A STUDY ON THE PERFORMANCE OF ICICI BANK LIMITED ...

262

A STUDY ON THE PERFORMANCE OF ICICI BANK LIMITED AND CUSTOMER SATISFACTION TOWARDS E-BANKING SERVICES IN CHENNAI METRO Thesis submitted to the BHARATHIDASAN UNIVERSITY, TIRUCHIRAPPALLI for the award of the degree of DOCTOR OF PHILOSOPHY IN COMMERCE Submitted by M. MOHAMED SIDDIK Reg. No: 8306/Ph.D./COMMERCE/PT/JULY 2007 ASST. PROFESSOR IN COMMERCE S.C.P. JAIN COLLEGE MINJUR, CHENNAI - 601203 Under the Guidance and Supervision of Dr. M. SELVACHANDRA M.COM., M.B.A., M.PHIL., PH.D., (RESEARCH GUIDE) ASSOCIATE PROFESSOR IN COMMERCE A.D.M COLLEGE FOR WOMEN (AUTONOMOUS) NAGAPPATINAM - 611001 BHARATHIDASAN UNIVERSITY TIRUCHIRAPPALLI - 620024 TAMIL NADU, INDIA JUNE - 2012

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of A STUDY ON THE PERFORMANCE OF ICICI BANK LIMITED ...

A STUDY ON THE PERFORMANCE OF ICICI BANK

LIMITED AND CUSTOMER SATISFACTION TOWARDS

E-BANKING SERVICES IN CHENNAI METRO

Thesis submitted to the BHARATHIDASAN UNIVERSITY, TIRUCHIRAPPALLI

for the award of the degree of

DOCTOR OF PHILOSOPHY IN COMMERCE

Submitted by

M. MOHAMED SIDDIK

Reg. No: 8306/Ph.D./COMMERCE/PT/JULY 2007

ASST. PROFESSOR IN COMMERCE

S.C.P. JAIN COLLEGE

MINJUR, CHENNAI - 601203

Under the Guidance and Supervision of

Dr. M. SELVACHANDRA M.COM., M.B.A., M.PHIL., PH.D.,

(RESEARCH GUIDE)

ASSOCIATE PROFESSOR IN COMMERCE

A.D.M COLLEGE FOR WOMEN (AUTONOMOUS)

NAGAPPATINAM - 611001

BHARATHIDASAN UNIVERSITY

TIRUCHIRAPPALLI - 620024

TAMIL NADU, INDIA

JUNE - 2012

M. MOHAMED SIDDIK M.COM., M.B.A., M.PHIL.,

ASST. PROFESSOR IN COMMERCE

S.C.P. JAIN COLLEGE

MINJUR - 601203

Cell : +919942693002 E-Mail : [email protected]

DECLARATION I do hereby declare that the thesis, entitled “A STUDY ON THE PERFORMANCE OF

ICICI BANK LIMITED AND CUSTOMER SATISFACTION TOWARDS

E-BANKING SERVICES IN CHENNAI METRO”, is carried out by me originally under

the guidance and supervision of Dr. M. SELVACHANDRA M.COM., M.B.A., M.PHIL., PH.D.,

ASSOCIATE PROFESSOR IN COMMERCE A.D.M COLLEGE FOR WOMEN

(AUTONOMOUS) NAGAPPATINAM. I declare that this work or any part thereof has not

been submitted elsewhere for the award of any other degree, diploma or fellowship.

(M. MOHAMED SIDDIK)

Dr. M. SELVACHANDRA M.COM., M.B.A., M.PHIL., PH.D.,

ASSOCIATE PROFESSOR IN COMMERCE

A.D.M COLLEGE FOR WOMEN (AUTONOMOUS)

NAGAPPATINAM - 611001

CELL : +919842639030

E-Mail: [email protected]

Date: __________

CERTIFICATE

This is to certify that the thesis entitled “A STUDY ON THE PERFORMANCE OF

ICICI BANK LIMITED AND CUSTOMER SATISFACTION

TOWARDS E-BANKING SERVICES IN CHENNAI METRO”, submitted to

the BHARATHIDASAN UNIVERSITY, TIRUCHIRAPPALLI in partial fulfilment of the

requirements for the award of the Degree of Doctor of Philosophy in Commerce is a record of original

research work done by M. MOHAMED SIDDIK ASST. PROFESSOR IN COMMERCE

S.C.P. JAIN COLLEGE MINJUR, CHENNAI, under my supervision and guidance and this

work or any part thereof has not been submitted elsewhere for any other purpose or degree.

(DR. M. SELVACHANDRA)

ACKNOWLEDGEMENT

First, I gratefully acknowledge my deep sense of gratitude to Almighty for his

spiritual guidance and blessings to complete the research work successfully.

It is my great pleasure to thank our honourable Vice Chancellor, Registrar, and

Controller of Examinations of Bharathdasan University, Tiruchirappalli for their support

provided to complete my research work successfully.

I thank Dr.A.SIVAKAMASUNDARI Principal, A.D.M College for women,

Nagapptinam, Dr.S.BABU, Principal S.C.P Jain College Minjur, Chennai,

Dr.ARUNACHALAM, Principal R.D.B College, Papanasam for their support and

encouragement.

The intellectual integrity and infinite patience of my research guide,

Dr. M. SELVACHANDRA, Associate professor in Commerce A.D.M College for women

(Autonomous) Nagappatinam, has always been the benchmark of my learning. I hope this thesis

proves of the many discussions we had conducted and the encouragement she has given me over the

years. But for her great help and cooperation, the research would not be completed successfully. I am

very much and always thankful to him for her scholarly guidance and kindness.

It is my bounden duty to express my deep sense of gratitude to Dr.A.Asick Iqbal,

Associate Professor of Commerce, Khadir Mohideen College, Adiramapattinam, Member of

the Doctoral Committee, for his valuable suggestions, support and encouragement in the

completion of my research work.

I would like to express my heartful appreciation and thanks to Mr.A.SURESH and

Mr.M.ANANTHAN, Ms.MAGESHWARI (avadi) ALPHA SYSTEMS Papanasam have

helped me in the accomplishment of my doctoral thesis.

I would like to extend my sincere and heartful thanks to my Family members,

Mr.K.MOHAMED IBRAHIM, M.MUMTHAJ BEGAM, M.MUNAR, MOHSINA

MUMTHA and THARA ABDUL KAEEM for their unconditional support and

encouragement.

I thank Mr M.SUNDARAKUMARAN and DR.MU.ARUMUGAM, Asst. Professor

,in economics ,SCP Jain college ,Chennai,

I extend my heartful thanks to all my colleagues, friends and relatives for their

unconditional support and encouragement.

M. MOHAMED SIDDIK

i

ABBREVIATION

ATM - Automated Teller Machine CDO - Collateralised Debt Obligations CRM - Customer Relationship Management DNA - Deoxyribo Nucleic Acid E-Commerce - Electronic Commerce EFT - Electronic Fund Transfer HDFC - Housing Development Finance Corporation IT - Information Technology ICDO - Indian Collateralised Debt Obligations IDBI - Industrial Development Bank of India NYSE - New York Stock Exchange RBI - Reserve Bank of India SWOT - Strength Weakness Opportunity and Threat UK - United Kingdom USA - United States of America USD - United States Dollar UTI - Unit Trust of India

CONTENTS

Chapter No.

Title Page No.

Abbreviation i

List of Tables ii

List of Figures v

1. Design and Execution of the Study 1

2. Review of Literature 21

3. Profile and performance of ICICI Bank Ltd., 55

4. Analysis of Customer Satisfaction Towards the

Services of ICICI Bank Ltd., 103

5. Summary of Findings, Suggestions and

Recommendation. 210

Bibliography i

Appendices :

Balance Sheet ix

Key Financial Ratio xi

Profit & Loss Statement xii

Interview Schedule xiv

ii

List of Tables

Table no.

Title

Page no.

3.1 Assets of ICICI Bank from 2006-07 to 2010-11 82

3.2 Projected Assets of ICICI Bank from 2010-11 to 2015-16 88

3.3 Liabilities of the Bank from 2006-07 to 2010-11 93

3.4 Projected Liabilities of the Bank from 2010-11 to 2015-16 98

4.1 Gender wise classification of Respondent 110

4.2 Age wise Distribution of Respondent 111

4.3 Education-wise classification of Respondent 113

4.4 Occupation-wise Classification of Respondent 115

4.5 Income-wise Classification of Respondent 117

4.6 Martial Status of Respondent 119

4.7 Who motivated to open the Account 120

4.8 Types of Account Maintained 121

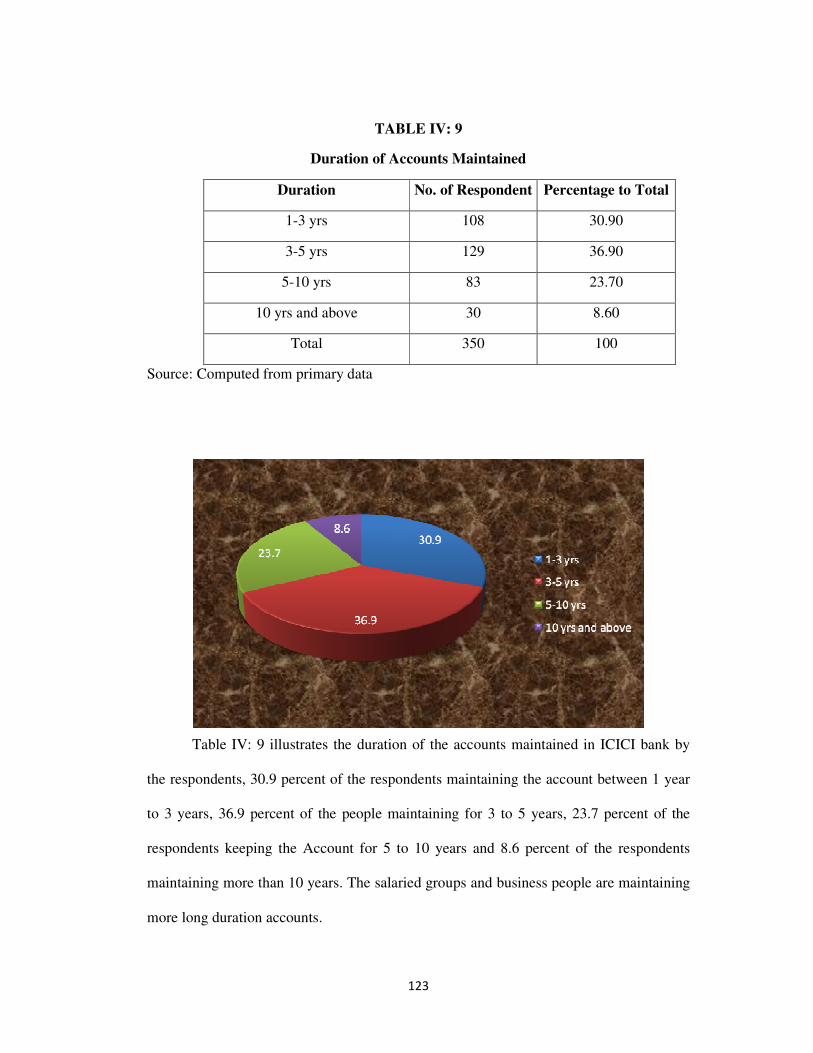

4.9 Duration of Accounts Maintained 123

4.10 Reason for Selecting the Branch/Bank 124

4.11 Opinion about the banking Environment 126

4.12 Frequency of receiving Personalized service 127

4.13 Physical Facilities of the ICICI Bank Branch which deserved 129

iii

Appreciation of the Respondents

4.14 Frequency of Visit to Branches 131

4.15 Opinion of the respondents about the working hours of the Bank 133

4.16 Facilities provided during waiting time in the ICICI Bank ltd., 135

4.17 Opinion on the rate of interest charged 136

4.18 Opinion on various service charges of the ICICI Bank Ltd. 137

4.19 Common problem encountered in the bank 141

4.20 Opinion on the process to resolve the problem in ICICI bank Ltd. 145

4.21 Opinion about financial services of the respondents 148

4.22 Opinion about Non – financial services 152

4.23 Opinion about approach with Customer 156

4.24

Opinion about attitude of bank employees in rendering service to the customers

157

4.25

Opinion about awareness of staff members on various schemes of ICICI Bank Ltd.

158

4.26 Staff members reciprocation to the customer’s enquiry 160

4.27 Opinion about Active presence of bank staff during banking hours 162

4.28 Opinion about Timely opening and closing of branches 164

4.29 Opinion about Entries in the pass book 167

4.30 Opinion about Depository Services 169

4.31 Opinion about Cheque services 171

4.32 Opinion about Demand Draft Services 173

4.33

Perceptions of the customer on the availability of the physical infrastructure

175

4.34 Opinion about Other Services 177

v

List of Figures

Table no. Title Page no.

3.1 Assets of ICICI Bank from 2006-07 to 2010-11 83

3.2 Projected Assets of ICICI Bank from 2010-11 to 2015-16 89

3.3 Liabilities of the Bank from 2006-07 to 2010-11 94

3.4 Projected Liabilities of the Bank from 2010-11 to 2015-16 99

4.1 Gender wise classification of Respondent 110

4.2 Age wise Distribution of Respondent 111

4.3 Education-wise classification of Respondent 113

4.4 Occupation-wise Classification of Respondent 116

4.5 Income-wise Classification of Respondent 117

4.6 Martial Status of Respondent 119

4.7 Who motivated to open the Account 120

4.8 Types of Account Maintained 121

4.9 Duration of Accounts Maintained 123

4.10 Reason for Selecting the Branch/Bank 124

4.11 Opinion about the banking Environment 126

4.12 Frequency of receiving Personalized service 127

4.13Physical Facilities of the ICICI Bank Branch which deserved Appreciation of the Respondents

129

4.14 Frequency of Visit to Branches 131

4.15 Opinion of the respondents about the working hours of the Bank 133

4.16 Facilities provided during waiting time in the ICICI Bank ltd., 135

4.17 Opinion on the rate of interest charged 136

vi

4.18 Opinion on various service charges of the ICICI Bank Ltd. 138

4.19 Common problem encountered in the bank 142

4.20 Opinion on the process to resolve the problem in ICICI bank Ltd. 145

4.21 Opinion about financial services of the respondents 149

4.22 Opinion about Non – financial services 153

4.23 Opinion about approach with Customer 156

4.24

Opinion about attitude of bank employees in rendering service to the customers

157

4.25

Opinion about awareness of staff members on various schemes of ICICI Bank Ltd.

158

4.26 Staff members reciprocation to the customer’s enquiry 160

4.27 Opinion about Active presence of bank staff during banking hours 162

4.28 Opinion about Timely opening and closing of branches 164

4.29 Opinion about Entries in the pass book 167

4.30 Opinion about Depository Services 169

4.31 Opinion about Cheque services 171

4.32 Opinion about Demand Draft Services 173

4.33

Perceptions of the customer on the availability of the physical infrastructure

175

4.34 Opinion about Other Services 177

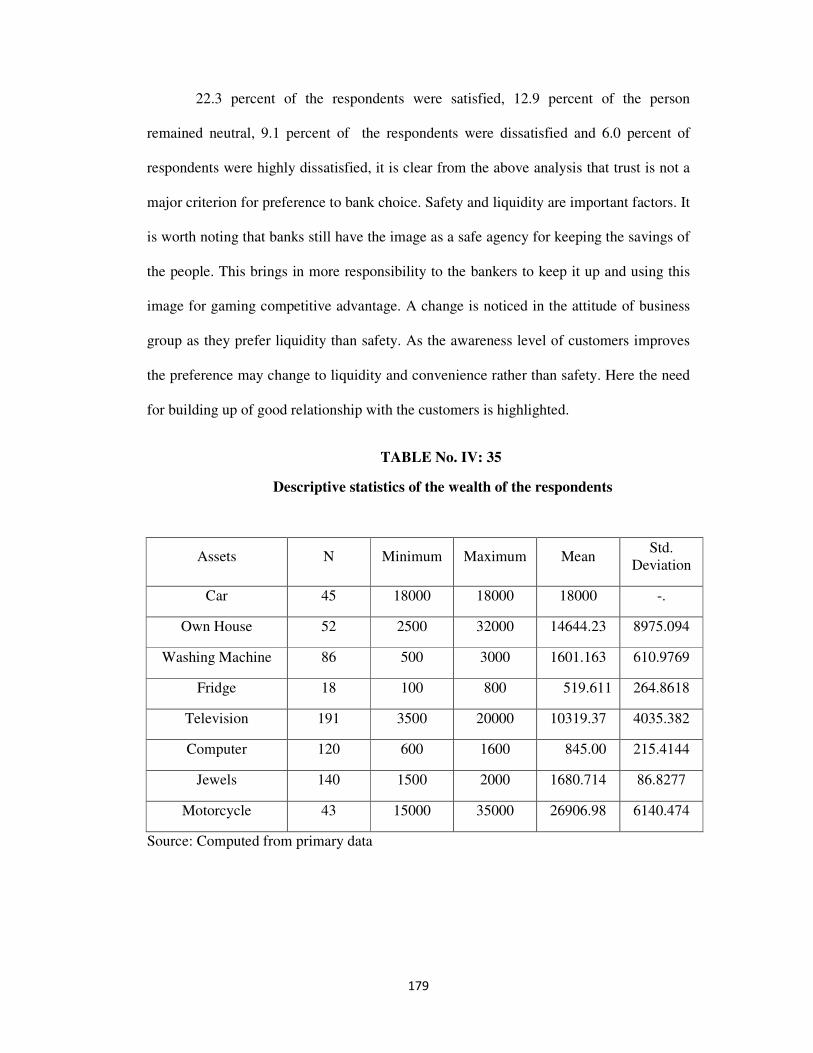

4.35 Descriptive statistics of the wealth of the respondent 179

4.36 Opinion about Frequency of the usage of ATM 181

4.37 Time taken to wait in queue for ATM transaction 182

4.38 Opinion about Time taken for process in ATM transaction 183

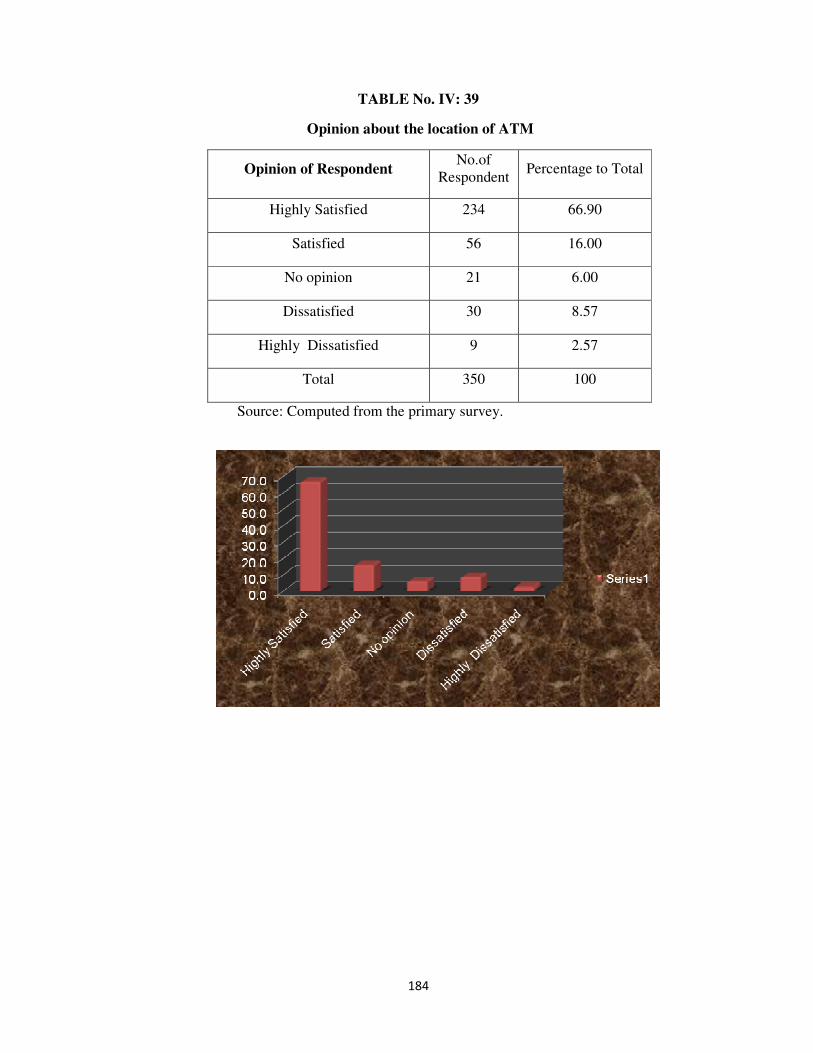

4.39 Opinion about the location of ATM 184

vii

4.40 Opinion about the denomination required 186

4.41 Opinion about Run out of cash in ATM 187

4.42 Opinion about Frequency of Out of Order of ATM 188

4.43

Opinion about notification displayed about the non-availability of the service

189

4.44 Opinion about Card get struck in the ATM machine 190

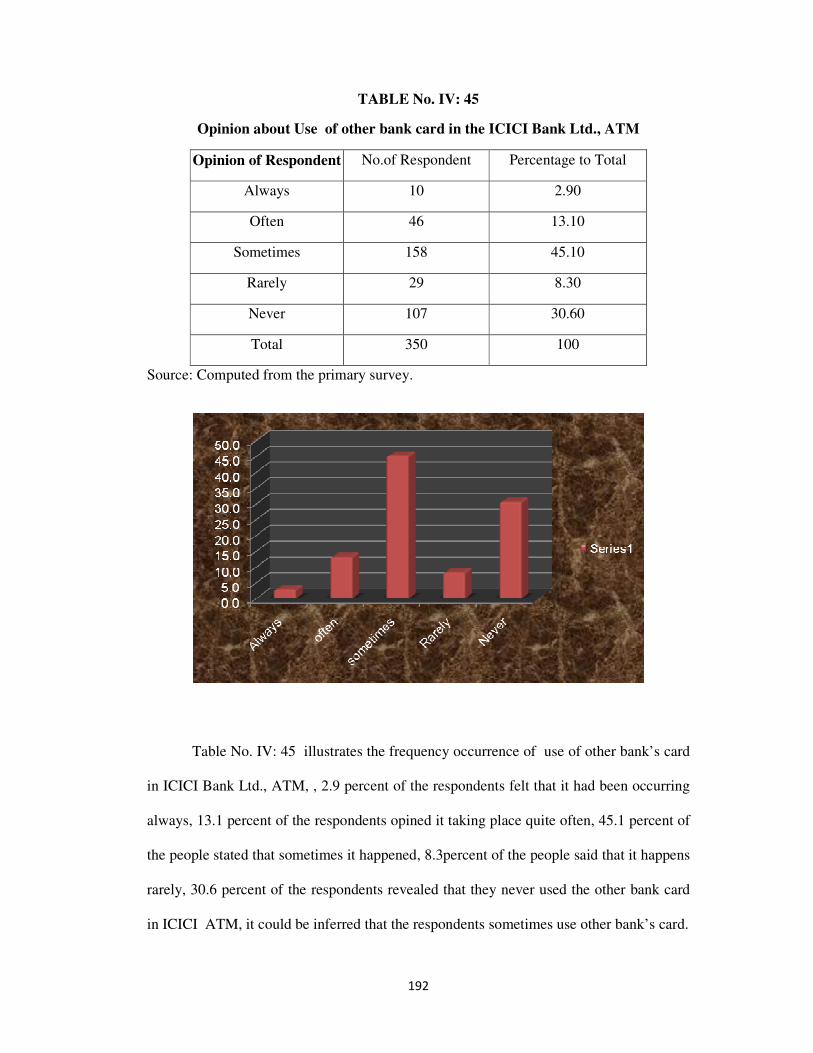

4.45 Opinion about Use of other bank card in the ICICI bank ATM 192

4.46

Opinion about Provision of transactions statement after every transaction

193

4.47

Opinion about Bank employees commitment to instant rectification of problem occurred in ATM

195

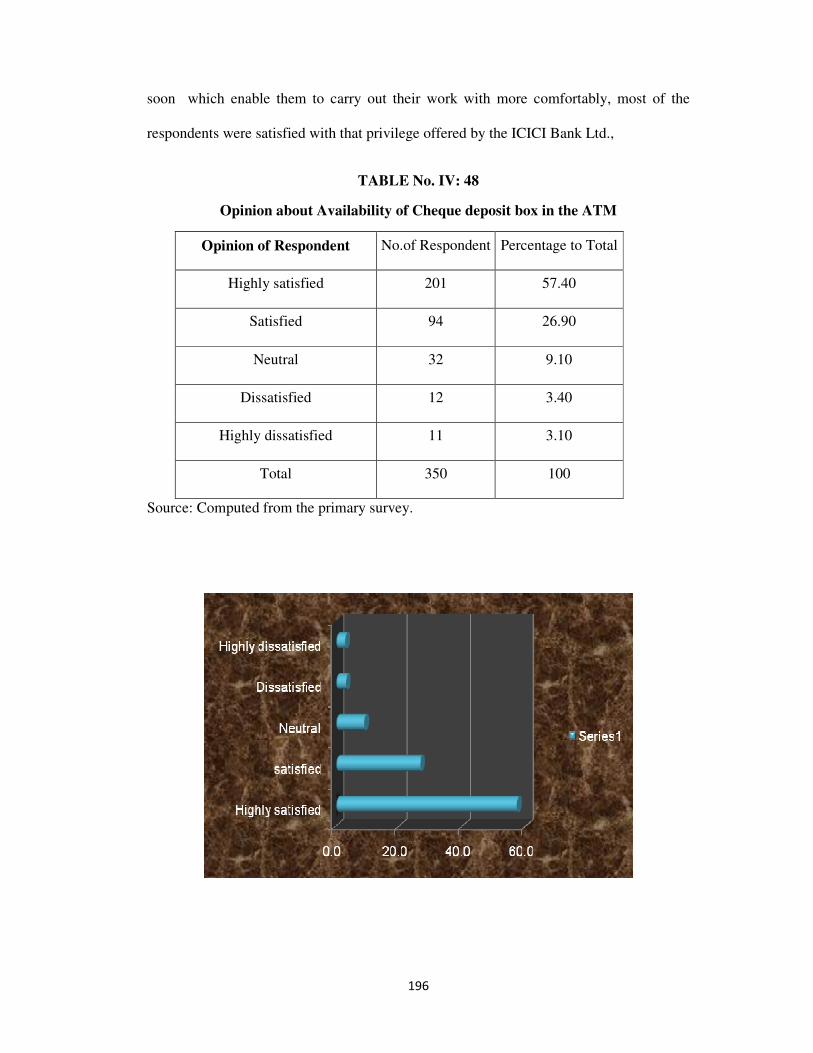

4.48 Opinion about Availability of cheque deposit box in the ATM 196

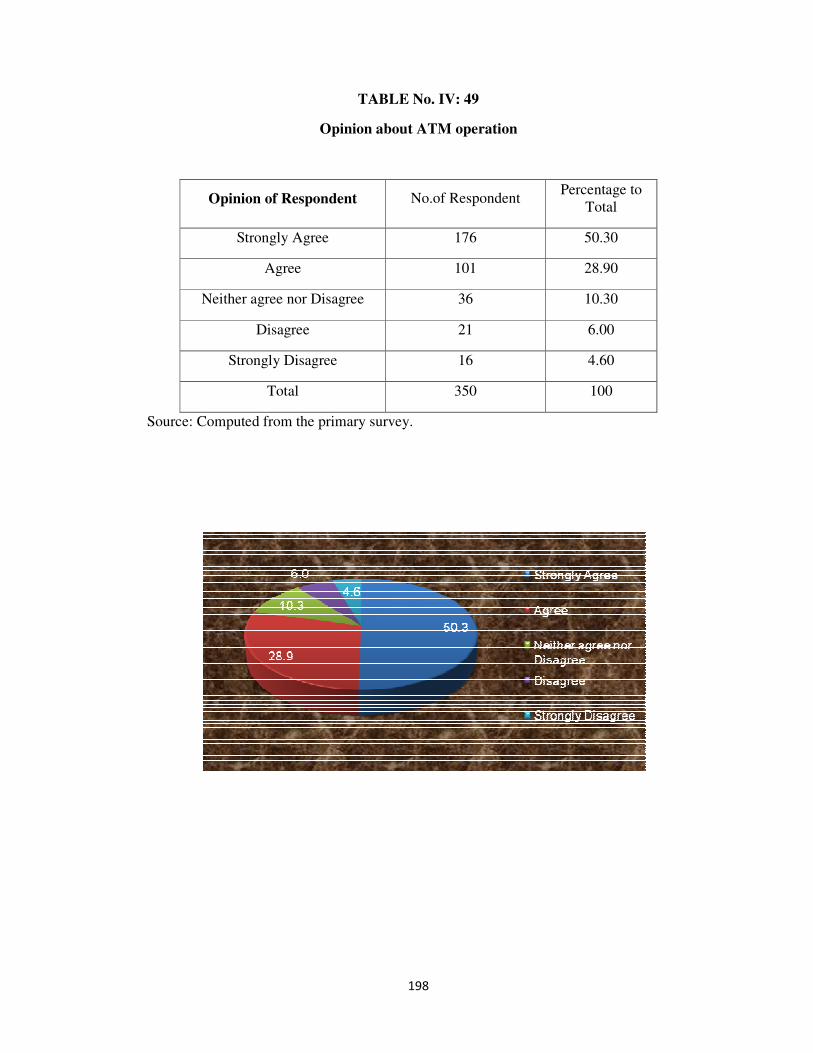

4.49 Opinion about the ATM operation 198

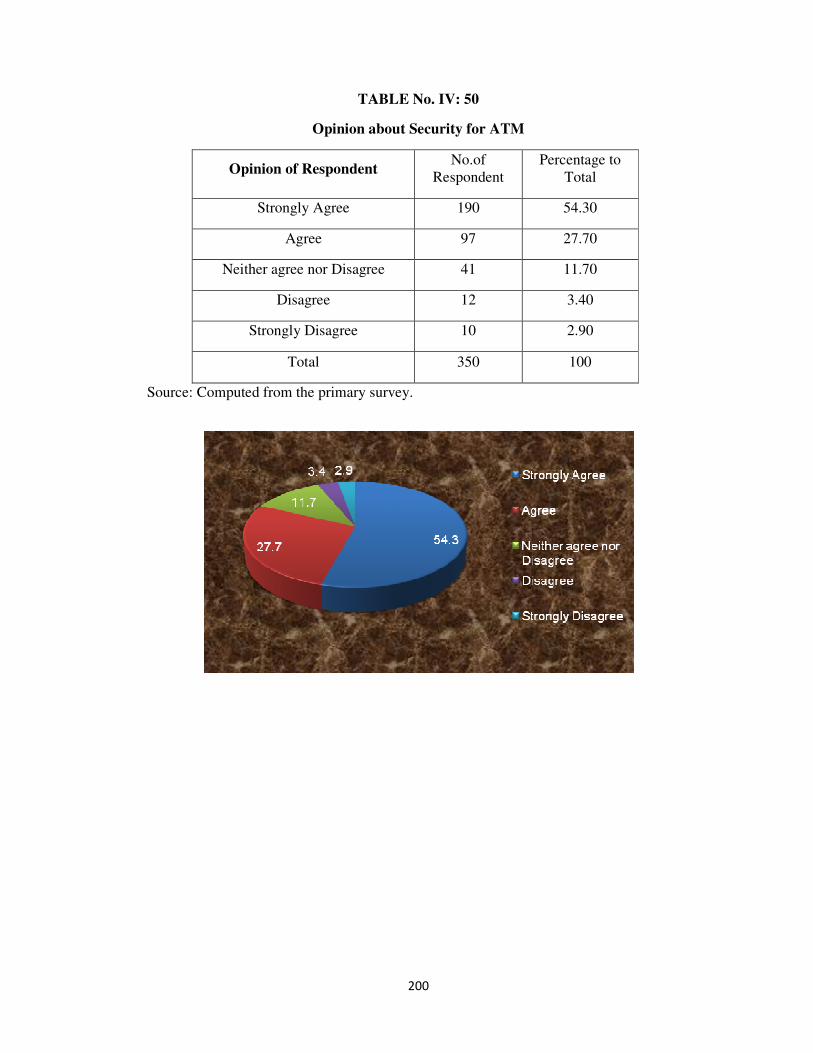

4.50 Opinion about Security for ATM 200

4.51 Expectation of customers on enhancement of ATM services 202

1

CHAPTER – I

DESIGN AND EXECUTION OF THE STUDY

Introduction

Indian banking scenario has underwent dramatic changes after the

implementation of the new economic policy which triggered out the economy in rapid

speed and as a result of that drastic changes have taken place in money transactions.

The growth in the number of banks has on the one hand increased competition and on

the other hand heightened the standards that need to be met in order to gain a

competitive advantage. In addition, the competition between banks is a premise of

customers’ ever growing expectations. Customers are now more informed and they

expect their banks to meet their needs when, how and where they want. Otherwise,

there is the risk that a bank loses the market share in favour of its competitors.

Considering these issues, one major concern of the banks is the customer retention. A

long-term relationship between a bank and its customers is a proof of the financial

institution’s efforts to offer high quality services that satisfy customers’ demands.

Moreover, the customer retention is a necessary input for improving business

performance. It is therefore necessary that the banks concentrate their efforts towards

improving the quality of their services and satisfying their customers’ needs. ‘High

service quality results in customer satisfaction; high service quality leads to

competitive advantage as customers feel satisfied and thus are more probable to

further buy the company’s services, to recommend them to others and to ignore the

competitors’ offer. It is therefore necessary to continuously measure the service

quality in order to establish those areas that need improvement.

2

Moreover, it is important to know whether customers are satisfied with the

offer and with the quality of the services in order to decide if improvements need to

be made. Nevertheless, it is important to find out which are the aspects that influence

customers’ satisfaction most. From a bank’s perspective, it is necessary to seek out

the ‘most influential determinants of customer satisfaction and to determine

customers’ perceptions regarding these determinants’ quality level. Thus, they

increase their chances to differentiate from their competitors and to retain their

customers. Services may be referred to as benefits or experiences and therefore, when

customers decide whether they are satisfied or not with a bank, they actually evaluate

their experiences with ATMs, Internet Banking etcetera, or the experiences they have

within a bank unit. Hence, we may say that service quality is an evaluation of the

bank’s delivery system and satisfaction refers to customers’ experiences with the

delivery system.

Innovative Role of Banks

Application of marketing techniques to banking business is a relatively new

development. Academically and professionally it forms a part of services marketing

and in more precise terms a division of marketing of financial services. While the role

of financial services offered by banks have grown continuously, there have been

mounting pressures on the economies of western countries for a more effective

marketing management of the financial services offered by the banks. Since the

banking sector represents the most important financial sector not only in terms of

turnover, profits and employment, but also on its paramount impact on the other

spheres of the economy, it has become inevitable to recognize marketing.

3

The financial services provided to-day is very different from what they were in

the past both for business and trade customers and in the personal financial services

field. In the personnel sector for instance the market has broadened immensely with

the introduction of new payment methods, investment methods, insurance methods

etc.; and have all changed in response to wider financial knowledge. The growth of

disposable income and cultural changes

In this background of growing markets for financial services, increasing

competition and improving the level of financial awareness and sophistication by the

end users, both personnel and corporate, the banks had to develop their marketing

skill at least to maintain their marketing share and profitability levels.

Thus it becomes apparent that, of all the challenges confronting to-days banker

none is more serious or demanding of action than the proliferation of aggressive new

competitors. Not only are there more of them, but they are generally more

strategically focused and marketing driven. They have identified specific market

segments to gain competitive advantage and are creative in positively differentiating

their product offerings and exploit the weakness of their bank competitors. The

consumer will buy the bank or service that provides the best service for him.

In that sense banks are not different from most other marketers of goods and

services to-day they face the same problems of communicating with and motivating

consumers who are better educated, financially savvy and deluged by all forms of

media, Obviously, owing to the very nature of banking it cannot be treated in exactly

the same way as that of a manufacturing firm. These are two fundamentally different

functions that bank marketing must perform It must attract deposits on one hand and

attract borrowers and users of services on the other.

4

This double-sided nature of banking business brings marketing problems that

are more complex than those that normally face commercial concerns. . Considering

the importance and role of banks in the society and the economic development of a

nation it will not be appropriate to adopt the marketing techniques in other business to

banking without modifications.

The marketing concept, as put forward by most-marketing practitioners, is a

business philosophy which says that the purpose of any business is to satisfy the

wants and needs of consumers at a profit. Successful firms have recognized that

customers are fast becoming more sophisticated and the industry's traditional product

orientation cannot respond to this change. No longer can the industry produce

whatever it is capable of producing, and offer the product unmodified to customers.

Within a regulated environment that practice may have worked well. But with the

relaxing of controls it was no longer viable. Innovative business firms found that

products and services had to be expressly designed to meet customer needs and their

line divisions have accepted marketing as a way of life.

Electronic banking and its various forms

Banking is done through electronic systems for customer’s transactions (front

office computerization) and /or internal accounting and book-keeping (back office

computerization), as against the traditional manual system. The new private sector

banks, which began operating in 1994 with front office and back office

computerization, spurred a trend towards complete-computerization and electronic

banking in public sector banks.

5

Today, most of the banks have computerized front offices in metros/cities and

their back office and information management systems are also fast getting

computerized. Recent advancements in information and communication technologies

have virtually replaced manual banking with electronic banking. Electronic banking

has enabled banks to improve their customer service quality by speeding up most of

the routine banking transactions and by providing ‘anywhere, anytime banking’. New

banking channels are opened up in the form of ATMs, Tele-Banking and Internet

Banking, although the conventional ‘brick and mortar’ banking is also available at all

branches.

Electronic Banking has also improved internal book-keeping and management

information systems of the banks. Inter-connectivity between the branches is also

done to achieve economy, centralizing the core banking operations on a common

electronic platform, enabling the banks to achieve economies of scale and to further

improvise ‘anywhere banking’. Electronic banking makes use of electronic currency.

Check cards or debit cards, smart cards or stored-value cards, digital cash and digital

checks are the different types of electronic currency. If you use a check card to make

purchases, the funds are transferred immediately from your account to the store’s

account. Smart cards have a specific amount of credit embedded in it. The chip in the

card contains both personal and financial information. Digital checks are used with

electronic bill paying services. Consumers could use personal finance software

packages or use software provided by a bank. On line banking or PC banking offers a

wider outreach for smaller institutions. Electronic banking offers consumers the

convenience of accessing and transferring funds between their accounts, paying their

bills and other purchase, twenty four hours a day, seven days a week.

6

Automated Teller Machine (ATMs) have become very popular for dispensing

cash to customers on-site and off-site, 24 hours a day, 365 days a year. However,

these have certain limitations as regards quantum of withdrawals and denomination of

notes disbursed. Further, these do not issue cheques books or drafts, like a

teller/assistant at the bank counter, does not can these respond to an un-programmed

query of a customer. These do not have a human face, nor do these show any empathy

to a customer who has run into some problem. Mobile Banking goes to the customers

for banking transactions, rather than the other way round (as in conventional

banking). Mobile banks have either computerized system or manual banking system.

In either case, it reaches the customers on designated days/hours on specified places.

It involves less capital investment, but has problems of security and safety, unlike a

conventional branch, which provides safety, security and comfort coupled with

complete banking facilities.

Tele banking provides ‘anywhere and anytime’ banking, but only to a limited

extent. It provides general information about the account to a customer, but it too does

not issue a cheques book or a draft instantly, which is possible in branch banking.

Internet banking enables customers to access and view their ledger accounts and make

limited transfer of funds from one account to another. However, Internet banking has

not yet gained momentum in India, as it requires certain infrastructure, which is not

yet possessed by most customers. There are certain issues that require to be tackled

before it gains popularity in cities and towns. Electronic Funds Transfer has made

fund-transfer from one center to another in the same country or to another country

faster and safer. Electronic Clearing System has enabled the banks abroad to handle

the clearing of cheques and interbank settlement faster and in large volumes.

7

In India the clearing system is not fully automated. This results in credit

clearance to customer’s accounts being done on the third day after the cheque is

deposited. Electronic credit/debit systems have saved the customers from the tedium

involved in receiving/making payments by cheques. The corporate and banks also

prefer to adopt this hassle-free, cheque-less system of payments and receipts, by

issuing mandates to the bankers for making periodic payments from accounts of the

specified company.

Forms of E-Banking

• Mobile Banking

• Tele Banking

• ATM

• Internet Banking

Mobile Banking

Technology has a major impact in helping banks service their customers with

the introduction of Internet banking. It helps to give the customer’s anytime access to

their banks. Customers could check out their account details, get their bank

statements, perform transactions like transferring money to other accounts and pay

their bills sitting in the comfort of their homes and offices. However the biggest

limitation of internet banking is the requirement of a PC with an internet connection.

Mobile banking address this fundamental limitation of internet banking, as it reduces

the customer requirement to just a mobile phone. The main advantage of mobile

Banking over internet banking is that it enables ‘Anywhere Banking’.

8

Customers now do not need access to a computer terminal to access their

banks, they could do so on the go – when they are waiting for their bus to the work

place, when they are traveling or when they are waiting for their orders to come

through in a restaurant.

Tele Banking

In the current fast and active pace of our society, most people have less or no

time to go through the hassles of going to the bank just to perform some simple

transactions / inquiries. As such, telebanking through the telephone is the perfect

solution for people on the go. Telebanking system is an Interactive Voice Response

(IVR) application, which uses a telephone to access information from a database. It is

an easy to use, cost effective and innovative solution designed to meet user needs for

electronic banking application. It provides communication between information in

IVRS system and off-site telephone caller I customer. This solution bridges the gap

between digital data and human modality of listening and speaking.

Telebanking eases the hassle of going to the Bank or any Automatic Teller

Machines to perform day-to-day banking transactions.

Internet Banking

The Internet banking indicates the technological development in the banking

industry. Financial institutions started "home banking" business via a touch- tone

telephone in the 1970s. Cable television was introduced in the 1970s. Cable television

was considered as a possible medium for home banking in the 1980s. This approach

solved the graphic limitations of the telephone.

9

However, it had drawback the absence of two-way communication. Later, the

PC provided both visual display and two - way communication. It has been

considered an ideal device for modern banking medium.

Internet Deployment

To carryout transactions that are internal to a bank, between the bank and its

branches and subsidiaries, intranet deployment in banking is required. Extranet

permits a bank to have full control over the users of intranet and information to be

transmitted. The integration of the internal and external communications of banking

related information through banking internet and intranet for the development of the

financial sector requires extensive working on the part of the bankers.

E-Banking in India

In banking industry, e-services are revolutionizing the way business is

conducted. Electronic based business models are replacing conventional banking

system and almost of banks are rethinking business process designs and customer

relationship management strategies. It is also known as e-banking, online banking

which provides various alternative e-channels to using banking services i.e. ATM,

credit card, debit card, internet banking, mobile banking, electronic fund transfer,

electronic clearing services etc. however, in the Indian e-banking scenario ATM is

more acknowledged than other e-channels.

10

The first bank to introduce the ATM concept in India was the Hong Kong and

Shanghai Banking Corporation (HSBC) in the year 1987 followed by Bank of India in

1988. According to the R.B.I. annual report (2010-11) almost commercial banks are

providing ATM facilities to its customers and to date there are 45,520 ATMs installed

by public sector banks and 32,480 ATMs installed by private sector banks in India.

ICICI Bank Ltd., is the first bank introduce the ATM transaction in India, therefore

this bank got the important place in the process of technological revolution

undergoing in our country moreover it is the largest private bank of the country.

Needs of the study

The philosophy of a Bank demands the satisfaction of customer’s (consumers)

needs as the prerequisite for the existence and survival of the bank. So, bank

marketing is so basic that it cannot be considered as a separate function. It is the

whole business seen from the point of view of its final result that is the customer’s

point of view. This means that the central focus of all the activities of a bank is the

customer. The marketing function in a bank is required to be integrated with customer

centric operations. In India, the customer is now becoming increasingly

sophisticated and choosy, like his counterparts in the Western World. The customer

expects to get service packages to suit his diverse needs. He also expects advice and

guidance to meet his needs from the bank. Banking is the people staff interaction. The

efficiency with the service is delivered to a customer and the customer’s satisfaction

depends on the attitude, traits, orientation and training of the staff. It also depends

upon the system and procedures followed by the bank and the level of technology

used in banking transactions.

11

The advent of Six Sigma practices, it has become imperative that banking

solutions can be adverted. This paved the way for the banking industry taking

advantage of the Technology and IT based enabled solutions to shift from historical

banking methods to e-banking solutions. The e- banking solution is more focused on

the total services of the banking industry as whole as e-banking services.

The draw backs of the historical and the Traditional Banking services like

opening an account, depositing and withdrawal of cash, and other connected

operational facilities are time consuming with lot of formalities. These can be

addressed and resolved through e - banking services. E-banking services also

enhances the customer relationship with promotes better Human Relations.

Apart from ‘Service time’ and interaction with the bank’s staff, ambience and

infrastructure facilities play an important role in the customer service quality

perception. The ‘ambience and infrastructure’ includes variables such as ‘pleasant

atmosphere in the Bank’, spacious and uncluttered layout’, ‘location of bank’,

‘parking facility’, branching network’, ‘technology used by the bank technology

updated, speedy services, and ‘accessible and visible display of information are some

of the required/ expected facilities from the customers point of views. Providing

banking services involves interaction between the customers and the bank staff.

Banking services by their very nature are human - intensive. Therefore, in spite of

introduction of modern technology, there may be situations where non- involvement

of bank staff in attending to customers in person may generate customer distrust.

The banking system plays a crucial role in the development the economy. It is

necessary to improve the efficiency and to offer better customer friendly services

through personal banking at a reasonable cost to the customers.

12

The new generation, Private Sector banks are emerging with better and

upgraded technology, ambience, innovative banking products and services coupled

with faster efficient service, have contributed to the growth. These Technology

initiatives like ATMs, Credit, Debit Cards, E-Commerce, and tele-banking services

have posed a serious challenge to the public sector banks.

It has become imperative to study the performance of the private bank in

fulfilling the requirement of the increasing customer, whether the private sector bank

could provide the service with the help of IT development, Generally the public

sector banks have been functioning in the conservative structure which might not

have adequately support the changing requirement in a smooth way in such situation

it is became essential to look into the performance of the private bank in providing

the services in more comfortable way to the consumers, how the private bank

marketing their services to the consumers.

Statement of the problem

The crux of the earlier studies has revealed that automated service quality has

been identified to have a significant importance in the financial performance of a

bank. The current study extends the previous study and investigates whether there is

any relationship between automated service quality and customer satisfaction with the

financial performance of a bank along with the satisfaction level of the customer on

the services provided by the ICICI Bank Ltd.,

13

ATM, telephone banking, internet banking, price, and core service, five

factors of automated service quality of a bank are the key components of the financial

performance of a bank. In the general literature, service quality and customer

satisfaction have often been identified as significant predictors of business

performance. Therefore, this study explores how perceived quality of automated

service and level of customer satisfaction are related to profitability of the bank.

Technology, however has had a remarkable influence on the growth of

service delivery options. There are several competitive advantages associated with the

adoption of technology in service organizations, including the creation of entry

barriers, enhancement of productivity, and increased revenue generation from new

services Service quality is one of the main factors that determines the success or

failure of electronic commerce. However, automated service quality has tended to lag

behind because practitioners have focused mainly on issues of usability and

measurement of use, with little consideration for the outcomes.

Bank’s customers come from different strata of the society. These

customers belong to different economic, cultural and social back grounds, with

heterogeneous attitudes, and expectations and influenced by the environmental

background of the customers. In a developing economy, people migrating from the

rural and semi-urban localities to the metropolitan cities in search of opportunities

cannot be ignored. They add to an overall development including service sector.

Moreover, economic liberalization has resulted in the growth of private sector

especially in the field of banking. In today’s market economy the customer is the king

and only the more focused customer oriented services will survive. The Customer

perceives a product of service from cost benefit analysis.

14

Satisfying the needs of heterogeneous customers is indeed a difficult task.

Development in the field of IT and ITES offer solution to this problem. Hence the role

of banking has expanded incredibly, banks are also have equipped immensely with

the help of IT development in unleashing the services in better way to their consumers

in such context number of studies have been carried out to find out the consumer

satisfaction of the bank customer in order to enhance the service, most of the studies

have revealed that the IT development has better impact on the service delivery but

the propose study would like to encompass all the spheres of the banking services in

assessing the service delivery and the satisfaction level of the customer, hence it is

very much imperative to explore the consumer satisfaction at multi dimensional level.

Therefore, this study aims to investigate whether significant relationship exist

among the automated service quality, the customer satisfaction and the financial

performance and the level of consumer satisfaction on the various services provided

by the ICICI bank Ltd extensively and holistically.

15

OBJECTIVES OF THE STUDY

The following are the major objectives of the study:

1 To Study the profile of ICICI Bank Ltd;

2 To analyze the performance of ICICI Bank Ltd from 2006 -11;

3 To asses the customer satisfaction towards the services provided by ICICI

Bank Ltd. and

4 To test the following hypothesis:

� Ho: There is no significant influence of determinants on customer

satisfaction of ICICI Bank Ltd. :

� Ho: There is no significance distinction between educated customers

and the less educated customers in accessing the benefits of ICICI

Bank Ltd. ; and

� Ho: There is no significant difference among the business group and

employees on the perception on the service charges levied by ICICI

Bank Ltd.

16

LIMITATIONS OF THE STUDY

1. The Study is restricted to ICICI Bank Ltd. situated in Chennai Metro

only.

2. The Study is confined to a period of five years from 2006 – 11 for

assessing the performance of ICICI Bank Ltd.

3. The survey for the study was undertaken during the period January to

March 2011.

4. This study focuses on the account holders of ICICI Bank Ltd. only.

AREA OF THE STUDY

This district is listed as the "most advanced" district in Tamil Nadu. It has a

resident population of 4,681,087 as of 2011, yielding an average density of 26,903

persons per km, excluding the huge commuter traffic from neighbouring districts.

This is against a density of 24,963 persons per km in 2001, making it the district with

the second highest density in the country. The sex ratio is 1000:951. The average

literacy rate is 80.14%, much higher than the national average of 64.5%. It is 100%

urbanised as per Census 2011. Chennai District has 13.39 per cent of the urban

population in the state of Tamil Nadu. The decadal growth of population in Chennai

District during 2001-2011 is 7.77 percent.

17

Locations of ICICI Bank Ltd. Branches in Chennai Metro

18

RESEARCH METHODOLOGY

Sources of the data

Survey method was used for the study. Both Primary and Secondary data were

used for the study. Primary data were collected from the customer respondents of

ICICI Bank Ltd., through interview schedule. Secondary data were collected from

books, journals and the Annual Report of ICICI Bank Ltd., from 2006-2011.

Sampling

Stratified random sampling method was followed for the study. Chennai

Metro was stratified into three parts namely Central Chennai, South Chennai and

North Chennai. It was learned that the number of ICICI Bank branches in the three

parts were 20, 15 and 15 respectively. Hence, 140, 105 and 105 sample respondent

were selected. In each branch 7 sample respondent were selected for the study.

In proportion to the number of ICICI Bank branches located in the Central

Chennai, South Chennai and North Chennai.

Central Chennai South Chennai North Chennai Total

No. Of. ICICI

Bank Branches

20 15 15 50

No. of Samples 140 105 105 350

19

Data collection

The study is an empirical one based on sample survey method. The study has

basically depended on primary data. The required primary data were collected by

means of an interview schedule administered to customers of ICICI Bank ltd., at

Chennai Metro. Secondary data were collected from books, magazine, journal and

Annual Reports of the ICICI bank Ltd.,

Tools for data collection

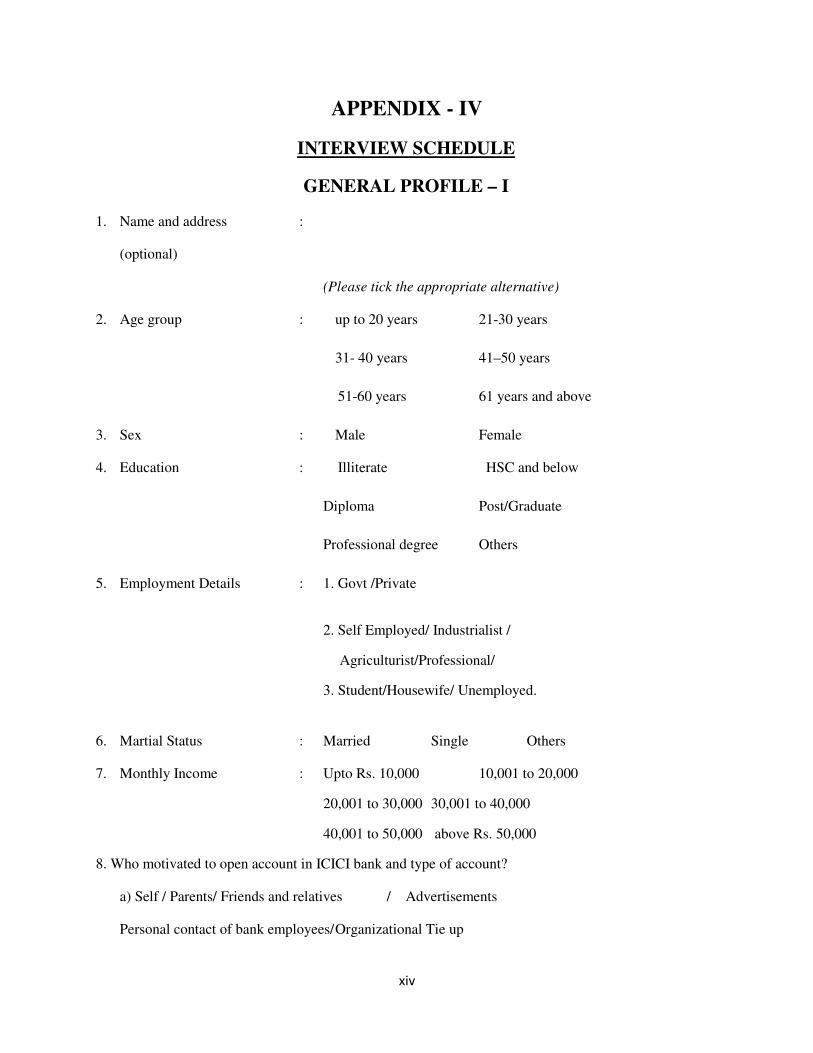

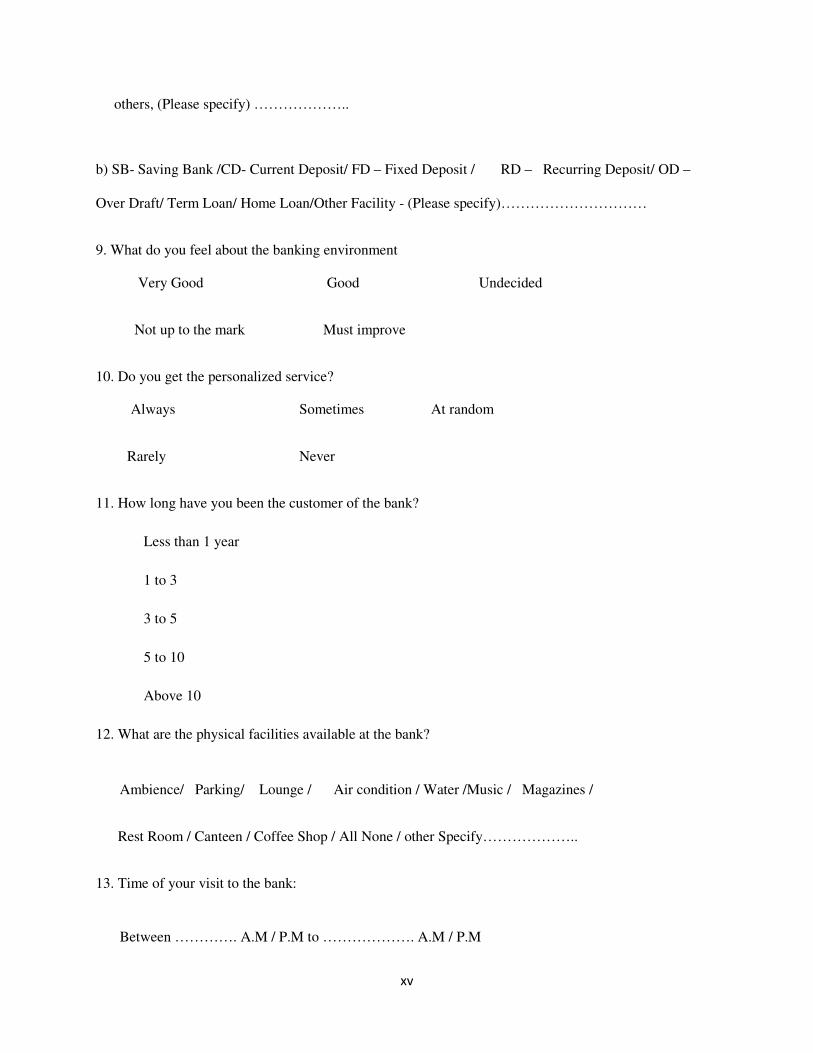

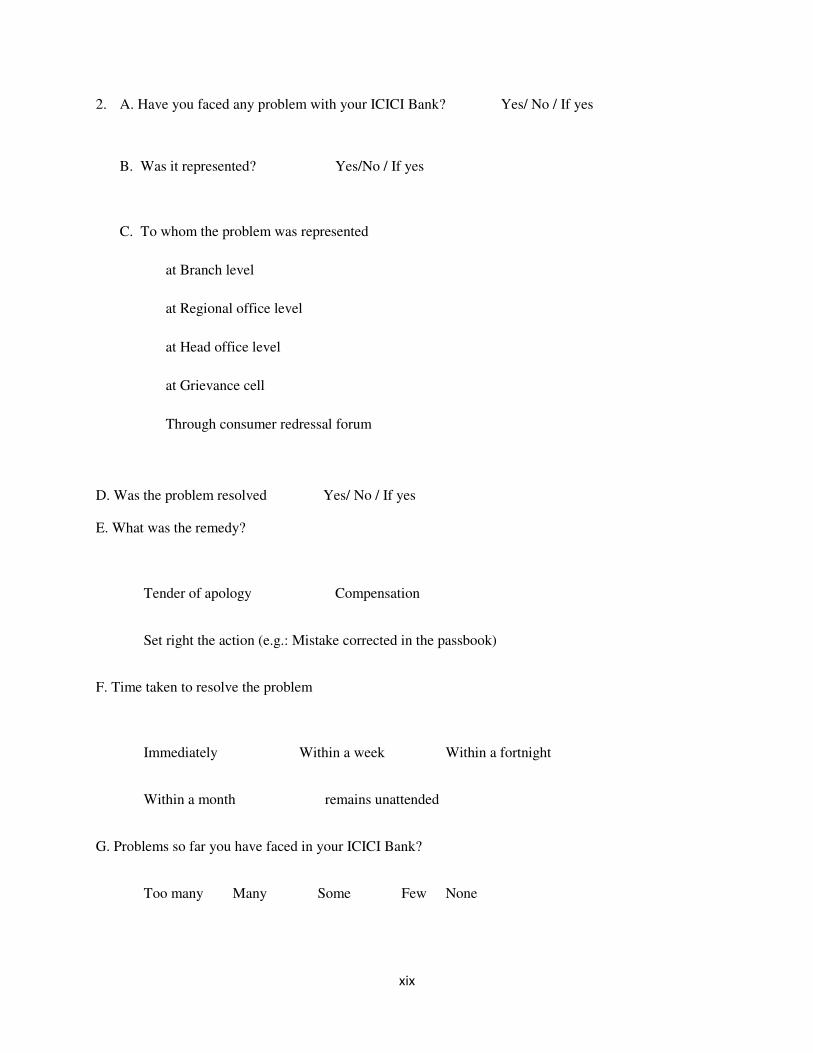

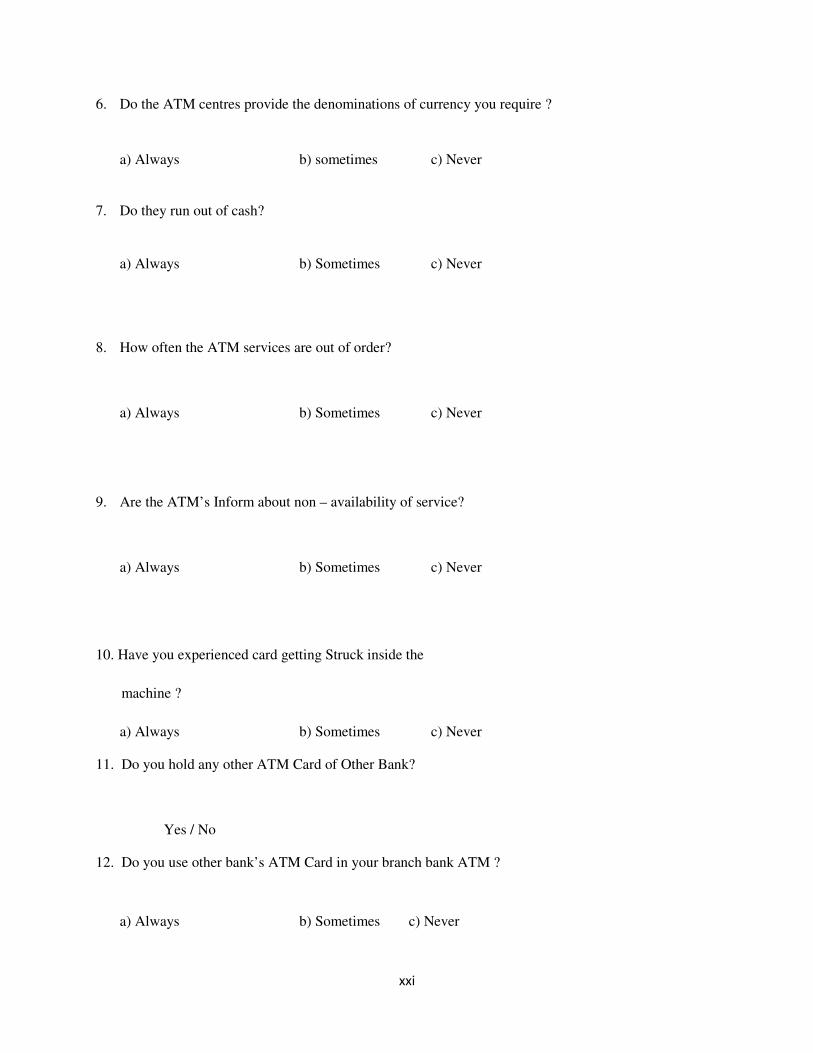

Interview schedule addressed to the customer respondents of ICICI Bank Ltd

was used to collect primary data. The interview schedule was developed mainly on

the basis of the studies of Lyman E.Ostuland ,John Croson and George Steiner and

Sandra L.Holmes. The interview schedule contained questions divided in to six

parts namely general profile, services study, ATM services, opinion survey (Financial

and Non Financial services) general operational opinion, and Customer satisfaction.

Questions were framed based on Likert five – point scale to obtain responses from

customers . A pilot study was conducted with a sample of 50 respondents to know the

feasibility of the study.

Tools for Analysis

Descriptive statistical tools such as frequency distribution, mean values,

quartile distribution and standard deviation have been used to describe the profiles of

respondents. Inferential analysis such as, ANOVA test, ‘t’ test, Multiple Regression

Test, other relevant tools ware used to the test the hypothesis. The data so collected

were tabulated analyzed and presented in this research report.

20

The interpretation of data has been used to draw inferences and findings of the

study. The hypotheses framed on the lines of the objective of the study, were tested

statistically for their significance.

Chapterization

The report of the research work is presented in five chapters as given below;

First Chapter deals with the design and execution of the study which includes the

introductory note, justification and selection of the study, statement of the research

problem, objectives, methodology and chapterisation.

Second Chapter deals with the review of literature of the related studies - the

literature review part divided into three categories namely studies pertaining to

customer satisfaction, E-banking Marketing strategies, and ATMs service delivery.

Third Chapter deals with the profile and performance of ICICI Bank Ltd.,

Fourth Chapter gives an extensive analysis of customer satisfaction of the services

of ICICI Bank Ltd., including ATM services.

Fifth Chapter brings out the summary of major findings, suggestions and conclusion

of the study.

21

CHAPTER - II

LITERATURE REVIEW

This systematic perusal of the literature on the selected domain has stemmed

in this chapter. The literature has been classified into three important categories like

literature pertaining to E-banking, studies pertaining to banking service and consumer

satisfaction and literature concerning to ATM of Banks.

E-Banking

1. Mookerji (1998) : Internet Banking is fast becoming popular in India. However, it

is still in its evolutionary stage. By the year 2005, large sophisticated and highly

competitive internet banking markets will develop. Almost all the banks operating in

India and having their websites but only a few banks provide transactional internet

banking.

2. Daniel (1999) :Customer’s value features in internet banking such as convenience,

increased choice of access to the bank, improved control over their banking activities

and finances, case of use, speed and security. From the banks prospective the main

benefits and electronic banking are cost savings, reaching new segments and the

population, efficiency, cross selling, Third –party integration, and customer

satisfaction.

22

3. Guru et al., (2000) : Examined the various electronic channels utilized by the

Malaysian banks and also assessed the consumers relations and reactions to these

delivery channels. It was found that either Internet banking was absent or it was not

successful in the local Malaysian banks due to lack and adequate legal frame work

and security purpose. However major percent of the respondents were having

internet access at home and this represented a positive indication for personal

computer based and e-banking in future.

4. Furst et al., (2000): Contributed data on the number & National banks in U.S

offering Internet banking and the product and services being offered. Only 30 percent

of National banks offered Internet banking in the Fourth quarter of 1999. However as

a groups these Internet banks accounted for almost 90 percent of National banking

systems assets, and 84 percent of small deposits banks in all size categories offering

Internet banking tend to accounts less on interest – yielding activities and core

deposits than do non internet banks, also institution with Internet banking out

performed non-Internet banks in Terms of Profitability.

5. Suganthi et, al., (2001): Conducted a review of Malaysian banking sites and

revealed that generally all banks are having a web access. Only Four banks out the ten

major banks were in the transactional sites. The rest of sites were at informal level.

There are various psychological and behavioral issues such as trust, security of

Internet Transaction, unwilling to change and preference for human interface which

appear to hinder and growth of Internet banking.

23

6. Janice et al., (2002): Based on the interviews with four banks in Hong Kong

reviewed that banks view the internet as being a supplementary distribution channel

for their products and services in addition to other forms of distribution channel such

as Automated Teller Machine (ATMs), Mobile Phone and Bank branches. Basic

transactions and Securities trading are the most popular types of operations that

customer’s carryout in internet banking.

7. Lustsik (2003): Based on the survey of experts of e-banking in Estonia banks

found that Estonia has achieved significant success in implementation of e-banking

and also on the top of the list in emerging countries. All the major banks are

developing e-business as one of the core strategies for future development.

8. Zeithmal and Bitner (2003): “Satisfaction is the consumer fulfillment response. It

is a Judgment that a product or service feature, or the product or service itself,

provides a pleasurable level of consumption related fulfillment.”

9. Hiltunen et al. (2004): Customers value features in internet banking such as

convenience increased choice of access to the bank, improved control over their

banking activities and finances, ease of use, speed and security. From the banks

prospective the main benefits of electronic banking are cost saving, reaching new

segments of the population, efficiency, cross selling, third party integration and

customer satisfaction

24

10. Chowdari Prasad (2004): Studied the performance of all private sector banks. As

per the criteria selected like efficiency, financial strength, profitability and size of

scale it is revealed that the private sector banks were in a better position to offer cost

effective, effective product and services to their customers using technology, best

utilization of human resources along with the professional management and the

corporate governance principles. -Chowdari Prasad (2004). "Private Sector Banks in

India-A SWOT ANALYSIS"

11. Sathye, Milind (2005): Sathye found that the performance of the public sector

banks was sounder as compared to the private sector banks.

12. Sanjay. J. Bhayani (2006): In his study analyzed the performance of new private

sector banks with the help of the CAMEL Model. The study covered 4 leading private

sector banks-ICICI, HDFC, UTI & IDBI for a period of 5 years from 2000-2004. It is

revealed that the aggregate performance of IDBI bank is the best among all the banks

followed by UTI. Sanjay J. Bhayani (2006). "Performance of the new Indian private

banks” -A Comparative Study.

13. Arabinda Saha (2008): States that the formal banking system can perhaps learn

something from the success of micro-credit. The steps to be taken to facilitate

increased earnings of the selected banks are more profitability, practical management,

follow-up of loans, Advisory services, customer information services, credit card

services, e-commerce technology and establishing of “Research cell” are in each of

the banks is important.

25

14. Ca. Lavanya Gupta (2009): The advent of the internet has provided great and

endless opportunities for the people all over the world and the importance of the

internet in the world of business and banking has grown astoundingly. This is why

most business today, from colossal corporations to petite family-owned enterprises,

has embraced the internet to avoid being edged out by their competitors. It is

inevitable to espouse the same and resort to the internet which opens the door to the

world.

15. Bernadette D.Silva et al., (2010): Conducted an Analysis for internet banking says

that the bank corporate to understand that there are certain Parameters in e-banking

which are affected by the demographic status like Gender, Income level and

Educational Qualification etc., for opening internet bank account. Bank operations

through internet can attract larger customer and it will enhance the brand image of

banks for usage of sophisticated technology.

16. MD. Mallya, (2010): Technology has changed the face of banking, more

particularly in the Last Five years. Banks have begun to provide virtual banking

services to customers. There is ‘anywhere banking’ through core banking systems,

‘Any time banking’ through new 24/7/365 delivery channels such as ATMs and Net

and Mobile banking facilities provided in some banks. Currently, 67% of bank

branches are on CBS mode, while around 35,000 ATMs are located off-site.

17. Manoranjan Mobapatra, et al., (2010): About Forty percent of the population in

India is un-banked. Since e-banking has evolved as a platform for future innovations

that can have long ranging socio-economic benefits for India and hence also be able to

capitalize on the Indian government’s dream of, one bank Account Per Indian;

established in the fact that e-banking is the need of the hour in India today.

26

It is a win-win situation for all concerned, operators banks and specialist companies

are gradually getting themselves organized to operate e-banking services. Banks are

able to reach remote areas without incurring the heavy expenses that opening a branch

entails and the ATM penetrating in rural areas is not that High with only forty ATM s

per million people in India.

18. KR. Kamath (2010): Banks may more towards universal banking driven by the

forces of deregulation, liberalizations, and technological advancement. The pressures

would emanate from super markets, utility service providers etc., Technology has

played and is playing a critical and arguably the most important role in redefining the

financial business. Banks are responding by offering alternative delivery channels like

ATMs, Tele banking, internet banking, mobile banking etc., Most of the banks have

already implemented core banking solution (CBS) across all offices to provide

“anytime anywhere” banking in true sense.

19. K.B.L Mathur (2010): Indian banks have shown a healthy growth rate as

improvement in performance as is evident from capital adequacy, asset quality,

earnings, efficiency indicators and new technological like E-Banking etc.,

20. Barna Maulick (2010) : Indian banks are hopeful of becoming global brands as

they are the major source of financial sector revenue and profit growth. The financial

services penetration in India continues to be healthy, thus the banking industry is also

not far behind. As a result of this, the profit for the Indian banking industry will

surely surge ahead.

27

21. Dr.Vijay M.Kumbhar (2011): This study evaluates that the major factors (i.e.

service quality, brand perception and perceived value) affecting on customers’

satisfaction in e-banking service settings. This study also evaluates influence of

service quality on brand perception, perceived value and satisfaction in e-banking.

Required data have been collected through customers’ survey. For conducting

customers’ survey likert scale based questionnaire has been developed. A result

indicates that, Perceived Value, Brand Perception, Cost Effectiveness, Easy to Use,

Convenience, Problem Handling, Security/Assurance and Responsiveness are

important factors in customers satisfaction in e-banking it explains 48.30 per cent of

variance. Contact Facilities, System Availability, Fulfillment, Efficiency and

Compensation are comparatively less important because these dimensions explain

21.70 per cent of variance in customers’ satisfaction. Security/Assurance,

Responsiveness, Easy to Use, Cost Effectiveness and Compensation are predictors of

brand perception in e-banking and Fulfillment, Efficiency, Security/Assurance,

Responsiveness, Convenience, Cost Effectiveness, Problem Handling and

Compensation are predictors of perceived value in e-banking.

22. Dr.Vijay Kumbhar (2011): This research is based on empirical evidences

collected through the customers’ survey regarding to the customers perception in

internet banking services provided by public and private sector banks. It is efforts to

examines that the relationship between the demographics and customers’ satisfaction

in internet banking, relationship between service quality and customers’ satisfaction

as well as satisfaction in internet banking service provided by the public sector banks

and private sector banks. Present research shows that the, demographics of the

customers’ are one of the most important factors which influence using internet

28

banking services. Overall results shows that the highly educated, a person who are

employees, businessmen and belongs to higher income group and younger group are

using this service, however, remaining customers are not using this services. Results

also shows that overall satisfaction of employees, businessmen and professionals are

higher in internet banking service quality. There is significant difference in the

customers’ perception in internet banking services provided by the public and private

sector banks. Private sector banks are providing better service quality of internet

banking than service provided by the public sector banks. Therefore, public sector

banks should improve their internet banking services according to the expectations of

their customers.

29

CUSTOMER SATISFACTION

1. Bearden, W.O. Teel., J.E. (1983): Used the data to examine the antecedents

and consequences of consumer satisfaction in an empirical consumer panel

based a two phase study of customer satisfaction. Their results supported

pervious findings that expectations and disconfirmation are plausible

determinants of satisfaction, and also suggested that complaint activity may be

included in satisfaction/dissatisfaction research. It highlights “A cognitive

model of the antecedents and consequences of satisfactions decisions”. The

study also concluded that there is a significant influence on customer

satisfaction.

2. Nessim Hanna and Wagle, J.S. (1989): Have provided an explanation on two

psychological theories on perceived expectation. Their work focuses on

“Effort Satisfaction Theory and Optimal Satisfaction theory”. They have

explained and provided evidence to show that effort/satisfaction is as much an

individualistic attribute as it is a universal trait of consumers. They have

studied these with the help of an experiment and have concluded that although

many personality traits have not proved to be related to marketing behavior, it

appears that optimal stimulation level may be one that they have suggested

that should be carefully studied.

3. Eugene W Anderson, Mary W Sullivan (1993): Claims that the firm’s future

profitability depends on satisfying customers in the present. If consistently

providing high satisfaction leads to higher repurchase intentions, then the

expected number of times a buyer will repurchase should rise accordingly, and

30

no satisfactory literal definition has yet been developed for consumer

satisfaction and dissatisfaction in the literature of marketing.

4. William L. Boyd, Myton Leonard and Cheries White (1994): In the paper

“Customer preferences for financial service An analysis” determined the

relative strengths of factors used in the selection process They also identified

the orientation of potential customers relative to those factors for financial

service The customers selected for the study were given a list of factor for

selecting a financial institution The weighting system was used to rank their

choices and it was concluded that many customer of financial institutions had

difficulty in determining the importance of one selection criterion over the

other.

5. Piercy, N.F. (1996): Observes that while customer satisfaction measurement is

currently one of the commonest prescriptions in both the marketing and the

management literatures, little attention has been paid to the effects of customer

satisfaction measurement, particularly in terms of the impact on the internal

market i.e. the employees and the manager inside the organization. A recent

study of the internal market effects of customer satisfaction measurement

identifies a number of ways in which the use of customer satisfaction

information may have negative effects within the organization, and may stand

in the way of the implementation of market strategies of service and quality.

This suggests a management agenda which extends far beyond the acquisition

of customer satisfaction data and reporting systems to consider the full impact

of such measurement systems.

31

6. Peter Kangis and Vassilis Voukelatos (1997): In their paper “Private and

Public banks A companion of customer expectations and perceptions”

reported the findings of a survey among customers of private and public sector

banks in Greece the study showed that service quality perceptions and

evaluation of services received were marginally higher in the private than in

the public sector in most of the dimensions measured. The dimensions were

the relative importance attached to each quality attributes. The perception of

the profile of the services received was different between the two sectors

Thus it suggested that they did deliver a different quality of service They

concluded that distinctiveness of the perceived service on offer was an

essential ingredient to competitive positioning in financial services.

7. Srinivasan, P.T. and Harish Kotadia; (1997): Have reviewed various theories

of customer satisfaction. They have stated that, “The theories are growing and

gaining more and more insight into the customer’s psyche”.

8. Sangeeta Aurora and Minakshi Maihotra (1997): In the paper entitled

“Customer Satisfaction A comparative analysis of public and private sector

banks”, analyzed the factors determining customer satisfaction They also

studied the level of satisfaction of customers and highlighted the marketing

strategies important for increasing the level of customer satisfaction The

sample of the study was selected from the cities of Amritsar, Ludhiana and

Chandigarh in India The sample consists of 100 public and 100 private sector

bank customers chosen randomly. The factor analytic technique was used to

determine factors representing satisfaction and dissatisfaction of public and

private sector bank customers The twenty variables with regard to different

32

aspects were employed for factor analysis The six factors identified for

determining satisfaction of public sector bank customers.They were routine

operations price situation, environment, technology and interactiveness In the

private sector bank customers the seven factors identified were staff, routine

operations, service, environment, interactiveness promotion and situation The

factor-wise average scores were calculated to measure the satisfaction level of

customers both in public and private banks The comparative result showed

that the public sector banks were lagging behind in all the areas The study

suggested that public sector bank has to adopt certain specific marketing

strategies to survive in the world of competition.

9. Thirumaran, R.M. (1998): Attempted to study the role of Co-operative

societies in mitigating the problem of housing in Chennai city A very brief

discussion on the Co-operative Society for housing like area of operation,

lending policy, growth in membership financial position, rate of interest

working results etc were studied The study suggested some ideas to improvise

the Co-operative societies in lending housing finance. The study has covered

the importance of housing, its components, housing shortage in urban and

rural areas, the role of Government, and the role of private and public sector in

housing He also discussed the problems of housing and housing finance in

India. The studies on housing finance covered the financial aspects like the

growth and financial performance of the housing finance companies in India.

In today’s housing finance market, due to severe competition, there is a need

for further research covering the marketing aspect of housing finance in India.

33

10. Nicholls, J.A.F. et.al, (1998): This paper develops a concise customer

satisfaction survey instrument to help organizations measure satisfaction with

their services. A seven – stage process was used to develop the instrument.

Following pilot studies, a preliminary instrument of 24 items was administered

to consumer of variety of business firms and government agencies providing

service to customers or clients. After further analysis, a revised instrument was

developed consisting of 18 statements. Additional analysis and further

purification led to an even more presise final version of the customer

satisfaction survey, employing nine statements in two factors; satisfaction with

the personal service (SatPers) and satisfaction with the service setting

(SatSett). Organizations could use the scale internally to identify their

strengths and weakness, as well as measuring their customer satisfaction.

11. Sidearm, N. (1998): Has argued that in an increasingly competitive world,

companies are finding that the recipe for success lies not in outmaneuvering

the customers and satisfying their every want.

12. “Customers familiarity and its effects on expectations, performance

perceptions and satisfaction A longitudinal study” is the title of the paper

where the authors Elisabeth Lundberg, Valerie Rzasnicki and Magnus

Soderlund (2000) examined the effects of customer familiarity on expectations

prior to the consumption of a service, performance perceptions after the

consumption and satisfaction of the customers Those who have traveled with

a particular tour operator from Sweden to Spain were selected as sample

respondents The customer familiarity was measured with regard to predictive

expectations and performance perceptions on personne’ The customer

34

satisfaction was measured with single question The correlation analysis used

in the study revealed that familiarity was associated with predictive

expectations The customer familiarity had a negative significant association

with performance perceptions as well as customer satisfaction The study

suggested that customer familiarity affected the post-purchase assessments of

the customers in terms of performance perceptions and their satisfaction.

13. Primal H. Vyas (2002): In his publication titled “Managing and measuring

consumers satisfaction” briefly conceptualized the review of consumer

satisfaction components of consumers satisfaction and dissatisfaction The

theories of consumers satisfaction process of consumers satisfaction and

dissatisfaction were highlighted He also gave suggestions about the

management of consumers satisfaction, methods of tracking and measuring

consumers satisfaction He has given valuable guidelines to use the

consumers’ satisfaction data and the effect of the price on consumers

satisfaction The study gave a brief idea about the models of consumers’

satisfaction The study finally gave some guidelines in measuring the

consumers’ satisfaction. This was evidenced by measuring the satisfaction of

consumers of housing finance, vehicle finance and in house consumer finance

in India.

The study was undertaken mainly to measure and evaluate consumers

current state of satisfaction or dissatisfaction from the conveniently drawn

sampling units The sample consists of consumers who have purchased

products like house. In home appliances and vehicles with the help of

consumer financing activities The study aimed at measuring the satisfaction

35

and dissatisfaction level of middle-income group consumers in Gujarat in

India The data was collected from 100 customers for housing finance and in-

home appliances each, and 120 for vehicle finance The hypotheses were

tested with the help of chi-square test The consumers of vehicle finance and

home appliances expected the detailed explanation about all the relevant

information But it not significant in housing finance The study also covered

the overall experience as a customer of consumer finance schemes consumers

satisfaction with the consumer finance agency product performance,

administrative facilities, and problems faced by consumers The post purchase

behavior of consumers was also studied.

14. “Satisfaction benchmarking and customer classification An application to the

branches of a banking organization” is the title of the paper in which

Grigoroudis. E, Politis. Y and Siskos. Y (2002) used the multi- criteria method

MUSA to measure and analyze customer satisfaction in different branches of a

banking organization The aim of this paper was to present a pilot customer-

satisfaction survey in the Cypriot private banking sector The customer

satisfaction survey consists of personnel image, service and access of the bank

The customer satisfaction evaluation was applied in different customer

segments in this particular application.

It has given that total banking customers did not appear homogenous

concerned to their preferences and expectations using cluster analysis The

results of the pilot survey indicated several extensions of the presented

application These extensions referred mostly to the installation of a

permanent customer-satisfaction barometer and the inclusion of competitors

36

performance in the customer satisfaction survey These results were also used

to benchmark these branches according to the provided services The

segmentation analysis was performed in order to identify the different groups

of customers The study also estimated the homogeneity of preferences in

distinct customer segments.

15. Ton Van der Wiele, Paul Boselie and Martijn Hesselink (2001): Focuses on

the analysis of empirical data on customer satisfaction and the relationship

with hard organizational performance data in the paper entitled “Empirical

evidence for the relation between customer satisfaction and business

performance?” The authors used a custome’ satisfaction database from Start

flex Company, one of major employment agencies in the Netherlands. Then it

related the customer satisfaction data gathered in 1998 with data on business

performance in 1998 and 1999. The customer satisfaction items used were the

satisfaction, complaints, overall satisfaction and the information about other

companies were collected. The measures of business performance were such

as sales volume, sales margin number of hours spent per customer and number

of placements per customer The data on customer satisfaction have been

analyzed through factor analysis in order to find the underlying concepts or

dimensions of customer satisfaction. The results showed a positive

relationship between customer satisfaction and organizational performance

indicators but the relationship was not strong.

37

16. Vidhyavadhi. K. (2002): In her paper entitled, “Role of urban housing finance

institution in Karnataka A Study of selected housing finance corporations in

Bangalore city” formulated the study in two different dimensions The first

dimension covered the evaluation of the performance of selected housing

finance corporations during 1989-99 This was evaluated in terms of various

business parameters as well as rations pertaining to profitability and efficiency

levels The second dimension attempted to measure the perception of the

borrowers about the housing loans provided by housing finance companies

The six housing finance institutions selected for the study were Housing

Development Finance Corporation Limited (HDFC). LIC Housing Finance

Corporation Limited, GIC Housing Finance Corporation Limited, Can Fin

Homes Limited, SBI Home Finance Limited and Dewan Housing Finance

Limited. The sample consists of 200 home loan borrowers through personal

interview method The annual reports and government reports were made used

for getting the financial ratios The statistical tools like chi-square test, ratios,

percentages rank correlation and averages were used for the study The study

concluded that the performance of HDFC was excellent and superior to other

housing finance companies The performance of Dewan Housing Finance Ltd

and Can Fin Homes was satisfactory But the performance of SBI was very

poor in terms of business parameters as well as profitability and efficiency

standards The second dimension concluded that the home loan borrowers

were influenced by the rate of interest speed of service, liquidity location,

advertisement, courtesy etc.

38

17. Vaishali DKK and Kumar, M.P. (2003): Studied five essential steps for

organizational transformation the first being leaders commitment, wherein,

change or cultural transformation begins with the personal transformation of

the leader. The next step was to scan the then culture, which would enable a

bank to analyze and evaluate the gap between the then and desired culture.

After this the employee personalities need to be profiled: therefore, the next

step proposed was personality profiling of the work force. It was then possible

to make the hiring decisions based on the quantitative assessment of the

compatibility between the candidate’s personality, values and behavior with

both the then and desired culture within the organization.

18. Sharma, R.D. and Gurjeet Kaur (2004 – 2005): Studied the nature and extent

of customer satisfaction in regional rural banks through customer opinion and

works out a strategic action plan. One regional rural bank from northern India,

viz., Shivali Kshetriya Gramin Bank, Hoshiarpur (Punjab) was selected to

work out the level of customer satisfaction in this bank measured with regard

to six Ps of bank marketing mix on 5-point Likert scale. Most commonly used

statistical tools viz., mean, factor analysis, multiple regression, multiple

correlation, coefficient of determination, were employed for analyzing the data

collected. Split – half reliability and convergent validity have also been

studied.

19. Parimal Vyas (2004): The empirical study based on descriptive research

design to measure customers’ satisfaction considering the prevalent state of IT

adoption among selected branches of sectoral banks. World over, the banking

sectors do face stiff competition not only among themselves, but also from a

39

host of other financial institutions. IT strategies therefore, need to be in proper

consonance with banks marketing strategies. Customers are now demanding,

individualistic and no longer willing to accept delay in transactions. A

customer centric view has replaced the earlier product centric view. IT is the

greatest equalizer. To the banks, it means changing the age-old style of

functioning and adopting innovative methods to serve their customers and

clients with utmost professionalism. The new age IT is bringing about

sweeping changes in the banking industry, forcing them to re-engineer many

of their basic processes and systems few of the technology driven electronic

banking services being offered are viz., ATM, ECS, EFT, Tele-banking,

Internet banking etc. the various sectoral banks are found as passing through

varying stages of IT adoption partly due to their different legacies and

strategic approaches towards computerization and technology adoption.

20. Chowdhary, (2004): This study is exploratory in nature, which was undertaken

to identify the constituent factors of service quality in banking industry. The

investigation is also focused at understanding the perceptual gaps amongst

stakeholders about service quality while comparing the employees and

customers of private and public sector banks respectively. Further he added

that bank’s customers’ service is followed by their demands for customization

and responses are to be shifted to their requirements by the frontline

personnel. Any service to be provided to the customer can be differentiated by

the service provider from the rest of the service providers, if it possesses some

unique selling proposition. In the banking services, the competition is

increasing every year with the dominance and popularity of foreign and

40

private banks. The present study is an attempt to identify the constituent

factors of service quality in private and public sector banks, in terms of the

perception of employees and customers separately. The inquiry will also

reveal gaps in the perceptions of employees and customers about the service

quality of private and public sector banks.

The multi-sampling approach was followed to collect data for the

study. In the first stage, a purposive sample of 40 judges was selected to

facilitate item selection for the measure developed for the measure developed

for the study. In the second stage, a sample of 30 respondents each was

selected on stratified random sampling basis to represent employees of private

and public sector banks respectively. Similarly, a sample of 45 respondents

each was selected on stratified random basis to represent the customers of

private and public sector banks respectively. Therefore, the study had a total

sample of 150 respondents in the second stage. The extraneous variables of

age, gender, education, marital status, occupation and area were controlled by

randomization and elimination.

21. Heryanto (2011): Discusses about the research are to know an influence of

service quality to customer satisfaction on Main Branch of Bank Nagari,

Padang. The population size amount 155.264 saving customer. The sample

size amount 100 saving customers. Collecting data through questionnaire with

using the accidental technique of random sampling. Data analysis techniques

have been used consisted of simple regression. The study shows that there was

an influence of service quality to customer satisfaction significantly. Service

quality are very important consisted easily in opening account, quick and on

41

the right time, to give the right service, commitment, staff available, polite,

campentency and capability, complaint solusion, customer attention, complete

facility, and staff performance. Meanwhile service quality are important

factors consisted of accurate, relax in taking compliance, customer need and

modern facility.

22. Uma Rani T.S (2011): States that change is the only constant factor in this

dynamic world and banking is not an exception. The changes staring in the

face of bankers relates to the fundamental way of banking-which is

undergoing rapid transformation in the world of today, in response to the

forces of completion productivity and efficiency of operations, reduced

operating margins better asset/liability management, risk management, any