Audit Procedures for Misappropriation of Assets Pertemuan XXIV Matakuliah: F0184/Audit atas...

22

-

date post

20-Dec-2015 -

Category

Documents

-

view

232 -

download

6

Transcript of Audit Procedures for Misappropriation of Assets Pertemuan XXIV Matakuliah: F0184/Audit atas...

Audit Procedures for Misappropriation of Assets

Pertemuan XXIV

Matakuliah : F0184/Audit atas KecuranganTahun : 2007

Bina Nusantara

• Mahasiswa diharapkan dapat melakukan audit kecurangan atas penyalahgunaan asset

Learning Outcomes

3

Bina Nusantara

• Audit Procedures for:– Account Receivable– Inventory– Purchasing and Payroll– Cash– Computer Scheme

Outline Materi

4

Account ReceivableTypical Fraud:• Lapping• Posting bogus credits to the account• Altering internal copies of invoices

Bina Nusantara

Account ReceivableWhat to look for:• Unexplained differences noted by customers on

their account receivable confirmations• Significant delays between the time when the

customer states a payment was made and the payment was recorded as received by the company

• A significant number of credit entries and other adjustments made to the accounts receivable records

• Unexplained or inadequately explained differences between the accounts receivable sub ledger and general ledger

Bina Nusantara

Account ReceivableExample Audit Procedures:• Confirm the account activity not just the balance with

the customer directly• Perform analytical reviews of credit memo and write

off activity• Vouch credit memos and other write offs to all related

supporting documentation• Investigate all differences between the payment date

reported by the customer and payment date recorded by the company

• Analyze recoveries of written off accounts• Check the nature of aging and who has the access to

thatBina Nusantara

Bina Nusantara

Extended Audit Procedures Misappropriation of Assets

Account ReceivableTypical Fraud

1. Common technique for this fraud are:– Lapping. Used another customer payment– Posting bogus credits. Posting credit memo or other non

cash reduction– Altering internal copies of invoice. Reporting lower

amount than actually billed 2. Closed an account with an overdue receivable3. Mutual arrangement between customer and employee

8

Bina Nusantara

9

What to Look For

– Difference on account receivable confirmation– Delays between customer payment and company record– Credit entries and adjustment to account receivable record– Difference between account receivable subsidiary ledger

and general ledger

Bina Nusantara

10

Example Audit Procedure– Confirm account activity to customer directly– Perform analytical reviews of credits memo and write-off

activity– Vouch credits memo and other write-offs– Check the different payment date between customer and

company record– Analyze recoveries of written-off accounts– Understand how account receivable aging and who is/are

responsible for it

Bina Nusantara

Extended Audit Procedures Misappropriation of Assets

InventoryTypical Fraud

1. For personal use. 2. Small, easy to steal and valued by employee as a customer3. For sale. 4. Steal from the receiving docks before physical custody5. Coalition between receiving and vendor’s delivery

personnel6. Theft of scrap

11

Bina Nusantara

12

What to Look For

– Large difference between physical and inventory records– Unusual increase in inventory turnover– Unusual entries in inventory records– Key inventory ratios– Shipping documents without corresponding sales

documentation

Bina Nusantara

13

Example Audit Procedure– Analyze inventory shortage, compare key inventory ratios,

look for unusual condition– Review receiving report– Review supporting documentation for reduction to

inventory record– Compare between shipping and corresponding documents

Bina Nusantara

Extended Audit Procedures Misappropriation of Assets

Purchasing and PayrollTypical Fraud

1. Payment of invoices to a fictitious company2. Coalition between vendors to company’s purchasing agent• Allow vendor submit fake / false billing and approving

payment• Excess purchasing of property or services• Bid-rigging3. The use of ghost or terminated employee

14

Bina Nusantara

15

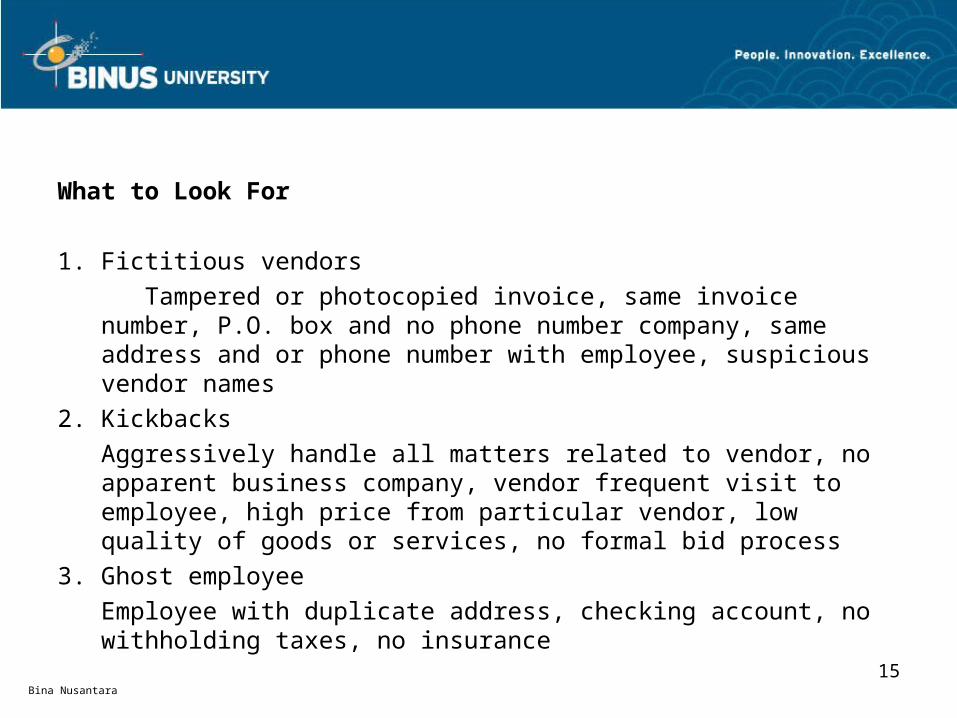

What to Look For

1. Fictitious vendors

Tampered or photocopied invoice, same invoice number, P.O. box and no phone number company, same address and or phone number with employee, suspicious vendor names

2. Kickbacks

Aggressively handle all matters related to vendor, no apparent business company, vendor frequent visit to employee, high price from particular vendor, low quality of goods or services, no formal bid process

3. Ghost employee

Employee with duplicate address, checking account, no withholding taxes, no insurance

Bina Nusantara

16

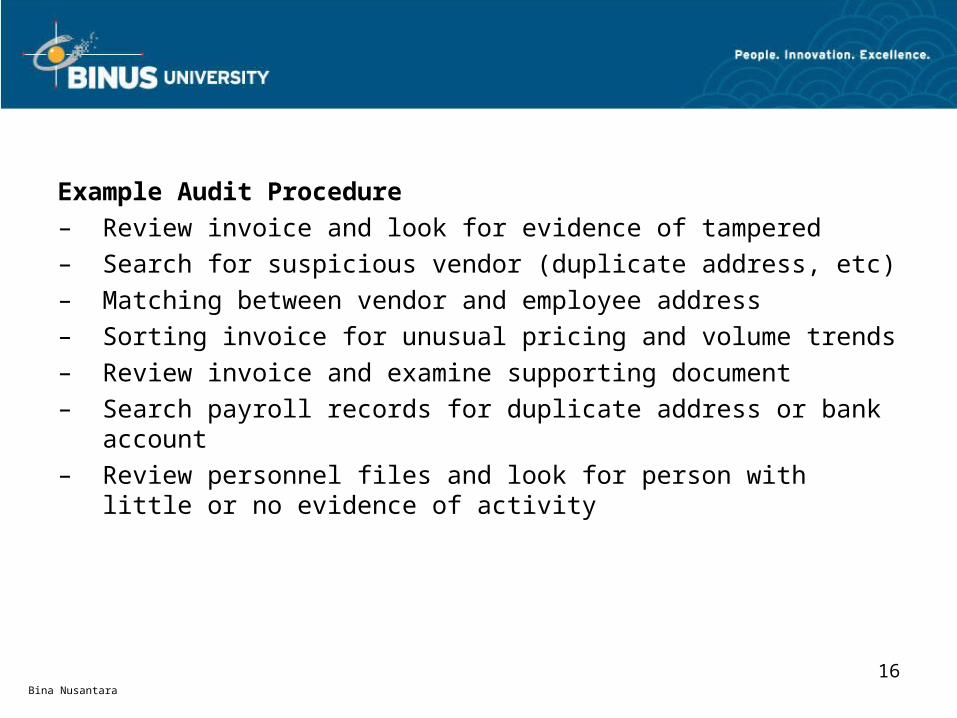

Example Audit Procedure– Review invoice and look for evidence of tampered– Search for suspicious vendor (duplicate address, etc) – Matching between vendor and employee address– Sorting invoice for unusual pricing and volume trends– Review invoice and examine supporting document– Search payroll records for duplicate address or bank

account– Review personnel files and look for person with little or no

evidence of activity

Bina Nusantara

Extended Audit Procedures Misappropriation of Assets

CashTypical Fraud

1. Withdraw cash directly for their own benefit2. To pay personal expenses3. Skimming. Cash is taken before entering system4. Substituting personal checks for cash. Take money and

substitute with personal checks5. Fictitious refunds and discounts. 6. Altered credit card receipts. Usually restaurant where he or

she or they intent to increase the tip on credit card receipt

17

Bina Nusantara

18

What to Look For

1. Large reconciling items in bank reconciliation2. Bank statement didn’t include cancelled checks3. Missing cancelled checks4. Unsupported disbursement5. Customer complaints 6. Altered or missing cash register tapes

Bina Nusantara

19

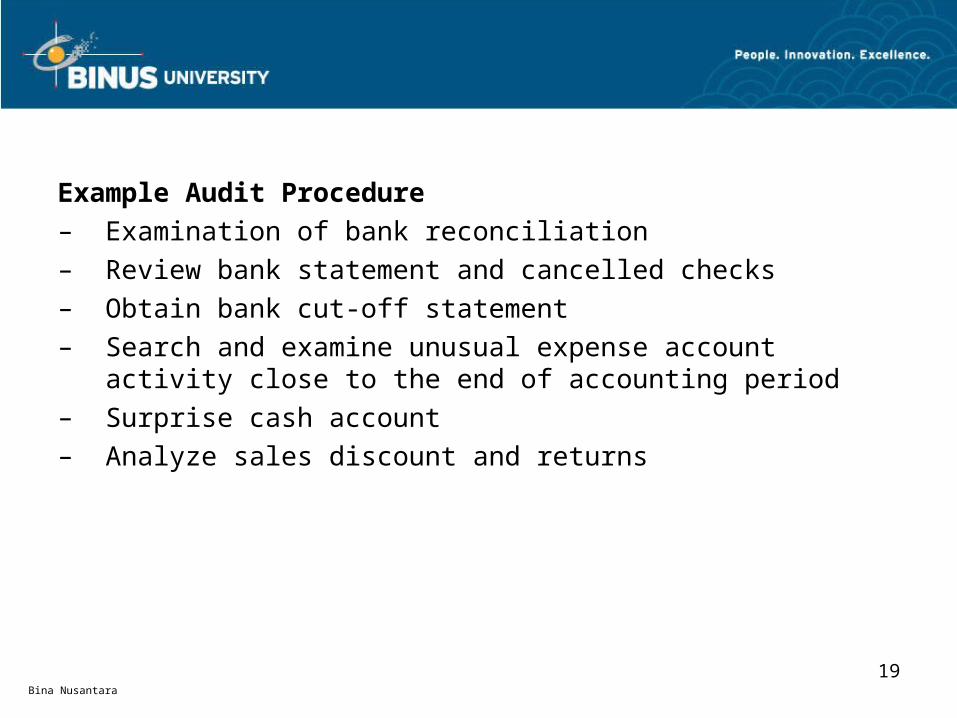

Example Audit Procedure– Examination of bank reconciliation– Review bank statement and cancelled checks– Obtain bank cut-off statement– Search and examine unusual expense account activity

close to the end of accounting period– Surprise cash account– Analyze sales discount and returns

Bina Nusantara

Extended Audit Procedures Misappropriation of Assets

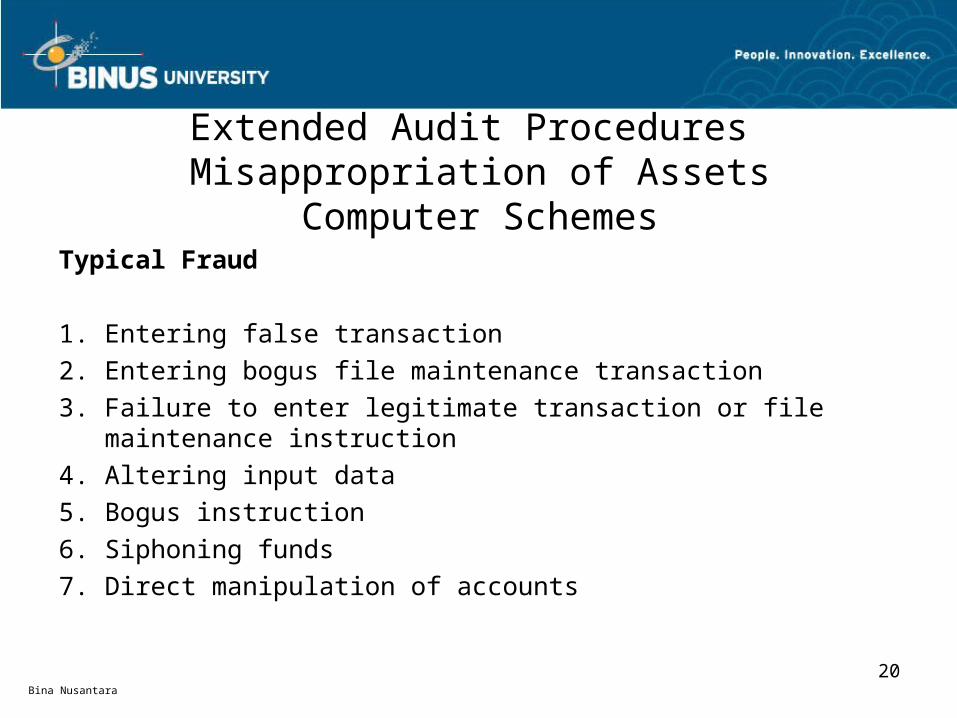

Computer SchemesTypical Fraud

1. Entering false transaction2. Entering bogus file maintenance transaction3. Failure to enter legitimate transaction or file maintenance

instruction4. Altering input data5. Bogus instruction6. Siphoning funds7. Direct manipulation of accounts

20

Bina Nusantara

21

What to Look For

1. Inability to process computer application2. Differences in batch or hash totals3. Undocumented or unauthorized account posting, file

changes, or modifications to program4. Differences between general ledger and computerized

accounting records5. Lack of segregation of duties6. Lack of logical access 7. Lack of adequate computer processing controls

Bina Nusantara

22

Example Audit Procedure– Reviews documentation supporting– Review control over input and processing of financial

transactions or file maintenance procedures– Reconstruct accounts or files from original source

documents