009 Progress Report,Brussels, 14 October 2006, SEC (2006) 1334.

European Commission (2008) Turkey 2008 Progress Report,Brussels, 5 November 2006, SEC (2006) 2699.

European Commission (2007a) Russian Federation: Country StrategyPaper 2007-2012, Brussels: European Commission,http://ec.europa.eu/external_relations/russia/docs/2007-2013_en.pdf (accessed 20 August 2010)

53

European Commission (2007b) Turkey 2007 Progress Report,Brussels, 6 November 2006, SEC (2007) 1436.

European Commission (2006a) ‘Green Paper: A EuropeanStrategy for Sustainable, Competitive and Secure Energy’,available at: http://ec.europa.eu/energy/green-paper-energy/doc/2006_03_08_gp_document_en.pdf, accessed 11November 2008.

European Commission (2006b) Turkey 2006 Progress Report,Brussels, 8 November 2006, SEC (2006) 1390.

European Commission (2005) Turkey 2005 Progress Report,Brussels, 9 November 2005, SEC (2005) 1201.

European Commission (2004) 2004 Regular Report on Turkey’sprogress towards accession, Brussels, 6 October 2004, SEC(2004) 1426.

International Energy Agency (2007) World Energy Outlook,International Energy Agency: Paris

Jong, J. and Van der Linde, C. (2008) ‘Energy Policy in aSupply Constrained World’, European Policy Analysis, Issue 11(October), pp.1-9

Kalicki, J. H. (2007) 'Rx For “Oil Addiction”: The MiddleEast And Energy Security', Middle East Policy, 14 (1), pp. 76-83.

54

Kalicki, J. H. (2005) Energy and security: toward a new foreign policystrategy, Washington, DC: Woodrow Wilson Center Press.

Karabulut, A. (2010) ‘Rusya Enerji Bakanı: Türkiye ileilişkilerimizde bahar havası yaşanıyor’ (Russian EnergyMinister: It is being lived spring time for Turkish-RussianRelations), Zaman, May 10, available at:http://www.zaman.com.tr/haber.do?haberno=983077&title=rusya-enerji-bakani-turkiye-ile-iliskilerimizde-bahar-havasi-yasaniyor

Kepperpütz, R. (2009) ‘EU-Russian Gas Relations-PipelinePolitics: Mutual Dependency and the Question ofDiversification’ in K. Liuhto (ed.) The EU-Russia gas connection:Pipes, politics and problems, Electronic Publications of Pan-European Institute 8/2009, pp. 92-108,http://www.tse.fi/FI/yksikot/erillislaitokset/pei/Documents/Julkaisut/Liuhto%200809%20web.pdf (accessed 20 August 2010)

Khalaf, R. and Gardner, D. (2010) 'Turkey says EUmembership is top priority', Financial Times, 8 July 2010.

Kilic, A. (2010) ‘Energy Minister Yildiz: We are ready toopen the energy chapter, but the EU is not’ Today’s Zaman,10 August available at: http://www.todayszaman.com/tz-web/news-218627-energy-minister-yildiz-we-are-ready-to-open-the-energy-chapter-but-the-eu-is-not.html

Kohen, A. (2008) ‘Russia: The Flawed Energy Superpower’ inin G. Luft and A. Korin (eds.) Energy Security Challenges for the 21st

Century, Santa Barbara, CA: Prager Security International.

55

Luft, G. and Korin, A. (2009) (eds.) Energy security challenges forthe 21st century: a reference handbook, Santa Barbara, CA: PraegerSecurity International.

Kreyenbühl, T. (2007) 'Iran-Turkey Gas Deal Gives New Hopefor EU Nabucco Pipeline', World Politics Review, 9 October2007, http://www.worldpoliticsreview.com/articles/1220/iran-turkey-gas-deal-gives-new-hope-for-eu-nabucco-pipeline(accessed 20 August 2010)

Kuchinsky, R. (2009) ‘LNG-Russia’s New Energy BlackmailTool’, The Jamestown Foundation Eurasia Daily Monitor, 22 April 2009,http://www.jamestown.org/single/?no_cache=1&tx_ttnews[tt_news]=34888 (accessed 20 August2010)

Turkish Energy and Natural Resources Ministry (2010) StrategicPlan for 2010-2014, Ankara.

Luft, G. and Korin, A. (2009) (eds.) Energy security challenges forthe 21st century:

a reference handbook, Santa Barbara, CA: Praeger SecurityInternational.

Lucas, E. (2008) The New Cold War: How the Kremlin Menaces both Russiaand the Wales, London: Bloomsbury.

56

Mangott, G. and Hamilton, D. (2008) (eds.), The Wider Black SeaRegion in the 21st Century: Strategic, Economic and Energy PerspectivesWashington, D.C.: Center for Transatlantic Relations

Mankoff, J. (2009) Eurasian Energy Security, New York: Council onForeign Relations

Matlary, J. H. (1997) Energy Policy in the European Union, New York:St. Martin’s Press.

Matthews, O. (2010) ‘Ankara in the Middle’, Newsweek, 2August 2010, http://www.newsweek.com/2010/07/26/ankara-in-the-middle.html (accessed 20 August 2010)

Mazarov, V. (2008) ‘Energy Dialogue and the Future ofRussia: Politics and Economics in the Struggle for Europe’,in P. Aalto (ed.) The EU-Russian Energy Dialogue: Europe’s Future EnergySecurity, Ashgate: Hampshire.

Meister, S. (2010) ‘The EU, Russia and Turkey- Prospects ofan Energy Triangle?’, in Lanke, K. and Vietor, M. (eds)‘Prospects of a Triangular Relationship? Energy RelationsBetween the EU, Russia and Turkey’ , Friedrich EbertStiftung International Policy Analysis, April.

Mitrova, T. (2010) ‘New Aproaches in Russian Energy Policy-East and West’ in Lanke, K. and Vietor, M. (eds) ‘Prospectsof a Triangular Relationship? Energy Relations Between theEU, Russia and Turkey’ , Friedrich Ebert Stiftung InternationalPolicy Analysis, April.

57

Monaghan, A. and Jankovski, L. (2006) ‘Europe-Russia EnergyRelations: The need for active engagement’, EPC Issue Paper 45,Brussels: European Policy Center.

Murinson, A. (2010) Turkey’s Entente with Israel and Azerbaijan, Oxon:Routledge.

Natorski, N. and Surralles, A. H. (2008) ‘Securitizing Movesto Nowhere? The Framing of the European Union’s EnergyPolicy’, Journal of Contemporary European Research, 4 (2), pp.71-89.

Oğuzlu, T. (2008) 'Middle Easternization of Turkey’s ForeignPolicy: Does Turkey Dissociate from the West?', TurkishStudies, 9 (1), pp. 3-20.

Orban, A. (2008) Power, Energy, And The New Russian Imperialism,Westport: Praeger Security International.

Öniş, Z. and Yilmaz, Ş. (2009) 'Between Europeanization andEuro-Asianism: Foreign Policy Activism in Turkey during theAKP era', Turkish Studies, 10 (1), pp. 7-24.

Pamir, N. (2009) ‘Turkey as an Energy Corridor’’ in Luft,G. and Korin, A. (2009) (eds.)

Energy security challenges for the 21st century: a reference

handbook, Santa Barbara, CA: Praeger Security International.

Perimani, H. (2001) The Caspian Pipeline Dilemma: Political Games andEconomic Losses, Westport: Praeger.

58

Perovic, J., Orttung, R. W. and Wenger, A. (2009) (eds.)Energy and the Transformation of International Relations: Towards a NewProducer-Consumer Framework, Oxford: Oxford University Press.

Pomfret, R. (2010), ‘Energy Security in the EU and Beyond’,CASE Network Studies and Analyses, No. 400/2010, http://www.case-research.eu/upload/publikacja_plik/28060953_CNSA_400.pdf(accessed 01 August 2010)

Radikal (2009), ‘AB Turkiye Nabucco’da yuzde 15’ten vazgectidiyor. Ankara Kabul etmiyor’ (EU says Turkey has given up on15% from Nabucco), May 13, p.7.

Roberts, J. (2009) ‘Energy Challenges for Europe’ inPerovic, J., Orttung, R. W. and Wenger, A. (eds.) Energy andthe Transformation of International Relations: Towards a New Producer-Consumer Framework, Oxford: Oxford University Press.

Saivetz, C. (2009) ‘Tangled Pipelines: Turkey’s Role inEnergy Export Plans’ Turkish Studies, 10: 1, p. 95- 108

Shaffer, B. (2009) Energy Politics, Philadelphia: University ofPennsylvania Press.

Sleivyte, J. (2010) Russia's European Agenda and the Baltic States, NewYork: Routledge.

59

Smith, K. C. (2008) Russia and European Energy Security: Divide andDominate, Washington: Center for Strategic and InternationalStudies.

Socor, V. (2010) ‘EU Supports Nabucco Against South Stream’,The Jamestown Foundation Eurasia Daily Monitor, 3 August 2010,http://www.jamestown.org/programs/edm/single/?tx_ttnews[tt_news]=36706&cHash=9b57650d47 (accessed 20August 2010)

Stuermer, M. (2008) Putin and the Rise of Russia, London:Weidenfeld & Nicholson.

Tassinari, F. (2009) Why Europe Fears its Neighbors, California:ABC-CLIO.

Trainer, I. (2009) ‘Europe's plan for alternative pipelinefaces big problems, Guardian, July 7.

Truscott, P. (2009) European Energy Security, Whitehall Papers:Abingdon

Tekin, A. and Williams, P. (2009) ‘EU-Russian Relations andTurkey’s Role as an Energy Corridor’, Europe-Asia Studies, 61:2,p. 337-356

Tekin A. and Williams, P. (2009) ‘ European External EnergyPolicy and Turkey’s Accession Process’, Center for EuropeanStudies Working Paper Series: 17

60

Tekin, A. and Walterova, I. (2007) ‘Turkey’s GeopoliticalRole: The Energy Angle’, Middle East Policy, 14 (1)

Undersecretariat of State Planning Organization (2009)Medium Term Programme 2010-2012,www.dpt.gov.tr/.../Medium_Term_Programme_(2010-2012).pdf(accessed 20 August 2010)

Vahtra, P. (2009) ‘Energy security in Europe in theaftermath of 2009 Russia-Ukraine gas crisis’, in K. Liuhto(ed.) The EU-Russia gas connection: Pipes, politics and problems,Electronic Publications of Pan-European Institute 8/2009,pp. 92-108,http://www.tse.fi/FI/yksikot/erillislaitokset/pei/Documents/Julkaisut/Liuhto%200809%20web.pdf (accessed 20 August 2010)

Westphal, K. (2008) 'Germany and the EU-Russia EnergyDialogue' in P. Aalto P. (ed.) The EU-Russian Energy Dialogue:Europe’s Future Energy Security, Hampshire: Ashgate.

Winrow, G. (2009), ‘Turkey, Russia and the Caucasus: Commonand Diverging Interests’, Chatham House Briefing Paper, November2009.

Yilmaz, H. (2008) 'Euroskepticism in Turkey: Parties, Elitesand Public Opinion, 1995-2006', South European Society andPolitics, 13 (4)

Yinanc, B. (2010) ‘South Stream to be Completed by 2015,says Gazprom CEO’, Hurriyet Daily News, 11 June 2010.

Youngs, R. (2009) Energy Security: Europe’s New Foreign Policy Challenge,New York: Routledge.

61

62