Automobiles - Prabhudas Lilladher

33

September 04, 2013 Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision. Please refer to important disclosures and disclaimers at the end of the report Automobiles Two Wheelers – Ahead in the race Sector Report Surjit Arora [email protected] +91-22-66322235 Sensex v/s. Hero Motocorp & Bajaj Auto 70 80 90 100 110 120 130 140 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Sensex Bajaj Auto Hero Motocorp Source: Bloomberg Stock Performance (%) 1M 6M 12M Sensex (3.1) (1.6) 6.5 Auto (0.1) (1.9) 10.7 Bajaj Auto (1.1) (5.0) 14.6 Hero Motocorp 6.9 17.6 6.6 Stock Data CMP (Rs) TP (Rs) PE (x) FY14E FY15E Bajaj Auto 1,889 2,083 15.9 13.6 Hero Motocorp 1,927 2,176 17.6 13.3 How we differ from Consensus EPS (Rs) PL Cons. % Diff. Bajaj Auto 2014 119.1 123.5 ‐3.6 2015 138.8 141.8 ‐2.1 Hero Motocorp 2014 109.3 109.4 0.0 2015 145.1 139.3 4.2 We believe that with the interest rate cycle reversing (read inching up) and robust rural economy, two‐wheeler stocks are likely to outperform over the next one year. Three key factors leading to our stance are a) strong rural economy led by good monsoon and increase in MSPs b) export potential ‐ Indian firms are better placed compared to Chinese counterparts (Africa & Latin America dominated by Chinese) on currency and labour cost front 3) Valuation attractive at 13‐14.0x 1yr fwd P/E, given the strong 18% earnings CAGR, coupled with strong balance sheet and better corporate governance. We upgrade Bajaj to ‘Accumulate’ from ‘Reduce’ mainly on account of higher export realization in FY14E and volume recovery from Jan’14. At the same time, with scooter volumes growing faster than motorcycle (women are increasing opting for the same), entry into the export market and strong rural sales (which account for ~45%), we upgrade Hero Motocorp from ‘Reduce’ to ‘Accumulate’. Recovery in two‐wheelers likely: According to Hero Motocorp management, recovery in two-wheeler industry demand is likely, given the good monsoon, coupled with possible increase in government spending ahead of 2014 national elections. We expect 12-13% CAGR in scooter volumes for the next two years. We expect two-wheeler volumes to grow at ~7% CAGR mainly led by 12.2% CAGR in scooter volumes and 6.0% CAGR in motorcycle volumes over FY13- FY15E period. Scooter share in the last three years has increased from 15% to 21% of two-wheeler volumes mainly driven by (a) growing acceptability of gearless scooters, particularly by women, (b) rising urbanization and increasing proportion of working women. Rural economy to spur demand: In the country's main cropping regions, monsoon has been timely and 20-30% above average so far, prompting farmers to expand cultivated area by 9% to 930 lakh hectares, with the biggest gains in pulses, oilseeds and coarse cereals. Going by the current trend of rising rural incomes with higher yields and minimum support prices, the outlook on two- wheelers is positive. Low penetration level, lack of adequate mode public transport and rising per capita income in rural India would lead to long-term healthy volume of two-wheelers. With rural economy accounting for 40-45% of the sales for two-wheelers, we expect good times ahead for two-wheeler manufacturers. Competitive intensity likely to slowdown: Over the last two years, HMSI has gained 450bps in motorcycles to 11.8% in FY13 and 520bps market share in scooters segment to 48.6% in FY13E. At the same time, HMCL has lost only 150bps market share in motorcycles to 53.6% in FY13E whereas it has gained market share of 210bps to 18.8% in FY13 in the scooter segment. Going forward, in our view, Hero would gain 180bps in market share in scooter segment thanks to ‘Maestro’ and ‘Pleasure’ to 21.6%, whereas it is likely to protect its turf in the motorcycle segment by maintaining its market share at 53.3% in FY15E. HMSI is likely to further gain market share to the tune of 260bps to 14.7% by FY15E at the cost of Bajaj Auto.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Automobiles - Prabhudas Lilladher

September 04, 2013

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Automobiles

Two Wheelers – Ahead in the race

Sector Report Surjit Arora

[email protected] +91-22-66322235

Sensex v/s. Hero Motocorp & Bajaj Auto

708090

100110120130140

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Sensex Bajaj Auto

Hero Motocorp

Source: Bloomberg

Stock Performance

(%) 1M 6M 12M

Sensex (3.1) (1.6) 6.5

Auto (0.1) (1.9) 10.7

Bajaj Auto (1.1) (5.0) 14.6

Hero Motocorp 6.9 17.6 6.6

Stock Data

CMP (Rs) TP (Rs) PE (x)

FY14E FY15E

Bajaj Auto 1,889 2,083 15.9 13.6

Hero Motocorp 1,927 2,176 17.6 13.3

How we differ from Consensus

EPS (Rs) PL Cons. % Diff.

Bajaj Auto

2014 119.1 123.5 ‐3.6

2015 138.8 141.8 ‐2.1

Hero Motocorp

2014 109.3 109.4 0.0

2015 145.1 139.3 4.2

We believe that with the interest rate cycle reversing (read inching up) and robust

rural economy, two‐wheeler stocks are likely to outperform over the next one year.

Three key factors leading to our stance are a) strong rural economy led by good

monsoon and increase in MSPs b) export potential ‐ Indian firms are better placed

compared to Chinese counterparts (Africa & Latin America dominated by Chinese)

on currency and labour cost front 3) Valuation attractive at 13‐14.0x 1yr fwd P/E,

given the strong 18% earnings CAGR, coupled with strong balance sheet and better

corporate governance. We upgrade Bajaj to ‘Accumulate’ from ‘Reduce’ mainly on

account of higher export realization in FY14E and volume recovery from Jan’14. At

the same time, with scooter volumes growing faster than motorcycle (women are

increasing opting for the same), entry into the export market and strong rural sales

(which account for ~45%), we upgrade Hero Motocorp from ‘Reduce’ to

‘Accumulate’.

Recovery in two‐wheelers likely: According to Hero Motocorp management, recovery in two-wheeler industry demand is likely, given the good monsoon, coupled with possible increase in government spending ahead of 2014 national elections. We expect 12-13% CAGR in scooter volumes for the next two years. We expect two-wheeler volumes to grow at ~7% CAGR mainly led by 12.2% CAGR in scooter volumes and 6.0% CAGR in motorcycle volumes over FY13-FY15E period. Scooter share in the last three years has increased from 15% to 21% of two-wheeler volumes mainly driven by (a) growing acceptability of gearless scooters, particularly by women, (b) rising urbanization and increasing proportion of working women.

Rural economy to spur demand: In the country's main cropping regions, monsoon has been timely and 20-30% above average so far, prompting farmers to expand cultivated area by 9% to 930 lakh hectares, with the biggest gains in pulses, oilseeds and coarse cereals. Going by the current trend of rising rural incomes with higher yields and minimum support prices, the outlook on two-wheelers is positive. Low penetration level, lack of adequate mode public transport and rising per capita income in rural India would lead to long-term healthy volume of two-wheelers. With rural economy accounting for 40-45% of the sales for two-wheelers, we expect good times ahead for two-wheeler manufacturers.

Competitive intensity likely to slowdown: Over the last two years, HMSI has gained 450bps in motorcycles to 11.8% in FY13 and 520bps market share in scooters segment to 48.6% in FY13E. At the same time, HMCL has lost only 150bps market share in motorcycles to 53.6% in FY13E whereas it has gained market share of 210bps to 18.8% in FY13 in the scooter segment. Going forward, in our view, Hero would gain 180bps in market share in scooter segment thanks to ‘Maestro’ and ‘Pleasure’ to 21.6%, whereas it is likely to protect its turf in the motorcycle segment by maintaining its market share at 53.3% in FY15E. HMSI is likely to further gain market share to the tune of 260bps to 14.7% by FY15E at the cost of Bajaj Auto.

September 04, 2013 2

Automobiles

Indian Manufactures to gain at the cost of Chinese: Two key export markets, mainly Africa and Latin America, are currently dominated by Chinese players, with ~75-80% market share and ~70% market share, respectively. While the Indian players have been gaining share from the Chinese mainly on account of their better quality, there is a likelihood of further market share gains on account of a) rising labour cost in China b) 16% rupee depreciation v/s 3% CNY appreciation against the USD.

Exports likely to grow in double‐digit led by Africa and LatAm: Given the low penetration in African and Latin American market relative to the Asian market, these regions are likely to drive double-digit growth over the next 4-5 years. Given that there are no plants in Africa, it is the largest importer of motorcycles globally, thereby, making it the most important export market for Indian players. With an overall population of ~1bn people and with the fastest population growth rate in the world, African market has a lot of potential. In Latin American markets like Argentina and Chile, market share gains are likely, given the currency as well as quality advantage. In our assessment, exports from Indian manufacturers are likely to grow in the region of 13-15% over the next five years.

Prefer Two‐wheelers over Four‐Wheelers; Upgrade Bajaj Auto & Hero

Motocorp to Accumulate: With exports, three-wheeler and spares accounting for ~55% of its FY14E turnover, we believe Bajaj Auto is better placed to mitigate the impact of slowdown in the two-wheeler industry. With earnings CAGR of 17-18% for FY13FY15E period, coupled with attractive dividend yields of 3%+ and ROEs in excess of 38%, we believe valuation at 13.6x FY15E EPS for Bajaj and 13.3x FY15E EPS for Hero Motocorp looks attractive. Given that interest rates are unlikely to come down, we believe two-wheelers are likely to outperform four-wheelers.

September 04, 2013 3

Automobiles

CONTENTS

Page No

Two wheeler segment - recovery likely ...................................................................... 4

Competitive intensity likely to slowdown .................................................................. 7

Scooters ............................................................................................................................................. 7

Motorcycles ....................................................................................................................................... 8

New / Recent Launches .............................................................................................. 9

Indian manufactures to gain at the cost of their Chinese counterparts .................. 11

Two-wheeler exports likely to grow in double-digit led by Africa and LatAm ......... 12

African Market – Motorcycles used as Taxis - Dominated by Chinese Players ............................... 13

Nigeria – Dominated by Chinese ................................................................................................ 13

Western Africa ........................................................................................................................... 15

Latin America – dominated by Japanese and Chinese Players ........................................................ 16

South Asia – Dominated by Indian Manufacturers ......................................................................... 17

Companies

Bajaj Auto ........................................................................................................................................ 20

Hero Motocorp ................................................................................................................................ 26

September 04, 2013 4

Automobiles

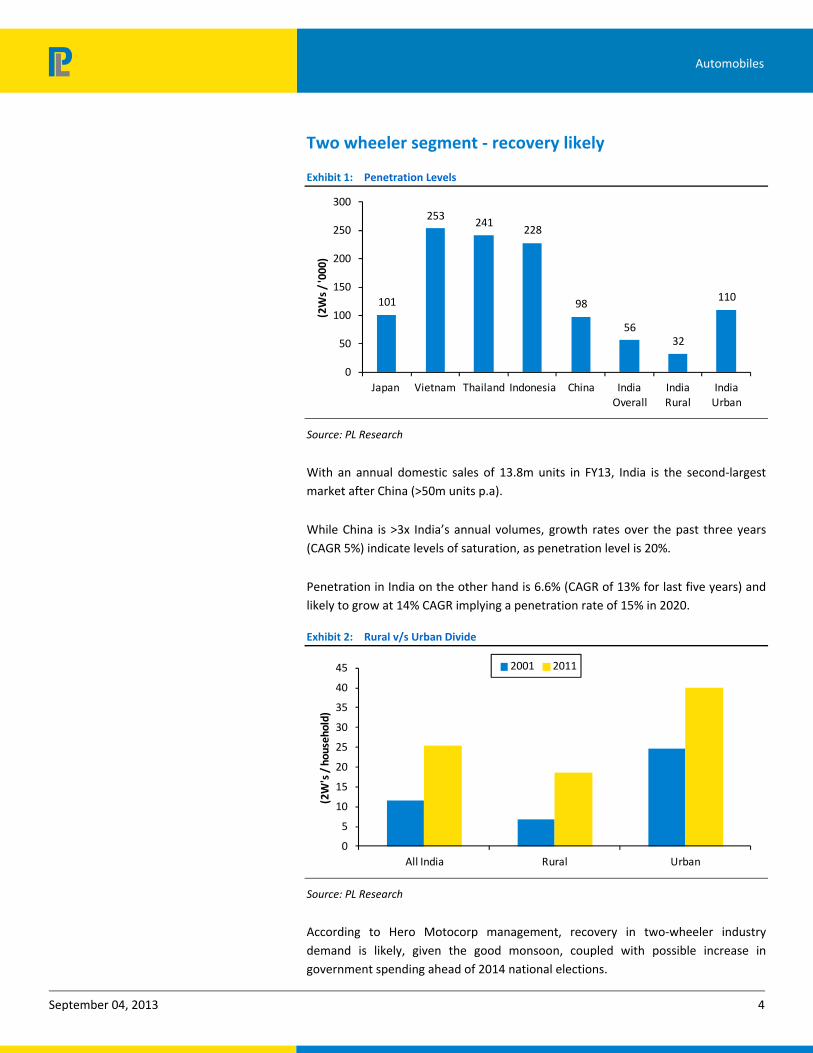

Two wheeler segment ‐ recovery likely

Exhibit 1: Penetration Levels

101

253 241228

98

5632

110

0

50

100

150

200

250

300

Japan Vietnam Thailand Indonesia China India Overall

India Rural

India Urban

(2Ws / '000)

Source: PL Research

With an annual domestic sales of 13.8m units in FY13, India is the second-largest market after China (>50m units p.a).

While China is >3x India’s annual volumes, growth rates over the past three years (CAGR 5%) indicate levels of saturation, as penetration level is 20%.

Penetration in India on the other hand is 6.6% (CAGR of 13% for last five years) and likely to grow at 14% CAGR implying a penetration rate of 15% in 2020.

Exhibit 2: Rural v/s Urban Divide

0

5

10

15

20

25

30

35

40

45

All India Rural Urban

(2W's / household)

2001 2011

Source: PL Research

According to Hero Motocorp management, recovery in two-wheeler industry demand is likely, given the good monsoon, coupled with possible increase in government spending ahead of 2014 national elections.

September 04, 2013 5

Automobiles

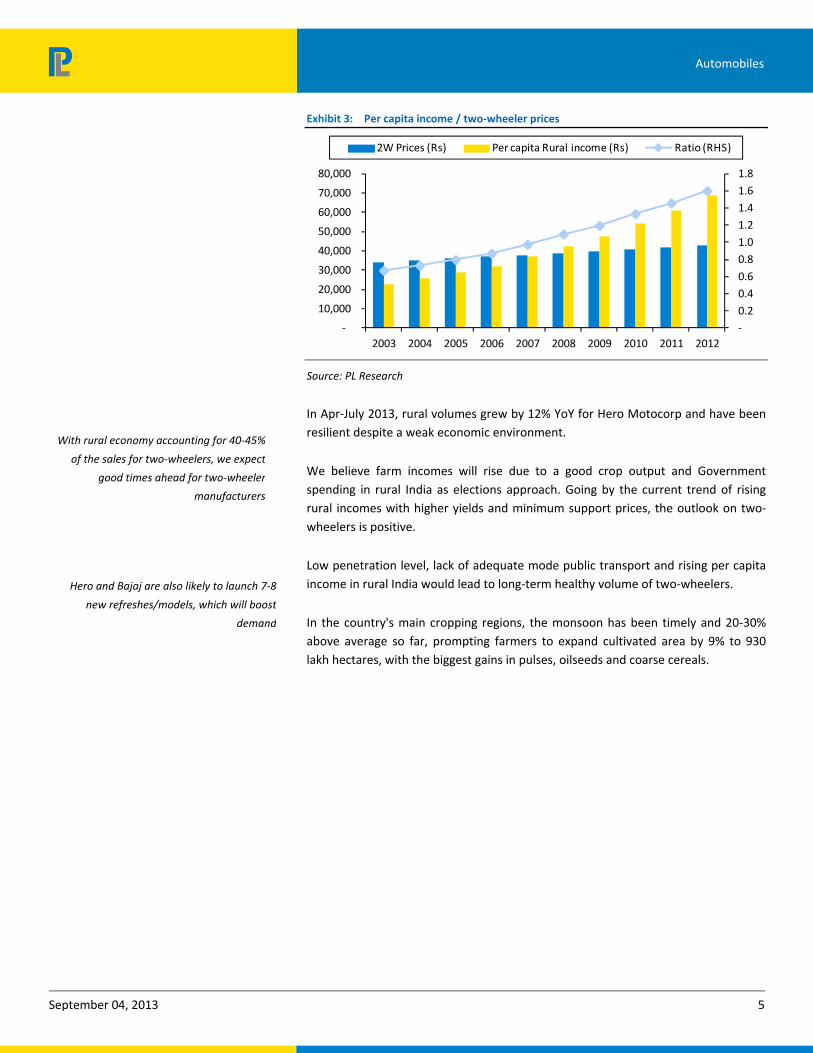

Exhibit 3: Per capita income / two‐wheeler prices

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

2W Prices (Rs) Per capita Rural income (Rs) Ratio (RHS)

Source: PL Research

In Apr-July 2013, rural volumes grew by 12% YoY for Hero Motocorp and have been resilient despite a weak economic environment.

We believe farm incomes will rise due to a good crop output and Government spending in rural India as elections approach. Going by the current trend of rising rural incomes with higher yields and minimum support prices, the outlook on two-wheelers is positive.

Low penetration level, lack of adequate mode public transport and rising per capita income in rural India would lead to long-term healthy volume of two-wheelers.

In the country's main cropping regions, the monsoon has been timely and 20-30% above average so far, prompting farmers to expand cultivated area by 9% to 930 lakh hectares, with the biggest gains in pulses, oilseeds and coarse cereals.

With rural economy accounting for 40‐45%

of the sales for two‐wheelers, we expect

good times ahead for two‐wheeler

manufacturers

Hero and Bajaj are also likely to launch 7‐8

new refreshes/models, which will boost

demand

September 04, 2013 6

Automobiles

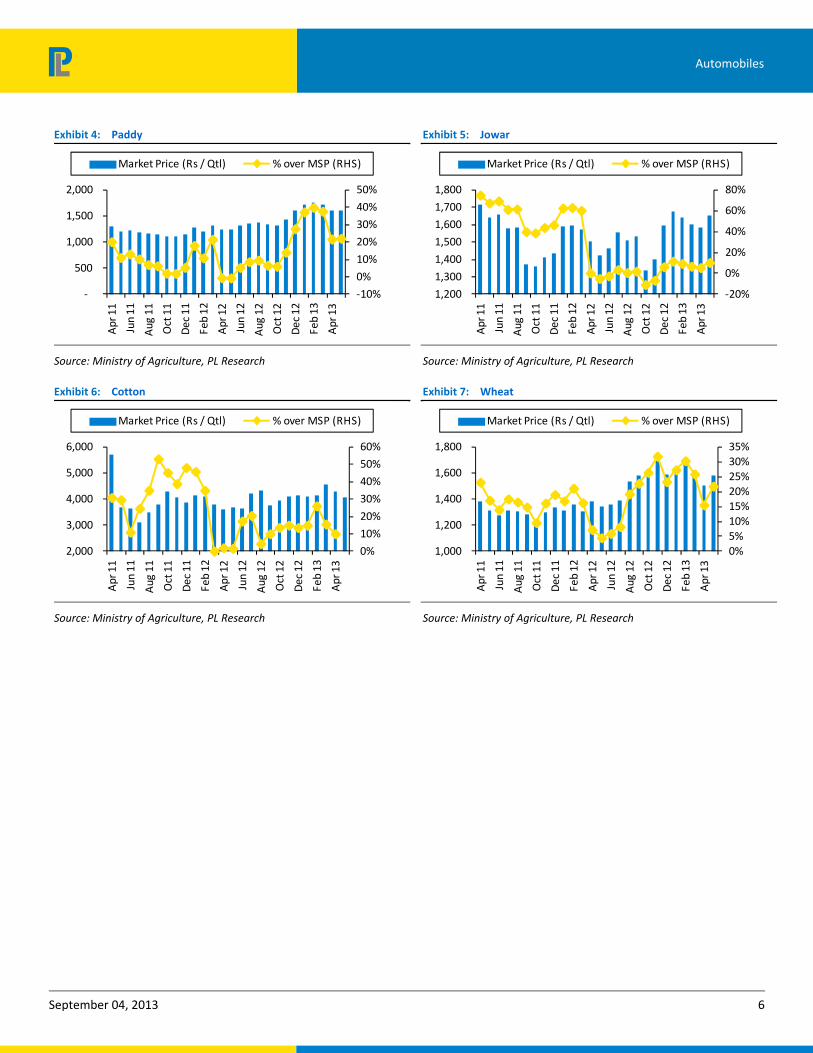

Exhibit 4: Paddy

-10%

0%

10%

20%

30%

40%

50%

-

500

1,000

1,500

2,000

Apr

11

Jun

11

Aug

11

Oct

11

Dec

11

Feb

12

Apr

12

Jun

12

Aug

12

Oct

12

Dec

12

Feb

13

Apr

13

Market Price (Rs / Qtl) % over MSP (RHS)

Source: Ministry of Agriculture, PL Research

Exhibit 5: Jowar

-20%

0%

20%

40%

60%

80%

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Apr

11

Jun

11

Aug

11

Oct

11

Dec

11

Feb

12

Apr

12

Jun

12

Aug

12

Oct

12

Dec

12

Feb

13

Apr

13

Market Price (Rs / Qtl) % over MSP (RHS)

Source: Ministry of Agriculture, PL Research

Exhibit 6: Cotton

0%

10%

20%

30%

40%

50%

60%

2,000

3,000

4,000

5,000

6,000

Apr

11

Jun

11

Aug

11

Oct

11

Dec

11

Feb

12

Apr

12

Jun

12

Aug

12

Oct

12

Dec

12

Feb

13

Apr

13

Market Price (Rs / Qtl) % over MSP (RHS)

Source: Ministry of Agriculture, PL Research

Exhibit 7: Wheat

0%5%10%15%20%25%30%35%

1,000

1,200

1,400

1,600

1,800

Apr

11

Jun

11

Aug

11

Oct

11

Dec

11

Feb

12

Apr

12

Jun

12

Aug

12

Oct

12

Dec

12

Feb

13

Apr

13

Market Price (Rs / Qtl) % over MSP (RHS)

Source: Ministry of Agriculture, PL Research

September 04, 2013 7

Automobiles

Competitive intensity likely to slowdown

Scooters

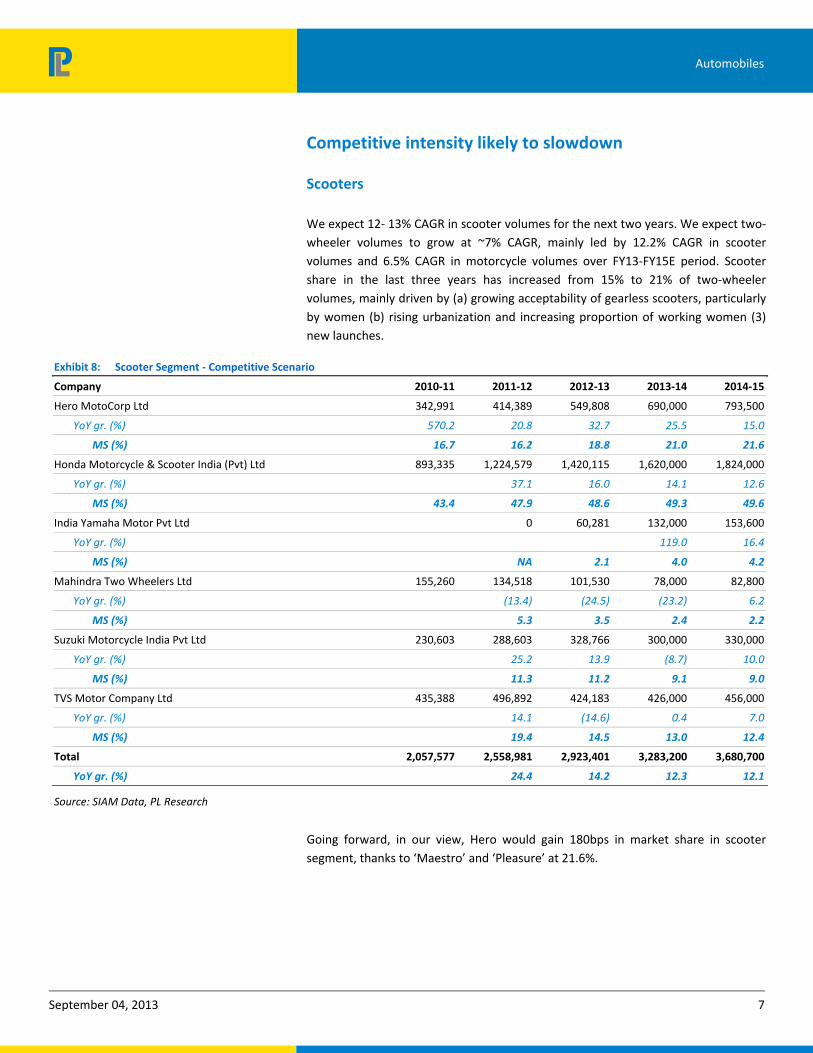

We expect 12- 13% CAGR in scooter volumes for the next two years. We expect two-wheeler volumes to grow at ~7% CAGR, mainly led by 12.2% CAGR in scooter volumes and 6.5% CAGR in motorcycle volumes over FY13-FY15E period. Scooter share in the last three years has increased from 15% to 21% of two-wheeler volumes, mainly driven by (a) growing acceptability of gearless scooters, particularly by women (b) rising urbanization and increasing proportion of working women (3) new launches.

Exhibit 8: Scooter Segment ‐ Competitive Scenario

Company 2010‐11 2011‐12 2012‐13 2013‐14 2014‐15

Hero MotoCorp Ltd 342,991 414,389 549,808 690,000 793,500

YoY gr. (%) 570.2 20.8 32.7 25.5 15.0

MS (%) 16.7 16.2 18.8 21.0 21.6

Honda Motorcycle & Scooter India (Pvt) Ltd 893,335 1,224,579 1,420,115 1,620,000 1,824,000

YoY gr. (%) 37.1 16.0 14.1 12.6

MS (%) 43.4 47.9 48.6 49.3 49.6

India Yamaha Motor Pvt Ltd 0 60,281 132,000 153,600

YoY gr. (%) 119.0 16.4

MS (%) NA 2.1 4.0 4.2

Mahindra Two Wheelers Ltd 155,260 134,518 101,530 78,000 82,800

YoY gr. (%) (13.4) (24.5) (23.2) 6.2

MS (%) 5.3 3.5 2.4 2.2

Suzuki Motorcycle India Pvt Ltd 230,603 288,603 328,766 300,000 330,000

YoY gr. (%) 25.2 13.9 (8.7) 10.0

MS (%) 11.3 11.2 9.1 9.0

TVS Motor Company Ltd 435,388 496,892 424,183 426,000 456,000

YoY gr. (%) 14.1 (14.6) 0.4 7.0

MS (%) 19.4 14.5 13.0 12.4

Total 2,057,577 2,558,981 2,923,401 3,283,200 3,680,700

YoY gr. (%) 24.4 14.2 12.3 12.1

Source: SIAM Data, PL Research

Going forward, in our view, Hero would gain 180bps in market share in scooter segment, thanks to ‘Maestro’ and ‘Pleasure’ at 21.6%.

September 04, 2013 8

Automobiles

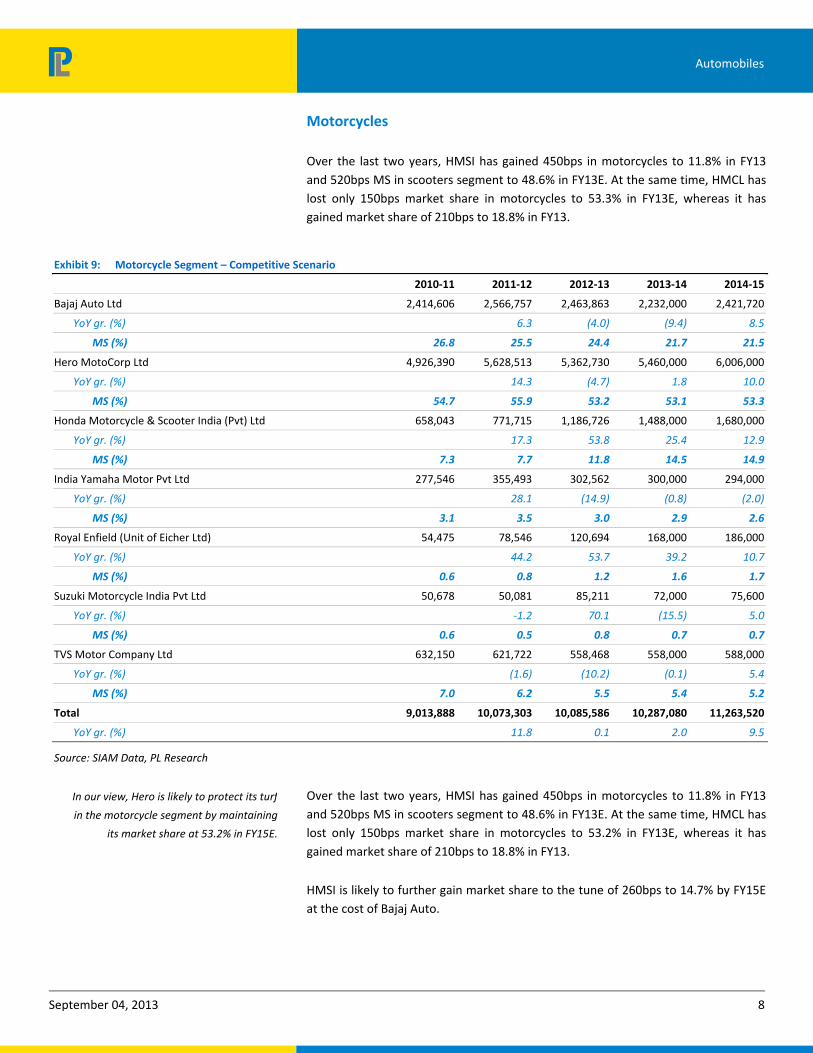

Motorcycles

Over the last two years, HMSI has gained 450bps in motorcycles to 11.8% in FY13 and 520bps MS in scooters segment to 48.6% in FY13E. At the same time, HMCL has lost only 150bps market share in motorcycles to 53.3% in FY13E, whereas it has gained market share of 210bps to 18.8% in FY13.

Exhibit 9: Motorcycle Segment – Competitive Scenario

2010‐11 2011‐12 2012‐13 2013‐14 2014‐15

Bajaj Auto Ltd 2,414,606 2,566,757 2,463,863 2,232,000 2,421,720

YoY gr. (%) 6.3 (4.0) (9.4) 8.5

MS (%) 26.8 25.5 24.4 21.7 21.5

Hero MotoCorp Ltd 4,926,390 5,628,513 5,362,730 5,460,000 6,006,000

YoY gr. (%) 14.3 (4.7) 1.8 10.0

MS (%) 54.7 55.9 53.2 53.1 53.3

Honda Motorcycle & Scooter India (Pvt) Ltd 658,043 771,715 1,186,726 1,488,000 1,680,000

YoY gr. (%) 17.3 53.8 25.4 12.9

MS (%) 7.3 7.7 11.8 14.5 14.9

India Yamaha Motor Pvt Ltd 277,546 355,493 302,562 300,000 294,000

YoY gr. (%) 28.1 (14.9) (0.8) (2.0)

MS (%) 3.1 3.5 3.0 2.9 2.6

Royal Enfield (Unit of Eicher Ltd) 54,475 78,546 120,694 168,000 186,000

YoY gr. (%) 44.2 53.7 39.2 10.7

MS (%) 0.6 0.8 1.2 1.6 1.7

Suzuki Motorcycle India Pvt Ltd 50,678 50,081 85,211 72,000 75,600

YoY gr. (%) ‐1.2 70.1 (15.5) 5.0

MS (%) 0.6 0.5 0.8 0.7 0.7

TVS Motor Company Ltd 632,150 621,722 558,468 558,000 588,000

YoY gr. (%) (1.6) (10.2) (0.1) 5.4

MS (%) 7.0 6.2 5.5 5.4 5.2

Total 9,013,888 10,073,303 10,085,586 10,287,080 11,263,520

YoY gr. (%) 11.8 0.1 2.0 9.5

Source: SIAM Data, PL Research

Over the last two years, HMSI has gained 450bps in motorcycles to 11.8% in FY13 and 520bps MS in scooters segment to 48.6% in FY13E. At the same time, HMCL has lost only 150bps market share in motorcycles to 53.2% in FY13E, whereas it has gained market share of 210bps to 18.8% in FY13.

HMSI is likely to further gain market share to the tune of 260bps to 14.7% by FY15E at the cost of Bajaj Auto.

In our view, Hero is likely to protect its turf

in the motorcycle segment by maintaining

its market share at 53.2% in FY15E.

September 04, 2013 9

Automobiles

New / Recent Launches

Exhibit 10: Scooter Segment – New Launches

New Launches Price (Rs ex showroom Delhi) Engine Displacement

Piaggio Vespa 60,000 125cc

Ray / Spark 47,102 125cc

Maestro 48,900 110cc

Activa 49,700 110cc

Dio 47,000 110cc

Source: Company Data, PL Research

September 04, 2013 10

Automobiles

Exhibit 11: Motorcycle segment – New Launches

New Launches Price (Rs ex showroom Delhi) Engine Displacement

Ignitor 63,800 125cc

Passion X pro 52,700 110cc

Super Splendor 53,900 125cc

Splendor NXG 49,000 100cc

Dream Yuga 52,400 110cc

Dream Neo 51,500 110cc

CBF Stunner 60,200 125cc

Source: Company Data, PL Research

September 04, 2013 11

Automobiles

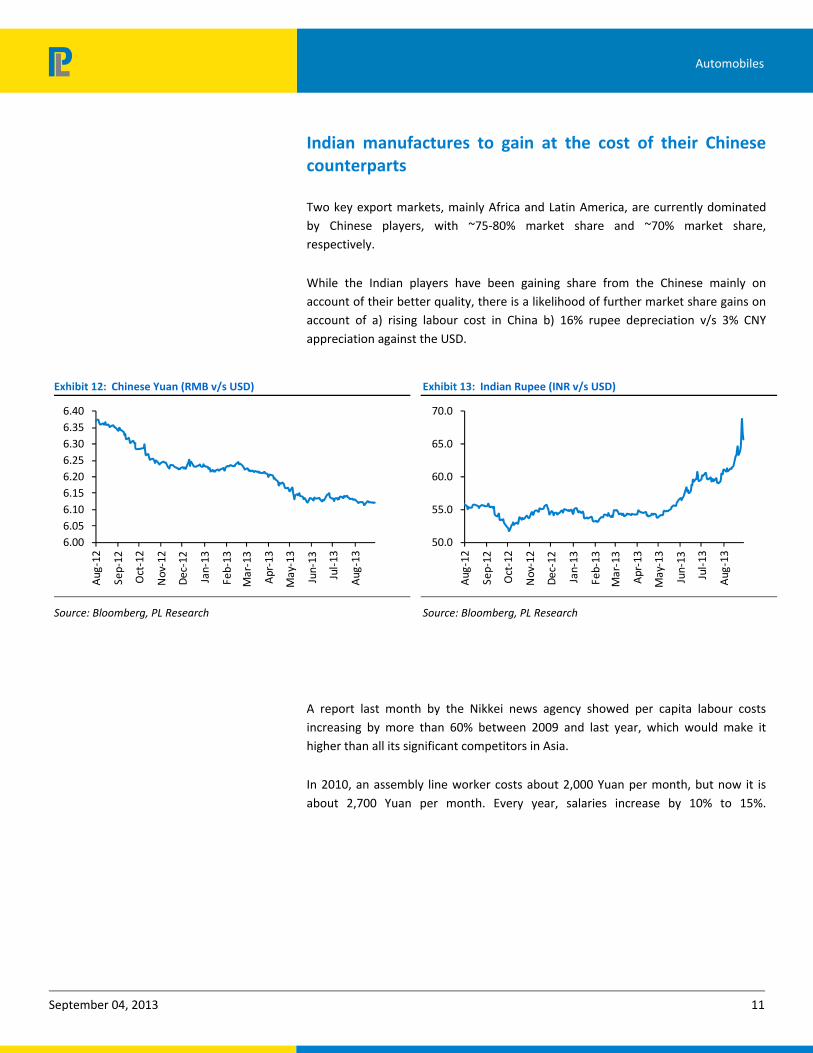

Indian manufactures to gain at the cost of their Chinese counterparts

Two key export markets, mainly Africa and Latin America, are currently dominated by Chinese players, with ~75-80% market share and ~70% market share, respectively.

While the Indian players have been gaining share from the Chinese mainly on account of their better quality, there is a likelihood of further market share gains on account of a) rising labour cost in China b) 16% rupee depreciation v/s 3% CNY appreciation against the USD.

Exhibit 12: Chinese Yuan (RMB v/s USD)

6.006.056.106.156.206.256.306.356.40

Aug

-12

Sep-

12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Source: Bloomberg, PL Research

Exhibit 13: Indian Rupee (INR v/s USD)

50.0

55.0

60.0

65.0

70.0

Aug

-12

Sep-

12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Source: Bloomberg, PL Research

A report last month by the Nikkei news agency showed per capita labour costs increasing by more than 60% between 2009 and last year, which would make it higher than all its significant competitors in Asia.

In 2010, an assembly line worker costs about 2,000 Yuan per month, but now it is about 2,700 Yuan per month. Every year, salaries increase by 10% to 15%.

September 04, 2013 12

Automobiles

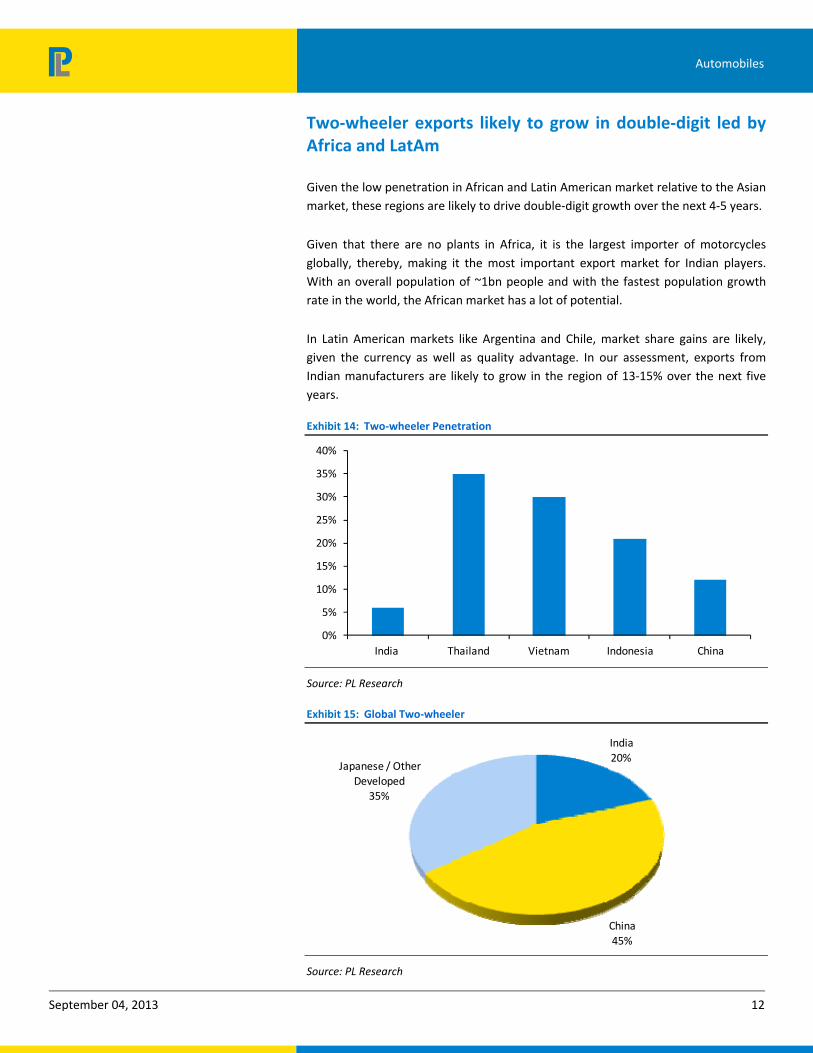

Two‐wheeler exports likely to grow in double‐digit led by Africa and LatAm

Given the low penetration in African and Latin American market relative to the Asian market, these regions are likely to drive double-digit growth over the next 4-5 years.

Given that there are no plants in Africa, it is the largest importer of motorcycles globally, thereby, making it the most important export market for Indian players. With an overall population of ~1bn people and with the fastest population growth rate in the world, the African market has a lot of potential.

In Latin American markets like Argentina and Chile, market share gains are likely, given the currency as well as quality advantage. In our assessment, exports from Indian manufacturers are likely to grow in the region of 13-15% over the next five years.

Exhibit 14: Two‐wheeler Penetration

0%

5%

10%

15%

20%

25%

30%

35%

40%

India Thailand Vietnam Indonesia China

Source: PL Research

Exhibit 15: Global Two‐wheeler

India20%

China45%

Japanese / Other Developed

35%

Source: PL Research

September 04, 2013 13

Automobiles

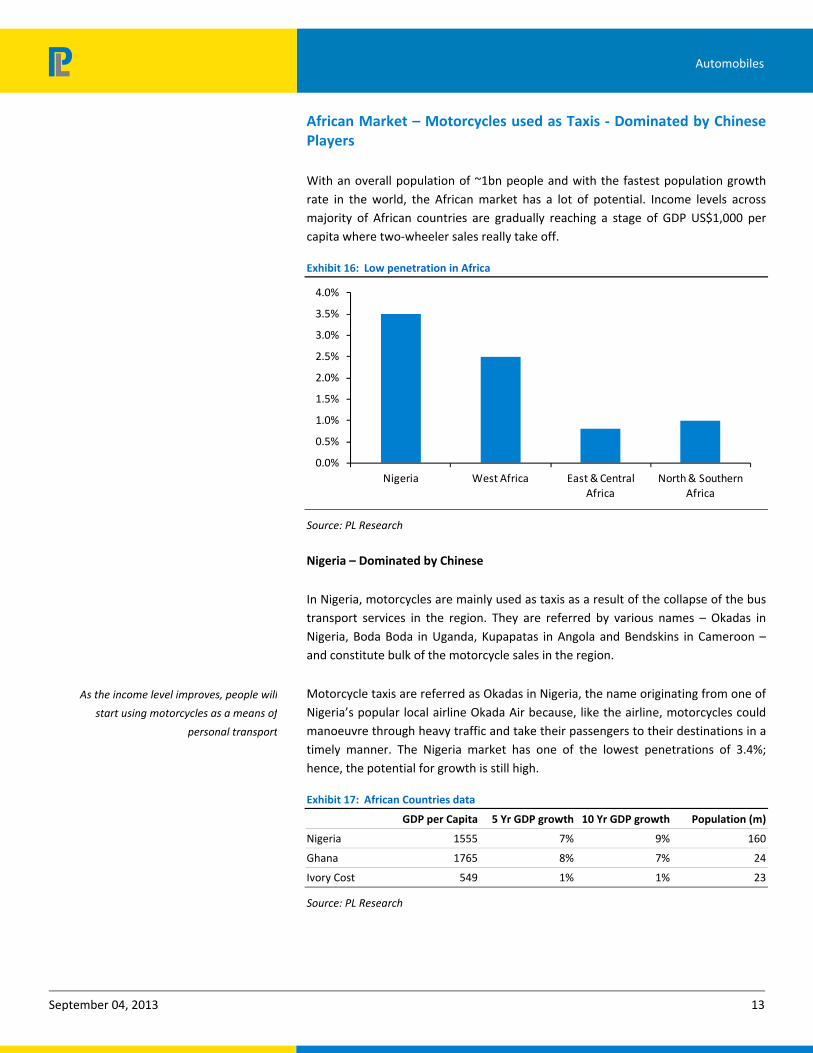

African Market – Motorcycles used as Taxis ‐ Dominated by Chinese Players

With an overall population of ~1bn people and with the fastest population growth rate in the world, the African market has a lot of potential. Income levels across majority of African countries are gradually reaching a stage of GDP US$1,000 per capita where two-wheeler sales really take off.

Exhibit 16: Low penetration in Africa

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Nigeria West Africa East & Central Africa

North & Southern Africa

Source: PL Research

Nigeria – Dominated by Chinese

In Nigeria, motorcycles are mainly used as taxis as a result of the collapse of the bus transport services in the region. They are referred by various names – Okadas in Nigeria, Boda Boda in Uganda, Kupapatas in Angola and Bendskins in Cameroon – and constitute bulk of the motorcycle sales in the region.

Motorcycle taxis are referred as Okadas in Nigeria, the name originating from one of Nigeria’s popular local airline Okada Air because, like the airline, motorcycles could manoeuvre through heavy traffic and take their passengers to their destinations in a timely manner. The Nigeria market has one of the lowest penetrations of 3.4%; hence, the potential for growth is still high.

Exhibit 17: African Countries data

GDP per Capita 5 Yr GDP growth 10 Yr GDP growth Population (m)

Nigeria 1555 7% 9% 160

Ghana 1765 8% 7% 24

Ivory Cost 549 1% 1% 23

Source: PL Research

As the income level improves, people will

start using motorcycles as a means of

personal transport

September 04, 2013 14

Automobiles

Given the fact that motorcycles are largely used as taxis here, cheap motorcycles are the norm here and hence, Chinese dominate the market. In fact till 2005, they were virtually the only players in the market.

Exhibit 18: Nigeria Market – Chinese players dominate

95%75% 78% 76%

4%25% 22% 23%

0%

20%

40%

60%

80%

100%

120%

2007 2009 2010 2011

Chinese Players Indian Players

Source: PL Research

Nigerians have started appreciating Bajaj’s quality and realising that though the upfront cost is higher with a Bajaj vehicle, the total cost of ownership on account of the lower maintenance and better mileage is lower than that of Chinese bikes.

The Boxer brand with its larger seats is suitable for usage as a taxi. Bajaj has recently launched the Boxer 150, which has been well received by the market.

But with the fact that motorcycles for personal use would be the next growth driver the volumes in this market can continue to grow at 8-10% CAGR over the next five years.

Opportunity for Bajaj Auto in the three‐wheeler segment: Given the increase incidence of Nigeria banning motorcycle taxis, we have assumed a 10% CAGR in volumes in Nigeria v/s a 20% CAGR in volumes in Eastern and Central Africa where penetration at 0.8% is very low.

Already, a number of these states which have banned three-wheelers have started replacing motorcycle taxis with tricycles from Bajaj Auto; hence, three-wheelers can be a big opportunity here.

Bajaj Auto entered the Nigerian market in

2005 and has had great success in the past

five years. Its market share has already

reached ~24% despite the fact that its

vehicles are almost 50% more expensive

than the Chinese bikes

September 04, 2013 15

Automobiles

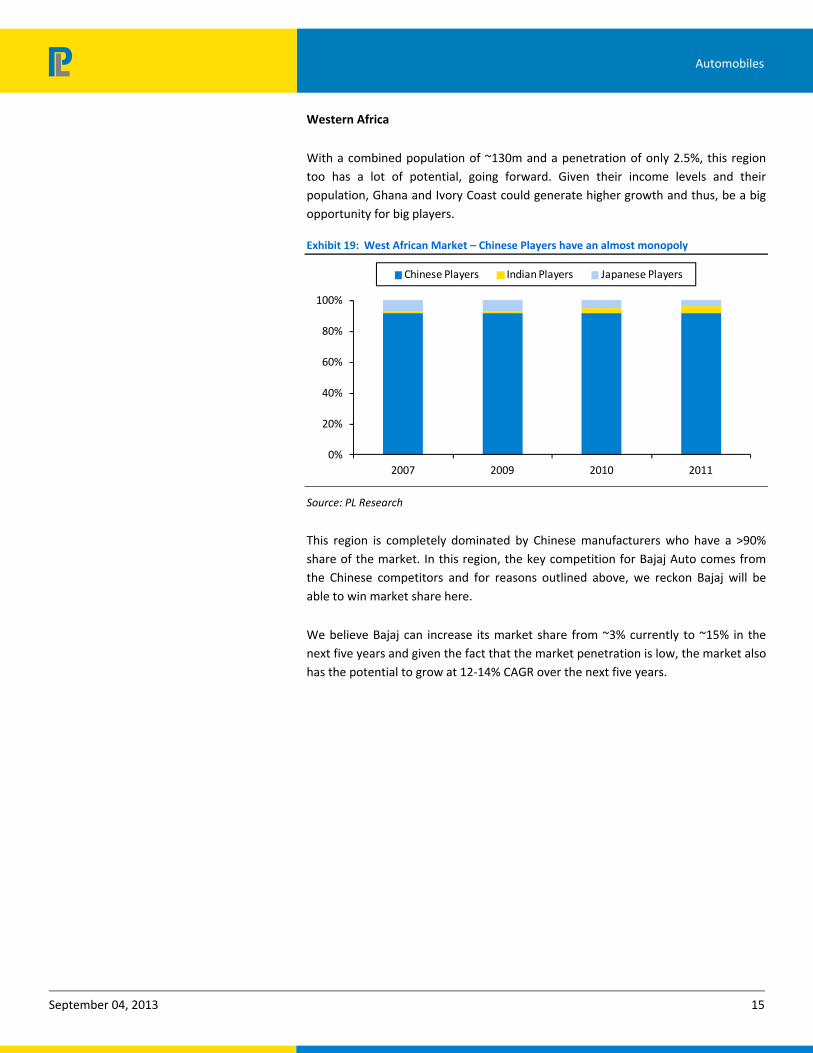

Western Africa

With a combined population of ~130m and a penetration of only 2.5%, this region too has a lot of potential, going forward. Given their income levels and their population, Ghana and Ivory Coast could generate higher growth and thus, be a big opportunity for big players.

Exhibit 19: West African Market – Chinese Players have an almost monopoly

0%

20%

40%

60%

80%

100%

2007 2009 2010 2011

Chinese Players Indian Players Japanese Players

Source: PL Research

This region is completely dominated by Chinese manufacturers who have a >90% share of the market. In this region, the key competition for Bajaj Auto comes from the Chinese competitors and for reasons outlined above, we reckon Bajaj will be able to win market share here.

We believe Bajaj can increase its market share from ~3% currently to ~15% in the next five years and given the fact that the market penetration is low, the market also has the potential to grow at 12-14% CAGR over the next five years.

September 04, 2013 16

Automobiles

Latin America – dominated by Japanese and Chinese Players

Overall, the Latin American export market excl. Brazil is similar in size to the African market at ~US$2bn. Brazil, which is the largest market in the region with an annual demand of 2m units is currently dominated by Honda with an 82% market share which has a local production base in Brazil as well.

With an overall population of 340m (one-third of Africa), the potential opportunity in Latin America is not as large as the one in Africa. However, Latin America is already in the midst of a very strong boom in two-wheelers and hence, represents a good near-term opportunity.

Latin American countries are a bit of a contradiction in the sense that with GDP per capita at ~US$10,000, countries normally start moving away from two-wheelers to passenger cars. Also, a number of these countries already have a higher passenger car penetration than two-wheeler penetration.

The reason attributed to a trend different from the norm is on account of very wide income inequality in these countries. Thus, despite these countries being “middle-income” countries, ~40% of the population in these countries is poor.

Exhibit 20: Latin America Market

GDP per Capita (PPP) 5 Yr GDP growth 10 Yr GDP growth Population (m)

Argentina 17,554 7% 6% 41

Chile 15,848 4% 4% 17

Columbia 9,124 4% 4% 46

Guatemala 4,396 3% 3% 15

Peru 9,429 7% 6% 30

Brazil 10,264 4% 4% 195

Source: PL Research

Most of the countries have witnessed strong growth led by investments by Governments in upliftment of poor and hence, a surge in employment in the 2000s has also helped. This reduction in inequality has resulted in the emergence of a strong middle class and this consequently has resulted in a strong demand for two-wheelers.

For e.g., Argentinean two‐wheeler market

today is 6x of what it used to be in 2005

and is the second largest importer of two‐

wheelers globally after Nigeria

September 04, 2013 17

Automobiles

Exhibit 21: Latin American Market

0% 20% 40% 60% 80% 100% 120%

Dominican

Chile

Paraguay

Guatemala

Venezuela

Colombia

Peru

Argentina

Indian MS Chinese MS

Source: PL Research

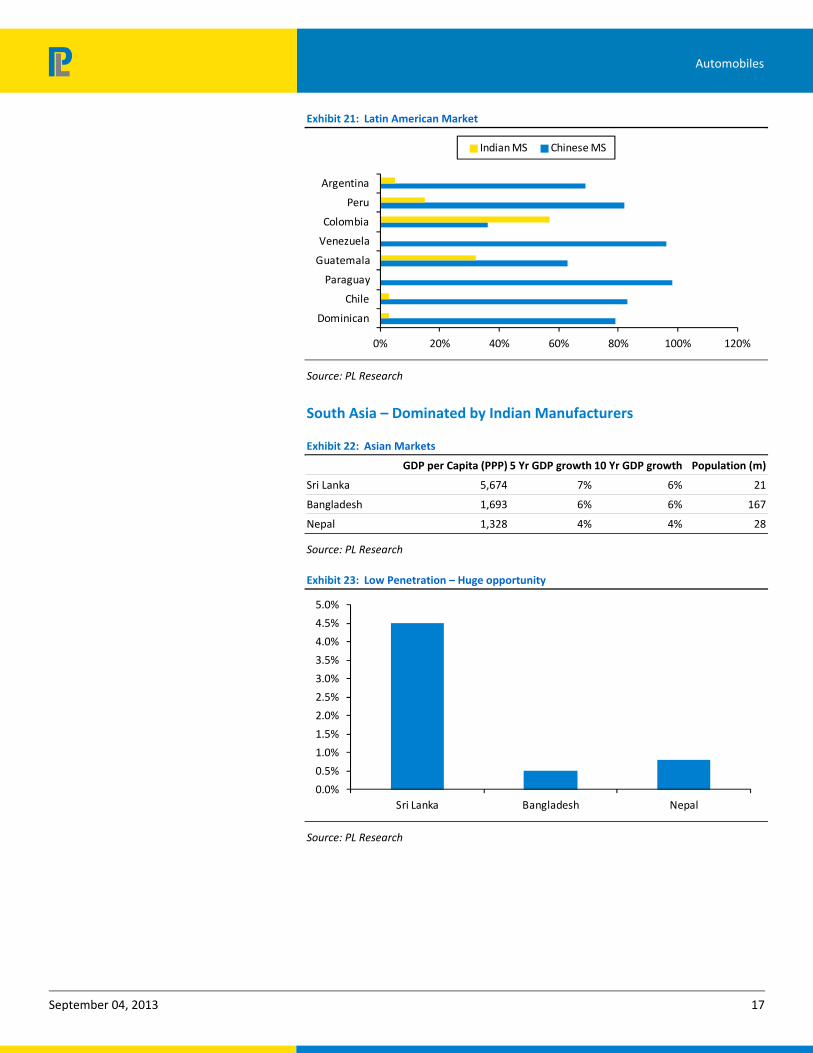

South Asia – Dominated by Indian Manufacturers

Exhibit 22: Asian Markets

GDP per Capita (PPP) 5 Yr GDP growth 10 Yr GDP growth Population (m)

Sri Lanka 5,674 7% 6% 21

Bangladesh 1,693 6% 6% 167

Nepal 1,328 4% 4% 28

Source: PL Research

Exhibit 23: Low Penetration – Huge opportunity

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Sri Lanka Bangladesh Nepal

Source: PL Research

September 04, 2013 18

Automobiles

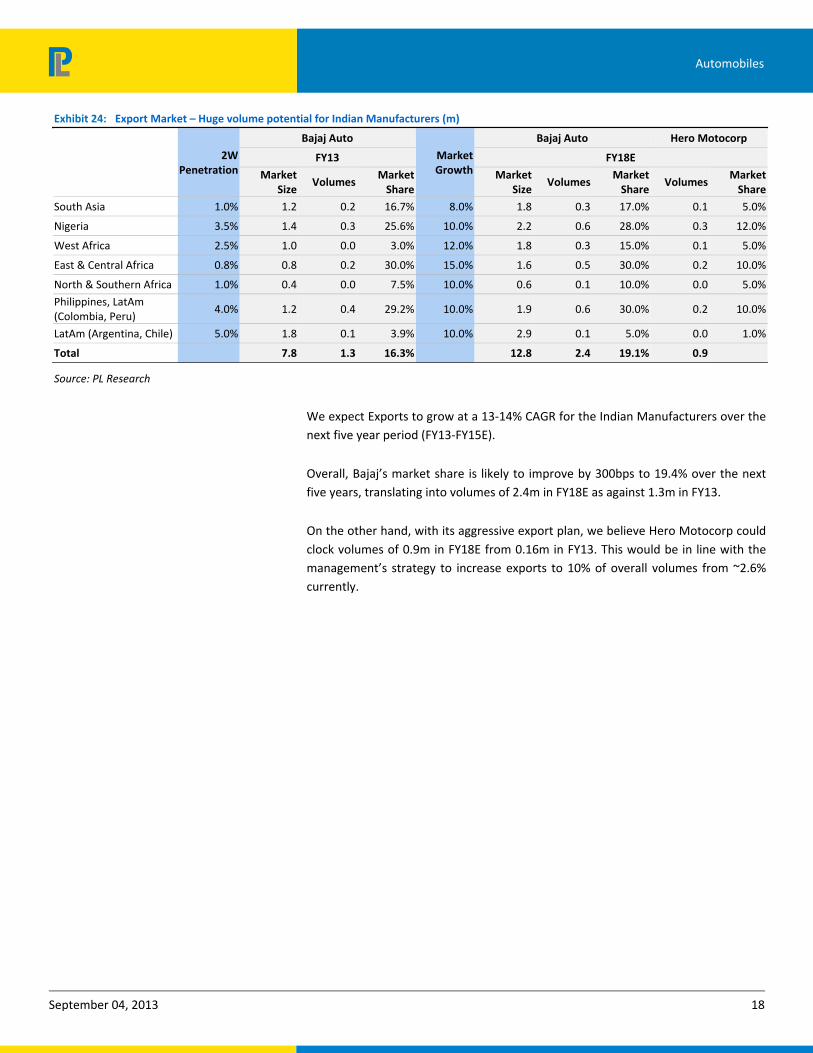

Exhibit 24: Export Market – Huge volume potential for Indian Manufacturers (m)

2W

Penetration

Bajaj Auto

Market Growth

Bajaj Auto Hero Motocorp

FY13 FY18E

Market Size

VolumesMarket Share

Market Size

Volumes Market Share

VolumesMarket Share

South Asia 1.0% 1.2 0.2 16.7% 8.0% 1.8 0.3 17.0% 0.1 5.0%

Nigeria 3.5% 1.4 0.3 25.6% 10.0% 2.2 0.6 28.0% 0.3 12.0%

West Africa 2.5% 1.0 0.0 3.0% 12.0% 1.8 0.3 15.0% 0.1 5.0%

East & Central Africa 0.8% 0.8 0.2 30.0% 15.0% 1.6 0.5 30.0% 0.2 10.0%

North & Southern Africa 1.0% 0.4 0.0 7.5% 10.0% 0.6 0.1 10.0% 0.0 5.0%

Philippines, LatAm (Colombia, Peru)

4.0% 1.2 0.4 29.2% 10.0% 1.9 0.6 30.0% 0.2 10.0%

LatAm (Argentina, Chile) 5.0% 1.8 0.1 3.9% 10.0% 2.9 0.1 5.0% 0.0 1.0%

Total 7.8 1.3 16.3% 12.8 2.4 19.1% 0.9

Source: PL Research

We expect Exports to grow at a 13-14% CAGR for the Indian Manufacturers over the next five year period (FY13-FY15E).

Overall, Bajaj’s market share is likely to improve by 300bps to 19.4% over the next five years, translating into volumes of 2.4m in FY18E as against 1.3m in FY13.

On the other hand, with its aggressive export plan, we believe Hero Motocorp could clock volumes of 0.9m in FY18E from 0.16m in FY13. This would be in line with the management’s strategy to increase exports to 10% of overall volumes from ~2.6% currently.

September 04, 2013 19

Automobiles

COMPANIES

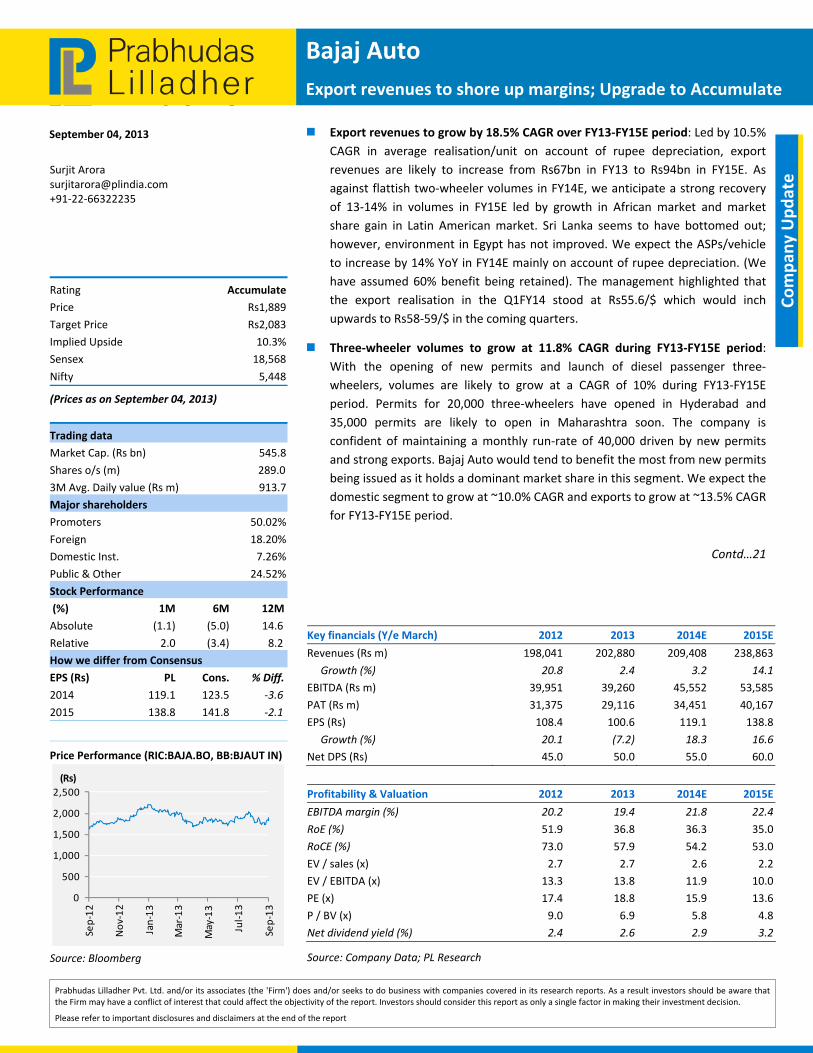

Bajaj Auto

Export revenues to shore up margins; Upgrade to Accumulate

September 04, 2013

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Compan

y Update Surjit Arora

[email protected] +91-22-66322235

Rating Accumulate

Price Rs1,889

Target Price Rs2,083

Implied Upside 10.3%

Sensex 18,568

Nifty 5,448

(Prices as on September 04, 2013)

Trading data

Market Cap. (Rs bn) 545.8

Shares o/s (m) 289.0

3M Avg. Daily value (Rs m) 913.7

Major shareholders

Promoters 50.02%

Foreign 18.20%

Domestic Inst. 7.26%

Public & Other 24.52%

Stock Performance

(%) 1M 6M 12M

Absolute (1.1) (5.0) 14.6

Relative 2.0 (3.4) 8.2

How we differ from Consensus

EPS (Rs) PL Cons. % Diff.

2014 119.1 123.5 ‐3.6

2015 138.8 141.8 ‐2.1

Price Performance (RIC:BAJA.BO, BB:BJAUT IN)

Source: Bloomberg

0

500

1,000

1,500

2,000

2,500

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

(Rs)

Export revenues to grow by 18.5% CAGR over FY13‐FY15E period: Led by 10.5% CAGR in average realisation/unit on account of rupee depreciation, export revenues are likely to increase from Rs67bn in FY13 to Rs94bn in FY15E. As against flattish two-wheeler volumes in FY14E, we anticipate a strong recovery of 13-14% in volumes in FY15E led by growth in African market and market share gain in Latin American market. Sri Lanka seems to have bottomed out; however, environment in Egypt has not improved. We expect the ASPs/vehicle to increase by 14% YoY in FY14E mainly on account of rupee depreciation. (We have assumed 60% benefit being retained). The management highlighted that the export realisation in the Q1FY14 stood at Rs55.6/$ which would inch upwards to Rs58-59/$ in the coming quarters.

Three‐wheeler volumes to grow at 11.8% CAGR during FY13‐FY15E period: With the opening of new permits and launch of diesel passenger three-wheelers, volumes are likely to grow at a CAGR of 10% during FY13-FY15E period. Permits for 20,000 three-wheelers have opened in Hyderabad and 35,000 permits are likely to open in Maharashtra soon. The company is confident of maintaining a monthly run-rate of 40,000 driven by new permits and strong exports. Bajaj Auto would tend to benefit the most from new permits being issued as it holds a dominant market share in this segment. We expect the domestic segment to grow at ~10.0% CAGR and exports to grow at ~13.5% CAGR for FY13-FY15E period.

Contd…21

Key financials (Y/e March) 2012 2013 2014E 2015E

Revenues (Rs m) 198,041 202,880 209,408 238,863

Growth (%) 20.8 2.4 3.2 14.1

EBITDA (Rs m) 39,951 39,260 45,552 53,585

PAT (Rs m) 31,375 29,116 34,451 40,167

EPS (Rs) 108.4 100.6 119.1 138.8

Growth (%) 20.1 (7.2) 18.3 16.6

Net DPS (Rs) 45.0 50.0 55.0 60.0

Profitability & Valuation 2012 2013 2014E 2015E

EBITDA margin (%) 20.2 19.4 21.8 22.4

RoE (%) 51.9 36.8 36.3 35.0

RoCE (%) 73.0 57.9 54.2 53.0

EV / sales (x) 2.7 2.7 2.6 2.2

EV / EBITDA (x) 13.3 13.8 11.9 10.0

PE (x) 17.4 18.8 15.9 13.6

P / BV (x) 9.0 6.9 5.8 4.8

Net dividend yield (%) 2.4 2.6 2.9 3.2

Source: Company Data; PL Research

September 04, 2013 21

Bajaj Auto

Two‐wheeler volumes to recover post CY13: As the slowdown in the domestic market continues and the competitive intensity increases, we don’t see a meaningful growth in the domestic market in FY14E for Bajaj Auto. However, given the six new variants of Discover to be launched over the next six months, there is likely to be recovery in volumes in H2FY14. We expect a 9.5% decline in domestic two-wheeler volumes in FY14E (YTD -14.0% decline) and build in 8.5% volume growth in FY15E (anticipating recovery in the two-wheeler sector).

Valuations attractive, given 17.5% earnings CAGR; Upgrade to ‘Accumulate’: We expect earnings to grow at a 17.5% CAGR over the next two years led by higher realisation in exports in FY14E and volume recovery in both export and domestic market in FY15E. We had a ‘Reduce’ rating on the stock in our post result note ((Stock Price: 1,985). However, with a positive outlook on the two-wheeler sector, the valuation at 15.9x FY12E EPS and 13.6x FY15E EPS seems attractive. Hence, we upgrade the stock to ‘Accumulate’ from ‘Reduce’ with a target price of Rs2,083 based on 15x FY15E EPS, a 10% premium to its average P/E of 13.5x 1 year fwd. (Earlier TP – Rs1,904 @14x FY15E EPS).

September 04, 2013 22

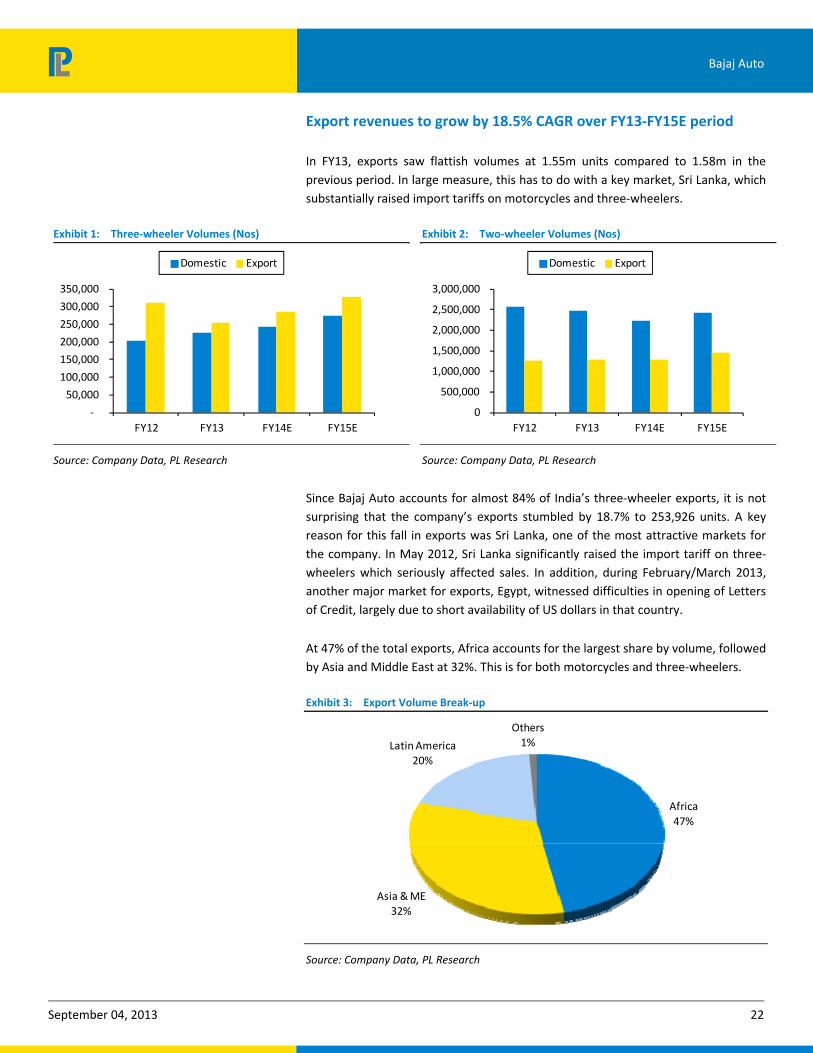

Bajaj Auto

Export revenues to grow by 18.5% CAGR over FY13‐FY15E period

In FY13, exports saw flattish volumes at 1.55m units compared to 1.58m in the previous period. In large measure, this has to do with a key market, Sri Lanka, which substantially raised import tariffs on motorcycles and three-wheelers.

Exhibit 1: Three‐wheeler Volumes (Nos)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

FY12 FY13 FY14E FY15E

Domestic Export

Source: Company Data, PL Research

Exhibit 2: Two‐wheeler Volumes (Nos)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

FY12 FY13 FY14E FY15E

Domestic Export

Source: Company Data, PL Research

Since Bajaj Auto accounts for almost 84% of India’s three-wheeler exports, it is not surprising that the company’s exports stumbled by 18.7% to 253,926 units. A key reason for this fall in exports was Sri Lanka, one of the most attractive markets for the company. In May 2012, Sri Lanka significantly raised the import tariff on three-wheelers which seriously affected sales. In addition, during February/March 2013, another major market for exports, Egypt, witnessed difficulties in opening of Letters of Credit, largely due to short availability of US dollars in that country.

At 47% of the total exports, Africa accounts for the largest share by volume, followed by Asia and Middle East at 32%. This is for both motorcycles and three-wheelers.

Exhibit 3: Export Volume Break‐up

Africa 47%

Asia & ME32%

Latin America20%

Others1%

Source: Company Data, PL Research

September 04, 2013 23

Bajaj Auto

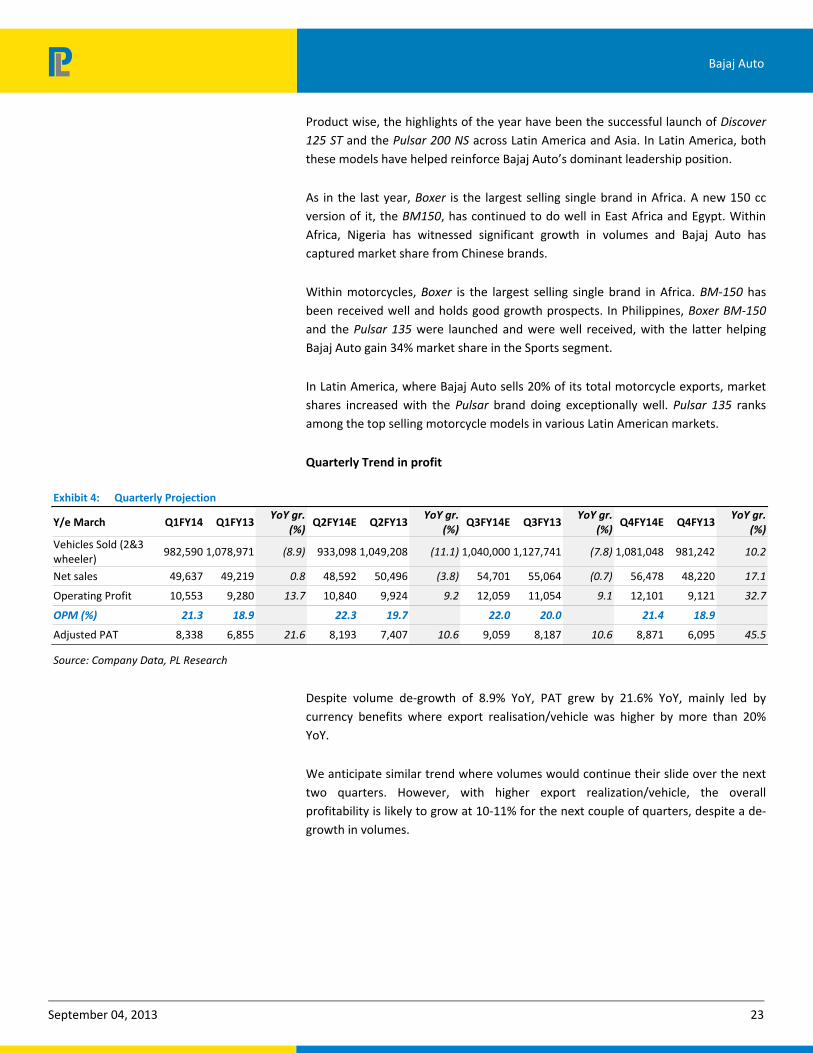

Product wise, the highlights of the year have been the successful launch of Discover 125 ST and the Pulsar 200 NS across Latin America and Asia. In Latin America, both these models have helped reinforce Bajaj Auto’s dominant leadership position.

As in the last year, Boxer is the largest selling single brand in Africa. A new 150 cc version of it, the BM150, has continued to do well in East Africa and Egypt. Within Africa, Nigeria has witnessed significant growth in volumes and Bajaj Auto has captured market share from Chinese brands.

Within motorcycles, Boxer is the largest selling single brand in Africa. BM‐150 has been received well and holds good growth prospects. In Philippines, Boxer BM‐150 and the Pulsar 135 were launched and were well received, with the latter helping Bajaj Auto gain 34% market share in the Sports segment.

In Latin America, where Bajaj Auto sells 20% of its total motorcycle exports, market shares increased with the Pulsar brand doing exceptionally well. Pulsar 135 ranks among the top selling motorcycle models in various Latin American markets.

Quarterly Trend in profit

Exhibit 4: Quarterly Projection

Y/e March Q1FY14 Q1FY13 YoY gr.

(%) Q2FY14E Q2FY13

YoY gr. (%)

Q3FY14E Q3FY13 YoY gr.

(%) Q4FY14E Q4FY13

YoY gr. (%)

Vehicles Sold (2&3 wheeler)

982,590 1,078,971 (8.9) 933,098 1,049,208 (11.1) 1,040,000 1,127,741 (7.8) 1,081,048 981,242 10.2

Net sales 49,637 49,219 0.8 48,592 50,496 (3.8) 54,701 55,064 (0.7) 56,478 48,220 17.1

Operating Profit 10,553 9,280 13.7 10,840 9,924 9.2 12,059 11,054 9.1 12,101 9,121 32.7

OPM (%) 21.3 18.9 22.3 19.7 22.0 20.0 21.4 18.9

Adjusted PAT 8,338 6,855 21.6 8,193 7,407 10.6 9,059 8,187 10.6 8,871 6,095 45.5

Source: Company Data, PL Research

Despite volume de-growth of 8.9% YoY, PAT grew by 21.6% YoY, mainly led by currency benefits where export realisation/vehicle was higher by more than 20% YoY.

We anticipate similar trend where volumes would continue their slide over the next two quarters. However, with higher export realization/vehicle, the overall profitability is likely to grow at 10-11% for the next couple of quarters, despite a de-growth in volumes.

September 04, 2013 24

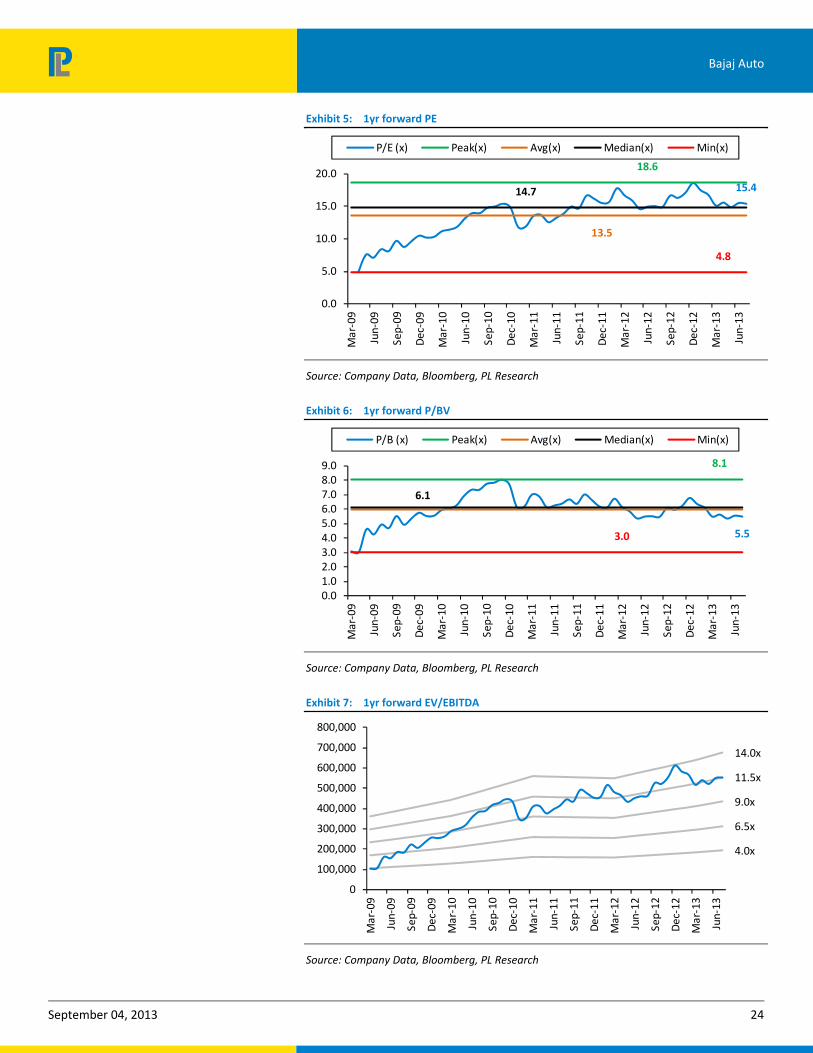

Bajaj Auto

Exhibit 5: 1yr forward PE

15.4

18.6

13.5

14.7

4.8

0.0

5.0

10.0

15.0

20.0

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

P/E (x) Peak(x) Avg(x) Median(x) Min(x)

Source: Company Data, Bloomberg, PL Research

Exhibit 6: 1yr forward P/BV

5.5

8.1

6.1

3.0

0.01.02.03.04.05.06.07.08.09.0

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

P/B (x) Peak(x) Avg(x) Median(x) Min(x)

Source: Company Data, Bloomberg, PL Research

Exhibit 7: 1yr forward EV/EBITDA

4.0x

6.5x

9.0x

11.5x

14.0x

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Source: Company Data, Bloomberg, PL Research

September 04, 2013 25

Bajaj Auto

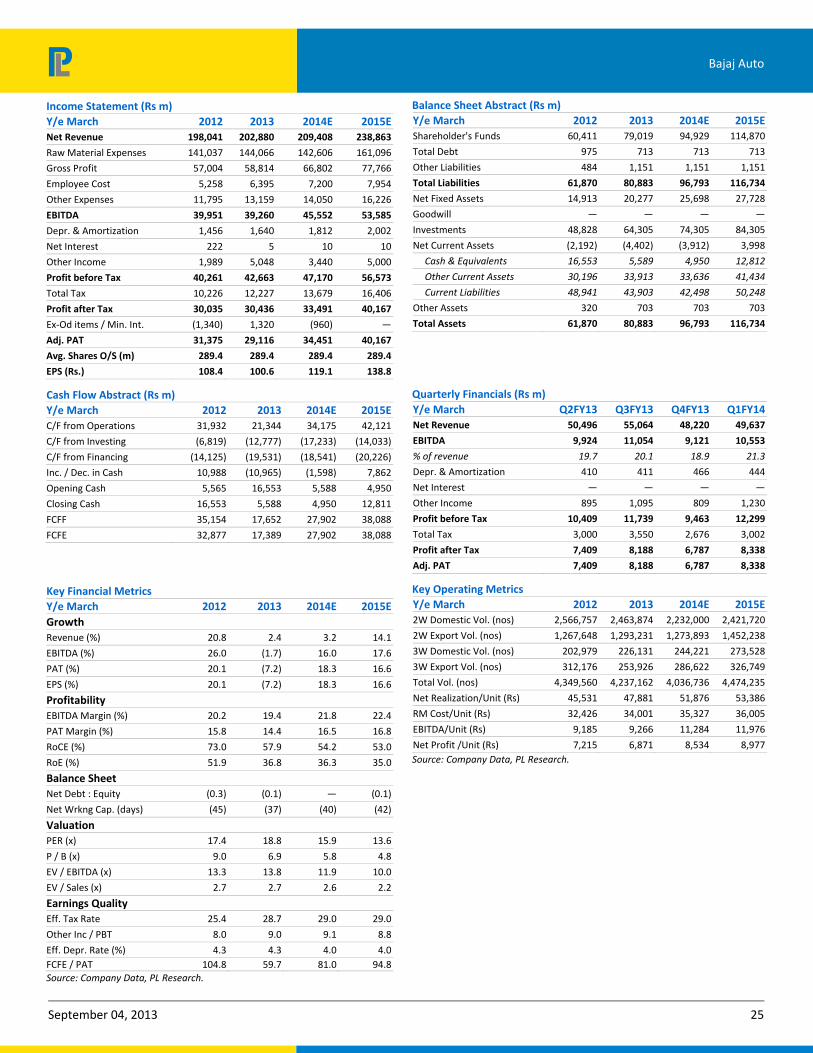

Income Statement (Rs m)

Y/e March 2012 2013 2014E 2015E

Net Revenue 198,041 202,880 209,408 238,863

Raw Material Expenses 141,037 144,066 142,606 161,096

Gross Profit 57,004 58,814 66,802 77,766

Employee Cost 5,258 6,395 7,200 7,954

Other Expenses 11,795 13,159 14,050 16,226

EBITDA 39,951 39,260 45,552 53,585

Depr. & Amortization 1,456 1,640 1,812 2,002

Net Interest 222 5 10 10

Other Income 1,989 5,048 3,440 5,000

Profit before Tax 40,261 42,663 47,170 56,573

Total Tax 10,226 12,227 13,679 16,406

Profit after Tax 30,035 30,436 33,491 40,167

Ex-Od items / Min. Int. (1,340) 1,320 (960) —

Adj. PAT 31,375 29,116 34,451 40,167

Avg. Shares O/S (m) 289.4 289.4 289.4 289.4

EPS (Rs.) 108.4 100.6 119.1 138.8

Cash Flow Abstract (Rs m)

Y/e March 2012 2013 2014E 2015E

C/F from Operations 31,932 21,344 34,175 42,121

C/F from Investing (6,819) (12,777) (17,233) (14,033)

C/F from Financing (14,125) (19,531) (18,541) (20,226)

Inc. / Dec. in Cash 10,988 (10,965) (1,598) 7,862

Opening Cash 5,565 16,553 5,588 4,950

Closing Cash 16,553 5,588 4,950 12,811

FCFF 35,154 17,652 27,902 38,088

FCFE 32,877 17,389 27,902 38,088

Key Financial Metrics

Y/e March 2012 2013 2014E 2015E

Growth

Revenue (%) 20.8 2.4 3.2 14.1

EBITDA (%) 26.0 (1.7) 16.0 17.6

PAT (%) 20.1 (7.2) 18.3 16.6

EPS (%) 20.1 (7.2) 18.3 16.6

Profitability

EBITDA Margin (%) 20.2 19.4 21.8 22.4

PAT Margin (%) 15.8 14.4 16.5 16.8

RoCE (%) 73.0 57.9 54.2 53.0

RoE (%) 51.9 36.8 36.3 35.0

Balance Sheet

Net Debt : Equity (0.3) (0.1) — (0.1)

Net Wrkng Cap. (days) (45) (37) (40) (42)

Valuation

PER (x) 17.4 18.8 15.9 13.6

P / B (x) 9.0 6.9 5.8 4.8

EV / EBITDA (x) 13.3 13.8 11.9 10.0

EV / Sales (x) 2.7 2.7 2.6 2.2

Earnings Quality

Eff. Tax Rate 25.4 28.7 29.0 29.0

Other Inc / PBT 8.0 9.0 9.1 8.8

Eff. Depr. Rate (%) 4.3 4.3 4.0 4.0FCFE / PAT 104.8 59.7 81.0 94.8Source: Company Data, PL Research.

Balance Sheet Abstract (Rs m)

Y/e March 2012 2013 2014E 2015E

Shareholder's Funds 60,411 79,019 94,929 114,870

Total Debt 975 713 713 713

Other Liabilities 484 1,151 1,151 1,151

Total Liabilities 61,870 80,883 96,793 116,734

Net Fixed Assets 14,913 20,277 25,698 27,728

Goodwill — — — —

Investments 48,828 64,305 74,305 84,305

Net Current Assets (2,192) (4,402) (3,912) 3,998

Cash & Equivalents 16,553 5,589 4,950 12,812

Other Current Assets 30,196 33,913 33,636 41,434

Current Liabilities 48,941 43,903 42,498 50,248

Other Assets 320 703 703 703

Total Assets 61,870 80,883 96,793 116,734

Quarterly Financials (Rs m)

Y/e March Q2FY13 Q3FY13 Q4FY13 Q1FY14

Net Revenue 50,496 55,064 48,220 49,637

EBITDA 9,924 11,054 9,121 10,553

% of revenue 19.7 20.1 18.9 21.3

Depr. & Amortization 410 411 466 444

Net Interest — — — —

Other Income 895 1,095 809 1,230

Profit before Tax 10,409 11,739 9,463 12,299

Total Tax 3,000 3,550 2,676 3,002

Profit after Tax 7,409 8,188 6,787 8,338

Adj. PAT 7,409 8,188 6,787 8,338

Key Operating Metrics

Y/e March 2012 2013 2014E 2015E

2W Domestic Vol. (nos) 2,566,757 2,463,874 2,232,000 2,421,720

2W Export Vol. (nos) 1,267,648 1,293,231 1,273,893 1,452,238

3W Domestic Vol. (nos) 202,979 226,131 244,221 273,528

3W Export Vol. (nos) 312,176 253,926 286,622 326,749

Total Vol. (nos) 4,349,560 4,237,162 4,036,736 4,474,235

Net Realization/Unit (Rs) 45,531 47,881 51,876 53,386

RM Cost/Unit (Rs) 32,426 34,001 35,327 36,005

EBITDA/Unit (Rs) 9,185 9,266 11,284 11,976

Net Profit /Unit (Rs) 7,215 6,871 8,534 8,977Source: Company Data, PL Research.

Hero Motocorp

Volume Recovery Ahead; Upgrade to Accumulate

September 04, 2013

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Compan

y Update Surjit Arora

[email protected] +91-22-66322235

Rating Accumulate

Price Rs1,927

Target Price Rs2,176

Implied Upside 12.9%

Sensex 18,568

Nifty 5,448

(Prices as on September 04, 2013)

Trading data

Market Cap. (Rs bn) 384.7

Shares o/s (m) 199.7

3M Avg. Daily value (Rs m) 898.9

Major shareholders

Promoters 52.21%

Foreign 30.57%

Domestic Inst. 8.46%

Public & Other 8.76%

Stock Performance

(%) 1M 6M 12M

Absolute 6.9 17.6 6.6

Relative 10.0 19.2 0.1

How we differ from Consensus

EPS (Rs) PL Cons. % Diff.

2014 109.3 109.4 0.0

2015 145.1 139.3 4.2

Price Performance (RIC: HROM.BO, BB: HMCL

IN)

0

500

1,000

1,500

2,000

2,500

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

(Rs)

Management commentary positive; Rural economy to drive volumes: In the recent Annual Report, the management was cautiously optimistic and expects a recovery in two-wheeler volumes driven by good monsoon and pre-election spending. In the country's main cropping regions, monsoon has been timely and 20-30% above average so far, prompting farmers to expand cultivated area by 9% to 930 lakh hectares, with the biggest gains in pulses, oilseeds and coarse cereals. Low penetration level, lack of adequate mode public transport and rising per capita income in rural India would lead to long-term healthy volume of two-wheelers. The company has benefited from stronger rural demand - rural forms 45% of Hero's sales versus 40% for the industry and beneficial impact of the warranty scheme (first to offer a 5-year warranty on two-wheelers).

Competitive intensity receding; Hero Motocorp to maintain its turf: Hero has made a strong come back in the recent months on the strength of its strong brands and distribution. Given the strong distribution reach and wider product portfolio, including scooters, we believe volumes could grow by ~4% in FY14E and 11% in FY15E, thereby, maintaining its turf in motorcycles with a market share of 53.6%. Going forward, in our view, Hero would gain 180bps in market share in the scooter segment thanks to ‘Maestro’ and ‘Pleasure’ at 21.6%. HMSI is likely to further gain market share to the tune of 260bps to 14.7% by FY15E at the cost of Bajaj Auto. Our channel checks suggest good traction for its products, both in scooters as well as motorcycle segments, whereas, Honda’s Dream series

has fizzled out and no longer a threat.

Contd…27

Key financials (Y/e March) 2012 2013 2014E 2015E

Revenues (Rs m) 235,789 237,681 255,095 291,110

Growth (%) 21.5 0.8 7.3 14.1

EBITDA (Rs m) 36,047 32,845 37,331 43,923

PAT (Rs m) 23,782 21,100 21,834 28,975

EPS (Rs) 119.1 105.7 109.3 145.1

Growth (%) 18.5 (11.3) 3.5 32.7

Net DPS (Rs) 45.0 60.0 65.0 70.0

Profitability & Valuation 2012 2013 2014E 2015E

EBITDA margin (%) 15.3 13.8 14.6 15.1

RoE (%) 65.6 45.6 39.2 42.4

RoCE (%) 55.7 46.3 51.6 58.6

EV / sales (x) 1.6 1.6 1.5 1.3

EV / EBITDA (x) 10.7 11.7 10.1 8.5

PE (x) 16.2 18.2 17.6 13.3

P / BV (x) 9.0 7.7 6.3 5.1

Net dividend yield (%) 2.3 3.1 3.4 3.6

Source: Company Data; PL Research

September 04, 2013 27

Hero Motocorp

Advanced R&D by tie‐ups with various international companies: During 2012-13, Hero Motocorp tied up with the Italian design firm Engines Engineering. The Bologna-based firm has been developing and designing scooters and motorcycles for various manufacturers over the years and is now sharing its expertise with Hero MotoCorp to help develop next generation two-wheelers. At the same time, R&D tie-up with AVL of Austria will help in developing new engines. It also tied up with EBR of the US to launch high-performance platform bikes for meeting domestic and international needs.

Entered high growth markets of Africa, LatAm and Asia: HMCL entered into a partnership with the reputed ABANS Group of Sri Lanka. Under the alliance, ABANS has been appointed as the sole distributor of Hero MotoCorp range of two-wheelers in Sri Lanka. HMCL has launched its range of two-wheelers in Guatemala City, El Salvador and Honduras, marking the iconic Indian brand’s first foray into new international markets. A partnership has been forged with Indy Motos Group of Guatemala to bring its two-wheelers to these markets. Under the alliance, Indy Motos has been appointed as the authorized distributor of Hero MotoCorp range of two-wheelers in Guatemala, Honduras and El Salvador. We expect exports to account for ~10% of volumes (0.9m) by FY18E end. We expect exports to grow by 40% in FY15E albeit at a lower base.

Earnings to grow at a CAGR of 18.0% for FY13‐FY15E period: We expect Hero to gain market share in scooters segment and maintain its market share in the motorcycle segment. We expect a 10.7% CAGR in revenues with margins likely to expand by 130bps (given the lower competitive intensity and cost cutting initiatives). At the same time, we expect savings of Rs4.5bn on account of royalty payments to Honda ending by March 2014. As a result, earnings are expected to grow at 18.0% CAGR for FY13-FY15E period. At the CMP, the stock trades at 17.6x FY14E EPS and 13.3x FY15E EPS. Hence, we upgrade the stock from ‘Reduce’ to ‘Accumulate’ with a TP of Rs2,176 based on 15x FY15E earnings, in line with its past 5 year average. The stock is likely to get re-rated given the strong rural economy and higher interest rates leading to a shift from four-wheeler stocks to two-wheelers.

September 04, 2013 28

Hero Motocorp

Competitive intensity receding; Hero Motocorp to maintain its turf

The company has benefited from stronger rural demand - rural forms 45% of Hero's sales versus 40% for the industry and beneficial impact of the warranty scheme (first to offer a 5-year warranty on two-wheelers).

Hero has made a strong come back in the recent months on the strength of its strong brands and distribution.

Given the strong distribution reach and wider product portfolio, including scooters, we believe volumes could grow by ~4% in FY14E and 11% in FY15E, thereby, maintaining its turf in motorcycles with a market share of 53.3%.

Going forward, in our view, Hero would gain 180bps in market share in the scooter segment thanks to ‘Maestro’ and ‘Pleasure’ at 21.6%.

HMSI is likely to further gain market share to the tune of 260bps to 14.7% by FY15E at the cost of Bajaj Auto. Our channel checks suggest good traction for its products, both in scooters as well as motorcycle segments, whereas, Honda’s

Dream series has fizzled out and no longer a threat.

September 04, 2013 29

Hero Motocorp

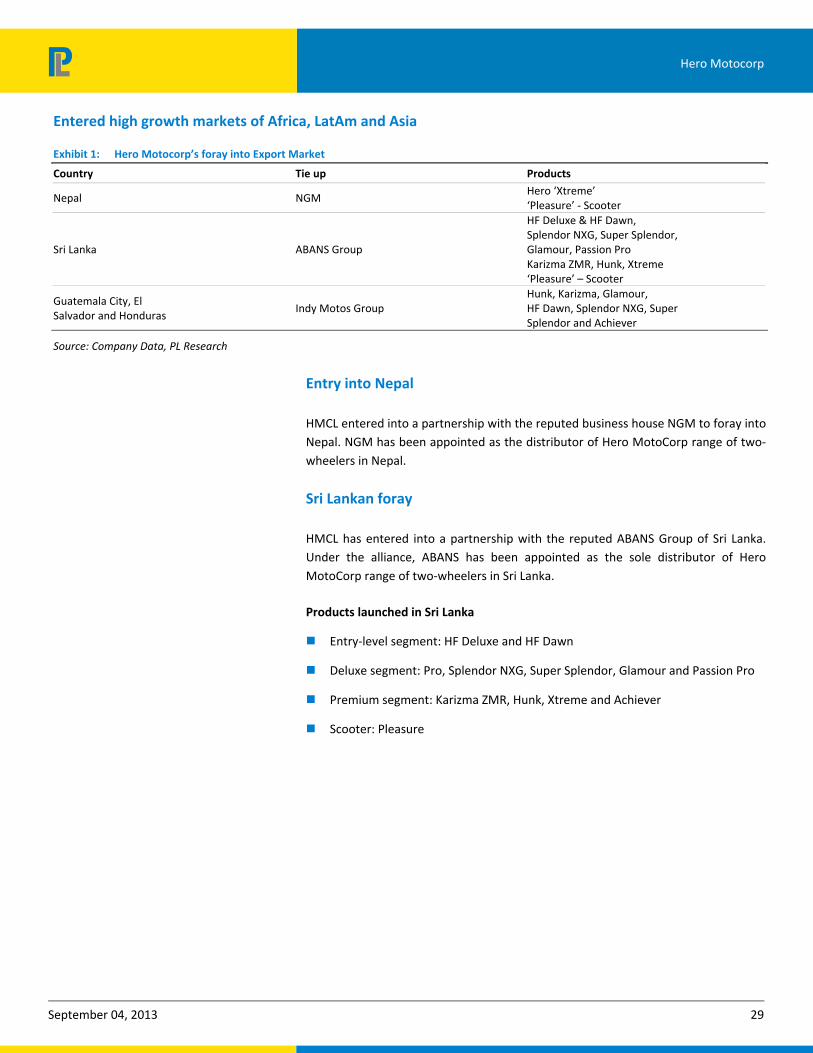

Entered high growth markets of Africa, LatAm and Asia

Exhibit 1: Hero Motocorp’s foray into Export Market

Country Tie up Products

Nepal NGM Hero ‘Xtreme’ ‘Pleasure’ - Scooter

Sri Lanka ABANS Group

HF Deluxe & HF Dawn, Splendor NXG, Super Splendor, Glamour, Passion Pro Karizma ZMR, Hunk, Xtreme ‘Pleasure’ – Scooter

Guatemala City, El Salvador and Honduras

Indy Motos Group Hunk, Karizma, Glamour, HF Dawn, Splendor NXG, Super Splendor and Achiever

Source: Company Data, PL Research

Entry into Nepal

HMCL entered into a partnership with the reputed business house NGM to foray into Nepal. NGM has been appointed as the distributor of Hero MotoCorp range of two-wheelers in Nepal.

Sri Lankan foray

HMCL has entered into a partnership with the reputed ABANS Group of Sri Lanka. Under the alliance, ABANS has been appointed as the sole distributor of Hero MotoCorp range of two-wheelers in Sri Lanka.

Products launched in Sri Lanka

Entry-level segment: HF Deluxe and HF Dawn

Deluxe segment: Pro, Splendor NXG, Super Splendor, Glamour and Passion Pro

Premium segment: Karizma ZMR, Hunk, Xtreme and Achiever

Scooter: Pleasure

September 04, 2013 30

Hero Motocorp

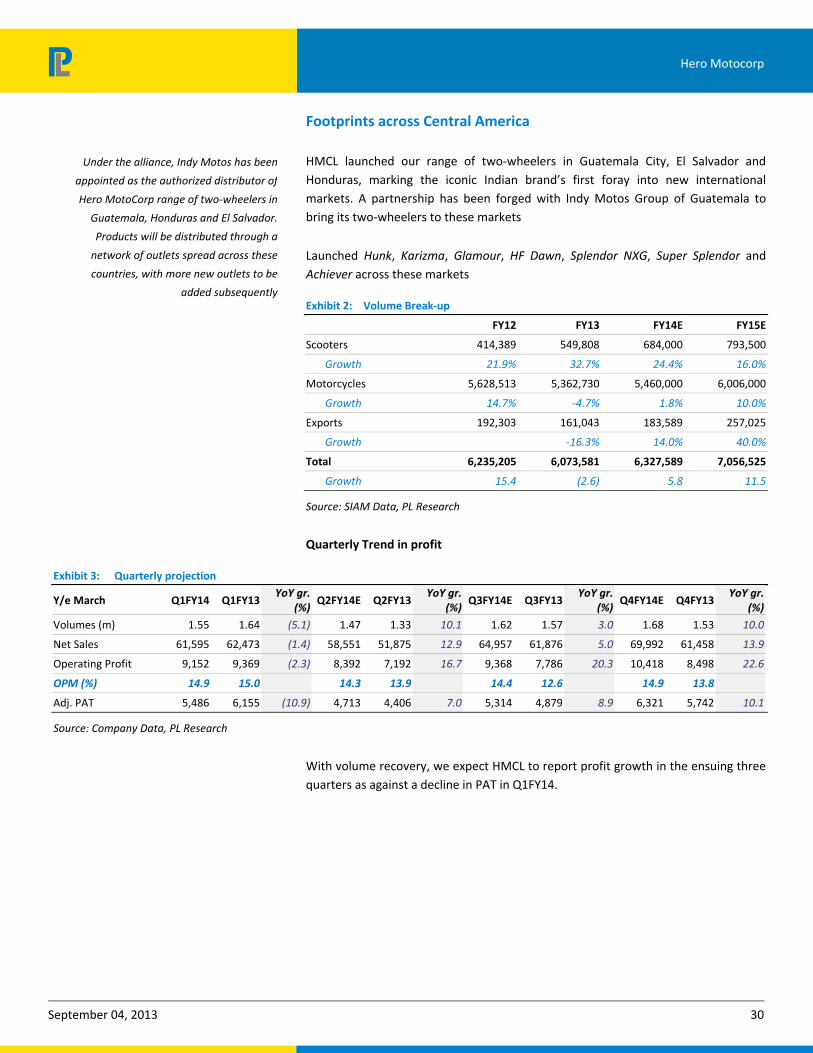

Footprints across Central America

HMCL launched our range of two-wheelers in Guatemala City, El Salvador and Honduras, marking the iconic Indian brand’s first foray into new international markets. A partnership has been forged with Indy Motos Group of Guatemala to bring its two-wheelers to these markets

Launched Hunk, Karizma, Glamour, HF Dawn, Splendor NXG, Super Splendor and Achiever across these markets

Exhibit 2: Volume Break‐up

FY12 FY13 FY14E FY15E

Scooters 414,389 549,808 684,000 793,500

Growth 21.9% 32.7% 24.4% 16.0%

Motorcycles 5,628,513 5,362,730 5,460,000 6,006,000

Growth 14.7% ‐4.7% 1.8% 10.0%

Exports 192,303 161,043 183,589 257,025

Growth ‐16.3% 14.0% 40.0%

Total 6,235,205 6,073,581 6,327,589 7,056,525

Growth 15.4 (2.6) 5.8 11.5

Source: SIAM Data, PL Research

Quarterly Trend in profit

Exhibit 3: Quarterly projection

Y/e March Q1FY14 Q1FY13 YoY gr.

(%) Q2FY14E Q2FY13

YoY gr. (%)

Q3FY14E Q3FY13YoY gr.

(%) Q4FY14E Q4FY13

YoY gr. (%)

Volumes (m) 1.55 1.64 (5.1) 1.47 1.33 10.1 1.62 1.57 3.0 1.68 1.53 10.0

Net Sales 61,595 62,473 (1.4) 58,551 51,875 12.9 64,957 61,876 5.0 69,992 61,458 13.9

Operating Profit 9,152 9,369 (2.3) 8,392 7,192 16.7 9,368 7,786 20.3 10,418 8,498 22.6

OPM (%) 14.9 15.0 14.3 13.9 14.4 12.6 14.9 13.8

Adj. PAT 5,486 6,155 (10.9) 4,713 4,406 7.0 5,314 4,879 8.9 6,321 5,742 10.1

Source: Company Data, PL Research

With volume recovery, we expect HMCL to report profit growth in the ensuing three quarters as against a decline in PAT in Q1FY14.

Under the alliance, Indy Motos has been

appointed as the authorized distributor of

Hero MotoCorp range of two‐wheelers in

Guatemala, Honduras and El Salvador.

Products will be distributed through a

network of outlets spread across these

countries, with more new outlets to be

added subsequently

September 04, 2013 31

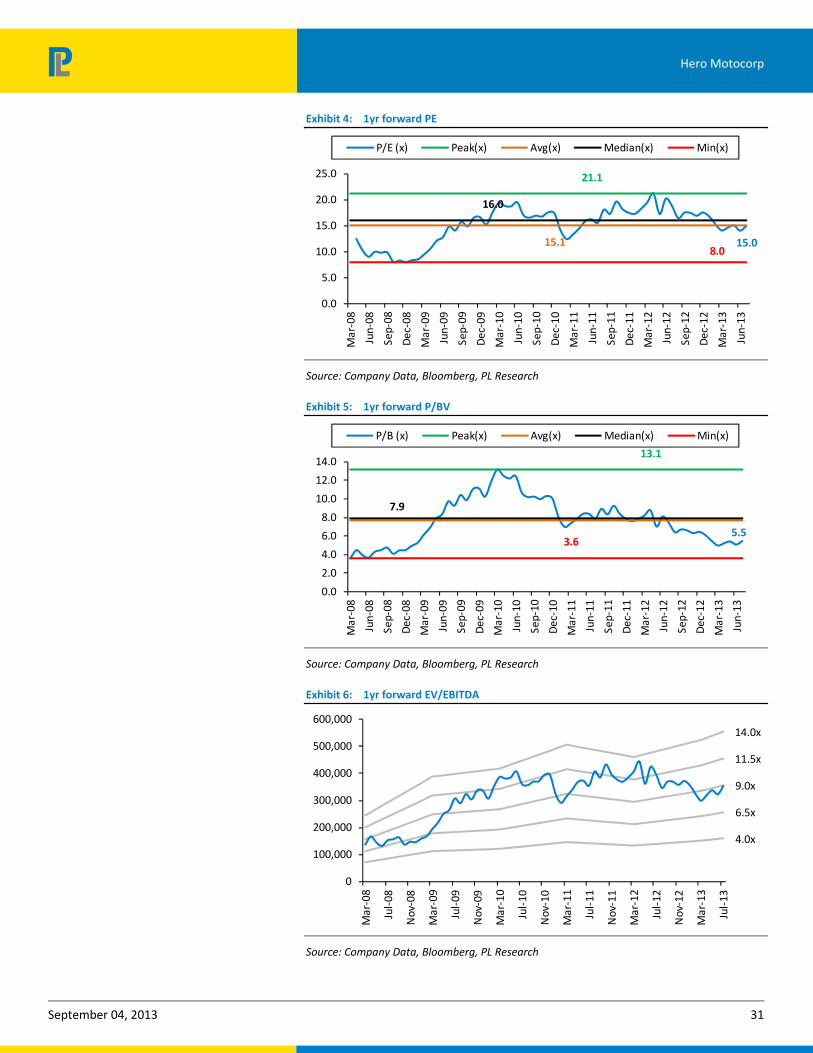

Hero Motocorp

Exhibit 4: 1yr forward PE

15.0

21.1

15.1

16.0

8.0

0.0

5.0

10.0

15.0

20.0

25.0

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

P/E (x) Peak(x) Avg(x) Median(x) Min(x)

Source: Company Data, Bloomberg, PL Research

Exhibit 5: 1yr forward P/BV

5.5

13.1

7.9

3.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

P/B (x) Peak(x) Avg(x) Median(x) Min(x)

Source: Company Data, Bloomberg, PL Research

Exhibit 6: 1yr forward EV/EBITDA

4.0x

6.5x

9.0x

11.5x

14.0x

0

100,000

200,000

300,000

400,000

500,000

600,000

Mar

-08

Jul-

08

Nov

-08

Mar

-09

Jul-

09

Nov

-09

Mar

-10

Jul-

10

Nov

-10

Mar

-11

Jul-

11

Nov

-11

Mar

-12

Jul-

12

Nov

-12

Mar

-13

Jul-

13

Source: Company Data, Bloomberg, PL Research

September 04, 2013 32

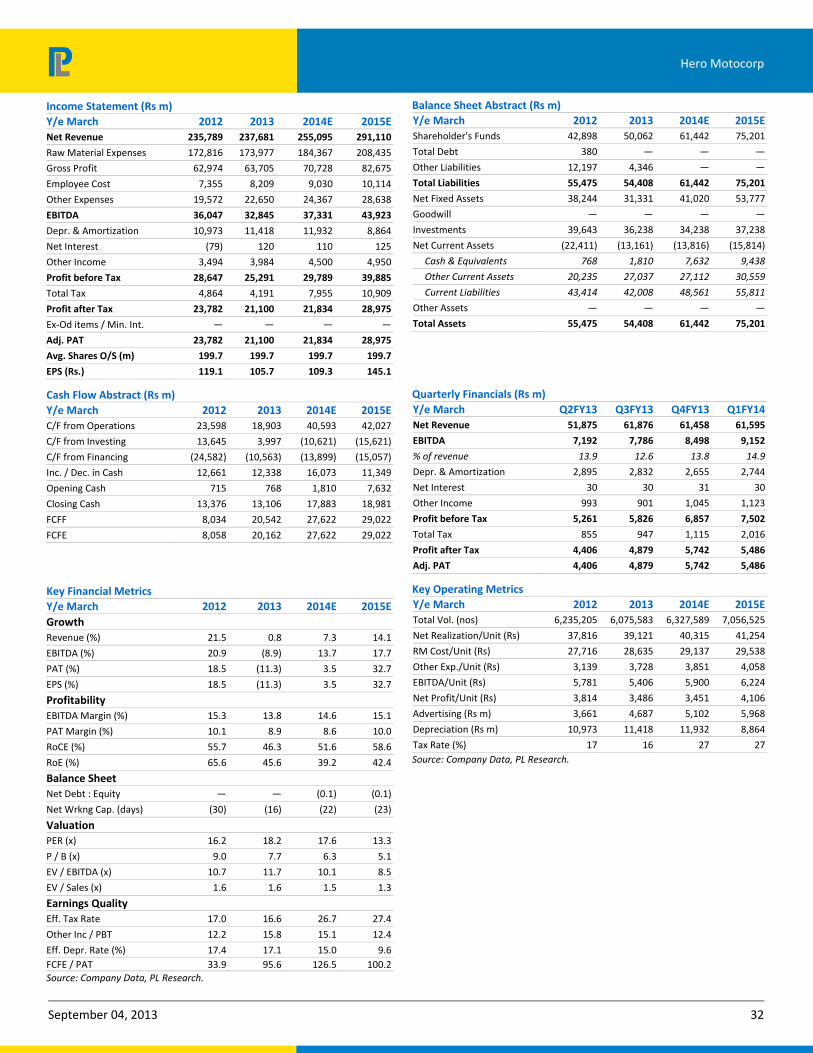

Hero Motocorp

Income Statement (Rs m)

Y/e March 2012 2013 2014E 2015E

Net Revenue 235,789 237,681 255,095 291,110

Raw Material Expenses 172,816 173,977 184,367 208,435

Gross Profit 62,974 63,705 70,728 82,675

Employee Cost 7,355 8,209 9,030 10,114

Other Expenses 19,572 22,650 24,367 28,638

EBITDA 36,047 32,845 37,331 43,923

Depr. & Amortization 10,973 11,418 11,932 8,864

Net Interest (79) 120 110 125

Other Income 3,494 3,984 4,500 4,950

Profit before Tax 28,647 25,291 29,789 39,885

Total Tax 4,864 4,191 7,955 10,909

Profit after Tax 23,782 21,100 21,834 28,975

Ex-Od items / Min. Int. — — — —

Adj. PAT 23,782 21,100 21,834 28,975

Avg. Shares O/S (m) 199.7 199.7 199.7 199.7

EPS (Rs.) 119.1 105.7 109.3 145.1

Cash Flow Abstract (Rs m)

Y/e March 2012 2013 2014E 2015E

C/F from Operations 23,598 18,903 40,593 42,027

C/F from Investing 13,645 3,997 (10,621) (15,621)

C/F from Financing (24,582) (10,563) (13,899) (15,057)

Inc. / Dec. in Cash 12,661 12,338 16,073 11,349

Opening Cash 715 768 1,810 7,632

Closing Cash 13,376 13,106 17,883 18,981

FCFF 8,034 20,542 27,622 29,022

FCFE 8,058 20,162 27,622 29,022

Key Financial Metrics

Y/e March 2012 2013 2014E 2015E

Growth

Revenue (%) 21.5 0.8 7.3 14.1

EBITDA (%) 20.9 (8.9) 13.7 17.7

PAT (%) 18.5 (11.3) 3.5 32.7

EPS (%) 18.5 (11.3) 3.5 32.7

Profitability

EBITDA Margin (%) 15.3 13.8 14.6 15.1

PAT Margin (%) 10.1 8.9 8.6 10.0

RoCE (%) 55.7 46.3 51.6 58.6

RoE (%) 65.6 45.6 39.2 42.4

Balance Sheet

Net Debt : Equity — — (0.1) (0.1)

Net Wrkng Cap. (days) (30) (16) (22) (23)

Valuation

PER (x) 16.2 18.2 17.6 13.3

P / B (x) 9.0 7.7 6.3 5.1

EV / EBITDA (x) 10.7 11.7 10.1 8.5

EV / Sales (x) 1.6 1.6 1.5 1.3

Earnings Quality

Eff. Tax Rate 17.0 16.6 26.7 27.4

Other Inc / PBT 12.2 15.8 15.1 12.4

Eff. Depr. Rate (%) 17.4 17.1 15.0 9.6FCFE / PAT 33.9 95.6 126.5 100.2Source: Company Data, PL Research.

Balance Sheet Abstract (Rs m)

Y/e March 2012 2013 2014E 2015E

Shareholder's Funds 42,898 50,062 61,442 75,201

Total Debt 380 — — —

Other Liabilities 12,197 4,346 — —

Total Liabilities 55,475 54,408 61,442 75,201

Net Fixed Assets 38,244 31,331 41,020 53,777

Goodwill — — — —

Investments 39,643 36,238 34,238 37,238

Net Current Assets (22,411) (13,161) (13,816) (15,814)

Cash & Equivalents 768 1,810 7,632 9,438

Other Current Assets 20,235 27,037 27,112 30,559

Current Liabilities 43,414 42,008 48,561 55,811

Other Assets — — — —

Total Assets 55,475 54,408 61,442 75,201

Quarterly Financials (Rs m)

Y/e March Q2FY13 Q3FY13 Q4FY13 Q1FY14

Net Revenue 51,875 61,876 61,458 61,595

EBITDA 7,192 7,786 8,498 9,152

% of revenue 13.9 12.6 13.8 14.9

Depr. & Amortization 2,895 2,832 2,655 2,744

Net Interest 30 30 31 30

Other Income 993 901 1,045 1,123

Profit before Tax 5,261 5,826 6,857 7,502

Total Tax 855 947 1,115 2,016

Profit after Tax 4,406 4,879 5,742 5,486

Adj. PAT 4,406 4,879 5,742 5,486

Key Operating Metrics

Y/e March 2012 2013 2014E 2015E

Total Vol. (nos) 6,235,205 6,075,583 6,327,589 7,056,525

Net Realization/Unit (Rs) 37,816 39,121 40,315 41,254

RM Cost/Unit (Rs) 27,716 28,635 29,137 29,538

Other Exp./Unit (Rs) 3,139 3,728 3,851 4,058

EBITDA/Unit (Rs) 5,781 5,406 5,900 6,224

Net Profit/Unit (Rs) 3,814 3,486 3,451 4,106

Advertising (Rs m) 3,661 4,687 5,102 5,968

Depreciation (Rs m) 10,973 11,418 11,932 8,864

Tax Rate (%) 17 16 27 27Source: Company Data, PL Research.

September 04, 2013 33

Hero Motocorp

Prabhudas Lilladher Pvt. Ltd.

3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai-400 018, India

Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209

Rating Distribution of Research Coverage

26.4%

52.8%

17.6%

3.2%

0%

10%

20%

30%

40%

50%

60%

BUY Accumulate Reduce Sell

% of Total Coverage

PL’s Recommendation Nomenclature

BUY : Over 15% Outperformance to Sensex over 12-months Accumulate : Outperformance to Sensex over 12-months

Reduce : Underperformance to Sensex over 12-months Sell : Over 15% underperformance to Sensex over 12-months

Trading Buy : Over 10% absolute upside in 1-month Trading Sell : Over 10% absolute decline in 1-month

Not Rated (NR) : No specific call on the stock Under Review (UR) : Rating likely to change shortly

This document has been prepared by the Research Division of Prabhudas Lilladher Pvt. Ltd. Mumbai, India (PL) and is meant for use by the recipient only as

information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of PL. It should not be

considered or taken as an offer to sell or a solicitation to buy or sell any security.

The information contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy

or completeness of the same. Neither PL nor any of its affiliates, its directors or its employees accept any responsibility of whatsoever nature for the information,

statements and opinion given, made available or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The

suitability or otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an

independent expert/advisor.

Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or

engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication.

We may from time to time solicit or perform investment banking or other services for any company mentioned in this document.