Carbon markets, carbon prices and innovation: Evidence from Interviews with Managers

42

Carbon markets, carbon prices and innovation: Evidence from Interviews with Managers * Ralf Martin † , Mirabelle Muûls ‡ and Ulrich Wagner § Preliminary Abstract Based on interviews with almost 800 manufacturing firms in six European countries, this study develops a firm level indicator of “clean” that is climate change related innovation and explores the impact of the EU Emissions Trad- ing System on such innovation. We find that the majority of firms engage in some form of climate change related innovation although this is primarily process rather than product innovation. We also find significant differences in the propensity to innovate between countries, even after controlling for poten- tially different industrial structures. Further, we find that firms expecting less generous allocations of free permits in the third phase of the EUETS tend to innovate more. We explore if this a causal effect of variations in allocations across sectors by devising a regression discontinuity design. We find a discrete drop in innovation effort around the thresholds - in terms of carbon and trade intensity - implied by EU Commission rules for free allocation. This suggests that allocating permits for free causes a reduction in clean innovation. This contradicts the hypothesis that permit allocation has only a distributional but no effect on real behaviour. We suggest that requiring firms to buy permits in an auction has an important signalling effect for senior management, which does not occur under free allocation. JEL Classification: D22, O31, Q48, Q54 * The authors thank Morgan Bazilian and Karsten Neuhoff for useful comments and suggestions. † Centre for Economic Performance and Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science, Houghton Street, London WC2A 2AE, phone: 020 7955 6975, email: [email protected] ‡ Grantham Institute for Climate Change, Imperial College London, South Kensington Campus, London SW7 2AZ and Research Associate, Centre for Economic Performance, London School of Economics and Political Science, phone: 020 7594 8452, email: [email protected] § Universidad Carlos III Madrid, Department of Economics, Calle Madrid, 126 28903 Getafe, Spain and Research Associate, Centre for Economic Performance, London School of Economics and Political Science, phone: +34 (0) 916 24 8488, email: [email protected] 1

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Carbon markets, carbon prices and innovation: Evidence from Interviews with Managers

Carbon markets, carbon prices and innovation:Evidence from Interviews with Managers∗

Ralf Martin†, Mirabelle Muûls ‡and Ulrich Wagner§

Preliminary

Abstract

Based on interviews with almost 800 manufacturing firms in six Europeancountries, this study develops a firm level indicator of “clean” that is climatechange related innovation and explores the impact of the EU Emissions Trad-ing System on such innovation. We find that the majority of firms engagein some form of climate change related innovation although this is primarilyprocess rather than product innovation. We also find significant differences inthe propensity to innovate between countries, even after controlling for poten-tially different industrial structures. Further, we find that firms expecting lessgenerous allocations of free permits in the third phase of the EUETS tend toinnovate more. We explore if this a causal effect of variations in allocationsacross sectors by devising a regression discontinuity design. We find a discretedrop in innovation effort around the thresholds - in terms of carbon and tradeintensity - implied by EU Commission rules for free allocation. This suggeststhat allocating permits for free causes a reduction in clean innovation. Thiscontradicts the hypothesis that permit allocation has only a distributional butno effect on real behaviour. We suggest that requiring firms to buy permitsin an auction has an important signalling effect for senior management, whichdoes not occur under free allocation.

JEL Classification: D22, O31, Q48, Q54

∗The authors thank Morgan Bazilian and Karsten Neuhoff for useful comments and suggestions.†Centre for Economic Performance and Grantham Research Institute on Climate Change and

the Environment, London School of Economics and Political Science, Houghton Street, LondonWC2A 2AE, phone: 020 7955 6975, email: [email protected]‡Grantham Institute for Climate Change, Imperial College London, South Kensington Campus,

London SW7 2AZ and Research Associate, Centre for Economic Performance, London School ofEconomics and Political Science, phone: 020 7594 8452, email: [email protected]§Universidad Carlos III Madrid, Department of Economics, Calle Madrid, 126 28903 Getafe,

Spain and Research Associate, Centre for Economic Performance, London School of Economicsand Political Science, phone: +34 (0) 916 24 8488, email: [email protected]

1

1 Introduction

In advanced economies, the industrial sector is directly responsible for about a thirdof greenhouse gas (GHG) emissions (IEA, 2009). Understanding the drivers andbarriers that affect company behavior related to climate change is therefore essentialto design effective policies for reducing emissions, to prevent dangerous levels ofglobal warming. At the same time, private-sector firms are also the key players whenit comes to investments in research and development (R&D); “clean” innovationis critical for achieving the transition to a low-carbon economy. The relationshipbetween “clean” R&D investments and climate change policy becomes all the morerelevant if the fruits of these investments spill over across international bordersand help to reduce emissions in countries with few or no climate change policies.Currently, some view this possibility as the main justification for European climatechange policy, given that EU emissions reductions alone would not be sufficient toprevent dangerous global climate change from occurring.

To date, the empirical evidence on what firms are doing (or not) to curb GHGemissions is rather limited and has been collected through either mail surveys orcase studies (McKinsey and Ecofys (2005), Kenber et al. (2009)). This paper exam-ines the link between climate change regulation, investment and innovation, usingdetailed survey data for a representative sample of firms. The data were collectedby interviewing managers on climate-change and energy related issues using a novelmethod that circumvents various types of bias that plague more traditional surveyformats. We applied this approach to a sample of approximately 800 manufacturingfirms in six European countries from August to October 2009.

Based on this dataset, we obtain a number of new descriptive results regardingthe behavior of businesses related to climate change. It appears that most (70%)firms are engaged in some formal or informal R&D, with the aim of curbing emis-sions and/or energy consumption (“clean process innovation”). A smaller proportion(40%) is also pursuing “clean product innovation”; i.e. R&D with the aim of de-veloping products that can help customers to reduce their emissions. There aresignificant differences between countries when it comes to clean innovation. Ac-cording to our study, most active on product innovation is Germany, on processinnovation is France with lowest levels of innovative activities observed in Hungaryand Poland. Also, this study shows that firms expect carbon prices to be consider-ably higher in the future, compared with current levels in the EU ETS. We find anaverage expected carbon price of €40 for the post-2012 trading period. And finally,ompared to the current trading period (Phase II, from 2008 to 2012), firms expectthe imposition of tighter caps for Phase III, starting in 2013. The proportion offirms reporting that their allowance allocation does not imply a binding emissionslimit falls from 40% in Phase II to less than 10% in Phase III.

Apart from descriptive statistics, we use regression analysis to analyze the effectof climate policy on innovation at the firms in our sample. We provide two piecesof evidence in support of a causal link between company-specific caps – i.e. theamount of allowances companies receive for free in the EU ETS – and “clean” R&D

2

by firms. First, we find a significant positive association between the expectationsfirms hold about the future stringency of their cap and “clean” innovation. Thisrelationship is robust to including a broad range of control variables.Second, wefind that firms within the EU ETS which are just below the thresholds establishedfor free allowances are engaging more strongly in climate change related productinnovation than firms that are just above the threshold (and thus will continue toreceive free allowances). There is a discontinuity in both expected stringency aswell as “clean” innovation at the thresholds that are implied by the latest set ofcriteria that the European Commission has proposed for allocating free emissionsallowances after 20121. This result suggests that the ongoing practice within theEU ETS, of generously allocating allowances for free to manufacturing sectors leadsto less innovation than would otherwise be the case.

The remainder of this paper is organized as follows: Section 2 describes the process ofinterviewing managers about various aspects of company behavior related to climatechange. Section 3 provides summary statistics of our innovation measures as wellas regarding future expectations. Section 4 examines the link between innovation,future expectations and climate policy. Section 5 concludes.

2 Interviewing managers

2.1 Interview Methodology

Our survey builds upon and substantially extends previous work on climate changepolicies and management practices by Martin et al. (2010). We conduct structuredtelephone interviews with managers at randomly selected manufacturing facilitiesin Belgium, France, Germany, Hungary, Poland and the UK. The interview setupfollows the management survey design pioneered by Bloom and van Reenen (2007),in that the interviewer engages interviewees in a dialogue with open questions thatare meant not to be answered by “yes” or “no”. On the basis of this dialogue, theinterviewer then assesses and ranks the company along various dimensions. Notethat our setup adopts a double-blind strategy: interviewees do not know that theinterviewers are scoring their answers and interviewers do not know performancecharacteristics of the firm they are interviewing. This interview format is designedto avoid several sources of bias common in conventional surveys (Bertrand andMullainathan, 2001). For instance, experimental evidence shows that a respondent’sanswers can be manipulated by making simple changes to the ordering of questions,to the way questions are framed, or to the scale on which respondents are supposedto answer. By asking open-ended questions and by delegating the task of scoring theanswers to the interviewer, we seek to minimize cognitive bias of this type. Possiblecognitive bias on the part of the interviewers can be controlled for using interviewer-fixed effects in the regression analyses. Another common observation with survey

1The Commission takes this decision for each sector based on whether it is sufficiently (i) carbonintensive, (ii) trade intensive or (iii) both.

3

Table 1: Interview response rates by country

Refused

Belgium 134 131 85 46 178 47 0.74France 141 140 92 48 238 98 0.59Germany 139 138 95 43 337 199 0.41Hungary 69 69 37 32 90 21 0.77Poland 78 78 57 21 140 62 0.56UK 209 205 63 142 468 264 0.44Total 770 761 429 332 1451 691 0.52

# of Interviews

# of Firms Interviewed

# of ETS Firms

Interviewed

# of Non ETS Firms

Interviewed

Total Firms Contacted

Response Rate

Notes: There are more interviews than interviewed firms as we conducted severalinterviews with different partners in a small number of firms.

data is that respondents are tempted to report attitudes or patterns of behaviorthat are socially desirable but may not reflect what they actually think and do.This problem may be exacerbated in situations where respondents do not have adefinite attitude toward the issues they are asked about but are reluctant to admitthat. Our research design addresses this issue in two ways. First, the interviewerstarts by asking an open question about an issue and then follows up with morespecific questions, or asks for some examples in order to evaluate the respondent’sanswer as precisely as possible. Second, the results of the interviews are then linkedto independent data on economic performance, as a validation exercise.

2.2 Interview Practice

Using the ORBIS database maintained by Bureau Van Dijk we obtained contact de-tails for 44,605 manufacturing firms in Belgium, France, Germany, Hungary, Polandand the UK2. We randomly selected companies from that list to solicit an interview.To ensure sufficient coverage of firms subject to the EU ETS (hereafter, EU ETSfirms), we also sampled manufacturing firms at random from the Community Inde-pendent Transaction Log (CITL) in these countries. Interviewers made “cold calls”to production facilities (not head offices), gave their name and affiliation with theLondon School of Economics and then asked to be put through to the environmentalmanager. In the case of EU ETS firms, interviewers asked for the person responsiblefor the EU ETS, as it is listed in the CITL. Table 1 reports the number of calls madeand various statistics about the response rates.

An ordinal scale of 1 to 5 was adopted to measure various management practicesrelated to climate change. For each aspect of management ranked in this way, inter-viewers were instructed to ask a number of open questions. Questions were orderedsuch that the interviewer started with a fairly open question about a topic andthen probed for more details in subsequent questions, if necessary. The goal was tobenchmark the practices of firms according to a few common criteria. For instance,

2For more details on the survey, see Anderson et al. (2011)

4

rather than asking the manager for a subjective assessment of the management’sawareness of climate-change issues, we gauged this by how formal and far-reachingthe discussion of climate-change topics is in current management. To verify the con-sistency of the interviewer’s scoring, a subset of randomly selected interviews wasdouble-scored by a second team member who listened in. The interviews seeks togather information on both the effectiveness and the competitiveness effects of cli-mate change policies, particularly of the EU ETS, in a random sample of Europeanmanufacturing firms. The questionnaire (see appendix) is divided in four sections.The first section examines the current and anticipated future effects of the EU ETS.The second section deals with prices for energy and CO2, competition and otherexternal drivers of climate-change related management practices. The third sec-tion inquires about specific measures that were adopted by firms and others whichwere considered but eventually discarded. The last section gathers information onrelevant company characteristics.

3 Descriptive evidence from interviewing managers

3.1 Clean Innovation

An important path for firms’ future GHG emissions abatement is to innovate: thecompany can either invest in finding cleaner production processes or develop newand cleaner products, thereby reducing their customers’ future emissions. Figure1 shows the distribution of the scores for clean process and product innovation3.An example of clean process innovation could be the development of a less energy-consuming way to transform limestone into quicklime. Clean product innovationwould for example be the invention of a new tyre with which cars consume lesspetrol. We see that almost 70% of firms are engaged in some form of clean processinnovation; only 40% engage in clean product innovation. Figure 2 shows that cleanproduct innovation is most likely to occur in firms that are also conducting cleanprocess innovation.

Figure 3 examines whether there are differences in clean innovation between coun-tries in our sample. There is clearly a gap between Western and Central/EasternEuropean countries, with Poland and Hungary lagging behind, both in terms ofprocess and of product R&D. France emerges as the leader in process, Germanyin product R&D. The second panel of Figure 3 explores whether these differencesare driven by differences in the specialization of the various economies across sec-tors. The figures report average differences between countries while controlling forthe 3-digit sector4. This makes the differences found in the first panel even more

3The clean process and product innovation measures are throughout this paper taken from thesurvey responses and we hereafter use interchangeably the term innovation and R&D.

4We use the NACE rev. 1.1 classification of the ORBIS data

5

Figure 1: Distribution of the Clean Innovation Scores

(a) Clean Process Innovation (b) Clean Product Innovation

Notes: The figures show a histogram of the scores for each of the two types of cleaninnovation reported by interviewed firms.

Figure 2: The relative frequency of clean process and product innovation

Notes: The figure shows a histogram of the types of clean innovation reported by inter-viewed firms.

6

Figure 3: Differences in clean innovative activities between countriesNo industry controls

(a) Process Innovation (b) Product innovation3-digit industry controls

(c) Process Innovation (d) Product innovationNotes: Each graph shows the average difference - conditional on noise controls - between firms fromdifferent countries in terms of the interview scores for process and product innovation describedin Figure 1. Stars indicate if these deviations are statistically significant and at what significancelevel: ***=1%, **=5%, *=10%.

pronounced, suggesting that they are not driven by differences in industrial com-position.

Figure 4 reveals sizeable differences in clean innovation across sectors and betweentypes of innovation. In Table 2, we use this information to group sectors accordingto their focus on clean technologies. Only three sectors – Glass, Other Mineralsand TV & Communication – have above-average scores in both product and processinnovation.

3.2 What firms expect

Investment decisions depend on the expectations held by investors. In order to elicitthis information, the interview included a number of questions on expectations.This section reports on our findings, starting with an examination of differences in

7

Figure 4: Differences in clean innovative activities between industries

(a) Process Innovation (b) Product innovationNotes: Each graph shows the average difference - conditional on noise controls - between firmsfrom different sectors in terms of the interview scores for process and product innovation describedin Figure 1. Stars indicate if these deviations are statistically significant and at what significancelevel: ***=1%, **=5%, *=10%.

Table 2: Sectors according to their focus on clean innovation

Clean Product Innovatonbelow average above average

below average

above average

Clean Process Innovaton

- Ceramics; - Fabricated Metals- Food & Tobacco- Publishing - Textle Leather

- Machinery & Optcs;- Other Basic Metals;- Vehicles

- Cement; - Chemicals & Plastc;- Fuels;- Iron & Steel; - Wood & Paper

- Glass- Other Minerals- TV & Communicaton

8

Figure 5: Distribution of price expectations

Notes: The figure shows a histogram of the price of a tonne of CO2 that interviewed firmsexpect on the EU ETS market.

these expectations between firms, countries and sectors. Subsequently, we discussexpectations about the future of the EU ETS.

3.2.1 Prices

Figure 5 reports the distribution of the expected price of emitting one tonne ofcarbon dioxide in 2020. Forecasts range between 0 and 500. The median pricereported is €30, the mean €40. There are substantial differences, not only betweendifferent firms but also between countries and sectors, as shown in Figure 6. Frenchfirms expect a much higher price, of €50 on average, whereas UK firms expect amore modest €28, on average. Across sectors, the highest price is expected by firmsin TV and Communication, with an average of €78, the lowest by firms in the Fuelssector, at close to €23. There is also a sizeable variation across sectors and countrieswith respect to the mere existence of a price expectation. Figure 7 shows that morethan 80% of interviewed Polish managers actually have a carbon price expectationversus less than 5% of the Hungarian managers that we interviewed. At the sectorlevel, the highest proportion of firms with an expectation occurs in the Glass sector(55%), whilst the lowest percentage is only 18%, in Machinery and Optics. We alsoasked interviewees about their knowledge of the current price of a tonne of CO2 onthe EU ETS, as a way of gauging their awareness of the market and the potentialintegration of this price in investment and trading decisions. Again, there is a lot ofvariation between sectors and countries, as shown in Figure 8, with Poland and theFuels industry exhibiting the largest shares of managers aware of the carbon price.

3.2.2 Expected stringency of EU ETS

We also asked firms about their expectations regarding the stringency of the cap onemissions implied by their participation in Phase III of the EU ETS. Put differently,we wanted to know how hard it would be for them to limit their future emissions to

9

Figure 6: Price expectations across industries and countries

(a) Across countries (b) Across sectorsNotes: The figures show average carbon price expectations for 2020 for all interviewed firms thatreported price expectations (i.e. both EU ETS and non EU ETS firms).

Figure 7: Existence of Price expectations

(a) Across countries (b) Across sectorsNotes: The figures show what proportion of firms in a country or a sector reported a carbon priceexpectation in our sample.

10

Figure 8: Knowledge about current prices

(a) Across countries (b) Across sectorsNotes: The figures show what proportion of firms in a country or a sector knew the current carbonprice in the EU ETS.

the amount they receive in free allowances (or how expensive if they do not reducetheir emissions, and need to buy allowances). A firm’s response to this questionwould depend on (i) how costly it would be to reduce its emissions, on (ii) howmany allowances it receives for free and on (iii) the price they expect on the marketand therefore the expected overall allocation. We asked a similar question regardingthe stringency of the cap imposed by the current Phase II of the trading system.Figure 9 reports on the resulting scores. Firms clearly expect more stringent capsfor Phase III. The proportion of firms answering that the cap they receive will allowthem to continue under business-as-usual terms declined, from almost 40% to lessthan 10%. That said, few firms expect, even for Phase III, that fundamental changeswould be needed in order to meet their cap.

4 What is driving investment in climate-change re-lated innovation?

Having described in section 3 firms’ investment in R&D related to climate changeand their expectations for the future, this section, examines whether there is a linkbetween the two . Table 3 reports results from regressions of the process innovationscore whereas Table 4 reports the equivalent regressions for product innovation.

In column 1 we start first by regressing the innovation scores on a set of dummyvariables indicating whether a firm is part of the EU ETS in either Phase II or IIIor both. For process innovation this does not lead to a significant coefficient. Forproduct innovation we find a coefficient that is significant at 10%, however only forparticipation in Phase 2. Hence there is no strong evidence that ETS firms in generaldiffer in their innovativeness from non-ETS firms. In column 2 we add both priceexpectations and expectations about the future stringency of the firm level cap asexplanatory variables. We find positive coefficients for both variables and with both

11

Figure 9: Expected stringency and current perceived stringency

(a) Trading Phase II (b) Trading Phase IIINotes: The figure for Trading Phase II shows how stringent firm-specific caps are perceived tobe. The figure for Trading Phase III shows what stringency firms expect for the Trading Phasestarting in 2013

types of innovation. However, we only get significant coefficients for the expectedstringency of the cap. Thus it seems that the stringency of the emissions cap is morerelevant for R&D decisions than the price. This is an interesting suggestion, as asimple model of company behavior would tend to predict the opposite: since the EUETS is a cap-and-trade system the only thing that should matter for firms’ alloca-tion and investment decisions is the (expected) emissions price. Company-specificcaps should only be relevant for determining the distribution of rents that emergefrom imposing scarcity on a formerly free good (GHG pollution). The notion thatallocation decisions are independent of the distribution of allowances has been re-ferred to as the “independence property” of emissions trading (?, Hahn and Stavins,2010).

An alternative explanation for the correlation between stringency and innovationcould be that we are picking up reverse causality or biases due to omitted variables.For example, a firm’s perception of stringency is certainly influenced by the avail-ability of cheap technological solutions to reduce emissions. When cheap solutionsare not available, a firm is likely to respond that the cap is more stringent. There-fore, such a firm might be more likely to conduct some R&D in response to highercarbon prices. In this case, a positive relationship between R&D and stringencymight emerge due to unobserved heterogeneity. We proceed by accounting for thisin a number of ways: First, by adding more control variables. Second, by examiningwhat happens when we include current (i.e. Phase II) perceived stringency, ratherthan future stringency. Third, we use process innovation as a control for un-observedfactors in the product innovation regressions. Fourth, rather than using the surveybased stringency measures we exploit variations in cap stringency implied by theEU Commission rules for continued free allocation – instead of the requirement topurchase allowances through auctioning. We discuss each approach in turn.

12

Table 3: Regressions of process innovation score

(1) (2) (3) (4) (5) (6) (7) (8)Dependent Variable. Process Innovation ScoreAnticipation of ETS Stringency in Phase 3 0.177** 0.107 0.122 0.144**

(0.079) (0.079) (0.076) (0.071)ETS Stringency in Phase 2 0.093* 0.078* 0.125**

(0.049) (0.046) (0.057)

0.100 -0.041 0.038 0.015

(0.074) (0.063) (0.063) (0.094)

0.064 0.115*** 0.071 0.078 0.139*** 0.103**

(0.048) (0.038) (0.051) (0.049) (0.037) (0.046)Multinational Enterprise 0.140 0.161 0.339 0.172 0.184 0.379*

(0.148) (0.132) (0.228) (0.144) (0.130) (0.228)R&D Intensive Facility 0.140 0.171* 0.039 0.166 0.197** 0.076

(0.106) (0.091) (0.147) (0.107) (0.095) (0.146)Employment 0.244*** 0.199*** 0.162** 0.254*** 0.213*** 0.187***

(0.046) (0.036) (0.072) (0.047) (0.037) (0.067)In ETS in Phase 2 -0.237 -0.285 -0.316 -0.129 . -0.490* -0.317 .

(0.198) (0.198) (0.241) (0.235) . (0.275) (0.278) .In ETS in Phase 3 0.225 -0.064 0.046 0.061 . 0.322 0.308 .

(0.304) (0.340) (0.350) (0.345) . (0.329) (0.357) .In ETS in Phase 2 and 3 0.388 0.128 -0.053 0.004 . 0.109 0.185 .

(0.359) (0.401) (0.392) (0.380) . (0.381) (0.378) .Observations 732 732 731 731 342 731 731 342

0.28 0.31 0.40 0.30 0.33 0.38 0.28 0.32Cluster 153 153 153 153 91 153 153 913-digit sector controls yes yes yes no no yes no noNoise Controls yes yes yes yes yes yes yes yes

CO2 Price expectation by 2020

ln(CO2 Price)

CO2 Intensity in 2008

ln(CO2/EMP)

ln(emp)

R2

Notes: All columns estimated by OLS with standard errors are in parentheses under coefficientestimates clustered by sector. The dependent variable is the interview score for process innovation.CO2 intensity data are derived from the CITL database while employment is taken from ORBIS. Allother variables are derived from the interviews. Noise controls include interviewer, country, time,day and month of the interview and manager background fixed effects. Stars indicate statisticalsignificance level: ***=1%, **=5%, *=10%.

13

Table 4: Regressions of product innovation score

Notes: All columns estimated by OLS with standard errors are in parentheses under coefficientestimates clustered by sector. The dependent variable is the interview score for product innovation.CO2 intensity data are derived from the CITL database while employment is taken from ORBIS. Allother variables are derived from the interviews. Noise controls include interviewer, country, time,day and month of the interview and manager background fixed effects. Stars indicate statisticalsignificance level: ***=1%, **=5%, *=10%.

14

4.1 More control variables

Column 2 in Tables 3 and 4 already includes 3-digit industry dummies. In column3 we add further controls, such as the size, CO2 intensity, foreign ownership, etc.of a firm. We note that the stringency coefficient remains positive and significantfor product innovation. For process innovation it remains positive but is no longersignificant. For completeness we also examine what happens when we drop industrycontrols in column 4 and when we restrict the sample to only firms that are particip-ating in Phase III5. For product innovation, the stringency-innovation relationship isrobust in all of these specifications. The results for process innovation are less clear-cut. The stringency coefficient remains insignificant when dropping sector controlsbut becomes significant when restricting to the ETS sample.

4.2 Using current stringency

Up until Phase II emission allowances have by and large been allocated for free toemitters. Current plans for Phase III stipulate that some firms will have to purchasean increasing fraction of their allowances through an auction or on the open market.Hence, if the relationship between stringency and innovation is driven by variationsin the cap rather than abatement cost heterogeneity, we expect that the relationshipis weaker or non-existent with current stringency. Again, this turns out to be thecase for product innovation where the current stringency coefficient is not significantin columns 6 to 8. For process innovation, the reverse seems to be the case with thecurrent stringency coefficient being positive and significant.

4.3 Using process innovation as a control variable

Product innovation should be less affected by any confounding variation that mightaffect the relationship between stringency and innovation. This is because producingand researching the design of wind turbines, for example, does not necessarily gen-erate knowledge that helps to reduce the emissions from producing wind turbines.Even so, we cannot rule out that there are complementarities in conducting processand product R&D. To account for that, Table 4 includes an additional column wherewe include process R&D as an additional regressor6. The future stringency relation-ship remains significant at 10% in column 9 and leads to an estimate comparable insize when including process R&D as an additional control variable7.

5Note that we have the expected stringency score variable only for firms that are regulated bythe EU ETS in Phase III. Thus in all columns the stringency effect is identified only from thosefirms. Including the other firms can be useful, however, to identify the impact of variables oninnovation that are relevant for all firms, such as sector, size or noise controls.

6If variations in the cap are driving both process and product R&D, this would likely lead toa downward bias in the estimated coefficient on stringency. But if the "cap" effect is stronger forproduct R&D, we should still be able to detect an effect.

7The results of Tables 3 and 4 are robust to including a control of whether the firm is tradingon the EU ETS or not.

15

Figure 10: Placebo and real thresholds

Notes: The Figure plots interviewed firms in the Value at Stake (y-axis) and Trade Intensity(x-axis) space according to the industry they belong to. The three lines correspond to theEU criteria for exemption of auctioning in Phase III and to two placebo threshold linesused in our analysis.

4.4 The effect of the EU Commission rules

As a further check of the robustness of the relationship between stringency andinnovation, we exploit the link between exogenous variations in free allowance al-location, rather than relying on the self-reported stringency score8. As mentionedbefore, Phase III will see radical changes in the number of allowances that are al-located for free to firms. Under current proposals, the European Commission willexempt certain 4-digit industries from allowance auctioning, based on two statistics,trade intensity (TI) and CO2 intensity (VaS) 9. Firms in a 4-digit industry will beexempt if the industry’s TI or VaS rates exceed 30%, or if the sector simultaneouslyexceeds a 10% threshold for TI and a 5% threshold for VaS. Figure 10 plots the firmsin our sample in the VaS-TI space, along with a line (labeled “actual”) indicatingthose thresholds.

However, in Tables 5 and 6, we examine whether there is a discrete jump in both thereported expected stringency as well as innovation as we move over the thresholds

8Of the three factors underlying a firm’s perception of stringency (see Section 3.2.2), we focushere on point (ii), the amount of permits the firm receives for free.

9The Value at Stake is defined as the ratio between the sum of the direct and indirect costs offull auctioning and the gross value added of a sector. The direct costs are calculated as the valueof direct CO2 emissions (using a proxy price of €30/t CO2), and the indirect costs capture theexposure to electricity price rises.

16

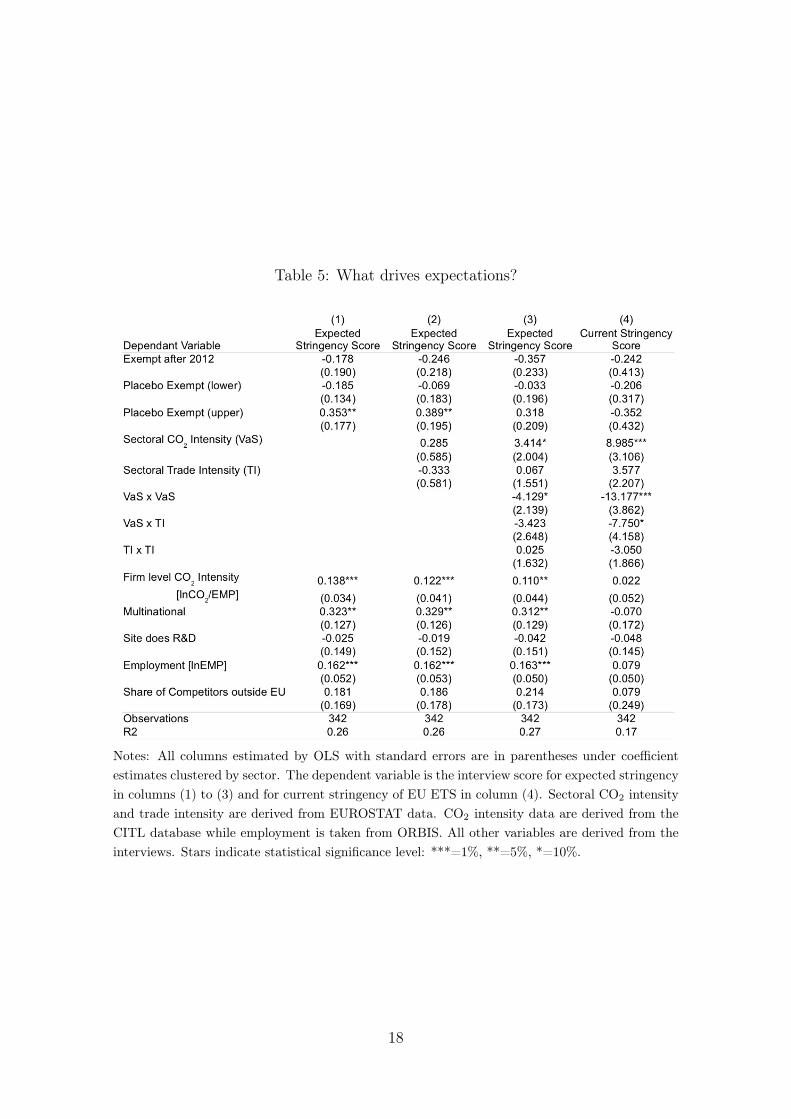

implied by the European Commission criteria10. We also test if such discrete jumpsare a feature of our data rather than the cause of exemptions from auctioning,by defining two “placebo” thresholds, which are also indicated in Figure 10. Onethreshold is slightly lower, the other slightly higher than the actual threshold. Weexperimented with a range of values here. The specific lines in Figure10 are definedso as to ensure that 5% of firms fall within the band on either side of the differentcut-off values. Let us consider first the regression results reported in Table 5, wherefuture stringency – derived from our survey - is the dependent variable. In column1, we include indicator variables that are equal to 1 if a firm exceeds any of thesethresholds as explanatory variables. We see that there is a negative and significantcoefficient for exceeding the actual threshold (“Exempt after 2012”) and a positivecoefficient for exceeding the upper threshold. In column 2, we include trade intensity(TI) and CO2 intensity (VaS) in addition as explanatory variables. This has littleeffect on the threshold parameters. As we include quadratic terms, however, incolumn 3, the actual threshold effect becomes stronger and more significant, whereasthe placebo effect becomes smaller and loses significance11. Moreover, we find incolumn 4 that there is no such threshold effect when looking at the current stringencyscore.

Table 6 shows the results from similar regressions for the innovation variables. Wefind a negative point estimate of passing the actual threshold for process innovation,but it is not statistically significant at conventional levels. On the other hand, we finda very clear and statistically significant threshold effect for product innovation. Thecoefficient estimate implies that passing the threshold for free allowance allocationimplied by the EU criteria leads to a drop in innovation on the order of 1 score point,on our score scale ranging from 1 to 5. As this corresponds roughly to 1 standarddeviation, we conclude that the effect of stringency on product innovation is alsoeconomically significant. In column 5, we see that this result is robust to includingonly the actual threshold. Column 6 reports negative point estimates for the placebothreshold when the actual threshold is excluded from the regression. This reflectsbias from omitting the relevant threshold as well as more noisy estimates, as theactual threshold is measured with error. Figure 11 illustrates the results of theregression in column 5: there is a clear discontinuity in product innovation impliedby the thresholds that define free allocation of allowances.

In sum, we find robust evidence that product innovation responds to the expectedstringency of the EU ETS. There is no clear evidence that the same is true forprocess innovation. An explanation for this could be that having to pay for allrequired emissions allowances has an important signaling function for companies indrawing the attention of more senior management levels to the issue of emissions. Itis only then that firms would take the more strategic decision to engage in productlines that are climate-change related, as opposed to process innovation, which is

10It is easy to think of reasons why trade and energy intensity might be correlated with thedegree of innovation a firm is undertaking, irrespective of these criteria. Indeed, in Figure 11 wefind that there is an inverse u-shaped relationship with respect to energy intensity for both productand process innovation.

11We also experimented with higher order terms, which gave similar results.

17

Table 5: What drives expectations?

Notes: All columns estimated by OLS with standard errors are in parentheses under coefficientestimates clustered by sector. The dependent variable is the interview score for expected stringencyin columns (1) to (3) and for current stringency of EU ETS in column (4). Sectoral CO2 intensityand trade intensity are derived from EUROSTAT data. CO2 intensity data are derived from theCITL database while employment is taken from ORBIS. All other variables are derived from theinterviews. Stars indicate statistical significance level: ***=1%, **=5%, *=10%.

18

Table 6: The effect of exemptions on innovation

(1) (2) (3) (4) (5) (6)Dependant Variable Process Innovation Score Product Innovation ScoreExempt after 2012 -0.294 -0.301 -1.106** -1.229** -0.927***

(0.291) (0.305) (0.454) (0.468) (0.340)Placebo Exempt (lower) 0.445** 0.390* 0.249 0.255 -0.240

(0.194) (0.226) (0.188) (0.256) (0.340)Placebo Exempt (upper) 0.120 0.195 0.664 0.424 -0.212

(0.288) (0.299) (0.521) (0.513) (0.404)

0.393 0.696 0.666 5.237 6.475* 2.498(0.740) (2.501) (0.560) (3.439) (3.517) (3.617)

Sectoral Trade Intensity (TI) -0.716 -1.964 -0.140 2.244 3.946* 2.238(0.432) (1.754) (0.609) (2.250) (2.284) (2.285)

VaS x VaS -1.563 -5.155 -6.642 -2.710(3.312) (4.303) (4.335) (4.680)

VaS x TI 4.299 -7.068* -7.297* -4.131(4.073) (3.628) (3.994) (3.782)

TI x TI 1.457 -1.968 -3.322 -2.285(1.688) (2.101) (2.285) (2.193)

0.098 0.094 0.032 0.013 0.009 0.010

(0.062) (0.063) (0.056) (0.055) (0.056) (0.059)Multinational 0.446* 0.423* 0.564*** 0.547*** 0.520** 0.530**

(0.233) (0.240) (0.191) (0.201) (0.202) (0.211)Site does R&D 0.041 0.046 0.173 0.140 0.128 0.133

(0.171) (0.174) (0.133) (0.130) (0.133) (0.125)0.192*** 0.187*** 0.112 0.113 0.117 0.120(0.064) (0.064) (0.068) (0.069) (0.071) (0.074)

Share of Competitors outside EU 0.288 0.338* 0.176 0.178 0.186 0.182(0.194) (0.202) (0.246) (0.231) (0.229) (0.234)

Observations 342 342 342 342 342 342R2 0.28 0.28 0.24 0.25 0.25 0.22

Sectoral CO2 Intensity (VaS)

Firm level CO2 Intensity

[lnCO2/EMP]

Employment [lnEMP]

Notes: All columns estimated by OLS with standard errors are in parentheses under coefficientestimates clustered by sector. The dependent variable is the interview score for process innovationin columns (1) to (3) and for product innovation in column (4). Sectoral CO2 intensity andtrade intensity are derived from EUROSTAT data. CO2 intensity data are derived from theCITL database while employment is taken from ORBIS. All other variables are derived from theinterviews. Stars indicate statistical significance level: ***=1%, **=5%, *=10%.

19

Figure 11: Discontinuity in Product Innovation

Notes: The figure gives a graphical impression of the regression results in column 5 of Table 6. Thehorizontal plane represents the CO2 and Trade Intensity Space. The vertical axis measures theinnovation score. We see that innovation responds to both Trade and CO2 intensity with a positivelinear and negative quadratic form. The figure shows the discontinuous decline in innovation thatis implied by the thresholds which allow for free allocation of allowances.

arguably more gradual. In such a scenario there could be information barriers thatprevent senior management from seeing these opportunities unless the issuance oftight, company-specific emissions caps forces them to focus on climate change issues.

5 Conclusion

This paper investigates climate-change related investment behavior among manufac-turing firms in Europe on the basis of approximately 800 interviews with managersin six European countries. We start by looking at climate-change related innovationand find that most (70%) firms are equally engaged in formal or informal R&D withthe aim of curbing emissions and/or energy consumption. A smaller proportion(40%) is also pursuing “Clean product innovation”; i.e. R&D with the aim of devel-oping products that can help customers to reduce their emissions. Almost all firmsthat report product R&D also report process R&D. We find that firms expect futurecarbon prices to be considerably higher than current levels in the EU ETS, averaging€40 in 2020. Compared to the current 2nd trading period, firms expect the impos-ition of tighter caps for the post-2012 EU ETS period. Whereas in Phase II 40% offirms reported that the EU ETS cap imposed on them was not binding, this propor-tion reduces to less than 10% for the post-2012 period. Firms that expect a morestringent EU ETS cap in Phase III are more likely to engage in product innovation.Such a correlation could potentially imply that in a trading system the allocationof emissions allowances might not be independent of other real factors, such as theinvestment in R&D. We examine this hypothesis further by examining whether there

20

is a discontinuity in innovative activity at the thresholds implied by the EuropeanCommission criteria for exemptions from auctioning post-2012. We find that firmsthat narrowly qualified for exemption from auctioning were conducting significantlyless product innovation than firms that narrowly missed being exempted from auc-tioning. This finding is consistent with the hypothesis that having a tight carbonbudget has an important signalling effect for firms in that it draws the attention ofhigher levels of management to the matter of GHG emissions. This in turn might bethe trigger of the decision to engage in climate-change related product R&D. On thewhole, our results support the view that allocating fewer allowances for free wouldlead to a stronger innovation response in an otherwise identical emissions tradingsystem.

ReferencesAnderson, B., Leib, J., Martin, R., McGuigan, M., Muuls, M., de Preux, L., and

Wagner, U. J. (2011). Climate change policy and business in europe: Evidencefrom interviews with managers. Technical report.

Bertrand, M. and Mullainathan, S. (2001). Do people mean what they say implica-tions for subjective survey data. American Economic Review Papers & Proceed-ings, 91(2):67–72.

Bloom, N. and van Reenen, J. (2007). Measuring and explaining management prac-tices across firms and countries. Quarterly Journal of Economics, CXXII(4):1351–1406.

Hahn, R. W. and Stavins, R. N. (2010). The effect of allowance allocations on cap-and-trade system performance. Social Science Research Network Working PaperSeries.

Kenber, M., Haugen, O., and Cobb, M. (2009). The effects of eu climate legislationon business competitiveness: A survey and analysis. Climate & Energy PaperSeries, The German Marshall Fund of the United States.

Martin, R., Muûls, M., De Preux, L. B., and Wagner, U. J. (2010). Anatomy of aparadox: Management practices, organizational structure and energy efficiency.CEP Discussion Paper Series, 1039.

McKinsey and Ecofys (2005). Review of emissions trading scheme: Survey high-lights. Technical report, European Commission Directorate General for Environ-ment, Brussels.

21

A Questionnaire

22

1 App

endix: Que

stionn

aire

Que

stions

Values

Coding

descriptio

n

I. Introd

uctio

n 1. A bit ab

out y

our b

usiness

(a) Is y

our firm

a m

ultin

ationa

l? If yes, w

here is th

e he

adqu

arters?

(b) O

n ho

w m

any prod

uctio

n sites do you op

erate (globa

lly)?

(c) H

ow m

any of th

ese sites are situated

in th

e EU

? (d) H

ow m

any of th

ese sites are situated

in th

e UK/B/FR

/...?

no, list of cou

ntrie

s, dk, rf

“No”, if n

ot a m

ultin

ationa

l; cou

ntry whe

re headq

uarters is located

if a

multin

ationa

l nu

mbe

r, dk, rf

numbe

r, dk, rf

Num

ber o

f site

s globa

lly (a

pproximate if un

sure)

Num

ber o

f site

s in the EU

numbe

r, dk, rf

Num

ber o

f site

s in curren

t cou

ntry

2. A bit ab

out y

ou

(a) Job

title

text

(b) T

enure in com

pany

numbe

r, rf

(c) T

enure in current post

numbe

r, rf

(d) M

anagerial backgroun

d commercial, techn

ical, law

, other

3. EU ETS involvem

ent

As you

might kno

w, the

Europ

ean Union

Emiss

ions Trading

System

(referred to as E

U ETS, h

ereafter) is a

t the

heart of

Europe

an clim

ate chan

ge policy.

(a) Is y

our c

ompa

ny (o

r parts th

ereo

f) regulated un

der the

EU

ETS?

(b) Since whe

n?

(c) H

ow m

any of you

r Europ

ean bu

siness s

ites a

re covered

by the

EU ETS?

no, list of years 200

5-‐20

09, yes dk

year, d

k, rf

numbe

r, dk, rf

Que

stions

Values

Coding

descriptio

n

4. Site

locatio

n For single plan

t firm

s and

interviewees b

ased at a

produ

ction site:

Could you tell me the po

stcode

of the

business s

ite whe

re you

are

based?

For m

ulti-‐plan

t firm

s where th

e interviewee is located at a non

-‐prod

uctio

n site:

Some of th

e qu

estio

ns I am

going to

ask you

next a

re sp

ecific to a

prod

uctio

n site with

in you

r firm

. Please choo

se a particular

prod

uctio

n site an

d an

swer m

y qu

estio

ns fo

r the

particular site

througho

ut th

e interview. The

site sh

ould be the on

e you know

be

st, the

largest o

ne, o

r the

one

nearest to

you

. If you

are in th

e EU

ETS, p

lease pick a site covered

by the EU

ETS. Co

uld you tell

me the po

stcode

of the

cho

sen site?

text

Records the

postcod

e

II. Im

pact of E

U ETS

5. EU ETS strin

gency (If not an EU

ETS firm

, con

tinue

with

que

stion 9)

(a) H

ow to

ugh is the em

issions cap

/quo

ta currently im

posed by th

e EU

ETS on your produ

ction site?

(b) C

an you

describe some of th

e measures y

ou put in place to

comply with

the cap?

1-‐5, dk, rf, n

a Low

Cap is at business a

s usual.

Mid

Some ad

justmen

ts se

em to

have taken place, how

ever nothing which

led to fu

ndam

ental cha

nges in practices; e.g. insulation, etc.

High

Measures w

hich led to fu

ndam

ental cha

nges in produ

ction processes;

e.g. fu

el sw

itching; rep

lacemen

t of e

ssen

tial plant and

machine

ry.

(c) W

hat is the

ann

ual cost b

urde

n of being part o

f the

EU ETS?

For e

xample, m

onito

ring, verificatio

n an

d tran

saction costs; th

e cost

of buying pe

rmits or red

ucing em

issions.

If the man

ager does n

ot und

erstan

d the qu

estio

n:

Imagine your installatio

n was not part o

f the

EU ETS th

is year, w

hat

cost sa

ving wou

ld you

r firm

do?

numbe

r

percen

tage

Absolute num

ber

Or p

ercentage of ann

ual ope

ratin

g cost

6. EU ETS m

anag

emen

t Ask on

ly m

ulti-‐plan

t firm

s:

site, other site, n

ationa

l firm

,

Que

stions

Values

Coding

descriptio

n

Is EU ETS com

pliance man

aged

on the prod

uctio

n site or

elsewhe

re?

europe

an firm

, dk, rf, n

a

7. ETS trad

ing

(a) In March of this y

ear (i.e. b

efore the compliance process), w

hat

was you

r allowan

ce position

on this site?

(b) W

ere you short o

r lon

g in allowan

ces?

long, sho

rt, b

alan

ced, dk, rf, n

a text

If the man

ager hap

pens to

men

tion the de

tailed nu

mbe

r of a

llowan

ces, m

ake a

note of it in this fie

ld.

(c) B

efore the compliance process in Ap

ril, d

id you

buy or sell

allowan

ces o

n the market o

r over the

cou

nter from

other firm

s?

(d) If n

ot, w

hy not?

buy, se

ll, both, no: only trad

ing

durin

g compliance pe

riod, no: no

need

, no: im

age concerns, n

o:

tran

saction costs, no: other, d

k, rf,

na

(e) If yes, h

ow freq

uently?

daily, w

eekly, m

onthly, q

uarterly,

bi-‐ann

ual, yearly, d

k, rf, n

a

(f) In

April this yea

r, wha

t was you

r position

after

the compliance process?

If an

swers "

long

": Did you

ban

k pe

rmits fo

r future

years? W

hy?

banking to emit more in fo

llowing

years, ban

king to

sell at a highe

r ETS pe

rmit price in fu

ture, b

anking

dk why, lon

g for p

ooling, dk, rf, n

a

Banking reason

.

If an

swers "

balanced/com

pliant" or "short": D

id you

bo

rrow

permits from

next y

ear's allowan

ce? Why?

borrow

ing to emit less in fo

llowing

years, borrowing to buy at a

lower

ETS pe

rmit price in fu

ture,

borrow

ing to be compliant,

borrow

ing dk why, rf, dk, n

a

Borrow

ing reason

. Note: Only choo

se "bo

rrow

ing to be compliant" if the

man

ager is very short sighted and

doesn't seem

to und

erstan

d he will

eventually have to eith

er emit less or b

uy permits

If an

swers "

short": W

hy did you

remain short?

short for poo

ling, sh

ort a

nd paid

fine, other, rf, dk, n

a Short reason.

text

If “other”: why?

(g) H

as th

is site exchan

ged em

ission pe

rmits with

other

installatio

ns belon

ging to

you

r com

pany th

at are part o

f the

EU

ETS? (p

ooling)

yes, no, rf, d

k, na

Que

stions

Values

Coding

descriptio

n

8. Rationa

lity of m

arket b

ehaviour

(a) H

ow do you de

cide

how

man

y pe

rmits to

buy or sell or trade

at

all?

(b) D

id you

base this de

cisio

n on

any fo

recast abo

ut pric

es and

/or

energy usage?

(c) D

id you

trad

e pe

rmit revenu

e off a

gainst emiss

ion redu

ction

costs in your plann

ing on

this iss

ue?

1-‐5, dk, rf, n

a Low

Take th

eir p

ermit allocatio

n as a ta

rget to

be met as s

uch an

d do

not

take into accou

nt th

e price of permits or the

cost o

f aba

temen

t. Just se

ll if there is a surplus o

r buy if th

ere is a de

ficit.

Mid

Are in th

e process o

f learning ho

w th

e market w

orks and

in th

e first

years d

id not have an

y market d

riven

attitu

de, b

ut now

have someo

ne

in cha

rge of m

anaging the ETS so as to minim

ize compliance cost. This

person

has experience in fina

ncial m

arkets and

sometim

es interacts

with

the prod

uctio

n man

ager.

High

Compa

ny has a th

orou

gh und

erstan

ding of the

site-‐spe

cific CO2

abatem

ent cost curve. Trading is used as a to

ol to

redu

ce com

pliance

cost and

to gen

erate extra revenu

es from

excess a

batemen

t. Moreo

ver,

compa

ny fo

rms e

xpectatio

ns abo

ut permit price an

d re-‐optim

izes

abatem

ent cho

ice if ne

cessary. Trade

r resorts to

futures a

nd derivatives

to m

anage ETS pe

rmits as a

fina

ncial asset.

9. Anticipation of pha

se III

(a) D

o you expe

ct to

be pa

rt of the

EU ETS from

201

2 on

wards?

If no

t, continue with

question 10

yes, no, dk, rf, n

a

(b) H

ow strin

gent do you expe

ct th

e ne

xt pha

se of the

EU ETS (from

2012

to 202

0) to

be?

(c) W

ill it be tough for y

our firm

to re

ach such a ta

rget? Ca

n you

describ

e some of th

e measures y

ou wou

ld have to put in place?

(d) D

o you be

lieve th

e allowan

ces w

ill be distrib

uted

through an

au

ctioning m

echa

nism

? (e) Is it likely that sa

nctio

ns fo

r non

-‐com

pliance will becom

e more

strin

gent?

1-‐5, dk, rf, n

a Low

Cap for p

hase III is a

nticipated

to be compa

rable to business a

s usual.

The man

ager believes the

re will be no

add

ition

al sa

nctio

ns and

that

they will re

ceive the pe

rmits fo

r free.

Mid

Phase III is likely to

trigger som

e ad

justmen

ts, h

owever nothing th

at will

lead

to fu

ndam

ental cha

nges in practices. O

nly a sm

all part o

f permits

will be au

ctione

d an

d sanctio

ns are not expected to be very high.

High

The presen

ce of stron

g sanctio

ns, exten

sive use of auctio

ning and

more

strin

gent ta

rgets in Ph

ase III is anticipated

. It is likely to im

ply the

adop

tion of m

easures w

hich will lead

to fu

ndam

ental cha

nges in

prod

uctio

n processes. It m

ight also

imply the closure of th

e plan

t, or

redu

ndan

cy of m

ore than

20%

of e

mploymen

t.

(f) Do you expe

ct to

tran

sfer unu

sed (ban

ked) ERU

s or C

ERs from

Phase II to Pha

se III ?

EUAs, ERU

s, CER

s, EUAs and

ERU

s,

EUAs and

CER

s, ERU

s and

CER

s, all

Que

stions

Values

Coding

descriptio

n

Note: ERU

s are Emiss

ion Re

duction Units stem

ming from

Joint

Implem

entatio

n projects. C

ERs a

re Certified Em

ission Re

ductions

stem

ming from

Clean

Develop

ment M

echa

nism

projects.

three, no, dk, rf, n

a

10. A

waren

ess

(a) A

re clim

ate chan

ge to

pics disc

ussed with

in you

r business? Can

you give examples?

(b) A

re clim

ate chan

ge re

lated iss

ues formally disc

ussed in

man

agem

ent m

eetin

gs? Ca

n you give examples?

(c) D

o your strategic ob

jectives m

entio

n clim

ate chan

ge?

(d) D

id you

com

miss

ion repo

rts o

r studies on ho

w clim

ate chan

ge

will affe

ct you

r business?

1-‐5, dk, rf, n

a Note: Give minim

um sc

ore of 3 to

ETS firm

s and

probe dire

ctly fo

r 4 or 5

, skipping

(a) a

nd (b

). Low

Don't k

now if th

reat or o

pportunity. N

o aw

aren

ess.

Mid

Some aw

aren

ess b

acked up

by eviden

ce th

at th

is is be

ing

form

ally disc

ussed by m

anagem

ent.

High

Eviden

ce th

at clim

ate chan

ge is an im

portan

t part o

f the

bu

siness s

trategy.

Men

tione

d po

sitive im

pact:

yes, no

III. Prices

11a En

ergy price expe

ctations

By how

man

y pe

rcen

t do you expe

ct ene

rgy prices to

go up

or d

own

by 202

0?

percen

tage, d

k, rf

percen

tage, d

k, rf

percen

tage, d

k, rf

Expe

cted

pric

e chan

ge in percent of tod

ay's price.

Note: This p

rice includ

es th

e effect of current and

future clim

ate chan

ge policies

on th

e energy price.

Upp

er bou

nd on expe

cted

pric

e chan

ge – re

cord only if interviewee m

entio

ns

it.

Lower bou

nd on expe

cted

pric

e chan

ge – re

cord only if interviewee m

entio

ns

it.

11b Ca

rbon

price expe

ctations

(a) A

s you

might kno

w, the

EU has com

mitted

to re

ducing

greenh

ouse gas emiss

ions by 20

%-‐30%

over the

next d

ecad

e. W

hat

price do

you

expect to pa

y for e

mitting on

e tonn

e of CO2 in 202

0?

percen

tage, d

k, rf

Expe

cted

pric

e in Euros per to

n of CO2.

percen

tage, d

k, rf

Or e

xpected price chan

ge in percent of tod

ay's price.

yes, no, rf, d

k Kn

ows tod

ay's price of CO2.

(b) W

hat p

rice do

you

expect in the worst-‐case scen

ario?

Upp

er bou

nd in Euros per to

n of CO2.

Que

stions

Values

Coding

descriptio

n

(c) W

hat p

rice do

you

expect in the be

st-‐case scen

ario?

Lower bou

nd in Euros per to

n of CO2.

12. Future im

pact of carbo

n pricing

(a) D

o you expe

ct th

at governm

ent e

fforts to pu

t a pric

e on

carbo

n em

issions will fo

rce you to outsource parts of the

produ

ction of th

is bu

siness s

ite in th

e foreseeable future, o

r to close do

wn completely? 1-‐5, dk, rf

Low

No im

pact of this k

ind.

Mid

Significant re

duction (>10

%) in prod

uctio

n/em

ploymen

t due

to

outsou

rcing.

High

Complete close-‐do

wn.

(b) W

hat carbo

n price do

you

associate with

this

scen

ario?(Assume that you

wou

ld have to pay fo

r all allowan

ces.)

Note: The price relates to the scenario given und

er (a

). If an

swered

"no im

pact" un

der (a), skip this qu

estio

n.

numbe

r, dk, rf, na

Eu

ros p

er to

n

(c) H

ow wou

ld you

r answer to

the previous que

stions cha

nge, if you

received

a free allowan

ce fo

r 80%

of you

r current emiss

ions?

Note: If answered "no

impa

ct" un

der (a), skip this qu

estio

n.

1-‐5, dk, rf, n

a Low

No im

pact of this k

ind.

Mid

Significant re

duction (>10

%) in prod

uctio

n/em

ploymen

t due

to

outsou

rcing.

High

Complete close-‐do

wn.

(d) N

ote: Only ask if an

swered "no

impa

ct" un

der (a).

At wha

t carbo

n price level w

ould you

be forced

to close you

r plan

t dow

n?

If the man

ager has no idea

or say

s it w

ould need to be very high,

try differen

t pric

es, starting high

, for example: If you

had

to pay

200 Eu

ros/ton of carbo

n, wou

ld you

need to close dow

n?

numbe

r, dk, n

a Eu

ros pe

r ton

(e) H

ow did you

reach this conclusio

n?

(f) How

con

crete are the plan

s for outsourcing or c

losure?

1-‐5, dk, rf, n

a Low

Gut fe

eling of th

e man

ager.

Mid

Respon

se is based

on a plau

sible argum

ent. For e

xample, interviewee

discusses a

vailable techno

logical options and

associated cost and

relates the

m to

profit m

argins.

High

Commiss

ione

d a de

tailed stud

y of aba

temen

t options and

associated

cost (in-‐ho

use or externa

l).

(g) W

hat fraction of an en

ergy pric

e or carbo

n price increase can

you pa

ss on to you

r customers?

percen

tage, d

k, rf

IV. C

ompe

tition and custom

ers

Que

stions

Values

Coding

descriptio

n

13. Com

petitors

(a) C

an you

tell me the nu

mbe

r of firm

s in the world which

compe

te with

you

in one

or m

ore local m

arkets?

Note: For m

ulti-‐prod

uct m

ulti-‐plan

t firm

s refer to

the market for

the prod

ucts created on the current site

referred to

during this

interview. For instan

ce, for m

ulti-‐plan

t firm

s start th

e qu

estio

n with

"For the produ

cts p

rodu

ced at th

e prod

uctio

n site, can

you

tell me ..."

numbe

r, dk, rf

(b) H

ow m

any of th

em are located with

in th

e EU

? nu

mbe

r, dk, rf

(c) H

ow m

any of th

em are located in you

r cou

ntry?

numbe

r, dk, rf

(d) Location of m

ain compe

titor (cou

ntry)

list o

f cou

ntrie

s, dk, rf, n

a

(e) D

o you know

in which cou

ntry you

r main compe

titor doe

s most o

f its produ

ction?

same, EU, n

on-‐EU, list of

coun

tries, dk, rf, n

a

14. Location of Customers

(a) Sha

re of sales exported (to the EU

and

the rest of the

world)

percen

tage, d

k, rf

(b) Sha

re of sales exported to EU cou

ntrie

s pe

rcen

tage, d

k, rf

(c) A

re you

r produ

cts s

old mainly to con

sumers o

r to othe

r bu

sinesses?

B2B, fina

l customer, d

k, rf

15. Customer pressure

(a) A

re you

r customers c

oncerned

abo

ut you

r GHG emiss

ions?

(b) H

ow do they voice th

is concern?

(c) D

o your customers req

uire hard da

ta on your carbo

n em

issions?

1-‐5, dk, rf

Low

"B2C

" -‐ N

ot aware that emiss

ions perform

ance is of significan

t con

cern

to con

sumers o

f the

ir prod

uct.

"B2B

" -‐ N

ot aware that businesses the

y supp

ly to

are con

cerned

abo

ut

the em

issions of the

plant; q

uality an

d price are the on

ly con

siderations.

Mid

"B2C

" -‐ T

he business is a

ware of th

e im

portan

ce of clim

ate-‐chan

ge

issue

s in gene

ral and

so are con

scious th

at th

eir c

ustomers m

ay

consider GHG perform

ance to

be im

portan

t, althou

gh th

ey do no

t expe

ct or req

uire data as proof.

"B2B

" -‐ C

ustomers s

et ISO 140

01 as a

precond

ition

to su

ppliers.

Que

stions

Values

Coding

descriptio

n

Eviden

ce of e

nviro

nmen

tal com

pliance is requ

ested, but details of

emiss

ions figures a

re not re

quire

d.

High

"B2C

" -‐ B

eing se

en to

redu

ce GHG emiss

ions is th

ought to be

impo

rtan

t in th

e pu

rcha

sing de

cisio

ns of the

firm

's consum

ers. This h

as been

determ

ined

by market research or con

sumers h

ave voiced

their c

oncern

through othe

r means. C

ustomers a

lso ask fo

r certified da

ta on

emiss

ions during prod

uctio

n or usage. A

customer-‐friend

ly sy

stem

to

recognize the be

st produ

cts in term

s of e

nergy efficiency is often

available in th

e market (e.g. EU ene

rgy efficiency grad

e for h

ome

appliances).

"B2B

" -‐ C

ustomers a

sk fo

r evide

nce of externa

l validation of GHG

figures. C

ustomers req

uest inform

ation on

carbo

n em

issions as p

art o

f their o

wn supp

ly cha

in carbo

n au

ditin

g. Customers c

onform

to PAS

20

50 or o

ther nationa

l stand

ard in carbo

n foot-‐prin

ting an

d so re

quire

de

tailed inform

ation on

a re

gular b

asis.

16 Clim

ate chan

ge re

lated prod

uct inn

ovation

(a) G

loba

lly, is y

our c

ompa

ny currently trying to

develop

new

prod

ucts th

at help your customers to redu

ce GHG emiss

ions?

(b) C

an you

give exam

ples?

(c) W

hat fraction of you

r Research & Develop

men

t fun

ds are used

for tha

t? (Less tha

n 10

%, m

ore than

10%

?)

1-‐5, dk, rf

Low

No efforts to de

velop clim

ate chan

ge re

lated

prod

ucts.

Mid

Some efforts b

ut it is not th

e main ob

jective of

the firms R

&D efforts.

High

The firm is fo

cusin

g all produ

ct R&D efforts

on clim

ate chan

ge.

V. M

easures

17. Ene

rgy mon

itorin

g

Que

stions

Values

Coding

descriptio

n

(a) H

ow detailed is your m

onito

ring of ene

rgy usage?

(b) H

ow often

do you mon

itor y

our e

nergy usage? Since whe

n?

(c ) De

scrib

e the system

you

have in place.

1-‐5, dk, rf

Low

No mon

itorin

g ap

art from looking at th

e en

ergy bill.

Mid

Eviden

ce of e

nergy mon

itorin

g as opp

osed

to looking at th

e en

ergy bill,

i.e. the

re is so

me consciou

sness a

bout th

e am

ount of e

nergy be

ing used

as a business o

bjectiv

e. How

ever, d

iscussio

ns are irregular a

nd not part

of a structured

process and

are m

ore freq

uent with

pric

e rises. Not

more than

qua

rterly m

onito

ring of ene

rgy.

High

Energy use is m

easured an

d mon

itored constantly and

is on the agen

da

in re

gular p

rodu

ction meetin

gs. Ene

rgy use in th

e plan

t is d

ivided

up in

space (by prod

uctio

n line, m

achine

or sim

ilar) and

mon

itored over time

(daily, h

ourly

or c

ontin

uously). Th

e am

ount of e

nergy rather th

an th

e cost is fo

cused on

.

2000

and

earlier, list o

f years

2001

-‐201

0, dk, rf, n

a Start d

ate (put “na

” if score is “1”)

18. Targe

ts on en

ergy con

sumption for m

anag

emen

t (a) D

o you ha

ve any ta

rgets o

n en

ergy con

sumption which

man

agem

ent h

as to

observe? (e.g. kWh of electric

ity)

no ta

rgets, re

lativ

e qu

antity

targets, absolute qu

antity targets,

absolute and

relativ

e qu

antity

targets, only expe

nditu

re ta

rgets,

dk, rf

Type

(b) C

an you

describe some of th

e challenges you

face in m

eetin

g the

targets?

(c) H

ow often

do you meet the

se ta

rgets? Do you think they are

tough?

Note: If th

e man

ager re

plies they ha

ve EU ETS/CCA

targets, ask

"have these been tran

slated into internal ta

rgets for m

anag

ement?"

1-‐5, dk, rf

Low

No targets.

Mid

Targets e

xist but se

em easy to achieve.

High

Eviden

ce th

at ta

rgets a

re hard to achieve. D

etailed.

(d) B

y ap

proxim

ately ho

w m

uch do

es th

is requ

ire re

ducing you

r curren

t ene

rgy consum

ption in th

e ne

xt 5 years (1

0%, 25%

, 50%

)?

Note the tim

etab

le fo

r the ta

rget (e

.g. 5 years or o

ther num

ber g

iven by

interviewee).

percen

tage, d

k, rf, n

a nu

mbe

r, dk, rf, na

Horizon

(num

ber o

f years)

(e) Since whe

n do

you

have these targets?

2000

and

earlier, list o

f years

2001

-‐201

0, dk, rf, n

a

Que

stions

Values

Coding

descriptio

n

19. G

HG m

onito

ring

(a) D

o you explicitly mon

itor y

our G

HG emiss

ions? Since whe

n?

(b) H

ow do you estim

ate your GHG emiss

ions?

(c) A

re you

r GHG estim

ates externa

lly validated

?

1-‐5, dk, rf

Low

No specific GHG m

onito

ring.

Mid

Detailed en

ergy m

onito

ring with

clear evide

nce for carbo

n accoun

ting

(at least firm

level). M

anager is aware that ene

rgy fig

ures need to be

scaled

by carbon

intensity

. High

Carbon

accou

nting of both direct and

indirect emiss

ions (sup

ply chain

emiss

ions). External validation of GHG figures.

20

00 and

earlier, list o

f years

2001

-‐201

0, dk, rf, n

a Start d

ate (put “na

” if score is “1”)

20. Targe

ts on GHG

emission

s for m

anag

emen

t (a) D

o you ha

ve any ta

rgets o

n GHG emiss

ions which

man

agem

ent h

as to

observe?

no ta

rgets, dire

ct emiss

ions,

indirect and

dire

ct, d

k, rf

(b) C

an you

describe some of th

e challenges you

face in m

eetin

g the

targets?

(c) H

ow often

do you meet the

se ta

rgets? Do you think they are

tough?

Note: If th

e man

ager re

plies they ha

ve EU ETS/CCA

targets, ask:

Have these be

en tran

slated into internal ta

rgets for m

anagem

ent?

1-‐5, dk, rf

Low

No targets for GHG emiss

ions.

Mid

There is some aw

aren

ess o

f the

con

tribution of differen

t ene

rgy sources

and prod

uctio

n processes to em

issions, b

ut th

is is a second

ary

consideration to cost focused

ene

rgy targets. The

re is so

me de

gree of

difficulty

in th

e targets.

HIgh

There are sepa

rate ta

rgets for GHGs, distinct from

ene

rgy use. GHG

emiss

ions are a KPI (K

ey Perform

ance In

dicator) fo

r the

firm

. The

contrib

ution of each en

ergy so

urce and

the prod

uctio

n process to GHG

emiss

ions is kno

wn an

d suggested im

provem

ent p

rojects for th

e prod

uctio

n are assessed

on their p

oten

tial impa

ct on carbon

as w

ell as

energy efficien

cy.

(d) B

y ap

proxim

ately ho

w m

uch do