eprints.undip.ac.ideprints.undip.ac.id/63417/3/Hersugondo_Disertasi_Terbuka... · Web viewAnalisis...

169

EFEKTIFITAS INVESTASI BERKOMITMEN PADA HUMAN CAPITAL DEVELOPMENT DALAM PERSPEKTIF GOOD CORPORATE GOVERNANCE DALAM MENENTUKAN KINERJA DAN NILAI PERUSAHAAN PADA PERUSAHAAN YANG TERDAFTAR DI BURSA EFEK INDONESIA DISERTASI Hersugondo NIM 12020113510027 i

-

Upload

nguyenhuong -

Category

Documents

-

view

224 -

download

0

Transcript of eprints.undip.ac.ideprints.undip.ac.id/63417/3/Hersugondo_Disertasi_Terbuka... · Web viewAnalisis...

EFEKTIFITAS INVESTASI BERKOMITMEN PADA HUMAN CAPITAL DEVELOPMENT

DALAM PERSPEKTIF GOOD CORPORATE GOVERNANCE DALAM MENENTUKAN

KINERJA DAN NILAI PERUSAHAAN PADA PERUSAHAAN YANG TERDAFTAR

DI BURSA EFEK INDONESIA

DISERTASI

HersugondoNIM 12020113510027

PROGRAM DOKTOR (S3) ILMU EKONOMIUNIVERSITAS DIPONEGORO

SEMARANGJanuari, 2018

i

Disertasi

EFEKTIFITAS INVESTASI BERKOMITMEN PADA HUMAN CAPITAL DEVELOPMENT DALAM

PERSPEKTIF GOOD CORPORATE GOVERNANCE DALAM MENENTUKAN KINERJA DAN NILAI

PERUSAHAAN PADA PERUSAHAAN YANG TERDAFTAR DI BURSA EFEK INDONESIA

Oleh:Nama : Hersugondo

NIM : 12020113510027

Telah Disetujui Untuk Dipertahankan dihadapan Sidang Terbuka Ujian Promosi Doktor Ilmu Ekonomi Bidang Manajemen Keuangan Pada Program Doktor Ilmu Ekonomi Universitas Diponegoro Semarang

Semarang, Januari 2018

Promotor Ko-Promotor

(Prof. Dr. H. Sugeng Wahyudi, MM.) (Dr. Harjum Muharam, ME.)

ii

PERNYATAAN KEASLIAN DISERTASI

Dengan ini, saya yang bertanda tangan dibawah ini:

Nama : Hersugondo

NIM : 12020113510027

menyatakan bahwa disertasi saya yang berjudul:

”EFEKTIFITAS INVESTASI BERKOMITMEN PADA HUMAN CAPITAL DEVELOPMENT DALAM PERSPEKTIF GOOD CORPORATE GOVERNANCE DALAM MENENTUKAN KINERJA DAN NILAI PERUSAHAAN PADA PERUSAHAAN YANG TERDAFTAR DI BURSA EFEK INDONESIA”,

adalah karya saya dan disertasi ini belum pernah digunakan untuk mendapatkan

gelar keilmuan dimanapun.

Karya ilmiah ini sepenuhnya hasil karya dan milik saya, semua

informasi yang berasal dari penulis lain telah diberi penghargaan dengan

mengutip sumbernya. Oleh karena itu, semua tulisan dalam disertasi ini menjadi

tanggung jawab saya sebagai penulis.

Kemudian apabila didapati unsur plagiasi, maka saya akan

berpertanggungjawab sesuai dengan ketentuan yang berlaku.

Penulis,

Hersugondo

iii

ABSTRAK

Penelitian ini bertujuan untuk menjembatani gap kesimpulan yang berbeda antara pengaruh corpotare governance terhadap nilai perusahaan dengan konsep baru sebagai variabel intervening Efektivitas Investasi Berkomitmen pada Sumber Daya Manusia (Investment Efectiveness Committed to Human Capital Development/IEHCD) yang dikembangkan dengan mensintesakan antara Agency Theory dan Resourses Base Theory. Penelitian ini menggunakan data sekunder dengan populasi pada perusahaan yang terdaftar di BEI Tahun 2013-2015, Sampel penelitian ini adalah 57 perusahaan yang terdaftar di BEI tahun 2013-2015. Data diperoleh dengan memanfaatkan An nu al Re po rt periode 2013-2015. Alat analisis yang digunakan dalam penelitian ini adalah dengan menggunakan SmartPLS. Penelitian ini menghasilkan simpulan, yaitu pertama variabel K epe m ilik an In st itu si, Ke pe m ilik an as in g berpengaruh positif dan signifikan (α 0.05) terhadap Nilai Perusahaan sedangkan variabel Proporsi Kepemilikan Manajemen memiliki koefisien regresi yang positif tetapi tidak signifikan. Kedua, IEHCD mampu memediasi pengaruh antara proporsi kepemilikan manajemen terhadap nilai perusahaan. Ketiga, IEHCD mampu memediasi pengaruh antara proporsi kepemilikan asing terhadap nilai perusahaan. dan Keempat, IEHCD mampu memediasi pengaruh antara Proporsi Kepemilikan institusi terhadap nilai perusahaan.

Kata kunci: Corpotare Governance, Investment Efectiveness Comitted to Human Capital Development (IEHCD), Nilai Perusahaan.

iv

ABSTRACT

The aim of the study was to bridge the gap of different conclusions between the effect of corporate governance on corporate value and new concept as the intervening variable. The Investment Effectiveness Committed to Human Capital Development (IEHCD) was developed by synthesizing Agency Theory and Resource Base Theory. The study used secondary data with the population of the companies listed on the Stock Exchange in 2013-2015. The research samples were 57 companies listed in the Stock Exchange in 2013-2015. The data were obtained by using the Annual Report of the period of 2013-2015. The analytical tool used in this research was SmartPLS. The research resulted in the conclusions: first, the variables of Institutional ownership and foreign ownership have positive and significant effect (α 0.05) on Corporate Value, and the variable of Management Ownership Proportion has positive insignificant regression coefficients. Second, IEHCD was capable of mediating the effect between the proportions of management ownership on company value. Third, IEHCD was capable of mediating the effect between the proportion of foreign ownership on corporate value. Fourth, IEHCD was capable of mediating the effect between the proportion of institutional ownership on corporate value.

Keywords: Corporate Governance, Investment Effectiveness Committed to Human Capital Development (IEHCD), Corporate Value.

v

RINGKASAN

Kemakmuran pemegang saham yang merupakan tujuan utama perusahaan, untuk mencapai tujuan tersebut maka fungsi-fungsi manajemen harus dilaksanakan dengan hati-hati dan akurat, mengingat setiap keputusan majemen yang diambil akan mempengaruhi keputusan keuangan yang lain yang berdampak terhadap nilai perusahaan. Dalam praktek pengelolaan perusahaan modern, terjadi pemisahan antara pemilik dan pengelola, dimana pemilik perusahaan tidak lagi sebagai fihak yang dapat mengendalikan jalannya operasional perusahaan secara langsung, tetapi pengelolaan perusahaan diserahkan pada manajer profesional (Agency Theory) yang dalam prakteknya selalu muncul masalah keagenan (agency problem), untuk itu perlu mekanisme Good Corporate governance.

Kajian ini berangkat dari perbedaan-perbedaan kesimpulan hasil kajian empirik tentang corporate governance terutama yang menyangkut struktur kepemilikan pengaruhnya terhadap nilai perusahaan. Kemudian diajukan masalah penelitian dalam disertasi ini adalah: “Bagaimana mengembangkan model teoritikal untuk mengisi gap pengaruh corporate governance terhadap nilai perusahaan?”. Permasalahan penelitian yang diajukan adalah bagaimana pengaruh proporsi kepemilikan manajemen (Mgt_Own), proporsi kepemilikan institusi (Inst_Own), proporsi kepemilikan asing (Forg_Own), terhadap kinerja perusahaan (CorPerfm) dan nilai perusahaan (CorValue), efektivitas investasi berkomitmen pada sumber daya manusia. Bagaimana pengaruh Efektivitas Investasi Berkomitmen pada Sumber Daya Manusia (Investment Efectiveness Committed to Human Capital Development/IEHCD) terhadap kinerja perusahaan dan nilai perusahaan dan apakah IEHCD merupakan variabel intervening yang memediasi pengaruh faktor tata kelola terhadap kinerja perusahaan dan nilai perusahaan.

Teori dasar yang digunakan dalam penelitian ini adalah Agency Theory dan Resources-Based Theory yang disintesakan menjadi konsep baru yaitu Efektivitas Investasi Berkomitmen pada Sumber Daya Manusia (Investment Efectiveness Committed to Human Capital Development/IEHCD). Theory Agency mengambarkan hubungan antara pemegang saham dengan pengelola perusahaan. Prinsip dari teori keagenan adalah mengkaitkan hubungan antara fihak yang memberi pekerjaan dalam hal ini adalah pemegang saham kepada manajer profesional yang diberi kewenangan untuk mengelola perusahaan agar dalam penelolaan perusahaan mampu meningkatkan kemakmuran pemegang saham. Sementara Resources Based Theory membahas mengenai bagaimana sumber daya yang dimiliki perusahaan dan bagaimana perusahaan tersebut dapat mengolah dan memanfaatkan sumber daya yang dimilikinya. Kemampuan perusahaan dalam mengelola sumber dayanya dengan baik dapat menciptakan keunggulan kompetitif sehingga dapat menciptakan nilai bagi perusahaan. Dari kedua teori tersebut kemudian diderivasi menjadi konsep baru Efekktivitas Investasi Berkomitmen pada Pengembangan SDM/Investment Efectiveness Committed to Human Capital Development (EIHCD). Investment Efectiveness Committed to Human Capital Development (EIHCD) adalah maksimalisasi

vi

keuntungan perusahaan dengan memadukan investasi pada asset yang mendatangkan keuntungan yang dibarengi investasi pada sumber daya manusia (Human Capital Development). Masalah penelitiannya adalah apakah EIHCD mampu memediasi pengaruh struktur kepemilikan dalam tata kelola perusahaan yang baik (good corporate governance) terhadap kinerja perusahaan dan meningkatkan nilai perusahaan, yang dimaksudkan untuk mengisi gap penelitian antara tata kelola perusahaan terhadap nilai perusahaan.

Jenis dan sumber data sekunder yaitu data yang bersumber dari sumber eksternal. Objek pada penelitian adalah perusahaan yang go public yang terdaftar di BEI. Populasi dalam penelitian ini adalah perusahaan yang terdaftar di Bursa Efek Indonesia selama tiga tahun sebanyak 530 perusahaan per tahun, yaitu tahun 2013 sampai dengan 2015 yang dipublikasikan oleh dalam Annual Report. Dengan purposive sampling didapat sampel sebanyak 57 perusahaan setiap tahun dengan. Variabel-variabel penelitian merupakan data time series dan cross section, dimana satu variable dalam penelitian saling mempengaruhi terhadap variable penelitian yang lain. Analisis data dilakukan dengan alat analisa Partial Least Square (PLS) dan analisis jalur (parth analysis).

Simpulan dalam penelitian ini tidak terjadi multikolineritas didalam model regresinya karena dari hasil perhitungan nilai VIF kurang dari 10. Uji Goodness of Fit adalah Model Fit , berdasarkan output model fit and quality indicates model mempunyai nilai SRMR = 0,023 < 0,08 ; NFI = 0,982, > 0,90 ; dan VIF < 3,3. Mengacu pada ketentuan tersebut, dapat disimpulkan bahwa model penelitin ini adalah fit. variabel nilai perusahaan (CorValue) yang di proksi dengan Tobin’q dan Price Book Value (PBV) dipengaruhi oleh variabel Kepemilikan manajemen (Mgt_Own), Kepemilikan institusi (Inst_Own), Kepemilikan asing (Forg_Own), EIHCD dan Kinerja Perusahaan (CorPerfm) yang diproxy Return On Asset (ROA) sebesar 60% sedangkan sisanya sebesar 40% dipengaruhi oleh faktor lain diluar variabel yang diteliti. Variabel EIHCD dipengaruhi oleh variabel proporsi kepemilikan manajemen (Mgt_Own), proporsi kepemilikan institusi (Inst_Own), proporsi kepemilikan asing (Forg_Own), sebesar 34% sedangkan sisanya sebesar 66% dipengaruhi variabel lain diluar variabel yang diteliti. Variabel kinerja perusahaan yang di proksi oleh CorPerfm dipengaruhi oleh variabel EIHCD sebesar 7,3% sisanya sebesar 92,7% dipengaruhi oleh variabel lain diluar variabel yang diteliti. Semua variabel berpengaruh terhadap Nilai Perusahaan kecuali Proporsi Kepemilikan Manajemen tidak berpengaruh terhadap Nilai Perusahaan karena t hitung yang dihasilkan adalah 0, 466 lebih kecil dari t tabel 1.960. Proporsi Kepemilikan Manajemen memiliki peran yang rendah terhadap variabel nilai perusahaan melalui variabel Efektivitas Investasi Berkomitmen pada Sumber Daya Manusia (Investment Efectiveness Committed to Human Capital Development/IEHCD). Nilai importance sebesar 0,004 bermakna bahwa variabel ini tidak memiliki peran mempengaruhi variabel proporsi kepemilikan manajemen. Hasil pengujian hipotesis penelitian dari 12 hipotesis yang diajukan semuanya diterima, kecuali Proporsi Kepemilikan Manajemen terhadap Investment Efectiveness Committed to Human Capital Development (EIHCD).

Penelitian ini menghasilkan simpulan pertama, Investment Efectiveness Committed to Human Capital Development (EIHCD) mampu memediasi

vii

pengaruh antara proporsi kepemilikan manajemen terhadap nilai perusahaan dapat diterima. kedua, Investment Efectiveness Comitted to Human Capital Development (EIHCD) mampu memediasi pengaruh antara proporsi kepemilikan investor asing terhadap nilai perusahaan dapat diterima, dan ketiga, Investment Efectiveness Committed to Human Capital Development (EIHCD) mampu memediasi pengaruh antara Proporsi Kepemilikan institusi terhadap nilai perusahaan.

Implikasi Penelitian secara keseluruhan konsep Investment Efectiveness Committed to Human Capital Development (EIHCD) yang merupakan sintesa antara kinerja investasi pada aktivitas investasi yang berbasis pada asset berwujud yang diproxy dengan ROA dengan human capital investment (HCI) yang diproxy dengan pengeluaran investasi untuk pengembangan SDM (human capital investment) dapat dipergunakan untuk memberikan alasan baru mengapa perusahaan mapan berinvestasi dalam modal manusia secara umum yang mampu menghasilkan ide-ide bisnis baru bagi perusahaan meskipun meningkatan risiko kehilangan karyawan. Implikasi Teoritis pada Grand Theory dalam penelitian ini adalah Agency Theory. Middle Theory pertama, diturunkan dari Agency Theory adalah Signaling Theory. Middle Theory kedua, diturunkan dari Teori Investasi adalah Konsep Investasi Industri Dinamis Berbasis Resource Based View.

viii

EXECUTIVE SUMMARY

Prosperity of shareholders is company’s main objectives. To achieve the goal, management functions must be carried out carefully and accurately since every management decision made will affect other financial decisions that affect corporate value. In the practice of modern company management, there is a separation between owners and managers in which company owner is no longer as the party who can control the company's operations directly, but the company management is handed over to professional managers (Agency Theory) which in practice always causes the problem of agency (agency problems). Therefore, it requires the mechanism for Good Corporate Governance.

The study started from the differences of empirical study conclusions on corporate governance, particularly with respect to the ownership structure and its effect on company value. Then, the study problem in this dissertation was: "How to develop a theoretical model to fill the gap of the effect of corporate governance on company value?" The proposed research was how the effects of the proportion of management ownership (Mgt_Own), the proportion of institutional ownership (Inst_Own), the proportion of foreign ownership (Forg_Own), corporate performance (CorPerfm) and corporate value (CorValue), and the investment effectiveness committed to human capital development. How the effect of the Investment Effectiveness Committed to Human Capital Development (IEHCD) on corporate performance and corporate value, and whether the IEHCD is the intervening variable that mediated the effect of governance on corporate performance and corporate value.

The basic theories used in this research were Agency Theory and Resource-Based Theory synthesized into a new concept of Investment Effectiveness Committed to Human Capital Development (IEHCD). Agency Theory describes the relationship between shareholders and corporate managers. The principle of agency theory is to link the relationship between the party who gives the job (shareholder) and the professional manager who is authorized to manage the company so that the company is able to increase the prosperity of shareholders. Meanwhile, Resources-Based Theory describes how the resources by a company and how the company is able to process and utilize its resources. The company's ability to manage its resources properly can create a competitive advantage and corporate value. A new concept on Investment Effectiveness Committed to Human Capital Development (EIHCD) is derived from the two theories. The Investment Effectiveness Committed to Human Capital Development (EIHCD) is the maximization of corporate profits by combining the investments in assets that make profit along with investment in Human Capital Development. The research problem was whether the EIHCD was capable of mediating the effect of ownership structure in good corporate governance (GCG) on corporate performance and increasing corporate value, which was intended to fill the research gap between corporate governance and corporate value.

The type and source of secondary data were the data obtained from external sources. The research objects were the go-public companies listed on the

ix

Indonesian Stock Exchange. The population in this study were 30 (thirty) companies registered in the Indonesian Stock Exchange for three years from 2013 to 2015, published by the Annual Report. Using purposive sampling, the samples obtained were 57 companies each year. The research variables was the time series data and cross section,in which one variable in the research influenced one another to the other research variables. The data analysis was conducted using the analytical instrument of Partial Least Square (PLS) and the path analysis.

The conclusions in this study did not have a multicolinearity in the regression models because the result of the calculation of the VIF value is smaller than 10. The test of Goodness of Fit is Model Fit based on output model fit and quality that indicates the model has the value of SRMR= 0.023 < 0.08; NFI = 0.982 > 0.90; and VIF < 3.3. Referring to the provisions, it can be concluded that the model of this experiment is fit. The variable of corporate value (CorValue) proxied with Tobin'q and Price Book Value (PBV) is affected by the variable of management Ownership (Mgt_Own), institutional ownership (Inst_Own), foreign ownership (Forg_Own), EIHCD, and Corporate Performance (CorPerfm) proxied with Return on Assets (ROA) of 60%, while the remaining 40% were influenced by other factors beyond the examined variables. The variable of EIHCD was influenced by the variables of the proportion of management ownership (Mgt_Own), the proportion of institutional ownership (Inst_Own), the proportion of foreign ownership (Forg_Own) by 34%, while the rest of 66% was influenced by other variables out of the examined variables. The variable of corporate performance proxied by CorPerfm was influenced by the variable of EIHCD by 7.3%, and the remaining 92.7% was influenced by other variables out of the examined variables. All variables affected Corporate Value except the Proportion of Management Ownership that did not affect Corporate Value because the t-count generated is 0.466 or smaller than t-table of 1.960. the Proportion of Management Ownership played a lower role low against the variable of corporate value through the variable of Investment Effectiveness Committed to Human Capital Development (IEHCD). The importance value of 0.004 means that the variable does not play a role to influence the variable of the proportion of management ownership. The results of the research hypothesis testings of the twelve hypothesis proposed were all accepted, except the proportion of Management Ownership to the Investment Effectiveness Committed to Human Capital Development (EIHCD).

This research resulted in several conclusions: first, the Investment Effectiveness Committed to Human Capital Development (EIHCD) which is capable of mediating the effect of the proportion of management ownership on corporate value is acceptable. Second, Investment Effectiveness Committed to Human Capital Development (EIHCD) which is capable of mediating the effect of the proportion of foreign ownership on corporate value is acceptable. Third, Investment Effectiveness Committed to Human Capital Development (EIHCD) is capable of mediating the effect of the proportion of institutional ownership on corporate value.

The research implications, as a whole, show that the concept of the Investment Effectiveness Committed to Human Capital Development (EIHCD)

x

which is a synthesis between the performance of investments in investment activities based on tangible assets proxied with ROA and the human capital investment (HCI) proxied with the investment expenditures for human capital investment can be used to provide a new reason why well- established companies invest in human capital in general is capable of generating new business ideas for the companies despite the increased risk of losing employees. The theoretical implication on the Grand Theory in this study is the Agency Theory. The first middle theory derived from Agency Theory is Signaling Theory and Peking Order Theory. The second middle theory derived from Investment Theory is the concept of Dynamic Industrial Investment based on Resource Based View.

xi

MOTO

"Sesungguhnya jika kamu bersyukur, pasti Kami akan menambah (ni'mat) kepadamu, dan jika kamu mengingkari (ni'mat-Ku), maka sesungguhnya azab-Ku sangat pedih". (QS: Ibrahim:7)

“Sebaik-baik Manusia Adalah Yang Paling Bermanfaat Bagi Orang Lain” (Al-Amin).

Anda tak akan bisa menghukum orang yang ikhlas. Karena apapun hukuman yang anda berikan, tak akan membuatnya tersiksa. Tapi justru akan membuatnya semakin bersyukur. (Orang Bijak)

Sahabat seperti hal dengan bintang, tak selalu nampak tapi selalu ada dihati, Sahabat akan selalu menghampiri ketika seluruh dunia menjauh, Persahabatan itu seperti tangan dengan mata, Ketika tangan terluka, mata menangis, Ketika mata menangis, tangan menghapusnya. Bahkan ketika kau akan menangis, sahabat melakukan sesuatu yang menjadi kau tersenyum (Orang Bijak)

Pandanglah sesuatu dari kacamata orang lain. Apabila hal itu menyakitkan hatimu, maka mungkin hal itu menyakitkan hati orang lain. (Orang Bijak)

xii

PERSEMBAHAN:

Karya Ilmiah ini saya persembahkan pada istri dan anak-anaku yang tercinta dan dunia untuk kemajuan ilmu pengetahuan

xiii

KATA PENGANTAR

Puji syukur ke hadirat Allah SWT yang telah melimpahkan banyak

kenikmatan, rahmat dan hidayah-Nya, sehingga penyusunan disertasi ini dapat

diselesaikan. Disertasi ini dapat saya selesaikan tidak lepas dari bantuan banyak

pihak, untuk itu saya mengucapkan banyak terima kasih dan penghargaan kepada:

1. Prof. Dr. Yos Johan Utama, M.Hum. selaku Rektor dan para wakil

Rektor dilingkungan Universitas Diponegoro, yang telah memberikan

kesempatan dan fasilitas kami untuk melakukan studi lanjut.

2. Dr. Suharnomo, M.Si. selaku dekan beserta para wakil dekan di

Fakultas Ekonomika dan Bisnis, Prof. Dr. Imam Ghozali, Akt. M.Com.

dan Prof. Waridin, Ph.D., selaku Ketua dan sekretaris Program Studi

Doktor Ilmu Ekonomi Universitas Diponegoro beserta seluruh Staf

Administrasi (mba Lina, mas Jo, dll.), yang telah dan selalu memberikan

pelayanan yang tulus dan prima selama saya menempuh tugas belajar.

3. Prof. Dr. H. Sugeng Wahyudi, MM., yang saya hormati dan saya

banggakan selaku promotor yang dengan kesabarannya telah meluangkan

waktu membimbing dan sekaligus keteladanannya serta memberi

kesempatan untuk belajar dalam riset, pengabdian masyarakat, konferensi

dan publikasi bahkan menulis buku. Dr. Harjum Muharam, ME., selaku

co-promotor yang dengan kesabarannya telah meluangkan waktu

membimbing dan keteladanannya.

xiv

4. Dosen-dosen Penguji antara lain Dr. Sugiono, MSIE, Dr. Irene D.P. ME.,

Dr. HM Chabahib, M.Si. Dr. Wisnu Mawardi, MM., Dr. Mutamimah,

M.Si., terima kasih masukan-masukan yang berharga yang telah mengisi

kekurangan-kekurangan dalam saya menulis disertasi ini.

5. Dosen-dosen Program Studi Doktor Ilmu Ekonomi Prof. Augusty T.

Ferdinand, Prof. Miyasto, Dr. Akhyar, Dr. Toto Susilo, yang telah

memberikan saya kesempatan untuk belajar dan menimba ilmu.

6. Kementerian Riset, Tekhnologi dan Pendidikan Tinggi, yang telah

memberikan Beasiswa Pascasarjana Dalam Negeri (BPDN), dan

Koordinator Kopertis Wilayah VI Jawa Tengah yang telah memberikan

penugasan kepada saya untuk mengikuti studi lanjut sehingga dapat

membantu dan melancarkan saya dalam menempuh tugas belajar.

7. Rektor Unisbank, Ketua YPPMI, Dekan, Sekretaris Fakultas, Ketua

Program Studi dan para tenaga kependidikan di lingkungan Fakultas

Ekonomika dan Bisnis Universitas Stikubank, terima kasih untuk

semuanya yang telah diberikan khususnya security kampus Kendeng

yang menemani saat-saat harus lembur hingga larut malam bahkan fajar.

8. Prof. Dr. Ibnu Khajar, Prof. Y. Sutomo, MM., Prof. Eric Santoso,

MBA., Dr. Bambang Sudiyatno, Dr. Alimudin, Dr. Agung Nusantara,

Dr. Herry Subagyo, Dr. Sih Darmi Astuti, Dr. Endang Tjahtjaningsih, Dr.

Basukianto, Dr. Bambang Suko, Dr. M. Fauzan, Dr. Tristiana, Dr. Euis

Soliha, Dr. Agus Budi, Dr. Cecilia Sri Mindarti, Dr. J. Widiyatmoko,

Dr. GN. Masdjojo, Dr. Sri Nawatmi, Dr. Elen P., Jaeni, MSi, Andi

xv

Kartika, MM., Marlien, MM., Mulyo Budi, MM., Dr. Isnowati, Askar

Yunianto, MSi., Sri Sudarsi, MSi., Ali Maskur, M.Kom., Pancawati H.

MSi., Alfasadun, MM. dan teman-teman lain di FEB Unisbank yang

tidak bisa disebut satu persatu, terima kasih untuk dukungan dan

motivasinya selama saya menempuh studi.

9. Rekan-rekan Program Studi Doktor Ilmu Ekonomi Universitas

Diponegoro Semarang, Dr. Eka Handriani, Dr. Robiyanto, Rio Dhani

Laksana, M.Sc. Siti Puryandani, Hartati Hadadi, Tony Heryana, Dian

Purna, Dr. Bertha, Dr. Nuryakin, Dr. Hendar, Dr. Gita, Dr. Ida, pa

Marno, mas Anta, mas Agus Prie, mas Prio, bu Lita, bu Ika, atas

dorongan motivasi dan solidaritas selama dalam menempuh studi di S3.

Mba Eka, Pa Roby, Mas Rio, bro Yon, gus Ipul, pa Riskin, dan Ounty

yang bersama-sama belajar di “Riset Center”, ayo lanjutkan.

10. Ayahanda Bapak H. Dasmad (almarhum) yang ingin

menyaksikan promosi har i ini , tapi sang Khal ik lebih

mencinta i , dan Ibunda Hj. Tarinah, yang telah mengasuh,

membesarkan, dan mendoakan serta dengan perjuangannya yang penuh

kesabaran, kasih sayang, keteladanan, dan pengorbanan yang tak

terhitung nilainya, mudah-mudahan sehat selalu dan mudah-mudahan

bisa menjadi waladun sholihan.

11. Istriku tercinta, Dr. Hermin Pancasakti Kusumaningrum, M.Si. dan

anak-anakku t e r s ayang , Hererapratita Aysha Hapsari (Rera),

Hertantya Muhamad Aulyasaktya (Anto) dan Heradita Kaniaazzahra

xvi

Doktorasaintifika (Kania), yang selalu mendorong, mendoakan dan

memotivasi agar saya dapat menyelesaikan studi, dan selalu tanya

“kapan papa selesai kuliahnya”, terjawab sudah pertanyaannya dan baru

sekarang menjawabnya.

12. Kakak-kakaku, H. Hendro Puspito, SH., MH. dan Hj. Eko Nurhayati,

SH., Prof. Dr. Ir. H.M. Zainuri, DEA dan Hj. Ir. Hj. Hadi Endrawati,

DESU., Drs. H. Dwi Husodo Sapto Hariadi, MM. dan Dra. Hj. Hernanik

Narimaningsih, Adik-adikku: Puji Hartono, AMd. dan Rihanah, Arif

Setiadi, SE., Akt., MSi. dan Lilis Anisah, SSt., MSi., Sri Hastuti, AMd.

dan Targono, SH. Ponakan-ponakanku: Andika Satya Pratama, SH.,

Reza, S.Sos., Aula ST., dr. Rifa, dr. Fully, dr. Rona, Fira, Lala, Afip,

Yoga, Anggie, Yusuf, Ais, Habibie, Nesya, Aira, Deren dan Bagas,

terimakasih atas dorongan dan motivasinya.

13. Berbagai Pihak yang tidak dapat saya sebutkan, yang telah membantu

saya dalam menyusun dan menyelesaikan disertasi.

Dengan penuh kesadaran penulis merasa bahwa disertasi ini masih banyak

kekurangannya dan ketidaksempunaan, sehingga masih membutuhkan masukan,

kritik dan saran untuk penyempurnaan tulisan ini. Oleh karena itu, bagi

bapak/ibu/sdr yang berminat membaca, saya mohon untuk memberikan saran dan

kritik demi penyempurnaan disertasi ini.

Semarang, Januari 2018Penyusun,

Hersugondo

xvii

DAFTAR ISI

halamanHalaman Sampul Depan.......................................................................................... i

Halaman persetujuan .............................................................................................. ii

Pernyataan keaslian disertasi................................................................................... iii

Abstrak.................................................................................................................... iv

Abstract................................................................................................................... v

Ringkasan................................................................................................................ vi

Executive Summary................................................................................................ ix

Motto ...................................................................................................................... xii

Persembahan ........................................................................................................... xii

Kata Pengantar........................................................................................................ xiv

Daftar Tabel............................................................................................................. xxv

Daftar Gambar......................................................................................................... xxvii

BAB

I P E N D A H U L U A N.............................................................................. 1

1.1. Latar Belakang Penelitian.................................................................. 1

1.2. Penelitian Terdahulu dan Research Gaps.......................................... 10

1.2.1. Research Gap1: Kepemilikan Manajemen dan Nilai

Perusahaan........................................................................... 21

1.2.2. Research Gap2: Kepemilikan Investor Institusional dan

Nilai Perusahaan.................................................................. 28

1.2.3. Research Gap 3: Kepemilikan Asing dan Nilai

Perusahaan .......................................................................... 30

1.3. Fenomena Bisnis, Tata Kelola Perusahaa dan Human Capital

Investment.......................................................................................... 36

1.4. Masalah Penelitian............................................................................. 49

1.5. Perumusan Masalah........................................................................... 49

1.6. Tujuan Penelitian............................................................................... 50

1.7. Manfaat Penelitian............................................................................. 51

xviii

1.7.1. Manfaat Teoritis .................................................................. 51

1.7.2. Manfaat Praktis.................................................................... 51

1.8. Orisinilitas ......................................................................................... 52

II TELAAH PUSTAKA DAN PENGEMBANGAN MODEL 53

2.1. Telaah Pustaka .................................................................................. 53

2.1.1. Agency Theory (Teori Keagenan)........................................ 53

2.1.2. Resources Based Theory (RBT) .......................................... 58

2.1.3. Market Based Theory (MBT) .............................................. 66

2.1.4. Signaling Theory (Teori Pensinyalan) ................................ 68

2.1.5. Struktur Kepemilikan (ownership structure) ...................... 71

2.1.5.1. Kepemilikan Manajemen (Manajerial Ownership) 72

2.1.5.2.Kepemilikan Saham Institusi (Institution

Ownership) ............................................................ 74

2.1.5.3. Kepemilikan InsvestorAsing (foreign Ownership) 79

2.1.6. Kinerja Perusahaan (Corporate Performance) ................... 81

2.1.7. Tata Kelola Perusahaan (Corporate Governance)............... 83

2.1.7.1. Definisi Tata Kelola Perusahaan............................. 96

2.1.7.2. Tujuan Tata Kelola Perusahaan.............................. 99

2.1.7.3. Mekanisme Tata Kelola Perusahaan....................... 102

2.1.8. Nilai Perusahaan (Firm Value) ........................................... 105

2.2. Pengembangan Proposisi................................................................... 110

2.2.1. Teori Agensi dan Kebijakan Investasi................................. 110

2.2.2. Sintesis Agency Theory dan Resources Based Theory.......... 127

2.2.3. Efektifitas Investasi Berkomitmen pada Human Capital

Development........................................................................ 130

2.2.4. Indikator Efektifitas Investasi Berkomitmen pada Human

Capital Development .......................................................... 133

xix

2.2.4.1. Kinerja Perusahaan (Corporate Financial

Performance) ......................................................... 134

2.2.4.2. Kinerja Human Capital Investment....................... 138

2.2.5. State of the Art Proposisi Efektifitas Investasi

Berkomitmen pada Pengembangan SDM (Investment

Efectiveness Comitted to Human Capital

Development(IECHCD)....................................................... 140

2.2.6. Proposisi Efektifitas Investasi Berkomitmen pada

Pengembangan SDM (InvestmentEfectiveness Comitted to

Human Capital Development/ IECHCD) ........................... 148

2.3. Model Teoritikal Dasar (Grand Theoritical Model) ......................... 149

2.4. Pengembangan Hipotesa.................................................................... 158

2.4.1. Pengaruh Kepemilikan Manajerial Terhadap Kinerja dan

Nilai Perusahaan.................................................................. 158

2.4.2. Pengaruh kepemilikan Institusi Terhadap Kinerja dan

Nilai Perusahaan.................................................................. 164

2.4.3. Pengaruh Kepemilikan Investor Asing Terhadap Kinerja

dan Nilai Perusahaan............................................................ 170

2.4.4. Pengaruh Kepemilikan Manajerial Terhadap Investment

Efectiveness Committed to Human Capital Development... 177

2.4.5. Pengaruh Kepemilikan Institusi Terhadap Investment

Efectiveness Committed to Human Capital Development... 183

2.4.6. Pengaruh Kepemilikan Investor Asing Terhadap

Investment Efectiveness Committed to Human Capital

Development ....................................................................... 188

2.4.7. Pengaruh Investment Efectiveness Committed to Human

Capital Development Terhadap Kinerja dan Nilai

Perusahaan .......................................................................... 194

2.4.8. Investment Efectiveness Committed to Human Capital

Development Memediasi Pengaruh Kepemilikan

Manajemen terhadap Nilai perusahaan............................... 205

xx

2.4.9. Investment Efectiveness Committed to Human Capital

Development Memediasi Pengaruh Kepemilikan Institusi

terhadap Nilai perusahaan........................................................ 212

2.4.10 Investment Efectiveness Committed to Human Capital

Development Memediasi Pengaruh Kepemilikan Investor

Asing terhadap Nilai perusahaan............................................ 218

III MOTODE PENELITIAN ................................................................................ 226

3.1. Desain Penelitian....................................................................................... 226

3.2. Obyek Penelitian....................................................................................... 228

3.3. Jenis Data dan Sumber Data.................................................................... 228

3.4. Populasi dan Sampel................................................................................. 229

3.5. Difinisi Konsep Variabel Penelitian....................................................... 229

3.5.1. Nilai Perusahaan (Firm Value) ............................................... 230

3.5.2. Kinerja Keuangan Perusahaan (Corporate Financial

Performance) ............................................................................. 231

3.5.3. Tata Kelola Perusahaan (Corporate Governance) ............... 232

3.5.3.1.Proporsi Kepemilikan Manajerial (Managerial

Ownership ) ................................................................. 232

3.5.3.2.Proporsi Kepemilikan Institusi (Institutional

Investor) ........................................................................ 237

3.5.3.3. Proporsi kepemilikan institusi asing......................... 244

3.6. Definisi Operasional dan Pengukuran Variabel.................................... 247

3.6.1. Definisi Operasional.................................................................. 247

3.6.1.1. Nilai Perusahaan......................................................... 247

3.6.1.2. Kinerja Perusahaan (Corporate Performance)....... 248

3.6.1.3. Tata Kelola Perusahaan (Corporate Governance). 249

3.6.1.4. Efektifitas Investasi Berbasis pada Human

Capital (EICHCD)................................................. 250

3.6.2. Pengukuran Variabel................................................................. 252

3.7. Teknik Analisis.......................................................................................... 254

xxi

3.7.1. Analisis Jalur (Path Analysis).................................................. 254

3.7.2. Analisis Model Dengan PLS.................................................... 258

IV ANALISIS DATA DAN PEMBAHASAN...................................................... 260

4.1. Pengantar.................................................................................................... 260

4.2 Analisis Deskriptif.................................................................................... 260

4.3. Pengujian Asumsi Model Penelitian Empiris........................................ 264

4.3.1. Uji Multikolineritas...................................................................... 264

4.3.2. Uji Goodness of Fit Model Penelitian Empiris........................ 265

4.4. Pengujian dengan SmartPLS 4.0............................................................. 266

4.4.1. Pengujian Full Model................................................................... 266

4.4.2. Hasil Estimasi Model................................................................... 270

4.4.3. Pengujian Model Mediasi............................................................ 278

4.4.3.1. Hasil Pengujian Model Mediasi dengan

Importance–Performance Map Analysis (IPMA)

for construct.................................................................... 280

4.4.4. Pengujian Hipotesis...................................................................... 282

4.4.4.1. Pengujian pengaruh struktur dan mekanisme

Corporate Governance terhadap nilai perusahaan.. 283

4.4.4.2. Pengujian pengaruh mediasi Investment

Efectiveness Committed to Human Capital

Development atas struktur dan mekanisme

Corporate Governance terhadap nilai perusahaan.. 286

V PEMBAHASAN HASIL PENELITIAN......................................................... 289

5.1. Pengantar.................................................................................................... 289

5.2. Pembahasan................................................................................................ 290

5.3. Pengujian pengaruh mekanisme Corporate Governance terhadap

nilai perusahaan................................................................................. 291

5.3.1. Pembahasan Hasil Pengujian Hipotesis 1................................. 292

xxii

5.3.2. Pembahasan Hasil Pengujian Hipotesis 2................................. 295

5.3.3. Pembahasan Hasil Pengujian Hipotesis 3................................. 295

5.3.4. Pembahasan Hasil Pengujian Hipotesis 4................................. 296

5.3.5. Pembahasan Hasil Pengujian Hipotesis 5................................. 299

5.3.6. Pembahasan Hasil Pengujian Hipotesis 6................................. 301

5.3.7. Pembahasan Hasil Pengujian Hipotesis 7................................. 303

5.3.8. Pembahasan Hasil Pengujian Hipotesis 8................................. 304

5.3.9. Pembahasan Hasil Pengujian Hipotesis 9................................. 306

5.3.10 Pembahasan Hasil Pengujian Hipotesis 10............................... 307

5.3.11 Pembahasan Hasil Pengujian Hipotesis 11............................... 311

5.3.12 Pembahasan Hasil Pengujian Hipotesis 12............................... 313

VI KESIMPULAN,IMPLIKASI DAN KETERBATASAN PENELITIAN 317

6.1. Pengantar....................................................................................................... 317

6.2. Kesimpulan Hasil Pengujian Hipotesis................................................ 318

6.2.1. Hubungan Kausalitas struktur corporate governance dengan

Nilai Perusahaan.............................................................................. 322

6.2.2. Hubungan struktur Corporate Governance dengan Investment

Efectiveness Committed to Human Capital Development......... 325

6.3. Kesimpulan dari permasalahan penelitian............................................ 331

6.3.1. Alternatif Pertama..................................................................... 331

6.3.2. Alternatif Kedua........................................................................ 332

6.3.3. Alternatif Ketiga....................................................................... 333

6.4. Temuan penelitian................................................................................ 335

6.4.1. Proporsi Kepemilikan Institusi→ nilai perusahaan.................... 335

6.4.2. Proporsi kepemilikan institusi asing→ nilai perusahaan........... 337

6.4.3. Proporsi Kepemilikan Manajerial→ Investment Efectiveness

Committed to Human Capital Development.............................. 338

6.4.4. Proporsi Kepemilikan Institusi→ Investment Efectiveness

Committed to Human Capital Development.............................. 340

6.4.5. Proporsi kepemilikan institusi asing→ Investment

xxiii

Efectiveness Committed to Human Capital Development......... 341

6.4.6. Investment Efectiveness Committed to Human Capital

Development → kinerja perusahaan......................................... 342

6.4.7. Investment Efectiveness Committed to Human Capital

Development → nilai perusahaan............................................. 343

6.4.8. Kinerja perusahaan → nilai perusahaan.................................... 345

6.4.9. Investment Efectiveness Committed to Human Capital

Development →Proporsi Kepemilikan Investor Asing →nilai

perusahaan.................................................................................. 347

6.5. Implikasi penelitian.............................................................................. 347

6.5.1. Implikasi Teoritis...................................................................... 350

6.5.2. Implikasi Manajerial................................................................. 361

6.5.3. Implikasi Praktis bagi Investor................................................. 372

6.5.4. Implikasi bagi Pemerintah........................................................ 377

6.5.5. Keterbatasan Penelitian dan Agenda Penelitian Mendatang..... 379

DAFTAR PUSTAKA............................................................................................ 383

LAMPIRAN-LAMPIRAN

xxiv

DAFTAR TABEL

Tabel. 1.1.

Tabel. 1.2.

Tabel. 2.1.

Research Gap antara Corporate Governance dengan Nilai

Perusahaan...............................................................................

Data Rata-Rata Struktur Kepemilikan dan Nilai Perusahaan

dari Tahun 2013-2015...................................................................

Tinjauan Teori Keagenan.............................................................

34

4

5

56

Tabel. 2.2. St State of the Art Investment Efectiveness Committed to Human

Capital Development (EIBHC)................................................ 141

Tabel. 2.3. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Manajemen Terhadap Kinerjadan Nilai Perusahaan................ 160

Tabel. 2.4. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Institusi Terhadap KinerjadanNilai Perusahaan....................... 167

Tabel. 2.5. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Investor Asing Terhadap Kinerja dan Nilai Perusahaan.......... 172

Tabel. 2.6. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Manajemen Terhadap Investment Efectiveness Committed to

Human Capital Development................................................... 178

Tabel. 2.7. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Institusi Terhadap Investment Efectiveness Committed to

Human Capital Development................................................... 184

Tabel. 2.8. Ringkasan Kajian Empirik Pengaruh Proporsi Kepemilikan

Asing Terhadap Investment Efectiveness Committed to

Human Capital Development................................................... 190

Tabel. 2.9. Ringkasan Kajian Empirik Pengaruh Investment Efectiveness

Committed to Human Capital Development Terhadap

Kinerja dan Nilai Perusahaan................................................... 201

xxv

Tabel.2.10

.

Ringkasan Kajian Empirik Investment Efectiveness

Committed to Human Capital Development Memediasi

Pengaruh Kepemilikan Manajemen terhadap Nilai

perusahaan............................................................................... 206

Tabel

2.11.

Ringkasan Kajian Empirik Investment Efectiveness

Committed to Human Capital Development Memediasi

Pengaruh Kepemilikan Institusi terhadap Nilai perusahaan.... 214

Tabel

2.12.

Ringkasan Kajian Empirik Investment Efectiveness

Committed to Human Capital Development Memediasi

Pengaruh Kepemilikan Investor Asing terhadap Nilai

perusahaan............................................................................... 219

Tabel 3.1. Pengukuran Variabel Penelitian............................................... 252

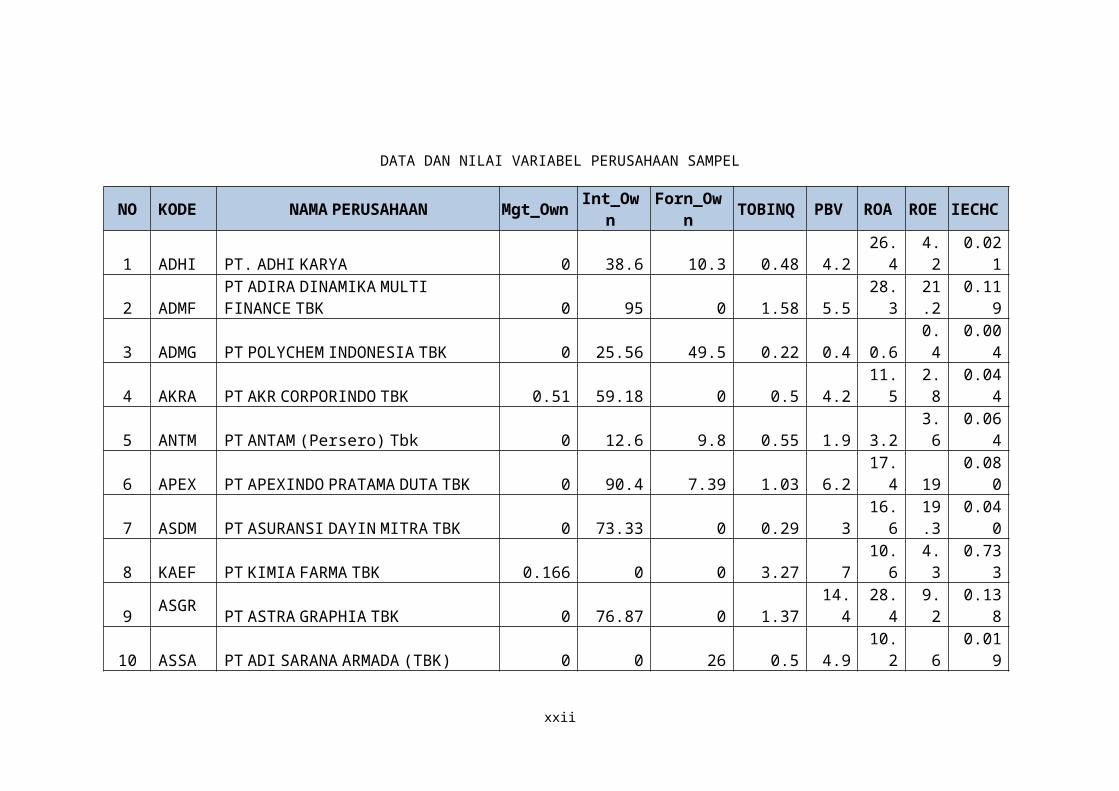

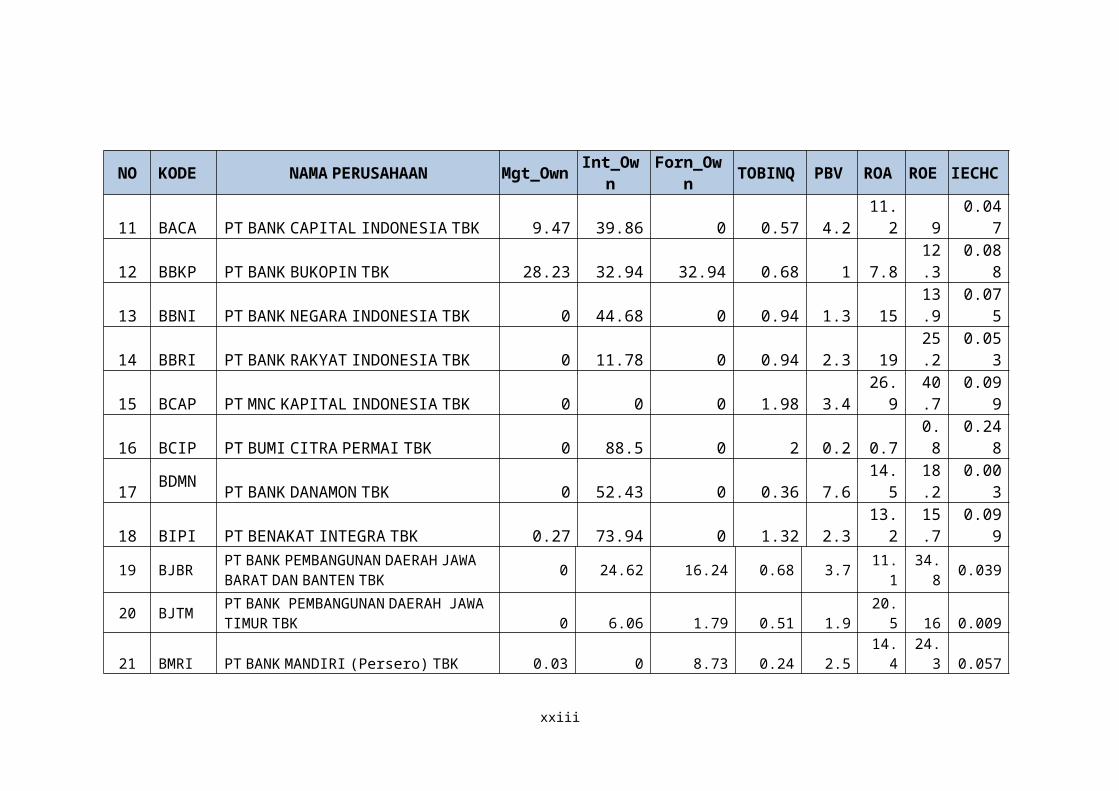

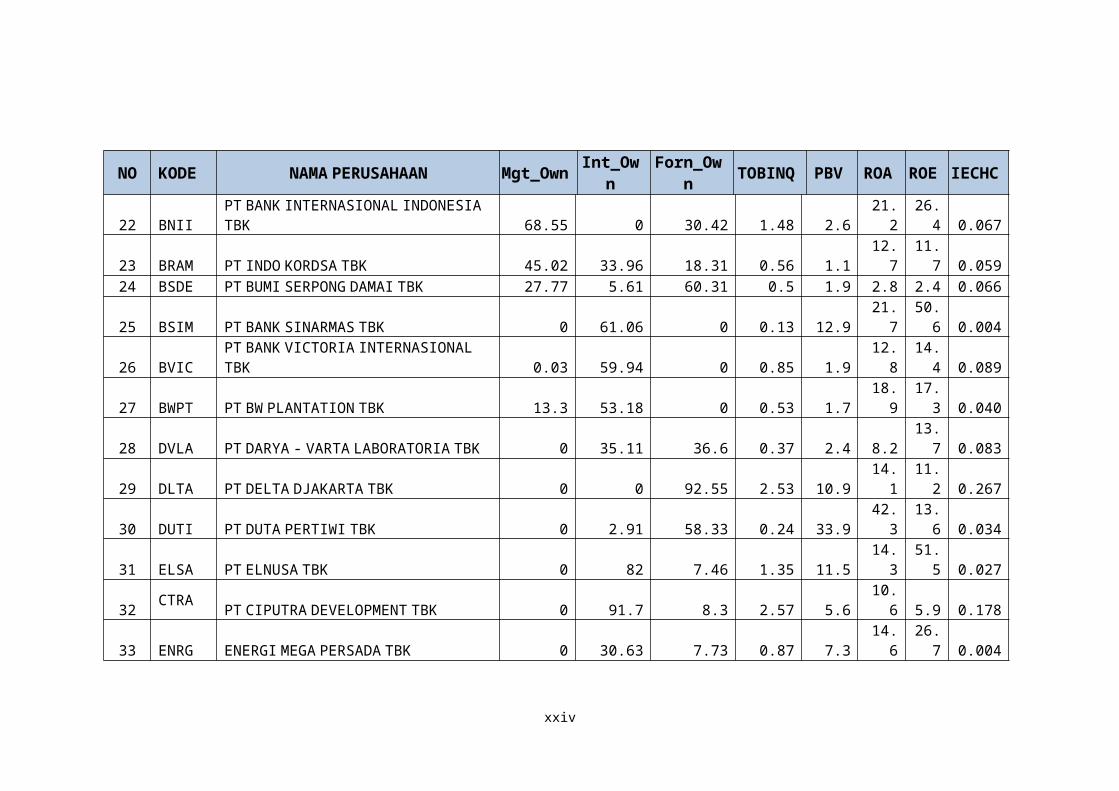

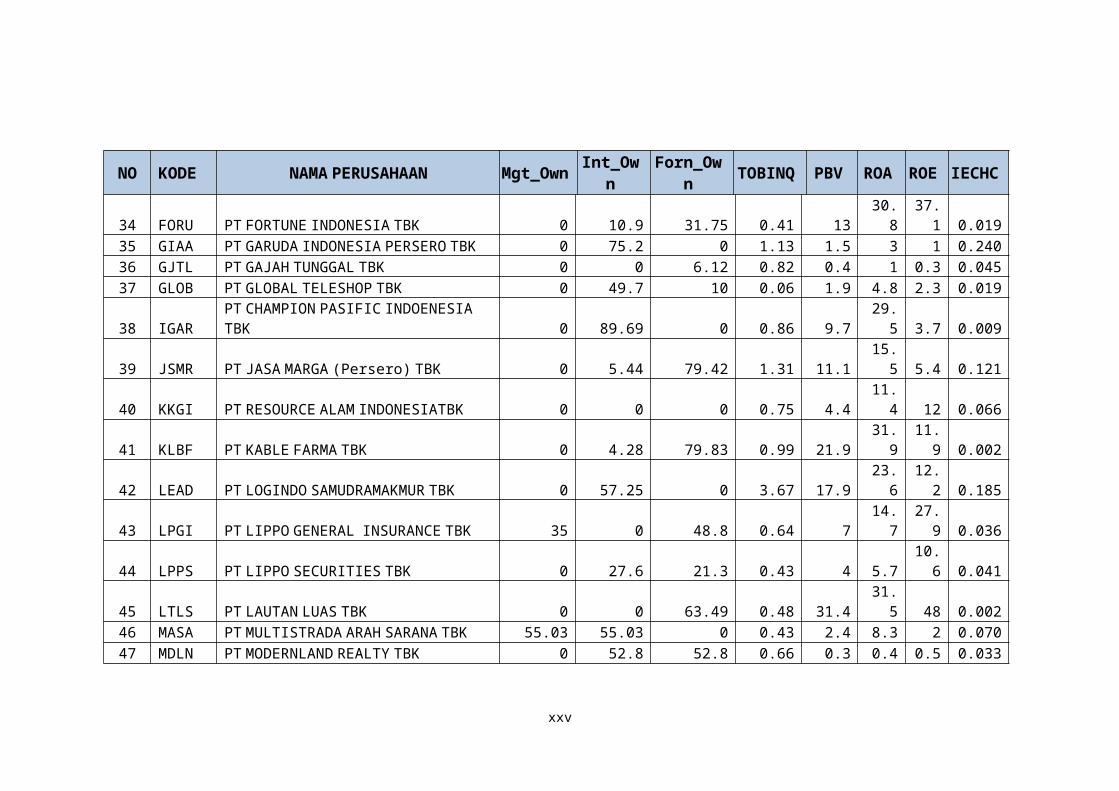

Tabel 4.1. Data Nama Perusahaan Objek Penelitian................................ 261

Tabel 4.2 . Statistik Deskriptif Data Penelitian Tahun 2012 – 2015......... 262

Tabel 4.3. Quality Criteria : Collinearity Statistic................................... 265

Tabel 4.4. Quality Criteria : Model Fit Summary.................................... 266

Tabel 4.5. Model Fit and Quality Indicates, Path Coefisiens dan ρ-

Value, Indirect Effect, Total Effect, Effect Size – Full Model.. 268

Tabel 4.6. R squared, Q squared dan full collinearity VIF...................... 269

Tabel 4.7 Final Result – Path Coefficient (Direct Effect) ....................... 273

Tabel 4.8 Pengaruh Langsung Proporsi Kepemilikan Investor Asing,

Proporsi Kepemilikan Manajemen, Proporsi Kepemilikan

institusi, Investment Efectiveness Committed to Human

Capital Development, Kinerja Perusahaan dan Nilai

Perusahaan............................................................................... 278

Tabel 4.9 Hasil Pengujian pengaruh tidak langsung................................ 279

Tabel 4.10 Importance–Performance Map Analysis (IPMA) for

construct................................................................................... 281

Tabel 4.11

Tabel 5.1

Hasil pengujian hipotesis penelitian........................................

Ringkasan hasil pengujian Hipotesis Penelitian......................

288

291

xxvi

Tabel 6.1. Temuan Hasil Penelitian dan Implikasi Teoritis...................... 353

DAFTAR GAMBAR

Gambar. 1.1. Proporsi Tangible dan Intangable Asset dalam Perusahaan.. 39

Gambar: 2.1. Mapping Human Capital Dalam Modal Perusahaan............. 123

Gambar 2.2. Proporsi Peran Asset tidak Berwujud (intangible asset) ...... 125

Gambar 2.3. Model Piktografis Proposisi.................................................. 132

Gambar.2.4. Diagram State of the Art Investment Efectiveness

Committed to Human Capital Development (EIBHC) ......... 147

Gambar 2.5. Model Teoritikal Dasar.......................................................... 153

Gambar 2.6. Model Penelitian Empirik...................................................... 225

Gambar 3.1. Analisis Jalur (Path Analysis)............................................... 255

Gambar 4.1 Output SmartPLS - Full Model.............................................. 271

Gambar 5.1. Sistematika Bab V................................................................. 289

Gambar 5.2. Pergerakan Peran Proporsi Kepemilikan Manajerial

(Manajerial Ownership) dan Nilai Perusahaan.................... 294

Gambar 5.3. Pergerakan Peran Proporsi Kepemilikan Manajerial

(Manajerial Ownership) dan Investment Efectiveness

Committed to Human Capital Development.......................... 298

Gambar 6.1. Sistematika Bab VI................................................................ 317

Gambar 6.2. Alternatif 1 Struktur Corporate Governance Terhadap

Nilai Perusahaan.................................................................... 332

Gambar 6.3.

Gambar 6.4.

Alternatif 2 struktur corporate governance terhadap

Investment Efectiveness Committed to Human Capital

Development .........................................................................

Struktur corporate governance Dimediasi Oleh Investment

EfectivenessCommitted to Human Capital Development

Terhadap Nilai Perusahaan....................................................

333

334

xxvii

DAFTAR PUSTAKA

Abdullah, L., Jaafar, S., and Taib, I. (2013). Ranking of Human Capital Indicators using Analytic Hierarchy Process. Procedia-Social and Behavioral Sciences, 107(2013), 22-28.

Abe, M. and Hoshi, T. (2004). Corporate Finance and Human Resource Management RIETI RIETI Discussion Paper Series 04-E-027

ADB. (2010). Operations Manual Bank Policies (BP). 2010.

Agbloyor, E. K., Abor, J., Adjasi, C. K. D., & Yawson, A. (2013). Exploring the causality links between financial markets and foreign direct investment in Africa. Research in International Business and Finance, 28, 118-134.

Aggarwal, A., and C. R. Knoeber. (1996). Firm Performance and Mecanisms to control Agency Problem Between Managers and Shareholders. Journal of Financial and Quantitative Analisys 31 (3):377-397.

Aggrawal, A., and G. N. Mandelker. (1990). Large Shareholders and The Monitoring of Managers: The Case of Antitakeover Charter Amendment. Journal of Financial and Quantitative Analysis 25:143-161.

Aggarwala, T. (2003). Innovative human resource practices and organizational commitment: An empirical investigation. International Journal of Human Resource Management, 14(2), 175–197.

Aghion, P., Van Reenen, J., and Zingales, L. (2013). Innovation and institutional ownership. The American Economic Review, 103(1), 277-304.

Ahesha, P. and Sujani, T. (2012). Impact of Human Capital Investment on Firm Financial Performances: An Empirical Study of Companies in Sri Lanka. DOI: 10.7763/IPEDR. 2012. V54. 3

Ahmad, Z., Abdullah, N. M. H., and Roslan, S. (2012). Capital structure effect on firms perfor

mance: Focusing on consumers and industrials sectors on Malaysian firms. International Review of Business Research Papers, 8(5), 137-155.

Ahn, S., Denis, D. J., and Denis, D. K. (2006). Leverage and investment in diversified firms. Journal of financial Economics, 79(2), 317-337.

xxviii

Alessandri, T. M., and Seth, A. (2014). The effects of managerial ownership on international and business diversification: Balancing incentives and risks. Strategic Management Journal, 35(13), 2064-2075.

Al Farooque, O., Tony van Zijl., Dunstan, K., and Karim, W, (2005), University of Auck-land Business School (Tamaki Division), Private Bag 92019, Auckland, New Zealand, Email: [email protected]., School of Accounting and Commercial Law, Victoria University of Wellington, PO Box 600, Welington New Zealand, http://www.accounting-research.org.nz, A Simultaneous Equations Approach to Analysing the Relationship Between Ownership Structure and Performance in Bangladesh.

Ali, S. M., Salleh, N. M., and Hassan, M. S. (2010). Ownership structure and earnings management in Malaysian listed companies: the size effect. Asian Journal of Business and Accounting, (2),1-10.

Al-Malkawi, H.-A. N., and Rekha. (2012). Internal Mechanisms of Corporate Governance and Firm Performance: A Review of Theory and Empirical Evidence. Journal of Modern Accounting and Auditing 8 (4):549-568.

Al-Najjar. D. (2015). The Effect of Institutional Ownership on Firm Performance: Evidence from Jordanian Listed Firms. International Journal of Economics and Finance; Vol. 7, No. 12.

Al‐Najjar, B., and Anfimiadou, A. (2012). Environmental policies and firm value. Business Strategy and the Environment, 21(1), 49-59.

Alves, C., and Mendes, V. (2004). Corporate governance policy and company performance: the Portuguese case. Corporate Governance: An International Review, 12(3), 290-301.

Amihud, Y., and B. Lev. (1981). Risk Reduction as Managerial Motive for Conglomerate Mergers. Bell Journal of Economics 12:605-617.

Armstrong, M. (2006). A Handbook of Human Resource Management Practice (10 ed.). London: Kogan Page.

Andras, T. L. and Srinivasan, S. S. (2003). Advertising Intensity and R&D Intensity: Differences across Industries and Their Impact on Firm's Performance. International Journal of Business and Economics, 2(2), 167-176.

xxix

An, H., and Zhang, T. (2013). Stock price synchronicity, crash risk, and institutional investors. Journal of Corporate Finance, 21, 1-15.

Anuchitworawong, C. (2004). Ownership-based Incentive, Internal Corporate Risk and Firm Performance. Dissertation, Institute of Economics Reseach, Hitotsubhasi University.

Apreda, R.. (2011). Corporate Governance And Intellectual Capital. University Del Cema. MCMLXXVIII.

Arslan-Ayaydin, Ö., Florackis, C., and Ozkan, A. (2014). Financial Flexibility, Corporate Investment and Performance: Evidence From Financial Crises. Review of Quantitative Finance and Accounting, 42(2), 211-250.

Arthur, J. B. (1994). Effects of Human Resource Systems on Manufacturing Performance and Turn Over. Academy of Management journal, 37(3), 670-687.

Ashour, A., and Bontis, N. (2007). Human capital and organizational performance: a study of Egyptian software companies. Management Decision, 45(4), 789-801.

Asiedu, E., and Esfahani, H. S. (2001). Ownership Structure in Foreign Direct Investment Projects. The Review of Economics and Statistics, 83(4), 647-662.

Asker, J., Farre-Mensa, J., and Ljungqvist, A. (2014). Corporate Investment and Stock Market Listing: A Puzzle?. The Review of Financial Studies, 28(2), 342-390.

Astuti, P.D. (2005). “Hubungan Intellectual Capital dan Business Performance.” Jurnal MAKSI. Vol 5, 34-58.

Attig, N., Cleary, S., El Ghoul, S., and Guedhami, O. (2013). Institutional investment horizons and the cost of equity capital. Financial Management, 42(2), 441-477.

Aukiyah, R., and A. Hamzah. (2006). Anallisa Karakteristik Perusahaan, Industri dan Ekonomi Makro Terhadap Return dan Beta Saham Syariah di BEJ. Paper read at Simposium Nasioanal Akuntansi 9 at Padang.

Bahjat, s. and Black B. (1999) The Uncertain Relation between Board Composition and Firm Performance. Business Law, 54, 921-963. Bhagat,

xxx

S., and B. Black.(2002) The non-correlation between board independence and long-term firm performance. Journal of Corporation Law 27 (Winter): 231-274.

Baker, H., and Powell, G. E. (2012). Dividend policy in Indonesia: survey evidence from executives. Journal of Asia Business Studies, 6(1), 79-92.

Bae, J., and Lawler, J. J. (2000). Organizational and HRM strategies in Korea: Impact on firm performance in an emerging economy. Academy of management journal, 43(3), 502-517.

Baños-Caballero, S., García-Teruel, P. J., and Martínez-Solano, P. (2014). Working capital management, corporate performance, and financial constraints. Journal of Business Research, 67(3), 332-338.

Barbosa, N., and H. Louri. (2005). Corporate Performance: Does Ownership Matter? A Comparison of Foreign and Domestic Owned Firm in Greece and Portugal. Review of Industrial Organization 27:73-102.

Barclay, M. J., and C. G. Holderness. (1992). The Law and Large-block Trades. Journal of Law and Economics 35:265-294

Barney, J.B. (1991). Firm Resources and Sustained Competitive Advantage. Journal of Management. Pp 99-120.

Bartel, Ann. (1994). Productivity Gains from the Implementation of Employee Training Programs. Industrial Relations. 33(4): 411-425.

Bartram, S. M., Griffin, J. M., Lim, T. H., and Ng, D. T. (2015). How important are foreign ownership linkages for international stock returns?. The Review of Financial Studies, 28(11), 3036-3072.

Bassi, L., Harrison, P., Ludwig, J., and McMurrer, D. (2004). The impact of US Firms’ investments in human capital on stock prices. unpublished, June.

Bassi, L., Harrison, P., Jens L.ig, and McMurrer, D. (2001). Human Capital Investments and Firm Performance. (www.bassi-investments.com/ downloads/Research Paper_June2001_.pdf).

Bassi, L., and McMurrer, D. (2006). Human capital and organizational performance: Next generation metrics as a catalyst for change. McBassi & Company white paper available online at www. McBassi. com.

xxxi

Bathala, C., and R. Rao. (1995). The Determinant of Board Composition: An Agency Yheory Perspective. Managerial and Decision Economics 5 (16):59-69.

Batten, J. A., and Vo, X. V. (2015). Foreign ownership in emerging stock markets. Journal of Multinational Financial Management, 32, 15-24.

Beasly, M. S. (1996). An Empirical Anaysis of The relation Between the Board of Directors Composition and Financial Statement Fraud. The Accounting Review 71.

Becker, B., Bergstresser, D., and Subramanian, G. (2013). Does shareholder proxy access improvefirm value? evidence from the business roundtable’s challenge. The Journal of Law and Economics, 56(1), 127-160..

Belden, T. Fister, and B. Knapp. (2005). Dividends and Directors : Do Outsiders Reduce Agency Cost? Business and Society Review 102 (2):171-180.

Belkhir, M. (2005). Board Structure, Ownership structure, and Firm performance: Evidence from Banking:http://www.uniy-orleans.fr/deg/GD Recomofi/Activ/belkhir_ strasbg05.pdf.

Bergstrom, C. and K. Rydqvist. (1990. The Determinants of Corporate Ownership, Journal of Banking and Finance. 14: 237–262.

Bena, J., and Hanousek. (2008). Rent Extraction by Large Shareholders: Evidence Using Dividend Policy in the Czech Republic. Journal of Economics and Finance 58 (3-4):106-130.

Bevan. A.A., and J. Danbolt. (2002). Capital structure and its determinants in the UK – a decompositional analysis. Applied Financial Economics, 12 pp.159-170

Bhagat, S., and B. Black.(2001) The non-correlation between board independence and long-term firm performance. Journal of Corporation Law 27 (Winter): 231-274.

Bhagat, S., Black, B., and Blair, M. (2004). Relational Investing And Firm Performance. Journal of Financial Research, 27(1), 1-30.

xxxii

Black, B., and Kim, W. (2012). The Effect Of Board Structure On Firm Value: A Multiple Identification Strategies Approach Using Korean Data. Journal of Financial Economics, 104(1), 203-226.

Black, F., and Scholes, M. (1974). The effects of dividend yield and dividend policy on common stock prices and returns. Journal of financial economics, 1(1), 1-22.

Black, Sandra, and Lisa Lynch. (1996). Human-Capital Investments and Productivity. American Economic Review. 86(2): 263-267.

Black, B., and Kim, W. (2012). The Effect Of Board Structure On Firm Value: A Multiple Identification Strategies Approach Using Korean Data. Journal of Financial Economics, 104(1), 203-226.

Blundell, R., (1999). Human Capital Investment: The Returns from Education and Training to the Individual, the Firm, and the Economy, Fiscal Studies (1999) vol 20.

Bodie, Z., Kane, A., and Marcus, A. J. (2014). Investments, 10e. McGraw-Hill Education.

Bolton, P., Chen, H., & Wang, N. (2013). Market Timing, Investment, And Risk Management. Journal of Financial Economics, 109(1), 40-62.

Bontis, N, Wiliam Chua Chong Keow dan Stanley Richardson. (2000). Intellectual Capital and Business Performance in Malaysian Industries. Journal of Intellectual Capital. Vol 1, No. 1, 85-100.

Bontis, and Fitz-Enz. (2002). Intellectual Capital ROI: A Casual Map of Human Capital Antecedents and Consequents. Journal of Intellectual Capital, 3(3), 223-247.

Bontis, N., & Fitz-Enz, J. (2002). Intellectual Capital ROI: A Causal Map of Human Capital Antecedents and Consequents. Journal of Intellectual capital, 3(3), 223-247.

Bosma, N., Praag, M. V., Thurik, R., & Wit, G. (2004). The Value of Human and Social Capital Investments for the Business Performance of Startups. SmallBusiness Economic, 23, 227-236.

xxxiii

Bos. S., Pendleton.,A and Tom, S. (2011). Governance Thresholds, Managerial Ownership and Corporate Performance: Evidence from the U.K. Working Paper No. 58 ISSN Number: 1743-4041

Boubakri, N. (2006). The Impact of Internal and External Governance on The Agency Cost of Debt: International Evidence URL: http://132.203.59.36/CIRPEE/conf-cirpee/JourneesCIRPEE29-30Sept06/

Boubakri, N., Cosset, J. C., and Saffar, W. (2013). The Role of State and Foreign Owners in Corporate Risk-Taking: Evidence From Privatization. Journal of FinancialEconomics, 108(3), 641-658.

Brealey, R. A., S. C. Myers, and A. J. Marcus. (2008). Dasar-Dasar Manajemen Keuangan Perusahaan. Jakarta: Erlangga.

Brennan, M. J. (1970). Taxes, market valuation and corporate financial policy. National tax journal, 23(4), 417-427.

Brickly, J. A., and C. M. James. (1987). The Takeover Market Corporate Board Composition, and Ownership Structure: The Case of Banking. Journal of Law and Economics 30.

Brigham, E.F. and Daves, P.R. (2007). Intermediate Financial Management. Ninth Edition, Thomson/South-Western.

Brigham, E. F., and J. F. Houston. (2007). Essentials of Financial Management . Singapore: Cengage Learning.

Brigham. E.F., Ehrhardt. M. C. (2014). Financial Management – Theory & Practice – 14th Edition. Publisher: South-Western.

Broussard, J. P., S. A. Buchenroth, and E. A. Filotte. (2004). CEO Incentive, Cash Flow and Investment. Financial Management:51-70.

Brown, L. D., and Caylor, M. L. (2004). Corporate governance and firm performance.

Buck, T., Filatotchev, I., Demina, N., and Wright, M. (2003). Insider Ownership, Human Resource Strategies and Performance in a Transition Economy. Journal of International Business Studies, 34(6), 530-549.

Bushee, B. J., Carter, M. E., and Gerakos, J. (2013). Institutional Investor Preferences For Corporate Governance Mechanisms. Journal of Management Accounting Research, 26(2), 123-149.

xxxiv

Buckley, P. J., and Casson, M. (2016). The Future of The Multinational Enterprise. Springer.

Cadbury, c. (1992). Report of The Committee on The Financial Aspeccts of Corporate Governance. London.

Cai, F., and Ghosh, A. (2003). Tests of Capital Structure Theory: A Binomial Approach. The Journal of Business and Economic Studies, 9(2), 20.

Callen, J. L., and Fang, X. (2013). Institutional Investor Stability and Crash Risk: Monitoring Versus Short-Termism?. Journal of Banking & Finance, 37(8), 3047-3063.

Card, David. (1999. The Causal Effects of Education on Earnings. In Orley Ashenfelter and David

Chan, S. H., Martin, J. D., and Kensinger, J. W. (1990). Corporate Research and Development Expen Ditures and Share Value. Journal of Financial Economics, 26(2), 255-276.

Che Haat, M., Abdul Rahman, R., and Mahenthiran, S. (2008). Corporate Governance, Transparency and Performance of Malaysian Companies. Managerial Auditing Journal, 23(8), 744-778.

Chen, C. J., and Yu, C. M. J. (2012). Managerial Ownership, Diversification, And Firm Performance: Evidence From An Emerging Market. International Business Review, 21(3), 518-534.

Chen. Carl.R, Weiyu Guo, and Vivek Mande, (2006). Corporate Value, Managerial Stockholdings and Investment of Japanese Firms. Journal of International Financial Management and Accounting, 17(1): 29-51.

Chen, C. R., and Steiner, T. L. (1999). Managerial Ownership And Agency Conflicts: A Nonlinear Simultaneous Equation Analysis Of Managerial Ownership, Risk Taking, Debt Policy, And Dividend Policy. Financial Review, 34(1), 119-136.

Chen, C. R., Guo, W., and Mande, V. (2006). Corporate Value, Managerial Stockholdings And Investments Of Japanese Firms. Journal of International Financial Management & Accounting, 17(1), 29-51.

xxxv

Chen, J., and Strange, R. (2006). The Determinants Of Capital Structure: Evidence From Chinese Listed Companies. Economic Change and Restructuring, 38(1), 11-35.

Chen. C.R. and Steiner T.L. (2000)Tobin’s Q, Managerial Ownership, and Analyst Coverage A Nonlinear Simultaneous Equations Model. Journal of Economics and Business 2000; 52:365–382

Chemmanur, T. J., Loutskina, E., and Tian, X. (2014). Corporate Venture Capital, Value Creation, and Innovation. The Review of Financial Studies, 27(8), 2434-2473.

Chen, C. J., and Yu, C. M. J. (2012). Managerial Ownership, Diversification, and Firm Performance: Evidence From an Emerging Market. International Business Review, 21(3), 518-534.

Chen, Z., Du, J., Li, D., and Ouyang, R. (2013). Does Foreign Institutional Ownership Increase Return Volatility? Evidence from China. Journal of Banking & Finance, 37(2), 660-669.

Cho, M.H. (1998): Ownership Structure, Investment, and The Corporate Value: An Empirical Analysis, Journal of Financial Economics, 47(1), 103–121.

Cho, G., and Kim, D. K. (2007). Efficiency Analysis and Ranking Of Major Container Ports in Northeast Asia: An Application of Data Envelopment Analysis. International Review of Business Research Papers, 3(2), 486-503.

Christensen, C. M. (2013). The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail. Harvard Business Review Press.

Chtouron, S. M., J. Bedard, and L. Courteau. (2001). Corporate Governance and Earning Management. Working Paper. The Social Sciences and Humannities Reseach Council of Canada.

Chung, M. F., and J.-b. Kim. (2005). FCF Agency Costs, Earning Management, and Investor Monitoring. Corporate Ownership & Control 2 (4):51-61.

Claessens, A. A., and J. L. Zimmerman. (2000). Expropriation of Minority Shareholders: Evidance from East Asia. Policy Reseach Working Paper The Word Bank 2008.

xxxvi

Claessens, S., and Yurtoglu, B. B. (2013). Corporate Governance In Emerging Markets: A Survey. Emerging markets review, 15, 1-33.

Claude, E., H. C. R., and V. T. E. (1996). Political Risk, Economic Risk, and Financial Risk Finacial Analysis Journal Nov-Dec:29-46.

Clay Dibrell, C., and Miller, T. R. (2002). Organization Design: The Continuing Influence of Information Technology. Management Decision, 40(6), 620-627.

Coles, J.L., Daniel, N.D., and Neveen, L. (2004). Departement of Finance W.P. Carey Scholl of Business Arizona State University, Email: [email protected], Departement of Fianance Robinson College of Business Georgia State University, email: [email protected], and Email: [email protected], Managerial Incentives and Risk Taking.

Coles, J. L., Lemmon, M. L., and Meschke, J. F. (2012). Structural Models and Endogeneity in Corporate Finance: The Link Between Managerial Ownership and Corporate Performance. Journal of Financial Economics, 103(1), 149-168.

Colombo, M. G., Croce, A., and Murtinu, S. (2014). Ownership Structure, Horizontal Agency Costs and The Performance of High-Tech Entrepreneurial Firms. Small Business Economics, 42(2), 265-282.

Corbetta, G., and Salvato, C. (2004). Self‐serving or Self‐actualizing? Models of Man and Agency Costs In Different Types Of Family Firms: A Commentary On “Comparing The Agency Costs Of Family and Non‐Family Firms: Conceptual Issues and Exploratory Evidence. Entrepreneurship Theory and Practice, 28(4), 355-362.

Copeland T.E., Weston J. F. and Shastri. K. (2014). Financial Theory and Corporate Policy. Pearson New International Edition.

Cronqvist, H., and Nilsoson, M. (2003). Agency Costs of Controlling Minority Shareholders, Journal of Financial and Quantitative Analysis, 38(4): 695-714.

Cubbin, J and Leech, D. (1983). The Effect of Shareholding Dispersion on the Degree of Control in British Companies: Theory and Measurement. The Economic Journal, 93: 351-369.

xxxvii

Cui, L., Meyer, K. E., and Hu, H. W. (2014). What Drives Firms’ Intent to Seek Strategic Assets by Foreign Direct Investment? A Study of Emerging Economy Firms. Journal of World Business, 49(4), 488-501.

Cull, R., Li, W., Sun, B., and Xu, L. C. (2015). Government Connections and Financial Constraints: Evidence From A Large Representative Sample of Chinese Firms. Journal of Corporate Finance, 32, 271-294.

Cunat, V., M., and M. Guadalupe (2012). The vote is cast: the effect of corporate governance on shareholder value, The journal of finance, 67(5), 1943–1977.

Dallas, George. (2004). Governance and Risk. Analitytical Hand books for Investors, Managers, Directors and Stakeholders. New York: McGraw Hill.

Dalton, D. R., Daily, C. M., Johnson, J. L., & Ellstrand, A. E. (1998). Number of Directors and Financial Performance: A Meta-Analysis. Academy of Management journal, 42(6), 674-686.

Dam, L., and Scholtens, B. (2013). Ownership Concentration and CSR Policy of European Multinational Enterprises. Journal of Business Ethics, 118(1), 117-126.

Damodaran, Aswath. (2012). Investment Valuation. New Jersey : John Wiley &Sons.

Darmawati, Deni, R.G. Rahayu and Khomsiyah. (2004), Hubungan Corporate Governance dan Kinerja Perusahaan, Simposium Nasonal Akuntansi VII Denpasar Bali.

David E. Guest, (1997). Human Resource Management and Performance: a Review and Research Agenda, The International Journl of Human Resource Management.

David, F. R. (2003). Strategic Management: Concept. edited by N. Edition. New Jersey 07458.: Prentice Hall Upper Saddle River.

Delaney, J. T., and Huselid, M. A. (1996). The Impact of Human Resource Management Practices on Perceptions of Organizational Performance. Academy of Management Journal, 39(4), 949–969.

De Miguel. A., J.Pindando and C. de la Torre. (2004). Ownership Structure and Firm Value: New Evidence from Spain. Strategic Management Journal. 25(12): 1119-207.

xxxviii

Demsetz, H., and K. Lehn. (1985). The Stucture of Corporate Ownership: Causes and Consequencies. Journal Political Economy:1155-1177.

Demsetz, H., and B. Villalonga. (2001). Ownership Structure and Corporate Performance. Journal of Corporate Finance 7:209-233.

Denis, D. J., D. K. Denis, and A. Sarin. (1997). Agency Problem, Equity Ownership Structure on Corporate Diversification Strategies. Strategic Management Journal 20:1071-1076.

Denis, D. K., and J. J. McCornell. (2003). International Corporate Governace”. Journal of Financial and Quantitative Analysis 38:1-36.

Dinga, A.K., Dixon,R and Stratling R, (2009). Ownership Structure and Firm Performance in the UK: Evidence from the Agency Perspective. Working Paper, Durham Business School, University of Durham.

Drakos, A. A. and Bekiris, F. V. (2010). Corporate Performance, Managerial Ownership and Endogeneity: A Simultaneous Equations Analysis for the Athens Stock Exchange. Research in International Business and Finance, 24(1), 24-38.

Dogan, Ergun and Russeli Smyth. (2002). Board Remuneration, Company Performance and Ownership Concentration: Evidance from Publicy Listed Malaysian Companies. ASEAN Economics Bulletin. 19(9):319-347

Dooley, M. P. (2000). A Model of Crises in Emerging Markets. The Economic Journal, 110 (460), 256-272.

Dornbusch, R., S. Fischer, and R. Startz. (2001). Macroeconomics. 8 ed. New York: McGraw-Hill.

Driffield, N., Mahambare, V., and Pal, S. (2007). How Does Ownership Structure Affect Capital Structure And Firm Value? Recent Evidence From East Asia. Economics of Transition, 15(3), 535-573.

Dulewicz, V., and Herbert, P. (2004). Does the Composition and Practice of Boards of Directors Bearany Relationship to The Performance of Their Companies?. Corporate Governance: An International Review, 12(3), 263-280.

xxxix

Dutta, S., and Jog, V. (2004). The Long-Term Performance of Acquiring Firms: A Re-Examination of An Anomaly. Journal of Banking & Finance, 33(8), 1400-1412.

Easterbrook, F. H. (1984). Two Agency-Cost Explanations of Dividends. American Economic Review 74:650-659.

Eisenhardt, K. M. (1985). Control: Organizational and Economic Approaches. Management Science 31 (2):134-149.

__________________ (1989), “Agency Theory: An Assessment and Review”. Academy of Management Journal, 14: 57-74.

Elloumi, F., and J.-P. Gueye. (2001). Financial Distress and Corporate Governance: An Empirical Analysis. Corporate Governance 1 (1):15-23.

Elsevier Choi, J. J., S. W. Park, and S. Sean. (2007). The Value of Outside Director: Evidance from Corporate Governance Reform in Korea. Journal of Financial and Quantitative Analysis 42 (2):941-962.

Fama, E. F. (1980). Agency Problems and Theory of The Firm. Journal of Political Economy 88 (21):288-307.

Fama, E. F., and K. R. French. (2001). Disapearing Dividends: Changing Firm Characteristics or Lower Propensity yo Pay? Journal of Financial Economics 60 (1):3- 44.

Fama, E. F., and M. C. Jensen. (1983). Separation of Ownership and Control. Journal of Law and Economics 26 327-349.

Fang, V. W., Maffett, M., and Zhang, B. (2015). Foreign Institutional Ownership and The Global Convergence of Financial Reporting Practices. Journal of Accounting Research, 53(3), 593-631.

Farrar, D. E., Farrar, D. F., and Selwyn, L. L. (1967). Taxes, Corporate Financial Policy and Return to Investors. National Tax Journal, 20(4), 444-454.

Filatotchev, I. (2006). Effects of Executive Gharacteristics and Venture Gapital Involvement on Board Gomposition and Share Ownership in IPO Firms. British foumal of Management 17: 75-92.

xl

Fisher, M. (1994). Accountancy for The 90’s: The Role of Audit Committee. The Malaysia Accountant:18-21.

Fleisher, B., Li, H., and Zhao, M. Q. (2010). Human capital, economic growth, and regional inequality in China. Journal of Development Economics, 92(2), 215-231.

Francis, J. C. (1988). Management Investment. Second ed. Singapore: McGraw-Hill International Editions Financial Series.

Giroud, X., and H. M. Mueller (2011): Corporate governance, product market competition, and equity prices, The Journal of Finance, 66(2), 563–600.

Garay, U., and González, M. (2008). Corporate Governance and Firm Value: The Case of Venezuela. Corporate Governance: An International Review, 16(3), 194-209.

Gary, R., dan Shiguang, M., (2011). Managerial Ownership, Capital Structure and Firm Value: Evidence From China’s Civilian-Run Firms, Australian Accounting Business and Finance Journal, 5 (3).

Garvey, G. T., and A. Mawani. (2005). Risk Taking Incentive of Executive Stock Option and The Asset subtitution Problem. Accounting and Finance:3-23.

Garza-Gil, M. D., Varela-Lafuente, M. M., Caballero-Miguez, G., and Álvarez-Díaz, M. (2011). Analysing the Profitability of the Spanish Fleet After the Anchovy Moratorium Using Boot Strap Techniques. Ecological Economics, 70(6), 1154-1161.

Greenaway, D., Guariglia, A., and Yu, Z. (2014). The More The Better? Foreign Ownership and Corporate Performance in China. The European Journal of Finance, 20(7-9), 681-702.

Giannetti, M. (2003). Do Better Institutions Mitigate Agency Problem? Evidence from Corporate Finance Choices. Journal of Finance And Quantitative Analysis 38 (1):185-212.

Ghazali, I. (2006). Structural Equation Modelling: Metode Alternatif dengan Partial Least Square. Badan Penerbit Universitas Diponegoro. Semarang

Ghozali, I. (2011). Aplikasi Analisis Multivariate dengan Program IBM SPSS 19. BP Undip. Semarang.

Ghozali, I and Irwansyah. (2002). Analisis Pengaruh Kinerja Keuangan Perusahaan dengan alat ukur EVA, MVA dan ROA Terhadap Return Saham

xli

pada Perusahaan Manufaktur di BEJ. Jurnal Penelitiam Akuntansi-Bisnis dan Manajemen. 9 (1):18-33

Ghazali, I. and Latan, H. (2012). Partial Least Squares: Konsep, Tehnik dan Aplikasi Menggunakan Program SmartPLS 3.0 Untuk Penelitian Empiris. Badan Penerbit Universitas Diponegoro. Semarang

Girma, S., Görg, H., and Pisu, M. (2008). Exporting, Linkages and Productivity Spillovers From Foreign Direct Investment. Canadian Journal of Economics/Revue Canadienne D'économique, 41(1), 320-340.

Goodstein, J., K. Gautam, and W. Boeker. (1994). The Effects of Board Size and Disersity on Strategic Change. Strategic Management Journal 15:241-250.

Grossman, S., and O. Hart. (1980). Takeover Bids, the Free Rider Problem and the Theory of the Corporation. Bell Journal of Economis:42-64.

Gomez‐Mejia, L. R., Campbell, J. T., Martin, G., Hoskisson, R. E., Makri, M., and Sirmon, D. G. (2014). Socioemotional Wealth as a Mixed Gamble: Revisiting Family Firm R&D Investments With the Behavioral Agency Model. Entrepreneurship Theory and Practice, 38(6), 1351-1374.

Goyal, P., Rahman, Z., and Kazmi, A. A. (2013). Corporate Sustainability Performance and Firm Performance Research: Literature Review and Future Research Agenda. Management Decision, 51(2), 361-379.

Grant, R.M. (1991). The Resources Base Theory of Competitive Advantage: Implications for Strategy Formulation. Calicornia Management Review. Vol. 33 (3). Pp. 114-135.