Corporate Ownership & Control / Volume 4, Issue 2, Winter ...

85

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued) 159 CORPORATE OWNERSHIP & CONTROL Editorial Address: Assistant Professor Alexander N. Kostyuk Department of International Economics Ukrainian Academy of Banking of National Bank of Ukraine Petropavlovskaya Str. 57 Sumy 40030 Ukraine Tel: +0038-0542-611025 Fax: +0038-0542-611025 e-mail: [email protected] [email protected] www.virtusinterpress.org Journal Corporate Ownership & Control is published four times a year, in September-November, December-February, March-May and June-August, by Publishing House “Virtus Interpress”, Kirova Str. 146/1, office 20, Sumy, 40021, Ukraine. Information for subscribers: New orders requests should be addressed to the Editor by e-mail. See the section "Subscription details". Back issues: Single issues are available from the Editor. Details, including prices, are available upon request. Advertising: For details, please, contact the Editor of the journal. Copyright: All rights reserved. No part of this publication may be reproduced, stored or transmitted in any form or by any means without the prior permission in writing of the Publisher. Corporate Ownership & Control ISSN 1727-9232 (printed version) 1810-0368 (CD version) 1810-3057 (online version) Certificate № 7881 Virtus Interpress. All rights reserved. КОРПОРАТИВНАЯ СОБСТВЕННОСТЬ И КОНТРОЛЬ Адрес редакции: Александр Николаевич Костюк доцент кафедры международной экономики Украинская академия банковского дела Национального банка Украины ул. Петропавловская 57 г. Сумы 40030 Украина Тел.: 0038-0542-611025 Факс: 0038-0542-611025 эл. почта: [email protected] [email protected] www.virtusinterpress.org Журнал "Корпоративная собственность и контроль" издается четыре раза в год в сентябре- ноябре, декабре-феврале, марте-мае, июне- августе издательским домом Виртус Интерпресс, ул. Кирова 146/1, г. Сумы, 40021, Украина. Информация для подписчиков: заказ на подписку следует адресовать Редактору журнала по электронной почте. Отдельные номера: заказ на приобретение отдельных номеров следует направлять Редактору журнала. Размещение рекламы: за информацией обращайтесь к Редактору. Права на копирование и распространение: копирование, хранение и распространение материалов журнала в любой форме возможно лишь с письменного разрешения Издательства. Корпоративная собственность и контроль ISSN 1727-9232 (печатная версия) 1810-0368 (версия на компакт-диске) 1810-3057 (электронная версия) Свидетельство КВ 7881 от 11.09.2003 г. Виртус Интерпресс. Права защищены.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Corporate Ownership & Control / Volume 4, Issue 2, Winter ...

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

159

CORPORATE

OWNERSHIP & CONTROL

Editorial Address: Assistant Professor Alexander N. Kostyuk Department of International Economics Ukrainian Academy of Banking of National Bank of Ukraine Petropavlovskaya Str. 57 Sumy 40030 Ukraine Tel: +0038-0542-611025 Fax: +0038-0542-611025 e-mail: [email protected] [email protected] www.virtusinterpress.org Journal Corporate Ownership & Control is published four times a year, in September-November, December-February, March-May and June-August, by Publishing House “Virtus Interpress”, Kirova Str. 146/1, office 20, Sumy, 40021, Ukraine. Information for subscribers: New orders requests should be addressed to the Editor by e-mail. See the section "Subscription details". Back issues: Single issues are available from the Editor. Details, including prices, are available upon request. Advertising: For details, please, contact the Editor of the journal. Copyright: All rights reserved. No part of this publication may be reproduced, stored or transmitted in any form or by any means without the prior permission in writing of the Publisher.

Corporate Ownership & Control

ISSN 1727-9232 (printed version)

1810-0368 (CD version)

1810-3057 (online version)

Certificate № 7881 Virtus Interpress. All rights reserved.

КОРПОРАТИВНАЯ

СОБСТВЕННОСТЬ И КОНТРОЛЬ

Адрес редакции: Александр Николаевич Костюк доцент кафедры международной экономики Украинская академия банковского дела Национального банка Украины ул. Петропавловская 57 г. Сумы 40030 Украина Тел.: 0038-0542-611025 Факс: 0038-0542-611025 эл. почта: [email protected] [email protected] www.virtusinterpress.org Журнал "Корпоративная собственность и контроль" издается четыре раза в год в сентябре-ноябре, декабре-феврале, марте-мае, июне-августе издательским домом Виртус Интерпресс, ул. Кирова 146/1, г. Сумы, 40021, Украина. Информация для подписчиков: заказ на подписку следует адресовать Редактору журнала по электронной почте. Отдельные номера: заказ на приобретение отдельных номеров следует направлять Редактору журнала. Размещение рекламы: за информацией обращайтесь к Редактору. Права на копирование и распространение:

копирование, хранение и распространение материалов журнала в любой форме возможно лишь с письменного разрешения Издательства. Корпоративная собственность и контроль

ISSN 1727-9232 (печатная версия)

1810-0368 (версия на компакт-диске)

1810-3057 (электронная версия)

Свидетельство КВ 7881 от 11.09.2003 г. Виртус Интерпресс. Права защищены.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

160

EDITORIAL BOARD

Alex Kostyuk, Editor, Ukrainian Academy of Banking (Ukraine); Sir George Bain, President and Vice-Chancellor, Queen's University (UK) –

honorary member; Sir Geoffrey Owen, London School of Economics (UK) - honorary member; Michael C. Jensen, Harvard Business School (USA) - honorary member;

Stephen Davis, President, Davis Global Advisors, Inc. (USA); Brian Cheffins, Cambridge University (UK); Bernard S. Black, Stanford Law School (USA); Simon Deakin, Judge Institute, Cambridge Business School (UK); David Yermack, New York University (USA); Joongi Kim, Graduate School of International Studies (GSIS), Yonsei University (Korea); Geoffrey Netter, Terry College of Business, Department of Banking and Finance, University of Georgia (USA); Ian Ramsay, University of Melbourne (Australia); Jonathan Bates, Director, Institutional Design (UK); Liu Junhai, Institute of Law, Chinese Academy of Social Sciences (China); Jonathan R. Macey, Cornell University, School of Law (USA); Fianna Jesover, OECD Corporate Governance Division; Yoser Gadhoum, University of Quebec (Canada); Alexander Lock, National University of Singapore (Singapore); Anil Shivdasani, Kenan-Flagler Business School, University of North Carolina at Chapel Hill (USA); Rado Bohinc, University of Ljubliana (Slovenia); Harry G. Broadman, Europe & Central Asia Regional Operations, The World Bank (USA); Rodolfo Apreda, University of Cema (Argentina); Hagen Lindstaedt, University of Karlsruhe (Germany); Andrea Melis, University of Cagliari (Italy); Julio Pindado, University of Salamanca (Spain); Robert W. McGee, Barry University (USA); Piotr Tamowicz, Gdansk Institute of Market Research (Poland); Victor Mendes, University of Porto (Portugal); Azhdar Karami, University of Wales (UK); Alexander Krakovsky, Ukraine Investment Advisors, Inc. (USA); Peter Mihalyi, Central European University (Hungary); Wolfgang Drobetz, University of Basle (Switzerland); Jean Chen, University of Surrey (UK); Klaus Gugler, University of Vienna (Austria); Carsten Sprenger, University of Pompeu Fabra (Spain); Tor Eriksson, Aarhus School of Business (Denmark); Norvald Instefjord, Birkbeck College (UK); John S. Earle, Upjohn Institute for Employment Research (USA); Tom Kirchmaier, London School of Economics (UK); Theodore Baums, University of Frankfurt (Germany); Julie Ann Elston, Central Florida University (USA); Demir Yener, USAID (Bosnia and Herzegovina); Martin Conyon, The Wharton School (USA); Geoffrey Stapledon, University of Melbourne (Australia); Eugene Rastorguev, Secretary of the Board (Ukraine).

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

161

CORPORATE OWNERSHIP & CONTROL

Volume 4, Issue 2, Winter 2006-2007 (continued)

CONTENTS

IPO BOARDS OF DIRECTORS AND FIRM PERFORMANCE: THRESHOLD FIRMS AND GOVERNANCE THEORY BOUNDARIES 162

Suzanne M. Carter, James H. Davis, Charles R. Young CORPORATE GOVERNANCE AND FIRM PERFORMANCE OF HIGHLY LEVERAGED TRANSACTIONS: EVIDENCE FROM LEVERAGED RECAPITALIZATIONS AND MANAGEMENT BUYOUTS 170

Sung C. Bae, Hoje Jo THE EFFECTS OF INVESTOR PROTECTION ON THE VENTURE CAPITAL INDUSTRY 181

Luis J. Sanz CIRCUMSTANCES RELATING TO INTERLOCKING DIRECTORATES IN ITALY: AN EXPLORATORY STUDY 192

Garen Markarian, Antonio Parbonetti, Gary John Previts CORPORATE GOVERNANCE IN INDONESIAN STATE-OWNED

ENTERPRISES: FEEDING WITH WESTERN INGREDIENTS 205

Frederik G. Worang, David A. Holloway CORPORATE GOVERNANCE AND FIRM PERFORMANCE IN AN EMERGING MARKET - AN EXPLORATORY ANALYSIS OF PAKISTAN 216

Mohammed Nishat, Rozina Shaheen ECONOMIC GROWTH IN AFRICA: THE ROLE OF CORPORATE GOVERNANCE AND STOCK MARKET DEVELOPMENTS 226 Anthony Kyereboah-Coleman MANAGEMENT CONTROL IN ENTERPRISE SYSTEM ENABLED ORGANIZATIONS: A LITERATURE REVIEW 233 Pall Rikhardsson, Carsten Rohde, Anders Rom

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

162

IPO BOARDS OF DIRECTORS AND FIRM PERFORMANCE:

THRESHOLD FIRMS AND GOVERNANCE THEORY BOUNDARIES

Suzanne M. Carter*, James H. Davis**, Charles R. Young***

Abstract

Past research examining the influence of boards of directors on firm performance has acknowledged, but typically failed to account for, the early life cycle stage of the firm. This study analyzes the effectiveness of board structure and behavior on firm performance in the early stages of the life-cycle for start-up IPO firms. Results suggest that the life-cycle of the firm is an important contextual variable to include when determining board effectiveness. Keywords: Corporate governance, firm life-cycle, IPO

*University of Notre Dame, 18993 Stonewater Blvd, Northville, MI 48167, (248) 924-2295; fax: (248) 924-2295, [email protected] **University of Notre Dame, Notre Dame, IN 46556, 574-631-8614; fax: 219-631-5255; [email protected] ***Success Academy, Milwaukee, Wisconsin 55127, 651-917-8185; fax: 651-917-8075, [email protected]

Introduction For decades, researchers have studied the effects of boards of directors (BOD) on various firm outcomes, such as strategy, strategic change, social performance and financial performance (Baysinger & Hoskisson, 1990; Dalton, Daily, Ellstrand & Johnson, 1998; Zahra & Pearce, 1989). The purpose of past work has been in part to determine how much value is created for the firm by the structure, process and control of the BOD. While this work has produced mixed results (Donaldson & Davis, 1994), the vast majority of governance research studies have focused primarily on large, well-established Fortune 500 companies. Many scholars acknowledge that examining other arenas, where managerial and board discretion is likely to be higher, may yield a different set of results (Dalton et al, 1998; Johnson, Daily & Ellstrand, 1996). Some speculate that the BODs in small or entrepreneurial firms at the beginning of their life-cycle are likely to differentially impact their firm’s financial performance compared to those in larger well-established firms (Daily & Dalton, 1993; Zahra & Pearce, 1989). Zahra and Pearce (1989), noting a dearth of studies outside of the Fortune 500 samples, call the life-cycle of the firm a critical contingency that should be accounted for when studying the influence of BOD on financial performance.

Recently, to fill this gap in our knowledge, scholars have begun to explore board composition and its relationship to performance at the early stage of a firm’s life cycle (Certo, Daily & Dalton, 2001; Finkle, 1998). Our study continues that effort by

exploring company financial and stock performance subsequent to the Initial Public Offering (IPO) stage to clarify boundaries where previously theorized effects of BOD-performance associations are most likely to occur. We examine exclusively those entrepreneurial-type firms that are at the stage of entering IPOs that raised less than $20 million. These threshold firms are defined as firms that are at (or near) the point of transition from entrepreneurial to professional management (Clifford, 1973; Daily & Dalton, 1992). Our research question is whether the composition and process of threshold firms’ boards of directors impact the future financial performance of their firms.

This study has several theoretical and practical implications. We add to the governance literature by enhancing our understanding of how board composition and processes may be differentially effective for early threshold stages of a firm’s life-cycle. Setting boundary conditions for previously theorized effects of corporate governance roles is an important aspect of theory refinement. From a practical standpoint, we challenge those scholars who have suggested various “best approaches” for board selection and board decision-making processes without taking into consideration the key contextual variable of life-cycle stage.

We begin with a brief review of prior research on BOD and financial performance of both large and small firms. Next, we present and test a set of hypotheses using a sample of 150 small-cap threshold firms. We discuss results of the empirical study, and set forth theoretical, empirical, and practical implications.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

163

Governance Theory Previous researchers have used a number of theoretical lenses to examine the BOD-financial performance relationship, including legalistic, resource dependence, class hegemony and agency theory perspectives, among others (see Johnson, Daily & Ellstrand, 1996 and Zahra & Pearce, 1989 for reviews). The empirical results of these studies have been equivocal. Dalton et al (1998) performed a meta-analysis of the effects of corporate governance on financial performance using 54 previous studies of board composition and 31 studies of board leadership structure and found little evidence of systematic governance/financial performance relationships. Importantly, however, Dalton et al reported that approximately 80% of their sample consisted of large, Fortune 500 firms. They concluded that generalizability of their results beyond large U.S. corporations may be misleading. But the question remains, are existing theories better able to explain the BOD-performance relationships in other settings where discretion may be higher, such as the early life-cycle stage of the firm? Examining the contingent aspect of governance issues may be an important next step towards understanding under what circumstances boards may be most influential.

The Life-Cycle Contingency and Board Influence on Performance

The needs of firms change as they age suggesting firm life-cycle to be a critical contingency (Jawahar & McLaughlin, 2001). For example, as a firm is getting established in a marketplace, it is important that it develop a favorable reputation that may provide an intangible source of resources to the firm over its lifetime (Zahra & Pearce, 1989). The development of this reputation likely requires a substantially different set of resources and capabilities than would the maintenance of a well-established reputation. Furthermore, threshold firms often require significant capital investment, as well as community support as they build their legitimacy and reputation among their various stakeholders (Suchman, 1995). It is likely that CEOs of threshold firms are less constrained by organizational structures and control than those in well-established firms (Daily & Dalton, 1993; Norburn & Birley, 1988). An important result is that the CEO may be at greater discretion to build a board according to his/her own set of criteria. Indeed, in new start-ups, founder/CEOs have significant influence on who sits on the board (Timmons, 1999). The ability for BODs to influence future financial performance effectively may be a key motivation behind the CEO’s nomination of directors. Indeed, some outsiders may bring a critical element to early board operations that CEOs are likely to not only need, but

also to desire. Thus, the types of directors that are selected at the IPO stage of a firm may ultimately influence the firm’s future financial performance.

Some effort has been made to understand the differential impact of BODs on small firms. For example, Daily and Dalton (1993) found that boards of small cap firms are likely to have significantly different board composition than might be evident at larger Fortune 500 firms and that BOD composition/ financial performance relationships were found to be more effective for those firms that followed typical board reform adoptions such as separating CEO and BOD roles, and adopting a greater number of outsiders to the board. The mean age of the firms in the Daily and Dalton sample was over 17 years and thus it is unclear whether similar effects might be found for firms at the threshold of going public.

Closer to the empirical examinations made in the present study, several scholars have examined the impact of board composition on IPO pricing (Certo et al, 2001; Finkle, 1998). These scholars found differential impact of board composition on IPO pricing using resource dependence and signaling theories. For example, Certo et al found a negative relationship between board size and IPO underpricing but a positive relationship between board independence and IPO underpricing, suggesting that underwriters may value those inside directors that have familiarity with the firm rather than more independent directors. Finkle (1998) explored biotechnology firms at the IPO stage and found that CEO expertise increased the size of the firm’s IPO, but had no impact on subsequent stock market valuation. Our study extends these efforts by examining additional board roles as well as the board’s association with subsequent financial and stock performance of the firm – key to understanding board effectiveness at this stage. We now turn to that issue. Governance scholars have agreed that several roles and responsibilities of the BOD are particularly important to their effectiveness. These roles can generally be divided into three key responsibilities - service, strategy and control (Zahra & Pearce, 1989). Each of the roles is expected to ultimately influence the company’s performance. The effects of the BOD may be more pronounced at the IPO life-cycle stage of the firm for a number of reasons. First, strong boards at the threshold stage are particularly critical as capital markets and investors assess the firm. Additionally, the management needs of the firm begin to shift from an entrepreneurial style to professional management, and thus board responsibilities play a greater role in managing this change. Finally, at this stage the effects of the board on a new venture are most salient in that firm performance can be assessed in market terms as well as in accounting terms. Hence, it is an ideal time to assess the impact of the board on firm performance.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

164

We will discuss these three main responsibilities and develop hypotheses specific to these roles below.

Service. The service component involves being a boundary spanner with the external environment, finding and obtaining necessary resources, and establishing networks to legitimize the organization and improve its reputation (Zahra & Pearce, 1989). The main theoretical stance taken in regard to this role is resource dependence (Pfeffer & Salancik, 1978). Scholars taking this perspective argue that directors are responsible for providing the firm with critical resources that may not otherwise be obtained. Selecting board members with the power to obtain these resources may be crucial to the firm's survival. Previous research generally supports the central argument of resource dependence for well-established firms (Pfeffer & Salancik, 1978; Zahra & Pearce, 1989). The need for reduced environmental uncertainty may be even greater for threshold firms. These firms are not likely to have established strong reputations in their community or in the broader community that will help them ensure long-term survival. Nor have these threshold firms had the opportunity to develop crucial contacts that will provide access to key scarce resources. Thus, to improve performance, having boundary spanners on the BOD will likely be critical in the IPO life-cycle stage.

Hypothesis 1: The greater the number of service

directors on the board of the threshold firm at its

IPO stage, the greater the increase in subsequent

firm performance.

Strategy. The second responsibility of the board is to help management with strategic decisions. The strategy role of directors includes giving counsel and advice to the CEO, initiating analyses, suggesting alternatives, guiding the articulation of the firm's mission and setting guidelines for implementation of the firm's strategy (Zahra & Pearce, 1989). Scholars emphasizing this role promote the importance of expertise and understanding of firm activities to ensure board effectiveness and improve firm performance. Evidence of the contribution that boards have given well-established companies for the strategy role has been limited (Henke, 1986). However, it is likely that management of threshold firms has a greater need for the expertise and advice of board members than would be necessary for well-established firms. Indeed, Finkle (1998) found that CEO expertise was associated with larger IPO offerings. Directors experienced with the firm’s services/products and customer markets may have a similar impact upon the firm’s future financial performance. Expertise in the industry is likely to be a key characteristic that the CEO is searching for in the IPO stage. Those firms that capitalize on this element of a board’s role are likely to have better performance than other firms.

Hypothesis 2: The greater the number of

strategy specialists on the board of the threshold

firm at its IPO stage, the greater the increase in

subsequent firm performance. The process by which the board operates can be

an important element to the effectiveness of the board of threshold firms. One measure of board activity is the number of meetings held by the board over the course of each fiscal year (Vafeas, 1999; Zahra & Pearce, 1989). There are opposing views on the likely benefit of board meetings. One view suggests that board meetings are indeed beneficial to shareholders (Conger, Finegold & Lawler; 1998). Alternatively, Vafeas (1999) found that shareholders place a lower value on firms whose boards meet more frequently. However, he also finds that years with abnormally high meeting frequencies are followed by improvements in operating performance, suggesting that these meetings were effective nonetheless. Companies that have recently been established are much more likely to need significant help from the board in establishing a credible place in the community, developing a favorable reputation, providing and sustaining funding needs, determining growth opportunities, etc. (Reingold, 1999). As such, numerous meetings by the BODs will likely be more effective for the firm's future performance. Moreover, as noted by Judge and Zeithaml (1992), recent institutional pressures have increased the expectation by stakeholders that BODs become more active in day-to-day activities of the firm. Thus, boards formed under this increased pressure are likely to attend to this issue to a greater extent than older more established boards.

Hypothesis 3: The greater the board activity of

the threshold firm at its IPO stage, the greater the

increase in subsequent firm performance.

Control. The final responsibility for the BOD is control. Agency theorists contend that the control role of the board is the most critical (Zahra & Pearce, 1989). However, the degree to which this control is influential or important at the IPO stage is still in question. While most empirical studies examining control issues have examined large firms exclusively, some research has examined firms in IPO situations. Beatty and Zajac (1996) argued that agency problems arise in all situations in which there is no single 100-percent owner/entrepreneur who incurs the full cost of his or her actions. Thus, they argue that this life-cycle stage may also be relevant for the control role of the BODs.

From this perspective, directors selected to the board are in a position to control upper management. A board whose membership is independent of management is best suited to control the decisions and activity of upper management. Independence is best gained by appointing outside directors who are neither employees of the firm, nor members of the top management team or past top management

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

165

groups (Jones & Goldberg, 1982). Yet outside directors are not necessarily placed on threshold boards by CEO/founders for control, but rather for collaboration, advice, expertise and boundary spanning capabilities. And indeed, venture capitalists are frequently considered to be “insiders” because of their lack of independence with management (Reingold, 1999). In many cases, the firm would likely be unable to reach the threshold stage without the venture capitalist’s financial backing, increasing the power of the venture capitalist to influence executive decision-making. Bertsch of TIAA-CREF indicates, “We would consider a founding venture capitalist to be an insider,” and feels that a “substantial majority” of directors should be outsiders [non-venture capitalists or employees] to avoid conflicts of interests.” (Reingold, 1999: 132). Independence seems to be the critical element that separates insiders from outsiders (Daily et al, 1999; Lorsch, Zelleke & Pick, 2001). While agency theory argues that outside directors in general improve firm performance through their control role, given the life-cycle context of threshold boards, we contend that simply having a larger contingency of outside directors is unlikely to provide the controls that agency theorists expect. Instead, the control function may be best attended to by directors that are

independent of management, thus excluding venture capitalists from the “outsider” category.

Hypothesis 4: The greater the ratio of independent directors to total directors of the BOD of the threshold firm at its IPO stage, the greater the increase in subsequent firm performance.

Methodology

Firms selected to test the hypotheses of our study were transitioning from start-up stages to their initial public offering in 1993. We specifically examine those entrepreneurial-type firms that are at the stage of entering IPOs that raised less than $20 million (deemed threshold firms, Clifford, 1973; Daily & Dalton, 1992). A sample of 150 firms was randomly selected from Standard and Poor’s Smallcap 600 guide for statistical analysis. Marketing, accounting, industry, and director composition data was collected from proxy reports and Standard and Poor’s Smallcap 600 guide and directory as well as through Primark financial services. Additionally a series of structured interviews with the top executive (founder) of each firm was conducted which provided key data on board of director background and experience.

Dependent Variables - Firm Performance

In order to test both market returns as well as accounting returns (Cochran & Wood, 1984; Daily & Dalton, 1993), we used both Market Value and Net Income as suggested by Zahra and Pearce (1989).

We study the influence of board characteristics on the change in both marketing and accounting measures of performance using a two-year lag, considered adequate to capture the impact of the independent variables on the dependent variables. This change measure is based on the suggestions of Zahra and Pearce (1989), who note that static performance measures have been overemphasized in BOD studies, and suggest that the dimension of change should be considered to a greater extent.

Market Value Change. The percentage change in market value over a two-year period was calculated by subtracting each firm’s year ending 1995 market value from its initial year ending 1993 market value and dividing by the 1993 value. This performance variable reflects the firm’s market performance over a two-year period.

Net Income Change. Most executives interviewed stated that net income is a measure of performance that was meaningful to their firm and was tracked by the board. A performance change score was calculated by dividing the difference between 1995-93 Net Income by 1993 Net Income. Thus the accounting measure was percentage change in net income using a two-year lag.

Independent Variables

Service. Directors that perform a service role are expected to enhance the company reputation and span boundaries between the firm and its external environment. These directors typically have alliances and networks that can be utilized by the firm. We contend that threshold firms gain this type of service in part by having venture capitalists on their boards. Venture capitalists typically have competencies that ensure that necessary resources become available to the company as needed (Jain, 2001). Most new ventures require networks of venture groups to obtain sufficient funding to grow to the point where an IPO is possible (Berlin, 1998). A venture capitalist often brings a strong understanding of the community resources available and the best means of obtaining these resources to the board (Reingold, 1999). Venture capitalists serving in the role of service directors can be strong assets towards securing critical resources and reducing environmental uncertainty. The measure used was the number of venture capitalists on the board and is labeled Venture Capital Directors.

Strategy. Directors who can help the firm strategically are those that have expertise with the firm’s product/service and/or industry. These directors have skills, knowledge and experience that the CEO/founder can tap to improve the competitive position of the firm in its markets. In the structured interviews, top executives were asked how many of their board’s directors had related firm and industry experience. The measure for strategy directors was the ratio of number of executives with related

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

166

expertise to the total number of board directors, and is labeled Percentage Related Directors.

Additionally, we examined the strategy responsibilities by testing the degree to which the intensity of board activity influenced firm performance measures. Thus, as measured in other studies of board activity, we used a proxy for board activity intensity by the total number of annual, ‘in person’ board meetings as reported in proxy reports (Vafeas, 1999), labeled Number of Board Meetings.

Control. One common way of assessing board control over the firm is with the ratio of outside directors to the total number of board directors (Daily, Johnson & Dalton, 1999; Pearce & Zahra, 1992). Independent outside directors are herein defined as those directors who are not employees of the firm and are considered to be independent of management, thus reducing conflicts of interest (Daily et al, 1999). Outside directors are thought to bring objectivity to critical organizational decisions and ensure that shareholder wealth and vision for the firm are protected. Thus, we measure control with the variable labeled Percentage Independent Outside

Directors, including only outsiders considered to be independent of management (thus excluding venture capitalists and insider employees).

Control Variables

Controls were selected to ensure that the variance accounted for in hypothesis testing could be attributed to the board and not other firm and industry factors. The Log of Sales was used as a control for firm size. Because multiple industries were examined, industry was controlled using a measure of Average Industry Net Income. Similar control measures have been used in other studies examining board variables (Judge & Zeithaml, 1992).

Data Analysis

A final sample of 134 (89% of the sample of 150 start-ups contacted) provided the information needed for statistical testing. The average board in our sample had 6 directors, 58.39% outside directors and met 5.79 times during the year. Threshold firms within our sample came from 80 different four-digit SIC codes. See Table 1 for a summary of means, standard deviations and correlations. [See appendices, Table 1].

Ordinary Least Squares (OLS) multiple regression was used for hypothesis testing. The two dependent variables of interest for performance were the percent change in Market Value from 1993 to 1995 as well as the percentage increase in Net Income from 1993-1995 (Table 2). We entered each set of hypothesized variables into the model according to their theorized impact on the level of firm performance (service, strategy and control). In each regression model, we include two control

variables, firm size and industry profitability. We report standardized coefficients and one-tailed tests. We then present a full model including all variables. Below we will describe the results of our tests on the service, strategy, and control hypotheses as well as those of the full model. [ See appendices, Table 2].

Results

The first hypothesis examined the effect of venture capital directors on firm performance. It was hypothesized that the networking and boundary spanning function of service directors would significantly increase the performance of the firm. There was a range of zero to four venture capital directors on the boards in our sample with an average of .81. This suggests that most boards in our sample had at least one service director. Venture capital directors were significantly positively related to both performance measures (β = .357, p< .001, for market value, and β = .198, p< .05 for net income). This result supports the first hypothesis, that service directors are associated with an increase in firm performance both from a market as well as an accounting perspective.

Hypothesis 2 examined whether directors with related experience with the products or services of the firm explained the variance in firm performance. As predicted, we found that these strategy directors had a positive relationship to both market value change β = .266, p<.05 and net income change (β = .277, p< .05), thus supporting hypothesis 2. Hypothesis 3 argued that the activity level of the board affects firm performance. Board activity showed no support of Hypothesis 3 with market value change and modest support with the change in net income (β = .165, p< .10). Thus, there is some limited, but mixed support for Hypothesis 3.

Hypothesis 4 posits a positive relationship between the percentage of independent outsider directors to firm performance. In this case, this ratio was not found to be significant when used to explain changes in market value, and was found to be negative and significant, in the opposite of the predicted direction, for net income (β = -.184, p<.05), giving no support to Hypothesis 4. That is, independent outside directors did not have the positive influence on firm performance as expected by agency theory predictions. In order to determine whether our results were due to the unique nature of the venture capitalists on the board (i.e., considered to be non-independent), we ran a post hoc regression analysis to compare total outsiders (including venture capitalists) with total directors. Our results showed that this measure of total outsiders failed to explain a significant amount of the variance in net income change. It did, however, explain a significant amount of the variance in market value change (β = .186, p < .05). If venture capitalists are considered outside directors their influence was

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

167

enough to change the relationship from significantly negative to significantly positive. Thus the venture capitalists significantly influenced financial performance (as found in hypothesis 1) above and beyond that of the other outside board members.

The full models are reported for both market value change and net income change as well. These full models had R-squared values of .154 and .118 respectively. The variables in the full model had similar results to those in the separate regression equations with only two exceptions. Specifically, in the full model for net income, the number of venture capitalists as well as the independent outsiders is each no longer significantly associated with net income change. Instead, it appears that the strategy variables exhibit the greatest influence over net income. The implications of these exceptions are discussed below.

Discussion and Implications

In this research we have tried to determine how the IPO stage of the firm contributes to our understanding of boundary conditions for corporate governance research. Our research examined whether the match between board attributes within the context of threshold firms affected firm performance. We found that service directors who span resource market boundaries as well as strategy directors who have related firm specific expertise influence both the market value and the net income of the threshold firm. However, we had mixed evidence as to whether threshold firms whose executives have more meetings with their boards (strategy process) have significantly higher performance than those that do not. Specifically, the number of meetings was modestly significant using an accounting performance measure but failed to explain a significant amount of market performance change suggesting perhaps that shareholders view threshold BOD meetings as being similarly ineffective as those of larger firm BOD meetings (Vafeas, 1999).

Control through the use of independent outside directors as prescribed by agency theory failed to improve either the market value or net income of the threshold firm. Indeed, independent board members had a negative and significant association with firm performance from an accounting perspective while they had no effect on market performance. Certo et al (2001) found that greater proportions of outside directors were positively associated with IPO underpricing suggesting that oversight of firm management may be considered by underwriters to be less critical in the IPO context. Consistent with Certo et al’s findings, our study adds further evidence that this consideration may be valid.

In addition, our complete model demonstrates the effect different types of directors have on different aspects of firm performance. Venture

capitalist directors explain the variance in market performance to the greatest extent and directors with related business experience explain the variance in net income to the greatest extent. Venture capitalists appear to bring market understanding and boundary spanning competencies to the firm translating into improved market performance at the IPO stage. Directors with related business experience bring tacit operational knowledge and mentoring experience that help the firm’s efficiency, effectiveness and ultimately, accounting performance at the IPO stage. Thus, based on our analysis of these threshold firms, there is some evidence confirming the proposition that the match between board form, function and context, and in particular, life-cycle, has merit (Zahra & Pearce, 1989). While we found evidence that independent outsiders actually may have harmed the effectiveness of firms at this stage of the life-cycle, other studies of outsiders of large companies have found similar negative effects (Rechner & Dalton, 1988; Chaganti, Mahajan & Sharma, 1985). These studies suggest that outsiders play only a minimalist role, refraining from active initiative-taking, reacting to managerial proposals and not exercising incisive questioning of management. In contrast, Daily and Dalton (1993) found a positive relationship between outsider ratio and firm performance for small firms (Their measure of outsiders included everyone not employed by the firm and thus may have included individuals who were not truly independent). Even so, as Daily and Dalton speculate, it is likely that the service and resource functions of those independent board members may be more critical to the small firm than the control functions. Indeed, why independent outsiders at the threshold stage are similarly ineffective to those outsiders in larger firms may be partially explained not by their lack of initiative- taking or incisive questioning, but instead by the differential boundary spanning and resource acquisition needs of the firm at this stage. Perhaps, as Certo et al (2001) suggest, the threshold stage of the firm is an arena in which the control function of the board is unnecessary. Indeed, at this stage of a firm’s life cycle, ownership may not yet be dispersed enough to require the need for management oversight prescribed to older, more established firms (Jensen & Meckling, 1976). This standard application of agency theory does not seem to apply to the threshold context. Thus, the IPO stage may demonstrate an important boundary condition to agency theory. From a practical standpoint, one must begin to question the value of independent outside board members if empirical evidence continues to mount that outsiders do not offer the improvements in firm performance that agency theorists would expect. Agency prescriptions have found a strong following within the business world. Institutional investors are successfully encouraging under-performing companies to improve their boards by

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

168

making them more independent of management through an increase in the representation of outside directors (Pearce & Zahra, 1992). And yet this control reform seems to have no bounds. Is control a necessary role for BODs in the IPO stage? Our results suggest that it may not be – at least not in our traditional understanding. However, we did find evidence that some outside directors who are not truly independent of the firm - venture capitalists, seem to add boundary spanning capabilities and knowledge that can be used by firm executives – specifically, it appears that venture capitalists are critical to the success of these threshold organizations. Our results suggest that it is not just outsiders in general, but the specific type of outsider, that matters when predicting performance. Collaboration efforts, not control, per se, seem to affect firm performance at the IPO stage of the life-cycle. Both theoretical and empirical studies in the future should attend to finer grained measures of outsiders versus insiders to understand the true implications of certain board members on firm performance. There are limitations to this study design that should be addressed. Causality is always a problem in governance research. We attempted to overcome this problem by using a change measure with a two-year performance lag. Shorter performance lags may not reflect the firm’s long-term performance but simply reflect the speculation and hype of the market. Additionally, our study only examined a limited number of roles that BODs serve. Future research should examine how important other characteristics of board members are to firm performance. For example, the prestige of board members may substantially influence not only market measures of performance but operating performance as well in the form of increased business while threshold firms are trying to establish their place in the market. These, as well as other characteristics, may prove to be differentially effective for firms at the early life-cycle stage and should be examined in future studies.

Conclusion

This research supports the notion that the life-cycle of the firm is an important contingency supporting Zahra and Pearce’s (1989) argument that context matters in governance research. This research is one of very few empirical investigations of threshold firms at the IPO stage of the life-cycle. Our study reveals several things about organizational governance that should influence future research. First, we find support for the proposal that successful board structure and process is context dependent. The performance of threshold firms is explained to some degree by the service and strategy attributes of skilled directors. Board control of executives through the use of independent directors does not seem to explain the performance of threshold firms. Firms in

the IPO stage of their life-cycle appear to need a more collaborative board that provides expert advice and bridges organizational boundaries than more mature organizations. We add our results to others that have concluded that a ‘one-best-way’ theory to organizational governance is incorrect (Donaldson & Davis, 1991). The correct governance structure and process is contingent upon the conditions of the firm. The mixed results that currently abound may be due to the homogenization of very different governance needs regardless of the context studied (Daily et al, 1999). Future research should further develop contingency frameworks to advance the governance literature in constructive ways.

References

1. Baysinger, B. & Hoskisson, R. E. 1990. The composition of boards of directors and strategic control: Effects on corporate strategy. Academy of

Management Review. 15 (1): 72-87. 2. Certo, S., Daily, C., & Dalton, D. 2001. Signaling

firm value through board structure: An investigation of Initial Public Offerings. Entrepreneurship Theory

and Practice.Winter.33-50. 3. Chaganti, R.S., Mahajan, V., & Sharma, S. 1985.

Corporate board size, composition and corporate failures in retailing industry. Journal of Management

Studies, 2: 400-416. 4. Clifford, D. K. 1973. Growth pains of the threshold

company. Harvard Business Review, 61 (3): 143-154. 5. Conger, J., Finegold, D. & Lawler, E.III. 1998.

Appraising boardroom performance. Harvard

Business Review, 76: 136-148. 6. Daily, C. & Dalton, D. 1992. Financial performance

of founder-managed vs. professionally managed small corporations. Journal of Small Business Management, April: 25-34.

7. Daily, C. M & Dalton, D. R. 1993. Board of director’s leadership and structure: Control and performance implications. Entrepreneurship Theory and Practice, Spring: 65-81.

8. Daily, C. M., Johnson, J. L. & Dalton, D. R. 1999. On the measurements of board composition: Poor consistency and a serious mismatch of theory and operationalization. Decision Sciences, 30 (1): 83-106.

9. Dalton, D. R., Daily, C. M., Ellstrand, A. E & Johnson, J. L. 1998. Meta-Analytic reviews of board composition, leadership structure, and financial performance. Strategic Management Journal, 19.

10. Donaldson, L., & Davis, J.H. 1991. Stewardship theory or agency theory: CEO governance and shareholder returns. Australian Journal of

Management, 16(1): 49-64. 11. Donaldson, L., & Davis, J.H. 1994. Boards and

company performance: Research challenges the conventional wisdom. Corporate Governance: An

International Review, 2 (3):151-160. 12. Finkle, S. 1998. The relationship between boards of

directors and Initial Public Offerings in the Biotechnology industry. Entrepreneurship: Theory

and Practice, Spring 22 (3): 5-30. 13. Henke, J. W., Jr. 1986. Involving the board of

directors in strategic planning. Journal of Business

Strategy, 7 (2): 87-95.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

169

14. Jain, B. A. 2001. Predictors of performance of venture capitalist-backed organizations. Journal of Business

Research. 52: 223-233. 15. Jawahar, I., & McLaughlin, G. 2001. Toward a

descriptive stakeholder theory: An organizational life cycle approach. Academy of Management Review, 26.

16. Jensen, M.C., & Meckling, W.H. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3: 305-360.

17. Johnson, J. L., Daily, C. M. & Ellstrand, A. E. 1996. Boards of directors: A review and research agenda. Journal of Management, 22 (3): 409-438.

18. Jones, T. M. & Goldberg, L. D. 1982. Governing the large corporation: More arguments for public directors. Academy of Management Review. 7.

19. Judge, W. & Zeithaml, C. 1992. Institutional and strategic choice perspectives on board involvement in the strategic decision process. Academy of

Management Journal, 35 (4): 766-794. 20. Lorsch, J.W., Zelleke, A. S. & Pick, K. 2001.

Unbalanced boards. Harvard Business Review, February, 79 (2): 28-30.

21. Norburn, D. & Birley, S. 1988. The top management team and corporate performance. Strategic

Management Journal, 7: 110-117.

22. Pearce, J. A. & Zahra, S. A. 1992. Board composition from a strategic contingency perspective. Journal of

Management Studies, 29 (4): 411-437. 23. Pfeffer. J & Salancik, G. R. 1978. The external

control of organizations: A resource-dependence

perspective. New York: Harper and Row. 24. Rechner, P.L., & Dalton, D.R. 1988. Board

composition and organizational performance: A longitudinal assessment. Paper presented at the annual meeting of the Academy of Management, Anaheim.

25. Reingold, J. 1999. Dot.Com boards are flouting the rules. Business Week, New York, December 20.

26. Shivdasani, A. & Yermack, D.1999. CEO involvement in the selection of new board members: An empirical analysis. The Journal of Finance, LIV (5): 1829-1853.

27. Suchman, M. C. 1995. Managing legitimacy: Strategic and institutional approaches. Academy of

Management Review, 20 (3): 571-610. 28. Timmons, J.A. 1999. New Venture Creation. Boston:

McGraw-Hill. 29. Vafeas, N. 1999. Board meeting frequency and firm

performance. Journal of Financial Economics. 30. Zahra, S. A. & Pearce, J. A. 1989. Boards of directors

and corporate financial performance: A review and integrative model. Journal of Management, 15 (2).

Appendices

Table1. Means, Standard Deviations & Correlations a

Means 1 2 3 4 5

1 Percent increase market value 93-95

1.123 2.373

2 Percent net income change 93 to 95

-.0973 3.351 .220

3 Venture Capitalist Directors

.8060 1.037 .339 .177

4 Percentage Independent Outside Directors

.450 .206 -.118 -.169 -.493

5 Percentage Related Director

.123 .179 .280 .264 .374 -.102

6 Number of Meetings

5.795 3.180 .070 .227 .285 -.114 .291

a p<.05 for all r>.14; p<.01 for all r>.18.

Table 2. OLS Regressions: Percentage Change in Market Value 1993-1995;

Percentage Change in Net Income 1993-1995 a

Variables

Service

MktVal

Strategy

MktVal

Control

MktVal

Full

MktVal

Service

NI

Strategy

NI

Control

NI

Full NI

Constant 0.00 (2.53)

0.00 (2.24)

0.00 (2.56)

0.00 (2.65)

0.00 (1.81)

0.00 (2.25)

0.00 (2.22)

0.00 (2.51)

Log of Sales

.063 (.564)

.116 (.464)

.044 (.550)

.124 (.482)

.003 (.394)

-.041 (.453)

.010 (.414)

.030 (.455)

Industry Net Income

-.046 (.002)

-.073 (.002)

-.042 (.002)

-.075 (.002)

-.055 (.002)

-.097 (.002)

-.065 (.002)

-.062 (.002)

Venture Capital Directors

.198* (.332)

.057 (.333)

.357*** (.242)

.361** (.331)

Percentage Related Director

.277* (.277)

.263* (.017)

.266* (.015)

.164+ (.016)

Number of Board Meetings

.165+ (.106)

.159+ (.109)

-.016 (.101)

-.069 (.100)

Percentage Independent Outside Directors

-.184* (1.73)

.018 (1.68)

-.078 (1.23)

.122 (1.51)

R-Squared

.038 .116 .035 .118 .131 .080 .023 .154

Standardized coefficients reported. Standard errors are in parentheses.

a + p < .10 ;* p < .05; ** p < .01; *** p < .001

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

170

CORPORATE GOVERNANCE AND FIRM PERFORMANCE OF HIGHLY

LEVERAGED TRANSACTIONS: EVIDENCE FROM LEVERAGED

RECAPITALIZATIONS AND MANAGEMENT BUYOUTS

Sung C. Bae*, Hoje Jo**

Abstract

We examine the effects of several corporate governance mechanisms on firm performance of two highly leveraged transactions (HLTs). Employing forty-one firms that implemented leveraged recapitalizations (LRs) and eighty-eight firms that undertook leveraged management buyouts (MBOs) during the period 1985-1990, we find that prior to their HLT, MBO firms tend to be smaller, be less profitable, have higher managerial ownership, have lower block ownership, and have a smaller fraction of independent outside directors on their board than LR firms. On the other hand, we observe no significant difference in board size or equity-based compensation between MBO and LR firms. Our regression results show that higher managerial ownership and greater equity-based compensation, which presumably help align managers’ incentives with shareholders, are strongly associated with operating performance of MBO firms, but only marginally with operating performance of LR firms. In contrast, greater outside representation on corporate boards, which presumably improves shareholder monitoring, is strongly associated with operating performance of LR firms, but only marginally with operating performance of MBO firms. Blockholders’ ownership, another effective mechanism of internal monitoring, is found to play a relatively insignificant role in enhancing operating performance of firms that go through a HLT. Our results are not attributed either to the difference in firm size or to an industry effect. Keywords: corporate governance, firm performance, management buyouts, leveraged recapitalizations

* Corresponding author: Department of Finance, 201 BA Bldg., College of Business Administration, Bowling Green State University, Bowling Green, OH 43402, USA; Tel) 419-372-8714; Fax) 419-372-2527; E-mail) [email protected]. ** Santa Clara University We thank Yaron Brook, Saeyoung Chang, Patric Hendershott, Michael Jensen, Jonathan Karpoff, Tim Opler, Young Seok Park, Atulya Sarin, Dennis Sheehan, Meir Statman, René Stulz and session participants at the Annual Korean Securities Research Institute Symposium for many valuable comments on earlier versions of our paper. Bae acknowledges financial support from the CBA summer research grant program at Bowling Green State University, and Jo acknowledges a Leavey Research Grant at the Leavey School of Business and the Dean Witter Foundation for financial support.

1. Introduction In modern corporations, stockholders rely on internal and external governance mechanisms to help resolve agency problems that arise from the separation of ownership and management. Boards of directors and blockholders are important internal control mechanisms whereas the takeover market is a major source of external control. In this context, a growing body of research has dealt with the effectiveness of alternative corporate governance systems such as the Anglo-Saxon market based system and the Continental-European bank based system.1 An active market for corporate control would make corporate governance ultimately market-based. Widespread

1Dennis and McConnell (2003) and Holmstrom and Kaplan (2003) review recent development of corporate governance issues.

corporate misconduct in the U.S. during the early 2000s, however, raises questions about its effectivenes.

In this study, we examine how various corporate governance mechanisms affect firm performance of highly leveraged transactions (HLTs). We take two HLTs that were widely used in the market for corporate control during the 1980s: leveraged management buyouts (MBOs), in which a company is purchased by a group of its managers with debt financing, and leveraged recapitalizations (LRs), in which a large debt-financed cash payout, generally either a special dividend or tender offer repurchase, is distributed to stockholders. These two HLTs share many similarities in that both often occur in response to a takeover threat and tend to substantially increase firm value, debt levels, and insider ownership. MBOs and LRs, however, lead to a very different post-HLT governance system. MBOs take a company private

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

171

with little or no publicly traded equity whereas LRs retain relatively diffuse outside ownership of publicly traded equity. Contrasting MBOs and LRs provides an excellent experiment for exploring the effectivenss of vastly different corporate governance systems and their effects on firm performance while controlling for increased leverage.

Previous research documents the characteristics of HLTs and their effects on securityholders' wealth and firm performance.2 These studies, however, pay little attention to the relation of various governance mechanisms of MBO and LR firms on firm performance. Although it would be interesting to examine the impact of pre-HLT corporate governance on post-HLT operating and stock performance, post-MBO performance data are difficult to obtain due to MBO firms’ private company status. Accordingly, we investigate the potential differences in corporate governance mechanisms of ownership structure (managerial ownership and blokcholder ownership), corporate boards, and executive compensation for the pre-HLT period and the empirical relations between pre-HLT corporate governance characteristics and pre-HLT firm performance of firms conducting MBOs and LRs. The four pre-HLT governance mechanisms of MBO and LR firms would all be closely related to the firm’s operating performance. Jensen and Meckling (1976) argue that increased equity ownership by managers provides them with incentives to make value-maximizing decisions. Morck, Shleifer, and Vishny (1988) and McConnell and Servaes (1990) document a curvelinear relation between management ownership and firm value. Jensen and Murphy (1990a, 1990b) argue that equity-based compensation provides managers with an incentive to maximize value. Additionally, large outside blockholders, recognizing that managers have a tendency to skew decisions in directions that would benefit themselves, have an incentive to monitor managers (Demsetz and Lehn (1985), Jensen (1989), and Shleifer and Vishny (1986)). Denis and Serano (1996) find that monitoring by active outside blockholders with substantial ownership stakes often promotes valuable internal control efforts. It has been suggested that the Anglo-Saxon regime shareholders may control management decision making through both the board and the market for corporate control. In the Continental-European system, alternately, shareholder control can only take place through corporate boards in the absence of the market for corporate control and the effective mechanisms for legal investor protection.3 Hence,

2See Palepu (1990) and Halpern, Kieschnick, and Rotenberg (1999) for a review of LBO research and Palepu and Wruck (1992) for a review of LR research. Bae, Hendershott, and Jo (2001) investigate factors determining a firm’s choice of an organizational form between a LBO and a LR. 3The Economist (January 29, 1994) argues that American corporate governance is improved by merger and takeover activity, while questioning the effectiveness of the German and

shareholders in both regimes will be seriously interested in board characteristics when it comes to the accountability of managements for corporate performance. As noted in the seminal study of Fama and Jensen (1983), boards can be effective mechanisms to monitor top management on behalf of dispersed shareholders by effectuating management appointment, dismissal, suspension, and reward. Several studies suggest that top managers are more vigorously monitored when the board of directors is controlled by independent outside directors (see, e.g., Berger, Ofek, and Yermack (1997), Brickley, Coles, and Terry (1994), Byrd and Hickman (1992), and Weisbach (1988)). Yermak (1996) also argues that board size has an impact on the quality of internal monitoring. In contrast, examining a two-tier board system of Netherlands, Ees, Postma, and Sterken (2003) find no evidence of a strong relation between firm performance and board size. They also report that the number of outside board members is negatively associated with firm performance, whose evidence is contrary to those from Bhagat and Black (1998), Dalton et al. (1998), and Hermalin and Weisbach (1991).4 Combined together, well-designed corporate governance systems would either align managers' incentives with shareholders through substantial managerial ownership and equity-linked compensation plans or promote active monitoring on managers’ decision making through outside block ownership and boards of directors. Hence, firms with good corporate governance should put greater emphasis on value maximization.5

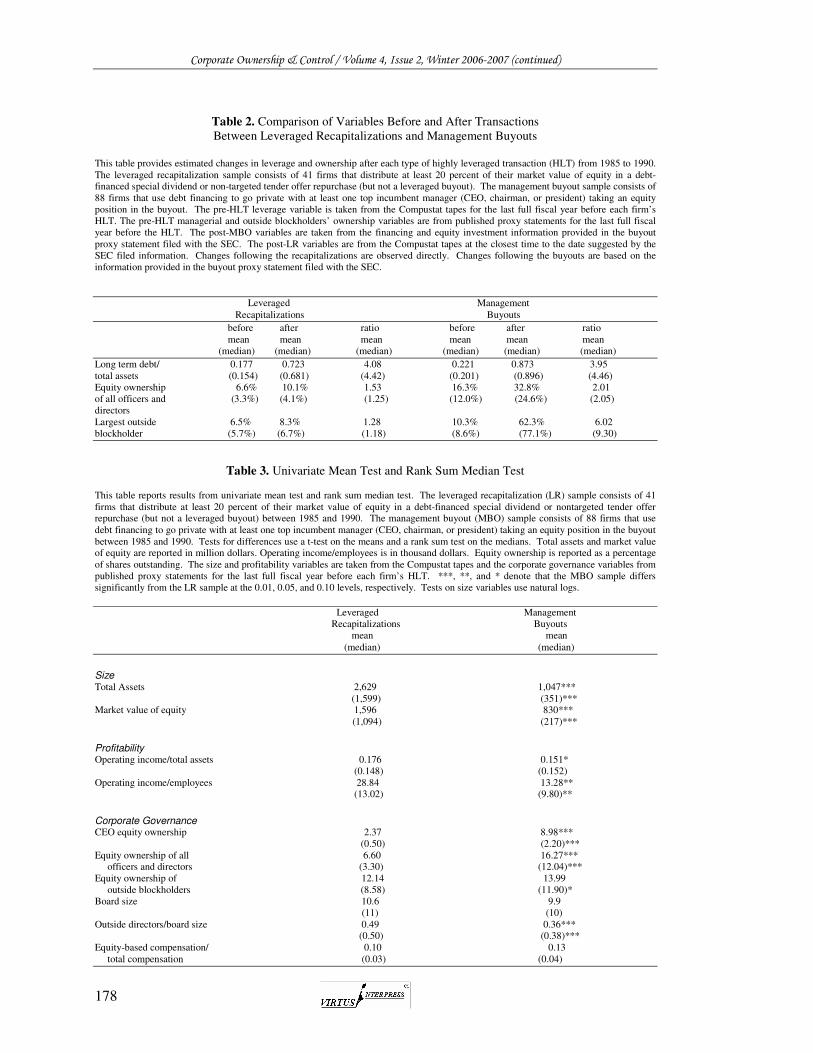

Based upon a sample of 41 LRs and 88 MBOs during the 1985-1990 period, our empirical results indicate the following. Prior to their HLT, MBO firms tend to be smaller, be less profitable, have higher insider ownership, have lower block ownership, and have a smaller fraction of independent outside directors on their board. A further analysis shows that these findings can not be attributed either to the difference in firm size or to an industry effect.

We perform regression analysis of two industry-adjusted measures of firm’s operating performance against four corporate governance mechanisms along with firm size as a control variable. The results show that CEO equity ownerhsip and the fraction of indenpendent outside directors on the board are significantly positively related to operating

Japanese corproate governance model. 4In a similar line of reasoning, Hartzell and Starks (2003) suggest that institutional investors also serve a monitoring role in mitigating the agency problem between shareholders and managers. 5Several studies examine the relation between foreced CEO turnover and firm performance (see, e.g., Allgood and Farrell (2000), Parrino (1997), Warner, Watts, and Wruck (1988)). Interestingly, Huson, Parrino, and Starks (2001) report that although there were significant changes in internal monitoring mechanisms from early 1970s to mid-1990s, the relation between the likelihood of forced CEO turnover and firm performance has not changed significantly over the time.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

172

performance for MBO firms, but marginally to operating performance for LR firms. On the contrary, board dependence, measured by the ratio of outside independent directors on the board, is strongly related to operating performance of LR firms, but only marginally to operating performance of MBO firms.

Our results suggest that higher managerial ownership and greater equity-based compenstion relative to total compensation, which presumably help align managers’ incentives with shareholders, are strongly associated with operating performance of MBO firms. In contrast, greater board independence measured by the number of outside directors on corporate boards, which presumably improves shareholder monitoring, is strongly associated with operating performance of LR firms. Blockholders’ ownership, another effective mechanism of internal monitoring, plays little, or relatively insignificant, role in enhancing operating performance of firms that go through a HLT.

Our paper proceeds as follows. Section II compares governance and ownership structures between LR and MBO firms, and Section III discusses our sample data and measurement of variables. Section IV presents empirical results with conclusions in Section V. 2. Governance and Ownership Structures Between LR Firms and MBO Firms Previous studies document a different ownership structure between LR and MBO (or LBO more generally) firms and provide evidence consistent with greater management incentive rationale for MBO firms. For a sample of 76 MBOs in 1980-1986, Kaplan (1989) reports that while the median pre-buyout ownership of all managers is 5.88 percent, the median post-buyout ownership increased by about three times the pre-buyout value to 22.63 percent. Smith (1990) provides similar evidence on the concentration of ownership that the median post-buyout ownership share of all officers, outsider directors and other major holders for MBO firms is 95.26 percent, compared to the corresponding pre-buyout ownership share of 75.45 percent. Kaplan and Stein (1993) find that for 124 large MBOs during the 1980s the managerial ownership increased from 5 percent prior to the buyout to 22.3 percent after the buyout.

Following a typical LR transaction, managerial ownership also increases, but in a much smaller magnitude. According to Gupta and Rosenthal (1991), the pre- and post-LR managerial ownership is 3.8 percent and 8.4 percent, respectively. Denis and Denis (1993) find that equity ownership of officers and directors increases from a median of 1.7 percent to a median of 3.6 percent. Similarly, Palepu and Wruck (1992) report that managerial ownership of defensive recapitalization firms increases from 2.9

percent to 5.9 percent. Denis (1994) provides similar evidence on the changes in managerial ownership for LBO and LR firms.6

The difference in ownership structure following MBOs and LRs appears to result in different compensation arrangements for top management. Conceivably, management ownership stake is more enhanced by MBO firms so that their incentives are stronger for improved performance than LR firms. Going-private MBOs facilitate compensation arrangements that induce management to undertake some investment proposals that would require disproportionate effort of managers, and hence disproportionate share of the proposal's income (DeAngelo, DeAngelo, and Rice (1984) and Travlos and Cornett (1990)). Muscarella and Vetsuypens (1990) provide evidence on management incentives following LBO transactions. They show that almost all firms in their sample (69 out of 72) implement at least one type of incentive plan under private ownership and that the two most popular types of incentive plans are stock option plans and stock appreciation rights. Their study also reports an elasticity of compensation (defined as salary plus bonus) to sales of 0.46 for the most highly paid officer in their sample. This finding is in contrast to the typical elasticity of about 0.3 found for public companies in Murphy (1985). By comparing the Kroger Co.'s LR with the Safeway Stores' LBO, Denis (1994) shows similar evidence that while Safeway relates managerial compensation more closely to firm performance, there was no such compensation scheme at Kroger.

Finance literature has also documented that MBOs (and LBOs in general) replace prior management and provide new management with large equity stakes, whereas LRs involve little change in governance of the firm. In an LBO, managers are frequently replaced and they are responsible to a small but powerful group of shareholders (e.g., LBO specialist or institutional investors). Jensen (1993) shows that following an LBO, boards of directors shrink to about seven or eight people and the sensitivity of managerial pay to performance rises. In a study of 42 firms that announced LRs during the 1985-1989 period, Handa and Radhakrishnan (1991) report that only five firms result in a change of CEOs following the firms' financial problems. Denis (1994) also shows a dramatic difference in the composition of the board of directors following Kroger's LR versus Safeway's LBO. While there were no changes in Kroger's board at a result of their LR, Safeway's board size was reduced from eighteen to five members; only two members of the old board remained following

6 Unlike these studies, Kleiman (1988) reports that average insider ownership increases to 29.5 percent after LRs from a pre-LR average of 8.1 percent.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

173

the buyout. It was also noted that Kroger's board held just 1.8 percent of the firm's equity after LR, whereas Safeway's board represented 92.6 percent of the firm's equity after the buyout.

The evidence suggests that the incentives for closer board monitoring of managerial behavior should be much stronger in MBOs than in LRs. Denis (1994) offers similar evidence on executive compensation for LR and LBO firms. There was no formal change in the structure of Kroger's executive cash compensation following LR. In contrast, there were major changes in executive compensation policy following Safeways' buyout which included bonuses as high as 110 percent (vs. 40 percent prior to buyout) of the executive's salary and also tied bonus payments to performance measures.

To put in perspective, there appear to be significant changes in ownership structure, board composition, and executive compensation policy following MBOs in a way that not only gives MBO firms' management more incentive, but also increases monitoring of top management. Hence, MBOs (especially induced by LBO specialists) would result in large changes in corporate governance and involve closer monitoring of management by the newly-formed board of directors. This suggests, as Denis (1994) points out, that given the small financial incentives of LR firms' officers and directors, these firms may choose the LR transaction as a means of avoiding these changes in governance system and monitoring. On the contrary, the increased ownership following LRs may improve managerial incentives and monitoring, but its effect is expected to be much smaller than for the case of MBOs. Hence, going private through MBOs enables the firm to institute more incentive compensation plans, which may not be possible for public firms due to the outside restrictions such as political process (Jensen and Murphy (1990b)).

In sum, leverage coupled with changes in governance structure appears to effectively eliminate the agency problem of free cash flow. While managers in recaps may waste resources to defend their position to potential takeover threat, going private MBOs may eliminate these costs. In many MBOs, the LBO specialists (e.g., KKR) retain a large equity stake and serve on the board. The equity stake and their desire to protect their reputation as efficient sponsors give them the incentive to closely monitor post MBO management. The concentrated ownership resulting from a MBO represents reunification of ownership and control. As documented in Denis (1994), the improved incentive structure and increased monitoring provided by the LBO specialists appear to lead managers to generate cash in a more productive manner than did the organizational structure of LR firms.

3. Data and Measurement of Variables

A. Data

We collect data from a sample of MBO and LR firms during the period 1985 to 1990, the period of greatest LBO and LR activities during the 1980’s. The recession of 1990-1991, combined with a collapse of the high-yield junk bond market in 1989, brought a substantial drop of LBO activity to $6.8 billion in 1991, less than 9 percent of the $76 billion in 1989. With the more favorable economic environment and the resurgence of the high-yield bond market since 1992, however, the LBO market has moved to an age of renewal, expanding its scope increasingly beyond mature slow-growing industries to high growth technology-driven industries (Allen (1996)). However, we use the 1985-1990 period because LRs first appeared in 1985, and LR activity dropped sharply after 1990 and there is almost no LRs after 1990.

Our sample of LRs comes from a search of the annual industrial Compustat tapes for large special dividends and stock repurchases. Each LR transaction indicating that there was an abrupt recapitalization is then confirmed from the news media. This process results in 41 sample LR firms that distribute at least 20 percent of their market value of equity in a debt-financed special dividend or nontargeted tender offer repurchase (but not a LBO).

We construct our sample of MBOs using a newspaper search of the Wall Street Journal abstracts over the same period for the keywords "LBO," "MBO," and "buyout," and selecting the resulting LBOs that meet criteria similar to those in Kaplan (1989). Specifically, (i) the firm must go private in a whole company LBO7; (ii) there cannot be a pre-MBO majority owner; and (iii) the firm must maintain its independence following the LBO. In addition, we categorize a LBO as a MBO when at least one top incumbent manager (CEO, Chairman, or President) is reported as taking an equity position in the buyout. If no top incumbent manager is reported as taking an equity position in the buyout, the firm is classified as a non-MBO LBO. We also require that sufficient Compustat data are available for our tests. This produces a sample of 88 MBO firms out of 106 LBO firms. Table 1 provides the sample distribution by year. The sample LR firms are most heavily concentrated in 1988-1989 and are very thin in 1990. The sample MBO firms are most heavily concentrated in 1987-1989 and are very thin in 1990. We use the Wall Street Journal Index to learn whether an active takeover threat exists prior to the initial MBO or LR proposal.

7We do not include divisional LBO firms in our sample because divisional LBO firms are believed to be more comparable with other corporate divestiture tactics, such as equity carve-outs, spin-offs, sell-offs, and asset sales.

Corporate Ownership & Control / Volume 4, Issue 2, Winter 2006-2007 (continued)

174

We define an active takeover threat as either an actual takeover offer or a large (>5 percent) toehold disclosure by a potential bidder along with published speculation about a possible takeover in the Wall

Street Journal.

B. Measurement of Variables

In our tests, all financial variables are taken from the Compustat tapes for the last full fiscal year before each firm's HLT. We measure pre-HLT performance using firms’ profitability. Since potential operating improvements can be the result of restructuring either capital or labor, we measure pre-HLT performance as both the ratio of operating income to total assets and the ratio of operating income to the number of employees. These are common performance measures in the HLT and governance literature (see, e.g., Allgood and Farrell (2000), Kaplan (1989), and Smith (1990)). We use four variables measuring the quality of corporate governance systems—managerial equity ownership, outside block ownership, board independence, and CEO equity-based compensation—and collect the governance data from published proxy statements for the last full fiscal year before the HLT.

We measure managerial equity ownership in two ways: CEO's beneficial ownership and the beneficial ownership of all officers and directors. Outside block ownership represents equity ownership of outside blockholders and is measured as the sum of greater-than-five percent owners that are unaffiliated with the firm. We measure board independence as the number of independent outside directors divided by the total number of directors on the board. We define independent outside directors following Hermalin and Weisbach (1988) as directors who have no past, present, or likely future financial ties to the firms other than compensation for being a director (investment bankers are assumed to have likely future financial ties). For the variable, we exclude gray directors who are relatives of former or current officers or have personal business relationship with the firm. Finally, following Mehran (1995), we measure CEO’s equity-based compensation as the sum of the value of CEO stock, pseudo-stock, and option grants expressed as a percentage of total compensation.

4. Empirical Results

A. Preliminary Comparison of MBO Firms and LR Firms

Before we examine the effects of various corporate governance mechanisms on firm performance of HLT firms, it will be beneficial to have some preliminary comparison of how the HLT transactions affect leverage and ownership in our sample firms. While changes following LRs are observed directly, changes following MBOs are based on the financing and equity investment information provided in the buyout proxy statement filed with the SEC.

Table 2 presents a preliminary summary of how HLTs change leverage and equity ownership. In both MBOs and LRs, debt levels roughly quadruple from relatively low levels (around 20 percent of total assets) to very high levels (around 80 percent of total assets). These findings demonstrate that both transactions are associated with dramatic (and similar) leverage increases. LRs have, however, a much more modest impact on firms’ organizational form. While remaining publicly traded corporations, LR firms are associated with only a modest increase in director and officer ownership and outside blockholdings. For LR firms, the median level of managerial ownership rises from 3.3 percent to 4.1 percent while the largest blockholder’s stake rises from a median level of 5.7 percent to 6.7 percent. On the other hand, MBO firms experience more dramatic organizational changes after going private. The median director and officer ownership rises from 12.0 percent to 24.6 percent, and the largest blockholder’s median stake rises from 8.6 percent to 77.1 percent. Our results clearly indicate that although MBOs and LRs result in similar capital structure changes, they produce very different organizational structures at least in terms of equity ownership structures.

B. Univariate Tests