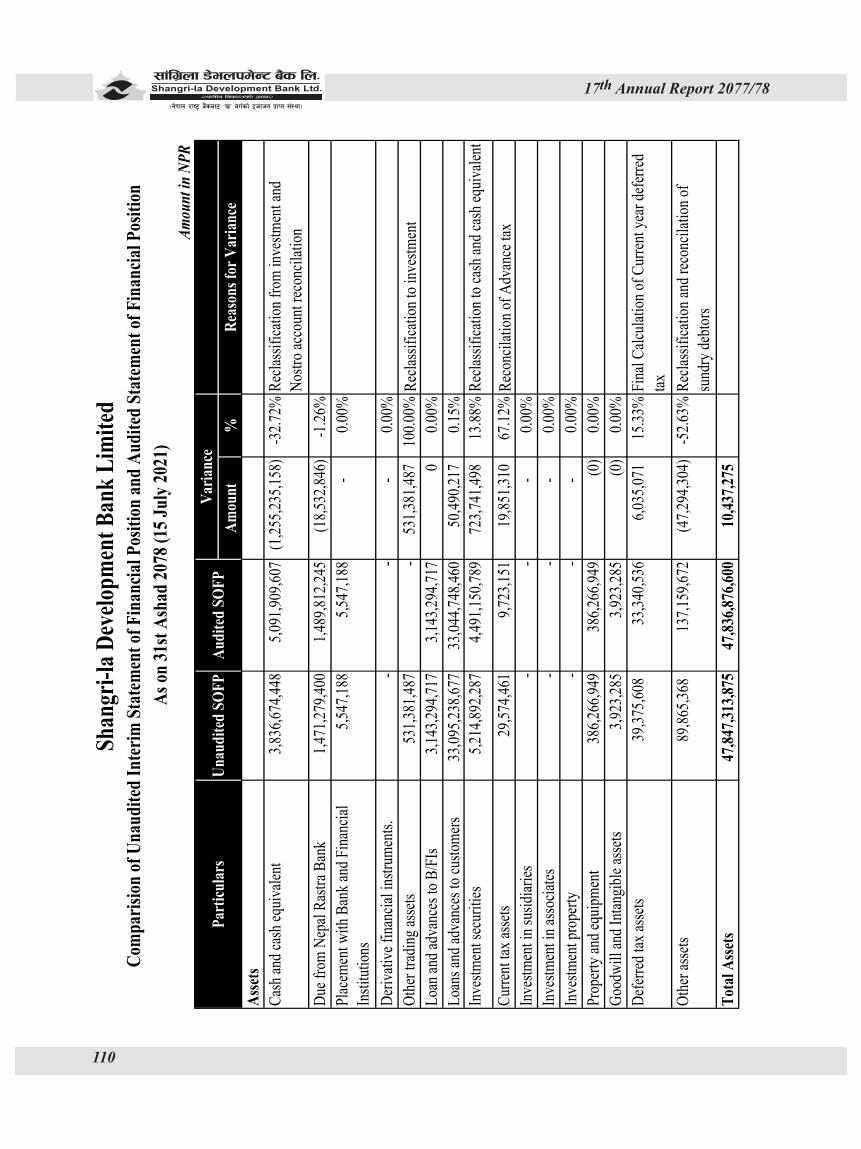

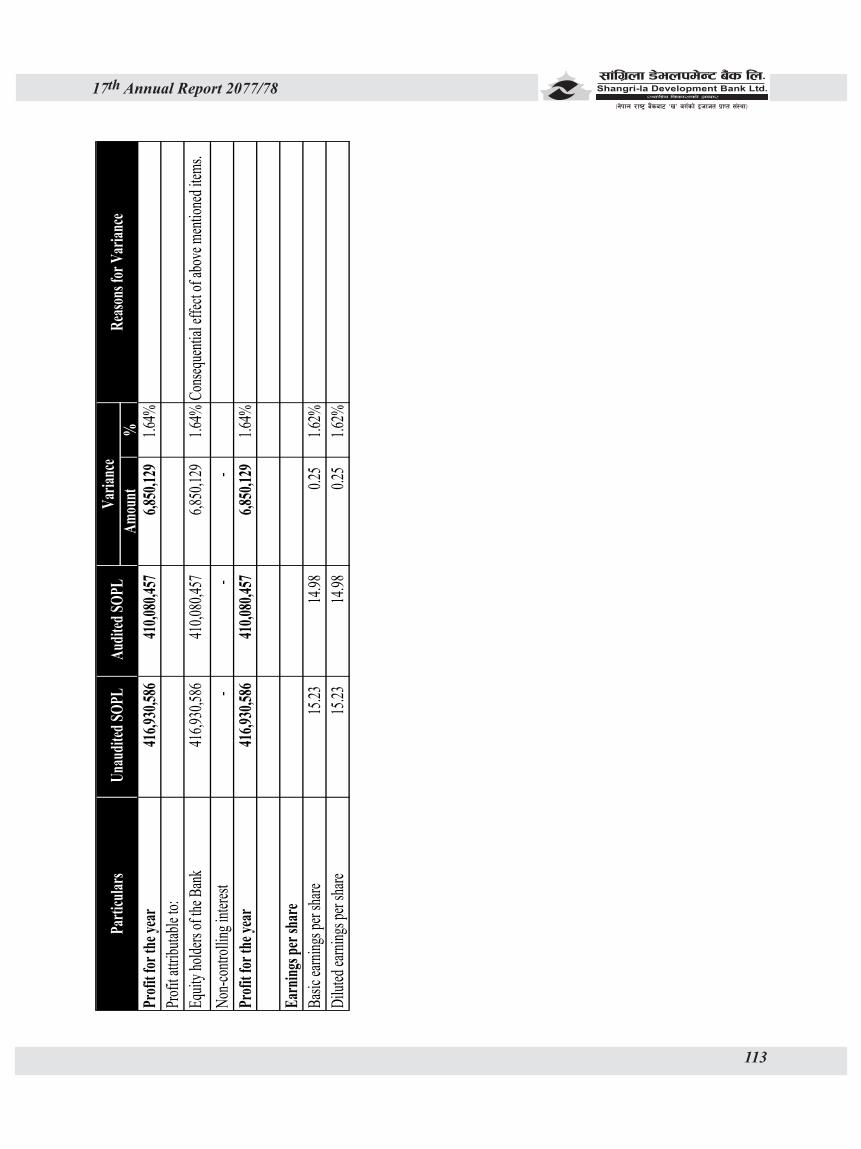

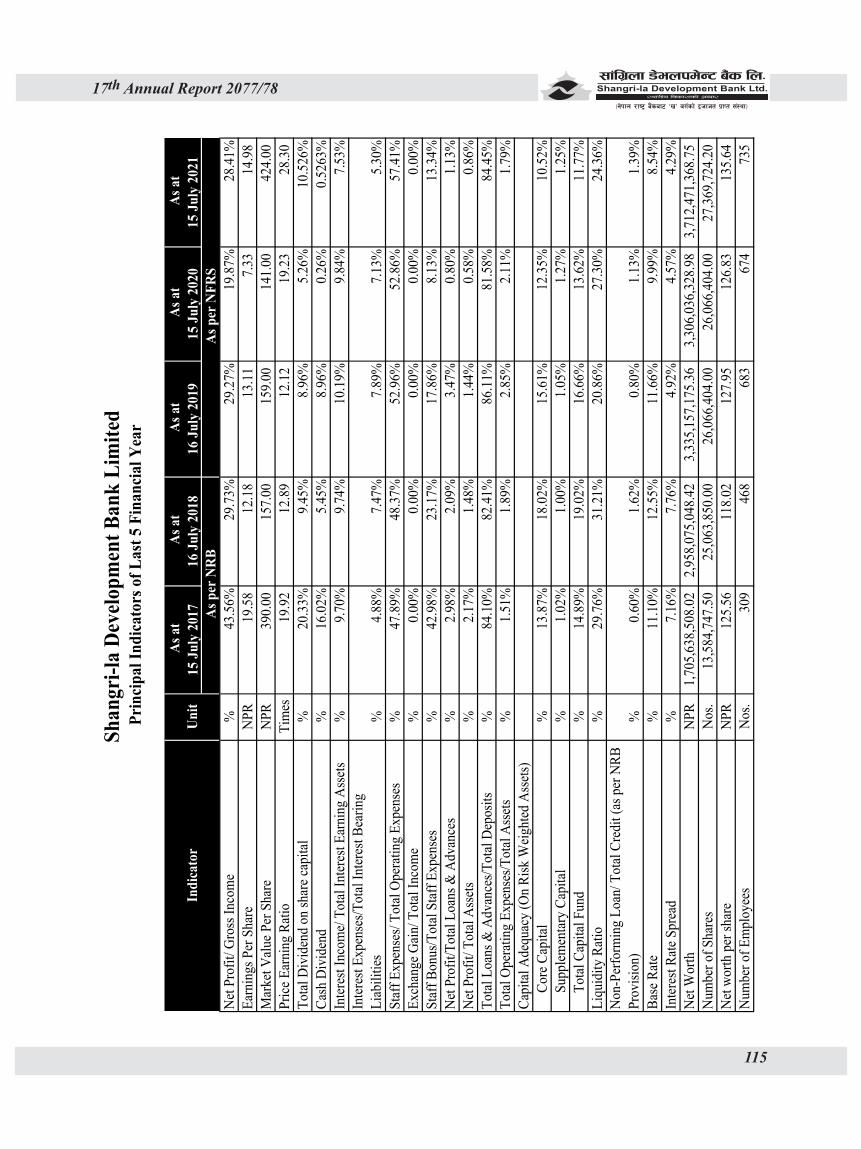

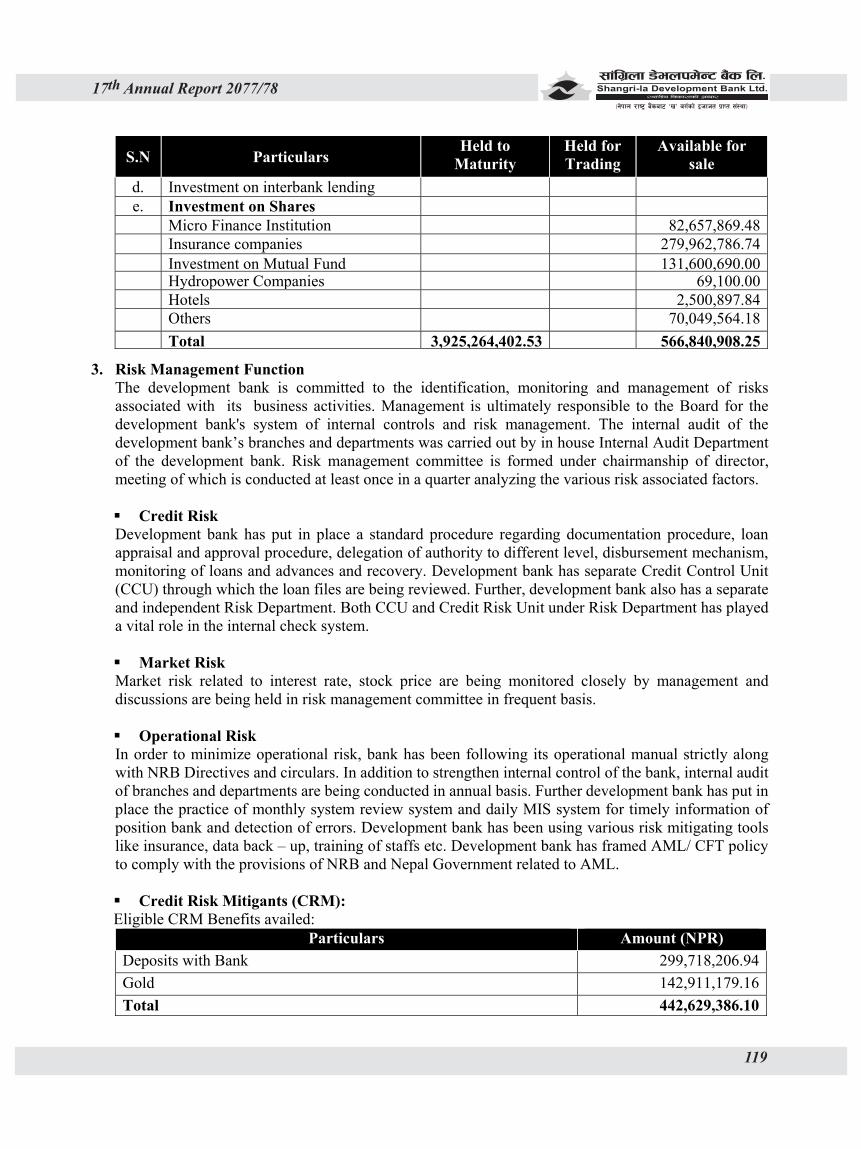

17th Annual Report 2077/78

152

Message from Chairman On the behalf of our Board of Director, I am delighted to express my sincere gratitude and warm regards to all our respected shareholders, representatives from regulatory bodies, auditors, legal advisors, Chief Executive Officer and entire stakeholders for your remarkable presence in this 17 th Annual General Meeting of the development bank. I take this opportunity to assure everyone that through this support of our stakeholders, we commit full dedication towards our responsibilities to achieve our stakeholders’ expectation and faith. It gives me immense pleasure to place before you the highlights of the bank’s performance during the financial year 2077.78. We have expanded our balance sheet size by 45.41% and reached to NPR 47.84 billion and generated net profit of NPR 410 million. Our Earning Per Share has increased from Rs. 7.33 to Rs. 14.98 in current fiscal year. As on 31 st Ashad 2078, the development bank has been providing its banking services to its stakeholders through 95 branches and 31 ATMs throughout the country. Similarly, by the end of 31 st Ashad 2078, the deposit customer base of this bank stood at around 360 thousand, mobile banking customers stood at 76 thousand, number of Debit card holders stood at 28 thousand. Similarly, by creating direct employment opportunity for 735 employees, the bank has contributed in bringing about positive changes in the lives of their dependents. The Board of Directors of our development bank is continuously engaged with the management to setup business goals which shall benefit to all the stakeholders. I express my gratitude to all the stakeholders for your contribution and cooperation with this development bank and keeping your trust in our mission. Thank You, Achyut Prasad Prasai Chairman

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 17th Annual Report 2077/78

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Message from Chairman On the behalf of our Board of Director, I am delighted to express my sincere gratitude and warm regards to all our respected shareholders, representatives from regulatory bodies, auditors, legal advisors, Chief Executive Officer and entire stakeholders for your remarkable presence in this 17th Annual General Meeting of the development bank. I take this opportunity to assure everyone that through this support of our stakeholders, we commit full dedication towards our responsibilities to achieve our stakeholders’ expectation and faith. It gives me immense pleasure to place before you the highlights of the bank’s performance during the financial year 2077.78. We have expanded our balance sheet size by 45.41% and reached to NPR 47.84 billion and generated net profit of NPR 410 million. Our Earning Per Share has increased from Rs. 7.33 to Rs. 14.98 in current fiscal year. As on 31st Ashad 2078, the development bank has been providing its banking services to its stakeholders through 95 branches and 31 ATMs throughout the country. Similarly, by the end of 31st Ashad 2078, the deposit customer base of this bank stood at around 360 thousand, mobile banking customers stood at 76 thousand, number of Debit card holders stood at 28 thousand. Similarly, by creating direct employment opportunity for 735 employees, the bank has contributed in bringing about positive changes in the lives of their dependents. The Board of Directors of our development bank is continuously engaged with the management to setup business goals which shall benefit to all the stakeholders.

I express my gratitude to all the stakeholders for your contribution and cooperation with this development bank and keeping your trust in our mission. Thank You, Achyut Prasad Prasai Chairman

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

Brief About Shangri-la Development Bank Ltd. It is formed after merger of two local level development banks named Bageshwari Development Bank Ltd. based in Nepalgunj and Shangri-la Development Bank Ltd. based in Pokhara. At present, Shangri-la Development Bank Ltd. is one of the largest National Level Development Banks with Branch network of 98 branches. Shangri-la Development Bank Ltd. had acquired Cosmos Development Bank Ltd. and started its joint operation from 30 Ashad, 2074.

We value our customers and our policies are adapted to meet the best interest of our customers and our stakeholders by catering pragmatic and reliable services. We are committed to provide the quality products and services to every customer with utmost courtesy and care.

As on Ashad end 2078, the bank has a noticeable Balance Sheet size of NPR 47.84 billion with 95 branches and 31 ATMs across the country serving more than 360 thousand happy customers from different age groups, communities and societies. Likewise, mobile banking customers stood at 76 thousand and number of Debit card holders stood at 28 thousand.

Similarly, the development bank has entered into an agreement with CDS and Clearing Ltd. to function as Depository Participant to facilitate its customers.

Our basic objective is to deliver quality banking services for the development of economy of the country through appropriate new and improved banking techniques.

No. of Branches FY

2076.77 91

Branches Opened

4

Total Branches

FY 2077.78 95

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Key Financial Highlights as on Ashad End 2078

BALANCE SHEET SIZE

(NPR)

• 47.84 BILLION• 45.41% growth

LOANS AND ADVANCES

(NPR)

• 36.18 BILLION• 51.63% growth

DEPOSITS (NPR)

• 42.84 BILLION• 46.48% growth

EPS

• Earning Per Share Rs.14.98• 104.37% growth

CAR

• Capital Adequacy Ratio 11.77%

Trend Analysis of Growth During Last Five Fiscal Years

13,872,84017,788,230

22,470,525

29,253,427

42,849,643

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

Am

ount

in '0

00

Fiscal Year

Deposit

2073/74 2074/75 2075/76 2076/77 2077/78

11,667,323 14,659,124

19,469,805

23,865,493

36,188,043

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

Am

ount

in '0

00

Fiscal Year

Loans and Advances

2073/74 2074/75 2075/76 2076/77 2077/78

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

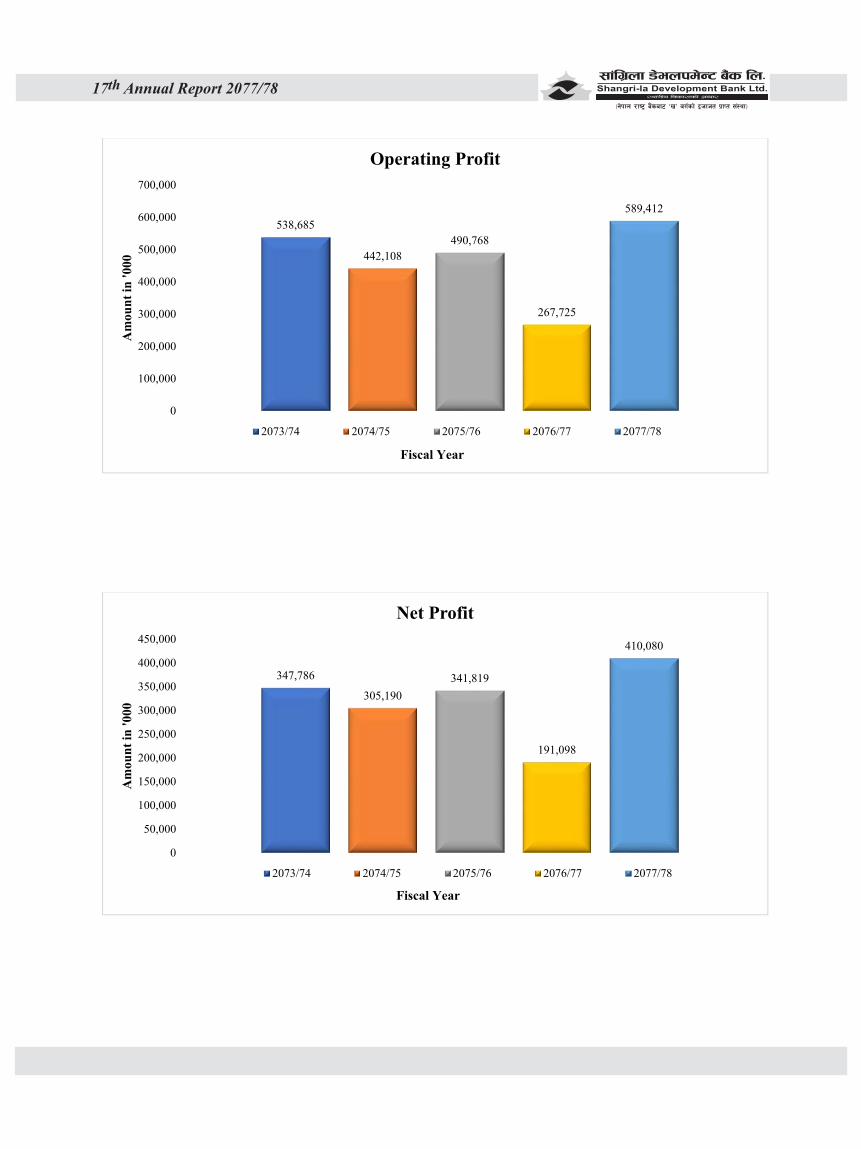

538,685

442,108490,768

267,725

589,412

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Am

ount

in '0

00

Fiscal Year

Operating Profit

2073/74 2074/75 2075/76 2076/77 2077/78

347,786

305,190341,819

191,098

410,080

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Am

ount

in '0

00

Fiscal Year

Net Profit

2073/74 2074/75 2075/76 2076/77 2077/78

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

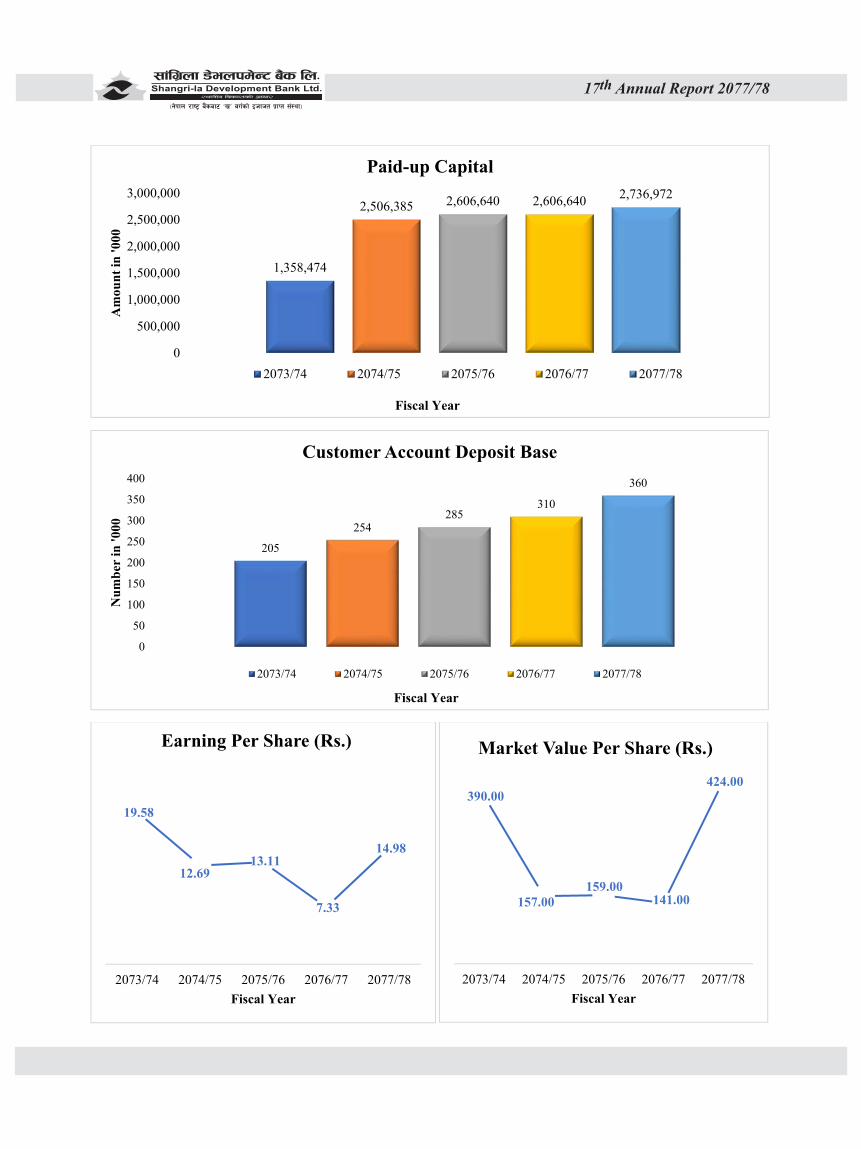

1,358,474

2,506,385 2,606,640 2,606,640 2,736,972

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Am

ount

in '0

00

Fiscal Year

Paid-up Capital

2073/74 2074/75 2075/76 2076/77 2077/78

205

254285

310

360

0

50

100

150

200

250

300

350

400

Num

ber i

n '0

00

Fiscal Year

Customer Account Deposit Base

2073/74 2074/75 2075/76 2076/77 2077/78

19.58

12.69 13.11

7.33

14.98

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Earning Per Share (Rs.)

390.00

157.00 159.00

141.00

424.00

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Market Value Per Share (Rs.)

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

125.56

118.02

127.95 126.83

135.64

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Net Worth Per Share (Rs.)

19.92

12.89 12.12

19.23

28.30

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Price Earning Ratio (Times)

20.33%

9.45% 8.96%

5.26%

10.53%

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Dividend Payout Ratio

309

468

683 674 735

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Number of Employees

36

54

86 91 95

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Number of Branches

14

23 26 27

31

2073/74 2074/75 2075/76 2076/77 2077/78Fiscal Year

Number of ATMs

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Board of Directors The Board of Directors have been acting in adherence to operate the development bank in interests of depositors, customers and general shareholders taking into consideration overall risk management of the development bank. The Board make assurance not to intervene into daily conduct of business. The Board of Directors comprise of seven members headed by Chairman, Mr. Achyut Prasad Prasai. The competent and experienced directors ensure a good governance and provide right direction to the management to achieve organization’s vision, mission and goals. There were 23 board meetings held in the fiscal year. Details of Directors with date of appointment is given below: Name Relationship Date of Appointment Mr. Achyut Prasad Prasai Chairman Appointed on 30th Poush 2075 Mr. Ganga Sagar Dhakal Director Appointed on 30th Poush 2075 Mr. Naresh Man Tuladhar Director Appointed on 9th Poush 2076 Mr. Sushil Kaji Baniya Director Appointed on 30th Poush 2075 Ms. Lisa Sherchan Director Appointed on 28th Magh 2076 Mr. Raju Nath Khanal Director Appointed on 26th Shrawan 2076Mr. Nitish Gupta Director Appointed on 25th Ashwin 2078

Mr. Achyut Prasad Prasai Mr. Achyut Prasad Prasai, resident of Nepalgunj 02, Banke district has done Master in Business Administration. He has been engaged with the bank as Chairman since 30th Poush 2075. He is also director at Nepalgunj Educational Foundation and also President of Radio Bheri Abbaj, Nepalgunj / Community Reform Committee, Nepalgunj. Mr. Ganga Sagar Dhakal Mr. Ganga Sagar Dhakal, resident of Aadhikhola 06, Syangja district has done Master Degree in Humanities & Social Science. He has been engaged with the bank as director since 30th Poush 2075. Also, he has worked as a Gazetted Third-Class Officer and Second-Class Officer in Government of Nepal. Mr. Naresh Man Tuladhar Mr. Naresh Man Tuladhar, resident of Ganabahal 21, Kathmandu district has done Master in Business Administration in Finance. He has been engaged with the bank as director since 9th Poush 2076. He has also worked in Group of Business Consultant Pvt. Ltd. (GBC), Asian Adhesive Pvt. Ltd. and Unique College of Management. Mr. Sushil Kaji Baniya Mr. Sushil Kaji Baniya, resident of Dhumbarahi 04, Kathmandu district has done Master of Laws and Master in Arts. He has been engaged with the bank as director since 30th Poush 2075. He has working experience as a legal consultant in various Multi-national and national companies/ in court litigations and in the area of legal research.

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

Ms. Lisa Sherchan Ms. Lisa Sherchan, resident of Tokha 03, Kathmandu district has done Master of Science in Business Analytics. She has been engaged with the bank as director since 28th Magh 2076. She has working experience as a Director in Three Sixty Education Solutions, Goldman Sach Asset Management (GSAM) in Bangalore, GSAM-Compliance Officer and Goldman Sach Asset Management in New York, GSAM Anti-Money Laundering Compliance Officer. Mr. Raju Nath Khanal Mr. Raju Nath Khanal, resident of Myagdi 1, Gunadhi Tanahu district has done Master in Business Administration. He is serving in the capacity of independent director and has been engaged with the bank since 26th Shrawan 2076. He has long period of working experience in Nepal Bank Ltd. Mr. Nitish Gupta Mr. Nitish Gupta, resident of Nepalgunj 01, Banke district has done Master in Business Administration in Finance and Marketing. He has been engaged with the bank as director since 25th Ashwin, 2078. He has also worked as Manager Sales and Market Analysis in Steel Trading since 2014 A.D. Committee of Directors: To take the informed decision in the best interest of the development bank, the Board has constituted various committees. These committees are formed as per the Unified Directives of the Nepal Rastra Bank (The Regulatory Authority) and work as per the terms of reference provided therein. Following are the Committees of Directors of the Bank: Audit Committee: The Audit Committee of the development bank is comprised of three members, one director from the Board as a coordinator. Head Internal Audit is the member secretary. The development bank has an independent Internal Audit Department under this committee. Internal Audit is an independent appraisal function within the development bank to examine and evaluate its activities. The basic objective of the development bank’s Internal Audit Department is to assist the management in the effective discharge of their responsibilities. It assists the development bank to accomplish its objectives by bringing a systematic and disciplined approach to evaluate and improve the effectiveness of risk management, internal control and governance process. During the year seven meetings of Audit Committee were held.

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Risk Management Committee Board of Directors (BoD) is the apex and supreme authority of the development bank and is responsible to frame and implement robust policies and framework for effective compliance of regulation and direction issued by the regulatory authority. BoD ensures the strategies, policies and procedure is in accordance with the risk appetite/tolerance limit for effective management of risk within the development bank. The Board understands the nature of risk of the development bank, and periodically reviews reports on risk management, including policies and standards, stress testing, liquidity and capital adequacy through the reporting by the Risk Management Committee.

During the year five meetings of Risk Management Committee were held. Assets Money Laundering Prevention Committee The committee ensures that the development bank complies with all the regulations under Asset (Money) Laundering Prevention Act, Asset (Money) Laundering Prevention Rule & the Directives on AML/CFT issued by Nepal Rastra Bank. It reviews the adequacy of the resources (including information technology tools) to identify, measure & mitigate the money laundering issues and reports the same to the Board. The committee also reviews and reports to the Board the existing methodology, policy, processes etc. and need for improvement to identify all kinds of money laundering risks on timely manner.

During the year four meetings of Assets Money Laundering Prevention Committee were held. Employee Service Benefit Committee The Employee Service Benefit Committee of the development bank works on the identifying and addressing policies and current trends of employee issues, including the changes in legislation as well as enhanced benefit programs, and use of the plans to remain competitive in market. The Committee is coordinated by a director of the Board having the Head Human Resource Department as a member secretary. The Committee reviews and recommends the Board for approval of the Human Resources strategy including key HR objectives, plans and workforce requirements, recruitment promotion, selection, transfer & placement norms and monitors the implementation of the same. During the year eight meetings of Employee Service Benefit Committee were held.

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

COVID-19: Diverging into Possibilities The Novel Corona Virus has changed our life drastically. The world economy has major breakthrough to deal with this situation. So, the model of doing business has changed and we have moved from Brick Banking to Click Banking.

Due to the gravity of the both pandemic and the lockdown; the constraint of movement of people, goods, resources and business, the economy was heavily affected. The general public had to face many difficulties during this period.

Despite the situation, we have always put our customer’s needs at the fore front including well-being of our employees. We have formulated different strategies to overcome the challenges and threats created by this unexpected situation. The initiatives taken by our bank during this pandemic are briefly presented below:

Branch and ATM Service Shangri-la Development Bank Ltd. has a vision to serve the customers at its level best despite of unfavorable circumstances. All our 31 ATMs were operated 24/7 for serving the customers. We had placed notice regarding emergency contact number to be coordinated, if any awkward situation arises. Branches and ATMs were thoroughly sanitized and precaution were used to verify the safety and security of our stakeholders. Branches operating schedule was published in our website on daily basis so, our customers would not face any difficulties. Disinfection and Social Distancing As our customers and employees are our important assets, their health is our prime matter of concern. Sanitation kits such as masks, gloves and face shield were provided to each employee from security guard to executive level. Sanitizer dispensing unit were also placed at branch premises for customers/visitors to use. Thermal gun was also kept for temperature check for both visitors and employees at branches. There was sufficient social distancing while doing banking transactions. Our staffs were also showing great concern to maintain the health protocol issued by the government.

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Work from Home Access and Staff Training To provide uninterrupted service to our customers, we had provided our staffs access from home to run day to day transaction smoothly. Customers were facilitated through phone calls and virtual meetings by our employees regarding any of their queries about our product and services. We had also conducted numerous trainings to our staffs through virtual platform to enhance their knowledge base in the banking sector.

Digital Marketing and Awareness

Shangri-la Development Bank Ltd. has been regularly updating messages, tips regarding COVID related issues. All the notices were made available in the bank’s website and social media platform for the customers to know about any information regarding the bank. As we are moving towards the digital era to cope with this fast-growing industry, we have installed the digital display at our corporate office building

to provide updated information regarding our products, services, festivals discounts, financial literacy and COVID awareness messages. Latest Product and Services During the pandemic situation, we have never compromised to provide top-most services to our valued customers. So, we had introduced brand new product and services. Deposit schemes for women (Shangri-la Nari Bachat), minor (Shangri-la Bal Bhabisya Bachat) and old-age individuals (Shangri-la Jestha Nagarik Bachat) were launched.

Work from Home Access and Staff Training To provide uninterrupted service to our customers, we had provided our staffs access from home to run day to day transaction smoothly. Customers were facilitated through phone calls and virtual meetings by our employees regarding any of their queries about our product and services. We had also conducted numerous trainings to our staffs through virtual platform to enhance their knowledge base in the banking sector.

Digital Marketing and Awareness

Shangri-la Development Bank Ltd. has been regularly updating messages, tips regarding COVID related issues. All the notices were made available in the bank’s website and social media platform for the customers to know about any information regarding the bank. As we are moving towards the digital era to cope with this fast-growing industry, we have installed the digital display at our corporate office building

to provide updated information regarding our products, services, festivals discounts, financial literacy and COVID awareness messages. Latest Product and Services During the pandemic situation, we have never compromised to provide top-most services to our valued customers. So, we had introduced brand new product and services. Deposit schemes for women (Shangri-la Nari Bachat), minor (Shangri-la Bal Bhabisya Bachat) and old-age individuals (Shangri-la Jestha Nagarik Bachat) were launched.

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

Our “Ek ko dui Muddati Khata” and “Recurring Deposit” product were very popular amongst our depositors as we had provided online account opening facilities so that our customers could easily open any accounts without visiting the branches. Our bank has also provided online fixed renewal services so anyone who have access to internet services can easily renew their fixed deposit account. Customers can also apply for online loan application. We have tried to push forward our digital services in an effective manner. We have installed “50 Reflective Highway Hoarding Board” from Nagdhunga to Pokhara which mainly focus on social awareness information to our stakeholders and promotes visibility of our brand.

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

Value Added Statement The Value-Added Statement (also known as an added-value statement) is a financial statement showing how much wealth (the value-added) has been created by the collective effort of capital, employees, and others resources and how it has been allocated to the stakeholders, employees, government, community, shareholder and expansion and growth of the bank within an accounting period.

Value Added Statement of the bank during the fiscal year 2077.78 and 2076.77 are depicted below:

Amount in million Particulars FY 2077.78 FY 2076.77 Change (%)

Interest earned 3,515.21 3,135.05 12.13%Other Income 479.92 176.20 172.37%Interest Expenses 2,308.69 2,084.75 10.74%Other Operating Expenses 290.61 254.58 14.15%Value Added by Banking Service 1,395.83 971.92 43.62%Impairment Charge for Loans and other losses 236.07 259.48 -9.02%Gross Value Added 1,159.77 712.44 62.79%Application Statement To Employees Salaries and Other Benefits 490.23 366.79 33.66%To Government Income Taxes 185.40 79.64 132.81%To Community Corporate Social Responsibility 4.10 1.91 114.59%To Shareholders Dividend and Bonus shares 288.10 137.19 110.00%To Expansion and Growth Reserves and Accumulated Profit 117.88 52.00 126.71%Depreciation and Amortization 80.93 77.34 4.64%Deferred Taxation (6.88) (2.42) 183.90%Total of Value Added Allocation 1,159.77 712.44 62.79%

The value added by the bank stood at NPR 1,159.77 million as on Ashad 2078 compared to NPR 712.44 million in the previous year.

For the year ended Ashad 2078, the application statement comprised of value addition to various stakeholders of the bank. The current value addition of 42.27% has been apportioned to the employees of the bank for the salaries and other benefits and 15.99% to the Government. Similarly, the community, shareholders and expansion & growth received 0.35%, 24.84% and 16.55% respectively of the total value addition.

Market Value Added

Market Value is the difference between the market value and total book value of the bank. It shows the difference between the current market value of the bank and capital contributed by investors. It is the sum

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

of all capital claims held against the bank plus the market value of debt and equity. Positive market value added depicts the bank has added value.

Amount in million Particulars FY 2077.78 FY 2076.77

Market Price Per Share (Rs.) 424.00 141.00Number of shares 27.37 26.07Total Market Value 11,604.76 3,675.36Book Value per share (Rs.) 135.64 126.83Number of shares 27.37 26.07Total Book Value 3,712.47 3,306.04Market Value Added 7,892.29 369.33

The total market value of the bank has increased by NPR 7,929.40 million and has reached to NPR 11,604.76 million. Similarly, the total book value of the shares has increased by NPR 406.44 million and has reached to NPR 3,712.47 million.

With the increase in the market value of shares and book value of shares, the total market value added in the FY 2077.78 has reached to NPR 7,892.29 million as compared to NPR 369.33 million in the previous year. Economic Value Added

Economic Value Added (EVA) is the financial performance measurement tool which is used to measure the value of a company generated from the fund invested in it. It is an estimate of bank’s economic profit or the value created in excess of the required return of the bank’s shareholders. Economic Value Added is the profit earned by the bank less the cost of financing the bank’s capital.

Amount in million Particulars FY 2077.78 FY 2076.77

Net Operating Profit after Tax 410.08 191.10Average Shareholder's Fund 3,509.25 3,320.60Cost of Capital Employed (%) 10% 10%Cost of Capital Employed (Amount) 350.93 332.06Economic Value Added 59.16 (140.96)

The bank has generated Economic Value Added of NPR 59.16 million as on Ashad end 2078 compared to NPR (140.96) million last year. Cost of Equity has been assumed to be 10%, slightly higher than the return on government bonds by considering the difference between the cost of equity and return on government bonds to be risk premium.

������ ������� ������ ������� ������ �� ������ ����� �

�� ����� ������� ������ �� ������ ��� ������� ���

�� ���� �� ����� � ����� �� �

�� ������� ���� ������ ������� ��� ������������ ������ ������ ������� ������� �������� ��� ����� ���� ���� ��� ���� ��� ��� ������ � ��������� ������� ����� ���� ������� ���� ��� ������� ������� ���� ��� ��� �� ��� ����� ��� ��

��� ������� �����¡� ��¢���������� �������� ���� ����� �������� ������� ����� ����� �� ��� ������ ����� ����� ��� ������ ���������� ����� ����� ��� �������� ����� ����� £� ���� ���� ���������� ����� ����� ������ ���¤� ����� �� ��� ��� ��������� ����� ����� ������� ��¢� ������ ����� �������� � ������� ����� �������� ����� ������ ���� ���� �������¢��� ���¢ ����� ��������� ����¡� ����� ¥ � ��������� ������� ��� ����� ����� � ����� ����¦ ������� ��£��� ��������� ������ ����� ����¦ ������� ��£��� ������� ��� ������ ������� ����� ������ �������� �������� ������� ���� ���� ����� ������ ��¢� ������� ������ ����� ���

����������

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

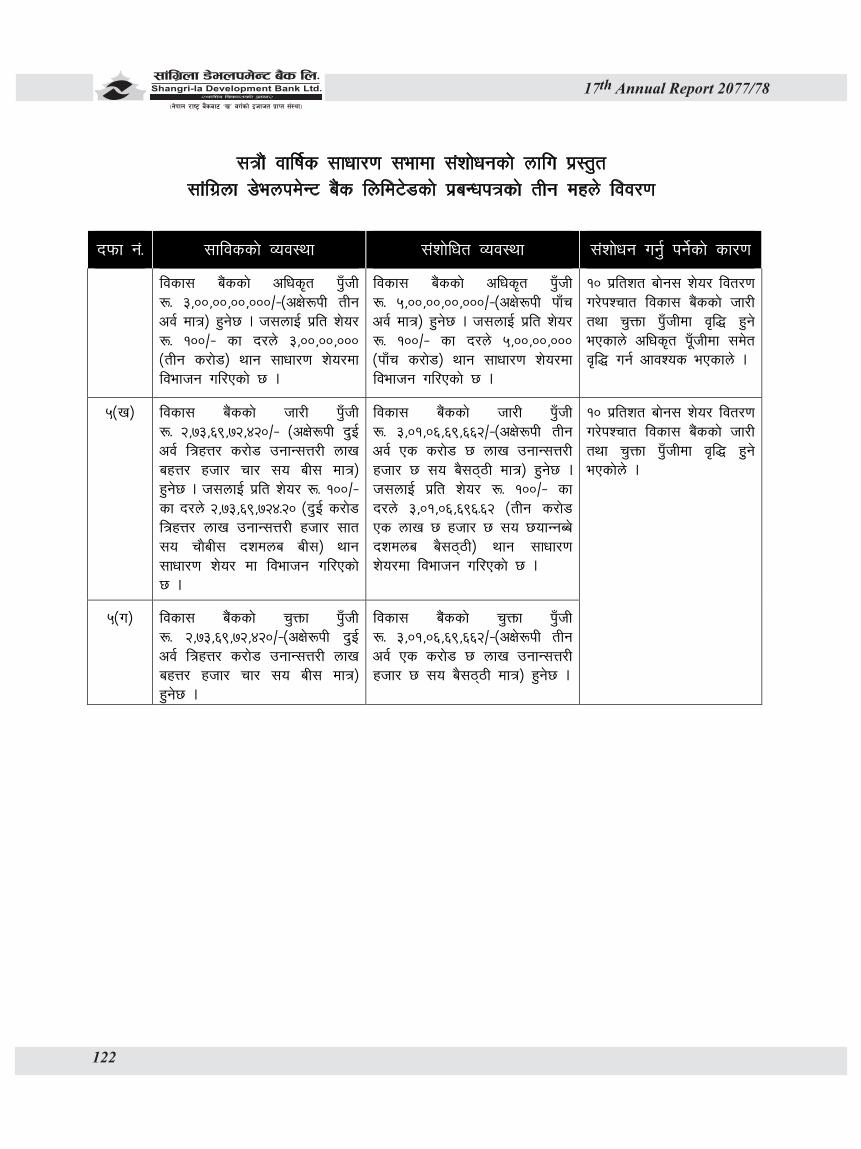

;f+lu|nf 8]enkd]G6 a}+s lnld6]8sf] ;qf}+ jflif{s ;fwf/0f ;ef a:g] ;DaGwL ;"rgf

cfb/0fLo z]o/wgL dxfg''efjx?, o; ;f+lu|nf 8]enkd]G6 a}+s lnld6]8sf] ;~rfns ;ldltsf] ldlt @)&*÷)^÷@% ut] -tb\g';f/ !! cS6f]j/ @)@!_ ;f]daf/sf lbg a;]sf] @&*cf}+ a}7ssf] lg0f{o cg';f/ o; 8]enkd]G6 a}+ssf] ;qf}+ jflif{s ;fwf/0f ;ef b]xfosf ljifox¿df 5nkmn ug{ lgDg ldlt, :yfg / ;dodf a:g] ePsf] x'Fbf sDkgL P]g, @)^# sf] bkmf ^& cg';f/ ;Dk"0f{ z]o/wgL dxfg'efjx¿sf] hfgsf/L Pj+ pkl:yltsf nflu of] ;"rgf k|sflzt ul/Psf] 5 .

;ef x'g] ldlt M @)&* ;fn sflQs !^ ut] -tb\g';f/ @ gf]e]Da/ @)@!_, d+unjf/ :yfg M n}grf}/ Aofª\Sj]6, n}grf}/, sf7df8f}+ . ;ef ;'? x'g] ;do M laxfg !)M)) ah] . 5nkmnsf] ljifo;"rL M s_ ;fwf/0f k|:tfj M -!_ cWoIfHo"sf] dGtAo ;lxt cfly{s jif{ @)&&÷)&* sf] ;~rfns ;ldltsf] jflif{s k|ltj]bg pk/ 5nkmn u/L

kfl/t ug]{ af/] . -@_ n]vfk/LIfssf] k|ltj]bg ;lxtsf] ldlt @)&* cfiff9 d;fGtsf] ljQLo cj:yfsf] ljj/0f tyf cfly{s jif{

@)&&÷)&* sf] gfkmf gf]S;fg lx;fa, cGo lj:t[t ljj/0f, gub k|jfx ljj/0f, OlSj6Ldf ePsf] kl/jt{g nufot ;Dk"0f{ ljQLo ljj/0fx¿ 5nkmn u/L kfl/t ug]{ af/] .

-#_ cfly{s jif{ @)&*÷)&( sf] nflu 8]enkd]G6 a}+ssf] n]vfk/LIf0f sfo{sf] nflu n]vfk/LIf0f ;ldltsf] l;kmfl/;

adf]lhd n]vfk/LIfs lgo'Qm ug]{ / lghsf] kfl/>lds lgwf{/0f ug]{ ;DaGwdf . -xfn jxfnjfnf n]vfk/LIfs >L /lGhj P08 P;f]l;o6\;, rf6{8 Psfp06]G6\; k'gM lgo'lQm x'g of]Uo x'g'x'G5._

-$_ ;~rfns ;ldltn] k|:tfj u/] adf]lhd 8]enkd]G6 a}+ssf] xfn sfod r'Qmf k"FhL @,&#,^(,&@,$@)÷– sf] !)

k|ltzt af]g; z]o/ ljt/0f ug]{ ;DjlGw ljz]if k|:tfj kfl/t x'Fbf ;f] af]g; z]o/ tyf s/ k|of]hgsf nflu k|:tfljt gub nfef+z ;d]t u/L s'n nfef+zdf nfUg] s/ e'QmfgL k|of]hgsf nflu 8]enkd]G6 a}+ssf] r'Qmf k"FhLsf] )=%@^# k|ltztn] x'g cfpg] /sd ?= !,$$,)%,!!*÷– -cIf]?kL Ps s/f]8 rjfnL; nfv kfFr xhf/ Ps ;o c7f/ dfq_ gub nfef+z ljt/0f ug]{ k|:tfj kfl/t ug]{ .

-%_ afFsL cjlwsf] nflu ul/Psf] ;+rfnssf] lgo'lQmsf] cg'df]bg ;DaGwdf .

v_ ljz]if k|:tfj M !_ xfn sfod clws[t k"FhL ? #,)),)),)),)))÷– -tLg cj{_ nfO{ j[l4 u/L ? %,)),)),)),)))÷– -kfFr cj{_

sfod ug]{ ;DjlGw k|:tfj kfl/t ug]{ . @_ ;~rfns ;ldltn] k|:tfj u/] adf]lhd xfn sfod r'Qmf k"FhL ? @,&#,^(,&@,$@)÷– -cIf]?kL b'O{ cj{ lqxQ/

s/f]8 pgfG;Q/L nfv jxQ/ xhf/ rf/ ;o jL; dfq_ sf] !) k|ltzt cyf{t /sd ?= @&,#^,(&,@$@÷– -cIf]?kL ;QfO{; s/f]8 5QL; nfv ;GtfgAa] xhf/ b'O{ ;o aofnL; dfq_ sf] af]g; z]o/ hf/L ug]{ ;DaGwL k|:tfj kfl/t ug]{ .

��

����������������������� ���������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

#_ 8]enkd]G6 a}+ssf] xfn sfod hf/L tyf r'Qmf k"FhL ? @,&#,^(,&@,$@)÷– -cIf]?kL b'O{ cj{ lqxQ/ s/f]8 pgfG;Q/L nfv jxQ/ xhf/ rf/ ;o jL; dfq_ /x]sf]df jf]g; z]o/ ljt/0f kZrft hf/L tyf r'Qmf k"FhL ? #,)!,)^,^(,^^@÷–-cIf]?kL tLg ca{ Ps s/f]8 5 nfv pgfG;Q/L xhf/ 5 ;o a};7\7L dfq_ k'¥ofpg] k|:tfj kfl/t ug]{ .

$_ ljz]if k|:tfj g+= -!_, -@_ / -#_ kfl/t eP adf]lhd x'g] u/L 8]enkd]G6 a}+ssf] k|jGwkq tyf lgodfjnLdf

cfjZos ;+zf]wg ug]{ ;DjlGw k|:tfj kfl/t ug]{ . %_ o; ;f+lu|nf 8]enkd]G6 a}+s / cGo O{hfhtkq k|fKt pko'Qm a}+s tyf ljQLo ;+:yf -x?_ Ps cfk;df

ufEg]÷ufleg] (Merger) tyf ;f+lu|nf 8]enkd]G6 a}+s lnld6]8n] cGo a}+s tyf ljQLo ;+:yf -x?_ k|flKt ug]{ (Acquisition) ;DaGwdf pko'Qm a}+s tyf ljQLo ;+:yf -x?_ vf]hL ug{, pko'Qm nfu]sf] a}+s tyf ljQLo ;+:yf;Fu ufEg]÷ufleg] (Merger) tyf k|flKt ug]{ (Acquisition) ;DaGwL ;xdltkq (Memorandum of Understanding) tof/ u/L x:tfIf/ ug{, ;Dk"0f{ rn crn ;DklQ tyf bfloTj d"Nof°g (Due Diligence Audit) u/fpg], tyf ufEg]÷ufleg] (Merger) jf k|flKt ug]{ (Acquisition) ;DaGwdf lgodgsf/L lgsfox?;Fu ;xdlt lng], ufEg]÷ufleg] (Merger) jf k|flKt ug]{ (Acquisition) ;DaGwL sfo{sf] nflu k|aGwkq tyf lgodfjnLdf cfjZos ;+zf]wg ug'{kg]{ ePdf ;f] ;d]t ug]{ nufotsf ;Dk"0f{ k|s[of cjnDag u/L Ps cfk;df ufEg]÷ufleg] (Merger) jf k|flKt ug]{ (Acquisition) ;Dk"0f{ sfo{ ug{ ;~rfns ;ldltnfO{ clVtof/L k|bfg ug]{ ;DaGwL k|:tfj kfl/t ug]{ .

^_ 8]enkd]G6 a}+ssf] k|aGwkq tyf lgodfjnLdf ePsf ;+zf]wgsf] :jLs[lt lng] qmddf g]kfn /fi6« a}+s, sDkgL

/lhi6«f/sf] sfof{no, g]kfn lwtf]kq af]8{ nufotsf lgodgsf/L lgsfoaf6 km]/abn, kl/dfh{g, yk36 tyf ;+zf]wg ug{sf] nflu lgb]{zg k|fKt ePdf ;f] sfo{ ug{sf nflu ;~rfns ;ldltnfO{ clVtof/L k|bfg ug]{ ;DalGw k|:tfj kfl/t ug]{ .

-u_ ljljw M

;~rfns ;ldltsf] cf1fn] sDkgL ;lrj

���

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

;qf}+ jflif{s ;fwf/0f ;ef ;DaGwL hfgsf/L

!= ;qf}+ jflif{s ;fwf/0f ;ef, ;f] ;efdf k]z x'g] !)=%@^# k|ltzt nfef+z k|of]hgsf nflu 8]enkd]G6 a}+ssf] z]o/ bflvn vf/]h -z]o/ btf{ lstfa_ ldlt @)&*÷)&÷% ut] b]lv ldlt @)&*÷)&÷!^ ut];Dd aGb /xg] 5 . z]o/ bflvn vf/]h aGb z'? x'g] ldlt eGbf cl3Nnf] lbg cyf{t ldlt @)&*÷)&÷)$ ut];Dd g]kfn :6s PS;r]~h lnld6]8df sf/f]jf/ eO{ lgodfg';f/ sfod z]o/wgLx?nfO{ ;fwf/0f ;efdf efu lng tyf !)=%@^# k|ltzt nfef+z k|fKt ug{sf nflu of]Uo x'g]5g\ .

@= z]o/wgL dxfg'efjx?nfO{ z]o/wgL nutdf sfod /x]sf] 7]ufgfdf ;~rfns ;ldltsf] k|ltj]bg / n]vfk/LIf0f

k|ltj]bg ;lxtsf] cfly{s jif{ )&&÷)&* sf] jflif{s k|ltj]bg k'l:tsf k7fOg]5 . s'g} sf/0fjz z]o/wgLn] ;dodf jflif{s k|ltj]bg k'l:tsf k|fKt ug{ g;s]df o; 8]enkd]G6 a}+ssf] s]Gb|Lo sfof{no afn'jf6f/, sf7df8f+} jf z]o/ /lhi6«f/ PgcfOljPn P; Soflk6n lnld6]8af6 k|fKt ug{ ;Sg'x'g]5 . pQm k|ltj]bg 8]enkd]G6 a}+ssf] j]j;fO6 www.shangrilabank.com df x]g{ / 8fpgnf]8 ug{ ;d]t ;lsg]5 .

#= ;efdf pkl:yt x'g] ;Dk"0f{ z]o/wgLx?n] z]o/ k|df0fkq jf l8Dof6 vftfsf] ljj/0f / cfkm\gf] kl/ro v'Ng] k|df0f

-h:t} gful/stf k|df0fkq jf cGo s'g} kl/rokq_ clgjfo{ ?kdf ;fydf lnO{ cfpg'x'g cg'/f]w 5 . ;fy} 8]enkd]G6 a}+ssf] ;qf} jflif{s ;fwf/0f ;efdf z]o/wgL dxfg'efjx?n] h'd ldl6ª (Zoom Meeting) k|ljlw dfkm{t ;d]t cjnf]sg ug{ ;lsg] Joj:yf ldnfO{Psf] 5 . o;sf] nflu 8]enkd]G6 a}+sn] z]o/wgL dxfg'efjx?nfO{ z]o/ /lhi6«f/ dfkm{t k|fKt x'g] clen]vdf pNn]lvt df]afOn gDa/df ldl6ª cfO{8L / kf;sf]8 ;DaGwL hfgsf/L pknAw u/fOg]5 . xfn ljZje/ km}ln/x]sf] sf]le8 !( sf] dxfdf/LnfO{ dWogh/ ub}{ oyf;So h'd ldl6ª (Zoom Meeting) k|ljlw dfkm{t ;xeflutf hgfpg k|f]T;fxg ul/g]5 . o;/L ePsf] pkl:ytLnfO{ ;ef xndf pkl:yt eP ;/x dfGotf k|bfg ul/g]5 .

$= ;efdf efu lngsf] nflu k|ltlglw -k|f]S;L_ lgo'Qm ug{ rfxg] z]o/wgLx?n] k|f]S;L kmf/d e/L ;ef ;'? x'g] egL

tf]lsPsf] ;do eGbf slDtdf $* 306f cufj} sf/f]jf/ ;do leq 8]endk]G6 a}+ssf] s]Gb|Lo sfof{nodf btf{ ul/;Sg' kg]{5 . o;/L lgo'Qm ul/Psf] k|ltlglw 8]endk]G6 a}+ssf] z]o/wgL x'g'kg]{5 . To;/L k|ltlglw lgo'Qm ul/;s]kl5 pQm k|ltlglw ab/ u/L csf]{ k|ltlglw d's// u/L ;ef z'? x'g] egL tf]lsPsf] ;do eGbf slDtdf $* 306f cufj} 8]enkd]G6 a}+ssf] s]Gb|Lo sfof{nodf sf/f]jf/ ;do leq btf{ u/]df jf cfkm' :jo+ ;fwf/0f ;efdf pkl:yt x'g cfPdf To:tf] z]o/wgLn] ul/lbPsf] cl3Nnf] k|f]S;L :jtM ab/ x'g]5 . s'g} z]o/wgLn] Ps eGbf a9L z]o/wgLnfO{ k|ltlglw lgo'Qm u/]sf] /x]5 eg] lgh :jo+n] cGo ab/ u/L Pp6f sfod u/]sf] cj:yfdf afx]s To:tf ;a} k|ltlglw kqx? :jtM ab/ x'g]5 . k|ltlglw d's// ubf{ cfkm\gf] ;Dk"0f{ z]o/sf] k|ltlglw Pp6} JolQmnfO{ lgo'Qm ug'{k5{ . s'g} lsl;daf6 5'6\ofO{ lbPdf pQm k|f]S;L ab/ ul/g]5 . o; ;DaGwdf ;fwf/0f ;efdf ljjfb ug{ kfO{g] 5}g .

%= ;+o'Qm ?kdf z]o/ u|x0f ug]{ z]o/wgLx?sf] xsdf ;fem]bf/x?åf/f lgo'Qm ;fem]bf/n] jf lghn] lgo''Qm u/]sf]

k|ltlglwn] / ;f] adf]lhd lgo'Qm x'g g;s]sf]df z]o/wgLx?sf] btf{ lstfadf gfd qmdfg';f/ cl3 n]lvPsf] ;fem]bf/n] dfq ;efdf efu lng, 5nkmn ug{ / dtbfg ug{ kfpg]5 .

^= gfafns jf dfgl;s ;Gt'ng l7s gePsf z]o/wgLsf] tkm{af6 sDkgLsf] z]o/wgL btf{ lstfadf ;+/Ifssf] ?kdf

btf{ ePsf] ;+/Ifsn] jf ;+/Ifsn] lgo'Qm u/]sf] k|ltlglwn] ;efdf efu lng tyf dtbfg ug{ kfpg]5g\ .

��

�������������������� ������������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

&= ;+ul7t ;+:yf jf sDkgL z]o/wgL ePsf]df To:tf ;+ul7t ;+:yf jf sDkgLn] dgf]lgt u/]sf] k|ltlglwn] ;efdf efu lng / dtbfg ug{ kfpg]5g\ .

*= ljljw zLif{s cGtu{t 5nkmn ug{ rfxg] z]o/wgLn] 5nkmn ug{ rfx]sf] ljifo ;ef x'g' eGbf & lbg cufj}

8]enkd]G6 a}+ssf] s]Gb|Lo sfof{no afn'jf6f/, sf7df8f}+df lnlvt ?kdf hfgsf/L u/fpg'kg]{5 . o;/L lnlvt ?kdf k"j{ hfgsf/L gu/fPsf] ljifodf ;efdf 5nkmn tyf lg0f{o ul/g] 5}g .

(= z]o/wgL dxfg'efjx?sf] ;'ljwfsf] nflu xflh/L k'l:tsf ;ef :yndf ;fwf/0f ;ef x'g] lbg ljxfg )(M)) ah]b]lv

g} v'Nnf ul/g]5 . ;fwf/0f ;efdf efu lng] k|To]s z]o/wgL dxfg'efjx?n] ;ef x'g] :yfgdf pkl:yt eO{ pQm :yfgdf /x]sf] xflh/L k'l:tsfdf b:tvt ug'{kg]{5 .

!)= ;fwf/0f ;efsf] sfd sf/jfxLx? sDkgL P]g @)^#, a}+s tyf ljlQo ;+:yf ;DaGwL P]g @)&# tyf 8]enkd]G6

a}+ssf] k|aGwkq, lgodfjnL adf]lhd x'g]5g\ . !!= zflGt ;'/Iffsf sf/0f ;fwf/0f ;efdf pkl:yt x'g] z]o/wgL dxfg'efjx?nfO{ oyf;So emf]nf÷Aofu gNofpg'x'g

cg'/f]w ul/G5 . ;efsf] ;'/Iffsf nflu vl6Psf ;'/IffsdL{x?n] z]o/wgL dxfg'efjx? nufot ;efsIfdf k|j]z ug]{ ;a}sf] emf]nf÷Aofu / z/L/ hfFr ug{ ;Sg]5g\ .

!@= ;fwf/0f ;ef ;DaGwL yk hfgsf/L 8]enkd]G6 a}+ssf] s]Gb|Lo sfof{no afn'jf6f/ sf7df8f}+af6 sfof{no ;do

leq k|fKt ug{ ;lsg]5 .

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

������������������������������������������ ������������������������������������

��������������� �������������������

������������������������������������������������������������������������������������������������������������������������������������������������ ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������ ���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������� ����������������������������������������������������������������������

���������������������� ������������������������������������������������������������������������������������������������������������������� ���������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�����������������������������������¡���������¢��£����¤����������������������������������������������¥

������������������������������������������������������������������������������������������������� ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

��� ����¡����������������������������������������������������������������������������������������������¦�����������������

������������������������������� ������������������ �������������������������¥�������������� ��������������������� �����§�������¨���������§���������� �����

����������������¦��������������������������������������¡�����¡���¤�������©��������������������¥

��������

����������������������������������������� ���

���������§�¥

�������������������������� �������������������������� ����

���������������������

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

8]enkd]G6 a}++s ;DaGwL hfgsf/L

8]enkd]G6 a}+ssf] gfd M ;f+lu|nf 8]enkd]G6 a}+s lnld6]8

sDkgLsf] k|sf/ M klAns lnld6]8 sDkgL

/lhi68{ sfof{no M afn''jf6f/, sf7df8f}F}

sDkgL /lhi6«f/sf] sfof{nodf btf{ ePsf] ldlt,btf{ g+ M *&!÷)^)÷^!, @)^)÷!)÷!$

g]kfn /fi6« a}+s af6 sf/f]af/ :jLs[lt k|fKt ldlt M @)^)÷!)÷@#

ljQLo sf/f]af/ z'? ePsf] ldlt M @)^!÷)&÷!#

sfo{ If]q M /fli6«o:t/

:yfoL n]vf gDa/ M #)!^%%@$*

k"FhL ;+/rgf M clws[t k""FhL M ?= #,)),)),)),)))÷—

Hff/L k""FhL M ?= @,&#,^(,&@,$@)÷–

r'Qmf k""FhL M ?= @,&#,^(,&@,$@)÷–

Zf]o/ ;+/rgf M ;+:yfks M %! k|ltzt

;j{;fwf/0f M $( k|ltzt

z]o/ wgLsf] ;+Vof M %@@ hgf, ;+:yfks @),&(* hgf ;j{;fwf/0f

k|ltj]bg tof/ kfbf{sf] ldlt;Dd ;+rfngdf /x]sf zfvf ;+Vof (*

s'n sd{rf/L ;+Vof M &#% -##* hgf dlxnf_

Zf]o/ ;'lrs/0f ldlt M @)^&÷!)÷!!

g]6jy{ -k|:tfljt nfef+z ;lxt_ M ?= #,&!,@$,&!,#^(÷–

g]6jy{ k|lt z]o/ -k|:tfljt af]g; z]o/ ;lxt_ M ?= !#^

s'n lgIf]k M ?= $@,*$,(^,$@,&$%=&(÷–22 638 219 075.91s'n shf{ tyf ;fk6L M ?= #^,!*,*),$#,!&^=$!÷–

Vf'b gfkmf M ?= $!,)),*),$%&=)$÷–

k|lt z]o/ cfDbfgL -af]g; z]o/ ;dfj]z ug'{ cl3_ M ?= !$=(*

Kf"FhLsf]if k|of{Kttf M !!=&& k|ltzt

shf{ / kF'hL tyf lgIf]k cg'kft -CCD Ratio_ M &*=@( k|ltzt

shf{ tyf lgIf]k cg'kft -CD Ratio_ M *$=&) k|ltzt

lgis[o shf{ cg'kft M !=#( k|ltzt

t/ntf cg'kft M @$=#^ k|ltzt

Aofhb/ cGt/ M $=@( k|ltzt

artstf{ ;+Vof M #^),*$^

C0fL ;+Vof M !(,$*%

n]vf k/LIfs M >L /lGhj P08 P;f]l;o6\;, rf6{8 Psfp06]G6\;

�

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

;f+lu|nf 8]enkd]G6 a}+s lnld6]8sf] ;qf}+ jflif{s ;fwf/0f ;efsf nflu ;~rfns ;ldltsf] tkm{af6

cWoIfHo"sf] k|ltj]bg -cf=j=@)&&÷)&*_

cfb/0fLo z]o/wgL dxfg'efjx?, o; ;f+lu|nf 8]enkd]G6 a}+s lnld6]8sf] cfhsf] o; ;qf} jflif{s ;fwf/0f ;efdf pkl:yt x'g' ePsf ;Dk"0f{ >4]o z]o/wgL dxfg'efjx?, ;~rfns ;ldltsf ;b:oHo"x?, xfd|f] lgdGq0ffnfO{ ;xif{ :jLsf/ u/L lgodgsf/L lgsfoaf6 kfNg' ePsf cltlyHo'x?, cfGtl/s tyf afx|o n]vfk/LIfs, sfg'gL ;Nnfxsf/, a}+ssf k|d'v sfo{sf/L clws[t tyf sfo{/t sd{rf/Lx? Pj+ pkl:yt ;Dk"0f{ eb| dlxnf tyf ;Hhgj[Gbx? k|lt cfhsf] o; ;fwf/0f ;efsf] z'e cj;/df d]/f] JolQmut tyf ;+rfns ;ldltsf tkm{jf6 xflb{s :jfut Pj+ clejfbg AoQm ub{5' .

cf=j= @)&&÷)&* Dff o; 8]enkd]G6 a}+sn] xfl;n u/]sf] k|ult Pj+ pknlAwx? ;dfj]z ul/Psf] @)&* cfiff9 d;fGt ;Ddsf] ljQLo cj:yfsf] ljj/0f, gfkmf jf gf]S;fg ljj/0f, lj:t[t cfosf] ljj/0f, gub k|jfx ljj/0f / OlSj6Ldf ePsf] kl/jt{gsf] ljj/0f tyf ;f];Fu ;DaGwLt cg';"rLx? ;lxtsf] ;~rfns ;ldltaf6 kfl/t tyf g]kfn /fi6« a}+saf6 l:js[t ljQLo ljj/0f oxfFx? ;dIf l:js[tLsf nflu k]z u/]sf] 5' .

o; ;fwf/0f ;efn] 8]enkd]G6 a}+sn] ut cfly{s jif{df u/]sf] pknlAwx? tyf rfn' cfly{s jif{df / eljiodf rfNg' kg]{ sbd tyf ckgfpg' kg]{ gLlt lgod / sfo{of]hgf ;DaGwdf ;Nnfx ;'emfj Pj+ dfu{ lgb]{zg ug]{5 eGg] ljZjf;sf ;fy oxfFx? ;Dk"0f{nfO{ Åbo b]lv xflb{s :jfut ub}{ o; ;qf}+ jflif{s ;fwf/0f ;efsf] k|ltj]bg 5nkmn tyf l:js[tLsf] nfuL oxfFx? ;dIf k]z ug]{ cg'dtL rfxG5' .

-!_ cf=j= )&&÷)&* sf] 8]enkd]G6 a}+ssf] sf/f]jf/ ;ldIff M– s_ ljQLo l:ytL M 8]enkd]G6 a}+ssf] cf=j= @)&&÷)&* tyf @)&^÷)&& sf] t'ngfTds ljQLo l:ytL lgDg cg';f/ 5 .

?= xhf/df

ljj/0f cf=j=)&&÷)&* cf=j=)&^÷)&& j[l4÷sdL/sddf k|ltzt

r'Qmf kF"hL -k|:tfljt af]g; z]o/ ;lxt_ 3,010,669 2,736,972 273,697 10.00%

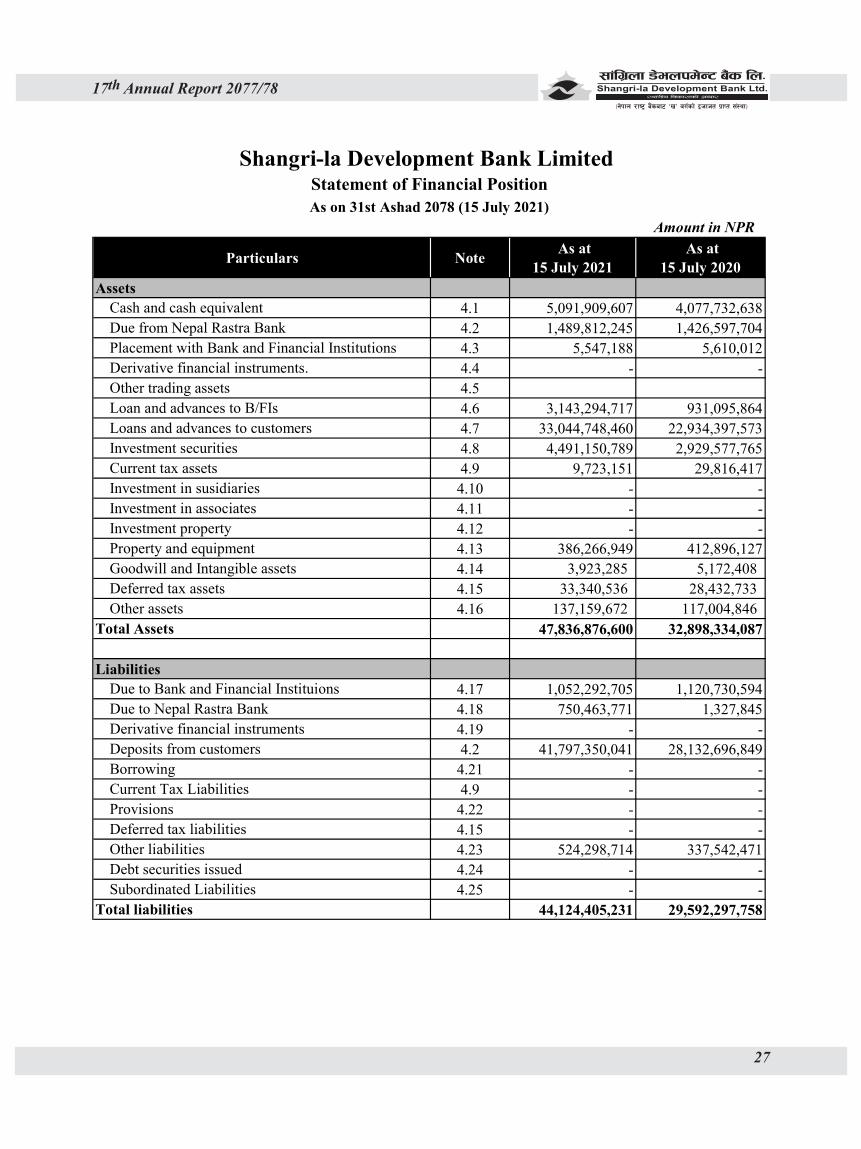

hu]8f tyf sf]ifx? 659,580 545,903 113,677 20.82% s'n ;DklQ 47,836,877 32,898,334 14,938,543 45.41% s'n lgIf]k 42,849,643 29,253,427 13,596,216 46.48% s'n shf{ tyf ;fk6 36,188,043 23,865,493 12,322,550 51.63% nufgL 4,491,151 2,929,578 1,561,573 53.30% Aofh cfDbfgL 3,515,206 3,135,051 380,155 12.13% Aofh vr{ 2,308,686 2,084,753 223,933 10.74% v'b Aofh cfDbfgL 1,206,520 1,050,299 156,221 14.87% sd{Rff/L vr{ 490,234 366,789 123,445 33.66% cGo ;+rfng vr{ 282,762 249,721 33,041 13.23% ;+rfng d'gfkmf 589,412 267,725 321,687 120.16% v'b d'gfkmf 410,080 191,098 218,982 114.59% Gff]S;fgL Aoj:yf yk -sdL_ 236,068 259,481 -23,413 -9.02% t/ntf k|ltzt 24.36% 27.30% - -10.77% lglis|o shf{ k|ltzt 1.39% 1.13% - 23.01% k|lt z]o/ cfDbfgL ?= 14.98 7.33 7.65 104.37% cfwf/ b/ k|ltzt 8.54% 9.99% - -14.51% k"FhL sf]if kof{Kttf k|ltzt 11.77% 12.93% - -8.97%

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

ljZjAofkL ?kdf km}lnPsf] sf]le8–!( sf] dxfdf/Ln] l;lh{t c;xh kl/l:ytLn] ubf{ ljZj cy{tGq g} ylnPsf] cj:yfdf clwsf+z pBf]u, Aofkf/ Joj;fox?df k|lts'n c;/ kg{ uPsf] oxf+x?nfO{ ljlbt} 5 . cf=j= @)&^÷&& sf] r}q dlxgfb]lv nfdf] ;do;Dd b]zAofkL ?kdf ePsf] aGbfaGbL / tt\ kZrft @)&&÷)&* j}zfv b]lv ePsf] lgif]wf1fsf] k|ToIf k|efj xfd|f] a}+snfO{ klg k/]sf] 5 . o;/L sf]le8–!( sf] sf/0f C0fLx?df k/]sf] c;/ Go"gLs/0f ug]{ p2]Zon] g]kfn /fi6« a}+såf/f sf]/f]gf k|efljt C0fLx?sf] ;'ljwfsf nflu ljleGg lgb]{zg hf/L eP adf]lhd u|fxsx?nfO{ ;dodf ls:tf /sd a'emfpg g;Sbf k]gfN6L /sd ltg{ gkg'{sf ;fy lgif]wf1fsf] cjlwe/ shf{ /sd c;'npk/sf] nflu lwtf] lnnfd ug{ gkfOg] Joj:yfn] ;d]t C0fLx?nfO{ /fxt k'Ug uPsf] 5 .

o:tf] ljifd kl/l:ytLsf afah't klg pk/f]Qm ljQLo ljj/0fx?sf] cfwf/df 8]enkd]G6 a}+ssf] ljQLo ;"rsf+sx? ;Gtf]ifhgs g} /x]sf 5g . 8]enkd]G6 a}+sn] o; cf=j= @)&&÷&* sf] d'gfkmfaf6 af]g; z]o/ ljt/0f ug]{ k|:tfj u/]sf]n] 8]enkd]G6 a}+ssf] r'Qmf k"+hLdf !) k|ltztn] j[l4 x'g] ePsf] 5 eg] k"+hLsf]if kof{Kttf, g]kfn /fi6« a}+sn] /fli6«o :t/sf] ljsf; a}+snfO{ tf]s]sf] !) k|ltzt eGbf !=&& k|ltztn] cem} clws /x]sf] 5 .

To:t} 8]enkd]G6 a}+ssf] v'b Aofh cfDbfgL !$=*& k|ltztn] j[l4 ePsf] 5 eg] sf]le8–!( dxfdf/Lsf] sf/0f ;dodf shf{sf] Aofh c;'nL x'g g;s]sf]n] ;Defljt gf]S;fgL Aoj:yfdf s]xL j[l4 eO{ lgis[o shf{ cg'kft ut cf= j= eGbf @#=)! k|ltztn] j[l4 ePsf] 5 .

ut cf= j= @)&^÷&& sf] s'n shf{ tyf ;fk6Ldf sl/j ?= !@ cj{ #@ s/f]8 yk shf{ k|jfx u/L 8]enkd]G6 a}+sn] o; cf= j= @)&&÷&* df s'n shf{ ?= #^ cj{ !* s/f]8 k'/\ofPsf] 5 h'g ut cf=j=sf] t'ngfdf %!=^# k|ltztsf] j[l4 xf] eg] lgIf]kdf ?= !# cj{ %( s/f]8 yk lgIf]k ;+sng u/L ?= $@ cj{ *$ s/f]8 k'/\ofPsf] 5 h'g ut jif{sf] t'ngfdf $^=$* k|ltztsf] j[l4 xf] . To;sf] ;fy} ;ldIff jif{df a}+sn] nufgL tkm{ em08} ?= ! cj{ $$ s/f]8 a/fa/sf] ljsf; C0fkq tyf 6«]h/L landf / Do"Rcn km08 tyf cGo ;+:yfx?sf] z]o/df ?= !! s/f]8 u/L s'n ?= ! cj{ %^ s/f]8 a/fa/ nufgL yk u/]sf]n] a}+ssf] cfDbfgLdf ljljwtf ug]{ tkm{ cu|;/ ePsf] 5 .

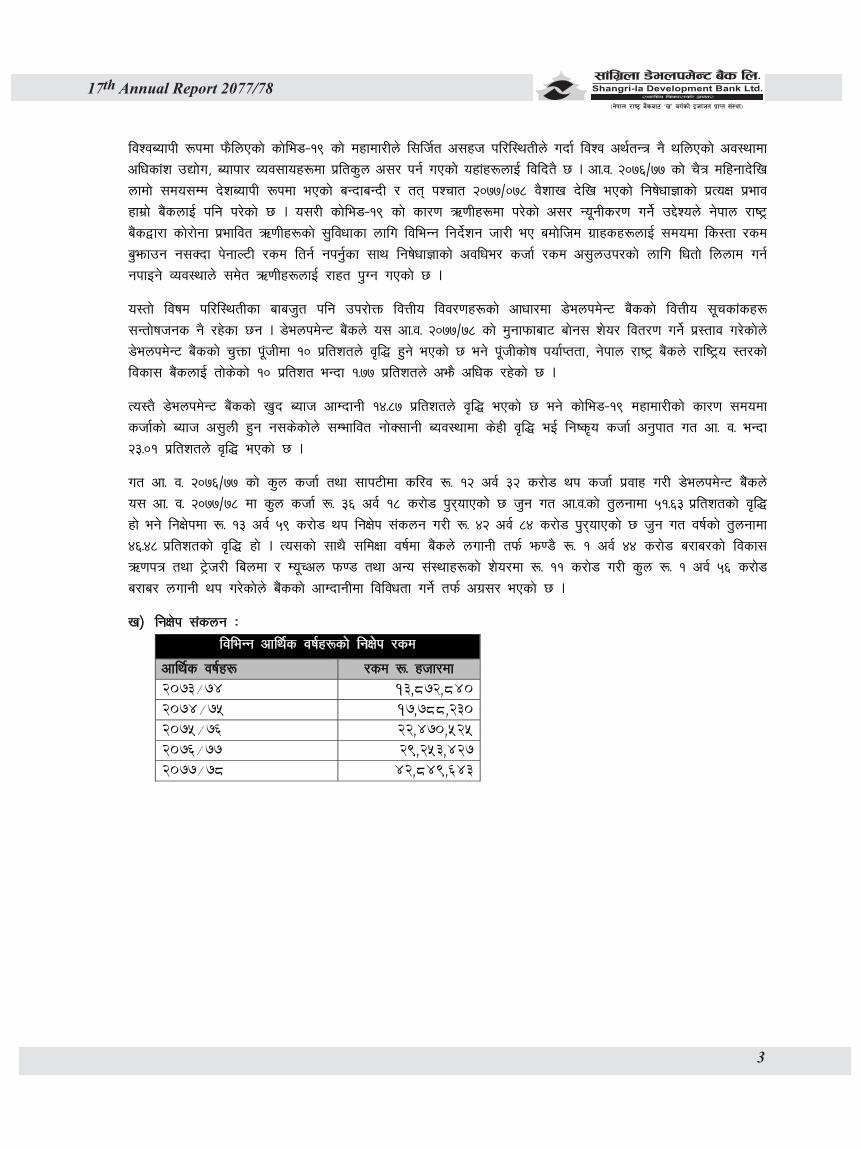

v_ lgIf]k ;+sng M ljleGg cfly{s jif{x?sf] lgIf]k /sd

cfly{s jif{x? /sd ?= xhf/df 2073÷74 13,872,840 2074÷75 17,788,230 2075÷76 22,470,525 2076÷77 29,253,427 2077÷78 42,849,643

�

����������������������� ���������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

ljut kfFr cf= j= b]lv xfn;Dd o; 8]enkd]G6 a}+ssf] lgIf]k /sdsf] j[l4b/ lgDgfg';f/ 5 M

cf=j= @)&^÷&& sf] cGTodf ?= @( cj{ @% s/f]8 lgIf]k /x]sf]df o; 8]enkd]G6 a}+sn] o; cf= j= @)&&÷&* sf] cfiff9 d;fGt;Dd cfO{k'Ubf sl/a !# cj{ %( s/f]8 yk lgIf]k ;+sng u/L ?= $@ cj{ *$ s/f]8 k'/\ofPsf] 5 h'g ut jif{sf] t'ngfdf $^=$* k|ltztsf] j[l4 xf] eg] ;f] cjlw;Dd 8]enkd]G6 a}+ssf sl/a # nfv ^) xhf/ eGbf al9 u|fxsx? /x]sf 5g\ .

xfn o; 8]enkd]G6 a+}ssf] lgIf]ksf] agf]6 o; k|sf/ /x]sf] 5 . ?= xhf/df

qm=;+= lgIf]ksf] k|sf/ )&&÷&* -?=_ k|ltzt )&^÷&& -?=_ k|ltzt!= dflh{g lgIf]k 18,650 0.04 22,448 0.08@= art lgIf]k 13,022,179 30.39 9,364,835 32.01#= d'2tL lgIf]k 23,891,451 55.76 15,723,976 53.75$= dfu]sf] avt ltg'{ kg{] lgIf]k 5,104,925 11.91 3,515,390 12.02%= rNtL lx;fa 812,438 1.90 626,778 2.14

hDdf ?= 42,849,643 100 29,253,427 100

13,872,84017,788,230

22,470,525

29,253,427

42,849,643

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

/sd

?= xh

f/df

cfly{s jif{

ljleGg cfly{s jif{x?sf] lgIf]k /sd

2073÷74 2074÷75 2075÷76 2076÷77 2077÷78

0.04%

30.39%

55.76%

11.91% 1.90%

cfly{s jif{ @)&&÷&* df lgIf]ksf] agf]6 -?=_

dflh{g lgIf]k art lgIf]k d'2tL lgIf]k dfu]sf] avt ltg'{ kg{] lgIf]k rNtL lx;fa

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

Dffly pNn]lvt lgIf]ksf] agf]6n] klg k|i6 kfb{5 ls 8]enkd]G6 a}+sdf d'2tL lgIf]k tyf art lgIf]k dfu]sf] avt ltg"{ kg]{ -sn vftf_ lgIf]ksf] t''ngfdf c+z al9 /x]sf]5 . o;/L o; 8]enkd]G6 a}+ssf] s'n lgIf]ksf] ^#=(^ k|ltzt lgIf]k ;j{;fwf/0f JolQmx?sf] /x]sfn] ubf{ 8]enkd]G6 a}+s t/ntfsf] b[li6«sf]0fn] Go""g hf]lvddf /x]sf] k|i6 x'G5 .

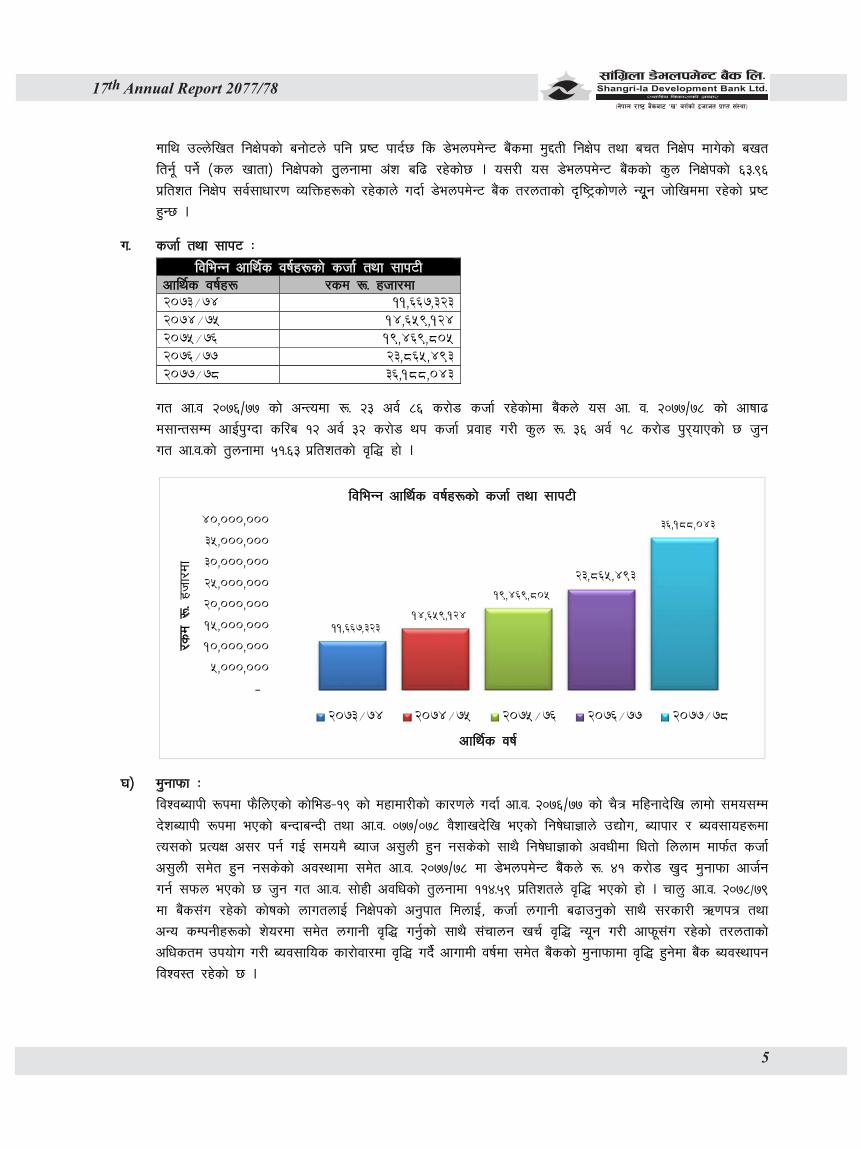

u= shf{ tyf ;fk6 M ljleGg cfly{s jif{x?sf] shf{ tyf ;fk6L

cfly{s jif{x? /sd ?= xhf/df2073÷74 11,667,3232074÷75 14,659,1242075÷76 19,469,8052076÷77 23,865,4932077÷78 36,188,043

ut cf=j @)&^÷&& sf] cGTodf ?= @# cj{ *^ s/f]8 shf{ /x]sf]df a}+sn] o; cf= j= @)&&÷&* sf] cfiff9 d;fGt;Dd cfO{k'Ubf sl/a !@ cj{ #@ s/f]8 yk shf{ k|jfx u/L s'n ?= #^ cj{ !* s/f]8 k'/\ofPsf] 5 h'g ut cf=j=sf] t'ngfdf %!=^# k|ltztsf] j[l4 xf] .

3_ d'gfkmf M ljZjAofkL ?kdf km}lnPsf] sf]le8–!( sf] dxfdf/Lsf] sf/0fn] ubf{ cf=j= @)&^÷&& sf] r}q dlxgfb]lv nfdf] ;do;Dd

b]zAofkL ?kdf ePsf] aGbfaGbL tyf cf=j= )&&÷)&* j}zfvb]lv ePsf] lgif]wf1fn] pBf]]u, Aofkf/ / Aoj;fox?df To;sf] k|ToIf c;/ kg{ uO{ ;dod} Aofh c;'nL x'g g;s]sf] ;fy} lgif]wf1fsf] cjwLdf lwtf] lnnfd dfkm{t shf{ c;'nL ;d]t x'g g;s]sf] cj:yfdf ;d]t cf=j= @)&&÷&* df 8]enkd]G6 a}+sn] ?= $! s/f]8 v'b d'gfkmf cfh{g ug{ ;kmn ePsf] 5 h'g ut cf=j= ;f]xL cjlwsf] t'ngfdf !!$=%( k|ltztn] j[l4 ePsf] xf] . rfn' cf=j= @)&*÷&( df a}+s;+u /x]sf] sf]ifsf] nfutnfO{ lgIf]ksf] cg'kft ldnfO{, shf{ nufgL a9fpg'sf] ;fy} ;/sf/L C0fkq tyf cGo sDkgLx?sf] z]o/df ;d]t nufgL j[l4 ug'{sf] ;fy} ;+rfng vr{ j[l4 Go"g u/L cfkm";+u /x]sf] t/ntfsf] clwstd pkof]u u/L Aoj;flos sf/f]jf/df j[l4 ub}{ cfufdL jif{df ;d]t a}+ssf] d'gfkmfdf j[l4 x'g]df a}+s Aoj:yfkg ljZj:t /x]sf] 5 .

11,667,323 14,659,124

19,469,805

23,865,493

36,188,043

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

/sd

?= xh

f/df

cfly{s jif{

ljleGg cfly{s jif{x?sf] shf{ tyf ;fk6L

2073÷74 2074÷75 2075÷76 2076÷77 2077÷78

�

����������������������� ���������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

ljleGg cfly{s jif{x?sf] ;+rfng d"gfkmf cfly{s jif{x? /sd ?= xhf/df

2073÷74 538,685 2074÷75 442,108 2075÷76 490,768 2076÷77 267,725 2077÷78 589,412

ljleGg cfly{s jif{x?sf] v'b d'gfkmf cfly{s jif{x? /sd ?= xhf/df

2073÷74 347,786 2074÷75 305,190 2075÷76 341,819 2076÷77 191,098 2077÷78 410,080

538,685

442,108490,768

267,725

589,412

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

/sd

?= xh

f/df

cfly{s jif{

ljleGg cfly{s jif{x?sf] ;+rfng d"gfkmf

2073÷74 2074÷75 2075÷76 2076÷77 2077÷78

347,786 305,190

341,819

191,098

410,080

-

100,000

200,000

300,000

400,000

500,000

/sd

?= x

hf/df

cfly{s jif{

ljleGg cfly{s jif{x?sf] v'b d'gfkmf

2073÷74 2074÷75 2075÷76 2076÷77 2077÷78

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

-@_ /fli6«o tyf cGt/f{li6«o kl/l:ytLjf6 sf/f]jf/nfO{ k/]sf] c;/ M

cGt/f{li6«o kl/b[io ;g\ @)@) df #=@ k|ltztn] ;+s'rg ePsf] ljZj cy{tGq ;g\ @)@! Dff ^=) k|ltztn] la:tf/ x'g] cGt/f{li6«o d'b|f sf]ifsf]

cg'dfg 5 . ;g\ @)!( df ljZj cy{tGq @=* k|ltztn] la:tf/ ePsf] lyof] . ;g\ @)@) df $=^ k|ltztn] ;+s'rg ePsf] ljsl;t d'n'sx¿sf] cy{tGq ;g\ @)@! df %=^ k|ltztn] la:tf/ x'g] k|If]k0f /x]sf] 5 . To;}u/L, ;g\ @)@) df @=! k|ltztn] ;+s'rg x'g] cg'dfg /x]sf] pbLodfg tyf ljsf;zLn cy{tGq ;g\ @)@! df ^=# k|ltztn] la:tf/ x'g] k|If]k0f 5 . ;g\ @)!( df ljsl;t cy{tGq / pbLodfg tyf ljsf;zLn cy{tGqsf] j[l4b/ qmdzM !=^ k|ltzt / #=& k|ltzt /x]sf] lyof] .

l5d]sL d'n'sx? dWo] rLgsf] cy{tGq ;g\ @)!( df ^=) k|ltztn] la:tf/ ePsf]df ;g\ @)@) df @=# k|ltztn] j[l4 ePsf] cGt/f{li6«o d'b|f sf]ifsf] cg'dfg 5 . To;} u/L, ef/tsf] cy{tGq ;g\ @)!( df $=) k|ltztn] la:tf/ ePsf]df ;g\ @)@) df &=# k|ltztn] ;+s'rg ePsf] sf]ifsf] cg'dfg 5 . ;g\ @)@! df rLgsf] cfly{s j[l4 *=! k|ltzt / ef/tsf] (=% k|ltzt /xg] k|If]k0f 5 . ;g\ @)@) df ljsl;t d'n'sx¿sf] d'b|f:kmLlt )=& k|ltzt /x]sf]df ;g\ @)@! df @=$ k|ltzt /xg] sf]ifsf] k|If]k0f 5 . pbLodfg tyf ljsf;zLn d'n'sx¿sf] d'b|f:kmLlt ;g\ @)@) df %=! k|ltzt /x]sf]df ;g\ @)@! df %=$ k|ltzt /xg] k|If]k0f 5 . ;g\ @)@) df ljZj Jofkf/ cfotg *=# k|ltztn] ;+s'rg ePsf]df ;g\ @)@! df (=& k|ltztn] la:tf/ x'g] k|If]k0f 5 . ;g\ @)@) df k]6«f]lnod kbfy{sf] d"Nodf #@=& k|ltztn] sdL cfPsf]df ;g\ @)@! df %^=^ k|ltztn] j[l4 x'g] k|If]k0f 5 .

sf]le8–!( dxfdf/Ln] ubf{ Psftkm{ clwsf+z d'n'sx?df /fh:j kl/rfng ;+s'lrt ePsf] 5 eg] csf]{ tkm{ ;fj{hlgs vr{df ePsf] a9f]Q/Lsf sf/0f s'n ufx{:Yo pTkfbg;Fu ;fj{hlgs C0fsf] cg'kft ljZjJofkL ?kdf a9]sf] 5 . ;g\ @)!( df o:tf] cg'kft *#=& k|ltzt /x]sf]df ;g\ @)@) df (&=# k|ltzt k'u]sf] 5 .

;dli6ut cfly{s l:ylt

cfly{s j[l4 cfly{s jif{ @)&^÷&& df @=)( k|ltztn] ;+s'rgdf uPsf] g]kfnsf] cy{tGq cfly{s jif{ @)&&÷&* df $=)! k|ltztn] la:tf/

x'g] s]Gb|Lo tYof° ljefusf] cg'dfg /x]sf] 5 . t/ rf}yf] qodf;df ePsf] ;+qmd0fsf] bf];|f] nx/n] of] j[l4b/ sfod x'g r'gf}tLk"0f{ b]lvPsf] 5 . cfly{s jif{ @)&&÷&* df s'n ufx{:Yo pTkfbg;Fusf] s'n ufx{:Yo artsf] cg'kft ^=^ k|ltzt / s'n /fli6«o artsf] cg'kft #!=$ k|ltzt /x]sf] cg'dfg 5 . cl3Nnf] jif{ oL cg'kftx? qmdzM ^=# k|ltzt / #@=^ k|ltzt /x]sf lyP . cfly{s jif{ @)&&÷&* df s'n ufx{:Yo pTkfbgdf s'n l:y/ k"FhL lgdf{0fsf] cg'kft @&=# k|ltzt /x]sf] cg'dfg 5 . cl3Nnf] jif{ o:tf] cg'kft @*=$ k|ltzt /x]sf] lyof] .

d"No l:ylt cfly{s jif{ @)&&÷&* df jflif{s pkef]Qmf d'b|f:kmLlt cf};t & k|ltztsf] ;Ldfleq /fVg] nIo /x]sf]df #=^) k|ltzt sfod

/x]sf] 5 . jflif{s laGb'ut cfwf/df @)&* c;f/df pkef]Qmf d'b|f:kmLlt $=!( k|ltzt /x]sf] 5 .

;/sf/L vr{, /fh:j / cfGtl/s C0f kl/rfng dxfn]vf lgoGqs sfof{noaf6 @)&* ;fpg ! df k|sflzt ljj/0f cg';f/ cfly{s jif{ @)&&÷&* df ;+3Lo ;/sf/sf]

s'n vr{ ?= !,!*) ca{ (% s/f]8 ePsf] 5 . o;dWo] rfn' vr{ ?= *%! ca{ ^* s/f]8, k"FhLut vr{ ?= @@* ca{ #) s/f]8 / ljQLo Joj:yftkm{sf] vr{ ?= !)) ca{ (& s/f]8 /x]sf] 5 . To;}u/L /fh:j ;+sng ?= (#* ca{ #@ s/f]8 ePsf] 5 . cfly{s jif{ @)&&÷&* df g]kfn ;/sf/n] s'n cfGtl/s C0f kl/rfng ?= @@$ ca{ ! s/f]8 / ;fFjf e'QmfgL ?= #^ ca{ () s/f]8 u/L v'b cfGtl/s C0f ?= !*& ca{ !! s/f]8 kl/rfng u/]sf] 5 . pQm /sd s'n ufx{:Yo pTkfbgsf] $=$ k|ltzt x'g cfpF5 .

�

����������������������� ���������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

j}b]lzs Jofkf/, ljk|]if0f cfk|jfx / zf]wgfGt/ l:ylt cfly{s jif{ @)&&÷&* df lgof{t $$=$ k|ltztn] a9]/ ?= !$! ca{ !@ s/f]8 / cfoft @*=& k|ltztn] a9]/ ?= !,%#( ca{

*$ s/f]8 k'u]sf]5 . o; cjlwdf j:t' Jofkf/ 3f6f @&=# k|ltztn] a9]sf] 5 . ljk|]if0f cfk|jfx (=* k|ltztn] j[l4 eO{ ?= (^! ca{ % s/f]8 k'u]sf] 5 . cfly{s jif{ @)&^÷&& df rfn' vftf 3f6f ?= ## ca{ &^ s/f]8 / zf]wgfGt/ art ?= @*@ ca{ $! s/f]8 /x]sf] t'ngfdf ;dLIff jif{df rfn' vftf 3f6f ?= ### ca{ ^& s/f]8 / zf]wgfGt/ art ?= ! ca{ @# s/f]8 /x]sf] 5 . @)&* c;f/ d;fGtdf s'n ljb]zL ljlgdo ;l~rlt ?= !#(( ca{ # s/f]8 -cd]l/sL 8n/ !! ca{ &% s/f]8_ /x]sf] 5 . @)&& c;f/ d;fGtsf] t'ngfdf @)&* c;f/ d;fGtdf cd]l/sL 8n/;Fu g]kfnL ?k}ofF !=!@ k|ltztn] clwd"Nog eO{ k|lt cd]l/sL 8n/ vl/b b/ ?= !!(=)$ k'u]sf] 5 .

ljQLo If]q l:ylt

a}lsË If]q tyf ;Demf}tLt art kl/rfng cfly{s jif{ @)&&÷&* df a}s tyf ljQLo ;+:yfsf] lgIf]k kl/rfng @!=$ k|ltztn] j[l4 eO{ ?= $,^^@ ca{ &# s/f]8

k'u]sf] 5 . cl3Nnf] jif{ lgIf]k kl/rfng !*=& k|ltztn] j[l4 eO{ ?= #,*#( ca{ &# s/f]8 /x]sf] lyof] . cfly{s jif{ @)&&÷&* df a}s tyf ljQLo ;+:yfsf] lghL If]qtkm{ nufgLdf /x]sf] shf{ @&=# k|ltztn] j[l4 eO{ ?= $,)*$ ca{ *! s/f]8 k'u]sf] 5 . cl3Nnf] jif{ o:tf] shf{ !@=) k|ltztn] a9]/ ?= #,@)( ca{ &( s/f]8 /x]sf] lyof] . a}+s tyf ljQLo ;+:yf -n3'ljQ ljQLo ;+:yf ;d]t_ sf] r'Qmf k"FhL @)&& c;f/ d;fGtdf ?= #%@ ca{ #& s/f]8 /x]sf]df @)&* c;f/ d;fGtdf !)=* k|ltztn] j[l4 eO{ ?= #() ca{ $# s/f]8 k'u]sf] 5 . @)&* c;f/ d;fGtdf jfl0fHo a}+sx¿sf] k"FhL sf]if kof{Kttf cg'kft !$=! k|ltzt, ljsf; a}+sx¿sf] !#=@ k|ltzt / ljQ sDkgLx¿sf] @@=) k|ltzt /x]sf] 5 . @)&& c;f/ d;fGtdf oL cg'kftx¿ qmdzM !$=) k|ltzt, !$=$ k|ltzt / !(=^ k|ltzt /x]sf lyP . @)&* c;f/ d;fGtdf jfl0fHo a}+sx?sf] lgliqmo shf{ cg'kft !=% k|ltzt, ljsf; a}+sx?sf] !=% k|ltzt / ljQ sDkgLx?sf] ^=@ k|ltzt /x]sf] 5 . @)&& c;f/ d;fGtdf oL cg'kftx? qmdzM !=* k|ltzt, !=% k|ltzt / ^=@ k|ltzt /x]sf lyP . @)&* c;f/ d;fGt;Dd s'n @@( a}+s tyf ljQLo ;+:yfx? ufEg]÷ufleg] k|lqmofdf ;fd]n ePsf 5g\. oLdWo] !&! ;+:yfx?sf] Ohfht vf/]h eO{ %* ;+:yf sfod ePsf 5g\ .

a}+s tyf ljQLo ;+:yfsf zfvf la:tf/;Fu} ljQLo kx'Fr a9]sf] 5 . a}+s tyf ljQLo ;+:yfx?sf] zfvf ;+Vof @)&& c;f/ d;fGtdf (,&^% /x]sf]df @)&* c;f/ d;fGtdf !),^*# k'u]sf] 5 . pQm cjlwdf k|lt a}+s zfvf hg;+Vof #,)&@ af6 36]/ @,*$$ sfod ePsf] 5 . jfl0fHo a}+ssf zfvf &%) :yfgLo txx?df k'u]sf 5g\ .

sd{rf/L ;~ro sf]ifsf] ;|f]t÷pkof]u @)&& c;f/ d;fGtdf ?= #*$ ca{ ! s/f]8 /x]sf]df @)&& r}t d;fGtdf ?= $@$ ca{ ( s/f]8 k'u]sf] 5 . pQm cjlwdf ;+rostf{x?sf] ;l~rt /sd *=* k|ltztn] j[l4 eO{ ?= #*) ca{ %$ s/f]8 k'u]sf] 5 eg] shf{ ;fk6L %=^ k|ltztn] j[l4 eO{ ?= @^^ ca{ %^ s/f]8 k'u]sf] 5 . gful/s nufgL sf]ifsf] ;|f]t÷pkof]u @)&& c;f/ d;fGtdf ?= !^! ca{ * s/f]8 /x]sf]df @)&& r}t d;fGtdf ?= !*! ca{ &( s/f]8 k'u]sf] 5 . ;f] cjlwdf sf]if ;+sng !)=( k|ltztn] j[l4 eO{ ?= !%^ ca{ &$ s/f]8 k'u]sf] 5 eg] shf{ ;fk6L *=( k|ltztn] j[l4 eO{ ?= $( ca{ ^@ s/f]8 k'u]sf] 5 . aLdf sDkgLx?sf] ;|f]t÷pkof]u @)&& c;f/ d;fGtdf ?= $#& ca{ @^ s/f]8 /x]sf]df @)&& r}t d;fGtdf !*=$ k|ltztn] j[l4 eO{ ?= %!& ca{ *@ s/f]8 k'u]sf] 5 .

k"FhL ahf/ @)&& c;f/ d;fGtdf !,#^@=$ /x]sf] g]K;] ;"rsf° @)&* c;f/ d;fGtdf @,**#=$ sfod ePsf] 5 . To;}u/L ahf/

k"FhLs/0f @)&& c;f/ d;fGtdf ?= !,&(@ ca{ &^ s/f]8 /x]sf]df @)&* c;f/ d;fGtdf !@#=& k|ltztn] j[l4 eO{| ?= $,)!) ca{ (^ s/f]8 sfod ePsf] 5 . cfly{s jif{ @)&&÷&* df g]kfn lwtf]kq af]8{n] ?= @# ca{ $ s/f]8 a/fa/sf] C0fkq, ?= !% ca{ !* s/f]8 a/fa/sf] ;fwf/0f z]o/, ?= !$ ca{ % s/f]8 a/fa/sf] xsk|b z]o/ / ?= ( ca{ $) s/f]8 a/fa/sf] Do'r'cn km08 u/L s'n ?= ^! ca{ ^& s/f]8 a/fa/sf] lwtf]kq ;fj{hlgs lgisfzg ug{ cg'dlt lbPsf] 5 . cfly{s jif{ @)&&÷&* df !^ jfl0fHo a}+s, $ ljsf; a}+s / ! ljQ sDkgL u/L @! a}+s tyf ljQLo ;+:yfx?n] ?= ^(

�

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

ca{ ^) s/f]8sf] C0fkq lgisfzg ug{ g]kfn lwtf]kq af]8{af6 :jLs[lt k|fKt u/]sf 5g\ . @)&* c;f/ d;fGtdf a}+s tyf ljQLo ;+:yfaf6 C0fkq dfkm{t\ ?= !)) ca{ #* s/f]8 ljQLo ;fwg kl/rfng ePsf] 5 .

;xsf/L ;+:yf @)&& c;f/ d;fGtdf ;xsf/L ;+:yfx?sf] art kl/rfng ?= #%) ca{ %* s/f]8 /x]sf]df @)&& r}q d;fGtdf

?= $&& ca{ (^ s/f]8 k'u]sf] 5 . ;f] cjlwdf ;xsf/L ;+:yfx?af6 k|jfx ePsf] C0f ?= #$! ca{ &! s/f]8af6 j[l4 eO{ ?= $@^ ca{ @^ s/f]8 k'u]sf] 5 .

ljkGg ju{ shf{ jfl0fHo a}+s, ljsf; a}+s / ljQ sDkgLn] cfkm\gf] s'n shf{ nufgLsf] Go"gtd % k|ltzt ljkGg ju{df k|jfx ug'{kg]{

Joj:yf /x]sf]df @)&* c;f/ d;fGtdf s'n shf{sf] & k|ltzt k|jfx ePsf] 5 .

;x'lnotk"0f{ shf{ pTkfbg clej[l4, /f]huf/L l;h{gf / pBdzLntf ljsf;sf nflu g]kfn ;/sf/sf] Aofh cg'bfgdf ;~rflnt ;x'lnotk"0f{

shf{ sfo{qmd cGtu{t @)&* c;f/;Dddf !,)$,!)( C0fLnfO{ ?= !^! ca{ $$ s/f]8 shf{ k|jfx ePsf] 5 . o;dWo] s[lif tyf kz'k+IfL Joj;fodf $^,)%& C0fLnfO{ ?= !)^ ca{ (* s/f]8 / %%,%%! dlxnf pBdLnfO{ ?= %) ca{ (* s/f]8 shf{ nufgL ePsf] 5 . ;x'lnotk"0f{ shf{sf cGo * zLif{s cGtu{t @,%)! C0fLx?;F+u ?= # ca{ $* s/f]8 shf{ nufgLdf /x]sf] 5 .

sf]le8–!( nlIft shf{

k'g/shf{ sf]le8–!( dxfdf/Laf6 k|efljt cy{tGqsf] k'g?Tyfgsf] nflu tf]lsPsf k]zf, pBd / Joj;fox?nfO{ Aofhb/df ;x'lnot

lbg] p2]Zon] sfof{Gjogdf NofOPsf] k'g/shf{ ;'lawfsf] Joj:yfaf6 @)&* c;f/ d;fGt;Dddf $*,*() C0fLnfO{ ?= !$* ca{ &% s/f]8 k'g/shf{ :jLs[t ePsf] 5 .

rfn' k"FhL shf{ sf]le8–!( af6 cltk|efljt pBf]u Joj;fo ;'rf? Ufg{ ;xhLs/0f ug]{ p2]Zon] rfn' k"FhL shf{ pkof]u u/]sf C0fLnfO{

rfn' k"FhL shf{sf] clwstd @) k|ltzt yk shf{ pknAw u/fpg ;Sg] Joj:yf ul/Psf]df !^,!*@ C0fLnfO{ ?= !$ ca{ @$ s/f]8 o:tf] shf{ k|jfx ePsf] 5 . cfjlws shf{ dfq pkof]u u/]sf C0fLnfO{ ;f]xL shf{sf] lwtf]df clwstd !) k|ltzt ;Dd yk shf{ pknAw u/fpg ;Sg] Joj:yf ul/Psf]df &,@^( C0fLnfO{ ?= ( ca{ #^ s/f]8 shf{ k|jfx ePsf] 5 .

shf{sf] u|]; cjlw yk sf]le8–!( sf] sf/0f kl/of]hgf lgdf{0f ;DkGg÷;+rfng x'g g;s]sf] cj:yfdf a}+s tyf ljQLo ;+:yfn] shf{sf] u|]; cjlw

yk ug{;Sg] Joj:yf ul/Psf]df ((# C0fLsf] hDdf ?= %@ cj{ shf{sf] u|]; cjlw yk ePsf] 5 . o;dWo], Go"g Kf|efljt !&$ C0fLsf] ?= # ca{ (% s/f]8 shf{ ^ dlxgf, dWod k|efljt #@! C0fLsf] ?= !* ca{ $! s/f]8 shf{ ( dlxgf / clt k|efljt $(* C0fLsf] ?= @( ca{ ^# s/f]8 shf{sf] u]|; cjlw ! jif{ yk ePsf] 5 .

shf{sf] e'QmfgL cjlw yk sf]le8–!( sf] sf/0f shf{sf] ;fFjf / Aofh e'QmfgL ug{ ;d:ofdf k/]sf C0fLx?sf nflu shf{ e'QmfgL cjlw yk ug]{

Joj:yf eP adf]lhd !(,&*^ C0fLsf] hDdf ?= (# cj{ ^# s/f]8 shf{sf] e'QmfgL cjlw yk ePsf] 5 . o;dWo], Go"g k|efljt ljleGg k]zf, pBf]u / Joj;fosf &,^** C0fLsf] ?= #) ca{ # s/f]8 shf{sf] e'QmfgL cjlw ^ dlxgf, dWod k|efljt &,**& C0fLsf] ?= @* ca{ @& s/f]8 shf{sf] e'QmfgL cjlw ( dlxgf / clt k|efljt $,)!@ C0fLsf] ?= !$ ca{

��

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

$& s/f]8 shf{sf] e'QmfgL cjlw ! jif{ yk ePsf] 5 . sf]le8–!( af6 clt k|efljt ko{6g nufot tf]lsPsf pBf]u Joj:ffo If]qsf !(( C0fLsf] ?= @) ca{ *^ s/f]8 shf{sf] e'QmfgL cjlw @ jif{sf] nflu yk ePsf] 5 .

shf{sf] k'g/;+/rgf tyf k'g/tflnsLs/0f shf{sf] k'g/;+/rgf tyf k'g/tflnsLs/0f ug{ ;Sg] Joj:yf adf]lhd @)&& k'; d;fGt;Dd sf]le8–!( af6 k|efljt If]qsf

@!,^!& pBdL Joj;foLsf] ?= !@( ca{ @! s/f]8 shf{ k'g/;+/rgf tyf k'g/tflnsLs/0f ePsf] 5 .

Joj;fo lg/Gt/tf shf{ sf]le8–!( k|efljt ko{6g / 3/]n', ;fgf tyf demf}nf pBd If]qsf] Joj;fo lg/Gt/tfdf ;xof]u k'¥ofpg tL If]qsf >lds

tyf sd{rf/Lsf] kfl/>lds e'QmfgLsf nflu g]kfn ;/sf/af6 Joj:yf ul/Psf] Joj;fo lg/Gt/tf shf{ sfo{qmd cGt/u{t @)&* c;f/ ;Dddf ?= (% s/f]8 ^& nfv :jLs[t eO{ ?= &# s/f]8 ^* nfv nufgLdf /x]sf] 5 .

-#_ rfn' cf= j= sf] pknJwL / eljiodf ug{'kg]{ s'/fsf] ;DaGwdf ;+rfns ;ldltsf] wf/0ff M

o; k|ltj]bg tof/ kfbf{sf] cjlw;Dd klxnf] q}df;sf] ljQLo ljj/0f tof/ gePsfn] o; lzif{sdf s]lx ;dfj]z gul/Psf] .

-s_ u|fxs ;]jf tyf ;'rgf k|ljwLsf] ;DaGwdf M cfhsf] o; k|lt:kwf{Tds ljZj jhf/df a}lsË If]qdf ;"rgf tyf k|ljlwsf] lta| ultdf eO{/x]sf] kl/jt{gnfO{

;dofgs'n cfTd;fy ub}{ o; a}+snfO{ ;jn, ;Ifd Pj+ k|lt:klw{ ;"rgf k|ljlwo''Qm agfO{ ;]jfu|fxLnfO{ ;/n, ;xh Pj+ l56f] 5l/tf] ?kdf a}lsË ;]jf k|bfg ug{] p2]Zon] ;"rgf k|ljlwsf] ;+oGqdf :t/ j[l4 ub}{ laleGg lsl;dsf cTofw''lgs ;]jfx? k|bfg ub]{{ cfO{/x]sf] 5 .

ATM ;]jf M u|fxsx?sf] ;''ljwfnfO{ dWogh/ ub}{ o; 8]enkd]G6 a}+sn] leiff 8]lj6 sf8{ ;+rfngdf NofO{ pQm sf8{df Chip based EMV ;]jf yk ul/Psf] 5 eg ] Paper based Pin nfO{ la:yflkt u/L u|fxsnfO{ Mobile OTP sf] dfWodaf6 Green Pin ;]jf ;d]t lbb}+ cfO/x]sf]5 . o;af6 u|fxsju{x?nfO{ ;xh ?kdf ;]jf k|bfg ug{ ;lsg] ljZjf; lnPsf] 5 . xfn;Dd o; 8]enkd]G6 a}+sn] cfkm\gf] #! :yfgjf6 ATM ;]jf k|bfg ub}{ cfO{/x]sf] 5 . ;fy}, 8]lj6 sf8{ k|fKt u/]sf u|fxs dxfg'efjx?nfO{ nfe xf];\ p2]Zon] ljleGg ;+:yfx? h:t} c:ktfn, xf]6n tyf cGo ;]jf k|bfos ;+:yfx?;Fu ;Demf}tf u/L pQm ;+:yfx?n] k|bfg ug]{ ;]jf pkef]u u/] jfkt lglZrt k|ltzt ;Ddsf] /sd 5'6 x'g] Joj:yf ;d]t ldnfOPsf] 5 . lgs6 eljiodf qm]l86 sf8{sf] ;d]t ;'ljwf lbg;Sg] u/L 8]enkd]G6 a}+sn] sfo{ cufl8 a9fPsf] 5 .

Bank Smart & SMS ;]jf M u|fxs dxfg'efjx?nfO{ ;lhnf] ?kdf cfkm\gf] 3/÷sfof{nodf j;L cfkm\gf] sf/f]jf/ jf/] hfgsf/L k|fKt ug{sf] ;fy} u|fxsn] o; a}+sdf /x]sf] cfkm\gf] vftfaf6 l;w} csf]{ a}+s tyf laQLo ;+:yfdf /x]sf] vftfdf tyf cGo a}+saf6 o; a}}+s /x]sf] vftfdf /sd /sdfGt/0f ug{ ;lsg] cfw'lgs Bank Smart ;]jf, Mobile Banking ;]jfnfO{ cku|]8 u/L Bio-metric Login, lan e'QmfgL ;]jf ;d]t yk u/]sf] 5 . o;/L u|fxsx?n ] I-Banking, E-Sewa, Khalti h:tf ;]jfx?af6 k};f k7fpg], lah''nL tyf 6]lnkmf]gsf] lan e''QmfgL h:tf ;]jfx? k|of]u ub}{ cfO{/x]sf 5g . o; a}+ssf sl/a ^!,&(& hlt ;]jfu|fxLx?n] pQm ;]jf pkef]u ub}{ b}lgs cfkm\gf] vftfdf ePsf] sf/f]jf/sf] ;xh} SMS ;]jfaf6 hfgsf/L k|fKt ub}{ cfO{/x]sf 5g\ . 8]enkd]G6 a}+sn] xfn;fn } Online Account Opening, Online Fixed Deposit, QR Payment, QR Scanner tyf Online Loan Application sf] Aoj:yf ;d]t u/]sf] 5 .

cGt/ a}+s e''QmfgL k|0ffnL ;]jf M o; 8]enkd]G6 a}+sn] g]kfn lSnol/Ë xfp; lnld6]8;+u ;Demf}tf u/L cGt/a}+s e'QmfgL k|0ffnL ;]jfaf6 cGo a}+s tyf laQLo ;+:yfx?af6 o; a}+sdf /x]sf] vftfdf l;w} /sd hDdf

��

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

�������������������������

ug{ ldNg] tyf o; a}+sdf /x]sf] cfkm\gf] vftfaf6 cGo a}+sdf /sd k7fpg'sf] ;fy} laleGg ;+:yfx?n] k|bfg ug]{ gub nfef+z o; a}+sdf /x]sf] vftfdf ;xh} hDdf ug{ ;Sg] h:tf ;]jfx? k|bfg ub}{ cfO{/x]sf] 5 . o;/L a}+sn] Connect IPS ;]jfdf Real Time Payment & Settlement ;]jf ;d]t yk u/L cfkmgf] a}+s vftfaf6 cgnfOg tyf df]afOn PK;af6 lan e''Qmfg tyf /sd 6fG;km/ ug{ ;lsg], /fh:j e''QmfgL, df]afOn jfn]6 z]o/ a|f]s/ e''QmfgL, qm]l86 sf8{ lan e''QmfgL RTGS ;]jf h:tf ;]jfx? k|bfg ub}{ cfO{/x]sf] 5 .

cfZjf ;]jf M 8]enkd]G6 a}+sn] cfkm\gf u|fxsx?nfO{ laleGg sDkgLx?sf] ;fj{hlgs z]o/ lgisfzgsf] qmddf cfZjf -ASBA) k|0ffnL dfkm{t tL sDkgLx?sf] z]o/ nufgLdf cfa]bg lbg ;Sg] ;fy} l;w} laB''tLo dfWodaf6 ;d]t cfa]bg eg{ ;Sg] Aoj:yf u/]sf] 5 . of] ;]jf o; 8]enkd]G6 a}+sdf vftf ePsf u|fxsx?n] 8]enkd]G6 a}+ssf] ;Dk""0f{ zfvfx?af6 k|fKt ug{ ;Sg] 5g\ .

lgIf]k ;b:o ;]jfM g]kfn lwtf]kq af]8{ / l;l8P; P08 lSnol/Ë lnld6]8af6 8]enkd]G6 a}+sn] lgIf]k ;b:osf] cg'dlt k|df0fkq k|fKt u/L lgIf]k ;b:on] lbg] ;]jf rfn' cfly{s jif{df z'? u/]sf] 5 . o; lsl;dsf] cg'dlt k|fKt u/];Fu} a}+sn] l8Dof6 vftf vf]Ng] sfo{ ;'rf? ul/;s]sf] 5 .

o;} u/L ljutsf jif{x?b]lv g} 8]enkd]G6 a}+sn] cfkm\gf u|fxsx?nfO{ ABBS ;]jf, s]xL zfvfx?af6 zlgaf/ tyf ;fj{hlgs labfsf lbgx?df ;d]t sfpG6/ vf]nL lgIf]k lng] tyf r]sx?sf] e''QmfgL lbg] h:tf #^% lbg] a}+lsË ;]jf tyf laleGg ljk|]if0f sDkgLx?;+u ;Demf}tf u/L laleGg d''n''sx?af6 k7fPsf] /sd e''QmfgL ug]{ tyf :jb]z leq Ps :yfgaf6 csf]{ :yfgdf /sd k7fpg] / k7fPsf] /sd e''QmfgL lbg] / u|fxsx?sf] ax'd"No ;fdfgx?, ;'g rfFbL tyf cGo sfuhftx?sf] ;'/Iffsf] nflu laleGg zfvfx?af6 ns/ ;]jf pknAw u/fpb} cfO{/x]sf] 5 .

-v_ zfvf ;~hfn lj:tf/ M :yfgLo ljsf;sf] cfwf/ eGg] cfkm\gf] d''n gf/fnfO{ cfTd;fy ub}{ 8]enkd]G6 a}+sn] :yfkgf sfn b]lv g}+ u|fdL0f

If]qsf hgtfx? lar cfw'lgs a}+lËs ;]jf, ;'ljwf k|bfg ub}{ cfO{/x]sf] oxfFx? ;fd' ;j{ljlwt g} 5 . ;fy} b]z ;+3Lotfdf uO{;s] kZrft g]kfn ;/sf/ tyf g]kfn /fi6« a}+ssf] :yfgLo :t/df zfvf ;~hfn k''/\ofpg] gLltnfO{ canDag ub}{ 8]enkd]G6 a}+sn] cfkm\gf] :yflkt zfvfx?sf] ljsf; tyf gofF Zffvf la:tf/ ug]{ gLlt cg'?k cfjZostfsf] klxrfg tyf laleGg :yfgx? 5gf}6 u/L ;ft} j6f k|b]zsf :yfgLo txx?df cfkm\gf] pkl:ytL dfkm{t zfvf ;+hfnnfO{ la:tf/ ub}{ ;ldIff jif{sf] clGtddf a}+ssf] zfvf ;+Vof hDdf (% /xsf] 5 eg] ;f] kZrft of] laQLo ljj/0f tof/ kbf{sf] lbgDd xflsdrf]s zfvf e/tk'/, lj/f6gu/ zfvf df]/Ë, lj/u+h zfvf jf/f u/L # j6f yk zfvfx? ;+rfngdf NofO{ xfn zfvf ;+Vof (* /x]sf 5g\ eg]] cffkm\gf] Aoj;fo j[l4 / lj:tf/sf nflu o;} rfn' cfly{s jif{df pkTosf leq / aflx/ u/L cGo yk !* j6f zfvf lj:tf/ ug]{ gLlt lnPsf] Joxf]/f ;DdfgLt ;ef ;dIf hfgsf/L u/fpFb5' .

-u_ cfGtl/s lgoGq0f k|0ffnLsf] ljj/0f M g]kfn /fi6« a}+ssf] lgb]{zg, a}+s tyf laQLo ;+:yf ;DaGwL P]g @)&# sf] bkmf !$ / !% df ePsf] Aoj:yf adf]lhd

;~rfns ;ldltn] cfkm\gf] hjfkmb]xLtfdf u}/ sfo{sf/L ;+rfnsx?sf] ;+of]hsTjdf cfGtl/s n]vf k/LIf0f ;ldlt, hf]lvd Joj:yfkg ;ldlt, sd{rf/L ;]jf ;'lawf lgwf{/0f ;ldlt / ;DklQ z'l4s/0f lgjf/0f ;DaGwL ;ldlt u7g u/L pQm ;ldltsf] a}+7sdf eP u/]sf sfd sf/jfxLx? ;+rfns ;ldltsf] a}+7sdf ;d]t hfgsf/L u/fO{ 5nkmn u/L cfjZos lgb]{zg lbg] u/]sf] 5 . To:t} Joj:yfkg :t/df kbk"lt{ ;ldlt, cfly{s k|zf;g pk–;ldlt, ;DkQL tyf bfloTj pk–;ldlt (ALCO) / vl/b pk–;ldlt u7g u/L 8]enkd]G6 a}+sn] cfGtl/s lgoGq0f k|0ffnLnfO{

��

������������������������� �������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

Jojl:yt ug{ ljleGg ljlgodfjnL, gLlt, lgb]{zg, sfo{ljlw tyf dfu{bz{gx? Kff/Lt u/L cfjZostf cg';f/ g]kfn /fi6« a}+saf6 :jLs[lt lnO{ tyf hfgsf/L u/fO{ nfu'' u/]sf] 5 .

o; 8]enkd]G6 a}+ssf u}/ sfo{sf/L ;~rfnssf] ;+of]hsTjdf ul7t n]vf k/LIf0f ;ldltn] 8]enkd]G6 a+}ssf] ljQLo sf/f]af/sf] q}dfl;s ?kdf a}+7s a;L cg'udg ug]{, cfGtl/s lgoGq0fnfO{ k|efjsf/L t'Nofpb} cfO/x]sf] 5 . a}+ssf] cfGtl/s n]vfk/LIf0f ljefun] b}lgs ?kdf sfo{ ;Dkfbg sf/f]jf/x?sf] n]vfhf]vf tyf hfFr ug]{ ;fy} d"Nof°g, cWoog tyf lgoGq0fsf] ?kdf cfGtl/s n]vf k/LIf0f u/L, lgoGq0f k|0ffnLnfO{ r':t / b'?:t /fVg] ul/Psf] 5 eg] pQm cfGtl/s n]vfk/LIfsn] cf}NofPsf s}lkmot tyf q''l6x?nfO{ tTsfn} ;''wf/ ub}{ cfO{/x]sf] 5 .

-3_ ;DklQ z'l4s/0f lgjf/0f tyf u|fxs klxrfg M ;DklQ z'l4s/0f tyf cft+safbL lqmofsnfkdf laQLo nufgL lgjf/0f ;DaGwL sfo{sf] k|efjsf/L lgoGq0fsf nflu

o; a}+sn] ;DklQ z'l4s/0f lgjf/0f P]g, @)^$, ;DklQ z'l4s/0f lgjf/0f lgodfjnL @)&#, g]kfn /fi6« a}+s, laQLo hfgsf/L OsfO{n] hf/L u/]sf lgb]{zg tyf kl/kq adf]lhd cfjZos gLlt k|lqmofsf] th'{df u/L lg/Gt/ ?kdf sfof{Gjog ub}{ cfPsf] 5 .

;f] sf] k|efjsf/L ?kdf sfof{Gjog ug{ a}+ssf ;~rfns >L ;'lzn sfhL aflgof+sf] ;+of]hsTjdf ;DklQ z'l4s/0f tyf cft+safbL sfo{df laQLo nufgL lgjf/0f ;DaGwL ;ldlt u7g ul/Psf] 5 . o; ;ldltn] u/]sf lg0f{ox? tyf ePsf sfo{x? ;~rfns ;ldltdf 5nkmn ug]{ ul/Psf] 5 . o; 8]enkd]G6 a}+sn] AML/CFT OsfO{ v8f u/L u|fxs klxrfg, go AML k|ljlwsf] ljsf;, AML and CDD Policy tyf CDD Procedures agfO{ pQm OsfO{n] k|To]s zfvfx?df cfjZos sd{rf/L tf]sL ;DklQ z'l4s/0f lgjf/0f ;DaGwL P]g tyf lgb]{zgx?sf] sfof{Gjog ub}{ cfPsf] 5 .

-$_ k"FhL j[l4 tyf ;+/rgf ;DaGwdf M cfly{s jif{ @)&&÷&* sf] cGTodf 8]enkd]G6 a}+ssf] r'Qmf k"FhL ?= @,&#,^(,&@,$@)÷– -b'O{ cj{ qLxQ/ s/f]8 pgfG;Q/L

nfv axQ/ xhf/ rf/;o aL;_ sfod /x]sf] 5 . ;+:yfks ;d"xsf] z]o/ :jfldTj %! k|ltzt /x]sf] 5 eg] ;j{;fwf/0f ;d"xsf] z]o/ :jfldTj $( k|ltzt /x]sf] 5 . ;f+lu|nf 8]enkd]G6 a}+s lnld6]8 / cGo O{hfhtkq k|fKt a}+s tyf laQLo ;+:yfx? Ps cfk;df ufEg] ufleg] tyf o; ;f+lu|nf 8]enkd]G6 a}+s lnld6]8n] cGo laQLo ;+:yfx?nfO{ k|flKt ug]{ sfo{ v'nf ?kdf cl3 a9fpg] 8]enkd]G6 a}+ssf] of]hgf /xg]5 .

-%_ dfgj ;+zfwg Joj:yfkg M ;ldIff jif{sf] cfiff9 d;fGtdf 8]enkd]G6 a}+sdf s'n &#% hgf sd{rf/Lx? sfo{/t /x]sf 5g\ . h;dWo] !@& hgf gofF

sd{rff/L lgo'lQm tyf ^% hgf sd{rf/Lx? ;]jfaf6 cnu ePsf 5g\ . 8]enkd]G6 a}+ssf] s'n sd{rf/L ;+Vof dWo] ##* hgf -$%=(( k|ltzt_ dlxnf sd{rf/Lx? /x]sf 5g\ . a}+s tyf laQLo ;+:yf eg]sf] b]z ljsf;sf] Ps lhDd]jf/ Pj+ cfly{s d]?b08 ePsf]n] /fi6«sf] x/]s cfly{s ultljlwx?df o;sf] k|ToIf k|efj kg]{ ub{5 . bIf hgzlQm ljgf s'g} klg ;+:yf ;kmntf k"j{s cuf8L a9\g g;Sg] ;fy} cfhsf] o; k|lt:kwf{Tds o'udf bIf hgzlQm lagf s'g} klg ;+:yfsf] ;kmntfsf] kl/sNkgf ug{ g;lsg] ePsf]n] cfkm\gf] hgzlQmnfO{ k|lt:kwL{x?sf] lar ;Ifd agfO{ cfkm\gf u|fxsx?nfO{ cfw'lgs ;]jf Pj+ ;'lawfx? k|bfg ug{ plrt k|lzIf0f Pj+ tflndsf] cfjZostfnfO{ b[li6ut u/L 8]enkd]G6 a}+sn] sfo{/t sd{rf/Lx?nfO{ cfjZostf cg';f/sf] afx|o tyf cfGtl/s tflndx? ljleGg ;dodf u/fpFb} cfO/x]sf] 5 . afx|o tfnLd cGtu{t ljleGg k|ltli7t ;+:yfx?n] ;~rfng ug]{ tfnLd tyf sfo{zfnf uf]i7Ldf cfjZostf cg';f/ slgi7 tx b]lv sfo{sf/L txsf sd{rf/Lx?nfO{ ;xefuL u/fpFb} cfO{/x]sf] 5 eg] Aoj:yfkg txsf sd{rf/Lx?nfO{ 8]enkd]G6 a}+ssf] cfjZostf cg';f/ a}b]zLs tflnd gLlt tof/ u/L lab]zdf ;d]t k7fpg] u/]sf] 5 . To:t} 8]enkd]G6 a}+sn] ljleGg ljefudf sfo{/t dfgj ;+zfwgsf] sf/f]jf/sf] k|s[tLsf] cfwf/df cfGtl/s ?kdf ;d]t tfnLd k|bfg ub}{ cfO{/x]sf]] 5 eg]

��

�������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

����������������������� ��

gofF lgo''Qm u/]sf slgi7 :t/sf sd{rf/Lx?nfO{ cfGtl/s tyf aflx/af6 ;d]t k|lzIfs NofO{ cled''lvs/0f ;DaGwL tflnd k|bfg ub}{ cfO{/x]sf 5 . ;fy} xfn sf]le8–!( sf] kl/l:ytLdf Online dfkm{t ;d]t tflnd k|bfg ul/Psf] / cfufdL lbgx?df klg o;nfO{ lg/Gt/tf lbg] gLlt a}+sn] lnPsf] 5 .

g]kfn /fi6« a}+saf6 a}}+s tyf laQLo ;+:yfx?nfO{ hf/L lgb]{zg cg''?k s''n sd{rf/L tna eQf vr{sf] tLg k|ltztn] x''g] /sd sd{rf/Lsf] tflnd tyf j[l4 ljsf;df vr{ ug''{kg]{ Aoj:yf eP adf]lhd ;ldIff jif{df 8]enkd]G6 a}+sn] cfGtl/s tyf afx|o u/L sl/a ;Dk"0f{ sd{rf/Lx?nfO{ tflnddf ;xeflu u/fO{ hgzlQm tfnLddf ?= @,*&*,@!&÷– vr{ u/]sf] 5 . dfl;s ?kdf pRr Joj:yfkg, ljefuLo k|d'v / zfvf k|d'v ljr ljleGg zfvfx?sf] sf/f]jf/, k|utL ljj/0f / ;d:ofx?jf/] 5nkmn tyf efjL of]hgf jf/] k|lzIf0f tyf cGt/lqmof ub}{ cfO{/x]sf] 5 .

-^_ ;+:yfut ;'zff;g M s''g} klg ;+:yfsf] ;kmntf d"n ?kdf To; ;+:yfn] cjnDag ug]{ s''zn ;+:yfut ;''zf;gsf cEof;x?df lge{/ x''g] ub{5 . ;+:yfut ;'zf;g lagf s'g} klg ;+:yf nfdf] ;do tyf lbuf] ?kdf cufl8 a9\g g;Sg] x''Fbf ljZj;gLo Joj;fo ;+rfngsf] nflu ;+:yfut ;'zf;g k|d'v cfwf/ xf] eGg] dfGotfdf a}+s k|lta4 /xL ;f]xL adf]lhd o;sf d'ne"t dfGotfx? hjfkmb]lxtf, kf/blz{tf / O{dfGbfl/tfnfO{ a}+sn] ;b}a kfngf ub}{ cfO{/x]sf] 5 . k|rlnt P]g lgod, g]kfn /fi6« a}+s tyf cGo lgodgsf/L lgsfox?af6 hf/L lgb]{zg tyf a}+ssf] cfkmg} gLlt lgod tyf lgb]{lzsf adf]lhd sfo{ ;+rfng ub}{ cfO{/x]sf] 5 . o;/L cfjZos gLlt lgodx? ;dofg's'n ;+zf]wg ;lxt cBfjlws u/L nfu' ug]{ sfd lg/Gt/ eO{/x]sf] 5 eg] a}+sn] cfkm\gf] ljQLo ljj/0fx? tyf lgodgsf/L lgsfo dfkm{t lgwf{/0f ul/Psf ;"rgf tyf k|ltj]bgx? ;/f]sf/jfnf lgsfox?;+u k]z ug{'sf] ;fy} k|sfzg u/L cfkm\gf] j]j;fO{6df ;d]t /fVb} cfO{/x]sf] 5 .

o;/L o; 8]enkd]G6 a}+sn] a}+s tyf laQLo ;+:yf ;DaGwL P]g, g]kfn /fi6« a}+s tyf cGo lgodgsf/L lgsfox?4f/f hf/L gLlt, lgb]{zg tyf kl/kqx?sf] ;~rfns tyf sd{rf/Lx?n] kfngf ug'{kg]{ cfr/0fx? pRr k|fyldstfsf ;fy kfngf ub]{ cfO{/x]sf] / eljiodf ;d]t k"0f{ ?kdf kfngf ul/g] 5 .

-&_ cf}Bf]uLs jf Joj;flos ;DaGw M 8]enkd]G6 a}+sn] cfkm\gf] Aoj;flos ;DaGw tyf sf/f]jf/ lj:tf/sf] nflu g]kfn pBf]u jfl0fHo dxf;+3, g]kfn pBf]u

kl/;+3, g]kfn r]Da/ ckm sd;{ sf7df08f}+sf] ;b:otf lng'sf] ;fy} :yfgLo :t/df /x]sf ;+3÷;+:yf, laleGg ;/sf/L tyf u}x| ;/sf/L sfof{no, sd{rf/Lx?;+u Joj;foLs / sf/f]jf/sf] ;DaGw km/flsnf] agfpb} cufl8 jl9/x]sf] 5 .

lgodgsf/L lgsfox? g]kfn /fi6« a}+s, sDkgL /lhi6«f/ sfof{no, g]kfn lwtf]kq jf]8{, g]kfn :6s PS;r]Gh, l;l8P; P08 lSnol/Ë lnld6]8, ljleGg a}+s tyf ljlQo ;+:yfx?, g]kfn ;/sf/ / ;/sf/L tyf u}/ ;/sf/L ;+3 ;+:yfx?, 8]enkd]G6 a}°;{ Pzf]l;P;g nufot 8]enkd]G6 a}+s;+u ;Da4 cGo ;+3 ;+:yfx? tyf ;/f]sf/jfnfx?;+usf] ;f}xfb{k""0f{ Aoj;flos ;DaGw la:tf/ ub{} nluPsf] / a}+s tyf u|fxs dxfg'efjx? ljrsf] sf/f]jf/ ;DaGw / ;'/IffnfO{ Wofgdf /fvL ;'dw'/ ;DjGw sfod ul/Psf] hfgsf/L u/fpFb5' .

-*_ ;+:yfut ;fdflhs pQ/bfloTj M a}+sn] cfkm\gf] d'gfkmfdf dfq s]lGb|t geO{ ;fdflhs If]qdf klg s]xL of]ubfg k'¥ofpg' kb{5 eGg] s'/fnfO{ cfTd;fy ub}{

lautsf jif{x?df em} o; sfo{nfO{ lg/Gt/tf lbb} ;+:yfut ;fdflhs pQ/bfloTj sfo{qmd cGt{ut ljleGg sfo{s|dx?df cfkm} k|ToIf jf k/f]If ?kdf tyf cGo ;+:yfx?n] u/]sf] sfo{qmddf cfly{s ?kdf ;xof]u u/L ;lqmo ;xeflutf hgfpb} cfO/x]sf]5 .

g]kfn /fi6« a}+ssf] O{=k|f= lgb]{zg g+= ^ sf] !^ adf]lhd a}+sn] ;dLIff jif{df v'b d'gfkmfsf] ! k|ltztn] x'g] ?= $!,)),*)%÷– ;+:yfut ;fdflhs pQ/bfloTj sf]ifdf ljlgof]hg u/]sf] 5 . h'g cl3Nnf] cf= j= df pQm sf]ifdf v'b d'gfkmsf] ! k|ltztn] x'g] ?= !(,!),(&*÷– ;+:yfut ;fdflhs pQ/bfloTj sf]ifdf ljlgof]hg u/]sf] lyof] . o;/L ;ldIff jif{df 8]enkd]G6 a}+sn] s]Gb|Lo sfof{no tyf ljleGg zfvf sfof{nox?af6 ;ft}j6f k|b]zdf g]kfn /fi6« a}+sn] a}+s tyf ljQLo ;+:yfx?nfO{ hf/L O{=k|f=lgb]{zg g+= ^ sf] !^ adf]lhd ljleGg lzIff, :jf:Yo, v]ns'b, wfld{s cg'i7fg, j[4fcf>fd, c;xfo tyf lk5l8Psf]

��

����������������������� ���������������������������� �������������������������� ����

���������������������

������������������������� ���������������������

If]qsf åGblkl8t afnaflnsf tyf laBfnox?sf c;xfo ljBfyL{x?nfO{ 5fqj[lt, ljQLo ;fIf/tf sfo{qmd, u}x| ;/sf/L ;+:yfx?n] ug]{ :jf:Yo ;DaGwL lzlj/ tyf jftfj/0fLo ;DaGwL sfo{qmdx?df ;+:yfut ;fdflhs pQ/bfloTj sfo{qmd cGtu{t ?= !(,!),(&*÷– a/fa/ vr{ u/]sf] 5 . o;/L eljiodf ;d]t ;fdflhs pQ/bfloTj sfo{x?df cem} lg/Gt/ ?kdf ;xof]u hf/L /xg] 5 .

-(_ ;~rfns ;ldltdf ePsf] x]/km]/ M o; 8]enkd]G6 a}+ssf] lgoddfjnLdf ePsf] Joj:yf adf]lhd ;+:yfks z]o/wgLx?sf] ;d"x æsÆ af6 # hgf, ;j{;fwf/0f

z]o/wgLx?sf] ;d"x ævÆ af6 # hgf / ! hgf :jtGq ;~rfns u/L s'n & ;b:oLo ;~rfns ;ldlt /xg] Aoj:yf 5 . cl3Nnf] cf= j=sf] t'ngfdf o; cf= j=df ;~rfns ;ldltdf s'g} x]]/km]/ ePsf] 5}g . xfn 8]enkd]G6 a}+sdf lgDg adf]lhd ;~rfnsx? /xg' ePsf] 5 .

ljj/0f M

s|=;+= Gffd Kfb 7]ufgf ! >L cRo't k|;fb k|;fO{ cWoIf g]kfnu+h –@, af+s]@ >L ;''lzn sfhL aflgof+ ;~rfns w''Da/fxL –$, sf7df08f}+ # >L g/]z dfg t'nfw/ ;~rfns u0faxfn –@!, sf7df08f}+$ >L u+uf ;fu/ 9sfn ;~rfns ;j{;fwf/0f tkm{af6 cflwvf]nf –^, :ofËhf % >L ln;f z]/rg ;~rfns ;j{;fwf/0f tkm{af6 6f]vf–#, sf7df08f}+ ^ >L /fh'gfy vgfn :jtGq ;~rfns DofUb] –!, u'0ffbL, tgx'+& >L lgltz u'Ktf ;~rfns ;j{;fwf/0f tkm{af6 g]kfnu+h –!, af+s]

-!)_ sf/f]jf/nfO{ c;/ kfg]{ d'Vo s'/fx? M 8]enkd]G6 a}+ssf] sf/f]jf/nfO{ c;/ kfg{ d'Vo s'/fx? lgDgfg';f/ /x]sf 5g M

s_ ljZj dxfdf/Lsf] ?kdf km}lnPsf] sf]le8 –!( sf] sf/0f ;dod} shf{ c;'nL tyf Aofh e'Qmfg x'g g;sL pTkGg x'g] hf]lvdx? .

v_ ;"rgf tyf k|ljlwsf] ljsf;;+u} a}+s tyf laQLo ;+:yfx?df cfly{s ck/flws ultljwLx? a9\b} uO{/x]sf] sf/0f x'g] hf]lvdx? .

u_ /fhgLlts kl/jt{gsf sf/0f pTkGg x'g] hf]lvdx? .

3_ k"+hL ahf/df cfpg] ptf/ r9fjsf] sf/0f x'g ;Sg] hf]lvdx? .

ª_ a}+lsË If]qdf x'g] cToflws k|lt:kwf{sf sf/0f x'g] hf]lvdx? .