7 redemption. Aero also granted Air Canada the ... - assets.kpmg

103

7 redemption. Aero also granted Air Canada the right to set off the Bills of Exchange against Aero payables if Aero failed to remedy its defaults. 23. On May 8, 2009, with Aero's consent, two Bills of Exchange were released from escrow and delivered to Air Canada to enable Air Canada to set-off the amounts payable under the Bills of Exchange against Air Canada's outstanding receivables from Aero. 24. In June of 2009, based on the declining volumes of consumption from the January Inventory Pool, Air Canada undertook an audit of the CAT 3 Inventory in the January Inventory Pool. Based on the results of the audit, Air Canada estimated that as much as US $40,000,000 of the CAT 3 Inventory in the January Purchase Pool would not be used by Air Canada within the period agreed to between the parties under the January Purchase Agreement and that the remaining January Inventory Pool was comprised of many spare parts that could not be used by Air Canada at all or would not be used for 24 months or so. Air Canada notified Aero of Aero's breach and demanded that the breach of warranty be remedied. 25. Aero acknowledged the breach and agreed to remedy the breach by replacing the non- conforming inventory with conforming inventory that Aero said it had on site in Canada. Aero agreed to pay Air Canada the difference between actual consumption and the average monthly consumption that would be necessary to meet the warranty requirements, namely US$8,500,000, if the new inventory was not delivered. 26. This became the basis for a Warranty Performance Agreement executed between the parties in October, 2009 (the "Warranty Performance Agreement"). Procedures were implemented immediately to begin to correct the composition of the January Inventory Pool. 27. As Aero's indebtedness to Air Canada increased throughout the summer of 2009, including indebtedness arising from its warranty performance obligations, Aero agreed, in August of 2009, to deliver three more Bills of Exchange into escrow and authorized Air Canada to set off the Bills of Exchange against its outstanding receivables from Aero. 28. Throughout the summer of 2009, negotiations continued between Air Canada and Aero with a view to settling their disputes and, in particular, agreeing on the terms and conditions

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 7 redemption. Aero also granted Air Canada the ... - assets.kpmg

7

redemption. Aero also granted Air Canada the right to set off the Bills of Exchange against Aero

payables if Aero failed to remedy its defaults.

23. On May 8, 2009, with Aero's consent, two Bills of Exchange were released from escrow

and delivered to Air Canada to enable Air Canada to set-off the amounts payable under the Bills

of Exchange against Air Canada's outstanding receivables from Aero.

24. In June of 2009, based on the declining volumes of consumption from the January

Inventory Pool, Air Canada undertook an audit of the CAT 3 Inventory in the January Inventory

Pool. Based on the results of the audit, Air Canada estimated that as much as US $40,000,000 of

the CAT 3 Inventory in the January Purchase Pool would not be used by Air Canada within the

period agreed to between the parties under the January Purchase Agreement and that the

remaining January Inventory Pool was comprised of many spare parts that could not be used by

Air Canada at all or would not be used for 24 months or so. Air Canada notified Aero of Aero's

breach and demanded that the breach of warranty be remedied.

25. Aero acknowledged the breach and agreed to remedy the breach by replacing the non-

conforming inventory with conforming inventory that Aero said it had on site in Canada. Aero

agreed to pay Air Canada the difference between actual consumption and the average monthly

consumption that would be necessary to meet the warranty requirements, namely US$8,500,000,

if the new inventory was not delivered.

26. This became the basis for a Warranty Performance Agreement executed between the

parties in October, 2009 (the "Warranty Performance Agreement"). Procedures were

implemented immediately to begin to correct the composition of the January Inventory Pool.

27. As Aero's indebtedness to Air Canada increased throughout the summer of 2009,

including indebtedness arising from its warranty performance obligations, Aero agreed, in

August of 2009, to deliver three more Bills of Exchange into escrow and authorized Air Canada

to set off the Bills of Exchange against its outstanding receivables from Aero.

28. Throughout the summer of 2009, negotiations continued between Air Canada and Aero

with a view to settling their disputes and, in particular, agreeing on the terms and conditions

8

under which Aero would exchange the Bills of Exchange that it held for the CAT 3 Inventory it

was purchasing from Air Canada or in payment of its warranty obligations.

29. Air Canada learned during this period that Aero PLC was showing a markedly improving

share price and, in October 2009, Aero PLC advised Air Canada that it was negotiating a major

equity issue and had applied for a listing on the senior board at the London Stock Exchange.

30. On October 9, 2009, a term sheet is agreed to between Air Canada and Aero providing

for the settlement of their disputes.

31. The settlement of the dispute between Air Canada and the Aero Companies involved

several key concessions by each of the parties:

(a) Air Canada would be bound to buy two Bills of Exchange and, except for

US$2,000,000 which would be used to set-off against Aero payables, the purchase

price would be paid to Aero; the discount rate in respect of the Bills of Exchange

to be purchased was fixed at 15%, generating proceeds of US$17,000,000 for

Aero;

(b) Aero would deliver to Air Canada the remaining Bills of Exchange in its

possession, except Bill of Exchange No. 10 which Aero would sell in a private

placement, generating additional cash proceeds;

(c) the discount rate for the five Bills of Exchange that had previously been delivered

to Air Canada, and which Air Canada had the right to set off against outstanding

Aero payables, would be fixed at 5%;

(d) to compensate Air Canada for the cost of capital relating to the foregone cash

payments under the January Purchase Agreement, the Holdback would be reduced

by US$4,000,000;

(e)

Air Canada agreed to purchase new CAT 3 Inventory from Aero, representing

new receivables for Aero in an aggregate amount of US$25,500,000 plus

applicable taxes, provided that the sales would be in instalments and that Air

9

Canada would have no obligation to pay for any instalment for at least 60 days;

and

(f)

the parties would memorialize and give effect to their agreement relating to

warranty performance in the Warranty Purchase Agreement.

32. The purpose of converting the Bills of Exchange maturing on February 8, 2010, into

obligations payable on demand was to accelerate Air Canada's indebtedness and to evidence the

discount rate negotiated and fixed by mutual agreement.

33. As part of the settlement transactions, the January Purchase Agreement, as amended, was

further amended by a Second Amending Agreement (the "Second January Agreement

Amendment"). The Second January Agreement Amendment reduced the Holdback under the

January 2009 Agreement from US$10,000,000 to US$6,000,000. This transaction compensated

Air Canada for the damages it suffered due to the loss of the cash flows that should have been

generated under the January Purchase Agreement.

34. The settlement transactions were concluded on October 23, 2009. Air Canada paid to or

to the order of Aero US$17,000,000 under the Demand Promissory Notes exchanged for Bills of

Exchange Nos. 8 and 9. Air Canada then set off the amounts owing under the Demand

Promissory Notes exchanged for Bills of Exchange Nos. 3-7 against amounts due and owing to

Air Canada as at September 30, 2009. After the conclusion of these transactions, the Aero

Companies continued to be net debtors to Air Canada for ongoing purchases of CAT 3 Inventory

from the January Purchase Pool and for warranty performance under the January Purchase

Agreement.

35. On October 23, 2009, the parties also entered into the Warranty Performance Agreement.

This agreement confirmed and extended the agreement already made and in force for the purpose

of remedying Aero's breach of warranty under the January Purchase Agreement.

36. Aero has defaulted in the performance of its obligations under the Line Maintenance

Agreement, the Warranty Performance Agreement and the October Purchase Agreement. Air

Canada has informed the Administrators that no payment would be made under the Line

Maintenance Agreement, the October Purchase Agreement or any other agreement between the

- 10 -

parties until the obligations owed by the Aero Companies to Air Canada have been discharged.

The Administrators have dismissed Aero's employees in Canada and refused to perform their

obligations, disrupting Air Canada's operations and causing it extensive damages.

37. Following the Recognition Order, the Administrators wrote to Air Canada, to inform Air

Canada that Aero did not consider itself to be bound by the Line Maintenance Agreement and

dictating new commercial terms for all transactions. Since the date of the Recognition Order,

Aero has failed to provide any of the services or support required under the Line Maintenance

Agreement, disrupting Air Canada's operations and causing it extensive damages.

38. Because Air Canada holds CAT 3 . Inventory purchased under the January Purchase

Agreement and the October Purchase Agreement, it has not needed to and has not purchased any

CAT 3 Inventory from Aero under the Line Maintenance Agreement since the date of the

Recognition Order. Air Canada has taken over the inventory procurement and management

functions that it had outsourced to Aero. The disruption of Air Canada's operations and the

increased costs are substantial, including a profound change in the implementation of Air

Canada's long-term strategic objectives to outsource the procurement and management of CAT 3

Inventory.

With respect to the relief sought in paragraph (c):

39. All material agreements between Air Canada and the Respondents are governed by the

law of Quebec. The January 2009 Purchase Agreement and the October 2009 Purchase

Agreement contain the following provisions:

"This Agreement shall be governed by and construed in accordance with the

laws of the Province of Quebec ahd the laws of Canada applicable therein. The

parties consent to the exclusive jurisdiction of the courts of the Province of

Quebec in connection with any civil action concerning any controversy, dispute

or claim arising out of or relating to this Agreement or the Transaction

Documents."

40. Section 40.19 of the Line Maintenance Agreement provides the parties choice regarding

both the law governing their relationship and the appropriate forum for resolving disputes:

9 z "Governing Law. This Agreement shall be governed by and construed in

accordance with the laws of the Province of Quebec and the federal laws of

Canada applicable therein, without regard to its choice of law principles. Subject

to the provisions for arbitration in Section 32.3, the courts of the province of

Quebec, judicial district of Montreal shall have exclusive jurisdiction in relation

to all Disputes."

General Provisions

41. Sections 9, 11, 21, 48 and 50 of the CCAA;

42. Section 97(3) of the BIA;

43. Rules 2.03 and 37 of the Rules of Civil Procedure, R.R.O. 1990, Reg. 194; and

44. Such further and other grounds as counsel may advise and this Flonourable Court may

permit.

THE FOLLOWING DOCUMENTARY EVIDENCE will be used at the hearing of

this motion:

1. The Affidavit of Alan Butterfield, solemnly declared and affirmed January 27 , 2010, and

the exhibits thereto ; and

2. Such further and other materials as counsel may advise and this Honourable Court may

permit.

- 12 -

January 27, 2010 HEENAN BLAIKIE LLP

2900 Bay Adelaide Centre 333 Bay Street Toronto, Ontario M5H 2T4

Kenneth D. Kraft, LSUC #31919P John Salmas, LSUC# 42336B Tel: 416.643.6822 / 416.360.3570 kkrafaheenan.ca / [email protected]

Fax: 416.360.8425

Montréal Office:

1250, boul. René-Levesque Ouest bureau 2500 Montréal, Québec H3B 4Y1

Keith D. Wilson, LSUC #37420A Tel: 514.846.2325 Fax: 514 846.3427 [email protected]

Solicitors for Air Canada

- 13 -

TO: OGILVY RENAULT LLP Suite 3800 Royal Bank Plaza, South Tower 270 Bay Street, P.O. Box 84 Toronto, Ontario M5J 2Z4

Orestes Pasparakis Tel: 416.216.4815 Fax: 416.216.3930 Email: [email protected]

Susan Rothfels Tel: 416.216.4033 Email: [email protected]

Fax: 416.216.3930

Canadian Counsel to the Applicants

AND TO: OSLER, HOSKIN & HARCOURT LLP P.O. Box 50 1 First Canadian Place Toronto, Ontario M5X 1B8

John A. MacDonald Tel:: 416 862-5672 Fax: 416 862-6666 Email: [email protected]

Canadian Counsel to Aveos Fleet Performance Services Inc.

AND TO : AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC 30 Lancaster Road New Barnet, Hertfordshire ENA 8AP United Kingdom

Paul Docker Tel: +44 (208)447.3372 - Fax: +44 (208) 447.3362 Email: [email protected]

Collin Trupp Tel: +61 4 0662.6670 Email: [email protected]

Respondents

- 14 - 9 5

AND TO :

AND TO :

KPMG INC. Suite 3300, 199 Bay Street Commerce Court West Toronto, Ontario M5L 1B2

Nicholas Brearton Tel: 1.416.777.3768 Fax: 1.416.777.3364 Email [email protected]

Information Officer

LLOYDS TSB COMMERCIAL FINANCE LIMITED Boston House, The Little Green Richmond, Surrey TW9 1QE United Kingdom

Jon Fenton-Jones Tel: +44 208 727 2023 Fax: 01295 702124 Fax: +44 208 332.7761 Email: j on. fenton-j ones@ltsbcf. co . uk

Commercial List No. 09-8456-00CL

IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF JAMES ROBERT TUCKER, RICHARD MIS AND ALLAN WATSON GRAHAM OF ICPMG LLP, AS JOINT ADMINISTRATORS

AND IN THE MATTER OF AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC

ONTARIO SUPERIOR COURT OF JUSTICE

(COMMERCIAL LIST) Proceeding commenced at Toronto

NOTICE OF MOTION

HEENAN BLAIKIE LLP 2900 Bay Adelaide Centre, 333 Bay Street Toronto, Ontario M5H 2T4

Kenneth D. Kraft, LSUC #31919P John Salmas, LSUC# 42336B

Tel: 416.643.6822 / 416.360.3570

[email protected] / [email protected]

Fax: 416.360.8425

Montréal Office:

1250, boul. René-Lévesque Ouest, bureau 2500 Montréal, Québec H3B 4Y1

Keith D. Wilson, LSUC #37420A Tel: 514.846.2325 Fax: 514 846.3427

Lawyers for Air Canada

1-IBdocs - 7594253v6

TAB 10

Court File No. 09-CL-8456-00CL

ONTARIO SUPERIOR COURT OF JUSTICE - COMMERCIAL LIST

IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF JAMES ROBERT TUCKER, RICHARD HEIS AND ALLAN WATSON GRAHAM OF KYMG LLP, AS JOINT ADMINISTRATORS

Applicants

AND IN THE MATTER OF AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC

Respondents

APPLICATION UNDER SECTIONS 46 AND FOLLOWING OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, C. C-36, AS AMENDED

SUPPLEMENTAL REPORT TO THE

REPORT OF THE INFORMATION OFFICER AND TRUSTEE IN BANKRUPTCY DATED FEBRUARY 4, 2010

FEBRUARY 9, 2010

cg

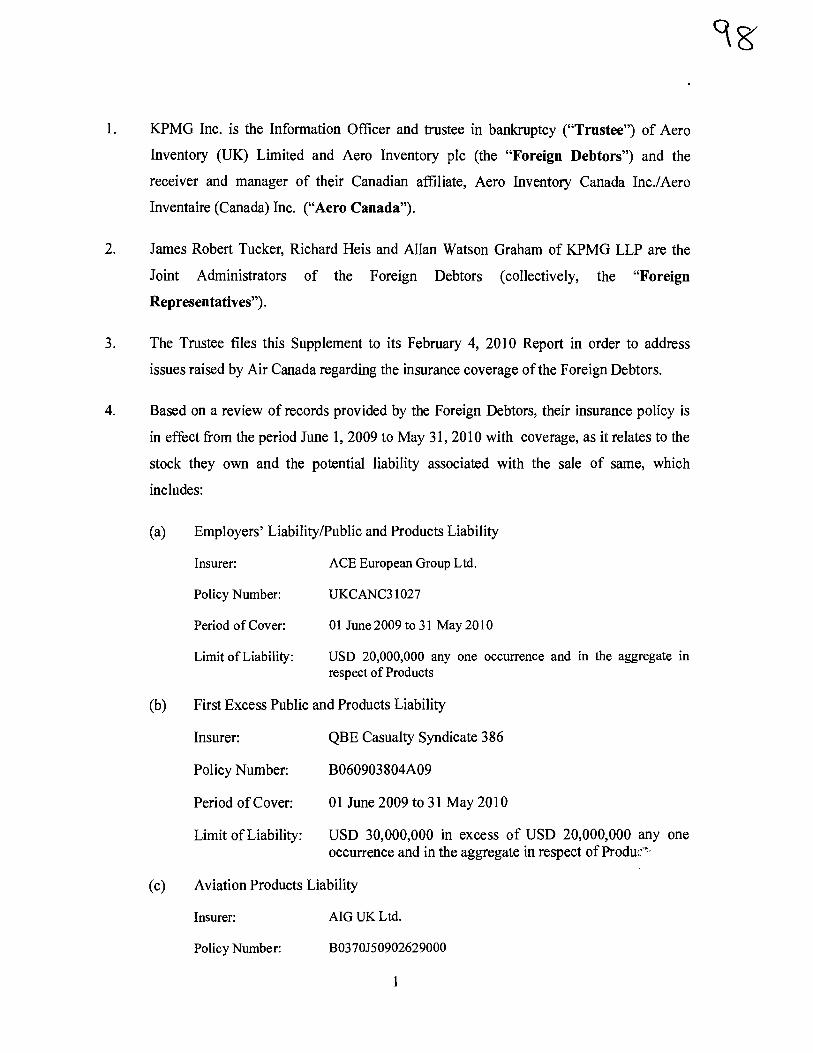

1. KPMG Inc. is the Information Officer and trustee in bankruptcy ("Trustee") of Aero

Inventory (UK) Limited and Aero Inventory plc (the "Foreign Debtors") and the

receiver and manager of their Canadian affiliate, Aero Inventory Canada Inc./Aero

Inventaire (Canada) Inc. ("Aero Canada").

2. James Robert Tucker, Richard Heis and Allan Watson Graham of KPMG LLP are the

Joint Administrators of the Foreign Debtors (collectively, the "Foreign

Representatives").

3. The Trustee files this Supplement to its February 4, 2010 Report in order to address

issues raised by Air Canada regarding the insurance coverage of the Foreign Debtors.

4. Based on a review of records provided by the Foreign Debtors, their insurance policy is

in effect from the period June 1, 2009 to May 31, 2010 with coverage, as it relates to the

stock they own and the potential liability associated with the sale of same, which

includes:

(a) Employers' Liability/Public and Products Liability

Insurer: ACE European Group Ltd.

Policy Number: UKCANC31027

Period of Cover: 01 June 2009 to 31 May 2010

Limit of Liability: USD 20,000,000 any one occurrence and in the aggregate in respect of Products

(b) First Excess Public and Products Liability

Insurer: QBE Casualty Syndicate 386

Policy Number: B060903804A09

Period of Cover: 01 June 2009 to 31 May 2010

Limit of Liability: USD 30,000,000 in excess of USD 20,000,000 any one occurrence and in the aggregate in respect of Produr

(c) Aviation Products Liability

Insurer: AIG UK Ltd.

Policy Number:

B0370J50902629000

oc s

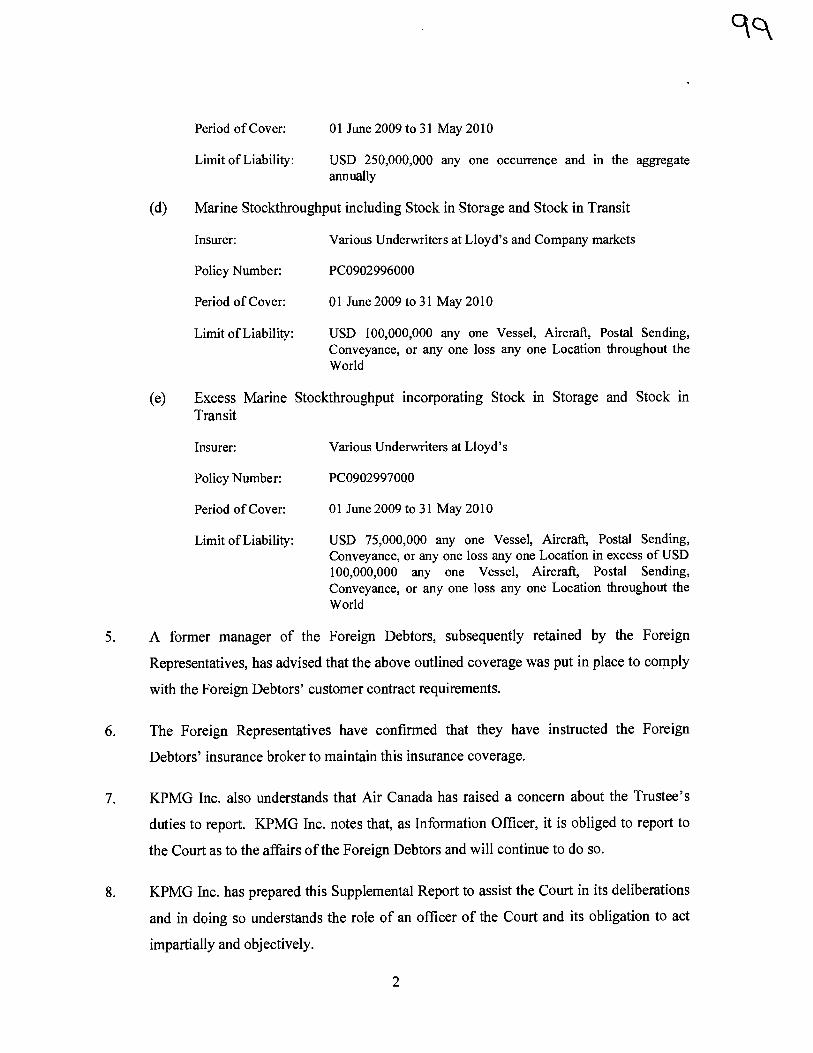

Period of Cover: 01 June 2009 to 31 May 2010

Limit of Liability: USD 250,000,000 any one occurrence and in the aggregate annually

(d) Marine Stockthroughput including Stock in Storage and Stock in Transit

Insurer: Various Underwriters at Lloyd's and Company markets

Policy Number: PC0902996000

Period of Cover: 01 June 2009 to 31 May 2010

Limit of Liability: USD 100,000,000 any one Vessel, Aircraft, Postal Sending, Conveyance, or any one loss any one Location throughout the World

(e) Excess Marine Stockthroughput incorporating Stock in Storage and Stock in Transit

Insurer: Various Underwriters at Lloyd's

Policy Number: PC0902997000

Period of Cover: 01 June 2009 to 31 May 2010

Limit of Liability: USD 75,000,000 any one Vessel, Aircraft, Postal Sending, Conveyance, or any one loss any one Location in excess of USD 100,000,000 any one Vessel, Aircraft, Postal Sending, Conveyance, or any one loss any one Location throughout the World

5. A former manager of the Foreign Debtors, subsequently retained by the Foreign

Representatives, has advised that the above outlined coverage was put in place to comply

with the Foreign Debtors' customer contract requirements.

6. The Foreign Representatives have confirmed that they have instructed the Foreign

Debtors' insurance broker to maintain this insurance coverage.

7. KPMG Inc. also understands that Air Canada has raised a concern about the Trustee's

duties to report. KPMG Inc. notes that, as Information Officer, it is obliged to report to

the Court as to the affairs of the Foreign Debtors and will continue to do so.

8. KPMG Inc. has prepared this Supplemental Report to assist the Court in its deliberations

and in doing so understands the role of an officer of the Court and its obligation to act

impartially and objectively.

2

All of which is respectfully submitted this 9 th day of February, 2010.

KPMG INC. INFORMATION OFFICER AND TRUSTEE OF THE ESTATES OF AERO INVENTORY (UK) LIMITED AND AERO INVENTORY PLC

Per: Nicholas Brearton Senior Vice President

1

TAB 11

[Transcribed]

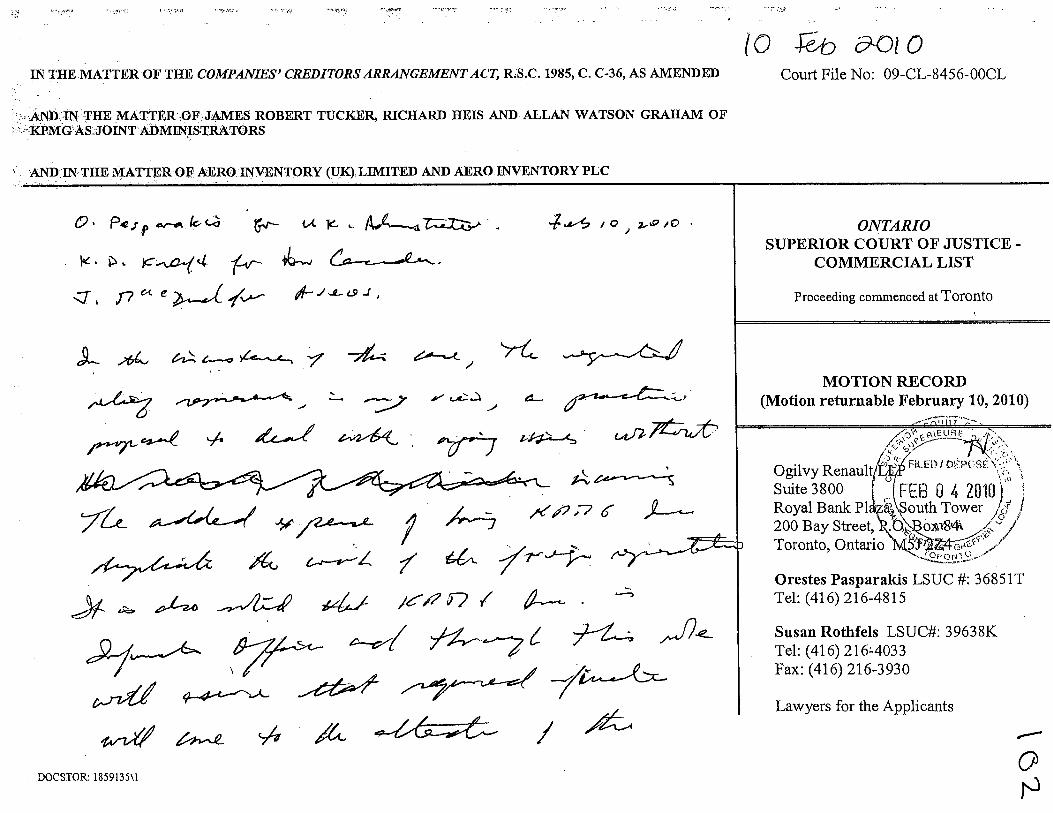

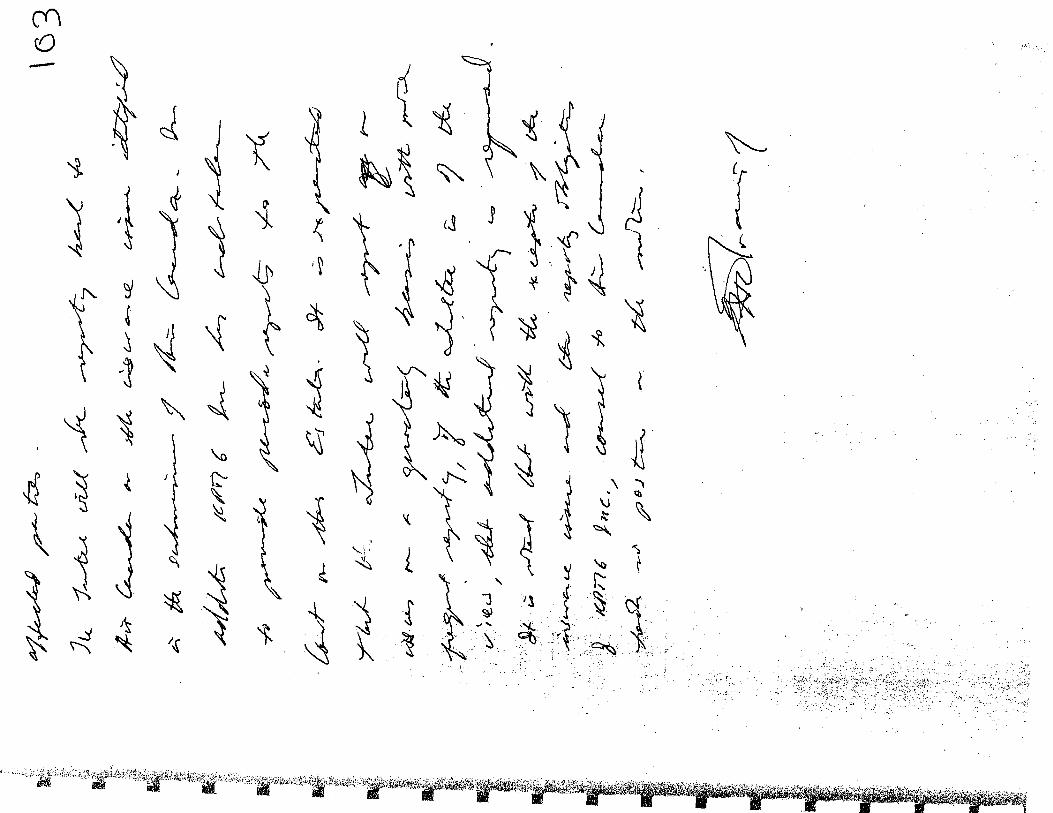

10 Feb 2010

0. Pasparakis for U.K. Administrator

K.D. Kraft for Air Canada

J. MacDonald for Aveos

In the circumstances of this case, the requested relief represents, in my view, a practical proposal to deal with ongoing issues without incurring the added expense of having KPMG Inc. duplicate the work of the foreign representatives. It is also noted that KPMG Inc. is Information Officer and through this role will ensure that required information will come to the attention of the affected parties.

The Trustee will be reporting back to Air Canada on the insurance issue identified in submissions of Air Canada. In addition, KPMG Inc. has undertaken t. provide periodic reports to the Court on the Estates. It is expected that the Trustee will report on issues on a quarterly basis with more frequent reporting, if the Trustee is of the view, that additional reporting is required. It is noted that with the exception of the insurance issue and the reporting obligations of KPMG Inc., counsel to Air Canada took no position in the motion.

"Morawetz J."

Av' •

7&Pu/t.".'

MOTION RECORD (Motion returnable February 10, 2010)

AL:

Ogilvy Renault \ FED 0 4 2010) ; Suite 3800-

Royal Bank PI VSouth Tower i d i

200 Bay Street, ‘g.CIA: oxi8/4k Toronto, Ontario

Orestes Pasparakis LSUC #: 36851T Tel: (416) 216-4815

Susan Rothfels LSUC#: 39638K Tel: (416) 2164033 Fax: (416) 216-3930

•

0 -re:40 o IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, RS.C. 1985, C. C-36, AS AMENDED Court File No: 09-CL-8456-00CL

AND- IN THE MATTER OF , JAMES ROBERT TUCKER, RICHARD HEIS AND ALLAN WATSON GRAHAM OF - KPNIG-AS JOINT'ADMINISTRATORS

AND1N THE MATTER'OF AERO INVENTORY (UK): LIMITED AND AERO INVENTORY PLC

o • P (K) tA 4 / 0 2,0 / 0 • ONTARIO SUPERIOR COURT OF JUSTICE -

COMMERCIAL LIST

Proceeding commenced at Toronto a f ,

.Av.„ -744

„(70, /e_ •-7

e

6-4----"Z 1(yt

2444j- .

,6';3t

./27je-

Lawyers for the Applicants

.tv-fret, ‘,4 jet,

DOCSTOR: 1859135 \1

C() 0

TAB 12

JUGDES ADMIX IX4- 170 .4.15 41 7 P,002A10.7. OLt

CITATION: Tucker v, Acts InVeritory (14K) Limited, 2010 ,ONSC 1196 COURT rat NO.: 09-CL-8456-00CL .

DATE: 20100224

SUPERIOR COURT OF "JUSTICE —

(COMMERC*LIJST)

IN 'PMMAuiiR OF TO iiRgr Tata:TORS litkiNOE ;€47 ACT, R.S.C. A* 0. ,c::30; ,AS AMENDED.

THE MAER OP JAMES- ROBERT TUCKER, tleflA0 - 11EIS - AND ALAN W.4003,1 ORAtiAbil Ok K1)..MG AS: ItiiNT APMJNI$TRATOR&I,A011OWs

AND ix mE• MATTER OF AEROINVENTORY ) LIMITED AERO INVENTORY FILC„ Respondents

11EPORE: MORAWETZ

COUNSEL: Dena:ck Tay ena Susan RI:Alders, Tor:the Applicants

Kenneth"). Xraft and John Salmas, fer.Air Can,acla

John MacDonald, fzsr Avcos Fleet Performance Inc.

mwsi.

kEttAgED:. JANow 2z zoo

ENDORSEMENT

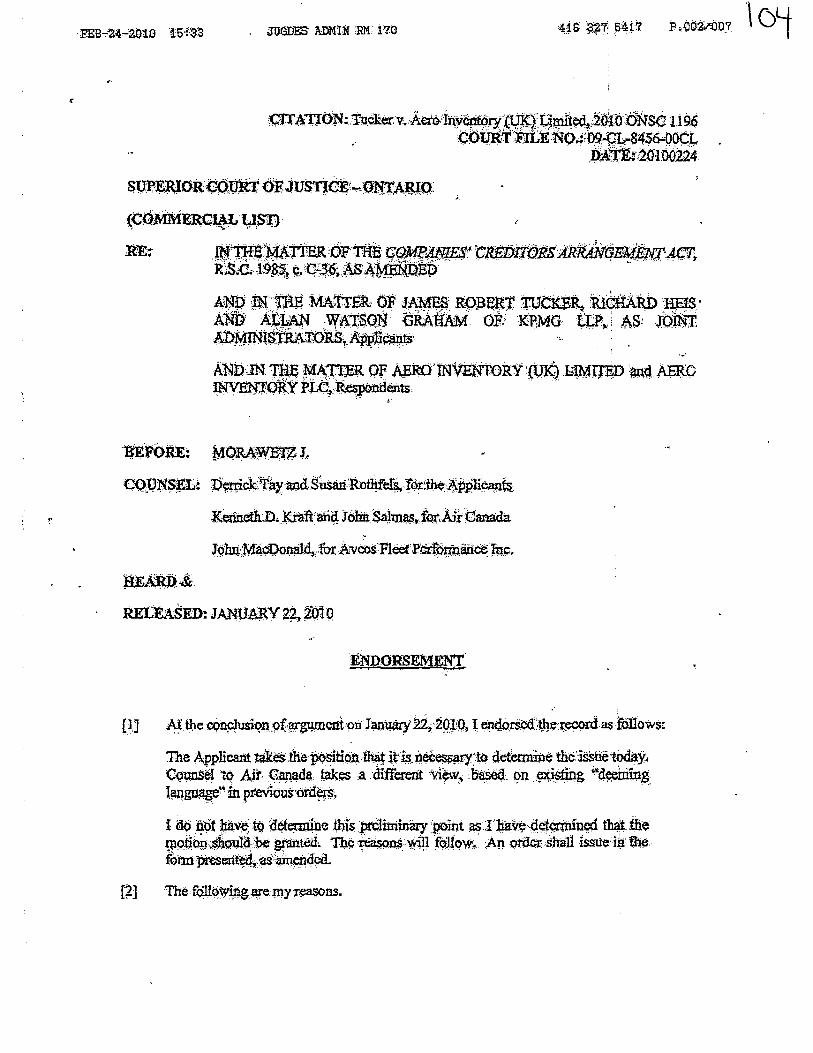

At the conclusion cf. opulent on January 22,•2010, I endorsed the recond 4 follows:

The Applicant tikes the poSition Slat it is necessary to determine the issue todaSt.. Counsel tq Air Canada takes a different View, based on existing "deeining language"in previousordem

I do not have tp determine this preliminary point as I haVe determined that the motion.shonlabe granted. The 'reasons will follow.. An order shall issue in the fvrm prtserted, asamendcd.

[21

The following are my reasons "

44- 6 327 47 \ P 303'007 5 FEB-2-2010 .15 It3 queDEs =ITN .RM 170

[3] The APPlicantsbrouglit this motion for an order lifting the stay granted in the initial order dated November j I, 2009 in these -proceedings and granting leave to John Robit. T Richard Heis and' Allan Watson -Graham of KPMG LLP (the "Foreign Represcniativess) -to an Assignment-in Banlcruptcy in Toronto for Aero Inventory (UK) Limited and Aero Inventory plc (both in Administration and, collectively, the "Foreign Debtors"), and restoring the stay thereafter.

[4] •The motion was opposed by Air Canada.

M. On NoVenibef I I* 20091 this PZnitt T .ecognited '.the Appointment of the- 1Apolitaho as Foreign R sentatjves of Acre! IPventgrilIptIlithitod vA11-40d.Aero Inventóry.plc (be*in-administration, and toilectively, the "fOrtign DebtO01, Under Part IV of the Cthiglithiee Creditef&All - ketOpitAct("cCAA"),(thellecognitiOn:C ,rderu):

In order tO fadilitate a preferenee attion under the .1J'enzretyptc-;,' and kz. 7.61-vCncl Act (131.A")? the Foreign Representatives teguire (a) &date br an initial bankl-optcy eye* and .:(17). a trnstee in bankruptcy.

[71 The Foreign Representatives bring this. motion for an order to temparari& lift the stay granted in the Recogfiltion Order and Zrleaveto assign thaToreign Debtort into'h,anicTIAPteY-

[8] The 'Foreign DebtOtS and tipitinterna,tiOnifi affiliates i,ineludinz Aero Invittory Canada 41cAeeq ,TA*0):144P- (canada)-.Ine;„.0ieso Cariadal; fOrny an intogi*ii4 and intcr,deperident group)SfeoMpanieS thatttipplY,parls*IbqArlit4.i44144S,

[9) ''The Fotago potoEs. , hnve a.ssets, Cana.* and then, canadfan 4e -rations tte . . , adininlitered by Agii Canada_ They itav61-00 key'Canadian,.4407ners: Air Canadarand Aveos Fleet PerformanceInc. eAyocin pn. October23, 2009 , Ai ana Air Canada entet4intoa.series of cOntracts inehiding;ngreeMents providingfetthe exeliange of n.teriek of bills of 40.1:awe; .40t-off agreements and a purchase ;64-saie.agreement *ithrespeetto ix•rtain inventory .

ROI On NpircalbOr 11, griOst, administration prodeeding§ (the "FAreiga _za") were eplquicnced:bythetbreign kireseOtatiVesJil r4gitti4a0.)4..OrtheToreign-Do3bbsktilb High C,eurt. of Jp$tioi-q',..,,tagle0d And Wales (Chancery - Divis. ION ck.anparadt Co*t) 'the "'grtgli§h C0147'att.d. the FOreiga ktpreSetitaiiVesr ;werela000#4* i0i4i,,a0initisirator$. Of the- affairs i business .and property -Of the .FOreign Debtors (Sometimes referred to the; "IJK Court Administrafere.),

1111 OnNovenbeill2 200g,'Ne*I7olial. gratitcd a Recognition Order, inter

(a) recOglilingOrderamade onNovember 14 2009 bythe Engush.rcont

(h) recognizing thc Foreign Pmceedings as "foreign mait. prt)ceediage• putsuant to s. 47 of the CCAA;

(c) recognizing-the Foreign Representatives as "foreign remsentatives" as defined in s. 45 of the CCAA;

Ytui--2472010 ZUGDE$ ADKOT-RN 170

41g 501 P;004/007 (0

- Page 3 -

(d) staying all prOcepdings,ip respect of the Foreign Debtors, the Foreign Represent2itives or theirbusiness or property; and

fej noobiting KPMG 1nc as Information.Officer in these prOceedings.

[1Z1 On December 1,-2009i..This court...Made an older appointing gaiNid inc:t.t.*;;ivet and managct;Ovet Aeros, Canada purstient.th-s.. 49 of the C-CAA and s 101 .,-of the rpzirts cf.hgtice, Ada.

1133 icemc 1n orted,that is.sues e arisen with Air Canadgs copcierning the status 01 it§ relationship vyith the Foreign Debtors inehiding the effect of the October 23, 2009 tranSadionS.

[14] Qn Janua#1,.201A -Cunmaing,1 made Mi Order:

_(a) op the consent of Air Canada, al It re, ates to Air Canada, deeming -the date of the FOreign Debtora'"ipithil bankruptcy eVentyilit liappered after3anuary, 2010 to have occurred ortianuary g;„2910 •

(h) se4et_laliAg a-00341:.a4e1,1dane9 for February 1„, 2010 and providing that the Foreign Representatives. Coulct attend earlier ta .file a banlcuptcy apPlicatio%i if 'teen to be neeeSSary,

' 05] The 'Foreign: Representatives viiskto -ascign the Foreign pebtors into bankruptcy:for the pwpose of preserving- theAr Yight to poriue any reviewable AranSactioni; ,Settlenients and prefetenet§ Ortridervaluetransiction which May taken place-dtring the statutory review' peried pres.P.ibed toy tc BIA •

[IQ Counsel . ..thó:i è tbde±eda§ whether it i§ appropriate for the court to Ii the stay io4 spitt woo to, tho Fereign Representativ0 tO 0 -§itt • t4e..Foreigo -Obbtoit intobanlcasptey„

1 1 71TheForeigu Rep .resentatives arc officers -appointed by the Ctç:inaiiage th -managd . _ ForeigoDebtorst affairs, butiness and property.

E13:1 lalthiS:eites,:tlierc-1.$11910,ing concenilantinets-and it appears that the seoored will suffer a shortfall!. 'Conniel to ow Fereign Representatives submits that the Statutory obligation of theUK Pk* AdMinistrators. in these ciretanstandeS is to MaxiMiZelecoveries ler the secured. Creditors and that the UK Court Administrators have the statutbry'role lof Managing the :Foreign Debtors for the purpOse of realizing property in Order to Make diStributions to secured Creditors. Further, counsel ..subtnits that ss 1 of the UK insotyen97 Act, vvhichissexptessly incorporated into the Etigii§h court ,-,tat4cr. recognized by this Court, set.S. oot _ . _ specre pOWers'including;the poWer to bring legal prinecedingS:in.the 4dministratOr's name:and op behalf Of-the Foreign Dtbtotsi : inehgling the ..power to wind,up debtor companies ina otaot relief

1191 The UK Court Administrators have been 'recognized as Foreign Representatives in. the Recognition Order: 'This court has already recoplized the UK Court Administrators' authority in

FEB-24-2010 15:34 aiGDES MI 170

416 5417 P.P.0611;e07\

P4e4

Canada and as offleers of the court to act as agent of the Fcreiga Debtors and/or brmg legal proceedings on -their behalf

[20) Coupsel to tile foreign:Representatives firtheriOrnits that:the IIKtourtAdminiStrators, vagent7 ofthe Pordivy'DebtorS, have the. autherity to bring proceedinp ,on their behal.f nnd sgs

'agent" Of the lereign Debtors have the ability:Undeie* 49 of 0413410 it*ke-na. assigrageniin bankruptcy.

Dij POPTIsel als0-zeferenceg' parar0 Of AO git-P0117.0.11: , w41:41 .410 satiits specifically contemplateS bankrnp patOci be initiated by The.; Coirt_Adininistratem

"Nothing in tlus order ishail. prevent the Foreign Representatives or the, Information bfficer Tim:4 icting as a trustee lit: haniUlipiey of -thegFordign :Mt*"

[22) Part IV (Idle CCAA addrestiesissna5,telating to pross=bordcr insolvendei and the eoUrt is given broad statutory discre6on in PartW and,in parikular, 4,49(1 ).:

If an order recogaizin' g a foreip Proceedift is lua4e, the allot maY, on applicati= by the foreign rvresentative who . applied for the order, ifthe aourt is satisfiedThat it is necessary foLthe protect:len 'of ihe dOloes c,oPipaniCs' PioPertY or the intereSts of -a creditor , or creditor, make any order that . it Considers aPPTPPtiate-..

[23] Tho purpose of Part IV Of the CCAA is fp promote cooperation between -41M dourta-anill other tompetent authoritieiinCanada with these of foreigajutiidictionaig et* of cross-hOrder insolvencies..:". See s. ,44-(a) CCAA.

1241 Counsel th theToreignilepresentatives submits that Part IV of the CCAA proVides naPchanism bY which the, tanadian court coordinates with forcizn CoUrts and,. fdrther, that the CCAA expressly conteraplatcs that Ishkrre cakbe;gowigxent :Canadian and foreigrriproccedings. Further, counsel to the Foreign Titoresentatives -submits that Tarfly is arSo cleat in that those Canadian insolvency proccedinp cnn inch* a BIA filing. S action 48 addresses recegnition of

-

a foreign main prnececling. Section. 48(4),reads:

"Iqo ' g in subsection -(1) precludes the,dehtor cornpany frora commenting or continuing:proceedings under thts 4c4 the Baida720,01: aildinoolvency Act or the Winding-up ipzd RestructuritigActin respect-of a debtor -tompany2i'

125] Since Part IV of the CCAA specifically contemplates a bankruptcy preceeding continuing during a Part Wproceedinz, counsel submits there cEuLbe noinconsiateneyin hayin both proceedings concurrently.

'26] Further, counSel submits that the coordination of Canadian insolvency proceedings with Foreign Proceedings was recoyi-led by Newbould J. at paragraph 15 of-the Recognition Order referred at [21] above

FEB-24-2010 i5 :26 JUGDES ADM I II RM AIS• 221 ,5417 P. Op 5/.0t717 aa

- Page 5—

[77] JustiCe turtmaingalS6 acknoWledged that a fl g Of•a -liankiliptey , iibation -could be Made before ,February 24.)11) If seen tO be nteess , as .re.fereneed fl4iAbdve:

[28] Counsel to 4ip canada,S‘Mitsthat the order of ',the 'English Court, which i the subjecx of .the Redognition, Opcier,-; shotild not be 'interpret -0d to include the ability of the- Petelko kepresehtatiske to 'fliiikelhe ass4mient. in the circulated= of thicise.,,i diSagreefat reasons sotOlit below.

fp] CCtunselJO ,Airtanada alSO:taiSed the;:ettreStibn.as :toliow bankruptcY isnSiitcgt with the-Nit IV stOte"Obn, lt%Se.ems: to me that Part N. conterriP14$4110 pogsibilitST-of 'Concurrent prOceedings inyolifing the 111A. E#rtheii, 41,0, *bititiity of moth:tent /3IK ptoCer;ding$ Was ctmttmplated,hytheprties*ltis reffeeted the ofitlefe:alitA .NokoVj.,:ard"....Commiagi,

_circunts.tanccs of this ease, tbe 104 of the SIAm ooncutrett :pkidetalgslo patt w is tonsistat with Con4oviiiiiikpoRcy. The preposed actionsofthc1JK Court*dininistratorS inkingtelinyoke Canadian iiankruptCy prOCccclings.10 t4e-ailitantaggettn**Piettft#00; proviSions ate fOz= the purpose of i/ix6rni4in& the b6bto-te proposed *di:0PS of the UK Administrators Ore 40:00 *bat a uedifor reptts4ittitip, *oula undertake it tina4k.

pn counSel to Air Canada were try bc succes,sfurin Opposing theJelief so theffci may-very well be that a transaction that Triay be prefurential in nature may escag review by a ereclitox rVreSentative. Snell an outcome ivould,belleonSistentivith Canadian' rilblie Policy , It seems to me that, in the circumstances Of thit - caSe, the &reign tepresentaave AO:0d, have the abliity tochallenge the traasaCtion under Canadian bankruptcy Iei*:;

[32] In my view, theitaerpretation urged by counsei.to Air Cana6 is =dilly reStdctive mth circumstance& The language of gip Q.C.AA is permissive. There is -rio going cor*En operatiOn. The stated purpose of the assignment is o engage in a ;'emiew .of a potential preference transaction and the only objection is being raised by ilk _party that is ;likely the sbjet of the -review,

P3] l am in.agreein.exit with ap submissions made by-connsei to Foreign Representative.

(341 the UK Conn AdmiriStritors see 1.5 to set aside-contracts gOvelrnOl by C,.44dian law and affecting assets in Canada. It is not necessary to deterMina tbe.appropriatenag or tlio remedy today nor to assess the various defences that May be available to:the responding party.. Rather, this court needs only to ensure that the UK Court Administrators ad consistently' with ?art IV and theirstatntory obligation to maximize the debtors* estate&

[35) in my view, in -the furtherance of these objectives,, it is appropriate fbr ,this court to exercise its discretion to -lift the stay to permit the bankruptcy Min&

MOMWETZ

FEB-24-20,10 15:15 MODES ADmuf RN 17.0 416 5417 P . 007/001 CCk

Pagefi

An._o_id0 -has bi* giv:e1T7d6k. to the foregov-rezigolik.

itatv-febttiag24_4_20,19 .

TOTAL P . Q07

TAB 13

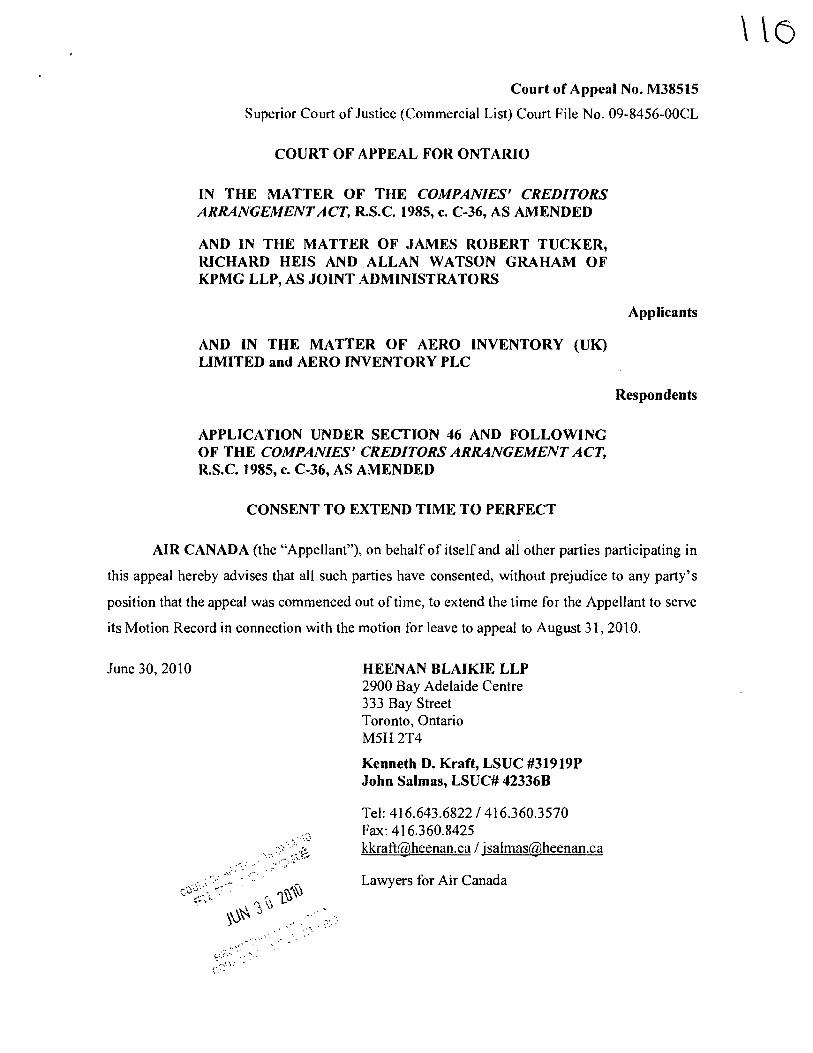

Court of Appeal No. M38515

Superior Court of Justice (Commercial List) Court File No. 09-8456-00CL

COURT OF APPEAL FOR ONTARIO

IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF JAMES ROBERT TUCKER, RICHARD HEIS AND ALLAN WATSON GRAHAM OF KPMG LLP, AS JOINT ADMINISTRATORS

Applicants

AND IN THE MATTER OF AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC

Respondents

APPLICATION UNDER SECTION 46 AND FOLLOWING OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

CONSENT TO EXTEND TIME TO PERFECT

AIR CANADA (the "Appellant"), on behalf of itself and all. other parties participating in

this appeal hereby advises that all such parties have consented, without prejudice to any party's

position that the appeal was commenced out of time, to extend the time for the Appellant to serve

its Motion Record in connection with the motion for leave to appeal to August 31, 2010.

June 30, 2010 HEENAN BLAIKIE LLP 2900 Bay Adelaide Centre 333 Bay Street Toronto, Ontario M5H 2T4

Kenneth D. Kraft, LSUC #31919P John Salmas, LSUC# 42336B

Tel: 416.643.6822 / 416.360.3570 Fax: 416.360.8425 [email protected] / [email protected]

Lawyers for Air Canada

TO: OGILVY RENAULT LLP Suite 3800 Royal Bank Plaza, South Tower 270 Bay Street, P.O. Box 84 Toronto, Ontario M5.1 2Z4

Orestes Pasparakis Tel: 416.216.4815 Email: opasparakisRogilvyrenault.com

Virginie Gauthier Tel: 416.216.4853 Email: [email protected]

Fax: 416.216.3930

Canadian Counsel to the Applicants and KPMG Inc.

AND TO: OSLER, HOSKIN & HARCOURT LLP P.O. Box 50 1 First Canadian Place Toronto, Ontario M5X 1B8

John A. MacDonald Tel:: 416 862-5672 Fax: 416 862-6666 Email: j m acdonaldQosler.com

Canadian Counsel to Aveos Fleet Performance Services Inc.

I ea - 3 -

THE UNDERSIGNED PARTIES, by their solicitors hereby consent, without prejudice

to any party's position that the appeal was commenced out of time, to an extension of time for

Air Canada to tile a Motion Record in connection with the motion for leave to appeal in this

matter to August 31,2010, or such further date as the parties may agree.

June , 2010 APPLICANTS and KPMG INC., by its solicitors, Ogilvy Renault LLP

/Per: ,;; 7 ,

Name: Orestes Pasparakis / Virginie Gauthier

June 0 , 2010 AVEOS FLEET PERFORMANCE SERVICES INC., by its solicitors, Osler, Hoskin & Harcourt LLP

Per: I) P.- 95; Name: John. A. MacDonald

Court of Appeal File No. M38515

Commercial List No. 09-8456-00CL

IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

AND IN THE MATTER OF JAMES ROBERT TUCKER, RICHARD HEIS AND ALLAN WATSON GRAHAM OF KPMG LLP, AS JOINT ADMINISTRATORS

AND IN THE MATTER OF AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC

COURT OF APPEAL FOR ONTARIO Proceeding commenced at Toronto

CONSENT TO EXTEND TIME TO PERFECT

HEENAN BLAIKIE LLP 2900 Bay Adelaide Centre 333 Bay Street Toronto, Ontario M5H 2T4

Kenneth D. Kraft, LSUC #31919P John Sattnas, LSUC# 42336B

Tel: 416.643.6822 / 416.360.3570

[email protected] / jsalmasheenan.ea

Fax: 416.360.8425

Lawyers for Air Canada

HBdocs - 8221127v6

TAB 14

C VS/ Cameron MeKenna

All Parties on the Service List

Your Ref. Our Ref NEJA/M1T2.62a

CMS Cameron mcKenna LIP

Mitre House 160 Aldersgate Street London EC1A 4DD

Tel +44(0)20 7367 3000 Fax+44(0)20 7367 2000 www.cms-cmck.com DX 135316 BARBICAN 2

Tel +44(0) 207 3667 3118 [email protected]

30 September 2010

Dear Sirs/Mesdames

Ontario Superior Court, File No. 09-CL-8456-00CL

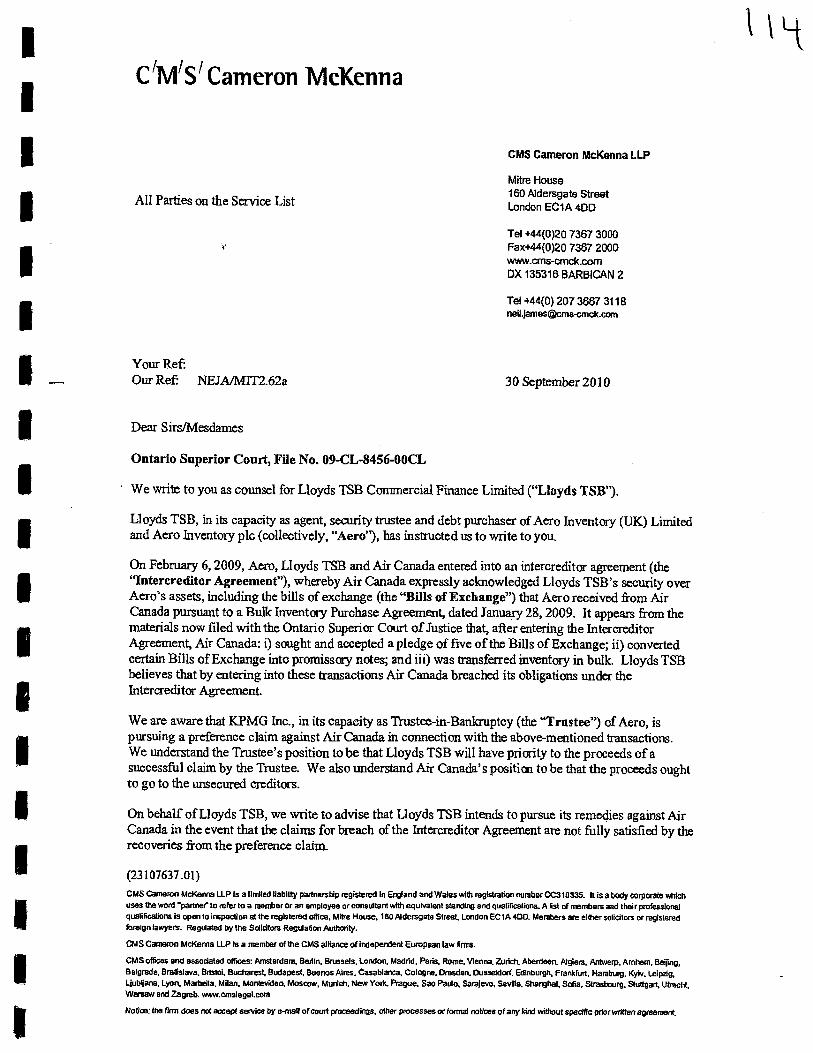

' We write to you as counsel for Lloyds TSB Commercial Finance Limited ("Lloyds TSB").

Lloyds TSB, in its capacity as agent, security trustee and debt purchaser of Aero Inventory (UK) Limited and Aero Inventory plc (collectively, "Aero"), has instructed us to write to you.

On February 6, 2009, Aero, Lloyds TSB and Air Canada entered into an intercreditor agreement (the "Intercreditor Agreement"), whereby Air Canada expressly acknowledged Lloyds TSB's security over Aero's assets, including the bills of exchange (the "Bills of Exchange") that Acro received from Air Canada pursuant to a Bulk Inventory Purchase Agreement, dated January 28, 2009. It appears from the materials now filed with the Ontario Superior Court of Justice that, after entering the Intercreditor Agreement, Air Canada: i) sought and accepted a pledge of five of the Bills of Exchange; ii) converted certain Bills of Exchange into promissory notes; and iii) was transferred inventory in bulk. Lloyds TSB believes that by entering into these transactions Air Canada breached its obligations under the Intercreditor Agreement.

We are aware that KPMG Inc., in its capacity as Trustee-in-Bankruptcy (the "Trustee") of Aero, is pursuing a preference claim against Air Canada in connection with the above-mentioned transactions. We understand the Trustee's position to be that Lloyds TSB will have priority to the proceeds of a successful claim by the Trustee. We also understand Air Canada's position to be that the proceeds ought to go to the unsecured creditors.

On behalf of Lloyds TSB, we write to advise that Lloyds TSB intends to pursue its remedies against Air Canada in the event that the claims for breach of the Intercreditor Agreement are not fully satisfied by the recoveries from the preference claim.

(23107637.01) CMS Cameron McKenna LLP Is a limited liability partnership registered In England and Wales with registration number 0C310335. It is a body corporate which uses the word "partner to refer to a member or an employee or consultant with equivalent standing and qualifications. A list of members and their professional qualificabons is open to inspection at the registered office, Mitre House, 160 Aldersgate Street, London EC1A 400. Members are either solicitors or registered foreign lawyers. Regulated by the Sdicitors Regulation Authority.

CMS Cameron McKenna LLP is a member of the CMS alliance of independent European law firms.

CMS offices end associated offices: Amsterdam, Berlin. Brussels. London, Madrid, Paris, Rome, Vienna, Zurich. Aberdeen, Algiers, Antwerp, Arnhem, Beijing, Belgrade. Bratislava. Bristol, Bucharest, Budapest, Buenos Aires. Casablanca, Cologne. Dresden, Dusseldorf. Edinburgh, Frankfurt, Hamburg, Kyiv. Leipirg, Ljubljana, Lyon. Marbella, Milan. Montevideo, Moscow, Munich. New York. Prague, Sao Paulo, Sarajevo, Seville, Shanghai, Sofia, Strasbourg, Stuttgart, Utrecht, Wasaw and Zagreb. ,,wow.cmslegaicom

Notice: the rum does not accept service by e-mail of court proceedings, other processes or formal notices of any kinl without specific prlorwrittenagreemert

H 5

C /M /S / Cameron iVicKenna

This letter is without prejudice to or waiver of any rights or remedies of Lloyds TSB against Air Canada.

Yours faithfully

cms cetAkeltr Nr\cKpAr\lkc

CMS Cameron'UcKenna LLP

2 (23107637.01)

TAB 15

Court File No. 09-8456-00CL

ONTARIO SUPERIOR COURT OF JUSTICE

(COMMERCIAL LIST)

IN THE MATTER OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED AND IN THE MATTER OF JAMES ROBERT TUCKER, RICHARD HEIS AND ALLAN WATSON GRAHAM OF KPMG LLP, AS JOINT ADMINISTRATORS

Applicants

AND IN THE MATTER OF AERO INVENTORY (UK) LIMITED and AERO INVENTORY PLC

Respondents

APPLICATION UNDER SECTION 46 AND FOLLOWING OF THE COMPANIES' CREDITORS ARRANGEMENT ACT, R.S.C. 1985, c. C-36, AS AMENDED

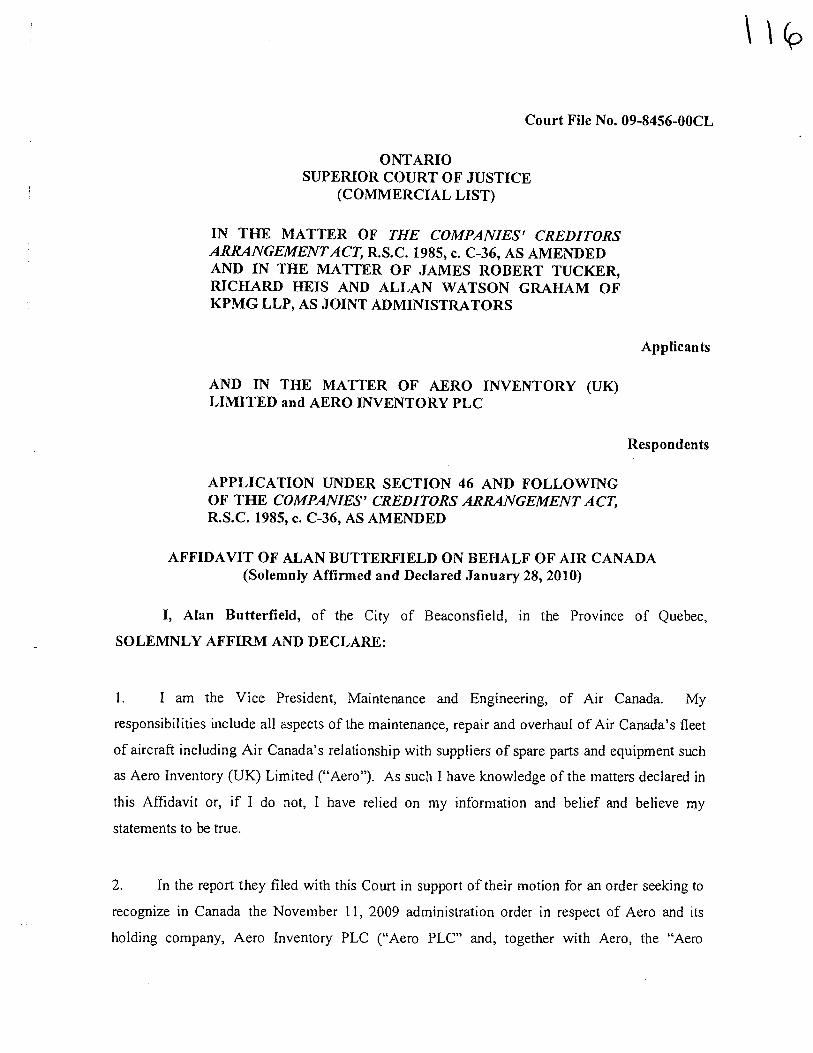

AFFIDAVIT OF ALAN BUTTERFIELD ON BEHALF OF AIR CANADA (Solemnly Affirmed and Declared January 28, 2010)

I, Alan Butterfield, of the City of Beaconsfield, in the Province of Quebec,

SOLEMNLY AFFIRM AND DECLARE:

1. I am the Vice President, Maintenance and Engineering, of Air Canada. My

responsibilities include all aspects of the maintenance, repair and overhaul of Air Canada's fleet

of aircraft including Air Canada's relationship with suppliers of spare parts and equipment such

as Aero Inventory (UK) Limited ("Aero"). As such I have knowledge of the matters declared in

this Affidavit or, if I do not, I have relied on my information and belief and believe my

statements to be true.

2. In the report they filed with this Court in support of their motion for an order seeking to

recognize in Canada the November I I, 2009 administration order in respect of Aero and its

holding company, Aero Inventory PLC ("Aero PLC" and, together with Aero, the "Aero

- 2 -

Companies") which motion was granted by the Ontario Superior Court of Justice that same day

(the "Recognition Order"), the UK administrators (the "Administrators") made numerous errors

of fact, many of which are detailed in this Affidavit, respecting the relationship between Air

Canada and the Aero Companies and the obligations and balances of account owing between

them.

3. Although it is possible the Administrators did not possess all information that was needed

to understand the relationship between Air Canada and the Aero Companies at the time the

Recognition Order was made, Air Canada has since given the Administrators all of the relevant

contracts, which, in any event, were in the possession of the Aero Companies, as well as the

financial information compiled by Air Canada, the responsibility for much of which was to be

borne by Acro under the agreements between Aero and Air Canada. Air Canada has also made

available to the Administrators, members of Air Canada's management and its maintenance

personnel to assist the Administrators in understanding the logistics, procurement and

management of the consumable and expendable spare parts and services supplied by Aero to Air

Canada and financial arrangements between the parties. Despite these efforts by Air Canada, the

Administrators continue to mischaracterize the agreements and relationship between Air Canada

and the Acro Companies and the steps taken by Air Canada since the Recognition Order,

including the extraordinary efforts required of Air Canada to mitigate the extensive damages

sustained by Air Canada as a result of the breach of the Aero Companies' obligations to Air

Canada, the interruption of all services provided to Air Canada and the dismissal of Aero's

employees assigned to service Air Canada.

4. The main focus of this Affidavit is the relief sought by Air Canada from the limitation

under the Recognition Order against the exercise of set-off rights. However, this Affidavit also

seeks to correct inaccuracies that Air Canada believes exist in the current Court record. Most

importantly, Air Canada was, at the date of the Recognition Order and throughout most of its

relationship with the Acro Companies, and Air Canada continues to be a net creditor of the Aero

Companies, not a net debtor.

5. As the Administrators acknowledge in the Report submitted with the motion for the

Recognition Order (par. 13):

- 3 -

"[the) principal activity of the Aero Group [is the] provision of a comprehensive procurement and inventory management service to companies in the aerospace industry. Specifically, [Aero] sources, distributes and sells consumable and expendable parts (e.g., bearings, fasteners and gaskets) required in the maintenance of aircraft, its customers being airlines and aerospace maintenance and repair companies around the world."

6. As between Air Canada and Aero, the expendable spare parts that Aero sold are known as

Category 3 Inventory ("CAT 3 Inventory"). Spare parts are classified as CAT 3 Inventory

because they are either single-use items that arc not capable of repair or items which, after the

performance of certain procedures, are re-certifiable for limited periods. Consumable spare

parts, such as machinc oils or fluid and other materials that breakdown with use, are entirely

consumed during the maintcnance or operation of aircraft. Expendable spare parts must be

traceable, warranted and certifiable. Tracking systems must record the entire life-cycle of each

expendable part from the time of manufacturing of the part until it is destroyed. Air Canada

requires tens of thousands of different types of CAT 3 Inventory to maintain its aircraft. Very

substantial stocks of CAT 3 Inventory must be maintaincd at all times and must be accessible at

each site where maintenance is performed. Thc efficient procurement and management of CAT

3 Inventory is a crucial and complex task, indispensable to Air Canada's operations and the

delivery of its services to customers.

7. In December, 2008, Air Canada and Aero entered into an Agreement for the Supply and

Management of Consumable and Expendable Spares (the "Line Maintenance Agreement"). Line

maintenance is generally considered to be minor or scheduled maintenance carried out on

aircrafts that are in service (such as overnight maintenance and maintenance between flights).

Under the Line Maintenance Agreement, Aero became Air Canada's exclusive supplier for

approximately 98% of CAT 3 Inventory used by Air Canada for line maintenance on its mainline

aircraft Acro also assumed responsibility for managing all aspects of the procurement and

delivery of CAT 3 Inventory for line maintenance, including monitoring and planning for Air

Canada's consumption and use of the inventory. A copy of the Line Maintenance Agreement is

attached as Exhibit "A".

8. The implementation of the Line Maintenance Agreement was part of Air Canada's long-

term strategy to focus on customer service and reduce operating expenses by outsourcing certain

- 4 -

supply and logistics functions, including the procurement and management of CAT 3 Inventory

for line maintenance. A key element of this strategy, implemented after Air Canada's successful

restructuring under the Companies' Creditors Arrangement Act in 2004, was to appoint Aveos

Fleet Performance Inc. ("Aveos") as Air Canada's sole supplier of certain maintenance services.

The Line Maintenance Agreement enabled Air Canada to pursue this strategy further, by

outsourcing the procurement and management of thc CAT 3 Inventory used in line maintenance

while nevertheless retaining responsibility itself for the maintenance performed.

9. Having concluded the Line Maintenance Agreement with Aero and previously

outsourced most procurement and maintenance functions to Aveos, Air Canada did not intend,

and until the default of the Aero Companies following the Recognition Order, was not required

to takc on any responsibility for the logistics, procurement or management of CAT 3 Inventory.

However, for the reasons explained in this Affidavit, and, specifically, what appeared to be Air

Canada's relatively lower cost of capital, it was beneficial for the Aero Companies and Air

Canada that Air Canada bear a portion of the capital cost of the CAT 3 Inventory required by

Aero to perform its services for Air Canada.

10. Air Canada financed a portion of the capital cost of the CAT 3 Inventory required by

Aero under two principal agreements. In February, 2009, Air Canada purchased

US$100,000,000 of Aero's then current stock of CAT 3 Inventory under a Bulk Inventory

Purchase Agreement dated January 28, 2009 between Air Canada and the Aero Companies

(the "January Purchase Agreement"). A copy of the January Purchase Agreement is attached as

Exhibit "B". In October, 2009, Air Canada agreed to purchase additional CAT 3 Inventory from

Aero's then current stock but in three equal instalments, each valued at USS8,500,000,

deliverable on October 23, 2009, November 1, 2009 and December 1, 2009, and each payable

approximately 60 days after delivery (the "October Purchase Agreement"). A copy of the

October Purchase Agreement is attachcd as Exhibit "C".

11 The January Purchase Agreement was proposed by the Aero Companies. The Acro

Companies informed Air Canada that under their proposal, Air Canada could procure a

guaranteed supply of CAT 3 Inventory matching Air Canada's requirements for I year and that

Air Canada could defer making any payment for thc inventory until the end of the year.

- 5 -

12. Thc Aero Companies were expanding aggressively and appeared to require massive

capital investments. By the fall of 2008, the Acro Companies' access to capital markets

appeared to be limited due to the collapse of credit and financial markets generally. The Aero

Companies advised Air Canada that Aero had the opportunity to become the exclusive supplier

of another major airline, a transaction that would reduce its overall operating costs and would

indirectly benefit Air Canada. The transaction with another major airline would be predicated on

the purchase of the airline's existing stock of CAT 3 Inventory and would require a significant

capital investment. Market conditions at the time seemed to preclude the Aero Companies from

raising sufficient funds independently for this purpose. Acro's proposal to Air Canada involved

the leveraging or monetization of a portion of Aero's stock of CAT 3 Inventory in Canada by

selling it to Air Canada. Air Canada concluded that, if it could purchase the CAT 3 Inventory in

bulk, pay the purchase price under negotiable bills or notes maturing in the future — after Air

Canada had consumed the inventory — the transaction would be strongly cash flow positive for

Air Canada. A purchase transaction bascd on payment instruments that the Aero Companies

could discount and sell on the London commercial paper market would achieve the parties'

objectives and creatc a source of new capital for the Aero Companies based on Air Canada's

credit rating.

13. More specifically, the January Purchase Agreement provided three advantages to Air

Canada. First, Air Canada would acquire CAT 3 Inventory necessary to meet its forecast

consumption for a year but would pay for that inventory only at the end of the year. Second,

because Aero would be buying back the inventory in order to supply Air Canada under the Line

Maintenance Agreement and to supply Aveos under its exclusive supply agreement with Aveos,

Air Canada would receive monthly payments from Aero before making any cash outlay itself on

account of the Purchase Price. Third, Air Canada could obtain certain discounts and volume

rebates under thc Line Maintcnance Agreement. For the Aero Companies, the January Purchase

Agreement held out the prospect of raising new capital undcr then prevailing market conditions

that limited the Aero Companies' access to the capital markets.

14. Under the January Purchase Agreement, Aero sold to Air Canada the CAT 3 Inventory

described in Schedule 2.1(c) to the agreement (the "January Inventory Pool"). Air Canada paid

an aggregate purchase price of US$100,000,000 plus applicable goods and services tax and

1 Z

- 6 -

provincial sales taxes, representing an aggregate purchase price of US$110,740,027 (the

"January Purchase Price"). The January Purchase Price, less a holdback (as provided for in the

January Purchase Agreement) in the amount of US$10,000,000 (the "Holdback"), was paid in

full at the time of the transaction closed on February 9, 2009.

15. The January Purchase Price, less the Holdback, was paid at closing by way of thc

acceptance by Air Canada and delivery to Aero of the following bills of exchange drawn by Aero

on Air Canada and payable on February 8, 2010 (the "Bills of Exchange"):

Principal Amount Number Maturity

US$10,000,000 1 February 8, 2010 US$10,000,000 2 February 8, 2010 US$10,000,000 3 February 8, 2010 US$10,000,000 4 February 8, 2010 US$10,000,000 5 February 8, 2010 US$10,000,000 6 February 8, 2010 US$10,000,000 7 February 8, 2010 US$10,000,000 8 February 8, 2010 US$10,000,000 9 February 8, 2010 US$10,740,026.72 10 February 8, 2010

Copies of the Bills of Exchange are attached as Exhibit "D".

16. The delivery of the Bills of Exchange by Air Canada to Aero at the closing of the

purchase and sale transaction under the January Purchase Agreement discharged and constituted

full and final payment by Air Canada of the January Purchase Price except the Holdback.

17. The January Purchase Agreement was amended as of February 6, 2009, in order to

specify the conditions for the closing of the transactions contemplated by the agreement. A copy

of the First Amending Agreement is attached as Exhibit "E".

18. As further consideration for the purchase of the CAT 3 Inventory under the January

Purchase Agreement, the Line Maintenance Agreement was amended in order to guarantee Air

Canada a monthly rebate of US$100,000. This amendment also provided for three additional

- 7 -

rebates to Air Canada of US$833,333.33 each, payable on July 1, 2009, and on July 1 of each

year thereafter until July 1, 2011. A copy of the relevant First Amending Agreement (the "LMA

First Amending Agreement") is attached as Exhibit "F".

19. Air Canada insisted on receiving extensive representations and warranties under the

January Purchase Agreement. Part of the benefit to it under the transaction accrued because it

would use the spare parts from the January Inventory Pool before being required to make any

payments under the Bills of Exchange. For this to occur, it was essential that the CAT 3

Inventory in the January Inventory Pool be of a nature and kind, and purchased in quantities, that

would meet Air Canada's requirements over the ensuing twelve (12) months. Thc Acre

Companies madc the following specific representation and warranty to Air Canada in section

3.6(e) of the January Purchase Agreement:

"(e) Supply Management. The Seller is a specialist in inventory management and planning for the aerospace industry. The Seller has made investigations of historical relevant data and has made enquiries necessary and has the data and software required to forecast the Buyer's consumption of Parts and other inventory of the same nature or kind as the Purchased Inventory in the ordinary course of business during the twelve (12) months following the Closing Date. Based on historical data and the forecast derived from the Seller's investigations, enquiries and expertise, the Purchased Inventory does not exceed the requirements of Air Canada for such period. Only "high usage" C&E and Parts form part of the Purchased Inventory and none of the Purchased Inventory is or will become obsolete or unusable during the twelve (I 2) months following the Closing Date".

20. In planning for the purchase and sale transaction under the January Purchase Agreement,

Air Canada took the steps necessary to verify and protect its interests in the January Inventory

Pool, including obtaining the consent of the Aero Companies' senior lenders and the discharge of

thcir security interests in the January Inventory Pool, taking its own security in the January

Inventory Pool, obtaining confirmation from Air Canada's auditors and the Aero Companies'

auditors that the transaction would be recorded as a sale and insisting on receiving the benefit of

the following representations, set out in section 3.5, 3.6 and 3.7 of the January Purchase

Agreement.

"3.5 Transfer of Title

- 8 -

At the Closing, the Buyer will acquire good, valid and marketable title to all the Purchased Assets, free and clear of any Lien, except any Lien in favour of the Buyer".

"16 Purchased Assets

(a) Description of Purchased Inventory. Schedule 2.1 contains an accurate and complete description of the Purchased Inventory.

(b) Related Assets. Schedule 3.6(b) contains an accurate and complete description of any material Related Assets.

(c) Location of Purchased Assets. All Purchased Assets are located at the premises identified in Schedule 3.6(e). The owner and any other person having any interest in or access to such premises, other than the Seller and the Buyer, is also identified in Schedule 3.6(c)".

"3.7 Financial Information and Accounting Treatment

(a) Financial Statements. The financial statements of each AI Party described in the Closing Agenda have been prepared from the books and records of each such Al Party in accordance with International GAAP and present fairly in all material respects the financial condition of such AI Party as at the date thereof.

(b) No Material Adverse Change. Since the date of the financial statements of each AI Party described in the Closing Agenda, there has been no Material Adverse Change.

(c) Solvency. Thc Aero Inventory Group is able to pay its liabilities as such liabilities become due. The fair market value of the assets of the Aero Inventory Group cxceed the liabilities of the Aero Inventory Group.

(d) Accounting Recognition. The Purchase Transaction will be recognized on the balance sheet and income statement of the Seller as a sale of the Purchased Assets."

- 9 -

21. Aero PLC made these representations and warranties jointly and severally (solidarily)

with Aero and agreed to indemnify Air Canada in connection with Aero's obligations under the

January Purchase Agreement.

22. For Aero, the commercial value in the transaction arose only if it succeeded in

discounting and selling the Bills of Exchange, raising thc capital it required. Air Canada learned

after the closing of the transaction that Aero had not taken any steps to pre-sell the Bills of

Exchange or obtain firm commitments to purchase them or a put option. It appears that the Aero

Companies entered into the January Purchase Agreement without any assurance that they would

be able to sell the Bills of Exchange.

23. After the closing of the transaction under the January Purchase Agreement, Acro

informed Air Canada that it was having difficult) , selling the Bills of Exchange.

24. Only weeks after the closing of the transaction under the January Purchase Agreement,

Acro sought to sell a number of Bills of Exchange to Air Canada. Because Air Canada was

concerned when it learned of the difficulty in selling the Bills of Exchange and had concluded

the January Purchase Agreement to conserve cash, it was reluctant to buy any Bills of Exchange.

Instead, it proposed that thc parties take the steps necessary to reverse the transaction. The Aero

Companies refused to consider unwinding the purchasc and sale. Air Canada agreed to purchase

two Bills of Exchange but subject to a discount of 50%. Bills of Exchange Nos. 1 and 2 were

thus acquired by Air Canada. Air Canada understands that the proceeds from the transaction

were used to make an interest payment to the Aero Companies' senior lenders. A copy of the

BofE Purchase Agreement dated February 23, 2009 is attached as Exhibit "G".

25. The first sales under the Line Maintenance Agreement occurred in Spring of 2009. All

sales of CAT 3 Inventory that occurred under the Line Maintenance Agreement and the purchase

price and other amounts payable by AC on account of the agreement are summarized in the

fo I I owing table:

a 3

- 10 -

Description Amount Taxes Total

May 2009 Consumption US$1,774,954.69 US$131,206.88 US$1,876,161.57

Jun. 2009 Consumption US$1,916,261.45 US$136,537.00 USS2,052,798.45

Jul. 2009 ConsAption US$1,658,397.13 US$100,405.58 US$1,758,802.71

Aug. 2009 Consumption US$1,792,465.66 US$132,544.29 US$1,925,009.95

Sept. 2009 Consumption US$1,874,126.24 US$152,694,69 US$2,027,090.93

Oct. 2009 Consumption* US$2,301,479.06 US$155,509.92 US$2,456,988.98

Nov. 1-10, 2009 Consumption* US$456,196.74 US$30,825.01 US$487,021.75

Total US$11,743,880.97 US$839,993.37 US$12,583,874.34

* It was the responsibility of Aero to generate and deliver invoices under the Line Maintenance Agreement. No invoices were given to Air Canada for October or November. These figures are based on Air Canada's own audit.

26. The cumulative rcbates payable to Air Canada based on the LMA First Amending

Agreement and the achievement of annual spend targets, are summarized in the following table:

Description Amount

May 2009 Line Mtce. Rebatc US$100,000.00

Jun. 2009 Line Mtce. Rebate US$100,000.00

Jul. 2009 Line Mtce. Rebate US$100,000.00

Aug. 2009 Line Mtce. Rebate US$100,000.00

Sep. 2009 Line Mtce. Rebate US$100,000.00

Oct. 2009 Line Mtce. Rebate US$100,000.00

Nov. 2009 Line Mtce. Rebate US$33,333.33

Line Maintenance Conditional Rebate US$833,333.33

Total US$1,466,666.66

27. The Line Maintenance Agreement, as amended by the LMA First Amending Agreement,

was in full force and effect as of the date of the Recognition Order. As at that date, Air Canada

was indebted to Aero in the amount of US$11,050,541.01, representing the difference between

the sales under the Line Maintenance Agreement and the cumulative rebates owing as at that

12,6

date. These balances do not include expenses which Air Canada is entitled to deduct from the

amount payable to Aero nor the damages caused by Acro's breach and disclaimer of the Line

Maintenance Agreement.

28. Contrary eo the evidence presented in the report of the Information Officer to this Court

at the time of the Recognition Order, Air Canada was entitled to approximately US$1,500,000 in

rebates under the Line Maintenance Agreement. More importantly, the Information Officer's

report omitted any reference to the obligations of Aero to Air Canada under the January Purchase

Agreement, the October Purchase Agreement and the other transactions that occurred in the

period until the end of October, 2009. The net effect of these transactions is that Aero was

indebted to Air Canada, not the other way around.

29. As explained, it is important to appreciate that in order to supply CAT 3 Inventory to Air

Canada under the Line Maintenance Agreement and to supply CAT 3 Inventory to Aveos, Acro

was buying CAT 3 Inventory from the January Inventory Pool throughout the period preceding

thc Recognition Order. In fact, Aero purchased CAT 3 Inventory from Air Canada daily until

the Administrators ceased making any such purchases.

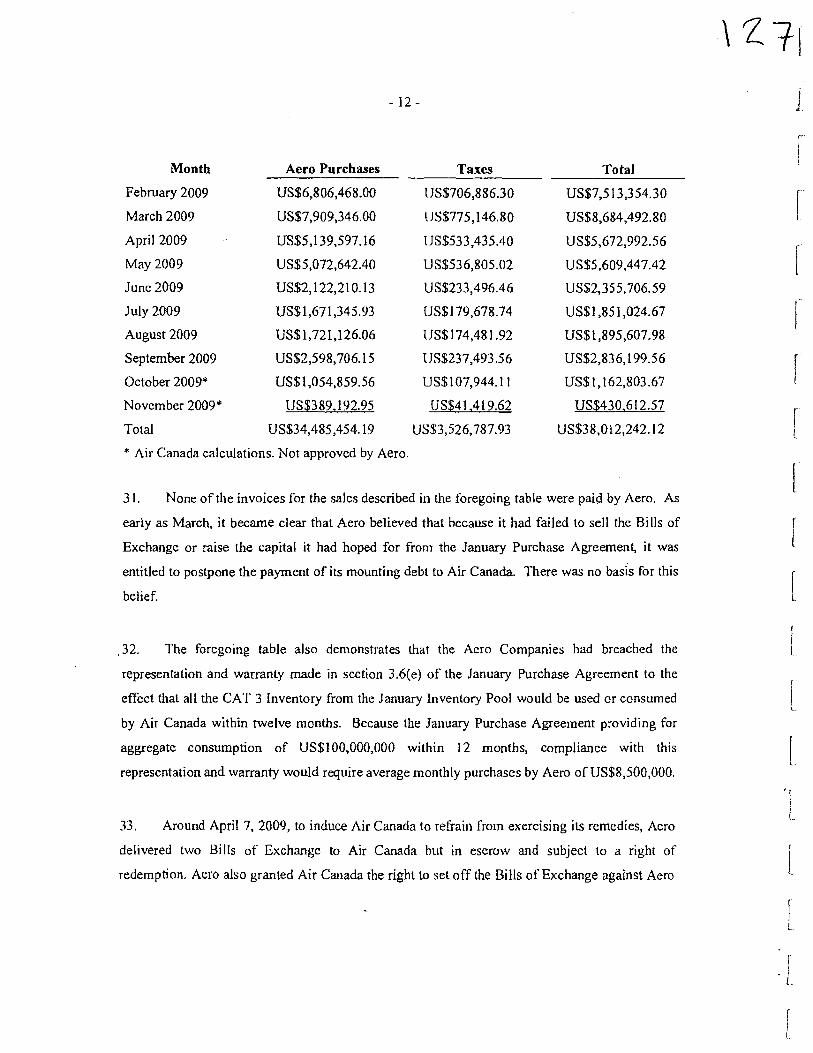

30. The following is a summary of the purchases made by Aero from the CAT 3 Inventory

Pool, based on the monthly invoices issued and approved by the parties:

- 12 -

Month Aero Purchases Taxes Total

February 2009 US$6,806,468.00 US$706,886.30 US$7,513,354.30

March 2009 US$7,909,346.00 US$775,146.80 US$8,684,492.80

April 2009 US$5,139,597.16 US$533,435.40 US$5,672,992.56

May 2009 US$5,072,642.40 US$536,805.02 USS5,609,447.42

Junc 2009 US$2,122,210.13 US$233,496.46 US$2,355,706.59

July 2009 US$1,671,345.93 US$179,678.74 US$1,851,024.67

August 2009 US$1,721,126.06 US$174,481.92 US$1,895,607.98

September 2009 US$2,598,706.15 US$237,493.56 US$2,836,199.56

October 2009* US$1,054,859.56 US$107,944.11 US$1,162,803.67

November 2009* US$389,192.95 US$41,419.62 US$430,612.57

Total US$34,485,454.19 US$3,526,787.93 US$38,012,242.12

* Air Canada calculations. Not approved by Aero.

31. None of the invoices for the sales described in the foregoing table were paid by Aero. As

early as March, it became clear that Aero believed that because it had failed to sell the Bills of

Exchange or raise the capital it had hoped for from the January Purchase Agreement, it was

entitled to postpone the payment of its mounting debt to Air Canada. There was no basis for this

belief.

, 32. The foregoing table also demonstrates that the Acro Companies had breached the

representation and warranty made in section 3.6(e) of the January Purchase Agreement to the

effect that all the CAT 3 Inventory from the January Inventory Pool would be used or consumed

by Air Canada within twelve months. Because the January Purchase Agreement providing for

aggregate consumption of US$100,000,000 within 12 months, compliance with this

representation and warranty would require average monthly purchases by Aero of US$8,500,000.

33, Around April 7, 2009, to induce Air Canada to refrain from exercising its remedies, Acro

delivered two Bills of Exchange to Air Canada but in escrow and subject to a right of

redemption. Aero also granted Air Canada the right to set off the Bills of Exchange against Aero

Z

12g

- 13 -

payables if Aero failed to remedy its defaults. A copy of the interim pledge and escrow is

attached as Exhibit "H".

34. On May 1, 2009, Air Canada sent a demand for payment to Aero, including a demand

that Acro make arrangements to pay for future purchases of CAT 3 Inventory by delivering

additional Bills of Exchange. A copy of the Air Canada demand is attached as Exhibit "I".

35. On May 8, 2009, with Aero's consent, two Bills of Exchange were released from escrow

and delivered to Air Canada to enable Air Canada to set-off the amounts payable under the Bills

of Exchange against Air Canada's outstanding receivables from Aero.

36. In March and May of 2009, based on the declining volumes of consumption from the

January Inventory Pool for the period from March 2009 through to May 2009, Air Canada

undertook an audit of the CAT 3 Inventory in the January Inventory Pool. Based on the results

of the audit, Air Canada estimated that as much as US$40,000,000 or more of the spare parts

remaining in the January Purchase Pool would not be used by Air Canada within the period

agreed to between the parties under the January Purchase Agreement and that the remaining

January Inventory Pool was comprised of many spare parts that could not be used by Air Canada

at all or would not be used for 24 months or more. Air Canada notified Aero of Aero's breach

and demanded that the breach of warranty be remedied. Aero acknowledged thc breach and

agreed to remedy the breach by replacing the non-conforming inventory with conforming

inventory that it said it had on site in Canada. It agreed to pay Air Canada any difference

between actual consumption and the average monthly consumption that would be necessary to

meet the warranty requirements, namely US$8,500,000, if the new inventory was not delivered.

This agreement was later memorialized in the Warranty Performance Agreement executed

between the parties in October, 2009 (the "Warranty Performance Agreement"). Based on the

agreement, procedures were implemented immediately to begin to correct the composition of the

January Inventory Pool. Beginning in June 2009, invoices included both the amount owed for

CAT 3 Inventory actually consumed and the amount owed for warranty performance. In

addition, a special invoice was issued for the aggregate difference between actual consumption

during the months of February through to May and the agreed monthly minimum consumption of

1Zei

- 14 -

US$8,500,000 necessary to comply with the warranty requirements. A copy of the Warranty

Performance Agreement is attached as Exhibit "J".

37. As Aero's indebtedness to Air Canada increased throughout the summer of 2009,

including indebtedness arising from its warranty performance obligations, Aero agreed, in

August of 2009, to deliver three more Bills of Exchange into escrow and authorized Air Canada

to set off the Bills of Exchange against its outstanding receivables from Aero. A copy of the

second interim escrow and set-off agreement is attachcd as Exhibit "K".

38. Throughout thc summer of 2009, negotiations continued between Air Canada and Aero

with a view to settling their disputes and, in particular, agreeing on the terms and conditions

under which Aero would exchange the Bills of Exchange that it held for the CAT 3 Inventory it

was purchasing from Air Canada or in payment of its warranty obligations. However, Aero and

Air Canada could not agree on the discount rate to be used to establish the fair market value of

the Bills of Exchange. During this period, Aero appeared to be seeking buyers for the Bills of

Exchange in the commercial paper market, relying on improvements in Air Canada's financial

condition.

39. Air Canada learned during this period that Aero PLC was showing a markedly improving

share price and, in October 2009, Aero PLC advised Air Canada that it was negotiating a major

equity issue and had applied for a listing on the senior board at the London Stock Exchange.

40. On October 9, 2009, a term sheet was agreed to between Air Canada and Aero providing

for the settlement of their disputes. A copy of the term sheet is attached as Exhibit "L".

41. The settlement of the dispute between Air Canada and the Acro Companies involved

several key concessions by each of the parties:

(a) Air Canada would be bound to buy two Bills of Exchange and, except for

US/$2,000,000 which would be used to set-off against AI payables; the purchase

- 15 -

pricc would be paid to Al; the discount rate in respect of the Bills of Exchange to

be purchased was fixed at 15%, generating proceeds of US$17,000,000 for Aero;

(b) Aero would deliver to Air Canada the remaining Bills of Exchange in its

possession, except Bill of Exchange No. 10 which Aero would sell in a private

placement, generating additional cash proceeds;

(c) the discount rate for the five Bills of Exchange that had previously been delivered

to Air Canada, and which Air Canada had the right to set off against outstanding AI

payables, would he fixed at 5%;

(d) to compensate Air Canada for the cost of capital relating to the foregone cash

payments under the January Purchase Agreement, the Holdback would be reduced

by US$4,000,000;

(e) Air Canada agreed to purchase new CAT 3 Inventory from Aero, representing new

receivables fbr Aero in an aggregate amount of US$25,500,000 plus applicable

taxes, provided that the sales would be in instalments and that Air Canada would

have no obligation to pay for any instalment for at least 60 days; and

(f) the parties would memorialize and give effect to their agreement relating to

warranty performance in the Warranty Purchase Agreement.

42. In certain pleadings, the Administrators suggest that Air Canada received a preference

under thc settlement transactions entered into in October, 2009 or that these transactions were

otherwise prejudicial to the Aero Companies or their creditors. As demonstrated in the table in

paragraph 48, if the settlement transactions had not been concluded, Air Canada would be a net

creditor of the Aero Companies at the time of the Recognition Order. If the financial impact of

these transactions is disregarded, the Aero Companies would be indebted to Air Canada at the

date of the Recognition Order, and excluding the damages suffered by Air Canada as a result of

the Acro Companies' breach of their agreement with Air Canada, in the amount of

VD-

- 16 -

US$23,949,829.95. As part of the settlement transactions, the Bills of Exchange delivered to Air

Canada were exchanged for Demand Promissory Notes. There should be no confusion regarding

the purpose of these exchanges, which was twofold: to convert thc Bills of Exchange which

matured on February 8, 2010 into obligations payable on demand, that is, to accelerate Air

Canada's indebtedness; and, to evidence the discount rate negotiated and fixed by mutual

agreement.

43. As previously stated, as part of the settlement transactions, the January Purchase

Agreement, as amended, was further amendcd by a Second Amending Agreement (thc "Second

January Agreement Amendment"). Thc Second January Agreement Amendment reduced the

Holdback under the January 2009 Agreement from US$10,000,000 to US$6,000,000. This

transaction compensated Air Canada for the damages it suffered due to the loss of the cash flows

that should have been generated under the January Purchase Agreement. A copy of the Second

January Agreement Amendment is attached as Exhibit "M".

44. The settlement transactions were concluded on October 23, 2009. Air Canada paid to or

to the order of Acro US$15,000,000 under the Demand Promissory Notes exchanged for Bills of

Exchangc Nos. 8 and 9. Air Canada then sct off US$2,000,000 and the amounts owing under the

Demand Promissory Notes exchanged for Bills of Exchange Nos. 3-7 against amounts due and

owing to Air Canada as at September 30, 2009. After the conclusion of these transactions, the

Aero Companies continued to be net debtors to Air Canada for ongoing purchases of CAT 3

Inventory from the January Purchase Pool and for warranty performance under the January

Purchase Agreement.

45. In summary, for the period beginning in February, 2009 and ending in October, 2009, Air

Canada purchased Bills of Exchange from Aero at thc dates and subject to discounting at or

above market rates, as set out below.

\r32

- 17 -

Discounted Date of Delivery Date of Purchase Principal Purchase to Air Canada by Air Canada Bill No. Amount Price

February 23, 2009 February 23, 2009 I US$10,000,000 US$5,000,000 February 23, 2009 February 23, 2009 2 US$ 1 0,000,000 US$5,000,000 May 8, 2009 October 23, 2009 3 US$10,000,000 US$9,500,000 May 8, 2009 October 23, 2009 4 US$10,000,000 US$9,500,000 August 19, 2009 October 23, 2009 5 US$10,000,000 US$9,500,000 August 19, 2009 October 23, 2009 6 US$10,000,000 US$9,500,000 August 19, 2009 October 23, 2009 7 US$10,000,000 US$9,500,000 October 23, 2009 October 23, 2009 8 US$10,000,000 US$8,500,000 October 23, 2009 October 23, 2009 9 US$10,000,000 US$8,500,000

Total US$90,000,000 US$74,500,00

46. As a result of the settlement transactions, including the Second January Agreement

Amendment, the balance of the Purchase Price payable by Air Canada under the January

Purchase Agreement, as at October 24, 2009, was as follows:

Description Amount

Original Purchase Price List: US$110,740,026.72

Amounts Prepaid by Air Canada by Discounting Bills of Exchange: US$90,000,000

Capital-cost of Non-payment US$4,000,000

Cash Proceeds for Aero US$27,000,000

Payment of Acro's Arrears on AC's Receivables US$47,500,000

Balance of Purchase Price: US$16,740,026.72

Amount Payable to Holder of Bill of Exchange No. 10: US$10,740,026.72

Amount Payable to Aero: US$6,000,000

47. As explained, on October 23, 2009 the parties also entered into the Warranty

Performance Agreement. This agreement confirmed and extended the agreement already made

- 18 -

and in force for the purpose of remedying Aero's breach of warranty under the January Purchase