Kebutuhan Dasar Layak dan Upah/ Pensiun -...

12

Kebutuhan Dasar Layak dan Upah/ Pensiun Hasbullah Thabrany Konsultan Dewan Jaminan Sosial Nasional Email: [email protected]

Transcript of Kebutuhan Dasar Layak dan Upah/ Pensiun -...

Kebutuhan Dasar Layak dan Upah/ Pensiun

Hasbullah Thabrany Konsultan

Dewan Jaminan Sosial Nasional

Email: [email protected]

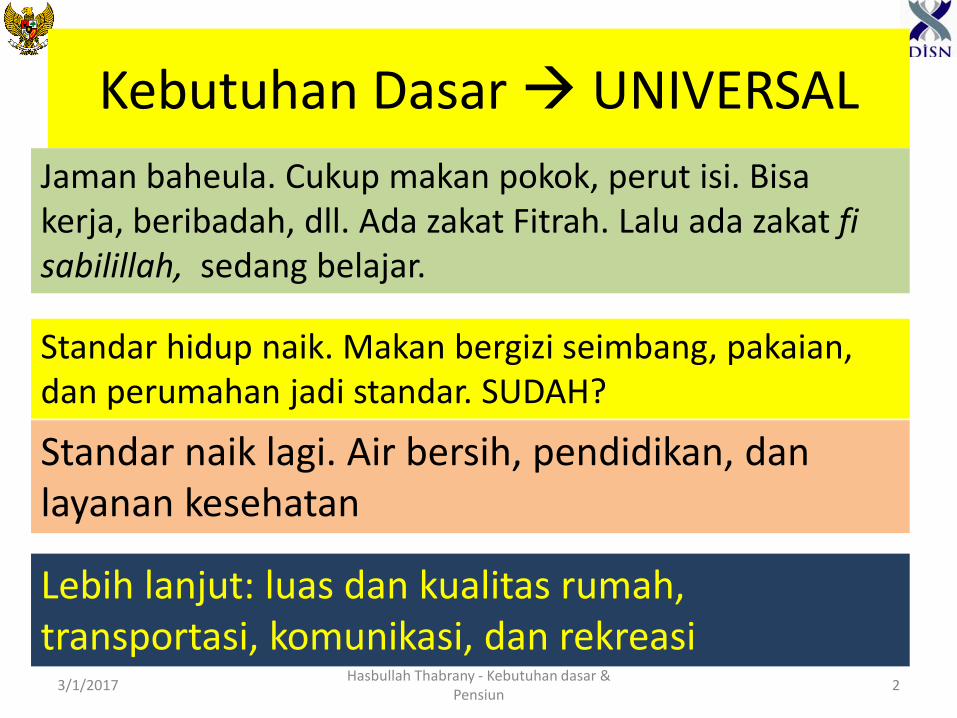

Kebutuhan Dasar UNIVERSAL

Jaman baheula. Cukup makan pokok, perut isi. Bisa kerja, beribadah, dll. Ada zakat Fitrah. Lalu ada zakat fi sabilillah, sedang belajar.

Standar hidup naik. Makan bergizi seimbang, pakaian, dan perumahan jadi standar. SUDAH?

Standar naik lagi. Air bersih, pendidikan, dan layanan kesehatan

Lebih lanjut: luas dan kualitas rumah, transportasi, komunikasi, dan rekreasi

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 2

Rasio klaim JKK sangat kecil, sekiar 20%. Buruh

mati atau cacad total tetap, TIDAK dapat pensiun bulanan.

Keluarga?

Kita sudah Merdeka?

Banyak pekerja belum!

Apalagi anggota keluarganya.

Perusahaan TIDAK MAMPU bayar UML,

Laba kecil? Atau Merugi?. Siapa yang

ungkap?

Sebagian hidup Merdeka Sekali.

Berlimpah.

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 3

Ketika Aktif – Kebutuhan Dasar Pekerja Terpenuhi

• Sebagian besar BELUM masuk tingkat III, pendidikan dan rumah layak.

• Ketika sakit, lumayan ada JKN, meskipun tahan penyakit ketika antri.

• Ketika masuk Lansia? Hanya Pegawai Negeri dan Wakil Rakyat yang Merdeka, meskipun belum bahagia – Haruskah pekerja mengandalkan anak? Hasil

tani/kebun ada? – Sampai tingkat dasar mana? Tingkat I? sekedar

makanan pokok??

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 4

Kita Peduli?

• Berapa % Lansia yang punya “income pensiun” (bulanan)

• Berapa % kebutuhan dasar pensiunan terpenuhi? Dasar yang mana?

• Berapa % yang sudah mengiur untuk Pensiun?

• Belum mampukah kita mengiur untuk pensiun?

• Apakah Negeri ini begitu miskin?

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 5

Peraturan Pensiun & JHT - BURUK

• Pemerintah belum hadir, baru mengintip pemenuhan kebutuhan sangat mendasar

• Pemerintah terjebak “pikiran pendek” pekerja. Masa depan? kumaha engke wae!

• Dana JHT, diambil sebelum Lansia. Pinjam boleh

• Iuran 3%, prediksi manfaat uang pensiun bulanan cukup apa?

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 6

Mari tengok dan Belajar dari Negara Lain Dana Pensiun, MENJAMIN Kebutuhan Dasar Lansia, SEKALIGUS menghimpun dana pembukaan lapangan kerja

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 7

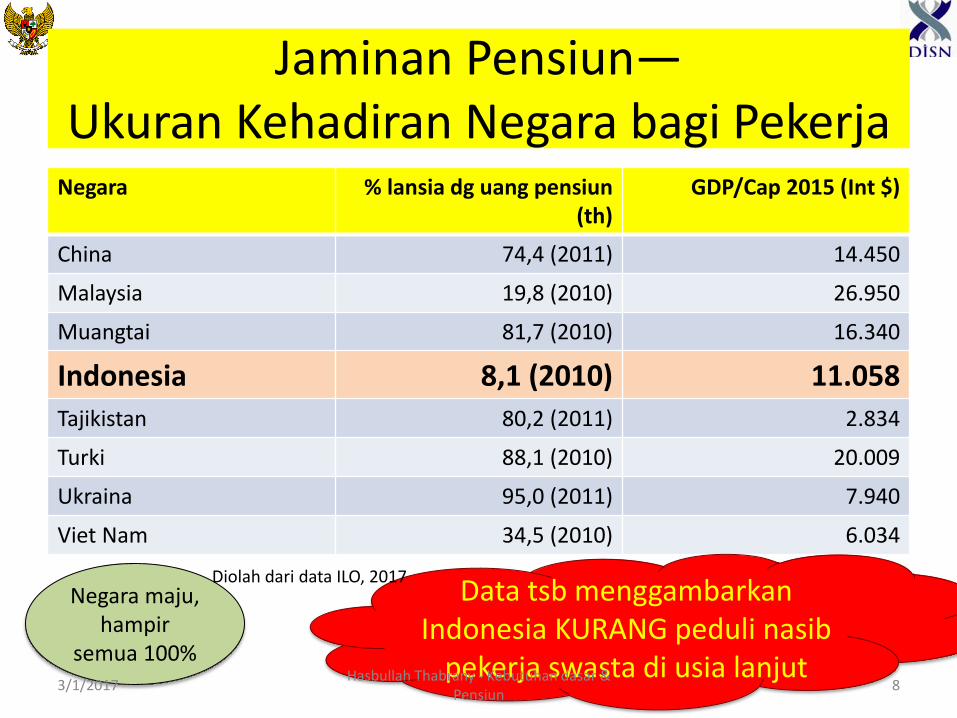

Jaminan Pensiun— Ukuran Kehadiran Negara bagi Pekerja

Negara % lansia dg uang pensiun (th)

GDP/Cap 2015 (Int $)

China 74,4 (2011) 14.450

Malaysia 19,8 (2010) 26.950

Muangtai 81,7 (2010) 16.340

Indonesia 8,1 (2010) 11.058

Tajikistan 80,2 (2011) 2.834

Turki 88,1 (2010) 20.009

Ukraina 95,0 (2011) 7.940

Viet Nam 34,5 (2010) 6.034

Negara maju, hampir

semua 100%

Data tsb menggambarkan Indonesia KURANG peduli nasib

pekerja swasta di usia lanjut

Diolah dari data ILO, 2017

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 8

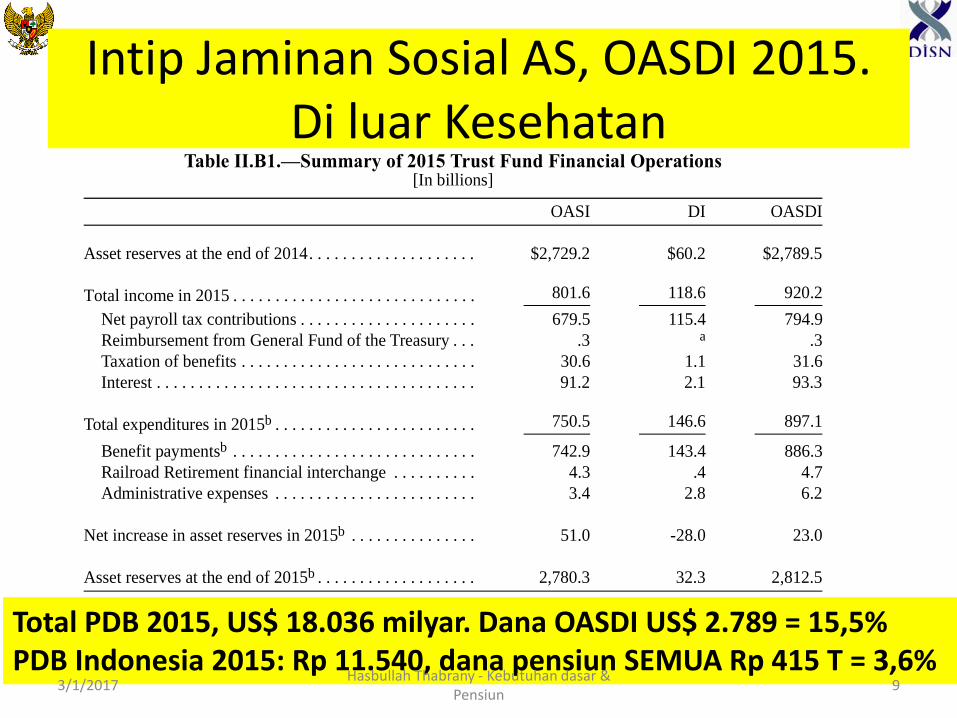

Intip Jaminan Sosial AS, OASDI 2015. Di luar Kesehatan

7

Calendar Year 2015 Operations

B. TRUST FUND FINANCIAL OPERATIONS IN 2015

Table II.B1 shows the income, expenditures, and asset reserves for the OASI,

the DI, and the combined OASI and DI Trust Funds in calendar year 2015.

Note: Totals do not necessarily equal the sums of rounded components.

In 2015, net payroll tax contributions accounted for 86 percent of total trust

fund income. Net payroll tax contributions consist of taxes paid by employ-

ees, employers, and the self-employed on earnings covered by Social Secu-

rity. These taxes are paid on covered earnings up to a specified maximum

annual amount, which was $118,500 in 2015. Table II.B2 shows the tax rates

for 2015.

In 2015, approximately 0.04 percent of OASI and DI combined Trust Fund

income came from reimbursements from the General Fund of the Treasury.

Public Laws 111-312, 112-78, and 112-96 account for most of the reimburse-

ment for the year. These acts specified General Fund reimbursement for tem-

porary reductions in revenue due to reduced payroll tax rates for employees

and for self-employed workers for 2011 and 2012.

Three percent of OASI and DI combined Trust Fund income in 2015 came

from subjecting up to 50 percent of Social Security benefits to Federal per-

Table II.B1.—Summary of 2015 Trust Fund Financial Operations[In billions]

OASI DI OASDI

Asset reserves at the end of 2014. . . . . . . . . . . . . . . . . . . . $2,729.2 $60.2 $2,789.5

Total income in 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 801.6 118.6 920.2

Net payroll tax contributions . . . . . . . . . . . . . . . . . . . . . 679.5 115.4 794.9

Reimbursement from General Fund of the Treasury . . . .3 a

a Less than $50 million.

.3

Taxation of benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30.6 1.1 31.6

Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.2 2.1 93.3

Total expenditures in 2015b . . . . . . . . . . . . . . . . . . . . . . . .

b Benefit payments which were scheduled to be paid on January 3, 2016 were actually paid onDecember 31, 2015 as required by the statutory provision for early delivery of benefit payments when thenormal payment delivery date is a Saturday, Sunday, or legal public holiday. The amount of these paymentsmade on an accelerated basis was approximately $19.7 billion for the OASI Trust Fund and $6.1 billion forthe DI Trust Fund. For comparability with the values for historical years and the projections in this report, alltrust fund operations and asset reserves reflect the 12 months of benefits scheduled for payment each year.

750.5 146.6 897.1

Benefit paymentsb . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 742.9 143.4 886.3

Railroad Retirement financial interchange . . . . . . . . . . 4.3 .4 4.7

Administrative expenses . . . . . . . . . . . . . . . . . . . . . . . . 3.4 2.8 6.2

Net increase in asset reserves in 2015b . . . . . . . . . . . . . . . 51.0 -28.0 23.0

Asset reserves at the end of 2015b . . . . . . . . . . . . . . . . . . . 2,780.3 32.3 2,812.5

Total PDB 2015, US$ 18.036 milyar. Dana OASDI US$ 2.789 = 15,5% PDB Indonesia 2015: Rp 11.540, dana pensiun SEMUA Rp 415 T = 3,6%

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 9

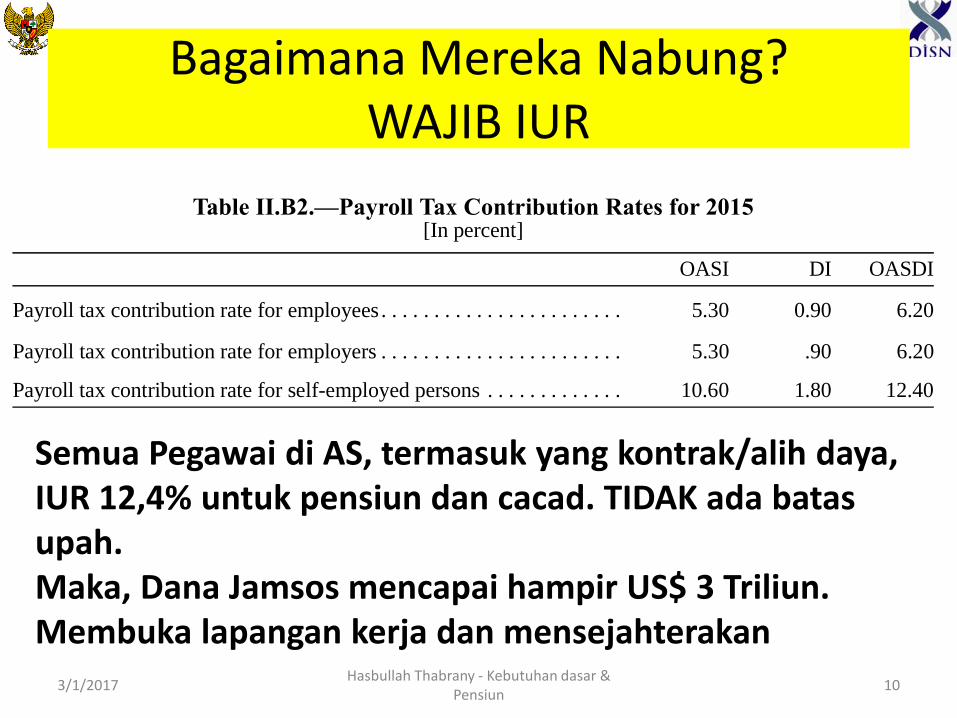

Bagaimana Mereka Nabung? WAJIB IUR

Overview

8

sonal income taxation for beneficiaries with income (including half of bene-

fits and all non-taxable interest) exceeding specified levels. Interest earned

on invested trust fund asset reserves accounted for 10 percent of OASDI

income. The Department of the Treasury invests trust fund reserves in inter-

est-bearing securities issued by the U.S. Government. In 2015, the combined

trust fund reserves earned interest at an effective annual rate of 3.4 percent.

Almost 99 percent of expenditures from the combined OASI and DI Trust

Funds in 2015 were retirement, survivor, and disability benefits totaling

$886.3 billion. A net payment of $4.7 billion was made to the Railroad

Retirement Social Security Equivalent Benefit Account from the combined

OASI and DI Trust Funds, which was about 0.5 percent of total OASDI

expenditures. The administrative expenses of the Social Security program

were $6.2 billion, which was about 0.7 percent of total expenditures.

The trust fund investments provide a reserve to pay benefits whenever total

program cost exceeds income. Trust fund reserves increased by $23.0 billion

for 2015 because total income to the combined funds, including interest

earned on trust fund reserves, exceeded total expenditures.1 At the end of

2015, the combined reserves of the OASI and the DI Trust Funds were

$2,813 billion, or 303 percent of estimated expenditures2 for 2016. In com-

parison, the combined reserves at the end of 2014 were 311 percent of expen-

ditures for 2015.

1 As noted in footnote b of table II.B1 and elsewhere in this report, asset reserves shown for the end of 2015reflect the 12 months of benefits scheduled for payment in 2015 and thus exclude the benefits scheduled forpayment on January 3, 2016, which were actually paid on December 31, 2015 as required by the law. 2 Estimated expenditures are based on the intermediate set of assumptions.

Table II.B2.—Payroll Tax Contribution Rates for 2015[In percent]

OASI DI OASDI

Payroll tax contribution rate for employees. . . . . . . . . . . . . . . . . . . . . . . 5.30 0.90 6.20

Payroll tax contribution rate for employers . . . . . . . . . . . . . . . . . . . . . . . 5.30 .90 6.20

Payroll tax contribution rate for self-employed persons . . . . . . . . . . . . . 10.60 1.80 12.40

Semua Pegawai di AS, termasuk yang kontrak/alih daya, IUR 12,4% untuk pensiun dan cacad. TIDAK ada batas upah. Maka, Dana Jamsos mencapai hampir US$ 3 Triliun. Membuka lapangan kerja dan mensejahterakan

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 10

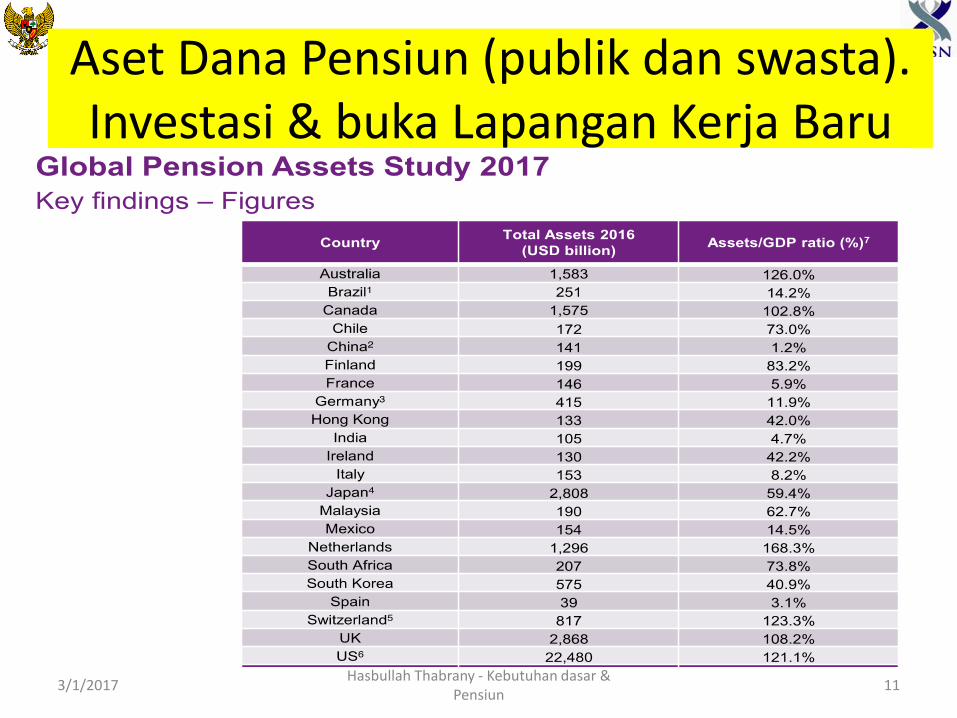

Aset Dana Pensiun (publik dan swasta). Investasi & buka Lapangan Kerja Baru

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 11

Tidak mampukah kita? Atau Tidak Mau dan

Tidak Peduli?

3/1/2017 Hasbullah Thabrany - Kebutuhan dasar &

Pensiun 12