1 SCHEME INFORMATION DOCUMENT L&T Mutual ... - SEBI

102

1 SCHEME INFORMATION DOCUMENT L&T Mutual Fund 309, 3rd Floor, Trade Centre, Bandra Kurla Complex, Bandra (East), Mumbai - 400 051 L&T Prudence Fund An Open Ended Balanced Scheme Offer of units at Rs.10/- per unit and at NAV based prices upon re-opening New Fund Offer opens on ___________2012 New Fund Offer closes on ___________2012 The Scheme shall Re-open for Continuous Sale and Repurchase within 5 Business Days of Allotment. SPONSOR L&T Finance Limited L&T House, Ballard Estate, P.O. Box 278, Mumbai – 400 001 INVESTMENT MANAGER L&T Investment Management Limited Registered Office*: Dare House, No. 2, N.S.C. Bose Road, Parry’s, Chennai - 600 001 Head Office: 309, 3rd Floor, Trade Centre, Bandra Kurla Complex, Bandra (East), Mumbai - 400 051 TRUSTEE COMPANY L&T Mutual Fund Trustee Limited Registered Office: ‘L&T House’, Ballard Estate, P.O.Box No. 278, Mumbai, 400001 Website of the Entity www.lntmf.com The particulars of the Scheme have been prepared in accordance with the Securities and Exchange Board of India (Mutual Funds) Regulations 1996, (herein after referred to as SEBI (MF) Regulations) as amended till date, and filed with SEBI, along with a Due Diligence Certificate from the AMC. The units being offered for public subscription have not been approved or recommended by SEBI nor has SEBI certified the accuracy or adequacy of the Scheme Information Document. The Scheme Information Document sets forth concisely the information about the Scheme that a prospective investor ought to know before investing. Before investing, investors should also ascertain about any further changes to this Scheme Information Document after the date of this Document from the Mutual Fund / Investor Service Centres / Website / Distributors or Brokers. The investors are advised to refer to the Statement of Additional Information (SAI) for details of L&T Mutual Fund, Tax and Legal issues and general information on www.lntmf.com

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 1 SCHEME INFORMATION DOCUMENT L&T Mutual ... - SEBI

1

SCHEME INFORMATION DOCUMENT

L&T Mutual Fund

309, 3rd Floor, Trade Centre, Bandra Kurla Complex, Bandra (East), Mumbai - 400 051

L&T Prudence Fund An Open Ended Balanced Scheme

Offer of units at Rs.10/- per unit

and at NAV based prices upon re-opening

New Fund Offer opens on ___________2012 New Fund Offer closes on ___________2012

The Scheme shall Re-open for Continuous Sale and Repurchase within 5 Business Days of Allotment.

SPONSOR

L&T Finance Limited L&T House, Ballard Estate, P.O. Box 278, Mumbai – 400 001

INVESTMENT MANAGER

L&T Investment Management Limited Registered Office*: Dare House, No. 2, N.S.C. Bose Road, Parry’s, Chennai - 600 001

Head Office: 309, 3rd Floor, Trade Centre, Bandra Kurla Complex, Bandra (East), Mumbai - 400 051

TRUSTEE COMPANY

L&T Mutual Fund Trustee Limited Registered Office: ‘L&T House’, Ballard Estate, P.O.Box No. 278, Mumbai, 400001

Website of the Entity

www.lntmf.com The particulars of the Scheme have been prepared in accordance with the Securities and Exchange Board of India (Mutual Funds) Regulations 1996, (herein after referred to as SEBI (MF) Regulations) as amended till date, and filed with SEBI, along with a Due Diligence Certificate from the AMC. The units being offered for public subscription have not been approved or recommended by SEBI nor has SEBI certified the accuracy or adequacy of the Scheme Information Document. The Scheme Information Document sets forth concisely the information about the Scheme that a prospective investor ought to know before investing. Before investing, investors should also ascertain about any further changes to this Scheme Information Document after the date of this Document from the Mutual Fund / Investor Service Centres / Website / Distributors or Brokers. The investors are advised to refer to the Statement of Additional Information (SAI) for details of L&T Mutual Fund, Tax and Legal issues and general information on www.lntmf.com

2

SAI is incorporated by reference (is legally a part of the Scheme Information Document). For a free copy of the current SAI, please contact your nearest Investor Service Centre or log on to our website www.lntmf.com. The Scheme Information Document should be read in conjunction with the SAI and not in isolation. This Scheme Information Document is dated ____________ 2012 * Consequent to change in controlling interest of the AMC, its registered office shall be shifted from the State of Tamil Nadu to the State of Maharashtra, upon receipt of requisite approvals. The registered office shall be shifted at L&T House, Ballard Estate, P.O. Box 278, Mumbai – 400 001.

3

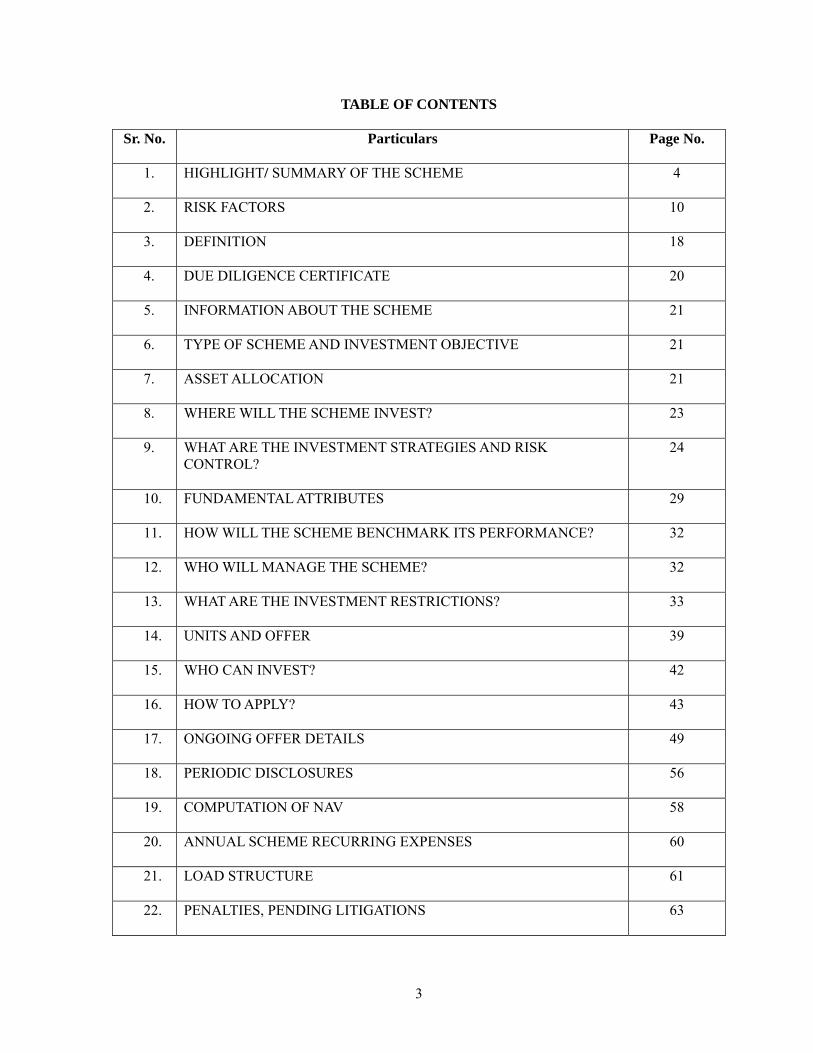

TABLE OF CONTENTS Sr. No. Particulars Page No.

1. HIGHLIGHT/ SUMMARY OF THE SCHEME

4

2. RISK FACTORS

10

3. DEFINITION

18

4. DUE DILIGENCE CERTIFICATE

20

5. INFORMATION ABOUT THE SCHEME

21

6. TYPE OF SCHEME AND INVESTMENT OBJECTIVE

21

7. ASSET ALLOCATION

21

8. WHERE WILL THE SCHEME INVEST?

23

9. WHAT ARE THE INVESTMENT STRATEGIES AND RISK CONTROL?

24

10. FUNDAMENTAL ATTRIBUTES

29

11. HOW WILL THE SCHEME BENCHMARK ITS PERFORMANCE?

32

12. WHO WILL MANAGE THE SCHEME?

32

13. WHAT ARE THE INVESTMENT RESTRICTIONS?

33

14. UNITS AND OFFER

39

15. WHO CAN INVEST?

42

16. HOW TO APPLY?

43

17. ONGOING OFFER DETAILS

49

18. PERIODIC DISCLOSURES

56

19. COMPUTATION OF NAV

58

20. ANNUAL SCHEME RECURRING EXPENSES

60

21. LOAD STRUCTURE

61

22. PENALTIES, PENDING LITIGATIONS

63

4

HIGHLIGHT/ SUMMARY FEATURES

Name the Scheme L&T Prudence Fund Nature of the Scheme An Open Ended Balanced Scheme Investment Objective

The investment objective of the Scheme is to provide medium to long term capital gains and/ or income distribution while at all times emphasizing the importance of capital appreciation.

Plans 1. Moderate Plan 2. Aggressive Plan

Options Following Options are available under each Plan:

Dividend Option: Dividend (Payout & Reinvestment**) Growth Option* Bonus Option***

* If no option is specified at the time of application, the default option is Growth Option.

** If no sub option is specified the default option is dividend reinvestment.

*** Declared as and when decided by the Trustees.

The Trustees reserves the right to declare dividend from time to time, subject to availability of distributable surplus.

Investment Pattern An indication of the asset allocation pattern of the portfolio in both the Plans is as follows:

Moderate Plan:

Asset Class Allocation Range (% of Net Assets)

Risk Profile

Large Cap Equity & Equity Related Instruments*

60% – 75% Medium to High

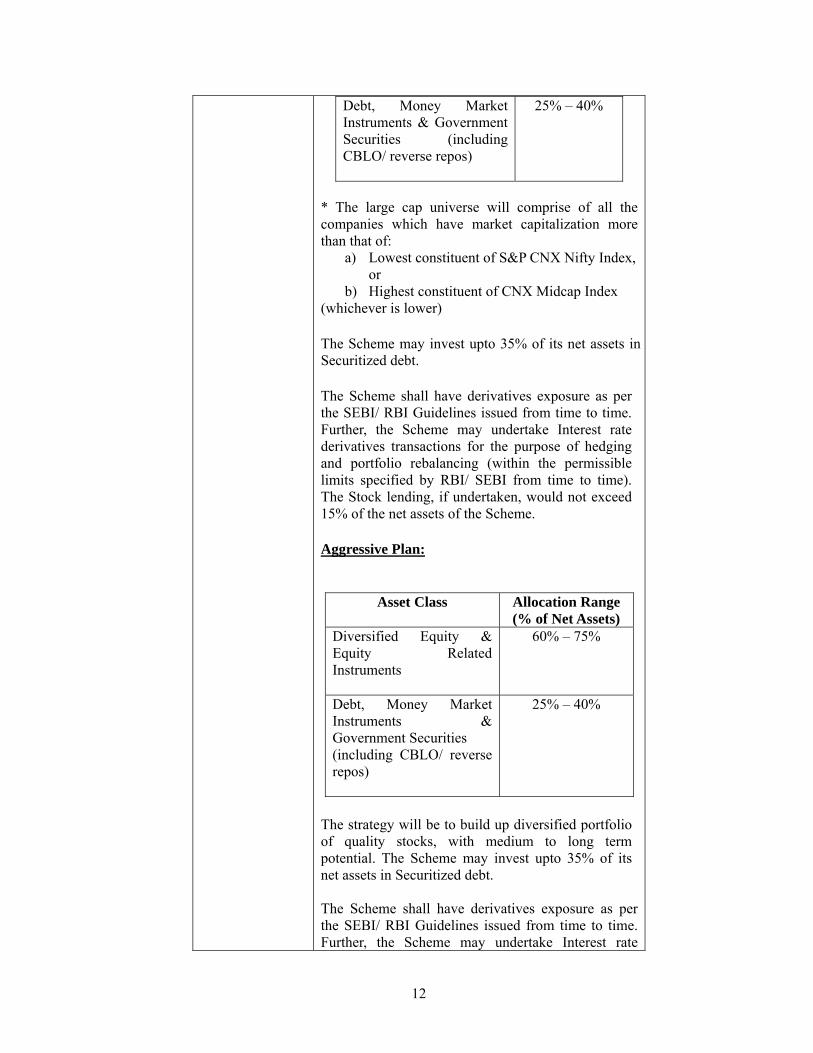

Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40% Low to Medium

* The large cap universe will comprise of all the companies which have market

5

Name the Scheme L&T Prudence Fund capitalization more than that of:

a) Lowest constituent of S&P CNX Nifty Index, or b) Highest constituent of CNX Midcap Index

(whichever is lower)

The Scheme may invest upto 35% of its net assets in Securitized debt.

The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The Stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme.

Pending deployment of the funds in securities in terms of investment objective of the Scheme, the AMC may park the funds of the Scheme in short term deposits of the Scheduled Commercial Banks, subject to the guidelines issued by SEBI vide its circular dated April 16, 2007, as may be amended from time to time.

The gross investments in securities under the Scheme which includes Debt, Money Market Instruments, Government Securities and Large Cap Equity & Equity Related Instruments including Securitized debt & Derivatives shall not exceed 100% of net assets of the Scheme. However, following will not be considered while calculating the gross exposure:

a) Instrument/ Security-wise hedged position and b) Exposure in Cash or cash equivalents with residual maturity of less than 91 days.

The exposure to derivatives will be calculated on notional value of the derivative contracts.

The above asset allocation pattern is not absolute and can vary depending upon the AMC’s perception of the debt, equity and money markets as well as the general view on interest rates. The asset allocation pattern indicated above may thus be altered only on defensive considerations and for a short period not exceeding 1 month.

Aggressive Plan:

Asset Class Allocation Range (% of Net Assets)

Risk Profile

Diversified Equity & Equity Related Instruments

60% – 75% Medium to High

6

Name the Scheme L&T Prudence Fund Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40% Low to Medium

The strategy will be to build up diversified portfolio of quality stocks, with medium to long term potential. The Scheme may invest upto 35% of its net assets in Securitized debt.

The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme.

Pending deployment of the funds in securities in terms of investment objective of the Scheme, the AMC may park the funds of the Scheme in short term deposits of the Scheduled Commercial Banks, subject to the guidelines issued by SEBI vide its circular dated April 16, 2007, as may be amended from time to time.

The gross investments in securities under the Scheme which includes Debt, Money Market Instruments, Government Securities and Diversified Equity & Equity Related Instruments including Securitized debt & Derivatives shall not exceed 100% of net assets of the Scheme. However, following will not be considered while calculating the gross exposure:

a) Instrument/ Security-wise hedged position and b) Exposure in Cash or cash equivalents with residual maturity of less than 91 days.

The exposure to derivatives will be calculated on notional value of the derivative contracts.

The above asset allocation pattern is not absolute and can vary depending upon the AMC’s perception of the debt, equity and money markets as well as the general view on interest rates. The asset allocation pattern indicated above may thus be altered only on defensive considerations and for a short period not exceeding 1 month.

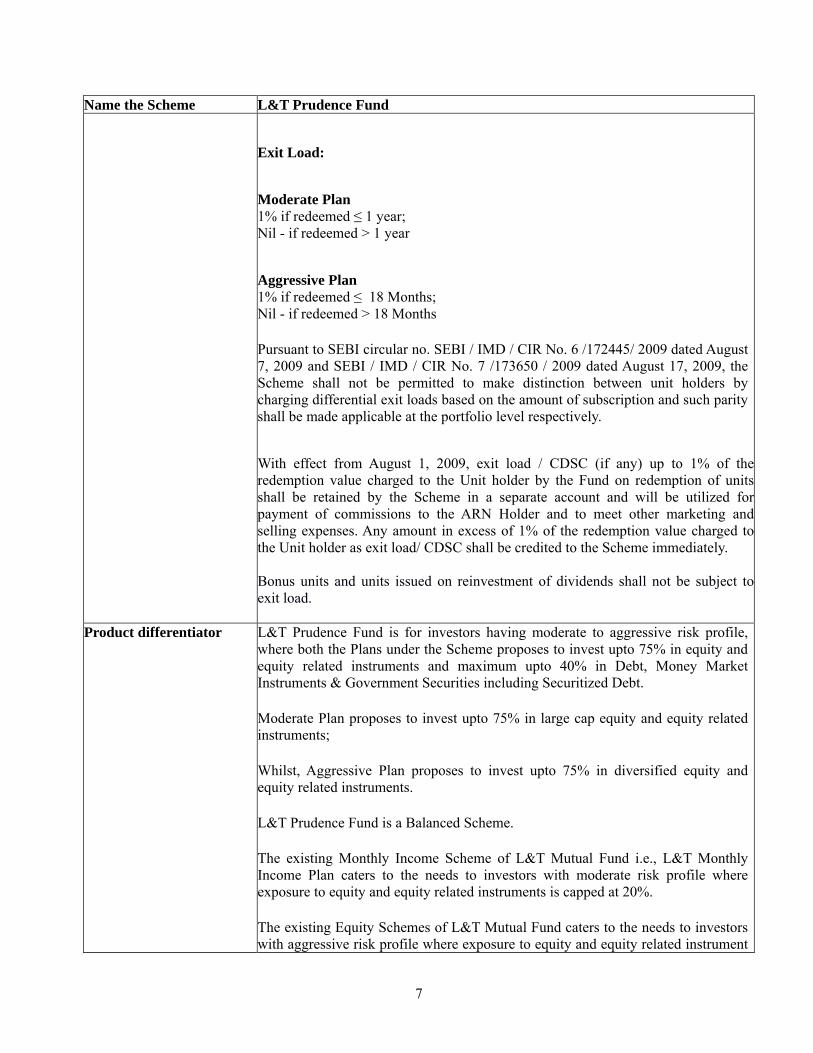

Entry/ Exit Load(including SIP/ STP/ SWP/DIP)

Entry Load: Nil

In terms of SEBI circular no. SEBI/IMD/CIR No.4/ 168230/09 dated June 30, 2009, no entry load will be charged by the Scheme to the investor effective August 1, 2009. Upfront commission shall be paid directly by the investor to the AMFI registered Distributors based on the investor’s assessment of various factors including the service rendered by the distributors.

7

Name the Scheme L&T Prudence Fund

Exit Load: Moderate Plan 1% if redeemed ≤ 1 year; Nil - if redeemed > 1 year Aggressive Plan 1% if redeemed ≤ 18 Months; Nil - if redeemed > 18 Months

Pursuant to SEBI circular no. SEBI / IMD / CIR No. 6 /172445/ 2009 dated August 7, 2009 and SEBI / IMD / CIR No. 7 /173650 / 2009 dated August 17, 2009, the Scheme shall not be permitted to make distinction between unit holders by charging differential exit loads based on the amount of subscription and such parity shall be made applicable at the portfolio level respectively. With effect from August 1, 2009, exit load / CDSC (if any) up to 1% of theredemption value charged to the Unit holder by the Fund on redemption of units shall be retained by the Scheme in a separate account and will be utilized forpayment of commissions to the ARN Holder and to meet other marketing andselling expenses. Any amount in excess of 1% of the redemption value charged to the Unit holder as exit load/ CDSC shall be credited to the Scheme immediately. Bonus units and units issued on reinvestment of dividends shall not be subject toexit load.

Product differentiator L&T Prudence Fund is for investors having moderate to aggressive risk profile, where both the Plans under the Scheme proposes to invest upto 75% in equity and equity related instruments and maximum upto 40% in Debt, Money Market Instruments & Government Securities including Securitized Debt.

Moderate Plan proposes to invest upto 75% in large cap equity and equity related instruments;

Whilst, Aggressive Plan proposes to invest upto 75% in diversified equity and equity related instruments.

L&T Prudence Fund is a Balanced Scheme.

The existing Monthly Income Scheme of L&T Mutual Fund i.e., L&T Monthly Income Plan caters to the needs to investors with moderate risk profile where exposure to equity and equity related instruments is capped at 20%.

The existing Equity Schemes of L&T Mutual Fund caters to the needs to investors with aggressive risk profile where exposure to equity and equity related instrument

8

Name the Scheme L&T Prudence Fund can be upto 100%.

New Fund Offer Price Rs. 10 per unit during New Fund Offer and at NAV based prices after the Scheme re-opens for ongoing sales.

New Fund Offer (NFO) expenses

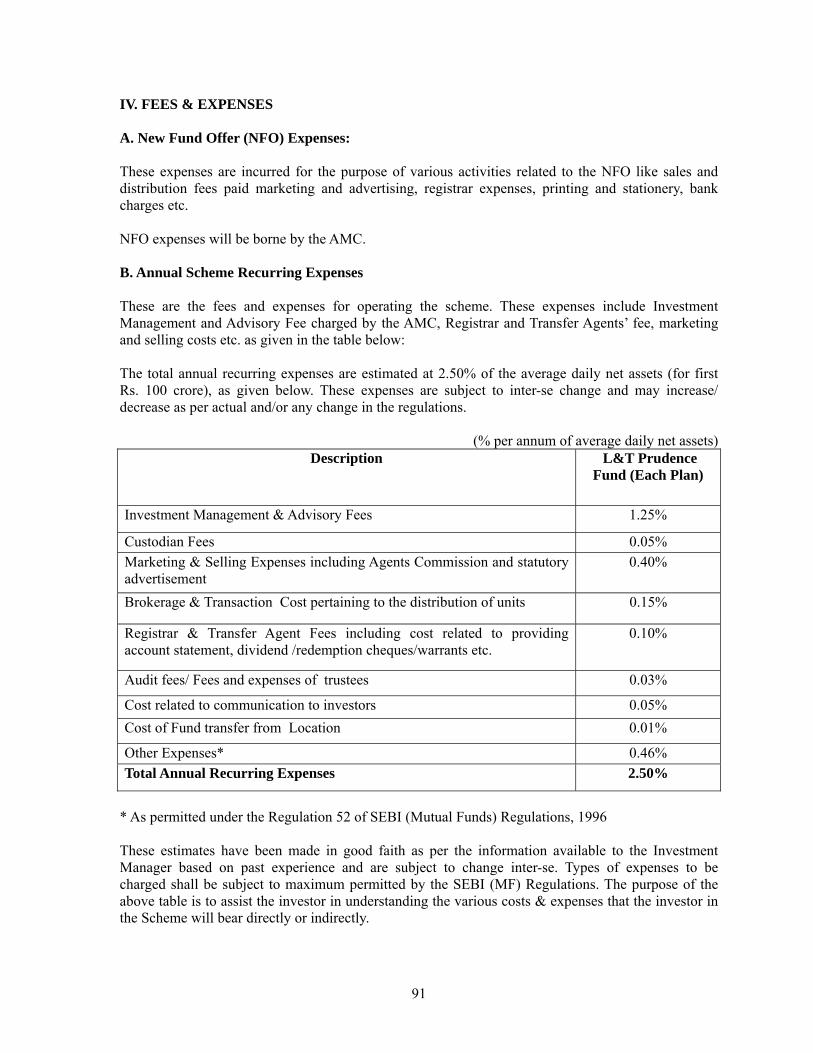

These expenses are incurred for the purpose of various activities related to the NFO like sales and distribution fees paid marketing and advertising, registrar expenses, printing and stationery, bank charges etc.

No NFO expenses will be charged to the Scheme. These expenses will be borne by the AMC.

Minimum ApplicationAmount for LumpsumInvestments under bothPlans (First Purchase):(During NFO and afterScheme opens for repurchaseand sale)

For Dividend Option: A minimum of Rs. 10,000/- per application and in multiples of Re. 1/- thereafter

For Growth/ Bonus Option: A minimum of Rs. 5,000/- per application and in multiples of Re. 1/- thereafter.

Additional Purchase by Existing Unitholders underboth Plans (after theScheme opens for repurchaseand sale)

For all Options - A minimum of Rs. 1,000/- per application and in multiples of Re. 1/- thereafter.

Minimum RepurchaseAmount/ Minimum Unitsunder both Plans (after theScheme opens for repurchaseand sale)

For all Options - A minimum of Rs. 500/- per application or 50 units.

Portfolio Plan-wise portfolio.

Cut Off Timing Before 3.00 p.m. for purchase, redemptions and switches of units of the Scheme, same business day’s NAV. Applications received after 3.00 p.m., next business day’s NAV.

NAV Declaration of NAV on all business days.

Liquidity The AMC will calculate and disclose the first NAV not later than 5 business days from the date of allotment of units. The Scheme will sell and redeem units on a continuous basis, subject to the prevailing load structure (if any).

9

Name the Scheme L&T Prudence Fund

However, units of the plans under the scheme can also be subscribed and redeemed additionally through: a) registered trading members/ stock brokers of recognized Stock Exchanges; b) clearing members of the registered Stock Exchanges; c) depository participants of registered Depositories (to process only redemptionrequest of units held in demat form).

Investors are requested to refer “Facility to hold units in Demat Form through Stock Exchange Mechanism”, mentioned in this Document.

Dematerialization The Unitholders of the plans under the scheme are given an option to hold the units by way of an Account Statement or in Dematerialized (‘Demat’) form.

The Unitholder intending to hold the units in Demat form are required to have a beneficiary account with the Depository Participant (DP) and will be required to indicate in the application the DP’s name, DP ID number and the beneficiary account number of the applicant with the DP. The AMC intends to register with both NSDL & CDSL. Investors to note that name provided in the application form must match with the name provided to the DP and in case of any discrepancies in this, the application will be processed under physical mode.

The AMC shall issue units in dematerialized form to a unitholder within two Business days of the receipt of valid request from the unitholder. In which case, the mode of holding of units would be in demat form.

In case Unitholders do not provide their demat account details in the application form, it shall be treated as investment under physical mode and they will not be able to transact on the eligible Stock Exchange until the holding are converted into demat mode and listed on the Stock Exchange.

Redemption of Units

The Scheme will sell and redeem units under each Plan on a continuous basis (subject to the prevailing Load Structure).

An endeavour shall be made by the AMC to dispatch the redemption proceeds within 3 working days of receipt of valid application at the AMC/ Registrars Office(s).

Disclosure Semi-annual disclosure of entire portfolios of each Plan (in SEBI prescribedformat).

Repatriation Facility Non-resident Indians (NRIs), persons of Indian origin residing abroad, and registered FIIs can invest in the Scheme on a repatriation basis.

Benchmark Index For both Plans:

10

Name the Scheme L&T Prudence Fund

CRISIL Balanced Fund Index

Custodian HDFC Bank Ltd.

Registrar & Transfer Agent Computer Age Management Services Pvt. Ltd.

Minimum Mobilizationunder each Plan

Rs. 1 crore

Banker HDFC Bank Ltd.

Fund Manager For both Plans: Mr. Anant Deep Katare (for Equity portion) and Ms. Bekxy Kuriakose (for Debt portion)

Recurring Expenses Expected to be incurred on an on-going basis not exceeding 2.50% of the daily average net assets upto Rs. 100 Crore, subject to SEBI regulations.

Investors are requested to refer Section on “Fees & Expenses” for detailed break-up.

11

COMPARISON BETWEEN EXISTING OPEN ENDED EQUITY SCHEMES

Schemes L&T Prudence Fund

Investment Objective

The investment objective of the Scheme is to provide medium to long term capital gains and/ or income distribution while at all times emphasising the importance of capital appreciation.

Differentiation

(1) L&T Prudence Fund is for investors having moderate to aggressive risk profile, where both the Plans under the Scheme proposes to invest upto 75% in equity and equity related instruments and maximum upto 40% in Debt, Money Market Instruments & Government Securities including Securitized Debt.

(2) Moderate Plan proposes to invest upto 75% in large cap equity and equity related instruments;

(3) Whilst, Aggressive Plan proposes to invest upto 75% in diversified equity and equity related instruments.

(4) L&T Prudence Fund is a Balanced Scheme. (5) The existing Monthly Income Scheme of

L&T Mutual Fund i.e., L&T Monthly Income Plan caters to the needs to investors with moderate risk profile where exposure to equity and equity related instruments is capped at 20%, whereas L&T MIP – Wealth Builder Fund is for investors with an aggressive risk profile, where the Scheme proposes to invest upto 30% in equity and equity related instruments.

(6) The existing Equity Schemes of L&T Mutual Fund caters to the needs to investors with aggressive risk profile where exposure to equity and equity related instrument can be upto 100%.

Asset Allocation

Moderate Plan:

Asset Class Allocation Range (% of Net Assets)

Large Cap Equity & Equity Related Instruments*

60% – 75%

12

* The large cap universe will comprise of all the companies which have market capitalization more than that of:

a) Lowest constituent of S&P CNX Nifty Index, or

b) Highest constituent of CNX Midcap Index (whichever is lower)

The Scheme may invest upto 35% of its net assets in Securitized debt.

The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The Stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme.

Aggressive Plan:

Asset Class Allocation Range

(% of Net Assets) Diversified Equity & Equity Related Instruments

60% – 75%

Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40%

The strategy will be to build up diversified portfolio of quality stocks, with medium to long term potential. The Scheme may invest upto 35% of its net assets in Securitized debt. The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate

Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40%

13

derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme. Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Live folios (as on December 8,

2011)

Not Applicable

Assets under Management (in Rs. Crore) (as on

November 30, 2011)

Not Applicable

14

Schemes L&T Tax Advantage Fund - Series I L&T Opportunities Fund

Investment Objective

The investment objective of the Scheme is to seek to generate long-term capital growth from a diversified portfolio of predominantly equity and equity-related securities and also enabling investors to get income tax rebate as per the prevailing Tax Laws and subject to applicable conditions. The investment policies shall be framed in accordance with SEBI (Mutual Funds) Regulations, 1996 and rules and guidelines for Equity Linked Savings Scheme (ELSS), 2005 (and modifications to them).

The Scheme will invest mainly to generate long term capital appreciation from a diversified portfolio of equity and equity related securities. The fund will invest in a universe of stocks, which will be identified using fundamental analysis. The fund will invest in a portfolio of both value and growth stocks. The strategy will be to build up diversified portfolio of quality stocks, with medium to long term potential.

Differentiation

1. The Scheme is a 10 years Close Ended Equity Linked Saving Scheme, subject to a lock in for a period of three years from date of allotment.

1. The Scheme invests mainly to generate long term capital appreciation from a diversified portfolio of equity and equity related securities. The Scheme invests in a portfolio of both value and growth stocks.

2. The Scheme is a Close-ended Equity Linked Tax Saving Scheme. Redemptions can be made only after completion of lock-in-period of 3 years from the date of allotment of the units proposed to be redeemed, at NAV based prices.

2. As per asset allocation pattern, the Scheme invests at least 80% of its corpus in equity and equity related instruments.

Asset Allocation

Instruments Min% - Max% Equity & equity related instruments *

80% - 100%

Debt Securities and money market instruments **

0% - 20%

* In accordance with the ELSS notification of November 2005, the Fund collected under the Scheme shall be invested in the equities, cumulative convertible preference shares and fully convertible debenture and bonds of the companies. Investment may also be made in partly convertible issues of debenture and bonds including those issued on rights basis subject to the condition that, as far as possible, the non convertible portion of the debenture so acquired or subscribed, shall be disinvested within a period of 12 months.

** Scheme will not engage in stock lending and will not invest in securitized debt unless as and when permitted by ELSS guidelines and clarification in this regard issued by SEBI. Please refer Scheme Information Document of

Instruments Min% - Max% Equity and equity related instruments

80% - 100%

Debt and Money Market Instruments (including cash/call money)

0% - 20%

Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

15

the Scheme for detailed Asset Allocation.

Live folios (as on December

8, 2011)

4538 41823

Assets under Management (in Rs. Crore)

(as on November 30,

2011)

2.84 96.13

16

Schemes L&T Hedged Equity Fund L&T Midcap Fund

Investment Objective

The investment objective of the fund is to generate long term capital appreciation by investing in equity, equity related and derivative instruments. The fund seeks to minimize risk by use of hedging instruments such as index and stock derivative instruments. The aim is to generate returns with a lower volatility.

The investment objective of the scheme is to generate capital appreciation by investing primarily in midcap stocks. The scheme will invest primarily in companies whose market capitalization falls between the highest and the lowest constituent of the CNX Midcap Index.

Differentiation

1. The Scheme seeks to minimize risk by extensive use of hedging instruments such as index and stock derivative instruments.

1. The Scheme seeks to generate return by investing primarily in midcap stocks as per the investment objective and asset allocation.

2. The aim is to generate returns with a lower volatility. Investment in equity derivative instruments can be upto 50% of net assets of the Scheme.

2. The scheme will invest primarily in companies whose market capitalization falls between the highest and the lowest constituent of the CNX Midcap Index.

Asset Allocation

Instruments Min% - Max% Equity and equity related instruments (including equity derivative instruments)#

65% - 100%

Debt and Money Market Instruments*

0% - 35%

# Investment in equity derivative instruments would not exceed 50% of the net assets of the scheme. * Investment in Securitized debt, if undertaken, would not exceed 30% of the net assets of the scheme. A maximum of 40% of net assets may be deployed in securities lending and the maximum single party exposure may be restricted to 10% of net assets outstanding at any point of time. Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Instruments Min% - Max% Equity & Equity related instruments

80% - 100%

Debt Securities, Securitized Debt & Money Market instruments (including cash/call money)

0% - 20%

Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Live folios (as on December

8, 2011)

3609 21528

Assets under Management (in Rs. Crore)

(as on November 30,

2011)

7.82 53.22

17

Schemes L&T Growth Fund L&T Tax Saver Fund

Investment Objective

The Scheme primarily seeks to generate long term capital appreciation income through investments in equity and equity related instruments; the secondary objective is to generate current income and distribute dividend. However, there is no assurance that the investment objective of the scheme will be achieved.

The Scheme seeks to provide long term capital appreciation by investing predominantly in equity and equity related instruments and also enabling investors to get income tax rebate as per the prevailing Tax Laws and subject to applicable conditions.

Differentiation

1. The Scheme seeks to generate long term capital appreciation through investment in equity and equity related instruments.

1. The Scheme follows a multi-cap investment approach i.e., the Scheme invests in a well-diversified portfolio of equity & equity related instruments across all ranges of market capitalization.

2. The Scheme focuses on investing in large cap companies.

2. The Scheme enables the investors to get income tax rebate as per the prevailing Tax Laws, subject to lock in period of 3 years from the date of allotment.

Asset Allocation

Instruments Min% - Max%

Equity & Equity related instruments

80% - 100%

Debt securities & Money Market instruments (including cash and call money)

0% - 20%

Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Instruments Min% - Max% Equity & Equity related instruments

80% - 100%

Debt* and Money market instruments

0% - 20%

* Investment in securitized debt, if undertaken, will not exceed 20% of corpus of the scheme. Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Live folios (as on December 8,

2011)

13632 9390

Assets under Management (in Rs. Crore)

(as on November 30,

2011)

32.17 25.74

18

Schemes L&T Contra Fund

Investment Objective

The objective of the scheme is to generate capital appreciation by investing in equity and equity related instruments by using a 'contrarian strategy'. Contrarian investing refers to buying into fundamentally sound scripts which have underperformed / not performed to their full potential in their recent past.

Differentiation

1. The Scheme invests in equity and equity related instruments by using a 'contrarian strategy'. Contrarian investing refers to buying into fundamentally sound scripts which have underperformed / not performed to their full potential in their recent past. 2. The Scheme may invest upto 30% of its net assets in Securitized debt.

Asset Allocation

Instruments Min% - Max% Equity & Equity related instruments#

65% - 100%

Debt and Money market instruments*

0% - 35%

# including investments in ADR / GDR upto 25% (subject to maximum of US$ 50 million as specified by SEBI), exposure in derivatives upto a maximum of 25% (subject to limit as specified by SEBI from time to time). At the time of investment, investments in derivative instruments may be done for hedging and portfolio balancing. * Investment in Securitized debt, if undertaken, would not exceed 30% of the net assets of the scheme. A maximum of 40% of net assets may be deployed in securities lending and the maximum single party exposure may be restricted to 10% of net assets outstanding at any point of time. Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Live folios (as on December 8,

2011)

4488

19

Assets under Management (in Rs. Lakhs)

(as on November 30,

2011)

833.23

Schemes L&T Infrastructure Fund

Investment Objective

The Scheme seeks to generate capital appreciation by investing predominantly in equity and equity related instruments of companies in the infrastructure sector.

Differentiation

1. The Scheme will predominantly invest in securities of the companies in the infrastructure sector.

Asset Allocation

Instruments Min% - Max% Equity and equity related instruments (including equity derivative instruments)

65% - 100%

Debt and Money Market Instruments*

0% - 35%

*Investment in Securitized debt, if undertaken, would not exceed 35% of the net assets of the scheme. Please refer Scheme Information Document of the Scheme for detailed Asset Allocation.

Live folios (as on December

8, 2011)

16875

Assets under Management (in Rs. Crore)

(as on November 30,

2011)

7.50

20

RISK FACTORS A. Standard Risk Factors

• Investment in Mutual Fund Units involves investment risks such as trading volumes, settlement risk, liquidity risk, price risk, default risk including the possible loss of principal.

• Mutual Funds and securities investments are subject to market risks and there is no assurance or guarantee that the objectives of the Scheme will be achieved.

• As the price / value / interest rates of the securities in which the Scheme invests fluctuate, the value of your investment in the Scheme may go up or down.

• Past performance of the Sponsor/AMC/Mutual Fund does not guarantee future performance of the Scheme.

• L&T Prudence Fund including its Plans does not in any manner indicate either the quality of the Scheme/ Plan or its future prospects and returns; and is only the name of the Scheme/ Plan.

• The Sponsor is not responsible or liable for any loss resulting from the operation of the Scheme beyond initial contribution of Rs. 1 lakh made by it towards setting up of the Fund.

• The Scheme/ Plan do not provide guarantee or assured return to the unitholders. Scheme Specific Risk Factors

1. Since the NAV of the Scheme/ Plan will be linked to the share price performance of

Companies where the Scheme will invest, they may outperform or under perform the benchmark index (CRISIL Balanced Fund Index) and/or the constituents of the said benchmark index.

2. Each Plan under the Scheme proposes to invest upto 75% in equity and equity related instruments (however, Moderate Plan shall invest upto 75% in large cap equity and equity related instruments), risk associated with it could be relatively more than an Income Scheme. Investors are requested to consult their legal, financial, tax advisor before investing.

3. Returns: Investors in the Scheme are not being offered any guaranteed or assured returns.

4. Performance Risk: Scheme/ Plan performance can decrease or increase, depending on a

variety of factors, which may affect the values and income generated by a Scheme’s portfolio of securities. The returns of a Scheme’s investments are based on the current yields of the securities, which may be affected generally by factors affecting capital markets such as price and volume, volatility in the stock markets, interest rates, currency exchange rates, foreign investment, changes in government and Reserve Bank of India policy, taxation, political, economic or other developments and closure of the stock exchanges. Investors should understand that the investment pattern indicated for the Scheme, in line with prevailing market conditions, is only a hypothetical example as all investments involve risk and there can be no assurance that the Scheme’s investment objective will be attained nor will the Scheme be in a position to maintain the model percentage of investment pattern/ composition particularly under exceptional circumstances so that the interest of the unitholders are protected. The AMC will endeavour to invest in researched growth companies, however the growth associated with equities is generally high as also the erosion in the value of the investments/ portfolio in the case of the capital markets passing through a bearish phase is a distinct possibility. A change in the prevailing rates of interest is likely to affect the value of the Scheme’s investments and thus the value of the Scheme’s Units. The value of money market instruments held by the Scheme generally will vary inversely with the changes in prevailing interest rates. Since the NAV of the Scheme will also be linked to share price

21

performance of Companies where the scheme will invest, they may outperform/ underperform the benchmark index and/or the constituents of the benchmark index.

5. Liquidity & Settlement Risk: Investors may note that AMC’s investment decisions may not be always profitable. The Plans under the Scheme proposes to invest upto 40% in Debt, Money Market Instruments & Government Securities including Securitized Debt. The Scheme will, substantially invest in Equity & Equity related instruments. Trading volumes, settlement periods and transfer procedures may restrict the liquidity of these investments. Different segments of the Indian financial markets have different settlement periods and such periods may be extended significantly by unforeseen circumstances. The inability of the Scheme/ Plan to make intended securities purchases due to settlement problems could cause the Scheme/ Plan to miss certain investment opportunities. By the same rationale, the inability to sell securities held in the Scheme’s portfolio due to the absence of a well developed and liquid secondary market would result, at times, in potential losses to the Scheme/ Plan, in case of a subsequent decline in the value of securities held in the Scheme/ Plan portfolio.

6. Derivative Risk: Derivative products are leveraged instruments and can provide

disproportionate gains as well as disproportionate losses to the investor. Execution of such strategies depends upon the ability of the fund manager to identify such opportunities. Identification and execution of the strategies to be pursued by the fund manager involve uncertainty and decision of fund manager may not always be profitable. No assurance can be given that the fund manager will be able to identify or execute such strategies.

The risks associated with the use of derivatives are different from or possibly greater than, the risks associated with investing directly in securities and other traditional investments.

As and when the Scheme/ Plan trades in the derivatives market there are risk factors and issues concerning the use of derivatives that Investors should understand. Derivative products are specialized instruments that require investment techniques and risk analyses different from those associated with stocks. The use of a derivative requires an understanding not only of the underlying instrument but of the derivative itself. Derivatives require the maintenance of adequate controls to monitor the transactions entered into, the ability to assess the risk that a derivative adds to the portfolio and the ability to forecast price or interest rate movements correctly. There is the possibility that a loss may be sustained by the portfolio as a result of the failure of another party (usually referred to as the “counter party”) to comply with the terms of the derivatives contract. Other risks in using derivatives include the risk of mis-pricing or improper valuation of derivatives and the inability of derivatives to correlate perfectly with underlying assets, rates and indices. Investors are requested to refer section on “Guidelines for investments in Securitized Debt”, mentioned in this Document.

7. Currency Risk: Investments in overseas securities (if undertaken after obtaining necessary approvals) are subject to currency risk. Returns to investors are the result of a combination of returns from investments and from movements in exchange rates. For example, if the Rupee appreciates vis-à-vis US dollar, the extent of appreciation will lead to reduction in the return to the investor to the extent of exposure in the overseas securities. In case the Rupee depreciates vis-à-vis the US dollar, the extent of depreciation will lead to a corresponding increase in the returns to the investor to the extent of exposure in the overseas securities.

22

Going forward, the Rupee may depreciate (lose value) or appreciate (increase value) against the currencies of the countries where the Scheme will invest.

8. Exchange Rate Risk: Companies with high export earnings may generate revenues and make investments in foreign currencies. Changes in exchange rates may have a positive or negative impact on the prospects of such companies.

9. Changes in Government Regulations: The businesses in which companies operate are

exposed to a range of government regulations, related to tax benefits, liberalisation, provision of infrastructure and the like. Changes in such regulations may affect the prospects of companies.

10. Political Risk: Whereas the Indian market was formerly restrictive, a process of deregulation

has been taking place over recent years. This process has involved the removal of trade barriers and other protectionist measures, which could adversely affect the value of investments. It is possible that future changes in the Indian political situation, including political, social, or economic instability, diplomatic developments and changes in laws or regulations could have an effect on the value of investments. Expropriation, confiscatory taxation, or other relevant developments could also affect the value of investments.

11. Securities/ Stock Lending Risks: It may be noted that Securities Lending activity would

have the inherent probability of collateral value drastically falling in times of strong downward market trends or due to it being comprised of tainted/ forged securities, resulting in inadequate value of collateral until such time as that diminution in value is replenished by additional security. It is also possible that the borrowing party and/ or the approved intermediary may suddenly suffer severe business setback and become unable to honour its commitments. This along with a simultaneous fall in value of collateral would render potential loss to the Scheme/ Plan. Besides, there can also be temporary illiquidity of the securities that are lent out and the Scheme may not be able to sell such lent out securities.

The risks in lending portfolio securities, as with other extensions of credit, consist of the failure of another party, in this case the approved intermediary, to comply with the terms of agreement entered into between the lender of securities i.e. the Scheme/ Plan and the approved intermediary. Such failure to comply can result in the possible loss of rights in the collateral put up by the borrower of the securities, the inability of the approved intermediary to return the securities deposited by the lender and the possible loss of any corporate benefits accruing to the lender from the securities deposited with the approved intermediary.

12. Dividends: The Scheme/ Plan do not guarantee or assure any dividend frequency. The Mutual Fund/ Trustee Company is also not assuring that it will make regular dividend distributions though it could have intention of doing so. The dividend distributions in each dividend options of the Scheme/ Plan will be dependent on the returns achieved through active management of the portfolio and subject to availability of distributable surpluses. Dividend frequency will be based on the investment results of the portfolio and Trustees reserves the right to declare the dividend. Investors should note that pursuant to the payment of dividend, the NAV of the respective Dividend Options of the Scheme/ Plan will fall to the extent of payout and statutory levy, if any.

Under dividend options of the Scheme/ Plan, in case of net dividend entitlement is less than Rs.250/- the dividend amount will be reinvested in the Scheme automatically.

23

13. Risk Factors Associated with investment in Equity and Equity Related Instruments:

1. Equity securities and equity related securities are volatile and prone to price fluctuations on a daily basis. The liquidity of investments made in the Scheme/ Plan may be restricted by trading volumes and settlement periods. Settlement periods may be extended significantly by unforeseen circumstances. The inability of the Scheme/ Plan to make intended securities purchases, due to settlement problems, could cause the Scheme/ Plan to miss certain investment opportunities. Similarly, the inability to sell securities held in the Scheme/ Plan portfolio would result at times, in potential losses to the Scheme/ Plan, should there be a subsequent decline in the value of securities held in the Scheme/ Plan portfolio.

2. The performance and the value of the Scheme/ Plan investments may be affected by factors affecting the securities markets such as price and volume volatility in the capital markets, currency exchange rates, changes in law / policies of the Government, taxation laws and political, economic or other developments which may have an adverse bearing on individual securities, a specific sector or all sectors. Consequently, the NAV of the Units may be affected.

3. The liquidity and valuation of the Scheme/ Plan investments due to its holdings of unlisted securities may be affected if they have to be sold prior to their target date of divestment.

4. The Scheme/ Plan may invest in securities which are not quoted on a stock exchange ("unlisted securities") which in general are subject to greater price fluctuations, less liquidity and greater risk than those which are traded in the open market. Unlisted securities may lack a liquid secondary market and there can be no assurance that the Scheme/ Plan will realize its investments in unlisted securities at a fair value.

14. Risks associated with investing in Fixed Income Securities and Money Market Instruments: Investment in Debt is subject to interest rate, credit, reinvestment and liquidity risk. The NAV of the Scheme/ Plan(s) may be affected, inter alia, by changes in the market conditions, changes in RBI policies, interest rates, trading volumes, settlement periods and redemptions. Investing in Bonds and Fixed Income securities are subject to the risk of an Issuer’s inability to meet principal and interest payments obligation (credit risk) and may also be subject to price volatility due to such factors as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity (market risk). The timing of transactions in debt obligations, which will often depend on the timing of the Purchases and Redemptions in the Scheme/ Plan(s), may result in capital appreciation or depreciation because the market value of debt and money market instruments generally varies inversely with the prevailing interest rates. Interest Rate Risk: As with all debt securities, changes in interest rates will affect the Scheme’s Net Asset Value as the prices of securities generally increase as interest rates decline and generally decrease as interest rates rise. Prices of longer-term securities generally fluctuate more in response to interest rate changes than do shorter-term securities. Interest rate movements in the Indian debt markets can be volatile leading to the possibility of large price movements up or down in debt and money market securities and thereby to possibly

24

large movements in the NAV. Liquidity or Marketability Risk: This refers to the ease at which a security can be sold at or near its true value. The primary measure of liquidity risk is the spread between the bid price and the offer price quoted by a dealer. Liquidity risk is characteristic of the Indian fixed income market. Credit Risk: Credit risk or default risk refers to the risk which may arise due to default on the part of the issuer of the fixed income security (i.e. will be unable to make timely principal and interest payments on the security). Because of this risk debentures are sold at a yield spread above those offered on Treasury securities, which are sovereign obligations and generally considered to be free of credit risk. Normally, the value of a fixed income security will fluctuate depending upon the actual changes in the perceived level of credit risk as well as the actual event of default. Reinvestment Risk: This risk refers to the interest rate levels at which cash flows received from the securities in the Scheme or from maturities in the Scheme(s) are reinvested. The additional income from reinvestment is the “interest on interest” component. The risk refers to the fall in the rate for reinvestment of interim cash flows. Liquidity Risk: This risk refers to the risk arising from selling or buying a debt security if its illiquid and does not have enough trading volumes. This can lead to a purchase or sale at above or below the fair market value. Such a risk typically arises at the time of sale which may be due to unforeseen conditions like redemptions and or change in market conditions due to which market preferences shift. This can make an exisiting liquid debt instrument illiquid and vice versa.

15. Risk Associated with Securitized Debt and PTC:

Scheme may invest in domestic securitized debt such as asset backed securities (ABS) or mortgage backed securities (MBS). Asset Backed Securities (ABS) are securitized debts where the underlying assets are receivables arising from automobile loans, personal loans, loans against consumer durables, etc. Mortgage backed securities (MBS) are securitized debts where the underlying assets are receivables arising from loans backed by mortgage of residential / commercial properties. ABS/MBS instruments reflect the undivided interest in the underlying pool of assets and do not represent the obligation of the issuer of ABS/MBS or the originator of the underlying receivables. The ABS/MBS holders have a limited recourse to the extent of credit enhancement provided. If the delinquencies and credit losses in the underlying pool exceed the credit enhancement provided, ABS/MBS holders will suffer credit losses. ABS/MBS are also normally exposed to a higher level of reinvestment risk as compared to the normal corporate or sovereign debt. Typically, investments in securitized debt carry credit risk (where credit losses in the underlying pool exceed credit enhancement provided, (if any) and the reinvestment risk (which is higher as compared to the normal corporate or sovereign debt).

Generally the following asset classes for securitization are available in India: (a) Commercial Vehicles (b) Auto and Two wheeler pools (c) Mortgage pools (residential housing loans) (d) Personal Loan, credit card and other retail loans (e) Corporate loans/receivables (f) Single Loan PTC

25

In terms of specific risks attached to securitization, each asset class would have different underlying risks, however, residential mortgages are supposed to be having lower default rates as an asset class. On the other hand, repossession and subsequent recovery of commercial vehicles and other auto assets is fairly easier and better compared to mortgages. Some of the asset classes such as personal loans, credit card receivables, etc., being unsecured credits in nature, may witness higher default rates. As regards corporate loans/receivables, depending upon the nature of the underlying security for the loan or the nature of the receivable the risks would correspondingly fluctuate. However, the credit enhancement stipulated by rating agencies for such asset class pools is typically much higher and hence their overall risks are comparable to other AAA rated asset classes. The rating agencies have an elaborate system of stipulating margins, over collateralization and guarantee to bring risk limits in line with the other AA rated securities.

A single loan PTC is a securitization transaction in which a loan given by an originator (Bank/ NBFC/ FI etc.) to a single entity (obligor) is converted into pass through certificates and sold to investors. The transaction involves the assignment of the loan and the underlying receivables by the originator to a trust, which funds the purchase by issuing PTCs to investors at the discounted value of the receivables. The PTCs are rated by a rating agency, which is based on the financial strength of the obligor alone, as the PTCs have no recourse to the originator.

The advantage of a single loan PTC is that the rating represents the credit risk of a single entity (the obligor) and is hence easy to understand and track over the tenure of the PTC. The primary risk is that of all securitized instruments, which are not traded as often in the secondary market and hence carry an illiquidity risk. The structure involves an assignment of the loan by the originator to the trustee who then has no interest in monitoring the credit quality of the originator. The originator that is most often a bank is in the best position to monitor the credit quality of the originator. The investor then has to rely on an external rating agency to monitor the PTC. Since the AMC relies on the documentation provided by the originator, there is a risk to the extent of the underlying documentation between the seller and underlying borrower.

Investors are requested to note the following additional risks associated with investments in securitized debt and PTC:

• Tenor risk: While building the planned amortisation schedule for a PTC there can be a

clause stating a minimum percentage of receivable by the issue to stick to the initial cash flows. If the receivables are less than the minimum stated receivables then the tenor of the PTC can get elongated or vice versa.

• Credit risk: The PTC holders/Contributors are taking a direct exposure to the repayment

ability of the underlying borrowers. Hence the timely payment on the PTCs/Contributions will depend on the credit quality of the pool borrowers. The credit-cum-liquidity enhancement stipulated for the PTCs/Contributions adequately covers the credit risk.

• Commingling risk: This risk arises on account of time lag between pool collections and

investor payouts, during which the Collection Agent continues to hold the pool collections. The risk of loss of cash flows on account of commingling depends on the credit standing of the issuer.

26

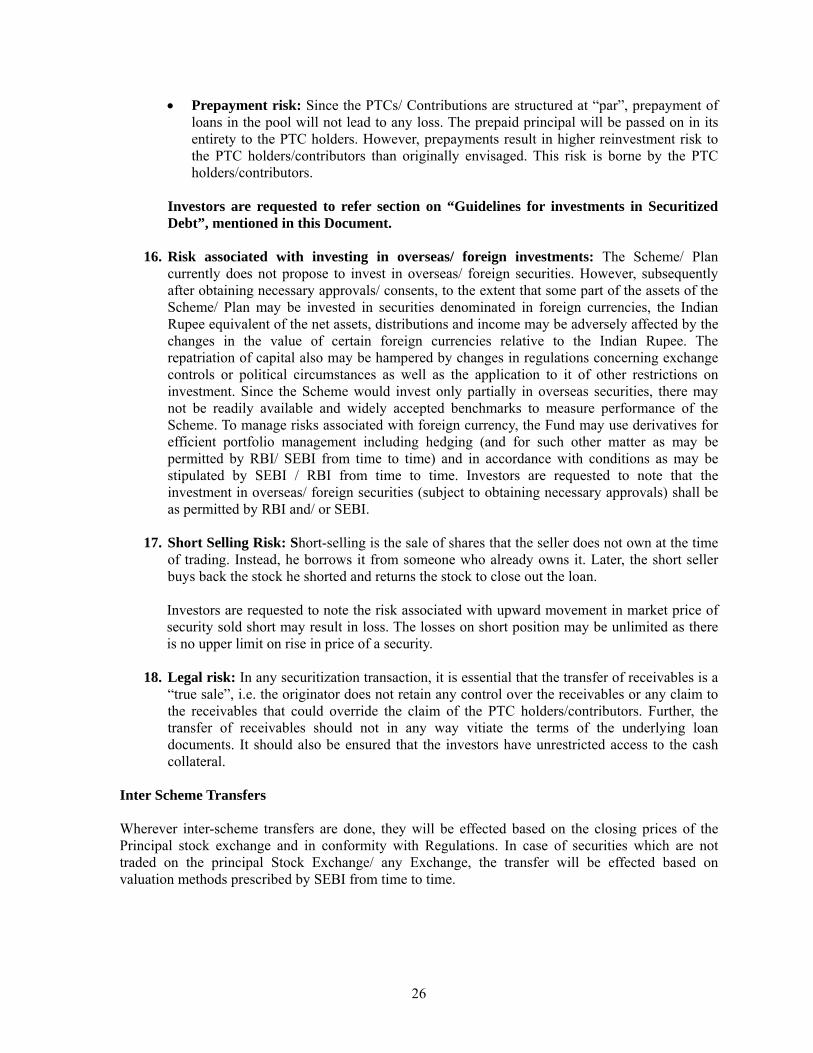

• Prepayment risk: Since the PTCs/ Contributions are structured at “par”, prepayment of loans in the pool will not lead to any loss. The prepaid principal will be passed on in its entirety to the PTC holders. However, prepayments result in higher reinvestment risk to the PTC holders/contributors than originally envisaged. This risk is borne by the PTC holders/contributors.

Investors are requested to refer section on “Guidelines for investments in Securitized Debt”, mentioned in this Document.

16. Risk associated with investing in overseas/ foreign investments: The Scheme/ Plan

currently does not propose to invest in overseas/ foreign securities. However, subsequently after obtaining necessary approvals/ consents, to the extent that some part of the assets of the Scheme/ Plan may be invested in securities denominated in foreign currencies, the Indian Rupee equivalent of the net assets, distributions and income may be adversely affected by the changes in the value of certain foreign currencies relative to the Indian Rupee. The repatriation of capital also may be hampered by changes in regulations concerning exchange controls or political circumstances as well as the application to it of other restrictions on investment. Since the Scheme would invest only partially in overseas securities, there may not be readily available and widely accepted benchmarks to measure performance of the Scheme. To manage risks associated with foreign currency, the Fund may use derivatives for efficient portfolio management including hedging (and for such other matter as may be permitted by RBI/ SEBI from time to time) and in accordance with conditions as may be stipulated by SEBI / RBI from time to time. Investors are requested to note that the investment in overseas/ foreign securities (subject to obtaining necessary approvals) shall be as permitted by RBI and/ or SEBI.

17. Short Selling Risk: Short-selling is the sale of shares that the seller does not own at the time

of trading. Instead, he borrows it from someone who already owns it. Later, the short seller buys back the stock he shorted and returns the stock to close out the loan.

Investors are requested to note the risk associated with upward movement in market price of security sold short may result in loss. The losses on short position may be unlimited as there is no upper limit on rise in price of a security.

18. Legal risk: In any securitization transaction, it is essential that the transfer of receivables is a

“true sale”, i.e. the originator does not retain any control over the receivables or any claim to the receivables that could override the claim of the PTC holders/contributors. Further, the transfer of receivables should not in any way vitiate the terms of the underlying loan documents. It should also be ensured that the investors have unrestricted access to the cash collateral.

Inter Scheme Transfers

Wherever inter-scheme transfers are done, they will be effected based on the closing prices of the Principal stock exchange and in conformity with Regulations. In case of securities which are not traded on the principal Stock Exchange/ any Exchange, the transfer will be effected based on valuation methods prescribed by SEBI from time to time.

27

Borrowing Powers As per SEBI Regulations, the Fund may borrow in order meet temporary liquidity needs of the Scheme for the purpose of repurchase, redemption, or payment of interest / dividend to Unit Holders. Further as per SEBI Regulations, the Fund may borrow upto 20% of the Net Assets of the Scheme for a period of upto 6 months. The Fund may enter into required arrangements with banks, financial institutions or other bodies corporate.

These loans will be secured, if necessary, by securities or assets of the Scheme or such other collateral security as may be agreed upon with the Bank at the time of borrowing. Such borrowing may have an impact of investment gains or losses on the NAV of the Scheme. The Scheme may bear the interest charged on such borrowings.

Measures to mitigate risks associated with the Scheme/ Plan

1) The overall portfolio structuring of the Scheme/ Plan would aim at controlling risk at

moderate level. 2) Stock/ Instrument specific risk shall be minimised by investing in those companies that have

been thoroughly researched in-house. 3) Risk would also be managed through broad diversification of the portfolios within the

framework of the Scheme/ Plan investment objective and policies. 4) The Scheme/ Plan may also invest in derivative products to reduce the volatility of the

portfolio. B. Requirement of Minimum Investor in the Scheme/Plan Each Plan of the Scheme shall have a minimum of 20 investors and no single investor shall account for more than 25% of the corpus of the Plan. However, if such limit is breached during the NFO of the Scheme/ Plan, the Fund will endeavour to ensure that within a period of three months or the end of the succeeding calendar quarter from the close of the NFO of the Scheme/ Plan, whichever is earlier, the Scheme/ Plan complies with these two conditions. In case any of the Plan does not have a minimum of 20 investors in the stipulated period, the provisions of Regulation 39(2)(c) of the SEBI (MF) Regulations would become applicable automatically without any reference from SEBI and accordingly the Plan shall be wound up and the units would be redeemed at applicable NAV. The two conditions mentioned above shall also be complied within each subsequent calendar quarter thereafter, on an average basis, as specified by SEBI. If there is a breach of the 25% limit by any investor over the quarter, a rebalancing period of one month would be allowed and thereafter the investor who is in breach of the rule shall be given 15 days notice to redeem his exposure over the 25 % limit. Failure on the part of the said investor to redeem his exposure over the 25% limit within the aforesaid 15 days would lead to automatic redemption by the Mutual Fund on the applicable Net Asset Value on the 15th day of the notice period. The Fund shall adhere to the requirements prescribed by SEBI from time to time in this regard. C. SPECIAL CONSIDERATIONS, if any Investors are requested to note that the income is not assured and is subject to availability of distributable surplus. There can be no assurance that the objective of the Scheme/ Mutual Fund will be achieved.

All the above factors not only affect the prices of securities but may also affect the time taken by the Fund for redemption of Units, which could be significant in the event of receipt of a very large

28

number of redemption requests or very large value of redemption requests. The liquidity of the assets may be affected by other factors such as general market conditions, political events, bank holidays and civil strike. In view of this, the Trustee has the right in its sole discretion to limit redemption (including suspension of redemption) under certain circumstances. Please refer to the para "Suspension of Sale and Redemption of Units” in Statement of Additional Information.

The liquidity of the Scheme's investments may also be restricted by trading volumes, settlement periods and transfer procedures. In the event of an inordinately large number of redemption requests or of a restructuring of the plan's portfolios, the time taken by the plan for redemption of Units may become significant. In view of this, the Trustee has the right in its sole discretion to limit redemption (including suspension of redemption) under certain circumstances.

Redemption due to change in the fundamental attributes of the Scheme or due to any other reasons may entail tax consequences. The Trustee, AMC, Mutual Fund, their directors, their employees or associates shall not be liable for any such tax consequences that may arise.

The tax benefits described in this Scheme Information Document/ Statement of Additional Information are as available under the present taxation laws and are available subject to conditions. The information given is included for general purpose only and is based on advice received by the AMC regarding the law and practice in force in India and the Unitholders should be aware that the relevant fiscal rules or their interpretation may change. As is the case with any investment, there can be no guarantee that the tax position or the proposed tax position prevailing at the time of an investment in the Scheme will endure indefinitely. In view of the individual nature of tax consequences, each unitholder is advised to consult his/ her own professional tax advisor.

No person has been authorised to give any information or to make any representation not confirmed in this Standard Information Document in connection with the scheme or the offer of Units, and any information or representation not contained herein must not be relied upon as having been authorised by the Mutual Fund or the Asset Management Company Since, the investments in mutual funds and secondary markets inherently involve risks, Investors are advised to consult their Legal, Tax, Finance and other Professional Advisors before making decision to invest in or redeem the units in regard to tax/ legal issues relating to their investments in the Scheme. Recipient of this Document should understand that statements made herein regarding future prospects may not be realized. Any performance information shown refers to the past should not be seen as an indication of future returns. The value of investments and any income from them can go down as well as up. The distribution of this Document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. Investors in the Scheme are not being offered any guaranteed returns. Please read SAI, this Document and KIM carefully before investing.

29

DEFINITIONS In this Scheme information Document the following words and expressions shall have the meaning specified herein unless the context otherwise requires:

Asset Management Company / AMC / Investment Manager

L&T Investment Management Limited, the asset management company set up under the Companies Act, 1956 and authorized by SEBI to act as Asset Management Company to the Schemes of L&T Mutual Fund.

Applicable NAV (after the Scheme opens for repurchase and sale)

Purchases/ Switch-ins: In respect of valid applications received up to 3.00 p.m. by the Mutual Fund

along with a local cheque or a demand draft payable at par at the place where the application is received, the closing NAV of the day on which application is received shall be applicable.

In respect of valid applications received after 3.00 p.m. by the Mutual Fund along with a local cheque or a demand draft payable at par at the place where the application is received, the closing NAV of the next business day shall be applicable.

However, in respect of valid applications with outstation cheques/demand drafts not payable at par at the place where the application is received, closing NAV of the business day on which cheque/ demand draft is credited shall be applicable. Redemptions/ Switch-out:

In respect of valid applications received upto 3.00 p.m. on a day, the same day’s NAV of receipt of application shall be applicable.

In respect of valid applications received after 3.00 p.m. on a day, the closing NAV of the next Business Day shall be applicable.

Business Day Any day other than:

1) Saturday; 2) Sunday; 3) Day on which any one of Banks / RBI in Mumbai or the Bombay Stock Exchange Ltd. or the National Stock Exchange of India Ltd. are required or obliged by law or executive order to remain close including the occasions when the functioning of any of the above banks or stock exchanges is affected due to a strike call made by a recognized union / management at any part of the country; 4) Day on which the sale and redemption of units is suspended by the Trustee / AMC.

CDSC Contingent Deferred Sales Charge permitted under the Regulations Custodian HDFC Bank Limited is acting as the Custodian of the Scheme.

HDFC Bank Limited – Custody Services, Lodha - I Think Techno Campus, Building - Alpha, 8th Floor, Next to Kanjur Marg Railway Station, Kanjur Marg (East), Mumbai – 400042.

Equity and Equity related Instruments

Equity and equity related instruments shall mean and include equity shares, convertible bonds and debentures, warrants carrying the right to obtain equity shares and other like instruments.

Entry Load Load on purchase of units by the investor

30

Exit Load Load on redemption of units by the investor other than CDSC Investment Management Agreement or IMA

The Investment Management Agreement dated October 23, 1996, executed between L&T Mutual Fund Trustee Limited and L&T Investment Management Limited.

ISC Investor Service Centre of the Asset Management Company Mutual Fund or Fund L&T Mutual Fund, a Trust set up under the provisions of Indian Trust Act, 1882

and registered with SEBI vide Registration No. MF/035/97/9 dated 03/01/1997. NAV Net Asset Value of the units of L&T Prudence Fund calculated in the manner as

may be prescribed by SEBI Regulations from time to time. Scheme information Document

This document issued by L&T Mutual Fund offering Units of L&T Prudence Fund.

Registrars & Transfer Agent

Computer Age Management Services Ltd., (CAMS) Chennai, performing the functions of a Registrar and is also Transfer Agent.

Regulations / SEBI Regulations

SEBI (Mutual Funds) Regulations, 1996, as amended from time to time, for the operation and management of Mutual Funds

Repo / Reverse Repo Sale/ purchase of Government securities with simultaneous agreement to repurchase/resell them at a later date.

RBI Reserve Bank of India, established under the Reserve Bank of India Act, 1934 SEBI Securities and Exchange Board of India established under Securities and

Exchange Board of India Act, 1992 Sponsor L&T Finance Limited, having its registered office at L&T House, Ballard Estate,

P.O. Box 278, Mumbai – 400 001 The Trustee L&T Mutual Fund Trustee Limited, a company set up under the Companies Act,

1956 Trust Deed The Registered Trust Deed dated October 17, 1996 establishing L&T Mutual

Fund as a Trust under the Indian Trusts Act, 1882 and amended from time to time

The Scheme L&T Prudence Fund The Plan The Scheme offers two Plans with separate Portfolios i.e., Moderate Plan and

Aggressive Plan Unit or Units The interest of an investor which consists of one undivided share in the NAV of

the relevant option of L&T Prudence Fund Unit holder A participant in L&T Prudence Fund L&T Prudence Fund The Scheme that is being offered under this Scheme Information Document for

subscription Interpretation For all purposes of this Scheme Information Document, except as otherwise expressly provided or unless the context otherwise requires: • The terms defined in this offer document include the plural as well as the singular. • Pronouns having a masculine or feminine gender shall be deemed to include the other. • All references to "dollars" or "$" refer to United States Dollars and "Rs." refer to Indian Rupees. • All references to timings relate to Indian Standard Time (IST). • Words and expressions used herein but defined in the SEBI Act, 1992 or the SEBI Regulations shall have the meanings respectively assigned to them therein.

31

DUE DILIGENCE CERTIFICATE

A Due Diligence Certificate duly signed by the Compliance Officer of L&T Mutual Fund has been submitted to SEBI, which reads as follows: It is confirmed that:

a. the draft Scheme Information Document forwarded to SEBI is in accordance with the SEBI (Mutual Funds) Regulations, 1996 and the guidelines and directives issued by SEBI from time to time.

b. all legal requirements connected with the launching of the scheme as also the guidelines, instructions, etc., issued by the Government and any other competent authority in this behalf, have been duly complied with.

c. the disclosures made in the Scheme Information Document are true, fair and adequate to enable the investors to make a well informed decision regarding investment in the proposed scheme.

d. the intermediaries named in the Scheme Information Document and Statement of Additional Information are registered with SEBI and their registration is valid, as on date.

For L&T Investment Management Limited

(Investment Manager to L&T Mutual Fund) Sd/- Date: January 2, 2012 Jaymeen Shah Place: Mumbai Compliance Officer

32

II. INFORMATION ABOUT THE SCHEME A. NATURE OF THE SCHEME An Open Ended Balanced Scheme B. INVESTMENT OBJECTIVE The investment objective of the Scheme is to provide medium to long term capital gains and/ or income distribution while at all times emphasising the importance of capital appreciation. C. ASSET ALLOCATION An indication of the asset allocation pattern of the portfolio in both the Plans is as follows:

Moderate Plan:

Asset Class Allocation Range

(% of Net Assets)

Risk Profile

Large Cap Equity & Equity Related Instruments*

60% – 75% Medium to High

Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40% Low to Medium

* The large cap universe will comprise of all the companies which have market capitalization more than that of

a) Lowest constituent of S&P CNX Nifty Index, or b) Highest constituent of CNX Midcap Index

(whichever is lower) The Scheme may invest upto 35% of its net assets in Securitized debt.

The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The Stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme.

Pending deployment of the funds in securities in terms of investment objective of the Scheme, the AMC may park the funds of the Scheme in short term deposits of the Scheduled Commercial Banks, subject to the guidelines issued by SEBI vide its circular dated April 16, 2007, as may be amended from time to time.

33

The gross investments in securities under the Scheme which includes Debt, Money Market Instruments, Government Securities and Large Cap Equity & Equity Related Instruments including Securitized debt & Derivatives shall not exceed 100% of net assets of the Scheme. However, following will not be considered while calculating the gross exposure:

a) Instrument/ Security-wise hedged position and b) Exposure in Cash or cash equivalents with residual maturity of less than 91 days.

The exposure to derivatives will be calculated on notional value of the derivative contracts. The above asset allocation pattern is not absolute and can vary depending upon the AMC’s perception of the debt, equity and money markets as well as the general view on interest rates. The asset allocation pattern indicated above may thus be altered only on defensive considerations and for a short period not exceeding 1 month.

Aggressive Plan:

Asset Class Allocation Range (% of Net Assets)

Risk Profile

Diversified Equity & Equity Related Instruments

60% – 75% Medium to High

Debt, Money Market Instruments & Government Securities (including CBLO/ reverse repos)

25% – 40% Low to Medium

The strategy will be to build up diversified portfolio of quality stocks, with medium to long term potential. The Scheme may invest upto 35% of its net assets in Securitized debt. The Scheme shall have derivatives exposure as per the SEBI/ RBI Guidelines issued from time to time. Further, the Scheme may undertake Interest rate derivatives transactions for the purpose of hedging and portfolio rebalancing (within the permissible limits specified by RBI/ SEBI from time to time). The stock lending, if undertaken, would not exceed 15% of the net assets of the Scheme.

Pending deployment of the funds in securities in terms of investment objective of the Scheme, the AMC may park the funds of the Scheme in short term deposits of the Scheduled Commercial Banks, subject to the guidelines issued by SEBI vide its circular dated April 16, 2007, as may be amended from time to time.

The gross investments in securities under the Scheme which includes Debt, Money Market Instruments, Government Securities and Diversified Equity & Equity Related Instruments including Securitized debt & Derivatives shall not exceed 100% of net assets of the Scheme. However, following will not be considered while calculating the gross exposure:

a) Instrument/ Security-wise hedged position and b) Exposure in Cash or cash equivalents with residual maturity of less than 91 days.

34

The exposure to derivatives will be calculated on notional value of the derivative contracts. The above asset allocation pattern is not absolute and can vary depending upon the AMC’s perception of the debt, equity and money markets as well as the general view on interest rates. The asset allocation pattern indicated above may thus be altered only on defensive considerations and for a short period not exceeding 1 month. Change in Investment Pattern Subject to the SEBI Regulations, the asset allocation pattern indicated above may change from time to time, keeping in view market conditions, market opportunities, applicable regulations and political and economic factors. It must be clearly understood that the percentages stated above are only indicative and not absolute. These proportions can vary substantially depending upon the perception of the Fund Manager; the intention being at all times to seek to protect the interests of the Unitholders. Such changes in the investment pattern will be for short term (not exceeding one month) and for defensive considerations only. D. WHERE WILL THE SCHEME INVEST? Subject to the Regulations, the corpus of the Scheme may be invested in all or any one of (but not exclusively) the following securities.

• Securities created and issued by the Central and State Governments and/or repos/reverse repos/in such Government Securities as may be permitted by RBI (including but not limited to coupon bearing bonds, zero coupon bonds and treasury bills);

• Securities guaranteed by the Central and State Governments (including but not limited to coupon bearing bonds, zero coupon bonds and treasury bills);

• Obligations of banks (both public and private sector) including term deposits with the banks as permitted by SEBI / RBI from time to time and development financial institutions;

• Debt obligations of domestic Government agencies and statutory bodies, which may or may not carry a Central/State Government guarantee;

• Corporate debt and securities (of both public and private sector undertakings) including Bonds, Debentures, Notes, Strips, Bills Re-discounting (BRDS) etc;

• Money market instruments permitted by SEBI/ RBI, in CCIL’s CBLO market or in alternative investments for deployment of cash surpluses as may be provided by RBI to meet the liquidity requirements;

• Certificate of Deposit (CDs); • Commercial Paper (CPs); • The non-convertible part of convertible securities; • Securitized Debt obligation; • PTCs (pass through certificates or pay-through security); • Equity and equity related instruments including preference shares, convertible bonds and

debentures and warrants carrying the right to obtain equity shares excluding equity linked debentures;

• Derivative instruments like Forward Rate Agreements and such other derivative instruments/ strategies (for both Debt and Equity) as may be permitted by SEBI/RBI from time to time;

• Overseas/ foreign securities (as and when proposed after obtaining necessary approvals/ consents). Investment in such securities shall be within the permissible limits as specified by SEBI/ RBI from time to time;

35

• Indian Depository Receipts, subject to compliance with applicable Rules, Regulations and Guidelines issued thereunder;

• Any other instruments/ securities as may be permitted by RBI/ SEBI or such other regulatory bodies from time to time;