AICPA Professional Standards - eGrove

42

University of Mississippi University of Mississippi eGrove eGrove AICPA Professional Standards American Institute of Certified Public Accountants (AICPA) Historical Collection 2006 AICPA Professional Standards: Statements on standards for tax AICPA Professional Standards: Statements on standards for tax services as of June 1, 2006 services as of June 1, 2006 American Institute of Certified Public Accountants. Tax Executive Committee Follow this and additional works at: https://egrove.olemiss.edu/aicpa_prof Part of the Accounting Commons, and the Taxation Commons Recommended Citation Recommended Citation American Institute of Certified Public Accountants. Tax Executive Committee, "AICPA Professional Standards: Statements on standards for tax services as of June 1, 2006" (2006). AICPA Professional Standards. 325. https://egrove.olemiss.edu/aicpa_prof/325 This Article is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in AICPA Professional Standards by an authorized administrator of eGrove. For more information, please contact [email protected].

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of AICPA Professional Standards - eGrove

University of Mississippi University of Mississippi

eGrove eGrove

AICPA Professional Standards American Institute of Certified Public Accountants (AICPA) Historical Collection

2006

AICPA Professional Standards: Statements on standards for tax AICPA Professional Standards: Statements on standards for tax

services as of June 1, 2006 services as of June 1, 2006

American Institute of Certified Public Accountants. Tax Executive Committee

Follow this and additional works at: https://egrove.olemiss.edu/aicpa_prof

Part of the Accounting Commons, and the Taxation Commons

Recommended Citation Recommended Citation American Institute of Certified Public Accountants. Tax Executive Committee, "AICPA Professional Standards: Statements on standards for tax services as of June 1, 2006" (2006). AICPA Professional Standards. 325. https://egrove.olemiss.edu/aicpa_prof/325

This Article is brought to you for free and open access by the American Institute of Certified Public Accountants (AICPA) Historical Collection at eGrove. It has been accepted for inclusion in AICPA Professional Standards by an authorized administrator of eGrove. For more information, please contact [email protected].

Am

er

ica

n

In

st

itu

te

o

f C

er

tif

ied

P

ub

lic

A

cc

ou

nt

an

ts

AICPAProfessionalStandardsVolume 2

Accounting and Review Services

Code of Professional Conduct

Bylaws

Consulting Services

Quality Control

Peer Review

Tax Services

Personal Financial Planning

Continuing Professional Education

As of June 1 , 2006

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Table of Contents 18,001

TS Section

TAX SERVICES

STATEMENTS ONSTANDARDS FOR TAX SERVICES

The Statements on Standards for Tax Services (SSTSs) and Interpre-tations, promulgated by the Tax Executive Committee, reflect the AICPA'sstandards of tax practice and delineate members' responsibilities to tax-payers, the public, the government, and the profession. The Statementsare intended to be part of an ongoing process that may require changesto and Interpretations of current SSTSs in recogition of the acceleratingrate of change in tax laws and the continued importance of tax practiceto members. Interpretation No. 1–2 was approved by the Tax ExecutiveCommittee on August 21, 2003; its effective date is December 31, 2003.

The SSTTs have been written in as simple and objective a manneras possible. However, by their nature, ethical standards provide for anappropiate range of behavior that recognizes the need for Interpreta-tions to meet a broad range of personal and professional situations. TheSSTTs recognize this need by, in some sections, providing relatively sub-jective rules and by leaving certain items undefined. These terms andconcepts are generally rooted in tax concepts, and therefore should bereadily understood by tax practitioners. It is, therefore, recognized thatthe enforcement of these rules, as part of the AICPA's Code of ProfessionalConduct Rule 201, General Standards, and Rule 202, Compliance WithStandards, will be undertaken with flexability in mind and handled ona case-by-case basis. Members are expected to comply with them.

TABLE OF CONTENTSSection Paragraph

100 Tax Return Positions .01-.12Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .02-.04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.12

9100 Tax Return Positions: Tax Services Interpretations of Section 100 .01-.931-1. Realistic Possibility Standard (8/00) . . . . . . . . . . . . . . . . . . . . .01-.411-2. Tax Planning (12/03) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42-.93

Contents

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,002 Table of Contents

Section Paragraph

200 Answers to Questions on Returns .01-.06Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .02Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .03-.06

300 Certain Procedural Aspects of Preparing Returns .01-.09Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .02-.04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.09

400 Use of Estimates .01-.07Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .02Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .03-.07

500 Departure From a Position Previously Concluded in an AdministrativeProceeding or Court Decision .01-.06

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01-.03Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.06

600 Knowledge of Error: Return Preparation .01-.09Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01-.02Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .03-.04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.09

700 Knowledge of Error: Administrative Proceedings .01-.08Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01-.02Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .03-.04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.08

800 Form and Content of Advice to Taxpayers .01-.11Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .01Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .02-.04Explanation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .05-.11

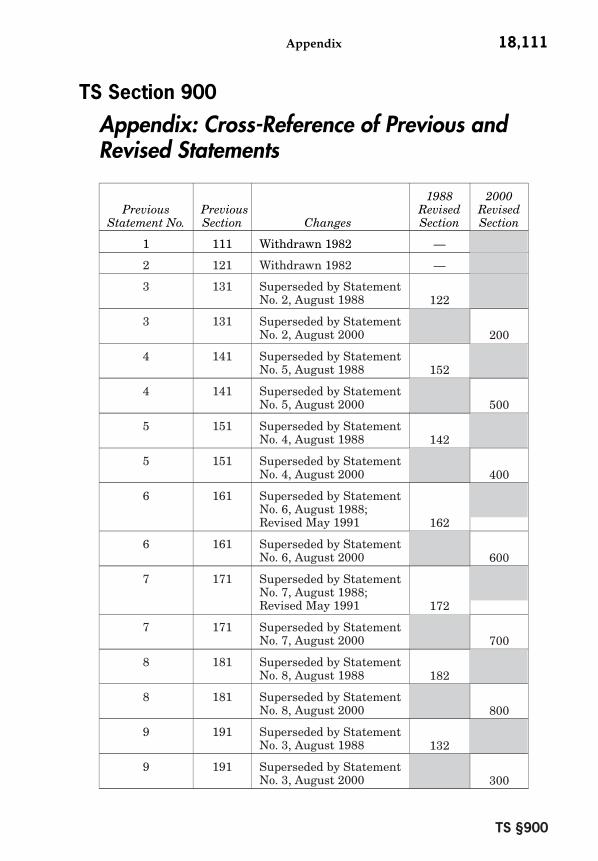

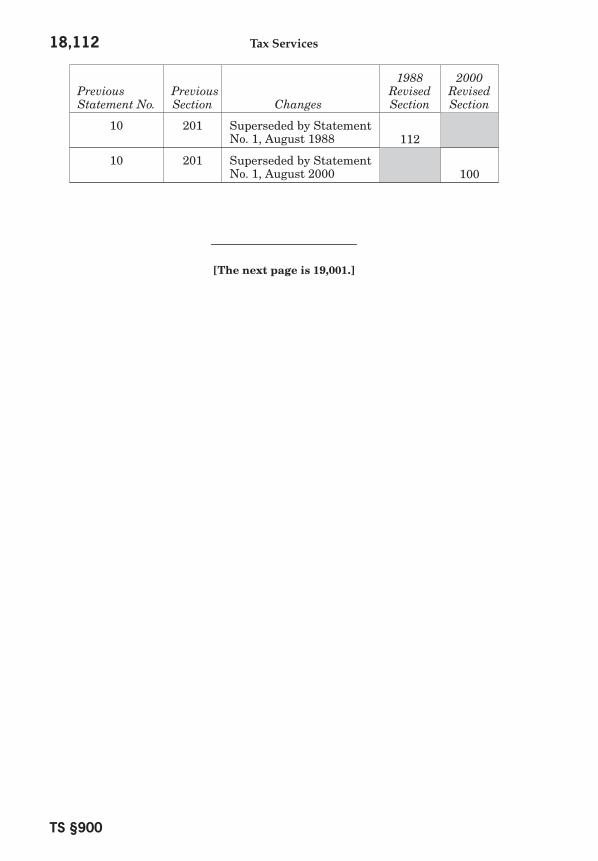

900 Appendix: Cross-Reference of Previous and Revised Statements

[The next page is 18,011.]

Contents

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,011

PrefacePractice standards are the hallmark of calling one's self a professional. Mem-

bers should fulfill their responsibilities as professionals by instituting andmaintaining standards against which their professional performance can bemeasured. Compliance with professional standards of tax practice also confirmsthe public's awareness of the professionalism that is associated with CPAs aswell as the AICPA.

This Publication sets forth ethical tax practice standards for members ofthe AICPA: Statements on Standards for Tax Services (SSTSs or Statements).Although other standards of tax practice exist, most notably Treasury Depart-ment Circular No. 230 and penalty provisions of the Internal Revenue Code(IRC), those standards are limited in that (1) Circular No. 230 does not providethe depth of guidance contained in these Statements, (2) the IRC penalty pro-visions apply only to income-tax return preparation, and (3) both Circular No.230 and the penalty provisions apply only to federal tax practice.

The SSTSs have been written in as simple and objective a manner as pos-sible. However, by their nature, ethical standards provide for an appropriaterange of behavior that recognizes the need for interpretations to meet a broadrange of personal and professional situations. The SSTSs recognize this needby, in some sections, providing relatively subjective rules and by leaving cer-tain terms undefined. These terms and concepts are generally rooted in taxconcepts, and therefore should be readily understood by tax practitioners. It is,therefore, recognized that the enforcement of these rules, as part of the AICPA'sCode of Professional Conduct Rule 201, General Standards [ET section 201.01],and Rule 202, Compliance With Standards [ET section 202.01], will be under-taken with flexibility in mind and handled on a case-by-case basis. Membersare expected to comply with them.

HistoryThe SSTSs have their origin in the Statements on Responsibilities in Tax

Practice (SRTPs), which provided a body of advisory opinions on good tax prac-tice. The guidelines as originally set forth in the SRTPs had come to play a muchmore important role than most members realized. The courts, Internal RevenueService, state accountancy boards, and other professional organizations recog-nized and relied on the SRTPs as the appropriate articulation of professionalconduct in a CPA's tax practice. The SRTPs, in and of themselves, had become defacto enforceable standards of professional practice, because state disciplinaryorganizations and malpractice cases in effect regularly held CPAs accountablefor failure to follow the SRTPs when their professional practice conduct failedto meet the prescribed guidelines of conduct.

The AICPA's Tax Executive Committee concluded that appropriate actionentailed issuance of tax practice standards that would become a part of theInstitute's Code of Professional Conduct. At its July 1999 meeting, the AICPABoard of Directors approved support of the executive committee's initiative andplaced the matter on the agenda of the October 1999 meeting of the Institute'sgoverning Council. On October 19, 1999, Council approved designating the TaxExecutive Committee as a standard-setting body, thus authorizing that com-mittee to promulgate standards of tax practice. These SSTSs, largely mirroringthe SRTPs, are the result.

The SRTPs were originally issued between 1964 and 1977. The first nineSRTPs and the Introduction were codified in 1976; the tenth SRTP was is-sued in 1977. The original SRTPs concerning the CPA's responsibility to sign

Preface

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,012

the return (SRTPs No. 1, Signature of Preparers, and No. 2, Signature of Re-viewer: Assumption of Preparer's Responsibility) were withdrawn in 1982 af-ter Treasury Department regulations were issued adopting substantially thesame standards for all tax return preparers. The sixth and seventh SRTPs,concerning the responsibility of a CPA who becomes aware of an error, wererevised in 1991. The first Interpretation of the SRTPs, Interpretation 1-1, "Re-alistic Possibility Standard," was approved in December 1990. The SSTSs andInterpretation supersede and replace the SRTPs and their Interpretation 1-1effective October 31, 2000. Although the number and names of the SSTSs, andthe substance of the rules contained in each of them, remain the same as in theSRTPs, the language has been edited to both clarify and reflect the enforceablenature of the SSTSs. In addition, because the applicability of these standardsis not limited to federal income-tax practice, the language has been changed tomirror the broader scope.

Ongoing ProcessThe following Statements on Standards for Tax Services [sections 100–800]

and Interpretations No. 1-1, "Realistic Possibility Standard," and No. 1-2, "TaxPlanning," [section 9100] to Statement No. 1, Tax Return Positions [section 100]reflect the AICPA's standards of tax practice and delineate members' responsi-bilities to taxpayers, the public, the government, and the profession. The State-ments are intended to be part of an ongoing process that may require changesto and interpretations of current SSTSs in recognition of the accelerating rateof change in tax laws and the continued importance of tax practice to members.

The Tax Executive Committee promulgates SSTSs. Even though the 1999-2000 Tax Executive Committee approved this version, acknowledgment is alsodue to the many members whose efforts over the years went into the develop-ment of the original statements.

[The next page is 18,021.]

Preface

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,021

TS Section 100

Tax Return Positions

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for members when

recommending tax return positions and preparing or signing tax returns (in-cluding amended returns, claims for refund, and information returns) filed withany taxing authority. For purposes of these standards, a tax return position is(a) a position reflected on the tax return as to which the taxpayer has beenspecifically advised by a member or (b) a position about which a member hasknowledge of all material facts and, on the basis of those facts, has concludedwhether the position is appropriate. For purposes of these standards, a tax-payer is a client, a member's employer, or any other third-party recipient of taxservices.

Statement.02 The following standards apply to a member when providing profes-

sional services that involve tax return positions:

a. A member should not recommend that a tax return position be takenwith respect to any item unless the member has a good-faith beliefthat the position has a realistic possibility of being sustained admin-istratively or judicially on its merits if challenged.

b. A member should not prepare or sign a return that the member isaware takes a position that the member may not recommend underthe standard expressed in paragraph .02a.

c. Notwithstanding paragraph .02a, a member may recommend a tax re-turn position that the member concludes is not frivolous as long asthe member advises the taxpayer to appropriately disclose. Notwith-standing paragraph .02b, the member may prepare or sign a returnthat reflects a position that the member concludes is not frivolous aslong as the position is appropriately disclosed.

d. When recommending tax return positions and when preparing or sign-ing a return on which a tax return position is taken, a member should,when relevant, advise the taxpayer regarding potential penalty con-sequences of such tax return position and the opportunity, if any, toavoid such penalties through disclosure.

.03 A member should not recommend a tax return position or prepare orsign a return reflecting a position that the member knows—

a. Exploits the audit selection process of a taxing authority.b. Serves as a mere arguing position advanced solely to obtain leverage

in the bargaining process of settlement negotiation with a taxing au-thority.

TS §100.03

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,022 Tax Services

.04 When recommending a tax return position, a member has both theright and responsibility to be an advocate for the taxpayer with respect to anyposition satisfying the aforementioned standards.

Explanation.05 Our self-assessment tax system can function effectively only if tax-

payers file tax returns that are true, correct, and complete. A tax return isprimarily a taxpayer's representation of facts, and the taxpayer has the finalresponsibility for positions taken on the return.

.06 In addition to a duty to the taxpayer, a member has a duty to the taxsystem. However, it is well established that the taxpayer has no obligation topay more taxes than are legally owed, and a member has a duty to the taxpayerto assist in achieving that result. The standards contained in paragraphs .02,.03, and .04 recognize the members' responsibilities to both taxpayers and tothe tax system.

.07 In order to meet the standards contained in paragraph .02, a membershould in good faith believe that the tax return position is warranted in existinglaw or can be supported by a good-faith argument for an extension, modifica-tion, or reversal of existing law. For example, in reaching such a conclusion, amember may consider a well-reasoned construction of the applicable statute,well-reasoned articles or treatises, or pronouncements issued by the applicabletaxing authority, regardless of whether such sources would be treated as author-ity under Internal Revenue Code section 6662 and the regulations thereunder.A position would not fail to meet these standards merely because it is laterabandoned for practical or procedural considerations during an administrativehearing or in the litigation process.

.08 If a member has a good-faith belief that more than one tax returnposition meets the standards set forth in paragraph .02, a member's adviceconcerning alternative acceptable positions may include a discussion of thelikelihood that each such position might or might not cause the taxpayer's taxreturn to be examined and whether the position would be challenged in anexamination. In such circumstances, such advice is not a violation of paragraph.03a.

.09 In some cases, a member may conclude that a tax return positionis not warranted under the standard set forth in paragraph .02a. A taxpayermay, however, still wish to take such a position. Under such circumstances, thetaxpayer should have the opportunity to take such a position, and the membermay prepare and sign the return provided the position is appropriately disclosedon the return or claim for refund and the position is not frivolous. A frivolousposition is one that is knowingly advanced in bad faith and is patently improper.

.10 A member's determination of whether information is appropriatelydisclosed by the taxpayer should be based on the facts and circumstances of theparticular case and the authorities regarding disclosure in the applicable taxingjurisdiction. If a member recommending a position, but not engaged to prepareor sign the related tax return, advises the taxpayer concerning appropriatedisclosure of the position, then the member shall be deemed to meet thesestandards.

.11 If particular facts and circumstances lead a member to believe that ataxpayer penalty might be asserted, the member should so advise the taxpayer

TS §100.04

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,023

and should discuss with the taxpayer the opportunity to avoid such penalty bydisclosing the position on the tax return. Although a member should advise thetaxpayer with respect to disclosure, it is the taxpayer's responsibility to decidewhether and how to disclose.

.12 For purposes of this Statement, preparation of a tax return includesgiving advice on events that have occurred at the time the advice is given if theadvice is directly relevant to determining the existence, character, or amountof a schedule, entry, or other portion of a tax return.

[The next page is 18,031.]

TS §100.12

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,024

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,031

TS Section 9100

Tax Return Positions: Tax ServicesInterpretations of Section 1001-1. Realistic Possibility Standard

Background

.01 Statement on Standards for Tax Services (SSTS) No. 1, Tax ReturnPositions [section 100], contains the standards a member should follow in rec-ommending tax return positions and in preparing or signing tax returns. Ingeneral, a member should have a good-faith belief that the tax return positionbeing recommended has a realistic possibility of being sustained administra-tively or judicially on its merits, if challenged. The standard contained in SSTSNo. 1, paragraph 2a [section 100.02a], is referred to here as the realistic possi-bility standard. If a member concludes that a tax return position does not meetthe realistic possibility standard:

a. The member may still recommend the position to the taxpayer if theposition is not frivolous, and the member recommends appropriatedisclosure of the position; or

b. The member may still prepare or sign a tax return containing the po-sition, if the position is not frivolous, and the position is appropriatelydisclosed.

.02 A frivolous position is one that is knowingly advanced in bad faith andis patently improper (see SSTS No. 1, paragraph 9 [section 100.09]). A member'sdetermination of whether information is appropriately disclosed on a tax returnor claim for refund is based on the facts and circumstances of the particularcase and the authorities regarding disclosure in the applicable jurisdiction (seeSSTS No. 1, paragraph 10 [section 100.10]).

.03 If a member believes there is a possibility that a tax return positionmight result in penalties being asserted against a taxpayer, the member shouldso advise the taxpayer and should discuss with the taxpayer the opportunity, ifany, of avoiding such penalties through disclosure (see SSTS No. 1, paragraph11 [section 100.11]). Such advice may be given orally.

General Interpretation

.04 To meet the realistic possibility standard, a member should have agood-faith belief that the position is warranted by existing law or can be sup-ported by a good-faith argument for an extension, modification, or reversal ofthe existing law through the administrative or judicial process. Such a beliefshould be based on reasonable interpretations of the tax law. A member shouldnot take into account the likelihood of audit or detection when determiningwhether this standard has been met (see SSTS No. 1, paragraphs 3a and 8[section 100.03a and .08]).

.05 The realistic possibility standard is less stringent than the substantialauthority standard and the more likely than not standard that apply underthe Internal Revenue Code (IRC) to substantial understatements of liabilityby taxpayers. The realistic possibility standard is stricter than the reasonablebasis standard that is in the IRC.

TS §9100.05

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,032 Tax Services

.06 In determining whether a tax return position meets the realistic pos-sibility standard, a member may rely on authorities in addition to those evalu-ated when determining whether substantial authority exists under IRC section6662. Accordingly, a member may rely on well-reasoned treatises, articles in rec-ognized professional tax publications, and other reference tools and sources oftax analyses commonly used by tax advisers and preparers of returns.

.07 In determining whether a realistic possibility exists, a member shoulddo all of the following:

• Establish relevant background facts

• Distill the appropriate questions from those facts

• Search for authoritative answers to those questions

• Resolve the questions by weighing the authorities uncovered by thatsearch

• Arrive at a conclusion supported by the authorities

.08 A member should consider the weight of each authority to concludewhether a position meets the realistic possibility standard. In determining theweight of an authority, a member should consider its persuasiveness, relevance,and source. Thus, the type of authority is a significant factor. Other importantfactors include whether the facts stated by the authority are distinguishablefrom those of the taxpayer and whether the authority contains an analysis ofthe issue or merely states a conclusion.

.09 The realistic possibility standard may be met despite the absenceof certain types of authority. For example, a member may conclude that therealistic possibility standard has been met when the position is supported onlyby a well-reasoned construction of the applicable statutory provision.

.10 In determining whether the realistic possibility standard has beenmet, the extent of research required is left to the professional judgment of themember with respect to all the facts and circumstances known to the mem-ber. A member may conclude that more than one position meets the realisticpossibility standard.

Specific Illustrations

.11 The following illustrations deal with general fact patterns. Accord-ingly, the application of the guidance discussed in the General Interpretationsection to variations in such general facts or to particular facts or circumstancesmay lead to different conclusions. In each illustration there is no authority otherthan that indicated.

.12 Illustration 1—A taxpayer has engaged in a transaction that is ad-versely affected by a new statutory provision. Prior law supports a positionfavorable to the taxpayer. The taxpayer believes, and the member concurs, thatthe new statute is inequitable as applied to the taxpayer's situation. The statuteis constitutional, clearly drafted, and unambiguous. The legislative history dis-cussing the new statute contains general comments that do not specificallyaddress the taxpayer's situation.

.13 Conclusion—The member should recommend the return position sup-ported by the new statute. A position contrary to a constitutional, clear, andunambiguous statute would ordinarily be considered a frivolous position.

TS §9100.06

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,033

.14 Illustration 2—The facts are the same as in Illustration 1 except thatthe legislative history discussing the new statute specifically addresses thetaxpayer's situation and supports a position favorable to the taxpayer.

.15 Conclusion—In a case where the statute is clearly and unambiguouslyagainst the taxpayer's position but a contrary position exists based on legisla-tive history specifically addressing the taxpayer's situation, a return positionbased either on the statutory language or on the legislative history satisfies therealistic possibility standard.

.16 Illustration 3—The facts are the same as in Illustration 1 except thatthe legislative history can be interpreted to provide some evidence or authorityin support of the taxpayer's position; however, the legislative history does notspecifically address the situation.

.17 Conclusion—In a case where the statute is clear and unambiguous,a contrary position based on an interpretation of the legislative history thatdoes not explicitly address the taxpayer's situation does not meet the realisticpossibility standard. However, because the legislative history provides somesupport or evidence for the taxpayer's position, such a return position is notfrivolous. A member may recommend the position to the taxpayer if the memberalso recommends appropriate disclosure.

.18 Illustration 4—A taxpayer is faced with an issue involving the in-terpretation of a new statute. Following its passage, the statute was widelyrecognized to contain a drafting error, and a technical correction proposal hasbeen introduced. The taxing authority issues a pronouncement indicating howit will administer the provision. The pronouncement interprets the statute inaccordance with the proposed technical correction.

.19 Conclusion—Return positions based on either the existing statutorylanguage or the taxing authority pronouncement satisfy the realistic possibilitystandard.

.20 Illustration 5—The facts are the same as in Illustration 4 except thatno taxing authority pronouncement has been issued.

.21 Conclusion—In the absence of a taxing authority pronouncement in-terpreting the statute in accordance with the technical correction, only a returnposition based on the existing statutory language will meet the realistic pos-sibility standard. A return position based on the proposed technical correctionmay be recommended if it is appropriately disclosed, since it is not frivolous.

.22 Illustration 6—A taxpayer is seeking advice from a member regardinga recently amended statute. The member has reviewed the statute, the leg-islative history that specifically addresses the issue, and a recently publishednotice issued by the taxing authority. The member has concluded in good faiththat, based on the statute and the legislative history, the taxing authority'sposition as stated in the notice does not reflect legislative intent.

.23 Conclusion—The member may recommend the position supported bythe statute and the legislative history because it meets the realistic possibilitystandard.

.24 Illustration 7—The facts are the same as in Illustration 6 except thatthe taxing authority pronouncement is a temporary regulation.

.25 Conclusion—In determining whether the position meets the realisticpossibility standard, a member should determine the weight to be given theregulation by analyzing factors such as whether the regulation is legislative or

TS §9100.25

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,034 Tax Services

interpretative, or if it is inconsistent with the statute. If a member concludesthat the position does not meet the realistic possibility standard, because it isnot frivolous, the position may nevertheless be recommended if the memberalso recommends appropriate disclosure.

.26 Illustration 8—A tax form published by a taxing authority is incorrect,but completion of the form as published provides a benefit to the taxpayer.The member knows that the taxing authority has published an announcementacknowledging the error.

.27 Conclusion—In these circumstances, a return position in accordancewith the published form is a frivolous position.

.28 Illustration 9—A taxpayer wants to take a position that a member hasconcluded is frivolous. The taxpayer maintains that even if the taxing authorityexamines the return, the issue will not be raised.

.29 Conclusion—The member should not consider the likelihood of auditor detection when determining whether the realistic possibility standard hasbeen met. The member should not prepare or sign a return that contains afrivolous position even if it is disclosed.

.30 Illustration 10—A statute is passed requiring the capitalization ofcertain expenditures. The taxpayer believes, and the member concurs, that tocomply fully, the taxpayer will need to acquire new computer hardware andsoftware and implement a number of new accounting procedures. The taxpayerand member agree that the costs of full compliance will be significantly greaterthan the resulting increase in tax due under the new provision. Because ofthese cost considerations, the taxpayer makes no effort to comply. The taxpayerwants the member to prepare and sign a return on which the new requirementis simply ignored.

.31 Conclusion—The return position desired by the taxpayer is frivolous,and the member should neither prepare nor sign the return.

.32 Illustration 11—The facts are the same as in Illustration 10 except thata taxpayer has made a good-faith effort to comply with the law by calculatingan estimate of expenditures to be capitalized under the new provision.

.33 Conclusion—In this situation, the realistic possibility standard hasbeen met. When using estimates in the preparation of a return, a membershould refer to SSTS No. 4, Use of Estimates [section 400].

.34 Illustration 12—On a given issue, a member has located and weighedtwo authorities concerning the treatment of a particular expenditure. A taxingauthority has issued an administrative ruling that required the expenditureto be capitalized and amortized over several years. On the other hand, a courtopinion permitted the current deduction of the expenditure. The member hasconcluded that these are the relevant authorities, considered the source of bothauthorities, and concluded that both are persuasive and relevant.

.35 Conclusion—The realistic possibility standard is met by either posi-tion.

.36 Illustration 13—A tax statute is silent on the treatment of an item un-der the statute. However, the legislative history explaining the statute directsthe taxing authority to issue regulations that will require a specific treatmentof the item. No regulations have been issued at the time the member mustrecommend a position on the tax treatment of the item.

.37 Conclusion—The member may recommend the position supported bythe legislative history because it meets the realistic possibility standard.

TS §9100.26

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,035

.38 Illustration 14—A taxpayer wants to take a position that a memberconcludes meets the realistic possibility standard based on an assumption re-garding an underlying nontax legal issue. The member recommends that thetaxpayer seek advice from its legal counsel, and the taxpayer's attorney givesan opinion on the nontax legal issue.

.39 Conclusion—A member may in general rely on a legal opinion on a non-tax legal issue. A member should, however, use professional judgment whenrelying on a legal opinion. If, on its face, the opinion of the taxpayer's attor-ney appears to be unreasonable, unsubstantiated, or unwarranted, a membershould consult his or her attorney before relying on the opinion.

.40 Illustration 15—A taxpayer has obtained from its attorney an opinionon the tax treatment of an item and requests that a member rely on the opinion.

.41 Conclusion—The authorities on which a member may rely includewell-reasoned sources of tax analysis. If a member is satisfied about the source,relevance, and persuasiveness of the legal opinion, a member may rely on thatopinion when determining whether the realistic possibility standard has beenmet.

[Issue Date: August, 2000.]

1-2. Tax PlanningBackground

.42 SSTSs are enforceable standards that govern the conduct of membersof the AICPA in tax practice. A significant area of many members' tax practicesinvolves assisting taxpayers in tax planning. Two of the eight SSTSs issuedas of the date of this Interpretation's release directly set forth standards thataffect the most common activities in tax planning. Several other SSTSs set forthstandards related to specific factual situations that may arise while a memberis assisting a taxpayer in tax planning. The two SSTSs that are most typicallyrelevant to tax planning are SSTS No. 1, Tax Return Positions [section 100],including Interpretation No. 1-1, "Realistic Possibility Standard" (paragraphs.01–.41), and SSTS No. 8, Form and Content of Advice to Taxpayers [section800].

.43 Taxing authorities, courts, the AICPA, and other professional organi-zations have struggled with defining and regulating tax shelters and abusivetransactions. Crucial to the debate is the difficulty of clearly distinguishing be-tween transactions that are abusive and transactions that are legitimate. Atthe same time, it must be recognized that taxpayers have a legitimate interestin arranging their affairs so as to pay no more than the taxes they owe. It mustbe recognized that tax professionals, including members, have a role to play inadvancing these efforts.

.44 This Interpretation is part of the AICPA's continuing efforts at self-regulation of its members in tax practice. It has its origins in the AICPA's desireto provide adequate guidance to its members when providing services in connec-tion with tax planning. The Interpretation does not change or elevate any levelof conduct prescribed by any standard. Its goal is to clarify existing standards.It was determined that there was a compelling need for a comprehensive Inter-pretation of a member's responsibilities in connection with tax planning, withthe recognition that such guidance would clarify how those standards wouldapply across the spectrum of tax planning, including those situations involvingtax shelters, regardless of how that term is defined.

TS §9100.44

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,036 Tax Services

General Interpretation

.45 The realistic possibility standard (see SSTS No. 1, paragraph 2a [sec-tion 100.02a], and Interpretation No. 1–1 [paragraphs .01–.41]) applies to amember when providing professional services that involve tax planning. Amember may still recommend a nonfrivolous position provided that the mem-ber recommends appropriate disclosure (see SSTS No. 1, paragraph 2c [section100.02c]).

.46 For purposes of this Interpretation, tax planning includes, both withrespect to prospective and completed transactions, recommending or expressingan opinion (whether written or oral) on (a) a tax return position or (b) a specifictax plan developed by the member, the taxpayer, or a third party.

.47 When issuing an opinion to reflect the results of the tax planningservice, a member should do all of the following:

• Establish the relevant background facts.

• Consider the reasonableness of the assumptions and representations.

• Apply the pertinent authorities to the relevant facts.

• Consider the business purpose and economic substance of the trans-action, if relevant to the tax consequences of the transaction.

• Arrive at a conclusion supported by the authorities.

.48 In assisting a taxpayer in a tax planning transaction in which thetaxpayer has obtained an opinion from a third party, and the taxpayer is lookingto the member for an evaluation of the opinion, the member should be satisfiedas to the source, relevance, and persuasiveness of the opinion, which wouldinclude considering whether the opinion indicates the third party did all of thefollowing:

• Established the relevant background facts

• Considered the reasonableness of the assumptions and representa-tions

• Applied the pertinent authorities to the relevant facts

• Considered the business purpose and economic substance of the trans-action, if relevant to the tax consequences of the transaction

• Arrived at a conclusion supported by the authorities

.49 In conducting the due diligence necessary to establish the relevantbackground facts, the member should consider whether it is appropriate to relyon an assumption concerning facts in lieu of either other procedures to supportthe advice or a representation from the taxpayer or another person. A membershould also consider whether the member's tax advice will be communicated tothird parties, particularly if those third parties may not be knowledgeable ormay not be receiving independent tax advice with respect to a transaction.

.50 In tax planning, members often rely on assumptions and representa-tions. Although such reliance is often necessary, the member must take careto assess whether such assumptions and representations are reasonable. Indeciding whether an assumption or representation is reasonable, the membershould consider its source and consistency with other information known to themember. For example, depending on the circumstances, it may be reasonablefor a member to rely on a representation made by the taxpayer, but not ona representation made by a person who is selling or otherwise promoting thetransaction to the taxpayer.

TS §9100.45

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,037

.51 When engaged in tax planning, the member should understand thebusiness purpose and economic substance of the transaction when relevantto the tax consequences. If a transaction has been proposed by a party otherthan the taxpayer, the member should consider whether the assumptions madeby the third party are consistent with the facts of the taxpayer's situation. Ifwritten advice is to be rendered concerning a transaction, the business purposefor the transaction generally should be described. If the business reasons arerelevant to the tax consequences, it is insufficient to merely assume that atransaction is entered into for valid business reasons without specifying whatthose reasons are.

.52 The scope of the engagement should be appropriately determined. Amember should be diligent in applying such procedures as are appropriate un-der the circumstances to understand and evaluate the entire transaction. Thespecific procedures to be performed in this regard will vary with the circum-stances and the scope of the engagement.

Specific Illustrations

.53 The following illustrations address general fact patterns. Accordingly,the application of the guidance discussed in the "General Interpretation" sectionto variations in such general facts or to particular facts or circumstances maylead to different conclusions. In each illustration, there is no authority otherthan that indicated.

.54 Illustration 1—The relevant tax code imposes penalties on substantialunderpayments that are not associated with tax shelters as defined in such codeunless the associated positions are supported by substantial authority.

.55 Conclusion—In assisting the taxpayer in tax planning in which anyassociated underpayment would be substantial, the member should inform thetaxpayer of the penalty risks associated with the tax return position recom-mended with respect to any plan under consideration that satisfies the realis-tic possibility of success standard, but does not possess sufficient authority tosatisfy the substantial authority standard.

.56 Illustration 2—The relevant tax code imposes penalties on tax shelters,as defined in such code, unless the taxpayer concludes that a position taken ona tax return associated with such a tax shelter is, more likely than not, thecorrect position.

.57 Conclusion—In assisting the taxpayer in tax planning, the membershould inform the taxpayer of the penalty risks associated with the tax returnposition recommended with respect to any plan under consideration that satis-fies the realistic possibility of success standard, but does not possess sufficientauthority to satisfy the more likely than not standard.

.58 Illustration 3—The relevant tax regulation provides that the detailsof (or certain information regarding) a specific transaction are required to beattached to the tax return, regardless of the support for the associated taxreturn position (for example, even if there is substantial authority or a higherlevel of comfort for the position). While preparing the taxpayer's return for theyear, the member is aware that an attachment is required.

.59 Conclusion—In general, if the taxpayer agrees to include the attach-ment required by the regulation, the member may sign the return if the mem-ber concludes the associated tax return position satisfies the realistic possi-bility standard. However, if the taxpayer refuses to include the attachment,the member should not sign the return, unless the member concludes the

TS §9100.59

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,038 Tax Services

associated tax return position satisfies the realistic possibility standard andthere are reasonable grounds for the taxpayer's position with respect to theattachment. In this regard, the member should consider SSTS No. 2, Answersto Questions on Returns, paragraphs 1 and 5, [section 200.01 and .05], whichprovides that the term questions, as used in the standard, "includes requestsfor information on the return, in the instructions, or in the regulations, whetheror not stated in the form of a question," and that a "member should not omit ananswer merely because it might prove disadvantageous to a taxpayer."

.60 Illustration 4—The relevant tax regulations provide that the detailsof certain potentially abusive transactions that are designated as "listed trans-actions" are required to be disclosed in attachments to tax returns, regardlessof the support for the associated tax return position (for example, even if thereis substantial authority or a higher level of support for the position). Underthe regulations, if a listed transaction is not disclosed as required, the taxpayerwill have additional penalty risks. While researching the tax consequences ofa proposed transaction, a member concludes that the transaction is a listedtransaction.

.61 Conclusion—Notwithstanding the member's conclusion that the trans-action is a listed transaction, the member may still recommend a tax returnposition with respect to the transaction if he or she concludes that the proposedtax return position satisfies the realistic possibility standard. However, themember should inform the taxpayer of the enhanced disclosure requirementsof listed transactions and the additional penalty risks for nondisclosure.

.62 Illustration 5—The same regulations apply as in Illustration 4. Themember first becomes aware that a taxpayer entered into a transaction whilepreparing the taxpayer's return for the year of the transaction. While research-ing the tax consequences of the transaction, the member concludes that thetaxpayer's transaction is a listed transaction.

.63 Conclusion—The member should inform the taxpayer of the enhanceddisclosure requirement and the additional penalty risks for nondisclosure. If thetaxpayer agrees to make the disclosure required by the regulation, the membermay sign the return if the member concludes the associated tax return positionsatisfies the realistic possibility standard. Reasonable grounds for nondisclo-sure (see the conclusion to Illustration 3) generally are not present for a listedtransaction. The member should not sign the return if the transaction is notdisclosed. If the member is a nonsigning preparer of the return, the membershould recommend that the taxpayer disclose the transaction.

.64 Illustration 6—The same regulations apply as in Illustration 4. Themember first becomes aware that a taxpayer entered into a transaction whilepreparing the taxpayer's return for the year of the transaction. While research-ing the tax consequences of the transaction, the member concludes that thereis uncertainty about whether the taxpayer's transaction is a listed transaction.

.65 Conclusion—The member should inform the taxpayer of the enhanceddisclosure requirement and the additional penalty risks for nondisclosure. Ifthe taxpayer agrees to make the disclosure required by the relevant regula-tion, the member may sign the return if the member concludes the associatedtax return position satisfies the realistic possibility standard. If the taxpayerdoes not want to disclose the transaction because of the uncertainty aboutwhether it is a listed transaction, the member may sign the return if the

TS §9100.60

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,039

member concludes the associated tax return position satisfies the realistic pos-sibility standard and there are reasonable grounds for the taxpayer's positionwith regard to nondisclosure. In this regard, the member should consider SSTSNo. 2, paragraph 4 [section 200.04], which indicates that the degree of uncer-tainty regarding the meaning of a question on a return may affect whetherthere are reasonable grounds for not responding to the question.

.66 Illustration 7—A member advises a taxpayer concerning the tax con-sequences of a transaction involving a loan from a U.S. bank. In the processof reviewing documents associated with the proposed transaction, the memberuncovers a reference to a deposit that a wholly owned foreign subsidiary of thetaxpayer will make with an overseas branch of the U.S. bank. The transac-tion documents appear to indicate that this deposit is linked to the U.S. bank'sissuance of the loan.

.67 Conclusion—The member should consider the effect, if any, of thedeposit in advising the taxpayer about the tax consequences of the proposedtransaction.

.68 Illustration 8—Under the relevant tax law, the tax consequences of aleasing transaction depend on whether the property to be leased is reasonablyexpected to have a residual value of 15 percent of its value at the beginning ofthe lease. The member has relied on a taxpayer's instruction to use a particularassumption concerning the residual value.

.69 Conclusion—Such reliance on the taxpayer's instructions may be ap-propriate if the assumption is supported by the expertise of the taxpayer, bythe member's review of information provided by the taxpayer or a third party,or through the member's own knowledge or analysis.

.70 Illustration 9—A member is assisting a taxpayer with evaluating aproposed equipment leasing transaction in which the estimated residual valueof the equipment at the end of the lease term is critical to the tax consequencesof the lease. The broker arranging the leasing transaction has prepared an anal-ysis that sets out an explicit assumption concerning the equipment's estimatedresidual value.

.71 Conclusion—The member should consider whether it is appropriate torely on the broker's assumption concerning the estimated residual value of theequipment instead of obtaining a representation from the broker concerning es-timated residual value or performing other procedures to validate the amountto be used as an estimate of residual value in connection with the member's ad-vice. In considering the appropriateness of the broker's assumption, the membershould consider, for example, factors such as the broker's experience in the area,the broker's methodology, and whether alternative sources of information arereasonably available.

.72 Illustration 10—The tax consequences of a particular reorganizationdepend, in part, on the majority shareholder of a corporation not disposing ofany stock received in the reorganization pursuant to a prearranged agreementto dispose of the stock.

.73 Conclusion—The member should consider whether it is appropriate inrendering tax advice to assume that such a disposition will not occur or whether,under the circumstances, it is appropriate to request a written representationof the shareholder's intent concerning disposition as a condition to issuing anopinion on the reorganization.

.74 Illustration 11—A taxpayer is considering a proposed transaction. Thetaxpayer and the taxpayer's attorney advise the member that the member is re-sponsible for advising the taxpayer on the tax consequences of the transaction.

TS §9100.74

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,040 Tax Services

.75 Conclusion—In addition to complying with the requirements of para-graph .47, the member generally should review all relevant draft transactiondocuments in formulating the member's tax advice relating to the transaction.

.76 Illustration 12—A member is responsible for advising a taxpayer onthe tax consequences of the taxpayer's estate plan.

.77 Conclusion—Under the circumstances, the member should review thewill and all other relevant documents to assess whether there appear to be anytax issues raised by the formulation or implementation of the estate plan.

.78 Illustration 13—A member is assisting a taxpayer in connection witha proposed transaction that has been recommended by an investment bank. Tosupport its recommendation, the investment bank offers a law firm's opinionon the tax consequences. The member reads the opinion, and notes that it isbased on a hypothetical statement of facts rather than the taxpayer's facts.

.79 Conclusion—The member may rely on the law firm's opinion whendetermining whether the realistic possibility standard has been satisfied withrespect to the tax consequences of the hypothetical transaction if the mem-ber is satisfied about the source, relevance, and persuasiveness of the opinion.However, the member should be diligent in taking such steps as are appropri-ate under the circumstances to understand and evaluate the transaction as itapplies to the taxpayer's specific situation by:

• Establishing the relevant background facts

• Considering the reasonableness of the assumptions and repre-sentations

• Applying the pertinent authorities to the relevant facts

• Considering the business purpose and economic substance of the trans-action, if relevant to the tax consequences of the transaction (Mere re-liance on a representation that there is business purpose or economicsubstance is generally insufficient.)

• Arriving at a conclusion supported by the authorities

.80 Illustration 14—The facts are the same as in Illustration 13 exceptthe member also notes that the law firm that prepared the opinion is one thathas a reputation as being knowledgeable about the tax issues associated withthe proposed transaction.

.81 Conclusion—The conclusion is the same as the conclusion to Illustra-tion 13, notwithstanding the expertise of the law firm.

.82 Illustration 15—A member is assisting a taxpayer in connection witha proposed transaction that has been recommended by an investment bank. Tosupport that recommendation, the investment bank offers a law firm's opinionabout the tax consequences. The member reads the opinion, and notes that(unlike the opinions described in Illustrations 13 and 14), it is carefully tailoredto the taxpayer's facts.

.83 Conclusion—The member may rely on the opinion when determiningwhether the realistic possibility standard has been met with respect to the tax-payer's participation in the transaction if the member is satisfied about thesource, relevance, and persuasiveness of the opinion. In making that determi-nation, the member should consider whether the opinion indicates the law firmdid all of the following:

• Established the relevant background facts

• Considered the reasonableness of the assumptions and repre-sentations

TS §9100.75

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Tax Return Positions 18,040-1

• Applied the pertinent authorities to the relevant facts

• Considered the business purpose and economic substance of the trans-action, if relevant to the tax consequences of the transaction (Mere re-liance on a representation that there is business purpose or economicsubstance is generally insufficient.)

• Arrived at a conclusion supported by the authorities

.84 Illustration 16—The facts are the same as in Illustration 15, exceptthe member also notes that the law firm that prepared the opinion is one thathas a reputation of being knowledgeable about the tax issues associated withthe proposed transaction.

.85 Conclusion—The conclusion is the same as the conclusion to Illustra-tion 15, notwithstanding the expertise of the law firm.

.86 Illustration 17—A member is assisting a taxpayer with year-end plan-ning in connection with the taxpayer's proposed contribution of stock in a closelyheld corporation to a charitable organization. The taxpayer instructs the mem-ber to calculate the anticipated tax liability assuming a contribution of 10,000shares to a tax-exempt organization assuming the stock has a fair market valueof $100 per share. The member is aware that on the taxpayer's gift tax returnsfor the prior year, the taxpayer indicated that her stock in the corporation wasworth $50 per share.

.87 Conclusion—The member's calculation of the anticipated tax liabilityis subject to the general interpretations described in paragraphs .49 and .50.Accordingly, even though this potentially may be a case in which the value of thestock substantially appreciated during the year, the member should considerthe reasonableness of the assumption and consistency with other informationknown to the member in connection with preparing the projection. The membershould consider whether to document discussions concerning the increase invalue of the stock with the taxpayer.

.88 Illustration 18—The tax consequences to Target Corporation's share-holders of an acquisition turn in part on Acquiring Corporation's continuance ofthe trade or business of Target Corporation for some time after the acquisition.The member is preparing a tax opinion addressed to Target's shareholders. Acolleague has drafted a tax opinion for the member's review. That opinion makesan explicit assumption that Acquiring will continue Target's business for twoyears following the acquisition.

.89 Conclusion—In conducting the due diligence necessary to establishthe relevant background facts, the member should consider whether it is ap-propriate to rely on an assumption concerning facts in lieu of a representationfrom another person. In this case, the member should make reasonable effortsto obtain a representation from Acquiring Corporation concerning its plan tocontinue Target's business and further consider whether to request a writtenrepresentation to that effect.

.90 Illustration 19—The member receives a telephone call from a taxpayerwho is the sole shareholder of a corporation. The taxpayer indicates that he isthinking about exchanging his stock in the corporation for stock in a publiclytraded business. During the call, the member explains how the transactionshould be structured so it will qualify as a tax-free acquisition.

.91 Conclusion—Although oral advice may serve a taxpayer's needs appro-priately in routine matters or in well-defined areas, written communications arerecommended in important, unusual, or complicated transactions. The membershould use professional judgment about the need to document oral advice.

TS §9100.91

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,040-2 Tax Services

.92 Illustration 20—The member receives a telephone call from a taxpayerwho wants to know whether he or she should lease or purchase a car. Duringthe call, the member explains how the arrangement should be structured so asto help achieve the taxpayer's objectives.

.93 Conclusion—In this situation, the member's response is in conformitywith this Interpretation in view of the routine nature of the inquiry and thewell-defined tax issues. However, the member should evaluate whether otherconsiderations, such as avoiding misunderstanding with the taxpayer, suggestthat the conversation should be documented.

[Issue Date: December, 2003.]

[The next page is 18,041.]

TS §9100.92

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Answers to Questions on Returns 18,041

TS Section 200

Answers to Questions on Returns

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for members when

signing the preparer's declaration on a tax return if one or more questions onthe return have not been answered. The term questions includes requests forinformation on the return, in the instructions, or in the regulations, whetheror not stated in the form of a question.

Statement.02 A member should make a reasonable effort to obtain from the taxpayer

the information necessary to provide appropriate answers to all questions on atax return before signing as preparer.

Explanation.03 It is recognized that the questions on tax returns are not of uniform

importance, and often they are not applicable to the particular taxpayer. Nev-ertheless, there are at least two reasons why a member should be satisfied thata reasonable effort has been made to obtain information to provide appropriateanswers to the questions on the return that are applicable to a taxpayer.

a. A question may be of importance in determining taxable income orloss, or the tax liability shown on the return, in which circumstancean omission may detract from the quality of the return.

b. A member often must sign a preparer's declaration stating that thereturn is true, correct, and complete.

.04 Reasonable grounds may exist for omitting an answer to a questionapplicable to a taxpayer. For example, reasonable grounds may include thefollowing:

a. The information is not readily available and the answer is not signif-icant in terms of taxable income or loss, or the tax liability shown onthe return.

b. Genuine uncertainty exists regarding the meaning of the question inrelation to the particular return.

c. The answer to the question is voluminous; in such cases, a statementshould be made on the return that the data will be supplied uponexamination.

TS §200.04

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,042 Tax Services

.05 A member should not omit an answer merely because it might provedisadvantageous to a taxpayer.

.06 If reasonable grounds exist for omission of an answer to an applicablequestion, a taxpayer is not required to provide on the return an explanationof the reason for the omission. In this connection, a member should considerwhether the omission of an answer to a question may cause the return to bedeemed incomplete.

[The next page is 18,051.]

TS §200.05

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Certain Procedural Aspects of Preparing Returns 18,051

TS Section 300

Certain Procedural Aspects ofPreparing Returns

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for members con-

cerning the obligation to examine or verify certain supporting data or to con-sider information related to another taxpayer when preparing a taxpayer's taxreturn.

Statement.02 In preparing or signing a return, a member may in good faith rely, with-

out verification, on information furnished by the taxpayer or by third parties.However, a member should not ignore the implications of information furnishedand should make reasonable inquiries if the information furnished appears tobe incorrect, incomplete, or inconsistent either on its face or on the basis of otherfacts known to a member. Further, a member should refer to the taxpayer's re-turns for one or more prior years whenever feasible.

.03 If the tax law or regulations impose a condition with respect to de-ductibility or other tax treatment of an item, such as taxpayer maintenanceof books and records or substantiating documentation to support the reporteddeduction or tax treatment, a member should make appropriate inquiries todetermine to the member's satisfaction whether such condition has been met.

.04 When preparing a tax return, a member should consider informationactually known to that member from the tax return of another taxpayer if theinformation is relevant to that tax return and its consideration is necessary toproperly prepare that tax return. In using such information, a member shouldconsider any limitations imposed by any law or rule relating to confidentiality.

Explanation.05 The preparer's declaration on a tax return often states that the infor-

mation contained therein is true, correct, and complete to the best of the pre-parer's knowledge and belief based on all information known by the preparer.This type of reference should be understood to include information furnished bythe taxpayer or by third parties to a member in connection with the preparationof the return.

.06 The preparer's declaration does not require a member to examine orverify supporting data. However, a distinction should be made between (a) theneed either to determine by inquiry that a specifically required condition, such

TS §300.06

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,052 Tax Services

as maintaining books and records or substantiating documentation, has beensatisfied or to obtain information when the material furnished appears to beincorrect or incomplete and (b) the need for a member to examine underly-ing information. In fulfilling his or her obligation to exercise due diligence inpreparing a return, a member may rely on information furnished by the tax-payer unless it appears to be incorrect, incomplete, or inconsistent. Although amember has certain responsibilities in exercising due diligence in preparing areturn, the taxpayer has the ultimate responsibility for the contents of the re-turn. Thus, if the taxpayer presents unsupported data in the form of lists of taxinformation, such as dividends and interest received, charitable contributions,and medical expenses, such information may be used in the preparation of atax return without verification unless it appears to be incorrect, incomplete, orinconsistent either on its face or on the basis of other facts known to a member.

.07 Even though there is no requirement to examine underlying documen-tation, a member should encourage the taxpayer to provide supporting datawhere appropriate. For example, a member should encourage the taxpayer tosubmit underlying documents for use in tax return preparation to permit fullconsideration of income and deductions arising from security transactions andfrom pass-through entities, such as estates, trusts, partnerships, and S corpo-rations.

.08 The source of information provided to a member by a taxpayer foruse in preparing the return is often a pass-through entity, such as a limitedpartnership, in which the taxpayer has an interest but is not involved in man-agement. A member may accept the information provided by the pass-throughentity without further inquiry, unless there is reason to believe it is incorrect,incomplete, or inconsistent, either on its face or on the basis of other factsknown to the member. In some instances, it may be appropriate for a memberto advise the taxpayer to ascertain the nature and amount of possible exposureto tax deficiencies, interest, and penalties, by contact with management of thepass-through entity.

.09 A member should make use of a taxpayer's returns for one or more prioryears in preparing the current return whenever feasible. Reference to prior re-turns and discussion of prior-year tax determinations with the taxpayer shouldprovide information to determine the taxpayer's general tax status, avoid theomission or duplication of items, and afford a basis for the treatment of similaror related transactions. As with the examination of information supplied forthe current year's return, the extent of comparison of the details of income anddeduction between years depends on the particular circumstances.

[The next page is 18,061.]

TS §300.07

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Use of Estimates 18,061

TS Section 400

Use of Estimates

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for members when

using the taxpayer's estimates in the preparation of a tax return. A member mayadvise on estimates used in the preparation of a tax return, but the taxpayerhas the responsibility to provide the estimated data. Appraisals or valuationsare not considered estimates for purposes of this Statement.

Statement.02 Unless prohibited by statute or by rule, a member may use the tax-

payer's estimates in the preparation of a tax return if it is not practical to obtainexact data and if the member determines that the estimates are reasonablebased on the facts and circumstances known to the member. If the taxpayer'sestimates are used, they should be presented in a manner that does not implygreater accuracy than exists.

Explanation.03 Accounting requires the exercise of professional judgment and, in

many instances, the use of approximations based on judgment. The applica-tion of such accounting judgments, as long as not in conflict with methods setforth by a taxing authority, is acceptable. These judgments are not estimateswithin the purview of this Statement. For example, a federal income tax regula-tion provides that if all other conditions for accrual are met, the exact amount ofincome or expense need not be known or ascertained at year end if the amountcan be determined with reasonable accuracy.

.04 When the taxpayer's records do not accurately reflect information re-lated to small expenditures, accuracy in recording some data may be difficultto achieve. Therefore, the use of estimates by a taxpayer in determining theamount to be deducted for such items may be appropriate.

.05 When records are missing or precise information about a transactionis not available at the time the return must be filed, a member may prepare atax return using a taxpayer's estimates of the missing data.

.06 Estimated amounts should not be presented in a manner that providesa misleading impression about the degree of factual accuracy.

.07 Specific disclosure that an estimate is used for an item in the returnis not generally required; however, such disclosure should be made in unusual

TS §400.07

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,062 Tax Services

circumstances where nondisclosure might mislead the taxing authority regard-ing the degree of accuracy of the return as a whole. Some examples of unusualcircumstances include the following:

a. A taxpayer has died or is ill at the time the return must be filed.b. A taxpayer has not received a Schedule K-1 for a pass-through entity

at the time the tax return is to be filed.c. There is litigation pending (for example, a bankruptcy proceeding) that

bears on the return.d. Fire or computer failure has destroyed the relevant records.

[The next page is 18,071.]

TS §400.07

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Departure From a Position 18,071

TS Section 500

Departure From a Position PreviouslyConcluded in an Administrative Proceedingor Court Decision

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for members in

recommending a tax return position that departs from the position determinedin an administrative proceeding or in a court decision with respect to the tax-payer's prior return.

.02 For purposes of this Statement, administrative proceeding also in-cludes an examination by a taxing authority or an appeals conference relatingto a return or a claim for refund.

.03 For purposes of this Statement, court decision means a decision by anycourt having jurisdiction over tax matters.

Statement.04 The tax return position with respect to an item as determined in an

administrative proceeding or court decision does not restrict a member fromrecommending a different tax position in a later year's return, unless the tax-payer is bound to a specified treatment in the later year, such as by a formalclosing agreement. Therefore, as provided in Statement on Standards for TaxServices (SSTS) No. 1, Tax Return Positions [section 100], the member mayrecommend a tax return position or prepare or sign a tax return that departsfrom the treatment of an item as concluded in an administrative proceeding orcourt decision with respect to a prior return of the taxpayer.

Explanation.05 If an administrative proceeding or court decision has resulted in a

determination concerning a specific tax treatment of an item in a prior year'sreturn, a member will usually recommend this same tax treatment in subse-quent years. However, departures from consistent treatment may be justifiedunder such circumstances as the following:

a. Taxing authorities tend to act consistently in the disposition of an itemthat was the subject of a prior administrative proceeding but generallyare not bound to do so. Similarly, a taxpayer is not bound to follow thetax treatment of an item as consented to in an earlier administrativeproceeding.

TS §500.05

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,072 Tax Services

b. The determination in the administrative proceeding or the court's de-cision may have been caused by a lack of documentation. Supportingdata for the later year may be appropriate.

c. A taxpayer may have yielded in the administrative proceeding for set-tlement purposes or not appealed the court decision, even though theposition met the standards in SSTS No. 1 [section 100].

d. Court decisions, rulings, or other authorities that are more favorableto a taxpayer's current position may have developed since the prioradministrative proceeding was concluded or the prior court decisionwas rendered.

.06 The consent in an earlier administrative proceeding and the existenceof an unfavorable court decision are factors that the member should considerin evaluating whether the standards in SSTS No. 1 [section 100] are met.

[The next page is 18,081.]

TS §500.06

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

Knowledge of Error: Return Preparation 18,081

TS Section 600

Knowledge of Error: Return Preparation

Issue date, unlessotherwise indicated:

August, 2000

Introduction.01 This Statement sets forth the applicable standards for a member who

becomes aware of an error in a taxpayer's previously filed tax return or of ataxpayer's failure to file a required tax return. As used herein, the term errorincludes any position, omission, or method of accounting that, at the time thereturn is filed, fails to meet the standards set out in Statement on Standardsfor Tax Services (SSTS) No. 1, Tax Return Positions [section 100]. The termerror also includes a position taken on a prior year's return that no longermeets these standards due to legislation, judicial decisions, or administrativepronouncements having retroactive effect. However, an error does not includean item that has an insignificant effect on the taxpayer's tax liability.

.02 This Statement applies whether or not the member prepared or signedthe return that contains the error.

Statement.03 A member should inform the taxpayer promptly upon becoming aware

of an error in a previously filed return or upon becoming aware of a taxpayer'sfailure to file a required return. A member should recommend the correctivemeasures to be taken. Such recommendation may be given orally. The memberis not obligated to inform the taxing authority, and a member may not do sowithout the taxpayer's permission, except when required by law.

.04 If a member is requested to prepare the current year's return andthe taxpayer has not taken appropriate action to correct an error in a prioryear's return, the member should consider whether to withdraw from prepar-ing the return and whether to continue a professional or employment relation-ship with the taxpayer. If the member does prepare such current year's re-turn, the member should take reasonable steps to ensure that the error is notrepeated.

Explanation.05 While performing services for a taxpayer, a member may become aware

of an error in a previously filed return or may become aware that the taxpayerfailed to file a required return. The member should advise the taxpayer of theerror and the measures to be taken. Such recommendation may be given orally.If the member believes that the taxpayer could be charged with fraud or othercriminal misconduct, the taxpayer should be advised to consult legal counselbefore taking any action.

TS §600.05

P1: JsY

AICP034-p18001-19004 AICPA034-Vol-II-PS.cls June 30, 2006 13:4

18,082 Tax Services

.06 It is the taxpayer's responsibility to decide whether to correct the error.If the taxpayer does not correct an error, a member should consider whether tocontinue a professional or employment relationship with the taxpayer. Whilerecognizing that the taxpayer may not be required by statute to correct anerror by filing an amended return, a member should consider whether a tax-payer's decision not to file an amended return may predict future behavior thatmight require termination of the relationship. The potential for violating Codeof Professional Conduct rule 301 [ET section 301.01] (relating to the member'sconfidential client relationship), the tax law and regulations, or laws on privi-leged communications, and other considerations may create a conflict betweenthe member's interests and those of the taxpayer. Therefore, a member shouldconsider consulting with his or her own legal counsel before deciding uponrecommendations to the taxpayer and whether to continue a professional oremployment relationship with the taxpayer.