Auditor's Report to the shareholders of Prime Bank Securities Limited

20

1 Auditor’s Report to the shareholders of Prime Bank Securities Limited We have audited the accompanying financial statements of Prime Bank Securities Limited (PBSL) which comprise the financial position as at 31 December 2012 and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended and a summary of significant accounting policies and other explanatory information disclosed in Notes 1-22 to the financial statements. Management’s Responsibility for the Financial Statements Management of PBSL is responsible for the preparation and fair representation of these financial statements in accordance with Bangladesh Financial Reporting Standards (BFRSs), and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Bangladesh Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain evidence about the amount and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risks assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion. Opinion In our opinion, financial statements which have been prepared in accordance with Bangladesh Financial Reporting Standards give a true and fair view of the state of affairs of the company as at 31 December 2012 and of its financial performance and cash flows for the year then ended in accordance with Bangladesh Financial Reporting Standards.

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Auditor's Report to the shareholders of Prime Bank Securities Limited

1

Auditor’s Report to the shareholders of Prime Bank Securities Limited

We have audited the accompanying financial statements of Prime Bank Securities Limited (PBSL)

which comprise the financial position as at 31 December 2012 and the statement of

comprehensive income, statement of changes in equity and statement of cash flows for the year

then ended and a summary of significant accounting policies and other explanatory information

disclosed in Notes 1-22 to the financial statements.

Management’s Responsibility for the Financial Statements

Management of PBSL is responsible for the preparation and fair representation of these financial

statements in accordance with Bangladesh Financial Reporting Standards (BFRSs), and for such

internal control as management determines is necessary to enable the preparation of financial

statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with Bangladesh Standards on Auditing. Those standards

require that we comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free from material

misstatement.

An audit involves performing procedures to obtain evidence about the amount and disclosures in

the financial statements. The procedures selected depend on the auditor’s judgment, including

the assessment of the risks of material misstatement of the financial statements, whether due to

fraud or error. In making those risks assessments, the auditor considers internal control relevant

to the entity’s preparation and fair presentation of the financial statements in order to design

audit procedures that are appropriate in the circumstances, but not for the purpose of expressing

an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating

the appropriateness of accounting policies used and the reasonableness of accounting estimates

made by management, as well as evaluating the overall presentation of the financial statements.

We believe that our audit provides a reasonable basis for our opinion.

Opinion

In our opinion, financial statements which have been prepared in accordance with Bangladesh

Financial Reporting Standards give a true and fair view of the state of affairs of the company as

at 31 December 2012 and of its financial performance and cash flows for the year then ended in

accordance with Bangladesh Financial Reporting Standards.

2

Emphasis of Matter

Without qualifying our opinion we draw attention to note # 06 to the financial statements where

the Company explains the measurement procedure of DSE and CSE memberships cost.

Report on Other Legal and Regulatory Requirements

We also report that:

• we have obtained all the material information and explanations which to the best of our

knowledge and belief were necessary for the purposes of our audit and made due

verification thereof;

• in our opinion, proper books of account as required by law have been kept by the Company

so far as it appeared from our examination of those books;

• the Company’s financial position and financial performance dealt with by the report are in

agreement with the books of account; and

• the expenditure incurred was for the purposes of the Company’s business.

Dated, Dhaka

26 February 2013 ACNABIN

Chartered Accountants

Prime Bank Securities Limited

Statement of Financial Position

As at 31 December 2012

2012 2011

SOURCES OF FUNDS

Share Capital 3 750,000,000 750,000,000

Retained Earnings 4 33,096,718 4,495,828

Shareholders equity 783,096,718 754,495,828

APPLICATION OF FUNDS

Non-Current Assets (A)

Fixed assets 5 7,492,430 9,326,599

Intangible assets 5 1,217,647 815,796

Membership at cost 6 664,000,000 664,000,000

672,710,077 674,142,395

Current Assets (B)

Advances, deposits and prepayments 7 313,800 231,300

Advance income tax 8 19,568,538 8,143,350

Investment in securities 9 77,051,850 32,472,977

Accounts receivable 10 7,658,920 27,780,279

Loan to customers 404,029,700 193,021,110

Preliminary expenses 11 614,121 1,228,243

Cash and cash equivalents 12 190,740 4,803,433

509,427,669 267,680,692

Current Liabilities (C)

Accounts payable 13 14,933,195 40,849,889

Secured overdraft 14 352,278,429 135,253,198

Provision for diminution value of investment in shares 9 4,221,798 988,820

Provision for impairment of margin loan 15.01 597,088 -

Provision for Taxation 15 23,855,427 8,170,117

Deferred tax liabilities 15 648,910 665,885

Provision for expenses 16 2,506,181 1,399,350

399,041,028 187,327,258

Net current assets D=(B-C) 110,386,641 80,353,434

Total assets (A+D) 783,096,718 754,495,828

____________________________

Chief Executive Officer Chairman

Dated, Dhaka ACNABIN26 February 2013 Chartered Accountants

_________________________

These financial statements should be read in conjunction with annexed notes 1 to 22.

Note Amount in Taka

Director

__________

3

Prime Bank Securities Limited

Statement of Comprehensive income

For the year ended 31 December 2012

2012 2011

Operating Income

Revenue from brokerage commission 17 52,419,765 20,187,773

Interest income 18 58,355,301 8,507,103

Capital gain from investment in shares 8,850,564 1,916,822

Dividend income 944,511 108,873

Other operating income 19 859,572 328,617

Total operating income (A) 121,429,712 31,049,188

Operating expenses 20 65,988,517 14,144,974

Direct expenses 21 7,341,905 2,583,564

Total operating expenses (B) 73,330,421 16,728,538

Operating profit before provision C=(A-B) 48,099,291 14,320,650

Less: Provision for diminution in value of investment in shares 9 3,232,978 988,820

Provision for impairment of margin loan 15.01 597,088 -

Total provision (D) 3,830,066 988,820

Operating profit before taxation E=(C-D) 44,269,225 13,331,830

Current tax 15 15,685,310 8,170,117

Deferred tax 15 (16,975) 665,885

Total provision for tax (F) 15,668,336 8,836,002 Net profit after tax [G=E-F] 28,600,890 4,495,828

Earnings per share 0.38 0.06

These financial statements should be read in conjunction with annexed notes 1 to 22.

____________________________

Chief Executive Officer Chairman

Dated, Dhaka ACNABIN

26 February 2013 Chartered Accountants

Note Amount in Taka

Director

_________________________

4

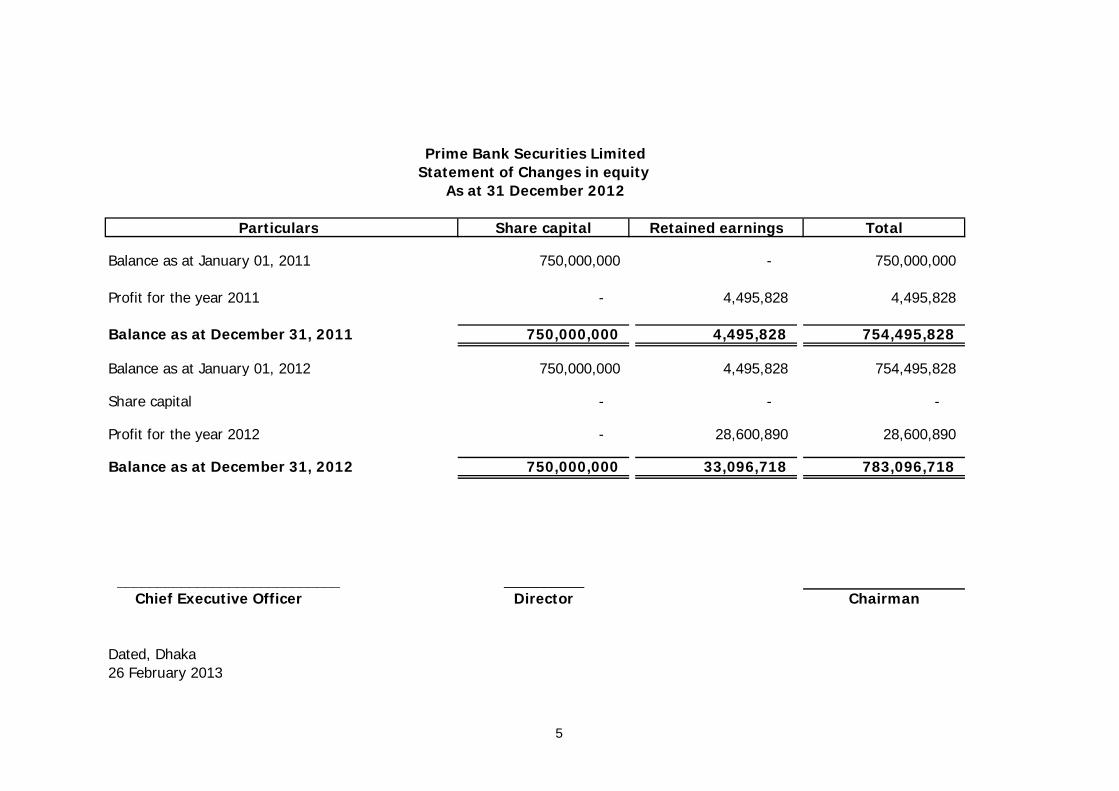

Particulars Share capital Retained earnings Total

Balance as at January 01, 2011 750,000,000 - 750,000,000

Profit for the year 2011 - 4,495,828 4,495,828

Balance as at December 31, 2011 750,000,000 4,495,828 754,495,828

Balance as at January 01, 2012 750,000,000 4,495,828 754,495,828

Share capital - - -

Profit for the year 2012 - 28,600,890 28,600,890

Balance as at December 31, 2012 750,000,000 33,096,718 783,096,718

____________________________ Chief Executive Officer Chairman

Dated, Dhaka

26 February 2013

Director

Prime Bank Securities Limited

Statement of Changes in equity

As at 31 December 2012

__________

5

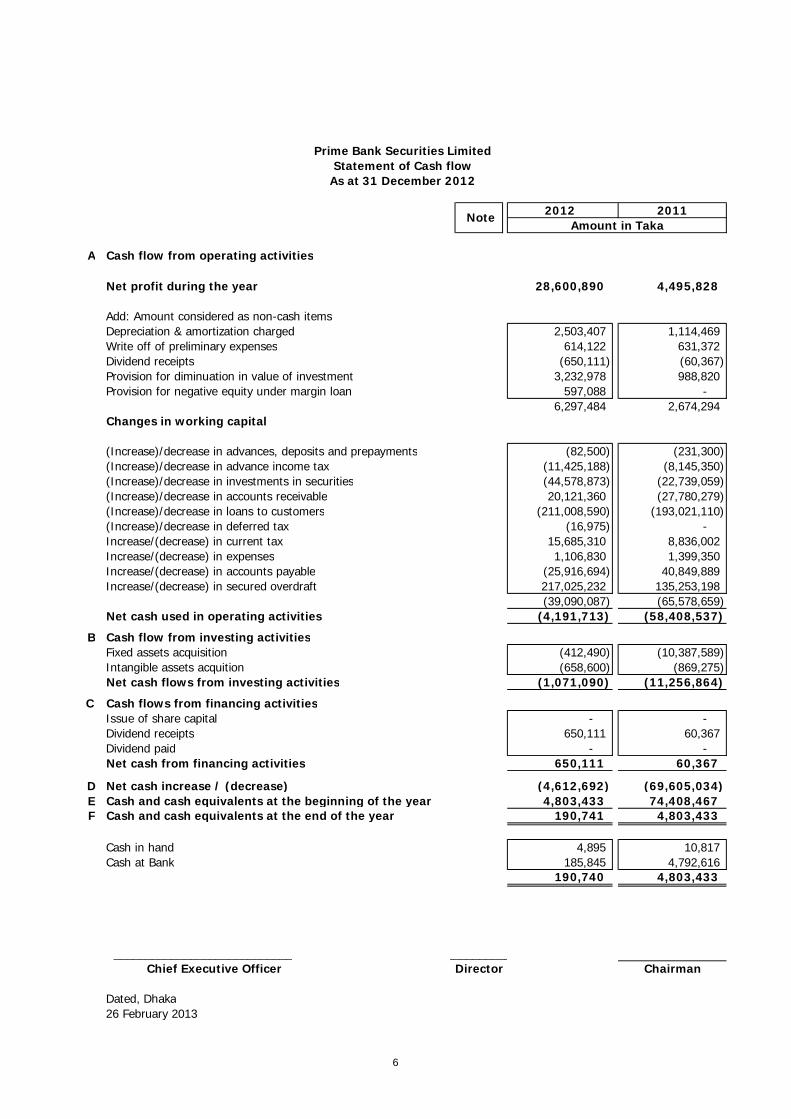

2012 2011

A Cash flow from operating activities

Net profit during the year 28,600,890 4,495,828

Add: Amount considered as non-cash items

Depreciation & amortization charged 2,503,407 1,114,469

Write off of preliminary expenses 614,122 631,372

Dividend receipts (650,111) (60,367)

Provision for diminuation in value of investment 3,232,978 988,820

Provision for negative equity under margin loan 597,088 -

6,297,484 2,674,294

Changes in working capital

(Increase)/decrease in advances, deposits and prepayments (82,500) (231,300)

(Increase)/decrease in advance income tax (11,425,188) (8,145,350)

(Increase)/decrease in investments in securities (44,578,873) (22,739,059)

(Increase)/decrease in accounts receivable 20,121,360 (27,780,279)

(Increase)/decrease in loans to customers (211,008,590) (193,021,110)

(Increase)/decrease in deferred tax (16,975) -

Increase/(decrease) in current tax 15,685,310 8,836,002

Increase/(decrease) in expenses 1,106,830 1,399,350

Increase/(decrease) in accounts payable (25,916,694) 40,849,889

Increase/(decrease) in secured overdraft 217,025,232 135,253,198

(39,090,087) (65,578,659)

Net cash used in operating activities (4,191,713) (58,408,537)

B Cash flow from investing activities

Fixed assets acquisition (412,490) (10,387,589)

Intangible assets acquition (658,600) (869,275)

Net cash flows from investing activities (1,071,090) (11,256,864)

C Cash flows from financing activities

Issue of share capital - -

Dividend receipts 650,111 60,367

Dividend paid - -

Net cash from financing activities 650,111 60,367

D Net cash increase / (decrease) (4,612,692) (69,605,034)

E Cash and cash equivalents at the beginning of the year 4,803,433 74,408,467 F Cash and cash equivalents at the end of the year 190,741 4,803,433

Cash in hand 4,895 10,817

Cash at Bank 185,845 4,792,616 190,740 4,803,433

0.92

____________________________

Chief Executive Officer Chairman

Dated, Dhaka

26 February 2013

Director

Note Amount in Taka

Prime Bank Securities Limited

Statement of Cash flow

As at 31 December 2012

__________

6

Prime Bank Securities LimitedNotes to the Financial Statements

as at and for the year ended 31 December 2012

1.1 Status of the Company

1.2 Nature of Business

1.3 Significant accounting policies and basis of preparation of financial statements

1.3.1 Basis of accounting

1.3.2 Statement of compliance

1.3.3 Components of Financial Statements

The financial statements referred to here comprises:

a) Statement of financial position

b) Statement of comprehensive income

c) Statement of change in equity

d) Statement of cash flows and

e) Notes to the financial statements

1.3.4

1.3.5 Statement of cash flows

1.4 Reporting period

These financial statements cover one calendar year from 1 January to 31 December 2012.

The Prime Bank Securities Limited ("the Company") was incorporated as a private limited company in

Bangladesh under Companies Act, 1994 vide certificate of incorporation no. C-84302 /10. It commenced its

broker business with one extension office from May 18, 2011 under the license issued by Bangladesh

Securities and Exchange Commission. Presently the company has 2 (two) offices including Head Office all

over Bangladesh.The registered office of the company is located at people's Insurance Bhaban (11th floor) 36, Dilkusha

Commercial Area, Dhaka-1000.

Use of estimates and judgments

The preparation of financial statements requires management to make judgments, estimates and

assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities,

income and expenses. It also requires disclosures of contingent assets and liabilities at the date of the

financial statements. Actual results may differ from these estimates.

The principal objectives of the Company are to act as a member of Dhaka Stock Exchange Ltd. and

Chittagong Stock Exchange Ltd. to carry on the business of stock brokers / dealers in relation to shares and

securities dealings and other services as mentioned in the Memorandum and Articles of Association of the

Company.

These financial statements have been prepared under the historical cost convention on a going concern

basis and in accordance with Bangladesh Financial Reporting Standards (BFRS), the Companies Act-1994,

Securities and Exchange Rules-1987 and other laws and rules applicable in Bangladesh.

Estimates and underlying assumptions are reviewed on an ongoing concern basis. Revisions to accounting

estimates are recognized in the period in which the estimate is revised and in any future periods affected.

Statement of cash flows is prepared in accordance with the Bangladesh Accounting Standard-7 " Statement

Cash Flows" and the cash flows from operating activities have been presented under indirect method.

7

1.5 Share capital

1.6 Property, plant and equipment

Category of assets Rate(%)

Furniture and fixtures 20

Office equipment 25

Air conditioners 25

Computer and hardwares 25

Vehicle 20

1.7 Intangible assets and amortization of intangible assets

On disposal of fixed assets, the cost and accumulated depreciation are eliminated from the fixed assets

schedule and gain or loss on such disposal is reflected in the income statement, which is determined with

reference to the net book value of the assets and net sale proceeds.

Ordinary shares are classified as equity when there is no contractual obligation to transfer cash or other

financial assets.

All fixed assets are stated at cost less accumulated depreciation as per BAS-16 " Property, Plant and

Equipment". The cost of acquisition of an asset comprises its purchase price and any directly attributable

cost of bringing the asset to its working condition for its intended use inclusive of inward freight, duties and

non-refundable taxes.

The Company recognizes in the carrying amount of an item of property, plant and equipment the cost of

replacing part of such an item when that cost is incurred if it is probable that the future economic benefits

embodied with the item will flow to the company and the cost of the item can be measured reliably.

Expenditure incurred after the assets have been put into operation, such as repairs and maintenance is

normally charged off as revenue expenditure in the period in which it is incurred.

Depreciation is charged on the basis of straight line method on all fixed assets at the following rate:

Software represents the value of computer application software licensed for use of the Company other than

those applied for the operating system of computers. Intangible assets are carried at their cost, less

accumulated amortization and impairment loss, if any.

For additions during the year, depreciation is charged for the remaining days of the year and for disposal

depreciation is charged up to the date of disposal.

An intangible asset is recognized if it is probable that the future economic benefits that are attributable to

the asset will flow to the entity and the cost of the assets can be measured reliably.

Expenditure incurred for software is capitalized only when it enhances and extends the economic benefits of

software beyond its original specification and life and such cost is recognized as capital improvement and

added to the original cost of software.

Software is amortized using the straight-line method over the estimated useful life of 5 (five) years

commencing from the date of the acquisition available for use over the best estimates of its useful economic

life.

Initial cost comprises license fees paid at the time of its acquisition and other directly attributable

expenditures that are incurred in customizing the software for its intended use.

8

1.8 Investment in Membership

1.9 Advance, deposits and prepayments

1.10 Advance Income tax

1.11 Investments in securities

1.12 Account receivables

1.13 Loans to customers

1.14 Preliminary and pre-operating expenses

1.15 Cash and cash equivalents

1.16 Provision for taxation

- Deposits are measured at payment value.

Investment in marketable and non-marketable ordinary shares has been shown at cost. Full provision for

diminution in value of shares as on closing of the year on an aggregate portfolio basis has been made in the

account.

The amount of advance income tax are mainly deduction at sources by DSE & CSE on daily transaction of

broker & dealer operation. Tax deduction on interest income and dividend income are also included here.

Receivables are recognized when there is a contractual right to receive cash or another financial asset from

another entity.

Investment in membership are stated at cost. The cost of acquisition of an membership comprises its

purchase price and any directly attributable cost of bringing the asset to its working condition for its

intended use inclusive of stamp duty and non-refundable taxes, etc.

- Prepayments are initially measured at cost. After initial recognition, prepayments are carried at cost less

charges to Statement of Comprehensive Income.

- Advances are initially measured at cost. After initial recognition, advances are carried at cost less

deductions, adjustments or charges to other account heads such as property, plant and equipment,

inventory, etc.

Provision for current income tax has been made in compliance with relevant provisions of Income Tax law.

Loans to customers are stated in the balance sheet on gross basis. Interest is calculated on a daily product

basis but charged and accounted for on accrual basis. Interest on customer loans is realized quarterly.

These are recognized as an asset if it is probable that future economic benefits that are attributable to the

asset will flow to the enterprise and cost of the asset can be measured reliably. These are amortized over 3

years from the year of their first utilization at the rate of Taka 631,372 per year.

Cash and cash equivalents include notes and coins on hand, unrestricted balances held with Banks and

highly liquid financial assets which are subject to insignificant risk of changes in their fair value, and are used

by the Company management for its short-term commitments.

9

1.17 Deferred taxation

1.18 Secured overdraft

1.19

1.20 Provision for liabilities

1.21 Brokerage commission

Brokerage commission is recognized as income when selling or buying order executed

1.22 Interest income on marginal loan

1.23 Capital gain on sale of share

1.24 Fees income

1.25 Dividend income on shares

Dividend income on shares is recognized when the shareholder's right to receive payment is established.

1.26 Interest paid and other expenses

1.27 Earnings per share

Fees income arises on services provided by the Company are recognized on accrual basis.

A provision is recognized in the balance sheet when the Company has a legal or constructive obligation as a

result of a past event and it is probable that an outflow of economic benefit will be required to settle the

obligations, in accordance with the BAS 37 "Provisions, Contingent Liabilities and Contingent Assets".

Borrowing fund include borrowings from Prime Bank Limited, which is stated in the statement of financial

position at secured overdraft. Interest on secured overdraft is recognized in statement of comprehensive

income.

Incentive bonus

In terms of the provisions of BAS-1 "Presentation of Financial Statements" interest and other expenses are

recognized on accrual basis.

Basic earnings per share has been calculated in accordance with BAS 33 "Earnings per Share" which has

been shown on the face of the profit and loss account. This has been calculated by dividing the profit

attributable to the ordinary shareholders by the weighted average number of ordinary shares outstanding

during the year.

Deferred tax liabilities are the amount of income taxes payable in future periods in respect of taxable

temporary differences. Deferred tax assets are the amount of income taxes recoverable in future periods in

respect of deductible temporary differences. Deferred tax assets and liabilities are recognized for the future

tax consequences of timing differences arising between the carrying values of assets, liabilities, income and

expenditure and their respective tax bases. Deferred tax assets and liabilities are measured using tax rates

and tax laws that have been enacted or substantially enacted at the balance sheet date. The impact on the

account of changes in the deferred tax assets and liabilities has also been recognized in the profit and loss

account as per BAS-12 "Income Taxes".

Prime Bank Securities Ltd. started a incentive bonus scheme for its employees. Maximum 10% of net profit

after tax is given to the employees in every year as incentive bonus. This bonus amount is being distributed

among the employees based on their performance. The bonus amount is paid annually, normally first

quarter of every following year and the cost are accounted for the period to which it relates.

Interest income on margin loan is recognized on accrual basis. Such income is calculated on daily margin

loan balance of the respective customers. Income is recognized on monthly but realized quarterly.

Capital gain on investments in shares is recognized when it is realized.

10

1.28 Events after the reporting period

1.29 Directors' responsibility on financial statements

1.30 Related party transaction

2.00 General

a)

b)

c)

Where necessary, all the material events after the reporting period date have been considered and

appropriate adjustment/disclosures have been made in the financial statements.

Related party transaction is a transfer of resources, services or obligation between related parties and here

the related party transactions are the loan taken from Prime Bank Limited and the brokerage transactions

done by the Company for Prime Bank Investment Ltd. as its client, within the financial period.

These financial statements are presented in Taka, which is the Company's functional currency.

Figures appearing in these financial statements have been rounded off to the nearest Taka.

The board of directors of the company is responsible for the preparation and presentation of these financial

statements.

Figures of previous year have been rearranged whenever necessary to conform to current years

presentation.

The expenses, irrespective of capital or revenue nature, accrued / due but not paid have been

provided for in the books of the Company.

11

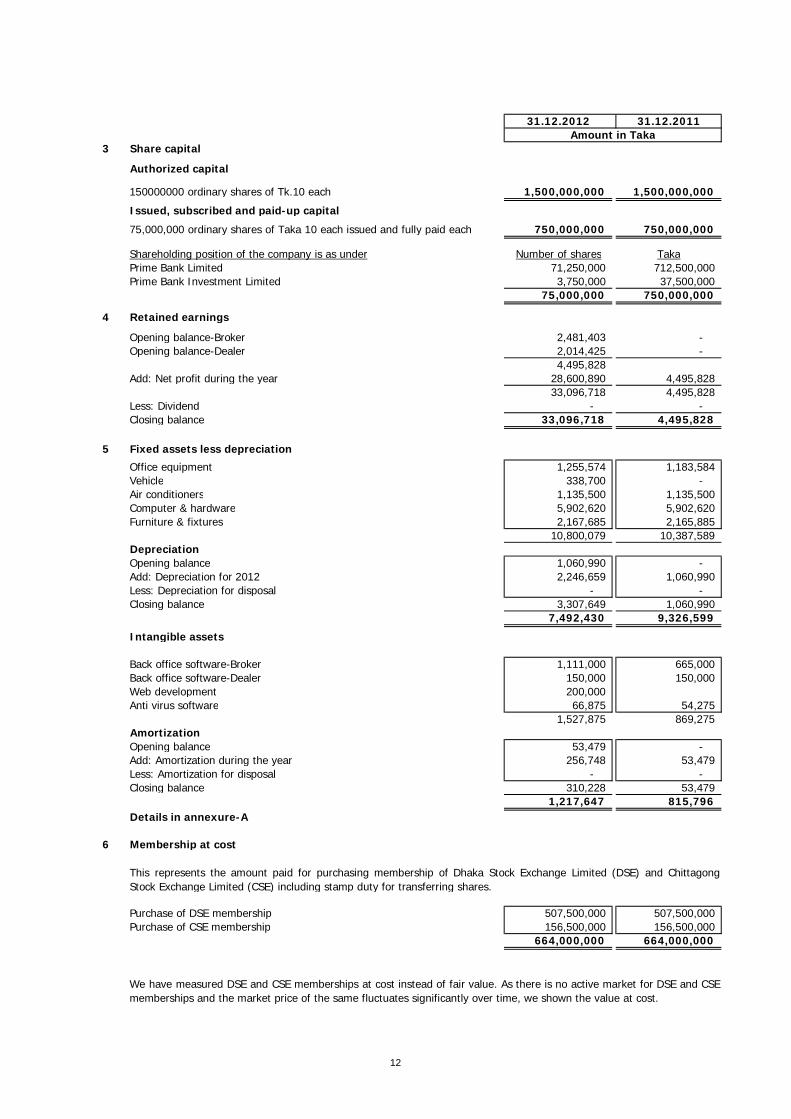

31.12.2012 31.12.2011

3 Share capital

Authorized capital

150000000 ordinary shares of Tk.10 each 1,500,000,000 1,500,000,000

Issued, subscribed and paid-up capital

75,000,000 ordinary shares of Taka 10 each issued and fully paid each 750,000,000 750,000,000

Shareholding position of the company is as under Number of shares Taka

Prime Bank Limited 71,250,000 712,500,000

Prime Bank Investment Limited 3,750,000 37,500,000

75,000,000 750,000,000

4 Retained earnings

Opening balance-Broker 2,481,403 -

Opening balance-Dealer 2,014,425 -

4,495,828

Add: Net profit during the year 28,600,890 4,495,828

33,096,718 4,495,828

Less: Dividend - -

Closing balance 33,096,718 4,495,828

5 Fixed assets less depreciation

Office equipment 1,255,574 1,183,584

Vehicle 338,700 -

Air conditioners 1,135,500 1,135,500

Computer & hardware 5,902,620 5,902,620

Furniture & fixtures 2,167,685 2,165,885

10,800,079 10,387,589

Depreciation

Opening balance 1,060,990 -

Add: Depreciation for 2012 2,246,659 1,060,990

Less: Depreciation for disposal - -

Closing balance 3,307,649 1,060,990

7,492,430 9,326,599

Intangible assets

Back office software-Broker 1,111,000 665,000

Back office software-Dealer 150,000 150,000

Web development 200,000

Anti virus software 66,875 54,275

1,527,875 869,275

Amortization

Opening balance 53,479 -

Add: Amortization during the year 256,748 53,479

Less: Amortization for disposal - -

Closing balance 310,228 53,479

1,217,647 815,796

Details in annexure-A

6 Membership at cost

Purchase of DSE membership 507,500,000 507,500,000

Purchase of CSE membership 156,500,000 156,500,000

664,000,000 664,000,000

This represents the amount paid for purchasing membership of Dhaka Stock Exchange Limited (DSE) and Chittagong

Stock Exchange Limited (CSE) including stamp duty for transferring shares.

We have measured DSE and CSE memberships at cost instead of fair value. As there is no active market for DSE and CSE

memberships and the market price of the same fluctuates significantly over time, we shown the value at cost.

Amount in Taka

12

31.12.2012 31.12.2011

7 Advances, deposits and prepayments

Security deposit with CDBL 200,000 200,000

Security deposit with CSE 25,000 25,000

Advances for software maintenance fees 82,500 -

Security deposit with T&T 6,300 6,300

313,800 231,300

8 Advance income tax

Opening balance 8,143,350 -

Add: Tax deduction during the year:

Advance income tax deducted by DSE on transaction-Broker 11,026,941 7,791,466

Advance income tax deducted by DSE on transaction-Dealer 197,994 32,894

Advance income tax deducted by CSE on transaction 23,535 132,300

Advance income tax deducted by Bank on deposits 9,217 174,409

Direct tax 26,767 -

Advance income tax deducted by Bank on deposits-Dealer 1,009 224

Advance income tax deducted on dividend 139,726 12,057

11,425,188 8,143,350

19,568,538 8,143,350

9 Investment in securities

Cost Price

The City Bank Ltd. 4,578,419 4,270,419

DESCO 10,721,200 -

IFIC Bank Ltd. - 7,468,135

Jamuna Oil 14,105,710

Lafas Surma Cement 4,276,300 -

Lankabangla Finance 8,763,100 -

National Housing Finance and Investment Ltd. 4,602,900 -

One Bank Ltd. 10,844,135 4,049,988

Phonix Finance and Investment Ltd. 6,546,850 6,070,050

Rupali Insurance Company Ltd. - 1,766,430

Square Pharmaceutical Ltd - 1,239,090

Unique Hotel 6,640,500

Uttara Bank Ltd. 5,972,735 -

M.I. Cement Factory Ltd. - 3,608,809

MJL Bangladesh Ltd. - 4,000,056

Total Cost price (A) 77,051,850 32,472,977

Market Price (B) 55,942,860 31,484,157

Loss for diminution in value of investment in shares (C=A-B) 21,108,990 988,820

20% provision for unrealized loss arising out of year end

(31/12/12) revaluation of shares purchased*(d=C X 20%)4,221,798 -

Less: Provision already kept in last year 988,820 -

Net provision 3,232,978 988,820

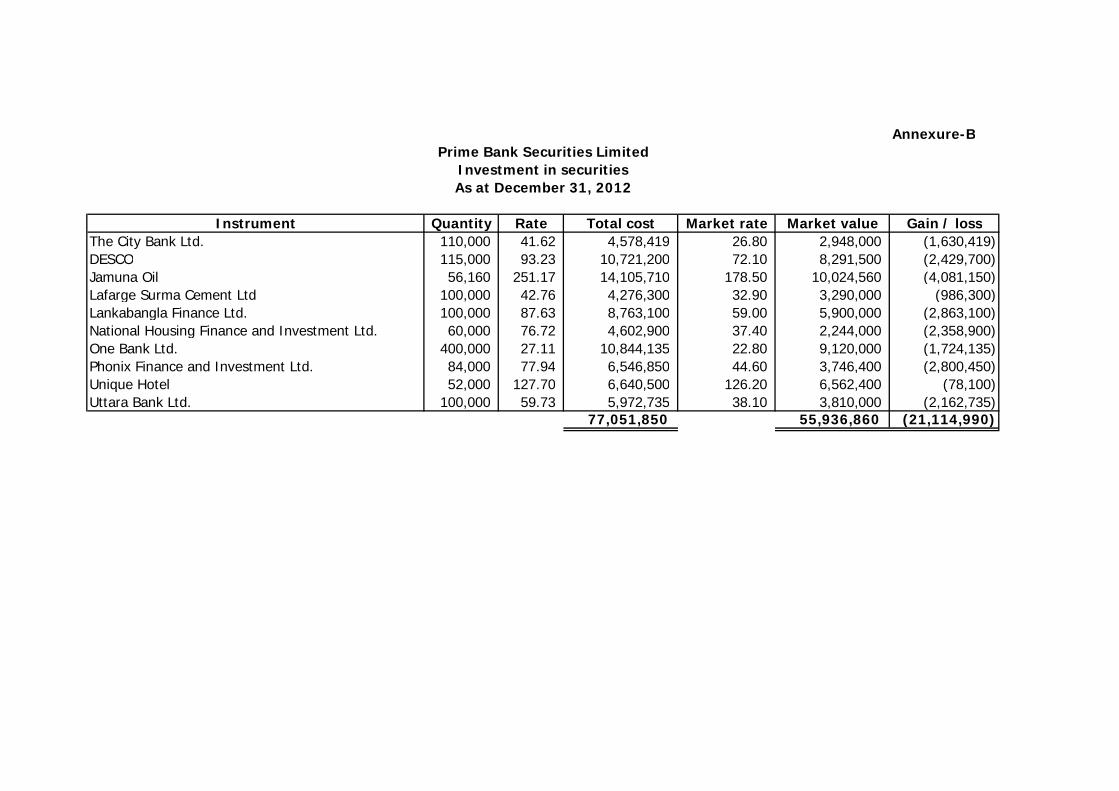

Details in annexure-B

10 Accounts receivable

Receivable from DSE 7,317,754 -

Receivable from DSE-Dealer 46,766 -

Receivable from PBIL - -

Dividend receivable 294,400 48,506

Receivable from clients - 27,731,774

7,658,920 27,780,279

Amount in Taka

*As per Press release# SEC/Mukhopatro/2011/696 dated 19 February 2013 of Bangladesh Securities and Exchange

Commission, 20% provision has been made for unrealized loss arising out of year-end (31.12.2012) revaluation of shares

purchased as dealer.

13

31.12.2012 31.12.2011

11 Preliminary expenses

`

Opening balance 1,228,243 1,859,615

Add: expenses made during the year - -

Less: Write-off in 2012 614,122 631,372

614,121 1,228,243

12 Cash and cash equivalent

Cash in hand 4,895 10,817

Cash at Bank:

One Bank Limited (SND)-DSE Broker 8,865 4,222,066

One Bank Limited (SND)-DSE Dealer 30,638 83,542

One Bank Limited (CD)-DSE Broker 102,647 335,801

Prime Bank Limited (CD)-Operation 5,340 120,858

Prime Bank Limited (CD)-DSE Broker 14,505 29,640

Prime Bank Limited (CD)-CSE Broker 23,850 708

185,845 4,792,616

190,740 4,803,433

13 Accounts payable

Payable to DSE 57,192 29,028,119

Payable to CDBL 159,892 23,356

Payable to clients 9,519,781 10,907,860

Security deposits 283,220 890,554

Payable to PBIL 4,913,110 -

14,933,195 40,849,889

14 Secured Overdraft from Prime Bank Ltd, Motijeel Branch 352,278,429 135,253,198

15 Provision for tax

Current tax

Opening balance 8,170,117 -

Add: Provision for the during year 15,685,310 8,170,117

Less: Provision adjusted during the year - -

Closing balance 23,855,427 8,170,117

Deferred tax

Opening balance 665,885 -

Add: Provision for the during year (16,975) 665,885

Less: Provision adjusted during the year - -

Closing balance 648,910 665,885

24,504,337 8,836,002

15.01 Provision for impairment of margin loan

Impaired margin loan as at 31st December 2012 2,985,439 -

20% provision for unrealized loss arising out of year end

(31/12/12) revaluation of shares purchased*.597,088 -

The above loan, overdraft (general), was taken from Prime Bank Ltd, Motijheel Branch bearing interest @ 14.50% per

annnum on quarterly basis vide reference no. Prime/MJ/CR/2011/33809 dated 04 September 2011.

Amount in Taka

*As per Press release# SEC/Mukhopatro/2011/696 dated 19 February 2013 of Bangladesh Securities and Exchange

Commission, 20% provision has been made for unrealized loss arising out of year-end (31.12.2012) revaluation of shares

purchased through margin loan.

14

31.12.2012 31.12.2011

16 Provision for expenses

Internet bill 265,000 33,000

Security and cleaning 63,250 52,000

Water bill 7,500 2,000

Telephone bill 25,000 28,000

Office rent 83,246 126,000

Electricity bill 55,000 60,000

Wasa bill 8,000 14,000

Salary-PF - 77,550

Salary arrear 395,100 500,000

Incentive bonus 1,459,085 449,000

Audit fee 69,000 41,800

Professional fees 69,000 -

Fuel 7,000 16,000

Provision for negative equity

2,506,181 1,399,350

Amount in Taka

15

2012 2011

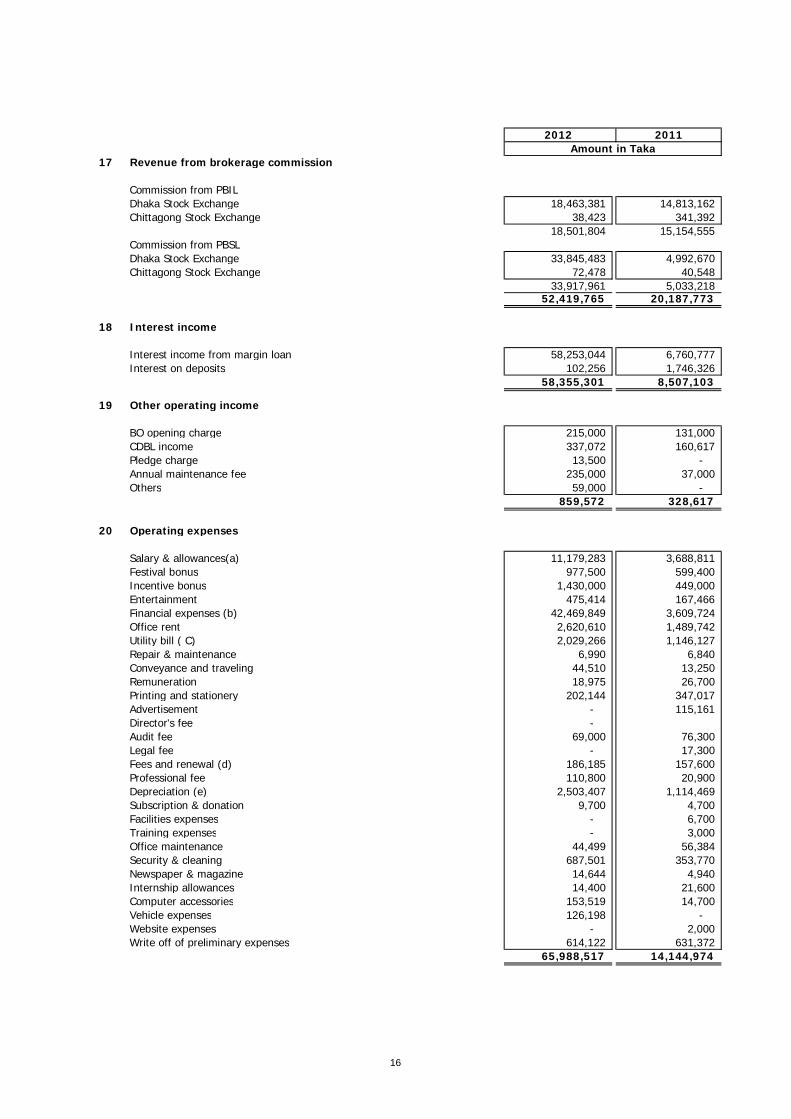

17 Revenue from brokerage commission

Commission from PBIL

Dhaka Stock Exchange 18,463,381 14,813,162

Chittagong Stock Exchange 38,423 341,392

18,501,804 15,154,555

Commission from PBSL

Dhaka Stock Exchange 33,845,483 4,992,670

Chittagong Stock Exchange 72,478 40,548

33,917,961 5,033,218 52,419,765 20,187,773

18 Interest income

Interest income from margin loan 58,253,044 6,760,777

Interest on deposits 102,256 1,746,326

58,355,301 8,507,103

19 Other operating income

BO opening charge 215,000 131,000

CDBL income 337,072 160,617

Pledge charge 13,500 -

Annual maintenance fee 235,000 37,000

Others 59,000 -

859,572 328,617

20 Operating expenses

Salary & allowances(a) 11,179,283 3,688,811

Festival bonus 977,500 599,400

Incentive bonus 1,430,000 449,000

Entertainment 475,414 167,466

Financial expenses (b) 42,469,849 3,609,724

Office rent 2,620,610 1,489,742

Utility bill ( C) 2,029,266 1,146,127

Repair & maintenance 6,990 6,840

Conveyance and traveling 44,510 13,250

Remuneration 18,975 26,700

Printing and stationery 202,144 347,017

Advertisement - 115,161

Director's fee -

Audit fee 69,000 76,300

Legal fee - 17,300

Fees and renewal (d) 186,185 157,600

Professional fee 110,800 20,900

Depreciation (e) 2,503,407 1,114,469

Subscription & donation 9,700 4,700

Facilities expenses - 6,700

Training expenses - 3,000

Office maintenance 44,499 56,384

Security & cleaning 687,501 353,770

Newspaper & magazine 14,644 4,940

Internship allowances 14,400 21,600

Computer accessories 153,519 14,700

Vehicle expenses 126,198 -

Website expenses - 2,000

Write off of preliminary expenses 614,122 631,372

65,988,517 14,144,974

Amount in Taka

16

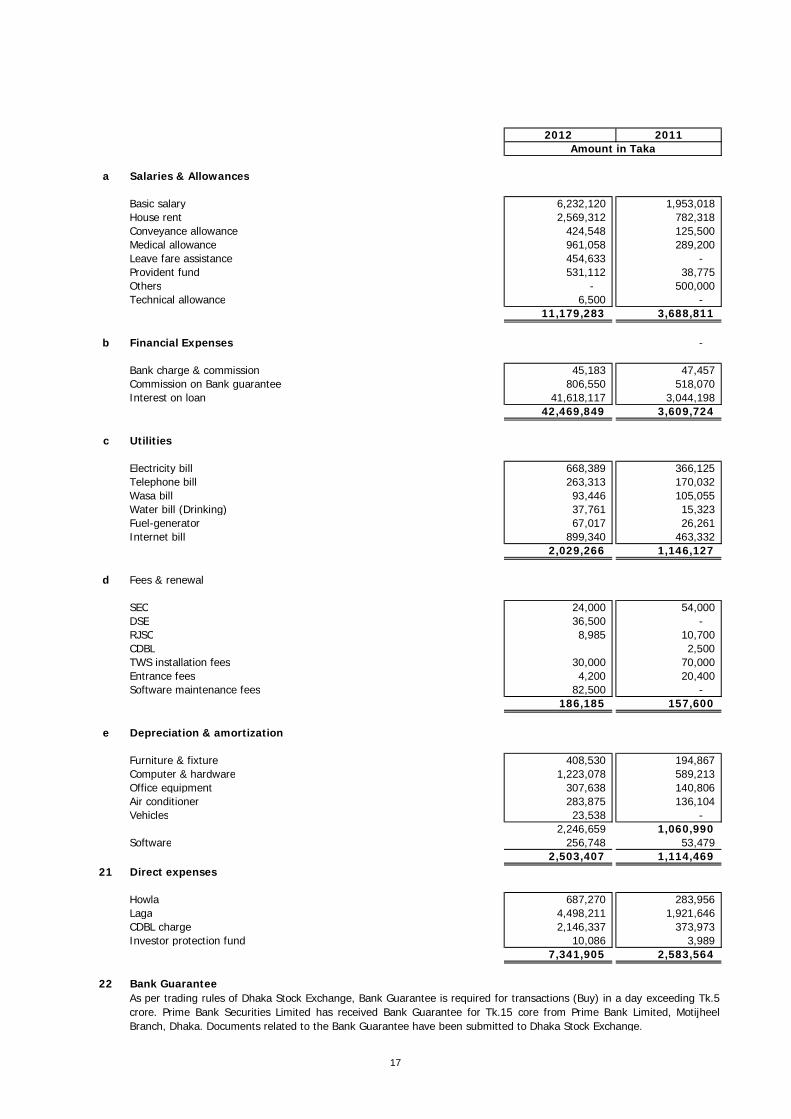

2012 2011

a Salaries & Allowances

Basic salary 6,232,120 1,953,018

House rent 2,569,312 782,318

Conveyance allowance 424,548 125,500

Medical allowance 961,058 289,200

Leave fare assistance 454,633 -

Provident fund 531,112 38,775

Others - 500,000

Technical allowance 6,500 -

11,179,283 3,688,811

b Financial Expenses -

Bank charge & commission 45,183 47,457

Commission on Bank guarantee 806,550 518,070

Interest on loan 41,618,117 3,044,198

42,469,849 3,609,724

c Utilities

Electricity bill 668,389 366,125

Telephone bill 263,313 170,032

Wasa bill 93,446 105,055

Water bill (Drinking) 37,761 15,323

Fuel-generator 67,017 26,261

Internet bill 899,340 463,332

2,029,266 1,146,127

d Fees & renewal

SEC 24,000 54,000

DSE 36,500 -

RJSC 8,985 10,700

CDBL 2,500

TWS installation fees 30,000 70,000

Entrance fees 4,200 20,400

Software maintenance fees 82,500 -

186,185 157,600

e Depreciation & amortization

Furniture & fixture 408,530 194,867

Computer & hardware 1,223,078 589,213

Office equipment 307,638 140,806

Air conditioner 283,875 136,104

Vehicles 23,538 -

2,246,659 1,060,990

Software 256,748 53,479

2,503,407 1,114,469

21 Direct expenses

Howla 687,270 283,956

Laga 4,498,211 1,921,646

CDBL charge 2,146,337 373,973

Investor protection fund 10,086 3,989

7,341,905 2,583,564

22 Bank Guarantee

As per trading rules of Dhaka Stock Exchange, Bank Guarantee is required for transactions (Buy) in a day exceeding Tk.5

crore. Prime Bank Securities Limited has received Bank Guarantee for Tk.15 core from Prime Bank Limited, Motijheel

Branch, Dhaka. Documents related to the Bank Guarantee have been submitted to Dhaka Stock Exchange.

Amount in Taka

17

Depreciation

Opening

balance

Addition

during the

year

Disposal

during

the year

Total cost Rate Opening

balance

Charged

during the

year

Disposal

during the

year

Total

depreciation

Office equipment 1,183,584 71,990 - 1,255,574 0.25 140,806 307,638 - 448,444 807,130

Air conditioners 1,135,500 - - 1,135,500 0.25 136,104 283,875 - 419,979 715,521

Vehicles - 338,700 - 338,700 0.20 - 23,537.54 - 23,538 315,162

Computer & hardwares 5,902,620 - - 5,902,620 0.25 589,213 1,223,078 - 1,812,291 4,090,329

Furniture & fixtures 2,165,885 1,800 - 2,167,685 0.20 194,867 408,530 - 603,397 1,564,288

10,387,589 412,490 - 10,800,079 1,060,990 2,246,659 - 3,307,649 7,492,430

Amortization

Opening

balance

Addition

during the

year

Disposal

during

the year

Total Cost RateOpening

balance

Charged

during the

year

Disposal

during the

year

Total

amortization

Software 869,275 658,600 - 1,527,875 0.20 53,479 256,748 - 310,228 1,217,647

869,275 658,600 - 1,527,875 53,479 256,748 - 310,228 1,217,647

Cost

Total written

down value

Schedule of amortization

As at December 31, 2012

Particulars

Annexure-A

Cost

ParticularsTotal written

down value

Prime Bank Securities Limited

Schedule of depreciation

As at December 31, 2012

Annexure-B

Instrument Quantity Rate Total cost Market rate Market value Gain / loss

The City Bank Ltd. 110,000 41.62 4,578,419 26.80 2,948,000 (1,630,419)

DESCO 115,000 93.23 10,721,200 72.10 8,291,500 (2,429,700)

Jamuna Oil 56,160 251.17 14,105,710 178.50 10,024,560 (4,081,150)

Lafarge Surma Cement Ltd 100,000 42.76 4,276,300 32.90 3,290,000 (986,300)

Lankabangla Finance Ltd. 100,000 87.63 8,763,100 59.00 5,900,000 (2,863,100)

National Housing Finance and Investment Ltd. 60,000 76.72 4,602,900 37.40 2,244,000 (2,358,900)

One Bank Ltd. 400,000 27.11 10,844,135 22.80 9,120,000 (1,724,135)

Phonix Finance and Investment Ltd. 84,000 77.94 6,546,850 44.60 3,746,400 (2,800,450)

Unique Hotel 52,000 127.70 6,640,500 126.20 6,562,400 (78,100)

Uttara Bank Ltd. 100,000 59.73 5,972,735 38.10 3,810,000 (2,162,735) 77,051,850 55,936,860 (21,114,990)

Prime Bank Securities Limited

Investment in securities

As at December 31, 2012

Operating profit before charging Tax 48,099,291

Less: Items for separate consideration

Dividend income 944,511 Capital gain 8,850,564 9,795,074

38,304,217 Add: Inadmisible items

Entertainment 475,414 Write off-Preliminary exp. 614,122 Accounting depreciation 2,503,407 Donation & subscription 9,700 3,602,643

41,906,860 Less: Admisible items as per tax lawSubscription 9,700 Depreciation 2,458,142

2,467,842 Profit before charging entertainment expenses 39,439,018

Less: Entertainmenton first Tk. 10 lac 40,000 on balance 768,780 808,780 Actual expenses 475,414 475,414 Total Income from Business or Profession 38,963,604

Add: Dividend income 944,511 Capital gain 8,850,564 Total income 48,758,679

Capital gain 8,850,564 0.100 885,056 Dividend income 944,511 0.200 188,902 Business income 38,963,604 0.375 14,611,352

15,685,310

Deferred tax assets for depreciation 45,265 0.375 16,975

Prime Bank Securities LimitedFor the year ended 31 december 2012

Calculation of Income tax