An organic growth story - Morgans

32

Food & Beverages │ Australia April 20, 2015 IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP An organic growth story Bellamy’s Australia (BAL) is a Tasmanian-based organic food business, specialising in premium baby food and formula. BAL is on a strong growth trajectory as its benefits from consumer’s preference for organic food and Asia’s demand for safe, high quality Australian food. We initiate coverage with an Add rating and A$3.85 price target. Bellamy’s – organic infant formula and food for infants BAL offers an organic food range for babies and children, with 32 products across infant formula and baby food. Importantly, both of these segments are growth categories. All of BAL’s products are Australian-made and 100% certified organic. Consequently, its products attract a premium price which parents are willing to pay for their children to have the best nutrition. Selling organic products provides BAL with a point of differentiation in a competitive market place. It also means that BAL is the fastest growing baby formula company in Australia with a market share of over 14%. The brand is well established in Australia and has a growing presence in China, Singapore, Hong Kong, Vietnam, Malaysia and New Zealand. BAL also has a user-friendly online store allowing consumers to purchase products conveniently. BAL operates a capital light business model in that it outsources the growing, manufacturing and packaging of its products. A key strength of the company is its deep understanding of the organic goods supply chain. Expect strong earnings growth BAL is on a strong earnings trajectory. Since listing in August 2014, the company has issued two profit upgrades within six months. We believe that BAL is well placed to report strong double digit grow for many years to come as consumers increasingly demand organic food and beverages, it launches new products and expands its distribution network both in Australia and overseas. Initiate coverage with an Add rating and A$3.85 price target We have a positive investment view on BAL due to its: (1) strong brand name; (2) point of differentiation; (3) leverage to favourable industry dynamics; (4) strong supplier relationships; (5) product and packaging innovation; (6) growing export business; (7) solid earnings growth; and (8) strong management team. Key share price catalysts include further profit upgrades, expansion in new markets or products and corporate activity. The main risks are BAL’s lack of ownership of the supply chain, raw material supply and the competitive environment. Belinda MOORE T (61) 7 3334 4532 E [email protected] BAL150420 Share price info Share price perf. (%) 1M 3M 12M Relative 12.9 80.7 Absolute 13.5 91.6 Major shareholders % held The Black Prince Private Foundation 14.7 Ellerston Capital 9.5 Quality Life 8.6 Bellamy's Australia BAL AU / BAL.AX Current A$3.20 Market Cap Avg Daily Turnover Free Float Target A$3.85 US$236.8m US$0.59m 81.5% A$304.0m A$0.76m 95.00 m shares Up/Downside 20.3% Conviction| | SOURCE: MORGANS, COMPANY REPORTS Financial Summary Jun-13A Jun-14A Jun-15F Jun-16F Jun-17F Revenue (A$m) 28.8 50.9 124.0 186.0 241.8 Operating EBITDA (A$m) 1.20 3.13 9.99 16.93 24.35 Net Profit (A$m) 1.71 1.28 6.51 11.65 16.71 Normalised EPS (A$) 0.01 0.02 0.07 0.12 0.17 Normalised EPS Growth 0% 34% 273% 62% 43% FD Normalised P/E (x) 216.4 161.7 43.4 26.7 18.6 DPS (A$) - - 0.021 0.042 0.060 Dividend Yield 0.00% 0.00% 0.64% 1.31% 1.88% EV/EBITDA (x) 253.4 95.9 29.2 18.0 12.6 P/FCFE (x) NA NA NA NA 120.1 Net Gearing 12.8% (25.9%) (27.0%) (10.4%) (4.9%) P/BV (x) 32.08 19.50 6.87 5.75 4.72 ROE 15.0% 23.4% 23.7% 27.9% % Change In Normalised EPS Estimates Normalised EPS/consensus EPS (x) 1.30 1.08 78 120 161 203 245 286 328 0.70 1.20 1.70 2.20 2.70 3.20 3.70 Price Close Relative to S&P/ASX 200 (RHS) Source: Bloomberg 2 4 6 8 10 Aug-14 Oct-14 Dec-14 Feb-15 Vol m 3.20 3.85 1.00 3.20 Target 52-week share price range Current

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of An organic growth story - Morgans

Food & Beverages │ Australia

April 20, 2015

IMPORTANT DISCLOSURES REGARDING COMPANIES THAT ARE THE SUBJECT OF THIS REPORT AND AN EXPLANATION OF RECOMMENDATIONS CAN BE FOUND AT THE END OF THIS DOCUMENT. MORGANS FINANCIAL LIMITED (ABN 49 010 669 726) AFSL 235410 - A PARTICIPANT OF ASX GROUP

An organic growth story Bellamy’s Australia (BAL) is a Tasmanian-based organic food business, specialising in premium baby food and formula. BAL is on a strong growth trajectory as its benefits from consumer’s preference for organic food and Asia’s demand for safe, high quality Australian food. We initiate coverage with an Add rating and A$3.85 price target.

Bellamy’s – organic infant formula and food for infants BAL offers an organic food range for babies and children, with 32 products across infant formula and baby food. Importantly, both of these segments are growth categories. All of BAL’s products are Australian-made and 100% certified organic. Consequently, its products attract a premium price which parents are willing to pay for their children to have the best nutrition. Selling organic products provides BAL with a point of differentiation in a competitive market place. It also means that BAL is the fastest growing baby formula company in Australia with a market share of over 14%. The brand is well established in Australia and has a growing presence in China, Singapore, Hong Kong, Vietnam, Malaysia and New Zealand. BAL also has a user-friendly online store allowing consumers to purchase products conveniently. BAL operates a capital light business model in that it outsources the growing, manufacturing and packaging of its products. A key strength of the company is its deep understanding of the organic goods supply chain.

Expect strong earnings growth BAL is on a strong earnings trajectory. Since listing in August 2014, the company has issued two profit upgrades within six months. We believe that BAL is well placed to report strong double digit grow for many years to come as consumers increasingly demand organic food and beverages, it launches new products and expands its distribution network both in Australia and overseas.

Initiate coverage with an Add rating and A$3.85 price target We have a positive investment view on BAL due to its: (1) strong brand name; (2) point of differentiation; (3) leverage to favourable industry dynamics; (4) strong supplier relationships; (5) product and packaging innovation; (6) growing export business; (7) solid earnings growth; and (8) strong management team. Key share price catalysts include further profit upgrades, expansion in new markets or products and corporate activity. The main risks are BAL’s lack of ownership of the supply chain, raw material supply and the competitive environment.

Belinda MOORE T (61) 7 3334 4532 E [email protected]

BAL150420

Share price info

Share price perf. (%) 1M 3M 12M

Relative 12.9 80.7

Absolute 13.5 91.6

Major shareholders % held

The Black Prince Private Foundation

14.7

Ellerston Capital 9.5

Quality Life 8.6

Bellamy's Australia BAL AU / BAL.AX Current A$3.20

Market Cap Avg Daily Turnover Free Float Target A$3.85

US$236.8m US$0.59m 81.5%

A$304.0m A$0.76m 95.00 m shares Up/Downside 20.3% Conviction| |

Sources: CIMB. COMPANY REPORTS

SOURCE: MORGANS, COMPANY REPORTS

Financial Summary

Jun-13A Jun-14A Jun-15F Jun-16F Jun-17F

Revenue (A$m) 28.8 50.9 124.0 186.0 241.8

Operating EBITDA (A$m) 1.20 3.13 9.99 16.93 24.35

Net Profit (A$m) 1.71 1.28 6.51 11.65 16.71

Normalised EPS (A$) 0.01 0.02 0.07 0.12 0.17

Normalised EPS Growth 0% 34% 273% 62% 43%

FD Normalised P/E (x) 216.4 161.7 43.4 26.7 18.6

DPS (A$) - - 0.021 0.042 0.060

Dividend Yield 0.00% 0.00% 0.64% 1.31% 1.88%

EV/EBITDA (x) 253.4 95.9 29.2 18.0 12.6

P/FCFE (x) NA NA NA NA 120.1

Net Gearing 12.8% (25.9%) (27.0%) (10.4%) (4.9%)

P/BV (x) 32.08 19.50 6.87 5.75 4.72

ROE 15.0% 23.4% 23.7% 27.9%

% Change In Normalised EPS Estimates

Normalised EPS/consensus EPS (x) 1.42 1.30 1.08

78

120

161

203

245

286

328

0.70

1.20

1.70

2.20

2.70

3.20

3.70

Price Close Relative to S&P/ASX 200 (RHS)

Source: Bloomberg

2

4

6

8

10

Aug-14 Oct-14 Dec-14 Feb-15

Vol m

3.20

3.85

1.00 3.20

Target

52-week share price range

Current

Bellamy's Australia April 20, 2015

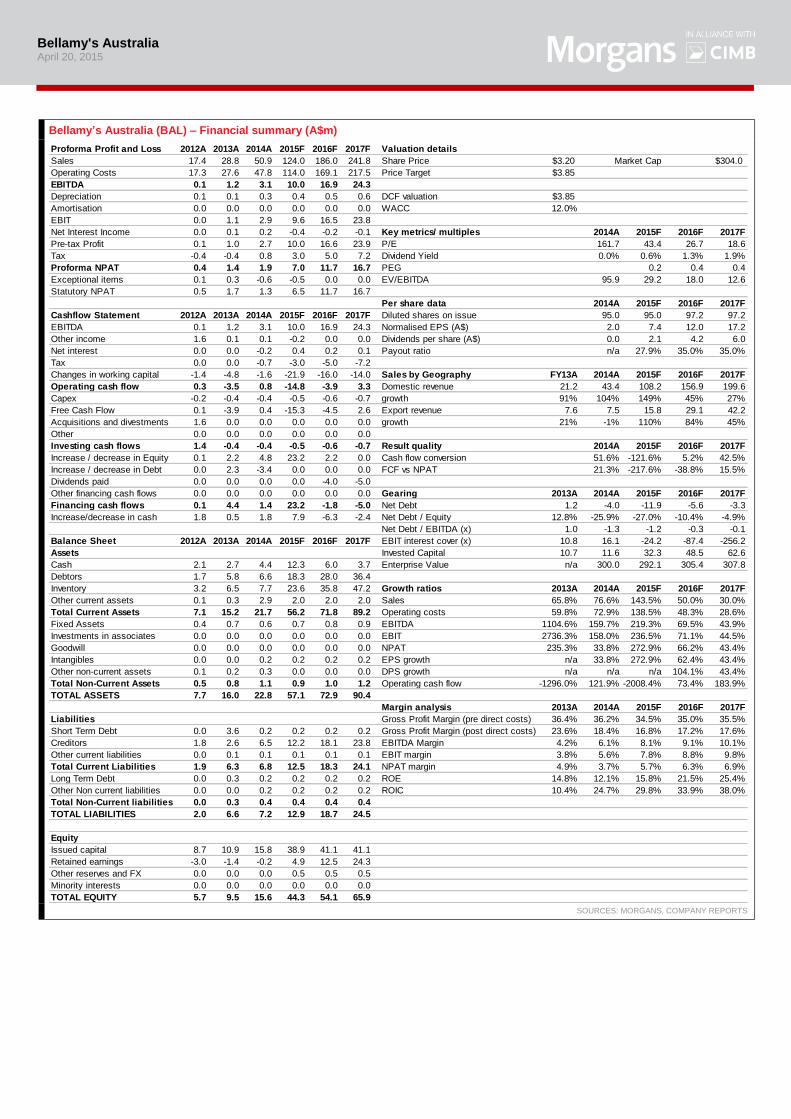

Bellamy’s Australia (BAL) – Financial summary (A$m)

SOURCES: MORGANS, COMPANY REPORTS

Proforma Profit and Loss 2012A 2013A 2014A 2015F 2016F 2017F Valuation details

Sales 17.4 28.8 50.9 124.0 186.0 241.8 Share Price $3.20 $304.0

Operating Costs 17.3 27.6 47.8 114.0 169.1 217.5 Price Target $3.85

EBITDA 0.1 1.2 3.1 10.0 16.9 24.3

Depreciation 0.1 0.1 0.3 0.4 0.5 0.6 DCF valuation $3.85

Amortisation 0.0 0.0 0.0 0.0 0.0 0.0 WACC 12.0%

EBIT 0.0 1.1 2.9 9.6 16.5 23.8

Net Interest Income 0.0 0.1 0.2 -0.4 -0.2 -0.1 Key metrics/ multiples 2014A 2015F 2016F 2017F

Pre-tax Profit 0.1 1.0 2.7 10.0 16.6 23.9 P/E 161.7 43.4 26.7 18.6

Tax -0.4 -0.4 0.8 3.0 5.0 7.2 Dividend Yield 0.0% 0.6% 1.3% 1.9%

Proforma NPAT 0.4 1.4 1.9 7.0 11.7 16.7 PEG 0.2 0.4 0.4

Exceptional items 0.1 0.3 -0.6 -0.5 0.0 0.0 EV/EBITDA 95.9 29.2 18.0 12.6

Statutory NPAT 0.5 1.7 1.3 6.5 11.7 16.7

Per share data 2014A 2015F 2016F 2017F

Cashflow Statement 2012A 2013A 2014A 2015F 2016F 2017F Diluted shares on issue 95.0 95.0 97.2 97.2

EBITDA 0.1 1.2 3.1 10.0 16.9 24.3 Normalised EPS (A$) 2.0 7.4 12.0 17.2

Other income 1.6 0.1 0.1 -0.2 0.0 0.0 Dividends per share (A$) 0.0 2.1 4.2 6.0

Net interest 0.0 0.0 -0.2 0.4 0.2 0.1 Payout ratio n/a 27.9% 35.0% 35.0%

Tax 0.0 0.0 -0.7 -3.0 -5.0 -7.2

Changes in working capital -1.4 -4.8 -1.6 -21.9 -16.0 -14.0 Sales by Geography FY13A 2014A 2015F 2016F 2017F

Operating cash flow 0.3 -3.5 0.8 -14.8 -3.9 3.3 Domestic revenue 21.2 43.4 108.2 156.9 199.6

Capex -0.2 -0.4 -0.4 -0.5 -0.6 -0.7 growth 91% 104% 149% 45% 27%

Free Cash Flow 0.1 -3.9 0.4 -15.3 -4.5 2.6 Export revenue 7.6 7.5 15.8 29.1 42.2

Acquisitions and divestments 1.6 0.0 0.0 0.0 0.0 0.0 growth 21% -1% 110% 84% 45%

Other 0.0 0.0 0.0 0.0 0.0 0.0

Investing cash flows 1.4 -0.4 -0.4 -0.5 -0.6 -0.7 Result quality 2014A 2015F 2016F 2017F

Increase / decrease in Equity 0.1 2.2 4.8 23.2 2.2 0.0 Cash flow conversion 51.6% -121.6% 5.2% 42.5%

Increase / decrease in Debt 0.0 2.3 -3.4 0.0 0.0 0.0 FCF vs NPAT 21.3% -217.6% -38.8% 15.5%

Dividends paid 0.0 0.0 0.0 0.0 -4.0 -5.0

Other financing cash flows 0.0 0.0 0.0 0.0 0.0 0.0 Gearing 2013A 2014A 2015F 2016F 2017F

Financing cash flows 0.1 4.4 1.4 23.2 -1.8 -5.0 Net Debt 1.2 -4.0 -11.9 -5.6 -3.3

Increase/decrease in cash 1.8 0.5 1.8 7.9 -6.3 -2.4 Net Debt / Equity 12.8% -25.9% -27.0% -10.4% -4.9%

Net Debt / EBITDA (x) 1.0 -1.3 -1.2 -0.3 -0.1

Balance Sheet 2012A 2013A 2014A 2015F 2016F 2017F EBIT interest cover (x) 10.8 16.1 -24.2 -87.4 -256.2

Assets Invested Capital 10.7 11.6 32.3 48.5 62.6

Cash 2.1 2.7 4.4 12.3 6.0 3.7 Enterprise Value n/a 300.0 292.1 305.4 307.8

Debtors 1.7 5.8 6.6 18.3 28.0 36.4

Inventory 3.2 6.5 7.7 23.6 35.8 47.2 Growth ratios 2013A 2014A 2015F 2016F 2017F

Other current assets 0.1 0.3 2.9 2.0 2.0 2.0 Sales 65.8% 76.6% 143.5% 50.0% 30.0%

Total Current Assets 7.1 15.2 21.7 56.2 71.8 89.2 Operating costs 59.8% 72.9% 138.5% 48.3% 28.6%

Fixed Assets 0.4 0.7 0.6 0.7 0.8 0.9 EBITDA 1104.6% 159.7% 219.3% 69.5% 43.9%

Investments in associates 0.0 0.0 0.0 0.0 0.0 0.0 EBIT 2736.3% 158.0% 236.5% 71.1% 44.5%

Goodwill 0.0 0.0 0.0 0.0 0.0 0.0 NPAT 235.3% 33.8% 272.9% 66.2% 43.4%

Intangibles 0.0 0.0 0.2 0.2 0.2 0.2 EPS growth n/a 33.8% 272.9% 62.4% 43.4%

Other non-current assets 0.1 0.2 0.3 0.0 0.0 0.0 DPS growth n/a n/a n/a 104.1% 43.4%

Total Non-Current Assets 0.5 0.8 1.1 0.9 1.0 1.2 Operating cash flow -1296.0% 121.9% -2008.4% 73.4% 183.9%

TOTAL ASSETS 7.7 16.0 22.8 57.1 72.9 90.4

Margin analysis 2013A 2014A 2015F 2016F 2017F

Liabilities Gross Profit Margin (pre direct costs) 36.4% 36.2% 34.5% 35.0% 35.5%

Short Term Debt 0.0 3.6 0.2 0.2 0.2 0.2 Gross Profit Margin (post direct costs) 23.6% 18.4% 16.8% 17.2% 17.6%

Creditors 1.8 2.6 6.5 12.2 18.1 23.8 EBITDA Margin 4.2% 6.1% 8.1% 9.1% 10.1%

Other current liabilities 0.0 0.1 0.1 0.1 0.1 0.1 EBIT margin 3.8% 5.6% 7.8% 8.8% 9.8%

Total Current Liabilities 1.9 6.3 6.8 12.5 18.3 24.1 NPAT margin 4.9% 3.7% 5.7% 6.3% 6.9%

Long Term Debt 0.0 0.3 0.2 0.2 0.2 0.2 ROE 14.8% 12.1% 15.8% 21.5% 25.4%

Other Non current liabilities 0.0 0.0 0.2 0.2 0.2 0.2 ROIC 10.4% 24.7% 29.8% 33.9% 38.0%

Total Non-Current liabilities 0.0 0.3 0.4 0.4 0.4 0.4

TOTAL LIABILITIES 2.0 6.6 7.2 12.9 18.7 24.5

Equity

Issued capital 8.7 10.9 15.8 38.9 41.1 41.1

Retained earnings -3.0 -1.4 -0.2 4.9 12.5 24.3

Other reserves and FX 0.0 0.0 0.0 0.5 0.5 0.5

Minority interests 0.0 0.0 0.0 0.0 0.0 0.0

TOTAL EQUITY 5.7 9.5 15.6 44.3 54.1 65.9

Market Cap

Bellamy's Australia April 20, 2015

Organic growth Bellamy’s Australia (BAL) gives investors direct exposure to the high-growth segments of the Fast Moving and Consumer Goods (FMCG) industry. BAL divides its product range amongst four age categories: 0-6 months, 6-12 months, 1-3 years and 3 years+. Its products include infant formula, ready to serve baby food, chewable baby foods, snacks and mixable cereals. Domestic revenue accounts for 85% of group revenue, with the majority of the remaining revenue from China. 89% of revenue comes from infant formula, while 11% is baby food.

Table 1: Bellamy’s product range

SOURCES: COMPANY REPORTS

INVESTMENT THESIS

BAL is on a strong earnings growth trajectory, backed by a market leading brand in the high-growth organic food and beverage industry. It is also benefiting from Asia’s strong demand for Australia’s safe and high quality food. We initiate coverage on BAL with an Add recommendation and A$3.85 target price.

BAL is well positioned to take advantage of an expanding market. Founded in only 2004, the company should deliver revenue in excess of A$120m in FY15, an increase from A$17.4m in FY12, with solid growth in the EBIT margin each year. BAL’s success is due to its unique position in the high growth organic infant formula and baby food market. The company is also well placed to take advantage of the rapidly changing demographics in China. BAL has an impressive management team which has achieved much success in a very short period of time.

The baby and infant food market has grown strongly in Australia, China and South East Asia. While the market grows with the number of births and the increasing number of women in the workforce, increased health-consciousness has become a strong driver of industry growth in recent years. The days of feeding a baby bland mush are gone, with demand for high quality and nutritious food skyrocketing. BAL has been quick to respond to these trends, developing organic, convenient and ready-to-serve meals in attractive and practical packaging.

All of BAL’s products are certified organic which is a key point of differentiation. Organic products are grown without the use of chemicals such as pesticides, herbicides, or growth hormones. BAL’s certified organic brand, is clearly displayed on all of its products. This factor combined with its powerful packaging design, builds trust and loyalty with its growing customer base.

Organic food is the fastest growing segment of the global food industry. It is worth approx. A$1.72bn in Australia and has been growing at a CAGR of over 15% since 2009. BAL’s products are well positioned to leverage this trend. While the demand for organic goods is strong nationally, there is also increasing demand internationally. The growth of China’s wealth has been unmatched in the past decade, leading to an enormous increase in the upper middle class population. The upper middle class is attracted to premium organic products given their aspiration to provide their children with the best possible upbringing,

Product age range Range

0-6 months Step 1 Infant formula

Ready to serve baby food

Mixable baby food

6-12 months Step 2 "follow-on" formula

Teething rusks

Ready to serve baby food

Chewable baby food

1-3 years Step 3 milk drink

Chewable baby food

Fruit snacks

Mixable cereals

3+ year "Ready2Go" milk drinks

Bellamy's Australia April 20, 2015

further inflating the demand for organic baby formula and baby food, considered superior to non-organic alternatives. In many cases, the income of the mother and father, as well as the grandparents is spent on the child, allowing families ranging from lower middle class to upper middle class to afford organic baby foods. Importantly, they are willing to pay a premium price.

Chinese market demand is further supported by the 2008 melamine incident in China, in which 54,000 babies were hospitalised and there was six deaths from contaminated baby formula. Following the incident, Chinese consumers sought to purchase and import baby formula from overseas companies. From the Chinese nationals’ perspective, Australia is a clean, green place with safe, high quality produce, meaning that baby formula from Australia is regarded highly. This is evidenced by the fact that BAL’s is one of the top searches on Taobao, an online Chinese marketplace, similar to eBay. BAL has an impeccable safety record bolstering the trust between the company and its consumers.

While BAL is growing strongly in the Australian market, over the medium term, we see huge potential for success in Asia. Between the growing middle class, the demand for overseas (safe) infant formula, low breastfeeding rates and the loosening of the Chinese One Child Policy, BAL is uniquely positioned to excel from its competitive advantage. In addition, BAL is one of few companies which has certified organic status by both the Australian and Chinese authorities, allowing it to directly export to China.

Key strengths

Growing market share. Bellamy’s Organics is the fastest growing brand in the Australian baby category. BAL now has over 14% of the Australian retail infant formula market, growing from about 10% at the time of its IPO (August 2014). Its market share in baby cereals and snacks in Australia is 12%. The speed of increase in its market share is an indication of the company’s appeal to consumers. Bellamy’s Organics is easily recognised on the shelf with its well-designed packaging.

Well regarded and trusted brand name – given all BAL’s products are 100% Australia made and are certified organic.

Offers the only Australian organic infant formula range. We see this as a key point of differentiation in this highly competitive market. Importantly, organic products sell for a premium price.

‘Organic’ is the fastest growing segment of the global food and beverage industry – The average growth projection for the coming years is 10-15% as there is strong demand for organic products. BAL is well positioned to benefit from this growing trend.

The infant formula category in Australia is one of the fastest growing categories in the grocery trade, despite the country’s relatively flat birth rate. Some of this growth rate has been spurred by overseas consumers purchasing Australian product to take back home given their lack of trust with their own food production standards.

Exposure to defensive end markets. The baby food market is relatively unaffected by a worsening economic climate. Providing the optimum start for children remains a high priority regardless of financial position.

Established offshore operations, leveraging Asia’s growth. BAL employs staff in China and Singapore. An important factor of the company’s offshore expansion is to have a strong team on the ground who understand the market and customers. BAL is well positioned to benefit from Asia’s rising middle class.

Strong customer relationships and a growing distribution base – Over many years, BAL has developed strong relationships with retailers/chemists both in Australia and offshore.

Bellamy's Australia April 20, 2015

Online presence. BAL has built an extensive website combining an online store. The company also operates an active social media profile on Twitter, Facebook, Weixin and Weibo where it is able to respond in real-time to customer queries and complaints. Monitoring online trends has proven an integral component to the direction and management of the company. Bellamy’s is a top 10 performer in the baby food category on Taobao, an online Chinese marketplace similar to eBay.

Focus on innovation and R&D. In a market of premium goods, quickly responding to consumer demands is a necessity. BAL recognises that many parents buying its products are time-poor, in reaction to this, the company has produced convenient plastic packaging with ready-to-serve quality food. It also has a track record of launching new products.

BAL is a low cost producer. Management has a focus on operational efficiency. The company has significantly grown its EBIT margins each year from 3.8% in FY13, to 5.6% in FY14 and 7.8% in FY15 (Morgans forecast).

Capital light business model. BAL has intentionally avoided purchasing a manufacturing facility. Instead, the company supplies its manufacturing partners with ingredients, raw materials and packaging. This means that BAL’s production capability can scale in line with rising demand.

As an Australian owned company, BAL is a beneficiary of ‘brand Australia’ – In Australia, there is increasing demand by grocery retailers to source both branded and private label products from Australian based companies due to food safety and quality assurances. In Asia, the fact that BAL’s products are supported by Australian retailers, is seen as a strong endorsement of the quality of its brand and has assisted with its entry into these markets. In addition, the recent decline in the AUD has made sourcing products domestically more cost effective. There is also an increasing consumer preference to support ‘Australian-made’ products. ‘Australian made’ is also a key selling point for international sales opportunities.

BAL is a beneficiary of Australia's FTA with China. Tariffs on infant formula into China will be phased out over four years. This will further improve Australian producers competitive position. Australia also secured FTA’s with South Korea and Japan during 2014. The government is now looking to secure a deal with India during 2015.

We expect BAL to generate strong profit growth over the next few years – Profit growth will reflect: 1) further market share gains in the Australian market, along with expanded distribution; 2) growth in offshore markets and entry into new markets; and 3) the launch of new innovative products.

Strong management team – BAL has an experienced management team lead by Laura McBain who was appointed CEO in 2011. In 2013, Laura was named Telstra Australian Business Woman of the Year (Private & Corporate).

One of the few direct branded food / FMCG companies on the ASX – BAL is one of a handful of companies listed on the ASX that offers investors direct exposure to the food and beverage industry.

Corporate appeal – We believe that BAL is an attractive takeover target to other dairy and/or large food companies, both in Australia and overseas. The Australian FMCG industry has consolidated significantly in the last 10 years given its quality, traceability and freight advantage into Asia. Australia has a reputation for high quality and safe food which helps it sell produce at premium prices overseas. In addition, food giants are taking advantage of the skyrocketing demand for organic and are buying up the smaller and independent companies. Large companies are also looking to acquire smaller more specialised companies to diversify their product lines and/or to expand in a growth category. In 2014, General Mills purchased

Bellamy's Australia April 20, 2015

Annie's Homegrown, a popular natural and organic brand. In 2013, Campbell Soup Co., bought the all-natural baby food brand Plum Organics. Across 2013 and 2014, PZ Cussons purchased Rafferty’s Garden (baby food) and five:am (organic yoghurt). The Hain Celestial Group was an early leader purchasing Earth’s Best Organic and it recently acquired Ella’s Kitchen organic baby food in 2013. The same year Danone forged a partnership with the Happy Family (formerly Happy Baby) organic product line. We expect these consolidation trends will continue.

Catalysts for share price performance

Earnings surprise on the upside – since listing in August 2014, BAL has had two profit upgrades in six months.

New distribution agreements.

Expansion in new markets.

Successful new product development.

Corporate activity.

Risks to consider

Potential loss of organic certification. BAL’s brand relies on its 100% organic status to retain its image as a premium product. If quality control issues arise and/or certifying bodies are not satisfied, this certification may be lost.

Concentration of manufacturing. The majority of BAL’s manufacturing is carried out by Tatura Milk Industries Limited (TMI) which is owned by Bega Cheese (BGA). There is no formal relationship between BAL and TMI, only trust from many years of working together. However, a formal contract is being discussed. Should there be an issue with TMI’s ability or desire to continue manufacturing for BAL, there may be a major disruption in the supply of its product. We also note that it is TMI which has the accreditation with the Chinese authorities, not BAL.

Shortage of raw material supply. BAL does not own any farms but rather maintains its certified organic status through rigid control of its supply chain. With rapid growing demand for organic produce and the instability of environmental factors in organic goods production, there is potential for a sudden supply shortage. We also note that the organic farming market is only small and that it takes three years for a conventional farmer to convert to an organic farm. Supply limitations would detrimentally impact BAL’s future financial prospects. BAL’s growth was constrained in FY12-14 due to limited supply of key ingredients.

Rising input costs – Input costs could increase significantly as agricultural producing regions of Australia suffer from extreme weather conditions. Also, with organic food being in such strong demand and given it is only a small market, organic ingredients could rise sharply in price. In a competitive market place, BAL may not be able to pass these costs onto customers.

Product concentration given about 89% of sales are infant formula and 85% of sales come from Australia.

Pricing pressure from the major retailers could pressure margins – The Australian grocery retailing market is one of the most consolidated and profitable markets in the world with the top two industry participants, Woolworths and Coles, accounting for about 70% of the market. They therefore have the buying/negotiating power to extract a disproportionate share of the value chain, exerting pressure on their suppliers. The major retailers competitive stance on lowest price leadership (eg. Coles' ‘Down, Down’ campaign and Woolworths’ ‘Cheap, Cheap’ campaign) are driving an increase in the percentage of food sold through supermarkets on promotion. This particularly affects branded products

Bellamy's Australia April 20, 2015

which are in direct competition with their private label offerings. Overall, we believe that BAL’s strong brand, organic status and growing market share provide it with reasonable negotiating power with the major retailers.

Private label push from the major retailers could limit growth - The major retailers have a strategy of increasing their private label product offering at the expense of branded product. Private label now represents approx. 25% of the retailers total sales and is forecast by IBISWorld to rise to 35% by the end of the decade. The retailers are also cutting the selling price of private label products. Shelf space availability to food manufacturers is being influenced by the supermarkets as they expand their private label offering. We highlight that BAL’s branded products have grown their market share in recent years in spite of private label. BAL does not have a private label offering.

Loss of a major customer or failure to attract new customers. In Australia, approx. 70% of BAL’s revenue comes from four large customers. If there is a change in behavior with these large customers, total sales could be significantly reduced. BAL’s performance is also dependent on its ability to attract new customers.

Competitive environment. It is no secret that the organic industry is booming. In a competitive market, there are materially larger competitors (eg. Nestle, Danone, Mead Johnston) with access to more capital. Should these companies try to copy BAL’s product range or exert increased competitive pressure, the company may struggle to maintain financial performance. All the major infant formula suppliers are trying to crack the Chinese market, obviously everyone can’t be successful. However we believe that BAL has key point of differentiation in that it is 100% Australian made and 100% certified organic. In addition, unlike its competitors, BAL offers a complete range of organic infant formula and food from birth.

Legal, economic, political and regulatory risks associated with operating in foreign countries, particularly China. The Chinese government has instituted an imported dairy food products regulatory regime that requires, among other things, that certain foreign manufacturing facilities complete a registration process. Late last year, BAL’s manufacturer, TMI, succeeded in achieving organic certification with China and was able to re-commence sales. However, removal of this licence due to unforeseen circumstances would have a major impact on BAL’s overseas sales.

Currency risks – BAL purchases a number of its ingredients from overseas, which means that it is exposed to currency movements with its purchasing activity. As the company’s offshore operations ramp-up, BAL’s FX exposure will further increase. We note that a falling AUD is a positive for export sales from a competitive point of view and can be from an earnings on translation point of view.

Success of new product development (NPD) – NPD is an important driver of growth for BAL. The success of new products depends on BAL’s ability to accurately anticipate consumer needs, ability to innovate, successfully launch new products in a timely manner, price products competitively and differentiate products to those of its major competitors. There is a risk that BAL’s NPD is not supported by sufficient market interest and demand. To date, BAL’s NPD has largely been successful however we note that it most recent launch of a new UHT supplementary milk drink, “Ready to Go”, did not reach management’s sales targets and the business reported a loss of A$0.7m in stock overproduced for the launch.

Brand damage: The reputation and value of a brand can be adversely affected by a number of factors such as loss of organic certification, contamination issues, product recall, or adverse reactions from consumers.

Bellamy's Australia April 20, 2015

BAL is required to comply with a range of laws and regulations. Regulatory areas which are of particular significance to the company include fair trading and consumer protection, employment, property and environment, customs, tariffs, taxation and food standards and labelling. Regulatory changes may materially reduce BAL’s revenue and/or increase its costs.

Key person risk – given the experience of the management team in successfully delivering on the company’s strategy.

Volatile market conditions and investor sentiment towards high PE stocks. With the company trading on an FY16 PE of 26.7x, there is no room for disappointment or the stock will be punished.

Bellamy's Australia April 20, 2015

MORGANS VALUATION & PEER ANALYSIS

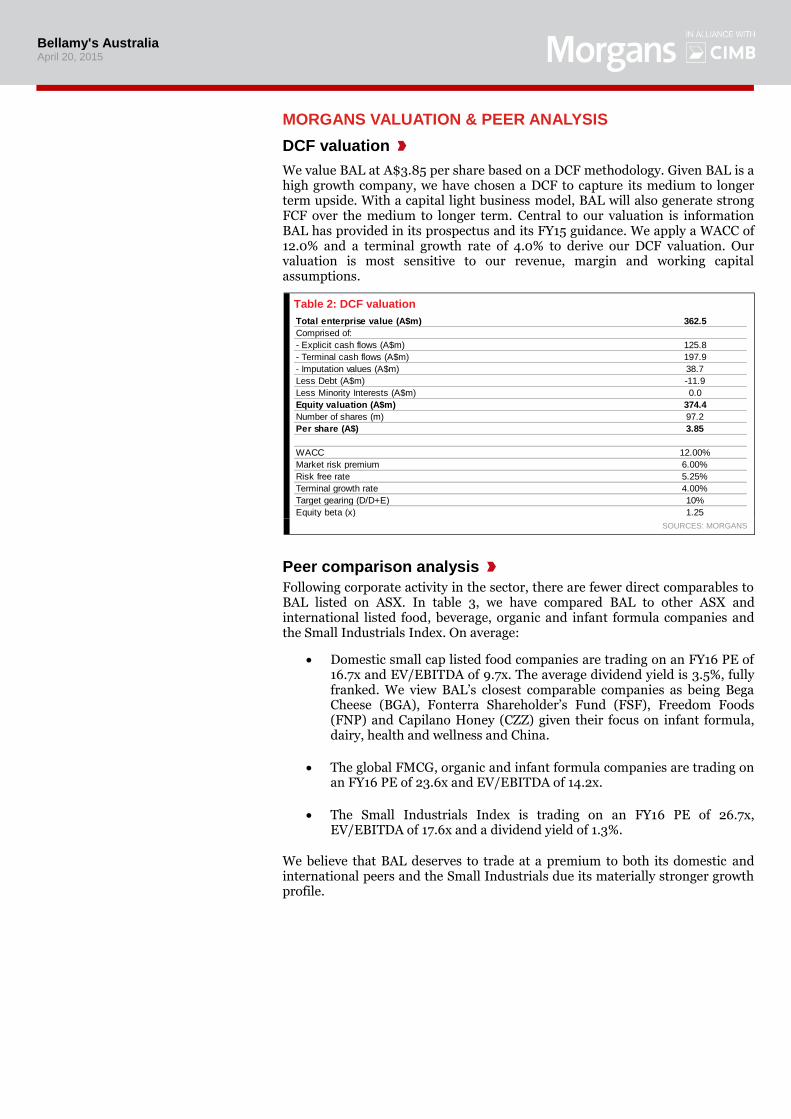

DCF valuation

We value BAL at A$3.85 per share based on a DCF methodology. Given BAL is a high growth company, we have chosen a DCF to capture its medium to longer term upside. With a capital light business model, BAL will also generate strong FCF over the medium to longer term. Central to our valuation is information BAL has provided in its prospectus and its FY15 guidance. We apply a WACC of 12.0% and a terminal growth rate of 4.0% to derive our DCF valuation. Our valuation is most sensitive to our revenue, margin and working capital assumptions.

Table 2: DCF valuation

SOURCES: MORGANS

Peer comparison analysis

Following corporate activity in the sector, there are fewer direct comparables to BAL listed on ASX. In table 3, we have compared BAL to other ASX and international listed food, beverage, organic and infant formula companies and the Small Industrials Index. On average:

Domestic small cap listed food companies are trading on an FY16 PE of 16.7x and EV/EBITDA of 9.7x. The average dividend yield is 3.5%, fully franked. We view BAL’s closest comparable companies as being Bega Cheese (BGA), Fonterra Shareholder’s Fund (FSF), Freedom Foods (FNP) and Capilano Honey (CZZ) given their focus on infant formula, dairy, health and wellness and China.

The global FMCG, organic and infant formula companies are trading on an FY16 PE of 23.6x and EV/EBITDA of 14.2x.

The Small Industrials Index is trading on an FY16 PE of 26.7x, EV/EBITDA of 17.6x and a dividend yield of 1.3%.

We believe that BAL deserves to trade at a premium to both its domestic and international peers and the Small Industrials due its materially stronger growth profile.

Total enterprise value (A$m) 362.5

Comprised of:

- Explicit cash flows (A$m) 125.8

- Terminal cash flows (A$m) 197.9

- Imputation values (A$m) 38.7

Less Debt (A$m) -11.9

Less Minority Interests (A$m) 0.0

Equity valuation (A$m) 374.4

Number of shares (m) 97.2

Per share (A$) 3.85

WACC 12.00%

Market risk premium 6.00%

Risk free rate 5.25%

Terminal growth rate 4.00%

Target gearing (D/D+E) 10%

Equity beta (x) 1.25

Bellamy's Australia April 20, 2015

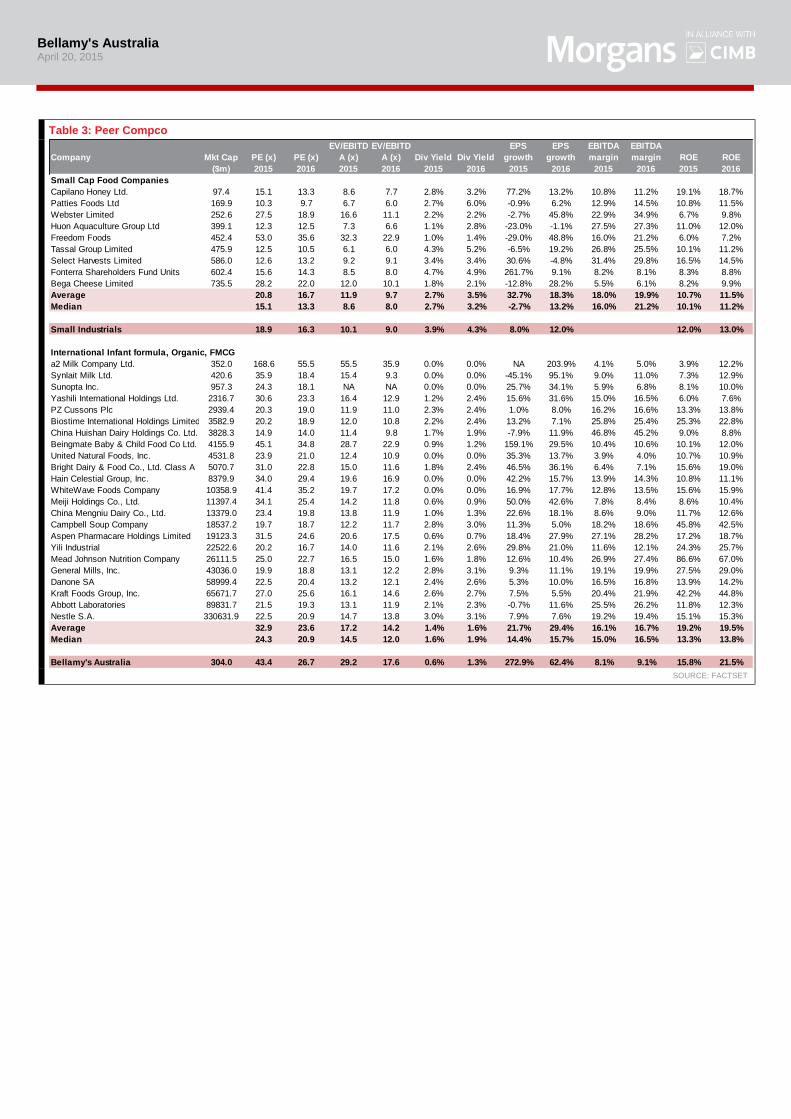

Table 3: Peer Compco

SOURCE: FACTSET

Company Mkt Cap PE (x) PE (x)

EV/EBITD

A (x)

EV/EBITD

A (x) Div Yield Div Yield

EPS

growth

EPS

growth

EBITDA

margin

EBITDA

margin ROE ROE

($m) 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016

Small Cap Food Companies

Capilano Honey Ltd. 97.4 15.1 13.3 8.6 7.7 2.8% 3.2% 77.2% 13.2% 10.8% 11.2% 19.1% 18.7%

Patties Foods Ltd 169.9 10.3 9.7 6.7 6.0 2.7% 6.0% -0.9% 6.2% 12.9% 14.5% 10.8% 11.5%

Webster Limited 252.6 27.5 18.9 16.6 11.1 2.2% 2.2% -2.7% 45.8% 22.9% 34.9% 6.7% 9.8%

Huon Aquaculture Group Ltd 399.1 12.3 12.5 7.3 6.6 1.1% 2.8% -23.0% -1.1% 27.5% 27.3% 11.0% 12.0%

Freedom Foods 452.4 53.0 35.6 32.3 22.9 1.0% 1.4% -29.0% 48.8% 16.0% 21.2% 6.0% 7.2%

Tassal Group Limited 475.9 12.5 10.5 6.1 6.0 4.3% 5.2% -6.5% 19.2% 26.8% 25.5% 10.1% 11.2%

Select Harvests Limited 586.0 12.6 13.2 9.2 9.1 3.4% 3.4% 30.6% -4.8% 31.4% 29.8% 16.5% 14.5%

Fonterra Shareholders Fund Units 602.4 15.6 14.3 8.5 8.0 4.7% 4.9% 261.7% 9.1% 8.2% 8.1% 8.3% 8.8%

Bega Cheese Limited 735.5 28.2 22.0 12.0 10.1 1.8% 2.1% -12.8% 28.2% 5.5% 6.1% 8.2% 9.9%

Average 20.8 16.7 11.9 9.7 2.7% 3.5% 32.7% 18.3% 18.0% 19.9% 10.7% 11.5%

Median 15.1 13.3 8.6 8.0 2.7% 3.2% -2.7% 13.2% 16.0% 21.2% 10.1% 11.2%

Small Industrials 18.9 16.3 10.1 9.0 3.9% 4.3% 8.0% 12.0% 12.0% 13.0%

International Infant formula, Organic, FMCG

a2 Milk Company Ltd. 352.0 168.6 55.5 55.5 35.9 0.0% 0.0% NA 203.9% 4.1% 5.0% 3.9% 12.2%

Synlait Milk Ltd. 420.6 35.9 18.4 15.4 9.3 0.0% 0.0% -45.1% 95.1% 9.0% 11.0% 7.3% 12.9%

Sunopta Inc. 957.3 24.3 18.1 NA NA 0.0% 0.0% 25.7% 34.1% 5.9% 6.8% 8.1% 10.0%

Yashili International Holdings Ltd. 2316.7 30.6 23.3 16.4 12.9 1.2% 2.4% 15.6% 31.6% 15.0% 16.5% 6.0% 7.6%

PZ Cussons Plc 2939.4 20.3 19.0 11.9 11.0 2.3% 2.4% 1.0% 8.0% 16.2% 16.6% 13.3% 13.8%

Biostime International Holdings Limited 3582.9 20.2 18.9 12.0 10.8 2.2% 2.4% 13.2% 7.1% 25.8% 25.4% 25.3% 22.8%

China Huishan Dairy Holdings Co. Ltd. 3828.3 14.9 14.0 11.4 9.8 1.7% 1.9% -7.9% 11.9% 46.8% 45.2% 9.0% 8.8%

Beingmate Baby & Child Food Co Ltd. Class A4155.9 45.1 34.8 28.7 22.9 0.9% 1.2% 159.1% 29.5% 10.4% 10.6% 10.1% 12.0%

United Natural Foods, Inc. 4531.8 23.9 21.0 12.4 10.9 0.0% 0.0% 35.3% 13.7% 3.9% 4.0% 10.7% 10.9%

Bright Dairy & Food Co., Ltd. Class A 5070.7 31.0 22.8 15.0 11.6 1.8% 2.4% 46.5% 36.1% 6.4% 7.1% 15.6% 19.0%

Hain Celestial Group, Inc. 8379.9 34.0 29.4 19.6 16.9 0.0% 0.0% 42.2% 15.7% 13.9% 14.3% 10.8% 11.1%

WhiteWave Foods Company 10358.9 41.4 35.2 19.7 17.2 0.0% 0.0% 16.9% 17.7% 12.8% 13.5% 15.6% 15.9%

Meiji Holdings Co., Ltd. 11397.4 34.1 25.4 14.2 11.8 0.6% 0.9% 50.0% 42.6% 7.8% 8.4% 8.6% 10.4%

China Mengniu Dairy Co., Ltd. 13379.0 23.4 19.8 13.8 11.9 1.0% 1.3% 22.6% 18.1% 8.6% 9.0% 11.7% 12.6%

Campbell Soup Company 18537.2 19.7 18.7 12.2 11.7 2.8% 3.0% 11.3% 5.0% 18.2% 18.6% 45.8% 42.5%

Aspen Pharmacare Holdings Limited 19123.3 31.5 24.6 20.6 17.5 0.6% 0.7% 18.4% 27.9% 27.1% 28.2% 17.2% 18.7%

Yili Industrial 22522.6 20.2 16.7 14.0 11.6 2.1% 2.6% 29.8% 21.0% 11.6% 12.1% 24.3% 25.7%

Mead Johnson Nutrition Company 26111.5 25.0 22.7 16.5 15.0 1.6% 1.8% 12.6% 10.4% 26.9% 27.4% 86.6% 67.0%

General Mills, Inc. 43036.0 19.9 18.8 13.1 12.2 2.8% 3.1% 9.3% 11.1% 19.1% 19.9% 27.5% 29.0%

Danone SA 58999.4 22.5 20.4 13.2 12.1 2.4% 2.6% 5.3% 10.0% 16.5% 16.8% 13.9% 14.2%

Kraft Foods Group, Inc. 65671.7 27.0 25.6 16.1 14.6 2.6% 2.7% 7.5% 5.5% 20.4% 21.9% 42.2% 44.8%

Abbott Laboratories 89831.7 21.5 19.3 13.1 11.9 2.1% 2.3% -0.7% 11.6% 25.5% 26.2% 11.8% 12.3%

Nestle S.A. 330631.9 22.5 20.9 14.7 13.8 3.0% 3.1% 7.9% 7.6% 19.2% 19.4% 15.1% 15.3%

Average 32.9 23.6 17.2 14.2 1.4% 1.6% 21.7% 29.4% 16.1% 16.7% 19.2% 19.5%

Median 24.3 20.9 14.5 12.0 1.6% 1.9% 14.4% 15.7% 15.0% 16.5% 13.3% 13.8%

Bellamy's Australia 304.0 43.4 26.7 29.2 17.6 0.6% 1.3% 272.9% 62.4% 8.1% 9.1% 15.8% 21.5%

Bellamy's Australia April 20, 2015

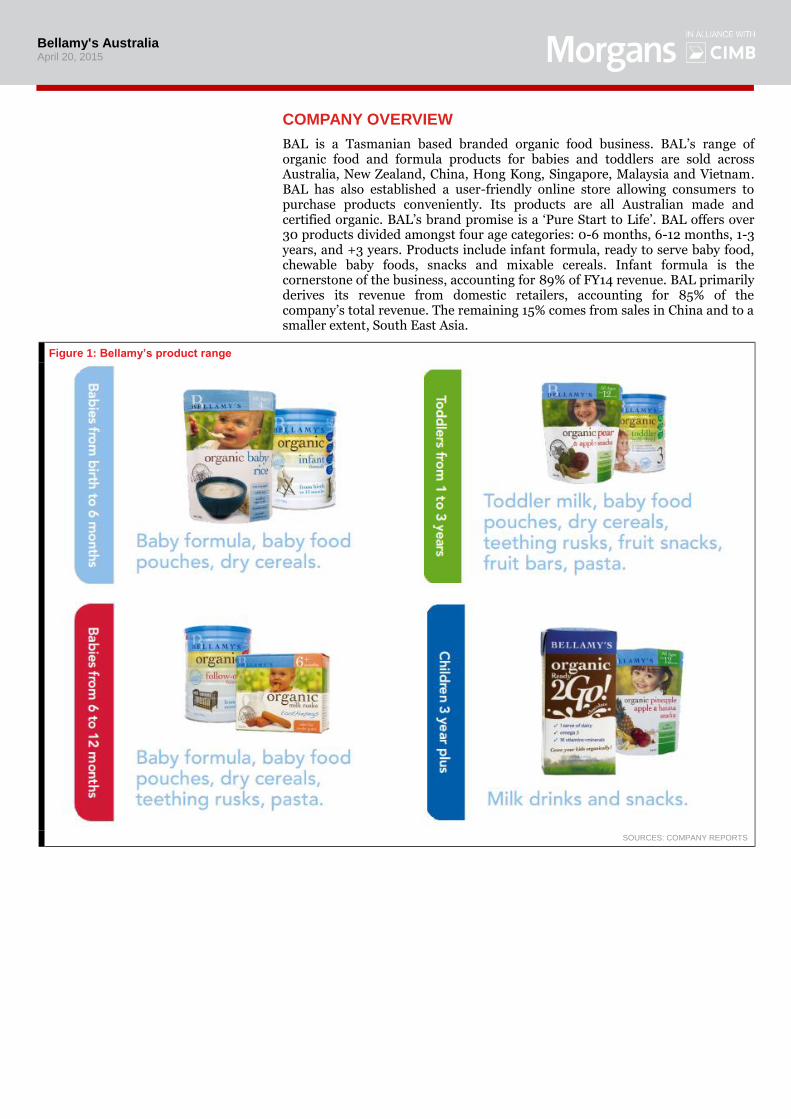

COMPANY OVERVIEW

BAL is a Tasmanian based branded organic food business. BAL’s range of organic food and formula products for babies and toddlers are sold across Australia, New Zealand, China, Hong Kong, Singapore, Malaysia and Vietnam. BAL has also established a user-friendly online store allowing consumers to purchase products conveniently. Its products are all Australian made and certified organic. BAL’s brand promise is a ‘Pure Start to Life’. BAL offers over 30 products divided amongst four age categories: 0-6 months, 6-12 months, 1-3 years, and +3 years. Products include infant formula, ready to serve baby food, chewable baby foods, snacks and mixable cereals. Infant formula is the cornerstone of the business, accounting for 89% of FY14 revenue. BAL primarily derives its revenue from domestic retailers, accounting for 85% of the company’s total revenue. The remaining 15% comes from sales in China and to a smaller extent, South East Asia.

Figure 1: Bellamy’s product range

SOURCES: COMPANY REPORTS

Bellamy's Australia April 20, 2015

Company history

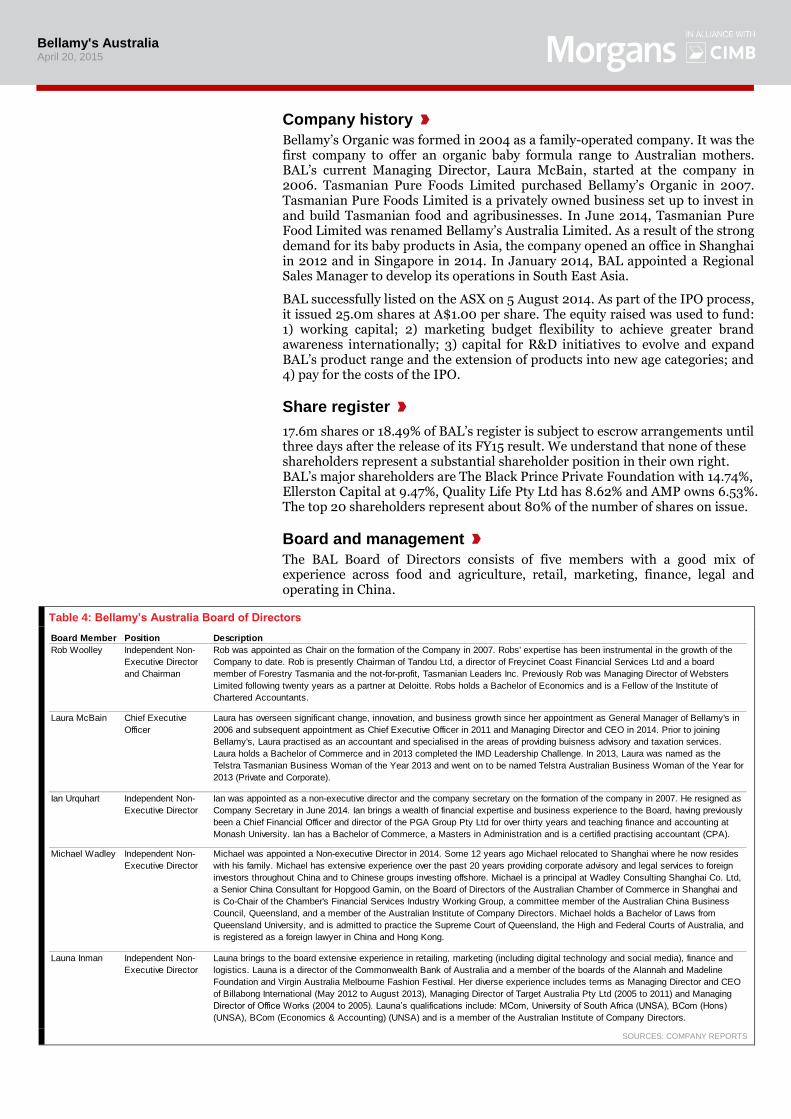

Bellamy’s Organic was formed in 2004 as a family-operated company. It was the first company to offer an organic baby formula range to Australian mothers. BAL’s current Managing Director, Laura McBain, started at the company in 2006. Tasmanian Pure Foods Limited purchased Bellamy’s Organic in 2007. Tasmanian Pure Foods Limited is a privately owned business set up to invest in and build Tasmanian food and agribusinesses. In June 2014, Tasmanian Pure Food Limited was renamed Bellamy’s Australia Limited. As a result of the strong demand for its baby products in Asia, the company opened an office in Shanghai in 2012 and in Singapore in 2014. In January 2014, BAL appointed a Regional Sales Manager to develop its operations in South East Asia.

BAL successfully listed on the ASX on 5 August 2014. As part of the IPO process, it issued 25.0m shares at A$1.00 per share. The equity raised was used to fund: 1) working capital; 2) marketing budget flexibility to achieve greater brand awareness internationally; 3) capital for R&D initiatives to evolve and expand BAL’s product range and the extension of products into new age categories; and 4) pay for the costs of the IPO.

Share register

17.6m shares or 18.49% of BAL’s register is subject to escrow arrangements until three days after the release of its FY15 result. We understand that none of these shareholders represent a substantial shareholder position in their own right. BAL’s major shareholders are The Black Prince Private Foundation with 14.74%, Ellerston Capital at 9.47%, Quality Life Pty Ltd has 8.62% and AMP owns 6.53%. The top 20 shareholders represent about 80% of the number of shares on issue.

Board and management

The BAL Board of Directors consists of five members with a good mix of experience across food and agriculture, retail, marketing, finance, legal and operating in China.

Table 4: Bellamy’s Australia Board of Directors

SOURCES: COMPANY REPORTS

Board Member Position Description

Rob Woolley Independent Non-

Executive Director

and Chairman

Rob was appointed as Chair on the formation of the Company in 2007. Robs' expertise has been instrumental in the growth of the

Company to date. Rob is presently Chairman of Tandou Ltd, a director of Freycinet Coast Financial Services Ltd and a board

member of Forestry Tasmania and the not-for-profit, Tasmanian Leaders Inc. Previously Rob was Managing Director of Websters

Limited following twenty years as a partner at Deloitte. Robs holds a Bachelor of Economics and is a Fellow of the Institute of

Chartered Accountants.

Laura McBain Chief Executive

Officer

Laura has overseen significant change, innovation, and business growth since her appointment as General Manager of Bellamy's in

2006 and subsequent appointment as Chief Executive Officer in 2011 and Managing Director and CEO in 2014. Prior to joining

Bellamy's, Laura practised as an accountant and specialised in the areas of providing buisness advisory and taxation services.

Laura holds a Bachelor of Commerce and in 2013 completed the IMD Leadership Challenge. In 2013, Laura was named as the

Telstra Tasmanian Business Woman of the Year 2013 and went on to be named Telstra Australian Business Woman of the Year for

2013 (Private and Corporate).

Ian Urquhart Independent Non-

Executive Director

Ian was appointed as a non-executive director and the company secretary on the formation of the company in 2007. He resigned as

Company Secretary in June 2014. Ian brings a wealth of financial expertise and business experience to the Board, having previously

been a Chief Financial Officer and director of the PGA Group Pty Ltd for over thirty years and teaching finance and accounting at

Monash University. Ian has a Bachelor of Commerce, a Masters in Administration and is a certified practising accountant (CPA).

Michael Wadley Independent Non-

Executive Director

Michael was appointed a Non-executive Director in 2014. Some 12 years ago Michael relocated to Shanghai where he now resides

with his family. Michael has extensive experience over the past 20 years providing corporate advisory and legal services to foreign

investors throughout China and to Chinese groups investing offshore. Michael is a principal at Wadley Consulting Shanghai Co. Ltd,

a Senior China Consultant for Hopgood Gamin, on the Board of Directors of the Australian Chamber of Commerce in Shanghai and

is Co-Chair of the Chamber's Financial Services Industry Working Group, a committee member of the Australian China Business

Council, Queensland, and a member of the Australian Institute of Company Directors. Michael holds a Bachelor of Laws from

Queensland University, and is admitted to practice the Supreme Court of Queensland, the High and Federal Courts of Australia, and

is registered as a foreign lawyer in China and Hong Kong.

Launa Inman Independent Non-

Executive Director

Launa brings to the board extensive experience in retailing, marketing (including digital technology and social media), finance and

logistics. Launa is a director of the Commonwealth Bank of Australia and a member of the boards of the Alannah and Madeline

Foundation and Virgin Australia Melbourne Fashion Festival. Her diverse experience includes terms as Managing Director and CEO

of Billabong International (May 2012 to August 2013), Managing Director of Target Australia Pty Ltd (2005 to 2011) and Managing

Director of Office Works (2004 to 2005). Launa’s qualifications include: MCom, University of South Africa (UNSA), BCom (Hons)

(UNSA), BCom (Economics & Accounting) (UNSA) and is a member of the Australian Institute of Company Directors.

Bellamy's Australia April 20, 2015

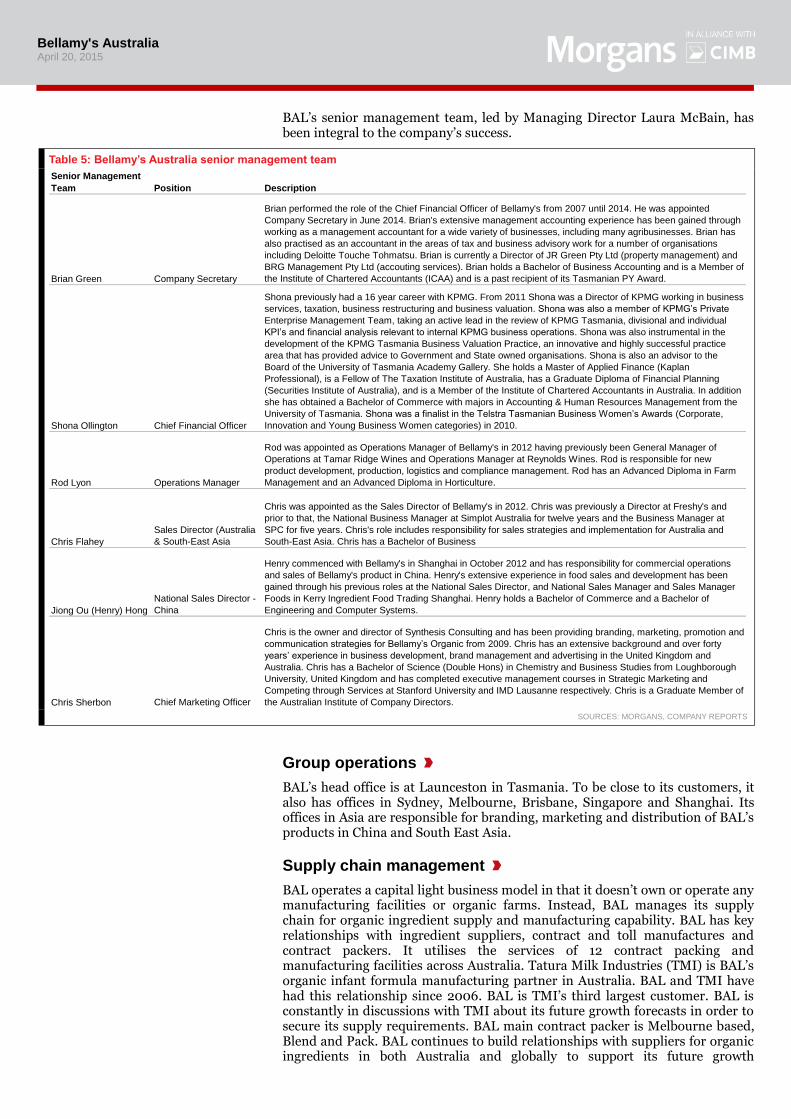

BAL’s senior management team, led by Managing Director Laura McBain, has been integral to the company’s success.

Table 5: Bellamy’s Australia senior management team

SOURCES: MORGANS, COMPANY REPORTS

Group operations

BAL’s head office is at Launceston in Tasmania. To be close to its customers, it also has offices in Sydney, Melbourne, Brisbane, Singapore and Shanghai. Its offices in Asia are responsible for branding, marketing and distribution of BAL’s products in China and South East Asia.

Supply chain management

BAL operates a capital light business model in that it doesn’t own or operate any manufacturing facilities or organic farms. Instead, BAL manages its supply chain for organic ingredient supply and manufacturing capability. BAL has key relationships with ingredient suppliers, contract and toll manufactures and contract packers. It utilises the services of 12 contract packing and manufacturing facilities across Australia. Tatura Milk Industries (TMI) is BAL’s organic infant formula manufacturing partner in Australia. BAL and TMI have had this relationship since 2006. BAL is TMI’s third largest customer. BAL is constantly in discussions with TMI about its future growth forecasts in order to secure its supply requirements. BAL main contract packer is Melbourne based, Blend and Pack. BAL continues to build relationships with suppliers for organic ingredients in both Australia and globally to support its future growth

Senior Management

Team Position Description

Brian Green Company Secretary

Brian performed the role of the Chief Financial Officer of Bellamy's from 2007 until 2014. He was appointed

Company Secretary in June 2014. Brian's extensive management accounting experience has been gained through

working as a management accountant for a wide variety of businesses, including many agribusinesses. Brian has

also practised as an accountant in the areas of tax and business advisory work for a number of organisations

including Deloitte Touche Tohmatsu. Brian is currently a Director of JR Green Pty Ltd (property management) and

BRG Management Pty Ltd (accouting services). Brian holds a Bachelor of Business Accounting and is a Member of

the Institute of Chartered Accountants (ICAA) and is a past recipient of its Tasmanian PY Award.

Shona Ollington Chief Financial Officer

Shona previously had a 16 year career with KPMG. From 2011 Shona was a Director of KPMG working in business

services, taxation, business restructuring and business valuation. Shona was also a member of KPMG’s Private

Enterprise Management Team, taking an active lead in the review of KPMG Tasmania, divisional and individual

KPI’s and financial analysis relevant to internal KPMG business operations. Shona was also instrumental in the

development of the KPMG Tasmania Business Valuation Practice, an innovative and highly successful practice

area that has provided advice to Government and State owned organisations. Shona is also an advisor to the

Board of the University of Tasmania Academy Gallery. She holds a Master of Applied Finance (Kaplan

Professional), is a Fellow of The Taxation Institute of Australia, has a Graduate Diploma of Financial Planning

(Securities Institute of Australia), and is a Member of the Institute of Chartered Accountants in Australia. In addition

she has obtained a Bachelor of Commerce with majors in Accounting & Human Resources Management from the

University of Tasmania. Shona was a finalist in the Telstra Tasmanian Business Women’s Awards (Corporate,

Innovation and Young Business Women categories) in 2010.

Rod Lyon Operations Manager

Rod was appointed as Operations Manager of Bellamy's in 2012 having previously been General Manager of

Operations at Tamar Ridge Wines and Operations Manager at Reynolds Wines. Rod is responsible for new

product development, production, logistics and compliance management. Rod has an Advanced Diploma in Farm

Management and an Advanced Diploma in Horticulture.

Chris Flahey

Sales Director (Australia

& South-East Asia

Chris was appointed as the Sales Director of Bellamy's in 2012. Chris was previously a Director at Freshy's and

prior to that, the National Business Manager at Simplot Australia for twelve years and the Business Manager at

SPC for five years. Chris's role includes responsibility for sales strategies and implementation for Australia and

South-East Asia. Chris has a Bachelor of Business

Jiong Ou (Henry) Hong

National Sales Director -

China

Henry commenced with Bellamy's in Shanghai in October 2012 and has responsibility for commercial operations

and sales of Bellamy's product in China. Henry's extensive experience in food sales and development has been

gained through his previous roles at the National Sales Director, and National Sales Manager and Sales Manager

Foods in Kerry Ingredient Food Trading Shanghai. Henry holds a Bachelor of Commerce and a Bachelor of

Engineering and Computer Systems.

Chris Sherbon Chief Marketing Officer

Chris is the owner and director of Synthesis Consulting and has been providing branding, marketing, promotion and

communication strategies for Bellamy’s Organic from 2009. Chris has an extensive background and over forty

years’ experience in business development, brand management and advertising in the United Kingdom and

Australia. Chris has a Bachelor of Science (Double Hons) in Chemistry and Business Studies from Loughborough

University, United Kingdom and has completed executive management courses in Strategic Marketing and

Competing through Services at Stanford University and IMD Lausanne respectively. Chris is a Graduate Member of

the Australian Institute of Company Directors.

Bellamy's Australia April 20, 2015

requirements. It also continues to support the growth and development of organic farming in Australia. In 2013, BAL worked with organic dairy farmers and processors to double their output of key ingredients. The outcome of this work was a doubling of BAL’s organic formula supply.

Table 6: Bellamy’s production matrix

SOURCE: COMPANY REPORTS

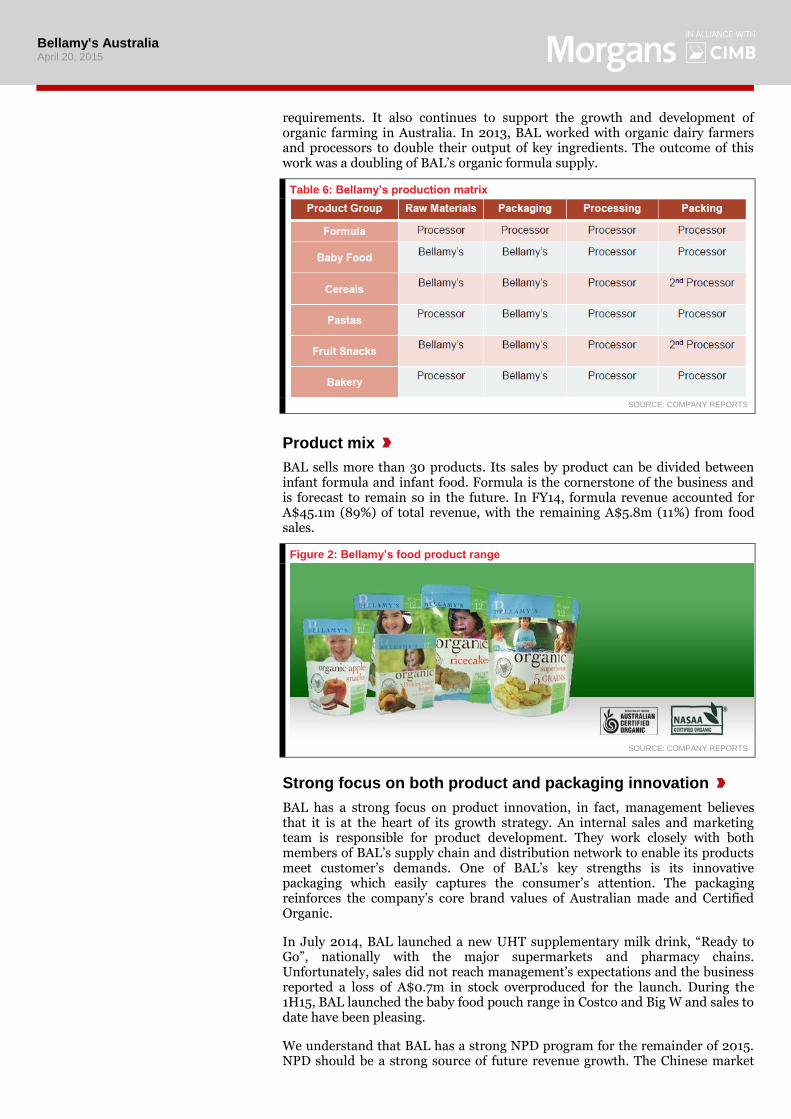

Product mix

BAL sells more than 30 products. Its sales by product can be divided between infant formula and infant food. Formula is the cornerstone of the business and is forecast to remain so in the future. In FY14, formula revenue accounted for A$45.1m (89%) of total revenue, with the remaining A$5.8m (11%) from food sales.

Figure 2: Bellamy’s food product range

SOURCE: COMPANY REPORTS

Strong focus on both product and packaging innovation

BAL has a strong focus on product innovation, in fact, management believes that it is at the heart of its growth strategy. An internal sales and marketing team is responsible for product development. They work closely with both members of BAL’s supply chain and distribution network to enable its products meet customer’s demands. One of BAL’s key strengths is its innovative packaging which easily captures the consumer’s attention. The packaging reinforces the company’s core brand values of Australian made and Certified Organic.

In July 2014, BAL launched a new UHT supplementary milk drink, “Ready to Go”, nationally with the major supermarkets and pharmacy chains. Unfortunately, sales did not reach management’s expectations and the business reported a loss of A$0.7m in stock overproduced for the launch. During the 1H15, BAL launched the baby food pouch range in Costco and Big W and sales to date have been pleasing.

We understand that BAL has a strong NPD program for the remainder of 2015. NPD should be a strong source of future revenue growth. The Chinese market

Bellamy's Australia April 20, 2015

also provides BAL with an opportunity to offer unique innovation with Australian made products that cater specifically for the Chinese lifestyle.

Domestic vs offshore sales mix

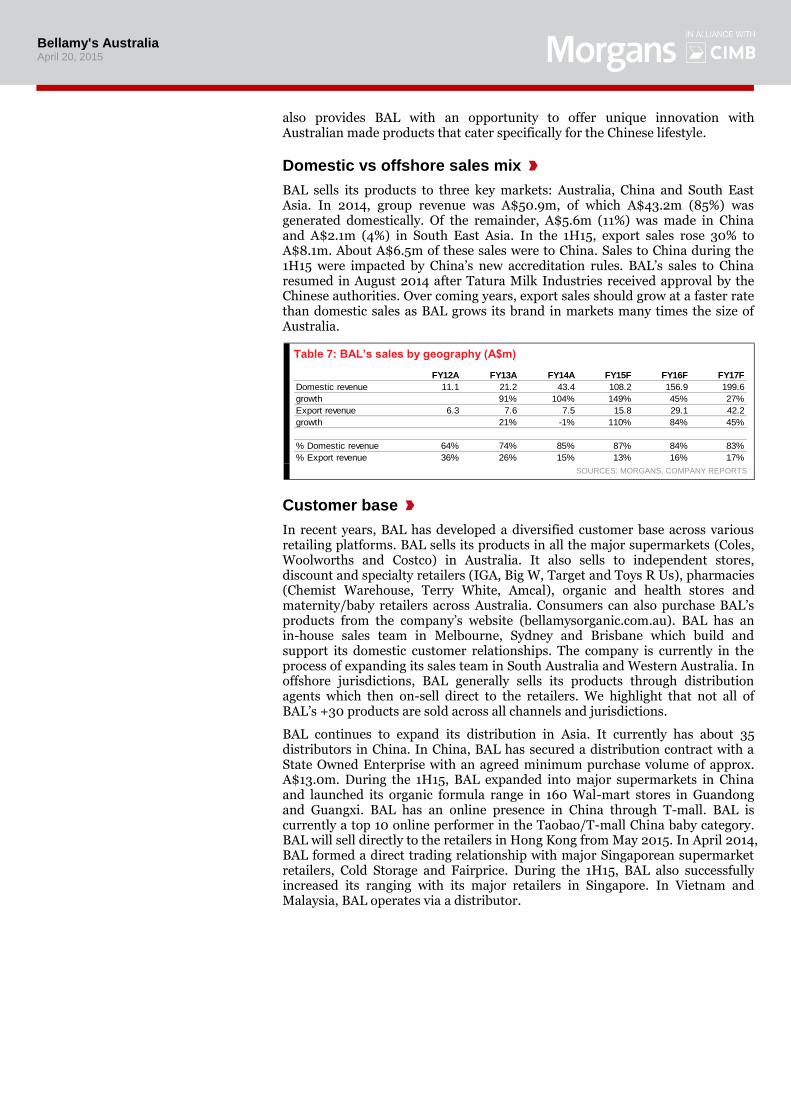

BAL sells its products to three key markets: Australia, China and South East Asia. In 2014, group revenue was A$50.9m, of which A$43.2m (85%) was generated domestically. Of the remainder, A$5.6m (11%) was made in China and A$2.1m (4%) in South East Asia. In the 1H15, export sales rose 30% to A$8.1m. About A$6.5m of these sales were to China. Sales to China during the 1H15 were impacted by China’s new accreditation rules. BAL’s sales to China resumed in August 2014 after Tatura Milk Industries received approval by the Chinese authorities. Over coming years, export sales should grow at a faster rate than domestic sales as BAL grows its brand in markets many times the size of Australia.

Table 7: BAL’s sales by geography (A$m)

SOURCES: MORGANS, COMPANY REPORTS

Customer base

In recent years, BAL has developed a diversified customer base across various retailing platforms. BAL sells its products in all the major supermarkets (Coles, Woolworths and Costco) in Australia. It also sells to independent stores, discount and specialty retailers (IGA, Big W, Target and Toys R Us), pharmacies (Chemist Warehouse, Terry White, Amcal), organic and health stores and maternity/baby retailers across Australia. Consumers can also purchase BAL’s products from the company’s website (bellamysorganic.com.au). BAL has an in-house sales team in Melbourne, Sydney and Brisbane which build and support its domestic customer relationships. The company is currently in the process of expanding its sales team in South Australia and Western Australia. In offshore jurisdictions, BAL generally sells its products through distribution agents which then on-sell direct to the retailers. We highlight that not all of BAL’s +30 products are sold across all channels and jurisdictions.

BAL continues to expand its distribution in Asia. It currently has about 35 distributors in China. In China, BAL has secured a distribution contract with a State Owned Enterprise with an agreed minimum purchase volume of approx. A$13.0m. During the 1H15, BAL expanded into major supermarkets in China and launched its organic formula range in 160 Wal-mart stores in Guandong and Guangxi. BAL has an online presence in China through T-mall. BAL is currently a top 10 online performer in the Taobao/T-mall China baby category. BAL will sell directly to the retailers in Hong Kong from May 2015. In April 2014, BAL formed a direct trading relationship with major Singaporean supermarket retailers, Cold Storage and Fairprice. During the 1H15, BAL also successfully increased its ranging with its major retailers in Singapore. In Vietnam and Malaysia, BAL operates via a distributor.

FY12A FY13A FY14A FY15F FY16F FY17F

Domestic revenue 11.1 21.2 43.4 108.2 156.9 199.6

growth 91% 104% 149% 45% 27%

Export revenue 6.3 7.6 7.5 15.8 29.1 42.2

growth 21% -1% 110% 84% 45%

% Domestic revenue 64% 74% 85% 87% 84% 83%

% Export revenue 36% 26% 15% 13% 16% 17%

Bellamy's Australia April 20, 2015

Marketing/trade spend strategy

BAL’s marketing/promotional spend can be split between direct costs (trade spend) and marketing and promotion expenses.

Direct costs (trade spend) - is the sum of trading discounts (retailer claims back from the supplier) and promotional allowances (short term and variable retail claims). In short, it is the amount of money BAL has to spend on promoting (discounting) its products on-shelf. It is a significant expenditure item within the business. We note that trade spend for Australian food and grocery manufacturers has increased in recent years to about 26% of gross sales.

Marketing and promotion expenses – BAL’s brand has been built by its online presence and by word of mouth. BAL’s own website (bellamysorganic.com.au) is a key source of information for its customers, including a regularly updated blog which answers its customer’s questions and helps guide them through their baby’s formative weeks and months and through the toddler years. In 2013, BAL launched a Chinese website, while the Singaporean website has recently been launched. This is important given consumers in Asia spend more time online. BAL focuses on social media marketing. The company actively markets its brand on Twitter, Facebook, Weixin and Weibo (Chinese social media sites). It currently has about 45,000 followers on Facebook. BAL also uses search engine optimisation (SEO). Management closely monitors the effectiveness of its online marketing activity and social media ROI.

Bellamy's Australia April 20, 2015

GROWTH STRATEGY

BAL’s growth strategy is based on growing its distribution channels both in Australia and offshore and continuing to innovate with new products while also enhancing its existing products. Below we explore BAL’s growth strategy in more detail.

Expansion in Asian markets - Sales revenue from China and South East Asia are expected to dramatically increase as BAL expands in these markets and increases its presence with existing customers and distributors. The company has already secured a A$13m deal with a Chinese State Owned Enterprise, which will double revenue in FY15 compared to FY14. Following the 2008 Melamine Scandal in China, the Chinese people switched from buying infant formula from local producers to offshore reputable companies. This trend is also prevalent across South East Asia. Consumers in Asia are also ‘trading up’ and buying more ultra-premium infant formula which is perfect for BAL as this is the category its products fit in. In May 2015, BAL will commence selling directly to retailers in Hong Kong. It has already had great success dealing direct in Singapore. BAL is also currently evaluating potential business partners in The Philippines and Indonesia.

Expansion in other new markets - BAL is also seeking to identify key markets for growth outside of Asia. While this option is not likely to occur in the short term, there will be long term consideration for entrance into other large overseas markets such as the US, UK and Middle East.

Developing products outside of the baby category – In the future, BAL aims to leverage its strong brand awareness by developing new products outside of the baby category. The recently launched “Ready to Go” drink is an example of an all-ages product designed to leverage brand awareness.

Developing new products within the baby category - Product innovation and development is a primary focus for BAL. Its internal sales and marketing team closely monitors the changing needs and specific cultural demands of its customers both in Australia and offshore to develop products which specifically meet their requirements. We understand that a range of new products will be launched shortly.

Achieving full distribution across Australia – In a short period of time, BAL’s infant formula market share in Australia has risen from 12% to 14.1% which highlights the company’s success in expanding its distribution network. BAL intends to continue to grow its distribution network across Australia and have more of its products with its existing retailer base. BAL will shortly begin selling its products in South Australia and Western Australia. There is also the opportunity to supply other large pharmacy chains.

Bellamy's Australia April 20, 2015

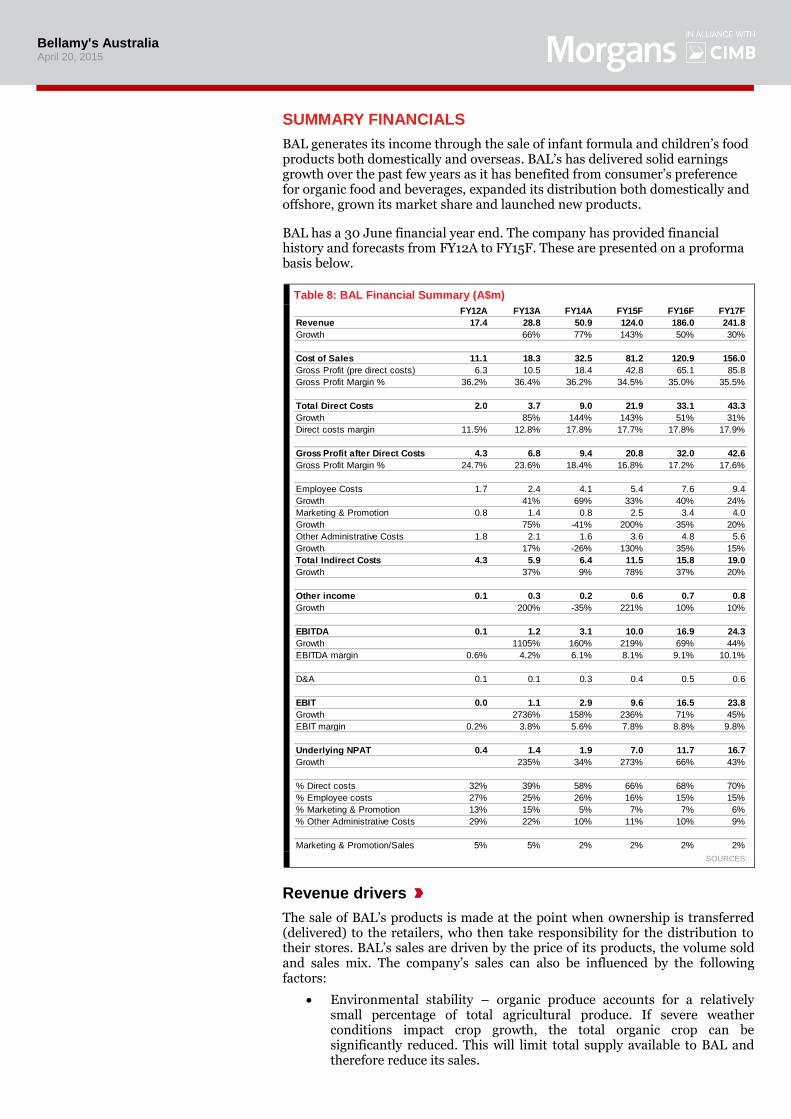

SUMMARY FINANCIALS

BAL generates its income through the sale of infant formula and children’s food products both domestically and overseas. BAL’s has delivered solid earnings growth over the past few years as it has benefited from consumer’s preference for organic food and beverages, expanded its distribution both domestically and offshore, grown its market share and launched new products.

BAL has a 30 June financial year end. The company has provided financial history and forecasts from FY12A to FY15F. These are presented on a proforma basis below.

Table 8: BAL Financial Summary (A$m)

SOURCES:

Revenue drivers

The sale of BAL’s products is made at the point when ownership is transferred (delivered) to the retailers, who then take responsibility for the distribution to their stores. BAL’s sales are driven by the price of its products, the volume sold and sales mix. The company’s sales can also be influenced by the following factors:

Environmental stability – organic produce accounts for a relatively small percentage of total agricultural produce. If severe weather conditions impact crop growth, the total organic crop can be significantly reduced. This will limit total supply available to BAL and therefore reduce its sales.

FY12A FY13A FY14A FY15F FY16F FY17F

Revenue 17.4 28.8 50.9 124.0 186.0 241.8

Growth 66% 77% 143% 50% 30%

Cost of Sales 11.1 18.3 32.5 81.2 120.9 156.0

Gross Profit (pre direct costs) 6.3 10.5 18.4 42.8 65.1 85.8

Gross Profit Margin % 36.2% 36.4% 36.2% 34.5% 35.0% 35.5%

Total Direct Costs 2.0 3.7 9.0 21.9 33.1 43.3

Growth 85% 144% 143% 51% 31%

Direct costs margin 11.5% 12.8% 17.8% 17.7% 17.8% 17.9%

Gross Profit after Direct Costs 4.3 6.8 9.4 20.8 32.0 42.6

Gross Profit Margin % 24.7% 23.6% 18.4% 16.8% 17.2% 17.6%

Employee Costs 1.7 2.4 4.1 5.4 7.6 9.4

Growth 41% 69% 33% 40% 24%

Marketing & Promotion 0.8 1.4 0.8 2.5 3.4 4.0

Growth 75% -41% 200% 35% 20%

Other Administrative Costs 1.8 2.1 1.6 3.6 4.8 5.6

Growth 17% -26% 130% 35% 15%

Total Indirect Costs 4.3 5.9 6.4 11.5 15.8 19.0

Growth 37% 9% 78% 37% 20%

Other income 0.1 0.3 0.2 0.6 0.7 0.8

Growth 200% -35% 221% 10% 10%

EBITDA 0.1 1.2 3.1 10.0 16.9 24.3

Growth 1105% 160% 219% 69% 44%

EBITDA margin 0.6% 4.2% 6.1% 8.1% 9.1% 10.1%

D&A 0.1 0.1 0.3 0.4 0.5 0.6

EBIT 0.0 1.1 2.9 9.6 16.5 23.8

Growth 2736% 158% 236% 71% 45%

EBIT margin 0.2% 3.8% 5.6% 7.8% 8.8% 9.8%

Underlying NPAT 0.4 1.4 1.9 7.0 11.7 16.7

Growth 235% 34% 273% 66% 43%

% Direct costs 32% 39% 58% 66% 68% 70%

% Employee costs 27% 25% 26% 16% 15% 15%

% Marketing & Promotion 13% 15% 5% 7% 7% 6%

% Other Administrative Costs 29% 22% 10% 11% 10% 9%

Marketing & Promotion/Sales 5% 5% 2% 2% 2% 2%

Bellamy's Australia April 20, 2015

Consumer switch to organic products – demand for organic produce has been increasing at double digit rates for a number of years and this is set to continue.

Fertility rates – the rate of births is stable in Australia, however in China fertility rates are influenced by government policy. Tightening or loosening of China’s One Child Policy will influence the number of newborns and thus the number of parents purchasing baby food and formula.

Growth of the number of women in the workforce.

Growth in BAL’s distribution network both domestically and offshore.

New products - generally increase total sales but similar products may result in some cannibalisation of previous products.

Currency – as more of BAL’s sales occur overseas, there will be an increased sensitivity to currency changes, in particular the Chinese yuan.

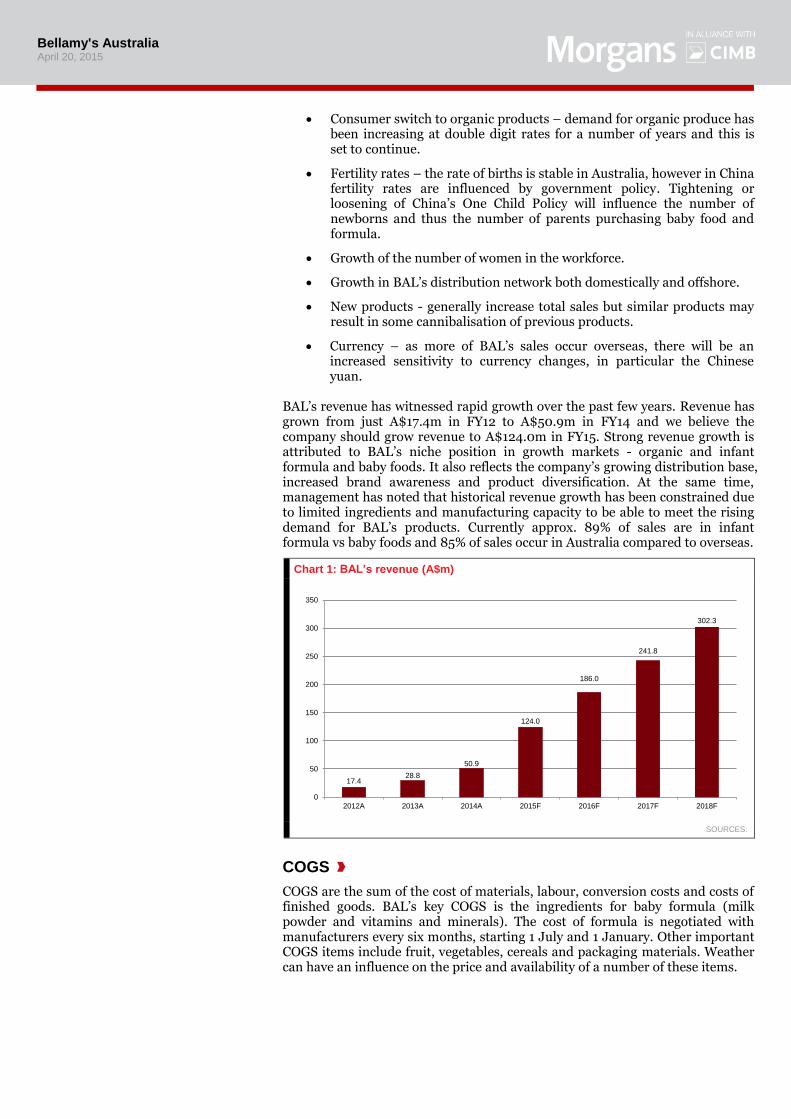

BAL’s revenue has witnessed rapid growth over the past few years. Revenue has grown from just A$17.4m in FY12 to A$50.9m in FY14 and we believe the company should grow revenue to A$124.0m in FY15. Strong revenue growth is attributed to BAL’s niche position in growth markets - organic and infant formula and baby foods. It also reflects the company’s growing distribution base, increased brand awareness and product diversification. At the same time, management has noted that historical revenue growth has been constrained due to limited ingredients and manufacturing capacity to be able to meet the rising demand for BAL’s products. Currently approx. 89% of sales are in infant formula vs baby foods and 85% of sales occur in Australia compared to overseas.

Chart 1: BAL’s revenue (A$m)

SOURCES:

COGS

COGS are the sum of the cost of materials, labour, conversion costs and costs of finished goods. BAL’s key COGS is the ingredients for baby formula (milk powder and vitamins and minerals). The cost of formula is negotiated with manufacturers every six months, starting 1 July and 1 January. Other important COGS items include fruit, vegetables, cereals and packaging materials. Weather can have an influence on the price and availability of a number of these items.

17.428.8

50.9

124.0

186.0

241.8

302.3

0

50

100

150

200

250

300

350

2012A 2013A 2014A 2015F 2016F 2017F 2018F

Bellamy's Australia April 20, 2015

Gross profit margin

BAL’s gross profit margin varies across its different products. Gross profit margin can be impacted by price realisation, sales mix and movements in COGS. BAL’s gross profit margin (pre direct costs) increased slightly in FY13 to 36.4%, however it then fell in FY14 to 36.2% and to 33.2% in the 1H15 due to increased ingredient pricing, in particular whole milk. Essentially BAL’s ingredient suppliers have issued price rises in FY15 given the strong demand for organic formula ingredients. However importantly, management has said that it has successfully undertaken several projects to address this change and expects to see the benefits in the 2H15. We forecast BAL’s margin to rise to 35.0% in FY16, 35.5% in FY17 and 36.0% in FY18.

Direct costs

Direct costs include trade term discounts and promotional deals, warehousing costs, freight and other incidental costs.

Indirect costs

BAL has a relatively fixed cost base which provides it with significant operating leverage when it experiences strong sales growth. The company breaks down its operating expenses into three key areas:

Employment costs - BAL employs about 37 people. As a percentage of sales, employment costs were 4.7% in 1H15, down from 6.2% in the 1H14.

Marketing & Promotion - We forecast BAL’s marketing budget to rise over the next few years as the company plans to grow its brand awareness across its target markets. Marketing & Promotion as a percentage of sales increased to 2.1% in the 1H15 compared to 1.4% in the 1H14 for this reason.

Other administrative costs - As a percentage of sales, other administrative costs (plus the costs of offshore expansion) were 3.1% in 1H15, down from 3.7% in the 1H14.

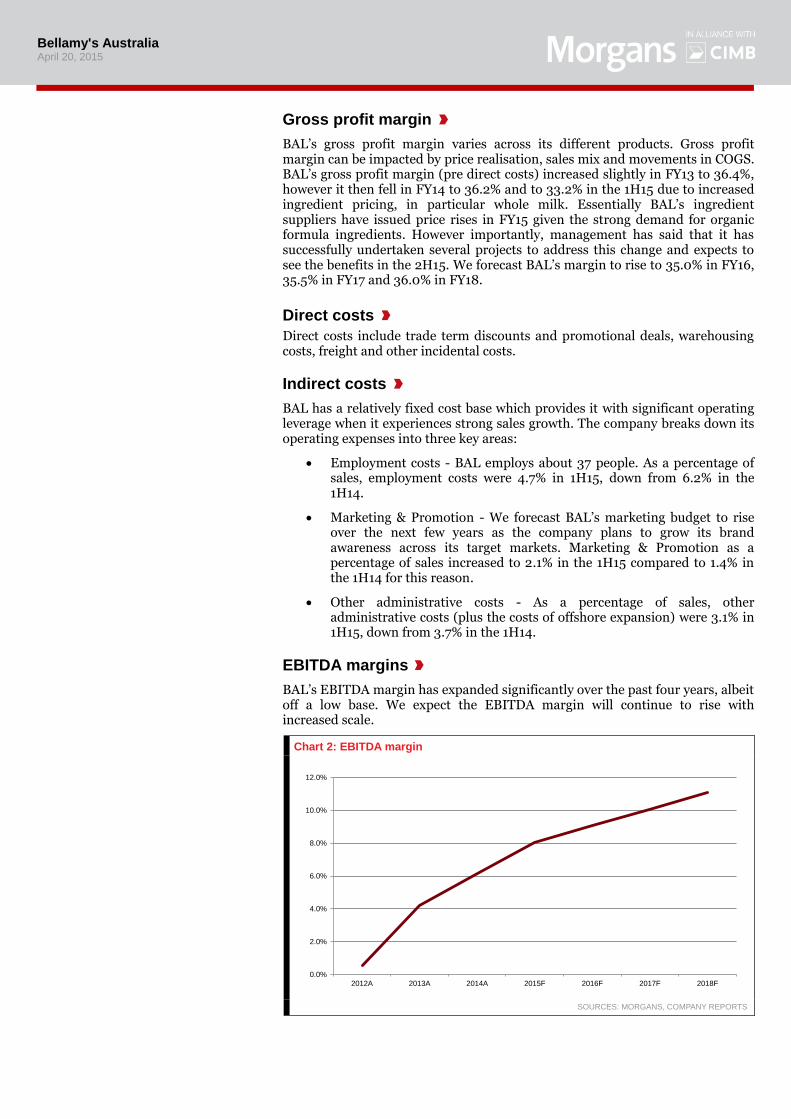

EBITDA margins

BAL’s EBITDA margin has expanded significantly over the past four years, albeit off a low base. We expect the EBITDA margin will continue to rise with increased scale.

Chart 2: EBITDA margin

SOURCES: MORGANS, COMPANY REPORTS

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2012A 2013A 2014A 2015F 2016F 2017F 2018F

Bellamy's Australia April 20, 2015

Depreciation and amortisation (D&A) expense

Depreciation is minimal given BAL’s capital light business model.

Tax rate

We forecast an effective tax rate of 30% in FY15 and beyond. This could prove conservative as BAL’s Asian operations gain scale given the much lower tax rate in these regions.

Seasonality of earnings

Earnings can be higher in the first half as December is BAL’s key trading month.

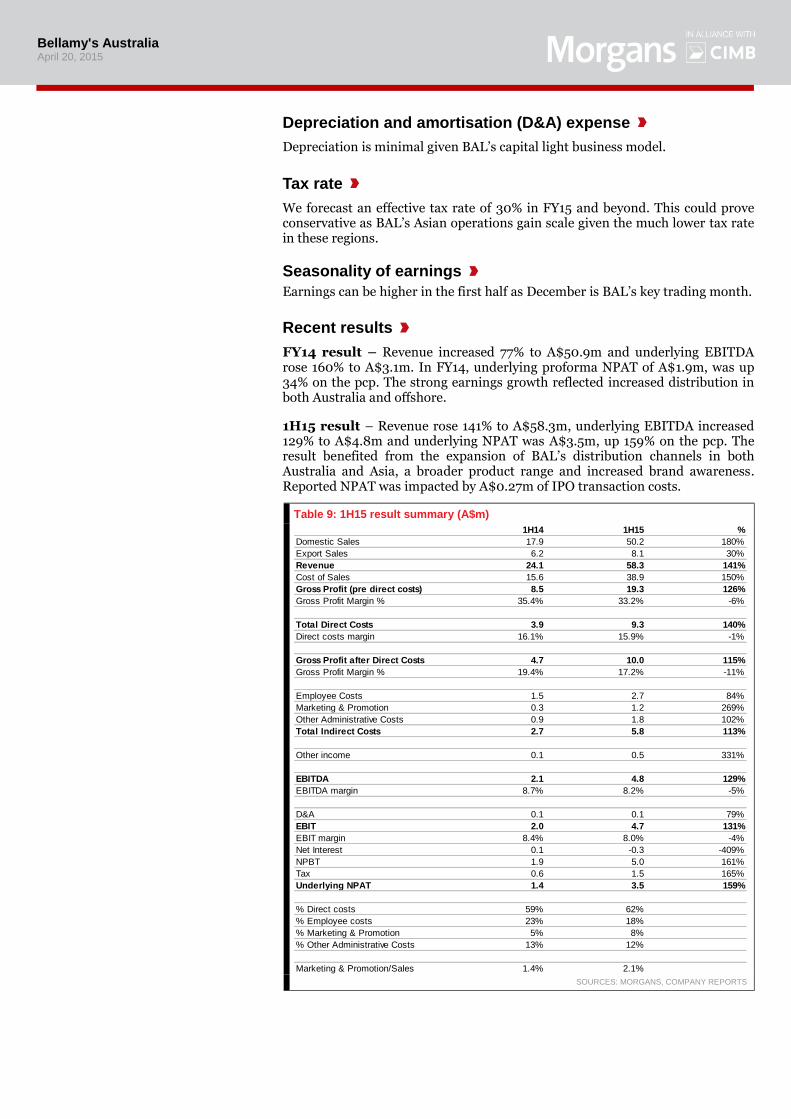

Recent results

FY14 result – Revenue increased 77% to A$50.9m and underlying EBITDA rose 160% to A$3.1m. In FY14, underlying proforma NPAT of A$1.9m, was up 34% on the pcp. The strong earnings growth reflected increased distribution in both Australia and offshore.

1H15 result – Revenue rose 141% to A$58.3m, underlying EBITDA increased 129% to A$4.8m and underlying NPAT was A$3.5m, up 159% on the pcp. The result benefited from the expansion of BAL’s distribution channels in both Australia and Asia, a broader product range and increased brand awareness. Reported NPAT was impacted by A$0.27m of IPO transaction costs.

Table 9: 1H15 result summary (A$m)

SOURCES: MORGANS, COMPANY REPORTS

1H14 1H15 %

Domestic Sales 17.9 50.2 180%

Export Sales 6.2 8.1 30%

Revenue 24.1 58.3 141%

Cost of Sales 15.6 38.9 150%

Gross Profit (pre direct costs) 8.5 19.3 126%

Gross Profit Margin % 35.4% 33.2% -6%

Total Direct Costs 3.9 9.3 140%

Direct costs margin 16.1% 15.9% -1%

Gross Profit after Direct Costs 4.7 10.0 115%

Gross Profit Margin % 19.4% 17.2% -11%

Employee Costs 1.5 2.7 84%

Marketing & Promotion 0.3 1.2 269%

Other Administrative Costs 0.9 1.8 102%

Total Indirect Costs 2.7 5.8 113%

Other income 0.1 0.5 331%

EBITDA 2.1 4.8 129%

EBITDA margin 8.7% 8.2% -5%

D&A 0.1 0.1 79%

EBIT 2.0 4.7 131%

EBIT margin 8.4% 8.0% -4%

Net Interest 0.1 -0.3 -409%

NPBT 1.9 5.0 161%

Tax 0.6 1.5 165%

Underlying NPAT 1.4 3.5 159%

% Direct costs 59% 62%

% Employee costs 23% 18%

% Marketing & Promotion 5% 8%

% Other Administrative Costs 13% 12%

Marketing & Promotion/Sales 1.4% 2.1%

Bellamy's Australia April 20, 2015

Outlook

FY15 earnings guidance – Since listing, BAL has twice upgraded its original prospectus forecast for an underlying NPAT of A$5.0m. Its most recent FY15 guidance is for 2H15 performance to be consistent with the 1H15 result or for an underlying NPAT of A$7.0m.

Morgans forecasts

Our FY15 forecast for an underlying NPAT of A$7.0m, up 273%, is in line with guidance. We forecast FY16 NPAT to rise by 66% to A$11.7m. We believe that BAL is well placed to report strong double digit grow for many years to come as consumers increasingly demand organic food and beverages, it launches new products and expands its distribution network both in Australia and overseas.

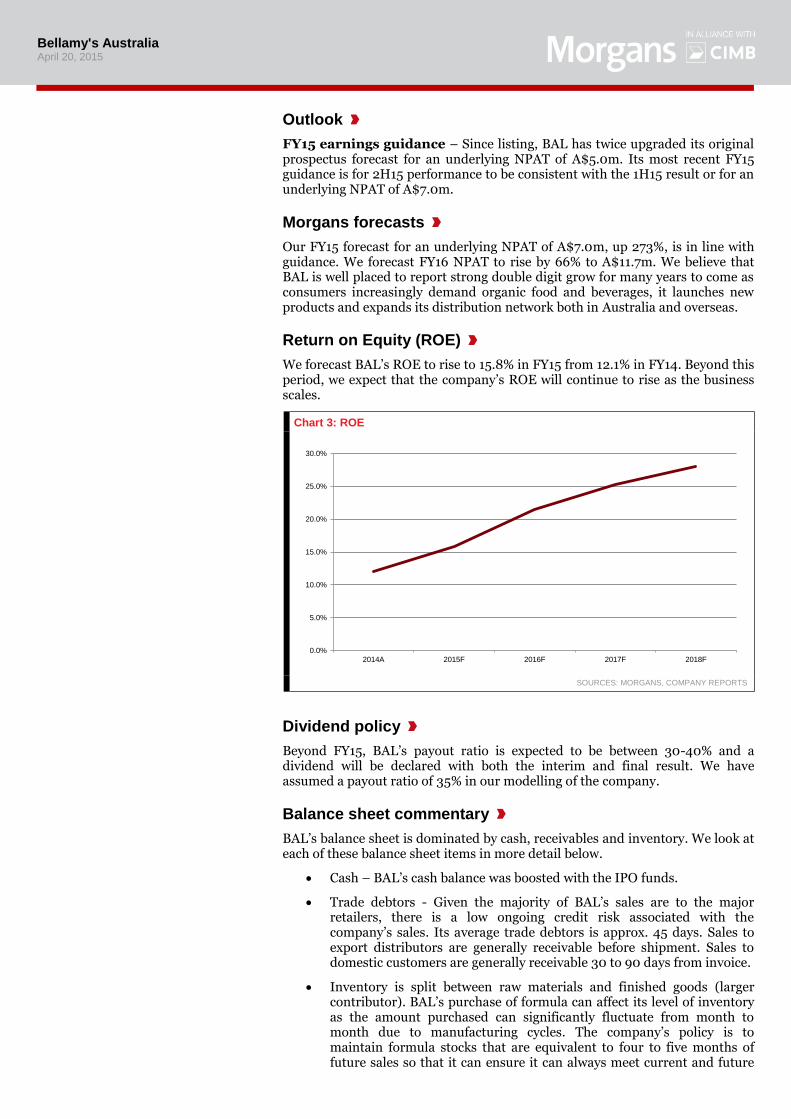

Return on Equity (ROE)

We forecast BAL’s ROE to rise to 15.8% in FY15 from 12.1% in FY14. Beyond this period, we expect that the company’s ROE will continue to rise as the business scales.

Chart 3: ROE

SOURCES: MORGANS, COMPANY REPORTS

Dividend policy

Beyond FY15, BAL’s payout ratio is expected to be between 30-40% and a dividend will be declared with both the interim and final result. We have assumed a payout ratio of 35% in our modelling of the company.

Balance sheet commentary

BAL’s balance sheet is dominated by cash, receivables and inventory. We look at each of these balance sheet items in more detail below.

Cash – BAL’s cash balance was boosted with the IPO funds.

Trade debtors - Given the majority of BAL’s sales are to the major retailers, there is a low ongoing credit risk associated with the company’s sales. Its average trade debtors is approx. 45 days. Sales to export distributors are generally receivable before shipment. Sales to domestic customers are generally receivable 30 to 90 days from invoice.

Inventory is split between raw materials and finished goods (larger contributor). BAL’s purchase of formula can affect its level of inventory as the amount purchased can significantly fluctuate from month to month due to manufacturing cycles. The company’s policy is to maintain formula stocks that are equivalent to four to five months of future sales so that it can ensure it can always meet current and future

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2014A 2015F 2016F 2017F 2018F

Bellamy's Australia April 20, 2015

demand. While this requires significant working capital, it provides assurance that the business can meet sudden increases in demand and also manage any unavoidable delays in the manufacturing of formula products.

Intangible items are small and relate to new product development costs such as the UHT supplementary milk drink. These costs are amortised over 2-5 years. There is no value for the Bellamy’s brand in the balance sheet, whereas in reality, this brand has significant value.

BAL’s trade creditors largely relate to suppliers of raw materials, packaging, freight and marketing. Payables are usually within 30 days.

BAL previously used a debtor finance facility to manage its monthly fluctuations in working capital. However the net cash raised from last year’s raising and IPO of A$28.7m, gives the company flexibility to manage its working capital requirements in FY15 without utilising its existing debtor finance facility.

Post the IPO funds, BAL is in a strong net cash position. As at 31 December 2014, BAL had A$16.6m of net cash.

Cashflow commentary

FY14 operating cashflow was A$0.8m compared to an outflow the pcp of A$3.5m. BAL reported a 1H15 operating cash outflow of A$10.3m compared to a cash inflow A$1.4m the pcp due to higher net working capital requirements (increased by A$27.0m). 1H15 trade and other receivables increased by A$13.0m and inventory levels rose by A$4.6m due to increased sales. Management stated that its debtor collection cycle remained consistent and in line with industry standards.

While the business is scaling and developing in new markets offshore, BAL’s working capital requirements are large. Consequently, accurately forecasting its operating cashflow is difficult. At this point, we forecast the company to start generating positive operating cashflow in FY17.

BAL has relatively limited capex requirements due to its capital light business model.

Employee Share Option Plan (ESOP)

BAL has 2.2m options on issue as part of its Employee Share Option Plan (ESOP). These were issued to the Managing Director and five members of the senior management team. The exercise price is A$1.00. The options can be exercised following the release of the FY15 result as long as BAL achieves its original prospectus forecast for a NPAT of A$5.0m. They must then be exercised no later than 31 August 2017. Our forecasts assume that the options are exercised during FY16, raising an additional A$2.2m.

Bellamy's Australia April 20, 2015

APPENDIX

BAL operates in the fast moving consumer goods (FMCG) industry. It is focused on two key segments being: 1) organic food; and 2) infant formula and baby food. Infant formula is the largest product within the baby segment.

Organic food industry

Organic is a certain way in which agricultural products are grown and processed. The agricultural farming and processing of the food products must meet specific requirements to be labelled as ‘organic’. Organic crops must always be grown in safe soil, with no modifications, no use of synthetic pesticides, bioengineered genes or genetically modified organisms (GMOs), petroleum-based fertilisers, and sewage sludge-based fertilisers. Also, the organic livestock must have access to the outdoors and be given organic feed. They may not be given antibiotics, growth hormones, or any animal-by-products.

Health AIM sites five reasons to add organic food to your diet:

Organic farming is better for the environment: Organic farming practices help in conserving water, reduce soil erosion, increase soil fertility and use less energy and thus are considered pollution free (air, water, soil).

Organic produce contains fewer pesticides: Pesticides which are widely used in conventional agriculture remain on (and in) the food in the form of residue and thus are harmful when consumed. Organic food is devoid of synthetic pesticides.

Organic food is Genetically Modified Organisms (GMO) free: In most countries, organic crops contain no GMOs and organic meat comes from animals raised on organic, GMO-free feed. GMOs are those whose DNA has been altered in the laboratory in order to be resistant to pesticides or produce an insecticide.

Organic food is considered fresh: Organic food doesn’t contain added preservatives to make it last longer because it is often produced on smaller farms near or where it is sold. Hence, it is fresh.

Organically raised animals are not given antibiotics, growth hormones, or fed animal by-products, thus have a lesser risk of acquired infections from antibiotic-resistant strains of bacteria.

There are nutritional benefits from consuming organic foods as well. A 2014 analysis of multiple studies by the British Journal of Nutrition concluded that organic crops contained higher antioxidant levels than their non-organic counterparts.

IBISWorld believes that two important factors determine the demand for organic produce including: (1) availability and (2) price. Both present challenges for the industry. Price premiums for organic foods stem from the higher costs of production and distribution and the relative level of supply and demand.