ACCA Paper P2

317

ACCA Paper P2 (International & UK) Corporate Reporting Class Notes June 2013

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of ACCA Paper P2

ACCA Paper P2

(International & UK) Corporate Reporting

Class Notes

June 2013

2 www.studyinteract ive.org

© Interactive World Wide Ltd, January 2013

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of Interactive World Wide Ltd.

www.studyinteract ive.org 3

Contents PAGE

INTRODUCTION TO THE PAPER 5

CHAPTER 1: BASIC GROUPS 25

CHAPTER 2: COMPLEX GROUPS 45

CHAPTER 3: FOREIGN CURRENCY TRANSLATION 57

CHAPTER 3: GROUP CASH FLOW STATEMENTS 69

CHAPTER 5: CORPORATE SOCIAL RESPONSIBILITY AND CURRENT ISSUES 83

CHAPTER 6: PERFORMANCE REPORTING 123

CHAPTER 7: PROVISIONS 131

CHAPTER 8: NON CURRENT ASSETS 139

CHAPTER 9: LEASES 149

CHAPTER 10: EMPLOYEE BENEFITS 155

CHAPTER 11: SHARE BASED PAYMENTS 161

CHAPTER 12: FINANCIAL INSTRUMENTS 167

CHAPTER 13: TAX 187

CHAPTER 14: UK CORPORATE REPORTING 201

APPENDIX: SUGGESTED SOLUTIONS TO QUESTIONS AND EXAMPLES 209

ACCA STUDY GUIDE 311

4 www.studyinteract ive.org

www.studyinteract ive.org 5

Introduction to the

paper

INTRODUCTION TO THE PAPER

6 www.studyinteract ive.org

AIM OF THE PAPER

The aim of the paper is to test your understanding of financial reporting and probably more importantly to test your ability to solve problems in accounting scenarios that are every bit as messy as real life.

FORMAT OF THE EXAM PAPER

The syllabus is assessed by a three hour paper-based examination. The paper has 15 minutes reading time. There are four questions of which you must do three as follows:

Section A (Compulsory Case Study)

(q1) The case will be based around a group scenario. There will be 35 marks of numbers and 15 marks of narrative.

(50 marks)

Section B (Choice of 2 from 3 questions)

(q2) Focus. Typically the second question in the exam focuses on a single technical subject, such as pensions, financial instruments or deferred tax. Often this question requires thorough technical knowledge.

(25 marks)

(q3) Mix. Usually there are roughly 5 mini scenarios, each valued at 5 marks and covering a wide range of financial reporting issues. These questions require problem solving and usually far less technical knowledge than question two.

(25 marks)

(q4) Current Issues and CSR. Whether you call this question “Corporate Social Responsibly”, “pure narrative” or another less polite phrase, there is no getting away from the very low technical content and the very high potential for letting your pen wander across a whole range of ideas. These questions have to be seen to be believed. So look at the chapter on Corporate Social Responsibility to get a feel for their style.

(25 marks)

In reality, the examiner plays with the flavour of the B section. For example, in June 2010 the examiner reversed the usual order of the middle two questions, so that q2 was mix and q3 was focus. Often the style of question 2, 3 and 4 can be so similar as to make distinction irrelevant.

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 7

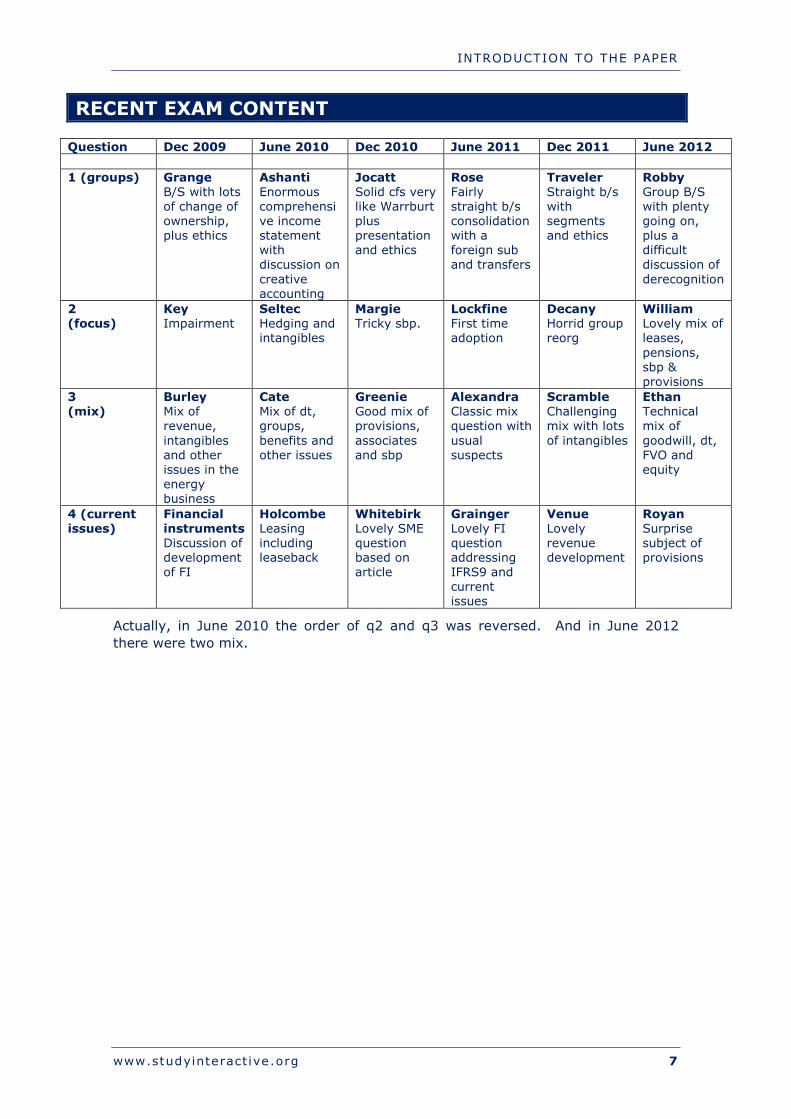

RECENT EXAM CONTENT

Question Dec 2009 June 2010 Dec 2010 June 2011 Dec 2011 June 2012 1 (groups) Grange

B/S with lots of change of ownership, plus ethics

Ashanti Enormous comprehensive income statement with discussion on creative accounting

Jocatt Solid cfs very like Warrburt plus presentation and ethics

Rose Fairly straight b/s consolidation with a foreign sub and transfers

Traveler Straight b/s with segments and ethics

Robby Group B/S with plenty going on, plus a difficult discussion of derecognition

2 (focus)

Key Impairment

Seltec Hedging and intangibles

Margie Tricky sbp.

Lockfine First time adoption

Decany Horrid group reorg

William Lovely mix of leases, pensions, sbp & provisions

3 (mix)

Burley Mix of revenue, intangibles and other issues in the energy business

Cate Mix of dt, groups, benefits and other issues

Greenie Good mix of provisions, associates and sbp

Alexandra Classic mix question with usual suspects

Scramble Challenging mix with lots of intangibles

Ethan Technical mix of goodwill, dt, FVO and equity

4 (current issues)

Financial instruments Discussion of development of FI

Holcombe Leasing including leaseback

Whitebirk Lovely SME question based on article

Grainger Lovely FI question addressing IFRS9 and current issues

Venue Lovely revenue development

Royan Surprise subject of provisions

Actually, in June 2010 the order of q2 and q3 was reversed. And in June 2012 there were two mix.

INTRODUCTION TO THE PAPER

8 www.studyinteract ive.org

INTERNATIONAL EXAMINABLE DOCUMENTS

For the official list of examinable documents check out the P2 web page under “examinable documents”. You will find detail there. All the examinable standards are covered herein. But frankly, P2 is not a list of documents to learn and regurgitate. P2 is about understanding and applying. The examiner perceives financial reporting as being largely problem solving and so rarely expects regurgitation of standards.

UK STREAM

Some students may wish to consider the UK stream. Do not do so without reading the chapter at the end of the notes on the UK stream. This stream does require extra work and this extra work is unlikely to be of use to you in your career unless you have a specific need for the UK stream syllabus.

Please read the final chapter for further information.

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 9

INTERACTIVE STUDENT ADVICE

The following is advice aimed at students using the on-line media to do battle with P2.

Firstly, I would advise that you treat this course as if it were a classroom course. Set an evening each week (or a half day each weekend) to study the subject. Sit yourself in front of your computer with paper, pen, calculator and these notes and copy what I am doing as if you and I were in class together.

Then rework the questions from the recorded lectures until you are happy with them. Any parts you are unsure about: review the relevant recording and rework the problem a couple of times.

Once you are satisfied with your understanding of the essentials as recorded to video, then provided time allows work the supplementary questions that have not been recorded. There are answers to all the questions in the back, but obviously it’s the answers to the unrecorded questions that will interest you most.

If you are really stuck, then post your problem to the discussion board. See if you can help others with their problems posted to the discussion board. I will review the boards when I can and point you and others in the right direction. My advice is that the little things with which you struggle are often so minor as to be near irrelevant. Concentrate on the big picture, make sure you can do all the basics and when you come back to the same question for the third or fourth time, the tricky issues that seemed hard then will resolve themselves.

Emails. Really I should not be corresponding through email as this denies other students the opportunity to see our correspondence. I can see that email is very tempting, but it is against the spirit of Interactive. You guys are supposed to interact with one another as well as with me. This is why the discussion board is the way to communicate.

When it comes to the text book, my advice is be wary. The text has been based on the following notes, however, it has not been authored by me. Of course, it is absolutely fine in theory to read widely in order to widen your knowledge. But in practice, because you have so little time before you will be in the exam hall sitting the P2 exam, my advice is stick to these class notes and you will benefit from the focus. There is everything you need to know in these notes and copious practice questions. So avoiding other sources will avoid the frustrations of differing opinions and other problems associated with drawing from text books.

Finally, I wish you very good luck with your online studies and with the exam at the end of term.

INTRODUCTION TO THE PAPER

10 www.studyinteract ive.org

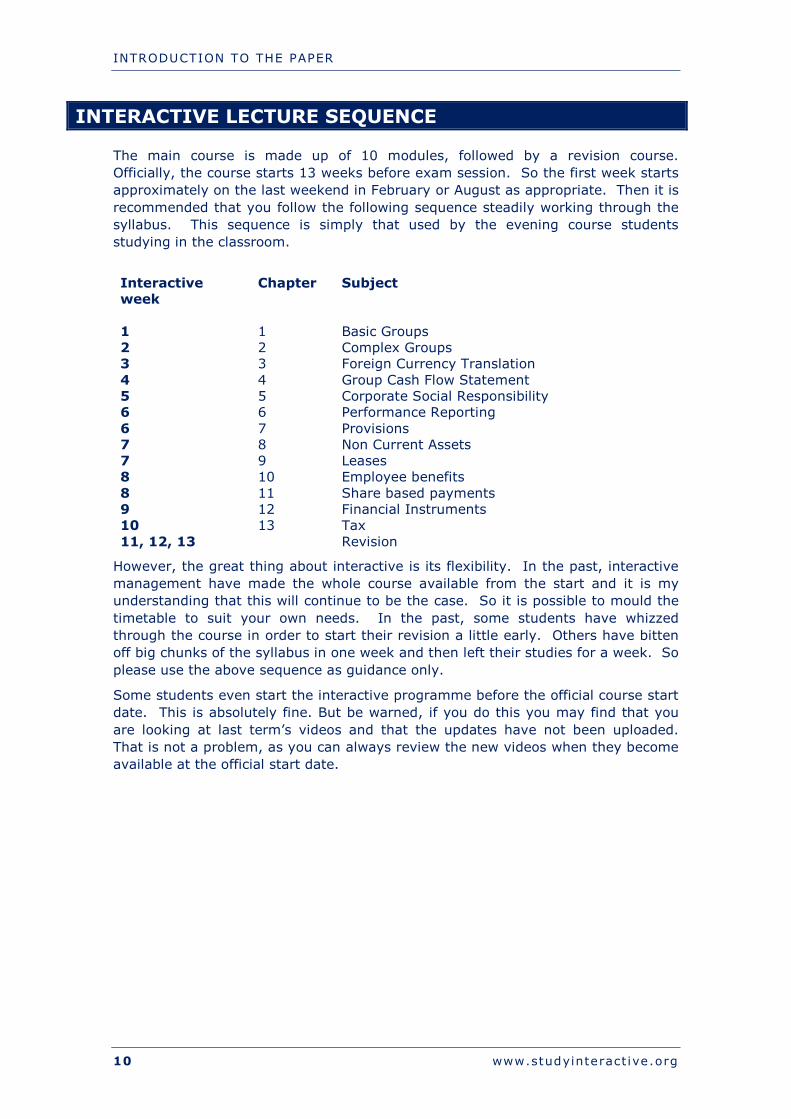

INTERACTIVE LECTURE SEQUENCE

The main course is made up of 10 modules, followed by a revision course. Officially, the course starts 13 weeks before exam session. So the first week starts approximately on the last weekend in February or August as appropriate. Then it is recommended that you follow the following sequence steadily working through the syllabus. This sequence is simply that used by the evening course students studying in the classroom.

Interactive week

Chapter Subject

1 1 Basic Groups 2 2 Complex Groups 3 3 Foreign Currency Translation 4 4 Group Cash Flow Statement 5 5 Corporate Social Responsibility 6 6 Performance Reporting 6 7 Provisions 7 8 Non Current Assets 7 9 Leases 8 10 Employee benefits 8 11 Share based payments 9 12 Financial Instruments 10 13 Tax 11, 12, 13 Revision

However, the great thing about interactive is its flexibility. In the past, interactive management have made the whole course available from the start and it is my understanding that this will continue to be the case. So it is possible to mould the timetable to suit your own needs. In the past, some students have whizzed through the course in order to start their revision a little early. Others have bitten off big chunks of the syllabus in one week and then left their studies for a week. So please use the above sequence as guidance only.

Some students even start the interactive programme before the official course start date. This is absolutely fine. But be warned, if you do this you may find that you are looking at last term’s videos and that the updates have not been uploaded. That is not a problem, as you can always review the new videos when they become available at the official start date.

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 11

VIDEO SCHEDULE

The following is the video schedule for interactive as at the start of term. It gives you a very good idea of what you will expect to see online.

Note the video style in the left column. I have used two styles of recording. First there is talking head. This style of video is an introduction to the subject. It is intended to give you a feel for the subject without going into the detail. Then there is worked example. As the name suggests, I use an example to illustrate the technical points I wish to make and draw out the detail.

P2 Introductory Session

Introduction to paper P2

Title Syllabus reference

Video style

Aim of the paper Talking head

Outline of the syllabus Talking head

Format of the exam Talking head

Structure of P2 interactive Talking head

Study style recommendations Talking head

Interacting on interactive Talking head

INTRODUCTION TO THE PAPER

12 www.studyinteract ive.org

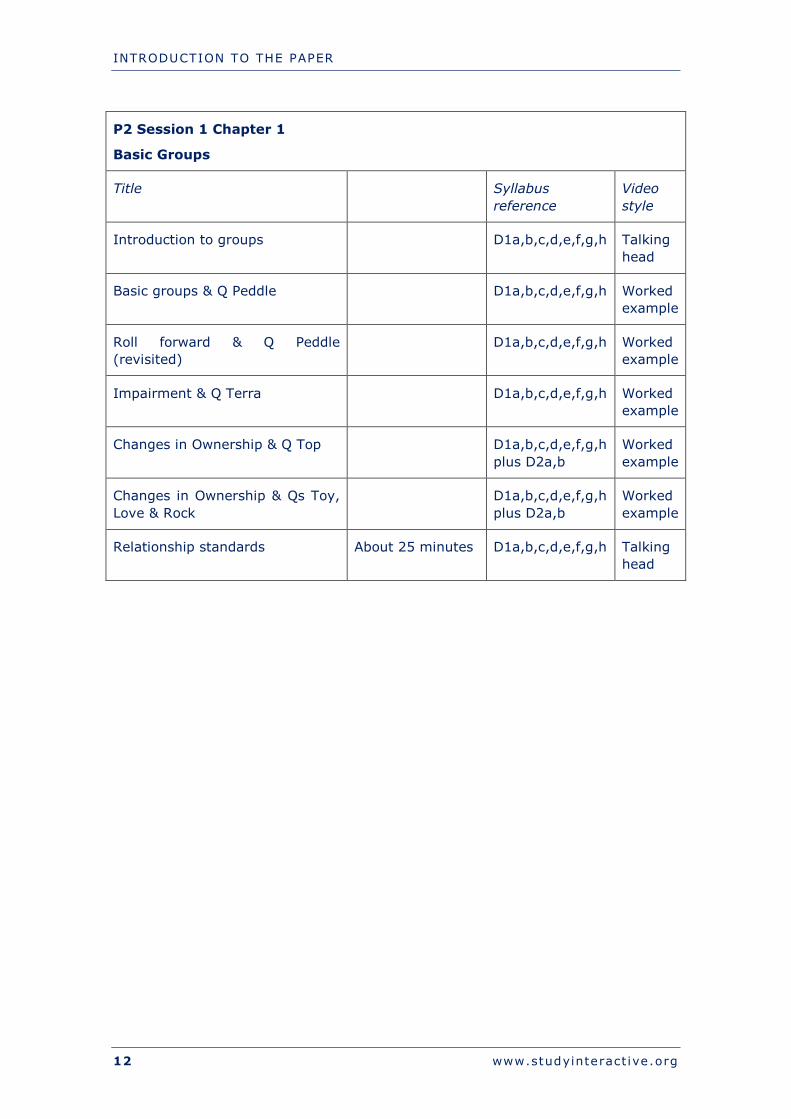

P2 Session 1 Chapter 1

Basic Groups

Title Syllabus reference

Video style

Introduction to groups D1a,b,c,d,e,f,g,h Talking head

Basic groups & Q Peddle D1a,b,c,d,e,f,g,h Worked example

Roll forward & Q Peddle (revisited)

D1a,b,c,d,e,f,g,h Worked example

Impairment & Q Terra D1a,b,c,d,e,f,g,h Worked example

Changes in Ownership & Q Top D1a,b,c,d,e,f,g,h plus D2a,b

Worked example

Changes in Ownership & Qs Toy, Love & Rock

D1a,b,c,d,e,f,g,h plus D2a,b

Worked example

Relationship standards About 25 minutes D1a,b,c,d,e,f,g,h Talking head

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 13

P2 Session 2 Chapter 2

Complex Groups

Title Syllabus reference

Video style

Introduction to complex groups D1a Talking head

Vertical group (Q Hendrix) D1a Worked example

D group (Q Dee) D1a Worked example

Question Rodney (explanation) D1a Worked example

Question Rodney (calculation) About 45 minutes D1a Worked example

Changes in group structure Remove D3a, b Talking head

Introduction to changes in group structure

About 10 minutes D3a, b Talking head

Changes in group structure (Q Desperate (a)(i) )

About 30 minutes D3a, b Worked example

Changes in group structure (Q Desperate (a)(ii) part one)

About 20 minutes D3a, b Worked example

Changes in group structure (Q Desperate (a)(ii) part two)

About 20 minutes D3a, b Worked example

Changes in group structure (Q Desperate (b) )

About 15 minutes D3a, b Worked example

INTRODUCTION TO THE PAPER

14 www.studyinteract ive.org

P2 Session 3 Chapter 3

Foreign Currency Translation

Title Syllabus reference

Video style

Introduction to foreign currency translation

D4a, b Talking head

Foreign transactions (Q Feature) D4a, b Worked example

Foreign subsidiaries (Q Kenya) D4a, b Worked example

Forex (Q Xenon) D4a, b Worked example

P2 Session 4 Chapter 4

Group Cash Flow Statements

Title Syllabus reference

Video style

Introduction to cfs D1i Talking head

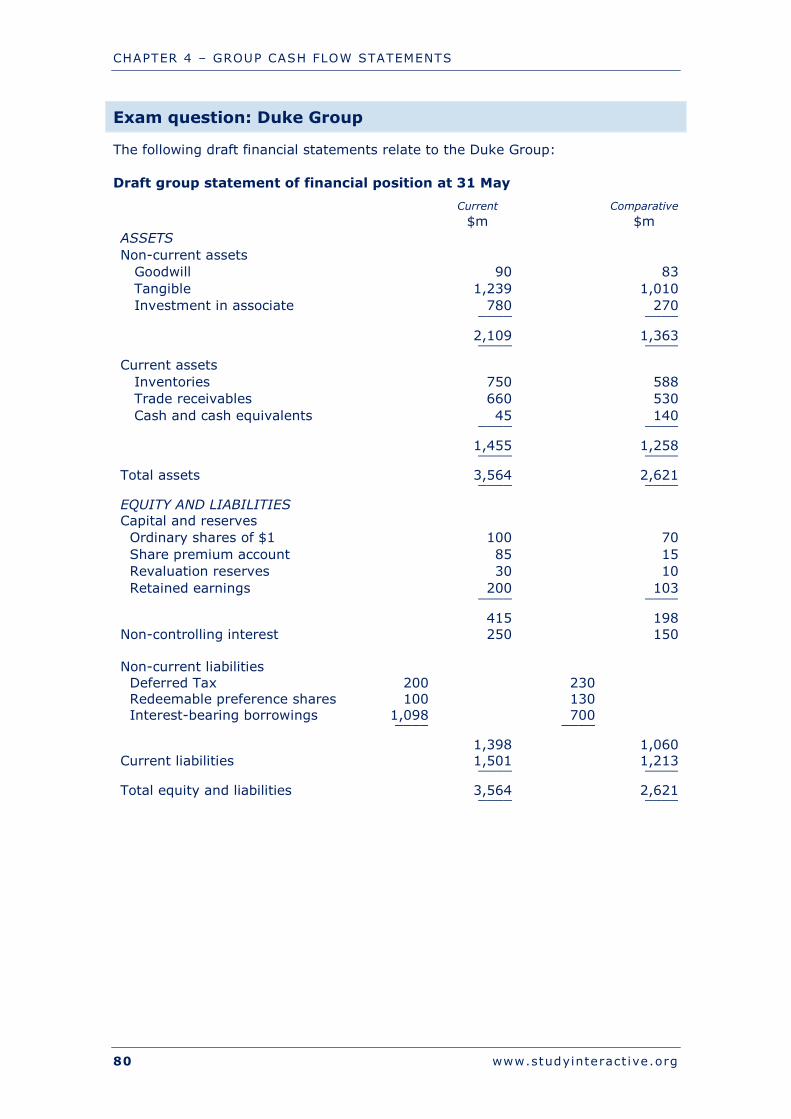

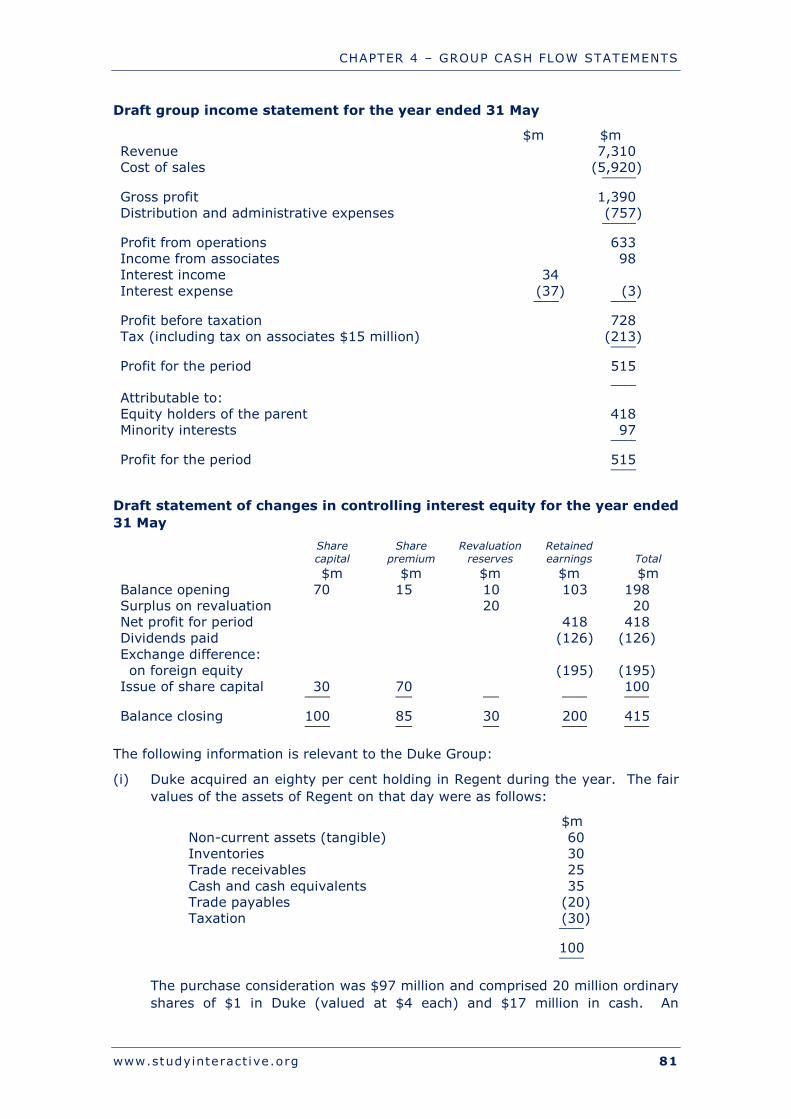

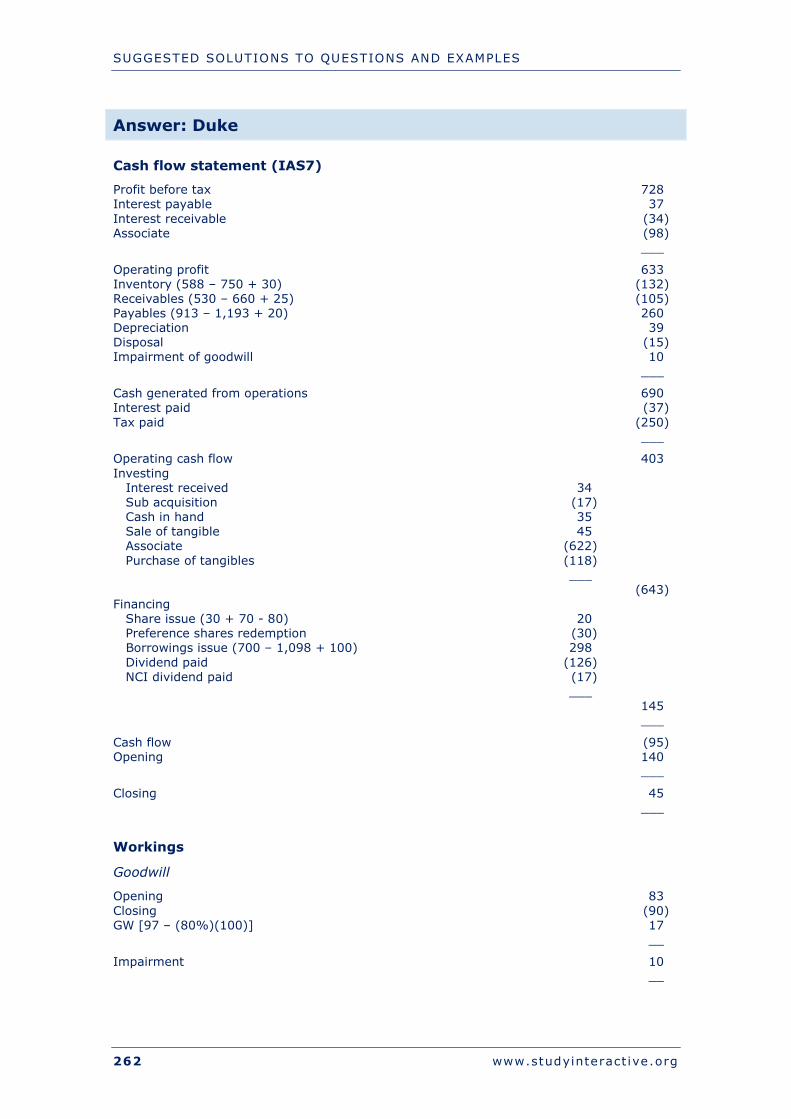

Working a cfs (Q Duke) Remove D1i Worked example

Formatting a cfs (Q Squire) Roughly 10 minutes

D1i Worked example

Working a cfs (Q Squire) Roughly 45 minutes

D1i Worked example

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 15

P2 Session 5 Chapter5

CSR & CI

Title Syllabus reference

Video style

Professional ethics A1a, b and A2a, b and A3a, b

Talking head

The framework for financial reporting

B1a, b, c and B2a, b

Talking head

Current reporting issues H3a and F2a Talking head

Convergence H2a, b and F1a Talking head

Environmental and social reporting

H1a, b, c Talking head

Appraisal G1a, b and G2a, b, c, d

Talking head

Specialised entities and specialised transactions

E1a and E2a, b, c

Talking head

Small and medium entities C11a, b, c, d, e Talking head

Current issues exam questions A,B,C,E,F,G,H Talking head

INTRODUCTION TO THE PAPER

16 www.studyinteract ive.org

P2 Session 6 Chapter 6

Performance Reporting

Title Syllabus reference

Video style

Performance reports & revenue C1a, b, c Talking head

Revenue example C1a, b, c Worked example

Held for sale and discontinued operations

C2a, b + D2a, b Talking head

Segments C5a, b Talking head

Discontinued example C2b + D2a, b Worked example

P2 Session 7 Chapter 7

Provisions

Title Syllabus reference

Video style

Provisions C8a, b Talking head

Events after the reporting period C8c, d Talking head

Related party disclosure C9a, b Talking head

Provisions exercises C8,a,b,c,d + C9a,b

Worked example

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 17

P2 Session 8 Chapter 8

Non-current assets

Title Syllabus reference

Video style

Non current asset basics C2a Talking head

Investment Properties C2c Talking head

Intangibles C2d Talking head

Non current asset examples C2a, c, d Worked example

P2 Session 9 Chapter 9

Leases

Title Syllabus reference

Video style

Lease accounting C4a Talking head

Sale and leaseback C4b Talking head

Leases exercises C4a, b Worked example

P2 Session 10 Chapter 10

Employee benefits

Title Syllabus reference

Video style

Pension accounting C6a, b, c, d Talking head

Pension exercises Remove C6a, b, c, d Worked example

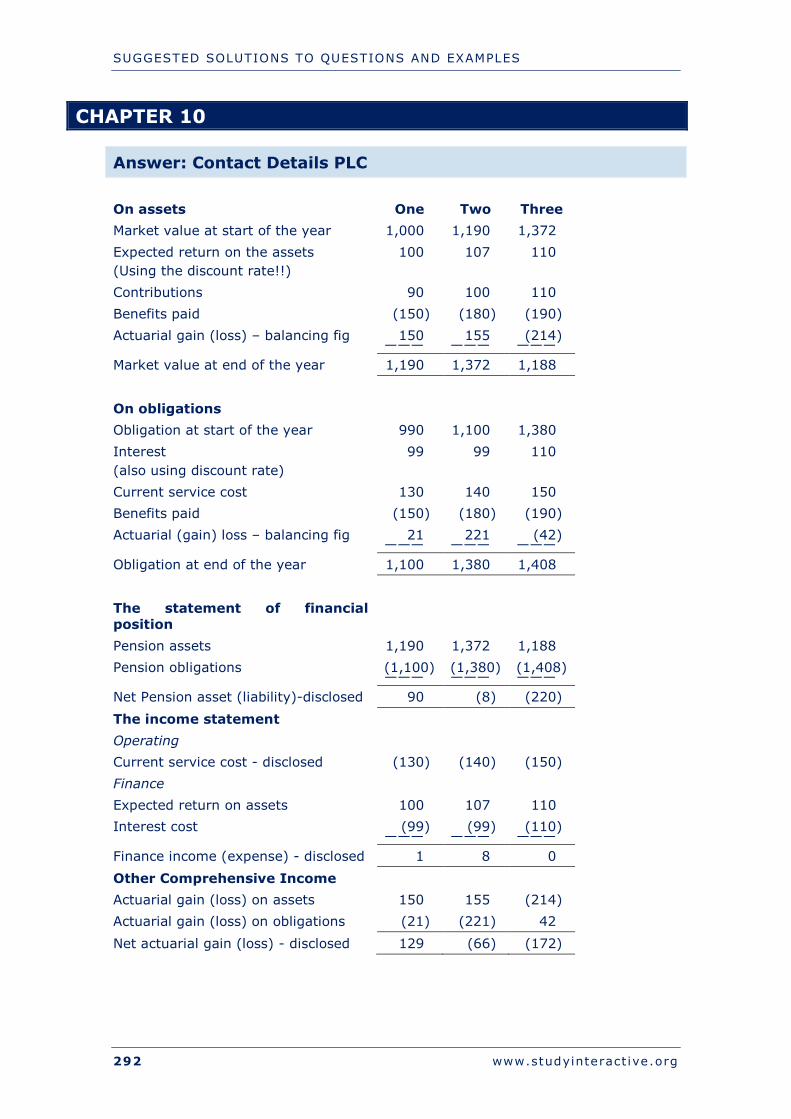

Pension exercise (Q Contact) About 25 minutes C6a, b, c, d Worked example

INTRODUCTION TO THE PAPER

18 www.studyinteract ive.org

P2 Session 11 Chapter 11

Share based payments

Title Syllabus reference

Video style

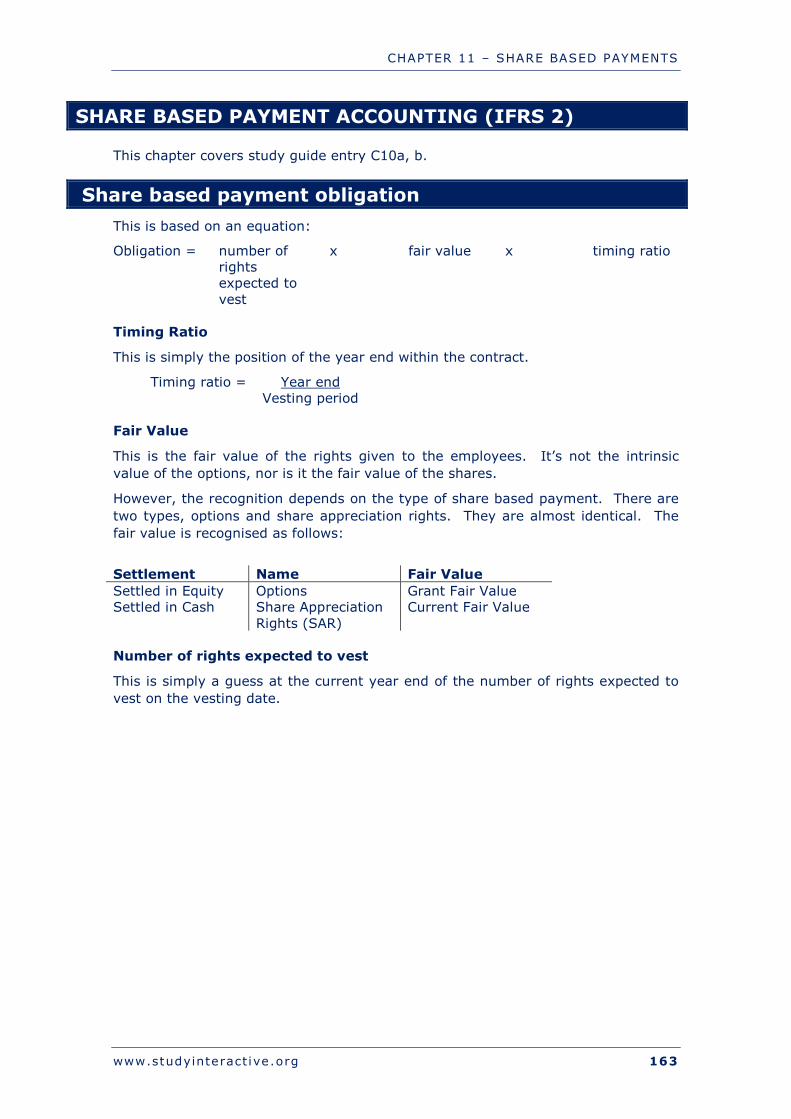

Share based payment obligation C10a, b Talking head

Share based payment exercises C10a, b Worked example

P2 Session 12 Chapter 12

Financial instruments

Title Syllabus reference

Video style

Financial instrument classification C3a, b, c, d, e, f Talking head

FA carried at amortised cost C3a, b, c Worked example

FA carried at fair value C3a, b, c Worked example

Fair Value Option About 15 minutes C3a, b, c, d,e,f Worked example

Fair Value Measurement About 20 minutes C3a, b, c, d, e, f Worked example

Impairment of FI About 30 minutes C3a, b, c, d, e, f Worked example

Hedging About 30 minutes C3a, b, c, d, e, f Worked example

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 19

P2 Session 13 Chapter 13

Tax

Title New (date recorded)

Old (source video)

Syllabus reference

Video style

Deferred Tax Formula C7a,b Worked example

Conceptual basis of deferred tax C7a,b Worked example

Specific temporary differences C7a,b Worked example

Group temporary differences C7a,b Worked example

Sbp & Tax losses C7a,b Worked example

P2 Session 14 Chapter 14

UK Corporate Reporting

Title New (date recorded)

Old (source video)

Syllabus reference

Video style

Introduction to P2 Corporate Reporting

P2 UK syllabus Talking Head

UK legislation for financial reporting

P2 UK B3a Talking Head

UK financial reporting divergence P2 UK C2f, C4c, C5c, C6e, C7e, C9c, C11f, D1j

Talking Head

INTRODUCTION TO THE PAPER

20 www.studyinteract ive.org

FULL TIME LECTURE SEQUENCE

Short Term

The course is made up of 11 days.

Day Chapter Subject 1 1 Basic Groups 2 Complex Groups 2 2 Complex Groups Continued 3 Foreign Currency Translation 3 4 Group Cash Flow Statement 5 Corporate Social Responsibility 4 6 Performance Reporting 7 Provisions 8 Non Current Assets 5 9 Leases 10 Employee benefits 11 Share based payments 6 12 Financial Instruments 13 Tax 7 Q2 revision 8 Q3 revision 9 Q4 revision 10 Q1 revision 11 Re-revision

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 21

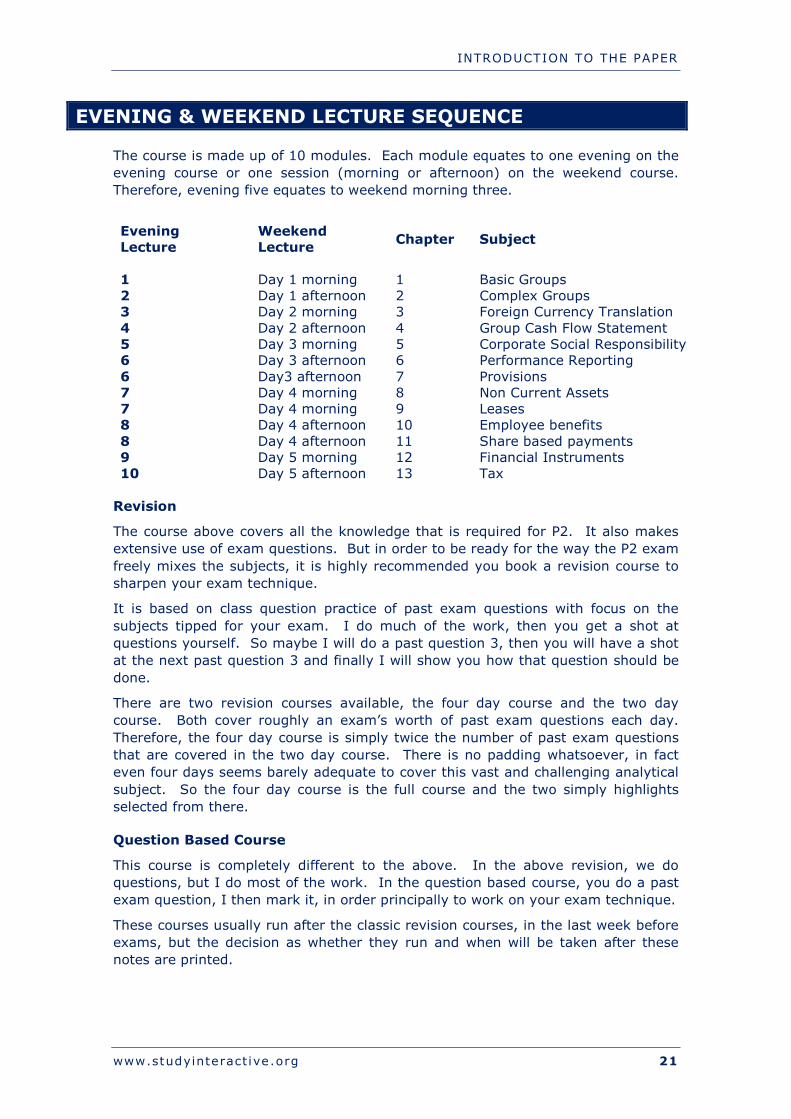

EVENING & WEEKEND LECTURE SEQUENCE

The course is made up of 10 modules. Each module equates to one evening on the evening course or one session (morning or afternoon) on the weekend course. Therefore, evening five equates to weekend morning three.

Evening Lecture

Weekend Lecture Chapter Subject

1 Day 1 morning 1 Basic Groups 2 Day 1 afternoon 2 Complex Groups 3 Day 2 morning 3 Foreign Currency Translation 4 Day 2 afternoon 4 Group Cash Flow Statement 5 Day 3 morning 5 Corporate Social Responsibility 6 Day 3 afternoon 6 Performance Reporting 6 Day3 afternoon 7 Provisions 7 Day 4 morning 8 Non Current Assets 7 Day 4 morning 9 Leases 8 Day 4 afternoon 10 Employee benefits 8 Day 4 afternoon 11 Share based payments 9 Day 5 morning 12 Financial Instruments 10 Day 5 afternoon 13 Tax

Revision

The course above covers all the knowledge that is required for P2. It also makes extensive use of exam questions. But in order to be ready for the way the P2 exam freely mixes the subjects, it is highly recommended you book a revision course to sharpen your exam technique.

It is based on class question practice of past exam questions with focus on the subjects tipped for your exam. I do much of the work, then you get a shot at questions yourself. So maybe I will do a past question 3, then you will have a shot at the next past question 3 and finally I will show you how that question should be done.

There are two revision courses available, the four day course and the two day course. Both cover roughly an exam’s worth of past exam questions each day. Therefore, the four day course is simply twice the number of past exam questions that are covered in the two day course. There is no padding whatsoever, in fact even four days seems barely adequate to cover this vast and challenging analytical subject. So the four day course is the full course and the two simply highlights selected from there.

Question Based Course

This course is completely different to the above. In the above revision, we do questions, but I do most of the work. In the question based course, you do a past exam question, I then mark it, in order principally to work on your exam technique.

These courses usually run after the classic revision courses, in the last week before exams, but the decision as whether they run and when will be taken after these notes are printed.

INTRODUCTION TO THE PAPER

22 www.studyinteract ive.org

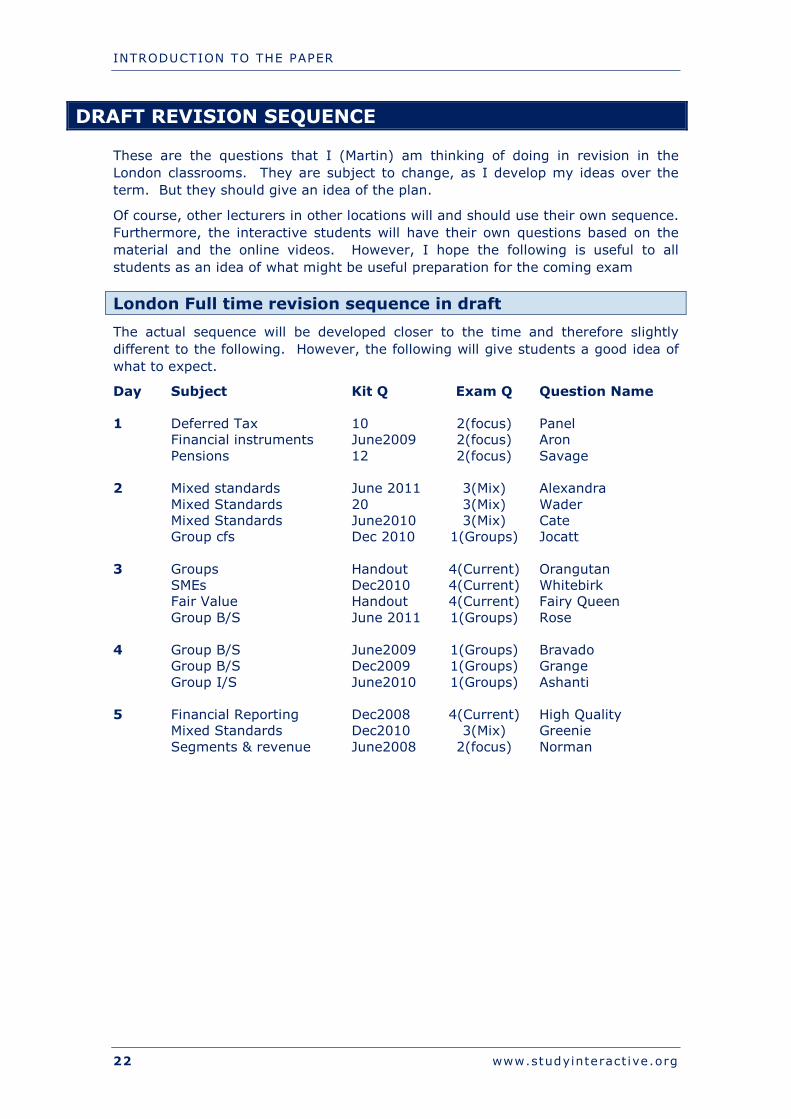

DRAFT REVISION SEQUENCE

These are the questions that I (Martin) am thinking of doing in revision in the London classrooms. They are subject to change, as I develop my ideas over the term. But they should give an idea of the plan.

Of course, other lecturers in other locations will and should use their own sequence. Furthermore, the interactive students will have their own questions based on the material and the online videos. However, I hope the following is useful to all students as an idea of what might be useful preparation for the coming exam

London Full time revision sequence in draft The actual sequence will be developed closer to the time and therefore slightly different to the following. However, the following will give students a good idea of what to expect.

Day Subject Kit Q Exam Q Question Name 1 Deferred Tax 10 2(focus) Panel Financial instruments June2009 2(focus) Aron Pensions 12 2(focus) Savage 2 Mixed standards June 2011 3(Mix) Alexandra Mixed Standards 20 3(Mix) Wader Mixed Standards June2010 3(Mix) Cate Group cfs Dec 2010 1(Groups) Jocatt 3 Groups Handout 4(Current) Orangutan SMEs Dec2010 4(Current) Whitebirk Fair Value Handout 4(Current) Fairy Queen Group B/S June 2011 1(Groups) Rose 4 Group B/S June2009 1(Groups) Bravado Group B/S Dec2009 1(Groups) Grange Group I/S June2010 1(Groups) Ashanti 5 Financial Reporting Dec2008 4(Current) High Quality Mixed Standards Dec2010 3(Mix) Greenie Segments & revenue June2008 2(focus) Norman

INTRODUCTION TO THE PAPER

www.studyinteract ive.org 23

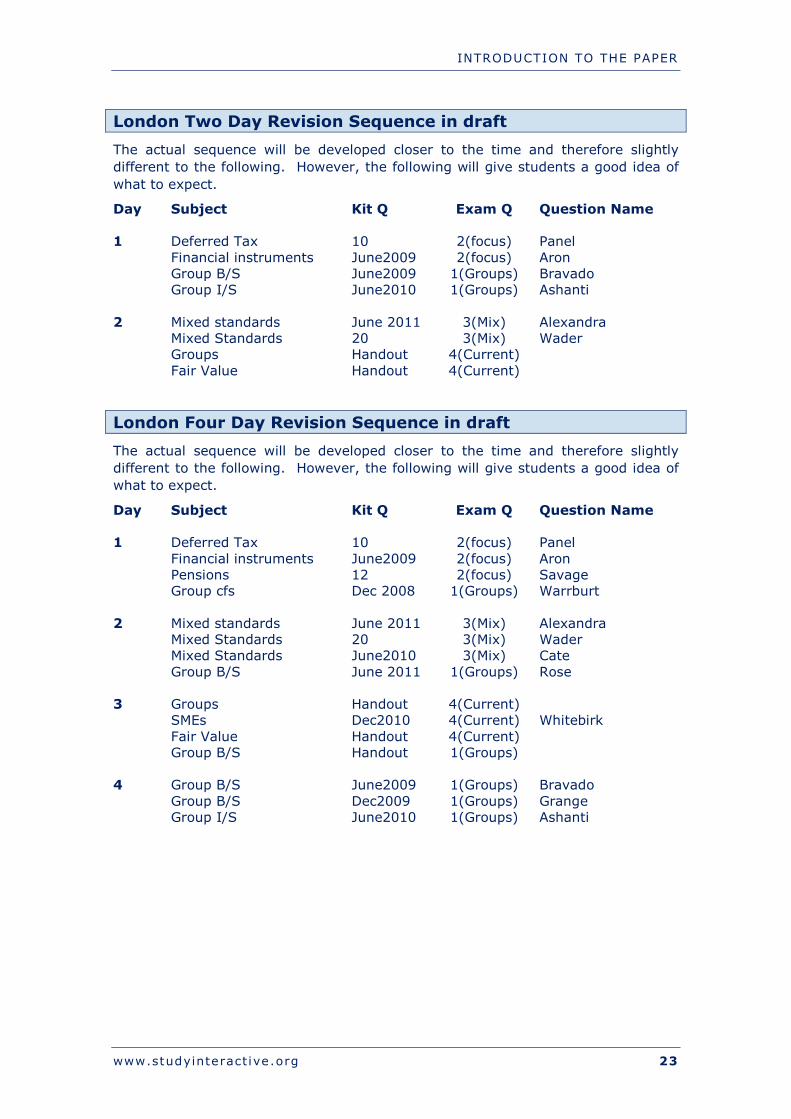

London Two Day Revision Sequence in draft The actual sequence will be developed closer to the time and therefore slightly different to the following. However, the following will give students a good idea of what to expect.

Day Subject Kit Q Exam Q Question Name 1 Deferred Tax 10 2(focus) Panel Financial instruments June2009 2(focus) Aron Group B/S June2009 1(Groups) Bravado Group I/S June2010 1(Groups) Ashanti 2 Mixed standards June 2011 3(Mix) Alexandra Mixed Standards 20 3(Mix) Wader Groups Handout 4(Current) Fair Value Handout 4(Current)

London Four Day Revision Sequence in draft The actual sequence will be developed closer to the time and therefore slightly different to the following. However, the following will give students a good idea of what to expect.

Day Subject Kit Q Exam Q Question Name 1 Deferred Tax 10 2(focus) Panel Financial instruments June2009 2(focus) Aron Pensions 12 2(focus) Savage Group cfs Dec 2008 1(Groups) Warrburt 2 Mixed standards June 2011 3(Mix) Alexandra Mixed Standards 20 3(Mix) Wader Mixed Standards June2010 3(Mix) Cate Group B/S June 2011 1(Groups) Rose 3 Groups Handout 4(Current) SMEs Dec2010 4(Current) Whitebirk Fair Value Handout 4(Current) Group B/S Handout 1(Groups) 4 Group B/S June2009 1(Groups) Bravado Group B/S Dec2009 1(Groups) Grange Group I/S June2010 1(Groups) Ashanti

INTRODUCTION TO THE PAPER

24 www.studyinteract ive.org

www.studyinteract ive.org 25

Chapter 1

Basic groups

CHAPTER 1 - BASIC GROUPS

26 www.studyinteract ive.org

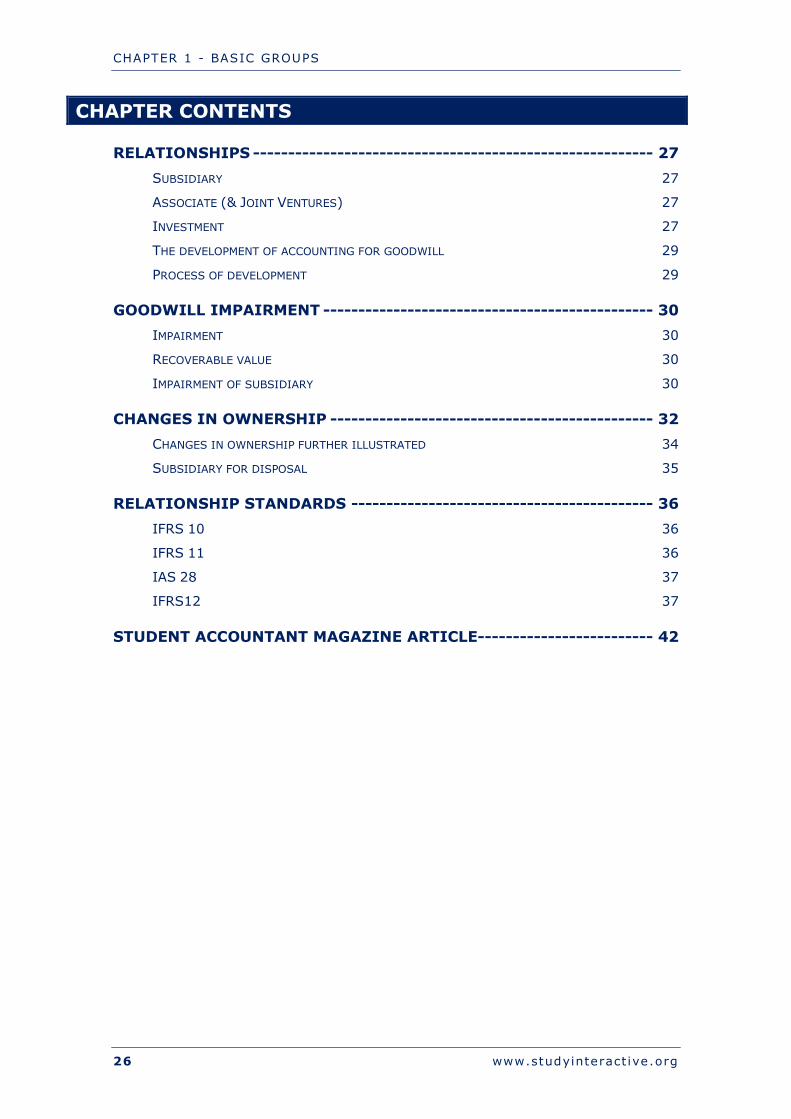

CHAPTER CONTENTS

RELATIONSHIPS --------------------------------------------------------- 27

SUBSIDIARY 27

ASSOCIATE (& JOINT VENTURES) 27

INVESTMENT 27

THE DEVELOPMENT OF ACCOUNTING FOR GOODWILL 29

PROCESS OF DEVELOPMENT 29

GOODWILL IMPAIRMENT ----------------------------------------------- 30

IMPAIRMENT 30

RECOVERABLE VALUE 30

IMPAIRMENT OF SUBSIDIARY 30

CHANGES IN OWNERSHIP ---------------------------------------------- 32

CHANGES IN OWNERSHIP FURTHER ILLUSTRATED 34

SUBSIDIARY FOR DISPOSAL 35

RELATIONSHIP STANDARDS ------------------------------------------- 36

IFRS 10 36

IFRS 11 36

IAS 28 37

IFRS12 37

STUDENT ACCOUNTANT MAGAZINE ARTICLE------------------------- 42

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 27

RELATIONSHIPS

This chapter covers the process of consolidation required in a group containing parent, subsidiary and associate. So this chapter covers study guide entry D1a, b, c, e, f, g, h.

The process is determined by the relationships between the entities. There are three relationships between entities:

● control

● influence

● passive.

The ideas are studied briefly below and in more detail in the Relationship Standards section later in this chapter.

Subsidiary When a parent has control of another entity, then that entity is known as a subsidiary and is consolidated using acquisition accounting.

This means the subsidiary’s assets and liabilities are added to those of the parent.

Associate (& Joint Ventures) When a parent has influence over another entity, then that entity is known as an associate and is brought into the group fs using equity accounting.

This means the group fs include a share of the profit on the income statement and a share of the net assets on the statement of financial position (in the UK we show three lines on the P&L, share of operating profit, finance and tax).

A joint venture is an entity over which the parent has joint control. Despite its name, joint control is taken to mean very significant influence. So a JV is accounted for as a 50% associate. There has never been a question in which students were required to consolidate a joint venture.

Investment When a parent has no relationship with another entity, then that entity is known as an investment and brought into the fs using investment accounting. This means that the shares are carried at fair value. Investment accounting is covered in much more detail later, in the chapter on financial instruments.

CHAPTER 1 - BASIC GROUPS

28 www.studyinteract ive.org

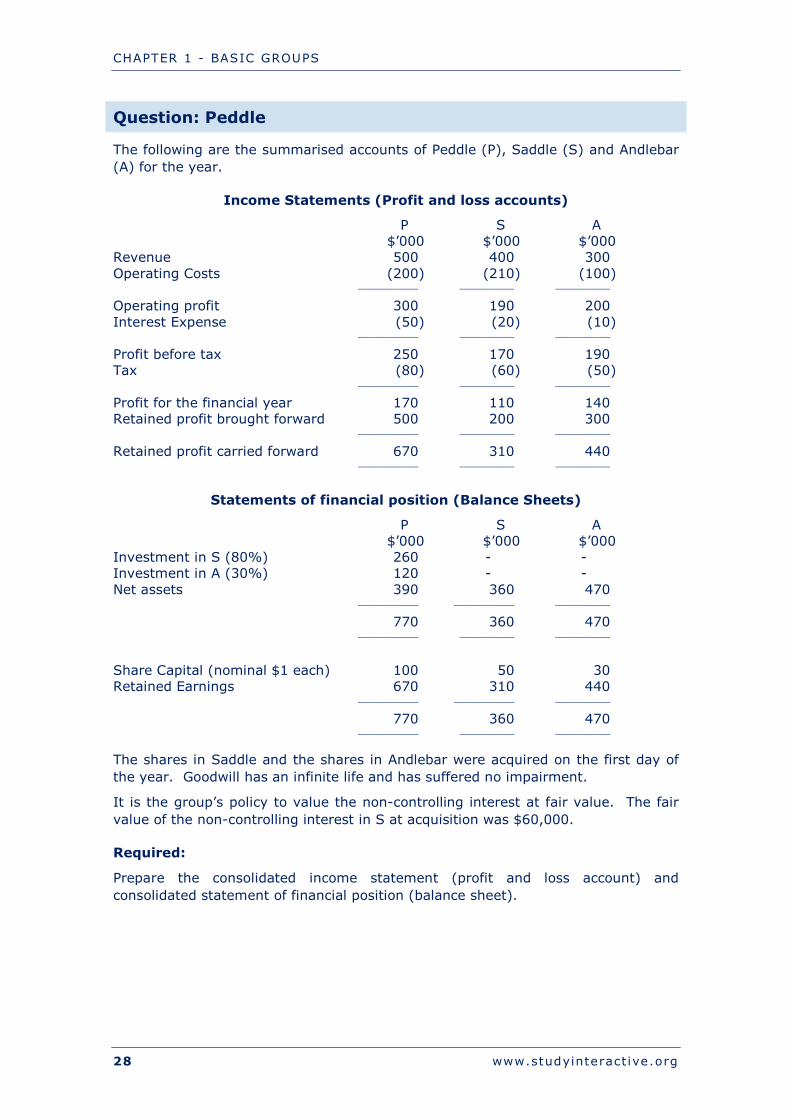

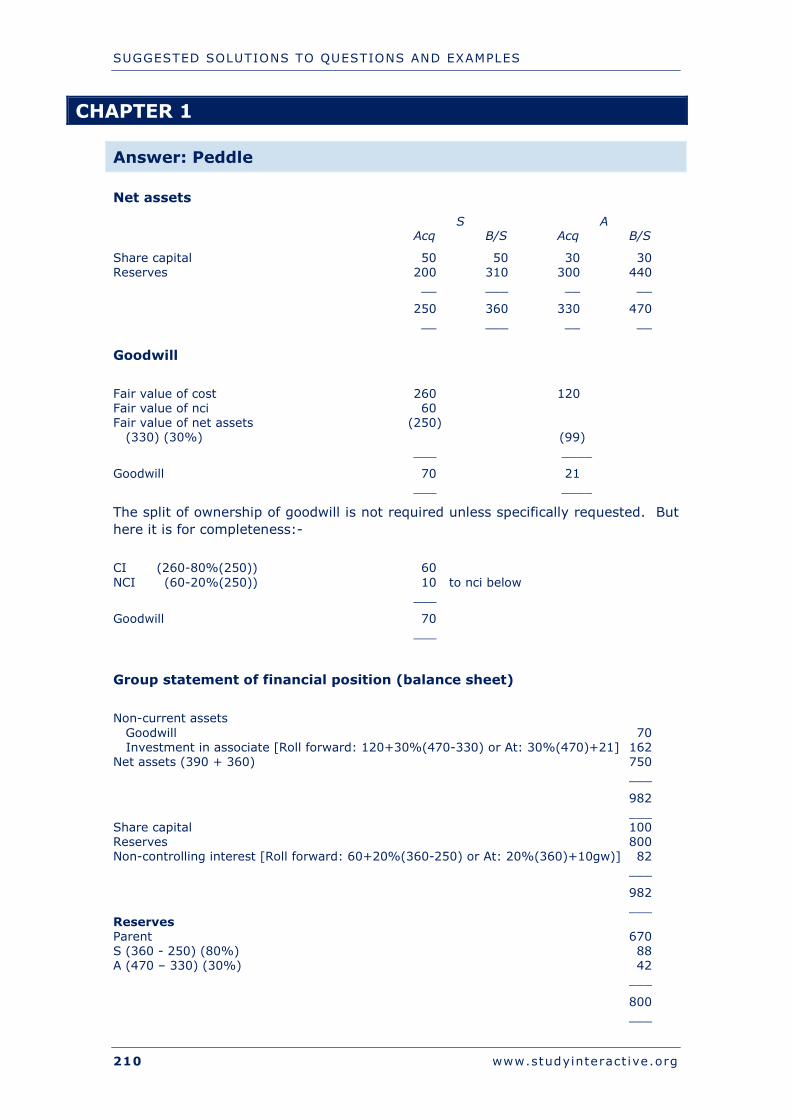

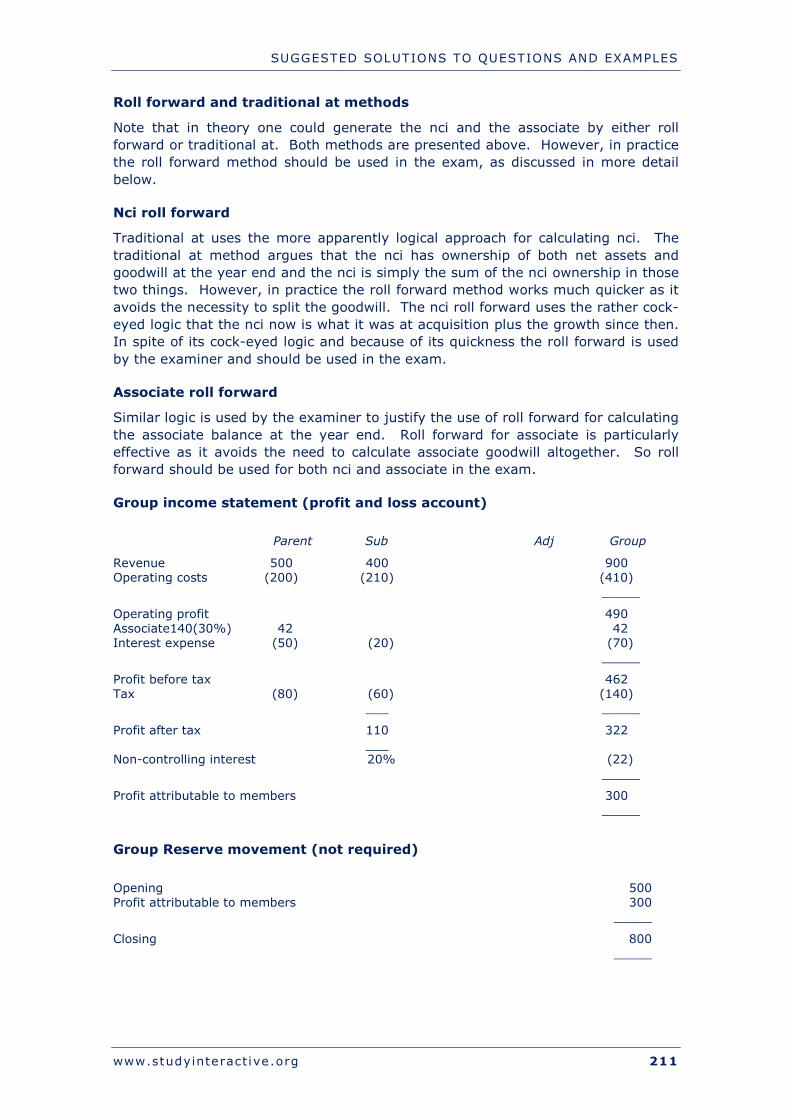

Question: Peddle

The following are the summarised accounts of Peddle (P), Saddle (S) and Andlebar (A) for the year.

Income Statements (Profit and loss accounts)

P S A $’000 $’000 $’000 Revenue 500 400 300 Operating Costs (200) (210) (100) ___________ __________ __________

Operating profit 300 190 200 Interest Expense (50) (20) (10) ___________ __________ __________

Profit before tax 250 170 190 Tax (80) (60) (50) ___________ __________ __________

Profit for the financial year 170 110 140 Retained profit brought forward 500 200 300 ___________ __________ __________

Retained profit carried forward 670 310 440 ___________ __________ __________

Statements of financial position (Balance Sheets)

P S A $’000 $’000 $’000 Investment in S (80%) 260 - - Investment in A (30%) 120 - - Net assets 390 360 470 ___________ ___________ __________ 770 360 470 ___________ __________ __________

Share Capital (nominal $1 each) 100 50 30 Retained Earnings 670 310 440 ___________ ___________ __________ 770 360 470 ___________ __________ __________

The shares in Saddle and the shares in Andlebar were acquired on the first day of the year. Goodwill has an infinite life and has suffered no impairment.

It is the group’s policy to value the non-controlling interest at fair value. The fair value of the non-controlling interest in S at acquisition was $60,000.

Required:

Prepare the consolidated income statement (profit and loss account) and consolidated statement of financial position (balance sheet).

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 29

The development of accounting for goodwill Until 2009, Goodwill disclosed on the statement of financial position was ‘our’ goodwill (that is until recently goodwill has shown ownership). This is often called ‘partial goodwill’ (or ‘proportional goodwill’). There is a newly reissued IFRS (IFRS3 (2008 revised)) that recommends goodwill disclosed be changed to the entire goodwill of the entity (so that goodwill would then show control). This is in order to make goodwill consistent with the rest of the statement of financial position where we already use control. This recommendation is usually called ‘full goodwill’. However, the new IFRS continues to allow partial goodwill, making the whole situation very confused.

Process of development The process of development is undertaken by the International Accounting Standards Board (IASB). There are three phases ending with an IFRS. The three phases are as follows:-

DP Discussion Paper ED Exposure draft IFRS Financial reporting standard

CHAPTER 1 - BASIC GROUPS

30 www.studyinteract ive.org

GOODWILL IMPAIRMENT

Some groups questions require students to conduct an impairment review on the subsidiaries at the year end. This results in a goodwill impairment.

Impairment An impairment occurs if the recoverable value of an asset falls below the carrying value.

Recoverable value This is the higher of VIU and NRV.

● VIV = Value in use

● NRV = Net realisable value (more strictly this is actually phrased as “fair value less cost to sell which is essentially the same idea as NRV)..

Impairment of subsidiary Goodwill impairment is identified by looking at the impairment of the whole subsidiary.

Question: Fakenstock

A parent, Fakenstock, bought 100% of the equity of a sub at the year start for $900m. Share capital was $100m, retained earnings were $400m and retained profits for the year were $200m.

Goodwill has in infinite life and an impairment review of the sub at the first year end revealed a value in use (VIU) of $780m and net realisable value (NRV) of $350m.

Required:

Goodwill.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 31

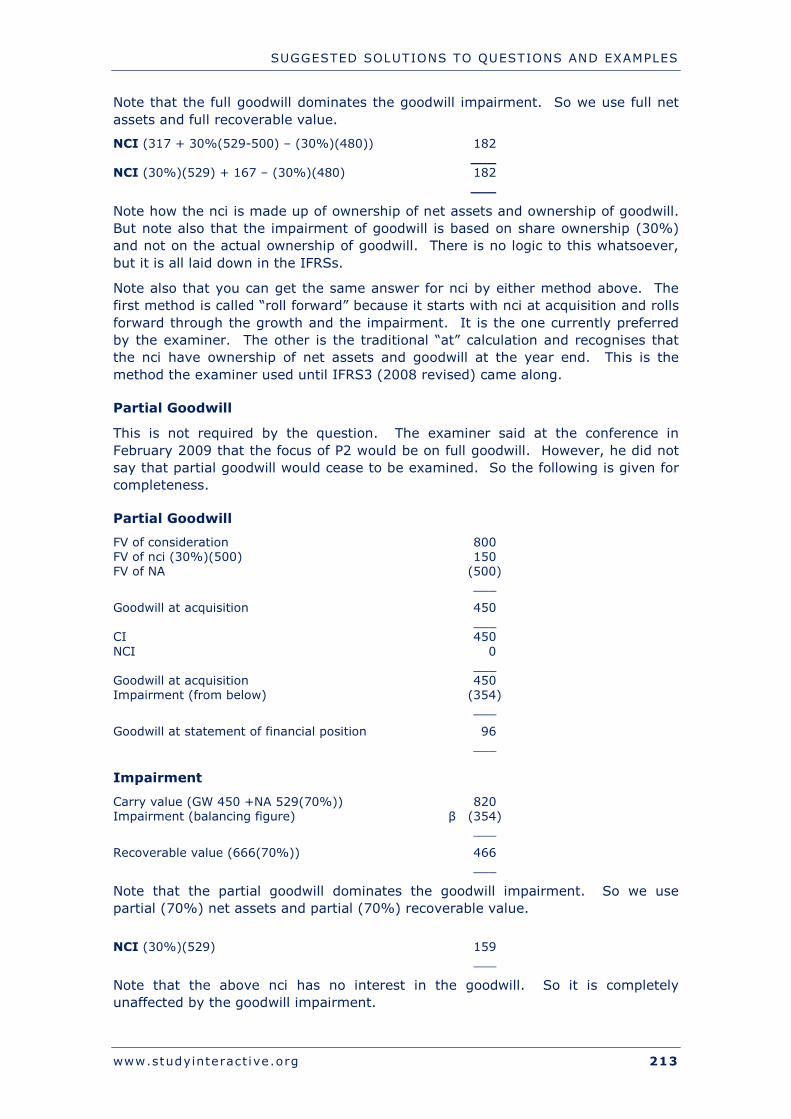

Question: Terra

A parent, Terra, buys 70% of a sub for $800m at the year start, when the share capital is $50m, retained earnings are $350m and a fair value adjustment (FVA) of $100m is required on machines with a life of five years. The fair value of the non-controlling interest is $317m

During the year the sub made profits retained of $50m and the sub sold goods valued at $12m to the parent with a margin of 25%; one third of which is still in inventory in the parent.

Goodwill has an infinite life and a year end review reveals a value in use (VIU) of $360m and net realisable value (NRV) of $666m.

It is the group’s policy to value the non-controlling interest at fair value (full goodwill).

Required:

Goodwill and NCI.

CHAPTER 1 - BASIC GROUPS

32 www.studyinteract ive.org

CHANGES IN OWNERSHIP

This is found in the study guide under paragraph D2a.

A parent may simply buy or sell shares. However, the group viewpoint is quite different. A group only acquires a sub when it gets control and only sells a sub when it loses control. Other share exchanges are simply changes in ownership and result in transfers. The examiner has written an article on this element of IFRS3. It was available at accaglobal.com within the P2 section under “Technical Articles” when this document went to print. It was published in February 2009. The following illustrative questions take their inspiration from that article.

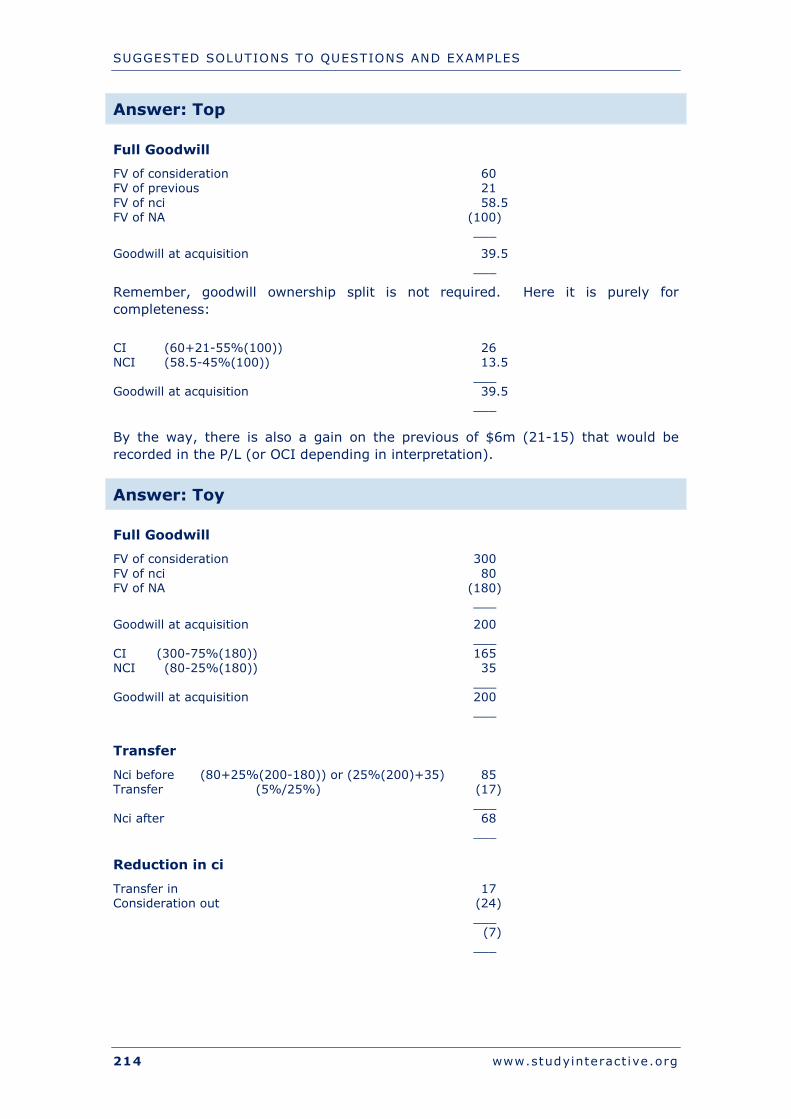

Question: Top

At the year start, Top acquired a 15% interest in Dog at a cost of $15m. At the year end Top acquired a further 40% interest in Dog at a cost of $60m and obtained control. The fair value of the initial 15% interest at this time was $21m and the fair value of the NCI was $58.5m. The fair value of the identifiable net assets was $100m. The group has recently changed the policy of recognising the non-controlling interest from valuation at fair value of identifiable net assets (partial goodwill) to valuing at fair value as indicated by market price at acquisition (full goodwill).

Required:

Goodwill.

Question: Toy

At the year start, Toy acquired 75% of Boy for $300m. The fair value of the identifiable net assets of Boy at the point of acquisition was $180m. The fair value of the NCI was $80m. The group has the policy of recognising the non-controlling interest at fair value.

Required:

(a) Goodwill.

At the year end, Toy acquires a further 5% of Boy for $24m. Boy has made profits and grown by $20m over the year and therefore the carrying value of identifiable net assets of Boy is $200m at the year end.

Required:

(b) Transfer from NCI and reduction in controlling interest.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 33

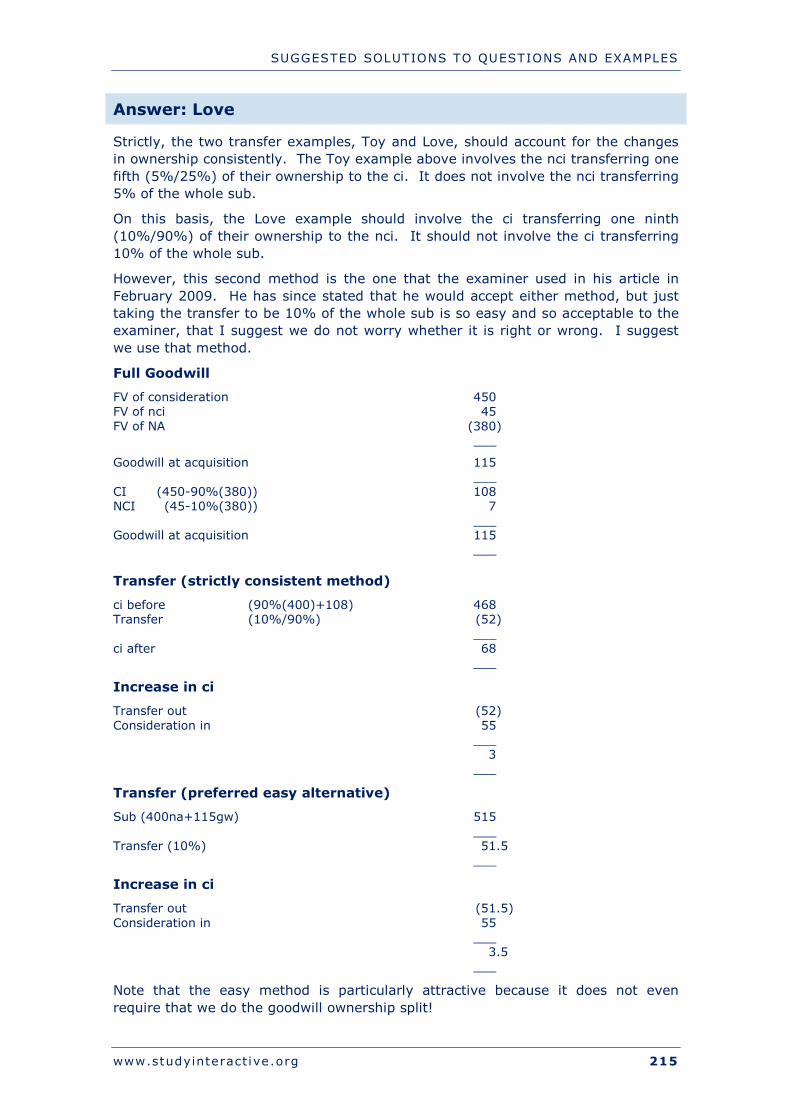

Question: Love

At the year start, Love acquired 90% of Rat for $450m. The fair value of the identifiable net assets of Rat at the point of acquisition was $380m. The fair value of the NCI was $45m. The group has the policy of recognising the non-controlling interest at fair value.

Required:

(a) Goodwill.

At the year end, Love disposes of 10% of the equity of Rat for $55m and so reduces its ownership to 80%. Rat has made profits and grown by $20m over the year and therefore the carrying value of identifiable net assets of Rat is $400m at the year end.

Required:

(b) Transfer to NCI and increase in controlling interest.

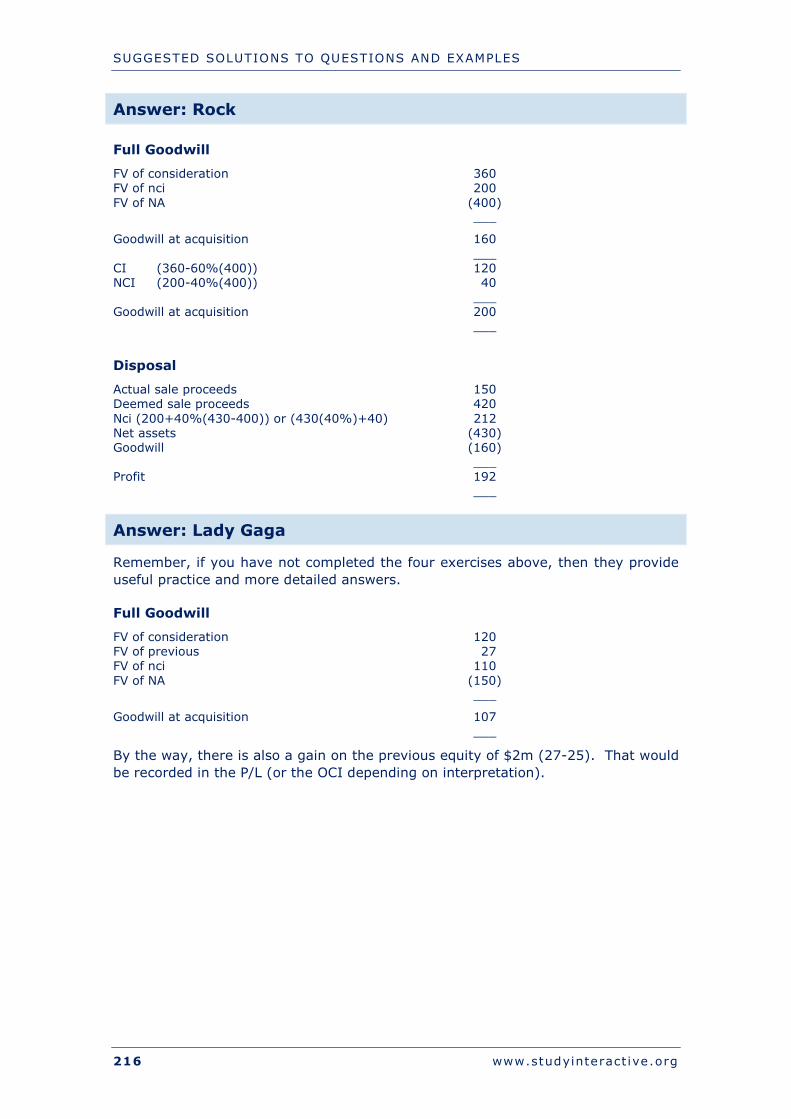

Question: Rock

At the year start, Rock acquired 60% of Star for $360m. Star had identifiable net assets with a fair value of $400m at acquisition and the fair value of the NCI was $200m. Rock has the policy of valuing NCI at the fair value of identifiable net assets, but on this occasion it chooses to recognise NCI at fair value.

At the year end, Rock sells 15% of Star for $150m and loses control, but retains influence through its remaining 45% ownership. The fair value of the associate retained is measured at $420m.

At the year end Star had identifiable net assets of $430m. The growth of $30m had been reported through the income statement.

Required:

Profit on disposal to be recognised in the income statement.

CHAPTER 1 - BASIC GROUPS

34 www.studyinteract ive.org

Changes in ownership continued Frankly, this basic accounting technique is such a cornerstone of group financial reporting that it is worth repeating. Here are four supplementary questions covering acquisition, disposal and the two transfers. Assume that full goodwill applies throughout.

Question: Lady Gaga

At the year start, Lady acquired a 10% interest in Gaga at a cost of $25m. At the year end Lady acquired a further 45% interest in Gaga at a cost of $120m and obtained control. The fair value of the initial 10% interest at this time was $27m and the fair value of the NCI was $110m. The fair value of the identifiable net assets was $150m.

Required:

Goodwill.

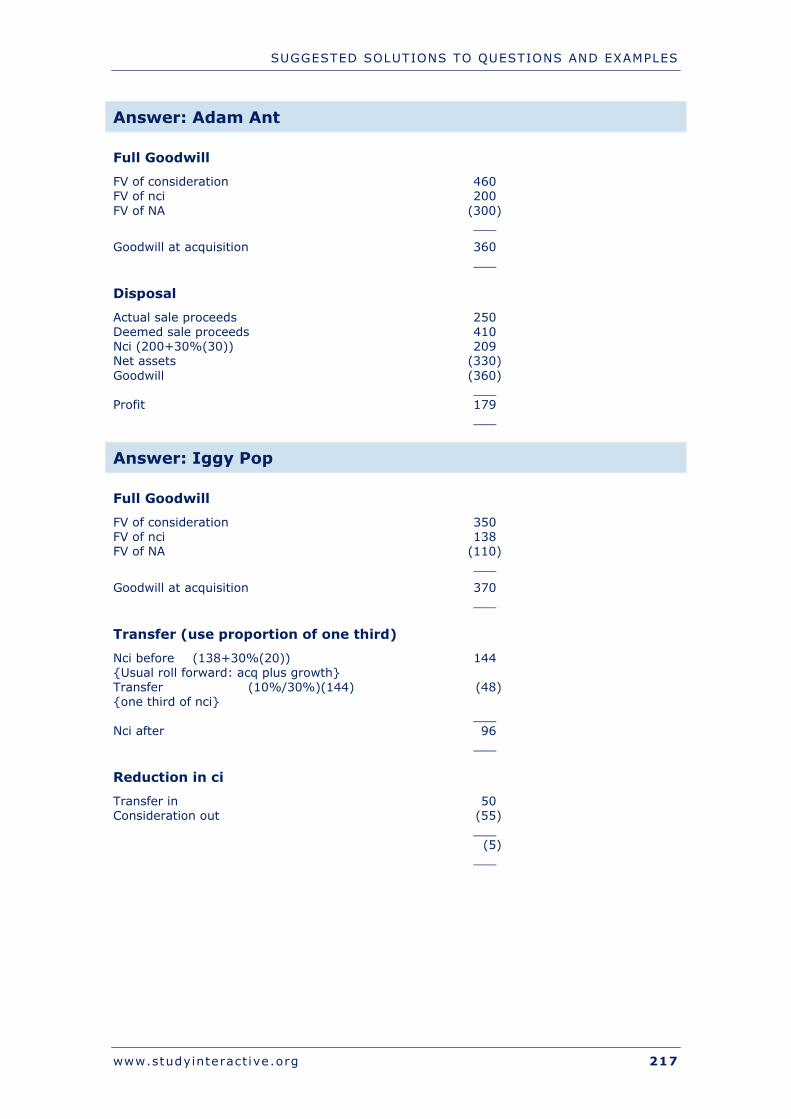

Question: Adam Ant

At the year start, Adam acquired 70% of Ant for $460m. Ant had identifiable net assets with a fair value of $300m at acquisition and the fair value of the NCI was $200m.

At the year end, Adam sells 25% of Ant for $250m and loses control, but retains influence through its remaining 45% ownership. The fair value of the associate retained is measured at $410m.

At the year end Ant had identifiable net assets of $330m. The growth of $30m had been reported through the income statement.

Required:

Profit on disposal to be recognised in the income statement.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 35

Question: Iggy Pop

At the year start, Iggy acquired 70% of Pop for $350m. The fair value of the identifiable net assets of Pop at the point of acquisition was $110m. The fair value of the NCI was $138m.

Required:

(a) Goodwill.

At the year end, Iggy acquires a further 10% of Pop for $55m. Pop has made profits and grown by $20m over the year and therefore the carrying value of identifiable net assets of Pop is $130m at the year end.

Required:

(b) Transfer from NCI and effect on controlling interest.

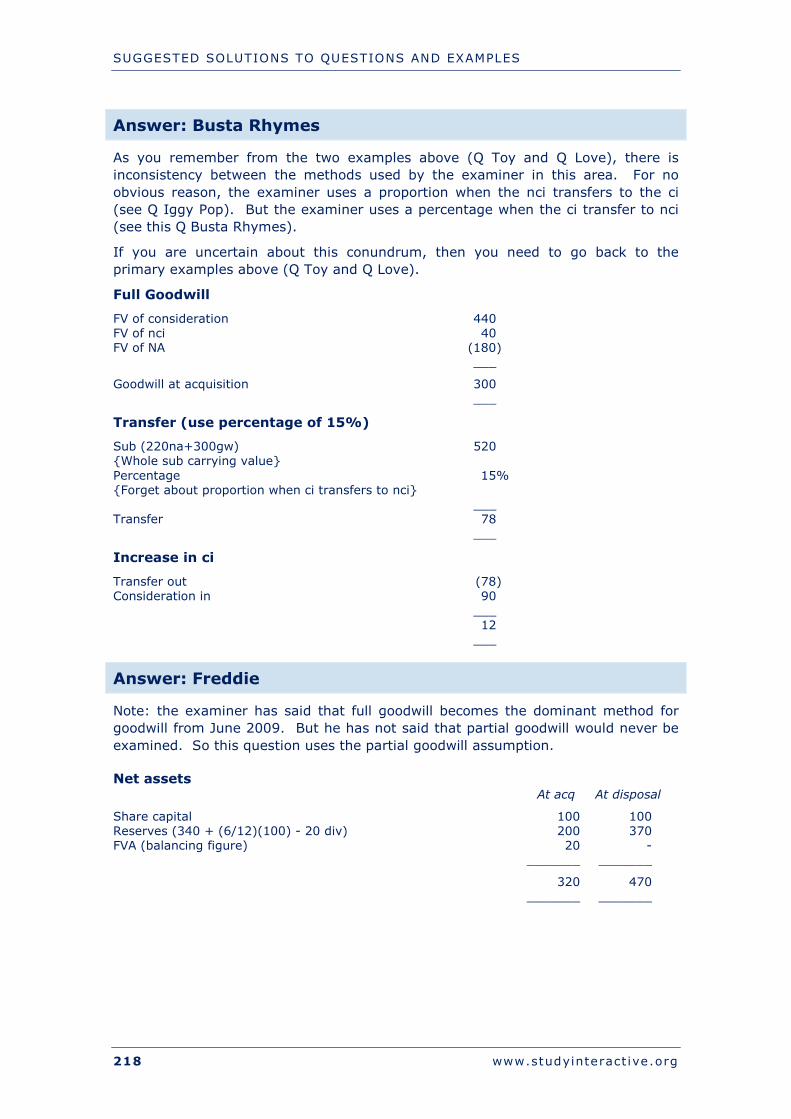

Question: Busta Rhymes

At the year start, Busta acquired 90% of Rhymes for $440m. The fair value of the identifiable net assets of Rhymes at the point of acquisition was $180m. The fair value of the NCI was $40m.

Required:

(a) Goodwill.

At the year end, Busta disposes of 15% of the equity of Rhymes for $90m and so reduces its ownership to 75%. Rhymes has made profits and grown by $40m over the year and therefore the carrying value of identifiable net assets of Rhymes is $220m at the year end.

Required:

(b) Transfer to NCI and effect on controlling interest.

Subsidiary for disposal This is study guide entry D2b.

As you might imagine, a subsidiary acquired exclusively with a view to subsequent disposal is still a subsidiary and must be consolidated for the short period of control.

CHAPTER 1 - BASIC GROUPS

36 www.studyinteract ive.org

RELATIONSHIP STANDARDS

There are various standards that govern group accounting and they are very rarely directly examined. However, it is possible that a question could expect a student to know a little of their content.

IFRS 10 IFRS 10 Consolidated Financial Statements defines control and tells us how to consolidate. Control is defined as the power to direct activities with exposure to variable returns. So the definition includes both the old ideas of risks and rewards and the new ideas of being able to make things happen. The new definition is so simple that it is hoped that it will be very difficult for parents to possess subsidiaries and ignore them. This was a big part of the Enron fraud and brought accounting for subs into disrepute.

Consolidation is essentially adding performance and position to the parent with adjustments (see Question Peddle for mechanics).

IFRS 11 IFRS 11 Joint Arrangements looks at entities under joint control. Joint control exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control. Joint control occurs when you and I together have control of another entity but individually have only influence. There are two arrangements:-

Joint operations In a JO, you and I share control of the operation, but my assets are mine and your assets are yours. The accounting follows the substance. My assets go on my balance sheet and yours on yours.

Joint Venture In a JV, you and I share control and everything else as well. Joint control is seen as very very significant influence. So a JV is simply accounted for as an associate. The detail of associate accounting remains in old IAS 28.

Incorporation It is not always true, but usually incorporation gives away the underlying nature. JVs are incorporated and JOs are not.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 37

Example: You and I

An example may help make it clear. You and I are working together selling petrol. We go into Japan and we both put $100m each into a newly incorporated company that will build a refinery and buy oil to refine and sell to the Japanese. You will have half the shares and I will have the other half. We also go into Russia. We agree to share the revenue half and half. But you put your Russian refinery into the deal and I put my trans-Siberian pipeline in. We agree that your refinery remains yours and my pipeline remains mine, although to repeat, the revenue is to be shared half and half.

Japan

The Japanese joint arrangement is a JV. Everything is shared 50/50. Nothing is yours absolutely and nothing is mine absolutely. Everything belongs to the JV and the JV belongs to us half and half. Backing this conclusion up is the incorporation of the JV.

So the Japanese arrangement will be recorded as a 50% associate in my books and the same in yours.

Russia

But the Russian deal is quite different. It is a JO. The pipeline is mine and not yours. The refinery is yours and not mine. We share the revenue and so operate jointly but we do not share everything.

So the pipeline will stay on my b/s and the refinery will stay on yours.

IAS 28 IAS 28 Associates defines significant influence as the power to participate and requires equity accounting for associates (including JVs). Equity accounting is essentially recognising a share of the associate profit in the i/s and a share of net assets in b/s. Equity accounting is also described as an equity investment initially recorded at cost and is subsequently adjusted to reflect the investor's share of the net profit or loss of the associate (see Question Peddle for mechanics).

IFRS 12 IFRS 12 Disclosure of Interests in Other Entities is a very cute piece of standard setting. The above standards define control, joint control and influence and together make it difficult to fake a relationship. But IFRS 12 makes it that bit harder. IFRS 12 requires that a parent lists all the entities with which it has a relationship and explain the basis of the parent conclusion. So the parent must list all its subs and say why it believes it has control and list all its associates and say why it believes it has influence and not control. This makes it even harder to pretend a sub is an associate.

CHAPTER 1 - BASIC GROUPS

38 www.studyinteract ive.org

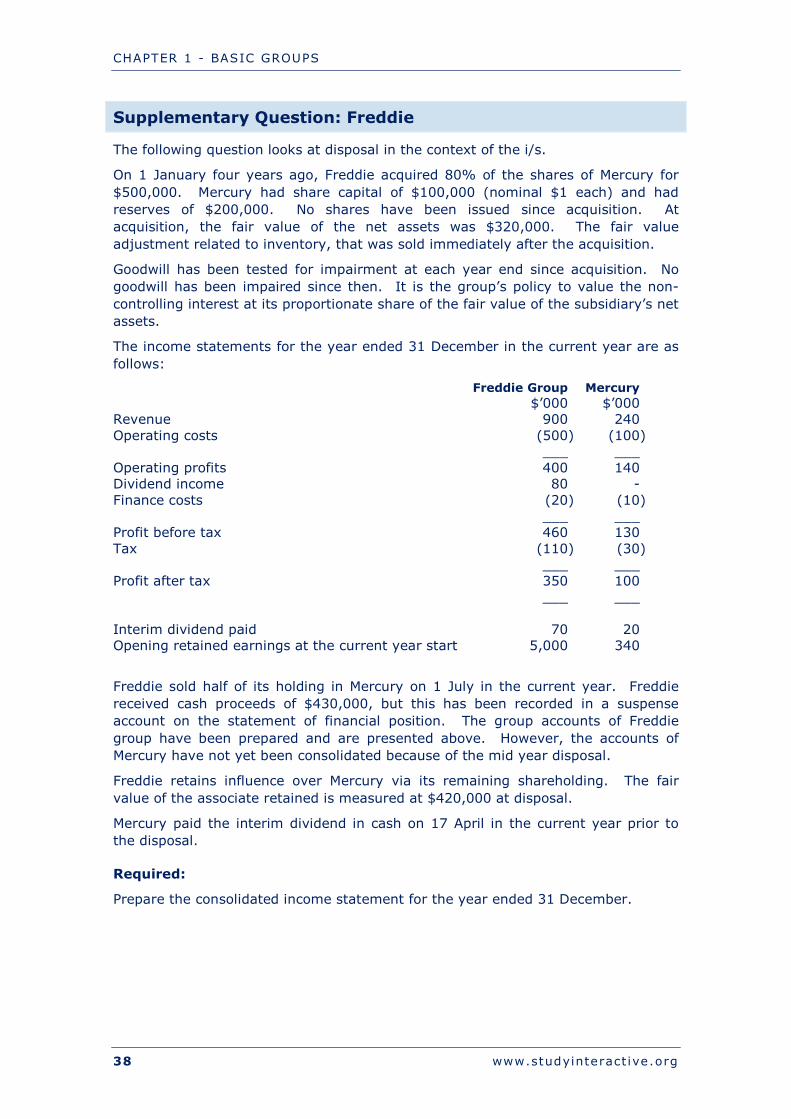

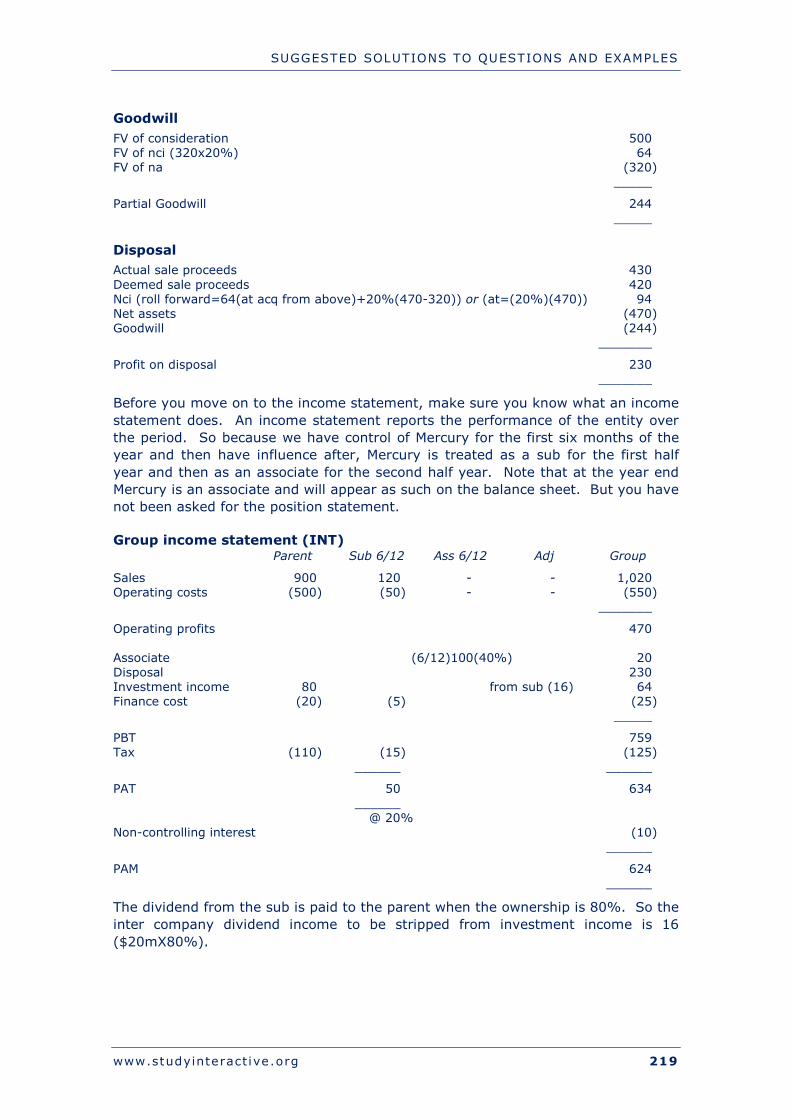

Supplementary Question: Freddie

The following question looks at disposal in the context of the i/s.

On 1 January four years ago, Freddie acquired 80% of the shares of Mercury for $500,000. Mercury had share capital of $100,000 (nominal $1 each) and had reserves of $200,000. No shares have been issued since acquisition. At acquisition, the fair value of the net assets was $320,000. The fair value adjustment related to inventory, that was sold immediately after the acquisition.

Goodwill has been tested for impairment at each year end since acquisition. No goodwill has been impaired since then. It is the group’s policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary’s net assets.

The income statements for the year ended 31 December in the current year are as follows:

Freddie Group Mercury $’000 $’000 Revenue 900 240 Operating costs (500) (100) ___ ___ Operating profits 400 140 Dividend income 80 - Finance costs (20) (10) ___ ___ Profit before tax 460 130 Tax (110) (30) ___ ___ Profit after tax 350 100 ___ ___ Interim dividend paid 70 20 Opening retained earnings at the current year start 5,000 340

Freddie sold half of its holding in Mercury on 1 July in the current year. Freddie received cash proceeds of $430,000, but this has been recorded in a suspense account on the statement of financial position. The group accounts of Freddie group have been prepared and are presented above. However, the accounts of Mercury have not yet been consolidated because of the mid year disposal.

Freddie retains influence over Mercury via its remaining shareholding. The fair value of the associate retained is measured at $420,000 at disposal.

Mercury paid the interim dividend in cash on 17 April in the current year prior to the disposal.

Required:

Prepare the consolidated income statement for the year ended 31 December.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 39

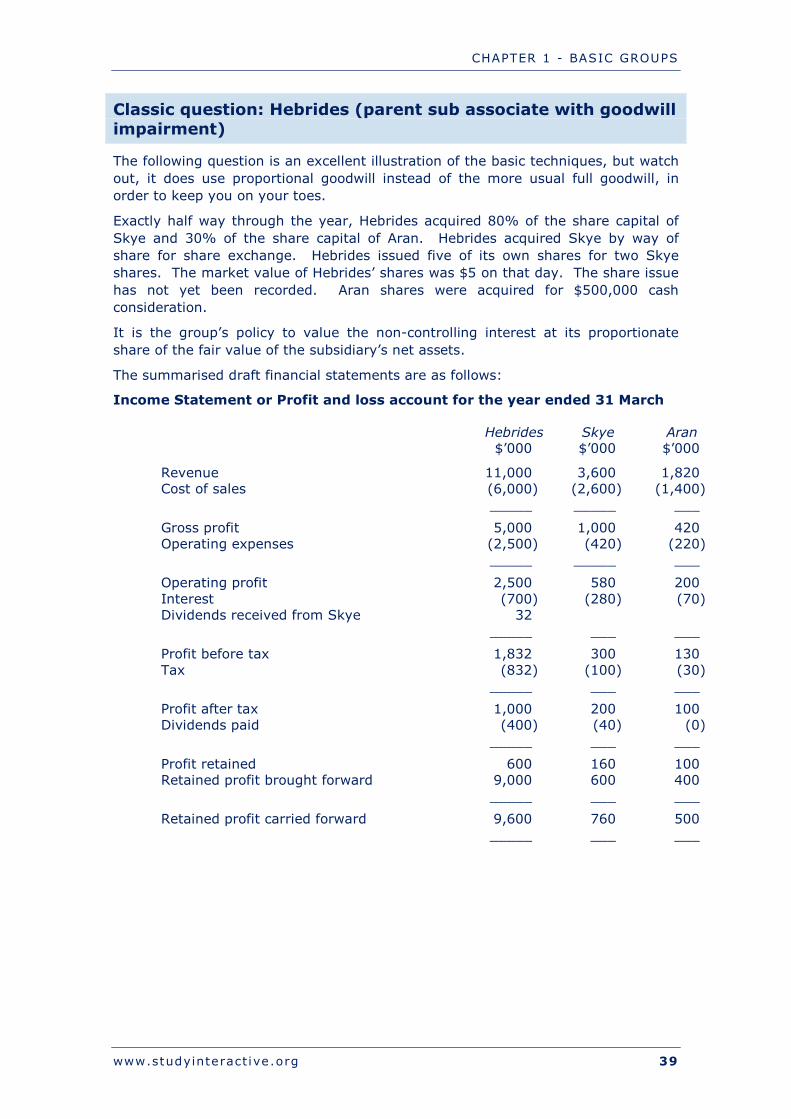

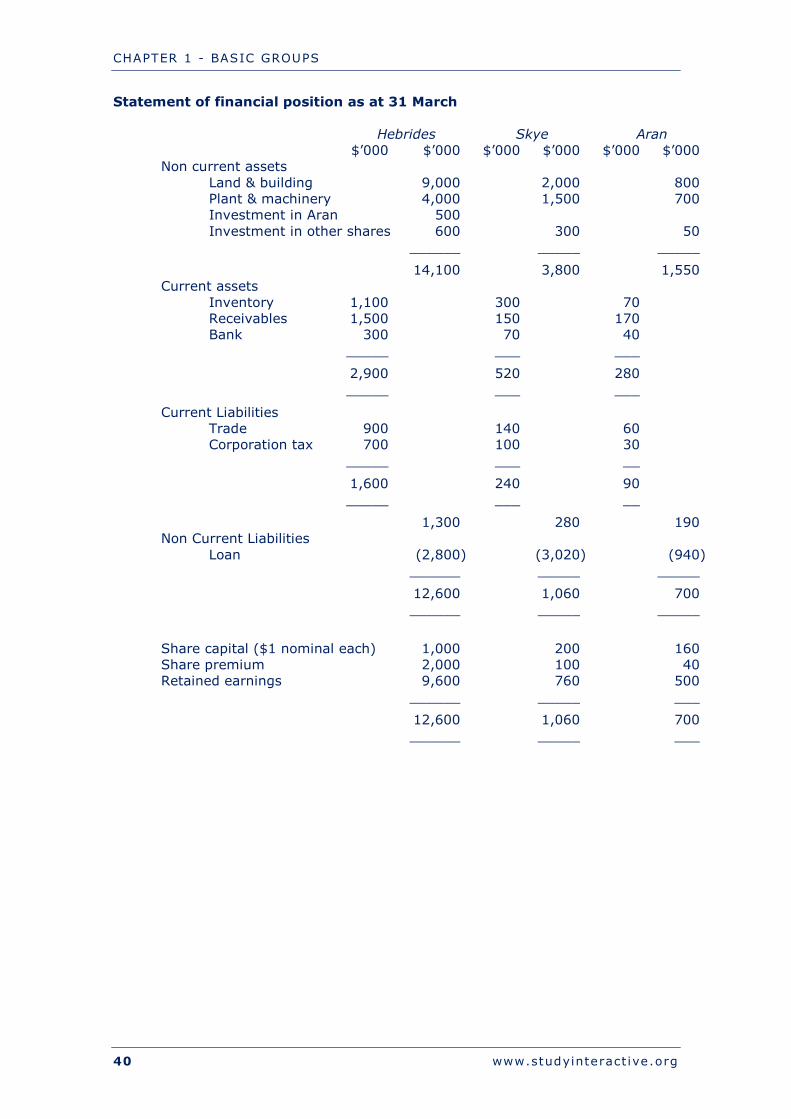

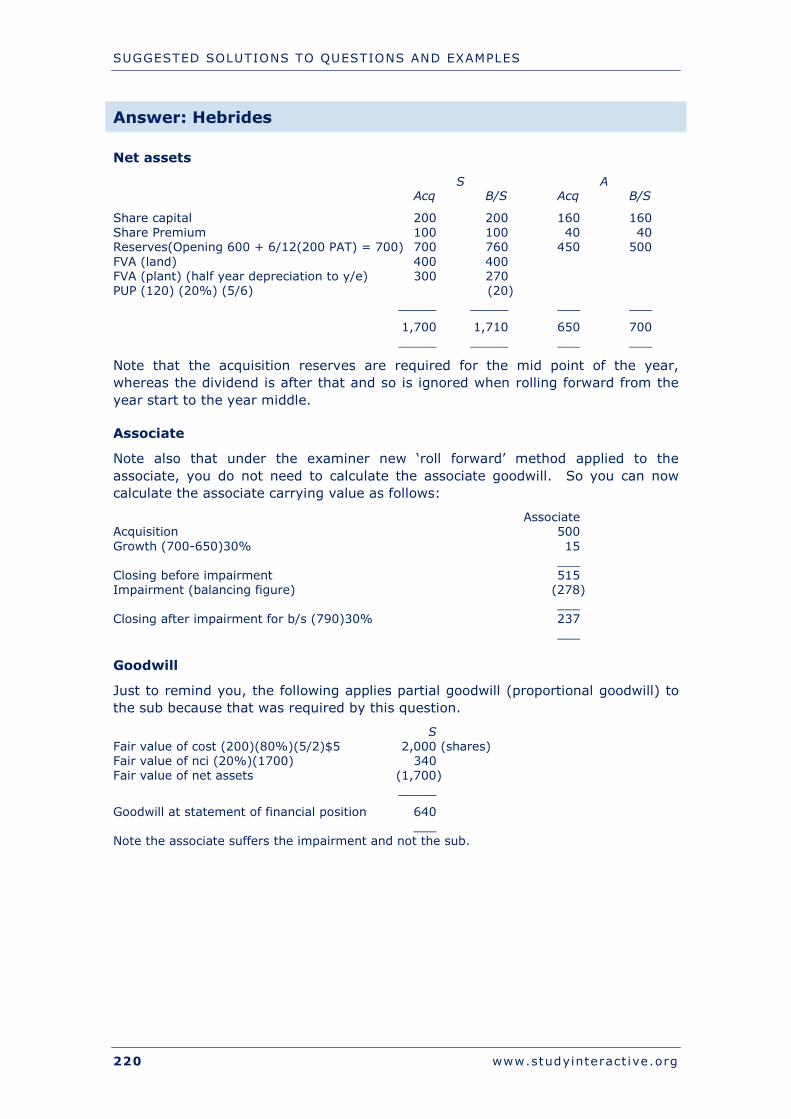

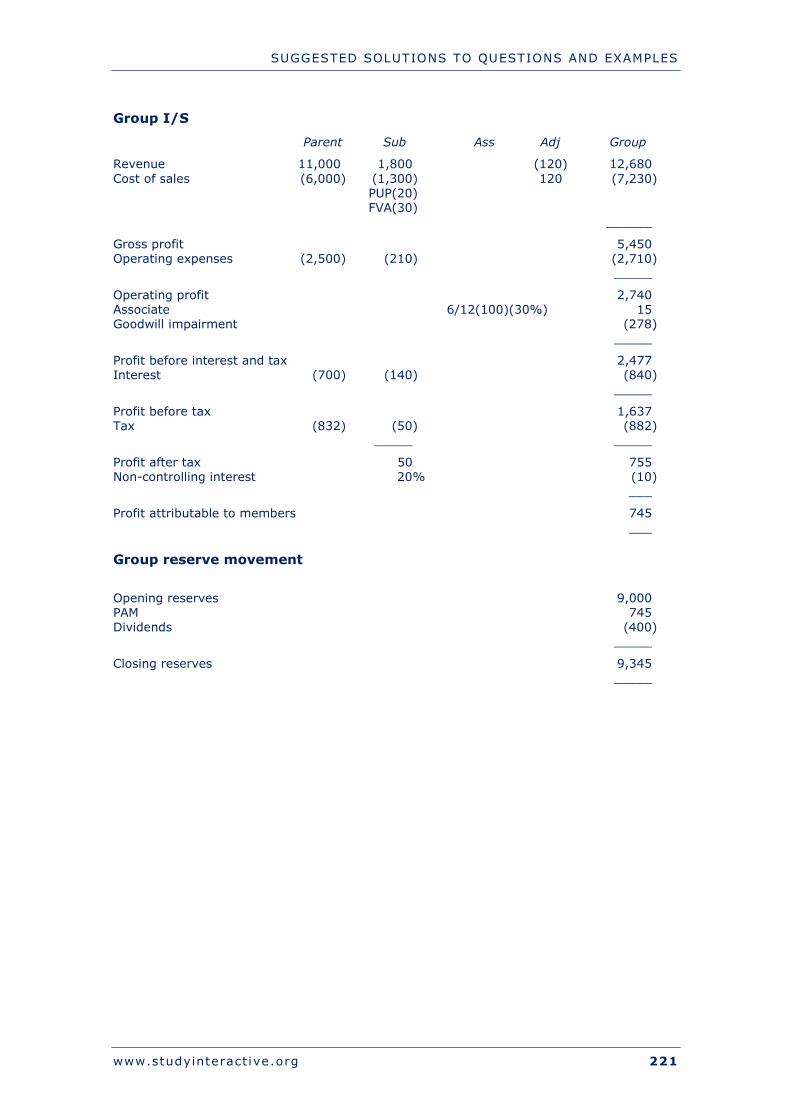

Classic question: Hebrides (parent sub associate with goodwill impairment)

The following question is an excellent illustration of the basic techniques, but watch out, it does use proportional goodwill instead of the more usual full goodwill, in order to keep you on your toes.

Exactly half way through the year, Hebrides acquired 80% of the share capital of Skye and 30% of the share capital of Aran. Hebrides acquired Skye by way of share for share exchange. Hebrides issued five of its own shares for two Skye shares. The market value of Hebrides’ shares was $5 on that day. The share issue has not yet been recorded. Aran shares were acquired for $500,000 cash consideration.

It is the group’s policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary’s net assets.

The summarised draft financial statements are as follows:

Income Statement or Profit and loss account for the year ended 31 March Hebrides Skye Aran $’000 $’000 $’000

Revenue 11,000 3,600 1,820 Cost of sales (6,000) (2,600) (1,400) _____ _____ ___

Gross profit 5,000 1,000 420 Operating expenses (2,500) (420) (220) _____ _____ ___

Operating profit 2,500 580 200 Interest (700) (280) (70) Dividends received from Skye 32 _____ ___ ___

Profit before tax 1,832 300 130 Tax (832) (100) (30) _____ ___ ___

Profit after tax 1,000 200 100 Dividends paid (400) (40) (0) _____ ___ ___

Profit retained 600 160 100 Retained profit brought forward 9,000 600 400 _____ ___ ___

Retained profit carried forward 9,600 760 500 _____ ___ ___

CHAPTER 1 - BASIC GROUPS

40 www.studyinteract ive.org

Statement of financial position as at 31 March Hebrides Skye Aran $’000 $’000 $’000 $’000 $’000 $’000 Non current assets Land & building 9,000 2,000 800 Plant & machinery 4,000 1,500 700 Investment in Aran 500 Investment in other shares 600 300 50 ______ _____ _____

14,100 3,800 1,550 Current assets Inventory 1,100 300 70 Receivables 1,500 150 170 Bank 300 70 40 _____ ___ ___

2,900 520 280 _____ ___ ___

Current Liabilities Trade 900 140 60 Corporation tax 700 100 30 _____ ___ __

1,600 240 90 _____ ___ __

1,300 280 190 Non Current Liabilities Loan (2,800) (3,020) (940) ______ _____ _____

12,600 1,060 700 ______ _____ _____

Share capital ($1 nominal each) 1,000 200 160 Share premium 2,000 100 40 Retained earnings 9,600 760 500 ______ _____ ___

12,600 1,060 700 ______ _____ ___

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 41

The following information is relevant:

(1) At acquisition the fair value of all Aran’s assets was reasonably represented by the book value. The same was true of Skye with the exception of some land and plant. These had fair values of $400,000 and $300,000 above book values. The plant had a remaining life of five years. Depreciation is charged to cost of sales.

(2) In the post acquisition period Skye sold goods to Hebrides at $120,000. Transfer transactions were calculated to give a margin of 20% (mark up of 25%). Skye held five sixths of these goods in inventory at the year end.

(3) Goodwill related to the Skye acquisition was subject to a brief impairment review and this was sufficient to confirm that there was no impairment. However, a similar review of the goodwill related to Aran revealed that there may be an impairment. So a more detailed review was conducted which revealed a value in use of $790,000 and a net realisable value of $560,000. Goodwill impairment is separately discloseable on the face of the income statement.

(4) The current account between Hebrides and Skye did not agree due to cash in transit from subsidiary to parent of $4,000. Hebrides recorded a receivable of $25,000 at the year end. Dividends were paid in the last month before the year end.

Required:

Income statement (Profit or loss report) and statement of financial position (balance sheet) for the group for the year ended 31 March.

CHAPTER 1 - BASIC GROUPS

42 www.studyinteract ive.org

STUDENT ACCOUNTANT MAGAZINE ARTICLE

Business Combinations as a Current Issue

This is an article I (Martin Jones) did for the Student Accountant Magazine. It was published in the May 2009 edition. It was a response to the two examiner articles which appeared in the Student Accountant Magazine in February and April 2009. The idea was to bring to life the technicalities covered by those examiner articles. The published version of this article can be found online by going to the ACCA website and delving into the Student Accountant Magazine archive to find the May issue. I (Martin Jones) have written a bucket load of articles for Student Accountant. So if you ever find yourself with time for study after you have worked these class notes, then go to the relevant articles section of the ACCA P2 webpage.

Current issues

Current issues are at the heart of P2 corporate reporting and permeate the entire exam. But it is the last question, Q4 that really delves into the political and intellectual mire that is current issues in financial reporting. Traditionally, this question has been the best answered over the years. However, in recent sittings the focus question, Q2 has caught up. This article is aimed at putting the current issues question back out in front.

The article will first take you through some of the hot topics in financial reporting. But then, by using an illustrative question, the article will show you how to use this information to formulate an answer to a current issues question. Here is your whirlwind tour of current issues.

The framework

The examiner’s advice is that if you are not sure where to start your answer to a current issues question, then start with the framework. So that is where I’ll start.

The framework for financial reporting sets out the conceptual basis for the development of standards and is itself based on the elements of assets and liabilities. To paraphrase the framework “an asset/liability is a right/obligation to a future economic outflow/inflow.” This focus on financial position has permeated all the standards issued in recent years and continues to dominate the current issues.

But the framework also talks to us of other concepts, such as relevance, reliability and entity.

Fair value

Which brings us smoothly to the hot topic in financial reporting, fair value. In order to make the position statement a genuine statement of financial position rather than simply a balance sheet, the IASB have been pushing financial reporting towards fair value. Fair value accounting attempts to present all assets and liabilities at market value and as such is highly subjective. But the IASB are prepared to accept the reduced reliability in favour of the increased relevance.

Convergence

Also red hot is the subject of convergence, which the IASB interpret essentially as the convergence of IFRS with American accounting. This process has taken a major boost over recent months with the United States of America Securities and Exchange Commission coming out in favour of fair value and the IASB.

CHAPTER 1 - BASIC GROUPS

www.studyinteract ive.org 43

Business combinations

Tangled up in the process of convergence is the project to make sense of group accounting. The IASB have long accepted that the American slant on groups was tuned better to the entity concept and the reality of acquisitions. So the IASB issued and reissued IFRS3 Business Combinations in order to reflect this. But perhaps the rarity of non-controlling interest in the US has led to the IASB creating unnecessary complications as regards the NCI goodwill. These complications are discussed below.

Management commentary

But the spiralling complexity of financial reporting has led to most companies translating the financial statements into a more digestible report tagged on to the financial statements in the annual report. This management commentary is largely unregulated at the moment, but the IASB have a standard under development that once issued will produce some standardisation in management commentaries.

CHAPTER 1 - BASIC GROUPS

44 www.studyinteract ive.org

www.studyinteract ive.org 45

Chapter 2

Complex groups

CHAPTER 2 - COMPLEX GROUPS

46 www.studyinteract ive.org

CHAPTER CONTENTS

VERTICAL GROUP STRUCTURE ----------------------------------------- 47

CHANGES IN GROUP STRUCTURE -------------------------------------- 53

CHAPTER 2 - COMPLEX GROUPS

www.studyinteract ive.org 47

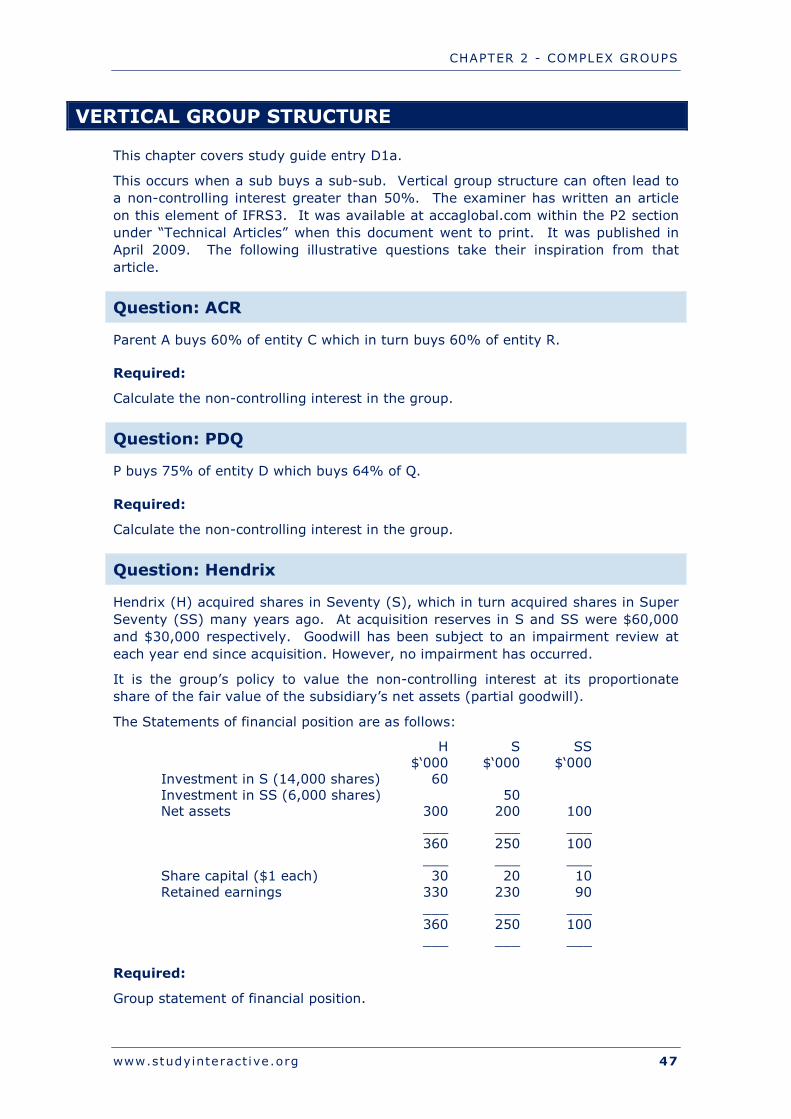

VERTICAL GROUP STRUCTURE

This chapter covers study guide entry D1a.

This occurs when a sub buys a sub-sub. Vertical group structure can often lead to a non-controlling interest greater than 50%. The examiner has written an article on this element of IFRS3. It was available at accaglobal.com within the P2 section under “Technical Articles” when this document went to print. It was published in April 2009. The following illustrative questions take their inspiration from that article.

Question: ACR

Parent A buys 60% of entity C which in turn buys 60% of entity R.

Required:

Calculate the non-controlling interest in the group.

Question: PDQ

P buys 75% of entity D which buys 64% of Q.

Required:

Calculate the non-controlling interest in the group.

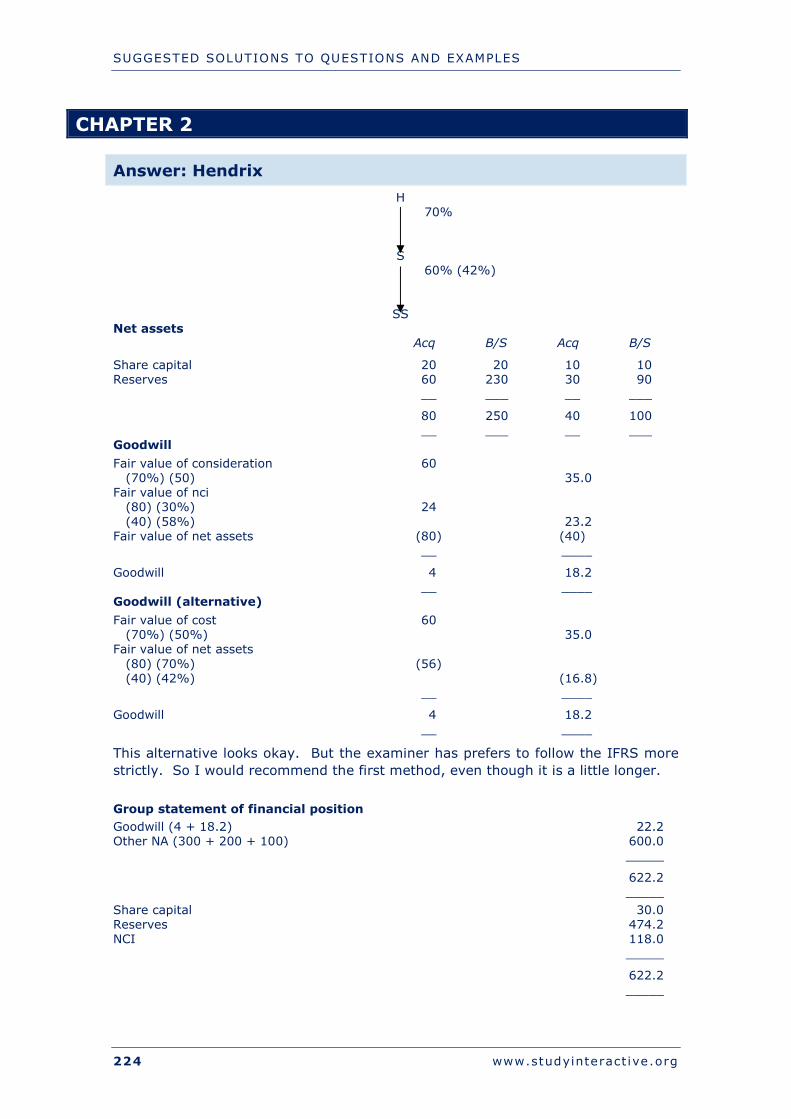

Question: Hendrix

Hendrix (H) acquired shares in Seventy (S), which in turn acquired shares in Super Seventy (SS) many years ago. At acquisition reserves in S and SS were $60,000 and $30,000 respectively. Goodwill has been subject to an impairment review at each year end since acquisition. However, no impairment has occurred.

It is the group’s policy to value the non-controlling interest at its proportionate share of the fair value of the subsidiary’s net assets (partial goodwill).

The Statements of financial position are as follows:

H S SS $‘000 $‘000 $‘000 Investment in S (14,000 shares) 60 Investment in SS (6,000 shares) 50 Net assets 300 200 100 ___ ___ ___ 360 250 100 ___ ___ ___ Share capital ($1 each) 30 20 10 Retained earnings 330 230 90 ___ ___ ___ 360 250 100 ___ ___ ___

Required:

Group statement of financial position.

CHAPTER 2 - COMPLEX GROUPS

48 www.studyinteract ive.org

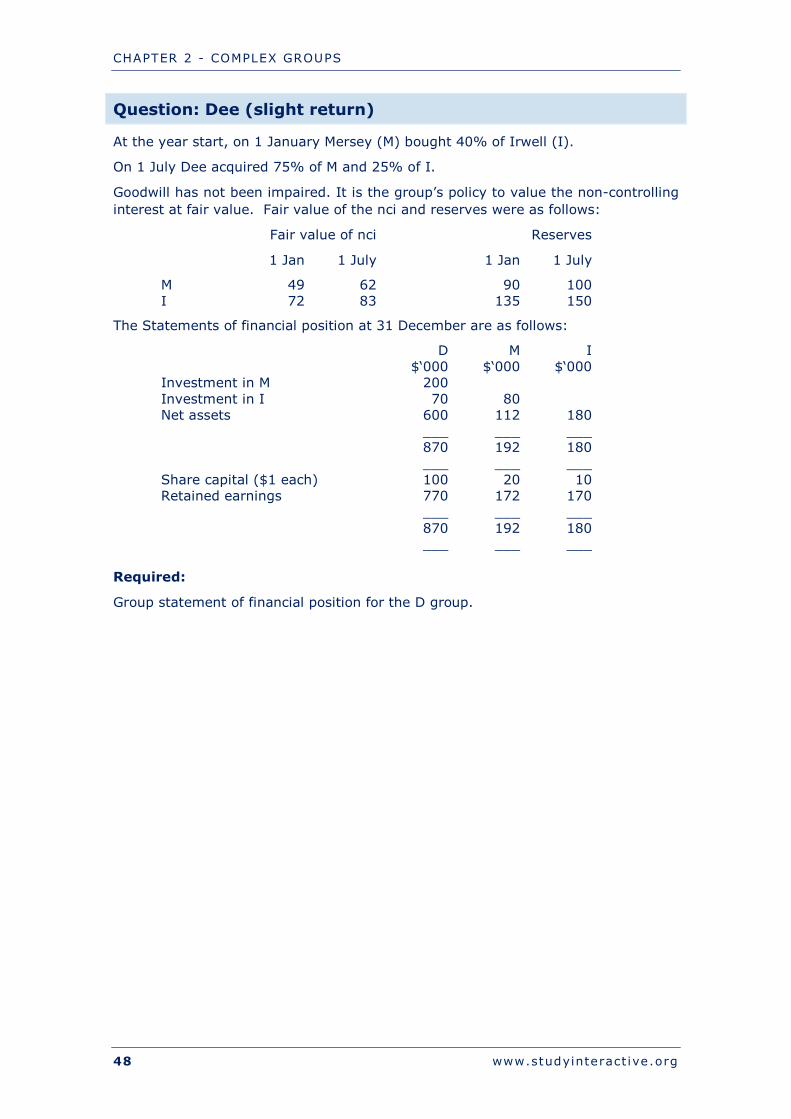

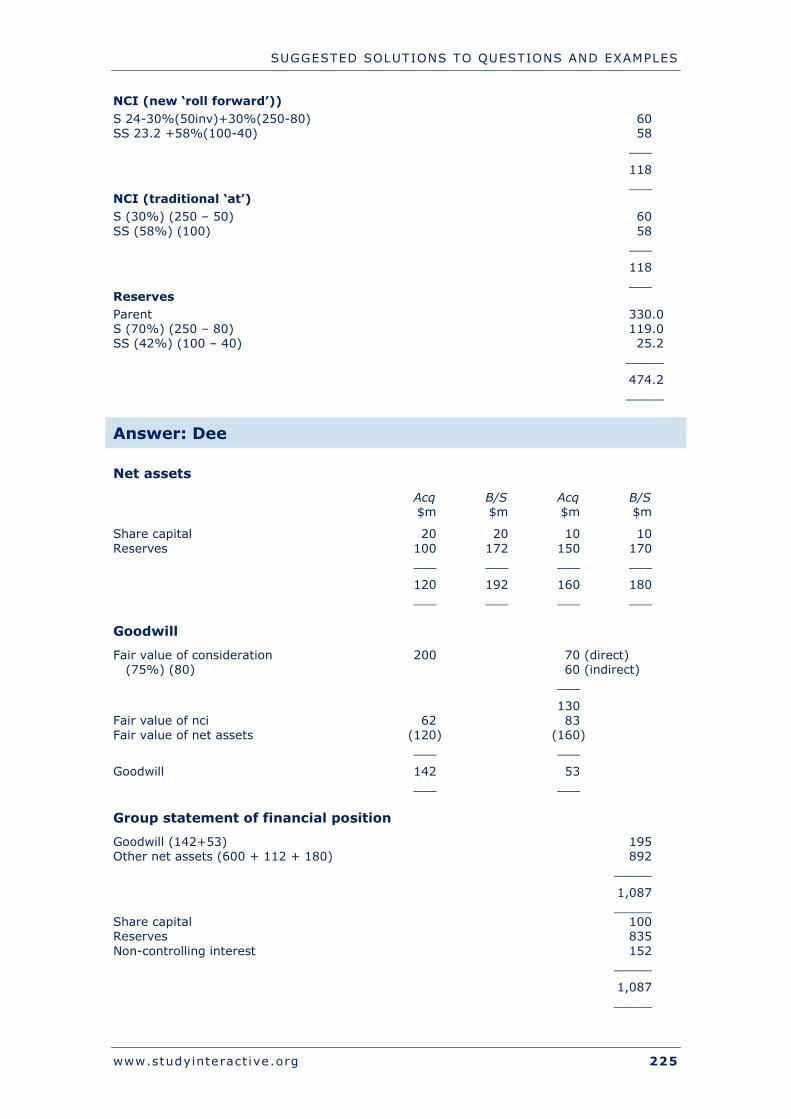

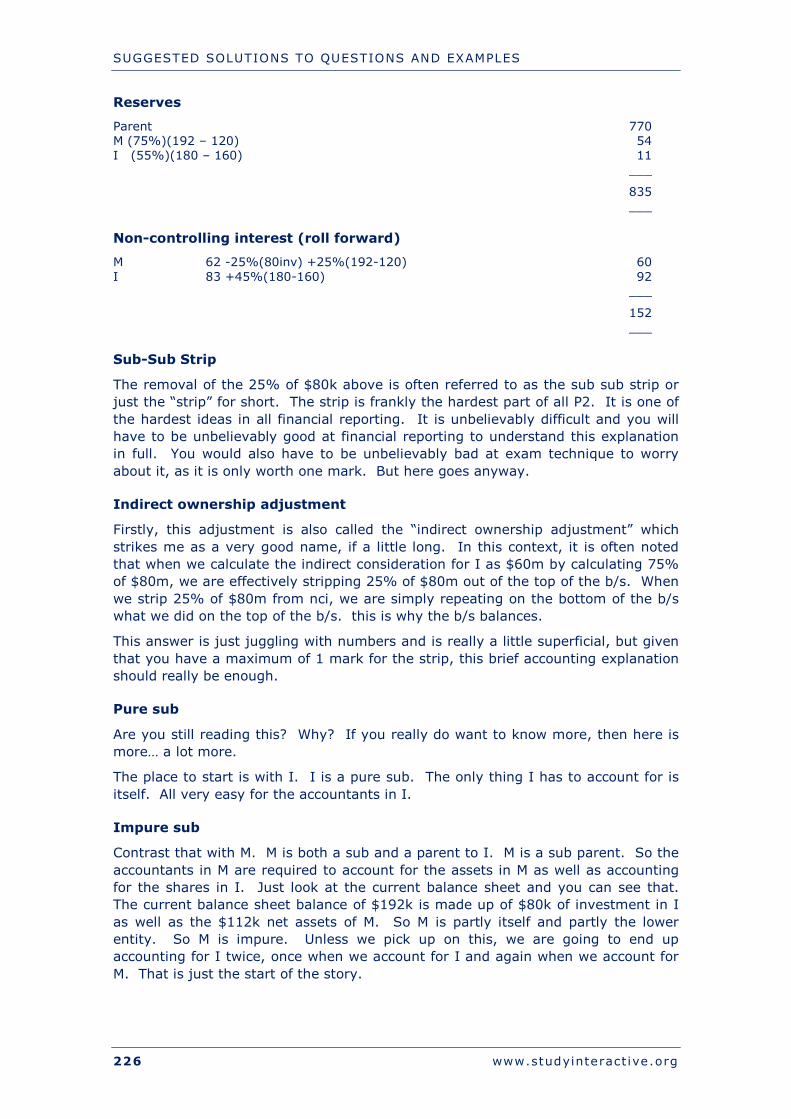

Question: Dee (slight return)

At the year start, on 1 January Mersey (M) bought 40% of Irwell (I).

On 1 July Dee acquired 75% of M and 25% of I.

Goodwill has not been impaired. It is the group’s policy to value the non-controlling interest at fair value. Fair value of the nci and reserves were as follows:

Fair value of nci Reserves

1 Jan 1 July 1 Jan 1 July

M 49 62 90 100 I 72 83 135 150

The Statements of financial position at 31 December are as follows:

D M I $‘000 $‘000 $‘000 Investment in M 200 Investment in I 70 80 Net assets 600 112 180 ___ ___ ___ 870 192 180 ___ ___ ___ Share capital ($1 each) 100 20 10 Retained earnings 770 172 170 ___ ___ ___ 870 192 180 ___ ___ ___

Required:

Group statement of financial position for the D group.

CHAPTER 2 - COMPLEX GROUPS

www.studyinteract ive.org 49

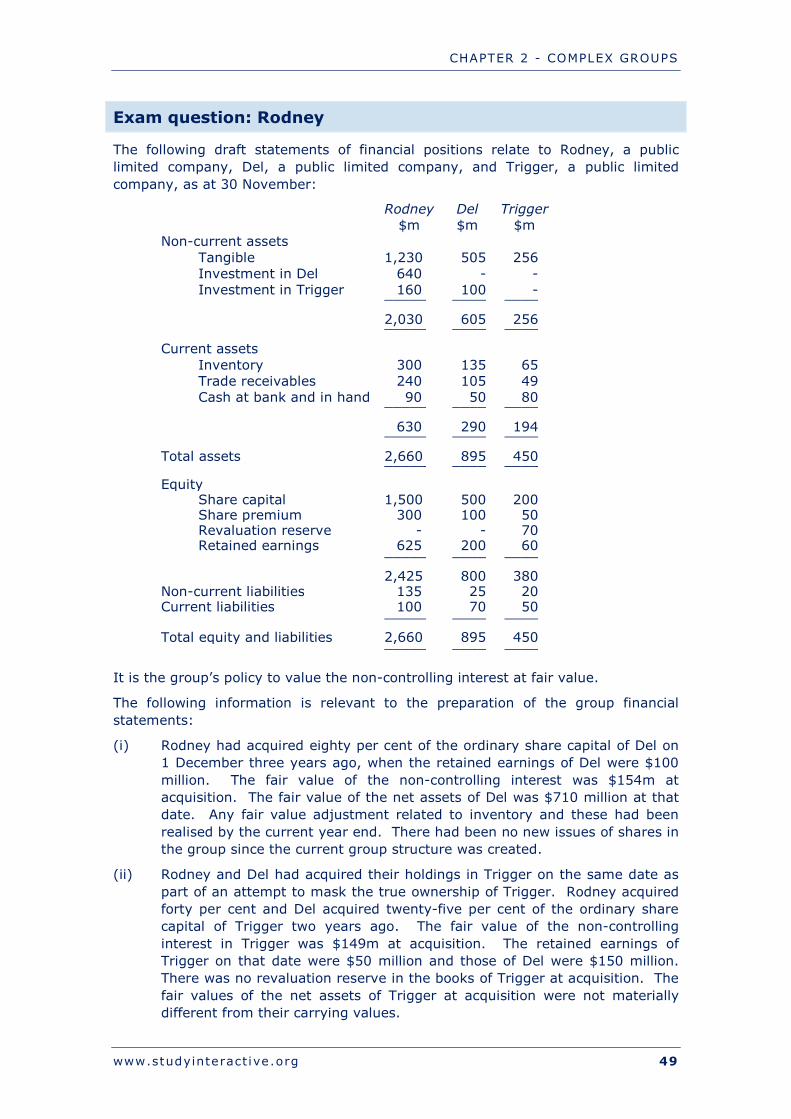

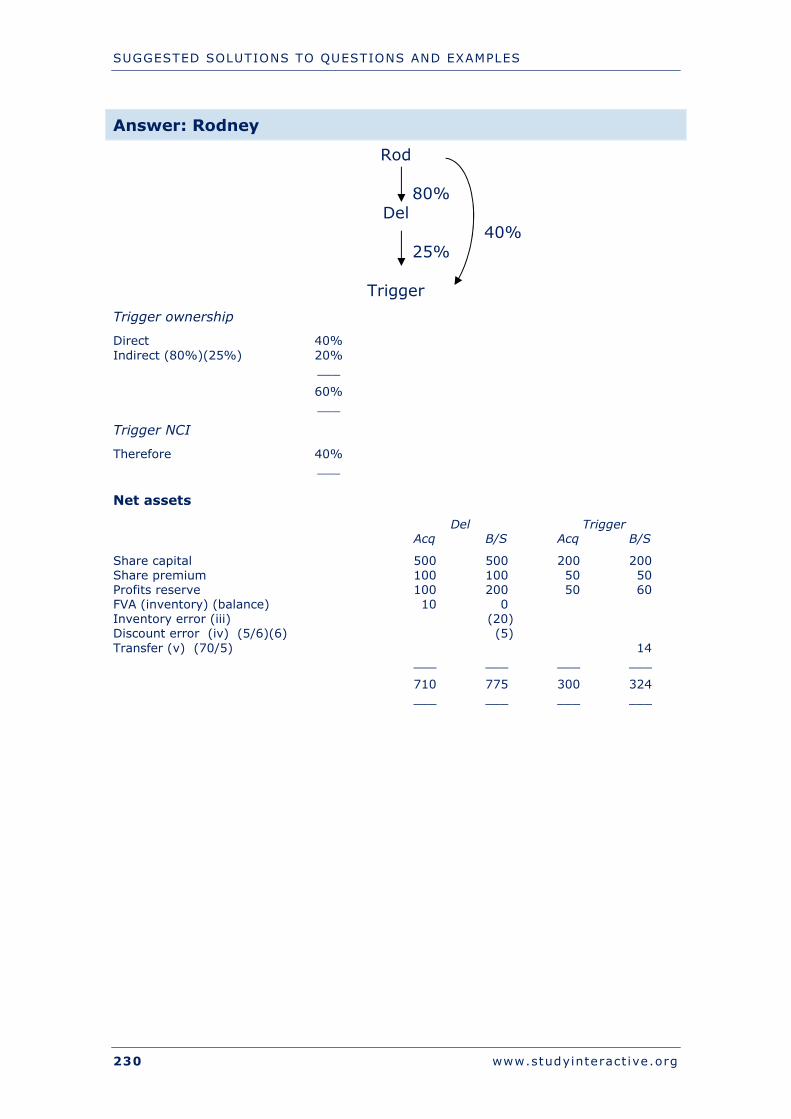

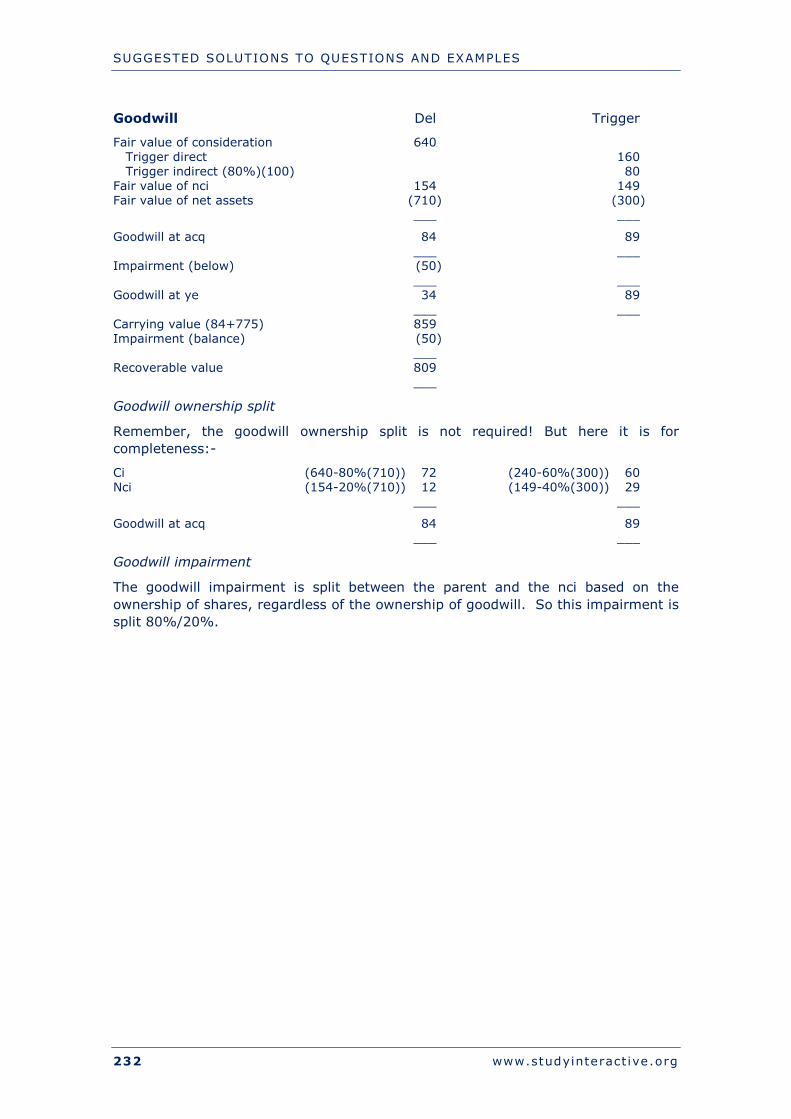

Exam question: Rodney

The following draft statements of financial positions relate to Rodney, a public limited company, Del, a public limited company, and Trigger, a public limited company, as at 30 November:

Rodney Del Trigger $m $m $m Non-current assets Tangible 1,230 505 256 Investment in Del 640 - - Investment in Trigger 160 100 -

_____ ____ ____

2,030 605 256

_____ ____ ____

Current assets Inventory 300 135 65 Trade receivables 240 105 49 Cash at bank and in hand 90 50 80

_____ ____ ____

630 290 194

_____ ____ ____

Total assets 2,660 895 450

_____ ____ ____

Equity Share capital 1,500 500 200 Share premium 300 100 50 Revaluation reserve - - 70 Retained earnings 625 200 60

_____ ____ ____

2,425 800 380 Non-current liabilities 135 25 20 Current liabilities 100 70 50

_____ ____ ____

Total equity and liabilities 2,660 895 450

_____ ____ ____

It is the group’s policy to value the non-controlling interest at fair value.

The following information is relevant to the preparation of the group financial statements:

(i) Rodney had acquired eighty per cent of the ordinary share capital of Del on 1 December three years ago, when the retained earnings of Del were $100 million. The fair value of the non-controlling interest was $154m at acquisition. The fair value of the net assets of Del was $710 million at that date. Any fair value adjustment related to inventory and these had been realised by the current year end. There had been no new issues of shares in the group since the current group structure was created.

(ii) Rodney and Del had acquired their holdings in Trigger on the same date as part of an attempt to mask the true ownership of Trigger. Rodney acquired forty per cent and Del acquired twenty-five per cent of the ordinary share capital of Trigger two years ago. The fair value of the non-controlling interest in Trigger was $149m at acquisition. The retained earnings of Trigger on that date were $50 million and those of Del were $150 million. There was no revaluation reserve in the books of Trigger at acquisition. The fair values of the net assets of Trigger at acquisition were not materially different from their carrying values.

CHAPTER 2 - COMPLEX GROUPS

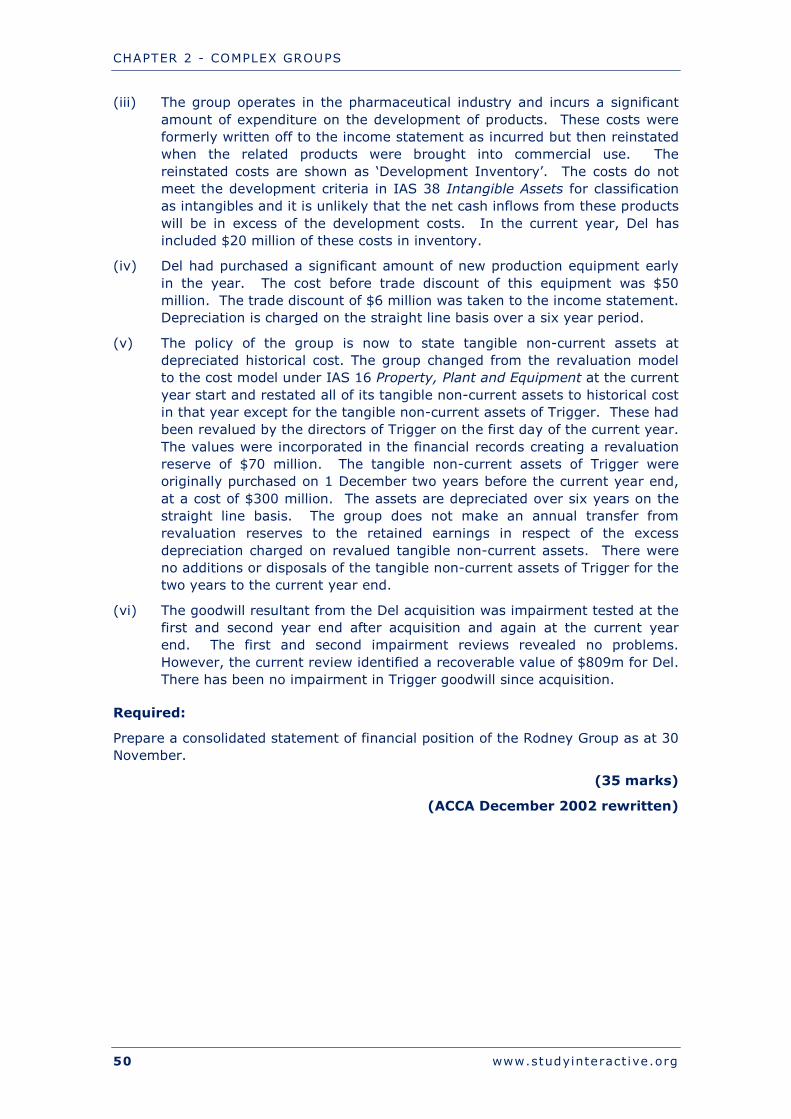

50 www.studyinteract ive.org

(iii) The group operates in the pharmaceutical industry and incurs a significant amount of expenditure on the development of products. These costs were formerly written off to the income statement as incurred but then reinstated when the related products were brought into commercial use. The reinstated costs are shown as ‘Development Inventory’. The costs do not meet the development criteria in IAS 38 Intangible Assets for classification as intangibles and it is unlikely that the net cash inflows from these products will be in excess of the development costs. In the current year, Del has included $20 million of these costs in inventory.

(iv) Del had purchased a significant amount of new production equipment early in the year. The cost before trade discount of this equipment was $50 million. The trade discount of $6 million was taken to the income statement. Depreciation is charged on the straight line basis over a six year period.

(v) The policy of the group is now to state tangible non-current assets at depreciated historical cost. The group changed from the revaluation model to the cost model under IAS 16 Property, Plant and Equipment at the current year start and restated all of its tangible non-current assets to historical cost in that year except for the tangible non-current assets of Trigger. These had been revalued by the directors of Trigger on the first day of the current year. The values were incorporated in the financial records creating a revaluation reserve of $70 million. The tangible non-current assets of Trigger were originally purchased on 1 December two years before the current year end, at a cost of $300 million. The assets are depreciated over six years on the straight line basis. The group does not make an annual transfer from revaluation reserves to the retained earnings in respect of the excess depreciation charged on revalued tangible non-current assets. There were no additions or disposals of the tangible non-current assets of Trigger for the two years to the current year end.

(vi) The goodwill resultant from the Del acquisition was impairment tested at the first and second year end after acquisition and again at the current year end. The first and second impairment reviews revealed no problems. However, the current review identified a recoverable value of $809m for Del. There has been no impairment in Trigger goodwill since acquisition.

Required:

Prepare a consolidated statement of financial position of the Rodney Group as at 30 November.

(35 marks)

(ACCA December 2002 rewritten)

CHAPTER 2 - COMPLEX GROUPS

www.studyinteract ive.org 51

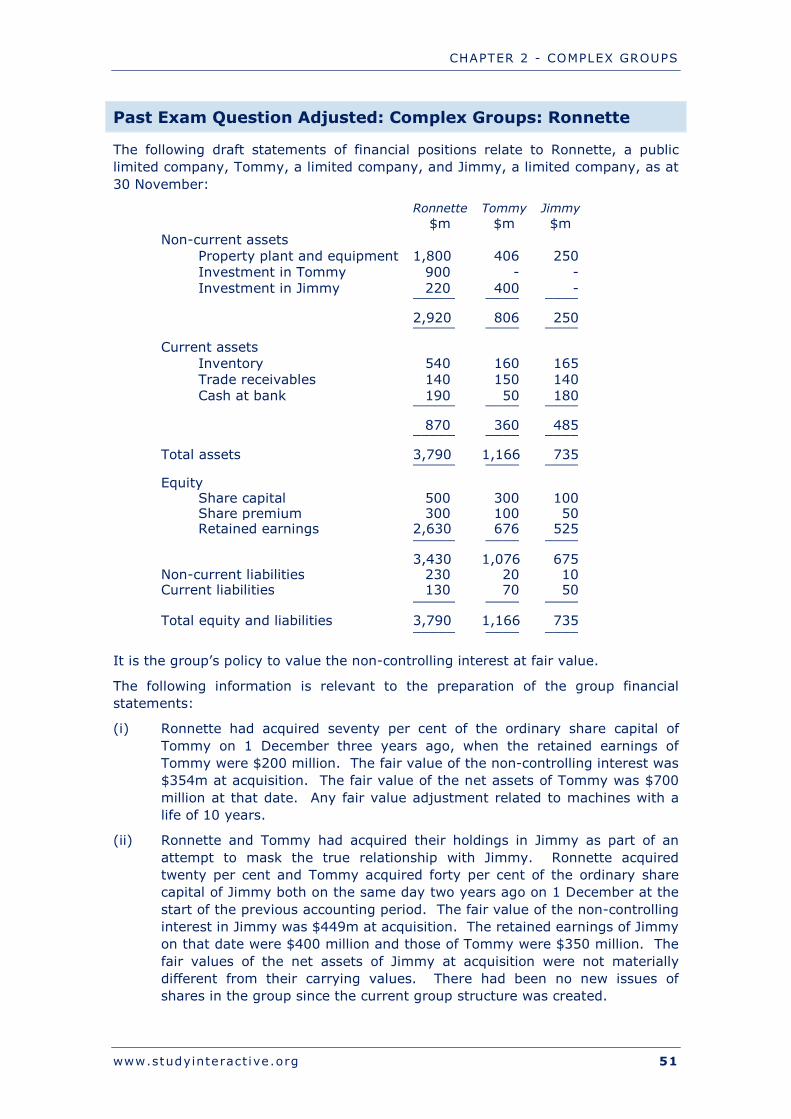

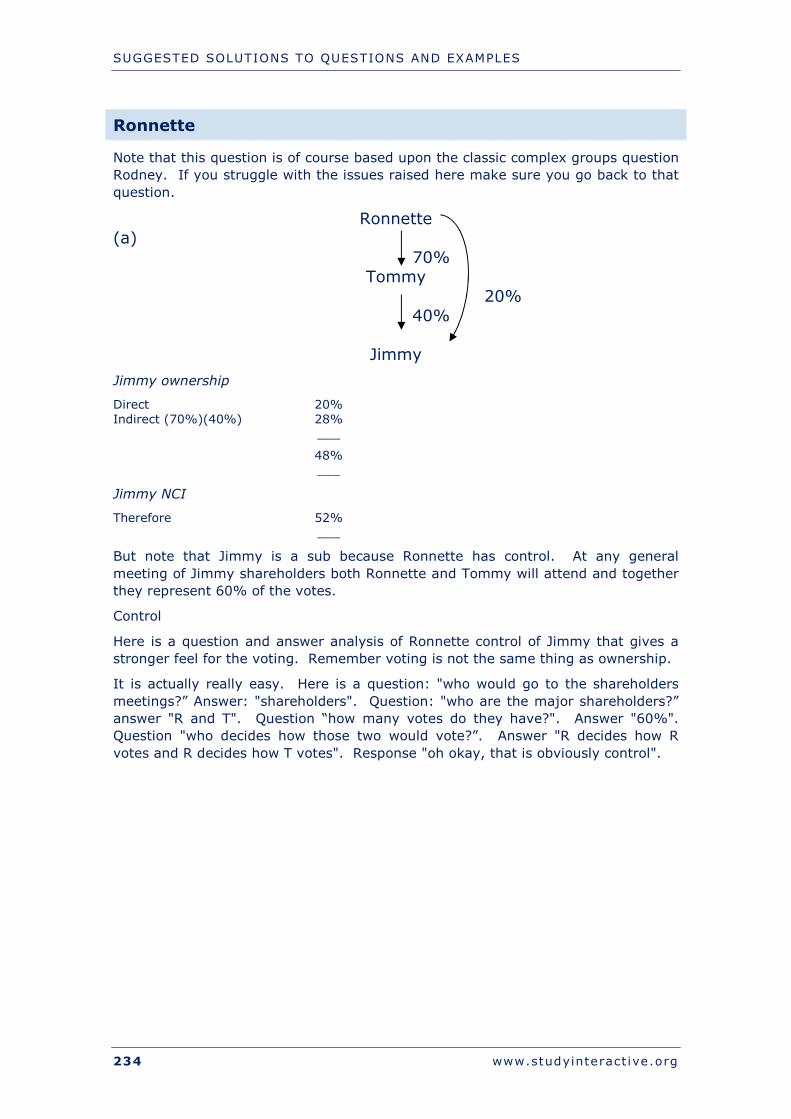

Past Exam Question Adjusted: Complex Groups: Ronnette

The following draft statements of financial positions relate to Ronnette, a public limited company, Tommy, a limited company, and Jimmy, a limited company, as at 30 November:

Ronnette Tommy Jimmy $m $m $m Non-current assets Property plant and equipment 1,800 406 250 Investment in Tommy 900 - - Investment in Jimmy 220 400 -

_____ ____ ____

2,920 806 250

_____ ____ ____

Current assets Inventory 540 160 165 Trade receivables 140 150 140 Cash at bank 190 50 180

_____ ____ ____

870 360 485

_____ ____ ____

Total assets 3,790 1,166 735

_____ ____ ____

Equity Share capital 500 300 100 Share premium 300 100 50 Retained earnings 2,630 676 525

_____ ____ ____

3,430 1,076 675 Non-current liabilities 230 20 10 Current liabilities 130 70 50

_____ ____ ____

Total equity and liabilities 3,790 1,166 735

_____ ____ ____

It is the group’s policy to value the non-controlling interest at fair value.

The following information is relevant to the preparation of the group financial statements:

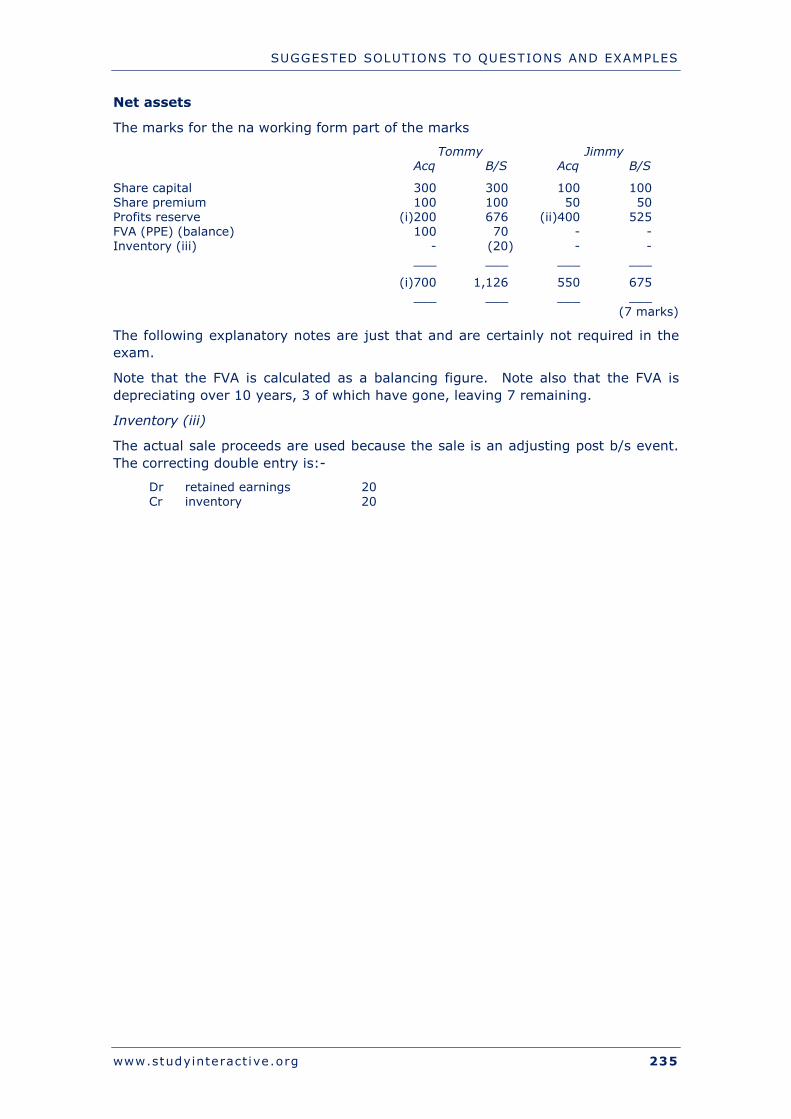

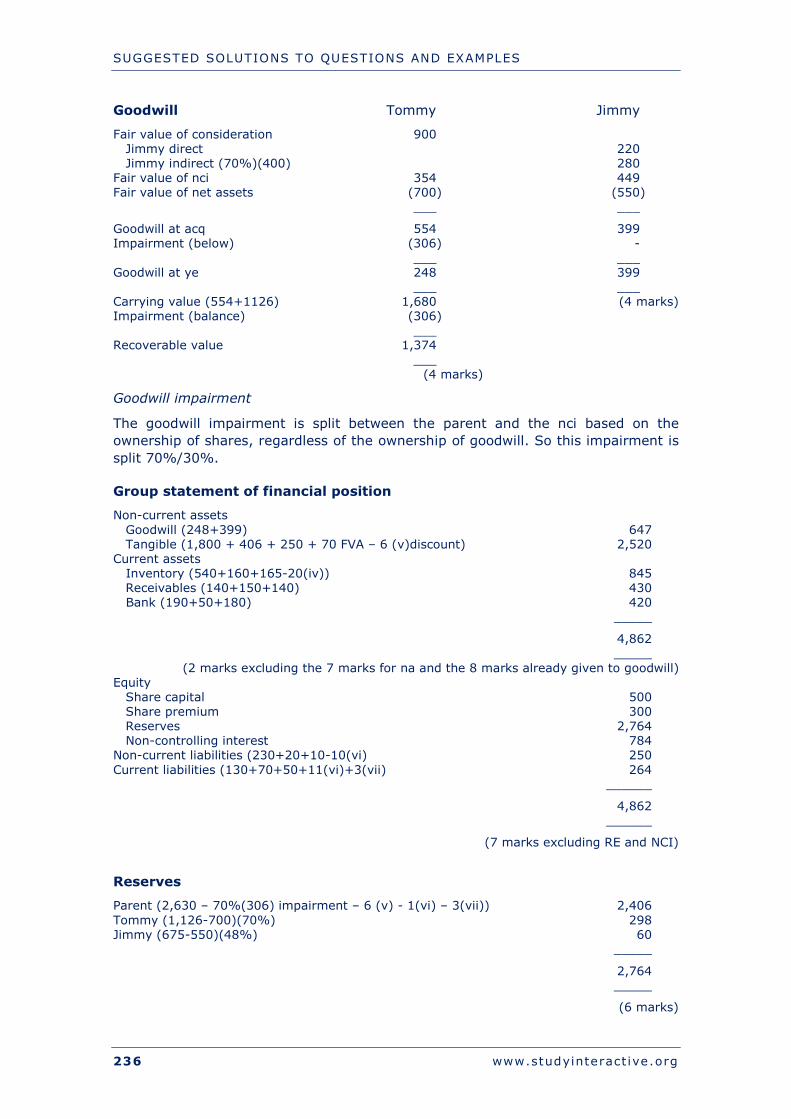

(i) Ronnette had acquired seventy per cent of the ordinary share capital of Tommy on 1 December three years ago, when the retained earnings of Tommy were $200 million. The fair value of the non-controlling interest was $354m at acquisition. The fair value of the net assets of Tommy was $700 million at that date. Any fair value adjustment related to machines with a life of 10 years.

(ii) Ronnette and Tommy had acquired their holdings in Jimmy as part of an attempt to mask the true relationship with Jimmy. Ronnette acquired twenty per cent and Tommy acquired forty per cent of the ordinary share capital of Jimmy both on the same day two years ago on 1 December at the start of the previous accounting period. The fair value of the non-controlling interest in Jimmy was $449m at acquisition. The retained earnings of Jimmy on that date were $400 million and those of Tommy were $350 million. The fair values of the net assets of Jimmy at acquisition were not materially different from their carrying values. There had been no new issues of shares in the group since the current group structure was created.

CHAPTER 2 - COMPLEX GROUPS

52 www.studyinteract ive.org

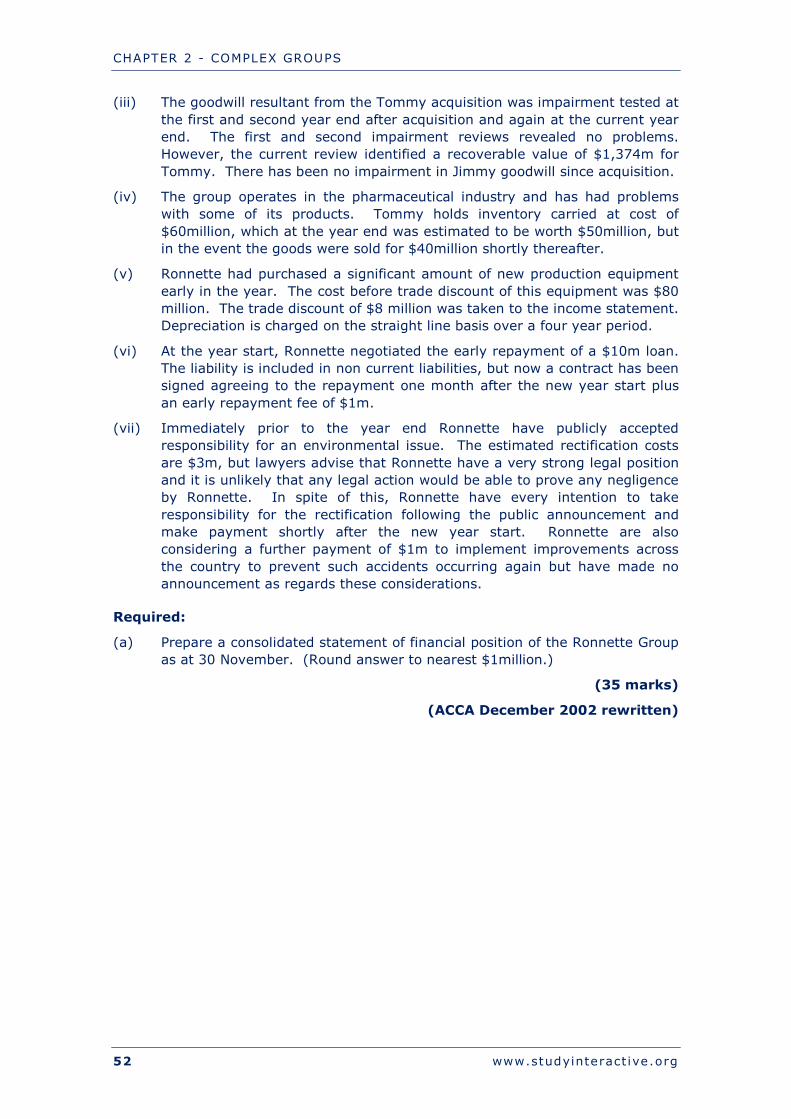

(iii) The goodwill resultant from the Tommy acquisition was impairment tested at the first and second year end after acquisition and again at the current year end. The first and second impairment reviews revealed no problems. However, the current review identified a recoverable value of $1,374m for Tommy. There has been no impairment in Jimmy goodwill since acquisition.

(iv) The group operates in the pharmaceutical industry and has had problems with some of its products. Tommy holds inventory carried at cost of $60million, which at the year end was estimated to be worth $50million, but in the event the goods were sold for $40million shortly thereafter.

(v) Ronnette had purchased a significant amount of new production equipment early in the year. The cost before trade discount of this equipment was $80 million. The trade discount of $8 million was taken to the income statement. Depreciation is charged on the straight line basis over a four year period.

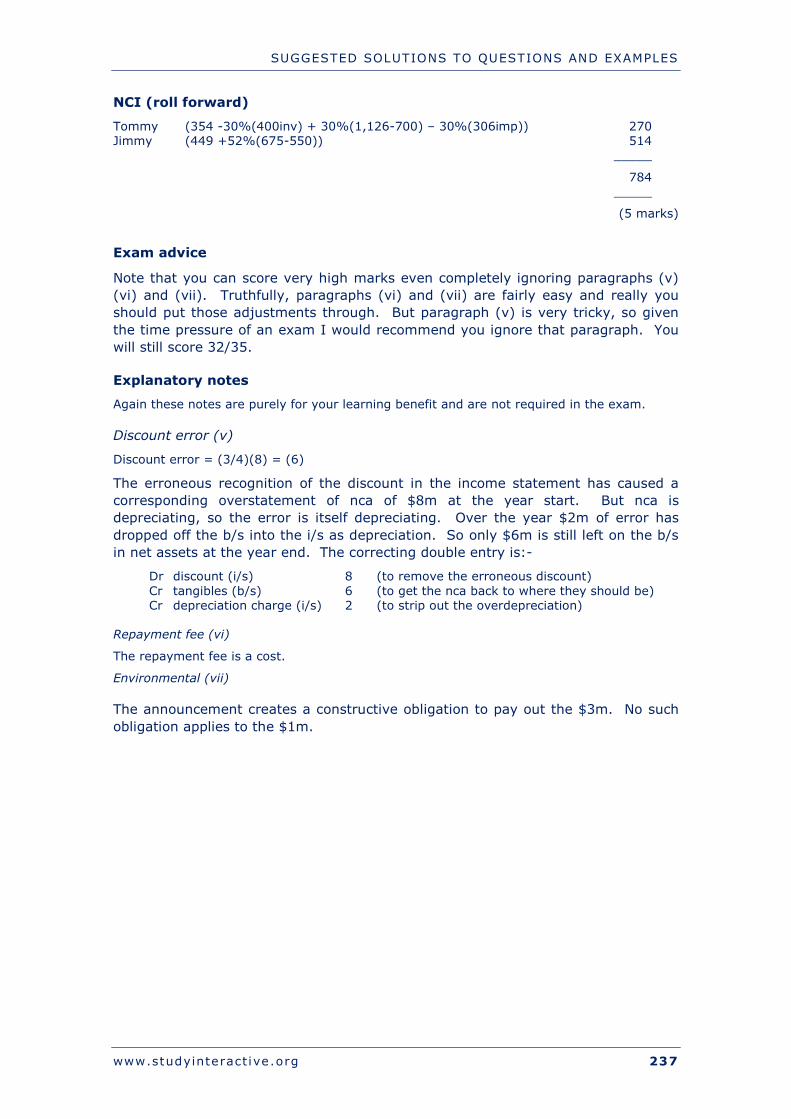

(vi) At the year start, Ronnette negotiated the early repayment of a $10m loan. The liability is included in non current liabilities, but now a contract has been signed agreeing to the repayment one month after the new year start plus an early repayment fee of $1m.

(vii) Immediately prior to the year end Ronnette have publicly accepted responsibility for an environmental issue. The estimated rectification costs are $3m, but lawyers advise that Ronnette have a very strong legal position and it is unlikely that any legal action would be able to prove any negligence by Ronnette. In spite of this, Ronnette have every intention to take responsibility for the rectification following the public announcement and make payment shortly after the new year start. Ronnette are also considering a further payment of $1m to implement improvements across the country to prevent such accidents occurring again but have made no announcement as regards these considerations.

Required:

(a) Prepare a consolidated statement of financial position of the Ronnette Group as at 30 November. (Round answer to nearest $1million.)

(35 marks)

(ACCA December 2002 rewritten)

CHAPTER 2 - COMPLEX GROUPS

www.studyinteract ive.org 53

CHANGES IN GROUP STRUCTURE

This is study guide entry D3a, b. The subject is properly called “group reorganisations” in IAS27. The subject is sometimes referred to by the somewhat old fashioned phrase “reconstructions”. However, students are advised to avoid using this phrase in the context of group reorganisations as the ACCA uses the phrase “entity reconstruction” to discuss the very different subject of changes in financial structure, discussed separately in chapter 5.

This rarely examined area of the syllabus relates to the change a parent may make in group structures. Occasionally a parent may want to move its subs around within a group. This only works if there is no nci. You are simply expected to know that whilst this does affect the individuals in the group it has no effect on the group fs. The rest comes down to double entry skills.

The possibilities There are three in particular:-

(1) Simple to vertical

One of the subs buys a sub from the ultimate parent.

(2) Vertical to simple

A sub parent sells a sub-sub to the ultimate parent.

(3) New ultimate parent

A new ultimate parent is created in the space between the original ultimate parent and the ultimate shareholders.

The effect As discussed above, because all these group reorganisation schemes have no effect on the underlying assets and liabilities, there is no effect on the group fs.

The individual entity fs Now this is the really challenging part of group reorganisation. The reorganisations have no effect on group fs, but they have substantial effects on the individual entities. There is nothing to learn in this context. The examiner will tell you what to record in a list of instructions. This is illustrated by the question Desperate which follows. However, you will have to be able to turn the instructions into double entry in order to execute the relevant reorganisation plan in the question. This will be a very stiff test of your double entry.

Truth is you will have to be brilliant at double entry to survive one of these questions. Almost certainly you will have to be so good at double entry that you can keep all the debits and credits in your head. The examiner is brilliant at double entry; but before selecting one of these questions in the exam, you must be sure that your technical expertise with debits and credits matches that of the examiner.

CHAPTER 2 - COMPLEX GROUPS

54 www.studyinteract ive.org

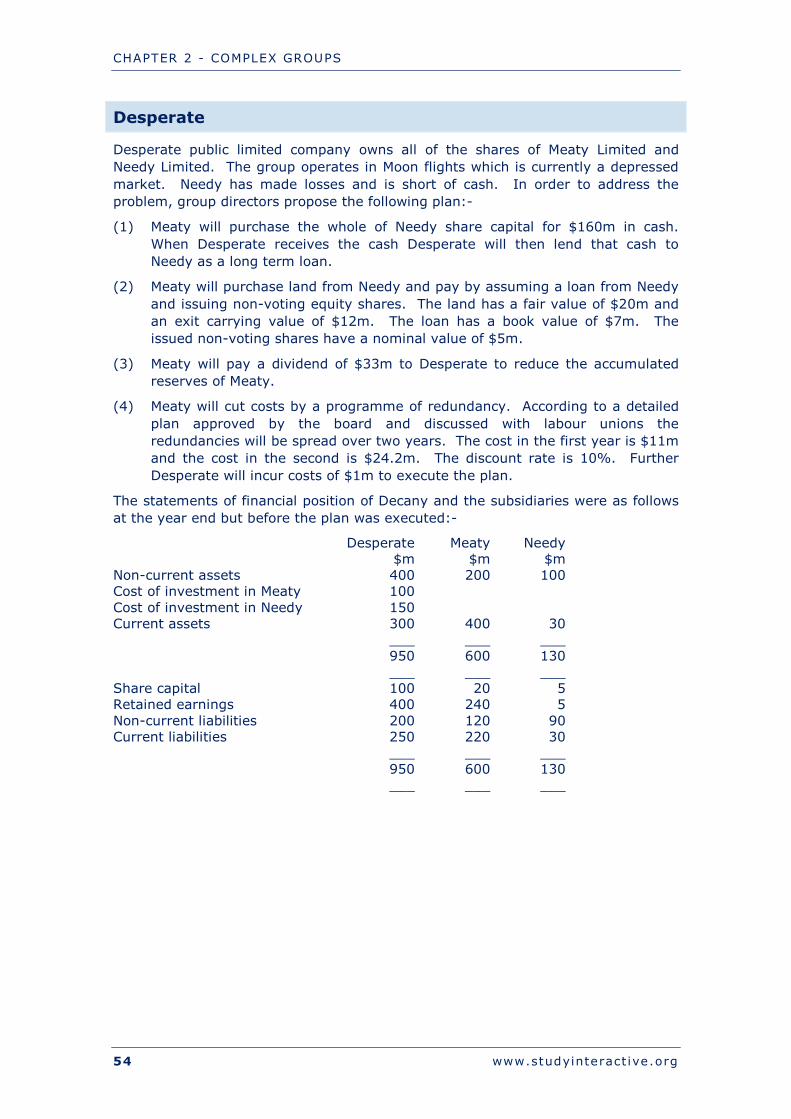

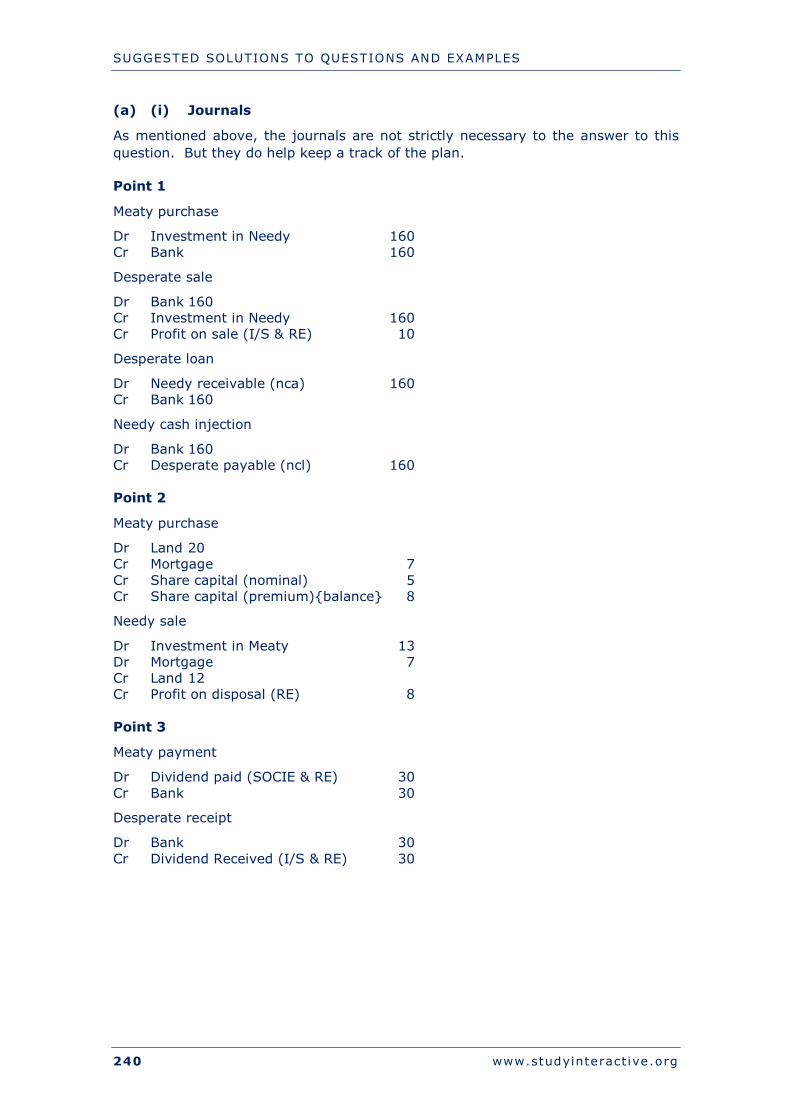

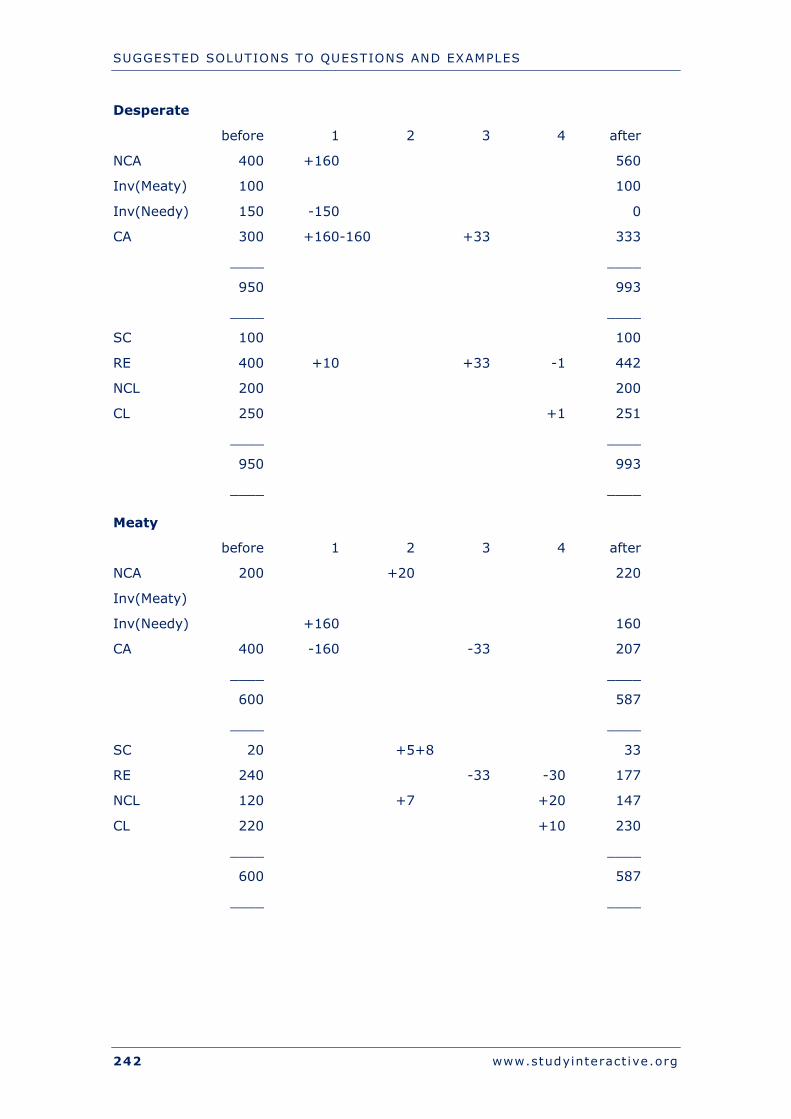

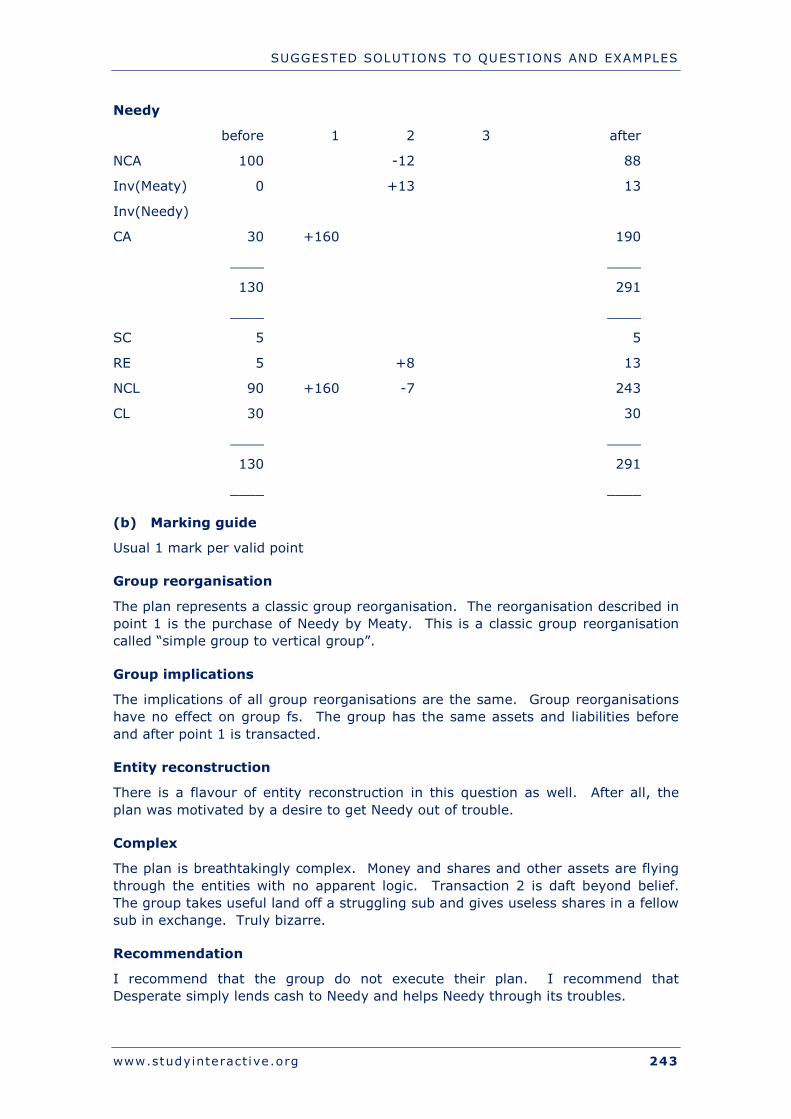

Desperate

Desperate public limited company owns all of the shares of Meaty Limited and Needy Limited. The group operates in Moon flights which is currently a depressed market. Needy has made losses and is short of cash. In order to address the problem, group directors propose the following plan:-

(1) Meaty will purchase the whole of Needy share capital for $160m in cash. When Desperate receives the cash Desperate will then lend that cash to Needy as a long term loan.

(2) Meaty will purchase land from Needy and pay by assuming a loan from Needy and issuing non-voting equity shares. The land has a fair value of $20m and an exit carrying value of $12m. The loan has a book value of $7m. The issued non-voting shares have a nominal value of $5m.

(3) Meaty will pay a dividend of $33m to Desperate to reduce the accumulated reserves of Meaty.

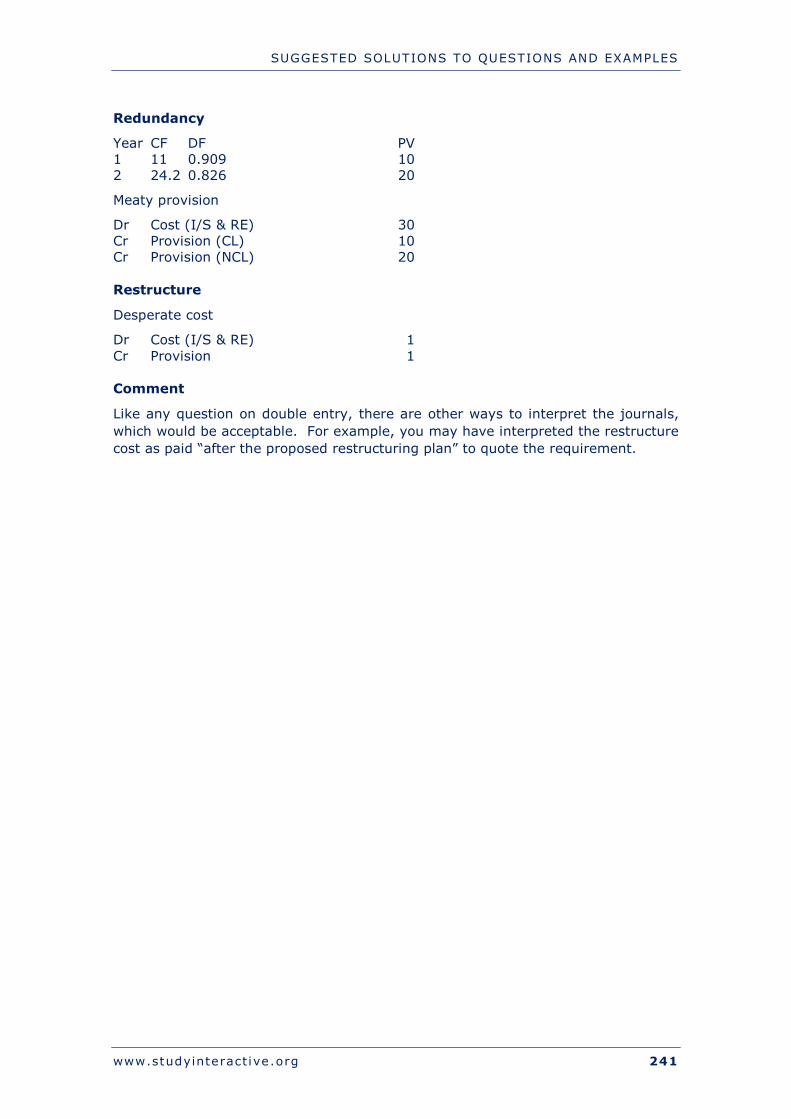

(4) Meaty will cut costs by a programme of redundancy. According to a detailed plan approved by the board and discussed with labour unions the redundancies will be spread over two years. The cost in the first year is $11m and the cost in the second is $24.2m. The discount rate is 10%. Further Desperate will incur costs of $1m to execute the plan.

The statements of financial position of Decany and the subsidiaries were as follows at the year end but before the plan was executed:-

Desperate Meaty Needy $m $m $m Non-current assets 400 200 100 Cost of investment in Meaty 100 Cost of investment in Needy 150 Current assets 300 400 30 ___ ___ ___ 950 600 130 ___ ___ ___ Share capital 100 20 5 Retained earnings 400 240 5 Non-current liabilities 200 120 90 Current liabilities 250 220 30 ___ ___ ___ 950 600 130 ___ ___ ___

CHAPTER 2 - COMPLEX GROUPS

www.studyinteract ive.org 55

Required:

(a) (i) Set out the requirements in IAS27 Separate Financial Statements as regards the payment of dividends from a subsidiary to a parent and as regards group reorganisation and apply those requirements to the individual entities in the Desperate group.

(5 marks)

(ii) Prepare the individual entity statements of financial position for all three entities as they would appear after the execution of the plan. (15 marks)

(b) Discuss the key implications of the plan on the group. (5 marks)

(25 marks)

Note: this question is based on the exam question Decany from December 2011 and gives you a very good idea of the standard of question to expect on group reorganisations. Unless you feel very confident with this question, you should be prepared to write off a question like this if it appears in your exam, and consider the rest of the exam compulsory.

CHAPTER 2 - COMPLEX GROUPS

56 www.studyinteract ive.org

www.studyinteract ive.org 57

Chapter 3

Foreign currency translation

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

58 www.studyinteract ive.org

CHAPTER CONTENTS

INTRODUCTION TO FOREIGN CURRENCY TRANSLATION ----------- 59

FOREIGN TRANSACTIONS ---------------------------------------------- 59

FOREIGN SUBSIDIARIES ----------------------------------------------- 61

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

www.studyinteract ive.org 59

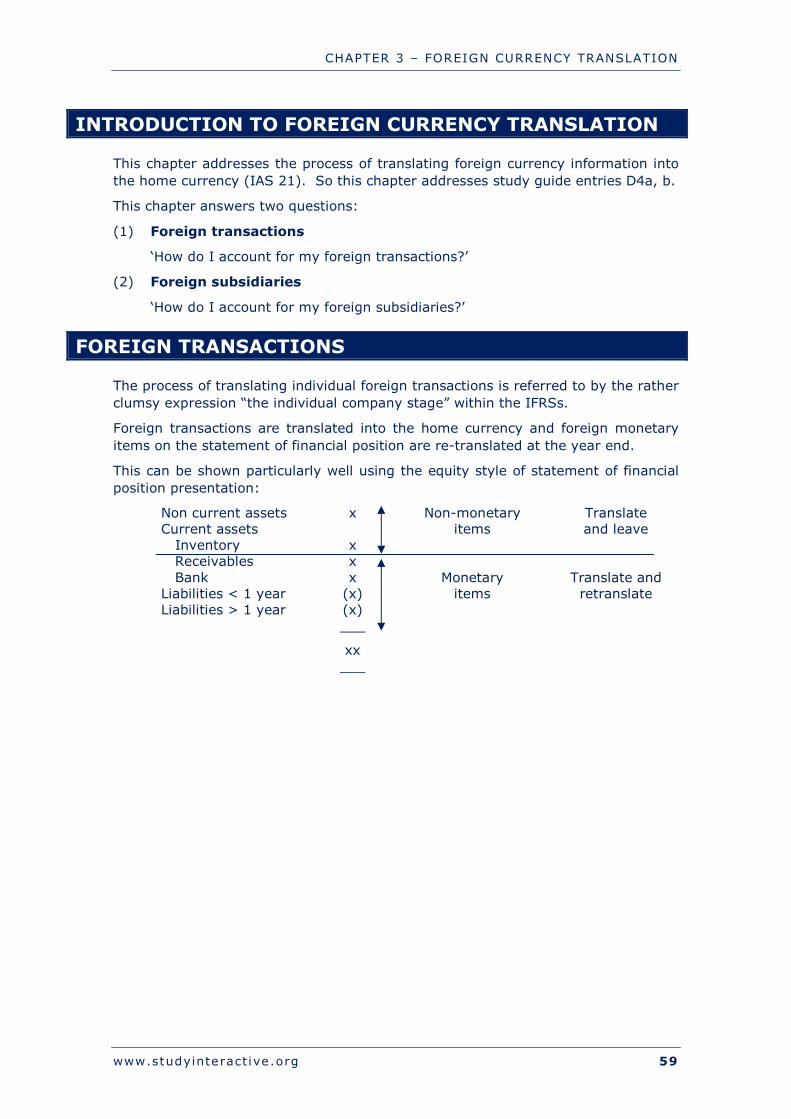

INTRODUCTION TO FOREIGN CURRENCY TRANSLATION

This chapter addresses the process of translating foreign currency information into the home currency (IAS 21). So this chapter addresses study guide entries D4a, b.

This chapter answers two questions:

(1) Foreign transactions

‘How do I account for my foreign transactions?’

(2) Foreign subsidiaries

‘How do I account for my foreign subsidiaries?’

FOREIGN TRANSACTIONS

The process of translating individual foreign transactions is referred to by the rather clumsy expression “the individual company stage” within the IFRSs.

Foreign transactions are translated into the home currency and foreign monetary items on the statement of financial position are re-translated at the year end.

This can be shown particularly well using the equity style of statement of financial position presentation:

Non current assets x Non-monetary Translate Current assets items and leave Inventory x Receivables x Bank x Monetary Translate and Liabilities < 1 year (x) items retranslate Liabilities > 1 year (x) ___

xx ___

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

60 www.studyinteract ive.org

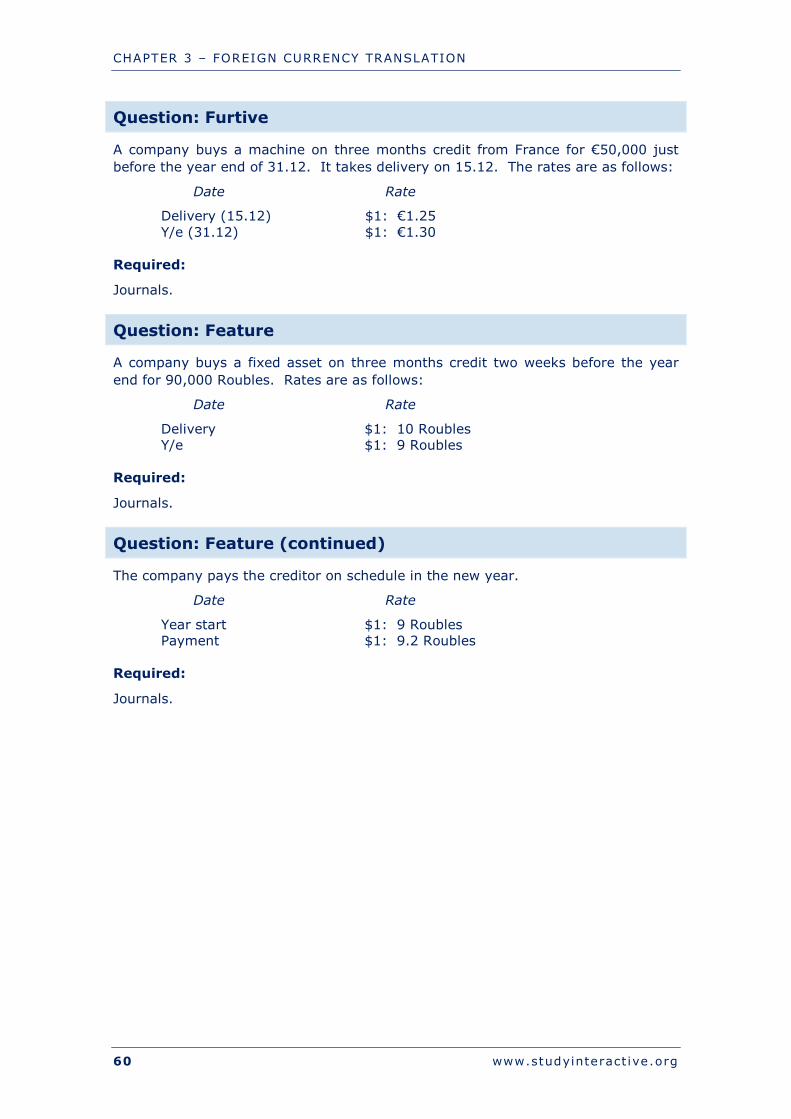

Question: Furtive

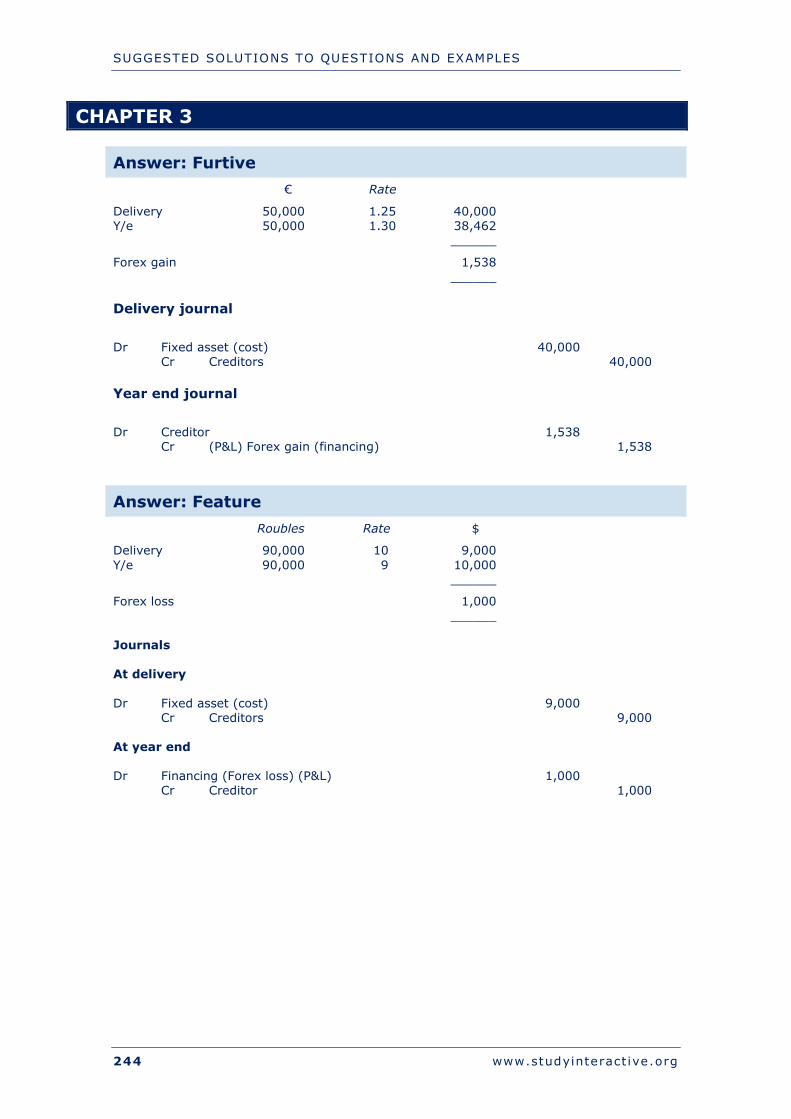

A company buys a machine on three months credit from France for €50,000 just before the year end of 31.12. It takes delivery on 15.12. The rates are as follows:

Date Rate

Delivery (15.12) $1: €1.25 Y/e (31.12) $1: €1.30

Required:

Journals.

Question: Feature

A company buys a fixed asset on three months credit two weeks before the year end for 90,000 Roubles. Rates are as follows:

Date Rate

Delivery $1: 10 Roubles Y/e $1: 9 Roubles

Required:

Journals.

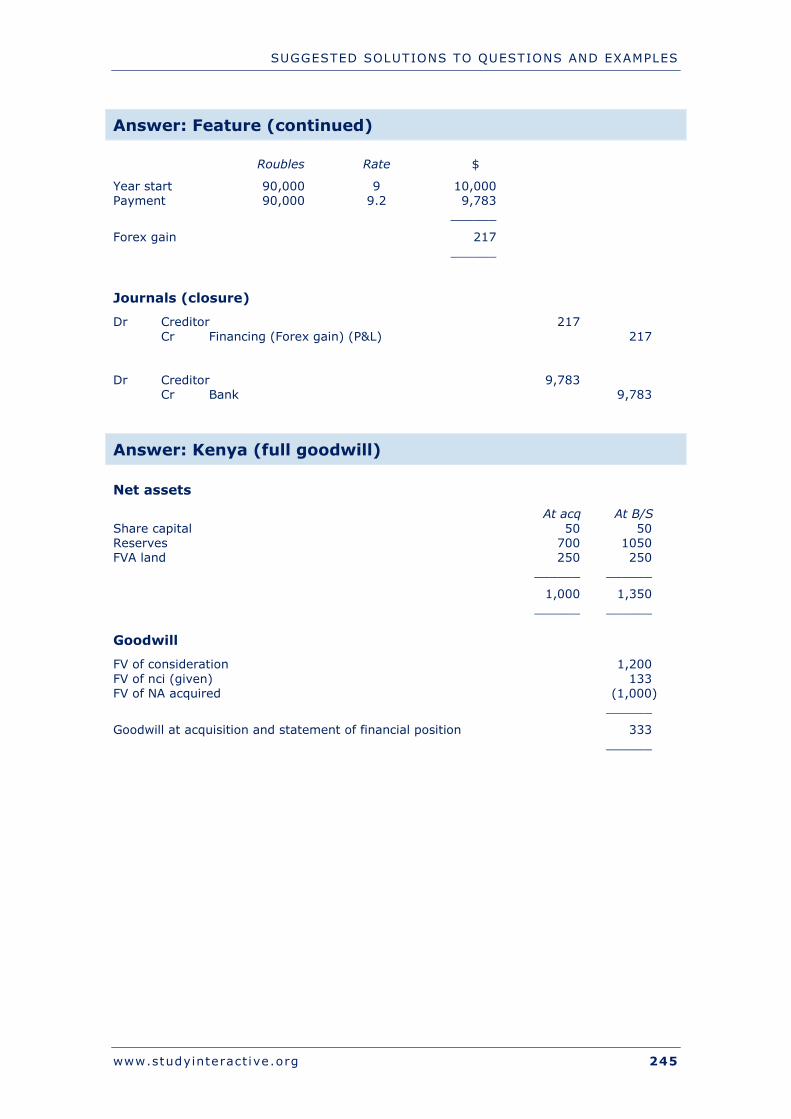

Question: Feature (continued)

The company pays the creditor on schedule in the new year.

Date Rate

Year start $1: 9 Roubles Payment $1: 9.2 Roubles

Required:

Journals.

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

www.studyinteract ive.org 61

FOREIGN SUBSIDIARIES

Group stage

A foreign subsidiary needs translation before consolidation:

Statement Rate

Statement of financial position Closing rate Profit and loss Average rate

Goodwill

Goodwill is a subsidiary asset so from the parent point of view it’s a foreign asset.

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

62 www.studyinteract ive.org

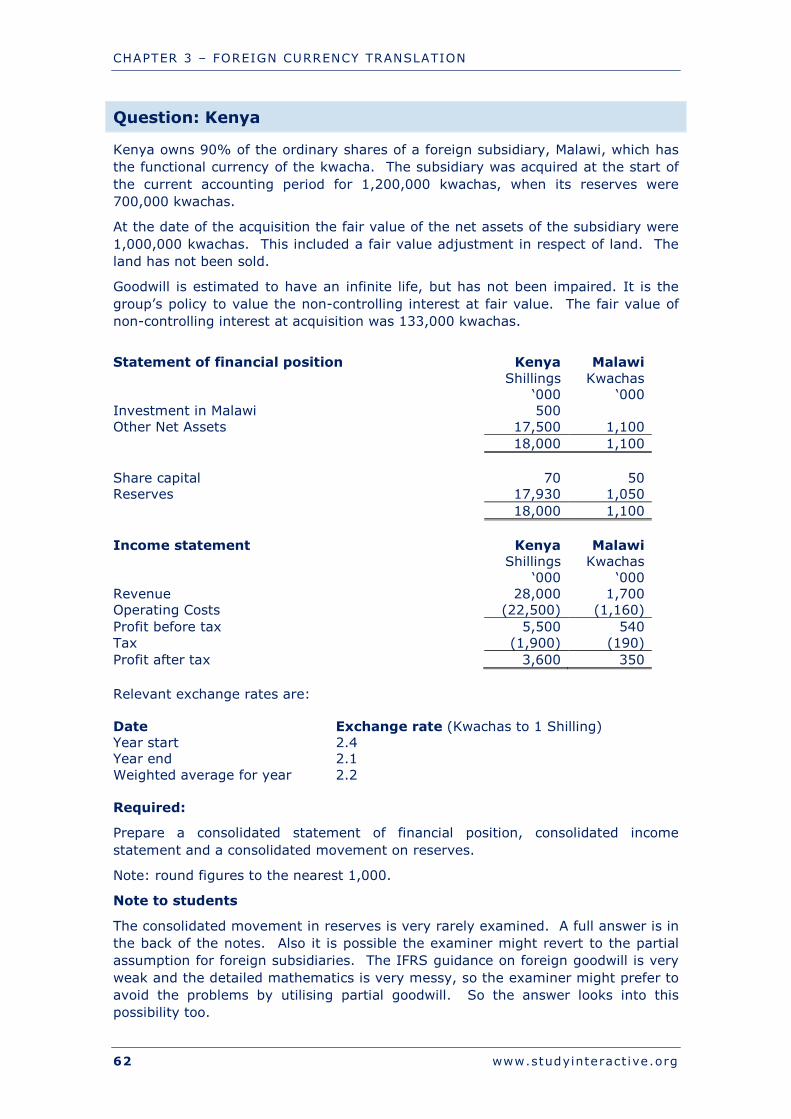

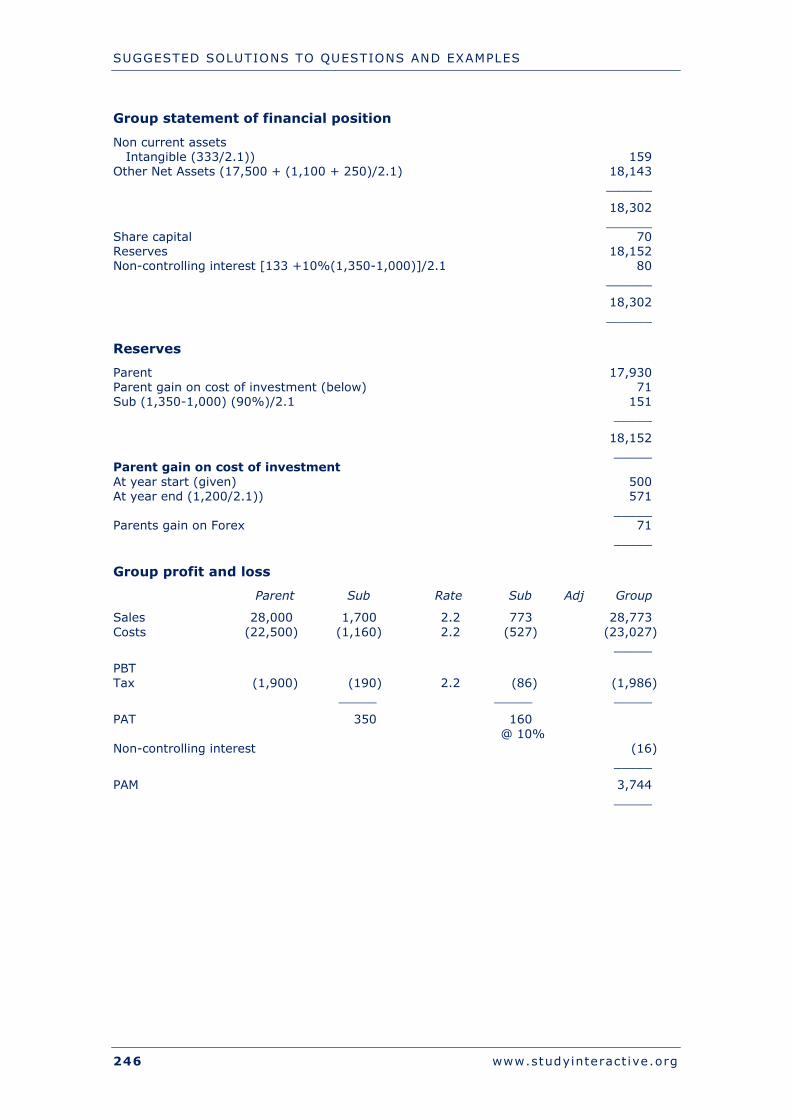

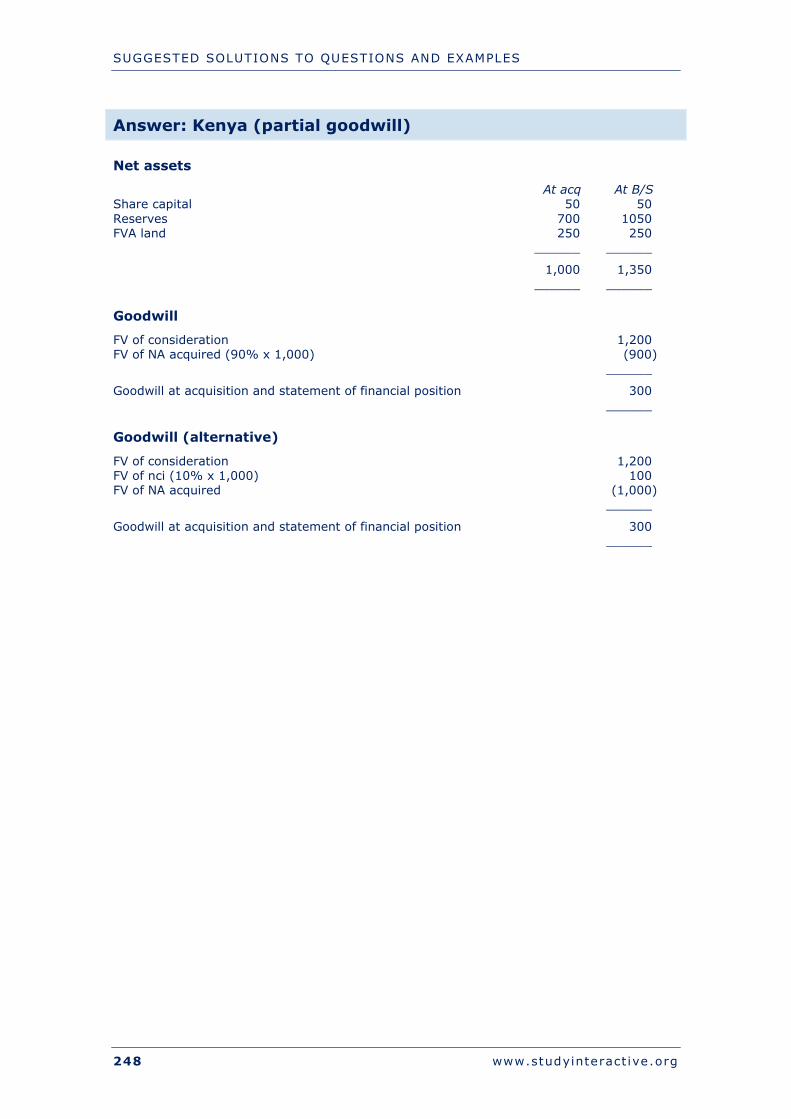

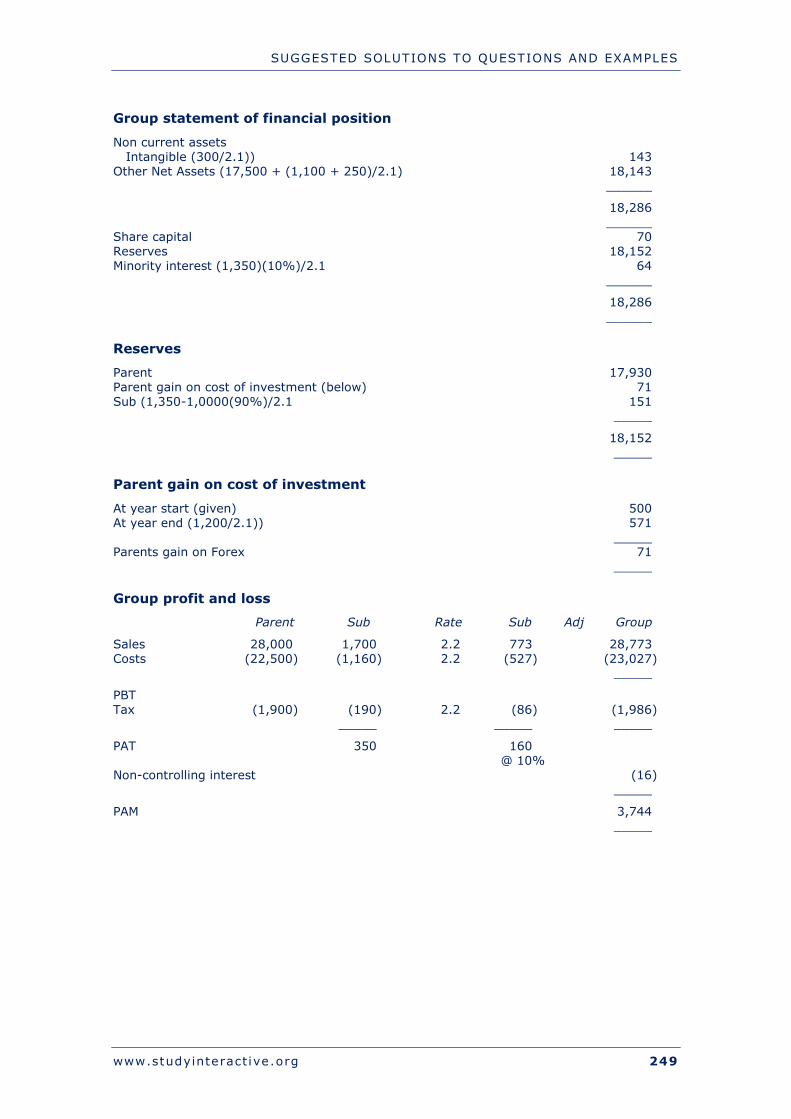

Question: Kenya

Kenya owns 90% of the ordinary shares of a foreign subsidiary, Malawi, which has the functional currency of the kwacha. The subsidiary was acquired at the start of the current accounting period for 1,200,000 kwachas, when its reserves were 700,000 kwachas.

At the date of the acquisition the fair value of the net assets of the subsidiary were 1,000,000 kwachas. This included a fair value adjustment in respect of land. The land has not been sold.

Goodwill is estimated to have an infinite life, but has not been impaired. It is the group’s policy to value the non-controlling interest at fair value. The fair value of non-controlling interest at acquisition was 133,000 kwachas.

Statement of financial position Kenya

Shillings ‘000

Malawi Kwachas

‘000 Investment in Malawi 500 Other Net Assets 17,500 1,100 18,000 1,100 Share capital 70 50 Reserves 17,930 1,050 18,000 1,100 Income statement Kenya

Shillings ‘000

Malawi Kwachas

‘000 Revenue 28,000 1,700 Operating Costs (22,500) (1,160) Profit before tax 5,500 540 Tax (1,900) (190) Profit after tax 3,600 350 Relevant exchange rates are: Date Exchange rate (Kwachas to 1 Shilling) Year start 2.4 Year end 2.1 Weighted average for year 2.2

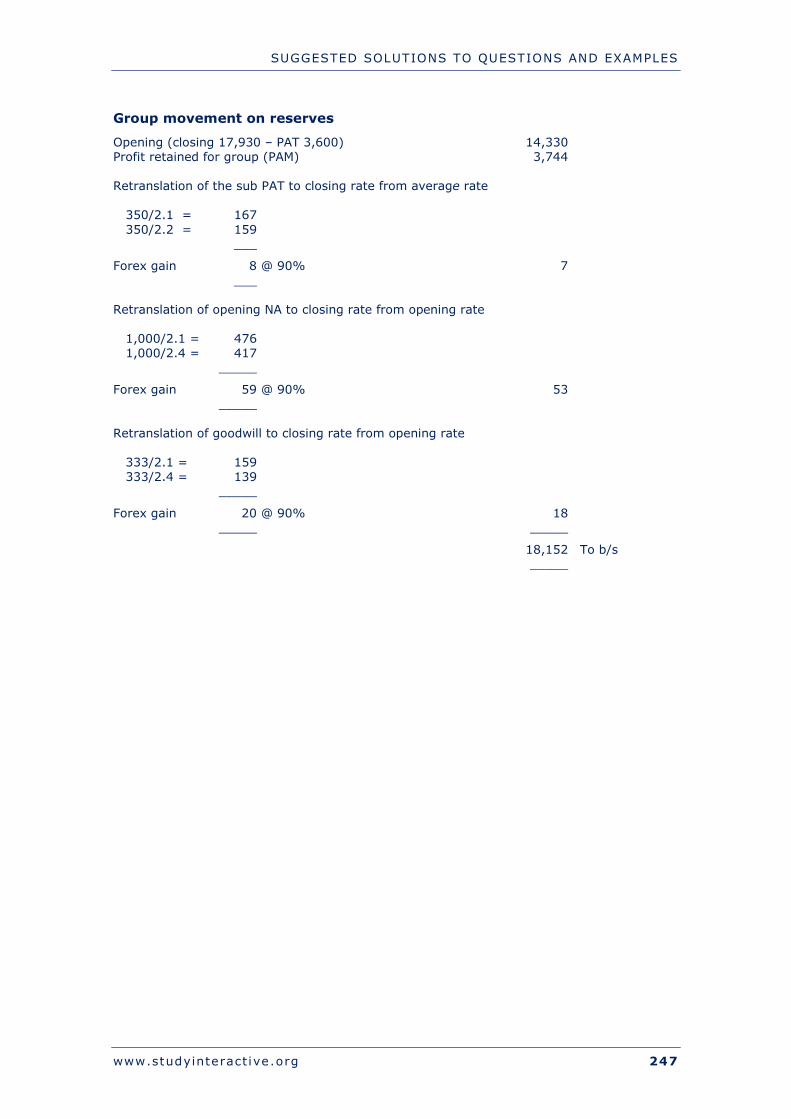

Required:

Prepare a consolidated statement of financial position, consolidated income statement and a consolidated movement on reserves.

Note: round figures to the nearest 1,000.

Note to students

The consolidated movement in reserves is very rarely examined. A full answer is in the back of the notes. Also it is possible the examiner might revert to the partial assumption for foreign subsidiaries. The IFRS guidance on foreign goodwill is very weak and the detailed mathematics is very messy, so the examiner might prefer to avoid the problems by utilising partial goodwill. So the answer looks into this possibility too.

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

www.studyinteract ive.org 63

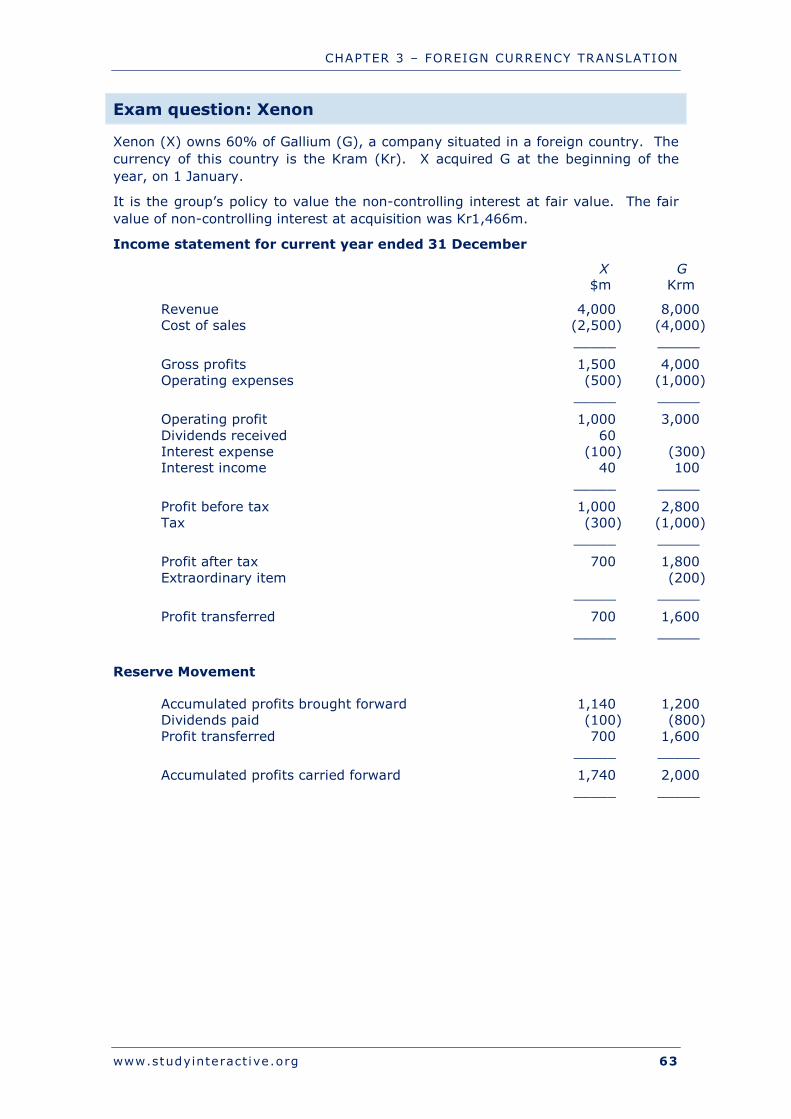

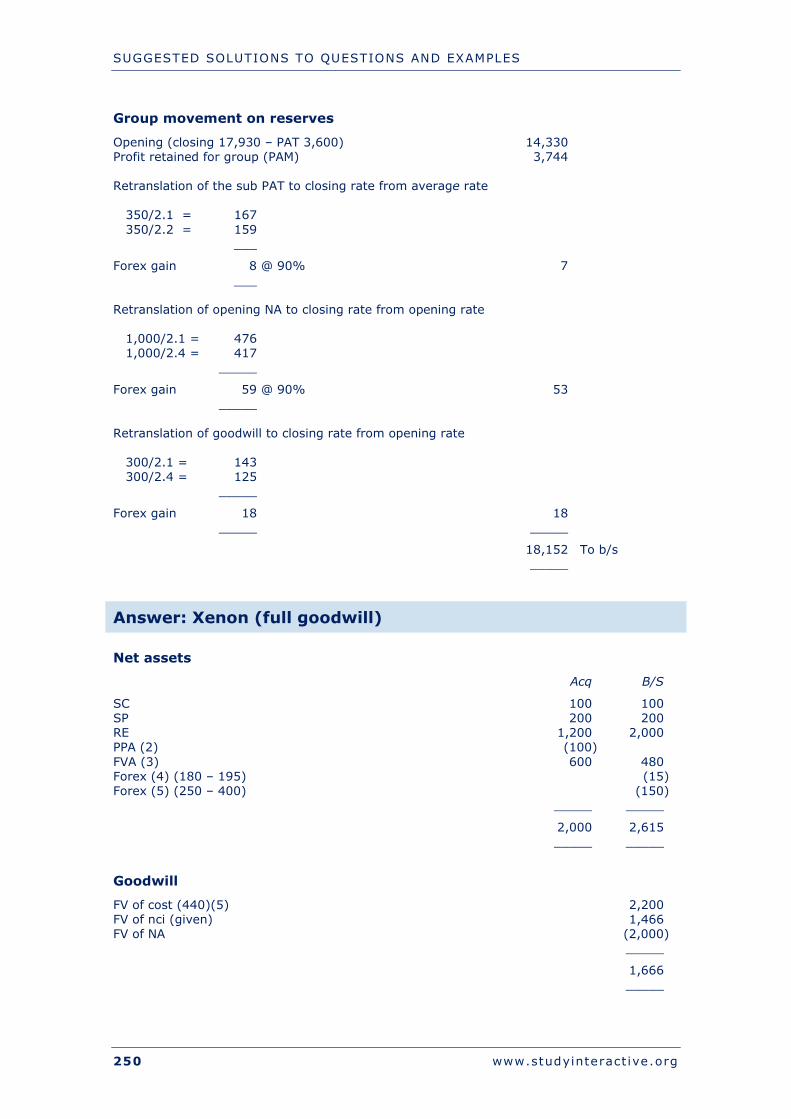

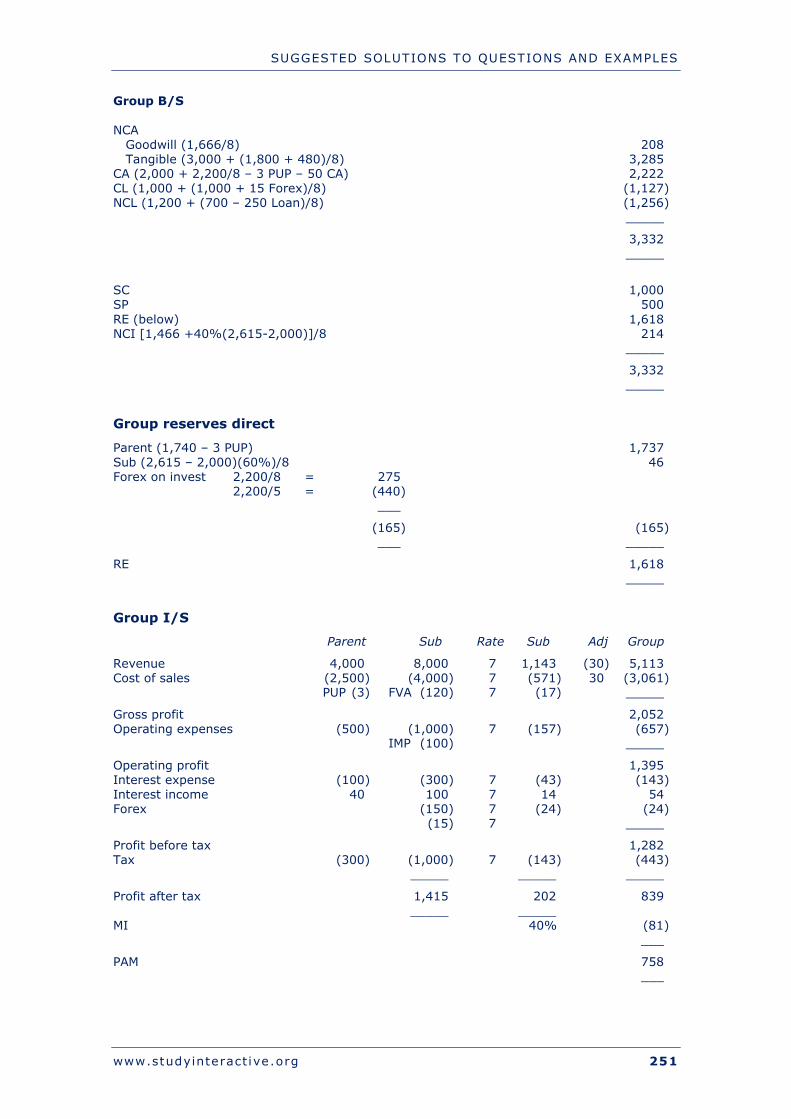

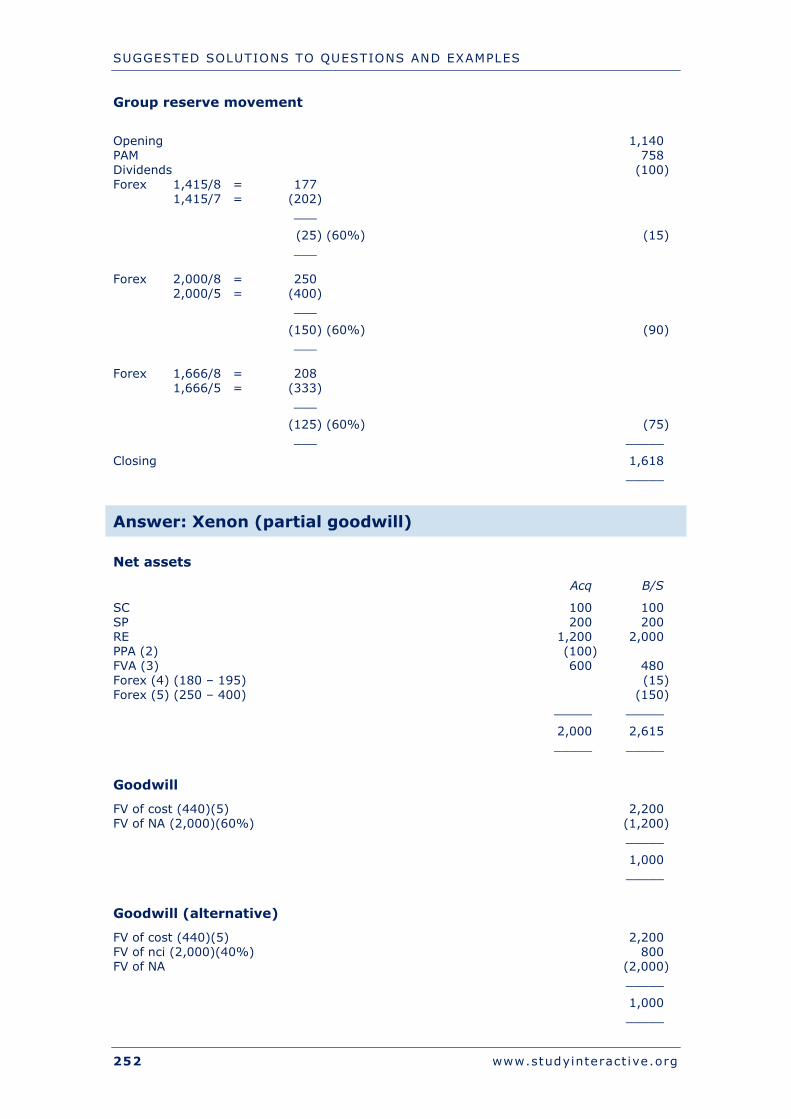

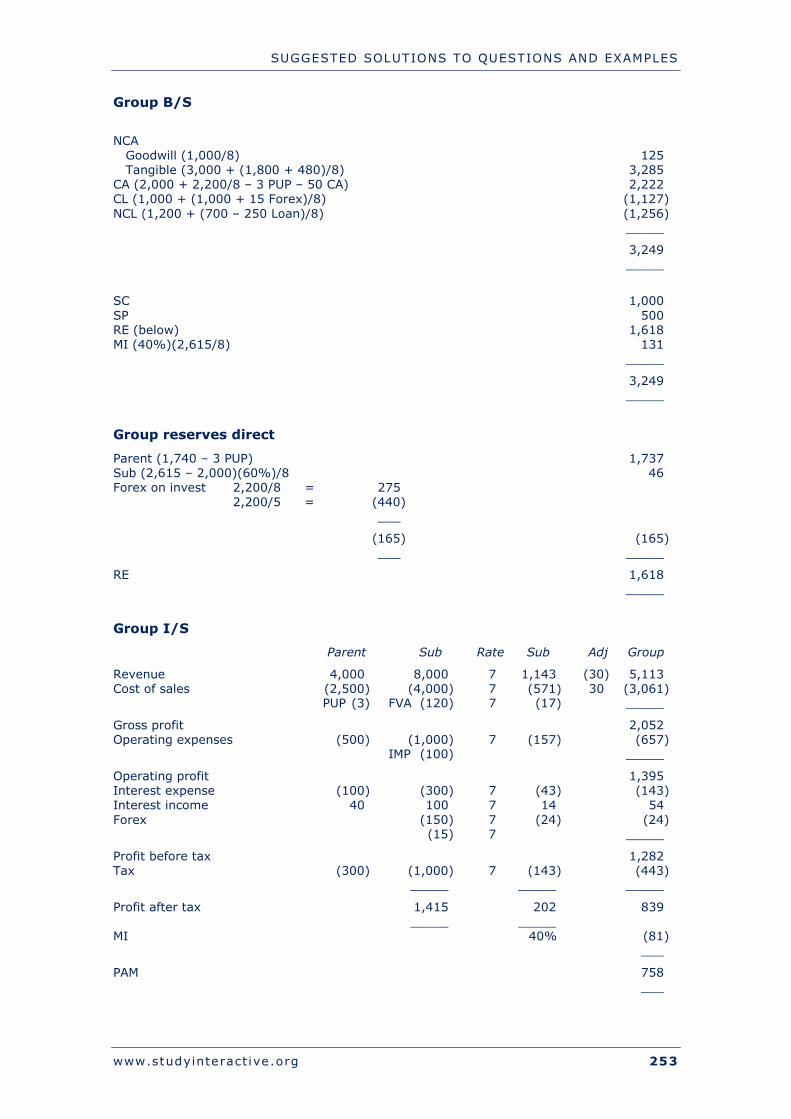

Exam question: Xenon

Xenon (X) owns 60% of Gallium (G), a company situated in a foreign country. The currency of this country is the Kram (Kr). X acquired G at the beginning of the year, on 1 January.

It is the group’s policy to value the non-controlling interest at fair value. The fair value of non-controlling interest at acquisition was Kr1,466m.

Income statement for current year ended 31 December

X G $m Krm

Revenue 4,000 8,000 Cost of sales (2,500) (4,000) _____ _____

Gross profits 1,500 4,000 Operating expenses (500) (1,000) _____ _____

Operating profit 1,000 3,000 Dividends received 60 Interest expense (100) (300) Interest income 40 100 _____ _____

Profit before tax 1,000 2,800 Tax (300) (1,000) _____ _____

Profit after tax 700 1,800 Extraordinary item (200) _____ _____

Profit transferred 700 1,600 _____ _____

Reserve Movement

Accumulated profits brought forward 1,140 1,200 Dividends paid (100) (800) Profit transferred 700 1,600 _____ _____

Accumulated profits carried forward 1,740 2,000 _____ _____

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

64 www.studyinteract ive.org

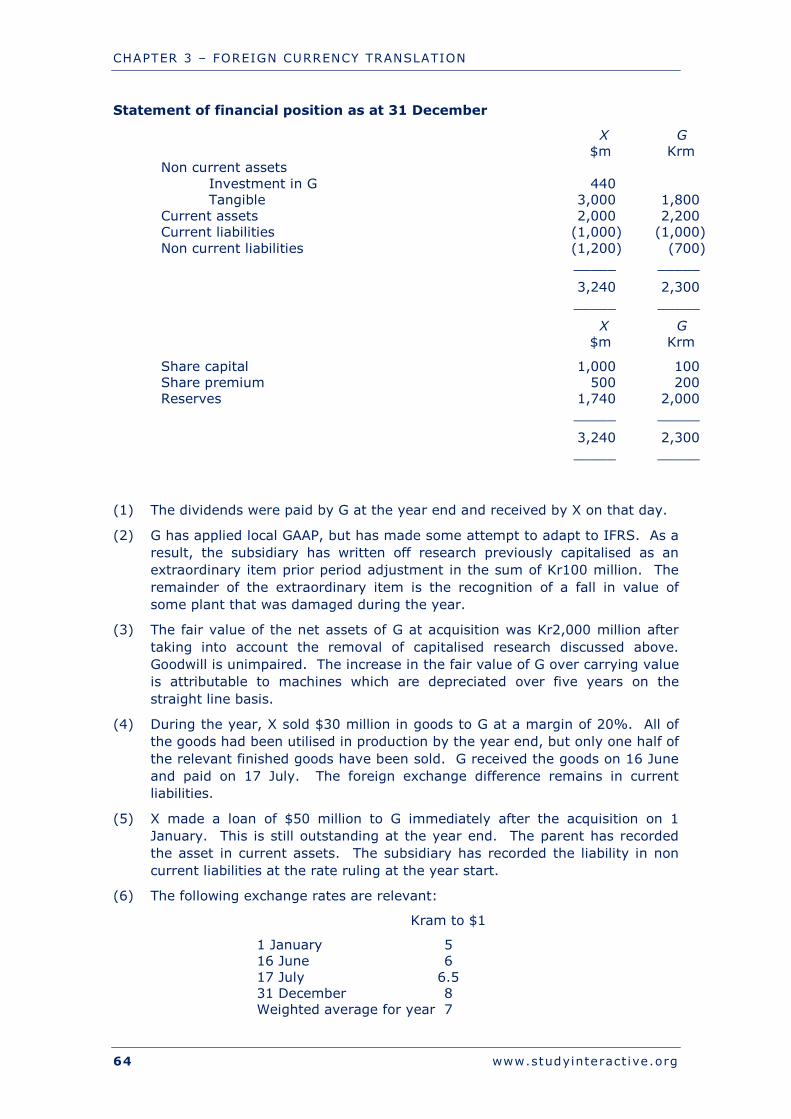

Statement of financial position as at 31 December

X G $m Krm Non current assets Investment in G 440 Tangible 3,000 1,800 Current assets 2,000 2,200 Current liabilities (1,000) (1,000) Non current liabilities (1,200) (700) _____ _____

3,240 2,300 _____ _____

X G $m Krm

Share capital 1,000 100 Share premium 500 200 Reserves 1,740 2,000 _____ _____

3,240 2,300 _____ _____

(1) The dividends were paid by G at the year end and received by X on that day.

(2) G has applied local GAAP, but has made some attempt to adapt to IFRS. As a result, the subsidiary has written off research previously capitalised as an extraordinary item prior period adjustment in the sum of Kr100 million. The remainder of the extraordinary item is the recognition of a fall in value of some plant that was damaged during the year.

(3) The fair value of the net assets of G at acquisition was Kr2,000 million after taking into account the removal of capitalised research discussed above. Goodwill is unimpaired. The increase in the fair value of G over carrying value is attributable to machines which are depreciated over five years on the straight line basis.

(4) During the year, X sold $30 million in goods to G at a margin of 20%. All of the goods had been utilised in production by the year end, but only one half of the relevant finished goods have been sold. G received the goods on 16 June and paid on 17 July. The foreign exchange difference remains in current liabilities.

(5) X made a loan of $50 million to G immediately after the acquisition on 1 January. This is still outstanding at the year end. The parent has recorded the asset in current assets. The subsidiary has recorded the liability in non current liabilities at the rate ruling at the year start.

(6) The following exchange rates are relevant:

Kram to $1

1 January 5 16 June 6 17 July 6.5 31 December 8 Weighted average for year 7

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

www.studyinteract ive.org 65

Required:

(a) Prepare the income statement and statement of financial position for the group for the current year. (30 marks)

(b) Prepare a movement in consolidated reserves for the current year. (5 marks)

(35 marks)

(ACCA June 1998)

(Note: round to the nearest million)

Note to students

The consolidated movement in reserves is rarely examined. A full answer is in the back of the notes.

CHAPTER 3 – FOREIGN CURRENCY TRANSLATION

66 www.studyinteract ive.org

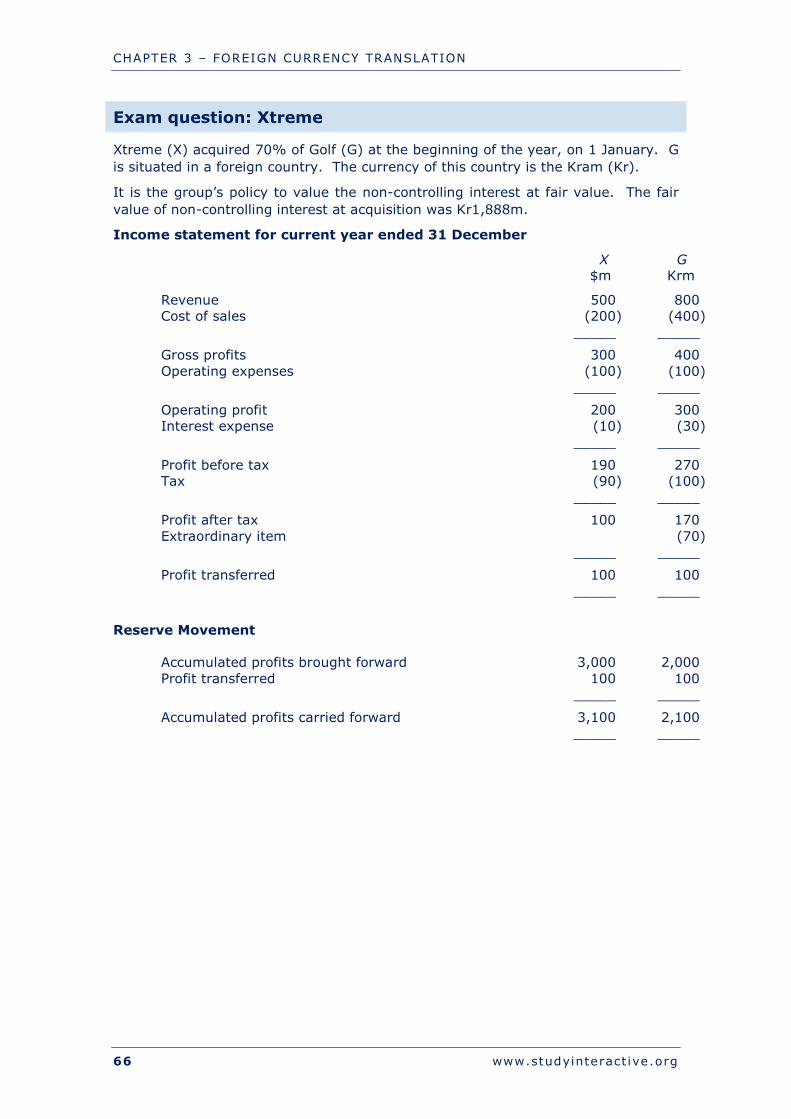

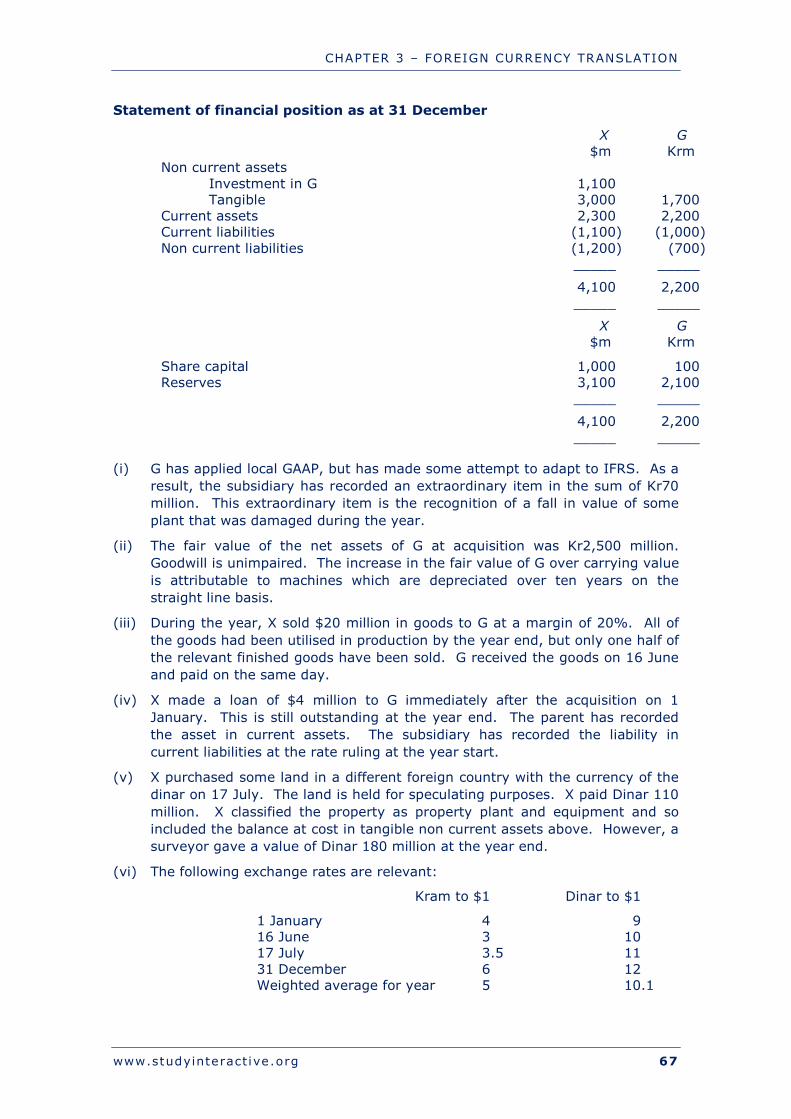

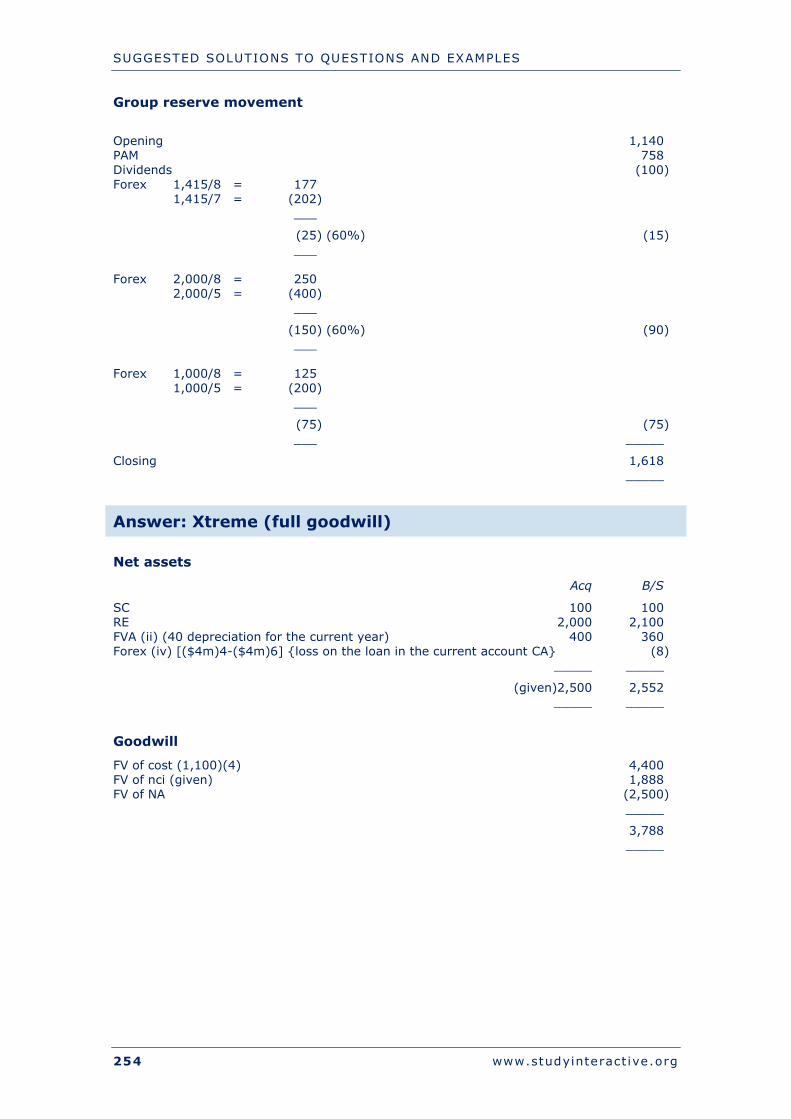

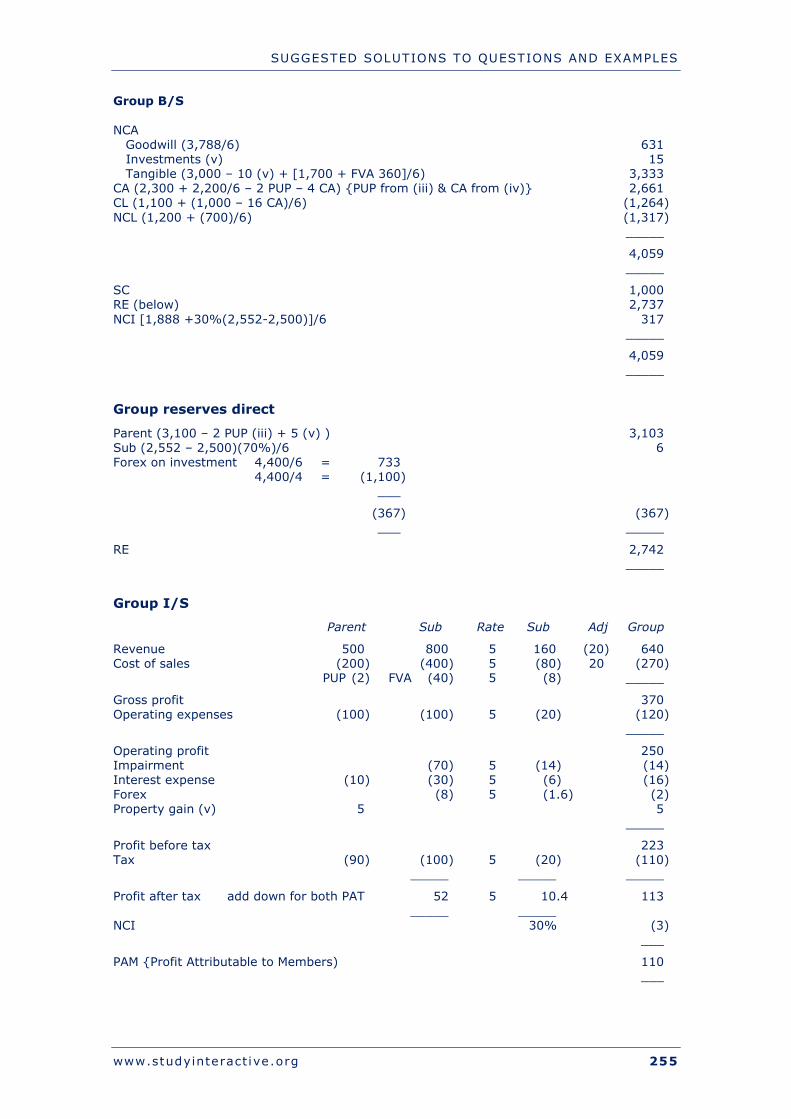

Exam question: Xtreme

Xtreme (X) acquired 70% of Golf (G) at the beginning of the year, on 1 January. G is situated in a foreign country. The currency of this country is the Kram (Kr).

It is the group’s policy to value the non-controlling interest at fair value. The fair value of non-controlling interest at acquisition was Kr1,888m.

Income statement for current year ended 31 December

X G $m Krm