DIRECTI NS 2015 - Australian Institute of Company Directors

36

Current issues and challenges facing Australian directors and boards DIRECTI NS 2015 supported by

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of DIRECTI NS 2015 - Australian Institute of Company Directors

Current issues and challenges facing Australian directors and boards

DIRECTI NS2015

supported by

2

King & Wood Mallesons / Directions 2015

Facts & Figures from our Survey

The uncertain road aheadAustralia’s business environment is currently subject to a range of countervailing economic forces including low interest rates, lower fuel prices, a lower Australian dollar, a soft labour market, rising house prices and weak business and consumer confidence. These conditions have been exacerbated by ongoing political instability at both the Federal and State Government levels, and perceived “sovereign risk” arising from uncertainties regarding the prospects for future government asset sales and proposed infrastructure projects. Furthermore, the Coalition Federal Government is still facing roadblocks in the implementation of key aspects of its 2014 Federal Budget, even as it heads into the Federal Budget cycle for 2015. The combination of these factors is contributing to a general unease and, at best, muted optimism among Australian directors and boards.

40.6% 41.4% 92.2%said independence restricts optimal board composition

had engagement with people they consider to be activists

said ‘repeal days’ have had minimal to no impact

AICD is proud to support the King & Wood Mallesons 2015 Directions report. As the voice of directors and the leader in corporate governance in Australia, the AICD has a clear interest in the insights the report offers on the issues and challenges facing the director community. We look forward to discussing the issues emerging from the 2015 Directions report with our members and to our continuing collaboration

with King & Wood Mallesons.

John Brogden Managing Director and Chief Executive Officer Australian Institute of Company Directors (AICD)

1 2015 Intergenerational Report: Australia in 2055, March 2015 2 http://www.smh.com.au/federal-politics/political-news/the-man-who-could-be-prime-minister-christian-porter-must-first-cut-through-red-tape-20150317-1m19w6.html

3

King & Wood Mallesons / Directions 2015

In light of these challenges, directors and boards need to continually assess whether they have (or have access to) the skills and experience necessary to navigate current uncertain times and take advantage of the opportunities for growth, including in the rapidly developing areas of technology and social media.

“Technology is changing the way we interact with each other and how we live our lives. It is changing the face of business, markets, governments and social engagement”.1

Directors and boards also continue to face significant regulatory and compliance burdens. Although directors expressed high hopes for the red tape reform agenda of the Federal Coalition Government, they have not seen tangible benefits from the ‘repeal

> 50% > 50% 72.2%want ‘big ticket’ reform of IR and tax laws

said IR laws and OH&S are top regulatory challenges for 2015

have not taken any steps to prepare for incoming FTAs

day’ legislation introduced to date seeking to abolish unnecessary regulation. The repeal of the carbon tax and the mining tax appears to have been largely forgotten, and directors continue to raise concerns about the lack of a considered policy debate and big ticket reform in areas such as tax regulation and industrial relations.

“The cuts to red tape are a “deregulatory diet” for the Australian economy”.2

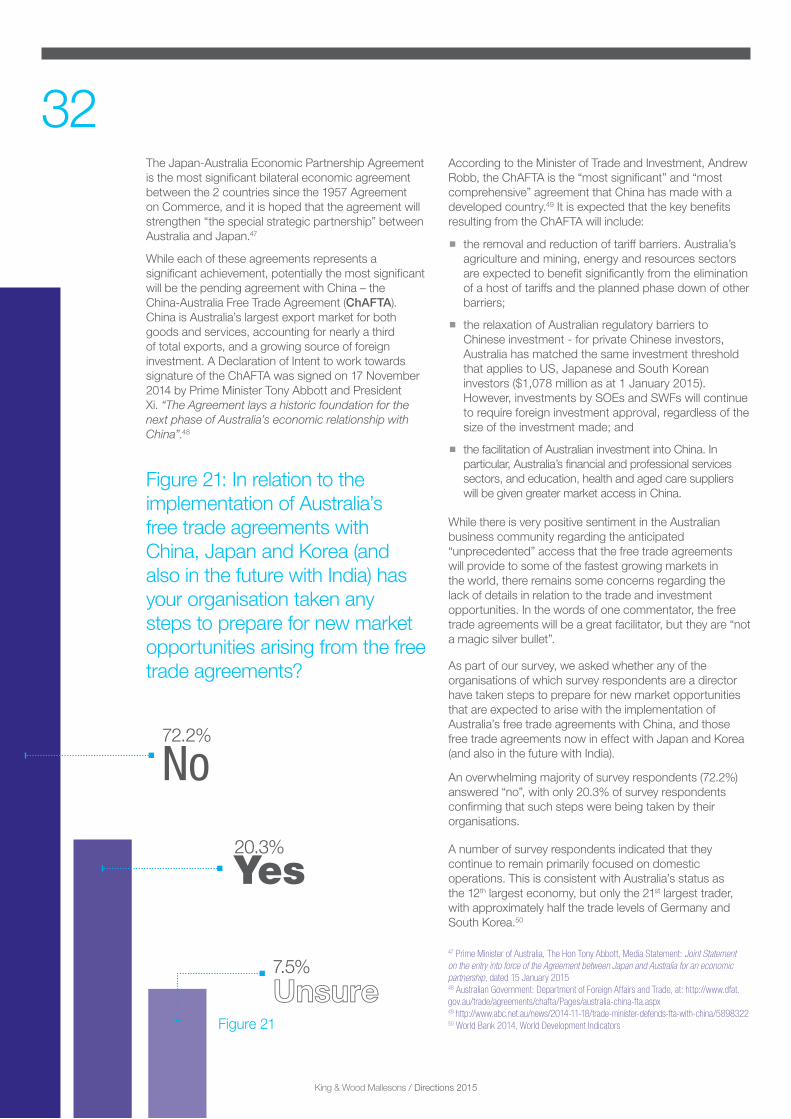

On a more positive note, Australia’s recently announced free trade agreements with China, Japan and South Korea are promoting some cautious optimism for future trade and investment opportunities. However, in the absence of further detail regarding these agreements, and in light of the various challenges in pursuing cross-border investments, many Australian companies remain primarily focused on their domestic operations.

Overview of the Report This is the fifth edition of the King & Wood Mallesons Directions Report. As in previous years, the 2015 Report focusses primarily on the legal and regulatory issues and challenges facing Australian directors and boards.

The Report begins with an analysis of the impact of the “best practice” Corporate Governance Principles and Recommendations published by the ASX Corporate Governance Council, the appropriateness of the independence criteria for the selection of directors, and the usefulness of the new board skills matrix.

We then go on to examine the 2014 AGM season and challenges faced by Australian directors and boards in relation to effective stakeholder engagement, including the influence of shareholder activism in the digital age.

We also reflect on the current regulatory landscape, and the key areas identified by survey respondents as either consuming directors’ time and attention, or requiring substantive reform.

This Report concludes by reflecting on the outlook for 2015 and the landscape for domestic and cross-border investment.

We trust that our Report makes a useful contribution to the ongoing debate regarding the issues, challenges and opportunities facing Australian directors and boards.

Meredith Paynter Partner, King & Wood Mallesons

Nicola Charlston Partner, King & Wood Mallesons

Australia’s corporate governance watershed?By the late 1990s, the corporate governance practices of Australia’s companies were, in the view of many commentators, outdated, anachronistic and not conducive to the provision of appropriate oversight of the management of Australian companies, or accountability to shareholders.

Corporate Governance

4

King & Wood Mallesons / Directions 2015

At that time, Australia had witnessed successive waves of corporate booms and busts most recently in the late 1980s and early 1990s fuelled by the opportunism, zeal and imagination of a range of high-profile entrepreneurs and CEOs, deregulation in the banking system, cheap debt, a buoyant stock market and asset bubbles.

Meanwhile, the boardroom had remained largely distant and mysterious, inhabited by predominantly male non-executive directors drawn from an exclusive pool of former senior executives and professionals. In 2001 a survey of the 300 largest institutional investors in six of the world’s stock exchanges asked those investors whether companies in their countries adhered to sound corporate governance practices. Australia ranked second last, with 63% responding ‘no’.3 This was certainly a remarkable vote of no confidence in the corporate governance system at the time.

In response to these failures, one of the key initiatives to reform and improve Australia’s corporate and business regulation was the Corporate Law Economic Reform Program (CLERP), which was first announced by the then Federal Treasurer, Peter Costello, in 1997 to promote business, economic development and employment. The policy framework developed under CLERP was intended to “contribute to the efficiency of the economy, while maintaining investor protection and market integrity”.

Among various reforms, some of the key changes in the areas of corporate governance included the introduction of the business judgement rule to “protect the authority of directors in the exercise of their duties of management” and to encourage them to “take advantage of business opportunities and not behave in an unnecessarily risk averse manner”, and a statutory derivative action to enhance shareholders’ rights.4

Subsequent reforms were (among other matters) directed to enhance financial reporting, audit oversight and auditor independence, in response to various regulatory shortcomings identified in the wake of further international (such as Enron and Worldcom) and domestic (such as HIH and One-Tel) corporate collapses in the early 2000s.

3 Russell Reynolds Associates Inc, ‘Russell Reynolds Associates’ Survey Finds increase in Institutional Investor Activism and Influence (Press Release, 19 June 2001) 4 Corporate Law Economic Reform Program, Policy Reforms, Treasury, 1998 at p 2-3

5

King & Wood Mallesons / Directions 2015

Coinciding with this process of review and reform of Australia’s corporate laws, including through the enactment of the Corporations Act in 2001, the ASX convened the ASX Corporate Governance Council (Governance Council) in 2002 with the objective of enhancing Australian corporate governance practices. Since 2003, the Governance Council has published the Corporate Governance Principles and Recommendations for listed entities (ASX Recommendations) in order to “promote investor confidence and to assist listed entities to meet stakeholder expectations”.5

The ASX Recommendations have been revised numerous times since their introduction, including to address various risk management and oversight matters following the most recent spate of corporate collapses arising from the global financial crisis in 2007-08, the subsequent global downturn and the European sovereign debt crisis.

The establishment of the Governance Council and the introduction of the ASX Recommendations coincided with ASIC taking a more active role in seeking to enforce corporate governance rules, including directors’ duties and continuous disclosure.6 Without undue hyperbole, this period of reform may fairly be called Australia’s corporate governance watershed.

Central to the original ASX Recommendations, and still at the core of Australia’s corporate governance framework, are the recommendations regarding board composition, including those recommending an independent chairman and that a majority on the board of a listed entity be independent. In 2014, in an environment where most discussion and commentary on board composition continued to be dominated by independence and diversity concerns, the Governance Council introduced a new recommendation that boards of listed entities disclose a board skills matrix, setting out the mix of skills and diversity that the board currently has, and/or is looking to achieve, in its membership.

Having regard to these recent changes to the ASX Recommendations, we sought to test directors’ views on the overall effectiveness of Australia’s corporate governance framework, with a focus on board composition.

A qualified endorsement?Our survey respondents indicated a general approval of the Australian corporate governance framework, with nearly 7 in 10 survey respondents indicating that the introduction of the Governance Council and the ASX Recommendations have been at least somewhat effective in improving governance outcomes for Australian listed entities. This has, in part, been through breaking down, in the words of one survey respondent, the “old mates clubs” that had previously characterised Australia’s boardrooms.

Figure 1: ASX Recommendations – Effective or not?

Very effective

7.6%

Somewhat effective 59.9%

Neutral 15.2%

Somewhat ineffective

12.0%

Unsure 2.3%

Very ineffective 3.0%

However, despite this overall endorsement, one of the most striking responses to our survey this year was that just over 40% of survey respondents indicated that they thought the ASX Recommendations with respect to independence restrict optimal board structure and inhibit the appointment of capable board members. This result indicates that, even if the overall corporate governance reform process as discussed previously has been positive, there are certain elements of the current governance framework which may require further thought.

5 ‘Corporate Governance Council’ at <http://www.asx.com.au/regulation/corporate-governance-council.htm> 6 Alan Dignam and Michael Galanis, ‘Australia Inside-Out: The corporate governance system of the Australian Listed Market’ (2004) 28 Melbourne University Law Review pp 645-646

6

King & Wood Mallesons / Directions 2015

Figure 2: Does independence restrict optimal board composition?

In many respects, the scepticism of our survey respondents regarding the unqualified benefit of independence echoes a number of international studies which have found that increased independence does not, by and large, enhance company value.7 Of course, the benefits and drawbacks of independence must be considered in the context of the independence regime of the relevant jurisdiction. Two key features of the Australian regime are relevant factors in considering whether the Australian independence requirements may, in certain instances, be counterproductive:

� the indicators of independence themselves (see Figure 3) including, notably, independence from both management and key shareholders; and

� the “comply or explain” (rather than strictly mandatory) nature of the ASX Recommendations as to independence.

When these features are considered together with other features of the Australian corporate governance landscape (for example, the shareholding structure of many listed entities and Australia’s relatively strong formal shareholder rights regime) the potential shortfalls in the current approach to director independence in Australia, in an age of increased media scrutiny and stakeholder activism, begin to emerge.

No 59.4%

Yes 40.6%

Figure 3: ASX Recommendations – Factors relevant to assessing independence

Examples of interests, positions, associations and relationships that might cause doubts about the independence of a director, as stated in the ASX Recommendations, include if the director:

� is, or has been, employed in an executive capacity by the entity or any of its child entities and there has not been a period of at least three years between ceasing such employment and serving on the board;

� is, or has within the last three years been, a partner, director or senior employee of a provider of material professional services to the entity or any of its child entities;

� is, or has been within the last three years, in a material business relationship (eg as a supplier or customer) with the entity or any of its child entities, or an officer of, or otherwise associated with, someone with such a relationship;

� is a substantial security holder of the entity or an officer of, or otherwise associated with, a substantial security holder of the entity;

� has a material contractual relationship with the entity or its child entities other than as a director;

� has close family ties with any person who falls within any of the categories described above; or

� has been a director of the entity for such a period that his or her independence may have been compromised.

7 For a summary of this view see Wolf-Georg Ringe, ‘Independent Directors: After the Crisis” (Oxford Legal Studies Research Paper No. 72/2013), <http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2293394>

7

King & Wood Mallesons / Directions 2015

The rationale for independence In assessing the effectiveness of the Australian independence requirements, it is relevant to consider the underlying rationale for corporate governance, and the purpose of independent directors and boards. In the broadest sense, corporate governance aims to ensure that the decision-making mechanisms within companies enable optimal decision making for the company, in the context of the economy and society as a whole.

One of the key functions of independent directors in this context is to mitigate the risk of conflicts of interest or duty, so that boards are able to bring a free and independent mind to the decisions before them. As one survey respondent noted, “independence of mind is a critical component in adding value to a board”.

This statement raises the following questions:

� Which conflicts need to be contained?

� If directors are to be independent, from whom do they need to be independent?

In the Anglo-American context, listed entities are typically characterised by a high degree of dispersed share ownership, with limited capacity for coordinated action among shareholders. This results in a separation of ownership (by shareholders) from control (by the board and management).

Under this structure, shareholders are vulnerable to the misdeeds of management and independence of the board from management is seen as key in ensuring good corporate decision making. The indicators of independence contained in the ASX Recommendations (see Figure 3) relating to current and previous experience in executive management, and providing for a time period for director tenure on a board before that director is likely to cease to be independent, are designed to manage this problem.

By contrast, in other jurisdictions (such as in the Continental European context), share ownership, even of listed entities, has historically been characterised by a high incidence of controlling shareholders or “block holders”. In that context, the issue is not shareholders having too little influence over management, but rather majority shareholders potentially having too much influence, and using this influence to the detriment of minority shareholders. Independence of the board from substantial shareholders (and not necessarily management) is therefore important, with independence from management regarded as being less critical.

Accordingly, the factors relevant to assessing independence in a given jurisdiction should reflect the conflict issues specific to that jurisdiction.

Too much independence?

What, then, are the primary conflicts of interest confronting Australian listed entities?Historically, Australia has been grouped together with the United States and the United Kingdom as a dispersed ownership jurisdiction, in which the principal focus is to ensure limited opportunities for management malfeasance. Board independence from management has therefore been seen as essential.

However, studies suggest that it may be more appropriate to characterise Australia as having a hybrid system, characterised by historically high levels of non-institutional block holders (giving rise to a shareholder-shareholder conflict) and the continued rise of institutional investors (giving rise to a shareholder-management conflict). See Figure 4 for further discussion of Australia’s shareholding structure. If this is the case then, perhaps more than other jurisdictions, there will be instances where certain characteristics of independence are particularly relevant for one entity, but less relevant for others.

In this respect, it is significant that the ASX Recommendations presently identify director associations both with executive management and with substantial shareholders as potentially indicating a lack of independence. Requiring this stringent level of independence clearly limits the pool of candidates available to be classified as independent, and may therefore unnecessarily lead to the appointment of directors who lack sufficient experience or knowledge of the business and/or industry, or sufficient incentive to take appropriate business risks, due to otherwise preferred candidates having current or prior associations that technically disqualify them as being independent. Especially for smaller listed entities, where the available pool of suitable candidates may be quite small, strict adherence to the ASX Recommendations may ultimately lead to a less than optimal board composition and decision making outcomes for the entity.

These issues were clearly at the heart of the concerns expressed by a number of survey respondents, captured in the statement that “independence per se can be a poor cousin of deep knowledge and industry expertise” and in the rise of the problem of “no conflict, no interest!”. A number of our survey respondents noted that this was a particular problem in smaller or emerging listed entities which may, more than large listed entities, “benefit from the continued involvement of some people who might not be viewed as independent”.

8

King & Wood Mallesons / Directions 2015

8 Asjeet Lamba and Geof Stapledon, ‘The Determinants of Corporate Ownership Structure: Australian evidence’ (Public Law and Legal Theory Working Paper No.20, Faculty of Law, The University of Melbourne 2001), p 24 <http://papers.ssrn.com/sol3/papers.cfm?abstract_id=279015> 9 Richard Mitchell et. al, ‘Shareholder Protection in Australia: Institutional Configurations and Regulatory Evolution’ (2014) 38 Melbourne University Law Review pp 71-74 10 See footnote 4, p 639 11 Geof Stapledon, ‘Share Ownership and Control in Listed Australian Companies’ (1999) 3 Corporate Governance International 17 12 See footnote 6, p 24-25

However, this conclusion is potentially complicated by the continued rise of institutional share ownership in Australia which, as early as 1997, was estimated at nearly 50% of the Australian listed share market.11 Historically, institutional shareholders have tended to act differently to non-institutional block holders. Their incidence of rent-seeking through related party transactions is far lower12

and, discouraged by coordination problems and free rider issues, they have traditionally preferred to vote with their feet and exit, rather than to intervene and agitate, in the case of perceived mismanagement. This lack of engagement can leave management relatively unchecked, as in a dispersed ownership model, even where share ownership concentration remains high.

Current trends in voting and participation at AGMs and shareholder activism are further discussed in this Report in the section entitled “AGMs, Stakeholder Engagement and the Digital Age”.

Figure 4: Concentrated or dispersed ownership?

Empirical studies indicate that Australia’s listed entity ownership structure defies easy characterisation as a dispersed or concentrated ownership jurisdiction.

In 1998, for instance, a study of a representative sample of 240 ASX-listed entities found that 72% had a non-institutional investor with at least a 10% holding, while 52% had a non-institutional investor with at least a 20% holding, and 16% were absolutely controlled by a non-institutional investor.8 When these shareholding numbers are viewed in the context of low shareholder turn out to vote on shareholder resolutions (allowing block holders with significantly less than a majority of total shares to routinely pass shareholder resolutions), formal shareholder rights which have been internationally recognised as among the strongest in the world9, historical levels of related party transactions with shareholders which have been described as “astounding by US or UK standards”10 and a less active takeover market than those countries, it is arguable that the key issue to be addressed by independence requirements in Australia is not the relationship between shareholders and management, but the relationship between block holders and minority shareholders.

King & Wood Mallesons / Directions 2015

The market signalling approachAn obvious response to the previous discussion is that, with its “comply or explain” approach - which allows listed entities to opt out of strict adherence to the independence recommendations if they explain why they are doing so - the ASX Recommendations already give listed entities sufficient flexibility to tailor independence requirements to their own circumstances.

The fundamental principle behind this approach is that, so long as appropriate disclosure is made, the market will ultimately judge whether a board is appropriately composed. Boards and shareholders are (theoretically) free to pick and choose, through the process of appointing and periodically re-electing directors, which characteristics of independence are most relevant in the particular context of the listed entity, and how independence as a criterion for board appointment is to be balanced against other factors.

Interestingly, a number of survey respondents suggested that, despite this technical flexibility, boards and nomination committees of listed entities nevertheless feel restricted by the ASX Recommendations in structuring their boards and committees, and identifying candidates for appointment.

Several survey respondents noted that the ASX Recommendations fail to provide “enough opportunity for circumstances specific to a company or any individual director” to be considered, while others commented on the existence of a “flawed obsession” with independence which can prevent well-qualified candidates with deep knowledge of the relevant company, business and/or industry from being nominated or appointed. It therefore appears that many boards and other stakeholders are effectively “reading the recommendations as rules”.

It is not entirely clear why this is the case. Some respondents suggested that a lack of strict adherence to the ASX Recommendations would provide fuel for the fire of shareholder activists (see the further discussion in the section entitled “AGMs, Stakeholder Engagement and the Digital Age”). Certainly, enhanced media scrutiny, and social media and digital technology which facilitate activism, may make any departure from “best practice” governance norms appear more difficult and risky.

The introduction of the board skills matrix The antidote to this predicament would be to ignite a more fulsome public discourse with stakeholders around the appropriate mix and relative value of skills and experience, beyond independence and diversity, which are necessary to optimise the effectiveness of listed boards in ever-changing and challenging domestic and international business environments. Given that directors of listed entities must be periodically elected or re-elected by shareholders (even when first appointed by directors to fill a casual vacancy), there is clear scope and opportunity for boards to make the case to shareholders regarding what board skills and experience are needed, and the extent to which the ASX Recommendations should be strictly followed.

By focusing attention on the key skills required, and the key current gaps on a listed entity’s board, the new board skills matrix should facilitate more rounded discussions regarding board composition and the desired attributes of potential candidates. In this respect, a majority of our survey respondents were optimistic that a board skills matrix would assist listed entities to structure their boards more optimally in the future.

Our survey results (summarised in Figures 5 and 6) indicate that industry knowledge and business skills have been the key priorities in board appointments in recent times and remain key identified gaps in board skills. As many of our survey respondents noted, the best place to find many of these skills and experience is in the existing or recent executive management of the listed entity. Further, many questioned the link between longevity on boards and non-independence.

Beyond independence considerations, it will be interesting to see the extent to which the board skills matrix facilitates director appointments which may be considered more daring or unconventional by historical standards.

This is particularly relevant in respect of experience and skills relating to digital technology and social media, which are transforming the economy, business practices and market behaviour, and creating considerable disruption and new opportunities. An increasing number of entities are appointing directors who have specific skills relevant to technology and/or the media environment. However, it is yet to be seen whether these types of skills and experience will become commonplace around the boardroom, or whether such skills and expertise better reside with executive management, with boards to be kept abreast of, but remaining somewhat detached from, the “Twittersphere”. We expect this will be different for different entities, and at different times, as the potential of digital technology and its impacts on various industries and businesses unfold.

If the board skills matrix can facilitate discussions which ultimately make desirable candidates more “viable” for appointment to listed boards, particularly in contexts where independence considerations are less critical, then it will have played an important part in ameliorating the concerns raised by our survey respondents. A key watch-out will be to ensure that board matrices do not ossify into de facto rules, embodying the latest fads in corporate governance, which are then used as “tick-a-box” exercises for future director appointments.

10

King & Wood Mallesons / Directions 2015

Diversity (gender and / or cultural)

0

25

50

75

100

Industry sector

knowledge

Independence Financial expertise

Business skills and

experience

Legal and regulatory expertise

Length of experience as a board member

Domestic experience

and knowledge

International experience

and knowledge

Other

55.6%

79.7%

39.1%43.6%

70.7%

19.6%16.5% 14.3%

25.6%

6.0%

Board skills: Priorities and gaps

Figure 5: In your view, which attributes were key priorities in any board appointments made during the past 12 months by the organisation/s of which you are a director?

Figure 6: Which attributes do you consider to be the primary gaps (if any) in the skill set of boards of organisation/s of which you are a director?*

Diversity (gender and / or cultural)

0

25

50

75

100

Industry sector

knowledge

Independence Financial expertise

Business skills and

experience

Legal and regulatory expertise

Length of experience as a board member

Domestic experience

and knowledge

International experience

and knowledge

Other

40.6%

22.6%

8.3%

17.3% 21.8%

9.8%8.3%

3.8%

28.6%

16.5%

*Survey participants were able to select multiple options. The percentages reflect the number of survey participants relative to the whole, who selected this skill.

11

King & Wood Mallesons / Directions 2015

The role and relevance of the AGM continues to be a focus for directors, with numerous survey respondents indicating that the AGM is “no longer an effective way of communicating with stakeholders” and “a waste of time and money because so few shareholders turn up”. The Australian Institute of Company Directors’ Director Sentiment Index findings for November 2014 indicated that 28% of directors believed the current system for conducting AGMs in Australia is dysfunctional.

12

King & Wood Mallesons / Directions 2015

These sentiments are consistent with the results from previous Directions surveys, and reflect concerns that the AGM, in its current form, is no longer filling its intended role as a forum for shareholders to ask questions, raise concerns, and engage with directors and management. Institutional shareholders typically have greater opportunities to engage with directors and management outside the AGM, given the size of their holdings, their resources and connections, and their perceived influence (including in relation to whether there is a “strike” recorded against a company’s remuneration report).

AGMs, Stakeholder

Engagement and the

Digital Age

13

King & Wood Mallesons / Directions 2015

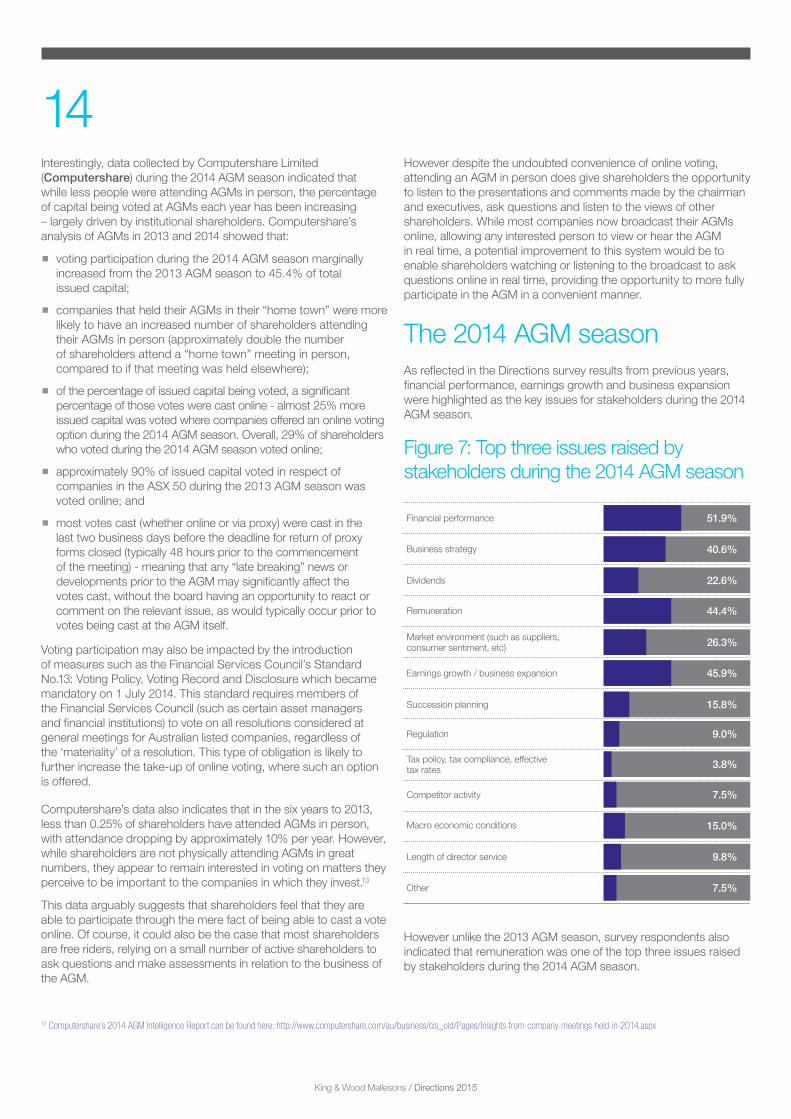

Interestingly, data collected by Computershare Limited (Computershare) during the 2014 AGM season indicated that while less people were attending AGMs in person, the percentage of capital being voted at AGMs each year has been increasing – largely driven by institutional shareholders. Computershare’s analysis of AGMs in 2013 and 2014 showed that:

� voting participation during the 2014 AGM season marginally increased from the 2013 AGM season to 45.4% of total issued capital;

� companies that held their AGMs in their “home town” were more likely to have an increased number of shareholders attending their AGMs in person (approximately double the number of shareholders attend a “home town” meeting in person, compared to if that meeting was held elsewhere);

� of the percentage of issued capital being voted, a significant percentage of those votes were cast online - almost 25% more issued capital was voted where companies offered an online voting option during the 2014 AGM season. Overall, 29% of shareholders who voted during the 2014 AGM season voted online;

� approximately 90% of issued capital voted in respect of companies in the ASX 50 during the 2013 AGM season was voted online; and

� most votes cast (whether online or via proxy) were cast in the last two business days before the deadline for return of proxy forms closed (typically 48 hours prior to the commencement of the meeting) - meaning that any “late breaking” news or developments prior to the AGM may significantly affect the votes cast, without the board having an opportunity to react or comment on the relevant issue, as would typically occur prior to votes being cast at the AGM itself.

Voting participation may also be impacted by the introduction of measures such as the Financial Services Council’s Standard No.13: Voting Policy, Voting Record and Disclosure which became mandatory on 1 July 2014. This standard requires members of the Financial Services Council (such as certain asset managers and financial institutions) to vote on all resolutions considered at general meetings for Australian listed companies, regardless of the ‘materiality’ of a resolution. This type of obligation is likely to further increase the take-up of online voting, where such an option is offered.

Computershare’s data also indicates that in the six years to 2013, less than 0.25% of shareholders have attended AGMs in person, with attendance dropping by approximately 10% per year. However, while shareholders are not physically attending AGMs in great numbers, they appear to remain interested in voting on matters they perceive to be important to the companies in which they invest.13

This data arguably suggests that shareholders feel that they are able to participate through the mere fact of being able to cast a vote online. Of course, it could also be the case that most shareholders are free riders, relying on a small number of active shareholders to ask questions and make assessments in relation to the business of the AGM.

However despite the undoubted convenience of online voting, attending an AGM in person does give shareholders the opportunity to listen to the presentations and comments made by the chairman and executives, ask questions and listen to the views of other shareholders. While most companies now broadcast their AGMs online, allowing any interested person to view or hear the AGM in real time, a potential improvement to this system would be to enable shareholders watching or listening to the broadcast to ask questions online in real time, providing the opportunity to more fully participate in the AGM in a convenient manner.

The 2014 AGM seasonAs reflected in the Directions survey results from previous years, financial performance, earnings growth and business expansion were highlighted as the key issues for stakeholders during the 2014 AGM season.

Figure 7: Top three issues raised by stakeholders during the 2014 AGM season

Financial performance

Business strategy

Dividends

Remuneration

Market environment (such as suppliers, consumer sentiment, etc)

Earnings growth / business expansion

Succession planning

Regulation

Tax policy, tax compliance, effective tax rates

Competitor activity

Macro economic conditions

Length of director service

Other

51.9%

40.6%

22.6%

44.4%

26.3%

45.9%

15.8%

9.0%

3.8%

7.5%

15.0%

9.8%

7.5%

13 Computershare’s 2014 AGM Intelligence Report can be found here: http://www.computershare.com/au/business/cis_old/Pages/Insights-from-company-meetings-held-in-2014.aspx

However unlike the 2013 AGM season, survey respondents also indicated that remuneration was one of the top three issues raised by stakeholders during the 2014 AGM season.

14

King & Wood Mallesons / Directions 2015

“The AGM process can be and is readily manipulated by shareholders with an agenda to push, particularly the two strikes rule on the REM report (in which they have little interest ... other than to use it as a mechanism to threaten boards).” Survey Respondent

While a number of companies received a second strike during the 2014 AGM season, the season also saw the first board spill. At the spill meeting of Liberty Resources Limited held on 14 January 2015, two incumbent directors were not re-elected. The other two incumbent directors were re-elected. The notice of meeting relating to the “spill meeting” noted that the reason that Liberty Resources Limited had received two strikes and that a resolution to hold a spill meeting was passed was due to “a small number of larger shareholders [who] voted against the Remuneration Report. Consequently the Company is required to convene this Spill Meeting…”14 Interestingly no other candidate was nominated for appointment as a director of Liberty Resources Limited. This may be because:

� those nominated for appointment may be seen as candidates who will pursue the agenda of their nominating shareholder; for example at Penrice Soda Holdings Limited’s 2013 “spill meeting”, five candidates stood for election comprising two spilled directors and three new candidates nominated by an activist shareholder. All the spilled directors were re-elected and none of the new candidates were elected; and

� voting against the re-election of a particular director may relate to an issue in respect of company performance or to that particular director, rather than a remuneration issue. As such, a shareholder can use the spill meeting to vote against re-electing a particular director, even if the company’s remuneration system is not an issue. It may also be the case that a new candidate nominated for appointment by a shareholder may not have the requisite skills and/or experience to sit on the board. Issues relating to board composition are further discussed in this Report in the section entitled “Australia’s Corporate Governance Watershed”.

There were approximately half the number of second strikes during the 2014 AGM season (10 second strikes) compared to the 2013 AGM season (18 second strikes). Of the companies that received a second strike in 2014, we are only aware of spill meetings being held by six of those companies. Three companies received a third strike in 2014. Further information on the impact of the two strikes rule is contained in the regulatory section of this report entitled “Looking back: key regulatory issues faced by directors in 2014”.

The gap between the number of companies receiving second strikes and the number of companies holding “spill meetings” may be attributable to the commonly-held view that voting to hold a spill meeting is not actually about removing directors from the board as much as it is a “show of strength” on behalf of shareholders. One survey respondent captured this recurring observation, stating “the remuneration vote is being used by some to push agendas other than remuneration”. Furthermore, while directors are excluded from voting on the remuneration report and spill meeting resolution, directors (the subject of the spill resolution) are permitted to vote in favour of their own re-election. This may be determinative in companies where directors hold or control a large percentage of voting securities. For example:

� James Packer indicated at the 2011 Crown AGM that a second strike would prompt him to use his holding to “ensure all directors are voted back in immediately”15; and

� at Globe International Limited’s 2013 “spill meeting”, three spilled directors (who between them held 65.9% of the voting capital) were re-elected (and no new candidates were nominated for appointment).

However while directors are technically able to vote on their own election/re-election, many directors of public companies appear to have adopted a practice of abstaining from voting on their own appointment at AGMs. As such, excluding directors from voting on the remuneration report and “spill meeting” resolution, but allowing directors to vote at the “spill meeting”, can potentially result in companies having to spend a substantial amount of time and money to convene a “spill meeting” at which the resolutions stand little chance of being passed.

14 Liberty Resources Limited (ACN 103 348 947) Notice of General Meeting and Explanatory Statement dated 9 December 2014 15 Crown pay rises risk second strike at AGM”, Andrew Cleary , Australian Financial Review (Online), 26 September 2012

15

King & Wood Mallesons / Directions 2015

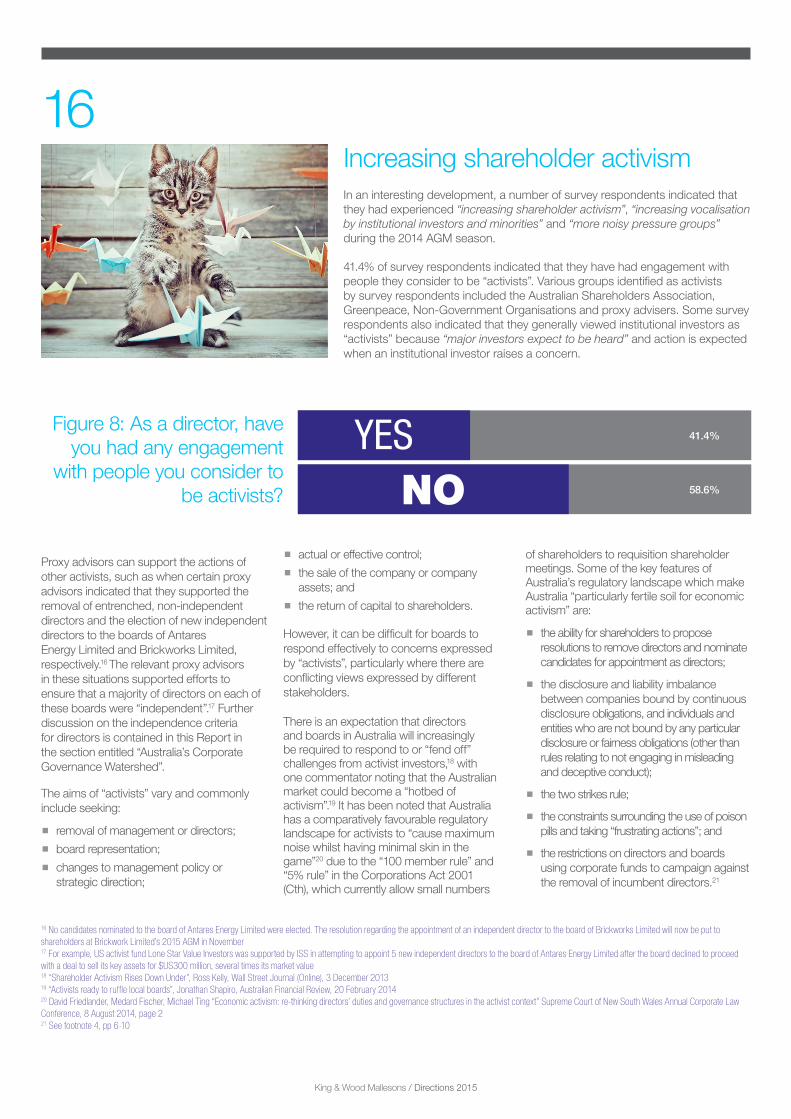

Figure 8: As a director, have you had any engagement

with people you consider to be activists?

41.4%

58.6%

YESNO

Increasing shareholder activismIn an interesting development, a number of survey respondents indicated that they had experienced “increasing shareholder activism”, “increasing vocalisation by institutional investors and minorities” and “more noisy pressure groups” during the 2014 AGM season.

41.4% of survey respondents indicated that they have had engagement with people they consider to be “activists”. Various groups identified as activists by survey respondents included the Australian Shareholders Association, Greenpeace, Non-Government Organisations and proxy advisers. Some survey respondents also indicated that they generally viewed institutional investors as “activists” because “major investors expect to be heard” and action is expected when an institutional investor raises a concern.

Proxy advisors can support the actions of other activists, such as when certain proxy advisors indicated that they supported the removal of entrenched, non-independent directors and the election of new independent directors to the boards of Antares Energy Limited and Brickworks Limited, respectively.16 The relevant proxy advisors in these situations supported efforts to ensure that a majority of directors on each of these boards were “independent”.17 Further discussion on the independence criteria for directors is contained in this Report in the section entitled “Australia’s Corporate Governance Watershed”.

The aims of “activists” vary and commonly include seeking:

� removal of management or directors;

� board representation;

� changes to management policy or strategic direction;

� actual or effective control;

� the sale of the company or company assets; and

� the return of capital to shareholders.

However, it can be difficult for boards to respond effectively to concerns expressed by “activists”, particularly where there are conflicting views expressed by different stakeholders.

There is an expectation that directors and boards in Australia will increasingly be required to respond to or “fend off” challenges from activist investors,18 with one commentator noting that the Australian market could become a “hotbed of activism”.19 It has been noted that Australia has a comparatively favourable regulatory landscape for activists to “cause maximum noise whilst having minimal skin in the game”20 due to the “100 member rule” and “5% rule” in the Corporations Act 2001 (Cth), which currently allow small numbers

of shareholders to requisition shareholder meetings. Some of the key features of Australia’s regulatory landscape which make Australia “particularly fertile soil for economic activism” are:

� the ability for shareholders to propose resolutions to remove directors and nominate candidates for appointment as directors;

� the disclosure and liability imbalance between companies bound by continuous disclosure obligations, and individuals and entities who are not bound by any particular disclosure or fairness obligations (other than rules relating to not engaging in misleading and deceptive conduct);

� the two strikes rule;

� the constraints surrounding the use of poison pills and taking “frustrating actions”; and

� the restrictions on directors and boards using corporate funds to campaign against the removal of incumbent directors.21

16 No candidates nominated to the board of Antares Energy Limited were elected. The resolution regarding the appointment of an independent director to the board of Brickworks Limited will now be put to shareholders at Brickwork Limited’s 2015 AGM in November 17 For example, US activist fund Lone Star Value Investors was supported by ISS in attempting to appoint 5 new independent directors to the board of Antares Energy Limited after the board declined to proceed with a deal to sell its key assets for $US300 million, several times its market value 18 “Shareholder Activism Rises Down Under”, Ross Kelly, Wall Street Journal (Online), 3 December 2013 19 “Activists ready to ruffle local boards”, Jonathan Shapiro, Australian Financial Review, 20 February 2014 20 David Friedlander, Medard Fischer, Michael Ting “Economic activism: re-thinking directors’ duties and governance structures in the activist context” Supreme Court of New South Wales Annual Corporate Law Conference, 8 August 2014, page 2 21 See footnote 4, pp 6-10

16

King & Wood Mallesons / Directions 2015

Figure 9: Australia’s favourable regulatory landscape for activists

Australia Comparable jurisdictions

Two strikes 25% “No” vote for remuneration report at two consecutive AGMs forces a vote on whether to “spill” the board

While “say on pay” legislation is common, there is no global equivalent to force a board spill as a result of a “say on pay” vote

Right to requisition meetings and remove directors Statutory right US – “classified” or “staggered” boards

Right to nominate directors on the company ballot Statutory right US – no general right to nominate directors on company ballot

Disclosure imbalance

Activists have no obligation to disclose intentions

No requirement to disclose derivative holdings (control transaction excepted)

US – Sch 13D filing requires disclosure of intentions

UK, HK, Singapore – derivative holdings must be disclosed

Poison pills constrainedNon pro-rata dilution limited to 15% for listed entities

Takeovers Panel “frustrating action”

US – commonly use poison pills with low trigger levels

US – can be implemented immediately following hostile approach

22 The Australian Financial Review, 28 January 2015, “ANZ, CBA urge activist shield”, Patrick Durkin, page 3 23 See footnote 18 24 See footnote 4 25 Shareholder Participation in the Modern Listed Public Company (June 2000), para 2.19

Of course, activists can also use non-legal strategies to spread their message including by persuading shareholders to direct proxy votes in their favour, placing pressure on the board through advertising and engagement with the media and/or through direct negotiation and engagement with senior management and the board.

The Federal Government is currently proposing to repeal the “100 member rule” as part of its effort to reduce red tape (which is further described in the regulatory section of this report entitled “Looking back: Key regulatory issues faced by directors in 2014”). A number of large institutions are supportive of this proposal due to the costs and time spent in preparing for and convening a meeting called by 100 members, “a frivolous waste of shareholders money … [shareholders are forced to] bear the ultimate cost of a fringe obsession.”22 However, there are a number of vocal supporters for maintaining the rule, even though the rule has not been used against an ASX 300 company for at least five years.23

The repeal of the “100 member rule” would remove a key tool in the arsenal of activists to force companies to hold general meetings which do not have the support of a significant number of shareholders. This is particularly pertinent in a situation where boards must be wary of how they respond to activists to ensure that they comply with their duties and legal obligations, including their continuous disclosure obligations. Unlike directors, activists have no duties to other shareholders, the company or to the market so are able to make broader statements (subject to defamation law and misleading and deceptive conduct restraints). “As activists are permitted to focus on personality as well as policy, directors are significantly disadvantaged by only being able to focus on the latter.”24

The Federal Government is proposing to leave the “5% rule” in place, such that members holding at least 5% of the issued capital of a company will be able to requisition a general meeting and legislation will remain to enable 100 members to require that a resolution be put to a general meeting. As the Corporations and Markets Advisory Committee (CAMAC) noted in its report released in 2000, abolishing the “100 member rule” and requiring shareholders to hold at least 5% of the issued capital of a company before they can requisition a general meeting would ensure that the cost of convening general meetings is only incurred when “there is a legitimate concern by a substantial number of shareholders who have an economic interest in the company”.25

17

King & Wood Mallesons / Directions 2015

King & Wood Mallesons / Directions 2015

“[Social media] is a threat if ignored but approached intelligently

can be an opportunity.” Survey Respondent

Activists are also increasingly using technology and social media to spread their messages. There have been recent examples of people tweeting from the floor of AGMs, such as Stephen Maynes at the Cabcharge Limited 2014 AGM (at which he nominated himself for appointment to the board) and at the Westfield Holdings Limited 2014 EGM. In this environment, it is becoming increasingly important for companies to have a fulsome media policy and for directors and boards to have a proper understanding of the social media environment.

This was recognised by the ASX in “Guidance Note 8 Continuous Disclosure: Listing Rules 3.1 – 3.1B” (Guidance Note 8) which states that a listed entity which is the subject of a blog would “often be aware of that fact from communications with its shareholders and, in ASX’s experience, would generally be monitoring the blog for an insight into what its shareholders are saying about it. Some (generally larger) listed entities would also be monitoring certain investor blogs, chat-sites and other social media sites through their investor relations function, again for the purposes of understanding what is being said about them on those sites”. Where a market sensitive announcement is pending, ASX considers that a listed entity should be actively monitoring those sites for any signs that confidential information in the pending announcement may have leaked.

Figure 10: Do the organisations of which you are a director have defined social media strategies in relation to external social media?

Social media has increasingly become a tool used by companies and other organisations for communicating and engaging with their stakeholders, and its use continues to grow. As one survey respondent observed “[Social media] is a threat if ignored but approached intelligently can be an opportunity.”

Approximately 70% of survey respondents indicated that the organisation(s) of which they are a director employ defined social media strategies through the various social media channels they use, a similar result to the survey responses for last year.

However, a number of survey respondents also highlighted the challenge of appropriately responding to social media and generally dealing with “digital disruption”. “Social media is predominated by either left wing activists or right wing nut jobs”. In particular, there is a risk that, in responding to social media comments, the board runs the risk of selective briefings (as not all people follow the same social media commentators or channels) and falling foul of continuous disclosure obligations.

One survey respondent commented that “the same approach should be used as with the ASX platform – avoid spin doctoring and ensure the full picture is provided.” However, given the reach of digital technology and the dynamic pace and volume of social media comments, even the most advanced media policy will not enable directors or boards to be able to respond in a timely yet considered fashion to all comments, in an environment where commentators are able to “make trouble for a living”.26 “Disentangling valid governance concerns from opportunistic activism is tricky business for both directors and those that sit in judgment of them.”27

Where to from here?As with so many other aspects of modern corporate life, it seems that the future of AGMs and shareholder engagement lies with digital technology.

While directors, boards and various stakeholders appear to be increasingly questioning the value of AGMs in their current form, shareholders clearly require a forum to “have a say” on the performance and direction of the companies in which they invest, and appear to be willing to do this via electronic means.

“General meetings are to companies what elections are to democracy.”28

It seems that the future of AGMs and stakeholder engagement lies in a mix of online direct voting coupled with shareholder briefings and, of course, the use of social media and other technology to continuously communicate with shareholders and other relevant stakeholders. However, this will require amendments to the Corporations Act 2001 (Cth) and the ASX Listing Rules, as well as regulators increasing their understanding of the broader environment in which directors and companies engage with their stakeholders.

26 See footnote 20 27 See footnote 22 28 See footnote 18

Like no Un Sure

69.2% 27.8% 3%

Figure 10

19

King & Wood Mallesons / Directions 2015

Regulatory

Looking back: Key regulatory issues faced by directors in 2014

Following a wave of regulatory reform, stemming from the global financial crisis in 2007-08 and its aftermath, corporate Australia has experienced relative calm over the past two years on the regulatory reform front.

This is reflected in this year’s survey results, with the top regulatory issues receiving director attention in the past 12 months being issues which have also featured prominently in previous years. This relative plateau in regulatory change has provided Australian companies and boards with some much needed time to consolidate and embed compliance practices, systems and processes necessitated by the earlier wave of reform.

However, as further described below, the regulatory burden for Australian business remains comparatively high, and regulatory compliance issues continue to consume a significant amount of director time and attention.

20

King & Wood Mallesons / Directions 2015

Initial hopes that the Coalition Federal Government’s proposed plans to reduce red and green tape and repeal redundant legislation would be effective to meaningfully reduce compliance costs and improve business efficiencies and productivity have faded. While a swathe of legislation has been repealed over the past 12 months through the Federal Government’s first bi-annual “repeal days”, our survey respondents overwhelmingly view the “repeal days” as having had minimal to no impact at all on their organisations or role as a director.

It is clear that corporate Australia is seeking more meaningful change to reduce regulatory and compliance burdens, in the hope that this will assist in facilitating much needed productivity improvements and breathe more life into Australia’s sluggish post-resources boom economy.

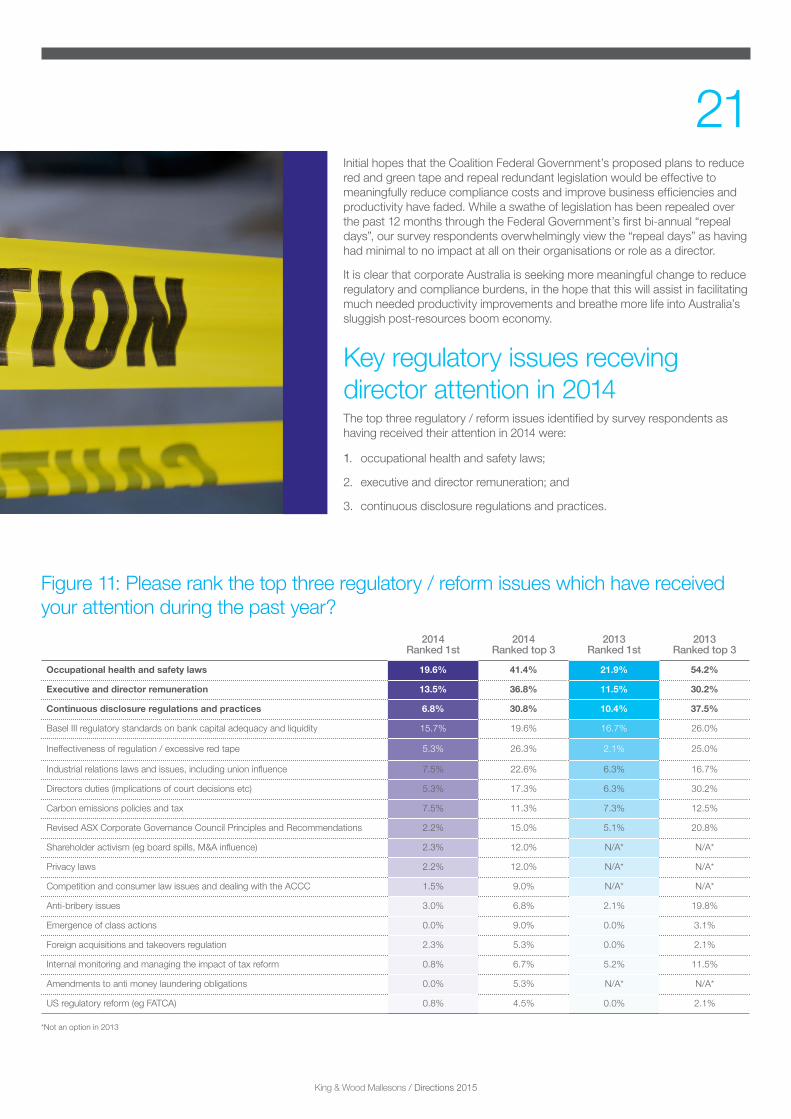

Key regulatory issues receving director attention in 2014The top three regulatory / reform issues identified by survey respondents as having received their attention in 2014 were:

1. occupational health and safety laws;

2. executive and director remuneration; and

3. continuous disclosure regulations and practices.

2014 Ranked 1st

2014 Ranked top 3

2013 Ranked 1st

2013 Ranked top 3

Occupational health and safety laws 19.6% 41.4% 21.9% 54.2%

Executive and director remuneration 13.5% 36.8% 11.5% 30.2%

Continuous disclosure regulations and practices 6.8% 30.8% 10.4% 37.5%

Basel III regulatory standards on bank capital adequacy and liquidity 15.7% 19.6% 16.7% 26.0%

Ineffectiveness of regulation / excessive red tape 5.3% 26.3% 2.1% 25.0%

Industrial relations laws and issues, including union influence 7.5% 22.6% 6.3% 16.7%

Directors duties (implications of court decisions etc) 5.3% 17.3% 6.3% 30.2%

Carbon emissions policies and tax 7.5% 11.3% 7.3% 12.5%

Revised ASX Corporate Governance Council Principles and Recommendations 2.2% 15.0% 5.1% 20.8%

Shareholder activism (eg board spills, M&A influence) 2.3% 12.0% N/A* N/A*

Privacy laws 2.2% 12.0% N/A* N/A*

Competition and consumer law issues and dealing with the ACCC 1.5% 9.0% N/A* N/A*

Anti-bribery issues 3.0% 6.8% 2.1% 19.8%

Emergence of class actions 0.0% 9.0% 0.0% 3.1%

Foreign acquisitions and takeovers regulation 2.3% 5.3% 0.0% 2.1%

Internal monitoring and managing the impact of tax reform 0.8% 6.7% 5.2% 11.5%

Amendments to anti money laundering obligations 0.0% 5.3% N/A* N/A*

US regulatory reform (eg FATCA) 0.8% 4.5% 0.0% 2.1%

*Not an option in 2013

Figure 11: Please rank the top three regulatory / reform issues which have received your attention during the past year?

21

King & Wood Mallesons / Directions 2015

1. Occupational health and safety lawsFor a third consecutive year, occupational health and safety laws remained the top regulatory issue identified by survey respondents as receiving their attention. 41.4% of survey respondents ranked OH&S in their top 3 issues, compared with 54.2% of survey respondents in 2013.

The harmonisation of State and Territory workplace laws in 2012 and 2013 resulted in additional obligations and liability being imposed on directors, with directors now required to actively monitor OH&S risks in their business. As the harmonisation process nears finalisation, directors are still adjusting to the “new normal” of pro-active and ongoing due diligence obligations, and increasing numbers of boards are working with legal and other advisers to design and implement systems which assist directors to discharge these obligations.

The impact of the positive due diligence obligations as a compliance issue, and the potential for personal director liability, remains at the forefront of directors’ minds. As one survey respondent stated, it is a “crucial element which directors cannot afford to get wrong.” It is also not surprising, from a business perspective, that this issue is a top focus for directors, given that every business should be seeking to provide a safe workplace for their employees with a target of “zero harm”.

2. Executive and director remunerationExecutive and director remuneration again featured as one of the top 3 regulatory issues receiving attention by survey respondents, moving up from 3rd position in 2013 to 2nd position in 2014 (with 36.8% of survey respondents ranking it in their top 3 issues compared with 30.2% of survey respondents in 2013). While there has not been the same degree of media focus on the topic in the past 12 - 18 months, one director noted that remuneration is “still causing a lot of angst” and that the “level of transparency is extraordinary”.

One reason for the continued level of director attention on remuneration is the rise of shareholder activism and the disclosure obligations relating to remuneration – as one director pointed out, the remuneration report is now typically the largest section of an annual report. This has resulted in a closer focus on ensuring that remuneration packages are structured so that they will be approved by shareholders, and to avoid the risk of strikes or spill motions. The “two strikes” rule has provided an additional incentive for directors to ensure remuneration reports are approved by shareholders, with a strike against the remuneration report generally regarded as being evidence of a material governance failure.

Proxy advisers have played a part in the ongoing prominence of remuneration as a key board concern. Their role in analysing remuneration structures and arrangements, and making recommendations to clients on how to vote on remuneration-related resolutions, means that companies and directors – especially the chairman of the remuneration committee – are spending considerable time with those proxy advisers explaining and justifying the appropriateness of their remuneration policies, performance conditions and their effectiveness (often compared to generic benchmarks or standards nominated by proxy advisers). Remuneration and the “two strikes” rule are further discussed in this Report in the section entitled “AGMs, Stakeholder Engagement and Digital Age”.

3. Continuous disclosure regulations and practicesContinuous disclosure remained one of the top 3 regulatory issues identified as receiving attention by survey respondents, being a top 3 issue for 30.8% of survey respondents compared with 37.5% of survey respondents in 2013. This reflects that continuous disclosure is an ever-present issue for directors of listed entities, particularly in relation to decisions on the timing and content of disclosure (especially in the case of corporate transactions, such as takeover offers). Decisions regarding when, and what, to disclose frequently require significant judgement – and those decisions are often heavily scrutinised with the benefit of hindsight.

The prominence of continuous disclosure as an issue capturing director attention also likely reflects the high-profile Newcrest case in mid-2014 and the release of updated (and soon to be further updated) continuous disclosure guidance by ASX.

Newcrest in a snapshot

In July 2014, the Federal Court imposed a $1.2 million penalty on Newcrest Mining Limited, the largest penalty imposed to date for a breach by a company of its continuous disclosure obligations. A class action on behalf of shareholders was later commenced on related grounds. The case related to disclosure of information concerning forecast gold production and capital expenditure which was provided to analysts before its release to the market.

22

King & Wood Mallesons / Directions 2015

Following the release by ASX of its revised Guidance Note 829 on continuous disclosure obligations in 2013, ASIC released a report in May 201430 which focussed on circumstances in which the confidentiality of market-sensitive information can be jeopardised and the way in which information can be selectively disclosed in an inappropriate way (see Figure 12). As a result of this review, ASIC indicated that it will focus less on providing guidance, and more on taking appropriate enforcement action where listed entities, advisers and analysts fail to implement consistent policies to prevent the leakage of confidential, market sensitive information.

“…listed entities are responsible for managing their confidential information and must take

special care during analyst and investor briefings. Selective disclosure has the potential

to undermine confidence in the market and ASIC will act to enforce the law in such cases.”

Cathie Armour ASIC Commissioner

On 6 March 2015, ASX released a consultation paper seeking public comment on further changes to Guidance Note 8. Developments such as the Newcrest case and ASIC Report 393 prompted ASX to consider that listed entities and their advisers would benefit from expanded guidance on analyst and investor briefings, analyst forecasts, consensus estimates and “earnings surprises” (in particular when an “earnings surprise” is disclosable) (see Figure 13).

The proposed amendments do not fundamentally change ASX’s existing position, but should provide some useful practical clarifications. While these clarifications are generally welcome, as the proposed new Guidance Note 8 runs to 85 pages (the relevant Listing Rules are one and a half pages), it is clear that this aspect of continuous disclosure will continue to be a tricky area for listed entities and their directors.

Figure 12: ASIC Report 393 – Key findingsASIC’s report focussed on the handling of potentially market-sensitive information:

(a) during briefings held by listed entities for analysts and institutional investors; and

(b) in the context of unannounced, market-sensitive corporate transactions.

In relation to analyst and institutional investor briefings, ASIC’s findings were not conclusive as its review of listed entities’ investor briefings was limited, but it did not find any evidence of selective disclosure of confidential, market-sensitive information.

In relation to unannounced market-sensitive corporate transactions, ASIC’s analysis found that since July 2010 there has been a reduction in the number of takeover-related leaks in the media. By contrast, since July 2010 there has been a slight increase in the number of leaks relating to equity capital raisings.

29 ASX Guidance Note 8 ‘Continuous Disclosure: Listing Rules 3.1 – 3.1B’ 30 ASIC Report 393: Handling of confidential information: Briefings and unannounced corporate transactions, May 2014

Figure 13: ASX Listing Rules Guidance Note 8 Consultation Paper – Key clarificationsSome of the key clarifications proposed in the consultation paper include:

� distinguishing between a “market sensitive earnings surprise” and a “lesser earnings surprise”. Only “market sensitive earnings surprises” trigger a disclosure obligation;

� confirming that listed entities are not under any obligation to bring earnings forecasts or consensus estimates of individual analysts or individual market data vendors in line with the entity’s internal projections;

� confirming that an entity is not required to release internal budgets or earnings projections provided they remain confidential, and that it remains acceptable for an entity to have a policy or practice of not providing earnings guidance to the market;

� ensuring that entities which do not give guidance take care in any communications with shareholders, analysts and the media to make sure that the confidentiality of their internal budgets and projections is preserved; and

� applying the 5% to 10% materiality variation range (as recommended by ASX) principally to situations where the entity itself has published guidance for the current reporting period.

23

King & Wood Mallesons / Directions 2015

Continued regulatory burden: Directors’ continued significant focus on regulationTime dedicated by directors to dealing with the top ranked regulatory issues remains high, with approximately 35% of survey respondents dedicating over 30 hours over the past 12 months to the relevant top issue.

While this level of focus on regulatory matters appears to be the “new normal”, it is still clearly a source of frustration for directors with “excessive bureaucracy, regulation and compliance burden” once again the top ranked issue concerning directors in fulfilling their role.

Reducing the regulatory burdenFollowing its promise prior to the 2013 Federal election to “reduce the red and green tape burden imposed on the Australian economy by $1 billion per year”31, the current Federal Government has now held three of its bi-annual “repeal days” (March and October 2014 and, at the time of writing this Report, March 2015). Legislation was introduced at the 2014 repeal days to abolish approximately 11,000 pieces of legislation, with a claimed $2.15 billion in net savings. The Federal Government has indicated that if the reforms proposed at the March 2015 repeal day are fully implemented, the total net savings since September 2013 will be approximately $2.45 billion (see Figure 15).32

10 to 20 hours 22.7%

Over 30 hours

35.6%

20 to 30 hours 24.2%

Less than 5 hours 0.8%

5 to 10 hours 16.7%

2014

10 to 20 hours 29.0%Over 30

hours 37.0%

20 to 30 hours 16.0%

Less than 5 hours 1.0%

5 to 10 hours 16.0%

2013Figure 15: Where are these “net savings” coming from?33

The total value of net savings from the two repeal days in 2014 is stated to be $2.1515 billion. The Coalition Federal Government has estimated that the deregulatory savings since the October 2014 repeal day, which include the March 2015 repeal day, will result in a further annual savings of $475.7 million. However, additional regulatory costs of $178.1 million from new regulations introduced in that time results in net savings for the period of $297.6 million, bringing the total for the estimated net savings from red tape cuts since September 2013 to $2.4491 billion.

31 ‘The Coalition’s Policy to Boost Productivity and Reduce Regulation’, July 2013, p2 32 www.cuttingredtape.gov.au 33 ‘The Australian Government Autumn Repeal Day March 2015’ consolidated list of deregulation initiatives available at www.cuttingredtape.gov.au

Figure 14: How many hours did you spend during the past twelve months dealing with the top ranked regulatory / reform issues you identified in the previous question?

24

King & Wood Mallesons / Directions 2015

impact

The search for productivity improvementsFollowing the Coalition Federal Government’s high-profile repeals of the carbon tax and mining tax, the attention for regulatory reform has now shifted to the cutting of red and green tape. A key driver behind cutting red and green tape is the benefit of reducing bureaucratic compliance costs. Furthermore, any new regulation should contribute to (or at least not adversely impact upon) enhanced productivity, innovation and efficiency.

The Business Council of Australia has identified regulation as the most common impediment to allowing Australia to continue to grow and prosper in a more globally competitive world. The slow speed of approvals and inconsistency between jurisdictions are also commonly noted as barriers. In making these assessments, the Business Council of Australia cites the IMD World Competitiveness Yearbook (2013), which ranks Australia 128th on regulatory burden, compared with 13th for New Zealand.34

Excessive red tape can result in over-regulation, delayed investments and foregone opportunities. Unnecessary regulation and red tape can force directors and boards to focus too much of their attention on regulatory compliance matters rather than the oversight of the strategic direction and business of the company.

To assist its red tape reduction agenda, the Federal Government has established “deregulation units” in each major federal department to drive red tape reduction and advise on deregulation priorities. The minister of each federal department has a committee, with a business representative, to advise on where regulation can be enhanced.

Beneficial progress or a slow start?The Federal Government’s push to remove red and green tape is a positive step. However, while the results of the repeal days so far appear impressive on paper, quantifiable benefits to business appear to remain elusive.

The overwhelming majority of this year’s survey respondents (92.2%) indicated that the repeal days have had minimal to no impact at all on their organisation or role as a director (see Figure 16).

It has been observed that much of the abolished legislation comprised “truly anachronistic laws and regulations that hardly apply to modern business”.35 It has also been observed that, “cutting redundant bills…won’t save anyone a single cent or make any business more productive”,36 given very few businesses would have had any exposure to the legislation repealed.

34 ‘ ‘Building Australia’s Comparative Advantages’, Business Council of Australia, July 2014 35 ‘Repeal day an exercise in deregulation smoke and mirrors’, John Wanna, The Conversation, 26 March 2014 36 ‘Red tape ritual doesn’t help’, Andrew Leigh, The Australian, 27 October 2014 37 ‘Reducing red tape to build a strong and prosperous economy’, Tony Abbott and Josh Frydenberg Media Release, 22October 2014 38 See footnote 37

There are, however, aspects of the repeal agenda which have practical utility. The Australian Taxation Office (ATO) released a new online tax return service, which pre-populates tax returns, which is estimated to save taxpayers $160 million in compliance costs annually,37 while businesses with no GST payable are no longer required to lodge a Business Activity Statement.38 While beneficial, this type of reform primarily provides efficiency benefits to individuals and small businesses as opposed to larger corporations and their boards and directors.

Figure 16: What level of impact have the Federal Government “Repeal Days” had on your organisation or to your role as a director?

34.4%No impact

at all

4.7%Some 57.8%Minimal

3.1%Reasonable

25

King & Wood Mallesons / Directions 2015

Clearing the way for real improvement?As early efforts to remove red tape seem to have targeted “predictable low-hanging fruit”,39 it will be interesting to monitor future repeal days to assess whether they bring tangible and lasting benefits to business and the community, and achieve the Coalition Federal Government’s aim of reducing the “cost of unnecessary or inefficient regulation imposed on individuals, business and community”.40

“The efforts to date have been commendable but while they have put a dent in the scope of the regulatory burden, they need to be the start of an ongoing process that reduces regulatory burdens and keeps them as low as possible.” Innes Willox, Chief Executive Australian Industry Group41

An emphasis on effective enforcement, and efficiency in the use of legislation and regulation, as opposed to a process focussed approach is particularly important for directors and business.

Figure 17: In which of the following areas would a reduction of red tape

be most beneficial to business?

However, the real benefit of the Coalition Federal Government’s red tape removal agenda will only be achieved when businesses experience a noticeable decrease in their regulatory and compliance burden. In particular, amendments to legislation and regulations which affect business on a daily basis, and the drive to improve the functions and actions of key regulators, is likely to have the most notable impact on businesses and consequently the Australian economy.

Director’s perspective: Where would a reduction in red tape be most beneficial?Tax regulation and compliance, OH&S and industrial relations were selected by survey respondents as the key areas where a reduction in red tape would be most beneficial. Directors commenting on the survey results found this unsurprising, noting that recent reform efforts have been “around the margins” and there has been no relief in areas of large burden on business. Directors are looking for “big reform” in substantive areas of regulation which will potentially provide real benefit to business and the community.

“[A] bigger concern is the mountain of industry specific

process constraining regulations, and especially,

detailed and non-value adding reporting of performance.”

Survey Respondent

Tax regulation and complianceCorporate tax rates in Australia have remained comparatively high. It is therefore no surprise that the survey shows tax regulation and compliance are at the forefront of directors’ minds. The rate of corporate tax in Australia (30%) is high in comparison with OECD rates (average 24.11%) and with regional competitors (Asian average 21.91%). While Australia’s franking system mitigates the headline rate to an extent, it is nevertheless the case that tax has a significant impact on doing business in Australia and impacts on investment decisions. With capital being highly mobile, investors may find lower tax rates, regulation and compliance requirements elsewhere that produce greater returns and the Australian tax regime may therefore be acting as a disincentive to investment in this country. Adopting a tax regime (and in particular a rate) more in line with international and regional standards may even see tax revenues increase for the Government.

39 ‘Slashing red tape requires a broader view of social costs’, Cassandra Wilkinson, The Australian, 31 May 2014. 40 www.cuttingredtape.gov.au 41 ‘Business welcomes fresh war on red tape’, John Ferguson, The Australian, 22 December 2014

Environmental policies

Tax regulation and

compliance

Occupational health and

safety

Corporate governance

28.6% 52.4% 38.1% 33.3%

26

King & Wood Mallesons / Directions 2015

Coupled with concerns about tax rate and regulatory compliance, the survey also indicates that tax uncertainty continues to be a dominant theme. This again is no surprise. There are many previously announced but un-enacted tax measures (eg managed investment trust taxation and the investment manager regime). Management of the ATO and the tax reform process also continue to be major challenges.

“…the tax system is way too complex for ordinary business people.” Survey Respondent

This is all occurring against a background where a company’s tax affairs will become more transparent and subject to greater scrutiny than ever before. Reports of taxes paid by large corporations commence in the second half of 2015 with the first report being made of taxes paid in 2014. The Senate is conducting inquiries into tax avoidance in March 2015 with a view to reporting to Parliament in June 2015. The Coalition Federal Government is also actively engaging with the international community to combat base erosion and profit shifting (known as BEPS). The ATO is leading this charge by actively sharing tax intelligence with G20 and OECD countries. It has already commenced with more than 200 risk reviews of multinationals in connection with BEPS related activity. To cap it off, the Federal Opposition has developed a policy which will limit gearing by international enterprises to their worldwide gearing level.